Economics 314 Make-up Assignment

21

Economics 314 Make-up Assignment Paul Robertson G11r1064 1. According to Smit (2008:89) South Africa has historically been influenced heavily by the balance-of-payments flows, this stems from it being a small open-economy as well has high in natural resources allowing large exports of raw materials. Because South Africa had a large share in the international trade of gold, a large portion of its GDP came from gold and other metals. Mining accounted for 21% of GDP in 1970, however in recent times it has fallen to only 6%, however because of the large share of GDP being from mining South Africa developed a dependency and a reliance on its exports of these metals in order to finance its spending (ADB, 2009:10). Another reason and through analysis of historical data SARB (28:2013) for South Africa’s dependency on foreign Capital inflows is that South Africa’s current deficit has historically been large and therefore has needed foreign direct investment in order to finance this debt and enable South Africa to still invest in infrastructure and technology in order to stimulate growth (Mohamed,2012:2).Since 1994 South Africa has also opened up the economy and implemented many orthodox economic policies, these were in the hopes of attracting even more FDI. Mohamed (2012:8) argues that opening up the economy results in South Africa’s economy becoming increasingly

Transcript of Economics 314 Make-up Assignment

Economics 314 Make-up Assignment

Paul Robertson

G11r1064

1. According to Smit (2008:89) South Africa has historically

been influenced heavily by the balance-of-payments flows,

this stems from it being a small open-economy as well has

high in natural resources allowing large exports of raw

materials. Because South Africa had a large share in the

international trade of gold, a large portion of its GDP

came from gold and other metals. Mining accounted for 21%

of GDP in 1970, however in recent times it has fallen to

only 6%, however because of the large share of GDP being

from mining South Africa developed a dependency and a

reliance on its exports of these metals in order to

finance its spending (ADB, 2009:10).

Another reason and through analysis of historical data

SARB (28:2013) for South Africa’s dependency on foreign

Capital inflows is that South Africa’s current deficit

has historically been large and therefore has needed

foreign direct investment in order to finance this debt

and enable South Africa to still invest in infrastructure

and technology in order to stimulate growth

(Mohamed,2012:2).Since 1994 South Africa has also opened

up the economy and implemented many orthodox economic

policies, these were in the hopes of attracting even more

FDI. Mohamed (2012:8) argues that opening up the economy

results in South Africa’s economy becoming increasingly

volatile, therefore it is increasingly important that

opening up the economy does indeed attract foreign

investment, or else the policy changes lead to more

volatility with nothing to show for it. Some of these

policy liberalisations included the abolition of exchange

controls on all current account transactions as well as

exchange controls on non-residents, Global leniency in

regards to outward FDI and overall progressive relaxation

of controls.

It is therefore clear that South Africa needs the FDI in

order to finance its current-account-deficit as well as

its public debt. As a developing country it also needs

access to capital and resources that other countries can

provide, therefore encouraging trade liberalising

policies as well as increasing our reliance on FDI as

this will enable us to finance the new technology and

capital acquired form developed countries. FDI also

allows capital to be allocated most efficient through

private markets instead of government allocation which is

susceptible to corruption and administrative costs

(Mohamed, 2012:11).

A problem with the capital inflows we receive is that the

majority of it comes from volatile portfolio flows. These

portfolio flows are volatile as they are easily

reversible, investors are free to buy and sell their

portfolios very easily, and therefore in the emergence of

a nominal shock or a global downturn, it is detrimental

for South Africa’s exchange rates. Appendex A shows how

the exchange rates adjust according to the supply and

demand of foreign capital.

2. There were a number of attributing factors that lead to

capital outflows in 1998 and 2001. Firstly the Asian

stock market collapses of 1997 which was mainly caused by

currency devaluations of Indonesia, Malaysia,

Philippines, South Korea, and Thailand. Another problem

was that people did not diversify their investments

therefore leading to larger losses due to concentration

of investments in the same markets that collapsed.

Because of the loss of funds this lead to capital being

drawn out of South Africa, due to the demand for

immediate funds in Asian countries (Garay: 2003:1). But

overall the main problem was due to rand depreciation,

causing weakened exchange rates.

