De' Longhi S.p.A. - Morningstar

293

OFFERING MEMORANDUM CONFIDENTIAL 37,500,000 Shares De' Longhi S.p.A. (nominal value 53 per share) This oÅering memorandum relates to a Global OÅering of the ordinary shares of De' Longhi S.p.A. (sometimes referred to as the ""Company'' or ""De' Longhi''), a limited liability company organized under the laws of Italy. We are oÅering 37,500,000 shares as part of the Global OÅering. The institutional underwriters are oÅering 27,900,000 shares (i) in the United States only to qualiÑed institutional buyers (as deÑned below) in reliance on Rule 144A under the U.S. Securities Act of 1933, as amended (the ""Securities Act'') and (ii) outside the United States in oÅshore transactions in reliance on Regulation S under the Securities Act. Additionally, the Italian underwriters are oÅering 9,600,000 shares to retail investors in Italy by way of a public oÅering pursuant to a separate prospectus in the Italian language. Investing in our shares involves risks. You should refer to ""Risk Factors'' beginning on page 13. The oÅering price is 43.4 per share. The shares are quoted on the Italian automated screen-based quotation system, the Mercato Telematico Azionario (""Telematico'') under the symbol ""DLG''. The shares have not been registered under the Securities Act and are being oÅered (i) in the United States only to qualiÑed institutional buyers in reliance on Rule 144A and (ii) outside the United States in reliance on Regulation S under the Securities Act. For a description of certain restrictions on resale or transfer, you should refer to ""Transfer Restrictions'' beginning on page 145. In addition, the Company has granted to the Joint Global Coordinators, on behalf of the institutional underwriters, the right to purchase up to an additional 3,750,000 shares solely to cover over-allotments, if any. The institutional underwriters expect to deliver the shares to purchasers on or about July 24, 2001. Joint Global Coordinators and Bookrunners Merrill Lynch International UniCredit Banca Mobiliare S.p.A. Co-Lead Manager Schroder Salomon Smith Barney Co-Manager EUROMOBILIARE SIM S.p.A. The date of this oÅering memorandum is July 19, 2001 Brought to you by Global Reports

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of De' Longhi S.p.A. - Morningstar

O F F E R I N G M E M O R A N D U M C O N F I D E N T I A L

37,500,000 Shares

De' Longhi S.p.A.(nominal value 53 per share)

This oÅering memorandum relates to a Global OÅering of the ordinary shares of De' Longhi S.p.A.(sometimes referred to as the ""Company'' or ""De' Longhi''), a limited liability company organized underthe laws of Italy. We are oÅering 37,500,000 shares as part of the Global OÅering. The institutionalunderwriters are oÅering 27,900,000 shares (i) in the United States only to qualiÑed institutional buyers(as deÑned below) in reliance on Rule 144A under the U.S. Securities Act of 1933, as amended (the""Securities Act'') and (ii) outside the United States in oÅshore transactions in reliance on Regulation Sunder the Securities Act. Additionally, the Italian underwriters are oÅering 9,600,000 shares to retailinvestors in Italy by way of a public oÅering pursuant to a separate prospectus in the Italian language.

Investing in our shares involves risks. You should refer to ""Risk Factors''beginning on page 13.

The oÅering price is 43.4 per share. The shares are quoted on the Italian automated screen-basedquotation system, the Mercato Telematico Azionario (""Telematico'') under the symbol ""DLG''.

The shares have not been registered under the Securities Act and are being oÅered (i) in the UnitedStates only to qualiÑed institutional buyers in reliance on Rule 144A and (ii) outside the United States inreliance on Regulation S under the Securities Act. For a description of certain restrictions on resale ortransfer, you should refer to ""Transfer Restrictions'' beginning on page 145.

In addition, the Company has granted to the Joint Global Coordinators, on behalf of the institutionalunderwriters, the right to purchase up to an additional 3,750,000 shares solely to cover over-allotments, ifany. The institutional underwriters expect to deliver the shares to purchasers on or about July 24, 2001.

Joint Global Coordinators and Bookrunners

Merrill Lynch International UniCredit Banca Mobiliare S.p.A.

Co-Lead Manager

Schroder Salomon Smith Barney

Co-Manager

EUROMOBILIARE SIM S.p.A.

The date of this oÅering memorandum is July 19, 2001

Brought to you by Global Reports

THIS OFFERING MEMORANDUM DOES NOT CONSTITUTE AN OFFER TO SELL, OR ASOLICITATION OF AN OFFER TO BUY, ANY SHARES OFFERED BY ANY PERSON IN ANYJURISDICTION IN WHICH IT IS UNLAWFUL FOR SUCH PERSON TO MAKE SUCH ANOFFER OR SOLICITATION. NEITHER THE DELIVERY OF THIS OFFERING MEMORANDUMNOR ANY SALE MADE HEREUNDER SHALL UNDER ANY CIRCUMSTANCES IMPLY THATTHERE HAS BEEN NO CHANGE IN OUR AFFAIRS OR THOSE OF OUR SUBSIDIARIES ORTHAT THE INFORMATION SET FORTH IN THIS OFFERING MEMORANDUM IS CORRECTAS OF ANY DATE SUBSEQUENT TO THE DATE HEREOF.

This oÅering memorandum is highly conÑdential and has been prepared by us solely for use inconnection with the proposed institutional oÅering of our shares. We and the institutional underwritersreserve the right to reject any oÅer to purchase, in whole or in part, for any reason, or to sell less than allof the shares oÅered hereby. This oÅering memorandum is personal to the person to whom it has beenoÅered and delivered by the institutional underwriters and does not constitute an oÅer to any person or tothe public in general to subscribe or otherwise acquire the shares. Distribution of this oÅeringmemorandum to any other person (including those persons, if any, retained to advise such person withrespect to the oÅering) is unauthorized, and any disclosure of any of its contents, without our prior writtenconsent, is prohibited. By accepting delivery of this oÅering memorandum, you agree to the aboveconditions and to make no photocopies of this oÅering memorandum.

You also acknowledge that (i) you have not relied on the institutional underwriters or any personaÇliated with the institutional underwriters in connection with any investigation of the accuracy of suchinformation or your investment decision and (ii) no person has been authorized to give any information orto make any representation concerning De' Longhi or the shares (other than as contained in this oÅeringmemorandum) and, if given or made, any such other information or representation should not be reliedupon as having been authorized by us, De' Longhi SoparÑ S.A. (as the controlling shareholder) or theinstitutional underwriters.

IN MAKING AN INVESTMENT DECISION, YOU MUST RELY ON YOUR OWN EXAMINA-TION OF THE COMPANY AND THE TERMS OF THE GLOBAL OFFERING, INCLUDING THEMERITS AND RISKS INVOLVED. THE SHARES HAVE NOT BEEN RECOMMENDED BY ANYFEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY. FUR-THERMORE, SUCH AUTHORITIES HAVE NOT CONFIRMED THE ACCURACY OR DETER-MINED THE ADEQUACY OF THIS DOCUMENT. ANY REPRESENTATION TO THECONTRARY IS A CRIMINAL OFFENSE IN THE UNITED STATES.

THESE SECURITIES ARE SUBJECT TO RESTRICTIONS ON TRANSFERABILITY ANDRESALE AND MAY NOT BE TRANSFERRED OR RESOLD EXCEPT AS PERMITTED UNDERTHE SECURITIES ACT AND APPLICABLE STATE SECURITIES LAWS, PURSUANT TOREGISTRATION OR EXEMPTION THEREFROM. YOU SHOULD BE AWARE THAT YOU MAYBE REQUIRED TO BEAR THE FINANCIAL RISKS OF THIS INVESTMENT FOR ANINDEFINITE PERIOD OF TIME.

NO REPRESENTATION OR WARRANTY, EXPRESS OR IMPLIED, IS MADE BY THEINSTITUTIONAL MANAGERS AS TO THE ACCURACY OR COMPLETENESS OF THEINFORMATION SET FORTH IN THIS OFFERING MEMORANDUM, AND NOTHING CON-TAINED IN THIS OFFERING MEMORANDUM IS, OR SHALL BE, RELIED UPON AS APROMISE OR REPRESENTATION, WHETHER AS TO THE PAST OR THE FUTURE. THEINSTITUTIONAL UNDERWRITERS HAVE NOT INDEPENDENTLY VERIFIED ANY SUCHINFORMATION AND ASSUME NO RESPONSIBILITY FOR ITS ACCURACY ORCOMPLETENESS.

We are not, and none of the institutional underwriters or any of their respective representatives is,making any representation to any oÅeree or purchaser of the shares oÅered hereby regarding the legality ofan investment by such oÅeree or purchaser under appropriate legal, investment or similar laws. Eachinvestor should consult with his or her own advisers as to the legal, tax, business, Ñnancial and relatedaspects of a purchase of the shares.

