FILE COPY - World Bank Documents & Reports

217

FILE COPY DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use Report No. 156-IN ECONOMIC SITUATIONAND PROSPECTS OF INDIA May 8, 1973 Asia Region South Asia Department This report was prepared for official use only by the Bank Group. It may not be published, quoted or cited without Bank Group authorization. The Bank Group does not accept responsibility for the accuracy or completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of FILE COPY - World Bank Documents & Reports

FILE COPYDOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

Report No. 156-IN

ECONOMIC SITUATION AND PROSPECTS

OF

INDIA

May 8, 1973

Asia RegionSouth Asia Department

This report was prepared for official use only by the Bank Group. It may not be published, quotedor cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY AND OTHER EQUIVALENTS

Currency

Prior to mid-December 1971 US $ 1.00 = Rs 7.50Rs 1.00 = US $ 0.1333

Mid-December 1971 toend June 1972 US $ 1.00 = Rs 7.27927

Rs 1.OO = US $ 0.1374

After end-June 1972 floating rate

Spot rate(March 31, 1973) approx. US $ 1.00 - Rs 7.59

approx, Rns 100 - US $ 0,13

For all projections in this report the exchange rateuS $ 1.00 = Rs 7.50 has been used, unless specified otherwise.

Weights

Unless otherwise specified all weight measures are metric.

Years

The Indian fiscal year runs from April 1 through March 31l

This report was prepared in the Office of the ResidentRepresentative of the World Bank in India by William M. Gilmartin,Bilsel H. Alisbah, Timothy King, Wolf Ladejinsky, Timothy P.Lankester, Peter E. Naylor, Norman E. Reynolds, N. S. Segal,Armand Van Nimmen, Sunanda Sengupta and Y. Satyanarayanan(Statistical Analyst).

ECONOMIf, SITTATION XAN) ̀ RCSPECTS CF' INDIA

Table of Contents

BASIC DATA .................. ..*. .

MAP .................................... ... ......... ...

SUFi4AP2fA.ND CONCLUSIONS ....................... . . ..............

1. INTRODUCTION

Historical Perspective ..................... ...... . 1Recent Developments .................... , .. ............ 7

2. 1T4?UATION 14

The Current Situation .,..... 17New Directions? . ... ................. C

3. UNEINPLODIP1NT AND POVERTY 21

'. AGRICULTURAL PRODUCTION

Growth Rate of total Agricultural Output. 2Foodgrains - 1. 1Theat ................. e ............... 27Foodgrains - 2. Rice 8.....2Foodgrains - 3. Other Toodgrains ., 30Foodgrains - 4. Total Seasonal and Regional Trends 31Non-Foodgrains Crops ...... ............ 32Livestock. . .. 3The Production Record in relation to Requirements . 34Implications of past trends for future growth ... 36

5. THE RURAI, SC'ENE

The Drought . .............. 40Illusory Drought Consequences . . .42Green Revolution's Gainers and Losers ..... O.......... 43Agricultural Prospects. .. 45New Land Ceiling Round 0............ ..Rural Programs .. . ............. .............. 52

G. INDUSTRY

HIistorical Perspective ........ .0* ...... 63Current Situation and Short Term Prospects ............. 67Longer Term Prospects .... .................... 69

7. STEEL, POWIER AND FERTILIZER: A BPLEF REVIEW 76

Table of Contents (continued) Page No.

u. DONIESTIC FINANCE

Domestic Resource Mobilization .............. .. .... 86Overall Budgetary Situation ............................... 90The Center ............ .......... O.!.......... 91State Finances ............. a. ...... , .... 96Plan Outlay ............. 98hioney and Prices ...... ............. 100

9. THE APPROAUCT TO TIIE FIFTH PLAN

Summary . .... . ......................... 102Faster Development . ................. 105n.edistribution . ................. ..... 106r ,omrjestic Financing ................ ......... 106'el.f Relia.ce.. ..... * g 109

10. EXPORTS

The Overall Record . . . ............ 112Direction of Exports .................... 0... . ... 1l11The Comxposition of Exports .................. . I .. 114Tr'aditional .. Exports . . . ....... ,. 115T.on-Traditional Ex.orts ................. . . . 117T..e I. ..ure . . . 124

11. YSTI;:ArTTD ACTD I.EQUIREJ1IET FOR 1 973/7)4

7lecent Trends in te Balance of Payments ..... ............ 125TIndia 1 s Trade and Aid el.atfionshin3 with East European

rountries ....... ........ 128Foreign Exchange Reserves . ..............................131External assistance .................. . . 1327lalance of Payments Projection and Aid Recor^mendation

for 1 973/714 ... 1............ ........ 135

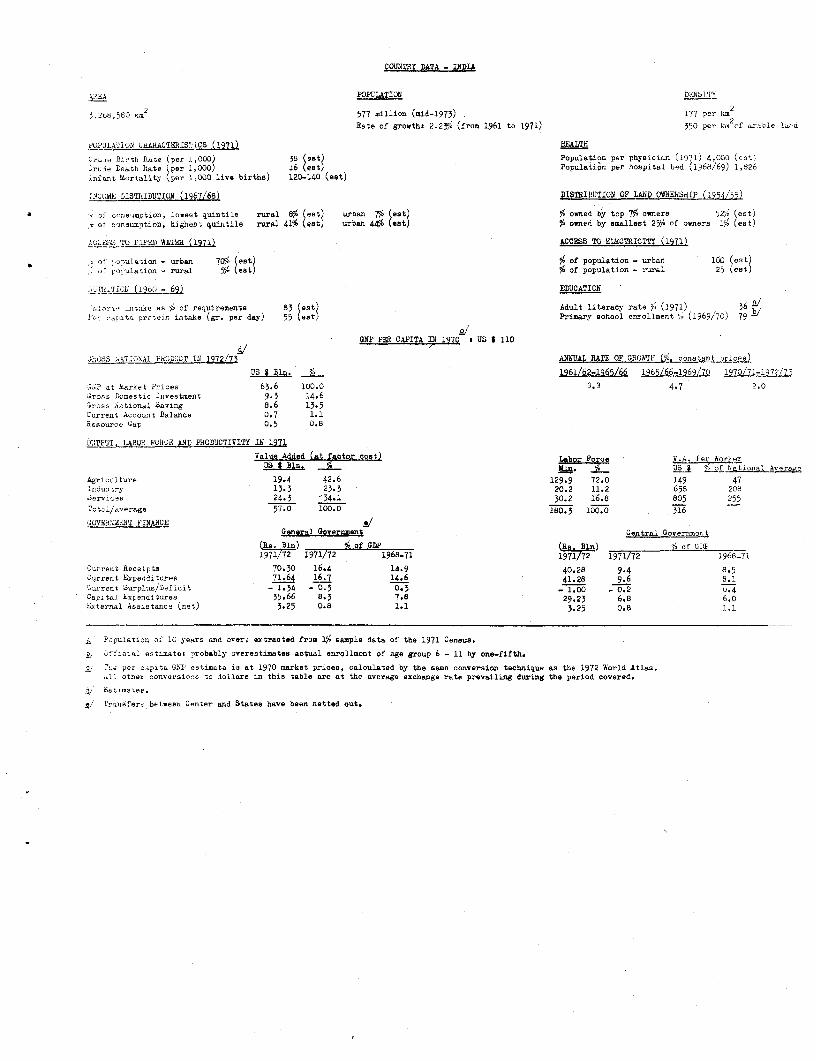

COUNTRY DATA - INDIA

]POPULATION DRl'.'TY

3 '68, 580 ,,2 577 million (mid-1973) 177 per kmRate of growths 2.2Yp% (from 1961 to 1971) 350 per km of arable 1nd

r UPLAT103 26ARACTRILS, CS (H)EALT

Brs ir ith reRe (per 1,000) 38 (eat) Population per phyatcian (1971) 4,000 (ast

1.rLie Death Rate per 1,000) 16 (eat) Populationr per hospital bed (1968/69) 1,826infant biortality per 1,000 live births) 120-140 (eat)

INCui& DlSTlibVTIOP (1967/68) DISTRIMJTION OF LAND OWNERSHIP (1954/55)

- of oonsumption, lowest quintile rural 8% (eat) urban 7e (eat) % owned by top 7% owners 12('6 (estjtol cnsumption, highest quintile rural 41% (est) urban 44% (eat) 56 owned by smallest 25%A of owners 19) (est)

A,;C-I 'O PIPED WATER (1971) CCESS TO ELECTRICITY (1971)

, of ;p,.laaion - urban 7VI6 (est) 56 of population - urban 100 (est).f rorulation - rural 556 (eat) 56 of population - rural 25 (eat)

.Ti.TOl; (i9 - 69) EDUCATION

-t. s 1o of requireoienta 83 (est) Adult literacy rate 74 (1971) 36Ir ,aitta protelr intake (gr. per day) 55 (est) Primary school enrollment 7/. (1969/70) 79

2/'GN? PEN CAPITA IN 1970 t US 4 110

hROSS N6TIONAL P0XO16T IN 1972/73 ANNIUAL RATE OF GROWTL (p/J constant prices)

US I Bln. % 1961/62-1965/66 1965/66-1969/70 1970/71-197?/75

11 at Lerket Irices 63.6 100.0 3.3 4.7 2.0Iro,s Domestic Investment 9.3 14.6^.ross ointional Saving 8.6 13.5Carrent Account Balance 0.7 1.1Resource Gap 0.5 0.8

OUTPUJT. LABOR FUH0E AND PRODUCTIVITY IN 1971

Value Added (at fastor oost) Labor Force V.A. Per WorkerUS t Bln. nc ____ L Rf National Averoe

kgrijul ture 19.4 42.6 129.9 72.0 149 47lndoi ry 13.3 23.5 20.2 11.2 658 208aervises 24.3 34.1 30.2 16.8 805 255Totl/.,erage 57-0 100-0 IO.3 100.0 316

.0VEW4IAriiT FINANCE 1/General GOvernment Central Governmen t

(Re. Bin) S of GDP (R ) B of GAL1971/72 1971/72 1968-71 1971/72 1971/72 1968_71

lurreat Receipts 70.30 16.4 14.9 40.28 9.4 8.5Current Expenditurse 71.64 16.7 14.6 41.28 9.6 8.1Corrent Surplucs/Deficit - 1.34 - -3 0.3 -_ 1.00 - 0.2 0.4lapotal iEx~enditnres 35.66 8.3 7.8 29.23 6.8 6.0Bxternal Ass:.otanoe (net) 3.25 0.8 1.1 3.25 0.8 1.1

M Population of 10 years and over; extracted from 156 sample data of the 1971 Census.

t*ffcial estimatet probably overestimates aotual enrollment of age group 6 - 11 by one-fifth.

c 2,s per CipltB GN2P estimate is at 1970 market prioces, caloulated by the same conversion technique as the 1972 World Atlas.Ai other conversiorns o dollars in this table are at the average exchange rate prevailing during the period covered.

