Chapter 17. Hybrid Intelligent Decision Support Systems and Applications for Risk Analysis and...

26

Chapter 17. Hybrid Intelligent Decision Support Systems and Applications for Risk Analysis and Discovery of Evolving Economic Clusters in Europe N. Kasabov , L. Erzegovesi , M. Fedrizzi , A. Beber , and D. Deng Dept. of Information Science, Univ. of Otago, Dunedin, New Zealand. E-mail: nkasabov, [email protected] Dept. of Informatics and Faculty of Economics, Univ. of Trento, Italy Abstract. Decision making in a complex, dynamically changing environment is a difficult task that requires new techniques of computational intelligence for build- ing adaptive, hybrid intelligent decision support systems (HIDSS). Here, a new ap- proach is proposed based on evolving agents in a dynamic environment. Neural network and rule-based agents are evolved from incoming data and expert knowl- edge if a decision making process requires this. The agents are evolved from meth- ods included in a repository for intelligent connectionist based information systems RICBIS (http://divcom.otago.ac.nz/infosci/kel/CBIIS.html) with the use of financial market data collected in an on-line mode, and with the use of macroeconomic data published monthly in the European Central Bank Bulletin. RICBIS includes different types of neural networks, including MLP, SOM, fuzzy neural networks (FuNN), evolving fuzzy neural networks (EFuNN), evolving SOM, rule-based sys- tems, data pre-processing techniques, standard statistical and financial techniques. A case study project on risk analysis of the European Monetary Union (EMU) is considered and a framework of a system EMU-HIDSS is presented, which deals with different levels of information and users, e.g. the whole world, Europe, clusters of nations, a single nation, companies/banks. It combines modules for final decision making, global and national economic development, exchange rate trend predic- tion, stock index trend prediction, etc. Some experimental results on real data are presented. Keywords. Intelligent decision support systems, risk analysis, connectionist-based informa- tion systems. 1 Introduction Complex decision making problems very often require considering enormous amount of information distributed among many variables. The decision support sys- tems (DSS) built to solve these problems should have advanced features such as [19]:

Transcript of Chapter 17. Hybrid Intelligent Decision Support Systems and Applications for Risk Analysis and...

Chapter 17. Hybrid Intelligent DecisionSupportSystemsand Applications for Risk AnalysisandDiscovery of Evolving EconomicClusters in Europe

N. Kasabov�, L. Erzegovesi

�, M. Fedrizzi

�, A. Beber

�, and D.

Deng�

�Dept.of InformationScience,Univ. of Otago,Dunedin,New Zealand.E-mail: nkasabov, [email protected]�Dept.of InformaticsandFacultyof Economics,Univ. of Trento,Italy

Abstract. Decisionmakingin a complex, dynamicallychangingenvironmentis adifficult taskthat requiresnew techniquesof computationalintelligencefor build-ing adaptive, hybrid intelligentdecisionsupportsystems(HIDSS).Here, a new ap-proach is proposedbasedon evolving agentsin a dynamicenvironment.Neuralnetworkandrule-basedagentsare evolvedfrom incomingdataandexpert knowl-edge if a decisionmakingprocessrequiresthis.Theagentsare evolvedfrommeth-odsincludedin a repositoryfor intelligentconnectionistbasedinformationsystemsRICBIS(http://divcom.otago.ac.nz/infosci/kel/CBIIS.html) with theuseof financialmarket data collectedin an on-line mode, and with the use of macroeconomicdata publishedmonthlyin the EuropeanCentral BankBulletin. RICBISincludesdifferent typesof neural networks,including MLP, SOM, fuzzyneural networks(FuNN),evolving fuzzyneural networks(EFuNN),evolving SOM,rule-basedsys-tems,datapre-processingtechniques,standard statisticalandfinancialtechniques.A casestudyproject on risk analysisof the EuropeanMonetaryUnion (EMU) isconsidered and a framework of a systemEMU-HIDSSis presented,which dealswith differentlevelsof informationandusers,e.g. thewholeworld, Europe, clustersof nations,a singlenation,companies/banks.It combinesmodulesfor final decisionmaking, global and national economicdevelopment,exchange rate trend predic-tion, stock index trendprediction,etc.Someexperimentalresultson real data arepresented.

Keywords. Intelligentdecisionsupportsystems,risk analysis,connectionist-basedinforma-tion systems.

1 Intr oduction

Complex decision making problems very often require consideringenormousamountof informationdistributedamongmany variables.Thedecisionsupportsys-tems(DSS)built to solve theseproblemsshouldhave advancedfeaturessuchas[19]:

� Goodexplanationfacilities,preferablypresentingthedecisionrulesused;� Dealingwith vague,fuzzy information,aswell aswith crispinformation;� Dealingwith contradictoryknowledge,e.g.,two expertspredictdifferenttrendsin thestockmarket;� Dealingwith largedatabaseswith alot of redundantinformation,orcopingwithlackof data.� Having hierarchicalorganisation,asdecisionmaking is usually not a single-level process,but involvesdifferent levels of processing,comparingdifferentpossiblesolutions,usingalternatives,sometimesin a recurrentway.

Techniquesof computationalintelligence,suchasartificial neuralnetworks,fuzzylogic systems,geneticalgorithms,advancedstatisticalmethods,hybrid systems,alongwith traditionalstatisticalandfinancialanalysismethods,have beenwidelyappliedon differentproblemsfrom financeandeconomics.Heresomeof themarereferencesandexplained.

1.1 Specialisedand AdvancedStatistical and EconometricModels

In [45] a modelfor risk analysison crashesof currenciesis introduced.It consid-ersa crashsituationwhena currency hasbeendevaluatedmorethan10%within amonthwhencomparedto the US dollar. Four parametersareusedto evaluatethelikelihoodof acrash(avalueof 0 or 1) in thefollowing month:measureof currencyovervaluation;expecteddomesticoutputgrowth; ratioof federalreservesversusex-ternaldebt; measuresof internationalfinancial contagion.The latter is measuredin risk appetite(a changein investorspreferencesbeforecrashesoccur),andclus-ters(whethercrashesof currenciesfrom thesameblock of countrieshave recentlyoccurred).Othermodelsarepresentedin [6].

Themethodsin this grouprequirea reliableknowledgeon theunderlyingrulesof thefinancialandeconomicsystemsandcannot beeasilyadjustedto a new eco-nomic or financial situation.They are applicablewhencrisesoccur accordingtorecurrentandknown patterns.

1.2 Symbolic and FuzzyRule-BasedSystems

Rule-basedsystemsandfuzzyrule-basedsystemsin particularhavebeenusedin fi-nancialandeconomicdecisionmaking(seepapersin [12][13]). Themainadvantageof rule-basedsystemsis that their functioningis basedon humanexpertrules.Themaindisadvantageis that thesesystemsarenot flexible enoughto reactto changesin thereality. Changingtherulesusuallyis difficult, andnobodycanarticulatetheperfectsetof rulesthatdonot have to changein a futuretime.

1.3 Artificial Neural Networks (ANN)

Extendedstudiesof usingANN for financialDSShave beendonein severalbooks(seefor example:[12][13][49][54]). Generally, the socallednon-parametricmod-els proved to outperformthe statisticalmethods,especiallywhen the underlyingrules were not known, or they changeover time. Different typesof ANN wereused,mainlymulti-layerperceptrons(MLP), radialbasisfunctions(RBF),andself-organisingfeaturemaps(SOM).

A MLP modelanda RBF modelon option pricing [16] provedto outperformseveral other models,that include a direct applicationof Black-Scholesformula,ordinaryleastsquares,andprojectionpursuit.Thetestdatawasthedaily S&P500futuresandoptionprices.Two inputvariables– theratiostockprice/strikepriceandtime to maturity, andoneoutputvariable- optionprice,wereused.This modelwasfurtherextendedinto amulti-modularANN modelwith theuseof hints[10].

In [5] a substantialstudyof applyingSOM to financialmarketsis presented.In[3] emergingandnew marketsaremappedinto aSOM thatshowsgroups(clusters)of similareconomies.

Thesofar developedandusedANN modelsprovedto beefficient,but they donot allow easily for dynamicon-line training, for changingthe parametersin anon-linemode,for combiningdataandknowledge(rules)into onesystem.

1.4 GeneticAlgorithms

Geneticalgorithms(GA) areheuristicmodelsthatarebasedon generatingpossiblesolutionsto aproblemandevaluatingtheir“goodness”basedonagoodness(fitness)function(e.g.goalfunction)thathasto bespecifiedin advance.GA useterminologyfrom thenaturalselectionandevolutionof species.Thereareseveralstudiesof usingGA for economicandfinancialdecisionmaking(seealsochaptersin this volume).Softwarebasedon GA simulation,that works directly on datain an Excel formathasbeenproduced[8].

The main advantageof GAs is that they do not requiremuch knowledgeontheunderlyingrules,formulas,etc.,but a goodnessfunction to evaluatehow goodsolutionsare.Themaindisadvantagesof GAsare:(i) they arecomputationallyslow;(ii) they do not necessarilyprovide with the bestsolutionasthey areheuristicallybased;(iii) they donot work in on-lineandrealtimemodes.

1.5 ModelsBasedon Dynamic SystemAnalysis

In [50] thestockmarketis modelledasacomplex dynamicsystemthatcanbein oneof four statesprojectedin a two-dimensionalspaceof groupthinking-fundamentalbias:randomwalk, chaoticmarket, coherentbull market, coherentbearmarket. In[38][39] astockindex predictionproblemis consideredasequivalentto thepredic-tion of a chaoticprocesswith differentcharacteristicsat differenttime scalesandahighfrequency index prediction(e.g.daily prediction)beingattemptedafterthelowfrequency one(e.g.,monthly, or annualprediction)is performed.

1.6 Hybrid Systems

Hybrid systemscombineseveral of the above methodsinto onesystem[19][20].They achieve this combinationeither in a “loose” way, e.g. differentmodulesinthesamesystemusedifferentmethods(seeexamplesof suchsystemsin [12][13]),or in a “tight” way - methodsaremixedat a low level, e.g.fuzzy neuralnetworks([18][29][42]). Thesemethodsarethemostpromisingamongthemethodsdiscussedabove,asthehybrid systemsintegratetheadvantagesof all themethodscombined,e.g. dealingwith both dataand expert rules, using both statisticalformulasandheuristicsor hints.

