Bull market, really? - Motilal Oswal

216

Company name January 2020 India Strategy Investors are advised to refer through important disclosures made at the last page of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital. Gautam Duggad – Research analyst ([email protected]); +91 22 6129 1522 Bull market, really?

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Bull market, really? - Motilal Oswal

Company name

10 December 2010 1

January 2020

India Strategy

Investors are advised to refer through important disclosures made at the last page of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Gautam Duggad – Research analyst ([email protected]); +91 22 6129 1522

Bull market, really?

Contents India Strategy – Bull market, really? ............................................................................................. 3-26

3QFY20 Highlights & Ready Reckoner ......................................................................................... 27-40

Sectors & Companies .................................................................................................................. 41-213 Automobiles .......................................... 42-54 Amara Raja Batt. ............................................. 46 Ashok Leyland ................................................. 46 Bajaj Auto ..................................................... 47 Bharat Forge ................................................... 47 Bosch .............................................................. 48 CEAT ................................................................ 48 Eicher Motors ................................................. 49 Endurance Tech. ............................................. 49 Escorts ............................................................ 50 Exide Inds. ....................................................... 50 Hero Motocorp ............................................... 51 Mahindra & Mahindra .................................. 51 Mahindra CIE .................................................. 52 Maruti Suzuki .................................................. 52 Motherson Sumi ............................................. 53 Tata Motors .................................................. 53 TVS Motor ....................................................... 54

Capital Goods.......................................... 55-63 ABB ............................................................... 58 Bharat Electronics ........................................... 58 BHEL ............................................................. 59 Blue Star .......................................................... 59 CG Consumer Elect.......................................... 60 Cummins India .............................................. 60 Engineers India................................................ 61 Havells India .................................................... 61 Larsen & Toubro ........................................... 62 Siemens........................................................... 62 Thermax ....................................................... 63 Voltas .............................................................. 63

Cement ................................................... 64-72 ACC ............................................................... 68 Ambuja Cements ............................................. 68 Birla Corporation ............................................. 69 Dalmia Bharat ................................................. 69 Grasim Industries ......................................... 70 India Cements ................................................. 70 J K Cements ..................................................... 71 Ramco Cements .............................................. 71 Shree Cement ................................................. 72 Ultratech Cement............................................ 72

Consumer ............................................... 73-85 Asian Paints ................................................. 77 Britannia ......................................................... 77 Colgate ............................................................ 78 Dabur .............................................................. 78 Emami ............................................................. 79 Godrej Consumer ............................................ 79 GSK Consumer ................................................ 80 Hind. Unilever ................................................. 80 ITC ................................................................... 81 Jyothy Labs ...................................................... 81 Marico ............................................................. 82 Nestle .............................................................. 82 P&G Hygiene ................................................... 83 Page Industries................................................ 83 Pidilite Inds. .................................................... 84 Tata Global ...................................................... 84 United Breweries ............................................ 85 United Spirits .................................................. 85

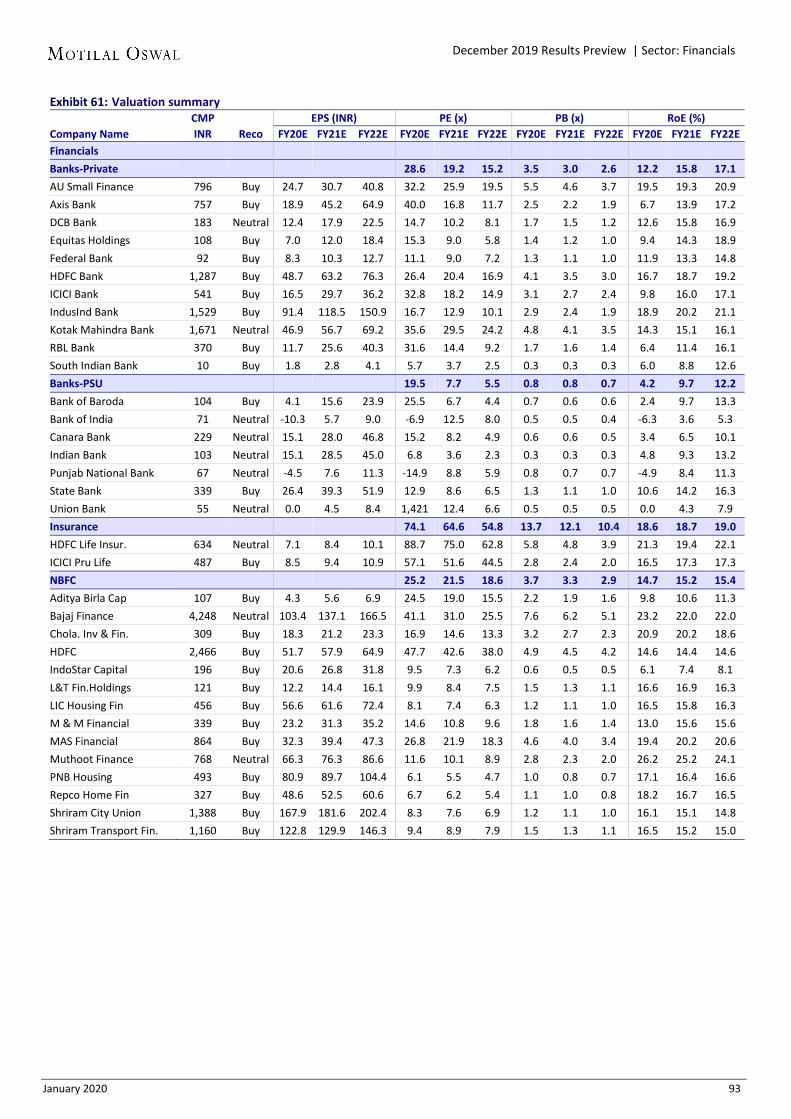

Financials ............................................... 86-101 AU Small Finance ............................................ 94 Axis Bank ......................................................... 94 Bank of Baroda ............................................. 95 DCB Bank......................................................... 95 Equitas Holdings.............................................. 96 Federal Bank ................................................... 96 HDFC Bank .................................................... 97 ICICI Bank ..................................................... 97 Indian Bank ..................................................... 98 IndusInd Bank ................................................. 98 Kotak Mahindra Bank ...................................... 99 Punjab National Bank ................................... 99 RBL Bank ....................................................... 100 State Bank of India ..................................... 100

HDFC Life Insur. ............................................. 101 ICICI Pru Life .................................................. 101 NBFC ................................................... 102-111 Bajaj Finance.................................................. 105 Chola. Inv & Fin. ............................................. 105 HDFC ........................................................... 106 IndoStar Capital ............................................. 107 L&T Fin.Holdings ............................................ 107 LIC Housing Fin .............................................. 108 M & M Financial ............................................ 108 MAS Financial ................................................ 109 Muthoot Finance ........................................... 109 PNB Housing .................................................. 110 Repco Home Fin ............................................ 110 Shriram City Union......................................... 111 Shriram Transport Fin. ................................... 111 Healthcare ........................................... 112-178 Ajanta Pharma ............................................... 115 Alembic Pharma ............................................ 115 Alkem Lab ...................................................... 116 Aurobindo Pharma ........................................ 116 Biocon ............................................................ 117 Cadila Health ................................................. 117 Cipla ........................................................... 118 Divis Labs ....................................................... 118 Dr Reddy’ s Labs ......................................... 119 Glenmark Pharma .......................................... 119 Granules India ............................................... 120 GSK Pharma ............................................... 120 IPCA Labs. ...................................................... 121 Jubilant Life ................................................... 121 Laurus Labs .................................................... 122 Lupin .............................................................. 122 Strides Pharma .............................................. 123 Sun Pharma ................................................... 123 Torrent Pharma ............................................. 124 Infrastructure ...................................... 125-128 Ashoka Buildcon ............................................ 127 IRB Infra ......................................................... 127 KNR Constructions ......................................... 128 Sadbhav Engineering ..................................... 128 Logistics .............................................. 129-133 Allcargo Logistics ........................................... 132 Concor ........................................................... 132 Gateway Distriparks ...................................... 133 Media .................................................. 134-142 D B Corp ......................................................... 139 Ent.Network .................................................. 139 Jagran Prakashan ........................................... 140 Music Broadcast ............................................ 140 PVR ................................................................ 141 Sun TV............................................................ 141 Zee Entertainment ......................................... 142 Metals ................................................. 143-215 Hindalco ...................................................... 147 Hindustan Zinc ............................................... 147 JSPL ................................................................ 148 JSW Steel ....................................................... 148 Nalco ............................................................. 149 NMDC ............................................................ 149 SAIL ................................................................ 150 Tata Steel ....................................................... 150 Vedanta ......................................................... 151 Oil & Gas ............................................. 152-165 Aegis Logistics ................................................ 158 BPCL ............................................................ 158 Castrol India................................................... 159 GAIL ............................................................ 159 Gujarat Gas .................................................... 160 Gujarat State Petronet .................................. 160 HPCL ........................................................... 161

Indraprastha Gas ........................................... 161 IOC ............................................................. 162 Mahanagar Gas ............................................. 162 MRPL ............................................................. 163 Oil India ......................................................... 163 ONGC ......................................................... 164 Petronet LNG ................................................ 164 Reliance Inds. ................................................ 165 Retail - A .............................................. 166-169 Jubilant Foodworks ....................................... 169 Titan Company .............................................. 169 Retail - B .............................................. 170-178 Aditya Birla Fashion ....................................... 175 Avenue Supermarts ....................................... 175 Future Lifestyle ............................................. 176 Future Retail.................................................. 176 Shoppers Stop ............................................... 177 Trent ............................................................. 177 V-Mart Retail ................................................. 178 Technology .......................................... 179-189 Cyient ............................................................ 183 HCL Technologies .......................................... 183 Hexaware Tech. ............................................. 184 Infosys ........................................................ 184 L&T Infotech .................................................. 185 Mindtree ....................................................... 185 MphasiS ........................................................ 186 NIIT Tech. ...................................................... 186 Persistent Systems ........................................ 187 TCS ................................................................ 187 Tech Mahindra .............................................. 188 Wipro .......................................................... 188 Zensar Tech ................................................... 189 Telecom ............................................... 190-196 Bharti Airtel ................................................... 195 Bharti Infratel ................................................ 195 Tata Comm .................................................... 196 Vodafone Idea ............................................... 196 Utilities ................................................ 197-202 CESC .............................................................. 199 Coal India ...................................................... 199 JSW Energy .................................................... 200 NHPC ............................................................. 200 NTPC ............................................................. 201 Power Grid Corp. ........................................... 201 Tata Power ................................................ 202 Torrent Power ............................................... 202 Others.................................................. 203-214 Brigade Enterpr. ............................................ 203 BSE ................................................................ 203 Coromandel International ............................. 204 Delta Corp ..................................................... 204 Godrej Agrovet .............................................. 205 Indian Hotels ................................................. 205 Info Edge ....................................................... 206 Interglobe Aviation........................................ 206 Kaveri Seed.................................................... 207 Lemon Tree Hotel .......................................... 207 MCX ............................................................... 208 Navneet Education ........................................ 208 Oberoi Realty ................................................ 209 P I Industries.................................................. 209 Phoenix Mills ................................................. 210 Quess Corp .................................................... 210 S H Kelkar ...................................................... 211 SRF ................................................................ 211 Tata Chemicals .............................................. 212 Team Lease Serv. ........................................... 212 Trident .......................................................... 213 UPL ................................................................ 213

January 2020 3

India Strategy | Bull market, really?

Earnings still tepid; Financials to drive aggregates

Another modest quarter of earnings ahead; tax cuts to provide some cheer With the Nifty near all-time highs and FII flows at a five-year high, one wouldn’t

be too amiss to conclude that India is in the midst of a major bull market. However, the reality is different. Economic growth momentum has decelerated, while corporate earnings have remained tepid for the last two years. CY19 turned out to be a year where the markets got further polarized in terms of both earnings and performance. While the Nifty delivered 12% returns, the Nifty Midcap-100 and Nifty Smallcap-100 were down 4% and 9%, respectively. Even within the Nifty, the divergence between the top 15 stocks by market cap and the rest has widened to 50%. Cumulatively over two years, the Nifty has now outperformed the Nifty Midcap-100 and Nifty Smallcap-100 by 35% and 51%, respectively. This to an extent is also a reflection of growth polarization and the heightened preference for quality in a slowing economy.

In our view, this polarization will reverse only if growth recovers and gets broad-based. From that perspective, CY20 holds some promise. The government and the RBI have taken some steps to revive growth, the effect of which will be visible with a lag. Some sectors are showing signs of stability/bottoming out with support from festive season demand and few macro indicators like Services PMI have also bounced. The forthcoming budget will be a crucial policy event with the market focus on: [a] potential near-term demand-booster from the government and [b] the contours of fiscal deficit arithmetic. Meanwhile, the recent geopolitical flare-up between the US and Iran has led to a spike in crude prices and intensified macro worries.

Corporate tax cuts have prevented a further slide in earnings estimates. Nonetheless, the FY20 corporate earnings story is all about Financials, with Nifty ex-BFSI earnings expected to decline 2% for the year. The upcoming earnings-report season will likely mark one more quarter of muted earnings.

