ch14 - Accounting for inflation and changing prices

28

Chapter 14: Accounting for Inflation and Changing Prices

Transcript of ch14 - Accounting for inflation and changing prices

Chapter 14:

Accounting for Inflation and Changing Prices

Lecture

Inflation definedPrice indicesInflation accountingIncome measurement systemsRelevant SFASs

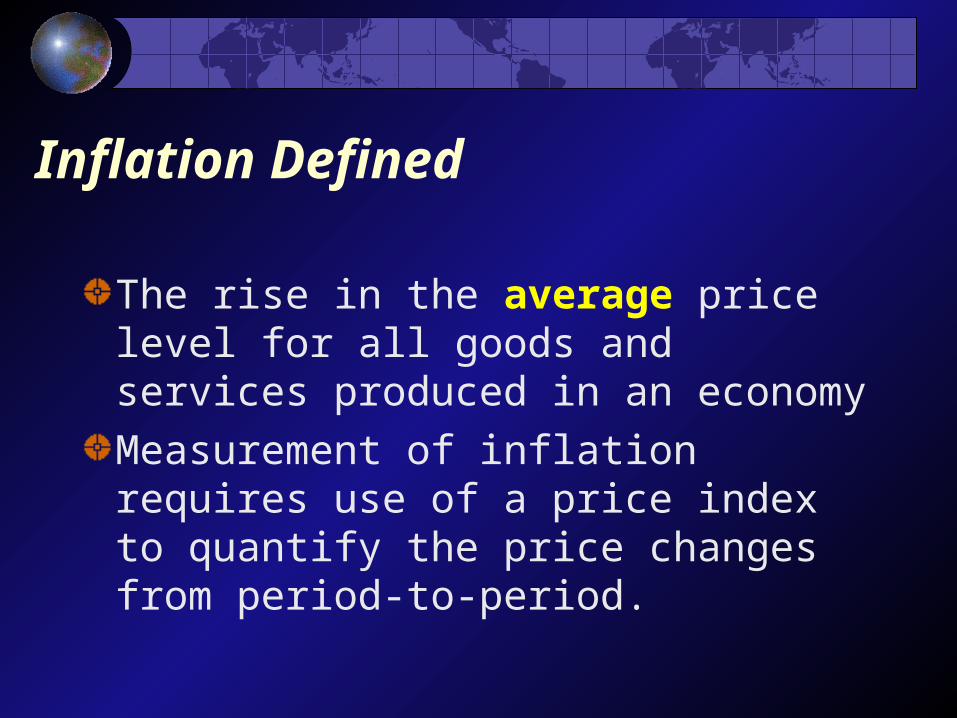

Inflation Defined

The rise in the average price level for all goods and services produced in an economyMeasurement of inflation requires use of a price index to quantify the price changes from period-to-period.

Price IndexIs a weighted average of the current prices of goods and servicesAverages are related to prices in a base period

