IMPORTANT NOTICE IMPORTANT: You must read the following ...

667

IMPORTANT NOTICE IMPORTANT: You must read the following disclaimer before continuing. The following disclaimer applies to the attached offering memorandum (the “Offering Memorandum”) received by e-mail or otherwise received as a result of electronic communication, and you are therefore advised to read this disclaimer page carefully before reading, accessing or making any other use of the attached Offering Memorandum. In accessing the Offering Memorandum, you agree to be bound by the following terms and conditions, including any modifications to them from time to time, each time you receive any information from us as a result of such access. Confirmation of Your Representation: By accepting the email and accessing the attached Offering Memorandum you will be deemed to have represented to each of Australia and New Zealand Banking Group Limited, Barclays Bank PLC, Singapore Branch, BNP Paribas, Citigroup Global Markets Singapore Pte. Ltd., Crédit Agricole Corporate and Investment Bank, Singapore Branch, DBS Bank Ltd., Deutsche Bank AG, Singapore Branch, First Abu Dhabi Bank PJSC, ING Bank N.V., Singapore Branch, J.P. Morgan Securities plc, Merrill Lynch (Singapore) Pte. Ltd., Morgan Stanley & Co. International plc, SMBC Nikko Capital Markets Limited, Société Générale, Standard Chartered Bank and The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch (collectively, the “Joint Lead Managers”), that (i) you are outside the United States and, to the extent you purchase the securities described in the attached Offering Memorandum, you will be doing so pursuant to Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”) and (ii) that you consent to delivery of the attached Offering Memorandum and any amendments or supplements thereto by electronic transmission. This Offering Memorandum has been sent to you in electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of transmission and consequently none of the Issuer, the Joint Lead Managers, the Trustee (as defined in this Offering Memorandum), the Agents (as defined in this Offering Memorandum) or any person who controls, or is a director, officer, employee, agent, representative or affiliate of, any such person accepts any liability or responsibility whatsoever in respect of any difference between the Offering Memorandum distributed to you in electronic form and the hard copy version available to you on request from the Joint Lead Managers. Restrictions : The attached Offering Memorandum is being furnished in connection with an offering exempt from registration under the Securities Act solely for the purpose of enabling a prospective investor to consider the purchase of the securities described in the Offering Memorandum. You are reminded that the information in the attached document is not complete and may be changed. Any investment decision should be made on the basis of a complete final Offering Memorandum. Nothing in this electronic transmission constitutes an offer of securities for sale in any jurisdiction where it is unlawful to do so. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE SECURITIES ACT, OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND MAY NOT BE OFFERED OR SOLD WITHIN THE U.S., EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND ANY APPLICABLE STATE OR LOCAL SECURITIES LAWS. You are reminded that you have accessed the attached Offering Memorandum on the basis that you are a person into whose possession this Offering Memorandum may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located and you may not nor are you authorized to deliver or forward this document, electronically or otherwise, to any other person. If you have gained access to this transmission contrary to the foregoing restrictions, you will be unable to purchase any of the securities described therein. Actions that You May Not Take : You should not reply by e-mail to this electronic transmission, and you may not purchase any securities by doing so. Any reply e-mail communications, including those you generate by using the “Reply” function on your e-mail software, will be ignored or rejected. THE ATTACHED OFFERING MEMORANDUM MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORIZED. You are responsible for protecting against viruses and other destructive items. Your use of this e-mail is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and other items of a destructive nature.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of IMPORTANT NOTICE IMPORTANT: You must read the following ...

IMPORTANT NOTICE

IMPORTANT: You must read the following disclaimer before continuing. The following disclaimer appliesto the attached offering memorandum (the “Offering Memorandum”) received by e-mail or otherwisereceived as a result of electronic communication, and you are therefore advised to read this disclaimer pagecarefully before reading, accessing or making any other use of the attached Offering Memorandum. Inaccessing the Offering Memorandum, you agree to be bound by the following terms and conditions,including any modifications to them from time to time, each time you receive any information from us asa result of such access.

Confirmation of Your Representation: By accepting the email and accessing the attached OfferingMemorandum you will be deemed to have represented to each of Australia and New Zealand Banking GroupLimited, Barclays Bank PLC, Singapore Branch, BNP Paribas, Citigroup Global Markets Singapore Pte.Ltd., Crédit Agricole Corporate and Investment Bank, Singapore Branch, DBS Bank Ltd., Deutsche BankAG, Singapore Branch, First Abu Dhabi Bank PJSC, ING Bank N.V., Singapore Branch, J.P. MorganSecurities plc, Merrill Lynch (Singapore) Pte. Ltd., Morgan Stanley & Co. International plc, SMBC NikkoCapital Markets Limited, Société Générale, Standard Chartered Bank and The Hongkong and ShanghaiBanking Corporation Limited, Singapore Branch (collectively, the “Joint Lead Managers”), that (i) you areoutside the United States and, to the extent you purchase the securities described in the attached OfferingMemorandum, you will be doing so pursuant to Regulation S under the U.S. Securities Act of 1933, asamended (the “Securities Act”) and (ii) that you consent to delivery of the attached Offering Memorandumand any amendments or supplements thereto by electronic transmission.

This Offering Memorandum has been sent to you in electronic form. You are reminded that documentstransmitted via this medium may be altered or changed during the process of transmission and consequentlynone of the Issuer, the Joint Lead Managers, the Trustee (as defined in this Offering Memorandum), theAgents (as defined in this Offering Memorandum) or any person who controls, or is a director, officer,employee, agent, representative or affiliate of, any such person accepts any liability or responsibilitywhatsoever in respect of any difference between the Offering Memorandum distributed to you in electronicform and the hard copy version available to you on request from the Joint Lead Managers.

Restrictions: The attached Offering Memorandum is being furnished in connection with an offering exemptfrom registration under the Securities Act solely for the purpose of enabling a prospective investor toconsider the purchase of the securities described in the Offering Memorandum. You are reminded that theinformation in the attached document is not complete and may be changed. Any investment decision shouldbe made on the basis of a complete final Offering Memorandum.

Nothing in this electronic transmission constitutes an offer of securities for sale in any jurisdiction whereit is unlawful to do so.

THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THESECURITIES ACT, OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHERJURISDICTION AND MAY NOT BE OFFERED OR SOLD WITHIN THE U.S., EXCEPT PURSUANTTO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATIONREQUIREMENTS OF THE SECURITIES ACT AND ANY APPLICABLE STATE OR LOCALSECURITIES LAWS.

You are reminded that you have accessed the attached Offering Memorandum on the basis that you are aperson into whose possession this Offering Memorandum may be lawfully delivered in accordance with thelaws of the jurisdiction in which you are located and you may not nor are you authorized to deliver orforward this document, electronically or otherwise, to any other person. If you have gained access to thistransmission contrary to the foregoing restrictions, you will be unable to purchase any of the securitiesdescribed therein.

Actions that You May Not Take: You should not reply by e-mail to this electronic transmission, and youmay not purchase any securities by doing so. Any reply e-mail communications, including those yougenerate by using the “Reply” function on your e-mail software, will be ignored or rejected.

THE ATTACHED OFFERING MEMORANDUM MAY NOT BE FORWARDED OR DISTRIBUTEDTO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER.ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLEOR IN PART IS UNAUTHORIZED.

You are responsible for protecting against viruses and other destructive items. Your use of this e-mail is atyour own risk and it is your responsibility to take precautions to ensure that it is free from viruses and otheritems of a destructive nature.

Thi

sP

reli

min

ary

Off

erin

gM

emor

andu

mis

subj

ect

toco

mpl

etio

nan

dam

endm

ent.

The

Not

esm

ayno

tbe

sold

nor

may

offe

rsto

buy

beac

cept

edpr

ior

toth

eti

me

afi

nal

Off

erin

gM

emor

andu

mis

com

plet

ed.

Thi

sP

reli

min

ary

Off

erin

gM

emor

andu

msh

all

not

cons

titu

tean

offe

rto

sell

orth

eso

lici

tati

onof

anof

fer

tobu

y,no

rsh

all

ther

ebe

any

sale

ofth

eN

otes

,in

any

juri

sdic

tion

inw

hich

such

offe

r,so

lici

tati

onor

sale

wou

ldbe

unla

wfu

lpr

ior

tore

gist

rati

on,

qual

ific

atio

nor

exem

ptio

nun

der

the

secu

riti

esla

ws

ofan

ysu

chju

risd

icti

on.

