Bahasa

Halaman

Hukum

ASIA-PACIFICHUMANDEVELOPMENTREPORT 2006

Trade on Human TermsTransforming Trade forHuman Developmentin Asia and the Pacific

Published for theUnited NationsDevelopment Programme

Copyright ©2006by the United Nations Development ProgrammeRegional Centre in Colombo, Human Development Unit

23 Independence Avenue, Colombo 7, Sri Lanka

All rights reserved. No part of this publication may be reproduced ortransmitted, in any form or by any means, without permission.Any person who does any unauthorised act in relation to this publicationmay be liable to criminal prosecution and civil claims for damages.

First published, 2006

Published for UNDP by Macmillan India Ltd.,this book is not for sale through commercial channels.

MACMILLAN INDIA LTD.Delhi Chennai Jaipur Mumbai Patna BangaloreBhopal Chandigarh Coimbatore Cuttack GuwahatiHubli Hyderabad Lucknow Madurai Nagpur PuneRaipur Thiruvananthapuram Visakhapatnam

ISBN CORP-000036

Published by Rajiv Beri for Macmillan India Ltd.2/10 Ansari Road, Daryaganj, New Delhi 110 002

Printed at Sanat Printers312 EPIP, Kundli 131 028

TEAM FOR THE PREPARATION OFAsia-Pacific Human Development Report 2006

Team LeaderAnuradha Rajivan

Core Team: C.P. Chandrasekhar,Ramesh Gampat, Achila Imchen andChune Loong Lum

Editor: Peter StalkerStatistics Advisor: Amitabh KunduStatistics Team: Rashmi Banga, KalpanaChoudhary and Niranjan SarangiCover Design: Rustam VaniaTechnical Editing and Production:Macmillan India Ltd.

The Asia-Pacific Human Development Unit(HDU), Regional Centre in Colombo (RCC)The Asia-Pacific Human DevelopmentReport 2006 is the result of a collaborativeeffort. Other members of the HDU whoworked on the Report include Susan Howesand Renata Rubian. The HDU adminis-trative team who supported the preparationof the Report include Ruwanthi Senarathneand Rehana Cuttilan. Kay Kirby Dorjiprovided assistance for advocacy and mediaoutreach.

International trade has been the engine of

growth for many countries of Asia and the

Pacific. The ‘economic miracle’ of the East

Asian ‘tigers’ is due in large part to their ability

to export to global markets and to develop

production at a scale, and with the technology,

that allows for higher returns. Poverty has

broadly declined in the region, and hundreds of

millions of people have experienced significant

improvement in the quality of their lives.

But some are being left behind. Several

smaller countries in the region, especially the

Least Developed Countries (LDCs), have not yet

experienced significant gains from trade. The

region’s rural poor have languished from

stagnation in agriculture, as the new riches of

the global marketplace fail to reach the

countryside, where most people live. Even in

fast-growing countries, trade has led to widening

disparities among regions, sectors and

households. Many economies, especially in East

Asia, are unable to create enough jobs for their

growing populations, especially for young

people and women.

The launch of the 2006 Asia-Pacific Human

Development Report, Trade on Human Terms,

comes at a critical time, with only a few months

left before the end-of-year deadline for the

completion of the Doha Development Round.

We are at the mid-point of the ten-year Brussels

Programme of Action for Least Developed

Countries, and have less than a decade to

achieve the targets of the Millennium Develop-

ment Goals.

As we see in the Report, daunting challenges

Foreword

remain. The link between trade, human develop-

ment and poverty reduction has weakened.

Incumbent WTO members have at times made

it difficult for developing countries to gain a

share in the benefits of globalization. China’s

stunning economic growth, in so many ways an

inspiration to its Asia-Pacific neighbors, is not

delivering reciprocal benefits to its regional

trading partners – and is in some cases creating

difficulties for them. One of the messages of this

report is that success in the global marketplace

brings with it new opportunities and responsi-

bilities as well, especially toward the least

developed nations.

The Report examines from an Asia-Pacific

perspective the changes required in the world’s

trading system, as envisioned in the Global

Partnership for Development and the Millen-

nium Development Goals. It draws on the

diverse experience of the region to propose a

comprehensive development strategy that

effectively combines trade liberalization with

the promotion of poverty reduction and human

development.

Trade on Human Terms also identifies the

types of national policies needed to ensure that

all people realize the potential benefits of trade.

Such policy recommendations include invest-

ments in infrastructure, higher education and

R&D for competitiveness; adoption of strategic

trade and industrial policies; a renewed focus

on agriculture and rural development; and

measures for combating “jobless growth.” The

ideas in this report can contribute to a better

globalization – a globalization with benefits for

v

all – both in the Asia-Pacific region and around

the world.

The launch of Trade on Human Terms

marks a turning point for UNDP too: the

evolution of Asia-Pacific Human Development

Reports into an annual series. We expect these

annual regional Reports to provide continuing

analysis of critical development issues that will

prove highly relevant at both the national and

international levels.

Kemal DervisAdministrator, UNDP

vi

The analysis and policy recommendations of this Report do not necessarily reflect the views of the UnitedNations Development Programme, its Executive Board or its Member States. The Report is an independentpublication commissioned by UNDP. It is the fruit of a collaborative effort by a team of eminent experts,stakeholders, and the Human Development Unit team of the Regional Centre in Colombo.

In Asia and the Pacific, trade has proved that itcan provide jobs and higher incomes formillions. At the same time, many people haveyet to benefit, including poor farmers margina-lized by trade barriers and distorted agriculturalprices; workers who lose jobs in domestic indus-tries due to the reduction of tariffs on competingimports; women, who deserve higher wages andbetter working conditions but face the risk ofdisplacement following the withdrawal of textilequotas; and overseas workers, who leave theirloved ones behind and face discrimination andexploitation in search of jobs that can lead toimproved lives back home.

The Asia-Pacific Human DevelopmentReport 2006 is by and for the people of the Asia-Pacific region. It seeks to demystify trade-relatedissues, making them more accessible to a widercross-section of people, thereby facilitating moreinformed debate and advocacy. In doing so, ithopes to promote human development in theregion, focusing especially on the attainment ofthe Millennium Development Goals.

I am proud that this Report is the product ofindigenous thinking by hundreds of people in theregion; experts, scholars, government officials,representatives of non-governmental organiza-tions, civil society and the private sector, andmany people from different walks of life.

Preface

The Report not only draws on many issue-and country-based studies and papers commis-sioned by UNDP, it also benefits from thefeedback on the approach and content obtainedfrom a number of regional workshops, stake-holder consultations and technical meetings.Thus, the process of gathering inputs and ideasfrom diverse, informed sources in the region hasbeen very full and rich.

Questions such as these provided themotivation for the Report: How does tradeliberalization affect the conditions of the worse-off sections of the population? Is trade expansioncontributing to higher employment and povertyreduction? The conclusion is that these links arenot automatic, and will need to be engineeredthrough favourable changes in the internationaltrading regime and appropriate domesticpolicies.

World leaders at the recent GlobalSummit of the United Nations resolved to spareno effort to free their fellow human beingsfrom the abject and dehumanizing conditions ofextreme poverty. We can make an enormouscontribution to fulfilling this pledge – and bene-fiting farmers, women, industrial labourers,overseas workers and others left out so far – byensuring that trade is on human terms andpromotes a better life for all.

Hafiz A. PashaDirector

Regional Bureau for Asia and the PacificUNDP

vii

This Report is the outcome of a truly collabora-tive venture. Persons deserving acknowledge-ment are so numerous, and have contributed inso many different ways, that no attempt to fullyrecognize their contribution can ever do justice.Nevertheless, it is necessary to acknowledge thecontribution of as many as possible. Hafiz Pashainspired and guided the work, and also providednumerous substantive inputs. The Report alsobenefited from specific suggestions from KemalDervis, UNDP Administrator. Colleagues inRCC provided ongoing inputs and support tothe process.

Contributors

Numerous background studies, papers, draftsand notes covering a wide range of issuescontributed to the Report. The main contribu-tors were: Ratnakar Adhikari, Homi S. Aibara,Anu Bhasin, Rupa Chanda, C.P. Chandrasekhar,Uttam Deb, Biswajit Dhar, Ramesh Gampat,Jayati Ghosh, Murray Gibbs, Komal Gopalani,Vu Quoc Huy, Sanath Jayanetti, MumtazKeklik, Mohan Kumar, Kamal Malhotra,Sebastian Mathew, Manuel Montes, SyedNawab Haider Naqvi, Omar Noman, PedroOrtega, Thangavel Palanivel, Hafiz Pasha,Minh Pham, Abdul Aziz Rahman, MustafizurRahman, Anuradha Rajivan, Miho Shirotori,Ruangrai Tokrisna, Lam Quoc Tuan, Tereso S.Tullao, Nguyen Viet Vinh and Swarnim Waglé.

Technical Consultations

The Report also draws on feedback and opinionsexpressed in regional technical consultationswhere inputs were obtained from experts within

Acknowledgements

and outside UNDP. Participants were RashmiBanga, Anuradha Bhasin, Elena Borsatti, JavedBurki, Jolita Butkeviciene, Rupa Chanda, C.P.Chandrasekhar, Kay Kirby Dorji, RameshGampat, Jayati Ghosh, Murray Gibbs, CherieHart, Cristina Hernandez, Susan Howes, AchilaImchen, T. Indrani, Mumtaz Keklik, Aileen Kwa,Marie Laberge, David Luke, Kamal Malhotra,Sebastian Mathew, Manuel Montes, B. Murali,Napoleon Navarro, Omar Noman, PedroOrtega, Thangavel Palanivel, Hafiz Pasha, MinhPham, Syed Ayub Qutub, Anuradha Rajivan,K.V. Ramani, Deepali Sharma, MargaritaSongco, Arusha Stanislaus, Trudy Tan, Thiyaga-rajan Velumail, Swarnim Waglé, YumikoYamamoto and Uchita de Zoysa.

Stakeholder Consultations

The Report benefited from views expressed bynumerous stakeholders in a series of focussedconsultations. Stakeholders were drawn fromacademia, government, private sector, CSOs,think tanks, UN entities, representatives ofworkers and consumers. Participants were ShirinAkhter, Primo Amparo, M.C. Arora, MariaFides Bagasao, T. Balan, Rashmi Banga,Anuradha Bhasin, Libran Cabactulan, RicardoCasco, Rupa Chanda, C.P. Chandrasekhar, BipulChatterjee, Wallace Shuaihua Cheng, XieCheng, Hla Phyu Chit, Srey Chanthy, KalpanaChoudhary, Verona Collantes, Michael AngeloCortez, Rodolfo de la Cruz, Pramod Dev,Maurice Dewulf, K. Dharmarajan, RameshGampat, Jayati Ghosh, Nguyen Thanh Giang,Murray Gibbs, K.M. Gopakumar, R. Gopalan,Komal Gopalani, Gopinath, Ganesh Gurung,Kanupriya Gupta, Tahir Hasnain, Minh Chien

ix

Ho, Susan Howes, Vu Quoc Huy, AchilaImchen, T. Indrani, Sanath Jayanetti, MarkusJelitto, Sitanon Jesdapipat, Kamol Kamoltrakul,Mumtaz Keklik, Makmur Keliat, ParasharKulkarni, Nagesh Kumar, Udaya Kumar,Nguyen Thi Phuong Lan, Leeber Leebouapao,Zhongzhou Li, S.H. Mahatre, Abdul Halim binMansor, Rajan Mohapatra, Manuel Montes,Monwer Mostafa, Samsen Neak, ShrawanNigam, Ernesto Ordonez, Pedro Ortega,Thangavel Palanivel, Balaji Pandey, K. SeetaPrabhu, Purnima Purohit, Atiur Rahman,Ananya Raihan, Anuradha Rajivan, SripriyaRanganathan, N.P. Samy, Husein Sawit, DeepaliSharma, Pradeep Sharma, Stanley Simpson,Photong Sliphong, Bounthone Soukavong,Farhana Faruqi Stocker, Indah Suksmanigsigh,Supanee Taneewut, Dikshya Thapa, RizaTjahjadi, Samar Verma, Gautam Vohra,Swarnim Waglé, Dushni Weerakoon, Ng LipYong, Uchita de Zoysa and B.K. Zutshi.

The team also wishes to acknowledge theactive participation of the Consumer Unity andTrust Society (CUTS) through the Centre forInternational Trade, Economics and Environ-ment (CITEE), including facilitation.

Statistical Work

Statistical information was compiled by RashmiBanga and Niranjan Sarangi with assistancefrom Kalpana Choudhary, Iori Kato and ChuneLoong Lum.

Reviewers

The RHDR benefited from expert reviewers

from within and outside of UNDP. Reviewersprovided general and specific inputs. Back-ground papers and draft chapters were putthrough a peer review process. The teamwould like to thank Anuradha Bhasin, JolitaButkeviciene, C.P. Chandrasekhar, CarolynDeere, Cristina Hernandez, Mumtaz Keklik,Aileen Kwa, Richard Leete, David Luke,Victor Ognivtsev, V.R. Panchamukhi, DwijenRangnekar, Miho Shirotori, Jan Vandemoorteleand Josef Yap. Amitabh Kundu, S.K. Nath,R. Ramachandran and Suranjana Vidyaratnereviewed the statistical work for which the Teamexpresses its thanks.

Production

UNDP India Country Office provided valuableoperational support during the production ofthis Report.

The promotion and dissemination of theReport benefited from the support of the UNDP-RCC Programme Advocacy and Media Unit, inparticular, Kay Kirby Dorji.

Suwansawan Baran, Dora Blessich, BarbaraLemoine and Siamak Moghaddam from theUNOPS Asia office, previously located in KualaLumpur and now in Bangkok, providedsupporting administrative services. UNDP-RCCBusiness Services Unit also provided support, inparticular, Lushantha Arsecularatne, ManojBasnyat and Vishwa Khanna.

The Report is the result of leadership anddedication of Anuradha Rajivan, who ablysteered this work through many twists and turns;without her, this work simply would not havebeen completed.

Minh PhamRegional Manager

UNDP Regional Centre in Colombo

x

Foreword v

Preface vii

Acknowledgements ix

Abbreviations xvii

OVERVIEWAn Era of Rapid Growth and Trade Liberalization 3Making Agricultural Trade Work for the Poor 4Adjusting to a New Era for Textiles and Clothing 5Selling Services Across Borders 6Trade Opportunities for the Least Developed Countries 7An Eight-Point Agenda 7Reaching a Different Frontier 11

CHAPTER 1: Using International Trade to Promote Human DevelopmentBalancing Growth and Human Development 16Pursuing Growth through Trade 17The Potential for State Action 18Multilateral, Regional and Bilateral Action 22The Human Development Imperative 25The Contours of the Report 26

CHAPTER 2: Trade and Human Development: The Asia-Pacific ExperienceTrends in International Trade 29The Energy Crunch 37The Implications for Human Development 38The Employment Channel 43

CHAPTER 3: Making Agricultural Trade Work for the PoorThe Pattern of Global Agricultural Trade 52Protectionism in the North 55Distorted Trade and Human Development 58Making Agricultural Trade Work for the Poor 59

Contents

xi

Agricultural Trade Policies of Developing Countries 61Intellectual Property 63Geographical Indications 64Fisheries and Human Development 66Policy Directions for Agricultural Trade 72Policy Priorities 74

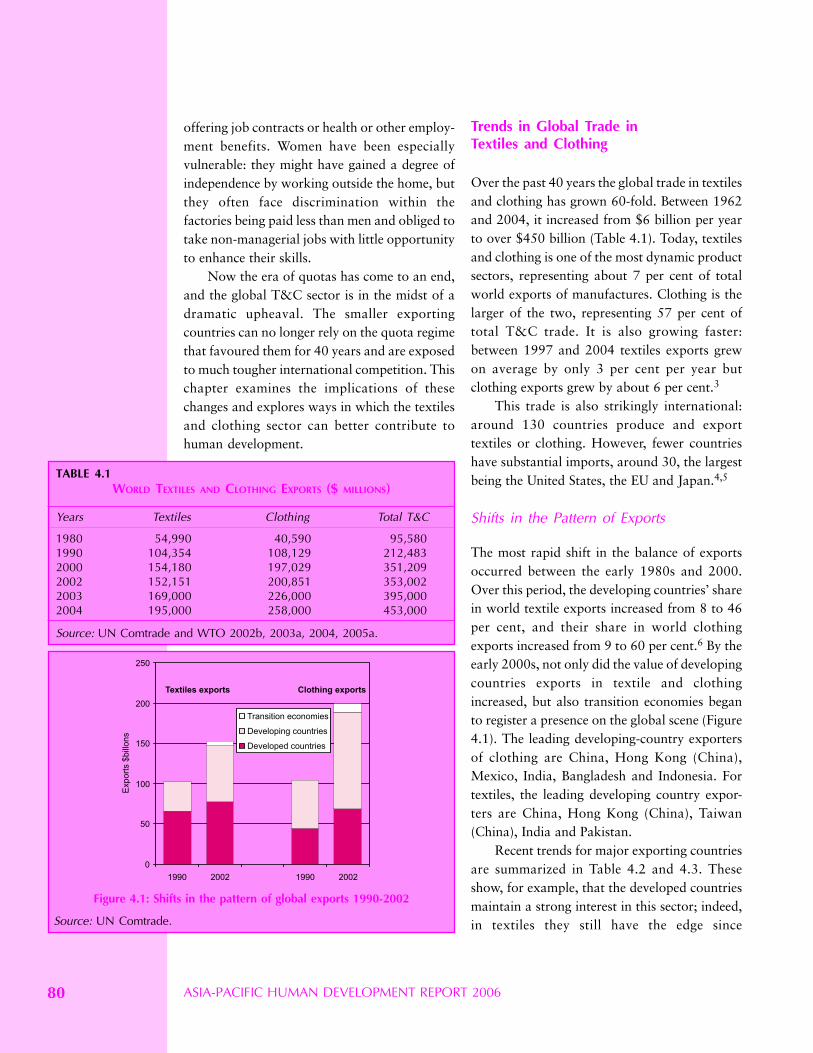

CHAPTER 4: Adjusting to a New Era for Textiles and ClothingTrends in Global Trade in Textiles and Clothing 80A Changing Trade Regime 84National Policy Directions 91International Measures to Increase Market Access 94Major Changes Ahead 95

CHAPTER 5: Selling Services Across FrontiersShort-term Migration 99Outsourcing Business Processes 108International Tourism 117The New Trade in Economic Services 123

CHAPTER 6: Trading Opportunities for the Least Developed CountriesWhy do LDCs not Benefit Sufficiently from Trade? 129Experience with Trade Integration 130Human Development Implications of Trade Integration 134Initiatives to Address LDC Vulnerability 136The Way Forward 140

CHAPTER 7: Trade for Human Development: An Eight-Point AgendaInvest for Competitiveness 147Adopt Strategic Trade Policies 148Restore a Focus on Agriculture 149Combat Jobless Growth 149Prepare a New Tax Regime 150Maintain Stable Exchange Rates 150Persist with Multilateralism 151Cooperate with Neighbours 151Reaching a Different Frontier 152