In 1998 one of the reasons for the weakening was

commodity prices, global demand for South African exports

decreased due to the Asian market collapse mentioned

above. Analysis reveals that a 1 percent fall of real

prices can account for 0.5 percent depreciation of real

exchange. Another reason for the deprivation of the rand

according to Bhundia (2004:167) was the role of Highly

Leveraged Institutions. Some of these institutions were

selling the rand short, and therefore driving up the

domestic interest rate, the rationale behind this was

that these same investors would sell government bonds

short and then make a profit as the interest rate spiked

on the government bonds.

Although not vital to the depreciation of the rand, it

must still be noted that the increases of AIDS and

unemployment increase the volatility of the rand to

sudden changes as well as presenting tough decisions to

policy makers. Because of the challenges these present,

it could consequently mean that a small shock results in

economic instability because of the fragility of our

workforce and the high unemployment rate Bhundia

(2004:167).

Another nominal shock that possibly could have affected

investors’ confidence in South Africa was contagion from

the events in Zimbabwe and its economic deterioration. It

is hard to pinpoint the exact shock that lead to South

Africa’s depreciating rand and weakening exchange rate,

however from the above it can be seen that it was a

combination of nominal shocks, relaxed monetary response

and financial market expectations (Bhundia,2004 164-167).

Lastly in 1998 Russian defaulted on domestic debt, which

gave international markets another reason to fear

investing in emerging markets. This resulted in more

capital outflows from South Africa as the fear was that

emerging markets are too risky to invest in (Keeton,

2013:57).

2001

As with the depreciation of the rand in 1998, it is hard

to determine which causes had the most impact, therefore

they need to need to be looked at collectively. The first

source of capital outflows stemmed from the slowing of

Economic reform. There was large pressure on South Africa

to open its market and this including privatisation of

Telkom. The reason that there was a delay was because of

the weakened global stock market, which would mean that

Telkom shares would be cheaply priced, therefore choosing

to wait until the stock market had recovered. However in

doing so, globally this was associated with not being

committed to economic reform, therefore losing out on a

lot of capital inflows and investors even withdrawing

capital from South Africa (Bhundia,2004 162).

Another reason was the enforcement of existing capital

controls. SARB announced that it would tighten

enforcement controls, and a number of observers including

those who testified in front of the Myburgh Commission

argued that the effect of this was perverse as it led to

a sharp deprivation of the Rand, because of reduced

market liquidity (Bhundia,2004 162).

A third possible reason for the increase of capital

outflows was the world decrease in world economic

activity which inevitably led to decrease demand for

South African exports and services. Furthermore

deteriorating economic conditions in Argentina may have

slightly affected South Africa, but only very marginally.

However the further decline of Zimbabwe may have deterred

foreign investment and foreigners may have thought South

Africa was going to end up like Zimbabwe. As mentioned

above Aids and unemployment rates may also have been seen

by foreigners as declining social state, and as pointed

out by Strauss (2013) that in order for economic growth,

the culture needs to be synonymous with economic growth

and heavy unemployment levels and aids may have been seen

as indicated as social instability.

Lastly a large reason of the capital outflows of South

Africa were attributed to Economic decline in America.

More specifically the dot-com bubble burst as well as the

Twin tower attacks. (Keeton,2013:66). The dot com bubble

bursting meant that many people lost out on their shares,

causing extreme losses on their investments, some of

these companies included pet.com, boo.com and

infospace.com where shares dropped from 1305 Dollars per

share to 22 Dollars per share. Because of the losses

people withdrew there offshore investments as they wanted

their money “closer to home” possibly also because they

did not want to lose money even further since it was

widely regarded that investing in emerging markets was

quite risky (BBC, 2001:1). Furthermore economic decline

in America decreased further after the 9/11 attacks, also

reiterating the point mentioned above about withdrawing

capital to safer developed markets (Keeton, 2013:66).

Empirical evidence:

Empirical evidence from an exchange rate model developed

by Clarida and Gali(1994) as well as a model from Bhundia

and Gottschalk(2003) of the dynamics of the rand found

that nominal shocks were the primary driving force in

both 1998 and 2001, and supply shocks and real demand

shocks were not statistically relevant (Bhundia,2004 164-

167).

