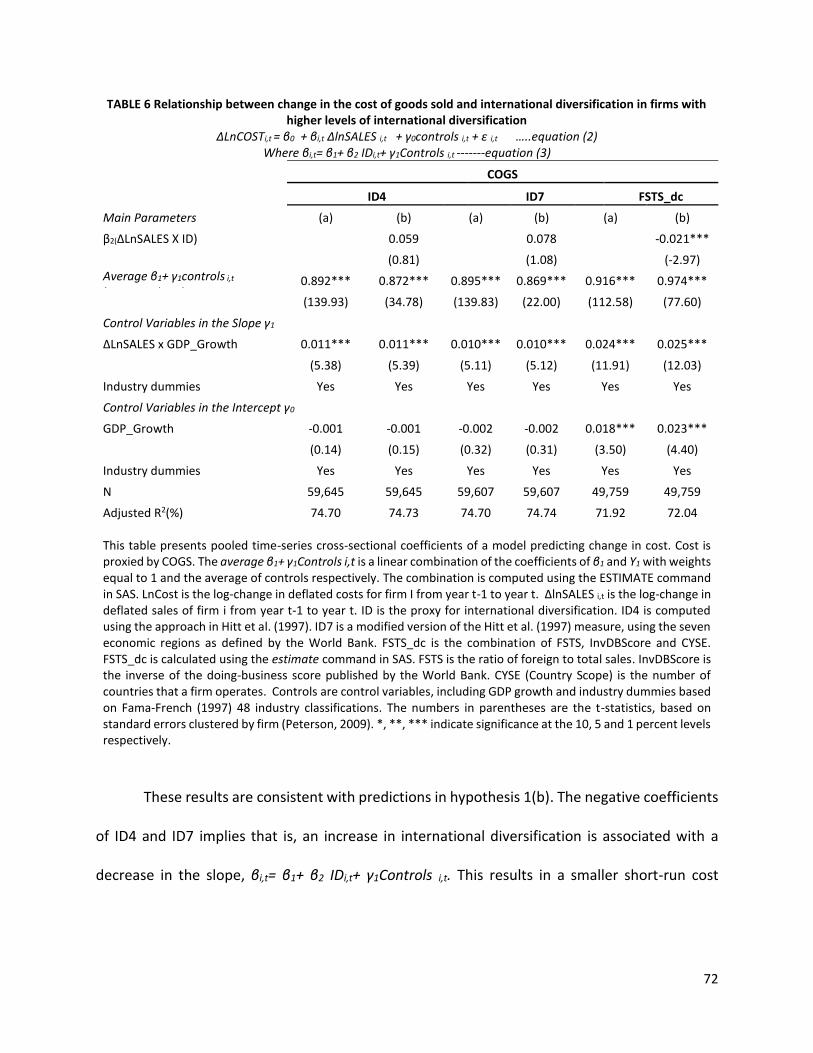

EFFECTS ON COST RIGIDITY AND INVESTMENT ...

155

INTERNATIONAL DIVERSIFICATION: EFFECTS ON COST RIGIDITY AND INVESTMENT CHARACTERISTICS Nancy Kangogo May, 2022 A dissertation submitted to the Kent State University Graduate School of Management in partial fulfilment of the requirements for the degree of Doctor of Philosophy

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of EFFECTS ON COST RIGIDITY AND INVESTMENT ...

INTERNATIONAL DIVERSIFICATION: EFFECTS ON COST RIGIDITY AND INVESTMENT CHARACTERISTICS

Nancy Kangogo

May, 2022

A dissertation submitted to the Kent State University Graduate School of Management in partial fulfilment of the requirements for the degree

of Doctor of Philosophy

ii

Dissertation written by:

Nancy Kangogo

Ph.D., Kent State University, 2022

MBA, Ohio University, 2005

MA, Ohio University, 2005

B. Commerce, Kenyatta University, 2002

Approved by:

Chair, Doctoral Dissertation Committee

Members, Doctoral Dissertation Committee

Accepted by:

Ph.D. Program Director

Graduate Dean,

College of Business Administration

iii

Table of Contents

List of Tables ............................................................................................................................................ iv

List of Appendices .................................................................................................................................... vi

Acknowledgements ................................................................................................................................. vii

CHAPTER 1: INTRODUCTION AND MOTIVATION .......................................................................................... 1

CHAPTER 2. LITERATURE REVIEW ................................................................................................................. 9

2.1 International Diversification ............................................................................................................... 9

2.2 International Diversification and Cost Rigidity ................................................................................. 10

2.3 International diversification and Investment Efficiency ................................................................... 15

2.4 International Diversification and R&D Intensity ............................................................................... 21

2.5 International Diversification and Uncertainty of Future Benefits from Investments ....................... 25

CHAPTER 3: HYPOTHESIS DEVELOPMENT ................................................................................................... 28

3.1 The Relation Between International Diversification and Cost Rigidity ............................................. 28

3.2 The Relation Between International Diversification and Investment Efficiency .............................. 35

3.3 The Relation Between International Diversification and R&D intensity ........................................... 41

3.4 International Diversification and Uncertainty of Future Benefits from R&D Investments .............. 45

CHAPTER 4. SAMPLE AND RESEARCH DESIGN ............................................................................................ 49

4.1 Sample ............................................................................................................................................... 49

4.2 Research Design ................................................................................................................................ 49

CHAPTER 5. RESULTS ................................................................................................................................... 61

5.1 Cost Rigidity- Results of Hypothesis Tests ........................................................................................ 61

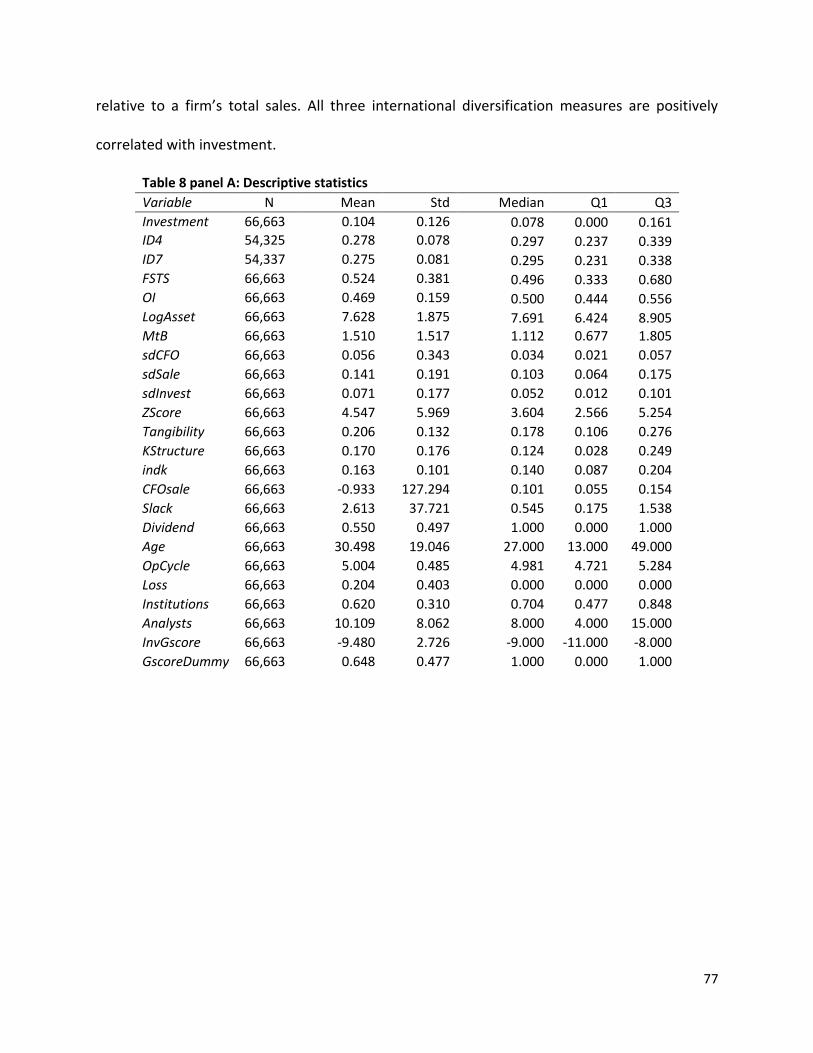

5.2 Investment Efficiency - Results of Hypothesis Tests ......................................................................... 76

5.3 Research and Development Intensity -Results of Hypothesis Tests ................................................. 99

5.4 Uncertainty of Future Benefits from Investments - Results of Hypothesis Tests ........................... 108

CHAPTER 6. CONCLUSION ......................................................................................................................... 118

Appendices ................................................................................................................................................ 130

References ................................................................................................................................................ 145

iv

List of Tables

Table 1: Cost Rigidity Descriptive Statistics ................................................................................. 63

Table 2: The Effect of International Diversification on The Rigidity Of SG&A For Firms with Low

to Medium Levels of International Diversification ...................................................................... 64

Table 3: The Effect of International Diversification on The Rigidity of COGS For Firms with Low

to Medium Levels of International Diversification ...................................................................... 66

Table 4: The Effect of International Diversification on The Rigidity of Changes in Number of

Employees for Firms with Low to Medium Levels of International Diversification ..................... 67

Table 5: The Effect of International Diversification on The Rigidity Of SG&A Costs for Firms with

Higher Levels of International Diversification .............................................................................. 70

Table 6: The Effect of International Diversification on The Rigidity of Cost of Goods Sold Costs

for Firms with Higher Levels of International Diversification ...................................................... 72

Table 7: The Effect of International Diversification on The Rigidity of Changes in Number of

Employees for Firms with Higher Levels of International Diversification ................................... 74

Table 8 Panel A: Investment Efficiency -Descriptive Statistics .................................................... 77

