WIN-dow to the week that was - Motilal Oswal

19

WIN – Week In a Nutshell 1 15 th March 2013 WEEK IN A NUTSHELL WIN-dow to the week that was Week in a Nutshell (WIN) The week gone by was a largely uneventful week even with 3 important economic data points released – WPI (6.84%), IIP (2.4%, after 2 months of de-growth) and trade deficit data (USD 15 Bn, 8 month low). Core inflation now at 3.8% is the big comforting factor. This month’s inflation also completely digests the fuel price rise. With almost all boxes ticked for RBI, a positive surprise would be welcome. COBRAPOST came out with a revealing sting operation on ICICI, Axis and HDFC Bank exposing money laundering modus operandi employed by these banks. The management of these banks did not deny the same but did assure that these are pockets of deviation and not a norm. TWO WHEELER – The news flow in the sector reminds us of the telecom sector a couple of years ago – INTENSE COMPETITION the constant theme. HMSI starts the battle against Bajaj now, launches all new 150 CC bike. Specs similar to Pulsar 150 CC, pricing the key. With the 100cc model to be launched in May and the 150 CC, FY14 could see a battle royale. They also said this – “We many now overtake Hero by 2015/16 and not 2020 as earlier planned”. IT SECTOR – With the US economy rebounding faster than most expectations, IT firms seem to be getting back into the pink of health. TCS, in its Analyst Meet retained 4Q outlook and indicated likely growth acceleration in FY14 on the back of better demand environment than that witnessed a year ago. Ashish’s note on Infosys likely Fy14 $ growth guidance is a MUST READ Our highlight event of the week was the discovery of ICE GAS. After 17 years of research, Japan extracts ice gas. Estimates of 40 Tn cu feet of methane. Necessity is the mother of invention! After the nuclear shut down and trade data turning -Ve, something had to give Some of the highlights of this edition: INDIA ENERGY: Landmark reforms … Oil PSUs to benefit Infosys: Making a case for growth convergence; Deals won, visible fruition of changed strategy increase growth confidence. INDIA AUTO (2W): HMSI’s profitability higher than Hero’s. Key WIN-dicators IIP moves back in to positive territory after two months HMSI earns higher margins than Hero Return ratios also superior than Hero Nifty (-1.2%) Week ended 15 th March 2013 WWW – WIN Weekend Wisdom PRICE IS EASY TO GET, VALUE IS DIFFICULT TO ASCERTAIN

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of WIN-dow to the week that was - Motilal Oswal

WIN – Week In a Nutshell 1 15th March 2013

WEEK IN A NUTSHELL

WIN-dow to the week that was Week in a Nutshell (WIN)

The week gone by was a largely uneventful week even with 3 important economic data points released – WPI (6.84%), IIP (2.4%, after 2 months of de-growth) and trade deficit data (USD 15 Bn, 8 month low). Core inflation now at 3.8% is the big comforting factor. This month’s inflation also completely digests the fuel price rise. With almost all boxes ticked for RBI, a positive surprise would be welcome. COBRAPOST came out with a revealing sting operation on ICICI, Axis and HDFC Bank exposing money laundering modus operandi employed by these banks. The management of these banks did not deny the same but did assure that these are pockets of deviation and not a norm. TWO WHEELER – The news flow in the sector reminds us of the telecom sector a couple of years ago – INTENSE COMPETITION the constant theme. HMSI starts the battle against Bajaj now, launches all new 150 CC bike. Specs similar to Pulsar 150 CC, pricing the key. With the 100cc model to be launched in May and the 150 CC, FY14 could see a battle royale. They also said this – “We many now overtake Hero by 2015/16 and not 2020 as earlier planned”. IT SECTOR – With the US economy rebounding faster than most expectations, IT firms seem to be getting back into the pink of health. TCS, in its Analyst Meet retained 4Q outlook and indicated likely growth acceleration in FY14 on the back of better demand environment than that witnessed a year ago. Ashish’s note on Infosys likely Fy14 $ growth guidance is a MUST READ Our highlight event of the week was the discovery of ICE GAS. After 17 years of research, Japan extracts ice gas. Estimates of 40 Tn cu feet of methane. Necessity is the mother of invention! After the nuclear shut down and trade data turning -Ve, something had to give

Some of the highlights of this edition:

INDIA ENERGY: Landmark reforms … Oil PSUs to benefit Infosys: Making a case for growth convergence; Deals won, visible

fruition of changed strategy increase growth confidence. INDIA AUTO (2W): HMSI’s profitability higher than Hero’s.

Key WIN-dicators IIP moves back in to positive territory after two months

HMSI earns higher margins than Hero

Return ratios also superior than Hero

Nifty (-1.2%)

Week ended

15th

March 2013

WWW – WIN Weekend Wisdom

PRICE IS EASY TO GET, VALUE IS DIFFICULT TO ASCERTAIN

WIN – Week In a Nutshell 2 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

*W+INside this week’s edition

WIN-teresting data points ................................................................................................................................... 3

WIN-ning charts & chats ..................................................................................................................................... 4

Human Development Index ............................................................................................................................................. 4

WIN-conomics .................................................................................................................................................... 5

ECONOMICS: Feb-13 trade deficit at 8-month low on falling non-oil imports; real INR appreciates .............................. 5

ECONOMICS: Jan-13 IIP growth at 2.4% after two months of de-growth ....................................................................... 5

INDIA ECONOMICS: Feb-13 WPI at 6.8% on fuel inflation; Core inflation at 3.8%. ......................................................... 6

Indian Transfer Pricing laws based on OECD guidelines; Belt tightened elsewhere too ................................................. 6

WIN-sights from management interaction ........................................................................................................... 8

UP Power Corporation - SK Agarwal, CFO ....................................................................................................................... 8

Nestle - Nandu Nandkishore, executive vice-president, head of Asia, Africa, Middle East and Oceania ...................... 10

WIN Sector Updates .......................................................................................................................................... 12

AUTO (2W): HMSI's launches CB Trigger (150cc) targeting Bajaj’s Pulsar; Aims for leadership by 2015-16 ................ 12

GASOLINE: The oil & gas monthly – March 2013 .......................................................................................................... 12

INDIA AUTO (2W): HMSI’s profitability higher than Hero’s. .......................................................................................... 12

INDIA ENERGY: Landmark reforms … Oil PSUs to benefit .............................................................................................. 12

IRON ORE: price outlook weakening once again; downside to NMDC estimates, valuations attractive ...................... 13

METALS WEEKLY: Iron ore and coking coal decline further; Base metals prices were mixed ....................................... 14

mPower (February 2013): Monthly round-up of power utilities .................................................................................... 14

WIN Corporate Corner ...................................................................................................................................... 15

AKZO NOBEL : Near term Paint industry demand at risk; RM softening is well entrenched. ........................................ 15

HAVELLS India: Proposed special resolution to hike FII limit / enter into new business segments ............................... 15

INFOSYS: Making a case for growth convergence; Deals won, visible fruition of changed strategy ............................ 15

ITC: Highlights from channel checks; Pricing ladder has never been so crucial; Maintain Buy ..................................... 16

RAIN COMMODITIES: Valuation attractive .................................................................................................................... 16

TATA MOTORS: JLR Feb-13 retails grew 3% YoY (-23% MoM) to 26,855 units. ............................................................ 17

TCS (Analyst meet takeaways): Retains 4Q outlook; Reiterates likely growth acceleration in FY14 ............................ 17

WIN Collage ...................................................................................................................................................... 18

Indian technology firms : Looking for India’s Zuckerberg .............................................................................................. 18

Nifty Valuations at a glance ............................................................................................................................... 19