We estimate MOFSL Universe’s 3QFY20 PBT/PAT to increase by 1%/9% YoY, led by BFSI (estimated to contribute 81% of incremental profit YoY), Automobile (low base effect) and Consumer (beneficiary of tax cuts). However, Metals/O&G are likely to drag the performance, given the underlying weak commodity prices. Telecom is expected to sharply reduce losses YoY, which will support earnings. Ex-BFSI, MOFSL Universe’s PBT is estimated to decline by 5% and PAT to increase by 2% YoY. We estimate Nifty PBT/PAT to increase 2%/8% YoY. Ex-BFSI, we expect Nifty PBT/PAT to decline 6%/2% YoY. Our FY20 Nifty EPS estimate has been stable at INR532. We now build in EPS growth of 10% for FY20.

Top Picks Large-Caps: ICICI Bank, SBI, Bharti Airtel, L&T, Infosys, Hindustan Unilever,

Eicher Motors, Ultratech. Mid-Caps: Indian Hotels, Ashok Leyland, ABFRL, L&T Infotech, Tata Global, JK

Cement, Alkem Labs, Crompton Consumer.

India Strategy BSE Sensex: 40,869 Nifty 50: 12,053

January 2020 4

India Strategy | Bull market, really?

Key sectoral trends/highlights Auto Universe’s PAT is expected to increase by 26% YoY in 3QFY20 off a weak

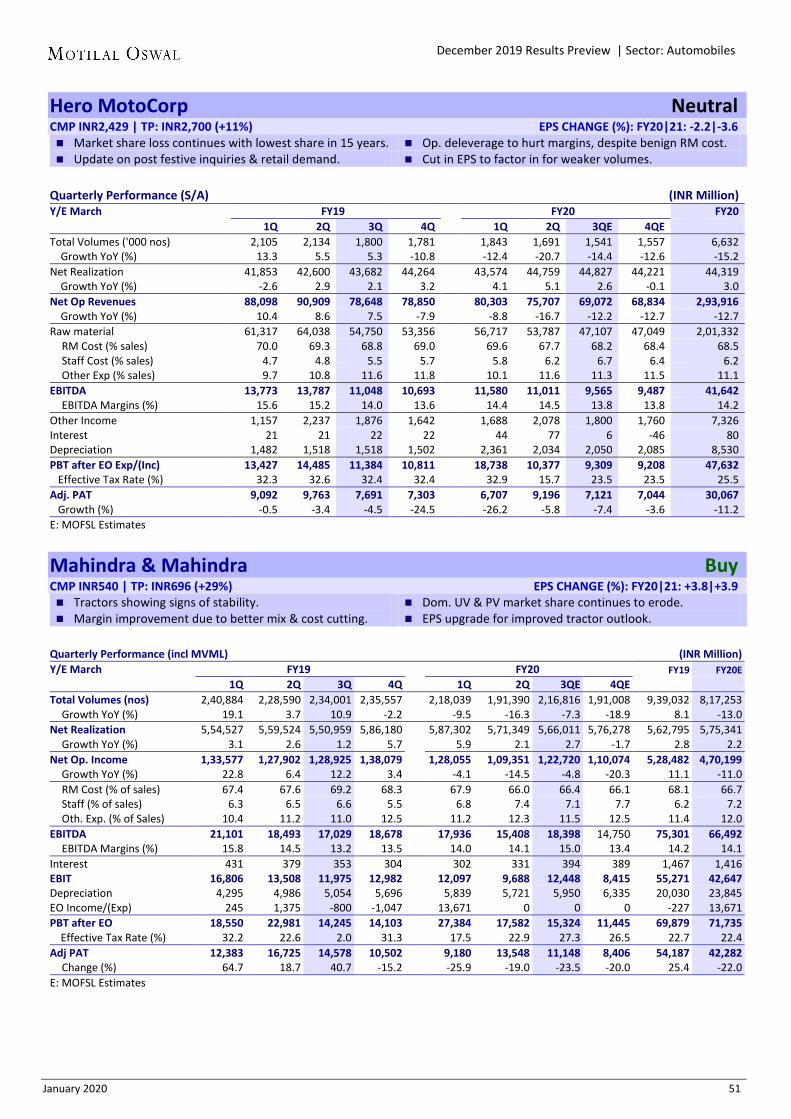

base (-23% YoY in 3QFY19) and entirely led by Tata Motors – first quarter of growth after six consecutive quarters of a profit decline. Ex-Tata Motors, Auto Universe’s PAT is expected to be down 7.5% YoY. We expect the EBITDA margin to expand by 180bp YoY/50bp QoQ to 12%. We expect Maruti and Bajaj Auto to report healthy double-digit profit growth, while Hero, M&M, TVS, Eicher and Ashok Leyland are expected to report a YoY profit decline.

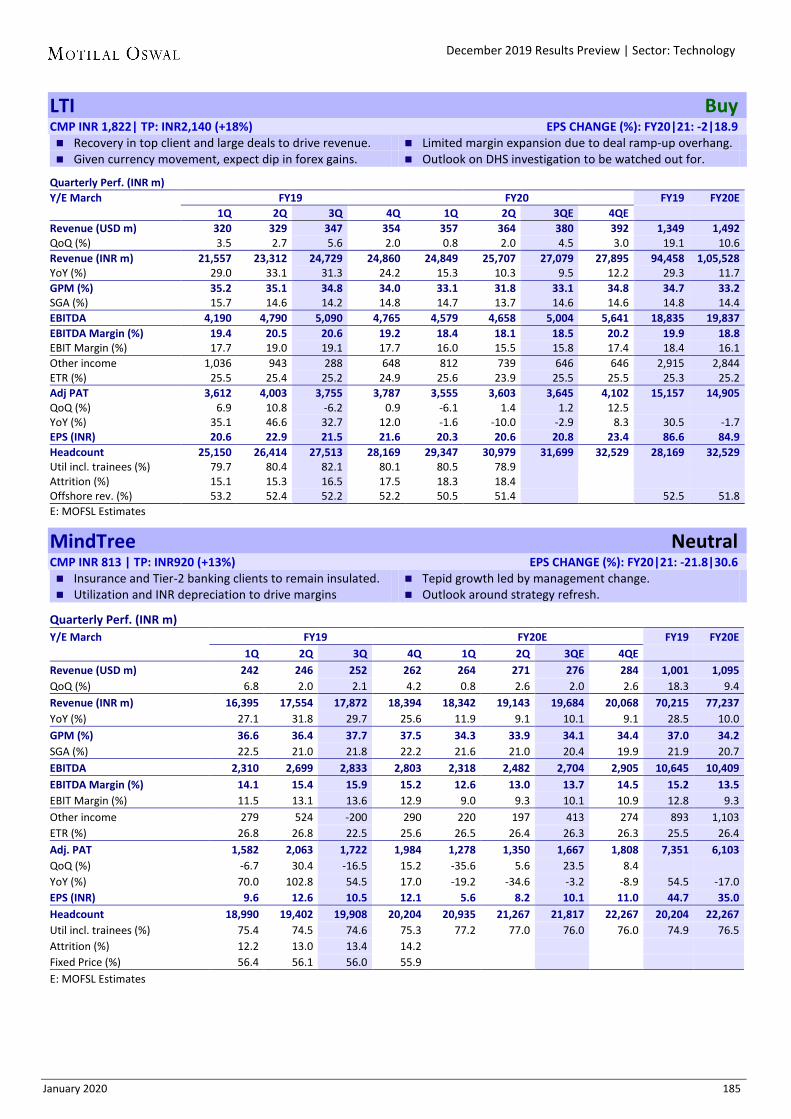

Technology Universe's revenue/EBITDA/PAT are estimated to grow 8%/8%/5% YoY in 3QFY20. We expect single-digit profit growth across tier-1, barring Infosys (one-off in base). Tech Mahindra/Wipro are likely to report a YoY profit decline.

Private Banks are expected to report a healthy quarter (15% PPoP, 28% PBT and 40% PAT growth). ICICI Bank, Kotak Mahindra Bank, IndusInd, AU and HDFC Bank are expected to deliver strong YoY PAT growth.

NBFCs are likely to post PBT/PAT growth of 7%/20% YoY, led by Bajaj Finance (BAF). Ex-BAF, PBT/PAT growth is estimated at 1%/13%. BAF is expected to post another strong quarter with 55% profit growth. Chola (31%), Muthoot (31%) and MMFS (22%) are expected to deliver healthy profit growth, while LTFH, MAS, SHTF and SCUF are likely to deliver subdued growth in profitability.

PSU Banks are expected to post profit of INR66b, driven by SBI (PAT of INR72b), while Telecom is expected to report a loss for the 10th straight quarter.

Consumer Universe profits are expected to increase 17% YoY, led by tax cuts. PBT growth is expected to be modest at 4% YoY. Nestle (34%), Pidilite (20% YoY) and ITC (23%) are expected to exhibit a strong performance, while Godrej Consumer, Marico and UBBL are expected to post weak results.

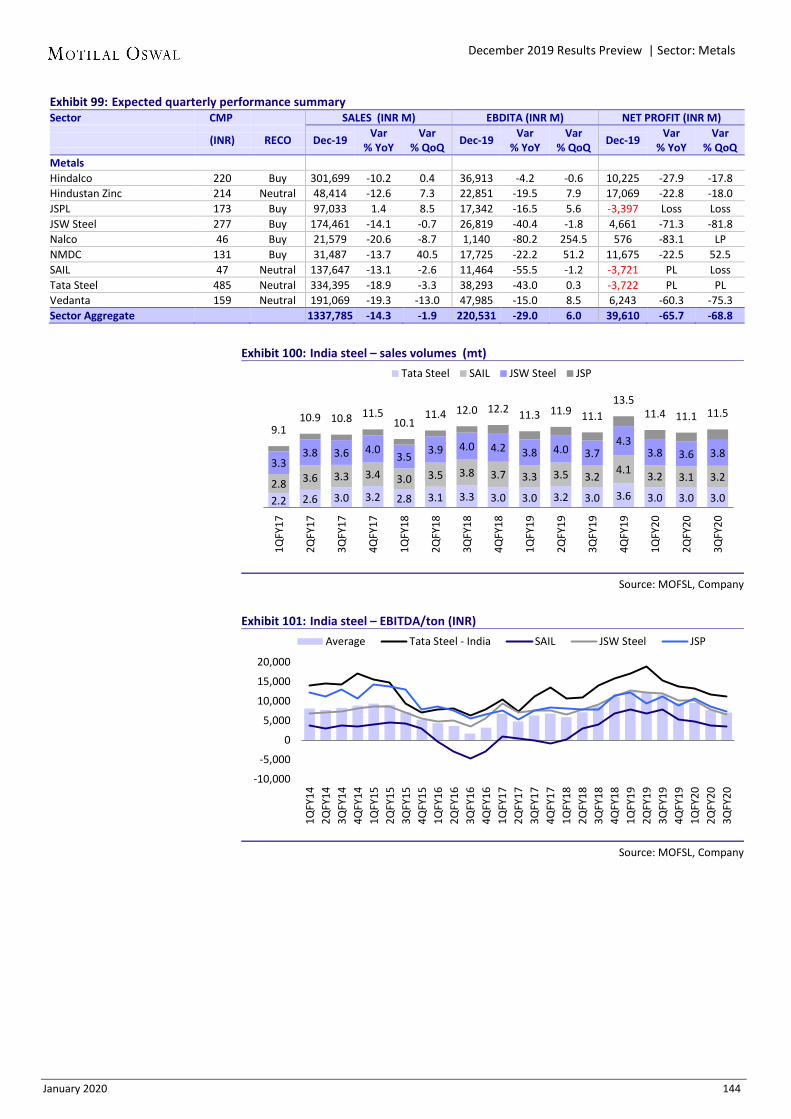

Metals are expected to post a decline of 29%/59%/66% YoY in EBITDA/PBT/PAT. We do not expect profit growth YoY for any of our Metal coverage company.

Oil & Gas is expected to report a flattish PBT/PAT performance, dragged by 40% YoY decline in ONGC PAT. OMCs are expected to post strong YoY profit growth off a benign base (inventory losses in base). RIL is expected to deliver a 3% EBITDA decline and flattish 4% profit growth. Ex-OMCs, we expect a 14% decline in profits for O&G.

Cement is expected to post 18%/24%/21% EBITDA/PBT/PAT growth YoY off a low base (1% profit decline in base), led by higher YoY realization and lower costs. Ultratech is expected to post 87% profit growth YoY, ex of which Cement Universe profits are expected to be up 4% YoY. ACC, Ambuja and Shree are expected to post 44%, 37% and 16% profit growth YoY, respectively.

Capital Goods Universe is expected to report flat PBT and 13% YoY profit growth, led by L&T (27% profit growth). Ex-L&T, profit is expected to decline 2.7% YoY. ABB/Thermax/Voltas are expected to post 34%/30%/34% YoY profit growth, while BEL (-39%), Cummins (-4%), Siemens (0%) and Havells (0%) are expected to report a subdued performance.

Utilities sector’s PBT is expected to decline 11%, while PAT is expected to stay flat YoY, dragged by Coal India (-39%/-26% YoY PBT/PAT). Power Grid (PAT: +8%) and NTPC (+21%) are expected to lead the performance.

