MASTER OF COMMERCE

67

RANI CHANNAMMA UNIVERSITY, BELAGAVI “FINANCIAL ANALYSIS OF DHANALAXMI CO-OP SUGAR FACTORY LTD: A CASE STUDY OF KHANAPETH SUGAR INDUSTR (RAMDURG)” A Project report submitted to RANI CHANNAMMA, UNIVERSITY, BELAGAVI of the partial fulfillment of degree of MASTER OF COMMERCE Submitted By Mr. AVINASH B MALAWAD Reg No. MC194404 M.Com 4 th Semester UNDER THE GUIDANCE OF Smt. KUSUMA HADAGALI Assistant professor and Project Guide, Dept. of Commerce Smt. I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G. STUDY CENTRE, RAMDURG. 2020-2021

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of MASTER OF COMMERCE

RANI CHANNAMMA UNIVERSITY, BELAGAVI

“FINANCIAL ANALYSIS OF DHANALAXMI CO-OP SUGAR FACTORY LTD:

A CASE STUDY OF KHANAPETH SUGAR INDUSTR (RAMDURG)”

A Project report submitted to

RANI CHANNAMMA, UNIVERSITY, BELAGAVI

of the partial fulfillment of degree of

MASTER OF COMMERCE

Submitted By

Mr. AVINASH B MALAWAD

Reg No. MC194404

M.Com 4th Semester

UNDER THE GUIDANCE OF

Smt. KUSUMA HADAGALI

Assistant professor and Project Guide, Dept. of Commerce

Smt. I.S. YADAWAD GOVT FIRST GRADE COLLEGE

AND P.G. STUDY CENTRE, RAMDURG.

2020-2021

PÁ¯ÉÃdÄ ²PÀët E¯ÁSÉ

²æêÀÄw. DAiÀiï. J¸ï. AiÀiÁzÀªÁqÀ ¸ÀPÁðj ¥ÀæxÀªÀÄ zÀeÉð PÁ¯ÉÃdÄ, gÁªÀÄzÀÄUÀð

(£ÁåPï¤AzÀ “©” UÉæÃqï ªÀiÁ£ÀåvÉ)

ªÉ¨ï¸ÉÊmï:https://gfgc.kar.nic.in/ramdurg E-ªÉÄïï: [email protected]

¸ÀASÉå :¸À¥ÀæzÀPÁgÁ/2021-22/project/ ¢£ÁAPÀ:

Certificate

This is to certify that Internship Report entitled “A STUDY ON FINANCIAL

ANALYSIS OF DHANALAXMI CO-OP SUGAR FACTORY LTD: AT. KHANAPETH

(RAMDURG)” is an individual work of Mr. AVINASH MALAWAD, RCU Examination

Registration No. MC194404 of M.com IV semester Smt. I S Yadawad Govt First College

and P.G. centre Ramdurg now being submitted in the partial fulfillment of requirement, for

the award of the Degree of Master of Commerce of Rani Channamma University, Belagavi

under my supervision and guidance.

Smt. KUSUMA HADAGALI

Assistant Professor and Project Guide, Dept. of Commerce

Smt. I. S. Yadawad First Grade Govt College

and P.G. Study Centre, Ramdurg

DECLARATION

Mr. Avinash Malawad the under signed hereby declare that the Project Report

entitled “A STUDY ON FINANCIAL ANALYSIS OF DHANALAXMI CO-OP SUGAR

FACTORY LTD: AT. KHANAPRTH (RAMDURG) ” has been prepared by me under the

guidance of Smt. Kusuma hadagali assistant professor of P. G. Department I. S. Yadawad

Govt College Ramdurg. The report submitted to Rani Channamma University, Belagavi in

partial fulfillment of the university rules and regulations for the award of the Degree of Master

of Commerce for Academic Year 2020-2021.

I further declare that this report is based on the original Research work undertaken by

me and has not formed a basis for the award of any other Degree / Diploma of RCU or any

other University.

Date: - Mr. Avinash Malawad

Place: - RAMDURG Reg. No. MC194404

ACKNOWLEDGEMENT

It is my proud privilege to release the feelings of my gratitude to several persons who

helped me directly or indirectly to conduct this research project work. I would like thank our

all teachers and my project guide Smt. Kusuma Hadagali assistant professor of P.G

Department. and. of commerce for having given me this opportunity and for his valuable

ever-patient guidance ever endeavoring support, timely help and constant encouragement and

also, I am thankful to all faculty members of our other departments for their valuable guidance

in completing this project successfully.

I am thankful to our Beloved Principal. Dr. A. S. Lalasangi for his strong inspiration

during the project period

I am thankful to Shambu Malawad Professional Director of dhanalaxmi co-op sugar

factory for his constant support and encouragement.

I would thanks to our Teaching and Non-Teaching staff in our college and library

dept. And I also express thanks to my parents, for their valuable support in completion of this

project successfully.

I also thank all my friends who have more or less contributed to the preparation of this

project report. I will be always indebted to them

The study has indeed helped me to explore more knowledgeable avenues related to my

topic and I am sure it will help me in my future.

Avinash Malawad

CONTENTS

Index Page no

CHAPTER – I INTRODUCTION

Introduction

Statement of the problem

Need of the study

Scope of the Study

Objective of the Study

Research Methodology

Limitation of the study

Review of literature

1-4

CHAPTER – II CONCEPTUAL FRAME WORK

Conceptual background

Advantages and disadvantages of sugar industries

5-16

CHAPTER-III COMPANY PROFILE

History

Present Board of Directors

Vision

Mission

17-32

CHAPTER- IV DATA ANALYSIS AND INTERPRETATION 33-52

CHAPTER – V FINIDINGS, CONCLUSION AND SUGGETION 58-61

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 1

CHAPTER - I

INTRODUCTION

“FINANCIAL ANALYSIS OF DHANALAXMI CO OP SUGAR FACTORY LTD: A

CASE STUDY OF KHANAPETH SUGAR FACTORY”

INTRODUCTION

The basis for financial analysis, planning and decision making reflects in scientific

analytical financial statement which mainly consists of Balance Sheet and Profit & Loss account

of a sugar factory. This summarized financial report provides the operating result and financial

position of a sugar factory and detailed analytical information contained therein is useful for

assessing the operational efficiency and financial soundness of a sugar factory

STATEMENT OF THE PROBLEM: -

Analyzing financial Position of the Dhanalaxmi Co-op sugar factory. In the form of

Ratio Analysis.

Techniques applied for the study:

Ratio Analysis

Linear Trend Analysis

NEED OF THE STUDY: -

The study has great significance and provides benefits to various parties

whom directly or indirectly with the company

To express the relationship between different financial aspects in such a way

that it allows the user to draw conclusions about the performance strengths

and weaknesses of the company

To diagnose the information contained in financial statement so as to judge

the profitability of the firm

The study Helps to know a liquidity, solvency, profitability and turnover

position of the company

Evaluation of operating efficiency

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 2

Scope of Study: -

Ratio analysis helps in Decision making from the information provided in

financial statement

Ratio analysis is of much help in financial forecasting.

To know the various factors affecting the profitability.

Ratio analysis even helps in making effective control of business.

OBJECTIVE OF THE STUDY: -

Aims at analyzing the Financial Position of Dhanalaxmi co-op Sugar factory

Ltd from the past records.

To suggest the feasible solution to improve the overall efficiency of the

Dhanalaxmi co-op sugar factory LTD

To analysis the profitability position of Dhanalaxmi co-op sugar factory LTD

Limitation of the study:

Profitability analysis is a wide study which involves numerous techniques.

As this is an external study, the results are not complete and clear as I’m

having a little idea about practical difficulties facing day today, except the

information provided by the Dhanalaxmi co-op sugar factory.

Lastly the study is purely academic. The experience makes this study less

precise when compared with a professional study.