1.7 What is Missing in the Methods fr om Above?

Thesix groupsof approachespresentedabove have beenpartially successful,withmajorproblemsaslistedbelow:

� They donotconsiderthecomplexity of theproblemin awholewith many hier-archicallevels for decisionmakingthat includeapplyinglow-level processingandhigherlevel expertknowledge;or� They do not consideruncertaintiesat differentlevelsof informationprocessingandcombiningthemor propagatingthemin a taskdependentway to thefinaldecisionmakingblock; or� They do not applysufficient varietyof techniquesandchoosethemostappro-priatefor eachsub-task;or� They do not offer adjustmentof variablesets,optimisationcriteria,rules,evenif therealsituationchangesover time.

2 From DSSto HIDSS

Hybrid systemscombinedifferent techniquesof computationalintelligencewithtraditionalstatisticalmethods.Hybrid systemsareespeciallysuitablefor buildingDSS.

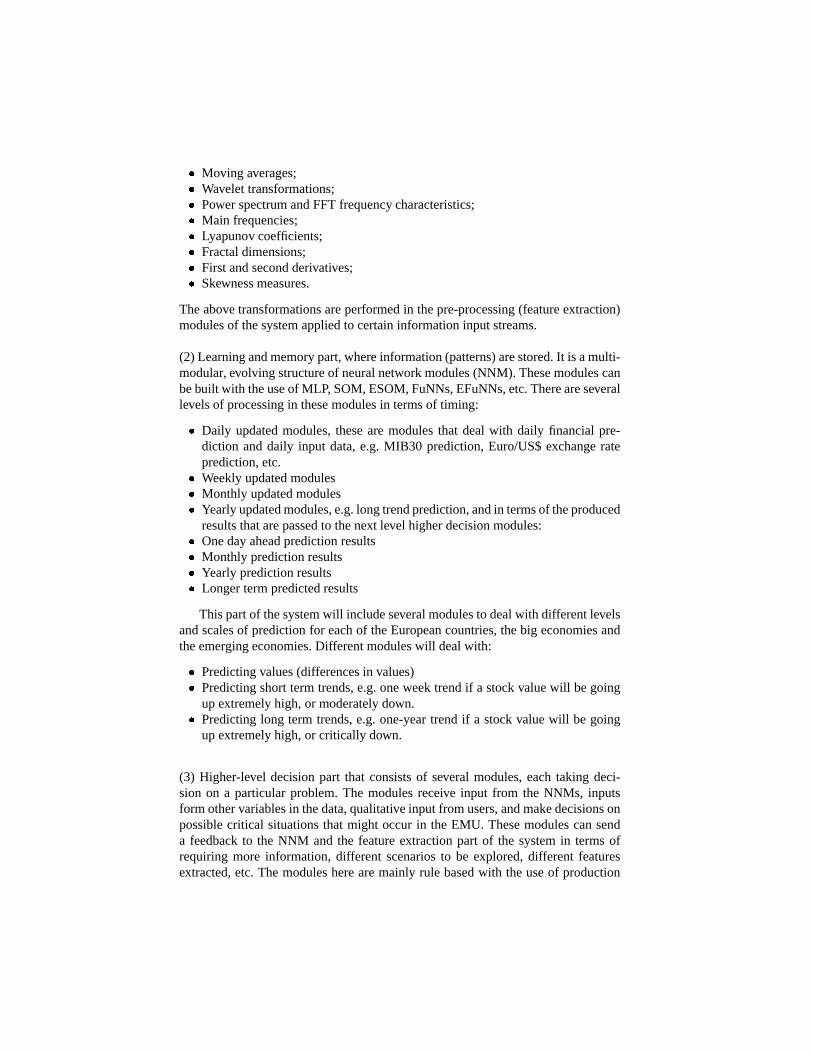

Stock market index predictionis a good exampleof a complex problemthatrequiresa hybrid system,as it is shown on the casestudy of the NZSE40stockindex in [19][38][39]. Several modulesare includedin the DSSsystempresentedthereas thereare several taskswithin the global one: datapre- processing(e.g.normalisation,moving averagescalculation,etc); predictingthe next valuefor theindex; predictinglonger-term valuesfor the NZES40,final decisionmaking thattakesinto accountruleson thepolitical andeconomicsituation;extractingtradingrules from the system- seeFig.1. A neuralnetwork is usedto predict the nextvalueof the index basedon thecurrentandtheprevious-dayvalues.Thepredictedvaluefrom theneuralnetwork moduleis combinedwith expertruleson thecurrentpolitical andeconomicsituationin a fuzzy inferencemodule.Thesetwo variablesarefuzzyby nature.Thefinal decisionis producedasafuzzyone,andasacrispone

- aftera defuzzificationprocess.Anothermodulein theDSSfrom Fig.1 is devotedto extractingfuzzy tradingrules,whichareusedto explain thecurrentbehaviour ofthemarket.

An environment,calledFuzzyCOPE/1,that canbe usedto createhybrid sys-tems,is describedin [19] andavailablefrom internetURL http://kel.otago.ac.nz/.Itconsistsof the following modulesthathave compatibleinterfacesandcanbecon-nectedin a DSSasa decisionmakingsequencethatrepresentsthelogic of therealdecisionmakingprocess:dataprocessingmodules(normalisation,fuzzification,fil-tering,etc.);multi-layerperceptron(MLP); self-organisingmap(SOM); fuzzyneu-ral network (FuNN)asintroducedby Kasabov in [18][19][28]; fuzzylogic inferenceengine(FLIE) basedon simplefuzzy rulesof Zadeh-Mamdanitype(Zadeh,1965);productionrule-basedsystemCLIPS and FuzzyCLIPSin particular. The Fuzzy-COPE/1environmenthasbeenextendedto FuzzyCOPE/3with theinclusionof newMLP andSOM learningmodes,andnew modesfor learning,rule extractionandrule insertionin FuNNs.Examplesof hybrid systemsbuilt with the useof Fuzzy-COPEaregiven in [19]. The two environmentsFuzzyCOPE/1andFuzzyCOPE/3areavailable from the following WWW site andcanbe usedfor building hybridDSS:http://divcom.otago.ac.nz/infosci/kel/CBIIS.html (Software � FuzzyCOPE).

Fig.1. An exampleof a hybridDSSfor stocktrading(from [19])

Thehybrid systemenvironmentsdevelopedsofar, andthehybrid systemsbuiltwith them,have beenvery usefultechniques,but thecomplexity andthedynamicsof thereal-world problems,especiallyin financeandeconomicsat present,requireevenmoreadvancedandsophisticatedmethodsandtoolsfor building hybrid intel-ligent decisionsupportsystems(HIDSS). Suchsystemsshouldbe ableto changeasthey operate,alwaysupdatingtheir knowledge,andto refinethemodelthroughinteractionwith theenvironment.Somemajorrequirementsto thepresentdayintel-ligent systems(IS), andto theHIDSSin particulararegivenin [21]-[25].

A framework for building adaptive intelligent systems,calledECOS(evolvingconnectionistsystems)hasbeenrecentlyintroducedin [21]-[25], alongwith its ar-

chitecture,learningandevolving algorithms,ruleextractionandrule insertionalgo-rithms,of anevolving fuzzy neuralnetwork EFuNN[23]-[25]. EFuNNscanlearnin an incremental,adaptive way throughone-passpropagationof any new dataex-amples.EFuNNsaremuchfasterthanFuNNsandMLPs andcanlearndatain anon-line mode.EFuNNsdo not have a fixed structure,on the contrary– they startevolving/learningwith no rule (hidden)nodesandthey grow asdatais presentedtothem.Pruningof nodesandnodereductionis achievedwith theuseof fuzzy prun-ing rules,e.g.:IF a node is not much used in a defined period, ANDit is old, THEN probability to prune the node is high.

EFuNNshave the following advantageswhencomparedwith traditionalMLPor SOM networks([24]:

1. they canlearnin anon-linemodeany new dataasthey aremadeavailableovertime;

2. they canwork in a complex environmentwith changingdynamics,e.g.a stockindex systemcanbe in a randomwalk state,thenit movesto a chaoticstate,and then - to quasiperiodic state,and an EFuNN that predictsfuture stockvalues,learnsall the time the new behaviour without any humaninterventionfor parameteradjustment.

3. they canbe usedto mix expert rulesanddataastherearealgorithmsfor ruleinsertionandrule extraction;

4. they canclusterdatain an on-line modewithout pre-definingthe numberofclusters,or thedimensionalityandthesizeof theproblemspace;

5. they canbeusedfor bothsupervisedandunsupervisedlearningmodes;assuper-visedsystemsthey canbeusedto predictfuturevaluesof theoutputvariables.

Examplesof usingFuNNsandEFuNNsfor adaptive, intelligent decisionsup-port systemsfor stock predictionand loan approval are given in [26]. Other ex-amplesinclude:imagerecognition[34]; speechandlanguagerecognition[24][33];mobilerobotcontrol[24].

Simulatorsof EFuNNareavailablefrom http://divcom.otago.ac.nz/infosci/kel/CBIIS.html(Software).

AnotherECOSalgorithm,calledEvolving Self-organizingMap (ESOM)[4], isproposedasavariationof theSOMalgorithmbasedontheECOSprinciples.ESOMusesalearningrulesimilarto SOM,but its network structureis evolveddynamicallyfrom inputdata.Simulationshaveshown thatESOMlearnsfasterthanSOMwith asmallerquantisationerrorfor featurevectors.

ECOS-basedmodulessuchasEFuNNsandESOMarepartof theNew ZealandRepositoryof IntelligentConnectionist-BasedSystems(RICBIS), which alsointe-gratesmodulesfrom the FuzzyCOPEenvironments,a Java versionof rule-basedsystemCLIPS(JESS),anda platform independentinterfacerunningasa Java ap-plet,which allows for dynamiccreationof new modulesduringtheoperationof anECOS,or anHIDSSin particular. RICBIS is availablefrom thefollowing URL:http://divcom.otago.ac.nz/infosci/kel/CBIIS.html (Software).

A new expert systemarchitecturecalledAdaptive Intelligent Expert Systems(AIES), basedon dynamicgenerationof interconnectedmodules(agents)from theRICBIS, is explainedin [34]. It is in sharpcontrastto theconventionalexpertsys-temsandDSSthatusuallyhave a fixedstructureof modulesanda fixedrule base.AlthoughtraditionalexpertsystemsandDSShavebeensuccessfulin somespecificandrestrictedareas,therewasno, or little flexibility left for the expert systemtoadaptto changesrequiredby theuser, or by thedynamicallychangingenvironmentin which theexpertsystemandtheDSSrespectively operated.

