Aberdeen Global - Morningstar Document Library

124

Aberdeen Global Interim Report and Accounts For the period ended 31 March 2008

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Aberdeen Global - Morningstar Document Library

Aberdeen Global Interim Report and Accounts

For the period ended 31 March 2008

Contents

Page

Incorporation...............................................................................................................................................................................................................................................................................1

Chairman’s Statement ............................................................................................................................................................................................................................................................2

Net Asset Value History .......................................................................................................................................................................................................................................................3

Summary of Historic Information ......................................................................................................................................................................................................................................5

Aberdeen Global - Combined Statements ......................................................................................................................................................................................................................6

American Opportunities Fund ..............................................................................................................................................................................................................................................7

Asia Pacific Fund .....................................................................................................................................................................................................................................................................11

Asia Pacific and Japan Fund ...............................................................................................................................................................................................................................................15

Asia Pacific and Australasian Bond Fund ......................................................................................................................................................................................................................17

Asian Smaller Companies Fund ........................................................................................................................................................................................................................................21

Australasian Equity Fund .....................................................................................................................................................................................................................................................25

China Opportunities Fund ..................................................................................................................................................................................................................................................29

Emerging Markets Fund .......................................................................................................................................................................................................................................................32

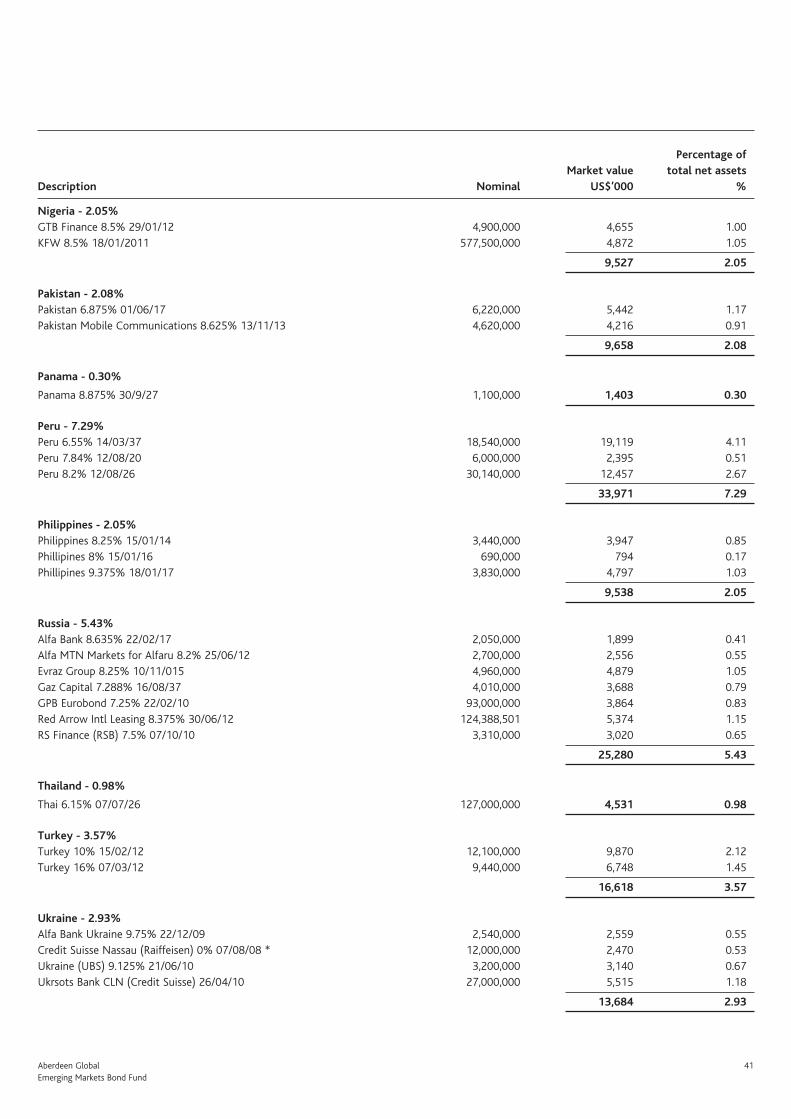

Emerging Markets Bond Fund ...........................................................................................................................................................................................................................................37

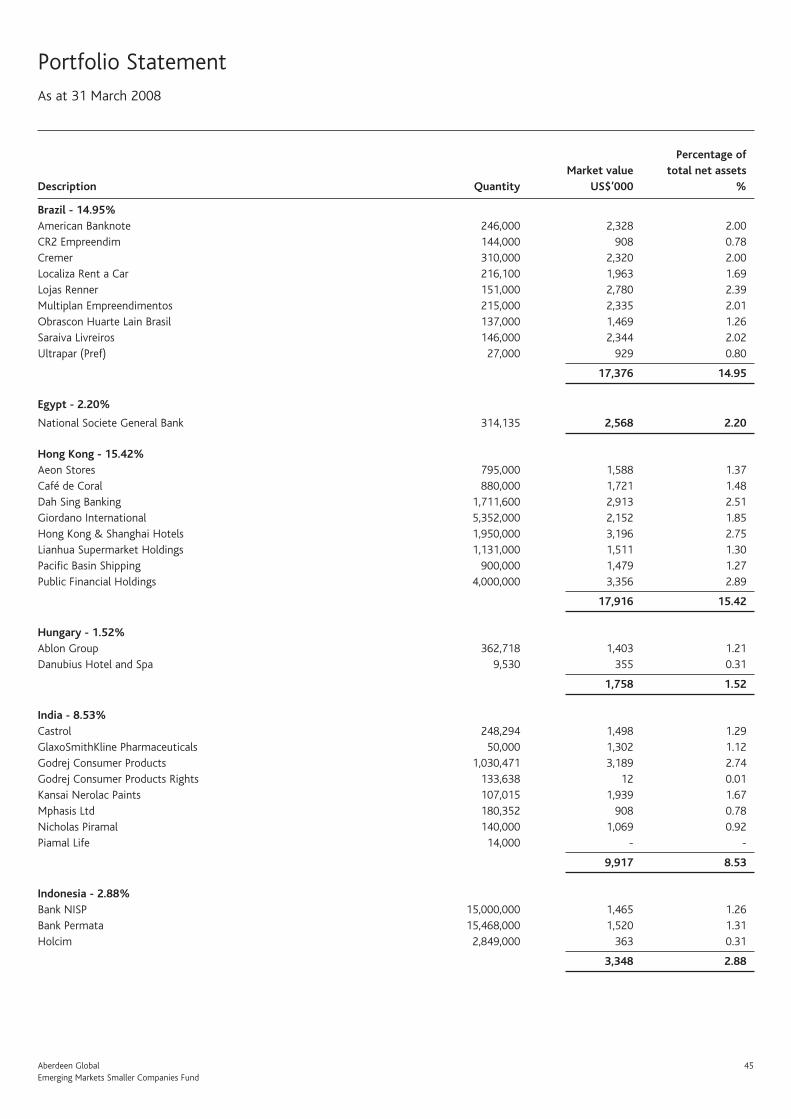

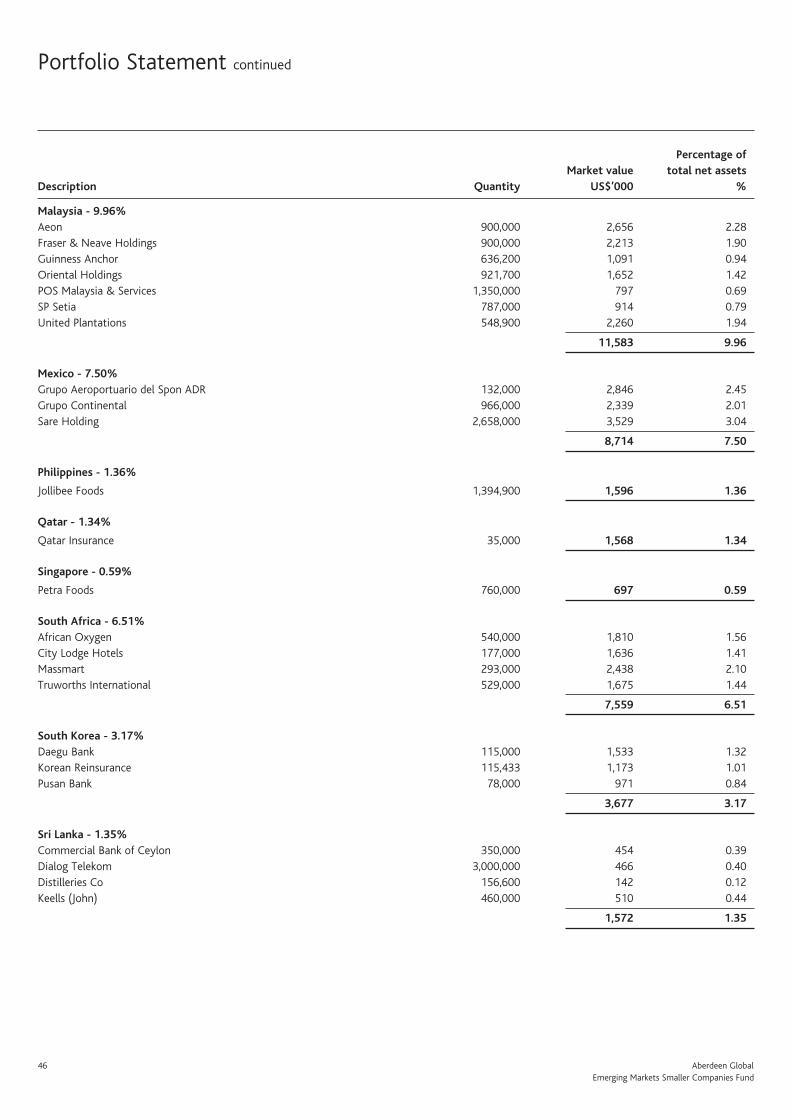

Emerging Markets Smaller Companies Fund ...............................................................................................................................................................................................................43

European Equity Fund ..........................................................................................................................................................................................................................................................48

European High Yield Bond Fund .......................................................................................................................................................................................................................................52

European Opportunities (ex UK) Fund ...........................................................................................................................................................................................................................58

High Yield Bond Fund ...........................................................................................................................................................................................................................................................62

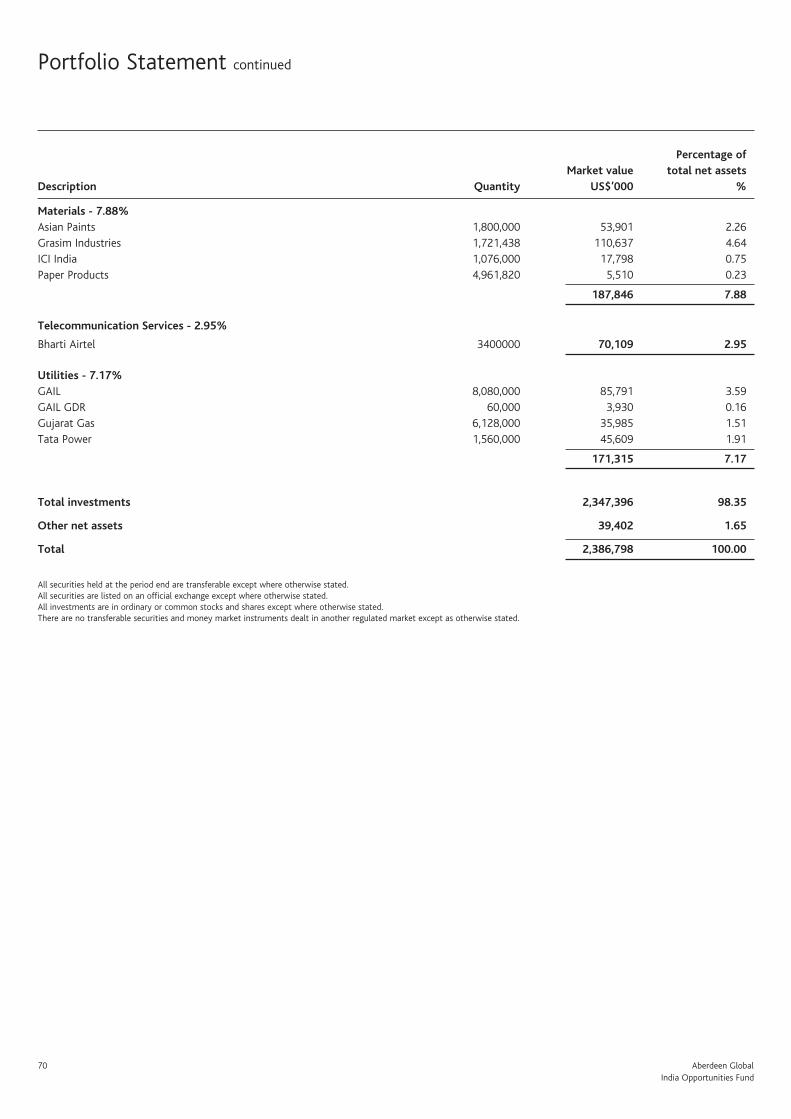

India Opportunities Fund ....................................................................................................................................................................................................................................................67

Japan Smaller Companies Fund ........................................................................................................................................................................................................................................71

Japanese Equity Fund ...........................................................................................................................................................................................................................................................75

Responsible World Equity Fund ........................................................................................................................................................................................................................................79

Sterling Corporate Bond Fund ...........................................................................................................................................................................................................................................84

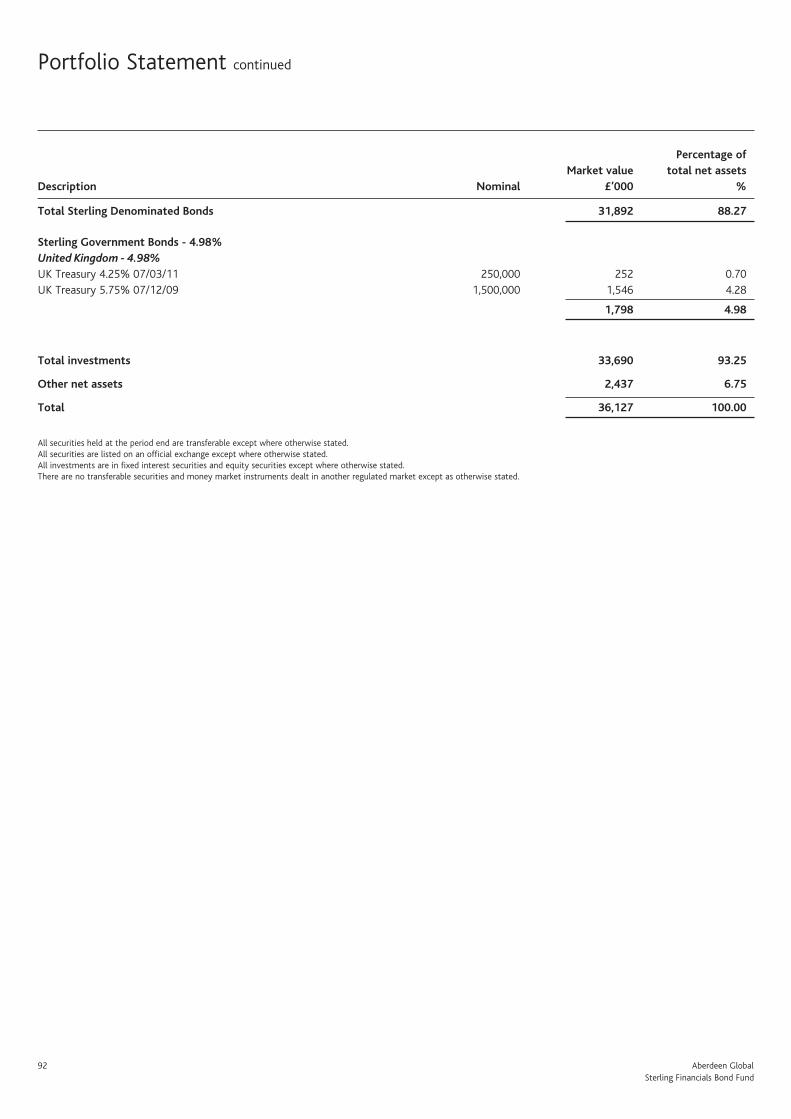

Sterling Financials Bond Fund ...........................................................................................................................................................................................................................................89

Technology Fund ....................................................................................................................................................................................................................................................................93

UK Opportunities Fund ........................................................................................................................................................................................................................................................97

World Bond Fund ................................................................................................................................................................................................................................................................ 102

World Equity Fund .............................................................................................................................................................................................................................................................. 105

Notes to the Financial Statements .............................................................................................................................................................................................................................. 110

Management and Administration ................................................................................................................................................................................................................................ 117

General Information ........................................................................................................................................................................................................................................................... 119

Further Information ............................................................................................................................................................................................................................................................ 121

Aberdeen Global 1

Aberdeen Global (“the Company” or “the Fund”) was incorporated as a société anonyme, qualifying as a société d’investissement à capital variable on 25 February 1988 for an unlimited period and commenced operations on 26 April 1988. It is registered under number B27471 at the Register of Commerce at the District Court of Luxembourg.

