F LE COPY 1Document of - World Bank Documents

35

F LE COPY 1Document of The World Bank FOR OFFICIAL USE ONLY Report No. P-2180-TUN REPORT AND RECOMMENDATION OF THE PRESIDENT OF THE INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT TO THE EXECUTIVE DIRECTORS ON AN INDUSTRIAL FINANCE PROJECT CONSISTING OF A PROPOSED SEVENTH LOAN TO BANQUE DE DEVELOPPEMENT ECONOMIQUE DE TUNISIE WITH THE GUARANTEE OF THE REPUBLIC OF TUNISIA AND A PROPOSED LOAN TO THE REPUBLIC OF TUNISIA December 6, 1977 This document has a restrited distributton and way be wed by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorizaton. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of F LE COPY 1Document of - World Bank Documents

F LE COPY 1Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-2180-TUN

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

TO THE

EXECUTIVE DIRECTORS

ON AN

INDUSTRIAL FINANCE PROJECT

CONSISTING OF A

PROPOSED SEVENTH LOAN

TO

BANQUE DE DEVELOPPEMENT ECONOMIQUE DE TUNISIE

WITH THE GUARANTEE

OF THE

REPUBLIC OF TUNISIA

AND A PROPOSED LOAN

TO THE

REPUBLIC OF TUNISIA

December 6, 1977

This document has a restrited distributton and way be wed by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorizaton.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

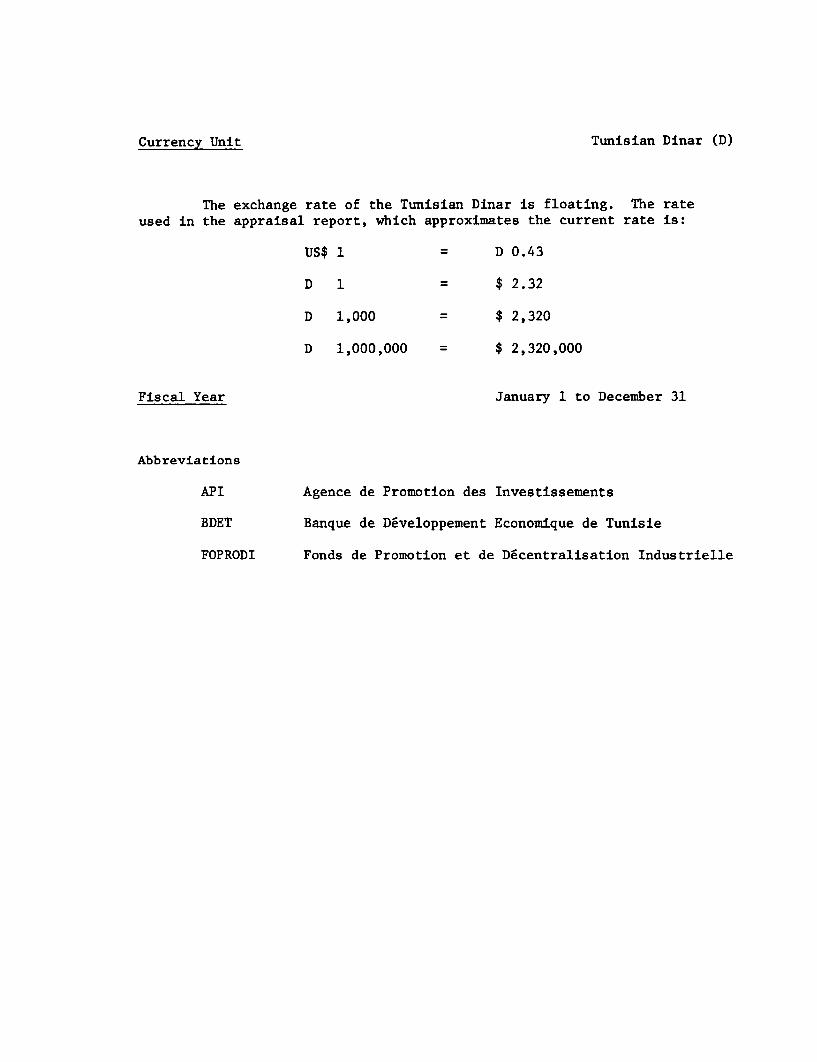

Currency Unit Tunisian Dinar (D)

The exchange rate of the Tunisian Dinar is floating. The rateused in. the appraisal report, which approximates the current rate is:

US$ 1 = D 0.43

D 1 $ 2.32

D 1,000 = $ 2,320

D 1,000,000 = $ 2,320,000

Fiscal Year January 1 to December 31

Abbreviations

API Agence de Promotion des Investissements

BDET Banque de Developpement Economique de Tunisie

FOPRODI Fonds de Promotion et de Dcentralisation Industrielle

FOR OFFRCIAL USE ONLY

TUNISIA

Loan and Project Summary

A. Loan to BDET

Borrower: Banque de Developpement Economique de Tunisie (BDET)o

Guarantor: Republic of Tunisia

Amount: US$30 million, in various currencies, including $2million for expansion of small-scale enterprises.

Terms: The Loan would be repayable in 13 years, including a4-year grace period, on a level principal paymentsbasis; interest at 7.9 percent per year; commitmentcharge of 3/4 of one percent .on the principal amountof the loan not withdrawn.

Relending Terms a) Interest rate of 9.0 percent per annum on sub-of loans to loans to medium and large scale industrial borrowers;BDET borrowers: amortization depends on individual sub-projects, and

may extend for industrial projects over a period ofup to fifteen years if justified in the individualcase by the forecast financial position of theborrower and the expected lifetime of the assets.Foreign exchange risk would be borne by Government.

b) Interest rate of 8.0-8.25 percent per annum onsub-loans to small-scale industrial borrowers.Amortization depends on individual sub-projectsand may vary between 7 and 11 years, with graceperiods between 2 and 3 years. FQreign exchangerisk would be borne by Government.

Project To meet part of BDET's requirements for the financingDescription: of import components of specific industrial enterprises

(US28 million), and to finance expansion of existingsmall-scale enterprises through BDET (US$2 million)0

Final date forsubproject December 31, 1979submission:

Free limit: About $705,000 equivalent for individual sub-loans.(DFC Component)

This documnt hs a rutricted distribution and nmy be wd by rciplanta only in tho perforninceof their official duties. Its contents may not othenrie be disclosed withut Word Bank autbonXazon.

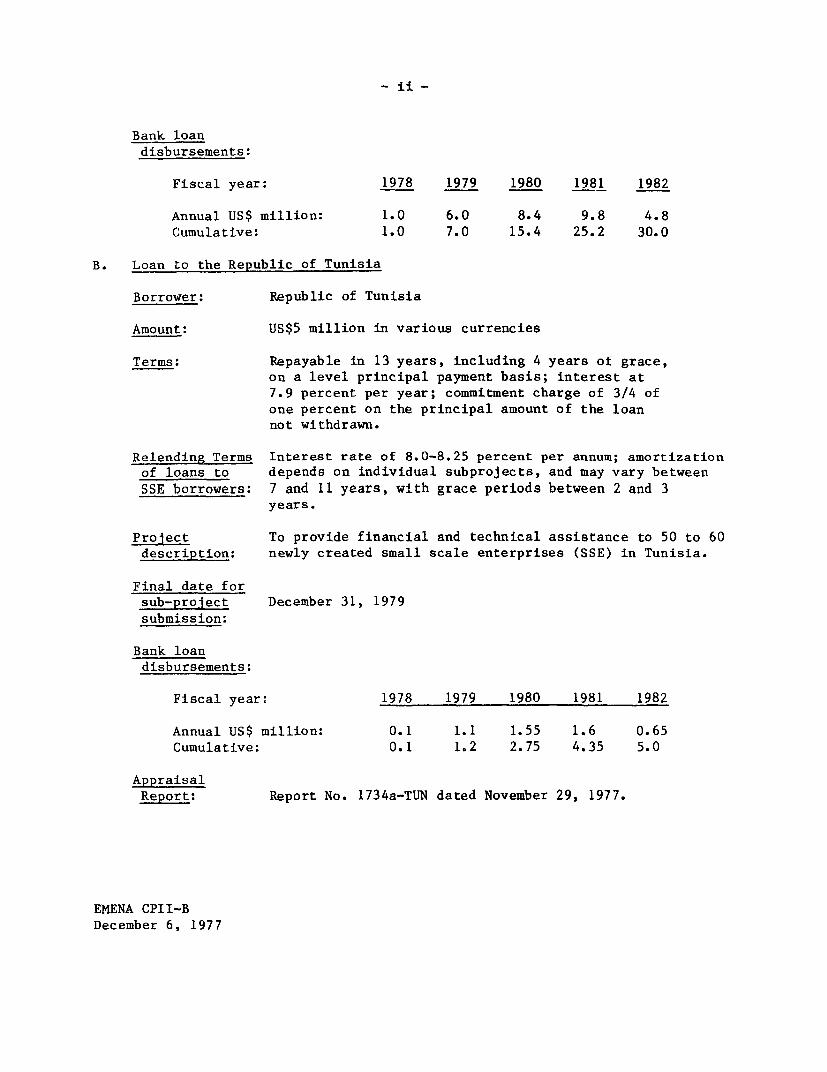

Bank loandisbursements:

Fiscal year: 1978 1979 1980 1981 1982

Annual US$ million: 1.0 6.0 8.4 9.8 4.8Cumulative: 1.0 7.0 15.4 25.2 30.0

B. Loan to the Republic of Tunisia

Borrower: Republic of Tunisia

Amount: US$5 million in various currencies

Terms: Repayable in 13 years, including 4 years of grace,on a level principal payment basis; interest at7.9 percent per year; commitment charge of 3/4 ofone percent on the principal amount of the loannot withdrawn.

Relending Terms Interest rate of 8.0-8.25 percent per annum; amortizationof loans to depends on individual subprojects, and may vary betweenSSE borrowers: 7 and 11 years, with grace periods between 2 and 3

years.

Project To provide financial and technical assistance to 50 to 60description: newly created small scale enterprises (SSE) in Tunisia.

Final date forsub-project December 31, 1979submission:

Bank loandisbursements:

Fiscal year: 1978 1979 1980 1981 1982

Annual US$ million: 0.1 1.1 1.55 1.6 0.65Cumulative: 0.1 1.2 2.75 4.35 5.0

AppraisalReport: Report No. 1734a-TUN dated November 29, 1977.

