ALFN TE@CH Regional Training Seminar September 9, 2015 ...

489

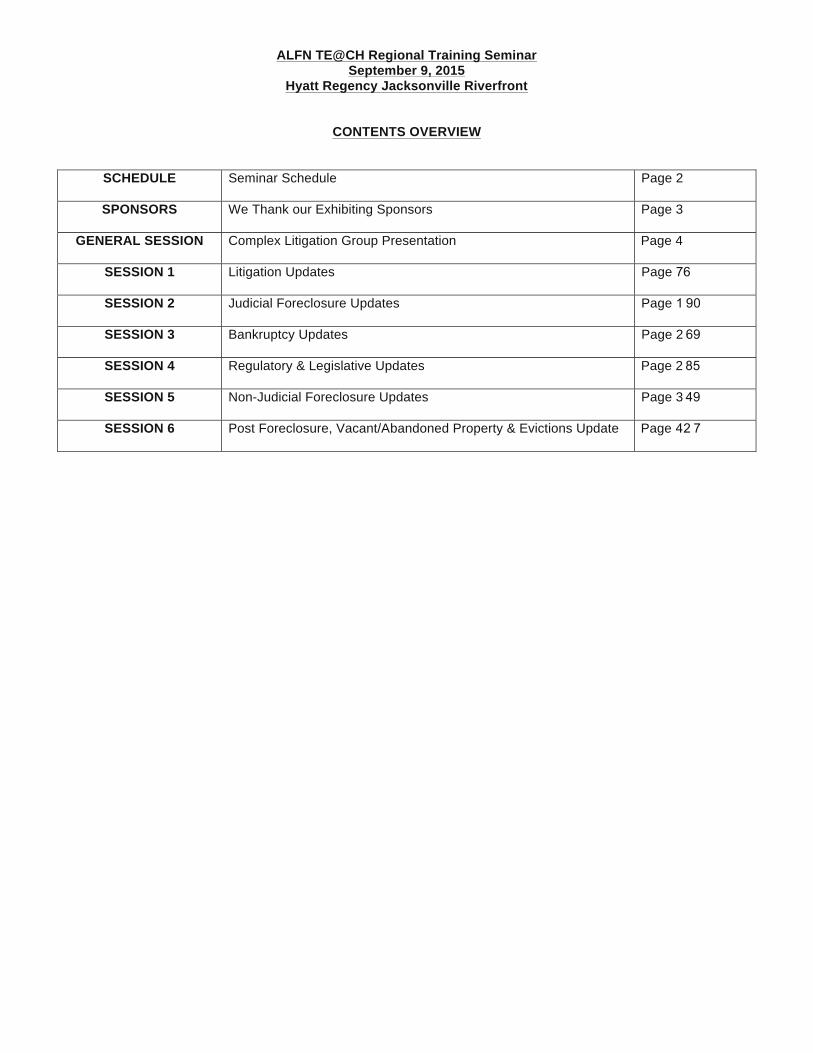

ALFN TE@CH Regional Training Seminar September 9, 2015 Hyatt Regency Jacksonville Riverfront CONTENTS OVERVIEW SCHEDULE Seminar Schedule Page 2 SPONSORS We Thank our Exhibiting Sponsors Page 3 GENERAL SESSION Complex Litigation Group Presentation Page 4 SESSION 1 Litigation Updates Page SESSION 2 Judicial Foreclosure Updates Page SESSION 3 Bankruptcy Updates Page 2 SESSION 4 Regulatory & Legislative Updates Page 2 SESSION 5 Non-Judicial Foreclosure Updates Page 3 SESSION 6 Post Foreclosure, Vacant/Abandoned Property & Evictions Update Page

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of ALFN TE@CH Regional Training Seminar September 9, 2015 ...

ALFN TE@CH Regional Training Seminar September 9, 2015

Hyatt Regency Jacksonville Riverfront

CONTENTS OVERVIEW

SCHEDULE Seminar Schedule Page 2

SPONSORS We Thank our Exhibiting Sponsors Page 3

GENERAL SESSION Complex Litigation Group Presentation Page 4

SESSION 1 Litigation Updates Page

SESSION 2 Judicial Foreclosure Updates Page

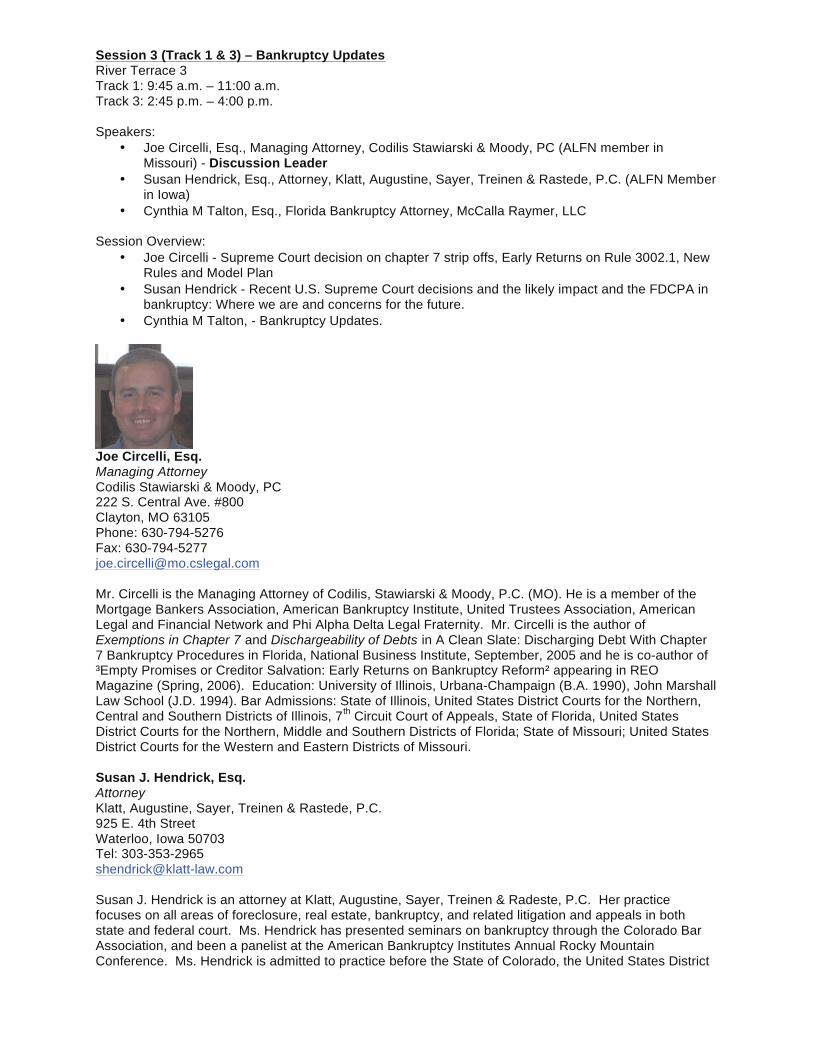

SESSION 3 Bankruptcy Updates Page 2

SESSION 4 Regulatory & Legislative Updates Page 2

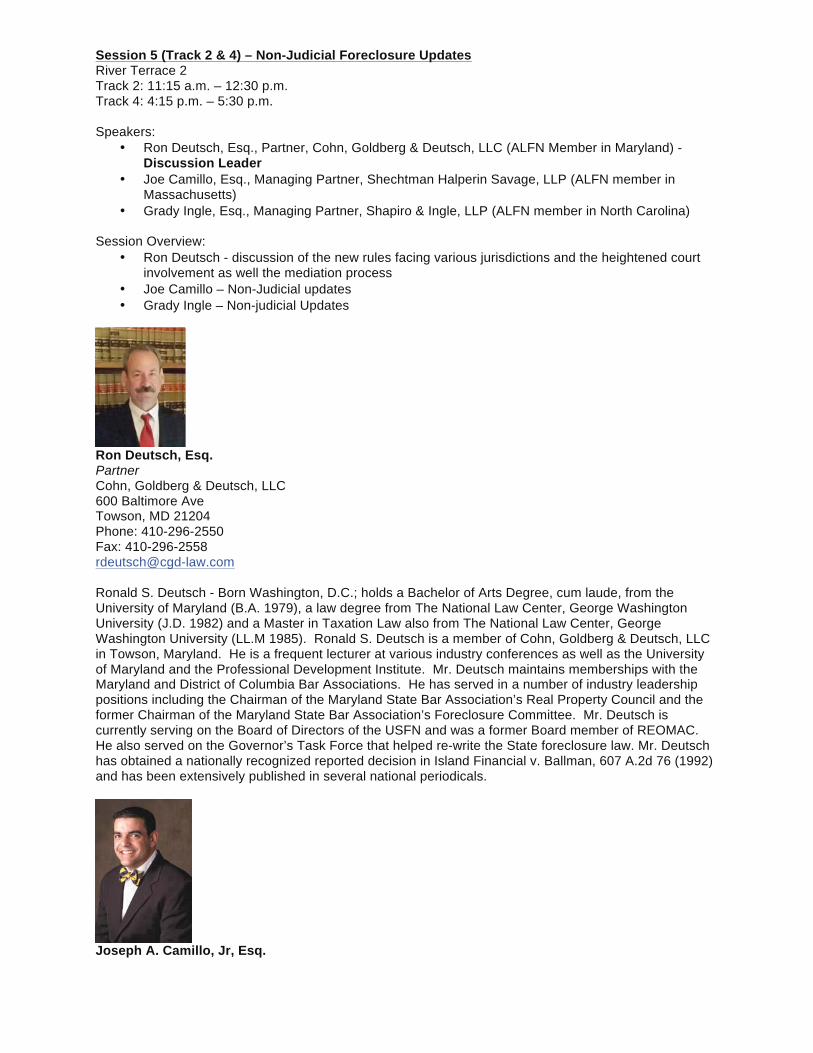

SESSION 5 Non-Judicial Foreclosure Updates Page 3

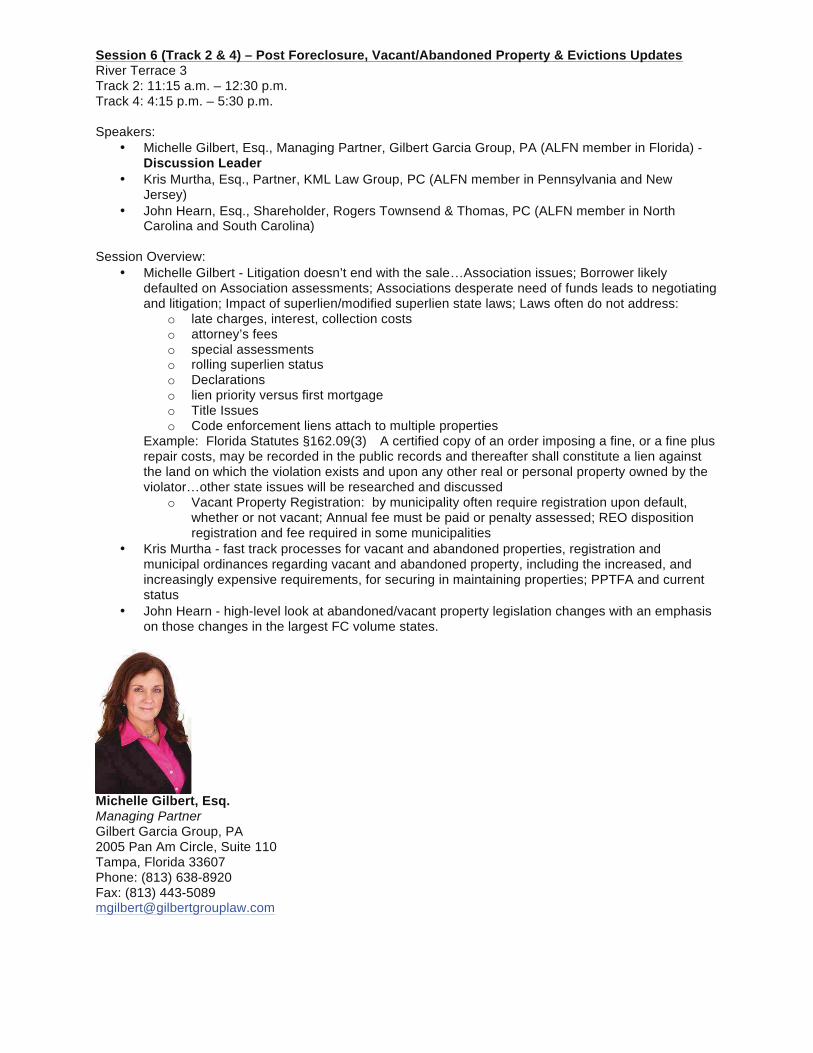

SESSION 6 Post Foreclosure, Vacant/Abandoned Property & Evictions Update Page

ALFN TE@CH Onsite Regional Training Seminar Schedule

6:30 a.m. – Staff & Exhibitor Arrivals & Setup

8:00 a.m. – 8:30 a.m. – Attendee Arrivals and Networking with Exhibiting Sponsors

7:30 a.m. – 5:00 p.m. – Registration Open (Skybridge – 3rd floor)

8:30 a.m. – 9:30 a.m. – General Session – Complex Litigation Group Presentation (River Terrace 1)

9:30 a.m. – 9:45 a.m. - Refreshment Break with Exhibiting Sponsors

9:45 a.m. – 11:00 a.m. - Track One• Session 1 – Litigation Updates (Conference Center B)• Session 2 – Judicial Foreclosure Updates (River Terrace 2)• Session 3 – Bankruptcy Updates (River Terrace 3)

11:00 a.m. – 11:15 a.m. – Refreshment Break with Exhibiting Sponsors

11:15 a.m. – 12:30 p.m. – Track Two• Session 4 – Regulatory & Legislative Updates (Conference Center B)• Session 5 – Non-Judicial Foreclosure Updates (River Terrace 2)• Session 6 – Post Foreclosure, Vacant/Abandoned Property & Evictions Updates (River Terrace

3)

12:30 p.m. – 1:30 p.m. – Lunch Provided & Networking with Speakers, Attendees & Exhibiting Sponsors (River Terrace 1)

1:30 p.m. – 2:30 p.m. – General Session – Complex Litigation Group Presentation (River Terrace 1)

2:30 p.m. – 2:45 p.m. - Refreshment Break with Exhibiting Sponsors

2:45 p.m. – 4:00 p.m. – Track Three – Repeat of Track One• Session 1 – Litigation Updates (Conference Center B)• Session 2 – Judicial Foreclosure Updates (River Terrace 2)• Session 3 – Bankruptcy Updates (River Terrace 3)

4:00 p.m. - 4:15 p.m. – Refreshment Break with Exhibiting Sponsors

4:15 p.m. – 5:30 p.m. – Track Four – Repeat of Track Two• Session 4 – Regulatory & Legislative Updates (Conference Center B)• Session 5 – Non-Judicial Foreclosure Updates (River Terrace 2)• Session 6 – Post Foreclosure, Vacant/Abandoned Property & Evictions Updates (River Terrace

3)

5:30 p.m. – Training Seminar Concludes

5:30 p.m. – 6:30 p.m. – Cocktail Reception at host hotel (River Terrace 1)

Other Details:

Lunch will be provided. Cocktail reception with hors d’oeuvres and drinks provided. Refreshments, snacks, mints, notepads and pens will be provided to all seminar attendees throughout seminar. Noprinted materials will be provided, as all session materials will be emailed to all registered attendees prior to the seminar.