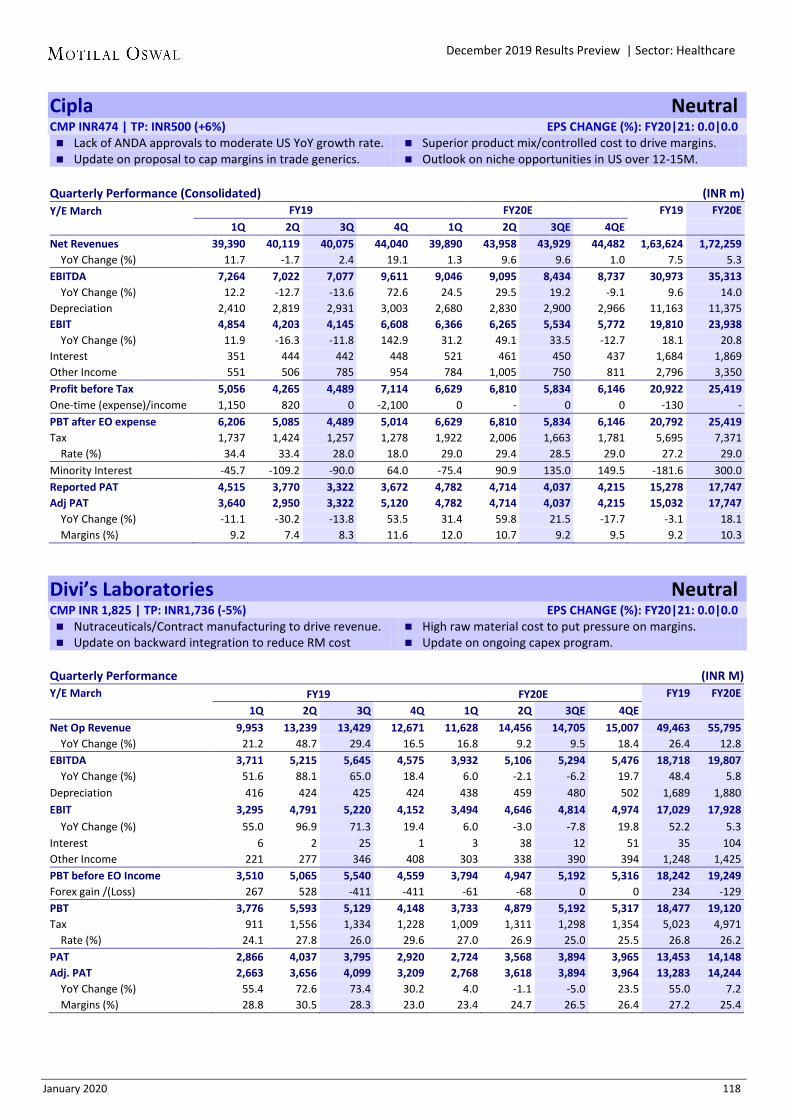

Healthcare is likely to deliver another muted quarter with 4% profit growth. Large-cap names like Lupin/Dr Reddy/Aurobindo are expected to post 1%/-7%/-2% profit growth, while Cipla/Sun’s profits are likely to grow by 22%/12% YoY.

Sources of exhibits in this report include Bloomberg, SEBI, NSE, Capitaline, Companies, and MOFSL database

January 2020 5

India Strategy | Bull market, really?

Model portfolio Our model portfolio construction is premised on earnings visibility, balance

sheet/cash flow comfort and market leadership position. Over the last two quarters, we have added/raised weights in a few high-quality Cyclicals in the portfolio, given their attractive valuations and improved business prospects. We maintain our positive stance on Financials, Consumption, IT and Telecom, and underweight stance on Commodities (Metals, Oil & Gas).

BFSI: We stay overweight on corporate banks. Our preferred picks are SBI, ICICI and Axis Bank. Large-ticket resolutions in IBC will boost the earnings of Corporate Banks in 3QFY20. In some Banks, value unlocking from subsidiaries is expected to provide further upside.

In NBFC, we maintain weights in HDFC, and replace MMFS with LTFH. Focused retailization strategy and reducing reliance on wholesale lending are likely to drive a re-rating of LTFH, in our view. It is one of the few NBFCs to maintain AAA credit rating across agencies, despite the higher share of wholesale loans. AMC business provides a strong option value.

Consumer: We retain HUL, ITC and Titan in the model portfolio. We continue liking HUL in staples, given the solid volume/margin outperformance versus industry. Integration with GSK Consumer will offer further margin synergies. ITC’s valuations at 18x FY21E EPS are attractive and discount most concerns. We are replacing Marico with Tata Global. TGB has shifted its focus back to the highly profitable India beverage business in order to build a dominant, natural beverages brand in the country.

Information Technology and Telecom: In IT, we are replacing Tech Mahindra with HCL Tech. As the trend of repatriation of workloads from public cloud to on-premise/hybrid cloud picks up, HCL will benefit the most given its stronghold in IMS. We expect up to ~5pp organic growth outperformance versus the top two over FY21-22. We are also introducing L&T Infotech in the portfolio. Over the past four years, LTI has continuously strengthened the moats around its business through a slew of measures. Client-specific issues – which had led to a muted performance over 9MCY18 – now appear to be largely behind. We further raise weights in Bharti Airtel, given the improving underlying business dynamics in the Telecom sector post the tariff hikes by key players.

In Oil & Gas, we are marginally cutting our weights in RIL after its recent sharp outperformance and the challenging context for the petrochemicals segment.

In Cement, we are raising the weight in Ultratech. Market mix has improved post-acquisition, with north/central India (both have better utilization outlook) contributing ~45% of volumes and the share of weaker regions (south/east) declining. We estimate a CAGR of 26% in EBITDA and 48% in EPS over FY19-21.

In Automobile, we are adding Eicher Motors. EIM is relatively well placed for BS6 transition due to the 5-7% price hike and more importantly the complete upgrade of the core portfolio post BS6 transition. We are raising the weight of Ashok Leyland. We believe worst is over for the CV industry, although volumes will remain volatile due to the upcoming BS6 transition. Unlike in the previous cycles, AL is on a very strong footing (lean cost structure/net cash balance sheet) and focused on adding new revenue/profit pools.

January 2020 6

India Strategy | Bull market, really?

Earnings still tepid; Financials to drive 3QFY20 Commodities continue to be a drag

Markets entered the new year after an eventful CY19 when the Nifty returned 12%, driven by USD14.2b FII inflows (highest in five years) even as GDP growth decelerated sharply and corporate earnings remained weak. Government announced several steps to revive growth, the impact of which is not yet visible.

After cutting repo rates by 135bp since Feb’19, the RBI maintained status quo in its latest meeting in Dec’19. It has also revised down the GDP growth estimate sharply to 5% for FY20 (~200bp revision since Aug’19). High frequency data remain weak yet. However, there are some silver linings to the dark clouds. Festive season in Oct-Nov’19 – although not blockbuster – was healthy. GST collections have moved up and came in at INR1t+ plus for Nov’19 and Dec’19. Better-than-expected monsoon and strong reservoir levels augur well for the Rabi season and rural India. Recent pick-up in inflation will also likely be positive for the rural pockets. We expect the government to unveil more steps to revive consumption demand in the forthcoming budget.

Overall, as far as the 3QFY20 earnings season is concerned, it will be more of the same with Financials driving the quarter and Commodities dragging it. Corporate commentary on the underlying demand scenario and any sequential improvement post government announcements will be the key monitorables. We believe that FY21 consensus estimates are factoring in a sharp recovery in earnings and have downside risks.

Financials to drive 3Q earnings; Ex-Financials, MOSL PBT to decline 5% YoY The reduction in the corporate tax rates will result in several adjustments in the

taxation charge in this quarter as well. Thus, we place more emphasis on analyzing PBT metrics for a more meaningful comparison.

MOFSL Universe's PBT is expected to grow by 1% and PAT by 9% YoY in 3QFY20, singularly led by Financials. Auto is also expected to rebound off a low base after six straight quarters of a profit decline. Consumers will benefit from tax cuts and post robust 17% profit growth. Reduction in losses in Telecom will also be accretive at the aggregate level. Metals will be a big drag with 59%/66% PBT/PAT decline YoY.

Ex-Financials, MOSL Universe PBT is expected to decline 5% YoY, while PAT is expected to increase 2% YoY. Ex-Metals, MOSL Universe PBT/PAT are expected to increase 7%/17% YoY.

Approximately 35% of MOFSL Universe are expected to post a YoY decline in PAT, while 41% are expected to deliver >15% growth.

Domestic Cyclicals are expected to contribute 42% of the profit pool, followed by Defensives (31%). The share of Global Cyclicals at 27% will be the lowest since Sep’16. Its share in the profit pool has been trending down after hitting a high of 53% in Mar'18.

3QFY20 PREVIEW

January 2020 7

India Strategy | Bull market, really?

We expect MOFSL Universe's revenue to decline 3% YoY (on the base of 21% growth in 3QFY19) – the worst in 14 quarters and the second consecutive YoY decline, largely due to (a) the correction in commodity prices, which is leading Metals to post the third consecutive quarter of a decline in YoY top-line performance (-14%) and Oil & Gas to post a 11% YoY decline and (b) the continued slowdown in Automobiles, where revenues are expected to be down 3% YoY – the third consecutive quarter of a decline.

MOFSL Universe EBITDA growth is estimated at 9% YoY – best in five quarters. The operating margin ex-Financials and OMCs is expected to expand by 40bp YoY to 19.3%.

Global Cyclicals are expected to post the fifth consecutive quarter of PAT decline (-16% YoY) after five straight quarters of strong double-digit growth, impacted by the correction in commodity prices.

Defensives are expected to post 21% YoY profit growth off a benign base (8% YoY decline in PAT in 3QFY19), as Telecom Universe is expected to post a sharp YoY reduction in its losses. Consumer Universe, however, is likely to post 17% growth in profit, aided by tax cuts.

For 3QFY20, Domestic Cyclicals' EBITDA and PAT are expected to grow by 16% and 22% YoY, respectively, off a high base, driven by Financials. Domestic Cyclicals have posted profit growth of 36%, 268%, 55% and 34% YoY in 3QFY19, 4QFY19, 1QFY20 and 2QFY20, respectively.

Earnings breadth weak; one third of universe to post PAT decline YoY Earnings breadth is likely to remain very weak, with 35% of the MOFSL Universe

expected to post a YoY decline in PAT. The number of companies reporting >30% growth is expected to decline from 31% to 22%, while that of companies reporting 0-15% growth will likely remain stable at ~23%.

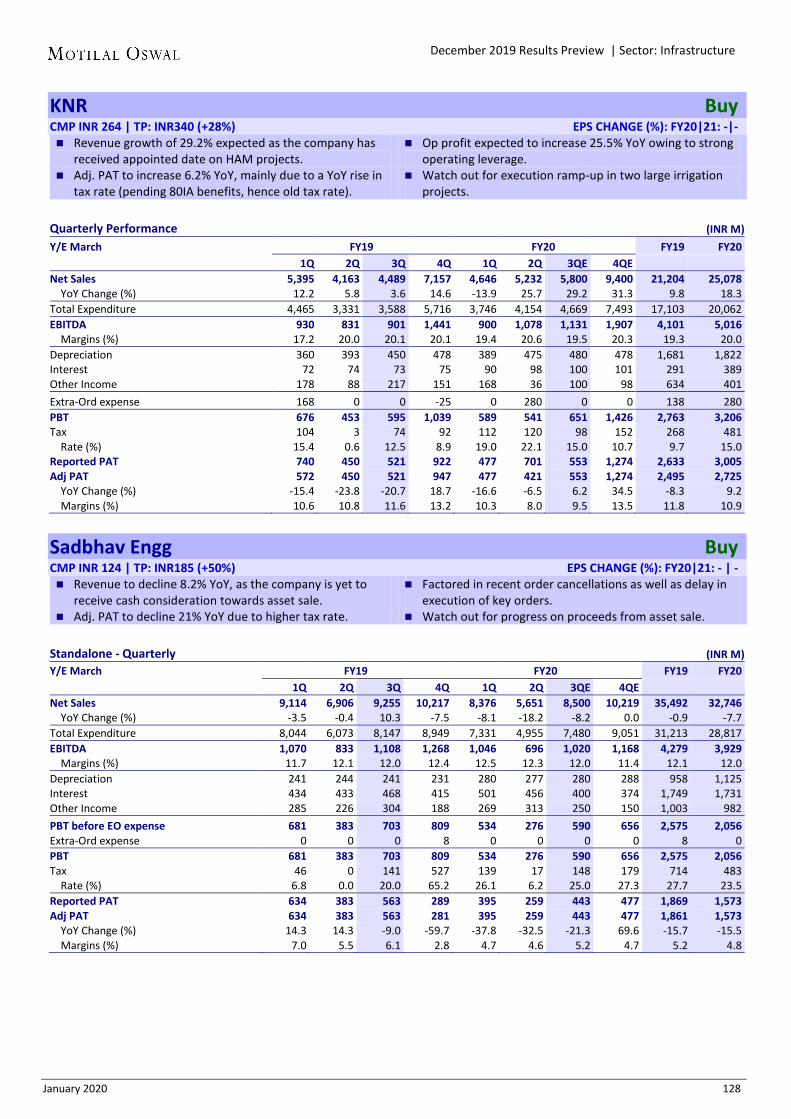

Financials are expected to contribute 81% of incremental earnings of the MOSL Universe in 3QFY20. Metals Universe is expected to post a sharp 66% YoY decline in profits, while Oil & Gas is expected to have a flattish quarter. Among other sectors, Capital Goods/Cement are expected to post 13%/21% profit growth, while Consumer, Pharma and Tech Universe are expected to deliver 17%, 4% and 5% YoY earnings growth, respectively

Nifty sales are expected to decline 3% YoY, while EBITDA/PBT/PAT are estimated to grow by 7%/2%/8% YoY in 3QFY20. Ex-Financials, Nifty PBT and PAT are expected to decline by 6% and 2% YoY, respectively.

