STE06 financial P90-195.indd - Morningstar

242

THE WINNING SPIRIT ANNUAL REPORT 2006 Global Reports LLC

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of STE06 financial P90-195.indd - Morningstar

THE WINNING SPIRIT

ANNUAL REPORT 2006

STE cover AW-OK.indd 1 6/3/07 3:42:50

Global Reports LLC

CONTENTS

01 The Winning Spirit10 Letter to Shareholders16 Financial Highlights22 Board of Directors26 Senior Management30 Organisation Chart32 Corporate Governance44 Environment, Health and Safety45 Corporate Social Responsibility46 Investor Relations48 Investor Relations Calendar 200648 Financial Calendar 200749 Share Price Performance50 Human Resources54 Awards and Commendations56 Operating Financial Review62 ST Engineering at a Glance89 Financial Report

STE cover AW-OK.indd 2 6/3/07 3:46:10

Global Reports LLC

The winning spirit entails more than performance. It is an active and adaptive mindset – one that defi es odds, embraces the courage to be different, and determination in the face of adversity.

ST Engineering empowers its people to direct positive energy into innovation and achievement. With the winning spirit, challenges are transformed into opportunities, problems into successes.

1

Global Reports LLC

ACCELERATING OUR INNOVATION

THE WINNING SPIRIT ST Engineering AR 2006

Global Reports LLC

Success in today’s challenging and unpredictable global marketplace is marked by the ability to push the boundaries of innovation – faster and more effectively. ST Engineering continually questions traditional assumptions and rules, and embraces fresh paradigms to redefi ne perspectives and create new solutions that transcend the ordinary.

3

Global Reports LLC

BUILDING OUR SCALE

THE WINNING SPIRIT ST Engineering AR 2006

Global Reports LLC

Scale is defi ned not just by an organisation’s numbers. As ST Engineering pursues scale to compete internationally, it is building a culture in its people – to achieve more, climb higher and go further.

5

Global Reports LLC

HARNESSING OUR TEAM POWER

THE WINNING SPIRIT ST Engineering AR 2006

Global Reports LLC

In a competitive and dynamic business environment, a collaborative culture engenders cohesiveness. ST Engineering believes in forming synergistic relationships with all its stakeholders – be they staff, business partners or customers – where each individual contributes to the overall achievement of the Group.

77

Global Reports LLC

ENHANCING OURCAPABILITIES

THE WINNING SPIRIT ST Engineering AR 2006

Global Reports LLC

ST Engineering seizes opportunities to acquire new capabilities while enhancing core competencies. This clear focus, coupled with an agility to adapt, enables the Group to continuously grow its portfolio of advanced, innovative and cost effective solutions.

9

Global Reports LLC

Dear ShareholdersGlobal markets continued their upward momentum in 2006, with Singapore’s growth at a new high compared to recent years. Higher interest rates and oil prices, however, threatened to hinder economic activity and exerted pressure on bottom lines for most industries. While higher oil prices have minimal direct impact on the Group, they affected the aviation industry, increasing the cost of operations for airlines already in a diffi cult market compounded by heightened competition from low cost carriers. China appears to have had some success in cooling its economy and growth continued to be strong, aided in part by the build up to the 2008 Olympics. India is another growing market where the Group seeks to increase its presence. Another area of opportunity is the booming Gulf States.

While various geographies pose different challenges, they serve as opportunities for the Group as we grow our presence globally.

Against this backdrop, the ST Engineering Group enjoyed another good year in 2006 with net profi t growing by 12% to $445.1m.

Becoming a Global EntityThe Group today is a global entity operating in fi ve continents, spanning 20 countries and 35 cities.

With our recent acquisitions, the profi le of our business mix is increasingly global and commercial, due to the nature and location of these new acquisitions. These new additions have steadily increased their contributions to the Group, enabling us to diversify our earnings stream. As a vital part of our total business mix, the Group’s defence business continues to grow with new solutions and product offerings. Customers are increasingly focused on the total cost of ownership and market best practices. Our fl exibility to leverage on the interplay between our defence and commercial businesses, and tapping the strengths of each, helps strengthen the Group’s ability to provide innovative and cost effective systems and solutions.

Group revenues outside of Asia has today grown to 47% from 28% in 2002, refl ecting our geographic spread and global customer base which covers more than 60 countries. Globalisation helps to diversify geographic-centric economic and political factors, thereby hedging the interests of the Group. Globalisation is the cornerstone of our strategy for growth and to build leading businesses to add vigour to the Group. We

The Group recorded double digit growth for a second straight year in 2006. Our net profi t rose by 12% to $445.1m on the strength of the Aerospace and Electronics sectors and higher contributions from our overseas acquisitions. Group turnover was up 34% to $4.49b, while profi t before tax increased 12% to $564.3m. Our earnings per share were 15.2 cents, an increase of 11%. Economic Value Added grew 13% to $327.8m. Return on equity was a very respectable 28.4%, higher than the 26.5% in 2005. Cash and cash equivalents, including funds under management, remained a healthy $1.4b.

Letter to Shareholders

THE WINNING SPIRIT ST Engineering AR 2006 10

Global Reports LLC

select each new addition carefully to enhance the value of our existing businesses, expand our technologies and capabilities, address new markets, enlarge our customer base, and infuse fresh talent into our cosmopolitan workforce.

In line with our globalisation thrust, this year we acquired two companies in the US – one in simulation and digital media, and another in specialty vehicles. In addition, a joint venture company was formed with Kalyani Group for the research, development and manufacture of military land-based products and solutions, specifi cally large calibre guns and small arms for India’s defence and security requirements. Our Aerospace sector is starting an aircraft maintenance facility in Panama in 2Q2007, which enhances our aerospace global network and complements the existing North American facilities in Mobile, Alabama, and San Antonio, Texas.

Growing by Double DigitThe Group recorded double digit growth for a second straight year in 2006. Our net profi t rose by 12% to $445.1m on the strength of the Aerospace and Electronics sectors and higher contributions from our overseas acquisitions. Group turnover was up 34% to $4.49b, while profi t before tax increased 12% to $564.3m. Our earnings per share were 15.2 cents,

an increase of 11%. Economic Value Added grew 13% to $327.8m. Return on equity was a very respectable 28.4%, higher than the 26.5% in 2005. Cash and cash equivalents, including funds under management, remained a healthy $1.4b.

ST Engineering’s market cap reached $9.07b as at end December 2006, compared to $8.33b at the close of 2005.

Recognising our ShareholdersThe ST Engineering Board of Directors is proposing to pay 100% of 2006 net profi t of $445.1m to our loyal shareholders as dividends. This will translate into a dividend of 15.11 cents per share, and a dividend yield of 5.1%. The dividends comprise an ordinary tax exempt (one-tier) dividend of 4 cents per share, and a special tax exempt (one-tier) dividend of 11.11 cents per share. The Group plans to start paying half-year interim ordinary dividends from 2007.

Winning the Trust of CustomersContracts announced during the year exceeded US$1.3b. The fi gure does not include smaller projects nor represent the Group’s total sales. These contract wins expanded our order book to an all time high of $7.37b by yearend.

Peter SEAH Lim Huat Chairman (left) TAN Pheng Hock President and CEO (right)

11

Global Reports LLC

Letter to Shareholders

We won several signifi cant contracts in 2006. Among them were the US$635m Airbus contract for total aviation support to Skybus, a new carrier in the US; two roll-on roll-off vessels to be used by Airbus to transport large aircraft components, including sections for their new A380 aircraft; and two shipbuilding contracts from the US Navy amounting to over US$360m, namely the Egyptian Navy fast missile craft project and a missile range instrumentation ship. The latter project is signifi cant as it marks the fi rst time we have won a contract from the US Navy since we acquired VT Halter Marine in 2002. Our Electronics sector’s foothold in the Chinese rail market now totals nearly $50m, including three projects in Guangzhou. It was also strengthened with the development of an integrated traffi c command centre system, the fi rst-of-its-kind aimed at effi ciently managing major rail lines in Beijing. This makes us the fi rst Singapore company to win a major Beijing Olympics related contract.

Many of the contracts for the Group came from existing customers. A repeat customer is a happy customer. For an organisation driven by performance and results, there is no better validation and recognition than having customers come back time after time.

Enhancing CapabilitiesThe Singapore Army commissioned into service an enhanced version of our Bionix armoured vehicle, BXII, in 2006. This latest Bionix boosts SAF’s 3rd Generation networked capability. Featuring innovations from the Electronics and Land Systems sectors, the BXII is integrated with the rest of the fi ghting forces through a battlefi eld management system and network-centric wireless communications systems. In support of the digitised army programme, this provides an integrated situation awareness capability, collaborative planning tools and knowledge-based command and control (C2). This enables ground commanders to make responsive decisions and exercise

highly effective C2 operations in a fast-moving battlefi eld – a prime example of how the Group delivers value to customers through innovation.

The need for continuous capability improvement is a given, particularly in an ever-evolving and competitive global market. This is supported by a corporate culture which encourages innovation in integrating technologies and collaboration with like-minded partners to add new solutions to meet our customers’ needs.

Some of these Group-wide capabilities and technologies were showcased at Asian Aerospace 2006. Many of these are dual-purpose or applicable to both the defence and commercial businesses, including a slew of homeland security solutions.

With our components companies in Scandinavia and the UK merged into one, our Aerospace sector has enlarged its product and services offerings in Europe, and added Scandinavian Airlines as a major customer. Together with the existing components repair capabilities, we now have expanded global coverage, as well as enhanced breadth and depth of our capabilities.

Living Up to Corporate CitizenryAs the Group expands, so does our Corporate Social Responsibility (CSR). Every country and every business has its own matrix of CSR hot buttons, ranging from the way we do business and preserve the environment to conservation/recycling practices, staff welfare and community programmes.

Good corporate governance is especially vital as the Group globalises. Transparent practices need to be applied with cultural and local sensitivity. ST Engineering constantly raises the bar in best practices, implementing a whistle-blowing process during the year.