WIN – Week In a Nutshell 3 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

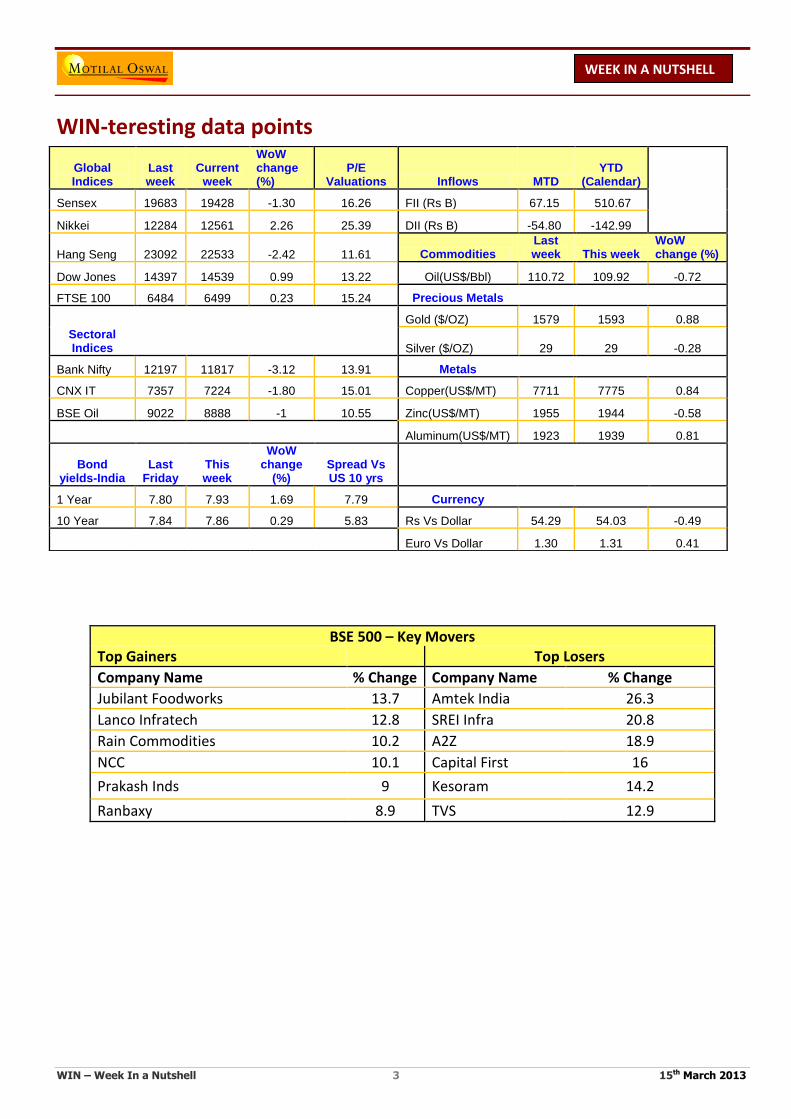

WIN-teresting data points

BSE 500 – Key Movers Top Gainers

Top Losers

Company Name % Change Company Name % Change

Jubilant Foodworks 13.7 Amtek India 26.3

Lanco Infratech 12.8 SREI Infra 20.8

Rain Commodities 10.2 A2Z 18.9

NCC 10.1 Capital First 16

Prakash Inds 9 Kesoram 14.2

Ranbaxy 8.9 TVS 12.9

Global Indices

Last week

Current week

WoW change (%)

P/E Valuations Inflows MTD

YTD (Calendar)

Sensex 19683 19428 -1.30 16.26 FII (Rs B) 67.15 510.67

Nikkei 12284 12561 2.26 25.39 DII (Rs B) -54.80 -142.99

Hang Seng 23092 22533 -2.42 11.61 Commodities Last week This week

WoW change (%)

Dow Jones 14397 14539 0.99 13.22 Oil(US$/Bbl) 110.72 109.92 -0.72

FTSE 100 6484 6499 0.23 15.24 Precious Metals

Gold ($/OZ) 1579 1593 0.88

Sectoral Indices Silver ($/OZ) 29 29 -0.28

Bank Nifty 12197 11817 -3.12 13.91 Metals

CNX IT 7357 7224 -1.80 15.01 Copper(US$/MT) 7711 7775 0.84

BSE Oil 9022 8888 -1 10.55 Zinc(US$/MT) 1955 1944 -0.58

Aluminum(US$/MT) 1923 1939 0.81

Bond yields-India

Last Friday

This week

WoW change

(%) Spread Vs US 10 yrs

1 Year 7.80 7.93 1.69 7.79 Currency

10 Year 7.84 7.86 0.29 5.83 Rs Vs Dollar 54.29 54.03 -0.49

Euro Vs Dollar 1.30 1.31 0.41

WIN – Week In a Nutshell 4 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN-ning charts & chats

Human Development Index GROSS domestic product, Robert F. Kennedy said, “measures everything…except that which makes life

worthwhile.”

In an attempt to redress the fixation with economic output alone, in 1990 the United Nations Development Programme (UNDP) launched the Human Development Index (HDI). This index combines life expectancy at birth, the average and expected number of years in education and economic output.

Only two countries, Zimbabwe and Lesotho, have seen their index scores fall since 1990, but elsewhere big strides have been made, particularly in China, Iran and India.

UNDP expects the world’s middle-class population—defined as households with incomes over $20,000 a year—to grow from 1.85 billion in 2009 to 3.25 billion in 2020. It predicts that by 2030, 80% of middle-class households will live in emerging and developing countries, accounting for 70% of global spending.

These figures mask some important difference within countries. The UNDP estimates that Latin Americans in America have an HDI of 0.75 (on a par with Kazakhstan). African-Americans have an HDI rating of 0.70, which is similar to China's. African-Americans in Louisiana score just 0.47 (equivalent to Nigeria).

WIN – Week In a Nutshell 5 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN-conomics ECONOMICS: Feb-13 trade deficit at 8-month low on falling non-oil imports; real INR appreciates During Feb-13, exports grew at a higher rate than imports after a gap of seven months. The value of exports at

USD26b was the highest in any month of FY13 so far; this level of exports was first achieved as far back as in Dec-10 and was much less than the highest exports of USD30b in Mar-11.

Imports on the other hand at USD41b was the lowest in six months. However, nearly the entire MoM decline was attributed by the fall in non-oil imports that declined to USD26b from USD30b a month back. Oil imports on the other hand at USD15b were closer to their all time high of USD16b a month back.

Feb-13 trade deficit at USD15b was at eight month low and fell significantly from the second highest level of USD20b just a month back.

Merchandise exports during Apr-Feb FY13 at USD266b de-grew 4% while imports were nearly static at USD448b. Trade deficit at USD182b already reached 9.9% of FY13 GDP, on course to reach a record high of 10.8% of GDP for FY13. We expect CAD-GDP to reach an all time high of 4.8% of GDP in FY13. However, trade deficit is expected to narrow to 9.6% of GDP during FY14 while CAD-GDP estimate is placed at 3.9% of GDP.

While trade data has improved, one need to be watchful on the capital flows front as the trade deficit still remains high near 1% of GDP on a monthly basis. Meanwhile real value of INR as measured by REER has risen in Feb-12 on account of lower trade deficit.

RBI has sounded higher current account deficit as a reason for holding back easing monetary policy further. The latest trade data and expected seasonal spike in exports in March is likely to yield the requisite space for RBI to cut rates in its 19th March policy measure

Exports growth finally exceeds import growth after seven months

ECONOMICS: Jan-13 IIP growth at 2.4% after two months of de-growth Jan-13 IIP growth recovered to 2.4% after two consecutive months of de-growth. Most sectors barring capital

goods recorded MoM improvement

Basic goods, which clocked positive growth in every single month of the year so far (a feat matched only by Electricity), consolidated their growth momentum further. Intermediate goods also accelerated but Capital goods continued to de-grow.

Consumer goods turned around led by non-durables; durables continued to de-grow for the second successive month.

The latest performance inched up the YTD IIP growth to 1% from 0.7% a month ago. The empty middle structure of industrial production is still visible YTD.

We have placed our FY13 IIP estimate at 1.1% and revised down our FY14 estimate to 3.7% from 5.6% earlier. This is consistent with our downward revision of FY14 GDP growth to 5.8% from 6.5% earlier.

The CPI (RU) for Feb-13 at 10.9% was persistently high, which we feel would drop significantly in Mar-13 aided by seasonal factors. Meanwhile, twin deficit risks have moderated somewhat as evidenced by latest Union Budget and trade data, increasing the policy space to RBI.

