IMPORTANT NOTICE

294

IMPORTANT NOTICE THIS PROSPECTUS MAY ONLY BE DISTRIBUTED TO PERSONS WHO ARE NOT U.S. PERSONS (AS DEFINED IN REGULATION S (REGULATION S) UNDER THE UNITED STATES SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT)) AND WHO ARE OUTSIDE OF THE UNITED STATES. IMPORTANT: You must read the following disclaimer before continuing. The following disclaimer applies to the attached prospectus (the Document) whether received by e-mail, accessed from an internet page or otherwise received as a result of electronic communication, and you are therefore advised to read this disclaimer carefully before reading, accessing or making any other use of the Document. In accessing the Document, you agree to be bound by the following terms and conditions, including any modifications to them from time to time, each time you receive any information from any of the Issuer and/or the Joint Lead Managers (each as defined below) as a result of such access. Restrictions: UNDER NO CIRCUMSTANCES SHALL THE DOCUMENT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR SHALL THERE BE ANY SALE OF THE SECURITIES IN THE UNITED STATES OR ANY OTHER JURISDICTION IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL. ANY SECURITIES TO BE ISSUED HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACT OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND MAY NOT BE OFFERED, SOLD, PLEDGED OR OTHERWISE TRANSFERRED DIRECTLY OR INDIRECTLY (I) AS PART OF THEIR DISTRIBUTION AT ANY TIME OR (II) OTHERWISE UNTIL 40 DAYS AFTER THE COMPLETION OF THE DISTRIBUTION, AS DETERMINED BY THE JOINT LEAD MANAGERS, OF ALL SECURITIES, WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE AND LOCAL SECURITIES LAWS. THE DOCUMENT MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON WITHOUT THE PRIOR WRITTEN CONSENT OF THE JOINT LEAD MANAGERS AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER. DISTRIBUTION OR REPRODUCTION OF THE DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE SECURITIES LAWS OF OTHER JURISDICTIONS. WITHIN THE UNITED KINGDOM, THE DOCUMENT IS DIRECTED ONLY AT (A) PERSONS WHO HAVE PROFESSIONAL EXPERIENCE IN MATTERS RELATING TO INVESTMENTS FALLING WITHIN ARTICLE 19(5) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION ) ORDER 2005 (THE FP ORDER), OR (B) WHO ARE PERSONS FALLING WITHIN ARTICLE 49(2)(a) TO (d) OF THE FP ORDER, OR (C) TO WHOM IT MAY OTHERWISE LAWFULLY BE DISTRIBUTED IN ACCORDANCE WITH THE FP ORDER (ALL SUCH PERSONS IN (A), (B) AND (C) ABOVE TOGETHER BEING REFERRED TO AS RELEVANT PERSONS). THE DOCUMENT MUST NOT BE ACTED ON OR RELIED ON BY PERSONS WHO ARE NOT RELEVANT PERSONS. ANY INVESTMENT OR INVESTMENT ACTIVITY TO WHICH THE DOCUMENT RELATES IS AVAILABLE ONLY TO RELEVANT PERSONS AND WILL BE ENGAGED IN ONLY WITH RELEVANT PERSONS. FOR A MORE COMPLETE DESCRIPTION OF RESTRICTIONS ON OFFERS AND SALES, SEE “SUBSCRIPTION AND SALE”. The Capital Securities are complex financial instruments and are not a suitable or appropriate investment for all investors. In some jurisdictions, regulatory authorities have adopted or published laws, regulations or guidance with respect to the offer or sale of securities such as, or with features similar to those of, the Capital Securities to retail investors. By purchasing, or making or accepting an offer to purchase, any Capital Securities from the Issuer and/or the Joint Lead Managers, each prospective investor represents, warrants, agrees with and undertakes to the Issuer and each of the Joint Lead Managers that: (a) it will not sell or offer the Capital Securities to retail clients in the European Economic Area (the EEA) (as defined in article (4)(1)(12) of the Markets in Financial Instruments Directive (2004/39/EC) (MiFID)) or do anything (including the distribution of this Document or the final prospectus in relation to the Capital Securities) that would or might result in the buying of the Capital Securities or the holding of a beneficial interest in the Capital Securities by a retail client in the EEA, other than in relation to any sale or offer to sell Capital Securities to a retail client in any EEA member state, where (i) it has conducted an assessment and concluded that the relevant retail client understands the risks of an investment in the Capital Securities and is able to bear the potential losses involved in an investment in the Capital Securities and (ii) it has at all times acted in relation to such sale or offer in compliance with MiFID to the extent it applies to it or, to the extent MiFID does not apply to it, in a manner which would be in compliance with MiFID if it were to apply to it; and (b) it has complied and will at all times comply with all applicable laws, regulations and regulatory guidance (whether inside or outside the EEA) relating to the promotion, offering, distribution and/or sale of the Capital Securities, including any such laws, regulations and regulatory guidance relating to determining the appropriateness and/or suitability of an investment in the Capital Securities by investors in any relevant jurisdiction.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of IMPORTANT NOTICE

IMPORTANT NOTICE

THIS PROSPECTUS MAY ONLY BE DISTRIBUTED TO PERSONS WHO ARE NOT U.S. PERSONS (AS DEFINED INREGULATION S (REGULATION S) UNDER THE UNITED STATES SECURITIES ACT OF 1933, AS AMENDED (THESECURITIES ACT)) AND WHO ARE OUTSIDE OF THE UNITED STATES.

IMPORTANT: You must read the following disclaimer before continuing. The following disclaimer applies to the attachedprospectus (the Document) whether received by e-mail, accessed from an internet page or otherwise received as a result ofelectronic communication, and you are therefore advised to read this disclaimer carefully before reading, accessing ormaking any other use of the Document. In accessing the Document, you agree to be bound by the following terms andconditions, including any modifications to them from time to time, each time you receive any information from any of theIssuer and/or the Joint Lead Managers (each as defined below) as a result of such access.

Restrictions: UNDER NO CIRCUMSTANCES SHALL THE DOCUMENT CONSTITUTE AN OFFER TO SELL OR THESOLICITATION OF AN OFFER TO BUY NOR SHALL THERE BE ANY SALE OF THE SECURITIES IN THE UNITEDSTATES OR ANY OTHER JURISDICTION IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL.ANY SECURITIES TO BE ISSUED HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACTOR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITEDSTATES AND MAY NOT BE OFFERED, SOLD, PLEDGED OR OTHERWISE TRANSFERRED DIRECTLY OR INDIRECTLY(I) AS PART OF THEIR DISTRIBUTION AT ANY TIME OR (II) OTHERWISE UNTIL 40 DAYS AFTER THE COMPLETIONOF THE DISTRIBUTION, AS DETERMINED BY THE JOINT LEAD MANAGERS, OF ALL SECURITIES, WITHIN THEUNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS EXCEPT PURSUANT TO ANEXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THESECURITIES ACT AND APPLICABLE STATE AND LOCAL SECURITIES LAWS.

THE DOCUMENT MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON WITHOUT THE PRIORWRITTEN CONSENT OF THE JOINT LEAD MANAGERS AND MAY NOT BE REPRODUCED IN ANY MANNERWHATSOEVER. DISTRIBUTION OR REPRODUCTION OF THE DOCUMENT IN WHOLE OR IN PART ISUNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIESACT OR THE APPLICABLE SECURITIES LAWS OF OTHER JURISDICTIONS.

WITHIN THE UNITED KINGDOM, THE DOCUMENT IS DIRECTED ONLY AT (A) PERSONS WHO HAVE PROFESSIONALEXPERIENCE IN MATTERS RELATING TO INVESTMENTS FALLING WITHIN ARTICLE 19(5) OF THE FINANCIALSERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION ) ORDER 2005 (THE FP ORDER), OR (B) WHO AREPERSONS FALLING WITHIN ARTICLE 49(2)(a) TO (d) OF THE FP ORDER, OR (C) TO WHOM IT MAY OTHERWISELAWFULLY BE DISTRIBUTED IN ACCORDANCE WITH THE FP ORDER (ALL SUCH PERSONS IN (A), (B) AND (C)ABOVE TOGETHER BEING REFERRED TO AS RELEVANT PERSONS). THE DOCUMENT MUST NOT BE ACTED ONOR RELIED ON BY PERSONS WHO ARE NOT RELEVANT PERSONS. ANY INVESTMENT OR INVESTMENT ACTIVITYTO WHICH THE DOCUMENT RELATES IS AVAILABLE ONLY TO RELEVANT PERSONS AND WILL BE ENGAGED INONLY WITH RELEVANT PERSONS. FOR A MORE COMPLETE DESCRIPTION OF RESTRICTIONS ON OFFERS ANDSALES, SEE “SUBSCRIPTION AND SALE”.

The Capital Securities are complex financial instruments and are not a suitable or appropriate investment for all investors. In somejurisdictions, regulatory authorities have adopted or published laws, regulations or guidance with respect to the offer or sale ofsecurities such as, or with features similar to those of, the Capital Securities to retail investors.

