1-510-338-9438 Meeting number (access code) - Grand ...

229

GRAND TRAVERSE COUNTY DEPARTMENT OF HEALTH AND HUMAN SERVICES BOARD 9:00 AM West Bay Beach, a Delamar Resort – Dayclub Room 615 East Front Street, Traverse City, MI 49686 On July 17, 2020 Governor Whitmer signed into effect Executive Order 2020-154. In an effort to reduce the spread of COVID-19 by limiting the number of people at public gatherings, this order suspends the rules and procedures for governmental entities requiring physical presence at meetings and hearings and it temporarily alters the rights of the public to be present at meetings. Due to the Board meeting in a space of 10 or under, a conference phone will be used for public comment and attendance. The Board Chair will announce when it is time for public comment and will give all call-in numbers the opportunity to speak during this time. This meeting will be recorded and saved on upnorthmedia.com and will also be shown on Charter cable channel 189. Conference number for the public Phone: 1-510-338-9438 Meeting number (access code): 126 717 4697 Meeting Password: 33685239 September 25, 2020 AGENDA 1. CALL TO ORDER – 9:00 a.m. Grand Traverse Pavilions – John Rizzo, Chair, Grand Traverse County Department of Health and Human Services Board 2. FIRST PUBLIC COMMENT/INPUT Any person shall be permitted to address a meeting of the Grand Traverse County Department of Health and Human Services Board which is required to be open to the public under the provisions of the Michigan Open Meetings Act, as amended. (MCLA 15.261, et.seq.) Public comment shall be carried out in accordance with the following Board Rules and Procedures: 1. Any person wishing to address the Board shall state his or her name and address. 2. Persons may address the Board on matters which are relevant to Grand Traverse Pavilions issues. 3. No person shall be allowed to speak more than once on the same matter, excluding time needed to answer Board Members questions. The Chairperson shall control the amount of time each person shall be allowed to speak, which shall not exceed three (3) minutes. (1) Chairperson may, at his or her discretion, extend the amount of time any person is allowed to speak. (2) Whenever a group wishes to address the Board, the Chairperson may require that the group designate a spokesperson; the Chairperson shall control the amount of time the spokesperson shall be allowed to speak, which shall not exceed fifteen (15) minutes. 3. COUNTY LIAISON REPORT 4. APPROVAL OF AGENDA 5. CONSENT CALENDAR The purpose of the consent calendar is to expedite business by grouping items to be dealt with by one Board motion without discussion. Any member of the Board, or staff may ask that any item on the consent calendar be removed and placed elsewhere on the agenda for discussion. Such requests will be automatically respected. Page 1 of 229

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 1-510-338-9438 Meeting number (access code) - Grand ...

GRAND TRAVERSE COUNTY

DEPARTMENT OF HEALTH AND HUMAN SERVICES BOARD 9:00 AM West Bay Beach, a Delamar Resort – Dayclub Room

615 East Front Street, Traverse City, MI 49686

On July 17, 2020 Governor Whitmer signed into effect Executive Order 2020-154. In an effort to reduce the spread of COVID-19 by limiting the number of people at public gatherings, this order suspends the rules and procedures for governmental entities requiring physical presence at meetings and hearings and it temporarily alters the rights of the public to be present at meetings.

Due to the Board meeting in a space of 10 or under, a conference phone will be used for public comment and attendance. The Board Chair will announce when it is time for public comment and will give all call-in numbers the opportunity to speak during this time. This meeting will be recorded and saved on upnorthmedia.com and will also be shown on Charter cable channel 189.

Conference number for the public

Phone: 1-510-338-9438 Meeting number (access code): 126 717 4697

Meeting Password: 33685239

September 25, 2020 AGENDA

1. CALL TO ORDER – 9:00 a.m. Grand Traverse Pavilions – John Rizzo, Chair, Grand Traverse County Department of Health and Human Services Board

2. FIRST PUBLIC COMMENT/INPUT Any person shall be permitted to address a meeting of the Grand Traverse County Department of Health and Human Services Board which is required to be open to the public under the provisions of the Michigan Open Meetings Act, as amended. (MCLA 15.261, et.seq.) Public comment shall be carried out in accordance with the following Board Rules and Procedures: 1. Any person wishing to address the Board shall state his or her name and address. 2. Persons may address the Board on matters which are relevant to Grand Traverse

Pavilions issues. 3. No person shall be allowed to speak more than once on the same matter, excluding time

needed to answer Board Members questions. The Chairperson shall control the amount of time each person shall be allowed to speak, which shall not exceed three (3) minutes. (1) Chairperson may, at his or her discretion, extend the amount of time any person is

allowed to speak. (2) Whenever a group wishes to address the Board, the Chairperson may require that

the group designate a spokesperson; the Chairperson shall control the amount of time the spokesperson shall be allowed to speak, which shall not exceed fifteen (15) minutes.

3. COUNTY LIAISON REPORT

4. APPROVAL OF AGENDA

5. CONSENT CALENDAR

The purpose of the consent calendar is to expedite business by grouping items to be dealt with by

one Board motion without discussion. Any member of the Board, or staff may ask that any item

on the consent calendar be removed and placed elsewhere on the agenda for discussion. Such

requests will be automatically respected.

Page 1 of 229

If any item is not removed from the consent calendar, the item on the agenda is approved by a

single Board action adopting the consent calendar.

A. Review and File HANDOUT#

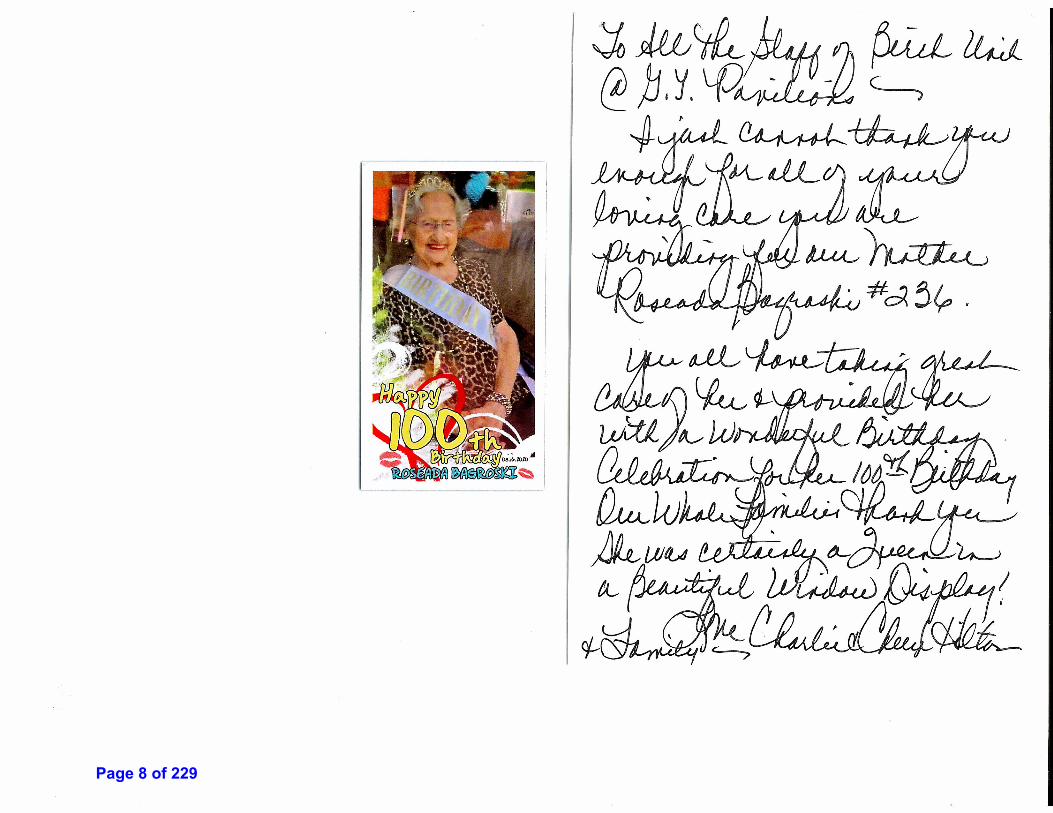

(1) Minutes of the 9/25/20 Board Meeting 1 (2) Weber Thank You 2 (3) Bagroski Thank You 3 (4) P.E.P. Talk Employee Newsletter – August 4 (5) Media Report – September 5

6. ITEMS REMOVED FROM CONSENT CALENDAR

(1)

7. GRAND TRAVERSE MEDICAL CARE -- Korvyn R. Hansen A. General Information

(1) COVID-19 Update 6 (2) Resident/family satisfaction Survey Report 7

B. Chief Executive Officer Board Report 8

C. Business

(1) Pension Bond Resolution 9

(2) Financial Report 10

D. Medical Staff (1)

G.T.P. Announcements

(1) September Service Excellence Award 11

8. SECOND PUBLIC COMMENT/INPUT Refer to Rules under First Public Comment/Input above.

9. CLOSED SESSION

(1)

10. ADJOURNMENT

Page 2 of 229

1

GRAND TRAVERSE COUNTY

DEPARTMENT OF HEALTH AND HUMAN SERVICES BOARD 1000 Pavilions Circle, Traverse City, MI 49684

MINUTES OF THE AUGUST 28, 2020 MEETING PRESENT: John Rizzo, Cecil McNally,Ralph Soffredine Board Kory Hansen, Rose Coleman, Robert Barnes, Lindsey Dood, Darcey Gratton Staff Gordie LaPointe Commission ABSENT: GUESTS: The regular meeting of the Grand Traverse County Department of Health and Human Services Board was called to order at 9:00 am by Board Chair John Rizzo in the Dayclub Room at the West Bay Beach, a Delamar Resort. On July 17, 2020 Governor Whitmer signed into effect Executive Order 2020-154. In an effort to reduce the spread of COVID-19 by limiting the number of people at public gatherings, this order suspends the rules and procedures for governmental entities requiring physical presence at meetings and hearings and it temporarily alters the rights of the public to be present at meetings. Due to the Board meeting in a space of 10 or under, Grand Traverse Pavilions provided a link on its website for public participation. This meeting was recorded and will be saved on upnorthmedia.com and also shown on Charter cable channel 189. Public Comment Andi Gerring Claudia Bruce County Liaison Report – LaPointe shared discussions of the most recent county board of commissioner meetings. Approval of Agenda – Chair Rizzo asked if there were additions, changes or corrections to the agenda. Motion was made by McNally to approve the Agenda as presented, seconded by Soffredine and carried unanimously. The purpose of the Consent Calendar is to expedite business by grouping items to be dealt with by one Board motion without discussion. Any member of the Board or staff may ask that any item on the Consent Calendar be removed and placed elsewhere on the agenda for discussion. Such requests will be automatically respected. REVIEW AND FILE

(1) Minutes of the 7/31/20 Board Meeting (2) Closed Minutes of the 7/31/20 Board Meeting

Page 3 of 229

dgratton

Text Box

1

2

(3) Mullen Thank You (4) P.E.P. Talk Employee Newsletter – August (5) Media Report – July

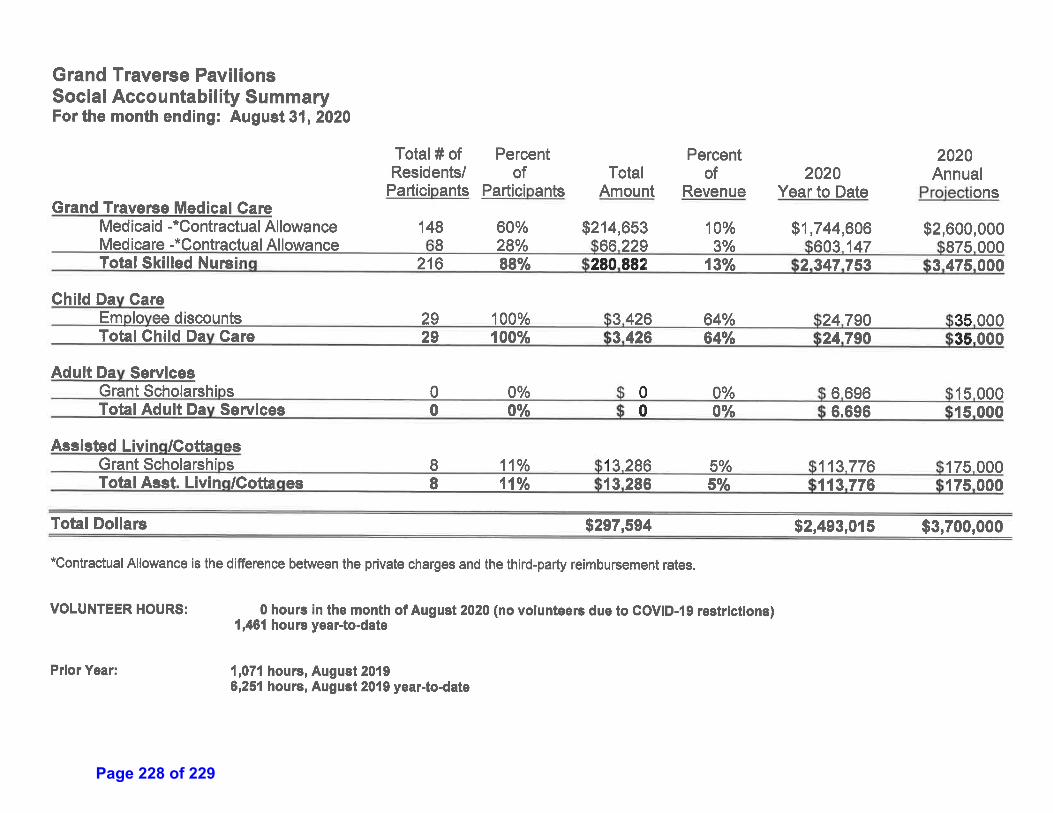

Motion was made by Soffredine to approve the Consent Calendar as presented. Motion seconded by McNally and carried unanimously. Items Removed From Consent Calendar – none COVID-19 Update – Coleman provided an update on the on-going status of COVID-related topics that affect the operation of the Pavilions. Hansen covered COVID-related relief payments and reimbursement that have been received to date. Reimbursement Update – Hansen shared that CMS issued a final rule that updates the Medicare payment rates and the value-based purchasing program for skilled nursing facilities for FY2021. The aggregate average increase to SNFs for Medicare under the PDPM methodology is 2.2%. Chief Executive Officer Report – Hansen reviewed his monthly report for July and answered board member’s questions. Financial Report – Dood reviewed the financial operations report for July, 2020. Dood outlined revenue and expenses compared to budget for each of the Pavilions’ programs that include the Medical Care Facility (skilled nursing), The Cottages (Assisted and Independent Living) and Adult Day Services. Additional information was provided on respective census and accounts receivable along with the total cash ending balance. Dood summarized the review of vouchers for the month that were in order without exception. The Social Accountability Summary was reviewed indicating the amount of uncompensated care provided and volunteer hours for the month. Motion made by Soffredine to accept the financial operations report as presented. Motion seconded by McNally and carried unanimously. MCACA Grant Submission Resolution 2020 - 2 - Hansen reviewed the Resolution to submit the grant application in the amount of $4,000 from the Michigan Council for the Arts and Cultural Affairs (MCACA) for funding towards the 2021 Concert on the Lawn concert series. Motion was made by McNally to approve the grant application to be submitted in the amount of $4,000 from the MCACA for funding towards the 2021 Concert on the Lawn concert series. Motion was seconded by Soffredine and carried unanimously. Lauren Reynolds, PA - Attending Privileges - Hansen reviewed the request of Lauren Reynolds, PA, to have attending privileges as recommended by Medical Director Dr. April Kirkowski, M.D. Lauren is joining Sound Physicians, to serve nursing homes and assisted living facilities. Motion was made by McNally to approve Lauren Reynolds, PA, for attending privileges, seconded by Soffredine and carried unanimously. Sarah Kristine White, NP - Attending Privileges - Hansen reviewed the request of Sarah Kristine White, NP, to have attending privileges as recommended by Medical Director Dr. April Kirkowski, M.D. Sarah is joining Sound Physicians, to serve nursing homes and assisted living facilities. Motion was made by McNally to approve Sarah Kristine White, NP, for attending privileges, seconded by Soffredine and carried unanimously.

Page 4 of 229

3

Jacob Vaughn White, PH.D - Consulting Privileges - Hansen reviewed the request of Jacob Vaughn White, PH.D, to have consulting privileges for psychology services as recommended by Medical Director Dr. April Kirkowski, M.D. Motion was made by McNally to approve Jacob Vaughn White, PH.D, for consulting privileges, seconded by Soffredine and carried unanimously. Grand Traverse Pavilions Announcements -

(1) July Service Excellence Award - Hansen reviewed weekly winners Public Comment/Input - none Meeting adjourned at 10:00 am Signatures:

John Rizzo – Chair Grand Traverse County Department of Health and Human Services Board

Korvyn R. Hansen, Assistant-Secretary Date: August 28, 2020 Approved Corrected and Approved

Page 5 of 229

Page 6 of 229

dgratton

Text Box

2

dgratton

Text Box

The Record-Eagle - 08/22/2020 Page : B04

Copyright (c)2020 The Record-Eagle, Edition 08/22/2020September 17, 2020 12:54 pm (GMT +4:00) Powered by TECNAVIA

4B Traverse CiTy reCord-eagle Saturday, August 22, 2020food/oBituaries

Elizabeth 'Liz' M. McGrathDied August 18, 2020

PESHAWBESTOWN— Elizabeth "Liz"Marie McGrath, of Pe-shawbestown, diedTuesday Aug. 18,2020, at home,surrounded by herchildren and grand-daughter.

Liz was known forher beautiful smileand her contagious laugh. Sheloved to spend time with herfamily and grandchildren; go-ing to mud bogs, camping andtubing down the river. Sheenjoyed playing bingo, lovedher casino time and going tolisten to her favorite bands, es-pecially Alan Turner, and danc-ing the night away.

Liz held the administrativeassistant position for theGrand Traverse Band HousingDepartment for the last 14years and became more than aworker; she became a lovedand valued member of thecommunity and will be misseddearly.

She is survived by her hus-

band, Paul McGrath,of Peshawbestown;her children, TamraNewton, of Pe-shawbestown, Curtis(Tiffany) Branch, ofGrand Rapids, John(Maria)Steed, of Tra-verse City, SarahSteed, of TraverseCity; grandchildren,

Mariah, Egypt, Jordyn, Kay-den, Ayden, Gunner, Jayden;her "special" grandson, Emit;siblings, Agnes (Charles)Cross, of Goshen, Indiana,Bernice Sineway, of Benzonia,Bertha (Marsh) Spaford, ofDaleville, Alabama, Ginger (Eu-gene) Zambon, of Arbor Vitae,Wisconsin; brother, Fred (Dar-lene) Weissert; and manynieces and nephews.

She was preceded in deathby her parents, John andAgnes Beaver; siblings, JoyceDuford, Bonnie Edinger, JudyKublick, Gerry Pamame, SarahLugg, Nancy Amy, Mike Sper-ling, Clifford Gerou, JohnBeaver and Mose Beaver.

Marian 'Midge' V. RytkonenDied August 12, 2020

CUMMING —Marian "Midge" ViolaRytkonen, 100,passed away,peacefully, on Aug,12, 2020, inCumming, Georgia.

She was born onJan. 1, 1920, to NinaBelle Burley and LeeWyatt, in Finley, Ohio.She lived most of her life inTraverse City, traveling toFlorida during the wintermonths but her last years werespent in Cumming, Georgia.

Marian was passionate aboutpeople, helping others, danc-ing, bowling and lemondonuts.

She joined the Women's Aux-iliary Army Core (WAAC) duringWorld War II, traveling exten-sively as a recruiter and gain-

ing fame by beingphotographed duringa recruitment effort ata Native AmericanReservation.

Consequently, sheproudly served andwas very active at herlocal Veterans ofForeign Wars post.

Midge will be sorelymissed and is survived by hersons, Rusty, Mark, AJ andRobert and their families;grandchildren; and great-grandchildren.

No services are scheduledright now, but in lieu of flowers,we the family, ask that you givegenerously to your local VFW.

Please visitwww.lifestorytc.com to shareyour thoughts and more.

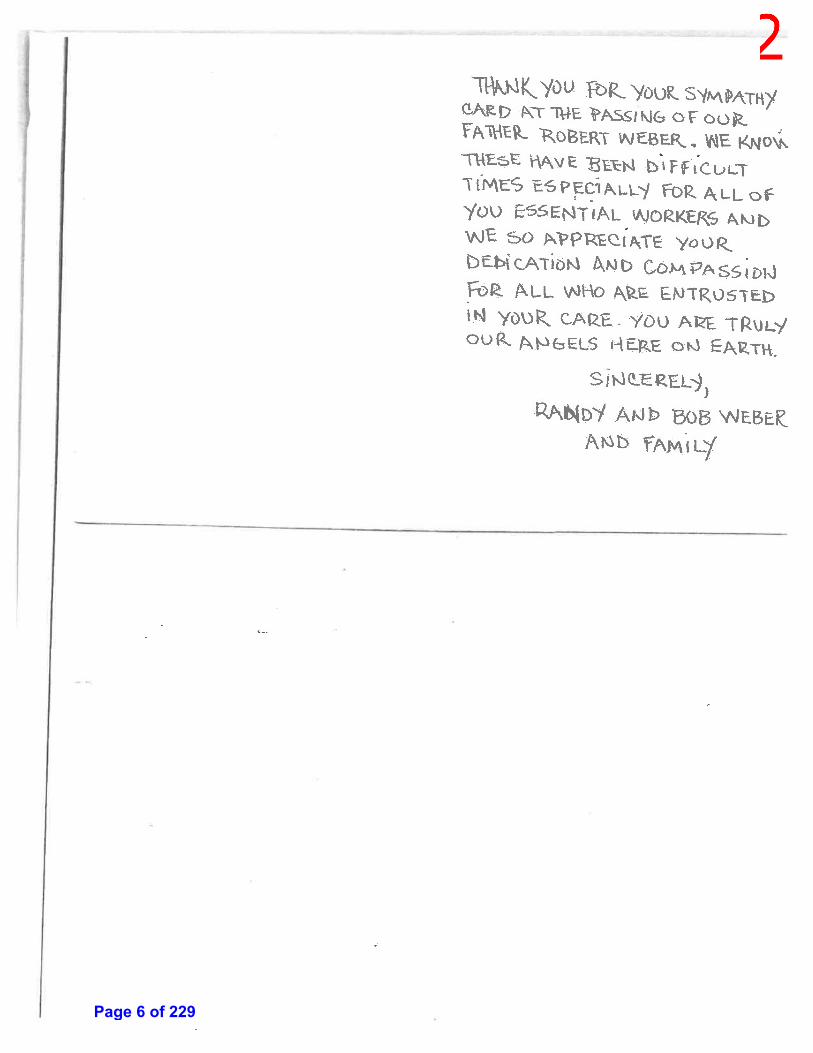

Robert J. WeberDied August 7, 2020

GRAWN — Robert JayWeber, 88, of Grawn, passedaway Friday, Aug. 7, 2020, atGrand Traverse Pavilions.

Bob was born on April 14,1932, in Buckley, to Julius andLeona (Pahl) Weber.

Bob attended BuckleyCommunity Schools andgraduated in 1950.