Notes 153

Bibliography 157

xii

BOXES1.1 Country Classifications Used in this Report 151.2 Recovering Revenue Losses from Trade Liberalization in Bangladesh 181.3 State Intervention in Trade – An Age-old Phenomenon 191.4 Strategic International Integration in a Globalizing World 201.5 Export Processing Zones 211.6 The Real Effective Exchange Rate: Regional Experiences 221.7 Varieties of Regional Trade Agreements 231.8 Established Regional Trade Agreements Involving Asia-Pacific Countries 242.1 Asia, the emerging factory of the world 302.2 From Food Surplus to Food Deficit 352.3 The Oil Shock 352.4 Trade and Growth in Malaysia’s Spectacular Poverty Decline 392.5 Including Women in Globalization 423.1 Agricultural Trade Liberalization in Indonesia 593.2 Geographical Indications in Asia 663.3 Food Safety Standards and Small-Scale Fisheries 693.4 CITES, The Shrimp-Turtle Dispute and Indian Fishworkers 714.1 Female Employment in the Bangladesh Garments Industry 834.2 Sweatshop Conditions in Delhi’s Garments Industry 834.3 LDCs: Major Beneficiaries of the Multifibre Arrangement 845.1 Movements of Unskilled Labour in the Asia-Pacific Region 1005.2 Use of Remittances in Bangladesh 1015.3 Discriminatory Work Visas 1025.4 Human Development Outcomes of Migration 1045.5 Government Promotion of Temporary Migration from Viet Nam 1055.6 Migration Options in the General Agreement on Trade in Services 1075.7 Outsourcing Business Processes – Implications for Widening Employment 1085.8 Outsourcing Services along the Value Chain 1085.9 Factors Shaping Competitiveness in Global Outsourcing 110

5.10 Human Development Outcomes of Outsourcing 1145.11 Domestic Measures to Promote Outsourcing 1155.12 Creating Comparative Advantage for Outsourcing in Malaysia 1165.13 The Significance of Domestic Tourism 1175.14 Harnessing Leisure Travel in the Maldives 1215.15 Rapid Tourist Development in a Remote Area: Angkor, Cambodia 1226.1 Nepal’s Cautious Approach to Liberalizing Services 1316.2 Special and Differential Treatment Provisions in the WTO 1326.3 TRIPS and the Looming Public Health Crisis in Cambodia 1336.4 Trade Between Asia-Pacific LDCs and China 1366.5 Aid-for-trade: The Way Forward 1386.6 Niche Products: An Opportunity for Least Developed Countries 140

xiii

TABLES2.1 Regional Growth Performance 292.2 Effective import duties for selected countries, 1990 and 2000 (%) 302.3 Growth Rates of Exports, 1980s and 1990s (%) 312.4 Growth Rates of Imports, 1980s and 1990s (%) 322.5 Composition of Merchandise Exports and Imports 342.6 Growth rates by sector and GDP growth rates 372.7 Trends in the Gini coefficient, 1960s to 1990s 382.8 Growth of Employment and Output, and Employment Elasticity by Sector 442.9 Factors Contributing to Changes in Rate of Employment Growth 44

2.10 Composition of Manufacturing Value-Added in China and Malaysia (%) 452.11 Growth of Output and Employment in the Services Sectors 452.12 Overall Growth of Employment and GDP and Employment Elasticity

in Selected Countries 462.13 Composition of Manufacturing Value-Added in India (%) 462.14 Growth in Total Factor Productivity in Selected Countries 463.1 Valued-Added in Agriculture as Percentage of GDP 513.2 Percentage Employment in Agriculture 513.3 Share of World Production of Selected Agricultural Products Traded

Across Borders 2005 523.4 Leading Agricultural Exporters in the Asia-Pacific Region 2003 543.5 European Union – Estimates of Support to Agriculture, $ Millions 563.6 United States – Estimates of Support to Agriculture, $ Millions 563.7 US Subsidies to Selected Agricultural Products, $ Millions 564.1 World Textiles and Clothing Exports ($ millions) 804.2 Leading Exporters of Textiles 2004 814.3 Leading Exporters of Clothing 2004 814.4 Textiles and Clothing Employment, Selected Asian Countries 824.5 US and EU Imports of Textiles and Clothing 2004 and 2005 864.6 Share in Value in Textiles and Clothing (%) 865.1 Tourist Arrivals in Asia-Pacific Countries, 2005 1185.2 Employment in the Tourist Industry 1196.1 Key Indicators of Asia-Pacific Least Developed Countries 128

FIGURES1.1 Trade and Human Development – A Schematic View 162.1 Import Tariffs, 1980–2000 292.2 The Asia-Pacific Region’s Share in World Trade, 1973-2000 (%) 312.3 Balance of Trade, East Asia and the Pacific, and South Asia, 1980s and 1990s 332.4 Composition of Merchandise Exports and Imports 342.5 Composition of Manufactured Exports, 1980-2000 362.6 Growth of Exports of Goods and Services and GDP in Asia and Pacific Countries 36

xiv

2.7 Income Poverty, 1981–2001, % of People Living on Less than $1 Per Day 392.8 LDCs and Developing Countries, Trade as % of GDP, 1970–2002 402.9 Annual Average Growth Rates, Developing Countries and LDCs, 1970–2000 40

2.10 Regional Unemployment Rates, 1993 and 2003 432.11 Education Level of the Unemployed 472.12 Unemployment Rate by Sex, 1990s 473.1 Commercial Food Import Bills 533.2 Exporter Rankings: A Comparison of those for Merchandise and Agricultural Goods 543.3 Tariffs Levied by Developed Countries on Imports from each Region (%) 574.1 Shifts in the Pattern of Global Exports 1990-2002 804.2 Share of Textiles and Clothing in Total Merchandise Exports in Selected Countries

of Asia 2004 814.3 Women’s Share in Paid Employment in Textiles and Clothing 824.4 Growth in Value of Exports of Textiles and Clothing to the EU and the US 2004-05 875.1 Flows of Remittances to Selected Asian Countries, 1983-2003, $ Billions 1015.2 Female and Male Migration from Sri Lanka 1025.3 Tourist Arrivals per 100 People, 2002 119