We won several signifi cant contracts in 2006. Among them were the US$635m Airbus contract for total aviation support to Skybus Airlines, a new carrier in the US; two roll-on roll-off vessels to be used by Airbus to transport large aircraft components, including sections for their new A380 aircraft; and two shipbuilding contracts from the US Navy amounting to over US$360m, namely the Egyptian Navy fast missile craft project and a missile range instrumentation ship. The latter project is signifi cant as it marks the fi rst time we have won a contract from the US Navy since we acquired VT Halter Marine in 2002. Our Electronics sector’s foothold in the Chinese rail market now totals nearly $50m, including three projects in Guangzhou. It was also strengthened with the development of an integrated traffi c command centre system, the fi rst-of-its-kind aimed at effi ciently managing major rail lines in Beijing. This makes us the fi rst Singapore company to win a major Beijing Olympics related contract.

Many of the contracts for the Group came from existing customers. A repeat customer is a happy customer. For an organisation driven by performance and results, there is no better validation and recognition than having customers come back time after time.

Enhancing CapabilitiesThe Singapore Army commissioned into service an enhanced version of our Bionix armoured vehicle, BXII, in 2006. This latest Bionix boosts SAF’s 3rd Generation networked capability. Featuring innovations from the Electronics and Land Systems sectors, the BXII is integrated with the rest of the fi ghting forces through a battlefi eld management system and network-centric wireless communications systems. In support of the digitised army programme, this provides an integrated situation awareness capability, collaborative planning tools and knowledge-based command and control (C2). This enables ground commanders to make responsive decisions and exercise

highly effective C2 operations in a fast-moving battlefi eld – a prime example of how the Group delivers value to customers through innovation.

The need for continuous capability improvement is a given, particularly in an ever-evolving and competitive global market. This is supported by a corporate culture which encourages innovation in integrating technologies and collaboration with like-minded partners to add new solutions to meet our customers’ needs.

Some of these Group-wide capabilities and technologies were showcased at Asian Aerospace 2006. Many of these are dual-purpose or applicable to both the defence and commercial businesses, including a slew of homeland security solutions.

With our components companies in Scandinavia and the UK merged into one, our Aerospace sector has enlarged its product and services offerings in Europe, and added Scandinavian Airlines as a major customer. Together with the existing components repair capabilities, we now have expanded global coverage, as well as enhanced breadth and depth of our capabilities.

Living Up to Corporate CitizenryAs the Group expands, so does our Corporate Social Responsibility (CSR). Every country and every business has its own matrix of CSR hot buttons, ranging from the way we do business and preserve the environment to conservation/recycling practices, staff welfare and community programmes.

Good corporate governance is especially vital as the Group globalises. Transparent practices need to be applied with cultural and local sensitivity. ST Engineering constantly raises the bar in best practices, implementing a whistle-blowing process during the year.

THE WINNING SPIRIT ST Engineering AR 2006 12

Global Reports LLC

Looking AheadAs the Group spreads its wings globally, we are constantly mindful of the multitude of risks each new market entry brings, be they natural, political, economic or socio-cultural. The risk and business management framework that we have put in place, which is constantly being refi ned and reviewed, helps mitigate such business risks.

Hurricane Katrina remains an important lesson of what could have been had we been less prepared. It is a reminder for us to stay vigilant and adaptive to an array of business challenges as we continue to grow our businesses globally.

Going global also means making tough and painful decisions when necessary. We closed our UK aircraft maintenance facility in Bournemouth this year after being unable to turn it around since its setup in 2001. This was decided together with our joint venture partner in the long term interests of both companies and stakeholders.

In 2007, we will continue to grow our business organically in new markets, with new products and systems innovation, as well as develop new capabilities to address changing customer needs. In addition, the Group will focus on creating synergies among our businesses and leverage economies of scale in all four sectors.

At the same time, the Group will continue to seek companies and partners that enhance our core business through acquisitions, joint ventures, partnerships and collaborations. We adopt a pragmatic approach when developing new markets, realistically appraising the key performance indicators and adopting a fl exible strategy for a particular environment which may require the Group to be a subcontractor, licensor, or supplier to local players.

As an innovative organisation, we increasingly develop intellectual property to serve as a defensive measure in our global thrust and as leverage for market entry strategy where it makes sense.

For the coming year, the Group expects to achieve a higher turnover and profi t before tax, barring unforeseen circumstances.

Expressing our AppreciationWe formally express our appreciation to shareholders at the AGM and in the annual report. In reality, our gratitude for your support extends throughout the year. In the same light, we thank our customers for their continuing support through the years.

Our Board of Directors is the beacon which steers Group strategy and sets Group directions. The Directors’ experience and depth of knowledge, willingly shared, have mapped our course and continue to guide our future.

We would like to record our deep appreciation to our Director, Lieutenant-General Ng Yat Chung, who will be retiring at our coming AGM.

Not least of all, our special thanks to our family of over 17,000 members around the world. Your dedication and loyalty have contributed to our success and winning spirit.

Peter SEAH Lim Huat TAN Pheng HockChairman President and CEO

16 March 2007

In 2007, we will continue to grow our business organically in new markets, with new products and systems innovation, as well as develop new capabilities to address changing customer needs. In addition, the Group will focus on creating synergies among our businesses and leverage economies of scale in all four sectors.

13

Global Reports LLC

THE WINNING SPIRIT ST Engineering AR 2006 14

Global Reports LLC

15

Global Reports LLC

Financial Highlights

Group turnover rose 34% to $4,486m. EBIT, PBT and PATMI were $457.6m, $564.3m and $445.1m, representing growth rates of 17%, 12% and 12% respectively. Order book rose to a new high at $7.37b. Return on equity improved from 26.5% for FY2005 to 28.4% for FY2006. The Board is proposing to pay 100% of net profi ts as dividends or 15.11 cents per share.

06

05

04

03

02

TURNOVER BY SECTOR ($m)

06

05

04

03

02

PROFIT BEFORE TAX BY SECTOR ($m)

06

05

04

03

02

PROFIT AFTER TAX BY SECTOR ($m)

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000

0 100 200 300 400 500 600

0 100 200 300 400 500

Aerospace Electronics Land Systems Marine Others

THE WINNING SPIRIT ST Engineering AR 2006 16

Global Reports LLC

Key Financial Data

2006 2005 2004 2003 2002

TURNOVER BY SECTOR ($m) 4,486 100% 3,338 100% 2,948 100% 2,819 100% 2,619 100%

Aerospace 1,673 37% 1,236 37% 1,118 38% 1,092 39% 1,043 40%

Electronics 951 21% 701 21% 626 21% 614 22% 571 22%

Land Systems 1,002 22% 600 18% 591 20% 717 25% 710 27%

Marine 702 16% 660 20% 484 16% 387 14% 280 11%

Others 158 4% 141 4% 129 5% 9 – 15 –

PROFIT BEFORE TAX BY SECTOR ($m) 564.3 100% 503.2 100% 446.2 100% 412.7 100% 413.0 100%

Aerospace 305.3 54% 255.4 51% 235.4 53% 225.2 55% 213.0 52%

Electronics 104.6 19% 76.0 15% 64.5 14% 61.4 15% 56.7 14%

Land Systems 70.0 12% 65.0 13% 71.5 16% 96.4 23% 96.9 23%

Marine 79.5 14% 87.9 17% 69.8 16% 35.2 9% 41.1 10%

Others 4.9 1% 18.9 4% 5.0 1% (5.5) (2%) 5.3 1%

PROFIT AFTER TAX BY SECTOR ($m) 445.1 100% 396.3 100% 354.2 100% 325.6 100% 330.7 100%

Aerospace 255.0 57% 210.3 53% 187.3 53% 176.3 54% 155.6 47%

Electronics 76.3 17% 58.0 15% 51.6 15% 48.0 15% 42.8 13%

Land Systems 51.9 12% 49.0 12% 58.1 16% 76.5 24% 100.6 30%

Marine 67.8 15% 70.3 18% 53.7 15% 30.8 9% 29.2 9%

Others (5.9) (1%) 8.7 2% 3.5 1% (6.0) (2%) 2.5 1%

1,043 40%

571 22%

710 27%

280 11%

15 –

1,092 39%

614 22%

717 25%

387 14%

9 –

1,236 37% 1,118 38%

701 21% 626 21%

600 18% 591 20%

660 20% 484 16%

141 4% 129 5%

213.0 52%

56.7 14%

96.9 23%

41.1 10%

5.3 1%

225.2 55%

61.4 15%

96.4 23%

35.2 9%

(5.5) (2%)

255.4 51% 235.4 53%

76.0 15% 64.5 14%

65.0 13% 71.5 16%

87.9 17% 69.8 16%

18.9 4% 5.0 1%

155.6 47%

42.8 13%

100.6 30%

29.2 9%

2.5 1%

176.3 54%

48.0 15%

76.5 24%

30.8 9%

(6.0) (2%)

210.3 53% 187.3 53%

58.0 15% 51.6 15%

49.0 12% 58.1 16%

70.3 18% 53.7 15%

8.7 2% 3.5 1%

17

Global Reports LLC

Key Financial Data

2006 2005 2004 2003 2002

Shareholders’ funds ($m) 1,565 1,493 1,358 1,324 1,452Total assets ($m) 5,514 4,566 4,042 4,122 4,351Net tangible assets ($m) 996.4 1,131 1,296 1,266 1,431Gross dividend per share (cents) 15.11 13.60 12.39 11.30 18.50Dividend yield (%) 5.09 5.24 5.67 6.12 9.25Dividend cover 1.00 1.00 1.00 1.00 0.74Earnings per share (cents) 15.15 13.64 12.26 11.29 11.47Return on turnover (%) 10.2 12.3 12.2 11.6 12.7Return on equity (%) 28.4 26.5 26.1 24.6 22.8Return on total assets (%) 8.3 9.0 8.9 7.9 7.7Net tangible assets per share (cents) 33.80 38.80 44.80 43.90 49.60

SHAREHOLDERS’ FUNDS ($m)

06

05

02

04

03

1,565

1,4931,452

1,358

1,324

RETURN ON EQUITY (%)

