advances in accounting behavioral research

247

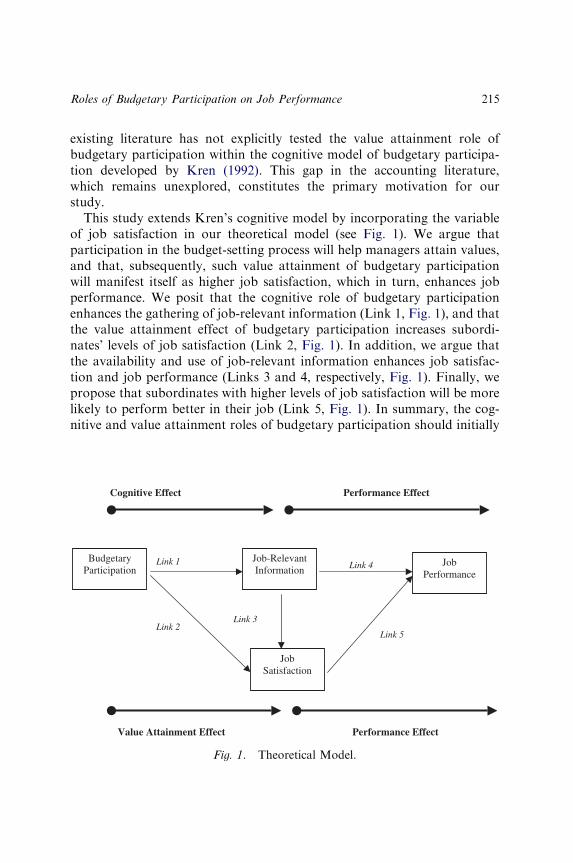

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of advances in accounting behavioral research

ADVANCES IN ACCOUNTING

BEHAVIORAL RESEARCH

i

ADVANCES IN ACCOUNTING

BEHAVIORAL RESEARCH

Series Editor: Vicky Arnold

Volumes 1–4: Series Editor: James E. Hunton

Volumes 5–7: Series Editor: Vicky Arnold

ii

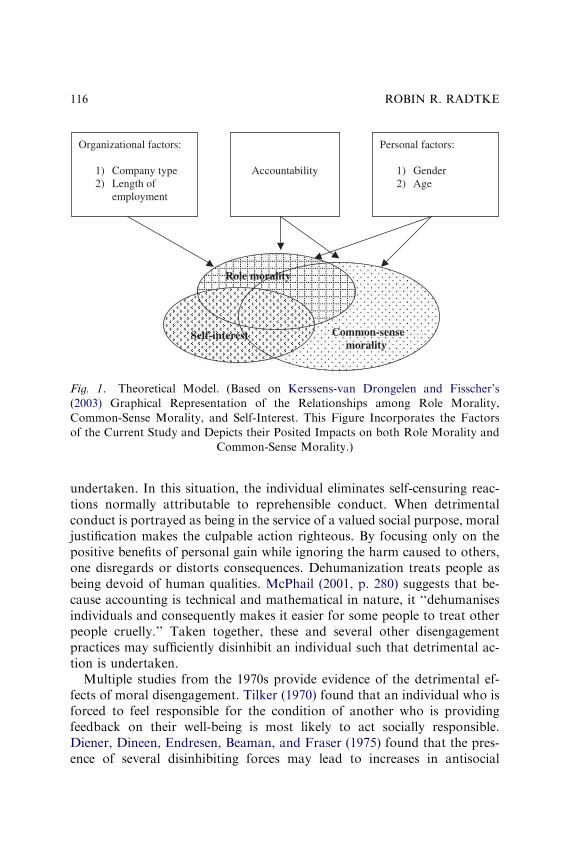

ADVANCES IN ACCOUNTING BEHAVIORAL RESEARCH VOLUME 8

ADVANCES INACCOUNTING

BEHAVIORAL RESEARCHEDITED BY

VICKY ARNOLD

Department of Accounting, School of Business, University of Connecticut, USA

and Department of Accounting and Business Information Systems, University of

Melbourne, Australia

Associate Editors:

B. DOUGLAS CLINTON

Northern Illinois University, USA

PETER LUCKETT

University of New South Wales, Australia

ROBIN ROBERTS

University of Central Florida, USA

CHRIS WOLFE

Texas A&M University, USA

SALLY WRIGHT

University of Massachusetts Boston, USA

Amsterdam – Boston – Heidelberg – London – New York – Oxford

Paris – San Diego – San Francisco – Singapore – Sydney – Tokyo

2005

iii

r 2005 Elsevier Ltd. All rights reserved.

This work is protected under copyright by Elsevier Ltd, and the following terms and conditions apply to its use:

PhotocopyingSingle photocopies of single chapters may be made for personal use as allowed by national copyright laws. Permissionof the Publisher and payment of a fee is required for all other photocopying, including multiple or systematic copying,copying for advertising or promotional purposes, resale, and all forms of document delivery. Special rates areavailable for educational institutions that wish to make photocopies for non-profit educational classroom use.

Permissions may be sought directly from Elsevier’s Rights Department in Oxford, UK: phone (+44) 1865 843830, fax(+44) 1865 853333, e-mail: [email protected]. Requests may also be completed on-line via the Elsevierhomepage (http://www.elsevier.com/locate/permissions).

In the USA, users may clear permissions and make payments through the Copyright Clearance Center, Inc., 222Rosewood Drive, Danvers, MA 01923, USA; phone: (+1) (978) 7508400, fax: (+1) (978) 7504744, and in the UKthrough the Copyright Licensing Agency Rapid Clearance Service (CLARCS), 90 Tottenham Court Road, LondonW1P 0LP, UK; phone: (+44) 20 7631 5555; fax: (+44) 20 7631 5500. Other countries may have a local reprographicrights agency for payments.

Derivative WorksTables of contents may be reproduced for internal circulation, but permission of the Publisher is required for externalresale or distribution of such material. Permission of the Publisher is required for all other derivative works, includingcompilations and translations.

Electronic Storage or UsagePermission of the Publisher is required to store or use electronically any material contained in this work, including anychapter or part of a chapter.

Except as outlined above, no part of this work may be reproduced, stored in a retrieval system or transmitted in anyform or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permissionof the Publisher.Address permissions requests to: Elsevier’s Rights Department, at the fax and e-mail addresses noted above.

NoticeNo responsibility is assumed by the Publisher for any injury and/or damage to persons or property as a matter ofproducts liability, negligence or otherwise, or from any use or operation of any methods, products, instructions orideas contained in the material herein. Because of rapid advances in the medical sciences, in particular, independentverification of diagnoses and drug dosages should be made.

First edition 2005

British Library Cataloguing in Publication DataA catalogue record is available from the British Library.

ISBN: 0-7623-1218-1ISSN: 1475-1488 (Series)

8 The paper used in this publication meets the requirements of ANSI/NISO Z39.48-1992 (Permanence of Paper).Printed in The Netherlands.

ELSEVIER B.V.

Radarweg 29

P.O. Box 211

1000 AE Amsterdam

The Netherlands

ELSEVIER Ltd

84 Theobalds Road

London

WC1X 8RR

UK

ELSEVIER Ltd

The Boulevard, Langford

Lane, Kidlington

Oxford OX5 1GB

UK

ELSEVIER Inc.

525 B Street, Suite 1900

San Diego

CA 92101-4495

USA

Working together to growlibraries in developing countries

www.elsevier.com | www.bookaid.org | www.sabre.org

iv

CONTENTS

LIST OF CONTRIBUTORS vii

REVIEWER ACKNOWLEDGEMENTS ix

EDITORIAL POLICY AND SUBMISSIONGUIDELINES

xi

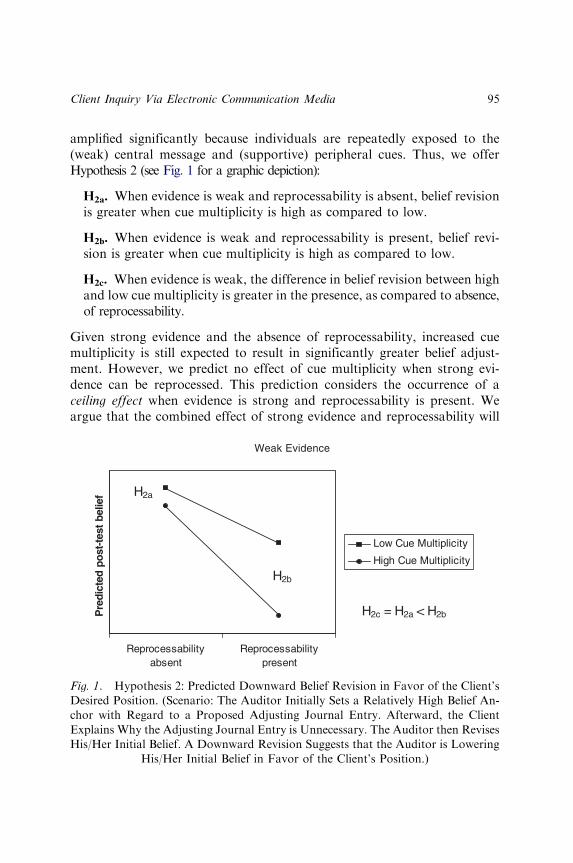

BELIEF REVISION IN ACCOUNTING: ALITERATURE REVIEW OF THE BELIEF-ADJUSTMENT MODEL

Jennifer Kahle, Robert Pinsker and Robin Pennington 1

AUDITOR CALIBRATION IN THE REVIEW PROCESSNoel Harding, Sally Hughes and Ken T. Trotman 41

