D. Mohanadas Thesis (Commerce 2014).pdf - Bharathidasan ...

264

Ph.D., Thesis Submitted to the Bharathidasan University for the Award of the Degree of Doctor of Philosophy in Commerce By D. MOHANADAS (Ref No. 025705) Assistant Professor, Department of Commerce, Sindhi College, Chennai – 77. Under the Supervision of Dr. M. RENGASAMY, Ph.D., Associated Professor and Head (Rtd.), PG and Research Department of Commerce, Poompuhar College (Autonomous), Melaiyur – 609107. BHARTHIDASAN UNIVERSITY TIRUCHIRAPPALLI – 620024 JULY – 2014

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of D. Mohanadas Thesis (Commerce 2014).pdf - Bharathidasan ...

Ph.D., Thesis Submitted to the Bharathidasan University

for the Award of the Degree of Doctor of Philosophy in Commerce

By

D. MOHANADAS

(Ref No. 025705)

Assistant Professor,

Department of Commerce,

Sindhi College, Chennai – 77.

Under the Supervision of

Dr. M. RENGASAMY, Ph.D.,

Associated Professor and Head (Rtd.),

PG and Research Department of Commerce,

Poompuhar College (Autonomous), Melaiyur – 609107.

BHARTHIDASAN UNIVERSITY TIRUCHIRAPPALLI – 620024

JULY – 2014

2

DDrr.. MM.. RREENNGGAASSAAMMYY,, M.Com., M.Phil., Ph.D., M.Ed.,DCPA.,

Research Supervisor, Associate Professor and Head (Rtd.), PG and Research Department of Commerce, Poompuhar College, (Autonomous),

Melaiyur – 608 107, Sirkali Taluk, Nagapattinam District, Tamilnadu, India.

Date:

CCeerrttiiffiiccaattee

This is to certify that the thesis entitled

“PERFORMANCE OF UTI MUTUAL FUND WITH

REFERENCE TO ITS SELECTED SCHEMES – A STUDY” is

a bonafide record of research work done by

Mr.D.Mohanadas, Part-Time Research Scholar, PG and

Research Department of Commerce, Poompuhar College

(Autonomous), Melaiyur, under my guidance for the award

of the degree of Doctor of Philosophy and that this thesis

has not previously formed the basis for the award of any

degree, diploma, fellowship, associateship or any other

similar title to the candidate.

This is also to certify that the thesis represents the

independent work of the candidate.

Candidate Supervisor

3

DECLARATION

I hereby declare that the thesis entitled,

“Performance of UTI Mutual Fund with Reference to Its

Selected Schemes – A Study”, submitted for the degree of

Doctor of Philosophy in Commerce is the result of my

original and independent research work carried out under

the guidance of Dr.M.RENGASAMY, Associate Professor

and Head (Retired), PG and Research Department of

Commerce, Poompuhar College (Autonomous), Melaiyur,

and it has not been submitted for the award of any

degree, diploma, associateship for fellowship of any

university or institution.

Place: Signature of the candidate

Date: [D. Mohanadas]

4

ACKNOWLEDGEMENT

First I would like to thank the Lord God, the Almighty for his

abundant benevolence and blessing and his grace has guided me up to this

level in my academic and research endeavours.

It is a pride and privilege to record my heartfelt and deep sense of

gratitude to my research guide, Dr. M. RENGASAMY, M.Com., M.Phil., Ph.D., M.Ed.,

Associate Professor Head (Rtd.), PG and Research Department of

Commerce, Poomphuhar College, Malaiyur, for his punctilious guidance,

continuous encouragement, valuable suggestions scientific freedom which

have helped me to proceed confidently and complete the study successfully

my Ph.D Research work. His approach, vision, hard work , honest and

guidance in research enabled me to gain a lot. This thesis is largely a result

of his diligent and meticulous approach to each and every step of my work.

I express my sincere thanks to Doctoral Committee Members,

Dr. PM. Meera Mohiadeen, Head of the Department of Commerce, Jamal

Mohammed Collage, Trichy, for providing me valuable suggestions to make

this study.

I am very much thankful to Dr. A. Panneerselvam Principal, and

Dr. G. Rajendran, Head of the Department of Commerce, Poompuhar

College (Autonomous) Melaiyur for their advice, direction and inspiration.

I convey my heartfull thanks to Dr. G. Shanmugasundaram,

Professor, Department Commerce, Pondicherry University for his advices

and encouragement.

My sincere thanks are also due to the members of the staff,

Department of Commerce for their encouragement.

My everlasting thanks are due to the Bharadhidasan University,

Tiruchirappalli, for permitting me to undertake this research work.

I am very much grateful to the officials of the TNIA, AMFI, UTI,

ICICI, Reliance, and HDFC Mutual funds for their full support while

gathering information.

5

I wish to thank to Dr. K. Sathyanarayana, Principal, Sindhi College,

Chennai-77, for his suggestions and kind co-operation which enable me to

complete my research work successfully.

I express my thankfulness to Mr. S. Sudharsan Assistant Professor,

Sindhi College, Chennai-77, for his help, pleasing words of encouragement

and who offered valuable suggestions.

I record my gratitude to Mr.R. Muthuraman, Mr.V. Sivaprakasam,

and Mr. A. Sairam, Faculty members of the Department of Corporate

Secretaryship, Sindhi college, for their timely help and co-operation which

enabled me to complete my research work successfully.

No words on earth can be enough to express my gratefulness to my

beloved parents, wife, my Children and members of my family who

helped me at every stage of this work.

I express my deep sense of gratitude to my beloved friends

Dr. V. Kannan and Mr. M. Dhamodharan, Assistant Professor, who have

provided accommodation facilities and for their support enabled me to

complete it successfully.

Also my special thanks to Bala-Sara computers, OP, Main Road

for their neat typing and execution of this research work.

[D.Mohanadas]

6

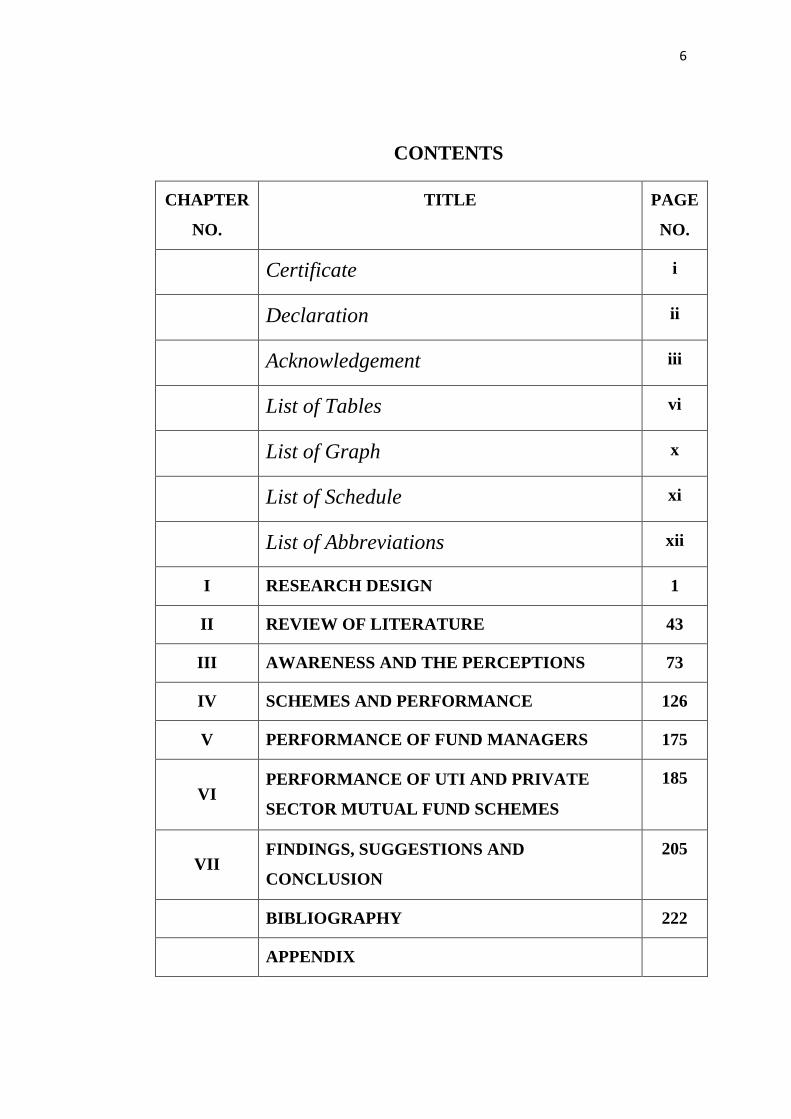

CONTENTS

CHAPTER

NO.

TITLE PAGE

NO.

Certificate i

Declaration ii

Acknowledgement iii

List of Tables vi

List of Graph x

List of Schedule xi

List of Abbreviations xii

I RESEARCH DESIGN 1

II REVIEW OF LITERATURE 43

III AWARENESS AND THE PERCEPTIONS 73

IV SCHEMES AND PERFORMANCE 126

V PERFORMANCE OF FUND MANAGERS 175

VI PERFORMANCE OF UTI AND PRIVATE

SECTOR MUTUAL FUND SCHEMES

185

VII FINDINGS, SUGGESTIONS AND

CONCLUSION

205

BIBLIOGRAPHY 222

APPENDIX

7

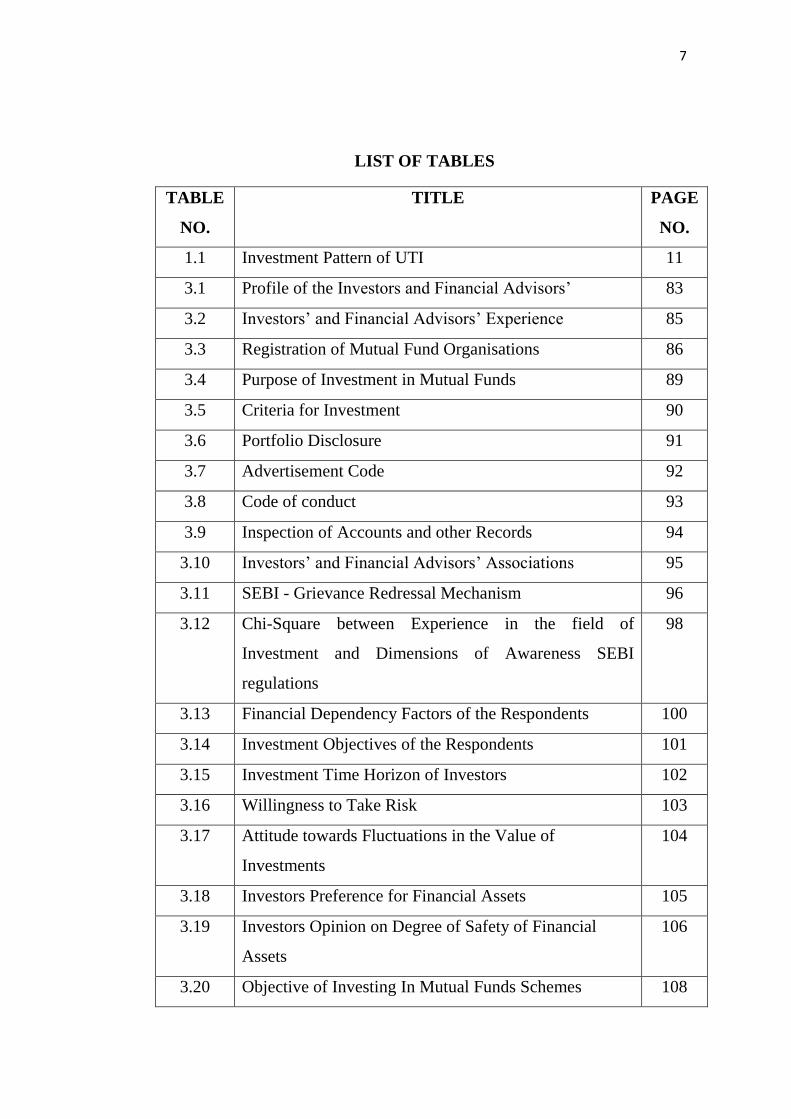

LIST OF TABLES

TABLE

NO.

TITLE PAGE

NO.

