An Introduction to Balanced Socrecard

60

Balanced Scorecard Introduction Overview & Examples

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of An Introduction to Balanced Socrecard

Balanced Scorecard IntroductionOverview & Examples

The BSC concept

- 3 -

Measurement Motivates Behaviour

“What you measure is

what you get”

“It’s not what you

expect … it’s what you inspect”

“If you can measure it,

you can manage it”

The Balanced Scorecard’s (BSC) fundamental premise is that measurement motivates behaviour

- 4 -

The scorecard differs substantially from traditional measurement approaches

• The BSC’s focus is on factors which create long-term economic value in an organisation, for example:– Customer focus.

– Organisational learning.

– Business processes.

• Traditional accounting measures are by definition backward looking:– Financial measures only reflect the results of actions already taken.

– Do not provide an indication of future financial performance.

– Do not indicate desired performance.

– Do not provide a basis for planning and target setting.

- 5 -

Criteria For A Good Balanced Scorecard

A Good Balanced Scorecard will “Tell the story” of your strategy

Cause and Effect Relationships:• Every measure should be part of a “cause

and effect” chain to determine if the measures correctly represents and drives the strategy.

Linked to Financials:• Every measure selected should ultimately

Drive Performance.• Focus on factors that create long-term

value.• A balance of lead and lag indicators:

Measures that Create Change:• Measures must cause the organisation to

change its behaviour in some way.

CompanyStrategy

As-Is

Vision

- 6 -

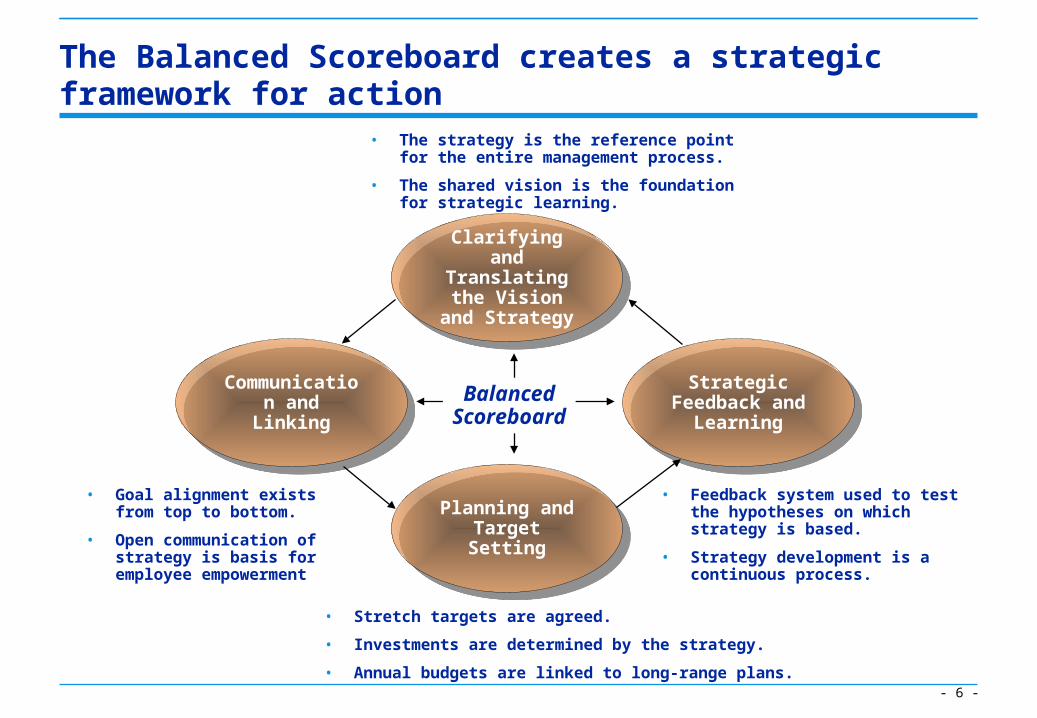

Clarifying and

Translating the Vision

and Strategy

Strategic Feedback and Learning

Planning and Target Setting

Communication and

Linking

• Feedback system used to test the hypotheses on which strategy is based.

• Strategy development is a continuous process.

• Stretch targets are agreed.• Investments are determined by the strategy.• Annual budgets are linked to long-range plans.

• Goal alignment exists from top to bottom.

• Open communication of strategy is basis for employee empowerment

BalancedScoreboard

The Balanced Scoreboard creates a strategic framework for action

• The strategy is the reference point for the entire management process.

• The shared vision is the foundation for strategic learning.

- 7 -

The Balanced Scorecard translates vision and strategy into four dimensions of performance

“When we achieve our vision, how will our organisation learn and

grow ?”

“When we achieve our vision, how will we look

to our business partners ?”

“When we achieve our vision, how will our internal business

processes operate ?”

“When we achieve our vision, how will we look to our shareholders ?”

Vision

Customers and Partners

Financial/Shareholder

Internal Processes

Learning and Innovation

- 8 -

For each of the four dimensions, objectives, measures and targets are explicitly defined

Financial / ShareholderObjectives Measures Targets

Customers and PartnersObjectives Measures Targets

Internal ProcessesObjectives Measures Targets

Learning and InnovationObjectives Measures Targets

Vision

- 9 -

The linkage between the four dimensions is crucial in ensuring long-term success

• Financial• Client satisfaction,

efficient and effective delivery of services will deliver financial results.

• Excellent processes and people will deliver client satisfaction.

• Good people in efficient processes support effectiveness.

• You need good people, people processes and structure to achieve high performance.

Shareholder Value

• Partners / Customers

• Internal Processes

• Learning & Growth

- 10 -

Alignment through the organisation will be achieved by cascading the scorecard

High Level Scorecard

Business Unit or Departmental Scorecards

Individual Scorecards

Shareholder / Parent / Requirements

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

- 11 -

When implemented well, the benefits of Balanced Scorecard can be significant

• Senior executives are focused and aligned around a small number of critical objectives and success measures.