06

05

04

03

02

28.4

26.5

26.1

24.6

22.8

NET TANGIBLE ASSETS PER SHARE (CENTS) 06

02

04

0305

33.8

49.6

44.8

43.938.8

THE WINNING SPIRIT ST Engineering AR 2006 18

Global Reports LLC

Productivity Data

2006 2005 2004 2003 2002

Average staff strength 15,912 13,099 11,684 11,702 11,413Sales per employee ($) 281,910 254,821 252,333 240,898 229,492Profi t after tax per employee ($) 27,974 30,255 30,316 27,823 28,977Employment costs ($m) 1,243.0 899.9 826.9 798.0 759.1Employment costs per $ of turnover ($) 0.28 0.27 0.28 0.28 0.29

Economic Value Added ($m) 327.8 290.6 234.5 240.9 190.2Economic Value Added spread (%) 12.3 16.2 13.7 13.9 11.3Economic Value Added per employee ($) 20,598 22,187 20,075 20,587 16,664

Value added ($m) 1,990.8 1,500.6 1,363.1 1,337.0 1,274.2Value added per employee ($) 125,112 114,559 116,668 114,253 111,646Value added per $ of employment costs ($) 1.60 1.67 1.65 1.68 1.68Value added per $ of gross property, plant and equipment ($) 0.99 1.02 1.03 1.05 1.03Value added per $ of turnover ($) 0.44 0.45 0.46 0.47 0.49

PROFIT AFTER TAX PER EMPLOYEE ($’000)

02 29.0

03 27.8

04 30.3 05 30.3

06 28.0

ECONOMIC VALUE ADDED PER EMPLOYEE ($’000)

02 16.7

03 20.604 20.1

05 22.2

06 20.6

VALUE ADDED PER EMPLOYEE ($’000)

02 111.6

03 114.3

04 116.7

05 114.6

06 125.1

19

Global Reports LLC

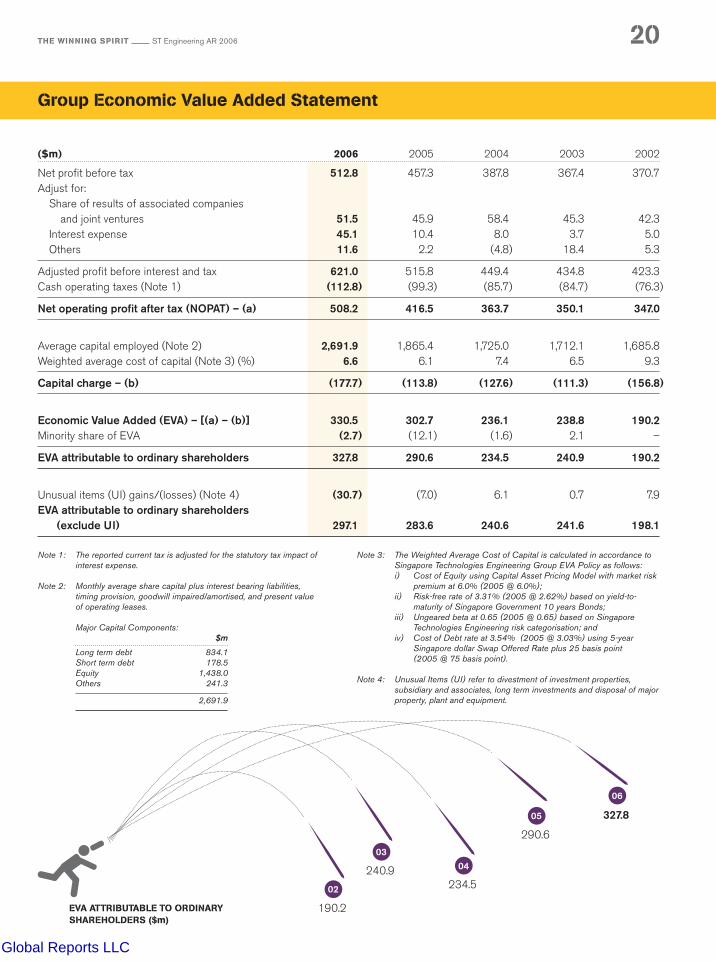

EVA ATTRIBUTABLE TO ORDINARY SHAREHOLDERS ($m)

02

190.2

04

234.5

03

240.9

05

290.6

06

327.8

Group Economic Value Added Statement

($m) 2006 2005 2004 2003 2002

Net profi t before tax 512.8 457.3 387.8 367.4 370.7Adjust for: Share of results of associated companies and joint ventures 51.5 45.9 58.4 45.3 42.3 Interest expense 45.1 10.4 8.0 3.7 5.0 Others 11.6 2.2 (4.8) 18.4 5.3

Adjusted profi t before interest and tax 621.0 515.8 449.4 434.8 423.3Cash operating taxes (Note 1) (112.8) (99.3) (85.7) (84.7) (76.3)

Net operating profi t after tax (NOPAT) – (a) 508.2 416.5 363.7 350.1 347.0

Average capital employed (Note 2) 2,691.9 1,865.4 1,725.0 1,712.1 1,685.8Weighted average cost of capital (Note 3) (%) 6.6 6.1 7.4 6.5 9.3

Capital charge – (b) (177.7) (113.8) (127.6) (111.3) (156.8)

Economic Value Added (EVA) – [(a) – (b)] 330.5 302.7 236.1 238.8 190.2Minority share of EVA (2.7) (12.1) (1.6) 2.1 –

EVA attributable to ordinary shareholders 327.8 290.6 234.5 240.9 190.2

Unusual items (UI) gains/(losses) (Note 4) (30.7) (7.0) 6.1 0.7 7.9EVA attributable to ordinary shareholders (exclude UI) 297.1 283.6 240.6 241.6 198.1

Note 1: The reported current tax is adjusted for the statutory tax impact of interest expense.

Note 2: Monthly average share capital plus interest bearing liabilities, timing provision, goodwill impaired/amortised, and present value of operating leases.

Major Capital Components: $m

Long term debt 834.1 Short term debt 178.5 Equity 1,438.0 Others 241.3

2,691.9

Note 3: The Weighted Average Cost of Capital is calculated in accordance to Singapore Technologies Engineering Group EVA Policy as follows:

i) Cost of Equity using Capital Asset Pricing Model with market risk premium at 6.0% (2005 @ 6.0%);

ii) Risk-free rate of 3.31% (2005 @ 2.62%) based on yield-to-maturity of Singapore Government 10 years Bonds;

iii) Ungeared beta at 0.65 (2005 @ 0.65) based on Singapore Technologies Engineering risk categorisation; and

iv) Cost of Debt rate at 3.54% (2005 @ 3.03%) using 5-year Singapore dollar Swap Offered Rate plus 25 basis point (2005 @ 75 basis point).

Note 4: Unusual Items (UI) refer to divestment of investment properties, subsidiary and associates, long term investments and disposal of major property, plant and equipment.

THE WINNING SPIRIT ST Engineering AR 2006 20

Global Reports LLC

02 1,274.203 1,337.0

04 1,363.1

05 1,500.6

06 1,990.8

TOTAL VALUE ADDED ($m)

Group Value Added Statement

($m) 2006 2005 2004 2003 2002

Value added from: Revenue earned 4,485.8 3,337.9 2,948.1 2,819.0 2,619.2Bought in materials and services (2,644.0) (1,959.0) (1,698.6) (1,578.5) (1,452.1)

1,841.8 1,378.9 1,249.5 1,240.5 1,167.1 Income from investments and interest 79.9 49.4 36.2 32.1 49.6Exchange loss (3.9) (1.8) (2.1) (1.2) (4.2)Other non-operating income 21.5 28.2 21.1 20.3 19.4Share of results of associated companies and joint ventures 51.5 45.9 58.4 47.3 43.8Amortisation of goodwill on acquisition of associated companies – – – (2.0) (1.5)

Total value added 1,990.8 1,500.6 1,363.1 1,337.0 1,274.2

Distribution of total value addedTo employees in wages, salaries and benefi ts 1,241.0 898.3 826.2 797.4 758.5To government in income and other taxes 116.8 99.6 93.8 93.1 83.8To providers of capital on: • Interest paid on borrowings 42.3 8.0 4.2 2.2 2.9• Dividends to shareholders 399.5 359.8 326.5 449.9 247.8

1,799.6 1,365.7 1,250.7 1,342.6 1,093.0

Balance retained in/(applied from) businessDepreciation 130.7 79.1 77.7 86.4 78.6Impairment of assets 9.3 16.5 1.0 1.1 1.9Retained profi ts (15.6) 5.3 (0.6) (149.7) 44.2

124.4 100.9 78.1 (62.2) 124.7

Non-production cost and incomeBad debts (9.2) (13.6) 0.2 25.7 11.1Income from investments and interest 79.9 49.4 36.2 32.1 49.6Exchange loss (3.9) (1.8) (2.1) (1.2) (4.2)

66.8 34.0 34.3 56.6 56.5

Total distribution 1,990.8 1,500.6 1,363.1 1,337.0 1,274.2

21

Global Reports LLC

Mr Peter SEAH Lim Huat, ChairmanMr Peter Seah Lim Huat, 60, was appointed non executive Chairman on 15 April 2002 and was last re-elected on 31 March 2006. He is currently a member of the Temasek Holdings Advisory Panel. Mr Seah was a banker for 33 years before retiring as Vice Chairman and CEO of the former Overseas Union Bank in 2001 and joining Singapore Technologies Pte Ltd as President and CEO. He held this position until 31 December 2004. Mr Seah is the Chairman of SembCorp Industries Limited* and Singapore Computer Systems Limited*. He also sits on the Boards of CapitaLand Limited*, Chartered Semiconductor Manufacturing Ltd#, STATS ChipPAC Ltd# and StarHub Ltd*.

Board of Directors

The names of the directors holding offi ce at the date of this report are set out below together with details of their academic and professional qualifi cations, age, date of fi rst appointment as director, date of last re-election as director as well as directorships in listed companies.

Mr Seah is also President Commissioner of PT Indosat Tbk, PT Bank Internasional Indonesia Tbk and Deputy Chairman of Global Crossing Limited and ST Telemedia Pte Ltd. His other appointments include being a member of the Board of Siam Commercial Bank Public Company Limited and the Government of Singapore Investment Corporation. He serves as a member of the Institute of Defence and Strategic Studies, Defence Science Technology Agency (DSTA), Singapore Chinese Chamber of Commerce and Industry and Singapore Business Federation Council. Mr Seah was awarded the Public Service Star (Bintang Bakti Masyarakat) in 1999 and made a Justice of the Peace in 2003. He graduated from the former University of Singapore (NUS) in 1968 with an Honours degree in Business Administration.