We Thank our SponsorsPlease take a moment to visit with our sponsors during the breaks in our session schedule at 9:30-

9:45am, 11:00-11:15 am, 12:30- 1:30 pm, & 2:30-2:45pm and 4:00-4:15pm or during the Networking Reception 5:30-6:30 p.m.

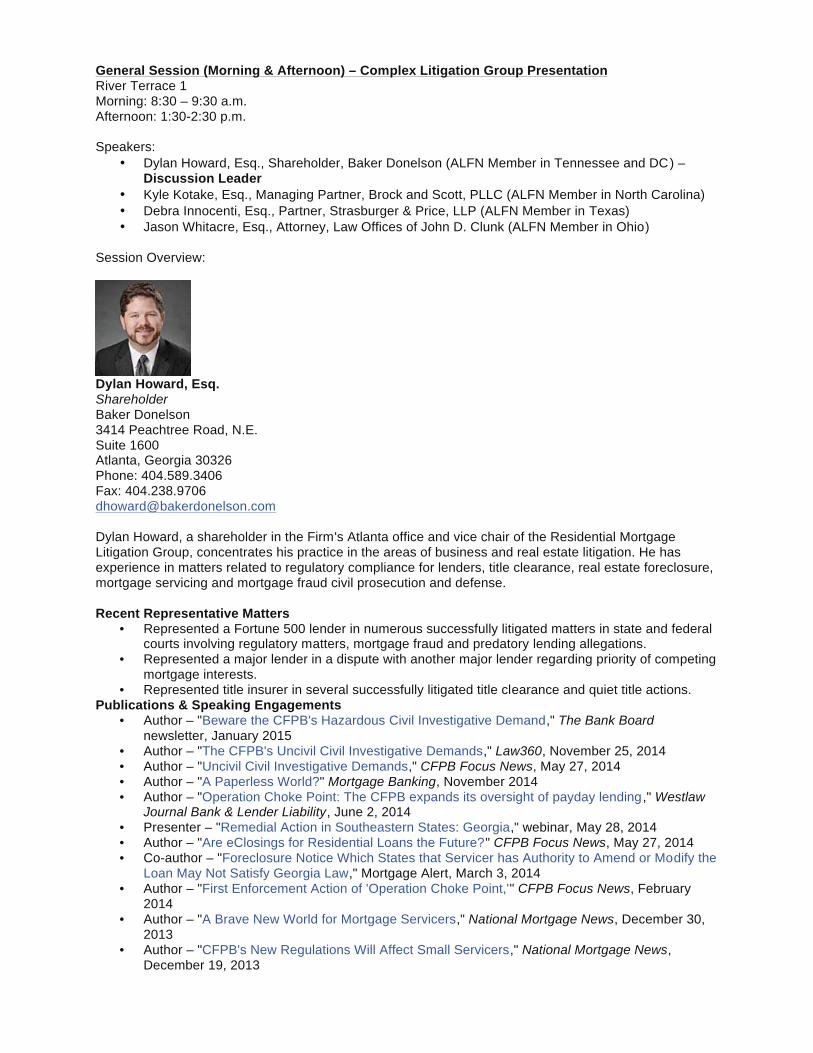

General Session (Morning & Afternoon) – Complex Litigation Group PresentationRiver Terrace 1 Morning: 8:30 – 9:30 a.m. Afternoon: 1:30-2:30 p.m.

Speakers:• Dylan Howard, Esq., Shareholder, Baker Donelson (ALFN Member in Tennessee and DC) –

Discussion Leader• Kyle Kotake, Esq., Managing Partner, Brock and Scott, PLLC (ALFN Member in North Carolina)• Debra Innocenti, Esq., Partner, Strasburger & Price, LLP (ALFN Member in Texas)• Jason Whitacre, Esq., Attorney, Law Offices of John D. Clunk (ALFN Member in Ohio)

Session Overview:

Dylan Howard, Esq.ShareholderBaker Donelson 3414 Peachtree Road, N.E. Suite 1600 Atlanta, Georgia 30326 Phone: 404.589.3406 Fax: 404.238.9706 [email protected]

Dylan Howard, a shareholder in the Firm's Atlanta office and vice chair of the Residential Mortgage Litigation Group, concentrates his practice in the areas of business and real estate litigation. He has experience in matters related to regulatory compliance for lenders, title clearance, real estate foreclosure, mortgage servicing and mortgage fraud civil prosecution and defense.

Recent Representative Matters • Represented a Fortune 500 lender in numerous successfully litigated matters in state and federal

courts involving regulatory matters, mortgage fraud and predatory lending allegations.• Represented a major lender in a dispute with another major lender regarding priority of competing

mortgage interests.• Represented title insurer in several successfully litigated title clearance and quiet title actions.

Publications & Speaking Engagements • Author – "Beware the CFPB's Hazardous Civil Investigative Demand," The Bank Board

newsletter, January 2015• Author – "The CFPB's Uncivil Civil Investigative Demands," Law360, November 25, 2014• Author – "Uncivil Civil Investigative Demands," CFPB Focus News, May 27, 2014• Author – "A Paperless World?" Mortgage Banking, November 2014• Author – "Operation Choke Point: The CFPB expands its oversight of payday lending ," Westlaw

Journal Bank & Lender Liability, June 2, 2014• Presenter – "Remedial Action in Southeastern States: Georgia," webinar, May 28, 2014• Author – "Are eClosings for Residential Loans the Future?" CFPB Focus News, May 27, 2014• Co-author – "Foreclosure Notice Which States that Servicer has Authority to Amend or Modify the

Loan May Not Satisfy Georgia Law," Mortgage Alert, March 3, 2014• Author – "First Enforcement Action of 'Operation Choke Point,'" CFPB Focus News, February

2014• Author – "A Brave New World for Mortgage Servicers," National Mortgage News, December 30,

2013• Author – "CFPB's New Regulations Will Affect Small Servicers," National Mortgage News,

December 19, 2013

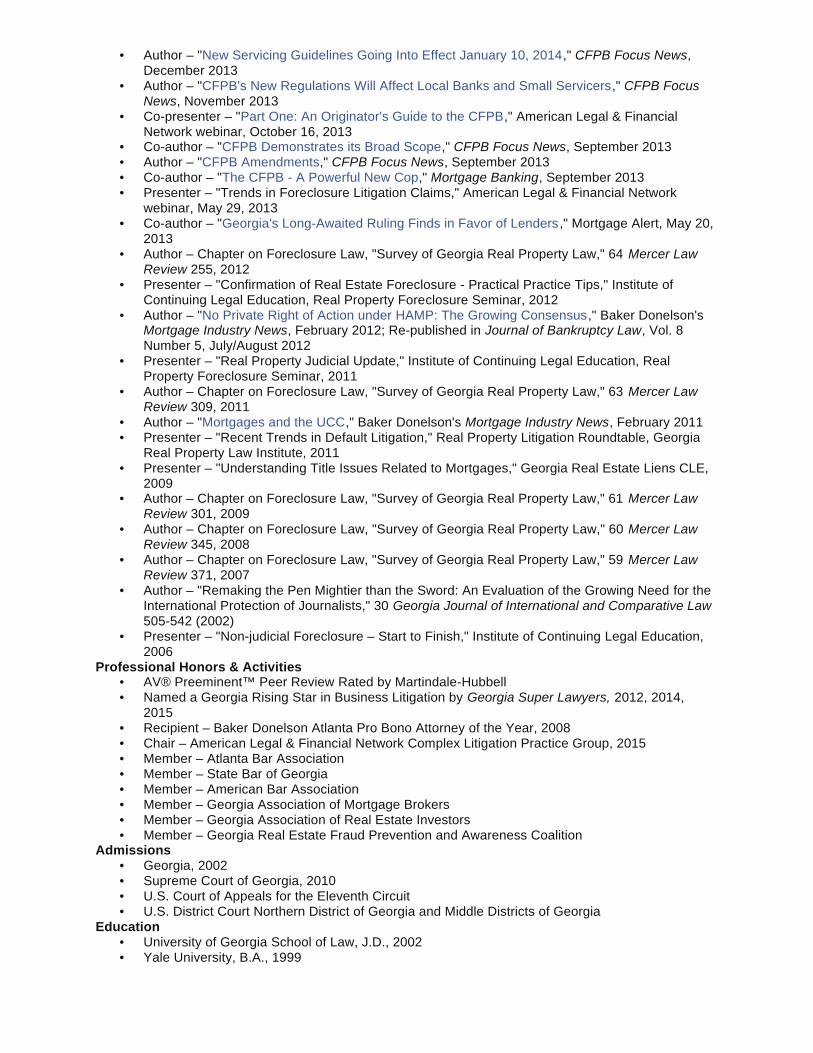

• Author – "New Servicing Guidelines Going Into Effect January 10, 2014," CFPB Focus News,December 2013

• Author – "CFPB's New Regulations Will Affect Local Banks and Small Servicers," CFPB FocusNews, November 2013

• Co-presenter – "Part One: An Originator's Guide to the CFPB," American Legal & FinancialNetwork webinar, October 16, 2013

• Co-author – "CFPB Demonstrates its Broad Scope," CFPB Focus News, September 2013• Author – "CFPB Amendments," CFPB Focus News, September 2013• Co-author – "The CFPB - A Powerful New Cop," Mortgage Banking, September 2013• Presenter – "Trends in Foreclosure Litigation Claims," American Legal & Financial Network

webinar, May 29, 2013• Co-author – "Georgia's Long-Awaited Ruling Finds in Favor of Lenders ," Mortgage Alert, May 20,

2013• Author – Chapter on Foreclosure Law, "Survey of Georgia Real Property Law," 64 Mercer Law

Review 255, 2012• Presenter – "Confirmation of Real Estate Foreclosure - Practical Practice Tips," Institute of

Continuing Legal Education, Real Property Foreclosure Seminar, 2012• Author – "No Private Right of Action under HAMP: The Growing Consensus," Baker Donelson's

Mortgage Industry News, February 2012; Re-published in Journal of Bankruptcy Law, Vol. 8Number 5, July/August 2012

• Presenter – "Real Property Judicial Update," Institute of Continuing Legal Education, RealProperty Foreclosure Seminar, 2011

• Author – Chapter on Foreclosure Law, "Survey of Georgia Real Property Law," 63 Mercer LawReview 309, 2011

• Author – "Mortgages and the UCC," Baker Donelson's Mortgage Industry News, February 2011• Presenter – "Recent Trends in Default Litigation," Real Property Litigation Roundtable, Georgia

Real Property Law Institute, 2011• Presenter – "Understanding Title Issues Related to Mortgages," Georgia Real Estate Liens CLE,

2009• Author – Chapter on Foreclosure Law, "Survey of Georgia Real Property Law," 61 Mercer Law

Review 301, 2009• Author – Chapter on Foreclosure Law, "Survey of Georgia Real Property Law," 60 Mercer Law

Review 345, 2008• Author – Chapter on Foreclosure Law, "Survey of Georgia Real Property Law," 59 Mercer Law

Review 371, 2007• Author – "Remaking the Pen Mightier than the Sword: An Evaluation of the Growing Need for the

International Protection of Journalists," 30 Georgia Journal of International and Comparative Law505-542 (2002)

• Presenter – "Non-judicial Foreclosure – Start to Finish," Institute of Continuing Legal Education,2006

Professional Honors & Activities • AV® Preeminent™ Peer Review Rated by Martindale-Hubbell• Named a Georgia Rising Star in Business Litigation by Georgia Super Lawyers, 2012, 2014,

2015• Recipient – Baker Donelson Atlanta Pro Bono Attorney of the Year, 2008• Chair – American Legal & Financial Network Complex Litigation Practice Group, 2015• Member – Atlanta Bar Association• Member – State Bar of Georgia• Member – American Bar Association• Member – Georgia Association of Mortgage Brokers• Member – Georgia Association of Real Estate Investors• Member – Georgia Real Estate Fraud Prevention and Awareness Coalition

Admissions• Georgia, 2002• Supreme Court of Georgia, 2010• U.S. Court of Appeals for the Eleventh Circuit• U.S. District Court Northern District of Georgia and Middle Districts of Georgia

Education• University of Georgia School of Law, J.D., 2002• Yale University, B.A., 1999

Kyle Kotake, Esq.Managing Partner Brock and Scott, PLLC 4360 Chamblee Dunwoody Road Ste 310 Atlanta, GA 30341 Phone: 404-789-2661 Fax: 404-294-0919 [email protected]

Kyle Kotake joined Brock & Scott, PLLC in October 2012 as Managing Partner of Evictions and Litigation in the Georgia office. Mr. Kotake is a litigator who practices in the areas of mortgage default litigation and eviction. He regularly represents lenders in both state and federal court.

