An Analysis of Model Parameter Uncertainty on Online Model ...

198

An Analysis of Model Parameter Uncertainty on Online Model-based Applications by Yingying Chen, M.S. A Dissertation In Chemical Engineering Submitted to the Graduate Faculty of Texas Tech University in in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy Approved Karlene A. Hoo Uzi Mann Mark W. Vaughn Xiaochang Wang Zdravko Stefanov Peggy Gordon Miller Dean of the Graduate School May, 2012

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of An Analysis of Model Parameter Uncertainty on Online Model ...

An Analysis of Model Parameter Uncertainty on Online

Model-based Applications

by

Yingying Chen, M.S.

A Dissertation

In

Chemical Engineering

Submitted to the Graduate Facultyof Texas Tech University in

in Partial Fulfillment ofthe Requirements for

the Degree of

Doctor of Philosophy

Approved

Karlene A. Hoo

Uzi Mann

Mark W. Vaughn

Xiaochang Wang

Zdravko Stefanov

Peggy Gordon MillerDean of the Graduate School

May, 2012

c©2012, Yingying Chen

Texas Tech University, Y. Chen, May 2012

Acknowledgements

I am greatly indebted to my research advisor, Dr. Karlene A. Hoo, for her sup-

port, advice and guidance during my doctoral study at Texas Tech University. I

appreciate Dr. Hoo for introducing me to the areas of multivariate statistical anal-

ysis, process control and optimization, process modeling, and the study of model

parameter uncertainty. I am very grateful to Dr. Hoo for the time she spent on re-

viewing and proofreading my various manuscripts and reports. It has truly been a

privilege for me to be her student.

I would like to thank Dr. Uzi Mann, Department of Chemical Engineering

at TTU, for his kindness in guiding my early study of reaction systems; and Dr.

Zdravko Stefanov for his assistance during my internship period. I also would like

to thank Dr. Mark Vaughn and Dr. Xiaochang Wang for agreeing to serve on my

doctoral committee. A special thank you goes to Dr. Shameem Siddiqui (Petroleum

Engineering) who gave me guidance on reservoir engineering. I also want to recog-

nize my fellow graduate students in the chemical engineering department for their

enthusiastic discussions and friendship during my studies at TTU.

Financial support for my graduate studies have been provided by TTU Process

Control & Optimization Consortium, National Science Foundation (#0927796) and

the Petroleum Research Fund (#49545-ND9).

ii

Texas Tech University, Y. Chen, May 2012

Finally, this research could never have been completed without the continuous

support, love and encouragement of my parents, Xinmin Chen and Qin Zhang. This

dissertation is entirely dedicated to them. My very special thanks to my husband,

Le Gao, for his love, patience and support in the past four years.

iii

Texas Tech University, Y. Chen, May 2012

Contents

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

Abstract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

LIST OF TABLES . . . . . . . . . . . . . . . . . . . . . . . . . . x

LIST OF FIGURES . . . . . . . . . . . . . . . . . . . . . . . . . x

I Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.1 Background . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.3 Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.4 Organization . . . . . . . . . . . . . . . . . . . . . . . . . . 13