Mr TAN Pheng Hock Mr Tan Pheng Hock, 49, is the President and CEO of ST Engineering and an executive Director. He was appointed Director on 1 May 2001 and was last re-elected on 31 March 2005. Mr Tan sits on the Board of SembCorp Marine Ltd* and Neptune Orient Lines Limited*. He is Chairman of the Nanyang Polytechnic Board of Governors and Deputy Chairman of the Singapore Workforce Development Authority. Mr Tan began his career with the Group as an engineer in ST Marine in 1981. He was previously Executive Vice President of ST Marine, President of ST Kinetics, President and Chief Operating Offi cer of ST Engineering and ST Engineering Group President. Mr Tan holds a Bachelor of Science (First Class Honours) in Marine Engineering from the University of Surrey, UK and a Master of Science in Management from Stanford University, USA.

Mr KOH Beng Seng Mr Koh Beng Seng, 56, is the CEO of Octagon Advisers Pte Ltd. He was appointed an independent non executive Director on 15 September 2003 and will be due for re-election at this coming AGM under Article 98 of the Company’s Articles of Association. Mr Koh was Deputy President of United Overseas Bank Ltd (UOB) until 31 January 2005. Prior to UOB, Mr Koh was Senior Advisor to Asia Pulp & Paper Co Ltd and Advisor to Bank of China and the International Monetary Fund. Mr Koh has extensive experience in the fi nancial services sector. He was with the Monetary Authority of Singapore from 1973 to 1998, where he served as Deputy Managing Director from 1988 to 1998. Mr Koh is a Director of Bank of China (Hong Kong) Limited^, Fraser & Neave Ltd* and Sing-Han International Financial Services Limited. Mr Koh holds a Bachelor of Commerce (First Class Honours) from the former Nanyang University, Singapore, and a Master of Business Administration from Columbia University, USA.

THE WINNING SPIRIT ST Engineering AR 2006 22

Global Reports LLC

Lieutenant-GeneralNG Yat ChungLG Ng Yat Chung, 45, is the Chief of the Defence Force1. He was appointed a non executive Director on 15 June 2003 and will retire at this coming AGM. He joined the Singapore Armed Forces (SAF) in 1979 and was awarded the SAF Overseas Scholarship in 1980. In the course of his military career, he has held various key command andstaff positions in the Ministryof Defence (MINDEF). LG Ng is the Deputy Chairman of SRCC Pte Ltd. He is also a member of the Board of Trustees of the National University of Singapore and a Director of DSTA. LG Ng holds a Bachelor of Arts (Honours) in Engineering Tripos and a Master of Arts (Mathematics) from the University of Cambridge, UK, as well as a Master of Business Administration from Stanford University, USA.

Dr TAN Kim SiewDr Tan Kim Siew, 52, is Permanent Secretary (Defence Development), MINDEF. He was appointed a non executive Director on 15 December 2003 and will be due for re-election at this coming AGM under Article 98 of the Company’s Articles of Association. Prior to his present appointment with MINDEF, he was the Deputy Secretary (Policy) with the Ministry of Finance. He was formerly the CEO and Chief Planner of the Urban Redevelopment Authority (URA) from 1996 to 2001. Dr Tan is the Chairman of DSTA and also a Director of Singapore Technologies Holdings Pte Ltd. Dr Tan holds a Bachelor of Arts in Engineering Tripos and a PhD in Engineering from the University of Cambridge, UK.

Professor LUI Pao ChuenProf Lui Pao Chuen, 64, is the Chief Defence Scientist in MINDEF. He was appointed a non executive Director on 1 October 1997 and was last re-elected on 31 March 2006. Prof Lui sits on the management boards of various scientifi c and research institutes. He is an Adjunct Professor in the Engineering Faculty of NUS. He is also the Chairman of SembCorp Design and Construction Pte Ltd, a subsidiary of SembCorp Industries Ltd, and Chairman of the Management Boards of Temasek Defence Systems Institute, NUS, and Temasek Laboratories, NUS and NTU. Prof Lui graduated from the former University of Singapore with a Bachelor of Science (Honours) in Physics and obtained a Master of Science degree in Operations Research & Systems Analysis fromthe Naval Postgraduate School, USA.

PAST DIRECTORSHIPS IN THE LAST THREE YEARS

Mr Peter SEAH Lim Huat• Civil Aviation Authority

of Singapore• Board of Commissioners

of Currency Singapore• AF (Indonesia) Pte Ltd• EDBV Management Pte Ltd• EDB Ventures 2 Pte Ltd• EDB Ventures Pte Ltd• PSA International Pte Ltd• Singapore Technologies

Pte Ltd• Singapore Technologies

Semiconductors Pte Ltd

Mr TAN Pheng Hock• TranSys Pte Ltd• ST Training & Simulation

Pte Ltd• Unicorn International

Pte Limited

Mr KOH Beng Seng• Chartered Semiconductor

Manufacturing Ltd• STATS ChipPAC Ltd.• Far Eastern Bank Limited• Industrial & Commercial

Bank Limited• Overseas Union Bank Limited• United Overseas Bank Limited• United Overseas Bank

(Canada)

Lieutenant-GeneralNG Yat Chung• Singapore Technologies

Kinetics Ltd• Trade Development Board• Public Utilities Board

Dr TAN Kim Siew• HDB Corporation Pte Ltd• Keppel Offshore & Marine Ltd

Professor LUI Pao Chuen• SembCorp Engineers and

Constructors Pte Ltd

1 until 23 March 2007

23

Global Reports LLC

Mr Winston TAN Tien Hin Mr Winston Tan Tien Hin, 58, is the Managing Director of Corporate Brokers International Pte Ltd. He was appointed an independent non executive Director on 1 October 1997 and was last re-elected on 31 March 2006. Mr Tan is also a member of the Salvation Army Advisory Board. He holds a Bachelor of Science in Physics from the former University of Singapore.

Mr Lucien WONG Yuen KuaiMr Lucien Wong Yuen Kuai, 53, is the Managing Partner of Allen & Gledhill. He was appointed an independent non executive Director on 1 October 1997 and will be due for re-election at this coming AGM under Article 98 of the Company’s Articles of Association. Mr Wong is a Director of Cerebos Pacifi c Limited*. He is also a member of the Monetary Authority of Singapore and Board of Trustees of NUS. Mr Wong graduated from the former University of Singapore with a Bachelor of Law degree.

Dr Philip PILLAI Dr Philip Pillai, 59, is the Senior Partner of Shook Lin & Bok. He was appointed an independent non executive Director on 1 April 2000 and was last re-elected on 31 March 2005. Dr Pillai is a Director of Singapore Press Holdings Limited*, Hotung Investment Holdings Limited* and International Board of Trustees of Haggai Institute, Atlanta. Dr Pillai obtained his Bachelor of Law (First Class Honours) from the former University of Singapore and a Master of Law and SJD from Harvard University, USA.

Board of Directors

THE WINNING SPIRIT ST Engineering AR 2006 24

Global Reports LLC

Mr QUEK Poh Huat Mr Quek Poh Huat, 60, is the Group CEO of Singapore Power Ltd. He was appointed a non executive Director on 15 April 2002 and was last re-elected on 31 March 2006. Mr Quek is a Director of Singapore Power Ltd, SP PowerAssets Limited, SP AusNet@ and SP Services Limited. He is also the Chairman of PowerGas Ltd, SPI Management Services Pty Ltd, SP PowerGrid Limited and Temasek Management Services Pte Ltd. He is also Singapore’s non resident Ambassador to Sweden. Mr Quek was awarded the Public Service Star award in August 1994. He obtained a Bachelor of Science in Chemical Engineering from the University of Leeds, UK, and a Master of Science in Management from the Naval Postgraduate School, USA.

Mr Venkatachalam KRISHNAKUMARMr Venkatachalam Krishnakumar, 57, is a Senior Advisor to Barclays Bank PLC, Global Retail and Commercial Banking. Prior to his present appointment, he was a Senior Advisor to McKinsey and Co. He was the Chief Operating Offi cer and Chief Financial Offi cer for the Asia Pacifi c Consumer Bank of Citigroup until his retirement on 28 February 2005, after a 31-year career with them. He was appointed an independent non executive Director on 15 April 2002 and was last re-elected on 31 March 2005. He is a Director of Singapore Computer Systems Limited* and also a member of the Board of the Singapore Land Authority. He holds a Bachelor of Engineering and a Master of Business Administration from the Indian Institute of Management, India.

Brigadier-General Bernard TAN Kok KiangBG Bernard Tan Kok Kiang, 40, is the Director, Joint Intelligence Directorate of MINDEF. He was appointed Alternate Director to LG Ng Yat Chung on 1 June 2003. He has held various positions in the last 17 years and assumed his present offi ce in 2002. He joined the SAF in 1984 and was awarded the President cum SAF Scholarship in 1985. He was also awarded the Lee Kuan Yew Scholarship in 2001. BG Tan is currently the Director of URA, Chairman of Sembawang Country Club and Board member of St Joseph’s Institution. BG Tan holds a Bachelor of Social Science (First Class Honours) in Economics and Political Science from the University of Birmingham, UK, and a Master of Business Administration from the Massachusetts Institute of Technology, USA.

* listed on Singapore Exchange Securities Trading Limited# listed on both Singapore Exchange Securities Trading Limited and NASDAQ^ listed on Stock Exchange of Hong Kong@ A stapled group comprising SP Australia Networks (Transmission) Ltd, SP Australia Networks (Distribution) Ltd and

SP Australia Networks (Finance) Trust, acting through its responsible entity, SP Australia Networks (RE) Ltd. It is dual-listed on the Australian Stock Exchange and the Singapore Exchange Securities Trading Limited.