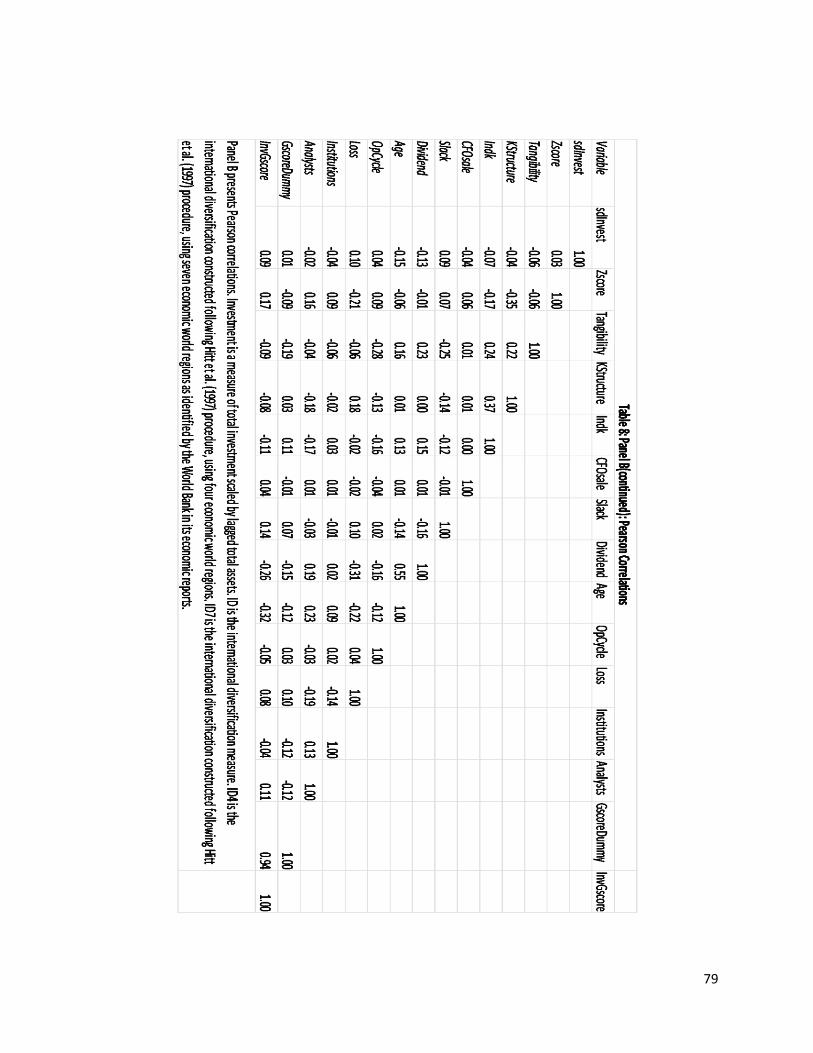

Table 8 Panel B: Investment Efficiency -Correlations .................................................................. 78

Table 8 Panel C: Investment Efficiency -Variable Definitions ...................................................... 80

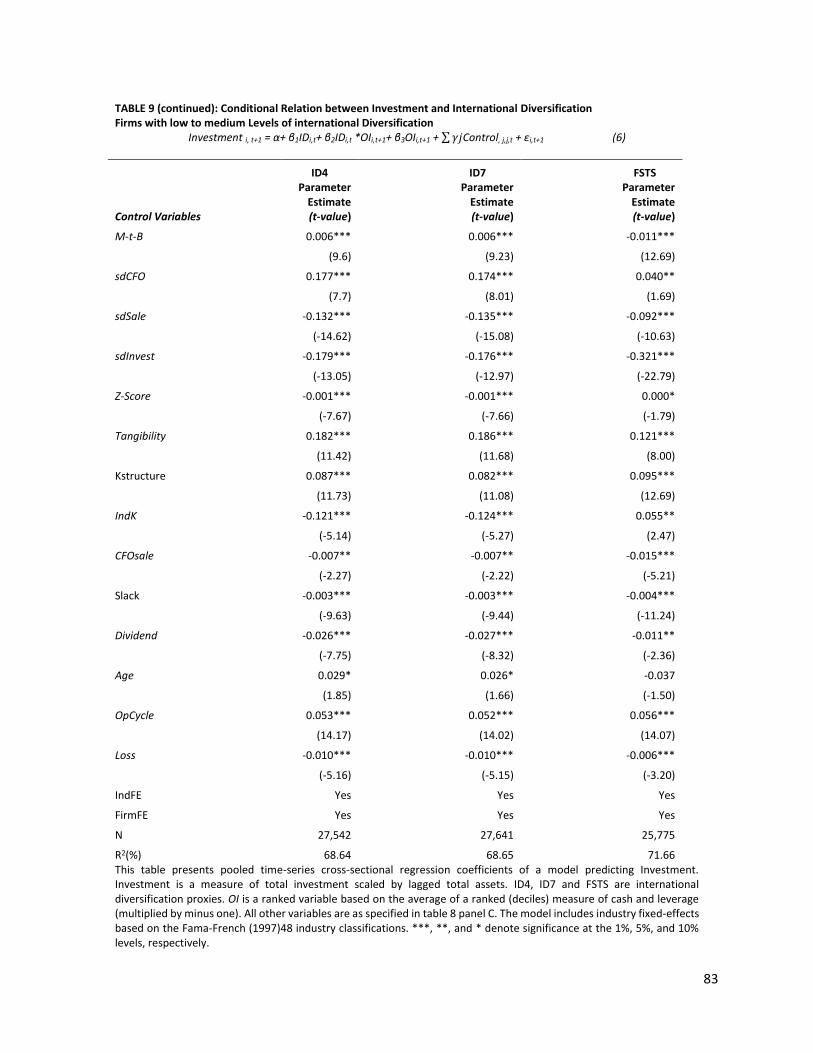

Table 9: Conditional Relation Between International Diversification and Investment for Firms

with Lower to Median Levels of International Diversification .................................................... 82

Table 10: Conditional Relation Between International Diversification and Investment for Firms

with Higher Levels of International Diversification ..................................................................... 86

Table 11: Deviation from Expected Level of Investment for Firms with Lower to Median Levels

of International Diversification: Under-investment Versus Normal Investment ........................ 90

Table 12: Deviation from Expected Level of Investment for Firms with Lower to Median Levels

of International Diversification: Over-investment Versus Normal Investment ........................... 92

Table 13: Deviation from Expected Level of Investment for Firms with Higher Levels of

International Diversification: Under-investment Versus Normal Investment ............................ 95

Table 14: Deviation from Expected Level of Investment for Firms with Higher Levels of

International Diversification: Over-investment Versus Normal Investment ............................... 97

Table 15: R&D Intensity Descriptive Statistics ........................................................................... 100

Table 16: R&D Intensity Correlations ......................................................................................... 101

Table 17: Effects of International Diversification On R&D Intensity-Fixed Effects .................... 104

v

Table 18: Effects of International Diversification On R&D Intensity: OLS Regressions ............. 105

Table 19: Uncertainty of Future Benefits from Investments -Descriptive Statistics ................. 110

Table 20: Effects of International Diversification on The Uncertainty of Earnings ................... 112

Table 21: Effects of International Diversification on The Uncertainty of Cash Flow from

Operations .................................................................................................................................. 115

Table 22: Effect of International Diversification on The Uncertainty of Sales Revenue ........... 117

vi

List of Appendices

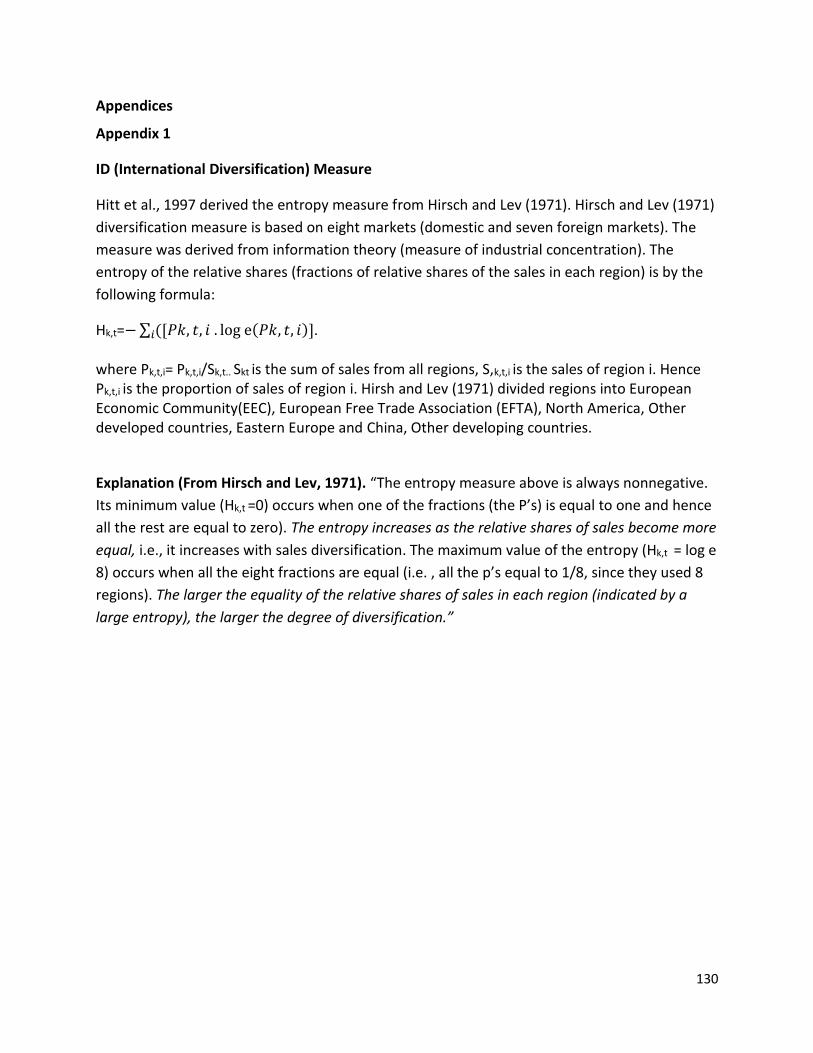

Appendix 1: International Diversification Measure ................................................................... 130

