01 mich Slide 8 rpk22

36

Intertemporal Macroeconomics Lecture 8 Government Spending and Taxes Pontus Rendahl [email protected] University of Cambridge Michaelmas, 2013

Transcript of 01 mich Slide 8 rpk22

Intertemporal MacroeconomicsLecture 8

Government Spending and Taxes

Pontus [email protected]

University of Cambridge

Michaelmas, 2013

Outline

Budget DeficitsA Ricardian Thought ExperimentAre Keynesians Ricardian?Are Neoclassicals Ricardian?Ricardian Equivalence

Distortionary TaxesOn Labour IncomeOn Investments

Summary

Next topic

Budget Deficits

I Newspapers would say that deficits are bad as thegovernment is a large borrower which implies r ↑.

I → Crowds out investments.I ⇒ lower growth.

I Is this true?

I Let’s study government deficits without changing G .

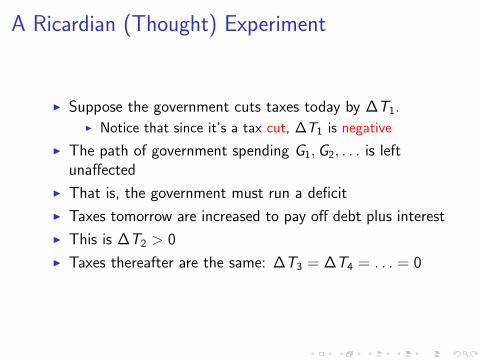

A Ricardian (Thought) Experiment

I Suppose the government cuts taxes today by ∆T1.I Notice that since it’s a tax cut, ∆T1 is negative

I The path of government spending G1,G2, . . . is leftunaffected

I That is, the government must run a deficit

I Taxes tomorrow are increased to pay off debt plus interest

I This is ∆T2 > 0

I Taxes thereafter are the same: ∆T3 = ∆T4 = . . . = 0

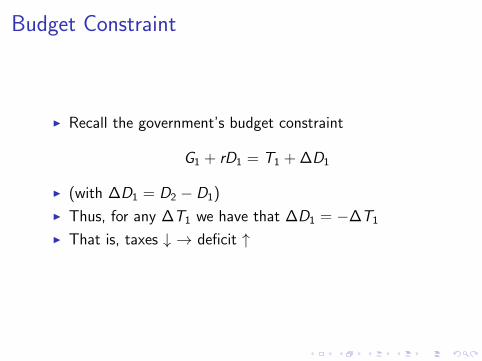

Budget Constraint

I Recall the government’s budget constraint

G1 + rD1 = T1 + ∆D1

I (with ∆D1 = D2 − D1)

I Thus, for any ∆T1 we have that ∆D1 = −∆T1

I That is, taxes ↓ → deficit ↑

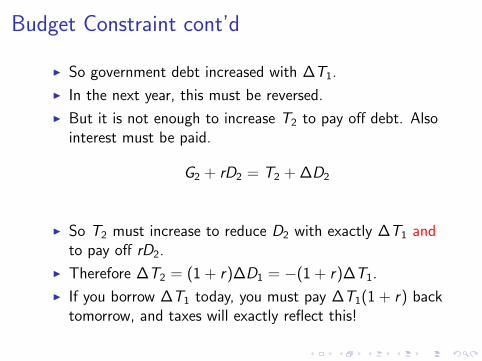

Budget Constraint cont’d

I So government debt increased with ∆T1.

I In the next year, this must be reversed.

I But it is not enough to increase T2 to pay off debt. Alsointerest must be paid.

G2 + rD2 = T2 + ∆D2

I So T2 must increase to reduce D2 with exactly ∆T1 andto pay off rD2.

I Therefore ∆T2 = (1 + r)∆D1 = −(1 + r)∆T1.

I If you borrow ∆T1 today, you must pay ∆T1(1 + r) backtomorrow, and taxes will exactly reflect this!

Are Keynesians Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Equilibrium

I No effect onsupply

I Direct effect ondemand (−β∆T1)

I New equilibrium.

