DSCL Janta doc 24.06.04.qxd - Morningstar

44

1 Shri Ajay S. Shriram Chairman & Senior Managing Director Shri Vikram S. Shriram Vice-Chairman & Managing Director Shri Rajiv Sinha Dy. Managing Director Shri Ajit S. Shriram Director (Sugar) Dr. S.S. Baijal Shri Arun Bharat Ram Shri Pradeep Dinodia Shri Vimal Bhandari Shri Sunil Kant Munjal Shri D. Sengupta Shri O.V. Bundellu IDBI Nominee Shri S.L. Mohan GIC Nominee Shri S.N. Chaturvedi UTI Nominee Company Secretary Shri V.P. Agarwal Audit Committee Dr. S.S. Baijal Chairman Shri Arun Bharat Ram Shri Pradeep Dinodia Shri O.V. Bundellu IDBI Nominee Bankers Punjab National Bank Bank of Baroda Oriental Bank of Commerce State Bank of India Auditors M/s. A.F. Ferguson & Co., New Delhi. Registered Office 6th Floor, Kanchenjunga Building, 18, Barakhamba Road, New Delhi – 110 001. Tel. No. :(91) 11-23316801 Fax No. :(91) 11-23357803 Email : [email protected] Stock Exchanges where the Securities of the Company are Listed National Stock Exchange of India Ltd., Exchange Plaza, 5th Floor, Plot No. C/1, G Block, Bandra-Kurla Complex, Bandra (East), Mumbai – 400 051. The Stock Exchange, Mumbai Pheroze Jeejeebhoy Towers, Dalal Street, Mumbai – 400 001. The Calcutta Stock Exchange Association Ltd., 7, Lyons Range, Kolkata – 700 001. (The Company’s application for delisting of its Equity Shares is pending with the Calcutta Stock Exchange Association Ltd.) (It is confirmed that annual listing fee has been paid by the Company to each of the above Stock Exchanges) Board of Directors DSCL Janta doc 24.06.04.qxd 9/18/04 4:46 AM Page 1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of DSCL Janta doc 24.06.04.qxd - Morningstar

1

Shri Ajay S. ShriramChairman & Senior Managing Director

Shri Vikram S. Shriram Vice-Chairman & Managing Director

Shri Rajiv SinhaDy. Managing Director

Shri Ajit S. ShriramDirector (Sugar)

Dr. S.S. Baijal

Shri Arun Bharat Ram

Shri Pradeep Dinodia

Shri Vimal Bhandari

Shri Sunil Kant Munjal

Shri D. Sengupta

Shri O.V. BundelluIDBI Nominee

Shri S.L. MohanGIC Nominee

Shri S.N. ChaturvediUTI Nominee

Company Secretary Shri V.P. Agarwal

Audit Committee Dr. S.S. BaijalChairman

Shri Arun Bharat Ram

Shri Pradeep Dinodia

Shri O.V. BundelluIDBI Nominee

Bankers Punjab National Bank

Bank of Baroda

Oriental Bank of Commerce

State Bank of India

Auditors M/s. A.F. Ferguson & Co.,New Delhi.

Registered Office 6th Floor, Kanchenjunga Building,18, Barakhamba Road, New Delhi – 110 001.Tel. No. : (91) 11-23316801Fax No. :(91) 11-23357803Email : [email protected]

Stock Exchanges where theSecurities of the Companyare Listed

National Stock Exchange of India Ltd.,Exchange Plaza, 5th Floor,Plot No. C/1, G Block, Bandra-KurlaComplex, Bandra (East), Mumbai – 400 051.

The Stock Exchange, MumbaiPheroze Jeejeebhoy Towers,Dalal Street, Mumbai – 400 001.

The Calcutta Stock ExchangeAssociation Ltd.,7, Lyons Range, Kolkata – 700 001.(The Company’s application for delistingof its Equity Shares is pending with theCalcutta Stock Exchange Association Ltd.)

(It is confirmed that annual listing fee has been paid bythe Company to each of the above Stock Exchanges)

Board of Directors

DSCL Janta doc 24.06.04.qxd 9/18/04 4:46 AM Page 1

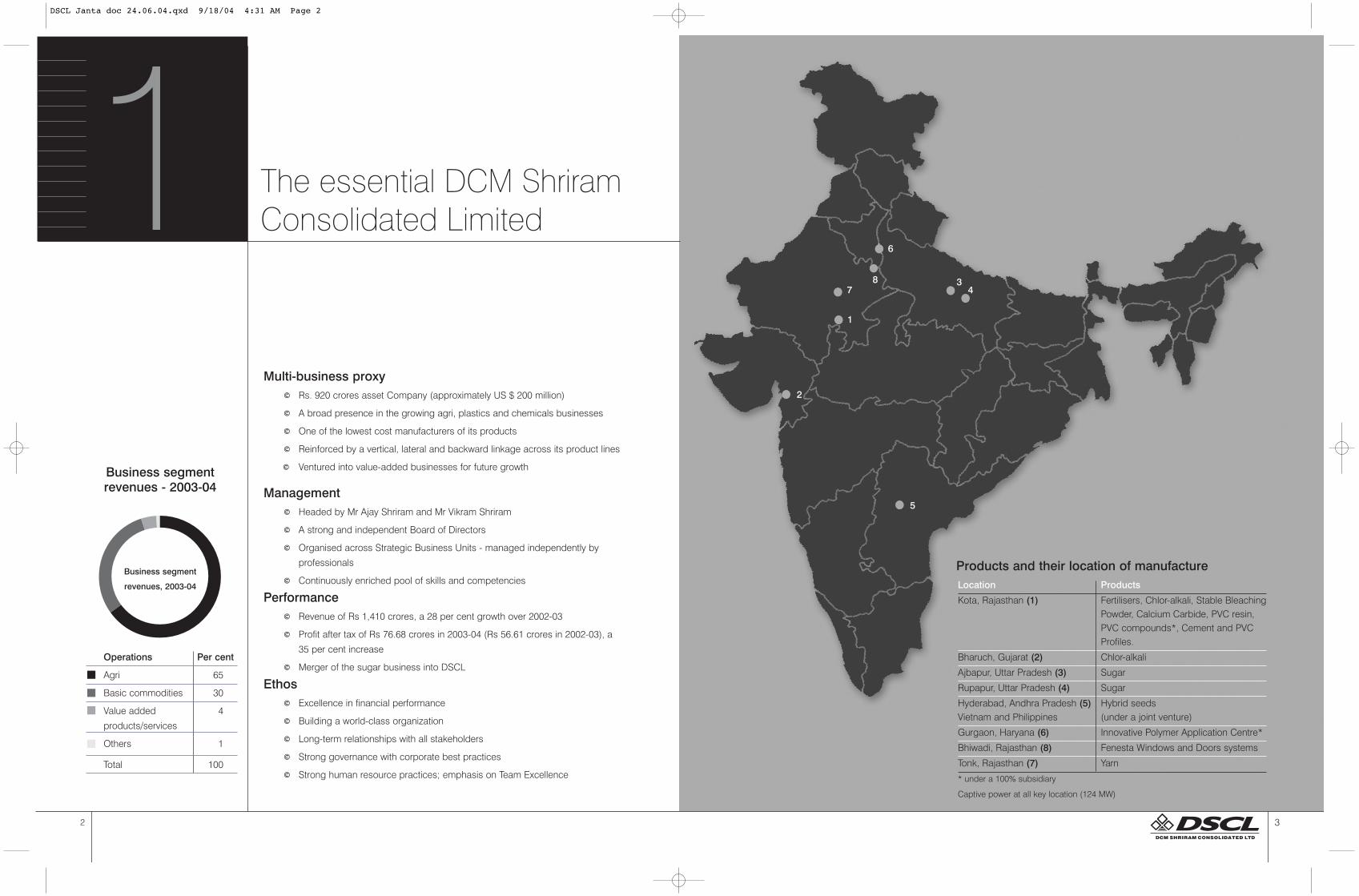

Multi-business proxy© Rs. 920 crores asset Company (approximately US $ 200 million)

© A broad presence in the growing agri, plastics and chemicals businesses

© One of the lowest cost manufacturers of its products

© Reinforced by a vertical, lateral and backward linkage across its product lines

© Ventured into value-added businesses for future growth

Management© Headed by Mr Ajay Shriram and Mr Vikram Shriram

© A strong and independent Board of Directors

© Organised across Strategic Business Units - managed independently by

professionals

© Continuously enriched pool of skills and competencies

Performance © Revenue of Rs 1,410 crores, a 28 per cent growth over 2002-03

© Profit after tax of Rs 76.68 crores in 2003-04 (Rs 56.61 crores in 2002-03), a

35 per cent increase

© Merger of the sugar business into DSCL

Ethos© Excellence in financial performance

© Building a world-class organization

© Long-term relationships with all stakeholders

© Strong governance with corporate best practices

© Strong human resource practices; emphasis on Team Excellence

The essential DCM ShriramConsolidated Limited

6

347

8

1

2

5

1

32

Products and their location of manufacture Location Products

Kota, Rajasthan (1) Fertilisers, Chlor-alkali, Stable BleachingPowder, Calcium Carbide, PVC resin, PVC compounds*, Cement and PVC Profiles.