• A simple, single management report makes progress towards financial, customer, internal processes and learning objectives clearly visible.

• The Plan-Do-Review principle establishes clear accountability for achieving objectives, for success and failure

• The BSC implementation establishes a strategic feedback / monitoring system that drives actions to excel in critical performance indicators

Focus

BalancedPerformance

Accountability

ContinuousImprovement

The BSC Process

- 13 -

Balanced Scorecard design is only a component of the overall process

Scorecard Design Scorecard Implementation / Roll-out

Strategic Intent

Develop & finalise Objectives

Develop & finalise Measures

Determine baselines and set targets

Incorporate scorecard review as

key item in business management meetings

Manage business according

to scorecard

Review/refine

score-card on a

regular basis

in conjunc-tion with strategy review process

Align/plan initiatives according

to scorecard

Develop and

implement BU and section

scorecards

Ensure scorecard alignment

Review & refine onan ongoing

basis

Manage BU, section etc.

according to

scorecard formatFeedback to high level scorecard to

ensure alignment

Corporate/Shareholder input where relevant

Communicate Scorecard to organisation

Cascade scorecard to individual level. To ensure individual

focus and alignment.Balanced Scorecard

Business Management Process

- 14 -

The Business Management Process (BMP) implements the Balanced Scorecard in a Plan-Do-Review Cycle

Link to Higher Level BSC

Financial

Learningand

Innovation

InternalProcesses

Customersand

Partners

MeasuresTargets

Objectives

Link to Lower Level BSC

Link to Higher Level BMP / Report

Link to Lower Level BMP / Report

ReviewBSC

• Take Action:– Initiatives– Plans – Budgets

• Measure Actuals against Targets

• Compile Report Target

• Plan-Do-Review session

• Determine Root Causes for Variances

• Define Action Steps

PDR Session

What makes a good Objective or Measure

- 16 -

We need to have clear and communicated definitions of the BSC components

• Objective:– Statement that defines what we must do to achieve the vision.– Linked to our strategy.

• Measure:– A numeric indicator that will indicate successful achievement of the objective. • Lead indicator – Indicates the likelihood of change (forward looking).• Lag indicator – Indicate that change has occurred (backward looking).

• Target:– Value of the measure that we would like to achieve in a given time frame.– Must be achievable.

- 17 -

Perspective

A “Good” Balanced Scorecard includes objectives, measurements and targets that promote changeExample:

Financial

Customer

Internal

Learning

BusinessObjectives

• Shareholder value

• Profit

• New revenue

• Differentiation

• Strategic alliances

• Customer service• Productivity

• New product development

• Segmentation

• People policy

• Alliance management

• Customer focus

Measurements

• % dividend growth

• Operating Margin

• Revenue from new services

• Target market-share

• Profits from alliances

• Customer satisfaction

• Revenue/work hour

• Product development cycle time

• Number of initiatives targeted at profitable segments

• Management span of control

• Number of “learning” partnerships”

• % management time interfacing with customers

Targets

• CPI + X% annually

• Top quartile

• 25% in three years

• Number one

• $M in five years

• Number one customer rating

• Best-in-class within five years

• Reduced by 50% in two years

• 60% within one year

• Triple in three years

• 10 in five years

• 20% in two years

Accountabilities

• Finance Director• CEO• Business Development Manager

• Marketing Director

• Business Development Manager

• Marketing Director• COO• Research and Development Manager

• Marketing Director

• Human Resources Director

• Business Development Manager

• CEO

. . . and clear accountabilities to ensure ownership.

- 18 -

The objectives define what the organisation must do to achieve the vision

Description of a good objective:

• Linked to, and descriptive of a component of the vision/strategy.

• Relevant to what the organisation wants to achieve.

• Action orientated:– Start statement with a verb.

• Measurable:– there must be a manner in which we can determine success in achieving the objective:

• Clear and concise.

• Understandable to the whole organisation.

• Must be able to assign overall accountability to a single person.

- 19 -

Measures must be the key indicators that register achievement of the objective

The SMART criteria defines a good measure:

• SS imple – relatively easy to access, collate and calculate.

• MM easurable – e.g: number of hours worked, lines installed, etc.

• AA actionable – ability to take action on variances to plan.

• RR elevant – ability to influence that which is being measured.

• TT imeous – must be determined/measured as frequently as

possible, or when relevant.

– the longer the delay in measuring the less the chance to allow timeous/appropriate action.

- 20 -

Targets must be set for each measure, and define goals for the organisation to achieve

Criteria for a good target:

• Must be achievable.

• Provide some stretch for the organisation.

• Set for a good fixed time period.

• Determine intermediate values, to evaluate progress.

• Aligned with what the organisation wants to achieve.

• Supported by and have buy-in of the executive team.

The objectives, measures, targets and accountabilities need to be defined at all levels of the organisation.