SUBJECT TO COMPLETIONPRELIMINARY OFFERING MEMORANDUM DATED JANUARY 14, 2018 CONFIDENTIAL

ABJA Investment Co. Pte. Ltd.(Incorporated in Singapore)

(Registration Number: 201309883M)US$ [●] [●]% Notes Due [●]US$ [●] [●]% Notes Due [●]

Each of the US$[●] [●]% Notes due [●] (the “[●] Notes”) and the US$[●] [●]% Notes due [●] (the “[●] Notes” and, togetherwith the [●] Notes, the “Notes”) will be the unsecured senior obligations of ABJA Investment Co. Pte. Ltd. (the “Issuer”), andwill rank pari passu with all of its other existing and future unsubordinated obligations and will be effectively subordinatedto its secured obligations and the obligations of its subsidiaries. Tata Steel has provided a non-binding letter of comfort to theTrustee on behalf of the noteholders in connection with the issuance of the Notes.

The [●] Notes will bear interest at a rate of [●]% per year. Interest will be paid on the [●] Notes semi-annually in arrear on[●] and [●] of each year, beginning on [●], 2018. Unless previously repurchased, cancelled, exchanged or redeemed, the [●]Notes will mature on [●]. The [●] Notes will bear interest at a rate of [●]% per year. Interest will be paid on the [●] Notessemi-annually in arrear on [●] and [●] of each year, beginning on [●], 2018. Unless previously repurchased, cancelled,exchanged or redeemed, the [●] Notes will mature on [●]. If a Change of Control (as defined herein) occurs, each Noteholder(as defined herein) shall have the right to require the Issuer to redeem all of such Noteholders’ Notes at 101% of their principalamount plus accrued and unpaid interest. Subject to the terms and conditions of the Notes (the “Conditions”), the Issuer mayalso redeem all of the Notes at 100% of their principal amount plus accrued and unpaid interest if at any time the Issuer becomesobligated to pay withholding taxes as a result of certain changes in tax law. Subject to the above and unless previouslyredeemed, purchased, exchanged or cancelled, the [●] Notes will mature and the Issuer will redeem the [●] Notes at theirprincipal amount on [●] and the [●] Notes will mature and the Issuer will redeem the [●] Notes at their principal amount on[●]. The Notes will not be guaranteed by Tata Steel or any other member of the Group.

For a more detailed description of the Notes, see “Terms and Conditions of the [●] Notes” and “Terms and Conditions of the[●] Notes” beginning on pages 175 and 199, respectively.

Issue Price for the [●] Notes: [●]%Issue Price for the [●] Notes: [●]%

Investing in the Notes involves certain risks. You should read “Risk Factors” beginning on page 39 before investing inthe Notes.

MiFID II product governance/Professional investors and ECPs only target market — For the purposes of Directive 2014/65/EU(as amended, “MiFID II”), any person offering, selling or recommending the Notes (a “distributor”) should take intoconsideration the target market in respect of the Notes which is eligible counterparties and professional clients only, each asdefined in MiFID II; however, a distributor subject to MiFID II is responsible for undertaking its own target market assessmentin respect of the Notes (by either adopting or refining the target market) and determining appropriate distribution channels.

Approval in principle has been granted for the listing and quotation of the Notes on the Singapore Exchange Securities TradingLimited (the “SGX-ST”). The SGX-ST takes no responsibility for the accuracy of any of the statements made or opinions orreports contained in this Offering Memorandum. Approval in-principle received for the listing and quotation of the Notes onthe SGX-ST is not to be taken as an indication of the merits of either us, this offering or the Notes. The Notes will be tradedon the SGX-ST in a minimum board lot size of US$200,000 for so long as any of the Notes are listed and quoted on the SGX-STand the rules of the SGX-ST so require.

The Notes have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “SecuritiesAct”), or any U.S. state securities laws. Accordingly, the Notes are being offered and sold only to persons outside theUnited States in compliance with Regulation S under the Securities Act (“Regulation S”). For a description of certainrestrictions on resales and transfers, see “Subscription and Sale”.

Each of the Notes will be represented by a global certificate (the “Global Certificate”) in registered form which will beregistered in the name of a nominee for a common depositary for Clearstream Banking, S.A. (“Clearstream, Luxembourg”) andEuroclear Bank S.A./N.V. (“Euroclear”) on or about [●]. Individual certificates evidencing holdings of the Notes will only beissued in certain limited circumstances described under “The Global Certificate”. The Notes are expected to be rated BB- byS&P.

Joint Lead Managers

ANZ Barclays BNP PARIBASBofA Merrill Lynch Citi DBS Bank Ltd.Crédit Agricole CIB Deutsche Bank First Abu Dhabi Bank

HSBC ING J.P. Morgan Securities plcMorgan Stanley SMBC Nikko Société Générale

Corporate & Investment BankingStandard Chartered Bank

The date of this Offering Memorandum is [●], 2018.

NOTICE TO INVESTORS

The Issuer, as well as the Joint Lead Managers, reserve the right to withdraw the offering of the Notesat any time or to reject any offer to purchase, in whole or in part, for any reason, or to sell less thanall of the Notes offered hereby.

This Offering Memorandum is personal to the prospective investor to whom it has been delivered bythe Joint Lead Managers and does not constitute an offer to any other person or to the public in generalto subscribe for or otherwise acquire the Notes. Distribution of this Offering Memorandum to anyperson other than the prospective investor and those persons, if any, retained to advise that prospectiveinvestor with respect thereto is unauthorized, and any disclosure of its contents without the Issuer’sprior written consent is prohibited. The prospective investor, by accepting delivery of this OfferingMemorandum, agrees to the foregoing and agrees not to make any photocopies of this OfferingMemorandum.

This Offering Memorandum is intended solely for the purpose of soliciting indications of interest inthe Notes from prospective investors and does not purport to summarize all of the terms, conditions,covenants and other provisions contained in any transaction documents described herein. Theinformation provided is not all-inclusive. The market information in this Offering Memorandum hasbeen obtained by the Issuer from publicly available sources deemed by it to be reliable.Notwithstanding any investigation that the Joint Lead Managers may have conducted with respect tothe information contained herein, the Joint Lead Managers do not accept any liability in relation tothe information contained in this Offering Memorandum or its distribution or with regard to any otherinformation supplied by or on the Issuer’s behalf.

The Issuer and the Group accept responsibility for the information contained in this OfferingMemorandum. To the best of the knowledge of the Issuer and the Group (having taken all reasonablecare to ensure that such is the case) the information contained in this Offering Memorandum is inaccordance with the facts and does not omit anything likely to affect the import of such information.

Prospective investors in the Notes should rely only on the information contained in this OfferingMemorandum. None of the Group, the Issuer, the Joint Lead Managers, the Trustee or the Agents hasauthorized the provision of information different from that contained in this Offering Memorandum.The information contained in this Offering Memorandum is accurate in all material respects only asof the date of this Offering Memorandum, regardless of the time of delivery of this OfferingMemorandum or of any sale of the Notes. Neither the delivery of this Offering Memorandum nor anysale made hereunder shall under any circumstances imply that there has been no change in the Issuer’saffairs and those of its subsidiaries or that the information set forth herein is correct in all materialrespects as of any date subsequent to the date hereof.

Prospective investors hereby acknowledge that (i) they have not relied on the Joint Lead Managers orany person affiliated with the Joint Lead Managers in connection with any investigation of theaccuracy of such information or their investment decision, and (ii) no person has been authorized togive any information or to make any representation concerning the Issuer or the Notes (other than ascontained herein and information given by the Issuer’s duly authorized officers and employees, asapplicable, in connection with investors’ examination of the Issuer and the terms of this offering) and,if given or made, any such other information or representation should not be relied upon as havingbeen authorized by the Group, the Issuer, the Joint Lead Managers, the Trustee or the Agents.

None of the Joint Lead Managers, the Group, the Issuer, the Trustee, the Paying Agent, theTransfer Agent and the Registrar or their respective affiliates or representatives is making anyrepresentation to any offeree or purchaser of the Notes offered hereby regarding the legality ofany investment by such offeree or purchaser under applicable legal investment or similar laws.None of the Joint Lead Managers, the Trustee, the Paying Agent, the Transfer Agent, the

i

Registrar or their respective affiliates or representatives makes any representation, warranty orundertaking, express or implied, or accepts any responsibility, with respect to the accuracy orcompleteness of any of the information in this Offering Memorandum. To the fullest extentpermitted by law, none of the Joint Lead Managers, the Trustee or the Agents accepts anyresponsibility for the contents of this Offering Memorandum or for any other statement made orpurported to be made by the Joint Lead Managers, the Trustee or the Agents or on their behalfin connection with the Issuer or the issue and offering of the Notes. Each of the Joint LeadManagers, the Trustee or the Agents accordingly disclaims all and any liability whether arisingin tort or contract or otherwise which it might otherwise have in respect of this OfferingMemorandum or any such statement.