Before joining Brock & Scott, Mr. Kotake spent 11 years in the Atlanta office of Johnson & Freedman, rising to partner responsible for complex litigation matters, where he gained extensive experience of Georgia foreclosure practice as well as handling numerous cases involving such matters as wrongful foreclosure, wrongful eviction, FDCPA violations, RESPA violations, asset forfeitures, code violations, tax sales, title reformation, declaratory judgments and quiet title actions. Throughout his time with the firm he also regularly appeared in the several bankruptcy courts in Georgia, in particular handling adverse matters and contested bankruptcy cases. For several years, Mr. Kotake managed a multi-state eviction practice, overseeing 19 other law firms and their handling of individual eviction cases.

He routinely speaks and provides training on the subjects of eviction and litigation. He was admitted into practice in the states of Georgia and Hawaii in 1999 and 1997, respectively.

ADMITTED TO PRACTICE • 1999 - Georgia Bar • 1997 - Hawaii Bar

EDUCATION • 1995 - Juris Doctor from Syracuse University. • 1992 - Bachelor of Business Administration from the University of Oklahoma.

AFFILIATIONS• American Legal & Financial Network - Co-Chair, Complex Litigation Committee • American Legal & Financial Network - Member, Default Services Practice Group

Debra L. Innocenti, Esq. PartnerStrasburger & Price, LLP 2301 Broadway Street San Antonio, TX 78215 Phone: 210.250.6127 Fax: 210.258.2734 [email protected]

Debra Innocenti maintains a diverse practice in specialty litigation and transactional law for financial services,technology, and Internet-related industries. In connection with her financial services practice, she assists investors, master servicers, special servicers, and sub-servicers in all real estate and litigation-related matters including issues related to MERS, common owner associations, mortgage-backed security trusts, title insurance, consumer protection law claims, and foreclosure matters.

In connection with her technology and Internet law practice, she assists startups, business owners, web developers, entrepreneurs, and artists with protecting and resolving disputes regarding their intellectual property, developing data security and data privacy policies and social media use policies, licensing software, and resolving online business defamation and cyber harassment. She is a member of Geekdom, and was an instructor in the English-Communications department at St. Mary’s University from 1997-2001.

PROFESSIONAL AFFILIATIONS • Admitted, Texas • Admitted, U.S. District Courts for Northern, Eastern, Western, and Southern Districts of Texas • Admitted, Supreme Court of The United States• American Bar Association – Science & Technology Law Section: Social Media Committee, Open • Source Software Committee, Cloud Computing Committees

o Litigation Section: former Chair, Membership Subcommittee, Bankruptcy and Insolvency Committee (2011); former Co-Chair, Appeals Subcommittee, Bankruptcy and Insolvency Committee (2010); former Co-Chair, Bankruptcy Litigation Subcommittee, Business & Commercial Litigation Committee (2008-2009)

• San Antonio Bar Association • State Board of Texas – Computer & Technology Section, Bankruptcy Section

o former member, Young Lawyers Committee (2008-2010); former Law School Liaison (2010)

• American Bankruptcy Institute o former Newsletter Editor, Mass Tort Committee (2009); former Editor, Fifth Circuit Update

(2009)• Greater San Antonio Chamber of Commerce

o former member, Board of Directors (2005-2007); former Council Chair, Area Business Councils (2007)

EDUCATION • The University of Texas School of Law, J.D., 2004, cum laude

o George Pierre Gardere Endowed Scholar o Phi Delta Phi, Legal Honors Society o American Journal of Criminal Law, Editor-in-Chief

• Sarah Lawrence College, M.F.A., 1995 • Our Lady of the Lake University, B.A.,1993, summa cum laude

EXPERIENCE Financial Services and Debtor/Creditor Law

• Litigation oversight and strategy in real estate and foreclosure matters;

• Investor, master servicer, special servicer and sub-Servicer representation in all real estate and foreclosure related disputes including, without limitation, issues related to MERS, common owner associations , title insurance and consumer protection law claims;

• Representation of clients in a diverse range of bankruptcy-related litigation, including avoidance actions, modifications of the automatic stay, claims estimation and allowance, discharge and dischargeability determinations, and executory contract disputes; and

• Representation of future claim representative (“FCR”) in chapter 11 bankruptcy of diversified mining firm subsidiary involved in the mining, processing and sale of raw asbestos and asbestos products.

Internet and Technology Law• Terms of use, terms of sale, and privacy policies for websites; • Software license agreements for startup software-as-a-service developers; Dispute resolution of

copyright infringement claims related to social media; • Creative clearance, including review of websites and social media for infringement issues;

Domain name/trademark searches and registration; • Cease and desist letters and take-down disputes; • Website development agreements to protect intellectual property ownership; and • Intellectual property license agreements.

PUBLICATIONS • Disclosing Material Connections in 140 Characters or Less , Strasburger Intellectual Property

Law• Blog (April 2015) • Co-author. An Educated Response to Cyberbullying, Texas School Business Magazine (March • 2015) • FTC Creates Office Of Technology Research & Investigation , Strasburger Intellectual Property

Law• Blog (March 2015) • The Top Three Things You Should Do to Manage Cybersecurity Risks , Strasburger Intellectual• Property Law Blog (February 2015) • FTC Issues Report on Privacy and Data Security Recommendations for Internet of Things ,

Strasburger Intellectual Property Law Blog (January 2015) • Obtaining Identities of Anonymous Online Defamers Just Got Harder , Circuits: Fall Newsletter of

the• Computer & Technology Section of the State Bar of Texas (November 2014) • FDA Releases Guidance on Medical Device Cybersecurity , Strasburger Intellectual Property

Blog• (October 2014) • Obtaining Identities of Anonymous Online Defamers Just Got Harder, Strasburger Intellectual • Property Blog (September 2014) • Like It or Not: Facebook Prohibits Like-Gating and Other Incentives, Strasburger Intellectual • Property Blog (August 2014) • Think Before You Tweet: Avoiding Liability in 140 Characters or Less , Strasburger Intellectual• Property Blog (August 2014) • Five Questions to Ask Your Webmaster and Your Lawyer, Strasburger Intellectual Property

Blog• (June 2014) • Four Steps in Responding to that Bad Online Review, Strasburger Intellectual Property Blog

(March • 2014)

MEDIA MENTIONS • Measure to Criminalize ‘Revenge Porn’ Will be Problematic for Lawmakers 1200 WOAI (May

2015) Monthly Tech Meetup to Feature IP Legal Education , San Antonio Business Journal (March 2015)

• Guest Voices: The Top Three Things You Should Do to Manage Cybersecurity Risks , San Antonio

• Express-News. Subscription required. (February 2015)• SCOTUS Seen Unlikely to Grant New Protections to Online Speech , 1200 WOAI (December

2014)

• Obtaining IDs of Anonymous Cyberbullies Just Got Harder , San Antonio Express-News. Subscription required. (September 2014)

• Unmasking Online Bullies Just Got Harder in Texas, 1200 WOAI (September 2014) • Product Review Legal Threat Could Be Start of ‘Mainstreaming’ Internet Speech , 1200 WOAI

(May • 2014) • San Antonio Artist Sues Over Public Art in Alabama , San Antonio Express News (December

2013)COMMUNITY

• San Antonio Pets Alive! , Founding Board Member • Leadership San Antonio, Class XXXI, Steering Committee and Class III and Class XXXV

RECOGNITION • Named among the Best Attorneys in Banking and Information Technology by San Antonio Scene • Magazine (2015)• Named among Texas Rising Stars by Thomson and Reuters (2007-2013) • Named a Rising Star in San Antonio’s Legal Community by San Antonio Scene Magazine (2009,

2013)• Named among the Best Bankruptcy and Workout Attorneys by San Antonio Scene Magazine

(2010- 2012)• Named a Top Forty Under 40-San Antonio Rising Star by San Antonio Business Journal (2006)

Jason Whitacre, Esq., AttorneyLaw Offices of John D. Clunk

• Case Western Reserve Law School (J.D. 2003) • Mount Union College (B.A. 2000) • Licensed in the Ohio State and Federal Courts since 2004.

ALFN Southeast TE@CH On-site Regional Training SeminarThe TCPASeptember 9, 2015 Hyatt Regency Jacksonville Riverfront

Dylan Howard, Co-Chair, ALFN Complex Litigation CommitteeShareholderVice Chair, Consumer Financial Litigation and Compliance Practice Group Baker Donelson [email protected]

2www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

What is it?

3www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

What is it?

Statutory scheme enacted by Congress to:

4www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

What is it?

Statutory scheme enacted by Congress to:

1. Confuse companies that have, as part of their business, the communication with large numbers of customers, or consumers.

5www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Statutory scheme enacted by Congress to:

1. Confuse companies that have, as part of their business, the communication with large numbers of customers, or consumers.

2. Give litigious customers/consumers another method for gaining leverage over their banks and mortgage servicers.

6www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

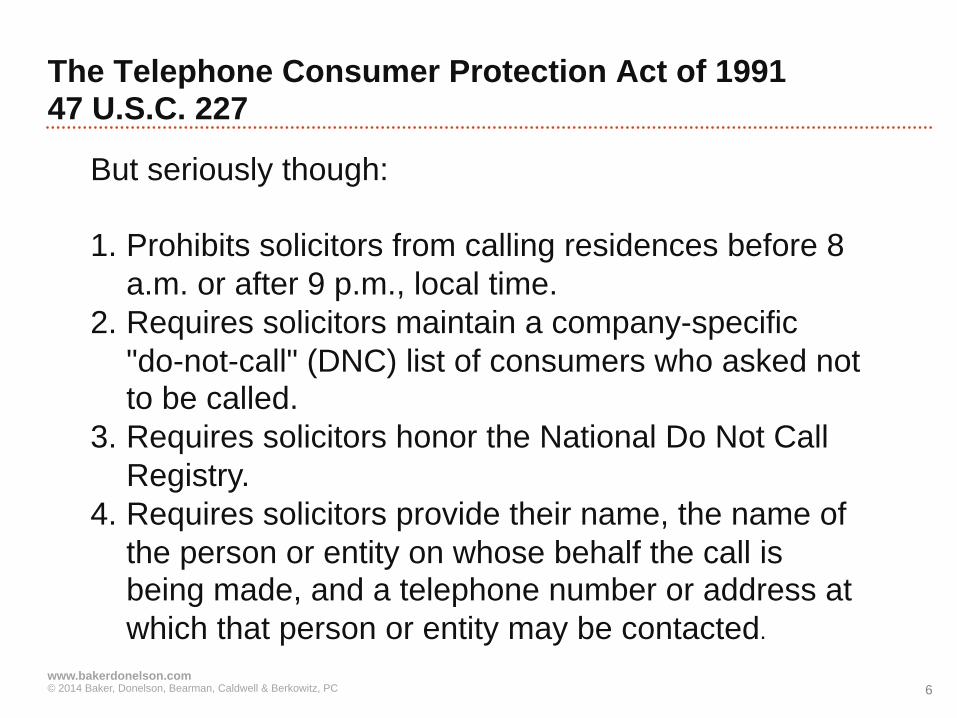

But seriously though:

1. Prohibits solicitors from calling residences before 8 a.m. or after 9 p.m., local time.

2. Requires solicitors maintain a company-specific "do-not-call" (DNC) list of consumers who asked not to be called.

3. Requires solicitors honor the National Do Not Call Registry.

4. Requires solicitors provide their name, the name of the person or entity on whose behalf the call is being made, and a telephone number or address at which that person or entity may be contacted.

7www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

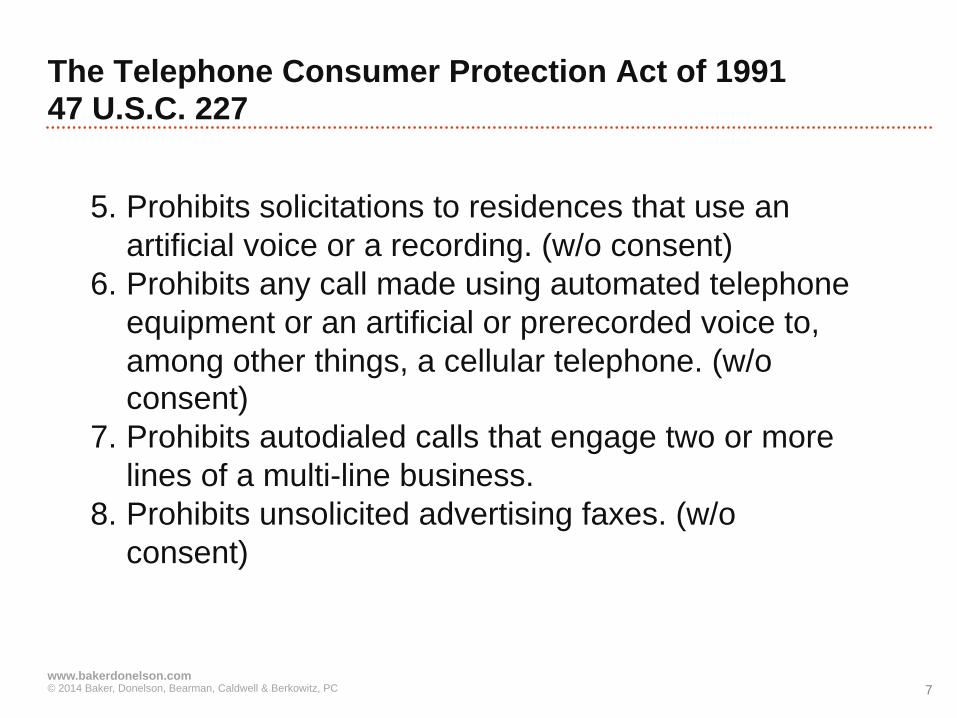

5. Prohibits solicitations to residences that use an artificial voice or a recording. (w/o consent)

6. Prohibits any call made using automated telephone equipment or an artificial or prerecorded voice to, among other things, a cellular telephone. (w/o consent)

7. Prohibits autodialed calls that engage two or more lines of a multi-line business.

8. Prohibits unsolicited advertising faxes. (w/o consent)

8www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Critical definition:

Automated telephone technology or auto dialer: dialing equipment that has the capacity to store or produce, and dial random or sequential numbers. Doesn’t matter if you are using that capability.

9www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Which companies are covered?

10www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Whichcompanies arearecovered?

YOURS!!!!