In connection with the Global OÅering, Merrill Lynch International or certain of its aÇliates oragents, on behalf of the institutional underwriters, may over-allot or eÅect transactions which stabilize ormaintain the market price of the ordinary shares at levels above those which might otherwise prevail in theopen market. Such transactions may be eÅected on the Telematico, in the over-the-counter markets orotherwise. Such stabilizing, if commenced, may be discontinued at any time and must in any event bediscontinued 30 calendar days after the commencement of trading of the shares on the Telematico.

i

Brought to you by Global Reports

NOTICE TO NEW HAMPSHIRE RESIDENTS ONLY

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FORA LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIREREVISED STATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT ASECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OFNEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE OF NEWHAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE ANDNOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION ISAVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OFSTATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, ORRECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION.IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PUR-CHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THEPROVISIONS OF THIS PARAGRAPH.

INFORMATION FOR PROSPECTIVE INVESTORS IN THE NETHERLANDS

Each institutional manager understands and agrees that any of the shares that are oÅered in TheNetherlands shall, in order to comply with the Netherlands Securities Market Supervision Act 1995 (Wettoezicht eÅectenverkeer 1995, hereinafter the ""WTE''), only be oÅered to individuals or legal entitiessituated in The Netherlands who or which trade or invest in securities in the conduct of a business orprofession (which includes banks, securities Ñrms, insurance companies, pension funds, investmentinstitutions, central governments, large international and supranational organizations, other institutionalinvestors and other parties, including treasury departments of commercial enterprises, which are regularlyactive in the Ñnancial markets in a professional manner), in which case (i) it must be made clear bothupon making the oÅer and in any document or advertisement in which a forthcoming oÅering of suchshares is publicly announced (whether electronically or otherwise) that such oÅer is exclusively made tothe said individuals or legal entities; and (ii) a copy of this oÅering memorandum must be submitted tothe Dutch Securities Board (Stichting Toezicht EÅectenverkeer) before the oÅer date.

JAPAN

The shares have not been and will not be registered under the Securities and Exchange Law of Japan.Accordingly, each institutional underwriter has represented and agreed that it has not, directly orindirectly, oÅered or sold and will not, directly or indirectly, oÅer or sell, shares in Japan or to any personresident in Japan for Japanese securities law purposes, including any corporation or other entity organizedunder the laws of Japan, except pursuant to an exemption from the registration requirements of, andotherwise in compliance with, the Securities and Exchange Law.

NOTICE TO PROSPECTIVE INVESTORS IN THE UNITED KINGDOM

Neither this oÅering memorandum nor any document issued in connection with the Global OÅeringmay be issued or passed on in the United Kingdom except to a person who is of a kind described inArticle 11(3) of the Financial Services Act 1986 (Investment Advertisements) (Exemptions) Order 1996or is a person to whom such document may otherwise lawfully be issued or passed on.

SALES OF SHARES IN CANADA

A prospectus has not and will not be Ñled to qualify the sale of the shares in Canada or any Provinceor Territory thereof. Shares are not and may not be oÅered or sold, directly or indirectly, in any Provinceor Territory of Canada or to or for the account of any resident of Canada except pursuant to an exemptionfrom the applicable registration and prospectus Ñling requirements, and otherwise in compliance with theapplicable securities laws and regulations of such Province or Territory.

ii

Brought to you by Global Reports

INFORMATION FOR PROSPECTIVE INVESTORS IN AUSTRALIA

This oÅering memorandum has not been lodged with any regulatory authority in Australia. Apurchaser of the shares in Australia may be required to prepare and lodge an Australian Corporations Lawcompliant prospectus in relation to the shares if such person on-sells the shares within 12 months of theirissue if the on-sale is to be made to a person who is a sophisticated or professional investor within themeaning of section 708(8) or 708(11) of the Australian Corporations Law.

BELGIUM

The shares will not be oÅered publicly, directly or indirectly, in Belgium at the time of the GlobalOÅering. The oÅering has not been notiÑed to, and this oÅering memorandum has not been approved by,the Belgian Banking and Finance Commission. The shares may only be sold in Belgium to professionalinvestors as deÑned in Article 3 of the Royal Decree of July 7, 1999 on the public nature of Ñnancialtransactions, acting for their own account, and this oÅering memorandum may not be delivered or passedon to any other investors.

SPAIN

The oÅering of our shares has been registered with the Spanish Securities Market Commission(Comisi πon Nacional del Mercado de Valores) as a partial exemption of a public oÅering addressed toinstitutional investors only and subject to a limited Ñling pursuant to Article 7.1(a) of Royal Decree 291 ofMarch 27, 1992 relating to issues and public oÅerings (the ""Royal Decree''). In Spain, this oÅering is,therefore, solely and exclusively addressed to institutional investors as deÑned under Article 7.1(a) of theRoyal Decree, and any subsequent transfers of our shares oÅered pursuant to this oÅering memorandummay be carried out only to other investors who also qualify as institutional investors for the purposes ofArticle 7.1(a) of the Royal Decree. Accordingly, each purchaser shall be deemed to accept and representthat it will not resell the shares other than to institutional investors.

ITALY

The oÅer of the shares in the institutional oÅering has been notiÑed together with the oÅer of aminimum of 9,600,000 shares to the public in Italy to the Commissione Nazionale per le Societ fia e laBorsa (or ""CONSOB''), the Italian Securities and Exchange Commission. This oÅering memorandum hasnot been and will not be submitted to the clearance procedures of CONSOB and accordingly may not beused in connection with any oÅer or sale of the shares in Italy. For the purposes of the Italian publicoÅering in Italy, we have prepared a prospetto informativo in the Italian language. Any sale of shares inthe institutional oÅering in Italy will only be made to ""Professional investors'' as deÑned in CONSOBRegulation No. 11522 of July 1, 1998, as amended and adopted pursuant to Legislative Decree No. 58 ofFebruary 24, 1998 (the ""UniÑed Financial Act''), other than asset management companies authorized tomanage investment portfolios in accordance with investment instructions given on a discretionary client-by-client basis and Ñduciary companies (societ fia Ñduciarie) managing portfolio investments (regulated bySection 60, paragraph 4 of Legislative Decree No. 415 of July 23, 1996). Any such oÅer or sale or anydistribution of this oÅering memorandum or any rendering of advice in respect of investment in the shareswithin Italy and in connection with this oÅering must be conducted either by registered securities dealingfirms (societ fia d'intermediazione mobiliare or ""SIMs'') or by authorized banks or investment Ñrms, asdescribed by the UniÑed Financial Act and CONSOB Regulation No. 11522 of July 1, 1998. After thecompletion of the distribution, each of the institutional underwriters is required promptly to give writtennotice to CONSOB of the names of each of their Italian professional investors and to give written noticeof the total number of shares they have sold to these professional investors.

ENFORCEMENT OF JUDGMENTS

We are a limited liability company (also referred to as a ""societ fia per azioni'' or ""S.p.A.'' in Italy)organized and existing under the laws of Italy. All of our directors and most of our executive oÇcers (andtheir equivalents) reside outside the United States, principally in Italy. In addition, a substantial portion ofour assets and the assets of such persons is located outside the United States. As a result, it may not bepossible for investors to eÅect service of process within the United States upon us or any such other personor to enforce in a United States court against us or such other persons any judgments obtained in suchcourts whether or not predicated upon the civil liability provisions of the federal or state securities laws ofthe United States.

iii

Brought to you by Global Reports

We have been advised by our Italian legal counsel, Bonelli Erede Pappalardo, that, subject to thequaliÑcations described below, recognition and enforcement in Italy of Ñnal judgments of U.S. courts,including judgments obtained in actions predicated upon the civil liability provisions of the U.S. federalsecurities laws, is automatic and will not require retrial on the merits if, among other things: (i) the U.S.courts have jurisdiction in accordance with Italian law and have rendered a Ñnal judgment; (ii) processhas been appropriately served on the defendant in accordance with applicable U.S. laws and nofundamental right of the defense has been violated; (iii) the parties have had an opportunity to be heardin accordance with applicable U.S. law or, if the judgment has been obtained by default, such default hasbeen declared in accordance with applicable U.S. laws; (iv) there is no conÖicting Ñnal judgment by anItalian court or an action pending in Italy that commenced prior to the commencement of the proceedingbefore the U.S. court among the same parties and arising from the same facts and circumstances; and(v) the content of the U.S. judgment does not violate Italian public policy.

We have also been advised by Bonelli Erede Pappalardo that in original actions brought before Italiancourts there is doubt as to the enforceability of liabilities based solely on the U.S. federal securities lawsand that, in original actions, Italian courts do not only apply Italian rules of civil procedure but also applycertain substantive provisions of Italian law that are regarded as mandatory.

FORWARD-LOOKING STATEMENTS

This oÅering memorandum includes forward-looking statements. In particular, forward-lookingstatements are included under ""Summary'', ""Risk Factors'', ""Use of Proceeds'', ""Dividends'', ""OurBusiness'' and ""Management's Discussion and Analysis of Financial Condition and Results of Operations''.When used in this oÅering memorandum, the words ""intend(s)'', ""aim(s)'', ""expect(s)'', ""will'', ""may'',""believe(s)'', ""should'', ""anticipate(s)'', and similar expressions are intended to identify forward-lookingstatements. We have based these forward-looking statements on our current expectations and projectionsabout future events. These forward-looking statements are subject to risks, uncertainties and assumptionsabout us which could cause actual results to diÅer materially from those projected, including, among otherthings, our ability to develop and expand our business; our ability to expand our product lines; our futurecapital spending and investments; our ability to control and reduce costs; our ability to develop, implementand maintain new technologies; our ability to improve the design of our products; and the eÅects ofregulation in Italy and in foreign jurisdictions in which we manufacture or sell our products.