E. Estimates.

c,' Prsofers between Center and States have been netted out.

C0OIISRY DATA - 31DIA

.O*bY 1h1*;lT AN3 P1UC8S 1965/66 1969/70 l 1 1971/72 October 1971 October 1972

( Billion Rs outstanding at end of period)

:o-OTy and quasi 2looey 61.4 93.3 105.6 122.3 113.7 130.4oank Credit to Publio Seotor 40.8 52.4 56.9 69.0 64.0 77.5Bank Credit to Private Sector 28.1 48.3 56.7 64.4 59-9 64.3

(Percentages or Index liumbers)

1965/66 1296 1970/71 1971/72 February 1972 February 1973

i,oney and .uasi Money as 31 of GPP 24.2 24 .3 24.8 26.5Yholebale Price Index (1961/62-100) 137.5 175.7 180.6 192.2 191.2 217.2

lh,uui percentage changee in?

ifolse61e Price Index 12.4 6.4 2.8 6.4 13.6oank Credit to Public Sector 12.9 1.5 8.6 21.3Snk Credit to Private Sector la.8 15.1 17.4 13.6

b i-jACa 0. PAYX1aTS

1969/70 1970/71 1971/72 DRCHANDISR EXPORTS (AVERAGE 1969/70-1971/72)(Million US S) US $ min. i

dicport of Goode 1,884 1,950 2,106 Jute Manufactures 291 15l-orts of GoodS ,109 2,179 2,436 Tea 188 9Trade Balance - 225 - 229 - 330 Cotton Textilee 161 8§sr 'net) 13 - 7 n.a. Iron Ore 139 7Ltouacur G4s - 212 - 236 n.a. Engineering Goods 136 7

Interest Payments (net) - 192 - 214 n.a. Others 1,968 1Cther Factor Payments (net) - 15 - 20 n.a. Total 1,9B0 100Set Transfers 79 83 n.a.

Galance on Current Account - 340 - 387 n.a. EXTERNAL MT. March 31. 1971OS $ bdn.

Official Aid (incl. grants) Repayeable in foreign currenoy 7,771Disbursementc 1,188 1,096 1,089 Repayable through export ofAmortization - 357 - 387 goods 782

birect Foreign Inveatment ) - 288 - 558 n.e. Total Outstanding 8,553Other Capital (net) )All Other Items ) DET BERjYIOB RATIO FOR 1971/72 30.6 percent

lncr.ase in Reserves 203-/ - 237-/ 39Gross Reserves (end year) 1,095 1, 052 1,277let Reserves (end year) 912 1,052 1,277 IBRD/IDA LENDING. March 31 1973 (UsS 1f4e S

hAT PE OF MC{APGR

Prior to mid-December 1971 a US 6 1.00 - Re. 7.5 IIRD IDARs, 1.00 - US 5 0.133333 Outstandirg and Disbursed 541 2,105

id-December 1971 to US 3 1.00 ' Ra. 7.27927 Undisbursed 66 755end June 1972 Rs. 1.00- lS 0.137376 Outstanding incl. Indisbursed 607 2,860

A-tor end June 1972 3 Floating Rate

Spot Rate (March 31, 1975) A app-rox, US $ 1,00 - RE. 7.59approx. Rs. 1.00 - US *0.13

, Allooations of SR' a and valuation changes reaulting solely from changes in exchange rates and the gold parity of the US dollar are treatedhere as exogenous to the balanoe of payments.

2/ 1530lization snd interest payments as a percentage of merohandise exports,

IBRD 10483

70 j soS;_Ms ,.S,,,a ra° 9O. May 1973

AFGHANISTAN u fit " ._' N'I rifl' /e!.r os ,ff I N D I A

JAMMU and KASHMIR

3 -~~~~~~sriaer grState and Union Territory Capitals

Si' - <~ >* National Capital

H S /1/MACHAL t.4 0 Other Cities

_t st .-' g PRADESH > State ond UnionTerritory Boundaries

.5 -.-.i-- _-- International Boundcries

PAKISTAN l c aandieerh

PUNJAB

YA/E/Af { \-| ~~~~~T I B E T._ ../ 1 Sl,DfZ~~~HI Zv

/A 'ANA EW DELHI p A BES

J -< ,3 u T rA P . NEPAL B HU 7 TAN

f B PRA DfESH .r. itCkIKKIM,P BHUTANDESHRAJA STHAN I4cknoc K 7.v

;aipur 0,Goreikhp.r ~\ 1 / X ~~~~~~ ~ ~~~Karpur Patnl({ 5t. s g > v

(( t*\ . .MG A Z A oi Y mp 01e

BIHAR hANGLADESH X /3 AgartaIX~

, -gGUJARAT D g u < BENGAL. : ~~~~~~M A D) H Y A P R A DEfS H />CiU8 9.% VIF

BURMA

t M~~A/IAA HBJA t>W-

$~~ ~~~~~ ~ ~~~~~~~~~~~ n g ofl\ J ( D~~~~~~Hyderabad ;Benga/

5 c/ )~A NDHRA rArab/an P PRADESH (4

Balngao @

\t ~~~~~~~~~~~~~~~~~~~~~~~ t),0. \ ) J~~~~~A MI Z NAODU

ffERA/At~ ~ ~ ~ ~ ~ ~~~~~1 Kp q 0 O 400 500 MILES

0 g > °cb > ~~~~~~~~0 O)l C 200 3070 400 5 60 7q) EqOO 0 KILOMETERS

Triwndru

7 ~ ~ ' 9 7De erzlunssS zON /11¢xnri doalolj iSRI L.AN,YAii ol,~~iio,jcqingrceleor -/rzr by i1tO I

1jDgii ¢'.dd 15t%/ lerk \ it jf.P

I

SULkARY AND CONCLUSIONS

i. The focus of this report is on the progress of India's developmenteffort during the 1y60s as a prelude to a discussion of next year's FifthFive Year Plan (1974/79). The record is a mixed one. In statistical termsand in relation to the immense needs of the world's second largest populationthe record is disappointing. It is nevertheless impressive not only for thevery considerable achievements but also when judged against India's inherentdevelopment difficulties and frequent disruptions caused by conflicts withneighboring countries and confrontations with nature.

ii. This year's poor agricultural harvest has provided a reminderof the ever-growing pressure of population on land and capital resourcesand the prospects of any great improvement in this regard are not bright.ACter several years of rising expenditure and declining performance therewas in some respects an improvement in family planning acceptance during1)71/72 and under the influence of a program of mass sterilization campsthis has continued in 1972/73. The ability to sustain this improvement mayhowever be hampered by the 1973/74 budget for family planning which has beencult sharply as part of the budget effort to curb inflation. In any case,there is considerable disagreement among experts as to the demographic effectof the program. Some feel that until the prospects for child survival toadulthood improve, it will be difficult to reduce family size. Nevertheless,the achievements of the family planning program are substantial and sincethere are no feasible alternatives as a way of tackling India's major longterm problem, the case for strengthening and expanding the program remainsstrong.

iii. Though it is not quite clear from the available statisticswhether the proportion of the population living below a very austere povertyline increased during the 1960s, there are reasons to believe that it did;in any case it is certain that the absolute number grew and may include40-50 percent of the population. Most of this is in the rural areas. Whilethere is substantial rural unemployment, low productivity of available em-ployment and partial employment is the principal cause of rural poverty.Urban poverty and underemployment and the employment problems of the recentlyeducated, which are compounded by both an excessive rate of growth in educa-tional enrolments at upper levels and a very slow increase in employment inthe private organized sectors, remain serious.

iv. In 1972/73, as often before, the weather has played havoc withIndia's agriculture. Foodgrain production has declined from a high of 108million tons in 1970/71 to at most 100 million tons; stocks of 9 milliontons which were accumulated during favorable years have been nearly depletedand orders were placed for about 2 million tons of imports in 1972/73. Thedrought however should not obscure the fact that domestic production is nowable to satisfy foodgrain demand during normal years. This has been made

- ii -

possible primarily by the breakthrough in wheat production which dominatesand explains most of the important agricultural trends of the latter 1960sincluding the productivity gains in foodgrain production and part of thesubstantial slowdown of the rate of growth of other crops because of shiftsto wheat. lt has also contributed to the increasing importance of the rabicrop and the considerably faster rise of agricultural production and in-comes in northern India as compared with the rest of the country.

v. One of the main challenges for the 1970s will be to improve thelot of the growing numbers of rural poor. This can best be achieved whereirrigation is possible by spreading the technology of the wheat revolutionto small as well as larger farmers and to other crops and regions. In ricea modest beginning has been made particularly in the eastern region. Inrain-fed areas a start has yet to be made and will probably require furthertechnological advances as well as institutional and infrastructure improve-mients. The prospects for helping the rural poor through land reform do notappear promising despite a new round of land ceiling legislation. The pre-occupation with the size of holdings and with a one shot redistribution havelead once again to the neglect of the broader and more lasting aspects ofagrarian reform. The rights and interests of the multitudes who can neverhope to ow. land are still poorly defined and Lnadequately defended. Theattempts to tackle the problem of extreme rural poverty through speciallydesigned rural works programs are certainly timely. There are however agreat many unanswered questions surrounding the existing schemes concerningdevelopment potentials of particular areas and the extent to which therural population are able and prepared to accept the work offered, and thebest way of organizing assistance schemles especially in the absence ofworthwhile district planning and of institutional channels oriented towardsthe problemins of the rural poor.

vi. In Indian industry the structure has changed dramatically since1956 when production was concentrated in light manufactures and consumergoods industries; today value added by capital and intermediate goods eachaccounts for nearly a third of total value added. The structural changehas also been accompanied by the substantial reduction of the dependence onimports. Partly as a consequence, however, the record of growth since 1965has been di-sappointing. Inadequate supplies of raw materials in some casesand in ot'121r cases insufficient demand have held back industrial growth.Contributing factors have been measures designed to curb the activities ofthe larger houses, and insufficient public savings for which the poorfinancial performance of some of the larger public sector industries is atleast partly responsible. Licensing procedures and price controls havealso hampered industrial growth.