11 www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

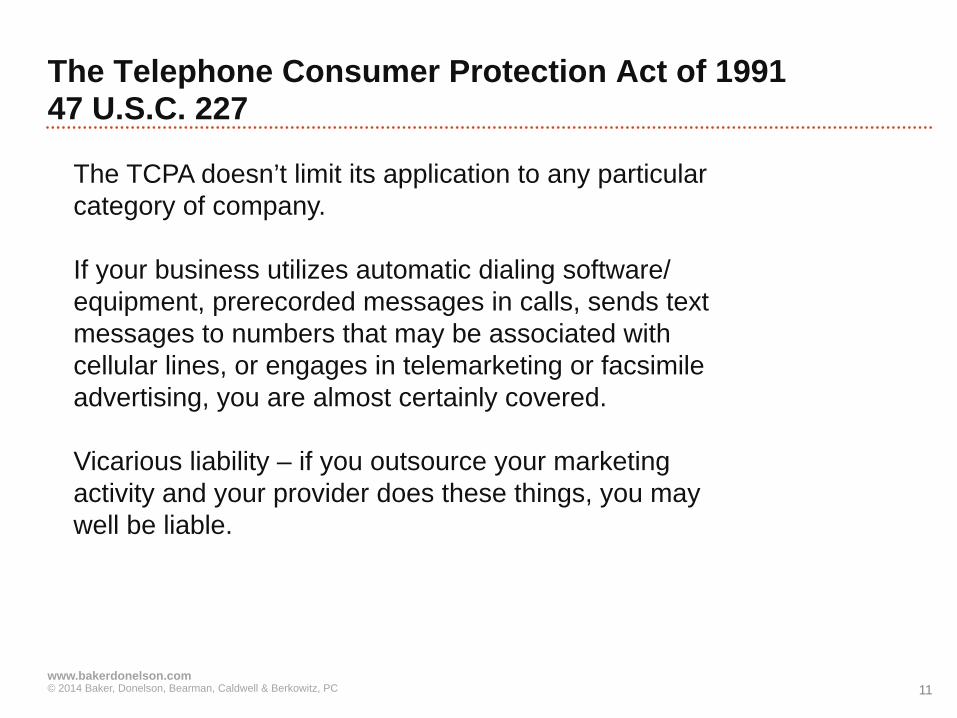

The TCPA doesn’t limit its application to any particular category of company.

If your business utilizes automatic dialing software/equipment, prerecorded messages in calls, sends text messages to numbers that may be associated with cellular lines, or engages in telemarketing or facsimile advertising, you are almost certainly covered.

Vicarious liability – if you outsource your marketing activity and your provider does these things, you may well be liable.

12www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

The TCPA and Litigation:

What’s the big deal?

13www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

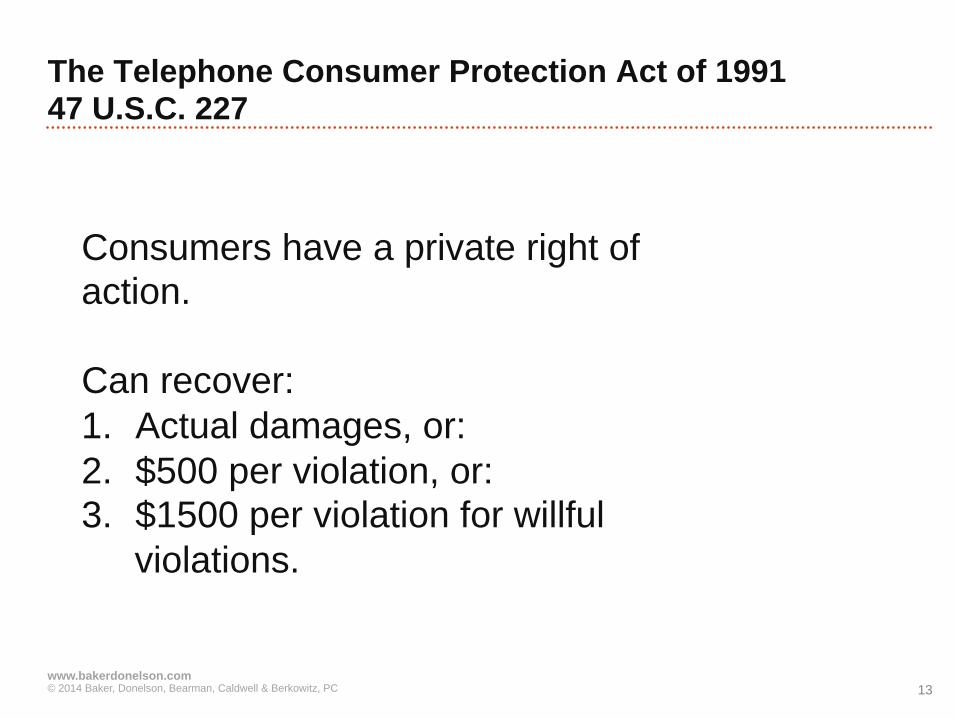

Consumers have a private right of action.

Can recover:1. Actual damages, or: 2. $500 per violation, or: 3. $1500 per violation for willful

violations.

14www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Not uncommon for consumers to allege several hundred phone calls. Damages can get substantial quickly!

15www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Even worse

16www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Class Actions!

17www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

In February, 2015, a Chicago Federal Court approved a TCPA class action settlement with Capital One Financial Corp. and its affiliates totaling $75.5 million.

18www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Pre-litigation Tips:

1. Verify whether your company engages in covered conduct.

19www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Pre-litigation Tips:

1. Verify whether your company engages in covered conduct.

2. Get familiar with prior express consent rules. Get a system in place to obtain and keep record of prior written consent.

20www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Pre-litigation Tips:

1. Verify whether your company engages in covered conduct.

2. Get familiar with prior express consent rules. Get a system in place to obtain and keep record of prior consent. Require written consent.

3. Require all 3rd party vendors to be in compliance with the TCPA.

21www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Pre-litigation Tips:

1. Verify whether your company engages in covered conduct.

2. Get familiar with prior express consent rules. Get a system in place to obtain and keep record of prior consent. Require written consent.

3. Require all 3rd party vendors to be in compliance with the TCPA.

4. Keep records of consent for at least four years.

22www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Pre-litigation Tips:

1. Verify whether your company engages in covered conduct.

2. Get familiar with prior express consent rules. Get a system in place to obtain and keep record of prior consent. Require written consent.

3. Require all 3rd party vendors to be in compliance with the TCPA.

4. Keep records of consent for at least four years.

5. Consistently work to verify that the telephone numbers you have for consumers remain accurate and that you know what kind of phone you are calling.

23www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Express Written Consent: Required for any communication involving “telemarketing”.

Telemarketing: a message that includes any form of advertising or otherwise encourages a consumer to purchase or use a service.

Non-telemarketing calls (purely informational) do not require written consent.

Danger: The lines are blurry

A consumer may revoke consent at any time by any reasonable means.

24www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Tips after the lawsuit is served:

25www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Tips after the lawsuit is served:

1. Hire experienced counsel.

26www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Tips after the lawsuit is served:

1. Hire experienced counsel.

2. Enter a litigation hold. Want any records about communications with the consumer preserved. Copies of consent documents and recordings of phone calls are the gold standard.

27www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Tips after the lawsuit is served:

1. Hire experienced counsel.

2. Enter a litigation hold. Want any records about communications with the consumer preserved. Copies of consent documents and recordings of phone calls are the gold standard.

3. Immediately investigate to determine scope of exposure.

28www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

Tips after the lawsuit is served:

1. Hire experienced counsel.

2. Enter a litigation hold. Want any records about communications with the consumer preserved. Copies of consent documents and recordings of phone calls are the gold standard.

3. Immediately investigate to determine scope of exposure.

4. If it’s a class action, you want your attorney to be diligent about attacking the eligibility of the case for class action status.

29www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

The Telephone Consumer Protection Act of 1991 47 U.S.C. 227

These rules are very much evolving.

On July 10, 2015, the FCC issued a 138 page declaratory ruling providing guidance.

More guidance is no doubt on the way!

30www.bakerdonelson.com © 2014 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Questions?

Please Contact:

Dylan Howard, ShareholderBaker Donelson [email protected]

Professional Limited Liability Company

o 24 CFR 203.604 • (b) The mortgagee must have a face-to-face interview with the

mortgagor, or make a reasonable effort to arrange such a meeting, before three full monthly installments due on the mortgage are unpaid. If default occurs in a repayment plan arranged other than during a personal interview, the mortgagee must have a face-to-face meeting with the mortgagor, or make a reasonable attempt to arrange such a meeting within 30 days after such default and at least 30 days before foreclosure is commenced, or at least 30 days before assignment is requested if the mortgage is insured on Hawaiian home land pursuant to section 247 or Indian land pursuant to section 248 or if assignment is requested under § 203.350(d) for mortgages authorized by section 203(q) of the National Housing Act.

HUD Regulations Face-to-Face Interview

o 24 CFR 203.604 • (c) A face-to-face meeting is not required if:

o (1) The mortgagor does not reside in the mortgaged property, o (2) The mortgaged property is not within 200 miles of the

mortgagee, its servicer, or a branch office of either, o (3) The mortgagor has clearly indicated that he will not

cooperate in the interview, o (4) A repayment plan consistent with the mortgagor's

circumstances is entered into to bring the mortgagor's account current thus making a meeting unnecessary, and payments thereunder are current, or

o (5) A reasonable effort to arrange a meeting is unsuccessful.

HUD Regulations Face-to-Face - Exceptions

• Most courts recognize that a violation of the HUD requirements can serve as a shield to a foreclosure action. See BAC Home Loans v. Taylor, 986 NE2d 1028. See also, Wells Fargo Bank, N.A. v. Gerst, 5th Dist. No. 13 CAE 05 0042, 2014-Ohio-80; Wells Fargo Bank, N.A. v. Aey, 7th Dist. No. 12 MA 178, 2013-Ohio-5381.

• However, there are a split of cases on whether violation of the HUD regulations may sustain a breach of contract claim. See Christenson v. CitiMortgage 2013 WL 5291947. But compare with Donlon v. Evolve Bank and Trust, 2014 WL 1330522.

• Jackson v. BANA, 2014 WL 5511017 is interesting because it states that even if the express incorporation of the HUD regulations into the Deed of Trust (usually in paragraph 9 of the standard form) creates a breach of contract claim, the claim was invalid (under MS law) because the borrower breached the contract first by failing to pay.

HUD Regulations Face-to-Face – Case Law

• Claim not properly preserved in pleadings

• Other defenses override claim

o Failure to Tender Amount Due

o Res Judicata

o Prior Breach

HUD Regulations Face-to-Face - Strategy

o Substantial Compliance • A common defense utilized by defense counsel in Florida – the

default letter failed to comply with the requirements of the mortgage. This defense had gained traction in Florida, especially in Central Florida. But, District Courts have recently been releasing opinions that apply a “substantial compliance” analysis.See Vasilevskiy v. Wachovia Bank, N.A., 2015 WL 4577415 (July 31, 2015).

o Bankruptcy Surrender • Issue of what “surrender” means within the bankruptcy context.

The court found that the term “surrender” means that debtors cannot thereafter take any overt action to defend or impede the foreclosure. In re Calzadilla, case no. 14-11318-RAM in the U.S. Bankruptcy Court, Southern District of Florida.

FLORIDA Recent Developments

o Notice of Transfer - FCCPA (Florida’s version of FDCPA)• While there are cases that find that some actions taken prior to or within the

context of a foreclosure may be deemed “debt collection” for the purpose of triggering the FCCPA (and FDCPA), the filing of a mortgage foreclosure lawsuit – standing alone – does not. Thus, 559.715 – a provision of the FCCPA that requires notice of debt transfer prior to initiating debt collection activity – is not a condition precedent to filing a lawsuit for mortgage foreclosure – which standing alone is not “an action to collect a debt.” U.S. Bank v. Vila, 2014 WL 10190153 (Fla.Cir.Ct., August 22, 2014).