II Preliminaries on Uncertainty Propagation . . . . . . . . . . . . . . 16

2.1 Sampling Techniques . . . . . . . . . . . . . . . . . . . . . 17

2.1.1 Monte Carlo Sampling . . . . . . . . . . . . . . . . . . 17

2.1.2 Latin Hypercube Sampling . . . . . . . . . . . . . . . . 18

2.1.3 Latin Hypercube Hammersley Sampling . . . . . . . . . 22

2.1.3.1 Hammersley sequence points . . . . . . . . . . . 22

2.1.3.2 Combination of Latin hypercube sampling and

Hammersley sequencing . . . . . . . . . . . . . . 24

2.2 Example: HDA Process . . . . . . . . . . . . . . . . . . . . 28

iv

Texas Tech University, Y. Chen, May 2012

2.2.1 HDA Process . . . . . . . . . . . . . . . . . . . . . . . 28

2.2.2 Propagation with Different Sampling Methods . . . . . 30

2.3 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

III Real-time State Prediction . . . . . . . . . . . . . . . . . . . . . . 41

3.1 PLS Regression . . . . . . . . . . . . . . . . . . . . . . . . 41

3.2 KL Expansion . . . . . . . . . . . . . . . . . . . . . . . . . 44

3.3 State Prediction with ROM . . . . . . . . . . . . . . . . . . 46

3.3.1 State Prediction of HDA Process . . . . . . . . . . . . . 48

3.4 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

IV Preliminaries on Uncertain Parameter Updating . . . . . . . . . . 55

4.1 Markov Chain Monte Carlo . . . . . . . . . . . . . . . . . . 56

4.1.1 Adaptive Metropolis Algorithm . . . . . . . . . . . . . 57

4.2 Ensemble Kalman Filter . . . . . . . . . . . . . . . . . . . 60

4.2.1 Forward Step . . . . . . . . . . . . . . . . . . . . . . . 61

4.2.2 Assimilation Step . . . . . . . . . . . . . . . . . . . . . 62

4.3 Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

4.4 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

V Real-time Model-based Optimization with Parameter Updating . . 68

5.1 Uncertain Parameter Updating in a Model-Based Optimiza-

tion Framework . . . . . . . . . . . . . . . . . . . . . . . . 68

5.2 Updating in a Reservoir Management Framework . . . . . . 68

v

Texas Tech University, Y. Chen, May 2012

5.2.1 Reservoir . . . . . . . . . . . . . . . . . . . . . . . . . 69

5.2.2 Basic Optimization Problem . . . . . . . . . . . . . . . 74

5.2.3 Markov Chain Monte Carlo Updating . . . . . . . . . . 77

5.2.4 Ensemble Kalman Filter Updating . . . . . . . . . . . . 80

5.2.5 Optimal Oil Production Results . . . . . . . . . . . . . 82

5.3 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

VI Robust Estimates of the Uncertain Parameters . . . . . . . . . . . 102

6.1 Robust Statistics Estimates . . . . . . . . . . . . . . . . . . 103

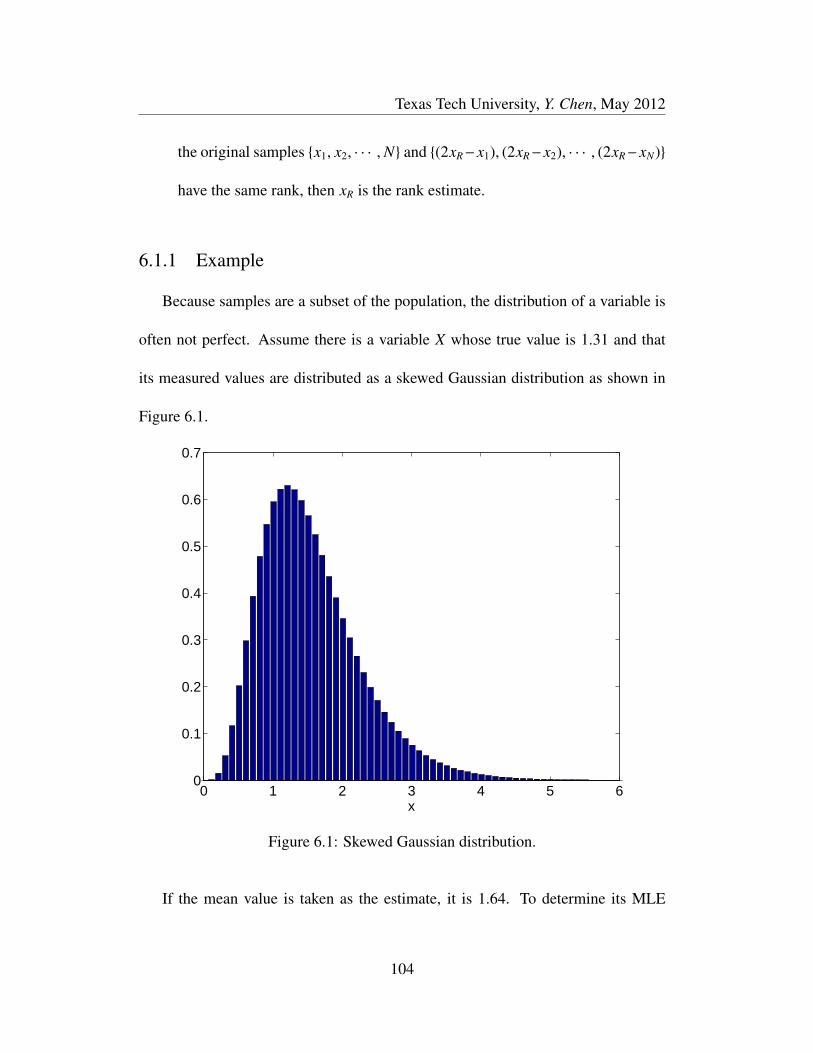

6.1.1 Example . . . . . . . . . . . . . . . . . . . . . . . . . 104

6.2 Preamble . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

6.3 Mathematical Foundation . . . . . . . . . . . . . . . . . . . 112

6.3.1 Example . . . . . . . . . . . . . . . . . . . . . . . . . 116

6.4 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

VII State Estimation & Model Predictive Control with a Maximum

Likelihood Model . . . . . . . . . . . . . . . . . . . . . . . . . . 121

7.1 Tubular Reactor . . . . . . . . . . . . . . . . . . . . . . . . 121

7.2 Determination of Robust Estimation of Uncertain Parame-

ters for State Estimation . . . . . . . . . . . . . . . . . . . . 123

7.2.1 Maximum Likelihood Model for Model Predictive Con-

trol . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

7.3 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

vi

Texas Tech University, Y. Chen, May 2012

VIII Summary, Contribution and Future Work . . . . . . . . . . . . . . 142

8.1 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

8.2 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . 145

8.3 Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . 145

BIBLIOGRAPHY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

APPENDICES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

I Preliminaries on Model-based Control . . . . . . . . . . . . . . . 160

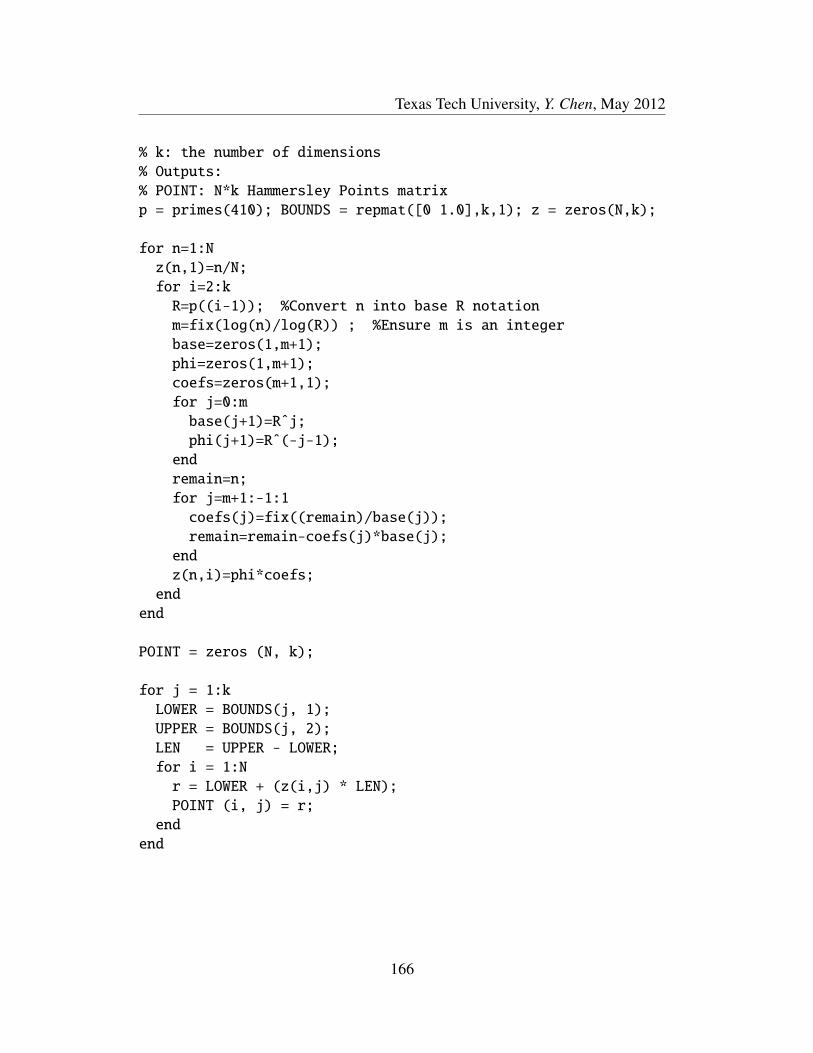

II Computer Programs . . . . . . . . . . . . . . . . . . . . . . . . . 165

B.1 Hammersley Points Generation . . . . . . . . . . . . . . . . 165

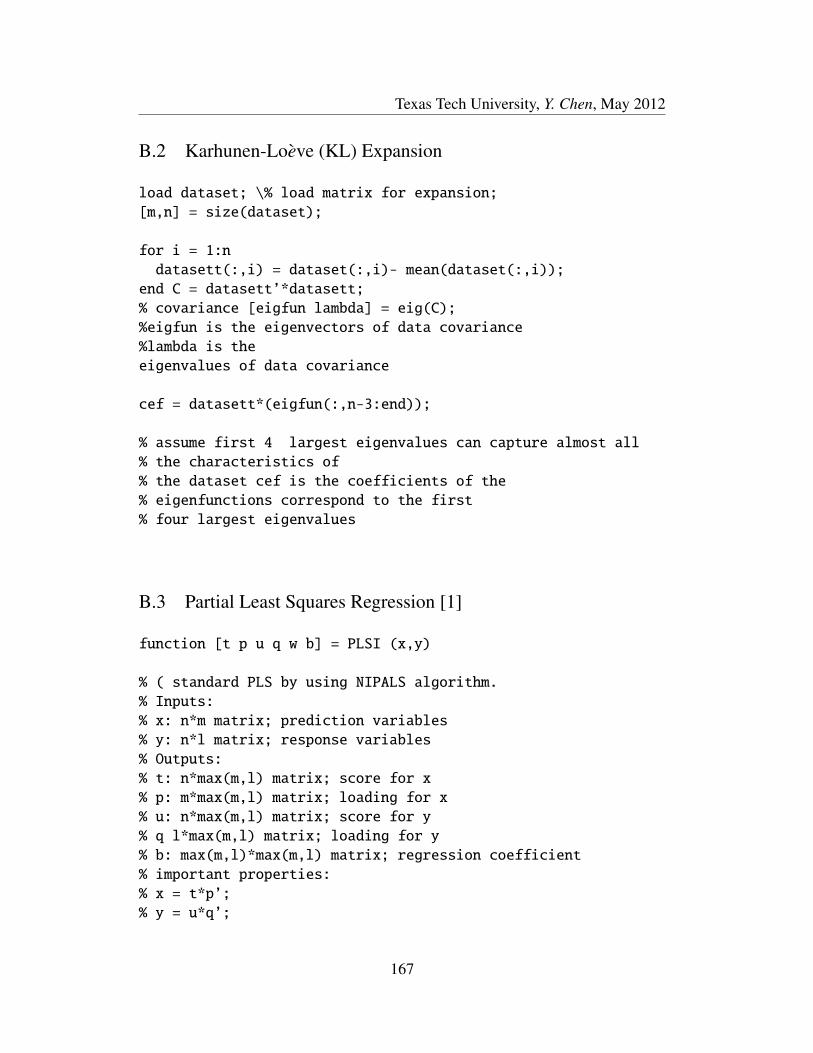

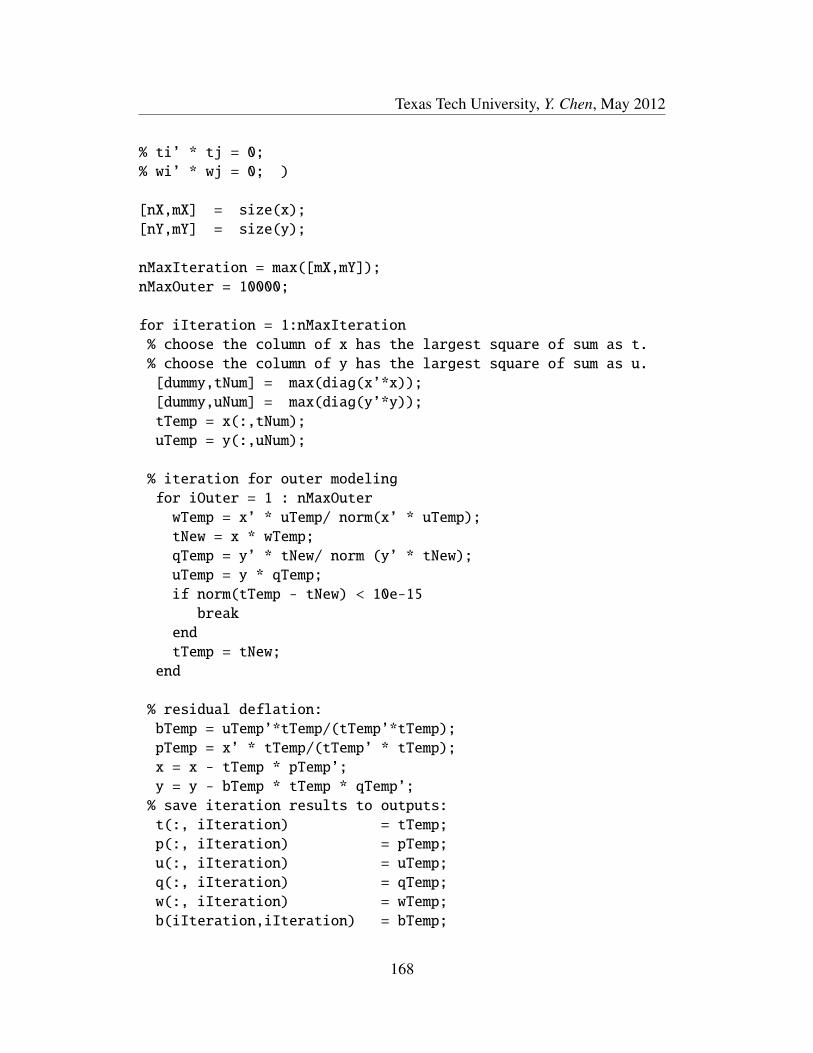

B.2 Karhunen-Loeve (KL) Expansion . . . . . . . . . . . . . . . 167

B.3 Partial Least Squares Regression [1] . . . . . . . . . . . . . 167

B.4 Markov Chain Monte Carlo . . . . . . . . . . . . . . . . . . 169

B.5 Generation of Monte Carlo Samples . . . . . . . . . . . . . 170

B.6 Ensemble Kalman Filter . . . . . . . . . . . . . . . . . . . 172

B.7 Robust Statistics . . . . . . . . . . . . . . . . . . . . . . . . 173

B.8 Model Predictive Control . . . . . . . . . . . . . . . . . . . 174

B.9 HDA Process . . . . . . . . . . . . . . . . . . . . . . . . . 177

B.10 Tubular Reactor . . . . . . . . . . . . . . . . . . . . . . . . 182

vii

Texas Tech University, Y. Chen, May 2012

Abstract

It is important to predict the behavior of an engineering process accurately and

timely. The predictions are usually achieved using a first-principles-based model

that describes the complex phenomena embodied in the process. However, no

model is an exact representation of the complex process for multiple reasons. The

primary goal of this research is to investigate one of the possible reasons, the un-

certainty of the model parameters from the viewpoint of their effect on the accuracy

of the model’s predictions. Other secondary goals of this research are updating the

uncertain parameter values and determination of robust estimates of the uncertain

parameters to improve the accuracy of a model.

The methodologies applied to understand propagation of the uncertain param-

eters through a model are Latin hypercube sampling coupled with Hammersley

sequencing (LHHS). These methods are selected because of their efficiency and

effectiveness when there are multiple uncertain parameters in a model.

Real processes experience unmeasured and unplanned disturbances. Even though

a model may come arbitrarily close to estimating the output of the process, because

of these types of disturbances there always will be process/model mismatch. This

study addresses this issue by investigating updating of the model uncertain param-

eters to minimize this mismatch. The updating methods designed in this research

viii

Texas Tech University, Y. Chen, May 2012

come from the class of particle filters (also referred to as sequential Monte Carlo

filters); they include a Markov chain Monte Carlo filter and an ensemble Kalman

filter.

As the number of uncertain parameters increase so does the computational bur-

den. While updating is one solution to improve model accuracy another potential

solution is to determine a robust estimate of the uncertain parameter using the the-

ory of robust statistics. This research will provide the theoretical proof that the

maximum likelihood estimate is the best statistic to provide a robust estimate.

The operational side of this research focuses on online model-based applications

such as model-based control and monitoring with processing of uncertain model

parameters. To demonstrate these research concepts, we employ simulations of a

continuous reactor system and an oil producing reservoir system. The results are

analyzed and discussed.

ix

Texas Tech University, Y. Chen, May 2012

List of Tables

2.1 Dimensionless parameters for the HDA process [2]. . . . . . . . . . 30

2.2 Computation time and number of samples at three spatial locations

that achieves 0.5% error of the true mean and variance of the ben-

zene concentration and reactor temperature. . . . . . . . . . . . . . 33

3.1 Maximum relative errors in the outputs between the physical model

and the ROM with and without uncertainty. . . . . . . . . . . . . . 49

5.1 Definition of Model Variables and Parameters. . . . . . . . . . . . . 71

5.2 Measurement uncertainties. [3] . . . . . . . . . . . . . . . . . . . . 74

5.3 Porosity, permeability and water injection ratio of four parts of

reservoir. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6.1 Estimates and errors . . . . . . . . . . . . . . . . . . . . . . . . . . 105

6.2 Robust estimates. y =2∑

j=1P j. . . . . . . . . . . . . . . . . . . . . . 118

6.3 Robust estimates. y = exp(P1) + P2 . . . . . . . . . . . . . . . . . . 118

7.1 Dimensionless parameters for the tubular reactor [4]. . . . . . . . . 123

7.2 Nominal values and robust estimates of the uncertain parameters . . 127

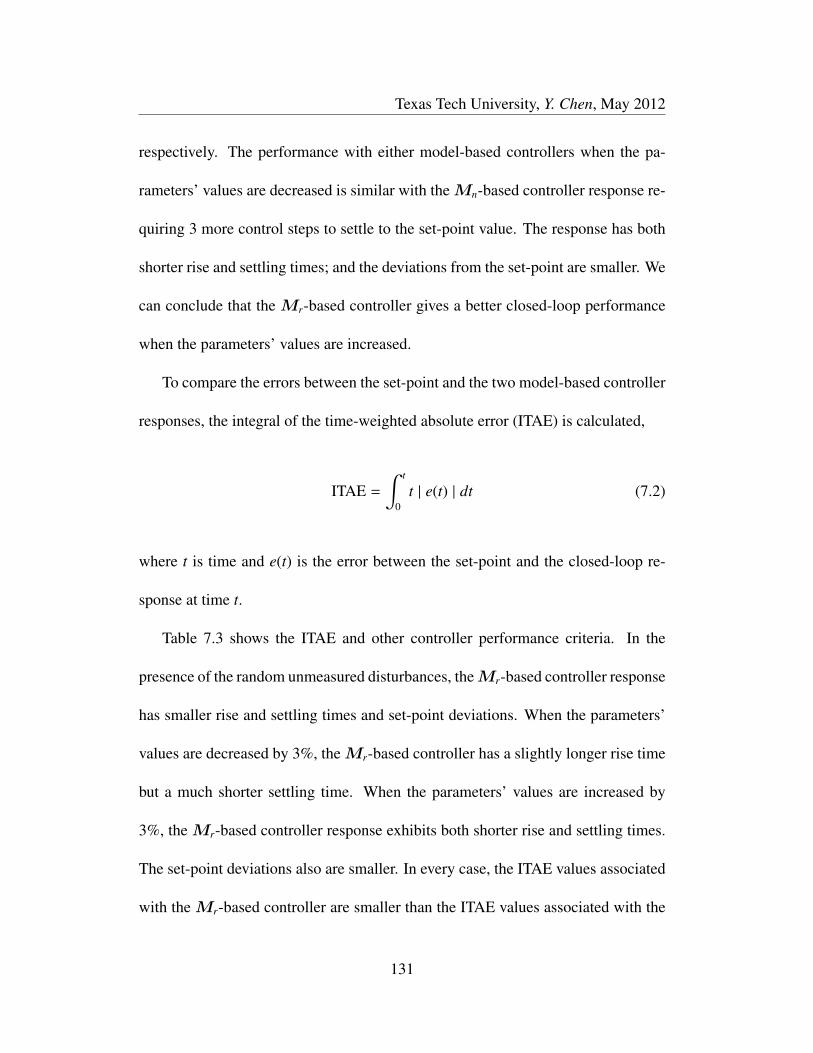

7.3 Closed-loop performance comparison betweenMr andMn . . . . . 132

7.4 Closed-loop performance comparison betweenMr andMn . . . . . 133

x

Texas Tech University, Y. Chen, May 2012

List of Figures

1.1 Road map. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.1 Selection of Pri. Top: MCS random selection. Bottom: LHS selec-

tion from equal probable intervals. . . . . . . . . . . . . . . . . . . 20

2.2 One-dimensional uniformity analysis with 20 sample points. Top:

MCS. Bottom: LHS. . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.3 One hundred sample points on a unit square with X,Y ∈ (0, 1). Top:

MCS. Bottom: LHS. . . . . . . . . . . . . . . . . . . . . . . . . . 23

2.4 One hundred sample points (sampled with LHHS) on a unit square

with x, y ∈ (0, 1). . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

2.5 One hundred sample points on a unit square with correlation 0.9.

Top: MCS. Middle: LHS. Bottom: LHHS. . . . . . . . . . . . . . . 36

2.6 Plug Flow Reactor. . . . . . . . . . . . . . . . . . . . . . . . . . . 37

2.7 Standard deviation of benzene concentration (left) and reactor tem-

perature (right) as a function of sample size. +: MCS. : LHS. ?:

LHHS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

2.8 Distribution of dimensionless benzene concentration and temperature. 39

3.1 Output of the ROM and physical model in the presence of a +5%

bias in the mean value of the uncertain parameters. Left: Benzene

concentration. Right: Reactor temperature. 4: Physical model. :

ROM generated with uncertain data. ∗: ROM without uncertainty. . 50

3.2 Output of the ROM and physical model in the presence of a -5%

bias in the mean value of the uncertain parameters. Left: Benzene

concentration. Right: Reactor temperature. 4: Physical model. :

ROM generated with uncertain data. ∗: ROM without uncertainty. . 51

xi

Texas Tech University, Y. Chen, May 2012

3.3 Output of the ROM and physical model in the presence of a +20%

error in the standard deviation of the uncertain parameters. Left:

Benzene concentration. Right: Reactor temperature. 4: Physical

model. : ROM generated with uncertain data. ∗: ROM without

uncertainty. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.1 Outputs of the logistic map. . . . . . . . . . . . . . . . . . . . . . . 65

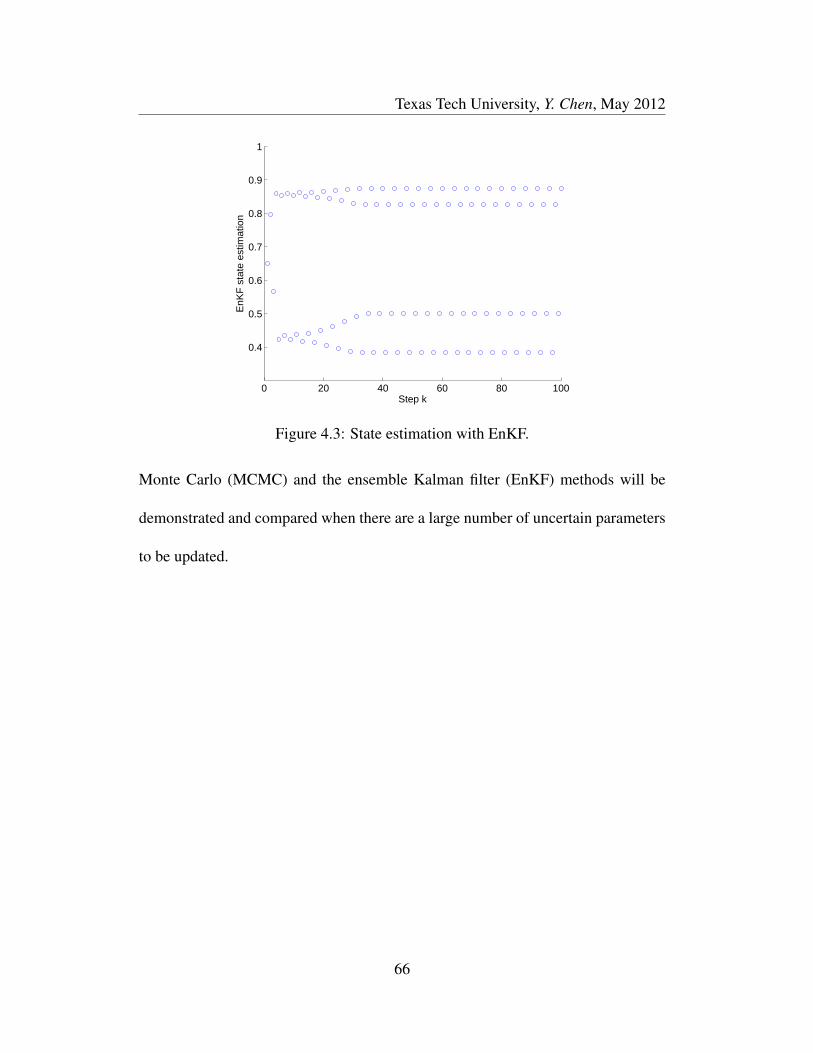

4.2 State estimation with MCMC. . . . . . . . . . . . . . . . . . . . . 65

4.3 State estimation with EnKF. . . . . . . . . . . . . . . . . . . . . . 66

5.1 Model-based optimization framework with parameter uncertainty

updating. y∗: set-points; u: outputs from the optimizer; d: dis-

turbances; ym: measurements; y(Θ): model outputs; Θ: model

uncertain parameters; e: errors between measurements and model

outputs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

5.2 Schematic of a two-dimensional reservoir and wells. ↓: water in-

jection well; ↑: oil production well. . . . . . . . . . . . . . . . . . . 69

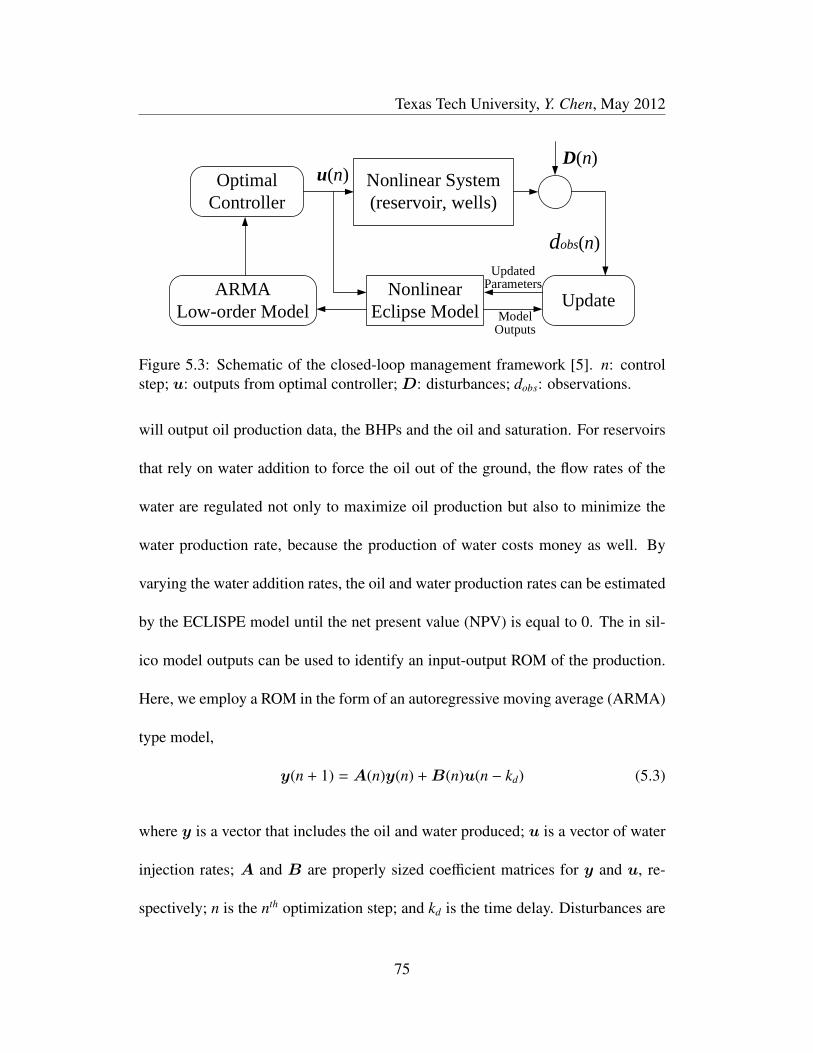

5.3 Schematic of the closed-loop management framework [5]. n: con-

trol step; u: outputs from optimal controller;D: disturbances; dobs:

observations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

5.4 Schematic of a two-dimensional reservoir and wells. ↓: water in-

jection well; ↑: oil production well. . . . . . . . . . . . . . . . . . . 78

5.5 Prior distributions of porosity and permeability. . . . . . . . . . . . 78

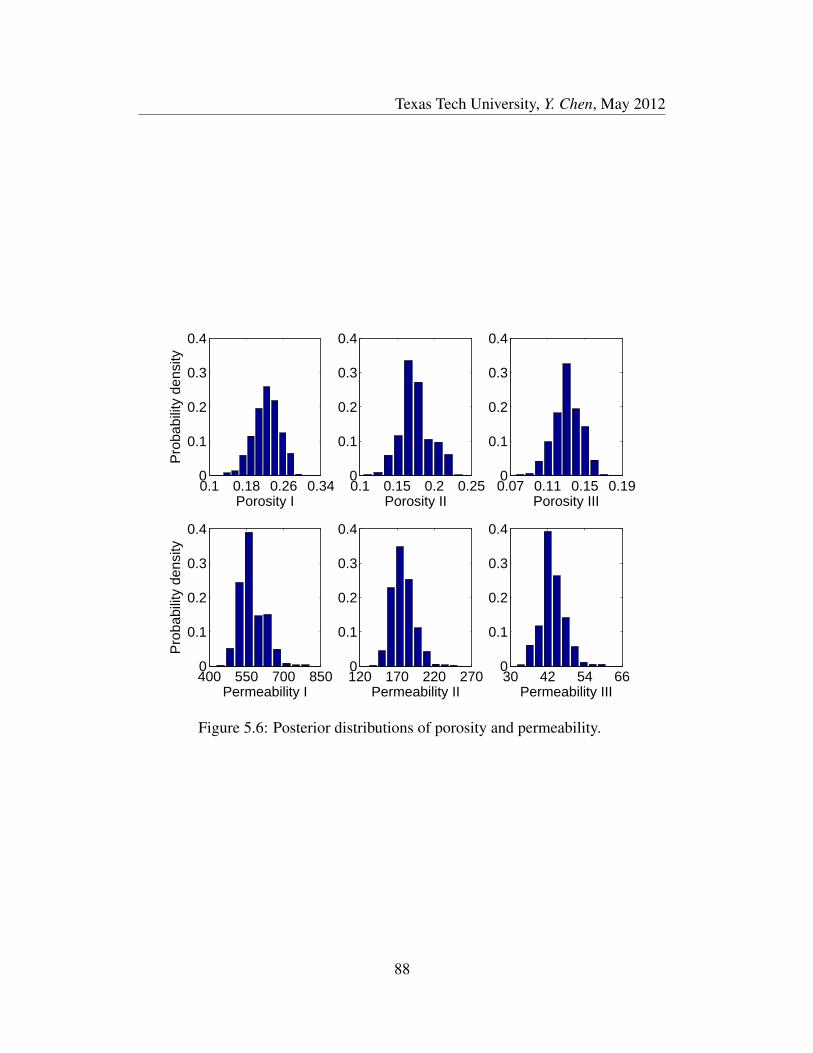

5.6 Posterior distributions of porosity and permeability. . . . . . . . . . 88

5.7 Initial, true and updated permeability of reservoir. . . . . . . . . . . 89

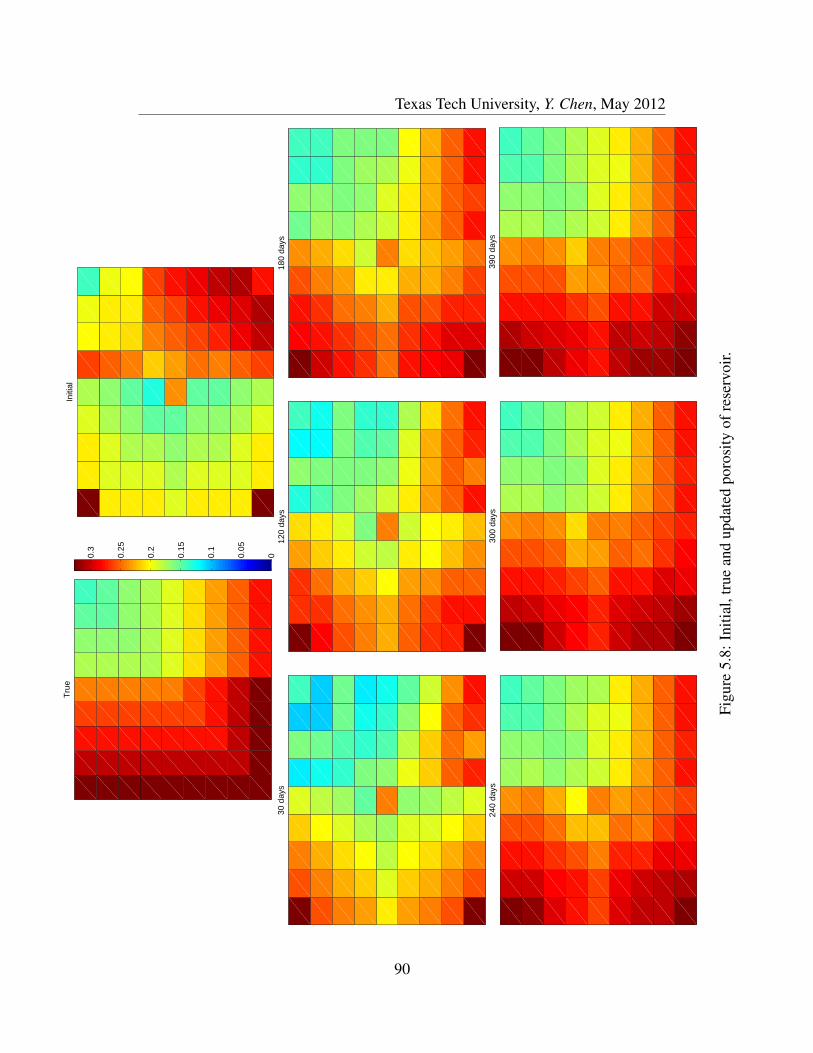

5.8 Initial, true and updated porosity of reservoir. . . . . . . . . . . . . 90

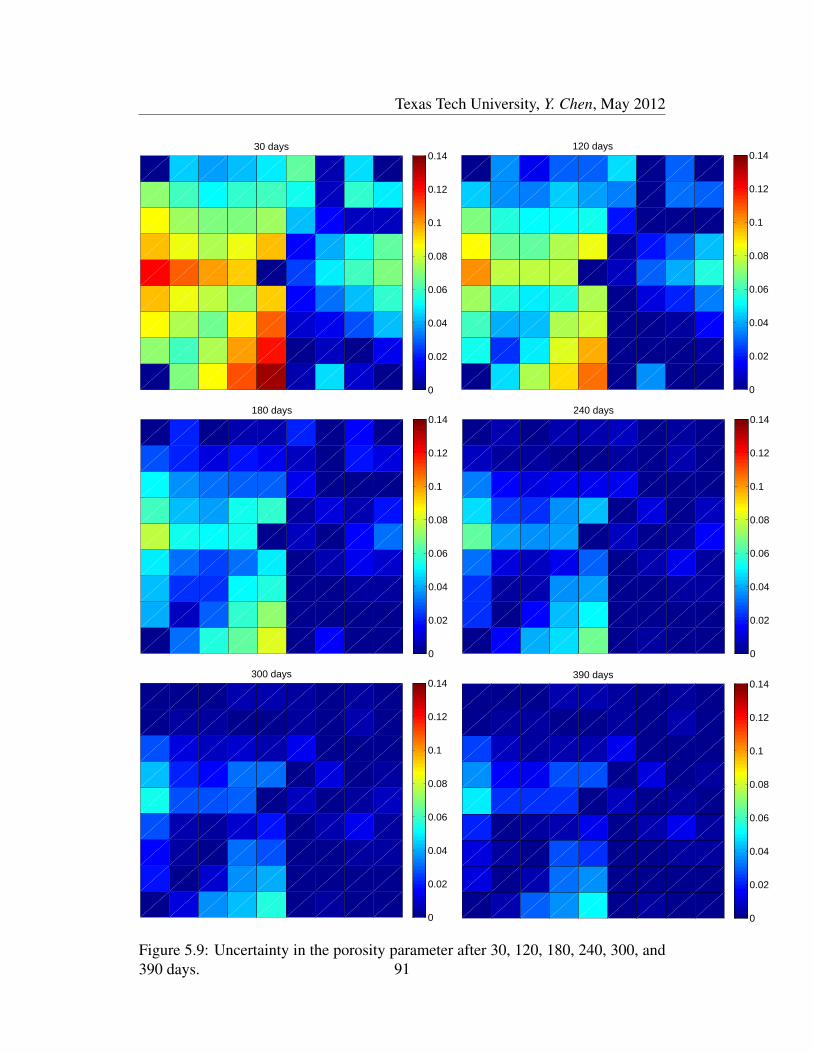

5.9 Uncertainty in the porosity parameter after 30, 120, 180, 240, 300,

and 390 days. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

5.10 Uncertainty in the permeability parameter after 30, 120, 180, 240,

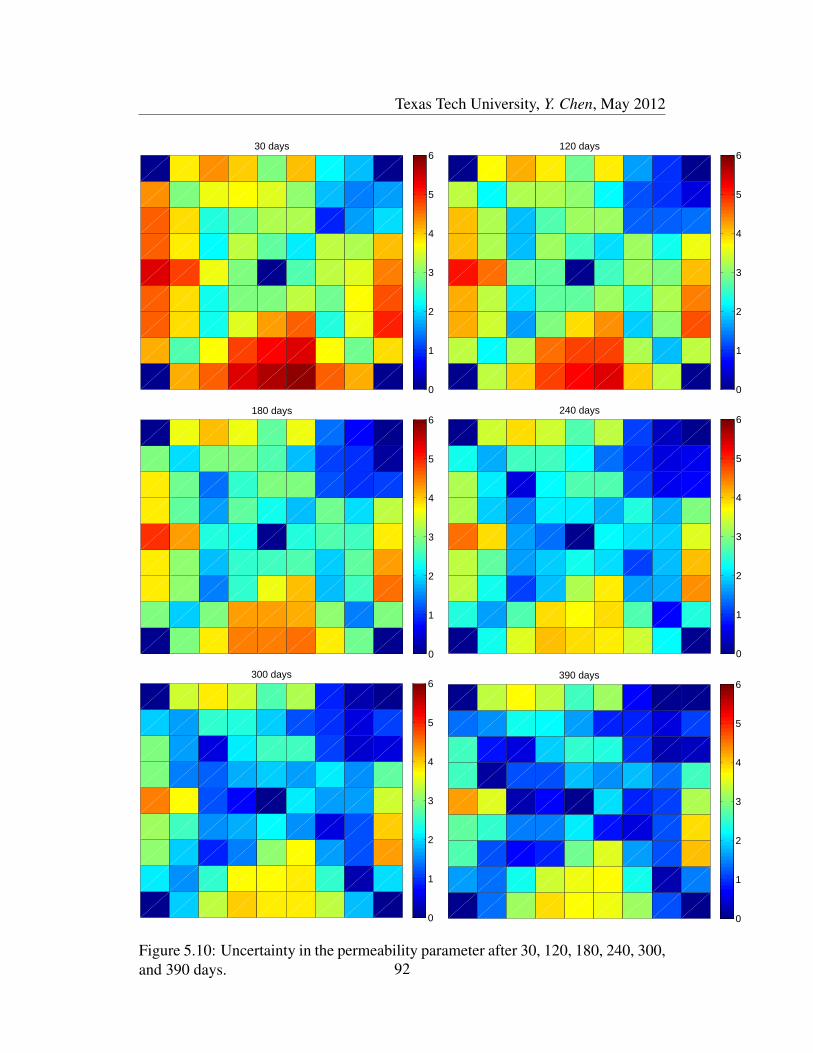

300, and 390 days. . . . . . . . . . . . . . . . . . . . . . . . . . . 92

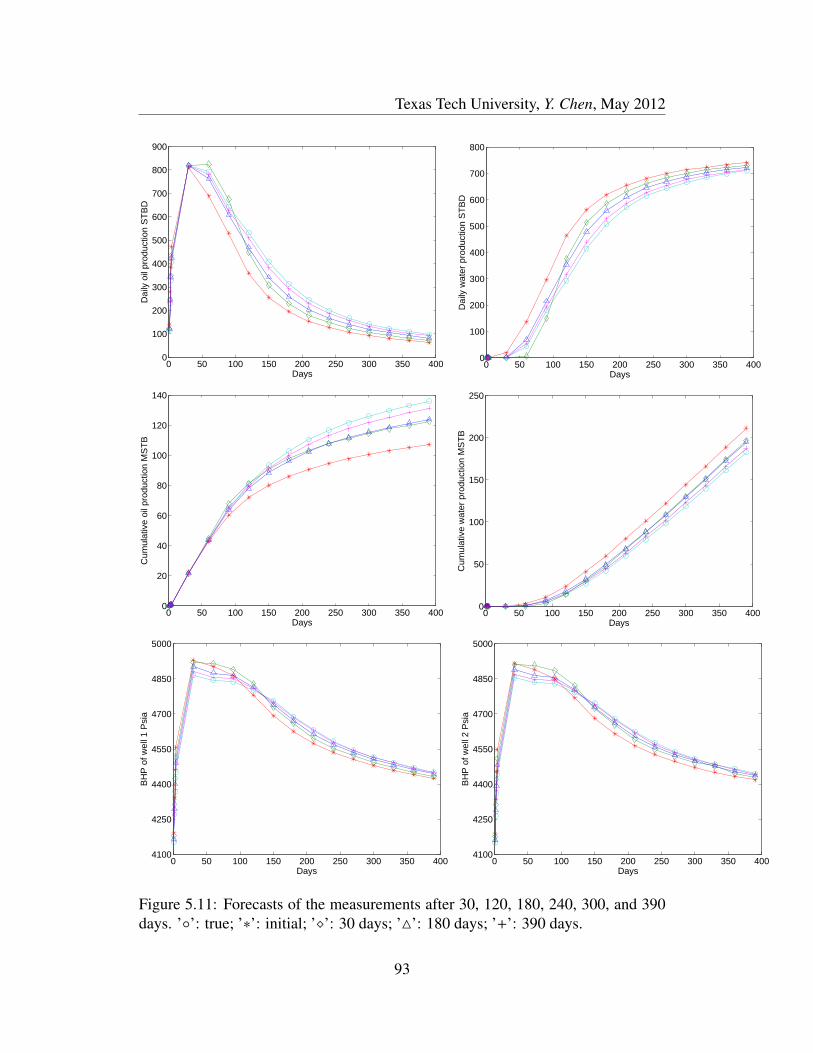

5.11 Forecasts of the measurements after 30, 120, 180, 240, 300, and

390 days. ’’: true; ’∗’: initial; ’’: 30 days; ’4’: 180 days; ’+’:

390 days. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

xii

Texas Tech University, Y. Chen, May 2012

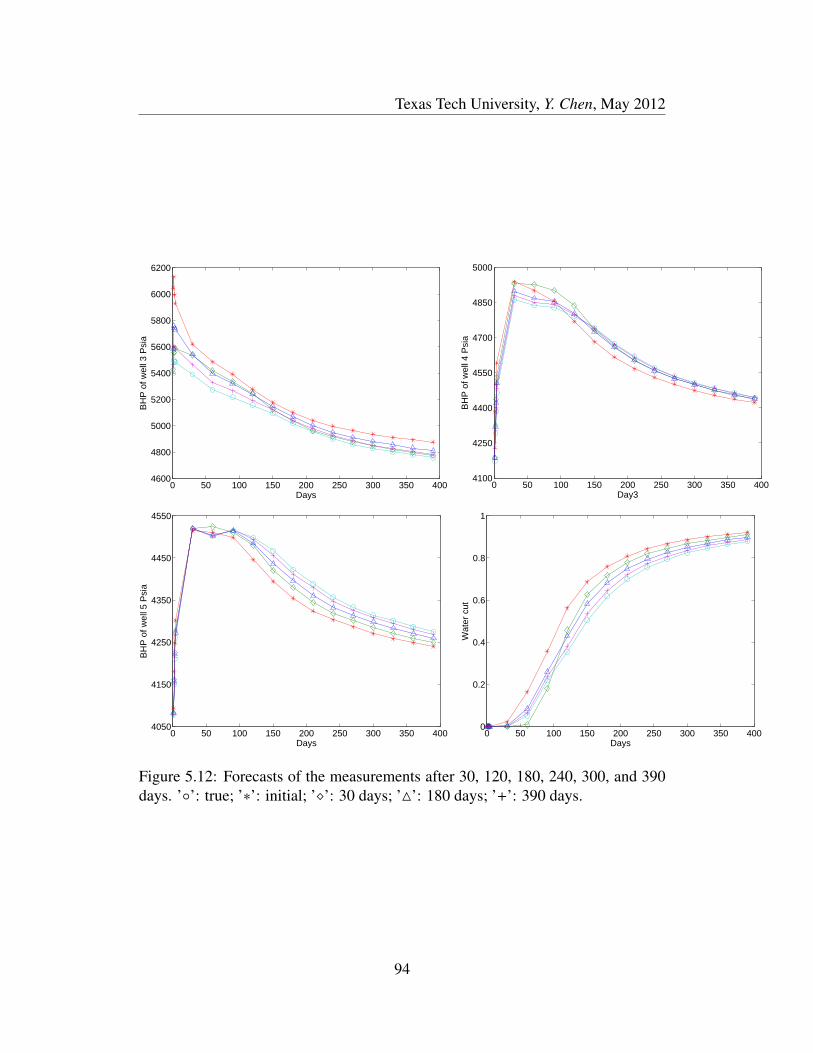

5.12 Forecasts of the measurements after 30, 120, 180, 240, 300, and

390 days. ’’: true; ’∗’: initial; ’’: 30 days; ’4’: 180 days; ’+’:

390 days. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

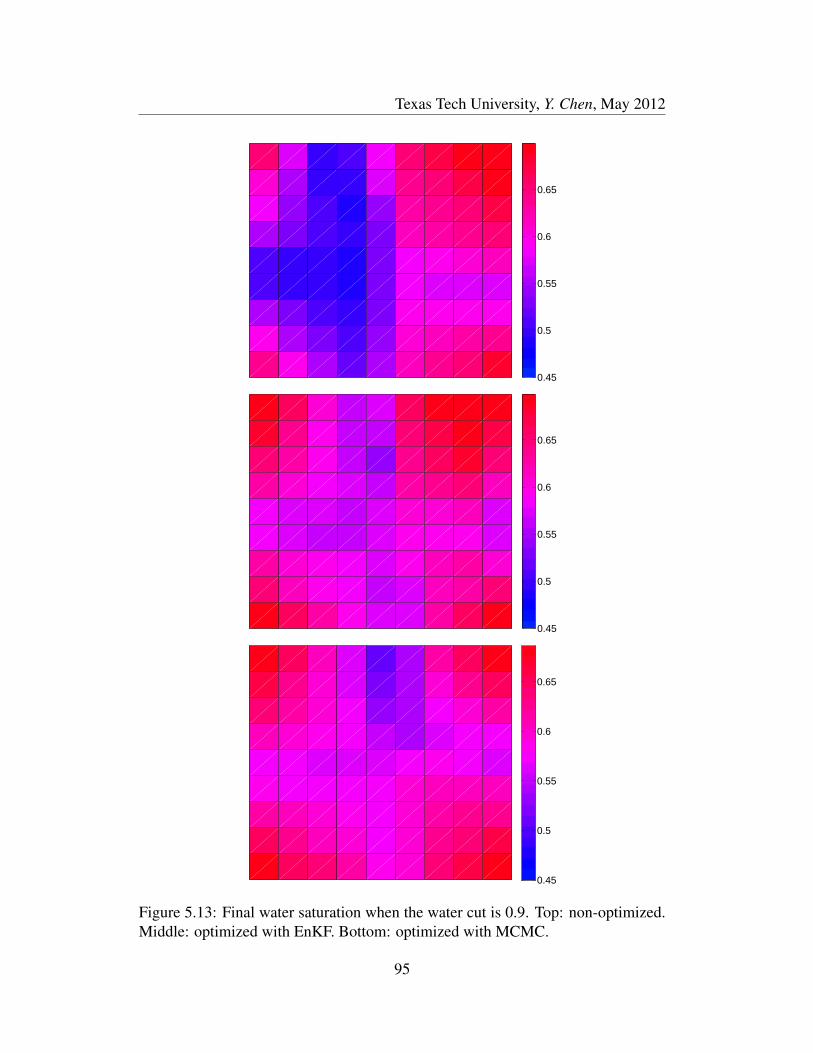

5.13 Final water saturation when the water cut is 0.9. Top: non-optimized.

Middle: optimized with EnKF. Bottom: optimized with MCMC. . . 95

5.14 Top: Comparison of cumulative production of oil and water. Op-

timized case: EnKF, oil () and water (5) production; MCMC, oil

(+) and water (4) production. Non-optimized case: oil () and (∗):

water production. Bottom: Cumulative NPV. Optimized: EnKF,

blue; MCMC, green. Non-optimized: red. . . . . . . . . . . . . . . 96

5.15 Optimal dimensionless injected water flow rate in the first well as

a function of the updating steps, and the average permeability (top)

and porosity (bottom) values. . . . . . . . . . . . . . . . . . . . . . 97

5.16 Optimal dimensionless injection water flow rate in the second well

as a function of the updating steps and average permeability (top)

and porosity (bottom) values. . . . . . . . . . . . . . . . . . . . . . 98

5.17 Optimal dimensionless injection water flow rate in the third well as

a function of the updating steps and average permeability (top) and

porosity (bottom) values. . . . . . . . . . . . . . . . . . . . . . . . 99

5.18 Optimal dimensionless injection water flow rate in the fourth well

as a function of the updating steps and average permeability (top)

and porosity (bottom) values. . . . . . . . . . . . . . . . . . . . . . 100

6.1 Skewed Gaussian distribution. . . . . . . . . . . . . . . . . . . . . 104

7.1 State estimation framework with a maximum likelihood model. . . . 124

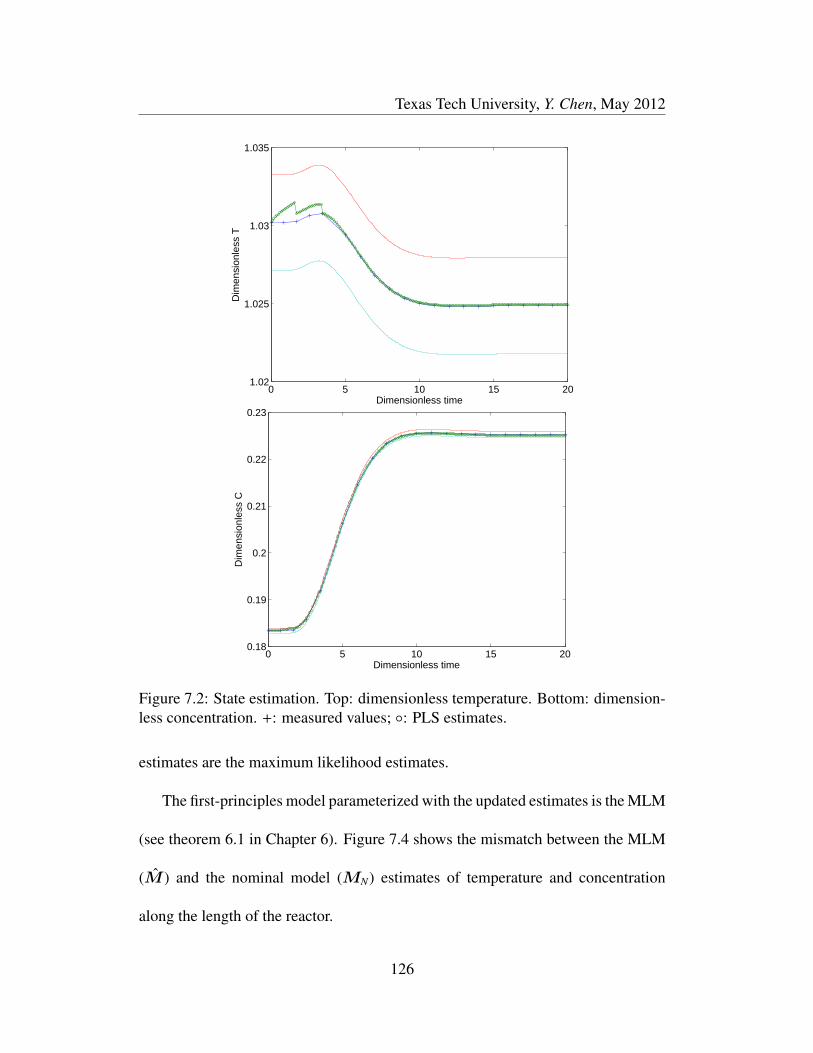

7.2 State estimation. Top: dimensionless temperature. Bottom: dimen-

sionless concentration. +: measured values; : PLS estimates. . . . 126

7.3 State estimation. Dimensionless concentration. +: plant measure-

ments; : PLS estimates. q: PLS estimates that violate the ±3σ

limits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

xiii

Texas Tech University, Y. Chen, May 2012

7.4 Outputs of the nominal and maximum likelihood models. Top: di-

mensionless temperature. Bottom: dimensionless concentration. :

states estimates from M ; ∗: states estimates fromMN . . . . . . . . 128

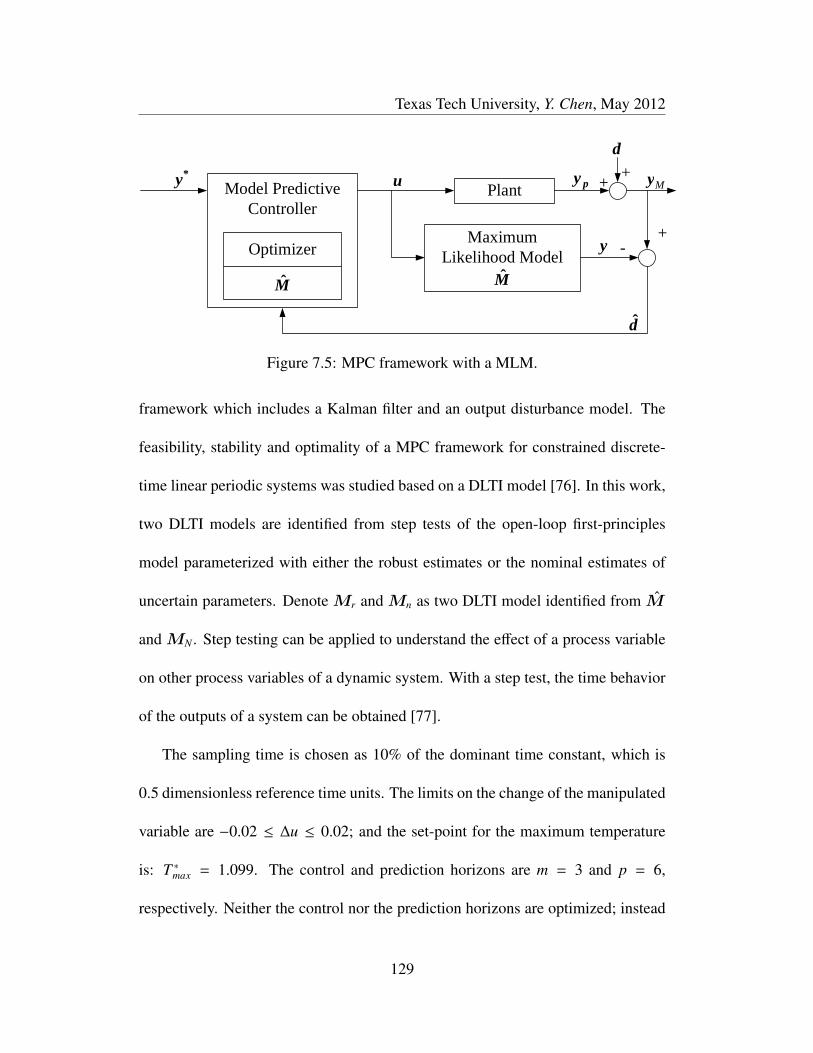

7.5 MPC framework with a MLM. . . . . . . . . . . . . . . . . . . . . 129

7.6 Model predictive control performance in the presence of distur-

bances: Top: Mr. Bottom: Mn. ∗: set-point. . . . . . . . . . . . . . 135

7.7 Model predictive control performance in the presence of distur-

bances and with 3% decrease in the value of the model’s param-

eters. Top: Mr. Bottom: Mn. ∗: set-point. . . . . . . . . . . . . . . 136

7.8 Model predictive control performance in the presence of distur-

bances and with 3% increase in the value of the model’s parameters.