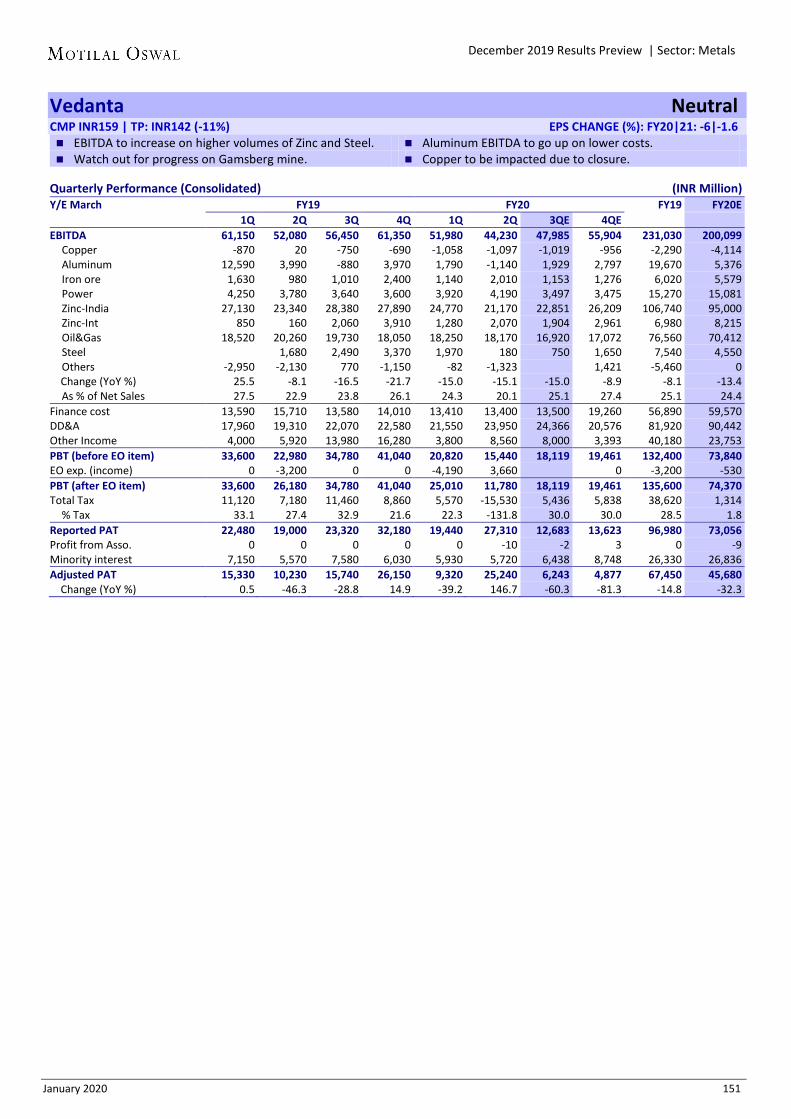

Nifty EPS marginally tweaked for FY20: Our FY20 Nifty EPS estimates have been marginally tweaked to INR532 (prior: INR538). We are now building in EPS growth of 10% for the Nifty for FY20. Financials are expected to account for 119% of incremental earnings. Excluding Financials, Nifty profits are likely to decline by 2% in FY20 – the worst in four years. Corporate Banks are likely to account for 82% of incremental profit growth for the Nifty in FY20. Excluding corporate banks, we are expecting 2% profit growth for the Nifty in FY20 – the worst in four years. For FY20, major earnings upgrades are in Tata Motors (L to P), Bharti (47%), Maruti (12%), SBI (9%) and Coal India (5%), while the major downgrades are in Grasim Inds (-43%), Axis Bank (21%), ONGC (18%), Vedanta (13%), Tata Steel (12%) and IOC (10%).

January 2020 8

India Strategy | Bull market, really?

Exhibit 1: Financials to account for 81% of incremental earnings of MOSL Universe in 3QFY20

SECTOR SALES EBITDA NET PROFIT PAT Delta EBITDA Margins

PAT Margins

(NO OF COMPANIES) Dec-19 Var % YoY

Var % QoQ Dec-19 Var %

YoY Var % QoQ Dec-19 Var %

YoY Var % QoQ

PAT Delta

Share %

Share %

Chg bp YoY

Chg bp YoY

High growth sectors 3,324 5 7 1,056 19 3 454 32 27 110 37 113 371 278 Others (22) 391 23 4 77 39 48 34 45 137 11 3 11 221 134 Private Banks (10) 386 17 4 324 15 2 167 40 55 48 13 49 -170 699 PSU Banks (4) 383 15 1 259 27 -9 66 36 42 17 5 18 656 268 Auto (17) 1,662 -3 11 199 15 15 82 26 10 17 7 17 184 112 Cement (10) 335 2 8 64 18 8 24 21 4 4 2 4 264 112 NBFC (13) 167 13 1 134 12 -1 81 20 -10 13 7 14 -68 287 Med/Low growth sectors 8,842 -4 3 1,415 8 3 781 5 -3 36 63 37 177 74 Consumer (18) 543 6 3 132 8 0 100 17 -7 14 8 15 41 175 Retail (9) 266 12 16 25 21 26 14 13 36 2 1 2 70 4 Capital Goods (12) 651 11 9 70 11 11 42 13 9 5 3 5 -1 10 Life Insurance (2) 171 19 10 6 19 -6 6 12 0 1 0 1 -1 -20 Technology (13) 1,191 8 3 281 8 6 204 5 3 10 16 10 -13 -54 Healthcare (19) 484 6 0 100 4 0 56 4 -3 2 4 2 -39 -22 Logistics (3) 40 9 2 6 26 0 3 3 0 0 0 0 213 -52 Media (7) 55 1 8 18 -6 15 11 2 -2 0 1 0 -245 10 Oil & Gas (15) 4,727 -11 2 517 12 2 245 1 -2 2 20 2 231 64 Utilities (8) 715 -3 0 257 1 0 101 0 -20 0 8 0 144 46 PAT de-growth sectors 1,791 -11 0 383 -8 6 6 -90 -92 -48 0 -50 48 -238 Infrastructure (4) 43 2 17 10 -9 -4 4 -16 6 -1 0 -1 -274 -176 Metals (9) 1,338 -14 -2 221 -29 6 40 -66 -69 -76 3 -78 -342 -443 Telecom (4) 411 3 3 153 57 6 -38 Loss Loss 28 -3 29 1,286 731 MOFSL (199) 13,958 -2.9 3.7 2,854 9.1 3.5 1,241 8.5 0.8 97 100 100 224 93 MOFSL Excl. OMCs (196) 11,545 0.8 4.0 2,735 5.3 2.8 1,193 5.7 -0.4 102 48 Sensex (30) 5,670 2.3 4.0 1,604 6.2 0.0 803 10.6 4.9 105 106 Nifty (50) 10,001 -3.3 4.1 2,242 7.3 2.4 1,005 7.7 2.5 221 102

Exhibit 2: MOFSL Universe: PBT is expected to grow by 1% and PAT by 9% YoY SECTOR PBT (INR b) Adjusted PAT (INR b)

(NO OF COMPANIES) Dec-18 Sep-19 Dec-19 Var % YoY

Var % QoQ Dec-18 Sep-19 Dec-19 Var %

YoY Var % QoQ

Auto (17) 94 98 112 19.9 14.0 65 75 82 25.9 10.0 Capital Goods (12) 61 55 61 0.4 10.3 37 39 42 12.5 8.8 Cement (10) 28 33 35 23.6 6.0 20 24 24 20.6 4.0 Consumer (18) 124 128 129 3.8 0.6 85 107 100 16.9 -6.9 Financials (29) 355 390 427 20.3 9.5 241 250 319 32.7 27.9 Private Banks (10) 173 208 222 28.2 6.7 120 108 167 39.8 54.7 PSU Banks (4) 79 74 95 20.2 28.6 48 46 66 35.8 42.0 Life Insurance (2) 6 6 6 14.9 0.5 5 6 6 12.4 -0.1 NBFC (13) 97 102 104 6.7 1.9 68 89 81 19.6 -9.7 Healthcare (19) 66 71 74 11.4 3.7 54 58 56 4.2 -3.2 Infrastructure (4) 6 5 5 -29.7 -7.9 4 3 4 -16.1 5.7 Logistics (3) 5 4 5 -8.8 1.0 3 3 3 2.8 0.2 Media (7) 17 13 15 -11.7 15.3 11 11 11 1.6 -1.7 Metals (9) 174 62 72 -58.6 16.5 115 127 40 -65.7 -68.8 Oil & Gas (15) 349 322 345 -1.1 7.3 242 250 245 1.0 -2.2 Excl. OMCs (12) 325 281 273 -15.9 -2.7 228 217 197 -13.7 -9.4 Retail (9) 17 13 18 5.1 35.7 12 10 14 13.2 35.7 Technology (13) 260 257 268 3.0 4.2 194 197 204 5.0 3.1 Telecom (4) -61 -57 -59 Loss Loss -66 -63 -38 Loss Loss Utilities (8) 142 152 126 -11.2 -17.4 101 126 101 0.1 -19.6 Others (22) 29 19 44 51.0 128.6 23 14 34 45.7 137.2 MOFSL (199) 1,667 1,568 1,676 0.6 6.9 1,143 1,231 1,241 8.5 0.8 Nifty (50) 1,358 1,268 1,379 1.5 8.8 934 981 1,005 7.7 2.5 Sensex (30) 1,035 1,024 1,082 4.6 5.6 726 766 803 10.6 4.9

January 2020 9

India Strategy | Bull market, really?

MOFSL Universe: Sales decline of 3%, PBT to grow 1%; PAT growth expected at 9% YoY

Exhibit 3: Commodities to drag top line

3

Exhibit 4: Earnings growth expected at 9% YoY despite flattish PBT

Exhibit 5: EBITDA margin to expand by 40bp YoY in 3QFY20

Source: MOFSL

Exhibit 6: PAT margin to stay flat YoY in 3QFY20

Source: MOFSL

Exhibit 7: Key assumptions Macro 1QFY20 2QFY20 3QFY20E 4QFY20E FY20E FY21E FY22E GDP Growth (%) 5.0 4.5 4.0 4.6 4.5 5.4 5.8 IIP Growth (%) 3.0 -0.3 -0.2 1.8 1.0 2.6 3.3 Inflation CPI-RU (%) 3.1 3.4 5.2 5.5 4.3 4.6 4.6 Currency: USD/INR 69.6 70.3 71.2 71.0 70.5 71.3 72.3 Repo Rate (%) 5.40 5.15 5.15 5.15 5.15 5.15 5.00 Interest Rate (%): 1Year CP Rate (Avg) 8.10 7.39 7.15 7.08 7.43 7.42 7.35 10Year G Sec (Avg) 7.21 6.56 6.55 6.51 6.71 6.50 6.42 Sectoral 1QFY20 2QFY20E 3QFY20E 4QFY20E FY20E FY21E FY22E Auto: CV Volume growth (%) -15.4 -42.8 -30.7 -39.8 -32.9 16.5 13.8 Car Volume growth (%) -14.4 -2.0 15.5 25.5 -20.8 16.6 11.1 Banking: Loan Growth (%) 12.0 10.5 8.6 9.0 9.0 12.5 14.2 Cement: Volume growth (%) -3.0 -2.0 3.0 5.0 1.0 6.0 6.0 Capital Goods: L&T order Intake (INRb) 387 483 450 618 1,938 2,146 2,404 Capital Goods: L&T order Intake (% YoY) 6.9 15.3 6.6 9.4 9.6 10.7 12.0 Metal: Steel (USD/Tonne) 656 619 605 613 627 629 632 Aluminum (USD/Tonne) 1,792 1,762 1,750 1,800 1,777 1,850 1,900 Zinc (USD/Tonne) 2,761 2,347 2,500 2,500 2,527 2,450 2,450 Oil: Brent (US$/bbl) 68.5 61.9 62.5 65.0 64.5 65.0 65.0 Oil & Gas: Under Recoveries (INRb) 91.4 50.7 52.2 53.8 248 253 256 Singapore GRM (USD/bbl) 3.5 6.5 1.7 4.0 3.9 6.0 6.0 Technology: $Revenue growth (%) 1.3 1.8 2.4 2.0 8.0 9.1 8.5

* CV volume for Tata Motors and Ashok Leyland; PV Volume for Maruti Suzuki (total volume growth)

14

5

0

-10 -4 -5 -4

4

-1

4 9

15 11 12 15 15

22 25 21

11 7

-2 -3

6

Jun-

14Se

p-14

Dec-

14M

ar-1

5Ju

n-15

Sep-

15De

c-15

Mar

-16

Jun-

16Se

p-16

Dec-

16M

ar-1

7Ju

ne-1

7Se

p-17

Dec-

17M

ar-1

8Ju

ne-1

8Se

p-18

Dec-

18M

ar-1

9Ju

ne-1

9Se

p-19

Dec-

19E

Mar

-20E

34

5

-6 -10

8 2 5

-8

2 7

16 16

-6

15 17

-8

13

3 1

27

3 12 9

18

Jun-

14Se

p-14

Dec-

14M

ar-1

5Ju

n-15

Sep-

15De

c-15

Mar

-16

Jun-

16Se

p-16

Dec-

16M

ar-1

7Ju

ne-1

7Se

p-17

Dec-

17M

ar-1

8Ju

ne-1

8Se

p-18

Dec-

18M

ar-1

9Ju

ne-1

9Se

p-19

Dec-

19E

Mar

-20E

18.9

18

.4

18.3

18

.9 20

.0

18.6

18

.9 20

.2 21

.1

19.8

20

.0

19.2

19

.3 20

.1

20.4

20

.0

20.1

19

.4

18.9

19

.0 19

.7

19.1

19.3

20.6

June

-14

Sep-

14De

c-14

Mar

-15

June

-15

Sep-

15De

c-15

Mar

-16

June

-16

Sep-

16De

c-16

Mar

-17

June

-17

Sep-

17De

c-17

Mar

-18

June

-18

Sep-

18De

c-18

Mar

-19

June

-19

Sep-

19De

c-19

EM

ar-2

0EMOFSL Universe EBITDA Margin LPA: 19.5%

9.9

9.6

9.0

9.7 10

.0

9.7

9.3

10.7

10

.3

9.8

9.4

10.3

9.

