You must read the following befo - Singapore Exchange

362

IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE UNITED STATES. Important: You must read the following before continuing. The following applies to the offering circular following this page (“ offering circular ”), and you are therefore advised to read this carefully before reading, accessing or making any other use of this offering circular. In accessing the offering circular, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “ SECURITIES ACT”), OR THE SECURITIES LAWS OF ANY STATE OF THE UNITED STATES OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES, EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THIS OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENT DECISION SHOULD BE MADE ON THE BASIS OF THE FINAL TERMS AND CONDITIONS OF THE SECURITIES AND THE INFORMATION CONTAINED IN AN OFFERING CIRCULAR THAT WILL BE DISTRIBUTED TO YOU ON OR PRIOR TO THE CLOSING DATE AND NOT ON THE BASIS OF THE ATTACHED DOCUMENTS. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED THEREIN. Confirmation of the Representation: In order to be eligible to view this offering circular or make an investment decision with respect to the securities, investors must not be located in the United States. This offering circular is being sent at your request and by accepting the electronic mail and accessing this offering circular, you shall be deemed to have represented to us that the electronic mail address that you gave us and to which this electronic mail has been delivered is not located in the United States and that you consent to delivery of such offering circular by electronic transmission. You are reminded that this offering circular has been delivered to you on the basis that you are a person into whose possession this offering circular may be lawfully delivered in accordance with the laws of jurisdiction in which you are located and you may not, nor are you authorised to, deliver this offering circular to any other person. The materials relating to any offering of securities to which this offering circular relates do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that such offering be made by a licensed broker or dealer and the underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, such offering shall be deemed to be made by the underwriters or such affiliate on behalf of the Issuer (as defined in the offering circular) in such jurisdiction. This offering circular has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently none of the Joint Lead Managers, the Trustee and the Agents (each as defined in the offering circular) or any person who controls such person or any director, officer, employee or agent of such person or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between this offering circular distributed to you in electronic format and the hard copy version available to you on request from any of the Joint Lead Managers. You are responsible for protecting against viruses and other destructive items. Your use of this e-mail is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and other items of a destructive nature.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of You must read the following befo - Singapore Exchange

IMPORTANT NOTICE

NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE UNITED STATES.

Important: You must read the following before continuing. The following applies to the offering circularfollowing this page (“offering circular”), and you are therefore advised to read this carefully before reading,accessing or making any other use of this offering circular. In accessing the offering circular, you agree tobe bound by the following terms and conditions, including any modifications to them any time you receiveany information from us as a result of such access.

NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FORSALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO.THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S.SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE SECURITIES LAWSOF ANY STATE OF THE UNITED STATES OR OTHER JURISDICTION AND THE SECURITIES MAYNOT BE OFFERED OR SOLD WITHIN THE UNITED STATES, EXCEPT PURSUANT TO ANEXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATIONREQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIESLAWS.

THIS OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHERPERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR,MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION ORREPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TOCOMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THEAPPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENT DECISION SHOULD BE MADEON THE BASIS OF THE FINAL TERMS AND CONDITIONS OF THE SECURITIES AND THEINFORMATION CONTAINED IN AN OFFERING CIRCULAR THAT WILL BE DISTRIBUTED TO YOUON OR PRIOR TO THE CLOSING DATE AND NOT ON THE BASIS OF THE ATTACHED DOCUMENTS.IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOINGRESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE ABLE TO PURCHASE ANY OFTHE SECURITIES DESCRIBED THEREIN.

Confirmation of the Representation: In order to be eligible to view this offering circular or make aninvestment decision with respect to the securities, investors must not be located in the United States. Thisoffering circular is being sent at your request and by accepting the electronic mail and accessing this offeringcircular, you shall be deemed to have represented to us that the electronic mail address that you gave us andto which this electronic mail has been delivered is not located in the United States and that you consent todelivery of such offering circular by electronic transmission.

You are reminded that this offering circular has been delivered to you on the basis that you are a person intowhose possession this offering circular may be lawfully delivered in accordance with the laws of jurisdictionin which you are located and you may not, nor are you authorised to, deliver this offering circular to anyother person.

The materials relating to any offering of securities to which this offering circular relates do not constitute,and may not be used in connection with, an offer or solicitation in any place where offers or solicitationsare not permitted by law. If a jurisdiction requires that such offering be made by a licensed broker or dealerand the underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction,such offering shall be deemed to be made by the underwriters or such affiliate on behalf of the Issuer (asdefined in the offering circular) in such jurisdiction.

This offering circular has been sent to you in an electronic form. You are reminded that documentstransmitted via this medium may be altered or changed during the process of electronic transmission andconsequently none of the Joint Lead Managers, the Trustee and the Agents (each as defined in the offeringcircular) or any person who controls such person or any director, officer, employee or agent of such personor affiliate of any such person accepts any liability or responsibility whatsoever in respect of any differencebetween this offering circular distributed to you in electronic format and the hard copy version available toyou on request from any of the Joint Lead Managers.

You are responsible for protecting against viruses and other destructive items. Your use of this e-mail is atyour own risk and it is your responsibility to take precautions to ensure that it is free from viruses and otheritems of a destructive nature.

Royal Capital B.V.(incorporated with limited liability in the Netherlands)

U.S.$350,000,000

Senior Guaranteed Perpetual Capital Securitiesunconditionally and irrevocably guaranteed by

International Container Terminal Services, Inc.(incorporated with limited liability in the Republic of the Philippines)

Issue price: 100%

U.S.$350,000,000 senior guaranteed perpetual capital securities (the “Securities”) will be issued by Royal Capital B.V. (the “Issuer”) andthe due and punctual payment of all sums payable by the Issuer in respect of the Securities will be unconditionally and irrevocablyguaranteed (the “Securities Guarantee”) by International Container Terminal Services, Inc. (the “Company” or the “Guarantor”). TheIssuer is a special purpose company which is an indirect subsidiary of the Company.

The Securities confer a right to receive distributions (each a “Distribution”) at the applicable rate described below. Subject to Condition4.5 (Optional Deferral of Distributions) of the Terms and Conditions of the Securities, Distributions are payable semi-annually in arrearon the Distribution Payment Dates of each year. “Distribution Payment Date” shall mean on 5 May and 5 November of each yearcommencing 5 May 2018. Unless previously redeemed in accordance with the terms of the Securities and subject to Condition 4.1 (Rateof Distribution) and Condition 4.4 (Increase in Rate of Distribution) of the Terms and Conditions of the Securities, Distributions fromand including 18 January 2018 shall accrue on the outstanding principal amount of the Securities at 5.875 per cent. per annum (the “Rateof Distribution”).

The Issuer or the Guarantor may, on any day which is not less than five Business Days (as defined below) prior to any DistributionPayment Date, resolve to defer payment of all or some of the Distribution which would otherwise be payable on that Distribution PaymentDate unless, during the six months ending on the day before that scheduled Distribution Payment Date, (i) a discretionary dividend,distribution, interest or other payment has been paid or declared on or in respect of any Junior Securities or (except on a pro-rata basis)Parity Securities (each, as defined below), other than a dividend, distribution or other payment in respect of an employee benefit planor similar arrangement with or for the benefit of employees, officers, directors and consultants of the Issuer and/or the Guarantor; or (ii)at the discretion of the Issuer or the Guarantor, any Junior Securities or Parity Securities have been redeemed, repurchased or otherwiseacquired by the Issuer or the Company. Any such deferred Distribution will constitute “Arrears of Distribution” and will not be due andpayable until the relevant Payment Reference Date. Distributions will accrue on each Arrears of Distribution for so long as such Arrearsof Distribution remains outstanding at the same Rate of Distribution (as defined below) as the principal amount of the Securities bearsat such time and will be added to such Arrears of Distribution (and thereafter bear Distributions accordingly) on each Distribution PaymentDate.

The Securities are perpetual securities in respect of which there is no fixed redemption date. Subject to applicable law, the Issuer mayredeem the Securities (in whole but not in part) on 5 May 2022 (the “First Call Date”) or on any subsequent Distribution Payment Dateat the Redemption Price (as defined below), on the giving of not less than 30 and not more than 60 calendar days’ irrevocable notice ofredemption to the Securityholders (as defined under “Terms and Conditions of the Securities”) in accordance with Condition 12.1 (Noticesto Securityholders) of the Terms and Conditions of the Securities and to the Trustee and the Principal Paying Agent in writing. TheSecurities may also be redeemed (in whole but not in part) at the option of the Issuer at the Redemption Price upon the occurrence ofcertain changes in the Dutch or Philippine tax law requiring the payment of Additional Amounts (as defined under “Terms and Conditionsof the Securities”). In addition, the Securities may be redeemed (in whole but not in part) at the option of the Issuer (A) upon theoccurrence of Change of Control Event (as defined under “Terms and Conditions of the Securities”) (i) at any time prior to (but excluding)the First Call Date at the Special Redemption Price (as defined under “Terms and Conditions of the Securities”) or (ii) on or at any timeafter the First Call Date at the Redemption Price, (B) upon the occurrence of a Reference Security Default Event (as defined under “Termsand Conditions of the Securities”) at any time at the Redemption Price, (C) upon the occurrence of an Accounting Event (as defined under“Terms and Conditions of the Securities”) (i) at any time prior to (but excluding) the First Call Date at the Premium Redemption Price(as defined under “Terms and Conditions of the Securities”) or (ii) on or at any time after the First Call Date at the Redemption Price,(D) upon the occurrence of a Tax Event (as defined under “Terms and Conditions of the Securities”) (i) at any time prior to (but excluding)the First Call Date at the Special Redemption Price or (ii) on or at any time after the First Call Date at the Redemption Price or (E) inthe event less than 25 per cent. of the aggregate principal amount of the Securities originally issued remain outstanding (i) at any timeprior to (but excluding) the First Call Date at the Premium Redemption Price (as defined under “Terms and Conditions of the Securities”)or (ii) on or at any time after the First Call Date at the Redemption Price, in each case on the giving of not less than 30 and not morethan 60 calendar days’ irrevocable notice of redemption to the Securityholders in accordance with Condition 12.1 (Notices toSecurityholders) of the Terms and Conditions of the Securities and to the Trustee and the Principal Paying Agent in writing.

Approval-in-principle has been received from the Singapore Exchange Securities Trading Limited (the “SGX-ST”) for the listing andquotation of the Securities on the SGX-ST. The SGX-ST assumes no responsibility for the correctness of any statements made, opinionsexpressed or reports contained herein. Admission of the Securities to the Official List of the SGX-ST is not to be taken as an indicationof the merits of the Issuer, the Company or the Securities. The Securities will be traded on the SGX-ST in a minimum board lot size ofU.S.$200,000 for as long as the Securities are listed on the SGX-ST and the rules of the SGX-ST so require.

The Securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”).The Securities are being offered in offshore transactions outside the United States in reliance on Regulation S under the Securities Actand, subject to certain exceptions, may not be offered or sold within the United States.

The Securities will be evidenced by a global certificate (the “Global Certificate”) in registered form which will be registered in the nameof a nominee of, and deposited with, a common depositary for Euroclear Bank SA/NV (“Euroclear”) and Clearstream Banking S.A.(“Clearstream, Luxembourg”).

The appointment of the Trustee and the Agents is subject to internal approvals by the entities named as such in this Offering Circular.

Investing in the Securities involves certain risks. See “Risk Factors” beginning on page 27.

Joint Lead Managers

Citigroup Credit Suisse Standard Chartered Bank

Offering Circular dated 10 January 2018.

In this Offering Circular, references to the “Company” are references to International ContainerTerminal Services, Inc. and its consolidated subsidiaries, as the context requires. References to the“Issuer” are references to Royal Capital B.V.

Each of the Issuer and the Company, having made all reasonable enquiries, confirm that: (i) thisOffering Circular contains all information with respect to the Issuer, the Company, the Securities andthe Securities Guarantee, which is material in the context of the issue and offering of the Securities;(ii) the statements contained in it relating to the Issuer and the Company are in every material respecttrue and accurate and not misleading; (iii) the opinions and intentions expressed in this OfferingCircular with regard to the Issuer and the Company are honestly held, have been reached afterconsidering all relevant circumstances and are based on reasonable assumptions; (iv) there are noother facts in relation to the Issuer, the Company, the Securities or the Securities Guarantee, theomission of which would, in the context of the issue and offering of the Securities, make any statementin this Offering Circular misleading in any material respect; and (v) all reasonable enquiries have beenmade by the Issuer and the Company to ascertain such facts and to verify the accuracy of all suchinformation and statements. In addition, each of the Issuer and the Company accepts full responsibilityfor the accuracy of the information contained in this Offering Circular.

No person has been or is authorised to give any information or to make any representation concerningthe Issuer, the Company, the Securities or the Securities Guarantee other than as contained herein and,if given or made, any such other information or representation should not be relied upon as havingbeen authorised by the Issuer, the Company, Citigroup Global Markets Limited, Credit Suisse (HongKong) Limited and Standard Chartered Bank (the “Joint Lead Managers”), Citicorp InternationalLimited as Trustee (the “Trustee”) or the Agents (as defined in the Terms and Conditions of theSecurities). Neither the delivery of this Offering Circular nor any offering, sale or delivery made inconnection with the issue of the Securities shall, under any circumstances, constitute a representationthat there has been no change or development reasonably likely to involve a change in the affairs ofthe Issuer or the Company or any of them since the date hereof or create any implication that theinformation contained herein is correct as of any date subsequent to the date hereof. This OfferingCircular does not constitute an offer of, or an invitation by or on behalf of, the Issuer, the Company,the Joint Lead Managers, the Trustee or the Agents or their respective affiliates, employees, directors,agents or advisers to subscribe for or purchase any of the Securities and may not be used for thepurpose of an offer to, or a solicitation by, anyone in any jurisdiction or in any circumstances in whichsuch offer or solicitation is not authorised or is unlawful.

In this Offering Circular, the Joint Lead Managers, the Trustee and the Agents have not separatelyverified all the information contained herein. Accordingly, no representation or warranty, express orimplied, is made or given by the Joint Lead Managers, the Trustee or the Agents or their respectiveaffiliates, employees, directors, agents or advisers as to the accuracy, completeness or sufficiency ofthe information contained in this Offering Circular, and nothing contained in this Offering Circular is,or shall be relied upon as, a promise, representation or warranty by the Joint Lead Managers, theTrustee or the Agents or their respective affiliates, employees, directors, agents or advisers, and noresponsibility or liability is accepted by the Joint Lead Managers, the Trustee or the Agents or theirrespective affiliates, employees, directors, agents or advisers as to the accuracy or completeness of theinformation contained in this Offering Circular of any other information in connection with theSecurities, their distribution or the offering of the Securities. This Offering Circular is not intendedto provide the basis of any credit or other evaluation nor should it be considered as a recommendationby any of the Issuer, the Company, the Joint Lead Managers, the Trustee, the Agents or their respectiveaffiliates, employees, directors, agents or advisers that any recipient of this Offering Circular shouldpurchase the Securities. Each potential purchaser of the Securities should determine for itself therelevance of the information contained in this Offering Circular and its purchase of the Securitiesshould be based upon such investigations with its own tax, legal and business advisers as it deemsnecessary. Investors may not reproduce or distribute this Offering Circular in whole or in part, andinvestors may not disclose any of the contents of this Offering Circular or use any information hereinfor any purpose other than considering an investment in the Securities. Investors agree to theforegoing by accepting delivery of this Offering Circular.

— 3 —

This Offering Circular has been prepared by the Issuer and the Company solely for use in connectionwith the proposed offering of the Securities described in this Offering Circular. The distribution of thisOffering Circular and the offering of the Securities in certain jurisdictions may be restricted by law.Persons into whose possession this Offering Circular comes are required by the Issuer, the Companyand the Joint Lead Managers to inform themselves about and to observe any such restrictions. TheSecurities have not been and will not be registered under the Securities Act or with any securitiesregulatory authority of any state or other jurisdiction of the United States. Subject to certainexceptions, the Securities may not be offered or sold within the United States. No action is being takento permit a public offering of the Securities or the distribution of this Offering Circular in anyjurisdiction where action would be required for such purposes. There are restrictions on the offer andsale of the Securities, and the circulation of documents relating thereto, in certain jurisdictionsincluding the United States, the United Kingdom, Japan, Singapore, the Philippines and Hong Kong,and to persons connected therewith. For a description of certain further restrictions on offers, sales andresales of the Securities and distribution of this Offering Circular, see “Subscription and Sale”.

MiFID II product governance / Professional investors and ECPs only target market — Solely forthe purposes of a manufacturer’s product approval process, the target market assessment in respect ofthe Securities has led to the conclusion that: (i) the target market for the Securities is eligiblecounterparties and professional clients only, each as defined in Directive 2014/65/EU (as amended,“MiFID II”); and (ii) all channels for distribution of the Securities to eligible counterparties andprofessional clients are appropriate. Any person subsequently offering, selling or recommending theSecurities (a “distributor”) should take into consideration the manufacturer’s target marketassessment; however, a distributor subject to MiFID II is responsible for undertaking its own targetmarket assessment in respect of the Securities (by either adopting or refining the manufacturer’s targetmarket assessment) and determining appropriate distribution channels.