PAST DIRECTORSHIPS IN THE LAST THREE YEARS

Mr Winston TAN Tien Hin• Singapore Technologies

Electronics Limited• Enersave Holdings Ltd• Gintic Technologies Pte Ltd• Ascendas Pte Ltd

Mr Lucien WONG• CapitaLand Limited• Raffl es Hotel (1886) Ltd• John Hancock International

(Southeast Asia) Pte Ltd• John Hancock Life Assurance

Company Ltd• Construction Exchange Pte Ltd• Raffl es Investments (1993)

Pte Ltd• Raffl es Investments

(Singapore) Pte. Limited• Raffl es Investments Limited

Dr Philip PILLAI • Lindeteves-Jacoberg Ltd*• PT Agro Indomas

Mr QUEK Poh Huat• Shangri-la Asia Ltd• S I Technology Fund Limited• PSA Corporation Ltd• Asia Financial Holdings Pte Ltd• Singapore Power International

(Pte) Ltd• Singapore Telecommunications

Limited• Other subsidiaries of Temasek

Holdings (Private) Limited

25

Global Reports LLC

Senior Management

THE WINNING SPIRIT ST Engineering AR 2006 26

Global Reports LLC

Leadership is a team effort, drawing on individual strengths united by a common goal.

27

Global Reports LLC

Senior Management

1 Mr TAN Pheng Hockis President and CEO of ST Engineering and a Director of the ST Engineering Board.(Mr Tan’s profi le is on page 22)

2 Mr WEE Siew Kim Mr WEE Siew Kim, 46, was appointed Deputy CEO in May 2004, overseeing the Aerospace and Marine sectors. He is concurrently the President, Defence Business of ST Engineering, a position he has held since 1 May 2002. Prior to his current position, Mr Wee was President of ST Engineering’s Europe operations from July 2001. He joined ST Aerospace as an engineer in 1984. He was President of ST Aerospace from December 1997 to July 2001. Mr Wee is also a Member of Parliament for the Ang Mo Kio Group Representative Constituency. He has a Bachelor of Science (First Class Honours) in Aeronautical Engineering from the Imperial College of Science & Technology, University of London, UK, and a Master in Business Administration from Stanford University, USA.

3 Mr SEAH Moon Ming Mr SEAH Moon Ming, 50, was appointed Deputy CEO of ST Engineering, overseeing the Electronics and Land Systems sectors, and President, International Business in May 2004. He is concurrently President, ST Electronics, a position he has held since 8 December 1997, after serving as Managing Director from 1 July 1997. Mr Seah was General Manager of CET Technologies, a subsidiary of ST Electronics, from July 1994 to July 1997. He is Chairman of the Board of Governors of Temasek Polytechnic. Mr Seah also serves as Vice Chairman of ECS Holdings Limited and Trek 2000 Limited. He is a Fellow of the Institution of Engineers Singapore, a senior member of IEEE and a member of Eta Kappa Nu. Mr Seah holds a Master of Science (with distinction) in Electrical Engineering from the Naval Postgraduate School, USA.

4 Mr Raphael CHIN Mr Raphael Chin, 42, is currently Acting Chief Financial Offi cer of the ST Engineering Group. He began his career at ST Engineering in 1990 as an accountant in the Group’s Aerospace sector. He subsequently held various fi nance positions in its subsidiaries, including SASCO, Perth Aerospace Engineering and STA Systems. In 1999, he took up the position of Financial Controller at ST Marine. The following year, he was appointed VP/Financial Controller of ST Engineering and became SVP/Group Financial Controller in 2006. Mr Chin holds a Bachelor of Economics from Monash University, Australia, and a Master of Commerce (Hons) from the University of Auckland, New Zealand. He is a Fellow of the Institute of Certifi ed Public Accountants of Singapore.

THE WINNING SPIRIT ST Engineering AR 2006 28

Global Reports LLC

5 Mr TAY Kok KhiangMr TAY Kok Khiang, 57, was appointed President of ST Aerospace on 10 July 2001. Mr Tay joined ST Aerospace as Vice President/General Manager of ST Aerospace Engineering Pte Ltd in 1993 and held many senior management appointments before becoming President. He was Deputy President & Chief Operating Offi cer prior to his current appointment. Mr Tay holds a Bachelor of Engineering (Honours) and a Master of Science in Industrial Engineering from the National University of Singapore.

6 Mr SEW Chee Jhuen Mr SEW Chee Jhuen, 43,was appointed President ofST Kinetics on 1 September 2006. Prior to his current position, Mr Sew was the Deputy President (Operations) and President, Defence Business, of ST Kinetics. He joined ST Aerospace as an aeronautical engineer in 1988 and has held various management appointments before becoming Deputy President (Operations). Mr Sew holds a Bachelor of Science (with distinction) in Aeronautical Engineering and Mechanics from the University of Minnesota and a Master in Business Administration from Stanford University, USA.

7 Mr SEE Leong Teck Mr SEE Leong Teck, 56, was appointed President of ST Marine in December 1997. He began his career with Vosper Thornycroft (Singapore) and joined ST Marine as a naval architect in 1980, rising through the ranks to become Deputy General Manager and eventually President. Mr See holds a Master of Science in Naval Architecture from the University of London, UK and a Master of Business Administration from the Cranfi eld School of Management, UK.

8 General (Retired)John G COBURN Gen (Ret) John G COBURN, 64, was appointed Chairman and CEO of ST Engineering’s US subsidiary, VT Systems, Inc on 1 December 2001. Gen (Ret) Coburn joined the Group after an illustrious 39-year career with the US Department of Defense. Prior to taking up this position, he was Commanding General of the US Army Materiel Command (AMC), one of the largest commands in the army with 50,000 employees and activities in 42 states and over a dozen foreign countries. Gen (Ret) Coburn holds a Juris Doctor from the University of Missouri, USA.

29

65 4 2 1 3 7 8

Global Reports LLC

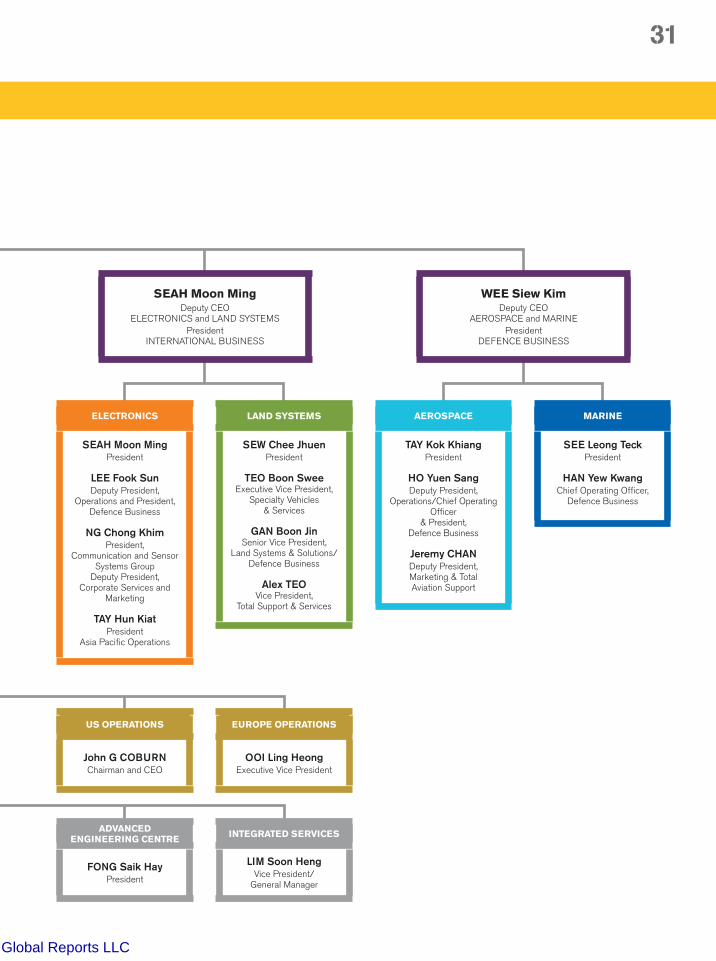

Organisation Chart AS AT 28 FEBRUARY 2007

Raphael CHINActing Chief Financial Offi cer

INTERNAL AUDIT

David EAWSenior Vice President

(Reporting to Audit Committee)

DEFENCE BUSINESS

LOW Yee KahSenior Vice President

INTERNATIONAL MARKETING

Patrick CHOYExecutive Vice President

TAN Pheng HockPresident and CEO

Members of Executive Offi ce

TECHNOLOGY

FONG Saik HayChief Technology Offi cer

NEW BUSINESS

Steven CHEONGSenior Vice President

HUMAN RESOURCE

TAN Nga KokSenior Vice President/

Director

LEGAL

LOW Meng WaiVice President/Director

INFORMATION TECHNOLOGY

TEO Chin SengChief Information Offi cer

STRATEGIC PLANS

Robin THEVATHASANSenior Vice President

CORPORATE COMMUNICATIONS

LIM Beng SeeVice President/Head

RISK MANAGEMENT

ONG Soon LeongVice President/Head

PROCUREMENT

GOH Bak NguanChief Procurement Offi cer/

Vice President

BUSINESSEXCELLENCE

Harnek SINGHVice President/Director

SPECIAL PROJECTS

WU Tzu ChienPresident

CHANG Cheow TeckPresident

THE WINNING SPIRIT ST Engineering AR 2006 30

Global Reports LLC

ADVANCED ENGINEERING CENTRE

FONG Saik HayPresident

INTEGRATED SERVICES

LIM Soon HengVice President/

General Manager

US OPERATIONS

John G COBURNChairman and CEO

EUROPE OPERATIONS

OOI Ling HeongExecutive Vice President

ELECTRONICS

SEAH Moon MingPresident

LEE Fook SunDeputy President,

Operations and President,Defence Business

NG Chong KhimPresident,

Communication and SensorSystems Group

Deputy President,Corporate Services and

Marketing

TAY Hun KiatPresident

Asia Pacifi c Operations

LAND SYSTEMS

SEW Chee JhuenPresident

TEO Boon SweeExecutive Vice President,

Specialty Vehicles & Services

GAN Boon JinSenior Vice President,

Land Systems & Solutions/Defence Business

Alex TEOVice President,

Total Support & Services

AEROSPACE

TAY Kok KhiangPresident

HO Yuen SangDeputy President,

Operations/Chief Operating Offi cer

& President,Defence Business

Jeremy CHANDeputy President, Marketing & Total Aviation Support

MARINE

SEE Leong TeckPresident

HAN Yew KwangChief Operating Offi cer,

Defence Business

WEE Siew KimDeputy CEO

AEROSPACE and MARINE President

DEFENCE BUSINESS

SEAH Moon MingDeputy CEO

ELECTRONICS and LAND SYSTEMSPresident

INTERNATIONAL BUSINESS

31

Global Reports LLC

Corporate Governance

THE WINNING SPIRIT ST Engineering AR 2006 32

Global Reports LLC

Board’s Conduct of Its Affairs (Principle 1)The Board’s corporate objective is the creation of long term value for shareholders. It strives to achieve this through its commitment to high standards of corporate governance by providing the leadership and guidance to management to develop and drive corporate strategy, business directions, acquisitions and divestments and risk policy for ST Engineering.