Appendix 2: Variable Definitions ............................................................................................... 132

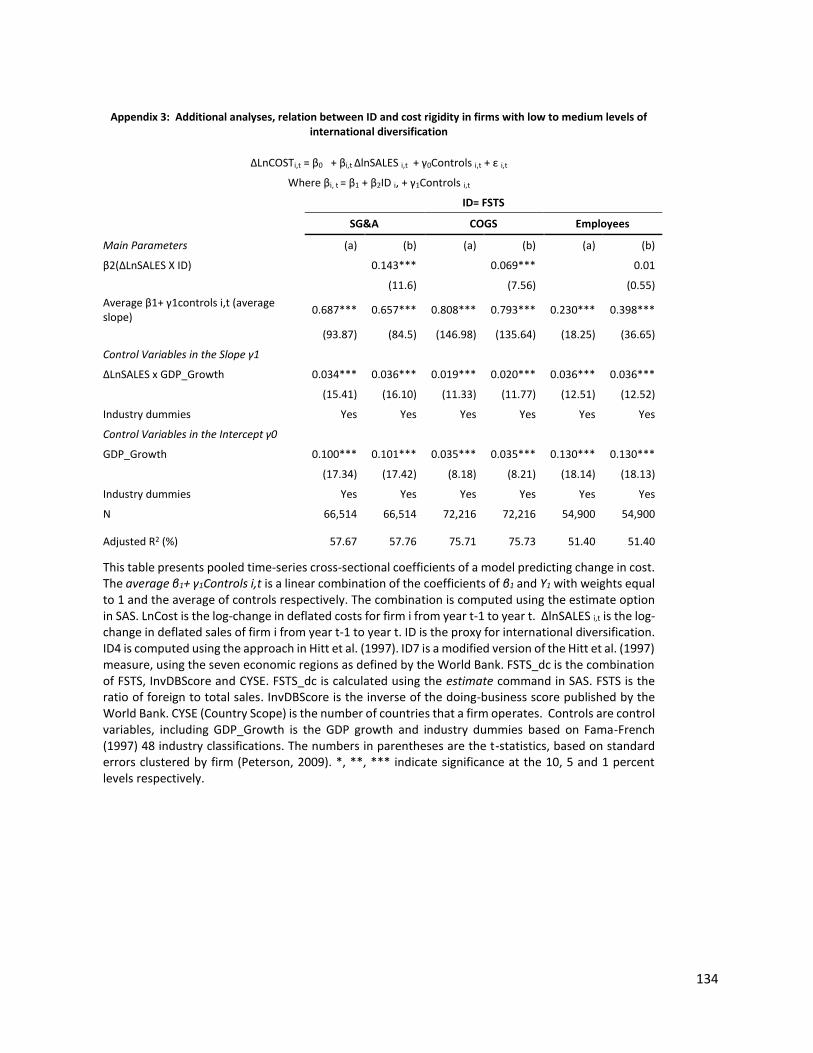

Appendix 3: Additional Analyses, Relation Between International Diversification and Cost

Rigidity in Firms with Low to Medium Levels of International Diversification .......................... 134

Appendix 4: Additional Analyses, Relation Between International Diversification and Cost

Rigidity in Firms with Higher Levels of International Diversification ......................................... 135

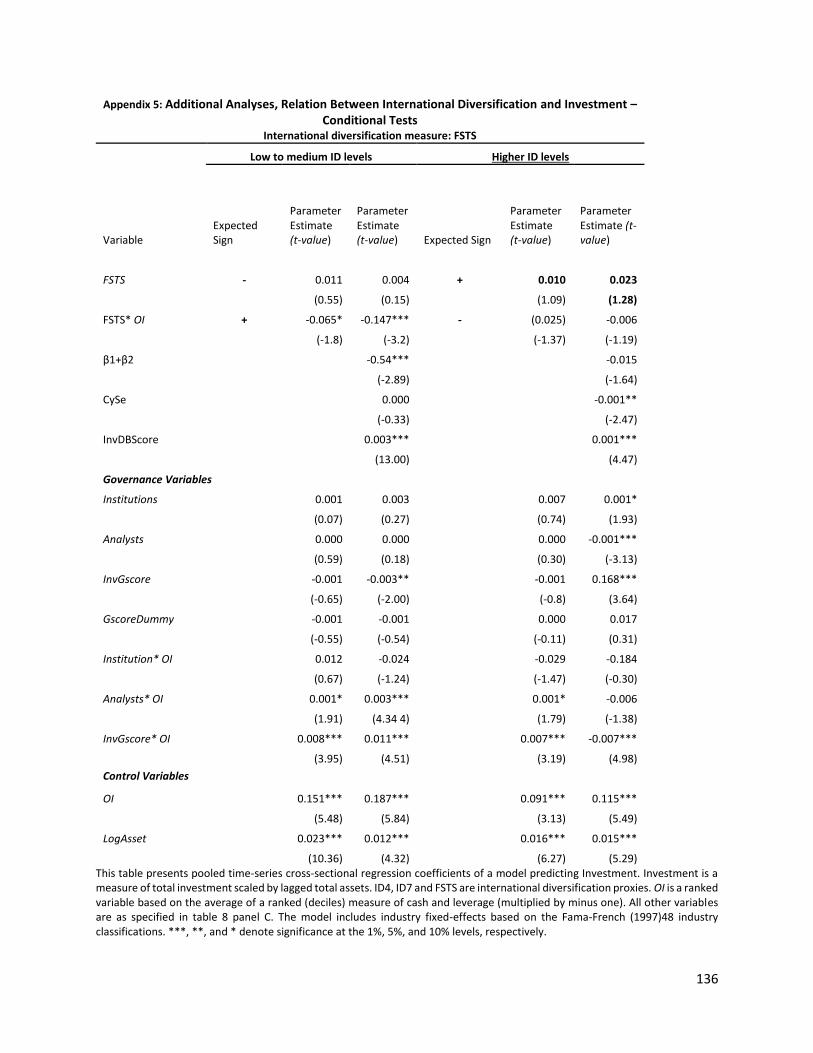

Appendix 5: Additional Analyses, Conditional Relation Between International Diversification and

Investment ................................................................................................................................. 136

Appendix 6: Additional Analyses, International Diversification and Deviations from Expected

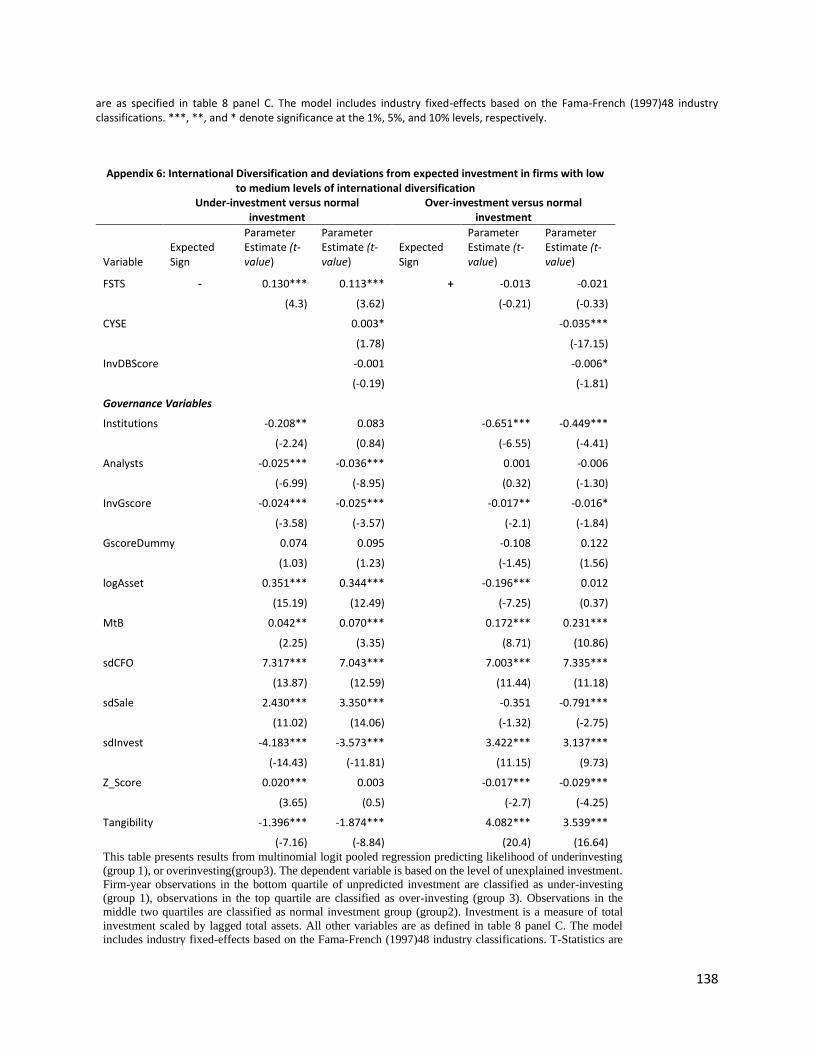

Investment in Firms with Low to Medium Levels of International Diversification ................... 138

Appendix 7: Additional Analyses, International Diversification and Deviations from Expected

Investment for Firms with Higher Levels of International Diversification ................................. 140

Appendix 8: Additional Analyses- Relation Between International Diversification and R&D

Intensity for Firms with Low to Medium Levels of International Diversification ...................... 142

Appendix 9: Additional Analyses- Relation Between International Diversification and R&D

Intensity for Firms with Higher Levels of International Diversification ..................................... 143

Appendix 10: Additional Analyses- Effect of International Diversification on the Variability of

Future Benefits from R&D Investments ..................................................................................... 144

vii

Acknowledgements

First, I would like to thank God for the opportunity to pursue my doctoral program at

Kent State University. It has been a great blessing that enabled me to pursue my dream.