By purchasing, or making or accepting an offer to purchase, any Capital Securities from the Issuer and/or the Joint LeadManagers, each prospective investor represents, warrants, agrees with and undertakes to the Issuer and each of the Joint LeadManagers that:

(a) it will not sell or offer the Capital Securities to retail clients in the European Economic Area (the EEA) (as defined inarticle (4)(1)(12) of the Markets in Financial Instruments Directive (2004/39/EC) (MiFID)) or do anything (including thedistribution of this Document or the final prospectus in relation to the Capital Securities) that would or might result in thebuying of the Capital Securities or the holding of a beneficial interest in the Capital Securities by a retail client in theEEA, other than in relation to any sale or offer to sell Capital Securities to a retail client in any EEA member state,where (i) it has conducted an assessment and concluded that the relevant retail client understands the risks of aninvestment in the Capital Securities and is able to bear the potential losses involved in an investment in the CapitalSecurities and (ii) it has at all times acted in relation to such sale or offer in compliance with MiFID to the extent itapplies to it or, to the extent MiFID does not apply to it, in a manner which would be in compliance with MiFID if itwere to apply to it; and

(b) it has complied and will at all times comply with all applicable laws, regulations and regulatory guidance (whether insideor outside the EEA) relating to the promotion, offering, distribution and/or sale of the Capital Securities, including anysuch laws, regulations and regulatory guidance relating to determining the appropriateness and/or suitability of aninvestment in the Capital Securities by investors in any relevant jurisdiction.

Where acting as agent on behalf of a disclosed or undisclosed client when purchasing, or making or accepting an offer topurchase, any Capital Securities from the Issuer and/or the Joint Lead Managers, the foregoing representations, warranties,agreements and undertakings will be given by and be binding upon both the agent and its underlying client.

CONFIRMATION OF YOUR REPRESENTATION: In order to be eligible to view the Document or make an investmentdecision with respect to the securities described herein, (1) each prospective investor in respect of the securities being offeredoutside of the United States in an offshore transaction pursuant to Regulation S must be a person other than a U.S. Person and(2) each prospective investor in respect of the securities being offered in the United Kingdom must be a Relevant Person. Byaccepting this e-mail and accessing, reading or making any other use of the Document, you shall be deemed to have representedto Goldman Sachs International, HSBC Bank plc and Morgan Stanley & Co. International plc (together, the Joint LeadManagers) and Ahli United Bank B.S.C. (the Issuer) (1) you have understood and agree to the terms set out herein, (2) you are(or the person you represent is) a person other than a U.S. Person, and that the electronic mail (or e-mail) address to which,pursuant to your request, the Document has been delivered by electronic transmission is not located in the United States, itsterritories, its possessions and other areas subject to its jurisdiction; and its possessions include Puerto Rico, the U.S. VirginIslands, Guam, American Samoa, Wake Island and the Northern Mariana Islands, (3) in respect of the securities being offered inthe United Kingdom, you are (or the person you represent is) a Relevant Person, (4) you consent to delivery by electronictransmission, (5) you will not transmit the Document (or any copy of it or part thereof) or disclose, whether orally or in writing,any of its contents to any other person except with the consent of the Joint Lead Managers and (6) you acknowledge that youwill make your own assessment regarding any legal, taxation or other economic considerations with respect to your decision tosubscribe for or purchase any of the securities described herein.

Neither the Joint Lead Managers nor any of their respective affiliates accepts any responsibility whatsoever for the contents of theDocument or for any statement made therein, in connection with the Issuer or the offer. The Joint Lead Managers and theirrespective affiliates accordingly disclaim all and any liability whether arising in tort, contract, or otherwise which they mightotherwise have in respect of such document or any such statement. No representation or warranty, express or implied, is made byany of the Joint Lead Managers or their respective affiliates as to the accuracy, completeness, verification or sufficiency of theinformation set out in the Document. The Joint Lead Managers are acting exclusively for the Issuer and no one else in connectionwith the offer. They will not regard any other person (whether or not a recipient of the Document) as their client in relation tothe offer and will not be responsible to anyone other than the Issuer for providing the protections afforded to its clients nor forgiving advice in relation to the offer or any transaction or arrangement referred to herein.

The materials relating to the offering do not constitute, and may not be used in connection with, an offer or solicitation in anyplace where such offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensedbroker or dealer and the Joint Lead Managers or any affiliate of the Joint Lead Managers is a licensed broker or dealer in thatjurisdiction the offering shall be deemed to be made by the Joint Lead Managers or such affiliate on behalf of the Issuer in suchjurisdiction.

Under no circumstances shall the Document constitute an offer to sell or the solicitation of an offer to buy nor shall there be anysale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful. Recipients of the Document whointend to subscribe for or purchase any securities to be issued are reminded that any subscription or purchase may only be madeon the basis of the information contained in the final version of the Document.

The Document has been made available to you in an electronic form. You are reminded that documents transmitted via thismedium may be altered or changed during the process of electronic transmission and consequently none of the Issuer, the JointLead Managers nor any person who controls or is a director, officer, employee or agent of the Issuer, the Joint Lead Managersnor any of their respective affiliates accepts any liability or responsibility whatsoever in respect of any difference between theDocument distributed to you in electronic format and the hard copy version. By accessing the Document, you consent to receivingit in electronic form. A hard copy of the Document will be made available to you only upon request to the Joint Lead Managers.

You are reminded that the Document has been delivered to you on the basis that you are a person into whose possession theDocument may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located and you may notnor are you authorised to deliver the Document, electronically or otherwise, to any other person and in particular to any U.S.Person or to any U.S. address. Failure to comply with this directive may result in a violation of the Securities Act or theapplicable laws of other jurisdictions.

If you received the Document by e-mail, you should not reply by e-mail to this communication. Any reply e-mailcommunications, including those you generate by using the “Reply” function on the e-mail software, will be ignored or rejected.Your receipt of the electronic transmission is at your own risk and it is your responsibility to take precautions to ensure that it isfree from viruses and other items of a destructive nature.

AHLI UNITED BANK B.S.C.(incorporated as a joint stock company under the laws of the Kingdom of Bahrain)

U.S.$400,000,000 Perpetual Tier 1 Capital SecuritiesThe U.S.$400,000,000 Perpetual Tier 1 Capital Securities (the Capital Securities) shall be issued by Ahli United Bank B.S.C. (AUB or theIssuer) on 29 April 2015 (the Issue Date). Distribution Payment Amounts (as defined in the Conditions) shall be payable subject to and inaccordance with terms and conditions set out in the “Terms and Conditions of the Capital Securities” (the Conditions) on the outstandingnominal amount of the Capital Securities from (and including) the Issue Date to (but excluding) 29 April 2020 (the First Call Date) at a rateof 6.875 per cent. per annum. If the Capital Securities are not redeemed or purchased and cancelled in accordance with the Conditions on orprior to the First Call Date, Distribution Payment Amounts shall be payable from (and including) the First Call Date subject to and inaccordance with the Conditions at a fixed rate, to be reset on the First Call Date and every five years thereafter, equal to the Relevant FiveYear Reset Rate (as defined in the Conditions) plus a margin of 5.387 per cent. per annum. Distribution Payment Amounts will (subject to theright of the Issuer to defer payments of interest in accordance with Condition 6.2 (Distribution Restrictions – Non-Payment Election)) bepayable semi-annually in arrear on 29 April and 29 October in each year, commencing on 29 October 2015 (each, a Distribution PaymentDate). Payments on the Capital Securities will be made without deduction for, or on account of, taxes, levies, imposts, duties, fees, assessmentsor other charges of whatever nature, imposed or levied by or on behalf of any Relevant Jurisdiction (as defined in the Conditions) (the Taxes)as described in Condition 12 (Taxation).

If a Non-Viability Event (as defined herein) occurs, a Write-down (as defined herein) shall occur on the relevant Non-Viability Event Write-down Date (as defined herein), as more particularly described in Condition 10 (Write-down at the Point of Non-Viability). In suchcircumstances, the rights of the holders of the Capital Securities to payment of any amounts under or in respect of the Capital Securities shall,as the case may be, be cancelled or written-down pro rata among the holders of the Capital Securities. See “Risk Factors — The rights of theholders of the Capital Securities to receive repayment of the principal amount of the Capital Securities and the rights of the holders of theCapital Securities for any further profit may be written-down upon the occurrence of a Non-Viability Event”.

The Issuer may elect, and in certain circumstances shall be required, not to make any distribution falling due on the Capital Securities. AnyDistribution Payment Amounts not paid as aforesaid will not accumulate and the holder of the Capital Security shall not have any claim inrespect thereof.

The Capital Securities are undated and have no final maturity. Unless the Capital Securities have previously been redeemed or purchased andcancelled as provided in the Conditions, the Capital Securities may, at the option of the Issuer, subject to the prior approval of the CentralBank of Bahrain (the CBB), be redeemed at par (in whole but not in part) on the First Call Date or any Distribution Payment Date thereafter.In addition, the Capital Securities may, in the event of a Tax Event or Capital Event (each as defined in the Conditions), be redeemed (inwhole but not in part), subject to the prior approval of the CBB.

An investment in the Capital Securities involves certain risks. For a discussion of these risks, see “Risk Factors”.