4 9.8 9.9 10.2

9.

1 9.

0 8.

5 9.

1 8.

0 9.

5 8.

4 9.

5

June

-14

Sep-

14De

c-14

Mar

-15

June

-15

Sep-

15De

c-15

Mar

-16

June

-16

Sep-

16De

c-16

Mar

-17

June

-17

Sep-

17De

c-17

Mar

-18

June

-18

Sep-

18De

c-18

Mar

-19

June

-19

Sep-

19De

c-19

EM

ar-2

0E

MOFSL Universe PAT Margin LPA: 9.5%

January 2020 10

India Strategy | Bull market, really?

Exhibit 8: 35% of the companies are likely to report PAT decline, while 41% are expected to post >15% PAT growth

41% of the companies would grow at >15% YoY, and 22% of the Universe would report >30% PAT growth. 35% of the Universe would report PAT de-growth.

Exhibit 9: Financials and loss reduction in Telecom to drive aggregate earnings; Metals to drag

Source: MOFSL

32 41 43 51

38 32 39 35 21 21 24 25 25 28 26 24 19 26 24 19 20 26 18 21 22 21 26 26 29 30 29 23 19 25 32 35 41

30 27 26 26 31 22

22 10 17

13 22

21 18 23

24 25 18 22 17 17 19 16 18 18 14 20 22

20 23 16 13

26 13 19 19 19 15

12 16 18

21 15 20

17 16 16 14

16 19

14 14 9 9 10 20 18 18

24 19 16 13 27 17 16 17 22

19 24 16 22

27 25 25

18 17

22 18 16 20 22 20 18

25 17 15

16

21 24 21 23 20 23

32 35 31 27 30 27

25 24 31 34

42 40 31 38 39 42 40 37 38 45

36 26 35 38 47

36 39 37 35 32 34 45 47

32 30 35 23

32 33 38 37 33 35

-15 -11

23

42

26

22

24

9

13

11

4

18

11

9

6

0

-3

8

12

9

17

7

-7

-9

-4

-3

-11

-13

-4

1

18

20

3

10 9

-21

7

5

11

23

8

14

6

June

09

Sep

09De

c 09

Mar

10

June

10

Sep

10De

c 10

Mar

11

June

11

Sep

11De

c 11

Mar

12

June

12

Sep

12De

c 12

Mar

13

June

13

Sep

13De

c 13

Mar

14

June

14

Sep

14De

c 14

Mar

15

June

15

Sep

15De

c 15

Mar

16

June

16

Sep

16De

c 16

Mar

17

June

17

Sep

17De

c 17

Mar

18

June

18

Sep

18De

c 18

Mar

19

June

19

Sep

19De

c 19

E

>30% >15-30% >0-15% <0% Ex OMCs (%)

% o

f MO

FSL

Uni

v. c

ompa

nies

Earnings Gr.

PAT Growth Ex OMCs (%)

1,24

1

1,14

3

48 28 17 17 14 13 11 10 5 4 2 2 2 1 0 0 0

-1 -76

MO

FSL

3QFY

19 P

AT (I

NRb

)

Priv

ate

Bank

s

Tele

com

PSU

Ban

ks

Auto

Cons

umer

NBF

C

Oth

ers

Tech

nolo

gy

Cap

Goo

ds

Cem

ent

Oil

& G

as

Heal

thca

re

Reta

il

Life

Insu

ranc

e

Med

ia

Util

ities

Logi

stic

s

Infr

a

Met

als

MO

FSL

3QFY

20 P

AT (I

NRb

)

January 2020 11

India Strategy | Bull market, really?

Share of Domestic Cyclicals in MOFSL Universe (excl. OMCs) earnings at 44%

Exhibit 10: PAT share of Global Cyclicals estimated at 24% (multi-qtr low) and of Domestic Cyclicals at 44% (multi-qtr high)

Defensives includes Consumer, Healthcare, Technology, Telecom and Utilities Global cyclicals includes Metals, Oil & Gas and JLR Domestic cyclicals includes Automobiles, Banks, Capital Goods, Infrastructure, Cement, Media, NBFCs, Real Estate and Retail

Nifty expected to post 2% PBT growth; PBT ex Financials to decline 6% Nifty PBT is expected to increase 2% YoY, while PAT is likely to grow by 8% YoY

off a similar base (+7% in the base quarter). Ex-Financials, Nifty PBT is likely to decline 6% YoY, while PAT is expected to be

down 2% YoY. Nifty sales are expected to decline 3% YoY off a strong base (+22% in 3QFY19) -

the second consecutive quarter of sales decline. Nifty EBITDA is expected to grow 7% YoY. 16 Nifty companies are expected to report a YoY decline in PAT, while 3 are

expected to post losses. Exhibit 11: Nifty sectoral 3QFY20 PAT change YoY (%)

Source: MOFSL

40

35

32

31

34

35 32

37

36

33

34

35

31

37

36

31

11 29

31

38

33 41

36

44

26

34

41

42

38

35 34

26

24

25

23 25

34

28

28

34

48

34

35 33

35

25

31 24

34 28

26

29

37

40

41

43

40

35 35

36

35

40

36

34 29

32

33

33

33

0%

25%

50%

75%

100%

Mar

-09

June

-09

Sep-

09De

c-09

Mar

-10

June

-10

Sep-

10De

c-10

Mar

-11

June

-11

Sep-

11De

c-11

Mar

-12

June

-12

Sep-

12De

c-12

Mar

-13

June

-13

Sep-

13De

c-13

Mar

-14

June

-14

Sep-

14De

c-14

Mar

-15

June

-15

Sep-

15De

c-15

Mar

-16

June

-16

Sep-

16De

c-16

Mar

-17

June

-17

Sep-

17De

c-17

Mar

-18

June

-18

Sep-

18De

c-18

Mar

-19

June

-19

Sep-

19De

c-19

E

Defensives

Global cyclicals

Domestic cyclicals

LP 82

52 36 31 27 20 14 9 8 8 5

-5 -5 -8 -17 -19

-75

Tele

com

Bank

s-PS

U

Auto

NBF

C

Bank

s-Pv

t

Cap

Goo

ds

Cons

umer

Reta

il

Cem

ent

Heal

thca

re

Nift

y

Tech

nolo

gy

Util

ities

Oil

& G

as

Agro

Che

m

Infr

a

Med

ia

Met

als

Metals, O&G to drag Nifty; BFSI, Auto,

Consumer and Capital Goods to support

Excl. OMCs

January 2020 12

India Strategy | Bull market, really?

Exhibit 12: Nifty Universe PBT and PAT change

PBT (INR M) PBT Adj. PAT (INR M) PAT

Company Sector Dec- 18 Sep-19 Dec- 19 YoY (%) QoQ (%) Dec- 18 Sep-19 Dec- 19 YoY (%) QoQ (%) Bajaj Auto Automobiles 15,591 16,089 16,549 6.1 2.9 11,019 14,024 12,411 12.6 -11.5 Eicher Motors Automobiles 7,479 5,922 6,515 -12.9 10.0 5,330 5,727 5,051 -5.2 -11.8 Hero MotoCorp Automobiles 11,384 10,979 9,309 -18.2 -15.2 7,691 9,196 7,121 -7.4 -22.6 Mahindra & Mahindra Automobiles 15,045 17,582 15,324 1.9 -12.8 14,578 13,548 11,148 -23.5 -17.7 Maruti Suzuki Automobiles 20,601 15,720 22,765 10.5 44.8 14,893 13,586 17,028 14.3 25.3 Tata Motors Automobiles -12,144 5,821 15,235 LP 161.7 -11,551 -1,949 11,144 LP LP Axis Bank Banks - Pvt 21,281 24,332 23,084 8.5 -5.1 16,809 -1,121 17,313 3.0 LP HDFC Bank Banks - Pvt 85,669 89,974 94,581 10.4 5.1 55,859 63,450 70,775 26.7 11.5 ICICI Bank Banks - Pvt 19,023 43,672 51,564 171.1 18.1 16,049 6,550 39,446 145.8 502.3 IndusInd Bank Banks - Pvt 15,103 18,857 20,170 33.6 7.0 9,850 14,010 15,087 53.2 7.7 Kotak Mahindra Bank Banks - Pvt 19,707 21,006 22,097 12.1 5.2 12,909 17,245 16,551 28.2 -4.0 State Bank Banks - PSU 66,187 50,598 105,083 58.8 107.7 39,548 30,117 71,981 82.0 139.0 Bajaj Finance NBFC 16,354 20,224 21,922 34.0 8.4 10,593 15,063 16,441 55.2 9.2 Bajaj Finserv NBFC 22,240 26,270 29,831 34.1 13.6 8,505 12,037 14,766 73.6 22.7 HDFC NBFC 27,502 26,451 28,157 2.4 6.4 20,422 29,805 22,638 10.8 -24.0 Larsen & Toubro Capital Goods 34,012 33,028 37,098 9.1 12.3 18,980 23,085 24,152 27.2 4.6 Grasim Industries Cement 8,770 6,510 4,813 -45.1 -26.1 6,082 5,265 3,465 -43.0 -34.2 Ultratech Cement Cement 5,912 8,962 11,369 92.3 26.9 4,076 5,790 7,617 86.9 31.6 Asian Paints Consumer 9,580 8,369 9,219 -3.8 10.2 6,472 8,450 6,989 8.0 -17.3 Britannia Consumer 4,664 4,994 4,622 -0.9 -7.4 3,007 4,038 3,467 15.3 -14.2 Hind. Unilever Consumer 20,120 23,550 21,983 9.3 -6.7 14,010 18,320 16,048 14.5 -12.4 ITC Consumer 48,212 48,077 48,675 1.0 1.2 32,091 40,231 39,427 22.9 -2.0 Nestle Consumer 5,854 7,080 7,222 23.4 2.0 4,049 6,035 5,408 33.5 -10.4 Cipla Healthcare 4,489 6,810 5,834 30.0 -14.3 3,322 4,714 4,037 21.5 -14.4 Dr Reddy’ s Labs Healthcare 5,805 2,835 5,798 -0.1 104.5 4,852 4,042 4,522 -6.8 11.9 Sun Pharma Healthcare 14,301 14,249 13,948 -2.5 -2.1 9,419 10,556 10,527 11.8 -0.3 Adani Ports Infrastructure 18,209 8,863 15,608 -14.3 76.1 14,086 10,541 11,761 -16.5 11.6 Zee Entertainment Media 8,109 6,760 5,676 -30.0 -16.0 5,247 5,604 4,246 -19.1 -24.2 Hindalco Metals 18,996 16,394 15,735 -17.2 -4.0 14,180 12,436 10,225 -27.9 -17.8 JSW Steel Metals 24,490 7,030 6,684 -72.7 -4.9 16,240 25,600 4,661 -71.3 -81.8 Tata Steel Metals 30,693 46 -80 PL PL 22,517 41,783 -3,722 PL PL Vedanta Metals 34,780 15,440 18,119 -47.9 17.3 15,740 25,240 6,243 -60.3 -75.3 BPCL Oil & Gas 5,895 16,551 16,656 182.5 0.6 4,951 17,084 11,110 124.4 -35.0 GAIL Oil & Gas 25,075 15,355 23,402 -6.7 52.4 16,496 10,643 15,691 -4.9 47.4 IOC Oil & Gas 13,446 8,145 29,870 122.1 266.7 7,168 5,634 19,924 177.9 253.6 ONGC Oil & Gas 120,630 90,383 74,728 -38.1 -17.3 82,627 62,631 49,844 -39.7 -20.4 Reliance Inds. Oil & Gas 144,210 150,010 142,899 -0.9 -4.7 103,760 113,520 107,517 3.6 -5.3 Titan Company Retail 5,997 4,270 6,013 0.3 40.8 4,111 3,143 4,690 14.1 49.2 HCL Technologies Technology 31,910 34,940 37,357 17.1 6.9 26,110 26,510 28,429 8.9 7.2 Infosys Technology 56,710 54,960 58,720 3.5 6.8 36,100 40,190 42,979 19.1 6.9 TCS Technology 107,270 105,290 108,771 1.4 3.3 81,210 80,420 83,050 2.3 3.3 Tech Mahindra Technology 14,838 13,374 13,455 -9.3 0.6 12,029 11,239 10,080 -16.2 -10.3 Wipro Technology 32,403 31,345 31,031 -4.2 -1.0 25,444 25,612 24,823 -2.4 -3.1 Bharti Airtel Telecom -12,135 -6,230 -11,628 Loss Loss -10,407 -11,229 -4,149 Loss Loss Bharti Infratel Telecom 10,375 9,802 10,466 0.9 6.8 6,484 9,662 7,832 20.8 -18.9 Coal India Utilities 70,281 42,785 43,168 -38.6 0.9 45,657 35,243 33,671 -26.3 -4.5 NTPC Utilities 33,467 45,746 40,664 21.5 -11.1 25,526 34,716 30,859 20.9 -11.1 Power Grid Corp. Utilities 29,758 32,827 30,974 4.1 -5.6 23,581 25,097 25,481 8.1 1.5 UPL Others 5,910 4,820 8,165 38.2 69.4 6,113 3,638 5,604 -8.3 54.1 Nifty (50) 1358,460 1268,088 1,379,076 1.5 8.8 933,850 980,761 1005303 7.7 2.5

January 2020 13

India Strategy | Bull market, really?