Bharuch, Gujarat (2) Chlor-alkali

Ajbapur, Uttar Pradesh (3) Sugar

Rupapur, Uttar Pradesh (4) Sugar

Hyderabad, Andhra Pradesh (5) Hybrid seedsVietnam and Philippines (under a joint venture)

Gurgaon, Haryana (6) Innovative Polymer Application Centre*

Bhiwadi, Rajasthan (8) Fenesta Windows and Doors systems

Tonk, Rajasthan (7) Yarn

* under a 100% subsidiary

Captive power at all key location (124 MW)

Operations Per cent

Agri 65

Basic commodities 30

Value added 4

products/services

Others 1

Total 100

Business segmentrevenues - 2003-04

Business segment

revenues, 2003-04

DSCL Janta doc 24.06.04.qxd 9/18/04 4:31 AM Page 2

54

DSCL is strengthening existingbusinesses while incubatingnewer and value-addedbusinesses for future growth.

From the Chairman and Vice Chairman's desk

Mr Ajay S Shriram and Mr Vikram S Shriram enunciate DSCL’s growth plan

The year 2003-04 was a satisfying one for the Company.

It was a year in which we benefited from the strategy that

your Company has been consistently practicing over the

years – ‘Strengthen our position in existing businesses while

incubating newer and value added business to provide future

growth’.

A sustained focus on cost rationalization and strengthening

competitive position, helped by a favourable price cycle in

our major businesses (plastics and chemicals), resulted in

your Company achieving an improved performance – a total

income of about Rs.1500 crs. and a profit after tax of Rs. 76

crs. (increase of 35% over the previous year).

As a continuation of this ongoing strategy, your Company is

implementing a capital expenditure programme of approxi-

mately Rs. 300 crs. over the next two years. This will:

© Provide volume growth in chemicals, PVC and cement at

a time when these businesses are going through an up-

cycle, while the increased power requirement will be

addressed by the augmentation of low cost captive power

generation capacity.

© Enhance our cost competitiveness across all businesses.

© Grow Hariyali Kisaan Bazaar, our newly

launched agri-retail initiative. The response

to its business model has been

encouraging, creating customer

excitement and a satisfactory financial

performance. In view of this, it is proposed

to increase the number of stores from 8 to

33 in two years.

© Grow Fenesta Building Systems, following

a positive response to its wimdow systems

launch in May 2003. In view of this, your

Company plans to extend it to an all India

presence.

The completion of these business-enhancing

programmes is expected to result in a

quantum jump in volumes and financial

performance.

We have all along recognized that people are

the key resources for the sucess of the

Company. We will, therefore, continue to give

highest priority to develop and strengthen the

human resources to meet future challenges.

Your Company continues to put strong

emphasis on environment, health and safety,

the results of which have received due

recognition. New initiatives are being

undertaken to further upgrade these areas.

We expect that these initiatives will provide

sustainable growth and lead to enhanced

value for all our stakeholders.

Friends, we deeply appreciate your support

and encouragement, which has contributed

to our attractive growth and hope that it will

continue to encourage our performance over

the coming years.

With best wishes,

The completion of these business-enhancingprogrammes is expected to result in a quantum

jump in volumes and financial performance.

(VIKRAM S. SHRIRAM) (AJAY S. SHRIRAM)Vice Chairman & Chairman &

Managing Director Sr. Managing Director

DSCL Janta doc 24.06.04.qxd 9/18/04 4:31 AM Page 4

visibility in the urban markets, while its ‘Shriram’ agri products

are directed towards rural community.

� Customer commitment: The Company’s commitment to

customers is reflected in its transparency, delivery and quality.

The Company’s website www.dsclpartners.com enables

transactions and customer interactions to be carried out

online.

The premium positioning of the Company’s products has

resulted in its products fetching a premium over competing

brands.

Ongoing de-risking A continuous de-risking is helping progressively insulate the

Company from diverse industry challenges. Over the years,

the Company has embarked on a number of initiatives

to do so:

� Improving cost position: The Company has continuously

focused on costs to enhance its competitive position, through

re-engineering as well as various technology and process

upgradations. This has enabled the Company to be amongst

the lowest cost producers in respective categories.

� Scaling up: The Company continues to build size at the

lowest cost to derive advantages of economies of scale and

costs. The manufacturing capacities have been aggressively

utilised to achieve the best efficiencies.

� Swing capability: Over the years, the Company has

developed a swing capability in its operations, wherein it is

able to change the product mix depending on the prevalent

market situation to derive the maximum value.

� Diversified portfolio: The Company’s product portfolio is

diversified, yet related. The diversification provides it with an

effective cushion against industry troughs, enhancing its

organisational stability.

� Fiscal conservatism: The Company’s preference for

internal accrual-driven expansion and the low cost

mobilisation of debt has strengthened its de-risking (please

read the financial section for more details).

� Controls: The Company’s control systems ensure a

proactive assessment of risks and steps to mitigate them.

These systems are periodically reviewed by external

professionals and upgraded continuously.

Human resources People represent the core of DSCL’s operations. Even as the

Company has been in business for over a century, it continues

to possess a refreshingly youthful spirit. This renewal and

rejuvenation is the result of a strong and relevant organization

structure, continuous training and development,

empowerment and working of cross-functional teams. The

benchmarking of its practices to the best standards of the day

has made it an exciting destination for achievers. Besides,

institution-building initiatives are pursued continuously across

the organisation. The Company recognises its employees as

key resource and has a long-standing and credible track

record in nurturing them.

� SBU structure: The SBU structure at DSCL, gives the

reqiured focus necessary to run the businesses and manage

performance effectively. This has led to a high level of

entrepreneurial ownership and involvement.

� Institution building: A strong culture of collaborative

working, team excellence, openness, transparency, sharing

and ethical working has been consciously developed through

an institution building exercise, including the use of cross-

functional teams and process labs.

� Progressive HR practices: The Company has always laid

an emphasis on training, including international exposure, for

continuous skill upgradation, recalibration to new

organizational and environmental needs. The Company’s

workforce can be characterized as committed and stable with

a high degree of varied skills and competencies.

� Excellent Industrial Relations: The Company has enjoyed

harmonious and constructive industrial relations track record

since inception. Its Industrial Relations policy is based on

fairness, firmness and concern for each person in the

organisation.

Information technologyIT continues to be the backbone of the organization.

The Company was amongst the first Indian companies to

implement SAP R/3 and mySAP.com in 1998 and 2002. Today,

all its processes are on SAP R/3, which allows the businesses

an effective decision-making support and adequate controls.

DSCL is a networked organization with an online connectivity

76

Our strengths

Integrated and Cost CompetitiveIntegration is DSCL’s biggest value-driver.

Over the years, the Company has integrated its operations across two

levels – locational and products.

� Locational integration: DSCL’s 800 acre complex at Kota comprises

the manufacture of Fertilisers, PVC resins, Calcium Carbide, Caustic soda,

Chlorine, Hydrochloric acid, Sodium hypochlorite, Cement, PVC

compounds, PVC Profiles, Captive Power and Steam. This locational

integration enables each business to share utilities and facilities, thereby

reducing overheads and other costs.

� Product integration: Operations at DSCL are also integrated across

products. The efficient utilization of products and by-products from one

plant to other and captive power and steam have enabled DSCL to emerge

among the lowest cost manufacturers in respective categories in the

country.

This approach has resulted in a reduction in operating cost/sales ratio from

94% in 1990-91 to 83% in 2003-04.

Premium positioningBranding helps DSCL’s products beat the commodity clutter of a

competitive marketplace.

� Recall: Most of the Company’s products are marketed under the

‘Shriram’ brand and represent distinct product identities, facilitating a clear

recall. The brand represents quality and reliability.

� Distribution: The Company’s products are backed by a strong

marketing and distribution network, e.g. its agri network comprises over 500

wholesalers and 5000 retailers primarily concentrated in India’s northern

states.

� Urban-rural coverage: The Company’s brands address the urban-rural

spread. For instance, its ‘Fenesta’ Windows and Doors Systems enhance

3Operations at DSCLare highly integratedon products. Efficientutilization of productsand by-products fromone plant to other andcaptive power andsteam has enabledDSCL to be amongstthe lowest costmanufacturer inrespective categories,in the country.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:32 AM Page 6

9

across 24 locations spread all over India and also with approximately 350

customers and vendors.

DSCL has been effectively using its IT network and facilities to its business

benefits from basic transactions to e-procurement, customer interaction, etc. The

focus is on to leverage the existing set-up more and derive even better values.

ProcessesDSCL is a process-driven organisation. Over the years it has strengthened

processes, which support the fulfillment of business objectives and goals. This

enables DSCL to handle diverse businesses with a unified focus, encourages

decentralisation and entrepreneurship, the sharing of information and best

practices while maintaining strong internal controls.

These processes extend from strategic planning to transaction processing, from

human assets to physical assets and from vendors to customers.

These processes have continuously been upgraded with inputs from the best

consultants and practitioners with a view to pro-actively respond to the emerging

requirements.

This approach prompted DSCL to go through a comprehensive Business

Process Re-engineering in early Nineties, adopt the best ERP package, upgrade

in accordance with SAP R/3 and continuously benchmark all its processes in line

with the best practices.

Environment, health and safetyEnvironment, health and safety has been a focus area at the Company. This

commitment has been recognized by way of several national awards. Over the

years, this concern has also been reflected in the following initiatives:

� Certifications: Company’s compliance has been validated by world-class

certifications - ISO 14001, OHSAS 18001 and SA 8000.