vii. Some of the serious problems of the last few years have beencaused by large shortfalls in the domestic production of a number of keyindusLries. Steel, electric power and fertilizers have been among the:LnMcbtstrles whose procuoction arnc general performance have been leastsatiac ctorJ, While there were differences in circumstances among theseaU-ee infdutstries and within each industry from one producing unit to another,

- iii -

a review of their record since about 19966 showis a number of vital, conmonfactors underlying their difficulties. First, the industries were all ina state of rapid expansion thro-ughout the period; and although this waslargely justified from the point of view of domestic derand, the continuingemphasis on expansion meant that insufficient attention was paid to con-solidation of initial operating experience, to preventive maintenance andto the development of a strong and balanced institutional structure in eachsector. Second, prices were controlled at levels which were not attractiveto new investment and which, in some cases, meant that existing operationscould not maintain an adequate rate of reinvestment for modernization andsimilar purposes and still be profitable. Third, the construction programswere adversely affected by delays in licensing and procurem-.ent, Dy rawmaterial shortages and so on. Fourth, there were serious labor problemsespecially in some parts of the country where political conditions weredisturbed.

vi-ii. The 7 percent growth of industrial production in 1972 has beenmade possible largely by the recoveries of textile and steel productionthough the growth is more broadlyg based. Tne prospects for sustaining t}lisrate of growth in the immediate future however are not encouraging in viewof the possible after-effects of the current drought and the serious powershortages which have emerged in recent years, and indeed there are indica-tions that industrial production has started to level off towards the endof 1972. In the longer term, however, it should be possible to restoreindustry as the leading growth sector of the economy. This of course cannotbe! taken for granted and will require action on a large number of fronts.Some of the key requirements will be: (i) policies and procedures whichwill boost exports; (ii) procedures which will reconcile India's aims ofgr-eater social and economic quality with the need for increased privatesector investment in new capacity and for modernization; (iii) furtherimprovem,ents in the efficiency of public sector enterprises; (iv) largerava i lability of foreign exchange for raw materials and components, includingthose required by the historically neglected small scale sector, in orderto utilize existing capacities more fully and to make up for shortfalls inthe production of key industrial and agricultural requirements. There issome progress on all these fronts but whether it will prove adequate remainstc be seen.

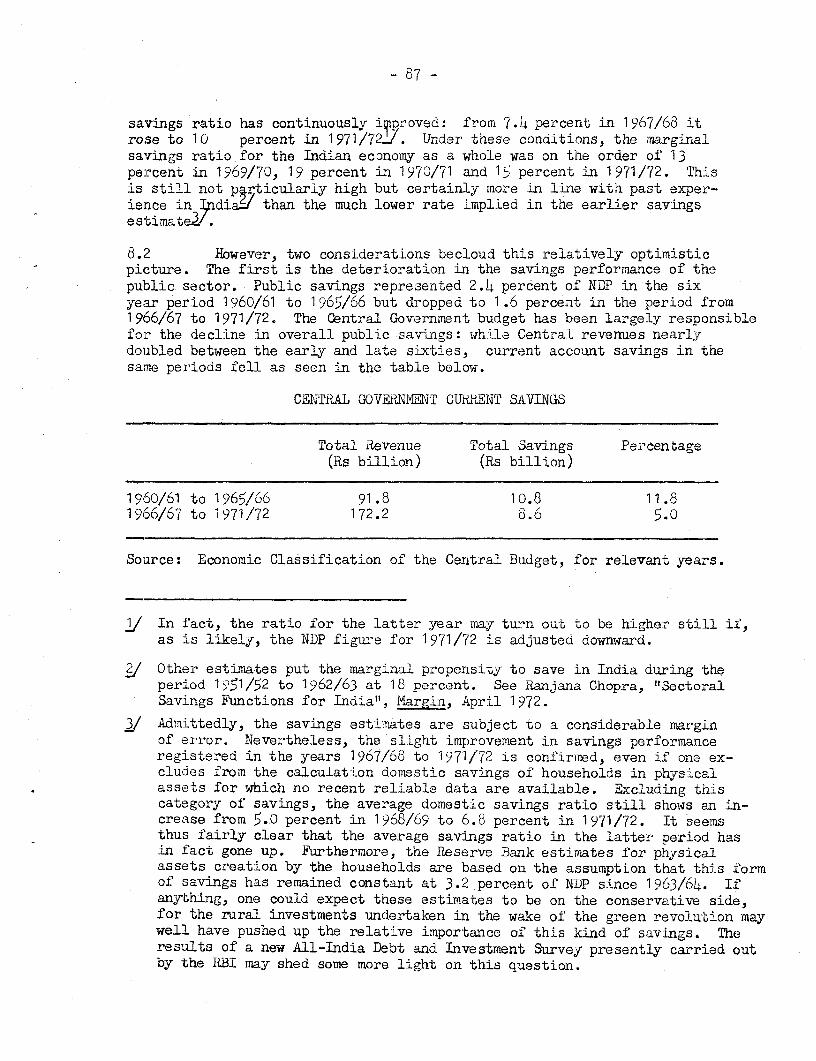

ix. One of the reasons for India's disappointing economic performanceduring the 1960s is undoubtedly the fact that the level of domestic savingshas hardly increased. The main explanation for this phenomenon is providedby fiscal developments. On the revenue side, India's revenue efforts havebeen outstanding and the country's overall tax revenues expressed as a per-centage of national income have increased by about 50 percent since 1)60.This has included increased direct taxation but has been largely on accountof Central excise duties and Sta-te sales taxes. Agricultural taxation hasremained minimal and its incidence may have declined. This rapid expansionin tax revenue, however, has been outpaced by the increase in current outlays,so that budget savings have in effect gone down in the period. Partly thisspurt in current outlays has been caused by extraneous elements, such aswars and droughts. Nevertheless, in relation to India's development needs

- iv -

the pu'blic savings performance remains fairly poor. Because of the narrowbase of State taxation, the States' reluctance to tax agriculture which isconstitutionally a State subject, and increasing demands on State expenditure,the States have become increasingly dependent on the Center for the provisionof financial resources. The Sixth Finance Cormission, appointed to allocatenon-Plan assistance in the next five years is giving particular attention tothis problem.

x. The recent budgetary situation of the Center has been marked in1971/72 by the war and the refugee problems and in 1972/73 by the severedrought conditions prevailing in large parts of the country. Both thesefactors have led to sigLificant annual budgetary deficits amounting to overRs 5 billion, equivalent to 7 percent of Central revenue. When Statestdeficits are added to these figures, the inflationary impact of Governmentactivities has been considerable. This combined with the foodgrain scarcityhas led, especially in 1972/73, to a considerable spurt in prices. TheGovernm.ent is acutely aware that the rapid price increases hit the poorerstrata of the population hardest. Therefore, much lower buidget deficitsare expected in the likely order of Rs 2.5 3 billion. This should bringabout a signif icant improvement in price trends, provided agricultural cropsthis year are satisfactory. Unfortunately, however, one of the consequencesof this year's budget improvement is a slowdown in the growth of Plan outlaywhich in real terms will be minimal after substantial increases in the lasttwo yeaLrs,

xi. The main objectives set by t1he Government for the next Plan, whichas currently under preparation, are: the acceleration of economic growth;the redistribution of consumption to pull up the sTandard of living of thepoorest 30 percent of the population to an acceptable minirnu.i level; andthe elimination by the end of the Plan period of India's dependence on netinflows of foreign assistance. These in turn will require among other thingsan impressive expoit performance; very large increases in key industrial andagricultural production to reduce imports and to keep growth balanced; anda greatly increased domestic saving effort. As compared with historicalachievements the -various targets seem ambitious indeed. However, the mairlesson of the past is that if India is to break the chains of poverty thelink with historical trends will have to be severed through a more concertede'fort in the future.

x.i. On the basis of need, it would seemJ in the interest of Indiandevelopzient to maintain throughout the Plan period a larger net inflow ofexternal assistance than seems to be implied by the assumptions of theApproach Paper. This is the case even if there are no poor harvests orexport disappointments. Of course, what actually happens will also dependon whether net external assistance corresponding to this larger need isactually available. This is a difficult question in view of' past and currentuncertaintnes. However, on the basis of current aid levels and of what isknnoiv about the short-term plans of most aid donors, it does not seem un-reasonable to assume an overall gross aid availability of at least US$5000million ovel the Plan period. While thlis is US$1000 million more than the

-v -

assessment in the Approach Paper, in relation to India's needs it is by nomeans an excessive figure, and in fact would realise a net transfer of onlyabout US$1500 million over the five year period.

xiii. The fifth Plan aim to increase exports by 7 percent a year wouldbe a major improvement over the 3 percent annual growth during the Sixties.The latter was much poorer than that achieved by most other developingcountries andi the export objective of the next Plan would be of irmmensebenefit in strengthening the econory and its capability for development.

* I.n this connection it is encouraging that export earnings in the last twoyears have increased substantially by about 8 percent in 1971/72 and anestimated i0 percent in 1)72/73. Unf:ortunately, India's non-traditionalexports and particularly engineering goods on which the hopes for thefuture are based and which have provided the main boost since the Wic-1Sixties,have not contributed to this recent acceleration. The pick up in domesticdemand for these goods, the serious shortage of steel and possibly decliningprofitability have all contributed to this phenomenon. Achievement of thetarget of 7 percent anmual growth in export earnings is likely to depend ongreater attention from policy rmakers ancd administrators in the provision ofincentives and other conditions conciucive to exports including ensuredpriority in the allocation of resources.

x-iv. As indicated, 1973/74 wiJl undoubtedly be a better year for theIndian economy in spite of obstacles like the power shortages, provided thereis a satisfactory monsoon. Nevertheless, the balance of payrnents can beexpected, as usual, to keep a check-rein on economic activity consideringInidia's mounting import needs of such critical items as petroleum, fertilizerand other chemicals, steel and non-ferrous metals, etc, as well as componentsand equipment for industrial and power expansion beyond domestic productioncapacities. We have assessed this year's minimum import requirements for themaintenance of current trends in the economy at about US$2540 million orUS$260 million more than the likely 1972/73 import level. This is wgithallowance for no more grain imports than the remainder from 1972/73 ordersdespite the depletion of stock after last year's poor harvest. Consideringthis stock depletion, it would seem inadvisable to draw on reserves for non-fcod imports in the event that adverse harvests might again require foodpurchases abroad.

xv. Hence, the possibility of larger non-food impolts will depend onthe export outlook and the level of foreign aid. Some increase in exportsis to be expected although not by as much as this year. Therefore the largerimport needs will depend on somewhat higher aid availabilities than last year.Taking account of the commodity aid pipeline and probable disbursement ratesfrom new aid commitments, the level of comirtrments required this year for non-.project aid may be estimated at US$700 million. This would allow for only amodest increase in the low non-project pipeline level. In addition we estimatethe need for new project aid commitments at about US$500 million. This takesaccount, on the one hand, of India's aim for a large expansion of the projectinvestment level in connection with Flfth Plan production targets and, on theother hand,, the linitations at present of projects which are likely to beprepared and ready for consideration this year and of uncertainties about

- vi -

Government policy in easing the import licensing of project equipment,On balance, US$500 million ofne project commitment may be a reasonableobjective for this year considering current project preparation effortsand the expectation that new project commitments by the Bank Group duringthe Indian fiscal year 1973/74 would be substantially more than the US$200million committed in 1972/73. Even if the proposed level of new non-projectand project commitments were to materialize, the net assistance of Consortiumcountries (excluding Bank Group) in 1973/74 would be only of the order ofUS$200 million.