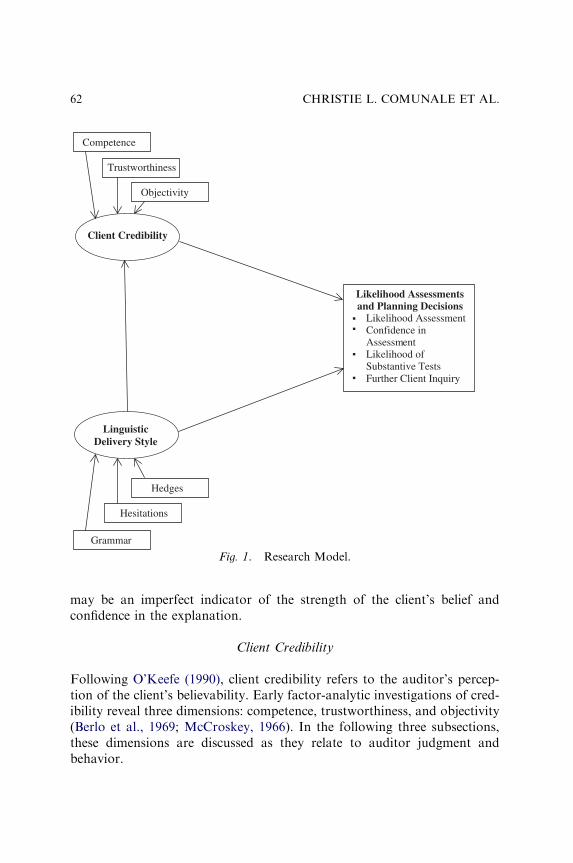

LINGUISTIC DELIVERY STYLE, CLIENTCREDIBILITY, AND AUDITOR JUDGMENT

Christie L. Comunale, Thomas R. Sexton andTerry L. Sincich

59

CLIENT INQUIRY VIA ELECTRONICCOMMUNICATION MEDIA: DOES THE MEDIUMMATTER?

Anna Noteberg and James E. Hunton 87

ROLE MORALITY AND ACCOUNTANTS’ETHICALLY SENSITIVE DECISIONS

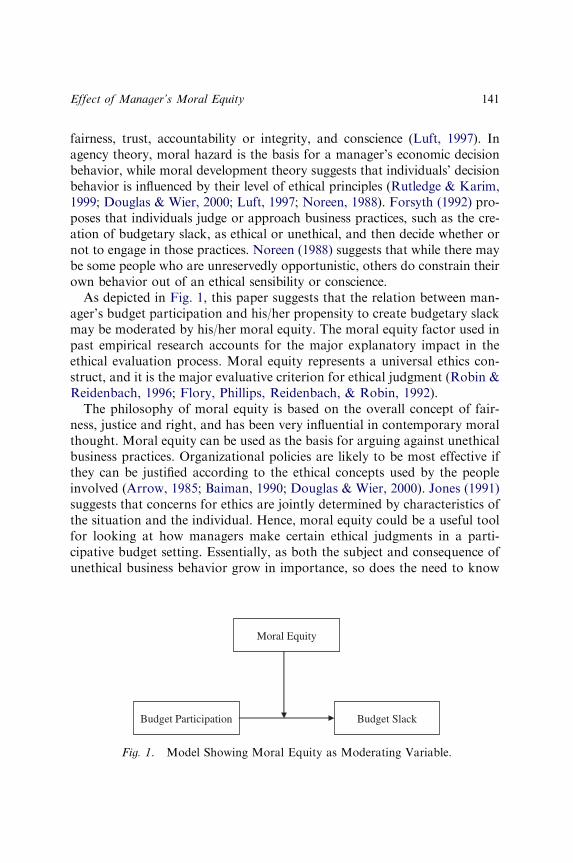

Robin R. Radtke 113

v

THE EFFECT OF MANAGER’S MORAL EQUITY ONTHE RELATIONSHIP BETWEEN BUDGETPARTICIPATION AND PROPENSITY TO CREATESLACK: A RESEARCH NOTE

Adam S. Maiga 139

ASYMMETRIC EFFECTS OF ACTIVITY-BASEDCOSTING SYSTEM COST REALLOCATION

M.G. Fennema, Jay S. Rich and Kip Krumwiede 167

EXAMINING THE ROLE OF CULTURE ANDACCULTURATION IN INFORMATION SHARING

Stephen B. Salter and Axel K.-D. Schulz 189

THE EFFECTS OF VALUE ATTAINMENT ANDCOGNITIVE ROLES OF BUDGETARYPARTICIPATION ON JOB PERFORMANCE

Vincent K. Chong, Ian R.C. Eggleton andMichele K.C. Leong

213

CONTENTSvi

LIST OF CONTRIBUTORS

Vincent K. Chong UWA Business School, The University ofWestern Australia, Australia

Christie L. Comunale School of Professional Accountancy, LongIsland University – C.W. Post Campus,USA

Ian R. C. Eggleton Waikato Management School, Universityof Waikato, New Zealand

M. G. Fennema Department of Accounting, Florida StateUniversity, USA

Noel Harding School of Accounting, University of NewSouth Wales, Australia

Sally Hughes School of Accounting, University of NewSouth Wales, Australia

James E. Hunton Accountancy Department, Bentley College,USA and Department of Accounting andInformation Management, UniversiteitMaastricht, The Netherlands

Jennifer Kahle School of Accountancy, University ofSouth Florida, USA

Kip Krumwiede College of Business and Economics, BoiseState University, USA

Michele K. C. Leong UWA Business School, The University ofWestern Australia, Australia

Adam S. Maiga School of Business Administration,University of Wisconsin – Milwaukee, USA

Anna Noteberg Department of Business Studies,Universiteit van Amsterdam, TheNetherlands

vii

Robin Pennington Department of Accounting andInformation Management, University ofTennessee, USA

Robert Pinsker College of Business and PublicAdministration, Old Dominion University,USA

Robin R. Radtke Department of Accounting, The Universityof Texas at San Antonio, USA

Jay S. Rich College of Business, Illinois StateUniversity, USA

Stephen B. Salter Universidad Adolfo Ibanez Escuela deNegocios, College of BusinessAdministration, University of Cincinnati,USA

Axel K-D. Schulz Department of Accounting and BusinessInformation Systems, The University ofMelbourne, Australia

Thomas R. Sexton College of Business, Stony BrookUniversity, USA

Terry L. Sincich Information Systems and Decision SciencesDepartment, University of South Florida,USA

Ken T. Trotman School of Accounting, University of NewSouth Wales, Australia

LIST OF CONTRIBUTORSviii

Mohammed AbdolmohammadiBentley College, USA

Elizabeth AlmerPortland State University, USA

Philip BeaulieuUniversity of Calgary, Canada

Jean BedardNortheastern University, USA

James BierstakerVillanova University, USA

Dennis M. BlineBryant College, USA

Wray BradleyUniversity of Tulsa, USA

Gary BraunUniversity of Texas at El Paso,USA

Rich BrodyUniversity of New Haven, USA

Shimin ChenUniversity of Louisiana atLafayette, USA

Vincent ChongThe University of WesternAustralia, Australia

Freddie ChooSan Francisco State University,USA

Janne ChungYork University, Canada

Bryan ChurchGeorgia Tech University, USA

Jeff CohenBoston College, USA

William N. DillaIowa State University, USA

Jesse DillardPortland State University, USA

Craig EmbySimon Fraser University, Canada

Dann FisherKansas State University, USA

Clark HamptonUniversity of Connecticut, USA

REVIEWER ACKNOWLEDGEMENTS

The Editor and Associate Editors at AABR would like to thank the many

excellent reviewers who have volunteered their time and expertise to make

this an outstanding publication. Publishing quality papers in a timely

manner would not be possible without their efforts.

ix

Joanne P. HealyKent State University, USA

Karen L. HooksFlorida Atlantic University, USA

Stacy KovarKansas State University, USA

Tanya LeeUniversity of North Texas, USA

Theresa LibbyWilfred Laurier University,Canada

Tim LindquistThe University of Northern Iowa,USA

Jill McKinnonMacquarie University, Australia

Mario MalettaNortheastern University, USA

Maureen MaschaMarquette University, USA

Elaine MauldinUniversity of Missouri, USA

Rob NieschwietzUniversity of Colorado at Denver,USA

Andreas NikolaouBowling Green State University,USA

Hossein NouriThe College of New Jersey, USA

Ed O’DonnellArizona State University, USA

Laurie PantSuffolk University, USA

Robert J. ParkerUniversity of New Orleans, USA

Will QuilliamUniversity of South Florida, USA

Randall RentfroFlorida Atlantic University, USA

Andrew J. RosmanUniversity of Connecticut, USA

Scott SummersBrigham Young University, USA

Steve SuttonUniversity of Connecticut, USA

Linda ThorneYork University, Canada

Kristin WentzelLa Salle University, USA

John WermertDrake University, USA

Patrick WheelerUniversity of Missouri, USA

Brett WilkinsonBaylor University, USA

Bernard Wong-On-WingWashington State University, USA

Alex YenUniversity of Connecticut, USA

REVIEWER ACKNOWLEDGEMENTSx

EDITORIAL POLICY AND

SUBMISSION GUIDELINES

Advances in Accounting Behavioral Research (AABR) publishes articles en-

compassing all areas of accounting that incorporate theory from and con-

tribute new knowledge and understanding to the fields of applied

psychology, sociology, management science, and economics. The journal

is primarily devoted to original empirical investigations; however, literature

review papers, theoretical analyses, and methodological contributions are

welcome. AABR is receptive to replication studies, provided they investigate

important issues and are concisely written. The journal especially welcomes

manuscripts that integrate accounting issues with organizational behavior,

human judgment/decision making, and cognitive psychology.

Manuscripts will be blind-reviewed by two reviewers and an associate editor.

The recommendations of the reviewers and associate editor will be used to

determine whether to accept the paper as is, accept the paper with minor re-

visions, reject the paper or to invite the authors to revise and resubmit the paper.