1.1 Investment Pattern of UTI 11

3.1 Profile of the Investors and Financial Advisors‟ 83

3.2 Investors‟ and Financial Advisors‟ Experience 85

3.3 Registration of Mutual Fund Organisations 86

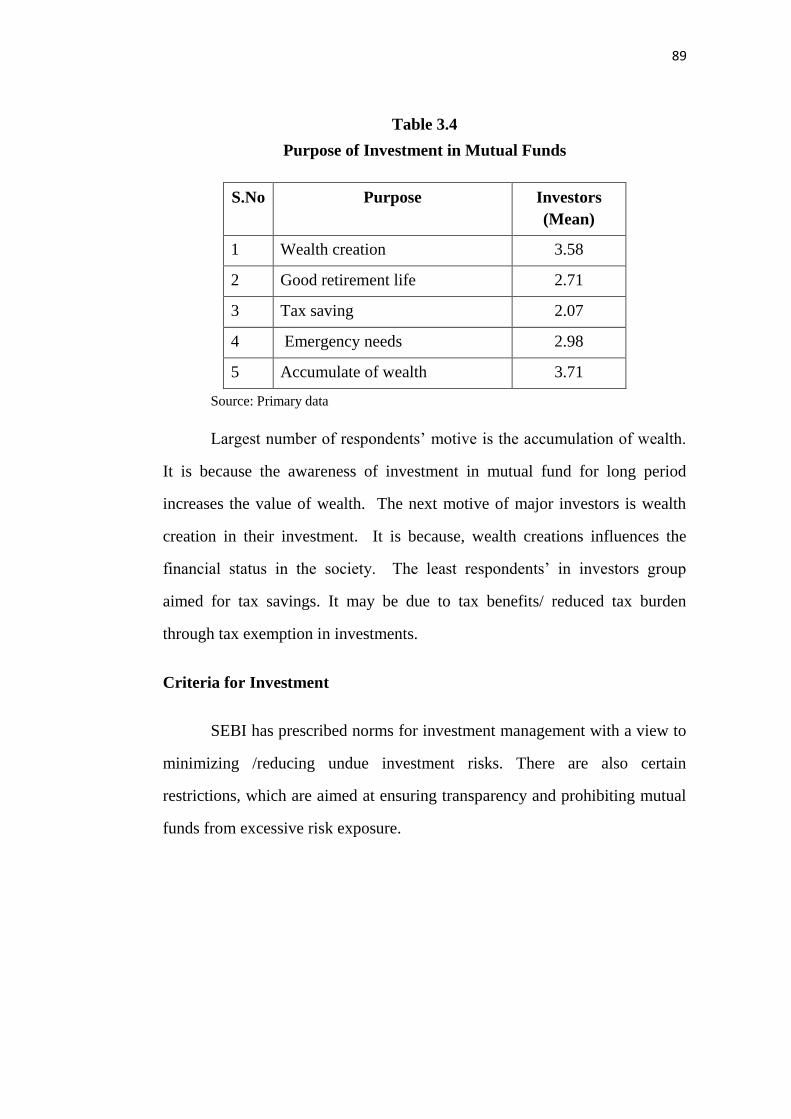

3.4 Purpose of Investment in Mutual Funds 89

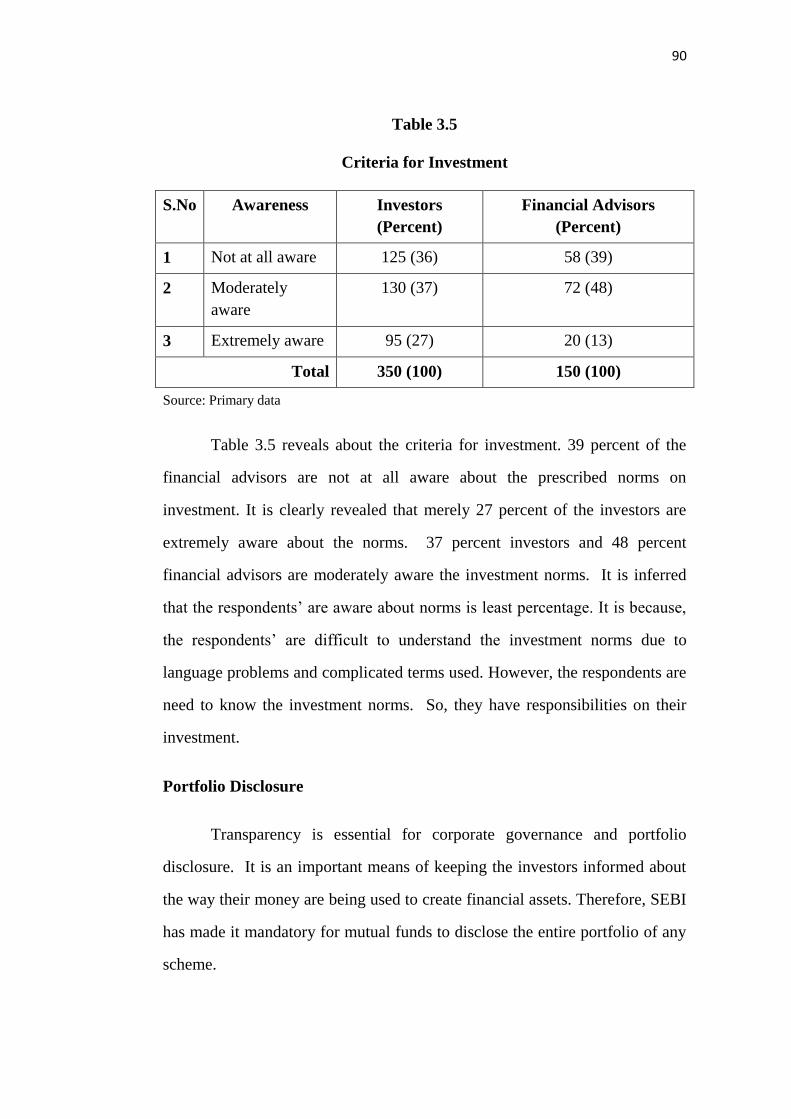

3.5 Criteria for Investment 90

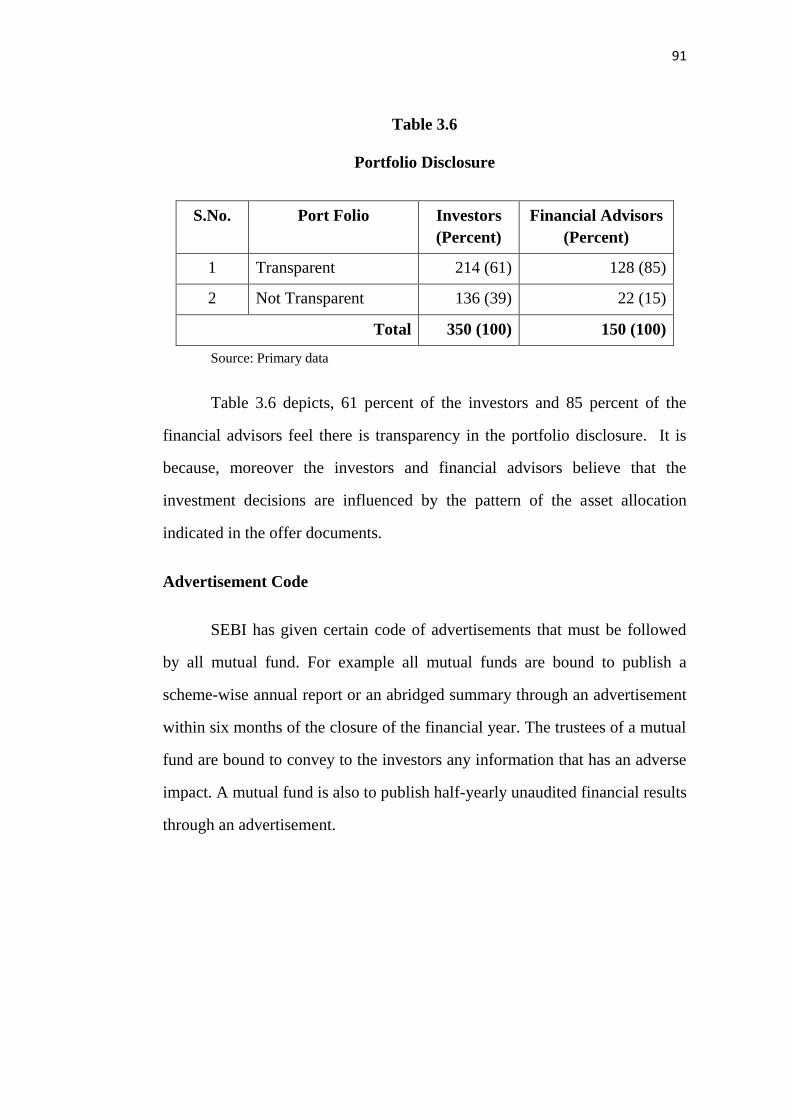

3.6 Portfolio Disclosure 91

3.7 Advertisement Code 92

3.8 Code of conduct 93

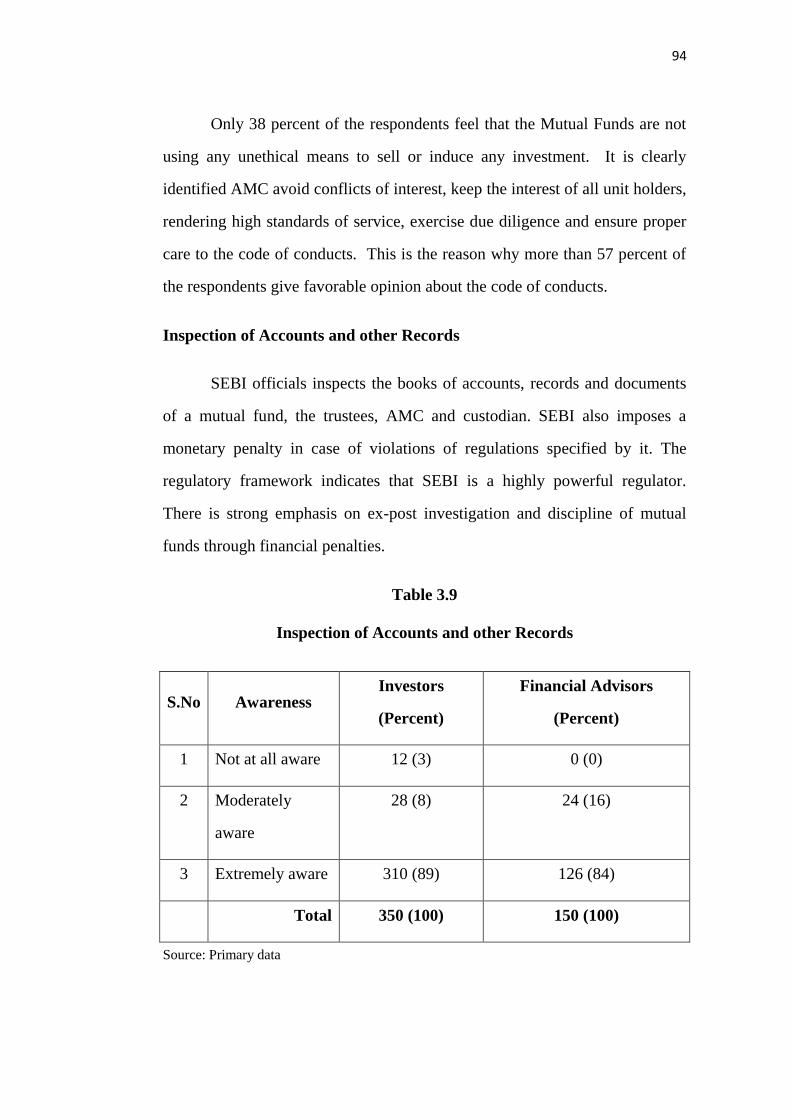

3.9 Inspection of Accounts and other Records 94

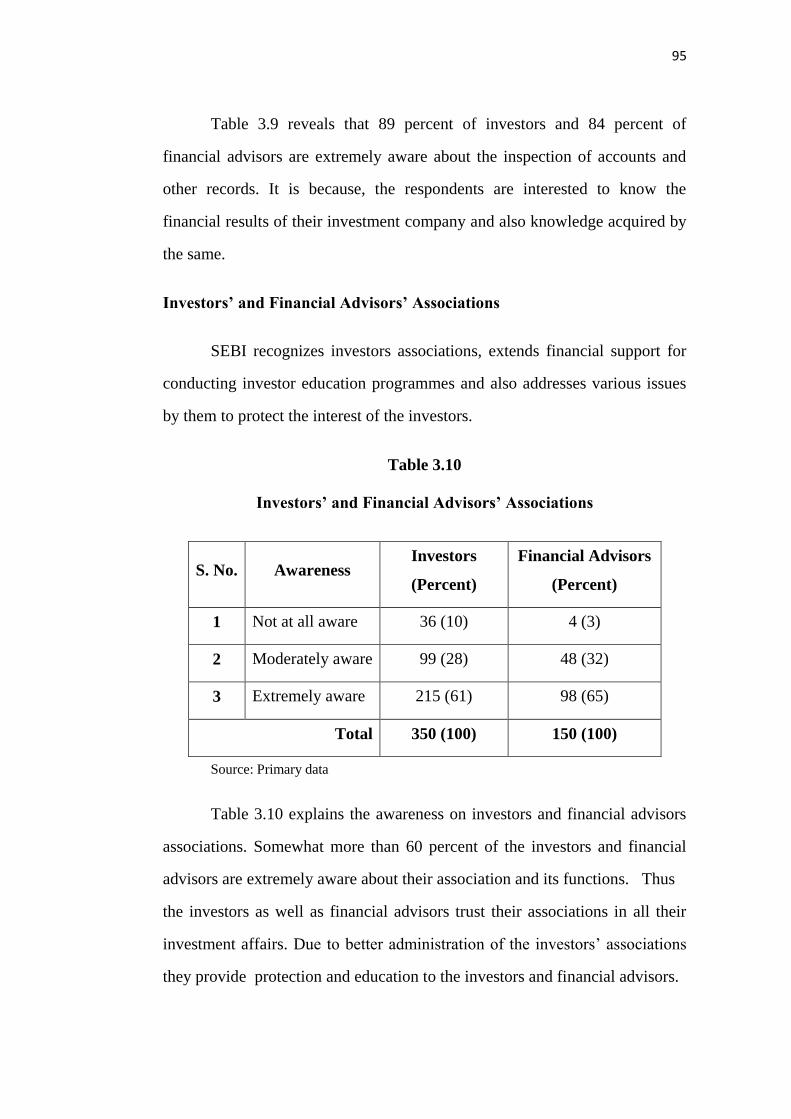

3.10 Investors‟ and Financial Advisors‟ Associations 95

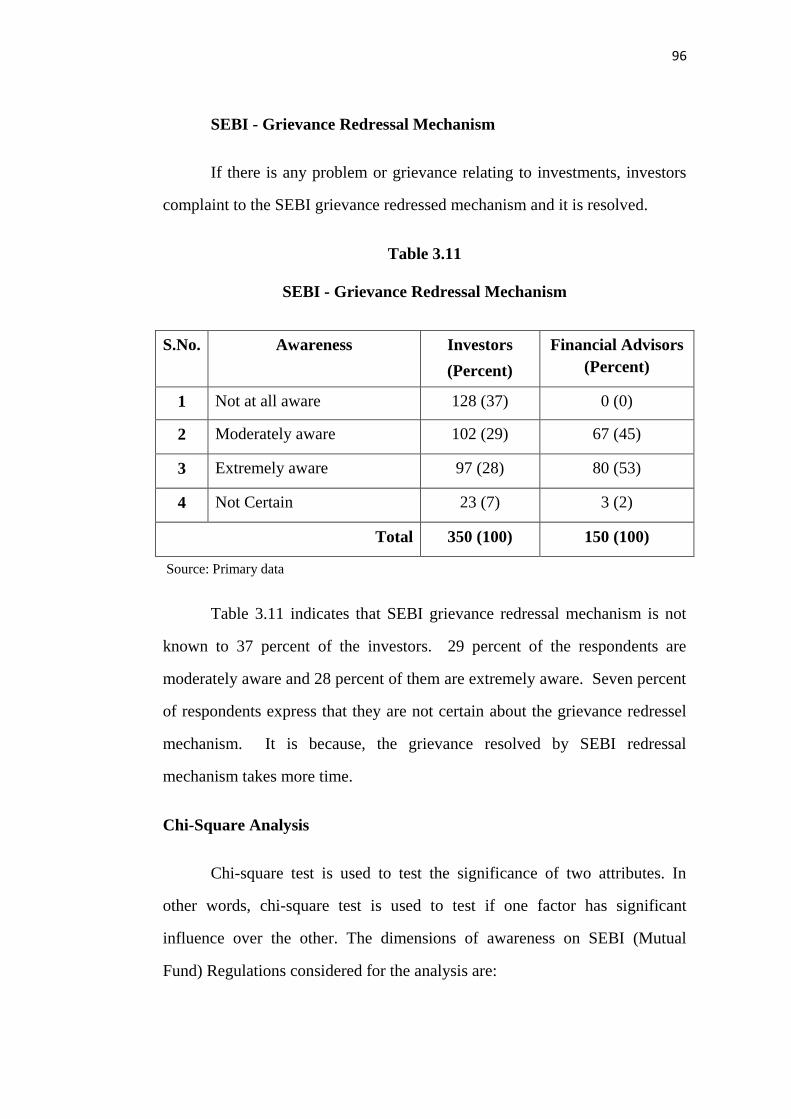

3.11 SEBI - Grievance Redressal Mechanism 96

3.12 Chi-Square between Experience in the field of

Investment and Dimensions of Awareness SEBI

regulations

98

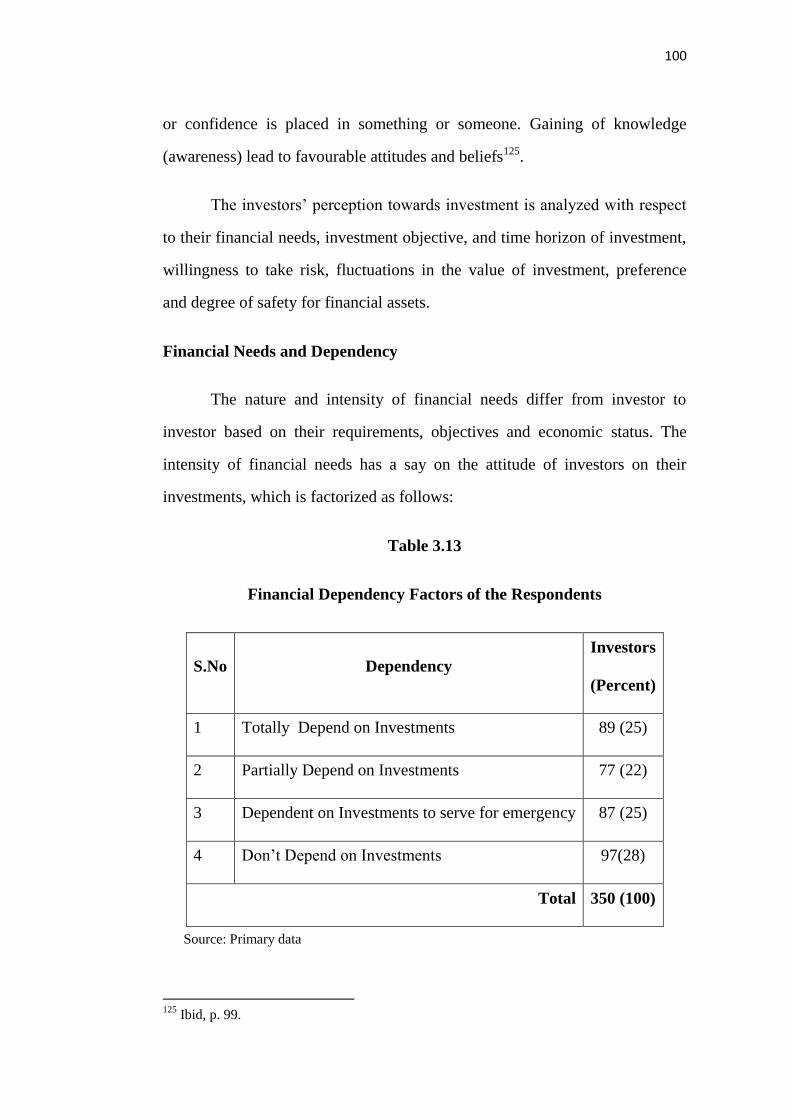

3.13 Financial Dependency Factors of the Respondents 100

3.14 Investment Objectives of the Respondents 101

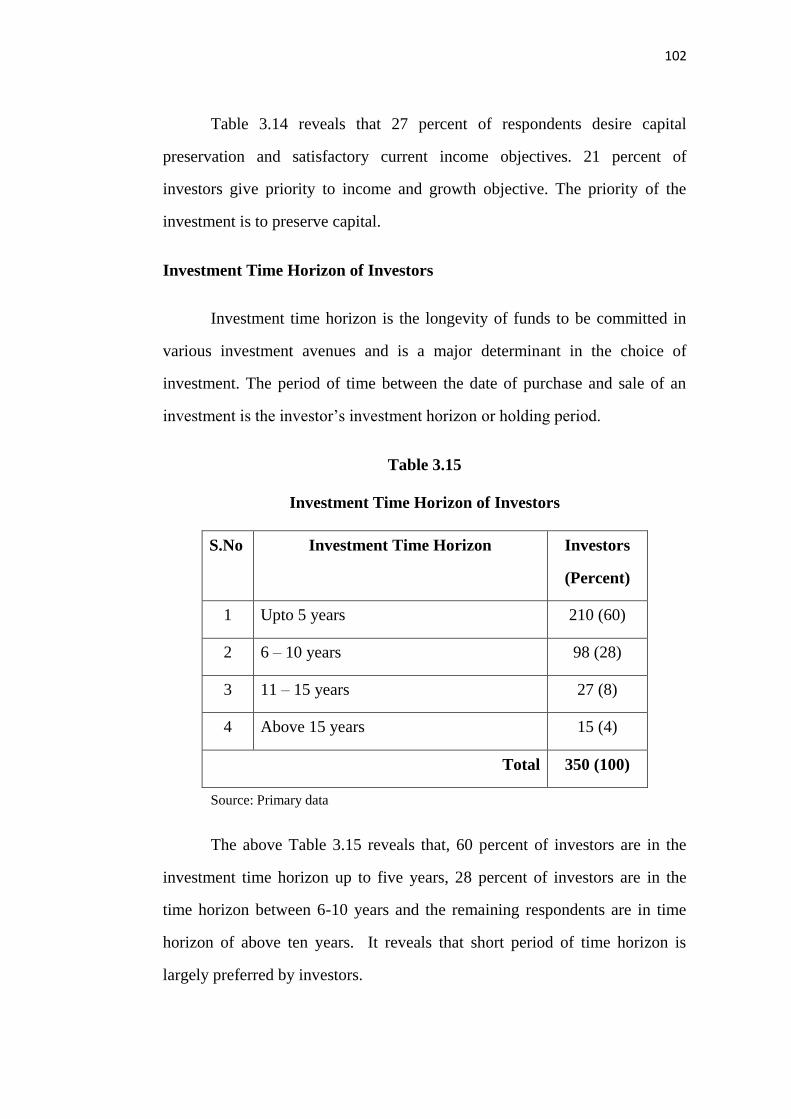

3.15 Investment Time Horizon of Investors 102

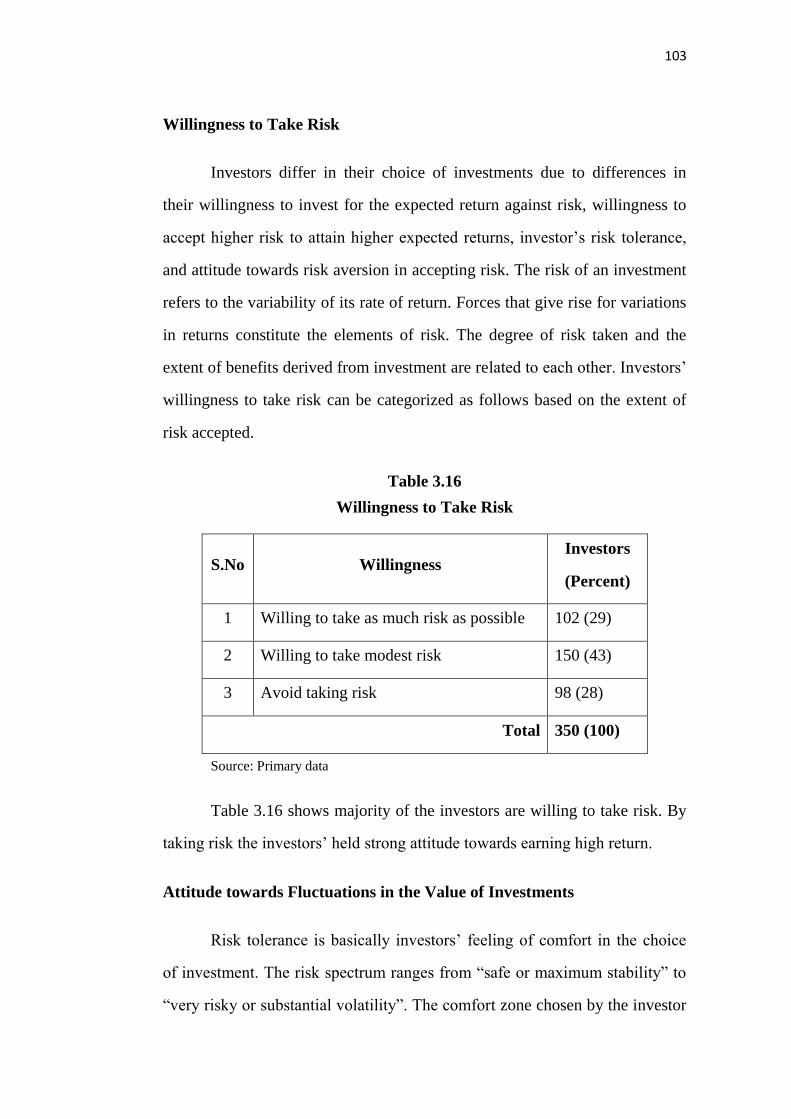

3.16 Willingness to Take Risk 103

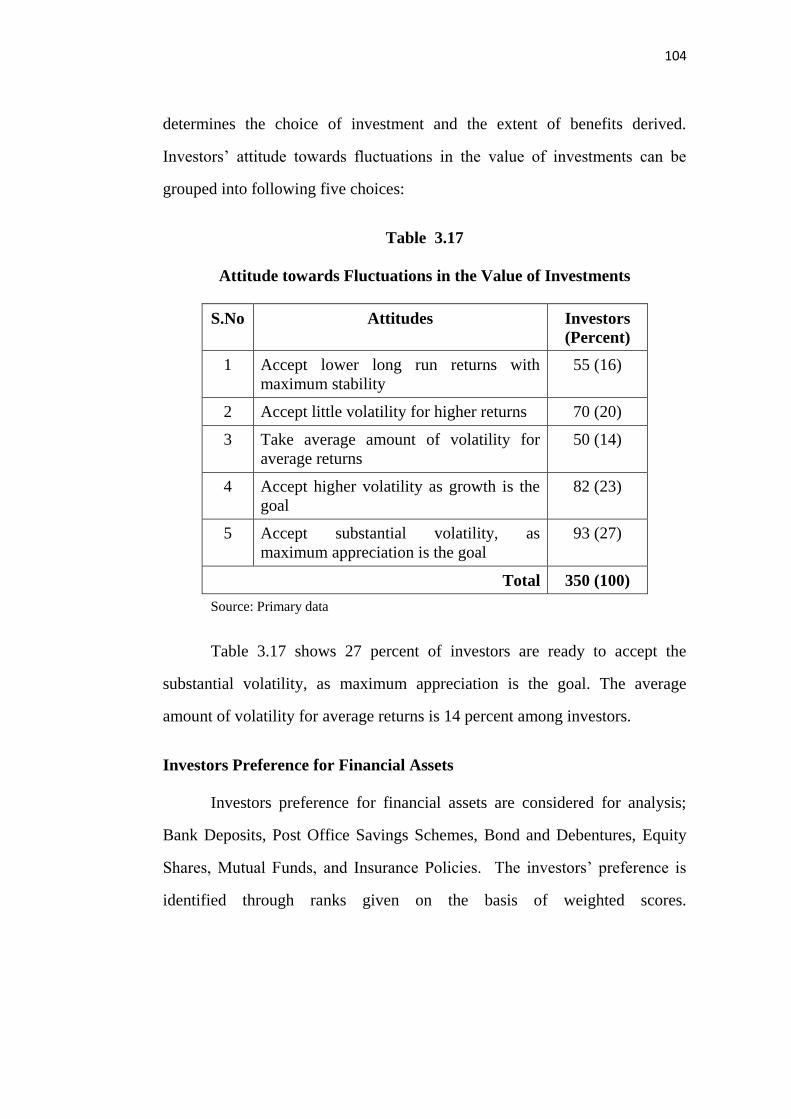

3.17 Attitude towards Fluctuations in the Value of

Investments

104

3.18 Investors Preference for Financial Assets 105

3.19 Investors Opinion on Degree of Safety of Financial

Assets

106

3.20 Objective of Investing In Mutual Funds Schemes 108

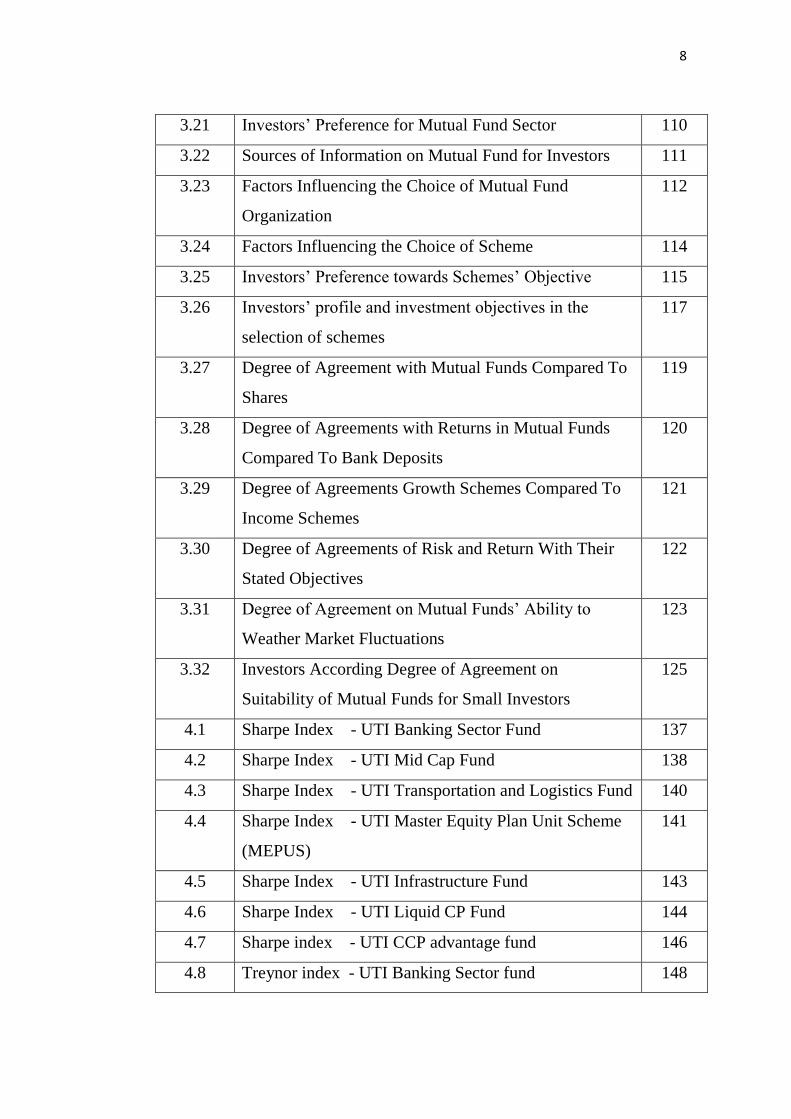

8