� Projects: The Company has initiated a number of water harvesting schemes

and extensive tree plantation programmes across several acres in and around its

manufacturing facilities in Kota, Bharuch, Ajbapur and Rupapur.

8

Financial highlightsOverviewDSCL has achieved a strong competitiveness in all its businesses, stability in itsearning stream and a sustained growth in topline / bottomline while ensuring aprudent level of leverage. This was done in line with the following objectives:

Continuing growth in Profits and profitability

DSCL focussed on cost rationalisation, exiting unviable businesses, technologyupgradation, increasing capacities and incubating/building new businesses. Whilethe investments have been continuous, they have been within prudent limits,resulting in:

© Turnover growth of 11.9% (CAGR) over 1990-91/2003-04.

© PBDIT growth of 18.9% (CAGR) over the same period.

© Operating margin enhancement from 6.7% in 1990-91 to 16.7% in 2003-04.

Stronger financial structure

Even as the total assets of the Company increased from Rs. 97 crs. to Rs. 921 crs.during this period, the leveraging ratios improved as given below:

© Total debt to net worth reduced from 2.63 in 1990-91 to 1.44 in 2003-04.

© Total outside liabilities to net worth declined from 5.10 to 2.33, and

© Interest cover strengthened from 2.03 to 4.74.

Reduction in interest costs

While funding asset growth through prudent debt management, the Company kepta tight control on interest cost. As a result, the Company was able to:

© Finance its working capital requirements at ~25 basis points higher than MIBOR i.e. effectively at rates substantially lower than the prime lending rates of banks in India.

© Progressively replace high cost long-term debt with low cost debt to achieve an effective intrest rate of ~7.75% on 31.03.04.

OutlookDSCL expects to strengthen its financials through the following:

© Enhanced credit rating: It expects to address the higher cost of feedstock inthe Urea business and upgrade its technology in Chlor-alkali, leading to lowered business risk. This, along with a further improvement in the leverage, should lead to an enhanced credit rating in the medium term.

© Extended debt maturity: The Company expects to increase its average high cost debt tenure and enhance its liquidity.

© Reduced borrowings cost: It will continue to restructure high cost debt throughdiverse financial instruments.

DSCL’s processesenable it to handlediverse businesseswith a unified focus,encouragesdecentralisation andentrepreneurship, thesharing ofinformation and bestpractices whilemaintaining stronginternal controls.

While funding thegrowth in assetsthrough prudent levelof debts, theCompany has kept itsfocus on tight controlon interest costs.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:32 AM Page 8

1110

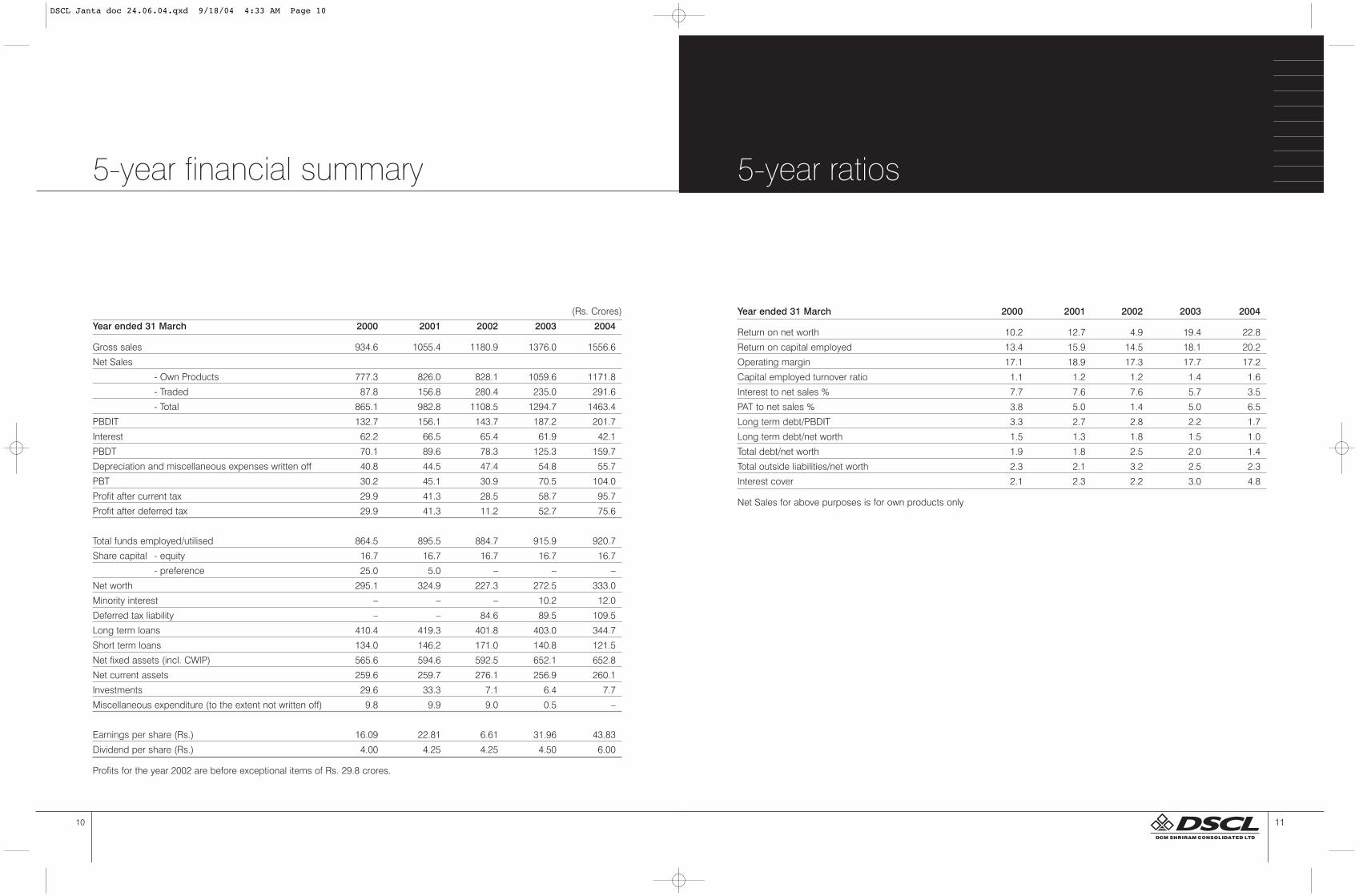

5-year financial summary

(Rs. Crores)

Year ended 31 March 2000 2001 2002 2003 2004

Gross sales 934.6 1055.4 1180.9 1376.0 1556.6

Net Sales

- Own Products 777.3 826.0 828.1 1059.6 1171.8

- Traded 87.8 156.8 280.4 235.0 291.6

- Total 865.1 982.8 1108.5 1294.7 1463.4

PBDIT 132.7 156.1 143.7 187.2 201.7

Interest 62.2 66.5 65.4 61.9 42.1

PBDT 70.1 89.6 78.3 125.3 159.7

Depreciation and miscellaneous expenses written off 40.8 44.5 47.4 54.8 55.7

PBT 30.2 45.1 30.9 70.5 104.0

Profit after current tax 29.9 41.3 28.5 58.7 95.7

Profit after deferred tax 29.9 41.3 11.2 52.7 75.6

Total funds employed/utilised 864.5 895.5 884.7 915.9 920.7

Share capital - equity 16.7 16.7 16.7 16.7 16.7

- preference 25.0 5.0 – – –

Net worth 295.1 324.9 227.3 272.5 333.0

Minority interest – – – 10.2 12.0

Deferred tax liability – – 84.6 89.5 109.5

Long term loans 410.4 419.3 401.8 403.0 344.7

Short term loans 134.0 146.2 171.0 140.8 121.5

Net fixed assets (incl. CWIP) 565.6 594.6 592.5 652.1 652.8

Net current assets 259.6 259.7 276.1 256.9 260.1

Investments 29.6 33.3 7.1 6.4 7.7

Miscellaneous expenditure (to the extent not written off) 9.8 9.9 9.0 0.5 –

Earnings per share (Rs.) 16.09 22.81 6.61 31.96 43.83

Dividend per share (Rs.) 4.00 4.25 4.25 4.50 6.00

Profits for the year 2002 are before exceptional items of Rs. 29.8 crores.

Year ended 31 March 2000 2001 2002 2003 2004

Return on net worth 10.2 12.7 4.9 19.4 22.8

Return on capital employed 13.4 15.9 14.5 18.1 20.2

Operating margin 17.1 18.9 17.3 17.7 17.2

Capital employed turnover ratio 1.1 1.2 1.2 1.4 1.6

Interest to net sales % 7.7 7.6 7.6 5.7 3.5

PAT to net sales % 3.8 5.0 1.4 5.0 6.5

Long term debt/PBDIT 3.3 2.7 2.8 2.2 1.7

Long term debt/net worth 1.5 1.3 1.8 1.5 1.0

Total debt/net worth 1.9 1.8 2.5 2.0 1.4

Total outside liabilities/net worth 2.3 2.1 3.2 2.5 2.3

Interest cover 2.1 2.3 2.2 3.0 4.8

Net Sales for above purposes is for own products only

5-year ratios

DSCL Janta doc 24.06.04.qxd 9/18/04 4:33 AM Page 10

15

Over the foreseeable future, the Company expects to grow horizontally and

vertically – horizontally in its core commodity businesses and vertically in

value-added products and services. These initiatives will require investments

in the short run, funded largely through accruals, and will begin yielding higher

revenues and margins across the medium to long-term.