Each prospective investor contemplating purchasing any Notes should make its own independentinvestigation of the financial condition and affairs, and its own appraisal of the creditworthinessof the Issuer and the terms of the Notes being offered, including the merits and risks involvedand its purchase of the Notes should be based upon such investigations with its own tax, legal andbusiness advisers as it deems necessary. See “Risk Factors” for a discussion of certain factors tobe considered. Any prospective investor in the Notes should be able to bear the economic risk ofan investment in the Notes for an indefinite period of time.

This Offering Memorandum does not constitute an offer to sell, or a solicitation of an offer to buy,

any Notes offered hereby by any person in any jurisdiction in which it is unlawful for such person to

make an offer or solicitation in such jurisdiction.

The distribution of this Offering Memorandum and the offer and sale of the Notes may, in certain

jurisdictions, be restricted by law. None of the Issuer, the Joint Lead Managers, the Trustee or the

Agents represents that this Offering Memorandum may be lawfully distributed, or that any Notes may

be lawfully offered, in compliance with any applicable registration or other requirements in any such

jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for

facilitating any such distribution or offering. In particular, no action has been taken by any of the

Issuer or the Joint Lead Managers which would permit a public offering of any Notes or distribution

of this Offering Memorandum in any jurisdiction where action for that purpose is required.

Accordingly, no Notes may be offered or sold, directly or indirectly, and neither this Offering

Memorandum nor any advertisement or other offering material may be distributed or published in any

jurisdiction, except under circumstances that will result in compliance with any applicable laws and

regulations.

Each purchaser of the Notes (each, a “Noteholder”) must comply with all applicable laws and

regulations in force in each jurisdiction in which it purchases, offers or sells the Notes or possesses

or distributes this Offering Memorandum, and must obtain any consent, approval or permission

required for the purchase, offer or sale by it of the Notes under the laws and regulations in force in

any jurisdiction to which it is subject or in which it makes purchases, offers or sales. Persons into

whose possession this Offering Memorandum or any Notes may come must inform themselves about,

and observe, any such restrictions on the distribution of Offering Memorandum and the offering and

sale of the Notes. In particular, there are restrictions on the offer and sale of the Notes, and the

circulation of documents relating thereto, in certain jurisdictions including the United States and the

European Economic Area and to persons connected therewith. See “Subscription and Sale”.

This Offering Memorandum has been prepared on the basis that all offers of the Notes will be made

pursuant to an exemption under Article 3 of the Prospectus Directive, as implemented in member

states of the European Economic Area, from the requirement to produce a prospectus for offers of the

Notes.

ii

This Offering Memorandum has not been and will not be registered as a prospectus with the MonetaryAuthority of Singapore. Accordingly, this Offering Memorandum and any other document or materialin connection with the offer or sale, or invitation for subscription or purchase, of the Notes may notbe circulated or distributed, nor may the Notes be offered or sold, or be made the subject of aninvitation for subscription or purchase, whether directly or indirectly, to persons in Singapore otherthan (i) to an institutional investor under Section 274 of the Securities and Futures Act, Chapter 289of Singapore (the “SFA”), (ii) to a relevant person pursuant to Section 275(1), or any person pursuantto Section 275(1A), and in accordance with the conditions specified in Section 275, of the SFA, or (iii)otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of theSFA.

Where the Notes are subscribed or purchased under Section 275 of the SFA by a relevant person whichis:

(a) a corporation (which is not an accredited investor (as defined in Section 4A of the SFA)) the solebusiness of which is to hold investments and the entire share capital of which is owned by oneor more individuals, each of whom is an accredited investor; or

(b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investmentsand each beneficiary of the trust is an individual who is an accredited investor,

securities (as defined in Section 239(1) of the SFA) of that corporation or the beneficiaries’ rights andinterest (howsoever described) in that trust shall not be transferred within six months after thatcorporation or that trust has acquired the Notes pursuant to an offer made under Section 275 of theSFA except:

(i) to an institutional investor or to a relevant person defined in Section 275(2) of the SFA, orto any person arising from an offer referred to in Section 275(1A) or Section 276(4)(i)(B)of the SFA;

(ii) where no consideration is or will be given for the transfer;

(iii) where the transfer is by operation of law;

(iv) as specified in Section 276(7) of the SFA; or

(v) as specified in Regulation 32 of the Securities and Futures (Offers of Investments) (Sharesand Debentures) Regulations 2005 of Singapore.

For a description of these and certain further restrictions on offers and sales of the Notes and thedistribution of this Offering Memorandum, see “Subscription and Sale”.

In connection with the issue of the Notes, Australia and New Zealand Banking Group Limited (the“Stabilizing Manager”) or any person acting on behalf of the Stabilizing Manager may, to the extentpermitted by applicable laws and directives, over-allot the Notes or effect transactions with a view tosupporting the price of the Notes at a level higher than that which might otherwise prevail, but in sodoing, the Stabilizing Manager or any person acting on behalf of the Stabilizing Manager shall act asprincipal and not as agent of the Issuer. However, there is no assurance that the Stabilizing Manageror any person acting on behalf of the Stabilizing Manager will undertake stabilization action. Any lossor profit sustained as a consequence of any such overallotment or stabilization shall be for the accountof the Joint Lead Managers.

MiFID II product governance/Professional investors and ECPs only target market

Solely for the purposes of each manufacturer’s product approval process, the target market assessmentin respect of the Notes has led to the conclusion that: (i) the target market for the Notes is eligible

iii

counterparties and professional clients only, each as defined in Directive 2014/65/EU (as amended,

“MiFID II”); and (ii) all channels for distribution of the Notes to eligible counterparties and

professional clients are appropriate. Any person subsequently offering, selling or recommending the

Notes (a “distributor”) should take into consideration the manufacturer’s target market assessment;

however, a distributor subject to MiFID II is responsible for undertaking its own target market

assessment in respect of the Notes (by either adopting or refining the manufacturer’s target market

assessment) and determining appropriate distribution channels.

iv

PRESENTATION OF FINANCIAL INFORMATION

Financial Data

The Issuer’s and the Group’s fiscal year ends on March 31. Accordingly, references in this OfferingMemorandum to a particular fiscal year are to the year ended March 31 of that year. References to ayear other than a “fiscal year” are to the calendar year ended December 31 of that year.

The Group is required to prepare its financial statements in accordance with Ind-AS with effect fromApril 1, 2016. Accordingly, the financial statements as at and for the year ended March 31, 2017,together with the comparative period data as at and for the year ended March 31, 2016, have beenprepared in in accordance with Ind-AS. The Issuer is required to prepare its financial statements inaccordance with Singapore Financial Reporting Standards (“SFRS”). Accordingly, all of the Issuer’sfinancial statements presented in this Offering Memorandum have been prepared in accordance withSFRS.

All historical consolidated financial information in this Offering Memorandum is that of the Group,its consolidated subsidiaries and joint ventures and associates. In this Offering Memorandum, unlessotherwise specified, all financial information is of the Group on a consolidated basis. All historicalnon-consolidated financial information in this Offering Memorandum is that of Tata Steel or theIssuer, as specified.

The annual financial statements of the Group, on a consolidated basis, and of Tata Steel, on astandalone basis, as at and for the years ended March 31, 2015, 2016 and 2017 (collectively, the“Annual Financial Statements”), and financial results for the six month periods ended September 30,2016 and 2017, have each been prepared in accordance with the following:

(i) with respect to the six months ended September 30, 2016 and 2017, prepared and presented inaccordance with Ind-AS;

(ii) with respect to the years ended March 31, 2016 and 2017, prepared and presented in accordancewith Ind-AS; and

(iii) with respect to the comparative period data for the years ended March 31, 2015 and 2016,prepared and presented in accordance with Indian GAAP.