The study was limited to only five years financial data

There is no set industry standard for comparison and hence the inference is

made on general Standards.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 3

RESEARCH METHODOLOGY: -

The project is based on the data collected during the following 5 years Viz

2015-2016

2016-2017

2017-2018

2018-2019

2019-2020

These figures for the five years were taken from Annual Reports &

Discussion with the company Guide.

DATA COLLECTION:

Primary Data:

The Data collected through financial statements like Balance sheet, Profit &

loss a/c for the 5 years

The information is collected from the personal interaction with the staff

of Dhanalaxmi co-op Sugars sugar factory Ltd.

Secondary Data:

Secondary data are those which are obtained from sources such as follows:

Annual reports of the company.

Information from the text sources.

Information from the internet sources.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 4

REVIEW OF LITERATURE

BARAN AND PASTY says in his research paper The financial situation of the business

subject is considered to be a complex output of their whole performance. This output is

presented through the ratio indicators of activity, profitability, liquidity, indebtedness and

market value. These indicators are based on the synthetic indicators of financial accounting

and they demonstrate the complexity of the business subject’s performance interpretation

PAUL BARNES Says in his article financial ratios are used for all kinds of purposes. These

include the assessment of the ability of a firm to pay its debts, the evaluation of business and

managerial success and even the statutory regulation of a firm's performance

STEVEN M. BRAGG says in his book A controller is responsible for a wide array of

functions Such as processing accounts payable and receivable and receivable transaction,

properly noting the transfer of assets and closing the books in a timely manner. Properly

completing these functions is critical to a corporation which relies on the accurate handling of

transactions and accurate financial statements. these activities clearly form the basis for

anyone’s successful career as a controller must acquire skills in the area of financial analysis

in order to be truly successful.

DAVID E. VANCE says in his book financial analysis is about shaping the future. It provides

the tools management needs to make sophisticated judgments about complex and challenging

business issues. As a corporate controller, chief financial officer, and retired CPA, I found that

outside auditors, purchasing managers, accountants, and corporate executives were making

bad decisions because they didn’t understand how to apply financial analysis to real-world

situations.

NISSIM AND PENMAN are said in their research practice Financial statement analysis has

traditionally been seen as part of the fundamental analysis required for equity valuation. But

the analysis has typically been ad hoc. Drawing on recent research on accounting-based

valuation, this paper outlines a financial statement analysis for use in equity valuation.

Standard profitability analysis is incorporated, and extended, and is complemented with an

analysis of growth. An analysis of operating activities is distinguished from the analysis of

financing activities.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 5

CHAPTER – II

CONCEPTUAL FRAME WORK

INDUSTRY OVERVIEW

The Historical Background Of The Indian Sugar Industry:

The sugar industry is proud to be an industry, which spreads the taste of sweetness to

the mankind. The history of origin of this industry is as old as the history of main it-self. Sugar

is generally made from sugarcane and beet. In India, sugar is produced mainly from sugarcane.

India had introduced sugarcane all over the worlds and is a leading country in the making sugar

from sugarcane.

‘Saint Vishwamitra’ is known as the research person of the sugarcane in religious

literature. We can find the example of sugarcane in Vedic literature also as well as sugarcane.

We can also find the reference of sugar and the sugarcane in Patanjali’s Mahabashya and the

treaty on the grammar of ‘Panini’. Greek traveler ‘Niyarchus’ and Chinese traveler ‘Tai-Sung’

have mentioned in their travelogue that the people of India used to know the methods of

making sugar and juice from sugarcane the great Emperor Alexander also carried sugarcane

with him while returning to his country. Thus, from different historical references and from

some ‘Puranas’ it can be concluded that method of making sugar from sugarcane was known

to the people of Bihar. The historical evidences of sugar industry prospering in ancient India

concrete and this has helped to develop and prosper the co-operative sugar movement in India.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 6

Contribution of sugar industry to Indian economy.

Sugar industry contributes about rs.1650 crores to the central exchequer as excise duty

and other taxes annually. In addition, about rs.600 crores is realized by the state governments

annually through purchase tax and cess on cane. At the prevailing sugarcane price, the total

sugar cane produced in the country value at about rs.24000 crores per year.

Indian sugar demand supply scenario

Total internal consumption for sugar in India has grown at a CAGR of 4.1% from 18.4

MMT in 2003 to 22.5 MMT in 2008. The production of sugar in India has grown from 20.1

MMT in 2003 to 26.3 MMT in 2008 at a CAGR of 5.5%. Apart from sugar, India also

consumes alternate sweeteners such as jiggery and khan sari. Sugar consumption is primarily

driven by population growth and the rise in per capita consumption. The consumption of sugar

in India is generally urban based. In rural areas, alternate sweeteners such as jaggery and

khandsari Are consumed in larger quantities. Rising income levels and the increasing

penetration of food and other retail products such as soft drinks and chocolates will aid the

increase of the per capita consumption of sugar.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 7

ADVANTAGES OF SUGAR INDUSTRIES

1. Ready market all year through. You can never fail to get market for your sugar.

2. High demand. Sugar has high demand

3. There is no low or high season in this industry

4. Ready products to use

DISADVANTAGES OF SUGAR INDUSTRIES

1. It is a capital intensive

2. High cost of production

3. Too much competition in the market

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 8

DETAILE STUDY OF PROJECT

WHAT IS FINANCIAL STATEMENT?

Financial statements are structured representation of the financial position and

financial performance of an entity. Financial statements provide information about an

entity’s (i) Assets (ii) Equity & Liabilities (iii) Income and expenses, including gains and

losses and (iv) Cash flows.

In the analysis, financial ratios were used to gain a critical review of the

specific areas of assessment of the company’s performance. The ratios were able to

provide a clear view of the overall performance of the company.

SIGNIFICANCE OF ANALYSIS OF FINANCIAL STATEMENTS

Financial analysis is useful and significant to different users in the following ways.

(a) Finance Manager: Financial analysis techniques enable the finance manager to make

constant reviews of the actual financial operations of the sugar factory for analyzing the

causes of major deviations, which may help in taking corrective action.

(b) Top Management: Financial analysis helps the Top Management in measuring the

success of the company’s operations, appraising the individual’s performance and

evaluating the system of internal control.

(c) Trade Payables: The traders are particularly interested in sugar factory’s ability to

meet their claims over a very short period of time, which evaluate factory’s liquidity

position.

(d) Lenders: Banks and Financial Institutions are concerned about the sugar factory’s

long-term solvency and survival. They analyze the historical financial statements to assess

its future solvency and profitability.

(e) Investors: Banks and Financial Institutions are concerned about the sugar factory’s

long-term solvency and future profitability to ascertain its effects on sugar factory’s

earning.

(f) Others: Economists, Researchers, Government etc., analyze the financial statements

to study the economic conditions for price regulations, taxation and other similar

purposes

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 9

TOOLS OF ANALYSIS OF FINANCIAL STATEMENTS

The most commonly used techniques of financial analysis are as follows:

(a) Comparative Statements: The comparative Profit & Loss account gives an idea of the

progress of business over a period of time. The changes in absolute money values and percentages

can be determined to analyze the profitability of the business. This analysis is also known as

‘horizontal analysis or Intra sugar factory analysis. Horizontal analysis compares each item with

an item for a selected base year.

(b) Common Size Statements: The common size statements analysis compares each item with a

base item of two different factories to realize where we actually stand as compared to other sugar

factories and what the exact reasons of deviation are. This analysis is also known as ‘Vertica l

analysis

(c) Trend Analysis: Trend analysis studies the financial history, operational results & financial

position of a sugar factory over a series of years using the historical data to observe the percentage

changes in selected data.

(d) Ratio Analysis: It is a tool for comparison of the previous year’s figures of the sugar unit,

other entities, and the industry. It helps the management to take proper decision after analysis.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 10

RATIO ANALYSIS

Ratio:

The ratio refers to numerical or quantitative relationship between two items.

Accounting/Financial Ratio:

It can be defined as the relationship between the items expressed in

mathematical form contained in the financial statements.

Ratio Analysis:

Ratio Analysis is an art of analysing the financial statements with the help

of different ratios.