Additional factors that could cause actual results, performance or achievements to diÅer materiallyinclude, but are not limited to, those discussed under ""Risk Factors''.

These forward-looking statements speak only as of the date of this oÅering memorandum.

We undertake no obligations to publicly update or revise any forward-looking statements, whether as aresult of new information, future events or otherwise. In light of these risks, uncertainties and assumptions,the forward-looking events discussed in this oÅering memorandum might not occur. Any statementsregarding past trends or activities should not be taken as a representation that such trends or activities willcontinue in the future. You are urged to carefully review and consider the various disclosures made by usin this oÅering memorandum which attempt to advise you of the factors which aÅect our business.

iv

Brought to you by Global Reports

TABLE OF CONTENTS

Page Page

Presentation of Financial and Other Description of Share Capital ÏÏÏÏÏÏÏÏÏÏÏÏ 125InformationÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1 Exchange Control PolicyÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 133

SummaryÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 5 Taxation of SharesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 134Risk Factors ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 13 Plan of Distribution ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 142Use of Proceeds ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 20 Transfer Restrictions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 145Market Information ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 21 Legal MattersÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 145Dividends and Dividends PolicyÏÏÏÏÏÏÏÏÏÏ 23 Independent Accountants ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 145Exchange Rates ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 25 Available Information ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 146Capitalization ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 27 Index to Financial Statements ÏÏÏÏÏÏÏÏÏÏÏ F-1Dilution ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 28 Annex AÌSummary of SigniÑcantSelected Financial and Other Data ÏÏÏÏÏÏÏ 29 DiÅerences Between Italian and U.S.

GAAP ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ A-1Management's Discussion and Analysis ofFinancial Condition and Results of Annex BÌSummary of SigniÑcantOperationsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 34 DiÅerences Between Italian and U.K.

GAAP With Respect to KenwoodOur BusinessÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 62Appliances plc Unaudited Restated

The Kenwood AcquisitionÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 102 Consolidated Financial InformationÏÏÏÏÏ B-1Unaudited Combined Pro Forma Financial Annex CÌExplanatory Note of

Statements ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 106 Aggregations in the OÅeringOur ManagementÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 113 Memorandum of the Kenwood

Consolidated Financial Statements ÏÏÏÏÏ C-1Our Principal ShareholdersÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 120

Certain Transactions with Related Parties 121

v

Brought to you by Global Reports

[THIS PAGE INTENTIONALLY LEFT BLANK]

Brought to you by Global Reports

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

The Ñnancial information contained in this oÅering memorandum, unless otherwise speciÑed, has beenprepared in accordance with accounting principles prescribed by Italian law, as supplemented by theaccounting principles promulgated by the Consiglio Nazionale dei Dottori Commercialisti e dei Ragionieri(together referred to as ""Italian GAAP''), which diÅer in certain material respects from generallyaccepted accounting principles in the United States (""U.S. GAAP'') or in the United Kingdom(""U.K. GAAP''). SigniÑcant diÅerences exist between Italian GAAP, U.S. GAAP and U.K. GAAPwhich might be material to the Ñnancial information contained herein. We have made no attempt toquantify the impact of those diÅerences. In making an investment decision, you should rely upon your ownexamination of the Company, the terms of the oÅering and the Ñnancial information relating to theCompany and the oÅering. You should consult your own professional advisers for an understanding of thediÅerences between Italian GAAP, U.S. GAAP and U.K. GAAP, and how these diÅerences might aÅectthe Ñnancial information herein. For descriptions of certain signiÑcant diÅerences between Italian GAAPand U.S. GAAP, as applicable to us, you should refer to ""Annex A Ì Summary of SigniÑcant DiÅerencesBetween Italian and U.S. GAAP''. For descriptions of certain signiÑcant diÅerences between ItalianGAAP and U.K. GAAP, as applicable to Kenwood, you should refer to ""Annex B Ì Summary ofSigniÑcant DiÅerences Between Italian and U.K. GAAP With Respect to Kenwood Appliances plcUnaudited Restated Consolidated Financial Information''.

During the course of 2000, we restructured our consolidated group with the aim of rationalizing ourorganizational structure and purchased certain companies which, although part of our core businesses,previously were owned by our parent company. As part of the restructuring process, we also sold certaincompanies which we believed were no longer strategic to our core businesses. You should refer to ""OurBusiness Ì Restructuring'' and ""Certain Transactions With Related Parties Ì Transactions with RelatedParties Involving Transfer of Group Securities'' for a more detailed description of this process.

On February 24, 2000, we acquired 91.66% of the share capital of Sile Corpi Scaldanti S.r.l., anItalian manufacturer and distributor of heating products, and on May 24, 2001, we completed our cashtender oÅer for all of the share capital of Kenwood Appliances plc (""Kenwood''), an English registeredcompany specializing in the manufacture and sale of small domestic appliances internationally under theKenwood and Ariete brand names. The acquisition of Kenwood was material. You should refer to ""OurBusiness Ì Recent Acquisitions'' and ""The Kenwood Acquisition'' for a more detailed description of theseacquisitions.

This oÅering memorandum contains the following Ñnancial statements:

(i) the ""Audited De' Longhi Consolidated Financial Statements'', comprising the auditedhistorical consolidated balance sheets of the Group at December 31, 1998, 1999 and 2000and the income statements and statements of changes in shareholders' equity and cash Öowstatements of the Group for the years ended December 31, 1999 and 2000 (including thenotes thereto). The Audited De' Longhi Consolidated Financial Statements have beenaudited by our independent auditor, PricewaterhouseCoopers S.p.A.(""PricewaterhouseCoopers''), whose audit reports are set forth elsewhere in this oÅeringmemorandum;

(ii) the ""Unaudited De' Longhi Pro Forma Consolidated Financial Statements'', comprising theunaudited pro forma balance sheets and income statements of the Group (including thenotes thereto) at and for the years ended December 31, 1998, 1999 and 2000, derived from:

‚ the Audited De' Longhi Consolidated Financial Statements;

‚ the audited annual Ñnancial statements of each of DL Radiators S.p.A. for 2000,De' Longhi Radiators S.r.l. for each of 1998 and 1999 and Climaveneta S.p.A. andErgoklima S.p.A. for each of 1998, 1999 and 2000, which have been audited by ourindependent auditor, PricewaterhouseCoopers; and

‚ the unaudited annual Ñnancial statements of De' Longhi Divisione Cucine S.p.A.,Micromax S.p.A. and Sile Corpi Scaldanti S.r.l.

1

Brought to you by Global Reports

The Unaudited De' Longhi Pro Forma Consolidated Financial Statements have beenadjusted to reÖect:

‚ the purchase on February 28, 2000 of a controlling interest in Sile Corpi Scaldanti S.r.l.,as if such acquisition had occurred on January 1, 1998. At the time of the acquisition,Sile Corpi Scaldanti S.r.l. represented approximately 0.4% of our total consolidated assets,0.6% of our total revenues and 0.9% of our net income, in each case as compared to ourconsolidated Ñnancial statements as of December 31, 1999 and for the year then ended;

‚ the purchase in December 2000, as part of our restructuring, of a controlling interest ineach of De' Longhi Divisione Cucine S.p.A., DL Radiators S.p.A., Climaveneta S.p.A.and Micromax S.p.A., together with 30% of the share capital of Ergoklima S.p.A., ineach case as if such acquisitions had occurred on January 1, 1998. At the time of theacquisition, these companies represented, in the aggregate, approximately 26.6% of ourconsolidated total assets, 25.0% of our total revenues and 17.5% of our net income, ineach case as compared to our consolidated Ñnancial statements as of December 31, 1999and for the year then ended;

‚ the sale in December 2000, as part of our restructuring, of Immobiliare FindomesticS.r.l., De' Longhi Radiators S.r.l., DL Canada Distributors Inc., 850721 Ontario Ltd. andE.S.C S.p.A., together with the sale of a controlling interest (equal to 60% of its sharecapital) of Nauta S.r.l., in each case as if such sale had occurred on January 1, 1998; and

‚ a capital increase of Lit. 250,587 million eÅected in April 2001 (thereby increasing ourtotal capitalization to Lit. 650,587 million), as if such capital increase had been eÅectedon January 1, 1998.

