ifile copy - World Bank Documents

132

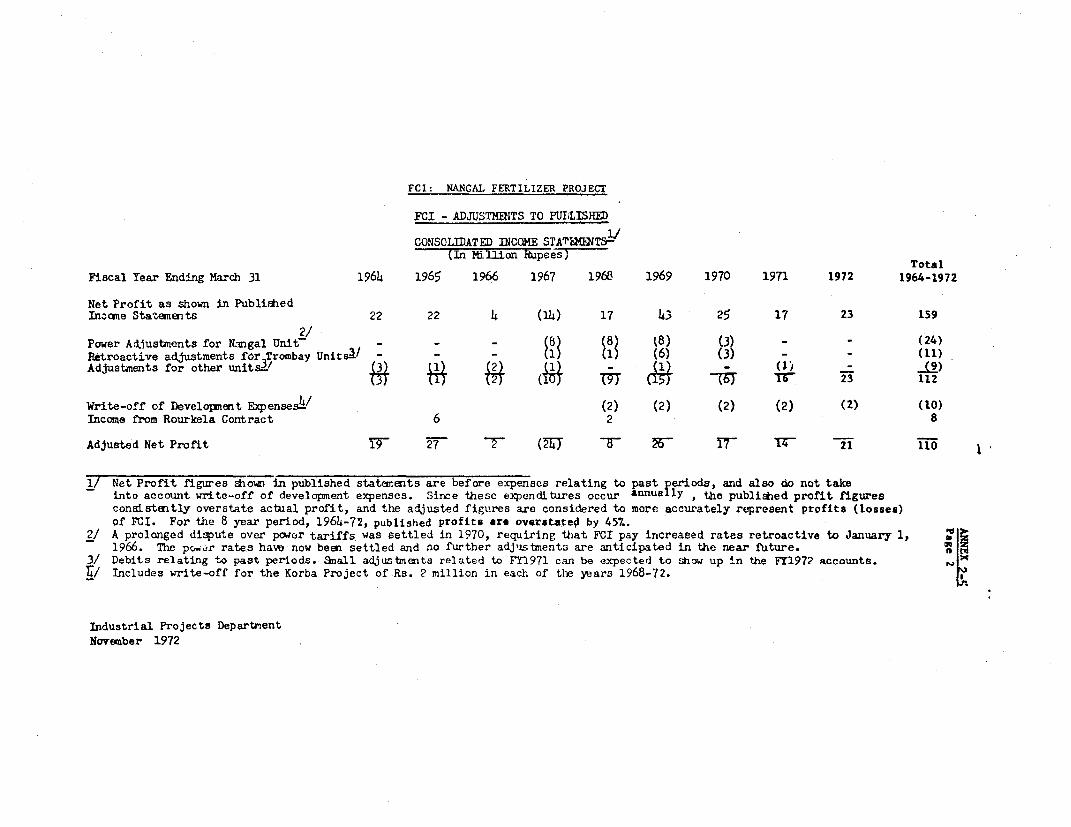

Las<-><7-TQ IFILE COPY DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATION):L DEVEL(2MENT ASSOCIATION Not For Public Ui; ,,,e, C$!e-E,' L~ '-"y TQ BL - 1 1z? ' U, zf :-- f; r-^ AReport No. 46-IN APPRAICAL OF NANGAL FERTILIZER PROJECT FERTILIZER CORPORATION OF INDIA INDIA January 2, 1973 Industrial Projects Department This report was prepared for official u se only by the Bank Group. It may not be published, quoted or cited without bink Group authorization. The Bank Group does not accept responsibility for the accuracy or completen;-sof thc report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of ifile copy - World Bank Documents

Las<-><7-TQ IFILE COPYDOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATION):L DEVEL(2MENT ASSOCIATION

Not For Public Ui;

,,,e, C$!e-E,' L~ '-"y

TQ BL - 1 1z? ' U, zf :-- f; r-^ AReport No. 46-IN

APPRAICAL OF

NANGAL FERTILIZER PROJECT

FERTILIZER CORPORATION OF INDIA

INDIA

January 2, 1973

Industrial Projects Department

This report was prepared for official u se only by the Bank Group. It may not be published, quotedor cited without bink Group authorization. The Bank Group does not accept responsibility for theaccuracy or completen;-sof thc report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURENCY EQIUVALEIUTS

, 1.0 = $0.137bls 7.28 $1.0Rs 1,000,000 = '137,40o

WEET=G. A,'D F7AURE.3

All weights and measures are in metric units1 Metric Ton (t) = 1,000 Kilograms (kg)1 Metric Ton (t) = 2,20L Pounds1 Kilometer (kn) = 0.62 Miles1 Hectare = 2.47 Acres

PRINCIPAL- ABRE7IATIOiS AND ACRq0I4YS USED

GOT, Government The Central Government of IndiaFCI, Coor-oration The Fertilizer Corooration of lndiaP & D Pia-in3ng and Development Divison of FCIFACT '-'ertilisers and Chernicals-Travancore-Ltd.indian Ujiil Indian Oil Corporation Ltd.P31:3 F-ILlPnjab 5tate Electricity PoardC mP 'Jnitad lations 1ievelonment Procran-eTPY 'etric Tons Per YearT7.D Metric Tons Per DayCIF Cost, lnsurance and iFreightF02 Free On Board

Fee l-egawattI4VH Megawatt "ourr%.i.' H Kilowatt hour4 '?Iitrogen

Fiscal fear

April 1 - March 31

NANGAL FERTILIZER PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS ................................ i

I. INTRODUCTION ...o ....................................... 1

II. FCI'S OPERATIONSA. History and Organization ........... .. 1............. B. FCI Management ...................... 2C. Financial Analysis of FCI - Past and Future ....... 3

III. NANGAL'S OPERATIONSA. Production Facilities ............................. 7B. Financial Analysis of Existing Nangal -

Past and Future ................................. 8C. Availability and Cost of Power .................... 9

IV. MA&KET AND MARKETINGA. Past Fertilizer Growth in India .... ............... 10B. Fertilizer Market Forecast for India .... .......... 11C. Fertilizer Markets in Northern India .... .......... 12D. Nangal Marketing System ........... a ............... 13

V. THE NANCAL EXPANSION PROJECTA. Project Scope .. ................................ 14B. Project Description ............................... 15C. Raw Materials and Utilities ........................ 15D. Employment ................... I .................... 16E. Ecology ........................................... 16

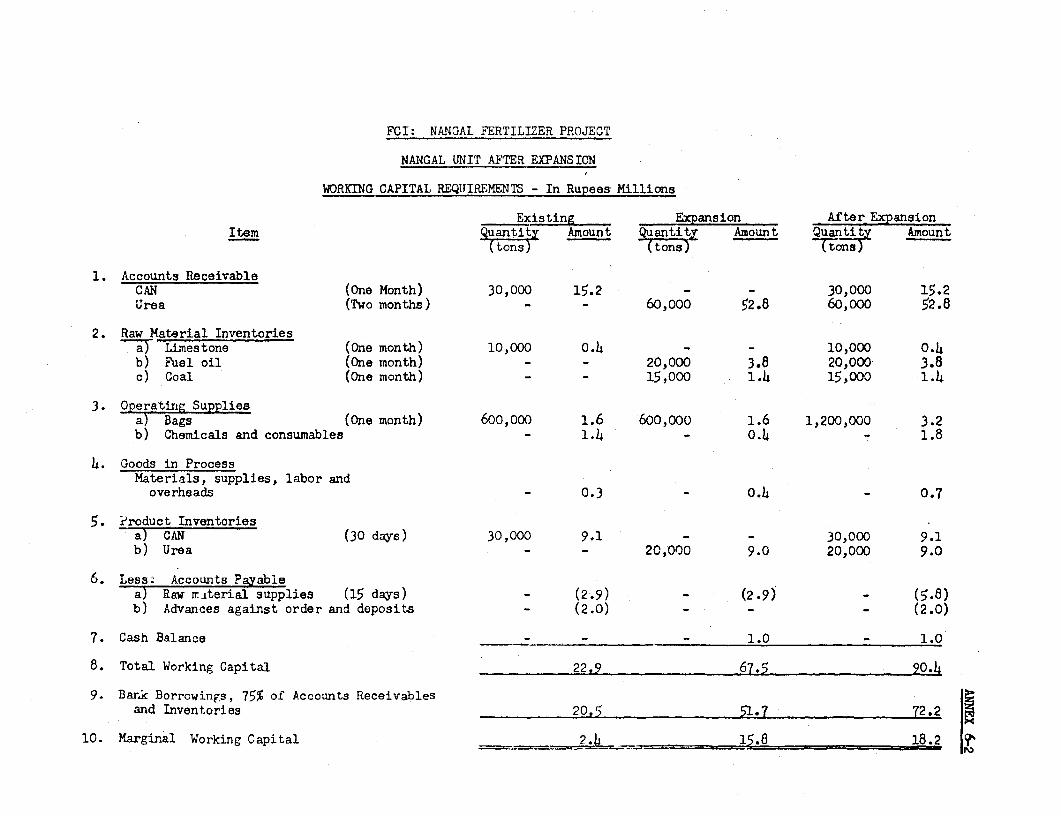

VI. PROJECT COST AND FINANCIAL PLANA. Capital Costs ..................................... 17B. Working Capital Requirements .. 18................... t8C. Financial Plan ... ..... e ........ .................. 18D. Allocation of IDA Credit ........... .. ............. 19

VII. PROJECT EXECUTIONA. Project Management and Execution .................. . 20B. Project Scheduling, Procurement and

Contractor's Guarantees ......................... 20

VIII. FINANCIAL ANALYSIS OF THE PROJECTA. Revenues and Operating Costs ...................... 21B. Feedstock Costs ................... 22C. Financial Forecasts ............................... 22D. Financial Return .................... I 24E. Risk ............. ................................. 24

IX. ECONOMIC ANALYSIS OF THE PROJECTA. Urea World Market Prices ........................ 26B. Economic Return and Competitive Position vis-a-vis

Imports ....................................... 26C. Foreign Exchange Aspects ........................ 27

X. RECONiiENDATIONS ....................................... 27

ANNEXES

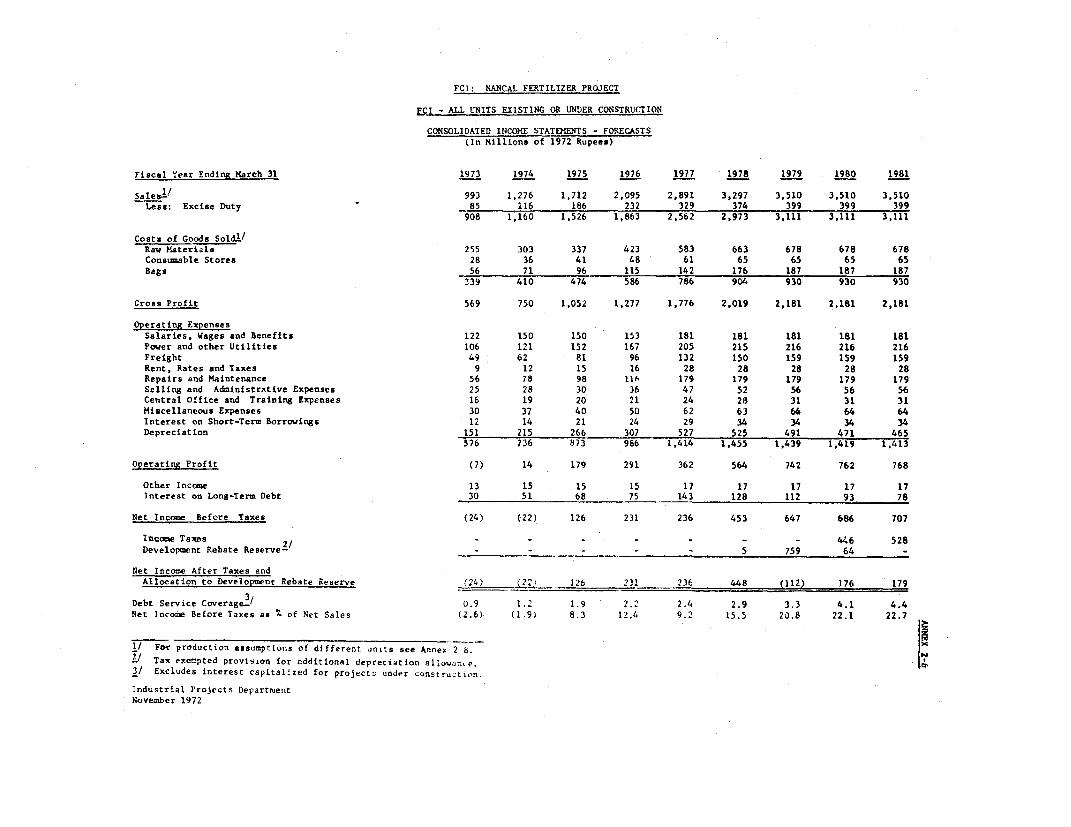

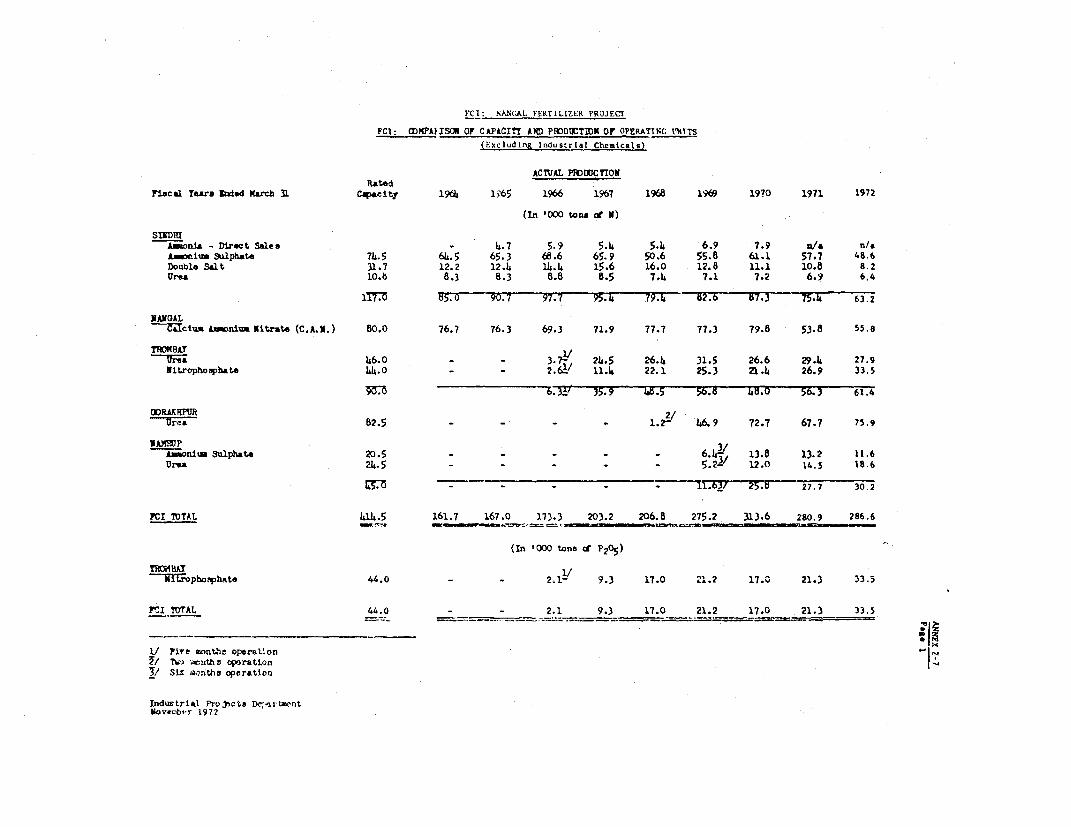

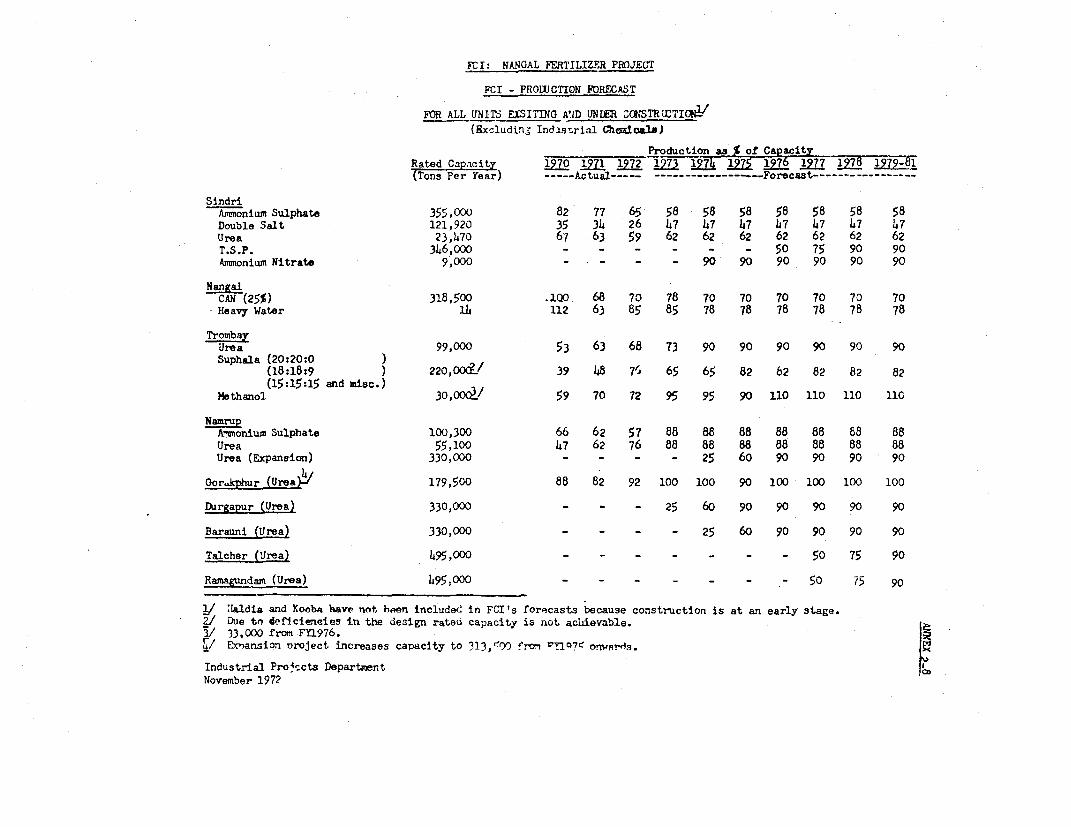

1 Technical Terms2-1 FCI - Description of the Corporation2-2 FCI - Existing Units and Planned Expansion Program2-3 FCI - Management - Board of Directors2-4 FCI - Organization Chart2-5 FCI - Consolidated Income StateAnents (1964-72)2-6 FCI - Consolidated Income Statements, Forecast2-7 FCI - Comparison of Capacity and Production of Operating Units2-8 FCI - Production Forecasts2-9 FCI - Consolidated Balance Sheets (1964-72)2-10 FCI - Consolidated Balance Sheets, Forecast2-11 FCI - Consolidated Source and Application of Funds (1964-72)2-12 FCI - Consolidated Lo'.rce and Application of Funds Statements,