Ratio analysis helps in assessing the solvency, efficiency and profitability

position of a business enterprise.

Window-dressing:

It is a technique used by companies and financial managers to manipulate financial statements

and reports to show more favourable results for a period.

Ratio can be expressed in three different ways. They are as follows:

1. Ratio as a pure e.g., debt equity ratio.

2. Ratio as a number of times e.g., stock turnover ratio;

3. Ratio as a percentage e.g., gross profit ratio.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 11

The four steps involved in ratio analysis are as follows:

1. Selection of relevant data from the financial statements depending upon the objective of

the analysis.

2. Calculation of appropriate ratios from the given data.

3. Comparison of the calculated ratios with the ratios of the same from in the past or a standard

ratio.

4. Interpretation of the ratios.

Significance/Advantages of Ratio Analysis:

1. Helps in decision making.

2. Helps in Financial Forecasting and Planning.

3. Helps in Comparison of performance.

4. Helps in simplifying accounting figures.

5. Helps in Communication and Control.

6. Utility to Shareholders, Creditors and Employees.

Limitations of Ratio Analysis:

1. Limits use of Single Ratio.

2. Lack of adequate standards.

3. Change of accounting procedure.

4. Price level changes.

5. Window dressing.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 12

USES OF RATIO ANALYSIS TO MANAGEMENT:

Helps in decision making:

Financial statements are prepared primarily for decision making. But the information

provided in financial statements in not an end in itself and no meaningful conclusions can

be drawn from these statements alone. Ratio analysis helps in decision making from the

information provided in these financial statements

Helps in financial forecasting and planning:

Ratio analysis is of much help in financial forecasting and planning. Planning is looking

ahead and the ratio calculated for a number of years work as a guide for the future,

meaningful conclusions can be drawn for future from these ratios. Thus, ratio analysis helps

in financial forecasting and planning.

Helps in communicating:

The financial strength and weakness of a firm are communicated in a more easy and

understandable manner by the uses of ratios. The information contained in the financial

statements is conveyed in a meaningful manner to the persons for whom it is meant. Thus,

ratios help in communication and enhance the value of the financial statements.

Uses of Ratio Analysis to investors:

Investors in the company will like to assess the financial position of the concern where he

is going to invest. His first interest will be the security of his investment and then a return in the

form of dividend or interest. For the first purpose he will try to assess the value of the fixed assets

and the loans rose against them. The investors will feel satisfied only if the concern has sufficient

amount of assets. Long-term solvency ratios will help him in assessing financial position of the

concern. Profitability ratios, on the other hand, will be useful to determined profitability position.

Ratio analysis will be useful to the investor in making up his mind whether present out financial

position of the concern warrants further investment or not.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 13

Helps in co-ordination:

Ratios help in co-ordination which is of utmost importance in effective business

management. Better communication of efficiency and weakness of an enterprise results in

better co-ordination in the enterprise.

Helps in control:

Ratio analysis helps in making effective control of the business. Standard ratio can be based

upon Performa of financial statements and variances or deviations, if any, can be found by

comparing the actual with the standards so as to take corrective action at the right time.

The weaknesses or otherwise, of any, come to the knowledge of the management which

help in effective control of the business.

Uses of Ratio Analysis to creditors:

The creditors or suppliers extend short-term credit to the concern. They are interested to

know whether financial position of the concern warrants their payments at a specified time or not.

The concern pays short-term creditors out of its current liabilities then the creditors will not hesitate

in extending credit facilities. Current and acid- test ratios will give an idea about the current

financial position of the concern.

Other uses:

There are so many other uses of ratio analysis. It is an essential part of budgetary control and

standard costing. Ratios are of immense importance in the analysis and interpretation of financial

statements as they bring out the strength or weakness of a firm.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 14

Limitations of ratio analysis:

Ratio analysis has been acclaimed as a very important tool in the kit of the financial management

helping several things at a time like simplifying financial information, measuring and studying the

financial health, helping inter-firm and intra firm comparison and above all helping in co-

ordination, communication and control. However, it is not without any limitations, which are listed

below:

1. Though ratio analysis serves the purpose of quantitative analysis, yet certain important

qualitative factors may be ignored. This may distort the purpose of analysis.

2. Ratios acquire significance only when they are studied along with other ratios. A ratio in

isolation can be meaningless by itself.

3. The data available are at best, only estimates which give an impression of accuracy and

precision. Therefore, the results of the analyst cannot claim total accuracy is based on

estimates which by themselves are not precise.

4. Information from ratio analysis can only be the beginning of the end and not an end in

itself. This can only be a fraction of information which must always be used with other

material information from various other sources for a dependable analysis.

5. Ratio analysis can be termed as historical documents, since they probe in to past financial

statements. They should not mislead in reflecting current conditions and may be able to

throw very little light on the future, particularly in the context of the expanding modern

business.

6. In the absence of a clear cut and predetermined standard and if accounting information is

not consistent to that extent ratio analysis becomes weak and helpless as a dependable tool

of financial analysis.

7. Ratio analysis ignores the topical problem of changes in price levels and the impact of

inflation.

8. Comparison of two variables with tool of ratio analysis will be fruitful when proper method

of valuation is adopted by the firms and the method is identical. But in actual practice

different methods are followed by different companies regarding the valuation of stock or

fixed assets or other current assets.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 15

PRECAUTIONS TO BE TAKEN WHILE USING RATIOS:

The calculation of ratio may not be a difficult task but their use is not easy. The information on

which these based, the constraints of financial statements, objectives for using them, the caliber of

the analyst, etc,.is important factors which influence the use of ratios. Following guidelines may

be kept in mind while interpreting various ratios:

ACCURACY OF FINANCIAL STATEMENTS:

The ratios are calculated from the data available in financial statements. The reliability of ratios is

linked to the accuracy of information in these statements. Before calculating ratios, one should see

whether proper concepts and convention have been used for preparing financial statement or not.

These statements should also be properly audited by competent auditors. The precautions will

establish the reliability of data given in financial statements.

OBJECTIVES OF ANALYSIS:

The type of ratio to be calculated will depend upon the purpose for which these are required; if

purpose is to study current financial position, then ratios relating to current assets and current

liabilities will be suited. The purpose of “user” is also important for the analysis of the ratios. A

creditor, a banker, an investor, a shareholder, has different objects for studying ratios.

The purpose for which ratio are required to be studied should always be kept in mind while

studying various ratios. Different objects may require the study of different ratios.

SELECTION OF RATIOS:

Another precaution in ratio analysis is the proper selection of appropriate ratios. The ratio should

match the purpose for which these are required. Calculation of large number of ratios without

determining their need in the present context may confuse things instead of solving them. Only

those ratios should be selected which can throw proper light on the matter to be discussed.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 16

USE OF STANDARD:

The ratio will give an indication of financial position only when discussed with reference

to certain standards. Unless otherwise these ratios are compared with curtained standards, one will

not be able to reach conclusions. These standards may be rule of thumb as in the case of current

ratio (2:1) and acid test ratio (1:1), may be industry standard, may be budgeted or projected ratios,

etc. the comparison of calculated ratios with the standards will help the analyst in forming his

opinion about financial situation of the concern.

CALIBER OF THE ANALYST:

The ratios are only tools of analysis and their interpretation will depend upon the caliber and

competence of the analyst. He should be familiar with various financial statements and the

significance of changes, etc., a wrong interpretation may create havoc for the concern since wrong

conclusions may lead to wrong decisions. The utility of ratio is linked to the enterprise of the

analyst.

Ratios provide only a base:

The ratios are only guidelines for the analyst. He should not base his decisions entirely on them.