STATISTICAL ANNEXESAbout the Data

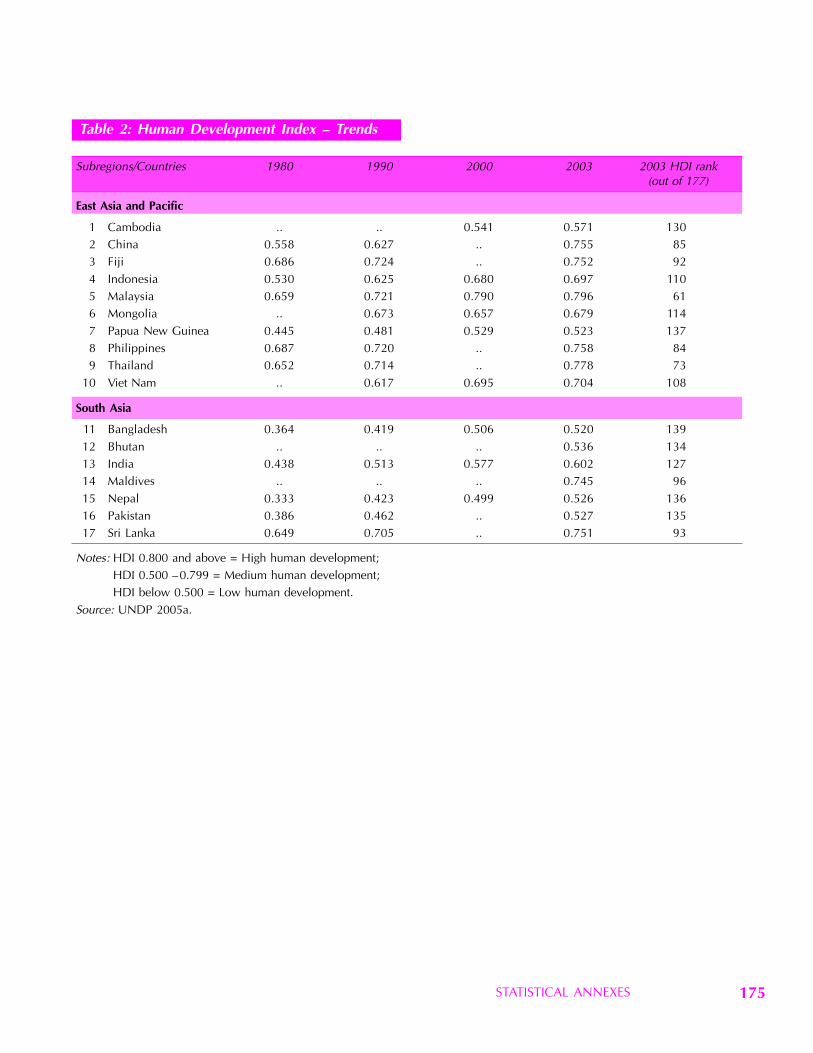

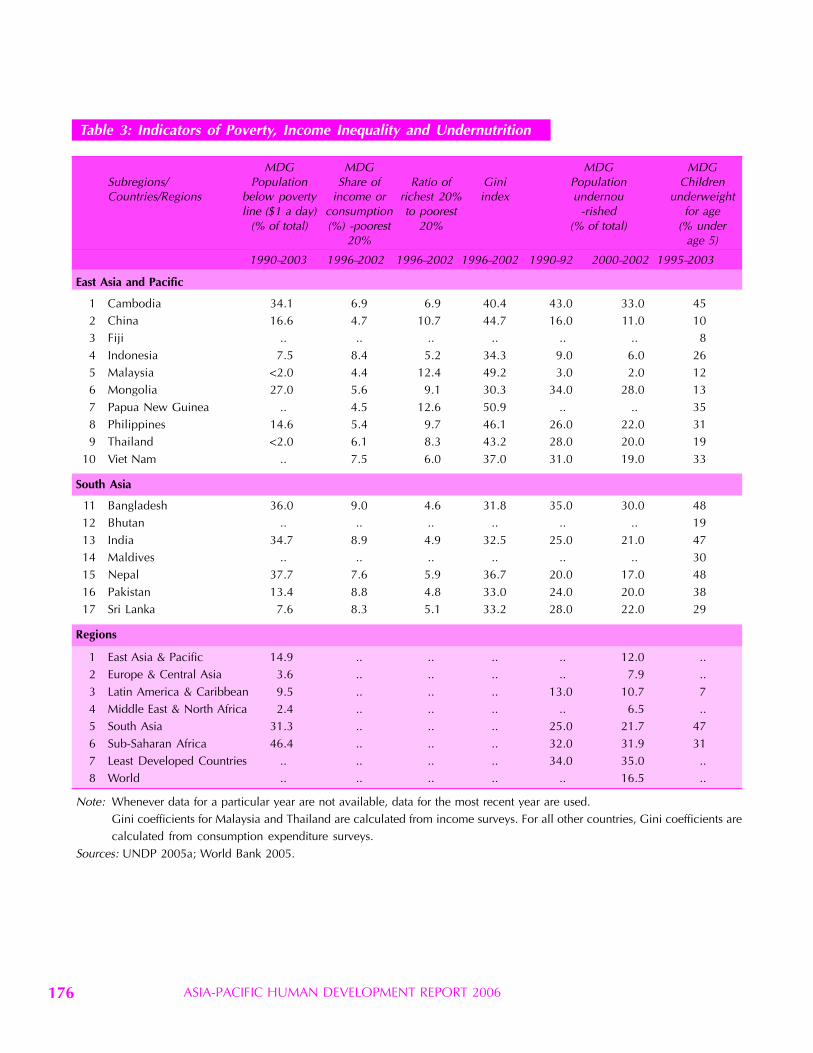

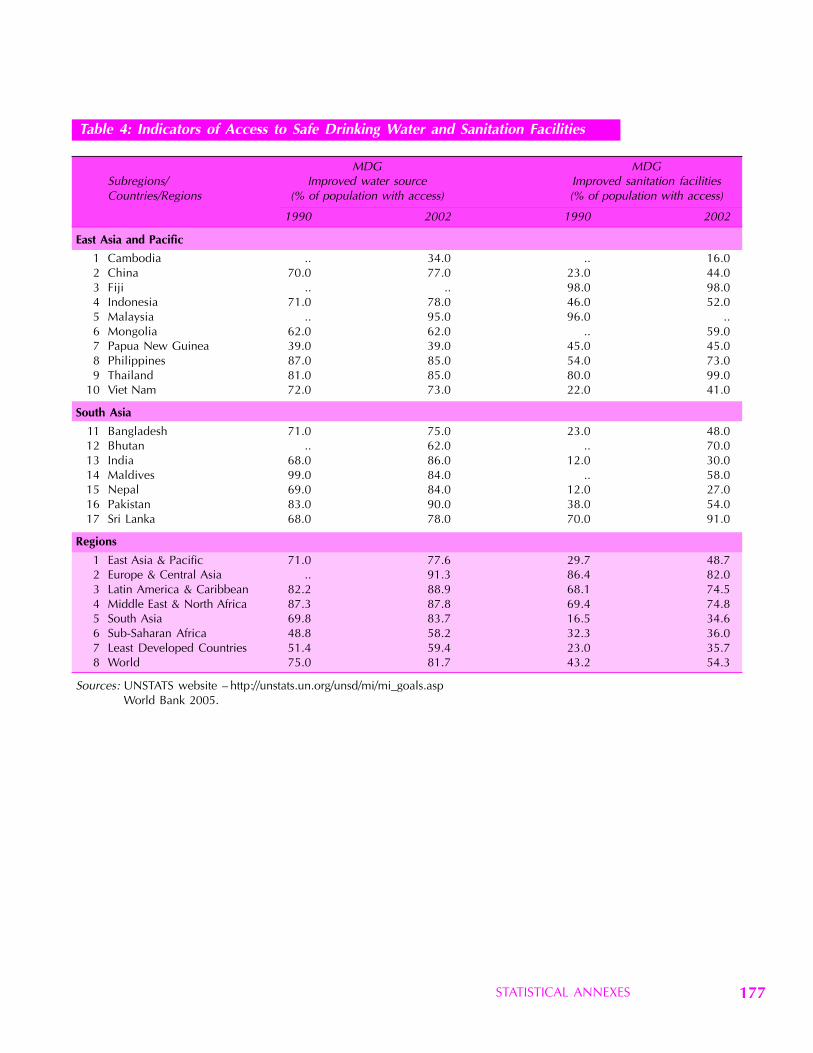

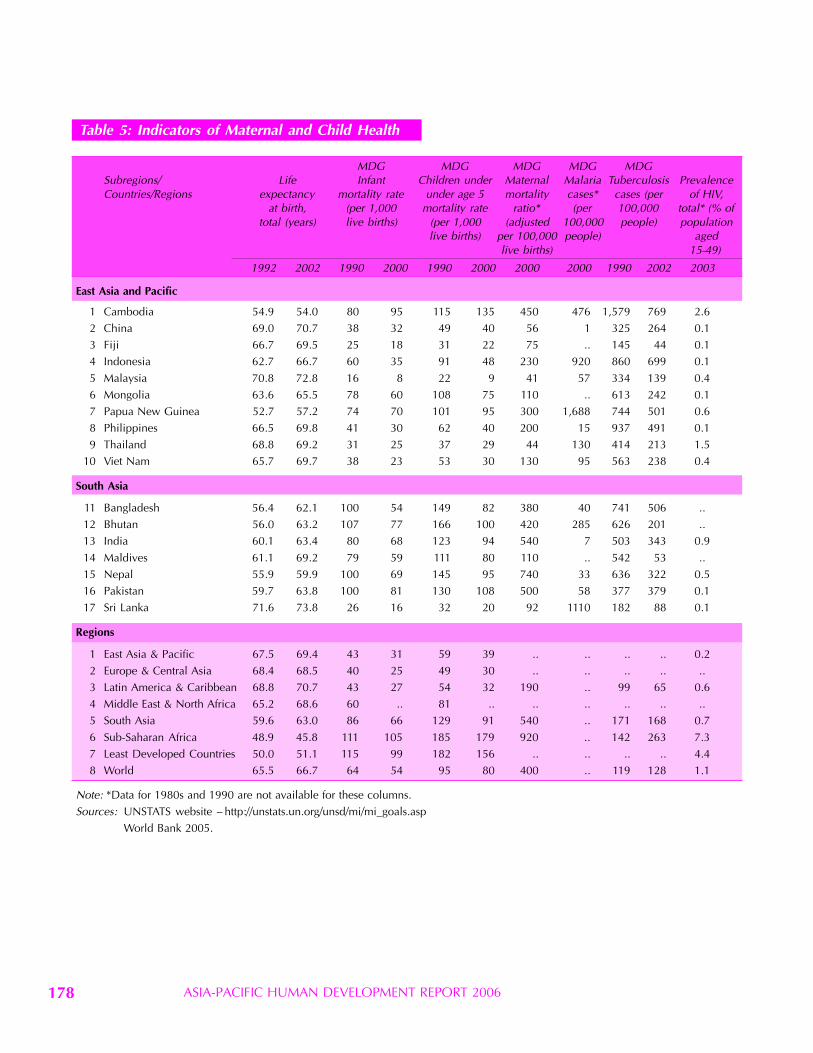

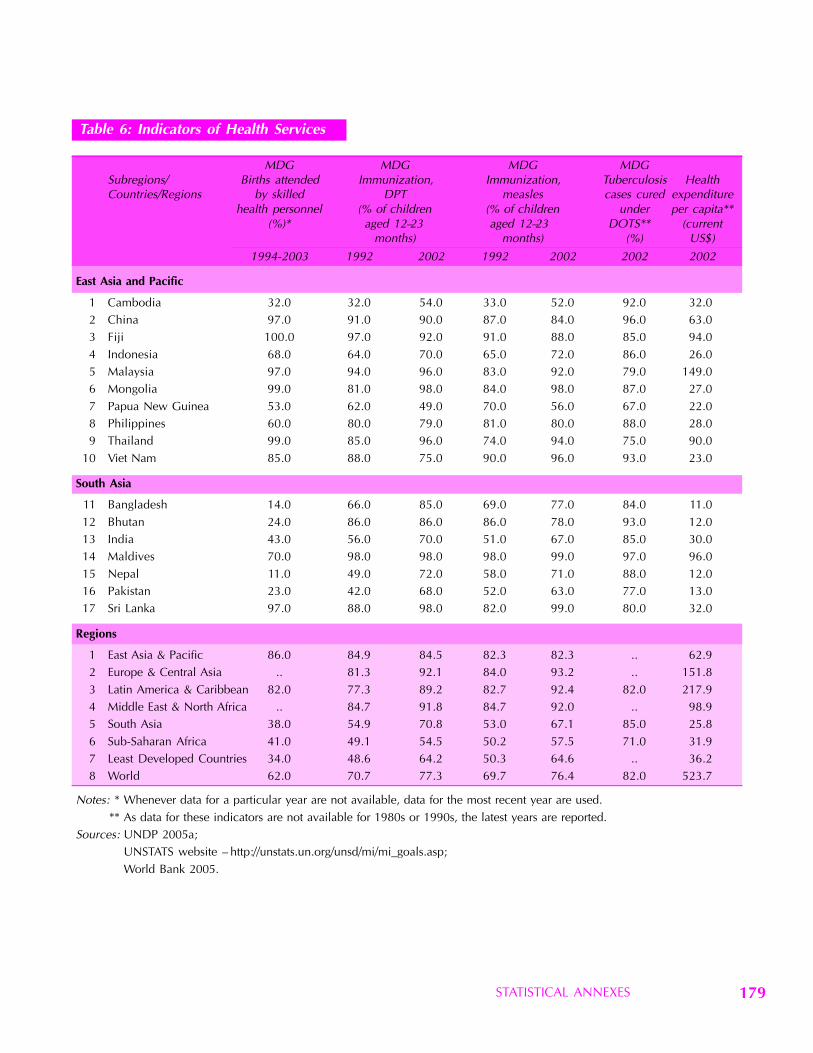

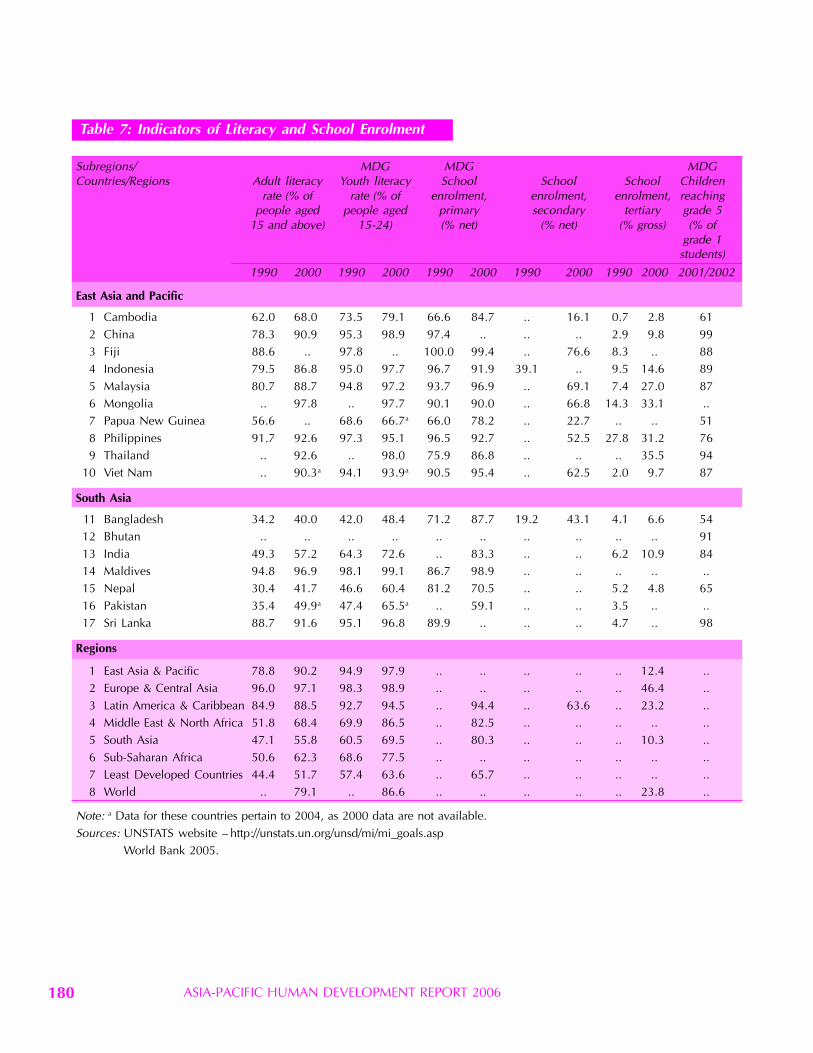

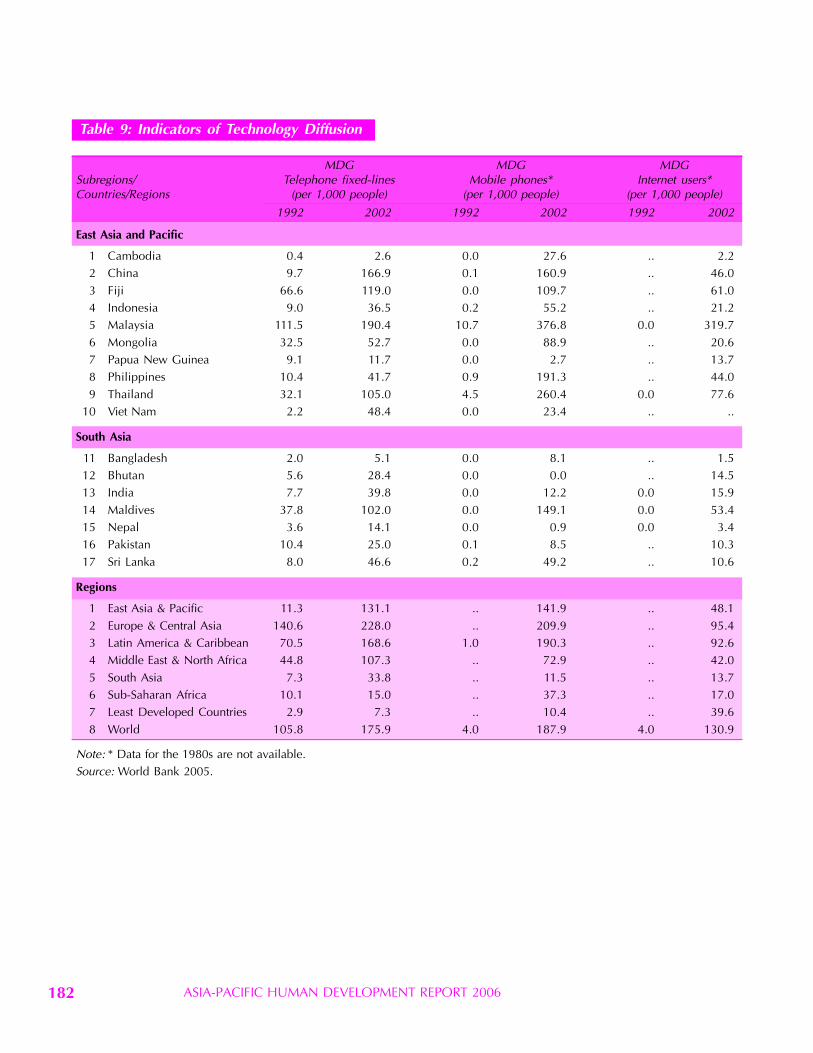

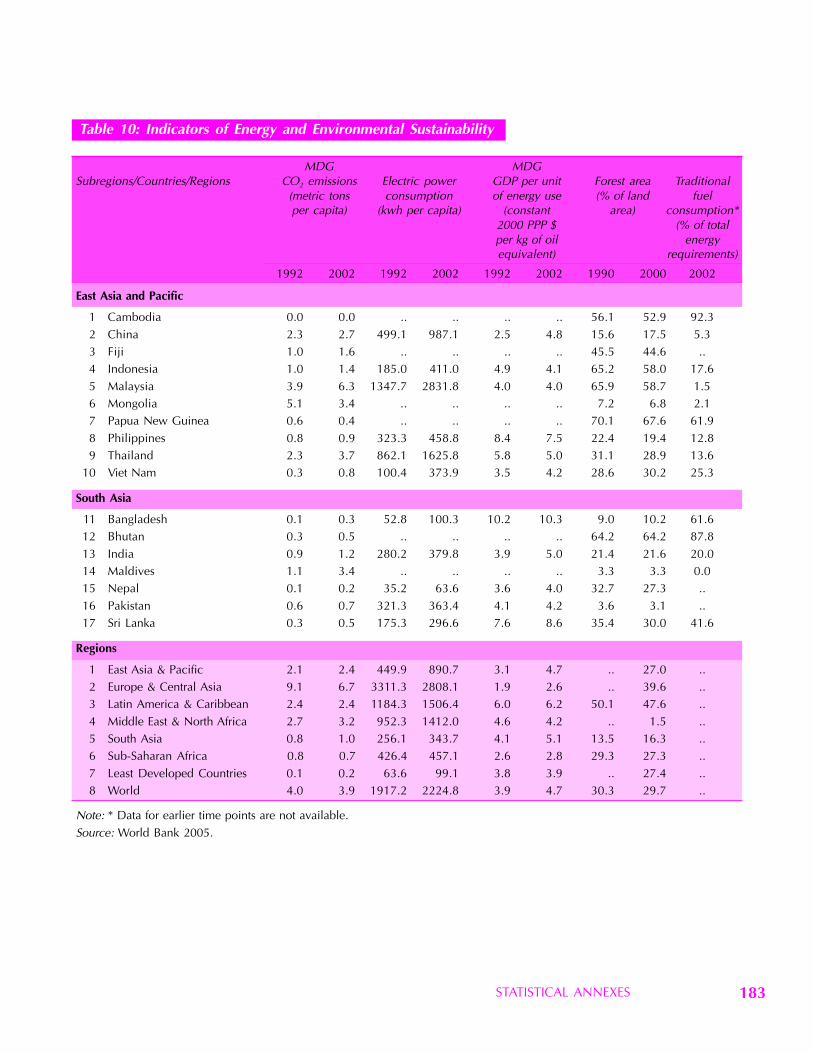

Table 1. Basic Indicators 174Table 2. Human Development Index – Trends 175Table 3. Indicators of Poverty, Income Inequality and Undernutrition 176Table 4. Indicators of Access to Safe Drinking Water and Sanitation Facilities 177Table 5. Indicators of Maternal and Child Health 178Table 6. Indicators of Health Services 179Table 7. Indicators of Literacy and School Enrolment 180Table 8. Indicators of Gender Development 181Table 9. Indicators of Technology Diffusion 182