- 21 -

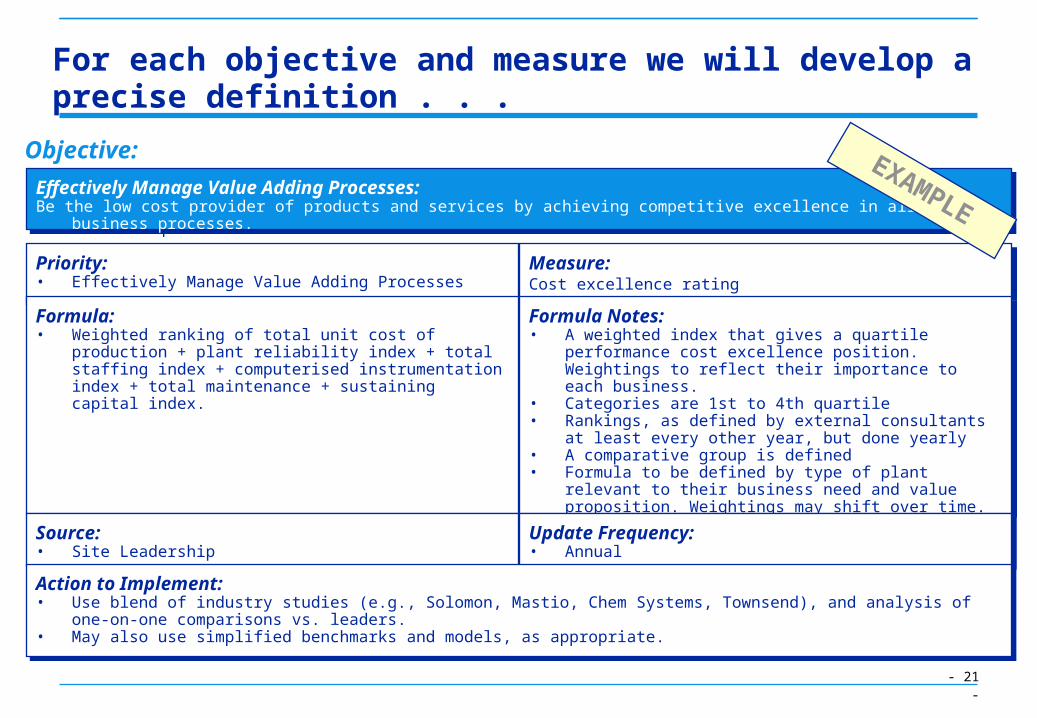

Priority: • Effectively Manage Value Adding Processes

Formula:• Weighted ranking of total unit cost of

production + plant reliability index + total staffing index + computerised instrumentation index + total maintenance + sustaining capital index.

Source:• Site Leadership

For each objective and measure we will develop a precise definition . . .

Measure:Cost excellence rating

Formula Notes:• A weighted index that gives a quartile

performance cost excellence position. Weightings to reflect their importance to each business.

• Categories are 1st to 4th quartile• Rankings, as defined by external consultants

at least every other year, but done yearly• A comparative group is defined• Formula to be defined by type of plant

relevant to their business need and value proposition. Weightings may shift over time.

Update Frequency:• Annual

Action to Implement:• Use blend of industry studies (e.g., Solomon, Mastio, Chem Systems, Townsend), and analysis of

one-on-one comparisons vs. leaders.• May also use simplified benchmarks and models, as appropriate.

Effectively Manage Value Adding Processes: Be the low cost provider of products and services by achieving competitive excellence in all our

business processes.

EXAMPLE

Objective:

- 22 -

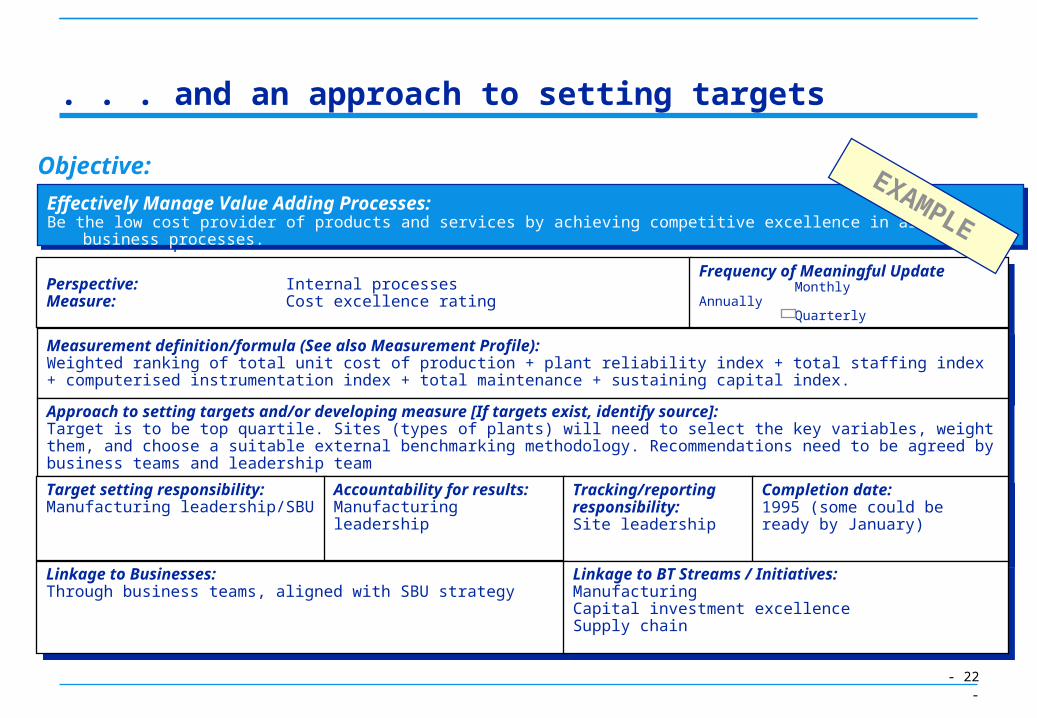

Perspective: Internal processesMeasure: Cost excellence rating ¦

. . . and an approach to setting targets

Effectively Manage Value Adding Processes: Be the low cost provider of products and services by achieving competitive excellence in all our

business processes.