CHAPTER I

1ThTODUCTION

Historical Perspective

1.1 Indiats record of economic developrnent during the 1960's andearly 1970's (the period of the Third and Fourth Five Year Plans) is asvaried as is the wide variety of life and environment in this vast,heavily populated and poorly endowed country. In such a context, averagesand generalizations are apt to be misleading. Yet there is, nevertheless,a broad impression of rather slow economic progress -- too slow -- andof large numbers of very poor Indians for whom the last fifteen years havebrought little improvement. The theme of this report is the course ofIndian economic development since about 1960, the achievements and short-comings of economic activity in this period, and some of the hobbles onthe pace of development with which the econorTr has had to contend. Infollowing this theme the report does not attempt to discuss all the importantsectors of the econonm or all of the influences which have tended to shapeIndia's development. Last year's economic report did provide a comprehensivecoverage of the main economic and social sectors including analysis of theircuirrent problem-;is. For this reason and also while awaiting the Fifth FiveYear Plan for review and comment in next year's economic report, it was felta(lvisable this time to review India's recent econoric past, and in so doingselect for comment only those facets of the econorr which have been criticalin liriting economic betterment for most Indians. In being selective, ourfocus has some glaring omissions like education and some other social servicesor transport or mining or certain important industries or others. This re-f'ects either our judgement about relative importance in influencing Indiandevelopment or a lack of anything substantial to add to last year's report.

1, - Whatever disappointrmients there may be in India's developmentrecord, they should not obscure the fact that there have been impressiveachievements. Indeed, the progress of some large regions of the country hasbeen satisfactory by any world standard. In the Punjab, Haryana and WesternUttar Pradesh, a region of about 50 million population which has been theheartland of the "green revolution", annual growth in output since 1965 hasbeen about 6 percent per year. (In Haryana alone about 12 percent during1965/66 - 1969/70.) Substantial progress as measured by economic growth hasalso been characteristic of other large parts of India including Mysore, Delhiand major sections of Maharashtra, and Tamil Nadu. These regional recordsare obviously not cited to minimize the significance of slow growth for thecountry as a whole; in fact as part of the national average they make it allthe more evident that the below-average parts of the country have been sluggishindeed. The better performing regions are worth noting however, not only fortheir own development, but to indicate capabilities for more rapid Indiandeveloprment given a reasonably satisfactory chance.

-2-

1.3 It is not only in selected regions that there has been substantialadvancement. The infrastructure of economic and social services has alsobeen greatly expanded since the beginning of the Sixties along with theimportant advances in agricultural technology and more rndern structure ofindustry.

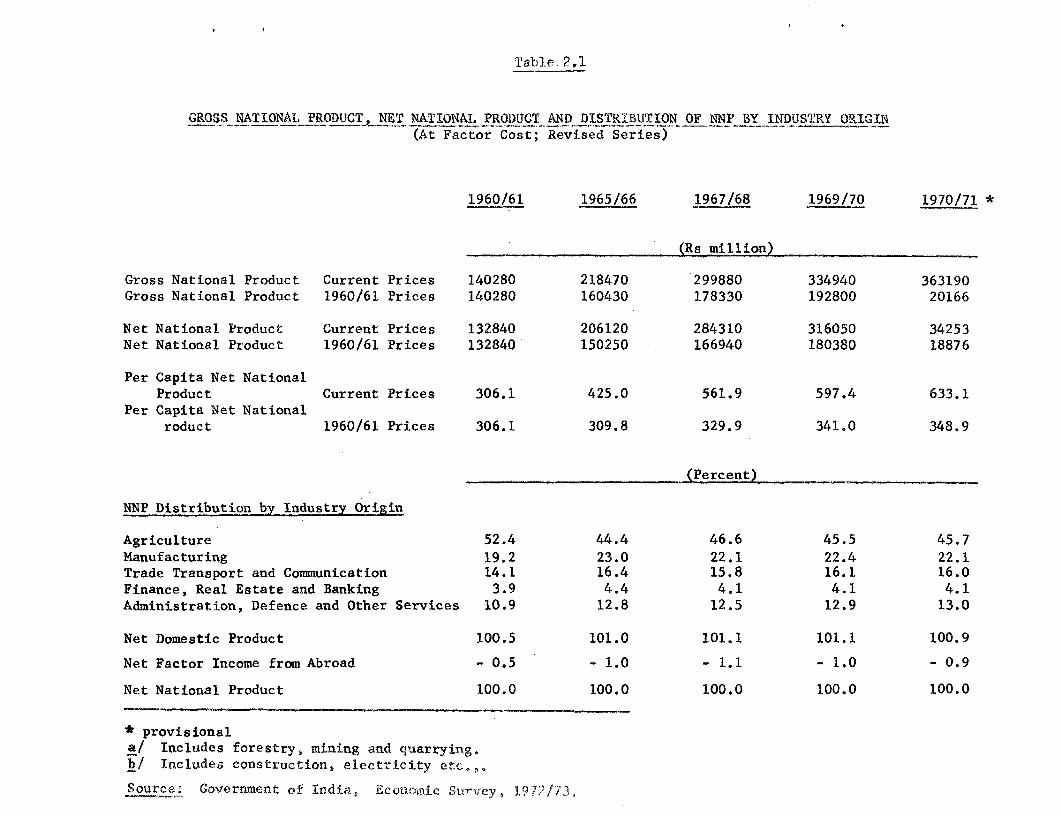

1.4 Just a few examples: Since the beginning of the Sixties,foodgrain production has increased by 30 percent, the irrigated area hasalmost doubled and fertilizer consumption has gone up more than 10 times.Power capacity is about 3½2 times greater. There is half again as muchsurfaced roads, about the same increase in railway freight, the number ofcommercial vehicles has considerably rsore than doubled, and port and shippingcapacity is greater by two to three times. In industry, the changing structureof the latter Fifties toward the manufacture of heavy capital goods, basicmetals and more sophisticated equipment continued, especially during thefirst half of the Sixties. By 1971 it is estinated that capital and inter-rmediate goods made up about 65 percent of industrial value added as com-pared with less than 50 percent in 1957. As a result the industrial sector(including mining, construction and electric power) increased from 19 to22 percent of the net national product between 1960 and 1970 while the shareof agriculture fell from 52 to 46 percent. Despite the substantial growthof the economyn, India now produces a far larger proportion of capitalgoods requirements as reflected in the impressive fact that capital goodsimports a-re now less in absolute value than they were in 1960.

1 X5 Some of the most substantial achievements have been in the socialserxice fields with primary education enrolment nearly doubling since 1960, andimticlo.e, secondary and university enrolment increasing proportionately by far more.Sinilarly there has been a large expansion in health services which have aboutdoubled since 1960 as measured by numbers of hospital beds, primary health centers,medical college enrolment and nuribers of doctors and nurses. Nevertheless,health facilities still remain grossly inadequzate to needs.

1.6 This record of advancement in the last decade or so is the moreimpressive, considering the difficulties of the environment, limitations onthe availability of domestic resources, the substantial decline of netforeign assistance, as well as the serious international crises that pun-ctuated the Sixties and early Seventies . The prolonged and severe droughtof 1 065 and 1966 was one of the worst in history. And in three years ofthe period 1962,1965 and 1971, India was at war. Perhaps, most persistentand intractable of all in dissipating the flow of potential human improve-ment from development has been India's annual increase in population. Atabout 2.25 percent a year this has thinned per capita benefits of developmentto about 1 percent on the average for the country at large; for the backwardregions -_-uhich are not backward in human fertility -- the incrementalper capita fare from development is much less if anything. In the face ofthese many economic, political and demographic difficulties, a high placeamong all of India's achievements must be given to the continuing preserva-tion, w-thout qualification or challenge, of free, democratic and tolerantpolit4ical and social institutions.

-3-

1.7 Yet with all these achievements of recent times -- the break-t hrough in agriculture, the creation in industry of a modern complexstructure, the advance of education and other social services, and theadherence to liberal political institutions -- the record of economicprogress remains disappointing when judged in relation to potentialitiesand especially to the depths of Indian poverty. Among the poor, as com-pared with 1960, those still living below an austerely drawn minimumacceptable consumption level are probably larger in number now, and perhapsthey are also a larger part of the population. Any improvement for thislarge segment of the population has been small at best, and for largenumbers of the very poorest conditions may have grown worse.

1.8 Actually this record of limited economic improvement is wellbelow the sights set for the economy by the Indian planners. Since 1 61/62when the Third Five Year Plan began, growth targets were over 5 percent ayear during the Third Plan period (1961/62 - 1965/66) and 5.5 percent duringthe Fourth Plan period ending this year (1969/70 - 1973/74). The plannersalso expected that growth in these amounts would be accompanied by signi-ficant inroads into low-end poverty and unemploymrent. The frustrations ofplanning, with actual growth at only about 3 percent a year, is obvious.

1.9 It is not only in relation to India's enormous needs and to theanticipations of the economic planners that the development record hasbeen disappointing. It is also disappointing in comparison with much of therest of the developing world. India t s growth in national product during theSixties was veyy low among developing countries. In addition there was asubstantial shortfall below planned objectives, which was not because plannedobjectives were unusually high.

1.10 Looking back on these frustrated development ambitions, thismray be a gooci time at the end of the Fourth Plan and just before theFifth to seek reasons for India's slow development.