We expect RBI to cut rates by 25bp in its 19th March policy, which should help sustain the moderate recovery in industrial production.

WIN – Week In a Nutshell 6 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

IIP moves back in to positive territory after a gap of two YTD performance – likely to improve marginally by Mar-13

The empty-middle structure of industrial production persists throughout FY13 Outstanding projects (cost adjusted) are yet to be in the positive territory

INDIA ECONOMICS: Feb-13 WPI at 6.8% on fuel inflation; Core inflation at 3.8%. Feb-13 inflation inched up to 6.8%, still the lowest in three years, barring Jan-13 reading of 6.6%.

Food and primary inflation eased on the base effect despite the underlying index recording noticeable increase. However, runaway inflation was noted in certain food items like potato and onion.

Sharp increase in fuel group inflation was solely responsible for pulling up the overall WPI inflation. This was both on account of a sharp rise in international oil price by 3.3% (only partially mitigated by 1% INR appreciation) and larger impact of deregulation of bulk diesel. Barring the fuel group, WPI inflation actually fell to 5.1% (from 5.4% in Jan-13), i.e., very close to the 5% tolerable level of RBI.

Manufacturing inflation eased further to 4.5%, while core inflation fell to 3.8% from 4.1% a month back, taking it closer to the previous low of 3.5% during Mar-10.

Reflecting the acceleration in food prices that was by the base and seasonal effect, CPI (Rural Urban) inflation for Feb-13 inched higher to 10.9% (from 10.8% in Jan-13).

We expect a sharp decline in both WPI and CPI in Mar-13 as the seasonal food inflation wanes. In particular, WPI inflation is likely to fall sharply to 6.3% level, well below the 6.8% estimate stated by RBI in its Jan-13 policy.

Low IIP growth and easing food and core inflation ahead provide a favorable backdrop to RBI to ease the monetary policy further. Moreover, easing twin deficit risks, as evidenced from the Union Budget release and the latest trade data, provide the necessary policy space to RBI to stay on the easing course. The choice of instruments may, however, give a due weightage to liquidity conditions too and its impact on transmission. Thus, we expect RBI to continue to ease policy (either through a 25bp CRR or Repo rate cut) in its 19th March policy measure.

Indian Transfer Pricing laws based on OECD guidelines; Belt tightened elsewhere too Indian transfer pricing (TP) laws are based on OECD guidelines which too are evolving.

Seen simply, transfer pricing laws prevent shifting profits from high tax jurisdiction to a lower one.

Indian TP laws are operational since 2001 that defines its applicability.

WIN – Week In a Nutshell 7 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

While a host of TP issues has affected companies and investors, belt tightening on TP laws in recent years is a worldwide phenomenon.

Devil is in the detail - specifics of India

Indian laws have detailed guidelines to determine the Arm's Length Price (ALP) based on five methods.

However, normally it is the Transactional Net Margin that is most widely used. It involves comparison of the margin earned by the tax payer vis-à-vis the net margin earned by comparable companies under similar circumstances.

The laws also prescribe procedures for the tax payer and tax department to compute tax liability and demand, respectively.

A detailed process of remedy for tax payers with various layers of appeal is also possible under the law. Disputes due to interpretation of economics, laws, implementation

As TP becomes important as a source of revenue, there are increased disputes.

In most cases it is the differing perspectives on the economic basis of transactions that result in disputes.

Thus, the choice of comparables to determine the Arm's Length Price (ALP) becomes the key issue to the dispute.

Lagged enactment of the law and proactive tax officials have increased the incidence of disputes.

This has resulted in a pile-up of disputed cases. Way forward - APA mechanism holds promise

The Advance Pricing Agreement holds the promise of a true game changer. This is an agreement that the tax payer enters with the Advanced Pricing Authority and it broadly ensures that the transfer prices worked out are not questioned again by the tax administration.

The 2012 changes in the Dispute Resolution Panel (DRP) rules, that makes it more even by allowing appeal by the tax department too, hold the promise of faster and more balanced orders (earlier only the tax payer was allowed to appeal thus making DRP biased towards the tax department).

Besides, tax payers need to be cautious and maintain a checklist.

As a specific example, the Vodafone issue is likely to be settled with some compromise. Incidentally, the Finance Minister in his post policy media interactions highlighted that the offer of conciliation from Vodafone is under Cabinet's consideration.

WIN – Week In a Nutshell 8 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN-sights from management interaction UP Power Corporation - SK Agarwal, CFO Q: Have you all started any negotiations with banks? This tripartite agreement whereby the UP state will accept some of your loans and the banks will convert the balance into long-term bonds, has the process kicked off? A: We have accepted the scheme announced by the Government of India and our total outstanding loans and the outstanding power purchase liabilities- the total was about Rs 30,000 crore, out of that Rs 15,000 crore is to be taken over by the state government. We have sent our consent to the Government of India and our cabinet has also approved that. The state government will take over loans worth Rs 15,000 crore and first we will issue the bonds in favour of the bank and then these bonds will be replaced by the state government bonds. Q: The biggest variable on which the success of this scheme hinges perhaps is the tariff hikes. In that, we learn that you have proposed somewhere like a 40 percent hike. Could you confirm those figures? In the recent budget you all have applied for about Rs 5.20 per unit? A: Rs 5.25 is the highest tariff that we have applied to the regulatory commission for 2013-14. For 2012-13 also we have implemented one hike. That in some cases goes up to even 35 percent. But the average works out to about 21 percent (this was approved in October 2012, no new tariff hike approved). Q: Along with this hike that you are proposing for the current year, what would have been the hike? A: The discoms will start getting about Rs 2,700 crore extra in one year. The hike that we have implemented in current fiscal will fetch us another Rs 2,500 crore in a year. So, two hikes will fetch us more than Rs 5,000 crore extra. Q: At the moment how much are your expenses over your revenues. What is the deficit you are running? A: We have a deficit of about Rs 10,000 crore, but the major portion was of interest burden because of the borrowings we have made in past. So far we have been paying the interest from our reserve of funds, but now this loan liability is being taken over by the state government. So that interest burden will be served by the state government out of budgetary resources. So once this burden goes away then our losses will come down and it will be easier for us to turnaround in the next 3-4 years. Q: What is the annual interest burden as of last year, as well if you take that out what will be the annual deficit? A: The annual interest burden is about Rs 3,500 crore and once this is taken over by the state government then our deficit will come down to about Rs 7,000 crore. Q: We have some reports suggesting that players like Reliance Power and Lanco have talked about terminating their supply because of their outstanding dues. Once this process gets cleared and the state government takes over, are the private companies-the independent power producers (IPPs) are going to start supplying again? At what stage are the talks with the IPPs? A: Rosa is already running three units out of four and Lanco recently has shut down two units. But the payment issue is not the only one issue, they have some other issues also because this was a Case II project in which they had quoted a bid price. I don't know somehow they have quoted a price, which was not viable for them so whatever we pay to them that’s not enough to meet their repayment obligations. So, they approached the regulatory commission for revision of tariff. We have recently discussed with Lanco, we have started making payment to them. We have paid immediately Rs 20 crore to them. So, they are starting the plants in the next two days. Q: I also wanted to find out about the Case II bidding norms. What have you heard, there were expectation that we could get some finalisation by March end; is it possible? Case II bidding projects in UP has been stuck. In Case I about 6 Gigawatt or so has been stuck in UP because of the lack of clarity, do you expect these norms to be finalised by the month end in Case II at least? A: I don't think that they will be finalised by the month end because many of the stake holders had issues in that. I think it will take another two months before they are finalised. Q: If you could outline what the key issues are? A: The major issue is the pass through of the coal price and the variable cost. In the earlier document, in the Case I bidding whatever the bidders were quoting that became the final price for assessing the variable cost. This became a problem for the bidders who had quoted earlier; they were not able to meet their obligations because the coal prices increased and so lot of increase in the variable cost. So, they want to be hedged in the new document. They want only fixed cost to be quoted by the bidder and variable cost to be made as a pass through. This is the crux of the new document that has been finalised by the ministry of power.