Top: Mr. Bottom: Mn. ∗: set-point. . . . . . . . . . . . . . . . . . 137

7.9 Closed-loop tracking. Top: Mr. Bottom: Mn. ∗: set-point. . . . . . 138

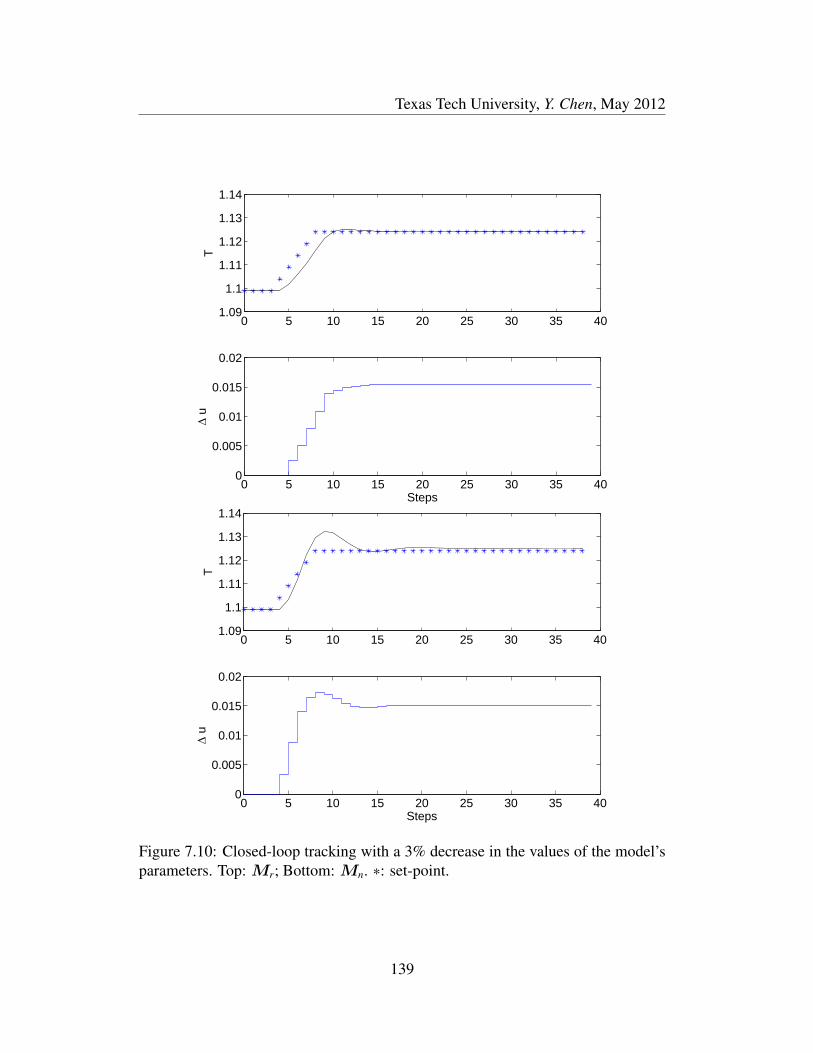

7.10 Closed-loop tracking with a 3% decrease in the values of the model’s

parameters. Top: Mr; Bottom: Mn. ∗: set-point. . . . . . . . . . . 139

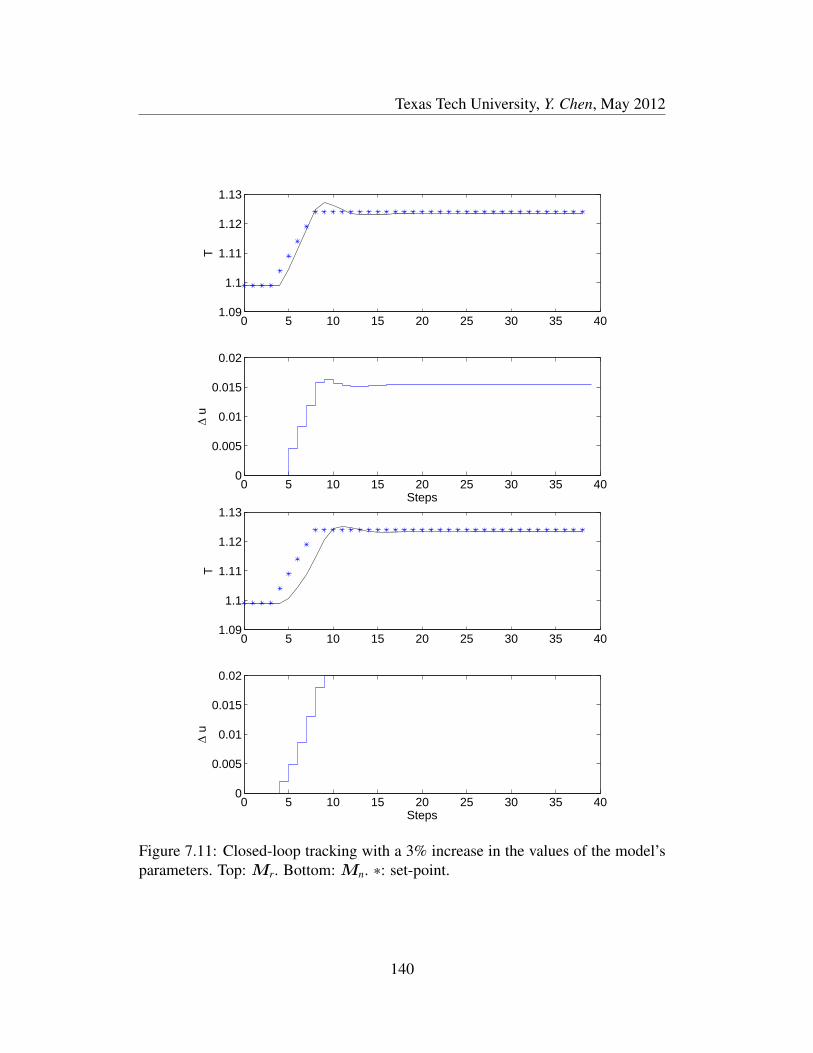

7.11 Closed-loop tracking with a 3% increase in the values of the model’s

parameters. Top: Mr. Bottom: Mn. ∗: set-point. . . . . . . . . . . 140

A.1 Internal model control framework [6]. y∗: desired set-points trajec-

tory, u: controller outputs, ym: process measurements, y: model

outputs, d: measured or unmeasured disturbances. . . . . . . . . . . 161

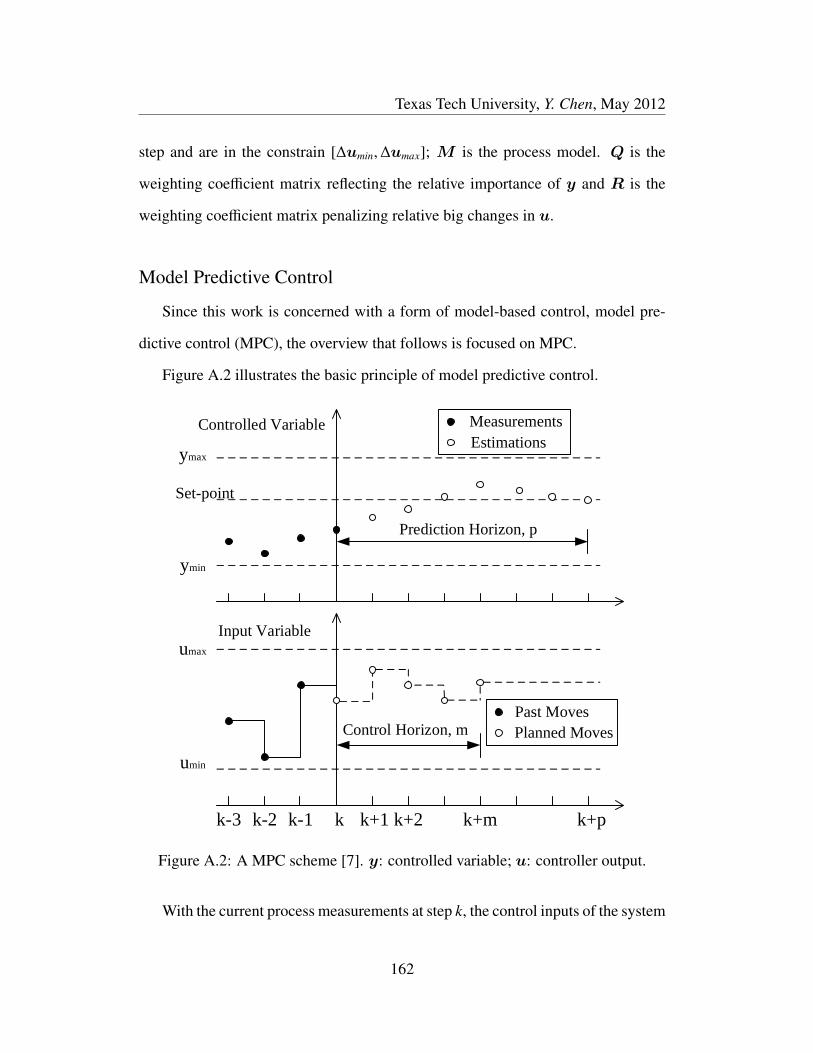

A.2 A MPC scheme [7]. y: controlled variable; u: controller output. . . 162

xiv

Texas Tech University, Y. Chen, May 2012

Chapter 1

Introduction

1.1 Background

Uncertainties exist inherently in real situations. Traditionally, cognitive heuris-

tics is applied to ascertain the appropriate management decisions. However, as real

systems have become increasingly complex the decisions to be made may have

higher associated risks, thus, heuristics while useful may not engender the required

level of certitude. An alternative is to use a mathematical model that describes the

dominant phenomena of these systems. Even though no model is an exact repre-

sentation of the system this approach may be more reliable and the confidence in

the model’s predictions can be quantified.

There are multiple reasons why a model is not exact. Primary among this is

the uncertainty associated with critical or sensitive model parameters that influ-

ence the final decisions. The study of the effect of model parameter uncertainty

on the model’s outputs is the primary objective of this research. Model parameter

uncertainty is common to many areas including, chemical, petrochemical, pharma-

ceutical industries, energy planing, power generation system planning, and so forth

[8, 9, 10].

Because of the widespread existence of uncertainties, their propagation has been

1

Texas Tech University, Y. Chen, May 2012

studied in many fields. The study of uncertainty propagation involves the develop-

ment of a mathematical model of the physical process and its numerical solution.

Xiu presented an algorithm of polynomial chaos to model the input uncertainty

and its propagation in incompressible flow simulations [11]. Polynomial chaos is a

non-sampling based method to determine evolution of uncertainty in the dynamical

system. Xiu stated that the polynomial chaos generalized for uncertainty promised

a substantial speed-up compared with Monte Carlo methods. However, in the case

study presented, there were only two uncertain parameters in a micro-channel flow

model. The precision depends on the order of the polynomials. For large numbers

of uncertain variables, polynomial chaos becomes very computationally expensive

making Monte Carlo methods more attractive. Tatang proposed a probabilistic col-

location method to analyze the uncertainty and its propagation in a geophysical

model [12]. With the orthogonal polynomials as functions of the uncertain pa-

rameters, the order of the model is reduced, which mitigates the computational

burden. Actually, the probabilistic collocation is a type of polynomial chaos that

approximates the response of the model with polynomial functions of the uncer-

tain parameters. For systems where a polynomial expansion cannot provide a good

approximation, sampling methods are needed.

Sampling of the uncertain parameter distributions followed by propagation of

the samples is a common and effective way to study the uncertainty effects on a

model’s outputs. The prior distribution of the uncertain parameters should be known

2

Texas Tech University, Y. Chen, May 2012

or assumed for sampling. Probability theory provides the foundation for sampling

uncertainty [13]. With a sample space that relates to the set of all probable outcomes

denoted by Ω, probability theory assumes that for each element θ ∈ Ω, an intrinsic

”probability” value from a function f (θ) satisfies the following properties:

• f (θ) ∈ [0, 1],∀θ ∈ Ω; and

•∑θ∈Ω

f (θ) = 1.

A probability distribution is a function f (θ) that describes the probability of a

random variable taking certain values. Based on the probability distribution func-

tion, various sampling techniques can be applied to sample the probable values of

uncertain variables for propagation.

Monte Carlo sampling (MCS) is one of the methods commonly used and is

considered to have high accuracy, but high computational burden. Because MCS

samples uncertain variables randomly, it needs a large number of sampling points

to cover the uncertain ranges. Thus, the model should be executed many times to

propagate these points. The corresponding computational efficiency is low. Related

to MCS is the Quasi Monte Carlo (QMC) sequences and the stratified technique

of Latin hypercube sampling (LHS). Both QMC and LHS have high accuracy but

they reduce the computational burden and improve the propagation efficiency [14].

However, as the number of uncertain variables increase, their efficiency decreases

noticeably.

3

Texas Tech University, Y. Chen, May 2012

Multiple dimensional uniformity of the samples can be applied to reduce the

number of samples and thus efficiency. Hammersley sequencing of points have

been shown to distribute the multiple variables samples regularly [15], and when

combined with LHS, together they provided an efficient sampling and sequenc-

ing technique called the Latin hypercube Hammersley sequence sampling (LHHS)

technique [16]. LHHS has been employed to study uncertainty propagation in var-

ious fields, such as health risk assessment process [14], estimation of greenhouse

gases emissions [17], off-line quality control of a reaction process [16], state esti-

mate of chemical processes [18, 19].

For unmeasurable parameters, updating is a necessary step to obtain an accurate

estimate of the state of the system by way of a model. Bayes’ theorem has been used

widely to estimate a variable from known conditions by determining the inverse

probability of this variable [20].

In probability theory and applications, Bayes’ theorem relates a conditional

probability to its inverse [21]. Consider A and B two events and denote the proba-

bility for each event happening by ℘(A) and ℘(B). Joint probability ℘(A, B) designs

the probability of both A and B occurring,

℘(A, B) = ℘(A|B)℘(B) = ℘(B|A)℘(A)

where ℘(A|B) and ℘(B|A) are conditional probabilities. ℘(A|B) is the probability of

4

Texas Tech University, Y. Chen, May 2012

A occurring given that B has already occurring. Bayes’ theorem in its simplest form

is given by,

℘(B|A) =℘(A|B)℘(B)℘(A)

To further elaboration on the use of this theorem, let Θ = (θ1, θ2, · · · , θd) be a

vector of model parameters with length d. Assume there are m observations y =

(y1, y2, · · · , ym). It follows that Bayes’ theorem in terms of probability distributions

is given by

℘(Θ|y) =℘(y|Θ)℘(Θ)℘(y)

℘(Θ|y) is the distribution of model parameters posterior to the observations,

y, and represents the probability that the model is correct given observations y.

℘(y|Θ) is called a likelihood function. Before y is observed, ℘(y|Θ) represents

the probability density function associated with the probable data realizations for

a fixed parameter vector Θ. Following an observation, ℘(y|Θ) is the likelihood of

obtaining the realization that was actually observed as a function of the parameter

vector Θ.

Based on Bayes’ theorem, a number of related approaches have emerged includ-

ing Markov chain Monte Carlo (MCMC) [22, 23, 24] and the ensemble Kalman

filter (EnKF) [25, 26, 27, 28, 29], especially to address updating in the presence

of multiple dimensional uncertain parameters in complex nonlinear models with

non-Gaussian distributions.

5

Texas Tech University, Y. Chen, May 2012

Uncertain parameter estimation and updating in a rainfall runoff model was

studied by [30, 31]. They introduced an adaptive Metropolis (AM) algorithm within

the MCMC framework. The AM algorithm was found to have several advantages

compared with the traditional Metropolis-Hastings algorithm. In the AM scheme,

the use of the parameter covariance matrix in the proposed distributions allows

the sampling of several uncertain parameters together, which provides a more effi-

cient exploration of the posterior distributions. Hassan used the AM algorithm in

the MCMC framework to update two uncertain parameters, recharge and hydraulic

conductivity, to quantify the parameters’ effect on the predictions of a groundwater

flow model [32]. The AM-based MCMC scheme was used successfully to obtain

the posterior distributions of the two uncertain parameters. However, a large num-

ber of model executions was required.

An EnKF was used to assimilate thickness (the difference in height between two

pressure levels in a weather forecast) data for operational numerical weather predic-

tion [33]. The quasi-geostrophic model was grided on a 64×32 two-dimension grid.

A series of 30-day data assimilation cycles were performed using ensembles of data

of different sizes. The result indicated that ensembles having an order of 100 mem-

bers or more were sufficient to describe the ensemble covariance accurately. In the

study by Heemink et al, an EnKF was designed to solve atmospheric chemistry data

assimilations problems [34]. The studied domain was divided into 30×30 grids and

the EnKF was able to provide a solution to the data assimilation problem. In recent

6

Texas Tech University, Y. Chen, May 2012

years, because of the successful use in the the above described complex geophys-

ical areas, the EnKF was introduced in the area of reservoir uncertain parameter

updating. In this application, the EnKF also showed good performance of updat-

ing critical geographic parameters of permeability and porosity of very large scale

reservoirs [3, 35, 36, 37, 38].

Updating of the uncertain model parameters is essential for the case where the

parameters are unmeasurable. However, the updating process is very time consum-

ing since it requires a large number of observations to make the uncertain param-

eters converge to their stationary distributions or stationary values. Even if there

is a parameter whose sampled values are known, it remains a nontrivial task to de-

termine an estimate of this uncertain parameter from its samples. The key point is

that an estimate of the uncertain parameter should be robust to prevent the effects

of outliers, insufficient number of samples, and so forth.

Robust statistics [39, 40, 41] is widely applied to obtain a robust estimate of an

uncertain variable. Olive did a study on the calculation of robust estimates based

on robust statistics for different kinds of usual distributions and nonparametric data

sets [42]. Daszykowski introduced robust statistics in chemometrics for data explo-

ration and modeling [43]. It was pointed out that when data contained outliers, the

data mean as well as its standard deviation were no longer reliable estimates, and

therefore, data preprocessing was required. The median and the absolute deviation

around the median were selected as robust estimates of a variable and its deviation;

7

Texas Tech University, Y. Chen, May 2012

these statistics then were used to scale the data sets and to screen for outliers.

The analysis of uncertain parameters’ propagation and updating are relevant

for model-based applications. In this work, the study of parameter uncertainties

is applied to the real-time application of model-based control, in particular model

predictive control (MPC).

Model-based control is a framework that explicitly uses a model of the process

to determine the optimal control input to regulate the real process. It is a well known

fact that the ideal feedback controller is the inverse of the process. This indirect

construction of the controller is known as internal model control (IMC) [6]. The

underlying assumption is that the inverse of the model is realizable. For models that

are not realizable, other model-based control designs have been proposed. Notable

ones are, model predictive control (MPC) [44], dynamic matrix control (DMC)

[45, 46], quadratic dynamic matrix control (QDMC), and generalized model-based

control (GMC) [47, 48]. The basic concepts remains the same – that of using a

model of the process in a constrained optimization formulation to determine the

optimal controller movers.