1.11 There is of course the fundamental handicap of a poor naturalendowment for such a large and rapidly growing population. Improvement ofthe environment relative to population is difficult indeed in a countrywhere fuel and mineral resources are far below needs, where rainfall ispoorly distributed and unreliable while water resource development is slowand complicated, and where transport in such a large and diverse countryis a demanding and heavy burden. Agricultural difficulties, becuase ofthe poor and uncertain environment, are well kmown. In combination with over-crowding, these difficulties condemn most farming to low output per personand per acre.

1,12 It is the overwhelming dominance in the lives of most Indiansof this poor, slow-moving and unreliable agriculture which should be perhapsthe starting point for considering why Indian development has not beenfaster.

1.13 In starting with agriculture, it is important to emphasize thatthis is no way to belittle or minimize the significance of the changes in

-4a-

agricultural technology that have been taking place in the last severalyears (the "green revolution"). Where this has taken place its remarkableeffect on production and modernization has opened a window on new horizonsfor agricultural development. But it still is a small window in theexpanse of Indian agriculture. The impact of the new technology has sofar been confined to wheat and millets, and to a few favorably located.rice growing areas. Thus far it has been a revolution in the technologyof irrigated land rather than rain-fed cultivation. Its big and growingimport has therefore been in the off-monsoon (rabi) season. The area asyet affected is about 15 million hectares out of a total cropped area ofabout 160 million hectares and a foodgrains area of almost 125 millionhectares. This obviously still leaves most of Indian agriculture and aneven larger part of the agricultural population untouched by technologicalchange. Regionally, Punjab, Haryana and Western Uttar Pradesh have beeneffected in a major way but for the rest of India regions of such changehave been very few, small and scattered.

1.14 As for its effect on trends in agricultural production, thebenefit from the expanded output fromw the "green revolution" has been tosustain an agricultural growth trend since the mid-Sixties which wouldotherwise have fallen. The rise in agricultural trends, including food-grirns, was no greater during the latter Sixties when the new agriculturaltechnology was spreading than it was during the Fifties. The reason forthis was that opening of new agricultural land, which had earlier been animportant growth factor, came nearly to a halt in the latter Sixties. Thusthe surge in wheat production in recent times offset a slowdown elsewhere.BLt regionally the slow own was a hard reality for those who were not partof the wheat expansioni.

1 .15 Thus even allowing for the "green revolution", agriculture inthe large has been a pretty slow growing part of the Indian econoV., Itis doubtful that a higher priority and a greater agricultural emphasis inofficial policies and programs would have pushed agriculture ahead verymuch laster in the Sixties. Even with hindsight it is not easy to see howany realistic potentials of importance were missed, considering the resistantand -ddependable environment, rural congestion, the disappearance of newland development opportunities, ancl above all the technological inhibitionsuntil the latter Sixties when the high yielding varieties came along. Itwould have been helpful if the development of rural institutions, e.g. thecooperatives and the extension services, had been a little more lively anduseful. Nevertheless there have been effective efforts for institutional,infrastructure and other improvements in agriculture such as the expansionand diversification of agricultural credit, the very large increase in publicas well as private groundwater facilities, some improvement in the distri-b-ution ol farm inputs like fertilizer, and above all the drive, organizationand imagination that went into the research, development and spread of the

21 For a more extended discussion of agricultural trends of the last decadesee Chapter II. See also Dharm Narain, "Growth and Imbalances in Indian1i'griculture", Journal of the Indian Society of Agricultural Statistics,Vol. XXIV, No 1, June 1972,

new high yielding technology.

1.16 Despite these welcome improvements, the limited progress inmost of Indian agriculture has had serious implications not only for economicgrowth but for rural welfare. It could hardly have been otherwise with70 percent of the population producing only half, and more recently less,of the national output. An overall increase in rural productivity wouldseem a pre-condition of sustained rural improvement. Agrarian reformcould helD if it were real agrarian reform, but this has not com-e of' inany substantial way. Other redistributi-ve measures and improvement ofrural social services would also help although these for India are tooexpensive to sustain on a rising course unless accompanied by real andsignificant gains in productivity. Arnd for such gains, the technologicalconstraints prescribe either adequate and effectively controlled water,or a major transformation of farming from a subsistence to a marketorientation, or both. Such agricultural changes on a scale of nationalsignificance within the available technology would have required muchmore than was available of water, water control, extensive marketinginfrastructure, and institutional mechanisms for planning and performringso complex a transforTmation. Without these, and with all the materialtechnological and institutional inhibitions, it is hardly surprising thatagriculture has been such a slow mover in the Indian economy, and thatthe economy in turn has had difficulty in reaching an acceptable momentumwith agriculture accounting for so much of the national output.

1.1 7 ?hus with the agriculturaL engine of development turning slowlyand unevenly it was a reasonable strategy to rely on the faster gearedindustrial engine to pull up the average pace of development. With theagricultural half of the economy on a 3 percent growth trend, the rest ofthe econony would have had to advance by about 8 percent a year for anovrerall annual growth rate of 5 or o percent. And this would imply alead frormi the industrial sector at something like 9 or 10 percent a year.Obviously, this pace could not be sustained if dependent mainly on anindustrial orientation toward the mass consumes market as constituted.This market is mainly agricultural and slow-groiwing and has only limitedlinks to rmanufacturing, mainly through food processing and textiles.Linkages between this market and heavy industr-y are even more tenuous.And so the strategy of rapid industrialization had to face in otherdirections -- toward the buildl-up of a heavy industrial base oriented to-ward import substitution and to the denand for capital equipment generatedby the rapid industrialization process itself -- "making machines to makemachines" as the strategy was sometimes described. Since it depended primarilyon the investment market rather than the consumption market, the process re-quired a substantial increase in investment resources, which -were to begenerated through increased budgetary saving, through saving generatedfrom earnings within the industrialization process itself and throughforeign saving supplied from external assistance. It might also haveleaned considerably on the export market but this possibility waslargely neglected.

-6-

1 .18 Qi The momentum of this strategy built up rapidly during the latterFifties and continued to the mid-Sixties. Between 1958 and 1965 valueadded in ,oanufacturing grew at an annual rate of about 7 percent. Itwas a strategy which was widely endorsed at the time both in India andabroad. And it served its objectives reasonably well for a time. Duringthe period 1960/61 to 1964/65 when agriculture was on its usual slow trend,the pull from- industry helped to carry the econozy along at an average rateof almost 5 percent.

1.19 As the mid-Sixties approached, the strategy was creaking in itsstructure of phys-cal output, inter-industrial lincages, and domestic andforeign resources. By 1965 the rate of industrial production was slackeningoff but not the trend of inflation with prices averaging almost a 10 per-cent increase in 1?64 and 1965. Then came the war with Pakistan in 1/$65an(d the seve-e drought of 1965 and 1966. Prices soared even faster in 19660and this ended the period of rising budget deficits. Even a sturdier in-dustrial expansion structure mnight have had difficulty in surviving thieseshodks;but they were certainly too much for the shaky state of the ind-us-rialization strategy by that time. Thus the drive for industry, as thekey to the accelerated develop-ment of an agrarian econotmv handicapped byslow moveiment of agriculture, foundered.

1.20 Since that ti-ne there has not really been a sustained industrialrevival. The reasons for continuing industrial lethargy are discussed inChapter VI. They include inefficiency and the shortfalls in domestic pro-duction and saving related thereto; insufficient foreign exchange fromexports and foreign assistance to supplement domestic production and com-pensate for domestic shortfalls; and slow development of exports not onlybecause of the adverse effect on import capability but also because of aninsufficient export supplement to domiestic demand for manufactures. Con-tracting inport subst-tution opportun ies relati ve to industrial capacity,and increasing difficulty in reconciling the obiective of greater socialand economic equality with expansion of the laxger private enterpriseshiave been increasingly important curbs on the industrial tempo of the lastseveral years, as have critical supply shortages like steel and othermetals and electric power.

1.21 If the past is any guide, this brief review of the Indian econoiyin recent times may suggest some of the keys to changing the pace of develop-ment in sise and distribution for the greater benefit of most Indians.

1.22 Clearly one of the most pressing demands for longer term welfareis an increasingly effective program of family planning. The record herels one of outstanding achievement in the dissemination of family planningknowledge, but it is less iapressive relative to the problem in theacceptance and application of this knowledge. This obviously continuesto be a first priority for the Indian develop,ment effort and inagination.

1 .23 In agriculture a large potential has been recently opened upb, tec.hnological advances which are well suited to small as well as largefarmlers, Currentu research suggests even larger future opportunities for

-7-

widespread participation in higher crop and livestock productivity bymeans of extended irrigation and other infrastructure and institutionaliraprove-ments. But this will still leave vast numbers of Indians in ruraldestitution unless the productivity of rain-fed crops and animal husbandrycan also be raised. Here the imperatives of technical, physical andinstitutional change are even more difficult and challenging than in thefurther spread of irrigation technology. But the rewards for achievementin this crucial part of Indiats struggle against poverty will be highindeed.

1.24 Along these two main lines of rural development emphasis, thereis every reason as subsequently discussed, to expect a better record ofproduction and distribution in agriculture during the next ten years thanin the last. Yet, even then agriculture is hardly likely to be the pacesetter if a more acceptabls size and pattern of development is to emergein the Seventies. Tne potentialities for the pace setter role are onlylikely to exist in a more lively industrial sector. For this there appearsstill the need to surmount the obstacles which have contributed to in-dustrial lethargy and which may be worth listing again: industrial in-efficiency, insufficient resource generation, poor export performance,shortages of materials -- imported and domestic -- and of infrastructureservices, contracting incentives for import substitution, and curbs onprivate industrial expansion attributable to cumbersome policy administra-tion and restraint on larger industrial establishments as the chosenmeans in this field for pursuing social objectives of grea-ter equality.

Recent Developments

1.25 The mass refugee influx and the war with Pakistan in 1971 andthe adverse turn of weather especially in 1972 have imposed severe strainson the Indian economy during the last two years. The recent reflection ofthese strains has been severe food shortages in large parts of Central andWestern India and an upswing in the general price level, particularly infood. Considering the difficulties, the fact that economic dislocationswere not more serious is a considerable tribute to the effective mobilizationof financial, material and human resources for support of the refugees andthe war, and to the accumulation in recent years of large food stocks totide over harvest failures like that of last year. And while the broadeconomic picture of 1 072 was not very bright, it did contain some brightspots including an improved industrial situation and a sharp rise in exports,mostly in some of the traditional commodities. A steady increase in realoutlays on development was also maintained through these difficult times.Because of the difficulties, however, the recent course of the Indian economyhas remained on the slow and uneven trend of the last ten or fifteen years.National output rose oy not more than 2 percent on average during 1971/72and 1972/73 and probably by less. This obviously allowed for no per capitagains and the very large numnber of Indians living in the drought areas orwhose incomes have lagged behind inflation are worse off today than theywere two years ago.