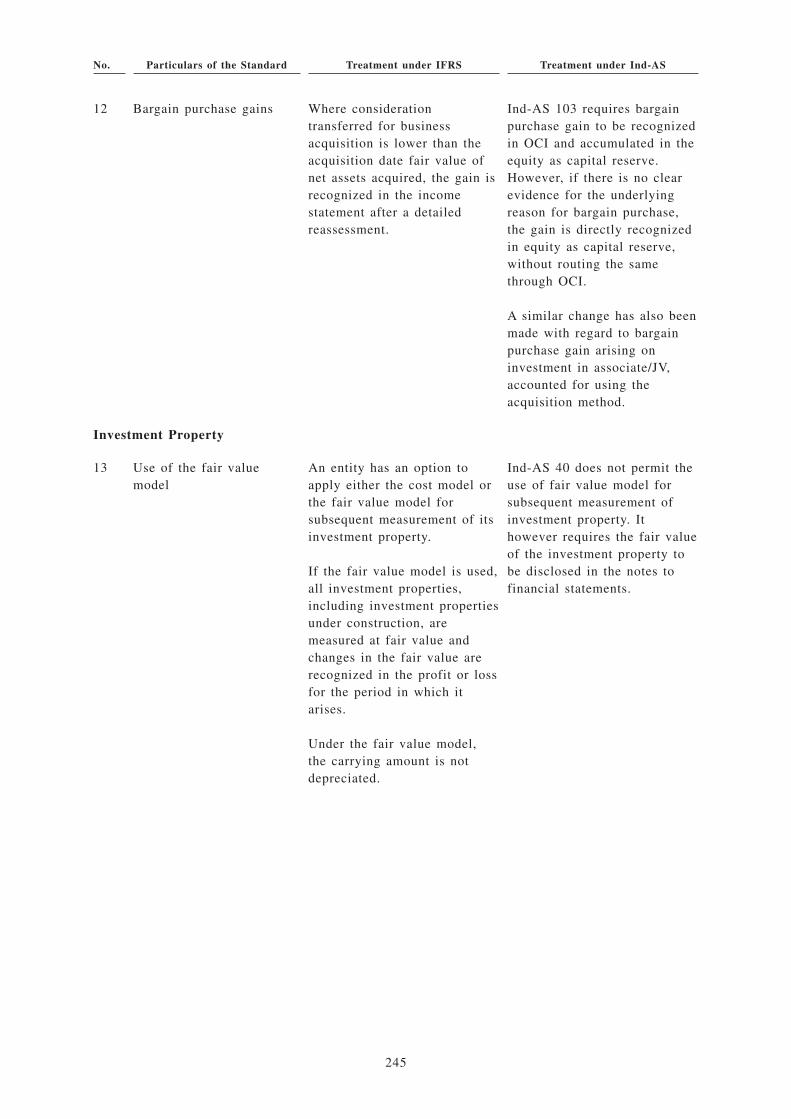

Ind-AS differs in certain respects from generally accepted accounting principles in the InternationalFinancial Reporting Standards (“IFRS”). For a discussion of certain significant differences betweenInd-AS and IFRS, see “Description of Certain Differences between Ind-AS and IFRS”. In making aninvestment decision, investors must rely on their own examination of the Group, the terms of theoffering and the financial information contained in this Offering Memorandum. Potential investorsshould consult their own professional advisers for an understanding of the differences between IndianGAAP and US GAAP or IFRS, and how these differences might affect their understanding of thefinancial information contained herein.

The Annual Financial Statements for the Group have been audited by Deloitte Haskins and Sells LLP,Chartered Accountants (“Deloitte”), as set forth in their audit reports included herein. For the financialyear beginning from April 1, 2017 onwards, Price Waterhouse and Co. Chartered Accountants LLP(“Price Waterhouse and Co.”) became the statutory auditor for the Group, andPricewaterhouseCoopers LLP became the auditors for the Issuer.

On January 10, 2018, SEBI imposed a two year ban on Price Waterhouse and Co network of firms inIndia (which includes Price Waterhouse & Co.) from auditing any publicly listed companies in Indiaas a result of their involvement as auditors in Satyam Computer Services Limited. The ban does notimpact Price Waterhouse & Co.’s ability to continue as statutory auditors of Tata Steel and the Groupfor financial year ending March 31, 2018. Price Waterhouse and Co network of firms in India have

v

proposed to appeal the SEBI ban, and should Price Waterhouse & Co. become legally incapable tocontinue the office of Tata Steel and the Group’s statutory auditors post March 31, 2018 Tata Steelwould evaluate to fill the vacancy in such eventuality, keeping in line with the requirements of theapplicable statutes in India.

The Annual Financial Statements for the Issuer have been audited by Deloitte, as set forth in theiraudit reports included herein. The unaudited interim financial statements of the Issuer for the sixmonths ended September 30, 2017, have been subject to limited review by PricewaterhouseCoopersLLP as set forth in their report dated January 12, 2018.

The standalone financial results of Tata Steel for the quarter and six months ended September 30, 2017have been audited by Price Waterhouse and Co. and the consolidated financial results of the Group forthe quarter ended September 30, 2017 have been subjected to a limited review by Price Waterhouseand Co. as set forth in their respective review reports included herein.

The unaudited interim financial statements of the Issuer for the six months ended September 30, 2017,have been subjected to a limited review by PricewaterhouseCoopers LLP as set forth in their reviewreport dated January 12, 2018.

Reporting Segments

The Group is engaged in the business of manufacturing steel products across the globe. The operatingsegments have been identified based on the different geographical areas where major entities withinthe Group operate, and the Chief Operating Decision Maker reviews and assesses the Group’sperformance based on the same.

The Group’s reportable segments and segment information is presented below:

• Tata Steel India

• Other Indian operations

• Tata Steel Europe

• Other trade related operations

• South East Asian operations

• Rest of the world

Non-GAAP Financial Measures

As used in this Offering Memorandum, a non-GAAP financial measure is one that purports to measurehistorical financial performance, financial position or cash flows, but excludes or includes amountsthat would not be so adjusted in the most comparable IFRS, Ind-AS and SFRS measures. From timeto time, reference is made in this Offering Memorandum to such “non-GAAP financial measures”,including EBITDA, or (unless otherwise specified) earnings before finance income and costs,taxation, depreciation, amortization and impairment and share of results of associates, and net debt,or (unless otherwise specified) non-current borrowings plus current borrowings minus cash and cashequivalents, current and non-current restricted cash, and short-term investments. The Group’smanagement believes that EBITDA, net debt, operating free cash flow, return on average net worth,return on average capital employed and other non-GAAP financial measures provide investors withadditional information about the Group’s performance, as well as ability to incur and service debt andfund capital expenditure, and are measures commonly used by investors. For more detailed

vi

information concerning EBITDA, see “Summary Financial and Operating Data”. The non-GAAP

financial measures described herein are not a substitute for IFRS, Ind-AS and SFRS measures of

earnings and may not be comparable to similarly titled measures reported by other companies due to

differences in the way these measures are calculated.

Rounding

Certain amounts and percentages included in this Offering Memorandum have been rounded.

Accordingly, in certain instances, the sum of the numbers in a column may not equal the total figure

for that column. Numbers have been rounded off to one decimal where the numbers on rounding off

amounted to zero.

vii

CERTAIN DEFINITIONS

In this Offering Memorandum, unless otherwise specified or the context otherwise requires, “the

Group” refers to Tata Steel Limited and its consolidated subsidiaries and joint ventures and associates.

References to the “Issuer” mean ABJA Investment Co. Pte. Ltd.

In this Offering Memorandum, unless otherwise specified, all financial statements and financial data

are of the Group on a consolidated basis. In this Offering Memorandum, unless otherwise specified

or the context otherwise requires, references to “$”, “US$” or “U.S. Dollars” are to United States

dollars, references to “Rs.”, “rupee”, “rupees” or “Indian rupees” are to the legal currency of India,

references to “GBP”, “pounds” or “£” are to the official currency of the United Kingdom, references

to “CAD” or “C$” are to the official currency of the Canada, references to “SGD” or “S$” are to

Singapore dollars, references to “THB” are to Thai baht and references to Euro, “Euros” or “ C= ” are

to the common currency of the Eurozone countries. References to a particular “Financial Year” are to

the financial year ended March 31 of such year. In this Offering Memorandum, references to “U.S.”

or “United States” are to the United States of America, its territories and its possessions. References

to “India” are to the Republic of India.

viii

EXCHANGE RATE INFORMATION

The following table sets forth, for the periods indicated, certain information concerning the exchange

rates between Indian rupees and U.S. Dollars. The exchange rates reflect the rates as reported by the

FEDAI.

Period Period end Average High Low

2012(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 51.16 47.95 54.24 43.95

2013(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 54.28 54.43 57.33 50.52

2014(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 59.89 60.47 68.85 53.67

2015(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 61.16 61.16 63.67 58.47

2016(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 65.45 65.45 68.72 62.19

2017(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . 67.08 67.08 68.77 64.85

July 2017 . . . . . . . . . . . . . . . . . . . . . . 64.19 64.46 64.88 64.11

August 2017 . . . . . . . . . . . . . . . . . . . . 63.91 63.96 64.16 63.59

September 2017 . . . . . . . . . . . . . . . . . . 65.29 64.46 65.72 63.79

October 2017 . . . . . . . . . . . . . . . . . . . . 64.75 65.06 65.50 64.75

November 2017 . . . . . . . . . . . . . . . . . . 64.47 64.86 65.43 64.32

December 2017. . . . . . . . . . . . . . . . . . . 63.88 64.24 64.58 63.88

January 2018 (through to January 8,2018) . . . . . . . . . . . . . . . . . . . . . . . . 63.51 63.50 63.68 63.37

(1) Represents the financial year ended March 31 of the year indicated.

The exchange rate on January 8, 2018 as reported by the FEDAI was Rs.63.51 per US$1.00.