Objective:

Frequency of Meaningful UpdateMonthly

AnnuallyQuarterly

Measurement definition/formula (See also Measurement Profile):Weighted ranking of total unit cost of production + plant reliability index + total staffing index + computerised instrumentation index + total maintenance + sustaining capital index.Approach to setting targets and/or developing measure [If targets exist, identify source]:Target is to be top quartile. Sites (types of plants) will need to select the key variables, weight them, and choose a suitable external benchmarking methodology. Recommendations need to be agreed by business teams and leadership teamTarget setting responsibility:Manufacturing leadership/SBU

Accountability for results:Manufacturing leadership

Tracking/reporting responsibility:Site leadership

Completion date:1995 (some could be ready by January)

Linkage to Businesses:Through business teams, aligned with SBU strategy

Linkage to BT Streams / Initiatives:ManufacturingCapital investment excellenceSupply chain

EXAMPLE

Example Objectives and Measures

- 24 -

Generally, BSC objectives focus around key themes in each of the four areas

Financial/Shareholder Themes

• Shareholder value.

• ROI.

• Profitability.

• Turnover/Revenue.

Learning & Innovation Themes

• Attract, retain and motivate employees.

• Clarify and communicate Roles and Responsibility.

• Building skills.• Manage resources

(leadership).• Knowledge management.

Internal Process Themes• Low costs.• Production efficiency.• Quality:

– ISO compliance.• Safety.• Production volume.• Environment.• Process effectiveness.

Customers & Partners Themes

• Retention.

• Satisfaction.

• Value-added to customers.

Vision

- 25 -

The Balanced Scorecard should contain a balance of lead and lag indicators

F1 Meet shareholder expectations

F2 Improve operating performance

F3 Achieve profitable growth

Return on Equity Combined Ratio Business Mix

C1 Improve agency performance

C2 Satisfy target policyholders

Acquisition/Retention(vs. plan)

Acquisition/Retention(by segment)

Agency Performance(vs. plan)

Policyholder Satisfaction Survey

I1 Develop target markets

I2 Underwrite profitablyI3 Align Claims with business

I4 Improved productivity

Business Mix (by segment)

Loss Ratio Claims Frequency Claims Severity Expense Ratio

Business Development (vs. plan)

Underwriting Quality Audit Claims Quality Audit

Headcount Movement Managed Spending Movement

L1 Upgrade staff competenciesL2 Access to strategic

information

Staff Productivity Staff Development (vs. plan) Strategic I/T Availability

(vs. plan)

ObjectivesMeasures

Lead Indicators(Performance Drivers)

Lag Indicators(Core Outcome Measures)

Lear

ning

Inte

rnal

Cust

omer

Fina

ncia

l

- 26 -

AREA PRODUCTION MANAGER

DIRECTOR

ZONE MANAGER

TEAM LEADER

Sample Target for Specific Time Window From To

21hours

19hours

Reduce area cycle time from

22 to 8 days

Reduce overall cycle time from 73 to 28 days

Strategic Business Objective

Reduce zone cycle time from

7 to 3 days

Reduce team cycle time from 30 to 11 hours

5.1days

4.6days

17days

15days

48days

44days

Top-Down and Bottom-Up

LinkedPLAN

ACTUAL

Quarterly Time Window Target

PLAN

ACTUAL

Quarterly Time Window Target

PLAN

ACTUAL

Quarterly Time Window Target

PLAN

ACTUAL

Quarterly Time Window Target

Objectives, measures and targets at each level have to be aligned top-down and bottom-up

Example: CarManufacturer Reduce overall

cycle time from 73 to 28 days

- 27 -

Measures should be cascaded as with this railway utility

• Managing Director

• Functional Managers

• Area Managers

• Department Managers

• Section Managers

• Work Group,Supervisors and Staff

Business objective:“92% of trains to

arrive within 5minutes of published

time”

Punctuality

% leave on time

Maintainschedule

Crewavailable

% trainsavailable

Trains inwrong

location

Trainsrejected byoperations

% trainsavailable

right formed

% trainsoperational

% trainspending

wheel sets

% wheel setsto plan

Wheel lathedowntime

Example BSC : TelcoSupp.

- 29 -

Client Key Issues

TelcoSupp’s vision is to be the most successful local telecommunications solutions provider

• Producer and supplier of products in the telecommunications industry.

• Vision is to be the most successful locally.

• Alignment of leadership to meet long-term goals.

• Increasing customer demands.

- 30 -

The TelcoSupp’s BSC objectives were designed to support the Vision

Financial / Shareholder• Deliver sustainable

growth in profitability.• Maximise shareholder

value.• Ensure financial

independence by funding future growth and initiatives internally.

Organisational Learning

• Attract and retain appropriate skills.

• Develop a learning culture.

• Communicate effectively.• Apply employment equity

principals.• Empower our employees.• Develop a company team

spirit.• Define, communicate and

live the values.

Internal

• Be the industry benchmark by any measure.

• Invest in the right projects to ensure our future

• Become a centre of competence.

• Develop a balanced relationship with the parent company.

Business PartnersCustomer:• Increase market share.• Broaden customer base.• Improve service quality to

exceed customer expectations.

• Build long term customer partnerships.

Alliances:• Pursue alliances to enable

us in our marketSuppliers:• Build long term supplier

relationshipsCommunity:• Actively support Southern

African development

A measurement system will assess progress towards the objectives.

Vision

- 31 -

Benefits Concerns

Comments on TelcoSupp’s BSC

• Cascaded into the organisation to create focus.

• Parent company has adopted BSC concept and suggested BSC development and implementation for other divisions.

• Strong ‘business partner’ and organisational learning focus.

• High number of objectives (21).

• Accountabilities rest with a few individuals.