3.21 Investors‟ Preference for Mutual Fund Sector 110

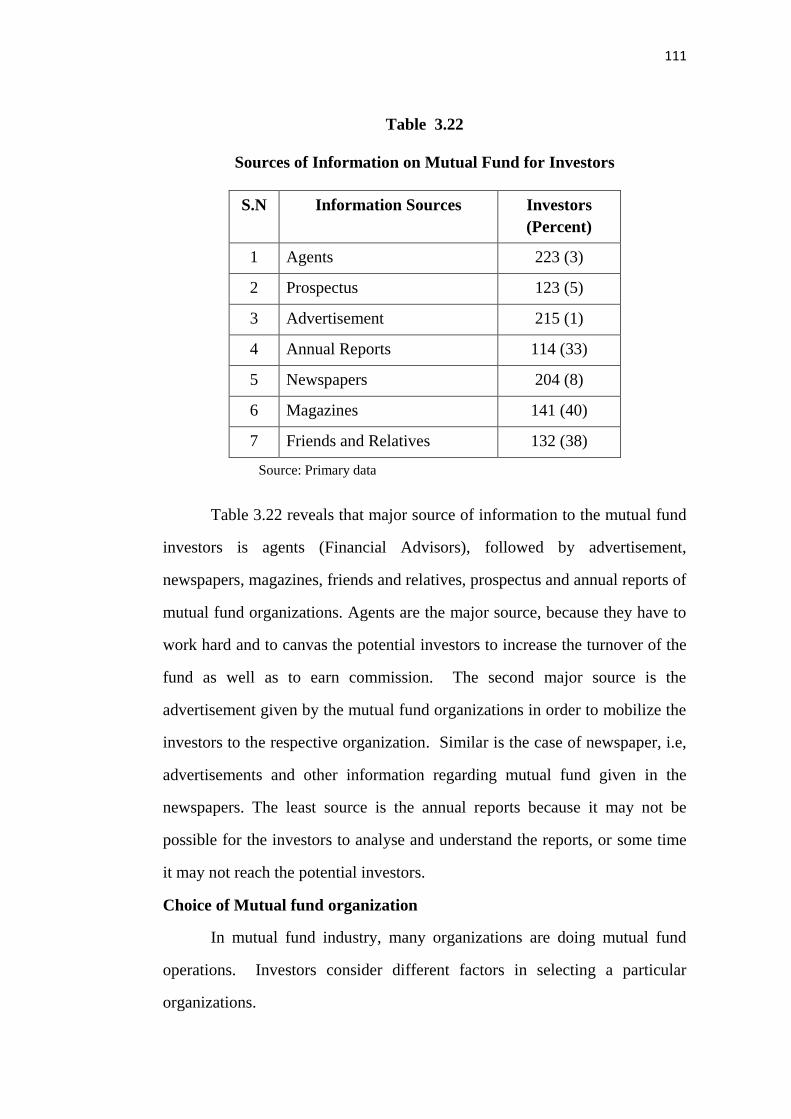

3.22 Sources of Information on Mutual Fund for Investors 111

3.23 Factors Influencing the Choice of Mutual Fund

Organization

112

3.24 Factors Influencing the Choice of Scheme 114

3.25 Investors‟ Preference towards Schemes‟ Objective 115

3.26 Investors‟ profile and investment objectives in the

selection of schemes

117

3.27 Degree of Agreement with Mutual Funds Compared To

Shares

119

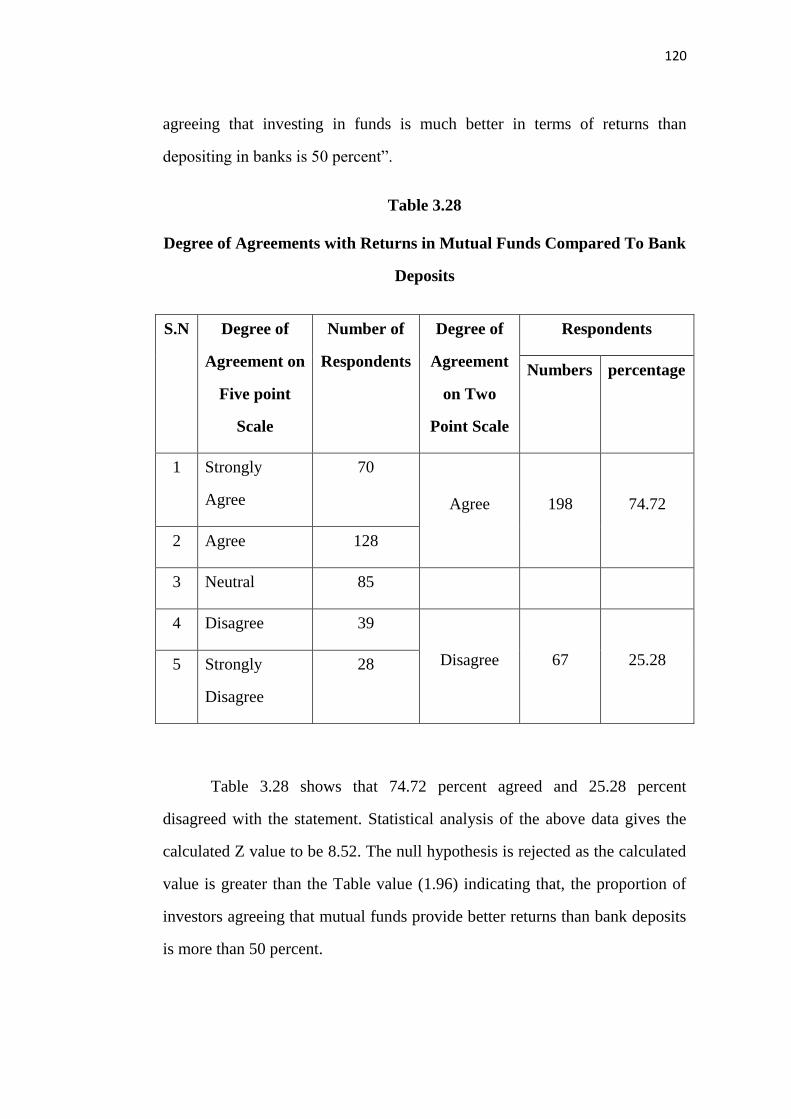

3.28 Degree of Agreements with Returns in Mutual Funds

Compared To Bank Deposits

120

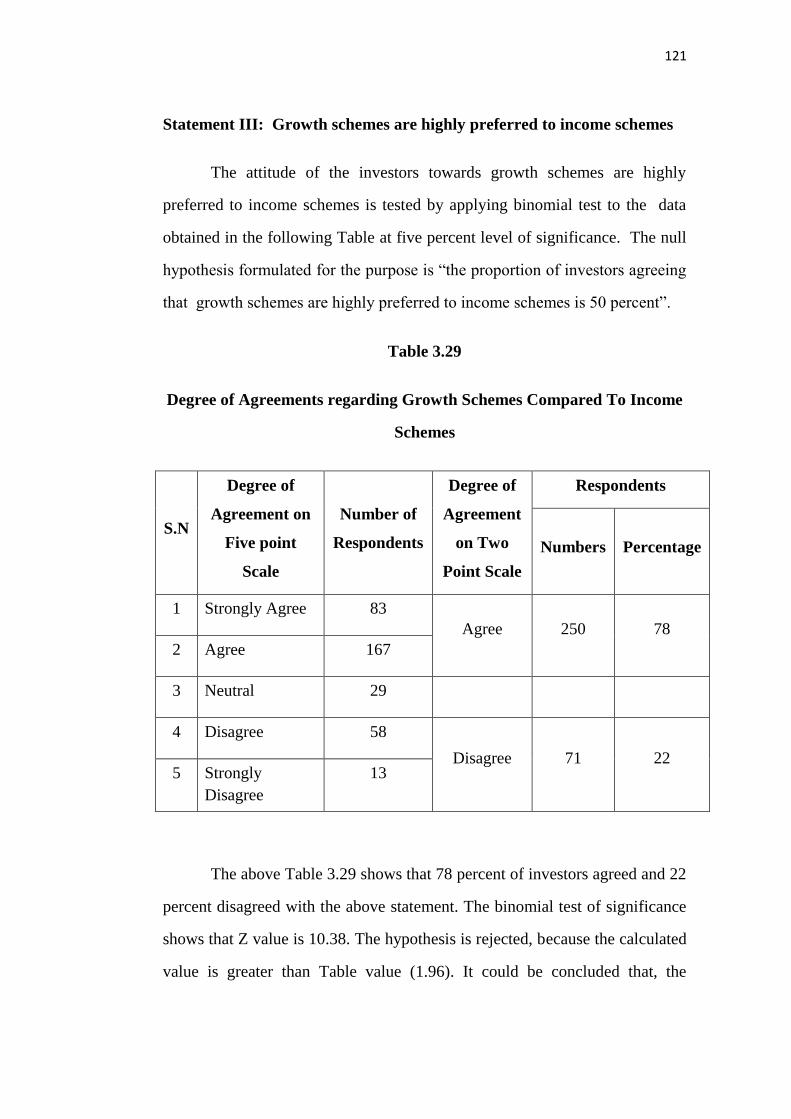

3.29 Degree of Agreements Growth Schemes Compared To

Income Schemes

121

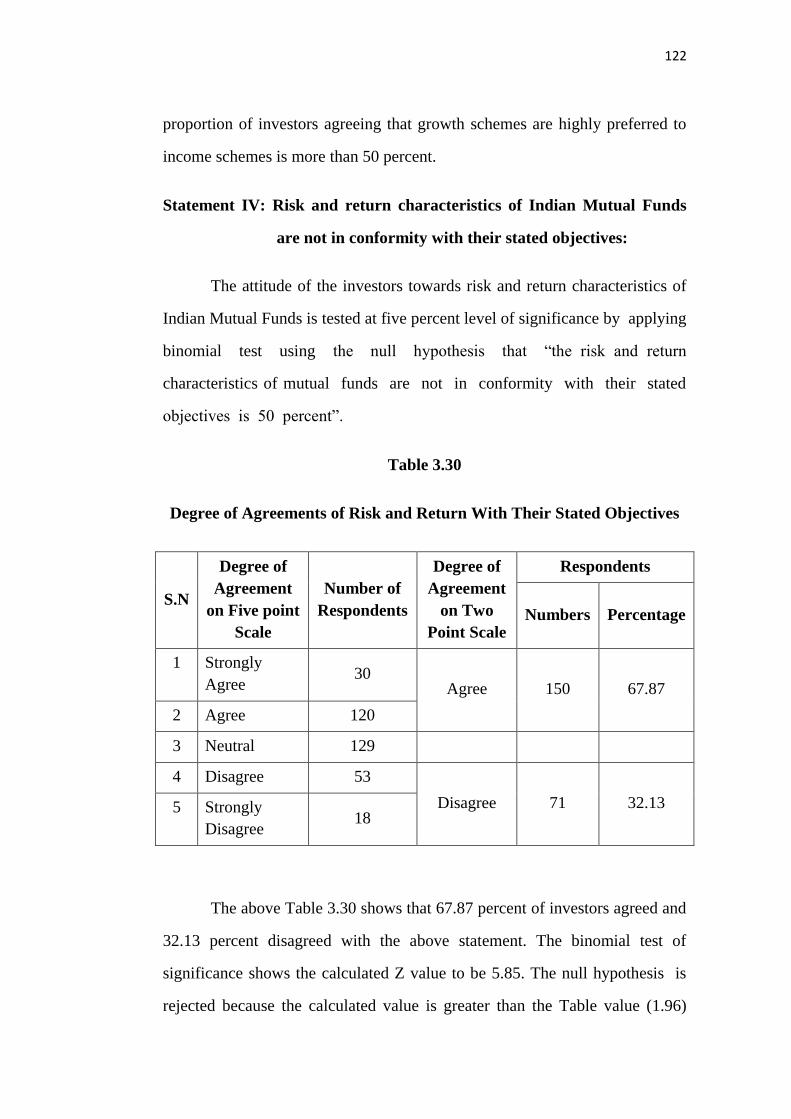

3.30 Degree of Agreements of Risk and Return With Their

Stated Objectives

122

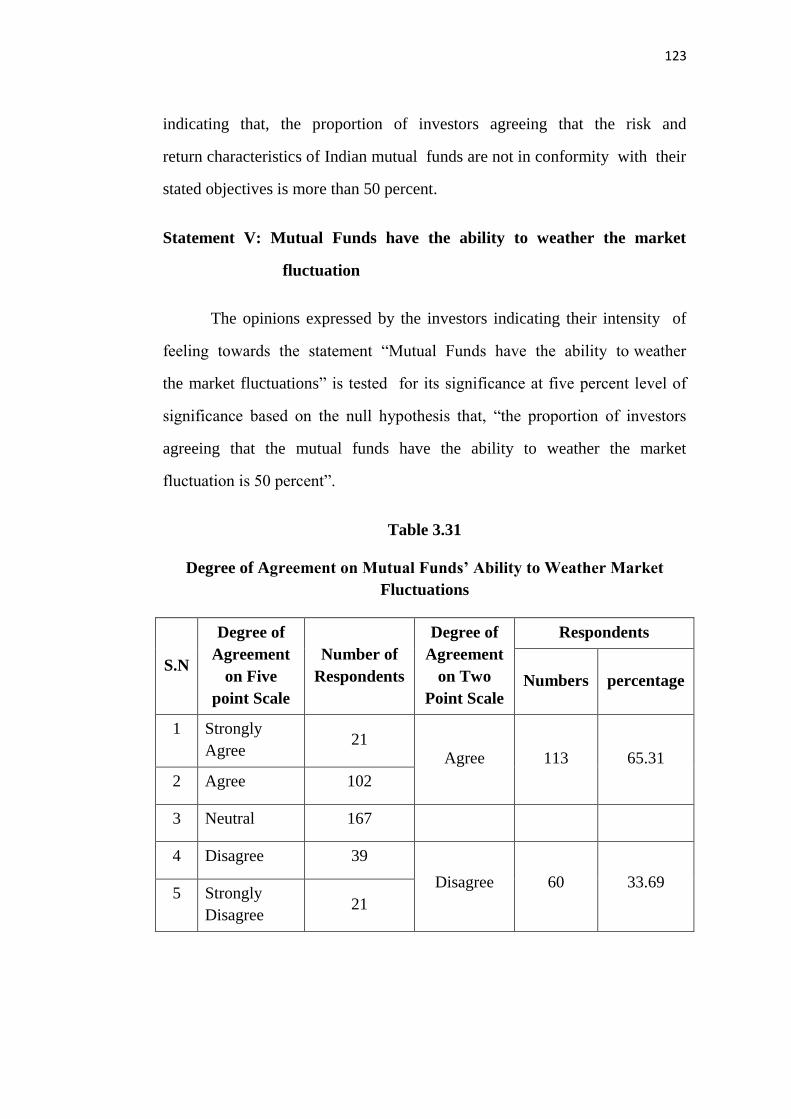

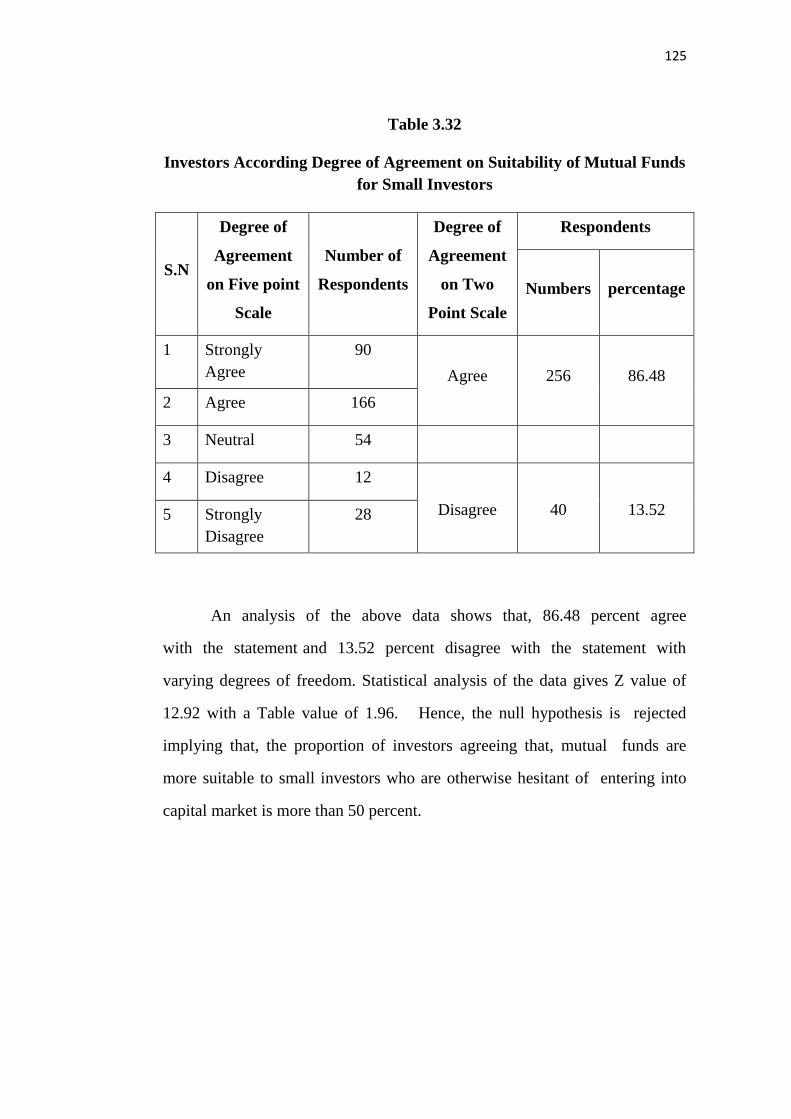

3.31 Degree of Agreement on Mutual Funds‟ Ability to

Weather Market Fluctuations

123

3.32 Investors According Degree of Agreement on

Suitability of Mutual Funds for Small Investors

125

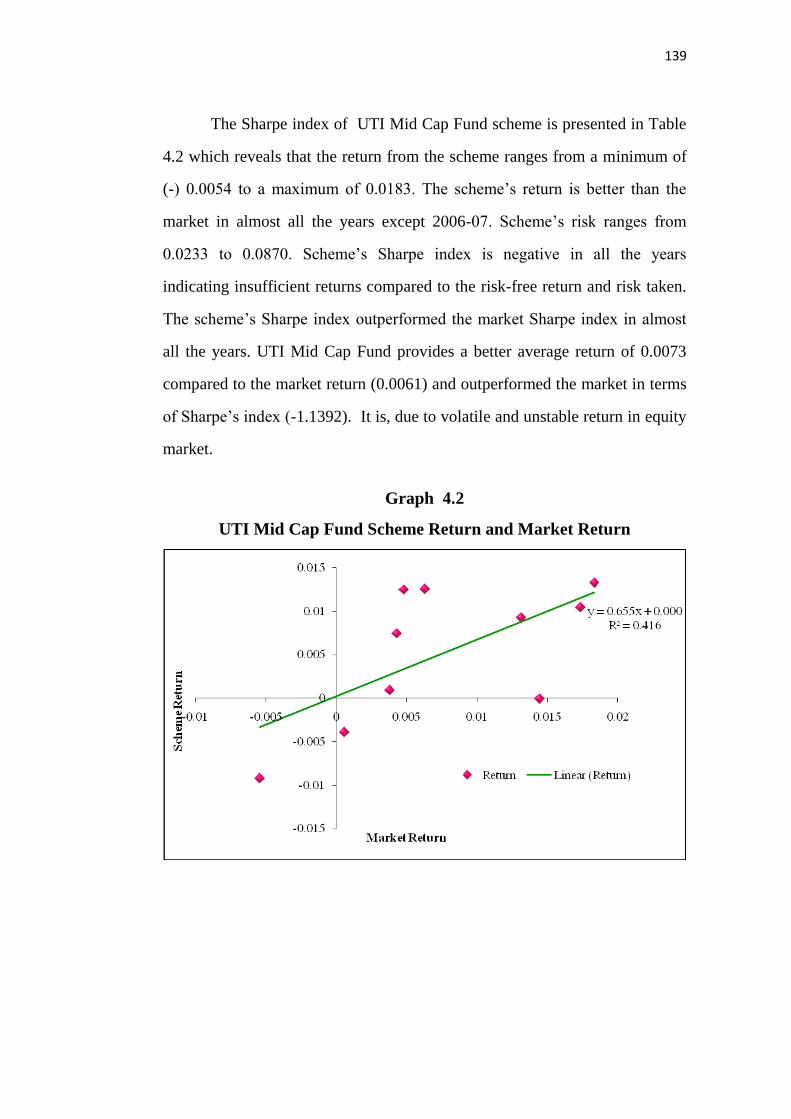

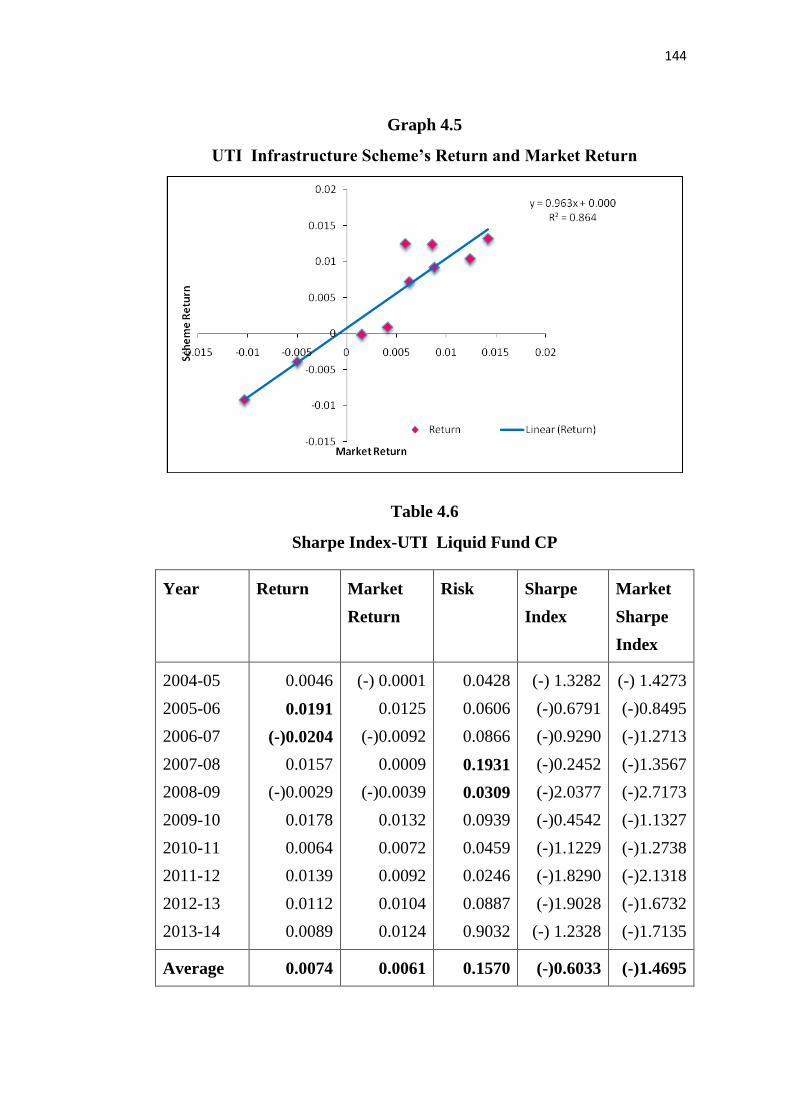

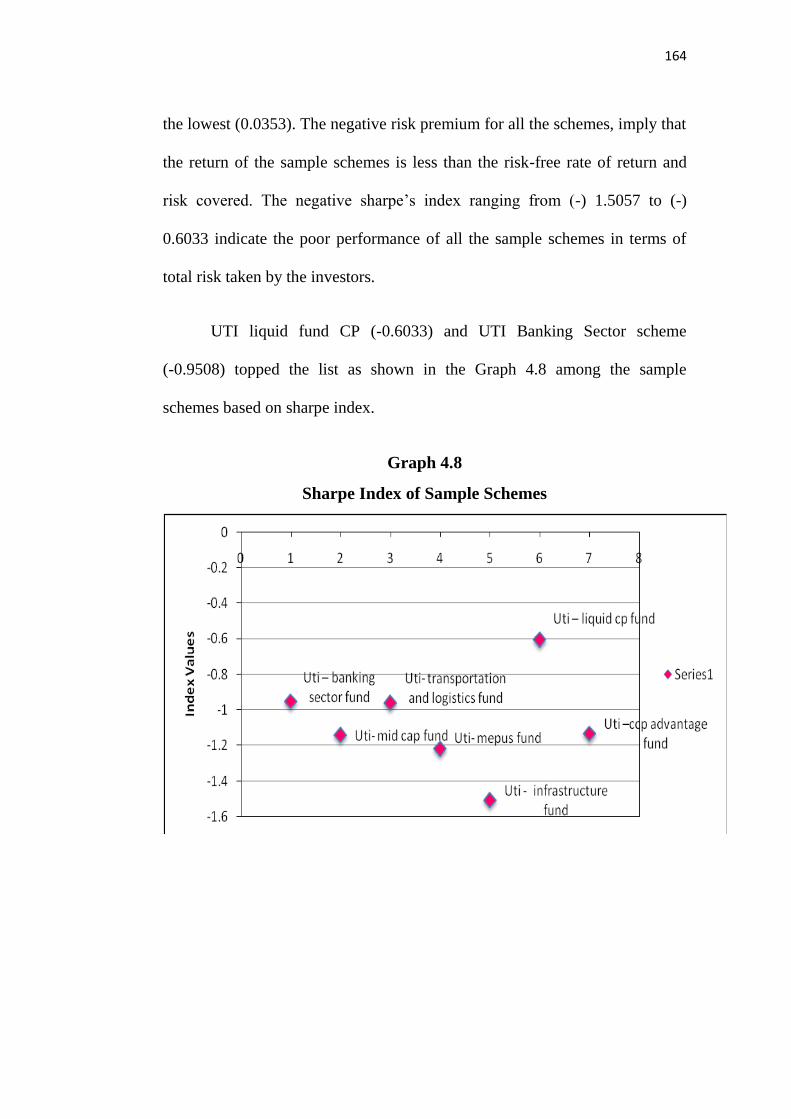

4.1 Sharpe Index - UTI Banking Sector Fund 137

4.2 Sharpe Index - UTI Mid Cap Fund 138

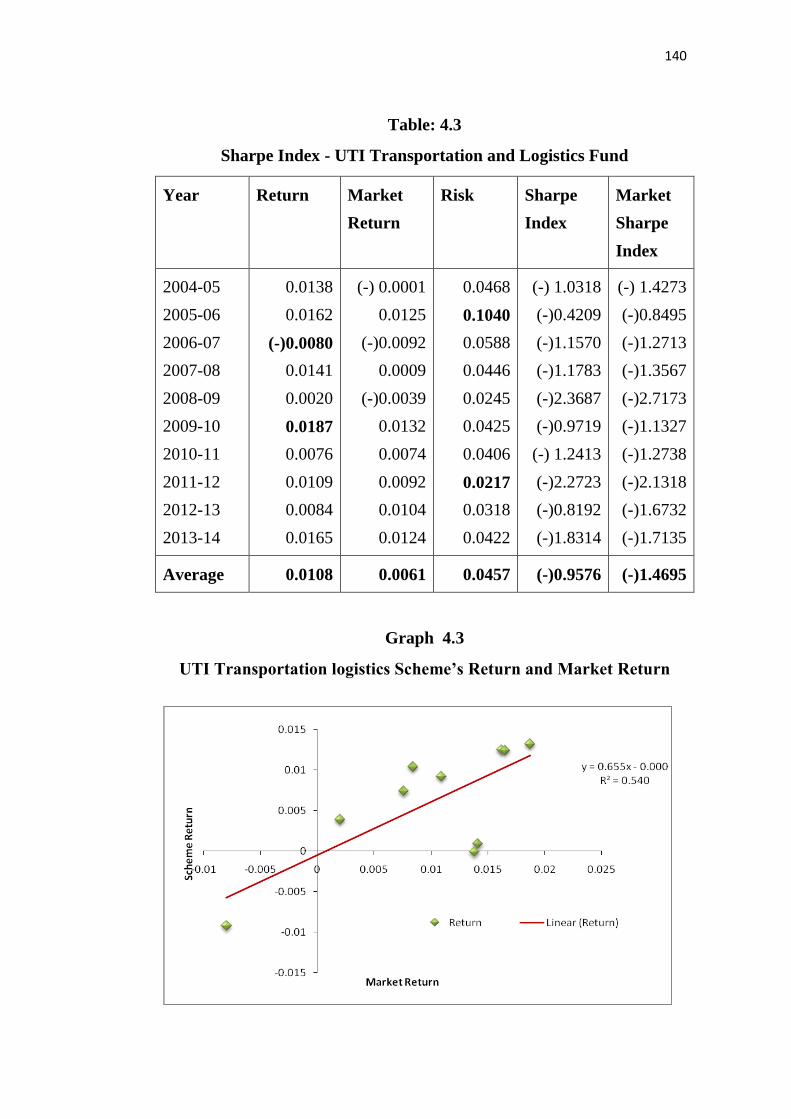

4.3 Sharpe Index - UTI Transportation and Logistics Fund 140

4.4 Sharpe Index - UTI Master Equity Plan Unit Scheme

(MEPUS)