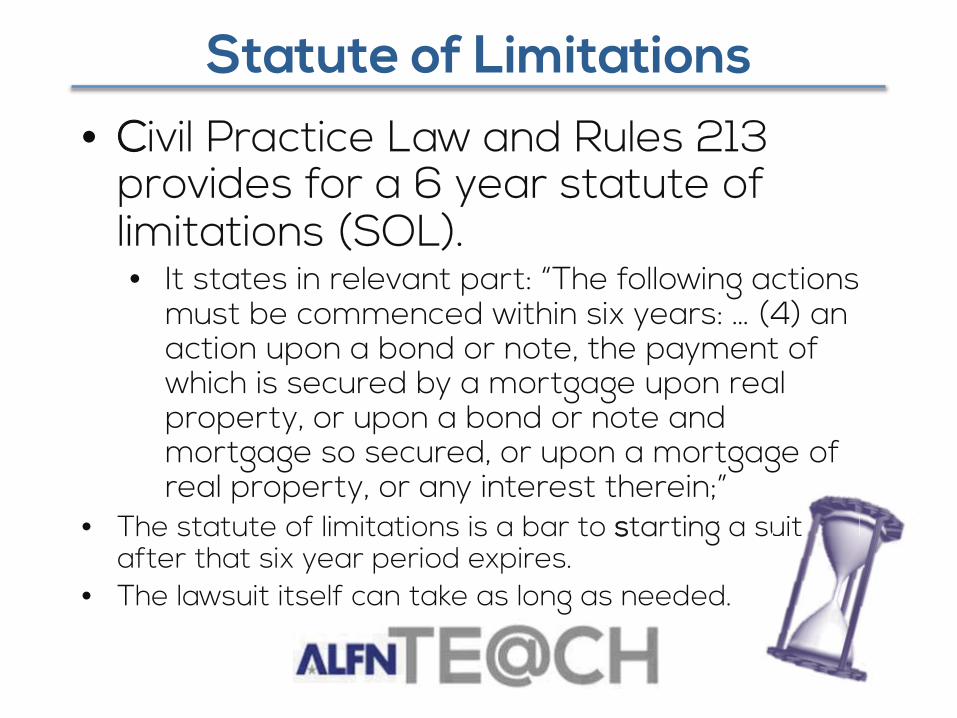

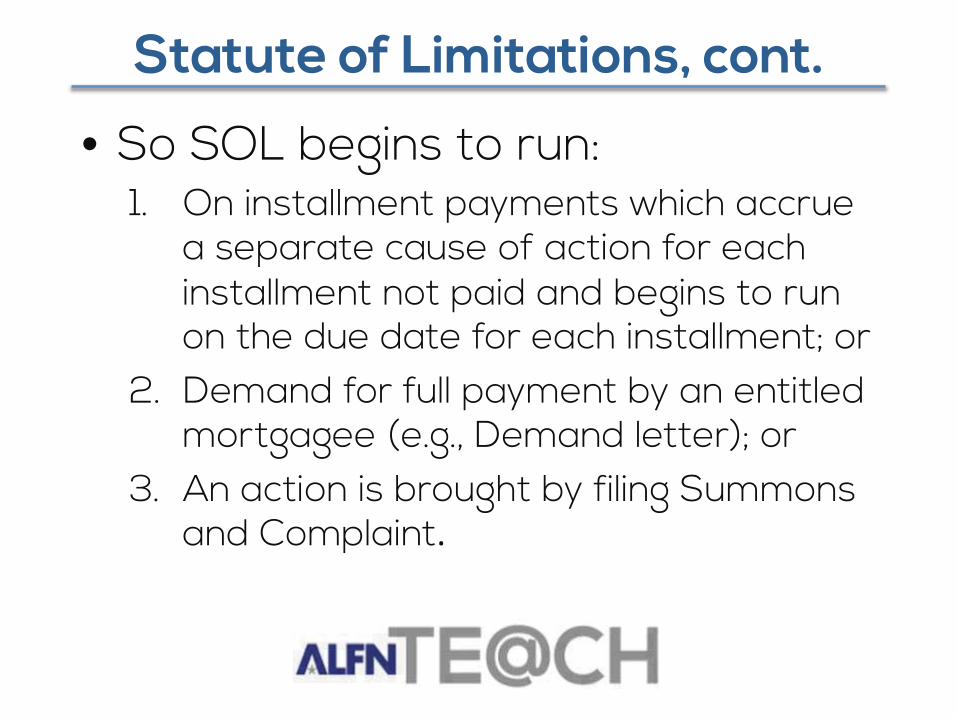

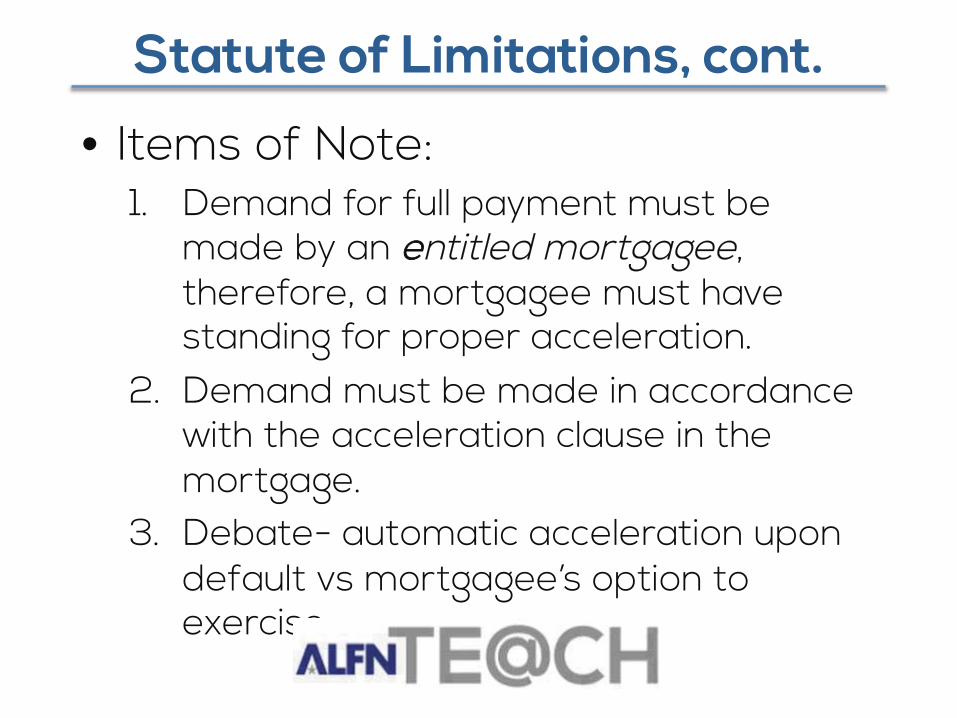

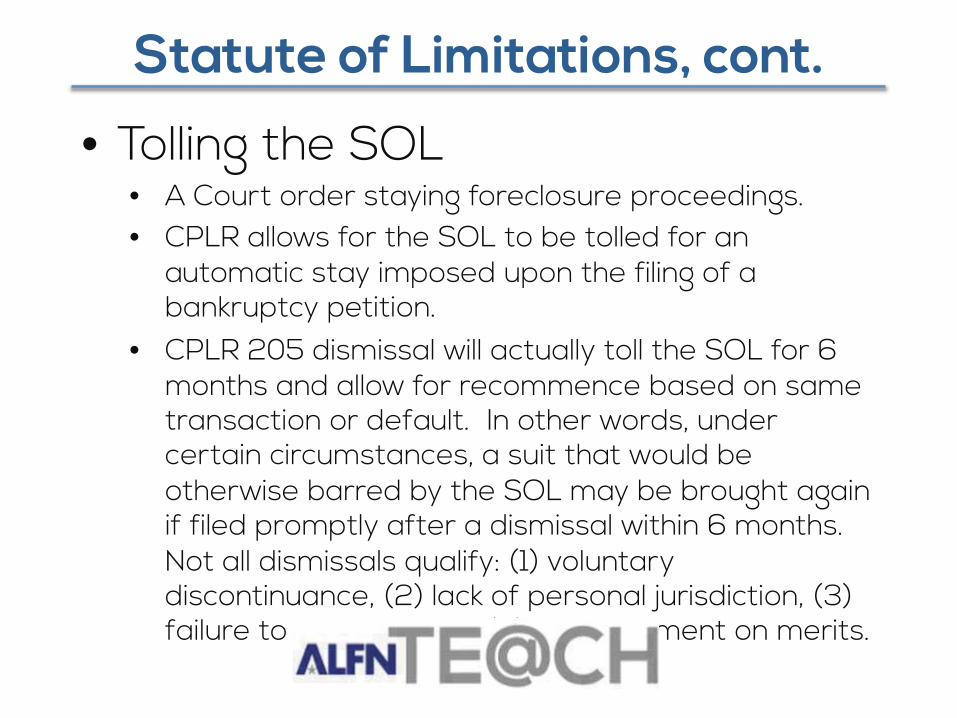

o Statute of Limitations • Two conflicting decisions in Florida. In Beauvais, 2014 WL 7156961, the Third

District holds no re-breach and re-file beyond the 5 year statute of limitations. In Bartram, 140 So. 3d 1007 (Fla. 5th DCA 2014) review granted, 160 So. 3d 892 (Fla. 2014), the Fifth District held a lender may re-breach and re-file. The Fifth District certified the question to the Florida Supreme Court and oral argument is scheduled in October. Interestingly, the Third District recently granted rehearing en banc in Beauvais, which means that the entire appellate bench will re-hear the issue. The oral argument in Beauvais is scheduled for the week after oral argument in Bartram. Everyone in Florida is watching these cases.

FLORIDA Recent Developments

General Session – ALFN Complex Litigation Group

September 9, 2015 – Jacksonville, FL

SESSION SPEAKERS

Jason A. Whitacre Lead Litigation Attorney The Law Offices of John D. Clunk Co., LPA [email protected]

HANDLING MILL LITIGATION IN

FORECLOSURE

Jason A. Whitacre, Esq. – The Law Offices of John D. Clunk Co., LPA

Common Tactics and Purposes First, what is mill litigation?

Litigation that uses the same or similar tactics in every case, regardless of the facts specific to that case, often by a for-profit law firm representing consumers

Why do it?

The tactic has a history of delaying cases; appears like real, fact-specific litigation; takes very little work (no customization from case-to-case); muddies the case waters.

Also increases the costs for mortgage servicers

The Face of Increased Costs Goal of removing file from foreclosure counsel to litigation

counsel using specific claims or tactics

Litigation counsel is perceived as having access to significantly greater settlement authority

Litigation counsel treats case as a litigated civil matter, helping the mill attorney earn fees and delay foreclosure judgment

“Discovery Bombs”: catch-all, overly extensive sets of discovery designed to prolong the case through an increase in the litigation timeline

Typical Counterclaims Regardless of claimed cause of action (and corresponding

elements), typically boils down to standing of foreclosing plaintiff.

FDCPA or State-equivalent consumer statutes

Fraud-on-the-court (seeks to invalidate assignments)

Quiet Title actions

CFPB Reg X and Notices of Error (often not based on specific complaints over servicing – cause of action manufacturing tool)

Settlement Conference vs. Mediation Typically in front of a judge or magistrate

Goal is to get the settlement process away from loss mitigation applications to corporate counsel for litigation resolution

Posturing and refusing to submit loss mitigation paperwork, knowing the servicer typically must first go through that step, to make the foreclosing plaintiff appear arbitrary and lacking in good-faith negotiations

How to Handle Mill Litigation DILIGENCE. Timely respond to notices of error; flag mill

litigators and track settlement demands, litigation claims.

COMPETENCE. Ensure your counsel and staff know how to handle these claims, can escalate the issues properly.

COMMUNICATION. Seek early opinion of counsel on viability of claims; troubleshoot potential problems in files.

PREPARE. As in, prepare the case. Flesh out the claims, real or imagined.

KEEP CONTROL. A major purpose of these tactics is to hijack the case and blow up or elongate the process.

Session 1 (Track 1 & 3) – Litigation UpdatesConference Center B Track 1: 9:45 a.m. – 11:00 a.m. Track 3: 2:45 p.m. – 4:00 p.m.

Speakers:• Linda Finley, Esq., Shareholder, Baker Donelson (ALFN member in Tennessee and DC) –

Discussion Leader• David Kluever, Esq., Managing Member, Kluever & Platt, LLC (ALFN Member in Illinois) • Denise Griffin, Esq., Senior Litigation Attorney, Shapiro, Swertfeger & Hasty, LLP (ALFN Member

in Georgia)

Session Overview: • Linda Finley - Coast to Coast Litigation Update • David Kluever - Litigation Updates • Denise Griffin - Breach letters (failure to send prior to accelerating); HUD regs incorporated into

security instruments.

Linda S. Finley, Esq. ShareholderBaker Donelson3414 Peachtree Road, N.E. Suite 1600 Atlanta, Georgia 30326 Phone: 404.589.3408 Fax: 404.238.9608 [email protected]

A shareholder in the Firm's Atlanta office, member of the Firm's board of directors and leader of the Residential Mortgage Litigation Group, Ms. Finley has tried more than 300 jury trials to verdict and concentrates her practice in business litigation involving the mortgage lending and servicing industries and litigation regarding real estate issues. Ms. Finley has experience in:

• Lender and servicer liability defense • Mortgage fraud civil prosecution and defense • Mortgage lending and servicing issues including foreclosure, bankruptcy, defense of wrongful

foreclosure and defense of predatory lending charges• QC/QA training and review • Real estate title clearance and litigation

Ms. Finley serves as a court appointed Special Master for purposes of adjudicating litigated real estate title issues. She is a frequent speaker regarding mortgage lending and servicing issues, and is called upon by clients as well as by law enforcement and prosecution offices to provide training on various topics including mortgage fraud investigation and prevention, quality control and loss mitigation. Before entering private practice, Ms. Finley served as an assistant district attorney for Atlanta, Georgia, and was tasked with the prosecution of major felonies.

Recent Representative Matters • Lead counsel in large scale mortgage fraud matter involving more than 250 loans. • Lead counsel in defense of mortgage related issues such as RESPA, TILA and defense of

charges of predatory lending.• Lead counsel in defense of lawsuits brought alleging wrongful foreclosure.• Lead counsel in Class Action suit against lender which alleged improper application of mortgage

fees in bankruptcy claim.

Publications & Speaking Engagements Since the 1990s Ms. Finley has been a national speaker and author on topics of mortgage servicing and real estate related issues. Her most recent engagements are below.