Over the next two years, the Company will invest Rs. 300 crs. across its various

businesses in capacity expansion, technology upgradation and growing value-

added products and services through the following initiatives:

Agri-businessThe Company expects to strengthen its competitive position in Urea and

expand Hariyali Kisaan Bazaar through proactive investments.

© Urea: DSCL intends to change its feedstock from Naphtha to LNG to

reduce costs and become more environment friendly.

© Hariyali Kisaan Bazaar: In its rural retail initiative, it plans to quadruple the

number of its Hariyali Kisaan Bazaar stores to 33, increasing its spread and

growing its volumes. It also plans to increase the offerings from each of its

stores.

Chemicals© Chlor alkali: The Company has embarked on a project to convert its

mercury cell technology at Kota to membrane cell and enhance its capacity

from 139 TPD to 200 TPD by 2006.

This will enhance energy efficiency

by 22 per cent and move to more

environment friendly technology.

PVCThe Company will expand its PVC

capacity from 115 TPD to 175 TPD

with a corresponding increase in its

carbide capacity, which will also

enhance the division’s cost

competitiveness.

CementWith an increased availability of sludge

through PVC/Carbide expansion, the

Company will increase its cement

capacity from 2.97 lac TPA to 4.0 lac

TPA, so as to drive volume cost

efficiencies.

PowerPower represents the heart of the

Company’s growth engine, especially

in view of the energy intensity of its

operations. The Company will

augment its power generation

capacity at Kota from 85 MW to 125

MW by 2006. The Company will be

able to generate power at

considerably lower cost than the

prevailing tariff of power sourced from

the state electricity grid. To secure its

raw material interests, the Company is

exploring lignite as a long-term

resource from mines in Rajasthan.

Fenesta Building SystemsThe launch of Fenesta Windows will be

extended from Northern India to

across India over the next two years, in

view of the housing construction and

infrastructure growth.

SugarSimultaneously, the Company is

evaluating options to further grow its

sugar business, a long-term growth

area.

Real EstateFollowing the Supreme Court order

directing the Company to shift its

textile operations from Delhi, the

Company has liberated 112 acres of

freehold property. This is being

developed as per the directives of the

Supreme Court through a joint venture

with an international Company, making

it one of the largest projects in the

Delhi region. DSCL will invest the

gains from this operation into its core

businesses.

14

The road ahead Strategy5 The Company expects to

grow horizontally in itscore commoditybusinesses and

vertically in value-addedproducts and services.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:34 AM Page 14

17

OverviewThe financial year 2003-04 was an excellent one for your Company. The

Company’s efforts to continuously improve the cost structures over the years

and the favourable commodity cycle helped it earn higher revenues and profits

during the year.

The strong demand growth in all the products has resulted in substantial

shrinking of the overhang of excess capacity in the country. In fact, for some

products like PVC, India turned into a net importer. Consequently, the prices of

almost all the products are on an upsurge leading to an improvement in margins

and capacity utilisations. Products like cement and sugar also recorded

improvement in prices and margins in the latter part of the year.

The up-trend in all these products is likely to last at least for a couple of years.

Your Company, therefore, has finalised a plan to increase capacities in the Chlor-

alkali, PVC, and Cement business along with adequate increase in power

generating capacity.

The Scheme of Arrangement for Merger of Ghaghara Sugar Ltd. into your

Company and de-merger of the Energy Services business into a separate

subsidiary, implemented during the current year, will facilitate the growth of the

sugar and energy services businesses and help them derive the benefits of

synergy and focus in operations.

Your Company has the following main business segments:

A Fertilisers

B Agri Merchandising

C Sugar

D Plastics

E Chemicals

F Other businesses

16

Management Discussion &Analysis Report6

The Company’s effortsto continuouslyimprove the coststructures over theyears and thefavourable commoditycycle helped it earnhigher revenues andprofits during the year.

A detailed analysis of the different

businesses is provided below:

A) Fertiliser businessi) Industry structure

Urea is the pre-dominant fertiliser used

by farmers in the country with an annual

demand of approx. 19.6 million TPA and

growing historically at a CAGR of ~5

per cent. Indigenous supplies primarily

meet the total demand. One of the

oldest industries in India, the fertiliser

industry has 32 players with plants of

differing vintage and varied feedstocks

(coal, fuel oil, naphtha, gas etc.). The

industry is regulated by the central

government through a Retention Price

System and Sales allocation under

Essential Commodities Act (ECA). In

2002-03, the government announced a

long-term pricing policy for urea,

thereby removing the uncertainty, which

was prevailing over the last 5-6 years.

During the current year, the government

announced policies for :

© Conversion of feedstock to

LNG/natural gas.

© De-bottlenecking of capacities and

expansion.

© Setting up of new urea plants.

The issue of LNG/NG pricing, however,

still remains to be resolved which is

delaying the efforts towards conversion

of feedstock.

In accordance with the long-term

pricing policy, the government

implemented the first phase w.e.f. 1st

April 2003 whereby the retention price

has been fixed based on the Group

Average or Company’s Retention Price,

whichever is lower. The second phase

has been implemented w.e.f. 1st April

2004, whereby energy consumption

norms have been further tightened and

expressed in terms of energy

consumed instead of quantity of inputs.

The ECA Sales Allocation has been

reduced to 50 per cent and companies

are free to sell the balance 50 per cent

in whichever market they want within the

country.

The earlier government had indicated its

decision to privatise some of the public

sector fertiliser companies which may

trigger consolidation in the industry.

Some of the existing manufacturers are

also setting up JVs in foreign countries

for the manufacture of urea for the

Indian market.

ii) Industry outlook India is expected to keep recording

positive growth in fertiliser consumption

for years to come. Fertiliser is an

essential ingredient to build a stronger

agriculture base and maintain self-

reliance in food supplies for a growing

population – the two stated objectives

of government policy.

However, in view of uncertainties in the

government policies, this sector does

not present an attractive environment

for committing major investments.

At the same time, it is expected that an

existing cost effective fertiliser

manufacturer can continue to ensure

reasonable returns provided it takes

pro-active steps to keep reducing cost

of production and strengthening market

position through the building of long-

term and fair relationships with farmers.

iii) Business performance The fertiliser business experienced

strong demand during the year,

supported by good monsoons. The

sales quantity at 3.80 lac tonnes (last

year 3.81 lac tonnes) was the maximum

permissible under the retention price

system.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:34 AM Page 16

The market for fertilisers, however, will

continue to face the uncertainty caused

by government policy. Other agriculture

inputs provide an attractive opportunity.

However, a long-term outlook and the

building of strong farmer relationships

will be the key drivers of success in this

business.

iii) Business performance

The turnover of this business grew by 24

per cent (from Rs.235.03 crs. to

Rs.291.62 crs.) during the year. It also

recorded positive margins primarily due

to a healthy growth in the non-fertiliser

agri-business (seeds - 19 per cent,

pesticides - 31 per cent) and gains due

to rupee appreciation. It also provided

low cost working capital funds, thus

contributing to the reduction in overall

interest costs of the Company.

The product basket was further

enhanced with the addition of

micronutrients and soluble fertilisers.

The single super phosphate business

grew from 50,940 tonnes to 1,18,736

tonnes, by tying up of reliable supply

sources.

The DAP and MOP business continues

to suffer due to uncertain government

policy which is a major hindrance in

realising the full potential of these

products.

iv) Business strategy

The turnover of SSP and non-fertiliser

agri-inputs (seeds, pesticides,

micronutrients etc.) has gone up in the

last few years. These products have

been the major focus areas in this

business. These are higher margin

products and, therefore, the Company

wants to grow their volumes

aggressively.

C) Sugar business

i) Industry structure

India is the largest consumer of sugar inthe world. The present demand is about18.5 million tonnes and growing at ahistorical CAGR of 4 per cent perannum. With improvement in thestandard of living and the rapidevolution of the food processingindustry in India, sugar demand isbound to accelerate.

India is also the second largestproducer of sugar in the world. Thereare over 450 sugar factories of varyingcapacities and vintage. The ownershippattern is also quite varied: publicsector, cooperative sector and privatesector companies co-exist in thisindustry. Similarly, there is a tremendousdiversity in sizes. Large corporategroups with over 20,000 TCD capacitiesrub shoulders with small standalone

mills of less than 2,000 TCD capacities.Geographically, sugar is produced inalmost all the major Indian statesthough Maharashtra and U.P. contributeover 50 per cent to the country’sproduction. Tamil Nadu, Karnataka,Punjab and Andhra Pradesh are theother major sugar producing States.

Imports and exports are not verysignificant in India, except in the yearsof major deficit and surpluses. Theseoccur as a part of the sugar cyclecaused by cane arrears/climatic factorsi.e. Bumper crop > fall in sugar prices> inability of the mills to pay cane pricesto farmers > shortfall in sugarcaneproduction as farmers divert land toother crops.