PRIIPs REGULATION / PROHIBITION OF SALES TO EEA RETAIL INVESTORS — TheSecurities are not intended to be offered, sold or otherwise made available to and should not beoffered, sold or otherwise made available to any retail investor in the European Economic Area(“EEA”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retailclient as defined in point (11) of Article 4(1) of MiFID II; (ii) a customer within the meaning ofDirective 2002/92/EC, where that customer would not qualify as a professional client as defined inpoint (10) of Article 4(1) of MiFID II. Consequently no key information document required byRegulation (EU) No 1286/2014 (the “PRIIPs Regulation”) for offering or selling the Securities orotherwise making them available to retail investors in the EEA has been prepared and thereforeoffering or selling the Securities or otherwise making them available to any retail investor in the EEAmay be unlawful under the PRIIPS Regulation.

In making an investment decision, investors must rely on their own examination of the Issuer, theCompany and the terms of the offering, including the merits and risks involved. See “Risk Factors”for a discussion of certain factors to be considered in connection with an investment in the Securities.

Each person receiving this Offering Circular acknowledges that such person has not relied on the JointLead Managers, the Trustee, the Agents or any of their respective affiliates, employees, directors,agents or advisers in connection with its investigation of the accuracy of such information or itsinvestment decision.

Forward-Looking Statements

This Offering Circular contains forward-looking statements and other information that involves risks,uncertainties and assumptions. Forward-looking statements are statements that concern plans,objectives, goals, strategies, future events or performance and underlying assumptions and otherstatements that are other than statements of historical fact, including, but not limited to, those that areidentified by the use of words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”,“plans”, “predicts”, “projects” and similar expressions. Such forward-looking statements include,without limitation, statements relating to expansion plans, changes in tariffs, capacity levels, the

— 4 —

competitive environment in which the Company operates, general economic and business conditions,political, economic and social developments in the jurisdictions in which the Company operates,changes in fuel prices, changes in governmental regulations relating to the container terminal sectoror other port-related industries, liability for remedial action under environmental regulations, the costand availability of adequate insurance coverage and financing, changes in interest rates and otherfactors beyond the Company’s control. Risks and uncertainties that could affect the Company include,without limitation:

• changes in global or regional economic conditions that could affect the demand for the productsthat are shipped through the terminals the Company operates;

• instability in the social, political and economic conditions in the countries in which the Companyoperates, particularly in the Philippines;

• fluctuations in throughput volume, utilisation rates or tariffs, resulting from fluctuations inglobal shipping capacity and shipping demand, and changing economic conditions in the regionsin which the Company operates;

• the risk of accidents, natural disasters or other adverse incidents in the operation of the terminalsthe Company operates;

• the time or cost that it may take to develop or acquire new terminals and commence fulloperations thereat;

• changes in the volume of containers the Company’s terminals handle;

• increases in fuel prices;

• the need for unexpected capital expenditures;

• changes in government regulations and increases in regulatory burdens in the jurisdictions inwhich the Company operates, including those pertaining to operational, health, safety andenvironmental standards;

• risks associated with the strategic expansion into new geographic markets;

• uncertainties relating to ongoing and future bids to operate additional terminals;

• difficulties in raising additional financing to fund future capital expenditures, acquisitions andother general corporate activities;

• changes in import or export controls, duties, levies or taxes, either in international markets orin the Philippines;

• threats to the Company’s concession contracts, whether as a result of litigation, changingregulations, breaches of contract provisions, public policy concerns or any other factors;

• increased competition by other port operators;

• the emergence of alternative means of cargo transportation; and

• other risks related to the business, the industry or the regions in which the Company operates.

Should one or more of such risks and uncertainties materialise, or should any underlying assumptionsprove incorrect, actual outcomes may vary materially from those indicated in the applicableforward-looking statements. Any forward-looking statement or information contained in this OfferingCircular speaks only as of the date the statement was made.

— 5 —

All of the Company’s forward-looking statements made herein and elsewhere are qualified in theirentirety by the risk factors discussed in “Risk Factors” and “Industry Overview”. These risk factorsand statements describe circumstances that could cause actual results to differ materially from thosecontained in any forward-looking statement in this Offering Circular.

The Issuer, the Company, the Joint Lead Managers, the Trustee and the Agents and their respectiveaffiliates, employees, directors, agents and advisers assume no obligation to update any of theforward-looking statements after the date of this Offering Circular to conform those statements toactual results, subject to compliance with all applicable laws. The Issuer, the Company, the Joint LeadManagers, the Trustee and the Agents and their respective affiliates, employees, directors, agents andadvisers assume no obligation to update any information contained in this Offering Circular or topublicly release any revisions to any forward-looking statements to reflect events or circumstances,or to reflect that the Company became aware of any such events or circumstances, that occur after thedate of this Offering Circular.

Industry and Market Data

The information contained in the section “Industry Overview”, including market and industrystatistical data, was provided by Drewry Shipping Consultants Limited (“Drewry”), a consultant firmspecialising in the shipping industry. In compiling the data for this section, Drewry relied on industrysources, published materials, its own private databanks and direct contacts with the industry. All ofthese sources were used to calculate the data and market information shown in this Offering Circular.

This data is subject to change and cannot be verified with complete certainty due to limits on theavailability and reliability of data and other uncertainties inherent in any statistical survey. Drewry hasconsented to the inclusion of data produced by it in this Offering Circular but did not prepare any dataspecifically for this Offering Circular.

In addition, other market data and certain industry forecasts used throughout this Offering Circularwere obtained from internal surveys, market research, publicly available information and industrypublications. Industry publications generally state that the information they contain has been obtainedfrom sources believed to be reliable but that the accuracy and completeness of that information arenot guaranteed. Similarly, internal surveys, industry forecasts and market research, while believed tobe reliable, have not been independently verified, and none of the Issuer, the Company, the Joint LeadManagers, the Trustee, the Agents or any of their respective affiliates, employees, directors, agents oradvisers make any representation as to the accuracy or completeness of that information.

Certain Defined Terms and Conventions

In this Offering Circular, references to “U.S.$” and “U.S. dollars” are to the lawful currency of theUnited States of America; references to “Philippine pesos” or “ P=” are to the lawful currency of theRepublic of the Philippines; references to “euros” or “EUR” are to the lawful currency of theEuropean Union; references to “Brazilian real” or “R$” are to the lawful currency of Brazil;references to “Polish Zloty” are to the lawful currency of Poland; references to “Japanese yen” or“¥” are to the lawful currency of Japan; references to the “Malagasy ariary” or “MGA” are to thelawful currency of Madagascar; references to “Mexican pesos” are to the lawful currency of Mexico;references to “kuna” are to the lawful currency of Croatia; and references to “Renminbi” or “RMB”are to the lawful currency of the People’s Republic of China.

All references to dates and times are to Manila dates and times, unless otherwise specified.

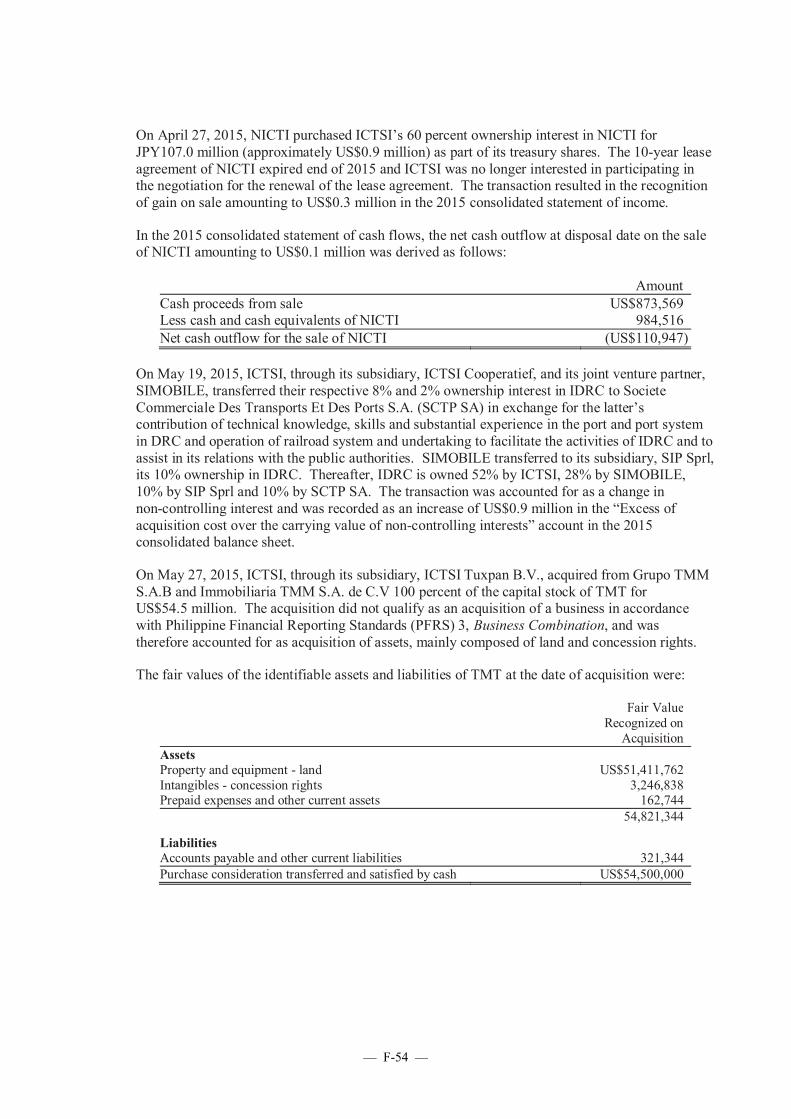

The Company’s audited consolidated financial statements as of 31 December 2014, 2015 and 2016 andfor each of the three years in the period ended 31 December 2016 and the unaudited, interimcondensed consolidated financial statements as of 30 September 2017 and for each of the nine monthsin the periods ended 30 September 2016 and 2017 included in this Offering Circular have beenprepared in accordance with the Philippine Financial Reporting Standards (“PFRS”). The Company

— 6 —

maintains its books and prepares and reports its consolidated financial statements using the U.S. dollarin accordance with the provisions of Philippine Accounting Standard 21, “The Effects of Changes inForeign Exchange Rates”, an accounting standard that became effective for annual periods beginningon or after 1 January 2005.

All references in this Offering Circular to the “Government” are to the government of the Republicof the Philippines and all references to the “Philippines” are to the Republic of the Philippines.References to “management”, “Directors” and “executive officers” refer to the management,Directors and executive officers of the Company. References to the “Articles of Incorporation” referto the Articles of Incorporation of the Company, as amended.

References to “financial year” in this Offering Circular are to the Company’s financial year ended orending 31 December.

References to the “United States” or “U.S.” in this Offering Circular shall be to the United States ofAmerica, its territories and possessions, any State of the United States and the District of Columbia.

In this Offering Circular, where information has been presented in percentages, thousands or millionsof units, amounts may have been rounded up or down. Accordingly, totals of columns or rows ofnumbers in tables may not be equal to the apparent total of the individual items and actual numbersmay differ from those contained herein due to rounding. References to information in billions of unitsare to the equivalent of thousand million units.

Presentation of Capacity Information

Information included in this Offering Circular regarding the throughput capacity of the terminals theCompany operates is based upon estimates the Company has made based upon, among other things:

• market conditions, such as the types of ships that utilise the terminal, call schedules andcontainer box exchange rates;

• the layout and availability of the physical infrastructure of the terminal, including the quaylength, the continuity of the berths, yard area and the time that containers remain on the yardafter being removed from the vessel; and

• equipment installed and available at the terminal.

Such estimates require significant subjective assessments and have not been audited or confirmed byany third party. The Company also produces estimates on a per year basis. The Company must alsomake similar subjective assessments in determining the capacity of terminals the Company bids forand acquires. While the Company believes that its methods for determination are consistent withindustry standards, there are no prescribed guidelines for estimating capacity levels and othercompanies in the container terminal industry may calculate and present capacity data in a differentmanner. Caution should be used in comparing its data with data presented by other companies or inmaking comparisons across the different terminals that it operates, as the data may not be directlycomparable.

Non-PFRS Financial Measures

The term “EBITDA” refers to earnings before interest expenses, taxes, depreciation and amortisation.EBITDA is a supplemental measure of the Company’s performance and liquidity that is not requiredby, or presented in accordance with, PFRS. Further, EBITDA is not a measurement of the Company’sfinancial performance or liquidity under PFRS and should not be considered as an alternative to netincome, gross revenues or any other performance measure derived in accordance with PFRS or as analternative to cash flow from operations or as a measure of the Company’s liquidity.

— 7 —

The Company believes that EBITDA facilitates operating performance comparisons from period to

period and from company to company by eliminating potential differences caused by variations in

capital structures (affecting interest expense), tax positions (such as the impact on periods or

companies of changes in effective tax rates or net operating losses) and the age and book depreciation

of tangible assets (affecting relative depreciation expense). In particular, EBITDA eliminates non-cash

depreciation expenses that arise from the capital-intensive nature of the Company’s business. The

Company also believes that EBITDA is a supplemental measure of its ability to meet debt service

requirements. Finally, the Company presents EBITDA because it believes it is frequently used by

securities analysts and investors in the evaluation of companies in its industry.

— 8 —

TABLE OF CONTENTS

Page

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Summary Financial Information and Throughput Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Summary of Offer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Terms and Conditions of the Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Exchange Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Capitalisation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

The Issuer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Selected Financial Information and Throughput Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

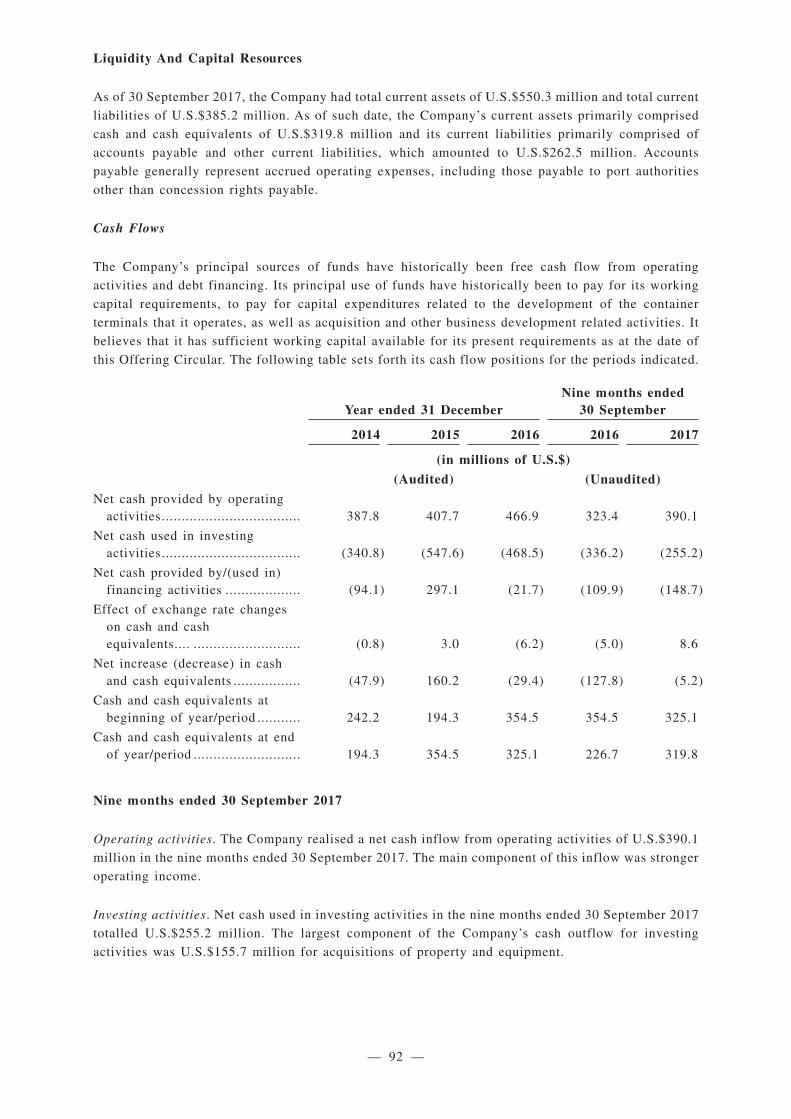

Management’s Discussion and Analysis of Financial Condition and Results of Operations . . 74