The Unaudited De' Longhi Pro Forma Consolidated Financial Statements have beenadjusted to reÖect an increase in our debt resulting from the payment for the companies wepurchased in 2000 and a reduction in our net debt due to the capital increase referred toabove. You should note that the purchase contracts for the companies we acquired inDecember 2000 as part of our restructuring process and referred to above includedapproximately Lit. 504,714 million in interest-free debt and, as a result, the Unaudited De'Longhi Pro Forma Consolidated Financial Statements do not include a charge for implicitinterest expense. In addition, the capital increase eÅected in April 2001 is treated as non-interest bearing for purposes of the Unaudited De' Longhi Pro Forma Consolidated FinancialStatements;

(iii) the ""Audited Kenwood Consolidated Financial Statements'', comprising the auditedhistorical consolidated balance sheets and income statements, statements of changes inshareholders' equity and cash Öow statements of Kenwood at and for the Ñscal years endedApril 2, 1999 and March 31, 2000 and 2001 (including the notes thereto). The AuditedKenwood Consolidated Financial Statements have been prepared in accordance with U.K.GAAP and have been audited by Ernst & Young, independent auditors, whose audit reportis set forth elsewhere in this oÅering memorandum;

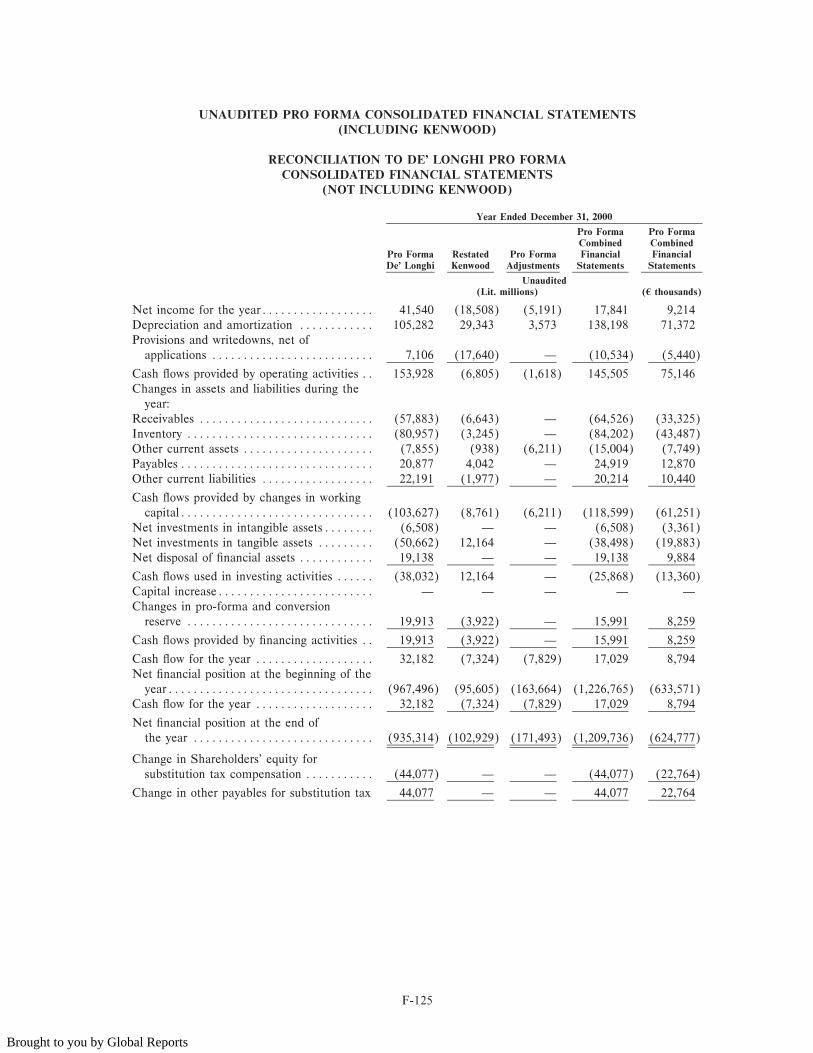

(iv) the ""Unaudited Combined Pro Forma Financial Statements'' of the Group, as at and for theyears ended December 31, 1998, 1999 and 2000 (referred to, together with the UnauditedDe' Longhi Pro Forma Consolidated Financial Statements, as the ""Unaudited Pro FormaFinancial Statements''), derived from:

‚ the Unaudited De' Longhi Pro Forma Consolidated Financial Statements; and

‚ the ""Unaudited Restated Kenwood Consolidated Financial Statements'' based on theAudited Kenwood Consolidated Financial Statements, which have been restated for eachyear to reÖect a Ñscal year ended December 31, 1998, 1999 and 2000 and to reÖectItalian GAAP. For a description of aggregations used to prepare such Ñnancial statementsunder Italian GAAP, you should refer to ""Annex C Ì Explanatory Note of Aggregationsin the OÅering Memorandum of the Kenwood Consolidated Financial Statements''.

The Unaudited Combined Pro Forma Financial Statements, in addition to the adjustmentsmade to the Unaudited De' Longhi Pro Forma Consolidated Financial Statements referred toabove, have been adjusted to reÖect the acquisition of Kenwood as if such acquisition hadoccurred on January 1, 1998; and

2

Brought to you by Global Reports

(v) the ""Unaudited Interim De' Longhi Consolidated Financial Statements'', comprising theunaudited interim historical consolidated balance sheets and income statements and cash Öowstatements of the Group at and for the three months ended March 31, 2000 and 2001(including the notes thereto).

The Unaudited Pro Forma Financial Statements have been prepared for informational purposes only.We did not control Sile Corpi Scaldanti S.r.l. or Kenwood on January 1, 1998 nor did we operate theirbusinesses in any period prior to the respective closing dates for such acquisitions. Consequently, theUnaudited Pro Forma Financial Statements do not purport either to represent what our consolidatedresults of operations would actually have been if the acquisitions had taken place on January 1, 1998 or toproject our consolidated results of operations at any future date or for any future periods. You should alsorefer to the notes to the Unaudited De' Longhi Pro Forma Consolidated Financial Statements and theUnaudited Combined Pro Forma Financial Statements for a description of the assumptions used in thepresentation of these Ñnancial statements.

In Italy, there are no standards governing the preparation of pro forma Ñnancial statements. Althoughthe Unaudited Pro Forma Financial Statements have been prepared using the best practices as identiÑedand disclosed by CONSOB, such Ñnancial statements do not take into account standards generallyaccepted in other jurisdictions, in particular the United States and the United Kingdom. Accordingly, thepresentation, assumptions and adjustments of the Unaudited Pro Forma Financial Statements may diÅersigniÑcantly from those in other jurisdictions. Investors are cautioned against placing undue reliance on theUnaudited Pro Forma Financial Statements. You should refer to ""Risk Factors Ì Risks Relating to theCompany and the Group Ì The pro forma Ñnancial information included in this oÅering memorandumdoes not represent our actual historical results of operations''. The Unaudited De' Longhi Pro FormaConsolidated Financial Statements have been examined by PricewaterhouseCoopers, to the extent and asmore fully described in the report of independent auditors relating thereto included elsewhere in thisoÅering memorandum.

For convenience only, we have translated certain Lira Ñgures into Euro at the Ñxed exchange rateestablished by the European Council of Ministers on December 31, 1998 between the Lira and the Euroof Lit. 1,936.27 • 41.00. The exchange rate between Lire and U.S. dollars represents the Lire equivalent(at the Ñxed Lira/Euro rate) of Lit. 2,265 • $1.00, the Noon Buying Rate in the City of New York forcable transfers in foreign currencies as announced by the Federal Reserve Bank of New York for customspurposes on July 16, 2001. To obtain a current formulation of the value of Italian Lira amounts in U.S.dollars, you must Ñrst convert Lire into Euro at the Ñxed Lira/Euro conversion of Lit. 1,936.27 • 41.00,and then convert the resulting Euro amount into U.S. dollars at the prevailing exchange rate. By includingconvenience currency translations in this oÅering memorandum, we are not representing that the Liraamounts actually represent the dollar amounts shown or could be converted into dollars at the ratesindicated. For information about the exchange rate between the Lire and U.S. dollar for periods from 1996through July 16, 2001 and between the U.S. dollar and the Euro since January 1, 1999, you should referto ""Exchange Rates and the European Monetary System''.

‚ References to ""dollars'', ""$'' and ""U.S. dollars'' are to United States dollars;

‚ References to ""pounds'' or ""'' are to the British pound sterling;

‚ References to ""Lire'', ""Lira'' or ""Lit.'' are to Italian Lire;

‚ References to ""4'' or ""Euro'' are to the Euro, the single currency established for participants inthe third stage of the European Monetary Union, or EMU. You should also refer to ""ExchangeRates and the European Monetary System''; and

‚ References to ""billion'' or ""bn'' mean a thousand million.

In preparing our Ñnancial statements, we present Ñnancial data in millions of Lire. For theconvenience of the reader in this oÅering memorandum, unless otherwise not available, we have roundedmost Ñnancial data to millions of Lire. As a result of this rounding, the totals of the data presented hereinmay vary slightly from the actual arithmetic totals of such data. In the tables herein, a dash (""Ì'')represents no value while the number ""0.0'' (or ""(0.0)'') represents a rounded amount. Additionally,percentage Ñgures that would otherwise be derived by dividing by zero have also been represented by adash.