Sugar is one of the largest agro-processing industries in India. Thefortunes of millions of farmers ride onthis industry. Moreover, sugar prices aresensitive from the common man’s pointof view. The sector, therefore, is highlyregulated, both by the central and stategovernments. It is the governmentwhich allots the area for cane plantationto mills, stipulates the cane prices anddecides how much sugar the mill cansell in the free market in a month.Besides, 10 per cent of sugar producedby a mill has to be sold at a fixed priceto the government’s public distributionsystem as a levy obligation.

19

The production at 3.64 lac tonnes (last

year 3.93 lac tonnes) was lower due to

carried-over stock since last year’s

production was higher than the

maximum permissible sales.

The lower production, a shutdown of the

power plant for about two months due

to technical failure, and accounting of

higher fertiliser subsidy arrears in last

year’s results led to a lower profit of the

business compared to last year.

The government implemented the first

phase of the long-term fertiliser policy

w.e.f. 1st April 2003 and the second

phase w.e.f. 1st April 2004.

The second phase of the policy, which

further reduces energy consumption

norms will cause a further squeeze in

margins in the coming year in spite of

your Company being the lowest cost

producer in its group. The management

is taking steps to reduce the impact as

much as possible. The Company has

taken up a scheme for conversion of its

urea plant, from naphtha to dual feed

(i.e. gas or naphtha).

The Company continued its efforts to

strengthen its relationship with farmers

and dealers through various initiatives,

including further growth in agri-

extension activities through Shriram

Krishi Vikas Kendras, kisan melas,

dealer promotion schemes etc. All these

have helped in maintaining the premium

brand positioning in the marketplace.

iv) Business strategy

During the last 35 years, the fertiliser

business of the Company has built

strong competitive advantages through

a premium positioning of Shriram brand

urea in north and central India (the

agricultural heart of the country) and a

4.2 lac MTPA naphtha-based plant

which is the lowest-cost urea producer

in its group (pre-1992 naphtha-based

plants).

These advantages enabled the

business to generate reasonable

returns despite pressures and

unfavourable developments. On the

marketing side, the Company intends to

further strengthen its relationships with

farmers and trade patrons. Your

Company continues to follow a cautious

approach towards committing major

investments in this sector.

B) Agri Merchandisingbusiness

i) Industry structure

With over two-thirds of the Indian

population engaged in agriculture,

coupled with the need to meet the

requirements of a large and growing

Indian population, the market for all

agriculture inputs -- fertilisers, seeds,

pesticides etc. – looks highly promising.

It will be characterised by an increasing

demand for valuable and better quality

agriculture inputs.

There are companies that started

business with one agriculture input and

over a period of time started offering the

complete basket through the same

channel. One of the major drivers of this

trend has been the leveraging of the

brand and distribution strength while

growing the overall volumes, which then

reinforces the brand and distribution

network - forming a virtuous cycle.

The other category of players has stuck

to its chosen field and provides only one

or two of the Agri inputs.

The central and state governments play

an important role for some of the inputs,

primarily fertilisers (DAP, MOP, SSP) and

their policies have an impact on the

business.

ii) Industry outlook

The demand for all agriculture inputs is

expected to keep growing at a healthy

rate carving an attractive profile for the

Indian market. Indian farmers have

shown great adaptability and

willingness to experiment with inputs to

increase agriculture productivity and

profitability.

18

DSCL Janta doc 24.06.04.qxd 9/18/04 4:34 AM Page 18

2120

Both the sugar factories had short 2003-04 sugar seasons due to low availabilityof cane. The cane crush was thussignificantly lower than the normallyachievable levels. The recovery wasalso adversely affected due to excessrainfall and waterlogging in the caneareas.

The Company has intensified its canedevelopment efforts to reduce theimpact of these adverse developmentsin the next season (2004-05).

The year started with very

unremunerative sugar prices due to

surplus production and large carry over

stock. The drop in sugar production has

seen improvement in sugar prices in the

second half of the year. The prices of

by-products, i.e. molasses and

bagasse also moved up. This upward

movement in prices enabled the sugar

business of your Company to record a

segment revenue of Rs.197 crs. and

EBIT margin of Rs.20.20 crs.

The project for addition of powergenerating capacity and setting up oftransmission lines for the supply ofpower from Ajbapur factory to the powergrid is progressing and the Companyexpects to be in a position to supplypower in the 2004-05 sugar season.

iv) Business strategy

Your Company has identified sugar asone of its growth areas and is aiming toemerge as one of the most efficient and

profitable sugar manufacturers in thecountry. Working closely with farmers toimprove cane production and canequality, and efficient factory operationsare key areas of focus for the Company.On the anvil is modular expansion ofsugar capacity in both the factories, inaccordance with the anticipated caneavailability. The Company is alsoaugmenting power generation capacityin order to supply power to the grid. Itwill explore the prospect ofalcohol/ethanol generation in duecourse.

D) Plastics business

i) Industry structure

The present demand of PVC resin is 9

lac MT which is expected to grow at a

rate of about 8 per cent per annum. PVC

is widely used in the country in various

applications such as pipes, cables,

footwear etc. There are however

significant application areas emerging,

such as automobiles, construction,

medical supplies and food packaging,

to name a few. The acceptance of PVC,

new uses and a stronger GDP growth

can further push the PVC demand

growth rate in the country.

There are five PVC manufacturers in the

country out of which Reliance and IPCL

account for 70 per cent of the total

capacity. The total production of PVC in

the country is about 8.8 lac tonnes and

the net imports are about 0.6 lac tonne

per year. Various manufacturers in the

country have announced plans to add

about four lac tonnes capacity during

2004-08. It is expected that even after

this capacity enhancement, India will

continue to be a net importer of PVC. All

the manufacturers, except your

Company, manufacture PVC through

the ethylene/EDC/VCM route. Your

Company on the other hand

manufactures PVC through the carbide

and acetylene route, a process widely

followed in China. This process

produces carbide as an intermediate

saleable product and creates immense

opportunity for the Company to simply

change the product mix between

Carbide and PVC based on prevalent

market situation to maximise value.

The landed cost of PVC imports is a

major determinant of India’s domestic

prices. Currently, PVC is subject to a

customs duty of 20 per cent, which is

expected to decline in the coming year.

ii) Industry outlook

PVC is experiencing buoyancy since

2003, led by a strong growth in demand

in China and other Asian countries. This

has resulted in an almost 50 per cent

increase in global prices of PVC during

the period.

It is expected that the buoyancy in the

PVC market will continue for the next

The recent order of the Hon’bleSupreme Court on cane prices hasprovided a new dimension to thealready difficult situation for the industry.We hope that both the state and centralgovernments will take a rational view inthe matter and initiate steps that help inbuilding a healthy and viable sugarindustry.

Over the last three to four years, surplusproduction and large inventory carry-over have been impacting the industry.The problem was further compoundedby the government’s increase ofsugarcane prices. It found favour withfarmers but disregarded the sugar mills’ability to afford such costs leading tohigh cane arrears. This, along withunfavourable climatic factors in some ofthe sugar cane producing States, hasled to a sharp drop in sugar productionin the sugar season of 2003-04. It isestimated that sugar production in thisseason will be about 15.5 million tonnescompared to over 20 million tonnes in

the last season. The sugar industry,incentivised by the government,exported over two million tonnes ofsugar in the last year. This has resultedin an increase in prices. In spite ofproduction declining sharply in a largenumber of mills, it is expected that theprofitability of sugar mills shouldimprove in the next couple of years.

Over the recent past, sugar mills havealso taken steps to become integratedplayers - producing power andalcohol/ethanol from by-products likebagasse and molasses, respectively.This would strengthen their operationsand improve sustainability over thelong-term.

ii) Industry outlookThe sugar season 2003-04 should endwith a reduction in carry over stock withthe industry, to bring it back to the levelsmaintained historically. It is expectedthat the country will continue to have ashortfall in sugar production vis-à-vis

demand for F.Y. 2004-05. This shouldresult in reasonable prices for sugar andthus reasonable returns to sugar mills,provided of course that the governmentfollows a rational policy on cane pricing.Thereafter, with the continuing increasein sugar demand in the country, aproduction excess is unlikely.

The process of evolving from a puresugar producer to an integrated sugarmill is likely to continue and strengthen.

iii) Business performance In accordance with the Scheme ofArrangement explained above, theoperations of the sugar business ofGhaghara Sugar Ltd. (GSL), a whollyowned subsidiary, have beentransferred to your Company w.e.f. 1stApril 2003.

The sugar season of 2003-04 (Octoberto September) is the first full season foryour Company though it also had part-operations in the previous season (Aprilto June 2003).