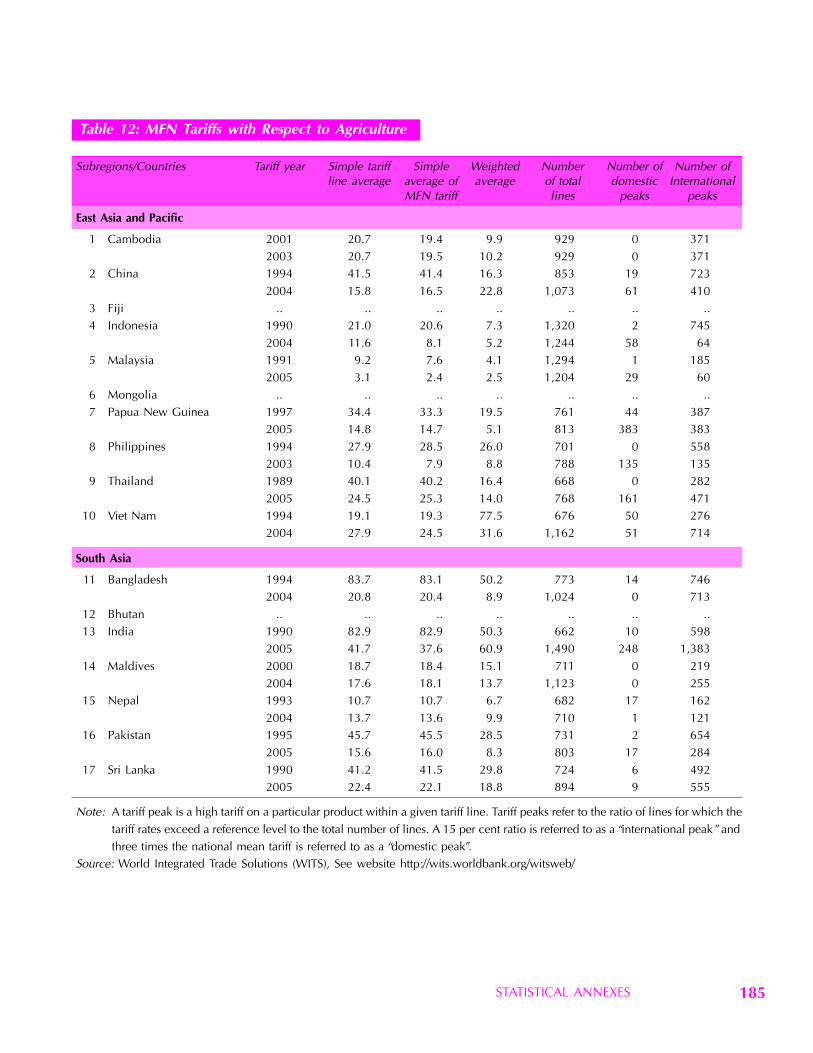

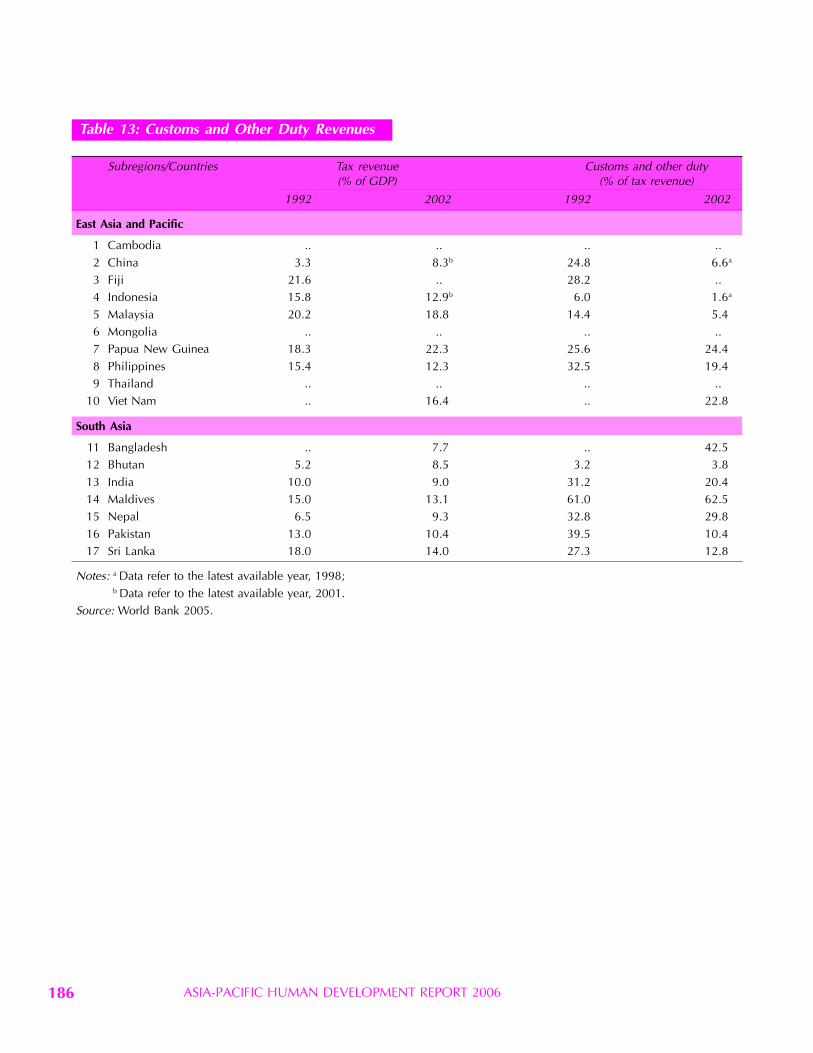

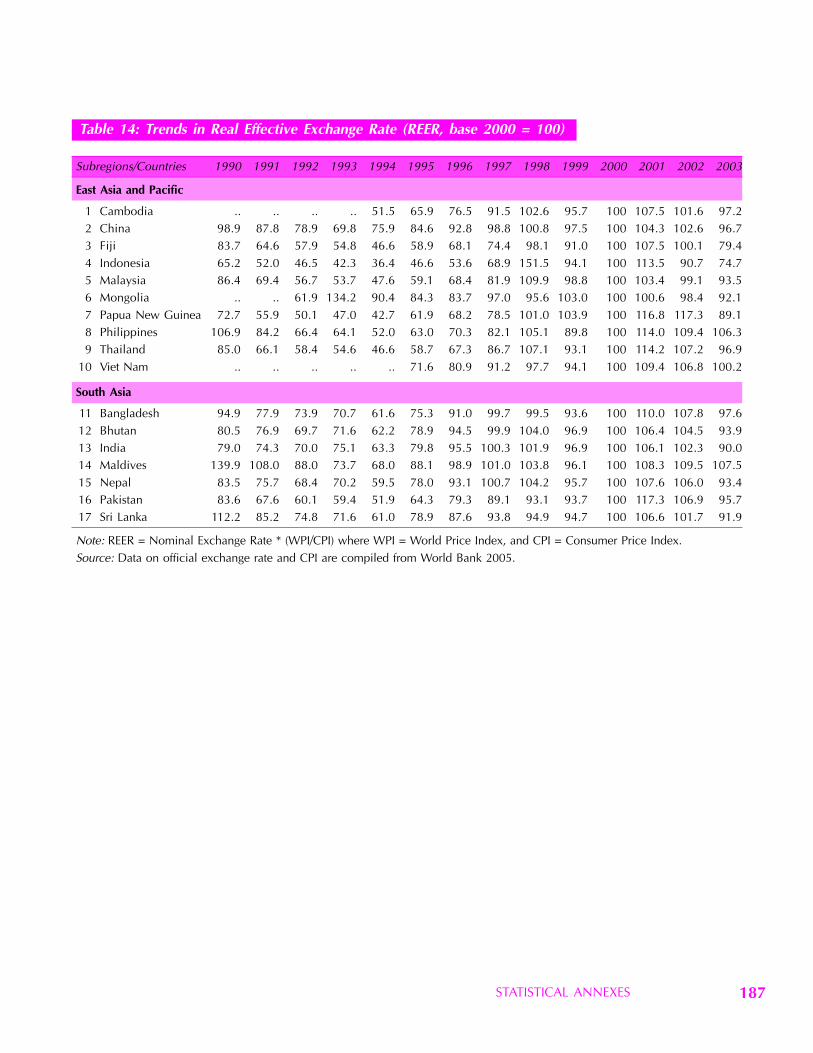

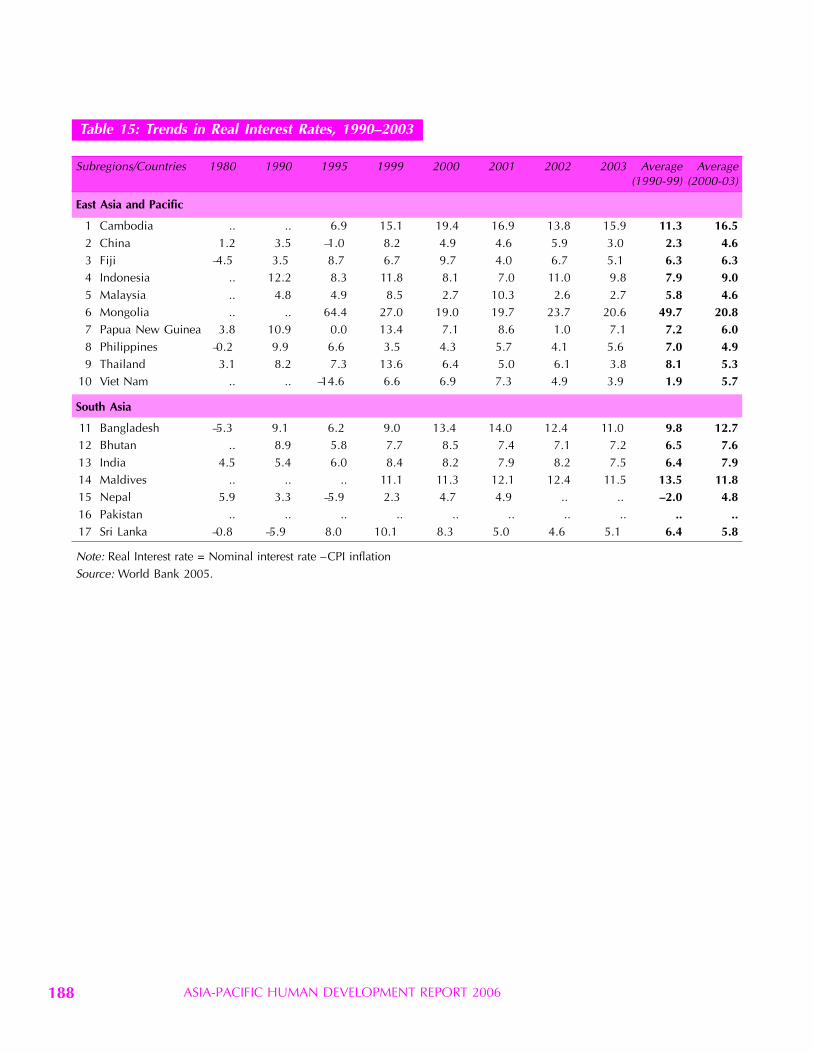

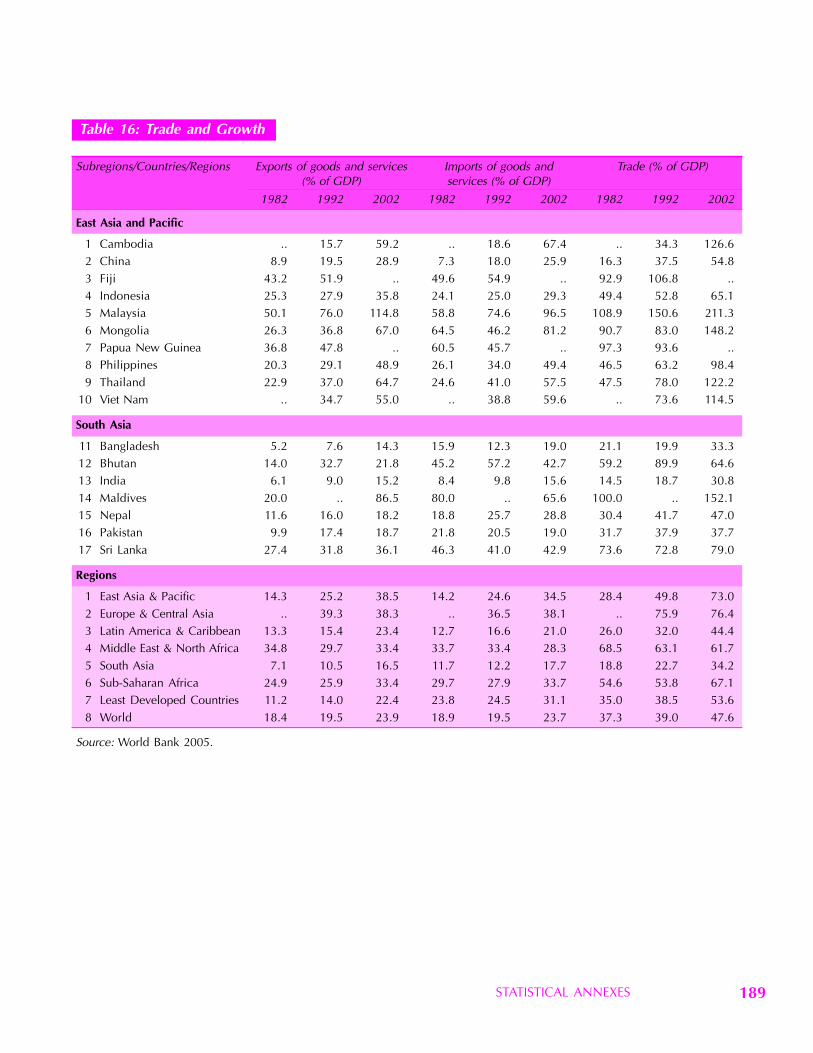

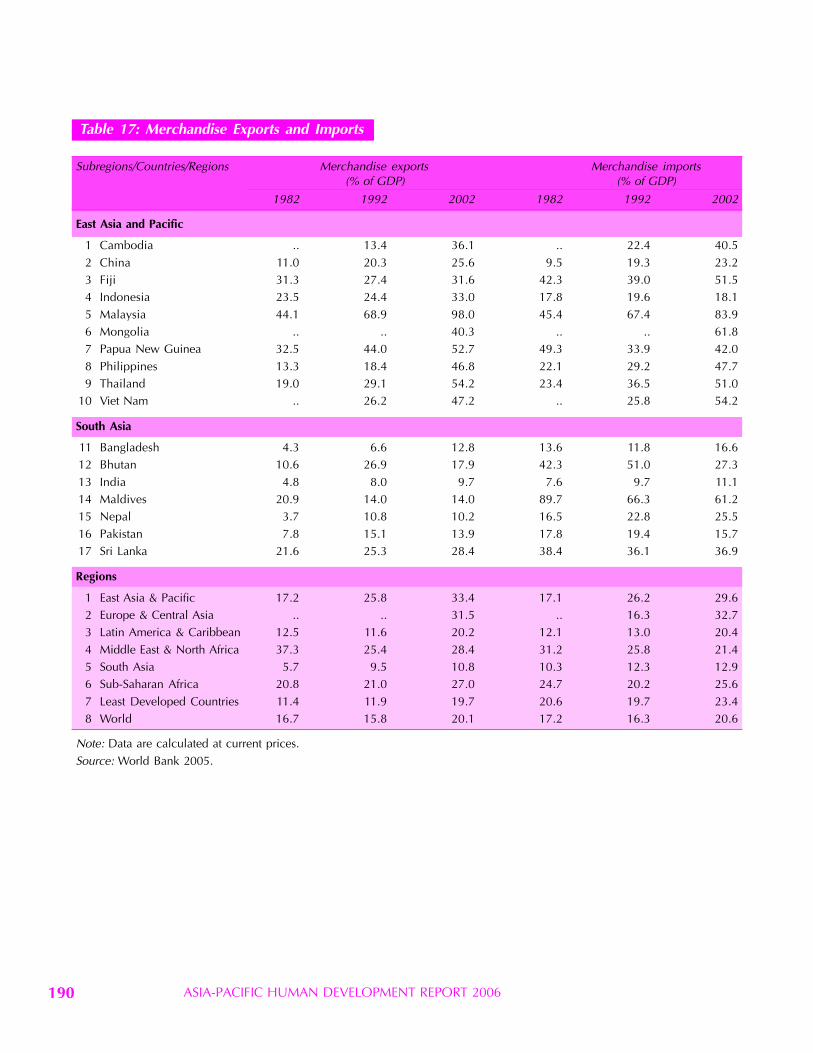

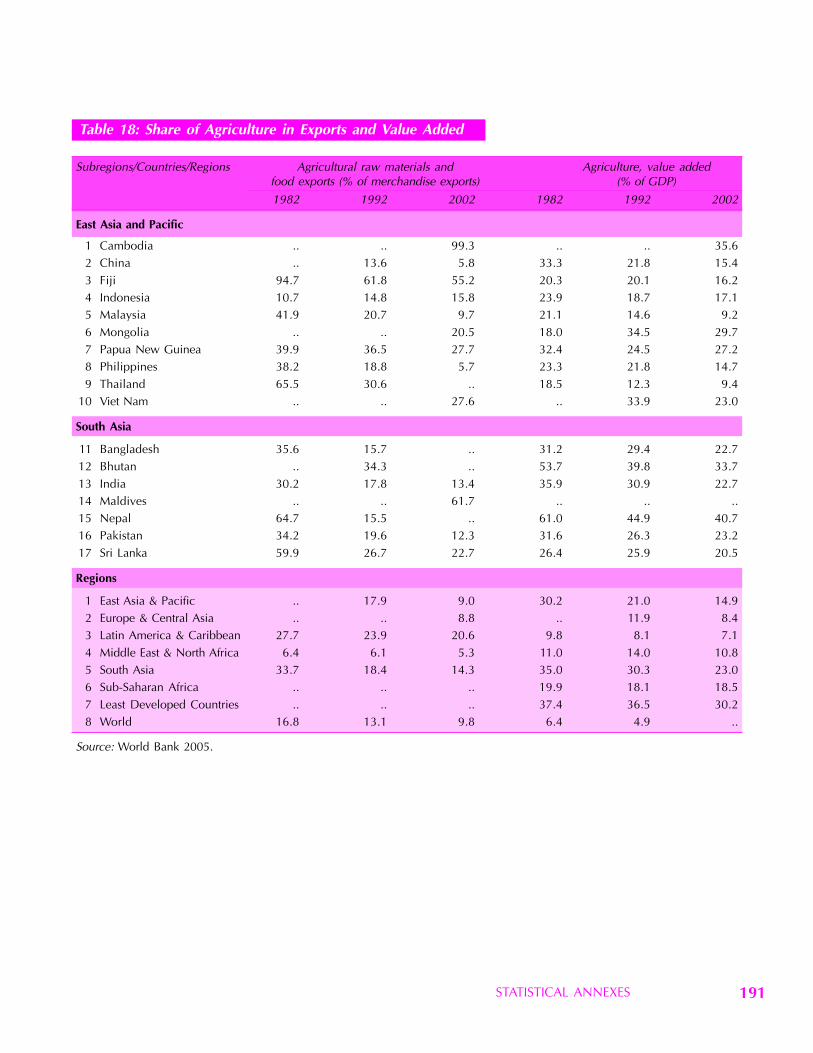

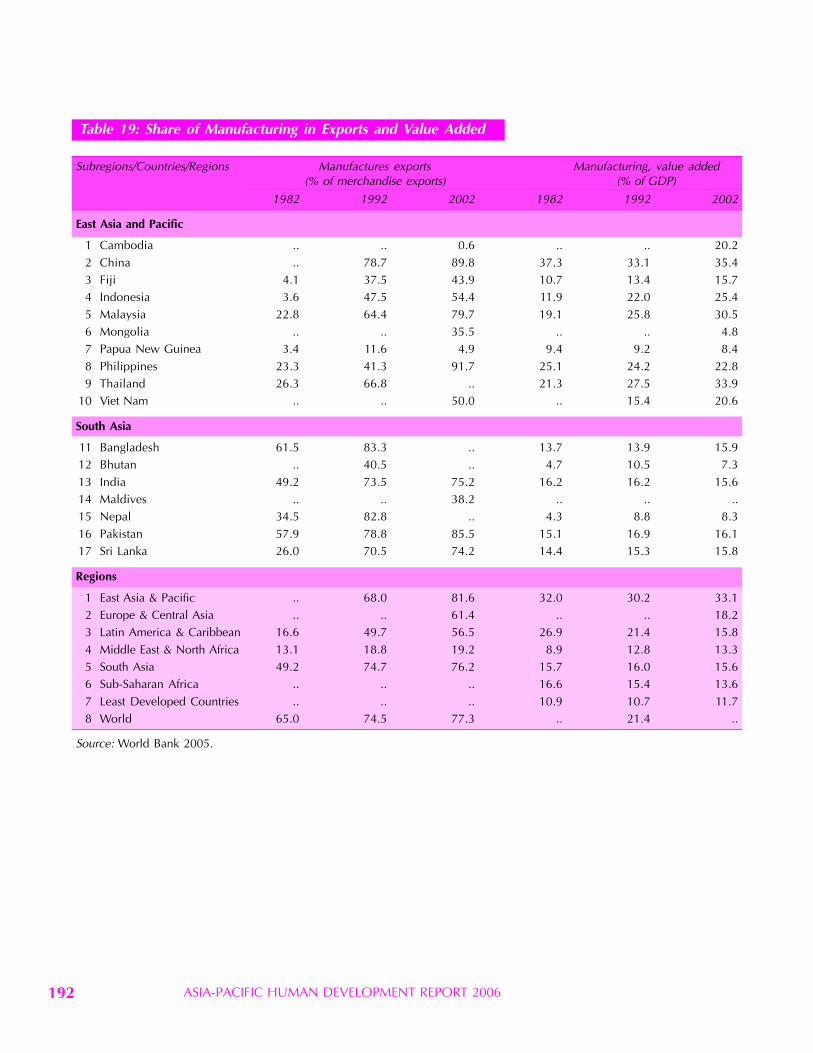

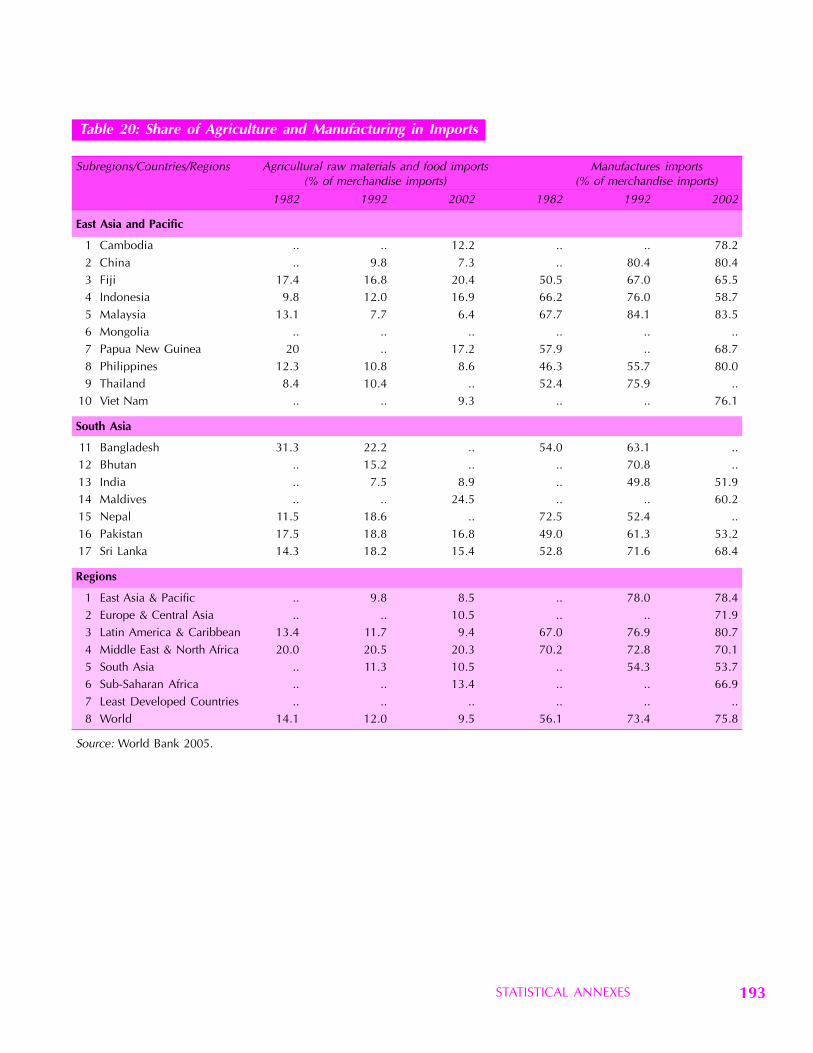

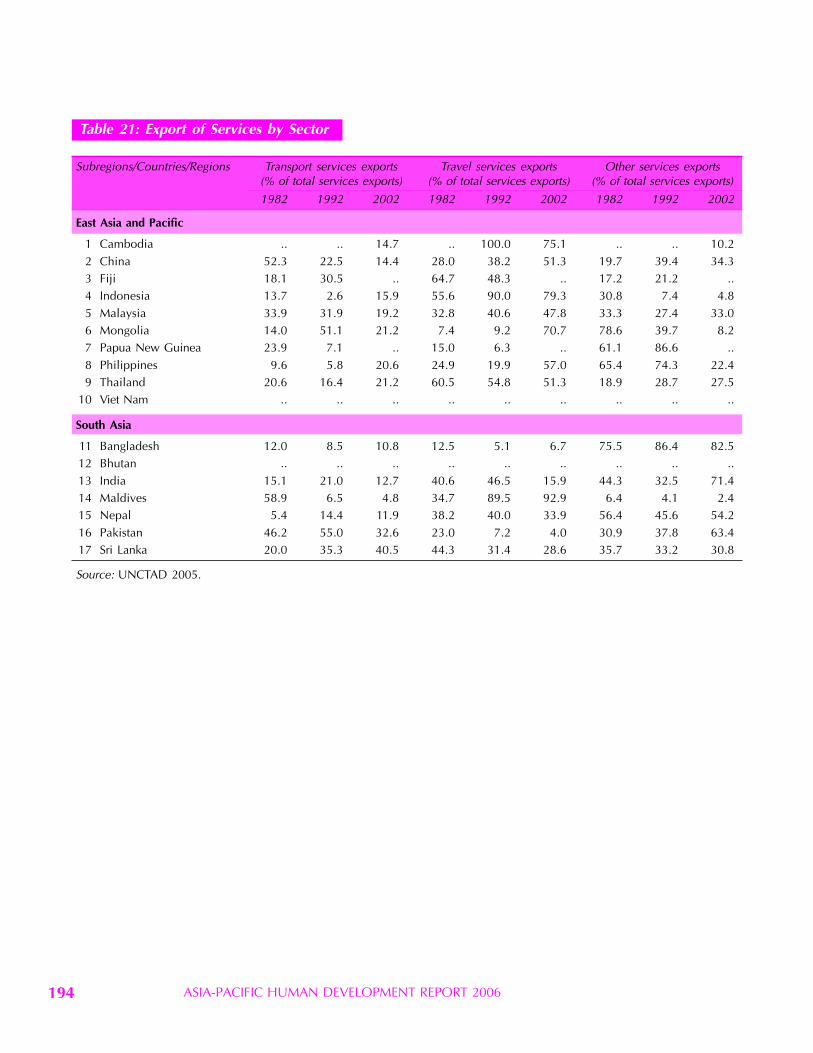

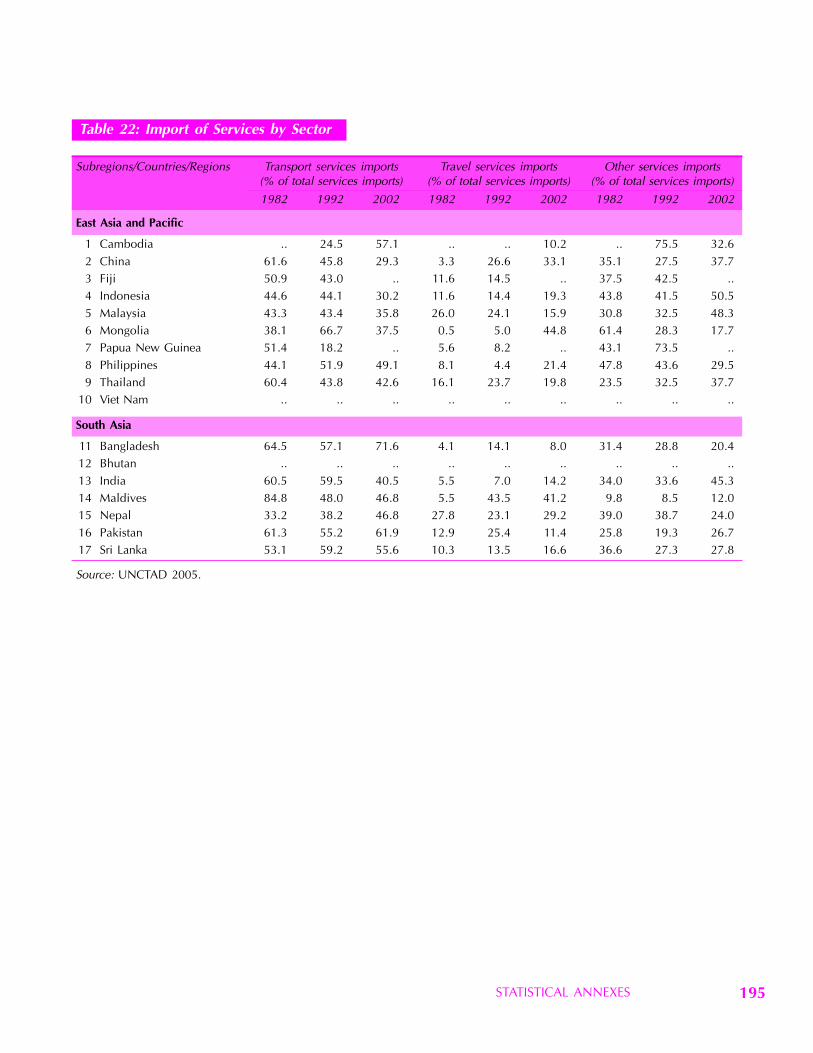

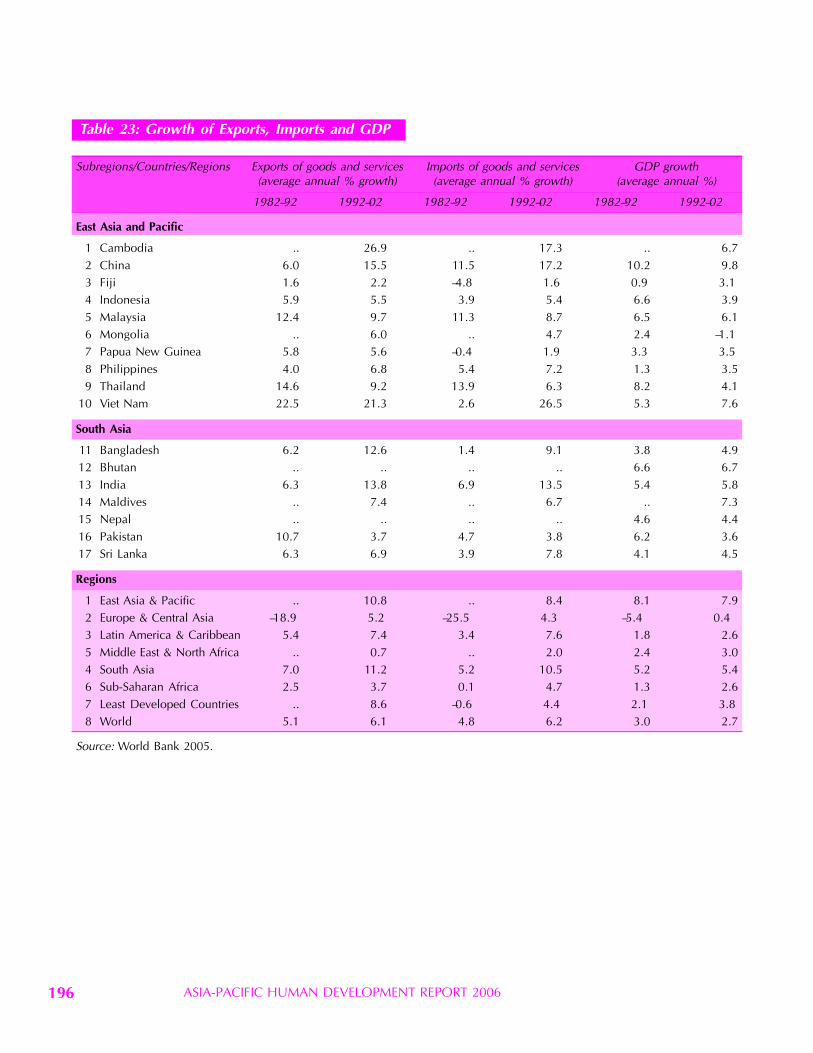

Table 10. Indicators of Energy and Environmental Sustainability 183Table 11. Tariffs, Domestic Peaks and International Peaks 184Table 12. MFN Tariffs with Respect to Agriculture 185Table 13. Customs and Other Duty Revenues 186Table 14. Trends in Real Effective Exchange Rate (REER, base 2000=100) 187Table 15. Trends in Real Interest Rates, 1990-2003 188Table 16. Trade and Growth 