He later joined the Army onJuly 16, 1952 and washonorably dischargedon June 25, 1954.

Bob worked as anLPN at the TraverseCity State Hospital for25 years and droveschool bus for TCAPSfor over 20 years.When not working,Bob spent his sparetime selling used cars,tires and snowmobiles atBob's Auto Sales.

He also enjoyed restoringantique cars; his greatestproject was a 1965 Mustangconvertible.

After retirement from theTraverse City State Hospital,Bob re-entered the job forceand worked as an LPN at theGrand Traverse Medical CareFacility, before retiring again.

Bob was preceded in deathby his father, Julius Weber;mother, Leona (Weber) Clous,step-father, Leonard Clous;and niece, Kim (Weber) Lint.

He is survived by his twinsons, Robert (Marilyn) Weber IIand Randall (Sharon) Weber,both of Kingsley; their mother,

Wilma, A. Weber; five grand-children, Nicholas, Christo-pher, Danielle, Hayley andLindsey Weber; two great-grandchildren, Eva Sky Giffordand Harvey Wayne Weber; aswell as many nieces; nephews;and cousins.

He leaves his wife and com-panion, Mary Kramer-Weber,who was at his side for over 25

years; a brother, Nor-man (Georgene) We-ber; and a sister, Jean(Bill) Walton. He alsoleaves behind Mary'schildren, Jeff (Diane)Kramer and their chil-dren and grandchild;Timothy (Judith)Kramer and their chil-dren and grandchil-dren; Susan (Steve)

Tompkins and their son,Steven, whom Bob lovingly re-ferred to as his special grand-son.

The family would like toexpress our deepest gratitudeto Comfort Keepers, MunsonMedical Center staff, GrandTraverse Pavilions staff, MaryFree Bed Rehabilitation staff,Hospice of Northern Michigan,Green Lake TownshipEmergency Services and to allwho touched Bob's life andcomforted him.

A burial and celebration oflife will be held at a later date.

Arrangements have beenentrusted to Kalkaska FuneralHome and Cremation Service.

Helene 'June' WhittakerDied August 21, 2020

ELK RAPIDS —Helene "June" Whit-taker, 100, of ElkRapids, passed awayat her home on Aug.21, 2020, with herfamily by her side.

June was born onJune 21, 1920, inMuskegon, to the lateRalph H. and Wadea(Nafe) Cederquist.

June married the love of herlife, James H. Whittaker Jr., onSept. 19, 1941, in St. Johns.They were childhoodsweethearts and united in mar-riage while Jim was on leavefrom the service. Following hishonorable discharge, theymoved from St. Johns toHiggins Lake. Together theyowned and operated the Whit-taker Shady Grove Resort andWhittaker Realty Company for23 years. They were wellknown for their hospitality andmade a lot of lifelong friends atthe resort whom June loveddearly.

After retirement, Jim andJune moved to Elk Rapids,where they have resided forthe last 40 years.

She was a devoted memberof the First PresbyterianChurch of Elk Rapids. Sheloved her church family andgreatly appreciated their con-tinued kindness and friendshipin her later years.

Jim and June traveled exten-sively after retirement and

wintered, at theirhome, in Sedona,Arizona.

June will be greatlymissed by all whoknew her. She trulywas a ray of light to allshe met.

June joins herbeloved husband,Jim, in heaven, who

preceded her in death; alongwith her son, David James; andbrothers, Jack (Shirley) andDavid Cederquist.

June is survived by herdaughter, Sue (Robert) VorBroker; grandchildren, Cynthia(Alan) Dessy, Kurt (Mallory) VorBroker, Scott Whittaker,Deborah (Ken) Camp and Keith(Briana) Whittaker; great-grandchildren, Lauren, Patrick,Benjamin, Brighton, Cielle andBobby; and sister, Mary Alice(Bob) Smith.

Graveside services for thefamily will be held at OakwoodCemetery, in Roscommon, onTuesday, Aug. 25, 2020 at 11a.m.

A memorial service andcelebration of June's life willbe held in June of 2021.

Memorial donations, in lieu offlowers, may be directed to theFirst Presbyterian Church inElk Rapids or to a charity ofyour choice.

Please visit www.reynolds-jonkhoff.com to share yourmemories and condolenceswith the family.

o b i t u a r i e s

To read obituaries online, go to www.record-eagle.com

WASHINGTON (AP) — Sometimes politics gives way to the personal at the White House. It has seen 18 weddings and at least 10 people are known to have died there, including two presidents and three first ladies.

It will serve Friday as a place of mourning for President Donald Trump and his family, with a private memorial service for the president’s young-er brother, Robert, who died last week at 71. The president has described Robert as “not just my brother. He was my best friend.”

Abraham Lincoln and Calvin Coolidge both mourned the loss of a son while serving as presi-dent, Willie Lincoln in 1862 and Calvin Coolidge Jr. in 1924. The memorial services for both children began in the White House.

Unlike Willie Lincoln and Calvin Coolidge Jr., Robert Trump did not live at the White House. Nev-ertheless, it’s completely within the president’s ability to honor him with a service there, said Anita McBride, who served in three presidential ad-ministrations, including as first lady Laura Bush’s chief of staff.

“The White House is a very complex place. It’s an office, it’s a museum and it’s a home,” McBride said. “We loan it to the president for the time he or she is living there. Coming from that per-spective, we need to be understanding of some decisions that they make in a case like this.”

When Trump explained why he wanted to have a

service for his brother at the White House, he said: “I think he’d be greatly honored. He loves our country. He loved our country so much. He was so proud of what we were doing and what we are doing for our country. So I think it would be appro-priate.”

Robert Trump, a busi-nessman, died Saturday after being hospital-ized in New York. The president had visited his brother in the hospital on Friday.

Robert Trump began his career on Wall Street working in corporate fi-nance but later joined the family business, manag-ing real estate holdings as a top executive in the Trump Organization.

“When he worked in the Trump Organization, he was known as the nice Trump,” Gwenda Blair, a Trump family biogra-pher, told The Associated Press. “Robert was the one people would try to get to intervene if there was a problem.”

In the 1980s, Donald Trump tapped Robert Trump to oversee an At-lantic City casino project, calling him the perfect fit for the job. When that project cannibalized his other casinos, though, “he pointed the finger of blame at Robert,” said Blair, author of “The Trumps: Three Genera-tions that Built an Em-pire.”

A Boston University graduate, Robert Trump later managed the Brook-lyn portion of his father Fred Trump’s real estate empire, which was even-tually sold.

White House to host rare memorial

r o b e r t t r u m p

LYNNWOOD, Wash. (AP) — On a warm sum-mer night, two food trucks pulled onto a tree-lined street in a hilltop neigh-borhood outside Seattle. The smell of grilled meat filled the air, and neigh-bors slurped on boba tea drinks. Toddlers, teens, their parents and dogs sat in the grass, chatting behind masks, laughing and mimicking imaginary hugs to stay socially distant while they waited for their food orders.

Long seen as an urban treasure, food trucks are now being saved by the suburbs during the corona-virus pandemic. No longer able to depend on bustling city centers, these small businesses on wheels are venturing out to where people are working and spending most of their time — home.

As food trucks hunt for customers that used to flock to them, they’re find-ing a captive audience thrilled to skip cooking dinner, sample new kinds of cuisines and mingle with neighbors on what feels like a night out while safely staying close to home.

“This is festival season, fun season. All the stuff we typically do as humans, we can’t do anymore,” said Matt Geller, president of the National Food Truck Association. “Walking out to a food truck is a taste of normalcy, and it feels re-ally good.”

YS Street Food Group owner Yuli Shen discov-ered the hilltop Seattle-area neighborhood through Facebook, and she and a friend who runs the Dreamy Drinks boba tea truck went out together re-cently and served custom-ers for three hours.

It’s a change and a relief for Shen. Before the pan-demic, she raked in money by parking at Amazon’s campus near downtown Seattle, where hordes of office workers would line up for lunchtime Chinese rice bowls. By July, she was frantically searching for somewhere to go.

“It’s very hard to find a location to park, and so we have to find a different place and different people. It’s harder to run the busi-ness, but we’re trying,” Shen said.

Weekday lunchtime busi-ness is the bulk of the rev-enue for an average food truck, which may make $800 to $1,200 a day, Geller said. And lucrative appearances at major summer festivals and community events pad-ded them for leaner winter months.

Since stay-at-home orders earlier this year emptied out city centers and can-celed gatherings, many food trucks — like brick-and-mortar restaurants — have gone out of business or aren’t sure when they’ll open again.

Food trucks adjusted their business model as

they headed to the suburbs: They focus on dinner, add-ing kid-friendly options and preparing for larger or-ders. A new neighborhood means being unsure how many customers they’ll get and gambling on how much food to bring. To avoid that, many trucks urge custom-ers to order ahead online.

Geller said the suburban shift has been a boon for food trucks in places like Seattle, Nashville, Tennes-see, and Austin, Texas. He said people in the suburbs have been good at staying connected with neighbors during COVID-19 through Facebook groups, where food truck gatherings are advertised.

B.J. Lofback decided to pivot his Nashville-area food truck and restaurant away from labor-intensive Korean food after laying off most of his staff when business dwindled. He rebranded as Pinchy’s Lobster Co. and now sells lobster rolls, which he can largely prep himself.

Without his usual down-town Nashville lunchtimes and music events, he and other truckers began reaching out to homeown-ers associations in large subdivisions. It’s been such a success, he doesn’t miss the “stressful, expensive” event schedule. Now, he can keep all the money he earns, instead of paying

up to 20% of his revenue in event fees.

“The economics just worked,” Lofback said. “Me personally, I’m hoping that even if a vaccine dropped tomorrow and herd im-munity was accomplished tomorrow, I hope neighbor-hoods still have us out.”

Piroshky Piroshky, a Seattle institution at the iconic Pike Place Market, lost 90% of its brick-and-mortar business when the pandemic hit, operations manager Brian Amaya said.

The bakery pivoted to online sales, home deliver-ies and food truck events. Some events featuring its famous hand pies have been as successful as a modest day in a store. The 28-year-old business is con-sidering adding a second food truck.

“It’s enough to pay our employees and cover the cost of it and make a little bit of revenue for us to keep going,” Amaya said.

The idea was also new to Julie Schwab before she created events that have practically become food truck lore near Lynnwood, Washington, about 16 miles (25 kilometers) north of Seattle.

Business owners ask if it’s true that one truck made $4,000 in one night. She tells them food trucks make between $1,000 to $4,000 a shift. The high school psy-chologist also advises other communities that want in on the food truck circuit.

“You look what’s happen-ing with everybody coming out, and people are get-ting to know each other,” Schwab said, adding that people wear masks and keep their distance. “It’s been really great to build a community despite what’s going on with this pan-demic.”

After hearing how the industry had dried up, Schwab took a stab at organizing an event in June for the only food truck she’d ever tried. Now, she’s scheduling trucks seven days a week and into De-cember.

Thanks to the trucks, Schwab discovered bibim-bap, a Korean rice bowl, and she relishes helping small businesses, many run by people of color.

But there’s been head-aches, too: hours of work scheduling trucks, promot-ing events and responding to neighbors with ques-tions. Occasionally, trucks are late, unprepared or no-shows.

Christine Thai, a hospital program coordinator, was surprised to learn about the food truck scene in her community when she went to one of Schwab’s events recently with her husband and baby. It was a rare out-ing for the family, and she got to enjoy a strawberry matcha latte.

“The suburbs are getting cool because people don’t want to travel anymore,” Thai said.

Saved by suburbs: Food trucks hit by virus find new foodiesf o o d

The Associated Press

Bobby Price, left, and Catherine vogt, right, stand with Catherine’s daughter avery, 8, and their dogs as they wait to order from the ys street Food food truck near the suburb of lynnwood, Wash., north of seattle. long seen as a feature of city living, food trucks are now finding customers in the suburbs during the coronavirus pandemic as people are working and spending most of their time at home.

Page 7 of 229

dgratton

Text Box

dgratton

Text Box

dgratton

Text Box

dgratton

Highlight

Grand TraversePavilionsstaff

Page 8 of 229

dgratton

Text Box

3

P E P T A L K V O L U M E 8 , I S S U E 9 , S E P T E M B E R 2 0 2 0

SEPTEMBER 2020 IN-SERVICES

Due September 30, 2020

Relias: Mandatory – All STAFF: HIPAA Essentials

Relias: Mandatory – All STAFF: COVID-19 Educational Course

Relias: Mandatory – ALL STAFF: All Page and Code Status

Relias: Mandatory – CERTIFIED NURSE AIDES: Range of Motion and Positioning

Relias: Mandatory – LICENSED NURSES: About Stroke

Relias: Mandatory –UNIVERSAL WORKERS: Oral Hygiene: Assisting with Brushing and Flossing

Relias Link: https://gtp.training.reliaslearning.com

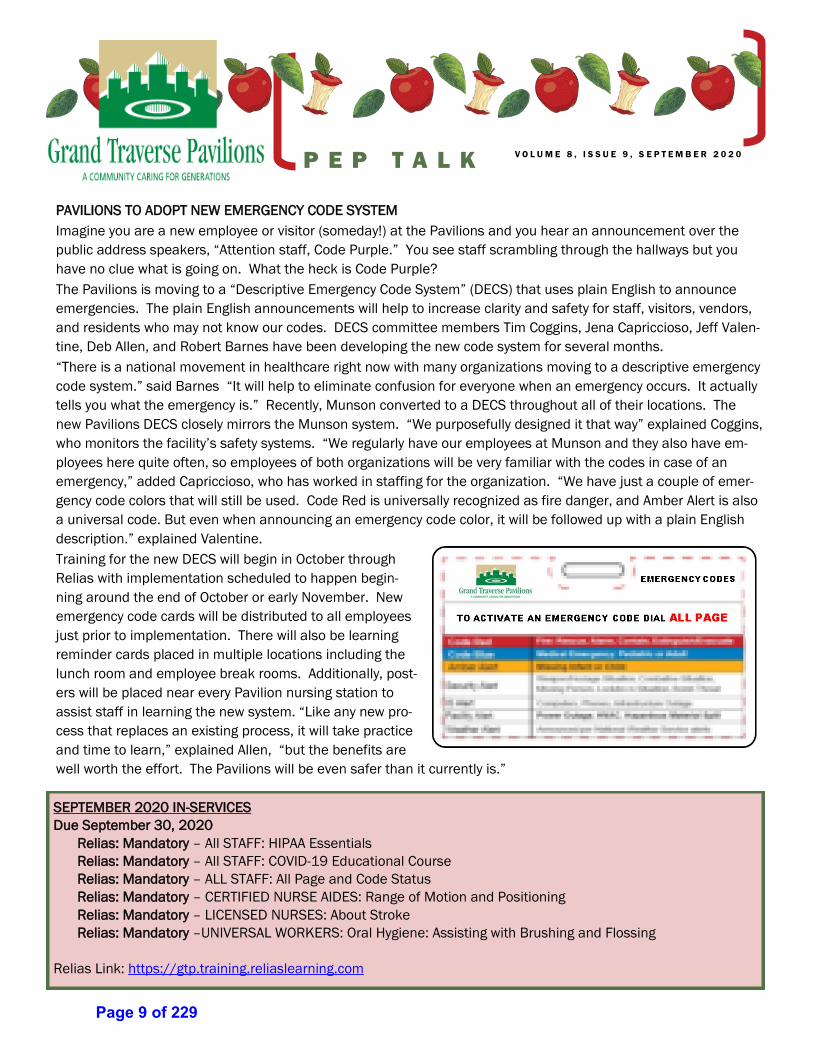

PAVILIONS TO ADOPT NEW EMERGENCY CODE SYSTEM

Imagine you are a new employee or visitor (someday!) at the Pavilions and you hear an announcement over the

public address speakers, “Attention staff, Code Purple.” You see staff scrambling through the hallways but you

have no clue what is going on. What the heck is Code Purple?

The Pavilions is moving to a “Descriptive Emergency Code System” (DECS) that uses plain English to announce

emergencies. The plain English announcements will help to increase clarity and safety for staff, visitors, vendors,

and residents who may not know our codes. DECS committee members Tim Coggins, Jena Capriccioso, Jeff Valen-

tine, Deb Allen, and Robert Barnes have been developing the new code system for several months.

“There is a national movement in healthcare right now with many organizations moving to a descriptive emergency

code system.” said Barnes “It will help to eliminate confusion for everyone when an emergency occurs. It actually

tells you what the emergency is.” Recently, Munson converted to a DECS throughout all of their locations. The

new Pavilions DECS closely mirrors the Munson system. “We purposefully designed it that way” explained Coggins,

who monitors the facility’s safety systems. “We regularly have our employees at Munson and they also have em-

ployees here quite often, so employees of both organizations will be very familiar with the codes in case of an

emergency,” added Capriccioso, who has worked in staffing for the organization. “We have just a couple of emer-

gency code colors that will still be used. Code Red is universally recognized as fire danger, and Amber Alert is also

a universal code. But even when announcing an emergency code color, it will be followed up with a plain English

description.” explained Valentine.

Training for the new DECS will begin in October through

Relias with implementation scheduled to happen begin-

ning around the end of October or early November. New

emergency code cards will be distributed to all employees

just prior to implementation. There will also be learning

reminder cards placed in multiple locations including the

lunch room and employee break rooms. Additionally, post-

ers will be placed near every Pavilion nursing station to

assist staff in learning the new system. “Like any new pro-

cess that replaces an existing process, it will take practice

and time to learn,” explained Allen, “but the benefits are

well worth the effort. The Pavilions will be even safer than it currently is.”

Page 9 of 229

dgratton

Text Box

4

V O L U M E 8 , I S S U E 9 , S E P T E M B E R 2 0 2 0 P A G E 2 P E P T A L K

ATTITUDE IS CONTAGIOUS

IS YOURS WORTH CATCHING?

Calling all Pavilions & Sodexo Employees! Have you been trying to get

healthier? Are you interested in helping your colleagues do the same? Do

you like friendly competition? Join TEAM PAVILIONS in a free, fun, weight-

loss challenge, Win by Losing, sponsored by Blue Care Network. The com-

petition runs from September 21 through November 20, 2020, with a

winner selected based on the team’s total percentage of weight loss at the end of the 9-week challenge. Team

Pavilions will compete against other BCN group customers for the coveted Team Trophy, weekly prizes, and brag-

ging rights. To sign up for the challenge visit the Employee Portal.

Employee Wellness Initiative 2020

Action Step #2: Preventative Dental Visit

Deadline: October 31, 2020

Action Step #3: Complete ONE Option Listed Below

Deadline: October 31, 2020

(1) Participate in a Win By Losing Challenge through Blue Care Network (dates to be announced)

(2) Attend a Wellness Educational Session (dates/times to be announced)

(3) Complete a Wellness Elective course on RELIAS

(4) Participate in 2020 Smart Commute Week—Dates: June 1—June 5, 2020

(5) Attend at least one (1) GTP Wellness Center Class

(6) Participate in a Community Fundraising Event (example: Walk to End Alzheimer’s, 5k walk/run, etc.)

*************************************

************************************* 12 Incredible Health

Benefits of Apples

� Stimulate Weight Loss

� Balance Blood Sugar Levels

� Strengthen Immunity

� Improve Your Eyesight

� Great for Your Teeth and Gums

� Build Stronger Bones

� Give You Energy

� Relieve Muscle Tension

� Improve Fertility in Women

� Improve Cardiovascular Health

� Improve Brain Function

� Incredibly Alkalizing

Page 10 of 229

V O L U M E 8 , I S S U E 9 , S E P T E M B E R 2 0 2 0 P A G E 3 P E P T A L K

THINGS YOU CAN CONTROL

1. Your beliefs

2. Your attitude

3. Your thoughts

4. Your perspective

5. How honest you are

6. Who your friends are

7. What books you read

8. How often you exercise

9. The type of food you eat

10. How many risks you take

11. How you interpret situations

12. How kind you are to others

13. How kind you are to yourself

14. How often you say “I love you”

15. How often you say “thank you”

16. How you express your feelings

17. Whether or not you ask for help

18. How often you practice gratitude

19. How many times you smile today

20. The amount of effort you put forth

21. How you spend/invest your money

22. Ho much time you spend worrying

23. How often you think about your past

24. Whether or not you judge other people

25. Whether or not you try again after a setback

26. How much you appreciate the things you have

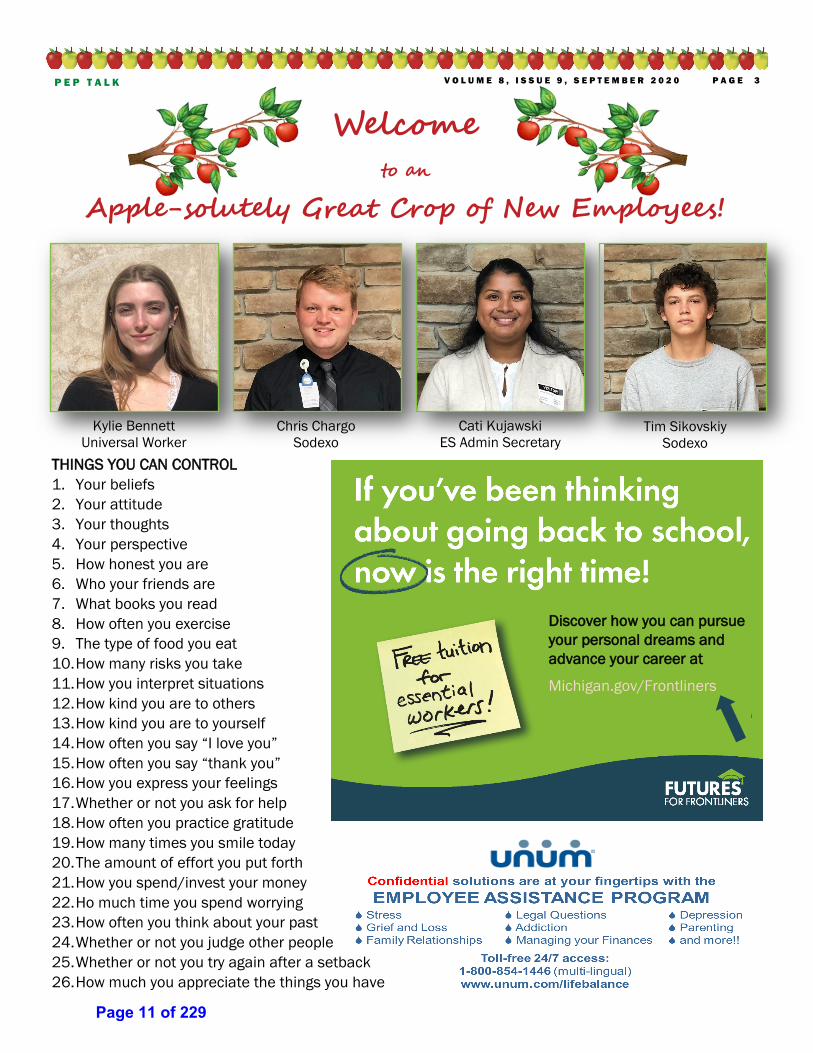

Kylie Bennett

Universal Worker

Chris Chargo

Sodexo

Cati Kujawski

ES Admin Secretary Tim Sikovskiy

Sodexo

Welcome

to an

Apple-solutely Great Crop of New Employees!