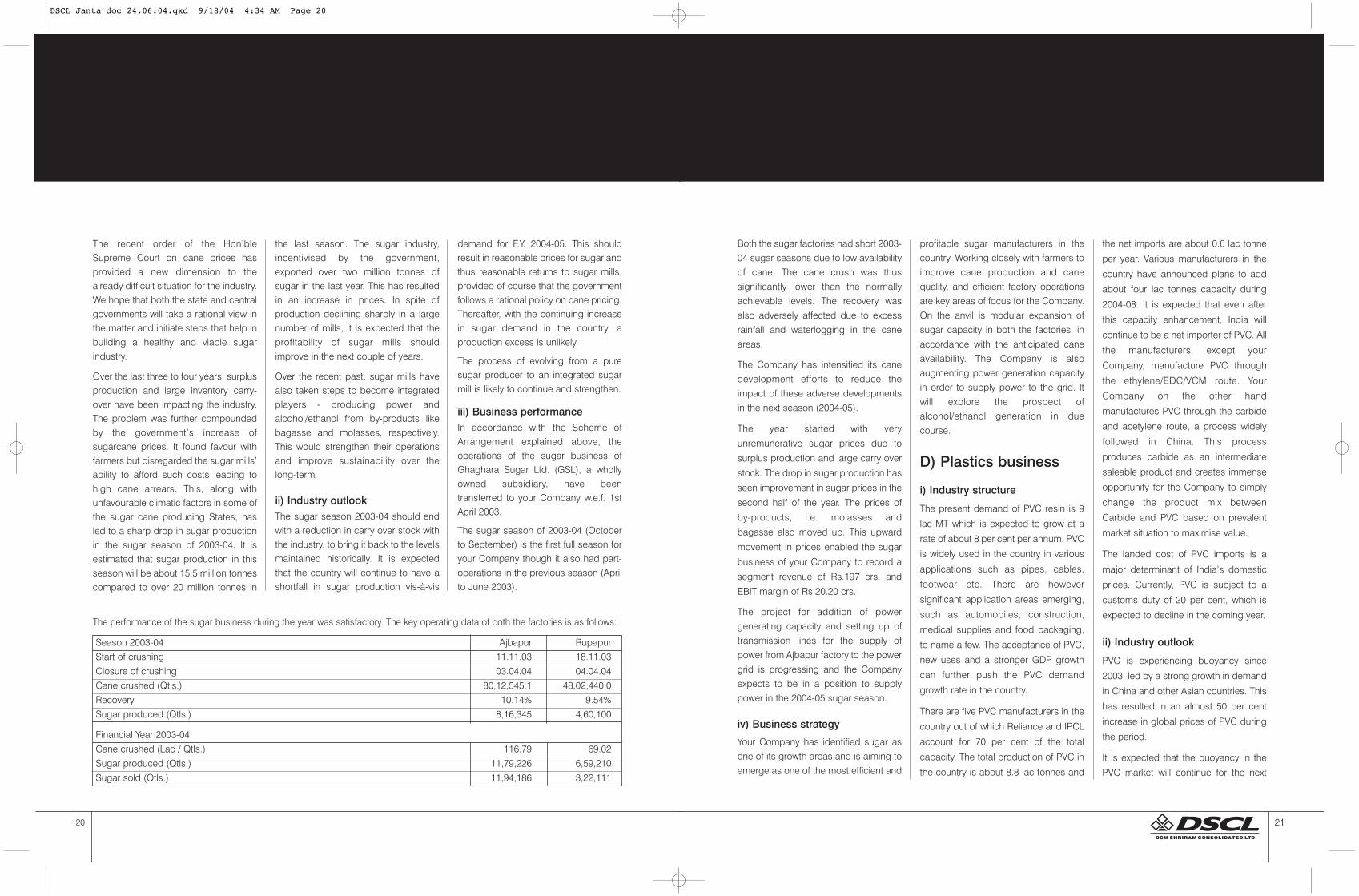

The performance of the sugar business during the year was satisfactory. The key operating data of both the factories is as follows:

Season 2003-04 Ajbapur RupapurStart of crushing 11.11.03 18.11.03Closure of crushing 03.04.04 04.04.04Cane crushed (Qtls.) 80,12,545.1 48,02,440.0Recovery 10.14% 9.54%Sugar produced (Qtls.) 8,16,345 4,60,100

Financial Year 2003-04Cane crushed (Lac / Qtls.) 116.79 69.02Sugar produced (Qtls.) 11,79,226 6,59,210Sugar sold (Qtls.) 11,94,186 3,22,111

DSCL Janta doc 24.06.04.qxd 9/18/04 4:34 AM Page 20

2322

ii) Industry outlook

Domestic chlor-alkali industry has been

experiencing surplus capacity for the

last five to six years. With the growth in

domestic demand, the surplus capacity

has gradually been absorbed. The

industry has reached a capacity

utilisation of about 80 per cent in F.Y.

2004. It is, therefore, expected that the

industry will have a more favourable

demand-supply balance in the coming

years, even after accounting for the new

capacity addition by some large

manufacturers and conversion of

mercury plants to membrane

technology.

The domestic prices of chlor-alkali

products have seen an upward trend

since the last two years based on better

demand-supply balance and upward

movement in chlorine prices

internationally. The buoyancy in

international prices is expected to

continue in the coming years led by

chlorine prices. Caustic Soda prices on

the other hand may remain soft.

The domestic prices may face some

downward pressure due to a reduction

in import tariff and hardening of the

rupee. The costs are also likely to see

upward movement primarily due to an

increase in energy prices like coal and

furnace oil, salt prices and other costs

elements.

iii) Business performance

The chemicals business recorded 12

per cent growth in segment revenue

(from Rs.196.33 crs. to Rs. 220.06 crs.)

during the year, with production

volumes going up by 4.1 per cent (from

1,06,927 tonnes to 1,11,353 tonnes). In

spite of sharp volatility in caustic soda

prices, the average ECU prices for the

year were higher by about 8 per cent

resulting in a 41.7 per cent growth in

profit from this segment.

During the last year, furnace oil prices

were volatile due to an increase in the

prices of crude oil, leading to a higher

operation cost. Despite the reduction of

peak duty by 20 per cent, no cut has

been made in the duty on furnace oil

which continues at 20 per cent. This

adversely affects the margins in one of

our plants where power is based on

furnace oil.

The Hydrogen sales volume and price

declined due to increased competition.

The softening in prices has been seen

on account of several manufacturers

setting up compression capacity,

without any significant increase in

demand.

Our market share of stable bleaching

powder increased further in the year,

with sales going up from 7,248 tonnes

to 7,508 tonnes.

The Company closed the operations of

its poly aluminium chloride business

and has sold the entire plant during the

year.

iv) Business strategy

Your Company is one of the lowest cost

and most efficient chlor-alkali

manufacturers in the country. It is also

the fourth largest in this industry. The

Company has been taking continuous

steps to improve its cost structures

through expansion and reduction in all

cost elements including energy. In line

with this, your Company is proactively

taking steps to implement a project to

convert its Chlor-Alkali Plant at Kota

from Mercury Cell to the latest

Membrane Cell based technology.

Simultaneously, the capacity of the plant

is being expanded from 139 TPD to 200

TPD. This project, expected to be ready

by the second quarter of 2005, would

further enhance the cost

competitiveness of this plant and

improve the profitability of chemical

operations.

F) Other businesses

Other businesses comprising some of

the older business i.e. cement and

textiles, and newer initiatives like Hariyali

Kisaan Bazaar and Fenesta building

systems have been discussed in this

segment.

couple of years, driven by the strong

demand and lack of new capacity

additions.

The Indian market has also seen strong

demand growth resulting in making

India a net importer of PVC. The prices

have also gone up in line with the

international trend in spite of

appreciation of the rupee and reduction

in customs duties. This trend is likely to

continue as India expects stronger PVC

demand growth in the coming years.

iii) Business performance

The buoyancy in the international and

domestic PVC market resulted in the

average prices for the year being higher

compared to last year, despite the

strengthening of the Rupee and a

reduction in customs duty.

The business experienced some cost-

push pressures particularly on charcoal

and coke but could still record a growth

in profit to Rs.47.22 crs. (last year

Rs.45.59 crs.), primarily due to a higher

sales quantity (35,554 tonnes vis-à-vis

34,616 tonnes last year) and higher

product prices. The sale of calcium

carbide during the year was 12,974

tonnes (last year 15,747 tonnes). The

prices were higher by ~7 per cent over

the last year.

iv) Business strategy

Your Company has built a strong and

enviable position in the PVC business

over the last 40 years. Based on its

business position and future outlook ,

your Company is proposing to grow in

this business in a cost efficient manner.

Accordingly, the Company has taken up

for implementation a scheme to expand

the production capacity of PVC resin at

Kota from 115 TPD to 175 TPD along

with the proportionate increase in

carbide capacity. This is expected to be

operational in the third quarter of 2005.

E) Chemicals businessgroup

i) Industry structure

The chlor-alkali industry is a worldwide

commodity industry encompassing

products such as caustic soda (lye and

flakes/prills/solid), Chlorine,

Hydrochloric Acid and Hydrogen.

Caustic Soda, one of the main

products, is used in several large

industries like Paper, Aluminium,

Dyestuffs, Soaps and Detergents,

Textiles, Pharmaceuticals, DM Water

Plants etc. Chlorine, the other product is

increasingly used in industries like PVC,

Organic Chemicals, Pesticides, Water

Treatment etc.

The present demand of caustic soda

and chlorine in the country is about 18

lac tonnes and 16 lac tonnes

respectively. Historically, it has grown in

line with the GDP growth rate. The

industry is widely held with over 40

manufacturers. There is no single

dominant manufacturer. There are sharp

differences amongst the manufacturers

in terms of technology, vintage and

backward and forward integration.

Power forms almost two-thirds of the

direct cost of production. Thus, cost

and efficiencies of power is one of the

major differentiators across the industry.

About 35-40 per cent of the capacity in

the country is based on purchased

power and thus less competitive than

others.

Caustic soda is an internationally traded

product, both in liquid and flakes/prill

form. Chlorine on the other hand is not

traded directly, though there is large

international trade in chlorine based

products. The international prices of

caustic soda as well as the major

chlorine carriers are highly volatile. India

does import and export small volume of

caustic soda. In recent years, there has

been import substitution of caustic soda

and this trend is expected to continue.