This dissertation is dedicated to my parents Mary Kangogo and the late Thomas

Kangogo Tegucho, and my sisters Lenah and Margaret. Without their assistance with my

upbringing, this journey would not have been possible. I thank my loving husband, Lewis, and

our kids, who have been very encouraging and patient with me throughout this journey.

I am eternally indebted to my dissertation committee, Rini Laksmana (Chair), Shunlan

Fang, and Murali Shanker for the time they invested in me and my success. Their enormous

support and guidance made this accomplishment possible.

I would like to acknowledge and appreciate the outstanding Kent State graduate faculty

that I had the pleasure to work with during my PhD program, including Pervaiz Alam, Mark

Altieri, Emmanuel Dechenaux, Arno Forst, Eric Johnson, Wei Li, John Rose, Drew Sellers, Wendy

Tietz, Jennifer Wiggins-Johnson, and Linda Zucca, among others.

A special thank you to my fellow accounting Ph.D. Students who were a great help and

company along the way.

1

CHAPTER 1: INTRODUCTION AND MOTIVATION

1. Introduction 1.1 Research Questions

Firms have been increasingly expanding their business activities across geographic regions

in pursuit of competitive advantages (Lu & Beamish 2004; Ramaswamy, 1995). Competitive

advantage result from economies of scale, access to resources, cost reduction, extension of

innovative capabilities, knowledge acquisition, location advantages and performance

improvements (Hitt et al., 1997). This research examines the relation between international

diversification1 and two factors: cost rigidity and investment characteristics. International

diversification can be defined as the expansion of a firms’ operation across country borders into

geographic locations that are new to the firm.

The research examines two questions. The first question is whether international

diversification is related to cost rigidity. Cost rigidity is an indication of the relative proportions

of variable-to-fixed costs ratio, and it is measured as the percentage change in cost for a

percentage change in sales revenue (Holzhacker et al., 2014; Banker et al., 2014). For example,

the percentage changes in selling and administrative expenses for a percentage change in sales

revenue.

The second question is whether international diversification affects investment

characteristics. I examine three investment characteristics: investment efficiency, uncertainty of

1 International M&A lead a level of international diversification depending on the number of foreign geographic

regions, sales per region among other factors.

2

future benefits from investments and R&D (research and development) intensity. R&D intensity

is used as a proxy for innovation.

1.2 Importance of the Research Questions

1.2.1 International diversification

This study’s focus on international diversification is due to four main reasons. First,

international diversification plays a pivotal role in corporate expansion and the strategic behavior

of large firms (Hitt et al., 1996) and has critical effects on firm outcomes relevant to global

competitiveness (Franko, 1989, Hitt et al., 1994) and firm performance (Lu and Beamish, 2004).

International diversification is therefore important for analyzing corporate strategy, goals, and

outcomes.

Secondly, the uniqueness of factors surrounding international diversification draws

further importance to this examination. International diversification presents unique benefits,

challenges, and costs due to the cross–border setting. A major source of benefits accrues to the

unique resource endowments and location-specific advantages in each host country (Lu and

Beamish, 2004). Internationalization provides opportunities to exploit imperfections in cross-

border use of firm assets (Caves 1989; Buckley, 1988), and improve knowledge base (Delios and

Henisz, 2000; Zahra et al., 2000). Alongside the opportunities, international diversification offers

great challenges (Child et al., 2001) and costs (Lu and Beamish 2004, Hitt et al., 1994).

Thirdly, there are trends towards increased international diversification despite

documented lower than expected performance and significant failures to realize the goals of the

3

international diversification (McGee, 2014). For example, over the past couple of decades there

has been dramatic increases in M&A activity and deal volume (Weber et al., 2013), as well as

huge increases in the number of deals (Shimizu et al., 2004). These trends are counterintuitive

given evidence that the rate of M&A failures is greater than 50 percent, with most of managers

reporting significant failures to achieve merger goals (Weber et al., 2013; Shimizu et al., 2004).

Lastly, the focus on international diversification is motivated by the voids in prior

literature. While the variation in firms’ performance following international diversification has

been widely documented in prior literature (e.g., Hitt et al., 1997), there are still voids in

understanding the reasons behind the variations in the findings. Studies document varying

patterns of association between international diversification and performance and other

measures of value. The mixed results have warranted calls by some scholars for the need to go

beyond investigation of the direct relations (e.g., Hitt et al., 2006). For example, studying

acquisition process and outcomes is an important step in understanding mergers and acquisitions

(Haspeslagh and Jemison, 1991; Child et al., 2001; Shimizu et al., 2004). This study heeds these

calls and aims to fill some of the voids in understanding the value creation effects of international

diversification by examining its interaction with cost rigidity and investment characteristics.

1.2.2 The relation between International Diversification and Cost Structure

In examining the relation between international diversification and cost structure, cost

rigidity is used as a proxy for cost structure. International diversification may affect cost rigidity

due to changes in firm resources and characteristics, the need to adjust to foreign territorial

conditions and changing market conditions (e.g., size, characteristics, opportunities, and threats).

4

An examination of the relation between international diversification and cost structure is

warranted by the pivotal role that cost structure plays in firm operations and ability to generate

profits. Cost rigidity is an important factor in firm performance because of its link to firm resource

commitment decisions in the face of adjustment costs (Banker et al., 2013). One of the main

reasons behind international mergers includes the potential benefits from economies of scale

and scope. A significant increase in productivity following mergers is from synergies. Synergies

arise from the sharing activities, and lumpy2 and intangible assets (Caves, 1989). Sharing affects

cost rigidity. Thus, there is an association between cost rigidity and the degree to which firms

gain from economies of scale and scope.

Evidence on the association between international diversification and cost rigidity is

useful to various stakeholders. Amihud et al. (2002) argues that cross-border operations lead to

increases in monitoring problems related to various factors including operating cost structure

among others. An examination of the relation between cost rigidity and international

diversification is useful to firms since it will shed light on firms’ success in adapting to changes in

geographic and other global market characteristics. Further, evidence on the relation between

international diversification and cost rigidity is useful for planning purposes. Management may

use such knowledge in increasing accuracy when estimating adjustment costs and potential gains

from economies of scale and scope.

2 Lumpy assets are those that represent a significant portion of total assets. Acquisition of lumpy assets involves significantly large cash or other financial resources.

5

1.2.3 International diversification and investment characteristics

International diversification may affect various investment characteristics including

investment efficiency, R&D intensity, and uncertainty of future benefits from investments.

International diversification may affect investment characteristics due its effects on various

factors. First, international diversification increases investment opportunities and organizational

goals. This is likely to affect investment efficiency, R&D intensity, and uncertainty of future

benefits from investments. For example, international diversification may lead to greater

investment efficiency due to an increased number of positive NPV projects available. Second,

international diversification increases organizational challenges from factors such as increased

demand fluctuations, institutional disruption (Kogut and Chang 1996; Allen and Pantzalis 1996),

information asymmetries and greater information processing costs (Kogut and Singh, 1988).

These challenges are likely to impact investment characteristics. For example, increased demand

fluctuations lead to increased uncertainty of future benefits from investments. Third,

international diversification fosters an environment that is more conducive to agency problems

due to increasing organizational goals, and greater information processing goals and information

asymmetries. These factors collectively affect firms’ investment strategies and choices which in

turn affect investment characteristics.

The importance of examining the relation between international diversification and

investment characteristics lie in role that the two factors and their interactions play in firm

operations and performance. Investment plays a critical role in firm performance. The quality

and quantity of investments relative to other firm factors is important as it affects long-term

6

operational sustainability and value creation through effects on revenue generation and cost

management.

Evidence on the relation between the degree of international diversification and

investment characteristics will also help illuminate puzzles presented by findings in prior

research. For instance, despite the strong evidence that diversification is value decreasing (e.g.,

Denis et al., 2002; Amihud and Lev; 1999), prior literatures document significant increases in

pursuit of global operations (e.g., Denis et al., 2002). Further, the results from the examination

of the relation between diversification and performance and other value measures are mixed.

This reinforces the importance of this examination since investment characteristics are related

to firm performance.

1.3 Contributions

The examination of international diversification and its relation to cost rigidity and

investment characteristics will provide insights into the variation in firms’ performance following

international mergers and acquisitions. This study heeds the calls in prior literature for evidence

on factors surrounding diversification (e.g., Hoskisson and Hitt, 1990; Rumelt, 1982; Haspeslagh

and Jemison, 1991; Child et al., 2001; Shimizu et al., 2004)). An examination of the relation

between international diversification and cost rigidity will contribute to the understanding of

corporate strategy and decisions. It will provide evidence whether firms are benefiting from

integration following international mergers and acquisitions. An examination of the relation

between international diversification and investment characteristics contributes to the

7

understanding of changes in firm performance following international diversification because

investment characteristics are linked to firm performance.

The evidence from this study will contribute to literature on international diversification.

There is scant literature examining the relation between international diversification and cost

rigidity as well as various investment characteristics. Despite the numerous studies on over-

investment (e.g., Richardson, 2006; Hubbard, 1998), there is scarcity of evidence on the link

between international diversification cost rigidity and investment efficiency3. This study is

valuable because it will provide various evidence from analyses based on a larger data set.