AIES, or HIDSS in particular, consistof a seriesof moduleswhich areagent-basedand are generated“on the fly” as they are needed.Fig.2 shows a generalarchitectureof anAIES [34]. Theuserspecifiestheinitial problemparametersandtasksto besolved.TheAIES thencreatesModulesthatmayinitially have no rulesor maybesetupwith rulesfrom theExpertKnowledgeBase.TheModulescombinetheruleswith thedatafrom theEnvironment.TheModulesarecontinuouslytrainedwith datafrom the Environment.Rulesmay be extractedfrom trainedFuNNsorEFuNNsfor later analysis,or for the creationof new Modules.The Modulesdy-namicallyadapttheir rulesetsastheenvironmentchangessincethenumberof rulesis dependenton the datapresentedto the Modules.Modules(agents)aredynami-cally created,updatedandconnectedin an on-line mode.They canbe removedifthey arenomoreneededata laterstageof theoperationof theAIES.

Agent 1

Adaptive Learning

Agent 2

ModuleGeneration

Solution

ResultsIntelligent Design Interface

User task specification

Data / Environment

Data Transformation

Neural Networks

Fuzzy Logic

Genetic Algorithm

Repository of Modules

EFuNNs

Web pages

Time series

Databases

Knowledge

Base

Fig.2. A block diagramof an agent-based,adaptive intelligent decisionsupportsystem–HIDSSthatusesthearchitectureof anAIES.

A very complex problem of risk analysisof the EuropeanMonetary Union(EMU) system,establishedin 1999to unify thecurrency andtheeconomicdevel-opmentof eleven Europeancountries,is the problemdiscussedandhandledhere.The restof the materialherepresentsfirst the problemandthena framework of aHIDSSfor its solution.It thendevelopssomespecificmodulesanddiscussessomepreliminaryexperimentalandimplementationissues.

3 The Problem of Risk Analysis in the EuropeanMonetary Union

Sinceits conception,therehavebeena lot of materialspublishedondifferentissuesconcerningEMU. Globalpolicy requirementsexist, suchasfor eachparticipatingcountryto haveadeficit lessthan3%of its GDPandexternaldebtlessthan60%oftheGDP. In theEMU framework, theEuropeanCentralBank(ECB) is in chargeofthemonetarypolicy, with priority andresponsibilityfor inflation control.TheECBpublishesa monthly bulletin containinga rich setof real,monetaryandfinancialdataregardingtheEMU economies,othercountriesthatwould bemembersof theEMU, USA andJapan,in orderto follow theevolutionof theEMU in aworld-widecontext. Importantfinancial and economicparametersare recordedandanalysedmonthly, quarterly, andannually, e.g.:Reservesandassets(gold, foreignexchange,other);Liabilities; Stockmarket indexesof the EMU, eachcountryseparatelyandthemajorworld indexes(Dow JonesEURO STOXX, S&P500– USA, Nikkei225–Japan);Interestrates;ExchangeratesEuro/US$,Euro/JY; Governmentbondyields(2, 3, 5, 7 and10years);Index of consumerprices;Industryandcommodityprices;GDP; Employment/unemployment; Saving, deficit/surplusratio (asa % of GDP);Grossnominal consolidatedebt (as a % of GDP); Balanceof payments(goods,services,income,capitalaccount).

Of a particular interest is the analysisof the EMU as a dynamic cluster ofeconomiesin termsof volatility, variations,change,tendencies,andprediction(e.g.,monthly, quarterly, yearly).Therearesmallersub-clustersthatevolvewith theeco-nomicdevelopmentof differentgroupsof Europeancountriesandworld economiesthatshouldbealsomodelledandpredictedin relationto theEMU cluster. All theseclustersmove quickly in a dynamicallychangingproblemspace,thusmakingtheproblemof their predictionandrisk analysisextremelydifficult.

Theproblemthis paperis dealingwith asa casestudy, canbedescribedasriskanalysisof theEMU system.Here,moredetailsaregiven.

With the EMU in effect, countriessharingthe Euro as a commoncurrencyshouldovercomethe risk of currency criseswithin the Euro area.However, theEuropeanmonetaryunificationhasnot ruledout possibleepisodesof financial in-stability in Europe.TheMaastrichtTreatyimposesrigid constraintson public bud-getdeficits.Theseconstraintsareaimedat preventinganexcessive debtburdenonnationalgovernments,which couldleadto a weaker Euro.On theotherside,EMUgovernmentscould put pressurein order to easesuchconstraintsin the presenceof externalshocks,suchasthecrisis in theBalkans.Moreover, Europeanfinancialmarketsarenot immunefrom shocksoriginatingin theworld economy.

In anextremescenario,risk of unilateralwithdrawal by weaker membercoun-tries (otherwisecalledbreakaway risk) cannotbe excludeda priori, sincethe po-litical costsassociatedwith respectof rigid fiscal andmonetaryconstraintsin ananchoredregime could make withdrawal imperative. Any withdrawal would be adisruptiveevent,anticipatedand/orfollowedby instabilityandcrashesin creditandassetmarkets.Credibility of EMU membershipwill beassessedandpricedby finan-

cial markets.In theEMU, expectationsof breakaway, unlikeexpectedrealignmentsor withdrawalsin theExchangeRateMechanismoperatingfrom 1979to 1998undertheEuropeanMonetarySystems,will nolongertranslateinto wider interestratedif-ferentialamongcurrencies,but into variationof creditspreadsappliedto sovereigndebt from differentcountries.Holdersof financial assetswill beara new sort ofmacrorisk, which will be differentfrom plain currency risk andmoredifficult toidentify andmeasure.Studiesoncurrency crises(e.g.[6]) mustbereinterpretedandextendedto thenew context. Earlywarningsystemsusedby centralbanksandspec-ulators,fedwith signalsof realandfinancialdis-equilibrium,mustberedesigned.

Thegoalof this projectis to developa computationalmodelfor analyzingandanticipatingsignalsof abruptchangesof volatility in financialmarkets.The sys-temwill beaimedat assessingthepossibilityof speculativeattacksagainstspecificEMU membercountries,prospective EMU membersor theEMU areaasa whole.Potentialusersof thesystemincludemonetaryauthorities,assetmanagers,traderson money, debt,currency andstockmarketsandcorporatefinancialmanagers.

Theconceptualmodelunderlyingthecomputationalmodelwill bederivedfromarepresentationof financialmarketsascomplex dynamicsystems,whosestochasticbehavior is influencedby exogenousshocksandendogenousuncertainty, the lattercausedby interactionamongmarketparticipants(degreeof consensusandtendencyto crowd behavior). Inspirationfor this approachcamefrom a paperby TonisVaga([50]). Thesystemwill befed with informationfrom differentsources,namely:- macroeconomicandmacro-financialindicators,suchasthe realexchangerateofthe Euro againstUS Dollar andJapaneseYen, inflation differentials,Governmentdeficit,aggregateliquidity andsolvency measures(debt/assetratio,reserve/debtra-tio);- risk spreadon debtsecuritiesissuedby sovereignandprivateborrowersin EMUcountries;- risk appetiteof investorsin securities,measuredonthebasisof correlationbetweenreturnsin “risky” and“safe” markets(risk appetiteis highwhenriskier marketsarerallying versus“safe” marketsandthecorrelationis highly positive);- returnsandhistoricalvolatility in financialmarkets(stock,currency, bond,money,derivatives);- signalsof trend,reversalandchangeof regimefrom technicalanalysisof financialprices(moving averages,resistanceandsupportlevels,relative strengthindicators,etc.);thesesignalswill serveasproxy variablesfor endogenousuncertainty;- implied volatility in option markets and expecteddistributions extractedfromthem;- recentepisodesof instability in other currency areasthat canexert a contagioneffecton theEMU area.

The logic of thesystemwill bedesignedasanextensionof existing event riskmodelsappliedto foreignexchangemarkets([45]). Thesystemwill be testedon asetof recentepisodesof marketcrash,andthenextendedtakingcareof uniquefea-turesof thenew EMU monetaryregime.Thesystemwill producearich informativeoutput,consistingof descriptivereportsandwarningsignals.

Firstly, thesystemwill provide anintelligent interfaceto informationcurrentlyanalyzedby economistsandtraders.Userswill beableto navigatethrougharich setof economicandfinancialdatapresentedin tablesandgraphs.Thepresentationwillfocusonphenomenapertainingto theeconomicperformancein theEMU area,em-phasizingdivergencesamongcountriesandsustainabilityof Maastrichtconstraintsbothat thenationalandtheEMU level.

Secondly, thesystemwill providesignalsandindicatorsreflectingthelikelihoodof a crashin EMU financialmarkets.An extensive set of symptomsof financialfragility will be monitoredin credit, bondandstockmarkets.New eventswill becheckedagainsttypical patternsof evolutionof financialcrises.

Thesystemwill provide a valuablesupportto analystsanddecisionmakersintwo ways:(1) selectingrelevantinformationto besubsequentlyanalyzedby humanexpertsand(2) extractingandsynthesizingsignalsfrom a vastarrayof informationsources.

4 Collecting Relevant Data for Risk Analysis on theEMU. The TrentoFinancial Data Dictionary

Thedatacollectionis animportantpartof theresearchproject,becausetheresultsandthe reliability of the hybrid systemdependcrucially on the quality of the rawdata.In factahugeamountof datais necessaryto monitortheso-calledbreakawayrisk in the EMU, in orderto detectthe solidity of the EMU system,the degreeofasymmetryandthepotentialexternalshocks.

Hugeamountof datais beingcollectedthatincludesdifferentlevel of informa-tion: macroeconomicinformation;financialdata.Macroeconomicdatais availablefrom many sourcesincluding EUROSTAT, the EuropeanCentralBank MonthlyBulletin, OECSand IMF. A vast amountof macroeconomicdata is madeavail-ablethroughDatastream.Financialdatais availablefrom differenton-linesources,suchasDataStreamandReuter. Differenttime-scalesof dataarepresentin thedatarepository(e.g.,yearly, quarterly, monthly, daily, irregulartime intervals,etc)

It is not easyto dealwith this relevantamountof datawithoutpreparingat leasta generalinitial structure.For this reasonwe have built two main prospects:the“sourcesdictionary”andthe“datadictionary”.