Industry Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

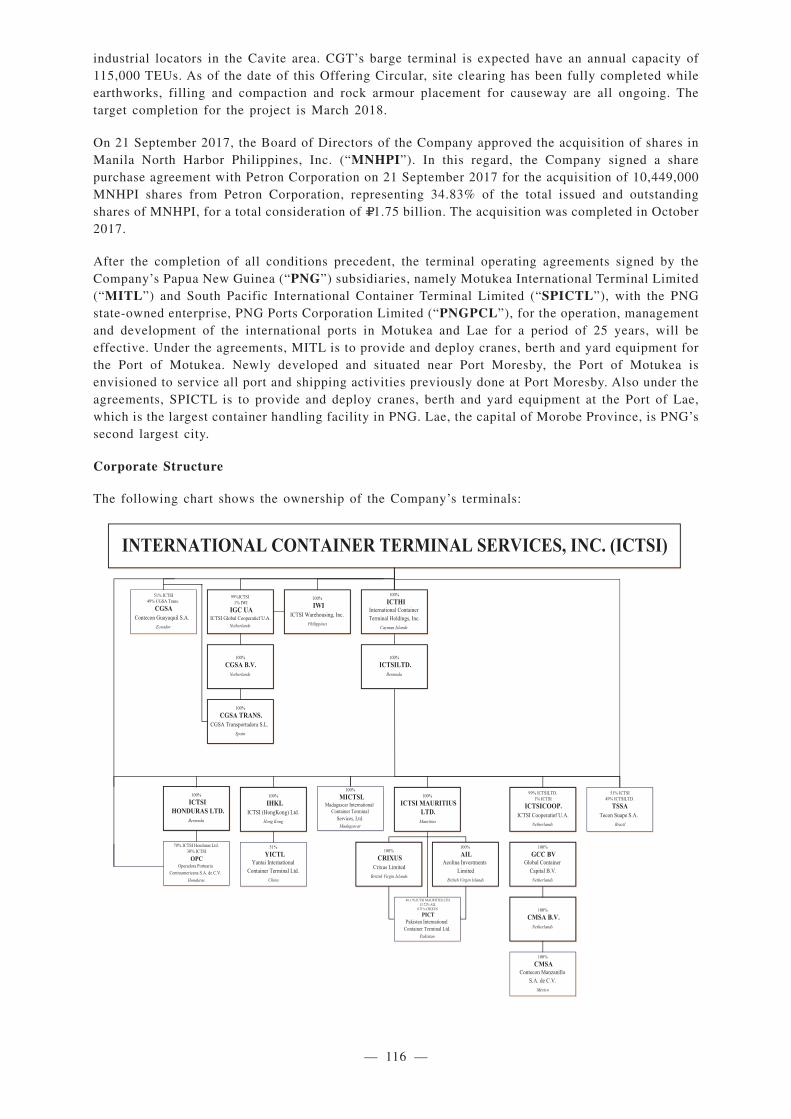

Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Description of Concession Agreements and Certain Indebtedness . . . . . . . . . . . . . . . . . . . . . 153

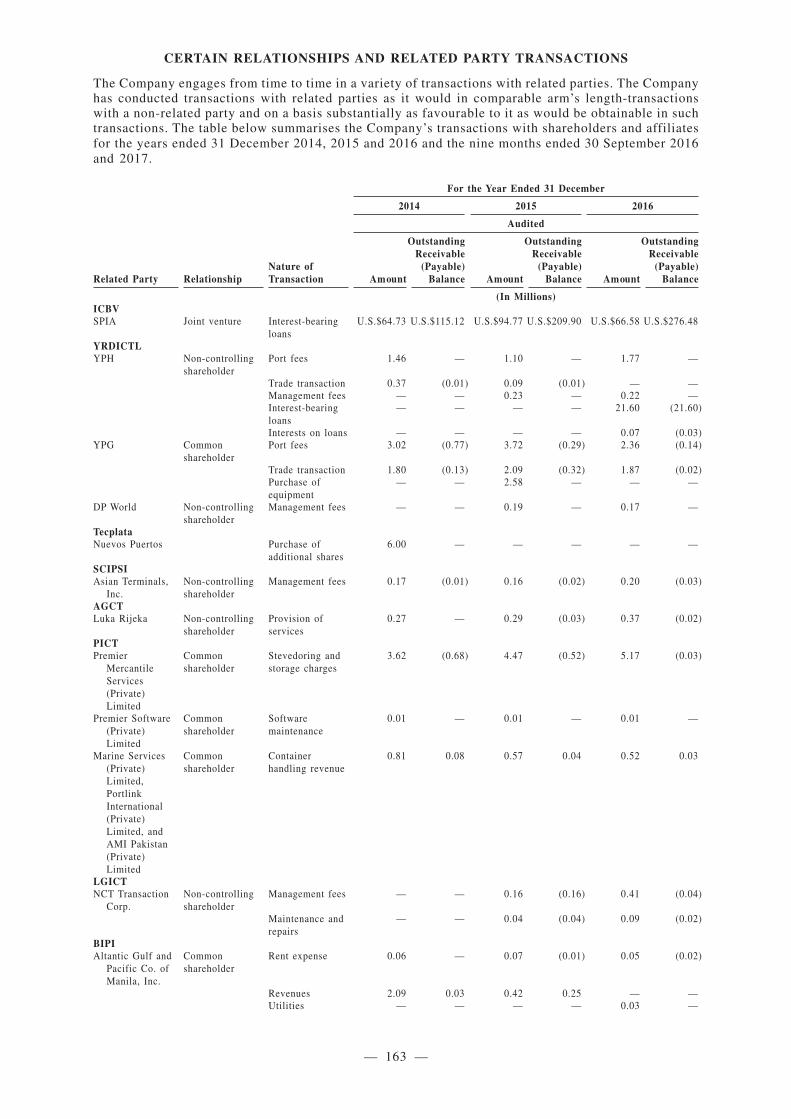

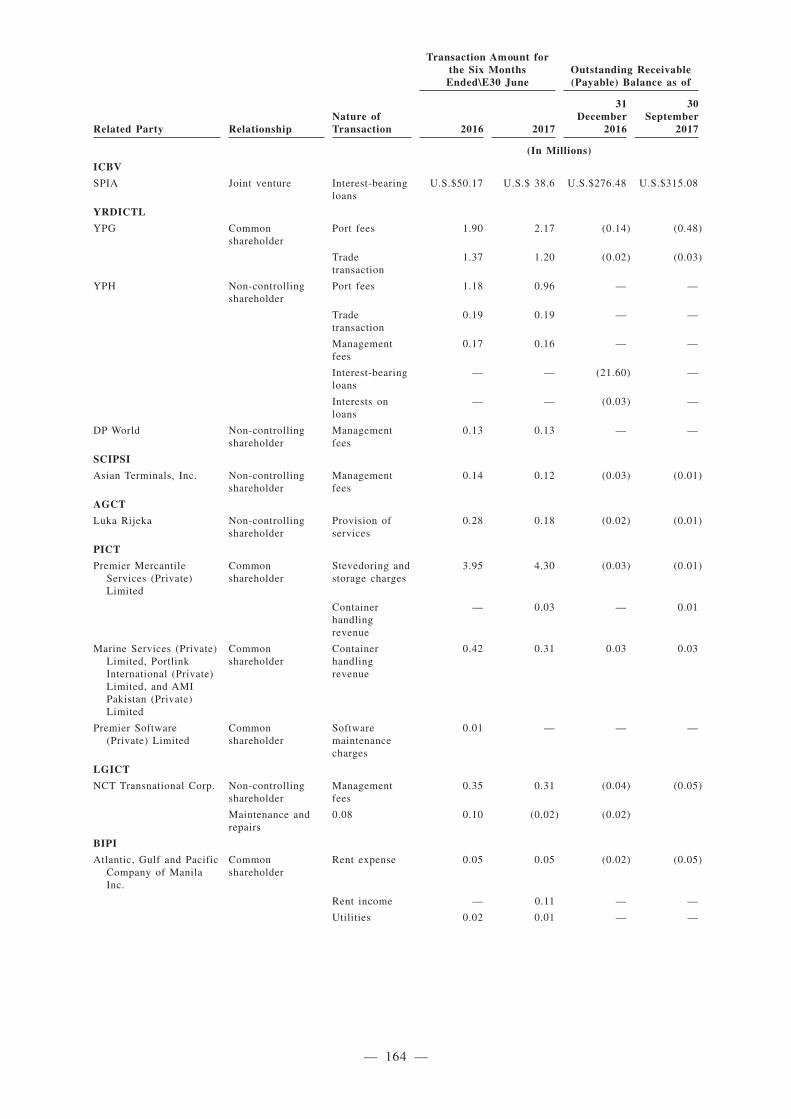

Certain Relationships and Related Party Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

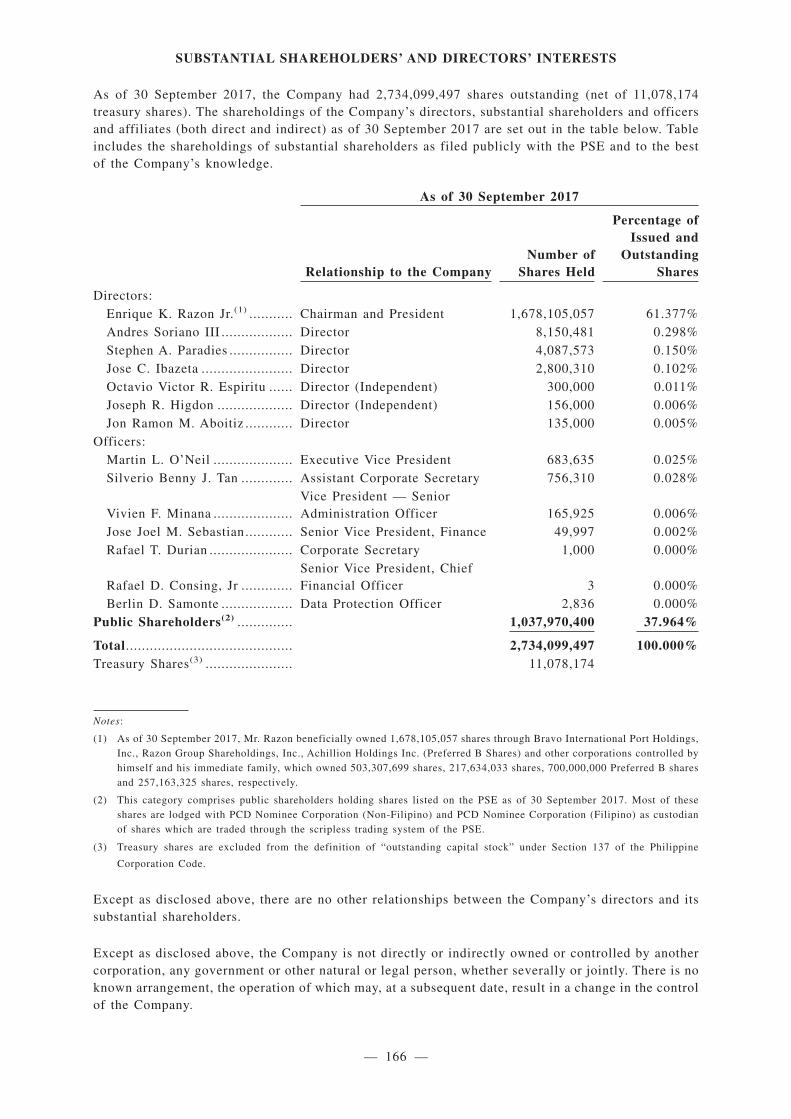

Substantial Shareholders’ and Directors’ Interests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166

Foreign Exchange and Foreign Investment Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

Clearance and Settlement of the Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173

Subscription and Sale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

General Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181

Index to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

— 9 —

SUMMARY

The following summary is qualified in its entirety, and is subject to, the more detailed information andthe financial information contained or referred to elsewhere in this Offering Circular. The meaningsof terms not defined in this summary can be found elsewhere in this Offering Circular.