Manuscript Submission

Manuscripts should be forwarded to the editor, Vicky Arnold, at

[email protected] via e-mail. All text, tables, and figures

should be incorporated into a Word document prior to submission. The

manuscript should also include a title page containing the name and address

of all authors and a concise abstract. Also, include a separate Word doc-

ument with any experimental materials or survey instruments. If you are

unable to submit electronically, please forward the manuscript along with

the experimental materials to the following address:

Vicky Arnold, Editor

Advances in Accounting Behavioral Research,

Department of Accounting U41A

School of Business

University of Connecticut

Storrs, CT 06269-2041

xi

References should follow the APA (American Psychological Association)

standard. References should be indicated by giving (in parentheses) the

author’s name followed by the date of the journal or book; or with the date

in parentheses, as in ‘suggested by Earley (2000)’.

In the text, use the form Rosman et al. (1995) where there are more than

two authors, but list all authors in the references. Quotations of more than

one line of text from cited works should be indented and citation should

include the page number of the quotation, e.g. (Dunbar, 2001 p. 56).

Citations for all articles referenced in the text of the manuscript should be

shown in alphabetical order in the Reference list at the end of the man-

uscript. Only articles referenced in the text should be included in the Ref-

erence list. Format for references is as follows:

For journals:

Dunn, C.L., & Gerard, G.J. (2001). Auditor efficiency and effectiveness with

diagrammatic and linguistic conceptual model representations. International

Journal of Accounting Information Systems, 2(3), 1–40.

For books:

Ashton, R.H., & Ashton, A.H. (1995). Judgment and decision-making research

in accounting and auditing. New York, NY: Cambridge University Press.

For a thesis:

Smedley, G.A. (2001). The effects of optimization on cognitive skill acquisition

from intelligent decision aids. Unpublished doctoral dissertation, University.

For a working paper:

Thorne, L., Massey, D.W., & Magnan, M. (2000). Insights into selection-

socialization in the audit profession: An examination of the moral reasoning

of public accountants in the United States and Canada. Working paper

York University, North York, Ontario.

For papers from conference proceedings, chapters from book, etc.:

Messier, W.F. (1995). Research in and development of audit decision aids. In:

R.H. Ashton, & A.H. Ashton (Ed.), Judgment and decision making in

accounting and auditing (pp. 207–230). New York: Cambridge University Press.

EDITORIAL POLICY AND SUBMISSION GUIDELINESxii

BELIEF REVISION IN

ACCOUNTING: A LITERATURE

REVIEW OF THE

BELIEF-ADJUSTMENT MODEL

Jennifer Kahle, Robert Pinsker and Robin Pennington

ABSTRACT

The belief-adjustment model has been an integral part of accounting

research in belief revision, especially in the examination of order effects.

Hogarth and Einhorn ((1992) Cognitive Psychology, 24, 1–55) created

the belief-adjustment model to serve as a theoretical framework for

studying individuals’ decision-making processes. The model examines

several aspects of decision-making, such as encoding, response mode, and

task factors. The purpose of this chapter is to provide a comprehensive

examination of the accounting studies that have used the theoretical

framework of the belief-adjustment model in auditing, tax, and financial

accounting contexts. Roberts’ ((1998) Journal of the American Taxation

Association, 20, 78–121) model of tax accountants’ decision-making is

used as a guideline to organize the research into categories. By using

Roberts’ categorization, we can better sort out the mixed results of some

prior studies and also expand the review to include a more comprehensive

look at the model and its application to accounting. While many variables

have been examined with respect to their effect on accounting professionals’

Advances in Accounting Behavioral Research

Advances in Accounting Behavioral Research, Volume 8, 1–40

Copyright r 2005 by Elsevier Ltd.

All rights of reproduction in any form reserved

ISSN: 1475-1488/doi:10.1016/S1475-1488(04)08001-9

1

belief revisions, most studies examine them in isolation and do not consider

the interaction effects that these variables may have. Our framework also

identifies areas of the belief-adjustment model that need further research.

INTRODUCTION

Professional judgment in accounting has been described in general terms as

a continuous and incremental process (Gibbins, 1984). Most judgment tasks

involve evidence that is evaluated in a sequential nature. Although

sequential processing can provide economy in decision-making in terms of

smaller demands on memory and information-processing load, it can also

have detrimental effects, such as order effects in belief updating. Order

effects, biases, and the use of heuristics resulting from the method by which

individuals update their beliefs have been found in various areas of

accounting, including auditing (e.g., Ashton & Ashton, 1988; Asare, 1992),

tax (e.g., Pei, Reckers, & Wyndelts, 1990), and financial reporting (Pinsker,

2004).

Much of the judgment and decision-making accounting literature has

been influenced by Hogarth and Einhorn’s (1992) theory of belief revision.

The theory accounts for order effects as they arise from the interaction of

information-processing strategies and task characteristics. In particular,

Hogarth and Einhorn’s belief-adjustment model assumes people handle

belief revision tasks by a general, sequential anchoring and adjustment

process in which current opinion, or the anchor, is adjusted by the impact of

succeeding pieces of evidence. The model predicts that under conditions of

evaluating a short series of simple information, a primacy effect will occur

(i.e., the decision-maker will place more weight on the earliest information

received) if the judgment is made after viewing all the evidence. However, if

a short series of mixed (i.e., both positive and negative relative to a current

hypothesis) information is evaluated piece-by-piece, differential weighting of

the mixed information will produce a recency effect (i.e., the decision-maker

will place more weight on the latest information received).

An abundance of accounting literature examining recency effects has been

motivated by the belief-adjustment model and findings of order effects in the

psychology literature. Findings suggest that, in the absence of some

mitigating influence, many accounting judgments are subject to recency

effects. From a normative perspective, the sequence of evidence evaluation

should not affect the conclusion drawn from the evidence (Christian &

Reneau, 1990). The implications for accounting professionals may be

JENNIFER KAHLE ET AL.2

systematic biases in judgments leading to reduced efficiency and effec-

tiveness.

The purpose of this chapter is to provide a comprehensive review of the

accounting studies that have used the theoretical framework of the belief-

adjustment model in auditing, tax, and financial accounting contexts. The

emphasis will be on the factors that have been shown to influence or mitigate

order effects. Roberts’ (1998) model of tax accountants’ decision-making will

be used as a guideline to organize the factors into five main categories,

including (1) individual psychological factors, (2) environmental factors, (3)

input task factors, (4) processing factors, and (5) output task factors. This

categorization is similar to that of Gibbins’ (1984) model of professional

judgment in public accounting, whose groups include the person, stimulus,

environment, decision, and judgment process. Categorization in this manner

recognizes the separate influences of both external (environmental and task)

and internal (individual) factors and reflects the recommendation by

Hogarth and Einhorn (1992) to study further procedural and task variables

that can affect belief revision. In an evaluation of recency effects in audit

judgments, Trotman and Wright (2000) noted that results have been mixed

across studies. By using Roberts’ (1998) categorizations, we can better

understand the mixed results of the prior auditing studies, and also expand

the review to include a more comprehensive look at the model and its

application to various areas of accounting.

The remainder of this chapter is organized into four sections. The first

section describes the belief-adjustment model as proposed by Hogarth and

Einhorn (1992). The following section discusses the general applications of

the belief-adjustment model to accounting. Next, factors tested for

association with belief revision are reviewed and categorized. The final

section provides some concluding remarks as well as suggested directions for

future research.

THE BELIEF-ADJUSTMENT MODEL

Order Effects

Bayes’ theorem was the dominant normative model of belief revision in

accounting prior to 1988. The theorem gained popularity because it is a

logical consequence of conditional probabilities. However, research in

behavioral decision-making suggests that it is incomplete as a descriptive

model of belief revision as it cannot adequately predict intuitive revision

Belief Revision in Accounting 3

(Ashton & Ashton, 1988). Some researchers suggest that the discrepancy

is due to the tendency for intuitive revisions to be driven by task charac-

teristics, such as presentation order of information, which are irrelevant to

the normative model (Pitz, Downing, & Reinhold, 1967). A large body of

literature in psychology and accounting (e.g., Hogarth & Einhorn, 1992;

Ashton & Ashton, 1988; Pei et al., 1992a, b; Kennedy, 1993) has confirmed

the existence of presentation order effects on individual belief revisions.

Hogarth and Einhorn (1992, p. 3) define order effects with the following

example:

There are two pieces of evidence, A and B. Some subjects express an opinion after seeing

the information in the order A–B; others receive the information in the order B–A. An

order effect occurs when opinions after A–B differ from those after B–A.

Primacy occurs when an individual places more weight on the earlier

evidence in the sequence, while recency occurs when an individual places

more weight on the latter (more recent) evidence in the sequence.

Hogarth and Einhorn (1992) developed a ‘‘belief-adjustment model’’ to

more fully explain how evidence is encoded and processed. They adapted the

general concept of anchoring and adjustment (i.e., forming a belief and then

adjusting it based on new information to form a new belief) to include

heuristics into the model. Research since 1988 has provided descriptive

validity for using the belief-adjustment model, rather than Bayes’ theorem,

to explain belief revision (e.g., Ashton & Ashton, 1988; Pei et al., 1990;

Bamber, Ramsay, & Tubbs, 1997).

There are four distinct aspects in which the belief-adjustment model differs

from Bayesian probability (Krishnamoorthy, Mock, & Washington, 1999).