Thefirst prospecthasathreedimensionalstructure.In thex-axiswehaveplacedthecountriesrelevantfor theEMU risk analysis;we have chosentheelevenpartic-ipatingcountries,thepotentialentrants,thebig world players,andsomeemergingcountriesto proxy for any contagioneffect. In the y-axiswe have setall the typesof datawhich couldbeusefulfor theresearchproject.Thethird dimensionis con-cernedwith thesourceof thegatheredinformation;every singlevariablerelatedtoeveryinvolvedcountryhasbeencollectedby aspecificsource.Thisaspectis impor-tantto evaluatemainly thereliability of thedata,but alsothedegreeof homogeneityin the dataset.In fact,choosingthe datasourcewhich coversthemostpartof theinvolvedcountriesallows to achievehigh degreeof similarity in themodellingpro-cedureandin theupdatingtiming andmethod.Consideringthespecificpurposeof

theanalysis,we rely uponofficial statisticsfrom Eurostatfor mostof the requireddata.

Thesecondprospect,named“datadictionary”,is formedasatablewith columnsreportingthespecificfeaturesof eachdataseries;the mostimportantonesarethefirst availabledate,thefrequency of collection,andthemnemoniccode,whichis analphanumericexpressionusefulto automatethe informationdownloadingprocess.We have distinguishedtwo broadcategoriesof datathat arebeingcollected.Thefirst level of information is concernedwith macroeconomicvariables;the secondlevel is morespecificandregardsfinancialmarket data.A third level of informa-tion, connectedwith qualitative knowledge,for examplethe political situationorparticularnews, is not formally consideredin this first modelimplementation.Thetypical featureof thefirst groupof variables– macroeconomicdata– is thelow fre-quency of collection,which is monthly, quarterlyor evenyearly, dependingon thespecificsector;anotherimportantfeatureis thepotentialvarietyof sourcesfor thesamekind of data.A third propertyis thepotentialdifferentcalculusandupdatingprocedurefor thesamesortof indices.Themostrelevantmacroeconomicdataaregenerallyavailableeitherashistoricaltimeseries,or asaconsensusforecast.

The financialmarket variablesarecollectedmore frequently, even on a dailybasis,andareusuallyreleasedofficially by theexchanges.In ourresearchprojectwehave tried to considernot only thepastevolution of thevariousfinancialseries,butalsothemarket expectationsimplied in option prices;thereis a growing literaturedealingwith thisaspectwith two mainapproaches.Thesimplerapproachis relatedto the calculationof implied volatility at differentmonetarydegreesasa forecastfor expectedvolatility. In the secondapproachthe underlyingrisk neutraldensityfunction is extractedfrom option market prices;it is very usefulsubsequentlytomonitortheevolutionof thevariousmomentof theprobabilitydistribution.

5 The EMU-HIDSS: Ar chitecture and Functionality

5.1 A GeneralFramework of the EMU-HIDSS

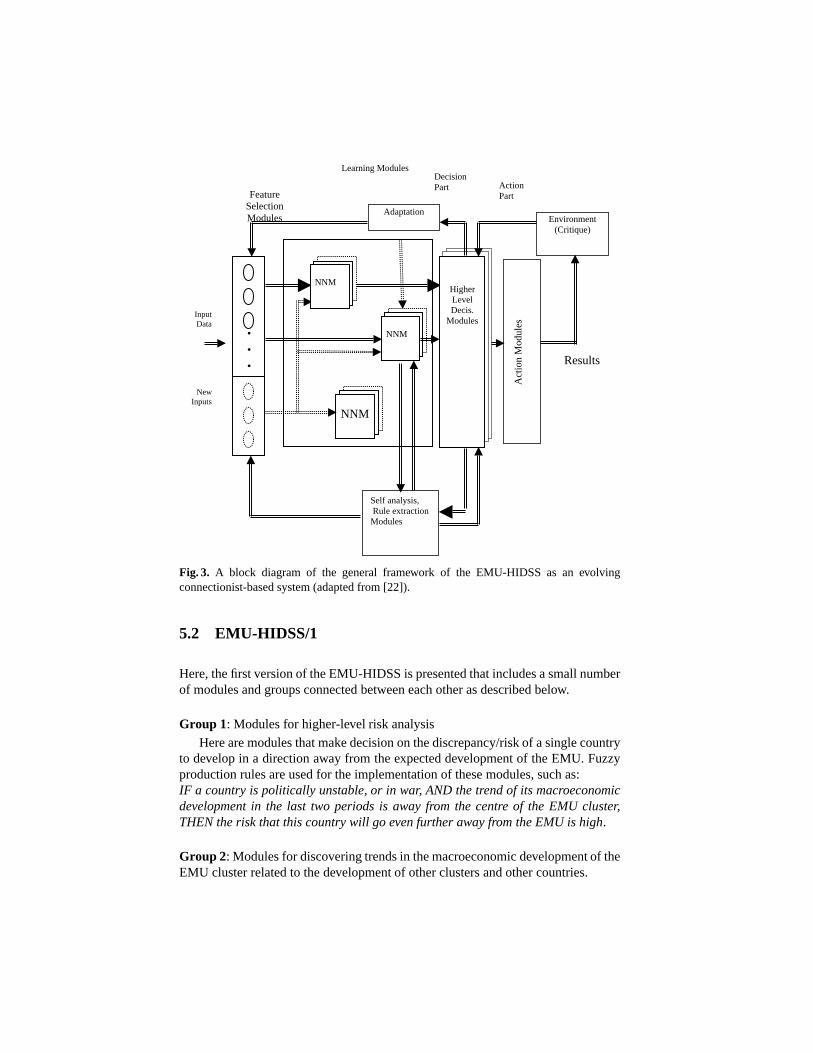

Hereapreliminarydesignof theEMU-HIDSSis presented(seeFig.3).It is amulti-level, multi-modularstructurewheremany neuralnetwork modules(denotedasNNM), rule-basedmodulesandothermodulesareconnectedwith inter-, andintra-connections.EMU-HIDSS doesnot have a clear multi-layer structure,but rathera modular, “open” structure.It is an evolving hybrid connectionist-basedsystem([22]).

Themainpartsof theEMU-HIDSSaredescribedbelow.(1) Featureselectionpart.It performsfiltering of theinput information,featureex-tractionandforming input vectors.Typical featuresextractedfrom the input dataeitherin anon-linemodeor from thealreadystoreddatain filesare:

� Basicstatisticalparameters;� Probabilitydistributionandclusterinformation;

� Moving averages;� Wavelettransformations;� PowerspectrumandFFT frequency characteristics;� Main frequencies;� Lyapunov coefficients;� Fractaldimensions;� First andsecondderivatives;� Skewnessmeasures.

Theabove transformationsareperformedin thepre-processing(featureextraction)modulesof thesystemappliedto certaininformationinputstreams.

(2) Learningandmemorypart,whereinformation(patterns)arestored.It is amulti-modular, evolving structureof neuralnetwork modules(NNM). Thesemodulescanbebuilt with theuseof MLP, SOM,ESOM,FuNNs,EFuNNs,etc.Thereareseverallevelsof processingin thesemodulesin termsof timing:

� Daily updatedmodules,thesearemodulesthat dealwith daily financialpre-diction anddaily input data,e.g.MIB30 prediction,Euro/US$exchangerateprediction,etc.� Weeklyupdatedmodules� Monthly updatedmodules� Yearlyupdatedmodules,e.g.longtrendprediction,andin termsof theproducedresultsthatarepassedto thenext level higherdecisionmodules:� Onedayaheadpredictionresults� Monthly predictionresults� Yearlypredictionresults� Longertermpredictedresults

Thispartof thesystemwill includeseveralmodulesto dealwith differentlevelsandscalesof predictionfor eachof theEuropeancountries,thebig economiesandtheemergingeconomies.Differentmoduleswill dealwith:

� Predictingvalues(differencesin values)� Predictingshorttermtrends,e.g.oneweektrendif a stockvaluewill begoingup extremelyhigh,or moderatelydown.� Predictinglong term trends,e.g.one-yeartrendif a stockvaluewill be goingup extremelyhigh,or critically down.

(3) Higher-level decisionpart that consistsof several modules,eachtaking deci-sion on a particularproblem.The modulesreceive input from the NNMs, inputsform othervariablesin thedata,qualitativeinput from users,andmakedecisionsonpossiblecritical situationsthat might occur in the EMU. Thesemodulescansenda feedbackto the NNM andthe featureextractionpart of the systemin termsofrequiring more information,different scenariosto be explored,different featuresextracted,etc.The modulesherearemainly rule basedwith theuseof production

systems,flat fuzzy rules,FuNNsandEFuNNsthat canrepresentboth fuzzy rulesanddata.Thereareseveralgroupsof in this part that interactbetweeneachother,for example:

(a)A groupof modulesthatdealwith a globalrisk evaluationproblems,e.g.:� Moduleevaluatingthedegreeof stability in theEMU;� Moduleevaluatingthedegreeof symmetry/ asymmetrybetweentheeconomies

within theEMU;� Moduleevaluatingthepolitical sustainabilityin theEMU;� Moduleevaluatingthedegreeof suitabilityof a new countryjoining theEMU;� Moduleevaluatingthedegreeof instability in theEMU basedon externalfac-tors(USA; Asia,Japan,India,Russia,wars,etc.)� others

(b) A group of modulesthat deal with importanteconomicfactorsand theirresultscanbeusedeitherseparately, or by themodulesof type(1) above:� GDP� Rateof unemployment� Internaldebt� Externaldebt� Shorttermglobaleconomictrends� Long termglobaleconomictrends� Solvency ratioof households,business,banksandgovernment� Indicationof reallocationof investmentsby globalassetmanagers� Sharpmovementsof acertaincommodityin a shortor in a long termpattern� Sharpfalls in shorttermor long termtrends� Evaluatingand indication of consecutive phaseshappeningover a period of

time, for exampleaneconomyhasbeenin threeconsecutivephasesthatsignala critical situationfor this economyandwill beinfluentialfor theEMU

(4) Action modules,thattaketheoutputfrom thehigher-leveldecisionmodulesandproduceoutput resultsor sendoutput (control) information in an on-line or in anoff-line modeto institutionsthatshouldbealertedon a critical situation.

(5) Self-analysis,and rule extractionmodules.This part extractscompressedab-stractinformationfrom theNNMs andfrom thedecisionmodulesin differentformsof rules,abstractassociations,etc.HereFuNNs’andEFuNNs’ruleextractioncapa-bilities will beutilised.

Initially theEMU-HIDSSwill haveapre-definedstructureof modulesandveryfew connectionsbetweenthemdefinedthroughprior knowledge.Gradually, thesys-temwill becomemoreandmore“wired throughself-organisation,andthroughcre-ationof new NNM andnew connections.