Overview

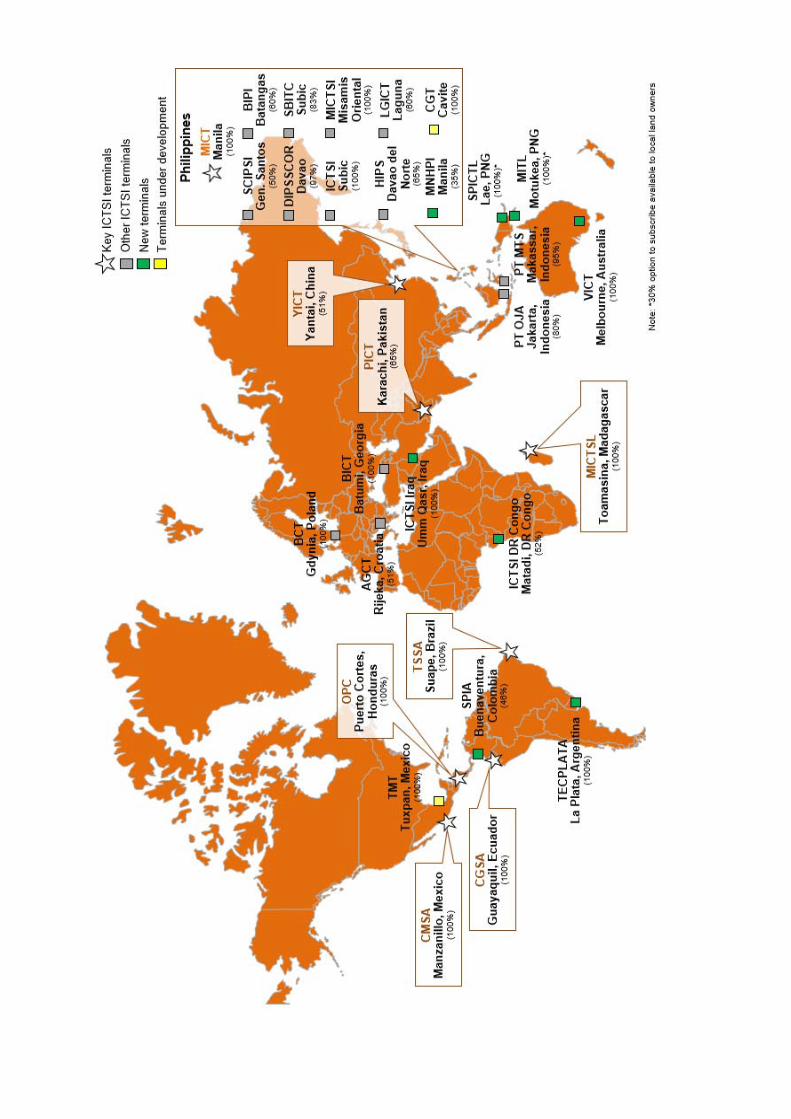

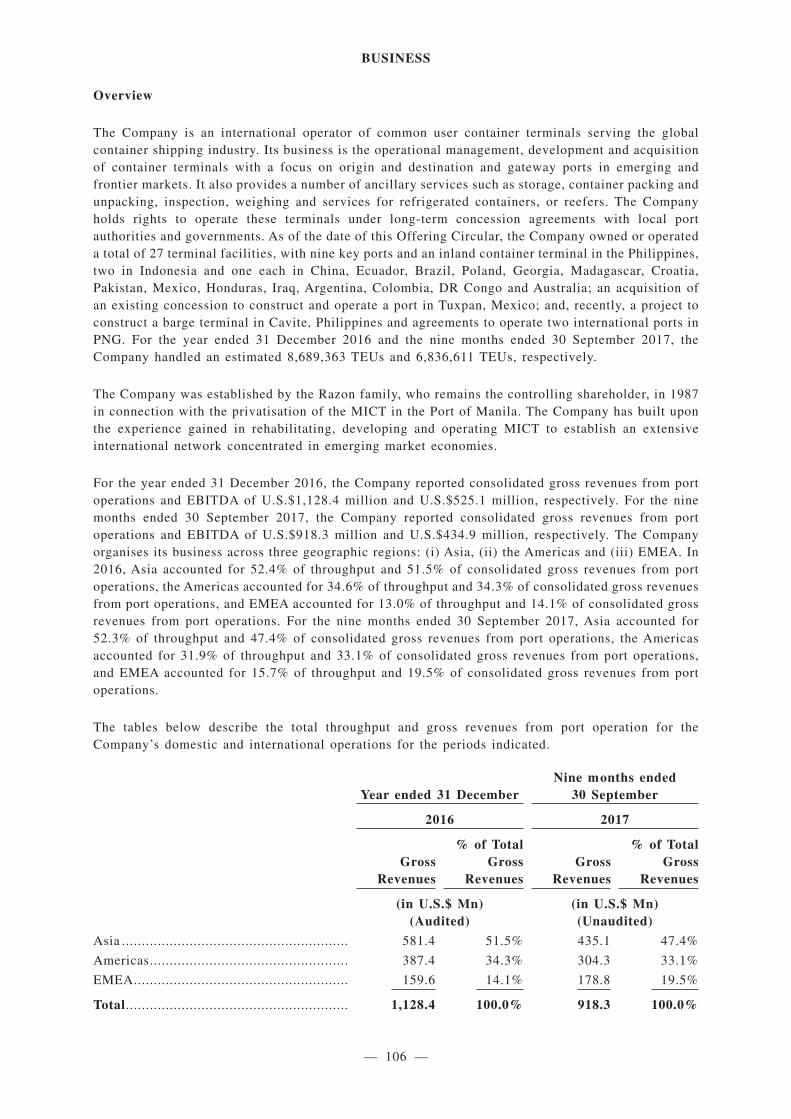

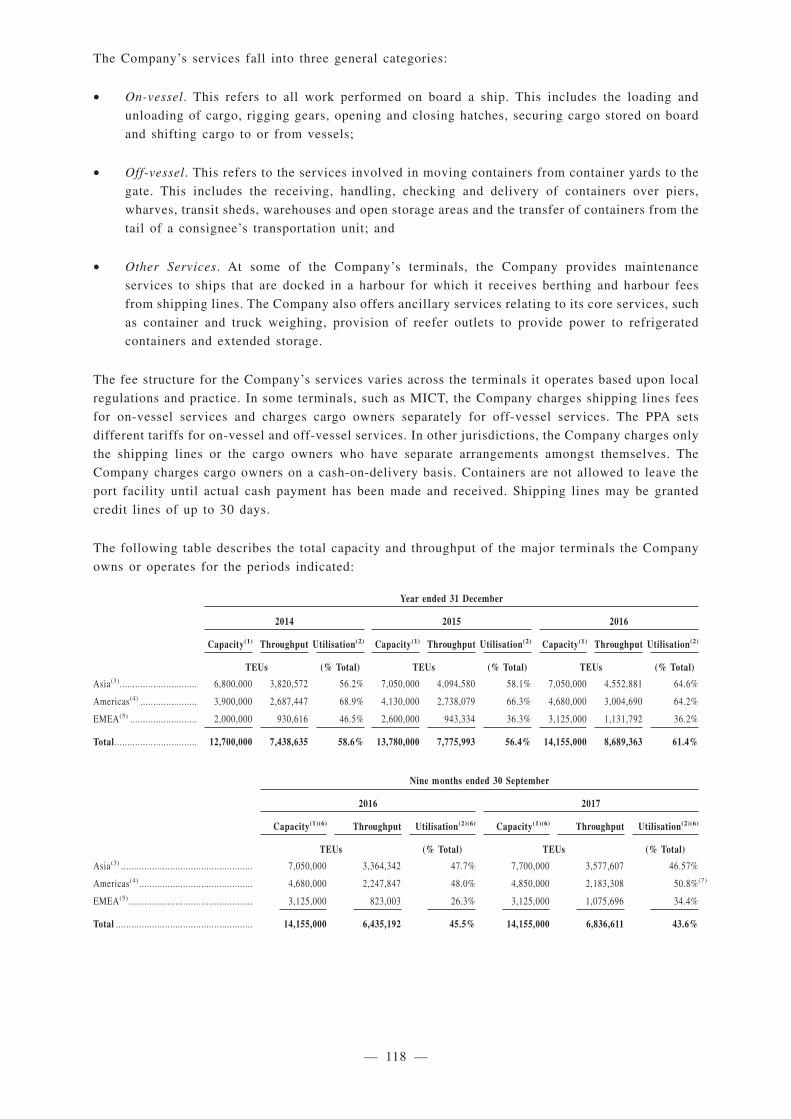

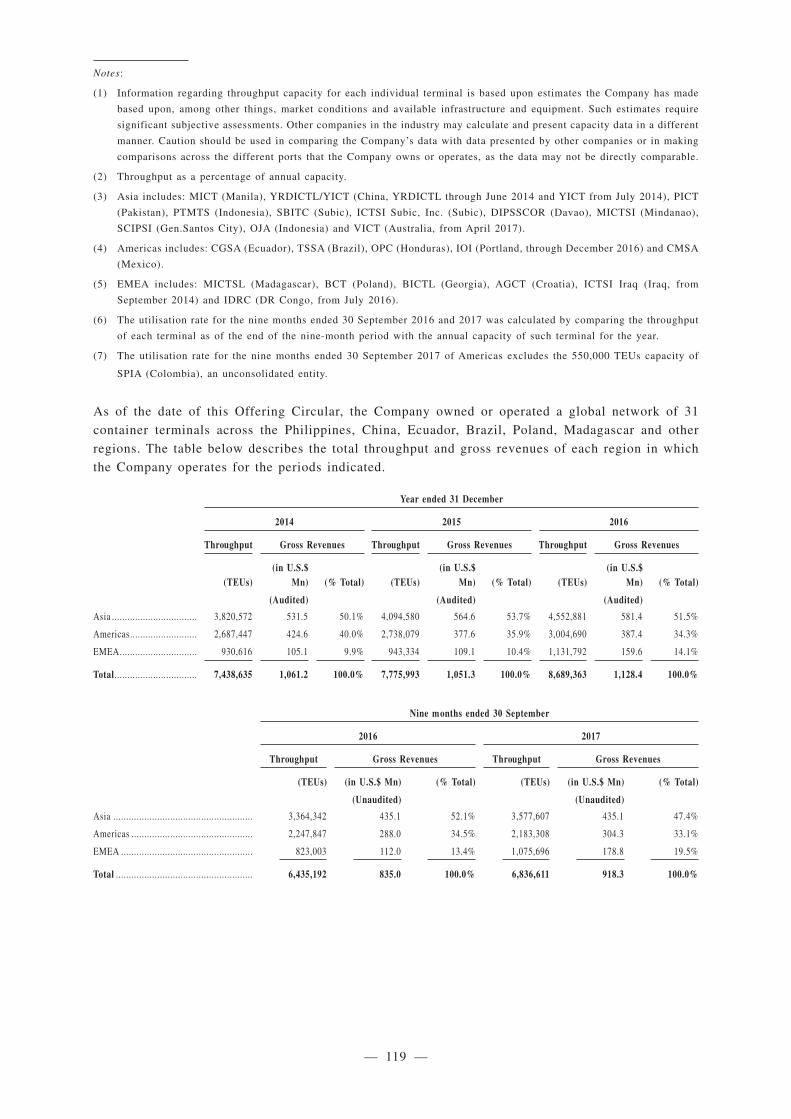

The Company is an international operator of common user container terminals serving the globalcontainer shipping industry. Its business is the operational management, development and acquisitionof container terminals with a focus on origin and destination and gateway ports in emerging andfrontier markets. It also provides a number of ancillary services such as storage, container packing andunpacking, inspection, weighing and services for refrigerated containers, or reefers. The Companyholds rights to operate these terminals under long-term concession agreements with local portauthorities and governments. As of the date of this Offering Circular, the Company owned or operateda total of 27 terminal facilities, with nine key ports and an inland container terminal in the Philippines,two in Indonesia and one each in China, Ecuador, Brazil, Poland, Georgia, Madagascar, Croatia,Pakistan, Mexico, Honduras, Iraq, Argentina, Colombia, DR Congo and Australia; an acquisition ofan existing concession to construct and operate a port in Tuxpan, Mexico; and, recently, a project toconstruct a barge terminal in Cavite, Philippines and agreements to operate two international ports inPNG. For the year ended 31 December 2016 and the nine months ended 30 September 2017, theCompany handled an estimated 8,689,363 TEUs and 6,836,611 TEUs, respectively.

The Company was established by the Razon family, who remains the controlling shareholder, in 1987in connection with the privatisation of the MICT in the Port of Manila. The Company has built uponthe experience gained in rehabilitating, developing and operating MICT to establish an extensiveinternational network concentrated in emerging market economies.

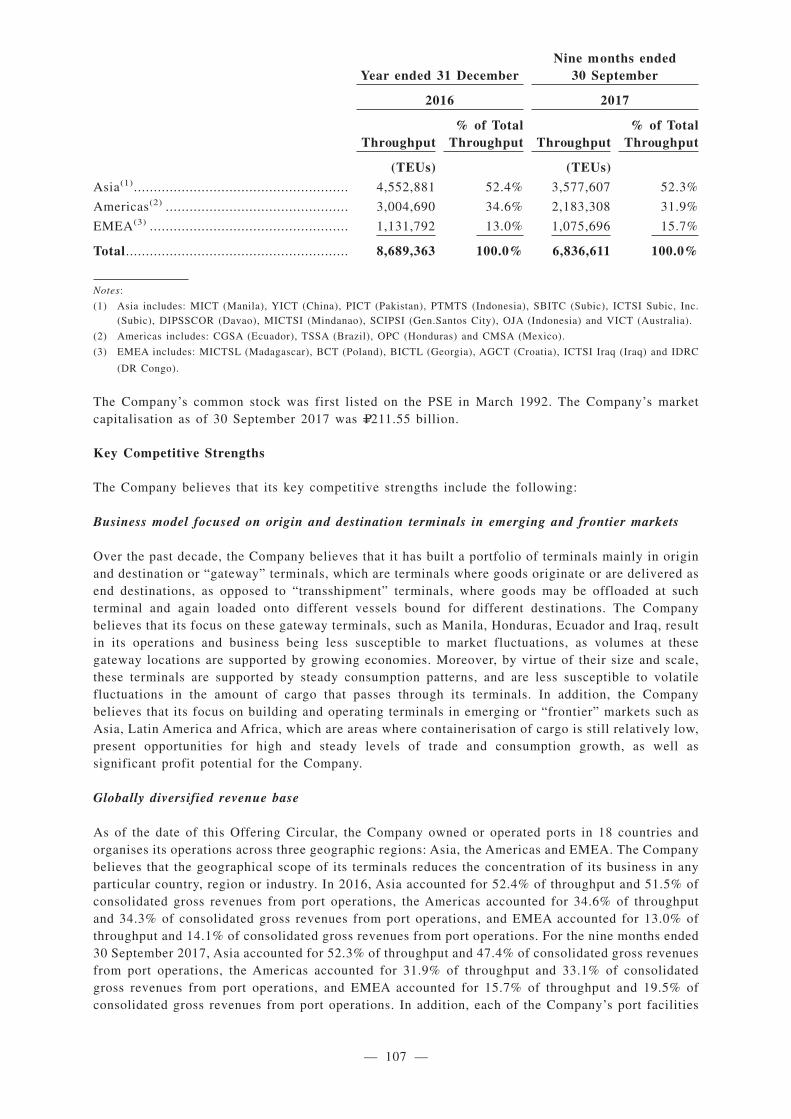

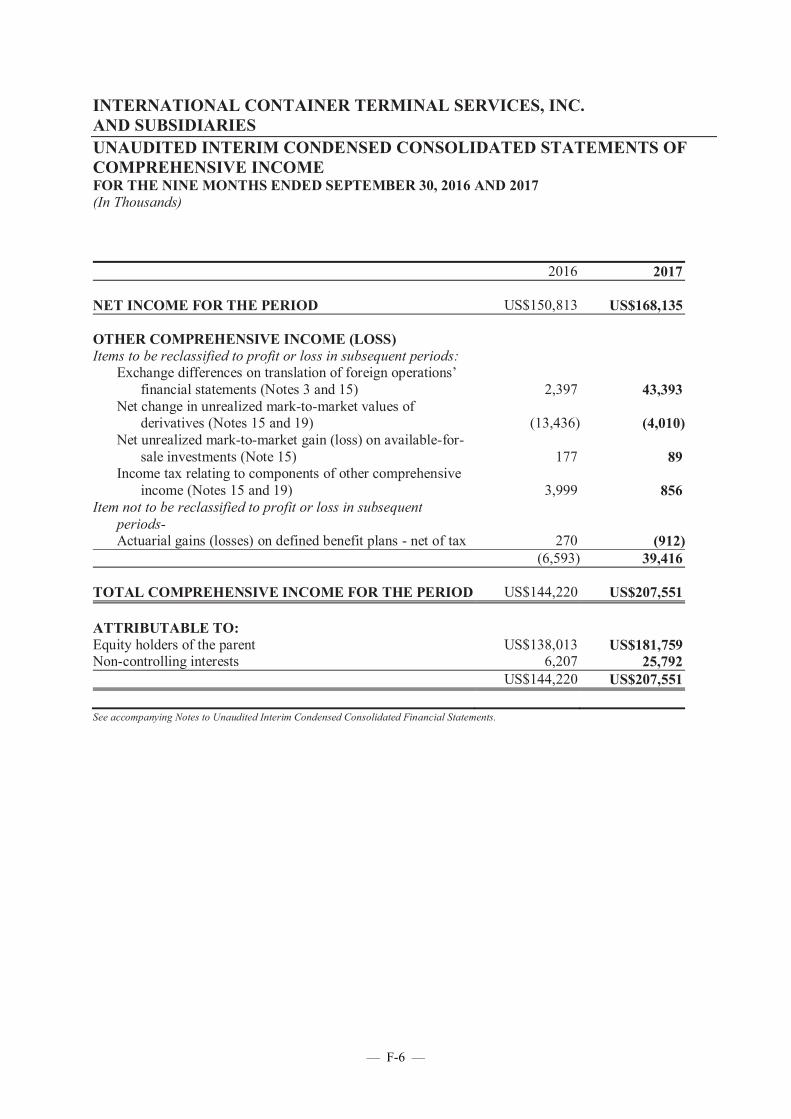

For the year ended 31 December 2016, the Company reported consolidated gross revenues from portoperations and EBITDA of U.S.$1,128.4 million and U.S.$525.1 million, respectively. For the ninemonths ended 30 September 2017, the Company reported consolidated gross revenues from portoperations and EBITDA of U.S.$918.3 million and U.S.$434.9 million, respectively. The Companyorganises its business across three geographic regions: (i) Asia, (ii) the Americas and (iii) EMEA. In2016, Asia accounted for 52.4% of throughput and 51.5% of consolidated gross revenues from portoperations, the Americas accounted for 34.6% of throughput and 34.3% of consolidated gross revenuesfrom port operations, and EMEA accounted for 13.0% of throughput and 14.1% of consolidated grossrevenues from port operations. For the nine months ended 30 September 2017, Asia accounted for52.3% of throughput and 47.4% of consolidated gross revenues from port operations, the Americasaccounted for 31.9% of throughput and 33.1% of consolidated gross revenues from port operations,and EMEA accounted for 15.7% of throughput and 19.5% of consolidated gross revenues from portoperations.

The Company’s common stock was first listed on the PSE in March 1992. The Company’s marketcapitalisation as of 30 September 2017 was P=211.55 billion.

Key Competitive Strengths

The Company believes that its key competitive strengths include the following:

Business model focused on origin and destination terminals in emerging and frontier markets

Over the past decade, the Company believes that it has built a portfolio of terminals mainly in originand destination or “gateway” terminals, which are terminals where goods originate or are delivered asend destinations, as opposed to “transshipment” terminals, where goods may be offloaded at suchterminal and again loaded onto different vessels bound for different destinations. The Companybelieves that its focus on these gateway terminals, such as Manila, Honduras, Ecuador and Iraq, result

— 10 —

in its operations and business being less susceptible to market fluctuations, as volumes at thesegateway locations are supported by growing economies. Moreover, by virtue of their size and scale,these terminals are supported by steady consumption patterns, and are less susceptible to volatilefluctuations in the amount of cargo that passes through its terminals. In addition, the Companybelieves that its focus on building and operating terminals in emerging or “frontier” markets such asAsia, Latin America and Africa, which are areas where containerisation of cargo is still relatively low,present opportunities for high and steady levels of trade and consumption growth, as well assignificant profit potential for the Company.

Globally diversified revenue base

As of the date of this Offering Circular, the Company owned or operated ports in 18 countries andorganises its operations across three geographic regions: Asia, the Americas and EMEA. The Companybelieves that the geographical scope of its terminals reduces the concentration of its business in anyparticular country, region or industry. In 2016, Asia accounted for 52.4% of throughput and 51.5% ofconsolidated gross revenues from port operations, the Americas accounted for 34.6% of throughputand 34.3% of consolidated gross revenues from port operations, and EMEA accounted for 13.0% ofthroughput and 14.1% of consolidated gross revenues from port operations. For the nine months ended30 September 2017, Asia accounted for 52.3% of throughput and 47.4% of consolidated gross revenuesfrom port operations, the Americas accounted for 31.9% of throughput and 33.1% of consolidatedgross revenues from port operations, and EMEA accounted for 15.7% of throughput and 19.5% ofconsolidated gross revenues from port operations. In addition, each of the Company’s port facilitiesserves a number of different shipping lines, which reduces its reliance on any one particular customer.In 2016 and the nine months ended 30 September 2017, revenue from the Company’s largest customerrepresented only 9.5% and 10.0% of its consolidated gross revenues from port operations for eachperiod, respectively. The Company believes that its diversified operations spanning the major regionsof the world, as well as its presence in areas where consumption and merchandise inventory aregrowing, mitigates the effect of regional or area-specific economic downturns on its business andresults of operations.

Leading market positions in key targeted markets

The Company’s major terminals enjoy leading positions in their respective geographic markets. TheCompany believes that its strong market position in the regions where it operates allows it to enhanceoperating efficiencies and maximise throughput, which increases profitability. The Company owns oroperates the largest container terminals in terms of volume throughput and capacity in the Philippines,Ecuador, the Brazilian state of Pernambuco, Madagascar, Yantai in China, Honduras, and morerecently Iraq and DR Congo. At these terminals, there are limited opportunities for competition fromother port operators, other ports or other terminals within the same ports due to high barriers to entry.Some of these barriers include the limited number of port sites, government controls and high terminalconstruction costs. This means that there are few substitutes for the Company’s services, which allowsit to maintain significant pricing power and thus helps to ensure robust margins. Many of these portsare in emerging markets, which generally exhibit stronger growth than developed markets; thus theCompany believes that its leading position in these markets will allow it to directly capture organicgrowth in line with the economies of these markets. Furthermore, all of the Company’s concessionagreements are long-term agreements that ensure continued benefits from long-term GDP growthtrends.