As at 31 March 2008, the Company has issued shares in the following Funds:

American Opportunities

Asia Pacific

Asia Pacific and Australasian Bond

Asian Smaller Companies

Australasian Equity

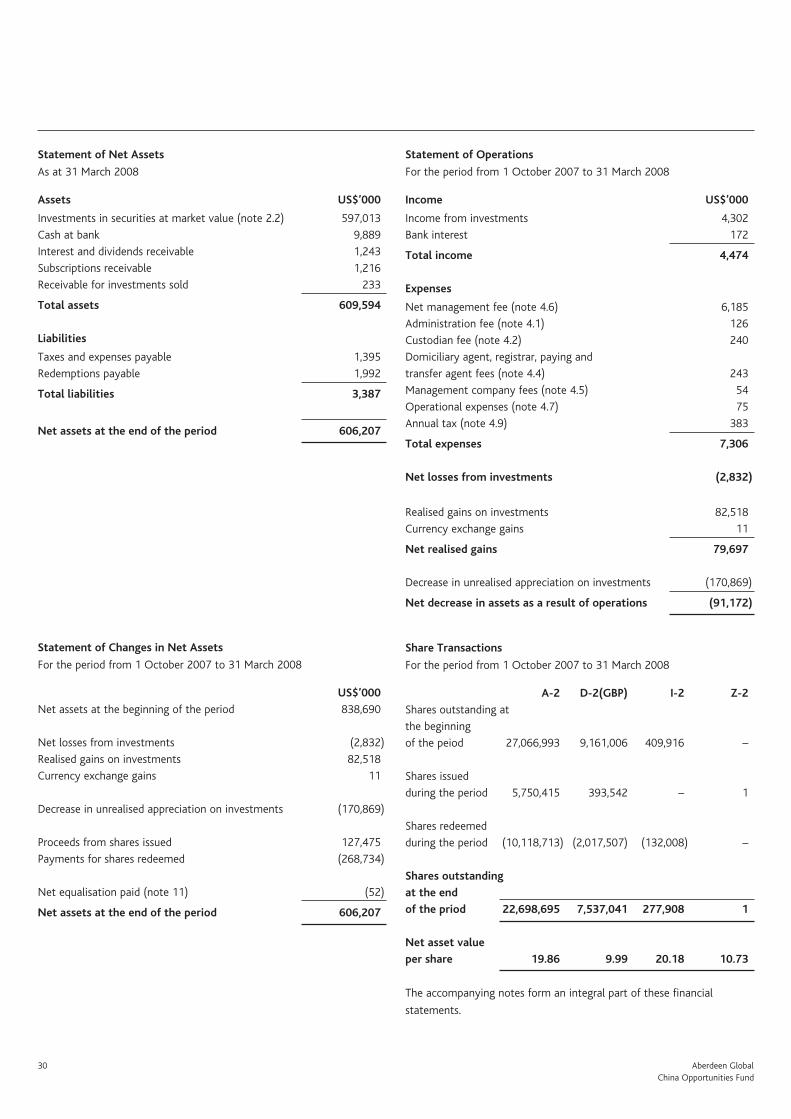

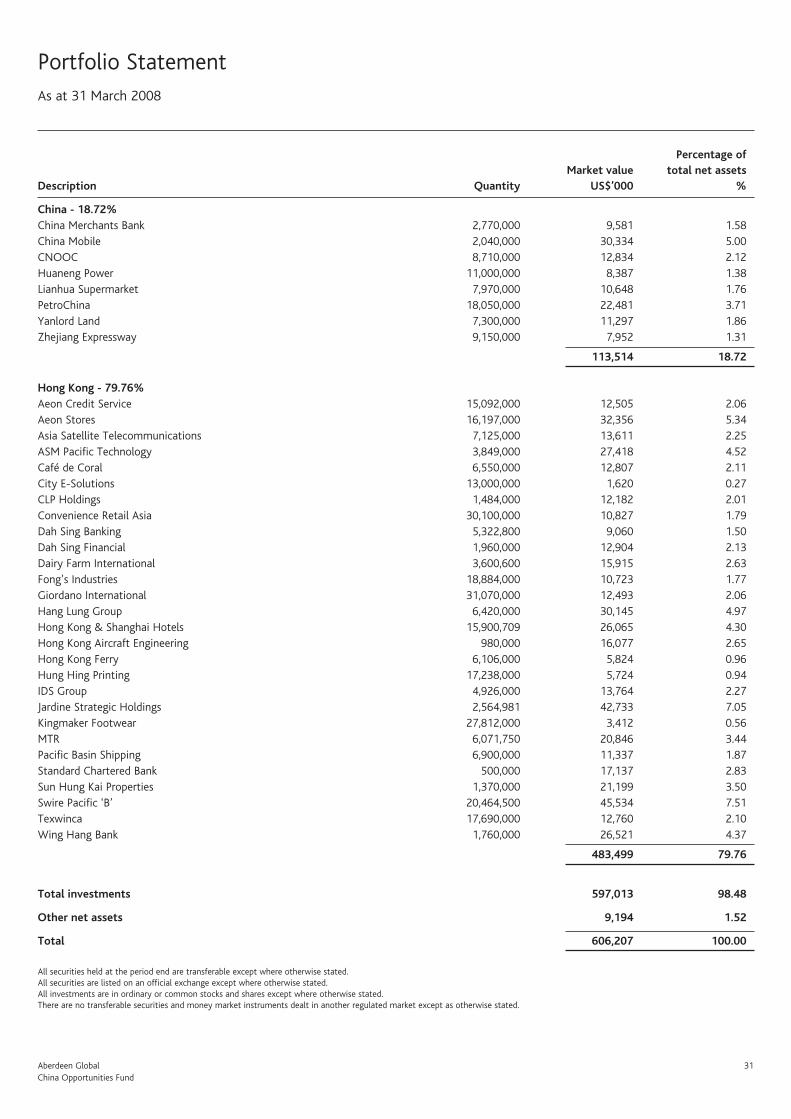

China Opportunities

Emerging Markets

Emerging Markets Bond

Emerging Markets Smaller Companies

European Equity

European High Yield Bond

European Opportunities (Ex UK)

High Yield Bond

India Opportunities

Japan Smaller Companies

Japanese Equity

Responsible World Equity

Sterling Corporate Bond

Sterling Financials Bond

Technology

UK Opportunities

World Bond

World Equity

The full name of each Fund is constituted by the name of the Company, Aberdeen Global, followed by a hyphen and then the specific name of the Fund. Throughout the Financial Statements, the Funds are referred to by their short names as indicated above.

No subscriptions can be received on the basis of this document. Subscriptions are only valid if made on the basis of the current prospectus.

Please see the Notes to the Financial Statements for changes during the year.

Incorporation

2 Aberdeen Global

Review of operationsAggregate funds under management for Aberdeen Global (“the Fund”) decreased from $15.4 billion to $12.6 billion during the period. This was mainly attributable to steep falls across stockmarkets, with the MSCI World index, for example, falling over 11% during the six months to end March 2008. The MSCI AC Asia Pacific ex Japan index fell further (by 14% over the same period) and, although the Aberdeen Global - Asia Pacific Fund significantly out-performed the index over the period, there was a knock-on impact to investor sentiment and to client asset allocation decisions, resulting in some net outflows to the Fund.

The Aberdeen Global - Responsible World Equity Fund was launched on 1 November 2007 and has since out-performed its peer group and secured some $64m in investment.

Investment reviewGlobal equity markets experienced increasing volatility in the six months under review, as the US sub-prime turmoil mutated into a full-blown financial crisis. After euphoria that saw markets, particularly in Asia and developing countries, rise to new highs last October, investor reaction turned to shock at the write-downs on Wall Street, as financial deleveraging intensified. This led to steep falls across stockmarkets, with high-fliers such as China and India the worst hit.

Initially, less developed markets had appeared immune to selling pressure because of their very limited exposure to credit derivatives. This, along with strong growth rates, fostered a belief that these emerging markets could “de-couple”. But global growth has been driven by closer economic integration, not less, particularly with the entry of China and India into the trading system.

While a slowdown among these newcomers has yet to materialise, exports have slowed in line with deteriorating US growth, which was apparent from the fourth quarter onwards. US consumer confidence slipped to a two-year low as falling house values and rising inflation squeezed consumption, affecting the job market in turn. In Europe, economic growth also started to decelerate, with a housing market downturn in the UK, Spain and Ireland while Germany alone appeared to make up for this weakness.

In comparison, Asian economies continued to expand at pace, helped by governments that have room to spend. The exception was Japan, where recovery stalled in the face of policy mistakes and flat incomes. Among emerging markets, GDP growth remained relatively healthy, buoyed by record prices for minerals, oil and soft commodities, led by demand from China. However, some of these countries are net importers of commodities, and they faced rising cost-push inflation.

Indeed, the conflicting winds of growth and inflation have made policymaking more difficult everywhere. The Federal Reserve’s first concern was to shore up liquidity in the financial system, as banks withdrew credit. It also cut interest rates aggressively. But like the Bank of England, it now faces rising prices that limit the scope for further stimulus - even as the slowdown bites. In both countries there is a debate over the legitimacy of bailing out firms such as the UK’s Northern Rock and Bear Sterns in America.

In Europe, the European Central Bank (ECB) maintained its hawkish stance and refused to budge from its policy rate. In Asia, responses varied. Many chose to keep the status quo, countering inflation by allowing their currencies to appreciate. This might be the correct response in that rising prices, food especially, are caused by supply side shocks rather than increases in demand but widespread use of subsidies

distorts the market. Should inflation become embedded, wage demands may follow.

Looking ahead, equity markets are likely to remain sensitive to the unravelling of the sub-prime issue in the near term. While the worst may soon be over in terms of provisioning for the banking sector, the effects on the global economy are only now being felt. The US is facing rising unemployment, mortgage foreclosures and slower consumer spending. This could have a significant impact on the world economy in the next quarter or two.

Meanwhile, financial markets are anything but settled. Bond market yields are at present anticipating rising inflation, suggesting that the pace of easing may decelerate, although we believe that rates in the US may continue to decline over the next 12 months. Further out, slower growth will cool demand. This makes today’s record high commodity prices less sustainable. As for equities, earnings growth forecasts are being revised down. Recent poor figures from General Electric, a popular proxy for the health of the US economy, took investors by surprise. Even with recent falls in equity markets, volatility is likely to persist as, on the one hand, hopes are raised that the worst is priced in, and, on the other, bad news continues to keep mainstream investors sidelined. Record withdrawals from mutual funds through the first quarter of the year say much about investors’ state of mind.

The recent sell-off across markets does however restore some order. Stock markets had appreciated strongly over the past five or so years and, in emerging markets, liquidity was a strong factor in demand. The current environment should see more focus on company fundamentals, which should suit the way our funds are managed. There is a natural defensiveness to portfolios, with a focus on company balance sheets, cashflow and operational gearing. We are hopeful that this will sustain relative outperformance across most funds in the first quarter, even if the immediate outlook remains choppy.

Fund developmentsAberdeen Global - Responsible World Equity Fund was launched on 1 November 2007 and has attracted some US$64 million of assets under management. The Fund will consider the environmental, social and governance policies of investee companies. Aberdeen has been providing Socially Responsible Investment management since the early ninties. On the other hand, Aberdeen Global - Asia Pacific and Japan Fund was closed on 26 October 2007 following a re-allocation of assets by the majority shareholder.

The range of sub-funds now offered by the Fund is 23, with 78 share classes available. Authorisations for distributions for many funds are either secured or actively being sought, from 24 territories worldwide.

Finally, it is pleasing to note that we have received a number of awards for our funds, even in light of turbulent market conditions. Aberdeen Global - European High Yield Bond Fund, has won Best Europe High Yield Bond Fund from Lipper over three and five years and also received an A rating by Standard and Poors. Aberdeen Global - World Equity Fund, received the Best Global Large-Cap Equity Fund Award 2008 from Morningstar and an A rating from Standard and Poors and Aberdeen Global - Emerging Markets Fund received a AA rating from Standard and Poors.

C G LittleChairman 20 May 2008

Chairman’s Statement

Aberdeen Global 3

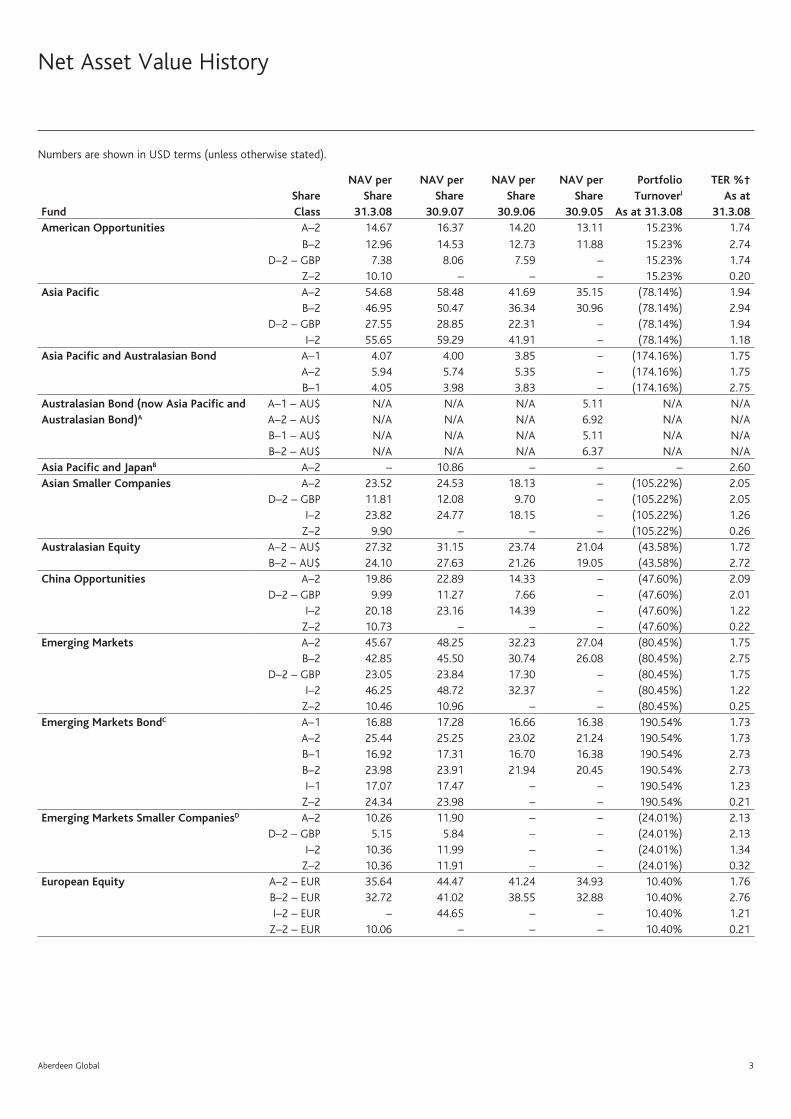

Net Asset Value History

Numbers are shown in USD terms (unless otherwise stated).

FundShare Class

NAV per Share

31.3.08

NAV per Share

30.9.07

NAV per Share

30.9.06

NAV per Share

30.9.05

Portfolio TurnoverI

As at 31.3.08

TER %† As at

31.3.08 American Opportunities A–2 14.67 16.37 14.20 13.11 15.23% 1.74

B–2 12.96 14.53 12.73 11.88 15.23% 2.74D–2 – GBP 7.38 8.06 7.59 – 15.23% 1.74

Z–2 10.10 – – – 15.23% 0.20Asia Pacific A–2 54.68 58.48 41.69 35.15 (78.14%) 1.94

B–2 46.95 50.47 36.34 30.96 (78.14%) 2.94D–2 – GBP 27.55 28.85 22.31 – (78.14%) 1.94

I–2 55.65 59.29 41.91 – (78.14%) 1.18Asia Pacific and Australasian Bond A–1 4.07 4.00 3.85 – (174.16%) 1.75

A–2 5.94 5.74 5.35 – (174.16%) 1.75B–1 4.05 3.98 3.83 – (174.16%) 2.75

Australasian Bond (now Asia Pacific and Australasian Bond)A

A–1 – AU$ N/A N/A N/A 5.11 N/A N/AA–2 – AU$ N/A N/A N/A 6.92 N/A N/AB–1 – AU$ N/A N/A N/A 5.11 N/A N/AB–2 – AU$ N/A N/A N/A 6.37 N/A N/A

Asia Pacific and JapanB A–2 – 10.86 – – – 2.60Asian Smaller Companies A–2 23.52 24.53 18.13 – (105.22%) 2.05

D–2 – GBP 11.81 12.08 9.70 – (105.22%) 2.05I–2 23.82 24.77 18.15 – (105.22%) 1.26

Z–2 9.90 – – – (105.22%) 0.26Australasian Equity A–2 – AU$ 27.32 31.15 23.74 21.04 (43.58%) 1.72

B–2 – AU$ 24.10 27.63 21.26 19.05 (43.58%) 2.72China Opportunities A–2 19.86 22.89 14.33 – (47.60%) 2.09

D–2 – GBP 9.99 11.27 7.66 – (47.60%) 2.01I–2 20.18 23.16 14.39 – (47.60%) 1.22

Z–2 10.73 – – – (47.60%) 0.22Emerging Markets A–2 45.67 48.25 32.23 27.04 (80.45%) 1.75

B–2 42.85 45.50 30.74 26.08 (80.45%) 2.75D–2 – GBP 23.05 23.84 17.30 – (80.45%) 1.75

I–2 46.25 48.72 32.37 – (80.45%) 1.22Z–2 10.46 10.96 – – (80.45%) 0.25

Emerging Markets BondC A–1 16.88 17.28 16.66 16.38 190.54% 1.73A–2 25.44 25.25 23.02 21.24 190.54% 1.73B–1 16.92 17.31 16.70 16.38 190.54% 2.73B–2 23.98 23.91 21.94 20.45 190.54% 2.73I–1 17.07 17.47 – – 190.54% 1.23