WIN – Week In a Nutshell 9 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Q: Do you think the state government has the Fiscal Responsibility and Budget Management (FRBM) room to accept Rs 15000 crore of your loans? A: FRBM prescribes the total loan limit -the loans that can be raised by the state government in a particular. So, suppose in case of Uttar Pradesh it is Rs 25000 crore. So, the total loans will remain within Rs 25000 crore and then state will utilise say about Rs 3500 crore for us and remaining about they will utilise for other development loans. They don’t have any problem on that. Q: They will take a lot of time to come to your Rs 15000 crore until then it will be on your books? A: This scheme provides for that. We will issue the bonds initially in favour of the banks and gradually the state will take it over. In our case we have proposed that in four years time the bonds issued by the discoms will be converted into state government bonds. Q: By when do you think the package will be finally ready and you will be issuing these bonds? A: Our package is ready and our FRP has also been prepared and we are sending it to the regulatory commission for approval. We have started the consultative process. Q: Who are the banks, which is the lead lender? A: In our case it is Punjab National Bank (PNB). Q: What is the exposure? A: Punjab National Bank's individual exposure is about Rs 2500 crore and there are 21 bankers in the consortium. Q: By when do you think you will be able to get fresh loans from the banks? Their argument was that if the loans taken over by banks were converted into bonds it will free-up some space for you to get more money. Do you see that happening in FY14? By when do you think you can get more money? A: Right now the banks have exhausted their exposure limits because these loans which are standing in our books they are the loan liability of the banks and once bonds are issued by us then this loan will get converted into the investment in the banker’s balance sheet. So that loan limit will get some space in there. Q: Some of your peers like Punjab have chosen to opt out of this scheme. What do you think is the driving force behind this and do you see any threat to the scheme itself because of some of the state electricity boards (SEBs) pulling out. Do you envisage some more states to back out? A: I personally feel that Punjab might be having some issues regarding the tariff and the other things and particularly the private sector participation. I suppose that is the one hindrance for their reluctance. If you see Rajasthan has already submitted the FRP and they have given their consent. We have given our consent. Andhra Pradesh has given its consent. So is the case with Haryana. So, most of the focused states have already participated in the scheme. So, Punjab also later on may decide to come and join the other states. Q: How much more power do you think you will buy in FY14, given the financial status that you envisage of your own profit and loss (P&L)? A: We have normally a growth of about 9-10 percent every year and in this year 2012-2013, we had bought about 76,000 million units. In the next year, we are having a plan of 84,000 million units. So, this much power we will necessarily buy and the main thrust of the debt recast scheme is that we have the liquidity in our hand. Q: That's exactly why I was coming to the liquidity part. When will the banks give you that liquidity? So in the summer months from say April to September, first half of the year? A: In summer months the demand is always 20 percent higher than what we have usually. So that necessarily we will buy because we cannot starve the people for power. Q: And you will have the liquidity for it, the banks will give you? A: Yes naturally because banks have not denied that they will not fund. This scheme has been finalized with the consent of the department of financial services. The scheme very clearly says that the funds will be provided till the utilities will turnaround. So, I don’t see any problem because whatever we have discussed with the banks in the consortium meeting - they have not said that they will not fund. The exact quantum of funds will be decided once we are through the FRP process and all these formalities are taken care of. Q: So when will the deadline be, when do you think the entire package will be implemented? A: 31st March is the deadline.

WIN – Week In a Nutshell 10 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Nestle - Nandu Nandkishore, executive vice-president, head of Asia, Africa, Middle East and Oceania Your emerging markets contribution has been growing consistently. Will that trend continue? We need to roll back a little and see that there’s been a fundamental shift in economic centre of gravity, that is moving away from north of Atlantic towards emerging economies. 2010 was a landmark year because 50% of the global GDP (gross domestic product) came from the emerging markets. There seems to be a de-linking of emerging economies from developed markets. However, to the extent some of the emerging markets were very reliant on exports from the developed markets, that has slowed. Therefore, there is a re-focusing that is happening in the emerging markets to channel more GDP growth towards domestic consumption. China and Thailand are doing that. Fundamentally, we would remain optimistic that emerging markets will be significant driver of growth in the years to come. 2010 was an inflection point for some reason. Fifty percent of humanity was living in urban areas. The projection is that for some reason mankind will migrate to cities and 70% of humanity will live in cities by 2025. Even in India, although it is a bit slower, the phenomenon will shape up. So the prognosis going forward is bright for the food processing industry. So, in fact, what we expect will happen over the course of this decade (starting 2010), globally we expect a billion people will move out of poverty and enter a universe where they can consume branded goods, moving away from unbranded; and, at the same time, half a billion will move out of the middle class into the affluence where they will be looking at luxury and premium goods and services. So, yes, there has been a slowdown in the North Atlantic and yes, we feel the effects in the emerging markets. Where does India fit in? We have five growth engines in the group; you have China, the South Asia region including India; you have Africa; the Middle East, and Oceania region. Each of these five growth engines are growing and we are investing. The expectation is that by 2020 India will be the fourth biggest economy in the world. We expect Nestle India to be the fourth biggest market for Nestle (by then), that’s the target we have. How do you plan to do that? Nestle SA is a shareholder in Nestle India. So, as a shareholder, what we have done is that we have invested directly in India in a research and development (R&D) centre in Manesar (in November) where we have invested Rs.280 crore. It is a global R&D centre and for India as well. We have helped Nestle India get approvals from shareholders for investments worth Rs.1,000 crore last year. We have basically invested in capacity. So how do we help Nestle India be our fourth biggest market by the end of the decade? We invest in R&D directly and we invest in people. We identify high potential resources and send them overseas and, at the same time, we bring expats in the Indian market. What is the rate of trading up among consumers in these markets and are you able to catch up? We are studying it. It’s something we’ve been coming to terms with. We typically sell coffee at about 10 US cents a cup and we find the same consumer is willing to go to a coffee shop down the road and pay $2 for it; now that’s an incredible stretch of value. But for us, indeed, it has been a bit of an eye-opener, to see how fast the emerging markets consumer is willing to pay that higher value for the value she receives, and that opens the doors for us to bring in more premium solutions as we have done in the developed markets, such as Dolce Gusto which offers a coffee shop experience at home. Are you then late at launching premium products and categories in India? Yes, we have been late in introducing a lot of these to India. But as part of our focus on India we will be making available a lot of these advanced technologies to Nestle India for premium products and start to tackle this premium opportunity, which is huge. Will this come from a manufacturing set-up or through imports? It will be a bit of both. Depends if we have the manufacturing capability locally. If we don’t, then there will be an import route first so as to get a commercial volume before we invest more. While the rural story is still intact in markets like India, is affluent, premium becoming increasingly relevant? Not outpacing, we have to do both the segments. They are both important. So we need to focus across the pyramid. In India we have been slower to address this (premium). Companies globally are focusing heavily on the health proposition; is the emerging market consumer really consuming such offerings? Yes, that’s where the technology and research come in. We have a technology that can do the micronutrient fortification without comprising the taste. So consumer gets the health benefits almost without realizing. And in the