Forecast

3-1 Nangal Unit - Existing Operations at Nangal3-2 Nangal Unit - Income Statements without Expansion3-3 Nangal Unit - Balance Sheets without Expansion3-4 Nangal Unit - Source and Applicaticn of Funds Statements,

without Expansion3-5 Nangal Unit - Availability and Cost of Power

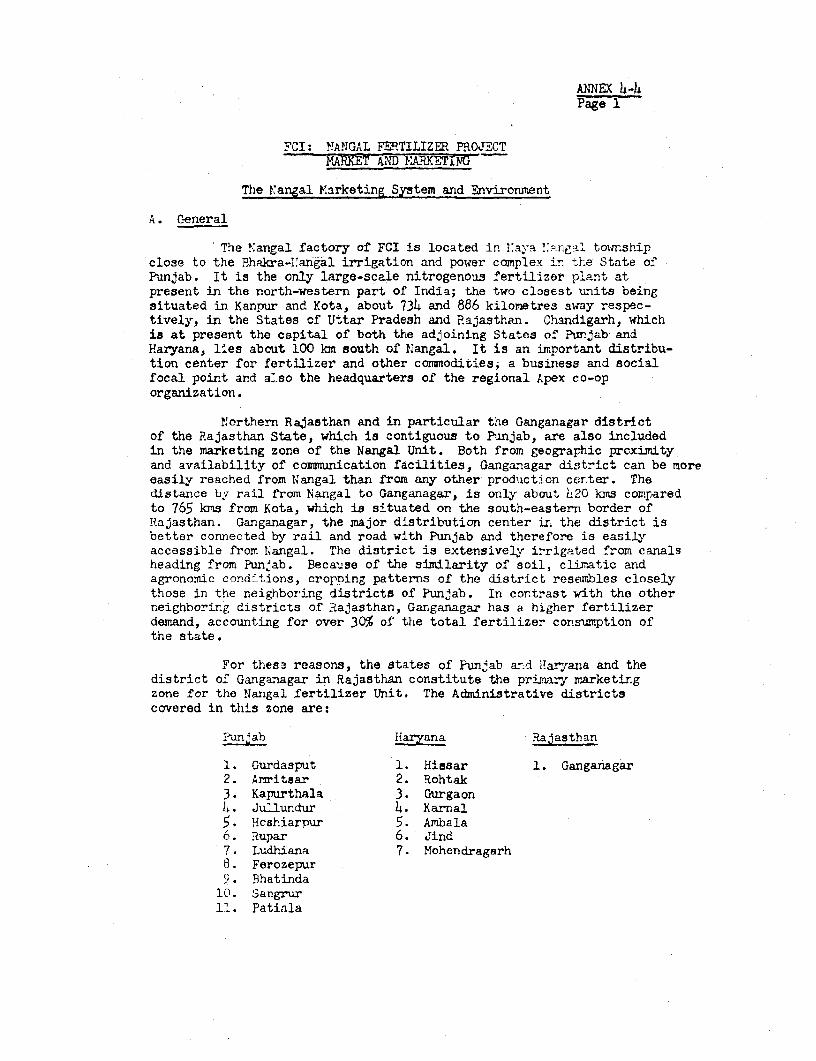

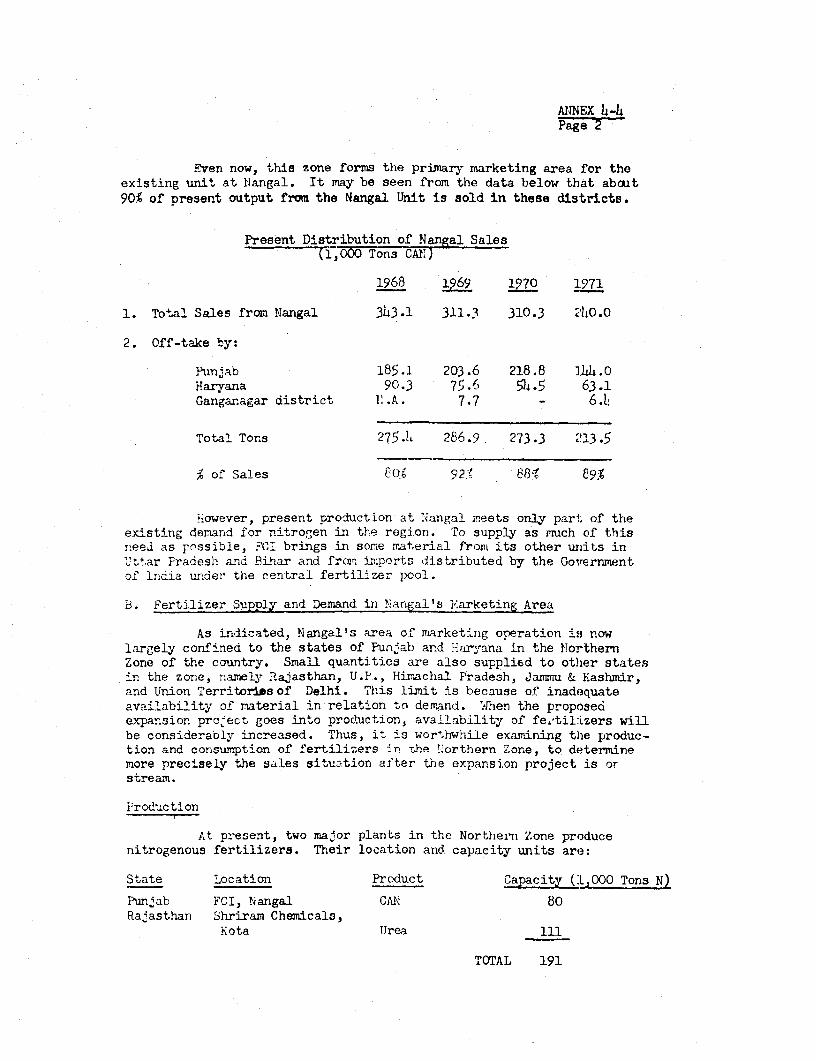

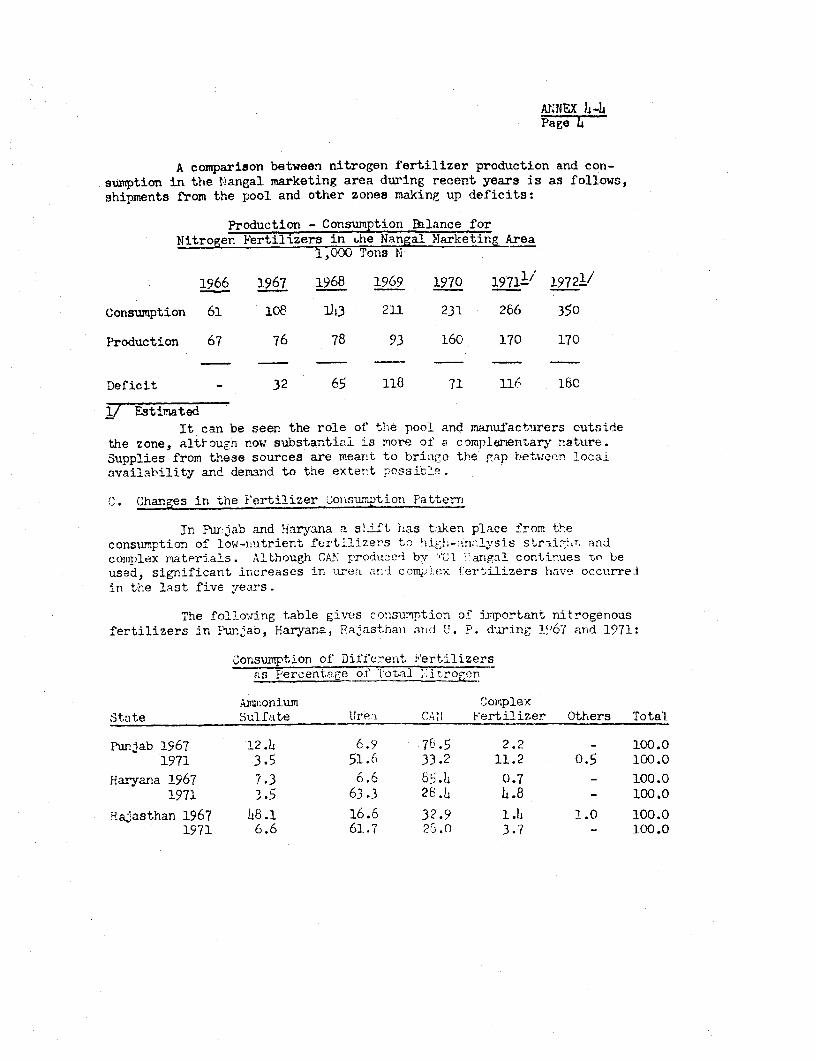

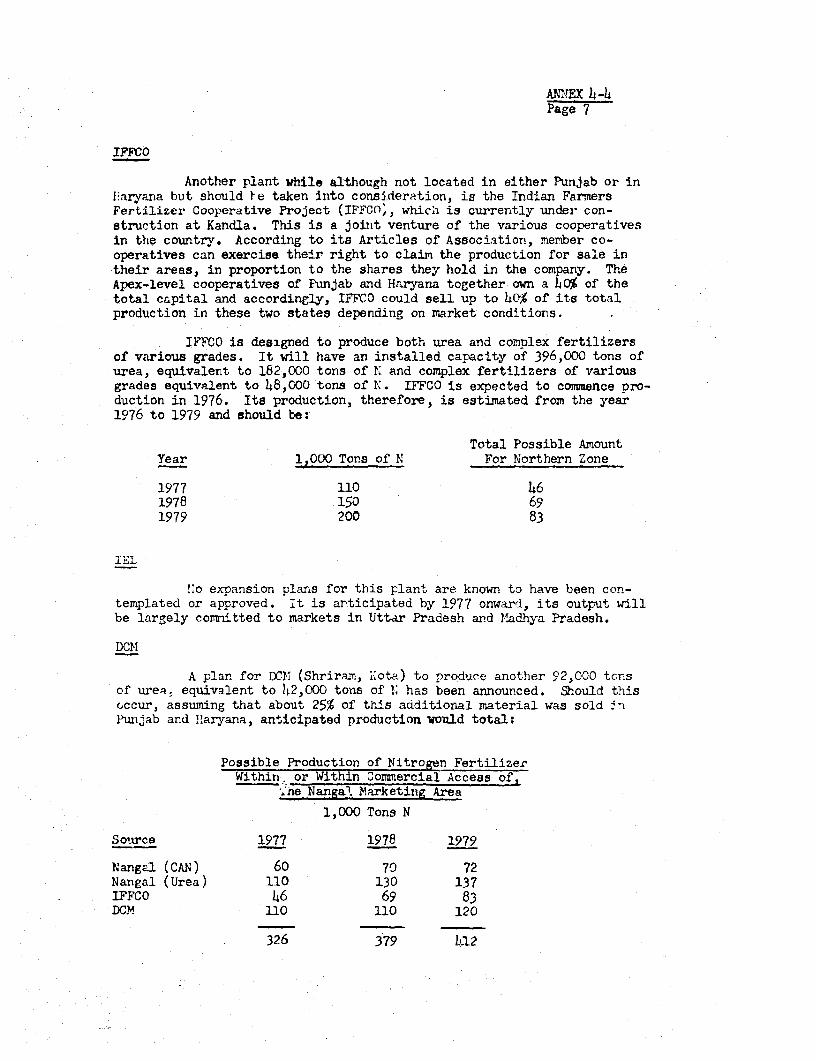

4-1 Past and Present Fertilizer Situation in India4-2 Market Forecast for India4-3 State of Agriculture in Lhe Nangal Marketing Area4-4 The Nangal Marketing System and Environment

5-1 Nangal Unit after Expansion - Schematic Flowsheet5-2 Nangal Expansion Project - Technical Description

6-1 Nangal Expansion Project Capital Cost Estimates6-2 Nangal Unit after Expansion - Working Capital Requirements6-3 Nangal Expansion Project - Projected Disbursement of IDA Crec t

7 Nangal Expansion Project - Implementation Schedule

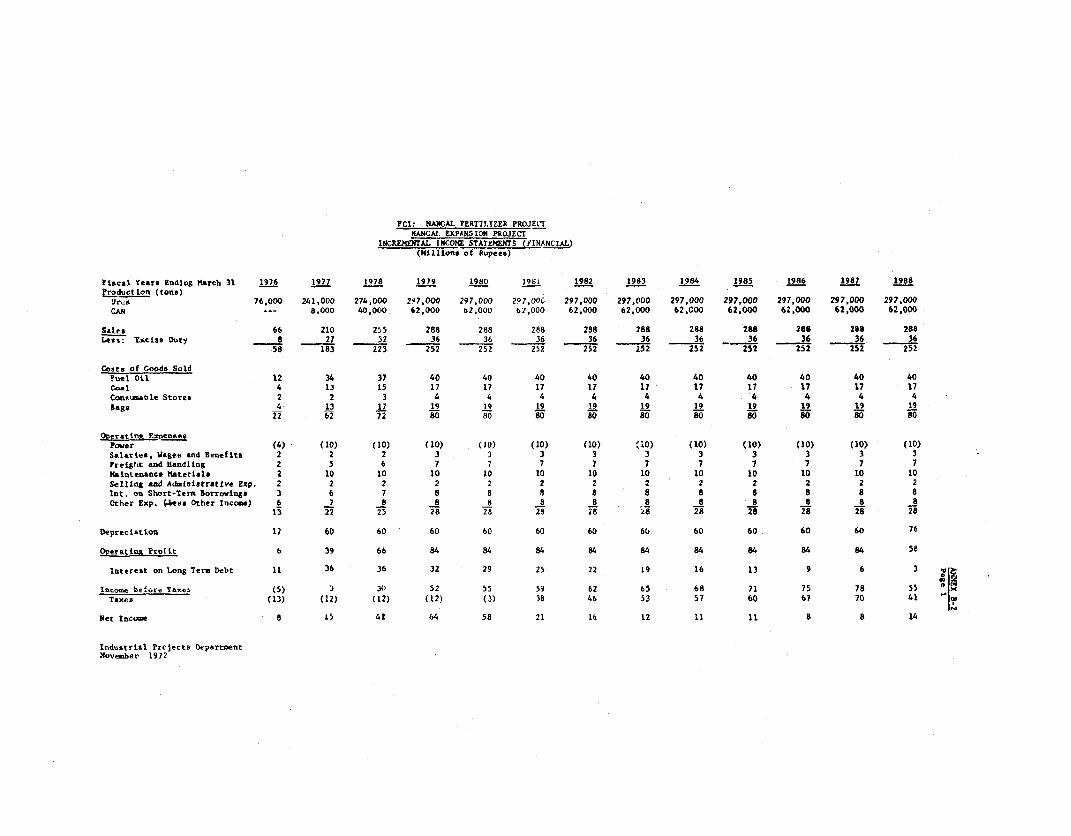

8-1 Nangal Unit before and after Expansion - Income Statements -Forecast

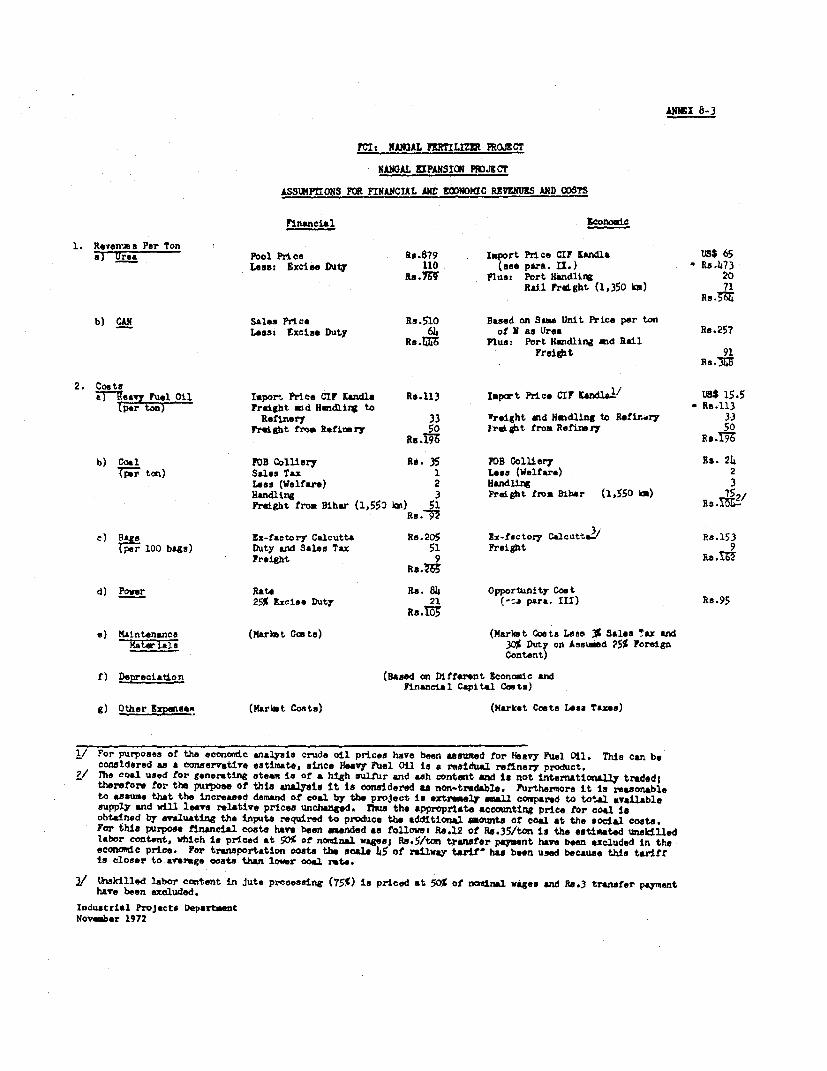

8-2 Nangal Expansion Project - Iocremental Income Statements8-3 Nangal Expansion Project - Assumptions for Financial and Economic

Revenues and Costs8-4 Nangal Unit after Expansion - Balance Sheets - Forecast8-5 Nangal Unit after Expansion - Source and Application of Funds

Statements - Forecast8-6 Nangal Unit after Expansion - Financial Break-Even Chart

9-1 Nangal Expansion Project - Rates of Return and Sensitivities9-2 Urea World Market Prices9-3 Nangal Expansion Project - Economic Return Sensitivity to Different

Price Assumptions for Urea (Chart)9-4 Nangal Expansion Project - Incremental Annu:" Foreign Exchange Savings

Map 1 Present and Proposed Major Fertilizer Plants in India.

This report has been prepared by Messrs. D. Brown, M. Ferber, R. Pigossiand C. Pratt of the Industrial Projects Department.

SUMMARY AND CONCLUSIONS

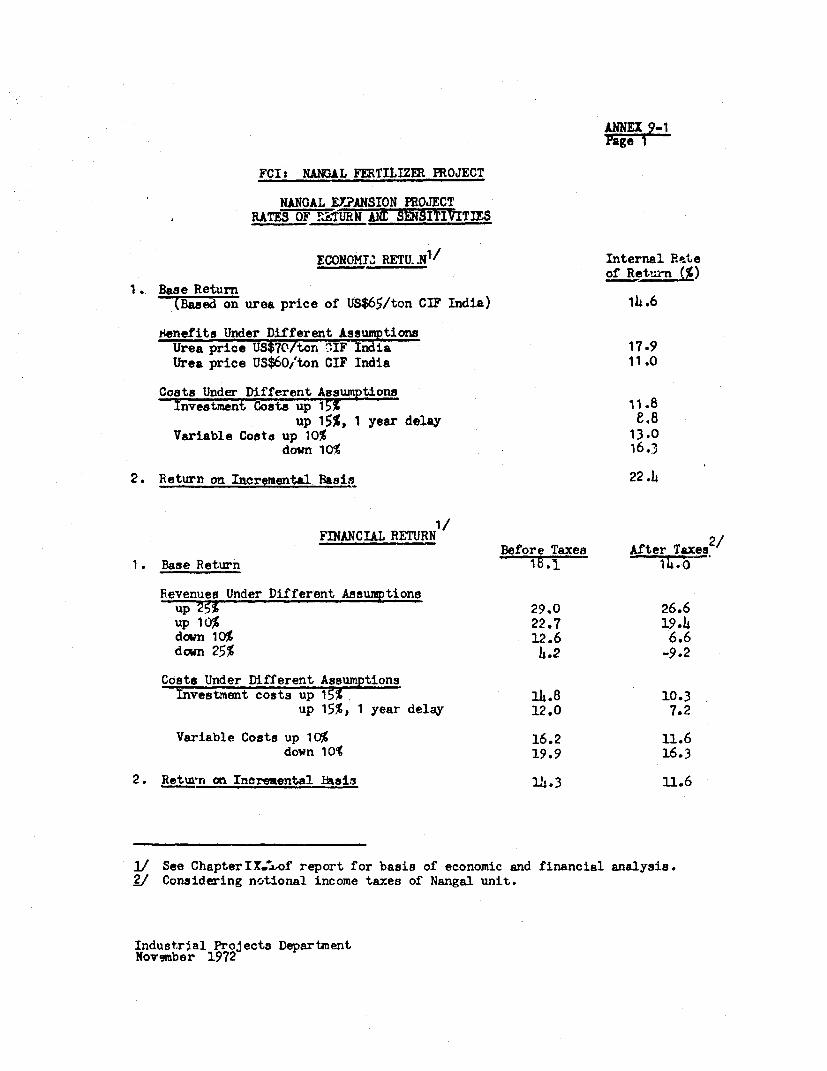

i. This report appraises a proposed project for the exparsion of theNangal unit of the Fertilizer Corporation of India (FCI), a Govf'rnment ofIndia (GOu) owned entity and the largest fertilizer producer ir the country.Estimated total cost of the project is US$105.6 million equivalent includinga mAximum of about US$58 million in foreLgn exchange, which the InternationalDevelopment Association has been asked ta provide. Ine proceeds of the IDAcredit would be re-lent to FCI at 8.5% and be used primarily to financeinternationally-bid equipment, engineerirg, erection and process licenses.The remainder of the financing required, about US$48. million, would be pro-vided by the Government as equity funds.

ii. Located in the State of Punjab in Northern India, the existingNangal - -nt has an annual design capacity of 80,000 tons per year of nitrogenin the t of calcium azmonium nitrate (CAN) fertilizer and 14 tons peryear of i zt heavy water. The expansion project would add 152,000tons per nitrogen in the form of urea, India's most popular andeffective LeL.' izer. This tonnage is adequate to stimulate production of10 million tons of food grains annually based on India's current nitrogento food giain ratio. Furthermore, the project by replacing the high powerconsuming, electrolysis section of the present, fully depreciated ammoniaplant, would permit the release of a large amount of hydroelectric powerfor more economic uses in the area. Manufacture of heavy water would bediscontinued, but existing fertilizer production (CAN) and off-site facili-ties would be retained. Thsefeedstock for the existing and additionalfertilizer production would be heavy fuel oil of which, in contrast tonaphtha, India has relatively ampYe quantities at its disposal.

iii. The Nangal unit Fegan operations in 1961 and has been FCI'smost profitable plant because it haa been operated efficiently and becauseof a low power price, of about one fourth of the present opportunity cost ofpower. The plant operated consistently at close to full capacity untilpower shortages arose about two years ago. These have reduced fertilizeroutput by about 30%. The power shortages are likely to continue and arean added reason for shutting dowa the existing electrolysis - ammonia plant.Nangal has no outstanding long-term debt.

iv. The project forms part of an ambitious expansion program of FCI,involving several plants now under construction and others in an advancedplanning stage, that by 1980 is to increase nitrogenous and phosphaticfertilizer production 5.4 and 9.3 times respectively over 1970 levels.While projects have been financed on a conservative 50:50 debt to equityratio, FCI's earnings record has been unsat4sfactory (about 1.5% returnon capital in recent years) due mainly to operating problems in existingplants and serious delays in plant construction. In the next two yearsannual losses of about Rs. 20 million are anticipated for FCI because ofcontinuing production difficulties plus the expected start-up losses ofthree large fertilizer plants which are more than two years behind schedule.