EMENA CPII-BDecember 6, 1977

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

REPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON AN INDUSTRIAL FINANCE PROJECT

CONSISTING OF A PROPOSED SEVENTH LOANTO THE BANQUE DE DEVELOPPEMENT ECONOMIQUE DE TUNISIE

WITH THE GUARANTEE OF THE REPUBLIC OF TUNISIA ANDA PROPOSED LOAN TO THE REPUBLIC OF TUNISIA

1o I submit the following report and recommendation on an industrialFinance Project in Tunisia consisting of: (i) a proposed seventh loan toBanque de Developpement Economique de Tunisie (BDET) to be guaranteed by theRepublic of Tunisia, for the equivalent of US$30.0 million co he^p financelending for industry, including US$2.0 million to finance the expansion ofsmall scale enterprises (SSEs); and (ii) a proposed loan to the Republic ofTunisia for the equivalent of US$5.0 million to finance the development of newsmall scale enterprises in industry. The interest rate for both loans wfouldbe 7.9 percent per annum. The proposed seventh BDET loan and the proposedloan to the Government would be repaid over a period of 13 years. includingfour years of grace, on a level principal payments basis.

PART I - THE ECONOMY

2. A special economic mission visited Tunisia in December 1976 toreview the draft Tunisian Fifth Plan, 1977-1981. A special economic reportentitled "Economic Position and Prospects of Tunisia, Review of the FifthDevelopment Plan, 1977-81" (No. 1539-TUN) was issued on May 2, 1977. Countrydata sheets are attached in Annex 1.

3. Tunisia is rather poorly endowed with natural resources, but it isclose to European markets and has large untapped labor reserves and tourismpotential. Much of the country is arid or semi-arid and there is an acuteshortage of surface water. Most of the agricultural activity is concentratedalong the coast and in a few oases. The main crop is wheat, which is subjectto sharp year-to-year fluctuations because of irregular rainfall. The mainexport crop is olives, but good olive harvests are also subject to a naturaloutput cycle. Tunisia's most important raw materials are phosphates, petro-leum and natural gas. However, except for phosphates, proven deposits arerelatively small. Tunisian phosphate rock is of low quality and e;:ploitationcosts are comparatively high. The production and export of petzoleum havebecome increasingly important. Recently, deposits of natura' gas were dis-covered off-shore in the Gulf of Gabes, which might become important for the-future development of the country. Industrial development, albeit auiteimpressive, has been hampered by a shortage of industrial entrepreneurs andskilled labor. The service sector, a quarter of which consists of governmentadministration, remains the most important one, generating about half of GDPin 1976. Tourism has developed rapidly and workers' remittances have becomea significant item in the balance of payments. Tunisia has enjoyed a l,.arge

amount of external aid and used it to expand economic and social infrastruc-ture, broaden the industrial base, make available a wide range of social andwelfare services to a large part of the population, and increase the rate ofgrowth.

4. Tunisia's overall economic performance during 1970-76 has been excel-lent0 Real GDP grew at an average annual rate of 9 percent, about twice asfast as during the 1960's. GNP per capita reached $840 in 1976, which in realterms is 60 percent above its level in 1969. The shift in policy orientationfrom the centrally controlled inward-looking investment strategy of the 1960'sto a freer export-oriented economy and the drive towards industrial develop-ment proved highly beneficial for the country. Two other factors also contri-buted to this performance: favorable weather conditions resulted in goodagricultural crops and the change in world commodity prices during 1973/74brought oizable windfalls. National savings during 1970-76 were high andon average amounted to about 22 percent of GNP. Savings, however, originatedmainly in the private sector and Government, and they were temporarily boostedby favorable changes in petroleum and phosphate prices since 1973. Publicenterprises, as a group, did not make a contribution to national savings thatwas commensurate with their importance in the economy, primarily because theirsale prices were not raised sufficiently to reflect cost increases, and alsobecause some enterprises were inefficiently managed. National savings financedabout 85 percent of investment during the period. Tunisia's dependence onexternal £inancing declined sharply from about 32 percent of investment in1969 to 21 percent in 1976. The balance of payments had been in continuousoverall surplus since 1967, but in 1975 and 1976 this was no longer the caseas the terms of trade deteriorated while imports continued to increase.

5e Tunisia has made impressive social gains. By 1976, primary schoolenrollment had reached 90 percents, and secondary enrollment 20 percent of therelevant age-groups. Public health services have been expanded with many pro-vided free. A family planning program has been introduced and has met withconsiderable success. Attempts have been made to tackle regional imbalancesand to improve income distribution. Total social expenditures during 1970-76increased by about 10 percent per annum and on average accounted for 9 percentof GDP and for 30 percent of total public expenditures. Nonetheless, majorsocial issues remain.

6. The most important problem facing the Tunisian economy is widespreadopen and hidden unemployment. Employment creation was one of the main objec-tives of the Fourth Plan. Chiefly because of the Government's generous incen-tives to - and the consequent growth in - labor intensive private investment,the planned creation of new jobs was exceeded by 37 percent0 However, someform of unemployment still affects close to one third of the labor force(about 22 percent of the non-agricultural labor force was unemployed in 1976and about 40 percent of the agricultural labor force was under-employed). In1976 there were some 265,000 people unemployed, 54 percent of whom were seek-ing employment for the first time. An increasing number of young people bornduring the high birth rate years are reaching working age. This is of majorconcern to the authorities, especially since the European outlets for Tunisian

- 3 -

surplus labor have been all but closed, and an increasing number of women isjoining the labor force. Concurrently there is a shortage of skilled labor,which has proven to be a major constraint to more rapid growth in the past.

7. Income distribution seems to have improved since 1966 in the wake ofincreased employment creation, minimum wage legislation, tax exemptions andfamily allowances for low income earners. The real impact of these measureswas safeguarded as domestic price inflation during 1966-76 was kept to an aver-age of 4.0 percent, mainly because of strict credit and price controls andgovernment subsidies for basic consumer goods, housing and services. Theincreased standard of living during the period is reflected in the reducedshare of food expenditure in the average household budget and in the increasedshare of housing expenditure. The share of the population living in absolutepoverty declined from 30 percent in 1966 to 18 percent in 1975. Because ofgreat internal migration, the majority (55 percent) of the population below theabsolute poverty line now lives in urban areas. Important disparities continueto exist between the income levels along the coast and in the interior. Percapita income in the poorest region amounts to about one third that of therichest region and that of-the rural population to about half that of theurban. Existing efforts to distribute the fruits of development more evenlyamong regions are still embryonic and insufficient to overcome the attractionof the capital and the coast.

During 1970-76, agriculture provided about half of total employ-.zent, 27 percent of merchandise exports and 21 percent of GDP. Food process-ing accounted for another 3 percent of GDP and over a third of value added inmanufacturing. During this period agricultural production rose substantially,largely as a result of favorable weather. Large infrastructure investmentswere made during the last decade. Current policy emphasizes projects thatmake a rapid and direct contribution to production and recognizes variousconstraints on agricultural development: absentee ownership, insecurity oftenure, inadequate access to agricultural credit, inadequate extension ser-vices, insufficient agricultural education, and underutilization of irrigationinvestments. Under the Fourth Plan, about $140 million has been allocated toa rural development fund which has been executed by the provincial adminis-trations.

During the 1960's, manufacturing production in Tunisia increased by8 percent annually. There has been a remarkable acceleration of growth in the

1970's due in part to record years for the olive oil processing industry andto favorable developments in the textile and chemical industries. The earlythrust of industrialization was supplied by large import substitution projectsin the social sector. These suffered, however, from the limited domesticmarket and shortages of experienced staff and management. More emphasis hasbeen put on export-oriented private industries since 1970. Under the FourthPlan, private manufacturing investment, particularly in food processing, tex-tiles, fertilizers and metals transformation, was expected to average D 25million per year, compared with D 12 million in 1972, and to account for two-thirds of total investment in manufacturing; these targets have been exceeded.Foreign and domestic private investment is now stimulated by a comprehensiveincentive framework, and facilitated by the streamlined approval procedures of

- 4 -

the investment promotion agency. Foreign investors are expected to contributeknow-how and overseas marketing. A new agreement between Tunisia and theEuropean Community was signed in April 1976. Although it provided for dutyfree entry into the countries of the Community of nearly all Tunisian indus-trial products, new restrictions have recently been imposed. The Governmenthas established a special fund to encourage growth of small industries andindustrial decentralization, and has started a program to establish industrialestates.

10. The development of tourism in Tunisia is relatively recent. Foreign-visitor arrivals reached 1 million in 19769 with an average annual rate ofgrowth during 1970-1976 of 15 percent, -- sharply higher than that of theMediterranean tourism market as a whole. Since 1970, earnings from tourismhave been a major source of foreign exchange, having reached $338 million in1976D more than twice the earnings from all manufacturing exports and slightlymore than petroleum exports. The rapid development of tourism in Tunisia hasunfortunately not been accompanied by adequate development of infrastructure(particularly recreational facilities), trained manpower and services. TheGovernment is endeavoring to alleviate these constraints through a varietyof measures, including revised investment incentives, increased marketing andtraining efforts, codes to enforce quality standards and more stringent zoninglaws.

11. The main objectives of the current Fifth Development Plan (1977-81)are (i) full employment of the additicnal labor force, (ii) self-sufficiencyin major foodstuffs, defined as a balanced trade account for agriculturalgoods, (iii) increases in the standard of living, and (iv) social stabilitythrough incomes policies and wage and price harmonization. To reach theseobjectives, the Plan foresees an average annual rate of real GDP growth of 7.6percent, the same as the one achieved during the Fourth Plan. This growth isto be generated by investments projected at D 4.2 billion ($9.8 billion) incurrent prices during the Plan. In real terms average annual investment wouldbe 54 percent greater during 1977-81 than during the preceding Plan, but owingto the high investment level reached in 1976, its annual growth would be 3percent only in real terms. The Fifth Plan's strategy emphasizes in particularexport-oriented industrial development and agricultural growth. Special atten-tion will be given to employment creation and to balance of payments considera-tions. Substantial investments are to be made in hydrocarbons, manufacturing,water development, transport and housirig. The Plan prescribes increaseddomestic production and processing of Tunisia's mineral resources (phosphates,petroleum) to export as much as possible. Extraction and distribution of thenewly discovered offshore gas deposits in the Gulf of Gabes rank prominentlyamong the list of major projects. This gas is to be used to substitute forpetroleum based fuels that would be freed for export. Eventually gas wouldalso be used as an input for the chemical industry. Private sector initiativeis expected to dominate investment in textiles, mechanical and electricalindustries and tourism. In these activities the authorities primarily expectemployment creation to take place. Education and training programs are to beexpanded sharply to meet more adequately the economy's skilled manpower needs

- 5 -

and worke-rs' expectations for upgraded jobs. The strategy proposed for theFifth Plan does not represent any major departure from the strategy pursuedsuccessfully during the preceding Plan.