There are matters which the Board has reserved for its own decision making. These include major acquisitions and investments, shareholder matters, policies relating to corporate governance, CEO appointment, approval of budgets, board changes and appointments on board committees. Board members receive monthly consolidated management reports on the fi nancial performance of each business sector, capital commitments and signifi cant operational highlights.

Other matters are delegated to Board committees and the Executive Offi ce for review and decision making. The Executive Offi ce comprises the President and CEO; Dy CEO, Electronics and Land Systems/President, International Business; Dy CEO, Aerospace and Marine/President, Defence Business; and CFO.

The Board comprises 11 directors and an alternate director. On appointment, a new director is issued a formal letter of appointment setting out his duties and responsibilities under the various regulations. A new director is also given a briefi ng by the President and CEO on the strategies and performance of the Company and its key subsidiaries as well as an introduction to the senior management team.

The Board consists of members with established track records in fi nance, banking, technology, legal and management skills. Each non executive director brings to the Board an independent and objective perspective based on his training and expertise to enable balanced and well considered decisions to be made.

From time to time, the Board is updated on the relevant laws, continuing listing obligations and standards requiring compliance, and their implications for the Group as part of ongoing training for existing directors.

The Board meets at least twice a year and convenes special board meetings where necessary. The Company’s Articles of Association allows Board meetings to be conducted by way of teleconference or video conference. The Chairman has a second or casting vote. The Board is supported in its tasks by Board Committees which have been established to focus on the key areas of corporate governance oversight.

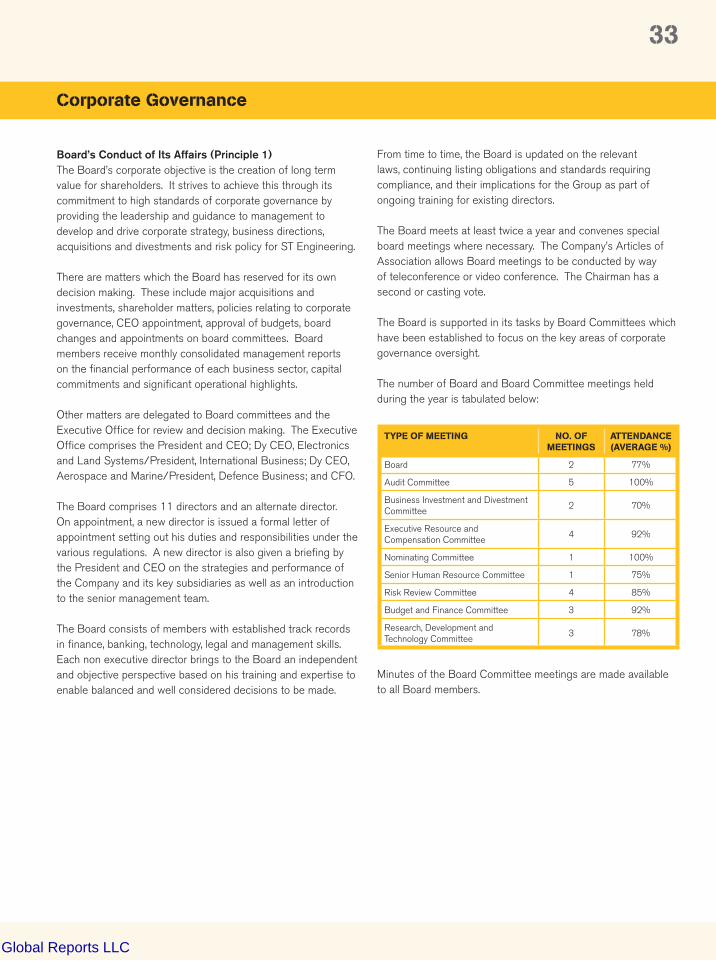

The number of Board and Board Committee meetings held during the year is tabulated below:

Minutes of the Board Committee meetings are made available to all Board members.

Corporate Governance

TYPE OF MEETING NO. OF MEETINGS

ATTENDANCE (AVERAGE %)

Board 2 77%

Audit Committee 5 100%

Business Investment and Divestment Committee

2 70%

Executive Resource and Compensation Committee

4 92%

Nominating Committee 1 100%

Senior Human Resource Committee 1 75%

Risk Review Committee 4 85%

Budget and Finance Committee 3 92%

Research, Development and Technology Committee

3 78%

33

Global Reports LLC

Corporate Governance

Independence of the Board (Principles 2 and 3)The Chairman of the Board is Mr Peter Seah, a non executive director. Mr Seah was appointed to the Board on 15 April 2002 as Chairman. He was re-elected at the 2006 AGM.

As a non executive director, Mr Seah is free from any relationship with the executive management of the Company that could materially interfere with the exercise of his independent judgment. However, as he is a Member of the Temasek Advisory Panel in Temasek Holdings, the Company’s major shareholder, he is not considered independent within the defi nition of the Corporate Governance Code (Code).

The President and CEO is Mr Tan Pheng Hock, who is an executive director. Save for Mr Tan Pheng Hock, our remaining 10 directors are non executive directors. The Nominating Committee (NC) has reviewed the provisions in the Code with regard to relationships and has concluded that fi ve directors are independent. The independent directors are Mr Koh Beng Seng, Mr Venkatachalam Krishnakumar, Dr Philip Pillai, Mr Winston Tan and Mr Lucien Wong. More than one third of the Board is independent as required under the Code.

According to the Corporate Governance Code guidelines, an independent director is one who has no relationship with the Company, its related companies or its offi cers that could interfere, or be reasonably perceived to interfere with the exercise of the director’s independent business judgment. Relationship tests aside, it is the quality of the governance that counts and that distinguishes an independent and effective board. While not all the non executive directors are considered independent based on relationship tests, the Board has, at all times exercised independent judgment in decision making using its collective wisdom and experience to act in the best interests of the Company.

The Board held a total of two meetings during the year, in accordance with its planning cycle, for the approval of the FY2005 results and release of half year results respectively.

Board Committees (Principles 4, 7 and 11)Supporting the Board are the following Board Committees:

• Audit Committee• Business Investment and Divestment Committee• Executive Resource and Compensation Committee• Nominating Committee• Budget and Finance Committee • Research, Development and Technology Committee • Senior Human Resource Committee • Risk Review Committee• Tenders Committee

The composition of the Board Committees is found on thenext page.

THE WINNING SPIRIT ST Engineering AR 2006 34

Global Reports LLC

Au

dit

Co

mm

itte

e(e

stbd

on

5/1

/19

98

)

Bu

sin

ess

Inve

stm

ent

and

Div

estm

ent

Co

mm

itte

e(e

stbd

on

8/9

/19

97)

Exe

cuti

ve R

eso

urc

e an

d C

om

pen

sati

on

C

om

mit

tee

(est

bd o

n 6

/12

/19

97)

No

min

atin

g C

om

mit

tee

(est

bd o

n 4

/12

/20

02

)

Bu

dg

et a

nd

Fin

ance

Co

mm

itte

e(e

stbd

on

5/1

/19

98

)

Res

earc

h D

evel

op

men

t an

d T

ech

no

log

y C

om

mit

tee

(est

bd o

n 1

/8/2

00

3)

Sen

ior

Hu

man

Res

ou

rce

Co

mm

itte

e(e

stbd

on

16

/1/1

99

8)

Ris

k R

evie

w C

om

mit

tee

(est

bd o

n 7/

12

/19

98

)

Ten

der

s C

om

mit

tee

(est

bd o

n 5

/1/1

99

8)

BOARD MEMBERS

Rol

ling

list o

f any

thre

e B

oard

Dire

ctor

s

Mr Peter SEAH Lim Huat C C M C

Mr TAN Pheng Hock M M M M M

Mr KOH Beng Seng C

Lieutenant-General NG Yat Chung M M M

Dr TAN Kim Siew M M

Professor LUI Pao Chuen C

Mr Winston TAN Tien Hin M M C

Mr Lucien WONG Yuen Kuai C M

Dr Philip Nalliah PILLAI M M C

Mr QUEK Poh Huat M M

Mr Venkatachalam KRISHNAKUMAR M M M M

Brigadier-General Bernard TAN Kok Kiang 1

NON BOARD MEMBER

Mr CHANG See Hiang CM

Denotes:C – Chairman M – Member CM – Co-opted Member

1 Alternate director to Lieutenant-General NG Yat Chung

Corporate Governance

BOARD COMPOSITION AND COMMITTEES AS AT 31 DECEMBER 2006

35

Global Reports LLC

Corporate Governance

Board Selection, Training and Evaluation of Performance (Principles 4 and 5)The NC is responsible for reviewing the composition of the Board regularly and identifying and selecting suitable candidates to the Board. The Committee also reviews the retirement and re-election of directors.

Dr Philip Pillai is the Chairman of the NC. The other members are Mr Peter Seah and Mr Venkatachalam Krishnakumar. Both Dr Pillai and Mr Krishnakumar are independent non executive directors.

The NC is charged with the responsibility of ensuring that the Company’s Board and its subsidiaries comprise individuals who are able to discharge their responsibilities as directors. The NC identifi es suitable candidates for appointment to the boards of the Group, in particular, candidates who can value add to the management through their contributions in the relevant strategic business.