- ii -

During that period, the ability of FCI to service debt out of its ownresources without help from the Government will be limited but GOI recognizesthis fact and is demonstrating not only a willingness to provide the neces-sary financing, but also attack the causes of the problem.

v. Thereafter, FCI's financial situation should show substantial im-provement provided it will devote a major portion of its energies to bring-Ing new plants into operation more quickly and to increasing overall utili-zation of existing capacity. An examination of the Corporation's furtherexpansion plans is needed to bring them better in line with FCI's resources -human, technical and financial. Therefore, FCI and GOI propose to takedecisive steps to overcome FCI's :resent and anticipated difficulties andurgently concentrate efforts directed primarily towards maximum use of exist-ing capacity with a critical review of proposed new plants.

vi. In executing the Nangal project, commercially proven processeswill be used and FCI will be the overal contractor; however, much of theengineering and procurement has been made the responsibility of the ammoniaplant contractor (Uhde, F.R. of Germany) and the urea plant contractor(Montedison, Italy). PCI has appointed a suitable project manager and hisresponsibilities plus a detailed project implementation plan have been jointlydefined by FCI and the contractors. Thus there is reasonable assurance thatthe project will be executed on schedule and without major technical diffi-culties. It is expected that the project will start commercial productionin December 1975 after a construction period of about 34 months.

vii. Based on detailed marketing studies, no problems in sellingNangal's urea are foreseen. India will continue to face a nitrogen fertili-zer shortage throughout the 1970's, especially in Nangal's main sales area -Punjab, Haryana and Northern Rajasthan - where most farmers are progressive,irrigation is extensive and nitrogen consumDtion ner unit of cropped area isover three times the national average. Well developed private dealer andcooperative distribution systems exist, backed by adequate storage, trays-portation and credit facilities. Furthermore, even if all approved ureaprojects within commercial reach of the marketing aLea were completed onschedule and operated as planned, there would still be a demand for fertil-izer .equivalent to the production of two more large nitrogen fertilizerplants in Northern India.

viii. Upon project complction, the Nangal unit is expected to have asatisfactory financial structure (debt/equity ratio of 35:65 and debt ser-vice coverage well above two). Export urea prices have recently significantlyincreased, reflecting in part rising investment costs and also operatingcosts in major supolying countries. Nevertheless, a conservative ureaimport price of US$65 per ton, c.i.f. India has been assumed to determinethe economic rate of return of the project. On this basis, the economicrate of return of the project is about 15%, which is very satisfactory fora fertilizer project. If revenues and costs of the project are consideredon an incremental basis, and thereby include the power savings from shut-ting down part of the existing plant the economic return would be even greater

- iii -

(about 22%). The return is sensicive to changes in sales prices, projectdelay3 and to a lesser degree, fluctuations in raw material prices, andoperating levels. Even if operating levels were reduced from 90% to 85% ofcapacity, and the project was delayed by one year - this probably being thesingle most serious risk the project faces - the economic return would stillbe about 10%.

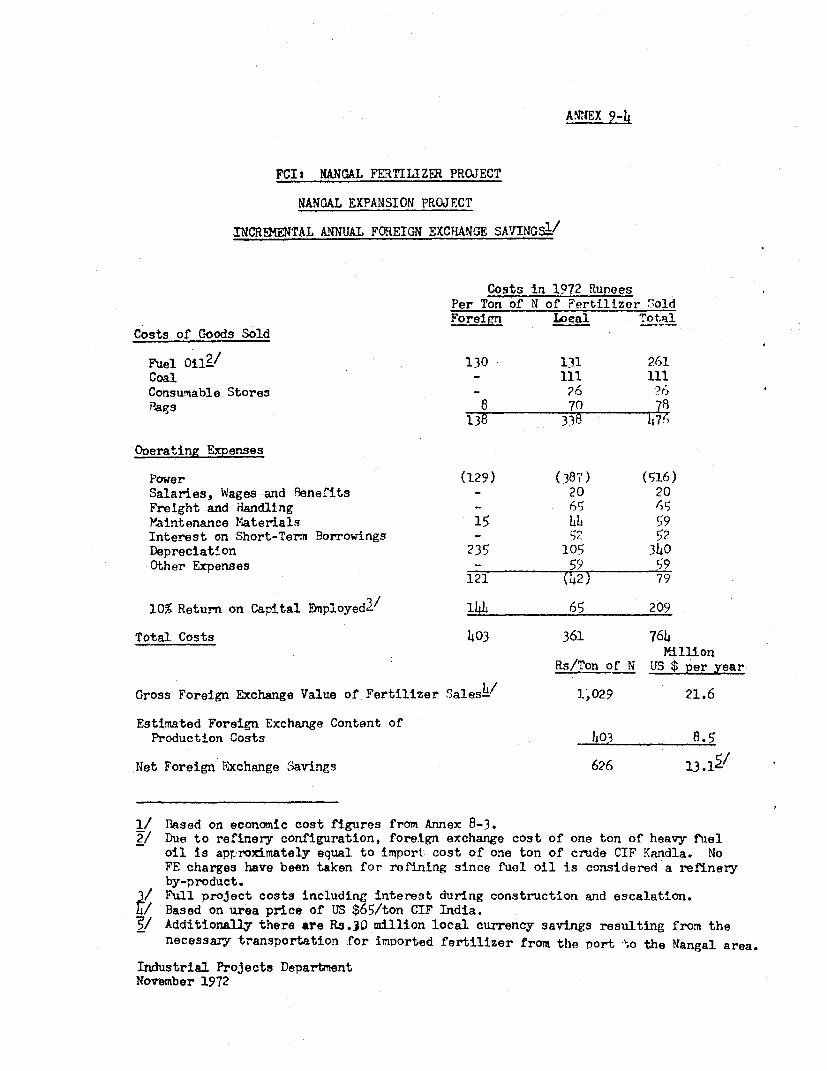

ix. Apart from the workers required during project construction and inthe fertilizer distribution system, the use of additional labor will be small,since existing labor from the phased-out ammonia plant will be largely usedto staff the expanded plant. There will be significant foreign exchangebenefits; the net annual foreign exchange savings are estimated at US$13million, once the plant is operating normally at its predicted level of 90%of capacity. The ecological effects of the proposed project have beenassessed and are considered minimal.

x. The Bank Croup has recently been active in the fertilizer fieldin India. IDA has made tno credits for expansions by the government-ownedFertilisers and Chemicals-Travancore-Ltd., (FACT) in Cochin and the FCIGorakhpur Unit. These have experienced some delays but are now proceedingsatisfactorily. IFC has participated in two private sector projects:Indian ExplDsives Ltd., in Kanpur, Uttar Pradesh and Zuari Agro ChemicalsLtd., in Coa. Indian Explosives, a competitor of Gorakhpur is alreadyoperating and Zuari Agro is about to commence operations. rhe Bank is alsoExecuting Agencv for a tN P project evaluating phosphate deposits inRajasthan. The Bank Group, in addition, is currently considering two otherfertilizer projects: FCI Trombay near Bombay and Tata Chemicals in GujaratState.

xi. Based on the agreements rea.hed during negotiations, the projectis suitable for an IDA credit of US$58 million.

I. INTRODJCrION

1.01 The Government of India (COI) has requested financing from theInternational Development Association (IDA) equivalent to USS58 millionwhich is the maximum estimated foreign exchange requirement to expandfacilities at the Nangal Unit of the Fertilizer Corporation of India (FCI).The expansion would add 330,000 metric tons per year (TPY) of urea capacity,equivalent to 152,000 TPY of nitrogen (N), to the existing calcium ammoniumnitrate (CAN) plant (80,000 TPY of N) and replace the ammonia section of theexisting plant at Nangal which is based on a power-intensive process.

1.02 Nangal, located in Punjab State, abotut 100.km north-west ofChandigarh, is one of five FCI operating units (Map IBRD 3559 R2). Theplant, which began production in 1961 1/ has until 1971 consistently oper-ated at high levels of available capacity and has significantly contributedto FCI's profits and cash generation. Nangal's profitability, however,largely results from the low price it pays for power. Conversely, *n recentyears capacity utilization and earnings have oeen substantially affected bypower shortages, which are expected to continue.

1.03 The Nangal project was identified by an IDA mission in June/July1969 and a feasibility study was submitted to the Bank in early 1971. Afterthe first appraisal mission in August/September 1971 three basic projecEalternatives were discussed between IDA, FCI and GOI out of which the alter-native now proposed emerged.

1.04 This appraisal report was prepared by Messrs. Donald Brown,Manfred Ferber, Richard Pigossi and Christopher Pratt of the IndustrialProjects Department, based on missions to India in August 1971, June andAugust 1972.

1.05 A glossary of technical terms used in the report is attached asAnnex 1.

II. TIE FERTILIZER CORPORATION OF INDIA (FCI)

A. History and Organization

2.01 FCI was incorporated in 1961 under the Companies Act of India,representing a merger of two existing public sector companies - SindriFertilizers and Chemicals Ltd. at Sindri, Bihar and Hindustan Chemicals ,andFertilizers Ltd. at Nangal, Punjab. These two companies began productionin 1948 and 1961, respectively. The Corporation's authorized share copitalat present is Rs 2,000 million (US$275 million) with Rs 1,375 nillion in

1/ All years refer to fiscal years ending March 31.

-2-

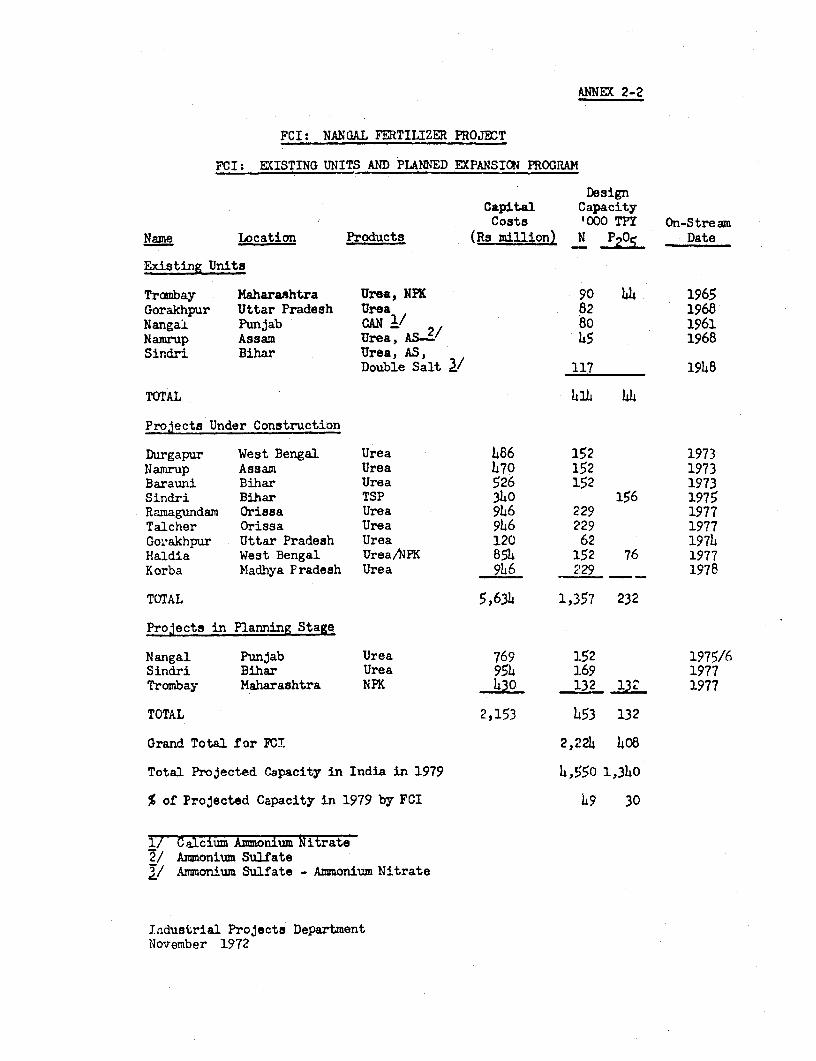

shares outstanding and paid in, all owned by GOI. FCI is the largest pro-ducer of fertilizer in India with 30% of nitrogen and 10% of phosphatecapacity. Given FCI's large expansion program, its market share will growsubstantially through the 1970's. a12.02 The operating units (or divisions) are (1) Trombay, (2) Nangal,(3) Gorakhpur, (4) Sindri and (5) Namrup. Another division, Planning andDevelopment (1 & D), is responsible for engineering, research and develop-ment. In addition, the Corporation has several major projects under con-struction: (1) Durgapur, (2) Barauni, (3) Namrup Expansion, (4) Ramagundam,(5) Talcher, (6) Sindri Rationalization, (7) Corakhpur Expansion, 2/ (8)Haldia, and (9) Korba. Three other projects are being actively consideredby FCI, namely (1) Nangal Expansion - the sublect of this report - (2) TrombayExpansion, and (3) Sindri Expansion. These divisions and projects are de-scribed in Annex 2-2 including capacities and capital costs. After cempletionof the expansion program in the late 1970's, FCI will have an installed fer-tilizer capacity of about 2.2 million TPY of N and 0.4 million TPY of phosphate(P?0'/ and should then be one of the largest fertilizer companies in the world.

2.03 Exlsting employment of the Corporation is approximately 19,000people; this is high even recognizirg that this figure includes not onlyoperating personnel but also ancillary employment for company-operatedschools, hospitals, town.hips and trainirg programs at each factory.

B. FCI Management

2.04 FCI is managed by a 12-member Board of Directors of which fiveare senior officers of FCI, three are from Government mi;uistries, two fromgovernment-owned corporations and two from other industries (Annex 2-3).The present Chairman of the Board is Mr. H. N. Sethna and the ManagingDirector is Dr. K. R. Chakravorty. The Board is designed to function as apolicy-making and controlling body and as a liaison and coordinating groupbetween FCI and the Government. The influence of GOI on operations, financeand expansion planning is felt strongly in the Corporation's management.

2.05 The Managing Director and four Functional Directors (Productionand Marketing, Project, Finance, and Personnel) direct the Corporation'soverall policy, growth and daily operations through a "Committee of Manage-ment." 3/ These officers, who are also on the Board, in effect are selectedby GOI although formally they are appointed bv the Board. The Functional

I/ A more detailed description of the Corporation is shown in Annex 2-1.,

'/ Partly financed by an IDA Credit of US$10 million (Credit No. 279 - IN,dated December 22, 1971).

I/ An organization chart of the Corporation is shown in Annex 2-4.

-3 -

Directors' posts are now filled by men with substaratial industrial experi-ence in FCI. Improvement in corporate management &iince the IDA mission inJune/July 1969 is evident, but, furtheL improvement is needed. f

2.06 Each unit is managed as a separate cost center and day-to-dayp:oduction functions are controlled by the Unit General Managers. FC'.senior management is aware of the continuing problems it faces in correct-ing deficiencies in operation and project implementation. These have serl-ously burdened management and financial results. The Cor,,ration's futurewill depend on the extent to which these deficiencies are overcom,e. Thelarge expansion program has created a need for a breat number o- experiencedstaff at the higher middle management level for both the execution of pro-jects and their operation. Filling these positions with qualified personneland improving iPS organization to implement new projects effectively, is oneof the biggest challenges currently facing FCI's senior management. The in-crease in operating activity and sales volume, resulting from great expan-sion projects expected to be completed during the forthcoming years, willalso require better management techniques, especially financial reportingand planning and the buildup of a more efficient marketing system in certainareas.

C. Financial Analvsis of FCI - Past and Future

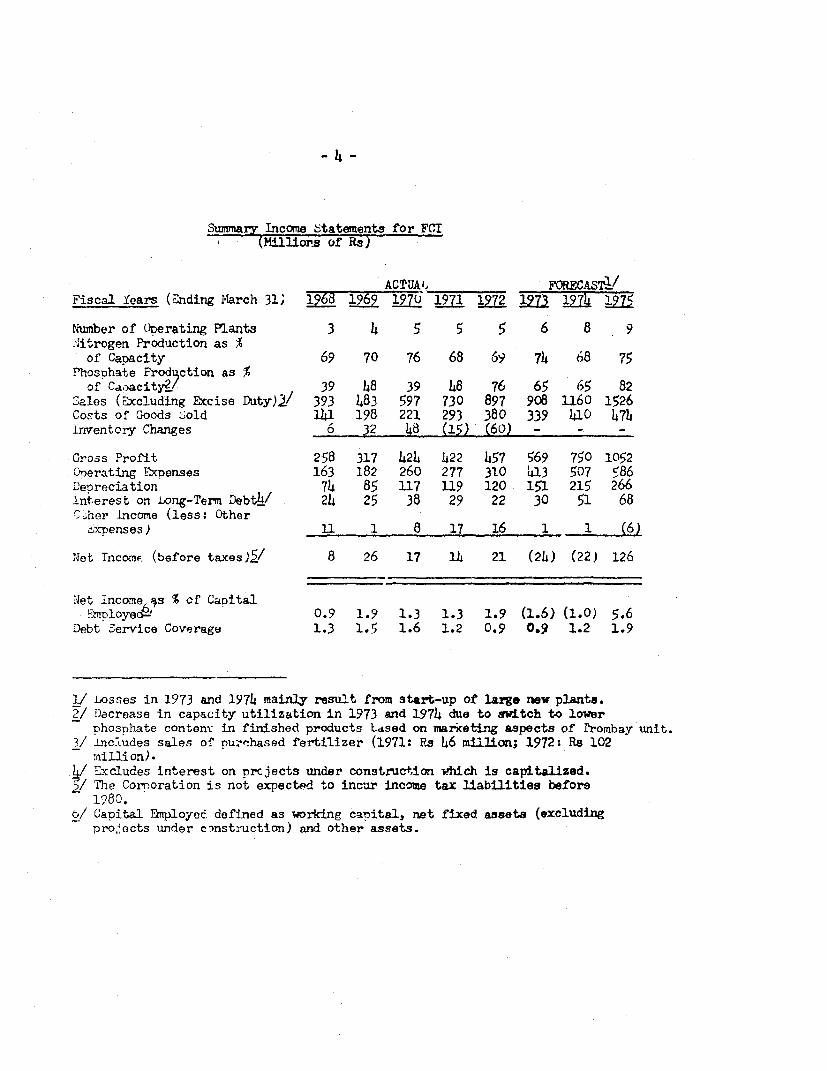

2.07 Historical and projected income statements for FCI throligh 1981are shown in detail in Annexes 2-5 and 2-6 and are summarized bSlow up to1975:

-4

Summary Income 'tatements for FCI(Millions of' Rs)

ACTUAiM FORECAST-./Fiscal Years (Ending lNarch 31; 1968 1969 1970 1971 1972 13 1974 1975

Number of perating Plants 3 4 5 5 5 6 8 9Aitrogen Production as %of Capacity 69 70 76 68 69 74 68 75

Phosohate Produ,ction as %of Ca,.acity2/ 39 48 39 48 76 65 65 82

.ales (axcluding Excise Duty)Y/ 393 483 597 730 897 908 1160 1526Costs of Goods $old 141 198 221 293 380 339 410 474inventory Changes 6 32 48 (15) (60) - - -

Gross Profit 258 317 424 422 457 569 750 1052C0erating Rxpenses 163 182 260 277 310 413 507 586Deoreciation 74 85 117 119 120 151 215 266Interest on tong-Term DebtV 24 25 38 29 22 30 51 68",her Income (less: OtherAxpenses) 11 1 8 17 16 1 1 (6)

Net Tncom. (before taxes)&/ 8 26 17 14 21 (24) (22) 126

N4et Incame 9s % of CapitalEmfloyecf' 0.9 1.9 1.3 1.3 1.9 (1.6) (1.0) 5.6

Debt Service Coverage 1.3 1.5 1.6 1.2 0.9 0.9 1.2 1.9

1/ tosses in 1973 and 1974 mainly result from start-up of large new plants.2/ Dacrease in capacity utilization in 1973 and 1974 due to switch t-o lower

nhosDhate content in finished products Ltsed on marketing aspects of 1rombay unit.3/ Lncludes sales of nurehased fertilizer (1971: Rs 46 million; 1972: Rs 102

m.iLlion).E Excludes interest on rrcjects under construction which is capitalized.

2/ The Cornoration is not expected to incur income tax liabilities before1980.

bi Capital Employec defined as working capital, net fixed assets (excludingTro.,Iects under construction) and other assets.