189Table 17. Merchandise Exports and Imports 190Table 18. Share of Agriculture in Exports and Value Added 191Table 19. Share of Manufacturing in Exports and Value Added 192Table 20. Share of Agriculture and Manufacturing in Imports 193Table 21. Export of Services by Sector 194Table 22. Import of Services by Sector 195Table 23. Growth of Exports, Imports and GDP 196

xv

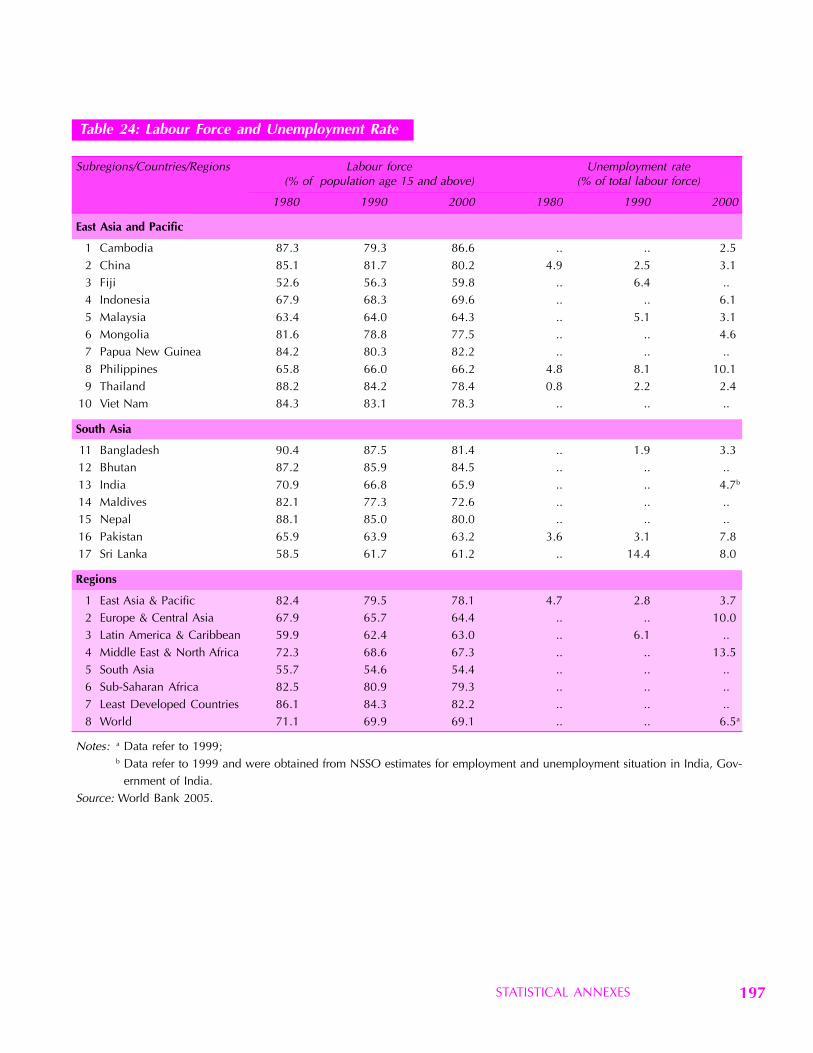

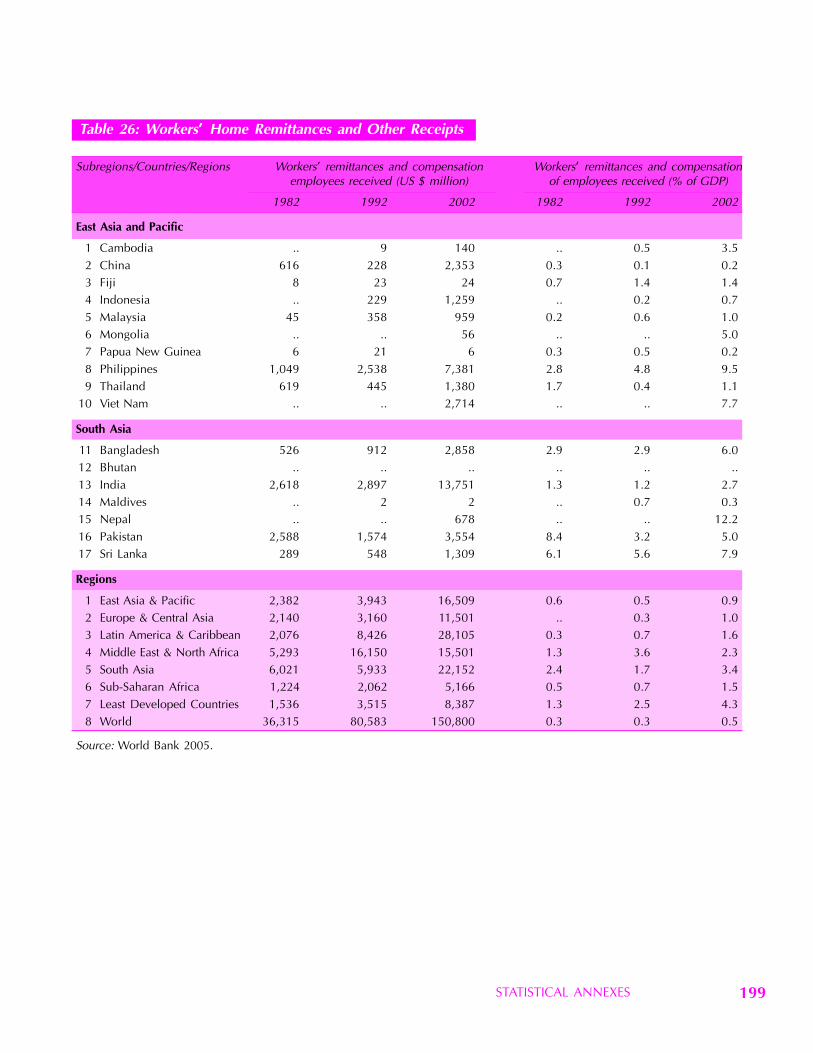

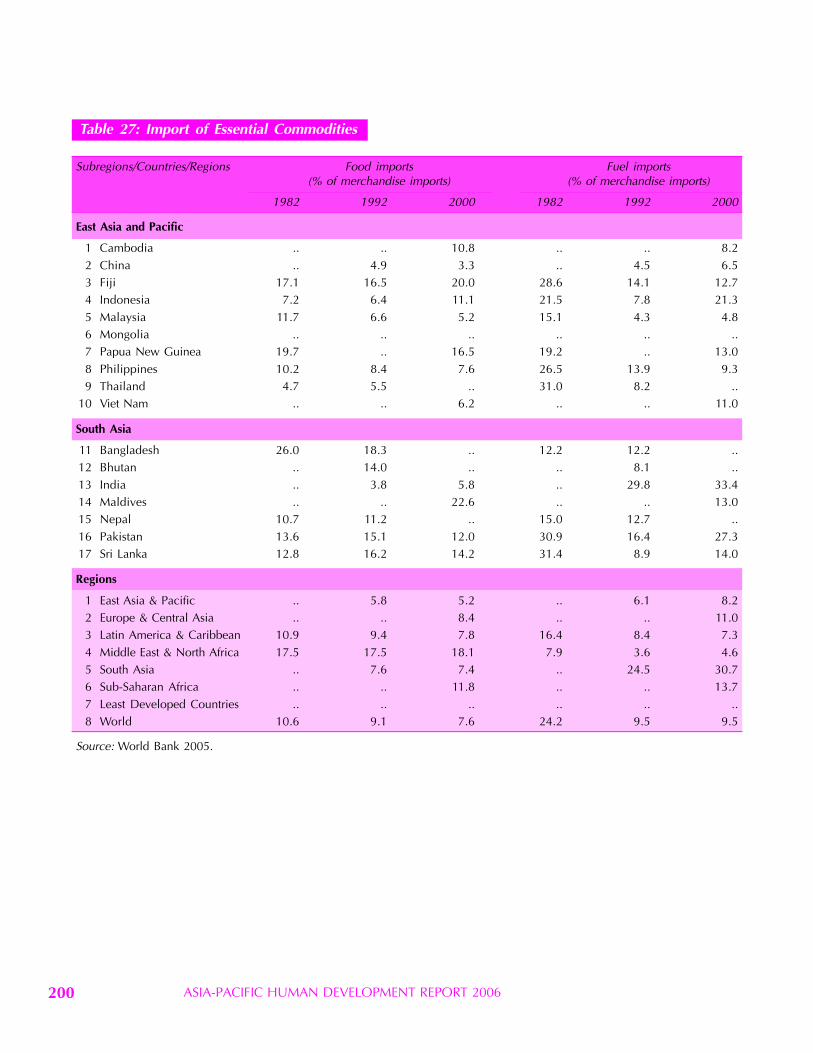

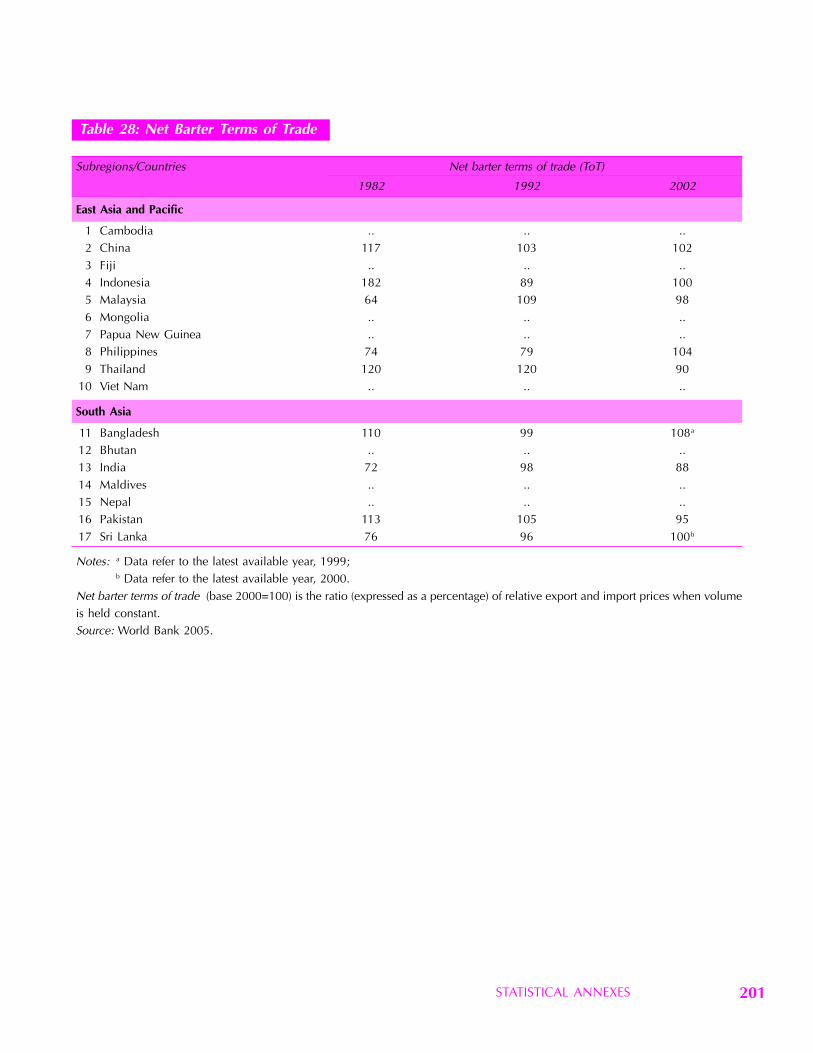

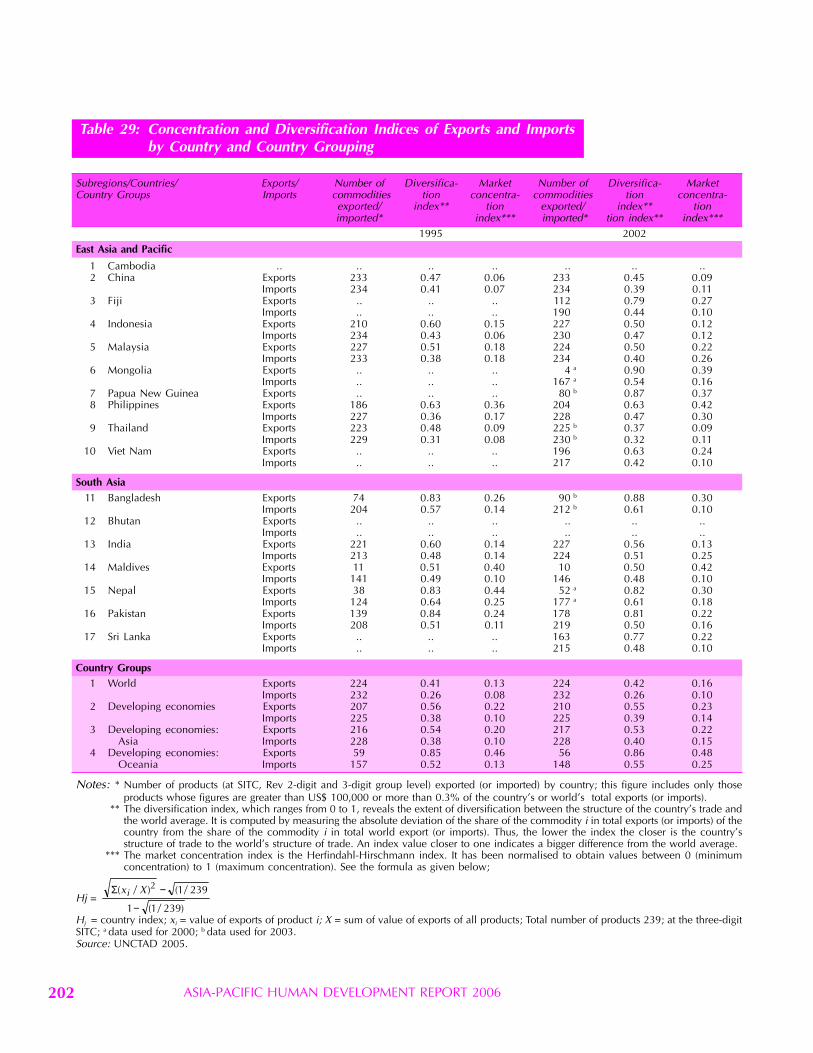

Table 24. Labour Force and Unemployment Rate 197Table 25. Structure of Employment 198Table 26. Workers’ Home Remittances and Other Receipts 199Table 27. Import of Essential Commodities 200Table 28. Net Barter Terms of Trade 201Table 29. Concentration and Diversification Indices of Exports and Imports by