The Capital Securities may only be offered, sold or transferred in registered form in minimum nominal amounts of U.S.$200,000 and integralmultiples of U.S.$1,000 in excess thereof. Delivery of the Capital Securities in book-entry form will be made on the Issue Date. The CapitalSecurities will be represented by interests in a global certificate in registered form (the Global Certificate) deposited on or about the IssueDate with, and registered in the name of a nominee for, a common depositary (the Common Depositary) for Euroclear Bank SA/NV(Euroclear) and Clearstream Banking, société anonyme (Clearstream, Luxembourg). Interests in the Global Certificate will be shown on, andtransfers thereof will be effected only through, records maintained by Euroclear and Clearstream, Luxembourg. Individual Certificates (asdefined in the Conditions) evidencing holdings of interests in the Capital Securities will be issued in exchange for interests in the GlobalCertificate only in certain limited circumstances described herein.

This Prospectus has been approved by the Central Bank of Ireland (the Central Bank) as competent authority under Directive 2003/71/EC, asamended (which includes the amendments made by Directive 2010/73/EU to the extent that such amendments have been implemented in arelevant Member State of the European Economic Area) (the Prospectus Directive). The Central Bank only approves this Prospectus as meetingthe requirements imposed under Irish and European Union law pursuant to the Prospectus Directive. Application has been made to the IrishStock Exchange plc (the Irish Stock Exchange) for the Capital Securities to be admitted to the official list (the Official List) and to tradingon its regulated market (the Main Securities Market). The Main Securities Market is a regulated market for the purposes of the Markets inFinancial Instruments Directive (Directive 2004/39/EC) (MiFID). References in this Prospectus to Capital Securities being listed (and all relatedreferences) shall mean that such Capital Securities have been admitted to the Official List and have been admitted to trading on the MainSecurities Market.

The Issuer has been assigned a long term foreign currency rating of A- (stable) and a short term foreign currency rating of A2 by CapitalIntelligence (Cyprus) Ltd (Capital Intelligence), a long term issuer default rating of BBB+ (stable) and a short term issuer default rating ofF-2 by Fitch Ratings Ltd. (Fitch) and a long term issuer rating of BBB+ (stable) and a short term issuer rating of A-2 (stable) by Standard &Poor’s Credit Market Services France S.A.S., a division of The McGraw-Hill Companies Inc. (Standard & Poor’s). Each of CapitalIntelligence, Fitch and Standard & Poor’s is established in the European Union and is registered under the Regulation (EC) No. 1060/2009 (asamended) (the CRA Regulation). As such each of Capital Intelligence, Fitch and Standard & Poor’s is included in the list of credit ratingagencies published by the European Securities and Markets Authority on its website (at http://www.esma.europa.eu/page/List-registered-and-certified-CRAs) in accordance with the CRA Regulation.

A rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, reduction or withdrawal at anytime by the assigning rating agency.

Prospective investors are referred to the section headed “Restrictions on marketing and sales to retail investors” on page iv of this Prospectusfor information regarding certain restrictions on marketing and sales to retail investors.

The Capital Securities have not been, nor will be, registered under the United States Securities Act of 1933, as amended (the Securities Act)or with any securities regulatory authority of any state or other jurisdiction of the United States and may not be offered, sold or deliveredwithin the United States or to, or for the account or benefit of, U.S. Persons (as defined in Regulation S under the Securities Act(Regulation S)) except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act andapplicable state securities laws. Accordingly, the Capital Securities may be offered or sold solely to persons who are not U.S. Persons outsidethe United States in reliance on Regulation S. Each purchaser of the Capital Securities is hereby notified that the offer and sale of CapitalSecurities to it is being made in reliance on the exemption from the registration requirements of the Securities Act provided by Regulation S.

Joint Lead Managers

Goldman Sachs International HSBC Morgan StanleyThe date of this Prospectus is 27 April 2015

i

IMPORTANT NOTICE

This Prospectus comprises a prospectus for the purposes of the Prospectus Directive.

The Issuer accepts responsibility for the information contained in this Prospectus. To the best ofthe knowledge of the Issuer (having taken all reasonable care to ensure that such is the case), theinformation contained in this Prospectus is in accordance with the facts and does not omit anythinglikely to affect the import of such information.

Certain information contained in “Risk Factors – Political Considerations in Bahrain” and“Description of the Issuer – Economic and Banking Environment” (as indicated therein) has beenextracted from the following independent, third party sources: in the case of “Risk Factors –Political Considerations in Bahrain”, from the CBB monthly statistical bulletin, the website of theBICI (www.bici.org.bh), the website of the Bahrain News Agency (www.bna.bh) and the website ofthe Bahrain Information Affairs Authority (www.iaa.bh) and, in the case of “Description of theIssuer – Economic and Banking Environment”, the Central Banks of Bahrain, Kuwait, Oman, Egyptand Iraq, the Economist Intelligence Unit and the International Monetary Fund.

The Issuer confirms that all third party information contained in this Prospectus has beenaccurately reproduced and that, as far as it is aware and is able to ascertain from informationpublished by the relevant third party sources, no facts have been omitted which would render thereproduced information inaccurate or misleading.

The Joint Lead Managers have not independently verified the information contained herein.Accordingly, no representation, warranty or undertaking, express or implied, is made and noresponsibility or liability is accepted by the Joint Lead Managers as to the accuracy orcompleteness of the information contained or incorporated in this Prospectus or any otherinformation provided by the Issuer in connection with the issuance of the Capital Securities. NoJoint Lead Manager accepts any liability in relation to the information contained in this Prospectusor any other information provided by the Issuer in connection with the issuance of the CapitalSecurities.

No person is or has been authorised by the Issuer to give any information or to make anyrepresentation not contained in or not consistent with this Prospectus or any other informationsupplied in connection with the issuance of the Capital Securities and, if given or made, suchinformation or representation must not be relied upon as having been authorised by the Issuer orany of the Joint Lead Managers.

Neither this Prospectus nor any other information supplied in connection with the issuance of theCapital Securities: (a) is intended to provide the basis of any credit or other evaluation; or (b)should be considered as a recommendation by the Issuer or any of the Joint Lead Managers thatany recipient of this Prospectus or any other information supplied in connection with the issuanceof the Capital Securities should purchase any Capital Securities. Each investor contemplatingpurchasing any Capital Securities should make its own independent investigation of the financialcondition and affairs, and its own appraisal of the creditworthiness, of the Issuer. Neither thisProspectus nor any other information supplied in connection with the issuance of the CapitalSecurities constitutes an offer or invitation by or on behalf of the Issuer or any of the Joint LeadManagers to any person to subscribe for or to purchase any Capital Securities.

Neither the delivery of this Prospectus nor the offering, sale or delivery of any Capital Securitiesshall in any circumstances imply that the information contained herein concerning the Issuer iscorrect at any time subsequent to the date hereof or that any other information supplied inconnection with the issuance of the Capital Securities is correct as of any time subsequent to thedate indicated in the document containing the same. The Joint Lead Managers expressly do notundertake to review the financial condition or affairs of the Issuer during the life of the issuanceor to advise any investor in the Capital Securities of any information coming to their attention.

This Prospectus does not constitute an offer to sell or the solicitation of an offer to buy anyCapital Securities in any jurisdiction to any person to whom it is unlawful to make the offer or

ii

solicitation in such jurisdiction. The distribution of this Prospectus and the offer or sale of CapitalSecurities may be restricted by law in certain jurisdictions. The Issuer and the Joint LeadManagers do not represent that this Prospectus may be lawfully distributed, or that any CapitalSecurities may be lawfully offered, in compliance with any applicable registration or otherrequirements in any such jurisdiction, or pursuant to an exemption available thereunder, or assumeany responsibility for facilitating any such distribution or offering. In particular, no action has beentaken by the Issuer or the Joint Lead Managers which is intended to permit a public offering ofany Capital Securities or distribution of this Prospectus in any jurisdiction where action for thatpurpose is required. Accordingly, no Capital Securities may be offered or sold, directly orindirectly, and neither this Prospectus nor any advertisement or other offering material may bedistributed or published in any jurisdiction, except under circumstances that will result incompliance with any applicable laws and regulations. Persons into whose possession this Prospectusor any Capital Securities may come must inform themselves about, and observe, any suchrestrictions on the distribution of this Prospectus and the offering and sale of any CapitalSecurities. In particular, there are restrictions on the distribution of this Prospectus and the offer orsale of any Capital Securities in Hong Kong, the United States, the United Kingdom, Japan, theUnited Arab Emirates (excluding the Dubai International Financial Centre), the Dubai InternationalFinancial Centre, the Kingdom of Saudi Arabia, the Kingdom of Bahrain (Bahrain) and the Stateof Qatar (see “Subscription and Sale”).

This Prospectus includes forward-looking statements. All statements other than statements ofhistorical facts included in this Prospectus may constitute forward-looking statements. Forward-looking statements generally can be identified by the use of forward-looking terminology, such as“may”, “will”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue” or similarterminology. Although the Issuer believes that the expectations reflected in their forward-lookingstatements are reasonable at this time, there can be no assurance that these expectations will proveto be correct.