Balanced Scorecard Comments

- 32 -

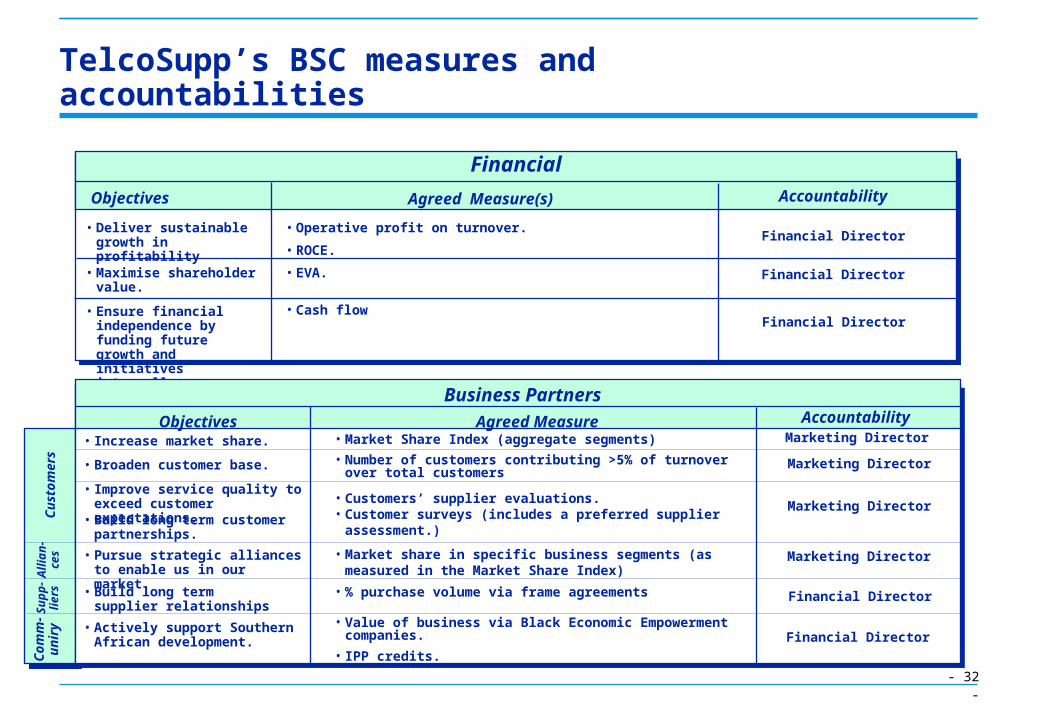

TelcoSupp’s BSC measures and accountabilities

Objectives

Financial

• Deliver sustainable growth in profitability

• Maximise shareholder value.

Agreed Measure(s)• Operative profit on turnover.• ROCE.• EVA.

• Ensure financial independence by funding future growth and initiatives internally.

• Cash flow

Accountability

Financial Director

Financial Director

Financial Director

Business PartnersObjectives

• Market Share Index (aggregate segments)

• Customers’ supplier evaluations.• Customer surveys (includes a preferred supplier assessment.)

• Number of customers contributing >5% of turnover over total customers

• Increase market share.• Broaden customer base.• Improve service quality to exceed customer expectations.• Build long term customer partnerships.

• Pursue strategic alliances to enable us in our market.

• Actively support Southern African development.

• Market share in specific business segments (as measured in the Market Share Index)

• Value of business via Black Economic Empowerment companies.

• IPP credits.

• % purchase volume via frame agreements• Build long term supplier relationships

Agreed MeasureMarketing DirectorMarketing Director

Marketing Director

Marketing Director

Financial Director

Financial Director

Accountability

Cust

omer

sAl

lian-

ces

Supp

-lie

rsCo

mm

-un

iry

- 33 -

TelcoSupp’s BSC measures and accountabilities (cont.)

Internal

• Be the industry benchmark by any measure.

• Become a Centre of Competence.

• Develop a balanced relationship with the parent company.

Objectives

• Refer to Quality Measurement System.

• Number of significant centres of competence.

• Proportion of own business versus commission business

• Invest in the right projects to ensure our future

• Net present value of all project business cases to be implemented

Agreed Measure

Operations Director

CEO

CEO

Executive Accountability

Marketing DirectorOrganisational LearningObjectives

• Staff turnover• Number of unfilled positions

• Training and education expenditure as % of payroll.

• Refer to Quality Measurement System.

• Attract and retain appropriate skills.

• Develop a learning culture.

• Communicate effectively.

• Apply employment equity principals.

• Empower our employees.

• Develop a Siemens team spirit.

• Define, communicate & live the values.

• % Black staff penetration.• % Black and gender representivity.

Agreed Measure

• Refer to Quality Measurement System.

• Refer to Quality Measurement System.

• Refer to Quality Measurement System.

HR Director

HR Director

HR Director

HR Director

HR Director

HR Director

HR Director

Executive Accountability

Example BSC : ChemCo

- 35 -

Client Key Issues

ChemCo needed a strategy to manage a diverse portfolio in a highly cyclical market

• Manufacturer of petrochemicals:– Polymers and monomers for use as industrial feedstocks

– Primarily commodity products

• Approximately 6000 employees

• One year into a two year Business Transformation™ project

• Highly cyclical market.

• Wide variety of product and customer types within the portfolio.

• Major leadership change underway.