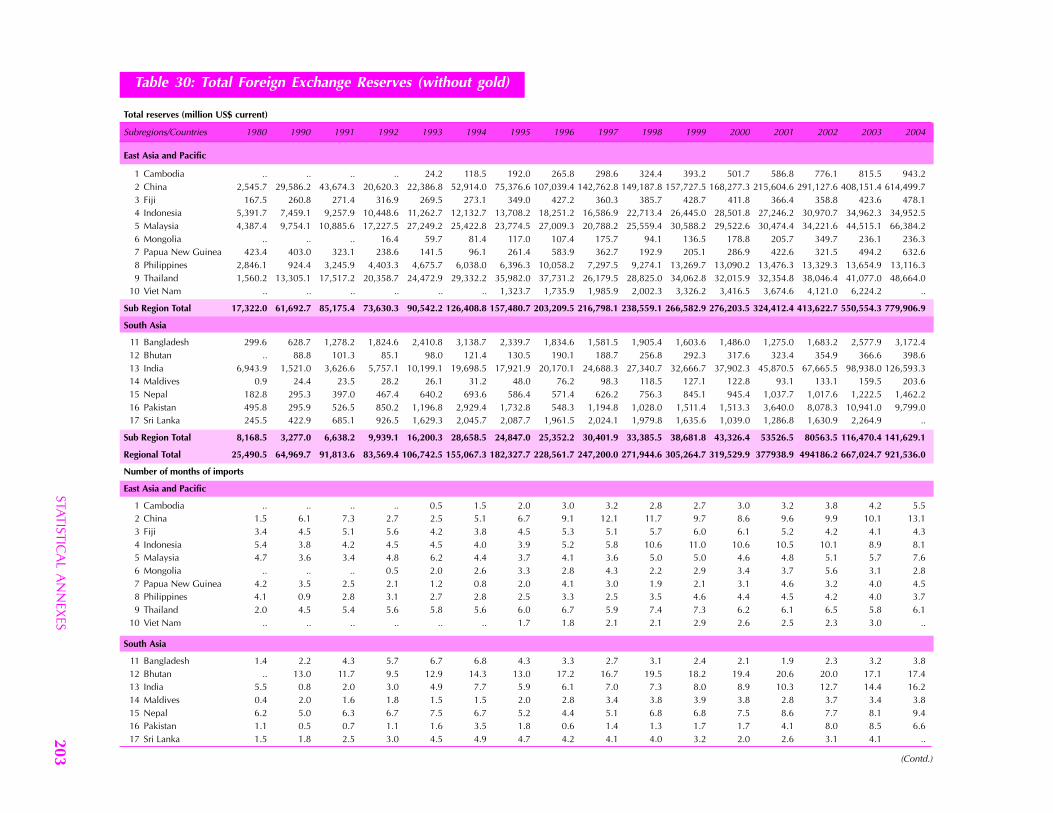

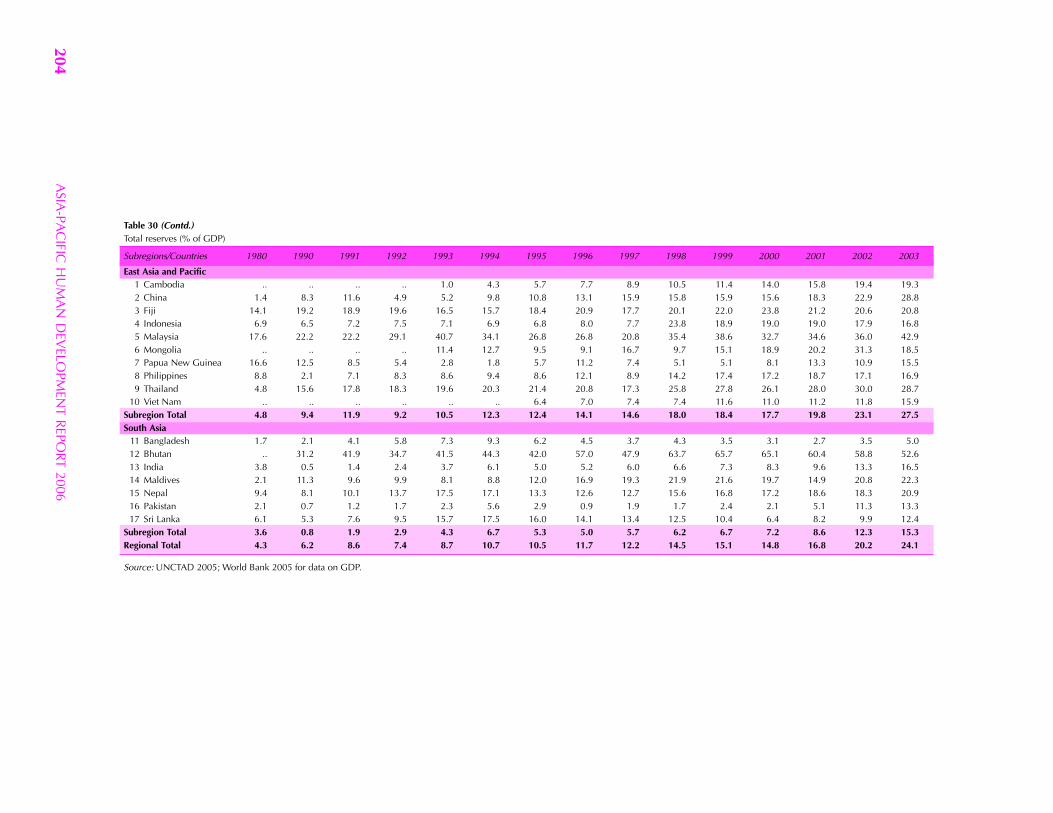

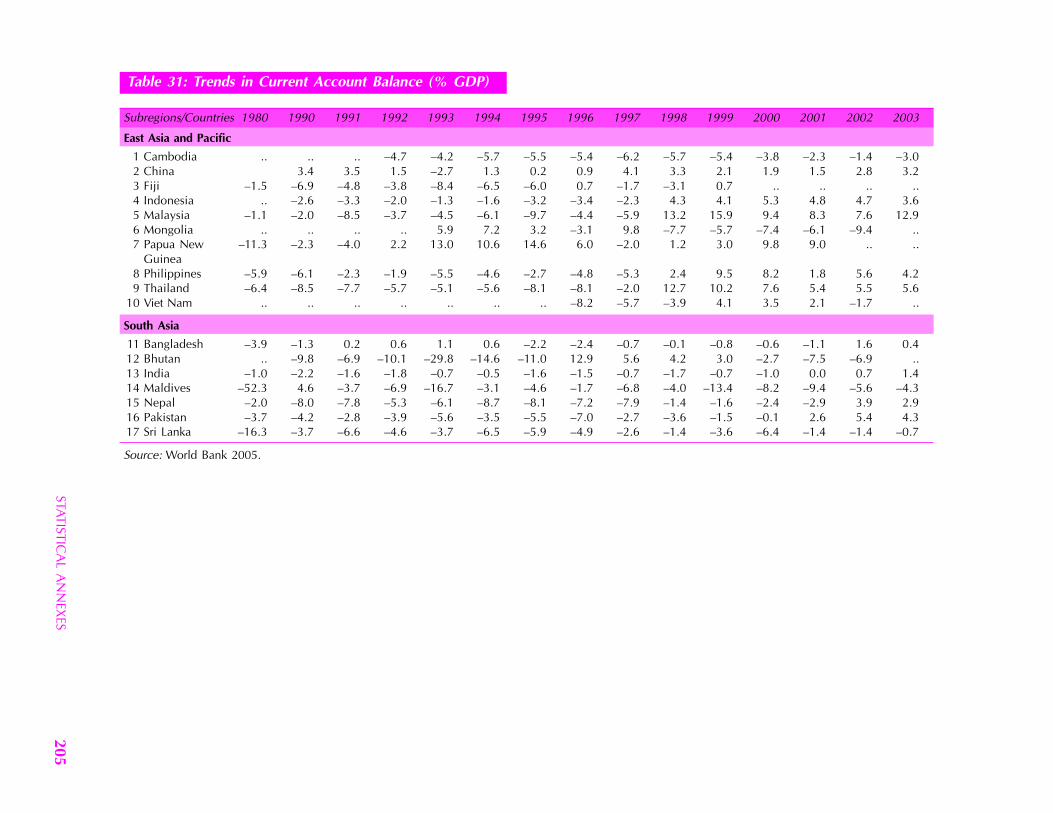

Country and Country Grouping 202Table 30. Total Foreign Exchange Reserves (without gold) 203Table 31. Trends in Current Account Balance (% GDP) 205Table 32. Trends in Capital Account Balance (% GDP) 206Table 33. Foreign Direct Investment 207Table 34. Official Development Asisstance 208Table 35. Exports by Main Regions of Origin and Destination 209Table 36. Imports by Main Regions of Origin and Destination 210Table 37. Regional and Bilateral Trading Agreements and WTO Membership 211

Definitions of Technical Terms 213

xvi

ACCEC ASEAN-China Comprehensive Economic CooperationADB Asian Development BankAFTA ASEAN Free Trade AreaAFTA-CER CEP AFTA-CER Closer Economic PartnershipAGOA African Growth and Opportunity ActAICEP ASEAN-India Comprehensive Economic PartnershipAJCEC ASEAN-Japan Comprehensive Economic CooperationAKCCP ASEAN-Korea Comprehensive Cooperation PartnershipAMS Aggregate Measure of SupportAO Appellation of OriginAPEC Asia Pacific Economic CooperationARF ASEAN Regional ForumARV Anti-retroviralASCM Agreement on Subsidies and Countervailing MeasuresASEAN Association of Southeast Asian NationsASEAN+3 ASEAN-China-Japan-KoreaATC Agreement on Textiles and ClothingATMI American Textile Manufacturers InstituteBIMSTEC-FTA Bay of Bengal Initiative for Multi-Sectoral Technical and Economic

Cooperation Free Trade AreaBIS Bank of International SettlementBPO Business process outsourcingBTA Bilateral Trade AgreementCAFTA Central American Free Trade AgreementCARP Comprehensive Agrarian Reform ProgrammeCBI Caribbean Basin InitiativeCEPT Agreement on the Common Effective Preferential TariffCER Closer Economic RelationsCET Common External TariffCITES Convention on International Trade in Endangered Species of Wild Flora

and FaunaCU Customs UnionDTIS Diagnostic Trade Integration StudyDAFEL Department of Administration of Foreign Employment Labour ForceDFID UK Department for International DepartmentEAEC East Asian Economic CouncilEAI Enterprise for ASEAN InitiativeEBA Everything But Arms Agreement

Abbreviations

xvii

ECO Economic Cooperation OrganizationEPZ Export Processing ZonesEU European UnionFAO Food and Agriculture Organization of the United NationsFAO-FISHSTAT FAO Fishery StatisticsFAS/USDA Foreign Agricultural Service/United States Department of AgricultureFDI Foreign Direct InvestmentFTA Free Trade AgreementFTAA Free Trade Area of the AmericasG-77 Group of 77GATS General Agreement on Trade in ServicesGATT General Agreement on Trade and TariffsGCI Growth Competitiveness IndexGDP Gross Domestic ProductGI Geographical IndicationsGSP Generalized System of PreferencesGSTP Agreement on Global System of Trade Preferences Among Developing

CountriesHACPP Hazard Analysis and Critical Control PointHIV/AIDS Human Immunodeficiency Virus/Acquired Immunodeficiency SyndromeHPLC High Performance Liquid ChromatographyIATP Institute for Agriculture and Trade PolicyICFTU International Confederation of Free Trade UnionsICSF International Collective in Support of FishworkersICTSD International Centre for Trade and Sustainable DevelopmentIF Integrated FrameworkIGG Inter-Governmental GroupILO International Labour OrganizationIMF International Monetary FundIOM International Organization for MigrationIP Intellectual PropertyIPA Integrated Programme of ActionIPN Integrated production networksIPR Intellectual Property RightsIS Indication of SourceISO International Standards OrganizationIT Information TechnologyITCB International Textiles and Clothing BureauLBD Learning by doingLDC Least Developed CountriesLICs Low Income CountriesMBA Master in Business AdministrationMDG Millennium Development GoalsMEA Multilateral Environmental Agreements

xviii

MFA Multifibre ArrangementMNC Multinational corporationsMOU Memorandum of UnderstandingMRA Mutual Recognition AgreementsNAFTA North American Free Trade AgreementNAMA Non-agricultural market accessNASSCOM National Association of Software and Service CompaniesNET Natural Economic TerritoriesNFIDC Net food importing developing countriesNGO Non-governmental organisationsNIC Newly Industrialised CountriesNIE Newly Industrializing EconomiesODC Other duties and chargesOECD Organisation for Economic Co-operation and DevelopmentOPEC Organization of the Petroleum Exporting CountriesPACER Pacific Agreement on Closer Economic PartnershipPIC Pacific Island CountriesPICTA Pacific Island Countries Trade AgreementPPB Parts per billionPPM Parts per millionPPT Parts per trillionPTA Preferential Trade AgreementPVP Plant Variety ProtectionQR Quantitative restrictionsR&D Research and DevelopmentRCD Regional Cooperation for DevelopmentREER Real Effective Exchange RateROO Rules of originRTA Regional Trade AgreementSAARC South Asian Association for Regional CooperationSAC South Asian CountriesSAFTA South Asian Free Trade AgreementSAPTA South Asian Preferential Trading AgreementSARC Declaration on South Asian Regional CooperationSARS Severe Acute Respiratory SyndromeSDT Special and Differential TreatmentSIDS Small Island Developing StatesSISs Small Island StatesSTD Short-term debtT&C Textiles and ClothingTBT Technical Barriers to TradeTED Turtle Excluder DeviceTFP Total Factor ProductivityTIFA Trade and Investment Framework Agreements

xix

TNC Transnational corporationsTPSEPA Trans-Pacific Strategic Economic Partnership AgreementTRIMs Agreement on Trade Related Investment MeasuresTRIPS Trade-Related Aspects of Intellectual Property RightsTSE Total Support EstimateUN United NationsUNCTAD United Nations Conference on Trade and DevelopmentUNDP United Nations Development ProgrammeUNDP-RCC UNDP Regional Centre in ColomboUNESCAP United Nations Economic and Social Commission for Asia and the PacificUNIDO United Nations Industrial Development OrganizationUPOV Union for the Protection of New Varieties of PlantsUSITC United States International Trade CommissionUSSR Union of Soviet Socialist RepublicsUSTR United States Trade RepresentativeVAT Value Added TaxWDI World Development IndicatorsWTO World Tourism OrganizationWTO World Trade OrganizationWTTC World Travel and Tourism Council$ refers to US dollars, unless otherwise specified¤ refers to the Euro, unless otherwise specified

xx

TRADE ON HUMAN TERMS: OVERVIEW 1

The Asia-Pacific region is at the forefront ofglobalization – with some of the world’s fastestrates of growth in international trade. East Asialed the way, but now South Asia too is makingits presence more strongly felt. Myriad goods,from shirts to footwear to computers, are criss-crossing the region – often in integrated inter-national production systems – before beingdispatched across the globe. Not just merchan-dise goods but services too: from Bangalore toManila, hundreds of thousands of workers areassisting customers and clients in Europe or theUnited States or Japan as though they weresitting in an office just down the street. Whenthe services cannot travel through the electronicether, the service workers are taking to the air,travelling across the region and beyond – asdomestic workers or nurses, construction wor-kers or engineers, factory workers or accoun-tants. Asia and the Pacific is thus rapidlybecoming not just the workshop of the world,but the back office too.

The rest of the world is watching thisprocess with some amazement and not a littleconcern. In the richer countries of the West, theIndustrial Revolution of the nineteenth centurycreated huge new centres of global economicconcentration: now, in the twenty-first century,the balance of power is not so much shifting asbeing far more widely dispersed. This is raisinghuge new questions: who will produce what,where and how? Above all, what impact will thishave on people’s lives – on their incomes, their

The Asia-Pacific region has embraced free trade, but free trade will not embrace the poorunless countries pursue a bold new policy agenda harnessing economic growth topromote human development.

health, their levels of education and their futureprospects, on who they are and what they canbecome? In sum: what will all this mean forhuman development? Looking at it from theother perspective, what contribution can higherstandards of human development make toexpanding trade and economic growth?

This Report responds to these questionsfrom inside Asia and the Pacific. An extensiveprocess of consultation among policymakers,academics, civil society groups, the privatesector and other stakeholders has examined themost recent developments on trade and eco-nomic growth and tried to assess the impact onhuman development – more specifically, theeffects on the region’s poorest countries and onits poorest people.

This is no simple task. This is, after all, ahuge region, accommodating more than 60 percent of the global population. Asia-Pacificcountries are also very diverse, ranging fromthird to 140th out of 177 countries rankedworldwide on the Human Development Indexfor 2003. Since the pace of social and economicchange is so rapid and the processes so complexacross one of the most dynamic regions in theworld, it is hard to encompass all of these.

This Report, therefore, narrows the focus,for although it does consider patterns of tradeand economic growth, it is primarily pre-occupied with the effects these are having onhuman development in the developing countriesof the region. But it goes further – emphasizing

Trade on Human TermsOverview

Asia and thePacific is rapidly

becoming notjust the

workshop of theworld, but the

back office too

ASIA-PACIFIC HUMAN DEVELOPMENT REPORT 20062

that neither trade nor growth can ever be ends inthemselves; instead, they are simply meanstowards the larger goals of expanded humandevelopment and combating poverty anddeprivation.

Trade can certainly enhance human deve-lopment – but it can also hinder it. Trade is, afterall, a profit-driven activity, and there are manyexamples from history that demonstrate whatcan happen when commercial gain takesprecedence over human well-being: slavery,colonialism and apartheid are some extremeforms. Today also, the drive to export andimport more goods and services typically triggersa series of complex and dynamic processes thatproduce both winners and losers. For just astrade liberalization can increase the opportu-nities for exports, it also exposes local producersto foreign competition that, particularly inpoorer countries, they may be unable to with-stand. So as well as creating new opportunities,especially in the modern sector, it can alsodestroy the livelihoods of people working insimple manufacturing processes or in agri-culture.

Faced with this potential damage, economicnationalists may argue for something close toautarchy – erecting higher trade barriers andaiming for national self-reliance; why depend onimports when you can make something verysimilar yourself? This has an emotional appealbut soon runs into practical limits. People in thetwenty-first century have social and economicrights that can only be met through interna-tional trade: some exports will always be neededto generate the foreign exchange for essentialimports, from pharmaceuticals, to food, to oil.

At the other extreme are the proponents offree trade who would opt for no barriers at all –letting the market dictate the most economicallysuitable production locations. This may seemmore seductive and plausible, but this too isfallacious, for it involves trade between unequalpartners, allowing the richest and most powerful

countries and companies to set the terms andleaving the poorer and weaker participants toaccept what they are offered, while riskingfurther inequalities both between countries andwithin countries.

An Active State

It might be thought that the best solution wouldbe a simple division of responsibilities: let freeand liberal markets take care of economicgrowth while requiring governments to addressmarket failure and take responsibility for theimplications of rising inequality – for socialconcerns and for human development prio-rities.

However, this division ignores the fact thattrade, economic growth and human develop-ment have a symbiotic relationship. Each needsthe other. One direct link is through tariffrevenue. Removing or reducing tariffs can havea damaging impact on human development sincemany countries rely on customs and other dutiesfor a high proportion of government income – insome Pacific Island countries, up to 70 per cent.Trade liberalization may thus demand dramaticcuts in public services as revenues fall.

A second link concerns sequencing. Coun-tries may need to achieve certain levels of humandevelopment to prepare the ground for liberali-zation. Boosting international trade requires notonly capital and technology but also a capablelabour force. For this the state needs to takeresponsibility – ensuring that the basic capacitiesare in place to enable the private sector to takefull advantage of liberalization.

Trade has thus never been a matter forprivate industry alone; it has always been subjectto active intervention from the state. Govern-ments usually recognize the value of the privatesector as the main engine for economic growth,but they also know that it needs to be harnessedor guided to some extent if it is truly to servehuman development.

There are manyexamples fromhistory thatdemonstratewhat canhappen whencommercial gaintakesprecedence overhuman well-being. Trade hasnever been amatter forprivate industryalone; it hasalways beensubject to activeinterventionfrom the state

TRADE ON HUMAN TERMS: OVERVIEW 3

An Era of Rapid Growth andTrade Liberalization

Keeping track of trade and economic develop-ment is a challenging task. These are often fast-moving processes, and Asia-Pacific has been theworld’s most rapidly-growing region. During theperiod 1990–2003, GDP grew annually onaverage by more than 7 per cent. Governmentscan take some credit for this since much of thisrapid economic growth has taken place during aperiod of steady trade liberalization. In East Asiaand the Pacific, liberalization started in the1970s, and by 2000 average tariffs had fallen to8 per cent. South Asia was slower to startliberalizing, but did so rapidly during the 1990sso that by 2000 average tariffs had fallen to 18per cent.

The lowering of tariffs has contributed to arapid growth in trade. During the earlier periods,export growth was faster in East Asia and thePacific than in South Asia, but in the 1990s itwas dispersed more across the region. Thus,between 1990 and 2003, while East Asia and thePacific continued to power ahead – and trade asa percentage of GDP increased from 45 to 81per cent – the proportion in South Asia alsoincreased: from 20 to 34 per cent. As a result, allAsian economies have become more open.

Accompanying the increases in volume oftrade have been dramatic transformations in thestructure of trade. Some countries have movedon from merchandise exports and are also sellingmore services. Those exporting primary pro-ducts are now turning more to manufacturedgoods; and within manufacturing many enter-prises are now climbing the technological laddertowards more sophisticated products, thoughthis is a phenomenon more evident in East Asiathan in South Asia.

What effect has the rapid increase in tradehad on human development? One of the mostdisturbing outcomes is that for most developingcountries in the region a greater engagement

with international markets has been accom-panied by a rise in income inequality. On a morepositive note, however, there has neverthelessbeen a substantial decline in poverty: between1990 and 2001, the number of people living onless than $1 a day dropped by nearly a quarter ofa billion.