Market Experience and Scale of Operations

The Company believes that its considerable expansion over the past decade has allowed it to gainsignificant experience in the regional markets in which it operates. This has resulted in the Companybeing more nimble to take advantage of acquisition, expansion and other business opportunities whicharise in those regions. For example, its experience operating in Latin America since 2007 and thepresence of a Latin America-based international team and operating unit helped it to identify andcapitalise opportunities to secure concessions in Argentina, Colombia and Mexico. The Company also

— 11 —

believes that its experience and relationships in the region with respect to operational aspects suchregulatory and labour allowed it to navigate necessary approvals and permits, as well as source themanpower and other requirements for its new terminals in a very efficient manner, often affordingsignificant savings, lower cost of capital and improved margins. In addition, the Company’s targetedand steady expansion has resulted in its operations achieving significant scale, which has translatedinto global relationships at the public and private sector levels which have allowed the Company toexert pricing influence over customers. The Company’s scale has also afforded it greater negotiatingpower with suppliers and other key third parties.

Dynamic and empowered management team

The Company’s management team has extensive experience in the acquisition, rehabilitation andoperation of container terminals. The Company has been able to deploy experienced management teammembers across its geographic operations to implement the start-up and takeover of new facilities. TheCompany’s management team is highly incentivised, as directors, company officers and related partieshave an approximate 62.0% equity interest in the Company as of the date of this Offering Circular.Its management structure is intentionally decentralised with broad authority delegated to individualoperating units, where management teams are closest to their customers and have the mostcomprehensive knowledge of the regulatory, labour and other key operating conditions prevailing intheir respective jurisdictions. The decentralised structure also allows for a lean and flat managementstructure organisation-wide, which reduces administrative costs. The Company’s senior managementat the corporate level focuses on providing overall strategy and direction as well as managing keyCompany-wide functions such as information technology, engineering and finance. The Companymaintains strong financial controls over each operating entity through standardised monthly reporting,its annual budget process, regular financial and operating audits, control over the external raising ofcapital and risk management.

Established track record of improving efficiency and performance

The Company has a strong track record of significantly improving the operating efficiency andfinancial performance of the terminals it acquires. The Company has developed robust financial andbusiness metrics to assess operational performance, search out inefficiencies and target areas forimprovement. The Company has made substantial investments in its terminals such as acquiring newhandling equipment to enhance handling capacity and efficiency, modernising information technologysystems and expanding and rehabilitating civil works. The Company also provides its know-howthrough enhanced training and the introduction of new work processes to streamline labour practices,and rational commercial strategies to achieve improvements in yield per TEU. The Company has beenable to improve efficiency measures that it believes shipping lines take into consideration whenchoosing a terminal, such as crane moves per hour and ship turnaround time. For example, at the portof Toamasina in Madagascar, prior to MICTSL’s takeover of operations, the average number ofcontainer moves per hour per vessel was 13 moves. After MICTSL assumed control, it implementedthe use of two mobile harbour cranes and increased the average number of moves to 36 per hour withina few months. This significantly decreased ship turnaround time. Similarly, at the Umm Qasr port,ICTSI Iraq improved quay crane productivity from 15 moves per hour to 53 moves per hour throughimproved maintenance, proper training and new/refurbished equipment. Likewise, lorry turn-aroundtime, in general, improved from approximately 24 hours to approximately two hours in the monthsafter MICTSL assumed control, and further decreased to under an hour in the following two years. TheCompany has received commendations and recognitions for its success in improving cargo handlingand assisting in the development of the private sector. For example, the Company has been cited bythe World Bank for its success in public-private partnerships in South America, Africa and Europe.The Company also believes that its recent improvements with respect to Enterprise Resource Planninginitiatives will also result in efficiencies and sustainable savings. Primarily as a result of these factorsthe Company has been able to maintain stable EBITDA margins (EBITDA as a percentage of grossrevenues from port operations) of 41.7%, 42.8%, 46.5%, 46.7% and 47.4% in the year ended 31December 2014, 2015 and 2016 and the nine months ended 30 September 2016 and 2017, respectively.

— 12 —

Strong capital structure and stable cash flows

The Company’s finances are supported by a strong capital structure and stable cash flows. As of 30September 2017, the Company’s total indebtedness was U.S.$1,468.8 million and its totalindebtedness to total equity ratio (interest-bearing debt over total equity, as shown in the consolidatedbalance sheet) was 0.79 times, providing head room for future financial leverage. The Companybelieves that its cash flows and debt structure will provide it with a solid platform to pursueinvestment opportunities, supported by its active balance sheet management strategies and liabilitymanagement initiatives which have helped streamline its debt maturity profile and interest paymentschedules significantly. Moreover, the Company believes that its major terminals provide stable cashflows because of its globally diversified operations focusing primarily on gateway locations andcharacterised by long-term concession agreements, which have an average remaining term ofapproximately 18 years weighted by capacity. In addition, the Company’s terminals generally focuson end destination cargo (which accounts for substantially all of the Company’s consolidatedthroughput volume) limiting concentration risk to individual container shipping lines in that if ashipping line that calls at one of its terminals ceases to operate, the cargo intended for that particulardestination will simply be transferred to another shipping line that is still calling at that terminal. TheCompany believes that focusing on this type of cargo results in a higher yield per TEU, as comparedto other operators. Primarily as a result of these factors, the Company’s operating cash flow hasincreased from U.S.$387.8 million in 2014 and U.S.$407.7 million in 2015 to U.S.$466.9 million in2016. The Company’s operating cash flow was U.S.$390.1 million in the nine months ended 30September 2017.

Strategies

The Company’s key strategies are set out below.

Continue prudent growth through targeted acquisitions, organic growth and select privatisation

The Company plans to continue its focus on terminals in origin and destination gateway ports,particularly in emerging and “frontier” markets. Gateway ports are the principal points of entry for acountry or a community and serve as the origin and destination points for cargo, and have higher profitmargins per unit moved than transshipment points for cargo. The Company also plans to continue tosearch for opportunities globally in emerging markets that will typically offer greater scope forimprovements to operational and financial performance, higher levels of volume growth due toincreases in containerisation rates, and favourable demographics which would support higher levelsof merchandise trade and consumption growth. The Company believes that the global containerterminal industry remains fragmented. The Company’s acquisition strategy is to consider opportunitieswith favourable valuations and scopes for operational improvements. Container terminals in lessdeveloped economies often experience higher rates of volume growth, and typically have lower coststructures due to more flexible labour practices. The Company has developed robust financial andbusiness criteria to assess potential acquisitions and have been able to procure financing on terms ithas found acceptable to fund acquisitions. In addition, the Company plans to continue to pursueopportunities for organic growth in its present locations, whether by expansion of facilities or additionof other services. Finally, the Company will look to continue to scout for privatisation opportunitiesto further bolster its operations portfolio.

Maintain a leadership position in the markets in which it operates

The Company expects to continue to improve its position as a leading terminal operator in origin anddestination user container terminals particularly in emerging and “frontier” markets with stronggrowth and profit potential. The Company believes it has the largest market share in the major marketsin which it currently operates terminals. The Company intends to maintain a leadership position inthese markets through improving its handling capacity, maintaining and improving operatingefficiencies, focusing on providing high levels of customer service and leveraging the knowledge andexperience gained from operations across multiple terminals.

— 13 —

Continue to optimise the benefits of existing ports

The Company will continue to look for opportunities to grow its revenues and profit margins, expand

and enhance efficiency at its existing port terminals, and will continue to focus on end-destination

cargo. The Company plans to optimise its operations to harness market trends, such as the increasing

containerisation of goods and the growth of emerging market economies. The Company also plans to

proactively manage its facilities to expand when maintaining and growing its margins. These

programmes may include cost reductions, equipment upgrades, and projects to improve labour

efficiencies and processes. As an example, the Company recently implemented its Terminal

Appointment Booking System (“TABS”), which helps to improve capacity and operational efficiency

in its terminals. Improvements to the labour pool also come from knowledge and experience sharing

across ports. The Company also plans to expand the handling capacity of its ports as needed, such as

the construction of new yard facilities at the MICT.

Continue to actively manage its balance sheet to optimise its yield curve and capital requirements

The Company plans to continue to actively and dynamically manage the principal redemption profile

of its liabilities to more closely align with its fluid cashflow requirements. As part of its balance sheet

management initiatives, the Company also plans to continue proactive management of its debt and

other financing covenants through periodic reviews, liability management exercises and other

measures, to ensure that such restrictions, covenants and the Company’s interest rate profile for its

liabilities more closely align with the Company’s rapid growth and improving profile with investors

and the financing markets. The Company experiences significant cashflow needs from time to time —

whether it be for greenfield port developments, targeted acquisitions or to ramp up volume and expand

operations at existing ports. The Company’s overall intention with its capital management initiatives

is to achieve a value accretive capital structure, wherein the deployment of capital for its various new

and existing projects does not impair its capacity to quickly secure financing for opportunistic

expansion or continuing improvements at existing ports.

Continue developing investor management initiatives and policies

The Company has developed fulsome and proactive investor management initiatives in recent years.

These initiatives are anchored on the core Company philosophy of transparency with its investors, the

number of which has steadily expanded over the years as the Company has accessed a wider market

base. The Company intends to continue periodic open dialogues and active engagement with its

investor base, with the aim of ensuring awareness of significant company developments and soliciting

regular feedback from stakeholders in the Company. The Company firmly believes that this policy of

active and regular engagement has allowed it to efficiently access its existing investor base from time

to time in relation to its financing and balance sheet management initiatives. The Company also

believes that these policies keep it informed of developments in the markets, as well as on issues and

concerns of investors with respect to similar companies and businesses.

Corporate Information

The Company is incorporated under the laws of the Philippines. The Issuer is incorporated under the

Laws of the Netherlands. They maintain their principal executive offices at ICTSI Administration

Building, Manila International Container Terminal, MICT South Access Road, Manila 1012,

Philippines. The telephone number at that address is +63-2-245-4101. The Company’s website is at

www.ictsi.com. Information on its website or websites is not incorporated by reference into this

Offering Circular and should not be relied on for the purposes of the Offering.

— 14 —

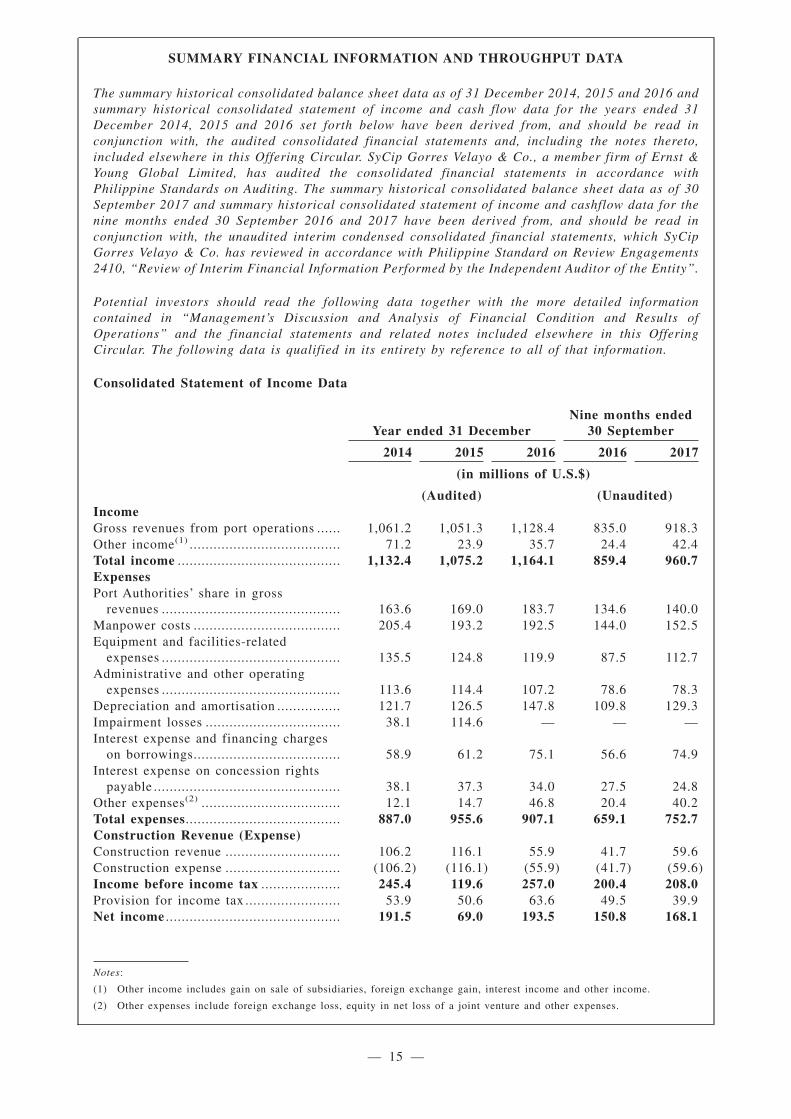

SUMMARY FINANCIAL INFORMATION AND THROUGHPUT DATA

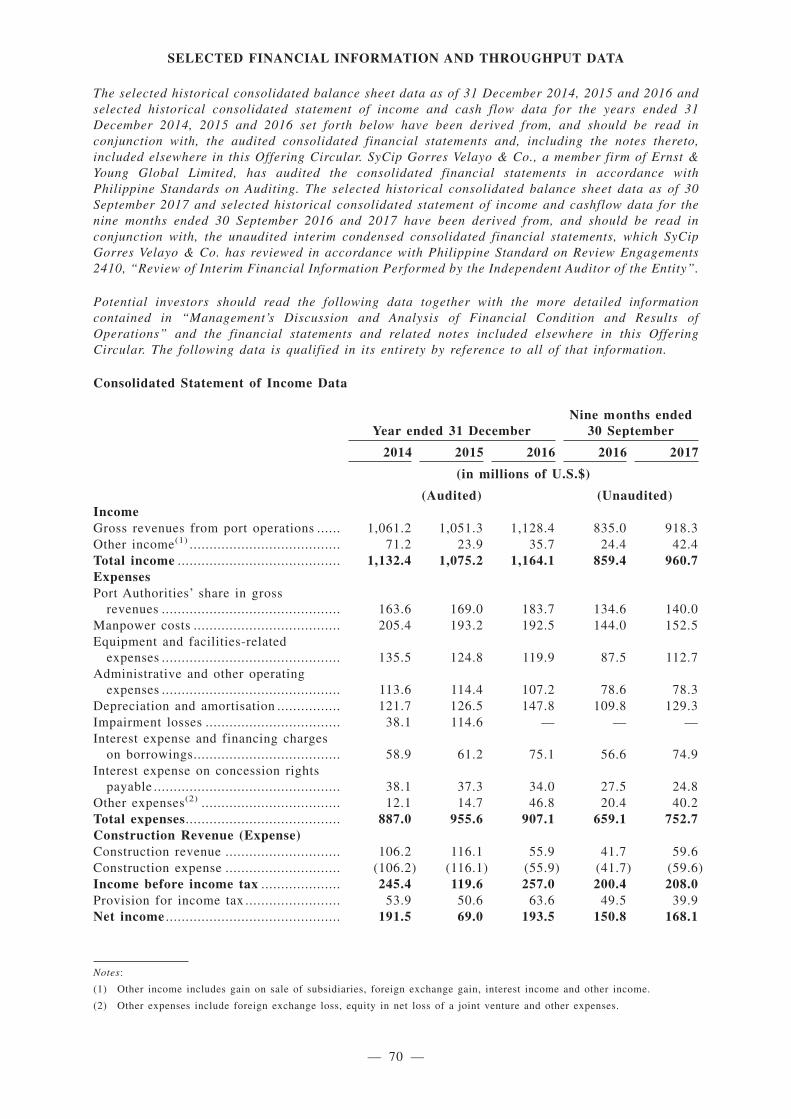

The summary historical consolidated balance sheet data as of 31 December 2014, 2015 and 2016 andsummary historical consolidated statement of income and cash flow data for the years ended 31December 2014, 2015 and 2016 set forth below have been derived from, and should be read inconjunction with, the audited consolidated financial statements and, including the notes thereto,included elsewhere in this Offering Circular. SyCip Gorres Velayo & Co., a member firm of Ernst &Young Global Limited, has audited the consolidated financial statements in accordance withPhilippine Standards on Auditing. The summary historical consolidated balance sheet data as of 30September 2017 and summary historical consolidated statement of income and cashflow data for thenine months ended 30 September 2016 and 2017 have been derived from, and should be read inconjunction with, the unaudited interim condensed consolidated financial statements, which SyCipGorres Velayo & Co. has reviewed in accordance with Philippine Standard on Review Engagements2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity”.

Potential investors should read the following data together with the more detailed informationcontained in “Management’s Discussion and Analysis of Financial Condition and Results ofOperations” and the financial statements and related notes included elsewhere in this OfferingCircular. The following data is qualified in its entirety by reference to all of that information.