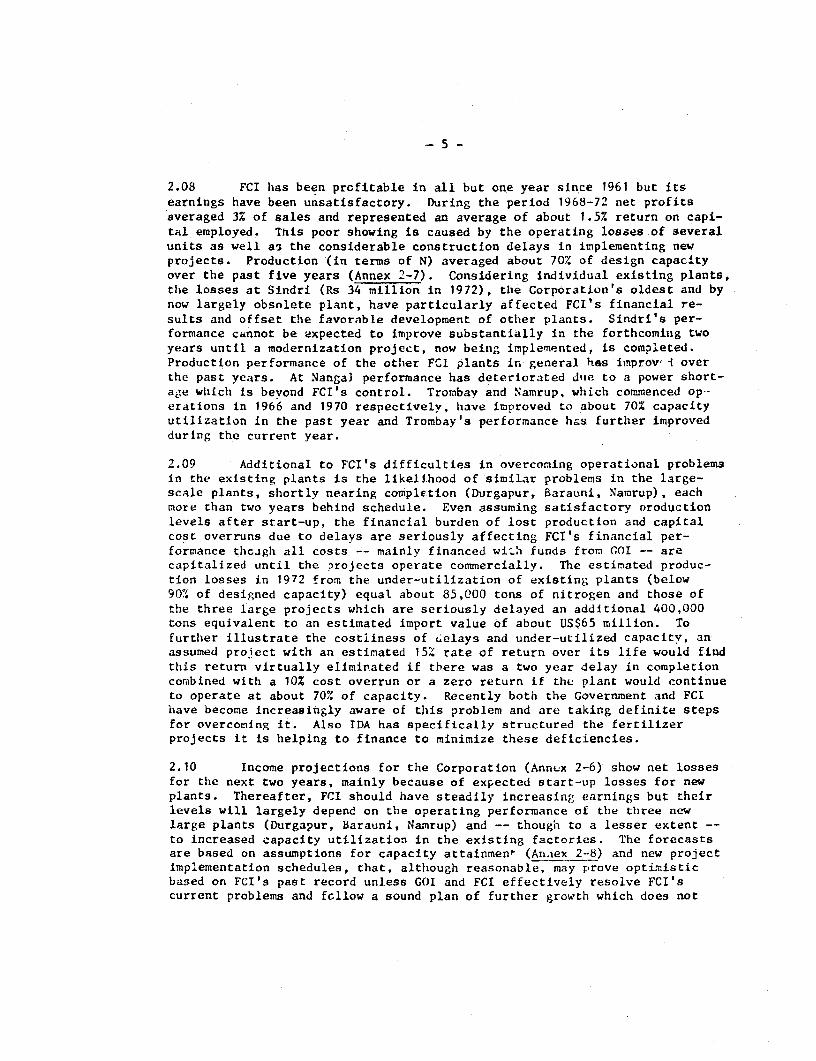

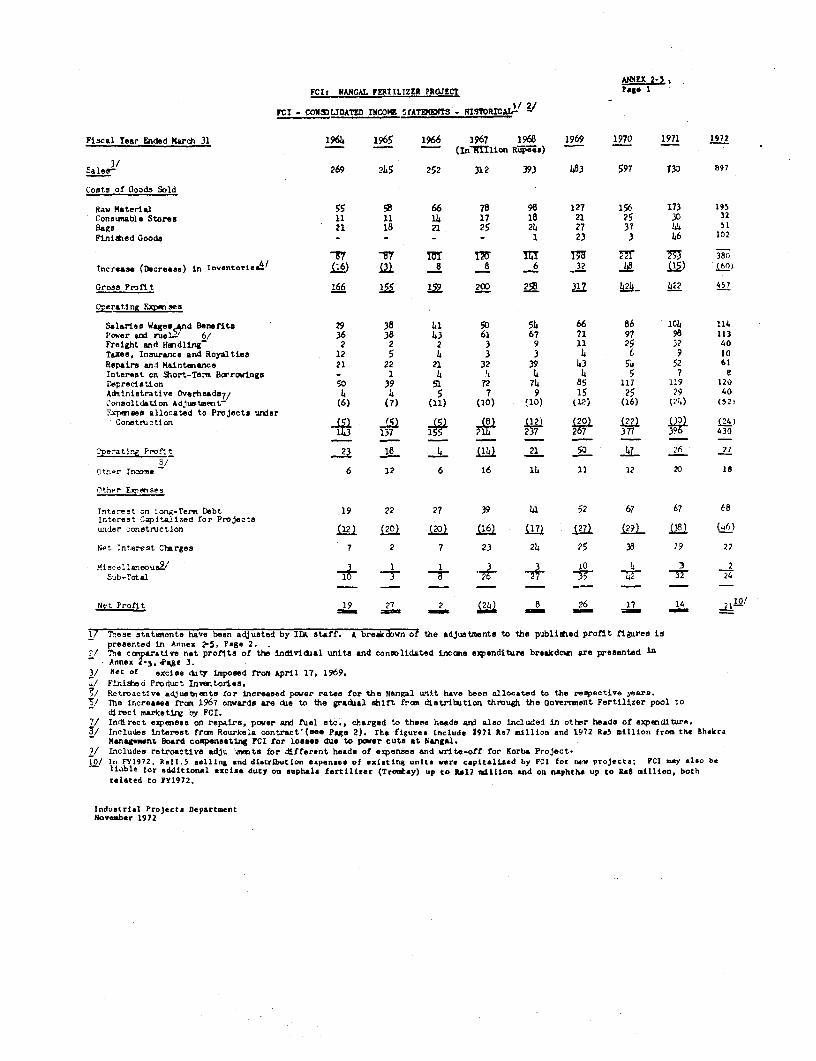

2.08 FCI has been profitable in all but one year since 1961 but itsearnings have been unsatisfactory. During the period 1968-72 net profitsaveraged 3% of sales and represented an average of about 1.5% return on capi-tal employed. This poor showing is caused by the operating losaes of severalunits as well as the considerable construction delays in implementing newproJects. Production (in terms of N) averaged about 70% of design capacityover the past five years (Annex 2-7). Considering individual existing plants,the losses at Sindri (Rs 34 million in 1972), the Corporation's oldest and bynow largely obsolete plant, have particularly affected FCI's financial re-sults and offset the favorable development of other plants. Sindri's per-formance cannot be expected to improve substantially in the forthcoming twoyears until a modernization project, now being implemented, is completed.Production performance of the other FC1 plants in general has improv'- overthe past years. At Nanga] performance has deteriorated d*ie to a power short-age which is beyond FCI's control. Trombay and Namrup, which commenced op-erations in 1966 and 1970 respectively, have improved to about 70% capacityutilization in the past year and Trombay's performance has further improvedduring the current year.

2.09 Additional to FCI's difficulties in overcoming operational problemsin the existing plants is the likelihood of similar problems in the large-scale plants, shortly nearing completion (Durgapur, Barauni, Namrup), eachmore than two years behind schedule. Even assuming satisfactory oroductionlevels after start-up, the financial burden of lost production and capitalcost overruns due to delays are seriously affecting FCI's financial per-formance theagh all costs -- mainly financed wi'2l funds from OI -- arecapitalized until the projects operate commercially. The estimated produc-tion losses in 1972 from the under-utilization of existing plants (below90a' of designed capacity) equal about 85,000 tons of nitrogen and those ofthe three large projects which are seriously delayed an additional 400,000tons equivalent to an estimated import value of about US$65 million. Tofurther illustrate the costliness of Gelays and under-utilized capacity, anassumed proiect with an estimated 15;' rate of return over its life would findthis return virtually eliminated if there was a two year delay in completioncombined with a 10% cost overrun or a zero return if the plant would continueto operate at about 70%1 of capacity. Recently both the Government and FCIhave become increasingly aware of this problem and are taking definite stepsfor overcoming it. Also IDA has specifically structured the fertilizerprojects it is helping to finance to minimize these deficiencies.

2.10 Income projections for the Corporation (Annex 2-6) show net lossesfor the next two years, mainly because of expected start-up losses for newplants. Thereafter, FCI should have stead.ly increasing earnings but theirlevels will largely depend on the operating performance of the three newlarge plants (Durgapur, Barauni, Namrup) and -- though to a lesser extent --to increased capacity utilization in the existing factories. The forecastsare based on assumptions for capacity attainmen' (Anaex 2-8) and new projectimplementation schedules, that, although reasonable, may prove optimisticbased on FCI's past record unless GOI and FCI effectively resolve FCI'scurrent problems and follow a sound plan of further growth which does not

-6-

overtax the Coporation's resources. Since FCI intends to increase its pro-durtion fourfold by 1979 from its present level, the importance of FCI'sexpansion program for its future financial position as well as for the fer-tilizer production in India becomes obvious. Also in view of FCI's respon-sibilities to optimize the use of its human, technical and capital resources,it should concentrate its efforts even more to overcome the difficulties en-countered in the implementation of current projects and operations and notconsider further expansion projects until these difficulties will have beenlargely overcome. In preparing its fertilizer program for the Fifth Five-Year Plan (April 1, 1974 - March 31, 1979) the Government is now systemat-ically studying the broader issues connected with it, including the organ-izational and management structure of the public sector. The Associationwill have an opportunity to discuss the issues with the Government withinthe next 'ew months.

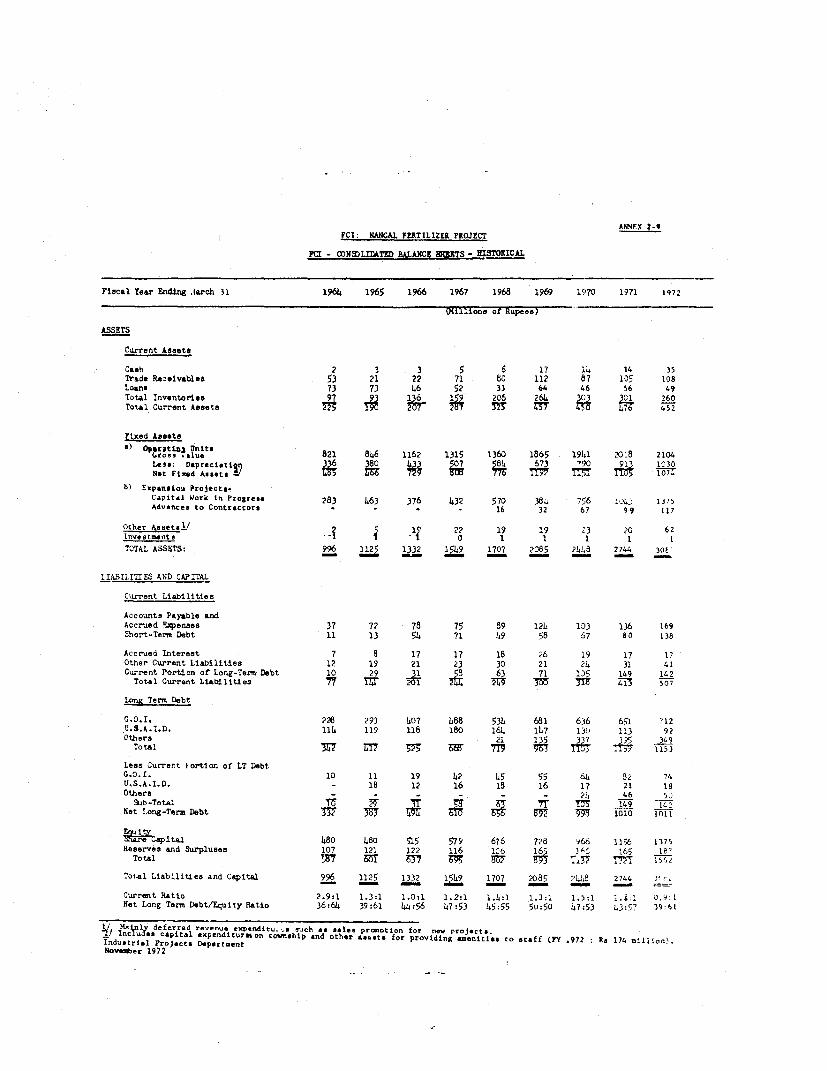

2.'1 Historical and projected balance sheets for FCI (Annexes 2-9 and2-1J) are summarized below:

Summary Balance Sheets for FCI(Millions of Rs)

Fiscal Years ACTUAL FORECAST'-(Ending March 31) 1968 1969 1970 1971 1972 1973 1974 1975

Current Assets 325 457 450 476 452 506 596 845Less:Current Liabilities 249 300 318 413 507 405 476 719

WorKing Capital 76 157 132 63 (55) 101 120 126Net Fixed AssetsOperating Plants 776 1192 1151 1105 1074 1439 2168 2103Projects Under

Construction 586 416 823 1142 1492 1772 1807 2436Other Assets 20 20 24 21 62 55 58 79

1458 1735 2130 2331 2573 3367 4153 4744Less:Net Long-Term Debt 656 892 998 1010 1011 1282 1584 1790Net Worth 802 893 1132 1321 1562 2085 2569 2954

Current Ratio 1.3:1 1.5:1 1.4:1 1.2:1 0.9:1 1.2:1 1.2:1 1.2:1Debt/Equity Ratio 45:55 50:50 47:53 43:57 39:61 38:62 38:62 38:62

/1 For Forecasts beyond 1975 see Annex 2-10.

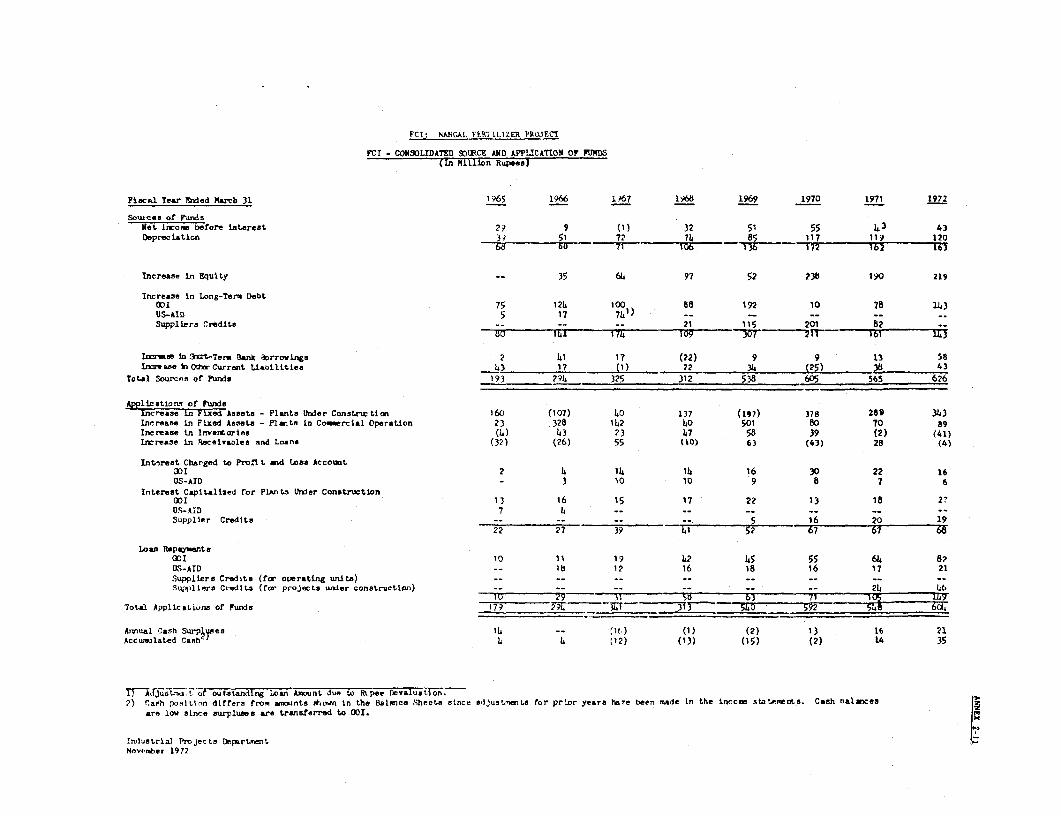

2.12 Historical balance sheets show that FCI has been financed on asound basis with a present debt/equity ratio of about 40:60 (Annex 2-11).As a rule GOI at present finances FCI's projects 50% by debt and 50% byequity after consideration of cash surpluses of existing operations on a

-7-

corporate basis. The fi::ed assets of FCI show the large amount for projectsunder construction (about Rs. 1.5 billion) as compared to a net value of theexisting plants of about Rs 1.1 billion. Total capital costs for the projectsunder construction (Annex 2-2) are estimated at about Rs 5.6 billion (US$770million) and for the projects under consideration at Rs 2.2 billion (US$290million).

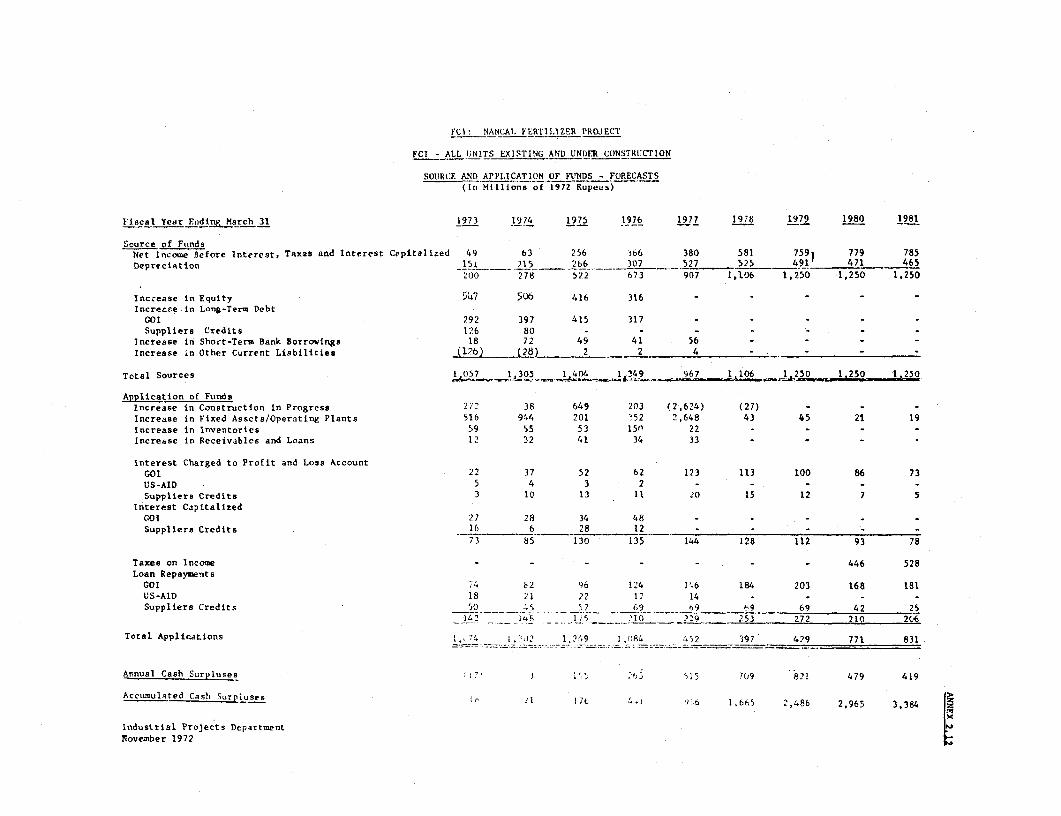

2.13 With low profits and high debt service obligations, partly causedby the delayed projects under construction, FCI would have difficulties asan independent company in meeting its debt service out of its own resourcesin the forthcoming year. However, since the Corporation's debt/equity ratiois low, the debt service ratio is expected to imprnve rapidly in future yearseven if FCI does not fully achieve the projected pro.its (Annex 2-12).

2.14 During negotiations, assurances were obtained that GOI will providethe necessary funds to FCI to meet its financial obligations, particularlyto maintain a current ratio of FCI of at least 1.2:1 and not declare dividendsor prepay any of its debt to GOI or others if such payments would reduce itscurrent ratio below 1.5:1, as already stated in the IDA Development Creditfor FCIts Gorakhpur fertilizer plant expansion.

III. NANGAL'S EXISTINC. OPERATIONS

A. Production Facilities

3.01 The present Nangal Unit, which began production !n 1961, has adesign capacity of 100,000 TPY of ammonia (310 TPD) based on the electrol-ysis of water (Annex 3-1). The ammonia is converted first to nitric acidand then to CAN, a rather low nutrient fertilizer (25% of N as compared to46% of N in urea) with a capacity of 80,000 TPY N. The electrolysis ofwater consumes a large amount of power (149 FW) and uses no natural gas orpetroleum feedstock as do most modern ammonia plants. The plant containsall necessary ancillary facilities such as maintenance shops, storage, powerand steam facilities, offices and township; it is located on the Sutlej Rivernear the Bakhra Dam in Punjab State. Transportation and distribution facil-ities in that area are well developed.

3.02 Heavy water (14,000 kg per year design), which is used in theatomic energy industry, is also produced from the hydrogen gas followingelectrolysis. All hydrogen (about 19,000 TPY) passes through the heavywater plant, but only a negligible fraction (2.5 TPY) is removed xnd con-verted to heavy water. The remaining hydrogen is processed into ammonia.

3.03 Except for the electrolysis and heavy water sections, the Nangalfactory represents conventional and commercially accepted technology (Annex3-1) although production units are small by today's standardis. Tne Nangalplant has always been operated and mnaintained well. Top management, recent-ly changed, is complemented by good middle management. No serious laborproblems have been experienced at Nangal in recent years.