Exhibit 13: Nifty sales to decline 3% in 3QFY20, dragged by Commodities and Auto

Exhibit 14: 3QFY20 Nifty PAT to grow 8% YoY

Exhibit 15: Nifty EBITDA to post 7% YoY growth – highest in five quarters

15.5

4.5

-1.7

-11.8 -6.2 -8.2 -6.2

1.3

-2.3

3.8 8.3

15.8 10.9 12.3 14.4 15.2

23.6 25.1 22.2

10.3 6.5

-2.5 -3.3

6.1

June

-14

Sep-

14

Dec-

14

Mar

-15

June

-15

Sep-

15

Dec-

15

Mar

-16

June

-16

Sep-

16

Dec-

16

Mar

-17

June

-17

Sep-

17

Dec-

17

Mar

-18

June

-18

Sep-

18

Dec-

18

Mar

-19

June

-19

Sep-

19

Dec-

19E

Mar

-20E

36.4

4.7

-3.2 -9.9

7.3 2.9

10.5

1.9 2.4 5.0 8.4

4.1

-5.2

13.9 15.9

6.8 10.3 10.7 7.3

14.7

4.5 8.3 7.7

21.1

June

-14

Sep-

14

Dec-

14

Mar

-15

June

-15

Sep-

15

Dec-

15

Mar

-16

June

-16

Sep-

16

Dec-

16

Mar

-17

June

-17

Sep-

17

Dec-

17

Mar

-18

June

-18

Sep-

18

Dec-

18

Mar

-19

June

-19

Sep-

19

Dec-

19E

Mar

-20E

17.9

2.6 4.5

-3.8

13.6

3.1

12.1 14.3 11.7

17.9 16.8

5.0

-5.3

18.4 14.4

21.4

30.7

13.8

6.4 6.1 3.0 2.1

7.3 11.1

June

-14

Sep-

14

Dec-

14

Mar

-15

June

-15

Sep-

15

Dec-

15

Mar

-16

June

-16

Sep-

16

Dec-

16

Mar

-17

June

-17

Sep-

17

Dec-

17

Mar

-18

June

-18

Sep-

18

Dec-

18

Mar

-19

June

-19

Sep-

19

Dec-

19E

Mar

-20E

January 2020 14

India Strategy | Bull market, really?

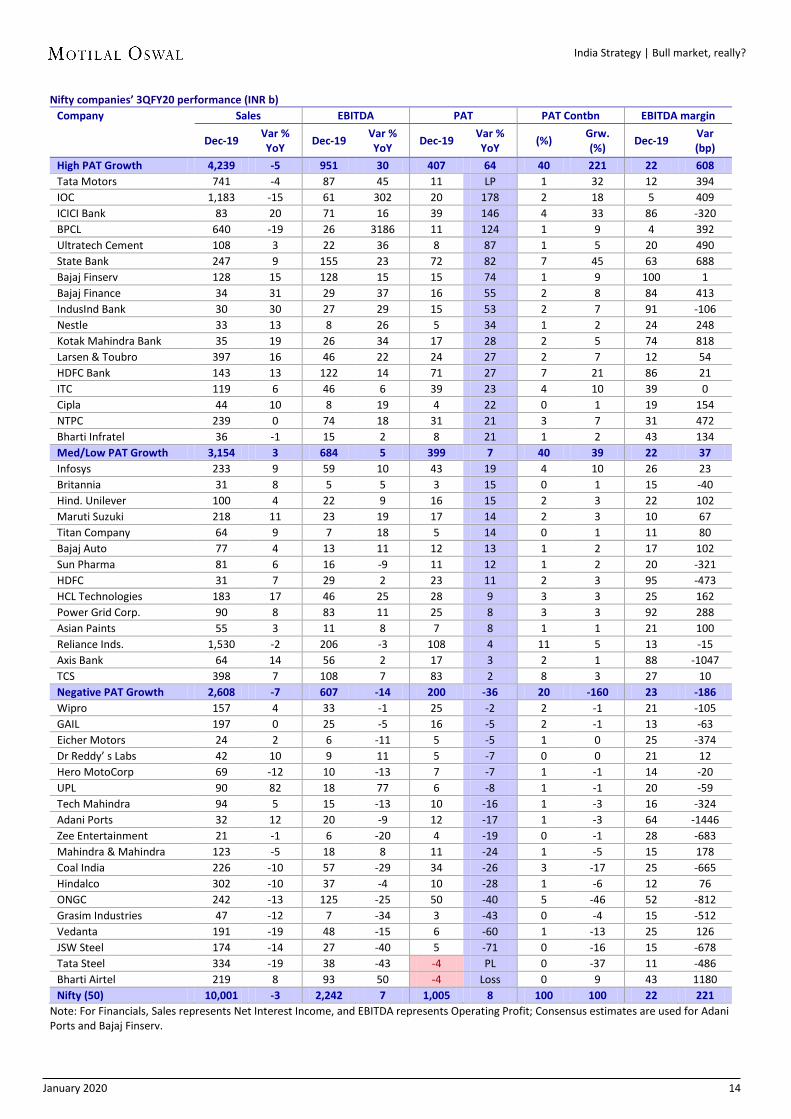

Nifty companies’ 3QFY20 performance (INR b) Company Sales EBITDA PAT PAT Contbn EBITDA margin

Dec-19 Var % YoY Dec-19 Var %

YoY Dec-19 Var % YoY (%) Grw.

(%) Dec-19 Var (bp)

High PAT Growth 4,239 -5 951 30 407 64 40 221 22 608 Tata Motors 741 -4 87 45 11 LP 1 32 12 394 IOC 1,183 -15 61 302 20 178 2 18 5 409 ICICI Bank 83 20 71 16 39 146 4 33 86 -320 BPCL 640 -19 26 3186 11 124 1 9 4 392 Ultratech Cement 108 3 22 36 8 87 1 5 20 490 State Bank 247 9 155 23 72 82 7 45 63 688 Bajaj Finserv 128 15 128 15 15 74 1 9 100 1 Bajaj Finance 34 31 29 37 16 55 2 8 84 413 IndusInd Bank 30 30 27 29 15 53 2 7 91 -106 Nestle 33 13 8 26 5 34 1 2 24 248 Kotak Mahindra Bank 35 19 26 34 17 28 2 5 74 818 Larsen & Toubro 397 16 46 22 24 27 2 7 12 54 HDFC Bank 143 13 122 14 71 27 7 21 86 21 ITC 119 6 46 6 39 23 4 10 39 0 Cipla 44 10 8 19 4 22 0 1 19 154 NTPC 239 0 74 18 31 21 3 7 31 472 Bharti Infratel 36 -1 15 2 8 21 1 2 43 134 Med/Low PAT Growth 3,154 3 684 5 399 7 40 39 22 37 Infosys 233 9 59 10 43 19 4 10 26 23 Britannia 31 8 5 5 3 15 0 1 15 -40 Hind. Unilever 100 4 22 9 16 15 2 3 22 102 Maruti Suzuki 218 11 23 19 17 14 2 3 10 67 Titan Company 64 9 7 18 5 14 0 1 11 80 Bajaj Auto 77 4 13 11 12 13 1 2 17 102 Sun Pharma 81 6 16 -9 11 12 1 2 20 -321 HDFC 31 7 29 2 23 11 2 3 95 -473 HCL Technologies 183 17 46 25 28 9 3 3 25 162 Power Grid Corp. 90 8 83 11 25 8 3 3 92 288 Asian Paints 55 3 11 8 7 8 1 1 21 100 Reliance Inds. 1,530 -2 206 -3 108 4 11 5 13 -15 Axis Bank 64 14 56 2 17 3 2 1 88 -1047 TCS 398 7 108 7 83 2 8 3 27 10 Negative PAT Growth 2,608 -7 607 -14 200 -36 20 -160 23 -186 Wipro 157 4 33 -1 25 -2 2 -1 21 -105 GAIL 197 0 25 -5 16 -5 2 -1 13 -63 Eicher Motors 24 2 6 -11 5 -5 1 0 25 -374 Dr Reddy’ s Labs 42 10 9 11 5 -7 0 0 21 12 Hero MotoCorp 69 -12 10 -13 7 -7 1 -1 14 -20 UPL 90 82 18 77 6 -8 1 -1 20 -59 Tech Mahindra 94 5 15 -13 10 -16 1 -3 16 -324 Adani Ports 32 12 20 -9 12 -17 1 -3 64 -1446 Zee Entertainment 21 -1 6 -20 4 -19 0 -1 28 -683 Mahindra & Mahindra 123 -5 18 8 11 -24 1 -5 15 178 Coal India 226 -10 57 -29 34 -26 3 -17 25 -665 Hindalco 302 -10 37 -4 10 -28 1 -6 12 76 ONGC 242 -13 125 -25 50 -40 5 -46 52 -812 Grasim Industries 47 -12 7 -34 3 -43 0 -4 15 -512 Vedanta 191 -19 48 -15 6 -60 1 -13 25 126 JSW Steel 174 -14 27 -40 5 -71 0 -16 15 -678 Tata Steel 334 -19 38 -43 -4 PL 0 -37 11 -486 Bharti Airtel 219 8 93 50 -4 Loss 0 9 43 1180 Nifty (50) 10,001 -3 2,242 7 1,005 8 100 100 22 221

Note: For Financials, Sales represents Net Interest Income, and EBITDA represents Operating Profit; Consensus estimates are used for Adani Ports and Bajaj Finserv.

January 2020 15

India Strategy | Bull market, really?

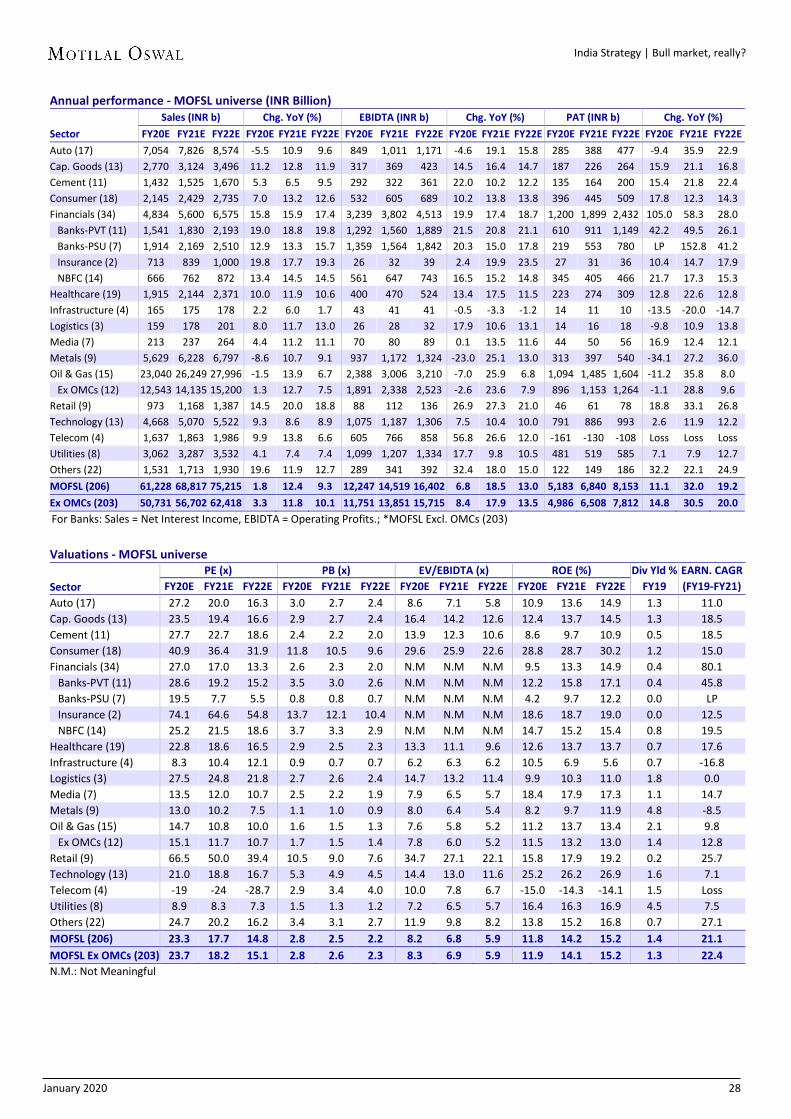

FY20 earnings recovery tepid Downside risks remain MOFSL earnings growth estimated at 11% for FY20, 32% for FY21: We estimate

FY20 revenue growth for our MOFSL Universe at 2% (v/s 14.4% CAGR over FY16-19) after three straight years of double-digit growth. Top-line performance will be impacted by Autos/Metals/O&G. We expect the EBITDA margin for our MOFSL Universe (ex-OMCs, Financials) to expand by 40bp to 18.5% in FY20. We expect profits to increase 11% YoY for the MOFSL Universe. Ex-PSU banks, the MOFSL Universe profits are estimated to increase 3% in FY20. Financials alone will likely account for 119% of incremental profits (72% contributed by PSU Banks, 35% by Private Banks), while Cement, Consumer and Capital Goods are expected to post 15%, 18% and 16% PAT growth, respectively. Ex-Financials, FY20 earnings growth for the MOFSL Universe is expected to be -2%. For FY21, we estimate MOFSL Universe sales/EBITDA/PAT growth of 12%/19%/32%.