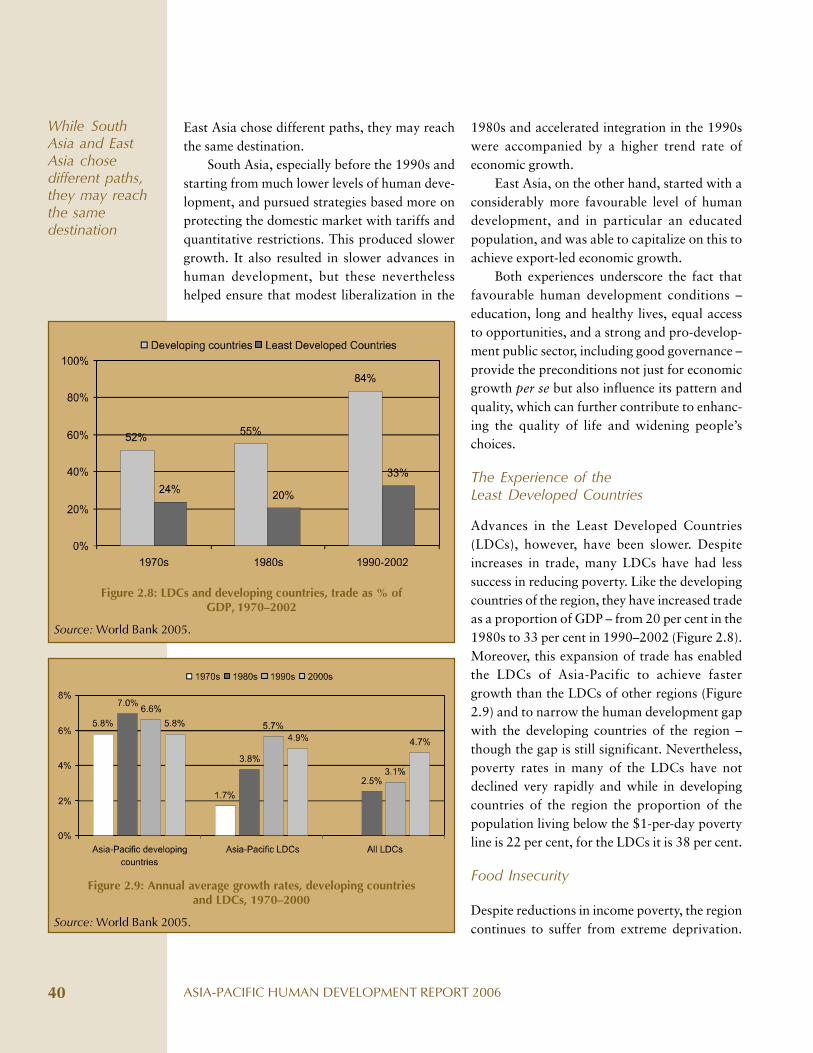

The slowest progress has been in the LeastDeveloped Countries (LDCs). Despite increasesin trade, many LDCs have had less success inreducing poverty. While in developing countriesof the region the proportion of the populationliving below the $1-per-day poverty line is 22 percent, for the LDCs it is 38 per cent.

Indeed, across the region there is still evi-dence of extreme deprivation. This is clear fromdata on food consumption. Liberalizing agricul-tural markets may have helped reduce the priceof food – particularly of crops produced with thebacking of agriculture subsidies in the US andthe EU. But this does not seem to have led to anyconsistent improvement in food security. Manymore countries now have food deficits, and Asiastill has more hungry people than any otherregion of the world – over 510 million.

On the health front, the picture is generallypositive. The period of trade-led growth has beenaccompanied by improvements in health, thoughthese seem to have slowed in recent years. Onelooming problem, however, is that the WTO-induced agreements on intellectual propertyrights could start to restrict supplies of essentialgeneric drugs.

Trade might have been expected to raiseeducation standards by giving people greaterincentives to improve their skills. But here tooprogress has been inadequate. The greatestproblems are in South Asia, where one child infive fails to enroll in primary school.

Trade has also had a strong influence ongender relations. East Asia’s export drive in the1960s and 1970s relied heavily on the mobili-zation of female workers. By being able to earnan independent income, many women thus

ASIA-PACIFIC HUMAN DEVELOPMENT REPORT 20064

obtained greater personal freedom – but only upto a certain point. Working women the worldover are all too familiar with the double burdenof housework and wage work outside the home.Within the workplace they are often second-classcitizens when it comes to the management andorganization of work, and can also find them-selves exposed to sexual harassment.

Expanding the Employment Channel

Indeed, for both men and women, the mainchannel for all these effects of trade on humandevelopment, for better or for worse, is throughemployment. Ideally, more trade should meanmore jobs and less unemployment. Unfortu-nately, in recent years this has often not been thecase.

Although Asian countries created jobs quiterapidly in the 1980s – 337 million in total – theycreated far fewer, 176 million, in the 1990s. Thishas not provided sufficient jobs for a risingpopulation: between 1993 and 2003 in South-East Asia, unemployment increased from 3.9 to6.3 per cent. Worryingly, the situation is oftenmore serious in some of the most trade-intensivecountries: China and Singapore, for example,have seen unemployment rates increase substan-tially. Most of this burden has fallen on youngpeople: in 2004, while those aged 15 to 24 madeup one-fifth of Asia-Pacific’s labour force, theyconstituted nearly half of the unemployed.Women too have lost out: in most countries theirunemployment rates are higher than men’s.

Why is the region experiencing ‘joblessgrowth’? Most of the problems are in East Asiaand especially in manufacturing, for althoughmanufacturing output increased by almost 180per cent in the 1990s, the associated employ-ment increased by only 3 per cent. This is princi-pally because manufacturing has been movingfrom low-tech, labour-intensive industries, suchas garments, to high-tech and more capital-intensive ones such as electronics – and even

within more labour-intensive manufacturing,companies have continued to invest in labour-saving equipment.

The employment situation is different inSouth Asia. Here, despite a slight deceleration inthe rate of economic growth, employment hascontinued to rise, if only modestly. This isbecause South Asia has yet to experience wide-spread structural change – continuing to rely ontraditional labour-intensive and natural-resource-based industries. This may have led toslower growth, but has at least spread the bene-fits more evenly.

The experience of the Asia-Pacific region hasthus clearly demonstrated that trade by itselfcannot address inequalities; indeed, it may wellmake them worse. Governments are increasinglyrecognizing that they must devise complemen-tary policies to ensure that increased engagementwith international markets also generates jobsand promotes human development.

Making Agricultural Trade Workfor the Poor

These jobs cannot be confined to the modernurban industrial or service sectors; they mustalso be generated in the rural areas and inagriculture. While setting their sights on inter-national trade, many governments in the regionhave been neglecting agriculture and investingfar less in rural development. In fact, tradeliberalization itself has often undermined natio-nal food production by allowing imports ofcheap food; these will benefit low-incomeconsumers, but they can also threaten the live-lihoods of poor farmers and fishing communi-ties, with serious implications for equity.

The most striking evidence of rural neglecthas been a serious deterioration in the balanceof agricultural trade. In the early 1960s, thedeveloping countries had an overall annualagricultural trade surplus of almost $7 billion,but since the beginning of the 1990s they have

The mainchannel for allthese effects oftrade on humandevelopment,for better or forworse, isthroughemployment

TRADE ON HUMAN TERMS: OVERVIEW 5

generally been net importers of agriculturalproducts, with a deficit in 2001, for example, of$11 billion.

Countries in the Asia-Pacific region havecontributed to this rising imbalance. True, inglobal markets they have never been majorplayers. Indeed, of the truly successful Asianexporters only China has earned that successeven partly through agricultural exports –though countries like Malaysia and the Republicof Korea have used surpluses from agricultureto invest in their export sectors. Even today, VietNam has agricultural exports as an importantsource of foreign exchange.

More worrying, however, is that a numberof countries are not just exporting less. They, andparticularly China, are likely to become majorimporters. As a result, global food supplies couldbecome much tighter. This raises questions offood security. Food is not like any other tradablecommodity, and most countries prefer some-thing closer to national self-sufficiency. This willmean, therefore, putting more emphasis on localproduction and giving greater protection forfarmers who find it difficult to compete at worldprices, especially when these are distorted bysubsidies in the US and the EU that have enabledthem to export below the cost of production.

Asia and the Pacific has much to gain bypromoting equitable agricultural trade gene-rally, but this is particularly true in fish trade.Countries in the region account for more thanone-third of global exports of fish and fishproducts. China is now the world’s largestexporter of fish, while Japan is the world’slargest importer, but the fish trade is importantthroughout the region. Indeed, the Asia-Pacificregion is home to 85 per cent of the world’sfishers and 95 per cent of its fish farmers.

In some respects, fishers are in a strongerposition than farmers because they sell a largerproportion of their output on a regular andconsistent basis. In other respects, however, theycan be more vulnerable, whether as a result of

natural factors such as variations in the fishcatch, bad weather, and exposure to cyclones, oras a result of economic factors such as pricefluctuations and variable access to markets.

Many fishing communities already have lowincomes, but their situation could get worse asstocks are exhausted. Intense competition inopen-access fisheries is leading to overfishing inseveral commercially important fisheries. TheAsian fishing sector also faces problems acces-sing markets in developed countries where thereare increasing demands for higher standards offood safety.

Developing countries face some complexchoices for policies on agricultural trade –deciding to what extent they can rely on imports.Some have chosen to invest outside agriculture,or even within agriculture, but have concen-trated on exportable commodities. This mayseem rational from the point of view of econo-mic efficiency, but it may be irrational from theperspective of human development. For whileincreasing agricultural trade might boost econo-mic growth and benefit poor consumers, it is alsolikely to depress local prices and undermine thelivelihoods of poor farmers.

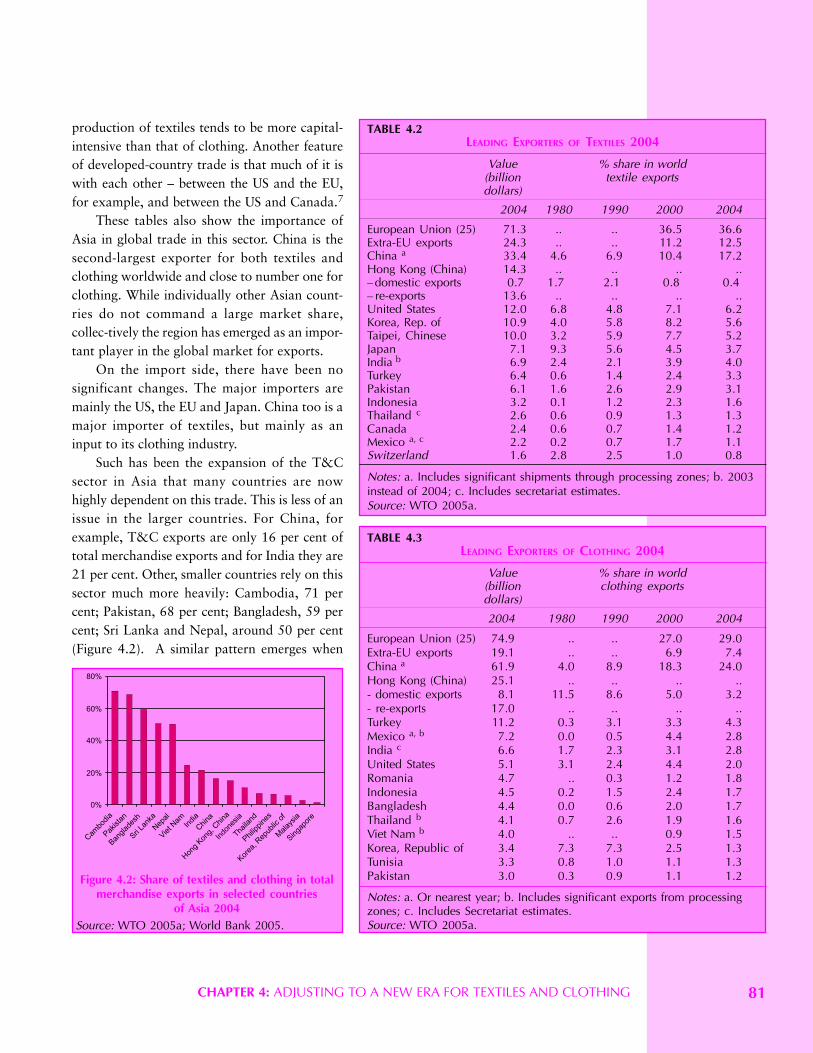

Adjusting to a New Era forTextiles and Clothing

Another area of critical importance to manypoor households is the textiles and clothingindustry, which in so many countries has servedas the launching pad for industrial development.In this case the Asia-Pacific region finds itself inthe midst of a potential upheaval now that theelaborate quota system under the MultifibreArrangement (MFA) has come to an end. TheMFA deliberately constrained imports from theregion’s larger producers, notably China andIndia, but offered quotas to many othercountries such as Bangladesh and Nepal, whichused them as the basis for new industries. Theoutcome was a highly dispersed textiles and

These jobscannot be

confined to themodern urban

industrial orservice sectors;they must also

be generated inthe rural areas

and inagriculture

ASIA-PACIFIC HUMAN DEVELOPMENT REPORT 20066

clothing industry across the region, providingemployment for hundreds of thousands ofdisadvantaged and lower-skilled workers, mostof whom were women – 90 per cent in bothBangladesh and Cambodia and 87 per cent inSri Lanka.

Since that era concluded at the end of 2004,many of these new producers are struggling toadjust to direct competition, particularly withChina. Thus far, the outcome for some countrieshas not been as bad as had been feared. Indeed,Asian producers overall have fared better thanthose in other regions and have increased theirshare of exports to the US and the EU. But, asexpected, the benefits were unequally shared.The main winners have been China and India;the main losers have been Nepal, Philippines,Thailand and Pakistan. Nevertheless, it isnotable that a number of countries that had alsorelied on quotas have been able to maintain oreven increase their shares – Cambodia, VietNam, Indonesia, Sri Lanka and Bangladesh.

Even now, however, it is difficult to envisagethe future shape of the textiles and clothingtrade, since the developed countries have beendefending themselves against rising imports withtemporary restrictions. What is clear, however,is that the only way to survive in a competitiveglobal market is by upgrading the industry andincreasing both the quality and quantity ofoutput. This will also mean improving workingconditions, not least because exporters arecoming under pressure from fair-trade organiza-tions to guarantee that their goods are notproduced under exploitative conditions. Higherlevels of trade in textiles and clothing can pro-mote human development, but only if govern-ments and employers take the necessary action.

Selling Services Across Borders

Asian countries continue to rely on the interna-tional trade in goods. But over the last threedecades they have been taking advantage of the

opportunities to boost the trade in services, andinternational trade has consequently becomemuch more complex. Three forms of cross-border services are discussed: either the sellermoves, as in international labour migration; orthe work moves, as with business outsourcing;or the buyer moves, as with internationaltourism.

All three types of movement have increasedsignificantly. For migration, millions of lower-skilled workers continue to travel abroad onshort-term contracts: an estimated 10 per centof the Philippines labour force and 12 per centof the Sri Lankan labour force now workoverseas. Many labour migrants have improvedtheir standard of life, and even some of thepoorest have earned enough to lift their familiesout of poverty. But they can also work underexploitative conditions and have their home livesseverely disrupted. Both source and destinationcountries can make migration a more productiveand fulfilling experience: source countries canensure that migrants are well-informed, financedand trained before they travel, and destinationcountries can make migration processes simplerand more trans-parent.

Asia has also been a pioneer in the off-shoring of IT and business process services: insome cases IT workers continue to travel over-seas on short-term assignments in developedcountries, but advances in information andcommunications technology, and falling inter-net connectivity costs, have allowed more andmore of these services to be delivered remotely –providing jobs for highly educated young peopleas well as drawing into the workforce othergroups such as retirees. However, this too hashuman costs: for example, long night shifts canlead to adverse health effects and preclude anormal social life, isolating workers from theircommunities. Moreover, the rapid growth of theoutsourcing industry is also widening regionaldisparities. Governments will also be concernedthat they are not producing enough skilled

The only way tosurvive in acompetitiveglobal market isby upgradingindustry andincreasing boththe quality andquantity ofoutput

TRADE ON HUMAN TERMS: OVERVIEW 7

people to keep expanding the industry. They do,however, have a range of policy options that canensure outsourcing makes a stronger contribu-tion to human development, including buildinginfrastructure, training the workforces andensuring the best regulatory and fiscal envi-ronment.

In tourism too, the Asia-Pacific region is oneof the global leaders – increasing its share ofglobal traffic from less than 10 per cent in the1950s to 40 per cent in 2004. Tourism can offernew sources of employment even to the remotestregions. But here too there are potential costs,for example, of cultural dislocation, and of envi-ronmental destruction. Many of the problemscan be resolved or minimized with proper plan-ning and management – for example, buildingthe appropriate infrastructure, providingtraining to people working in smaller enter-prises, and ensuring better economic linksbetween larger tourist operators and poor com-munities.

Trade Opportunities for theLeast Developed Countries

All of these trade issues have a particularresonance in the Least Developed Countries(LDCs). For many LDCs, trade represents asignificant proportion of economic activity. Infact, their trade-to-GDP ratios are often higherthan those in many developing countries, or evendeveloped ones. They also tend to have veryopen trade regimes, with low tariff or non-tariffbarriers.

Unfortunately, integrating with interna-tional trade does not seem to have produced acommensurate reduction in poverty. When itcomes to integrating into international trade, theLDCs are in a very vulnerable position –typically they have small economies, difficulttopographies, and are located far frominternational markets in which they are minorand weak players.

In these circumstances, why would LDCswant to gain access to the World Trade Organi-zation and the further liberalization that thisimplies? Because the likely alternative is worse –marginalization or bilateral control by one ortwo major powers. With all its limitations, themultilateral WTO is still a better option if itoffers some basic and consistent ground rules.

However, later entrents have found theprocess of accession to the WTO very arduous.They lack the trained people needed tounderstand the implications of trade agreements.And because the rules for accession to the WTOare vague, the incumbent members have beenable to exploit acceding members by imposingonerous conditions – generally narrowing theirfreedom of action on issues not just of tariffs butalso intellectual property rights, and even onhow they should run their economies, forexample, on the pace and extent of privatization.

The LDCs of the region can engage morefruitfully with the international trading system,but this will need more determined action atboth national and international levels. This willmean, for example, giving a higher priority totrade issues, increasing investment and buildingstronger alliances. But above all, both the LDCsand the developed countries should ensure thattrade initiatives and negotiations are based lesson reciprocity and more on a human develop-ment perspective, taking advantage of opportu-nities for ‘aid for trade’.

An Eight-Point Agenda

How should the countries of Asia and the Pacificrespond in a demanding new environment forinternational trade? Clearly, there can be nostandard blueprint, especially for such a hugeand diverse region. Nevertheless, there is a wayof encompassing this diversity by viewing tradeissues through a human development lens. Theanalysis in this Report suggests eight prioritiesthat have a degree of general application:

Asia has alsobeen a pioneer

in the offshoringof IT and

business processservices

ASIA-PACIFIC HUMAN DEVELOPMENT REPORT 20068

1. Invest for Competitiveness

In a globalizing world, public investment needsto take into account both national and inter-national considerations. Generally the type ofinvestment will remain much the same, but itmay need adjusting with an eye to internationalcompetitiveness. Thus, when looking at basicinfrastructure, governments will need to ensurethat they have the roads, railways, ports andtelecommunications systems that align withnational needs and also with the requirement ofgetting goods and services quickly and cheaplyto international markets.