• "Counsel's Corner: The Consumer's Use of Standing as a Defense in Foreclosure Cases ," DSNews, May 27, 2015

• "What's Fraud Got to Do with It? Seeking Civil Relief in Residential Mortgage Fraud Cases," Mortgage Finance Fraud Litigation Strategies, July 1, 2014

• "Walking Dead? Beware the Zombie Foreclosure," Baker Donelson's Mortgage News, Summer 2014; reprinted in National Mortgage News, August 6, 2014

• "Comply with Gen Y?" HousingWire Focus magazine, September 2013 • "From Coast to Coast: Hot Topics in Litigation," Moderator, ALFN Annual Leadership Conference,

Colorado Springs, Colorado, July 24, 2013• "Kicking the Boot Camps – Gaining an Edge in Default Servicing Defensive Litigation,"

Moderator, MBA National Mortgage Servicing Conference, February 2012 • "The Shoe Is On The Other Foot — Fraud Investigations Against Lenders For Document Fraud,"

Panelist, Mortgage Bankers Association National Fraud Issues Conference (March 29, 2011) • "Survey of Georgia Real Property Law," Mercer Law Review, 2002 – 2012• "Blame Enough for All - The Role of the Consumer, Lender and GSE's in the Mortgage Industry

Crisis," West First Focus™ Subprime Reform Actions of the Federal Reserve, September 2008 • "Subprime in the Prime Time," Institute of Continuing Legal Education, 2008 Real Property

Foreclosure Seminar, April 2008 • "Mortgage Fraud: Legislation & Remedies," Georgia Real Estate Fraud Prevention and

Awareness Coalition's Annual Seminar, April 2008 • "Consumers Were the Real Victims of Georgia's Predatory-Lending Law," The Subprime Crisis: A

Thomson West Special Report, April 2008• "Who, What, Where, When and How Much?, Investigating Mortgage Fraud and Preservation of

Evidence," Mortgage Fraud Blog Seminar, Las Vegas, Nevada, November 2007 • "Trials and Tribulations," Georgia Commercial Real Estate Seminar on Foreclosures, Workouts

and Related Litigation Matters, Atlanta, Georgia, November 2007 • "Here's a Subprime Primer," LegalTimes, September 24, 2007 • "Avoid the "F" Words – Fraud and Forgery That Is!" Institute of Continuing Legal Education,

Annual Real Property Law Winter Symposium, 2007 • "Introduction to Mortgage Fraud: From Start to a Successful Finish," American Conference

Institute, Las Vegas, Nevada, 2006• "Mortgage Fraud Recovery: Civil or Criminal?" Georgia Real Estate Fraud Prevention and

Awareness Annual Conference, 2006• "Beware of the Land Shark! Don’t Get Bitten by Mortgage Fraud," Institute of Continuing Legal

Education, Real Property Law Institute, 2006 • "Confirmation of Real Estate Foreclosure - Practical Practice Tips," Institute of Continuing Legal

Education, Real Property Foreclosure Seminar, 2006 • "Everything You Ever Wanted to Know about Title Examination, but Were Afraid to Ask," Legal

Issues for Georgia Professional Surveyors, 2006• "Preventing and Addressing Mortgage Fraud," Mortgage Banker's Association of Jacksonville,

Florida, 2005• "Beware of Land Sharks - Preventing Mortgage Fraud," Georgia Real Estate Fraud Prevention

and Awareness Coalition, Annual Conference, 2005• "Land Shark - Don’t Feel the Bite of Mortgage Fraud," SmartBusiness Magazine, 2005 • "Mortgage Fraud and Georgia," presented to the Georgia Senate Banking Committee and the

Georgia House of Representatives Banking Committee, 2005 • "Predatory Lending - What is it?" Fannie Mae, 2002

Professional Honors & Activities • Listed in The Best Lawyers in America® in Mortgage Banking Foreclosure Law, 2015 • Listed in Georgia Super Lawyers since 2009, listed as one of the top 50 female attorneys in

Georgia • Named to Georgia Trend Legal Elite in the area of Bankruptcy/Creditors' Rights, 2009 – 2011• Member – American and Atlanta Bar Associations• Board Member – Georgia Real Estate Fraud Prevention and Awareness Coalition, 2006 – 2008 • Fellow – American College of Mortgage Attorneys

• AV® Preeminent™ Peer Review Rated by Martindale-Hubbell • Former Assistant District Attorney – Major felony prosecution, Atlanta, Georgia

Admissions• Georgia, 1982 • Florida, 1986 • U.S. District Court for the Northern, Middle and Southern Districts of Georgia • U.S. Court of Appeals for the Eleventh Circuit • U.S. District Court for the Northern and Middle Districts of Florida • U.S. Supreme Court

Education• Mercer University Walter F. George School of Law, J.D., 1981 • Mercer University, B.A., 1978

David C. Kluever, Esq. PartnerKluever & Platt, LLC 65 East Wacker Place Suite 2300 Chicago, Illinois 60601 Phone: (312) 236-0077 Fax: (312) [email protected]

Education• Case Western Reserve University, J.D., 1983 John Marshall Law School, L.L.M. in Taxation,

1987 DePauw University, B.A. Economics, 1980

Admissions• Illinois, 1983 • United States District Court for the Northern District of Illinois,• including the federal trial bar, 1986 • United States District Court for the Southern District of Illinois, 2004 • United States District Court for the Central District of Illinois, 2009 • United States Court of Appeals for the Seventh Circuit, 2008 • United States Supreme Court, 2009

Affiliations• American Bar Association • Illinois Mortgage Bar • American Legal and Financial Network

Prior Experience • Cook County State’s Attorney’s Office 1983 – 1987 • Katz Randall & Weinberg (firm later named later Weinberg & Richmond) 1987-1988 • Gottlieb and Schwartz, Partner, 1988-1993

Mr. Kluever is an attorney specializing in the areas of commercial real estate transactions, secured financing transaction and all manner of real estate, creditor’s rights and commercial litigation. He has twenty five years experience in representing banks and institutional lenders in commercial loan transactions, creditor’s rights litigation and other compliance and contractual commercial litigation. Mr.

Kluever has had significant experience with failed institution litigation beginning with the RTC Crisis in 1989 and extending into the 1990’s. Kluever & Platt similarly operated under a legal services agreement and continues to handle litigation of a wide range of matters concerning failed institutions over the past five years.

His experience extends to the mortgage banking industry and currently includes the representation of three of the 5 major national banks subject to the National Mortgage Settlement decree, mortgage loan servicers some of which are subsidiaries of international banks and Wall Street firms, default industry process outsourcers, title companies and industry professionals.

While many firms specialize in handling only volume default-related litigation in actions to collect sums due under defaulted mortgage loans, Mr. Kluever leads Kluever & Platt’s separate team of litigators in handling all manner of related contested litigation and appeals. Such related litigation has included appraiser liability claims, loan origination and put-back claims, robo-signing litigation, MERS (standing) litigation, and other loan origination claims including TILA, HOEPA, Reg Z, and other contested claims and litigation.

Mr. Kluever represents clients not only in the trial courts but also in civil appeals. He has prevailed in appeals before the United States Seventh Circuit Court of Appeals, the Illinois Supreme Court and the First, Second, Third and Fifth Illinois Appellate Districts.

Mr. Kluever’s transactional clients include commercial real estate developers; developers of single family subdivisions, condominium and mixed use developments, low income tax credit and senior citizen multifamily housing developments; property management companies; condominium and homeowner’s associations; corporation, individual entrepreneurs and business owners; and accountants. It is noteworthy that a number of other attorneys practicing in Illinois hire Mr. Kluever to represent them in connection with their personal legal needs including both litigation and transactional matters.

Following graduation from law school, Mr. Kluever was a criminal prosecutor as an Assistant State’s Attorney under Richard Daley in Cook County, Illinois for four years from 1983 through 1987. During this time he tried hundreds of misdemeanor and felony cases throughout the Cook County criminal justice system and handled over twenty appeals in the Illinois First District Appellate Court and Illinois Supreme Court.

Denise Griffin, Esq. Senior Litigation Attorney Shapiro, Swertfeger & Hasty, LLP295 S. Culver Street, Suite BLawrenceville, GA 30046 Phone: 770-963-7147Fax: [email protected]

Denise Griffin has been a practicing litigation attorney since 1988. Ms. Griffin was of counsel with Shapiro & Swertfeger, LLP starting in 2002, and joined the firm as its senior litigation attorney in 2009.Her diverse legal background includes complex litigation involving mortgage lending and servicing, foreclosure, eviction, condemnation, quiet title, reformation, zoning and housing code matters, property owners association law, real property and title disputes, Georgia lien law, adverse possession, confirmation of sale and deficiency judgment actions, fraud, Truth-in-Lending Act, Fair Debt Collection Practices Act, Real Estate Settlement Procedures Act, Fair Credit Reporting Act, construction and development law, equitable subrogation, eminent domain, predatory lending, bankruptcy and the like.She regularly litigates in the trial and appellate courts. Ms. Griffin has ample experience representing mortgage lenders and servicers, title insurance companies, law firms, appraisers, developers, real estate brokers and agents, builders, investors, realtors, contractors and individuals with real estate-related

issues. Ms. Griffin is a 1988 graduate of Georgia State University College of Law. She is a member of the Georgia Bar Association and the Federal Bar Association, and is a former member of the Bleckley American Inn of Court. She is admitted to all Georgia state and federal courts, the Eleventh Circuit Court of Appeals, and the United States Supreme Court.

1

ALFN TE@CH Onsite Regional Training Seminar September 9, 2015 Hyatt Regency Jacksonville Riverfront Jacksonville, FL

2

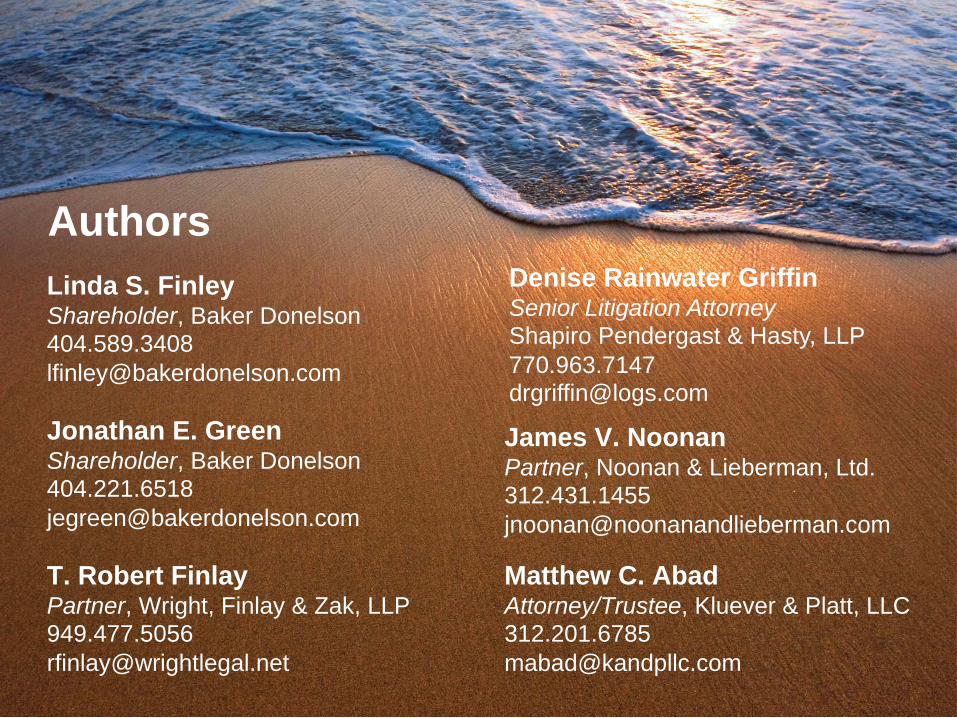

Jonathan E. Green Shareholder, Baker Donelson 404.221.6518 [email protected]

James V. Noonan Partner, Noonan & Lieberman, Ltd. 312.431.1455 [email protected]

Authors Linda S. Finley Shareholder, Baker Donelson 404.589.3408 [email protected]

Matthew C. Abad Attorney/Trustee, Kluever & Platt, LLC 312.201.6785 [email protected]

T. Robert Finlay Partner, Wright, Finlay & Zak, LLP 949.477.5056 [email protected]

Denise Rainwater Griffin Senior Litigation Attorney Shapiro Pendergast & Hasty, LLP 770.963.7147 [email protected]

3

Denise Rainwater Griffin Senior Litigation Attorney, Shapiro Pendergast & Hasty 770.963.7147 [email protected]

Moderator Speakers Linda S. Finley Shareholder, Baker Donelson 404.589.3408 [email protected]

David C. Kluever Partner, Kluever & Platt, LLC 312.201.6677 [email protected]

4

U.S. District Courts

5

Hot Topics Across the Country

• Standing • Statutes of Limitation • HUD Regulations • Homeowner’s and Condo Associations are Becoming Aggressive • Municipalities are Becoming Aggressive, Too • Regulations! Regulations!

6

FORECLOSURE ISSUES

7

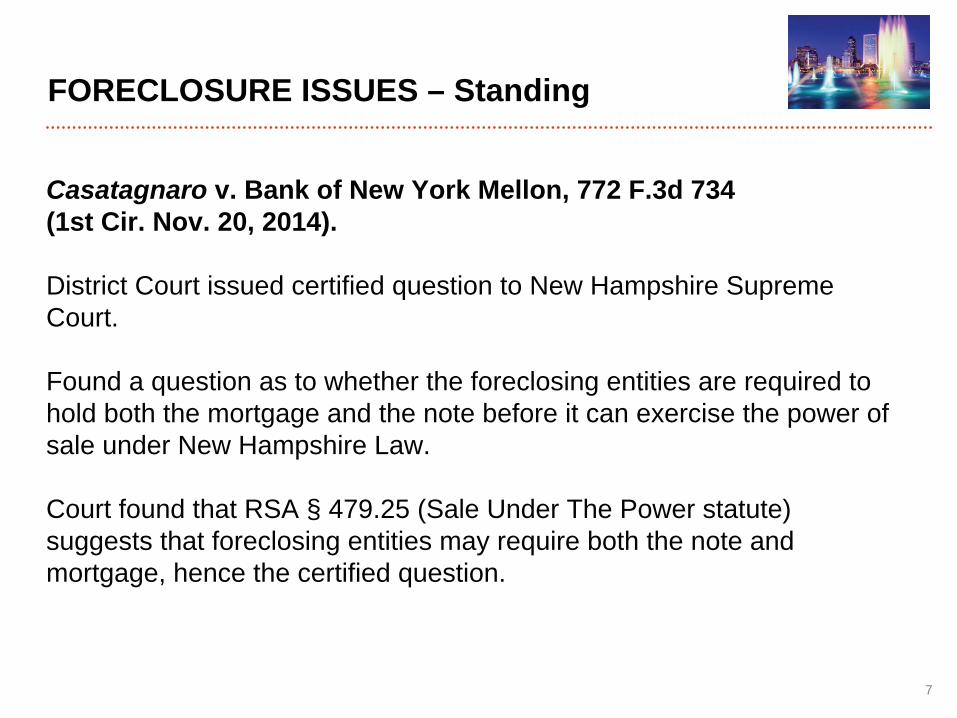

FORECLOSURE ISSUES – Standing

Casatagnaro v. Bank of New York Mellon, 772 F.3d 734 (1st Cir. Nov. 20, 2014). District Court issued certified question to New Hampshire Supreme Court. Found a question as to whether the foreclosing entities are required to hold both the mortgage and the note before it can exercise the power of sale under New Hampshire Law. Court found that RSA § 479.25 (Sale Under The Power statute) suggests that foreclosing entities may require both the note and mortgage, hence the certified question.