Are Keynesians Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

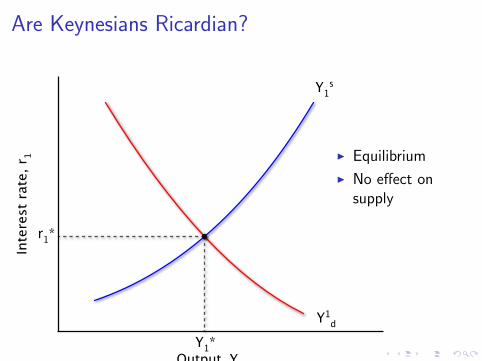

I Equilibrium

I No effect onsupply

I Direct effect ondemand (−β∆T1)

I New equilibrium.

Are Keynesians Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

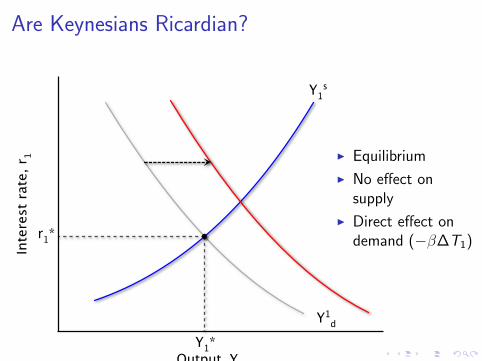

I Equilibrium

I No effect onsupply

I Direct effect ondemand (−β∆T1)

I New equilibrium.

Are Keynesians Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

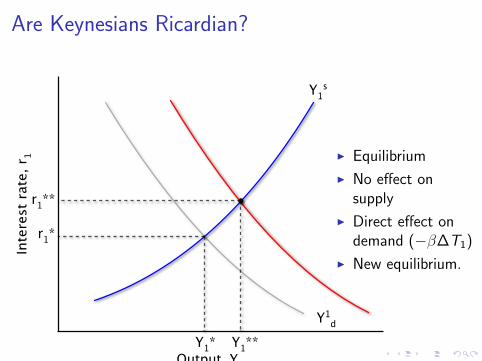

r1**

Y1**

I Equilibrium

I No effect onsupply

I Direct effect ondemand (−β∆T1)

I New equilibrium.

Are Keynesians Ricardian?

I By financing G through debt instead of taxes, individual’scurrent disposable income goes up

I In a Keynesian world this increases consumption demand,increasing output.

I However, as r goes up as well, investments must fall

I ⇒ lower growth in the future

Are Neoclassical Ricardian?

I In a famous article titled “Are Government Bonds NetWealth?”, Barro (1974) showed that Neoclassicalconsumers don’t act like this.

I Recall that private consumption only responds topermanent income changes and not temporary.

I While taxes will fall today, they will increase tomorrow,potentially leaving permanent income unchanged.

Are Neoclassicals Ricardian?

Consumption in period 1

Con

sum

ptio

n in

per

iod

2

C2*

C1*Y1

Y2

-T1

-T2I Equilibrium

I No effect onpermanent income

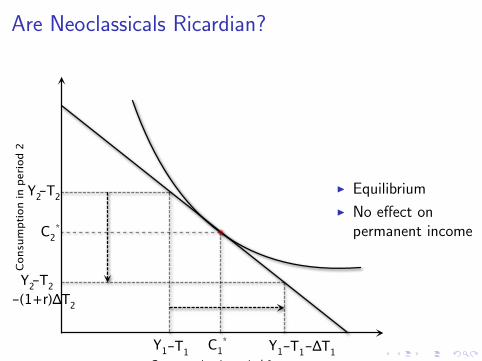

Are Neoclassicals Ricardian?

Consumption in period 1

Con

sum

ptio

n in

per

iod

2

C2*

C1*Y1

Y2

-T1

-T2

-T1Y1 -ΔT1

Y2-T2-(1+r)ΔT2

I Equilibrium

I No effect onpermanent income

Are Neoclassicals Ricardian?

I Look at the individuals’ present value income

Y1 − T1 +Y2 − T2

1 + r

I So any ∆T1 with ∆T2 = −∆T1(1 + r) will leave presentvalue income unchanged.