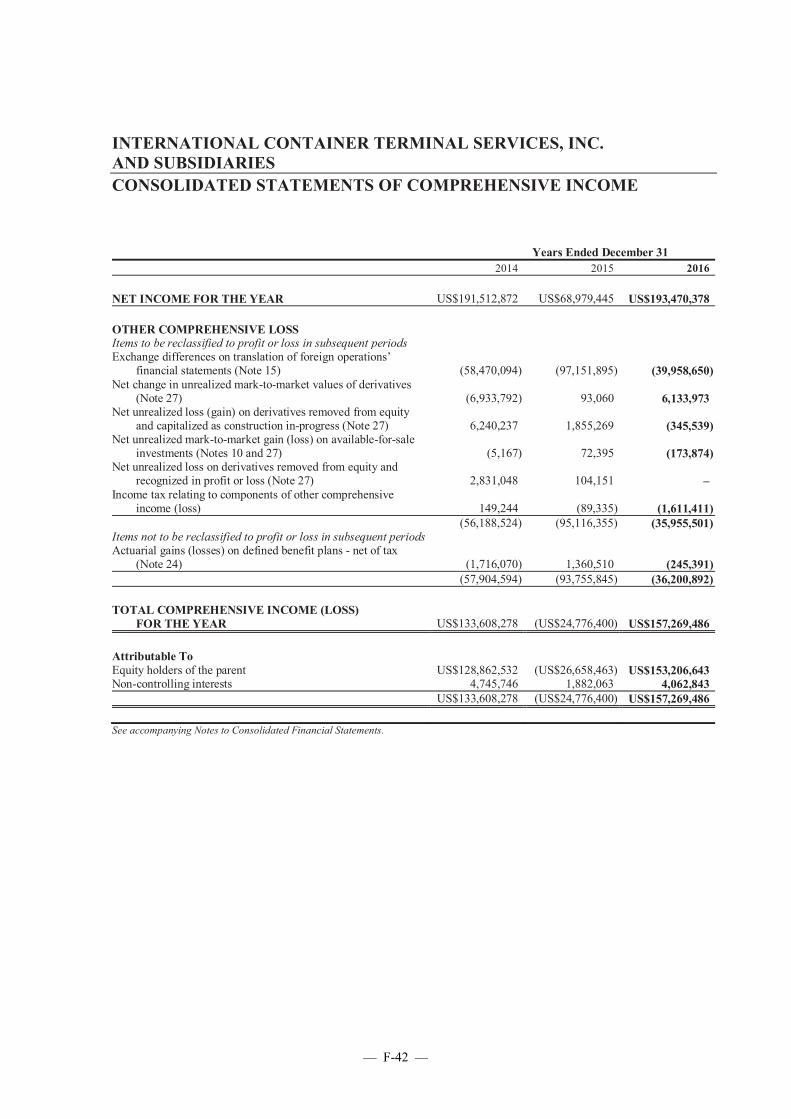

Consolidated Statement of Income Data

Year ended 31 DecemberNine months ended

30 September

2014 2015 2016 2016 2017

(in millions of U.S.$)

(Audited) (Unaudited)IncomeGross revenues from port operations ...... 1,061.2 1,051.3 1,128.4 835.0 918.3Other income(1) ...................................... 71.2 23.9 35.7 24.4 42.4Total income ......................................... 1,132.4 1,075.2 1,164.1 859.4 960.7ExpensesPort Authorities’ share in gross

revenues ............................................. 163.6 169.0 183.7 134.6 140.0Manpower costs ..................................... 205.4 193.2 192.5 144.0 152.5Equipment and facilities-related

expenses ............................................. 135.5 124.8 119.9 87.5 112.7Administrative and other operating

expenses ............................................. 113.6 114.4 107.2 78.6 78.3Depreciation and amortisation ................ 121.7 126.5 147.8 109.8 129.3Impairment losses .................................. 38.1 114.6 — — —Interest expense and financing charges

on borrowings..................................... 58.9 61.2 75.1 56.6 74.9Interest expense on concession rights

payable ............................................... 38.1 37.3 34.0 27.5 24.8Other expenses(2) ................................... 12.1 14.7 46.8 20.4 40.2Total expenses....................................... 887.0 955.6 907.1 659.1 752.7Construction Revenue (Expense)Construction revenue ............................. 106.2 116.1 55.9 41.7 59.6Construction expense ............................. (106.2) (116.1) (55.9) (41.7) (59.6)Income before income tax .................... 245.4 119.6 257.0 200.4 208.0Provision for income tax ........................ 53.9 50.6 63.6 49.5 39.9Net income ............................................ 191.5 69.0 193.5 150.8 168.1

Notes:

(1) Other income includes gain on sale of subsidiaries, foreign exchange gain, interest income and other income.

(2) Other expenses include foreign exchange loss, equity in net loss of a joint venture and other expenses.

— 15 —

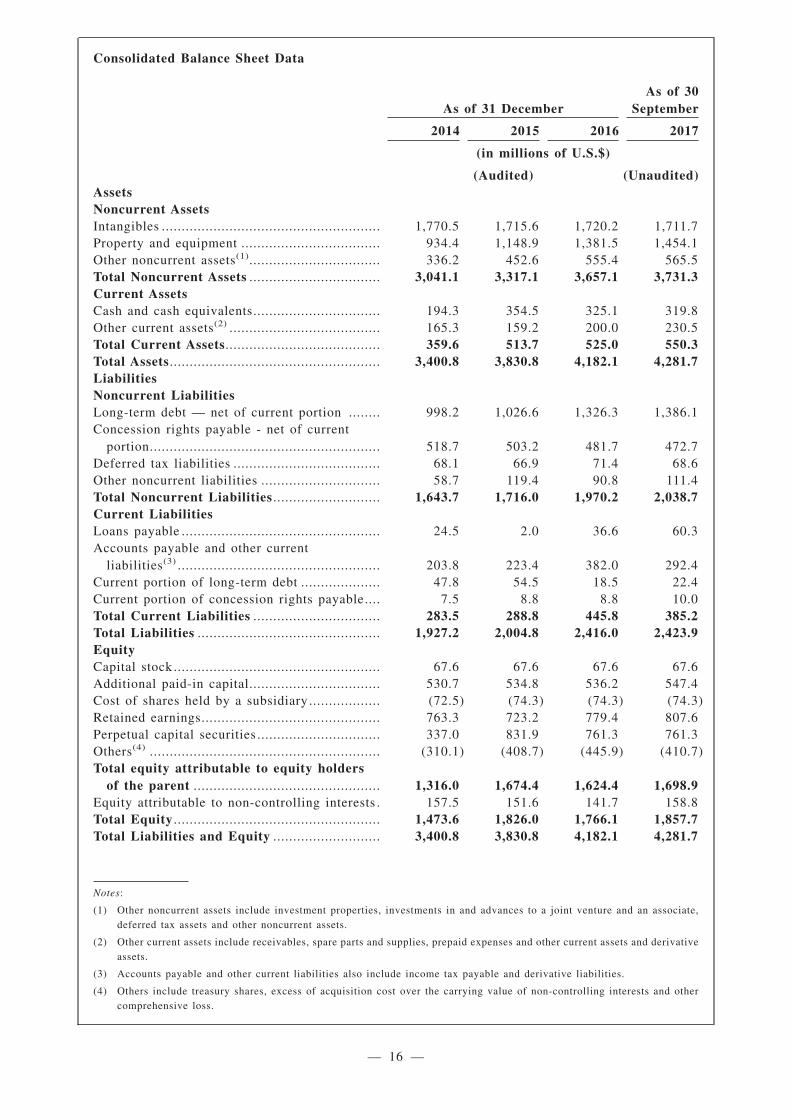

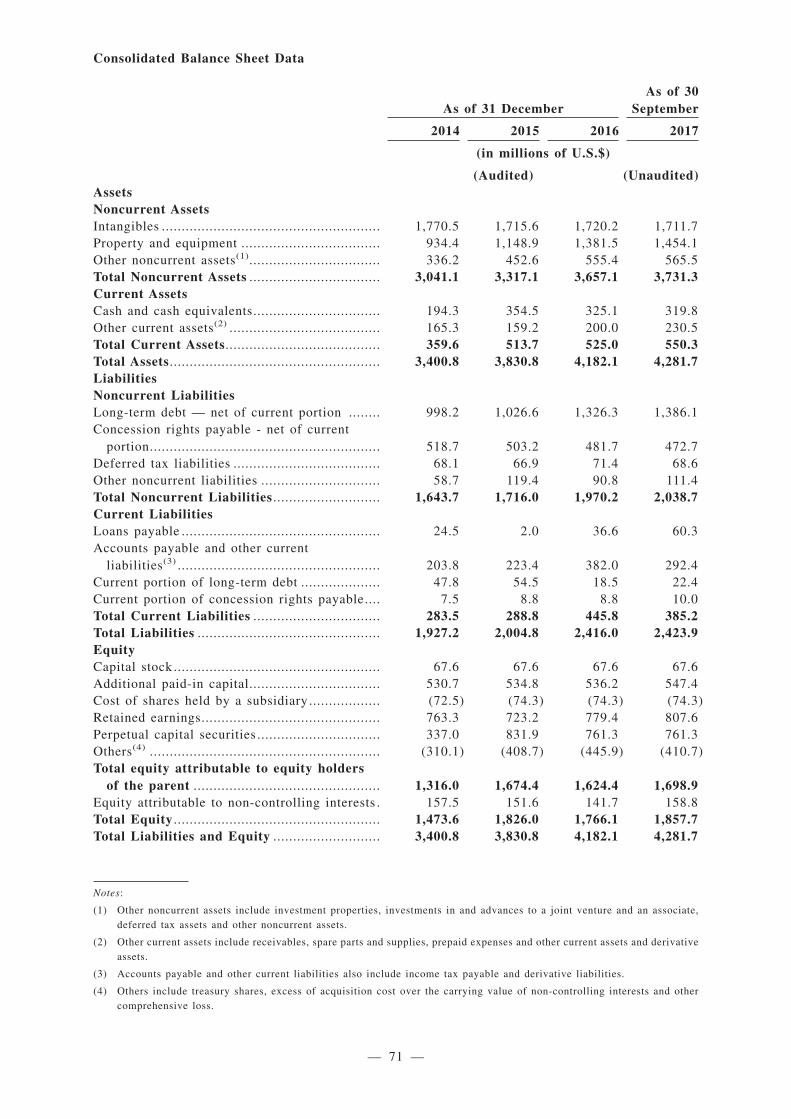

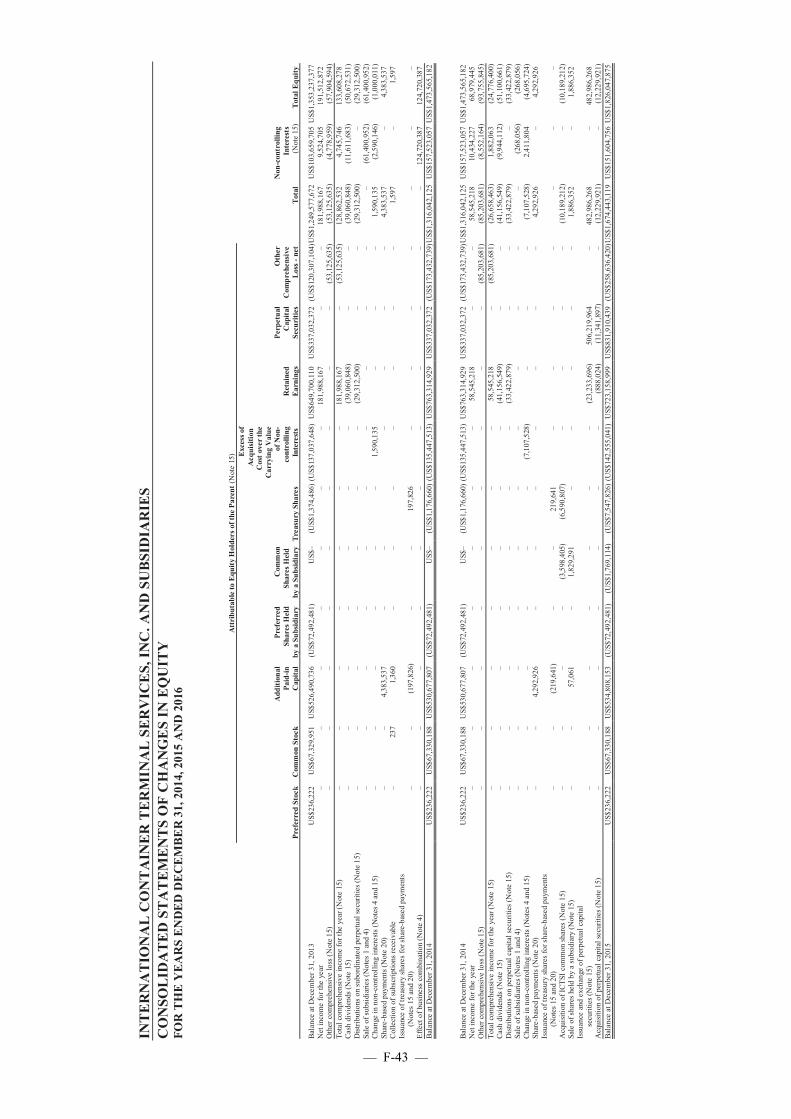

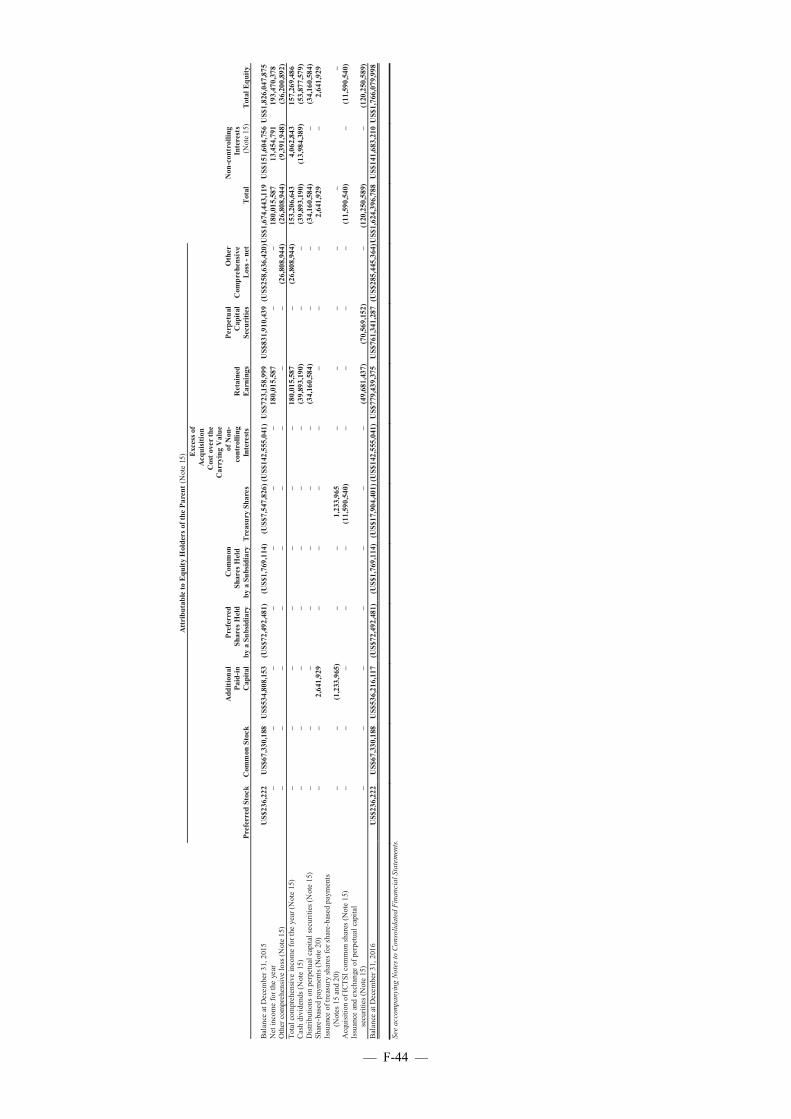

Consolidated Balance Sheet Data

As of 31 DecemberAs of 30

September

2014 2015 2016 2017

(in millions of U.S.$)

(Audited) (Unaudited)AssetsNoncurrent AssetsIntangibles ....................................................... 1,770.5 1,715.6 1,720.2 1,711.7Property and equipment ................................... 934.4 1,148.9 1,381.5 1,454.1Other noncurrent assets(1)................................. 336.2 452.6 555.4 565.5Total Noncurrent Assets ................................. 3,041.1 3,317.1 3,657.1 3,731.3Current AssetsCash and cash equivalents................................ 194.3 354.5 325.1 319.8Other current assets(2) ...................................... 165.3 159.2 200.0 230.5Total Current Assets....................................... 359.6 513.7 525.0 550.3Total Assets..................................................... 3,400.8 3,830.8 4,182.1 4,281.7LiabilitiesNoncurrent LiabilitiesLong-term debt — net of current portion ........ 998.2 1,026.6 1,326.3 1,386.1Concession rights payable - net of current

portion.......................................................... 518.7 503.2 481.7 472.7Deferred tax liabilities ..................................... 68.1 66.9 71.4 68.6Other noncurrent liabilities .............................. 58.7 119.4 90.8 111.4Total Noncurrent Liabilities ........................... 1,643.7 1,716.0 1,970.2 2,038.7Current LiabilitiesLoans payable .................................................. 24.5 2.0 36.6 60.3Accounts payable and other current