Z–2 24.34 23.98 – – 190.54% 0.21Emerging Markets Smaller CompaniesD A–2 10.26 11.90 – – (24.01%) 2.13

D–2 – GBP 5.15 5.84 – – (24.01%) 2.13I–2 10.36 11.99 – – (24.01%) 1.34

Z–2 10.36 11.91 – – (24.01%) 0.32European Equity A–2 – EUR 35.64 44.47 41.24 34.93 10.40% 1.76

B–2 – EUR 32.72 41.02 38.55 32.88 10.40% 2.76I–2 – EUR – 44.65 – – 10.40% 1.21

Z–2 – EUR 10.06 – – – 10.40% 0.21

4 Aberdeen Global

FundShare Class

NAV per Share

31.3.08

NAV per Share

30.9.07

NAV per Share

30.9.06

NAV per Share

30.9.05

Portfolio TurnoverI

As at 31.3.08

TER %† As at

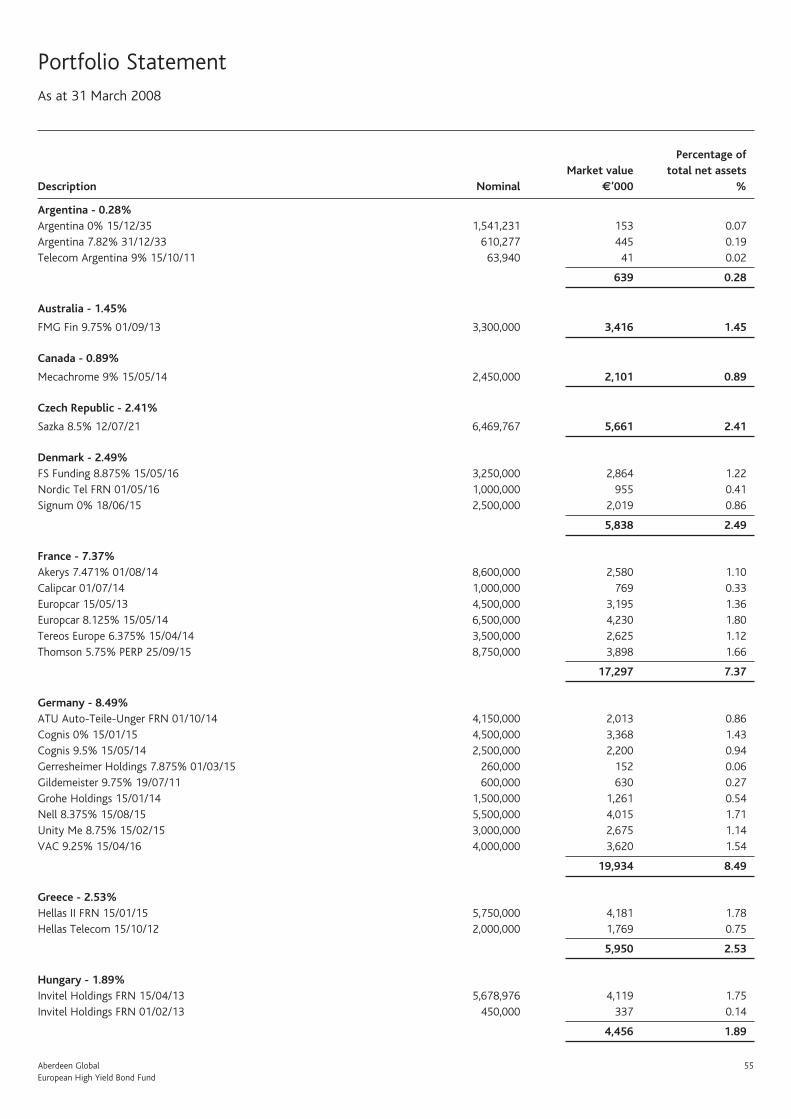

31.3.08 European High Yield Bond A–1 – EUR 6.75 8.73 8.85 8.83 (122.05%) 1.46

A–2 – EUR 11.37 14.05 13.46 12.58 (122.05%) 1.46A–2H – USD 8.11 – – – (122.05%) 1.46

B–1 – EUR 6.73 8.69 8.85 8.83 (122.05%) 2.46B–2 – EUR 10.52 13.10 12.69 11.97 (122.05%) 2.46

D–1 – GBP 5.40 6.07 – – (122.05%) 1.46I–2 – EUR 7.92 – – – (122.05%) 0.92

Z–2 – EUR 11.44 – – – (122.05%) 0.17European Opportunities (Ex UK) A–2 – EUR 9.22 11.07 10.44 – 29.82% 1.70

D–2 – GBP 7.32 7.74 7.07 – 29.82% 1.70Fixed Interest OpportunitiesE D–1 – GBP – – 1.05 – – –High Yield Bond D–1 – GBP 0.9940 1.0944 1.08 – 20.23% 1.48India Opportunities A–2 76.19 82.96 57.09 – (72.85%) 2.16

D–2 – GBP 38.36 40.85 30.55 – (72.85%) 2.16I–2 77.38 83.85 57.37 – (72.85%) 1.37

Z–2 8.49 – – – (72.85%) 0.37Japan Smaller CompaniesF A–2 – JPY 595 772 – – 13.09% 1.74

D–2 – GBP 3.00 3.30 – – 13.09% 1.74I–2 – JPY 546 773 – – 13.09% 1.20

Japanese Equity A–2 – JPY 270 365 391 349 40.71% 1.71B–2 – JPY 233 315 340 307 40.71% 2.71

D–2 – GBP 1.37 1.56 – – 40.71% 1.71Sterling Corporate Bond D–1 – GBP 0.9805 1.0069 1.05 – 50.07% 1.46Sterling Financials Bond A–2 – GBP 1.7334 1.6925 1.64 – 59.25% 0.97Responsible World EquityG A–2 9.23 – – – 3.86% 1.79

I–2 9.08 – – – 3.86% 1.25Z–2 9.08 – – – 3.86% 0.25

Technology A–2 2.79 3.35 2.70 2.40 (29.48%) 2.14B–2 2.57 3.10 2.53 2.28 (29.48%) 3.14

D–2 – GBP 1.40 1.65 1.44 – (29.48%) 2.14UK Opportunities A–2 – GBP 13.86 16.13 14.76 12.55 (9.50%) 1.66

B–2 – GBP 12.18 14.24 13.16 11.31 (9.50%) 2.66D–1 – GBP 13.47 15.79 14.70 – (9.50%) 1.66

World Bond D–1 – GBP 1.2811 1.1405 1.20 – 106.59% 1.12World Equity A–2 14.17 15.11 12.56 10.68 (33.26%) 1.71

B–2 13.08 14.01 11.77 10.10 (33.26%) 2.71D–2 – GBP 7.13 7.44 6.72 – (33.26%) 1.71

I–2 9.28 – – – (33.26%) 1.17Z–2 14.35 15.18 – – (33.26%) 0.17

Net Asset Value History continued

† Source: Aberdeen Asset Management.A The Fund changed its base currency from Australian Dollars to US Dollars from 1 March 2006.B New Fund launched 17 April 2007 and then subsequently closed on 26 October 2007.C The Fund changed its name from Sovereign High Yield Bond from 30 March 2007.D New Fund launched 26 March 2007.E The Fund liquidated on 10 July 2007.F New Fund launched 20 April 2007.G New Fund launched 1 November 2007.H Hedged share classI (Purchase of securities and sales of securities) - (Subscription of units and Redemptions of units)

= Portfolio Turnover(Average fund value over 12 months) x100

Exchange Rates 31.3.08 30.9.07 30.9.06 30.9.05£ - US$ 1.988750 2.031300 1.870000 1.765537US$ - AUD 1.093627 1.134003 1.340856 1.313700£ - € 1.257450 1.431800 1.475950 1.464866€ - US$ 1.581570 1.418704 1.266977 1.205255US$ - JPY 99.590190 115.207010 117.951872 113.4345

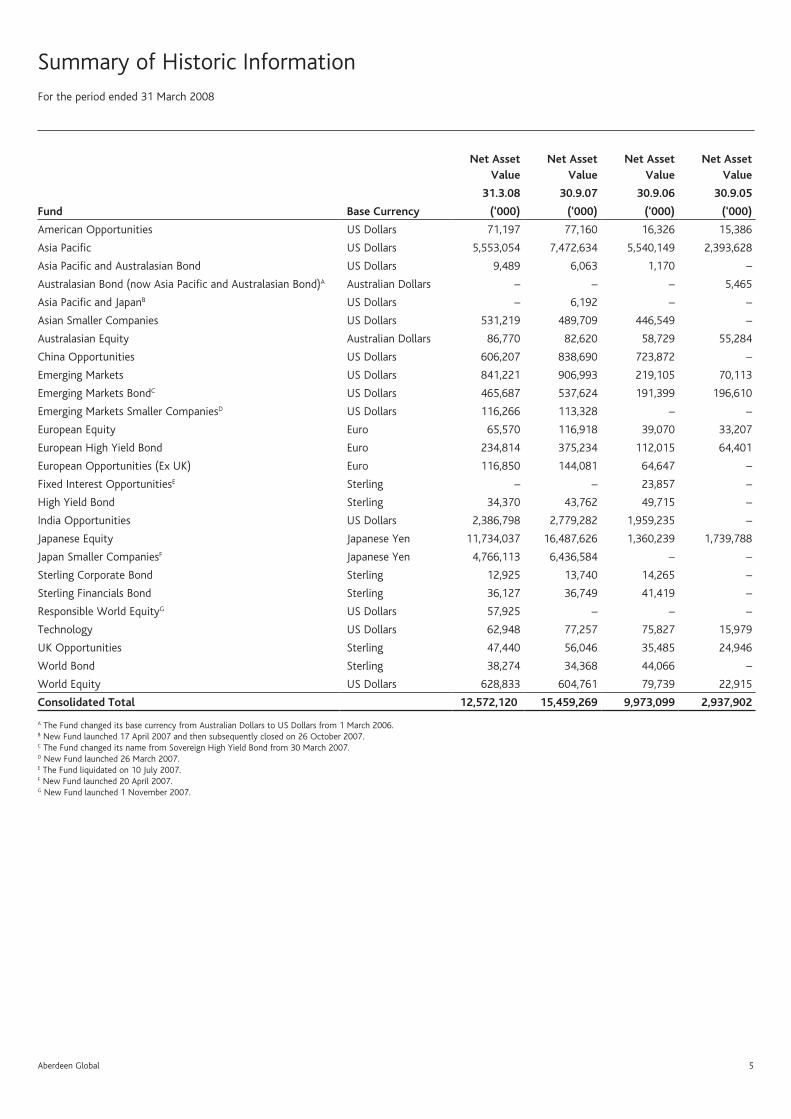

Aberdeen Global 5

Net Asset Value

Net Asset Value

Net Asset Value

Net Asset Value

31.3.08 30.9.07 30.9.06 30.9.05

Fund Base Currency (‘000) (‘000) (‘000) (‘000)

American Opportunities US Dollars 71,197 77,160 16,326 15,386

Asia Pacific US Dollars 5,553,054 7,472,634 5,540,149 2,393,628

Asia Pacific and Australasian Bond US Dollars 9,489 6,063 1,170 –

Australasian Bond (now Asia Pacific and Australasian Bond)A Australian Dollars – – – 5,465