Discover how you can pursue

your personal dreams and

advance your career at

Michigan.gov/Frontliners

Page 11 of 229

V O L U M E 8 , I S S U E 9 , S E P T E M B E R 2 0 2 0

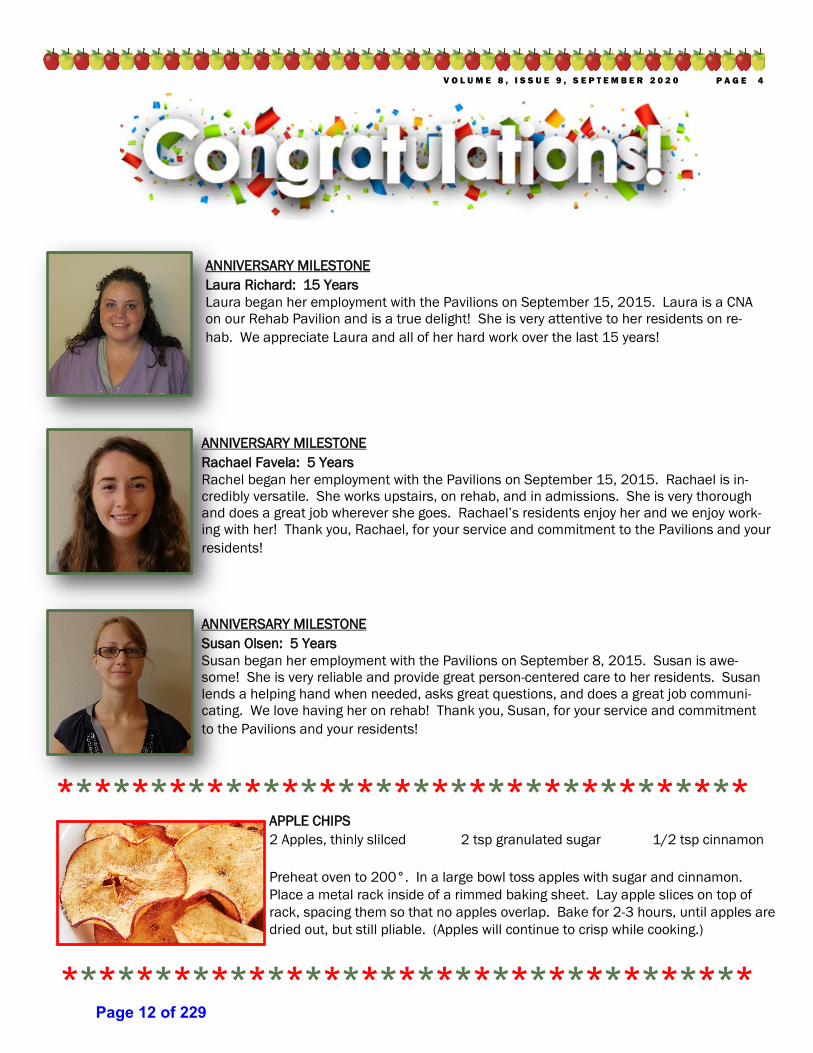

ANNIVERSARY MILESTONE

Laura Richard: 15 Years

Laura began her employment with the Pavilions on September 15, 2015. Laura is a CNA

on our Rehab Pavilion and is a true delight! She is very attentive to her residents on re-

hab. We appreciate Laura and all of her hard work over the last 15 years!

ANNIVERSARY MILESTONE

Rachael Favela: 5 Years

Rachel began her employment with the Pavilions on September 15, 2015. Rachael is in-

credibly versatile. She works upstairs, on rehab, and in admissions. She is very thorough

and does a great job wherever she goes. Rachael’s residents enjoy her and we enjoy work-

ing with her! Thank you, Rachael, for your service and commitment to the Pavilions and your

residents!

P A G E 4

ANNIVERSARY MILESTONE

Susan Olsen: 5 Years

Susan began her employment with the Pavilions on September 8, 2015. Susan is awe-

some! She is very reliable and provide great person-centered care to her residents. Susan

lends a helping hand when needed, asks great questions, and does a great job communi-

cating. We love having her on rehab! Thank you, Susan, for your service and commitment

to the Pavilions and your residents!

APPLE CHIPS

2 Apples, thinly slilced 2 tsp granulated sugar 1/2 tsp cinnamon

Preheat oven to 200°. In a large bowl toss apples with sugar and cinnamon.

Place a metal rack inside of a rimmed baking sheet. Lay apple slices on top of

rack, spacing them so that no apples overlap. Bake for 2-3 hours, until apples are

dried out, but still pliable. (Apples will continue to crisp while cooking.)

*************************************

*************************************Page 12 of 229

August, 2020 Media Report

Broadcast Report:

WTCM-FM:

Wellness Broadcast advertising ran from August 1 - 30, 2020.

Dialysis Services Broadcast advertising ran from August 13 - 30, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 3-6, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 10-13, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 17-20, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 24-27, 2020.

WTCM-AM:

Live Read – Wellness Broadcast advertising ran on August 6, 11, 21, and 24 of 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 3-6, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 10-13, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 17-20, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 24-27, 2020.

WKLT-FM/WBCM-FM:

Wellness Broadcast advertising ran from August 1 - 30, 2020.

Dialysis Services Broadcast advertising ran from August 13 - 30, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 3-6, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 10-13, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 17-20, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 24-27, 2020.

WCCW-AM (ESPN):

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 3-6, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 10-13, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 17-20, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 24-27, 2020.

WCCW-FM

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 3-6, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 10-13, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 17-20, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 24-27, 2020.

WJZQ-FM

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 3-6, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 10-13, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 17-20, 2020.

Concerts on the Lawn – Goes Radio Retro Broadcast (gratis) advertising ran from August 24-27, 2020.

Page 13 of 229

dgratton

Text Box

5

August, 2020 Media Report (CONT.)

Record Eagle:

A Career that Loves you Back.. August 2, 2020.

Concerts on The Lawn – Radio Retro – Jimmy Buffet Tribute August 5, 2020.

Concerts on The Lawn – Radio Retro – The Backroom Gang August 12, 2020.

A Family of Caregivers – Adult Day August 16, 2020.

Concerts on The Lawn – Radio Retro – Dig A Pony: A Beatles Tribute August 19, 2020.

The Convenience of On-Site Dialysis August 23, 2020.

Concerts on The Lawn – Radio Retro – Elvis Tribute Artist Jake Slater August 26, 2020.

Concerts on The Lawn – Radio Retro – Thank you to Sponsors August 30, 2020.

Make it Grand-Parent Video Charity Challenge August 30, 2020.

NorthCoast:

Our team has your back … - Wellness Center August 8, 2020.

The Convenience of On-Site Dialysis August 22, 2020.

Page 14 of 229

COVID 19 Report –September 2020

Testing Results

We are still receiving our COVID results within 48 hours of receipt. We admitted a rehab patient from

Munson this month who was without any symptoms only to be informed after admission that they were

COVID positive. This prompted isolation for this patient and initiated residents weekly testing for 2

weeks. We tested immediately upon learning of the positive COVID status and have tested again on

September 9. Additionally, four staff members were found to be COVID positive with one member

having symptoms and the other three without symptoms. These staff members are unrelated to the

rehab patient admission and with the exception of the two staff members who are roommates, are

unrelated to each other. We completed testing on September 14 and 16 for all staff, SNF residents and

Cottage residents. All tests were negative. Per the requirements we tested all staff and residents on

September 21 and are awaiting results.

Staff Screening

Staff are required to enter the building through the employee tunnel wearing their mask. Employees

have their temperature and photo taken via the thermal camera. If a temperature is outside of the

acceptable range of 94-100 degrees, an alert is sent to the nursing supervisor as well as administration.

An assessment is conducted by nursing at this time. If the temperature is acceptable, the screen on

the thermal camera flashes green. Staff proceeds to the questionnaire kiosk to complete the screening.

Should staff check yes to any symptoms, the system prevents them from completing the screening

process. A nursing assessment is completed at this time as well.

Visitation

We continue with a large volume of electronic visits between the families and their families. Window

visits continue weekly and we are looking at options for when the weather changes. As of now, we

provide golf cart transportation if needed, tents are up at the visit sites and chairs. The State has

published guidance that allows nursing homes to engage in outdoor visits. We are working on the policy

and procedure to offer these types of visits. It is unfortunate that this has taken the State so long to

determine as the weather is turning cooler and we foresee outdoor visits cut short due to dropping

temperatures and snow.

Communication

In addition to phone conferences between families and staff, COVID information and facility happenings

can be found on our website under the Weekly Family Update tab, the Neighborhood News and the

Legacy. In the event that families need to be notified of a positive COVID case a ROBO call is sent out

with information needed and direction to review the facility update page.

Infection Control

Employee and any resident illness is tracked through our infection control processes to ensure that staff

and residents are not exposing otherwise healthy individuals to potential germs. Staff and residents

practice strict hand hygiene. Facility surfaces are disinfected several times daily and as needed. Staff

are continually provided education on infection control practices at work, out in the community, and at

home. Staff are also required to wear eye protection while in the resident areas.

Page 15 of 229

dgratton

Text Box

6

Personal Protection Equipment (PPE)

Currently we have an adequate supply of gowns, face shields and masks. There is a shortage of

gloves in all sizes nationwide. We order continually and sometimes the order is received and others we

are placed on a wait list. We received the additional shipment from FEMA which included masks,

gowns and hand sanitizer. We were not given any gloves as this product ran out prior to distribution to

all facilities. We are (or will be) the recipients of a grant to cover PPE and have been able to place

large orders for masks, goggles and gloves for future use. This will provide a robust inventory through

the influenza season and COVID.

COVID Surveys

We have not had any further COVID Infection Control focused surveys however we are working with

the Quality Improvement Organization as required by CMS on two separate projects. The first project

is regarding antibiotic usage and the second is environmental disinfection practices. This is in its early

stages with no data to report yet. On September 2, during a Facility Reported Incident survey, we

received a citation for isolation procedures. There are conflicting published guidance between the

various regulating bodies regarding admissions and readmissions and the type of PPE that should be

worn. Our policy as a facility, in accordance with the guidance from our medical director, all new

admissions and readmissions were placed in droplet precautions. The state disagreed with this and is

mandating full PPE. This citation resulted in a directed plan of correction per the new CMS

requirements. We are currently working with an approved consultant on the requirements surrounding

a directed plan of correction. As interpreted by MDHHS, all new admissions, readmissions and those

residents who leave the facility for appointments must be quarantined (preferably on the same unit) for

14 days with staff utilizing full PPE regardless of a resident’s COVID status. The Rehab unit is being

utilized for this purpose with three separated areas. One area for admissions/readmissions, one area

for those residents who have left the facility for an appointment and the last area reserved for known

positive COVID residents.

COVID Funding Relief

Since the last board meeting, Grand Traverse Pavilions received a $358,000 distribution from the

Federal CARES Act through CMS, representing the $2.5 billion Phase 1 allocation of Provider Relief

Funds dedicated to Skilled Nursing Facilities. Another $2 billion allocation will be distributed to nursing

homes covering the last four months of 2020 based on infection control incentive outcomes related to

COVID infection and mortality rates. The Pavilions continued to receive reimbursement for COVID-

related costs, including $50,150 from the MDHHS towards the $2/hour wage premium for direct-care

staff; and $52,769 from the MDHHS towards weekly COVID testing administration of residents and

staff. The Pavilions also submitted a $250,000 grant towards PPE through a $25 million grant program

of CARES Act funds made available from the State of Michigan. An additional grant application for

$18,500 was submitted through the Michigan Department of Health and Human Services (MDHHS) for

infection prevention and control equipment. Finally, A Medicare payment advance of $735,000 applied

for back in April, was just approved and distributed in September. The advance payment will be

recouped from future Medicare receipts after 90 days.