Unless otherwise indicated, information and statistics presented herein regarding market trends,market volumes, our market share and our market share relative to competitors are based primarily on

3

Brought to you by Global Reports

data derived from publicly available sources. This oÅering memorandum speciÑcally contains marketinformation and data relating to the business segments and geographic areas in which we operate. Theprincipally available source used by us for Italy, AC Nielsen, tracks sales for relevant products and marketsegments with respect to the retail distribution channel only. On a pro forma basis (excluding Kenwood),our sales to retailers represented approximately 71.4% of our consolidated sales revenues in 2000. Youshould refer to ""Our Business Ì Marketing and Sales''. Homogenous sources for market data are notavailable for all of our products and geographic segments. In order to provide statistically signiÑcantinformation on the size and performance of the market segments in which we operate, we have prepareddata based on a comparison, regrouping and combination of data reported by a number of oÇcial andindependent sources. Market data and estimates with respect to the diÅerent market segments in whichwe operate have been derived, in part, from AC Nielsen, Air Conditioners Index (September 2000);AC Nielsen, Durable Service Italia (September 2000); Gesellschaft F ur Konsumforschung, Durable GoodsPanel (October 2000) and RIC Research Corp. Year Data Book (1999 and 2000). For certain marketswhere independent public sources are not available, we have prepared estimates based on available dataderived from our distributors or other sources which we deemed relevant. As a result, you should note thatthe market data presented in this oÅering memorandum, as it applies to individual market segments, maybe only a partial representation of the broader market to which the product segment belongs.

In this oÅering memorandum, the terms the ""Company'' or ""De' Longhi'' refer to De' Longhi S.p.A.Unless the context indicates otherwise, the terms ""we,'' ""us'', ""our'', ""the Group'' and the ""De' LonghiGroup'' refer to us and our consolidated subsidiaries as a combined entity. The terms the ""GlobalOÅering'' and ""oÅering'' refer to the international institutional oÅering and the Italian retail public oÅeringtogether. The term ""the shares'' refers to our ordinary shares, unless the context indicates otherwise, whichare being oÅered to you in this oÅering memorandum as part of this oÅering.

Unless otherwise speciÑed, statements contained in this oÅering memorandum assume no exercise ofthe institutional underwriters' over-allotment option.

4

Brought to you by Global Reports

SUMMARY

This summary contains basic information about this oÅering. It likely does not contain all theinformation that may be important to you. You should refer to this entire oÅering memorandum, includingthe Ñnancial data and the related notes, before making an investment decision. In particular, you shouldconsider carefully the factors set forth under the heading ""Risk Factors.''

Introduction

We are the Italian parent company of an international group of companies that manufactures anddistributes around the world quality leading products generally related to health and well-being under theDe' Longhi, Kenwood, Vetrella, Ariete, La Supercalor, Radel, Elba, Ariagel, Simac and Climaveneta brandnames, among others. Our product oÅerings comprise the following four market segments and businessareas:

‚ heating products, including portable heating units (such as oil-Ñlled radiators, electric convectorsand fan heaters), in which we believe we are a world leader, and terminal units for central heatingsystems (such as multi-column radiators, steel radiators and bathroom radiators);

‚ air conditioning and air treatment products (including portable and Ñxed-wall air conditioners,humidiÑers, dehumidiÑers and air puriÑers for both residential and industrial use), in which we area leader in Italy (Source: AC Nielsen, Air Conditioners Index, September 2000) and, with respectto our portable products, in which we believe we are a world leader;

‚ cooking and food preparation products (including electric ovens, deep-fryers, toasters, electricbarbecues, coÅee machines, free-standing stoves and food processors), in which we are the leaderin Italy and a leader in the United Kingdom (Source: AC Nielsen, Durable Service Italia,September 2000 and Gesellschaft F ur Konsumforschung, Durable Goods Panel, October 2000);and

‚ household cleaning and ironing products, including vacuum cleaners, steam cleaners and ironingsystems, in which we are generally recognized as a leader in Italy (Source: AC Nielsen, DurableService Italia, September 2000).

Competitive Strengths

We believe that our competitive strengths include the following:

‚ a focus on innovation;

‚ our experienced marketing network;

‚ our brand name recognition;

‚ state-of-the-art manufacturing capabilities;

‚ an extensive distribution and sales network;

‚ our signiÑcant experience in integrating companies into our group; and

‚ manufacturing and distribution synergies resulting from our recent acquisition of Kenwood.

Strategy

Our objective is to strengthen our position in markets where we have achieved leadership and toincrease our market share in other areas, with the aim of maximizing the return on investment for ourshareholders and achieving higher levels of proÑtability. In order to achieve these goals, we intend to:

‚ continue to develop innovative products;

‚ expand geographically by leveraging our distribution network and increasing our distributionchannels;

‚ strengthen our brand names;

‚ maintain control over key manufacturing processes and focus on our research and developmentprograms;

‚ increase our eÇciency; and

‚ continue to evaluate strategic opportunities.

5

Brought to you by Global Reports

Our Restructuring Process

During the course of 2000, we restructured the Group with the aim of rationalizing our organizationalstructure, and we purchased certain companies which, although part of our core businesses, were previouslyowned directly and indirectly by our parent company. As a result of the restructuring, we acquired,through our wholly owned subsidiary De' Longhi Pinguino S.A., a controlling interest in each of De'Longhi Divisione Cucine S.p.a., DL Radiators S.p.A., Climaveneta S.p.A. and Micromax S.p.A., togetherwith 30% of the share capital of Ergoklima S.p.A., for an aggregate amount equal to Lit. 538,889 million.At the time of our acquisition in December 2000, such companies represented, in the aggregate,approximately 26.6% of our consolidated total assets, 25.0% of our total revenues and 17.5% of our netincome, in each case as compared to our consolidated Ñnancial statements as of December 31, 1999 andfor the year then ended.

In addition, as part of the restructuring process, we sold certain companies which we believed were nolonger strategic to our core businesses to related parties for an aggregate amount equal to Lit. 32,301million (or approximately 416,682 thousand). This included the sale of all of the share capital ofImmobiliare Findomestic S.r.l., De' Longhi Radiators S.r.l., DL Canada Distributors Inc., 850721 OntarioLtd. and I.S.C. Ì Industrie Scambiatori di Calore S.p.A., together with a controlling interest (equal to60% of its share capital) of Societ fia Nauta S.r.l. You should refer to ""Certain Transactions With RelatedParties Ì Transactions with Related Parties Involving Transfers of Group Securities'' for a more detaileddescription of each of these companies, the terms and conditions of the above transactions and of ourrestructuring process generally.

Recent Acquisitions

On May 24, 2001, we completed the acquisition of Kenwood, an English company specializing in themanufacture and sale of small domestic appliances internationally under the Kenwood and Ariete brandnames. The aggregate total purchase price for the Kenwood shares was equal to 45.9 million (orapproximately Lit. 143,000 million), plus the assumption of approximately 18 million (or approximatelyLit. 56,000 million) of debt. At the time of the acquisition, Kenwood's total assets represented 12.5% ofour consolidated total assets, and Kenwood's revenues represented 37.8% of our total revenues, in eachcase as compared to our consolidated Ñnancial statements as of December 31, 2000 and for the year thenended. As of December 31, 2000, Kenwood's net debt position was equal to Lit. 102,928 million. Youshould refer to ""The Kenwood Acquisition'' for a more detailed description of Kenwood and its principalactivities.

In addition, on February 24, 2000, we acquired 91.66% of the outstanding share capital of Sile CorpiScaldanti S.r.l., an Italian manufacturer and distributor of heating products, for an aggregate purchaseamount equal to Lit. 4,583 million. At the time of the acquisition, Sile Corpi Scaldanti S.r.l.'s total assetsrepresented 0.4% of our consolidated total assets, its revenues represented 0.6% of our total revenues andits net income represented 0.9% of our total net income, in each case as compared to our consolidatedÑnancial statements as at December 31, 1999, and for the year then ended.

6

Brought to you by Global Reports

The Global OÅering

The Global OÅeringÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ The Global OÅering comprises the International OÅering andthe Italian Retail OÅering. The Global OÅering includes37,500,000 shares of capital stock of the Company, nominalvalue 43 per share, before the exercise of the over-allotmentoption referred to below. The closing of the Italian RetailOÅering and the International OÅering are conditional upon eachother.

International OÅering ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 27,900,000 shares are being oÅered by the institutional under-writers (the ""International OÅering'') (i) only to qualiÑedinstitutional buyers in the United States in reliance onRule 144A under the Securities Act and (ii) outside the UnitedStates in reliance on Regulation S under the Securities Act. Youshould refer to ""Plan of Distribution''.

Italian Retail OÅering ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 9,600,000 shares are being oÅered in Italy by way of a publicoÅering to retail investors (the ""Italian OÅering''), subject tominimum lots of 250 shares or multiples thereof.

OÅering Price ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Euro 3.4 per share.

Over-Allotment Option ÏÏÏÏÏÏÏÏÏÏÏÏÏ The Company has granted to Merrill Lynch International and toUniCredit Banca Mobiliare S.p.A. (for the beneÑt of theinstitutional underwriters) an option to purchase up to 3,750,000additional shares to cover any over-allotments. This option maybe exercised from the date of determination of the oÅering priceuntil 30 days after the commencement of trading of the shareson the Telematico. You should refer to ""Plan of Distribution''.

Ordinary Shares Outstanding beforethe Global OÅering ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 112,000,000 shares. You should refer to ""Description of Share

Capital''.

Ordinary Shares Outstanding afterthe Global OÅering ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 149,500,000 shares.