Asia Pacific and JapanB US Dollars – 6,192 – –

Asian Smaller Companies US Dollars 531,219 489,709 446,549 –

Australasian Equity Australian Dollars 86,770 82,620 58,729 55,284

China Opportunities US Dollars 606,207 838,690 723,872 –

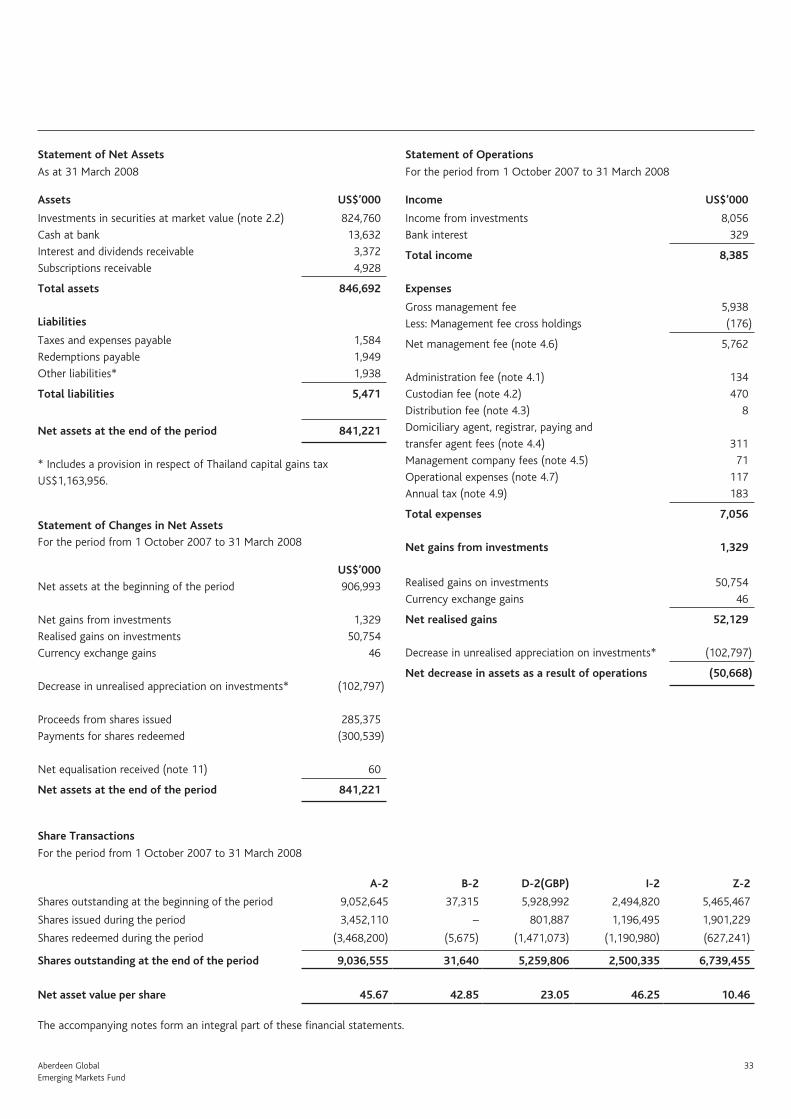

Emerging Markets US Dollars 841,221 906,993 219,105 70,113

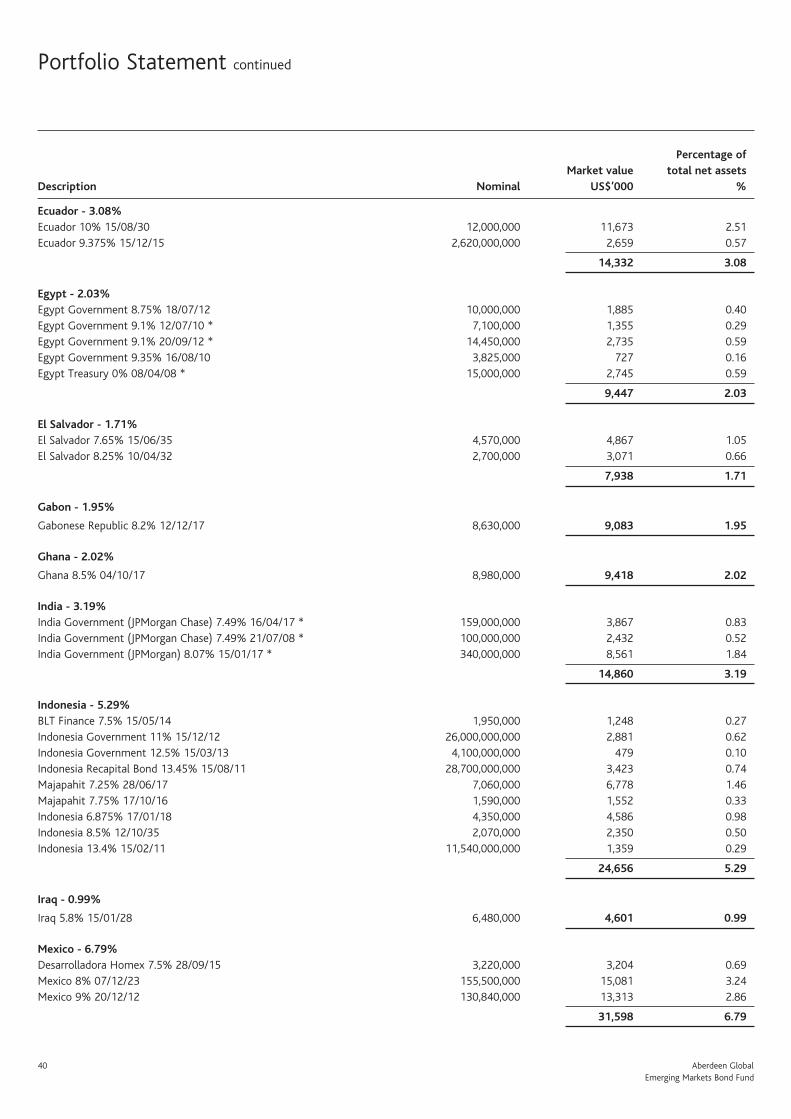

Emerging Markets BondC US Dollars 465,687 537,624 191,399 196,610

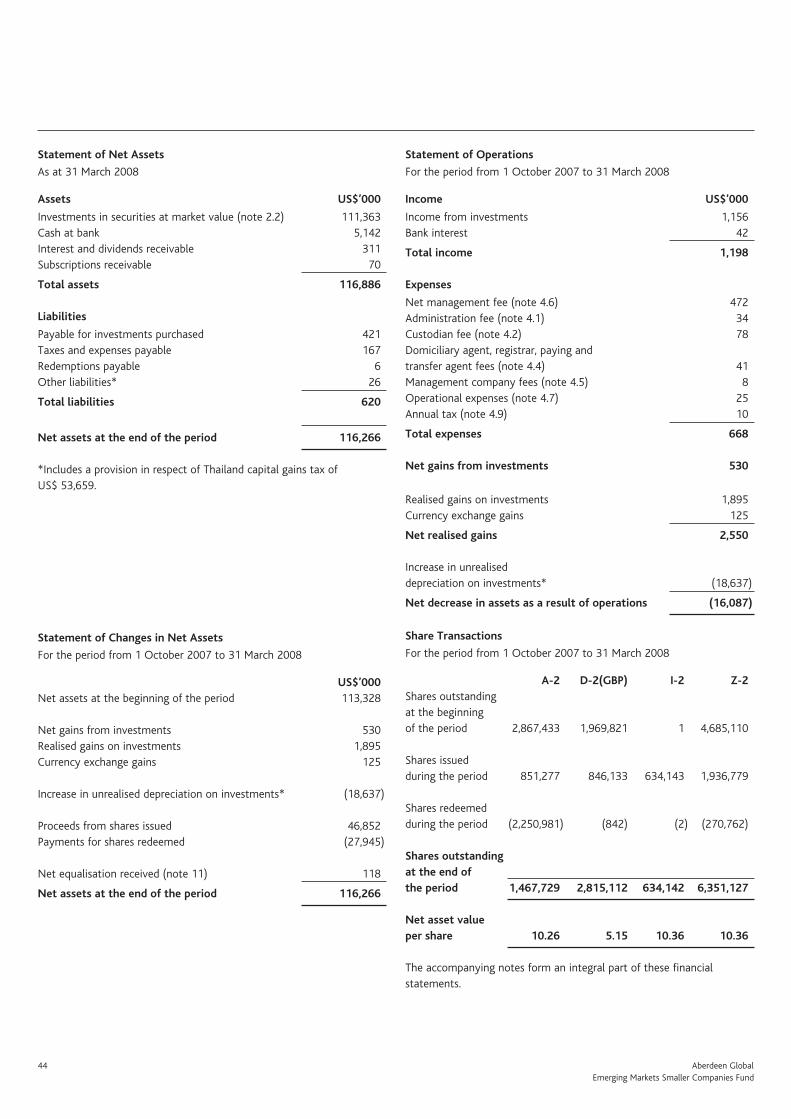

Emerging Markets Smaller CompaniesD US Dollars 116,266 113,328 – –

European Equity Euro 65,570 116,918 39,070 33,207

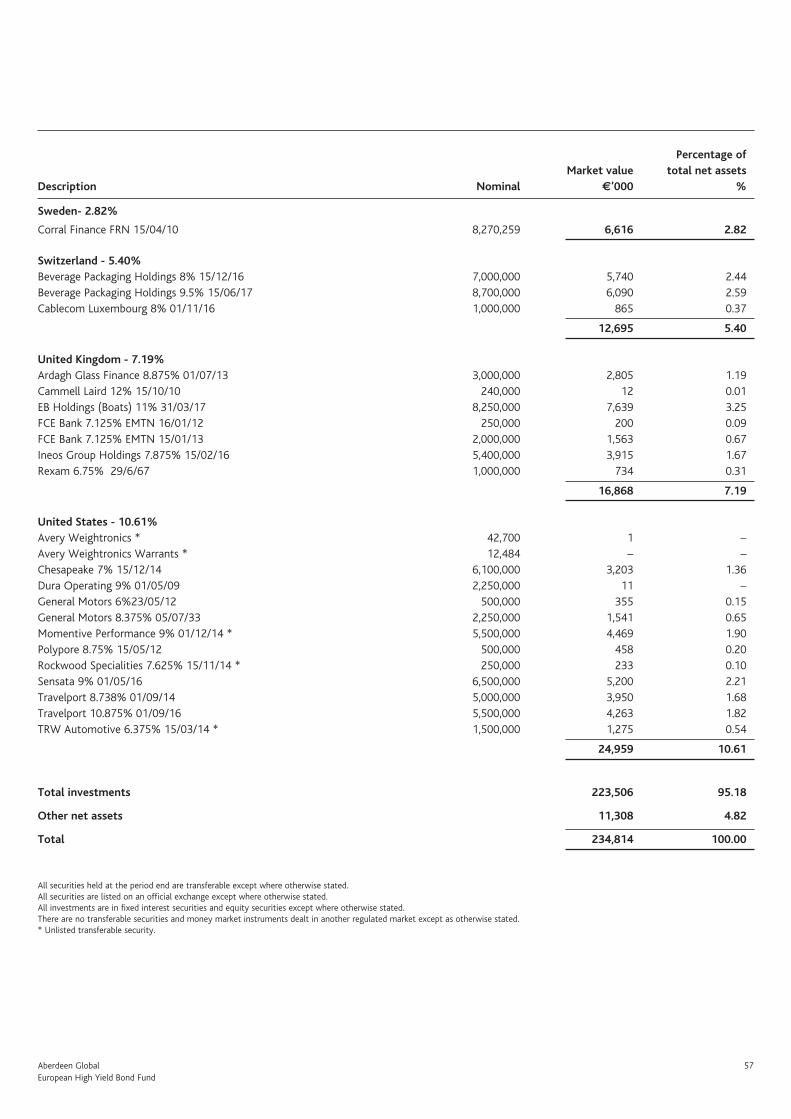

European High Yield Bond Euro 234,814 375,234 112,015 64,401

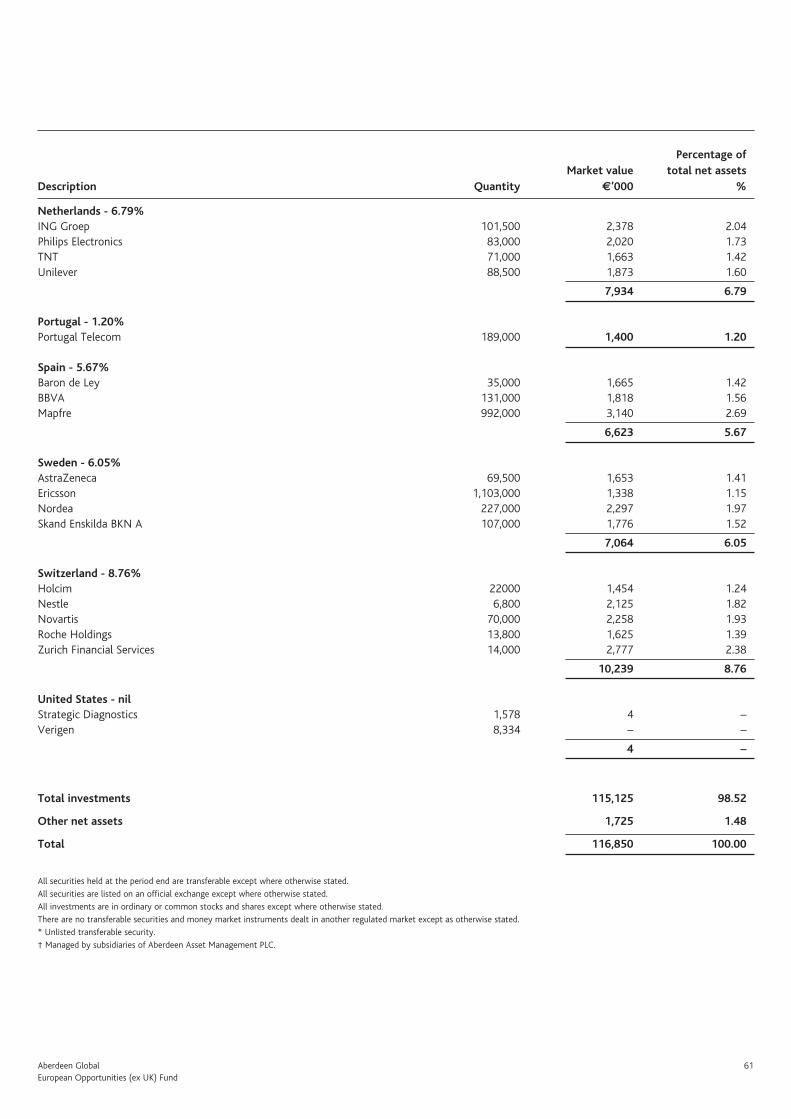

European Opportunities (Ex UK) Euro 116,850 144,081 64,647 –

Fixed Interest OpportunitiesE Sterling – – 23,857 –

High Yield Bond Sterling 34,370 43,762 49,715 –

India Opportunities US Dollars 2,386,798 2,779,282 1,959,235 –

Japanese Equity Japanese Yen 11,734,037 16,487,626 1,360,239 1,739,788

Japan Smaller CompaniesF Japanese Yen 4,766,113 6,436,584 – –

Sterling Corporate Bond Sterling 12,925 13,740 14,265 –

Sterling Financials Bond Sterling 36,127 36,749 41,419 –

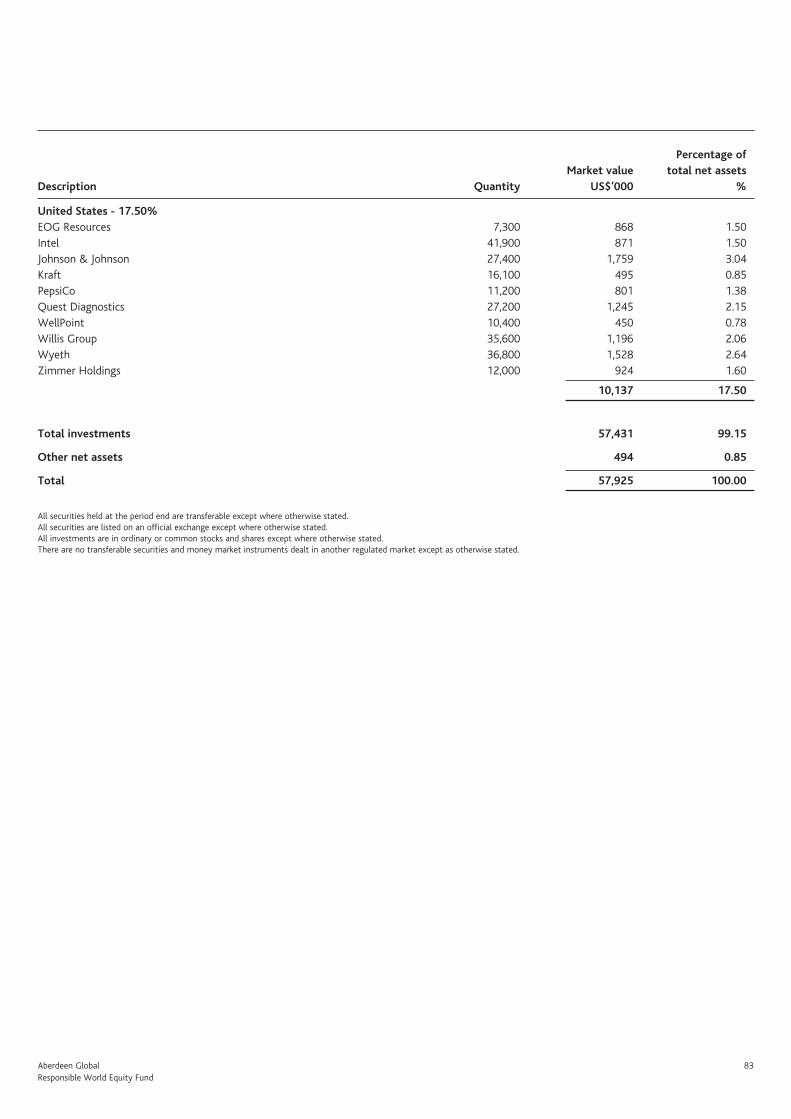

Responsible World EquityG US Dollars 57,925 – – –

Technology US Dollars 62,948 77,257 75,827 15,979

UK Opportunities Sterling 47,440 56,046 35,485 24,946

World Bond Sterling 38,274 34,368 44,066 –

World Equity US Dollars 628,833 604,761 79,739 22,915

Consolidated Total 12,572,120 15,459,269 9,973,099 2,937,902 A The Fund changed its base currency from Australian Dollars to US Dollars from 1 March 2006.B New Fund launched 17 April 2007 and then subsequently closed on 26 October 2007.C The Fund changed its name from Sovereign High Yield Bond from 30 March 2007.D New Fund launched 26 March 2007.E The Fund liquidated on 10 July 2007.F New Fund launched 20 April 2007.G New Fund launched 1 November 2007.

Summary of Historic InformationFor the period ended 31 March 2008

6 Aberdeen Global

Combined Statement of Net Assets

As at 31 March 2008

Assets US$’000

Investments in securities at market value (note 2.2) 12,316,062

Cash at bank 287,973

Interest and dividends receivable 60,273

Subscriptions receivable 46,458

Receivable for investments sold 9,975

Unrealised gain on forward foreign exchange contracts (note 9) 714

Other assets 407

Total assets 12,721,862

Liabilities

Payable for investments purchased 34,049

Taxes and expenses payable 27,245

Redemptions payable 50,671

Unrealised loss on forward foreign exchange contracts (note 9) 3,670

Other liabilities 34,107

Total liabilities 149,742

Net assets at the end of the period 12,572,120

Combined Statement of Changes in Net Assets

For the period from 1 October 2007 to 31 March 2008

US$’000

Net assets at the beginning of the period 15,459,269

Exchange rate effect on opening net assets 129,659

Net gains from investments 22,579

Realised gains on investments 1,220,319

Currency exchange losses (12,379)

Decrease in unrealised appreciation

on investments (2,310,967)

Decrease in unrealised depreciation

on open forward currency positions 510

Proceeds from shares issued 4,438,468

Payments for shares redeemed (6,364,285)

Net equalisation paid (note 11) (576)

Dividends paid (note 5) (10,477)

Net assets at the end of the period 12,572,120

Combined Statement of Operations

For the period from 1 October 2007 to 31 March 2008

Income US$’000

Income from investments 149,692

Bank interest received 3,427

Total income 153,119

Expenses

Gross management fee 112,414

Less: Management fee cross holdings (2,346)

Net management fee (note 4.6) 110,068

Administration fee (note 4.1) 1,811

Custodian fee (note 4.2) 7,227

Distribution fee (note 4.3) 370

Domiciliary agent, registrar, paying and

transfer agent fees (note 4.4) 4,743

Management company fees (note 4.5) 1,088

Operational expenses (note 4.7) 1,678

Expense cap to be refunded by management company (note 4.8) (9)

Mauritius income tax (note 12) 223

Annual tax (note 4.9) 3,311

Bank interest paid 30

Total expenses 130,540

Net gains from investments 22,579

Realised gains on investments 1,220,319

Currency exchange losses (12,379)

Net realised gains 1,230,519

Decrease in unrealised

appreciation on investments (2,310,967)

Decrease in unrealised depreciation

on open forward currency positions 510

Net decrease in assets as a result of operations (1,079,938)

The accompanying notes form an integral part of these financial

statements.

Aberdeen Global - Combined Statements

Aberdeen Global 7American Opportunities Fund

American Opportunities FundFor the period ended 31 March 2008

PerformanceFor the six-month period ended 31 March 2008, the value of the Aberdeen Global - American Opportunities Fund - A Accumulation shares decreased by 10.4% compared to a decrease of 12.5% in the benchmark, the S&P 500 Index.

Manager’s reviewThe six months under review saw the return of volatility to domestic equity markets. Although US equities performed strongly in early October, that positive momentum was short lived as declining house prices and poor underwriting standards exposed the weakness in complex credit derivatives. The write-downs of investment banks were exacerbated across Wall Street as well, totalling US$150bn to date. Financial de-leveraging intensified, culminating in the Bear Stearns debacle as concerns over the investment bank’s liquidity turned to contagion, which led to the Federal Reserve’s intervention and its takeover by JPMorgan Chase.

Despite US equities having posted negative returns, the consumer staples, energy and materials sectors gained on strong global demand. In addition, investors used commodities to hedge against inflation and the weak dollar, with the latter supporting exports. Conversely, financials underperformed.

During this period, the Fed provided unorthodox support to the financial markets, cutting interest rates five times by 2.5% to 2.25%, amid concerns that the mortgage-backed meltdown would slow growth. Additionally, the Fed and other central banks injected liquidity into the markets to control inflation.

Data on the economic front increased the likelihood of an economic recession, which added to anxiety in fragile markets. Fourth-quarter economic growth was weaker than expected: the unemployment rate rose to a two-year high while the manufacturing sector grew at its slowest pace in 10 months. Additionally, consumer confidence fell to a two-year low. Meanwhile, falling house values and rising petrol prices continue to weigh on economic growth, while inflation and a weak dollar affected spending.

Portfolio reviewDuring the period under review, the Fund fell by 10.4%, outperforming the S&P 500 by 2.1%.

In portfolio activity, we trimmed our exposure to energy and industrials where they showed early signs of weakening fundamentals and rich valuations. We added to our under-represented consumer related names, which had significantly discounted weaker consumer activity. In the same vein, we also initiated a position in homebuilder Toll Brothers and airline US Airways. Against this, we sold Trane after Ingersoll Rand made a bid for the maker of heating and air-cooling systems.