Page 16 of 229

Page 17 of 229

dgratton

Text Box

7

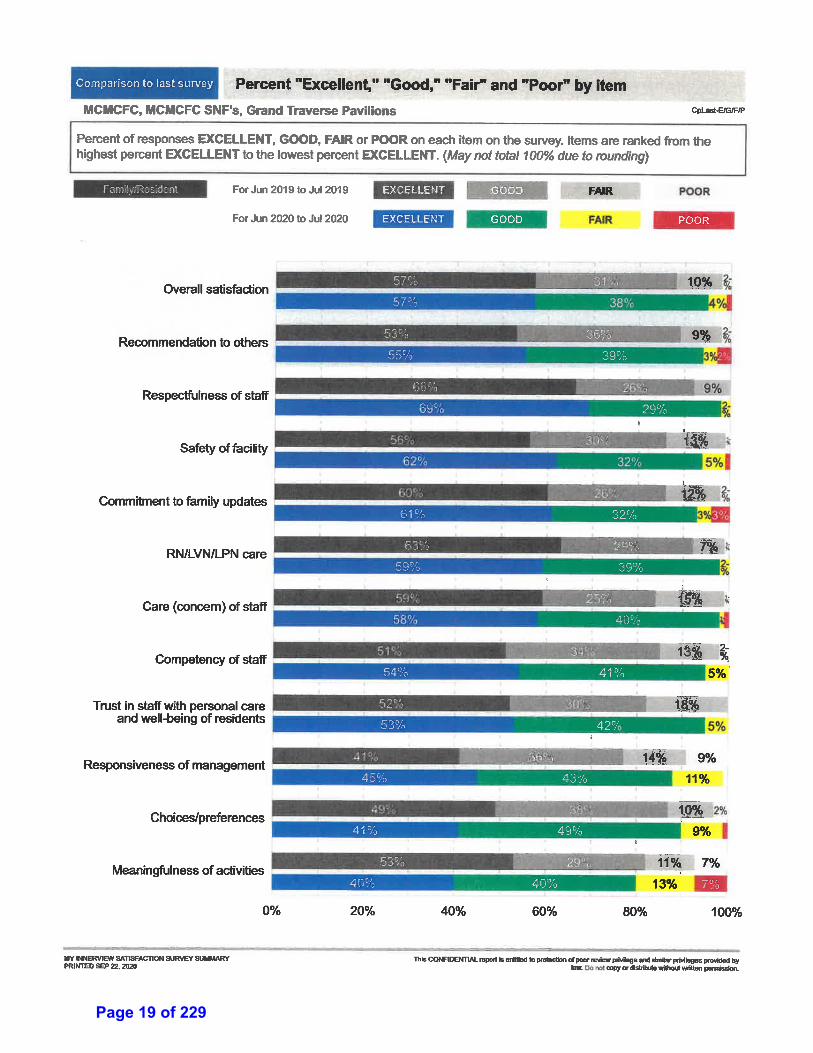

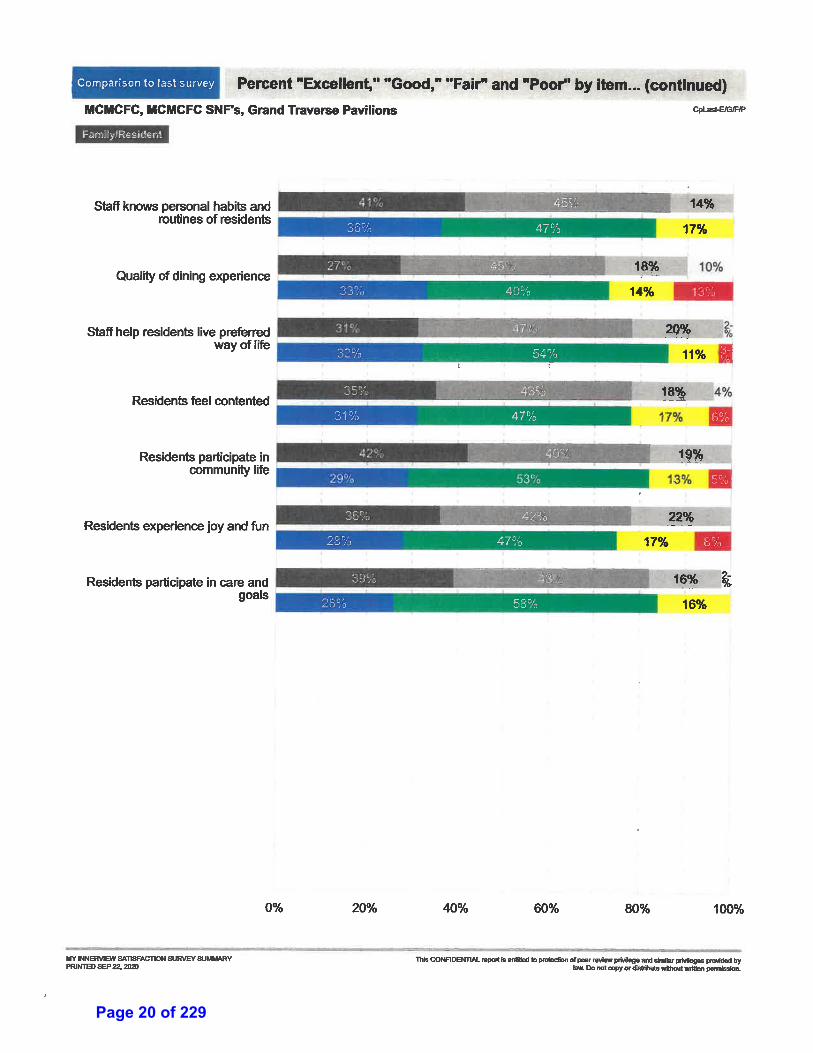

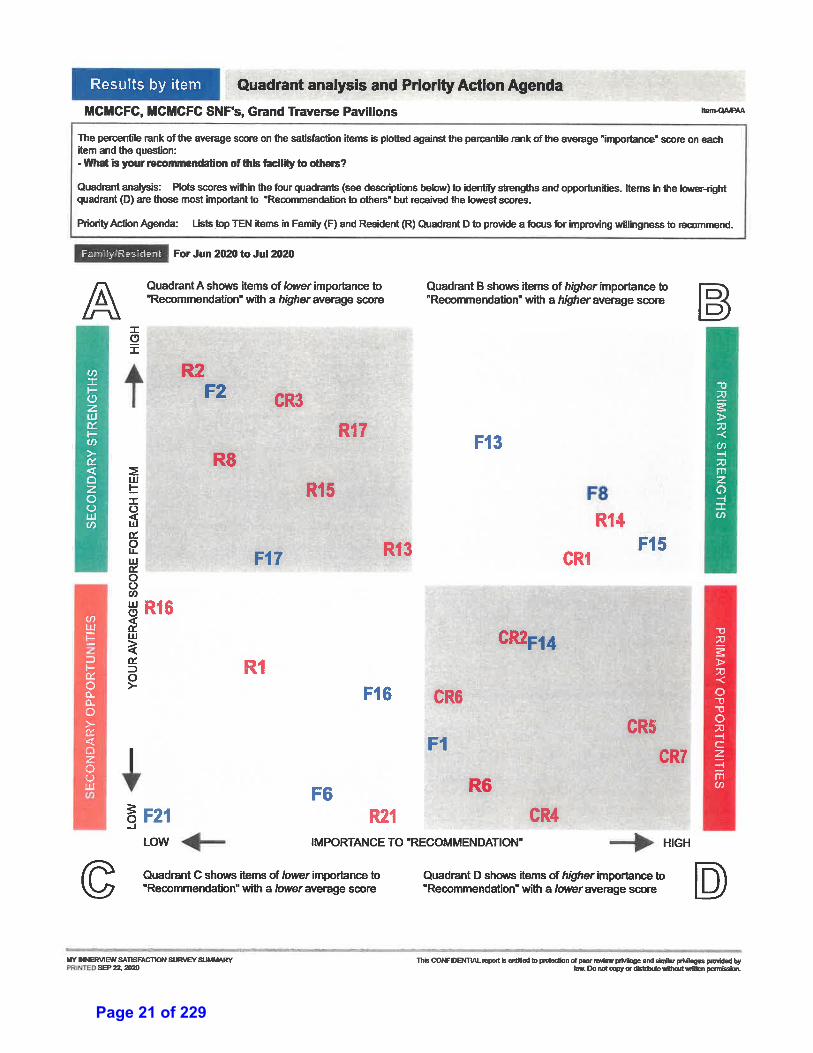

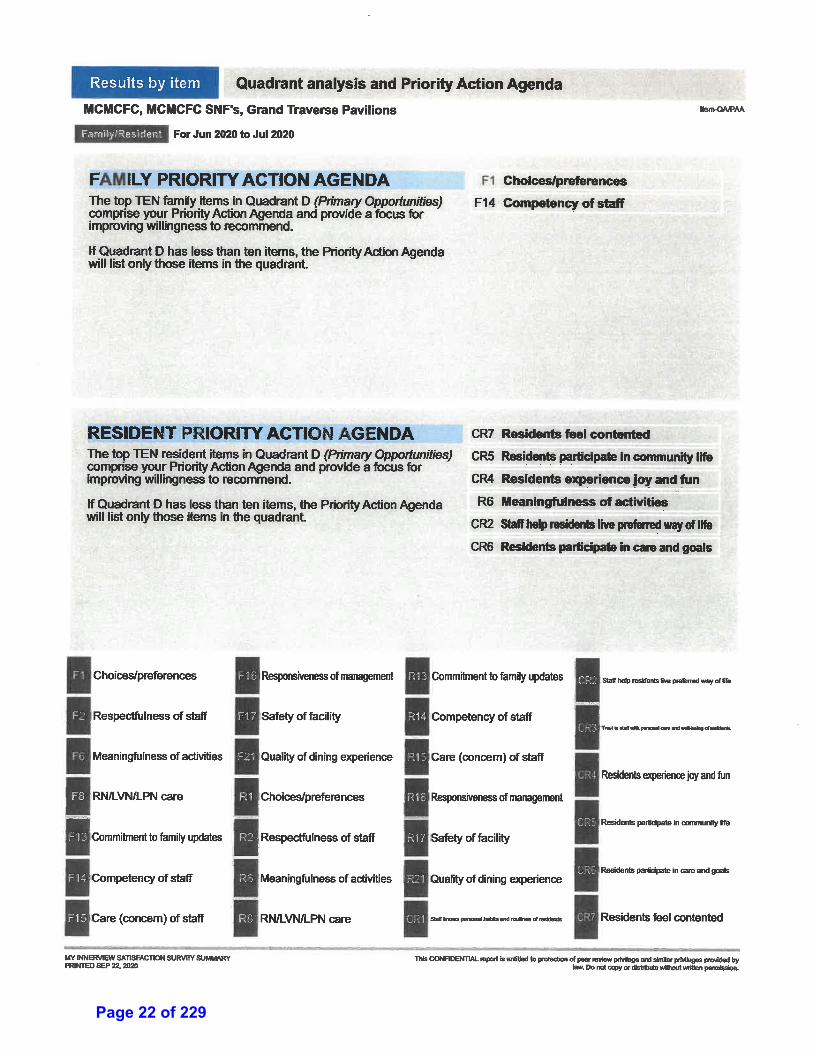

Page 18 of 229

Page 19 of 229

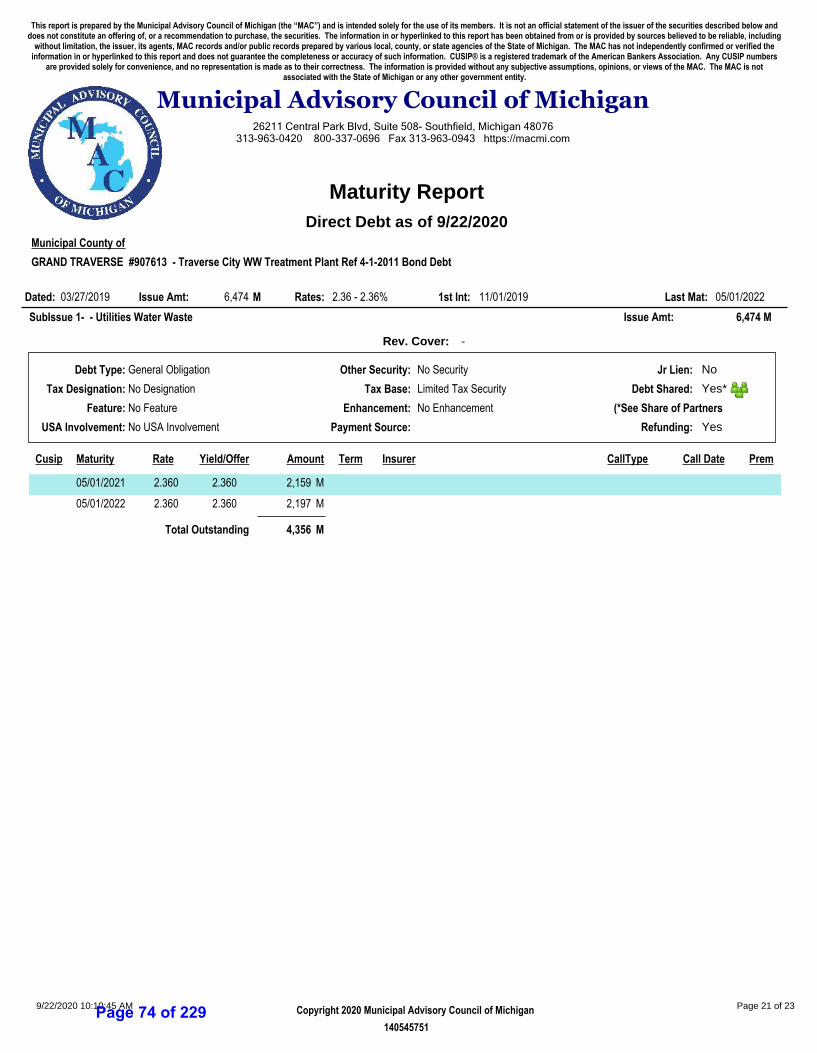

Page 20 of 229

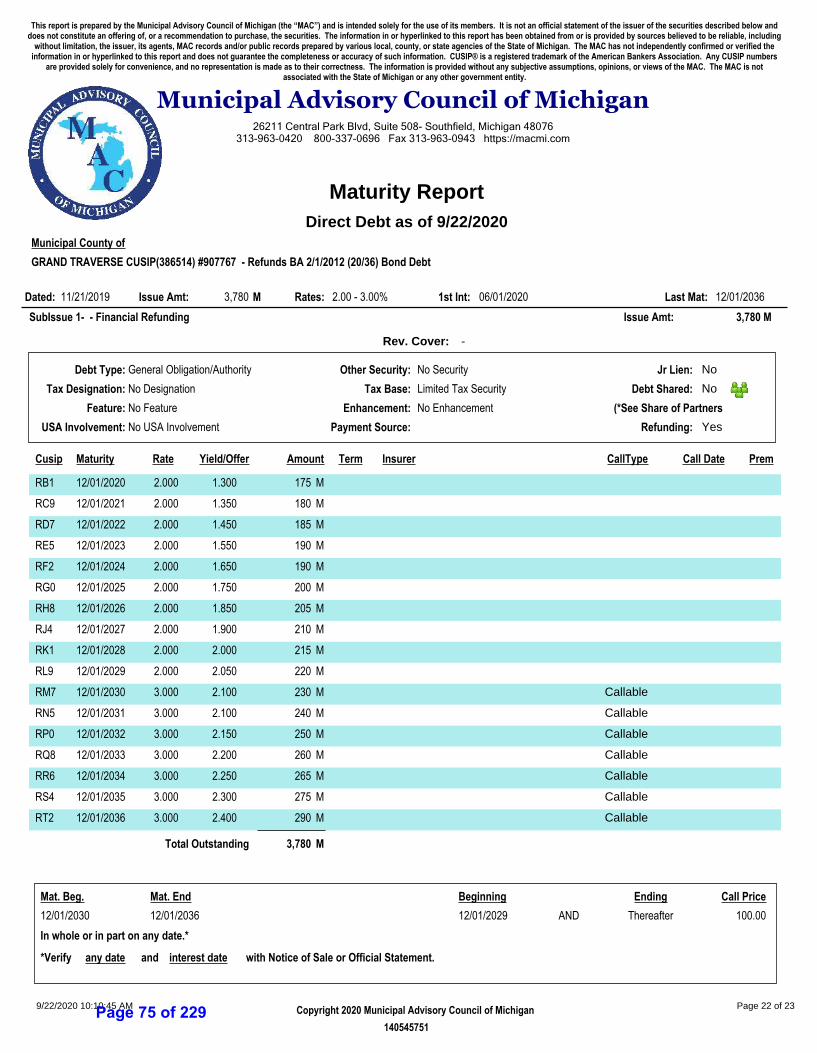

Page 21 of 229

Page 22 of 229

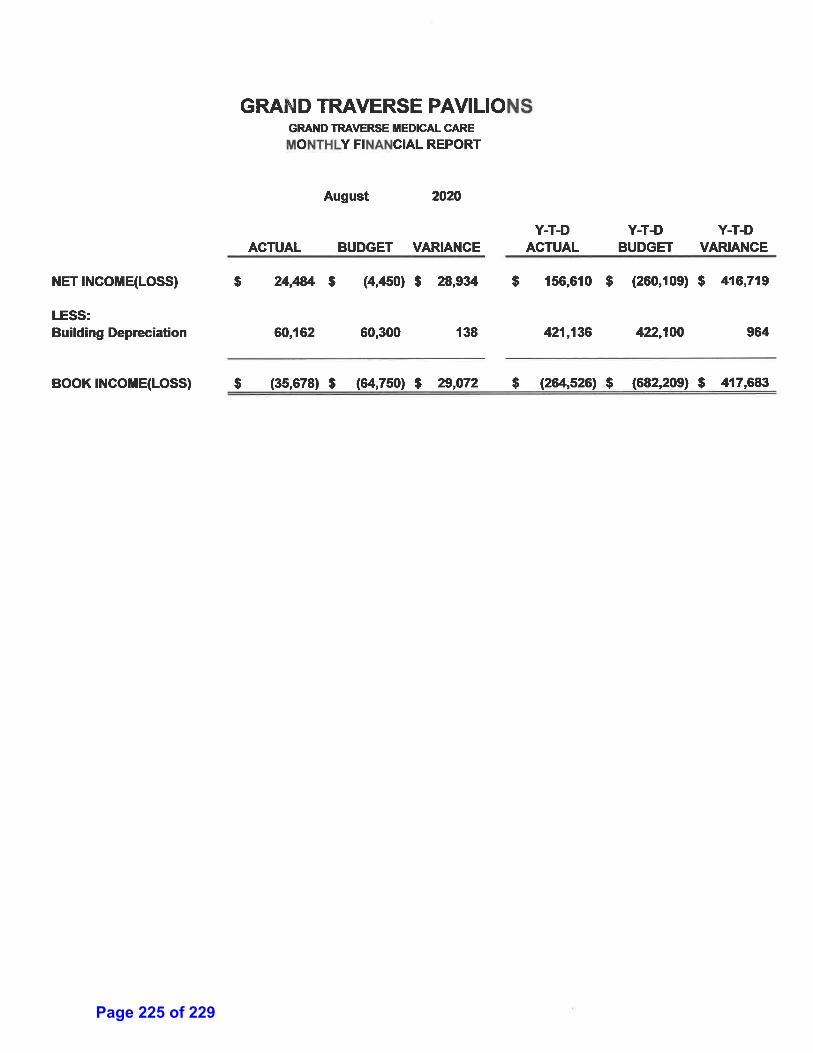

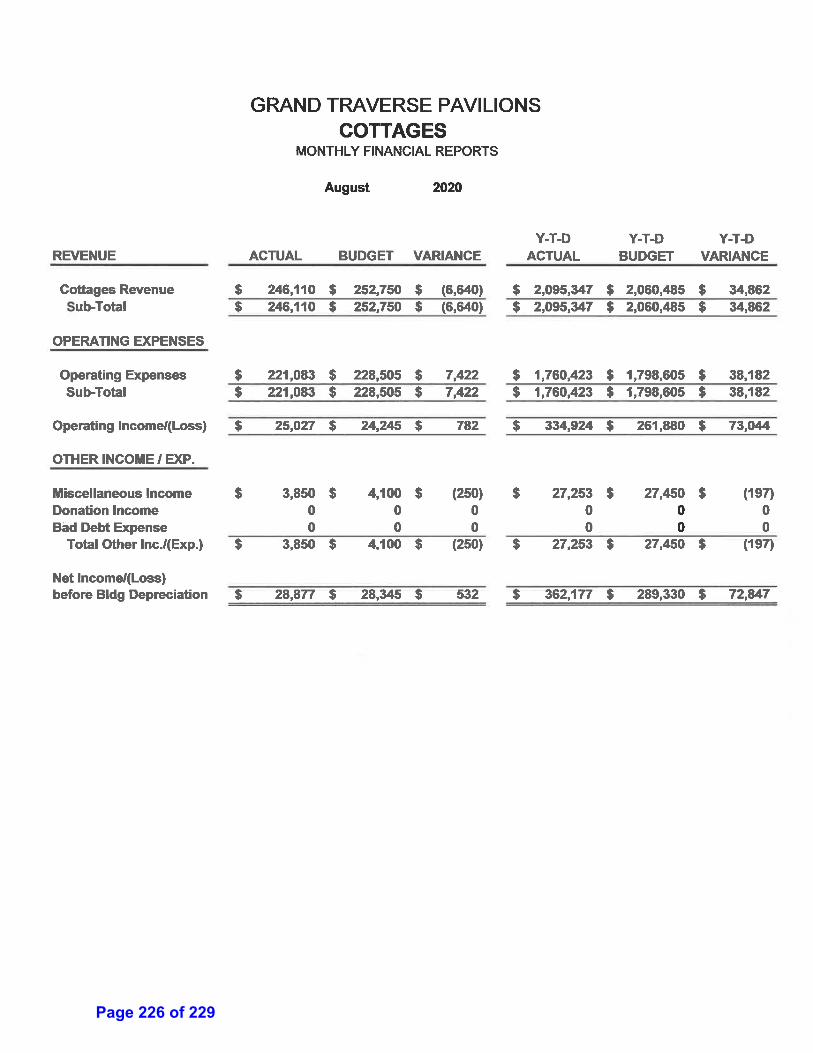

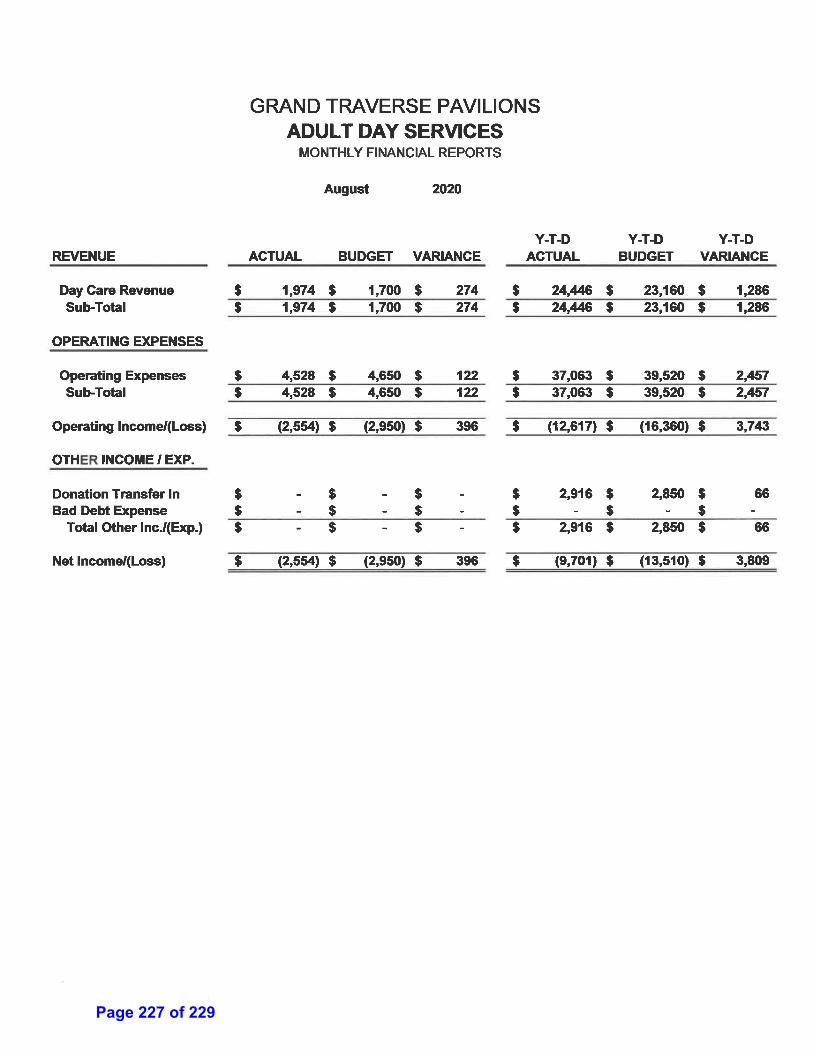

September 21, 2020 TO: Grand Traverse County Department of Health and Human Services Board FROM: Korvyn R. Hansen Administrator/CEO RE: August Report Hansen and Rose Coleman, COO-Clinical Services, continue to attend daily/weekly conference calls with Centers for Disease Control, Centers for Medicare and Medicaid, Grand Traverse County, Michigan County Medical Care Facility Council, Leading Age of Michigan and various other entities addressing the issues surrounding the COVID-19 pandemic. On August 4, Hansen attended the Recruiting and Retention committee meeting. Current open positions were identified as 15 CNA, 2 Nurses, 1 Custodians, and 1 Laundry. Universal Worker positions are all filled, however 2 of the UWs will be going back to college in early September. The idea of advertising for open positions on the side of a BATA bus was discussed, as was potentially using a Pavilions bus in the same way. Current media being used for open position advertising is WTCM, WKLT, Record Eagle, Michigan for Hire, The TC Ticker, Facebook, and Instagram. On August 5, Hansen and Holly Kazim, LMSW Dementia Services Director, Social Work supervisor, participated in a webinar with My Innerview to review the report generator features relating to the annual satisfaction survey results. On August 6, 12, 19 & 25, Hansen participated in the state’s Nursing Home Task Force on staffing issues related to COVID. The work groups finding will become part of a larger Task Force report to the Governor. On August 6, Hansen virtually attended the Area Agency on Aging of Northwest Michigan board meeting. On August 20, Hansen and Lindsey Dood, Chief Financial Officer, attended a virtual meeting with representatives of Plante Moran, PLLC (Jon Lanczak, Senior Manager and Megan Schaefer, Senior Consultant) to review analysis based on the cost reports filed for 2019 including projected rates and comparative costs. Also discussed report estimating the Medicaid reimbursement resulting from funding the pension plan with bond proceeds and proposed changes to the reimbursement system that could negatively impact the projected benefits.

Page 23 of 229

dgratton

Text Box

8

2

On August 24, Hansen and Allen met along with members of the Foundation Investment Committee. Huntington Bank representatives attended to provide an update on Foundation investment performance for the first half of 2020. On August 31, Hansen, Dood, Coleman, Robert Barnes, COO-Support Servivces, and Diane Mallory, Human Resources Director, met to review various COVID-19 related grant opportunities, develop an action plan for compiling the information necessary to apply for the grants and prepare a plan for spending grant funds to maximize resident outcomes and staff satisfaction. The monthly Safety Committee meeting was held on August 11. Mallory presented a summary of July’s employee incident/ accident statistics. There were 6 employee incidents during July. There were 89 restricted days and 2 lost time days. On August 3, Deborah Allen, Chief Development and Community Engagement Officer and Kory Hansen, Administrator/CEO for Grand Traverse Pavilions attended the funeral service for long time Pavilions supporter and Foundation Board Member Emeritus, Clara McManus. Clara passed away earlier this year in Florida. Plans were to celebrate her life this past May, but due to COVID-19 restriction the ceremony was postponed to early August. On August 3, Allen and Jessi Weir, Development/Marketing Assistant held a final production meeting with TV 9&10 Marketing Director, Michael Ramsey to discuss the launch of the “Make It Grand-parent Video Charity Challenge” on their Facebook and event platform. On August 7, Allen, Weir and Jena Capriccioso, Development/Marketing Administrative Assistant conducted a phone conference meeting for the Foundation Annual Events Committee. The status of the Concerts on the Lawn Goes Radio Retro and plans for the “Make it GRAND-Parent Video Charity Challenge” were vetted and shared with the committee. On August 11, Allen and Weir met with Jean Derenzy and Downtown TC staff Nick Viox, and Katy McCain to review plans for the Make It GRAND event and to request a $500 donation for the event to match PNC’s $500 contribution for the event to give a GRAND ($1,000) value of Downtown TC gift certificates. The proposals was well received and the staff was able to focus on a more robust promotional effort. On August 11, Hansen, Allen, Barnes, Tim Coggins, Environmental Services Director and Darcey Gratton, Administrative Services Director, reviewed plans for the re-installation of the “To Every Season” Sculpture that was originally dedicated to the Grand Traverse Medical Care Facility. On August 13, Allen submitted the Make it Grand Press Release to the media. On August 13, Allen prerecorded an interview with TV9&10 Anchor for “The Four” to feature the Make it Grand-Parent Video Charity Challenge in partnership with PNC Bank, 9&10 News, and Grand Prize sponsor Downtown TC. On August 14, “The Four” on TV 9&10 featured the Make it Grand promotion.

Page 24 of 229

3

On August 19, Allen was the scheduled presenter for the Bay Area Senior Advocates (BASA) meeting to offer an update on the Pavilions response to COVID-19 and to share information on the Make it Grand event. On August 20, Allen pre-recorded that final “Thank you” interview for the 2020 Concerts on the Lawn Goes Radio Retro Concert season to air on Thursday, August 27, 2020. On August 21, Allen virtually attended the Association of Fundraising Professionals of West Michigan Board meeting. All internal volunteer activity continued to be suspended during August. One hundred and eight three (183) letters were sent to Pavilions volunteers to recruit individuals who would be willing to send notes, messages and letters of good will to Pavilions residents during the pandemic. The total Social media post reach for August was 9,956 individuals. There were 21 “Page Followers” in August. The Facebook announcement featured on August 17: “On Sunday, August 16, 2020 Roseada Bagroski celebrated her 100th birthday here on our Birch Pavilion with her family on the other side of the window!” Had a reach of 2,338 people and 16 shares with an engagement of 836. The Facebook post featured on August 24: “Grand Traverse Pavilions is hiring!! Join the team of Nurses, Certified Nurse Aides, Universal Workers, Custodians and Laundry Service Staff and improve the quality of life for seniors in our community!” had reach of 294 and had 96 engagements. Grand Traverse Pavilions Website received 13,652 visitors (page views) for the month of August. Employment Opportunities page views totaled 1,131 for the month of August. Coleman continues to lead and facilitate the Incident Command Team in efforts to prevent the spread of COVID 19 to our facility. Part of August was spent with the core team comprised of Coleman, Kristen Packard, Director of Nursing, Holly Kazim, Dementia Assessment Coordinator/Social Worker Supervisor, Dan Butler, Director of Information Systems, and Emily Ball, Financial Management Assistant setting up KPI Dashboards through Netsmart. This module will allow staff to monitor key indicators through the electronic medical record system, MyUnity. On August 17, Coleman and Amy Coneset, Wellness Center Director, met with Dr. Jacob White neuropsychologist to review potential services to the Pavilions. In August, there were five facility reported incidents. Throughout the month of August, we had 58 admissions, including re-admissions from Munson Medical Center. Two of those admissions were admitted from our waiting list and one was admitted from our continuum of care. We received 118 referrals from Munson and 6 from other hospitals in the surrounding area. Four of our Rehab Center residents transferred up to long term care.

Page 25 of 229

4

In the month of August there were 57 discharges. Thirty – two residents were discharged to home, 20 to Munson, and 5 residents passed away. There were nine Medical record requests completed in the Month of August for Blue Cross and Blue shield of Michigan and Priority Health PPO insurance, Aetna Medicare advantage, various long-term care insurance carriers and individual record requests. Holly Edmondson, Clinical Case Manager, actively participates in the Incident Command Team as the organizations Infection Preventionist, maintaining daily pre-admission screening for all potential admissions, COVID-19 daily timeline and employee health screening, monitoring and follow up. In August this also included assisting the ICT with resident testing on August 7 and staff COVID-19 required testing on August 3, 10, 17, 24 and 31. The daily interdisciplinary team meetings continue to benefit all involved with discussions of current issues involving resident care in the last 24 hours or 72 hours over a weekend/Holiday. Topics reported include the following: falls, skin incidents, abnormal blood sugars, weight loss, behavioral issues, pressure ulcers, and any other pertinent issues. With each meeting new and current issues with residents are discussed and reviewed and new information is shared. In-services for August include: All Staff: All Page and Code Status, Understanding Alzheimer’s disease and Dementia and In-Person Annual Clinical Skills Competency. Licensed Nurses: Waived Testing: Hemoccult, Uristix, Blood Glucose. Certified Nurse Aides: Safe Transfers. Universal Workers: Assisting with Dressing. Jamie Wilson, Director of Certified Nurse Aids and Katy Leach, Staff Development Coordinator, continue the employee monitoring system with 15 visits to staff that are systematically followed up with during their first 3 months of employment or on an as needed basis. Staff Development created and distributed daily COVID-19 updates, assisted with weekly COVID-19 testing for staff and residents, and created COVID Education for all staff members. In-Person Annual Clinical Skills Competency Evaluations we held for all nurses with the following skills: Handwashing, Isolation, CPR Drill/All Page, Tracheostomy Care, CPAP Machine, Nebulizer Machine, Wound Vac, and Waived Testing: Blood Glucose Machine, Uristix, Hemoccult. All of the in-house clinics in the nursing home were cancelled in August. Restorative and Functional maintenance program monitoring continued including daily Restorative program documentation by the Certified Nurse Aide (CNA) or therapist completing the program. In lieu of Group Exercise, Therapists have been doing Restorative programs and 1:1 exercise programs. Quality Assurance (QA) Studies Completed for August included; monitoring medication storage/ refrigerators, call light response times, infection control and prevention, Nurse All Page system and Independent Safety of Resident. Packard and nursing administration continue to complete weekly COVID-19 testing for

Page 26 of 229

5

staff and residents. In addition, we are completing testing for 48 providers and vendors that are regularly inside the building. A flu vaccine clinic has been scheduled for October 27. Resident rosters have been provided to the ADON’s and letters with consents have been mailed to families. Yearly labs for creatinine clearance are to be obtained shortly in preparation for potential Tamiflu dosing. We continue to condense the admission process and work towards having more nurses familiar with completing admissions. At this time, we are trialing splitting the admission process between CQI and the floor nurses. The sections were divided in a way as to give the nurse a better overview of their new admission while allowing the CQI nurse to build the electronic medical record (EMR) chart while keeping in mind facility policies and the individual needs of each patient. James Hunter Dietary Manager participated in the Nursing Home Task Force Quality of Life workgroup. This committee proposed 13 different recommendations for improved quality of life for our residents including a return to a small level of communal dining for the residents and some small group social gathering activities. It is hopeful that these efforts will lead to a better food consumption experience for snacks and all meals in the near future. Life Enrichment staff continue assisting residents on the pavilions with individual social visits, manicures, reading, playing board games, writing letters and more. During the month of August, Kari Belanger, Linda Burton and Holly Kazim saw approximately 7-8 residents a day (all pavilions, Monday-Friday) to assist them in video chatting with their family members either by FaceTime, Google Duo, Facebook Messenger or ZOOM. In August, we had 227 social video chat visits with family members, 6 video chat visits included hospice visits, court appointments, telehealth, funerals, attorney visits, and counseling appointments with Community Mental Health, and a palliative care consult. Kari worked with IS and the Rehab Department in setting up an iPad (with FaceTime and Google Duo) so that the therapy staff can have a session(s) with Rehab residents and their family members prior to discharging home. Family members continue to contact their pavilion social worker or the recreational therapists to schedule the video chat. Residents continue to share that they are enjoying staying in touch with their family members this way. We have also assisted in celebrating birthdays over video chats. Kari Belanger continues to work on one of the two self-study programs through EVOLVE, that is facilitated by The Eden Alterative. This platform was developed in light of the Eden International Conference that was cancelled in April due to the coronavirus, as a way to offer educational classes for conference compensation. Currently, two classes are being offered with a third class to be launched in August or September. The weekly Prize Bingo continues to be successful for the residents, as approximately 9-13 residents winning each week by utilizing the Osborn Visual Solutions (OVS) television channel. Residents have asked to continue this way of playing bingo even when the COVID restrictions are lifted and they are able to play their beloved game in a group setting again.