I No effect on consumption.

Are Neoclassicals Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

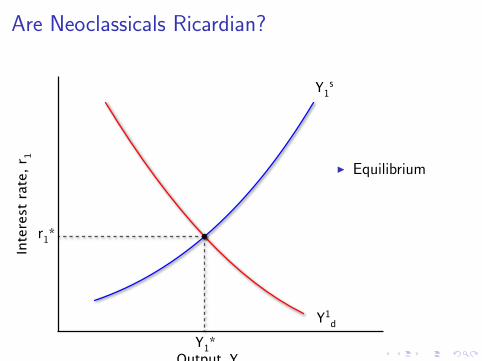

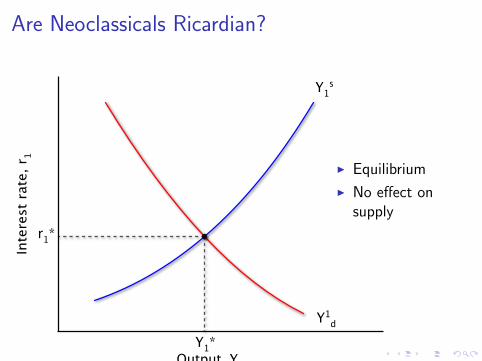

I Equilibrium

I No effect onsupply

I No effect ondemand.

Are Neoclassicals Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Equilibrium

I No effect onsupply

I No effect ondemand.

Are Neoclassicals Ricardian?

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Equilibrium

I No effect onsupply

I No effect ondemand.

Ricardian Equivalence

I Debt Neutrality Theorem:

I If consumers choose consumption intertemporally, andgiven a certain level of G , a decline in lump-sum taxestoday financed by (a deficit and) an increase in taxestomorrow, has no real effects on the economy.

I Timing of taxes do not matterI Only the level of G is importantI Government bonds are not net wealth

Ricardian Equivalence

I The intuition is quite simple

I Future taxes are like debt that you owe!

I So if taxes are lowered today, but increased tomorrow:I Keynesians go out partyingI Neoclassicals stay at home and save

I Note: This has nothing to do with any price-stickiness orso, but on planning horizon.

Taxes

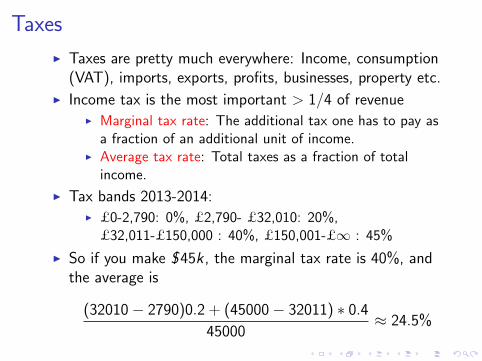

I Taxes are pretty much everywhere: Income, consumption(VAT), imports, exports, profits, businesses, property etc.

I Income tax is the most important > 1/4 of revenueI Marginal tax rate: The additional tax one has to pay as

a fraction of an additional unit of income.I Average tax rate: Total taxes as a fraction of total

income.