The NC has the same members as the Executive Resource & Compensation Committee. This is because both committees share similar objectives of searching for talent and expertise for Board renewal and to strengthen management. During the year, the NC reviewed and affi rmed the independence of the Company’s independent directors and reviewed the composition of the Board and the profi le of Board members in relation to the needs of the ST Engineering Board. The NC also assessed the current board size and determined that it is adequate for the effective functioning of the Board. The NC also reviewed the directors who were due for retirement and re-election.

At each AGM, one third of the directors with the longest term in offi ce is required to retire and submit themselves for re-election. Mr Koh Beng Seng, LG Ng Yat Chung, Dr Tan Kim Siew and Mr Lucien Wong will retire. LG Ng has confi rmed that he will not be seeking re-election. Save for LG Ng, the retiring directors, being eligible, have offered themselves for re-election. The NC has reviewed their contributions and recommended that each of the retiring Directors be re-elected at the Company’s forthcoming AGM.

Access to Information (Principle 6) The Board receives monthly reports providing updates on key operational activities and fi nancial analysis. The Board also has unrestricted access to the President and CEO, the CFO, management and the Company Secretary as well as the internal and external auditors and the risk management team. The Board can also seek independent professional advice if deemed necessary.

Level and Mix of RemunerationDisclosure on Remuneration (Principles 7, 8 and 9) The Executive Resource & Compensation Committee (ERCC) performs the role of the Remuneration Committee. The Committee comprises Mr Peter Seah as Chairman, Dr Philip Pillai and Mr Venkatachalam Krishnakumar. The majority of members of the ERCC have held senior positions in large organisations and are experienced in the area of executive remuneration.

All the ERCC members are non executive directors. Apart from Mr Peter Seah, the other members of the ERCC are independent directors.

The ERCC has access to professional advice from appropriate external advisors where necessary. The ERCC may meet with these external advisors without the presence of management. All decisions at any meeting of the ERCC shall be decided by a majority of votes of the ERCC members present and voting (the decision of the ERCC shall at all times exclude the vote, approval or recommendation of any member who has a confl ict of interest in the subject matter under consideration).

The ERCC has been authorised by the Board to carry out the following key duties and responsibilities:

• Review and establish executive remuneration policy• Approve the remuneration package and service terms

for senior executives• Set targets for senior executives and approve equity based

incentive share plans and the granting of performance share awards

• Approve non executive director remuneration structure

THE WINNING SPIRIT ST Engineering AR 2006 36

Global Reports LLC

Corporate Governance

The ERCC met four times in 2006. Its key activities were centred on the assessment and development of the management team, target setting, and the determination of their compensation and incentive awards. In determining the overall remuneration package, the ERCC assesses executives’ contribution to the Group relative to preset targets, the performance of the Group, and the compensation and employment conditions of various industries.

During the year, the ERCC reviewed and approved the granting of share options. In accordance with the rules of the ST Engineering Share Option Plan (ESOP), share options are priced at market value, on a volume-weighted average for the shares on the Singapore Exchange (SGX) over the three consecutive trading days immediately preceding the date of grant. The computation is referenced against the daily offi cial list of the SGX and verifi ed by Finance. The subscription price of the share options granted cannot be modifi ed

during the term of the options, except for adjustments arising from variations to the share capital, as the ERCC considers appropriate.

As standing procedure, the ERCC, as the Plan Administrator, has determined that share options shall be granted twice a year on fi xed dates following the release of the audited FY end results and fi rst half year results, respectively. In the event that any announcement on any matter of an exceptional nature involving price-sensitive information is made, the ESOP rules require that options be granted on or after the fourth market day following release of the announcement.

During the year, the ERCC decided on conditional performance share awards under ST Engineering’s approved share plans as well as Economic Value Added-based incentives for senior executives.

The following information relates to remuneration of directors of ST Engineering:

NUMBER OF DIRECTORS IN REMUNERATION BANDS 2006 2005

Remuneration Bands $500,000 and above 1 1$250,000 to $499,999 – –Below $250,000 10 10

Total 11 11

37

Global Reports LLC

Corporate Governance

Summary compensation table for the year ended 31 December 2006 (Group):

STOCK OPTIONS DIRECTORS’ GRANTED EXERCISE NAME OF DIRECTOR SALARY * BONUS * FEES TOTAL IN 2006 PRICE EXERCISABLE PERIOD $ $ $ $ $

Peter Seah Lim Huat – – 182,000 182,000 44,500 3.01 10.2.2007 to 9.2.2011 44,500 2.84 11.8.2007 to 10.8.2011

Tan Pheng Hock 1,090,275 1,711,991 # 2,802,266 200,000 3.01 10.2.2007 to 9.2.2016 200,000 2.84 11.8.2007 to 10.8.2016

Koh Beng Seng – – 94,000 94,000 27,500 3.01 10.2.2007 to 9.2.2011 27,500 2.84 11.8.2007 to 10.8.2011

LG Ng Yat Chung – – 10,000✣ 10,000 – – –

Dr Tan Kim Siew – – 10,000✣ 10,000 – – –

Professor Lui Pao Chuen – – 97,500† 97,500 29,000 3.01 10.2.2007 to 9.2.2011

Winston Tan Tien Hin – – 142,000† 142,000 37,000 3.01 10.2.2007 to 9.2.2011 37,000 2.84 11.8.2007 to 10.8.2011

Lucien Wong Yuen Kuai – – 86,000 86,000 21,500 3.01 10.2.2007 to 9.2.2011 21,500 2.84 11.8.2007 to 10.8.2011

Dr Philip Nalliah Pillai – – 123,000† 123,000 33,000 3.01 10.2.2007 to 9.2.2011 33,000 2.84 11.8.2007 to 10.8.2011

Quek Poh Huat – – 128,000† 128,000 33,000 3.01 10.2.2007 to 9.2.2011 33,000 2.84 11.8.2007 to 10.8.2011

Venkatachalam Krishnakumar – – 116,000 116,000 25,500 3.01 10.2.2007 to 9.2.2011 25,500 2.84 11.8.2007 to 10.8.2011

BG Bernard Tan Kok Kiang (Alternate to LG Ng Yat Chung) – – – – – – –

1,090,275 1,711,991 988,500 3,790,766 873,000

* The salary and bonus amount shown is inclusive of allowances, CPF and performance shares earned.✣ Fees for public sector Directors are payable to government agencies.† Includes fees for directorship in subsidiary(ies).# Fees payable to Mr Tan Pheng Hock of $168,750 includes fees for directorship in subsidiaries and are payable to Singapore Technologies Engineering Ltd.

THE WINNING SPIRIT ST Engineering AR 2006 38

Global Reports LLC

Corporate Governance

The Board has delegated authority to the ERCC to determine the remuneration of the President and CEO and the senior management. The remuneration package for non executive directors is reviewed by the Board annually and the fees to be paid to Board members are subject to approval at the AGM.

A revised directors’ fee policy commensurate with the increased responsibilities of the Board was endorsed by the Board.

The Group has set out a group-wide cross section of executives’ remuneration by number of employees from $100,000 upwards in bands of $50,000 up to $250,000.

The Senior Human Resource Committee, chaired by Mr Peter Seah, comprises Mr Tan Pheng Hock, LG Ng Yat Chung and Dr Tan Kim Siew. The Committee reviewed the talent management and leadership development for the organisation and its senior staff. Through its support for and direction of the Group’s talent management and leadership initiatives, the Committee has helped to enhance the process of identifi cation and development of talents to be groomed for senior positions. The Committee has also reviewed the succession plans for key positions in the Group. Another signifi cant initiative that has materialised from the Committee’s support and direction is the establishment of the inaugural ST Engineering Overseas Scholarship and ST Engineering Scholarship in China.

Accountability (Principle 10)In September 2006, the SGX introduced a new requirement for directors to issue a Negative Assurance Statement to accompany its interim fi nancial results announcement, confi rming that nothing has come to the attention of the Board that may render the interim fi nancial results to be false or misleading. Certain internal procedures have been put in place that enable each member of the Board reviewing the interim fi nancial statements to immediately raise any material information known to him which would impact the accuracy of the statements prior to their release to SGX. Should there be any signifi cant adverse issue(s) raised by the Audit Committee (AC) or Board member which may affect the results in a material way, the scheduled date of the results announcement will be postponed to allow time for investigation or further review.

The re-appointment of auditors is subject to approval at each AGM. In making its recommendations to shareholders on the appointment and re-appointment of auditors, the Board relies on the review and recommendations of the AC.

Remuneration Data for Year 2006

Remuneration data for employees earning $100,000 and above per annum (as at 31 Dec 2006).

TOTAL COMPENSATION BANDS ($) TOTAL NO. OF EMPLOYEES TOTAL DOLLAR VALUES ($)

100,000 to 149,999 843 100,059,481 150,000 to 199,999 252 43,235,882200,000 to 249,999 81 17,950,249250,000 to 499,999 91 30,606,716500,000 to 749,999 10 5,789,157750,000 to 999,999 5 4,380,4331,000,000 to 1,249,999 1 1,116,0741,250,000 to 1,499,999 3 4,086,7851,500,000 to 1,749,999 1 1,611,420=> 1,750,000 4 7,934,048

Total 1,291 216,770,245

Note: Total compensation comprises all staff salaries (including CPF for Singapore staff), overtime pay, variable bonuses, special bonuses, annual wage supplement (13th month), dollar contribution by the Group under the Employees’ Share Ownership Scheme, benefi ts-in-kind plus overseas postees’ cost of living allowance.

39

Global Reports LLC

During the year, the Board convened an EGM to adopt new Articles of Association updating changes made to the Companies Act (Chapter 50).

Directors and key senior executives of the Group are prohibited from dealing in ST Engineering shares two weeks before the announcement of ST Engineering’s fi rst quarter, half year, third quarter and full year results up to the date of the announcement of the results. Additionally, all directors of the Group and its employees are reminded not to trade in situations where the insider trading laws and rules would prohibit trading.