Page 27 of 229

6

Social services handed out 36 discharge surveys in August. On August 7, Kazim facilitated telemedicine rounds with Dr Engel. On August 13 and 27, Kazim facilitated Palliative Care rounds with residents. August resident council did not take place however social workers met with residents individually to check in and completed minutes. August family council also did not take place. Social workers continue to conduct follow up phone calls to discharged patients on the rehab pavilion, to proactively reduce hospital readmissions 30-days post-discharge. The Wellness Center saw the following patients this month: Medicare A: 47; Medicare B: Outpatient: 36; Medicare B: Inpatient: 21; Private Insurance: Outpatient: 4; Private Insurance: Inpatient: 4; Work compensation: Outpatient: 0; Private pay: Outpatient: 0; Private pay: Inpatient: 0. Auto: Outpatient: 5; Auto: Inpatient: 1. For the Cottages in August, there were 2 admissions, 4 respite stays, 3 in-house transfers, 5 discharges, and 2 deaths. Ten information packets were mailed and four were handed out. Nurse Practitioner Beth McNutt visited The Cottages on August 4, 11, 18, and 25 with a current case load of 39 patients including, 2 newly acquired in August. A Foot Clinic was held on August 12 with 32 residents participating by individual appointments. Cottage resident meetings resumed in August, one was held at each cottage on separate dates. Residents were able to share suggestions with the Dietary Director. The Adult Day Program had regular participants 3 days a week with 1 new participant enrolled, and 1 information packet was mailed.

On August 4, Dood participated in a call with Roger Swets, Member, Dickinson Write, Warren M. Creamer III, Managing Director-Public Finance, Robert W Baird and Steven Burke, CFA, President, MFCI, LLC to discuss the moving forward to develop an actionable presentation on pension bonding for the DHHS Board and County Board of Commissioners for consideration. On August 21, Dood participated in a conference call with Provinet representatives to review their preliminary assessment of the Pavilions financial configuration of myUnity and the estimated effort to change that configuration to enable the Pavilions to bill all payers using the software. On August 28, Dood participated in another conference call with Provinet representatives. Financial Management staff have reviewed Provinet’s reconsidered opinions and provided details on current process, developed project objectives and requested proposal for assistance in achieving objectives. Objectives identified included dashboard functionality, in source billing, create electronic closing process, receive recommendations on electronic PO and AP approval software and related GL software, electronic cash receipts posting and other process efficiencies as the department prepares for future retirements.

Page 28 of 229

7

On August 26, Dood attended training on the myUnity Dashboard. On August 5, 12 and 19 Dood attended the Safe and Calm webinars by Leading Age. During August, the Descriptive Emergency Call System Committee met to finalize plans for the roll out, tentatively scheduled for September. The committee consists of Jeff Valentine/Residential Services Coordinator, Jena Capriccioso/Marketing Development Administrative Assistant, Tim Coggins/Environmental Services Director, Deb Allen/Chief Development and Community Engagement Officer, and Robert Barnes/COO-Support Services. Capriccioso has been instrumental in developing all the presentation materials needed for the rollout. A review of the new DECS will be presented to the executive staff at the September meeting. On August 6, Barnes attended a Leading Age webinar. A federal judge has struck down several DOL regulations in the FFCRA. Interpretations should be coming out in early September to see if there will be any impact on the Pavilions. During August, the new temperature monitoring system worked very well. It is much quicker than the previous hand held process was. Also, if an employee temperature reading does not fall within the set parameters of the system, a photo of that employee is immediately sent to Nursing Administration and the employee will be evaluated for further determination. On August 25, D. Mallory and R. Barnes attended a Zoom meeting with Smartlinx new Customer Service Manager Xanthia Ellis. After reviewing the needs of Pavilions for employee performance management evaluations, Mallory, Ellis and Barnes all agreed that the Smartlinx performance evaluation module will work for the Pavilions. Ellis will submit a quote to the Pavilions within the next two weeks. Joshua Chubbs, Information Systems Intern, has been working on a new ticket tracking system. This system will allow staff to submit a ticket, track the work being requested and even communicate with the department. This will allow for future troubleshooting and potentially create a knowledge base for end users to use to troubleshoot their own issues. A total of 16 external interviews were scheduled for the month of August. Of the 16 external interviews scheduled in August, 5 individuals were extended conditional offers of employment. Recruitment is underway for the following open positions: 24 CNA; 5 Licensed Nurse; 8 Universal Workers; 2 Child Care; 2 Lauderers and 1 Custodian. Five employees were hired in August. Four (4) New Employee Orientations were held and included 2 Custodians, 1 CNA, 1 Physical Therapist and 1 UW. (78) people have been hired in 2020. In August, Pavilions job opportunities were posted on Michigan4Hire, Awesome Job Alert, Michigan Talent Bank, Black Diamond Broadcasting, Pure Michigan Talent, LinkedIn, Craigslist, Leelanau Enterprise and Indeed.

Page 29 of 229

8

There were 71 applications received in August. Up from 61 in July and up from 57 in June. For the month of August, there were a total of 18 terminations. Of those 18 terminations, 15 were voluntary and 3 were involuntary. There have been 112 terminations in 2020. In the month of July, the CNA Bonus Program yielded payments of $50.00 to 27 CNAs; $100.00 to 2 CNA’s; $150.00 to 17 CNAs that met the requirements. There was one employee referral received through our Employee Referral Bonus Program. To date we have paid the bonus to 35 employees for referring individuals and we have distributed 12 $25 gift cards for referring an applicant who were not considered for employment. In August, 44 employees utilized the Beech Gym. The maintenance team completed 706 separate work orders during June. Additionally, there were 40 wheelchair work orders completed. The monthly fire drill for the main building was August 22 at 6:00 PM. For the Cottages, fire drills occurred August 25 at 10:00 for Evergreen, August 6 at 4:00 PM for Hawthorn and August 19 at 7:00 PM for Willow. There were no actual fire codes in August. There were 56 room preparations at the main building. Of the main building preparations, 47 were for Rehab and 9 were from units Aspen through Elm. In addition, there were 3 room preparations at the cottages due to room vacancies from discharges and residents moving between rooms. During the month of August, there were 116 appointment bus runs and 2 group bus runs. On August 4, Tim Coggins, Environmental Services Director, met with Ashley Curtis of the Grand Traverse Health Department to perform the annual inspection on the therapy pool. There were no issues with the inspection. Ashley also commented that our pool is one of the best that she has inspected. On August 5, Coggins met with Joe Berry, Grand Traverse County Facilities Director, to review the preventive maintenance / work order software they are using for their operations. They are using a software called MVP Plant. We are looking at options to use for our maintenance techs that will be more efficient and accurate than the system we are using now.

Page 30 of 229

4834-6357-6523 v1 [90129-4]

GRAND TRAVERSE COUNTY

DEPARTMENT OF HEALTH AND HUMAN SERVICES BOARD

(Grand Traverse County, Michigan)

RESOLUTION NO. ______

RESOLUTION TO AUTHORIZE ACTIONS WITH RESPECT TO

PENSION BONDS

Minutes of a regular meeting of the Grand Traverse County Department of Health and

Human Services Board, Grand Traverse County, Michigan, held on September ____, 2020, at

_____ p.m., local time.

PRESENT: Members:

ABSENT: Members:

The following resolution was offered by Member ____________________ and supported

by Member ____________________:

WHEREAS, the Grand Traverse County Department of Health and Human Services Board

(the “Board”) deems it to be in the best in interest of the Grand Traverse Pavilions (the “Pavilions”)

for the County of Grand Traverse (the “County”) to issue its limited tax general obligation bonds

(the "Bonds") to finance part of the cost of the Pavilions’ unfunded pension liability for its defined

benefit plan retirement program as authorized by Section 518 of Act 34, Public Acts of Michigan,

2001, as amended (“Act 34”);

WHEREAS, the issuance of the Bonds would significantly fund Division 41 and Division

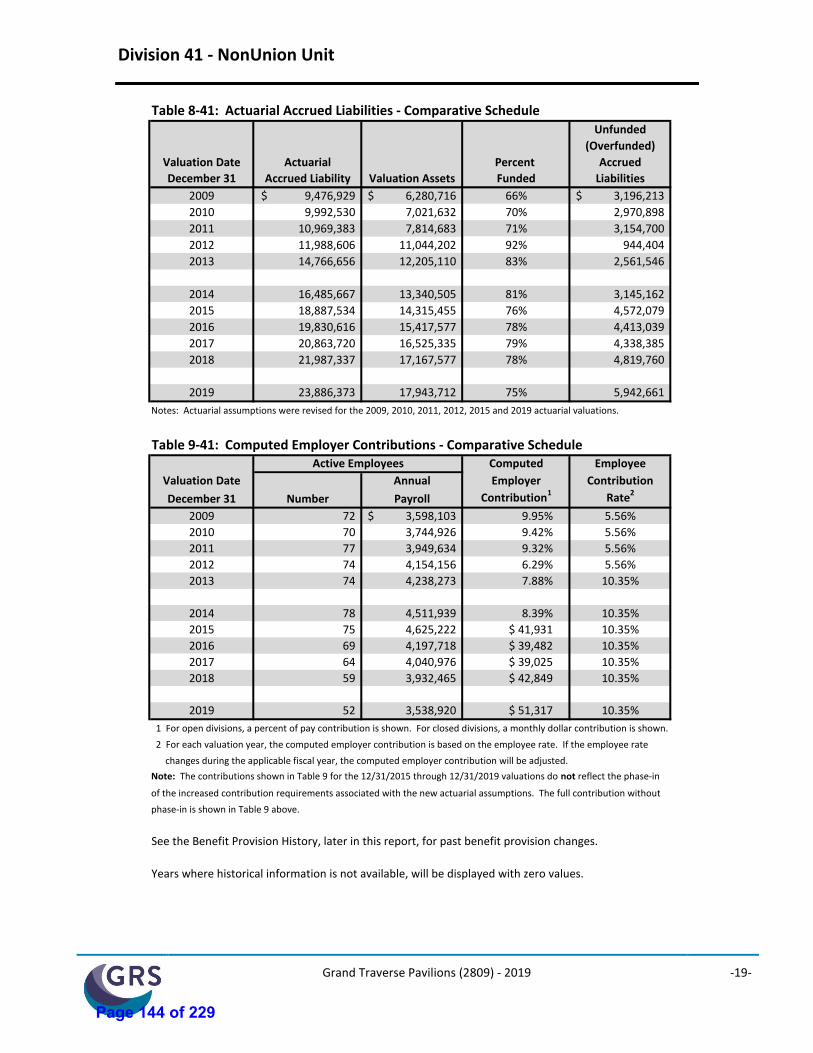

43 of the defined benefit retirement plan, providing assurance to the participants in such divisions

of their pension benefits thereunder;

WHEREAS, Act 34 requires the preparation of a comprehensive financial plan and other

actions and certain certifications prior to filing an application with the Department of Treasury for

approval for the issuance of Bonds;

WHEREAS, a comprehensive financial plan has been prepared pursuant to Section 518(5)

of Act 34 (the “Comprehensive Financial Plan”) and presented to the Board; and

WHEREAS, the Board has reviewed the Comprehensive Financial Plan and desires to

approve and recommend the Comprehensive Financial Plan to the County, along with a request

that the County consider issuance of the Bonds for the benefit of the Pavilions.

Page 31 of 229

dgratton

Text Box

9

4834-6357-6523 v1 [90129-4]

NOW, THEREFORE, BE IT RESOLVED that:

1. The Board finds that the issuance of the Bonds would be in the best interests of the

Pavilions, hereby approves the form of the Comprehensive Financial Plan as presented to the

Board, with such additions, completions and changes as may be approved by any officer of the

Pavilions and recommends it to the County Board of Commissioners for consideration.

2. The Board requests that the County consider undertaking the issuance of the Bonds

for the purpose of providing funding to Division 41 and Division 43 of the defined benefit

retirement plan and proceed with such actions as are required for that purpose.

3. The officers of the Pavilions are authorized and directed to take all necessary

procedures required to assist in the issuance of the Bonds, should the County determine to proceed.

Such officers, or any one or more of them, are authorized to execute any documents or certificates

necessary to effectuate such issuance.

4. All resolutions and parts of resolutions insofar as they conflict with the provisions

of this resolution be and the same are hereby rescinded.

YEAS:

NAYS:

ABSTAIN:

RESOLUTION DECLARED ADOPTED.

CERTIFICATION

I hereby certify that the foregoing is a true and complete copy of a Resolution adopted by

the Grand Traverse County Department of Health and Human Services Board at a regular meeting

held on September ___, 2020 and that the public notice of the meeting was given pursuant to

Act 267, Public Acts of Michigan, 1976, as amended.