I Tax bands 2013-2014:I £0-2,790: 0%, £2,790- £32,010: 20%,

£32,011-£150,000 : 40%, £150,001-£∞ : 45%

I So if you make $45k , the marginal tax rate is 40%, andthe average is

(32010− 2790)0.2 + (45000− 32011) ∗ 0.4

45000≈ 24.5%

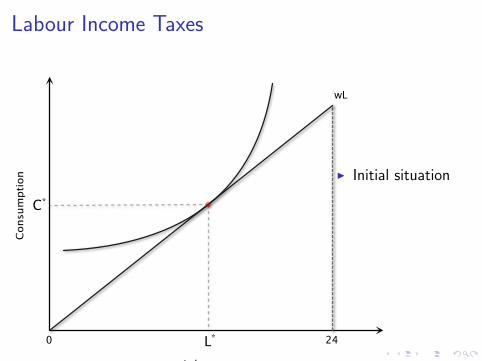

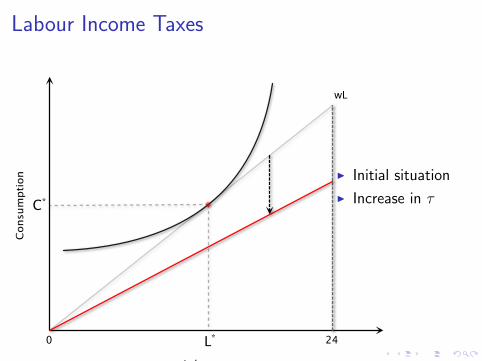

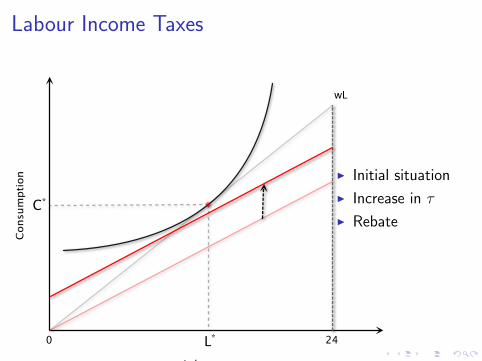

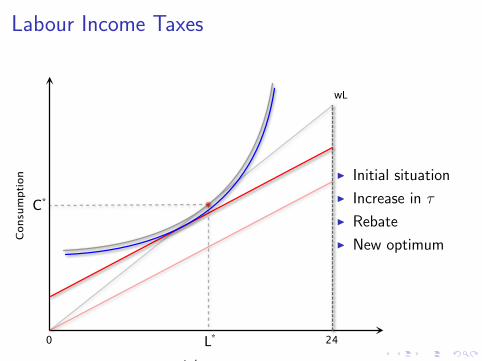

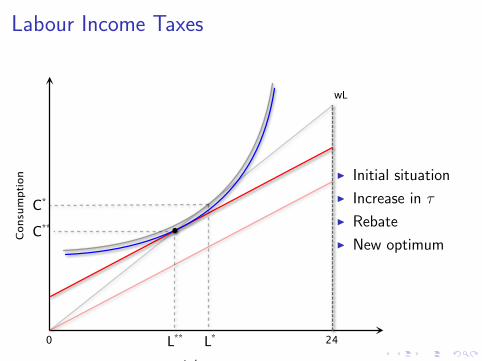

Labour Income Taxes

I Consider the static model

C = w(1− τ)L + b

I To isolate the effect of distortions, consider an increase inτ (from zero) which is rebated back to the consumersthrough an increase in b (from zero) in a lump-sum way.

I b must then equal wτL.

I Therefore, b will depend on L, but this is not internalizedby the consumers (as otherwise it wouldn’t be lump-sum).

Labour Income Taxes

0 24

Labour

Con

sum

ptio

n

L*

C*

wL

I Initial situation

I Increase in τ

I Rebate

I New optimum

Labour Income Taxes

0 24

Labour

Con

sum

ptio

n

L*

C*

wL

I Initial situation

I Increase in τ

I Rebate

I New optimum

Labour Income Taxes

0 24

Labour

Con

sum

ptio

n

L*

C*

wL

I Initial situation

I Increase in τ

I Rebate

I New optimum

Labour Income Taxes

0 24

Labour

Con

sum

ptio

n

L*

C*

wL

I Initial situation

I Increase in τ

I Rebate

I New optimum

Labour Income Taxes

0 24

Labour

Con

sum

ptio

n

L*

C*

wL

L**

C**

I Initial situation

I Increase in τ

I Rebate

I New optimum

Capital Gains Tax

I Taxes on earnings from investments

I Optimal investments

(1− τ)[A2MPK2 − δ] = r

I Since MPK2 is decreasing in I , investments will fall if τ ↑I Thus

I d(r , τ,A2, . . .)