OutlookDomestic equities still face near-term risks. Despite improved liquidity in the market, volatility is likely to continue in the coming months. Though the potential for unwelcome surprises in the credit markets has lessened, further write-downs may yet be announced as banks continue to de-leverage. Attention has meanwhile shifted to the knock-on effects in the broad economy. Tight credit conditions will restrict spending growth, compounding weak consumer sentiment. While the market appears to be looking past much of this, it is much too early to speak of a market bottom, let alone a recovery. As such, we remain cautious on our outlook, and will look to top up our favoured holdings only when valuations become more attractive.

8 Aberdeen Global American Opportunities Fund

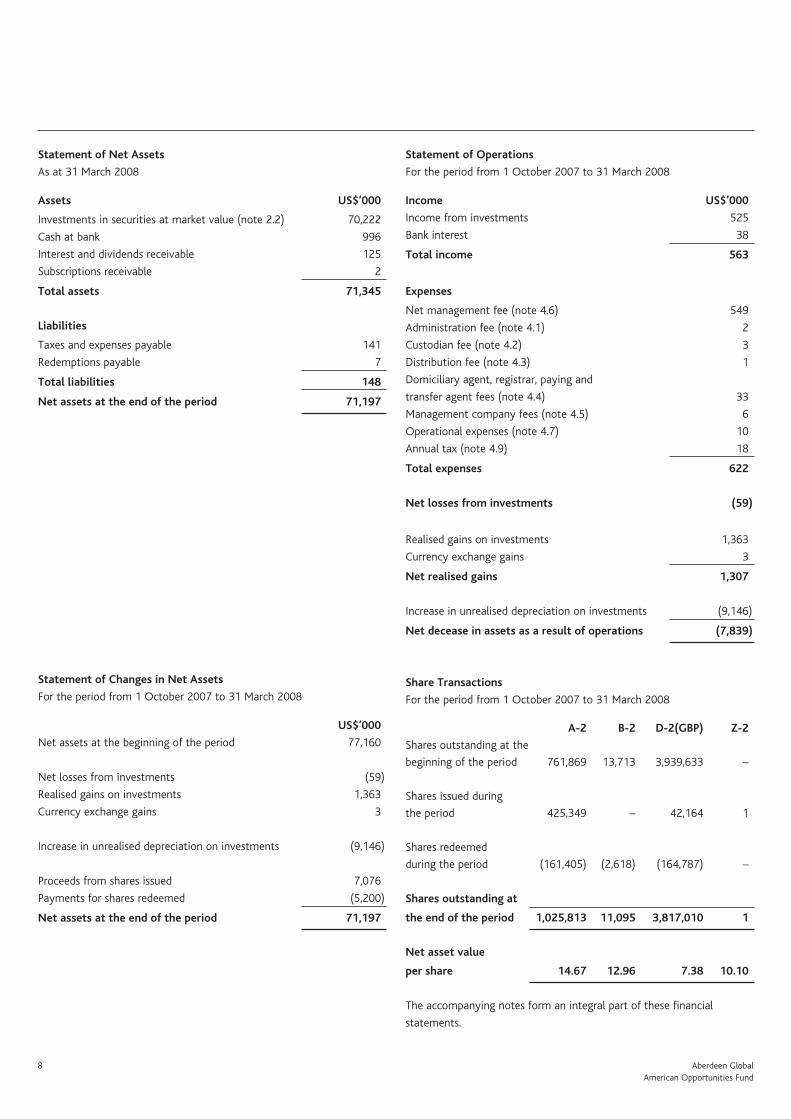

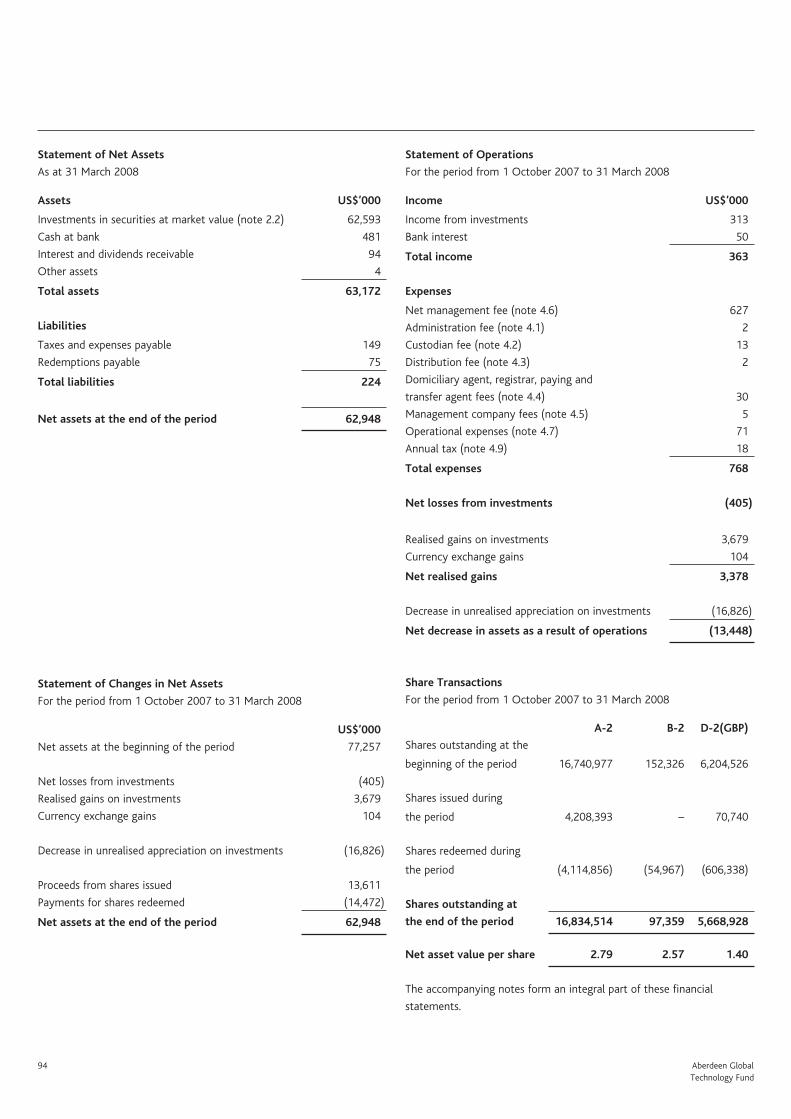

Statement of Net Assets

As at 31 March 2008

Assets US$’000

Investments in securities at market value (note 2.2) 70,222

Cash at bank 996

Interest and dividends receivable 125

Subscriptions receivable 2

Total assets 71,345

Liabilities

Taxes and expenses payable 141

Redemptions payable 7

Total liabilities 148

Net assets at the end of the period 71,197

Statement of Changes in Net Assets

For the period from 1 October 2007 to 31 March 2008

US$’000

Net assets at the beginning of the period 77,160

Net losses from investments (59)

Realised gains on investments 1,363

Currency exchange gains 3

Increase in unrealised depreciation on investments (9,146)

Proceeds from shares issued 7,076

Payments for shares redeemed (5,200)

Net assets at the end of the period 71,197

Statement of Operations

For the period from 1 October 2007 to 31 March 2008

Income US$’000

Income from investments 525

Bank interest 38

Total income 563

Expenses

Net management fee (note 4.6) 549

Administration fee (note 4.1) 2

Custodian fee (note 4.2) 3

Distribution fee (note 4.3) 1

Domiciliary agent, registrar, paying and

transfer agent fees (note 4.4) 33

Management company fees (note 4.5) 6

Operational expenses (note 4.7) 10

Annual tax (note 4.9) 18

Total expenses 622

Net losses from investments (59)

Realised gains on investments 1,363

Currency exchange gains 3

Net realised gains 1,307

Increase in unrealised depreciation on investments (9,146)

Net decease in assets as a result of operations (7,839)

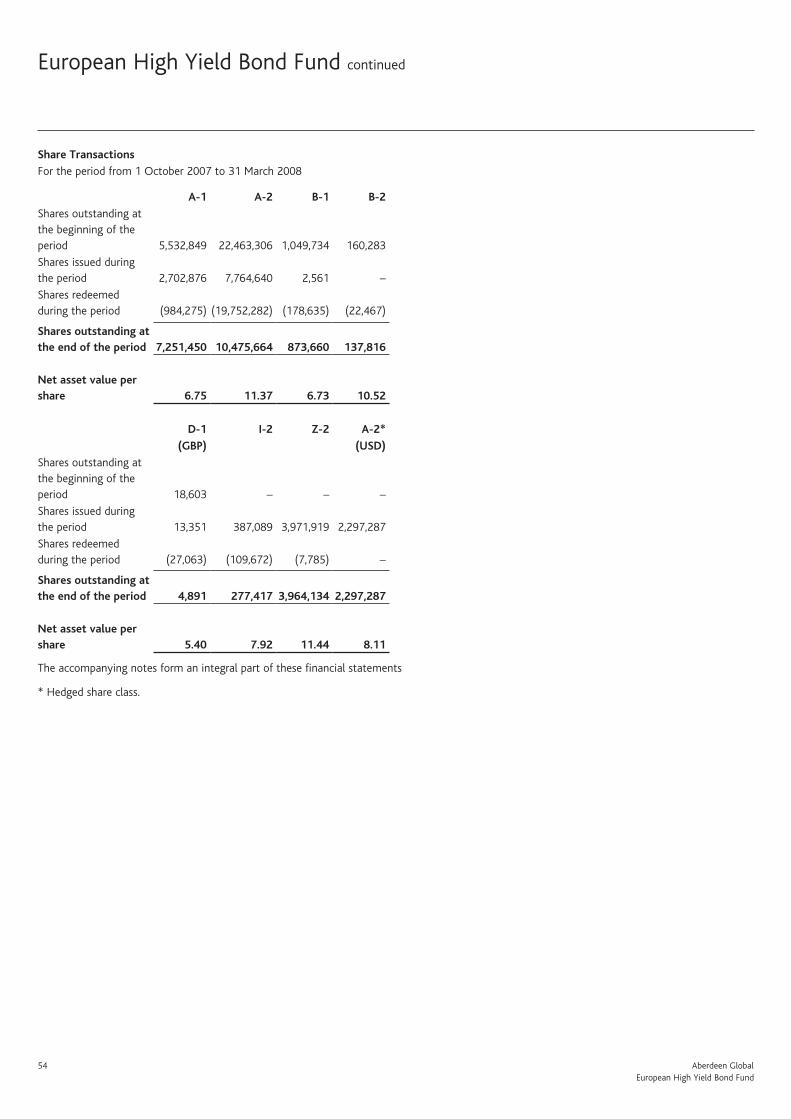

Share Transactions

For the period from 1 October 2007 to 31 March 2008

A-2 B-2 D-2(GBP) Z-2

Shares outstanding at the

beginning of the period 761,869 13,713 3,939,633 –

Shares issued during

the period 425,349 – 42,164 1

Shares redeemed

during the period (161,405) (2,618) (164,787) –

Shares outstanding at

the end of the period 1,025,813 11,095 3,817,010 1

Net asset value

per share 14.67 12.96 7.38 10.10

The accompanying notes form an integral part of these financial

statements.

Aberdeen Global 9American Opportunities Fund

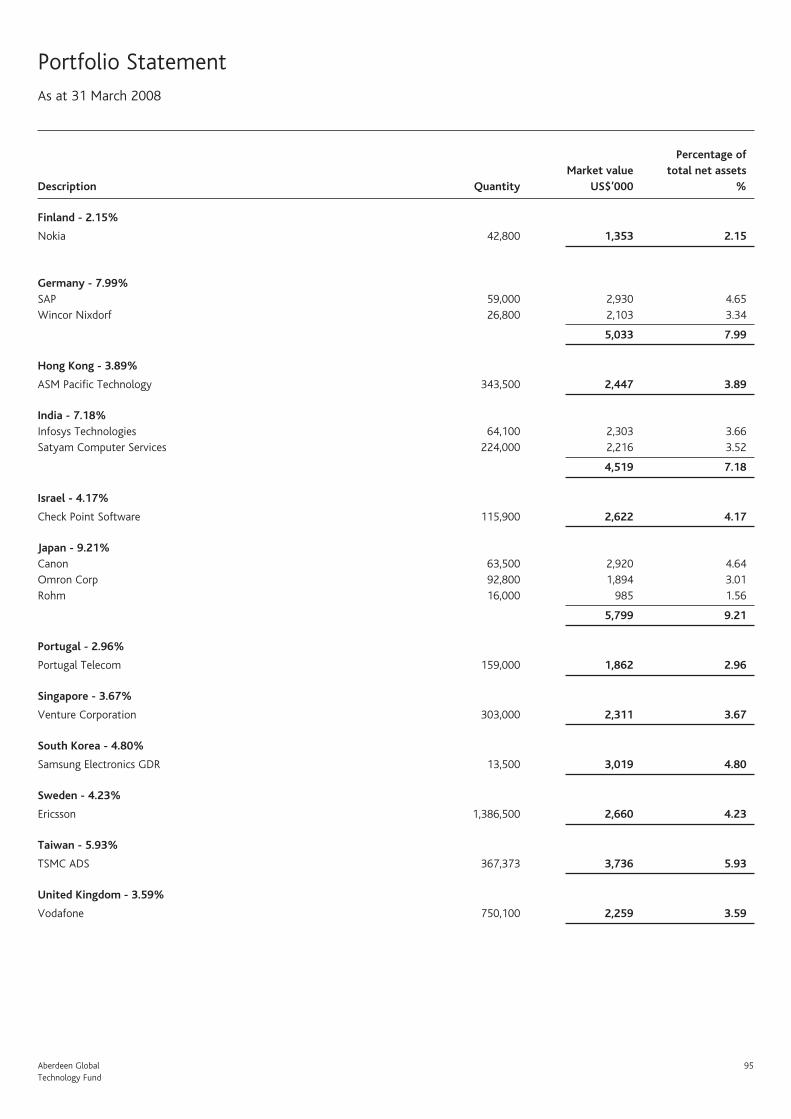

Portfolio StatementAs at 31 March 2008

Percentage of Market value total net assets Description Quantity US$’000 %

Consumer Discretionary - 11.72%BorgWarner 29,000 1,213 1.70Harley Davidson 29,900 1,134 1.59Macys 39,650 871 1.22Stanley Works 20,050 945 1.33Staples 45,300 1,015 1.43TJX Companies 32,411 1,059 1.49Toll Brothers 42,450 953 1.34VF Corp 15,200 1,152 1.62

8,342 11.72

Consumer Staples - 11.65%Altria 17,300 1,277 1.80Kraft 17,300 1,019 1.43PepsiCo 14,500 1,038 1.46Procter & Gamble 20,480 1,422 2.00Reynolds American 24,050 1,460 2.05Supervalu 32,800 952 1.34UST 20,200 1,119 1.57

8,287 11.65

Energy - 13.18%Apache 17,250 2,054 2.89Chevron 17,730 1,498 2.10Ensco 17,500 1,048 1.47EOG Resources 14,950 1,777 2.50Exxon Mobil 21,882 1,865 2.62Hess Corp 12,900 1,140 1.60

9,382 13.18

Financials - 15.86%Aflac 15,811 1,017 1.43Allstate 27,300 1,299 1.82Assurant 21,650 1,304 1.83Citigroup 34,750 724 1.02Goldman Sachs 6,050 995 1.40JPMorgan Chase 32,650 1,395 1.96Royal Bank of Canada 29,445 1,323 1.86Wells Fargo 46,550 1,366 1.92Willis Group 26,850 902 1.27Zions Bancorp 20,900 962 1.35

11,287 15.86

Health Care - 13.80%Aetna 27,100 1,153 1.62Johnson & Johnson 23,450 1,505 2.11Pfizer 48,500 994 1.40Quest Diagnostics 30,700 1,406 1.97St Jude Medical 18,600 806 1.13United Health Group 26,850 924 1.30WellPoint 17,070 738 1.04Wyeth 29,450 1,223 1.72Zimmer Holdings 13,991 1,077 1.51

9,826 13.80

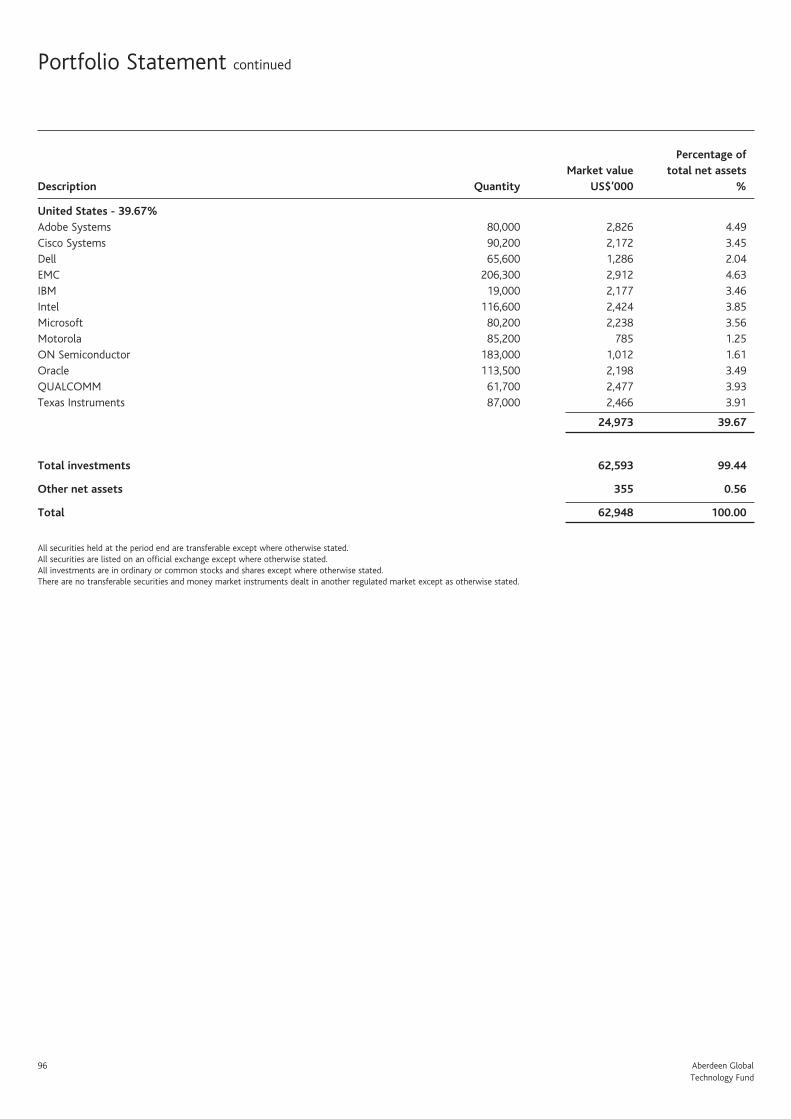

10 Aberdeen Global American Opportunities Fund

Industrials - 10.78%3M 16,489 1,285 1.80Canadian National Railway 27,550 1,347 1.89General Electric 35,057 1,283 1.80ITT Corp 22,700 1,173 1.65Textron Inc 19,100 1,043 1.46United Technologies 22,615 1,550 2.18

7,681 10.78

Information Technology - 11.41%Anixter 14,900 935 1.31Cisco Systems 61,300 1,476 2.07EMC 78,150 1,118 1.57Intel 52,850 1,099 1.54Microsoft 59,600 1,663 2.34Motorola 107,800 993 1.39ON Semiconductor 153,750 850 1.19

8,134 11.41

Materials - 2.85%Dow Chemical 29,450 1,080 1.51Rohm & Haas 17,749 953 1.34

2,033 2.85

Telecommunication Services - 2.79%Telus 20,550 877 1.23Windstream Corp 95,300 1,113 1.56

1,990 2.79

Transport - 0.51%US Airways Group 42,000 360 0.51

Utilities - 4.08%Allegheny Energy 18,000 901 1.27Constellation Energy 10,700 947 1.33PPL Corp 22,900 1,052 1.48

2,900 4.08

Total investments 70,222 98.63

Other net assets 975 1.37

Total 71,197 100.00

All securities held at the period end are transferable except where otherwise stated.All securities are listed on an official exchange except where otherwise stated.All investments are in ordinary or common stocks and shares except where otherwise stated.There are no transferable securities and money market instruments dealt in another regulated market except as otherwise stated.