3. Policy responses in 1998

The policy’s around 1990 were mainly dominated by GEAR.

The Growth, Employment and Redistribution plan (GEAR) was

a basic social development plan which focused on

redistribution of wealth, increase in job creation and

overall economic growth (Knight, 2001:1). This included a

policy response of Austerity, which included large cuts

in government expenditure, and an overall cut in the

national budget deficit. They also tightened fiscal

policies as well as implementing more cost-effective

civil services. Although GEAR was hoping to increase the

scope subsidies of grants, because of the economic

pressure it was currently experiencing, they had to also

cut down on the subsidy scope as well as a decrease in

overall jobs ensued, partly because of cutting on the

public sector expenditure (knight,2001:1).

Because of the depreciation of the rand, policy makers in

South Africa opted for an interventionist approach. This

included borrowing foreign currency in the forward market

and sold in the spot market, in the hopes that this would

stem the pressure of the rand (Bhundia, 2004 164-167)..

According to Keeton (2013:62) the reserve bank intervened

heavily in order to try protecting the value of the rand,

this was actually the opposite of what GEAR stated. They

borrowed 10 Billion Dollars from the forward book and in

reference to appendix A, was in order to shift the supply

curve right in order to stop the Rand’s slide, a

rightward shift would mean an increase the supply of

foreign capital in South Africa, which would bring down

the interest rates.

This resulted in the net foreign position (which is

basically the international reserves - the forward

liabilities of the central bank) being reduced by 10

billion US dollars between April and September 1998. This

soon proved to be unsuccessful, which led to the central

bank needing to increase its repo-rate to approx. 22% in

September 1998, in order to try and reduce current

account deficits by crushing investment and domestic

expenditure as well as to attract foreign capital. The

long-term government bonds rate also increased from 13

percent to 18 percent (Bhundia, 2004 164-167).

The South African reserve Bank was also stressing

monetary policy that would ensure stability over economic

growth, even though economic growth had slowed-down,

reasons for this included keeping high interest-rates in

order to avoid more International capital leaving the

country. High interest rates were also maintained due to

the weakening exchange rate and the high inflation. This

policy was partly successful as there was dwindling

fiscal deficits which allowed the pressure on South

Africa’s capital market to finance large government

needs, however the high interest rates did have a

negative effect on the economic growth (Khamfula,

2005:9)..

According to Khamfula (2005:10) the South African Reserve

Bank continued in its pursuit of its existing policy

goals which included growth as well as stabilizing the

exchange rate, while keeping the capital account

liberalized. In order to keep a competitive exchange rate

however they required a combination of increased real

interest rates and a decrease in the capital inflows in

order to limit money growth, this turned out to be a

terrible move, as the net capital inflows fell abruptly

in 1998, in order to try and absorb exchange rate-risk

the Reserve bank tried to reduce this outflow by selling

dollars into the market and increasing real interest

rates to 7% in 1998, in a desperate attempt to attract

foreign portfolios back (Khamfula, 2005:10).

Because of the increase in the repo rate by the reserve

bank, Commercial banks had to respond by increasing their

prime overdraft rate to an all-time high of 25% in the

third quarter, however by the end of the fourth quarter

they had decreased down to 21%. It must also be noted

that another reason the reserve bank raised interest

rates as mentioned earlier is that it discourages

investors from borrowing rands for the sole purpose of

taking speculation spots on the currency. Maphumulo

(1999:24) also argues that the reserve bank initially

thought that the short-term volatility of the rand was a

short-term weakness that would soon reverse, which

allowed them to borrow dollars from the forward market

and to sell in the spot marker. In July the total foreign

credit reached 18.5 billion rand, while during the same

time period the net forward position of the bank

increased from 12.8 billion rand to 25 Billion rand. In

order to change investor perception, SARB needed to

stabilize interest rates and limit its intervention in

the market; however a decrease in interest rates would

fuel more speculative positions on the currency. Appendix

3 shows the relationship between Net foreign reserves and

net open forward position (Maphumulo,1999:25).