-8-

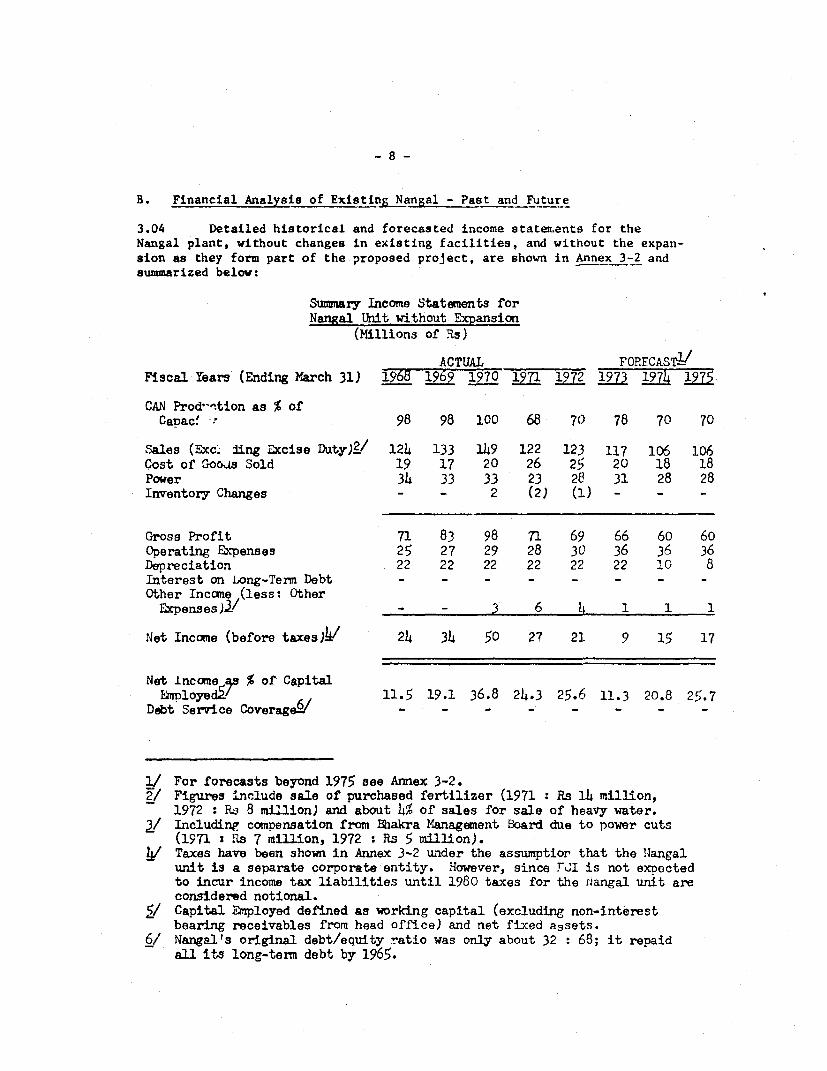

B. Financial Analysis of Existing Nangal - Past and Future

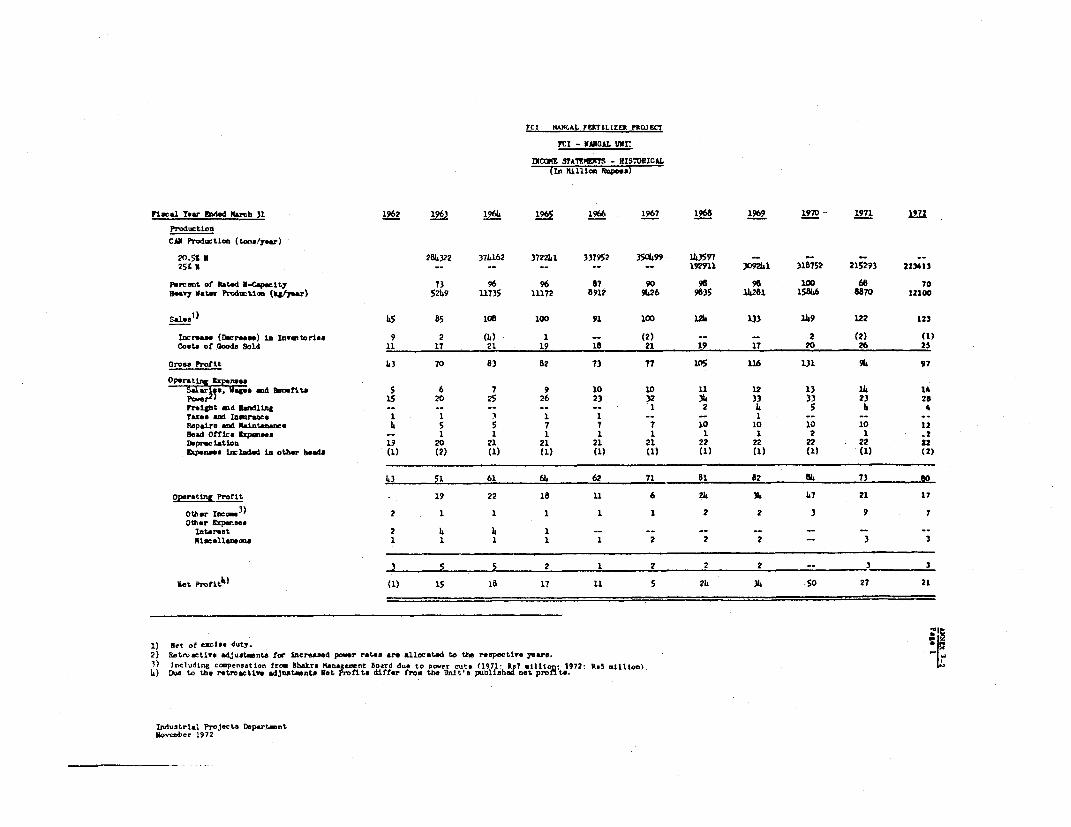

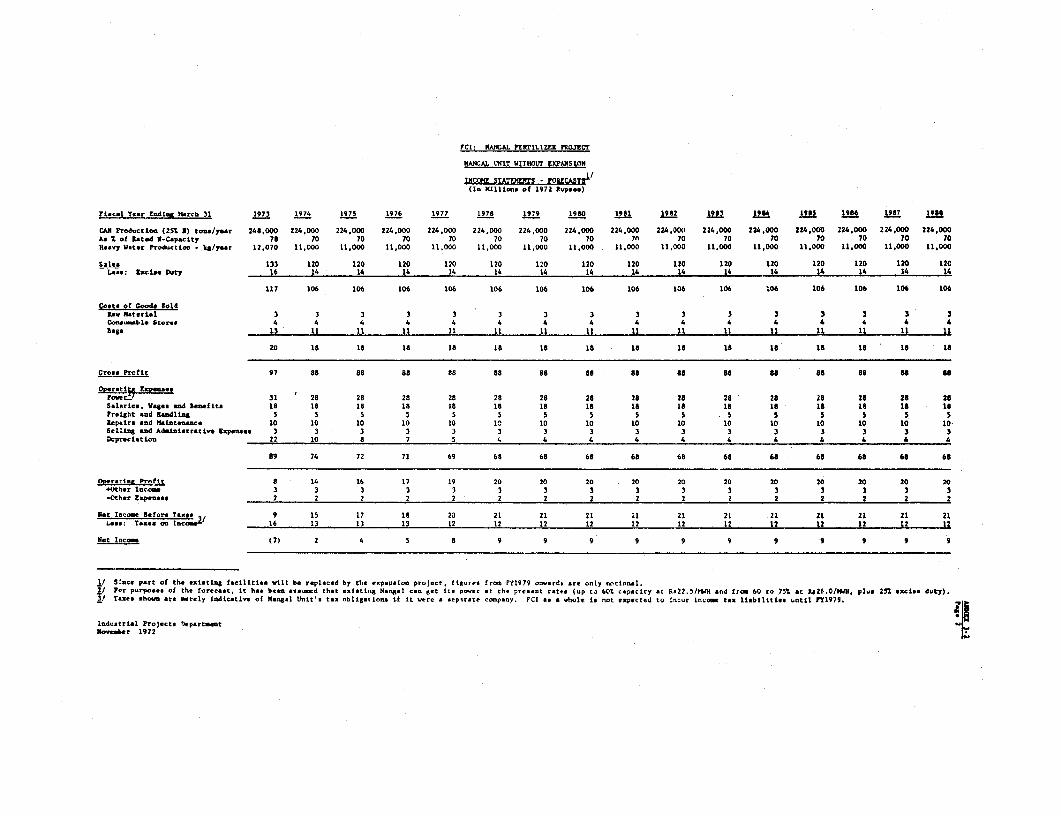

3.04 Detailed historical and forecasted income statements for theNangal plant, without changes in existing facilities, and without the expan-sion as they form part of the proposed project, are shown in Annex 3-2 andsummarized below:

Summary Income Statements forNangal Unit without Expansion

(Millions of Rs)

ACTUAL FORECAST "'Fiscal Years (Ending March 31) 1968 1969 1970 1971 1972 1973 1914 U72

CAN Prod'-ntion as % ofCarac! r 98 98 100 68 70 78 70 70

Sales (Exc:. ding Excise Duty)Z/ 124 133 149 122 123 117 106 106Cost of Goods Sold 19 17 20 26 25 20 18 18Power 34 33 33 23 28 31 28 28Inventory Changes - - 2 (2) (1) - - -

Gross Profit 71 83 98 71 69 66 60 60Operating Expenses 25 27 29 28 30 36 36 36Depreciation 22 22 22 22 22 22 10 8Interest on Long-Term Debt - - - - - - - -Other Income (less: Other

ExpensesJW/ - - 3 6 4 1 1 1

Net Income (before taxes)l 24 34 50 27 21 9 15 17

Net Income % of CapitalEIployed' 11.5 19.1 36.8 24.3 25.6 11.3 20.8 25.7

Debt Service Coverage6/ - - - - - -

1/ For forecasts beyond 1975 see Annex 3-2.2/ Figures include sale of purchased fertilizer (1971 : Rs 14 million,

1972 R: 8 million) and about 4%5 of sales for sale of heavy water.3/ Including compensation from Bbakra Management Board due to power cuts

(1971 : Rs 7 million, 1972 : Rs 5 million).v Taxes hav been shown in Annex 3-2 under the assumptior that the Nlangal

unit is a separate corporate entity. However, since FJI is not exDectedto incur income tax liabilities until 1980 taxes for the Aangal unit areconsidered notional.

/ Capital Employed defined as working capital (excluding non-interestbearing receivables from head office) and net fixed a3sets.

6/ Nangal's original debt/equity ratio was only about 32 : 68; it repaidall its long-term debt by 1965.

-9-

3.05 From 1964-1970 Nangal operated on average at 95% of capacityreaching 100% in 1970 and generated average net annual income of Rs 23million (US$3.2 million), or approximately 11% return on capital and 20%on sales. Production was down to about 70% in 1971 and 1972 due to powershortage (para. 3.07) but profits were still satisfactory, averaging Rs24 million per year, as compared to Rs 36 million during the three previ-ous years. As enlarged upon below, the relatively high earnin-s are dueto the low power rates Nangal has been paying. During the 1968-1972period Nangal accounted for about 25% of the Corporation's nutrient sales.

3.06 Although continuing power shortages would not allow plant utiliza-tion to rise above 70% over extended periods, projected income statementsshow satisfactory profits mainly because the plant will be almost fully de-preciated in 1973. Nangal has no outstanding long-term debt; with result-ing low capital charges, the profit and cash break-even points after 1973will be about 44% of capacity 1/.

C. Availability and Costs of Power

3.07 The existing Nangal plant consumes about 164 W of power at fullcapacity, 149 S. in the ammonia section alone. The original decision forchoosing this power-intensive process to produce ammonia, was based on theample availability of hydro-power in North India at prices which economicallyand financially justified the process at the time Nangal was built (Annex 3-5Subsequently, the supply and demand situation has changed, power demand hasincreased and generating cost of new facilities has gone up substantially.

3.08 Nangal has not only been experiencing power shortages since 1971which have severely limited production (para. 3.04), but from 1966 onwardhas had to pay power prices above those stipulated in the original 25 yearcontract; further increases are under discussion. At present, Nangal ispaying Rs 23/MWH (3.1 US mi'ls/KWH) 2/ based on a renegotiated contract asat January 1971. The normal rate for large industrial coLLsumers in thearea is Rs 84/MWH.

3.09 The future power shortage for Nangal is a function of supply as wellas of cost. The cost of supplying power to Nangal is estimated to be aboutRs 40/MWH from new hydro facilities and about Rs 95/kWH from thermal plants,the latter also being considered the economic cost of power (..nnex 3-5). IfNangal could afford to pay the regular rate for industrial consumers (Rs 84/.MWH)it could probably obtain its full power requirements relatively easily; butNangal could only pay about double its present power rate (or about Rs 40-45/WMH), before incurring losses, even with its almost fully depreciatedplant. At present Nangal, therefore, is receiving highly subsidized~ powerin both financial and economic terms.

1/ Detailed historical balance sheets and source and application of fundsstatements for Nangal are shown in Annexes 3-3 and 3-4.

2/ Quoted power prices exclude 25% excise tax levied against all consumers.

- 10 -

3.10 In view of the changed power situation, continued use of thepower-intensive process of producing ammonia in the existing Nangal plantis neither financially nor economically viable. However, the likelihood ofGOI and FCI shutting down the plant is remote, because of the urgent needfor fertilizer and the existence of a trained labor force plus supporting in-frastructure. Hence, closing the uneconomic part of the existing plant canonly be realized in combination with a new project that includes replacementof the ammonia section.

IV. FERTILIZER MARKET AND MARKETING

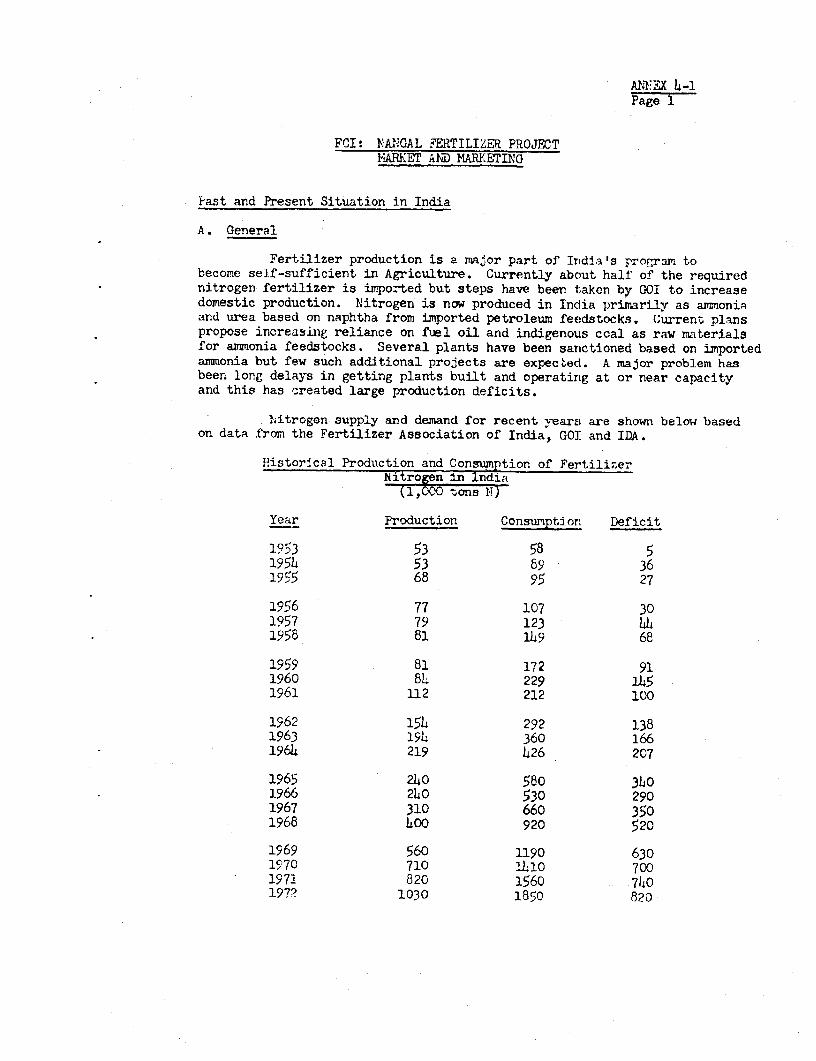

4.01 Past and future developments of fertilizer demand and supply inIndia and especially in Nangal's marketing area as well as the major fac-tors, including fertilizer pricing policies, that have contributed to thesedevelopments are discussed in detail in Annex 4. The Annex also containsan international comparison in fertilizer consumption (Annex 4-1).

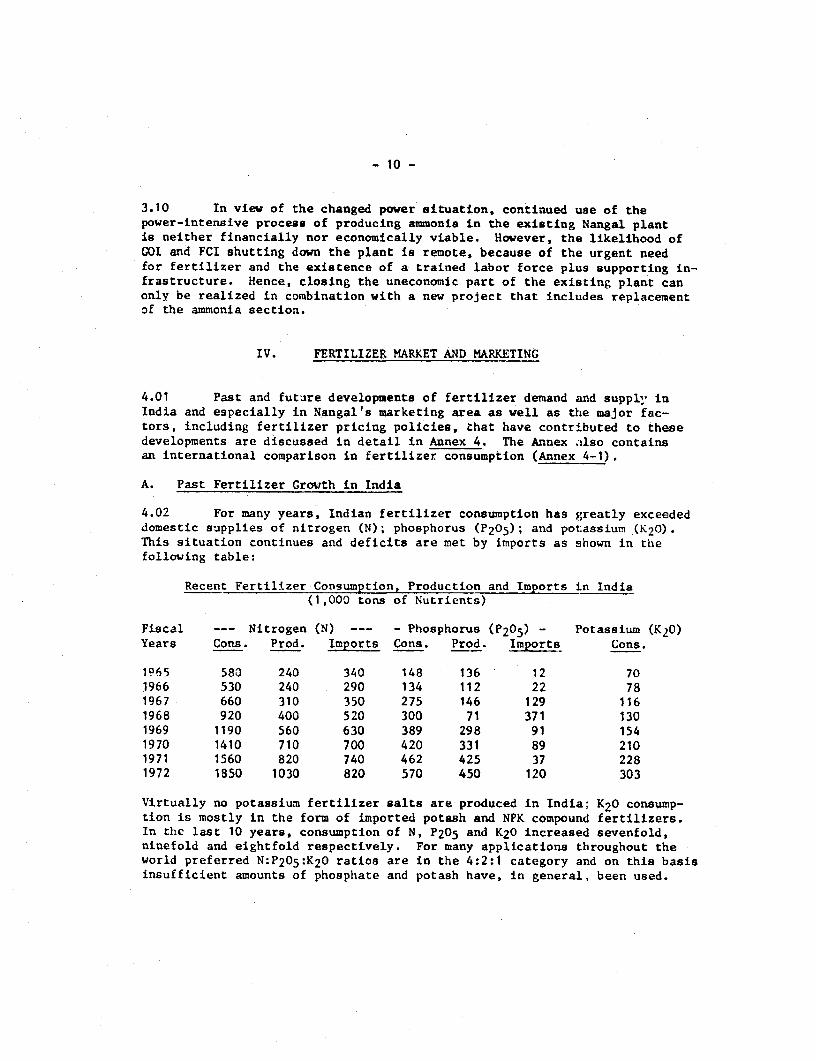

A. Past Fertilizer Growth in India

4.02 For many years, Indian fertilizer consumption has greatly exceededdomestic supplies of nitrogen (N); phosphorus (P205); and potassium (K20).This situation continues and deficits are met by imports as shown in thefollowing table:

Recent Fertilizer-Consumption, Production and Imports in India(1,000 tons of Nutrients)

Fiscal --- Nitrogen (N) --- - Phosphorus (P205) - Potassium (K20)Years Cons. Prod. Imports Cons. Prod. imports Cons.

1965 583 240 340 148 136 12 701966 530 240 290 134 112 22 781967 660 310 350 275 146 129 1161968 920 400 520 300 71 371 1301969 1190 560 630 389 298 91 1541970 1410 710 700 420 331 89 2101971 1560 820 740 462 425 37 2281972 1850 1030 820 570 450 120 303

Virtually no potassium fertilizer salts are produced in India; K20 consump-tion is mostly in the form of imported potash and NPK compound fertilizers.In the last 10 years, consumption of N, P205 and K20 increased sevenfold,ninefold and eightfold respectively. For many applications tbroughout theworld preferred N:P205:K20 ratios are in the 4:2:1 category and on this basisinsufficient amounts of phosphate and potash have, in general, been used.

- 11 -

B. Fertilizer Market Forecast for India

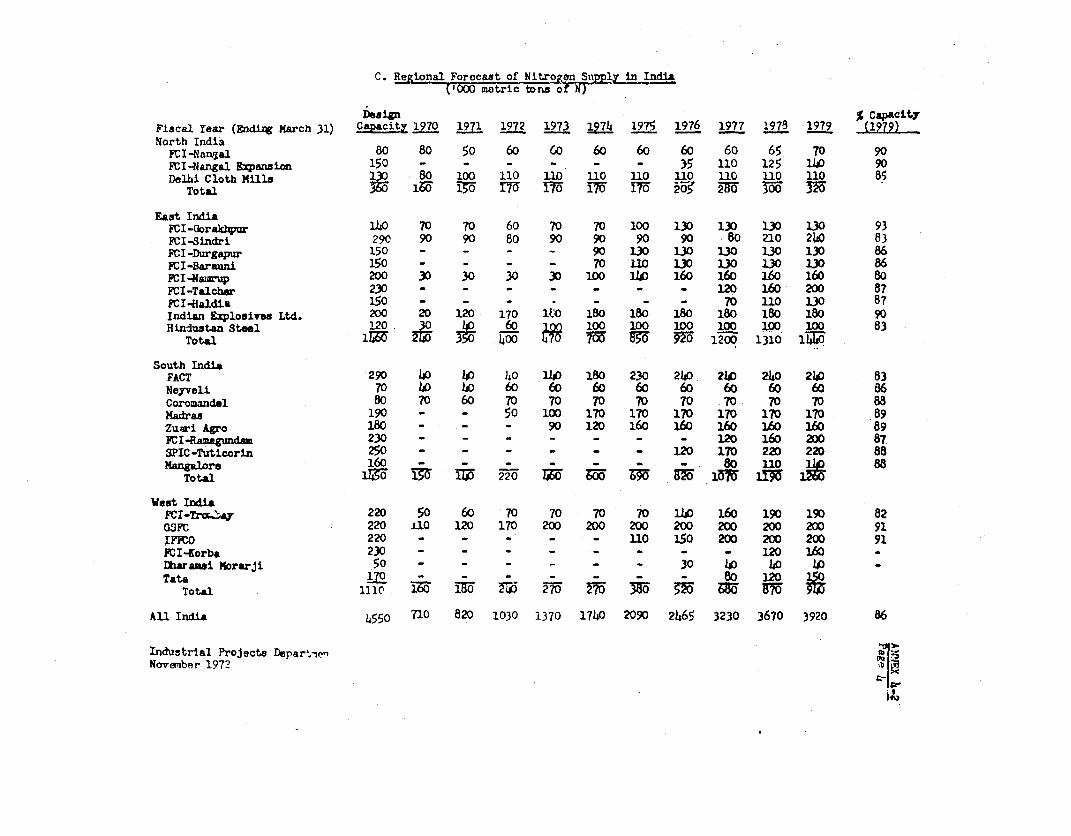

4.03 Demand/supply projections for N, P and K fertilizers are discussedin Annex 4-2 and are summarized below:

Projected Fertilizer Demand-Supply for India(1,000 tons of Nutrients)

Fiscal -- Nitrogen (N) -- -- PhosphorLS (P205) -- Potassium (K-3)Year Demand Supply Deficit Demand Supp:v Deficit Demand

1973 2300 1370 930 830 540 290 3201974 2650 1740 910 1000 650 350 3851975 2960 2090 870 1150 780 370 4601976 3320 2465 855 1320 940 380 5,01977 3720 3230 490. 1520 1130 390 6601978 4160 3670 490 1750 1370 380 8001979 4600 3920 680 2000 1630 370 960

Nitrogen projections a_e based on Bank studies 1/ plus data from the IndianPlanning Commission and the Mini .ry of Agriculture. Phosphate and potashdemand forecasts cannot readily be made on the basis of historical projec-tions because of irregular previous patterns. Indicated figures correspondto likely future attempts to bring P205 and K20 consumption more in linewith the previously mentioned, desirable 4:2:1 nutrient balance. Phosphateproduction includes ground rock and other products of indigenous origins.