12. Tunisia's existing resource base, its institutional and infrastruc-tural framework, its excellent performance in the earlier part of this decade,and the desire of the authorities to promote further development and to sup-port it with appropriate policy measures and institutions, are fundamentalingredients pointing towards continued rapid economic growth during the FifthPlan. The 7.6 percent target set for the average annual real growth of GDPi.n the Plan is in line with the possibilities of the Tunisian economy. Theinvestment priorities formulated in the Plan are considered necessary to sup-port the sectoral strategies. There are some less favorable signs, however.Tunisia's development recently benefited from the structural changes in world

market prices and excellent weather conditions. It would be unreasonable toexpect that these fortuitous factors will continue to work in Tunisia's favorto the same extent as in the past. Substantial efforts in domestic and ex-ternal resource mobilization will therefore be of crucial importance to financethe planned level of investment. On the domestic side, there is a great needfor increased savings and improved financial intermediation. The Governmentsector, in particular, will again be called upon to contribute substantiallyto the savings effort. The Plan suggests that this should be done by prudentexpenditure policies and increased revenue collections (selective tax increasesand better tax collection). In addition, the public enterprise sector willhave to increase substantially its contribution to public savings throughmanagement improvements, and especially through cost-related increases in thesale prices of selected enterprises. Externally, Tunisia would have totalfinancing requirements (disbursement basis) of some $3.5 billion during 1977-81.Given the country's creditworthiness, it seems reasonable to assume that Tunisiashould be able to mobilize such an amount without putting undue strain on thecountry's debt servicing capacity (para. 14).

13. Since the early 1960's, Tunisia has obtained relatively large amountsof official aid. A Consultative Group chaired by the Bank has provided aforum for aid-coordination among major donors (see para. 22). During 1970-76,annual loan commitments from public sources averaged $1.77 million, or about$33 per capita. About 72 percent of these commitments came from bilateralpublic sources, chiefly from France, Canada, and the Federal Republic ofGermany. About 20 percent came from oil-producing countries, whose sharerapidly increased from 8 percent in 1970 to 21 percent in 1976. Commitmentsfrom the Bank Group during 1970-76 accounted for 24 percent of total publiccommitments. Most aid has been obtained on concessionary terms; during1970-76, the average terms of borrowing from bilateral sources were 3.5percent interest and 23 years to maturity, including 6 years of grace; frommultilateral sources, they were 6.0 percent interest and 26 years to maturity,including 5 years of grace. During the same period, Tunisia also receivedannually some $43 million in grants. Loan commitments from private sourcesaveraged $35 million a year. Direct foreign private investment has been com-paratively small, but recently it has picked up momentum following increasedactivity in the petroleum sector and new incentives offered to foreign in-vestors in manufacturing. Thus, net direct foreign investment increased from$19 million in 1970 to $63 million in 1976.

- 6 -

14. At the end of 1976, total foreign debt disbursed and outstandingwas estimated at about $1.3 billion or 27 percent of GDP, compared withsome 40 percent in 1970. The debt service ratio in 1976 was 8.3 percent,compared with 20 percent in 1970. This significant decline in the debt ser-vice ratio was mainly due to the sharp increase in export earnings followingthe changes in world market prices in 1973/74. In the future, the externalborrowing requirements of the 1977-81 Plan (para. 12) will again increase debtservice obligations in relation to exports, to around 13.3 percent by 1981 and16.9 percent by 1986 according to current Bank projections. While these arerelatively high levels, debt service would be a manageable burden on the eco-nomy and balance of payments, particularly when considering Tunisia's longrecord of prudent and skillful external debt management. Tunisia is consideredcreditworthy for further Bank lending.

PART II - BANK GROUP OPERATIONS IN TUNISIA

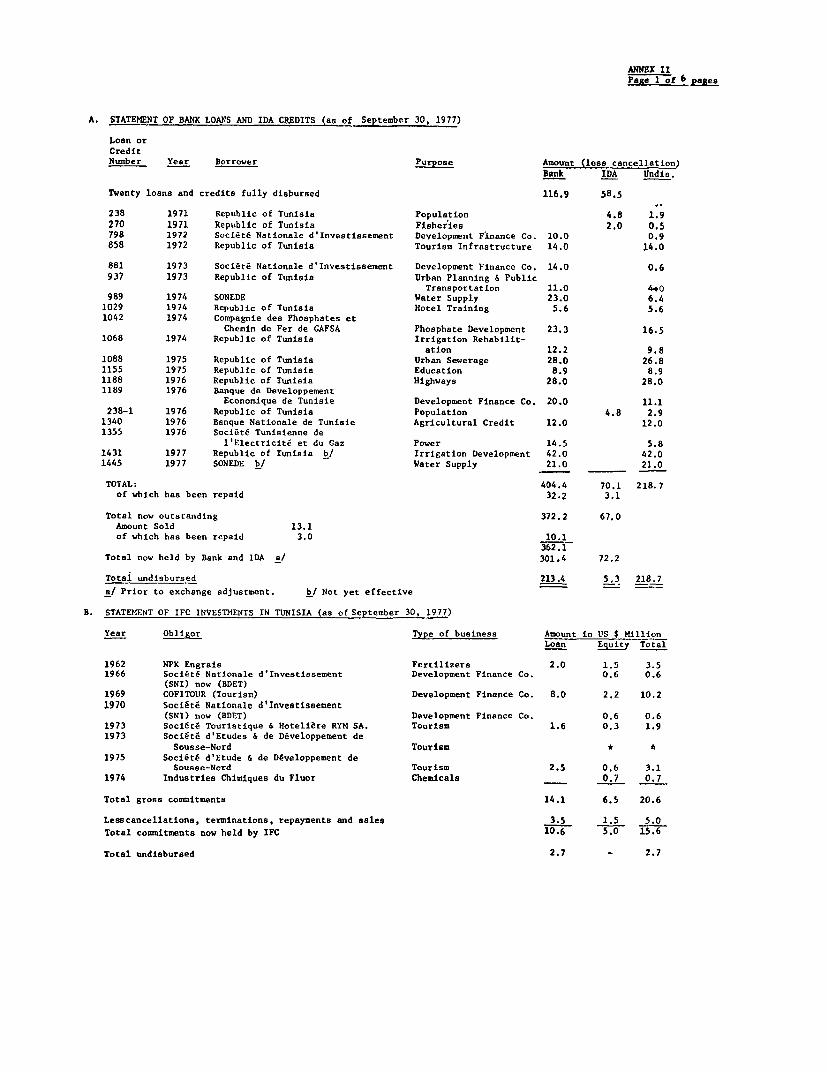

15. Since 1962, Tunisia has received a total of twenty-nine loans andeleven credits amounting respectively to $404.4 million and $70.1 million, netof cancellations and refundings. Annex II contains a summary statement ofBank loans, IDA credits and IFC investments as of September 30, 1977, andnotes on the execution of ongoing projects. While disbursements of some loansand credits have been slower than foreseen at appraisal, on the whole, projectexecution has been satisfactory. In a number of sectors, important institu-tional improvements have been achieved and independent agencies have beencreated or strengthened.

16. The Bank's lending strategy ia Tunisia aims at supporting Governmentefforts to (a) increase employment, (b) encourage more balanced growth anddistribution of income among regions and income groups, (c) promote export-oriented policies and investments, and (d) provide selective support for thedevelopment of infrastructure and for institution building in key public serv-ices. The main supporting feature of this lending strategy is to encouragethe Tunisian authorities in timely and well-coordinated preparation of proj-ects, with emphasis on technical assistance. The Bank is also cooperatingwith the Government in its efforts to increase the mobilization of domesticand foreign resources, in part through encouraging project cofinancing; thelatter is particularly important in view of the extent of Tunisia's externalresource needs, the large size of many priority projects, and the limitedavailability of Bank resources relative to the country's needs.

17. Within this broad framework, past Bank Group lending has emphasizedsupport for long-term investments in infrastructure and social development.Lending for urban and social development, including water supply, education,family planning and the Tunis urban planning and public transport projecthas accounted for 30 percent of Bank/IDA commitments in Tunisia. Lendingfor transport, power and tourism infrastructure has accounted for 32 percent.Agriculture and fisheries have receivnd 21 percent of total commitments.

Industrial and hotel financing through the Banque de Developpement Econo-mique de Tunisie (BDET) has accounted for 13 percent, and the Gafsa phos-phate development project received 4 percent of total commitments.

18. Lending for industry has so far been largely through the mainTunisian Development Finance Company, BDET, and has mostly benefited medium-size companies. The Bank has encouraged BDET to diversify its sources offunds and BDET has made significant progress in this respect. Such lendingis expected to continue, but at a declining rate as BDET diversifies itssources of funds. The Bank has also lent directly for the Gafsa phosphatemining project. Further direct Bank loans for priority industrial subsectorsin which Tunisia has a comparative advantage would depend on the progressachieved in the formulation of sound projects. Emphasis is now placed ondevelopment of small-scale enterprises (SSE). The SSE component describedbelow would be experimental and would serve as a vehicle to prepare furtherBank assistance for SSE development in Tunisia.

19. Lending in the current fiscal year and in the period ahead emphasizesprojects promoting agricultural and industrial production, such as the MishkarGas Development Project for the development and transmission of Tunisia'soff-shore gas resources, and a rural roads project with complementary agri-cultural investments; both projects are expected to be presented to theExecutive Directors later this fiscal year. Complementary to this primaryfocus, the program would also finance selected priority urban and socialdevelopment and infrastructure projects. Projects under discussion with theauthorities include a second fisheries project, a second population project,a second sewerage project, and an urban development project.

20. The Bank Group accounted for about 24 percent of total public com-mitments to Tunisia during 1970-76. The Bank Group's shares in total debtoutstanding and disbursed at the end of 1976 (including loans from privatesources) and in debt service during 1976 were 15 percent and 14 percentrespectively. The Bank Group's share in Tunisia's disbursed external debtby 1981 is expected to remain unchanged from about 15 percent in 1976, andits share in debt service would amount to about 10 percent.