Lastly because of the borrowing that South Africa did in

order to try and stabilize the exchange rates and because

of its ineffectiveness it lead to South Africa being in a

worse position due to the fact that it now had to repay

its debt with a depreciated currency, this contradicted

GEAR’s goal of trying to escape the debt trap (Keeton,

2013:62). Another reason that the exchange rate did not

attract capital flows even after borrowing was because

interest rates can move from 2-3 percent a day, whereas

interest rates for FDI are annualised.

2001

In 2001 we were currently not face a current account

deficit, however because of the reasons mentioned

earlier, the rand started depreciating affecting the

exchange rate. However Because of the unsuccessful

attempts at stabilizing the exchange rate in 1998, as

well as the new policy of targeting inflation, South

Africa decided to not try and directly influence the

exchange rate through direct intervention. The exchange

was also not increased until Jan 2002, which also saw a

modest increase to 17% rather than the 25.5% peak we saw

in 1998. (Keeton, 2013:66).

According to Bhundia (2004:166), one of the reasons for

the success in combating the economic downturn of 2001,

was that overall South Africa had better macro-economic

policy. An example of this is that the foreword book was

disbanded, as well as the inflation targeting framework

rather than focusing on the exchange rate proved to be a

more credible anchor for exchange rate fluctuations.

The Reserve Bank (2013:1) states that inflation targeting

was officially implemented in February 2000. This

includes bring greater transparency to monetary policy.

They note however that monetary policy does not directly

contribute to the growth and employment in the long-run

however a stable financial environment is synonymous with

the attainment of growth and development.

Inflation targeting also creates a co-ordination between

all economic policies and it targets a specific goal. It

also makes monetary policy less volatile due to the

accountability of the central bank. If the clear

inflation targets are not met, the central bank is held

accountable, this leads to better monetary decisions

being made, as well as more public awareness and

therefore confidence and trust, stemming from the fact

that transparency decreases impulsive responses by the

public (SARB,2004:2).

It must however be noted that although South Africa has

changed its policy framework to that of inflation

targeting is still is aware that changes in the exchange

rate are an important determination of monetary policy,

especially since South Africa is a small open economy.

Another reason why exchange rates are still important in

South Africa is that still rely heavily on foreign

investment therefore rand depreciation can easily lead to

a financial crisis(SARB,2004:13). It is for this reason

that South Africa has still chosen to focus narrowly on

exchange rate stability, hence the narrow increase of

17%. It is not always a clear-cut decision in which

policy’s to change, for example when the rand was

depreciating, South Africa could have opted to decrease

interests rates which according to SARB (2004:13) could

have benefited economic growth due to increased exports,

however it would of led to increase of inflation and

therefore because of the choice to target inflation, was

not implemented. South Africa also chose to not install a

crawling-peg or fixed-band exchange rate; they chose a

freely floating exchange rate policy with moderate

intervention by the central bank.

Therefore overall in the crisis of 2001 there was

definitely not as much intervention as in 1998. This

definitely seemed to help South Africa reach economic

stability sooner than in 1998. Therefore overall in 2001

the rand was mostly left to the supply and demand

conditions of the market of foreign exchange.

4. Question 4 has partly been answered above due to the

complexity of explaining the macro-economic policies.

However from the evidence and analysis done in question

1-3 it is clear that the response to the crisis in 1998

was not as effective as the policy response in 2001.

In 1998 South Africa opted for a heavy interventionist

approach whereby the central bank tried to control the

exchange rate. This was because South African policy

framework was centralised around the exchange rate.

However in February 2000 it was formally announced that

South Africa was switching to an inflation target

framework. This proved successful and thereby showing

that for South Africa, interfering with the exchange rate

too much leads to further economic instability and

therefore inflation targeting was more successful.

Another reason they differed is the fact that exchange

rate policies include a lot of intervention from the

central bank. Whereas inflation targeting includes less

intervention such as leaving the foreign funds market

open to supply and demand determinants that occurred

naturally in the market with modest control from the

central bank (SARB,2004:13). Appendix 2 (Keeton, 2013:71)

shows that South African GDP grows more through inflation

targeting than exchange rate control.