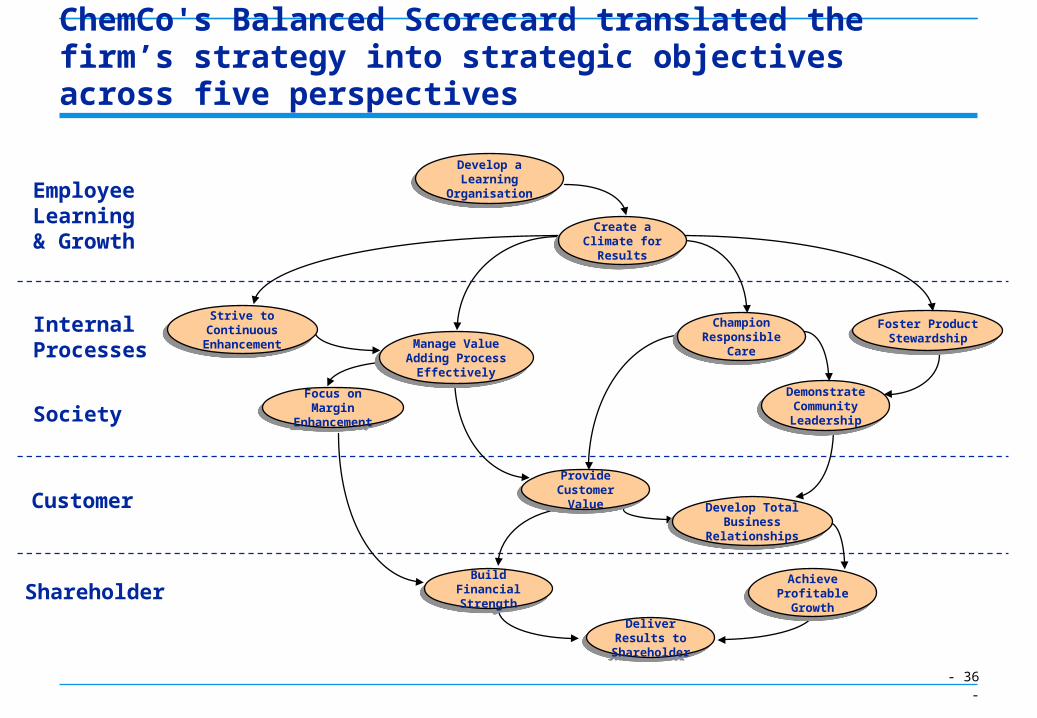

- 36 -

Shareholder

Customer

Internal Processes

Society

Employee Learning & Growth

Develop a Learning

Organisation

Focus on Margin

Enhancement

Strive to Continuous Enhancement Manage Value

Adding Process Effectively

Champion Responsible

Care

Foster ProductStewardship

Demonstrate CommunityLeadership

Provide CustomerValue Develop Total

Business Relationships

Build FinancialStrength

Achieve Profitable Growth

Deliver Results to Shareholder

Create a Climate for Results

ChemCo's Balanced Scorecard translated the firm’s strategy into strategic objectives across five perspectives

- 37 -

Benefits Concerns

Comments on ChemCo’s BSC

• Defined linkages to ultimately provide shareholder returns.

• Introduced “society” dimension to indicate community responsibility.

• Reduce focus to thirteen key objectives.

Balanced Scorecard Comments

• Broad and generic objectives and measures:– Not specific to the organisation.– Could apply to other companies.

- 38 -

Employee Learning & Growth Perspective

Society Perspective

Internal Processes Perspective

Shareholder Perspective

Customer Perspective

The objectives were translated into into a set of key strategic measures

•Provide superior value to our customers by supplying them with products and services that meet their needs (total value package).

•Form relationships with customers which allow us to fully understand and address their needs.

C1 Provide Customer Value

C2 Develop Total Business Relationships

SH1 Deliver Results to Shareholders

SH2 Build Financial Strength

SH3 Achieve Profitable Growth

DefinitionStrategic Priority•Develop and use our leadership to empower and gain commitment from all employees thus achieving exceptional business results.

•Improve our skills and knowledge by developing people and adapting best practices found within ChemCo and from external sources to realise all of our priorities.

•Be a leader in our industry by our achievements in safety, health, environment and risk management.

•Qualify as an industry leader by developing mutually supportive relationships with the communities in which we conduct business.

•Integrate health, safety, environment, economic, and ethical considerations at every stage in the life cycle of our products.

•Effectively manage the selection of customers and product offerings (including technology & service) so as to maximise margins.

•Be the low cost provider of products and services by achieving competitive excellence in all our business processes.

•Continuously seek ways to improve and simplify ChemCo’s processes to achieve our strategic business objectives.

•Manage our businesses to achieve the returns expected by shareholders.

•Manage our business so that we are cash positive and able to meet capital funding requirements to sustain ChemCo through the business cycle.

•Achieve increased size in our business to provide increased value to shareholders.

E1 Create a Climate for Results

E2 Develop a Learning Organisation

S1 Champion Responsible Care

S2 Demonstrate Community Leadership

S3 Foster Product Stewardship

I1 Focus on Margin Enhancement

I2 Effectively Manage Value Adding Processes

I3 Strive for Continuous Enhancement

Shareholder

Customer

InternalProcesses

Society

Employee Learningand Growth

Customer satisfaction index

Retention of targeted customers

Measures Leadership effectiveness

� survey rating� communications

Employee satisfaction Best practices identified Employee contribution

Safety,health, environment & risk results.

Community opinion rating Product stewardship

participation

Contribution margin

Cash flow cycle time Cost excellence rating Fixed cost productivity Product development cycle

time Business Transformation/SAP

benefits

Return on capital employed

Economic value added Net cash flow

Total revenue

Example BSC: ManCo

- 40 -

Client Key Issue

ManCo required a tool to focus and align the organisation

• Large petrochemical manufacturer.

• BSC was a component of a large two year transformation™ project.

• Significant cost reduction required to maintain profitability.

• Need to focus and align the organisation.

- 41 -

Accountability and targets are seen as key components of ManCo’s BSC

Shareholder / Financial Customer

Growth / Learning Internal Processes

KPI (Area) A Target CommentsReturn on Net Assets

PBIT/ Net assets (Qtr)

Profit after tax

Cash flow 4 -12 months projection (Mth)

Unit cost

KPI (Area) A Target CommentsCustomer satisfaction index

% Conformance to agreed offering per customer.(Qtr)

Product Mix Optimisation

KPI (Area) A Target CommentsValue created by Project Portfolio

NPV ofnew and developing projects at 22% discount rate (WACC) vs target NPV (Qtr)

Core competencies Taken off

until a suitable measure is defined

KPI (Area) A Target CommentsProcess efficiency

Environment Index: releases, resource consumptions, re-mediation & compliance (Mth)

Safety and Health

Production Value (Mth)

DIIR including occupational diseases

Total Cost per ton of product (Mth)

% Adherence to Target Mix (Mth)

Ton marketable product per gigajoule (Mth)

Actual vs target (Mth)

PeopleKPI (Area) A Target Comments

Employee satisfaction / climate windowAffirmative Action

Index : Leadership values,Job satisfaction and Development Productivity (Qtr)AA spectrum % (Qtr)

Production

Technical Integrity

Index: to be defined

Note: Accountabilities and targets not shown to maintain client confidentiality.