21. IFC has invested in NPK Engrais (a fertilizer plant), in BDET, inCompagnie Financiere et Touristique (COFIT, a company to promote and investin tourism projects), in Societe Touristique et Hoteliere RYM (a large hoteldevelopment) and in Industries Chimiques du Fluor, which will produce alumin-ium fluoride from local fluorspar for export. IFC's most recent investment,in May 1975, was in the Sousse-Nord integrated tourism development project.IFC's net commitments in Tunisia total $15.8 million. IFC's Board has ap-proved the sale of IFC shares in NPK Engrais to the Tunisian Government.

22. Since 1962 the Bank has chaired a Consultative Group for Tunisiabringing together the principal donor countries and institutions concernedwith the country's development. The most recent meeting of the Group, heldin Paris in June 1975, welcomed new participants which included Saudi Arabia,Japan, the Arab Fund for Economic and Social Development and the Commission

- 8 -

of the European Communities. This year, a development conference was organizedby the Government in Tunis in early July, in lieu of a meeting of the Consulta-tive Group.

PART III - THE INDUSTRIAL SECTOR IN TUNISIA

Background

23. Given Tunisia's relatively small endowment with natural resources,development of manufacturing industries is a major vehicle for economic growthand employment creation. During the 1960's, the stress was on import substitu-tion. Since the early 1970's, the stress has increasingly shifted towardsexport oriented manufacturing industries to prevent the expansion of import-substitution activities beyond the limits of efficiency set by the smalldomestic market. Simultaneously, the public sector's role as entrepreneurwas de-emphasized and its share in manufacturing investment declined from86 percent in the late 1960's to less than half during the Fourth Plan (1973-1976). Domestic and foreign private investment in manufacturing were stimu-lated by generous incentives, such as the Export Promotion Law of 1972 andthe revised Investment Code of 1974, and by the establishment of new insti-tutions to assist industry, such as API (Agence de Promotion des Investis-sements), which is responsible for the administration of the investment laws,and AFI (Agence Fonciere Industrielle), which is responsible for acquiringand developing industrial land.

24. Overall, manufacturing industry performed well during the FourthPlan. Value added increased at an average annual rate of 6.5 percent. Thetotal investment target of the Plan was exceeded by 20 percent in real terms,mainly because of greater than expected private investment. Employment crea-tion also exceeded the target by creating 61,000 new jobs, or 50 percent morethan expected. By 1976, the manufacturing sector accounted for 11.2 percentof GDP compared with 8 percent in 1960. A breakdown by sub-sectors shows apredominance of food processing (33 percent), textiles and leather (25 per-cent) and, mechanical and electrical industries (13.6 percent).

Industrial Objectives

25. The Fifth Plan (1977-1981) objectives for the manufacturing sectorare essentially the same as those of the Fourth Plan. Value added is expectedto grow in real terms at 11.7 percent per year, with non-agricultural indus-tries growing at 15.9 percent per year. Investment in manufacturing is ex-pected to reach D 950 million, or 23 percent of total planned investment.Manufacturing exports are to increase from D 151 million in 1976 to D 327 mil-lion in 1981. About 90,000 new industrial jobs are to be created, or 43 per-cent of all non-agricultural employment during the Plan period. The publicsector will continue to play a leading role in implementing strategic projectsof a capital-intensive and high-technology nature,

- 9 -

26. The Fifth Plan's targets can be achieved, provided that project

identification, preparation and execution capabilities are further strengthened.At present, only about 70 percent of the expected manufacturing investment for1977-81 is properly identified. Most of such investment is relatively capital-intensive. Furthermore, despite the existing incentives, Tunisian privateentrepreneurs have shown so far limited interest in export-oriented activities.The government is aware of this problem. It intends to stimulate and supportthe initiatives of Tunisian enterprises in foreign markets. It is alsoencouraging the location of new manufacturing industries in the interior byoffering fiscal and financial incentives and assuming certain expenses forinfrastructure. The AFI has begun working towards this end through itsprogram for the establishment of industrial estates.

Industrial Finance

27. The large industrial development projects in Tunisia are gener-ally sponsored by public sector enterprises, and financed by the government orthrough direct foreign borrowings. The authorities rely on the banking systemto finance medium and small scale industrial projects. BDET, which held atthe end of 1976 about 30 percent of total term credit extended to the indus-trial and tourism sectors, plays a central role in this respect. Commercialbanks are also encouraged to participate in the development financing effortby the requirement that 18 percent of their deposits be placed in medium-term(up to seven years) private loans, and by rediscounting facilities for refi-nancing further commercial bank lending to the private sector.

28. Inflation in Tunisia has been moderate in recent years (4.1 percentin 1974, 9.6 percent in 1975 and 5.4 percent in 1976) and the overall levelof interest rates has been kept low. Medium term lending rates for the indus-trial and tourism sectors have been in the range of 6.25 percent to 8 percent.BDET's rate for long term- loans (over seven years) was set at 9 percent in1976 (including a 1 percent Government interest rebate on loans to residentindustrial borrowers). The rather low interest rate structure has discouragedsavings in the form of long term financial instruments and led, on the demandside, to some credit rationing and a possible sub-optimal allocation of medium-and long-term credit. Partly as a result of discussions with the Bank, IFCnd the IMF, the government has prepared a study on the interest rate levelsand structure in Tunisia. This study led the Central Bank to increase as ofSeptember 1, 1977 both borrowing and lending rates by up to 1-3/8 percentagepo::rnts. Medium-term lending rates for rediscountable loans to the industrialand tourism-sectors have been increased from a range of 6.25-8 percent tof^-8025 percent. The medium-term rate applicable to loans for resident export-oriented enterprises and enterprises located in the least developed regionswas kept, however, within a range of 6.75 percent to 7 percent to encourageindustrial decentralization. As of January 1, 1978, the Government's rebateon BDET loans to -resident industrial borrowers will be abolished, These aresteps in the right direction. The declared aim of the authorities is graduallyto harmonize domestic interest rates with those prevailing in the internationalcapital markets.

- 10 -

29. The Ministry of Finance has also prepared a study on the domesticcapital market; the study recommends legislative measures to foster the devel-opment of the market. The implementation of these measures has not yet beendecided. The conclusions of both studies as well as the rigid Central Bankcontrol over credit and interest rates and the tightness of trade and exchangecontrols are the object of discussions between the Bank and the Tunisianauthorities.

Small Scale Enterprises

30. Tunisians have a long tradition of craftsmanship and commerce andthe number of small non-agricultural enterprises, defined as those employingless than 50 workers, is estimated to be close to 80,000, including 18,000in the manufacturing sector. Yet Tunisia's past administrative, fiscal andfinancial policies have not favored the development of such enterprises.Indeed, the industrial development strategy in the last two decades has givenpriority to large scale public enterprises and, more recently, to modernmedium-sized privately owned enterprises. As a result of limited access toindustrial credit and inadequate technical assistance, the entrepreneurialdynamism and investment potential of a large number of small scale Tunisianentrepreneurs has gone unrealized.

31. A change in the government's previous attitude was marked by thecreation in 1974 of the FOPRODI (Fonds de Promotion et de DecentralisationIndustrielle), a budget-financed fund intended to provide financial assistancefor small industrial projects (especially those outside the Tunis metropolitanarea) sponsored by Tunisian investors with adequate technical qualificationsbut limited means. Under the FOPRODI scheme, eligible entrepreneurs obtainfrom FOPRODI subsidized personal loans to help them acquire majority owner-ship in the capital of the new enterprises. Wnen the ceiling on total in-vestment cost was raised in October 1977 from D 200,000 to D 500,000, thesepersonal loans were set at 70 percent of equity for projects not costing morethan D 250,000, including working capital; sponsors are expected to provide10 percent of equity. For projects costing between D 250,000 and D 500,000(including working capital), personal loans represent up to 45 percent ofequity and the sponsor's contribution represents at least 20 percent ofequity. The equity base under this FOPRODI credit facility amounts to upto 30 percent of total project costs. These personal loans have terms of12 years including 5 years of grace and bear interest at 3 percent. Medium-and long-term loans are also extended to SSEs under FOPRODI for new projectscosting up to D 75,000 (including working capital) or expansion projectscosting up to D 45,000 (excluding working capital). The term loans cannotexceed 70 percent of total project costs. These loans have terms of 10 yearsincluding 3 years of grace for new projects, and seven years with no graceperiod for expansion projects; they bear interest at 4 percent. Eligibilityfor FOPRODI assistance is determined by API. From December 1975, when itbecame operational, until May 1977, FOPRODI financed 81 projects, with totalinvestments of about D 7 million and creation of 2,553 new jobs. An SSEpolicy unit is being established in the Ministry of the National Economy, andAPI has decided to set up a countrywide system of technical assistance to SSEs(see para. 52)

- 11 -

PART IV - THE PROJECT

32. The proposed project consists of two components: (i) a DFC-typeloan of $30 million to BDET, including $2 million to be earmarked for finan-cing the expansion of existing small scale enterprises; and (ii) a line ofcredit of $5 million to the Government to provide financial and technicalassistance to newly created SSEs in Tunisia. Negotiations were held inWashington in November 1977. Mr. Fakhfakh, BDET's Director-General, ledthe Tunisian negotiating team. An appraisal report on BDET (No. 1734-TUN),dated November 29, is being distributed separately.

33. Objectives of the Proposed Project. Under the proposed project,and in line with the Government's Fifth Plan strategy, the Tunisian authori-ties and BDET plan to give priority to the following categories of industrialprojects: (i) projects creating at least one job for every D 4600 at 1976prices ($10,670 equivalent) of investment; (ii) export oriented projectspromoted by Tunisian sponsors, (iii) projects sponsored by new entrepreneurswith adequate technical qualifications; (iv) projects outside the TunisMetropolitan area; and (v) small scale industrial projects. BDET's intentionto give priority to these categories of projects is reflected in a StrategyStatement which was approved by BDET's Board in October 1977. During nego-tiations, an understanding was reached with BDET that at least 75 percent ofthe proceeds of the proposed loan would be earmarked for such projects. Theobjectives of the Bank's involvement would be firstly to assist in the financ-ing and development of these priority categories of industrial projects;secondly, to continue supporting the development of BDET and, particularly,helping it to establish itself as a viable borrower in the internationalfinancial markets; thirdly, to pursue the ongoing dialogue with Tunisia onfinancial policies, especially regarding interest rates. The institution-building objectives of the SSE component are described in para. 47; theyrepresent the most innovative feature of the proposed project.