WIN – Week In a Nutshell 11 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

same portion, sizes play a key role; and if that means that at some point we won’t have to sell large pack sizes, that’s ok. In what categories is Nestle looking to expand in India? All the categories that we operate in globally. We are evaluating all categories, breakfast cereals, chocolates, coffee, evaluating all categories. We will go one by one, from Nestle SA’s point of view, we will make these technologies available to India and we will bring these products and make them available to Nestle India. There have been reports claiming that the parent firm has a sense of indifference towards the India operations. Is that correct? Not true at all, as I explained already. Look at what we are doing. We have invested $500 million in the past three years and set up an R&D plant in Manesar. India remains one of the key markets we look for growth. We expect this market to be the top four-five markets for Nestle, so we continue to invest in this country. We are making investments across all markets and India is one of the top important markets which has a lot of potential for us. Analysts are not particularly happy with Nestle’s stock performance in India, calling it “range bound” and lacking substantial action. How do you plan to rectify that? Am I happy with the growth that Nestle India has? I would say I want more. Let’s look at the CAGR (compounded annual growth rate). Over the last four years, we have been growing at 17.7%, ITC at 18.8%, Britannia 15.3% and HUL (Hindustan Unilever Ltd) at 13%. So in this benchmark I don’t see this as bad performance. And second thing is that (the) Nestle India business is more profitable and it is not something we are worried about; we see this profitability as important. Because we see this commitment we have to the shareholders at the same time, there is a realization that unless you have a profitable business it is difficult to invest in quality at a time when commodity prices are going up, it is difficult to invest capital in capacity. So we are not ashamed of these margins. We are growing, we are growing well and can grow better and faster, and there is a whole segment of opportunity in the premium segment that we have missed and will now focus on. Which means more investments? Absolutely, but we can’t give you numbers off the hand. But we’ve just gone through $500 million of investments in the last three years, let’s digest that. We have created capacities. Once we start filling those capacities with some more growth we will come in with some more accelerated investments. Globally, you have the largest breakfast alliance with General Mills called “Cereal partners worldwide”, yet you have stayed far away from this category in India. Any plans? We are late. You are right, it’s a category we should have entered and it’s a category we are evaluating to see what would be the right time and method to enter this. The success of western-style breakfast cereal is not an easy role in India because the Indian breakfast habit is a hot breakfast habit and to have cereals in cold milk (and that) has not worked. That has been one of the things that have held us back, which is hot breakfast habits. It’s something we are looking at because as urbanization catches pace and more and more young people enter the yuppy category, this segment is bound to go grow because of convenience matters. How is inflation and the overall bleak consumer confidence affecting growth of the firm globally? Look, inflation is here to stay both in India and globally, make no mistake. Today the global population is seven billion, which is expected to grow to nine billion by 2050, and that’s because of ageing, not because of more births. So when the population goes from seven to nine billion, you need a 50% increase in food production and at the same time there will be people emerging from poverty to middle class. And typically all over the world, and even in India, the moment that happens they want to consume more animal protein, and that needs far more land and water to produce the same kilo as vegetable protein. So, fundamentally, the world is looking at doubling food production over the next few years. I believe as food production doubles we are in for a sustained period of commodity prices. There will be road bumps and volatility but the underlying trend is going to be upwards. http://www.livemint.com/Companies/xBxGxG5fHCAIDg8Brn0wyH/Nestle-expects-India-to-become-its-fourth-biggest-market-by.html

WIN – Week In a Nutshell 12 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN Sector Updates

AUTO (2W): HMSI's launches CB Trigger (150cc) targeting Bajaj’s Pulsar; Aims for leadership by 2015-16 HMSI launched a new 150cc commuter motorcycle CB Trigger this week. Honda claims an outstanding 60

Kmpl fuel economy figure for the CB Trigger. Pricing will be announced in Apr-13.

The Honda CB Trigger puts out 13.81 Bhp of peak power at 8,500 rpm and 12.5 Nm of peak torque at 6,500 rpm. The 150cc air cooled motor is a derivative of the four stroke engine that powers the likes of the Honda CB Unicorn and the CB Dazzler.

The Honda Trigger CB150R essentially is replacement for CB Dazzler, which failed to ramp-up volumes. The CB Trigger is more sharply styled than the CB Dazzler and comes with an improved braking system.

Bookings for the Honda CB Trigger will begin from April 2013, with deliveries slated to begin from May-13.

The Honda CB Trigger is aimed at the 150cc commuter motorcycle segment, competing with Bajaj Pulsar 150 DTSi and the Honda Unicorn.

GASOLINE: The oil & gas monthly – March 2013 SUMMARY - February 2013 o Cut in OPEC supply strengthens crude prices: Brent prices moved up to USD 116/bbl (+3% MoM) in Feb-13,

mainly due to supply cuts by OPEC (~1 mmbbl/d) and returning positive sentiments on the demand front. o Reuters Singapore GRM up 48% MoM to USD10.5/bbl: Driven by high auto fuel cracks and large

shutdowns. Medium-term GRM outlook continues to be subdued due to over capacity and sluggish global demand. Expect GRM to be volatile (occasional spurts) due to occasional bunching up of shutdowns.

o Petchem margins seem to be in recovery mode: Key product margins are marginally up MoM (except PVC) and seem to be in the recovery mode. Domestic price premium in PP/PVC improved marginally MoM while premium to PE reduced.

o Valuation and view:

On the back of ongoing reforms, we continue our positive stance on upstream (ONGC/OIL) and OMC’s.

BPCL is top pick among OMC’s for its E&P upside potential.

RIL’s new refining/petchem projects likely to add to earnings from end-FY15/FY16, but medium-term outlook on core business remain weak with RoE reaching sub-13%, Neutral.

Neutral on GAIL/GSPL due to headwinds on incremental gas.

However, domestic gas scarcity augurs well for Petronet LNG.

INDIA AUTO (2W): HMSI’s profitability higher than Hero’s. We analyzed the financial performance of Honda Motorcycle & Scooters India (HMSI) for FY12 and following

are our key observations:

Considering focus on scooters and executive segment, realizations are similar to Hero but lower than Bajaj. Despite lower volumes/scale, higher import content (our estimate) and higher dealer margins, HMSI enjoys superior profitability (adj for royalty) and return ratios than Hero. HMSI’s EBITDA margins/RoCE for FY12 were at 15%/58.9% v/s 12.2%/51.5% for Hero.

Strong brand equity together with healthy demand for its popular brands [Activa (110cc scooter) & Shine (125cc motorcycle)] and lower advertising are the key reasons for superior financial performance. Recent JPY depreciation can further boost HMSI’s profitability as we estimate relatively higher import content for HMSI compared to Hero. HMSI plans 2-3 launches in the entry level motorcycle segment and aims to be No.1 player (30% market share) in the Indian 2W market.

INDIA ENERGY: Landmark reforms … Oil PSUs to benefit Under-recovery likely to halve in 2 years:

Diesel reforms (INR0.45/ltr price hike per month) to cut under-recovery by 50% to INR864b in FY15E v/s INR1.6t in FY13E. Upstream subsidy sharing in FY11 and FY12 stood at 39% and 40% and in 9MFY13 at ~36%.

Expect reform benefits to incentivize; Government to pursue the announced reforms: Diesel reforms will not only better oil PSUs financials, but benefit the government through: 1) increased revenues (taxes/dividend), 2)

WIN – Week In a Nutshell 13 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

lower expenditure (subsidies) and 3) higher valuations for its stake in PSUs (positive for divestments – IOC’s OFS likely in FY14).

Likely gas price hike, another trigger for upstream companies: Rangarajan Committee’s formula on domestic gas pricing implies a likely gas price of USD8/mmbtu v/s USD4.2/mmbtu now. And a likely APM gas price increase ahead of RIL’s scheduled KG-D6 price revision in March-14 will be another trigger for ONGC and Oil India (we model USD7/mmbtu from FY15E).

Expect auto fuel deregulation to improve OMCs’ marketing business profitability: In a deregulated scenario, while OMCs will lose some market share to private retailers (RIL, Shell, Essar Oil), they are likely to benefit more from a likely increase in retail marketing margins from the current cap of INR1.2/litre to at least INR2/litre. In FY04 (small period of deregulation), OMCs auto fuel marketing margin was at ~INR2.5/litre, that too when the pump prices of auto fuels were at ~INR35/litre.

Valuation and view:

On the back of ongoing reforms, we continue our positive stance on upstream (ONGC/OIL) and OMCs. BPCL is our top pick among OMCs for its E&P upside potential.

RIL's new projects are likely to add to earnings only from FY15/FY16, and medium term core business outlook remains weak.

Maintain Neutral on GAIL and GSPL due to headwinds for incremental gas in the medium term. However, domestic gas scarcity augurs well for Petronet LNG.