Real-time applications impose the requirement of reliable, stable, and timely

computational solutions. A complex, nonlinear, high-dimensional process model

usually in the form of a system of partial differential-algebraic equations, may not

be suitable for these types of applications. One means of addressing this limi-

tation is to employ an appropriate reduced-order model (ROM). Zheng and Hoo

8

Texas Tech University, Y. Chen, May 2012

combined the characteristics of singular-value decomposition and the Karhunen-

Loeve (KL) expansion to arrive at a ROM that captured the dominant characteris-

tics of a distributed parameter system [2, 4, 49, 50]. A proportional-integral (PI)

controller, a dynamic matrix controller (DMC) and a quadratic dynamic matrix

controller (QDMC) were designed based on this ROM and all showed good per-

formance for disturbance rejection. Astrid studied reduction of process simulation

models using a proper orthogonal decomposition (POD) approach for missing point

estimation and model-based control [51]. In Astrid’s work, heat conduction models

and a computational fluid dynamics (CFD) model of an industrial glass melt feeder

were used to demonstrate the model reduction technique. Based on a principal com-

ponent analysis (PCA), Lang reduced CFD models of a gas turbine combustor and

an entrained-flow coal gasifier to ROMs for process simulation and optimization

[52]. As a data-based latent variable method, partial least squares (PLS) regression

was analyzed and applied for process analysis, monitoring and control [53]. The

implementation of control policies for autoregressive moving average exogenous

(ARMAX) models was studied [54]. The control scheme implemented was a feed-

back strategy, with white noise control. The ARMAX models were shown to be

valuable for examining the closed-loop stability.

9

Texas Tech University, Y. Chen, May 2012

1.2 Motivation

In order to manage a physical process, it is very important to understand and

accurately predict the phenomena of this process fully. It would involve developing

a process model consisting of mass, moment and energy balances that can be ex-

pressed in a mathematical framework. The accuracy of the model parameters will

affect the solution results. Studying the effect of parameter uncertainties and their

validation in a simulation (or in silico) model play a critical role in managing the

process.

There are multiple reasons why model parameter uncertainties exist. For in-

stance, measurement error (uncalibrated sensors), the parameter cannot be esti-

mated reliably (bulk effective value versus local values), the parameter simply can-

not be measured given the current state-of-the-art sensors, or the experimental con-

ditions to carry out the measurements are dangerous. Since model parameter uncer-

tainties affect the numerical results, state estimates and other process management

applications (e.g., model based control, online monitoring, process optimization), it

would be very prudent to quantify the effect of parameter uncertainty on the model

outputs by way of propagation of the uncertainty, developing criteria and meth-

ods that provide robust parameter values, and designing an online framework for

efficient model parameter updating to maintain model accuracy.

10

Texas Tech University, Y. Chen, May 2012

1.3 Objectives

As stated previously, there are multiple reasons that contribute to model uncer-

tainty. These include, the model assumptions, the model parameter uncertainties,

the functional forms assumed to represent the phenomena, and so forth. The focus

of this research is to investigate the model parameter uncertainties and the road map

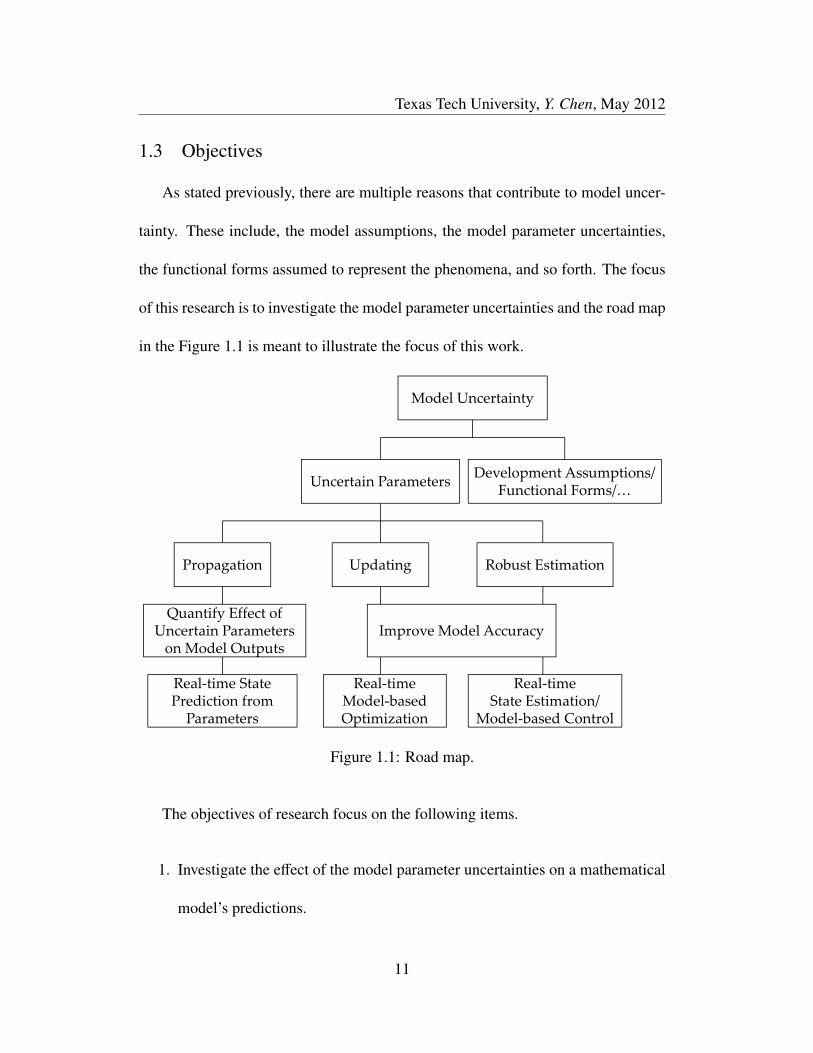

in the Figure 1.1 is meant to illustrate the focus of this work.

Model Uncertainty

De elo e t A u tio /Uncertain Parameters Development Assumptions/ Functional Forms/…

Propagation Updating Robust EstimationPropagation Updating Robust Estimation

Quantify Effect of Q yUncertain Parameters on Model Outputs

Improve Model Accuracy

Real‐time State Prediction from Parameters

Real‐time Model‐based Optimization

Real‐time State Estimation/

Model based ControlParameters Optimization Model‐based Control

Figure 1.1: Road map.

The objectives of research focus on the following items.

1. Investigate the effect of the model parameter uncertainties on a mathematical

model’s predictions.

11

Texas Tech University, Y. Chen, May 2012

By propagating uncertain parameters through a model, the effect of the model

parameter uncertainties on a mathematical model’s predictions can be quan-

tified. By capturing the relationships between the uncertain parameters and

the real-time state prediction, more accurate state estimation can be real-

ized. In this work, Monte Carlo sampling (MCS), Latin hypercube sampling

(LHS) and Latin hypercube sampling with Hammersley sequencing (LHHS)

are used to establish propagation efficiency. Partial least squares regression

is applied to capture the relationships between the uncertain parameters and

the model outputs. Once the relationships are determined, the PLS model

can be used to predict the process states from known values of the parame-

ters. Usually, the process states are of a higher dimension than the number of

uncertain parameters. To make the PLS feasible and efficient, an application

of the Karhunen-Loeve expansion is employed to reduce the dimension but

retain the dominant temporal and spatial characteristics of the process.

2. Update the uncertain parameters efficiently.

When the uncertain parameters are not readily measurable, an initial guess

of their values is unavoidable. However, for accuracy of the application, up-

dating the initial guess of the parameter uncertainties is justified. One of the

objective of this work is to update the uncertain parameters and thus improve

the estimate of the system states. For very complex and nonlinear models, as

12

Texas Tech University, Y. Chen, May 2012

described above, MCMC and EnKF have been used successfully. They will

be embedded in a model-based optimization framework in this work and their

performance will be compared.

3. Estimate robust values of uncertain parameters.

Robust statistics seeks to provide estimating methods that emulate popular

statistical methods, but which are not unduly affected by outliers or other

small departures from model assumptions. Three types of robust estimates

will be studied for robust estimation. They are, the maximum likelihood type

estimates (MLE), the linear combinations of order statistics (L-Estimate), and

the rank estimates derived from suitable rank tests (R-Estimate). This work

will demonstrate that models parameterized by robust estimates of the uncer-

tain parameters can provide more accurate state estimates.

1.4 Organization

The rest of the dissertation is organized as follows. Chapter 2 presents Monte

Carlo Sampling (MCS), Latin hypercube sampling (LHS) and Latin hypercube

sampling with Hammersley sequence (LHHS) techniques for uncertainty propa-

gation. The production of benzene from hydro-dealkylation (HDA) of toluene is

employed in this chapter to compare the propagation efficiency of these sampling

techniques. To study real-time state prediction from uncertain parameters, partial

13

Texas Tech University, Y. Chen, May 2012

least squares (PLS) regression and Karhunen-Loeve (KL) expansion are introduced

in Chapter 3. The performance of the real-time state prediction from uncertain pa-

rameters also is demonstrated using the HDA process. Chapter 4 introduces and

compares two updating techniques, Markov chain Monte Carlo (MCMC) and en-

semble Kalman filter (EnKF). In Chapter 5, the updating techniques are embed-

ded in a real-time model-based optimization framework. A five-spot pattern oil

reservoir system is introduced to demonstrate and compare the MCMC and EnKF

updating methods. Chapter 6 presents an overview of the theory of robust statis-

tics. Based on robust statistics, a new theorem about a maximum likelihood model

is introduced and proven. In Chapter 7, the robustness feature of the maximum

likelihood model is demonstrated in a model predictive control (MPC) framework.

Lastly, Chapter 8 summarizes the contributions of the research and suggests future

work.

14

Texas Tech University, Y. Chen, May 2012

Nomenclature

AM adaptive Metropolis

ARMAX autoregressive moving average exogenous

CFD computational fluid dynamics

DMC dynamic matrix control

EnKF ensemble Kalman filter

GMC generalized model-based control

HDA hydro-dealkylation

IMC internal model control

L-estimate linear combinations of order statistics

KL Karhunen-Loeve

LHS Latin hypercube sampling

LHHS Latin hypercube Hammersley sequence sampling

MCMC Markov chain Monte Carlo

MCS Monte Carlo sampling

MLE maximum likelihood type estimates

MPC model predictive control

PCA principal component analysis

PLS partial least squares

POD proper orthogonal decomposition

QDMC quadratic dynamic matrix control

QMC quasi Monte Carlo

R-estimate estimates derived from rank tests

ROM reduced-order model

15

Texas Tech University, Y. Chen, May 2012

Chapter 2

Preliminaries on Uncertainty Propagation

This chapter presents an overview of sampling methods of Monte Carlo, Latin

hypercube sampling, and Latin hypercube sampling with Hammersley sequencing

for uncertainty propagation. The production of benzene from hydro-dealkylation

(HDA) of toluene is then introduced to compare the propagation efficiency of these

sampling methods.

With known distributions, for example from historical data, of the multiple un-

certain variables, efficient and effective sampling are reasonable expectations to

propagate the large number of sequences through the complex model to determine

the state estimates and their distributions.

The conventional sampling method of Monte Carlo sampling (MCS) is known

to have low efficiency for uncertainty propagation. As a stratified sampling tech-

nique, Latin hypercube sampling (LHS) technique, is more accurate and efficient

than MCS when there is a single uncertain variable. But in the case of multiple

uncertain variables it has been demonstrated that the efficiency of LHS decreases

noticeably. Another sequencing method, Hammersley sequencing, when combined

with Latin hypercube sampling (LHHS) has been shown to be very efficient when

there are multiple uncertain variables [14].

16

Texas Tech University, Y. Chen, May 2012

2.1 Sampling Techniques

2.1.1 Monte Carlo Sampling

There is no consensus on how Monte Carlo should be defined. For example,

Ripley [55] reserved Monte Carlo for most probabilistic modeling as stochastic

simulation. Sawilowsky [56] distinguished between Monte Carlo method and a

Monte Carlo simulation. A Monte Carlo method can be used to solve a mathe-

matical or statistical problem but a Monte Carlo simulation repeated sampling to

investigate the properties of a phenomenon. Anderson [57] defined Monte Carlo

as the art of approximating an expectation by the sample mean of a function of

simulated random variables.

Monte Carlo sampling (MCS) method is one of the best known methods for

sampling a probability distribution that is based on the use of a pseudo-random

number generator [16]. This simple random sampling involves repeatedly forming

random values of a variable from a prescribed probability distribution. Because the

characteristic of Monte Carlo samples is random, to sample the distribution of an

uncertain variable means a very large number of sample points to cover the distri-

bution range and approximate the real expectation. The large number of sample

points is the primary reason that causes the computational burden for uncertainty

propagation.

To sample an uncertain variable X with MCS, the cumulative distribution func-

17

Texas Tech University, Y. Chen, May 2012

tion (CDF) F of X should be known. The values of the CDF are Pri = F(xi), where

F is the cumulative density function. The procedure is as follows.

• Randomly sample N values of Pri with uniform distribution ranging from 0

to 1, U (0, 1) (i = 1, · · · ,N), where N is the number of sample points and Pri

is a value of the cumulative probability.

• Transform the probability values Pri into the value xi using the inverse of the

distribution function F−1 : xi = F−1(Pri).

2.1.2 Latin Hypercube Sampling

Latin hypercube sampling (LHS) is a stratified-random 1 procedure which pro-

vides an efficient way of sampling a variable from its distribution. The LHS in-

volves sampling N values from the prescribed distribution of the variable X. The

cumulative distribution for this variable is divided into N equally probable intervals.

From each interval a value is selected randomly. Unlike simple random sampling

of MCS, this method ensures a full coverage of a variable by maximally stratifying

its marginal distribution 2 The procedure is as follows.

• Divide the cumulative distribution of the variable into N equal probable in-

1Stratified means that the range of a variable’s distribution has been separated in several intervals.Stratified-random means from each of the divided interval a sample is collected randomly.

2A distribution function may be for more than one variables for example f(x,y) which is the jointdistribution of x and y, the marginal distribution refers to the distribution of one of them f (x) =∫

y( f (x, y)dy. Stratifying the marginal distribution means separating the marginal distribution rangeaveragely according to the number of samples that we want.

18

Texas Tech University, Y. Chen, May 2012

tervals.

• Randomly select a value from each interval. The sampled cumulative proba-

bility can be written as [58]

Pri = (1/N)ru + (i − 1)/N

where ru is a uniformly distributed random number, ru ∼ U (0, 1).

• Transform the probability value Pri into the value Xi using the inverse of the

distribution function F−1 : Xi = F−1(Pri).

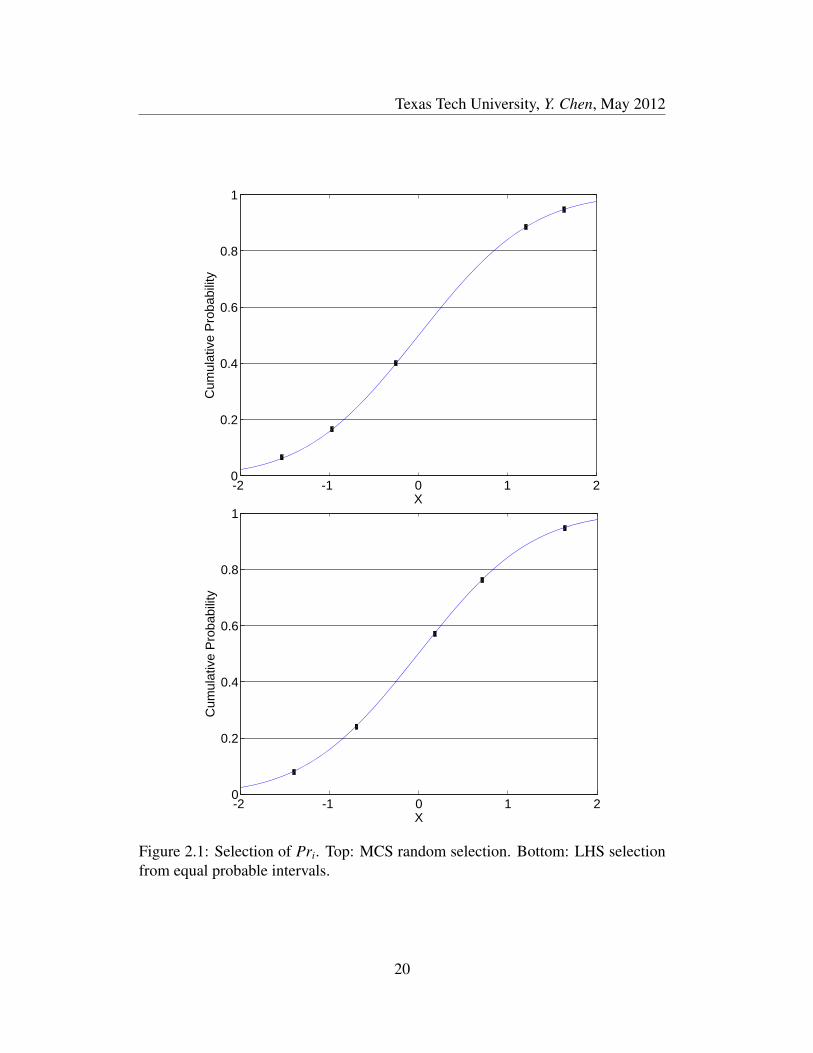

Assume 5 sample points of a normal distribution variable X are sampled with

MCS and LHS. X ∼ N (0, 1). Figure 2.1 shows how MCS and LHS select values

for Pri.