Dated: September ___, 2020

Page 32 of 229

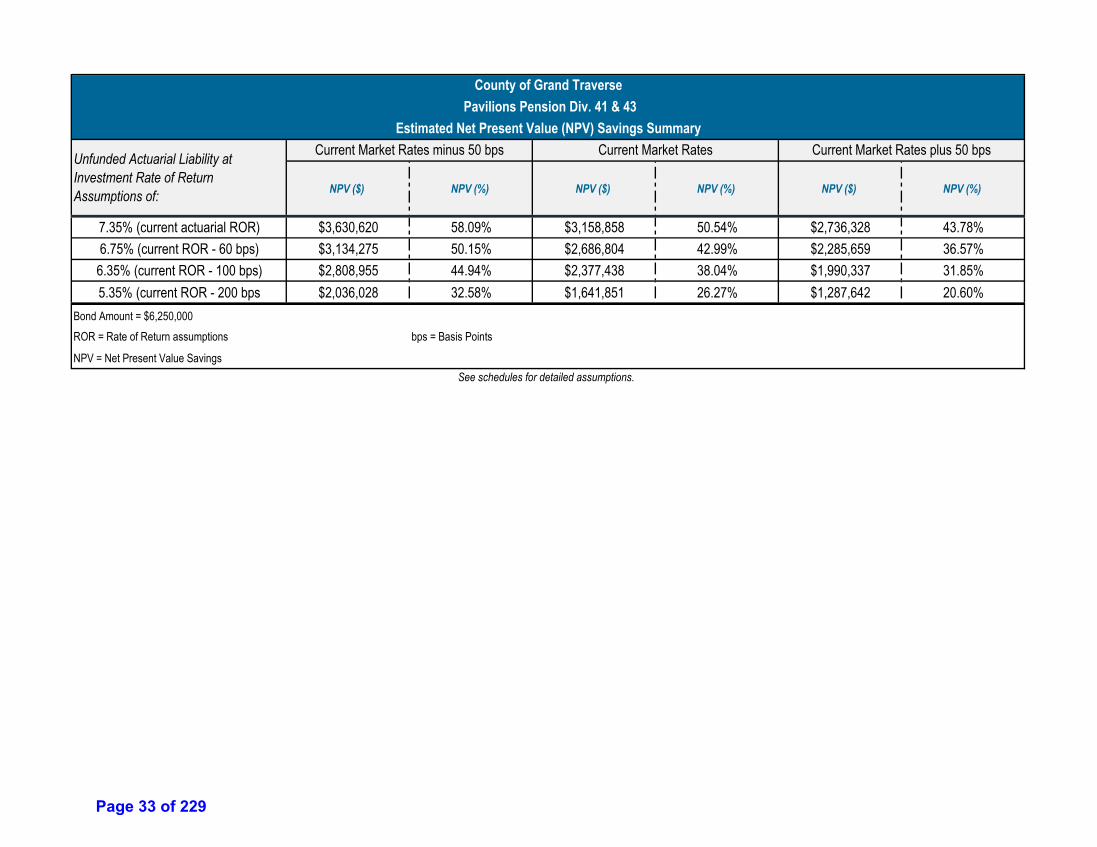

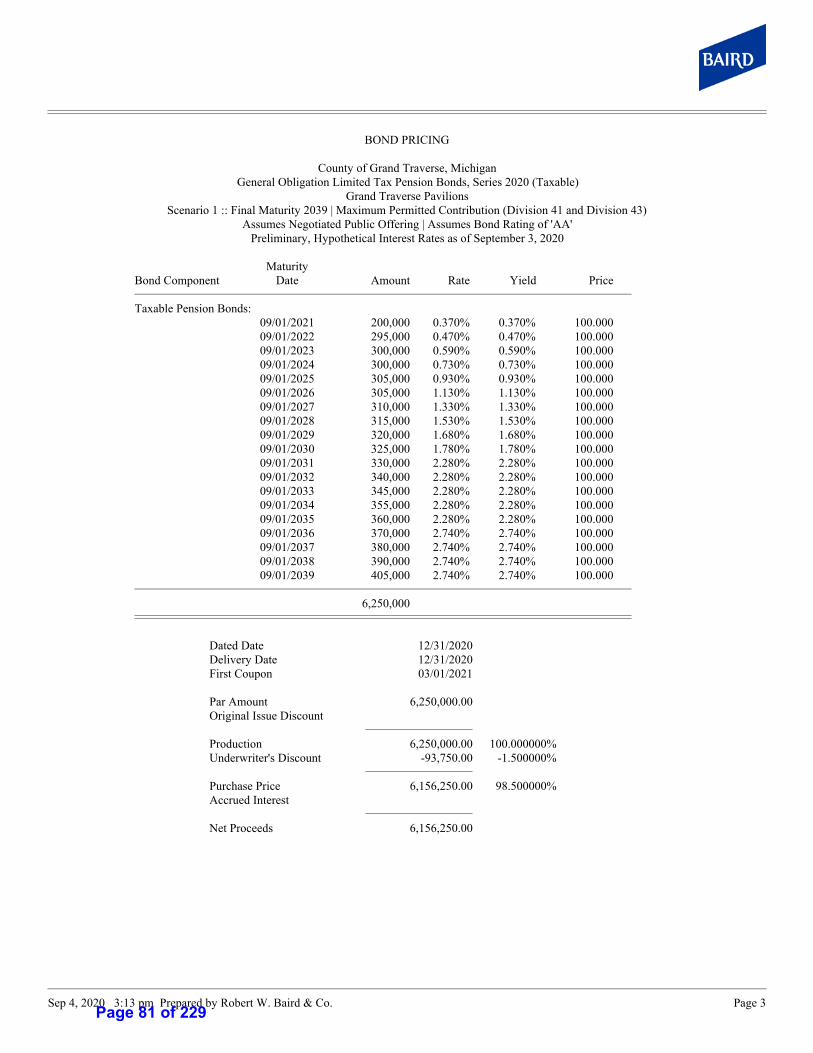

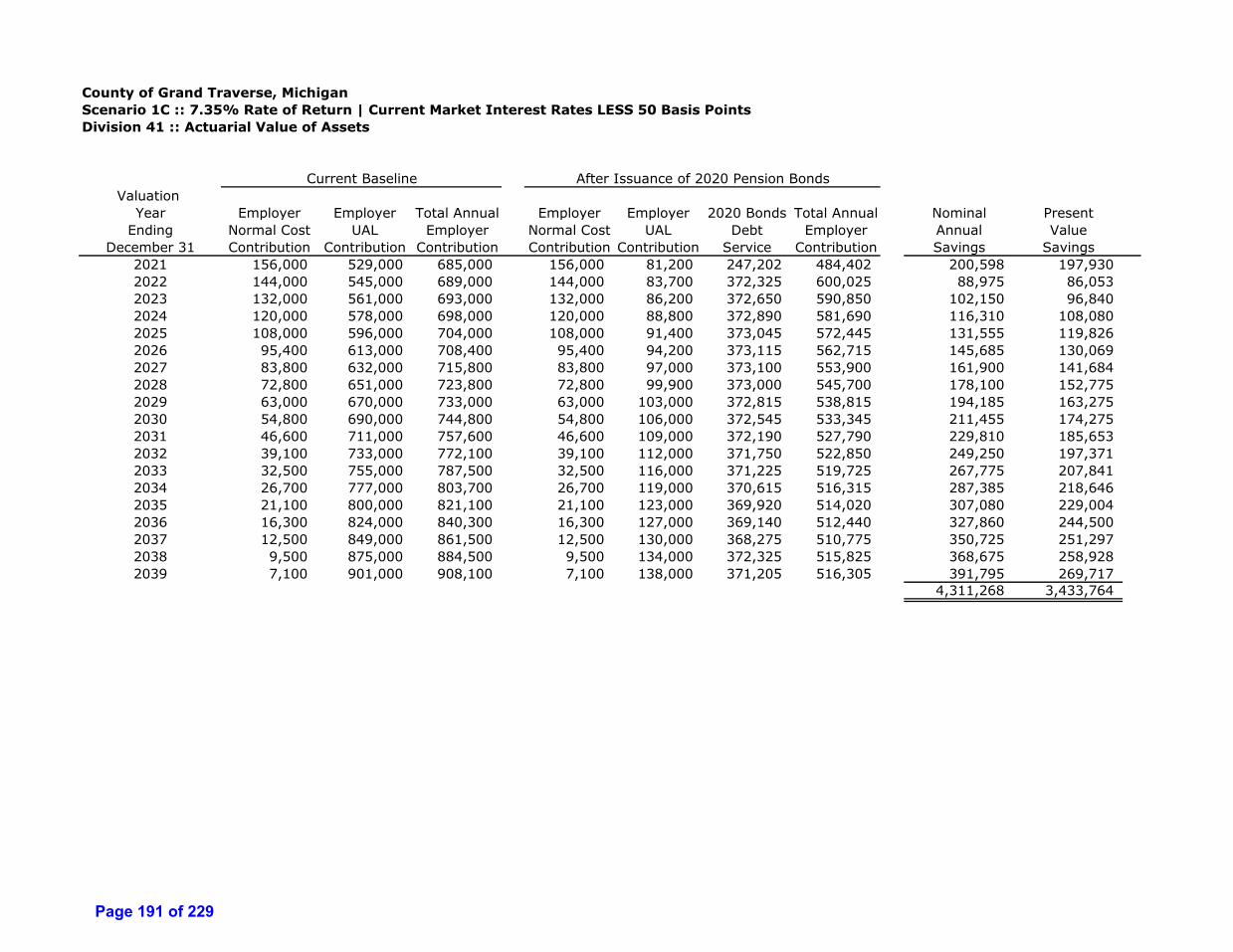

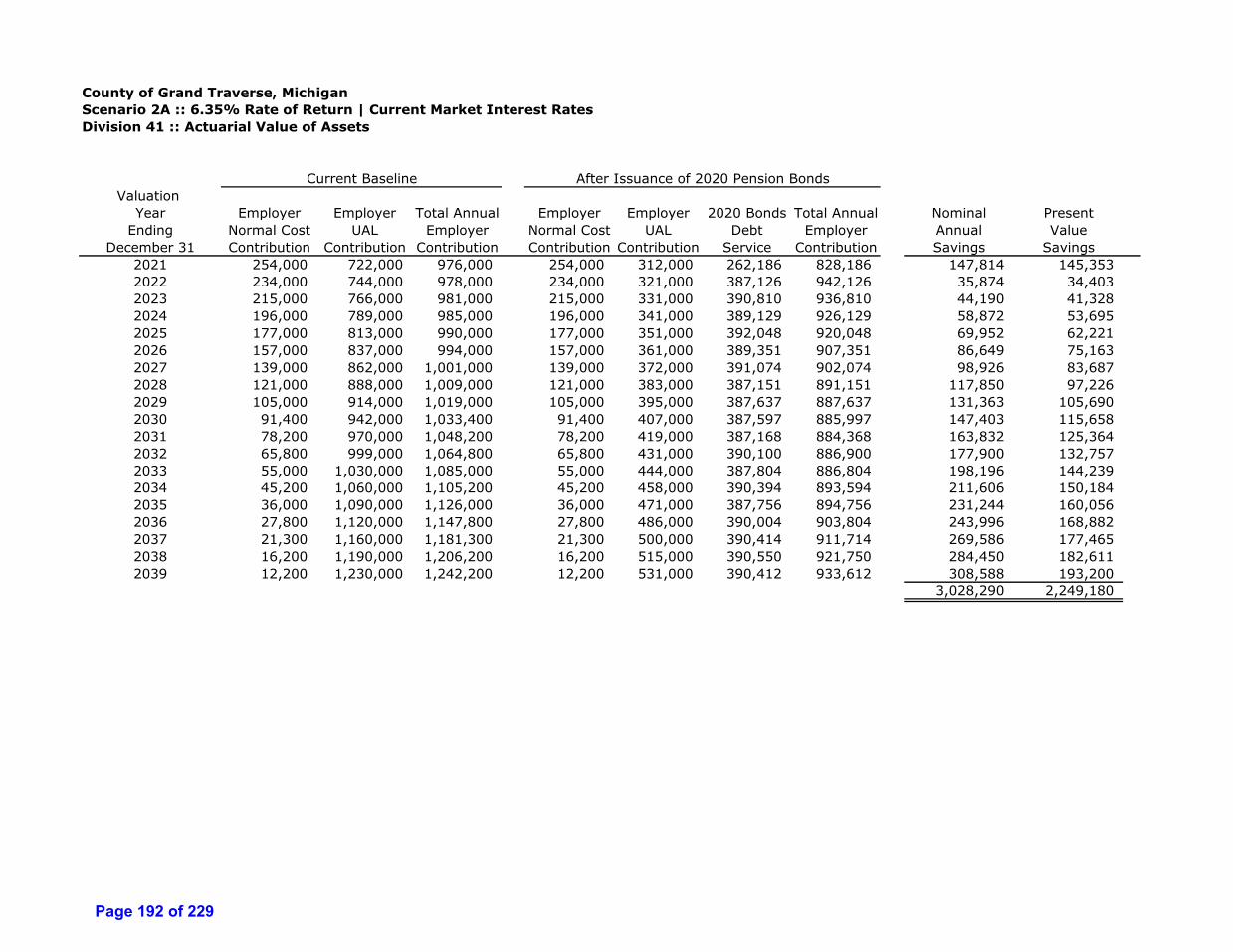

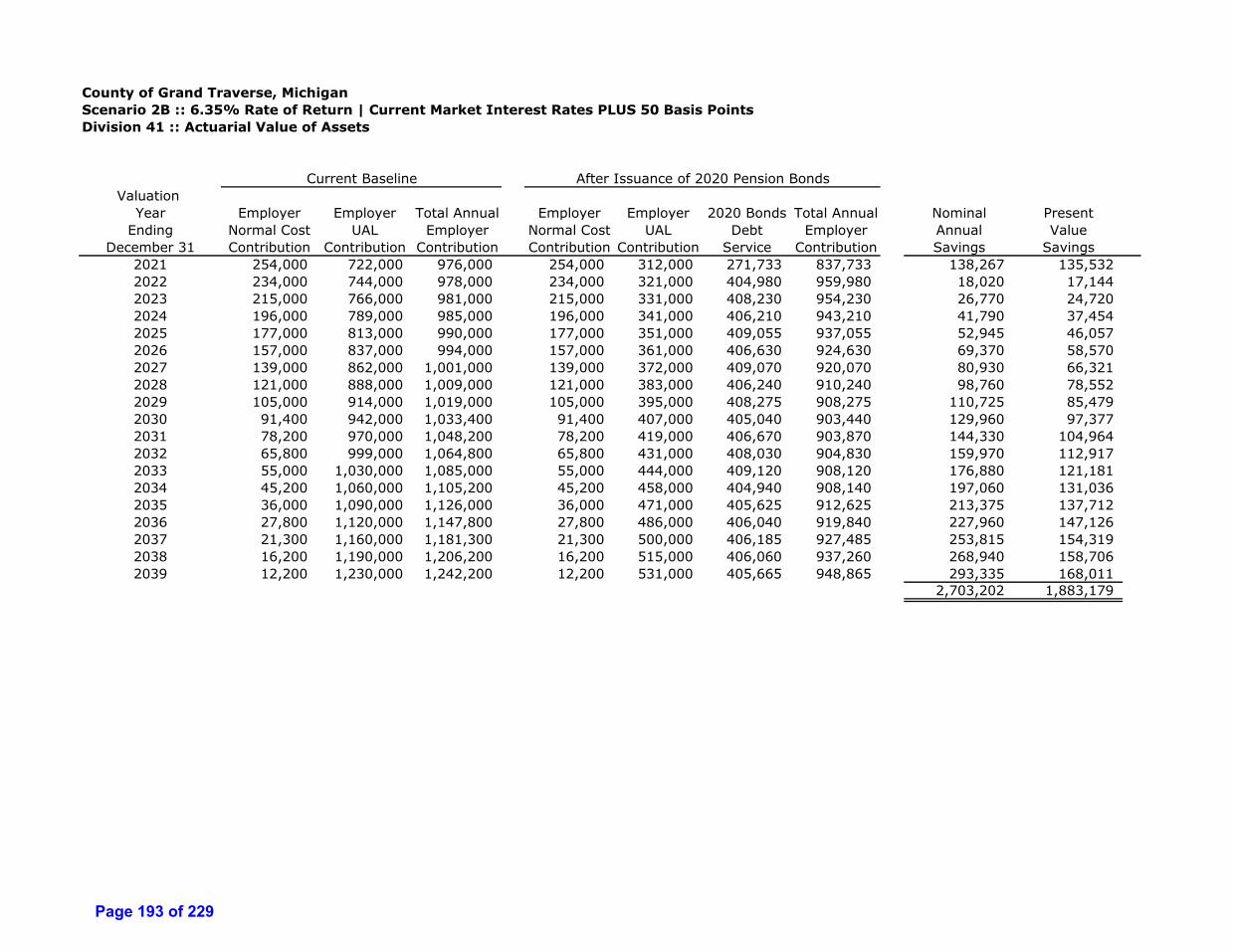

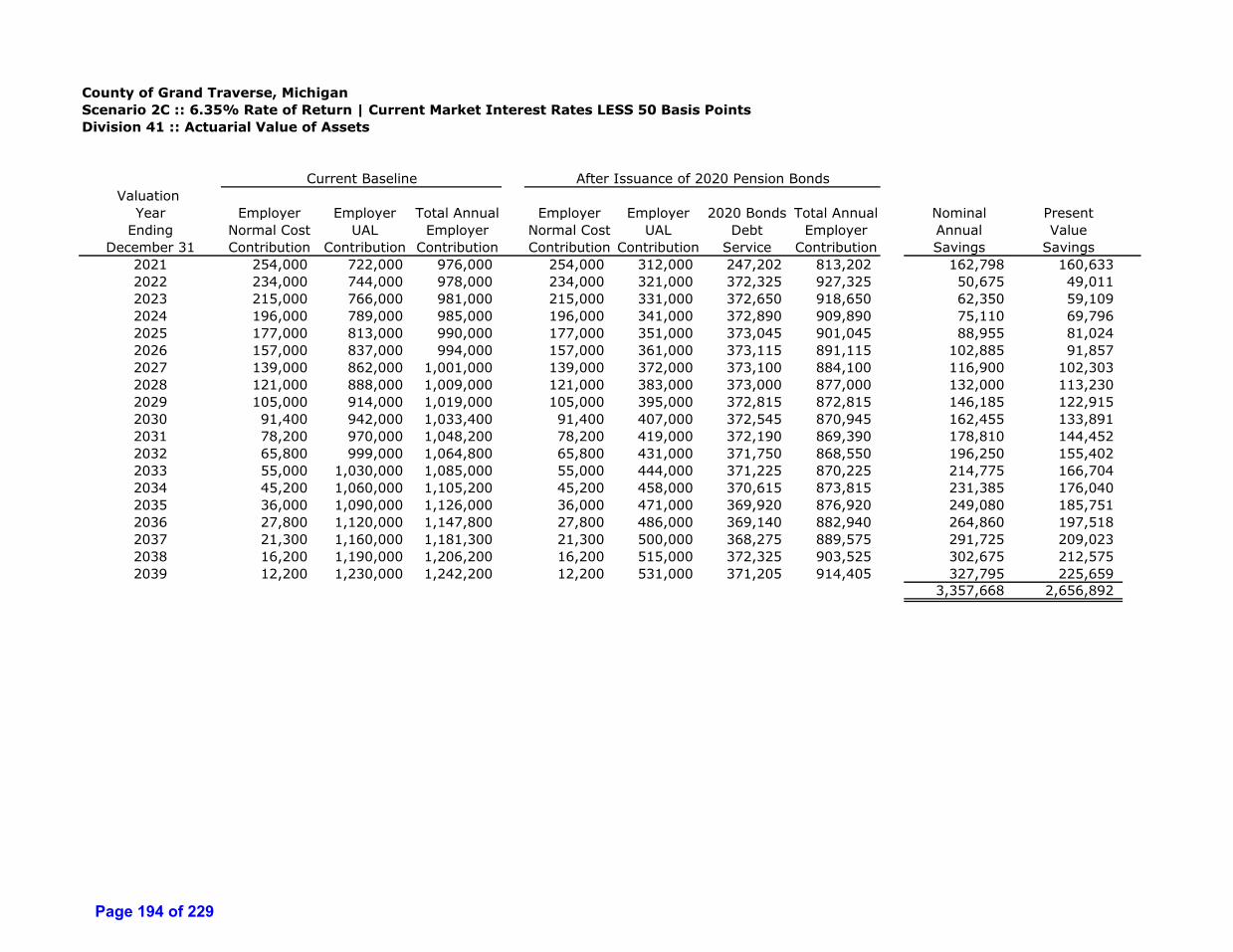

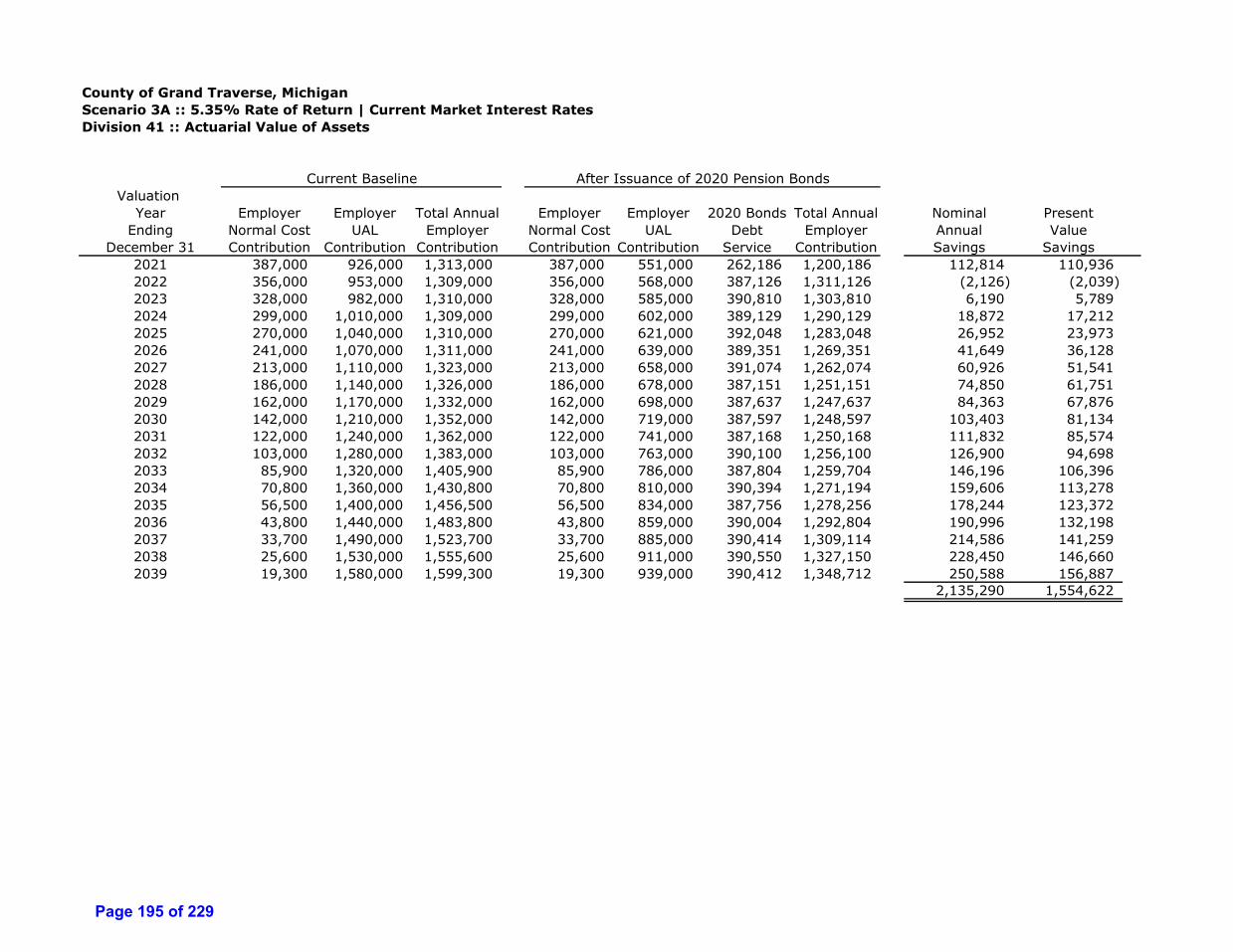