Portfolio Statement continued

Percentage of Market value total net assets Description Quantity US$’000 %

Aberdeen Global 11Asia Pacific Fund

Asia Pacific FundFor the period ended 31 March 2008

PerformanceFor the six-months ended 31 March 2008, the value of the Aberdeen Global - Asia Pacific Fund - A Accumulation shares decreased by 6.5% compared to a decrease of 14.0% in the benchmark, the MSCI AC Asia Pacific ex Japan Index.

Manager’s reviewAsian equities fell in the six months under review, as stock markets worldwide grew more volatile as the US housing and credit markets imploded, worsening global economic growth prospects. What started out as an issue of illiquidity quickly turned into a full-blown financial crisis. The US Federal Reserve resorted to unprecedented market measures to support the financial system, as well as reducing interest rates five times, to 2.25% which put further downward pressure on the dollar, complicating policy for Asia’s export-driven economies.

Meanwhile, more expensive oil and food prices saw inflation spike across the region, touching multi-year highs in China, Hong Kong and Singapore. Most central banks kept interest rates unchanged, relying on subsidies and price controls to curb headline price growth. Australia, China, Korea, Indonesia, India and Taiwan hiked rates; only the Philippines eased policy.

On the economic front, fourth-quarter GDP growth across the region generally exceeded expectations. In contrast, 2008 growth forecasts were downgraded as the fall out from the credit crunch became more apparent. Thailand, which underperformed because of political paralysis, upgraded its forecast. Elsewhere, India’s budget waived US$15bn in loans to farmers, while Hong Kong and Singapore offered tax breaks, all in an effort to boost growth.

In politics, several countries saw a changing of the guard. In Australia, the opposition Labor Party swept to victory; a pro-Thaksin party formed the government after Thailand’s first general election since the military coup and ex-premier Thaksin returned home after 17 months, but pledged to stay out of politics. Korea’s president Lee Myung-Bak began his term; Taiwanese opposition candidate Ma Ying-jeou won the presidential vote on a pro-growth platform, as expected; but Malaysia’s ruling Umno party suffered a shock loss of its two-third parliamentary majority at the general election, which prevents it now from pushing through laws at state level. The assassination of Pakistan’s opposition leader Benazir Bhutto delayed the general elections.

Portfolio review The Fund fell by 6.5% during the period, whereas the benchmark MSCI AC Asia Pacific ex Japan Index fell 14%.

In portfolio activity, we sold our small holding in Taiwanese lender, Sinopac, whose management failed to live up to expectations. We also top-sliced several holdings after strong runs in their share price, including China’s PetroChina and China Mobile, Australia’s Rio Tinto, Indian utility GAIL and Hong Kong-based Sun Hung Kai Properties.

Conversely, we initiated a position in Singapore-listed Fraser and Neave, a regional food and beverages company with additional interests in property and publishing. We also added to ASM Pacific Technology in Hong Kong and Singapore’s Venture Corp.

OutlookMarket volatility is expected to persist in the near term. A rebound at the end of the period, on optimism that the worst of the credit crisis was over, proved short-lived. The ongoing turmoil has hit not only the key players in the sub-prime segment, but appears now to have permeated the broader economy, with General Electric, widely seen as a proxy, posting its first fall in quarterly results in five years.

Various data would appear to suggest the slowdown is accelerating, with rising job losses, mortgage foreclosures and slower consumer spending in the US. In Asia, exports are experiencing slower demand, fuel and food inflation is squeezing corporate margins and household incomes are being eroded by negative real interest rates. Further downgrades of growth forecasts are likely. However, the portfolio has a natural defensiveness, given our focus on company balance sheets and cashflow. Therefore, we have needed to make few adjustments to the portfolio since markets peaked last October. With the recent price tumbles, we are looking anew at various stocks with a view to adding to positions should prices fall another 10-15%.

12 Aberdeen GlobalAsia Pacific Fund

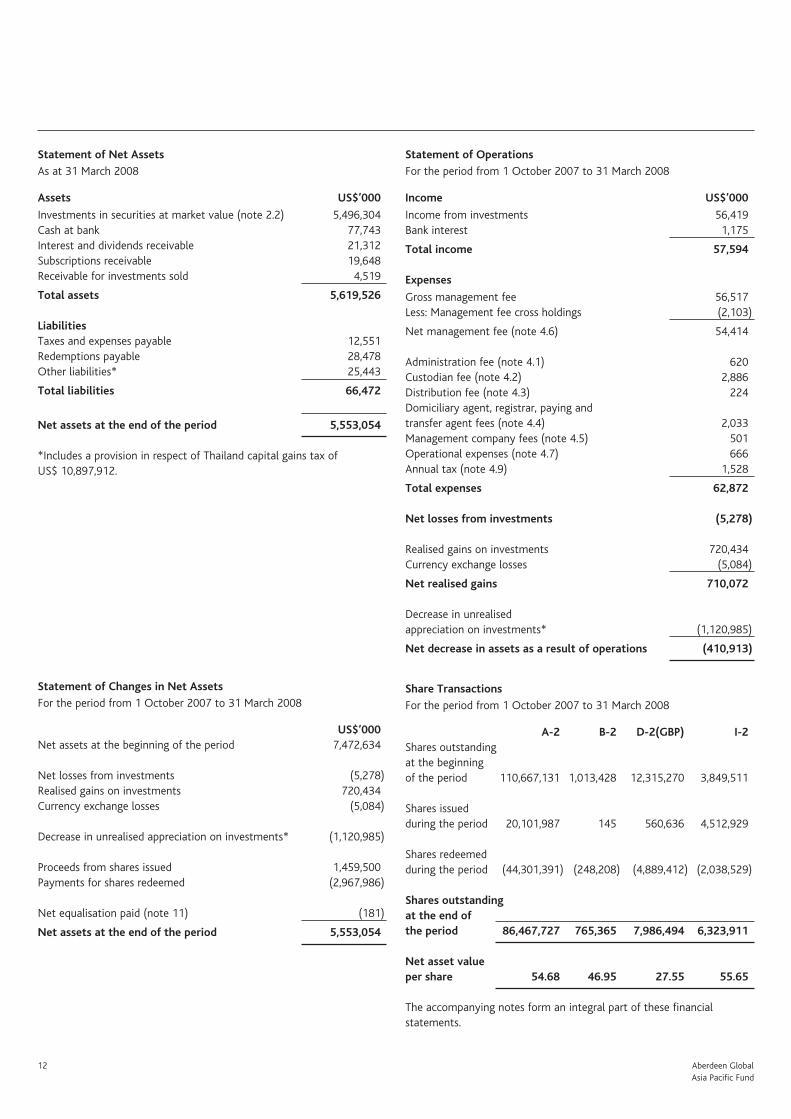

Statement of Net Assets

As at 31 March 2008

Assets US$’000

Investments in securities at market value (note 2.2) 5,496,304 Cash at bank 77,743 Interest and dividends receivable 21,312 Subscriptions receivable 19,648 Receivable for investments sold 4,519

Total assets 5,619,526 Liabilities Taxes and expenses payable 12,551 Redemptions payable 28,478 Other liabilities* 25,443

Total liabilities 66,472

Net assets at the end of the period 5,553,054

*Includes a provision in respect of Thailand capital gains tax of US$ 10,897,912.

Statement of Changes in Net Assets

For the period from 1 October 2007 to 31 March 2008

US$’000Net assets at the beginning of the period 7,472,634

Net losses from investments (5,278) Realised gains on investments 720,434 Currency exchange losses (5,084)

Decrease in unrealised appreciation on investments* (1,120,985)

Proceeds from shares issued 1,459,500 Payments for shares redeemed (2,967,986)

Net equalisation paid (note 11) (181)

Net assets at the end of the period 5,553,054

Statement of Operations

For the period from 1 October 2007 to 31 March 2008

Income US$’000

Income from investments 56,419 Bank interest 1,175

Total income 57,594

Expenses

Gross management fee 56,517 Less: Management fee cross holdings (2,103)

Net management fee (note 4.6) 54,414

Administration fee (note 4.1) 620 Custodian fee (note 4.2) 2,886 Distribution fee (note 4.3) 224 Domiciliary agent, registrar, paying and transfer agent fees (note 4.4) 2,033 Management company fees (note 4.5) 501 Operational expenses (note 4.7) 666 Annual tax (note 4.9) 1,528

Total expenses 62,872

Net losses from investments (5,278)

Realised gains on investments 720,434 Currency exchange losses (5,084)

Net realised gains 710,072

Decrease in unrealisedappreciation on investments* (1,120,985)

Net decrease in assets as a result of operations (410,913)

Share Transactions

For the period from 1 October 2007 to 31 March 2008

A-2 B-2 D-2(GBP) I-2Shares outstanding at the beginning of the period 110,667,131 1,013,428 12,315,270 3,849,511

Shares issued during the period 20,101,987 145 560,636 4,512,929

Shares redeemed during the period (44,301,391) (248,208) (4,889,412) (2,038,529)

Shares outstanding at the end ofthe period 86,467,727 765,365 7,986,494 6,323,911 Net asset value per share 54.68 46.95 27.55 55.65

The accompanying notes form an integral part of these financial statements.

Aberdeen Global 13Asia Pacific Fund

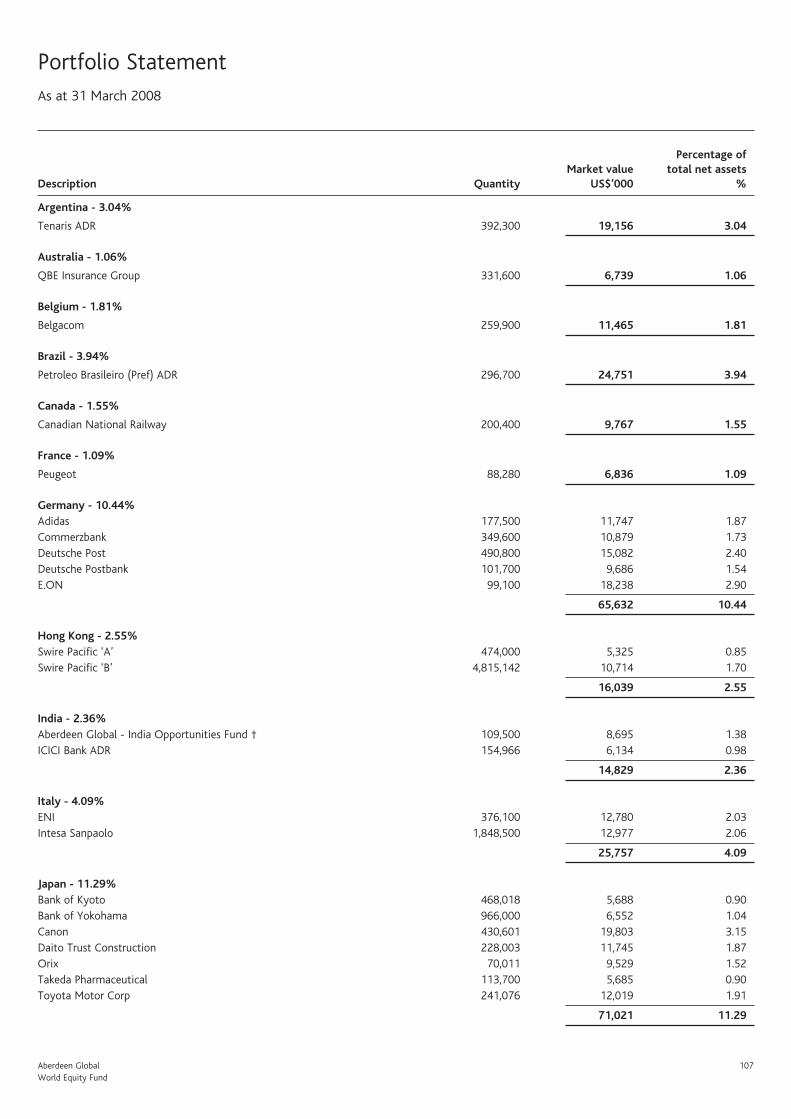

Portfolio StatementAs at 31 March 2008

Percentage of Market value total net assets Description Quantity US$’000 %

Australia - 8.48%QBE Insurance Group 8,804,220 178,922 3.22Rio Tinto 2,100,000 218,550 3.94Tabcorp Holdings 5,710,956 73,683 1.32

471,155 8.48

China - 4.64%China Mobile 9,000,221 133,832 2.41PetroChina 74,798,810 93,160 1.68Zhejiang Expressway 35,000,170 30,417 0.55

257,409 4.64

Hong Kong - 19.69%ASM Pacific Technology 9,815,120 69,917 1.26CLP Holdings 6,500,926 53,366 0.96Dah Sing Banking 10,099,621 17,191 0.31Dah Sing Financial 6,563,009 43,210 0.78Dairy Farm International 15,106,163 66,769 1.20Giordano International 49,557,573 19,927 0.36Hang Lung Group 16,514,186 77,541 1.40Hang Lung Properties 16,500,442 58,452 1.05Jardine Strategic Holdings 10,155,039 169,183 3.05Standard Chartered Bank 3,750,404 129,444 2.33Sun Hung Kai Properties 6,685,426 103,448 1.86Swire Pacific ‘A’ 900,491 10,116 0.18Swire Pacific ‘B’ 77,208,092 171,789 3.09Wing Hang Bank 6,843,239 103,120 1.86

1,093,473 19.69

India - 13.17%Aberdeen Global - India Opportunities Fund † 23,175,093 205,795 3.71GAIL 3,100,060 32,915 0.59GAIL GDR 300,000 19,650 0.35GlaxoSmithKline Pharmaceuticals 1,261,550 32,844 0.59Grasim Industries 1,080,560 69,448 1.25Hero Honda 3,135,500 54,349 0.98Housing Development Finance Corp 1,190,000 70,674 1.27ICICI Bank 2,557,048 49,099 0.88Infosys Technologies 2,100,600 75,484 1.36New India Investment Trust † 4,780,000 13,190 0.24Satyam Computer Services 10,940,500 108,218 1.95

731,666 13.17

Indonesia - 1.10%Unilever Indonesia 82,060,036 61,238 1.10

Malaysia - 5.98%British American Tobacco 4,721,920 63,024 1.13Bumiputra Commerce 22,500,030 70,278 1.27Malayan Banking 22,174,011 58,844 1.06Public Bank (Alien) 41,250,714 140,146 2.52

332,292 5.98

14 Aberdeen GlobalAsia Pacific Fund

Portfolio Statement continued

Philippines - 2.42%Ayala Land 286,209,322 72,885 1.31Bank of the Philippine Islands 48,432,854 61,813 1.11

134,698 2.42

Singapore - 21.10%City Developments 19,400,779 154,828 2.79Fraser & Neave Limited 25,800,000 90,419 1.63Oversea-Chinese Banking Corp 36,069,215 211,640 3.81Singapore Airlines 9,900,600 111,521 2.01Singapore Technologies Engineering 66,710,971 163,923 2.95Singapore Telecommunications 58,750,862 166,295 2.99United Overseas Bank 13,150,929 182,354 3.28Venture Corp 11,876,030 90,559 1.64

1,171,539 21.10

South Korea - 10.69%Daegu Bank 2,924,490 38,989 0.70Hyundai Motor (Pref) 550,290 17,211 0.31Kookmin Bank 2,110,901 117,997 2.12Pusan Bank 3,663,570 45,611 0.82Samsung Electronics (Pref) 539,714 242,524 4.37Shinsegae 208,900 131,303 2.37

593,635 10.69

Sri Lanka - 0.82%Commercial Bank of Ceylon 3,554,187 4,611 0.08DFCC Bank 6,108,073 7,075 0.13Dialog Telekom 73,606,300 11,424 0.21Keells (John) 15,737,023 17,462 0.31National Development Bank 2,857,725 4,406 0.09

44,978 0.82

Taiwan - 6.45%Fubon Financial 69,016,000 78,424 1.41Taiwan Mobile 50,922,975 97,964 1.76TSMC 87,500,000 181,576 3.28

357,964 6.45

Thailand - 4.44%PTT Exploration & Production (Foreign) 23,800,045 114,455 2.06Siam Cement (Foreign) 19,223,036 131,802 2.38

246,257 4.44

Total investments 5,496,304 98.98

Other net assets 56,750 1.02

Total 5,553,054 100.00

All securities held at the period end are transferable except where otherwise stated.All securities are listed on an official exchange except where otherwise stated.All investments are in ordinary or common stocks and shares except where otherwise stated.There are no transferable securities and money market instruments dealt in another regulated market except as otherwise stated.† Managed by subsidiaries of Aberdeen Asset Management PLC.