- 42 -

Benefits Concerns

Comments on ManCo’s BSC

• Significant management buy-in and use of the BSC.

• Two years after introduction the BSC remain the key focus/management tool for the executive committee.

• ‘People’ dimension added to indicate a key focus area.

• BSC focused on measures not objectives.

• After two years, executives consider fifteen objectives/measures too many to focus on simultaneously.

Balanced Scorecard Comments

Example BSC: OilCo

- 44 -

Client Key Issue

OilCo need to address internal soft issues

• Significant player in the downstream oil business.

• Successful organisation looking to maintain and grow position.

• Low employee moral and lack of confidence in leadership.

• Lack of understanding of organisations vision and strategy.

• Growth in market place.

- 45 -

Vision

BSC of a large downstream Oil CompanyFinancial / Shareholder Objectives

Customers and Partners Objectives Internal Processes Objectives

Learning and Innovation Objectives

• Maximise shareholder value.

• Real growth in operating profit with a long term objective of 10%.

• Keep unit cost increase below inflation.

• Increase Market Share

• Add significant value to customers.

• Ensure clear roles, responsibilities and accountabilities for all our people.

• Mobilise the organisation towards the vision.

• Ensure strategic advantage through IT.

• Ensure effective performance management.

• Increase diversity in the workforce.

• Empower our employees.

• Stimulate creativity and innovate.

- 46 -

Benefits Concerns

Comments on OilCo’s BSC

• Half the objectives focus on soft issues, to address current internal issues.

• Reduced number of objectives to allow for greater focus.

• No objective to determine/focus on internal efficiencies.

Balanced Scorecard Comments

- 47 -

OilCo designs measures and assigned accountability for all their objectives

Learning and InnovationObjective Measures Accountable

Person• Ensure effective

performance management1) Employees with development plans (lead)2) Level of acceptance of merit appraisal system

(lag)3) Percentage of employees receiving

quarterly performance reviews (lead)

4) Level of belief that performance drives reward and recognition (lag)

HR Director

• Increase diversity in the workforce

1) Staff mix (lag)2) Diversity awareness / attitude (lag)

CEO

• Empower our employees 1) Employee belief that they are empowered (lag) Operations Director

• Stimulate creativity and innovate

1) Number of new ideas (lag)2) Financial impact of new value - adding ideas

(lag)Technology Director

• Increase market share. 1) Market share (lag) Strategy director

• Add significant value to customers

1) Number of value adding plans for top 20% of customers (lead)

2) Customer belief that OilCo adds value to them (lag)

Marketing director

Customers and PartnersObjective Measures Accountable

Person

- 48 -

OilCo designs measures and assigned accountability for all their objectives

Internal Processes

• Ensure clear roles, responsibilities and accountabilities for all our people

1) Percentage of employees with agreed performance charters (lead)

2) Degree to which employees believe that their roles, responsibilities and accountabilitiesare clearly defined (lag)

Operations director

• Mobilise the organisation towards the vision

1) Percentage of employees who attended a Vision / Mission roll-out session (lead)

2) Percentage of monthly business meetings where Vision / Mission is a fixed agenda item and is discussed (lead)

3) Employee belief that OilCo is adhering to its stated value system (lag)

4) Percentage of employees responding “Yes” to vision / mission understanding and acceptance (lag)

HR director

• Ensure strategic advantage through IT

1) Return on total cost of ownership as an investment indicator (lag)

IT director

Objective Measures Accountable Person

Financial / ShareholderObjective Measures Accountable Person

• Maximise shareholder value 1) E.V.A. CEO

• Real growth in operating profit with a long term objective of 10%

CEO

• Keep unit cost increase below inflation

1) Increase in unit cost / vs. CPI. CFO

1) Real annual growth in operating profit

Example BSC: Aluminum Smelter

- 50 -

Client Key Issue

Aluminium Smelter introduced a BSC concept to monitor the progress of their “STAR” project

• International Aluminium Smelter.

• BSC development was part of an improvement project.

• Need to demonstrate financial performance to attract further investment:– Investment required for incremental expansion.

– No investment would force the Smelter to close in eight years’ time.

- 51 -

The management team BSC is displayed in a dashboard format

Performance ofRetrofitted

potsNet

shareholder value

PerformanceagainstSTAR

deliverables

Potlineinternalenv’t

Product/processdev’t

Profit

Rate of

return

Unit cost(addedvalues)

Accidentrate

Currentefficiency

• External environmental index.

• Environmental permit exceedances.

• Sickness rate.

• Potline output.

• Saleable output.

- 52 -

Benefits Concerns

Comments on Aluminium Smelters BSC

• The dashboard format indicates importance of each measure:– Large indicators represent key measures.

– Small indicators represent secondary measures.

– Bullet points indicate “warning lights”. Notice only when warning light flashes.

• Focus on few key themes.• Significant detail was

developed for each theme.

• Lack of balance in the scorecard:– Little focus on ‘customers’ and ‘innovation and learning’.

– Little need for customer focus as most product sold to shareholder.

– Focus on financial measures, as these are key for long term survival.

Balanced Scorecard Comments

Lessons Learned

- 54 -

The BSC must be driven from the top

• Leadership/management long-term buy-in and commitment to the Balanced Scorecard process is critical to ensuring success.

• The scorecard needs to be a living document:– Modified/reviewed in line with business/environmental changes.– Scorecard modification/review in conjunction with a strategic review process.

• Agree on a final limited set of key objectives:– Too many objectives will ‘de-focus’ the organisation and spread resources too thinly.