Nifty profits to grow 9% in FY20, entirely led by Financials: Nifty sales growth is expected to be muted at 2% YoY in FY20. Nifty EBITDA/PAT are likely to grow 6%/9% in FY20. In FY20, 119% of incremental Nifty profits are likely to be contributed by BFSI. In fact, 82% of incremental FY20 profit in the Nifty is expected to accrue from three corporate lenders – Axis, ICICI and SBI. Ex-Corporate Banks, Nifty FY20 profits are likely to grow 2% – lowest in four years. Ex-BFSI, Nifty FY20 profits are expected to decline 2%, again worst in four years.

Exhibit 16: Expect Nifty PAT CAGR of 18% over FY19-21

Sales CAGR (%)

EBIDTA CAGR (%)

EBIDTA Margin

(%)

PAT (INR b)

PAT Gr. / CAGR (%)

PAT Delta Share (%)

Sector (FY19-21) (FY19-21) FY21E FY20E FY21E FY22E FY20E FY21E FY22E (FY19-21) (FY19-21) High PAT CAGR (>20%) 16 19 50.2 1,368 2,110 2,696 91 54 28 72 64 Financials (34) 16 19 67.9 1,200 1,899 2,432 105 58 28 80 60 Banks-PVT (11) 19 21 85.2 610 911 1,149 42 50 26 46 22 Banks-PSU (7) 13 18 72.1 219 553 780 LP 153 41 LP 32 Insurance (2) 19 11 3.8 27 31 36 10 15 18 13 0 NBFC (14) 14 16 84.9 345 405 466 22 17 15 20 6 Others (22) 16 25 19.9 122 149 186 32 22 25 27 3 Retail (9) 17 27 9.6 46 61 78 19 33 27 26 1 Medium PAT CAGR (10-20%) 6 10 13.5 2,364 3,032 3,419 -1 28 13 12 29 Cement (11) 6 16 21.1 135 164 200 15 22 22 19 2 Cap. Goods (13) 12 15 11.8 187 226 264 16 21 17 19 3 Healthcare (19) 11 15 21.9 223 274 309 13 23 13 18 3 Consumer (18) 10 12 24.9 396 445 509 18 12 14 15 5 Media (7) 8 7 33.5 44 50 56 17 12 12 15 1 Auto (17) 2 7 12.9 285 388 477 -9 36 23 11 3 Oil & Gas (15) 6 8 11.5 1,094 1,485 1,604 -11 36 8 10 12 Ex OMCs (12) 7 10 16.5 896 1,153 1,264 -1 29 10 13 11 Low PAT CAGR (up to 10%) 5 11 26.2 1,451 1,698 2,038 -7 17 20 5 7 Utilities (8) 6 14 36.7 481 519 585 7 8 13 7 3 Technology (13) 9 9 23.4 791 886 993 3 12 12 7 5 Logistics (3) 10 14 16.0 14 16 18 -10 11 14 0 0 Metals (9) 1 -2 18.8 313 397 540 -34 27 36 -8 -4 Infrastructure (4) 4 -2 23.5 14 11 10 -14 -20 -15 -17 0 Telecom (4) 12 41 41.1 -161 -130 -108 Loss Loss Loss Loss 2 MOFSL (206) 7 13 21.1 5,183 6,840 8,153 11 32 19 21 100 MOFSL Ex OMCs (203) 7 13 24.4 4,986 6,508 7,812 15 31 20 22 NA Nifty (50) 7 12 21.7 4,173 5,339 6,302 9 28 18 18 NA Sensex (30) 8 14 27.5 3,299 4,205 4,980 18 27 18 23 NA Note: For Banks: Sales = Net Interest Income, EBIDTA = Operating Profits; Note: Sensex & Nifty Numbers are Free Float.

EARNINGS FY20-21

January 2020 16

India Strategy | Bull market, really?

Exhibit 17: Expect Nifty ex corporate lenders PAT CAGR of 12% over FY19-21

Exhibit 18: Nifty profits expected to grow 9% in FY20, entirely led by Financials Profit (INR b) FY17 FY18 FY19 FY20E FY21E Nifty (50) 3,263 3,453 3,821 4,173 5,339 Growth YoY (%) 9 6 11 9 28 Financials 509 459 596 1,013 1,475 Growth YoY (%) -16 -10 30 70 46 Nifty - Ex Financials 2,754 2,994 3,226 3,160 3,864 Growth YoY (%) 15 9 8 -2 22 Corporate Banks 137 25 103 393 670 Growth YoY (%) -55 -82 314 280 71 Nifty - Ex Corporate Banks 3,126 3,428 3,718 3,780 4,669 Growth YoY (%) 16 10 8 2 24 Incremental Nifty PAT 273 190 369 352 1,166 Incremental Corp Banks PAT -165 -112 78 289 277 Incremental Financials PAT -96 -50 137 417 462 Incre. Financials PAT/ Incre. Nifty PAT (%) -35 -26 37 119 40 Incre. Corp Bank PAT/ Incre. Nifty PAT (%) -60 -59 21 82 24

MOFSL Universe earnings to grow 11% in FY20 aided by banks For the MOFSL Universe, we estimate PAT growth of 11% for FY20 (off a base of

12% in FY19), led by a continued recovery in Financials (profits expected to jump 2.1x YoY and contribute ~119% of incremental profits in FY20). Other sectors that are expected to do well are Capital Goods/Cement/Consumer/Retail (+16%/15%/18%/19%).

Auto, Metals, O&G, Technology and Utilities are expected to have a subdued year with earnings growth of (9%), (34%), (11%), 3%, and 7%, respectively.

Nifty EPS stable at INR532 for FY20 Our Nifty EPS estimates are stable at INR532 for FY20 (prior: INR538) but

upgraded by 1.5% to INR693 for FY21 (prior: INR683). We are now building in EPS growth of 10% for the Nifty in FY20. Corporate

Banks are likely to account for 82% of incremental profit growth for the Nifty in FY20, and Financials for 119%. We expect Nifty profit growth of 2% ex-corporate banks and a profit decline of 2% ex-BFSI in FY20.

For FY20, major earnings upgrades are in Tata Motors (L to P), Bharti (47%), Maruti (12%), SBI (9%) and Coal India (5%), while the major downgrades are in Grasim Inds (-43%), Axis Bank (21%), ONGC (18%), Vedanta (13%), Tata Steel (12%) and IOC (10%).

3

15

2

9

16

10 8

2

24

5

13

3 6

9

6

11 9

28

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E

Nifty Ex Corp. Banks PAT chg. YoY (%) Nifty-50 PAT chg. YoY (%)

January 2020 17

India Strategy | Bull market, really?

Exhibit 19: Top Nifty companies’ EPS upgrades/downgrades since 2QFY20 review (%)

Company FY20E Tata Motors LP Maruti Suzuki 11.6 State Bank 8.8 Coal India 5.3 GAIL -5.1 Bajaj Finserv -6.8 UPL -9.4 IOC -10.4 Tata Steel -12.0 Vedanta -13.3 ONGC -18.4 Axis Bank -21.2 Grasim Industries -43.5

Exhibit 20: Nifty stock absolute FY20E PAT change (INR b)

Exhibit 21: Nifty stock absolute FY21E PAT change (INR b)

4,17

3

3,82

1 21

2 73

62

54

29

26

22

22

20

18

18

18

17

15

15

9 9 9 8 8 6 6 6 4 4 4 3 3 3 3 3 2 1 1 1 2 4 8 9 11

11

15

16

18

22

26

44

62

85

Nift

y-50

FY1

9…SB

IIC

ICI B

kRe

lianc

e In

dHD

FC B

kIT

CIn

dusI

nd B

kBa

jaj F

inan

ceL&

TBh

arti

Airt

elBa

jaj F

inse

rvHD

FCTa

ta M

otor

sKo

tak

Mah

Bk

NTP

CU

ltrat

ech

TCS

Bhar

ti In

frat

elPo

wer

Grid HU

LSu

n Ph

arm

aW

ipro

Asia

n Pa

ints

Adan

i Por

tsAx

is Bk

Baja

j Aut

oZe

e En

tN

estle UPL

Info

sys

Cipl

aHC

L Te

chBr

itann

iaTi

tan

CoDr

Red

dy’s

Te

ch M

ahEi

cher

Mot

Hero

Mot

oCo

al In

dia

M&

MGA

ILHi

ndal

coM

arut

i Suz

uki

Gras

imJS

W S

teel

Veda

nta

BPCL

Tata

Ste

elO

NGC IO

CN

ifty-

50 F

Y20E

…

Nift

y50

FY19

PAT

Nift

y50

FY20

E PA

T 5,

339

4,17

3 17

1 116

86

83

79

76

57

41

32

31

26

24

24

21

20

19

19

18

17

16

14

13

13

11

10

10

10

9 8 7 7 6 6 6 6 5 5 4 4 3 3 3 3 3 3 2 1 1

Nift

y-50

FY2

0E…

Relia

nce

Ind

SBI

ICIC

I Bk

IOC

HDFC

Bk

Axis

BkO

NGC

Tata

Mot

ors

TCS

BPCL

Info

sys

Indu

sInd

Bk

L&T

NTP

CBa

jaj F

inan

ceM

arut

i Suz

uki

Kota

k M

ah B

kJS

W S

teel

HCL

Tech

Tata

Ste

elHU

LHD

FCU

ltrat

ech

Pow

er G

ridBh

arti

Airt

elBa

jaj F

inse

rvM

&M

Sun

Phar

ma

Gras

imAd

ani P

orts

GAIL

UPL ITC

Wip

roHi

ndal

coTe

ch M

ahTi

tan

CoEi

cher

Mot

Hero

Mot

oCo

al In

dia

Zee

Ent

Dr R

eddy

’s

Nes

tleCi

pla

Baja

j Aut

oBr

itann

iaVe

dant

aBh

arti

Infr

atel

Nift

y-50

FY2

1E…

Nift

y50

FY20

E PA

T

Nift

y50

FY21

E PA

T

January 2020 18

India Strategy | Bull market, really?

Exhibit 22: Nifty performance - expect FF PAT CAGR (FY19-21) of 21%

Sales (INR b) Sales EBIDTA Margin (%) EBITDA PAT (INR b) PAT YoY (%) PAT Contbn to

Company FY20E FY21E FY22E CAGR % 19-21 FY20 FY21 FY22 CAGR %

19-21 FY20E FY21E FY22E FY20 FY21 FY22 CAGR % 19-21 Delta %

High PAT Gr. (20%+) 14,487 16,474 18,393 11 26 28 29 21 1,612 2,307 2,800 53 43 21 48 83 Tata Motors 2,885 3,164 3,397 2 12 13 13 16 3 44 60 LP 1,255 35 LP 4 State Bank 977 1,118 1,288 12 69 70 71 19 235 351 463 924 49 32 291 22 ICICI Bank 326 385 456 19 85 85 86 18 106 192 234 216 81 22 139 10 Axis Bank 251 296 351 17 92 95 97 22 51 127 183 9 149 44 65 5 IndusInd Bank 118 143 175 27 91 95 97 30 59 83 107 79 40 29 58 3 Ultratech Cement 449 486 532 8 23 24 24 25 40 52 65 61 31 23 45 2 Bajaj Finance 132 170 210 32 83 84 84 37 62 82 100 55 33 21 43 3 Bajaj Finserv 164 206 249 30 80 74 68 25 51 60 65 57 19 9 37 2 HDFC Bank 560 662 787 17 85 86 87 20 265 344 416 26 30 21 28 9 Reliance Inds. 6,175 7,069 7,834 12 15 17 17 21 460 631 707 16 37 12 26 15 Larsen & Toubro 1,555 1,779 2,002 15 12 13 13 22 102 125 148 27 23 18 25 3 Kotak Mahindra Bank 136 160 191 19 75 77 78 21 90 108 132 24 21 22 23 2 Sun Pharma 325 359 397 12 20 22 22 18 44 53 59 21 21 10 21 1 Zee Entertainment 85 98 112 11 32 32 32 11 20 23 26 24 17 16 20 0 UPL 348 380 412 32 20 22 22 42 24 30 36 15 25 19 20 1

Med. PAT Gr. (10-20%) 3,285 3,661 4,084 10 32 32 33 18 653 730 832 19 12 14 15 12 Titan Company 219 261 314 15 11 12 12 23 15 20 25 9 30 29 19 0 Cipla 172 188 208 7 21 21 21 12 18 21 23 18 16 12 17 0 Asian Paints 214 244 279 12 20 20 20 17 28 30 35 26 9 16 17 1 Nestle 125 141 161 12 24 24 24 11 21 24 27 20 14 16 17 0 HDFC 125 139 156 10 98 98 98 11 105 118 133 21 12 12 16 2 Hind. Unilever 405 458 517 9 24 25 26 16 71 85 97 13 19 15 16 1 Britannia 118 133 151 10 15 16 16 11 14 16 18 18 14 16 16 0 Adani Ports 123 139 153 13 64 65 64 17 45 53 52 14 16 -1 15 1 NTPC 994 1,100 1,211 10 31 33 35 35 130 151 173 13 16 15 15 2 Bharti Infratel 144 150 157 1 42 43 44 4 34 33 49 35 -4 49 14 0 ITC 480 529 583 8 39 38 38 8 154 160 176 24 4 10 13 2 Dr Reddy’ s Labs 165 179 195 9 21 22 21 15 18 21 23 6 16 6 11 0