Another reason that the policy responses in 2001 were

better than in 1998 was because South Africa borrowed

money to pump into the supply of foreign capital, however

this had the perverse effect of increasing the debt at a

lower exchange rate, making repayments more expensive.

Another reason is that currencies can move easily up to

2-3% per day and therefore eliminating any incentives

that foreigners would have in investing because bond and

share rates are determined annually (Keeton, 2013:62).

This is also a good example of how the policies differed

and how much less intervention there was in 2001.

Lessons we learn from the above are that Its better to

target the inflation rate rather than the exchange rate

during rand exchange weakness. We also learn that

interest rates needed to combat inflation are far less

those needed to combat exchange weaknesses. Therefore

during this exchange rate weakness we expect no policy

response due to inflation targeting, however if the

central bank does not think that they will meet the

inflation targets, then they will change the exchange

rate policy (Keeton, 2013:70-80)

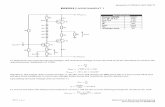

Appendix A

A decrease in capital flows causes

Supply curve to shift leftward. An

increase causes the supply curve to

shift rightwards.

An increase in capital outflows

causes the demand curve to shift

rightward, and a decrease in capital

outflows causes the demand curve to

shift leftward.

As the demand curve shifts leftward

or the supply curve shifts rightward

the interest rate will increase.

Indicated on our diagram is the

situation whereby there is a decrease

of capital inflows, and an increase

in capital outflows, pushing up the

exchanger rate.

Appendix 2

Appendix 3

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

84 86 88 90 92 94 96 98 00 02 04 06 08

SA GDP growth (% )

'84-93= 1% pa '94-'08 = 3.5% pa

'04-'07 = 5.1% pa

'09 = Reuters Consensus

References

AFRICAN DEVELOPMENT BANK.2012.”Results-Based Country Strategy

Paper”, [Online]. Available:

http://www.webcitation.org/65y0uU0lN [Accessed

02/10/2013].

BBC.2001.Warren Buffett:”I told you so”.[Online]. Available:

http://news.bbc.co.uk/2/hi/business/1217716.stm [Accessed

03/10/2013].

BHUNDIA, A., J.2006. The Rand Crises of 1998 and

2001: What Have We Learned? [Online]. Available:

http://www.imf.org/external/pubs/nft/2006/soafrica/eng/pa

soafr/sach10.pdf

[Accessed 04/10/2013].

GARAY,U.,2003. The Asian Financial Crisis of 1997 - 1998 and the

Behavior of Asian Stock Markets.[Online]. Available:

http://www.westga.edu/~bquest/2003/asian.htm [Accessed

03/10/2013].

KEETON,G.2013. Lecture Slides Week 10 Inflation Targeting.

KHAMFULA,Y.,2004.Macroeconomic policies, shocks and

economic growth in

south Africa. University of the Witwatersrand. [Online].

Available:

http://www.imf.org/external/np/res/seminars/2005/macro/

pdf/Khamfula.pdf [Accessed 03/10/2013].

KNIGHT.R. 2001. South Africa: Economic Policy and Development.

[Online]. Available:

http://richardknight.homestead.com/files/sisaeconomy.htm

[Accessed 04/ 10/2013].

MOHAMED, S.2012. The impact of capital flows on the South African

economic growth path since the end of apartheid. [Online].

Available:

http://www.augurproject.eu/IMG/pdf/The_impact_of_capital_

flows_on_the_South_African_economic_growth_path_since_the

_end_of_apartheid_LH_ed_WP2-2.pdf. [Accessed 03/10/2013].

SOUTH AFRICAN RESERVE BANK.2013. Supplement March 2013:

Government Finance Statistics of South Africa: 1994–2012. [Online].

Available:

http://www.resbank.co.za/Publications/Detail-Item-View/

Pages/Publications.aspx?sarbweb=3b6aa07d-92ab-441f-b7bf-

bb7dfb1bedb4&sarblist=21b5222e-7125-4e55-bb65-

56fd3333371e&sarbitem=5664

[Accessed 03/10/2013)

STRAUSS,C.2013.Rhodes Economics Department Centenary speech.