Chlorine-based products like EDC are

also imported in large quantities in to

the country. Here too, in the last one or

two years, there has been import

substitution leading to domestic

sourcing of chlorine for EDC. However,

the trend is still to stabilise.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:35 AM Page 22

2524

implementing a scheme to increase the

power generating capacity at Kota by

40 MW to meet the anticipated captive

requirements consequent to increase in

chlor-alkali and PVC capacities and 7.5

MW at the sugar factories to supply

power to the grid.

IT initiativeYour Company and its subsidiaries

continue to use and benefit extensively

from the SAP package, including

Enterprise Resource Planning, Data

Warehousing and Customer

Relationship Management solutions.

During the year, your Company has

completed the IT-enablement of the

Fenesta Building Systems business by

establishing the required

communication and IT infrastructure at

the manufacturing and marketing

locations and rolling out SAP at these

locations. In Shriram Bioseed Genetics

India Ltd. (a subsidiary), e-enablement

of business processes is underway

through the implementation of Navision

ERP solution from Microsoft. An

elaborate and secure IT infrastructure

has also been created which shall help

in transacting and communicating

across all international locations.

Plans are underway to create an IT

infrastructure in Rupapur sugar factory

and the Hariyali Kisaan Bazaar.

With the objective of leveraging IT for

business benefit, your Company had

initiated the customer relationship

initiative of moving IT beyond the

organisation’s boundaries. More

customers have been added to our

customer website

www.dsclpartners.com. Your Company

has also undertaken the employee-

related initiative of

www.dsclemployeenet.com that is

helping enhance the productivity of its

sales staff.

Efforts at environmentalprotectionThe Company continues to accord a

very high priority to environmental

protection as part of its social

responsibilities and is committed to

substantially improving the environment

in and around its manufacturing units.

During the year, the water harvesting

scheme at SAC, Bharuch was operated

fully and substantial savings achieved.

Both the Kota and Bharuch units have

continued efforts in water conservation

and effluent reduction and achieved

further savings during the year.

Both chlor-alkali units have received

OHSAS 18000 certification.

As a further step towards environment

improvement, the Company has taken

up the project of converting the Kota

chlor-alkali unit from mercury

technology to membrane technology.

Internal control systemsand adequacyThe Company has adequate internal

control systems and procedures

commensurate with its size and nature

of business. The systems are designed

to ensure that all assets are

safeguarded and protected against

unauthorised use or loss and the

transactions are authorised, recorded

and reported correctly.

The use of SAP provides a high degree

of system-based checks and controls

and has helped in enhancing the

effectiveness and efficiency of the

Company’s internal control systems.

The internal control systems span the

entire gamut of operations of the

Company spanning all locations,

businesses and functions. During the

Hariyali Kisaan Bazaar

The Company had embarked on a

pioneering venture for the setting up of

a chain of rural retail stores in the last

financial year. A total of 8 stores have

been set up on a pilot basis in different

formats. As reported last year, the

response of farmers to this concept has

been encouraging.

Based on the feedback from customers,

additional categories in selected areas

are being planned to increase the

basket of offerings to rural customers. A

petrol/diesel pump has been added at

one of the locations, on a pilot basis, to

understand the economics and

synergise with the core proposition of

agri inputs. Pilots have also been run on

the output side, in the form of contract

farming, to provide higher value

addition to target customers and

improve the business model.

The learnings from the business are

being continuously assimilated and the

venture is being scaled up to the next

level. It is now proposed to set up an

additional 25 stores in the next 2 years.

Fenesta building systems

As reported last year, your Company

has been implementing a new project to

launch Fenesta Windows and Door

Systems in the country. The Company

had entered into a technology and

marketing collaboration agreement with

M/s. HW Plastics, UK for this purpose.

The Company launched Fenesta

Windows System in May 2003. The

Company has set up a fabrication shop

in Bhiwadi and is setting up more

fabrication shops at Mumbai and

Bangalore. It is also setting up a profile

extrusion plant at Kota. The logistics

and installation capabilities are also

being developed simultaneously.

The response to the Fenesta Windows

System has been highly encouraging

and the Company is taking steps to

rapidly grow this business.

Cement business

The production of cement during the

year was marginally higher at 2,95,101

tonnes against 2,94,317 tonnes in the

previous year. The prices picked up in

the last quarter of the year, enabled the

average realisation for the year to be

about 6.7 per cent higher than last

year.

The Company achieved a substantial

reduction in production costs and

rationalised distribution costs during the

year. Consequently, the business could

achieve substantial improvement in

margins.

Textiles

The operations of Swatantra Bharat

Mills, Tonk are constrained by outdated

technology and small capacity. The

Company has taken various steps to

reduce costs, improve efficiency and

change product mix, which has resulted

in better performance during the year.

DCM Silk Mills did not have any

manufacturing activities or business

operations last year.

Captive powerThe Company possesses captive power

facilities at all its manufacturing

locations to meet near total power

requirements. The total power

generating capacity is 124 MW -

including 85 MW coal-based at Kota, 24

MW furnace oil-based at Bharuch and

15 MW bagasse-based at the sugar

factories.

Captive power provides key competitive

strength to the Company in all its

businesses and thus continues to be a

main focus area. We are now

DSCL Janta doc 24.06.04.qxd 9/18/04 4:35 AM Page 24

2726

year, the Company has further strengthened the

internal audit and risk management organisation

to give further impetus to the internal control

function.

The internal control systems are supplemented

by periodic reviews by external professional

firms. Audit findings and recommendations are

reviewed by the top management and the audit

committee of the Board.

Human resources / IndustrialrelationsThe Company has continued with its focus on

HR initiatives and strengthening of the HR

processes and systems during the year.

Training and development There has been a focused and structured effort

aimed at creating an all-round culture of learning

and development within the Company, which

would foster a continuous upgradation of skills

and competencies of employees. A variety of

training programmes have been conducted all

through the year. Along with the customised

training and development modules that address

individual and organisational needs, there have

been sessions on sharing of best practices and

learning from industry leaders to obtain an

update on the latest trends and thought

processes. It has also promoted professional

development and overall networking of

employees.

HR processes and systems The HR processes and systems encompassing

recruitment, performance management, training

and development, compensation management,

employee involvement and others have been

continuously strengthened and upgraded. The

Company has been able to derive considerable

benefit from the implementation of the SAP HR

module.

Organisation development has been pursued in

a very focused manner in the various

businesses and functions to deal with change

management and strengthen the renewal

processes of the Company. Attempts have been

made to institutionalise the improvements

coming out of the various organisational

development initiatives.

Industrial relationsThe organisation has had very harmonious and

cordial employee relations through the year.

DSCL is actively monitoring and managing the use of scarce natural resources,

helping it protect the environment.

DSCL’s environmental objectives

© To proactively comply and excel in all applicable environmental legislations and

regulations with due consideration to national and international protocols and

business charters relevant to our operations.

© To conserve all resources especially water, oil and energy to ensure a long-term

sustainability of the enviroment and minimise enviromental footprint of our

operations.

© To strengthen pollution prevention in all our activities and operations.

© To handle and dispose all inevitable wastes in an environmentally sound and

innovative manner.

© To enhance employee participation in environment protection.

© To keep its facilities and surroundings clean and green.

© To support and co-operate with regulatory agencies in national programmes.

© To consciously enhance the quality of life in surrounding habitats.

Environment management achievements

© A progressive decline in the consumption of energy, raw material and water.

© A lower discharge of effluents.

© Responsible ecological balance.

© A rigorous documentation and implementation discipline leading to world-class

certifications.

© The award of several national recognitions.

Energy conservation

Energy optimisation and conservation represent a critical business process in the

7A responsible corporate citizen

DSCL is aiming toensure long-termsustainability of theenvironment andminimise theenvironmental footprint of operations.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:35 AM Page 26

2928

8Community development

face of DSCL’s energy-

intensive Kota operations.

The formation of cross-

functional teams represents

the Company’s principal

initiative in rationalised

energy consumption. Over

the years, this teamworking

has translated into ongoing

energy audits, technology

upgradation, increased

equipment availability and a

proactive strong preventive

maintenance. These have

resulted in the following:

© Reduction in fuel, coal and

furnace oil consumption.

© Reduction in power

consumption.

© Reduction in feedstock

(naphtha) consumption is

being considered.

Water conservation

Water conservation also

continues to be a focus area

at DSCL through an ongoing

monitor of its consumption

and harvesting. The results of

this have been:

© Aggressive waste-water

re-use and recycling.

© Substantial decline in

water consumption.

© Substantial decline in

effluent generation.

Water harvesting

DSCL’s man-made reservoir

at Kota accommodates 4.5

lac cubic metres of water,

adequate to provide for 21

days of production. In

Bharuch, located in water-

starved Gujarat, the

Company’s sound water

collection and harvesting

system holds 20,000 cubic

metres that is effectively

deployed at its caustic soda

plant.

Ecological balance

Approximately 10 hectares

out of the 46.73 hectares at

the Company’s Bharuch

plant have been reserved for

green belt eco-development.

Over 75,000 tree saplings

have been planted in this

factory, covering 33 per cent

of its green belt. Tree survival

rate touched 95 per cent -

215,000 – in arid Kota. Some

100,000 trees have been

planted across the Ajbapur

and Rupapur sugar factories.