The belief-adjustment model (1) predicts that belief revision is influenced by

the order in which evidence is evaluated; (2) entails an anchoring and

adjustment strategy where the extent of belief revision is based on the size of

the anchor (current opinion), a strategy that violates the fundamental tenets

of Bayesian probability theory; (3) explicitly models the decision-maker’s

sensitivity toward evidence; and (4) allows one to increase or decrease

support for a hypothesis (e.g., that an account is fairly stated) without

affecting support for its complement (e.g., that an account is not fairly

stated). In an examination of four theoretical models of belief revision,

including a version of Bayesian inference, Krishnamoorthy et al. found that

the belief-adjustment model is the only model that captures both the

direction and magnitude of auditors’ belief revisions. Hogarth and Einhorn’s

(1992) theory of belief revision accounts for order effects by examining the

interaction of task characteristics and information processing strategies.

JENNIFER KAHLE ET AL.4

Task Variables

In forming their model, Hogarth and Einhorn (1992) considered three task

variables: (1) the complexity of the individual items of evidence to be

processed, (2) the length of the series of items, and (3) the manner in which

judgments are elicited, which will be referred to as response mode.1

Complexity is a function of the amount of information for each piece of

evidence that needs to be processed as well as the lack of familiarity with the

task (i.e., less familiar equals more complex and vice versa). Complexity is

important to belief revision since it relates to human processing ability. As

complexity increases, people may resort to simplifying strategies to ease

cognitive strain (Hogarth & Einhorn, 1992).

Length of series refers to the number of pieces of evidence to be evaluated.

Based on their review of several studies, Hogarth and Einhorn (1992)

consider a series of between 2 and 12 items to be ‘‘short’’ and a series of 17

or more items ‘‘long.’’ To distinguish length of series from complexity,

remember that complexity results from the amount of information

processing required and not necessarily the length of the series. As Arnold,

Collier, Leech, and Sutton (2000) indicate, a ‘‘complex’’ task is one that is

unfamiliar to the decision-maker (as noted in the previous paragraph) or

one that requires heavy information processing (defined as either a large

number or a long series of items). Therefore, a complex task could result

from a short series of evidence (if unfamiliar or full of detail) or

automatically from a long series. A ‘‘simple’’ task results from a short

series of familiar items.

Response mode concerns the manner in which judgments are elicited. Hogarth

and Einhorn (1992) consider two types: Step-by-Step (SbS) and End-of-Sequence

(EoS). The SbS mode is a ‘‘sequential’’ procedure whereby participants express

their beliefs each time they integrate a new piece of evidence. On the other hand,

the EoS mode is a ‘‘simultaneous’’ procedure in which participants express their

opinions only after all the information has been presented.

Encoding

Hogarth and Einhorn (1992) also acknowledge the impact of the method by

which individuals encode or process information on their subsequent

judgments. Accordingly, the predictions of the belief-adjustment model are

affected by two additional encoding variables: (1) processing mode (SbS

versus EoS), and (2) task type (evaluation versus estimation).

Belief Revision in Accounting 5

While related, the processing mode cannot be solely determined by the

required response mode. When the task is completed in an SbS response

mode, the individual must employ an SbS process by adjusting his or her

opinion incrementally for each piece of evidence processed. However, if a

task is completed in an EoS response mode, an individual can employ either

an SbS or an EoS processing mode. The EoS processing mode requires an

individual to aggregate all items prior to integrating them with the anchor,

which can be cognitively demanding. Thus, the processing mode should

depend on the cognitive demands of the task. Generally, the SbS processing

mode will be used when the task is more complex. This allows the individual

to continually integrate information with the anchor. The EoS mode is

expected to be used for a simpler task where aggregating the latter

information is cognitively easier.

In addition to task complexity, psychology and accounting research have

examined processing mode with respect to level of experience. Specifically,

Yates (1990) indicated less experienced individuals employ a sequential

(SbS) decision-making process. As individual decision-makers gain experi-

ence, they develop more ‘‘sophisticated’’ decision-making processes,

consistent with an EoS processing mode (Anderson, 1988). Further, less-

experienced individuals may employ an SbS processing mode to reduce

cognitive load (Arnold et al., 2000) or to reduce the effort necessary to

process a task (Hunton & McEwen, 1997).

Hogarth and Einhorn (1992) also make a distinction between evaluation

and estimation tasks. In evaluation tasks, information is encoded as positive

or negative relative to the hypothesis under consideration. Here, evidence is

seen as bipolar relative to the hypothesis and can be expressed by some

value on the continuum between ‘‘false’’ and ‘‘true.’’ On the other hand,

estimation tasks involve assessing a ‘‘moving average’’ that reflects the

position of each new piece of evidence relative to current opinion (involving

a unipolar scale). Research in accounting judgments has generally required

and found support for the use of the evaluation form of the model (Ashton

& Ashton, 1988; Tubbs, Messier, & Knechel, 1990).

To our knowledge, no accounting study has used the estimation task. As

Hogarth and Einhorn (1992, p. 9) indicated, estimation tasks use data that

fit ‘‘averaging models;’’ whereas, evaluation tasks use data that fit ‘‘adding

models.’’ In the auditing domain (where the majority of belief-adjustment

model research has taken place), Messier and Tubbs (1994) contend that an

auditor would evaluate an item and its relationship to an audit assertion

before revising beliefs about the assertion. Thus, auditors in particular are

assumed to generally employ an additive model when revising beliefs

JENNIFER KAHLE ET AL.6

(consistent with an evaluation task). Although there have been accounting

studies that used only positive or negative information in their tasks (e.g.,

Ashton & Ashton, 1988; Tubbs et al., 1990), the results obtained were

measured and analyzed in an additive fashion.2

Anchoring and Adjustment Process

The belief-adjustment model assumes that people revise beliefs through a

sequential anchoring and adjustment process in which the current opinion (an

anchor) is adjusted by the impact of subsequent pieces of information. The

algebraic form of the belief-adjustment model can generally be written as3

Sk ¼ Sk�1 þ wk½sðxkÞ � R�

where

Sk ¼ degree of belief in some hypothesis, after evaluating k pieces of

evidence (0pSkp1)

Sk�1 ¼ anchor or prior belief. The initial strength of belief is denoted S0

sðxkÞ ¼ subjective evaluation of the kth piece of evidence (Different

people may accord the same evidence, xk, different evaluations)

R ¼ the reference point against which the impact of the kth piece of

evidence is evaluated

wk ¼ the adjustment weight for the kth piece of evidence (0pwkp1).

The adjustment weight for the kth piece of evidence, wk, can be further

defined as

wk ¼aSk�1 when sðxkÞpR

bð1� Sk�1Þ when sðxkÞ4R

(

where

a ¼ the sensitivity toward negative evidence, and

b ¼ the sensitivity toward positive evidence.

The formula implies that wk is related to the strength of the anchor

through a ‘‘contrast’’ effect such that large anchors are ‘‘hurt’’ more than

smaller ones by the same negative evidence. Thus, the magnitude of the

belief revision is proportional to the prior belief, Sk�1; for negative

evidence and proportional to the inverse of the prior belief, 1� Sk�1; forpositive evidence. The a and b variables are constants, which represent an

Belief Revision in Accounting 7

individual’s sensitivity toward negative and positive evidence, respec-

tively, and are posited to be functions of both individual and external

variables.

For SbS processing, the adjustment weight, wk, will depend on the sign of

the new evidence and the level of the anchor, Sk�1; as described above.

However, under an EoS processing mode, the individual makes only one

adjustment, and the model can be simplified to

Sk ¼ S0 þ wk½sðx1; :::; xkÞ � R�,

where s(x1,y, xk) is some function, possibly a weighted average of the items

that follow the anchor.

The contrast assumption makes a prediction regarding the information

being evaluated. Specifically, it predicts whether primacy, recency, or no

order effect will occur in belief revision (Table 1). Under a short series of

simple information evaluated with EoS processing, the model always

predicts primacy. Conversely, the model predicts recency for SbS processing

of mixed evidence and no effect for consistent evidence. Under a short series

of complex information (i.e., full of details), the model always predicts

recency for the evaluation of mixed evidence and no order effect for the

evaluation of consistent evidence. Finally, as more information is processed

(long series), decrements in a and b are expected, which eventually leads to

predictions of primacy.

Table 1. Order Effect Predictionsa.

Type of Evidence Response mode Mixed Consistent

EoSb SbSc EoSb SbSc

Short series

Simple Primacy Recency Primacy No effect

Complex Recency Recency No effect No effect

Long series Toward primacy Toward primacy Primacy Primacy

aPredictions assume the evaluation mode (R ¼ 0) of encoding, which is consistent with studies

in accounting (see Note 1). Predictions under the estimation mode for both mixed and

consistent evidence would be exactly the same as the above predictions for mixed evidence

under the evaluation mode.bEoS ¼ End-of-Sequence or simultaneous processing.cSbS ¼ Step-by-Step or sequential processing.

JENNIFER KAHLE ET AL.8

BELIEF REVISION IN ACCOUNTING

Research in accounting examining the belief-adjustment model, with the

exception of Anderson and Maletta (1999), has generally been interested in

the predicted recency effects for a short series of mixed evidence where

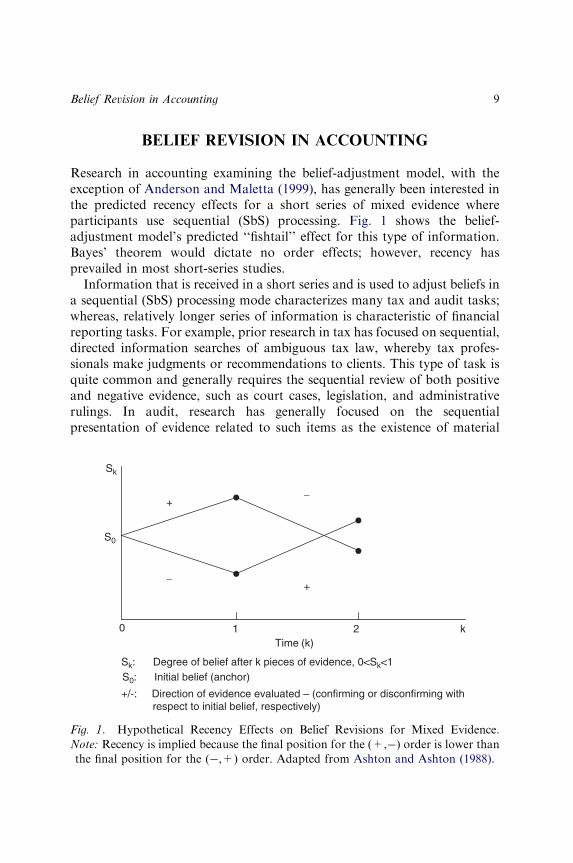

participants use sequential (SbS) processing. Fig. 1 shows the belief-

adjustment model’s predicted ‘‘fishtail’’ effect for this type of information.