8

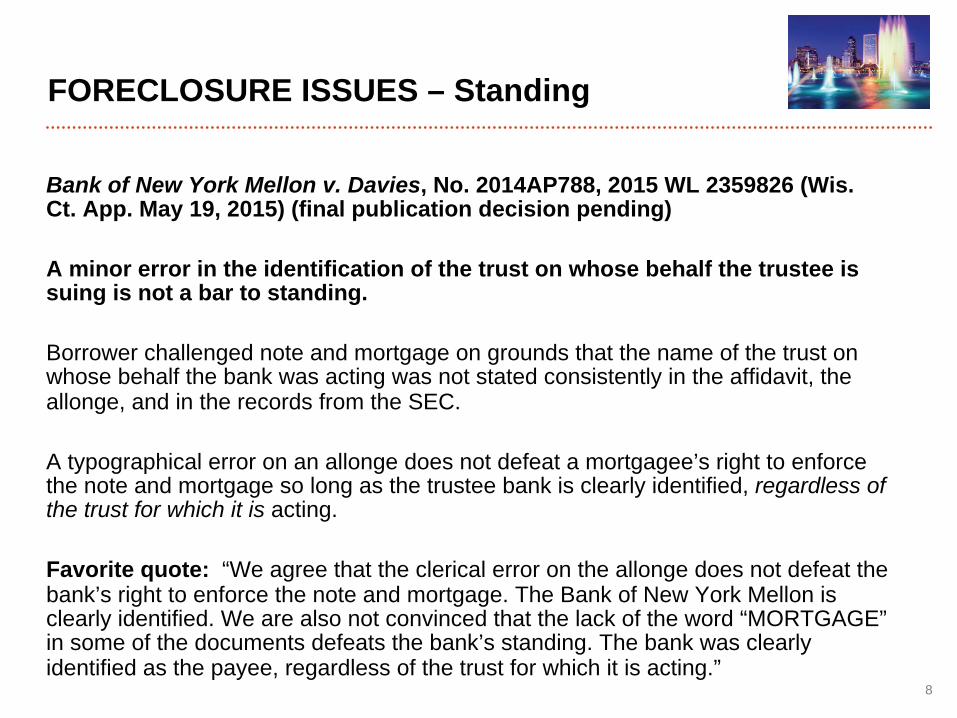

FORECLOSURE ISSUES – Standing

Bank of New York Mellon v. Davies, No. 2014AP788, 2015 WL 2359826 (Wis. Ct. App. May 19, 2015) (final publication decision pending) A minor error in the identification of the trust on whose behalf the trustee is suing is not a bar to standing. Borrower challenged note and mortgage on grounds that the name of the trust on whose behalf the bank was acting was not stated consistently in the affidavit, the allonge, and in the records from the SEC. A typographical error on an allonge does not defeat a mortgagee’s right to enforce the note and mortgage so long as the trustee bank is clearly identified, regardless of the trust for which it is acting. Favorite quote: “We agree that the clerical error on the allonge does not defeat the bank’s right to enforce the note and mortgage. The Bank of New York Mellon is clearly identified. We are also not convinced that the lack of the word “MORTGAGE” in some of the documents defeats the bank’s standing. The bank was clearly identified as the payee, regardless of the trust for which it is acting.”

9

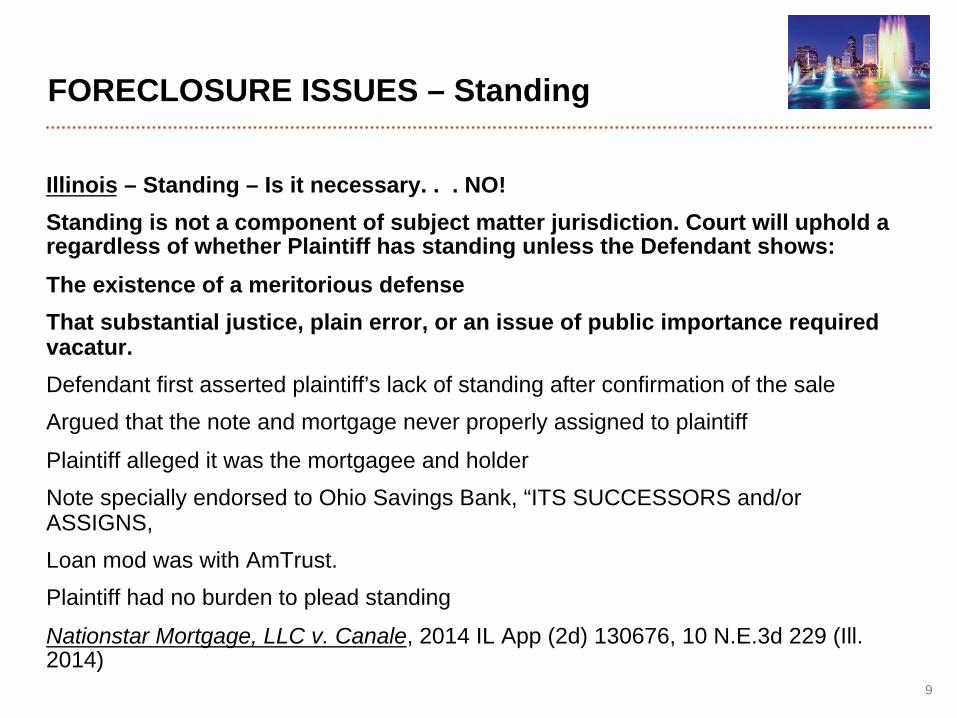

FORECLOSURE ISSUES – Standing

Illinois – Standing – Is it necessary. . . NO! Standing is not a component of subject matter jurisdiction. Court will uphold a regardless of whether Plaintiff has standing unless the Defendant shows: The existence of a meritorious defense That substantial justice, plain error, or an issue of public importance required vacatur. Defendant first asserted plaintiff’s lack of standing after confirmation of the sale Argued that the note and mortgage never properly assigned to plaintiff

Plaintiff alleged it was the mortgagee and holder Note specially endorsed to Ohio Savings Bank, “ITS SUCCESSORS and/or ASSIGNS, Loan mod was with AmTrust. Plaintiff had no burden to plead standing

Nationstar Mortgage, LLC v. Canale, 2014 IL App (2d) 130676, 10 N.E.3d 229 (Ill. 2014)

10

FORECLOSURE ISSUES – Standing

Illinois Does failure to plead standing deprive the trial court of subject matter jurisdiction?

To invoke court’s jurisdiction, an initial pleading need only state a justiciable matter. “A claim for foreclosure, even if defectively stated, presents a justiciable matter.”

Deustche Bank National Trust Company v. Petitti, 2014 IL App (2d) 130607-U *unpublished*

11

FORECLOSURE ISSUES - Standing

Georgia Johnson v. Bank of America, N.A., No. A15A0688, 2015 WL 4231861 (Ga. Ct. App. July 14, 2015). The Georgia Court of Appeals held the borrower who claimed that his security deed had been relinquished, had standing to sue for quiet title to remove it and its assignments from his title.

12

FORECLOSURE ISSUES – Statutes of Limitation

Deutsche Bank Trust Co. Americas v. Beauvais, 40 Fla. L. Weekly D1 (Fla. 3d DCA Dec. 17, 2014).

Statute of limitations barred second foreclosure action because that action was filed more than five years after the initial foreclosure complaint was filed/accelerated, and the first foreclosure was dismissed without prejudice so that the acceleration caused by the filing of the first complaint was not decelerated, so that the statute of limitations continued to run. The court certified conflict with Evergrene from the 4th DCA. However, the court also stated that, while the loan could not be foreclosed due to the SOL, the mortgage lien remained under Fla. Stat. 95.281(1)(a) until 5 years past the maturity date of the loan (i.e., the year 2041). This case is not final as the bank moved for rehearing and rehearing en banc but has not been ruled upon. Arguably, trial courts in the Third DCA should be following Evergrene until Beauvais is final, under Pardo v. State, 596 So.2d 665 (Fla. 1992).

LNB-017-13, LLC v. HSBC Bank USA, 2015 WL 1546150 (S.D. Fla. Apr. 7, 2015).

Federal judge sharply criticizes Beauvais’ SOL holding and ruled that such directly conflicts with cases “with the overwhelming amount of authority” in the Southern and Middle Districts of Florida and decisions from Florida courts.

13

FORECLOSURE ISSUES – Statutes of Limitation

FLORIDA - U.S. Bank Nat. Ass'n v. Bartram, 140 So. 3d 1007, 1008 (Fla. Dist. Ct. App. 2014) review granted, 160 So. 3d 892 (Fla. 2014)

The trial court granted summary judgment finding that the note and mortgage should be cancelled based on a failed attempt to foreclose the same note and mortgage in a prior foreclosure action filed by the Bank. The Bank appealed.

On appeal, the issue decided was whether acceleration of payments due under a note and mortgage in a foreclosure action that was dismissed pursuant to rule 1.420(b), Florida Rules of Civil Procedure, triggered application of the statute of limitations to prevent a subsequent foreclosure action by the mortgagee based on payment defaults occurring subsequent to dismissal of the first foreclosure suit. The District Court of Appeals concluded that the statute of limitations does not bar the subsequent foreclosure action. Review has been granted in Bartram v. U.S. Bank Nat. Ass'n, 160 So. 3d 892 (Fla. 2014).

14

FORECLOSURE ISSUES – Statutes of Limitation

U.S. Bank Nat. Ass'n v. Lamb, No. 14-1536 (Iowa Ct. App. May 20, 2015)(final publication decision pending). Although bank had rescinded early in rem judgment, borrower was unsuccessful in setting aside a foreclosure judgment on the basis that under Iowa Code section 615.1 any rights the bank as the mortgage and note holder held after it failed to enforce its judgment or file its notice of rescission within two years was nullified. Court ruled that this section applies only to judgment liens and notwithstanding it remains the rule that a creditor does not lose its lien on the debtor's property by taking a judgment. The mortgage remains a lien until the debt it was given to secure is satisfied. Thus, a mortgage is not affected by a judgment taken on the note.

15

FORECLOSURE ISSUES – Statutes of Limitation

Slorp v. Lerner, Sampson & Rothfuss, 587 F. App'x 249, 260 (6th Cir. 2014).

Is continuing to prosecute a wrongful suit a continuing violation that tolls the statute of limitations?

Circuit court declined to apply the continuing-violation doctrine

Found that the filing of the allegedly wrongful foreclosure suit was the actionable event under the FDCPA.

“Although the subsequent prosecution of that suit may exacerbate the damages, the continued accrual of damages does not diminish the fact that the initiation of the suit was a discrete, immediately actionable event.”

16

FORECLOSURE ISSUES – MERS

Illinois Deutsche Bank Nat. Trust v. Cichosz, 2014 IL App (1st) 131387, ¶¶ 16-17, 19 N.E.3d 134 In a foreclosure that was brought originally by MERS, the Illinois appellate court rejected the defense that the action was void because MERS was an unlicensed debt collector in violation of the Illinois Collection Agency Act. 225 ILCS 4251 et seq. Appellate court affirmed because the Act did not apply to MERS and the type of business MERS operates is not equivalent to debt collection.

17

FORECLOSURE ISSUES – MERS

Lockhart v. HSBC Fin. Corp., No. 13 C 9323 (N.D. Ill. Aug. 1, 2014). According to at least one U.S. District Court in Illinois, MERS and MERSCORP are not creditors or assignees so plaintiff cannot proceed against them under TILA and HOEPA. However, if plaintiff’s rescission claim is successful in unwinding the transaction, and the parties are to be returned to the status quo, MERS and MERSCORP may be necessary parties for that to occur. They therefore remain in the case.

18

FORECLOSURE ISSUES – MERS

Boyd Cnty. ex rel. Hedrick v. MERSCORP, Inc., No. 14-5647 (6th Cir. June 5, 2015). Forty-one of Kentucky's 120 counties brought suit against MERS alleging that assigned and continue to assigns mortgage liens among each other without recording those assignments, in violation of Kentucky law. The district court dismissed the lawsuit on the ground that the counties lacked the power to enforce the statute as lacking a private right of action. On appeal the dismissal was affirmed. The Sixth Circuit also refused to consider the counties “novel theory” that they have the power, as subdivisions of the state, to enforce mandatory provisions of Kentucky's recording statute through civil litigation, without support from the Kentucky courts. Court also refused to certify the question to the Kentucky Supreme Court.

19

FORECLOSURE ISSUES – MERS

Plymouth County, Iowa v. Merscorp, Inc., 774 F.3d 1155 (8th Cir. Dec. 19, 2014); County of Ramsey v. MERSCORP Holdings, Inc., 776 F.3d 947 (8th Cir. Dec. 19, 2014). Where there is no duty to record a mortgage county recorder county has no claim for unjust enrichment against MERS. No claim for civil conspiracy can lie either because in the absence of a mandatory recording requirement, there is no unlawful conduct.

20

FORECLOSURE ISSUES – Wrongful Foreclosure

Georgia Ames v. JP Morgan Chase Bank, N.A., No. 2013-CV-230620 (Apr. 30, 2013), cert. granted, No. S-15-G1007 (Sept. 2015).

Georgia Supreme Court will examine whether a borrower lacks standing to challenge the assignment of a security deed.

Could result in a reversal of a key line of cases which held that a debtor who is not a party to an assignment does not have standing to challenge it because the assignment was a contract and the debtor was not a party to the contract. See, Montgomery v. Bank of Am. (321 Ga.App. 343, 740 S.E.2d 434 (2013).

21

FORECLOSURE ISSUES – Wrongful Foreclosure

Georgia Stewart v. SunTrust Mortg., Inc., 331 Ga. App. 635 (Ga. Ct. App. Mar. 27, 2015).

Reversed grant of dismissal of wrongful foreclosure claim because allegation that lender mislead borrower by stating that the foreclosure would be postponed suggested a breach of a legal duty.

Applied standard of care for a fiduciary to the lender based on the Power-of-Sale clause appointing lender as attorney-in-fact.

22

FORECLOSURE ISSUES – Miscellaneous

Fannie Mae v. Hicks, 2015-Ohio-1955.

Ohio – LOST NOTE AFFIDAVIT – Not the only thing that was lost!

A mortgage may be enforced only by a person who is entitled to enforce the obligation the mortgage secures. Only after the court determines liability on the underlying obligation, can it proceed to the foreclosure analysis under the mortgage.

FNMA could not establish it was entitled to enforce the note where the note was specifically endorsed to Fannie Mae FNMA was not in possession of the note when it was lost.

Ohio has not adopted an amended to section 3-309 of the U.C.C, which allows for enforcement “if the person either (A) was entitled to enforce the instrument when loss of possession occurred, or (B) has directly or indirectly acquired ownership of the instrument from a person who was entitled to enforce the instrument when loss of possession occurred.”