Evidence on the relation between international diversification and cost rigidity as well as

investment characteristics is beneficial to various stakeholders including management, investors,

and researchers. The evidence will be useful for managers evaluating risks, potential

opportunities, and value from international diversification, making decisions about international

diversification, and setting future corporate strategies. This knowledge could provide more

insights for estimating expected values from foreign mergers and generating better analyses and

decisions for international diversification pursuits.

The findings from this study are useful for investors assessing risk and choosing firms to

invest in. For example, investors may prefer to avoid investing in firms with a high level of

diversification if there is evidence that they exhibit high level of investment inefficiencies. The

findings from this study will provide valuable insights for researchers. For instance, relationships

between international diversification and cost rigidity and/or investment characteristics can be

3 Fuegebbayn et al (1997) examines the relation between international diversification and R&D intensity. The research however focuses only on 104 US firms with operations in the Middle East. Hitt et al. (1997) examines the relation between diversification and R&D intensity. The paper, however, uses only three years of data.

8

used in analyzing the documented evidence of variations in performance following international

mergers. The findings will provide leads into research areas that can narrow the research gaps in

documenting international diversification. For example, finding a positive correlation between

international diversification and uncertainty of future benefits may draw attention to research

into the specific causes leading to the uncertainty and potential remedies.

1.4 Research Approach

In addressing the research questions above, archival data will be used. The sample will

include US firms that are internationally diversified. The sample period will be for the years 1990

and 2018 Using a sampling period of two decades present an opportunity to examine the

variables of interest in the long run as some firms continue to increase their diversification levels

while others decrease it through divestitures or other means. Further, it facilitates comparisons

across periods using sub-samples. The restrictions to only US acquirers ensure a level of similarity

of the acquirer firms underlying factors such as management expertise and company resources

among others.

9

CHAPTER 2. LITERATURE REVIEW

2.1 International Diversification

International diversification (ID) is a strategy through which a firm expands the sales of its

goods or services across the borders of global regions and countries into different geographic

locations or markets (Hitt et al., 2007). International diversification is reflected by the number of

geographical markets and the firms’ degree of influence on the market. For instance, the firm’s

market share percentage in a country. Large-scale changes in the global environment over the

decades have made international diversification a very important strategic option for firms

seeking competitive advantage (Nachum and Zaheer, 2005) and value-creation opportunities

(Cartwright and Schoenberg, 2006). Hoskisson and Hitt (1990) present three market

imperfections that enable or drive firms to diversify4; firm resource heterogeneity, external and

internal firm incentives for diversification, and managerial incentives for diversification.

The imperfections also drive international diversification. International diversification

offers greater means for value creation through access to foreign stakeholders, resources, and

institutions (Hitt et al., 2006). Literature examining international diversification firm success in

achieving value creation document inconsistent results. Some studies documented positive

association between international diversification and various measures of firm value, such as

combined value of target and acquiring firms (Bradley et al., 1988), and market value (Ramirez-

Aleson and Espitia-Escuer, 2001). On the contrary, other studies found negative association

between international diversification and firm value (Berger and Ofek, 1995; Denis et al., 2002)

4 Authors argue imperfection is necessary for diversification; that is, diversification cannot be expected by firms acting in perfectly competitive markets.

10

and other related measures, such as earnings persistence (e.g., Riahi- Belkaoui, 2002; Riahi-

Belkaoui, 1998). Other studies document no impact of international diversification on total firm

value (e.g., Lins and Servaes, 1999).

Similarly, the results on the relation between international diversification and

performance are mixed. There is evidence of positive relationships (e.g., Geringer et al., 1989;

Delios and Beamish, 19995), and non-linear6 relationships (e.g., Hitt et al., 1997; Lu and Beamish,

2004; Capar and Kotabe, 2003; Ruigrok and Wagner, 2003; Lu and Beamish, 2001; Gomes and

Ramaswamy, 1999; Hitt et al., 1997; Lu and Beamish, 2004; Contractor et al., 2003; Quan and Li,

2002; Thomas and Eden, 2004; Qian and Li, 2002). The mixed results show that the association

between international strategies and both firm value and performance remain complex (Hitt et

al., 2006; Gomes and Ramaswamy, 1999). Further, it alludes to differences in other factors linked

to value creation and firm performance. The factors include cost and investment characteristics,

among other variables that are critical to success of internationally diversified firms.

2.2 International Diversification and Cost Rigidity

Cost rigidity is an indication of the relative proportions of variable-to-fixed costs ratio. It

is measured as the percentage change in cost for a percentage change in sales revenue

(Holzhacker et al., 2014; Banker et al., 2014). My examination of cost rigidity is motivated by the

fact that it is an attribute of cost behavior.7 Prior literatures specifically highlight the strategic

role of cost and its importance in strategic choices. For instance, Porter (1985) argues that cost

leadership is a main strategy to gaining competitive advantage.

5 Uses geographical scope instead of diversification. 6 Various forms of non-linear relationships 7 Cost behavior is the resource adjustment in response to changes in activity (Banker et al., 2014)

11

Cost is even more critical to internationally diversified firms. In fact, many motives for

international diversification are linked to cost factors. Motives for international diversification

include access to new resources, synergy from economies of scale and scope, performance

improvements (Hitt et al., 1997; Hitt et al., 2006) and exploitation of tax reduction opportunities

(Mudambi, 1995). All these motives are linked to firm cost factors or the objective of gaining

value through cost reduction. In line with these motives, Cullinan (2004) argues that some major

factors to consider when evaluating acquisitions include cost advantages and potential

improvements in costs that can be achieved. In line with the highlighted motives, international

diversification firms undergo changes and face unique factors that affect cost relationships.

Specifically, they experience changes in resources, firm internal capital market, among other

factors. In addition, they find opportunities for internalization, synergy realizations and efficiency

gains.

Arguments and findings in prior literature point to resource availability and the quest for

more resources as some of the main drivers of diversification. For instance, there are arguments

that diversification is driven by endowment of resources (Delgado-Gomez et al., 2004) and

availability of resources (Porter, 1987) including slack resources (Banker et al., 2011). RBV

(resource-based view or resource-based theory) has been widely used in diversification studies.

According to Rindova and Fombrun (1999: 694):

“Resource-based theory (Penrose, 1959; Barney, 1991) attributes advantage in an industry to a firm's control over bundles of unique material, human, organizational and locational resources, and skills that enable unique value-creating strategies (Barney, 1991).” Peteraf, (1993) notes that “heterogeneous resources create distinct strategic options for a firm that, over time, enable its managers to exploit different levels of economic rent. A firm's resources are said to be a source of competitive advantage to the degree that they are scarce, specialized, appropriable (Amit and Schoemaker, 1993), valuable, rare, and difficult to imitate or substitute (Barney, 1991).”

12

In the quest to gain resources, location is one of the core factors to firms undertaking

international diversification (Hymer, 1976). Location theory posits that multinational

corporations (MNCs) stand to achieve significant cost benefits because they can access cheaper

labor and material in overseas markets (Gomes and Ramaswamy, 1999). The variation in MNC

firm operating regions, offers MNCs the potential to take advantage of arbitrage opportunities in

factor cost differentials across multiple locations (Kogut, 1985). There is evidence that MNCs take

advantage of variation in country resource endowments such as availability of cheap labor (e.g.,

Kravis and Lipsey, 1982). Arbitrage opportunities facilitate changes to capacity and other factors

related to firm cost rigidity. There is evidence that firms shift their cost structure and tend to

have more labor intensive instead of capital-intensive operations in countries with lower cost of

labor (Kravis et al., 1978).

Extant literature commonly points to economics of internal capital markets as one of the

major advantages from diversification (e.g., Jones and Hill, 1998). International diversification

enables firms to increase their internal capital markets and their financing ability. International

diversification strategies such as acquisition, lead to an increase in both tangible and intangible

assets including goodwill, technical knowledge, and managerial skill set among others. This leads

to increases the ability to borrow as well as increase other resources. Greater resource availability

is particularly important, because a significant portion of firms’ tangible and intangible assets

that can only be acquired or increased in discrete and relatively large lumps (Caves, 1989).

Resources are crucial to cost decisions as capacity building and adjustments to manage overall

costs requires cash and other capital resources.

13

International diversification facilitates internalization. A firm can be viewed as an

internalized buddle of resources that can be allocated between product groups and markets

(Buckley and Casson, 1976). Literature point to internationalization as a means through which

internationally diversified firms gain efficiency (e.g., Hennart, 1982; Hitt et al., 1997). Firms are

prompted to enter international markets where transactions are not efficiently conducted

(Hennart, 1982) and gain from improving efficiency by internalizing acquired business units

(Caves, 1996). Moving transactions within the firm improves control, facilitates the dissemination

of information, and offers means of dispute resolution (Caves, 1996). Further, it facilitates

changes in management and agency related costs through reorganization of business units and

displacement of inefficient managers. Consequently, it may reduce agency costs relating to

subsidiaries.

Changes in resources and internalization promote efficiencies and synergistic gains.

Larsson and Finkelstein define synergy realization as “the actual net benefits (such as reduced

cost per unit, increased income) created by the interaction of two firms involved in a merger or

acquisition” (Larson and Finkelstein, 1999, p3). Lubatkin (1983) presents three main sources of

synergies8 including technical economies, pecuniary economies, and diversification economies.

Harrison et al., (1991) attribute synergy to two main sources; improved operating efficiencies

due to economies of scale or scope, and skill transfers. Similarly, internalization enables firms to

achieve corporate level synergy through marketing, R&D and other corporate level activities

8Lubatkin (1983) examines mergers in general, I expect similar patterns with international diversification.

14

(Yavitz and Newman, 1982) and overcome transaction difficulties in exploiting synergy through

the market forces (Jones and Hill, 1998)9.