He should study any other relevant information, situation in the concern, general economic

environment, etc., before reaching final conclusions. The study of ratios in isolation may not

always prove useful. A businessman will not afford a single wrong decision because it may have

for reaching consequences. The interpreter should use the ratios as guide and try to solicit any

other relevant information which helps in taking the correct decision.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 17

CHAPTER - III

COMPANY PROFILE

Name : Shri Dhanlaxmi Shakari sakkare

Karkhane niyamith –khanpet Ramdurg

Residence : khanpet

At post: khanpet

Tq: Ramdurg dist.: Belgaum

Type of ownership : Co-operative

Nature of company : Co-operative sector

Main product : white crystal sugar

By product : A) cogeneration power (electricity)

B) molasses

C) press-mud

Production capacity : Medium

Finished product : Sugar

Land covered : 55 acre

Contact number : 08335-253475

Fax number : 08335-253475

Email id : [email protected]

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 18

ABOUT OF COMPANY

The “Dhanalaxmi Co-op sugar factory Limited” will established by B. B. Hirereddy on

1995, the construction was started on 1995. The factory estimation was started on 1995 and

this factory was established on 1997.

Dhanalaxmi co-op sugar factory LTD is registered under Karnataka cooperative society Act

1959

Dhanalaxmi co-op sugar factory has entered in to agreement with EID Parry India Ltd, public

limited company under BOOT system.

BOOT = Build, Own, Operate, transfer.

At 24 October 2007 the PSIL industry limited took this industry on lease bases and

they made lease up to 25 years. This PSIL industry limited was started by G. M. Rao from

Hyderabad.

But this PSIL industry limited can lead this industry only 2 years.

On the 1st year, in trial session the crushing occurs 54,000 metric ton.

On the 2nd year, in trial session the crushing occurs 2, 05,000 metric ton.

After this PSIL industry limited and E.I.D parry’s industry limited both are made

partnership. The partnership is based on percentage is 26% of PSIL industries limited and 74%

of E.I.D. parry’s sugar industries limited is made.

On 21/06/2017 E.I.D parry’s made agreement for crushing the cane from 4000 TCD TO 5000

TCD.

This project contains only information about Dhanalaxmi co-op Sugar Factory Ltd.

During the year under review, Industry turnover was Rs.1048.47 lakhs as against Rs.1025.98 lakhs

for the previous year. The profit before interest and depreciation of Rs.722.13 Lakhs. It generates

electricity up to 12 to 15MW. And 6MW is used for captive consumption. Every day cane crushing

is Up to 5000TCD

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 19

PRESENT BOARD OF DIRECTORS

1 Mr. Mallanna S Yadawad Chairman

2 Mr. Basangouda G Dyamangoudr Vice President

3 Mr. M S Yadawad Director

4 Mr. A S Surag Director

5 Mr. I S Haranatti Director

6 Mr. B M Tuppad Director

7 Mr. Mahadevappa M Aathar Director

8 Mr. D N Devaraddi Director

9 Mr. S G Patil Director

10 Mr. B V Patil Director

11 Mr. T B Patil Director

12 Mr. Sureshgouda L Dullolli Director

13 Mr.N S Chakalabbi Director

14 Mr. Chandru S Rajaput Director

15 Miss. N T Muragod Director

16 Miss. S B Somgond Director

17 Mr. Yallapp I Chippalkatti Director

18 Mr. S R Karadin Director

19 Mr. Shambhu G Malawad Professional

Director

20 Mr. Balappa Hanji Professional

Director

21 Mr. Sahina Akthar Managing Director

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 20

NATURE OF BUSINESS CARRIES:

Nature of Business carried at PSIL is involved in the activity of manufacturing white crystal sugar

products which is the main product. The process of production involve conversion of -

1) Raw sugarcane to sugar,

2) Raw sugar into refined sugar

3) Molasses, Bagasse are its by products.

MOLASSES:

Molasses is mainly used for the manufacture of ethyl alcohol (ethanol), Yeast and cattle feed.

BAGASSES:

Bagasse’s is usually used as a combustible in the furnaces to produce steam, which in turn is used

to generate power; it is also used as raw materials for production of paper and as feedstock for

cattle.

The company is having rich German technology machines and equipment that are installed

in the production area. The power plant machines and Turbines are of Bharath Heavy Electricals

Limited and Thriveni made.

VISION:

“To become the most efficient sugarcane processor and the largest marketer of sugar and

ethanol in the country.”

MISSION

“Its mission in meeting these objectives are to expand its installed capacity, achieve end-

to-end integration for all its plant to improve margins and reduce cyclicality of business achieve

greater raw material security, increase its focus of corporate and high value customers to reduce

price –risk in sugar by hedging, maintain a strong presence in export market and expand a market

for Ethanol”.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 21

OWNERSHIP PATTERN

BOD

Managing Chairman Vice-President

Shareholders

Class B Class A

Producer member Non producer member

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 22

PRODUCT PROFILE

SUGAR:

The sugar produced in Parry’s sugar industries limited is both refined confirming to EC II

grade with negligible sulfur content as well as plantation grade white sugar.

Sugar is sweet, white or brown, usually crystalline substance obtained mainly from

sugar cane or sugar beets and used commonly in food products. Sugar means something sweet in

form of taste.

Formula: 12CO2+11H2O=C12H22O11+12O2

Carbon Dixio+water=sucrose oxygen

In chemistry sugar refers to any of the class of carbohydrates to which this substance belongs.

Glucose, lactose, and maltose are sugar most plants manufacturing sugar is solute in water, sweet

to the taste and either directly or indirectly for men table.

Sugar is controlled commodity in India under the essential commodities Act,1955. The

government controls sugar capacity additions through industrial licensing determines the price to

the major input sugarcane, decides the quantity that can be sold in the open market, fixes the prices

of the levy quarter sugar and determines maximum stock level for wholesalers etc.

Nature of Business Carried:

Nature of Business carried by SRSL is involved in the activity of manufacturing white crystal

sugar products which is the main product. The process of production involve collection of

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 23

Raw sugarcane to sugar,

Raw sugar into refined sugar

Molasses, Bagasse’s are it’s by products

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 24

BY PRODUCTS OF SUGARCANE:

a) Molasses:

Molasses is the final effluent obtained in the preparation of sugar by repeated crystallization. It is

the end product from a refining process carried out yield sugar. Sucrose and invert sugars constitute

a major portion of molasses. The yield of molasses per ton of sugarcane varies in the range of 3.5%

to 4.5%

b) Bagasse’s:

Bagasse’s is a fibrous residue of cane stalk that is obtained after crushing and extraction of juice.

It consists of water, fiber and relatively small quantities of soluble solids; the composition of

bagasse’s varies based on the variety of sugarcane, maturity of cane, method of harvesting and the

efficiency of the sugar mill.

Bagasse’s is usually as a combustible in the furnaces to produce steam, which in turn is used to

generate power; it is also used as raw materials for production of paper and as feed stock for cattle.

By making use of bagasse’s, sugar mills have been successful in reducing dependence on state

electric boards for power supply.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 25

c) Power:

In the process of crushing sugar cane, bagasse’s, a fibrous by product is produced which is used in

the boilers to generate steam. The company produces power from Bagasse’s which is used in the

manufacturing process as well as sold to the state electricity boards. Further, this bagasse’s-based

cogeneration plant is eligible for carbon credit compensation.

d) Ethanol:

The company produces alcohol from the molasses (Molasses is the brown colored residue after

sugar has been extracted from the juice. Molasses still contains some quantity of sugar, but this

sugar cannot be extracted by usual technology) left after the extraction of sugarcane juice, which

can be used for both for table purposes well as an industrial chemical. Further, this alcohol can

again be purified to produce fuel grade ethanol that can be blended with petrol.

e) Bio-fertilizers:

The residue product from distillery operations blended with chemicals is being sold as bio-

fertilizers.

Area of operation:

In a business with diverse manufacturing, there is a premium on production, process and capacity

selection leading to competitiveness.

Shree Parry’s sugars consciously selected to integrate sugar manufacture with downstream

possibilities in its factories across Maharashtra and Karnataka. It invested in integration within a

year of inception, emphasizing its understanding of multi-product profitability. The Company

processes co-products to generate ethanol, power and bio-fertilizers. Of its five factories, three

possess integrated facilities, while the rest are in the process of integration.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 26

INFRASTRUCTURE FACILITIES

The various Infrastructural facilities provided by Dhanalaxmi co-op sugar factory Ltd are as

follows.