The Capital Securities may not be a suitable investment for all investors. Each potentialinvestor in the Capital Securities must determine the suitability of that investment in light ofits own circumstances. In particular, each potential investor may wish to consider, either on itsown or with the help of its financial and other professional advisers, whether it:

(a) has sufficient knowledge and experience to make a meaningful evaluation of the CapitalSecurities, the merits and risks of investing in the Capital Securities and the informationcontained in this Prospectus;

(b) has access to, and knowledge of, appropriate analytical tools to evaluate, in the context of itsparticular financial situation, an investment in the Capital Securities and the impact theCapital Securities will have on its overall investment portfolio;

(c) has sufficient financial resources and liquidity to bear all of the risks of an investment in theCapital Securities, including Capital Securities with principal or distributions payable in oneor more currencies, or where the currency for payments of principal or distributions isdifferent from the potential investor’s currency;

(d) understands thoroughly the terms of the Capital Securities and is familiar with the behaviourof any relevant indices and financial markets; and

(e) is able to evaluate possible scenarios for economic, distribution rate and other factors thatmay affect its investment and its ability to bear the applicable risks.

The Capital Securities are complex financial instruments. Sophisticated institutional investorsgenerally do not purchase complex financial instruments as stand-alone investments. They purchasecomplex financial instruments as a way to reduce risk or enhance yield with an understood,measured, appropriate addition of risk to their overall portfolios. A potential investor should notinvest in the Capital Securities unless it has the expertise (either alone or with a financial adviser)

iii

to evaluate how the Capital Securities will perform under changing conditions, the resulting effectson the value of the Capital Securities and the impact this investment will have on the potentialinvestor’s overall investment portfolio.

Legal investment considerations may restrict certain investments. The investment activities ofcertain investors are subject to legal investment laws and regulations, or review or regulation bycertain authorities. Each potential investor should consult its legal advisers to determine whetherand to what extent: (a) the Capital Securities are legal investments for it; (b) the Capital Securitiescan be used as collateral for various types of borrowing; and (c) other restrictions apply to itspurchase or pledge of any Capital Securities. Financial institutions should consult their legaladvisers or the appropriate regulators to determine the appropriate treatment of Capital Securitiesunder any applicable risk based capital or similar rules.

Restrictions on marketing and sales to retail investors

The Capital Securities are complex financial instruments and are not a suitable or appropriateinvestment for all investors. In some jurisdictions, regulatory authorities have adopted or publishedlaws, regulations or guidance with respect to the offer or sale of securities such as, or withfeatures similar to those of, the Capital Securities to retail investors.

By purchasing, or making or accepting an offer to purchase, any Capital Securities from the Issuerand/or the Joint Lead Managers, each prospective investor represents, warrants, agrees with andundertakes to the Issuer and each of the Joint Lead Managers that:

(a) it will not sell or offer the Capital Securities to retail clients in the European Economic Area(the EEA) (as defined in article (4)(1)(12) of MiFID) or do anything (including thedistribution of the Prospectus) that would or might result in the buying of the CapitalSecurities or the holding of a beneficial interest in the Capital Securities by a retail client inthe EEA, other than in relation to any sale or offer to sell Capital Securities to a retailclient in any EEA member state, where (i) it has conducted an assessment and concludedthat the relevant retail client understands the risks of an investment in the Capital Securitiesand is able to bear the potential losses involved in an investment in the Capital Securitiesand (ii) it has at all times acted in relation to such sale or offer in compliance with MiFIDto the extent it applies to it or, to the extent MiFID does not apply to it, in a manner whichwould be in compliance with MiFID if it were to apply to it; and

(b) it has complied and will at all times comply with all applicable laws, regulations andregulatory guidance (whether inside or outside the EEA) relating to the promotion, offering,distribution and/or sale of the Capital Securities, including any such laws, regulations andregulatory guidance relating to determining the appropriateness and/or suitability of aninvestment in the Capital Securities by investors in any relevant jurisdiction.

Where acting as agent on behalf of a disclosed or undisclosed client when purchasing, or makingor accepting an offer to purchase, any Capital Securities from the Issuer and/or the Joint LeadManagers, the foregoing representations, warranties, agreements and undertakings will be given byand be binding upon both the agent and its underlying client.

STABILISATION

In connection with the issue of the Capital Securities, HSBC Bank plc (the StabilisationManager) (or persons acting on behalf of the Stabilisation Manager) may over-allot CapitalSecurities or effect transactions with a view to supporting the market price of the Capital Securitiesat a level higher than that which might otherwise prevail. However, there is no assurance that theStabilisation Manager (or persons acting on behalf of a Stabilisation Manager) will undertakestabilisation action. Any stabilisation action or over-allotment may begin on or after the date onwhich adequate public disclosure of the terms of the offer of the Capital Securities is made and, ifbegun, may be ended at any time, but it must end no later than the earlier of thirty (30) days afterthe issue date of the Capital Securities and sixty (60) days after the date of the allotment of the

iv

Capital Securities. Any stabilisation action or over-allotment must be conducted by the StabilisationManager (or persons acting on behalf of any Stabilisation Manager) in accordance with allapplicable laws and rules.

NOTICE TO THE RESIDENTS OF THE KINGDOM OF SAUDI ARABIA

This Prospectus may not be distributed in the Kingdom of Saudi Arabia except to such persons asare permitted under the Offers of Securities Regulations issued by the Capital Market Authority ofthe Kingdom of Saudi Arabia (the Capital Market Authority).

The Capital Market Authority does not make any representations as to the accuracy orcompleteness of this Prospectus, and expressly disclaims any liability whatsoever for any lossarising from, or incurred in reliance upon, any part of this Prospectus. Prospective purchasers ofthe Capital Securities should conduct their own due diligence on the accuracy of the informationrelating to the Capital Securities. If a prospective purchaser does not understand the contents ofthis Prospectus they should consult an authorised financial adviser.

NOTICE TO THE RESIDENTS OF THE KINGDOM OF BAHRAIN

EACH POTENTIAL INVESTOR INTENDING TO SUBSCRIBE FOR ANY CAPITALSECURITIES (EACH, A POTENTIAL INVESTOR) MAY BE REQUIRED TO PROVIDESATISFACTORY EVIDENCE OF IDENTITY AND, IF SO REQUIRED, THE SOURCE OFFUNDS TO PURCHASE THE CAPITAL SECURITIES WITHIN A REASONABLE TIMEPERIOD DETERMINED BY THE ISSUER AND THE JOINT LEAD MANAGERS.PENDING THE PROVISION OF SUCH EVIDENCE, AN APPLICATION TO SUBSCRIBEFOR ANY CAPITAL SECURITIES WILL BE POSTPONED. IF A POTENTIAL INVESTORFAILS TO PROVIDE SATISFACTORY EVIDENCE WITHIN THE TIME SPECIFIED, ORIF A POTENTIAL INVESTOR PROVIDES EVIDENCE BUT NEITHER THE ISSUER NORTHE JOINT LEAD MANAGERS ARE SATISFIED THEREWITH, ITS APPLICATION TOSUBSCRIBE FOR ANY CAPITAL SECURITIES MAY BE REJECTED IN WHICH EVENTANY MONEY RECEIVED BY WAY OF APPLICATION WILL BE RETURNED TO THEPOTENTIAL INVESTOR (WITHOUT ANY ADDITIONAL AMOUNT ADDED THERETOAND AT THE RISK AND EXPENSE OF SUCH POTENTIAL INVESTOR). IN RESPECTOF ANY BAHRAINI POTENTIAL INVESTORS, THE ISSUER WILL COMPLY WITHBAHRAIN’S LEGISLATIVE DECREE NO. (4) OF 2001 WITH RESPECT TOPROHIBITION AND COMBATING OF MONEY LAUNDERING AND VARIOUSMINISTERIAL ORDERS ISSUED THEREUNDER INCLUDING, BUT NOT LIMITED TO,MINISTERIAL ORDER NO. (7) OF 2001 WITH RESPECT TO INSTITUTIONS’OBLIGATIONS CONCERNING THE PROHIBITION AND COMBATING OF MONEYLAUNDERING AND ANTI-MONEY LAUNDERING AND COMBATING OF FINANCIALCRIME MODULE CONTAINED IN THE CBB RULEBOOK, VOLUME 6.

THIS OFFER IS A PRIVATE PLACEMENT. IT IS NOT SUBJECT TO ALL OF THEREGULATIONS OF THE CBB THAT APPLY TO PUBLIC OFFERINGS OF SECURITIES.THIS PROSPECTUS IS THEREFORE INTENDED ONLY FOR “ACCREDITEDINVESTORS” AS DEFINED HEREIN. THE CAPITAL SECURITIES HEREBY OFFEREDBY WAY OF PRIVATE PLACEMENT ARE OFFERED IN MINIMUM DENOMINATIONSOF U.S.$200,000.