Use of Proceeds ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ We intend to use the net proceeds from this oÅering for generalcorporate purposes, including, among other things, to expand ouroperations, reduce our debt and for working capital needs. Youshould refer to ""Our Principal Shareholders''.

DividendsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Holders of the shares will be entitled to all dividends, if any,declared in subsequent Ñscal years. The declaration, payment andamount of any dividend is subject to the approval of theshareholders at the annual shareholders' meeting and will bedependent upon, among other things, the Ñnancial condition,results of operations, prospects, cash Öow, capital requirementsand reserves of the Company. You should refer to ""Dividends''and ""Description of Share Capital''.

7

Brought to you by Global Reports

Substitute Tax ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Dividends payable by the Company to non-residents of Italy aresubject to Italian substitute tax at a rate of 27%, which may bereduced by applicable treaties or conventions. You should referto ""Taxation of Shares Ì Italian Tax Considerations''.

Voting Rights ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Under Italian law, shareholders are entitled to one vote for eachshare held and are entitled to vote and attend ordinary andextraordinary meetings of the Company. You should refer to""Description of Share Capital Ì NotiÑcation of the Acquisitionof Shares and Voting Rights''.

Listing and Trading ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Prior to this oÅering, our shares have not been traded on anyexchange. An application has been made to list our shares on theTelematico. It is expected that trading on the Telematico willbegin on or around three working days after the date of pricing.You should refer to ""Risk Factors Ì Risks Relating to OurShares'' and ""Market Information''.

Joint Global CoordinatorsÏÏÏÏÏÏÏÏÏÏÏ Merrill Lynch International and UniCredit BancaMobiliare S.p.A. are joint global coordinators in respect of theGlobal OÅering. Merrill Lynch International and UniCreditBanca Mobiliare S.p.A. will act as joint lead managers and jointbookrunners of the International OÅering. UniCredit BancaMobiliare S.p.A. will act as lead manager of the Italian RetailOÅering.

Payment, Delivery and Settlement ÏÏÏÏ Payment for and delivery of the shares are expected to be madeon or about July 24, 2001. The shares will settle against paymentin Euro through the facilities of Monte Titoli (a centralizedsecurities depositary system) as well as through Euroclear andClearstream, Luxembourg. You should refer to ""Market Infor-mation Ì Clearance and Settlement in Italy''.

The ISIN for our shares is IT0003115950.

The Common Code for our shares is 132 77 877.

Lock-Up ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Each of the Company and De' Longhi SoparÑ S.A. (a companyindirectly controlled by Giuseppe De' Longhi), as the controllingshareholder, has agreed to certain restrictions relating to theissue or sale or other disposal of shares or other securitiesconvertible or exchangeable into the shares, subject to certainexceptions, during the period extending up to and including thedate falling 180 days after the Ñrst day of trading of the shareson the Telematico. See ""Plan of Distribution''.

Risk Factors ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ You should refer to ""Risk Factors'' and other informationincluded in this oÅering memorandum for a discussion of factorsthat should be considered before investing in our shares.

8

Brought to you by Global Reports

Summary Pro Forma and Historical Consolidated Financial Data

The selected unaudited pro forma and historical Ñnancial information set forth below has been derivedfrom the following Ñnancial statements included elsewhere in this oÅering memorandum:

‚ the Unaudited De' Longhi Pro Forma Consolidated Financial Statements as at and for the yearsended December 31, 1998, 1999 and 2000, derived from the Audited De' Longhi ConsolidatedFinancial Statements; the audited annual Ñnancial statements of DL Radiators S.p.A. for 2000,De' Longhi Radiators S.r.l. for each of 1998 and 1999, and Climaveneta S.p.A. and ErgoklimaS.p.A. for each of 1998, 1999 and 2000; and the unaudited annual Ñnancial statements of De'Longhi Divisione Cucine S.p.A., Micromax S.p.A and Sile Corpi Scaldanti S.r.l.

‚ the Unaudited Combined Pro Forma Financial Statements of the Group as at and for the yearsended December 31, 1998, 1999 and 2000, derived from the Unaudited De' Longhi Pro FormaConsolidated Financial Statements and the Unaudited Restated Kenwood Consolidated FinancialStatements based on the Audited Kenwood Consolidated Financial Statements (which have beenrestated for each year to reÖect a Ñscal year ended December 31 instead of March 31 and toreÖect Italian GAAP); and

‚ the Unaudited Interim De' Longhi Consolidated Financial Statements at and for the three monthsended March 31, 2000 and 2001.

The Unaudited Pro Forma Financial Statements have been adjusted, among other things, to reÖectthe purchase in 2000 of a controlling interest in each of De' Longhi Divisione Cucine S.p.A., DLRadiators S.p.A., Climaveneta S.p.A., Micromax S.p.A., Ergoklima S.p.A. and Sile Corpi Scaldanti S.r.l.,in each case as if such acquisitions had occurred on January 1, 1998. In addition, the Unaudited ProForma Consolidated Financial Statements have been adjusted to reÖect an increase in our debt resultingfrom the payment for the companies we purchased in 2000 and a corresponding reduction in our net debtdue to a capital increase of Lit. 250,587 million eÅected in April 2001. You should note that the purchasecontracts for the companies we acquired in December 2000 as part of our restructuring process andreÖected in such Ñnancial statements included approximately Lit. 504,714 million in interest-free debt and,as a result, the Unaudited Pro Forma Consolidated Financial Statements do not include a charge forimplicit interest expense. In addition, the capital increase eÅected in April 2001 is treated as non-interestbearing for purposes of the Unaudited De' Longhi Pro Forma Consolidated Financial Statements.

The foregoing Ñnancial statements have been prepared in accordance with Italian GAAP, whichdiÅers in signiÑcant respects from U.S. GAAP and U.K. GAAP. For descriptions of certain signiÑcantdiÅerences between Italian GAAP and U.S. GAAP, as applicable to the Company, you should refer to""Annex A Ì Summary of SigniÑcant DiÅerences Between Italian and U.S. GAAP''. For descriptions ofcertain signiÑcant diÅerences between Italian GAAP and U.K. GAAP, as applicable to Kenwood, youshould refer to ""Annex B Ì Summary of SigniÑcant DiÅerences Between Italian and U.K. GAAP WithRespect to Kenwood Appliances plc Unaudited Restated Consolidated Financial Information''. You shouldalso read the notes to the Unaudited De' Longhi Pro Forma Consolidated Financial Statements and theUnaudited Combined Pro Forma Financial Statements for a description of the assumptions used in thepresentation of these Ñnancial statements. The selected consolidated Ñnancial data set forth below shouldalso be read in conjunction with ""Presentation of Financial and Other Information'' and ""Management'sDiscussion and Analysis of Financial Condition and Results of Operations''.

9

Brought to you by Global Reports

Year ended December 31,

Unaudited De' Longhi Unaudited Combined Pro FormaPro Forma(1) (including Kenwood)(2)

1998 1999 2000 2000 1998 1999 2000 2000

(Lit. millions) (5 thousands) (Lit. millions) (5 thousands)

Income Statement Data:

Revenues:

Net sales ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,269,314 1,374,841 1,561,334 806,362 1,724,722 1,799,725 2,042,711 1,054,972

Other revenues ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 21,384 18,979 23,158 11,960 21,384 18,979 29,470 15,220

Total revenuesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,290,698 1,393,820 1,584,492 818,322 1,746,106 1,818,704 2,072,181 1,070,192

Operating costs:

Materials, consumables and

goods ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 630,240 637,305 714,053 368,778 869,195 885,304 1,026,265 530,022

Services ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 263,697 288,996 354,763 183,220 367,348(3) 375,627(3) 450,831(3) 232,835(3)

Rents, leases and related costs ÏÏÏ 13,016 12,467 14,379 7,426 Ì Ì Ì Ì

Other costs ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 21,128 17,874 10,867 5,612 21,128 17,874 10,867 5,612

Total production costs ÏÏÏÏÏÏÏÏ 928,081 956,642 1,094,062 565,036 1,257,671 1,278,805 1,487,963 768,469

Value added margin(4) ÏÏÏÏÏÏÏÏ 362,617 437,178 490,430 253,286 488,435 539,899 584,218 301,723

Wages, salaries and beneÑts ÏÏÏÏÏ 202,160 213,311 235,795 121,778 279,603 275,942 290,807 150,189

Gross operating margin ÏÏÏÏÏÏÏ 160,457 223,867 254,635 131,508 208,832 263,957 293,411 151,534

Depreciation and amortization ÏÏÏ 70,834 77,084 75,030 38,750 89,589 94,872 94,075 48,586

Amortization of goodwill ÏÏÏÏÏÏÏÏ 30,251 30,311 30,252 15,624 43,142 43,417 44,123 22,788

Provisions and write-oÅs ÏÏÏÏÏÏÏÏ 28,576 15,942 17,806 9,196 31,714 18,169 17,806 9,196

Operating proÑtÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 30,796 100,530 131,547 67,938 44,387 107,499 137,407 70,964

Net Ñnancial loss ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (73,187) (33,399) (45,418) (23,456) (98,580) (55,203) (68,856) (35,561)