Although certain rupee amounts in this Offering Memorandum have been translated into U.S. Dollars

for convenience, this does not mean that the rupee amounts referred to could have been, or could be,

converted into U.S. Dollars at any particular rate, the rates stated below, or at all. Except as otherwise

stated, Indian Rupee amounts as at and for the financial year ended March 31, 2017, and as at and for

the six months ended September 30, 2017, were converted to U.S. Dollars at the exchange rate of

US$1.00 = Rs.64.85 and US$1.00 = Rs.65.28, respectively.

ix

FORWARD-LOOKING STATEMENTS AND ASSOCIATED RISKS

Certain statements in this Offering Memorandum are not historical facts and are forward-lookingstatements. This Offering Memorandum may contain words such as “believe”, “could”, “may”, “will”,“target”, “estimate”, “project”, “predict”, “forecast”, “guideline”, “should”, “plan”, “expect” and“anticipate” and similar expressions that are intended to identify forward-looking statements, but arenot the exclusive means of identifying these statements. All statements regarding the Group’s expectedfinancial condition and results of operations and business plans and prospects are forward-lookingstatements. In particular, “Summary”, “Management’s Discussion and Analysis of Financial Conditionand Results of Operations of the Group”, “Management’s Discussion and Analysis of FinancialCondition and Results of Operations of the Group” and “Business” contain forward-lookingstatements, including relating to market trends, capital expenditure and other factors affecting theGroup that are not historical facts.

Forward-looking statements are subject to certain risks and uncertainties, including, but not limitedto:

• changes in global economic, political and social conditions;

• changes in economic and political conditions and increases in regulatory burdens in India andother countries in which the Group operates, transacts business or has interests;

• the Group’s substantial indebtedness and ability to meet its debt service obligations;

• the risk of a potential fall in steel prices or of price volatility;

• accidents and natural disasters in India or in other countries in which the Group operates orglobally, including specifically India’s neighboring countries;

• the Group’s business and operating strategies and its ability to implement such strategies;

• the Group’s ability to successfully implement its growth and expansion plans, technologicalchanges, exposure to market risks and foreign exchange risks that have an impact on its businessactivities;

• the Group’s ability to ensure continuity of senior management and ability to attract and retainkey personnel;

• the implementation of new projects, including future acquisitions and financings;

• the availability and terms of external financing;

• the Group’s ability to meet its capital expenditure requirements or increases in capitalexpenditure requirements;

• the Group’s inability to successfully compete with other steel manufacturers;

• cost overruns or delays in commencement of production from the Group’s new projects;

• changes in the Group’s relationship with the Government and the governments of the countriesin which the Group operates;

• changes in exchange controls, import controls or import duties, levies or taxes, either ininternational markets or in India;

• changes in laws, regulations, taxation or accounting standards or practices that affect the Group;

x

• changes in prices or demand for the products produced by the Group both in India and in

international markets;

• changes in the value of the rupee against major global currencies and other currency changes;

• the ability of third parties to perform in accordance with contractual terms and specifications;

• any adverse outcome in legal proceedings in which the Group is or may become involved

including, with respect to product liability claims;

• acquisitions and divestitures which the Group may undertake;

• changes in interest rates;

• significant fluctuations of the prices of raw materials;

• the estimated reserves of the Group’s iron ore mines; and

• other factors, including those discussed in “Risk Factors”.

Forward-looking statements involve inherent risks and uncertainties. If one or more of these or other

uncertainties or risks materialize, actual results may vary materially from those estimated, anticipated

or projected. Specifically, but without limitation, capital costs could increase, projects could be

delayed, and anticipated improvements in capacity, performance or profit levels might not be fully

realized. Although the Group believes that the expectations of its management as reflected by such

forward-looking statements are reasonable based on information currently available to it, no

assurances can be given that such expectations will prove to have been correct. Accordingly, you are

cautioned not to place undue reliance on the forward-looking statements, which speak only as of the

date they are made. Neither the Issuer nor the Group undertakes any obligation to update or revise any

of them, whether as a result of new information, future developments or otherwise.

xi

TABLE OF CONTENTS

Page

DEFINITIONS AND GLOSSARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

SUMMARY FINANCIAL AND OPERATING DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

THE OFFERING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

CAPITALIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

SELECTED CONSOLIDATED FINANCIAL DATA AND OTHER INFORMATION . . . . . . . 70

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS OF THE GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS OF TATA STEEL . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

DESCRIPTION OF THE ISSUER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135

MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

SHARE OWNERSHIP OF THE GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

REGULATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166

DESCRIPTION OF MATERIAL INDEBTEDNESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

TERMS AND CONDITIONS OF THE [●] NOTES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

TERMS AND CONDITIONS OF THE [●] NOTES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 199

THE GLOBAL CERTIFICATE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223

TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 224

CLEARANCE AND SETTLEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 229

SUBSCRIPTION AND SALE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230

TRANSFER RESTRICTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

INDEPENDENT AUDITORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 236

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237

DESCRIPTION OF CERTAIN DIFFERENCES BETWEEN IND-AS AND IFRS . . . . . . . . . 238

INDEX TO FINANCIAL STATEMENTS AND AUDITORS’ REPORTS . . . . . . . . . . . . . . . . F-1

xii

DEFINITIONS AND GLOSSARY

In addition to the terms that are otherwise defined in this Offering Memorandum, the following setsout the definitions of certain terms used in this Offering Memorandum.

Act or Companies Act or IndianCompanies Act . . . . . . . . . . . . .

Companies Act, 2013, together with rules and regulationsthereunder or, where applicable, the Companies Act, 1956,together with the rules and regulations thereunder, each asamended, supplemented or reenacted from time to time

Board or Board of Directors . . . . Board of Directors of Tata Steel, unless otherwise specified

brownfield . . . . . . . . . . . . . . . . . . Land occupied by defunct or under-utilized commercial orindustrial facilities

CAGR . . . . . . . . . . . . . . . . . . . . . Compounded Annual Growth Rate

crude steel . . . . . . . . . . . . . . . . . . Cast, solidified steel before further treatment

Directors . . . . . . . . . . . . . . . . . . . Directors of Tata Steel

downstream . . . . . . . . . . . . . . . . . Further processing of crude steel to produce finished steelproducts

EBITDA . . . . . . . . . . . . . . . . . . . Earnings before finance income and costs, taxation,depreciation, amortization and impairment and share ofresults of associates (unless otherwise specified). It is not aIFRS (GAAP) measure

Eurozone . . . . . . . . . . . . . . . . . . . The members of the European Union that have adopted theEuro as their common currency

FEDAI . . . . . . . . . . . . . . . . . . . . . Foreign Exchange Dealer’s Association of India

finished product . . . . . . . . . . . . . . Steel ready for construction or manufacturing use

GDP. . . . . . . . . . . . . . . . . . . . . . . gross domestic product

GoI or Government or CentralGovernment . . . . . . . . . . . . . . .

Government of India

greenfield project . . . . . . . . . . . . . a project that lacks any constraints by prior work

Group . . . . . . . . . . . . . . . . . . . . . Tata Steel Limited, its subsidiaries and joint ventures andassociates

Hazardous Wastes Rules. . . . . . . . The Hazardous and Other Wastes (Management andTransboundary Movement) Rules, 2016

IFRS . . . . . . . . . . . . . . . . . . . . . . International Financial Reporting Standards

I D Act . . . . . . . . . . . . . . . . . . . . Industrial Disputes Act, 1947, as amended

Indian GAAP . . . . . . . . . . . . . . . . Generally Accepted Accounting Practices in India

Ind-AS . . . . . . . . . . . . . . . . . . . . . Indian Accounting Standards

km . . . . . . . . . . . . . . . . . . . . . . . . Kilometers

1

kt . . . . . . . . . . . . . . . . . . . . . . . . . 1,000 tons

LIBOR . . . . . . . . . . . . . . . . . . . . . London Interbank Offered Rate

Minimum Wages Act . . . . . . . . . . Minimum Wages Act, 1948, as amended

mt . . . . . . . . . . . . . . . . . . . . . . . . Million tons

mtpa . . . . . . . . . . . . . . . . . . . . . . Million tons per annum

RBI . . . . . . . . . . . . . . . . . . . . . . . Reserve Bank of India

Re.. . . . . . . . . . . . . . . . . . . . . . . . One Indian Rupee

Rs. or Rupees . . . . . . . . . . . . . . . Indian Rupees

SEBI . . . . . . . . . . . . . . . . . . . . . . Securities and Exchange Board of India constituted under theSEBI Act, 1992

SFRS . . . . . . . . . . . . . . . . . . . . . . Singapore Financial Reporting Standards

Supreme Court . . . . . . . . . . . . . . . Supreme Court of India

tpa . . . . . . . . . . . . . . . . . . . . . . . . Tons per annum

TSE . . . . . . . . . . . . . . . . . . . . . . . Tata Steel Europe and its subsidiaries

Tata Steel. . . . . . . . . . . . . . . . . . . Tata Steel Limited as a standalone entity

ton . . . . . . . . . . . . . . . . . . . . . . . . Metric ton or 1,000 kilograms

Upstream . . . . . . . . . . . . . . . . . . . Processing of raw materials and production of crude steel

US GAAP . . . . . . . . . . . . . . . . . . Generally accepted accounting principles in the United Statesof America

2

SUMMARY

This overview highlights certain information contained in this Offering Memorandum. This overview

does not contain all the information you should consider before investing in the Notes. You should read

this entire Offering Memorandum carefully, including the sections entitled “Forward-Looking

Statements and Associated Risks”, “Risk Factors”, “Management’s Discussion and Analysis of

Financial Condition and Results of Operations of the Group” and “Business” included elsewhere in

this Offering Memorandum and the financial information and the notes thereto set forth herein. To

understand the terms of the Notes, you should carefully read the sections of this Offering Memorandum

entitled “Terms and Conditions of the Notes”.