A COPY OF THIS PROSPECTUS HAS BEEN SUBMITTED AND FILED WITH THE CBB.FILING OF THIS PROSPECTUS WITH THE CBB DOES NOT IMPLY THAT ANYBAHRAINI LEGAL OR REGULATORY REQUIREMENTS HAVE BEEN COMPLIEDWITH. THE CBB HAS NOT IN ANY WAY CONSIDERED THE MERITS OF THESECURITIES TO BE OFFERED FOR INVESTMENT WHETHER IN OR OUTSIDE OFTHE KINGDOM OF BAHRAIN.

NEITHER THE CBB NOR THE LICENSED EXCHANGE ASSUMES RESPONSIBILITYFOR THE ACCURACY AND COMPLETENESS OF THE STATEMENTS ANDINFORMATION CONTAINED IN THIS PROSPECTUS AND EACH EXPRESSLY

v

DISCLAIMS ANY LIABILITY WHATSOEVER FOR ANY LOSS HOWSOEVER ARISINGFROM RELIANCE UPON THE WHOLE OR ANY PART OF THE CONTENTS OF THISPROSPECTUS.

THE ISSUER ACCEPTS RESPONSIBILITY FOR THE INFORMATION CONTAINED INTHIS PROSPECTUS. TO THE BEST OF THE KNOWLEDGE OF THE ISSUER (HAVINGTAKEN ALL REASONABLE CARE TO ENSURE THAT SUCH IS THE CASE) THEINFORMATION CONTAINED IN THIS PROSPECTUS IS IN ACCORDANCE WITH THEFACTS AND DOES NOT OMIT ANYTHING LIKELY TO AFFECT THE IMPORT OFSUCH INFORMATION.

NOTICE TO RESIDENTS OF THE STATE OF QATAR

This Prospectus does not and is not intended to constitute an offer, sale or delivery of bonds orother debt financing instruments under the laws of the State of Qatar. The Capital Securities havenot been and will not be authorised by the Qatar Financial Markets Authority, the Qatar FinancialCentre Regulatory Authority or the Qatar Central Bank in accordance with their regulations or anyother regulations in the State of Qatar. The Capital Securities are not and will not be traded on theQatar Exchange.

PRESENTATION OF FINANCIAL INFORMATION

The Issuer prepared its audited consolidated financial statements for the years ended 31 December2014, 31 December 2013 and 31 December 2012 in accordance with International FinancialReporting Standards as issued by the International Accounting Standards Board (IFRS). TheIssuer’s selected historical consolidated financial data as at and for the years ended 31 December2014 and 31 December 2013 have been extracted from the audited consolidated financialstatements (including the related notes thereto), as at and for the year ended 31 December 2014.The Issuer’s selected historical consolidated financial data as at and for the year ended31 December 2012 have been extracted from the audited consolidated financial statements(including the related notes thereto), as at and for the year ended 31 December 2013 and are setout elsewhere in this Prospectus (collectively, the audited consolidated financial statements for theyears ended 31 December 2014 and 31 December 2013, the Consolidated Financial Statements).The Issuer adopted IFRS 9: Financial Instruments (IFRS 9) with effect from 1 January 2012.Based on the transitional provisions of IFRS 9, the new accounting standard was adoptedretrospectively and adjustments made to the consolidated balance sheet numbers as at 1 January2012, without requiring the restatement of the prior year numbers, as permitted by the standard.The transition to IFRS 9 resulted in the reclassification of financial instruments and an increase inthe equity attributable to the owners of the Issuer by U.S.$112.9 million as at 1 January 2012 asdetailed in Note 3.1 of the consolidated financial statements for the year ended 31 December 2012.Certain figures and percentages included in this Prospectus have been subject to roundingadjustments. Accordingly, figures shown in the same category presented in different tables mayvary slightly and figures shown as totals in certain tables may not be an arithmetic aggregation ofthe figures which precede them. In February 2013, the Group completed the sale of its 29.4 percent. shareholding in its associate, Ahli Bank Qatar. Accordingly, income from Ahli Bank Qatarthat was either classified as “share of profit from associates and joint venture” or “fees andcommission” for the year ended 31 December 2012 was reclassified as “gain/income relating toinvestment held for sale” in the comparative period of the consolidated financial statements for theyear ended 31 December 2013.

In this Prospectus, unless otherwise specified or the context otherwise requires, references to U.S.dollars, U.S.$, USD and United States dollars are to the lawful currency of the United States ofAmerica, its territories and possessions; references to BD, BHD and Bahrain dinars are to thelawful currency of Bahrain; references to ID, IQD and Iraqi dinars are to the lawful currency ofthe Republic of Iraq; references to KD, KWD and Kuwaiti dinars are to the lawful currency ofthe State of Kuwait; references to EGP and Egyptian pound are to the lawful currency of theArab Republic of Egypt; references to QR and QAR are to the lawful currency of the State ofQatar; and references to RO, OMR and Omani rial are to the lawful currency of the Sultanate ofOman.

vi

Translations of amounts from Bahrain dinars to U.S. dollars and Iraqi dinars to U.S. dollars in thisProspectus are solely for the convenience of the reader. The Bahrain dinar has been pegged to theU.S. dollar at a fixed exchange rate of 0.376 Bahrain dinars per U.S. dollar and, accordingly,unless otherwise indicated, translations of amounts from Bahrain dinars to U.S. dollars have beenmade at this exchange rate for all periods presented in this Prospectus. The exchange rate betweenthe Iraqi dinar and the U.S. dollar was, on 31 December 2014, U.S.$1.00 = IQD 1,166.

Such translations should not be construed as representing that Bahrain dinar and the Iraqi dinaramounts referred to in this Prospectus have been or could have been converted into United Statesdollars at this or any other rate of exchange.

The exchange rates used for various currencies are given below:

Profit & Loss Balance Sheet

For the For the For theyear ended year ended year ended As at As at As at

Equivalent per USD 31-Dec-14 31-Dec-13 31-Dec-12 31-Dec-14 31-Dec-13 31-Dec-12

KWD ................................ 0.285 0.284 0.280 0.293 0.282 0.281IQD .................................. 1,164 1,162 1,163 1,166 1,163 1,164EGP .................................. 7.092 6.899 6.093 7.150 6.939 6.365OMR ................................ 0.385 0.385 0.385 0.385 0.385 0.385QAR .................................. 3.640 3.640 3.640 3.640 3.640 3.640BHD .................................. 0.376 0.376 0.376 0.376 0.376 0.376LYD .................................. 1.221 1.262 1.254 1.197 1.234 1.262

CONTENTS

Page

RISK FACTORS.............................................................................................................................. 1

OVERVIEW OF THE ISSUANCE ............................................................................................ 18

TERMS AND CONDITIONS OF THE CAPITAL SECURITIES ...................................... 22

USE OF PROCEEDS .................................................................................................................... 43

DESCRIPTION OF THE ISSUER ............................................................................................ 44

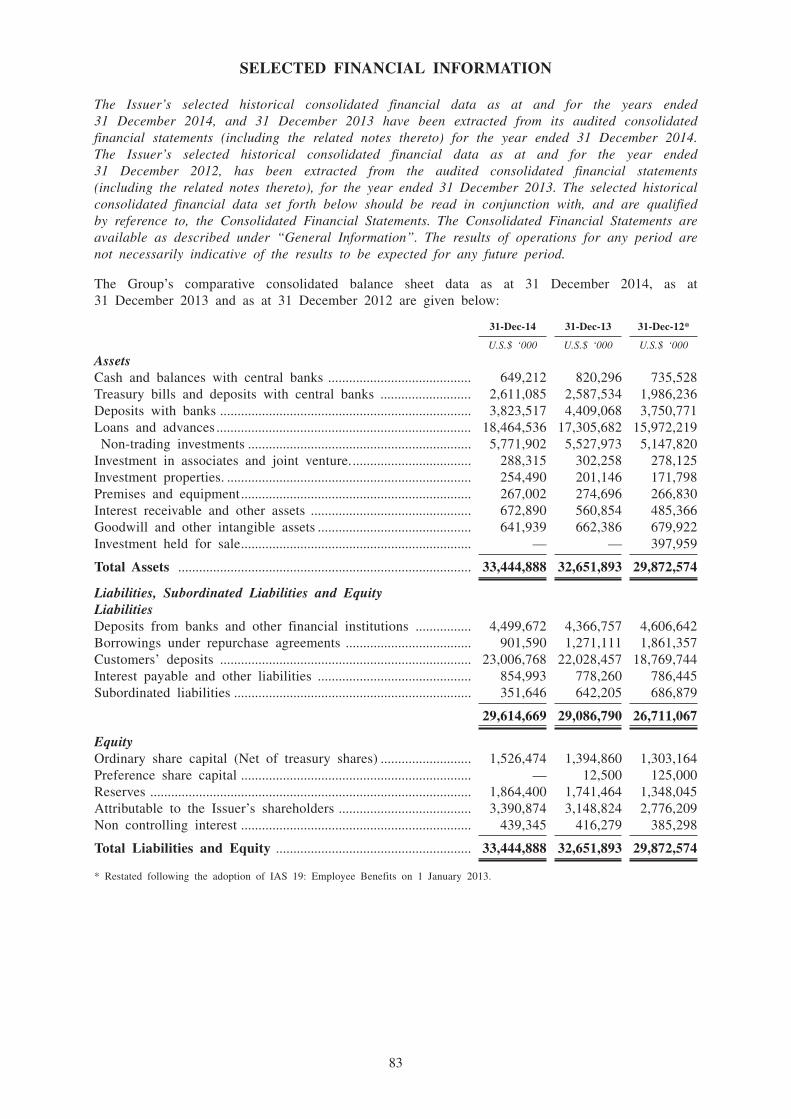

SELECTED FINANCIAL INFORMATION .............................................................................. 83

TAXATION ...................................................................................................................................... 90

SUBSCRIPTION AND SALE ...................................................................................................... 93

GENERAL INFORMATION ........................................................................................................ 96

FINANCIAL INFORMATION .................................................................................................... F-1

RISK FACTORS

The Issuer believes that the following factors may affect its ability to fulfil its obligations underthe Capital Securities. All of these factors are contingencies which may or may not occur and theIssuer is not in a position to express a view on the likelihood of any such contingency occurring.