Eachof themodulesin thesystemarebuilt, or automaticallygeneratedfrom theagentmodulesavailablefrom RICBIS,e.g.:dataprocessingmodules(e.g.normal-isation,moving averages,FFT, filtering, wavelet transformation,fractal analysis,chaosanalysis,etc); productionrules in JESS;fuzzy inferencerules,MLP, SOM,ESOM,FuNNs,EFuNNs,Hidden-Markov Models,etc.

Self analysis, Rule extractionModules

Act

ion

Mod

ules

•

•

•

ActionPart

DecisionPart

FeatureSelectionModules

Learning Modules

InputData

NewInputs

Environment(Critique)

HigherLevelDecis.

Modules

Adaptation

NNM

NNM

NNM

Results

Fig.3. A block diagramof the generalframework of the EMU-HIDSS as an evolvingconnectionist-basedsystem(adaptedfrom [22]).

5.2 EMU-HIDSS/1

Here,thefirst versionof theEMU-HIDSSis presentedthatincludesasmallnumberof modulesandgroupsconnectedbetweeneachotherasdescribedbelow.

Group 1: Modulesfor higher-level risk analysis

Herearemodulesthatmakedecisiononthediscrepancy/risk of asinglecountryto developin a directionaway from theexpecteddevelopmentof theEMU. Fuzzyproductionrulesareusedfor theimplementationof thesemodules,suchas:IF a countryis politically unstable, or in war, AND thetrendof its macroeconomicdevelopmentin the last two periodsis away from the centre of the EMU cluster,THENtherisk that this countrywill go evenfurther awayfromtheEMU is high.

Group 2: Modulesfor discoveringtrendsin themacroeconomicdevelopmentof theEMU clusterrelatedto thedevelopmentof otherclustersandothercountries.

Herethe conceptof EMU clusteris introducedbasedon the EMU aggregateddataprojectedfrom a multidimensionalspaceinto a two (or a three)dimensionaltopologicalmapwith the useof self-evolving, self-organisingmaps.The vectorsof the used8 parametersfor the last 5-6 yearof all the EMU countries,the otherEuropeancountries,someemergingmarketcountries,andalsotheUSA andJapan,aremappedinto oneSOM or ESOM.

The neuron(the point in the two-dimensionalmap space)wherethe current-periodEMU vectoris projectedis consideredto be thecenterof theEMU cluster.Theclusterincorporatesall pointswherethedataof the individual EMU countriesaremapped.Theform of theclusterandits movementfrom oneperiodto thenextonecanbe observedon the mapsandthe informationwill be quantifiedbasedonthedistancebetweenthepoints.Theshapeof theEMU clusterandits dynamicscansuggestfurtherpolitical andeconomicdevelopmentin theEMU.

Themovementof thecenterof theEMU clustercanbecomparedwith themove-mentof thepointswherethedifferentcountriesaremapped.A quantitativemeasureon thedifference(thedistancein thetopologicalspace)betweendifferentcountriesfrom theEMU, andoutsidetheEMU, is evaluatedthat is usedasa separateinfor-mationresultsaswell asan input informationto thehigher- level decisionmakingmodules.

Different clustersare formed on a SOM: the EMU cluster; the emergingeconomiescluster(e.g.,Poland);theclusterof thenon-Europeandevelopedcoun-tries (e.g.theUSA, Japan,Canada,Australia,New Zealand);theclusterof under-developedcountries;theclusterof thedevelopednon-EMUcountries(e.g.theUK);theclusterof thedevelopingnon-EMUcountries(e.g.,Bulgaria,Romania).A vectorof fuzzy membershipdegreesto which eachcountrybelongsto eachof theclustersis calculatedandtracedover time.

Modulesfrom group2 coverdifferenttime-scales:annualmacroeconomicmap-ping,quarterlymacroeconomicmapandmonthlymacroeconomicmapping.

The following variablesdescribethe macroeconomicstateof a country in agivenperiodandall thevectorsfor all therelevantperiods(years,quarters,months)areusedin theunsupervisedtraining:GDP, debt,deficit, inflation rate,interestrate,unemployment,balanceof payment,productiongap.

Group 3: Modulesfor evaluatingtrendsin theexchangerateEuro/US$Themainmoduleherepredictsthetrendof theexchangeratebetweenEuroand

the US dollar, but othermodulesdealwith nationalcurrenciesthatarenot part oftheEMU.

The following 10 input variables for example can be used to predict therate R(t+1) of Euro/US$,wheret is the currentperiod: R(t), R(t-1), Euro/JY(t),Euro/JY(t-1),ratio inflation ratein EMU/inflation ratein theUSA for both (t) and(t-1) periods;ratio interestratesin EMU/interestratesin USA for both(t) and(t-1)periods;ratioGDPin EMU/GDPin USA for both(t) and(t-1) periods.

Two typesof modelsareused- FuNNsandEFuNNs.Thetwo modelsusediffer-enttechniquesfor extractingrulesandthemeaningof theextractedrulesis different.

In therulesextractedfrom FuNNstheconditionandconclusionelementshave im-portancefactorsattachedto thempointingto theimportanceof thedifferentpartsofa rule. Therulesextractedfrom EFuNNsarealsofuzzy, but they point to theclus-tersin the input andtheoutputspacethatarelinkedtogetherin the rule. EFuNNsrequirelesstime for trainingandcanbeupdatedvery quickly with new datain anon-linemode.

Thepredictedtrendsof theexchangeratescanbeusedeitherasseparateoutputresults,or asinput valuesfor the higher-level decisionmodulesfor bothquarterlyandmonthlytrendsprediction.

Group 4: Modulesfor evaluatingtrendsin majorstockindexesandstockmarketsHereamapof thedifferentstatesof astockmarketaccordingto [50] is created.

Thetransitionbetweenrandomwalk state,chaoticstate,or a coherentstatewill bemodelledby the useof differenttechniques,that include:hiddenMarkov models;evolving fuzzyneuralnetworksEFuNNs;productionrules.

Anothermodulefrom thisgroupevaluatesthevolatility of monthlytrendsin theDow JonesEuroSTOXX50 index (DJE).Othermodulesevaluateweeklytrendsanddaily values.Thefollowing14inputvariablescanbeusedtoevaluatetheDJE

������ ,

where�

is thecurrenttimeperiod:DJE����

; DJE��������

; ����������� ���� ; ����������� ��� ��! ; Euro/US$

���� ; Euro/US$

�����"�! ; Euro/JY

���� ; Euro/JY

���#�$�� ; Inflation rate

���� ;

Inflation rate�����%�!

; GDP����

; GDP��������

; Interestrate����

; Interestrate��������

.Othermodulesevaluatethetrendsin majorEuropeanstockmarkets,suchasthe

ItalianMIB30 index (Milano).

6 Implementation and Curr ent ExperimentalResultswith the EMU-HIDSS

Theimplementationof theconceptualmodelof theEMU-HIDSSfrom section5 isaverycomplicatedtaskanda long-termobjective.Here,differentmodulesfrom theEMU-HIDSS/1conceptualmodelthatfollow thegeneraldescriptionandthelogicallinks presentedin theprevioussection,aredevelopedandresultsareexplained.

6.1 Group 1 Module for Statistically-BasedHigher-Level RiskAnalysis

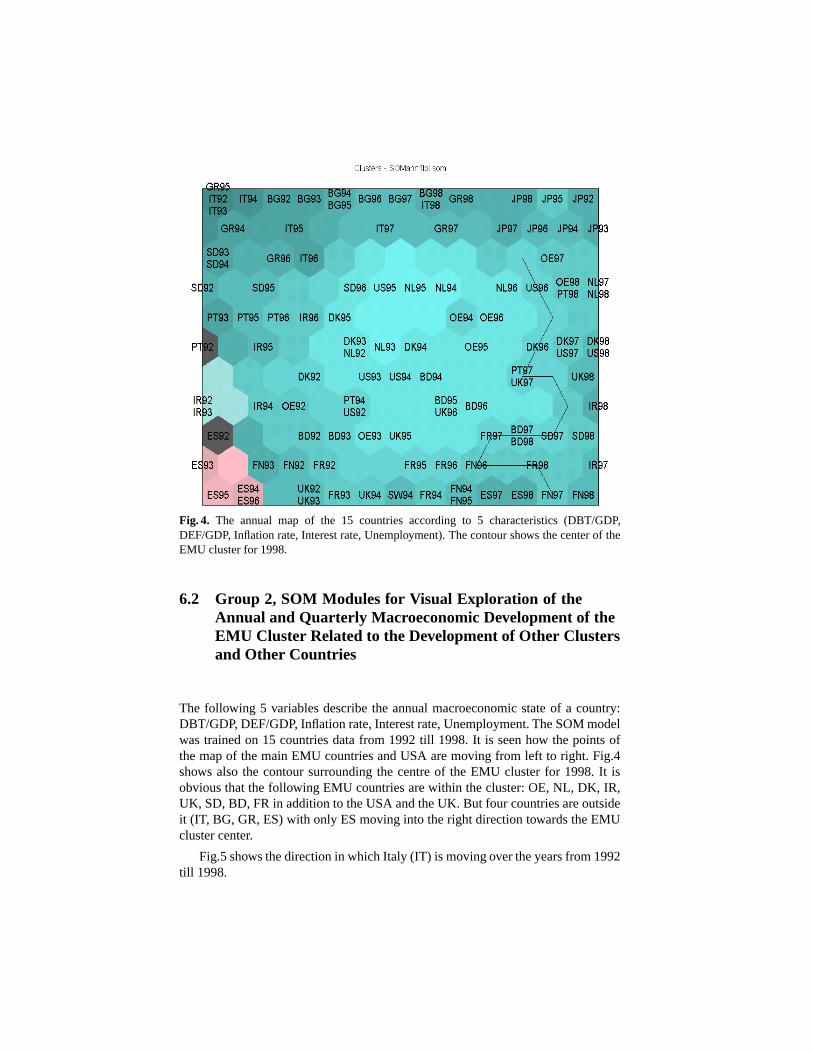

Thismoduletakesdynamicinput informationfrom theclustermapsof thepreviouslevel of processingandcalculatesthe Euclideandistancebetweeneachcountry’srepresentationvectorandthecenterof theEMU clusteroverconsecutiveperiodsoftime(years,quarters).In thiswaythecountriesthataremoving awayfrom theEMUclusterareindicatedalongwith thespeedatwhichthey aremoving.For examplethedistancebetweenthe clustercenterof the main EMU countriesandItaly for 1997canbe evaluatedas3.8 andfor 1998 as3.3, while the samedistancebetweenITandJPfor thesameperiodscanbeevaluatedas1.2and0.7respectively (seeFig.4).