Purpose is to determine how much change has occurred

Types of price indicesSpecific price indexGeneral price index

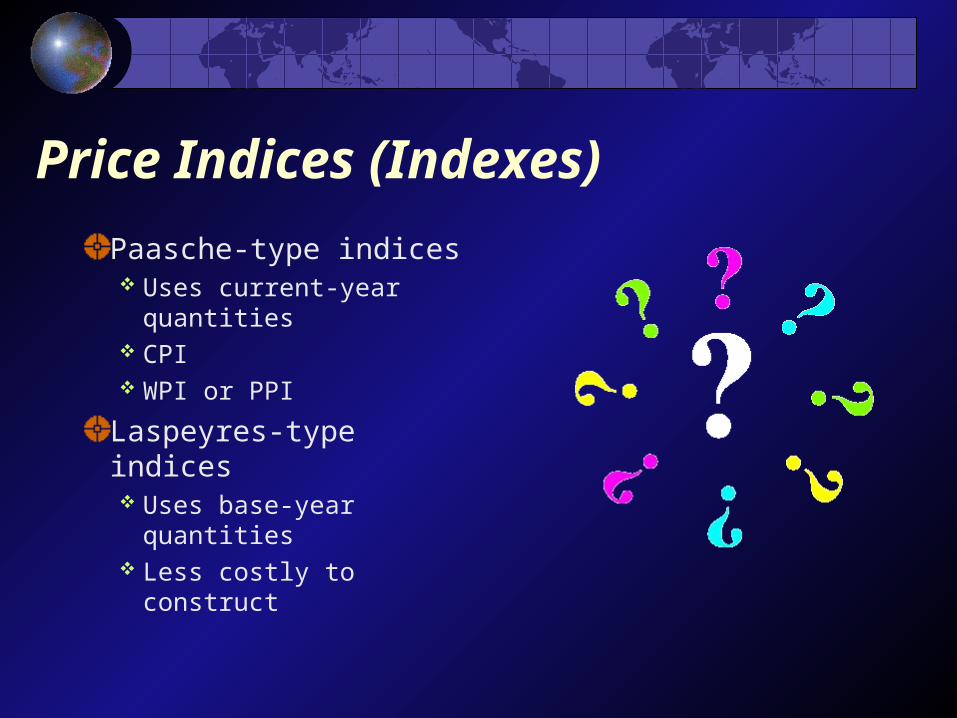

Price Indices (Indexes)Paasche-type indices Uses current-year quantities

CPI WPI or PPILaspeyres-type indices Uses base-year quantities

Less costly to construct

Accounting HistoryAs early as the 1920s, some U.S. corporations restated their primary financial statements for the effects of changes in specific prices.AAA and AICPA strongly supported the historical cost model in the mid-1930s.However, by the early 1950s both the AAA and AICPA began to modify their positions.

Accounting HistoryShortly after its inception, the Financial Accounting Standards Board (FASB) issued an exposure draft entitled “Financial Reporting in Units of General Purchasing Power.” Proposed to require the presentation, as supplementary information, of the balance sheet and income statement restated in units of general purchasing power.

The FASB deferred action on its exposure draft because the Securities and Exchange Commission (SEC) issued Accounting Series Release (ASR) 190, which reversed the SEC’s long- standing position of forbidding the presentation of information other than historical cost.

ASR 190Accountants in general and accounting organizations, such as the AAA, AICPA, and FASB, tended to favor price-level restated historical cost until the SEC’s rather dramatic action of issuing ASR 190. FASB immediately reconsidered its position (general price-level restatement at that time) and led to the dual approach eventually adopted in SFAS No. 33.

Traditional AccountingUnder a historical cost-based system of accounting, inflation leads to two basic problemsMany historical numbers are not economically relevant

Historical numbers are not additivePrice changes (inflation) are problematic

Inflation and Historical CostingLikely predictive value is diminishedComparability among financial statements of different firms is limitedCapital maintenanceIncome usually overstated relative to amounts that can be distributed to stockholders

Many dividends are really liquidating in nature

Inflation AccountingGeneral purchasing power adjustment translates historical dollars into dollars having equivalent purchasing powerCurrent valuation, also called current cost, attempts to derive the specific value or worth for a particular point ...Entry valuesExit values

Entry vs. Exit ValuesEntry valuesValue in use is best represented by replacement costs

Strong argument in support of use Exit values Are a form of opportunity costsThe balance sheet becomes the principal financial statement