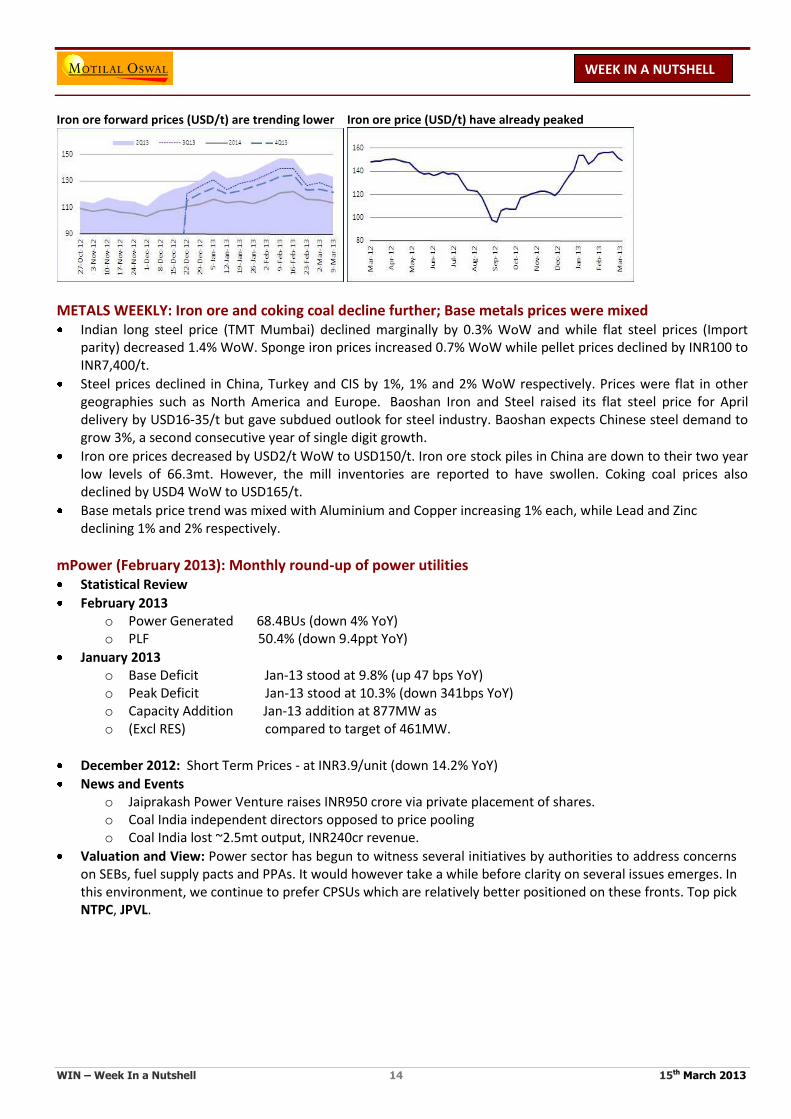

IRON ORE: price outlook weakening once again; downside to NMDC estimates, valuations attractive Event

The price outlook for globally traded iron ore (~1175m tons seaborne trade in 2012) has started weakening once again along with the peaking of spot prices of iron ore.

Recent rally in iron ore prices from bottom of USD96/dmt (cfr China, 63% Fe) by 64% to USD157/dmt over last 6 months has resulted in revival of many shelved projects and restart of high cost iron ore mines in China.

Nearly 210mtpa of new low cost iron ore supply is expected to hit seaborne trade over next 6-9 months.If prices remain strong , revival of high cost Chinese mines will add another ~50-60m tons of supply. China, sole driver of pig iron production and iron ore demand, is likely to consume 2-3% or 30-35m tons more in 2013. Global Supply will far outstrip demand growth in 2HCY13.

Impact

Coking coal, another raw material in steel making, too is turning in over supply with prices trending lower. Falling iron ore and coking coal prices will have disruptive impact on the Chinese steel market and thereby on global steel prices. Steel prices may correct by USD100-150/t over 9-12 months.

Indian steel market has been sluggish with demand growth decelarating to ~4%, which new capacities have come on stream.

Indian steel prices have barely participated in recent global steel price recovery during Oct 2012- Feb 2013. Therefore, there is a head room of ~USD40/t in Indian steel market to absorb some of the global steel price correction. This will definitely squeeze the margins of integrated steel producers like Tata Steel, SAIL.

Prices of iron ore lumps will have more direct impact, while prices of iron ore fines will be more resilent

NMDC drives 50% of revenue from lumps (35% by volume) and remaining from fines (65% by volume). The revenue from iron ore lumps will be vulnerable to steel prices, while other half revenue will be more resilient.

WIN – Week In a Nutshell 14 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Iron ore forward prices (USD/t) are trending lower Iron ore price (USD/t) have already peaked

METALS WEEKLY: Iron ore and coking coal decline further; Base metals prices were mixed Indian long steel price (TMT Mumbai) declined marginally by 0.3% WoW and while flat steel prices (Import

parity) decreased 1.4% WoW. Sponge iron prices increased 0.7% WoW while pellet prices declined by INR100 to INR7,400/t.

Steel prices declined in China, Turkey and CIS by 1%, 1% and 2% WoW respectively. Prices were flat in other geographies such as North America and Europe. Baoshan Iron and Steel raised its flat steel price for April delivery by USD16-35/t but gave subdued outlook for steel industry. Baoshan expects Chinese steel demand to grow 3%, a second consecutive year of single digit growth.

Iron ore prices decreased by USD2/t WoW to USD150/t. Iron ore stock piles in China are down to their two year low levels of 66.3mt. However, the mill inventories are reported to have swollen. Coking coal prices also declined by USD4 WoW to USD165/t.

Base metals price trend was mixed with Aluminium and Copper increasing 1% each, while Lead and Zinc declining 1% and 2% respectively.

mPower (February 2013): Monthly round-up of power utilities Statistical Review

February 2013 o Power Generated 68.4BUs (down 4% YoY) o PLF 50.4% (down 9.4ppt YoY)

January 2013 o Base Deficit Jan-13 stood at 9.8% (up 47 bps YoY) o Peak Deficit Jan-13 stood at 10.3% (down 341bps YoY) o Capacity Addition Jan-13 addition at 877MW as o (Excl RES) compared to target of 461MW.

December 2012: Short Term Prices - at INR3.9/unit (down 14.2% YoY)

News and Events o Jaiprakash Power Venture raises INR950 crore via private placement of shares. o Coal India independent directors opposed to price pooling o Coal India lost ~2.5mt output, INR240cr revenue.

Valuation and View: Power sector has begun to witness several initiatives by authorities to address concerns on SEBs, fuel supply pacts and PPAs. It would however take a while before clarity on several issues emerges. In this environment, we continue to prefer CPSUs which are relatively better positioned on these fronts. Top pick NTPC, JPVL.

WIN – Week In a Nutshell 15 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN Corporate Corner AKZO NOBEL : Near term Paint industry demand at risk; RM softening is well entrenched. We attended the analyst meet of Akzo Nobel. Following are key takeaways and potential implications for Asian

Paints.

Akzo Nobel’s vision is to reach EUR 1 bn revenues in medium term. For 9MFY13, it clocked revenues of INR16.9bn and as per management; the Indian business contributes ~3% of parent’s turnover.

It targets to become the second largest player in Decorative Paints segment (currently at number 4). Driving shares in mid-lower end of the Paints industry is a key focus area (Akzo is number 2 in Premium segment with 20% plus market share). Management expects a challenging near term environment for the Decorative paints industry and believes near term growth will be driven by volumes.

Pricing environment is expected to remain stable and may even see some softening as raw material prices (especially Tio2) has seen the top, as per management.

Akzo’s focus is on improving dealer network strength (currently at 8500), building brands (higher ad-spends) and sustained innovation efforts.

Despite significant capacity build up by incumbents company does not see concern for medium term volume growth in the industry.

From Asian Paint’s perspective, we believe the softening of RM environment augurs well. However challenging near term demand environment can have implications for Decorative paints volume growth. We have a BUY rating on Asian Paints with TP of INR 5000. We do not have a rating on Akzo Nobel.