Bayes’ theorem would dictate no order effects; however, recency has

prevailed in most short-series studies.

Information that is received in a short series and is used to adjust beliefs in

a sequential (SbS) processing mode characterizes many tax and audit tasks;

whereas, relatively longer series of information is characteristic of financial

reporting tasks. For example, prior research in tax has focused on sequential,

directed information searches of ambiguous tax law, whereby tax profes-

sionals make judgments or recommendations to clients. This type of task is

quite common and generally requires the sequential review of both positive

and negative evidence, such as court cases, legislation, and administrative

rulings. In audit, research has generally focused on the sequential

presentation of evidence related to such items as the existence of material

0 1 2 k

Time (k)

Sk: Degree of belief after k pieces of evidence, 0<Sk<1

S0: Initial belief (anchor)

+/-: Direction of evidence evaluated – (confirming or disconfirming with respect to initial belief, respectively)

S0

+

Sk

−+

−

Fig. 1. Hypothetical Recency Effects on Belief Revisions for Mixed Evidence.

Note: Recency is implied because the final position for the (+,�) order is lower than

the final position for the (�,+) order. Adapted from Ashton and Ashton (1988).

Belief Revision in Accounting 9

errors or fraud, going concern judgments, inventory write-downs, or internal

control evaluations. As mentioned by Trotman and Wright (2000), due to

time constraints, a short series of information is relevant since auditors

typically are not expected to obtain an extended set of evidence (e.g., over 15

items) for a particular assertion. In financial reporting, the sequential release

of a longer series of information items is characteristic of the new online

business-reporting model favored by the American Institute of Certified

Public Accountants (AICPA) and other regulatory constituents (2002).

Initial studies of the belief-adjustment model in accounting were primarily

concerned with testing the applicability of the model to a particular

accounting area (e.g., audit or tax). The initial belief revision study in

accounting by Ashton and Ashton (1988) tested the strength of the evidence

presented, the response mode, and the initial anchor. Since then, a variety of

other individual and external variables have been included as factors

important in the prediction of order effects. Recency effects consistent with

the belief-adjustment model have generally been found to be robust in the

absence of some mitigating factor.

FACTORS TESTED FOR ASSOCIATIONWITH BELIEF

REVISION EFFECTS

The factors that have been tested for association with belief revision effects

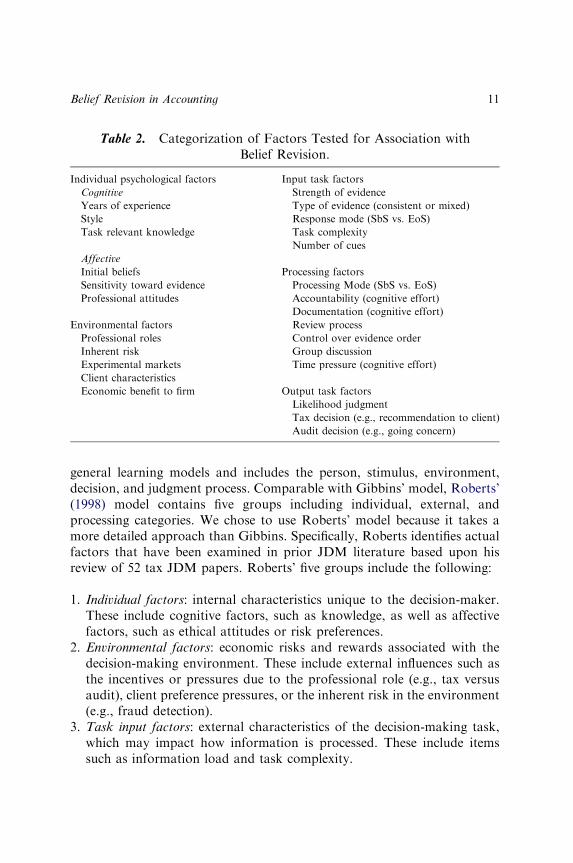

in accounting have been categorized in Table 2 using Roberts’ (1998)

economic psychology-processing (EPP) model that was developed for tax

accountants’ judgment and decision-making (JDM). The EPP model

emphasizes the cognitive decision-making process, with both individual

(internal) and economic (external) factors having varying degrees of

influence on cognitive processing for specific tasks. By using Roberts’

model as a framework, we begin with a solid foundation of the factors which

have been examined in prior literature, and we have an organization that

follows Hogarth and Einhorn’s (1992) suggestion to consider the influence

of individual and external factors on belief revision. While Roberts’ model

was created to better understand tax JDM, the categories are not tax

specific. The factors within each group (e.g., experience and task complex-

ity) also have been examined in audit JDM and, more specifically, the

overall belief revision process.

From a broad perspective, the EPP model is similar to Gibbins’ (1984)

model of professional judgment in public accounting, which is derived from

JENNIFER KAHLE ET AL.10

general learning models and includes the person, stimulus, environment,

decision, and judgment process. Comparable with Gibbins’ model, Roberts’

(1998) model contains five groups including individual, external, and

processing categories. We chose to use Roberts’ model because it takes a

more detailed approach than Gibbins. Specifically, Roberts identifies actual

factors that have been examined in prior JDM literature based upon his

review of 52 tax JDM papers. Roberts’ five groups include the following:

1. Individual factors: internal characteristics unique to the decision-maker.

These include cognitive factors, such as knowledge, as well as affective

factors, such as ethical attitudes or risk preferences.

2. Environmental factors: economic risks and rewards associated with the

decision-making environment. These include external influences such as

the incentives or pressures due to the professional role (e.g., tax versus

audit), client preference pressures, or the inherent risk in the environment

(e.g., fraud detection).

3. Task input factors: external characteristics of the decision-making task,

which may impact how information is processed. These include items

such as information load and task complexity.

Table 2. Categorization of Factors Tested for Association with

Belief Revision.

Individual psychological factors Input task factors

Cognitive Strength of evidence

Years of experience Type of evidence (consistent or mixed)

Style Response mode (SbS vs. EoS)

Task relevant knowledge Task complexity

Number of cues

Affective

Initial beliefs Processing factors

Sensitivity toward evidence Processing Mode (SbS vs. EoS)

Professional attitudes Accountability (cognitive effort)

Documentation (cognitive effort)

Environmental factors Review process

Professional roles Control over evidence order

Inherent risk Group discussion

Experimental markets Time pressure (cognitive effort)

Client characteristics

Economic benefit to firm Output task factors

Likelihood judgment

Tax decision (e.g., recommendation to client)

Audit decision (e.g., going concern)

Belief Revision in Accounting 11

4. Decision-processing factors: strategies used by decision makers to simplify

the judgment process. These strategies generally have been found to

influence cognitive effort through such pressures as accountability,

decision aids, or the review process.

5. Task output factors: type of decision required. For instance, consulting

and reviewing tasks are expected to influence the decision-making process

differently.

Similar to the broader JDM literature, the extant belief revision literature

has examined a multitude of variables and their effects on belief revision.

However, until now, there has been no clear, overall organization of these

variables. Using Roberts’ (1998) groupings will allow future research to

more directly draw conclusions about any general effects of each group and

potential interactions between the groups of factors. A solid organizational

framework will allow us to identify which areas are in need of additional

research. It also will enable researchers to better ensure that they have

considered (or controlled for) all possible influences on the belief revision

process. Finally, this categorization may allow future research to examine

the belief revision process as a whole by simultaneously examining factors

from each fundamental group mentioned earlier.