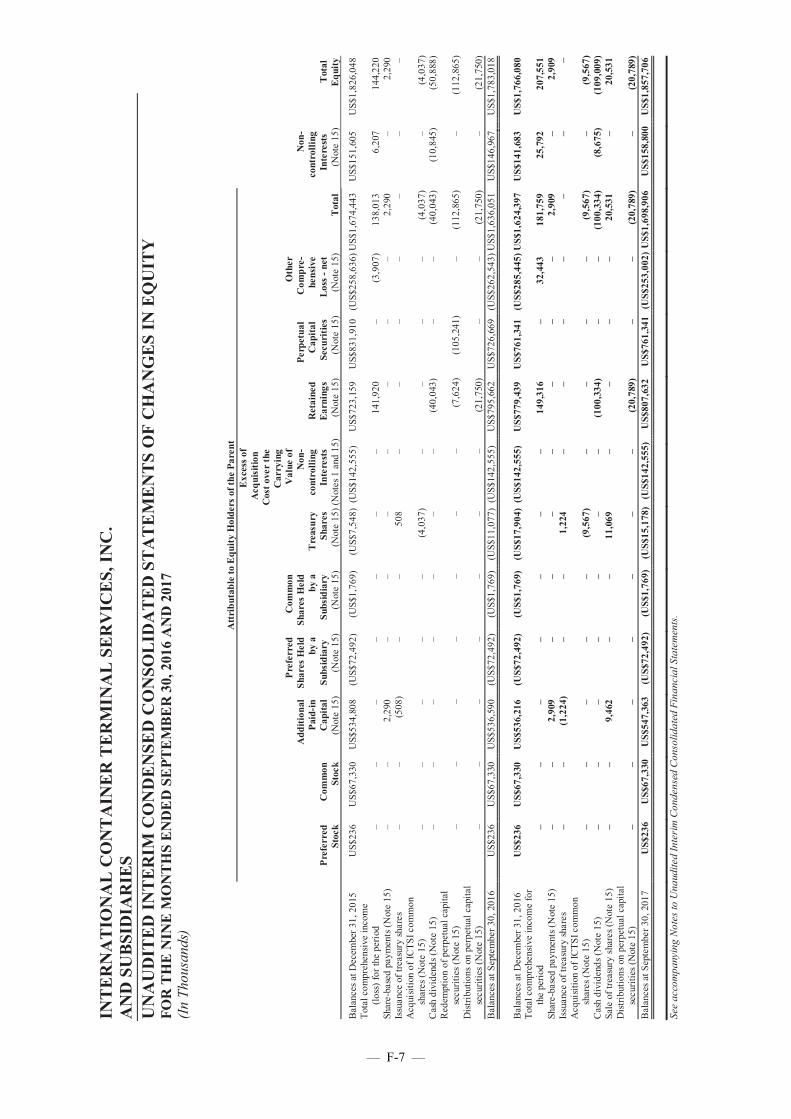

liabilities(3) ................................................... 203.8 223.4 382.0 292.4Current portion of long-term debt .................... 47.8 54.5 18.5 22.4Current portion of concession rights payable.... 7.5 8.8 8.8 10.0Total Current Liabilities ................................ 283.5 288.8 445.8 385.2Total Liabilities .............................................. 1,927.2 2,004.8 2,416.0 2,423.9EquityCapital stock .................................................... 67.6 67.6 67.6 67.6Additional paid-in capital................................. 530.7 534.8 536.2 547.4Cost of shares held by a subsidiary .................. (72.5) (74.3) (74.3) (74.3)Retained earnings............................................. 763.3 723.2 779.4 807.6Perpetual capital securities ............................... 337.0 831.9 761.3 761.3Others(4) .......................................................... (310.1) (408.7) (445.9) (410.7)Total equity attributable to equity holders

of the parent ............................................... 1,316.0 1,674.4 1,624.4 1,698.9Equity attributable to non-controlling interests . 157.5 151.6 141.7 158.8Total Equity .................................................... 1,473.6 1,826.0 1,766.1 1,857.7Total Liabilities and Equity ........................... 3,400.8 3,830.8 4,182.1 4,281.7

Notes:

(1) Other noncurrent assets include investment properties, investments in and advances to a joint venture and an associate,deferred tax assets and other noncurrent assets.

(2) Other current assets include receivables, spare parts and supplies, prepaid expenses and other current assets and derivativeassets.

(3) Accounts payable and other current liabilities also include income tax payable and derivative liabilities.

(4) Others include treasury shares, excess of acquisition cost over the carrying value of non-controlling interests and othercomprehensive loss.

— 16 —

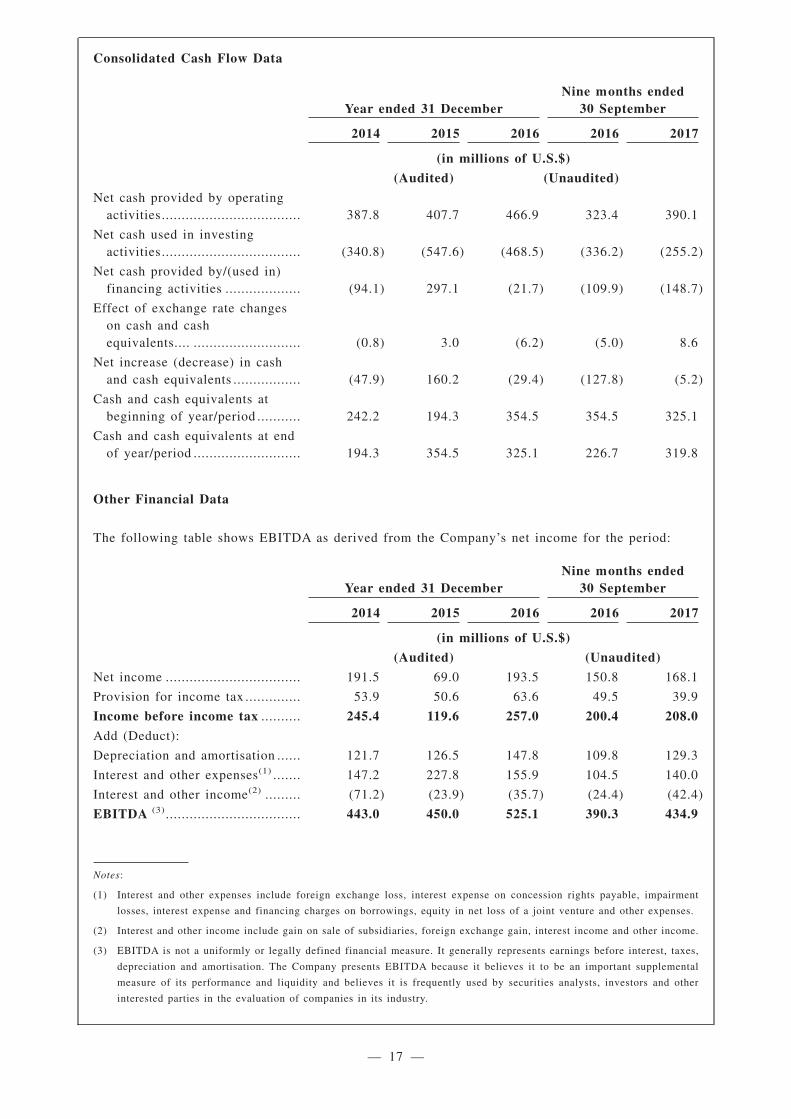

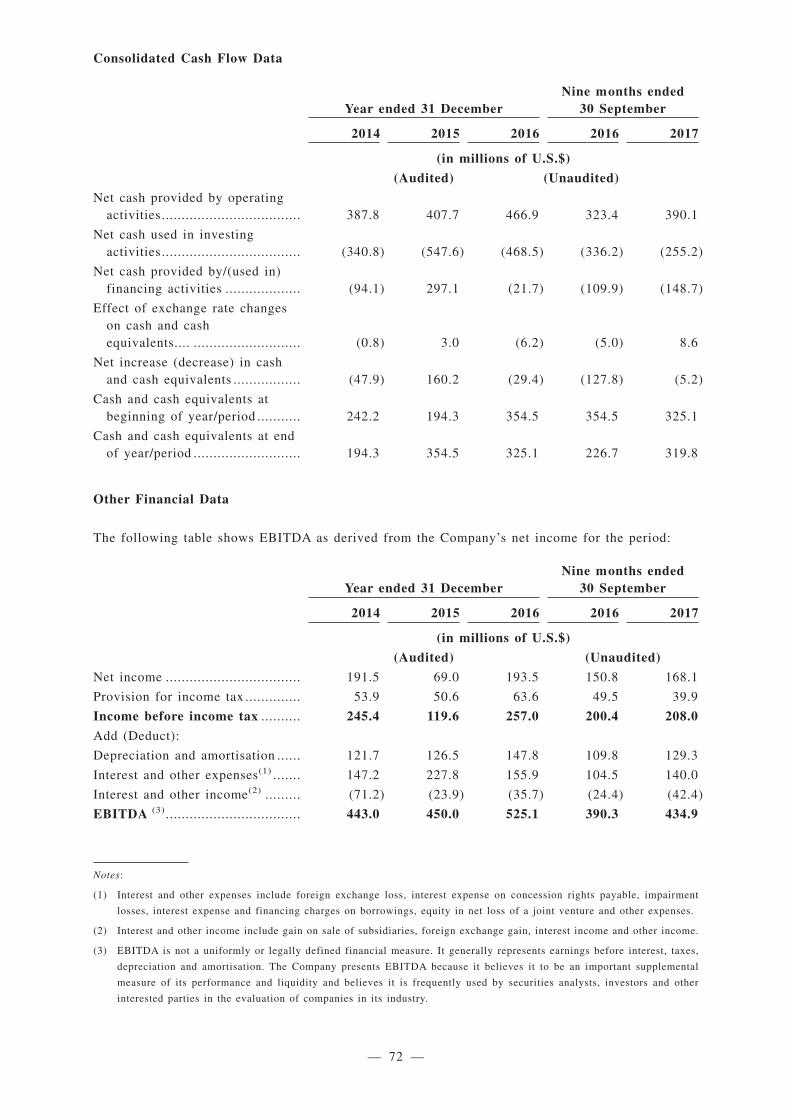

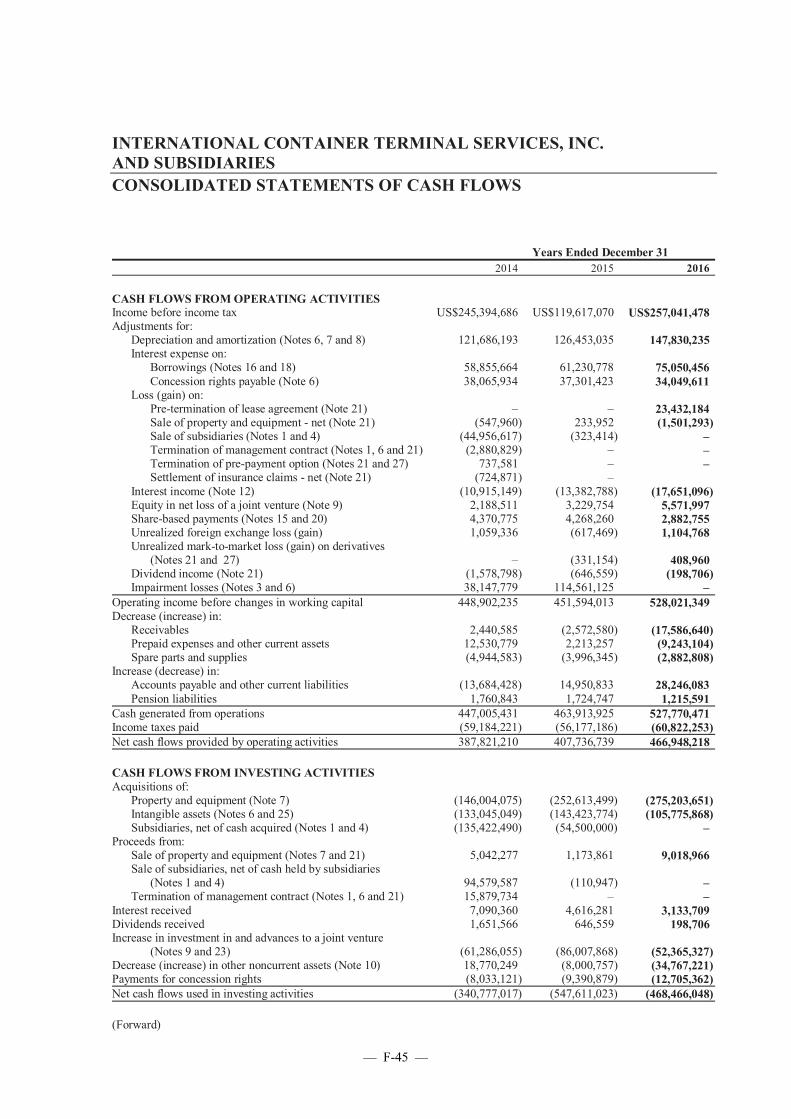

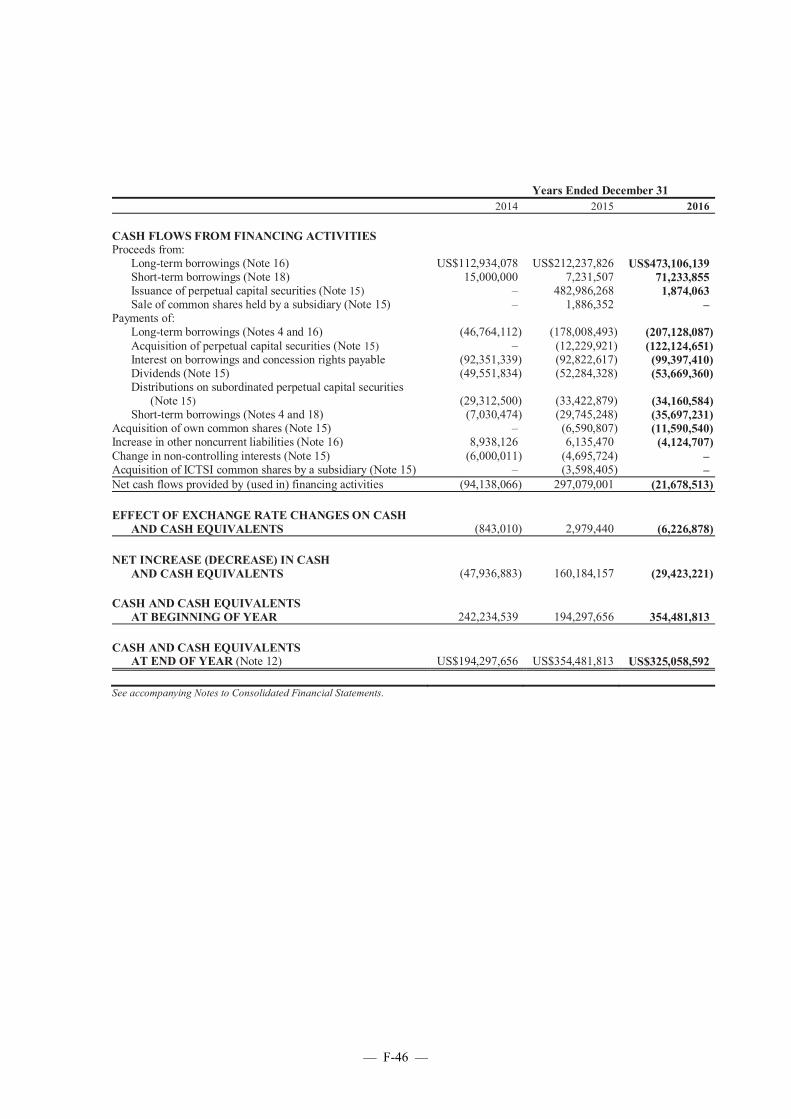

Consolidated Cash Flow Data

Year ended 31 DecemberNine months ended

30 September

2014 2015 2016 2016 2017

(in millions of U.S.$)

(Audited) (Unaudited)