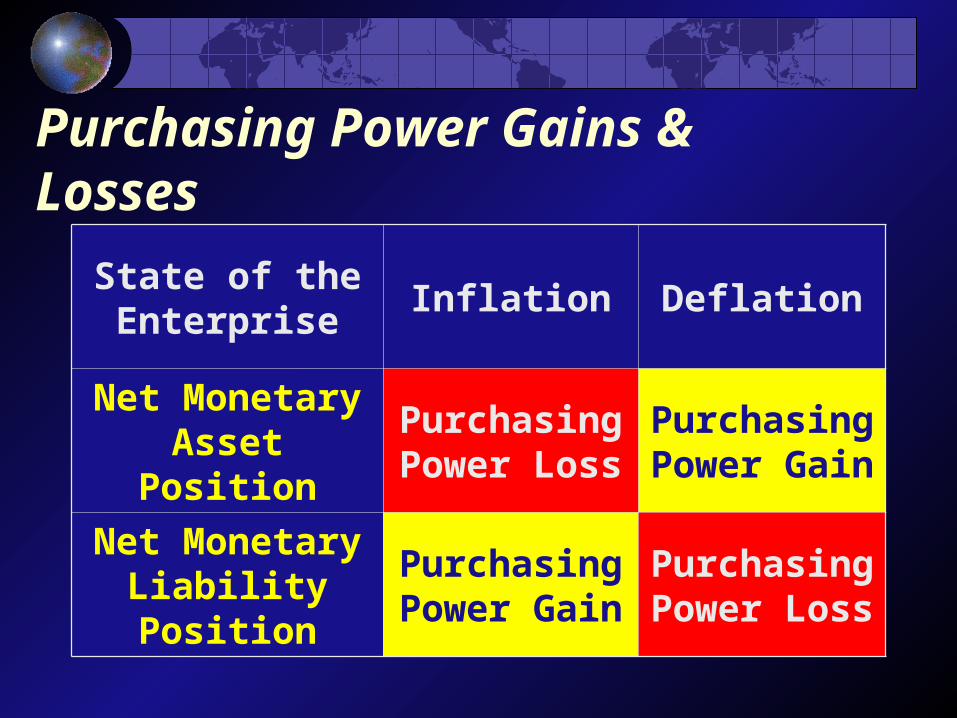

Purchasing Power Gains & Losses

Arise as a result of holding net monetary assets or liabilities during a period when the price level changes Monetary assets and liabilities include cash itself and other assets and liabilities that are receivable or payable in a fixed number of dollars

Purchasing Power Gains & Losses

State of the Enterprise Inflation Deflation

Net Monetary Asset

PositionPurchasing Power Loss

Purchasing Power Gain

Net Monetary Liability Position

Purchasing Power Gain

Purchasing Power Loss

Holding Gains & LossesHolding gains and losses on real (nonmonetary) assets can be divided into two parts monetary holding gains and losses, which arise purely because of the change in the general price level during the period; and

real holding gains and losses, which are the difference between general price-level-adjusted amounts and current values.

Are capital adjustments only; they are not a component of income

The Gearing AdjustmentSomewhat related to the holding gainWas used in Great Britain as part of that country’s inflation accounting mechanism Results in gains to equity capital during inflation because debt capital does not have any claim on holding gains proved to be an extremely confusing concept

Income Measurement SystemsCurrent Value ApproachesDistributable Income (DI) Realized Income (RI) Earning Power Income (EPI) Methods differ in terms of disposition of real holding gains and the resulting type of capital maintenance measure

SFAS No. 33FASB decided to keep nominal historical costs as the basis of primary financial statementsSpecified that the effects of changing prices should be presented as supplementary information in annual reportsFASB realized that a consensus could not be obtained on which method of accounting should be adopted

SFAS No. 33Not all enterprises had to comply with SFAS No. 33 For constant dollar reporting, the SFAS required disclosure ofInformation on income from continuing operations for the current fiscal year on a historical cost/constant dollar basis . . .

The purchasing power gain or loss on net monetary items for the current fiscal year. .

SFAS No. 33’s FailureThere was a dramatic decline of inflation during the early 1980sMeasurement problems were presentQuestions of understandability and usefulness for predictive purposes

SFAS No. 82 issued in 1984Eliminated the constant dollar income disclosures that had previously been required by SFAS No. 33 SFAS No. 33 information confused users may have caused “information overload” because of the presence of similar current cost income disclosures

SFAS No. 89 issued in 1986Two parts of SFAS No. 33 remained in effect; were “encouraged” but not required current cost income measurement, purchasing power gain or loss, and

holding gain informationFASB beat a hasty retreat from the problem of accounting for changing prices

SFAS No. 157 issued in 2006Grounded in the belief that current values (now called fair values) are more relevant for decision-making purposes than historical costing for all users and user groups. Fair value system of SFAS No. 157 is basically an exit value system.