141

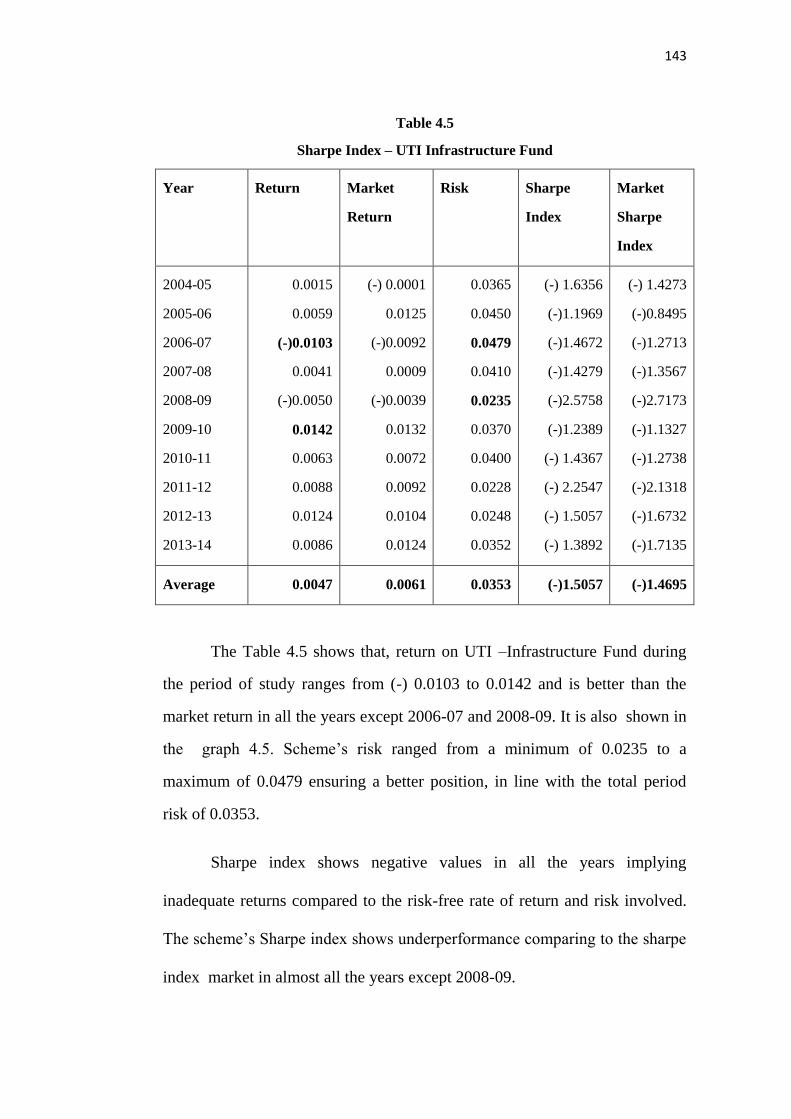

4.5 Sharpe Index - UTI Infrastructure Fund 143

4.6 Sharpe Index - UTI Liquid CP Fund 144

4.7 Sharpe index - UTI CCP advantage fund 146

4.8 Treynor index - UTI Banking Sector fund 148

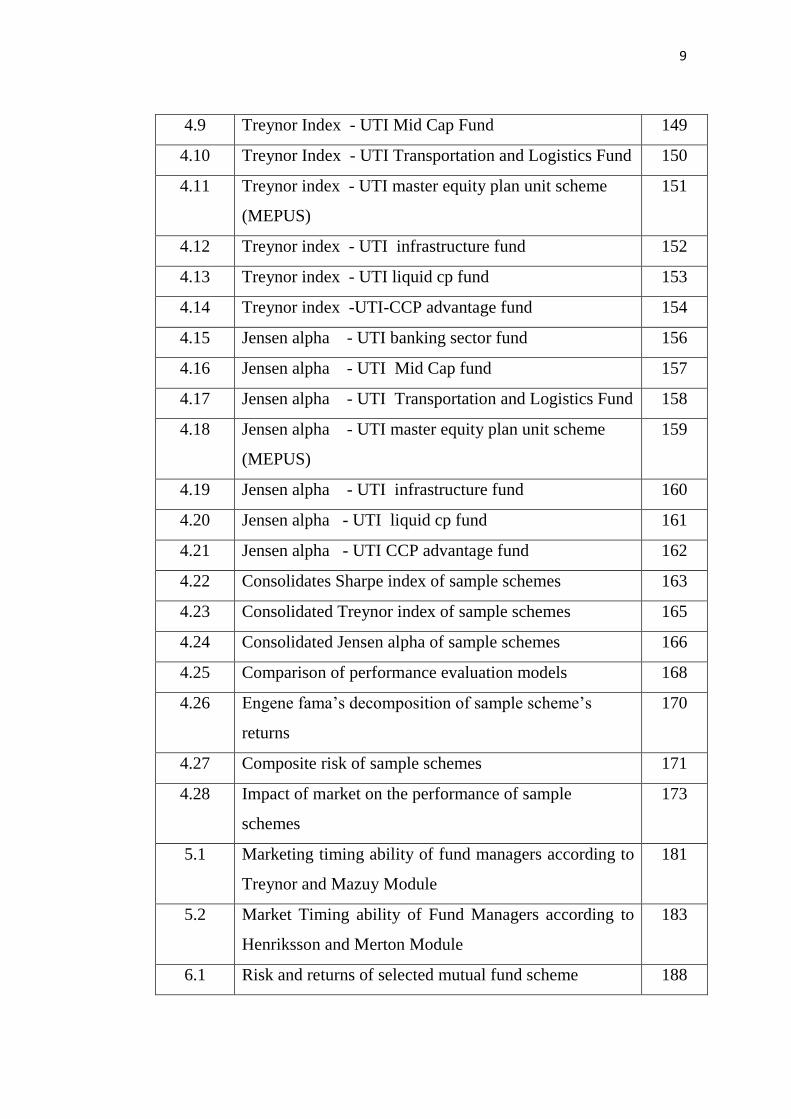

9

4.9 Treynor Index - UTI Mid Cap Fund 149

4.10 Treynor Index - UTI Transportation and Logistics Fund 150

4.11 Treynor index - UTI master equity plan unit scheme

(MEPUS)

151

4.12 Treynor index - UTI infrastructure fund 152

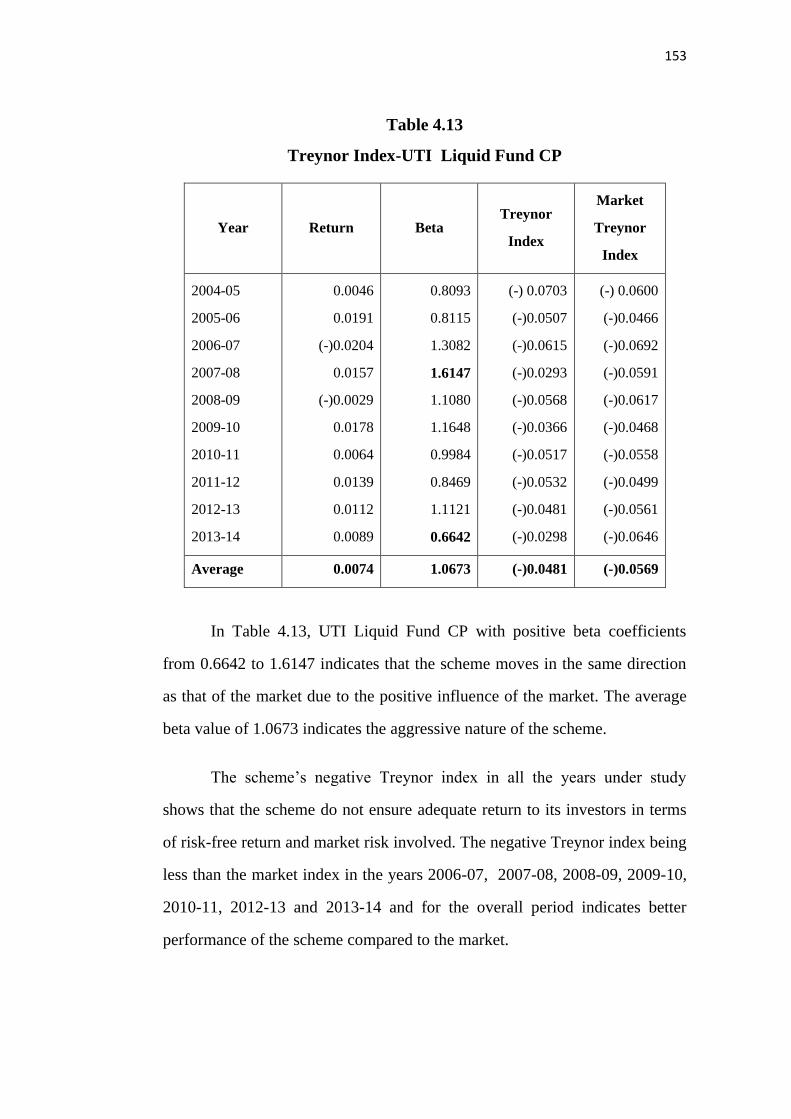

4.13 Treynor index - UTI liquid cp fund 153

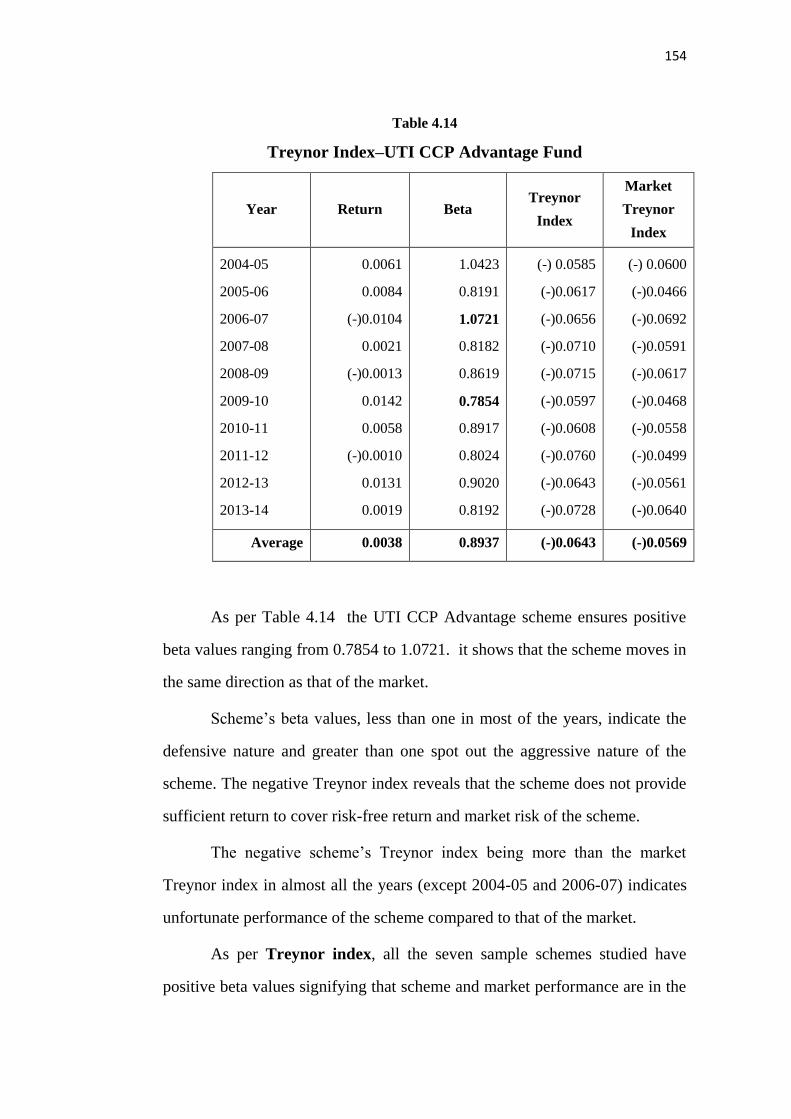

4.14 Treynor index -UTI-CCP advantage fund 154

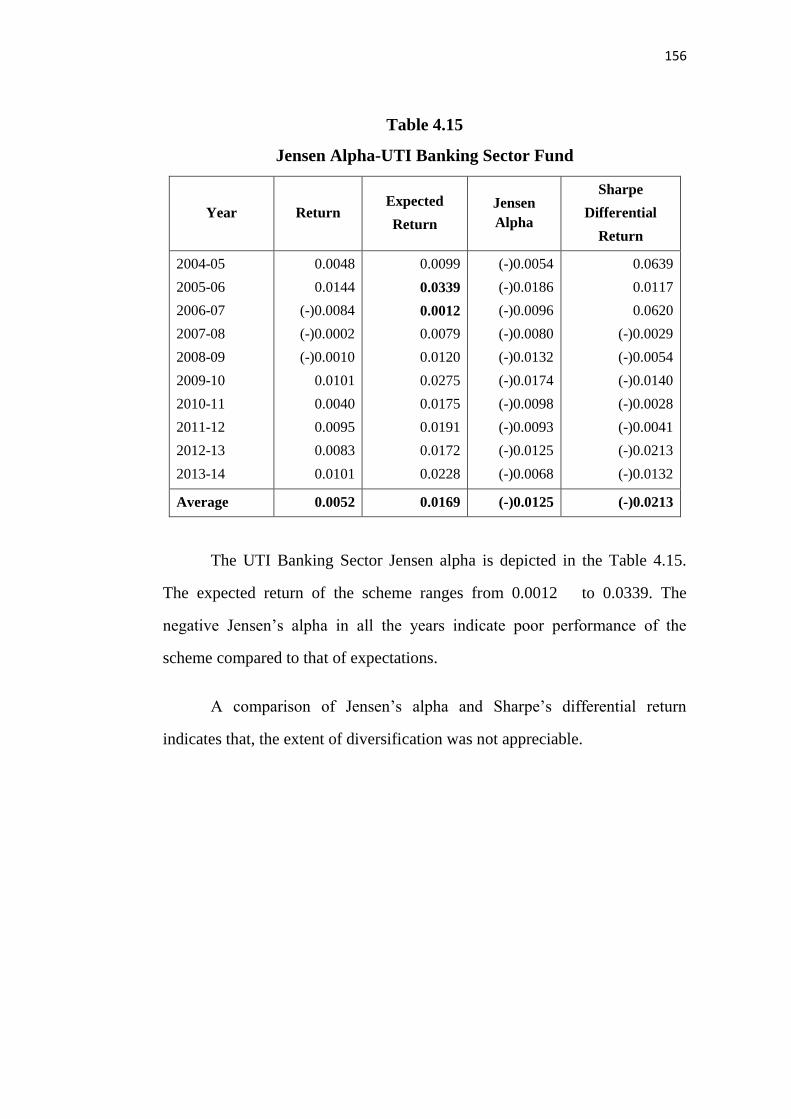

4.15 Jensen alpha - UTI banking sector fund 156

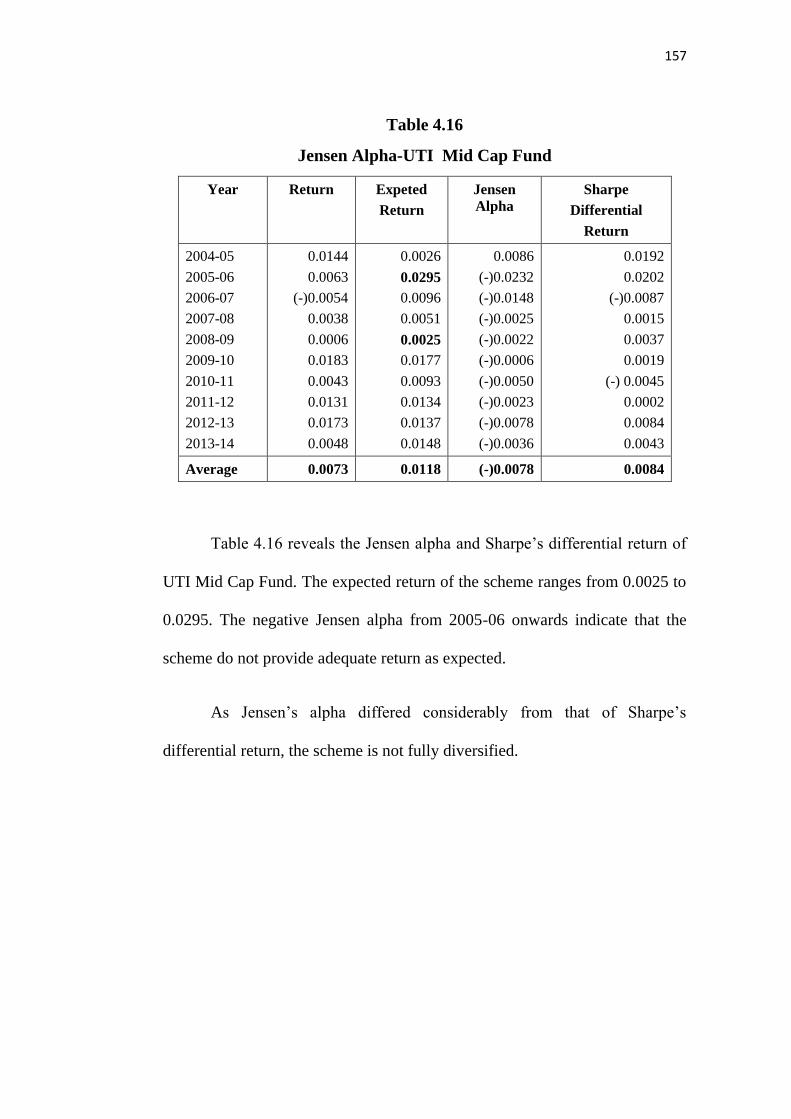

4.16 Jensen alpha - UTI Mid Cap fund 157

4.17 Jensen alpha - UTI Transportation and Logistics Fund 158

4.18 Jensen alpha - UTI master equity plan unit scheme

(MEPUS)