1 .26 The adverse effects of weather are reflected in the decline inthe kharif foodgrain crop from the bumper level of 69 million tons in 1970to 62 million in 1971 and down to around 52-54 million in 1972. Part of

this fall has probably been offset by the record rabi crop which has justbeen harvested. This has been partly the result of favorable rainfall inthe past winter and spring, and partly the result of a "crash" effort toboost the rabi crop which could have been even more effective but for in-sufficient fertilizer and power to operate tubewells and pumps. On balance,for the 1972/73 crop year as a whole production statistics will probably showno more than 100 million tons and possibly a little less, compared with 108million in 1970/71 and 105 million in 1971/72. The deprivation in thedrought-affected areas has been severe -- in drinking water as well asfood for both huian beings and livestock. It has been reflected in intensehuman suffering, migration and crowding into cities from the countryside,and heavy losses of cattle. The situation has been bad enough but it mighthave been even worse but for the grain stocks, which were drawn down fromabout '9 million tons to working levels of 2 or 3 million tons at the endof March, and by imports which had totalled 680,000 tons by the end of March1972 out of 1.65 million tons on order. With these additions to the supplyIndia may get along in 1973/74 without further critical difficulty providedthe 1973 monsoon is satisfactory and the distribution of wheat and rice flowswell through the newly nationalized channels.i/

1.27 Along with foodgrains, other crop production was also off in1)72/73 -- only marginally in tne case of cotton, jute and mesta but quiteseriously in the case of oilseeds. There was a slight rise in sugarcaneproduction. By and large there has been little recent evidence of spreading

1/ The Government has decided that the wholesale trade in wheat and rlceis to be taken over by government agencies this year. Accordingly StateGovernmen-ts have abolished private wholesale trade in wheat from the startof the current wlheat marketing season (from April 1I73). This is to befollowed by nationalization of the wholesale trade in rice in the latterpart of this year. As a supporting measure interstate movements of wheaton private account have been banned and this presumably will be followedby similar measures for rice. Government agencies will stand ready topurchase all the wheat and rice offered for sale by farmers to theseagencies at fixed procurement prices. No attempt is to be made to procurethe total marketable surpluses through levies or compulsory purchase.The private retail trade is not to be touched and farmers may makce salesd!irectly to licensed retailers.

The stated purpose of this nationalization of the wholesale trade is toreduce distribution margins and speculative seasonal price fluctuations,as well as to control an increasing volume of grain in the interest ofL;ul1d.ni up buffe- stocks and otherwise improving the distribution system.

Intended government procurement of wheat this season for official distri-bution through the nationalized channels is 7.5 million tons (or about 25percent of the expected production) compared with about 5 million tonslast year. It was still too early in the season at the timne of writing(rmiid-April) to judge the effectiveness of the newly nationalized system andits influence on flows of wheat through official and non-official channelsand on price patterns in the grain markets. The prospects for a favorablewheat harvest should make the difficult nationalization task somewhat easier.

-9-

dymamism or a new breakthrough in agriculture. The "green revolution" issuill going strong in reglons conducive thereto which means the regions andfarms with controlled irrigation and which have not been otherwise seriouslyhandicapped by fertlizer and power shortages. It is these regions whichare steadily boosting the i-mportance of the non-monsoon (rabi) crop comoaredto the monsoon crop. But indications of an early and significant upwarddeparture from the slow long term agricultural trend have not been evidentin the last two years.

1 .28 As so often happens, the direction of Indian industry was againcontrariwise to that of agriculture in 1972. A considerable range of i-ndus-trial production emnerged from the industrial doldrums prevail-ing since 1969to push up the industrial index by about 7 percent. This was twice theaverage annual gain in industrial production in 1970 and 1971. The indexleaves out a large share of industrial activity carried on in small scaleplants, but indications are that these also were considerably more busy in1 972.

1 .29 The industrial upswing appears to have been fairly broadly based,although particular pockets of industry were of special importance inboosting production. The textile industry -- cotton and jute -- ran alrmost10 percent above the low levels of 1)71 during most of 1972, and thisindustry accounts for more than a quarter of the industrial productionindex. It had been cramped in 171 by insufficient raw materials, butthis was not the case last year, thanks to the excellent harvests of cottonand jute in 1971/72. Favorable foreign markets for jute goods in theabsence of full production in Bangladesh, and government operation ofailing cotton mills previously closed all helped to raise textile produc-tion. In addition to textiles, other major branches of industry whichshared in the upswing were chemicals, electricity, transport equipment,machinery, mining and metals, non-metallic mineral products. The onlyimportant branches of industry which failed to expand production in 1972were food manufacturing and metal products.

1.30 There were several factors which helped last year to dispelthe previously prevailing industrial lethargy. More raw materials wasone factor, not only in raw cotton and jute but in metal and fuels as well.Steel, though still below demand, was in larger supply than in 1971. Domesticcoal production was also larger. Some further reduction in labor disputes,continuing after the considerable improvement in labor relations in 1971contributed to industrial advancement.

1.31 There were also bu-oyant influences from the demand side. Im-portant in this respect were substantial increases in development spendingby the Government in the last two years. Central budget outlays on directinvestment increased by 18 percent a year in both 1970/71 and in 1971/72,while total plan expenditure for the public sector (including Central andState Governments, public undertakings and financial institutions) may havegone up by 19 and 20 percent respectively in the same two years. These in-creases were not only a direct stimulus to manufacturing but also spurredindustrial expansion in indirect ways including some expansion of activity

- 10 -

in the private sector. Capital raised by private companies in 1972 wasabove that of the previous two years, and capacity utilization in a widerange of private industries was considerably improved, including most linesof chemicals, electrical goods, machinery (other than machine tools),rubber goods and metal products.

1.32 On the other hand, for a variety of reasons including supplyand operational constraints and demand deficiencies, large portions ofcapacity were still unutilized in many parts of the industrial sector,especially in engineering industries, in metals, fertilizer, and a varietyof electrical and metal manufactures. The amount of licensing of new andexpanded capacity was not indicative of any particularly buoyant outlookby private industry. Rather, even the short'er term outlook was clouded byuncertainties toward the end of the year including increasingly seriousshortages of industrial power and doubts about the ability of the Governmentto sustain the upward course of developnent spending.

1.33 P1eanwhile the development of exports as a supplementary marketfor Indian manufactures has continued to be disappointing. Manufacturesthat contributed to export expansion in 1972 were all in traditional lineslike jute and cotton textiles and leather goods. Exports of engineeringgoods, on which hopes have been pinned for improvement in Indian exportperformaance, actually fell. And this again reflected on export policiesand promotion measures which see.n unable to cope with the relative attrac-tions of the domestic market as opposed to export markets.

1 .34 By and large, industrial production in 1972 was encouragingindeed by comparison with the sluggish behavior in 1970 and 1971. But itwas still lacking in prornise of the drive necessary from the side of in-dus-try to bolster export growth and a sustained and satisfactory developmentoi the Indian economy.