Germany Technology made are main infrastructure for the production process

The ware housing is built in order to pressure for fore coming seasonal changes due to

which the material will be loss. (Capacity-5000 tons,2 ware house)

Canteen facilities is keep provided within a campus of the company so that workers will

continue their speed in work by saving their time in traveling from company to their house.

(Seating Capacity-70people)

Food is provided as subsidized rates to employees (50%)

One guest house

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 27

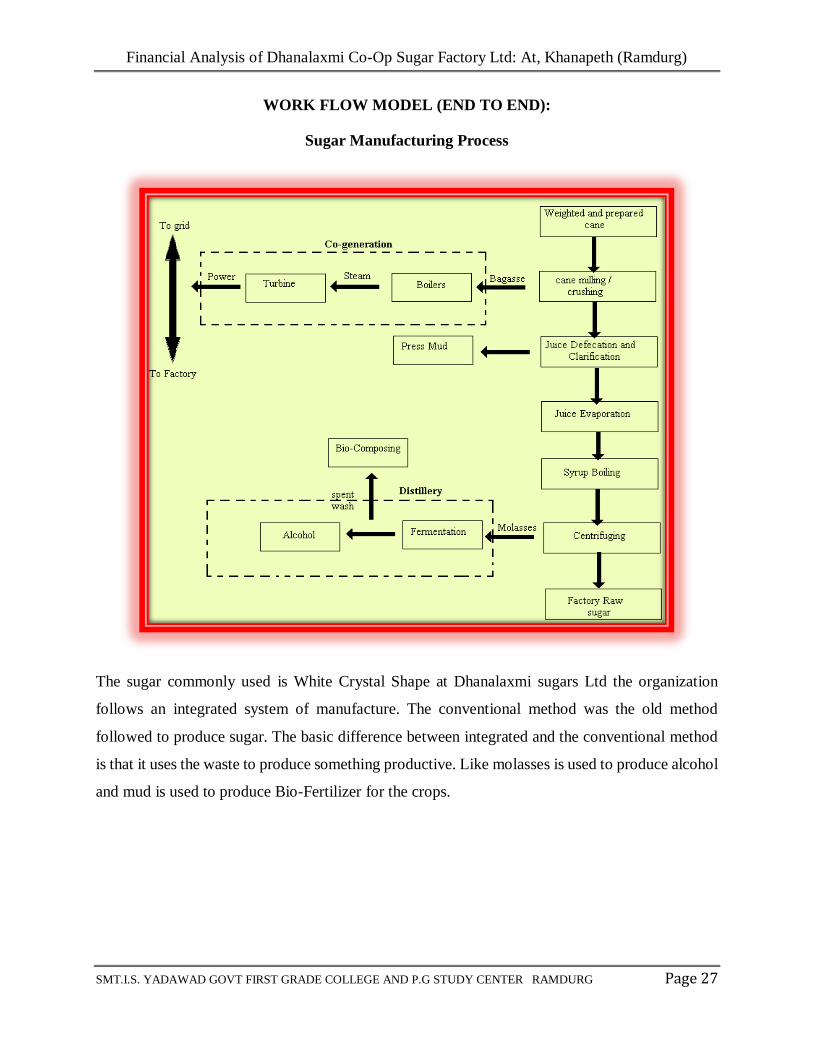

WORK FLOW MODEL (END TO END):

Sugar Manufacturing Process

The sugar commonly used is White Crystal Shape at Dhanalaxmi sugars Ltd the organization

follows an integrated system of manufacture. The conventional method was the old method

followed to produce sugar. The basic difference between integrated and the conventional method

is that it uses the waste to produce something productive. Like molasses is used to produce alcohol

and mud is used to produce Bio-Fertilizer for the crops.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 28

To produce different types of sugar different methods are used in the sugar factory. The

present system of sugar manufacturing is sub division into following stages.

1. Extraction of juice from sugarcane by milling

2. Clarification of juice.

3. Concentration of juice by evaporation to syrup.

4. Crystallization of sugar by vacuum pan boiling.

5. Centrifugation or separation of sugar and molasses from the massecuite.

6. Drying and cooling of sugar.

7. Sugar grading and packing.

The harvested vegetable material is crushed and the juice is collected and filtered. The liquid is

then treated (often with lime) to remove impurities; this is then with sulfur dioxide. The juice is

then boiled, sediment settles to the bottom and can be dredged out, scum rises to the being stirred

to produce sugar, which can be poured of sugar simultaneously some by-products are produced

namely.

PRODUCTION PROCESS OF WHITE CRYSTAL SUGAR

1)CANE PREPARATION:

Sugarcane is harvested and clean cane is loaded in the vehicles and brought to the factory.

The Gross weight is taken and loaded on the feeder table with electric crane. The weight of the

vehicle is taken to arrive at the weight of the cane. Cane is feed to cane carrier from the feeder

table. The preparatory devices viz. kicker, cutter, fiberize etc. is installed on the carrier for the

preparation of cane.

2) CANE MILLING:

Carrier takes the prepared cane to mills; to where the juice is extracted using compound

ambition process and hot water is applied to it for maximum extraction of the juice before the last

mill.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 29

3.RAW JUICE HEATING:

Mixed juice is strained and sent for processing and Water for imbition. Mixed juice and

water both are weighted in automatic weighing scales separately. Bagasse (residues of cane after

juice extraction) is used as fuel in the boiler and surplus Bagasse’s saved in the form of bales is

sent for storage.

4.SULPHITATION:

Mixed juice is clarified by sulphination process by heating at 75.C in a juice heater. Milk

of lime and sulphur dioxide gas, which is produced by burning sulphur, is used as clarificants.

They are thoroughly mixed in the juice sulphiter. Then the sulphited juice is heated to 102.C in

another juice heater.

5.CLARIFICATION:

This juice is passed on to continuous clarifier through flash tank for settling. The settled

mud is filtered with the help of vacuum filter where filters are separated and sent for clarification

treatment plant. The washed filter cake with minimum sugar content is sent out as by products.

6. EVAPORATION AND SYRUP BOILING:

Decanted clear juice from clarifier is taken to evaporators (multiple effects). The

concentration is increased to syrup consistency. The heat required for heating and evaporation is

used for exhaust steam and the vapors from evaporators. Exhaust steam is obtained from prime

mover turbines sent for further clarification treatment in the integrated plant. The sugar is produced

from further concentration of this syrup and sugar melt by evaporation in vacuum pan. The

necessary seed crystals are taken in the pan and boiled with syrup. This gives ‘A’ massecuite. ‘A’

massecuite from the pan is discharged in to crystallizers.

7.CENTRIFUGATION AND MOLASSES:

Then the sugar crystals are separated from the surrounding film of mother liquor in

centrifugal machine. The separated liquor is called as a molasses and sugar well washed and dried

with superheated water wash is dropped on the hopper from centrifugal machine

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 30

8. GRADING AND BAGGING:

The sugar is conveyed on hoppers and elevated to the top of grader by bucket elevator

and graded accordingly to the size and then bagged in twin mills bags of 50kgs net.

9. PRODUCTION OF ETHANOL:

A heavy molasses is subject to second boiling to get ‘B’massecute there by B sugar and B heavy

molasses. B sugar is used as seed or melted. B heavy molasses is subject to third boiling to get ‘C’

massecuite and there by C sugar and final molasses is weighted and stored in storage tanks. Factory

has set up 20.5 mw Cogeneration project.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 31

SWOT ANALYSIS OF DHANALAXMI CO OP SUGAR FACTORY LIMITED

STRENGTHS:

Well-developed industry with strong manufacturing base.

Track record of successful acquisition.

Better working facilities & conditions for workers.

The largest sugar refinery in India.

Reduced impact of the seasonality of the sugarcane corps.

Excellent relationship with sugarcane farmer.

Financial health of the company is good.

Power generation.