– Differentiate between nice-to-have and must have objectives.

• Measures must be carefully selected to reflect/determine the objective’s core intent.

• Do not develop a system with high running/maintenance costs, i.e. measurement cost outweighs benefit:– Use the 80:20 principle.

- 55 -

The final BSC must focus on the few key objectives required to achieve the strategy

• Too many objectives:– Confuse & de-focus the organisation.– Spread energy to thinly.

• Ensure a balance of objectives between the four dimensions .

• Clear accountabilities must be assigned for each objective.

• Assign only key measures for each objective:– As few measures per objective, ideally only one.– Distinguish between critical and nice-to-have measures.– Ensure balance between lead and lag indicators.

• Ensure the objective for the high level scorecard are strategic in nature, and crucials for all departments.– Operational or department specific objectives must be moved to departmental scorecards.

- 56 -

Successful BSC development will depend in placing objectives and measures at the correct level in the BSC structure

Most of Hillside’s present KPA are departmental measures.

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Financial

Customers& Partners

InternalProcessesVision

Learning& Innovation

Departmental Scorecards

High level or organisation scorecard:

- 57 -

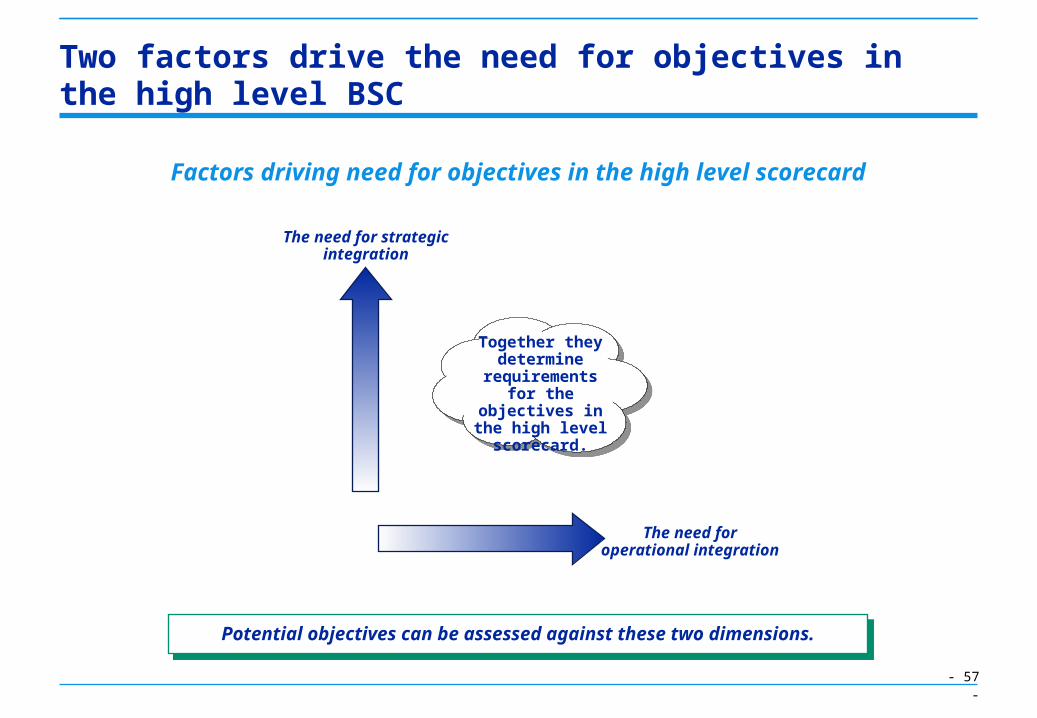

Two factors drive the need for objectives in the high level BSC

Factors driving need for objectives in the high level scorecard

Potential objectives can be assessed against these two dimensions.

Together they determine

requirements for the

objectives in the high level

scorecard.

The need for strategic integration

The need for operational integration

- 58 -

The high level scorecard must focus on strategic issues which integrate across several departments

High

LowHigh

Objectives fordepartmentalscorecardsTh

e ne

eds f

or s

trat

egic

inte

grat

ion

The needs for operational integration

Objectives for

the high level

scorecard

- 59 -

There are many potential pitfalls to successful implementation

Scorecard Design Scorecard Implementation / Roll-out

Strategic Intent

Develop & finalise Objectives

Develop & finalise Measures

Determine baselines and set targets

Incorporate scorecard review as

key item in business management meetings

Manage business according

to scorecard

Review/refine

score-card on a

regular basis

in conjunc-tion with strategy review process

Align/plan initiatives according

to scorecard

Communicate Scorecard to organisation

Develop and

implement BU and section

scorecards

Ensure scorecard alignment

Review & refine onan ongoing

basis

Manage BU, section etc.

according to

scorecard format

Cascade scorecard to individual level. To ensure individual

focus and alignment.

Feedback to high level scorecard to ensure alignment

Corporate/Shareholder input where relevant

Inappropriate strategy

Measures not aligned to objectives

Targets too soft

or ambitious

Scorecard not used

as business

management/focus toolScorecard

not communicated

Review process

inadequate or poorly

timed

Poor alignment between levelsFeedback

not taken into

account

- 60 -

PhilosophyProcess

Strategic Intent

Poor BSC design and implementation can lead to a multitude of problems

• Industry generic, not strategic.• Perspectives “unintegrated”.• What customer values not

defined.• Missing internal, operational

link.• Levels in organisation not

distinguished.

Measurement

• Too many measures.• Unrealistic, unrepeatable.

• Activities instead of measures.

• Misleading.• All financial.

• No executive consensus - not top down.

• Roll out before completion.• Tie to incentives too quickly.• Too many people, too long.• Lose momentum.

• Control, not communication.• Strategic report vs. strategic

agenda.• Strategic planning vs.

improvisation.