Major sources of cost synergies include resource sharing (Hitt et al., 1994), resource

combinations (Marks and Mirvis, 2010). Firms combine resources following combinations and

share activities and resources such as personnel, plant and equipment, sales force, and

distribution channels for multiple products (Marks and Mirvis, 2010). For example, Procter and

Gamble uses the same physical distribution system for both diapers and paper towels. Sharing

promotes competitive advantage through either differentiation or lowered costs (Porter, 1996).

There are arguments and evidence that synergistic efficiencies increase market power over

competitors (Stewart et al., 1984; Montgomery, 1985).

Despite the factors discussed above which present opportunities for cost reductions,

firms diversifying internationally face cost trade-offs of doing business abroad (Hymer, 1976;

Caves, 1996). As US firms progressively diversify into foreign markets, they are likely to

experience increases in information impactedness10 due to greater physical, technological, and

psychic distance (Qian and Li, 2002; Markides, 1995; Habib and Victor, 1991). For example, for

firms diversify internationally, coordination, distribution, communication, and other related costs

will increase considerably and may exceed diversification gains (Hitt et al., 1997). Therefore, the

extent of gains from additional resources, internalization, improved efficiencies, and synergistic

9Jones and Hill (1998) identify that, economic benefits arise when internalization leads to decrease in production costs due to investment in specialized assets, decreased misallocation of resources and decreased need for complex contracts. 10 asymmetric distribution of information between parties to a transaction (Jones and Hill 1988)

15

gains is largely dependent on the firm’s ability to manage opportunities and control the costs of

international diversification.

2.3 International diversification and Investment Efficiency

Investment efficiency is critical to the success of internationally diversified firms.

According to Biddle et al. (2009) “a firm is investing efficiently if it undertakes projects with

positive net present value (NPV) under the scenario of no market frictions such as adverse

selection or agency costs. Thus, under-investment includes passing up investments with positive

NPV in the absence of adverse selection. Correspondingly, over-investment is investing in

projects with negative NPV.”

As a firm diversifies internationally there are various factors within the firm and its

operating environments that may affect investment efficiency. These factors center around their

effects on financial and other resources or other factors that have either direct or indirect impact

on firm investment activities. The following subsections discuss some of these factors.

2.3.1 Factors that encourage investment efficiency

Firms diversifying internationally experience various factors that are conducive to optimal

investing. These include increases in resources, tax incentives, managerial cultural diversity,

investment opportunities, market size, market needs, and opportunities for synergistic gains in

the global environment. International diversification leads to increases in financial and non-

financial resources that are critical to firm investment initiatives. The financial resources include

cash and debt capacity. A common argument in prior literature is that international

diversification increases debt capacity due to combination of businesses with imperfectly

16

correlated earnings streams (Ofek and Berger, 1995; Lewellen, 1971). In addition to increased

debt capacity, international diversification provides the flexibility for firms to borrow capital in

countries with lower borrowing costs (Denis, Dennis, and Yost, 2010) and it also creates

additional tax benefits through interest deductions (Berger and Ofek, 1995).

Tax provisions and incentives not only influences international diversification decisions,

but also MNE investment decisions. Tax advantages arise due to factors such as differences in tax

rates across countries and investment related tax incentives in various countries. Lower tax rates

and provision of infrastructure are important to investment decisions (Mudambi, 1995).

International diversification increases opportunities for tax avoidance using strategies such as

income shifting.

As firms diversify internationally, they can attract a more culturally diverse top

management team (Hitt et al., 1997). Managerial talent and skill pool are essential to the

formulation, implementation and monitoring of firm strategies including those related to

investments. Hoskisson et al. (1994) discusses that better knowledge of diverse market facilitates

coordination and the use of strategic controls.

International diversification increases potential investment opportunities arising from the

need to exploit market imperfections (Caves, 1989; Buckley, 1988). An increase in investment

opportunities emanates from the expansion into other geographical regions as well as other

sectors. Caves (1971) highlights that the initial impetus to a firm’s internationalization comes

from the opportunity to exploit market imperfections in the cross-border use of its intangible

assets. The opportunity to exploit market imperfections in the use of firm intangible assets is

17

indeed a main driver in most cases, even for firms with different initial motivations for

diversifying internationally.

Access to foreign markets raises the need for additional investments to take advantage

of the additional market opportunities. Specifically, additional investments are necessary to meet

the demands of the growing market as well as unique or modified demands of newer markets.

The need for additional investments is fueled by the fact that success in the global market relies

on innovations (Hitt et al., 1997). Further, customers expect higher quality products at lower

costs.

International diversification provides avenues for increased efficiencies and synergies.

Cross border mergers may speed new market access and promote globalization synergies

(Forsgren, 1989; Olie, 1990). Increased efficiencies may lead to accumulation of additional

financial and other resources that may be used for investments. Further, cross border mergers

and acquisitions can enhance combination potential in ways not available domestically. For

example, a firm may acquire an overseas target with complementary technology that is not

available locally.

2.3.2 Factors that may hinder optimal investment choices

Despite the various factors that are conducive to investment efficiency, MNEs face other

variables that may hinder optimal investment choices or encourage suboptimal investments.

Some of these factors include increases in excess cash, organizational complexity, information

asymmetry and coordination costs, diversity of investment options, agency problems, and

cross-subsidization.

18

International diversification leads increases in excess free cash due to direct increases in

cash and increases a firm’s internal capital market. Larger internal capital market creates greater

borrowing power and access to cash. There is consensus that overinvestment is prevalent

(Blanchard et al., 1994; Hubbard 1998; Bates 2005). Firms with free cash flows show greater

tendencies of wasteful expenditure (Jensen 1986; Stulz, 1990) and suboptimal acquisition choices

(Hartford 1999). The presence of excess cash in addition to other factors such as increasing

organizational complexity makes it conducive for investment inefficiencies.

International diversification increases organizational complexity due to greater

geographical, cultural, legal, communication, and other distances. These lead to greater

challenges and uncertainties in the international market (Child et al., 2001). Challenges and

foreign market factors will make it harder for firms to manage their investments. Kogut (1985)

notes that institutional and cultural factors hamper transfer of competitive advantage across

country borders. The complexities related to these factors may also make it harder for firms to

transfer knowledge on management of investments. Further, it may lead to sup-optimal

investment strategies, declines in value and eventual business unit failures. Ravenscraft and

Scherer (1989) attribute some of the declines in value following acquisitions to control loss owing

to complex organizational structures. Declines in value and divestures of acquired business units

may suggest presence of failures stemming from sup-optimal investment strategies.

Increasing organizational complexity may be worsened by a larger number of investment

options together with increasing number of managerial objectives, making it harder to choose

between various projects. Stultz (1990) argues that diversified firms make poor investments in

business units with poor investment opportunities. The problem may be more prevalent with

19

internationally diversified firms especially those facing an increasingly complex environment.

These issues are intensified by the higher governance requirements. There are arguments in prior

literature that governance exceeds management capabilities at high levels of product

diversification (Tallman and Li, 1996)11.

Diversifying into foreign countries increases information asymmetry and coordination

costs (Harris, Kriebel and Raviv, 1982). International diversification increases the number of units

across geographical regions as well as physical and psychic distance (Qian and Li, 2002). Greater

geographic dispersion increases coordination and management challenges (Hitt et al., 1994).

Other factors such as cultural, psychic distance, legal, and communication barriers, heighten

coordination costs. Some prior literature further document that diversification creates

inefficiencies. For example, Chandler (1977) points to additional inefficiencies created by

additional managerial levels charged with coordinating divisions in diversified firms. Along the

same line, as international diversification increases, firms may venture more into investments

that are not related to its core business. This may lead to significant negative synergies across

the business segments and misallocation of management time and other resources (Jayasuriya

and Shambora, 2009). Anecdotal evidence links increasing geographical diversification to

significant cost increases. For example, Geringer et al. (1989) discuss that managers

communicated those costs began to escalate as their firm’s geographic market became

increasingly broad. A significant part of increasing costs is due to coordination and

communication challenges.

11 Thou Tallman and Li’s (1996) argument is based on product diversification, I expect international diversification will present similar and greater challenges to management.

20

Like other corporations, firms diversifying internationally face agency problems. Based on

agency theory and moral hazard models, managers pursuing their personal welfare may tend to

make investments that are not consistent with maximizing shareholder value (Jensen and

Meckling, 1976). For instance, they may invest in negative NPV projects. Managerial empire

building is widely documented in prior literature as one of the important drivers of diversification.

For instance, Jensen (1986) argues that even though diversification may be inefficient, managers

choose to diversify when they have free cash flow in order to build empires (Jensen, 1986). On a

similar note, Doukas and Lang (2003) indicate that the negative valuation effects of foreign direct

investment activity of US firms seem consistent with empire building and over-investment.

Agency problems may be greater in international diversified firms due to greater

monitoring difficulties, information asymmetries, and availability of free cash flows, among other

factors. Managers with more free cash flows due to effects12 of international diversification

undertake more investments in negative NPV projects (Jensen, 1986). Evidence shows that the

problem is more prevalent with diversification13. For example, Rajan, Servaes and Zingales (2000)

model and test the prediction that diversity in resources and opportunities increase flow of

resources toward the most inefficient division, leading to more inefficient investment and less

valuable firms.

International diversification may provide avenues for cross-subsidization- a factor that

is detrimental to value creation (Meyer et al., 1992). The evidence of well performing segments

12 Effects such as increase in firm size and greater borrowing ability among others. 13 I expect that the problem would generally be worse with international diversification (relative to diversification within one country) due to greater complexities, geographic distance, firm size, and information asymmetry among others.

21

subsidizing underperforming segments in diversified firms (Lamont, 1997), suggests that

diversification may have effects on investment efficiency. Cross-subsidization may affect

investment behavior through various means. For instance, high performing units will be less

motivated to maximize their performance when their surplus is used to support underperforming

divisions. Meyer et al. (1992) found evidence that some profitable segments did not strive as

hard as they might for higher earnings because their surplus was transferred into money losing

operations. These tendencies would foster under investment among well performing divisions

that have positive NPV investment options.