34. BDET Establishment and Resources. BDET was established in 1959 andreorganized in 1965 with Bank Group assistance. Since then, the Bank has madesix loans to BDET totalling $69 million. IFC holds 10 percent of BDET's sharecapital. The last of the Bank loans, amounting to $20 million, was made inearly 1976 and is now fully committed. Over the past few years, BDET has beensuccessful in borrowing new domestic and foreign long-term resources, permit-ting a decline of the share of Bank funds from 37.4 percent of its long termresources at the end of 1974 to 24.9 percent at the end of 1976. In 1976,BDET placed a bond issue on the international capital market, which was under-written by the Kuwait Investment Company (KIC) and guaranteed by the Tunisiangovernment. This operation is the first of its kind undertaken by a Tunisianfinancial institution and illustrates BDET's determination to gain access tothe international capital market (see para. 44).

35. BDET doubled its share capital to D 3 million in 1971, and againto D 6 million in 1974. A further share capital increase from D 6 millionto D 10 million was authorized by BDET shareholders in June 1976, and isexpected to take place over the 1978-80 period. As of end 1976, the Tunisian

- 12 -

government held 12.1 percent of BDET's share capital, other Tunisian publicsector institutions 17.4 percent, the Tunisian private sector 28.2 percent,IFC 10 percent, and other foreign shareholders 32.3 percent. For the purposeof BDET's new capital increase, the government agreed in 1976 to act as a sub-scriber of last resort by converting into shares, to the extent necessary, aD 4 million subordinated loan made to BDET in 1975 to make up for that portionof the capital increase that would not be subscribed by other shareholders orby other new private sector subscribers. Most foreign and domestic privateshareholders are expected to exercise their preemptive rights.

36. Management, Organization and Procedures. The composition of BDET'sBoard of Directors reflects BDET's ownership structure. As agreed duringnegotiations for the sixth Bank loan, BDET has taken measures to improve man-agement effectiveness. BDET's organization was restructured in 1976, in aneffort to decentralize decision-making at the middle management level. Thereare now six departments (instead of three), four of which are headed by youngTunisian professionals promoted from the ranks. Experience with the new orga-nization over the last fifteen months has been positive. BDET's appraisalwork has further improved over the past two years and overall, BDET's appraisalreports are generally comprehensive and sound. Further improvement can beachieved in BDET's market studies, in assessing the project's employment crea-tion capacity, and in evaluating physical and financial contingencies. Duringnegotiations on the proposed loan, an understanding was reached with BDET onways to improve on these weaknesses.

37. Project supervision remains the weak link in BDET's organization.To improve its project supervision, BDET has agreed to strengthen the staffingof its supervision division, to implement procedures and information flowswhich would improve this division's integration within BDET, and to prepare acomprehensive and detailed work program for the supervision division (DraftBDET Loan Agreement, Section 3.08). An understanding was reached duringnegotiations on the work program of BDET's supervision division for 1978.

38. Operations. BDET's policies, established at the time of its 1965reorganization provide that BDET is to stimulate industrialization and tourismdevelopment in Tunisia through the financing of sound and productive projects,and to help develop the capital market. In the manufacturing sector, BDET'sdisbursements accounted for about 15 percent of total investment both in 1975and 1976. BDET's involvement in tourism, which represented 41 percent of itsportfolio at end 1974 and about 25 percent at end 1976, is expected furtherto decline as industrial sector financing has become the primary objectiveof BDET. The proportion of BDET's new approvals in the public sector hasremained well below the ceiling of 30 percent of total BDET financing whichis reflected in BDET's policy statement. The distribution of BDET's opera-tions by industrial subsectors is fairly evenly spread. Almost half of BDET'soperations are concentrated in the Tunis area. Much remains to be done inpromoting projects in the less developed areas of the interior. During nego-tiations on the proposed loan, an understanding was reached that at least60 percent of the proceeds of the proposed Bank loan would finance projectslocated outside Tunis.

- 13 -

39. Financial Situation. BDET's auditors, the Tunisian firm CabinetFinor and Peat, Marwick, Mitchell and Company (PMM) issued an unqualifiedopinion on the 1975 and 1976 accounts, with only two minor reservations. Thefirst reservation concerned the inadequate reporting on 50 of BDET's clients,accounting for 3.2 percent of portfolio at end-1976; the second reservationconcerned a loan (D 877,500) to a hotel which has been in deficit since 1975.The work program of BDET's supervision division (see para. 37) includes mea-sures to improve information collection on BDET-financed sub-projects orinvestments. An understanding was reached with BDET on measures to fullyrecover BDET's loan to hotel El-Kebir as well as to validate the mortgageon this loan by June 1978.

40. BDET's portfolio at the end of 1976 amounted to D 61.4 million,including D 6.6 million in the form of equity investments. The arrears situa-tion, particularly in the tourism sector, has improved since 1974, followinga strong resurgence of tourism in 1975 and 1976, assertive action on thepart of BDET in collecting loans in arrears and the rescheduling of loans inarrears representing 17.8 percent of total loan portfolio at end-1976. Loanreschedulings were largely due to delays in the implementation of projectsapproved in the 1974 industrial investment boom, for many of which BDET hadgranted inadequate grace periods. An understanding was reached that BDET'ssupervision division would follow up closely the performance of clientshaving obtained reschedulings; in case reschedulings should affect in anygiven fiscal year more than 15 percent of BDET's loan portfolio, agreementwas reached to the effect that a special report would be submitted to BDET'sBoard (draft BDET Loan Agreement, Section 4.12).

41. BDET's loans to industrial customers are backed by chattel mortgageswhich are generally valid and sufficient to cover risks. Substantial progresshas been made since 1975 in validating mortgages of hotel borrowers, in linewith the timetable agreed with the Bank for the sixth Bank loan. Duringnegotiations it was agreed that, in future, BDET's hotel sub-loans would besecured by a valid mortgage, failing which the contracts for such sub-loanswould include a timetable, to be approved by BDET's Board, for the mortgagevalidation process (Draft BDET Loan Agreement, Section 3.07).

42. BDET's total assets grew from D 43.1 million in 1974 to D 73.4 mil-lion in 1976. The maximum debt/equity ratio agreed between BDET and the Bankwas raised from 5:1 in 1975 to 7:1 in 1976 following a change in the defini-tion of equity, which now excludes the government subordinated loan of D 4million. The ratio is expected to exceed 7:1 in 1977 and to stabilize there-after slightly below 8:1 as BDET's capital increase takes place in the 1978-80period. Given BDET's improved financial situation, an agreement was reachedduring negotiations that BDET would maintain at all times its debt/equityratio within the limit, of 8:1 (Draft BDET Loan Agreement, Section 4.06).

43. Projected Operations and Resource Requirements. BDET's businessprospects for the medium term are good. Yearly approvals are expected toincrease progressively from D 30.7 million in 1977 to D 39.5 million in 1981.Emphasis in BDET's financing will, however, be affected by the new prioritiesoutlined in the Plan for the manufacturing sector (see para. 26). This is

- 14 -

reflected in the Strategy Statement referred to in para. 33 above. It isexpected that in the period 1978-79, 50 percent of BDET's new approvals wouldbe for projects located outside Tunis, 35 percent for labor-intensive proj-ects, and 15 percent for projects of new entrepreneurs and for SSE projects.BDET would make all efforts to promote export-oriented projects, but the uncer-tainty of the international situation (European Community tariff policies)makes it difficult for BDET to set a specific target for the expected results.In any case, an understanding was reached that BDET would give priority tosub-projects belonging to these categories and submit yearly progress reportsto its Board of Directors and to the Bank.

44. To finance its operations during the Fifth Plan (1977-81), BDET willhave to mobilize about D 143 million of new financial resources (on a commit-ment basis). About 40 percent of the resource requirements for the 1978-79period, estimated at D 56.2 million have been identified (excluding the pro-posed Bank loan to BDET). These include besides cash generation, and thepartial payment of the capital increase, two new French lines of credit(partly at concessionary conditions), one new loan from Qatar, one new loanfrom the Arab fund for Social and Economic Development, and a local bondissue. The proposed Bank loan of $30 million to BDET would represent about21 percent of total resources to be raised for the 1978-79 period. Thiswould leave a financing gap of up to D 22.1 million which BDET plans to fillthrough borrowings in the foreign open markets. Preliminary contacts betweenBDET and lenders in the Euro-currency market and in the Gulf States indicatethat this objective can be achieved. Initially, at least, the guarantee ofthe government will be necessary to contain the cost of such borrowings. BDEThas prepared, in cooperation with the government, a program and timetable forresource mobilization for the period 1977-79. An understanding was reachedthat the Government and BDET would mobilize the required resources for 1977-79in accordance with the program and timetable which were reviewed duringnegotiations.

45. Projected Profitability. Under current circumstances, net profitsin percentage of average net worth would decline from a range of 8.3 percentto 9.7 percent in 1973-76 to 8 percent in 1977 and 1978. This is largelydue to government regulations having imposed on BDET low lending rates of 8percent in 1974 and 1975, and 9 percent (including a 1 percent Governmentinterest rebate on loans to resident industrial borrowers) in 1976 and 1977,despite steadily increasing costs of BDET's borrowed resources. An agreementwas reached during negotiations that the nominal rate of interest on BDET'slong-term loans to industrial borrowers would be raised as of January 1, 1978by at least one percentage point above the rate applicable to medium-termrediscountable commercial bank loans (Draft BDET Loan Agreement, Section 4.13).The Government would no longer provide as of January 1, 1978, the one percentrebate it provided on the rate payable by resident industrial borrowers onBDET's long-term loans. An understanding was also reached that the nominalrate of interest on BDET long-term loans for tourism would be increased from 9percent to 9.5 percent. Taking into account interest prepayment, commissionsand fees (other than commitment fees), the effective cost of BDET's long-termresources to industrial borrowers would be about 9.65 percent, and that oftourism loans would be about 10.15 percent. Although a step in the right

- 15 -

direction, the proposed increases in BDET's term-lending rates will not besufficient to guarantee BDET an adequate profitability. Further increases inthe rates of BDET's long-term industrial loans are not desirable, however, aslong as medium-term lending rates on commercial bank loans remain in the pre-sent range, because such increases would jeopardize BDET's competitive posi-tion. *To further strengthen BDET's-profitability while encouraging BDET tomaximize its spreads an understanding was reached during negotiations that theGovernment would subsidize ex-ante the cost of selective BDET non-concessionaryforeign borrowings so as to ensure an adequate margin of profit for BDET.