Overview

The Group is one of the world’s largest steel companies with a steel production capacity of

approximately 27.5 mtpa. According to the World Steel Association (“WSA”), the Group was the

world’s 10th largest steel maker by crude steel production volume in 2016. The Group is also one of

the most geographically diversified steel producers, with operations in 26 countries and a commercial

presence in more than 50 countries. As of March 31, 2017, the Group had over 70,000 employees.

Tata Steel was established as India’s first integrated steel company in 1907 by Jamsetji N. Tata and

is one of the flagship companies of the Group. The Group has a presence across the entire value chain

of steel manufacturing, including producing and distributing finished products as well as mining and

processing iron ore and coal for its steel production. The Group’s operations are primarily focused in

India, Europe, and South East Asia. For the year ended March 31, 2017, the Group’s operations in

India and Europe represented approximately 43% and 39%, respectively, of the revenue of the Group,

and for the six months ended September 30, 2017, represented approximately 45% and 46%,

respectively, of the revenue of the Group.

The steel production capacity of the Group has increased from approximately 5.0 mtpa in the year

ended March 31, 2006 to approximately 27.5 mtpa as of March 31, 2017. In India, as of September

30, 2017, the Group has steel production facilities located in Jamshedpur and Kalinganagar, with a

total steel production capacity of 12.7 mtpa. The Group’s operations in India also include captive iron

ore and coal mines. Additionally, the Group has significant operations in the United Kingdom and the

Netherlands, where the Group has a total steel production capacity of 12.4 mtpa. The remaining steel

production capacity of the Group is located in South East Asia.

For the year ended March 31, 2017, the Group’s business in India recorded sales of 10.97 mt,

recording a growth of 15.0% over the year ended March 31, 2016 and a growth of 22.0% for the six

months ended September 30, 2017, compared to the six months ended September 30, 2016. This

increase was largely due to the ramping up of operations at the Kalinganagar plant in Odisha, which

is now operating at full capacity.

The Group offers a broad range of steel products including a portfolio of high value-added

downstream products such as hot rolled, cold rolled and coated steel, sections, plates, rebars, wire

rods, tubes, rails and wires. The Group is also a large producer of ferro-chrome in India.

The Group’s main markets for its products are India and Europe, which together accounted for

approximately 82% and 83% of the Group’s revenue for the year ended March 31, 2016 and 2017,

respectively, with the remaining sales primarily taking place in other markets in Asia. The Group’s

customers are primarily in the construction, infrastructure, automotive, consumer goods, material

handling, aerospace and general engineering industries.

3

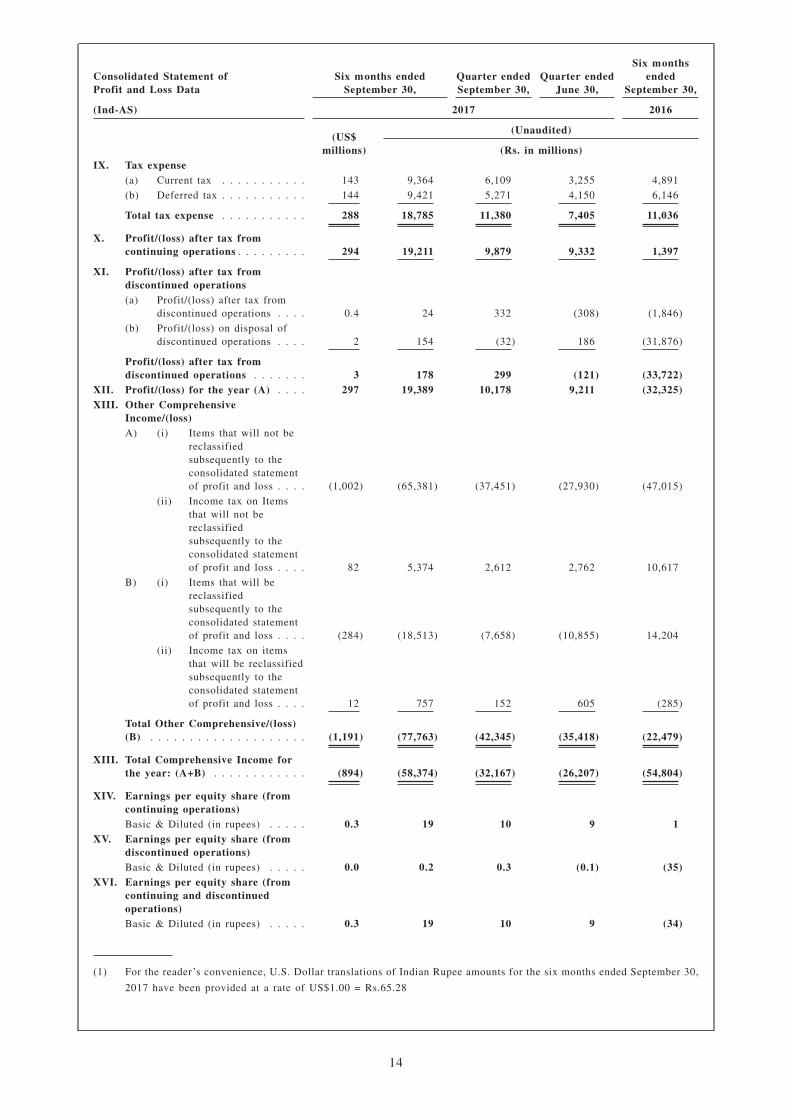

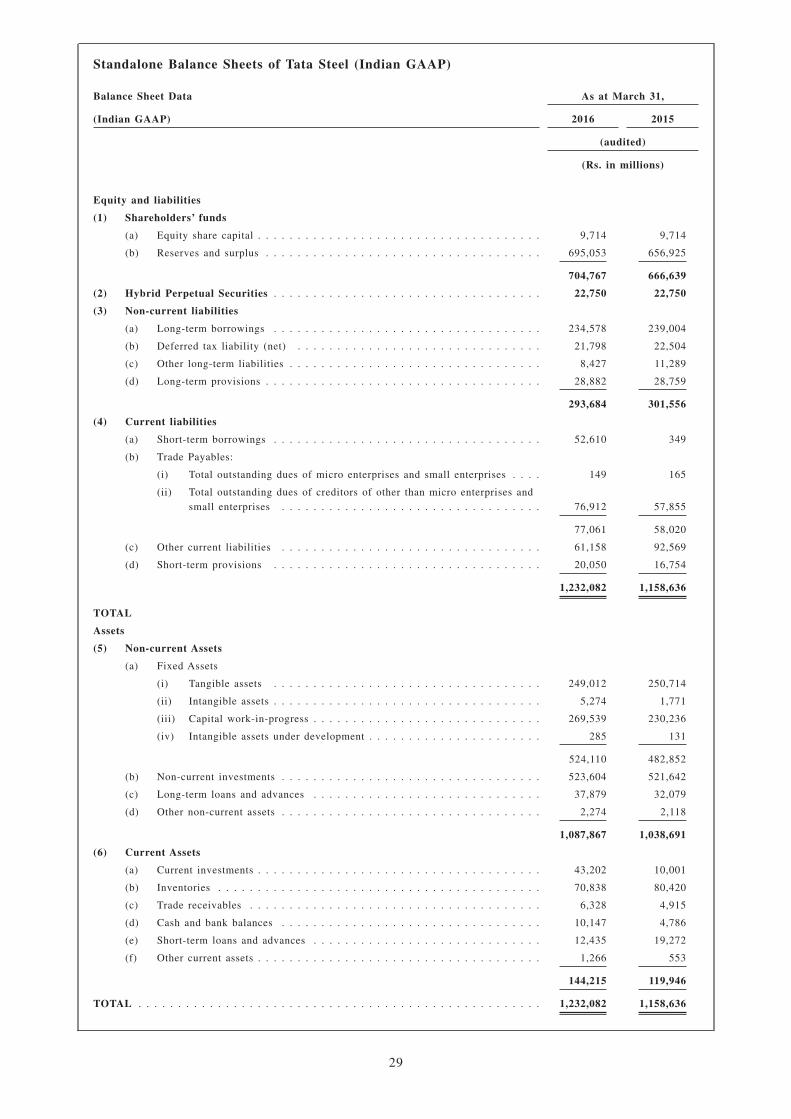

For the years ended March 31, 2016 and 2017, the Group recorded revenues of Rs.1,063,399 millionand Rs.1,174,199 million, respectively. The Group recorded a loss of Rs.4,971 million for the yearended March 31, 2016, a loss of Rs.41,686 million for the year ended March 31, 2017, a profit ofRs.19,389 million for the six months ended September 30, 2017 against a loss of Rs.32,325 millionfor the six months ended September 30, 2016. The Group had total assets of Rs.1,733,332 million asof March 31, 2017 and Rs.1,742,203 million as of September 30, 2017.