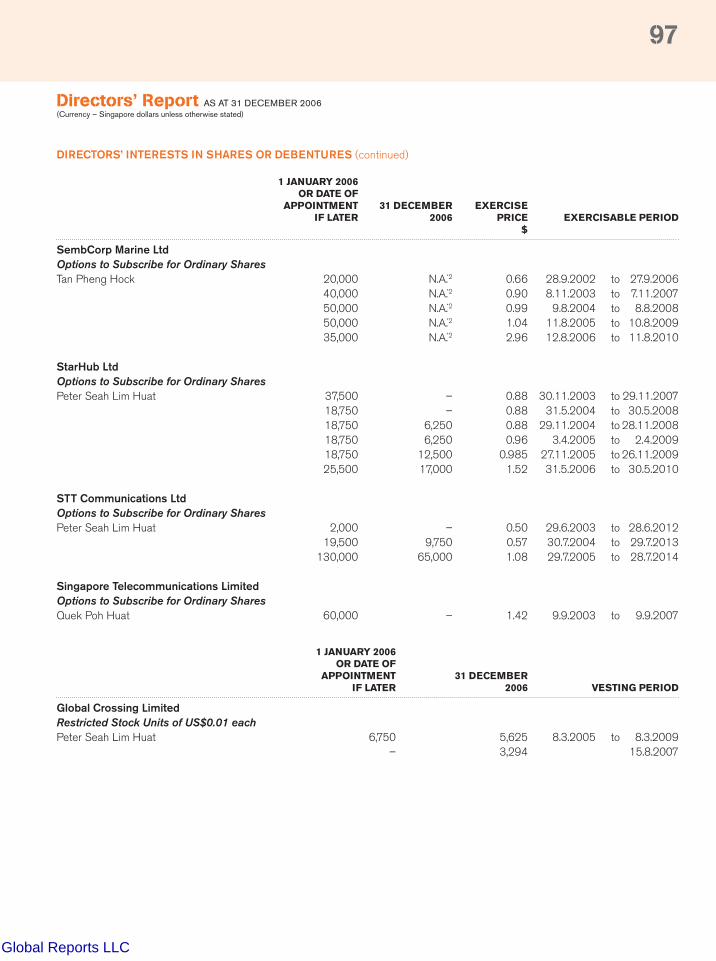

The directors’ interests in shares of ST Engineering and its related companies during the year are found on pages 91 to 99 of this Report.

Audit Committee (Principle 11)The AC is supported in its work by the audit committees of the four main business sectors. The respective chairmen of the audit committees of the four business sectors are invited to attend the AC meetings of ST Engineering so as to have a clear understanding of policies made at the holding company level and to give feedback from the sectors’ audit committees.

The AC has full authority to commission and review fi ndings of internal investigations into matters where it is alerted of any suspected fraud or irregularity or failure of internal controls or infringement of any law likely to have a material impact on the listed Group’s operating results. It can investigate any matter within its terms of reference and with the full cooperation of management.

During the year, the Board adopted a Whistle Blowing Policy with the objective of providing a process for staff to raise, in confi dence and without fear of retaliation, incidents of possible wrongdoing or breach of applicable laws, regulations or policies to the respective chairmen of the audit committees in the Group.

The AC comprises Mr Koh Beng Seng as Chairman, Dr Philip Pillai and Mr Venkatachalam Krishnakumar. All the members of the AC are independent directors. The AC held fi ve meetings during the year, including a January 2006 session with the external and internal auditors, without management, to review the FY2005 results.

During the year, the AC reviewed and recommended to the Board the release of the full year and half year fi nancial statements, and considered and approved the 2006 Audit Plan and the 2006 Internal Audit (IA) Plan. It also reviewed the adequacy of internal control procedures, Interested Person transactions and the issues raised in IA reports with IA being given the authority to rate risk issues according to different risk levels, and to follow up with remedial actions by the management.

During the year, the AC was briefed on the external auditors’ appointment of a US coordinating partner to coordinate the audit of the US group of companies with the local offi ce partner who would be overall in charge of both the local and overseas companies’ audits.

The AC also focused on the need to bring new acquisitions into alignment with policies in the ST Engineering Group and to integrate practices and activities with the Group post acquisition.

The AC reviewed the level of non audit services performed by its external auditors to satisfy itself that non audit services performed by the auditors did not compromise their independence under regulatory requirements.

Having been delegated authority by the Board, the AC approved the release of the fi nancial results for the fi rst quarter and third quarter of 2006.

In February 2007, the AC reviewed the audit observations on the fi nancial statements for FY2006 audit with the external auditors. The AC also met with the external and internal auditors, without management, to review 2006 results. There were no major issues highlighted and the auditors confi rmed that they would provide an unqualifi ed report.

The AC also reviewed the performance of the external auditors. It recommended to the Board the re-appointment of Ernst & Young as auditors for FY2007, after having been satisfi ed with its standard of audit, independence and objectivity.

Corporate Governance

THE WINNING SPIRIT ST Engineering AR 2006 40

Global Reports LLC

Corporate Governance

Internal Controls (Principle 12)Internal Audit (Principle 13)The AC oversees and appraises the quality of the audit effort of the Company’s IA function. The Board, through the AC, the President and CEO and the CFO, considers that the Group’s framework of internal controls and procedures is adequate to provide reasonable assurance of the integrity, confi dentiality and availability of critical information, and the effectiveness and effi ciency of operations, safeguarding of assets and compliance with applicable rules and regulations. It is also satisfi ed that problems are identifi ed on a timely basis and there is in place a process for best practices and follow up actions to be taken promptly to minimise unnecessary lapses and for the identifi cation and containment of business risks.

The IA supports the AC in reviewing the adequacy of the Company’s internal control system.

Staffed by qualifi ed auditors, IA has unrestricted direct access to the AC. The Head of IA’s primary line of reporting is to the Chairman of the AC, although he reports administratively to the CFO of the Company.

IA plans its internal audit schedules in consultation with, but independently of, management and its IA Plan is submitted to the AC for approval at the beginning of each year. The AC also meets with IA at least once a year without the presence of management to gather feedback on management’s level of cooperation and other matters that warrant AC’s attention. All audit reports are submitted to the AC for deliberation with copies of these reports extended to the relevant senior management, for prompt corrective actions, as recommended. Furthermore, IA’s summary of fi ndings, recommendations and updates on management’s actions taken are discussed at the quarterly AC meetings. There were no signifi cant control issues highlighted by IA in 2006.

During the year, IA briefed the AC on its plan to carry out surprise audits across the Group. The IA continued with its system of rating a company at the end of an internal audit for the purpose of differentiating the high risk issues which require more serious attention.

As part of the Group’s effort to continually improve on its control framework, IA has also introduced a quarterly Control Self Assessment Declaration for all auditable entities to sign off and declare that Management has reviewed and complied with all the requirements and that there are no material matters or issues that have not been highlighted.

On an ongoing basis, IA ensures that good practices are shared within the Group.

Risk ManagementThe Risk Review Committee, chaired by Mr Winston Tan, comprises LG Ng Yat Chung, Mr Lucien Wong, Mr Venkatachalam Krishnakumar, Mr Tan Pheng Hock and Mr Chang See Hiang, a co-opted member and Board Director of ST Aerospace. The Committee oversees the risk management framework and reviews key risk exposures, including business continuity management.

The Committee met four times during the year to review the key risks and the measures put in place as well as the key risk indicators of each sector. Emerging risk perspectives facing the Group were also discussed.

Budget and FinanceChaired by Mr Lucien Wong, the Budget and Finance Committee members include Mr Tan Pheng Hock, Mr Quek Poh Huat and Dr Tan Kim Siew.

Budgets prepared by the respective subsidiaries are consolidated at the ST Engineering level and presented to the Budget and Finance Committee for review and recommendation to the Board for approval.

During the year, the Budget and Finance Committee held three meetings to review the FY2006 budget assumptions and forecast. The Committee also met to review the 2007 Plan and recommended to the Board for approval.

41

Global Reports LLC

Corporate Governance

Business Investment and Divestment CommitteeThe Business Investment and Divestment Committee comprises Mr Peter Seah as Chairman, Mr Tan Pheng Hock, LG Ng Yat Chung, Mr Winston Tan and Mr Quek Poh Huat.

During the year, the Business Investment and Divestment Committee held two meetings to consider major investments by the Group.

Communication with Shareholders (Principle 14)Greater Shareholder Participation (Principle 15)The Group has a comprehensive investor programme aimed at providing existing and potential investors with comprehensive and prompt information to enable them to have a better understanding of the Group’s businesses, direction and performance. ST Engineering maintains a regularly updated website which provides a chronology of the latest press releases and highlights of corporate events of each of its sectors and their respective capabilities.

In 2006, ST Engineering hosted more than 300 investor meetings, including participation in 11 international investor roadshows and conferences in 25 cities. ST Engineering is committed to timely disclosures to ensure that the investing community receives a balanced and updated view of the Group’s performance and businesses.

Board members attended the AGM and EGM in 2006 where shareholders present were given an opportunity to seek clarifi cation or question the Board on issues pertaining to the resolutions proposed before they were voted on. The external auditors were also present at the AGM to assist the directors in answering questions on audit related matters from shareholders. The Group fully supports the Code’s principle to encourage active shareholder participation. More on Investor Relations can be found on pages 46 to 49.

Financial and other information are made available on the Company’s website at http://www.stengg.com and these are regularly updated.

THE WINNING SPIRIT ST Engineering AR 2006 42

Global Reports LLC

CODE PRINCIPLE REFERENCEPAGES

1 The Board’s Conduct of its Affairs Every company should be headed by an effective Board to lead and control the company. The Board is collectively responsible for the success of the company. The Board works with management to achieve this and the management remains accountable to the Board.

33

2 Board Composition and Guidance There should be a strong and independent element on the Board, which is able to exercise objective judgement on corporate affairs independently, in particular, from management. No individual or small group of individuals should be allowed to dominate the Board’s decision making.

34 and 35

3 Chairman and Chief Executive Offi cer There should be a clear division of responsibilities at the top of the company – the working of the Board and the executive responsibility of the company’s business – which will ensure a balance of power and authority, such that no one individual represents a considerable concentration of power.

34 and 35

4 Board Membership There should be a formal and transparent process for the appointment of new directors to the Board.

34 and 35