Percentage of Market value total net assets Description Quantity US$’000 %

Aberdeen Global 15Asia Pacific and Japan Fund

Asia Pacific and Japan FundFor the period ended 31 March 2008

Closure of FundThe Fund was closed on 26 October 2007. The Manager is in the process of winding the Fund up.

PerformanceFor the period 1 October 2007 to 26 October 2007, the value of the Aberdeen Global - Asia Pacific and Japan Fund - A Accumulation shares increased by 1.6% compared to an increase of 3.0% in the benchmark, the MSCI AC Asia Pacific Index.

Manager’s reviewAsian equities fell in the period under review, as stock markets worldwide faced increasing volatility amid heightened credit fears and worsening prospects for global economic growth. As financial market de-leveraging intensified, bond insurers and investment banks faced massive write-downs. Evidence of that distress was JP Morgan’s purchase of beleaguered Bear Stearns for a knock-down sum. Further underlining the severity of the situation, the US Federal Reserve resorted to unprecedented measures to boost liquidity in the financial system, as well as reducing interest rates five times, to 2.25%.

Inflation rose sharply across the region, touching multi-year highs in China, Hong Kong and Singapore, while Japanese prices accelerated at their fastest in a decade. Food and fuel prices were the main causes. Most central banks kept interest rates steady, using subsidies and price controls to suppress headline price growth. Still, Australia, China, Korea, Indonesia, India and Taiwan hiked rates, while the Philippines eased policy.

While fourth-quarter GDP growth generally exceeded expectations across the region, 2008 growth forecasts were downgraded on weakening export demand. Only Thailand raised its forecast. To boost growth, India’s budget waived US$15bn in loans to farmers, while Hong Kong and Singapore offered tax breaks to help the less well off.

In politics, Korea’s president-elect Lee Myung-Bak began his term; Taiwanese opposition candidate Ma Ying-jeou won the presidential vote on a pro-growth platform, as expected; but Malaysia’s ruling Umno party suffered a shock loss of its two-third parliamentary majority at the general election. In Japan, opposition MPs rejected the ruling LDP’s candidates to run the central bank, leaving it rudderless. Former Thai premier Thaksin Shinawatra returned home after 17 months, but pledged to stay out of politics.

Portfolio reviewDuring the review period, the Fund rose by 1.6%, compared to the benchmark MSCI AC Asia Pacific Index’s rise of 3.0%.

The Fund was terminated on 26 October 2007, following the redemption of a major shareholder, and all positions were closed out.

16 Aberdeen GlobalAsia Pacific and Japan Fund

Statement of Net Assets

As at 31 March 2008

Assets US$’000

Cash at bank 45

Other assets 33

Total assets 78

Liabilities

Taxes and expenses payable 9

Other liabilities 69

Total liabilities 78

Net assets at the end of the period -

Statement of Changes in Net Assets

For the period from 1 October 2007 to 31 March 2008

US$’000

Net assets at the beginning of the period 6,192

Net gains from investments 11

Realised gains on investments 518

Currency exchange losses (4)

Decrease in unrealised appreciation on investments (405)

Proceeds from shares issued 176

Payments for shares redeemed (6,487)

Net equalisation paid (note 11) (1)

Net assets at the end of the period –

Statement of Operations

For the period from 1 October 2007 to 31 March 2008

Income US$’000

Income from investments 16

Bank interest 4

Total income 20

Expenses

Net management fee (note 4.6) 9

Administration fee (note 4.1) 9

Domiciliary agent, registrar, paying and

transfer agent fees (note 4.4) 13

Operational expenses (note 4.7) (22)

Total expenses 9

Net gains from investments 11

Realised gains on investments 518

Currency exchange losses (4)

Net realised gains 525

Decrease in unrealised

appreciation on investments (405)

Net increase in assets as a result of operations 120

Share Transactions

For the period from 1 October 2007 to 31 March 2008

A-2

Shares outstanding at the beginning of the period 570,137

Shares issued during the period 12,856

Shares redeemed during the period (582,993)

Shares outstanding at the end of the period –

Net asset value per share –

The accompanying notes form an integral part of these financial

statements.

Aberdeen Global 17Asia Pacific and Australasian Bond Fund

Asia Pacific and Australasian Bond FundFor the period ended 31 March 2008

PerformanceFor the six-months ended 31 March 2008, the value of the Aberdeen Global - Asia Pacific and Australasian Bond Fund - A Accumulation shares increased by 3.5% compared to an increase of 6.2% in the benchmark, the iBoxx Pan-Asia (ex China) Index.

Manager’s reviewThe majority of local currency Asian fixed income markets over the six month period to end March 2008 saw yields moving lower. This was somewhat counterintuitive given that this period was characterised by a sharp rise in regional inflation, driven first and foremost by considerable food price inflation and by record highs in oil prices. In addition, fourth quarter 2007 GDP growth numbers showed reassuring resilience to the US and global slowdown and emerged stronger than expected. The clear trend has been a steepening of yield curves, in most cases a bullish steepening, led by a rally in shorter dated bonds. Longer dated bonds have been under more pressure given the inflation threat, most particularly so in Indonesia where the trend rise in CPI data has been most noticeable and where the market remains vulnerable to weak global sentiment.

There were a number of supporting factors for Asian bond markets. At the start of the period the market was already ignoring the US Fed’s less dovish statements that pointed to potentially a lesser need for policy easing given the latent inflation threat. Instead it firmly focussed on the deteriorating economic data which among other things showed continued housing market weakness, deterioration in Consumer Confidence indices and marked worsening in employment data. Momentum behind the financial market crisis also picked up with key global financial institutions announcing larger than expected asset write-downs. This moved the Fed to ease rates a further fifty basis points to 4.25% during the review period before the year end and an additional two hundred basis points during the review period after the year end, which led to a sharp rally in US yields.

Indonesia, Malaysia, South Korea and Thailand were affected by the marked trend rise in inflation data in the fourth quarter and saw their bond markets selling off. But in the case of the latter three markets, the emergency Fed easing and prevalence of bearish sentiment at the start of 2008 allowed even these markets to recover. At the start of the year, with regional growth forecasts being revised down and pricing pressures expected to stabilise as new food supplies came online and oil prices stabilised, CPI inflation was forecast to recover as well. Further support for bond yields came from a continued sell off in Asian equity markets, with the MSCI Asia Pacific equity index down 15% over the period and continued spikes in volatility.

By February oil prices surged through US$100 pressuring fuel costs and in addition there had been a general pick up in vegetable, grain, cooking oil, livestock and rice prices, a result of dry weather in Europe, drought in Australia and flooding in China aggravating food supplies and prices.

Given the risks to growth from a global slowdown moving forward, policymakers clearly have a preference for easing rates. The inflation risk has largely kept policy rates on hold up till now with policymakers pointing to the supply side nature of the shock as the key reason for not having to tighten policy rates at least in the near term, even as real yields have been seen moving lower or substantially negative, with the exceptions of India and Indonesia. However central banks potentially face a stagflation dilemma should inflation broaden as growth slows moving into the second half of the year. This has meant that some of the recovery in yields was eroded over the last couple of months of the period in review as bond markets priced in a transition from a neutral/easing policy bias to a neutral/tightening policy bias. Lastly given the prevalence of subsidised goods, the higher cost of food and oil has substantially increased the subsidy costs to governments leading to fiscal pressures, again most notably in Indonesia, with the ramifications of higher than expected bond issuance set to hit the market.

Asian currencies have generally performed well against the US dollar. The key drivers have been a) marked dollar bearishness on deteriorating US fundamentals, b) a policy preference to use stronger currency appreciation to counter higher imported prices, and c) better balanced Asian growth drivers and better than expected fourth quarter growth. The main exceptions were India, South Korea and Indonesia. India has been vulnerable to the spike up in oil prices with the market, given higher aversion generally, having a bias against current account deficit currencies. This also impacted the South Korean won, where economic fundamentals have also been seen rolling over. The Indonesian rupiah was hit by poor global sentiment and risk from a foreign bond investor capitulation, which however hasn’t occurred even as bond yields spiked up.

Portfolio reviewThe bias for bond trades over the period were for risk reduction, in particular reducing market exposure to Indonesia rates and increasing it to Singapore, a more defensive allocation. The duration of the overall portfolio was also reduced by 0.65, again primarily via a reduction in both Indonesia and Singapore duration. On the currency side we added risk to Singapore dollar, Thai baht, Philippine peso and Malaysian ringgit and reduced it to Indonesian rupiah.

OutlookReal bond yields are mostly negative across the region. And while tighter monetary policy will not solve supply side shortages particularly in food, we note that many countries still suffer from excessive money supply growth and overly generous credit conditions given the level of domestic growth momentum in their economies. Combined with potentially broader inflation there is a risk central banks have to hike rates as growth slows unless the price pressures ease.

18 Aberdeen GlobalAsia Pacific and Australasian Bond Fund

However we expect growth and inflationary pressures to ease in the second half of 2008 and to see a shift towards more relaxed monetary policy for many countries and a more constructive outlook for fixed income markets.

Overall, we continue to expect potential weakness across the region to be seen firstly in the export sectors of most countries. While numerous policy makers are likely to pin their hopes on China as a buffer to weaker global growth in 2008, we suspect that Chinese imports will also soften as global growth slows. Recent trade data suggests that several Asian countries have managed to diversify their export base towards the middle-east and various emerging markets. The region approaches the pending slowdown in global growth in a much better position than in previous cycles. Positive fiscal balances, strong external accounts, firm corporate balance sheets and ample liquidity support the region’s need to further develop infrastructure in coming years. This should cushion Asia’s growth profile in the coming 12-18 months as global growth slows.

Asian fundamentals remain very positive, however we have seen substantial currency appreciation already so there is a risk that should accommodative policy in the US gain traction and data improves as Asia’s softens, Asian currencies may enter a softer couple of quarters against the US dollar. However it is unlikely that we have seen the end of the US economic and financial market crisis that has driven the dollar bearishness, and with the US Fed still set to ease policy rates substantially, interest rate differentials will increasingly favour Asian currencies.

Aberdeen Global 19Asia Pacific and Australasian Bond Fund

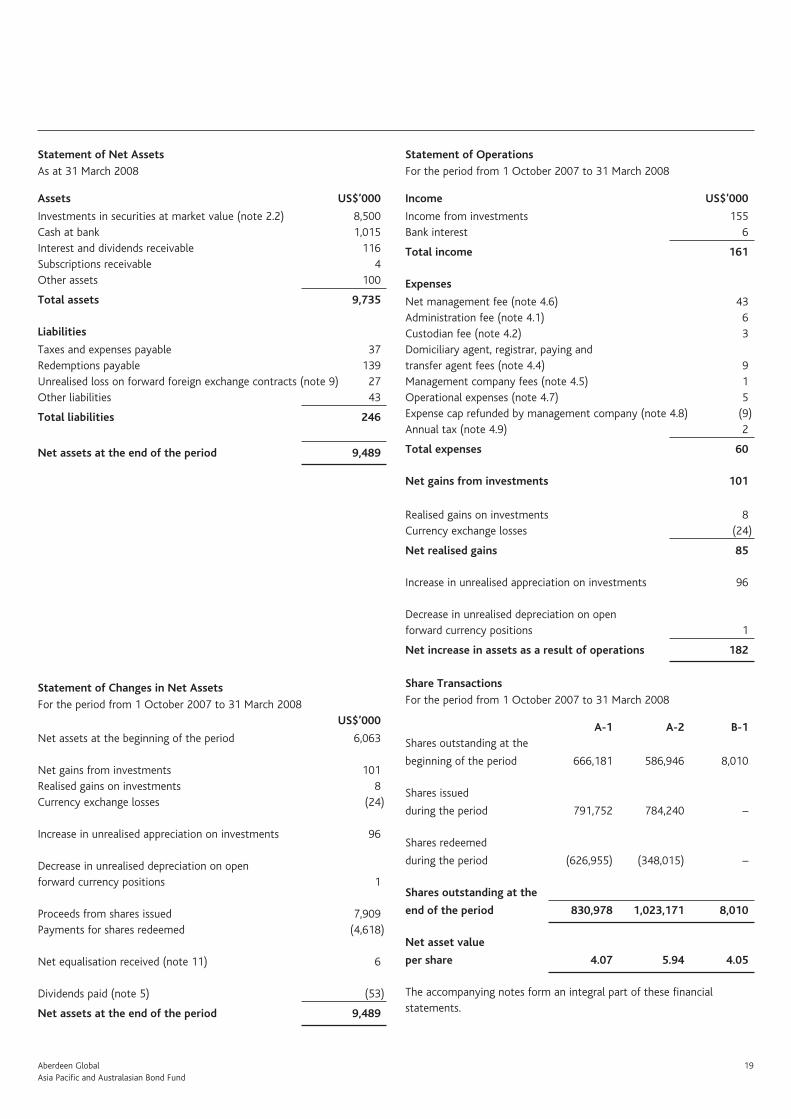

Statement of Net Assets

As at 31 March 2008

Assets US$’000

Investments in securities at market value (note 2.2) 8,500 Cash at bank 1,015 Interest and dividends receivable 116 Subscriptions receivable 4 Other assets 100

Total assets 9,735

Liabilities

Taxes and expenses payable 37 Redemptions payable 139 Unrealised loss on forward foreign exchange contracts (note 9) 27 Other liabilities 43

Total liabilities 246

Net assets at the end of the period 9,489

Statement of Changes in Net Assets

For the period from 1 October 2007 to 31 March 2008 US$’000

Net assets at the beginning of the period 6,063

Net gains from investments 101 Realised gains on investments 8 Currency exchange losses (24)

Increase in unrealised appreciation on investments 96

Decrease in unrealised depreciation on open forward currency positions 1

Proceeds from shares issued 7,909 Payments for shares redeemed (4,618)

Net equalisation received (note 11) 6

Dividends paid (note 5) (53)

Net assets at the end of the period 9,489

Statement of Operations

For the period from 1 October 2007 to 31 March 2008

Income US$’000

Income from investments 155 Bank interest 6

Total income 161

Expenses

Net management fee (note 4.6) 43 Administration fee (note 4.1) 6 Custodian fee (note 4.2) 3 Domiciliary agent, registrar, paying and transfer agent fees (note 4.4) 9 Management company fees (note 4.5) 1 Operational expenses (note 4.7) 5 Expense cap refunded by management company (note 4.8) (9) Annual tax (note 4.9) 2

Total expenses 60

Net gains from investments 101

Realised gains on investments 8 Currency exchange losses (24)

Net realised gains 85

Increase in unrealised appreciation on investments 96

Decrease in unrealised depreciation on open forward currency positions 1

Net increase in assets as a result of operations 182

Share Transactions

For the period from 1 October 2007 to 31 March 2008

A-1 A-2 B-1Shares outstanding at the

beginning of the period 666,181 586,946 8,010

Shares issued

during the period 791,752 784,240 –

Shares redeemed

during the period (626,955) (348,015) –

Shares outstanding at the

end of the period 830,978 1,023,171 8,010

Net asset value

per share 4.07 5.94 4.05

The accompanying notes form an integral part of these financial statements.