WEAKNESS:

Absence of motivating incentives.

Lack of training for subordinate staff.

High labor turnover.

Seasonal product fortunes swing from one extreme to another.

OPPORTUNITIES:

Scope to improve the profitability.

Can acquire more and more sick units in co-operative sector.

Well, placed for exports.

International markets can be tapped.

Expansion.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 32

THREATS:

Advancement of technology and changing job profile.

Huge Competition.

Pricing policy of the Government.

Open market system for Ethanol and alcohol.

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 33

CHAPTER - IV

DATA ANALYSIS AND INTERPRETATION

BALANCE SHEET OF DHANALAXMI CO-OP SUGAR FACTORY LTD 2015-16 TO 2019-20

PARTICULAR 2016 2017 2018 2019 2020

ASSETS

I. CURRENT ASSETS

Cash in hand

Cash at Bank

B.D.C Bank -220 Ramdurg

B.D.C Bank -141 Ramdurg

S B M Ramdurg

S B I Bank

S B I Estro

Syndicate Bank Ramdurg

Receivables

Receivable Sugar sales

T D S

Parry Sugars

Accrued Interest

Advance purchase of machinery

Prepaid expenses

Advance Income Tax

Yadawad Petroleum

Renuka sugars

CGST

SGST

IGST

OTHER

99,361,568.85

102283.98

1233.00

99245843.66

12208.21

6002921.00

750000.00

1098167.00

1643135.00

2511619.00

123340019.89

129015.98

1396.00

123197112.16

12495.75

8991172.34

8991172.34

24911304.81

3715102.98

1452.0

17808089.66

42945.00

3343715.17

9018768.71

9018768.71

399957055.00

450000.00

216.00

13318716.31

3887642.98

1511.00

5890288.66

41428.00

3497844.75

12179533.71

10183246.71

766000.00

444984.00

378861.00

35477.00

370965

7237.00

50098327.87

50826366.98

-892904.34

40779.00

124086.23

11995640.71

10561446.71

628274.00

766000.00

32420.00

7500.00

Total Current assets

105364489.85

132331192.23

434337128

25498465.31

62101205.58

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 34

II. NON-CURRENT ASSETS

Fixed Assets

Building

Plant & Machinery

Vehicle

Computer

Other Assets

Investments

Apex Bank BLR –

-Share

D C C Bank BGM

SBM Deposit

Syndicate Bank F D

SBM Deposit

(VAT register)

Accrued interest

Reddy cooperative bank share

Business Deposits

Irrigation Account

Postal Department

211181420.96

94144362.37

116500141.60

536916.99

50360100.00

10000.00

250100.00

30000000.00

20000000.00

100000.00

100388.00

96600.00

3788.00

184211425.96

84729926.13

99025120.36

456379.47

53353904.25

10000.00

250100.00

30000000.00

20000000.00

100000.00

2993804.25

100388.00

96600.00

3788.00

162352483.96

76256933.13

84171352.36

1924198.47

460488.00

10000.00

250100.00

100000.00

100388.00

96600.00

3788.00

566181379.9

6

133884857.1

3

430372324.3

6

1924198.47

460488.00

10000.00

250100.00

100000.00

100388.00

96600.00

3788.00

567096696.72

133884857.13

431246624.62

1924198.47

41016.50

3461388.00

10000.00

3250000.00

100000.00

1000.00

100388.00

96600.00

3788.00

Total Noncurrent assets 261641909.81 237665718.44 162812972 566641868.6

7

570558084.72

Total Assets

367006398.81

369996910.44

597150100.48

592140333.9

8

632659290.30

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 35

Particular 2016 2017 2018 2019 2020

Equity And liabilities

I. Shareholders fund

A. Share Capital Share A Share B Share C (Govt) Share D

B. Reserve Reserve Fund

Ceremony Fund Furniture Fund Depreciation on -Vehicle Depreciation on -Building Depreciation On Machinery Depreciation On -Computer

II. Noncurrent Liability

III. Current Liabilities

A. Trade Payables Contractor Deposit Election Nomination Audit Fees Govt.Payables -Guarantee Commission VidyaNidhi Account

Career Tax Staff Future Fund Payable For ‘ B’ Members Sugar Parry sugar Expansion Credit Subsidy Fund Suppliers of Machinery GST Payable (On lease Rent )

Staff Salary Earned Leaves Professional Fees Payable Postage management Allowance Payable TDS Payable GST Advance