4.04 The nitrogen demand projectior. assumes nitrogen consumption willgrow at 20% compounded annually to 1974 and at 11.7% subsequently. Annex4-2 shows how demand is expected to develop in each of the four major re-gions in India. The production estimate was made by IDA using informationobtained from GOI; Annex 4-2 also shows individual plant contributions andthe expectation that FCI's contribution to the domestic production of Nwill increase from 30Z in 1970 to 56Z in 1979. Average annual compoundgrowth rate is 28% to 1974 and 17.5% thereafter, based on optimistic butattaiinable start-up schedules and operating performances of new projects.Should these goals nit be met, production could be 10% to 20% less. Whileprecise forecasts canmot he made, substantial nitrogen fertilizer productionshortages are indicated tlhroughout the period 1972 to 1979. In this period,anticipated urea production will rise from about 60% to 74% in terms of totalN reflecting its popul.rity in terms of results and lowest delivered nitrogencost.

1/ "Effective Demand f^r Fertilizer in India" by W.B. Donde (COI) andDorris D. Brown (IBRD), May 1971.

- 12 -

C. Fertilizer Markets in Northern India

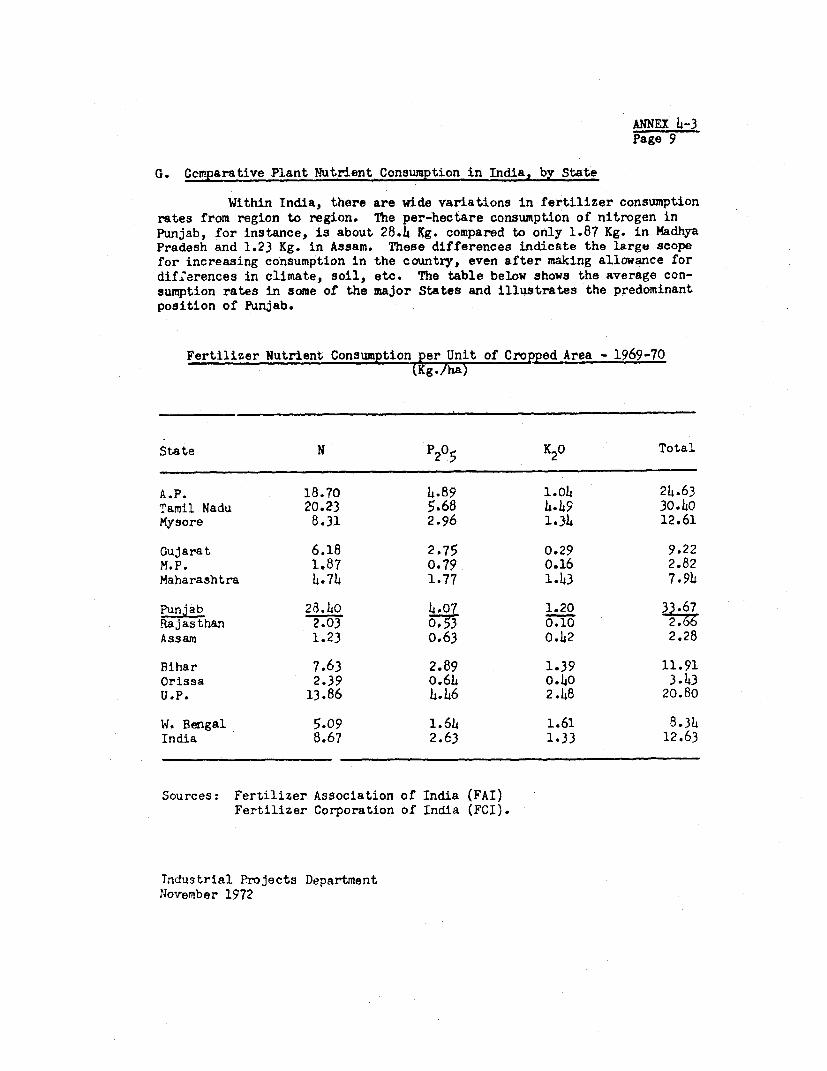

4.05 Fertilizer consumption per unit of cropped area is much greater

in Punjab than in all India, as the following comparison for 1970 shows:

Kg per Hectare

N P205 K20 Total

Punjab 28.4 4.1 1.2 33.7

All India 8.7 2.6 1.3 12.6

In both cases low application rates for P205 and K20 are evident comparedto the generally advisable 4:2:X balance and greater amounts of phosphorus

and potassium will be needed in the future as these elenents are graduallyremoved from the soil by intensive cropping. Because CAN and urea arethe only materials under consideration for Nangal, thib report will cover

in detail only nitrogen fertilizers.

4.06 The main marketing area for the Nangal plant is Punjab, Haryana,

Himachal Pradesh, Jammu and Kashmir states, plus Delhi and parts ofRajasthan. Due to present supply limitations, about 80% of Nangal's pro-

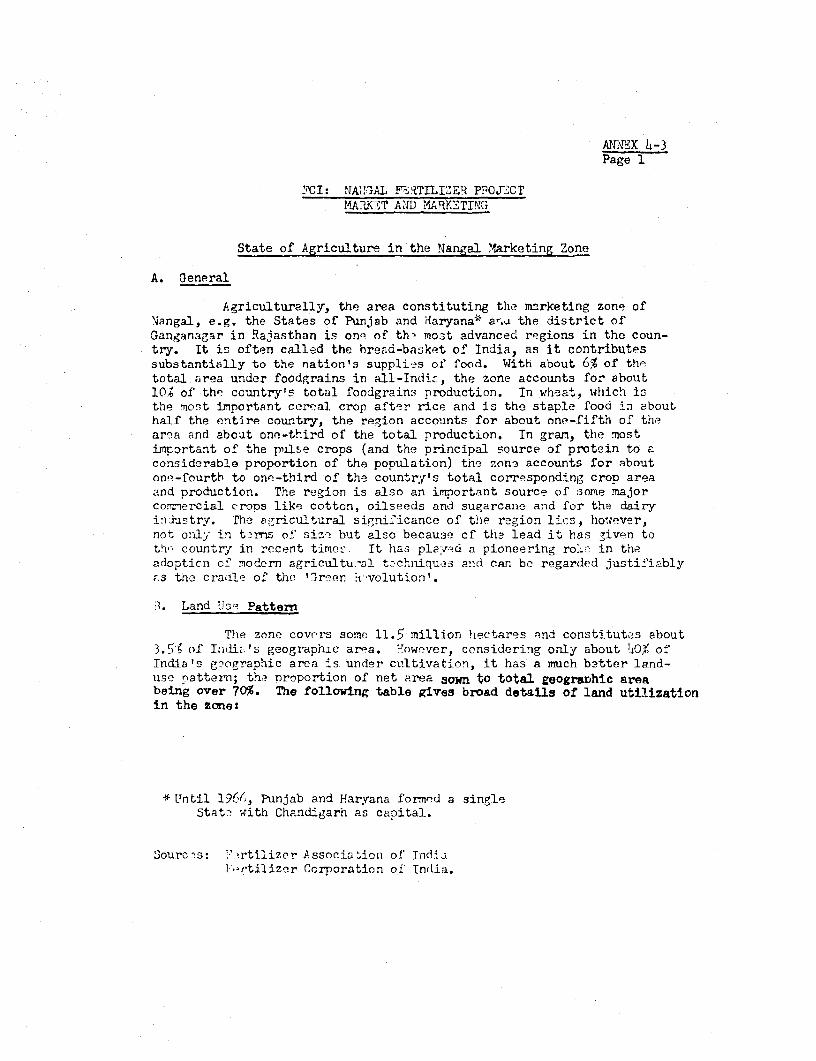

duction (CAN) is sold in Punjab and Haryana. As reviewed in Annex 4-3,these states represent one of the most advanced farming regions in India;

while comprising only 6% of the national area under foodgrains, theyproduce 10% of the nation's corresponding crops.

4.07 The demand-supply forecast for nitrogen fertilizer for northern

India is shown in greater detail in Annex 4-2. Projections for 1972-1979

including possibly available shipments from other regions (except: the dis-

tant southern states) are:

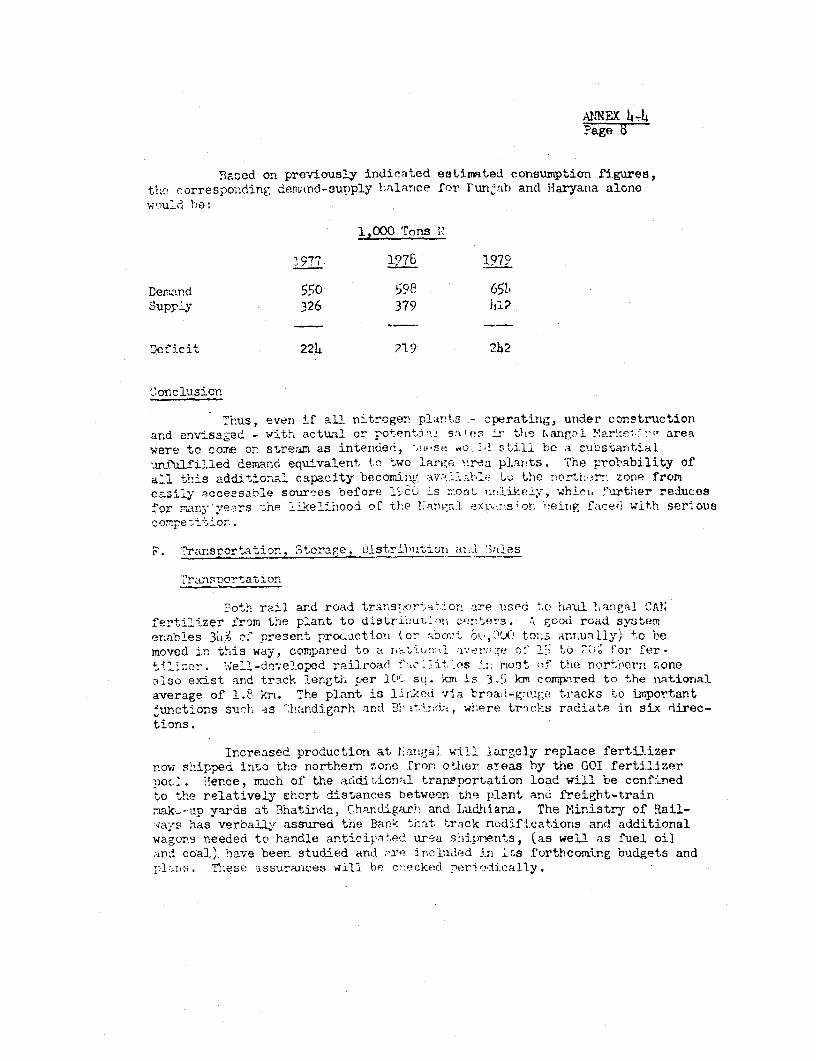

Demand-Supply Balance for Nitrogen Fertilizer in Northern Iodia(1,000 tons N)

Fiscal Years 1972 1975 1976 1977 1978 1979

Demand 350 570 630 690 760 840Supply 170 170 205 280 300 320

Possible Surplusesfrom East andWest India 0 0 0 130 250 170

Net Deficit 180 400 425 280 210 350

4.08 It is unlikely that all projected apparent surpluees in the eastand west regions would ever be shipped to the north; however, even if they

were, a shortage equivalent to two additional large urea plants would still

persimt an ihowi in Antiex 4-4. Accordingly, no problems in selling Nangaluroa are foreseen.

- 13 -

D. Nangal Marketing System

4.09 FCI has recently establislei tour mar'leting zotons [UgiOU InJla.Each is responsible for promotion, publicity and market research, and all arecoordinated at hcad office level under guidance from FCI's Director of Produc-tion and Marketing in New Delhi.

1. Transport and Storage

4, 10 Both rail and road haulage are used between the plant and maindistribution centers; good roads enable 34% of present CAN production tobe moved via truck compared to a national average of 20% for fertilizer.Well-developed railroads also exist and the Ministry of Railways has assuredFCI and IDA that corresponding facilities ;o accommodate additional raw ma-terials a,d products after expansion will be provided on tim.e. Extra trafficwill only amount to three trains daily and no problems are fcreseen. Fer-tilizer consumption in Nangal's marketing area if; fairly unifarm throughoutthe year because of double cropping and crop variety. Also, distributionand discount systems used by co-ops and private dealers have helped FCIavoid storing large tonnages in less-active months. Ample additional fac-tory storage (20,000 tons) will be installed, and adequate extra co-op anddealer capacity is available.

2. Distribution Networks

4.11 In Punjab and Haryana, fertilizers reach farmers via two distribu-tion networks: co-ops and private dealers. Competition between these twogroups is more related to obtaining material to sell than price reductionand is likely to remain so. FCI's policy is to make equal quanttites avail-able to both and to limit each private dealer to 500 tons annually.

3. Credit Facilities

4.12 Fertilizers handled "y co-ops and private cealers are sold tovarious groups ranging from large commercial estates to very low-Incomecultivators. Recently, steps have been taken by GOI to provide appropri-ate credit facilities to all levels of the agricultural community parti-cularly low-income groups whose coaly previous recourse was the villagemoney lender. Now, farmers can obtain loans from two major sources:state banks and co-op "banks" or lending agencies. Similarly, additionalcredit facilities have been extended to the growing number of pr-.vatedealers. Such available financing facilities will help to ensure tnat salesof Nangal urea will not be re-.tricted by payment problems, especially asmuch of the market lies in the well-developed States of Punjab and Haryanawhere farmers are relatively prosperous and purchase a subscantial proportionof their agricultural requirements with cash.

- 14 -

4. Urea Pricing

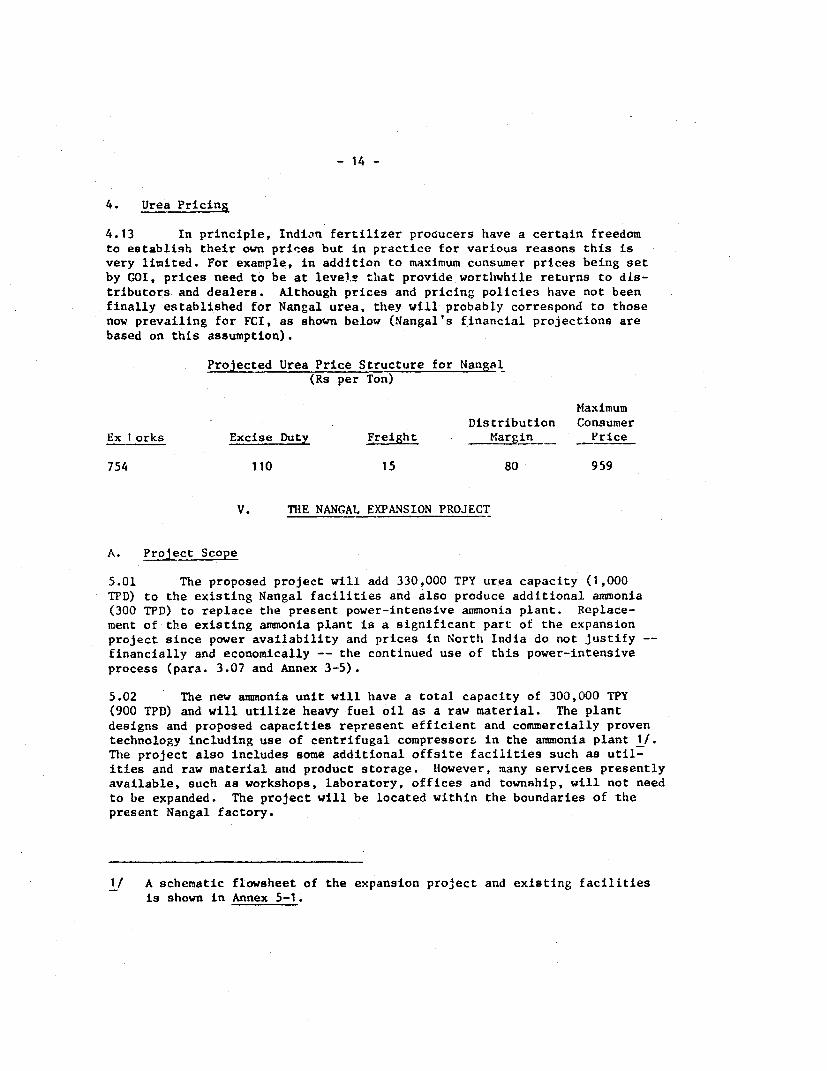

4.13 In principle, Indian fertilizer producers have a certain freedomto establish their own prines but in practice for various reasons this isvery limited. For example, in addition to maximum consumer prices being setby GOI, prices need to be at leve1.E that provide worthwhile returns to dis-tributors and dealers. Although prices and pricing policies have not beenfinally established for Nangal urea, they will probably correspond to thosenow prevailing for FCI, as shown below (Nangal's financial projections arebased on this assumption).

Projected Urea Price Structure for Nangal(Rs per Ton)

MaximumDistribution Consumer

Ex 1orks Excise Duty Freight Margin__ Price

754 110 15 80 959

V. THE NANGAL EXPANSION PROJECT

A. Project Scope

5.01 The proposed project will add 330,000 TPY urea capacity (1,000TPD) to the existing Nangal facilities and also produce additional ammonia(300 TPD) to replace the present power-intensive ammonia plant. Replace-ment of the existing ammonia plant is a significant part of the expansionproject since power availability and prices in North India do not justify --financially and economically -- the continued use of this power-intensiveprocess (para. 3.07 and Annex 3-5).

5.02 The new ammonia unit will have a total capacity of 300,000 TPY(900 TPD) and will utilize heavy fuel oil as a raw material. The plantdesigns and proposed capacities represent efficient and commercially proventechnology including use of centrifugal compressor& in the ammonia plant 1/.The project also includes some additional offsite facilities such as util-ities and raw material and product storage. However, many services presentlyavailable, such as workshops, laboratory, offices and township, will not needto be expanded. The project will be located within the boundaries of thepresent Nangal factory.

1/ A schematic flowsheet of the expansion project and existing facilitiesis shown in Annex 5-1.

- 15 -

B. Project Description

5.03 Anmonia production will be based on the partial oxidation of heavyfuel oil. Several processing steps are required, which arr> described in Annex5-2 and are summarized below together with the relevant process licensors.

Air Separation Plant - To be bi.1 internationl1lyPartial Oxidation - Shell (Netherlands)Sulfur Removal - Lurgi (F.R. of Germany'Shift Conversion - FCI (India) and Lurgi kF.R. o

Germany)C°2 Removal - Lurgi (F.R. of Germany)Nitrogen Wash - To be bid inzernationiallyAmmonia Synthesis - Uhde (F.R. of Germany)/Topsoe

(Denmark)

The use of Shell and Lurgi licensed processes, with which FCI has had p-ev-ious experience, and the Shift Conversion step by FCI are oased on utilizationof FCI engineering and know-how. The ammonia contractor, Ulde (Germany) whowas chosen after international bidding, will use its own anmonia synthesistechnology in conjunction with Haldor Topsoe.

5.04 The ammonia plant will be a single train unit with the exceptionof Partial Oxidation which will require three units and Air Separation whichmay require two units.

5.05 The urea plant will he based on the Montedison (Italy) design andpartly represents an extension of an existing license dgreement betwee.AMontedison and FCI for supply of urea technology. The urea design is con-ventional; total recycle technology being based on an operating plant inthe Netherlands, and will be a single unit. A similar plant, incorporatingtwo 500 [I'D units, is part of FCI's Durgapur and FACT's Cochin plan.s -hichare nearing completion.

C. Raw Materials and Utilities

5.06 The principal raw material required is heavy fuel cii wbizh will bepurchased through Indian Oil Corporation from a refinery that is to be bui'tnear Delhi, some 200 rail km from the Nangai plant and presently ?xpected tobe completed in late 1977 (some two years after the scheduled completion ofthe project). However, the ammonia plant will be designed to process anyliquid hydrocarbon material. Initially, fuel oil will be supplied from anexisting refinery (also owned by Indian Oil) in barauni (Bihar) or will beimported and will be transported to Nangal in heated cank cars. To confirmthe understanding that sufficient feedstock and rolling stock will be avail-able to meet the requirements of the expanded plants it was agreed to duringnegotiations that FCI will enter into satisfactory arrangements wi,h IndianOil and the Railway Authorities.

- 16 -

5.07 The major utilities required e:e power, coal and water. About 30MW of power will be needed, which will be supplied by Punjab Scate Electri-city Board (PSEB) from Bhakra at a normal industrial rate of 84 Rs/MWH.Since Nangal will release about 149 MW of power utilized by the existing unit(at full capacity) and because of Nangal's proximity to the power generatir.gsource (20 Km), no power supply problems are anticipated at Nangal. However,FCI has been asked to enter into satisfactory arrangements with PSEB for itspower requirements.

5.08 Coal, required for steam generation, will be transported by railfrom existing coal mines in-Bihar and Madhya Pradesh. No supply difficultyis anticipated and FCI has been a3ked to obtain satisfactory contracts withthe coal suppliers. Water, for both process and cooling uses will be obtaiaedfrom the adjacent Sutlej River. Ample supply is available and no problem isanticipated.

D. Employment

5.09 About 3,800 people (including about 1,200 for township and generalservices) are currently employed at Nangal and this number will not increasesubstantially after expansion. Operators from phased-out units will be em-ployed in the new plant. Provision has been made in cost calculations foran additional 200 employees to handle increased quantities of raw materialsand products, and also to undertake any additional maintenance and yard work.During plant construction, civil works labor needs are estimated to be about5,000 man years, equivalent to some 2,500 workers over a two year period.

5.10 The Nangal expansion will also create incremental indirect employ-ment in the coal, oil, bag-making and transportation industries but this isdifficult to measure. Urea distribution and sales will require incrementallabor and clerical help of about 300 extra dealers plus perhaps 1,000 part-time distributors. In addition, it is likely that about half of these num-bers will be required to distribute and sell via the co-op organizations.