I Clearing of the goods market:

C d(r ,PV (Y ), . . .) + I d(r , τ,A2, . . .) = Y s(r , τ,A2)

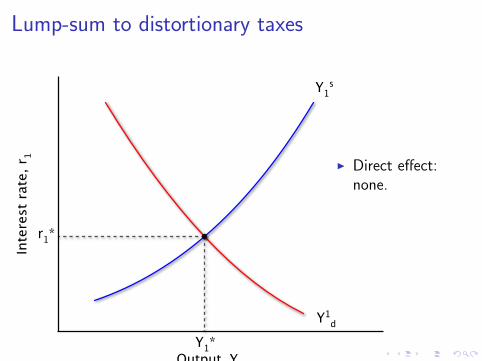

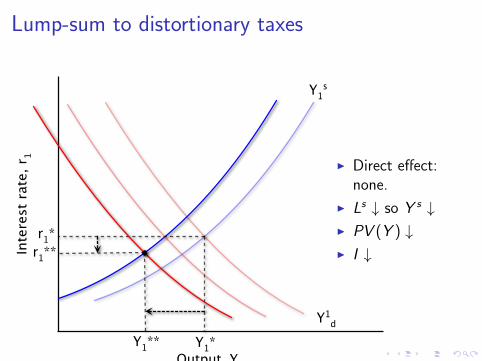

Lump-sum to distortionary taxes

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Direct effect:none.

I Ls ↓ so Y s ↓I PV (Y ) ↓I I ↓

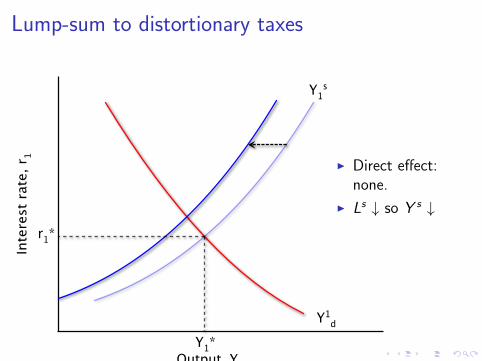

Lump-sum to distortionary taxes

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Direct effect:none.

I Ls ↓ so Y s ↓

I PV (Y ) ↓I I ↓

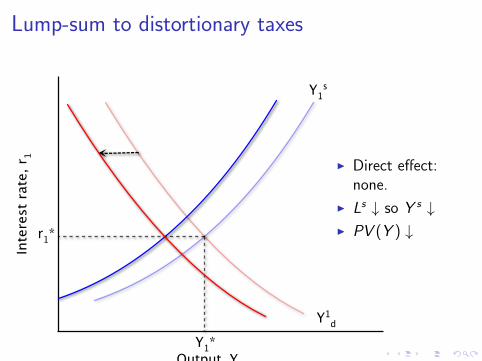

Lump-sum to distortionary taxes

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Direct effect:none.

I Ls ↓ so Y s ↓I PV (Y ) ↓

I I ↓

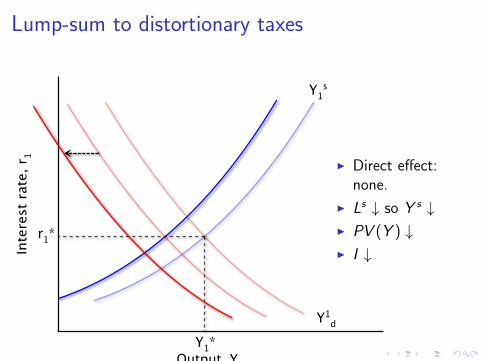

Lump-sum to distortionary taxes

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

I Direct effect:none.

I Ls ↓ so Y s ↓I PV (Y ) ↓I I ↓

Lump-sum to distortionary taxes

Output, Y1

Inte

rest

rat

e, r

1

Y1*

r1*

Y1s

Y1d

Y1**

r1**

I Direct effect:none.

I Ls ↓ so Y s ↓I PV (Y ) ↓I I ↓

Lump-sum to distortionary taxes

I Total effects:I Y ↓I r ↓I I ↓I C , ?

Summary

I Budget Deficits

I Ricardian Equivalence

I Effect of distortionary taxes onI Consumption/leisure choiceI InvestmentsI Equilibrium in goods market

Next Topic

Unemployment and Labour Markets