2.4 International Diversification and R&D Intensity

R&D intensity is a proxy for innovation, and it is measured as the ratio between R&D

expenditure to total number of employees (Hitt et al., 1997; Hill and Snell, 1988). R&D is an

important determinant of firm performance (Hitt et al., 1997; Jensen, 1986), because it affects

process and product innovation. There are findings in prior literature that R&D investments are

positively correlated with various performance measures. There is evidence of positive relation

between R&D investments and profitability (e.g., Severn and Laurence, 1974) and firm

productivity (Hill and Snell, 1989).

Process and product innovation are crucial to gaining competitive advantage in

international markets (Porter, 1991; Hitt et al., 1994; Hitt et al., 1997). This reinforces the

importance of examining the relation between international diversification and R&D

investments. Internationally diversified firms have various incentives for innovations (Hitt et al.,

1994) and other factors that may encourage investments in R&D. The incentives center around

the need to adapt and take advantage of market opportunities and investment opportunities in

22

international markets. International markets come with increases in demand for high quality and

low cost (Prahalad, 1990). In addition, companies may experience additional push from markets

demanding unique products or products tailored to the specific regions.

In addition to creating incentives, international diversification leads to increases in

resources-a critical element to R&D investments. International diversification may be necessary

to generate enough resources for large scale R&D operations (Kobrin, 1991). Resources are

directly used in R&D investments. Further, greater financial and other resources enable firms to

internalize and integrate their global operations, which is also pivotal to R&D investments. There

is evidence that US firms that have achieved significant integration are able to retain their

innovative abilities (Kotabe, 1990). Retention of innovative abilities may suggest existence of

significant R&D investments. Along similar lines, some prior literature document positive relation

between international diversification and other factors related to R&D. For instance, Zahra et al.

(2000) found that international diversification improves technological learning, which in turn

fosters innovation, differentiation, and market expansion speed.

Despite the incentives and factors that may foster investments in R&D, there are others

that may hamper investments in R&D. These factors include the use of acquisition as an

alternative to R&D investments, appropriation of innovations, decreased focus on specific

business units, and challenges with coordination and extending skillset and expertise across

countries.

Prior research finds evidence that firms may make tradeoffs between various strategies

(Hoskisson and Hitt, 1990; Geringer et al., 1989) including acquisitions and R&D investments. For

example, Banker et al. (2011) finds that firms with a high degree of diversification are likely to

23

innovate through acquisition, rather than through investment in R&D. Large firms often acquire

smaller firms due to the target’s technical and other capabilities. Acquisitions therefore help to

increase technical and other knowledge resources and may thus decrease the need for additional

R&D investments.

Kotabe (1990) argues that international diversification facilitates appropriation of

innovations. With appropriation, firms can apply competencies from their local market to

international markets to increase their performance (Bartlett and Ghoshal, 1999). Some of the

competencies emanate from R&D investments from the host country. In addition, international

diversification enables firms to tap into selective advantages of other countries (Porter, 1990)

and use it to fill the increasing market needs in other regions. Appropriation of innovations and

R&D resources decreases the need for additional R&D investments. In line with the preceding

arguments, Banker et al. (2011) finds that IT firms with a high degree of diversification14 tend to

innovate through acquisition rather than R&D.

In a firm with multiple business units, no single unit may feel responsible for maintaining

a viable position in core products nor be able to justify R&D investments required to build

leadership in their products (Prahalad, 1990). This situation is particularly critical in the context

of international diversification because such diversification is likely to decrease the weight of

specific business units given the increase in the number of business units. A company’s focus on

its core products is essential to its competitiveness and survival. Therefore, the increase in

14 Thou Banker et al. (2011) focused on diversification in general, I expect the same tendencies with international diversification.

24

business units due to international diversification may lead to decreases in the R&D investment

for each core product.

Greater geographic dispersion presents coordination and communication challenges

amongst internationally diversified companies. With greater dispersion, coordination and

communication barriers arise (Porter, 1990; Hitt et al., 1997). Dispersion may hamper

collaboration among divisions in various regions due to coordination, communication, and other

related challenges. Yeoh (2004) finds that geographic diversity of exports has negative effect on

technological learning. This may be an indication of coordination and communication challenges

on innovations.

There may be limits to the transferability of firm knowledge and its acceptance across

regions (Rugman and Verbeke, 2004). Differences in legal and cultural characteristics across

nations exacerbate difficulties when adapting to foreign markets and impose transferability

limits. In addition to limiting transferability, the differences may also limit firm ability to take

advantage of resource disparities across geographic regions. These differences reiterate the need

for additional investments in innovations and other capacities. Limited ability to transfer and

apply managerial and other skill may hamper innovations, because skill and expertise are critical

in a firm’s endeavors to innovate and remain competitive.

Extant literature documents evidence that large investments often fail in new areas

because of lack of appropriate management and production. Caves (1989) discusses that the

evidence of some divestures following acquisitions, is consistent with multiple business having

certain skills, controls and structures that work on a subset of firms, but crumble when applied

to new areas. He further argues that divestures may be the result of insufficient investment in

25

technical and other forms of learning to gain value from the acquired business units. This points

to the need for additional investments to achieve the appropriate knowledge and structures to

increase competitiveness as the market becomes more complex and diversified. Investments in

R&D play a pivotal role in this endeavor.

2.5 International Diversification and Uncertainty of Future Benefits from Investments

Firms, standard setters, and other users of financial information are concerned about the

likelihood that future benefits will be realized from investments and other resource outlays. For

instance, FASB uses the degree of uncertainty of future benefits as a criterion of determining

whether a cost should be expensed or capitalized (Statement of Financial Accounting Standards

No. 6, 1980). In this study, the uncertainty of future benefits from investment is measured by

future variability in value from investment (Kothari et al., 2002; Asdemir et al., 2012)15.

Ravenscraft and Scherer (1989) found evidence that, except for mergers involving pooling of

interest between firms of relatively similar sizes, the acquired business units experienced decline

in performance. They point to investment changes as possible causes of the documented decline.

This highlights the importance of investment quality to the performance of internationally

diversified companies.

One objective of this study contributes to the understanding of the variations in the

performance of internationally diversified firms. The examination of the uncertainty of future

benefits from investments by internationally diversified firms provides insights on the link

between firm inputs and financial outcomes, a lens into firms’ global effectiveness and value

15 In these papers, future variability in value is proxied by standard deviation of future earnings, sales revenue, and operating cash flows.

26

creation. Uncertainty in future benefits from investments is an important indicator of investment

quality. A common argument in prior literature is that international diversification results in

combination of imperfectly correlated earnings streams (Ofek and Berger, 1995; Lewellen, 1971).

The evidence of reduced risk of revenue stream variability (e.g., Hisey and Caves, 1985; Hwang

and Burgers, 1993) among diversified firms coincides with this argument.

Due to its critical role in firm performance and survival, R&D has received considerable

focus in the investment literature. R&D is an increasingly important productive input (Aboody

and Lev, 2000). The findings reiterate the central role that R&D plays in organizational growth

and performance. For instance, there is documented evidence that R&D expenditure is

associated with future performance (e.g., Deng and Lev, 2006) and market values (e.g., Hirschey

1982; Hirschey and Weygandt, 1985; Shevlin, 1991). Further, prior studies have documented that

the market assigns value to R&D activities (e.g., Lev and Sougiannis, 1996; Deng and Lev, 1997).

Despite the association between R&D and variables associated with firm value, FASB

requires that R&D expenses to be expensed immediately (SFAS No. 2) because of the high

uncertainty of future benefits from R&D investments. In SFAS No. 4, FASB specifically points to

the high degree of uncertainty of R&D expenditures in providing future benefits. The uncertainty

of R&D expenditure is especially greater for R&D intensive industries (Amir et al., 2007; Asdemir

et al., 2012). Comparing earnings variability of R&D versus that of capital expenditures, Kothari

et al. (2002) documents that the variability of R&D is about three-to-four times as large as that

of capital expenditures (Kothari et al., 2002, p. 357).

27

For manufacturing firms, while R&D may not constitute significant portion of the

investment outlays16. However, R&D remains a critical component to firm success. Amir et al.

(2007) argues that the capitalization of R&D should only be allowed in CAPEX-intensive firms

because the volatility of subsequent operating profitability is equally influenced by R&D and

CAPEX. There is evidence of significant correlation between R&D and future earnings (e.g.,

Kothari et al., 2002).

For internationally diversified firms R&D and other factors play a role in determining the

relation between the investments and uncertainty of future benefits. These factors include

geographical dispersion, market characteristics (e.g., similarity to home market), infrastructure

quality, and distribution networks among others.

16 I expect that investments in R&D are lower because they are mostly aimed at relatively small product and process improvements.

28

CHAPTER 3: HYPOTHESIS DEVELOPMENT

3.1 The Relation Between International Diversification and Cost Rigidity

Prior literature does not provide conclusive evidence on the relationship between

international diversification and cost rigidity. There are no studies that specifically delve into the

relative changes in variable versus fixed costs as firms diversify internationally. However, extant

literature present various arguments that are directly or indirectly related to the relationship

between international diversification and cost and cost rigidity. Ex-ante, there is consensus that

cost advantages is one of the drivers of international diversification (Hitt et al., 1997; Kogut,

1985). Ex-post, international diversification will drive changes in cost due to several factors that

differ across phases as firms expand from low levels through higher levels of international

diversification17. Through international diversification phases, firms face various factors

including, location choices, changes in resources, synergy and economies of scale, integration,

organizational learning and changes in governance, and environmental complexity.