E. Ecology

5.11 The effect of a modern ammonia-urea plant on its environment isminimal, and in the case of the Nangal project, no appreciable amounts ofharmful wastes will be discharged. The plant will use a high sulfur fueloil but the project includes desulfurization and sulfur recovery facilities.About 6,600 TPY elemental sulfur will be recovered, as a saleable product,which represents about 99.5% of the initial sulfur feed. No ammonia wouldbe discharged to the atmosphere except for accidental spills or leaks whichare an uncommon occurrence.

5.12 Liquid effluents can contain a small amount of absorbed ammonia,and this would be neutralized before discharging to the Sutlej River, Thedownstream use of the river is primarily for irrigationi, with no lakes sothere is no possibility of a build-up of nitrogen. In any case, the quan-tity of nitrogen is so small that the quality of water is not affected.Urea solids (as a fine dust) are a potential effluent but scrubbing equip-ment is to be installed to recover urea which is a valuable product. Theecological facilities included in the project are estimated to cost aboutUS$2 million equivalent, or about 2% of total project costs.

- 17 -

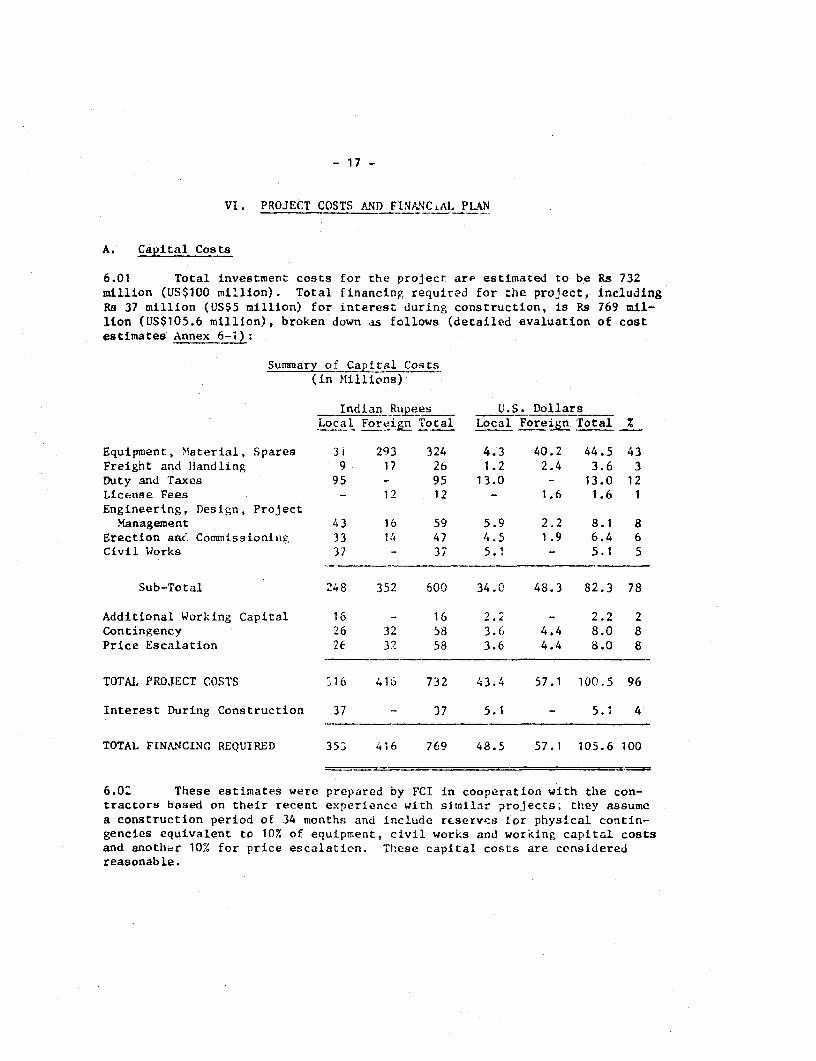

VI. PROJECT COSTS AND FINANCiAL PLAN

A. Capital Costs

6.01 Total investment costs for the project are estimated to be Rs 732million (US$100 million). Total financing required for the project, includingRs 37 million (US$5 million) for interest during construction, is Rs 769 mil-lion (US$105.6 million), broken down as follows (detailed evaluation of coatestimates Annex 6-t):

Summary of Ca ital Costs(in M1illions)

Indian Rupees U.S. DollarsLocal Foreign Total Local Foreign Total %

Equipment, Material, Spares 3i 293 324 4.3 40.2 44.5 43Freight and Handling 9 17 26 1.2 2.4 3.6 3Duty and Taxes 95 - 95 13.0 - 13.0 12License Fees - 12 12 - 1.6 1.6 1Engineering, Design, Project

Management 43 16 59 5.9 2.2 8.1 8Erection aae Commissioning 33 14 47 4.5 1.9 6.4 6Civil Works 37 - 37 5.1 - 5.1 5

Sub-Total 248 352 600 34.0 48.3 82.3 78

Additional Working Capital 16 - 16 2.2 - 2.2 2Contingency 26 32 58 3.6 4.4 8.0 8Price Escalation 26 32 58 3.6 4.4 8.0 8

TOTAL PROJECT COSTS ;16 415 732 43.4 57.1 100.5 96

Interest During Construction 37 - 37 5.1 - 5.1 4

TOTAL FINANCING REQUIRED 353 416 769 48.5 57.1 105.6 100

6.0 These estimates were prepared by FCI in cooperation with the con-tractors based on their recent experience with similar projects; they assumea construction period of 34 months and include reserves for physical contin-gencies equivalent to 10% of equipment, civil works and working capital costsand anothcr 10% for price escalation. These capital costs are consideredreasonable.

- is -

6.03 The expected foreign exchange costs of US$57 million are based. on

4% of equipment belng re arved for Irdian procurement and the expectation

that Indian suppliers will win 10% of the remaining equipment, all to be bid

internationallv (except US$2.2 million proprietary equipment). The foreign

exchange costs would in^rcr.se to U'S$58 million or drop to US$55 million were

Indian supn-iitrs tc Win raspectively 5i or 20% of the intcrnationally procured

equipment. Tae proioct cost est'.mates iinclude the likely effect of a 15% rar-

gin of preferente '-o- trie>rred domestic. bids when comparing domestic bids

with those from fore-,.n suppliers.

B. WorkinK_LGapltal Recuire.nen:s

6.04 Wor'ir' capi:cl requieamencs for the exOansioni project wil., be

Rs 68 mil o1l, cf .iti ' 's 52 ;mi'1.ion '_5' et7 inventories and receivables)can be carriie- as Slo-~:-:e cot Žrc. 5,tnk credit fronY the State Bank of

Indla (Annex_'-2). Thus, marginal working capital requiring long-termfileanicin, is 6 , i Ll 4c S. o 19 li on)

C. Financil '1?an6.05~ ~ _' . 6'm i'Wt r

6.05 2Ti S \; nl>.ou) pro Jecc financing would be

Drovicct a _C! - ' SO out 55:45 1ebt tr C eqt;Ity as shownb')Iov:

USS titllion

'-ttR, nrl , : 0s'r_

.r.)io-ve. TOX ;r:2di.: 58.0

47.6

Tutal 105.6

6.35 Ihe pF' p' Bsed au ,ount. of USi`8 million for the lI)A credit would

eover the 1e V"' ov^epc! ±oneijn exchange cost. un-ler international com-

petitive bld"-n r . :.½.o-). 'the IDA credit would be relent from GOI to

FCl; it reDreen's .';e -- rl r;bt shown in the proposed financial plan

for t'he prci'ec'-. t 1%i 'y 7cL S neW projects have been financed at 50:50

debt to equity. 'owevor, since existing Nangat has no outstanding long-term

debt. tl'he ie e det to ec,uity ratio of 55:45 for the project financingis accepza:'e -)L .. ro etquitr ratto of Nangal after expansion is not

c xp I ' }.I to { '\ < ( 'ds .~ : #)5.

- 19 -

6.07 Existing Nangal has generated attout Ka 3't) mtIlln if vi.li £:UIu ice

depreciation and earning since 1961. Cash generation during the co.istructionperiod of the project (1974-1976) is estimated at about Rs 40 milliorn (afterconsideration of notional taxes). According to the practice of COI-owi.edcompanies, Nangal's cash surpluses have been transferred to FCI;s head officeand, in turn, any corporate surplus from FCI has been zransferred to GO1.Therefore, Nangal's generated cash, cannot be reused for the financirZ ' theexpansion project, and the equity of the expansion project of US$47.6 millionequivalent will be provided by GOI as new equity.

6.08 The Government would on-lend the proceeds of the IDA credit toFCI as a loan for 15 years, from the date of etfectiveness of 6he credit,including a 5 year period of grace and repayment ir. iO equal annual ins .all-ments, at an interest rate of 8.5%. These terms are similar to those appliedto the recent IDA credits for the Cochin II and Gorakhpur fertilize; expan-sion projects. The credit proceeds would be denominated in rupees, and theexchange risk would remain with GOI.

6.09 To protect against an unexpected overrun in project costs (bothforeign exchange and local costs) GOl will provide additional funds as neces-sary to complete the project.

D. Allocation of the IDA Credit

6.10 Froceeds of the IDA credit woild be used as follows:

Allocation of IDA. Credit(Millions of US$)

1. Equipment and Materials, internationally bid 42.22. Imported Equipment for Standardization 2.53. Engineering, Design, Erection and Commissioning 7.54. Unallocated 5.8

58.)

6.11 The IDA credit will cover CIF costs of all imported equipment ('n-cluding US$2.2 million proprietary equipment) and ex-factory irice (excludingtaxes) of locally procured equipment that is internationallv bid. It willalso include total foreign exchange costs of process licenaes and cousultants'services and a portion of FCI's local costs for engineering and equipnenterection. The project's foreign exchange content is about US$57 million asdiscussed in para. 6.03. Any unused portion of the crediL will be reallo-cated by the Association to FCI's local expenditures for engineering andequipment erection. Projected disbursement schedule for tne IDA credit isgiven in Annex 6-3.

- 20 -

VII. PROJECT EXECUTION

A. Project Management and Execution

7.01 Difficulties experienced by FCI in undertaking projects withinoriginally established time and cost limits have been mentioned previously(para. 2.14). The relatively small urea expansion and debottleneckin- proj-ect at Gorakhpur (financed by IDA in 1971) has, as expected, not imposed astrain on the Company's engineering or management resources. hiowever, theproposed large ammonia and urea project at Nangal is of much greater magni-tude. Accordingly, to reduce the corresponding additional workload for FCI,GOI, FCI and IDA have agreed that the contractors chosen to supply the am-monia and urea processes will respectively be given major responsibility forexecuting substantial parts of the project. Also FCI has appointed an ex-perienced Project Manager, with adequate responsibilities as well as quali-fied senior engineering staff. FCI has been asked to consult with IDA be-fore changing the Nangal general manager or the project manager.

7.02 'rhe Planning and Development Division (P & D) of FCI will act asoverall prime contractor for the project. Design, and erection supervisionof the ammonia plant will be subcontracted to Uhde and similar responsibil-ities for the urea plant subcontracted to Montedison. Uhde was selected viainternational bidding by FCI in consultation with IDA. Montedison was com-mitted to the project before IDA involvement and undertook the design a.ndengineering of the FCI urea plant at Durgapur. This has not yet come onstream, because the ammonia plant is delayed; however, the urea process isoperating successfullv elsewhere.

7.03 P & D staff at Sindri will undertake as much detailed engineeringwork as possible on the ammonia and urea units under the guidance of Uhdeand Montedison specialists. Simultaneously, specialized design work will beperformed in the offices of Uhde and Montedison at Dortrund, and Milan respec-tively, assisted by selected FCI personnel. If it becomes evident that FCI'sstaff at Sindri cannot meet planned deadlines, the balance of work will promptlybe moved to Dortmund or Milan. Uhde and Montedison have agreed to acceptresponsibility for completing design and detailed engineering on time, in-cluding all such work undertaken by FCI staff on the ammonia and urea units.Offsite design and all field conetruction will be undertaken by FCI with theassistance of proven subcontractors. Specialists from Uhde and Montedisonwill supervise the erection of the ammonia and urea units and subsequentstart up, running-in and guarantee tests.

B. Project Scheduling, Procurement and Contractor's Guarantees

7.04 In consultation with Uhde and Montedison, FCI has prepared a de-tailed project schedule network and a project implementation plan. 1/ These

1/ A summarized implementation schedule is shown in Annex 7.

- 21 -

show respectively the critical timing ot all major activitius .,nd Lhe resiukl-sibilities for project execution and management within FCI asd berween FCI andthe contractors. Both documents have been reviewed by IDA and founo realistic.

7.05 The starting date of the project will be January 15, 1973. It i:;anticipated that completion will require 34 months and comiercial productionwill commence in December, 1975. Project scheduling snd cost conLrol will bethe responsibility of FCI, but Uhde and Montedison will act. in £1 consultingrole to assure completion on time and within the calculated budget. Tirae andcost controls will be maintaince by computer-aided critical path proceduresoperated separately by FCI anc the contractorb.

7.06 Equipment procurement responsibility will be shared between FCI,tThae and Montedison. Criticai, long delivery and proprietary itens will betendered, evaluated and expedited from Dortmund and Milani buz purchased ,romFCI, Delhi. Procurement will be aid-d by an agreement letween GOI and IDAthat all necessary import licenses w7ill be promptly issued and processed.Assurances have been givien by GOI that any item orcered in India that isdelayed unreasonably can be procured itmnediately from other countries toavoid possible adverse effects on project completion. As FCI is now familiarwith. IDA procedures; procurement should proceed without difficulty.

7.07 Uhde and Montedison have each agreed to furnish P & D withi completedesign and purchasing data within specified periods. Failure -o meet chesedeadlines will subject the contractors to penalty paymnents. Also, plantperformance guarantees in terms of capacity, product quality and utilityrequirements have been obtained from the contractors, partiy in conjunctionwith the process licensors, furnishing key sections of the ammonla plant(Shell, Lurgi, Haldor-Topsoe). inability to meet these performances willsubject contractors and licensors to penalties if adjustments made in tllefield at their expense prove ineffective.

VIII. FINANCIAL ANALYSIS OF THE PtQO.ECT

A. Revenues and Operating Costs

8.01 Revenues and opeL-ting costs for the modified exf.sting faciliciesand proposed expansion project are shown in Annexes 8-1 and 8-2.

8.02 A comparison of revenues and costs for Nangal before and after ex-pansion (Annex 8-1) shows that production at the unchanged existing facilitieswould be more expensive than after modification even with a fully depreciatedplant and the present low power rate. Assuming the present rate for powerwere to double (Annex 3-5) profits for existing Nangai would, as rLientionedpreviously, almost disappear, even at an increased capacity utilization of90%.

- 22 -

8.03 Marginal labor costs for the expansion project are low, since thereis some overstaffing in the existing plant and many of its labor-intensiveactivities (e.g. repair shop, township facilities, etc.) will not need tobe expanded. The other cost items are directly related to output and wereallocated to the CAN and urea plants to show the approximate costs of pro-ducing each product.

8.04 Raw materials necessary to supply the operations of the expansionproject are desLribed in Chapter V and their prices are shown in Annex 8-3.Fertilizer prices in India are high compared to other countries (Annex 4-1)but they are necessary to partly offset high duties and taxes on capital andoperating costs. Total Indian duties and taxes on imported equipment aloneamount to about 11% of Na'igal's total project tnsts (30% on imported equip-ment). Resulting increased capital charges from these duties on a per tonof finished product (urea) basis are estimated at about Rs 28 (US$3.8).

B. Feedstock Costs

8.05 The main difference in raw materials and operating costs as com-pared to international standards results from high feedstock costs; costsfor other main input materials, such as coal and bags are in line with inter-national prices. Costs for fuel oil or naphtha as feedstock substantiallyexceed costs of natural gas, which is readily available for fertilizer pro-ducers in some countries but not in India. Naphtha, now the feedstock ofmost of the modern urea plants in India, is in short supply and will partlyhave to be imported in the future. Accordingly, it is now GOI policy to basefuture ammonia production on alternative feedstock such as heavy-fuel oil orcoal. Nangal will have the first heavy-fuel based ammonia plant in India.GOI has recertly adjusted heavy fuel oil prices to make lheavy fuel basedfertilizer .roduction at Nangal competitive with that based on naphtha, alsotaking into account higher investment costs (about 10% of total project costs)for heavy-fuel oil process.

C. Financial Forecasts

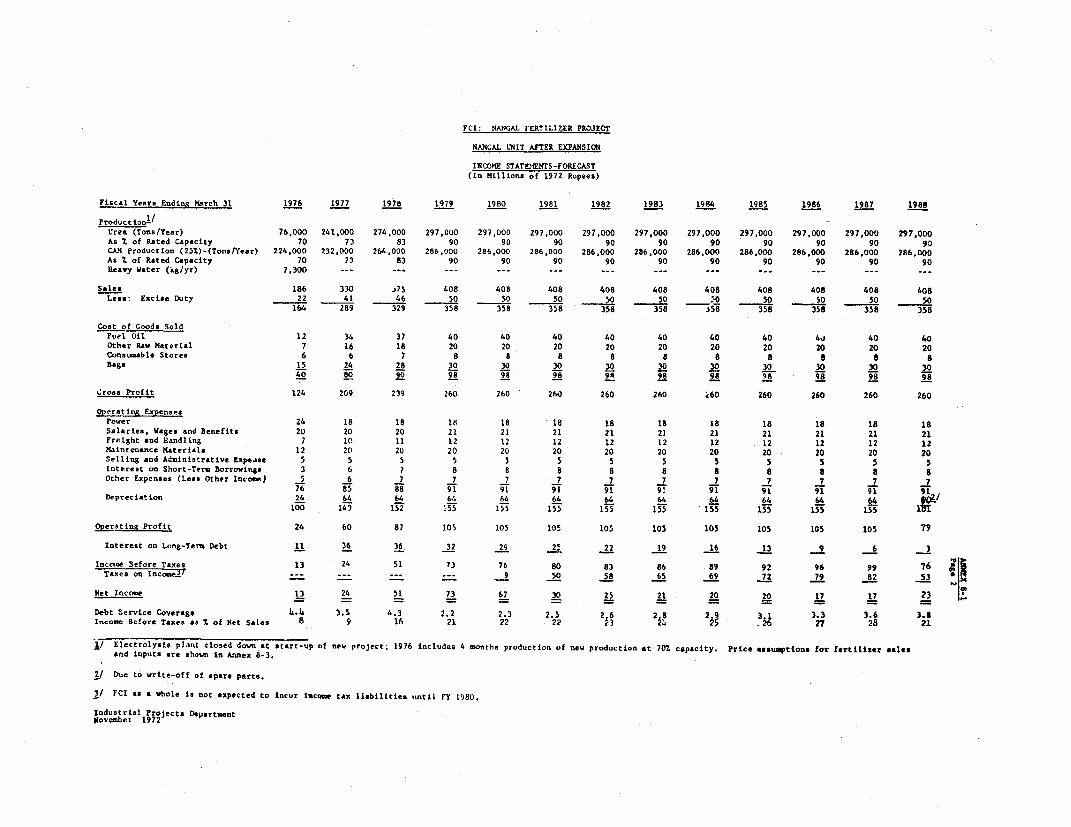

8.06 Forecasted Income Statements for the Nangal Unit before and afterexpansion given in Annexes 3-2 and 8-1, are summarized below: 1/

1/ 1972 figures are actual and 1973-1976 figures are forecasted for exist-ing Nangal Unit. Construction of the Expansion Project starts in 1973but income statements of the Nangal Unit will onl. be affected from thestArt of commercial production of the Expansion Project in December1975.

- 23 -

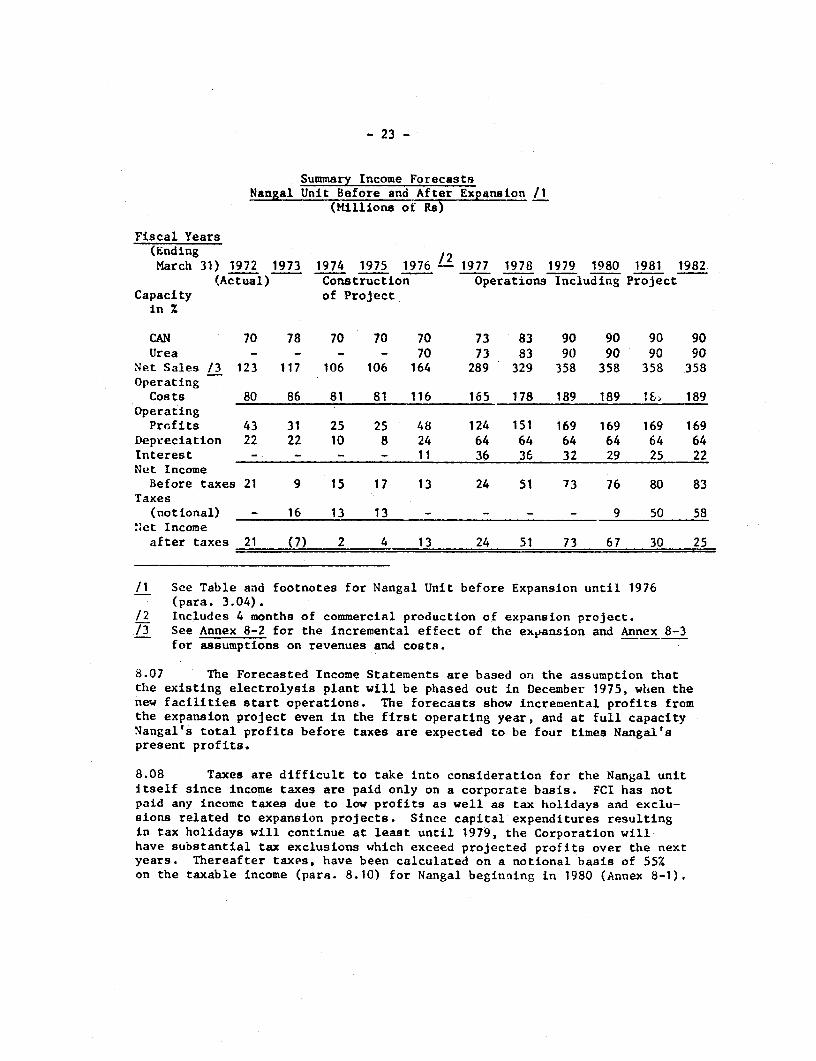

Summary Income ForecastsNangal Unit Before and After Expansion /1

(Millions of Rs)

Fiscal Years(Ending /2March 31) 1972 1973 1974 1975 1976- 1977 1978 1979 1980 1981 1982

(Actual) Construction Operations Including ProjectCapacity of Projectin Z

CAN 70 78 70 70 70 73 83 90 90 90 90Urea - - - - 70 73 83 90 90 90 90

Net Sales /3 123 117 106 106 164 289 329 358 358 358 358OperatingCosts 80 86 81 81 116 165 178 189 189 1E, 189

OperatingProfits 43 31 25 25 48 124 151 169 169 169 169

Depreciation 22 22 10 8 24 64 64 64 64 64 64Interest - - - - 11 36 36 32 29 25 22Net Income

Before taxes 21 9 15 17 13 24 51 73 76 80 83Taxes(notional) - 16 13 13 - - - - 9 50 58

.:et Incomeafter taxes 21 (7) 2 4 13 24 51 73 67 30 25

/1 See Table and footnotes for Nangal Unit before Expansion until 1976(para. 3.04).