It is easy to demonstrate that LHS can use less sample points than MCS to

cover the full range of a variable distribution. Better one-dimensional uniformity

is indicated by the closeness of the sample points to the 45 line with a uniform

interval between the adjacent sample points [14]. As shown in Figure 2.2, for 20

sample points selected by MCS and LHS, the latter shows better uniformity than

the former.

The attractive uniformity property of the LHS method can provide efficient

propagation of LHS sample points for a one dimension uncertain parameter. How-

19

Texas Tech University, Y. Chen, May 2012

-2 -1 0 1 20

0.2

0.4

0.6

0.8

1

X

Cum

ulat

ive

Pro

babi

lity

-2 -1 0 1 20

0.2

0.4

0.6

0.8

1

X

Cum

ulat

ive

Pro

babi

lity

Figure 2.1: Selection of Pri. Top: MCS random selection. Bottom: LHS selectionfrom equal probable intervals.

20

Texas Tech University, Y. Chen, May 2012

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

X

Cum

ulat

ive

Pro

babi

lity

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

X

Cum

ulat

ive

Pro

babi

lity

Figure 2.2: One-dimensional uniformity analysis with 20 sample points. Top:MCS. Bottom: LHS.

21

Texas Tech University, Y. Chen, May 2012

ever, it has been shown that for multiple uncertain distributions, LHS cannot retain

this advantage. Assume there are two variables X and Y and both have uniform dis-

tributions between 0 and 1, that is, X ∼ U (0, 1), Y ∼ U (0, 1). Figure 2.3 compares

the uniformity property of MCS and LHS in two dimensions. One hundred sample

points are generated on a unit square by each sampling method. The figure shows

that the sample points of both MCS and LHS are not ordered.

2.1.3 Latin Hypercube Hammersley Sampling

To combine sample points of multiple dimension variables, the conventional

approach is to pair them randomly. It is in this step that Hammersley sequencing

has better multi-dimensional uniformity [15, 59].

2.1.3.1 Hammersley sequence points

The definition of Hammersley points and an explanation of the procedure to

generate the Hammersley points are as follows [15, 16].

Let any nonnegative integer K be expanded using a prime base p,

K = k0 + k1 p + k2 p2 + · · · + km pm (2.1)

where each k j, j = 1, · · · ,m, is an integer in [0, p-1], m = [logKp ] (square brackets

denote the integral part).

22

Texas Tech University, Y. Chen, May 2012

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

x

y

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

x

y

Figure 2.3: One hundred sample points on a unit square with X,Y ∈ (0, 1). Top:MCS. Bottom: LHS.

23

Texas Tech University, Y. Chen, May 2012

Inverse of prime numbers can be used to define a function φp(K):

φp(K) =k0

p+

k1

p2 + · · · +km

pm+1

The sequence of Hammersley points of dimension d is given by,

(KN, φp1(k), φp2(k), · · · , φpd−1(k)

), K = 1, · · · ,N

where N is the number of samples and p1, · · · , pd−1 are the first d-1 prime numbers.

2.1.3.2 Combination of Latin hypercube sampling and

Hammersley sequencing

In order to retain the uniformity of LHS for multiple dimensions variables,

Hammersley sequence is applied to arrange the LHS sample points of each vari-

able [14, 17]. This sampling method is Latin hypercube Hammersley sampling

(LHHS). Based on the use of rank correlations [60], the LHS sample points for

multi-dimensional variables can be arranged according to the order of the multiple

dimensional Hammersley sequence points.

Suppose X is an N × d matrix that consists of N sets of d uncorrelated pa-

rameters (sampled with LHS). Then the correlation matrix is an identity matrix I .

24

Texas Tech University, Y. Chen, May 2012

Let

C = Γ × Γ′

be the desired correlation matrix ofX where Γ is a lower triangular matrix obtained

by Cholesky factorization. The transformed matrixXΓ′ then has the desired corre-

lation matrix C. This is the theoretical basis for transforming a desired correlation

to an uncorrelated matrix.

Because X is to be rearranged according to the Hammersley sequence points,

these points should be a matrix with the same dimension as X , N × d. Denote

the Hammersley sequence points by the matrixH . With the desired correlation C,

transformH to the rank matrixH∗ whose correlation matrix is C.

To avoid the problem that the correlation matrix of H is not I but R, a matrix

S should be found out that

SRS′ = C

With Cholesky factorization,

R = QQ′

Therefore, the solution of S can be obtained,

S = ΓQ−1

25

Texas Tech University, Y. Chen, May 2012

and correspondingly the transformation factor for the rank matrix is S and the rank

matrix becomes

H∗ =HS′

As a result the correlation matrix of H∗ is exactly equal to the desired matrix

C. The sample matrixX therefore can be paired according to the rank matrixH∗.

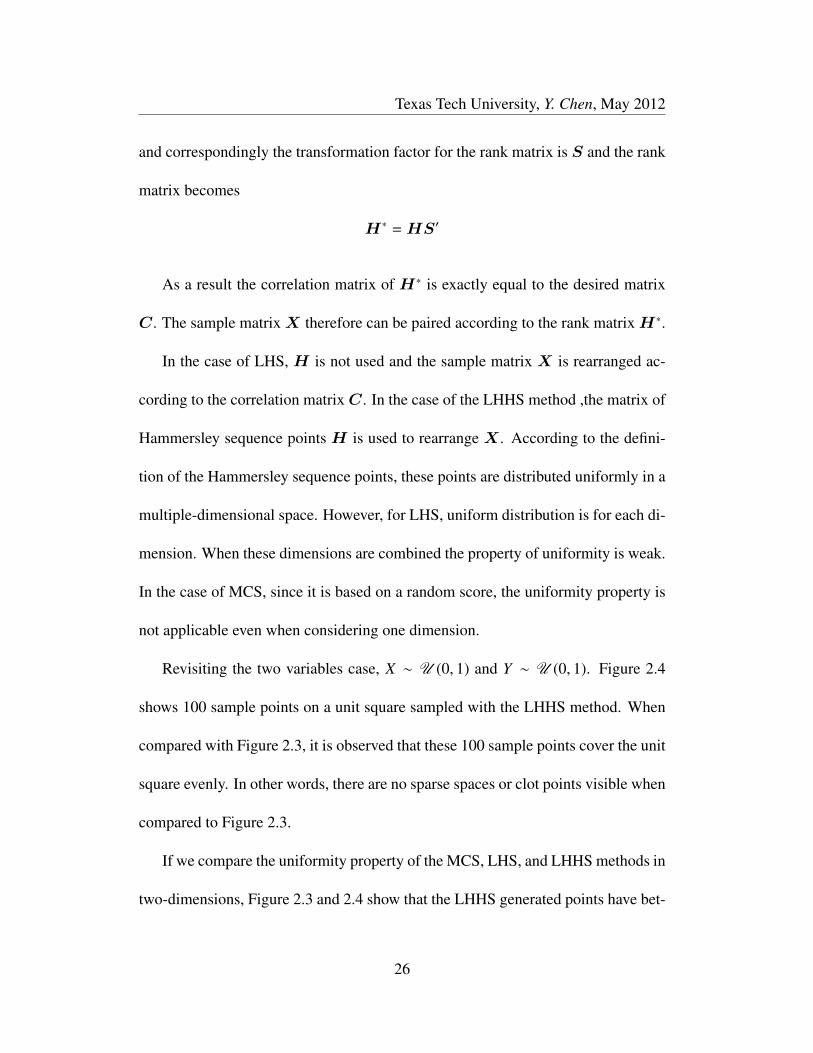

In the case of LHS, H is not used and the sample matrix X is rearranged ac-

cording to the correlation matrixC. In the case of the LHHS method ,the matrix of

Hammersley sequence points H is used to rearrange X . According to the defini-

tion of the Hammersley sequence points, these points are distributed uniformly in a

multiple-dimensional space. However, for LHS, uniform distribution is for each di-

mension. When these dimensions are combined the property of uniformity is weak.

In the case of MCS, since it is based on a random score, the uniformity property is

not applicable even when considering one dimension.

Revisiting the two variables case, X ∼ U (0, 1) and Y ∼ U (0, 1). Figure 2.4

shows 100 sample points on a unit square sampled with the LHHS method. When

compared with Figure 2.3, it is observed that these 100 sample points cover the unit

square evenly. In other words, there are no sparse spaces or clot points visible when

compared to Figure 2.3.

If we compare the uniformity property of the MCS, LHS, and LHHS methods in

two-dimensions, Figure 2.3 and 2.4 show that the LHHS generated points have bet-

26

Texas Tech University, Y. Chen, May 2012

ter uniformity properties. The main reason is that the Hammersley sequence places

the sampled points on a multi-dimensional hypercube in an ordered fashion. In con-

trast, the LHS method while designed for uniformity along a single dimension in the

case of multiple dimensions, it randomly pair the sampled points for placement on a

multi-dimensional hypercube. In the case of MCS, even for a single dimension, the

uniformity property is not applicable. Therefore, the likelihood that the MCS and

LHS methods can provide good uniformity property on multi-dimensional cubes is

extremely small.

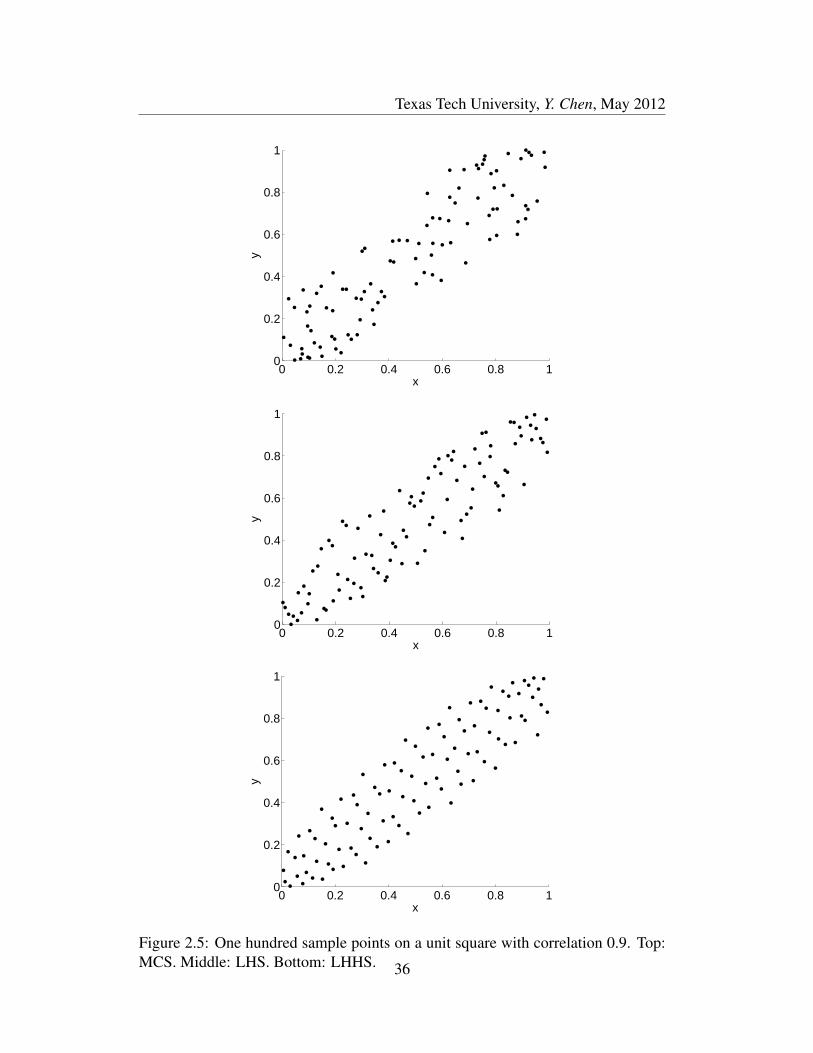

In the case that there are correlations between the multiple parameters, the

LHHS method still shows the best uniformity property when compared to the MCS

and LHS methods. Once again revisiting the two variables X and Y case, X ∼

U (0, 1), Y ∼ U (0, 1). Assume the correlation matrix between X and Y is

C =

1 0.9

0.9 1

A rank correlation H∗ = HC can be used to design each dimension. Figure

2.5 shows the uniformity property when there is a desired correlation matrix C for

a two-dimensional uniform distribution of 100 sample points with the imposed 0.9

correlation. As before, it is not difficult to conclude that the LHHS generated points

have better uniformity property when compared to the other methods. The reason

27

Texas Tech University, Y. Chen, May 2012

for this is that the Hammersley sequence preserves the uniformity property.

2.2 Example: HDA Process

The chemical process of benzene production from hydro-dealkylation (HDA)

of toluene [61] is introduced to demonstrate the sampling methods.

2.2.1 HDA Process

The hydro-dealkylation of toluene occurs in a nonlinear plug-flow reactor (PFR)

system (see Figure 2.6) which has been studied extensively by Zheng and Hoo

[7, 2].

Two reactions are known to occur, namely

C7H8 + H2 → C6H6 + CH4

2C6H6 C12H10 + H2

The first reaction is irreversible and the second is an equilibrium reaction. A

28

Texas Tech University, Y. Chen, May 2012

first-principles model can be developed to describe the major reaction phenomena.

∂ε1

∂τ= −υ

(∂ε1

∂τ1+ε1

θ

∂θ

∂τ1

)− ε1ε

0.52 θ

1.5eγ(θ−1/θ)1

∂ε2

∂τ= −υ

(∂ε2

∂τ1+ε2

θ

∂θ

∂τ1

)− ε1ε

0.52 θ

1.5eγ(θ−1/θ)1 + κ2(ε3θ)2eγ

(θ−1/θ)2 − κ3ε2ε5θ

2eγ(θ−1/θ)3

∂ε3

∂τ= −υ

(∂ε3

∂τ1+ε3

θ

∂θ

∂τ1

)+ ε1ε

0.52 θ

1.5eγ(θ−1/θ)1 − 2κ2(ε3θ)2eγ

(θ−1/θ)2 + 2κ3ε2ε5θ

2eγ(θ−1/θ)3 + FBm

∂ε4

∂τ= −υ

(∂ε4

∂τ1+ε4

θ

∂θ

∂τ1

)+ ε1ε

0.52 θ

1.5eγ(θ−1/θ)1

∂ε5

∂τ= −υ

(∂ε5

∂τ1+ε5

θ

∂θ

∂τ1

)+ κ2(ε3θ)2eγ

(θ−1/θ)2 − κ3ε2ε5θ

2eγ(θ−1/θ)3

∂θ

∂τ=

1ζ

[Hr1∂ε1

∂τ− Hr2

∂ε5

∂τ+ Q(θF − θ) − v

(ζ∂θ

∂τ1− Hr1

∂ε1

∂τ1+ Hr2

∂ε5

∂τ1

)]− FBmζB

(2.2)

where ζ = (Cp/CP0)(P0/Pr), υ(z) = (Fin + Fin j)/(P/RT ), Fin is the feed to the reac-

tor, εi is the concentration of the ith component and θ is the dimensionless reactor

temperature. The initial feed concentrations (mole fraction) of toluene, hydrogen,

and methane are ε1,0 = 0.0807, ε2,0 = 0.4035, ε4,0 = 0.5158. Table 2.1 provides

the definition and values of the parameters and variables, and subscript 0 is the

reference condition.