HAVELLS India: Proposed special resolution to hike FII limit / enter into new business segments HAVL has proposed the following resolutions for the shareholders approval: i) Increase in FII limit from 24% to

40%, with the cap of single FII at 10% ii) Entry into several new segments like kitchenware, stabilizers, UPS, inverters, batteries, dispensers, water purifiers, utensils, consumer durables, FMCG products, lifestyle products, etc.

Over the past few years, HAVL has added new product lines/segments which have become ~INR5b revenue product categories: i) company entered the lighting segment in 2003 and the business contributed INR5.5b to revenues in FY12 and ii) it entered the fans market in 2005 and contributed revenues of INR4.9b in FY12.

Going forward, we believe that new product portfolios, including consumer/kitchen appliances (launched in FY11) and Reo switches (mass market segment, launched in FY13), are likely to be in the INR5b+ category.

HAVL's stock has outperformed the BSE mid cap index by 40% over the past year. Going forward, we believe the key stock price drivers are: 23% consolidated earnings CAGR till FY15E, strong balance sheet, improving free cash generation and potential increase in dividend payout ratio. Management had increased the dividend payout to 25% in FY12 from ~12% in FY11 and we believe that given the robust free cash generation, payout ratios can further increase

INFOSYS: Making a case for growth convergence; Deals won, visible fruition of changed strategy Infosys' stock saw a spike in response to its 3QFY13 results and has moved in a range ever since. We believe that

3QFY13 may only have been the first quarter of a visible momentum in the company's growth, and that there is further upside in the stock from current levels.

We present a series discussing Infosys' potential to build upon its impressive 3Q performance. In this first one, we make a case for revenue growth convergence.

TCV of deals in outsourcing and PPS imply acceleration in FY14: Exit rate of USD 1,925m (INFY's 4QFY13 guidance) implies 4.8% organic revenue growth in FY14. Factoring 3Q outsourcing deals TCV of USD731m (assumed to accrue over five years and factoring revenues from TCV in PPS work out to organic growth rate of 7.5% in FY14. Including full year revenues at Lodestone implies growth of 9.2%.

Obvious upside to base assumptions makes a case for convergence

We see an obvious upside to the above growth number because it assumes: o TCV of outsourcing deals only in 3QFY13, while INFY bagged 4 large outsourcing deals in 1Q and 6 deals in 2Q o No growth at Lodestone in FY14 o Revenue recognition from PPS over five years v/s guidance of 3-5 years

WIN – Week In a Nutshell 16 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Infosys' pipeline in 2HCY12 improved over 1HCY12. This was largely an outcome of measures taken by the company to ensure growth revival, than any macro improvement. This is reflected in two metrics in particular:

o Growth outperformance at Business IT Services (BITS) segment v/s other segments in five out of the last seven quarters.

o Decline in constant currency realization in three out of the last four quarters.

Nasscom's guidance of 12-14% growth in exports in FY14 is unlikely without growth acceleration at Infosys and Wipro. Cognizant guided for a deceleration in CY13 growth and even 17% growth at TCS explains only negligible acceleration at Nasscom. 23%+ of the rest of the exports comes from Infosys and Wipro.

While the management continues to guide cautiously, following factors bolster our confidence on sanguine growth, going forward: [1] recovery in under-spent discretionary budgets, [2] uncertainty and not ability driving cautious stance (healthy cash reserves with clients), and [3] better pipeline YoY.

ITC: Highlights from channel checks; Pricing ladder has never been so crucial; Maintain Buy No price hikes yet but sections of trade have increased prices: Our channel checks with Cigarette distributors

and trade indicate no price hikes from ITC yet. However, some retailers/wholesalers have started charging higher rates for selective brands (Classic, Gold Flake). Even wholesalers have increased rates and artificial shortage is being created in certain sections of the trade to benefit from the pricing arbitrage. We note that VAT increases announced in the state budgets so far (WB, Gujarat, Bihar, Assam, J&K, Rajasthan) add up to 140bp increase in VAT to 22.2%. Key states for ITC – Maharashtra, AP, Kerala and TN – accounting for 45% of its Cig business will be announcing budgets over 15-21 March.

ITC needs to take 15% price hikes to nullify the 18% excise increase: In Union Budget and VAT increase (assuming wtd avg VAT to move to 23% in FY14) to post 15% Cig EBIT growth in FY14, as per our estimates.

Our assumptions: 2% volume growth, 15% Cig EBIT growth: We are building in 2% Cig volume for FY14E and 14% price hikes. However, we note that Cig prices would increase ~35% in two years which is unprecedented and hence it won’t be surprising if Cig volumes remain flat or even post a decline in the event of hostile consumer reaction to price hikes. Nonetheless, earnings won’t be impacted as pricing tends to have disproportionate influence in Cigarette business economics (3% EPS change for 1% price change; 1% EPS change for 1 % volume change).

Valuation & View: Maintain BUY with a TP of INR340; downside risks to our volume assumption; pricing will decide the earnings as always: We are keenly watching the pricing action on Gold Flake and whether ITC vacates the INR5 price point for this single largest selling brand in its portfolio. Despite the harsh policy measures, we believe ITC offers the best earnings visibility in our staples universe as it remains insulated from competitive headwinds and RM price fluctuation. Improving profitability in non-Cig FMCG can augment cash flows and payout ratios. BUY with a TP of INR340.

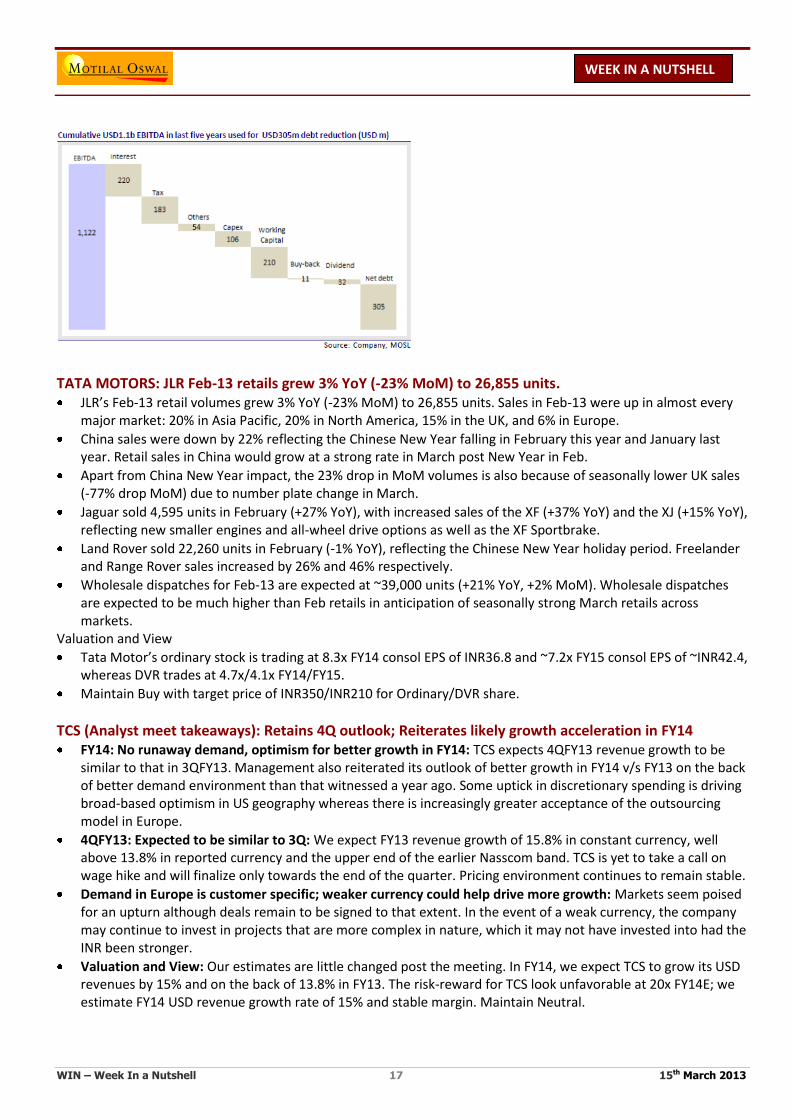

RAIN COMMODITIES: Valuation attractive In January 2013, Rain Commodities Ltd (RCOL) completed the acquisition of Europe-based coal tar distiller

Rutgers for a gross enterprise value of Euro702m. We believe the acquisition will add significant value to RCOL's business due to the following reasons: o Post acquisition, RCOL's product diversification to improve; no product will contribute more than 37% to

revenues. o Potential synergies on complimentary nature of CPC and CT pitch. o Rutgers business operating performance has been robust despite challenging business environment. EBITDA

posted a CAGR of 14% over CY09-12. o Severstal JV to result in additional supply of coal tar to European operations. This will take care of ~28% of

European operations' coal tar needs, thus mitigating the effect of declining European supplies. o Acquisition to result in EPS accretion of 13% and 16% in CY13E and CY14E respectively.