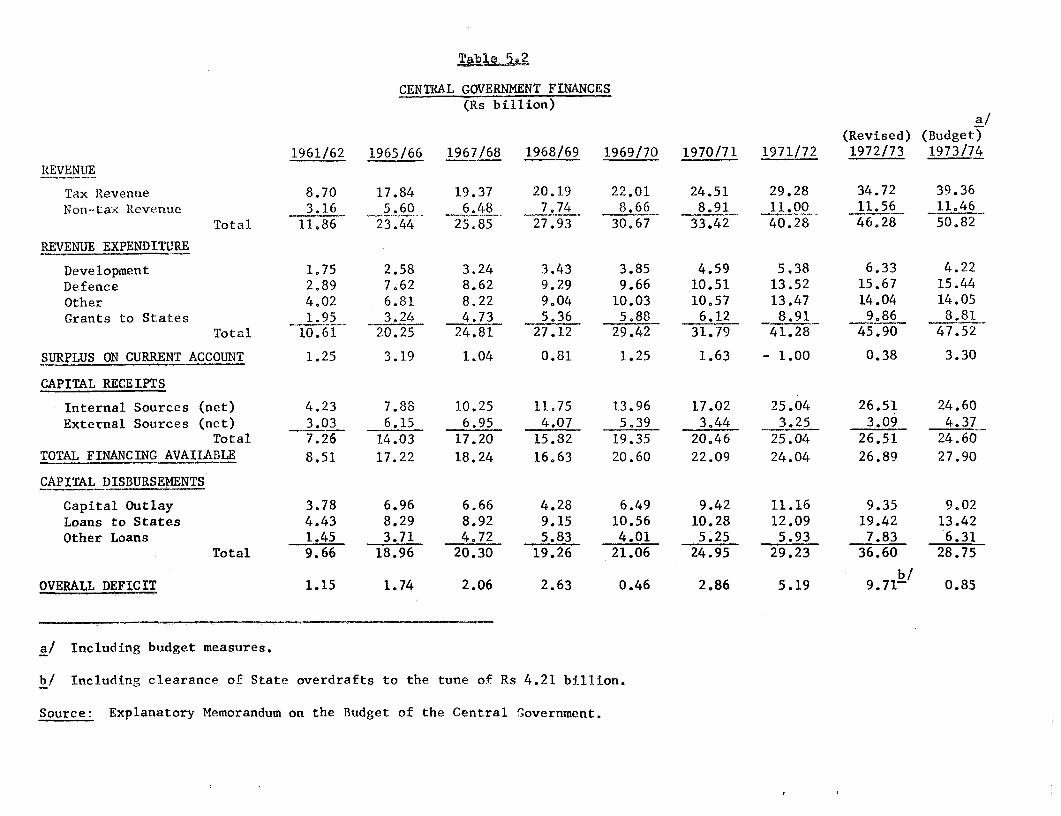

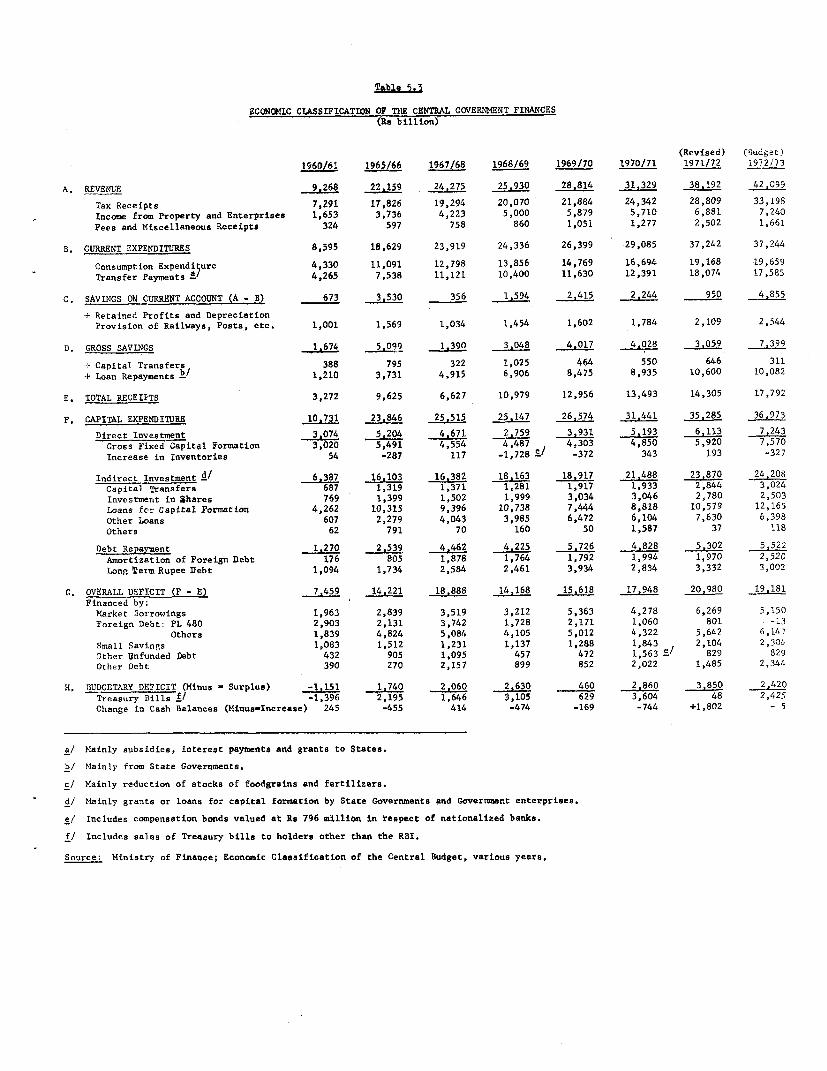

1.39 It is hardly surprising that the international crises of 1971and the agricultural setback of 1972 have been accompanied by financialdifficulties -- both internal and external -- which are persisting into1973. Government expenditures in 1971/72 (Central and State) ran far overthe budget estimates, and were nearly Rs 107 billion or 20 percent morethan in the pre8rious year. Heroic revenue efforts and other means of non-inflationary financing covered most of the increases but there was stillheavy inflationary financing of Central and State deficits by the ReserveDuak of over Rs o billion (about 10 percent of the money supply.

1.36 Financing problems, stemming from the war and aggravated by the1972 crop failures of last year continued into 1972/73. In addition to somne

contmnuation of refugee and Bangladesh aid expenditures, the past year hasaiso brought large emergency outlays for drough-t relief and for the crashmeasures to boost the rabi harvest. Development spending, including pro-grams for the poorer rural population, was also considerably expanded inIthe last two years as previously noted. Again, there were large offsettingMnirovements in revenues in 1972/73 which, with some further additional

taxataon and a full year of the wartimes revenue measures taken in 1971,

- 11 -

reached more than Rs 70 billion for 1972/73 which was about a third more thanin 1970/71. Despite this, there was again heavy deficit financing in 1972/73of about Rs 5.5 billion (Central Government only).

1.37 These fiscal deficits of the last two years have had substantialmonetary consequences, and, in combination with the poor harvests andgensrally slow real output growth, have contributed to rising prices. Themoney supply increased by about 14perceriL in fiscal 1971/72 and went upby about 11 percent in the calendar year 1972. It was in 1972, however,that most of the effect on prices has been felt, partly because of lags inthe monetary influences but especially because of food and other commodityshortages. The wholesale price index in December 1972 was higher thanDecember 1571 by nearly 14 percent and the average increase for the yearwas about 8 percent. Tnese increases have continued into 1973. Food ledthe price increase with an average rise for 1972 of 11 percent. Therewiere also increases of lesser magnitude in most other commodities with theoutstanding exception of raw cotton which declined in price following thefavorable 1971/73 crop.

1 .38 In such circumstances of upward price pressures, the extensivegovernment intervention into the price mechanism has been particularlydifficult with substantial trading in excess of publicly controlled orinfluenced price levels. Tnis has been especially so in a number of fooditems -- wheat, rice and other foodgrains, sugar and vegetable oils. Lnpast years the government procurement price for foodgrains has tended toserve as a floor in time of rising production. Last year, however, much ofthe grain was traded at prices well beyond the official procurement level,which of course aggravated the difficulties in a shortage year of reachingofficial grain procurement targets. In these and other respects, the upwardcours.e of the price index, which attem,pts to relfect free as well as con-t,rolled or othexrvise administered prices, was testimony to the frustrationsof goverrnment price administration.

1.39 Some fiscal pressure on money and prices seems likely to continuethis year. While the 1973/74 budget aims to limit deficit financing far belowthe previous two years, the GovernLment expects additional spending require-ments (mainly to meet expected pay increases) to boost the expansionarydeficit well above the budgeted Rs 850 million. There are also other pro-visions which .may be insuLficient, such as food subsidies and contributionsuo State budgets which by and large have substantial uncoverea dificits. Onthe other hand revenues are also likely to exceed budget estimates, and onbalance the expansionary influences of public finance this year, while pro-bably much larger than bud5eted are also likely to be well below last year' sfiscal expansion. Just what the price effects are likely to be will dependas much or more on agriculture production. In this respect it is encouragingthat the rabi harvest of 1973 is good, but itis still too early to say anythingabout this year's monsoon and the critical autumn harvest. One further noteof significance about this year's budget is the provision for Plan expenditure.For the first time since 1969/70 this would allow for little if any real in-

- 12 -

crease if budgeted intentions are adhered to. Once again it is India'schronically difficult choice to forego badly needed development outlays inan effort to curb the price instability which bears so heavily on poorerparts of the population.

1.40 The tight resource situation of the last two years, describedabove, had only limited relief from external developments. By far the mostfavorable aspect of recent external transactions was the substantial increasein Indian exports by 8 percent in 1971/72 and about 9 percent in 972/73.This was a rmlarked improvement from the 3h-4 percent growth rate of the pre-vious two years, even though the impact on India's purchasing power has beenmore limited due to rising import prices. In addition, there was specialinternational help in 1971 in support of the refugees in an amo-unt of aboutUS$230 million.

I .LjI Yet despite the improvement in exports, the broad balance of pay-men-ts situation has continued to be difficult. Increasing pressures onIndian import capability have stemmed from the contracting margin betweendeclining foreign assistance on the one hand and rising external debt serviceon -the other. At the same time there have been added recent import require-ments arising from shortfalls in domestic production, especially i grain,steel and fertilizer, which has meant tightening of import policy on otheritems.

1.42 For these and other reasons India has been losing foreign exchangereserves in the last,year for the first time since 1964. The drop in re-serves in 1972/73 amounted to US$46 million of which US$13 million was arepayment to Bangladesh and US$33 million was due to other balance of paymentsnet deficits.

1 .43 A continuing tight exchange situation and possibly further lossesof reserves are in prospect for the near future. This is on the assumptionof no substantial reversa'l of adverse trends in foreign aid and debt servicerequirements. There will contiuue to be large Lmport requirements -- muchof it available only at higher prices than in 1972 -- of steel, fertilizer,and petroleum as well as other current supplies. Further grain imports mayalso be needed, certainly if the 1973 monsoon is again unsatisfactory, andpossibly in any case if the decision is taken to start rebuilding the stocksof foodgrains depleted by last year's drought. There is also great uncer-tainty about sustaining last year's export expansion. Satisfaction aboutthe expansion was necessarily qualified by the fact that gains were almostentirely in traditional exports for reasons which are not necessarily likelyto be sustained. On the other hand newer exports in lines of manufacturelike the engineering industries, which are India's best hope for continuingexport strength, failled to contribute to the expansion. Part of the reasonhas been shortage of essential raw materials like steel. But there are otherreasons including the difficulties of world market competition, which in theabsence of adequate incentives and other export promotion measures, appearto give potential exporters an understandably strong preference for the pro-tected domestic market over the harsh exposures of foreign markets.

- 13 -

1.44 Broadly then 1972 was a mixed experience for the Indian economy.Agriculture was in one of its off years, and this, in combination with themonetary expansion left behing from the Pakistan war, gave prices one oftheir largest boosts in recent times. In this financial atmosphere budgetingfor 1973/7h was a difficult exercise which limited the scope for continuingincreases in Plan expenditures. It was also a mixed year for internationalaccounts with a welcome increase in traditional exports but disappointingforeign sales of non-traditional manufactures. Manufacturing for the domesticmarket did have some considerable revival, mainly in textiles but also in anumber of other lines of production. This did not, however, have promise ofanry great or sustained dynamism. On balance then 1972 was somewhat below butstill in the pattern of India's longer run trend of slow and uneven econormiicgrowth. Handicapped by sluggish and irregular agricultural development andwithout adequate thrust from the industrial side, the economy continued tofall short of adequate and socially acceptable patterns of development.