Income from equity investmentsÏÏ 1,818 3,857 8,321 4,297 1,818 3,857 8,321 4,297

Extraordinary (loss) income ÏÏÏÏÏ (3,410) (4,116) 4,707 2,431 (14,391) (44,657) (4,520) (2,334)

Earnings before taxes and

minority interests ÏÏÏÏÏÏÏÏÏÏ (43,983) 66,872 99,157 51,210 (66,766) 11,496 72,352 37,366

Income taxesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 427 26,355 57,413 29,651 37 25,269 54,307 28,047

Net (loss) income before

minority interests ÏÏÏÏÏÏÏÏÏÏ (44,410) 40,517 41,744 21,559 (66,803) (13,773) 18,045 9,319

Minority interests ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 271 72 (204) (105) 271 72 (204) (105)

Net (loss) income ÏÏÏÏÏÏÏÏÏÏÏ (44,139) 40,589 41,540 21,454 (66,532) (13,701) 17,841 9,214

Other Financial Data:

EBITDA(5) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 131,881 207,925 236,829 122,312 177,118 245,788 275,605 142,338

Capital expendituresÏÏÏÏÏÏÏÏÏÏÏÏ 72,990 37,259 52,394 27,059 89,757 54,765 63,768 32,933

Net working capital ÏÏÏÏÏÏÏÏÏÏÏÏ 553,934 524,255 638,194 329,600 688,820 651,026 779,286 402,468

Total assets ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 2,288,484 2,312,542 2,371,235 1,224,641 2,779,113 2,769,282 2,800,185 1,446,174

Net Ñnancial position ÏÏÏÏÏÏÏÏÏÏÏ 1,208,825 967,496 935,314 483,049 1,476,153 1,226,765 1,209,735 624,776

Shareholders' equity ÏÏÏÏÏÏÏÏÏÏÏÏ 551,765 706,348 723,724 373,772 623,246 736,179 725,519 374,699

(1) Prepared to give pro forma eÅect to the restructuring of the Group (including the acquisition and sale of various companies)

eÅected in 2000 and a capital increase of Lit. 250,587 million at nominal value in April 2001. You should refer to the

Unaudited De' Longhi Pro Forma Consolidated Financial Statements (including the notes thereto) for a discussion of the

assumptions used to prepare these Ñnancial statements.

(2) Prepared to reÖect the acquisition of all of the share capital of Kenwood in early 2001 as if such acquisition had occurred on

January 1, 1998. You should also refer to ""The Kenwood Acquisition'' and ""Unaudited Combined Pro Forma Financial

Statements''.

(3) Services expenses include rents, leases and related costs.

(4) Total revenues less total production costs.

(5) Operating earnings before interest, taxes and depreciation and amortization.

10

Brought to you by Global Reports

The summary consolidated historical Ñnancial information in the following table has been derivedfrom unaudited interim consolidated Ñnancial statements prepared by our management at and for the threemonths ended March 31, 2000 and 2001 and is not included in, and does not form part of, the UnauditedPro Forma Consolidated Financial Statements. Our results of operation and Ñnancial condition as at andfor the three months ended March 31, 2001 include the eÅects of our acquisition of Kenwood as ofJanuary 1, 2001 and have been prepared in accordance with Italian GAAP. You should also referto""Management's Discussion and Analysis of Financial Condition and Results of Operations Ì Results ofOperations for the Three Months Ended March 31, 2000 and 2001''. You should be aware that theinformation presented below may not be indicative of the results of the Group at year-end 2001. Youshould read the whole of this oÅering memorandum and not rely solely on the selected information set outbelow.

Unaudited Historical Consolidated

Three Months ended March 31,

2000(1) 2001(2) 2001

(Lit. millions) (5 thousands)

Income Statement Data

Revenues:

Net salesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 211,820 467,186 241,281

Other revenuesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6,493 4,967 2,565

Total revenues ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 218,313 472,153 243,846

Operating costs:

Materials, consumables and goodsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 91,577 239,868 123,881

Services, rents, leases and related costs ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 64,604 102,847 53,116

Other costs ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 3,366 2,923 1,510

Total production costsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 159,547 345,638 178,507

Value added margin(3) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 58,766 126,515 65,339

Wages, salaries and beneÑts ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 40,942 73,913 38,173

Gross operating marginÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 17,824 52,602 27,166

Depreciation and amortization ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 13,946 23,259 12,012

Amortization of goodwill ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 455 10,356 5,348

Provisions and write-oÅsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 2,356 (199) (103)

Operating proÑt ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,067 19,186 9,909

Net Ñnancial lossÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (11,640) (15,225) (7,863)

Extraordinary (loss) income ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (68) 2,598 1,342

Earnings before taxes and minority interests ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (10,641) 6,559 3,388

Income taxes ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,774 4,738 2,447

Net (loss) income before minority interests ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (12,415) 1,821 941

Minority interestsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Ì Ì Ì

Net (loss) incomeÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (12,415) 1,821 941

(1) Does not include the eÅects of the restructuring of the Group (including the acquisition and sale of various companies)

eÅected in 2000 or the capital increase of Lit. 250,587 million in April 2001.

(2) Includes the eÅects of the restructuring of the Group (including the acquisition and sale of various companies) eÅected in

2000 and the acquisition of Kenwood. You should also refer to the Unaudited De' Longhi Pro Forma Consolidated Financial

Statements for a discussion of the assumptions used in preparing the Ñnancial statements as well as ""Management's

Discussion and Analysis of Financial Condition and Results of Operations''.

(3) Total revenues less total production costs.

11

Brought to you by Global Reports

AuditedHistorical Unaudited Historical

Consolidated Consolidated

At December 31, At March 31,

2000 2001(2) 2001

(Lit. millions) (5 thousands)

Other Financial Data:

EBITDA(1)ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 180,485 52,801 27,269

Capital expenditures ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 34,810 8,960 4,627

Net working capitalÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 611,364 632,875 328,402

Total assets ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 2,402,205 2,980,992 1,539,554

Net Ñnancial position ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,192,801 1,340,992 692,565

Shareholders' equity ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 468,792 472,249 243,896

(1) Operating earnings before interest, taxes and depreciation and amortization.

(2) Includes the eÅects of the restructuring of the Group (including the acquisition and sale of various companies) eÅected in

2000 and the acquisition of Kenwood. You should also refer to the Unaudited De' Longhi Pro Forma Consolidated Financial

Statements for a discussion of the assumptions used in preparing the Ñnancial statements as well as ""Management's

Discussion and Analysis of Financial Condition and Results of Operations''.

12

Brought to you by Global Reports

RISK FACTORS

An investment in our shares involves risk. Prospective investors should carefully consider the risksdescribed below before investing in our shares. If any of the risks described below actually occur, ourbusiness, Ñnancial condition or results of operations could be materially adversely aÅected and,accordingly, the value and trading price of our shares may decline, resulting in a loss of all or part of anyinvestment in our shares. Furthermore, the risks and uncertainties described may not be the only ones weface. Additional risks and uncertainties not presently known to us or that we currently consider immaterialmay also impair our business operations.

Risks Relating to the Company and the Group

We face risks related to our international activities.

Our future growth is expected to come from countries in Western Europe (such as Great Britain andGermany) as well as other markets around the world, including the United States, Eastern Europe, Japanand, as a result of our acquisition of Kenwood, the Far East and South Africa. As part of our acquisitionof Kenwood, we acquired a manufacturing facility in the People's Republic of China (""China'') as well asa small assembly facility in England, countries in which we had not previously manufactured or assembledproducts. Moreover, most of our sales are transacted abroad. For the year ended December 31, 2000,approximately 67% of our consolidated revenues, or 71% of our combined pro forma revenues (includingthe Kenwood acquisition), were attributable to sales outside of Italy. Because we manufacture ourproducts and conduct our business in diÅerent countries, we are aÅected by several factors, includingmacroeconomic, political, business and legal conditions in these countries. Adverse changes inmacroeconomic conditions or changes in the political, business or legal environment (such as increasedduties, higher taxation, currency conversion limitations, restrictions on the transfer of funds, limitations onimports or exports, or the expropriation of private enterprises) could have a material adverse eÅect on ourbusiness, Ñnancial condition or results of operations.

The pro forma Ñnancial information included in this oÅering memorandum does not represent our actual

historical results of operations.

The Unaudited Pro Forma Financial Statements have been prepared for informational purposes onlyand present the balance sheets and income statements derived from the Audited Historical ConsolidatedFinancial Statements and from the audited and unaudited balance sheets and income statements of thecompanies acquired by the Group in 2000 and 2001, in each case adjusted as if each of the acquisitionshad been completed on January 1, 1998. You should refer to the notes to the Unaudited Pro FormaFinancial Statements for a description of the assumptions used to prepare such Ñnancial statements and""Presentation of Financial and Other Information.''

On January 1, 1998 we had not eÅected the restructuring process and therefore had neither purchasedDe' Longhi Divisione Cucine S.p.A., DL Radiators S.p.A., Climaveneta S.p.A., Micromax S.p.A. andErgoklima S.p.A.; nor had we sold Immobiliare Findomestic S.r.l., De' Longhi Radiators S.r.l., DLCanada Distributors Inc., 850721 Ontario Ltd., I.S.C. Ì Industrie Scambiatori di Calore S.p.A. and NautaS.r.l. At the time of the acquisitions, these companies represented, in the aggregate, approximately 26.6%of our consolidated total assets, 25.0% of our total revenues and 17.5% of our net income, in each case ascompared to our consolidated Ñnancial statements as of December 31, 1999 and for the year then ended.