3.1.1 Low to moderate levels of international diversification

In the initial phases of international diversification18, firms consider location choice due

to its pivotal role on costs, among other factors (Hitt et al., 1997). Location choice literature posit

that firms choose locations based on psychic, cultural and geographic distance (Papadopoulos

17 This study follows the approach Hitt and Middlemist (1978) and Hitt et al. (1997) in measuring level of international diversification. I use an entropy measure of international diversification that factors both the number of global market regions and the relative importance of each global region. The specific calculation is presented in eq. (1) in chapter 4. Based on the measure, firms are categorized into low-to-medium international diversification subgroup if they have an international diversification score(measure) of less than 0.30. Firms with a score of 0.30 and above are classified as categorized into the higher international diversification group. 18 Location factors are also considered in further international expansion decisions

29

and Dennis, 1988). Research has found support for market familiarity concept where firms give

preference to familiar markets (e.g., Davidson, 1983). In line with this prediction, David (1980)

finds that US firms prefer to start with Canada and the U.K when venturing into global expansion.

Similarly, Hisey and Caves (1985) predicts that firms prefer expanding in countries where they

already have operations due to experience in host country. These expansion choices help firms

to limit costs such as fixed cost related to finding new sites of operations (Hisey and Caves, 1985).

This is because familiar markets have similar distribution, administrative and marketing

characteristics, which enables appropriation of home country competencies and cost reductions

(Gomes and Ramaswamy, 1999, p 176). Expansion into familiar markets facilitates activity sharing

which may facilitate decreases in fixed costs and cost rigidity.

Location choice also affects firms’ abilities to take advantage of resource availability and

resource costs (Caves, 1989). U.S firms’ initial expansion into familiar markets such as Canada

and U.K, may not create significant differences in labor abundance and cost- a critical

manufacturing variable cost factor. Companies are therefore not likely to have significant shifts

towards a higher variable -to-fixed cost approach19. However, as they continue to medium levels

of diversification, they gain incremental opportunities to take advantage of resource availability

and prices. For instance, firms may adopt approaches substituting capital for direct labor due to

abundance and lower cost of human resources in foreign countries (Kravis and Lipsey, 1982). This

may move the company towards lower cost rigidity.

Another consequence of increased firm size is the increase in power over suppliers and

other supply chain participants. The impact of increased firm power on cost rigidity is unclear

19 Shifts would occur if firms changed their capital and labor ratios.

30

because it may create opportunities to decrease both variable and fixed costs. For example,

purchasing fixed assets at lower cost and variabilization of fixed costs would decrease cost

rigidity. Lower cost of raw materials could reduce variable costs relative to fixed costs and cause

increases in cost rigidity20.

Extant literature highlights that the desire for synergistic gains and economies of scale

affects initial and subsequent international expansion decisions (e.g., Larsson and Finkelstein,

1999, Lubatkin, 1983; Chartejee, 1986). Synergistic gains are attributable to improved operating

efficiencies (Jensen, 1993) due to economies of scale or scope, and skill transfers (Harrison et al.,

1991), among other factors. At lower to moderate levels of international diversification21, firms

may significantly benefit from sharing asset advantages and resources such as distribution,

marketing, and administrative resources (Gomes and Ramaswamy, 1999) across more markets.

Low to moderate international diversification is specifically conducive to asset sharing,

synergistic gains and other related benefits because of relatively higher business and market

similarity (due to related diversification). Hisey and Caves (1985) note that firms will tend to

pursue related diversification until the point at which marginal cost starts to exceed returns. At

which point they branch out to new product or geographic region. Sharing assets is likely to lead

to relative22 decreases in fixed costs. I expect relatively larger decreases in fixed costs because

sharing in activities that significantly drive fixed cost including administrative and marketing

human resources23 as well as production facilities among others. For example, when a U.S firm

20 BCG defines variabilizations as the conversion of fixed costs into variable costs. For example, selling fixed assets back to the manufacturer and renting them at a fee that varies with revenue or usage 21 Firms with low-to-moderate levels of international diversification are those with an international diversification that is less than the median. Similar to Hitt et al. (1997), I find that median is approximately 0.3(rounded). 22 Fixed cost relative to variable cost 23 For example, sharing of managers and other personnel will help decrease overall salaries.

31

expands to Canada, divisions in the US and Canada can share distribution resources such as

trucks, personnel, and other resources. This leads to decreases in the proportion of fixed costs24

relative to variable costs. Variable costs will generally increase in proportion to the increased

activity level. Such changes would decrease cost rigidity.

Organizational learning plays an important role in firm success (Barkema and Vermeulen,

1998; Hitt et al., 1994). Given challenges in the global environment, experience and

organizational learning are particularly critical as firms expand internationally. Firms at lower

level of international diversification encounter liabilities of newness and foreignness. These firms

tend to have low product diversification. As firms expand, moving from low to medium levels of

international diversification, they have experiential learning curve on establishment and running

of subsidiaries (Hisey and Caves, 1985). Increased knowledge and experiential learning enable

firms to better manage and reduce relative25 fixed and variable costs. However, the impact on

cost rigidity is unclear given the lack of evidence on the relative changes of fixed and variable

costs.

3.1.2 Higher levels of international diversification

Hitt et al. (1997), describes high diversification firms as those with an international

diversification score above 0.30. International diversification score is calculated based on

number of sales regions, as well as sales amount per region. For each firm, an increase in the

number of sales regions and/or activity on a sales region(s) leads to a higher international

24 Such as depreciation expense and salaries. 25 In relative terms such as per unit basis or in comparison to activity level.

32

diversification score. Beyond medium levels of international diversification26, firms still face the

factors above; that is, location factors, synergistic gains, experiential learning, market complexity

among others. However, firms face more challenges that affect the nature and effects of these

factors and cause significant increases in costs. For instance, cross-border mergers may impede

integration and coordination needed to realize synergies because of geographic distance as well

as legal, financial, psychic, and other country differences (Marks and Mirvis, 1993; Hitt et al.,

1997; Qian and Li, 2002). Once firms enter unfamiliar territories requiring major reconfiguration

of internal processes, structures, and mechanisms, the costs of internalization dramatically

increase to exceed benefits (Ruigrok and Werner, 2003).

As firms expand from medium to higher levels of diversification, there are greater

opportunities to take advantage of arbitrage opportunities in factor cost differentials across

multiple locations (Kogut, 1985). This is especially the case as firms expand into less developed

countries. Early research finds evidence that firms used more labor-intensive technologies in

countries with cheaper labor cost (Kravis and Lipsey, 1982). Shifts from capital-intensive towards

labor-intensive approaches, leads to greater increases in total variable cost relative to the

increases in total fixed costs hence a decrease in the proportion of fixed costs relative to variable

costs27. For such shifts would lead to disproportionately higher increases in total direct labor cost

relative to increase in total depreciation costs. Hence leading to decreases in cost rigidity.

26 International diversification is calculated based on number of sales regions, as well as sales regions. Increase in the of sales regions and/or activity on a sales region. Such that firms operating in a greater international diversification score. 27 Or relative to total cost.

33

Despite available opportunities to benefit from lower labor cost and abundance of other

resources, when MNCs expand beyond optimal level of international diversification, control and

coordination costs, cultural and other operating environment dissimilarity is expected to lead to

higher costs that exceed potential returns to multinational growth (Gomes and Ramaswamy,

1999). For instance, greater geographic and other dispersion which makes it more challenging to

share assets such as production facilities, distribution networks, and personnel among others

(Hitt et al., 1997). This is escalated by differences in customer tastes and increasing product

diversification and less focus which similarly creates a need for additional and specific assets.

Difficulty sharing assets makes it necessary to increase such assets in multiple regions or

countries. An increase in assets such as productions facilities and equipment among others is

likely to cause greater increases in fixed costs hence leading to an increase in cost rigidity.

Differences in legal and other regulatory systems will create significant governance

challenges. Increasing firm size and the limits to applicability of managerial skill to certain

countries, regions or business units worsens governance challenges. In addition, with increasing

differences between home country and foreign market, firms will face greater challenges

purchasing and installing facilities (Lu and Beamish, 2004). Governance challenges and

complexities necessitate hiring of foreign managers, leading to salary increases among other

costs. I expect that this would lead to greater increases in fixed cost relative to variable costs

hence leading to greater cost rigidity.

Expansion into new regions or territories, changes the operating environment of the firm

including uncertainty and risk levels (Lee and Caves, 1998). Uncertainty and risk levels are pivotal

factors to manager decisions including those linked to cost rigidity. Prior literature examining the

34

relationship between uncertainty and cost rigidity yielded inconclusive results. Using hospital

data, Kallapur and Eldenburg (2005) find evidence that hospitals increased cost flexibility

(increased cost rigidity) when they faced greater uncertainty. On the contrary, Banker et al.

(2014) found evidence of positive association between uncertainty and cost rigidity (higher fixed-

to-variable costs). Their findings coincided with their arguments that when firms are faced with

uncertain demand, they increase their capacity, to take advantage of future high demand28.

Increasing capacity leads to an increase in fixed cost hence a greater cost rigidity.

In sum, the relationship between international diversification and cost rigidity is not clear.

This is due multiple conflicting direction of effects of factors that affect cost making the overall

direction less clear. Further, the evidence on magnitudes of changes in fixed and variable costs

as firms diversify internationally is unclear. The overall changes in cost rigidity will depend on the

cost shifts directions and magnitudes as firms diversify internationally. At lower to medium levels

of international diversification, expansion into relatively similar markets29, activity sharing,

synergistic gains, among other the factors appear to point more towards decreasing cost rigidity.

This is because these factors lead to lower increases in total fixed costs relative to the increases

in total variable costs. I therefore predict a lower cost rigidity at low to medium levels of

international diversification. With higher international diversification, market complexity,

difficulty sharing activities, other factors within the MNCs and their operating environment are

likely to necessitate greater capital outlays30, leading to greater increases in total fixed costs