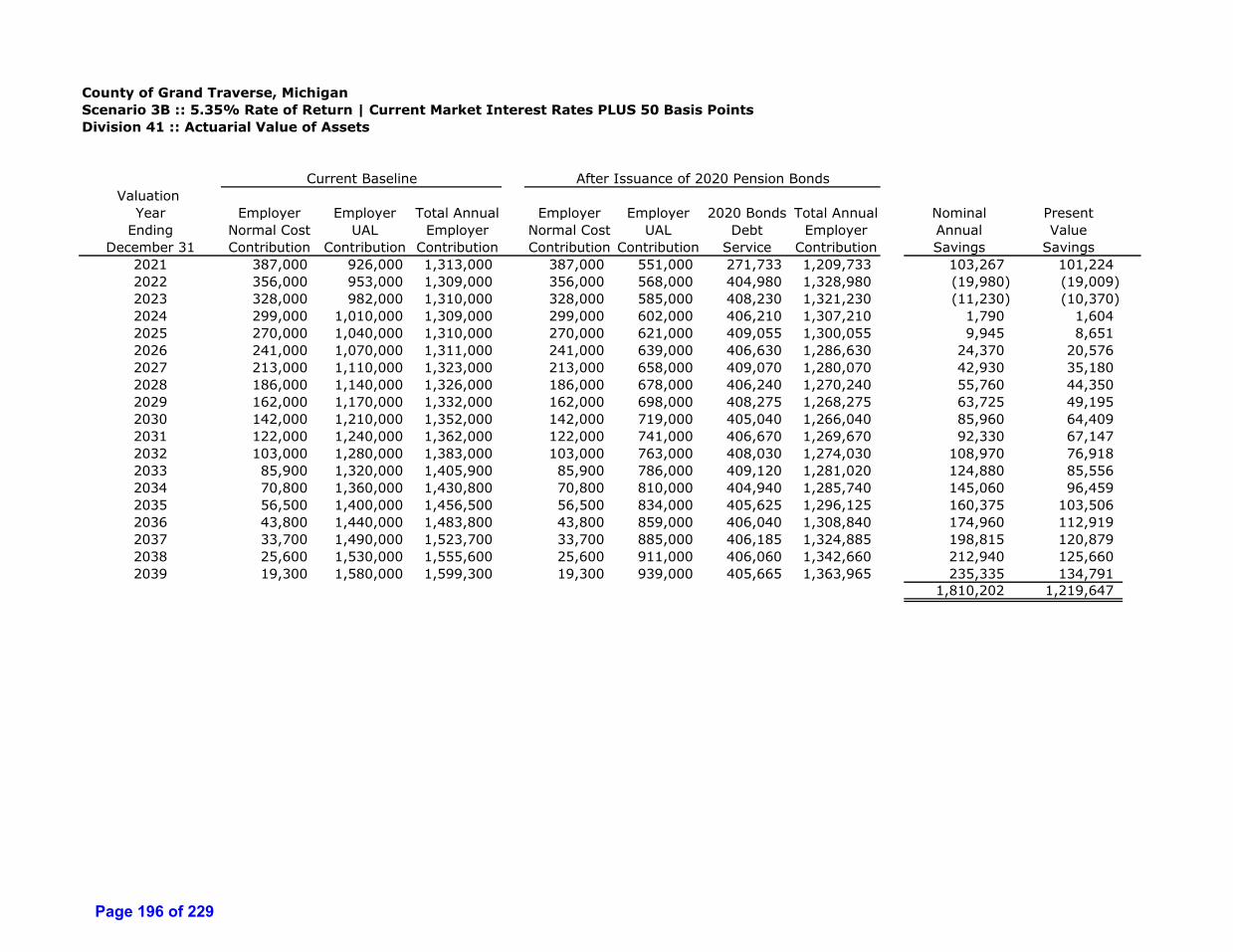

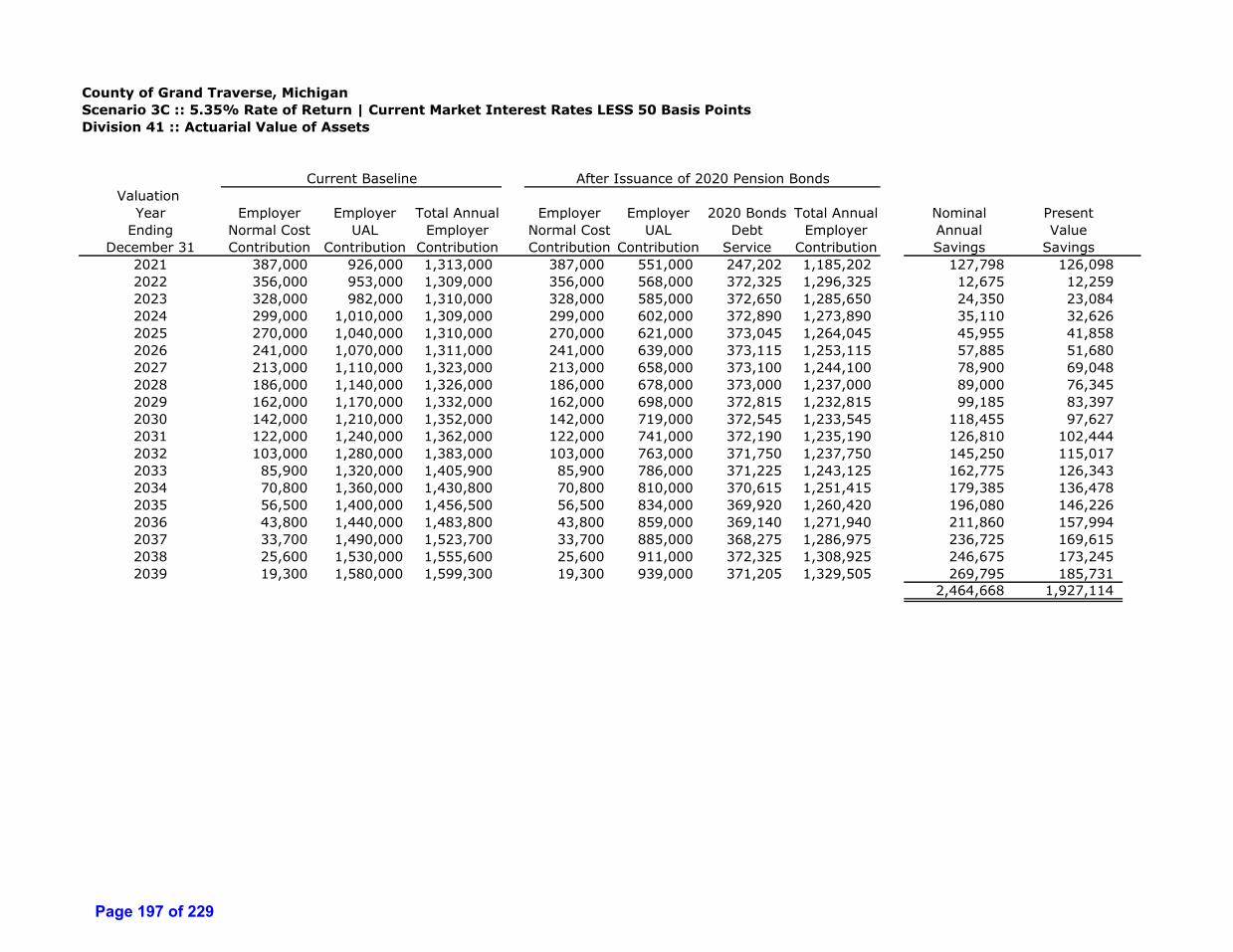

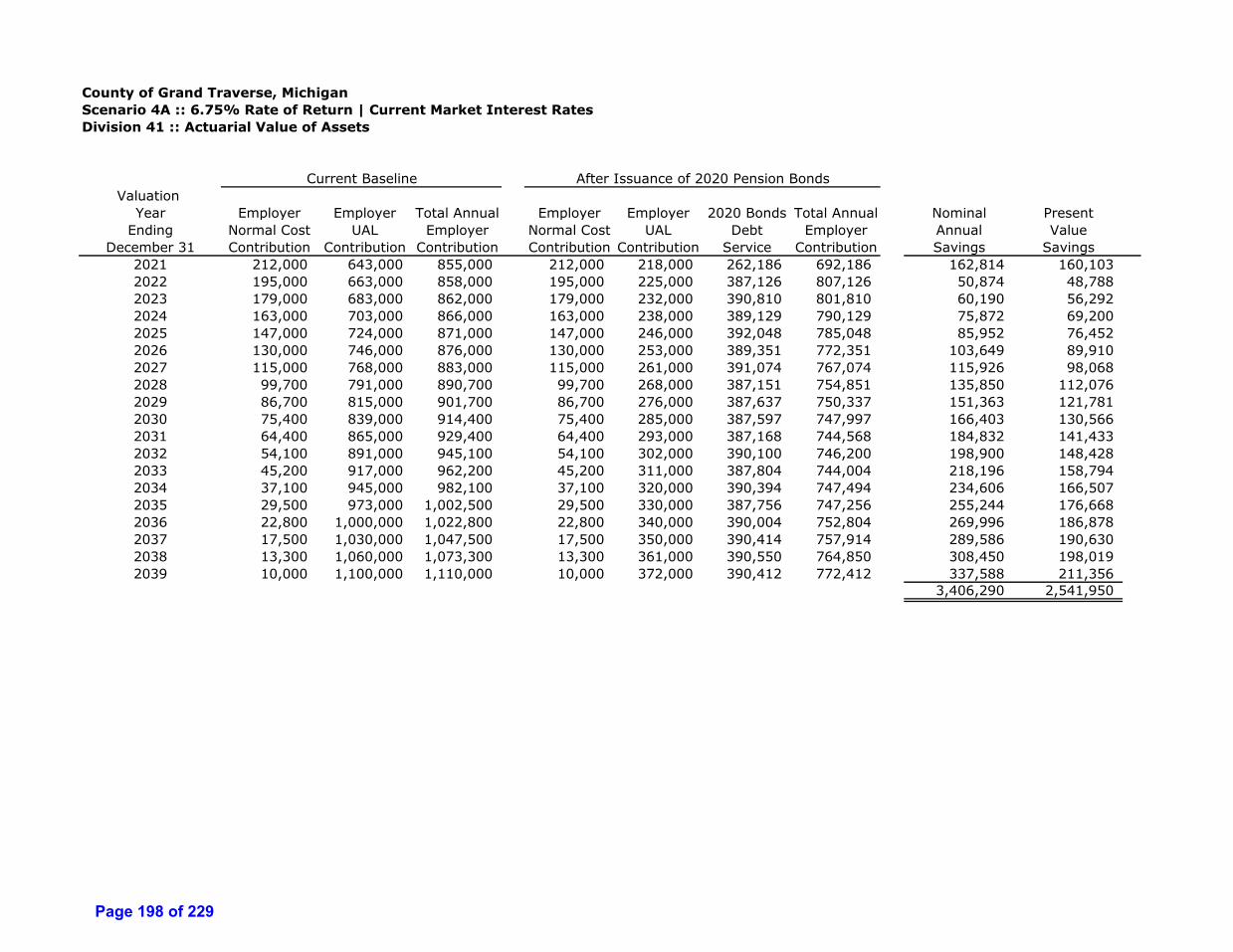

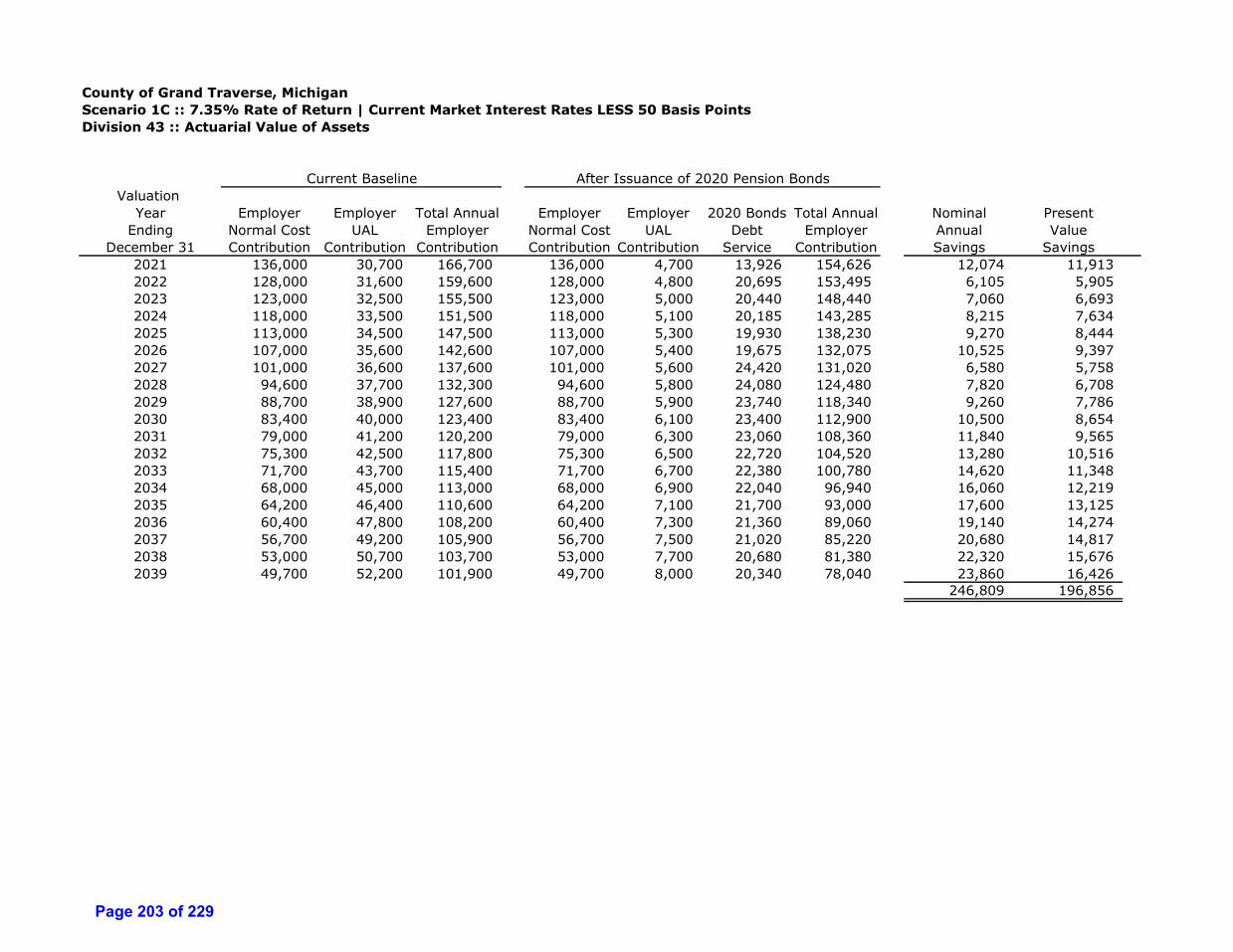

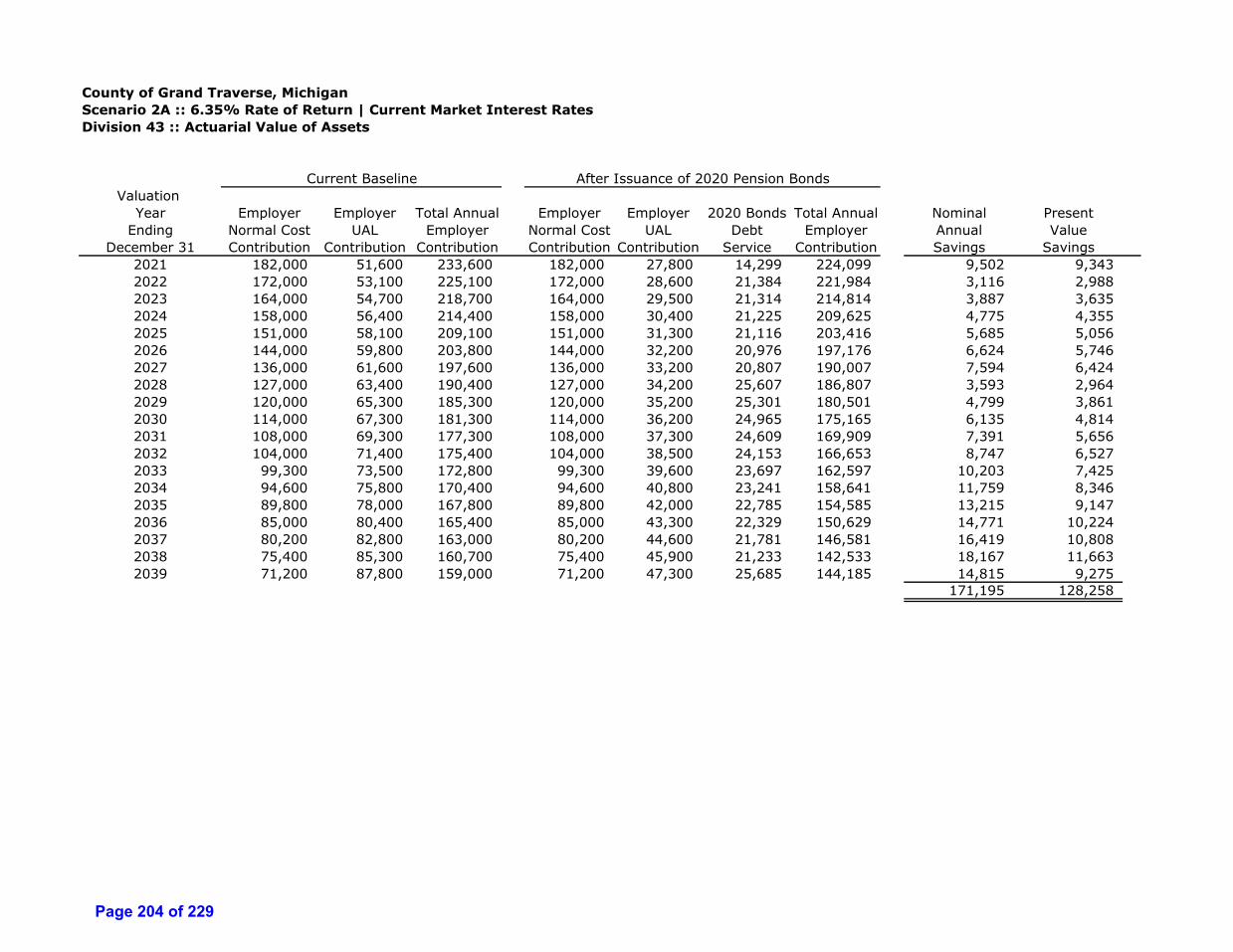

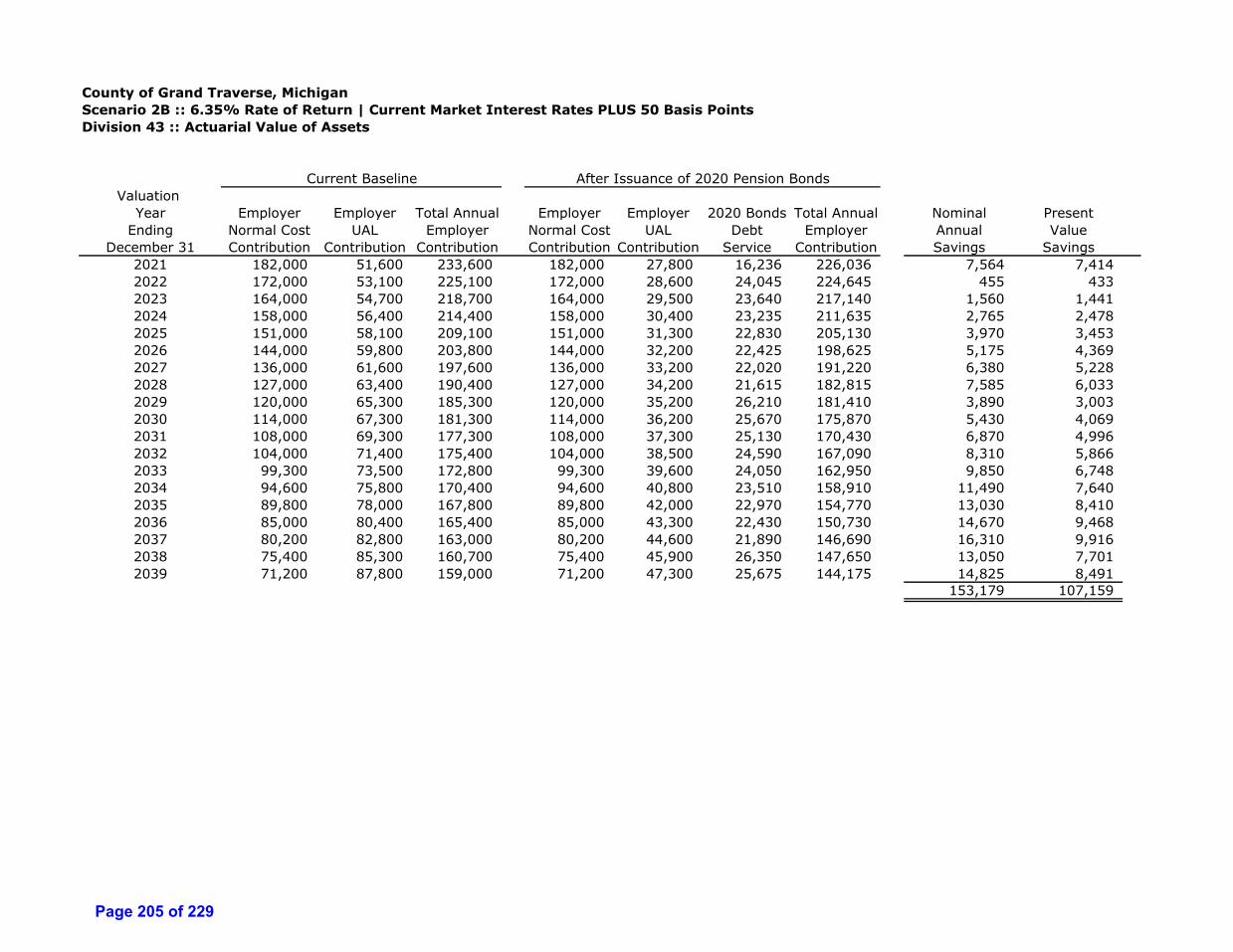

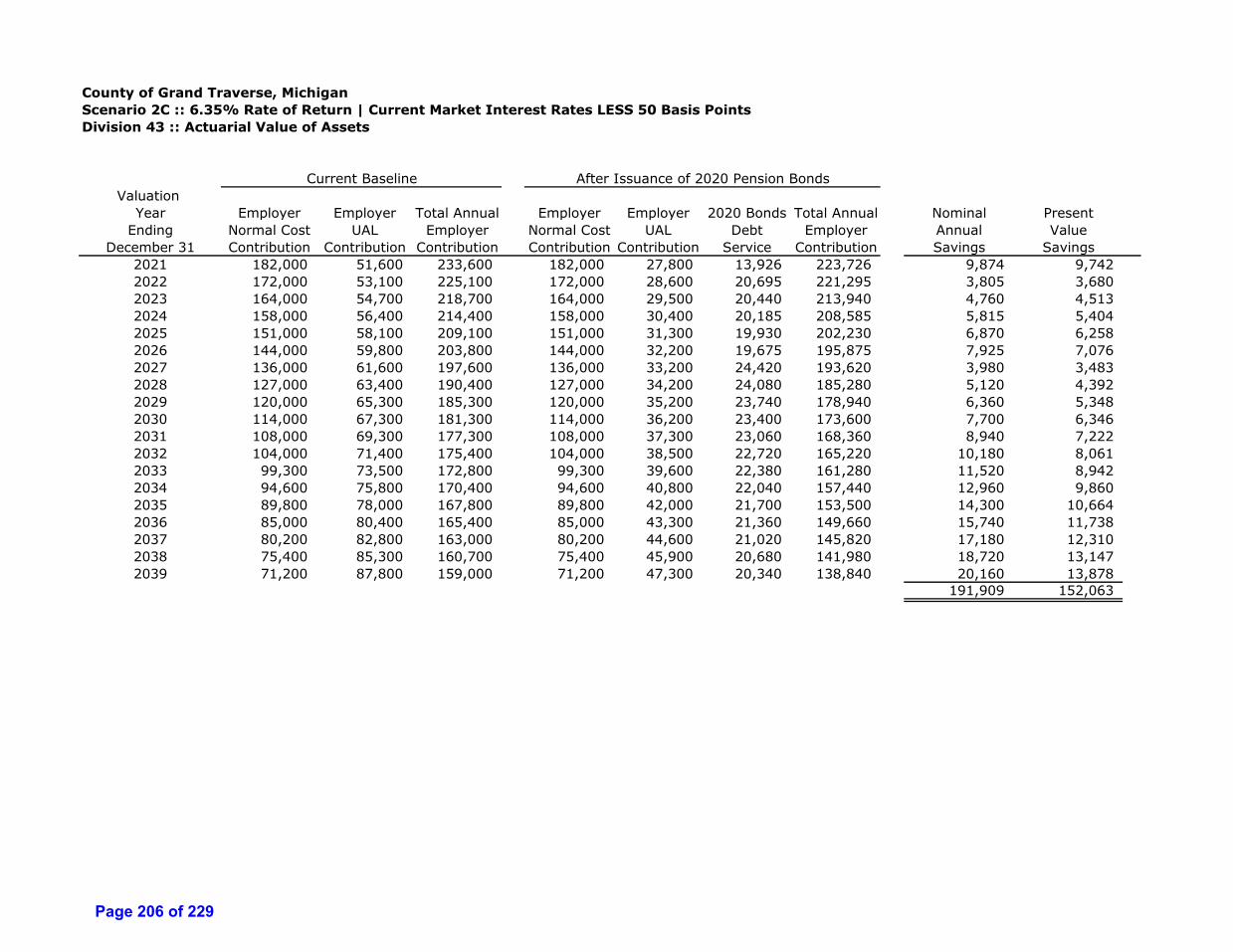

NPV ($) NPV (%) NPV ($) NPV (%) NPV ($) NPV (%)