Contingent Liabilities Service Tax Liabilities

255628000

103550000 1260000

150000000 818000

86660

142762 1789550

1151224.27

50000000

2000 652146

14037500

11777220

17249

255628000

103550000 1260000

150000000 818000

86660

142762 1789550 1151224

50000000

387646

14037500

528706 2200

118448

419580

255628000

103550000 1260000

150000000 818000

86660

142762 1789550 1151224

50000000

400000

14037500

530906

118448 406000

200000000

255628000

103550000 1260000

150000000 818000

86660

142762 1789550

1439853.27

13385171

64555848

50000000

500000

530906

3778 406000

160000000 307428

6095598

39533 197500

14037500

255628000

103550000 1260000

150000000 818000

86660

142762 1789550

1728483.27

26773657

129242842

6152

50000000

500000

530906

5428

120000000

6095598

40255

459000 40532

1134639

18731018.50 50000

14037500

Total Current liabilities 76486115 65494080 281557134 22118243 41624876.50

P & L Account

Accumulated and

-Current year Profit

31722087.54

45704634.17

56794770.21

22994246.71

5636307.53

Total Equity and Liabilities

367006398.81

369996910.44

597150100.48

592140333.98

632659290.30

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 36

Profit and Loss account for the period of 2016 & 2017

Particular Income Expenses 2016 2017 2016 2017

Sugar sales

Factory lease rental

Interest on deposits

Apex bank dividend

D.C.C bank dividend

Interest on savings

deposits

Sugar purchase

Sugar sales return

Staff salary

Printing and stationery

Election cost

Traveling expense

Fuel

Vehicle repair

Vehicle insurance

Annual general meeting

Police security

Postal and courier cost

Advertising

Service tax fine

Meeting allowance

Legal advisory cost

VAT register cost

Sugar distribution cost

General assembly

subscription

Death Subsidy

Suicide subsidy

Donation for adoption

Congregation cost

Telephone cost

Staff subordinate

Bank services fee

Income tax

Deprecation

Net income

2,60,10,000

8,41,23,000

51,34,933.21

950

25,618

940,46,996

412,00,000

33,20,276.59

900

22,509

4,673.54

4,75,76,100

81,500

4,45,110

5,86,071

20,38,008

1,92,634

1,37,655

15,330

4,68,637

14,850

2,60,000

4,18,960

4,10,000

2,500

3,99,350

6,774

7,99,000

95,000

1,56,000

36,000

36,113

1,29,060

3,240

3,11,16,335.33

2,98,70,158.88

759,18,580

9,17,246

4,51,051

20,000

233,555

1,77,624

15,446

3,44,350

1,00,000

98,710

1,40,080

49,500

4,92,050

4,43,000

1,45,000

55,000

36,525

989.50

180,04,107

269,69,995

139,82,546.63

Total 11,52,94,501 13,85,95,355 11,52,94,501 13,85,95,355

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 37

Profit and Loss account for the period of 2018 & 2019

Particular Income Expenses

2018 2019 2018 2019

Sugar sales

Factory lease rental

Interest on deposits

Apex bank dividend

D.C.C bank dividend

Death subsidy

Net loss

Interest on savings deposits

Sugar purchase

Sugar purchase associations

Sugar sales return

Staff salary

Staff future fund

contributions

Temporary staff salary

Temporary staff breakfast

Software cost

Printing and stationery

Election cost

Traveling expense

Interest on project loan

Fuel

Vehicle repair

Vehicle insurance

Annual general meeting

Police security

Postal and courier cost

4,01,35,870

8,92,46,000

29,27,813.88

800

22,571

3,71,58,724

10,20,16,000

5,59,723.58

500

22,500

84,000.00

3,38,00,523.5

7,99,26,840

8,82,786

9,02,391

3,22,533

60,000

3,30,00

1,01,481

2,92,971

2,52,546

16,332

1,80,600

28,500

1,00,000

1,59,00

93,000

4,62,354

2,40,348

6,59,20,000

3,71,008

5,88,296

54,048

1,83,150

1,15,000

70,000

2,83,123

20,920

1,55,07,397

2,44,243

1,04,284

61,074

1,80,690

58,200

1,00,000

1,90,752

34,416

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 38

Advertising

Service tax fine

Meeting allowance

Legal advisory cost

VAT register cost

Sugar distribution cost

General assembly

subscription

Death Subsidy

Suicide subsidy

Donation for adoption

Congregation cost

Telephone cost

Staff subordinate

Staff subdivision

Earned leave

Bank services fee

Income tax

Deprecation

Net income

13,09,000

1,75,000

2,80,000

26,630

1,918.50

1,14,35,342

2,36,66,326

1,10,90,136

1,33,000

5,41,145

2,16,418

1,33,000

7,79,000

25,000

51,000

37,183

3,07,428

1,97,500

926.08

90,37,122

7,82,29,648

Total 132333054 173641971 132333054 173641971

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 39

Profit and Loss account for the period from 01-04-2019 to 31-3-2020

INCOME AMOUNT EXPENDITURE AMOUNT

Factory lease rental

Sugar sales

Interest on deposits

Apex bank dividend

Selling scrap things

Staff salary

Fuel

Other incomes

Net loss

10,37,82,000.00

3,79,71,050.00

3,14,260.82

600.00

7,50,000.00

39,533.00

32,420.00

1,000.00

1,73,57,939.18

Sugar purchase

Sugar purchase

associations

Sugar distribution cost

Interest on project loan

Staff salary

Staff future fund

contributions

Assignment management

allowance

Staff future fund

subscription letter fee

Software cost

Printing and stationery

Traveling expense

Fuel

Vehicle repair

Annual general meeting

Police security

Unpaid income source

deduction

Advertising

Audit fees

Pre-election expenses

Death subsidy

Suicide subsidy

Meeting cost

Other expenses

Telephone, post, internet

cost

Bank services fee

Income tax

Deprecation

6,54,16,000.00

3,02,400.00

2,16,500.00

1,12,00,000.00

5,11,259.00

85,951.00

1,77,321.00

50,882.00

41,990.00

38,486.00

1,21,459.00

3,46,815.00

2,93,332.00

6,23,065.00

32,500.00

2,71,986.74

1,62,869.00

8,17,475.00

44,852.00

6,65,000.00

1,50,000.00

1,01,000.00

36,740.34

1,25,604.00

38,244.92

6,809.00

7,83,70,262.00

TOTAL 16,02,48,803.00 TOTAL 16,02,48,803.00

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 40

1) CURRENT RATIO:

This is most widely used ratio. It is the ratio of current assets to current liabilities

with its current assets.

Generally, 2:1 is considered ideal for concern i.e., current assets should be twice of

the current liabilities, there will be no adverse effect on the business when the payment of current

liabilities is made. If the ratio is less than two, difficulty may be experienced in the payment of

current liabilities & day-today operations of the business may be safer. It is expressed as follows,

Current Ratio = Current Assets

Current Liabilities

The Table 4.1 Showing Current Ratio:

Year Current Asset Current Liability Current Ratio

2015-2016 105364489 76486115 1.38

2016-2017 132331192 65494080 2.02

2017-2018 434337128 281557134 1.54

2018-2019 25498466 22118243 1.15

2019-2020 62101205 41624876 1.49

SOURCES: Collected from Annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 41

The chart showing current Ratio

INTERPRETATION:

From the above table reveals the current ratio of the year 2015-16, 2017-18, 2018-

19, 2019-20 it indicates that would not reach up to the mark (i.e., less than the standard of 2:1) But

the year 2016-17 Reveals that the current ratio of (2.02) it is much higher than the Standard Ratio.

0

0.5

1

1.5

2

2.5

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Current Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 42

2) LIQUID OR ACID TEST OR QUICK RATIO:

Liquidity ratio is the measure of the instant debt paying ability of the

business enterprise, hence it is also called ‘Quick Ratio ‘This ratio establishes the relationship

between liquid current assets and current liabilities.

Liquid liabilities include all items except bank overdraft. Quick assets included all current

assets except inventory and prepaid expenses Advance income Tax cannot be converted in to cash.

Generally, 1:1 ratio is considered ideal ratio for a concern because it is wise to keep the liquid

assets at least equal to liquid liabilities at all times. It is calculated as follows,

Liquid Ratio = Liquid Assets

Liquid Liabilities

The Table 4.2 Showing Quick Ratio

Year Quick Asset Current Liability Quick Ratio

2015-2016 105364489 76486115 1.38

2016-2017 132331192 65494080 2.02

2017-2018 433887127 281557134 1.54

2018-2019 24732465 22118243 1.12

2019-2020 61335205 41624876 1.47

SOURCES: Collected from Annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 43

The chart showing quick ratio

INTERPRETATION:

The above table gives an idea about the quick assets held by the company as

against their current liabilities. Investing more in the liquid assets would affect the profitability.

In the above all years (2016,2017,2018,2019,2020) the ratios of the company are more than the

standard ratio (1:1) and it indicates the sufficient liquidity. The instant Debt paying ability of the

business enterprises is satisfactory in all years. the financial position of the firm seems to be sound

and good

0

0.5

1

1.5

2

2.5

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Quick Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 44

3. ABSOLUTE LIQUID RATIO:

Cash is most liquid assets, although receivable & bills receivables or

generally better realizable than inventories still there are doubts regarding their realization

more so in time. so, they are not considered immediately available for making payments

and so exclude for the calculation of Absolute Liquid Ratio. A Standard of 0.5:1 in absolute

liquidity ratio is an acceptable norm, because fifty paisa worth of absolute liquid assets are

considered sufficient for one rupee worth of current liabilities.

Absolute liquid ratio = Absolute liquid assets

Liquid Liabilities

The Table 4.3 Showing Debtors Turnover Ratio

Year Absolute liquid

assets

Liquid Liabilities Ratio

2015-2016 99361568 76486115 1.30

2016-2017 123340019 65494080 1.88

2017-2018 433887127 281557134 1.54

2018-2019 13318932 22118243 0.60

2019-2020 50105564 416924876 1.20

SOURCES: Collected from Annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 45

The chart showing absolute liquid ratio

INTERPRETATION:

From the above table the data reveals that from the all years (i.e.,2016, 2017,

2018, 2019, 2020) super quick ratios are 1.30 , 1.88 , 1.54 , 0.60 , 1.20 respectively these years

high funds are deployed in super quick ratio , because all these years absolute ratios are quite

higher than the accepted standard (0.5:1) these all year liquidity position of the company is sound

.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Absolute Liquid Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 46