The boundary conditions are:

z = 0, εi = εi(t = 0), i = 1, · · · , 5, θ = θ(t = 0)

z = 1,∂εi

∂z= 0, i = 1, · · · , 5,

∂θ

∂z= 0

The pure benzene stream is injected at the start of the reactor. The finite difference

solution of this system serves as the true solution.

29

Texas Tech University, Y. Chen, May 2012

Table 2.1: Dimensionless parameters for the HDA process [2].

Parameter Nominal values Definition

P = Pr/P0 1.0 Reactor pressure

FBm = Fin j/Fin 0.008 Dimensionless benzene injection

θF = TF/T0 1.0 Jacket temperature

κ1 = k1(T0)/k1(T0) 1.0 Dimensionless reaction 1 rate constant

κ2 = k2(T0)P20/k1(T0)P1.5

0 0.995 Ratio of reaction 1 to reverse reaction 2

κ3 = k3(T0)P20/k1(T0)P1.5

0 5.34 Ratio of reaction 1 to reverse reaction 3

Hr1 = HR1/Cp0T0 -1.51 Heat of reaction 1

Hr2 = HR2/Cp0T0 -0.473 Heat of reaction 2

Q 0.0 Heat transfer coefficient

γ1 = Ea/RT0 29.26 Reaction 1 activation energy

γ2 = Ea/RT0 29.68 Reaction 2 activation energy

γ3 = Ea/RT0 33.49 Reaction 3 activation energy

τ ∈ <+ > 0 Dimensionless time

z ∈ Ω [0,1] Dimensionless space

2.2.2 Propagation with Different Sampling Methods

Each parameter in the HDA process is not exact, but not all of the parameters

have a pronounced effect on the system solution. Using a parametric sensitivity

analysis, the outputs are found to be most sensitive to the rate constant of reaction 1

(κ1), the fresh benzene injection rate (FBm), and the heat of reaction 1 (Hr1). These

parameters are uncorrelated.

Assume that a Gaussian distribution can represent each of these three param-

30

Texas Tech University, Y. Chen, May 2012

eters with mean values 1.0, 37.34, -1.51 and error levels of 20% ((σi/ui)100%),

where ui and σi represent the mean and standard deviation of the ith uncertain pa-

rameter, respectively. Here, the three sampling methods, Monte Carlo sampling

(MCS), Latin hypercube sampling (LHS), and Latin hypercube Hammersley sam-

pling (LHHS) are implemented and their efficiency and accuracy are compared.

The true mean and variance are needed to make a worthwhile comparison.

These statistics are estimated by propagating a very large number of samples, for

example MCS 50,000 samples, LHS 10,000 samples and LHHS 10,000 samples.

When these three methods provide the same (or similar) estimates for the mean

and variance, these values are accepted as the true values. Otherwise, the number

of samples is increased until this criterion is satisfied. Once the true values are

obtained, the efficiency of the different sampling techniques is compared by esti-

mating the number of samples required to obtain the true mean and variance to be

within a 0.5% error.

The finite difference solution of the above system of partial differential equa-

tions gives the spatial and temporal values of the dimensionless reactor temperature

and component concentrations. Consider three spatial locations, z = 1/3, 2/3, 1,

the number of samples and the computation time needed for the three methods to

be within a 0.5% error of the true mean and variance of the benzene concentra-

tion and reactor temperature are tabulated in Table 2.2. The results show that the

LHHS method requires a smaller number of samples (approximately 7 times less)

31

Texas Tech University, Y. Chen, May 2012

when compared to the LHS and is superior to the MCS (approximately 60 to 70

times less samples). For the same accuracy, LHHS is most efficient of these three

methods.

Figure 2.7 shows the standard deviations of the dimensionless benzene concen-

tration and reactor temperature that result with the implementation of the different

sampling methods at the exit of the reactor. The upper and lower solid lines give

the error limits of ± 0.5% of the true standard deviation. True standard deviation

of the benzene concentration is 1.033 × 10−3 and that of the reactor temperature is

1.782 × 10−3. It can be found that the LHHS method uses least number of sample

points to be within the error range and to have the fastest convergence rate.

The effect of the propagation of the parameter uncertainties through the model

is shown in Figure 2.8, which shows the distributions of the dimensionless ben-

zene concentration and reactor temperature at the reactor exit. The probability of

the model output uncertainties caused by uncertain parameters can be obtained by

propagation.

2.3 Summary

This chapter introduced three sampling techniques, Monte Carlo sampling (MCS),

Latin hypercube sampling (LHS), and Latin hypercube sampling with Hammersley

sequencing (LHHS). Their uniform property are explained to compare their sam-

pling efficiency. These three sampling techniques are applied in hydro-dealkylation

32

Texas Tech University, Y. Chen, May 2012

Tabl

e2.

2:C

ompu

tatio

ntim

ean

dnu

mbe

rofs

ampl

esat

thre

esp

atia

lloc

atio

nsth

atac

hiev

es0.

5%er

roro

fthe

true

mea

nan

dva

rian

ceof

the

benz

ene

conc

entr

atio

nan

dre

acto

rtem

pera

ture

.

z=1/

3z=

2/3

z=1

Met

hod

MC

SL

HS

LH

HS

MC

SL

HS

LH

HS

MC

SL

HS

LH

HS

Tim

eB

enco

nc15

2.1

15.6

2.1

114.

113

1.9

86.9

131.

9(m

in)

Tem

p18

7.3

15.6

2.1

182

15.6

1.9

14.1

15.6

1.9

Sam

ple

Ben

conc

5600

600

9042

0050

080

3200

500

80Te

mp

6900

600

9067

0060

080

4200

600

80

33

Texas Tech University, Y. Chen, May 2012

(HDA) of toluene process which illustrates the advantage of LHHS over MCS and

LHS. The product of LHHS technique is the generation of the outputs and their

uncertainty distributions that are functions of the uncertainty in the parameters.

34

Texas Tech University, Y. Chen, May 2012

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

x

y

Figure 2.4: One hundred sample points (sampled with LHHS) on a unit square withx, y ∈ (0, 1).

35

Texas Tech University, Y. Chen, May 2012

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

x

y

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

x

y

0 0.2 0.4 0.6 0.8 10

0.2

0.4

0.6

0.8

1

x

y

Figure 2.5: One hundred sample points on a unit square with correlation 0.9. Top:MCS. Middle: LHS. Bottom: LHHS. 36

Texas Tech University, Y. Chen, May 2012

Feed

FB BenzeneQuench

z = 0 z = 1

51 L=iiε

Outputcomponents

C7H8

H2 CH4

C7H8 H2

C6H6 CH4

C12H10

Figure 2.6: Plug Flow Reactor.

37

Texas Tech University, Y. Chen, May 2012

0 1000 2000 3000 4000 50001.015

1.025

1.035

1.045

1.055

1.06 x 10-3

Number of sample points

Sta

ndar

d de

viat

ion

of b

enze

ne c

once

ntra

tion

0 1000 2000 3000 4000 50001.72

1.74

1.76

1.78

1.8

1.82

1.84 x 10-3

Number of sample points

Sta

ndar

d de

viat

ion

of d

imen

sion

less

tem

pera

ture

Figure 2.7: Standard deviation of benzene concentration (left) and reactor temper-ature (right) as a function of sample size. +: MCS. : LHS. ?: LHHS.

38

Texas Tech University, Y. Chen, May 2012

0.04 0.05 0.06 0.07 0.08 0.090

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Dimensionless benzene concentration

Pro

babi

lity

1.02 1.04 1.06 1.08 1.1 1.120

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

Dimensionless temperature

Pro

babi

lity

Figure 2.8: Distribution of dimensionless benzene concentration and temperature.

39

Texas Tech University, Y. Chen, May 2012

Nomenclature

CDF cumulative distribution function

HDA hydro-dealkylation

LHHS Latin hypercube Hammersley sampling

LHS Latin hypercube sampling

MCS Monte Carlo sampling

PDE partial differential equation

C correlation matrix H matrix of Hammersley pointsH∗ rank matrx K integer

N number of sample points Pr probability value

X random variables Y random variablesd dimension of uncertain variables ru uniformly distributed random valueφp function of Hammersley points N normal distributionU uniform distribution

40

Texas Tech University, Y. Chen, May 2012

Chapter 3

Real-time State Prediction

Chapter 3 investigates real-time state prediction as a function of the set of un-

certain parameters using partial least squares regression (PLS) and the Karhunen-

Loeve (KL) expansion. These concepts are demonstrated using the HDA process

that was introduced in Chapter 2.

As stated previously, a first-principles model that describes the behavior of a

process is a system of nonlinear partial differential equations (PDEs) in which the

variables are function of space and time. Solving such systems is time consuming

and the solutions are an infinite series that cannot be used readily for real-time

applications such as real-time state prediction. However, if there are data that carry

the relationships between the process state variables and the uncertain parameters,

then a technique such as partial least squares (PLS) regression may be suitable to

capture these relationships in a less computationally-burdensome regression-type

model to enable real-time prediction.

3.1 PLS Regression

In order to consider the effects of uncertain parameters on the state variables, it

is necessary to determine the relationships between the uncertain parameters and the

41

Texas Tech University, Y. Chen, May 2012

data set of solutions generated from the first-principles model. Partial least squares

(PLS) regression is an often used method to determine the relationships between

the prediction variables and response variables.

The following is excerpted from [62]. Let XN×I be a matrix of I predictors

collected on N observations that describe J response variables, Y N×J. Decompose

both X and Y as a product of a set of orthogonal factors (T ) and a set of loadings

(P ),

X = TP ′ +E

Y = TBC′ + F

(3.1)

The columns of T are the latent vectors, P is the coefficient matrix of X , the

diagonal elements ofB are the regression weights,C represents the weights of the

response variables, and E and F are the matrices of residual errors.

To specify the latent vectors in T , two sets of weights w and c are needed to

create a linear combination of the columns of X and Y such that their covariance

is maximized. The goal is to obtain a pair of vectors t = Xw and u = Y c with

constraints such that w′w = 1, t′t = 1. It then follows that p =X ′t.

Procedurally, let Q = X and R = Y . Then column center and normalize R

andQ.

Step 1: Initialize the vector u with random values

Step 2: Estimate weights forX , w ∝ Q′u

42

Texas Tech University, Y. Chen, May 2012

Step 3: EstimateX factor scores, t1 = Qw1

Step 4: Estimate weights for Y , c1 ∝ R′t1

Step 5: Estimate Y scores, u1 = Rc1

Step 6: Return to step 2 if t1 has not converged. Otherwise continue.

Step 7: Calculate b = t′1u1

Step 8: Compute the loadings forX: p1 = Q′T .

Step 9: Subtract the effect of t1 from both Q and R: Q = Q − t1p′1 and R =

F − bt1c′1. b is a diagonal element ofB.

Step 10: Repeat from step 1 until the matrixQ becomes null.

The symbol ∝ represents a normalization of the result. The above relations

show thatw1 is the first right singular vector ofX ′Y and c1 is the first left singular

vector of X ′Y . Similarly, t1 and u1 are the first eigenvectors of XX ′Y Y ′ and

Y Y ′XX ′, respectively [62].

The prediction of the dependent variables is based on a multivariate regression

given by,

Y = TBC′ =XBPLS (3.2)

whereBPLS = (P ′)−1BC′.

43

Texas Tech University, Y. Chen, May 2012

3.2 KL Expansion

In some chemical processes such as a reactor, the states, for example, temper-

ature, concentration and so forth are functions of time and space whose data sets

have a larger dimension than the dimension of the uncertain parameters. To make

the PLS model feasible initial pre-processing of the data with a method such as

Karhunen-Loeve (KL) expansion is necessary, since the KL method can reduce the

dimension of the state data sets.

The basic concept behind the KL expansion is to find those modes that repre-

sent the dominant character of the system such that the basis set corresponding to

these modes comprise what is called the empirical eigenfunctions (EEFs) of the

system. The number of EEFs is usually small, which brings about a dimensionality

reduction without a loss in the complexity that is inherent to distributed parameter

systems [63].

Consider Equations (3.3) and (3.4) that represent the state and measured out-

puts, respectively of a simple one-dimensional (1D) PDE that can be used to repre-

sent a variety of nonlinear phenomena. Here, z is the spatial variable defined on a

closed and compact domain Ω, t is time, y(z, t) are the outputs, x(z, t) are the state

44

Texas Tech University, Y. Chen, May 2012

variables, and u(z, t) are distributed forcing functions.

∂x(z, t)∂t

= Ax(z, t) + u(z, t) (3.3)

y(z, t) = C(z)x(z, t) z ∈ Ω, t ≥ 0 (3.4)

A = α∂2

∂z2 − υ∂

∂z+ b α, ν > 0

Equation (3.3) usually is solved numerically. The solution, y(z, t), is the data from

which to develop the KL expansion. When t is fixed, the data points at this time are

said to represent a snapshot of the state of the process.

Let y(z, t) denote the mean of the y and v(z, t) = y(z, t)− y(z, t). The covariance

function of these data can be obtained from

R(z, ζ) = limM→∞

1M

∫ M

0,Ωv(z, t)v(ζ, t) dt z, ζ ∈ Ω (3.5)

For D snapshots, the empirical spatial correlation function is given by [64],

R(z, ζ) =1D

D∑k=1

vk(z)vk(ζ) (3.6)

where k is the time sequence number. The eigenvalue, λk ∈ Λ, and corresponding

eigenfunction, ψk ∈ Ψ, of the covariance matrix can be found. The KL expansion

45

Texas Tech University, Y. Chen, May 2012

of the system defined in Equation (3.3) is given by,

y(z, t) = y(z, t) +∞∑

k=1

√λk ψk(z)ςk(t) (3.7)

where ςk are the projections of y onto ψk. It has been shown that a small number

of EEFs can capture more than 95% of the system’s energy [65] in many instances

indicting a high degree of correlation among the data or a small number of degrees

of freedom in the data [60].

3.3 State Prediction with ROM

In this work, PLS regression is applied to determine the relationships between

the uncertain parameters and the state data sets obtained from the first-principles

model. The dimension of the state data sets is reduced using a KL expansion to

build a reduced-order model (ROM). Since Latin hypercube Hammersley sequence

(LHHS) has good multiple-dimensional uniformity property, it is used to sample

the set of uncertain parameter distributions. The sample sequences are propagated

through the first-principles model. By averaging the resulting state data sets, the

dominant empirical eigenfunctions (EEFs) of the averaged data matrix can be de-

termined. The EEFs serve as the basis for propagation of the state data. Usually a

small number of EEFs can capture the dominant characteristics of the data. With

a small number of dominant EEFs, the corresponding coefficients also is small.

46

Texas Tech University, Y. Chen, May 2012

These coefficients are the response variables for PLS regression. With the sampled

sets of uncertain parameters as predictors, the relationships between the uncertain

parameters and the coefficients of the corresponding propagated data matrices can

be determined with PLS regression to identify a predictive model. Then, given any

set of uncertain parameters, the ROM coefficients can be calculated from the iden-

tified PLS model. It then follows that the ROM’s outputs which are the states can

be predicted directly by projection of the coefficients onto the EEFs. Thus, with

the combination of PLS regression and KL expansion execution of the complex,

nonlinear first-principles model is avoided. To summarize, the procedural steps are

as follows.

• Step 1: Sample multiple uncertain parameters with LHHS technique.

• Step 2: Propagate samples of uncertain parameters (sampled in Step 1) through

first-principles model. Solve models with samples of uncertain parameters to

obtain the corresponding model outputs.

• Step 3: Average the model outputs and use KL expansion to reduce the di-

mension of averaged matrix to determine its dominant EEFs.

• Step 4: Calculate the corresponding coefficients of all the model outputs ob-

tained in step 2 based on the EEFs calculated in step 3.

• Step 5: Determine the relationships between the samples of uncertain param-

47

Texas Tech University, Y. Chen, May 2012

eters (sampled in Step 1) and the corresponding coefficients of model outputs

(calculated in Step 4) to build a PLS model.

• Step 6: Predict the process states from known values of the parameters with

the PLS model obtained in step 5.

3.3.1 State Prediction of HDA Process

The HDA process that was introduced in Chapter 2 will be used to demonstrate

state prediction using a ROM generated from the combination of PLS regression

and KL expansion. The uncertain parameters are the rate constant of reaction 1

(κ1), the fresh benzene injection rate (FBm) and the heat of reaction 1 (Hr1). The