But just as important as the physical infra-structure is human capital. The most successfultrading countries have invested heavily in thebasics of human development – generating ahealthy and well-educated workforce that hasthe stamina, the skill and the flexibility to copewith a changing trading environment. Educa-tion has to start with strong and universal pri-mary schooling, but nowadays all countries needto make sure they have sufficient people withtechnical and managerial skills. People withgood primary or secondary education can onlymake use of their potential for internationaltrade if they have the support of others withhigher levels of education, for example, in engi-neering, telecommunications, or accountancy.

At the same time, many countries will needto invest more in research and development thatraises productivity and specifically addresses theneeds of poor people – continually assessing themost appropriate technologies that can capita-lize on national strengths. Some of this can becarried out through public-private partnerships,though most of the research into opportunitiesspecifically for the poor is likely to take place inthe public sector.

2. Adopt Strategic Trade Policies

In a world of giant global players and fiercecompetition, no developing country now has the

luxury of entering global markets and hoping forthe best. Instead, states have to identify a fewsectors and industries that have both short- andlong-term potential in international markets andguide enterprises towards them. The chosenindustries will vary from country to country butshould be those with the greatest potentiallinkages with other industries so that they canalso train more people in essential skills and thusoffer important spillover benefits for the rest ofthe economy.

Picking ‘winners’ is not, of course, a simpletask. The aim should be to achieve a transparentpolicy compact between government and theprivate sector that uses a carrot-and-stickapproach. The carrot will include the opportu-nity to operate behind tariff walls until com-panies are strong enough to compete interna-tionally. The stick is that such industries will beclosely scrutinized to ensure that they are livingup to their side of the bargain and are deve-loping steadily more competitive products andservices for export. Enterprises should also besubject to a domestic competition policydesigned to prevent them from abusing amonopoly position.

The essential requirement for engagement ininternational trade, however, is that the processshould be strategically planned and carefullysequenced. Thus, higher tariffs should be rigidlytime-bound: in order to avoid creating cosymonopolies that never mature into vigorousexport enterprises, tariffs should automaticallybe scaled down after a predetermined period.

3. Restore a Focus on Agriculture

A trade strategy based on human developmenthas to have agriculture at its core. This is notbecause agriculture offers export opportunities,but because in many countries farming is still theprimary source of income for the poor; so notrade strategy that undermines rural livelihoodscan claim to be promoting human development.For food-importing countries in particular, it will

The mostsuccessfultrading countrieshave investedheavily in thebasics of humandevelopment

TRADE ON HUMAN TERMS: OVERVIEW 9

often, make sense to maintain tariffs on foodimports so as to protect poor producers. If thisresults in higher prices that cause hardship forthe poorest consumers, governments will needto prepare appropriate social safety nets. Thisalso has the strategic advantage of preservingnational food security in a world that in just afew years could be moving towards higher foodprices. As well as protection, farmers also needprogress. In many countries investment in ruraldevelopment has been on a steep downwardcurve. This has to be reversed – particularlythrough investment: for example, in irrigation,in village electrification and in farm-to-marketroads.

4. Combat Jobless Growth

Most countries that embark on industrializationtypically do so with labour-intensive productionin industries like garments, textiles and foot-wear that take advantage of ample supplies oflow-cost labour. But as industrialization pro-ceeds, they tend to move higher up the valuechain and also become more capital-intensive.As a result, the most successful trading coun-tries, primarily in East Asia, are now creatingjobs far more slowly – the phenomenon of‘jobless growth’.

To some extent this process is understand-able. Less comprehensible, however, is whygovernments should exacerbate this trend bymaintaining low interest rates – effectively giv-ing capital preference over labour. This mayseem like the best strategy for rapid growth butit is storing up problems for the future. By allmeans allow enterprises to choose the lowest-cost option for production, but this choiceshould not be biased away from labour: interestrates should, therefore, reflect the real price ofcapital, not the rate that industrialists wouldprefer. In a similar vein, states should phase outfiscal incentives to enterprises since these raisethe return on capital and again encouragecapital-intensive investments.

Another reason why enterprises may bereluctant to take on new workers is that labourcontracts can be too rigid. This creates a persis-tent duality – a small and protected group of‘insiders’ with secure employment influenced bynational regulations, and a large casual, andoften exploited, workforce employed on piecerates. Instead, more workers should steadily beabsorbed into formal employment but oncontracts sufficiently flexible that they canreadily be deployed to other sectors or compa-nies as trading conditions change. Governmentscan assist in this process by providing somesupport for workers through health insuranceand social security and by active labour marketpolicies to encourage retraining and redeploy-ment.

5. Prepare a New Tax Regime

Liberalization is a common prescription foreconomic success, but it has a debilitating sideeffect – it means foregoing a predictable andeasy-to-collect source of government revenue.Instead governments need to have an alternativetax regime in place before embarking onliberalization.

Care will need to be taken, however, toensure that these new taxes are progressive anddo not hurt the poor. Customs duties, forexample, are often quite progressive since theyare typically highest on the luxury items that areof greater interest to the rich. Corporate taxestoo can be levied progressively, though manypeople escape the net since the lawyers of thelargest corporations are skilled at techniques oftax planning, while most enterprises in theinformal sector simply evade tax collectors alto-gether. Much the same is true for income tax,which tends to be paid more by middle-incomeworkers in government or the formal sector.

Garnering more income from corporate orincome tax will mean overhauling the tax codesto close loopholes and also considering otheroptions such as ‘withholding taxes’. In addition,

States have toidentify a few

sectors andindustries that

have both short-and long-term

potential ininternationalmarkets and

guideenterprises

toward them

ASIA-PACIFIC HUMAN DEVELOPMENT REPORT 200610

governments can consider taxes on real estate oron capital gains. And the more advanced canadopt value added tax (VAT) – though thisassumes a thoroughly documented economy andneeds to be developed with care; in any case, itshould exempt food and other necessities of thepoor.

The key point is that these new sources ofrevenue should be up and running prior toliberalization or countries face the risk of severecuts in public services that will harm humandevelopment.

6. Maintain Stable andRealistic Exchange Rates

One thing that hampers international trade anddiscourages investment is a volatile exchangerate that makes it difficult for states or enterpri-ses to plan ahead. But it is important too thatthe rate is realistic: too high and it will jeopardizeemployment prospects for the poor by penalizingexporters as well as farmers and other localproducers who will face increased competitionfrom imports; too low and it will raise thedomestic price level and affect the cost of livingof the poor.

Exchange rates are likely to fluctuate,especially in small and open economies that arepowerless against the rise or fall in internationalcommodity prices. With floating exchange rates,these economies are also susceptible to the‘Dutch disease’ in which inflows of capitalwithout sufficient investment opportunities toabsorb them can appreciate the exchange rate tounrealistic levels. This may happen as a result ofrising commodity prices as, for example, withthe oil price for Timor-Leste. But it can also bethe result of inflows of aid, say, or of the arrivalof funds for disaster relief as with the tsunami.

Most of the successful Asian trading coun-tries have benefited from long periods of relativeexchange-rate stability based on active currencymanagement. For this purpose, during the initialprocess of liberalization, rather than having

freely floating exchange rates, countries that arebecoming more involved with internationaltrade can consider ‘managed floats’ that permittheir currencies to depreciate gradually – sincein the early stages of liberalization importstypically rise faster than exports. The overallpriority, however, is to ensure that the exchangerate remains stable and realistic.

7. Persist with Multilateralism

The slow pace of progress in the Doha round ofmultilateral trade negotiations has discouragedmany developing countries. They can see this‘development round’ running into some familiarimpediments, especially the resistance from thedeveloped countries over agricultural subsidies.This is leading at best to pessimism and at worstto a crisis of falling expectations that could causethe developing countries to abandon multilatera-lism altogether.

Despairing of the WTO negotiations, manycountries are also seeking bilateral trade agree-ments with the developed countries. Some wouldargue that in trade terms these are better becausethey give preferential access. But in human deve-lopment terms they may impose high costs:bilateral agreements typically involve muchdeeper tariff concessions from the developingcountries and make demands on issues likeintellectual property rights that go far beyondwhat WTO members require of each other, andcan threaten the health and livelihoods of thepoor.

Many countries of the region would dobetter to resist the immediate temptations of abilateral embrace and build up slower but ulti-mately more productive multilateral relation-ships that can lead to more durable humandevelopment outcomes.

8. Cooperate with Neighbours

Another good alternative is to seek trade andother agreements with other countries in their

Better to resistthe immediatetemptations of abilateralembrace andbuild up slowerbut ultimatelymore productivemultilateralrelationships

TRADE ON HUMAN TERMS: OVERVIEW 11

region or subregion. These could include regio-nal pacts such as the South Asian Free TradeAgreement, the ASEAN Free Trade Agreement,or the Pacific Island Countries Trade Agreement.These have the advantage of being quicker tonegotiate than multilateral agreements whileposing less of a risk to human development thanbilateral ones. In addition, they dovetail wellwith the region’s many integrated cross-nationalproduction systems and lead to trade creation.

Regional trade agreements can also be com-plemented by other forms of cooperation, parti-cularly in the financial area. Many countries inthe region have accumulated vast foreign ex-change reserves – $1.9 trillion in total, half ofwhich is in China – partly to protect themselvesagainst another Asian financial crisis. Thesefunds could be put to better use if they werepooled so that countries facing sudden balanceof payments crises caused, say, by a spike in oilprices could draw on this shared Asian resource.Governments can also consider using thereserves to expand the Asian Development Fund,which could put resources to work for invest-ment in large-scale infrastructure and in humandevelopment priorities such as health and edu-cation.

Reaching a Different Frontier

With or without new multilateral agreements,globalization will continue to power ahead. Andmillions more workers in the Asia-Pacific region

will find themselves producing goods for peopleon the other side of the globe as well as buyingat lower prices goods their parents could scarcelyhave dreamed of.

The main hazard, however, is that millionsof others will fall by the wayside – abandoned inrural areas whose agricultural economies havedrifted into decline, or scratching a living on thefringes of Asia’s megacities as a permanentunderclass. Even those currently in work mayfind themselves later discarded from ever-moresophisticated production systems. This not onlydenies people their basic rights to decent workand a reasonable standard of living, it alsoheightens the risk of future unrest: globalizationdoes not just distribute products; it also dissemi-nates new ideas and information that changepeople’s expectations.

The countries of the Asia-Pacific region arerenowned for the speed at which they havedeveloped economically. Now they find them-selves at a different frontier – trying to combineaccelerated trade-driven economic growth withequally rapid poverty reduction and, morebroadly, human development. In many ways thisis a more complex and difficult task, and just asbefore, they will need to work out their ownsolutions. Some of these are highlighted in thisReport; others will only emerge in the light ofexperience. One thing is certain – that Asia andthe Pacific will remain at the forefront of globaldevelopment and will offer fresh lessons to therest of the world.

Asia and thePacific will

remain at theforefront of

globaldevelopment

and will offerfresh lessons to

the rest of theworld

CHAPTER 1: USING INTERNATIONAL TRADE TO PROMOTE HUMAN DEVELOPMENT 15

The early years of the new millennium havewitnessed a robust expansion in world trade. In2004, global merchandise trade recorded its bestperformance since 2000, growing in volume by9 per cent and in value by 21 per cent.1

Manufacturing took the lead: although globalmanufacturing output grew by only 4 per cent,an increasing proportion of this output is tradedinternationally, and as a result the volume ofmanufactured exports rose by 10 per cent.

Nevertheless, trade in agricultural productsalso grew in value, by 15 per cent. At the sametime, there was a substantial increase in trade incommercial services, which increased in value by18 per cent. These figures build on an alreadycreditable growth performance for 2003.

An increasingly integrated world has clearlybeen expanding the opportunities for globaltrade. But what contribution can trade make todevelopment? The dominant view has been thatengagement with international markets is notjust unavoidable but also beneficial: that tradecan facilitate, promote and sustain the develop-ment process. Indeed, for individual nationstrade is seen as a prerequisite for sustainedgrowth. Governments taking that view havetherefore devised policies to promote trade, andto shape the nature and degree of nationalengagement with the international economy. Thelarger developing countries in the Asia-Pacificregion (Box 1.1) have also made the greatestimpact, but the smaller ones too have been

Deeper integration with international markets can boost economic growth and generatemillions of new jobs. But it also brings new risks – of further marginalizing the LeastDeveloped Countries and undermining the most vulnerable communities. The challengeis to build a trading regime that is not just more balanced and equitable but also activelycombats poverty and promotes human development.

exploiting new opportunities for trade inservices, through tourism, for example, themigration of workers and the outsourcing ofbusiness processes.

This Report argues, however, that tradeneed not be – indeed, should not be – an end initself. Rather, it should realize a broad range ofhuman development objectives, and especially inthe poorest and Least Developed Countries(LDCs) it should help to alleviate poverty andreduce human deprivation. Human developmentin this sense refers to expanding people’s choicesand enabling them to lead longer and healthierlives: by ensuring that they are well-nourished

Chapter

Using International Trade toPromote Human Development

BOX 1.1COUNTRY CLASSIFICATIONS USED IN THIS REPORT

This Report gathers data from a range of sources that often use differentgroupings for regions and subregions. For consistency, the followingclassification has been used in this Report. Overall, the region is referred toas Asia and the Pacific or, for stylistic purposes, the Asia-Pacific region. Themain subregions are South Asia, the Pacific, and East Asia. Whereappropriate, East Asia is subdivided into South-East Asia and North-EastAsia. The countries within these subregions are as follows.

North-East Asia. China, Democratic People’s Republic of Korea, Mongolia,Republic of Korea.

South-East Asia. Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar,Philippines, Timor-Leste, Thailand, Viet Nam.

South Asia. Afghanistan, Bangladesh, Bhutan, India, Iran, Maldives, Nepal,Pakistan, Sri Lanka.

Pacific. Cook Islands, Federated States of Micronesia, Fiji, Kiribati, MarshallIslands, Nauru, Niue, Palau, Papua New Guinea, Samoa, Solomon Islands,Tokelau, Tonga, Tuvalu, Vanuatu.

1

Trade need notbe – indeed,

should not be –an end in itself

ASIA-PACIFIC HUMAN DEVELOPMENT REPORT 200616

and have access to safe drinking water, sanita-tion facilities and shelter; by providing themequal opportunities to participate in economicactivity through education and decent work; andby affording them the freedoms to exercise thesechoices and fulfil their potential.

Trade can certainly enhance human deve-lopment, but it can also hinder it. Trade is, afterall, a profit-driven activity, and there are manyexamples from history that demonstrate whathappens when commercial gain takes precedenceover human well-being – for example, slavery,colonialism and apartheid. Today too the driveto export and import more goods and servicestypically triggers a series of complex and dyna-mic processes that produce both winners andlosers. For just as trade liberalization can incre-ase the opportunities for exports, it also exposes

local producers to foreign competition that, par-ticularly in poorer countries, they may be unableto withstand. So as well as creating new oppor-tunities, particularly in the modern sector, it canalso destroy the livelihoods of people working inbasic manufacturing or in agriculture.

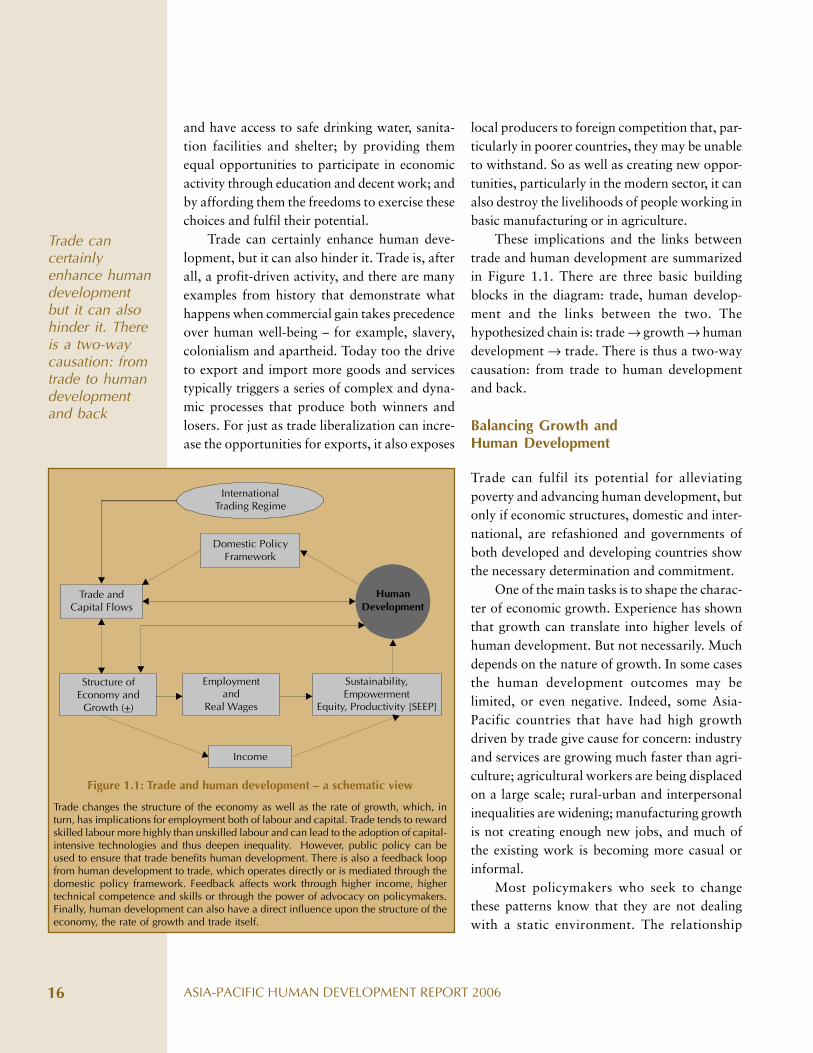

These implications and the links betweentrade and human development are summarizedin Figure 1.1. There are three basic buildingblocks in the diagram: trade, human develop-ment and the links between the two. Thehypothesized chain is: trade → growth → humandevelopment → trade. There is thus a two-waycausation: from trade to human developmentand back.

Balancing Growth andHuman Development

Trade can fulfil its potential for alleviatingpoverty and advancing human development, butonly if economic structures, domestic and inter-national, are refashioned and governments ofboth developed and developing countries showthe necessary determination and commitment.

One of the main tasks is to shape the charac-ter of economic growth. Experience has shownthat growth can translate into higher levels ofhuman development. But not necessarily. Muchdepends on the nature of growth. In some casesthe human development outcomes may belimited, or even negative. Indeed, some Asia-Pacific countries that have had high growthdriven by trade give cause for concern: industryand services are growing much faster than agri-culture; agricultural workers are being displacedon a large scale; rural-urban and interpersonalinequalities are widening; manufacturing growthis not creating enough new jobs, and much ofthe existing work is becoming more casual orinformal.

Most policymakers who seek to changethese patterns know that they are not dealingwith a static environment. The relationship

Figure 1.1: Trade and human development – a schematic view

Trade changes the structure of the economy as well as the rate of growth, which, inturn, has implications for employment both of labour and capital. Trade tends to rewardskilled labour more highly than unskilled labour and can lead to the adoption of capital-intensive technologies and thus deepen inequality. However, public policy can beused to ensure that trade benefits human development. There is also a feedback loopfrom human development to trade, which operates directly or is mediated through thedomestic policy framework. Feedback affects work through higher income, highertechnical competence and skills or through the power of advocacy on policymakers.Finally, human development can also have a direct influence upon the structure of theeconomy, the rate of growth and trade itself.

Trade cancertainlyenhance humandevelopmentbut it can alsohinder it. Thereis a two-waycausation: fromtrade to humandevelopmentand back

InternationalTrading Regime

Domestic PolicyFramework

Structure of Economy and

Growth ( )+

Income