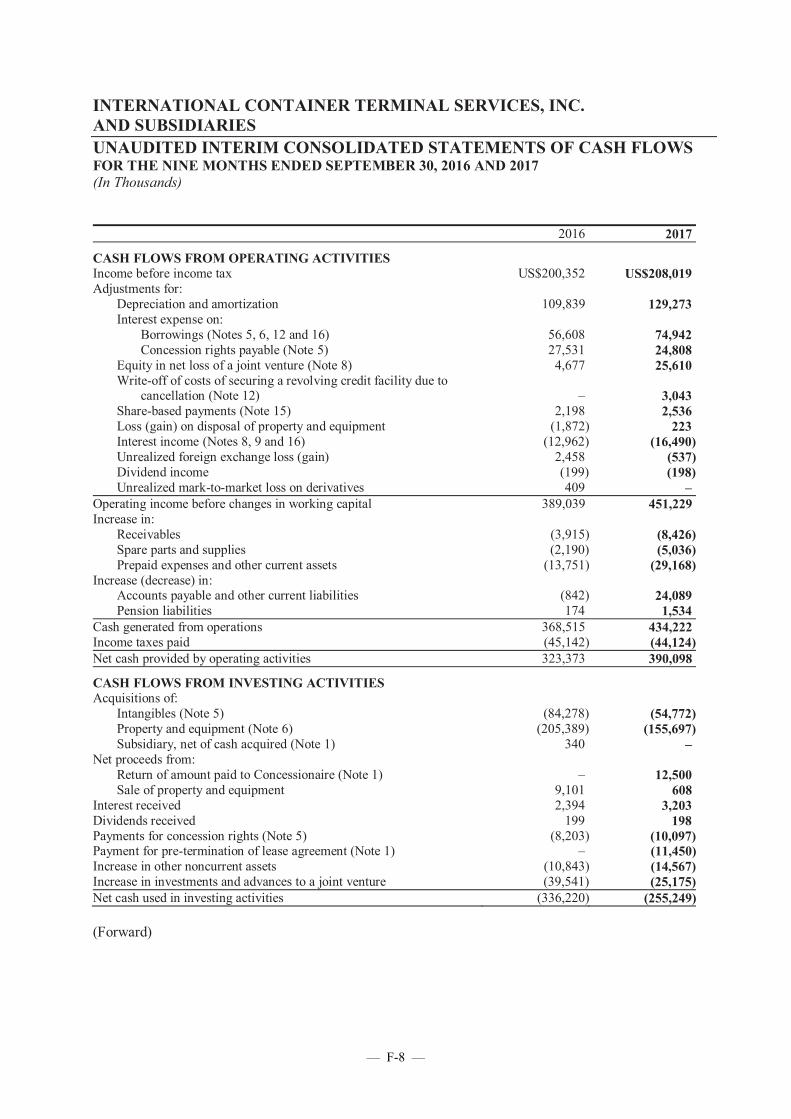

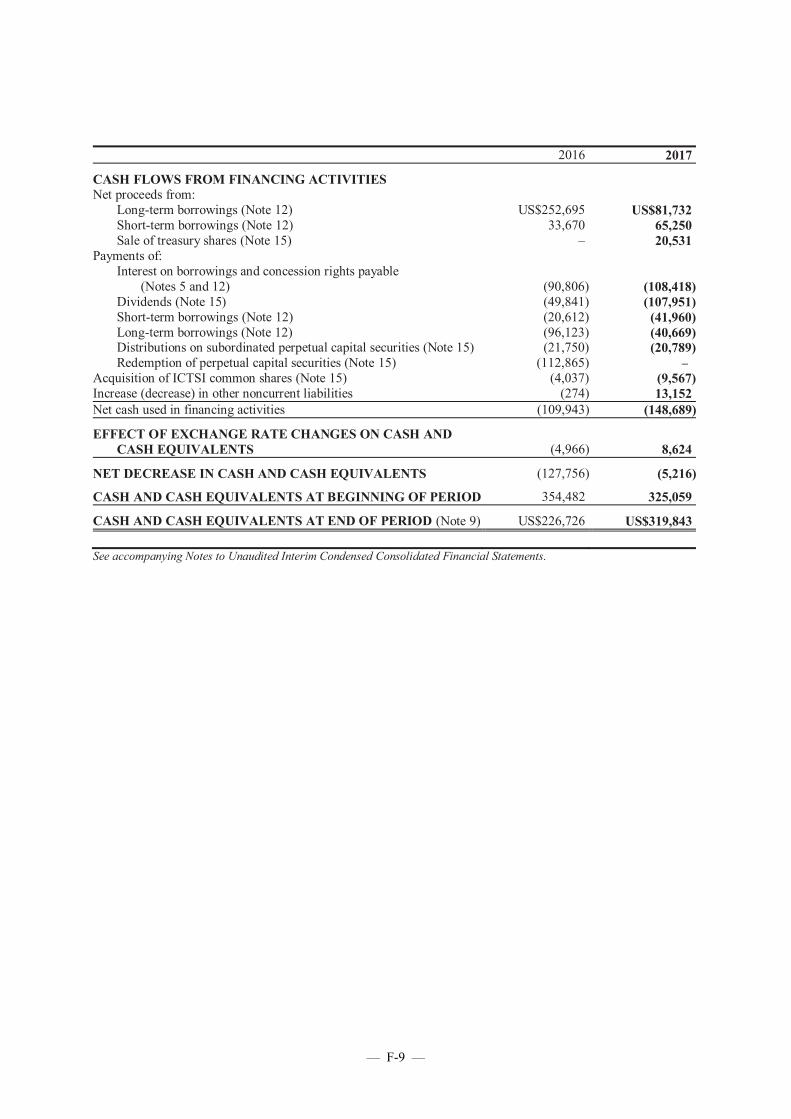

Net cash provided by operatingactivities................................... 387.8 407.7 466.9 323.4 390.1

Net cash used in investingactivities................................... (340.8) (547.6) (468.5) (336.2) (255.2)

Net cash provided by/(used in)financing activities ................... (94.1) 297.1 (21.7) (109.9) (148.7)

Effect of exchange rate changeson cash and cashequivalents.... ........................... (0.8) 3.0 (6.2) (5.0) 8.6

Net increase (decrease) in cashand cash equivalents ................. (47.9) 160.2 (29.4) (127.8) (5.2)

Cash and cash equivalents atbeginning of year/period ........... 242.2 194.3 354.5 354.5 325.1

Cash and cash equivalents at endof year/period ........................... 194.3 354.5 325.1 226.7 319.8

Other Financial Data

The following table shows EBITDA as derived from the Company’s net income for the period:

Year ended 31 DecemberNine months ended

30 September

2014 2015 2016 2016 2017

(in millions of U.S.$)

(Audited) (Unaudited)

Net income .................................. 191.5 69.0 193.5 150.8 168.1

Provision for income tax .............. 53.9 50.6 63.6 49.5 39.9

Income before income tax .......... 245.4 119.6 257.0 200.4 208.0

Add (Deduct):

Depreciation and amortisation ...... 121.7 126.5 147.8 109.8 129.3

Interest and other expenses(1) ....... 147.2 227.8 155.9 104.5 140.0

Interest and other income(2) ......... (71.2) (23.9) (35.7) (24.4) (42.4)

EBITDA (3) .................................. 443.0 450.0 525.1 390.3 434.9

Notes:

(1) Interest and other expenses include foreign exchange loss, interest expense on concession rights payable, impairment

losses, interest expense and financing charges on borrowings, equity in net loss of a joint venture and other expenses.

(2) Interest and other income include gain on sale of subsidiaries, foreign exchange gain, interest income and other income.

(3) EBITDA is not a uniformly or legally defined financial measure. It generally represents earnings before interest, taxes,

depreciation and amortisation. The Company presents EBITDA because it believes it to be an important supplemental

measure of its performance and liquidity and believes it is frequently used by securities analysts, investors and other

interested parties in the evaluation of companies in its industry.

— 17 —

The EBITDA figures are not, however, readily comparable to other companies’ EBITDA figures, as they are calculated

differently and must be read in conjunction with the related additional explanations. EBITDA has limitations as an

analytical tool and potential investors should not consider it in isolation or as a substitute for analysis of its results as

reported under PFRS. Some of the limitations concerning EBITDA are:

• EBITDA does not reflect the Company’s cash expenditures or future requirements for capital expenditures or

contractual commitments;

• EBITDA does not reflect changes in, or cash requirements for, the Company’s working capital needs;

• EBITDA does not reflect the interest expense, or the cash requirements necessary to service interest or principal

payments, on the Company’s debt;

• Although depreciation and amortisation are non-cash charges, the assets being depreciated or amortised will often

have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; and

• Other companies in the industry may calculate EBITDA differently than the Company does, limiting its usefulness

as a comparative measure.

Because of these limitations, EBITDA should not be considered as a measure of discretionary cash available to the

Company to invest in the growth of its business. The Company compensates for these limitations by relying primarily on

its PFRS results and using EBITDA only supplementally.

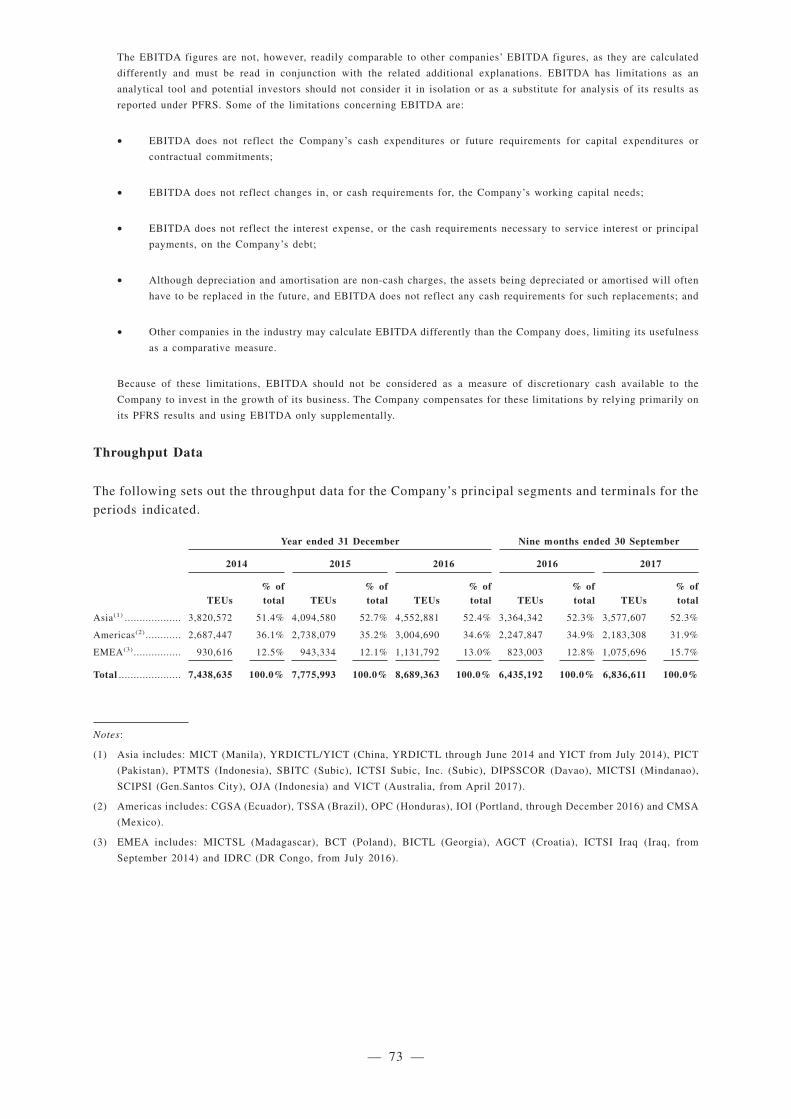

Throughput Data

The following sets out the throughput data for the Company’s principal segments and terminals for the

periods indicated.

Year ended 31 December Nine months ended 30 September

2014 2015 2016 2016 2017

TEUs% oftotal TEUs

% oftotal TEUs

% oftotal TEUs

% oftotal TEUs

% oftotal

Asia(1) ................... 3,820,572 51.4% 4,094,580 52.7% 4,552,881 52.4% 3,364,342 52.3% 3,577,607 52.3%

Americas(2) ............ 2,687,447 36.1% 2,738,079 35.2% 3,004,690 34.6% 2,247,847 34.9% 2,183,308 31.9%

EMEA(3) ................ 930,616 12.5% 943,334 12.1% 1,131,792 13.0% 823,003 12.8% 1,075,696 15.7%

Total ..................... 7,438,635 100.0% 7,775,993 100.0% 8,689,363 100.0% 6,435,192 100.0% 6,836,611 100.0%

Notes:

(1) Asia includes: MICT (Manila), YRDICTL/YICT (China, YRDICTL through June 2014 and YICT from July 2014), PICT

(Pakistan), PTMTS (Indonesia), SBITC (Subic), ICTSI Subic, Inc. (Subic), DIPSSCOR (Davao), MICTSI (Mindanao),

SCIPSI (Gen.Santos City), OJA (Indonesia) and VICT (Australia, from April 2017).

(2) Americas includes: CGSA (Ecuador), TSSA (Brazil), OPC (Honduras), IOI (Portland, through December 2016) and CMSA

(Mexico).

(3) EMEA includes: MICTSL (Madagascar), BCT (Poland), BICTL (Georgia), AGCT (Croatia), ICTSI Iraq (Iraq, from

September 2014) and IDRC (DR Congo, from July 2016).

— 18 —

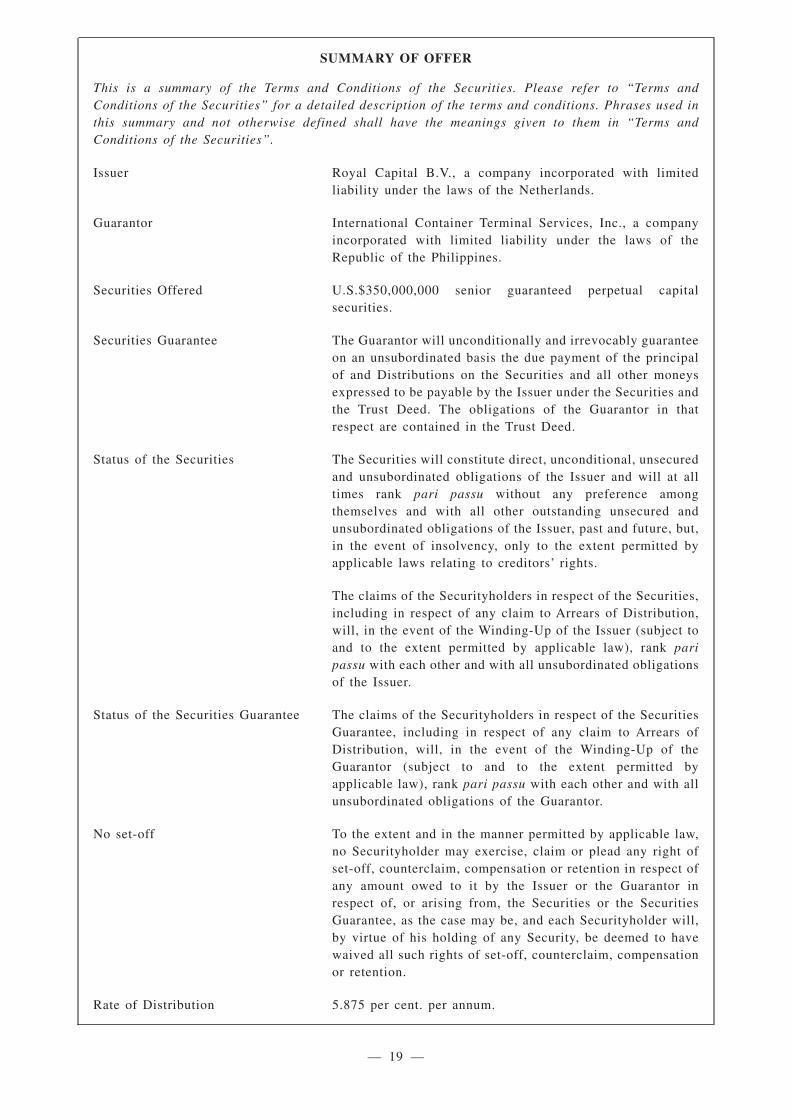

SUMMARY OF OFFER

This is a summary of the Terms and Conditions of the Securities. Please refer to “Terms andConditions of the Securities” for a detailed description of the terms and conditions. Phrases used inthis summary and not otherwise defined shall have the meanings given to them in “Terms andConditions of the Securities”.

Issuer Royal Capital B.V., a company incorporated with limitedliability under the laws of the Netherlands.

Guarantor International Container Terminal Services, Inc., a companyincorporated with limited liability under the laws of theRepublic of the Philippines.

Securities Offered U.S.$350,000,000 senior guaranteed perpetual capitalsecurities.

Securities Guarantee The Guarantor will unconditionally and irrevocably guaranteeon an unsubordinated basis the due payment of the principalof and Distributions on the Securities and all other moneysexpressed to be payable by the Issuer under the Securities andthe Trust Deed. The obligations of the Guarantor in thatrespect are contained in the Trust Deed.

Status of the Securities The Securities will constitute direct, unconditional, unsecuredand unsubordinated obligations of the Issuer and will at alltimes rank pari passu without any preference amongthemselves and with all other outstanding unsecured andunsubordinated obligations of the Issuer, past and future, but,in the event of insolvency, only to the extent permitted byapplicable laws relating to creditors’ rights.

The claims of the Securityholders in respect of the Securities,including in respect of any claim to Arrears of Distribution,will, in the event of the Winding-Up of the Issuer (subject toand to the extent permitted by applicable law), rank paripassu with each other and with all unsubordinated obligationsof the Issuer.

Status of the Securities Guarantee The claims of the Securityholders in respect of the SecuritiesGuarantee, including in respect of any claim to Arrears ofDistribution, will, in the event of the Winding-Up of theGuarantor (subject to and to the extent permitted byapplicable law), rank pari passu with each other and with allunsubordinated obligations of the Guarantor.

No set-off To the extent and in the manner permitted by applicable law,no Securityholder may exercise, claim or plead any right ofset-off, counterclaim, compensation or retention in respect ofany amount owed to it by the Issuer or the Guarantor inrespect of, or arising from, the Securities or the SecuritiesGuarantee, as the case may be, and each Securityholder will,by virtue of his holding of any Security, be deemed to havewaived all such rights of set-off, counterclaim, compensationor retention.

Rate of Distribution 5.875 per cent. per annum.

— 19 —

Issue Price 100 per cent.