RCOL has demonstrated the ability to sustain large acquisitions; CII acquisition added significant value

RCOL saw a net debt reduction of USD305m in the last 5 years; USD400m of equity value generation unnoticed.

Net debt/EBITDA at comfortable levels of 3.5x; major debt repayment to start only in 2018.

RCOL trades at 3.8x CY14E EV/EBITDA. Valuation multiple are much below its peers; US listing will further rerate the stock.

WIN – Week In a Nutshell 17 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

TATA MOTORS: JLR Feb-13 retails grew 3% YoY (-23% MoM) to 26,855 units. JLR’s Feb-13 retail volumes grew 3% YoY (-23% MoM) to 26,855 units. Sales in Feb-13 were up in almost every

major market: 20% in Asia Pacific, 20% in North America, 15% in the UK, and 6% in Europe.

China sales were down by 22% reflecting the Chinese New Year falling in February this year and January last year. Retail sales in China would grow at a strong rate in March post New Year in Feb.

Apart from China New Year impact, the 23% drop in MoM volumes is also because of seasonally lower UK sales (-77% drop MoM) due to number plate change in March.

Jaguar sold 4,595 units in February (+27% YoY), with increased sales of the XF (+37% YoY) and the XJ (+15% YoY), reflecting new smaller engines and all-wheel drive options as well as the XF Sportbrake.

Land Rover sold 22,260 units in February (-1% YoY), reflecting the Chinese New Year holiday period. Freelander and Range Rover sales increased by 26% and 46% respectively.

Wholesale dispatches for Feb-13 are expected at ~39,000 units (+21% YoY, +2% MoM). Wholesale dispatches are expected to be much higher than Feb retails in anticipation of seasonally strong March retails across markets.

Valuation and View

Tata Motor’s ordinary stock is trading at 8.3x FY14 consol EPS of INR36.8 and ~7.2x FY15 consol EPS of ~INR42.4, whereas DVR trades at 4.7x/4.1x FY14/FY15.

Maintain Buy with target price of INR350/INR210 for Ordinary/DVR share.

TCS (Analyst meet takeaways): Retains 4Q outlook; Reiterates likely growth acceleration in FY14 FY14: No runaway demand, optimism for better growth in FY14: TCS expects 4QFY13 revenue growth to be

similar to that in 3QFY13. Management also reiterated its outlook of better growth in FY14 v/s FY13 on the back of better demand environment than that witnessed a year ago. Some uptick in discretionary spending is driving broad-based optimism in US geography whereas there is increasingly greater acceptance of the outsourcing model in Europe.

4QFY13: Expected to be similar to 3Q: We expect FY13 revenue growth of 15.8% in constant currency, well above 13.8% in reported currency and the upper end of the earlier Nasscom band. TCS is yet to take a call on wage hike and will finalize only towards the end of the quarter. Pricing environment continues to remain stable.

Demand in Europe is customer specific; weaker currency could help drive more growth: Markets seem poised for an upturn although deals remain to be signed to that extent. In the event of a weak currency, the company may continue to invest in projects that are more complex in nature, which it may not have invested into had the INR been stronger.

Valuation and View: Our estimates are little changed post the meeting. In FY14, we expect TCS to grow its USD revenues by 15% and on the back of 13.8% in FY13. The risk-reward for TCS look unfavorable at 20x FY14E; we estimate FY14 USD revenue growth rate of 15% and stable margin. Maintain Neutral.

WIN – Week In a Nutshell 18 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN Collage Indian technology firms : Looking for India’s Zuckerberg A pioneer in outsourcing but a laggard in the internet era, can India become a leader in mobile technology? INFORMATION technology has been a mighty force for good in India. Its first tech revolution began 30 years ago, when a few engineers came up with the unlikely idea of doing back-office IT work for far-off Western firms. Today that outsourcing industry is a capitalist marvel. It has annual sales of $100 billion, mostly from abroad, and these export earnings have been vital in a country with a weak balance of payments. Millions of good jobs in India have been created. Young Indians have seen that globalisation creates winners. India’s reputation in the world has changed, too: Bangalore’s shining IT campuses have become as famous as the Ganges and the Gandhis. Yet India has been a comparative failure in terms of innovation over the past decade. You might have expected India’s many advantages (the English language, abundant engineers and a thriving diaspora in Silicon Valley) to pay off spectacularly on the internet. But only a few start-ups have made clever technical innovations that have been sold abroad. And at home e-commerce is in its infancy, with sales only 6% of China’s. Thanks to lousy infrastructure, useless regulation and a famously corrupt telecoms sector, the web is available to only 10% of Indians, many of them squinting at screens in cafés. India boasts no big internet firms to compare with Chinese giants such as Alibaba, Baidu and Tencent, nor start-up stars like Facebook’s Mark Zuckerberg. Instead, it has seen a succession of false dawns, from its version of the dotcom bubble in 1998-2002 to more recent hype over deal-of-the-day websites and text-based cricket updates. In 2010-11 lots of start-ups raised cash, but they have struggled since. Venture capitalists grumble that their returns have been poor. The original emerging-market tech pioneer has fallen behind in the internet era. Feeling luckier Catching up should be a priority for India—not least because its outsourcing champions are now reaching middle age. As the wages of India’s engineers rise, its IT industry cannot rely for ever on doing straightforward work cheaply for foreigners. The good news is that India now has a chance to lead again; the bad news is that this opportunity relies in part on Delhi’s bureaucrats not messing it up. Optimism springs, first, from a healthy stock of young entrepreneurs . Many have gained valuable experience working in America or for multinational firms. Many are battle-hardened through previous ventures that flopped, from dairy farms to bowling alleys. As in California, failure is no longer frowned upon in India. New firms such as Flipkart and Redbus are adapting Western e-commerce models to deal with India’s rickety logistics and cash-based economy. They are transforming mundane areas such as bus tickets, and opening up scores of smaller cities to modern retailing. Tens of millions of people are benefiting as a result. The second change is the mobile internet. India’s fixed-line system may be abysmal, but cheap smartphones and fast wireless networks are rapidly spreading. India is poised to leapfrog the era of the personal computer and go straight to the mobile-internet age. Already a quarter of internet traffic is from phones, compared with a seventh worldwide. E-commerce sites are getting a surge in activity from phone-users. But this budding revolution needs clever regulation. Outsourcing boomed in part because it avoided government: the product was exported through global networks. The mobile internet needs capital, payment systems and wireless capacity. In all three areas the government is in the way. The e-commerce industry appears stymied by the same restrictive rules on foreign investment that have bedevilled bricks-and-mortar retailing. Only a fifth of Indians have credit or debit cards—and using them online is a nightmare, again thanks to regulations (India could learn a lot from Africa’s use of mobile money). And India needs more and better wireless networks; some big players such as Mukesh Ambani, India’s richest man, have been tempted in, but the telecoms regime is a tangle of overcomplicated rules and graft. India has the talent to lead in the mobile internet, as it did in outsourcing. But so long as Indians struggle to get a signal or to make payments, the revolution will be held back.

WIN – Week In a Nutshell 19 15th March 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Nifty Valuations at a glance