46. Terms of the Development Finance Company Component. The proceeds ofthe proposed $30 million BDET loan (excluding the $2 million to be earmarkedfor expansion of SSE projects) would be used for financing: (a) the full costof directly imported equipment or services for eligible subprojects, and (b)70 percent of the cost of previously imported equipment. The free limit forsubloans not subject to prior Bank approval would be D 300,000 ($705,000equivalent). Exposure to a single customer would not exceed 25 percent ofBDET's equity. The foreign exchange risk on the Bank funds and BDET's otherforeign borrowings would be assumed by the Government (Draft Guarantee Agree-ment, Section 3.04). Taking into account that the loan will be committed overa 2-year period, and that the average term of BDET's loans is about 12 years,with a 2-year grace period, the loan should be repaid in a period of 13 years,including a 4-year grace period, on a level principal payments basis.

The Small-Scale Enterprises Component

47. Assistance for small-scale enterprises ($7 million) would aim, onan experimental basis, to coordinate and strengthen ongoing initiatives in thefield of financial and technical assistance to SSEs. It is expected that thisassistance would lead to the identification of the most suitable institutionalarrangements for a possible future Bank-financed SSE project. Of the amountearmarked for SSE development, $5 million would be lent to the Government forthe financing of newly-created SSEs through FOPRODI (see para. 31) and $2million would be lent-to BDET to finance expansion of existing SSE projects.Both SSE sub-components would benefit from a country-wide decentralized,technical assistance scheme for SSEs to be set up by API.

48. The $5 million loan would be channelled through an account with theCentral Bank, which would be separate from the existing FOPRODI credit facili-ties (Draft Government Loan Agreement, Section 3.01(b)(iii)). Establishmentof this account would be a condition of loan effectiveness (Draft GovernmentLoan Agreement, Section 6.01(c)). Agreement was reached during negotiationson the following financing scheme for new SSE projects (Draft Government LoanAgreement, Schedule 2, para. 5): the four commercial banks currently partici-pating in the FOPRODI scheme, as well as BDET would draw from this account anamount not exceeding 50 percent of total project costs to provide term loansto newly created SSEs which qualify for concessionary FOPRODI assistance forthe constitution of their equity capital. The participating bank would pro-vide out of its own resources a term loan to newly created SSEs in an amountof about 20 percent of total project costs. Individual promoters are expectedto provide the remaining 30 percent of total project costs, which can be

- 16 -

partly financed through the existing FOPRODI concessionary loan facility.Agreement was also reached on eligibility criteria of SSE sub-projects to theproceeds of the proposed Bank loan (Draft Government Loan Agreement, Schedule2, para. 3): (i) total project costs of the newly-created SSE (includingworking capital) would not exceed D 200,000 in 1976 prices; (ii) the cost ofjob created or maintained would be about D 4,600 in 1976 prices, which is inline with the accepted criteria of Bank's Urban Poverty Program and (iii) theentrepreneur would be willing to use, if needed, available technical assis-tance. These eligibility criteria would be more restrictive than eligibilitycriteria currently established for FOPRODI. As a condition of loan effective-ness, the Government would amend its existing agreements with commercial banksparticipating in the FOPRODI scheme to reflect the agreed criteria and opera-tional arrangements (see para. 49), and conclude a similar agreement with BDET(Draft Government Loan Agreement, Section 3.01 b(i), (ii)). API would providetechnical assistance to promoters (Draft Government Loan Agreement, Schedule 2,para. 13).

49. Promotion, identification, iritia' screening and appraisal of eli-gible SSE irojects wiould be the responsiMility of the banks administering theFOPRODI scr.eme assisted, as needec, by API. Once the SSE project and itsfinancing plan have been approved by the supporting bank and API, BDET wouldver4ry that the project complies with the Bank"s eligibility criteria, submitapproval and disbursement applications to the Bank, and maintain the necessarydocumentation (particularly as regards disbursement) available for inspectionby Bank supervision missions. The repayment obligation for the Bank-financedSSE sub-lo:-is wo-_:;c.e ._.wre the government but the responsibility for loancollection wou.-: :emn'4n with ,h2 bank sponsoring the project, which will shareequally with the gcvernment the risk of loss on both term loans financed outof the Bank funds ar. tern loans made out of the bank's own resources for SSEsub-projects. This arraz.gement, which is an improvement over the existingFOPRODI systems is eesigned zo 4nduce greater participating bank involvementin financing new SSE projects. Tha participating banks will be compensatedfor their services by Government commissions as currently provided under theexisting FOPRODI credit facilities, i.e. a flat commission on disbursementsand a commission based on the amount of principal and interest recovered onbehalf of FOPRODI.

50. The second SSE sub-component, amounting to $2 million, would be partof the BDET loan but would be earmarked to finance the expansion of existingSSEs with production facilities valued (before expansion and excluding land)at less than D 100,000 in 1976 prices ($232,000 equivalent). The terms andconditions of subloans for such expansion projects are expected to be similarto those applying on subloans for the new SSE sub-component, but the borrowingSSE's obligations would be toward BDET with BDET fully covering the risk. Inorder to ensure that SSE expansion projects will receive appropriate attention,BDET agreed to set up a special unit staffed by two SSE specialists (Draft BDETLoan Agreement, Section 3.09(c)); establishment of this unit is a condition ofloan effectiveness (Draft BDET Loan Agreement, Section 6.01a). The unit wouldbe responsible for the processing of expansion SSE projects as well as foradministering Bank funds to be channelled through the FOPRODI scheme.

- 17 -

51. Terms of the Sub-loans for SSEs. The term of Bank-financed FOPRODIor BDET sub-loans for SSEs is expected to be between 7 and 11 years, with graceperiods between 2 and 3 years. Correspondingly, loans for the new and expan-sion SSE projects would be repayable to the Bank, by the Government and BDETrespectively, over a period of 13 years, including 4 years of grace, on alevel principal payments basis. The cost of funds to SSE borrowers would beequal to the average interest rate charged by commercial banks on medium-termindustrial loans at the time of sub-loan signinLg (Draft Government Loan Agree-ment, Schedule 2, para. 8 and Draft BDET Loan Agreement, Section 4.13(b));currently, this rate is 8 to 8.25 percent except for loans financing invest-ments in less developed regions of Tunisia (6.75 to 7 percent). The foreignexchange risk on the Bank funds would be assumed by the Government (DraftGuarantee Agreement, Section 3.04). Although Bank funds would be used tofinance up to one-half of the full investment cost of SSE projects, withoutdistinguishing between foreign and local currency expenditures, it is expectedthat on average this will imply little, if any, local currency financing withBank funds, as the foreign exchange costs of SSE investments in Tunisia areestimated to vary between one-third and two-thirds of total costs, averagingabout 40 percent of total.

52. Technical Assistance to SSEs. Technical assistance to support SSEsis a key element to ensure the success of the SSE component of the proposed1oan. API would be responsible for establishment and implementation of thetechnical assistance program, both for SSE projects financed by the Bank loans,and other SSE projects in Tunisia. Initially, API's technical assistancestaff would concentrate on identifying SSE projects and assisting sponsors inpreparing their projects, obtaining the financing and properly implementingthe projects. Later, the API-centered extension service would provide follow-up assistance, especially in the areas of production and financial management,marketing and improvement of productivity. During negotiations on the proposedBank loan, the Government agreed to prepare a plan of action and a timetablefor providing technical assistance services to SSEs (Draft Government LoanAgreement, Schedule 2, para. 13); an understanding was reached during negotia-tions on this plan of action and the timetable for its implementation. TheGovernment also agreed to implement this plan of action and to periodically--eview its content and implementation with the Bank (draft Government LoanAgreement, Section 3.06(b)). An understanding was also reached that API wouldstrengthen by July 1, 1978 its existing central unit and its four regionaloffi-.2s through recruitment of at least eight qualified Tunisian specialists.About 69 man-months in specialized expertise wbuld be required initially toassist API in establishing the central core of SSE experts and to train expertsfor API's regional offices. The Government has agreed to complete by July 1,1978, financing arrangements for the foreign exchange costs of expatriate spe-cialists (about $300,000), failing which these costs would be financed underthe proposed $5 million loan to the Government (Draft Government Loan Agree-ment, Section 3.06(a)).

53. Benefits and Risks. Through the proposed project, the Bank wouldcontinue helping BDET to improve its financial management and portfolio, andthe Government to further liberalize credit and develop domestic capital mar-kets. Sub-projects financed by the proceeds of the Loan would contribute

- 18 -

to employment creation, export promotion, development of entrepreneurship anddecentralization of industrial activities (para. 33). The SSE component ofthe proposed project is expected to finance between 50 and 60 new, and 20 and30 expansion, sub-projects and to create about 2,300 new jobs at an averagecost per job created of about $7,000. This component would, in addition,contribute to laying appropriate grounds for Government financial and tech-nical assistance for SSE development throughout Tunisia. The relative lack ofexperience, in the Bank and in Tunisia, in assisting SSEs entails a moderaterisk that the SSE institution-building targets may not be fully achieved. Therisk is worth taking, however, since adequate mechanisms would be set up underthe project to ensure that only worthwhile projects are financed by the pro-posed loan.

PART V - LEGAL INSTRUMENTS AND AUTHORITY

54. The draft Loan Agreement between the Republic of Tunisia and theBank, the draft Loan Agreement between the Bank and Banque de DeveloppementEconomique de Tunisie, the draft Guarantee Agreement between the Republicof Tunisia and the Bank, the Report of the Committee provided for in ArticleIII, Section 4 (iii) of the Articles of Agreement and the text of a resolu-tion approving the proposed loans are being distributed to the ExecutiveDirectors separately. Features of the loans of particular interest are men-tioned in paragraphs 47 through 53 of this report. Special conditions ofeffectiveness are: (i) amendment of the FOPRODI Agreement between the Govern-ment and Participating Banks to reflect the negotiated operational arrange-ments for SSEs, and conclusion of a similar agreement between the Governmentand BDET (para. 48); (ii) establishment within BDET of a unit to administerSSE expansion sub-projects (para. 50); and (iii) establishment in the CentralBank of a Project Account for the Bank-financed new SSE operations (para. 48).The draft agreements conform to the normal pattern for loans for developmentfinance companies.

55. I am satisfied that the proposed loan would comply with the Articlesof Agreement of the Bank.

PART VI - RECOMMENDATION

56. I recommend that the Executive Directors approve the proposed loan.

Robert S. McNamaraPresident

AttachmentsDecember 6, 1977Washington, D.C.