In addition, factors which are material for the purpose of assessing the market risks associatedwith the Capital Securities are also described below.

The Issuer believes that the factors described below represent the principal risks inherent ininvesting in the Capital Securities, but the inability of the Issuer to pay interest, principal or otheramounts on or in connection with any Capital Securities may occur for other reasons and theIssuer makes no representation that the statements below regarding the risks of holding anyCapital Securities are exhaustive. Prospective investors should also read the detailed informationset out elsewhere in this Prospectus and reach their own views prior to making any investmentdecision.

Words and expressions defined in “Terms and Conditions of the Capital Securities” shall have thesame meanings in this section.

Factors that may affect the Issuer’s ability to fulfil its obligations under or in connection withthe Capital Securities

Economic, Political and Related Considerations

The Issuer is a bank, headquartered in the Kingdom of Bahrain (Bahrain), which is primarilyfocused on the financial markets of the six countries of the Gulf Cooperation Council (GCC),particularly Bahrain, Kuwait and Oman. The Issuer also has operations in Egypt, Iraq, Libya andthe United Kingdom. A significant part of the Issuer’s assets are located within the GCC, includingthe majority of its loan assets and deposit base. The Issuer has implemented various strategies tomitigate the impact of the political and social unrest in the Middle East and North Africa region(MENA) during 2011, popularly termed the “Arab Spring” (see further “Political considerationsrelating to the countries in which the Issuer operates” below).

However, there can be no assurance that the Issuer’s financial performance can be sustained in thefuture, or that growth and stability in the Issuer’s main markets will continue. Investors should alsonote that the Issuer’s business and financial performance could be adversely affected by political,economic and related risks both within and outside the GCC and the wider MENA. Any or all ofthe GCC countries could be further adversely affected by a worsening of general economicconditions in the global markets in which it operates. In addition, changes in investment markets,including changes in interest rates, exchange rates and returns from equity, property and otherinvestments, or a decrease in demand for oil and gas, or a sustained period of low oil prices mayalso adversely affect the economies of the GCC countries in which the Issuer operates, whichcould in turn affect the ability of the Issuer to perform its obligations in respect of the CapitalSecurities.

Ongoing Challenging Environment

Since the second half of 2007, disruptions in global capital and credit markets, coupled with there-pricing of credit risk and the deterioration of the real estate markets in the United States,Europe, Bahrain, the other countries of the GCC and elsewhere, have created difficult conditions inthe financial markets. These conditions have resulted in historically high levels of volatility acrossmany markets (including capital markets) and the failure of a number of financial institutions inthe United States and Europe. Further market disruption may be caused by certain Europeancountries experiencing debt servicing problems. Regional disturbances, such as localised creditfailures and the “Arab Spring”, have also affected the financial markets in the MENA region.

The countries of the GCC were affected by the global financial crisis in the second half of 2007;however, the most significant adverse effects only impacted the region in the second half of 2008.Since then, there has been a significant slowdown or reversal of the high growth rates that had

1

been experienced by many countries within the GCC. Consequently, certain sectors of the GCCeconomy that had benefited from the high rate of growth, such as real estate, construction andfinancial institutions, have been materially adversely affected by the crisis.

In response to the global financial crisis, governments and regulators in the GCC countries,Europe, the United States and other jurisdictions enacted legislation and took measures intended tohelp stabilise the financial system and increase the flow of credit to their economies. Thesemeasures included recapitalisation through the purchase of securities issued by financial institutions(including ordinary shares, preferred shares and other hybrid or quasi-equity instruments),guarantees by governments of debt issued by financial institutions and government-sponsoredmergers and acquisitions of and divestments by financial institutions. There can be no assurancethat any or all of these measures will continue to positively affect volatility and credit availabilityor that governments will continue to support recovery in this way.

Although growth has returned to certain global and MENA markets, investors should note that acontinuation or worsening of current financial market conditions could lead to further decreases ininvestor and consumer confidence, further market volatility, further economic disruption and, as aresult, this could have an adverse effect on the business, results of operations, financial conditionand prospects of the Issuer irrespective of steps currently taken to control these risks adequately.

Since mid-2014, international oil prices have fallen significantly, with the monthly average price ofthe OPEC reference basket falling from U.S.$105.61 in July 2014 to a low of U.S.$44.38 inJanuary 2015. On 9 April 2015, the OPEC reference basket price was U.S.$53.52. A sustained lowoil price environment may potentially adversely impact the economic growth in the key markets inthe GCC in which the issuer operates in 2015, which could materially adversely affect many of theIssuer’s borrowers and contractual counterparties. This, in turn, could adversely affect the Issuer’sbusiness, financial condition, results of operations and prospects, in particular through increasedprovisions for credit losses and reduced demand for loans and other banking services.

Emerging markets

The majority of the Issuer’s operating markets are emerging markets. Investors in emerging marketsshould be aware that these markets are subject to greater risks than more developed markets,including, in some cases, significant legal, economic and political risks. Accordingly, investorsshould exercise particular care in evaluating the risks involved in investing in the Capital Securitiesand must decide for themselves whether, in light of those risks, their investment is appropriate.Generally, investment in emerging markets is only suitable for sophisticated investors who fullyappreciate the significance of the risk involved.

Political considerations relating to the countries in which the Issuer operates

The Issuer has operations in Bahrain, Kuwait and Oman in the GCC, and in Egypt, Iraq, Libyaand the United Kingdom. Any political disturbances leading to turbulence in the financial marketsin these countries may have an adverse impact on the operations and profitability of the Issuer. Ofthese key markets, Bahrain and Egypt were primarily impacted by protests against the governmentsthroughout the MENA region, termed as the “Arab Spring”. Libya, albeit a less material market forthe Issuer, was also impacted by the “Arab Spring” and is witnessing continued civil unrest. Morerecently, Iraq and Libya have been impacted by an insurgency led by the terrorist group “IslamicState of Iraq and Al-Sham (ISIS)” (see further “Political Considerations in Iraq” and “PoliticalConsiderations in Libya” below).

Political Considerations in Bahrain

Protests against the Bahrain Government were held during February and March 2011. On 16 March2011, His Majesty, King Hamad bin Isa Al Khalifa of Bahrain issued Royal Decree No. 18 of2011, declaring a “State of National Safety” for three months, which was scheduled to end on15 June 2011. The provisions of the Royal Decree No. 18 included, amongst other things,measures aimed at maintaining security and public order, regulating public meetings and prohibiting

2

gatherings of people if they were deemed a threat to public order or national security. On 1 June2011, ahead of the scheduled date, His Majesty declared an end to the “State of National Safety”with the goal of encouraging national dialogue and reconciliation.

The Bahrain Independent Commission of Inquiry (the BICI) was established by Royal Order inJune 2011. The BICI was assigned the task of reporting on the protests in February and March2011 and their aftermath. The BICI produced its report on 23 November 2011, setting out adetailed narrative regarding the events that had taken place and presented a series ofrecommendations involving comprehensive, structural reform and a process of nationalreconciliation. The government pledged to implement the BICI recommendations in their entirety. Ahigh-level National Commission was formed to monitor and oversee the government’s progress inimplementing the BICI recommendations. Its report dated 20 March 2012 found that thegovernment had made substantial progress towards fully implementing the BICI recommendations.

In December 2013, the government issued a follow up-report outlining the further implementationof the BICI recommendations. The report stated that, as at December 2013, 19 recommendationswere fully implemented and the government had begun work to implement the remaining sevenrecommendations. The government published a further follow-up report in February 2014 thatconcluded that the government had implemented the majority of the BICI recommendations;however, the extent to which the recommendations have been implemented has been disputed.

Elections for the National Assembly were held in November 2014. Talks between the governmentand opposition aimed at reaching a political compromise ahead of the elections were unsuccessfuland the opposition boycotted the elections. There continues to be unrest with protests beingreported in February 2015 and the possibility of future protests cannot be ruled out.

The Issuer’s operations were unaffected during the unrest in Bahrain, except for one working day,while it met all of its settlement obligations by implementing its Business Continuity Planningframework. Any future unrest in Bahrain or the wider MENA could have an adverse effect on thebusiness, results of operations, financial condition and prospects of the Issuer irrespective of stepscurrently taken to control these risks adequately.