For the years ended March 31, 2016 and 2017, the Group had total steel production of 22.9 mt and24.2 mt, respectively. Similarly, the Group had steel production of 11.5 mt and 12.5 mt for the sixmonth periods ended on September 30, 2016 and September 30 2017, respectively.

Key Strengths

Sustainable and highly cost efficient operations in India

The Group is one of the lowest cost steel producers in India and it has successfully maintained its costleadership over several years. The cost of production of the Group’s Indian operations ranks amongthe lowest for hot rolled coils globally. The Group derives its competitive advantage through accessto raw materials from their captive mines and a highly skilled workforce with a relatively low cost oflabor at its operations in India. This advantage is especially valuable given the difficulty of achievingraw materials cost pass-through in the steel industry. In India, the Group has significant captive ironore, coking coal, chrome ore and manganese ore mines that accommodate a majority of its currentrequirements.

These factors have enabled the Group’s Indian operations to maintain robust operating margins inIndia. For the year ended March 31, 2017, with respect to its Indian operations, the Group obtained100% of its iron ore requirements and approximately 36% of its coking coal requirement from captivemines leased by the Group.

As a result, the Group expects that its exposure to volatility in prices of commodities such as iron oreand coking coal, for the Group’s Indian operations will be limited.

To expedite projects related to operational excellence across the value chain, in 2014, the Grouplaunched the SHIKHAR 25 program. The focus of SHIKHAR 25 is to improve process efficiency,speed and throughput, reliability, energy efficiency, value-in-use, supply chain and logistics and otherprocesses. Performance benchmarking at each of these processes allows the Group to readily identifyareas in need of improvement. The ultimate goal of SHIKHAR 25 is to improve overall processefficiency that would translate into EBITDA improvement. These initiatives resulted in approximatelyRs.34,000 million of cost savings in the year ended March 31, 2017.

Leading position across operations

The Group has significant market positions in its principal markets, India and Europe, across mainareas of operations in upstream and downstream steel products.

In India, the Group produces flat products used in the automotive and engineering industries and longproducts used in the construction industry, including in the industrial, commercial, infrastructure andhousing sectors. According to the Joint Plant Committee (a committee formed by the Indian Ministryof Steel to collect data on the industry), the Group’s Indian operations produced approximately 12%of sales of all the finished steel in India and was the third largest producer of crude steel for year endedMarch 31, 2017. According to the Joint Plant Committee, the Group had a market share of 15.7% ofsales in flat products for carbon steel for the year ended March 31, 2017.

In addition, the Group also benefits from being identified with the Tata brand, which is a widelyrecognized brand in India.

4

India is principally the largest market for the Group’s operations, representing approximately 43% of

its total revenue for the year ended March 31, 2017. The Group believes that its diversified customer

sector portfolio and strategic focus on creating customer relationships will continue to generate

customer loyalty and enable it to maintain its market share position in the construction, packaging, rail

and automotive sectors.

Global scale

The Group is one of the world’s largest steel companies and operates a global suite of integrated steel

making facilities, mining complexes and distribution companies. It has a commercial presence in over

50 countries, including both developed and emerging markets, and principal markets in Europe, India

and South East Asia. The Group believes that its global scale and reach enhances its ability to service,

retain and attract multi-national customers and, in particular, customers from the automotive,

packaging and construction industries. As major customers continue to globalize their operations and

are increasingly relying on a select few global suppliers for their products (such as in the automotive

sector), the Group believes it can attract new customers and better retain its existing customers

through its diversified downstream operations, product range and strong product branding, as well as

its extensive distribution and production capabilities.

The Group also benefits from its global scale operations, procurement, production plants and

distribution network, which allow the Group to achieve greater economies of scale and improve its

cost efficiencies across the supply chain, from raw material sourcing to product deliveries and support

functions.

Diversified product base targeting multiple end user segments

The Group has a wide range of product offerings that cater to diversified end-markets across

geographies. Over the years, the Group has significantly expanded its product portfolio through a mix

of acquisitions, downstream capacity expansions and joint ventures with other leading steel

companies.

The Group has significantly enhanced its portfolio of downstream steel products to differentiate itself

from competitors, including through its acquisition of Corus and downstream capacity expansions in

India. With its capacity expansions in India, the Group has further strengthened its ability to provide

a greater variety of value-added products.

Furthermore, the Group has entered into joint ventures with downstream foreign steel specialist

producers, including BlueScope Steel Limited and Nippon Steel and Sumitomo Metal Corporation, for

finishing plants that produce color coated steel and automotive cold rolled flat products, respectively.

In addition, the Group continues to invest in research and development and explore opportunities to

further improve their product offerings to customers.

Efficient project implementation

The Group has a proven track record of implementing significant projects, including cost reduction

plans and expansion plans for its major production facilities. The Group expanded its existing

brownfield crude steel capacity at Jamshedpur from 6.8 mtpa to 9.7 mtpa in December 2012 and

established a greenfield project of 3.0 mtpa in Kalinganagar, Odisha which increased crude steel

capacity in India from 9.7 mtpa to 12.7 mtpa. In addition, the Group has rebuilt one of the blast

furnaces at the Group’s facility in Port Talbot.

5

Uniquely positioned to undertake acquisitions opportunistically

The Group is uniquely positioned to undertake acquisitions opportunistically, in particular

opportunities with respect to companies in India undergoing the corporate insolvency resolution

process under the IBC.

The Group evaluates acquisition opportunities based on possibilities for synergies, broadening its

customer base, access to raw materials, manufacturing facilities, infrastructure, new geographic

locations and advanced technology, widening its product offerings and growth opportunities that such

acquisition may offer. The Group’s extensive operations in different parts of India and across various

verticals in the steel industry enhance possibilities for synergies from such acquisition opportunities.

The combination of the Group’s domain expertise of the Indian steel industry, coupled with its

knowledge of the global steel industry and its experience with acquisitions, enables it to better

evaluate strategic acquisition opportunities. Further, due to its track record of successful acquisitions,

the Group’s internal teams have experience and expertise in complex domestic and international

competitive acquisitions which can be leveraged in evaluating acquisition opportunities and executing

them in an efficient and timely manner. Additionally, the Group’s extensive experience in various

industries and acquisitions will help it evaluate acquisition opportunities.

If the Group pursues any acquisition opportunities, its robust balance sheet can potentially enable it

to avail internal and external funding options, which will enhance its ability to submit competitive

bids. Further, the brand name of the Group, and the reputation of the “Tata Group”, also provide it with

competitive advantages in acquisition processes.

The above factors differentiate the Group from its competitors and contribute to its unique position

to capitalize on acquisition opportunities in India, especially with respect to opportunities arising from

the corporate insolvency resolution process under the IBC.

Skilled workforce led by experienced management team

The Group’s senior management team is comprised of members with professional qualifications and

extensive experience in the steel industry. The senior management team’s rich experience and

understanding of the Group has been essential in building a sustainable global operation which

employs over 70,000 individuals, while the Group’s employee policies and welfare programs have

been instrumental in recruiting and retaining the high caliber workforce.

The Group seeks to nurture internal talent for senior management positions by hiring recent graduates

from top universities as entry-level employees, and then identifying and promoting the most promising

candidates through the management ranks. The employee welfare program is developed from the

Group’s philosophy that people are its greatest asset. The program affirms the rights to trade union

representation and collective consultation, ensures an ethical, just and fair workplace, encourages

work-life balance and provides managerial and functional training opportunities for all employees.

The Group’s commitment to building an ethical organisation through a committed workforce was

reaffirmed as it received the “World’s Most Ethical Company Award” in 2017 from Ethisphere USA

for the fifth time.