Fig.4. The annual map of the 15 countriesaccordingto 5 characteristics(DBT/GDP,DEF/GDP, Inflation rate,Interestrate,Unemployment).Thecontourshows thecenterof theEMU clusterfor 1998.

6.2 Group 2, SOM Modules for Visual Exploration of theAnnual and Quarterly MacroeconomicDevelopmentof theEMU Cluster Relatedto the Developmentof Other Clustersand Other Countries

The following 5 variablesdescribethe annualmacroeconomicstateof a country:DBT/GDP, DEF/GDP, Inflationrate,Interestrate,Unemployment.TheSOMmodelwastrainedon 15 countriesdatafrom 1992till 1998.It is seenhow the pointsofthemapof themainEMU countriesandUSA aremoving from left to right. Fig.4shows alsothe contoursurroundingthe centreof the EMU clusterfor 1998.It isobviousthat thefollowing EMU countriesarewithin thecluster:OE, NL, DK, IR,UK, SD,BD, FR in additionto theUSA andtheUK. But four countriesareoutsideit (IT, BG, GR,ES)with only ESmoving into theright directiontowardstheEMUclustercenter.

Fig.5showsthedirectionin whichItaly (IT) is moving overtheyearsfrom 1992till 1998.

Fig.5. Iso-graphsof the15countriesannualdevelopmentmapandthedirectionof thedevel-opmentof Italy.

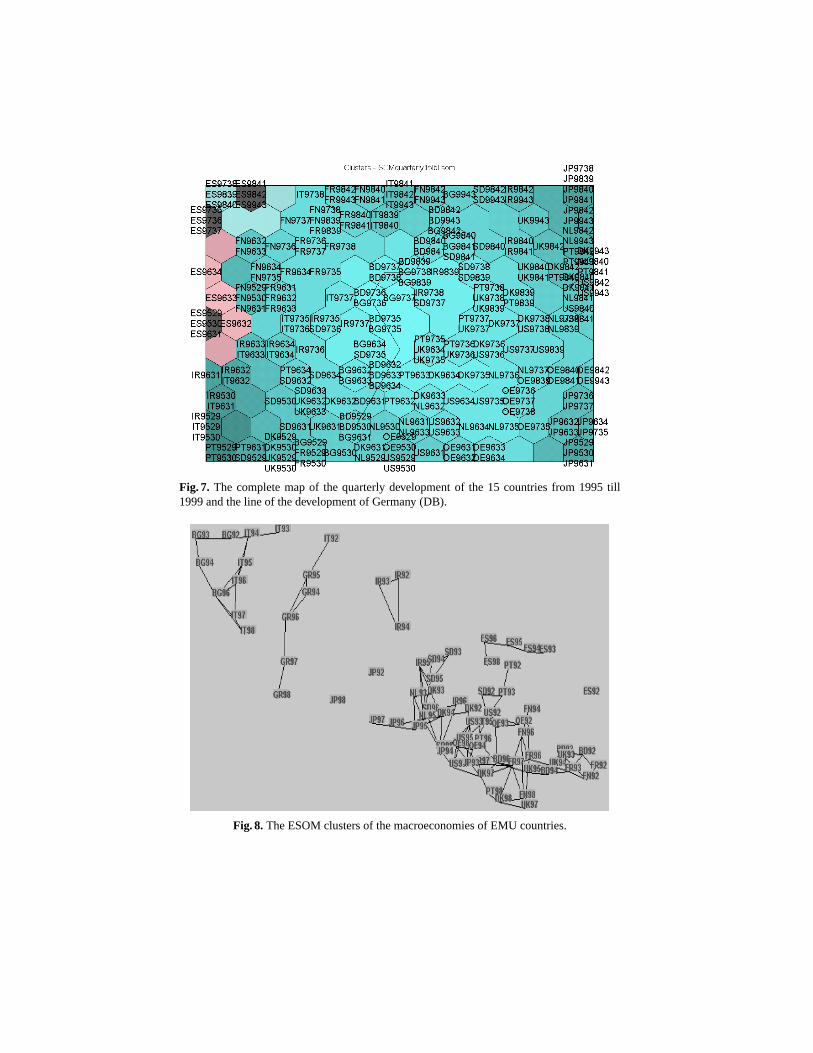

AnotherSOM moduleis trainedon quarterlydataof the following threevari-ables:Inflation rate,Interestrate,Unemployment.Fig.7shows themapandthelineof thequarterlydevelopmentof Germany (BD).

TheSOM modulesaresuitablefor visualexplorationasSOMsprovidewith anefficienttool for vectorquantisation,i.e.turningann-dimensionalspaceusuallyintotwo dimensionalspacepreservingthesimilarity betweentheinputvectorsacrossalltheattributesastopologicaldistancebetweenpointsof themap.SOMshave somedifficulties,mainly: (a) they haveafixedstructure;(b) they cannot toleratemissingvalues;(c) learningusuallytakesa long time.

In orderto overcomethelimitationsof theSOMs,hereevolving SOM modulesarealsoused.

6.3 Group 2, ESOM Module for Dynamic Mapping ofMacroeconomicAnalysis

Anotherannualmapis evolvedwith thesamedatasetasin theSOM modulesandis shown in Fig.8.Themapis first clusteredusingESOMalgorithm,andthenpro-jectedonto a two-dimensionalplanefor visualisationusingSammon’s algorithm.Henceboth clusteringanddatastructureareavailablewithin the map.The layoutof labellednodesis very similar to that of Fig.4, but the ESOM mapgivesmore

(a)

(b)

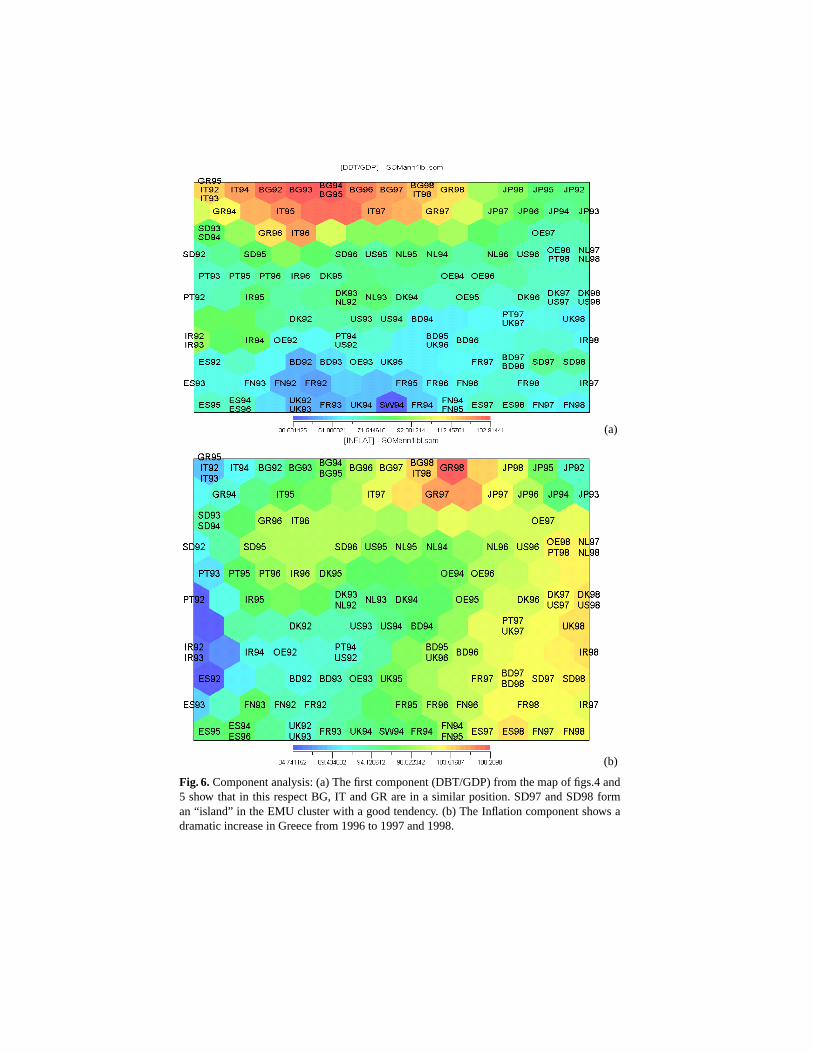

Fig.6. Componentanalysis:(a) Thefirst component(DBT/GDP)from themapof figs.4and5 show that in this respectBG, IT andGR arein a similar position.SD97andSD98forman“island” in theEMU clusterwith a goodtendency. (b) The Inflation componentshows adramaticincreasein Greecefrom 1996to 1997and1998.

Fig.7. The completemapof the quarterlydevelopmentof the 15 countriesfrom 1995 till1999andtheline of thedevelopmentof Germany (DB).

Fig.8. TheESOMclustersof themacroeconomiesof EMU countries.