l

- 14 -

CHAPTER II

POFULATION

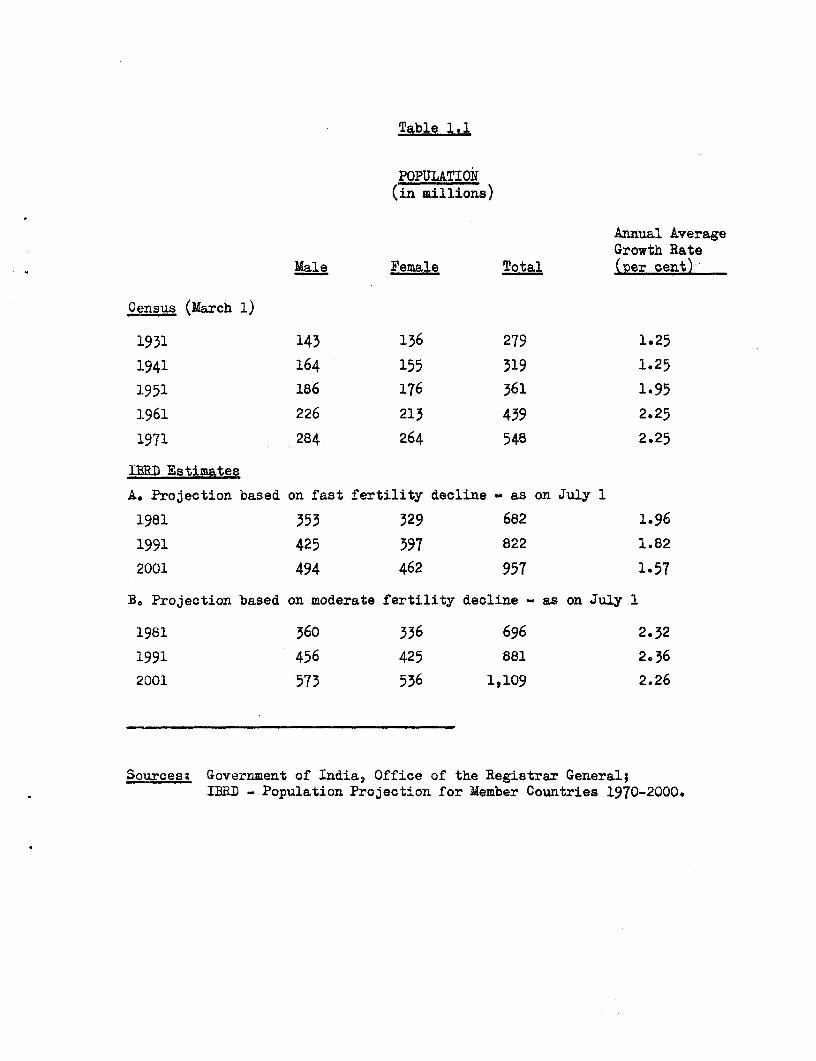

2.01 It should scarcely need stressing that population growth is one ofthe most important contributors to India's major economic and social problemsin the long run, probably the most important of all. This year the ghost ofI4althus has returned for one of its periodic visitations. Indeed, it isapparent that this ghost has never really departed, when one looks at region-ally disaggregated data on agricultural output, examines the statistics onmalnutrition and the obvious contribution it makes to infant and childmortality, or realizes that for at least the first eight years of the 1960snot merely the numbers but probably also the proportion of those livingbelow a most austerely-defined poverty line actually increased, and nowcomprise roughly half the population. 1/ Of course, population growth isnot the sole cause of India's poverty -- this year in the drought-hit areasmany of the very largest farms were as barren as the smallest plots, andlandowTners were as destitute as the landless -- but the two are intertwined.Incomes were so low, less because of an absence of employment opportunitiesthan because of their low productivity, and this reflects the remorselesspressure of population upon cultivable land and capital resources.

2.02 This pressure is going to continue to increase for the foreseablefuture. Which side of the billion mark the pop.lation will be at the end of

1/ It is possible to debate endlessly how to resolve the statistical problemsin using the National Sample Survey data (the orny source available on theconsuamption of the poor) -- what subsistence level to take, what price indexto use, etc. This does affect bot.h magnitudes and trends, but not theappalling nature of the problem, and the debate is bound to be inconclusive.The most disturbirg estimate is.also one of the most careful and convincing;"using NSS data on persons in different expenditure groups, the percentageof rural people below this alternative minimum level (Rs 14 per head monthlyin 1600/61) went up from somewhat less than 38 percent in 1960/61 to about53t percent in 1968/69". Pranab K. 1Bardhan, "On the Incidence of Poverty inRural Tndia of the Sixties", Economic and Political Weekly2 Annual Number,173 p i-254. This i r1)3,pp 211 5-. . hs level is base-d on an estimate of a nutritionallya. -iillU diet olus the same small nroportion of total expendit-re on non--food items that the bottom f-ifty percent of the rural population spent in1 C,0/61; it worked out at Rs 14 in 11 60/61 and Rs 28 in 1968/69. Theau-thor notes that there may be unreported consLmption of food and fueliterts - h-unted, fished, collected, or gleaned -- and that the imputed-alle of the consumption of home produced items may be under-estimated.

availa-bilt-y of cheaper local foodgrains might also affect the costoi a 1 mnirnLo diet. These adJus`ments would affect the proportion of thepopulation below any partic'llar level, but not the startling trend. Thewidely quoted estimate by V.I. Dandekar and Nilakerntha Rath was that in1967/68 nearly 40 percent of rural population and half the urban populationweere 1viin g below a povertyr line defined in terms of an adequate calorieint-a're plus rinimal non-food expenditure; see Poverty in India (IndiankIchool of Political Economy, 1971). On these estimates the rural poor,excent for the poorest, were marginally better off than in 1960/61, but the'7-ba; ooor substantially worse off.

- 15 -

this century is a matter for conjecture. It depends on the rate at whichfertility drops in an unprecedented situation; in the extreme, if it failedto drop at all, but mortality declined at a plausible rate, the populationwould reach the formidable figure of 1 ,230 million by 2 000.

2.03 The problem has been acknowledged for a great many years and therehas been an official family planning program since 1951 -- for longer thananywhere else. Only since the mid-1960s has it amounted to anything signi-ficant, either by way of total expenditure or in numerical measures offamily planning acceptance. A separate Department of Family Pla-nning wasestablished i-n 1966. In terms of acceptance, the program at that timeenjoyed a brief flowering; in 1965/66 and in 1966/67 the number of IUDinsertions was over 800,000 and 900,000 respectively; while sterilizationswent from 477,000 in 1965 to 1.8 million in 1967/68. Expenditure alsoroserapidly; from Rs 22 million in 1963/64 and Rs 65 million in 1964/65, itrose to Rs 265 million in 1967/68 and Rs 305 million in 1968/69. It hascorLtinued to rise ever since, as a huge network of health centers and sub-centres have been established through rural and urban areas alike, employingmarLy thousands of doctors, and paramedical staff and others involved insupplying both services and extension education. Very considerable propa-garnda efforts through mass media have also been made. But in spite ofthis increased expenditure the program seemed to be on a downward slide innumbers of acceptors, except of condoms, at least until 1971/72.

2.C4j 1971/72 was a somewhat more promising year. Dramatic gains wereachieved in the sterilization program with a 64 percent rise over i970/71,reversing a steady fall since 1967/68 and achieving the best year ever.Modest gains (1.5 percent) occurred in the I-TD program for the second yearrunning, though still leaving the program only a little over half its1966/67 level. Conventional contraceptive distribution, mainly condoms,continued to show encouraging growth, with a 14 percent increase. Theperiod April-November ,972, however, showed only a L.5 percent increase insterlizations over the corresponding period in 1971 and IUD insertions andconventional contraceptive distribution fell by 16 percent and 11 percentrespectively. The latter may in part reflect a shlortage of condoms. Bythe end of the financial year the sterilization performance is expected tobe much better in relation to 1971/72 than the April-November figures suggest.

2.05 The rise in sterilization in 1971/72 was undoubtedly the result ofa number of district-wide vasectomy camps, in which the whole of the admini-stration of a district participated, and which, for the most part, offeredmuch larger firnancial incentives to participants than the regular program. 1/In Gujarat these were held in all districts and the regular sterilizationprogram suffered. In Kerala, a very iwidely publicized single camp drew manyparticipants from outside the district and there was a similar drop. Elsewhere

1/ In 1971/72 there were wide difference between the levels of incentivesoffered by vasectomy camps in different states. The regular program paidan acceptor of a vasectomy Rs 10-16, except in Tamil Nadu where it wasRs 30. In the camps the total value of the payment to the acceptor wasin some states Rs 80-100, though some were significantly lower. In 1972/73the Central paymrents to states for camp acceptors was standardized atRs 100 of which not more than Rs 60 was to be paid to the acceptor himself.

- 16 -

the regular sterilization program roughly maintained its 1970/71 level. In1972/73, the camps were continued on a larger scale, covering over half thedistricts of India, though with some changes in organization. The principalchange has been to insist that the newly vasectomized remain at the camp forseveral days -- in principle a week, in practice more usually two days -- inorder to prevent infections from leading to deaths, as happened in UttarPradesh last year. At the time of writing, the 1972/73 camp results have notbeen issued but individually they are reported to be less good than last year's.However, by mid-February 1973 over 1.5 m.illion had been sterilized at the camps.

2.06 The camps have been a major factor in leading to increased expenlitureon the nrogram. This is expected to amount to nearly Rs 750 million, up fromELs 590 million in 1971/72 and about Rs 110 million above the initial budgetoutlay. The old situation in which the program was unable to spend its entirebudget has vanished with a vengeance. Rising costs and only modest progresshave regrettably led to an apparent cutback in financial support for theprogram -- only Rs 550 million have been budgeted for 1973/74. This meansthat total Plan expenditure for the Fourth Plan will be well below the ori-ginally proposed outlay of Rs 3,150 million. Unfortunately the easiestprogram to cut wxill be the vasectomy camps even though these are perhapsthe most promising of recent innovations, if no substitute for the regularprogram. It might be possible, however, to get equivalent results by thesame organizational pattern without such large incentives. In any case,having a different pattern of incentives for the camps for the regular programhas no justification -- if these are thought worthwhile for camps they mustequally be so for the regular program.

2.07 This year's Economic Report does not repeat the analysis of theproblens of the regular family planning program, which have been treated atsomne length in our two previous Reports. There would appear to be fewchang-es in these. It might be useful to no-te, however, that the programand its problems received a very thorough discussion in the ThirteenthReport of the Estimates Conmittee (1971/72) of the Lok Sabha, published inApril 1 972.

2.08 We argued last year, but it is worthwhile repeating, that the down-ward trend in acceptance from 1967/68 through 1970/71 could not be taken asa sign that diminishing returns to expenditure were firmly established.There is some evidence that inter-state variation in program acceptance issignificantly determined by family planning inputs, though environmentalfactors are also important. 1/ This argues strongly that the prograna shouldbe carried on to the fullest extent possible. It is at present the onl ysignif-icant weapon a' the disposal of the government in its desperate need toslow the iate of population growtlh, and i-t must, at this stage, be given theben fit of ar,y doubt.