23

FORECLOSURE ISSUES – HUD Regulations

The Federal Housing Administration (FHA) under the Department of Housing and Urban Development (HUD) insures loans made by lenders to qualifying homebuyers. FHA requires certain servicing practices for FHA-insured loans. These servicing practices are described in HUD regulations set out in the Code of Federal Regulations ( C.F.R. ) at 24 CFR Part 203, Subpart C ( Servicing Responsibilities ) Litigation: There has been a substantial amount of foreclosure-related litigation whereby borrowers with FHA-insured loans sue their lenders for violating HUD regulations incorporated into their loan documents, or defend foreclosures on such basis. Primary litigation argument: Language in loan documents limits the lender s ability to accelerate and foreclose upon property in the event of default.

24

FORECLOSURE ISSUES – HUD Regulations

Note 6. BORROWER'S FAILURE TO PAY

(B) Default If Borrower defaults by failing to pay in full any monthly payment, then Lender may, except as limited by regulations of the Secretary in the case of payment defaults, require immediate payment in full of the principal balance remaining due and all accrued interest. In many circumstances, regulations issued by the Secretary will limit Lender's rights to require immediate payment in full in the case of payment defaults. This Note does not authorize acceleration when not permitted by HUD regulations. As used in this Note, "Secretary" means the Secretary of Housing and Urban Development or his or her designee.

25

FORECLOSURE ISSUES – HUD Regulations

Deed of Trust / Security Deed 9. Grounds for Acceleration of Debt. (a) Default. Lender may, except as limited by regulations issued

by the Secretary, in the case of payment defaults, require immediate payment in full of all sums secured by this Security Instrument if:

(i) Borrower defaults by failing to pay in full any monthly payment required by this Security Instrument prior to or on the due date of the next monthly payment, or

(ii) Borrower defaults by failing, for a period of thirty days, to perform any other obligations contained in this Security Instrument.

26

FORECLOSURE ISSUES – HUD Regulations

Deed of Trust / Security Deed – Grounds for Acceleration of Debt – cont’d

d) Regulations of HUD Secretary. In many circumstances

regulations issued by the Secretary will limit Lender's rights, in the case of payment defaults, to require immediate payment in full and foreclose if not paid. This Security Instrument does not authorize acceleration or foreclosure if not permitted by regulations of the Secretary.

27

FORECLOSURE ISSUES – HUD Regulations

Regulations § 203.500 Mortgage servicing generally. This subpart identifies servicing practices of lending institutions that HUD considers acceptable for mortgages insured by HUD. Failure to comply with this subpart shall not be a basis for denial of insurance benefits, but failure to comply will be cause for imposition of a civil money penalty, including a penalty under § 30.35(c)(2), or withdrawal of HUD's approval of a mortgagee. It is the intent of the Department that no mortgagee shall commence foreclosure or acquire title to a property until the requirements of this subpart have been followed.

28

FORECLOSURE ISSUES – HUD Regulations

§203.602 Delinquency notice to mortgagor. The mortgagee shall give notice to each mortgagor in default on a form supplied by the Secretary or, if the mortgagee wishes to use its own form, on a form approved by the Secretary, no later than the end of the second month of any delinquency in payments under the mortgage. If an account is reinstated and again becomes delinquent, the delinquency notice shall be sent to the mortgagor again, except that the mortgagee is not required to send a second delinquency notice to the same mortgagor more often than once each six months. The mortgagee may issue additional or more frequent notices of delinquency at its option.

29

24 CFR § 203.604(b) Contact with the mortgagor. [Face-to-face interview] With certain limited exceptions, the mortgagee must have a face-to-face interview with the mortgagor, or make a reasonable effort to arrange such a meeting, before three full monthly installments due on the mortgage are unpaid.

FORECLOSURE ISSUES – HUD Regulations

30

EXCEPTIONS TO THE FACE-TO-FACE MEETING REQUIREMENT:

- The mortgagor does not reside in the property, - The property is not within 200 miles of the mortgagee,

its servicer, or a branch office of either, - The mortgagor has clearly indicated that he will not

cooperate in the interview, - A repayment plan consistent with the mortgagor's

circumstances is entered into to bring the mortgagor's account current thus making a meeting unnecessary, and payments thereunder are current, or

- A reasonable effort to arrange a meeting is unsuccessful.

24 CFR § 203.604(c)

FORECLOSURE ISSUES – HUD Regulations

31

WHAT CONSTITUTES A REASONABLE EFFORT TO ARRANGE A MEETING? - at least one letter to the mortgagor sent by certified mail; and - at least one trip to see the mortgagor at the mortgaged property, unless the mortgaged property is more than 200 miles from the mortgagee, its servicer, or a branch office of either, or it is known that the mortgagor is not residing in the mortgaged property. 24 CFR § 604(d)

FORECLOSURE ISSUES – HUD Regulations

32

FORECLOSURE ISSUES – HUD Regulations

24 CFR § 203.605(a) Loss mitigation performance. Before four full monthly installments due on the mortgage have become unpaid, the mortgagee shall evaluate on a monthly basis all of the loss mitigation techniques provided at § 203.501 to determine which is appropriate. Based upon such evaluations, the mortgagee shall take the appropriate loss mitigation action.

33

24 CFR § 203.605(c). Loss mitigation performance. Assessment of civil money penalty. A mortgagee that is found to have failed to engage in loss mitigation as required under paragraph (a) of this section shall be liable for a civil money penalty as provided in § 30.35(c) of this title.

FORECLOSURE ISSUES – HUD Regulations

34

FORECLOSURE ISSUES – HUD Regulations

24 CFR §203.606(a) Pre-foreclosure review.

Before initiating foreclosure, the mortgagee - must ensure that HUD-mandated servicing

requirements have been met - must, prior to initiating foreclosure, notify the

mortgagor in an approved format that mortgagor is in default and mortgagee intends to foreclose unless the mortgagor cures the default.

Mortgagee may not commence foreclosure for a monetary default unless at least 3 full monthly installments are unpaid after first applying any partial payments that may have been accepted.

35

FORECLOSURE ISSUES – HUD Regulations

24 CFR §203.606(b) Pre-foreclosure review.

If any of the following apply, foreclosure may be initiated without the foreclosure delay required by §203.606(a): - The property has been abandoned, or has been vacant for more than 60 days;- The mortgagor, after being clearly advised of the options available for relief, has clearly stated in writing that he or she has no intention of fulfilling his or her mortgage obligation;- The property is not the mortgagor's principal residence and it is occupied by tenants who are paying rent, but the rental income is not being applied to the mortgage debt;- The property is owned by a corporation or partnership.

36

FORECLOSURE ISSUES – HUD Regulations

RAMIFICATIONS OF FAILING TO COMPLY WITH HUD REGULATIONS PRIOR TO ACCELERATING AND FORECLOSING Litigation Claims / Defenses

Equitable defense Wrongful Foreclosure Breach of Contract / Failure of condition precedent Fair Debt Collection Practices Act Injunctive Relief Wrongful Eviction State Law Consumer Law Claims Class Action Claims

Penalties

37

FORECLOSURE ISSUES – HUD Regulations

FLORIDA - Laws vs. Wells Fargo Bank, N.A., Florida District Court of Appeal, First District; Case No. 1D14-620 (Feb. 27, 2015) Appeal of order granting lender summary judgment in judicial foreclosure action. As an affirmative defense, borrower argued the lender’s failure to give HUD-mandated notice of intent to accelerate. Lender argued HUD regulations are not generally considered conditions precedent to foreclosure. Held: The issue is not whether Wells Fargo met all conditions necessary to initiate foreclosure, but whether summary judgment was proper despite this affirmative defense.

38

FORECLOSURE ISSUES – HUD Regulations

Laws holding - cont’d. Since the note incorporated HUD regs requiring written notice of acceleration, Laws was entitled to raise failure to send such notice as a valid defense to foreclosure. See Real Estate Mortg. Network, Inc. v. Knight, 149 So.3d 121 (Fla. 4th DCA 2014) (holding a valid defense of noncompliance with HUD regulations that require a notice of acceleration existed, where the mortgage expressly provided that it “does not authorize acceleration or foreclosure if not permitted by regulations of the [HUD] Secretary.”) (citing Cross v. Federal National Mortgage Ass'n, 359 So.2d 464, 465 (Fla. 4th DCA 1978) (holding that non-compliance with HUD regulations may be asserted as an equitable defense in mortgage foreclosure proceedings)).”

39

FLORIDA - Cross v. Fed. Nat. Mortgage Ass'n, 359 So. 2d 464, 465 (Fla. Dist. Ct. App. 1978)

It seems clear now that the HUD guidelines are not mandatory procedures constituting conditions precedent to foreclosure. Encarnacion Hernandez v. Prudential Mortgage Corporation, 553 F.2d 241 (1st Cir. 1977). However, a mortgage foreclosure is an equitable action and thus equitable defenses are most appropriate. Thus, it appears , as suggested in [FNMA] v. Ricks, 83 Misc.2d 814, 372 N.Y.S.2d 485 (S.Ct.1975), that given the purpose of this federal Act and the recommended efforts to obviate the necessity of foreclosure, any substantial deviation from the recommended norm might be considered by the trial court under the heading of an equitable defense.

FORECLOSURE ISSUES – HUD Regulations

40

FORECLOSURE ISSUES – HUD Regulations

TEXAS - Sanchez v. Bank of Am., N.A., 3:14-CV-2571-B, 2015 WL 418084, at *8-9 (N.D. Tex. Jan. 30, 2015) Lender moved to dismiss borrower’s claims for specific performance and breach of contract. Borrower argued that Lender breached loan documents by failing to conduct a face-to-face meeting or make reasonable efforts to schedule the same; failing to inform of assistance options as required by 24 C.F.R. § 203.604(e)(2); and by failing to accept partial payments after default and to apply partial payments as mandated by 24 C.F.R. § 203.556(b)). Lender argued: Since the borrower admitted default, he could not show performance. Held: The HUD regs contemplate the borrower’s default and specify the lender’s obligations after such default.

41

GEORGIA - Eleventh Cir. - Bates v. JPMorgan Chase Bank, NA, 768 F.3d 1126, 1131 (11th Cir. 2014) District Court ruled that because a borrower may not directly sue for violations of HUD regs, he may not claim breach of contract based on alleged violations thereof. The Eleventh Circuit Court of Appeals disagreed based upon its reading of Georgia law that powers of sale in deeds are to be strictly construed. Held: “We believe Georgia courts would hold that HUD regulations clearly referenced in a deed as conditions precedent to the power to accelerate and [foreclose] could form the basis of a breach of contract action.” Therefore, Bates had asserted a duty owed to her by the lender.”

FORECLOSURE ISSUES – HUD Regulations

42

FORECLOSURE ISSUES – HUD Regulations

The following decision is entirely contrary to the Eleventh Circuit Court’s ruling in Bates. TEXAS - Klein v. Wells Fargo Bank, N.A., A-14-CA-861-SS, 2014 WL 5685113, at *5-6 (W.D. Tex. Nov. 4, 2014) aff'd, --- Fed.Appx. ----, 5th Cir.(Tex.), Aug. 20, 2015 Klein argued the lender violated HUD regs incorporated in her DOT by failing to have a face-to-face interview or making a reasonable effort to arrange such a meeting.

43

Klein – cont d

The court considered an earlier Texas state court decision (Hornbuckle v. Countrywide Home Loans, Inc., 02-09-00330-CV, 2011 WL 1901975, at *5 (Tex. App. May 19, 2011)) wherein the borrower had argued the lender breached the DOT, among other things, by failing to obtain HUD approval before attempting to foreclose. In that case, the Texas appeals court had held that the borrower had no private right of action regarding the lender s alleged failure to follow HUD regulations, even those incorporated into the deed of trust.

On this basis (and because Klein admitted default), the Klein court denied her breach of contract claim reasoning that HUD regulations govern the relations between the lender and the government. Therefore, Klein could not argue the lender breached a duty owed to her.

FORECLOSURE ISSUES – HUD Regulations

44

FORECLOSURE ISSUES – HUD Regulations

TEXAS – FIFTH CIR. - Johnson v. JP Morgan Chase Bank, 570 Fed. Appx. 404, 406 (5th Cir. June 4, 2014) Johnson argued her lender breached a contract by failing to comply with HUD regs incorporated in her loan documents by failing to conduct a face-to-face meeting, and by failing to perform loss mitigation.

Held: Although the HUD regulations were incorporated in the loan documents, since Johnson was already more than four months in default when Chase purchased the loan, and since Chase did not assume the liabilities of WAMU from which it acquired the loan, Chase could not be held responsible for WAMU’s alleged failure to comply with the relevant HUD regulations. The breach of contract claim thus failed.

45

FORECLOSURE ISSUES – HUD Regulations

OHIO - Bank of Am., N.A. v. Michko, 2015-Ohio-3137, Aug. 6, 2015, Ohio

Borrower argued BANA was not entitled to accelerate or foreclose unless it showed it complied with the HUD regs incorporated in her loan docs. The lender argued that since the Borrower did not specifically raise this defense, this was not made an issue, and it did not have to prove compliance with HUD regs on summary judgment. Held: When HUD regs are incorporated in the loan documents, compliance therewith is a condition precedent to foreclosure. Under Ohio law, the foreclosing lender must plead that conditions precedent have been satisfied. The borrower must then counter this allegation. But here, the borrower did not specifically and with particularity deny that the lender had failed to meet conditions precedent, so this was not made an issue in the case.

46

FORECLOSURE ISSUES – HUD Regulations

TEXAS - Fifth Cir. - Rabe v. Wells Fargo Bank, N.A., 14-40931, 2015 WL 3918906, at *2-3 (5th Cir. June 26, 2015)

Borrowers argued WF was barred from accelerating and foreclosing because it failed to conduct or make a reasonable effort to arrange a face-to-face meeting. WF argued no meeting was required. WF argued that the regulation does not define “branch office,” and HUD’s web site explains that because such meeting must be conducted by trained staff, the regulation only applies to mortgagors living within 200 mile of a servicing office.

47

FORECLOSURE ISSUES – HUD Regulations