159

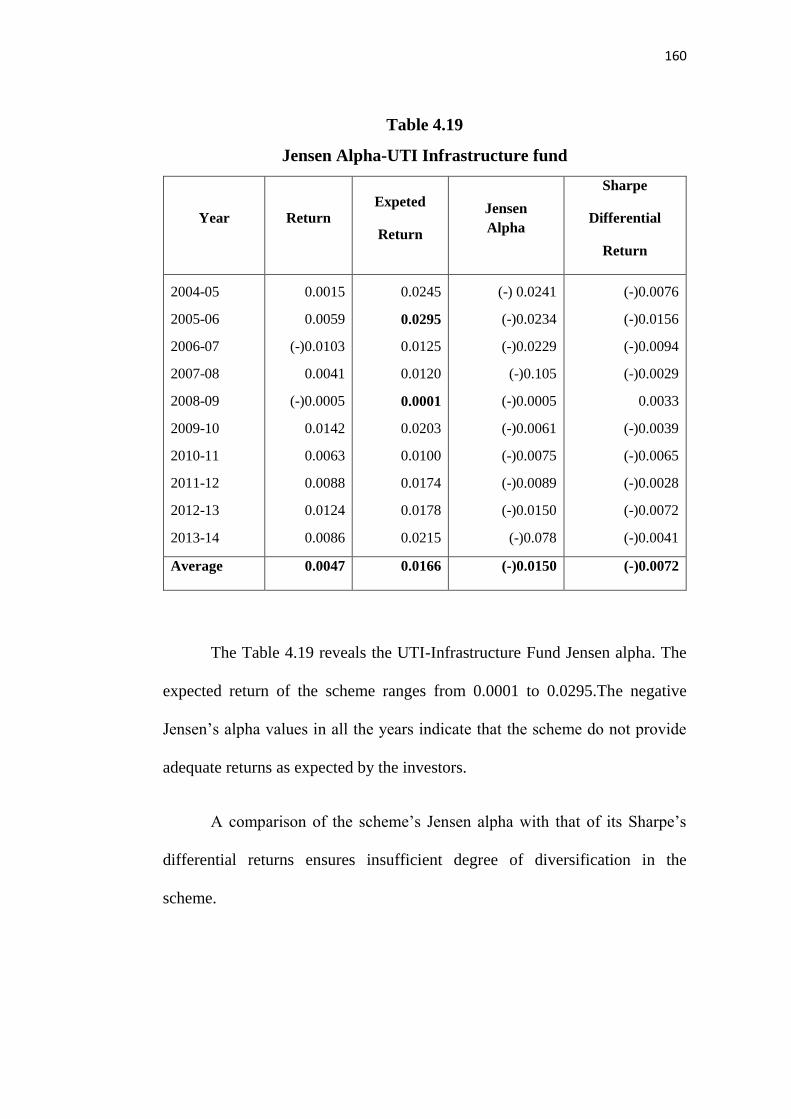

4.19 Jensen alpha - UTI infrastructure fund 160

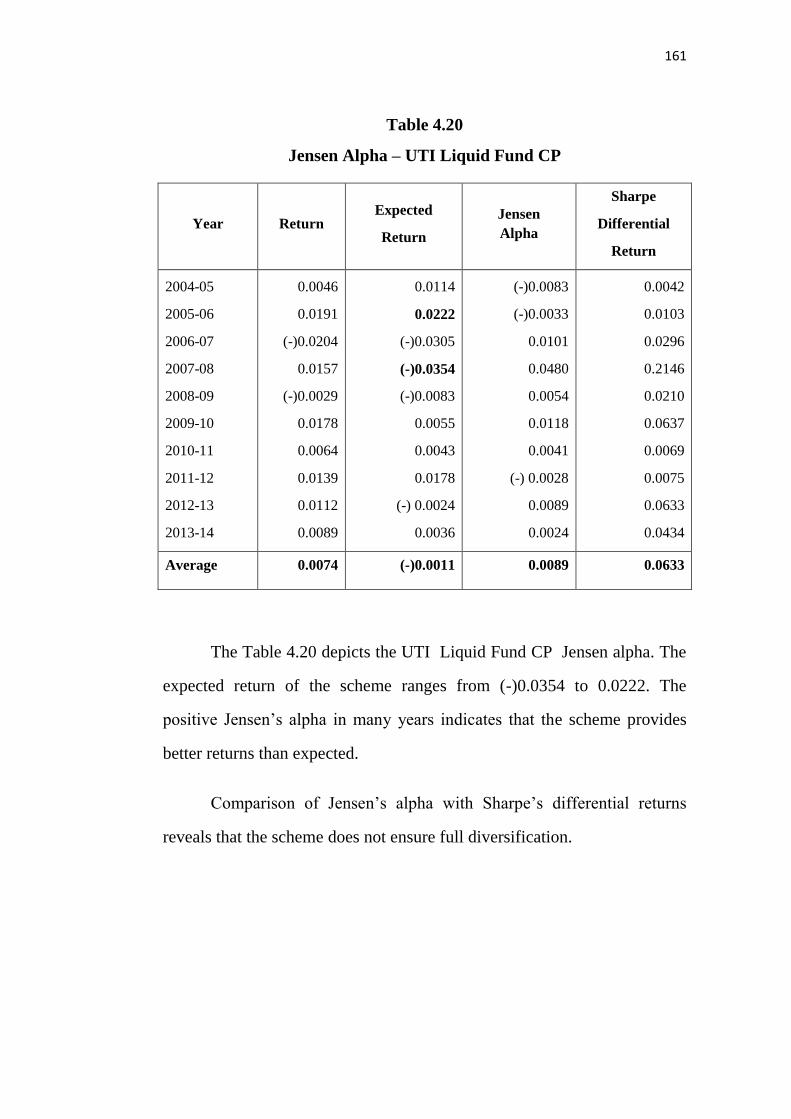

4.20 Jensen alpha - UTI liquid cp fund 161

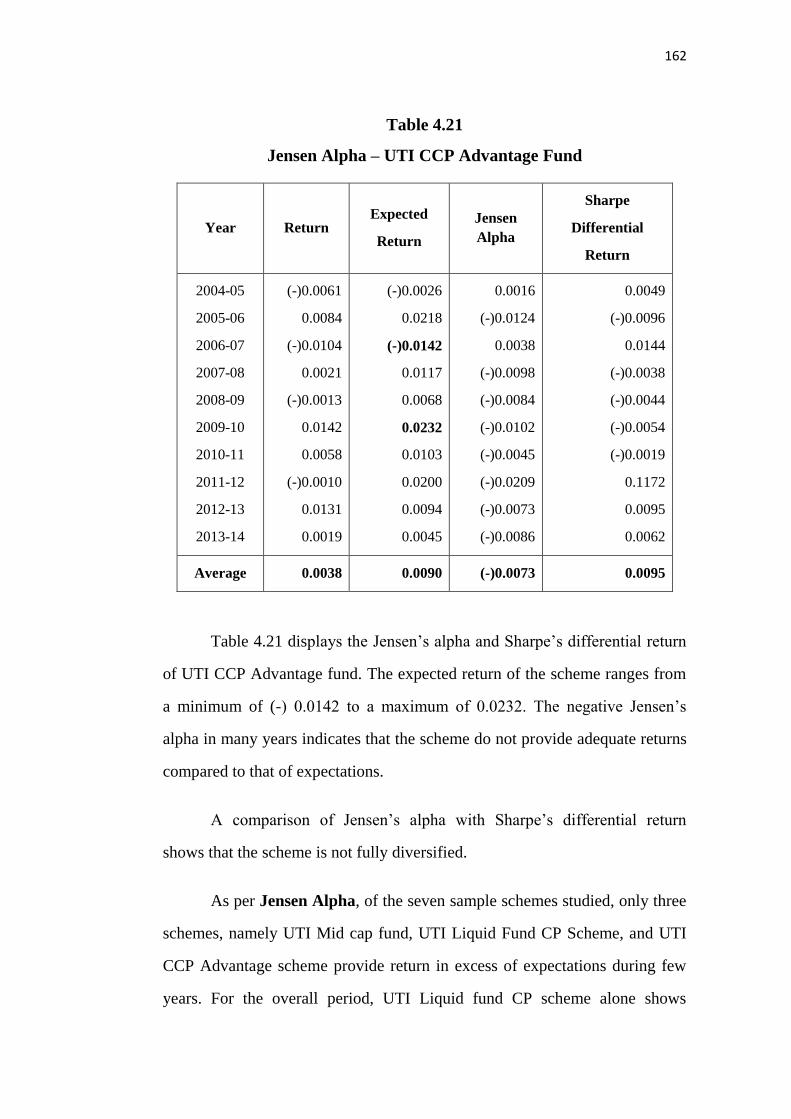

4.21 Jensen alpha - UTI CCP advantage fund 162

4.22 Consolidates Sharpe index of sample schemes 163

4.23 Consolidated Treynor index of sample schemes 165

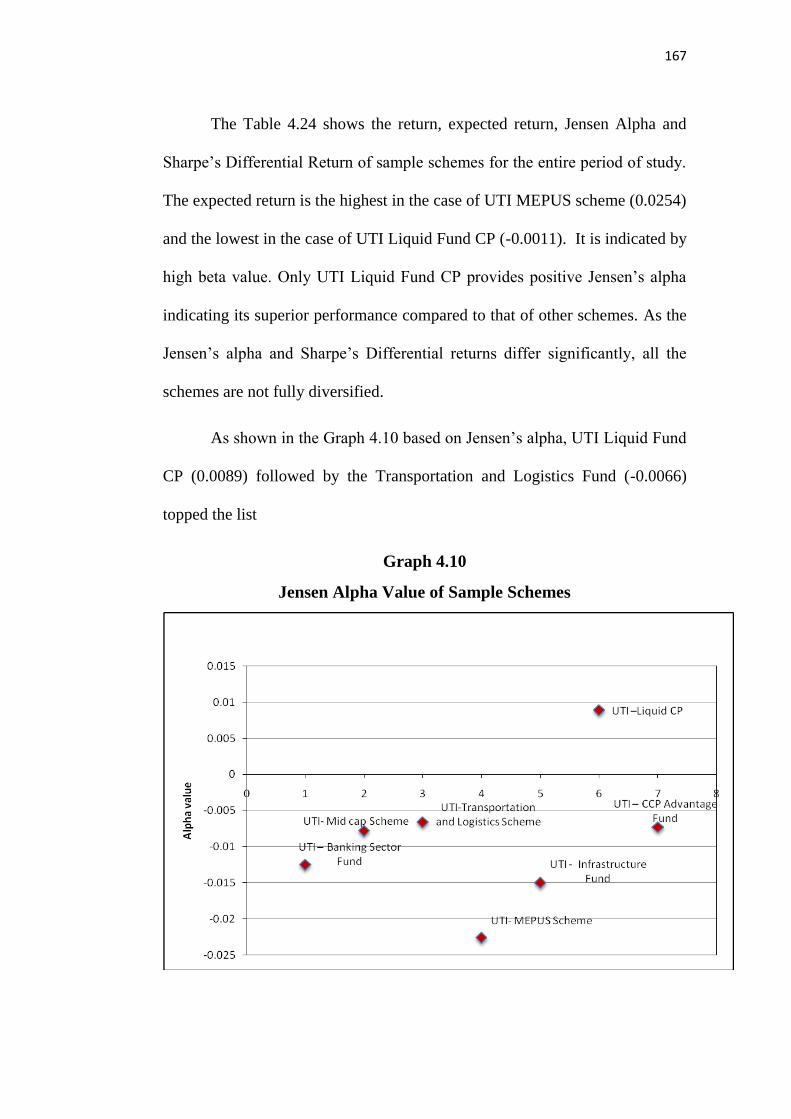

4.24 Consolidated Jensen alpha of sample schemes 166

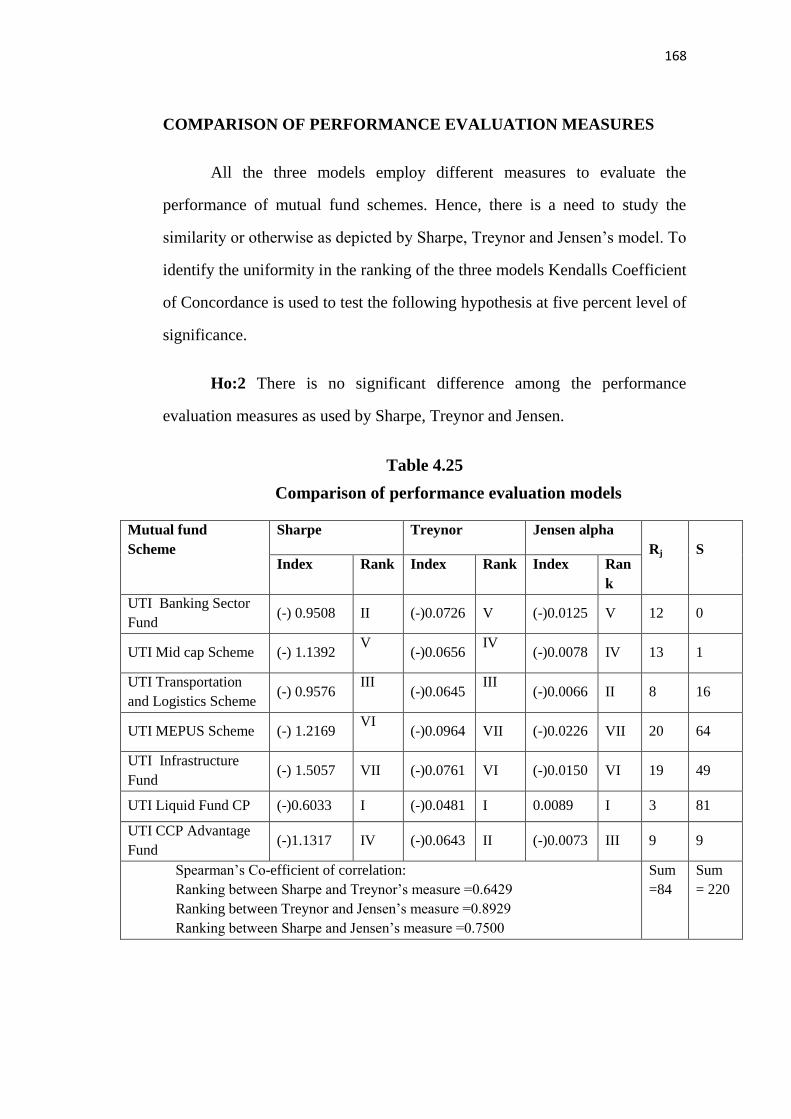

4.25 Comparison of performance evaluation models 168

4.26 Engene fama‟s decomposition of sample scheme‟s

returns

170

4.27 Composite risk of sample schemes 171

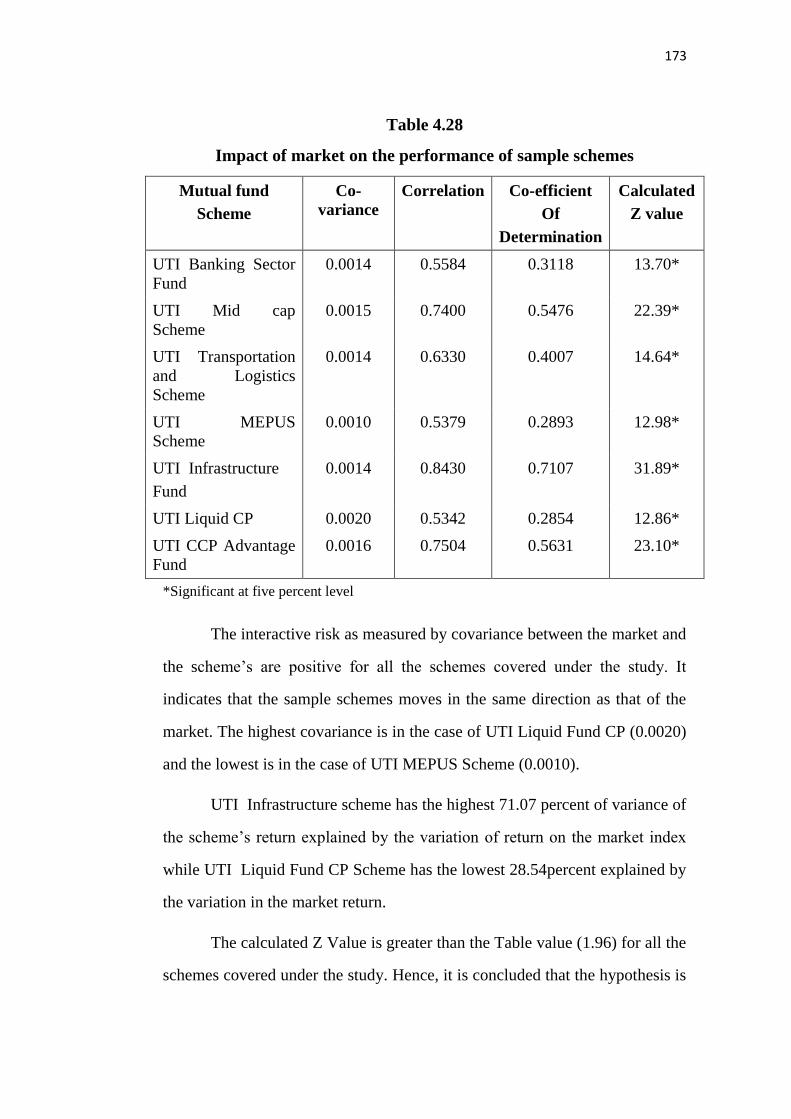

4.28 Impact of market on the performance of sample

schemes

173

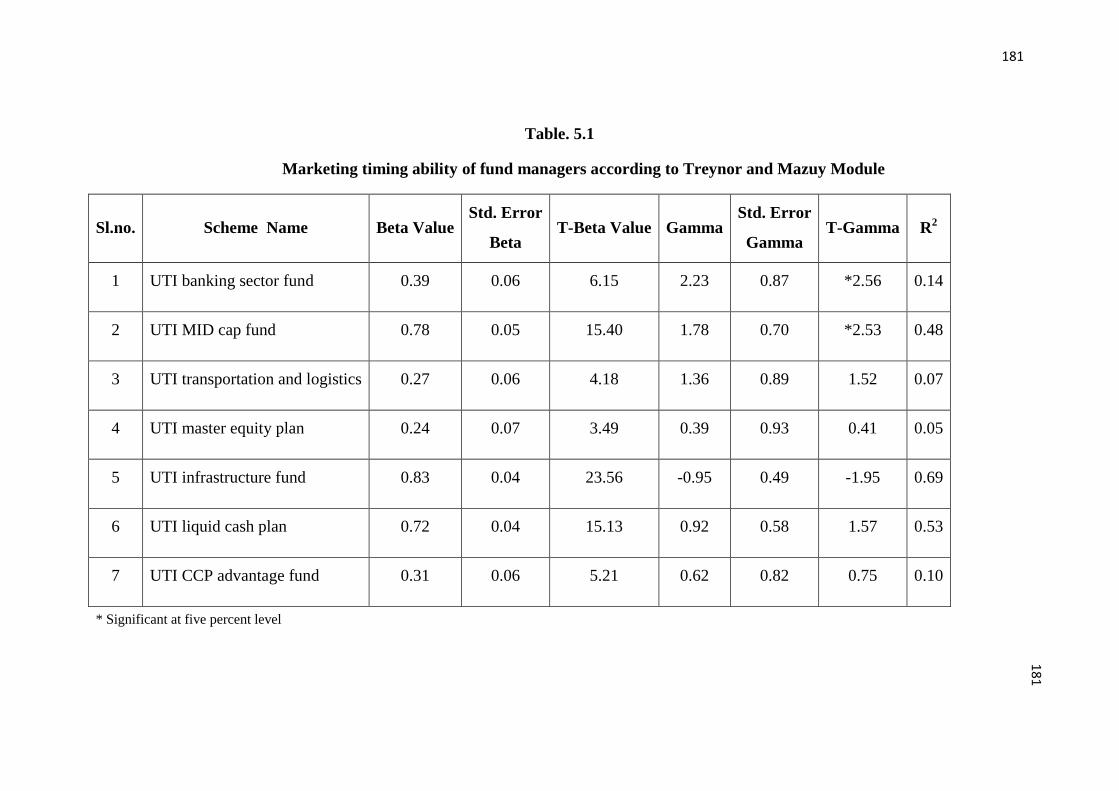

5.1 Marketing timing ability of fund managers according to

Treynor and Mazuy Module

181

5.2 Market Timing ability of Fund Managers according to

Henriksson and Merton Module

183

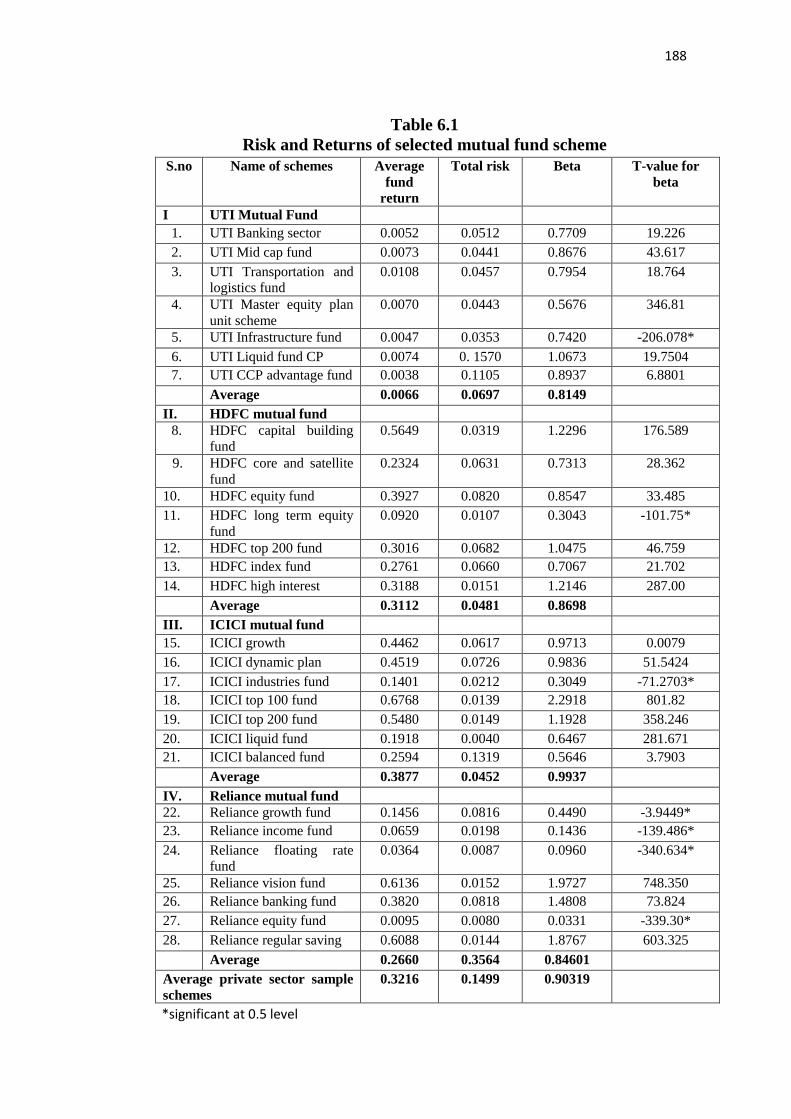

6.1 Risk and returns of selected mutual fund scheme 188

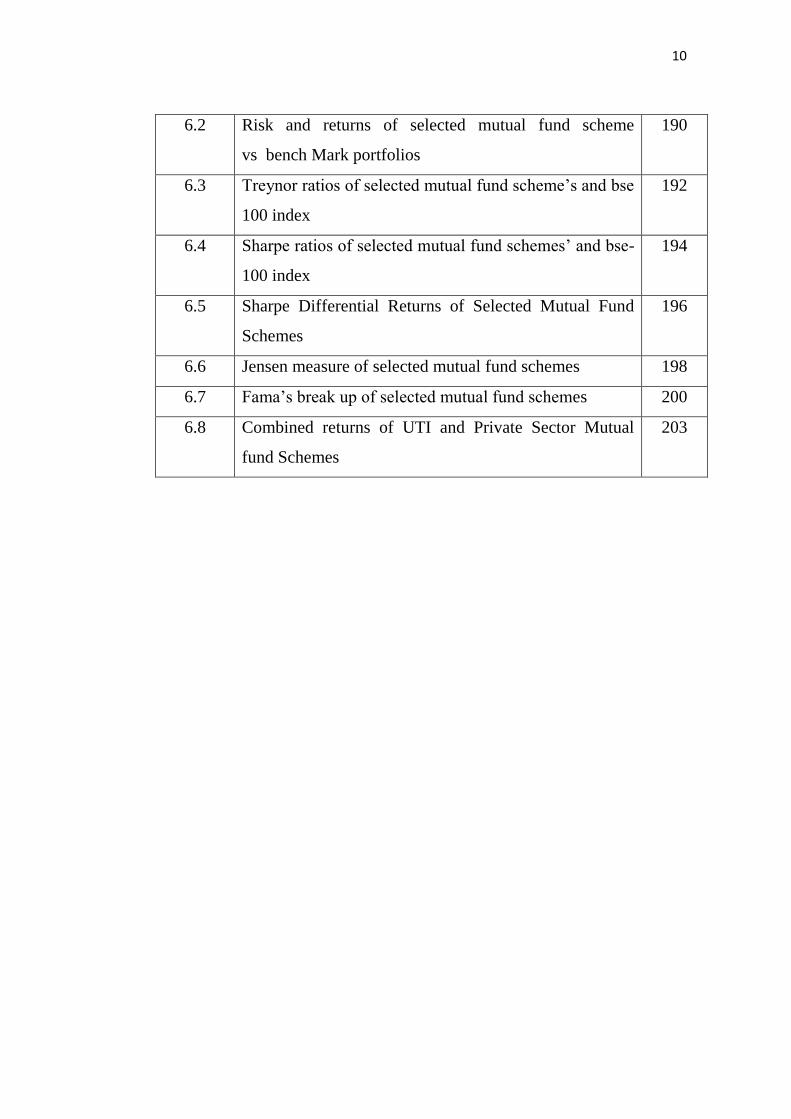

10

6.2 Risk and returns of selected mutual fund scheme

vs bench Mark portfolios

190

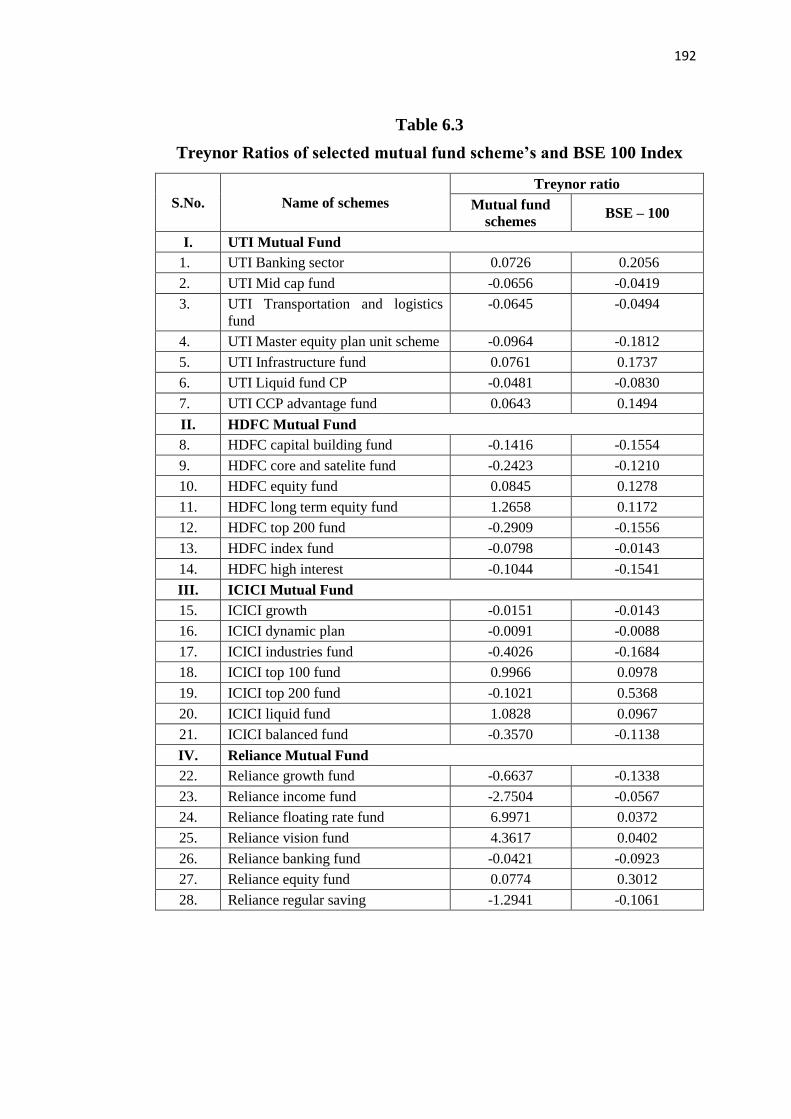

6.3 Treynor ratios of selected mutual fund scheme‟s and bse

100 index

192

6.4 Sharpe ratios of selected mutual fund schemes‟ and bse-

100 index

194

6.5 Sharpe Differential Returns of Selected Mutual Fund

Schemes

196

6.6 Jensen measure of selected mutual fund schemes 198

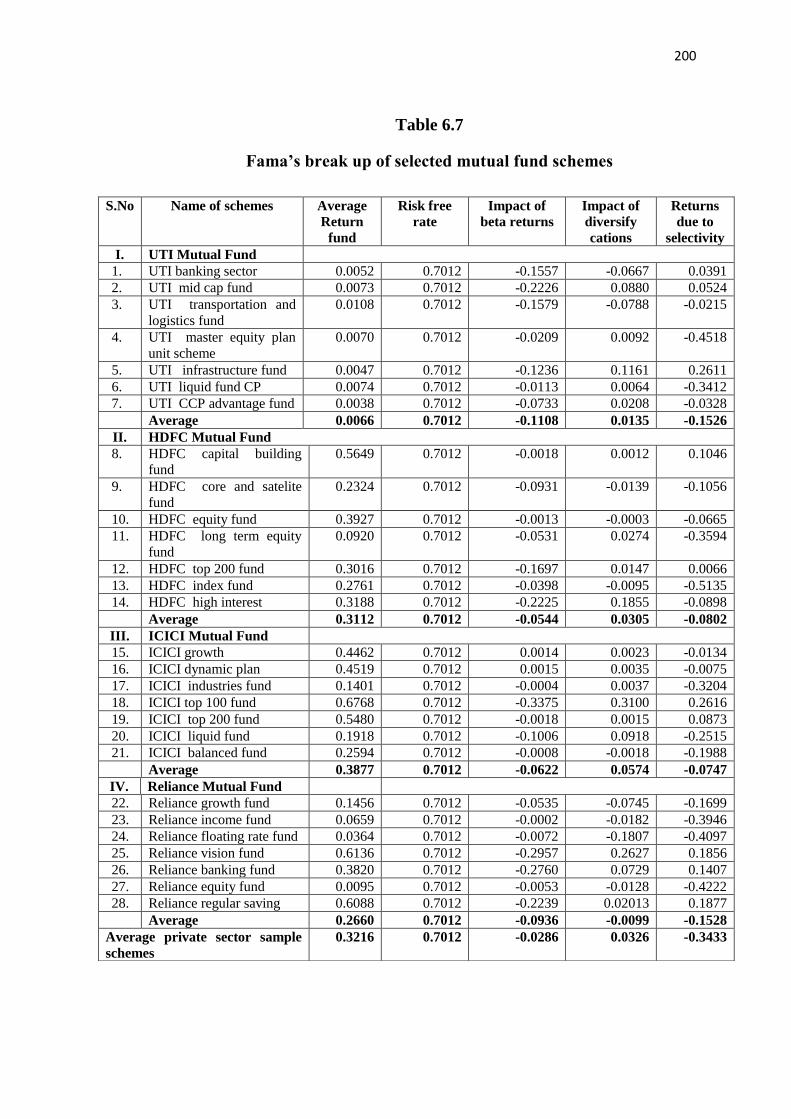

6.7 Fama‟s break up of selected mutual fund schemes 200

6.8 Combined returns of UTI and Private Sector Mutual

fund Schemes

203

11

LIST OF GRAPH

GRAPH

NO.