/2 Includes 4 months of commercial production of expansion project./3 See Annex 8-2 for the incremental effect of the expaasion and Annex 8-3

for assumptions on revenues and costs.

8.07 The Forecasted Income Statements are based on the assumption thatthe existing electrolysis plant will be phased out in December 1975, whlen thenew facilities start operations. The forecasts show incremental profits fromthe expansion project even in the first operating year, and at full capacityNangal's total profits before taxes are expected to be four times Nangal'spresent profits.

8.08 Taxes are difficult to take into consideration for the Nangal unititself since income taxes are paid only on a corporate basis. FCI has notpaid any income taxes due to low profits as well as tax holidays and exclu-sions related to expansion projects. Since capital expenditures resultingin tax holidays will continue at least until 1979, the Corporation willhave substantial tax exclusions which exceed projected profits over the nextyears. Thereafter taxes, have been calculated on a notional basis of 55%on the taxable income (para. 8.10) for Nangal beginaing in 1980 (Annex 8-1).

- 24 -

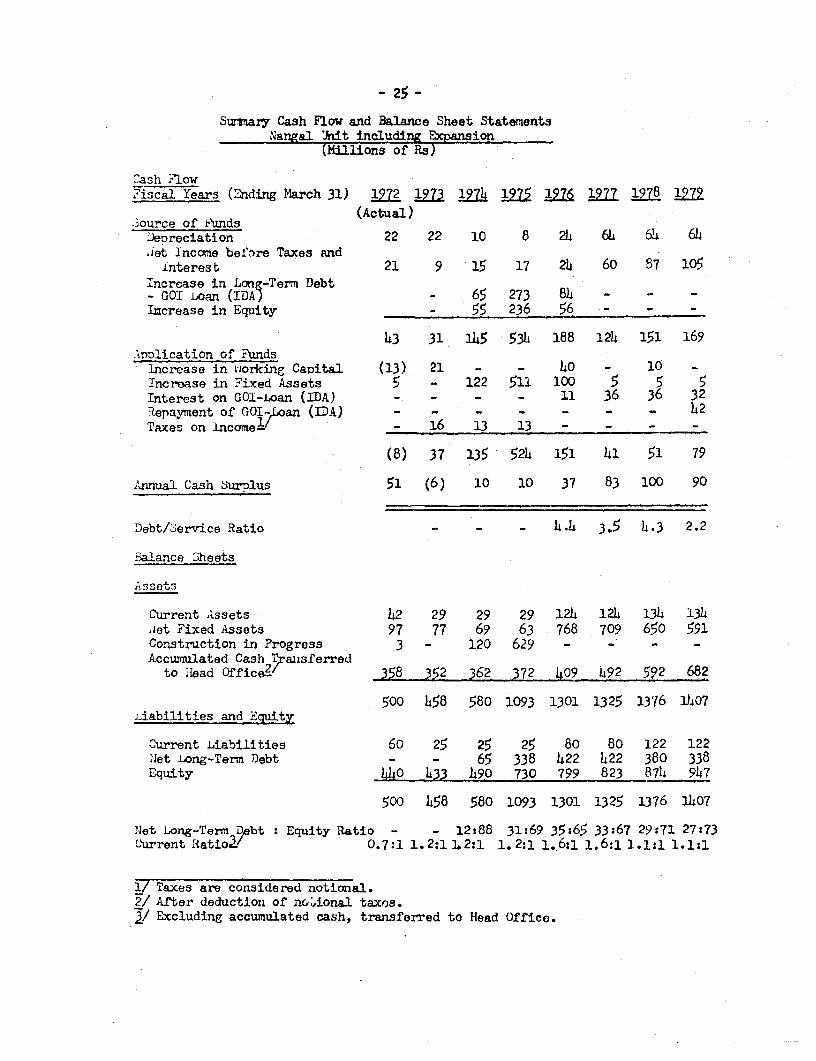

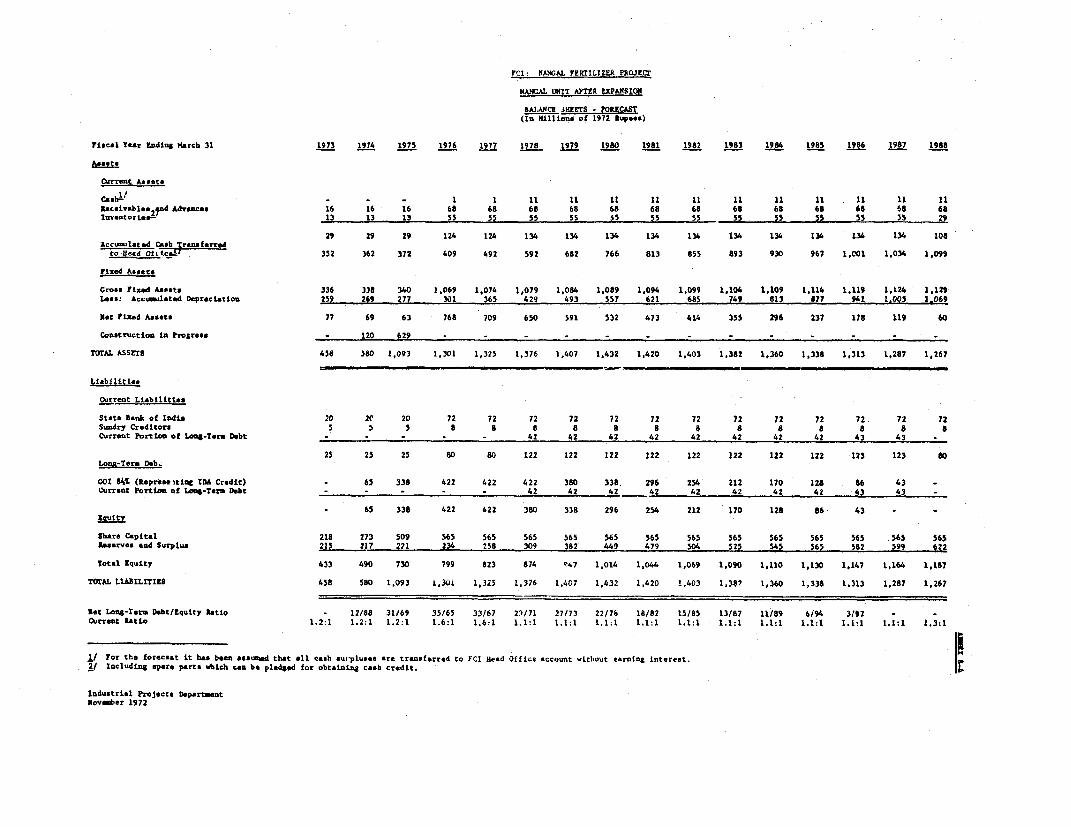

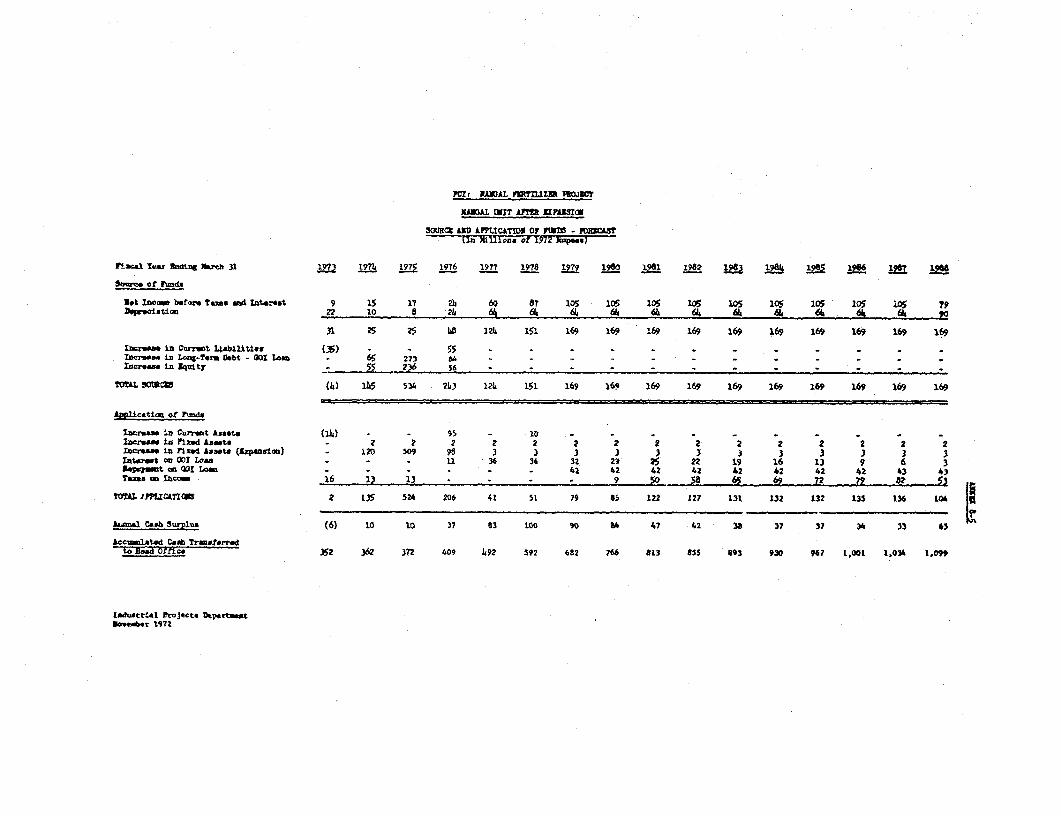

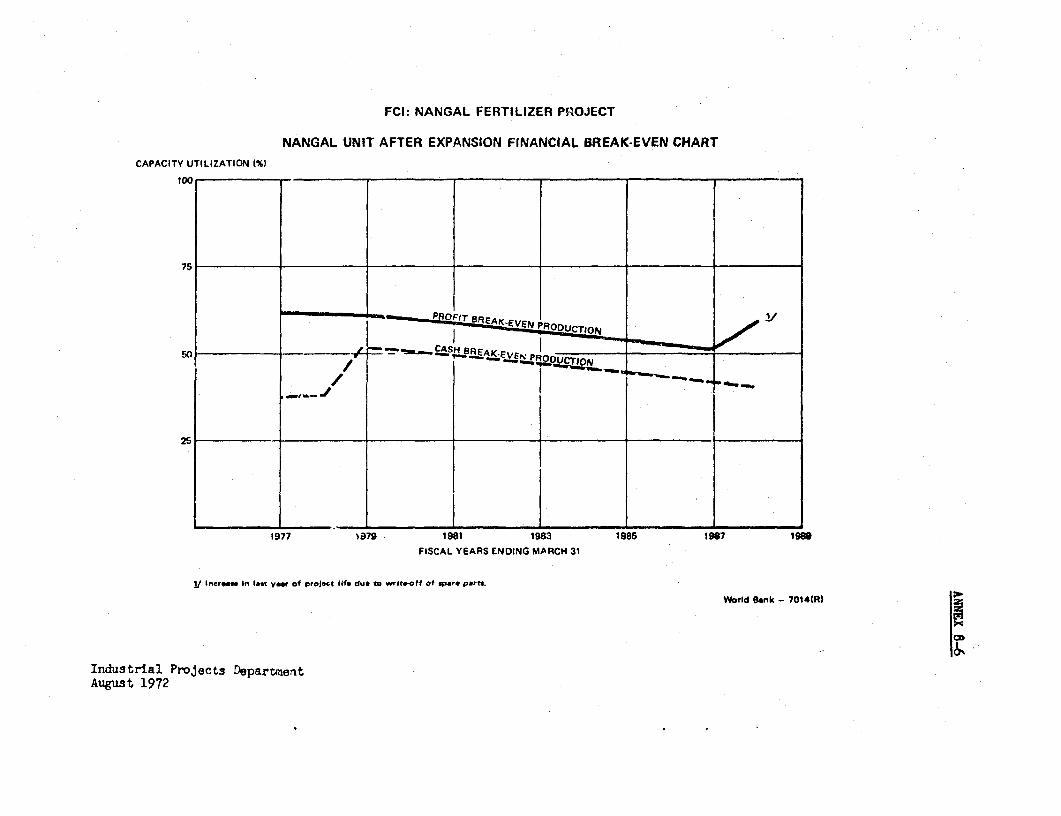

8.09 Projected balance sheet and cash flow statements for Nangal areshown in Annexes 8-4 and 8-5 and are summarized on the following page.These statements show that the project would be soundly"financed with theNangal unit having a debt to equity ratio of 35:65 at the end of construc-tion. Due to the high cash generation and the low debt/equity ratio, pro-jected debt service coverage always exceeds 2.2. The cash break-even pointof Nangal after expansion is expected to be less than 50% of capacity, where-as the profit break-even point declines from about 60% to 50% of capacityduring the life of the project (Annex 8-6). Nangal is an operating unit ofFCI and is thus liable to have its cash surpluses transferred to head office.However, assurances have been obtained during negotiations that Nangal shouldnot be called upon by FCI to transfer funds to FCI if by so doing its c :rentratio would fall below 1.1:1.

D. Financial Return

8.10 The base fiaancial rate of return for the project is 18.1% beforetaxes and 14.0% after taxes. 1/ The project's financial return would besensitive to changes in urea price, rising to 22.72 or falling to 12.6X withprice fluctuations of plus and minus 10% (Annex 9-1). A feedstock price in-crease of 10% would reduce the return to 16.2X and a. one year start-up delay.together with a 15% cost overrun, would lower the return to 12.0,'. With theexception of project completion delays and changes in the urea price, whicthis controlled by GOI, variations in other factors are not likely to underminethe financial viability of the expansion project.

E. Risk

8.11 The project design is based on commercially proven technologywhich should minimize technical risks with regard to design and efficientoperation. The major difficulty of projects in India, particularly in thepublic sector, is in implementation. The association of the two engineer-ing firms, Uhde and Montedison, which have major responsibility for theNangal project implementation including design, procurement, erection andstart-up, should reduce the risk of a project delay.

8.12 There is no appreciable commercial risk since urea is expected tocontinue being in short supply in India, especially in North India, and pricesare virtually controlled by Government policy. FCI's marketing system inNorth India is well developed and no problem is anticipated in selling Nangal'sproduction. The Nangal project itself has a high debt service coverage, al-though FCI may experience financial difficulties over the next few years(para. 2.10).

1/ Taxes are considered notional since income taxes are paid only on acorporate basis (para. 8.08). Therefore financial returns in thischapter refer to ft.iancial returns before taxes. Detailed returncalculations before and after income taxes of 55% are shown inAnnex 9-1.

- 25 -

Suwmary Cash Flow and Balance Sheet StatenientsNanRal Unit including Expansion

(Millions of Rs)

Cash Flow.7iscal Years (2nding March 31) 1972 1973 1974 1975 17 1977 1978 1972

2'ource of tunds (Actua1)Deoreciation 22 22 10 8 24 64 614 64.iet Income befere Taxes and

Lnterest 21 9 15 17 24 60 87 1o5Incroase in Long-Term Debt- GOI Loan (IDA) - 65 273 84 - - -

Iucrease in Equity - 55 236 56 - _ -

43 31 145 53h 188 124 151 169Application of Funds

Increase in wJorking Capital (13) 21 - - 40 - 10 -

Incroase in Fixed Assets 5 - 122 511 100 5 5 5Interest on GOI-,oan (IDA) - - - - 11 36 36 32Repayntent of GOI-,oan (IDA) - - - - - - - h2Taxes on 1nconae - 16 13 13 - - - -

(8) 37 135 524 151 41 51 79

Annual Cash SurDlus 51 (6) 10 10 37 83 100 90

Debt/Service Ratio - - - 4-A 3.5 4.3 2.2

ialance Theets

Asset3

Current Assets 42 29 29 29 124 124 1314 1344et Fixed Assets 97 77 69 63 768 709 650 591

Construction in Progress 3 - 120 629 - - - -Accumulated Cash Transferred

to Head Offic e!2 358 352 362 372 409_ 492 592 682

500 458 580 1093 1301 1325 1376 1407Liabilities and Equity

Current Liabilities 60 25 25 25 80 80 122 122Net Long-Term Debt - - 65 338 422 422 380 338Equity 440 433 1490 730 799 823 874 947

500 458 580 1093 1301 1325 1376 1407

Net Long-Term D bt : Equity Ratio - - 12288 31:69 35:65 33:67 29s71 27:73Current Ratioz' 0.7:1 1. 2:1 2 2:1 1. 2:1 1. 6:1 1.6:1 1.1:1 1. 1:1

1/ Taxes are considered notional.2/ After deduction of ncUional taxos.3/ Excluding accumulated cash, transferred to Head Office.

- 26 -

IX. ECONOMIC ANALYSIS OF THE PROJECT

A. Urea World Market Prices

9.01 International urea prices have behaved similarly to those of manyother man-made commodities, moving from an initial high to an unrealisticlow, and then to more rational levels as oversupply diminishes. In the early1960's some export prices for bagged urea, CIF, India, from small plants tnenexisting exceeded US$100 per ton. By 1970, corresponding prices for urea madein plants ten times bigger had fallen in some cases to the US$55-60 range.Recently, however, FOB prices have begun to rise and shipping rates havefallen. In the first half of 1972, India imported 120,000 tons from '.uropeat US$56-59 FOB (US$67-69 CIF) and 270,000 tons from the Middle East at aboutUS$60 FOB (US$65 CIF). These recent Cir (untied) purchases reflect unusuallylow freight rates, which are expected to return to higher levels. In thelatter half of the year, some contracts with untiecd funds were let in the US$75to US$80 per ton CIF range because of generally tight markVet conditions.

9.02 Reasons for rising urea FOB prices include: increasing naturalgas and petroleum ammonia feedstock prices, escalating plant constructionand start-up costs, and higher bag and bagging costs, as reviewed inAnnex 9-2. No major economies of scale or technical breakthroughs are fore-seen that would appreciably reduce these costs. Recent discussions withbrokers and international e-ganizations suggest typical world urea prices,bagged, CIF, India are likely to be at least in the US$65 to US$70 per tonrange for several years and could go US$5 per ton higher, especiaLly forEuropean material. In this appraisal (and for purposes of the economicproject evaluation) a conservative figure of US$65 per ton of urea, hagged,CIF, India has been used, bearing in mind the probability of increased im-ports from the Middle East and their correspondingly lower shipping costs.

B. Economic Return and Competitive Position vis-a-vis Imports

9.03 Indian fertilizer factories have to use fuel oil or naphtha, andtherefore, have higher feedstock costs than plants based on natural gas, inthe United States or the Middle East. However, on the offsetting side, theNangal Project will make use of existing infrastructure and the new invest-ment will also allow the economic use of existing fertilizer production ca-pacity which is now too costly to use economically (i.e., which is now yield-ing a negative economic rate of return). This economic loss could be eliminated,and the overall situation improved, merely by closing down the existing facil-ities. The whole production of the new Nangal complex, as it will stand afterthe completion of the proposed project, as well as its total production costs,can therefore, be properly attributed to the proposed project. Thus, in arepresentative full year of production, the planned investment would allowthe production of about 210,000 tons of nitrogen per year, at an annual eco-nomic cost of US$22 million. Assuming a c.i.f. price of US$65 per ton for urea,the project would generate annual gross revenues of US$37 million, and netrevenues of US$15 million. Taking into account the lag before full capacity

-27-

is achieved as well as the timing of expenditures and revenues, the economicreturn of the project is 14.6% (Annex 9-1). This rate is used as the baserate of economic return in this report.

9.04 The e)isting Nangal unit is still quite profitable financially,because of the artificially low cost of power charged to it. It is a majoradvantage of the proposed project that it allows FCI to improve the economicefficiency of its operations without depressing its financial returns. Itcould well be argued that, had it not been given this opportunity, FCI wouldnot have felt able to close down the existing Nangal unit, because of acutefertilizer needs and also the resulting labor disruption. If so, tihe savingrealized by closing down the existing electrolysis ammonia unit could alsobe attributed to the proposed project. This would raise the project's eco-nomic rate of return to about 22%.

9.05 The calculation of the economic return i6 based on investment andoperating costs, valued at world market prices as far as these goods aretradeable, and on their estimated economic costs where non-tradeable localsupplies are involved (Annex 8-3). For that purpose the identifiable transferpayments, such as excise duty and other direct or indirect taxes, were ex-cluded from the local costs and major components of unskilled labor containedin investment and operating costs have been evaluated at 50Z of the nominalwage rate.