In addition, on January 1, 1998 we had neither purchased Sile Corpi Scaldanti S.r.l. and Kenwood,nor had we eÅected a capital increase of Lit. 250,587 million. At the time of the respective acquisition,Sile Corpi Scaldanti S.r.l. represented 0.4% of our consolidated total assets, 0.6% of our total revenues and0.9% of our net income, in each case as compared to our consolidated Ñnancial statements as ofDecember 31, 1999 and for the year then ended; and Kenwood represented (on a restated basis) 12.5% ofour consolidated total assets and 37.8% of our total revenues, in each case as compared to our consolidatedÑnancial statements as of December 31, 2000 and for the year then ended. The results of operations andÑnancial condition of Sile Corpi Scaldanti S.r.l. and Kenwood reÖected the strategies of each of thecompanies' prior management, which we did not control. We were not responsible for the strategiesemployed by such prior management and our strategies may diÅer materially from those implemented inthe past.

As a result of the above, the Unaudited Pro Forma Financial Statements do not purport to representwhat our results of operations or Ñnancial position actually would have been if such purchases, sales and

13

Brought to you by Global Reports

capital increase had occurred on January 1, 1998 or to project our results of operations for any futureperiod.

In Italy, there are no standards governing preparation of pro forma Ñnancial statements. Although theUnaudited Pro Forma Financial Statements have been prepared using the best practices as identiÑed anddisclosed by CONSOB, such Ñnancial statements do not take into account U.S. or U.K. GAAP orstandards generally accepted in other jurisdictions. Accordingly, the presentation of, and the assumptionsand adjustments used to prepare, the Unaudited Pro Forma Financial Statements may diÅer signiÑcantlyfrom those in other jurisdictions. You are cautioned against placing undue reliance on the Unaudited ProForma Consolidated Financial Statements. The Unaudited De' Longhi Pro Forma Consolidated FinancialStatements have been examined by PricewaterhouseCoopers, to the extent and as more fully described inthe report of independent auditors relating thereto included elsewhere in this oÅering memorandum. Youshould also refer to the assumptions used to prepare the Unaudited Pro Forma Financial Statements setforth elsewhere in this oÅering memorandum.

Kenwood has incurred losses in the past and may not be able to achieve the objectives set forth in its

restructuring plan.

In early 2001, we acquired all of the capital stock of Kenwood, an English company specializing inthe manufacture and sale of small domestic appliances internationally under the Kenwood and Arietebrand names. You should also refer to ""The Kenwood Acquisition''. Prior to our acquisition, for therestated Ñscal years ended December 31, 1998, 1999 and 2000, Kenwood recorded consolidated net lossesequal to approximately Lit. 16,894 million, Lit. 49,358 million and Lit. 18,508 million, respectively. Forthe restated three months ended March 31, 2001, Kenwood recorded consolidated net losses equal toapproximately Lit. 2,535 million. Since 1997, Kenwood has been implementing a restructuring processaimed at transforming itself into a brand business and at reducing its exposure to manufacturing operationsin the United Kingdom. As a result of such plan, Kenwood has streamlined its operations in the UnitedKingdom, thereby reducing its committed cost base by an amount Kenwood estimates to be approximatelyLit. 47,000 million (or 14.6 million); it has improved and expanded the range of products it oÅers; and ithas refocused its marketing eÅorts. Although we believe that Kenwood's net losses were also due toextraordinary restructuring costs that were associated with the restructuring process, which has beensubstantially completed, and that it will improve its proÑtability levels and contribute to increased synergieswithin the Group in the future, we cannot assure you that Kenwood will be able to maintain or increase itsproÑts or that market conditions will not change in the future, which could, in turn, result in a materialadverse eÅect on our business and results of operation.

We face risks typical of acquisitions and, as a result, may not be able to fully realize potential synergies

with Kenwood.

We believe that the acquisition of Kenwood will contribute to signiÑcant manufacturing anddistribution synergies for the Group and will improve our competitive position. Nevertheless, ouracquisition requires us to assimilate the operations of Kenwood into our operations and may require us toincur certain expenditures and restructuring expenses. We cannot assure you that we will be able tointegrate Kenwood's business into our existing organization as planned, which could, in turn, result in aloss of part of Kenwood's customer base or its key personnel. Similarly, we may not achieve all of theexpected results, cost savings or other synergies from our acquisition. This, in turn, could have a materialadverse eÅect on our business and results of operations. In addition, there can be no assurance that ourrecent acquisition of Kenwood will not carry unforeseen liabilities. To the extent any customer or otherthird party asserts any material legal claims against Kenwood, our business, Ñnancial condition and resultsof operations could be materially and adversely aÅected.

We are exposed to price volatility of raw materials.

Our raw materials primarily consist of metals and plastics such as steel and acrylonite butadienestyrene (known as ""ABS''). Because the majority of these materials are commodity based, they areavailable from various independent suppliers. We are not dependent on any single foreign source for suchmaterials. However, we are subject to price volatility. For the year ended December 31, 2000, raw materialcosts increased by 18.7% largely due to a general increase in prices for such materials, especially steel(which increased from an average price of Lit. 650/kilogram in 1999 to Lit. 830/kilogram in 2000). Inorder to mitigate risks associated with price volatility, we typically enter into quarterly or six-monthforward supply agreements at Ñxed prices for certain materials. As a result, prices for our raw materials are

14

Brought to you by Global Reports

subject, in part, to exchange rate Öuctuations. You should refer to ""Ì We are exposed to foreign exchangerate Öuctuations.'' In addition, we cannot assure you that our current or future sources will continue toprovide raw materials to us at attractive prices, or at all, or that we will be able to obtain such rawmaterials in the future from these or other providers on the scale and within the time frames which werequire. Any failure to obtain such raw materials on a timely basis at an aÅordable cost, or any signiÑcantdelays or interruptions in supply, could have a material adverse eÅect on our business, Ñnancial conditionand results of operations.

We face risks associated with product recalls and product liability claims.

The sale and use of our products involve a risk of warranty and product liability claims, particularly inthe United States where product liability claims grounded on personal injuries are more common than inother countries. We are subject to possible claims for personal injury or property damage, which couldresult from the failure or alleged failure of our products or of components incorporated in products that wehave manufactured or sold. These claims could cause damage to our reputation and to the image of ourbrand names, negatively aÅecting our results of operations. While we make every eÅort to select reliablesuppliers for product components and although we rigorously control the quality of such goods, the risk ofdefects and product recalls cannot be completely eliminated. We have obtained insurance coverage forthese types of liabilities in amounts which we believe to be adequate. However, we may not be able toobtain such insurance on acceptable terms in the future, if at all; claims not covered by our insurance mayarise in the future; and our coverage may not be adequate to insure against all product liability claims. Apartially or completely uninsured claim, if successful and of signiÑcant magnitude, could have a materialadverse eÅect on our Ñnancial condition and results of operations.

We are exposed to foreign exchange and interest rate Öuctuations.

While we transact business largely in Euro zone currencies, a portion of our sales and operating proÑtsare aÅected by the impact of Öuctuations in foreign currency exchange rates on product prices and certainoperating expenses, including costs of raw materials and components. We believe that our exposure toÖuctuations in any particular currency is limited as a result of our diversiÑed business portfolio and due tothe fact that, for certain principal currencies such as the U.S. dollar, most of our net sales revenues areoÅset by our costs in the same currencies. Nevertheless, Öuctuations in the exchange rates of certainforeign currencies relative to the Euro may have an adverse impact on our sales and operating results andthe international competitiveness of our Italian-based manufacturing operations. We typically engage incertain foreign exchange transactions to hedge portions of our transactional exposure to Öuctuations inexchange rates between the Euro and the U.S. dollar, the pound sterling, the Canadian dollar and theJapanese Yen. We cannot assure you that our foreign exchange transactions will adequately protect usfrom the eÅects of currency Öuctuations or that, if signiÑcant Öuctuations were to occur, this would nothave an adverse eÅect on our Ñnancial position.

We also are subject to interest rate Öuctuations as a result of our debt position (which is generallysubject to variable market interest rates). As a result, we typically enter into interest rate contracts inconnection with our Ñnancial transactions with the aim of hedging a portion of our interest rate risk. As atDecember 31, 2000, we were party to interest rate contracts covering approximately 42.9% (or 4207,000thousand) of our total consolidated debt at such date (equal to 4483,000 thousand). Although weperiodically monitor the interest rate market and may subsequently enter into further hedging contractscovering some or all additional interest rate risks, we cannot assure you that such transactions willadequately protect us from the eÅects of interest rate Öuctuations or that, if signiÑcant Öuctuations were tooccur, this would not have an adverse eÅect on our Ñnancial position. You should also refer to""Management's Discussion and Analysis of Financial Condition and Results of Operations Ì Impact ofChanges in Exchange and Interest Rates''.

We rely upon certain key personnel.