Annex IPage 1 of 4 pages

TUNISIA - SOCIAL INDICATORS DATA SHEETLAND AREA (THOU KM2) ---------------------------------------------------------------- TUNISIA REFERENCE COUNTRIES (1970)

TOTAL 164.2 MOST RECENTAGRIC. 76.1 1960 1970 ESTIMATE UORDAN IRAQ GREECE***

GNP PER CAPITA (USs) 230.0* 370.0* 840.0* /a 350.0* 640.0* 1360.0*

POPULATION AND VITAL STATISTICS_______________________________

POPULATION (MID-YR, MILLION) 4.1 5.0 5.7 /a 2.3 9.4 8.8

POPULATION DENSITYPER SQUARE KM. 25.0 30.0 35.0 /a 24.0 22.0 67.0PER sQ. KM. AGRICULTURAL LAND 54.0 67.0 75-0 -a 165.0 92.0 96.0

VITAL STATISTICSCRUDE BIRTH RATE (/THOU, AV) 46.6 44.7 40.0 47.5 49.1 18.1CRUDE DEATH RATE (/THOU,AV) 21.5 16.9 13.8 17.8 17.9 8.0INFANT MORTALITY RATE (/THOU) .. 125.0 62.6 b 36.3 /abc 104.0 29.6LIFE EXPECTANCY AT BlRTH (YRS) 46.1 51.6 54.1 50.7 50.2 70.9GROSS REPRODUCTION RATE 3.1 3.4 3.4 3.5 3.5 1.0

POPULATION GROWTH RATE (%)TOTAL 1.8** 2.3** 2.3** 3.1 3.2 0.URBAN *- 3.0/a 4.7/C .6. .0 1.5

URBAN POPULATION (% OF TOTAL) 35.6 /a 40.1/b 47.0 .. 58.0 62.6

AGE STRUCTURE (PERCENT)0 TO 14 YEARS 42.4 46.3 42.1 47.0 /a 48.0 24.9

15 TO 64 YEARS 52.6 50.2 53.8 49.5 a 48.0 64.065 YEARS ANO OVER 5.0 3.5 4.1 3.5 ^ 4.0 11.1

AGE DEPENDENCY RATIO 0.9 1.0 0.9 1.o /a 1.1 0.6ECONOMIC DEPENDENCY RATIO 1.3/a.b 1.8/b.c 1.4 2.4 7.d 1.8 /a

FAMILY PLANNINGACCEPTORS (CUMULATIVE. THOU) .. 112.2 281.5USERS (% OF MARRIED WOMEN) .. 12.0 .. .. .

EMPLOYMENT

TOTAL LABOR FORCE (THOUSAND) 1400.0/a 1300.o/b 188o.0 350.0 /a 2700.0LABOR FORCE IN AGRICULTURE (%) 69.07 5 7.07S' 37.4 33.0 7a 52.0UNEMPLOYED (% OF LABOR FORCE) 1i .07 12.07 14.0 14.0 r 6.0

INCOME DISTRIBUTION

% OF PRIVATE INCOME REC'D BY-HIGHEST 5% OF HOUSEHOLDS .. .. ..HIGHEST 20% OF HOUSEHOLDS .. .. ..LOwEST 20% OF HOUSEHOLDS .. .. .. .. .LOWEST 40% OF HOUSEHOLDS .. .. ..

DISTRIBUTION OF LAND OWNERSHIP______________________________

% OWNED BY TOP 10% OF OWNERS .. 53.0 /d ..% OWNED BY SMALLEST 10% OWNERS .. o.s .. . ..

HEALTH AND NUTRITION

POPULATION PER PHYSICIAN 10000.0 /c s9so.o 5560. 0 /e f 2680.0 3270.0 620.0POPULATION PER NURSING PERSON .. 730.0 /e 670.0 7tR1 1050.0 5490.0 1140.0POPULATION PER HOSPITAL BED 360.0 /d 410.07T 410-0 960.0 520.0 160.0

PER CAPITA SUPPLY OF -CALORIES (% OF REQUIREMENTS) 86.0 94.0/8 94.0 /i 94.0 93.0 116.0PROTEIN (GRAMS PER DAY) 54.0 63.0 67.0 71 60.0 62.0 99.0

-OF WHICH ANIMAL AND PULSE 13.0 14 .0 I . 18.0/e 17. 0 b 52.0/a

DEATH RATE (/THDU) AGES 1-4 .. .5 /b,i s.o/b

EDUCATION

ADJUSTED ENROLLMENT RATIOPRIMARY SCHOOL 67.0 100.0 95.0 73.0/a 67.0 106.0SECONDARY SCHOOL 13.0 23.0 18.0 33.07 24.0 66.0

YEARS OF SCHOOLING PROVIDED(FIRST AND SECOND LEVEL) 13.0 13.0 13.0 12.0 12.0 12.0

VOCATIONAL ENROLLMENT(% OF SECONDARY) 24.0 12.0/h 28.0 3.0/ 3.0 20.0

ADULT LITERACY RATE (%) .. .. 55.0 .. 26.0 82.0

HOUSING

PERSONS PER ROOM (URBAN) .. 2.7/b .

OCCUPIED DWELLINGS WITHOUTPIPED WATER (%) 60.0/b * .. . .

ACCESS TO ELECTRICITY(% OF ALL DWELLINGS) . 24.0/b .. .. . .

RURAL DWELLINGS CONNECTEDTO ELECTRICITY (%) .. .. .. .. . ,

CONSUMPT ION

RADIO RECEIVERS (PER THOU POP) 41.0 77.0 74.0 160.0 180.0 111.0PASSENGER CARS (PER THOU POP) 11.0 13.0 18.0 7.0 7.0 26.0ELECTRICITY (KWH/YR PER CAP) 84.0 155.0 233.0 72.0 291.0 1072.0NEWSPRINT (KG/YR PER CAP) 0.3 0.1 0.1 0.3 0.3 1.6

SEE NOTES AND DEFINITIONS ON REVERSE

Aniex IFage 2 Qf 4 pages

U.loe. othe-is. acoted, doto far 1960 refer to aoy Fear bet-C.e 1959 aod 1MI, for 1970 between 1968 cod 1970, and for M-ost Rmeent Estimate betweeno19 73 and 1975.

A GNP9 per c.Pit. dote ore booed on the World Rock Atlaa mthodology (1974-76 basis).

0* ..u to oigr-tion popul.tion growth rate is liter thon the rote of naturalinrse

*0G-eece he. been selected as .n objective coontry, on the basis of the ite of It. population, nediterre.e.. geographical eltuotion and it.-cn-y, which tr .ne.t. 050 similarity with oT-ili's, with respect to n,tione1 rescortes, narket ese., agricu1toe end cerices activities.

TUNISIA1 1960 I 1956; /b Rotio of populotton under 15 aod 69 and over to total labor force; /. 1963; /d 1962, i..ludiog -rurahonpit.1.7

1970 0 1956-66; /b 1966; /c Ratio of population -nder 15 end h5 aod wver to toto1 labor force-; /d Co-eing 4.5 nillionhectoros of privete 1aed, eccluding 0.8 million hectares is public ownership, and 2.1 million hectare of collective land;/ePersonnelt to govenmet services only; If Governensst hospital ..tehli.faantot only; /& 1964-66; /h ft.l.ding

tehio coonmy nod technical indutry. Li- Registered only.K-ISl lECIIT ET iINHATE; Ia 1976; /b 1966-75; Ic Registered only; /d Ratio of population under 15 and 65 cod over to total

laber force.; /o lo-1Jdig dentista; /f 1972; /& Psrsonnel tn government services only;/b Govonolnt boopit.1 sstablictmients only; /t 1969-71 average.

JORDORJ 1970 I fEe.t lank only;. /b 1966; /. Registered only; /d Ratio of Popolatton under 5 cod 65 and over to total labor force;/. 1964-66; /f Including ti9fRA schools.

IRAQ 1970 /c tiol of popu1ction undsr 15 and 65 cod over to total labor force; /b 19646-6.

CRtici 1970 1967.

g13, September 23, 1977

OEf33=TOMn OPF SOCIAL IDICATMR

Lantd Ares (then k. I PoonlatIon ocr nursse carson - P.Puletion divided by n,fhr If practlclofTotal Tool nurf.oe orca cuyrlinig loand or endtland atere. sale and fcsale gr.duste .oues, "trained" or 'certified" 51.,andAsric. m ost re....c osti-ct. of sgricultsr1 area used tmoaiyor patin- s-itliary proronmel with training or speriesoe.

meetly for crps, pautures, sorkt & kitches gardens or to ILe fallow. Poewi.ttee par hmoeIno bed - Pepalation divided by s,ab.r of boepica1 tedsavailable is publilnand priest. general sod epeci.lised hospit.l and

GNP par -uit. (17S1) - GN? per capltc soI.ctiet at correct -kcht prices, rehabilitation centoer; omldsa oursing hoess and aatablishlnents fcr..c.lcu -to by sme onvr, o mthdi ae World Book Atlce (1973-75 hosts); custedil end preventive sees.1960; 1970 cod 1975 datc. Par ..pita .omPly of calorie. ft afrcuemnb- CaMuted fre, energy

equi-alent of set faod supplIes aeil.bls is cotno ps capita per dwy,P.pul.tion 4nd vitul -ttitctlc evileble euppli.s caspria. dboatic prduction, Ispot lese .epoot, andPopnlation (id-yeart! milo) A. of July firnt: if net aroiloble. over.ge ohe.Se in stack; met .. pplieo eccinde aelc.l food, seeds, quontities usad

of two end-year e tloaee 1-60, 1970 and 1975 dot.. In fend processeing and looses to distribution; requirnre.t woos .tisatodby FAO baeed on physlologi-Il seeds for som1 activity end health conid-

Populotiem dbbsiro per sour. lee - Mid-year pepoletiosi per squcr killnter ering -mironamtal temperature, body .sights, age end sea distributiono, of(100 hactrt) of total ero., pepuliati, cod allowing 105 for wstsate hIcs- hoohld leve.