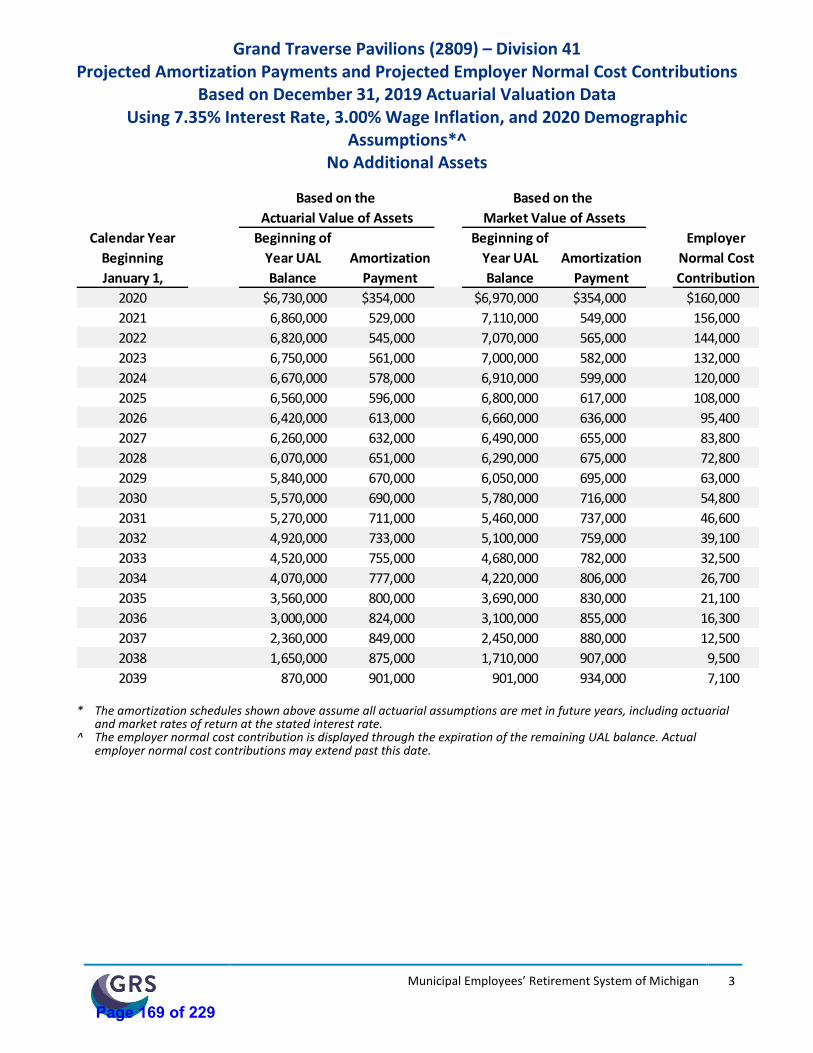

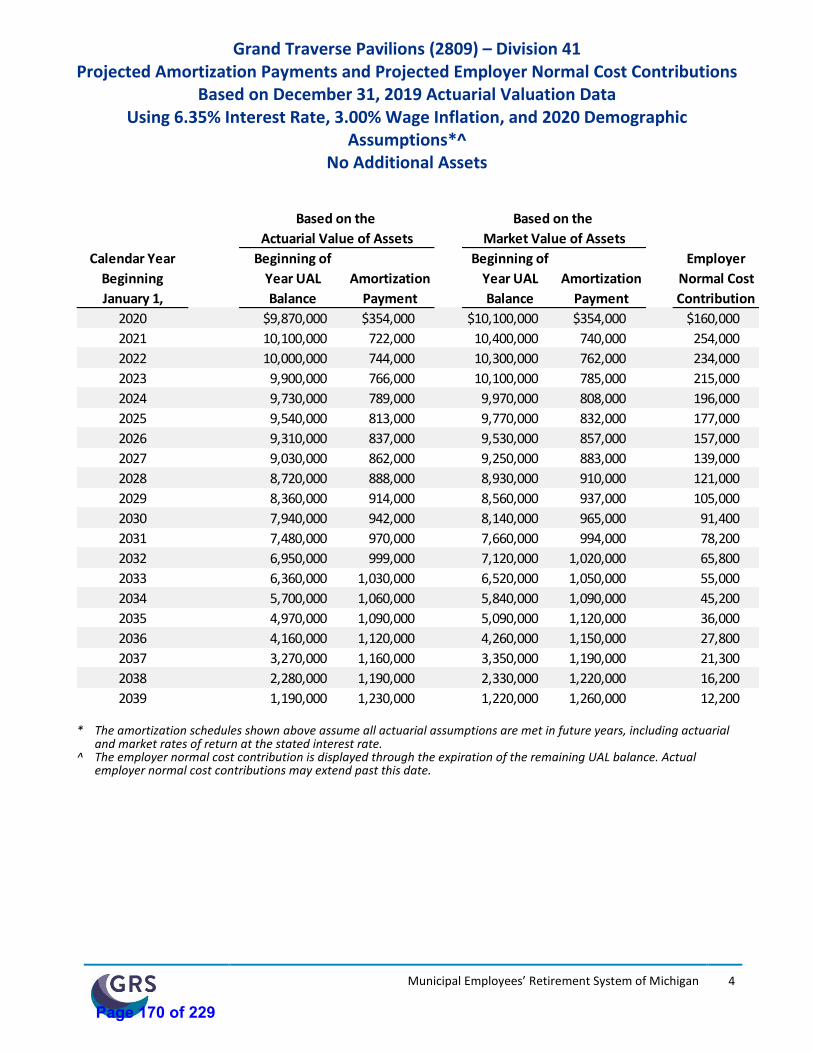

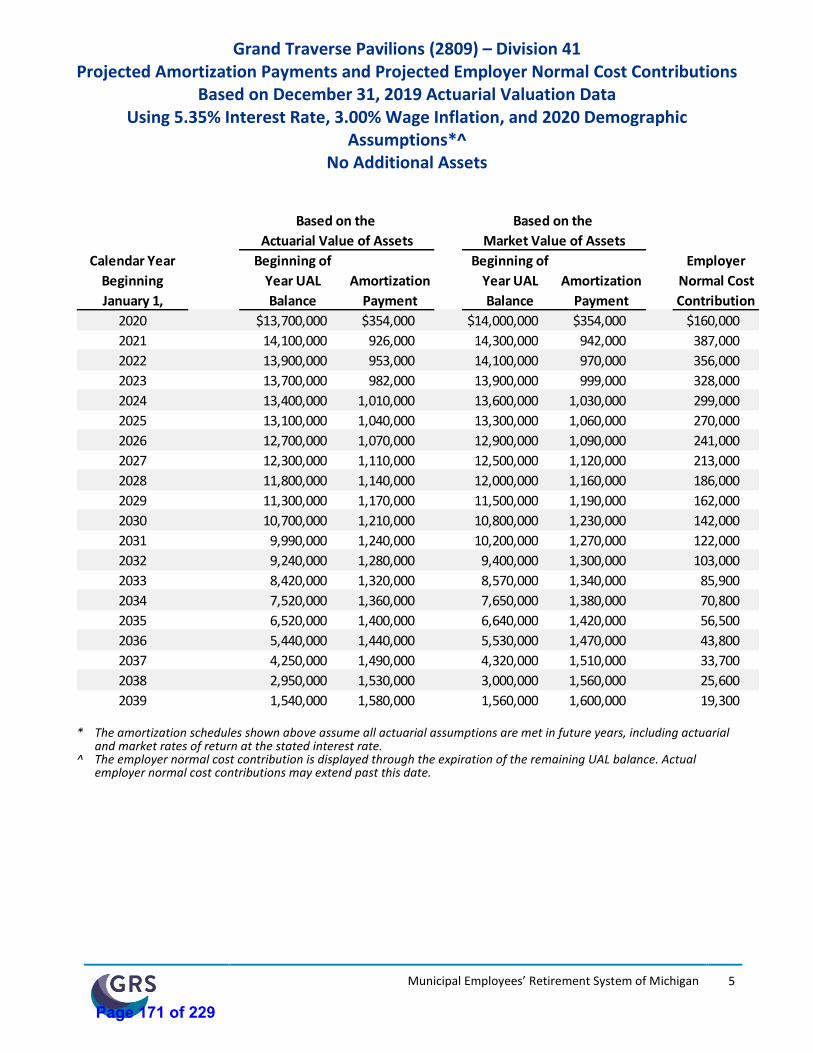

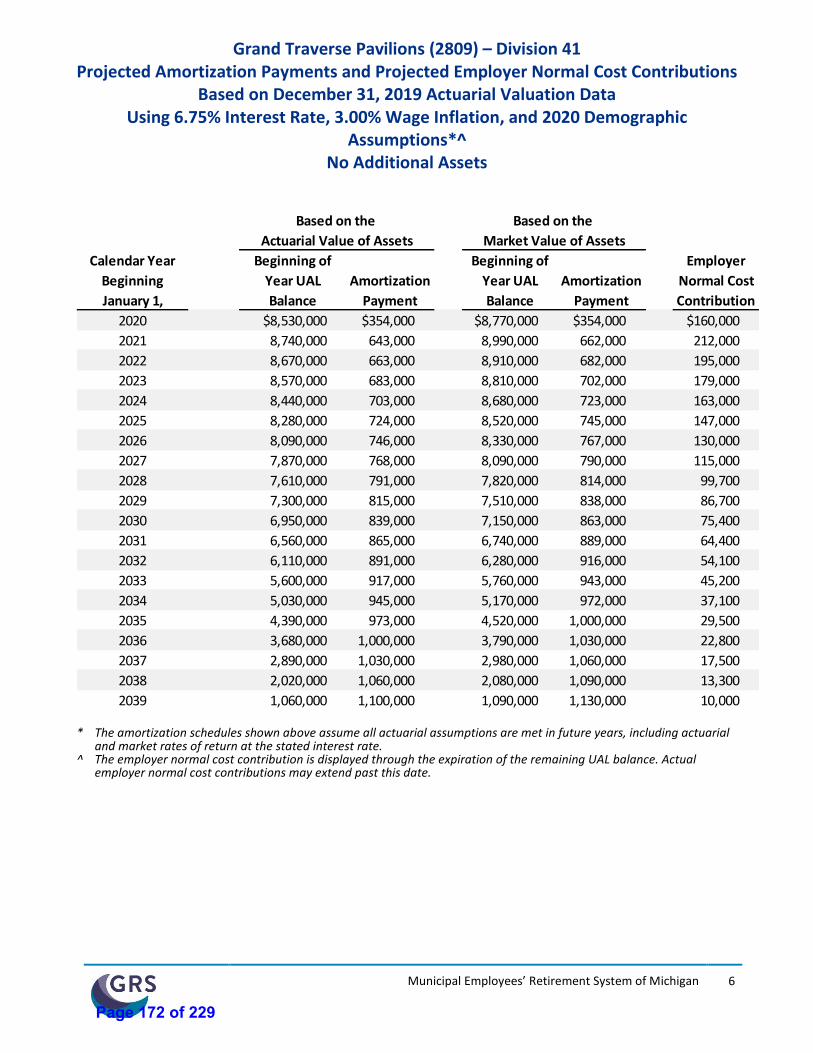

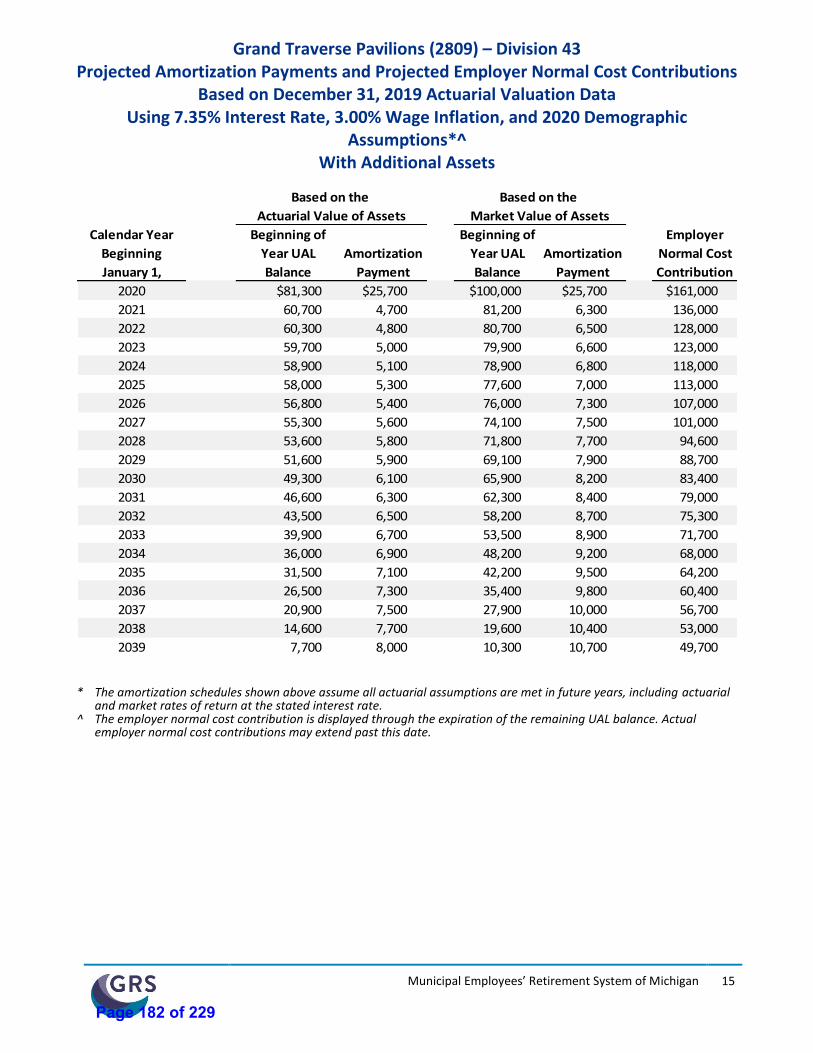

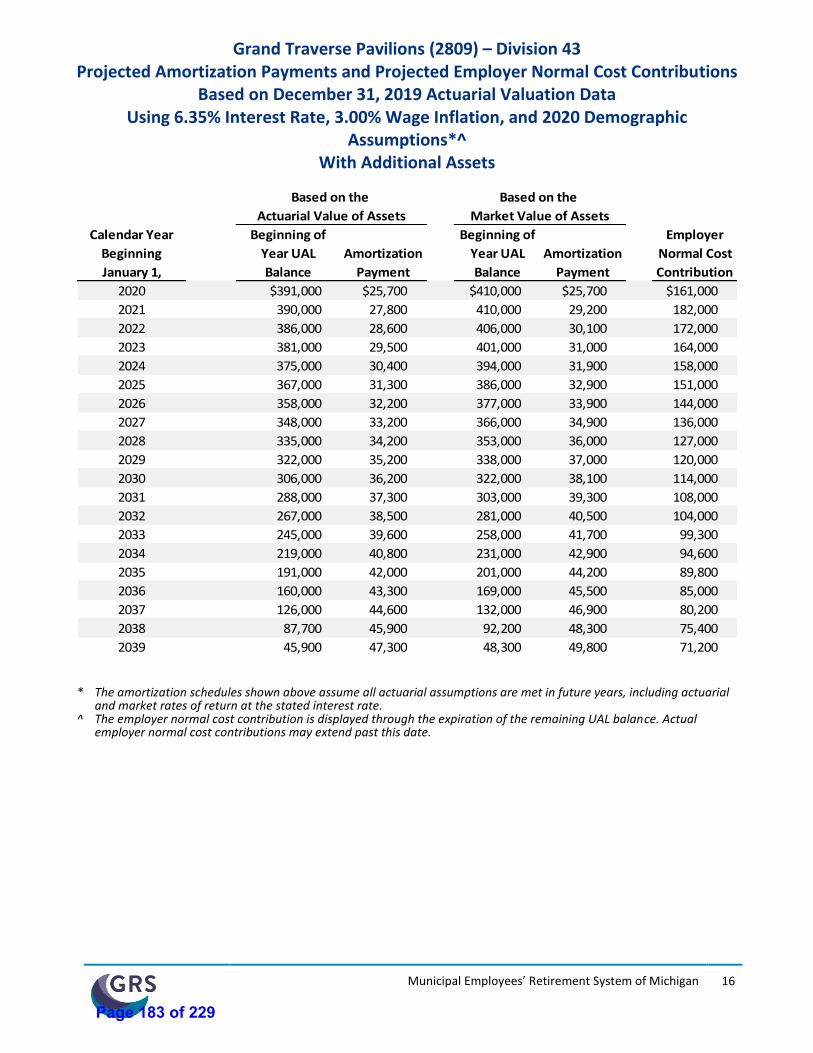

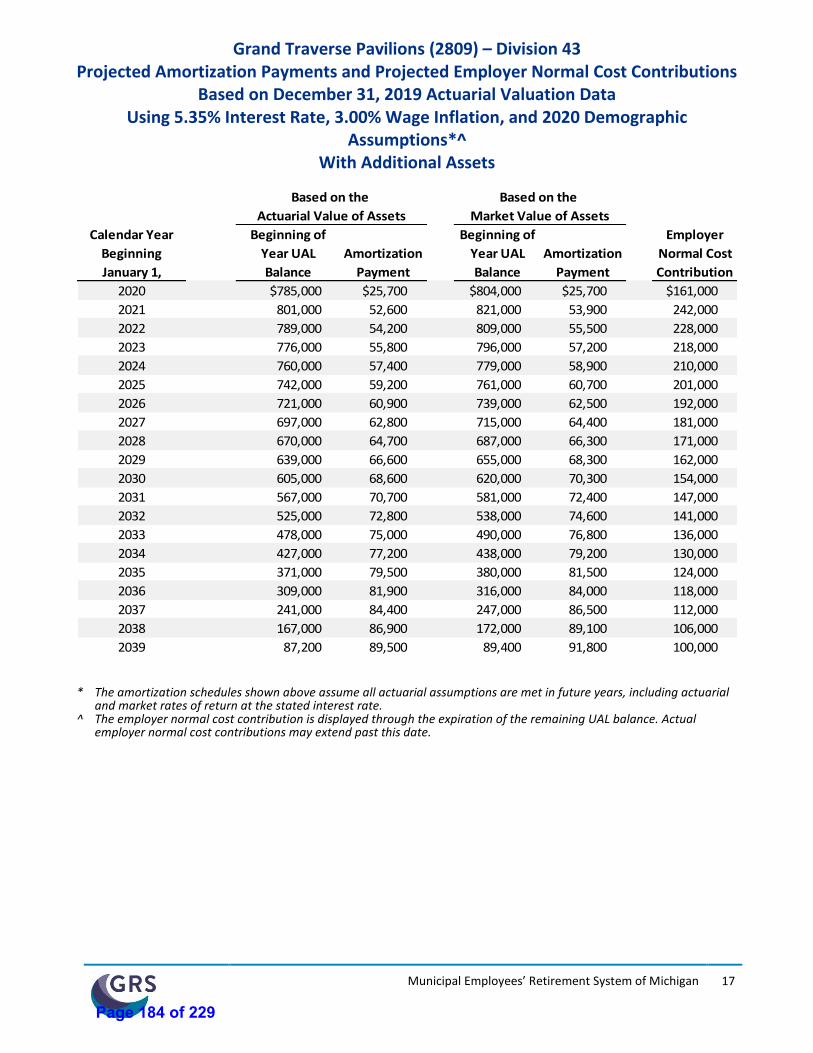

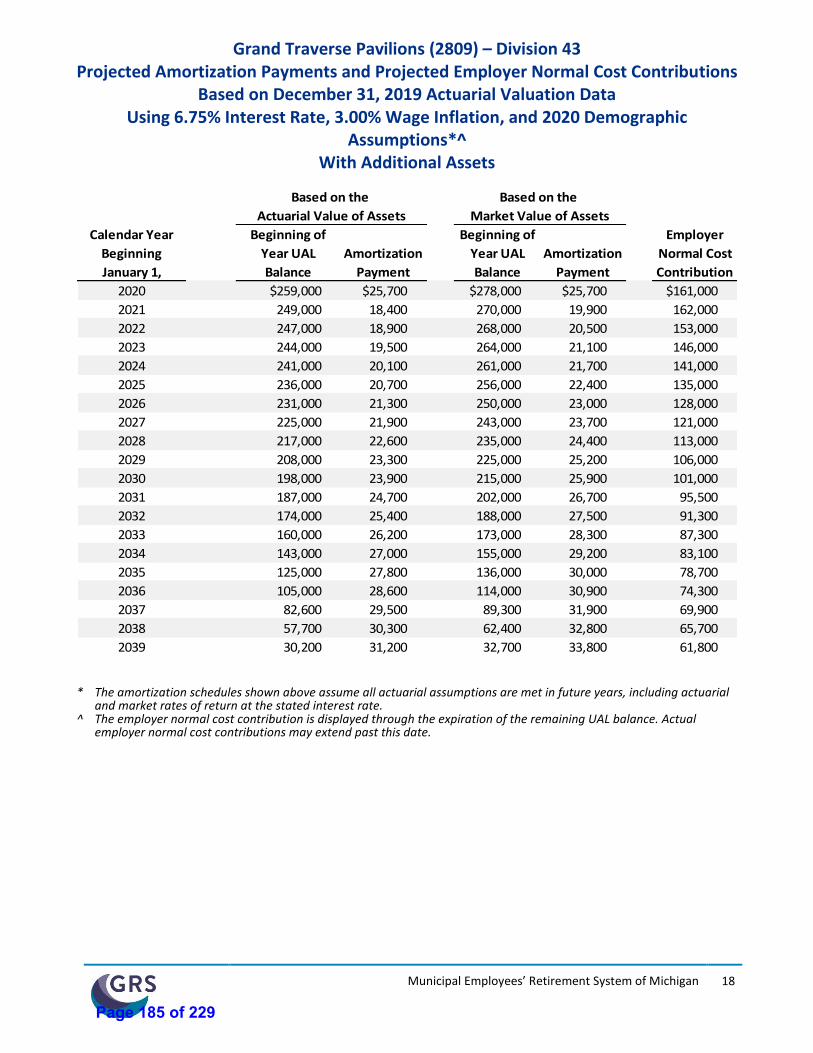

7.35% (current actuarial ROR) $3,630,620 58.09% $3,158,858 50.54% $2,736,328 43.78%6.75% (current ROR - 60 bps) $3,134,275 50.15% $2,686,804 42.99% $2,285,659 36.57%6.35% (current ROR - 100 bps) $2,808,955 44.94% $2,377,438 38.04% $1,990,337 31.85%5.35% (current ROR - 200 bps $2,036,028 32.58% $1,641,851 26.27% $1,287,642 20.60%

Bond Amount = $6,250,000ROR = Rate of Return assumptions bps = Basis Points

NPV = Net Present Value SavingsSee schedules for detailed assumptions.

County of Grand Traverse Pavilions Pension Div. 41 & 43

Estimated Net Present Value (NPV) Savings Summary

Unfunded Actuarial Liability at Investment Rate of Return Assumptions of:

Current Market Rates minus 50 bps Current Market Rates Current Market Rates plus 50 bps

Page 33 of 229

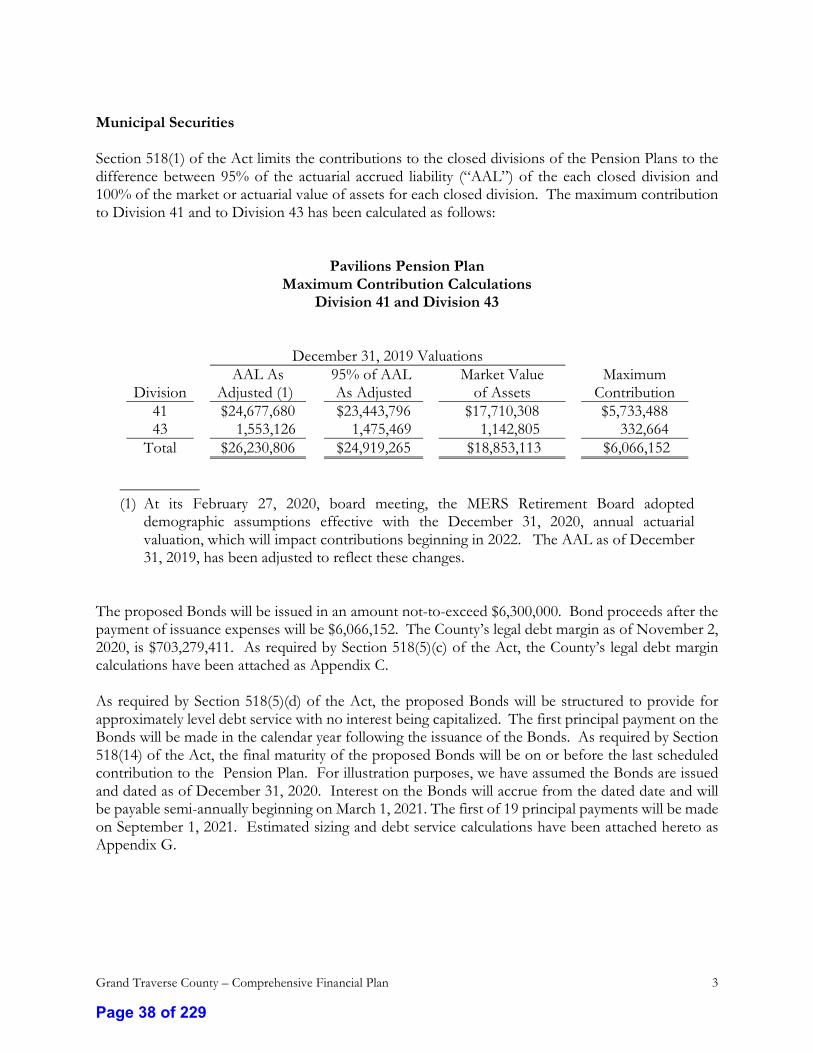

Grand Traverse County - Comprehensive Financial Plan

Grand Traverse County State of Michigan

Comprehensive Financial Plan for

Pension Bonds (Grand Traverse Pavilions)

October 6, 2020

Page 34 of 229

Grand Traverse County - Comprehensive Financial Plan

Table of Contents

Introduction ....................................................................................................................................................... 1

Application Requirements ............................................................................................................................... 2

Municipal Securities .......................................................................................................................................... 3

Application Documentation, Review and Consideration ........................................................................... 4

Letter Regarding Qualifying Statement ......................................................................................Appendix A

Notice of Intent Resolution .......................................................................................................... Appendix B

Legal Debt Margin ......................................................................................................................... Appendix C

Debt Statement ............................................................................................................................. Appendix D

Direct Debt Detail ......................................................................................................................... Appendix E

Estimated Bond Sizing and Debt Service Calculations ............................................................ Appendix F

Standard & Poor’s Rating Report Dated October 24, 2019 ................................................... Appendix G

Post-Retirement Medical Plan Accounting Report Dated December 31, 2019 .................. Appendix H

Pension Plan Actuarial Report Dated December 31, 2019 ...................................................... Appendix I

Pension Plan Supplemental Actuarial Report Dated September 1, 2020 ............................... Appendix J

Debt Service, UAAL Amortization and Present Value Schedules ........................................ Appendix K

Page 35 of 229

Grand Traverse County – Comprehensive Financial Plan 1

Comprehensive Financial Plan