TITLE PAGE

NO.

1.1 Assets Under Management of The Indian Mutual Fund

Industry (Since 1964)

8

4.1 UTI Banking Sector Fund Scheme Return and Market

Return

138

4.2 UTI Mid Cap Fund Scheme Return and Market Return 139

4.3 UTI Transportation logistics Scheme‟s Return and

Market Return

140

4.4 UTI MEPUS Scheme Return and Market Return 142

4.5 UTI Infrastructure Scheme‟s Return and Market

Return

144

4.6 UTI Liquid Schemes Return and Market Return 145

4.7 UTI – CCP Advantages Scheme‟s Return and Market

Return

147

4.8 Sharpe Index of Sample Schemes 164

4.9 Treynor Index of Sample Schemes 166

4.10 Jensen Alpha Value of Sample Schemes 167

12

LIST OF SCHEDULE

SCHDULE

NO.

TITLE PAGE

NO.

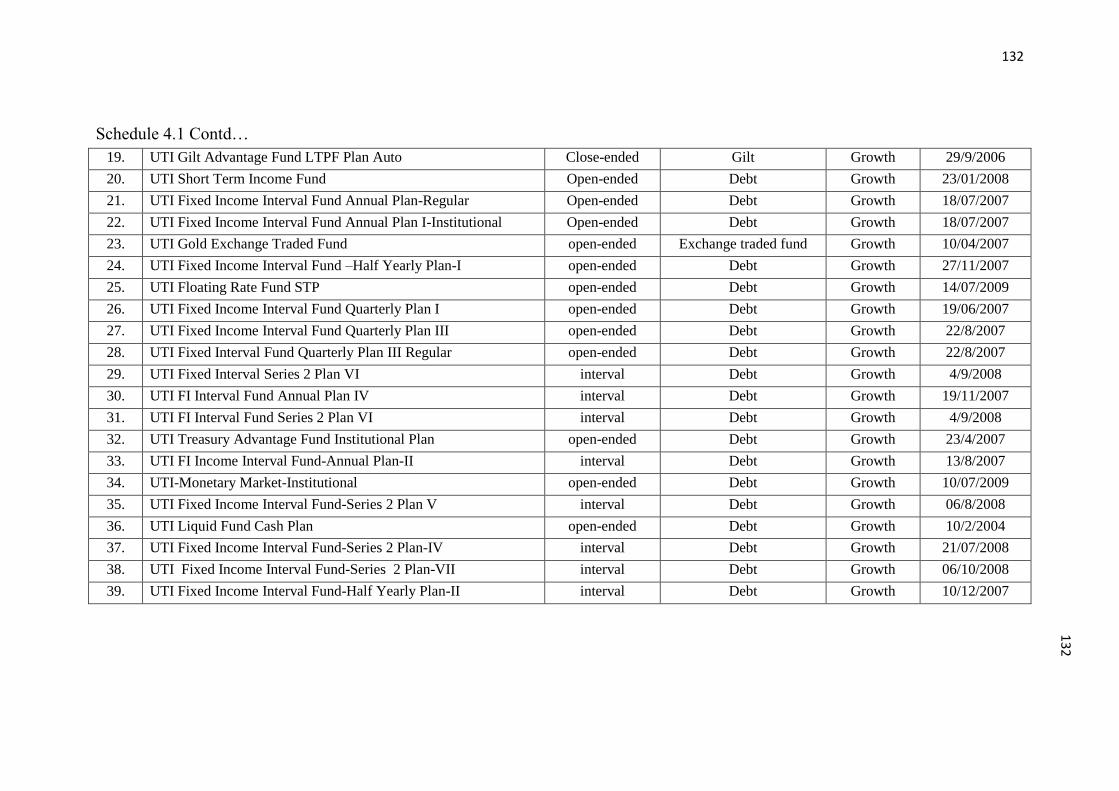

4.1 Various schemes offered by UTI Mutual Fund

(Since 2004)

131

6.1 Mutual Fund Schemes selected for Comparative

Performance

186

13

LIST OF ABBREVIATIONS

AMC : Asset Management Company

AMFI : Association of Mutual Funds of India

ARN : AMFI Registration Numbers

AUM : Assets Under Management

BSE : Bombay Stock Exchange

CAGR : Compound Annual Growth Rate

CAPM : Capital Asset Pricing Model

CGR : Compound Growth Rate

CRL : Characteristic Regression Line

GDP : Gross Domestic Product

DJIA : Dow Jones Industrial Average

ELSS : Equity Linked Savings Scheme

GDS : Gross Domestic Savings

IMFI : Indian Mutual Fund Industry

IPO : Initial Public Offer

NAV : Net Assets Value

SEBI : Securities and Exchange Board of India

SIP : Systematic Investment Plan

SWP : Systematic Withdrawal Plan

UTI : Unit Trust of India

UTIMF : UTI Mutual Fund

LIC : Life Insurance Corporation

GIC : General Insurance Corporation

CHAPTER – I

RESEARCH DESIGN

INTRODUCTION

The growth of any economy depends on the extent of promoting

investments in the corporate sector. The savings of the investors (or) the

public have to be mobilized for a productive use and this is possible only by

certain specialized agencies, who must also have the technique of attracting

the investments. It is in this manner that the mutual funds came into existence

to provide an investment opportunity to such people who do not want to take

any risks. So, mutual funds, after mobilizing the deposits, invest them in

various securities in such a manner that the investors are able to get a higher

return without much risk. In addition to this, they also enjoy the benefits for

their income.

There is large number of investment avenue in India. The investor is

to choose the best avenue for his investment considering his investment

objective.

The ideal investment objective of a rational investor is expected to be

maximization of returns and minimization of risk. The investor has to choose

proper investment depending on his objectives, preferences, needs and

abilities to take a minimum risk and obtain maximum returns.

2

Concept of Mutual Fund

SEBI (Mutual Funds) Regulations 1993 define Mutual fund as “a fund

established in the form of a trust by a sponsor to raise monies by the trustee

through the sale of units to the public under one or more schemes for investing

in securities in accordance with these regulations”1.

A mutual fund is a company that invests, may of its money, in public

traded securities, stocks and bond of business corporations. A mutual fund

obtains its capital by issuing and selling its schemes to investors, typically

small individual investors, who are company‟s shareholders2.

MUTUAL FUND INDUSTRY IN THE WORLD

At the very dawn of commercial history, Egyptians and Phoenicians

were selling shares in vessels and caravans in order to spread the risk of these

perilous ventures. The idea of pooling money dates back to 1822, when

groups of people in Belgium established a company to finance investments in

national industries under the name of „Societe Generale de Belgique‟

incorporating the concept of risk sharing3. The institution acquired securities

from a wide range of companies and practiced the concept of mutual fund for

risk diversification. The word „mutual‟ denoted something to be done

collectively by a group of people with the common objective of having mutual

faith and understanding among themselves. „Fund‟ was used in monetary

terms, to collect some money from the members for a common objective like

earning profits with joint efforts.

1 Jayadev, M. Investment policy and performance of Mutual funds, Kanishka Publishers

Distributors, New Delhi, 2004, p.44. 2 Grolieten Academic Encyclopedia. P.687.1983.

3 Mestholioma Resource centre, the Free Encyclopedia, p.698, 2004.

3

Mutual fund in America is basically the concept of Unit Trust of

Britain. In U.S.A. mutual funds have come a long way since March 21, 1924

when the first fund, „Massachusetts Investment Trust‟ was organised by the

professors of Harvard University and offered shares to the public in 1926. But

it was Sherman L Adams, the father of modern mutual fund, along with

Charles Learoyd and Ashton Carr established a modest portfolio of 45

common stocks worth USD 50,0004.

The enactment of Securities Act of 1933, Investment Company Act of

1940 and Investment Advisors Act of 1940, led to the revival of mutual funds

in U.S.A. The value of securities owned by U.S.A. funds in 1950 was 2.5

billion USD. So, the accepting houses started rapidly to build up their skills

and knowledge to deal with enlarged capital.

The Mutual fund industry in Japan dates back to 1937. But an

investment trust modeled on the unit trusts of U.K. was established only in

l941. Investment trusts in Japan were set up under the Securities Investment

Law of 1951 with the three important characteristics namely contractual

nature, open-end and flexibility5.

Prior to 1960s, the U.S.A. provident fund professional investment

authorities were abhorrent of investing in equities as they are of in India

today. In 1980s, because of high mutual fund returns, employees individual

retirement accounts (IRA) enmasse shifted to equity option for their

retirement fund. In stark contrast, Japan saw a 60 percent decline in Nikkei

from 40,000 to 16,000 as a consequence of Japanese retail investors‟ aversion

to equities. With the increasing inflation and interest rates during 1990s, the

4Sudhkar A a nd Sasikumar K, “Globalisation of Mutual Fund Industry: Challenges and

Implications” , Southern Economist, Vol 42, Nov 15, 2004, p22. 5Benjamin Graham and David L. David, “Security Analysis”: The classic edition, 1951, Principle

and Techniques, Books, pp. 698.

4

individual and institutional investors became extremely sensitive to the true

value of money. The shift started towards non-intermediation, resulting in the

growth of mutual funds.

Retail investments in US mutual funds were low because of the

flatness of the market since 1966 till 1982. The value of securities owned by

U.S.A. fund houses increased from $ 60 billion in 1960 to more than $100

billion in 1983. Since the beginning of 1990, investors have poured over half a

trillion dollars into stock and bond mutual funds. In 1990, U.S.A. mutual fund

industry consisted of 2,362 mutual funds with 39,614 thousands of investors

holding $ 570.8 billions of assets. American investors embraced mutual funds

with a fervor that even the most optimistic fund executives could not have

predicted. By the end of 1994 in U.S.A., mutual funds had become the second

largest financial institution, after the banking sector, holding assets worth

$2161.4 billion. In 1995, U.K. equity income category had the highest number

of account holders (11,86,365)6.

The popularity of mutual funds among retail investors was further

driven by changes in retirement fund investment norms where employees at

large were allowed to choose asset allocation between equities and debt. In

December 1995, the European community issued a directive to coordinate

laws, regulations and the administrative provisions relating to mutual funds

and was popularly known as Undertakings for Collective Investment in

Transferable Securities. The directive established a common regulatory

scheme for investment policies, public disclosure, structure of organisation,

and regulations to encourage the growth of mutual funds all over the world,

6 Fredman, Albert J, et.al , “How Mutual funds Work”, Prentice Hall of India Private Limited,

New Delhi, 1997, p 293.

5

which led the momentum in many countries in the Asia-Pacific region with a

big bang, including Hong Kong, Thailand, Singapore and Korea.

The mutual fund in its present structure is a Twentieth Century

phenomenon. Globally there were thousands of funds offering varied schemes

with different investment objectives and options. Mutual funds emerged as the

most important investment vehicle for household investments in U.S.A. with

the basic objective of allowing small investors to partake in the capital market

by investing in a wide portfolio of stocks so as to reduce risk. At the end of

first quarter of 2013, the assets of worldwide mutual funds stood at $ 27.86

trillion while the assets of equity funds contributed for 41 percent. The asset

share of bond fund was 26 percent, and the asset share of balanced, and mixed

funds was 12 percent, money market fund assets represented 17 percent, and

others four percent of the world wide total7.

MUTUAL FUND INDUSTRY IN INDIA

The mutual fund industry in India started in 1963 with the formation of

Unit Trust of India, at the initiative of Government of India and Reserve Bank

of India. The history of mutual funds in India can be broadly divided into four

distinct phases.

First Phase (1964-87)

Unit Trust of India (UTI) was established on 1963 by an Act of

Parliament. It was set up by the Reserve Bank of India and functioned under

the Regulatory and administrative control of the Reserve Bank of India. In

1978 UTI was de-linked from the RBI and the Industrial Development Bank

of India (IDBI) took over the regulatory and administrative control in place of

RBI. The first scheme launched by UTI was Unit Scheme 1964. At the end

of 1988 UTI had Rs. 6,700 crores of assets under management.

7 Tripathy, Naliniprava, Financial Instruments and Services, Prentice Hall of India Private Ltd.,

New Delhi, 2013, pp. 51-52.

6

Second Phase (1987-1993)

1987 marked the entry of non-UTI, public sector mutual funds set up

by public sector banks and Life Insurance Corporation of India (LIC) and

General Insurance Corporation of India (GIC). SBI Mutual Fund was the first

non-UTI Mutual Fund established in June 1987 followed by Canbank Mutual

Fund (December, 1987), Punjab National Bank Mutual Fund (August, 1989),

Indian Bank Mutual Fund (November 1989), Bank of India (June, 1990),

Bank of Baroda Mutual Fund (October, 1992). LIC established its mutual

fund in June 1989 while GIC had set up its mutual fund in December, 1990.

At the end of 1993, the mutual fund industry had assets under management of

Rs. 47, 004 crores.

Third Phase (1993-2003)

With the entry of private sector funds in 1993, a new era started in the

Indian mutual fund industry, giving the Indian investors a wider choice of

fund families. Also, 1993 was the year in which the first Mutual Fund

Regulations came into being, under which all mutual funds, except UTI, were

to be registered and governed. The erstwhile Kothari Pioneer (now merged

with Franklin Templeton) was the first private sector mutual fund registered in

July, 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more

comprehensive and revised Mutual Fund Regulations in 1996. The industry

now functions under the SEBI (Mutual Fund Regulations 1996.

The number of mutual fund houses went on increasing, with many

foreign mutual funds setting up funds in India and also the industry has

witnessed several mergers and acquisitions. As at the end of January 2003,

there were 33 mutual funds with total assets of Rs. 1,21,805 crores. The Unit

Trust of India with Rs. 44, 541 crores of assets under management was way

ahead of other mutual funds.

7

Fourth Phase (Since February 2003)

In February 2003, following the repeal of the Unit Trust of India Act

1963 UTI was bifurcated into two separate entities. One is the Specified

Undertaking of the Unit Trust of India with assets under management of

Rs.29, 835 crores as at the end of January 2003, representing broadly, the

assets of Unit Scheme (US)-64, assured return and certain other schemes. The

Specified Undertaking of Unit Trust of India, functioning under an

administrator and under the rules framed by Government of India, does not

come under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund, sponsored by SBI, PNB, BOB,

and LIC. It is registered with SEBI and functions under the Mutual Fund

Regulations. With the bifurcation of the erstwhile UTI which had in March

2000 more than Rs. 76,000 crores of assets under management and with the

setting up of a UTI Mutual Fund, conforming to the SEBI Mutual Fund

Regulations, and with recent mergers taking place among different private

sector funds, the mutual fund industry has entered its current phase of

consolidation and growth.

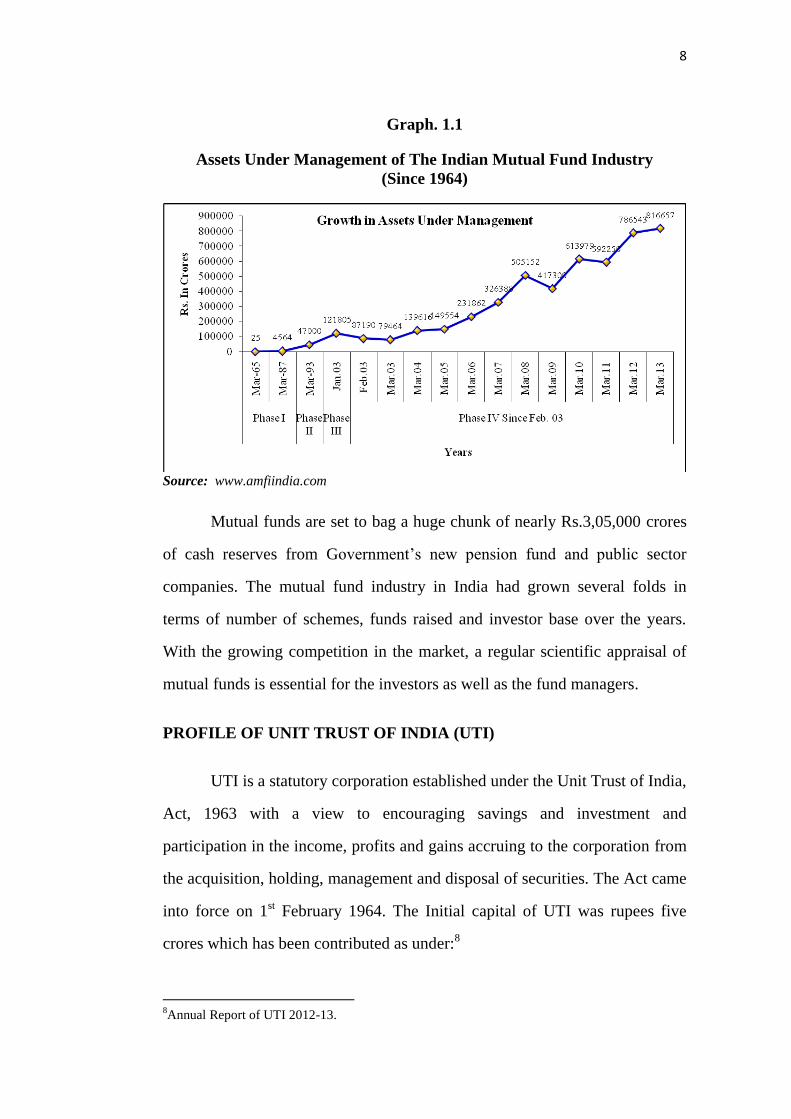

In India, mutual funds as vehicles of mobilization and channels of

funds towards the securities market, as exposed in the graph indicates

improvement in total net assets from Rs.25 crores, by the end of 1964-65 to

Rs.47,734 crores as on March 31, 1993, and touched Rs.2,31,862 crores as on

March 31, 2006 as shown in the graph 1.4. The industry held total net assets

worth Rs.8,16,657 crores as on March 31, 2013 through 1294 schemes.

8

Graph. 1.1

Assets Under Management of The Indian Mutual Fund Industry

(Since 1964)

Source: www.amfiindia.com

Mutual funds are set to bag a huge chunk of nearly Rs.3,05,000 crores

of cash reserves from Government‟s new pension fund and public sector

companies. The mutual fund industry in India had grown several folds in

terms of number of schemes, funds raised and investor base over the years.

With the growing competition in the market, a regular scientific appraisal of

mutual funds is essential for the investors as well as the fund managers.

PROFILE OF UNIT TRUST OF INDIA (UTI)

UTI is a statutory corporation established under the Unit Trust of India,

Act, 1963 with a view to encouraging savings and investment and

participation in the income, profits and gains accruing to the corporation from

the acquisition, holding, management and disposal of securities. The Act came

into force on 1st February 1964. The Initial capital of UTI was rupees five

crores which has been contributed as under:8

8Annual Report of UTI 2012-13.

9

i. Reserve Bank of India Rs. 2.50 crores

ii. Life Insurance Corporation of India Rs. 0.75 crores

iii. State Bank of India and its Subsidiary Banks Rs. 0.75 crores

iv. Schedule Banks and notified financial

institutions

Rs. 1.00 crores

Total Rs. 5.00 crores

The contribution of initial capital of the UTI as per Sec(2) of the UTI

Act, 1963 by its original owners. The initial capital forms part of Unit

Scheme-64 and the subscribers hold units in that schemes. In 1975, the UTI

Act was amended and by virtue of the amendment, the Industrials

Development Bank of India (IDBI) took over the rights and responsibilities of

RBI under the Act and the share of the initial held by RBI was transferred to

and vested in IDBI.

The general superintendence, direction and management of the affairs

and business of UTI rests in a Board of Trustees which exercised all powers

and does all acts and functions which may be exercised by UTI. The

composition of the Board of Trustees is as follows.

The Chairman to be appointed by the Central Government in

Consultation with Industrial Development Bank of India (IDBI, the Leader in

the Indian Capital Market). One trustee to be nominated by RBI. Four

trustees to be nominated by IDBI of whom not less than three persons having

special knowledge of/or experience in commerce, industry, banking, finance

or investment. One trustee each to be nominated by LIC and SBI. Two

trustees to be elected by other contributing institutions viz., scheduled banks

and their subsidiary banks and notified financial institutions. An executive

trustee to be appointed by IDBI, provided that such an appointment may not

10

necessary if the chairman is whole time. The board meets not less than six

times in a year and at least once in two months.

Executive Committee of UTI

The UTI operates through an executive committee structure. The

committee is given powers subject to such general and or special directions as

the Board may feel fit, from time to time. It has the power to deal with any

matter with the competence of UTI. The Executive Committee consists of the

Chairman of the Board and two other trustees nominated by IDBI. The

executive committee usually meets once in a month.

The day to day business operations of UTI are looked after by the full

time Chairman. He is assisted by a team of Executive Directors and Chief

General Managers. Presently eight Executive Directors and twelve Chief

General Managers are involved in the business9.

UTI has a three-tier organizational set up with a corporate office, Four

Zonal Offices and Fifty Four Branch offices. It has about 6.71 crores unit

holding accounts under 46 domestic schemes having investible funds at

market value as on 31st December 2013 of Rs.700.57 billion10. In addition, it

has six off shore funds and four venture capital funds. Its management

expenses amount to about one percent of the investible funds.

There is an Audit Committee consisting of five trustees, which reviews

the systems and control and interacts with the internal and external auditors.

In addition to the Board and committee, there are a number of committees

constituted by the executives of the UTI.

9 UTI Annual Report, 2012.

10 www.Amfi.com.

11

A first-tier audit committee reviews the reports of all sections and

department of UTI and initiates necessary corrective action. An investment

valuation committee reviews the systems and practice the valuation of

securities. Primary market investment committee handles primary market

proposals. Property management committee appraises proposals approved by

building committee and an internal committee for settlement dues.