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 10

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

OE98

BG98

FN98

FR98BD98

IR98

IT98

NL98

PT98ES98

DK98

UK98

GR98

SD98US98

JP98

OE97 BG97

FN97

FR97

BD97

IR97

IT97

NL97

PT97 ES97

DK97

UK97

GR97

SD97

US97

JP97OE96

BG96

FN96

FR96

BD96

IR96

IT96

NL96

PT96

ES96

DK96

UK96

GR96

SD96

US96

JP96

OE95

BG95

FN95FR95

BD95

IR95

IT95

NL95

PT95

ES95

DK95

UK95

GR95

SD95

US95

JP95

OE94 BG94

FN94FR94

BD94

IR94

IT94

NL94

PT94ES94

DK94

UK94

GR94SD94

SW94

US94

JP94

OE93

BG93

FN93

FR93

BD93

IR93

IT93

NL93

PT93

ES93

DK93

UK93

SD93

US93

JP93OE92

BG92

FN92

FR92

BD92IR92

IT92

NL92

PT92

ES92

DK92

UK92

SD92

US92

JP92

1

2

34

5

67

8

9

1011

12

13

14

15

16

17

18

19

2021

22

23

24

Distribution of Rule Nodes in Input-Input Space (Training )

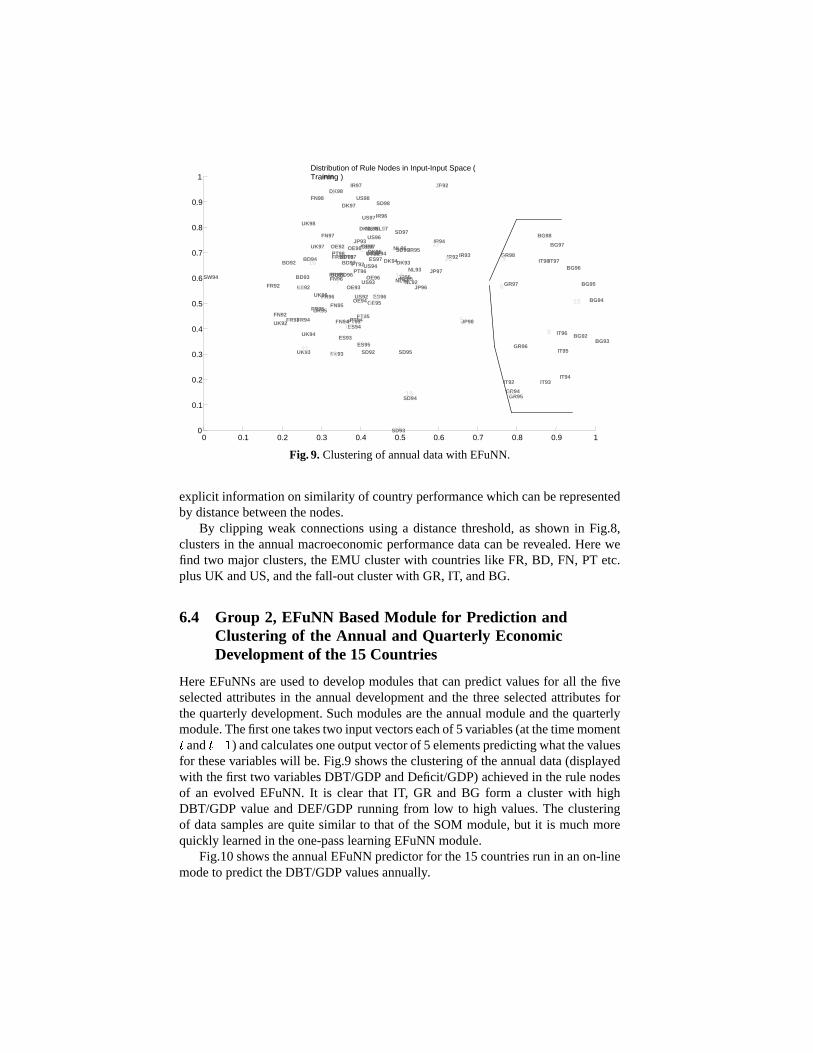

Fig.9. Clusteringof annualdatawith EFuNN.

explicit informationonsimilarity of countryperformancewhichcanberepresentedby distancebetweenthenodes.

By clipping weak connectionsusing a distancethreshold,asshown in Fig.8,clustersin the annualmacroeconomicperformancedatacanbe revealed.Herewefind two major clusters,the EMU clusterwith countrieslike FR, BD, FN, PT etc.plusUK andUS,andthefall-outclusterwith GR, IT, andBG.

6.4 Group 2, EFuNN BasedModule for Prediction andClustering of the Annual and Quarterly EconomicDevelopmentof the 15 Countries

HereEFuNNsareusedto developmodulesthat canpredictvaluesfor all the fiveselectedattributesin the annualdevelopmentandthe threeselectedattributesforthequarterlydevelopment.Suchmodulesarethe annualmoduleandthequarterlymodule.Thefirst onetakestwo inputvectorseachof 5variables(atthetimemoment�

and�&�'�

) andcalculatesoneoutputvectorof 5 elementspredictingwhatthevaluesfor thesevariableswill be.Fig.9shows theclusteringof theannualdata(displayedwith thefirst two variablesDBT/GDPandDeficit/GDP)achievedin therule nodesof an evolved EFuNN. It is clear that IT, GR and BG form a clusterwith highDBT/GDP valueandDEF/GDPrunning from low to high values.The clusteringof datasamplesarequite similar to that of the SOM module,but it is muchmorequickly learnedin theone-passlearningEFuNNmodule.

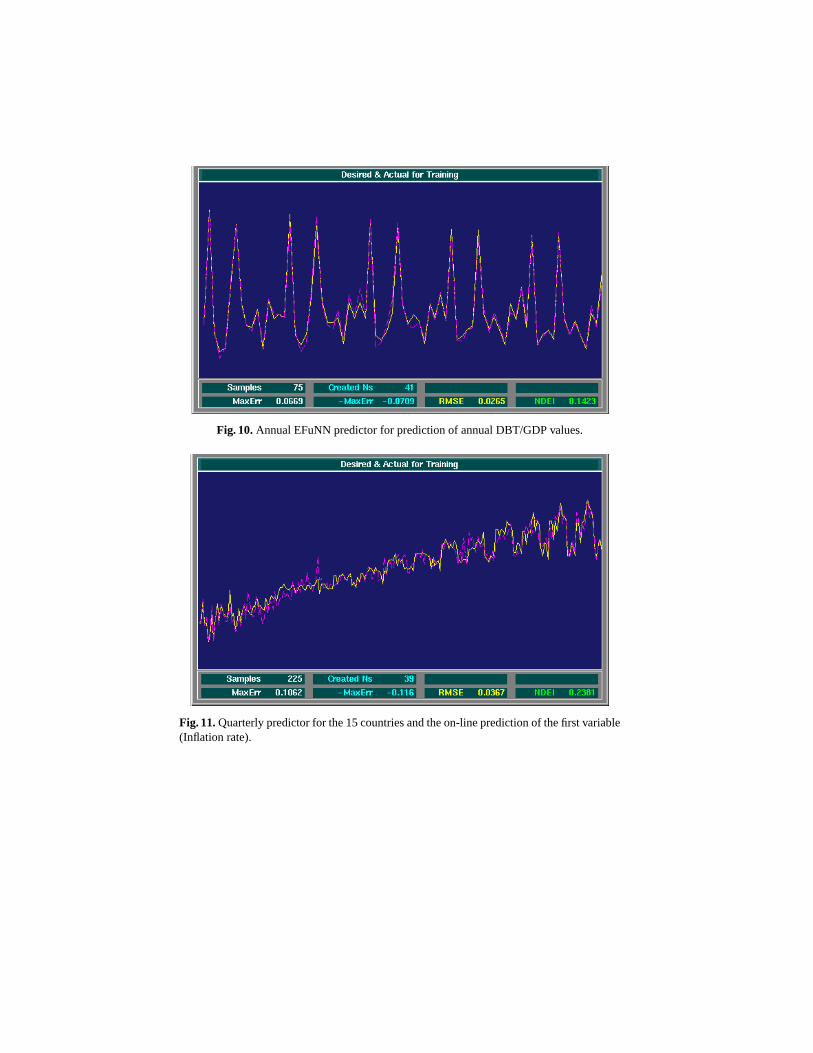

Fig.10shows theannualEFuNNpredictorfor the15countriesrun in anon-linemodeto predicttheDBT/GDPvaluesannually.

Fig.10.AnnualEFuNNpredictorfor predictionof annualDBT/GDPvalues.

Fig.11.Quarterlypredictorfor the15countriesandtheon-linepredictionof thefirst variable(Inflation rate).

Rulescanbeextractedfrom EFuNNsthatarefuzzy, andthey pointto theclustersin theinputandtheoutputspacethatarelinkedtogetherin therule.EFuNNsrequirelesstime for trainingandcanbeupdatedvery quickly with new datain anon-linemode.

Fig.11shows the 15 countriesquarterlypredictor, which canpredictvaluesofthethreeselectedvariablesInflationrate,Interestrate,Unemploymentfor any of thecountriesin thefollowing quartergiventhedatafor thecurrentandpreviousquarterandalsothe annualDBT/GDP andthe previous yearDBT/GDP areentered.Thefirst outputvariableis shown aspredictedin anon-linemode.Thesystemimprovesits predictionover time.

6.5 Group 4, EFuNN Module to Evaluate Trendsin theExchangeRateEuro/US$

Themainmoduleherepredictsthemonthlytrendof theexchangeratebetweenEuroandtheUS dollar. Thefollowing 10 input variablesareusedin orderto predicttherate ( ���&)�! of Euro/US$,where

�is thecurrentperiod: ( ���� , ( �����*�! , Euro/JY

���� ,

Euro/JY�����+�!

, ratio inflationratein EMU/inflationratein theUSA for both����

and���,�-�! periods;ratio interestratesin EMU/interestratesin USA for both

���� and��������

periods;ratioGDPin EMU/GDPin USA for both����

and��������

periods.

6.6 Group 4, EFuNN Module to EvaluateTrendsin the DJE501Major Stock Index

This moduleevaluatesthemonthlytrendsin theDow JonesEuroSTOXX50 index(DJE).Thefollowing 14 inputattributesareusedto evaluatetheDJE

���.%�! , where�

is the currenttime period:DJE����

; DJE���/�0�!

; ����������� ���� ; ����������� ���1�0�! ;

Euro/US$����

; Euro/US$�����"�!

; Euro/JY����

; Euro/JY���#�$��

; Inflation rate����

; In-flation rate

���#�%�! ; GDP

���� ; GDP

�������� ; Interestrate

���� ; Interestrate

���#���� .

Besidesthe moduleslisted above, several other modulesare currently underdevelopment.

7 Conclusionsand Dir ectionsfor Further Research

A framework of hybrid intelligent decisionsystemis presentedin the paper. Byapplyinga repositoryof intelligent informationprocessingmodulesimplementedin an agent-basedarchitecture,a casestudysystemEMU-HIDSS is built for riskanalysisandpredictionof evolving economicclustersin Europe.

The EMU-HIDSS is designedto be usedat different levels of analysisanddecision making about the EMU and about the relevant changesin the eco-nomic clusters of Europe and the world, that includes: the EuropeanUnionlevel; the global world economieslevel; national level; company and banklevel. Data and someof the developedmodelsare available from internetURL

http://divcom.otago.ac.nz/infosci/kel/CBIIS.html (Software- FinancialRiskAnaly-sisandPrediction).

Acknowledgements

Thiswork is supportedbyaresearchgrantof theDepartmentof ComputerandMan-agementSciences,Universityof Trento,andalsoby agrantPGSF-UOO808fundedby theNew ZealandFoundationfor Science,ResearchandTechnology(FRST).