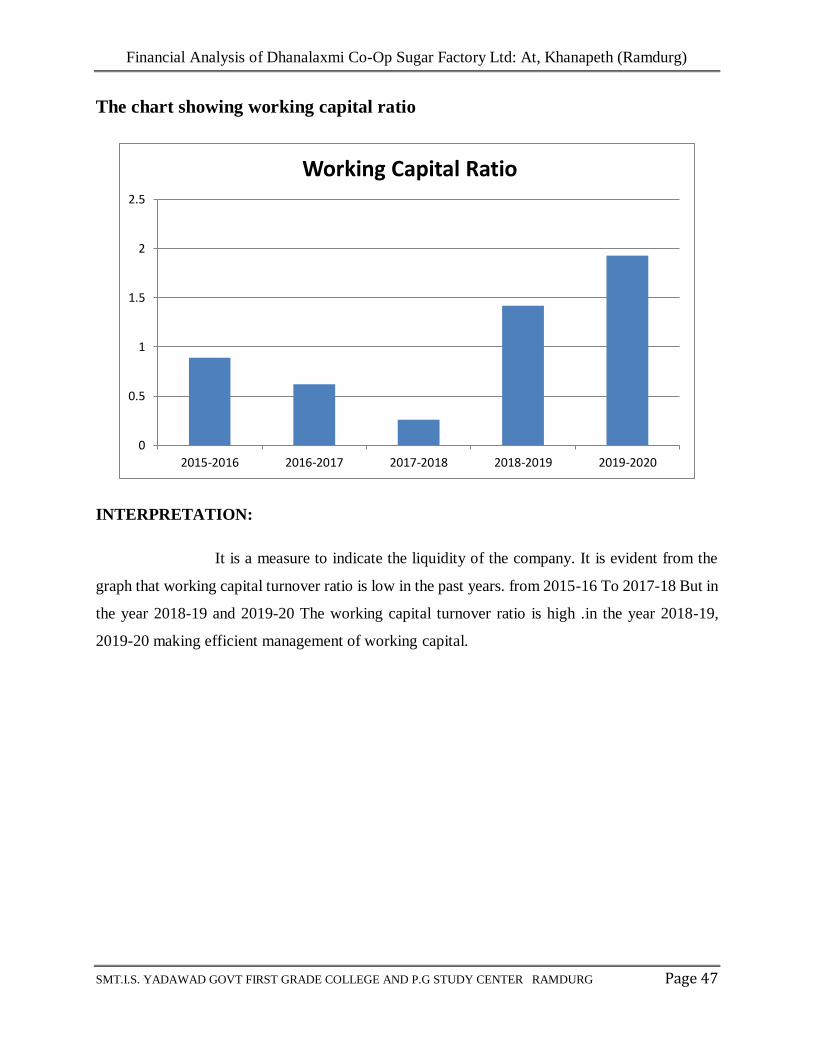

4.WORKING CAPITAL TURNOVER RATIO:

This ratio establishes the relationship between net working capital

and net sales. It is calculated by dividing the net sales by net working capital. This ratio is used

to assess the efficiency with which the working capital is being used in making sales.

Working capital ratio = Net sales

Net working capital

Net working Capital = (Current assets – Current Liabilities)

The Table 4.4 Showing Working capital Ratio:

Year Net sales Net working capital Working capital

ratio

2015-2016 25928500 28878374 0.89

2016-2017 41200000 66837112 0.62

2017-2018 40135870 152779994 0.26

2018-2019 37158724 26142233 1.42

2019-2020 37971050 20476329 1.93

SOURCES: Collected from annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 47

The chart showing working capital ratio

INTERPRETATION:

It is a measure to indicate the liquidity of the company. It is evident from the

graph that working capital turnover ratio is low in the past years. from 2015-16 To 2017-18 But in

the year 2018-19 and 2019-20 The working capital turnover ratio is high .in the year 2018-19,

2019-20 making efficient management of working capital.

0

0.5

1

1.5

2

2.5

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Working Capital Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 48

5. TOTAL ASSETS TURNOVER RATIO:

This ratio expresses the relationship between net sales and total assets. It is also called as

Total Investment turnover ratio. This ratio indicates the number of times the assets are turned over

in a year in relation to sales. The asset turnover Ratio measures the efficiency of a company’s

assets in generating revenue or sale according to Helfert only operating assets are considered

i.e., Investments are also excluded.

Total assets turnover Ratio = Net sales

Total assets

The Table 4.5 Showing Total assets turnover Ratio

Year Net sales Total assets Total assets

turnover Ratio

2015-2016 25928500 316646298 0.08

2016-2017 41200000 316643006 0.13

2017-2018 40135870 596689612 0.06

2018-2019 37158724 591679846 0.07

2019-2020 37971050 629197902 0.06

SOURCES: Collected from Annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 49

The chart showing total assets turnover ratio

INTERPRETATION:

In the year 2016-17 Dhanalaxmi sugar factory is highest effective utilisation of

investment in assets, it is 0.13 times assets are turned over in a year in relation to sales. Remaining

four years that assets are not properly utilized in comparison to sales.

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Total Assets Turnover Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 50

6.FIXED ASSETS TURNOVER RATIO :

This ratio expresses the relationship between fixed assets ( Less depreciation ) and net

sales .Since Investment in fixed assets is made for the ultimate purpose of efficient sales , the

ratio is used to measure the fulfilment of that objective . As such investment are excluded from

fixed assets as they do not affect sales . This ratio measure the efficiency and profit earning

capacity of the firm .

Fixed assets Turnover Ratio = Net Sales

Fixed Assets

The Table 4.6 Showing Fixed assets Turnover Ratio

Year Net sales Fixed assets Fixed assets

turnover Ratio

2015-2016 25928500 180065085 0.14

2016-2017 41200000 157241430 0.26

2017-2018 40135870 138686157 0.29

2018-2019 37158724 487951731 0.07

2019-2020 37971050 488726434 0.08

SOURCES: Collected from Annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 51

The chart showing fixed assets turnover ratio

INTERPRETATION:

In the year 2017-18, The factory is the greater intensive utilization of fixed assets.

because it has higher the Ratio. and in the year 2018-19 is underutilization of fixed assets and

excessive investment in these assets. Because the ratio is lower (0.07) comparatively remaining

four years. Remaining years not reach up to the optimum level comparative 2017-18.

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Fixed Assets Turnover Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 52

7. CURRENT ASSETS TURNOVER RATIO:

This ratio expresses the relationship between current assets and net sales. this ratio

reflects the efficiency and capacity of working capital it is a very

useful technique for non- factoring unit or those manufacturing units requiring lesser working

capital.

Current assets turnover Ratio = Sales

Current Assets

The Table 4.7 Showing current assets turnover Ratio

SOURCES: Collected from Annual reports

Year Sales Current assets Current assets

turnover Ratio

2015-2016 25928500 105364489 0.25

2016-2017 41200000 132331192 0.31

2017-2018 40135870 434337128 0.09

2018-2019 37158724 25498466 1.46

2019-2020 37971050 62101205 0.61

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 53

The chart showing current assets turnover ratio

INTERPRETATION:

In the year 2018-19, The factory is the greater intensive utilization of Current assets

because it has higher the Ratio that is 1.46. And in the year 2018 is underutilization of Current

assets that is (0.09) and excessive investment in these assets. Because the ratio is lower (0.09)

comparatively remaining four years. Remaining years not reach up to the optimum level

comparative 2018-19.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Current Assets Turnover Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 54

8. CAPITAL TURNOVER RATIO:

This ratio establishes the relationship between net sales and capital employed. The

efficiency and effectiveness of the operations are judged by comparing the sales or cost of

sales with the amount of capital employed in the business and not with the assets held in the

business. Therefore, this ratio is a better measurement of efficient use of capital employed.

No idle standard can be fixed for this ratio as turnover is different in different

types of industries.

Capital turnover ratio = sales

Capital employed

The Table 4.8 Showing Capital turnover ratio

Year Net sales Capital employed Capital turnover

ratio

2015-2016 25928500 240160183 0.11

2016-2017 41200000 251148925 0.16

2017-2018 40135870 315132478 0.13

2018-2019 37158724 568795602 0.07

2019-2020 37971050 586807026 0.06

SOURCES: Collected from Annual reports

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 55

The chart showing capital turnover ratio

INTERPRETATION:

Profit earning capacity and managerial efficiency is good in the Year 2016-17 because

its 0.16 times quicker rotation of capital to generate higher sales which leads to higher

profitability and good utilization of capital employed in the business and in the year 2019-20

has lower ratio, lower ratio will indicate that either the capital is not being used infinity to

generate enough sales. Remaining years not reached up to the mark comparatively 2016-17.

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Capital Turnover Ratio

Financial Analysis of Dhanalaxmi Co-Op Sugar Factory Ltd: At, Khanapeth (Ramdurg)

SMT.I.S. YADAWAD GOVT FIRST GRADE COLLEGE AND P.G STUDY CENTER RAMDURG Page 56

9. PROPRIETARY RATIO: