Budget implemtation

99

CHAPTER ONE INTRODUCTI ON 1.1 BACKGROUND OF THE STUDY A budget is a financial and a statement prepared prior to a defined period of time of the policy to be pursued for the purpose of attaining a given objective. Budget is a plan quantified in monetary terms, prepared and approved prior to a defined period of time, usually showing planned income to be generated and or expenditure to be incurred during that period and the capital to be employed to attain a given objective. Furthermore a budget is an attempt made at the beginning of each financial year to plan the profit and loss account for the year and to aim for a definite balance sheet. This profit planning must be a well thought- out operational plan with its financial implication expressed as both long and short range profit plans. In any community where budget is used as a means of planning many alternative plans have to be considered and the most profitable one will be adopted, because where the plan chosen in great 1

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Budget implemtation

CHAPTER ONE

INTRODUCTI

ON

1.1 BACKGROUND OF THE STUDY

A budget is a financial and a statement prepared

prior to a defined period of time of the policy to be

pursued for the purpose of attaining a given

objective. Budget is a plan quantified in monetary

terms, prepared and approved prior to a defined period

of time, usually showing planned income to be generated

and or expenditure to be incurred during that period

and the capital to be employed to attain a given

objective. Furthermore a budget is an attempt made at

the beginning of each financial year to plan the profit

and loss account for the year and to aim for a definite

balance sheet. This profit planning must be a well

thought- out operational plan with its financial

implication expressed as both long and short range

profit plans.

In any community where budget is used as a

means of planning many alternative plans have to be

considered and the most profitable one will be

adopted, because where the plan chosen in great1

expectations, then the best use must be made of the

available resources. On the other hand budgetary

implementation is the establishment of policies and

the periodic review or comparison of the actual

result with the budgeted performances either to

secure approval for individual action or to serve

as a remedial course of action. Budgetary

implementations whereby actual state of affairs can

be compared with that planned for by the

management, so that appropriate action may be taken

to correct adverse situation that may occur before

it is too late. It is also used to fix

responsibility. A budget systems serve the needs of

management in respect of the Judgments and

decisions it is fruited to make and to provide a

basis for the management functions of planning and

control. Developing a budget is a critical step in

planning any economic activity. This includes

business, governmental agencies and individuals.

Therefore businesses of all types and governmental

units at every level must make financial plans to

carry out routine operations, to plan for major

expenditures and to help in making financial2

decisions. On this back ground, every community no

matter the nature has a plan for the future, simply

because the success of any community depends on the

level of plan that is put into the community.

1.2 STATEMENT OF THE PROBLEM

The main problem with budgeting is that it

reflects data from the past and present, and will

only enable predictions and forecasts to be made

out the future. At the same time, numerous

pressures in the towns may impose constraints upon

Nasarawa Eggon local government which affect the

quality of information they collect. The problem

can be numerous; clearly, nothing can be forecasted

with absolute certainty. No matter what financial

and marking researches take place every the

community has to take risks. Though accounting

information may reduce the unpredictability of

event in the future. It will never eliminate it.

The study is aimed at accessing budget

implementation in Nasarawa eggon local government.

1.3 RESEARCH QUESTION

3

Can effective Budgets plan be a guide towards the

growth and development of Nasarawa Eggon Local

Government Area?

Can Budgets be a means to control and synchronize

Nasarawa Eggon local

1.4 OBJECTIVES OF THE STUDY

The objective of budgeting and budgetary

implementation in Nasarawa Eggon Community

includes;

To know how effective Budgets guide can lead to

growth and development of Nasarawa Eggon Local

Government Area.

To know if Budget can be a means to control and

synchronize Nasarawa Eggon local government.

To know if Corruption can be a major problem of

budget implementation In Nasarawa eggon local

government area.

To study and know if there are penalty when budget

are not implemented.

1.5 SIGNIFICANCE OF THE STUDY

These study will be of great important to the

government, private sector, public sectors, however

the specific objective are listed below.4

It will help the government to know how effective

Budgets guide can and lead to growth and

development of Nasarawa Eggon Local Government

Area.

It will help the government to know if Budget can

be a means to control and synchronize Nasarawa

Eggon local government.

It will help the private sector, public sector and

the government to know if Corruption can be a major

problem of budget implementation so to stop

corrupted practices by the local government

officials responsible for the implementation of

budget.

The study will also help to know if there are

penalty when budget are not implemented in the

local government area, not only in the study area

but over the state and the nation at large.

This study is Budgeting and budgetary

implementations it will be of great importance to

Nasarawa Eggon local government because;

The preparation of budget helps in the delegation

of responsibilities to each executive and induces

early consideration of basic policies. It also5

assists in the focusing of attention on the

contribution which may be made by each product and

market to the total profit and reveals any

opportunity which may be made by each product and

market to the total profit and reveals any

opportunity which may be made in maximizing profit.

It provides a means of ensuring that capital

invested in the community is kept to a minimum

level justifiable with the level of activities. It

also ensures that adequate liquid resources are

made available at anytime.

It defines goals and objectives that can serve as

benchmarks for evaluating subsequent performance.

Better control of current operations is helped by

regular, systematic monitoring and reporting of

activities.

It regulates the spending of money and expose loss,

waste and inefficiency and through this corrective

action will be taken to improve the adverse

situation.

It encourages management to decentralize

responsibilities without losing control, especially

6

where a company has many branch offices or

factories.

It provides for the co-ordination of sales

production and other activities of the business and

forces all members of management team to plan in

harmony and consider all relevant factors before a

decision is taken.

Where budgetary implementation is in operation,

cost consciousness is always increased and through

this means, waste and inefficiency will be reduced.

It also gives lower levels of management to also

take part in the management of the business.

It provides a means of communicating management’s

plans to the host community.

It uncovers potential bottle necks before they

occur.

1.6 RESEARCH HYPOTHESIS

H0: Effective Budget plan is a guide towards the

growth and development of Nasarawa Eggon Local

Government Area

7

H1: Budgets is a means to control and synchronize

Nasarawa Eggon local Government management and

personnel functions

1.7 SCOPE AND LIMITATION OF THE STUDY

The study of “budgeting and budgetary

implementation” in Nasarawa Eggon local

government Communities could have been extended to

cover the whole of the accounting and financial areas

of Nasarawa Eggon local government . But because

there are some limiting factors such lack of capital

shortage of time , the scope of the study will be

limited to only the facts on the budgeting and

budgetary implementation in Nasarawa Eggon local

government

Though budgeting and budgetary implementation has

many impressive and far reaching advantages, but it

also has certain limitations and pitfalls which the

Nasarawa Eggon local government must consider.

Other factors limiting the study are; the system

requires the co-operation and participation of all

members of the Nasarawa Eggon local government

project supervising team to supervise al project and

make sure that they are implemented and carried out8

appropriately and not only that, the basis for

success is executive managements absolute adherence

and enthusiasm for the budget. This is really very

important; but most often budgetary implementation

has failed because some of the members of the

Nasarawa Eggon local government who have paid lip

services to its execution.

CHAPTER TWO

LITERATURE REVIEW AND THEORETICAL FRAME WORK

2.1 INTRODUCTION

Finance is it is very paramount in any local

government, be it private, public or quasi-public.

This is always the case in all polities of the

world irrespective of the system of local

Government or ideological beliefs or persuasion

(Akindele 2000). Finance plays an important role in

the life of any organization. It embodies all

actions of raising and spending money through

9

prudent budgeting, management of available

resources and efficient allocation of values

(Mukoro, 2000). It is a vital ingredient that

sustains the life and motion of a local Government

that enable it to perform its most essential

function (Aluko 1987). Finance dictates the

development trends, shapes the real topography of

the political landscape of all polities and its

operational tool – (money) – has been, in the view

of Akindele (2000) variously in euphemistic

context, described as the “root of all evil” on one

hand and, as the “conqueror of all evil” on the

other hand, meaning that what money could not do

will be permanently left undone.

The above eulogies of money as the principal

component of finance according to Akindele (2000)

are not mere flukes but real promoter of its

indispensability to the economic survival of

mankind and its multiplier effects on other aspects

of man’s systemic existence, a combination of which

calls for its proper sourcing and management

especially within the public sector of the

political economy. Thus, the issue of public10

finance particularly as it concerns the healthy

relation of revenue with expenditure is crucial to

the success or otherwise of any sector of an

economy and the prosecution of the imperative of

its existence within any polity of the world.

This relation of revenue with expenditure, in

economic parlance denotes fiscal policy defines as

the use of local Government tax and expenditure

patterns to influence economic activities with a

view to avoiding fiscal stress or crisis. This is

always prosecuted through a balanced budget and its

neutral effect on total spending (Akindele, 2000).

2.2 CONCEPTUAL ISSUES

The basic and essential responsibilities of

public financial management include the planning,

financing, safeguarding, utilization, analyses and

reporting and at the centre of this process is the

government budget (Awe, 2001). Therefore any

systemic discussion of public finanacial management

must start with the institutional issues

surrounding the budget process (NISER, 1977).

Besides, formulation of public policies would not

be meaningful, effective and efficient if the11

financial resources needed to transform them into

concrete and practical realities through budgeting

are not available. Public budgeting, although

characterized by a lot of confusion due to many

different and often conflicting ways in which it

has been defined by different authors (Omopariola,

1997), is the allocation of financial resources

among the multifarious alternative policies,

programmes and activities of government (Alabi,

1987).

Budgeting involves not only allocation but also

planning, management and control. This position

tallies with that expressed by the United Nations

Manual for programme and Performance Budgeting

which are virtually the same, according to

Omopariola, (nd), is the most appropriate

definition for governments in developing country

like Nigeria. According to UNM- PPB (1956),

budgeting is an “operational activities” that must

be contrasted to a plan which is a “blue print for

action”. By this definition, economic policy

questions are not expected to be dealt with by

budgeting only but rather, by planning (Omopariola,12

1997). Patterson (1972) in his own defined

budgeting as the “translation of the longer term

performance and resource use plan in to a more

detail and precise plan for the year ahead” while

Nigrot (1969) sees it as “the process of converting

the goals, programmes and projects into money

terms” Budgeting is more than a mere economic term.

For the purpose of this paper it has to be

understood in its most inclusive politico –

administrative sense. It is on the basis of the

above that Wildavsky (1976) views budgeting as a

part of political process. Decision strategies are

premise on each agency’s historical base and

involve:

i. defending the base against the cuts in old

programme;

ii. increasing the base by inching ahead with

existing programmes and;

iii. expanding the base by adding new programmes;

These strategies are used by different agencies in

competing for the scarce resources of government.

Budgeting is, thus, not a static phenomenon. It is

a process and a lot of politics goes into its13

formulation. It is on the basis of this that

patience and caution have to be exercised by those

involved in its formulation and implementations as

its process reflects the dynamics of political

forces in the system or organization. A budget,

which is the output of budgeting is derived from

old French word “bougette” (meaning a small bag),

has been tentatively used to describe fiscal

expectation, expenditure and future planning of an

individual, organization, or government within a

given period of time .Comparison of the relative

values of alternative uses of funds allows decision

makers to know the opportunity costs of funding

alternative courses of action. According to

Dempster and Wildavsky (1979), a new budget

represents an ‘added on’ or ‘incremental change’

over its predecessor. Along the same line, Charles

Lindblom (1959) posits that because it is never

possible to identify all actions or alternative

policies for accomplishing results, incremental

decision-making becomes inevitable in budgeting.

This method of incremental analysis can be employed

in considering how to allocate scarce resources14

among alternative uses by dividing available

resources into increments and considering which of

alternative uses of each increment would yield the

greatest return. This is the concept of utility.

Natchez and Bupp (1973) do not reason along this

line. They argued that by concentrating on the

underlying regularities of the administrative

process, Wildavsky (1964, 1975) and Lindblom miss

the real changes in programme priorities which

occur within the total budget. Also John Wanat

(1974, 1978) argues for a shift in emphasis from

aggregate descriptive representative on to the

pragmatic portion of the budget. In concrete term,

budget analysis asks the question: On what basis

will it be decided to allocate X naira to project A

instead of allocating them to project B? The worth

of any public expenditure programme concerns not

only its individual virtues but also and more

importantly the return from every money spent on it

must worth its cost in terms of sacrificed

alternatives. It is in this sense that budget

analysis is construed to be “basically a comparison

of relative merit of alternative uses of funds” and15

is designed to enable governments and entrepreneurs

allocate resources for projects and other cost

items (Alabi, 1987).

From the foregoing, it is clear that public

finance, its sourcing, spending and management

through budgeting and budgetary process cannot be

ignored or taken for granted without severe and

detrimental economic and political consequences

within any polity. This is particularly so, because

the budget is usually the pillar upon which the

finances of the state or organization is fully

erected for any given year.

In other words, finance as viewed within the

context of this discussion and the need for its

prudent management as well as its indispensability

to effective governance, brought about the need for

proper and appropriate budgetary decision-making

process. This budgetary decision-making goes

through different phases thus:

i. executive preparation and submission of budget

proposals to the budget office:

ii. legislative authorization and appropriation;

the approval by the legislature, in its16

capacity as the “cheglem writer”, of the

appropriation bill(s) of the executive.

iii. the execution of the approved estimates.

iv. auditing of accounts to ensure that the budget

is executed as approved (Alabi, 1987).

The budgetary process is not without its own

problem which (may) hinder its successful

undertaking. Some of these hindrances include the

difficulty and near impossibility of getting

necessary data in precise figures for budget

compilation. Budget decision entails forecasting of

the future needs which may be right or wrong;

accomplishments in relation to costs cannot be

precisely measured even after the programme might

have been implemented; and that administrators have

no means of calculating the relative usefulness of

governmental activities because the activities have

no prices in the market place. These hindrances

notwithstanding, budget and budgetary process is

still a mechanism through which a particular system

is given meaningful financial, economic and

political directions.

17

From the discussions in the immediate last two

paragraphs it becomes obvious that two major

institutions/actors are traditionally and

constitutionally involved in budgetary decision-

making process in Nigeria and indeed in most

polities of the world. These actors, the executives

and the legislature, in the view of Akindele (2000)

could be regarded as the institutions or organs of

government responsible for making budgetary

decision. Besides, it also clearly shows from our

discussion that the budgetary procedure/process

must be dedicatedly pursued in accordance with laid

down historical, constitutional, legislative,

political, economic and administrative procedures

as can be discerned from the phases involved

(Akindele, 2000).

2.3 MAIN TYPE OF BUDGET

2.3.1 FIXED & FLEXIBLE BUDGET

A fixed budget is a budget which is designed to

remain unchanged irrespective of the volume of

output or turnover attained. That is, it is a

single budget with no analysis of cost. The major

purpose of a fixed budget is at the planning stage18

when it serves to define the broad objectives of

the Organization where there is no analysis of cost

into fixed and variable. The fixed budget is

unlikely to be of any real value for control

purpose except if the level of activity turned out

to be exactly as planned.

Flexible budget is a budget which by

recognizing different cost behavior patterns, is

designed to change as the volume of activity

changes for control purpose, it is vital that

flexible budgeting is used only by comparing what

the cost should have been with the expenditure

incurred at the actual activity level can any

control be exercised.

A flexible budget often reflects, increases or

decreases in business activity throughout an

Organization In some Organizations, changes may be

greater in some departments and smaller in others.

In some departments ability to produce more units

are there without incurring high additional costs.

While in anther cost increase or decrease in direct

proportion to production increase or decrease. The

flexible budget attempts to deal with this19

situation with a fair degree of accuracy. It keeps

the expense to the level of activity possible and

so facilitates the control of expenditure and

comparison of expense with revenue or volume of

production.

In order to be able to prepare flexible budgets

with some degree of accuracy, it is necessary to

classify overhead cost into fixed, variable and

semi-variable. With variable cost, a specific sum

per unit of output or standard hour is set and so

total variable cost is obtained by multiplying the

unit cost by units or hours.

2.3.2 OTHER TYPES OF BUDGET

The specific types of budget to be prepared by

the management of an Organization will depend on so

many factors such as the nature, size, complexity,

operation, etc. of the Organization. But in

practice, the following types of budget are common;

BUDGET-A cash budget involves detailed estimate of

anticipated cash receipts and payments for the

fourth coming year or period. This is because while

it may be possible for an Organization to exist and

continue to survive without profit, the existence20

of an Organization is doubtful without liquidity. A

cash budget identities potential period of cash

deficit or cash surplus to the Organization. This

Organization will therefore assist the adverse

effect of cash squeeze(lack of cash) by arranging

for an overdraft facility or to maximize the

benefit associated with surplus fund through short-

term investment.

MASTER BUDGET-The master budget also known as

profit plan is a comprehensive set of budgets

covering all phases of an Organizations operations

for a specified period of time. The master budget

is the principal output of a budgeting system.. It

is a comprehensive profit plan, that ties together

all phases of an Organizations operations. It is

comprised of many separate budgets that are

interdependent. They are

- Operational budget

- Financial budget.

OPERATIONAL BUDGET: Shows how operations will be

carried out to produce an Organizations goods and

services. The essence of operational budget is

21

for the Organization to be able to meet the demand

of its goods and services

FINANCIAL BUDGET: This shows how an Organization

will acquire financial resources during the budget

period.

SALES BUDGET: Sales budget shows the quantities of

each product that the company plans to sale and the

intended selling price. This budget is very important

because it is an estimate of the revenue to be

generated by the Organization from its operations. It

provides the prediction of the total revenue from

which cash receipts from customers will be estimated

and it also supplies the basic data for constructing

budgets for production cost and for selling,

distribution and administrative expenses. The sales

budget is the foundation of all other budgets since

all expenditure is ultimately dependent on the volume

of sales. This budgets also serves as a tool for

inventory management i. How to understand failure of

control in management of government establishments,

ii. How failure occur,

iii. How to analyze deviations,

iv. How to correct deviations, 22

v. And how to prevent failures in control

relationship of the above variables.

2.4 EMPIRICAL FRAME WORK There was a study carried out by Mullins (1993)

on the topic titled “Corporate Budgetary Control

and Accounting Practice in Nigeria’s Oil-Drivers

Economy: Survey of Government Owned Business

Investments” aimed at identifying the problems of

government owned industries in Nigeria. It was a

survey research by which he adopted the use of

questionnaire for data generation. He analyzed the

responses of the respondents (the Staff of Rivers

State government industries Budgetary Section)

using chi-square method. The outcome showed that

government owned industries in Nigeria have been

hampered by inadequate/ineffective accounting

practice/system, worsened by weak budgetary

control system, poor product marketing system and

finally defective deficit financial system. He

recommended that Government owned industries should

23

have up-to-date accounting practice and adequate

plan for budgetary implementation.

In another study carried out by Okemini and Uranta

(2008) on the topic “Government Owned Business

Investments (GOBIs)” aimed at assessing the

accounting practice and financial performance of

GOBIs in developing countries. The study adopted

survey research and used questionnaire to generate

data. The researcher administered questionnaires on

140 public enterprises and 50 private enterprises

proprietors at Delta State. They made use of

chisquare in their analysis. Okemini and Uranta

(2008) found out that GOBIs has negative financial

performance as a result of poor accounting

practice and that many operate at substantial

losses due to weak budgetary implementation.

Fubara (2004) in a publication titled “Poor

Performance on GOBI”. This publication revealed the

major problems facing GOBI in Nigeria. It was an

exposing research into poor practice of accounting

in GOBI in Nigeria. He noted that this was as a

result of insufficient funds arising from

restrictive ownership, scarcity of technology,24

conflict of objectives between government and

firm’s management, and general managerial

inefficiency. Akinsanya (1992) on the topic

“Educating the performance of Public Enterprises in

a changing environment” identified high incidence

of fraud, poor product marketing, pervasive

political affiliations, defective appointment of

board members, overstaffing, financial

indiscipline and dishonesty to be the major cause

of poor accounting practices and budgetary

implementation in government industries in Nigeria.

It can be observed from the above studies that poor

accounting practices on budget implementation is a

existing problem in Government owned industries in

Nigeria. Nevertheless, more of the researcher

pointed clearly a concrete machinery to put in

place to handle the poor accounting practices on

budget implementation caused by numerous factors

thus: high incidence of fraud, pervasive political

affiliations, defective appointment of board

members financial indiscipline and dishonesty etc.

2.5 PROBLEM OF BUDGET IMPLEMENTATION IN NASSARAWA

EGGON LOCAL GOVERNMENT 25

Many problems have bedeviled Nasarawa Eggon

local Government budget implantation . As such,

they have not been able to meet with their

statutory obligations of bringing the gains of

democracy closer to the citizens.

Some of these problems include:

Corruption and mismanagement

Corruption is one of the major problems facing

the Nasarawa Eggon local Governments. In fact, a

mere mention of the local government exudes

corruption. The popular myth propagated by the

council officials is that the councils are always

short of funds. No doubt, the heavy funding that

runs into billions of Naira as seen from the tables

may not be enough because of the high level of

corruption in the councils. It has also been

observed that Nasarawa Eggon local Governments do

not accord adequate regard to the budget process.

The fall out of this situation is the

indiscriminate and unplanned execution of projects.

The state governments which would have served as a

check are not free from this cankerworm. Evidently,26

there is contract scams in all local government

councils in Nigeria. These contracts are inflated

and worse still, the projects are not executed and

thereby defeating the essence of budgets.

Skilled Manpower

Nasarawa Eggon local Governments today is

manned by officials who do not possess the

requisite leadership and managerial skills to

deliver the gains of democracy to the people.

Section 7(4) of the 1999 constitution makes

provision that the qualification for election into

the offices of the Chairman and Councilors shall be

the same as that of the election into the Houses of

Assembly of a state.

The constitution puts the minimum educational

qualification for the election into the House of

Assembly of a state as school certificate.

However, this principle have not been followed and

as such, made the councils the dumping ground for

illiterates or a starting point for political

toddlers.

Lack of Civil Society Participation

27

The level of participation by the people ishighly limited especially Nasarawa Eggon localGovernments and other rural areas in the country.The reason is attributed to high illiteracy leveland the poverty rate. Thus, the psyche of thepeople is very low. In addition, there is no lawthat encourages civil society participation ingovernance and also no access to information andparticipation. In the absence of this, the civilsociety, no matter how vibrant and enlightened,cannot achieve anything.

Central/State Government’s InterferenceThe 1999 Constitution confers powers that

relegate the local governments to both the federal

and state governments. Evidently, this has created

friction leading to the neglect of local bodies.

The council is not given the necessary independence

as practice in a true federal structure. In

addition, elections into the councils in most

states have not taken place more than a year after

they were dissolved. It shows that democracy in

Nigeria today is not practiced at the local

government level.

Finance

Finance is another area of concern. Most of the

local council’s sources of revenue with referece to

28

Nasarawa Eggon have been taken over by the state

government. Some of these councils also are too

small in size and thus, have little or no resources

from which to generate revenue internally. The

internally generated revenue of these councils is

too small to pay the wages and salaries of their

junior staff not to talk of embarking on any

meaningful projects. Moreover, the 10% of the

internally generated revenue of the state that is

supposed to be given to local council is not

forthcoming. Worse still, the federal government

statutory allocation does not usually come to the

local councils regularly and the state government

at times divert the allocation to satisfy other

areas. In fact, it is in line with this situation

that the 774 local governments under the aegis of

the National Union of Local Government

Employees (NULGE) demanded for succor during

President Olusegun Obasanjo’s administration. The

union was assured for an existing constitutional

backing in its quest for fiscal and administrative

autonomy.

Prospects 29

Evidently, Nasarawa Eggon local Government

cannot overcome its problems without the supports

of both federal and state governments. However, the

local government should be allowed to discharge

some of its responsibilities without direct

intervention by these higher tiers of governments.

In the area of budgeting, the whole process should

be the responsibility of the local Chairman and

assisted by the local Supervisory councilors as

well as others like the Secretary and Finance

officer. The period for budget preparation should

be fixed. It may be between July 15 and October 15

of the current year. The document should be

transmitted to the local council not later than

October 16. The document also must consist of the

estimates of income and details of the total

appropriations to cover current operating

expenditures and capital outlays. Also, in

preparing the budget, certain requirements must be

followed.

These requirements which are like a form of

expenditure control include:

30

i. General limitations that

influence the total expenditures.

ii. Specific limitations which

mandate local governments to fund particular

expenditure items.

The legislative discussion of the budget estimate

should be able to commence between October 16 and

November 17 of the current year. This would enable

the chairman to issue an ordinance on or before the

current fiscal year. The budget review should

commence immediately after the authorization of the

document. The document should be submitted within

two weeks, for review by the reviewing office which

is the Department of Budget and Management. The

essence is to ensure compliance with budgetary

requirement and consistency with the local

development plan. The review should not last more

than 90 days. Once the budget passes review, it

goes to the implementation. It involves the release

and actual disbursement for funds for the specified

functions and projects. The programming of fund

disbursement should be the duty of work and

financial plan and request of allotment.31

At this level, emphasis is placed on prudent

disbursement of funds. Notably, it is always better

that no cash overdraft is incurred at the end of

the fiscal year and due process should be adopted

in disbursing fund (that is, appropriate

certificate of the local budget officer, local

accountant and treasurer required). The next level

is the budget implementation accountability. It

involves recording and reporting of actual income

and expenditure as well as the evaluation of the

performance. Accountability should be shared among

the department heads who participated in the use of

the fund, the local treasurer, local accountant and

budget officer. There is also the need to carry the

people along during budget preparation and

implementation. It could be in form of people’s

organizations and non-governmental organizations

within the local councils. The organizations should

be accredited by the local council and among them

either select or elect who will represent the group

in the special committees comprising the chairman,

members of the council and heads of concerned local

32

departments. This is mainly to bring home the

government priorities to the people.

2.6 REVENUE ALLOCATION IN NIGERIA

Discussions on local government finance most

of necessity in most cases touch the issue of

revenue allocation in Nigeria. The term “revenue

allocation” is often used in association with such

terms as fiscal federalism, resource control, and

fiscal decentralization. It has been broadly

defined to include the allocation of tax powers and

the revenue sharing arrangements not only among the

three tiers of government, but among state

governments as well (Olowononi, 1998: 247). Fiscal

federalism is a system of taxation and public

expenditure in which revenue-raising powers and

control over expenditure are vested in the various

tiers of government within a nation, ranging from

the national government to the smallest unit- the

local government (Anyafo, 1996 cited in Dang,

2013). Basically, fiscal federalism emphasizes on

how revenues are raised and allocated to different

levels of government for development (Dang, 2013).

33

According to Nyong (1999), fiscal federalism

concerns the relationship among the various levels

of government with respect to the sharing of the

national cake, assigned functions and tax powers to

the constituent units in a federation. He asserts

that the important issue in fiscal federalism is

revenue allocation formula, sharing of the national

revenue among various tiers of government (vertical

revenue sharing) as well as the distribution of

revenue among states (horizontal revenue

allocation).

For Ekpo (2003), fiscal federalism is a

mechanism in which relations arising from the

political decentralization of the public sector

functions and responsibilities are resolved. The

term deals with the allocation of resources among

the three tiers and units of government, and

institutions for the discharge of responsibilities

assigned to each jurisdictional authority. The

nature and well fashioned fiscal relations in any

federal system are crucial to the continual

existence of such systems. One of the cardinal

principles of federalism is that no level of34

government is subordinate to one another, though

there must be a central government for this

arrangement. The important features of federalism

are:

Division of powers among levels of government

Coordinate supremacy of each level of government.

Financial autonomy of each level of government

35

Wheare (1943 cited in Olowononi, 1998:248), the

chief exponent of federalism has emphatically argued

that all the tiers of government are coordinate in

status. This implies as he maintained that if state

authorities, for example, find that the services

allotted them are too expensive for them to perform,

and if they call on the federal authority for grants

and subsidy to assist them, then they are no longer

coordinate with the federal government but

subordinate to it. Consequently, in Wheare’s

contention, the financial subordination of the state

and local governments as the case in the Nigerian

experience from 1999 to 2013 “makes mockery of

federalism no matter how carefully the legal forms

may be preserved”.

36

Although the question of how to generate, increase,

allocate and expand revenue has constituted an

issue in the Nigerian politics and governance since

1914, it was from 1946 that the issue of revenue

sharing and allocation began to raise serious

national debate since there was real fusion of

fiscal operation in the country with the coming

into effect of the Richards Constitution which

provided for Legislative Council for the whole

country and Regional Councils with large devolution

of powers and functions. Consequently, various

Revenue Allocation Commissions were set up at

different times to examine and settle the issue of

revenue allocation among the three tiers of

government- the federal, state and local

(Onwioduokit, 2002). Thus, it is apt to say, that

the concept of fiscal federalism was first

introduced in Nigeria in 1946 following the

adoption of Richards Constitution (Vincent,

2000;http://www.doiserbia.nb.rs/ft.aspx?id=0013-

32641189027S_br). The period 1947 to 1952 is a

watershed in the beginning of sub-national

governments because financial responsibilities were37

devolved to three regions-North, West and East. As

Adesina (1998:232) puts until Nigeria’s

independence, the most contentious aspect of the

nation’s federalism, revenue allocation, remained

the responsibility of the colonial masters. Then,

politicians accepted compromise as the price of

access to the state office and thus to the revenue

of the state.

Fiscal federalism became deepened during the

military epoch of 1966 to 1990s following the

creation of states and local government perhaps as

a means of spreading development across the country

and satisfying agitations from potential ethnic

groups. The era of military rule began with the

creation of twelve states in 1967. As observed by

some commentators on Nigerian government and

politics, the creation of more states and local

governments was a deliberate tactics and technique

to compel dependency of state and local governments

on the federal government. As at present, there is

a Federal Government, 36 States, Federal Capital

Territory and 774 Local Governments in Nigeria.

Nigeria has engaged various commissions and38

committees since the colonial days, and yet this

issue continues to be in the front burner of

national discourse and debate. From 1946 to 2000,

nine Commissions, six Military Decrees, one act of

the Legislature and two Supreme Court judgments

have been resorted to in defining and modifying

fiscal relationships among the component parts of

the federation (Egwaikhide and Isumonah, 2001; Fiscal

Federalism - Dawodu.Com - The Premier website on(n.d.).

Retrieved from http://dawodu.com/eson1.htm_br).

Among these commissions re Philipson Commission

(1946), Hicks-Philipson Commission (1951), Louis

Chick Commission (1953, Jeremy Raisman Commission

(1958), the Binns Commission (1964), Dina

Commission (1968), the Aboyade Technical Committee

on Revenue Allocation (1977), the Okigbo Commission

(1980), and Danjuma Fiscal Commission,1988 (Ekpo,

2004; Jimoh, 2003; Akindele, 2002; Udeh,

2002;Olowononi, 1998; Ovwasa, 1995).

2.7 SOURCES OF LOCAL GOVERNMENT FINANCE IN NIGERIA

Source of local government finance implies the

various means through which local governments in

Nigeria generate financial resources to meet their39

financial obligations in the course of discharging

their constitutional functions and duties. There

are two major sources of local government finance

in Nigeria, namely, internally generated revenue

(which is revenue generated within the local

government area of administration and it entails

local tax or community tax, poll tax, or tenement

rates, user fees and loans); and externally

generated revenue which refers to the local

government funds generated outside the local

government area of administration (Alo, 2012: 23).

Internally generated revenue is a strategic source

of financing local governments operation and which

can be explored given the enabling environment and

political will. The level of internally generated

revenue by each local government depends on the

size of the local government, nature of business

activities, urban or rural nature of the council,

rate to be charged, instruments used in the

collection of revenue, political will and

acceptability by the people to pay based on the

legitimacy of the council and the socio-cultural

beliefs of the citizens regarding the issue of40

taxation (Anifowose and Enemuo, 1999). Local

governments are constitutionally empowered to

control and regulate certain activities in their

jurisdiction, and in so doing; they impose some

taxes and rates on these economic activities as a

way of generating funds for their operations.

The various ways Nasarawa Egon Local Government

generate revenue internally are community tax and

rates; property (tenement) rates;

general/development rates; licenses, fees and

charges like marriage registration fees, cart/truck

licenses; interest on revenues such as deposits,

investments, profits from the sale of stocks,

shares, etc; departmental recurrent revenues from

survey fees, repayment of personal advances,

nursery and day-care centres fees, rents on local

government quarters, etc ( Atakpa,

Ocheni, and Nwankwo, 2012). From the foregoing, tax

is an imperative ingredient of revenue generation,

development and transformation. As Olaoye (2008),

puts it, it is a compulsory levy imposed by the

government on individuals, companies for the

various legitimate functions of the state (and41

local government). The 1999 Constitution of the

Federal Republic of Nigeria provides tax

jurisdiction of federal, state and local

governments (see table below). The table also shows

the precarious position of local governments in

generating revenue internally for projects

execution and other financial commitments.

2.8 THE MANAGEMENT OF LOCAL GOVERNMENT FINANCE IN

NIGERIA

For the management and control of local

government finance, the 1999 Constitution of the

Federal Republic of Nigeria provides for the

establishment of State Joint Local Government

Account in each state of the federation where funds

from the Federal Account are lodged before

disbursement to the local government councils in

the state. This arrangement has been hijacked by

state governments to starve local governments in

their jurisdiction the needed funds for project

implementation and rural development. This point is

aptly acknowledged by Mbam, the Chairman of the

Revenue Mobilization Allocation and Fiscal

Commission (RMAFC) when he observed that42

information at the disposal of the Commission show

unethical practice in the disbursement of funds

from the State Joint Local Government Account in

various states of the federation. As he maintained,

allocations from the Federation Account, most times

do not actually reach the Local Government

Councils. There are numerous allegations of

manipulation of the Account at the point of

disbursement. States hardly make their own

contributions as stipulated by Section 162 (7) of

the Constitution of the Federal Republic of

Nigeria. In view of the above challenges, it is the

position of the RMAFC that Local Governments should

be granted fiscal autonomy by paying statutory

allocations from the Federation Account directly to

their coffers in which case the State Joint Local

Government Account should be abolished through

appropriate reforms (see “RMAFC Canvasses for

Direct Funding of LGAs”).

There are a number of financial management and

control under democratic setting in Nigeria. One of

such is the legislative control. Local governments

operate under a legislative framework established43

by the constitution of the country. These

legislative provisions are meant to guide the

disbursement of funds in the system. Technically,

local governments in Nigeria operate under three

levels of legislative frameworks. There are

National Assembly, State Assembly and the

Legislative Councils. But practically they operate

more under the latter as legislative councils are

directly responsible for the budget of councils and

implementation of the local government financial

vision. These checks and controls are “toothless

bulldog that barks but cannot bite”. Despite these

checks and control, poor funding remains the most

cited reason for the inefficient implementation of

public policies and programmes at the grassroots.

Budgeting and Budgetary Control in the Local

Government

Budgeting and budgetary control is another means of

managing and controlling local government finance

in Nigeria. An effective budgetary control

mechanism ensures the existence of a sound

financial planning and control which is a pivotal

for sustainable growth and development in Nigeria44

especially at the grassroots.

Budgetary control involves a periodic

comparison of actual expenditures with planned

expenditure and whether budgetary disbursement is

in compliance with the provisions of the financial

regulations and other relevant financial

authorities in the country.

Thus, Nigerian local governments must embark on

annual budget monitoring and evaluation to

ascertain the level of budget performance. The

results of this annual budget monitoring and

evaluation exercise will provide the needed

statistical input for the preparation of a more

functional budget in the subsequent or succeeding

year. In most local governments in the country,

disbursement of funds is based on political need

instead of appropriation. An appropriation is a law

passed by the legislature authorizing expenditures

for a subsequent financial year or defined period.

Local governments are to ensure that funds

allocated to various projects under different sub

heads in the appropriation are utilized for their

intended purpose since any alteration of resources45

allocation results in virement which may be a

cumbersome process. The movement of funds from one

subhead or project to another must not be

undertaken except with the approval of the

legislature through the passage of a supplementary

appropriation law called virement. Strict adherence

to these budgetary control procedures ensures that

funds are utilized only for the purpose for which

they are allocated in the annual budget.

2.9 FACTORS AFFECTING LOCAL GOVERNMENT FINANCE IN

NIGERIA

A number of factors affecting local government

finance in Nigeria have been identified by scholars

and professionals. Fundamental among these factors

are the issues of unequal share of resources,

absence of fiscal autonomy, overdependence in

allocations from the Federation Account, creation

of non-viable local governments, dishonesty and

corruption, etc.(Alo, 2012). There are only very

few local government councils (mostly urban

located) in the country that are economically

viable, thus, survive without financial allocation

from the Federation Account. King (1988:197),46

succinctly notes that local governments will be

dynamic vehicles of rural transformation and

development if they are well financed, as well as,

ably staffed. He further states that staff and

revenue are profoundly interlinked. Local

governments with inadequate financial resources can

hardly recruit and retain competent workers who

demand competitive salaries and fringe benefits.

Efficient and well motivated workers can make

positive contributions that can boost revenue

generation at the grassroots. In addition to

the above factors, local governments in Nigeria

suffer from the following challenges (Alo, 2006;

Adewunmi, 1999;Oviasuyi, Idada, Isiraojie, 2010)

(1) Inadequate and Poor Budgetary Process:

Budgeting is the nerve centre in the management of

financial resources in both public and private

organizations. A budget is a financial plan that

shows in detail the proposed estimate of revenue

and expenditure for a defined period, usually one

year Onah, 2005; Adamolekun, 1983). It is one of

the powerful instruments for effective financial

management and control in both developed and47

developing countries. With regards to local

governments in Nigeria, a budget stipulates the

financial objectives of the local government for a

period of one year and set out strategies for their

accomplishment. If adequate plan is made for

revenue generation in the budget, more revenue will

be generated, if not, the result will be low income

generation. Local governments in Nigeria are known

to suffer from inadequate and poor budgetary

process.

(2) Ineptitude to work and low quality of manpower:

The control of public funds in the local government

is achieved through the career principal accounting

officers like council Chairman, Treasurer, Head of

Personnel Management, Internal Auditor and the

Local Government Service Commission. Unfortunately,

the men that ought to protect the system through

exemplary conducts are known to be involved in

bureaucratic politics to guarantee the siphoning of

funds through frivolous activities and fictitious

contracts. The successful provision of services as

contained in the annual budgets of local

governments in Nigeria depends on whether the48

targeted revenue is actually realized and

effectively utilised. This in turn depends on the

competence, honesty and diligence of the key

financial officers of the local government like

treasurer, internal auditor, council chairman who

is the accounting officer and other financial

officers. The challenge is that local governments

in Nigeria in most cases recruit persons who do not

possess the requisite leadership and managerial

skills to deliver their constitutional

responsibilities. The provision that makes the

minimum educational qualification for chairmen and

councilors positions to be post primary education

has made “local government councils the dumping

ground for semi-literates or a starting point for

political toddlers”.

(3) Administrative Inefficiency: Local governments

in Nigeria suffer from administrative inefficiency

and ineffectiveness resulting from low educational

qualifications of staff, poor motivation,

autocratic leadership, poor work environment, etc.

The management and control of finance is a central

factor in the management of local governments. The49

quality and promptness/effectiveness of local

government services depend on the quality and

quantity of workers in the system. Politically,

politicians divert from their campaign promises

through scheming of ways to remain in office and

swell their private financial bank accounts with

public funds of the local government. They abandon

principles of good governance and democratic ideals

that are fundamental in promoting administrative

efficiency and effectiveness for selfish. A case in

point is the indictment of some state governors and

local government officials by Economic and

Financial Crime Commission (EFCC) for diverting

finance of local governments.

(4) Quest for Local Government Creation: The

unbridled agitation for local government creation

in Nigeria is often perceived as a means benefiting

from the “national cake”. The proliferation of

local government councils without consideration to

independent economic viability has produced

interethnic crises and political instability in the

country. Thus, a scholar has cautioned that local

government must not be seen as a gift on a platter50

of gold from the state or federal government but

must be striven for and conceived essentially as a

means of developing the rural areas. Locality

clamouring for a local government unit must be

mature and must demonstrate readiness to sustain

the local government through sufficient internally

generated revenue (Mabogunje 1995:9).

Akpan (1965:126) posits that the bottom line in

judging the effectiveness of local government in

discharging its constitutional responsibilities

amount to funds at its disposal. The services

rendered by local government councils cost money

which most of them cannot boast. It is important to

note that the financial crisis in the local

governments has worsened because the federal

government has failed to recognize the new local

governments and development centers created by some

state governors. Governors of such states use part

of the statutory allocations meant for the

recognized local governments to pay staff salaries

of the new ones (Zwingina, 2003).

2.10 THE BUDGET PERIOD

51

The conventional approach is that once the

manager of the local government and budget centre

prepares a detailed budget for one year. The budget

is divided into either twelve monthly or thirteen

four – weekly periods for control purposes. The

preparation of budget on an annual basis has been

strongly criticized on the grounds that it is too

rigid and ties a company to a twelve months

commitment. This can be risky because the budget is

based on uncertain forecast.

An alternative approach is for the annual

budget to be broken down by months for the first

three months, and by quarters for the remaining

nine month. The quarterly budget are then develop

on a monthly basis as the year proceeds, Example ,

during the first quarters the monthly budget for

the second quarters will be prepared and during the

second quarters, the monthly budget for the third

quarter will be prepared.

2.10.1 The Budget Committee

The budget committee consists of high-level

executives who represents the major segments of the

business its major task is to ensure that budgets52

are realistically established and that they are co-

ordinated satisfactorily. The normal procedure is

for the functional heads to present their budget to

the committee for approval. If the budget does not

reflect a reasonable level of performance, it will

not be approved and the functional head will be

required to adjust the budget and re-submit it for

approval. It important that the person whose

performance is being measured should agree that the

revised budget can be achieved. Otherwise if it is

considered to be impossible to achieve, it will not

act as a motivational device.

The budget committee should appoint a budget

officer, who will normally be the accountant. The

role of the budget officer is to co-ordinate the

individual budget into a budget for the whole

local government so that the budget committee and

the budgetee can see the impact of an individual

budget on the local government as a whole.

2.10.2 The Budget Manual

A budget manual is prepared by the accountant-

it will describe the objectives and procedures

involved in the budgeting process and will provide53

a useful reference source for managers responsible

for budget preparation. In addition, the manual may

include a timetable specifying the order in which

the budget should be prepared and the dates when

they should be presented to the budget committee.

The manual should be circulated to all individuals

who are responsible for preparing budgets.

2.10.3 Stages In The Budgeting Process

The important stages in the budgeting process are

as follows,

1. Communicating details of budget policy and guide

lines to those people responsible for the

preparation of budgets.

2. Determining the factor that restricts outputs

3. Preparation of the sales budget.

4. Initial preparation of various budgets.

5. Negotiation of budgets with superiors.

6. Co-ordination and review of budgets.

7. Ongoing review of budgets.

2.11 THEORETICAL FRAMEWORK

This study was based on the theory of budget

control. The theory of control was first formulated

by Henri Fayol in (1916) and published in the54

management Sciences Journal in 1949. This theory of

control specifies the obligations of government in

providing social and basic amenities to the

citizenry. It indicates that government owned s is a

basic principle of control on those scarce resources

they are meant to manage. Robert (1970) on a journal

of management control function on government enter

press states the relevance of effective management

control in government. Shields and Young (2009)

contends that government s ought to provide both

resources and employment to the citizens for

meeting the laid down objectives. This implies that

government of Nasarawa Eggon local Government

members and staff have joint responsibility to

ensure proper budget implementation practices and

timely budgetary implementation and appropriations

by building effective management controls and

directions.

8.The General Accepted Accounting Practice (GAAP)

should be uphold in all government establishments in

order to and the third tier of government which is

local government should meet the desired objectives.

Rittenbery and Schwieger (1997) states “several55

corporate failures which adversely affect both

budgeting, accounting and profitability. Adequate

control is very essential to every organization be

it individual or government owned all over the

world. It is because if there is no adequate control

of resources in the local government it will be

practically impossible to appropriate budgets and

accounting practices becomes a waste. The idea

behind proper accounting practices and timely

budget implementation and appropriations in the

above referenced research work seem to agree with

our opinion for the appointment minded individuals

into board members of government s in Nasarawa Eggon

local goverment State for adequate control,

acceptable accounting practices and above all

budgetary implementation in order to address the

problem of impact of accounting on budgetary

implementation.

9.Going by the theory of control with emphasis on its

principle of obligations of government s in

providing social and basic amenities to her

citizenry, government owned s are expected to live

to its responsibility of establishing standards,56

adequate controlling mechanism and acceptable

accounting practices. In view of Canard (2003),

government enterprises need not to have unethical

persons acting outside controls. Thus ineffective

control system in

every organization is negatively affects organizatio

nal profitability and sustainability as well as comp

any’s resources and performance. Many studies had

indeed established link between the accounting

practices and corporate financial performance

underscoring centrality and criticality of the poor

budget performance in government s especially in a

developing economics where corporate governance

might not be focused. This study, however, focused

mainly on the affairs of government owned in

Nasarawa eggon local goverment State. This theory is

relevant to the study because appreciation of

failure of control, how it occurred and how to

analyses and interpret the failure is necessary if

the correct thing must be done; and this is

directly correlated to the objectives of the study.

57

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 INTRODUCTION

Research work is of necessity in any academic

discipline and it requires a methodology to arrive

at its logical conclusions or desired objectives.

It provides ways of analyzing data so that theories

can be tested, accepted or rejected. The absence of

such systematic way of providing knowledge renders

research findings as mere chanced occurrence.

In an attempt to investigate budget implementation

in Nasarawa Eggon Local Government Area of Nasarawa

State

3.2 RESEARCH DESIGN

The design for this study is survey research

design. It involved the sampling of the factors

affecting the growth and development of Nasarawa

Eggon Local Government . According to Sambo (2001)

a survey is a description of the state of affairs.58

It is usually done through direct observation or

such instrument as questionnaires, opinions and

oral interviews.

3.3 POPULATION OF THE STUDY

The population for this research work comprises of

top management staffs, middle management staffs and

lower level management staffs of Nasarawa Eggon

Local Government management board branch. This

gives a total population of forty five (400) staffs

of the local government.

3.4 SAMPLE OF THE STUDY

Since it not possible to study the entire

population of staff of the local government the

researcher have decide to choose 40 out of the 400

staff of Nasarawa Eggon local Government as the

sample size of the study so collection of data can

be accurate and conclusion can be drawn at the of

the study

To determine the sampling size, the Yaro Yamane’s

technique was used. The formula stated as-

n= N

1+N(e)2

Where; n=desired sample size59

N = Population size under study

E = Level of significance of error.

Assumed to be 5%

I = Constant

Therefore,

n=?

N=45

Sample size (n) = 45

1+45(0.05)2

n= 45

1.1125

n = 40

The next step is to determine the minimum number of

staffs/respondents to be chosen from each department.

The bowlegs proportional formula is used which is

given as

NH= n*nh

N

Where,

NH = number of questionnaires allocated to

each

department/no of staffs to be chosen from each

department.60

N = Total sample size

Nh = Number of staffs in the department.

N = Total population size

Security Department

Nh= 40*10 = 9

45

Audit Department

NH = 40*12 = 11

45

Finance Department

Nh= 40*9 = 8

45

Personnel Department

Nh= 40*7 = 6

45

Maintenance Department

Nh= 40*7 =

6

45

3.5 METHOD OF DATA COLLECTION

The researcher employ the use of questionnaires and di

stributed them to staff of Nasarawa Eggon local

government to both educated and on educated61

staff and guided the non educated staff who were illit

erate filling and completing the questionnaire to make

the collection of data simple and accurate.

3.6 SOURCES OF DATA.

The researcher obtained the in formations contained

in this project from the following sources;

Primary source

Secondary source

3.6.1 PRIMARY SOURCES – These are data I generated from

surveys conducted. They are original in character.

I went to local government and got some facts

through oral interview and use of questionnaire

with the staffs of the local government

management board.

3.6.2 SECONDARY SOURCE – These are information’s the

researcher gathered from data which are already

collected by some other persons and have passed

through some statistical process of at least once.

The researcher gathered them from both published

and unpublished sources.

The sources of the researcher unpublished data

include materials obtained found from Official

publications of the government. Reports and62

publications of federal, state and local

government, public organization, banks, trade

unions, manufacturers, and professional bodies.

Technical Journals that is books and news papers.

Textbooks and well as different web site from the

internet.

3.7 METHOD OF DATA ANALYSISIn analyzing the data collected using the

questionnaire; the researcher used the simple

percentages method of data analysis. The analysis was

represented in tabular form for easy understanding and

it consist the number of respondents and the

corresponding percentage and chi – square was used as

the statistical tools used for testing more than two

population using data base on two independent random

samples.

The test statistical thus becomes

X2 = (o∑ 1 – e1)2

e1

Where o1 = observed frequency

e1= expected frequency

This test is based strictly on the primary data

gotten from the use of questionnaire.

63

DECISION RULE: Reject Null Hypothesis if calculated

value of (X2) is greater than the critical value and

accept Null Hypothesis if calculated value of (X2) is

less than the critical value.

The Degree of freedom = (n - 1) (k - 1)

Where Df =Degree of freedom

n = Number of rows and

k=number of colunm

3.8 LIMITATION OF RESEARCH METHODOLOGY

In these study the methods of data collection and

analysis are limited by the following

factors;

The questionnaires given to the respondents were

not treated as important documents and tools for a

research work.

Time constraint, a longer time would have allowed

for greater explanation of facts.

It was also difficult to retrieve the

questionnaires from some the respondents.

Some respondents were hostile to this researcher.

Some of the respondents were reluctant to reveal

some vital information that was termed informal

sector secrets.

64

CHAPTER FOUR

DATA PRESENTATION AND ANALYSIS

4.1 INTRODUCTION

In this chapter the researcher inclined to

measure data not as numerical values but in

categories. In presenting the data that way, it is

easier to determine from examination of the data,

the level, if there is any of dependencies between

the two tested variables. In this type of study,

the chi-square (or contingency table test) method

of data analysis will be used. A chi-square test

makes it imperative to emulate a null hypothesis,

which assumes that there two objects of interest

and their methods of classification. It is then my

65

task as the researcher through data analysis, to

prove the assumption wrong. In other words to

reject the null hypothesis.

The chi-square statistics can be computed from the

data in a chi-square table by comparing the

observed and expected frequencies in each cell of

the table, if the margins between the observed ends

expected frequencies are large, the chi-square

statistics will be large and the null hypothesis is

rejected if however, the difference is small, a

small chi-square value will result and the null

hypothesis is accepted. Finally compare the chi-

square statistics of the decision rule to accept or

reject the null hypothesis.

The detailed procedure and computations

required in chi-square test would be presented step

by step as the hypothesis is tested.

The data to be used in testing the hypothesis will

result from the analysis of questionnaires.

The simple percentage method data analysis is used

to analyze the questionnaires, the formular for it

is,

66

A% = a * 100

n 1

Whenn = Total number of response to a question.

a = Number of respondents ticking a

particular answer option to the

question.

A% = “a” expressed as a percentage of N.

In all 50 questionnaires were issued out, but only

40 were collected back

4.2 DATA ANALYSIS (QUESTIONAIRES)

This analysis is restricted to ten (11) questions

only, which I consider being of direct relevance in

testing the hypothesis. The questions are grouped

into three parts.

Each group of questions is expected to provide

relevant information to test a hypothesis. Each

relevant question is first presented and data

collected on it analysis. Then the data that result

from the analysis of all the questions in the group

are combined into a single set tabulated data on

which the hypothesis is tested. At the end of any

group of is hypothesis and the response are

weighed.67

QUESTION NO. 1

Can effective Budgets plan be a guide towards the

growth and

development of Nasarawa Eggon Local Government?

Table 4.1 Responses on effective budget plan Responses NO. OF RESPONDENTS (A) PERCENTAGES OF RESPONSE (A%)

To plan and

develop local

government

38 95

To keep proper

account

2 5

No idea 0 0Total (n) 40 100

From the above table 38(95%) staff of the local

responded that Budgets plan be cam be a guide

towards the growth and development of Nasarawa

Eggon Local Government Area while 2(5%) of the

staff responded that the management of Nasarawa

Eggon local Government should keep proper account

of all budget while 0(%) responded no idea. It is

seen clearly from the table keeping budget plan can

help develop Nasarawa Eggon Local Government .

QUESTION NO. 2

68

Why do you think Budgets can be a means to control

in Nasarawa Eggon local Government management and

personnel functions?

Table 4.2 Responses on a means of local government

control?RESPONSES NO.OF RESPONDENTS PERCENTAGES RESPONSES

38 98It does not control and

synchronize personnel

functions

0

-

TOTAL 38 100

From the above table 38(98%) staff of the local Budgets

responded that budget can be a means to control and

synchronize Nasarawa Eggon local government management

and personnel functions 0(0%) of the staff responded

that it does not

control and synchronize Nasarawa Eggon local government

management and personnel functions

69

QUESTION 3 Why do feel corruption can be a

major problem of budget

implementation in Nasarawa Eggon local government

Table 4.3 Responses on corruption and budget

implementation? RESPONSES NO. OF RESPONDENTS PERCENTAGES

RESPONSES (A%)Cause failure of

budget implementation

32 80

Cause under

development

8 20

TOTAL 40 100

From the above table 32 (80%) of responded the

responded that Corruption is the major problem that

cause the failure of budget implementation In

Nasarawa eggon local government while 8 (20%) of

responded the responded that corruption cause

under development in Nasarawa eggon local

government.

QUESTION 5 Do your duties as junior staff conflict

with those staff at the top management

office in the local government?

70

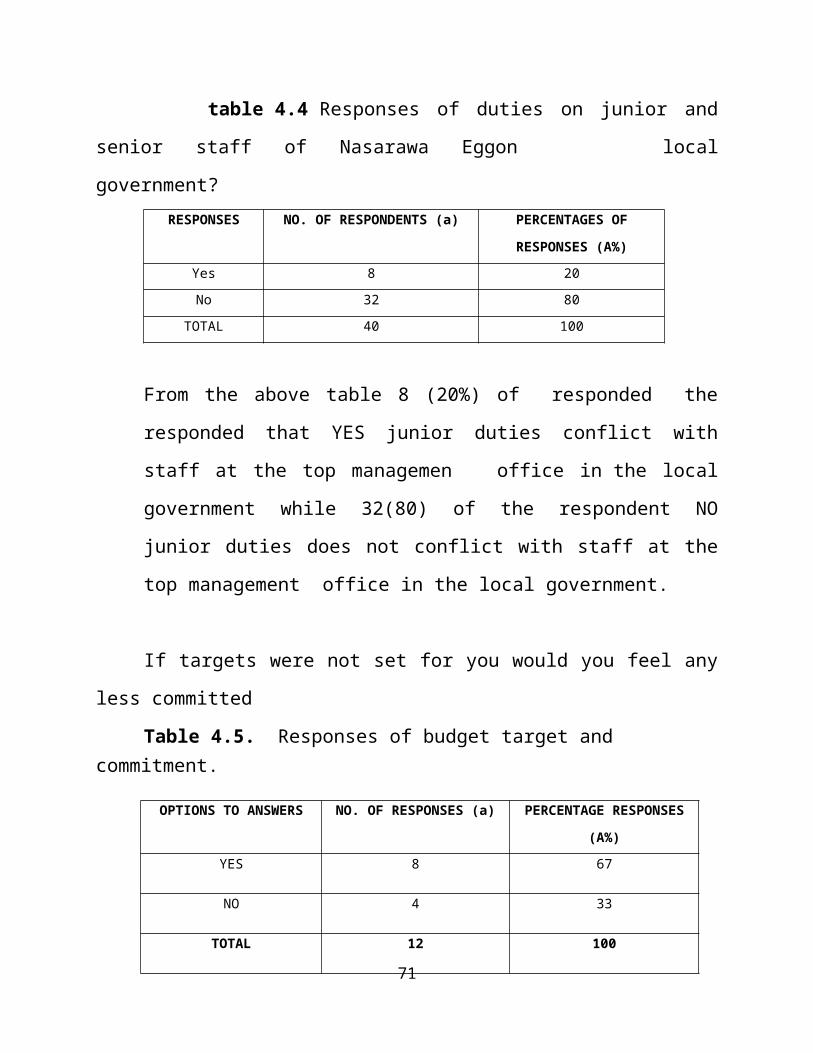

table 4.4 Responses of duties on junior and

senior staff of Nasarawa Eggon local

government? RESPONSES NO. OF RESPONDENTS (a) PERCENTAGES OF

RESPONSES (A%)Yes 8 20No 32 80

TOTAL 40 100

From the above table 8 (20%) of responded the

responded that YES junior duties conflict with

staff at the top managemen office in the local

government while 32(80) of the respondent NO

junior duties does not conflict with staff at the

top management office in the local government.

If targets were not set for you would you feel any

less committed

Table 4.5. Responses of budget target and commitment.

71

OPTIONS TO ANSWERS NO. OF RESPONSES (a) PERCENTAGE RESPONSES

(A%)YES 8 67

NO 4 33

TOTAL 12 100

From the table is seen that it is seen that 8(67%) of

the respondent were of the opinion that if target were