20 Aberdeen GlobalAsia Pacific and Australasian Bond Fund

Portfolio StatementAs at 31 March 2008

Percentage of Market value total net assets Description Nominal US$’000 %

Hong Kong - 6.51%Hong Kong Government 3.52% 22/03/10 1,950,000 262 2.76Hong Kong Government 4.33% 07/12/15 1,350,000 197 2.08Hong Kong Government 4.40% 22/08/13 1,100,000 158 1.67

617 6.51

Indonesia - 8.01%Indonesia Government 11% 15/12/12 1,450,000,000 161 1.70Indonesia Government 12.5% 15/03/13 4,137,000,000 483 5.09Indonesia Recapital 10.75% 15/05/16 1,077,000,000 116 1.22

760 8.01

South Korea - 19.72%Korea Treasury Bond 4.75% 10/03/12 1,083,000,000 1,072 11.30Korea Treasury Bond 5.00% 10/09/16 430,200,000 422 4.45Korea Treasury Bond 5.25% 10/12/10 375,100,000 377 3.97

1,871 19.72

Malaysia - 13.94%Malaysia Government 3.50% 31/05/27 450,000 127 1.34Malaysia Government 3.756% 28/04/11 2,941,000 930 9.80Malaysia Government 4.262% 15/09/16 340,000 111 1.17Malaysia Government 4.72% 30/09/15 465,000 155 1.63

1,323 13.94

Philippines - 6.61%Philippine Government 8.50% 17/02/09 2,920,000 72 0.76Philippine Government 7.125% 02/11/13 10,100,000 249 2.62Philippine Government 9.125% 04/09/16 1,920,000 52 0.55Philippine Government 8.5% 03/03/11 10,000,000 254 2.68

627 6.61

Singapore - 19.48%Asia Development Bank 3.27% 08/02/12 1,000,000 760 8.01Singapore Government 3.75% 01/09/16 451,000 364 3.83Singapore T Bills 0% 17/04/08 1,000,000 725 7.64

1,849 19.48

Thailand - 15.31%Asia Development Bank 5.54% 18/09/16 15,000,000 505 5.32Thailand Government 4.5% 11/03/12 13,000,000 428 4.51Thailand Government 5.25% 12/05/14 11,000,000 372 3.92Thailand Government 5.375% 15/05/09 4,550,000 148 1.56

1,453 15.31

Total investments 8,500 89.58

Other net assets 989 10.42

Total 9,489 100.00

All securities held at the period end are transferable except where otherwise stated.All securities are listed on an official exchange except where otherwise stated.All investments are in fixed interest securities and equity securities except where otherwise stated.There are no transferable securities and money market instruments dealt in another regulated market except as otherwise stated.

Aberdeen Global 21Asian Smaller Companies Fund

Asian Smaller Companies FundFor the period ended 31 March 2008

PerformanceFor the six-months ended 31 March 2008, the value of the Aberdeen Global - Asian Smaller Companies Fund - A Accumulation shares decreased by 4.1% compared to a decrease of 15.4% in the benchmark, the MSCI AC Asia Pacific ex Japan Small Cap Index.

Change in benchmarkThe Fund changed its benchmark from the MSCI AC Asia Pacific ex Japan Index to the MSCI AC Asia Pacific ex Japan Small Cap Index on 1 October 2007.

Manager’s reviewIn the half year under review, Asian equities, like their global counterparts, fell amid increasingly volatile market conditions. Sentiment was roiled by rapidly deteriorating economic growth prospects that resulted from the imploding US housing and credit markets. What started out as an issue of illiquidity quickly turned into a full-blown financial crisis. To support the financial system, the US Federal Reserve resorted to unprecedented measures, including five interest rate cuts that brought the policy rate to 2.25%. This, however, led to more downward pressure on the dollar, compounding the difficulty Asian policymakers faced as export competitiveness was eroded.

Meanwhile, inflation, caused by more expensive oil and food prices, spiked across Asia, touching multi-year highs in China, Hong Kong and Singapore. In response, Australia, China, Korea, Indonesia, India and Taiwan hiked rates; only the Philippines eased policy. Most other central banks were happy to keep interest rates stable, relying instead on subsidies and price controls to curb headline price growth.

Regional economic growth generally exceeded expectations in the fourth quarter. In contrast, 2008 forecasts were lowered as the fall out from the credit crunch became more apparent. Only Thailand upgraded its forecast, as it had underperformed its peers while political paralysis gripped the country since the bloodless coup in December 2006. Meanwhile, India’s budget waived US$15bn in loans to farmers, while Hong Kong and Singapore offered tax breaks, all in an effort to boost growth.

Portfolio reviewThe Fund fell by 4.1% over the period, compared to the benchmark MSCI AC Asia Pacific ex Japan Small Cap Index’s 15.4% decline, testimony to our defensive style and earlier unwillingness to chase the market.

In portfolio activity, we sold Hong Kong footwear-maker Kingmaker for better opportunities elsewhere, and stock exchange operator Bursa Malaysia, after a strong run-up in its share price. We also accepted the takeover offers for Singapore’s Robinson & Co, the Ascott Group and Straits Trading, which provided us with good exits. We took partial profits in dry bulk shipper Pacific Basin, Korean Reinsurance, plantations company MP Evans, and Sri Lanka’s Distilleries Co after a strong run.

Conversely, we initiated a holding in Hong Kong’s ASM International, and took advantage of market volatility to top up several holdings, including the Philippines’ Cebu Holdings, India’s Castrol, Malaysia’s Oriental Holdings and WBL Corp in Singapore.

OutlookRecent economic data would appear to suggest the slowdown is accelerating. This is reflected in rising job losses, mortgage foreclosures and slower consumer spending in the US. For smaller companies that generally cater to domestic demand, slower global growth may not be felt as acutely as for their larger counterparts, although they are more susceptible to inflationary pressure due largely to their inability to pass on cost increases, given their lack of pricing power. Meanwhile, negative real interest rates has further eroded household incomes.

We are not overly concerned about the portfolio, because it has a natural defensiveness, given our sharp focus on company balance sheets and cashflow. Accordingly, few adjustments to the portfolio have been required since markets peaked last October. With the recent price tumbles, we are looking anew at various stocks with a view to adding to positions, particularly if prices fall a further 10-15%.

22 Aberdeen GlobalAsian Smaller Companies Fund

Statement of Net Assets

As at 31 March 2008

Assets US$’000

Investments in securities at market value (note 2.2) 481,184

Cash at bank 58,208

Interest and dividends receivable 793

Subscriptions receivable 35

Total assets 540,220

Liabilities

Payable for investments purchased 5,346

Taxes and expenses payable 867

Redemptions payable 54

Other liabilities * 2,734

Total liabilities 9,001

Net assets at the end of the period 531,219

* Includes a provision in respect of Thailand capital gains tax of

US$1,898,184.

Statement of Changes in Net Assets

For the period from 1 October 2007 to 31 March 2008

US$’000

Net assets at the beginning of the period 489,709

Net gains from investments 1,032

Realised gains on investments 30,420

Currency exchange losses (370)

Decrease in unrealised appreciation on investments * (50,859)

Proceeds from shares issued 338,198

Payments for shares redeemed (277,109)

Net equalisation received (note 11) 198

Net assets at the end of the period 531,219

Statement of Operations

For the period from 1 October 2007 to 31 March 2008

Income US$’000

Income from investments 5,307

Bank interest 189

Total income 5,496

Expenses

Net management fee (note 4.6) 3,793

Administration fee (note 4.1) 81

Custodian fee (note 4.2) 230

Domiciliary agent, registrar, paying and

transfer agent fees (note 4.4) 160

Management company fees (note 4.5) 36

Operational expenses (note 4.7) 66

Annual tax (note 4.9) 98

Total expenses 4,464

Net gains from investments 1,032

Realised gains on investments 30,420

Currency exchange losses (370)

Net realised gains 31,082

Decrease in unrealised appreciation on investments * (50,859)

Net decrease in assets as a result of operations (19,777)

Share Transactions

For the period from 1 October 2007 to 31 March 2008

A-2 D-2(GBP) I-2 Z-2

Shares outstanding at

the beginning of the

period 8,213,582 11,573,192 175,868 –

Shares issued

during the period 4,457,733 120,602 20,707 22,769,645

Shares redeemed

during the period (1,770,304) (9,786,854) – –

Shares outstanding

at the end

of the period 10,901,011 1,906,940 196,575 22,769,645

Net asset value

per share 23.52 11.81 23.82 9.90

The accompanying notes form an integral part of these financial

statements.

Aberdeen Global 23Asian Smaller Companies Fund

Portfolio Statement As at 31 March 2008

Percentage of Market value total net assets Description Quantity US$’000 %

Hong Kong - 19.48%Aeon Credit Service 7,430,000 6,157 1.16Aeon Stores 4,100,000 8,190 1.54Asia Satellite Telecommunications 5,166,500 9,869 1.86ASM International 300,000 5,433 1.02Café de Coral 5,000,000 9,776 1.84Convenience Retail Asia 15,950,000 5,737 1.08Fong’s Industries 9,000,000 5,110 0.96Giordano International 33,009,000 13,273 2.49Hong Kong & Shanghai Hotels 2,436,258 3,994 0.75Hong Kong Aircraft Engineering 280,000 4,593 0.86Hong Kong Ferry 5,000,000 4,769 0.90Hung Hing Printing 7,202,000 2,392 0.45Pacific Basin Shipping 2,630,000 4,321 0.81Public Financial Holdings 16,346,000 13,712 2.58Texwinca 8,700,000 6,276 1.18

103,602 19.48

India - 7.51%Aventis Pharma 160,299 3,061 0.58Castrol 800,000 4,827 0.91Godrej Consumer Products 3,000,000 9,284 1.75Godrej Consumer Products Rights 360,000 33 0.01Gujarat Gas 734,659 4,314 0.81Jammu & Kashmir Bank 200,000 3,444 0.65Kansai Nerolac Paints 557,035 10,093 1.90Mphasis BFL 950,000 4,783 0.90

39,839 7.51

Indonesia - 5.31%Bank NISP 141,748,674 13,848 2.61Bank Permata 9,970,500 979 0.18Bank UOB Buana 36,391,659 4,345 0.82Dynaplast 12,093,000 1,011 0.19M.P. Evans 900,250 8,021 1.51

28,204 5.31

Malaysia - 15.55%Aeon 5,100,000 15,051 2.83Fraser & Neave Holdings 1,220,900 3,001 0.56Guinness Anchor 5,180,400 8,881 1.67LPI Capital 2,500,900 8,810 1.66Manulife Insurance 3,511,800 3,161 0.60Oriental Holdings 6,812,000 12,212 2.30Panasonic Manufacturing 892,000 2,975 0.56POS Malaysia & Services 10,000,000 5,902 1.11Star Publications 3,463,100 3,730 0.70United Malacca 2,531,400 6,044 1.14United Plantations 3,123,800 12,863 2.42

82,630 15.55

24 Aberdeen GlobalAsian Smaller Companies Fund

Portfolio Statement continued

Philippines - 3.61%Asian Terminals 58,148,000 4,808 0.91Cebu Holdings 91,646,000 4,745 0.89Ginebra San Miguel 5,080,000 2,420 0.46Jollibee Foods 6,250,200 7,153 1.35

19,126 3.61

Singapore - 22.47%Bukit Sembawang Estates 4,000,500 25,750 4.85Eu Yan Sang 19,554,000 8,043 1.51FJ Benjamin Holdings 10,000,000 2,990 0.56Hong Leong Finance 4,620,000 12,792 2.41Robinson & Co 3,672,000 18,378 3.45SBS Transit 5,251,500 9,478 1.78Sembcorp Marine 1,880,000 5,199 0.98Singapore Food Industries 7,597,000 4,171 0.79Singapore Post 6,000,000 4,980 0.94WBL 4,724,000 18,388 3.46Wheelock Properties 6,650,000 9,231 1.74

119,400 22.47

South Korea - 2.88%Daegu Bank 390,000 5,199 0.98Jeonbuk Bank 798,200 5,934 1.12Korean Reinsurance 408,000 4,144 0.78

15,277 2.88

Sri Lanka - 3.00%Aitken Spence 512,700 2,043 0.38Chevron Lubricants Lanka 3,559,600 3,241 0.61Commercial Bank of Ceylon 2,740,600 3,555 0.67Dialog Telekom 1,660,340 258 0.05Distilleries Co of Sri Lanka 3,201,900 2,908 0.55Keells (John) 3,543,797 3,932 0.74

15,937 3.00

Thailand - 10.77%Bumrungrad Hospital (Foreign) 4,678,200 5,049 0.95Central Pattana (Foreign) 9,400,000 8,317 1.57Hana Microelectronics (Foreign) 22,450,300 13,148 2.47Minor Corporation (Foreign) 870,900 406 0.08Regional Container Line (Foreign) 11,504,800 8,911 1.68Siam Makro (Foreign) 3,600,000 11,399 2.15Tisco Bank (Foreign) 10,751,000 9,939 1.87

57,169 10.77

Total investments 481,184 90.58

Other net assets 50,035 9.42

Total 531,219 100.00

All securities held at the period end are transferable except where otherwise stated.All securities are listed on an official exchange except where otherwise stated.All investments are in ordinary or common stocks and shares except where otherwise stated.There are no transferable securities and money market instruments dealt in another regulated market except as otherwise stated

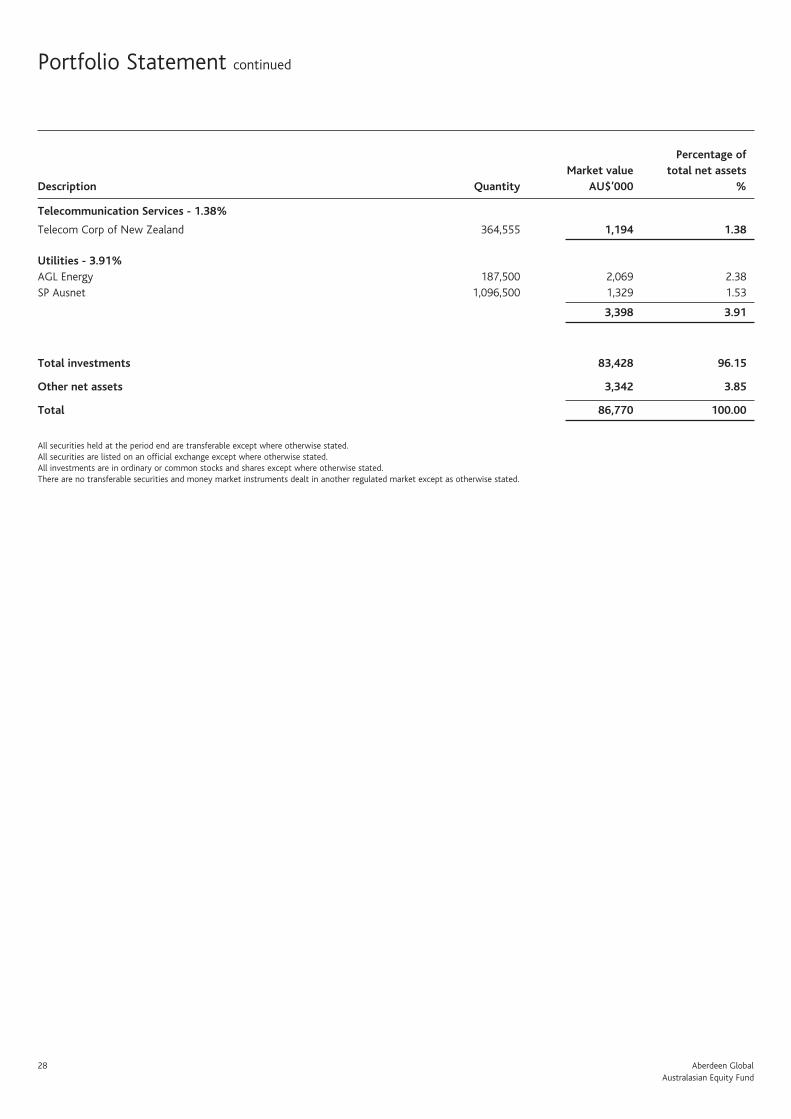

Percentage of Market value total net assets Description Quantity US$’000 %

Aberdeen Global 25Australasian Equity Fund

Australasian Equity FundFor the period ended 31 March 2008

PerformanceFor the six-months ended 31 March 2008, the value of the Aberdeen Global - Australasian Equity Fund - A Accumulation shares decreased by 12.4% compared to a decrease of 16.2% in the benchmark, the Australia All Ordinaries Index.

Manager’s reviewOver the six months under review, the domestic market experienced extreme volatility, having risen to a record high in October. Although the benchmark fell 16.2% over the period, the last few months were the worst that the markets had seen in 19 years owing to the escalating credit crisis. Global bond insurers and investment banks faced unprecedented write-downs, as financial market de-leveraging intensified and money markets seized up. Underlining the severity of the situation, the US Federal Reserve was forced to inject billions of dollars of emergency funding into the financial system, as well as reducing interest rates five times to 2.25%.

In response to global credit concerns, which drove up corporate borrowing costs, the Reserve Bank of Australia (RBA) injected liquidity into domestic money markets. But unlike in the US, with inflation accelerating, thanks to fuel prices and home rents, the RBA raised rates thrice over the period to a 12-year high of 7.25%. However, the demand for commodities remained resilient, with oil prices rising above US$100 a barrel and gold prices at one stage closing above US$1,000 an ounce.

Economic data presented a mixed picture: on the one hand, business investment rebounded on increased Chinese demand for iron ore; and retail sales rose as higher wages and jobs growth fuelled spending. The housing sector remained strong as well. On the other hand, economic growth decelerated to its slowest in more than a year, as construction declined and bottlenecks at ports hurt exports. In addition, high interest rates caused consumer and business borrowing growth to slow, dragging down confidence.

In politics, the Australian Labor Party ended John Howard’s 11-year rule in the November national elections, with Kevin Rudd becoming prime minister.

Portfolio reviewFor the period under review, the Fund fell by 12.4%, outperforming the benchmark Australia All Ordinaries Index by 3.8%. The top three contributors to performance were Incitec Pivot, Rio Tinto and Woodside Petroleum. Incitec Pivot announced it will acquire all the shares in Dyno Nobel, and continued to benefit from strong fertiliser prices. Rio Tinto’s shares were boosted by the bid from BHP Billiton and strong commodity prices, while Woodside was aided by rising spot oil prices.

Stocks that detracted from performance included QBE, ANZ and Bendigo Bank. QBE’s results were below market expectations although