6

Strategy

Capacity Expansion in Growing Indian Steel Markets

In recent years, the Group has successfully implemented significant projects focused on expanding thecapacity of its Indian operations through brownfield and greenfield projects, such as expanding itsfacility at Jamshedpur and establishing the Kalinganagar facility. The Group intends to continue toincrease the size of its operations in India in view of the growing steel market, and its competitiveadvantage as a low-cost producer, through its brownfield and greenfield expansion projects.

Restructuring of European portfolio

As part of the process of the Group’s restructuring of its European operations, on September 20, 2017,Tata Steel and Thyssenkrupp AG signed a memorandum of understanding to create a new 50:50 jointventure company called Thyssenkrupp Tata Steel. This joint venture is expected to be the next stagein the transformation of the Group’s European business. The joint venture is intended to create a largerworld-class and globally competitive strip steel business, which, if successful, will be the secondlargest steel company in Europe.

This joint venture follows other restructuring initiatives, including the following:

• On May 31, 2016, Longs Steel UK Limited and other subsidiaries of TSE, which were involvedwith the long steel business, were sold to Greybull Capital LLP;

• On May 1, 2017, TSE completed the sale of the Specialty Steels business to Liberty SpecialtySteels Ltd.;

• On July 31, 2017, TSE completed the sale of its 42 and 84 inch pipe mills in Hartlepool toLiberty Specialty Steels Ltd. Pursuant to these portfolio changes, activities of TSE will befocused on the manufacture and sale of strip products; and

• The British Steel Pension Scheme (“BSPS”) is the principal defined benefit pension scheme ofthe Group in the United Kingdom. On March 31, 2017 the BSPS was closed to future accrual andreplaced by a defined contribution scheme. On September 11, 2017 the BSPS separated from TataSteel UK (“TSUK”) and a number of affiliated companies on completion of a RegulatedApportionment Arrangement (“RAA”). TSUK has also agreed to sponsor a proposed new pensionscheme (“BSPS2”), subject to certain qualifying conditions being met. Since the RAA hascompleted, all members of the BSPS will be invited to transfer to the new scheme. If thequalifying conditions are met, members may choose to be transferred to BSPS2. The BSPS2scheme would have lower future annual increases for pensioners and deferred members comparedto the BSPS, giving it an improved funding position which is expected to improve the risk profilefor TSUK.

Increase Sales of High Value-Added Products and Branded Sales

The Group plans to increase sales of its specialized solutions, high value products and brandedproducts to improve its product mix and generate higher and sustainable margins. In India, the Groupplans to continue increasing its production and sales of high value-added steel products such as coldrolled coil, automotive-grade sheets, coated products such as tinplate, color-coated steel andgalvanized steel.

To consolidate gains from retail growth, the Group is also offering services and solutions whichprovide spin-off benefits that could potentially open new revenue streams in the future and keep retailsales from hitting a plateau. Simultaneously, the Group has increased its production and sales throughthe commencement of new manufacturing capacities at the Kalinganagar plant, which commencedoperations in June 2016 and has recently ramped up to full capacity. The Group’s steel-based solutions

7

include Pravesh (wood-finished steel doors), Nest-In (modular housing), toilets and water ATMs andRoof Junction (a complete roofing solution). The Group is also exploring the possibility of offeringservices or solutions for the furniture space which has wood-like finishes on blended steel structures.

To further enhance the high value-added product portfolio, the Group intends to increase productionthrough its various joint ventures, including the following:

• Tata BlueScope Steel Limited manufactures coated steel coils, steel building solutions andrelated building products;

• The Group’s joint venture with Nippon Steel and Sumitomo Metal Corporation;

• Jamshedpur Continuous Annealing & Processing Company Private Limited has a continuousannealing and processing line to produce automotive cold rolled flat products; and

• The Group’s joint venture with Nichia Steel Works, Japan through its subsidiary Siam IndustrialWire Co., Thailand to set up a high-end galvanized wires facility which including galvanizedwires for cable stay strands and zinc-aluminum coated wires.

Enhance Competitiveness through Continuous Improvement

The Group continues to improve its competitiveness through a number of initiatives and programsaimed at enhancing operational efficiencies and optimizing asset and material flows. The Group seeksto benefit from sharing experiences and best operational practices across its business units in India,Europe and South East Asia.

Operational Stability

Significant capital expenditure has been committed to support the strategic growth of differentiated,high value products in the automotive, lifting and excavating, and oil and gas market sectors. TheGroup is leveraging its market position in downstream products to aid margin improvement. TheGroup is also focused on streamlining its logistical operations in Europe through a supply chaintransformation improvement initiative which commenced in September 2016.

Further, to improve its operations in Europe, TSE approved the Strategic Asset Roadmap program in2015, to increase the sales of differentiated, high value products in several market segments includingautomotive, lifting and excavating and energy and power. This has required revamping and upgradingthe facilities to produce high quality products.

Raw Materials Security

The Group seeks access to raw materials for its operations in India and internationally in order toachieve economic returns and to optimize its costs by securing off-take rights. The Group believes thatbecoming increasingly self-sufficient in raw materials procurement will enable it to better respond tocyclical fluctuations in the demand for products and reduce volatility in production costs. For the yearended March 31, 2017, with respect to its Indian operations, the Group obtained 100% of its iron orerequirements and approximately 36% of its coking coal requirement from captive mines.

The Group’s various coking coal and iron ore assets across geographies include a 64% stake in SouthAfrica’s Sedibeng Iron Ore Company and a joint venture in Canada in relation to a project spread overvarious iron ore deposits in the provinces of Quebec and Newfoundland and Labrador.

The Group intends to continue to work with its partners to pursue its current initiatives and, ifopportunities arise, to pursue new initiatives, subject to market conditions, in effort to becomeincreasingly self-sufficient in its raw material procurement.

8

Strategic Control Over Logistics and Supply Chain

The Group continues to differentiate itself from competitors in India with various initiatives inlogistics and supply chain management. With a particular focus on the automotive, construction andsmall and medium enterprise customer segments, the Group has enhanced its distribution channels.The principal goal of these initiatives was to be able to provide supplies on an “on time in full” basis.

In India, the Group has developed a nationwide network of exclusive distributors and dealers. Toincrease efficiencies, the Group redesigned its supply network using the hub-and-spoke mode ofoperations and information technology enabled color-based dispatch priority systems. As a result, theGroup has been able to increase sales in the retail segment.

Other principal supply chain improvement initiatives include:

• Supply chain enhancements such as deploying theory of constraints, improving deliverycompliance via steel service center management and the availability of ready to use materialfrom certified service centers;

• Standardization and availability of information; and

• Convenience through the development of information technology systems across the distributionchannels, channel authentication through an authorized dealer network, conducive shoppingexperience through exclusive retail outlets and improved reach to largest consumption centers.

To further enhance its supply chain and enhance control over logistics, the Group entered into a jointventure with NYK Lines, a Japanese shipping company, to provide logistics solutions such as portoperations, ship agency, custom clearance, in-land logistics, warehousing, shipping and freightforwarding for dry bulk, containerized, break-bulk and project cargo.

Strategic Alliances with Joint Venture Partners

The Group’s expansion plans have benefitted from strategic alliances with joint venture partnersthroughout its chain of operations, including for raw material procurement (primarily for mining),steel production, product diversification and shipping. For example, through the Group’s strategicpartners it has developed:

• Mining operations in Canada;

• Downstream value-added steel production pursuant to joint ventures with BlueScope SteelLimited;

• Product diversification pursuant to a joint venture with Nippon Steel and Sumitomo MetalCorporation; and

• Shipping operations with NYK Line and Martrade.

The Group continues to expand its capacity and operations through joint ventures including throughits memorandum of understanding on September 20, 2017, with Thyssenkrupp AG to create a new jointventure company, namely, Thyssenkrupp Tata Steel.

Continue to pursue inorganic growth opportunities, including with respect to distressed assets

The Group intends to continue to pursue inorganic growth opportunities, with a particular focus onacquisitions that generate greater synergies and production capacity, manufacturing facilities,infrastructure and advanced technology, and which allow it to diversify its product and customer base.

9

In addition, the Group is pursuing and may continue to pursue opportunities for acquisition of

financially stressed assets, including with respect to companies that are undergoing a corporate

insolvency resolution process under the IBC. In considering such acquisition opportunities, the Group

has and may continue to rely on its deep experience and knowledge generally for evaluating

acquisitions, including the cost benefit and financing of such acquisitions.

The IBC Process is a statutory process for insolvency resolution of corporate entities in a time-bound

manner to maximize the value of assets of such entities. Currently, certain Indian steel manufacturing

companies such as Bhushan Steel Limited, Electrosteel Steels Limited, Essar Steel India Limited,