Political Considerations in Egypt

Protests against President Hosni Mubarak of Egypt began in January 2011 and led to Mubarak’sresignation on 11 February 2011. Political power was handed over to the Supreme Council of theArmed Forces (SCAF) which led to the dissolution of parliament and the suspension of theconstitution.

The Central Bank of Egypt (CBE) ordered all banks in Egypt to remain closed from 30 January2011 to 3 February 2011 and from 14 February 2011 to 17 February 2011. Further, reducedopening hours for banks were decreed from 6 February 2011 to 10 February 2011. The Issuercomplied with the CBE directive, resulting in operations being disrupted during this period. Normaloperations resumed from 20 February 2011.

Egypt experienced continued political uncertainty and instability over the course of 2012.Presidential elections were held in June 2012 and were won by the Freedom and Justice Partycandidate, Mohammed Morsi, who took office on 30 June 2012. On 22 November 2012, PresidentMorsi issued a decree which tasked a constitutional assembly with drafting a new constitution. Thisdecree sparked protests leading the president to rescind the majority of the decree on 20 December2012. The new constitution was approved by parliament on 30 November 2012 and it was signedinto law by President Morsi on 26 December 2012.

On 3 July 2013, protests calling for President Morsi’s immediate resignation culminated in thedeposition of President Morsi by the Egyptian army and the suspension of the Egyptianconstitution. The Egyptian army appointed the head of the Supreme Constitutional Court, ChiefJustice Adly Mansour, as Interim President. These events led to an escalation in protests and

3

violence by both pro and anti Morsi factions. After two successive interim governments in the firstquarter of 2014, presidential elections were conducted in May 2014. Abdel Fatah el-Sisi, formerEgyptian Defence Minister was elected President.

The High Elections Committee (the body responsible for conducting parliamentary elections inEgypt) announced in January 2015 that the parliamentary election will take place over two stagesin March and April 2015. The successful staging of the election is a prerequisite to furthernegotiations with the IMF over a proposed credit facility.

The challenges faced during the transition period, together with the incidents of social and politicalunrest and violence in Egypt and across the MENA region, have had a significant adverse effecton the Egyptian economy and there can be no assurance that further incidents of political or socialinstability, terrorism, protests or violence will not directly or indirectly affect Egypt and itseconomy.

Although as at 31 December 2014, the Issuer’s operations had not suffered any material adverseeffect as a consequence of these events, any future uncertainty in the Egyptian political situationmay have a negative impact on the Issuer’s operations in Egypt.

Political Considerations in Iraq

ISIS is a terrorist group whose main operations are in Syria and Iraq, among other states. InAugust/September 2014 the United States of America and certain of its western allies, with co-operation from various Arab allies, launched an air campaign against ISIS. The effect of the strikesto the capabilities of ISIS is unknown and as at 31 December 2014, ISIS still held large parts ofNorth Eastern Iraq.

The incidents of social and political unrest, terrorism and violence in Iraq have had an adverseeffect on the Iraqi economy and there can be no assurance that ISIS will be defeated by thecurrent military campaign.

The Issuer’s operations in Iraq are conducted through its branch network in Baghdad and Basra,which have not been directly impacted by the ISIS threats. The Issuer does not anticipate anymaterial adverse impact on its financial position from political developments in Iraq as Iraqcontributes less than 2 per cent. of the Issuer’s consolidated profit. Moreover, 96.6 per cent. ofIssuer’s total assets in Iraq are held in the form of cash and cash equivalents or governmentsecurities, reducing volatility in the Issuer’s performance in Iraq.

Political Considerations in Libya

It has been widely reported in the media that ISIS is steadily advancing its operations in Libya,facilitated by the current political turmoil in the country. ISIS now controls the Libyan cities ofDarna and Sirte, and has carried out suicide bombings and attacks on civilians across the rest ofthe country. In February/March 2015, ISIS launched a series of attacks on Libya’s oil fields,forcing the state-run oil corporation to declare 11 fields non-operational and causing oil productionto drop to approximately 25 per cent. of normal levels. These incidents of terrorism and violenceare highly likely to have an adverse effect on the Libyan economy.

Any continued and future unrest in Libya may have a negative impact on the Issuer’s operations inLibya.

The GCC may enter into a monetary union

There is the possibility that Bahrain, the State of Kuwait, the Kingdom of Saudi Arabia and theState of Qatar may each abandon their respective national currencies in favour of a single GCCcurrency within the next few years. If a single GCC currency is adopted, the necessaryconvergence of laws, policies and procedure will bring significant changes to the economic andpolitical infrastructure in each of the GCC states. As yet, there has been no announcement of anofficial timetable for the progression of monetary union and there are currently no details of new

4

legislation or policies. Investors should, however, be aware that new legislation and any resultingshift in policy and procedure in Bahrain could affect the ability of the Issuer to perform itsobligations under the Capital Securities.

Ownership and Legal Status

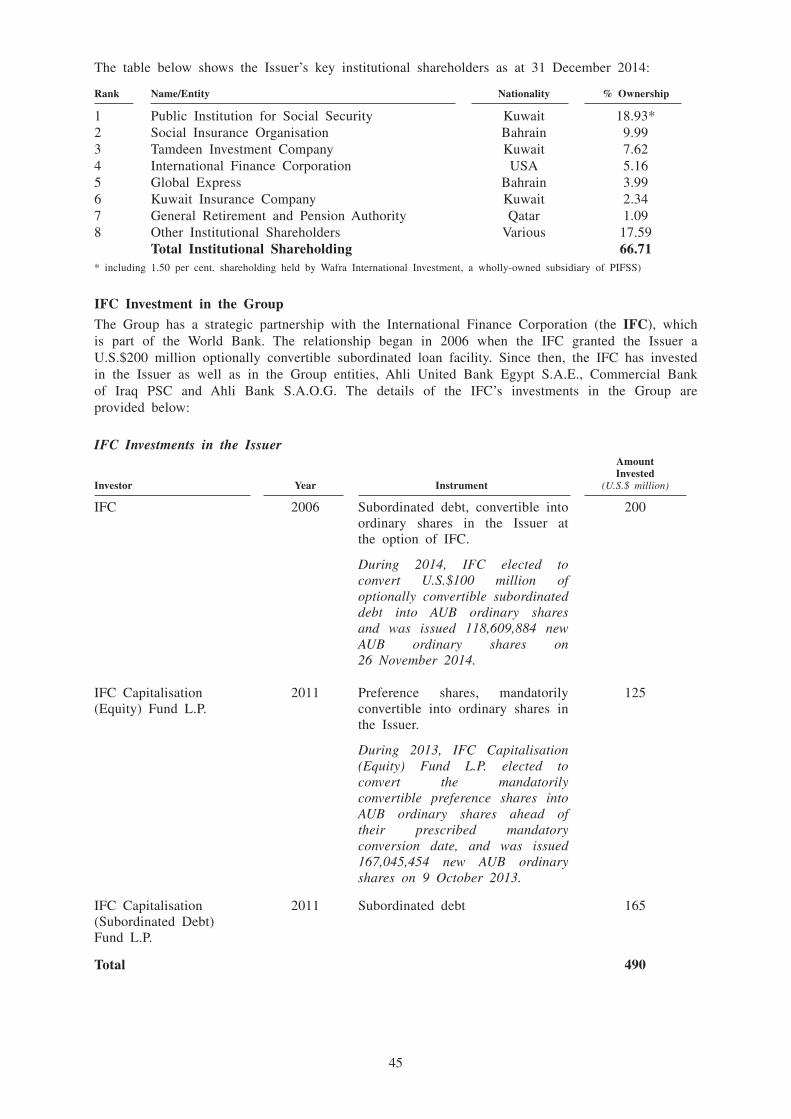

As at 31 December 2014, the Government of Kuwait, through the Public Institution for SocialSecurity (PIFSS), and Wafra International Investment (a wholly-owned subsidiary of PIFSS), own18.93 per cent. of the Issuer’s ordinary shares, Social Insurance Organisation, Bahrain (an amalgamof the Pension Fund Commission and the General Organisation for Social Insurance) owns 9.99 percent., Tamdeen Investment Company (the investment vehicle of certain private Kuwaiti investors)owns 7.62 per cent. and International Financial Corporation along with the IFC Capitalization(Equity) Fund LP owns 5.16 per cent. Other key institutional shareholders include Global Express(Bahrain) with 3.99 per cent. ownership, Kuwait Insurance Company (Kuwait) with 2.34 per cent.ownership and General Retirement & Pension Authority (Qatar) with 1.09 per cent. ownership.There can be no assurance however that the Issuer’s shareholders will continue to maintain theexisting levels of their ownership of the shares of the Issuer.

The Governments of Bahrain and Kuwait do not explicitly or implicitly guarantee the financialobligations of the Issuer, nor do they have any obligation to provide any support or additionalfunding for the Issuer’s future operations. The Governments may sell their shareholding in theIssuer to third parties and may cease to do business with the Issuer, including maintaining deposits.This may impact the Issuer’s ability to provide funding for its operations and may cause significantliquidity stress.