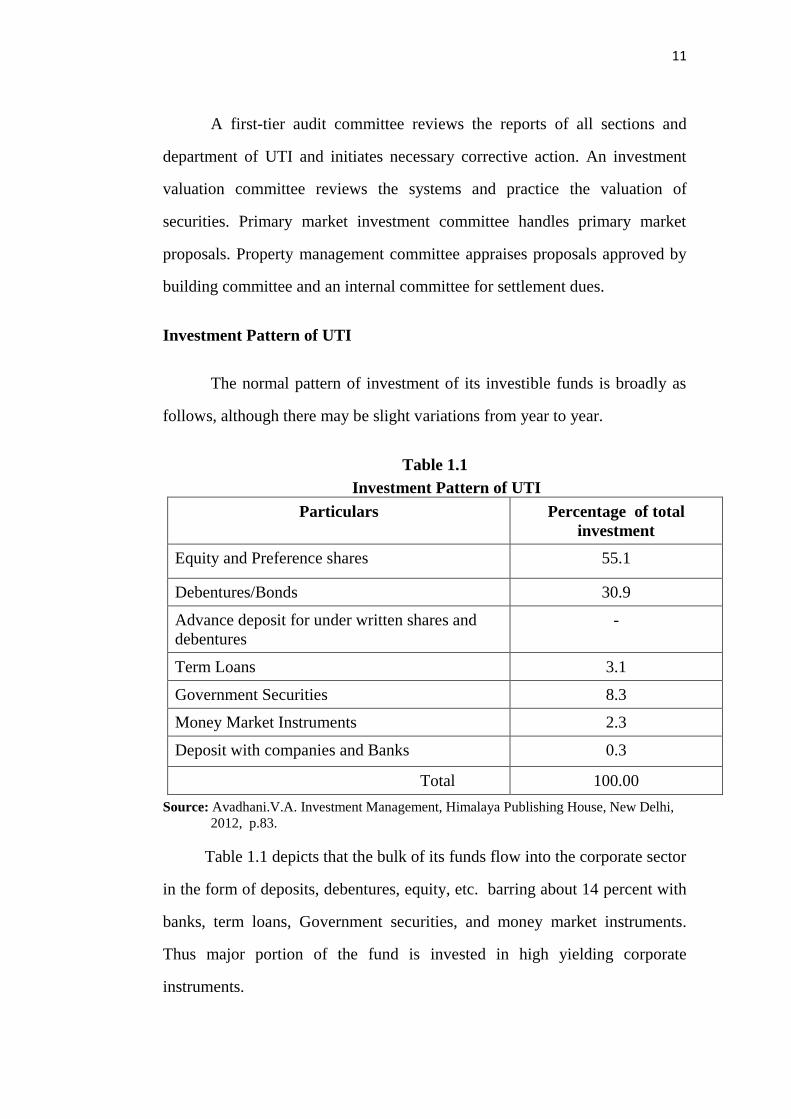

Investment Pattern of UTI

The normal pattern of investment of its investible funds is broadly as

follows, although there may be slight variations from year to year.

Table 1.1

Investment Pattern of UTI

Particulars Percentage of total

investment

Equity and Preference shares 55.1

Debentures/Bonds 30.9

Advance deposit for under written shares and

debentures

-

Term Loans 3.1

Government Securities 8.3

Money Market Instruments 2.3

Deposit with companies and Banks 0.3

Total 100.00

Source: Avadhani.V.A. Investment Management, Himalaya Publishing House, New Delhi,

2012, p.83.

Table 1.1 depicts that the bulk of its funds flow into the corporate sector

in the form of deposits, debentures, equity, etc. barring about 14 percent with

banks, term loans, Government securities, and money market instruments.

Thus major portion of the fund is invested in high yielding corporate

instruments.

12

Objectives of UTI

Its main objectives are to mobilize savings, particularly from the low

and middle income groups, to channelize these savings into productive

investment and to provide an assured income to savers. It provides the savers

with expert investment services, portfolio management and assured income.

Borrowing Power

There may be occasions for the trust to buy in bulk the shares and

debentures of many industrial concerns and institutions. When the resources

are found to be inadequate to meet its requirements, the UTI is authorized to

borrow from the Reserve Bank of India, or the Government or any other

authority.

Power to make schemes

Under sec.21(1) of the Unit Trust of India Act, 1963, the Board of

Trustees has been authorized to offer various schemes to the public for the

purpose of providing facilities for participation in the income, profits and

gains arising out of the acquisition, holding, management or disposal of

securities by the UTI.

Network of UTI

The core strength of UTI has been to build a large number of small

investors who have remained with UTI for long years. In all, as on 31st March,

2013 UTI has 76 schemes in operation with above 6.71 crores unit holding

accounts. UTI is well entrenched among investors and savers in each and

every district of the country. UTI has wide marketing network of 54 branches,

292 main branches, 190 collection centres 53 franchise offices and over

13

90,000 agents11. UTI has a well-knit distribution network to attract and

provide sufficient service to unit holders in all parts of the country. They are

committed to strengthen their marketing network and make give it a total

investment trusts to quicken and better the investor‟s services.

UTI Mutual Fund has a track record of managing a variety of schemes

catering to the needs of every class of citizens. It has a nationwide network

consisting of 146 UTI Financial Centres (UFCs) and UTI International offices

in London, Dubai, Bahrain and Singapore.

Reliability

UTI Mutual Fund (UTIMF) has consistently reset and upgraded

transparency standards. All the branches, UFCs and registrar offices are

connected on a robust IT network to ensure cost-effective quick and efficient

service. All these have evolved UTIMF to position as a dynamic, responsive,

restructured, efficient and transparent entity, fully compliant with SEBI

regulations.

STATEMENT OF THE PROBLEM

India has become the world‟s fourth largest economy besides U.S.A.,

China, and Japan12. Although the Indian capital market witnessed some

significant changes during the eighties, both the primary and the secondary

segments continued to suffer from some serious deficiencies. Many unhealthy

practices prevailed in the primary market to attract retail investors. High

pricing of new issues, difficulties in analyzing the prospects of a company,

under pricing of shares in the market after listing have discouraged and

11

www. Utimf.com. 12

Sudhakar A and Sasikumar K, “Globalization of Mutual Fund Industry: Challenges and

Implications”, Southern Economist, Vol. 42, Nov. 15, 2004, p.22.

14

aroused hesitation among many investors to enter into the stock market. The

secondary market had become highly volatile and technical for small

investors.

Markets for equity shares, real estate, derivatives and other assets have

become highly dynamic. Unprecedented global and national events have

brought in substantial changes in the securities market. Capital market, being

the major supplier of corporate finance, ought to grow in a healthy manner to

pump in more and more money. Investment in corporate securities demands

investors to understand the complexities of market, to keep track of market

movements and to make scientific investment decisions. The growing

popularity of mutual funds prove that it is an ideal investment vehicle for

small investors having limited information and knowledge to enter the today‟s

complex and modern capital market. Out of the household investors in

Mutual Fund, Bond, Debentures, IPO, Secondary Market, and Derivative

market, household investors in Mutual Fund stands first by holding

0.51 million followed by house holding investors in Bonds 0.16 billion,

Debentures 0.08 million, IPO 0.10 million, Secondary market 0.025 million,

and derivative 0.04 million13. The domestic mutual fund industry has grown

by 50 percent particularly through Systematic Investment Plan (SIP) from

retail participants. But, there is still a long way to go as only five percent of

the households are investing in mutual fund schemes.

Liberalization of economic policies, metamorphic changes in the

Indian Financial System, brought out increase in the share of household

savings, changes in investment attitude and preferences. It was estimated that,

the Gross Domestic Savings for 2007-08 to 2012-13 ranges from 33.4 percent

13

How House holds save and invest, National council of Applied Economic Research Report,

July 2011, p.29. Sponsored by SEBI.

15

to 34.7 percent, under the growth scenarios of seven to nine percent

respectively, against 27.1 percent in 2004-05. Household sector‟s financial

savings for 2011-12 to 2014-15 is expected to be in the range of 33.7 percent

to 37.7 percent, with household financial and physical savings projected in the

range of 11.3 percent to 11.4 percent and 12.9 percent to 13 percent

respectively14. As the household sector‟s share in financial assets is expected

to go much higher in the country‟s savings, it is of utmost importance to show

a right path to individual investors. With an emphasis on increase in domestic

savings and improvement in deployment of investible funds into the market,

the need and scope for mutual fund operations have increased and is expected

to increase tremendously in future. Mutual funds seek to serve those

individuals, who have the inclination to invest but lack the background,

expertise and sufficient resources to diversify their investment among various

sectors.

UTI is considered a leader in the mutual funds scenario, being the first

to have been established in India and is also the largest and a providing wide

range of products patronized by investors, both individual and institutional

large way. The product life cycle of these schemes has not been studied

properly. But during the later nineties, UTI faces severe challenges with it unit

schemes US-64 due to mismanagement. The problems of US-64 that has snow

balled has been hogging all the head lines in all dailies during nineties.

With the entry of private sector mutual funds offer with attractive

schemes, UTI confronted competition from several fronts. As a results, shares

of UTI investment in the industry is gradually decreasing as the private sector

14

Srinivasan G (2011), “Household, corporate savings seen rising on income growth”, The Hindu

Business Line: Economy, May 27, 2011. p 6.

16

mutual funds capture a substantial portion of total resource mobilization in the

industry.

In view of the above problem of UTI, the cabinet approved and passed

to repeal the UTI Act, 1963 and the SEBI Act. This paves the way for recast

of the UTI and overhaul of market watch dog and SEBI hence organizational

structure.

The setting up of a UTI mutual fund conforming to the SEBI mutual

fund regulations, led the UTI Mutual Fund to merge lot of existing schemes

into new schemes which have been effected since March 2003.

However, mutual fund have emerged as an important segment of

financial market in India, leading to merger and acquisitions in UTI Mutual

fund schemes. The present work is concentrated on, after the mergers and

acquisition undertaken by UTI Mutual Fund, the performance of its schemes

over a period of operations under the SEBI mutual fund regulated

environments. Specifically, the researcher attempts to bring out performance

of selected schemes where investors invest in terms of huge value of funds

involved in the UTI mutual fund. It would be of useful to the investors.

OBJECTIVES OF THE STUDY

The study is carried out with the following objectives;

1. To study the role of SEBI in regulating Mutual Funds and thereby to

know the investors‟ and financial advisors‟ awareness on regulation

and perception about Mutual Funds.

2. To know the various schemes offered by the UTI Mutual Fund and to

evaluate the performance of selected schemes on the basis of return

17

and risk by using Sharpe, Treynor, Jensen and Fama‟s measures of

portfolio evaluation.

3. To know the performance of the selected schemes by UTI Mutual

Fund based on market timing abilities of the fund managers by using

Treynor and Mazuy and Henriksson and Merton models.

4. To know the comparative performance of selected schemes of UTI

Mutual Fund and selected schemes of private sectors‟ mutual fund

through Sharpe, Treynor, Jensen and Fama‟s measures of portfolio

evaluation.

HYPOTHESIS OF THE STUDY

Based on the above objectives suitable hypothesis are framed for

analysis and are tested.

1. There is no significant relationship between investors and financial

advisors experience in the field of investment and awareness of SEBI

regulations on Mutual funds.

2. There is no significant difference among the performance evaluation

measures as used Sharpe, Treynor and Jensen.

3. The fund managers are not a successful market timers as suggested by

Treynor and Mazuy and Henricksson and Merton.

4. There is no significant difference between the performance of UTI

Mutual Fund and private sector mutual fund schemes.

18

METHODOLOGY

The present research is both descriptive and analytical in nature. It

focuses on mutual fund investors, financial advisors and performance of

selected schemes.

Investors‟ and Financial advisors‟ awareness on regulation and

perception about mutual fund study considered Chennai city. Performance of

selected Schemes and comparative performance are measured at all India

level. The researcher adopted proportionate stratified sampling technique for

selecting investors and financial advisors. The technique is suitable for

yielding a representative sample from homogenous Mutual Fund Investors

Population.

SAMPLING

1. Investors

In India, the estimates of savers households, in region wise, in

Northern Region stands first (10.20 million), followed by Western Region

(8.93 million), Southern region (5.75 million), Eastern Region (5.28 million),

Central Region (2.70 million), and North-Eastern region (0.66 million). But

the estimates of investor households respectively are: 1.42 million,

4.84 million, 5.88 million, 2.62 million, 0.14 million, and 1.42 million15. A

careful look at the figures shows that the maximum of saver households in

Southern Region invest their savings. Hence, for the purpose of the present

study southern region is preferred by the researcher.

There are two types of investors in mutual funds. The first one is

direct investors who invest in the mutual fund and deal their shares in the

15

Ibid, p.14.

19

stock market directly. The second one is indirect investors who invest in the

mutual fund through Investors Associations formed themselves and their share

in the stock market through associations. It is tedious to locate all the investors

and after all they are located there may be a chance of non-response that at

presently they are not dealing with mutual funds. In order to avoid such

problems the registered investors with the investors association is preferred

for the study. In southern region, there are three Investors‟ Association,

recognized by SEBI. Tamil Nadu possess the largest number of associations

in Southern Region16. Hence, once again the selection of sample is confined

to Tamilnadu. Tamilnadu Investors Association located at Chennai has 710

registered members, Kovai Investors‟ Association, located at Coimbatore has

360 registered members, and Coimbatore District Consumer Protection

Council, Coimbatore, has 296 registered members17. As the Tamilnadu

Investors Association has the largest registered members, the sampling is once

again confined to registered members in Tamilnadu Investors Association.

Out of the 710 registered members in Tamilnadu Investors Association

predominantly 675 (95 percent) of them are residing in Chennai and the

remaining members belong to other areas. So, as per the predominance and

feasibility of the study, samples are drawn only from Chennai, divided into

three areas (Northern, Southern and Central). So as to avoid

non-representative sampling and statistical errors in sampling. 350 number of

sampling investors is taken by proportionate stratified sampling method using

proportionate ratio among three areas of Chennai to collect desired data for

the study.

16

List of Investors‟ Association recognized by SEBI as on December, 2013. 17

Ibid.

20

2. Financial Advisors

Similarly, large number of financial advisors are working under

various assets management companies registered with Association of Mutual

Funds in India (AMFI). As per the registration number holder, 795 holders

are located in Chennai, which is the highest AMFI Registration Numbers

(ARN) holders compared to other areas of Tamil Nadu. Hence, the financial

advisors in Chennai are considered for data collection in the study. Again

based on the strength of the financial advisors in three areas of Chennai. So as

to avoid non-representative sampling and statistical errors in sampling 150

sample financial advisors are selected by the proportionate sampling method

using proportionate ratio to collect information for the study.

As per the requirement for the study sample size adopted by the

researcher, both the investors (350) and financial advisors (150) is totally 500.

In particular as per the need of the study the investors has been given

appropriate weight because it is more important for the study to identify the

perception of mutual funds among investors in wide range by using diverse

variables.

3. Selection of Samples Schemes

To evaluate the performance of selected schemes of UTI mutual fund,

the schemes introduced after February, 2003, the year in which the UTI

mutual fund registered with SEBI mutual fund regulations, 1996 was

implemented uniform regulations, are taken into consideration. Totally, there

are 51 schemes introduced by UTI mutual funds till March 2014, the period

which is considered as worth for analysis. Out of the 51 schemes, only seven

schemes are long term schemes considered for analysis, because, only long

21

term period analysis will give fruitful result and can be the basis for

forecasting the future.

Out of the 51 schemes the close ended schemes are merely five (10

percent) and the remaining 46 (90 percent) are open ended schemes. The life

of close ended schemes ranges from five to seven years and are considered not

fit for the analysis pertaining to long period (10 years). Hence they are

excluded for analysis. Only the schemes the life of which is not less than ten

years and that too are open ended, are selected for the study. This period is

generally considered to be sufficient enough to cover all upswings and down

swings of markets.

Open ended mutual fund schemes (46) comprises of Equity Growth

schemes 22 (43 percent), Debt Growth schemes 23 (45 percent) and Balanced

schemes one (Two percent). Out of 22 Equity Growth Schemes, 12 schemes

are young introduced in 2009-10 and after. Out of the remaining 10 schemes,

five (23 percent) schemes are in short-term maturity period (quarterly, half

yearly and annually), Remaining five equity growth open ended schemes are

long term in nature and are selected for the study. Out of the 23 (45 percent)

Debt Growth schemes, 21 (91 percent) schemes are young introduced in

2009-10 and after, and hence the rest Two Debt Schemes (9 percent) are

selected for the study. Balanced scheme (one) is not considered for the study

because it is not actively traded in the mutual fund industry.

The entire seven short listed schemes were initially open-end schemes.

Thus the sampling frame for the purpose of the study constitutes:

22

UTI Banking Sector Fund (Equity)

UTI Mid Cap Fund (Equity)

UTI Master Equity Plan Unit Scheme (Equity)

UTI Transportation and Logistics(Equity)

UTI Infrastructure Fund (Equity)

UTI Liquid Fund Cash Plan (Debt)

UTI CCP Advantage Fund (Debt)

In order to compare the performance of mutual fund schemes of the

UTI with the schemes introduced by the other private mutual funds, only the

dominating mutual fund industry, namely; ICICI, HDFC and Reliance are

taken into consideration. In consonance with the schemes introduced by the

UTI, seven schemes in each of the three industries were chosen, and totally 21

schemes were chosen for comparative analysis.

PERIOD OF STUDY

As the study is confined to the performance of UTI Mutual Fund with

the reference to its selected schemes, the period of study is from

April 2004 to March 2014.

SOURCES OF DATA

The study is blend of both primary and secondary data.

Primary Data: The researcher collected primary source of data from

investors and financial advisors by using questionnaire.

Secondary Data: The secondary data were collected from different reports,

Net Assets value, resale prices and repurchases prices announced by the

institution and published widely from time to time. The secondary data were

also collected from the published documents of UTI, HDFC, ICICI, and

23

Reliance Mutual Funds. To identify the performance of selected schemes, the

data are collected from the records of Centre for Monitoring Indian Economy

(CMIE), reports of SEBI and Credit Rating and Information Services of India

Ltd., (CRISIL). The Economic Times, The Business Time, and Association

of Mutual Fund Industry (AMFI) Newsletters and websites of respective

mutual funds were also used to collect the secondary data.

TOOLS FOR DATA COLLECTION

The researcher used well structured questionnaire as a tool for

collecting primary data from investors. In order to find out the applicability

and validity of the tool a well prepared questionnaire was tested with five

sample respondents. Based on the pretesting the researcher added and edited

some questions on those heads.

TOOLS OF ANALYSIS

The data collected from various sources have been analyzed by using

different technique as under.

1. Basic statistical technique like simple averages, percentages and

graphs.

2. Statistical formulae like standard deviation, alpha and beta to find the

intensity of risk.

3. The information collected by secondary source was analysed using

simple and sophisticated techniques as follows: (a) Compound Annual

Growth Rate (CAGR), (b) Compound Growth Rate (CGR), (c) Rank

Correlation, (d) Kendalls Coefficient of Concordace and (e) Binomial

Test.

4. (a) Rate of return (b) Sharp ratio (c) Treynor Ratio (d) Jensen

Differential Return, (g) Treynor and Mazuy Module, (h) Henriksson

24

and Merton Module and (i) Rank Order Scoring were used to measure

the financial performance of various sample mutual fund schemes.

5. Chi-square test has been employed to test the significance of

differences of opinions and perceptions of investors.

6. Correlation analysis, t-test and Z-test have been used to know the

degree of relation and significance between inter dependent variables

like different investment avenues and others.

TECHNIQUES OF ANALYSIS

In analyzing the risk-return relationship the Capital Asset Pricing

Model (CAPM) is used. The CAPM uses the concept of beta to link risk

with return. Beta as a measure of systematic risk shows how the Net

Asset Value (NAV) of a growth scheme responds to changes in market

performance. Using the beta concept the CAPM helps to define the required

return on a security. The equation for calculating the expected return based on

CAPM is as follows:

Ri = Rf + Rm-Rf)

Ri = Expected return

Rf = Risk-free return

= Measure of systematic risk

Rm = Market return

NAV values on every Monday of the sample schemes for the

period of (April 2004 to March 2014) ten years were used based on the data

available.

Portfolio Return refers to the yield from the selected growth

schemes with growth option. Portfolio returns (Rp) are calculated on the basis

25

of changes in the NAV on a weekly basis. Average of such weekly returns

(ARp) is calculated on a yearly basis and for the entire period of study as

follows:

1t

1ttp

NAV

NAVNAV R

Where t = Total period.

Market Return is calculated on the basis of the changes in the BSE

100 Index on a weekly basis (Rm) and the averages of such weekly

returns (ARm) are arrived at for every year and for the total period of study.

BSE 100 index is used as a benchmark for the selected growth schemes as it is

widely considered as a market proxy or benchmark for the purpose of

academic, research by practicing fund managers. BSE 100 index is a

broad based index, consisting of 100 actively traded equity shares

representing more than 70 percent of the total market capitalization in

Mumbai Stock Exchange. The market return is calculated as follows:

1-t

1-tt

IndexMarket

IndexMarket IndexMarket = Rm

Risk-free return (Rf) is the return available from zero risk investment

avenues like treasury bills and bank deposits. The current RBI bank rate of

9.00 percent is assumed as the risk-free rate of return and is related with

the most commonly preferred investment avenue namely bank deposits.

Risk is the uncertainty and variability of returns / capital appreciation

or loss of both. Total risk is measured with the help of standard deviation of

both scheme and market returns. The total risk of an investment consists of

two components: Diversifiable and non-diversifiable risk.

26

Diversifiable (Unsystematic) risk represents that portion of an

investment‟s risk that can be eliminated by holding enough number of

varied types of securities. Unsystematic risk is that portion of total risk

calculated as follows:

Unsystematic Risk = ( p2) – ( 2 - m

2)

p Standard Deviation of the Scheme

m Standard Deviation of the Market

Non-diversifiable (Systematic) risk is that part of total variability

in returns caused by factors due to economic, social and political

causes. Systematic risk is unavoidable. Each security possesses its own

level of systematic risk, which is measured using beta coefficient.

Systematic 2 x 2

Beta reflects how volatile the return from an investment in response to

market swings. It measures the impact of the market forces on return

expected from funds. Beta is calculated by relating portfolio return with

market return using regression analysis. Beta values greater than one depicts

high sensitivity of scheme‟s returns against market being aggressive. Beta

values less than one indicates defensive nature of the scheme. The regression

slope coefficient from the Characteristic Regression Line (CRL) measures the

systematic risk of an asset. The CAPM is applied to compute the beta value

from the following formula:

Ri = + Rm+e

Co-variance reflects the degree to which the market and scheme

returns vary. A positive covariance means that the market and scheme

27

returns move in the same direction whereas a negative covariance implies

that the return moves in the opposite direction. Covariance is calculated using

the formula:

C.V = (( p/ pX ) x 100)

pX is the mean return of the scheme

Coefficient of Correlation (r) measures the nature and the extent

of relationship between stock market index return and the scheme‟s return for

a particular period. The co-movement of schemes performance with that of

market index is studied with the help of a simple linear regression analysis

using the following formula:

22 yx x

xy =r

)X(X X

)Y(Y X

Coefficient of Determination (R2) is the square of the correlation

co-efficient and indicates the degree of diversification. It gives the percentage

variation in the scheme‟s return as explained by the variation in the market‟s

return. A low R2 indicates that scheme has further scope for diversification

and a high R2 indicates that the scheme is well diversified.

Compound Annual Growth Rate (CAGR) calculates the growth in

variables (number of funds, funds mobilized, assets under management,

number of schemes) on a yearly basis.

CAGR = [((P1 / P0) (1/n)– 1) × 100]

28

P1, P0, n are the variable in the current period, base period and the

number of years.

Compound Growth Rate (CGR) calculates the growth in variables

for the entire period of study. CGR is a superior measure of calculating

compounded return than simple return with the following formula:

CGR = [(Pn/ P0) (1/n)– 1) × 100]

Rank Correlation is used when information is sufficient to rank the

data. The rank correlation coefficient is a measure of correlation that

exists between two sets of ranks. It is a measure of association that is based on

the ranks of the observations and not on the numerical values of the data as

calculated using the following formula:

1)N(N

D61 R

2

2

R denotes coefficient of rank correlation

D refers to the difference of rank between the paired items in two

series.

Kendall’s Coefficient of Concordance is a non-parametric measure

of relationship determining the degree of association among several (k) sets of

ranking of N objects.

N)(N(1/12)k

)Rj(R W

32

2

j

k is the number of sets of rankings

N is the number of objects ranked

Rj is the sum of ranks assigned by all the k judges

29

(1/12) k2 (N3 – N) is the maximum possible sum of the squared

deviations.

Chi-square test is a non-parametric test explaining whether or not two

attributes are associated or not, using the following formula:

ij

2

ijij2

E

)E(O χ

Oij is the observed frequency of the cell in ith row and jth column

Eij is the expected frequency of the cell in ith row and jth column.

Z Test is used to verify the extent of relationship between the market

and the scheme using the correlation coefficient with the help of the formula:

nxr-1

r test Z

2

Student’s T-test is applied for the two populations when (sample)

mean and (Sample) variance is unknown. It is a measure of significance of

the difference between the mean of combined return of UTI and Private sector

mutual fund scheme using the following formula:

2

2

2

1

2

1

21

n

S

n

SS

XX t

Binomial Test of Significance is used to test the probability

model to make inference about population proportion from observations

satisfying the Bernoulli trials using Z test. The proportion of investors

agreeing with the specific attitude statements has been tested using the

30

following formula to identify the attitude towards mutual fund industry in

India and the extent of distribution of investors accepting with the specific

attitude statements:

(pxq)/n

Px/n= Z

x is the number of respondents agreeing

p, q and n is the proportion of acceptance, non acceptance and number

of Bernouls trails.