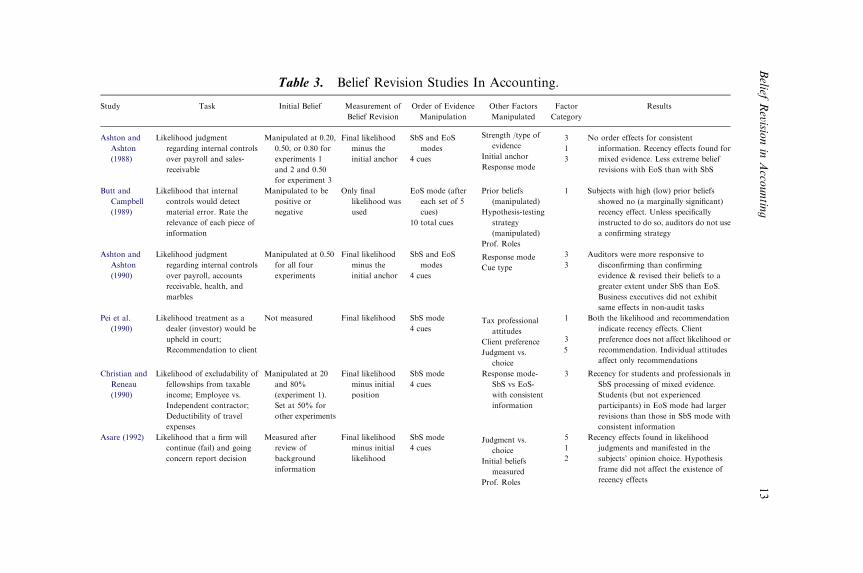

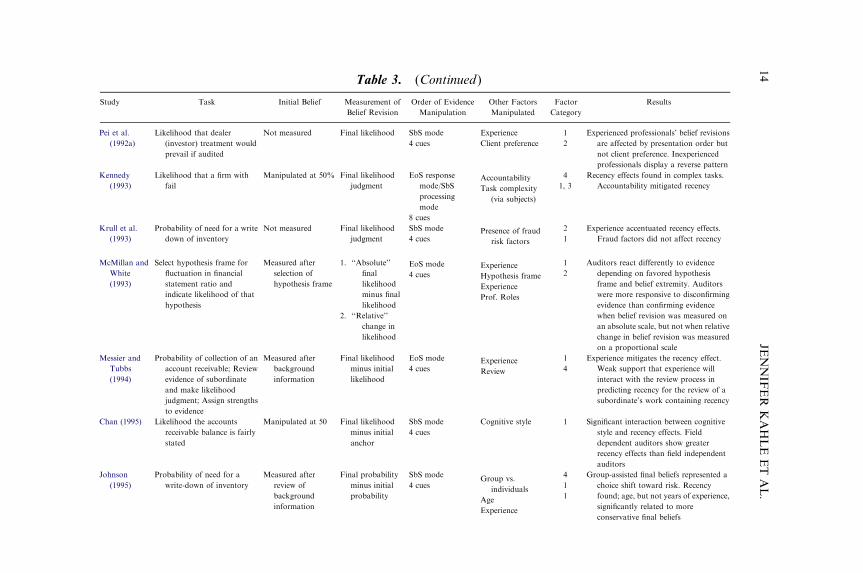

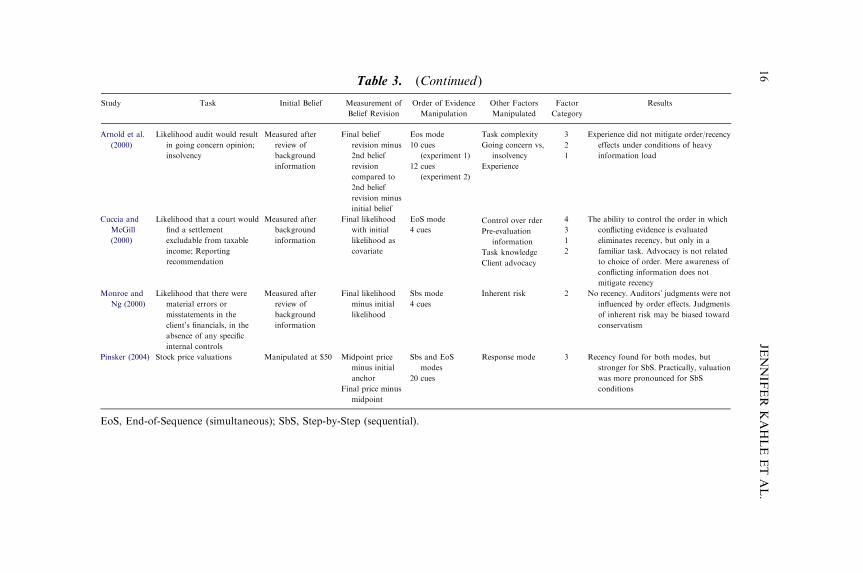

Table 3 provides chronologically a list of belief revision studies in

accounting and highlights the factors listed in Table 2. Specifically, of the 25

accounting studies listed, 19 have used the SbS processing mode. While a

few studies have used the EoS mode or consistent information, these have

generally been examined in addition to the SbS mode and mixed

information for comparison purposes. All but one of the studies have used

a short series of information (between 4 and 10 cues), with 4 cues being the

most common choice. These studies, along with the related findings, will be

discussed as they relate to the following sections.

Individual Psychological Factors

Individual psychological factors include both cognitive and affective factors.

Sixteen of the 25 studies listed examine, directly or indirectly, at least one

individual psychological factor. Studies of individual factors in accounting

have primarily focused on experience, a cognitive factor, and sensitivity

toward evidence, an affective factor. Task-relevant knowledge and

individual attitudes, including prior beliefs, have also been examined.

JENNIFER KAHLE ET AL.12

Table 3. Belief Revision Studies In Accounting.

Study Task Initial Belief Measurement of

Belief Revision

Order of Evidence

Manipulation

Other Factors

Manipulated

Factor

Category

Results

Ashton and

Ashton

(1988)

Likelihood judgment

regarding internal controls

over payroll and sales-

receivable

Manipulated at 0.20,

0.50, or 0.80 for

experiments 1

and 2 and 0.50

for experiment 3

Final likelihood

minus the

initial anchor

SbS and EoS

modes

4 cues

Strength /type of

evidence

Initial anchor

Response mode

3 No order effects for consistent

information. Recency effects found for

mixed evidence. Less extreme belief

revisions with EoS than with SbS

1

3

Butt and

Campbell

(1989)

Likelihood that internal

controls would detect

material error. Rate the

relevance of each piece of

information

Manipulated to be

positive or

negative

Only final

likelihood was

used

EoS mode (after

each set of 5

cues)

10 total cues

Prior beliefs

(manipulated)

Hypothesis-testing

strategy

(manipulated)

Prof. Roles

1 Subjects with high (low) prior beliefs

showed no (a marginally significant)

recency effect. Unless specifically

instructed to do so, auditors do not use

a confirming strategy

Ashton and

Ashton

(1990)

Likelihood judgment

regarding internal controls

over payroll, accounts

receivable, health, and

marbles

Manipulated at 0.50

for all four

experiments

Final likelihood

minus the

initial anchor

SbS and EoS

modes

4 cues

Response mode

Cue type

3 Auditors were more responsive to

disconfirming than confirming

evidence & revised their beliefs to a

greater extent under SbS than EoS.

Business executives did not exhibit

same effects in non-audit tasks

3

Pei et al.

(1990)

Likelihood treatment as a

dealer (investor) would be

upheld in court;

Recommendation to client

Not measured Final likelihood SbS mode

4 cuesTax professional

attitudes

Client preference

Judgment vs.

choice

1 Both the likelihood and recommendation

indicate recency effects. Client

preference does not affect likelihood or

recommendation. Individual attitudes

affect only recommendations

3

5

Christian and

Reneau

(1990)

Likelihood of excludability of

fellowships from taxable

income; Employee vs.

Independent contractor;

Deductibility of travel

expenses

Manipulated at 20

and 80%

(experiment 1).

Set at 50% for

other experiments

Final likelihood

minus initial

position

SbS mode

4 cues

Response mode-

SbS vs EoS-

with consistent

information

3 Recency for students and professionals in

SbS processing of mixed evidence.

Students (but not experienced

participants) in EoS mode had larger

revisions than those in SbS mode with

consistent information

Asare (1992) Likelihood that a firm will

continue (fail) and going

concern report decision

Measured after

review of

background

information

Final likelihood

minus initial

likelihood

SbS mode

4 cuesJudgment vs.

choice

Initial beliefs

measured

Prof. Roles

5 Recency effects found in likelihood

judgments and manifested in the

subjects’ opinion choice. Hypothesis

frame did not affect the existence of

recency effects

1

2

Belief

Revisio

nin

Acco

untin

g13

Pei et al.

(1992a)

Likelihood that dealer

(investor) treatment would

prevail if audited

Not measured Final likelihood SbS mode

4 cues

Experience

Client preference

1 Experienced professionals’ belief revisions

are affected by presentation order but

not client preference. Inexperienced

professionals display a reverse pattern

2

Kennedy

(1993)

Likelihood that a firm with

fail

Manipulated at 50% Final likelihood

judgment

EoS response

mode/SbS

processing

mode

8 cues

Accountability

Task complexity

(via subjects)

4 Recency effects found in complex tasks.

Accountability mitigated recency1, 3

Krull et al.

(1993)

Probability of need for a write

down of inventory

Not measured Final likelihood

judgment

SbS mode

4 cuesPresence of fraud

risk factors

Experience

2 Experience accentuated recency effects.

Fraud factors did not affect recency1

McMillan and

White

(1993)

Select hypothesis frame for

fluctuation in financial

statement ratio and

indicate likelihood of that

hypothesis

Measured after

selection of

hypothesis frame

1. ‘‘Absolute’’

final

likelihood

minus final

likelihood

2. ‘‘Relative’’

change in

likelihood

EoS mode

4 cues Hypothesis frame

Experience

Prof. Roles

1 Auditors react differently to evidence

depending on favored hypothesis

frame and belief extremity. Auditors

were more responsive to disconfirming

evidence than confirming evidence

when belief revision was measured on

an absolute scale, but not when relative

change in belief revision was measured

on a proportional scale

2

Messier and

Tubbs

(1994)

Probability of collection of an

account receivable; Review

evidence of subordinate

and make likelihood

judgment; Assign strengths

to evidence

Measured after

background

information

Final likelihood

minus initial

likelihood

EoS mode

4 cuesExperience

Review

1 Experience mitigates the recency effect.

Weak support that experience will

interact with the review process in

predicting recency for the review of a

subordinate’s work containing recency

4

Chan (1995) Likelihood the accounts

receivable balance is fairly

stated

Manipulated at 50 Final likelihood

minus initial

anchor

SbS mode

4 cues

Cognitive style 1 Significant interaction between cognitive

style and recency effects. Field

dependent auditors show greater

recency effects than field independent

auditors

Johnson

(1995)

Probability of need for a

write-down of inventory

Measured after

review of

background

information

Final probability

minus initial

probability

SbS mode

4 cuesGroup vs.

individuals

Age

Experience

4 Group-assisted final beliefs represented a

choice shift toward risk. Recency

found; age, but not years of experience,

significantly related to more

conservative final beliefs

1

1

Table 3. (Continued)

Study Task Initial Belief Measurement of

Belief Revision

Order of Evidence

Manipulation

Other Factors

Manipulated

Factor

Category

ResultsJE

NNIF

ER

KAHLEET

AL.