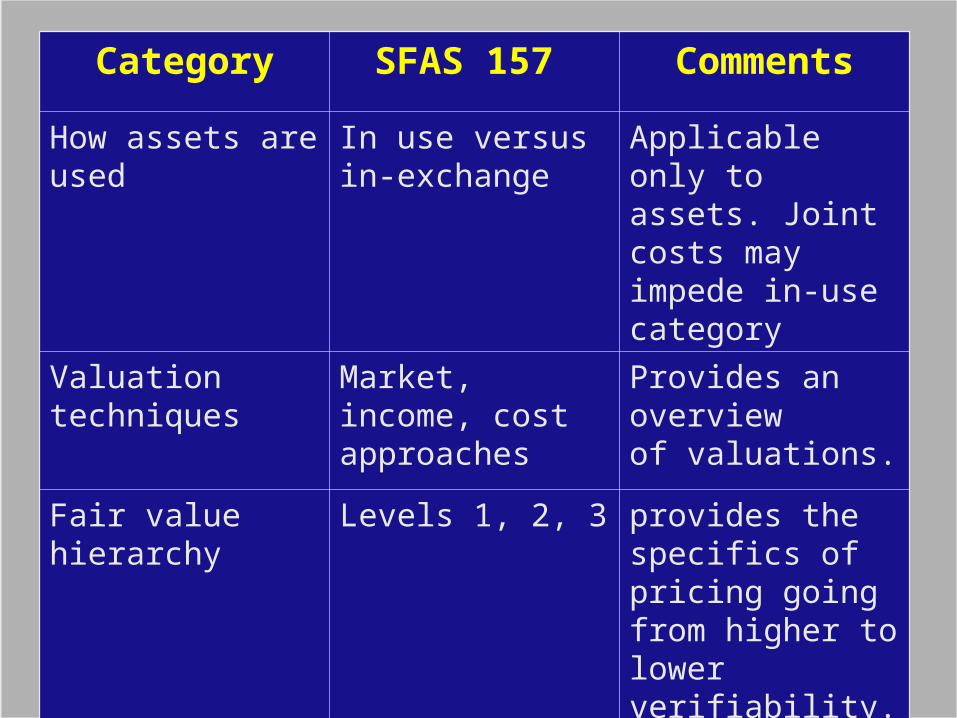

SFAS No. 157 issued in 2006Measurement ConsiderationsValuation TechniquesMarket approachIncome approachCost approachThe Fair Value Pricing Hierarchy, 3 levels

Category SFAS 157 CommentsHow assets are used

In use versus in-exchange

Applicable only to assets. Joint costs may impede in-use category

Valuation techniques

Market, income, cost approaches

Provides an overviewof valuations.

Fair value hierarchy

Levels 1, 2, 3 provides the specifics ofpricing going from higher to lower verifiability.

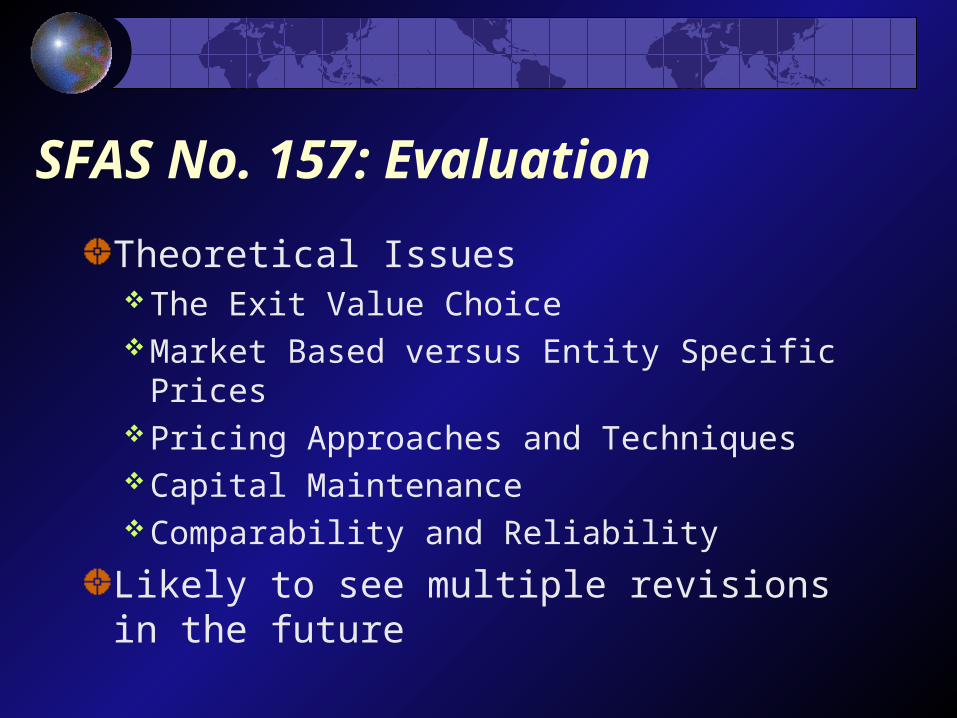

SFAS No. 157: EvaluationSFAS No. 157 affected…24 FASB standards 3 APB OpinionsOmissionsIncome StatementHolding Gains and Losses

SFAS No. 157: EvaluationTheoretical IssuesThe Exit Value Choice Market Based versus Entity Specific Prices

Pricing Approaches and Techniques Capital Maintenance Comparability and Reliability Likely to see multiple revisions in the future

LectureInflation Price indexesInflation accountingIncome measurement systemsSFAS No. 33 82 89 157