'Poocltiotn 'Caiy Pars seme he of coric- land - Ceepucd as shov for 9cr capitt sopply of"ot I er ocrdcv - Protei. contest of Per copisaagricoltural loand only. net soply of food po day; net eapy ffodi defined ce shove; require-

semis for all co,natroes eetablLshd by USDA ERooneme Receore Serei.eeVital stottatice Provid. for a minimis allowance of 60 Sr,was of total Pretein per day, codC-odo birth rats per thouosed. swerase - Amnoal lies birthe per thousand of 20 grosa of asime cod pales Prortei, of which 10 grean hbsu1d b. enlmoI

sid-yeer popolotion; ten-ye.r -rithostic overages ending in 1960 and 1970, protein; thece etondrda ere loser than those of 71 gr,aa of tate1 protsincod five-yea evaroge endIng in 1975 for meet recet satimat-. sod 23 gre. of anImal protein as en averag for the werld. Proposed by PA0

Crude det rot ncr tbo,cand. average - Asmuol denthe Per thoowend of mid-year in the Third World Peed Survey.populotion; ten-yeor arit testic overeges ending in 1960 and 1970 and flee- Per CoPit' oro':in onol,free amilso p'lse - Protein supply of fondyoar co ssding in 1975 for meat retest eatimets. derivd fre siml sod pcs. in gre.. pe day.

ttturoity rare /thou) A--IAna dZatba of infeste undr one year of ego Death rate f/thou) aese 1-4 - Ammual deethe per thousand is age group 1-4Per thouas..di!ve birth'. y-sr. to childans in this age grsup; suggested s as . indicator of

Life ..poct..cy as bIrth fees) A-tAerge -abcr of yeers of life renaming at neltrition.birth; ususlly five-year averagea ending in 196, 1970 sod 1971 for develop-

Cros rsorTod-ction rot - uverags nmber of Iive dauhtere . oann will beer Adjused erollment ratio erimere school - Esrellashat of all ag.. as par-1s her -ooc _rerductivepriod If she perinoos Pree...t ge-ope-ific cantos of potnery aseles populaIon. inclod.. children agod 6-11 yearsferi i ly rates; -sus1y five-yccr evesge ending in 1960, 1970 and 1971 bat adjusted for diffsreot length. of primary edustion. for cousriac withfor dwvclpn c, -trla. univrersal dcetin, enrollment e.y emceed 1007. since eons pupils are blow

1opulotionurputh rots Cl 6 -totol.- Conpoosd sensI grvth rtes, of mid-year or ab=v the officiml scoo agtpopulation for1950-60, 96-7 and 1970O-75. Adiusted wor,s1lmoot retto aeondre school- Conput.d as above. setondary

Poouiet on Arowth rots t -uban - Coaputed like groth rate of totn1 education requirec at leaset four ye.ar of spprovsd primary isatrution;populetion; dfeetdfotocfuraarecsay afetaparabtllty of provide general, vocatieal or teacher training ietructions for pupilsdatc aIn oetfcf 12 ta 17 y..r. of age; crepdccours.. f e ..genrally ...ciuded

Ura opltion ft of t-tal) - Ratio of urban to total populstion; different Ysorso cholis provided (first anscod lvels) - Total Is.,. ofdefinitione of urb.n r-s say effect ..omparbility of data 4-4 cbont-otr . schooin; at G.,condar le,vetIe instruction say be partially or

conplensly xcld.,aced sircot-ro (oprcet) - Childreo. (0-14cy..rc) , -kring-age (15-64 years), vonstionol =oolms fl of enodo m fctiona l.cjtiouinn inclod.

an rtired (65 yeors codonr) es per ctages of mid-year pspulati-n te-heice-Hindustrial or other pr-gran, which oper.s.toidapande-ly or A00 dependec ratio - atio of popoistion usder 15 and 65 sod over to these d.partoat of secondary inatituti-no

of ages 15 thrOugh 64. Adult it-sroc rete M5 - Lit.r.t. adults (able to rocd and write) as per-ico cdenpodence ratio - Ratio of population under 15 end 65 and ovr to ceotage of tetal edu1t population aged 15 y.ers end ovr.

the labor force I ago group of 1-h4 years.Fanil elentcoactstors(ctsuleive. thou) C-1Cuulti- .metr of ...teptore lionoin

of birth-actrol devices undr eup oof nainlfenily pl.aning progre. Psrs naocr roe. furb-ol - Average oeber of person per roe In oc-pied

amily p ..annlno users CZ of sar-iod aoe)-Pecnec of ried -we of structure. end unoncpiad parts.obi1d-bearing age (15-44 yeas-) whosebtb-on ldero n lsrie cuied dell wtou spte atr l) -Occupied convenia dwelling

Inme inan age group. inuba o rurl ee without meildsor outeida Piped ester f-cillitieas psruetege of .11 oc-pied dwellings.

noeloymeot Access is electritito ft~~~~~~~~(' of all den1ltg C- ConetIoa dwelings withTote1 labor force (thounend) - ftcononcally active Paras, inuloding rawnd lcff tricity i lIvin qusrer asPsret of total dwellings to urbao eedforces end uoeployed hot encluding housewives, students, etc.; dinfton.as mruralreas.to vrious coutries ar- oot cemprable. Rural delioga connected te electricity ft) - Ceeptned as above for rural

Labor force narcltr 1 grlcutura1 lobar force (Is fseno., forsstry, dwlig onybunting sod fichIng) es percentage of total labor forc..

U._mPloved It of labor force) U- ne.pl 4s sre usually d.fised aP--prsn hbe Consoniaeable end willing to teke eJob, out of a job on a given day, remand out Rdorctce(ocr thou All -1 type. of rec-ivsrs for radis b-nd-te

of a Job, end ...eking wn-k for a specifisd ninina period not seceding ft. to general publi petouad of populsttn; ...olodes oniceoed receiverweek, say not he ompeabl7 between.. outriee due to different deftoitiona is countries sod in yss.rs when registration of r.di. sets was La effect;of unemPloyed end sourceofdet, ,s;.g -emplymnt office statistics, .-nPI. date for recent years say sact he nnParable since nest ourisabolished.. _.eye, cnpolso..y unempleynstoI inusc..Pcetg

c "I c~~~~~~~~~~~~Paes orre (ocr thou p-e) - Passenge.r cars conpries sate .roar seatingIn.- diotributio - Per ctage of private incons (both In each end kind) less then eight Pn peesa emludee anbulance heerses wsd ilIturyreceived by riohsst it. richest S0t, poorest 201, and pooret 4Ot of hos-.-bciaholds. Pacrit (o/ror --P) - AnnuI alnconeption of industrial, - -riaj,

pulc adprlvets electrIcIty in kilowatt hour Per cepita, go...r-11yDistribation of lasd ownrsip - Percestages of land ow-d by wealthiest lOt base.d an prod..tion dais, without allwanc far loases In grIds bar allo-.

ssd poorestlO of lend wners tog for tmPerta mod Wrt. of electricity.

R srit kheyr ocr cop) - Per espit. c.n..I -xptlapio is kilogermHeeith and Nutrition e.timatsd gr- disasati prodactiop p1ue net imports of newsprint.Popu1:t on or physician - Populstion divIded by amb,er of prutcticig

physician q qulified fran s cdical school at univ-reity level.

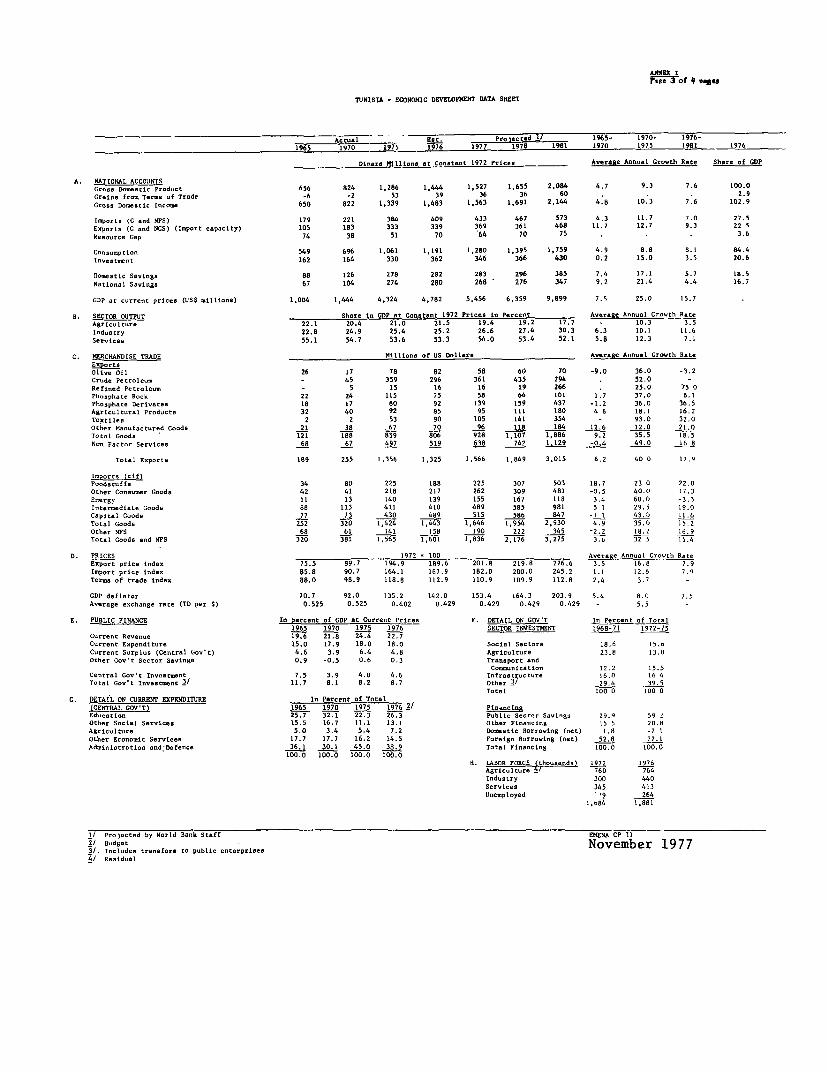

TUNISIJA -ECONOMIC DEVEI.PMENT! DATA SHEET

Autual R~~~ ~~at. Pr eRd /1965- I90 1976-1965 1970 1975 1976 1977 1978 1981 ~~~~~~1970 1975 1981 1976

Dloars Milllios tCotn 92Plr Awear6e Aon..l Growth Rate Share of GDP

A. RATIONAL ACCOUNTSGr..o D-owti Prodont 656 824 1,286 1,444 1,527 1,655 2.084 4.7 9.3 7.6 100.0Grains fron T-ro of Tr.de -6 -2 53 39 36 36 60 ... 2.9Gross Do,oetlc Intone 650 822 1,339 1,483 1,563 1,691 2,144 4.8 10.3 7.6 102.9