Risks Related to the Issuer’s Business

In the course of its business activities, the Issuer is exposed to a variety of risks, the mostsignificant of which are credit risk, market risk, operational risk, liquidity risk and concentrationrisk (each of which is described below). Investors should note that any failure to adequatelycontrol these risks could result in adverse effects on the business, results of operations, financialcondition and prospects of the Issuer.

Credit Risk

Risks arising from adverse changes in the credit quality and recoverability of loans and amountsdue from counterparties are inherent in a wide range of the Issuer’s businesses, principally in itslending and investment activities. Credit risks could arise from a deterioration in the credit qualityof specific borrowers, issuers and counterparties of the Issuer, or from a general deterioration inlocal or global economic conditions, or from systematic risks within financial systems. Such creditrisks could affect the recoverability and value of the Issuer’s assets and require an increase in theIssuer’s provisions for the impairment of loans, securities and other credit exposures.

The markets in which the Issuer operates, including the GCC economies, have been negativelyaffected by the global economic slowdown, which has impacted the various key industry sectorsincluding manufacturing, trade, tourism and real estate. As a result of these recent adverse marketconditions, certain of the Issuer’s customers to whom credit facilities have been extended by theIssuer have experienced, and may continue to experience, decreased revenues, financial losses,difficulty in obtaining financing, increased funding costs and problems servicing their debtobligations as they become due. Accordingly, the Issuer may experience a higher level of creditdefaults (including impaired loans and consequential rise in the charge for doubtful loans andadvances) in the future, which could have a material adverse effect on its results of operations.

Market Risk

The most significant market risks to which the Issuer is exposed are interest rate, foreign exchangeand bond and equity price risks associated with its trading, investment and asset and liabilitymanagement activities. The Issuer’s major markets, including Bahrain, Kuwait, Oman and theUnited Kingdom have free market economies, with no restrictions on capital movements, foreignexchange, foreign trade or foreign investment. However, changes in interest rate levels, yield curves

5

and spreads may affect the interest rate margin realised between the Issuer’s lending andinvestment activities and its borrowing costs, and the values of assets that are sensitive to interestrate and spread changes. Changes in foreign exchange rates may affect the values of assets andliabilities denominated in foreign currencies and the income from foreign exchange dealing.Changes in bond and equity prices may affect the value of the Issuer’s investment and tradingportfolios. A worsening of current financial market conditions could cause further market volatilityand further economic disruption. It is difficult to predict changes in economic and marketconditions accurately and to anticipate the effects that such changes could have on the Issuer’sfinancial performance and business operations.

Operational Risk

The Issuer faces the risk of losses resulting from fraud, errors by employees, failure to documenttransactions properly or to obtain proper internal authorisation, failure to comply with regulatoryrequirements and conduct of business rules, systems and equipment failures, natural disasters or thefailure of external systems (for example, those of the Issuer’s counterparties or vendors). Althoughthe Issuer has implemented risk controls and loss mitigation strategies under its Operational RiskSelf-Assessment regime, and substantial resources are devoted to developing efficient proceduresand to staff training, it is not possible to eliminate each of the operational risks entirely. TheIssuer is therefore exposed to operational risk that could negatively impact its business and resultsof operations.

Notwithstanding anything in this risk factor, this risk factor should not be taken as implying thatthe Issuer will be unable to comply with its obligations as a company with securities admitted toa regulated stock exchange.

Liquidity Risk

Liquidity risk could arise from the inability of the Issuer to anticipate and provide for unforeseendecreases or changes in funding sources which could have adverse consequences on the Issuer’sability to meet its obligations when they fall due.

The Issuer obtains its funding from diverse retail and wholesale sources, primarily from non-bank/financial institution depositors in the GCC, Egypt and the United Kingdom, as well as fromthe inter-bank market and term financing facilities. As at 31 December 2014, 75.6 per cent. of itstotal liabilities were derived from the GCC, comprising primarily of customer and inter-bankdeposits. Whilst the high proportion of deposits from GCC sources may protect the Issuer fromany sudden change in international sentiment towards the MENA region, it nevertheless contributesto the risk of a geographically concentrated depositor base. A failure to diversify the Issuer’sdepositor base beyond the MENA region could expose the Issuer to potential economic, politicaland cultural changes in that area which, in turn, could have a material adverse effect on thebusiness, results of operations, financial condition and prospects of the Issuer.

Concentration Risk

Concentrations in the loan/financing receivables and deposit portfolio of the Issuer subject it torisks from default by its larger borrowers, from exposure to particular industry sectors and fromthe withdrawal of any large deposits. The loans and receivables portfolio of the Issuer showsindustry and borrower concentration.

The ten largest private sector borrowers (which excludes those borrowers which are either whollyor majority owned by the Government) represented 12.3 per cent. of its total gross loans andadvances as at 31 December 2014. As at 31 December 2014, the Issuer’s largest funded exposureto a private sector borrower group, including connected exposures, was U.S.$377 million, whichconstituted 2.0 per cent. of its total gross loans and advances as at 31 December 2014.

In terms of the industry concentration of the loans and advances of the Issuer and its network ofsubsidiaries, as at 31 December 2014, banks and other financial institutions accounted for 5.5 percent., consumer/personal loans and advances accounted for 18.7 per cent., real estate loans andadvances accounted for 24.8 per cent., trading and manufacturing loans and advances accounted for

6

22.4 per cent., services loans and advances accounted for 16.7 per cent., government/public sectorloans and advances accounted for 1.4 per cent. and residential mortgages accounted for 9.1 percent. (of which 69 per cent. is accounted for in the United Kingdom).

As at 31 December 2014, banks and other financial institutions accounted for 15.8 per cent. of theIssuer’s total deposits and customers’ deposits accounted for 81.0 per cent. with the remaining 3.2per cent. coming from borrowings under repurchase agreements (Repo). The Issuer’s fundingbenefits from a wide and diversified deposit base, albeit skewed toward corporations, and largeshareholder deposits. Most depositors are longstanding clients, and the largest are GCC quasi-government entities. Although the Issuer considers that it has adequate access to sources offunding, the withdrawal of a significant portion of these large deposits may have an adverse effecton its financial condition or results of operations. A downturn in the financial condition orprospects of any of the Issuer’s depositors, or in the sectors in which they operate, could have amaterial adverse effect on the financial condition or results of operations of the Issuer.

Depositor concentration

As at 31 December 2014, 24.4 per cent. of customers’ deposits were deposits from GCCgovernment-owned institutions which have been shareholders of the Issuer since its incorporation(as compared with 28.5 per cent. as at 31 December 2013). These deposits have historically beenmaintained in a diverse range of accounts with the Issuer and its network of subsidiaries, and theIssuer understands these deposits to comprise the institutions’ funds for investment in the bankingsector in the GCC. Whilst the Issuer considers that it currently has adequate access to variousfunding sources (including, amongst other things, tested ability and capacity to carry out Repotransactions as part of ongoing liquidity management, and a diversified customer deposit baseamongst the Corporate Banking, Treasury and Investments and Retail Banking Divisions), thewithdrawal of all or a significant portion of such deposits may result in a material adverse effecton the business, results of operations, financial condition and prospects of the Issuer.

Real Estate Exposure

As at 31 December 2014, the Issuer’s total real estate exposures (excluding residential mortgages)amounted to 14.7 per cent. of total assets (U.S.$4.92 billion). These are mostly secured by incomeproducing properties and the portfolio’s average loan-to-value ratio at the end of December 2014was 57 per cent. Real estate prices in most of the markets in which the Issuer operates havegenerally declined since 2009, with a gradual recovery noted during 2013, which has continued todate in 2015, reflecting the slowdown in economic growth as well as uncertainty and loweravailability of credit. These factors have also led to a significant slowdown in the constructionsector in the markets in which the Issuer operates. Economic and other factors could lead tocontraction in the residential mortgage and commercial lending market and to further decreases inresidential and commercial property prices.

Strategic Risks

The Issuer is exposed to strategic risks in the markets in which it operates. The Issuer’s businessstrategy involves growth through acquisitions in target markets in the GCC and the MENA region(see “Business Description of the Issuer – Strategy”). The execution of this strategy is dependenton regional regulations and the central banks of the countries in which the Issuer wishes toexpand. The implementation of this strategy may be impacted due to regulatory restrictions orrefusals to grant approvals to the Issuer for the acquisitions, participation in capital increases andother related transactions.

Furthermore, in addition to the normal business and related risks associated with organic expansion,when suitable opportunities present themselves and the Issuer decides to make acquisitions, thismay entail additional risks, including in respect of the integration of such acquisitions. While theIssuer seeks to mitigate these risks by completing a detailed expansion opportunity analysis andcommissioning due diligence reviews as well as inserting the necessary conditions precedent in anyacquisition agreement, there is no guarantee that such mitigation will be effective. A failure on the

7

Issuer’s part to manage its future growth efficiently and effectively could have a material adverseeffect on the business, results of operations, financial condition and prospects of the Issuer andthereby affect its ability to make payments in respect of the Capital Securities.

Competition