References1. Amari, S., Kasabov, N., Eds.(1998)Brain-like ComputingandIntelligent Information

Systems.SpringerVerlag.2. Bollacker, K., LawrenceS., Giles L. (1998)CiteSeer:An autonomousWeb agentfor

automaticretrieval andidentificationof interestingpublications.Proc.of the2ndInter-nationalACM conferenceonautonomousagents.ACM Press,116-123.

3. Deboeck, G. (1999) Investment maps for emerging markets. In: N.Kasabov andR.KozmaEds.Neuro-fuzzytechniquesfor intelligentinformationsystems.PhysicaVer-lag (Springer),373-395.

4. Deng,D., Kasabov, N. (1999)Evolving Self-organizingMapandits Applicationin Gen-eratingA World MacroeconomicMap. Proc.of ICONIP/ANZIIS/ANNES’99 Interna-tionalWorkshop,Universityof Otago,7-12.

5. Deboeck,G., Kohonen,T. (1998) Visual exploration in financewith self-organizingmaps,SpringerVerlag.

6. Eichengreen,B., Rose,A., Wyplosz, C. (1995) Exchangemarket mayhem:the an-tecedentsandaftermathof speculative attacks.EconomicPolicy, 251-312.

7. Monthly Bulletin (1999)EuropeanCentralBank.8. Evolver softwarepackagefor Excel,

http://www.palisade.com/html/evolver body.html.9. Farmer, J.D.,Sidorowitch J. (1987)Predictingchaotictime series.Phys.Rev. Lett., 59,

845-848.10. Garcia,R., GencayR. (1997)Pricingandhedgingderivative securitieswith neuralnet-

worksandahomogeneityhint.TechnicalReport,Departmentof ScienceandEconomics,Universityof Montreal,Canada.

11. Goodman,R.,Higgins,C.M., et.al. (1992)Rule-basedneuralnetworksfor classificationandprobabilityestimation.NeuralComputation,14,781-804.

12. Goonatilake,S.,KhebbalS.Eds.(1995).IntelligentHybrid Systems.JohnWiley & SonsLondon.

13. Goonatilake, S.,Trelevan P. (1995)IntelligentSystemsfor FinanceandBusiness.JohnWiley & Sons.

14. Hashiyama,T., Furuhashi,T., Uchikawa, Y. (1992)A decisionmakingmodelusingafuzzy neuralnetwork. Proceedingsof the2ndInternationalConferenceon FuzzyLogic& NeuralNetworks,Iizuka,Japan,1057-1060.

15. Heskes,T.M., KappenB. (1993)On-linelearningprocessesin artificial neuralnetworks.Mathematicalfoundationsof neuralnetworks,Elsevier, Amsterdam,199-233.

16. Hutchinson,J.,Lo A., PoggioT. (1994)A nonparametricapproachto pricing andhedg-ing derivative securitiesvia learningnetworks.TheJournalof Finance,vol.XLIL, No.3,851-890.

17. Ishikawa,M. (1996)Structurallearningwith forgetting.NeuralNetworks,9, 501-521.18. Kasabov, N. (1996) Adaptableconnectionistproduction systems.Neurocomputing,

13(2-4)95-117.19. Kasabov, N. (1996)Foundationsof NeuralNetworks, FuzzySystemsandKnowledge

Engineering.TheMIT Press,CA, MA.20. Kasabov, N. (1996) Learningfuzzy rules and approximatereasoningin fuzzy neural

networksandhybrid systems.FuzzySetsandSystems,82(2),2-20.21. Kasabov, N. (1998)TheECOSFramework andtheECOLearningMethodfor Evolving

ConnectionistSystems.Journalof AdvancedComputationalIntelligence,2(6),1-8.22. Kasabov, N. (1998) ECOS:A framework for evolving connectionistsystemsand the

ECOlearningparadigm.Proc.of ICONIP’98,Kitakyushu,Japan,IOSPress,1222-1235.23. Kasabov, N. (1998)Evolving fuzzy neuralnetworks- algorithms,applicationsandbio-

logical motivation. In Yamakawa andMatsumotoEds.,Methodologiesfor theConcep-tion, DesignandApplicationof SoftComputing.World Scientific.271-274.

24. Kasabov, N. (1999)Evolving connectionistandfuzzy connectionistsystemsfor on-lineadaptive decisionmakingandcontrol. In: Advancesin Soft Computing- EngineeringDesignandManufacturing,R.Roy, T. FuruhashiandP.K. ChawdhryEds.Springer, Lon-don.

25. Kasabov, N. (1999) Evolving fuzzy neural networks for adaptive, on-line intelligentagentsandsystems.In: O. Kaynak,S.TosunogluandM.Ang Eds.RecentAdvancesinMechatronics.Springer, Berlin.

26. Kasabov, N. Fedrizzi,M. (1999)Fuzzyneuralnetworksandevolving connectionistsys-temsfor intelligentdecisionmaking.Proc.of the8th InternationalFuzzySystemsAsso-ciationWorld Congress,Taiwan,17-20.

27. Kasabov, N., Kozma,R. (1999)Multi-scaleanalysisof timeseriesbasedonneuro-fuzzy-chaosmethodologyappliedto financialdata.In Refenes,A., Burges,A. andMoody, B.Eds.ComputationalFinance1997.Kluwer Academic.

28. Kasabov, N., Kim J.S.et.al. (1997) FuNN/2- a fuzzy neuralnetwork architectureforadaptive learningandknowledgeacquisition.InformationSciences,101(3-4),155-175.

29. Kasabov, N., Kozma,R. (1997)Neuro-fuzzy-chaosengineeringfor building intelligentadaptive informationsystems.In: Intelligent Systems:FuzzyLogic, NeuralNetworksandGeneticAlgorithms. Da RuanEds.Kluwer AcademicBoston/London/Dordrecht,213-237.

30. Kasabov, N., Israel,S.,Woodford,B. (1999)Methodologyandevolving connectionistar-chitecturefor imagepatternrecognition.In: Pal,GhoshandKunduEds.SoftComputingandImageProcessing,Physica-Verlag(Springer)Heidelberg, accepted.

31. Kasabov, N., Song,Q. (1999)Dynamic,evolving fuzzyneuralnetworkswith ‘m-out-of-n activationnodesfor on-lineadaptive systems.TechnicalReportTR99-04,Departmentof InformationScience,Universityof Otago.

32. Kasabov, N., WattsM. (1997)Geneticalgorithmsfor structuraloptimisation,dynamicadaptationandautomateddesignof fuzzy neuralnetworks. In: Proc.of theInter. Conf.onNeuralNetworks(ICNN97), IEEE Press,Houston.

33. Kasabov, N., Watts,M. (1999)Spatial-temporalevolving fuzzy neuralnetworks STE-FuNNsandapplicationsfor adaptive phonemerecognition,TechnicalReportTR99-03,Departmentof InformationScience,Universityof Otago.

34. Kasabov, N., Woodford,B. (1999)Ruleinsertionandruleextractionfrom evolving fuzzyneuralnetworks: algorithmsand applicationsfor building adaptive, intelligent expertsystems.Proc.of Int. Conf.FUZZ-IEEE,Seoul.

35. Kawahara,S., Saito,T. (1996) On a novel adaptive self-organisingnetwork. CellularNeuralNetworksandTheirApplications,41-46.

36. Kohonen,T. (1990)TheSelf-OrganizingMap.Proceedingsof theIEEE,78,1464-1497.37. Kohonen,T. (1997)Self-OrganizingMaps,secondedition.Springer.38. Kozma,R.,Kasabov, N. (1998)Chaosandfractalanalysisof irregulartimeseriesembed-

ded into connectioniststructure.In: Brain-like Computingand Intelligent InformationSystems.S.Amari, N. Kasabov Eds.SpringerSingapore,213-237.

39. Kozma,R., Kasabov, N. (1999) Genericneuro-fuzzy-chaosmethodologiesand tech-niquesfor intelligenttime-seriesanalysis.In: Soft Computingin FinancialEngineering,R. Ribeiro,R. Yager, H.J.Zimmermann,J.Kacprzyk(Eds.),Physica-VerlagHeidelberg.

40. Krogh, A., Hertz, J.A. (1992)A simpleweight decaycanimprove generalisation.Ad-vancesin NeuralInformationProcessingSystems4, 951-957.

41. Le Cun,Y., Denker J.S.,Solla,S.A. (1990)OptimalBrain Damage.In Touretzky, D.S.Ed.Advancesin NeuralInformationProcessingSystems,2, 598-605.

42. Lin, C.T., LeeC.S.G.(1996)NeuroFuzzySystems.PrenticeHall.43. Mitchell, M.T. (1997)MachineLearning,MacGraw-Hill.44. Moody, J.,Darken,C. (1989)Fastlearningin networksof locally-tunedprocessingunits.

NeuralComputation,1, 281-294.45. Persaud,A. (1998)Global foreign exchangeresearch.In: Event Risk IndicatorHand-

book,JPMorgan,London,44-171.46. Saad,D. Ed.(1999)On-lineLearningin NeuralNetworks.CambridgeUniversityPress.47. Sankar, A., Mammone,R.J. (1993) Growing andpruning neuraltreenetworks. IEEE

Trans.Comput.,42(3),291-299.48. Swope, J.A., Kasabov, N., Williams, M. (1999) Neuro-fuzzymodelling of heart rate

signalsandapplicationsto diagnostics.In: SzepanjukEd.,FuzzySystemsin Medicine,PhysicaVerlag,accepted.

49. Trippi, R., TurbanE. Eds.(1993)NeuralNetworksin FinanceandInvesting.Irwin Pro-fessionalPublications,New York.

50. Vaga,T. (1990)Thecoherentmarkethypothesis.FinancialAnalystsJournal,November-December, 36-49.

51. Watts,M., Kasabov, N. (1998)Geneticalgorithmsfor the designof fuzzy neuralnet-works.In: Proc.of ICONIP’98,Kitakyushu,Japan,21-23.

52. Watts, M., Kasabov, N. (1999) Neuro-genetictools and techniques.In: Neuro-FuzzyTechniquesfor IntelligentInformationSystems,N.Kasabov andR.Kozma,Eds.,PhysicaVerlagHeidelberg, 97-110.

53. Woldrige,M., Jennings,N. (1995)Intelligentagents:Theoryandpractice.TheKnowl-edgeEngineeringReview, 10.

54. Zirilli, J.(1997)FinancialPredictionUsingNeuralNetworks.ThomsonComputerPress,London.