14

Cushing and

Ahlawat

(1996)

Likelihood that a firm will

continue and going

concern report decision

Measured after

background

information

Final likelihood

minus initial

likelihood

SbS mode

4 cues

Documentation

requirement

Judgment vs.

choice

4 Recency effect in the audit judgments of

no-documentation subjects, but not

among subjects who performed the

documentation task. No recency effect

on decision for type of report to issue

5

Hite and

Stock

(1996)

Probability of employee vs.

independent contractor;

Rate the strength of each

piece of evidence

Measured after

background

information

Final likelihood

minus initial

likelihood

SbS and EoS

modes

4 cues

Response mode

prior beliefs

3 Recency effects for SbS mode, even when

subjects have internalized prior beliefs.

Taxpayers were more sensitive to

negative than positive information.

Assigning (rather than measuring)

prior beliefs can lead to incorrect

inferences

1

Trotman and

Wright

(1996)

Likelihood that a firm will

continue; Assess the

strength of internal

controls

Measured after

background

information

Final likelihood

minus initial

likelihood

SbS and EoS

4 cuesResponse mode

Experience

3 Experienced managers do not display

recency effects. Students exhibit

recency for both tasks and both

response modes. Seniors exhibit

recency in all cases except EoS mode

for control evaluation task

1

Bamber et al.

(1997)

Likelihood that Inventory

fraud exists and likelihood

of collecting account

receivable; Rate each piece

of evidence

Manipulated at 50% Final likelihood

minus the

initial anchor

SbS mode

2 cuesExperience

Task (within subj)

1 Recency supported. Confirmation

proneness holds over both experience

levels and both contexts. Auditors are

also more sensitive to evidence when

the possibility of fraud exists

3

Tuttle et al.

(1997)

Stock trades in experimental

market (revise security

price beliefs)

Measured as initial

security price

Final price minus

initial price

SbS mode

4 cues

Experimental

market setting

2 Recency effect was found in experimental

asset markets

Ahlawat

(1999)

Likelihood of viability of

client (going concern)

Measured after

background

information

Final likelihood

minus initial

likelihood

SbS mode

6 cues

Group vs.

individual

accuracy,

confidence, and

severity of

recency

4 Recency found in individual auditors, but

not groups. Group memory was more

accurate and groups were more

confident than individuals

Anderson and

Maletta

(1999)

Likelihood of a material error

in sales/receivables and

number of planned audit

hours

Measured after

review of

background

information

Final likelihood

minus initial

likelihood

SbS mode

4 cuesInherent risk

Proportional vs.

Absolute

Measure

2 Auditors are susceptible to primacy effects

in settings that are relatively low in

inherent risk

1

Mayper et al.

(1999)

Likelihood that court will

uphold deduction of

worthless security; Final

recommendation to client

Measured after

background

information

Final likelihood

judgment with

initial

likelihood as a

covariate

EoS mode

4 cues

Staff conclusion 4 Order of arguments did not affect

reviewers’ likelihood assessments or

final recommendation. Staff conclusion

did affect likelihood assessment

Belief

Revisio

nin

Acco

untin

g15

Arnold et al.

(2000)

Likelihood audit would result

in going concern opinion;

insolvency

Measured after

review of

background

information

Final belief

revision minus

2nd belief

revision

compared to

2nd belief

revision minus

initial belief

Eos mode

10 cues

(experiment 1)

12 cues

(experiment 2)

Task complexity

Going concern vs,

insolvency

Experience

3 Experience did not mitigate order/recency

effects under conditions of heavy

information load

2

1

Cuccia and

McGill

(2000)

Likelihood that a court would

find a settlement

excludable from taxable

income; Reporting

recommendation

Measured after

background

information

Final likelihood

with initial

likelihood as

covariate

EoS mode

4 cues

Control over rder

Pre-evaluation

information

Task knowledge

Client advocacy

4 The ability to control the order in which

conflicting evidence is evaluated

eliminates recency, but only in a

familiar task. Advocacy is not related

to choice of order. Mere awareness of

conflicting information does not

mitigate recency

3

1

2

Monroe and

Ng (2000)

Likelihood that there were

material errors or

misstatements in the

client’s financials, in the

absence of any specific

internal controls

Measured after

review of

background

information

Final likelihood

minus initial

likelihood

Sbs mode

4 cues

Inherent risk 2 No recency. Auditors’ judgments were not

influenced by order effects. Judgments

of inherent risk may be biased toward

conservatism

Pinsker (2004) Stock price valuations Manipulated at $50 Midpoint price

minus initial

anchor

Final price minus

midpoint

Sbs and EoS

modes

20 cues

Response mode 3 Recency found for both modes, but

stronger for SbS. Practically, valuation

was more pronounced for SbS

conditions

EoS, End-of-Sequence (simultaneous); SbS, Step-by-Step (sequential).

Table 3. (Continued)

Study Task Initial Belief Measurement of

Belief Revision

Order of Evidence

Manipulation

Other Factors

Manipulated

Factor

Category

ResultsJE

NNIF

ER

KAHLEET

AL.

16

Cognitive-Experience

A large amount of accounting literature has found support for the idea that

a decision-maker’s experience has an effect on his or her judgment,

particularly for complex tasks (e.g., Davis & Solomon, 1989; Church, 1990;

Libby & Luft, 1993). Specifically, society expects more experienced

professionals to make higher quality judgments. Arguably, this should

occur because experienced decision-makers possess richer knowledge and

memory structures, as well as higher levels of confidence, which leads to

lower levels of sensitivity toward evidence received (Trotman & Wright,

2000). Based on this prior research, studies in belief revision posit that

greater order effects (lower performance) should occur among less

experienced individuals. However, findings in the belief revision literature

generally have not supported this view.

Experience in belief revision has been studied by examining the number of

years of experience (Pei et al., 1992a; Krull et al., 1993), age (Johnson, 1995),

experience titles (McMillan & White, 1993; Messier & Tubbs, 1994;

Trotman & Wright, 1996; Bamber et al., 1997), and task-related

experience/knowledge (Kennedy, 1993; Arnold et al., 2000; Cuccia &

McGill, 2000). Task-related experience, however, may be confounded with

input task factors. For example, an individual who has less experience with a

task is likely to consider the task more complex. Further, Trotman and

Wright (2000) argue that besides the task, experience is likely to have an

interactive effect with response mode and amount of information.

Measuring any single factor in isolation may be a cause of the lack of

consistent results supporting recency effects in experience studies. The

studies that examined task-related experience with task complexity will be

discussed later in conjunction with the discussion of input task factors.

Pei et al. (1992a) examined the impact of tax professionals’ experience on

belief revisions about ambiguous tax treatments. They found a significant

recency effect for experienced (5–13 years) tax managers, but not for

inexperienced (2–4 years) tax managers. One explanation for this result is

that a second manipulated factor, client preference, may have dominated the

results for the inexperienced participants. (Client preference is an environ-

mental factor and will be discussed in greater detail in the section

‘‘Environmental Factors.’’)

Krull et al. (1993) found similar results, whereby more experienced audit

managers exhibited greater recency effects than less experienced managers.

They, however, expected these somewhat counter-intuitive results. They

provided their participants with little background information, leading them

to predict that experienced participants would be more likely to recognize

Belief Revision in Accounting 17

the inadequacy of this information and place greater weight on the

subsequent information received.

Asare (1992) investigated order effects with different hypothesis frames

(viable or failing audit client) using audit partners and managers. He used

four pieces of evidence (two contrary and two mitigating) in both frames.

Significant recency order effects were found for both frames for these

experienced auditors.

Messier and Tubbs (1994) contend that the magnitude of the contrast

effect could be reduced if the participants had additional experience with the

stimuli. Consistent with this reasoning, they found that experience mitigated

recency effects. Only weak support was found for the proposition that

experience and the review process interacted to reduce recency effects. The

inconsistencies were arguably due to their use of different experience levels

(seniors and managers), task differences (more versus less background

information), and response mode (SbS versus EoS).

While not specifically hypothesized, McMillan and White (1993) found

that experience level (staff, seniors, and manager/partners) had no signi-

ficant effect on belief revisions for auditors after they evaluated confirming

or disconfirming evidence relative to a chosen hypothesis frame. Similarly,

Bamber et al. (1997) examined experience as it related to evidence sensi-

tivity. They concluded that inexperienced auditors (staff) were not more

sensitive to confirming evidence than experienced auditors (seniors).

Johnson (1995) examined two measures of experience: years on the job

and age of the participant. Age, but not years of experience, was signifi-

cantly associated with more conservative final beliefs. Despite the conser-

vatism related to age effect, recency did exist in an inventory write-down

task.

In sum, the majority of studies find either no recency effect for experi-

enced participants or more of a recency effect with experience. Therefore, we

conclude that the evidence suggests that experience does not necessarily

mitigate recency. However, task and response mode differences, the use of

different experience manipulations, and interactions between individual and

external factors make interpretation of the results across studies difficult.

Future research should continue to consider experience as an important

cognitive factor and seek to determine if experience only fails to mitigate

recency bias or actually increases recency bias.

Cognitive–Style

One accounting study manipulated cognitive style to find out if there was an

interaction with order effects. Chan (1995) had professional auditors assess

JENNIFER KAHLE ET AL.18

the likelihood that the accounts receivable balance of a fictional company

was fairly stated. Using the Group Embedded Figure Test (GEFT), he

separated auditors into field-dependent (those that have ‘‘spectator’’

learning approaches and are not able to separate items of information

from their contexts) and field-independent (those who have ‘‘active’’

learning approaches and tend to differentiate information into well-

distinguished components). Results indicated a significant interaction

between cognitive style and order effects, as the field-dependent auditors

showed greater recency effects than their field-independent counterparts.