Low PAT Gr. (<10%) 26,363 29,522 31,697 4 16 17 17 4 1,908 2,302 2,670 -14 21 16 2 6 Power Grid Corp. 388 422 452 14 90 90 90 17 109 119 131 9 10 9 9 1 HCL Technologies 706 801 884 15 23 24 24 17 104 120 135 3 16 12 9 1 Infosys 913 982 1,069 9 25 26 26 10 165 191 213 2 16 12 9 2 Bajaj Auto 301 332 366 5 16 16 16 1 52 54 61 8 5 13 7 0 TCS 1,573 1,680 1,844 7 26 27 27 6 328 360 413 3 10 15 6 3 Wipro 614 652 685 5 20 20 20 6 97 103 108 6 6 5 6 1 Eicher Motors 92 109 128 6 25 27 28 0 20 24 31 -9 20 27 5 0 Tech Mahindra 370 404 428 8 16 17 17 3 42 47 51 -3 12 9 4 0 BPCL 2,765 3,015 3,105 1 5 6 6 5 59 91 94 -30 53 4 3 0 Maruti Suzuki 782 878 996 1 10 12 14 0 60 79 102 -20 32 29 3 0 Mahindra & Mahindra 1,015 1,109 1,197 3 14 14 15 2 42 52 62 -17 23 19 1 0 JSW Steel 752 849 1,087 0 18 23 22 1 58 77 110 -24 32 44 0 0 Hero MotoCorp 294 326 355 -2 14 14 14 -4 30 34 38 -11 12 12 0 0 IOC 5,134 6,227 6,739 9 5 6 6 3 88 171 178 -49 95 4 -1 0 ONGC 4,270 4,697 4,858 2 17 17 17 -2 286 343 364 -18 20 6 -1 0 Coal India 965 1,022 1,099 1 23 23 24 -4 166 170 195 -5 2 15 -1 0 GAIL 772 865 929 7 11 12 12 3 53 59 65 -17 13 10 -3 0 Hindalco 1,259 1,442 1,450 5 12 12 12 5 44 50 49 -20 13 0 -5 0 Grasim Industries 201 206 221 0 15 15 15 -13 27 35 44 -37 30 25 -10 -1 Tata Steel 1,415 1,543 1,803 -1 14 16 18 -7 58 74 122 -43 29 65 -15 -2 Vedanta 821 854 778 -4 20 22 22 -1 46 45 68 -32 -2 52 -18 -1 Bharti Airtel 867 1,004 1,100 11 42 45 46 33 -15 -5 9 Loss Loss LP Loss 2

Nifty (PAT free float) 44,134 49,658 54,175 7 21 22 22 12 2,199 2,865 3,421 13 30 19 21 100

January 2020 19

India Strategy | Bull market, really?

SECTOR WEIGHT / PORTFOLIO PICKS

BSE 100

MOST WEIGHT

WEIGHT RELATIVE TO BSE100

EFFECTIVE SECTOR STANCE

Financials 39.5 39.0 -0.5 Neutral Private 24.2 23.0 -1.2 Underweight HDFC Bank 9.5 8.0 -1.5 Buy ICICI Bank 6.0 8.0 2.0 Buy Axis Bank 3.0 5.0 2.0 Buy Federal Bank 0.3 2.0 1.7 Buy PSU 2.6 5.0 2.4 Overweight SBI 2.2 5.0 2.8 Buy NBFCs 12.7 11.0 -1.7 Underweight HDFC 7.3 6.0 -1.3 Buy L&T Finance Holdings 0.0 2.0 2.0 Buy ICICI Prudential Life 0.0 3.0 3.0 Buy Technology / Telecom / Media 13.1 15.0 1.9 Overweight Infosys 4.8 6.0 1.2 Buy Bharti Airtel 1.5 5.0 3.5 Buy HCL Tech 1.1 2.0 0.9 Buy L&T Infotech 0.0 2.0 2.0 Buy Consumption / Retail 12.4 10.0 -2.4 Underweight ITC 3.5 3.0 -0.5 Neutral HUL 2.4 3.0 0.6 Buy Titan 0.8 2.0 1.2 Neutral Tata Global Beverages 0.2 2.0 1.8 Buy Energy 11.4 7.0 -4.4 Underweight Reliance Inds 8.4 5.0 -3.4 Buy IOC 0.5 2.0 1.5 Buy Cap Goods, Infra & Cement 6.7 7.0 0.3 Neutral Larsen & Toubro 2.8 4.0 1.2 Buy Ultratech 0.8 3.0 2.2 Buy Auto 6.5 6.0 -0.5 Neutral Maruti 1.7 2.0 0.3 Buy Eicher Motors 0.5 2.0 1.5 Buy Ashok Leyland 0.2 2.0 1.8 Buy Healthcare 3.6 4.0 0.4 Neutral Lupin 0.3 2.0 1.7 Buy Alkem Labs 0.0 2.0 2.0 Buy Utilities / Metals 4.9 4.0 -0.9 Neutral NTPC 0.9 2.0 1.1 Buy Hindalco 0.6 2.0 1.4 Buy Midcaps 1.9 8.0 6.1 Overweight Indian Hotels 0.0 1.0 1.0 Buy ABFRL 0.0 1.0 1.0 Buy CG Consumer Electrical 0.2 1.0 0.8 Buy Voltas 0.3 1.0 0.7 Buy Colgate 0.3 1.0 0.7 Buy JK Cement 0.0 1.0 1.0 Buy Motherson Sumi 0.3 1.0 0.7 Buy Future Retail 0.0 1.0 1.0 Buy Cash 0.0 0.0 0.00 TOTAL 100.0 100.0

MOFSL model portfolio

January 2020 20

India Strategy | Bull market, really?

Nifty ends year near record high; Mid-caps underperform again FII flows highest since CY14

Buoyed by the strong rally after the corporate tax cuts in Sep’19, the Nifty ended 2019 with impressive 12% gains. Healthy FII inflows and a benign global backdrop too worked in favor of the markets.

CY19 was characterized by sharp polarization between the Nifty and the Nifty Midcap/Smallcap as well as within the benchmark. This trend is likely to continue until earnings recover and more importantly become broad-based.

In CY19, all the key global markets – Brazil (+32%), the US (+29%), Russia (+28%), Taiwan (+23%), Japan (+18%), the UK (+12%), India-Nifty (+12%), China-HSCEI (+10%) and Korea (+8%) – closed higher in local currency terms.

India’s share in the world market cap (2.5%) is at its historical average. In CY19, the world’s market cap was up by 24.9% (USD17.3t) and India’s market cap by 3.4% (USD0.1t).

Among sectors, Private Banks (+31%), Real Estate (+27%), PSU Banks (+19%), NBFCs (+15%), Technology (+10%) and Oil (7%) were the positive performers for CY19. Metals (-12%), Automobiles (-11%), Capital Goods (-10%), Utilities (-4%), Consumer (-4%), Healthcare (-4%), and Cement (-2%) were the key laggards.

Market breadth was balanced with 25 Nifty stocks closing higher in the year. Bajaj Finance (+60%), Bharti Airtel (+59%), ICICI Bank (+50%), Bajaj Finserv (+45%) and BPCL (+35%) were the top performers. Yes Bank (-74%), Zee Ent (-39%), M&M (-34%), GAIL (-33%) and Vedanta (-25%) were the top laggards.

FIIs got back in action, infusing USD14.2b in CY19 – the highest since CY14. However, DII inflows were weak at USD6b compared to USD15.9b in the previous year. Domestic MF inflows moderated to USD7.6b from USD17.5b in the previous year. Notably, CY19 marked the eighth straight year of DII ex-MF outflows (USD35.4b over CY12-19).

Nifty P/E is valued at 18.4x, above its historical average of 18.1x. At 2.7x, the Nifty P/B is marginally above the historical average of 2.6x. Market-cap-to-GDP at 75% (FY20E GDP) is near its long-term average.

Exhibit 23: CY19 returns impressive post a muted CY18

Exhibit 24: Nifty QoQ change (%) — gains strength toward year-end

5,20

1

6,13

5

4,62

4

5,90

5

6,30

4

8,28

3

7,94

6

8,18

6

10,5

31

10,8

63

12,1

68

76 18 -25 28 7 31 -4 3 29 3 12

84 23 -37 24 -5 29 -8 0 37 -5 10

CY09

CY10

CY11

CY12

CY13

CY14

CY15

CY16

CY17

CY18

CY19

Trend in Nifty

Annual Return in INR (%)

CAGR in INR: 8.9% CAGR in USD: 4.3%

Annual Return in USD (%)

4 3

-1

-5

0

-3

7

4

-5

12

4 3

8

-4

6

2

-1

7

1

-3

6

Dec-

14M

ar-1

5Ju

n-15

Sep-

15De

c-15

Mar

-16

Jun-

16Se

p-16

Dec-

16M

ar-1

7Ju

n-17

Sep-

17De

c-17

Mar

-18

June

-18

Sep-

18De

c-18

Mar

-19

Jun-

19Se

p-19

Dec-

19QoQ Return (%)

MARKETS & FLOWS

Refer our latest India Strategy report on The Decade That

Was

January 2020 21

India Strategy | Bull market, really?

All major economies end higher in CY19 In CY19, all the key global markets – Brazil (+32%), the US (+29%), Russia (+28%),

Taiwan (+23%), Japan (+18%), the UK (+12%), India-Nifty (+12%), China-HSCEI (+10%) and Korea (+8%) – closed higher in local currency terms.

Exhibit 25: World equity indices (CY19) – local currency (%)

Exhibit 26: World equity indices (CY19) – USD (%)

India’s share in world market cap at historical average India’s share in the world market cap (2.5%) is at its historical average. In CY19,

the world’s market cap was up by 24.9% (USD17.3t) and India’s market cap by 3.4% (USD0.1t).

Exhibit 27: Trend in India's contribution to world market cap

Exhibit 28: Market cap change in CY19 (%)

8

10

12

12

15

18

23

28

29

32

South Korea

China (HSCEI)

India - Nifty

UK

MSCI EM

Japan

Taiwan

Russia MICEX

S&P 500

Brazil

4

10

11

15

17

20

26

27

29

43

South Korea

India - Nifty

China (HSCEI)

MSCI EM

UK

Japan

Taiwan

Brazil

S&P 500

Russia MICEX

3.3

1.6

2.5

1.5

2.0

2.5

3.0

3.5

Dec-

09Ju

n-10

Nov

-10

Apr-

11Se

p-11

Feb-

12Au

g-12

Jan-

13Ju

n-13

Nov

-13

Apr-

14O

ct-1

4M

ar-1

5Au

g-15

Jan-

16Ju

n-16

Dec-

16M

ay-1

7O

ct-1

7M

ar-1

8Au

g-18

Jan-

19Ju

l-19

Dec-

19

India's Contribution to World Mcap (%)

Average of 2.5%

3 5 8

14 16

26 28 28

37 39

2.1 1.4 0.5 3.5 6.3 1.3 34.4 1.1 7.3 0.8

Indi

a

Kore

a

Indo

nesiaU

K

Japa

n

Taiw

anUS

Braz

il

Chin

a

Russ

ia

Mkt cap chg CY19 (%) Curr Mcap (USD Tr)

January 2020 22

India Strategy | Bull market, really?

Sector performance: Financials, Real Estate, Technology and Oil end higher In the sectoral space, Private Banks (+31%), Real Estate (+27%), PSU Banks

(+19%), NBFCs (+15%), Technology (+10%) and Oil (7%) were the positive performers for CY19.

Metals (-12%), Automobiles (-11%), Capital Goods (-10%), Utilities (-4%), Consumer (-4%), Healthcare (-4%), and Cement (-2%) were the key laggards.

Mid-caps continued underperforming the benchmark for the second year.

Exhibit 29: Trend in sector performance YoY (%) — Private Banks, Real Estate, PSU Banks and NBFCs top outperformers Return YoY (%) CAGR (%) Sector CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18 CY19 CY09-CY19 CY14-CY19 Pvt - Banks 98 36 -26 63 1 61 2 5 47 18 31 21 19 Real Estate 70 -26 -52 53 -32 8 -14 -6 106 -31 27 -5 8 PSU - Banks 73 33 -39 46 -26 79 -30 9 38 -6 19 7 4 NBFC 109 38 -27 48 -8 49 -8 4 33 10 15 13 10 Nifty 50 76 18 -25 28 7 31 -4 3 29 3 12 9 8 Technology 133 32 -16 -1 60 17 5 -8 11 25 10 12 8 Oil 73 1 -29 13 4 12 -3 27 34 -16 7 3 8 Cement 84 37 5 41 -14 37 1 17 46 -17 -2 13 7 Healthcare 69 34 -13 39 23 47 15 -13 0 -6 -4 10 -2 Consumer 40 32 10 47 11 18 1 3 32 11 -4 15 8 Utilities 74 -6 -40 11 -15 23 -6 2 20 -16 -4 -5 -2 Nifty Midcap100 99 19 -31 39 -5 56 6 7 47 -15 -4 9 6 Capital Goods 104 9 -48 35 -6 50 -9 -3 40 -2 -10 2 2 Auto 204 38 -20 40 7 52 -1 9 32 -22 -11 10 0 Metal 234 1 -47 19 -10 8 -31 37 48 -21 -12 -5 -1

Breadth balanced in CY19 – 25 Nifty stocks closed higher Market breadth was balanced with 25 Nifty stocks closing higher in the year.

Bajaj Finance (+60%), Bharti Airtel (+59%), ICICI Bank (+50%), Bajaj Finserv (+45%) and BPCL (+35%) were the top performers.

Yes Bank (-74%), Zee Ent (-39%), M&M (-34%), GAIL (-33%) and Vedanta (-25%) are the top laggards.

Exhibit 30: Best and worst Nifty performers for CY19 (%)—25 companies in the Nifty delivered positive returns