Certifications

DSCL’s Kota plant

represents best-in-line

environment practices,

reflected in world-class

certifications: ISO 14001 by

KPMG in 2001 and the

OHSAS (Occupational Safety

and Health Standards)

18001. The Company’s

Bharuch plant has also

received the OHSAS and SA

8000 certifications.

Commitment

Right from inception, DSCL has been aware of its commitment beyond factory

gates and office portals – to society at large. This responsibility recognises the

importance of the health and happiness of fellow human beings in the long-term

sustainability of its enterprise.

As a result, social responsibility is an integral part of DSCL’s corporate philosophy.

It has translated into a mosaic of meaningful contributions to society across long-

term developmental issues like health care, family planning, education, cultural

heritage and sport.

Agriculture extension activities

Shriram Krishi Vikas Kendras (SKVKs) impart scientific knowledge to farmers across

subjects like crop cycles and harvesting, helping them achieve richer harvests and

profitable returns. SKVKs have also been active in addressing the needs of the local

populace through the adoption of villages and krishi centres.

Water to the people

DSCL has periodically responded to water needs during periods of drought in and

around its factories through the digging of bore wells, the installation of submersible

pumps and the construction of water storage tanks, etc around Kota. For instance,

around Kota bore wells and overhead tank systems were provided in a dozen

villages; in Ajbapur and Rupapur, the Company helped finance more than 650 wells.

The Company also facilitated water supply to drought-hit villages of the Mandsana

region during the sweltering summer.

Infrastructure

The most effective means of development are those that involve partnerships

between the donor and the recipient. DSCL has partnered with the local community

DSCL recognises theimportance of thehealth and happinessof fellow humanbeings in the long-term sustainability ofany human enterprise.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:36 AM Page 28

31

Directors’ Report

The Directors have pleasure in presenting the 15thAnnual Report of the Company along with AuditedAccounts for the year ended 31st March, 2004.

Scheme of Arrangement

The Company implemented a Scheme of Arrangementapproved by the Hon’ble High Court of Delhi under Sections391-394 of the Companies Act, 1956 for demerger of itsEnergy Services (ESCO) business to its subsidiary DSCLEnergy Services Company Limited and for merger of itssubsidiary Ghaghara Sugar Ltd. into the Company w.e.f. 1stApril, 2003. This scheme has been given full effect in theAnnual Report and Financial Statements for the year ending31st March, 2004 and thus the data for previous year is notcomparable.

The Scheme of Arrangement will further improve the businesssynergies and focus and will strengthen the financials of theCompany.

Financial Highlights

The working results for the year ended 31.3.2004 and31.3.2003 are as under:

31.3.2004 31.3.2003 (Rs. in Crores) (Rs. in Crores)

Sales (Gross) 1,475.62 1,150.14Other Income 20.83 17.93Profit before depreciation, misc. expenditure written off, interest and tax 195.09 169.23Interest 41.39 48.99Gross Profit 153.70 120.24Depreciation & misc. expenditure written off 50.72 45.03Provision for current tax 7.92 11.85Provision for deferred tax 18.38 6.75Profit for the year after tax 76.68 56.61

31.3.2004 31.3.2003 (Rs. in Crores) (Rs. in Crores)

Transfer from Debenture Redemption Reserve 10.82 8.65Balance brought forward from previous year 77.56 47.88Net Profit available for appropriation 165.06 113.14

Appropriations– Debenture Redemption

Reserve 0.56 2.40– Proposed Dividends on

Equity Shares 10.05 7.54– Tax on Dividends 1.29 0.64– General Reserve 35.00 25.00– Balance Carried Forward 118.16 77.56

Dividend

Your Company has paid an interim dividend @ 20% on1,73,70,332 Equity Shares of Rs.10/- each for the year ended31st March, 2004.

Your Directors are pleased to recommend total dividend @ 60% (including the interim dividend paid earlier) on1,73,70,332 Equity Shares of Rs.10/- each for the year ended31st March, 2004.

Performance

The Company’s sales grew by over 28% from Rs.1150.14Crores in the previous year to Rs.1475.62 Crores during thecurrent year. The operating profit of the Company for the yearincreased to Rs 195.09 Crores from Rs.169.23 Crores lastyear, reflecting an increase of over 15%. The Company’s profit

30

to build vast stretches of roads

benefiting the entire region in and

around its cane-growing areas.

Education

For the well being of the community

around its manufacturing locations,

DSCL continues to support education

activities by running various schemes at

primary and professional levels with a

special focus on protecting the future of

the girl child. It has instituted

scholarships in various educational

institutions to encourage meritorious

students achieve the best in the fields of

engineering, medicine, agriculture and

management.

The Company invested in Sanskar

Pariyojana around its sugar operations

in UP. This integrated education

programme, conducted in collaboration

with the Vinobha Bhave Trust inculcated

Shiksha (education), Swasth (health),

Safaai (cleanliness) and Swabhimaan

(self reliance) in individuals. It deputed

trainers and officers across 10 villages

covering a population in excess of

10,000.

In Kota, DSCL instituted scholarship

programmes that encourage students

to pursue advance academic studies.

The infrastructure of a number of

schools in the plants’ vicinities were

strengthened through the introduction

of basic facilities, including safe

drinking water. The Company built a

school at Nimoda Mines for students up

to class 10.

In Bharuch, it funded a degree college

and instituted a scholarship programme

that extends to several villages around

its facility. In another scheme, to provide

financial security and protect the future

of young individuals, meritorious

students were awarded ‘fixed deposits’

every year that can be encashed after

he/she turns 18 or on the students’

marriage/higher education.

DSCL responded to earthquake-torn

Kutch region of Gujarat and re-built a

school in the location.

Sport

DSCL launched the DSCL Open

National Tennis Championship to

motivate sportspersons and help India

carve a niche in the international tennis

arena. In appreciation of the Company’s

ability to organise a tournament of such

a stature, the game was awarded the

National status in 1996. Since then, the

DSCL Open National Tennis

Championship has emerged as one of

lndia’s most prestigious tournaments,

playing host to thousands of players

annually. The prize money, the largest in

its category for a national tournament,

comprehensively covers the men’s,

ladies, boys and girls (under 18,16 and

14 respectively) categories.

Health

DSCL helped equip the Maharao Bhim

Singh Hospital at Kota with a state-of-

the-art intensive care unit called ‘The

Shriram ICU’ and private wards called

‘The Shriram Wards’. The Company

encourages and promotes family

planning as a national imperative,

running incentive schemes in the

villages surrounding its facilities. It also

provided medical assistance –

consulting, medicines and camps – to

select villages in eastern Uttar Pradesh

and conducted medical camps in

villages around Kota.

DSCL Janta doc 24.06.04.qxd 9/18/04 4:36 AM Page 30

32

Companies Act, 1956 form part of thisreport. However, as per the provisions ofSection 219(1)(b)(iv) of the Act, the reportand accounts are being sent to all theMembers and the Trustee(s) for theholders of the debentures of theCompany, excluding the statementcontaining the particulars to be providedunder Section 217(2A) of the Act. Thisstatement shall be made available forinspection by any Member and/or anyTrustee(s) during working hours for aperiod of 21 days before the date of theAnnual General Meeting. Any Memberand/or the Trustee(s) interested inobtaining a copy of the said statementmay write to the Company Secretary atthe Registered Office of the Company andthe same will be sent by post.

Directors' Responsibility Statement

It is hereby affirmed that

1. in preparation of annual accounts, allapplicable accounting standards havebeen followed.

2. the accounting policies of theCompany have been consistentlyfollowed. Wherever circumstancesdemanded, estimates have beenmade that are reasonable andprudent so as to give a true and fairview of the state of affairs of theCompany at the end of the financialyear and of the profit or loss of theCompany for that period.

3. proper and sufficient care has beentaken for maintenance of accountingrecords in respect of assets of theCompany and proper internal controlsare in place for preventing anyirregularities or detection of frauds,and

4. annual accounts have been preparedon a going concern basis.

Conservation of Energy, TechnologyAbsorption and Foreign ExchangeEarnings/Outgo

The information required under Section217(1)(e) of the Companies Act, 1956read with the Companies (Disclosure ofParticulars in the Report of the Board ofDirectors) Rules, 1988 with respect tothese matters is appended hereto andforms part of this report.

Industrial Relations

The Company continued to maintainharmonious and cordial relations with itsworkers in all its Divisions, which enabledit to achieve this performance level on allfronts.

Acknowledgements

The Directors wish to thank customers,the Government authorities, financialinstitutions, bankers, other businessassociates and shareholders for thecooperation and encouragementextended to the Company. The Directorsalso place on record their deepappreciation for the contribution made bythe employees at all levels.

On behalf of the Board

(AJAY S. SHRIRAM)Chairman & Sr. Managing Director

New Delhi30th June, 2004

before tax for the year at Rs.102.98 Crores has grown by over36% as against Rs. 75.21 Crores achieved last year.

Improved performance was witnessed in Plastics andChemicals business segments, however the performance ofthe Fertilisers business was adversely affected due tobreakdown of one of the power plants of the Company duringthe last quarter of the year.

The performance of various businesses of the Company forthe year ended 31st March, 2004 has been stated in theManagement Discussion and Analysis Report, which appearsas a separate statement in the Annual Report.

Subsidiary Companies