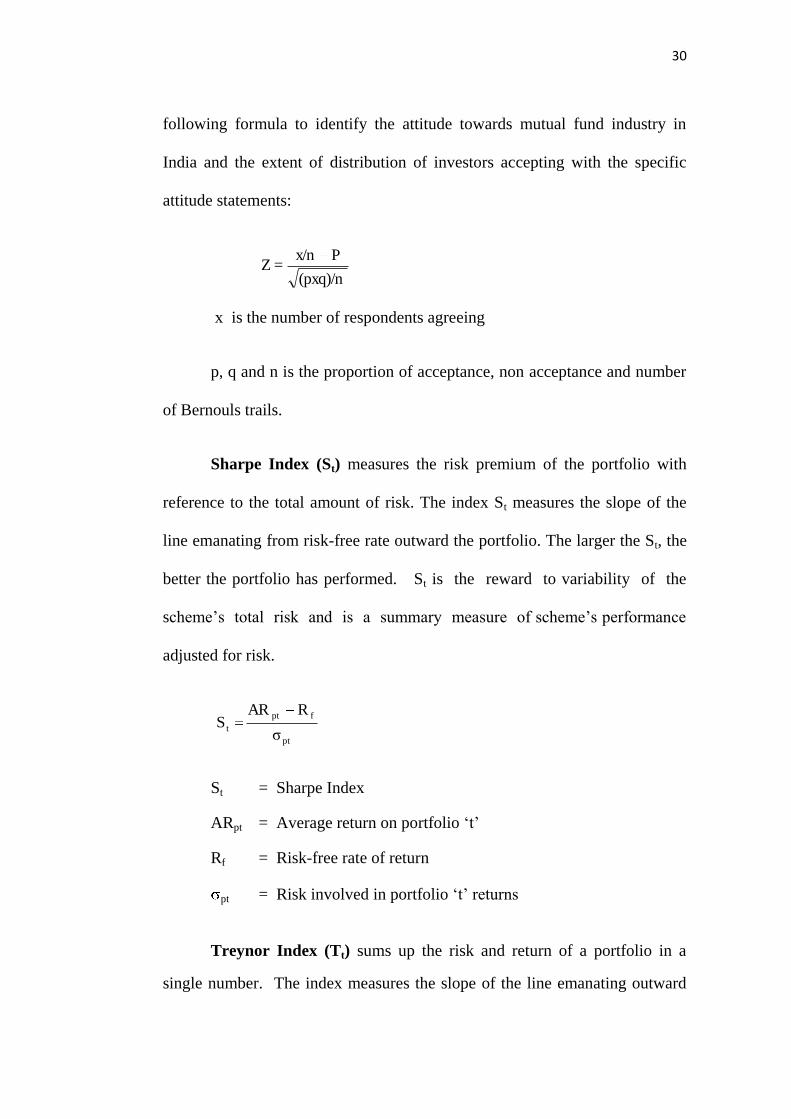

Sharpe Index (St) measures the risk premium of the portfolio with

reference to the total amount of risk. The index St measures the slope of the

line emanating from risk-free rate outward the portfolio. The larger the St, the

better the portfolio has performed. St is the reward to variability of the

scheme‟s total risk and is a summary measure of scheme‟s performance

adjusted for risk.

pt

fpt

tσ

RAR S

St = Sharpe Index

ARpt = Average return on portfolio „t‟

Rf = Risk-free rate of return

pt = Risk involved in portfolio „t‟ returns

Treynor Index (Tt) sums up the risk and return of a portfolio in a

single number. The index measures the slope of the line emanating outward

31

from the risk-free rate to the portfolio under consideration. Treynor index is a

reward to volatility of the portfolio. The characteristic line relates the market

return to a specific portfolio return without any direct adjustment for risk.

This line can be fitted through a least square regression involving a single

market portfolio. To use Treynor‟s measure first the Characteristics

Regression Line (CRL) of portfolios are fixed by estimating the following

equation:

Rp = ap + bp Rm + ep

Rp Return on portfolio „p‟

ap Intercept coefficient for portfolio

bp Portfolio‟s beta coefficient

Rm Return on market index

ep Random error term for portfolio „p‟

p

fp

tβ

RAR T

Jensen constructed a measure of absolute performance on a

risk-adjusted basis while Sharpe and Treynor models provided measures

for ranking the relative performance of various portfolios on a risk-

adjusted basis. Equilibrium average return on a portfolio is the benchmark.

Equilibrium average return is the return of the market portfolio for a given

systematic risk calculated with the following formula:

EARp = Rf + (Rm - Rf) Bp

EARp is the equilibrium average return of the portfolio „p‟ indicating

superior / inferior. Performance of the portfolio‟s alpha ( ) Jensen‟s Alpha is

the intercept of the CRL. If alpha is positive, the portfolio has performed

better and if it is negative, scheme performance is not up to the

32

benchmark. In a well-diversified portfolio, the average value of alpha of all

stocks turns out to be zero.

Eugene Fama’s Decomposition Of Total Returns Eugene Fama

provides an analytical framework, which enables for a detailed analysis of

scheme performance popularly known as Fama‟s Decomposition of Total

Return. The total return on a portfolio comprises risk-free return (Rf) and

excess return.

The excess return arises from different factors such as risk accepted

and stock selection. The excess return can be decomposed into two

components, namely risk premium (reward for bearing risk) and for stock

selectivity (return from stock selection).

Each portfolio will have both systematic risk and unsystematic risk.

Hence risk premium can be decomposed into two components namely,

return for bearing systematic risk (market risk) and return for bearing

unsystematic risk.

Return for Systematic Risk (R1) = p(Rm - Rf)

Return for Unsystematic Risk (R2) = [( p/ m) - p] × (Rm- Rf)

The return from pure stock selectivity (R3) is the difference between

the actual return and the sum of the other three components. The return for

pure (net) selectivity is the additional return obtained by a portfolio

manager for his superior stock selection ability over and above the return

mandated by the total risk of the portfolio.

33

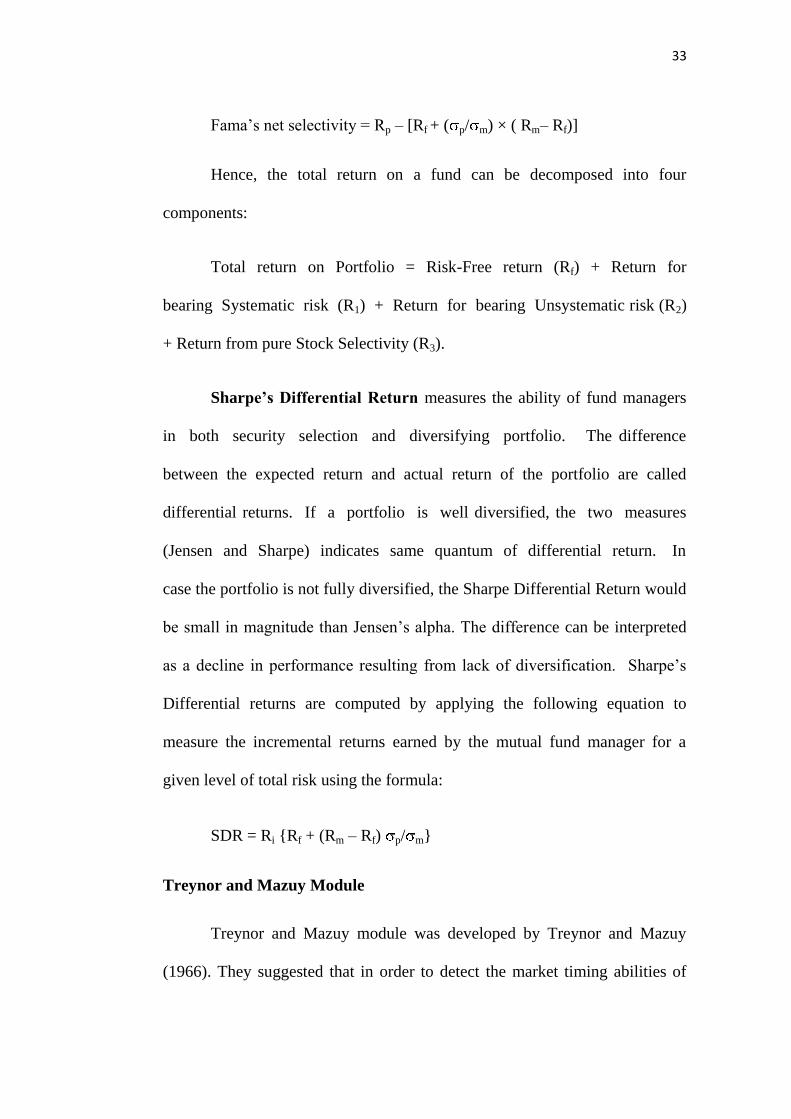

Fama‟s net selectivity = Rp – [Rf + ( p/ m) × ( Rm– Rf)]

Hence, the total return on a fund can be decomposed into four

components:

Total return on Portfolio = Risk-Free return (Rf) + Return for

bearing Systematic risk (R1) + Return for bearing Unsystematic risk (R2)

+ Return from pure Stock Selectivity (R3).

Sharpe’s Differential Return measures the ability of fund managers

in both security selection and diversifying portfolio. The difference

between the expected return and actual return of the portfolio are called

differential returns. If a portfolio is well diversified, the two measures

(Jensen and Sharpe) indicates same quantum of differential return. In

case the portfolio is not fully diversified, the Sharpe Differential Return would

be small in magnitude than Jensen‟s alpha. The difference can be interpreted

as a decline in performance resulting from lack of diversification. Sharpe‟s

Differential returns are computed by applying the following equation to

measure the incremental returns earned by the mutual fund manager for a

given level of total risk using the formula:

SDR = Ri {Rf + (Rm – Rf) p/ m}

Treynor and Mazuy Module

Treynor and Mazuy module was developed by Treynor and Mazuy

(1966). They suggested that in order to detect the market timing abilities of

34

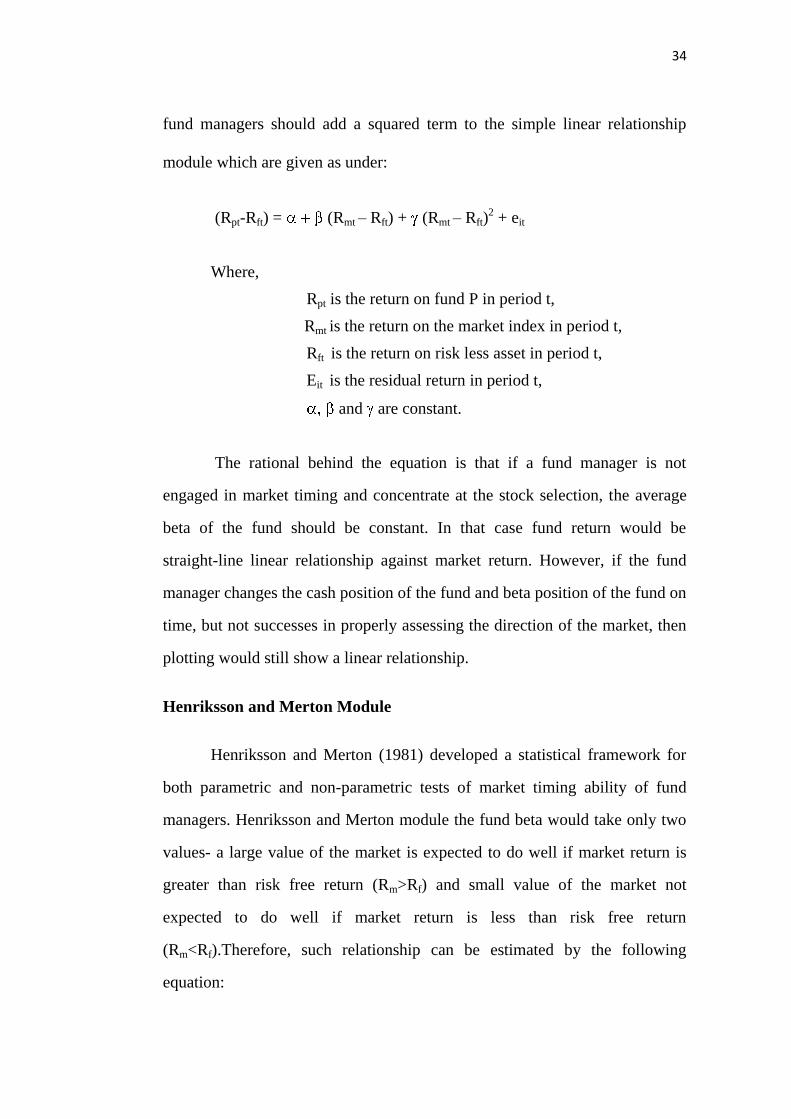

fund managers should add a squared term to the simple linear relationship

module which are given as under:

(Rpt-Rft) = (Rmt – Rft) + (Rmt – Rft)2 + eit

Where,

Rpt is the return on fund P in period t,

Rmt is the return on the market index in period t,

Rft is the return on risk less asset in period t,

Eit is the residual return in period t,

and are constant.

The rational behind the equation is that if a fund manager is not

engaged in market timing and concentrate at the stock selection, the average

beta of the fund should be constant. In that case fund return would be

straight-line linear relationship against market return. However, if the fund

manager changes the cash position of the fund and beta position of the fund on

time, but not successes in properly assessing the direction of the market, then

plotting would still show a linear relationship.

Henriksson and Merton Module

Henriksson and Merton (1981) developed a statistical framework for

both parametric and non-parametric tests of market timing ability of fund

managers. Henriksson and Merton module the fund beta would take only two

values- a large value of the market is expected to do well if market return is

greater than risk free return (Rm>Rf) and small value of the market not

expected to do well if market return is less than risk free return

(Rm<Rf).Therefore, such relationship can be estimated by the following

equation:

35

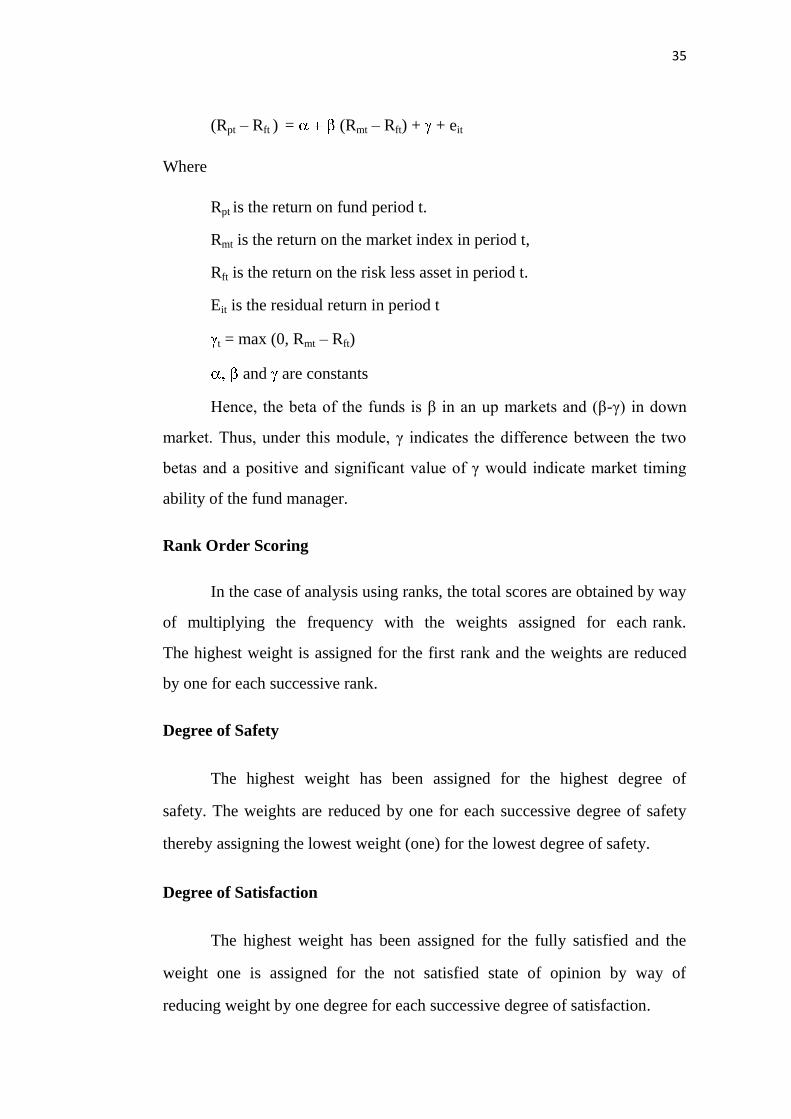

(Rpt – Rft ) = (Rmt – Rft) + + eit

Where

Rpt is the return on fund period t.

Rmt is the return on the market index in period t,

Rft is the return on the risk less asset in period t.

Eit is the residual return in period t

t = max (0, Rmt – Rft)

and are constants

Hence, the beta of the funds is β in an up markets and (β-γ) in down

market. Thus, under this module, γ indicates the difference between the two

betas and a positive and significant value of γ would indicate market timing

ability of the fund manager.

Rank Order Scoring

In the case of analysis using ranks, the total scores are obtained by way

of multiplying the frequency with the weights assigned for each rank.

The highest weight is assigned for the first rank and the weights are reduced

by one for each successive rank.

Degree of Safety

The highest weight has been assigned for the highest degree of

safety. The weights are reduced by one for each successive degree of safety

thereby assigning the lowest weight (one) for the lowest degree of safety.

Degree of Satisfaction

The highest weight has been assigned for the fully satisfied and the

weight one is assigned for the not satisfied state of opinion by way of

reducing weight by one degree for each successive degree of satisfaction.

36

Degree of Importance

The highest weight has been assigned for very important and the

weight one is assigned for not at all important as reduced by one point of

weight for each successive degree of importance.

Degree of Agreement

The highest weight of five points was assigned for strongly

agreeing and the lowest weight of one point was assigned for strongly

disagreeing statement. For each successive degree of agreement one point of

differentiation was assigned. Total scores are arrived by way of multiplying

the frequencies with their respective weights. Average scores are calculated

by way of dividing the total score by the total number of observations in each

case.

SCOPE OF THE STUDY

The present study is confined to study the perception and awareness

level of investors and financial advisors in the Mutual fund market and SEBI

mutual fund regulations. This will root to understand the investment process

and strategies followed by UTI Mutual Fund and private sector mutual fund

industries. Performance evaluation is restricted to seven growth schemes

launched during the study period and the industry brought under the regulated

environment by passing the SEBI (Mutual Funds) Regulations 1996.

Performance in terms of NAV of growth schemes with growth option alone is

studied from the angle of risk and return in comparison with the benchmark

(BSE 100) index of April 2004 to March 2014. Comparison of UTI mutual

fund and private sector selected schemes is done to know the financial

performance only and other aspects have not been considered.

37

LIMITATIONS OF THE STUDY

1. The study is confined only to the Mutual Fund Industry in India. Therefore

it has not focused on the mutual funds of other countries.

2. The sample size in the case of mutual fund investors and financial advisors

has been restricted to the limits of Chennai areas as it is highly difficult to

identify them in other areas because they are wide spread population. So

the research confined the sample with AMFI and Tamil Nadu Investors

Association records.

3. Brokerage commission, entry load, exit load and taxes are not considered

for performance evaluation because they are not practiced for all the

schemes.

4. Only the open-ended mutual fund (Seven short listed) schemes have been

included for measuring the financial performance as these are actively

traded in the Mutual Fund industry.

5. Though the techniques used for analyzing the data are traditional, these

were more appropriate as many researchers in India are following at

present.

DEFINITIONS OF CONCEPTS

Asset Management Company (AMC) means a company formed and

registered under the companies Act, 1956 (1 of 1956) and approved as such by

the SEBI under sub-regulation (2) of regulation 21; the company which

handles the day to day operations and investment decisions of a mutual fund

trust18.

18

SEBI Mutual Funds Regulation, 1996, pp.6-8.

38

Sponsor means any person who, acting alone or in combination with

another body corporate, establishes a mutual fund19.

Custodian means a person who has been granted a certificate of

registration to carry on the business of custodian of securities under the SEBI

Regulations, 1996. Legal custodian is who looks after all the monies invested

in a unit trust or mutual fund20.

Trustees means the board of trustees or a trustee company who hold

the property of the mutual fund in trust for the benefit of the unit holders21.

Mutual fund scheme refers to the IMFI products launched

representing a category with specific objective and varied options. A scheme

can belong to open or close - end type of operation. The objective of the

scheme can relate to any category like income, growth, balanced money

market and equity linked saving scheme22.

Portpolio means a collection of securities owned by an individual or

an institution (such as a mutual fund) that may include stocks, bonds and

many market securities23.

Units means the share of holding of an investor in a mutual fund

scheme. Each unit represents one undivided share in the assets of a scheme24.

Unit holders means a person holding unit in a schemes of a mutual

fund25.

19

Ibid, p.37. 20

Ibid 21

Ibid 22

Ibid 23

NCAER Survey, 2011, Glossary, p.107 24

Ibid p.38 25

Ibid

39

Growth Schemes Invest primarily in shares and also might hold

fixed-income securities in a smaller proportion26.

Growth option of a mutual fund schemes is an option for long term

growth of resources mobilized as it invest primarily in shares with significant

growth potential. Dividend is not paid to the investors but ploughed back into

the fund increasing the NAV of the units27.

Net Asset Value (NAV) is the value of a fund‟s asset less the value of

its liabilities per unit.

Fund Manager the person(s) responsible for implementing a fund's

investing strategy and managing its portfolio trading activities. A fund can be

managed by one person, by two people as co-managers and by a team of three

or more people. Fund managers are paid a fee for their work, which is a

percentage of the fund's average assets under management28.

Investors: An investor is a person who allocates capital with the

expectation of a financial return. This definition makes no distinction

between those in the primary and secondary markets. That is, someone who

provides a business with capital and someone who buys a stock are both

investors. Since those in the secondary market are considered investors,

speculators are also investors29.

26

Ibid, p.39 27

Ibid 28

www. investopedia.com 29

From Wikipedia, the free encyclopedia.

40

Financial Advisors A financial advisor (or advisor) is a professional

who renders financial services to clients. According to the U.S. Financial

Industry Regulatory Authority (FINRA), terms such as financial

adviser and financial planner are general terms or job titles used by investment

professionals and do not denote any specific designations. FINRA describes

the main groups of investment professionals who may use the term financial

advisor to be: brokers, investment advisors30.

Market Timing Ability: The act of attempting to predict the future

direction of the market, typically through the use of technical indicators or

economic data. The practice of switching among mutual fund asset classes in

an attempt to profit from the changes in their market outlook31.

Stock Selection: Stock selection criteria are methods for selecting a

stock(s) for investment. The stock investment or position can be "long" (to

benefit from a stock price increase) or "short" (to benefit from a decrease in a

stock's price), depending on the investor's expectation of how the stock price

is going to move. The stock selection criteria may include systematic stock

picking methods that utilize computer software and/or data32.

30

Ibid, p.40. 31

Ibid. 32

Ibid.

41

CHAPTER SCHEMES

The present study is broadly divided into seven chapters:

1. The first chapter „Research Design‟ being this chapter dealt with

the Introduction, mutual funds concepts, worldwide mutual funds,

mutual fund in India and an overview of the UTI mutual fund,

statement of the problem, objectives, methodology, analysis of

data, scope and limitation of the study.

2. The second chapter „Review of Literature‟ presents the previous

research works relating to the present study in a nutshell. It also

explains how the present study differs from the earlier studies.

3. The third chapter „Awareness and Perceptions‟ consists of

Awareness on SEBI Mutual Fund Regulations, Perceptions of

investors on the mutual fund industry, Investors preference on the

mutual fund industry, and Attitude of Investors towards mutual

fund industry.

4. The fourth chapter „Schemes and Performance‟ presents the

schemes offered by the UTI Mutual Fund, performance of return

and risk of selected schemes analysis using by Sharpe Index,

Treynor index, Jensen Alpha, and Sharpe Differential Return,

Composite risk-return Analysis, Comparative performance

evaluation of Sharpe, Treynor and Jensen Alpha model. Eugene

Fama‟s Decomposition of performance, Risk analysis, and