These results add credence to understanding the learning and processing

behaviors of decision-makers and perhaps even training them to be more

active in learning about task procedures.

Affective–Sensitivity to Evidence

Hogarth and Einhorn (1992) discuss the importance of an individual’s

sensitivity to negative and positive evidence. These parameters are often

described as sensitivity toward disconfirming and confirming evidence,

respectively. Confirming or disconfirming evidence is determined with

respect to a professional’s initial hypothesis. Similarly, an individual who is

sensitive to negative or positive evidence may be paralleled to someone who

is an advocate or a skeptic, respectively. That is, the individual views

information as positive or negative with respect to the client-favored

position.

Sensitivity is a critical element of the belief-adjustment model. It is posited

to be a constant for each individual decision-maker. The contrast effect,

which determines whether there will be an order effect, is diluted as one’s

sensitivity to evidence decreases. Sensitivity, as posited by Hogarth and

Einhorn (1992), is a function of both individual factors (e.g., experience) and

external factors (e.g., client preference).

The model suggests that in the absence of prior information or biases,

people will be highly sensitive to evidence, but as they become more

committed to their beliefs, as with a long series of information, sensitivity

will decline. For example, as discussed by Messier and Tubbs (1994),

individuals with more experience (an individual factor) should be more

confident in an initial impression of a problem. This higher confidence

should lead the individual to be less sensitive toward confirming and

disconfirming evidence, resulting in a smaller recency effect. Messier and

Tubbs’ research supports this theory. However, Krull et al. (1993) found

opposite results for their experienced versus inexperienced participants.

They suggest that differences in the ambiguity of the initial information

Belief Revision in Accounting 19

provided to the participants may help explain the seemingly conflicting

results. Experienced auditors may have been better able to appreciate the

inadequacy of the initial information and were more sensitive, in general, to

subsequent information.

An individual may inherently be more prone to a particular sensitivity

toward evidence, or the individual’s professional role may affect his or her

sensitivity. There is evidence from psychology as well as accounting that

individuals have a general tendency to search for or give more weight to

evidence that confirms an initial hypothesis (e.g., Church, 1990; Klayman &

Ha, 1987) and is often referred to as a confirmation bias. Conversely, some

evidence from the auditing literature supports disconfirmation bias,

arguably due to the auditor’s role requiring professional skepticism (e.g.,

Ashton & Ashton, 1990; McMillan & White, 1993). These biases affect an

individual’s weighting of evidence, and consequently, can affect the

predictions of Hogarth and Einhorn’s (1992) model. In fact, recency effects

may become negligible if the decision-maker maintains an extremely

asymmetrical sensitivity toward evidence (Pei et al., 1990).

Eight accounting studies in belief revision have looked at an individual’s

sensitivity toward evidence. These studies primarily looked at sensitivity as

it is influenced by the accountant’s professional role. For example, several

studies examined whether auditors were more sensitive to disconfirming

evidence or whether tax professionals exhibited biases related to their

professional roles as client advocates. The studies will be detailed in the

discussion for ‘‘Professional Roles’’ in the section on ‘‘Environmental

Factors.’’

Bamber et al. (1997) attempted to measure an individual’s sensitivity to

evidence. By controlling for the subjective strength of evidence and the

degree of the contrast, they examined whether auditors were more sensitive

to a particular type of evidence. Bamber et al. discussed five possible

sensitivities, including evidence neutrality, confirmation bias, disconfirma-

tion bias, positive evidence bias, and negative evidence bias. They found that

auditors were more sensitive to confirming evidence, which is consistent with

the confirmation bias findings from the psychology literature (e.g., Lord,

Ross, & Lepper, 1979; Nisbett & Ross, 1980).

Affective–Professional Attitudes

Pei et al. (1990) suggested that tax preparers’ attitudes might affect their

recommendations to clients and possibly their decision processes as well.

They explored tax professionals’ attitudes relative to (1) the relative

frequency of evasion, (2) the morality of evasive or aggressive tax reporting,

JENNIFER KAHLE ET AL.20

(3) the individual’s self-insight as to their aggressiveness, and (4) the

perception of the tax professional’s responsibilities to client and govern-

ment. In the study, tax professionals were asked to express a belief about the

likelihood of an ambiguous tax treatment (dealer versus investor classifica-

tion) prevailing upon an audit and to provide a recommendation to the

client. A significant recency effect was found for both the likelihood and

recommendation. Only the morality and self-insight attitudes were

associated with the client recommendation, and none were significantly

related to the likelihood judgment. Therefore, this study provides some

evidence that individual attitudes can impact a tax professional’s final

judgment.

Affective–Initial Beliefs

Accounting studies have recognized the importance of correctly measuring

the initial anchor (belief) and the participants’ belief revisions. The belief-

adjustment model relies heavily on prior beliefs as an input into the model.

Prior beliefs provide an anchor from which decision-makers adjust when

presented with additional evidence (Butt & Campbell, 1989).

Originally, many studies used background facts to manipulate a

participant’s initial belief. Ashton and Ashton (1988) manipulated initial

belief by describing the likelihood that controls would prevent or detect

material error to be 20, 50, or 80%. They found support for Hogarth and

Einhorn’s (1992) contention that smaller (larger) anchors are helped (hurt)

more by positive (negative) evidence than larger (smaller) anchors. Many

later studies (Ashton & Ashton, 1990; Kennedy, 1993; Bamber et al., 1997;

Pinsker, 2004) assigned an initial belief to the participants in order to

provide a consistent starting point for measuring recency.

Rather than assigning an initial belief, Butt and Campbell (1989)

recognized that having participants come to their own conclusions about

the initial belief gave more assurance that the researcher had actually

captured their priors. They measured participants’ initial beliefs after

presenting them with background information designed to induce either low

or high priors, and found recency effects only for participants with induced

low prior beliefs. Asare (1992) recognized that there also could be possible

source credibility issues in manipulating initial beliefs and similarly,

measured participants’ initial beliefs on likelihood scales. Unlike Butt and

Campbell, Asare found recency effects in both groups examined.

Hite and Stock (1996) found significant differences between belief

revisions for participants receiving assigned prior beliefs and those whose

prior beliefs were measured. They theorized that participants do not

Belief Revision in Accounting 21

internalize an assigned prior belief, therefore, the mean belief revision for

these participants may include measurement error. Hite and Stock

concluded that assigned prior beliefs are appropriate only when: (1) actual

priors are close to those assigned, (2) participants have no prior beliefs, or

(3) participants have weak internal priors.

McMillan and White (1993) recognized the possible scale effects that

could result from the strength of the initial belief in measuring a

participant’s belief revision. They pointed out, for example, that if a

participant’s initial likelihood score was 70% and the participant evaluates

confirming evidence, a 30-point range is available for upward revision.

Conversely, if the participant evaluates disconfirming evidence, a 70-point

range is available for downward revision. To control for scale effects, they

used a proportional measure for the participants’ belief revisions in addition

to the usual absolute measure. They found that the two measures of belief

revision do not provide consistent results for the effect of evidence direction

on the magnitude of belief revision. However, Anderson and Maletta (1999)

found that the scaled (proportional) measure of belief revision is consistent

with the unscaled (absolute) measure in their study of primacy effects.

With the exception of the last two studies mentioned above, the vast

majority of the accounting studies have used the final judgment minus the

beginning judgment as the measurement of belief revision. However, it is

important for future research to recognize the potential limitation of an

absolute measure due to the scale effects discussed above. Furthermore, a

comparison of the proportional measure to the belief-adjustment model’s

measurement of belief revision (as used by Bamber et al., 1997) reveals that

both have a similar method for examining belief revision processes when the

strength of evidence is constant for all evidence.

In general, the research to date suggests that individual psychological

factors, such as experience, fail to mitigate recency bias. However, limited

research concerning cognitive learning style shows active learning approaches

may mitigate some recency bias. Affective factors such as sensitivity to

evidence, professional attitude, and initial belief have been shown to affect

final judgments either directly or indirectly. Both confirmation and

disconfirmation biases have been documented with respect to sensitivity to

evidence and professional role. Initial beliefs have been shown to effect belief

revision differentially depending on whether the initial belief has been

assigned or measured. With respect to cognitive and affective factors, limited

research demonstrates that experience does not necessarily reduce sensitivity

to evidence. Studies have provided conflicting results, which indicates the need

for future research in the area of individual affective psychological factors.

JENNIFER KAHLE ET AL.22

Environmental Factors

As previously discussed, Hogarth and Einhorn’s (1992) model outlines a

framework explaining how external variables and processing factors interact

to produce order effects in belief updating. There are two types of external

variables – environmental and input task factors. Environmental factors

concern risks and rewards that are present in the decision-maker’s

environment. This may be due to the role of the decision-maker, the

particular characteristics of the client she/he is serving, or the inherent risk

present in the decision environment. Decision-makers do not operate in a

vacuum, and cognitive models should reflect the potential influence of items

such as the client, regulatory agencies, and professionals’ employers

(Roberts, 1998). Studies which have examined these environmental factors

are discussed below. Input task factors are described and discussed in the

following section.

Professional Roles

Hogarth and Einhorn (1992) suggest that an individual’s professional role

might produce differential ‘‘sensitivities’’ to evidence, and they discuss how

these differential sensitivities are considered to be advocate or skeptic

attitudes. Within each decision context, accounting professionals face

pressures that may cause them to be differentially sensitive to positive and

negative evidence. Accountants are charged with professional skepticism in

audit and assurance services (AICPA, 1995, AU, 316.16). On the other

hand, tax professionals have an obligation to act as a client advocate and to