You must read the following before contin - Singapore Exchange

533

IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE U.S. IMPORTANT: You must read the following before continuing. The following applies to the note offering circular dated 4 August 2016 (the Note Offering Circular and, together with the offering circular dated 4 November 2015, the Offering Circular) following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the Offering Circular. In accessing the Offering Circular, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S., EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE FOLLOWING OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENT DECISION SHOULD BE MADE ON THE BASIS OF THE TERMS AND CONDITIONS OF THE SECURITIES AND THE INFORMATION CONTAINED IN THE OFFERING CIRCULAR. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED THEREIN. Confirmation of your Representation: This Offering Circular is being sent at your request and by accepting the e-mail and accessing this Offering Circular, you shall be deemed to have represented to us that the electronic mail address that you gave us and to which this e-mail has been delivered is not located in the U.S. and that you consent to delivery of such Offering Circular by electronic transmission. You are reminded that this Offering Circular has been delivered to you on the basis that you are a person into whose possession this Offering Circular may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located and you may not, nor are you authorised to, deliver this Offering Circular to any other person. The materials relating to any offering of securities described in the Offering Circular do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by the underwriters or such affiliate on behalf of the Issuer in such jurisdiction.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of You must read the following before contin - Singapore Exchange

IMPORTANT NOTICE

NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE U.S.

IMPORTANT: You must read the following before continuing. The following applies to the note

offering circular dated 4 August 2016 (the Note Offering Circular and, together with the offering

circular dated 4 November 2015, the Offering Circular) following this page, and you are therefore

advised to read this carefully before reading, accessing or making any other use of the Offering

Circular. In accessing the Offering Circular, you agree to be bound by the following terms and

conditions, including any modifications to them any time you receive any information from us as a

result of such access.

NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF

SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE

IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE,

REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE

SECURITIES ACT), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER

JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE

U.S., EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT

SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND

APPLICABLE STATE OR LOCAL SECURITIES LAWS.

THE FOLLOWING OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED

TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER

WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S.

ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS

DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH

THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE

APPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENT DECISION SHOULD

BE MADE ON THE BASIS OF THE TERMS AND CONDITIONS OF THE SECURITIES AND

THE INFORMATION CONTAINED IN THE OFFERING CIRCULAR. IF YOU HAVE GAINED

ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING

RESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE ABLE TO PURCHASE

ANY OF THE SECURITIES DESCRIBED THEREIN.

Confirmation of your Representation: This Offering Circular is being sent at your request and by

accepting the e-mail and accessing this Offering Circular, you shall be deemed to have represented to

us that the electronic mail address that you gave us and to which this e-mail has been delivered is not

located in the U.S. and that you consent to delivery of such Offering Circular by electronic

transmission.

You are reminded that this Offering Circular has been delivered to you on the basis that you are a

person into whose possession this Offering Circular may be lawfully delivered in accordance with the

laws of the jurisdiction in which you are located and you may not, nor are you authorised to, deliver

this Offering Circular to any other person.

The materials relating to any offering of securities described in the Offering Circular do not constitute,

and may not be used in connection with, an offer or solicitation in any place where offers or

solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed

broker or dealer and the underwriters or any affiliate of the underwriters is a licensed broker or dealer

in that jurisdiction, the offering shall be deemed to be made by the underwriters or such affiliate on

behalf of the Issuer in such jurisdiction.

This Offering Circular has been sent to you in an electronic form. You are reminded that documents

transmitted via this medium may be altered or changed during the process of electronic transmission

and consequently neither Axis Bank, Singapore Branch, The Hongkong and Shanghai Banking

Corporation Limited, MUFG Securities EMEA plc, Standard Chartered Bank nor any person who

controls each of them nor any director, officer, employee nor agent of each of them or affiliate of any

such person accepts any liability or responsibility whatsoever in respect of any difference between the

Offering Circular distributed to you in electronic format and the hard copy version available to you on

request from Axis Bank, Singapore Branch, The Hongkong and Shanghai Banking Corporation

Limited, MUFG Securities EMEA plc and Standard Chartered Bank.

You are responsible for protecting against viruses and other destructive items. Your use of this e-mail

is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses

and other items of a destructive nature.

To the fullest extent permitted by law, neither Axis Bank, Singapore Branch, The Hongkong and Shanghai Banking Corporation Limited, MUFG Securities EMEA plc, Standard Chartered Bank nor

any person who controls each of them nor any director, officer, employee nor agent of each of them or

affiliate of any such person accept any responsibility for the contents of this Offering Circular or for

any other statement, made or purported to be made by Axis Bank, Singapore Branch, The Hongkong and Shanghai Banking Corporation Limited, MUFG Securities EMEA plc, Standard Chartered Bank

or by any person who controls each of them, or by any director, officer, employee or agent of each of

them or affiliate of any such person in connection with the Issuer, or the Offering. Axis Bank, Singapore Branch, The Hongkong and Shanghai Banking Corporation Limited, MUFG Securities

EMEA plc and Standard Chartered Bank accordingly disclaims all and any liability whether arising in

tort or contract or otherwise which it might otherwise have in respect of this Offering Circular or any such statement.

The Offering Circular has not been and will not be registered, produced or made available to all as an

offer document (whether a prospectus in respect of a public offer or an information memorandum or private placement offer letter or other offering material in respect of any private placement under the

Companies Act, 2013 or any other applicable Indian laws) with the Registrar of Companies of India

(RoC) or the SEBI or any other statutory or regulatory body of like nature in India,

In addition, holders and beneficial owners shall be responsible for compliance with restrictions on the

ownership of the Rupee Denominated Notes imposed from time to time by applicable laws or by any

regulatory authority or otherwise. In this context, holders and beneficial owners of Rupee

Denominated Notes shall be deemed to have acknowledged, represented and agreed that such holders

and beneficial owners are eligible to purchase the Rupee Denominated Notes under applicable laws

and regulations and are not prohibited under any applicable law or regulation from acquiring, owning

or selling the Rupee Denominated Notes. Potential investors should seek independent advice and

verify compliance with FATF Requirements prior to any purchase of the Rupee Denominated Notes.

The holders and beneficial owners of Rupee Denominated Notes shall be deemed to confirm that

for so long as they hold any Rupee Denominated Notes, they will meet the FATF Requirements

and will not be an offshore branch of an Indian bank.

Further, all Noteholders represent and agree that the Rupee Denominated Notes will not be

offered or sold on the secondary market to any person who does not comply with the FATF

Requirements or which is an offshore branch of an Indian bank.

0012018-0003086 HK:20704050.1

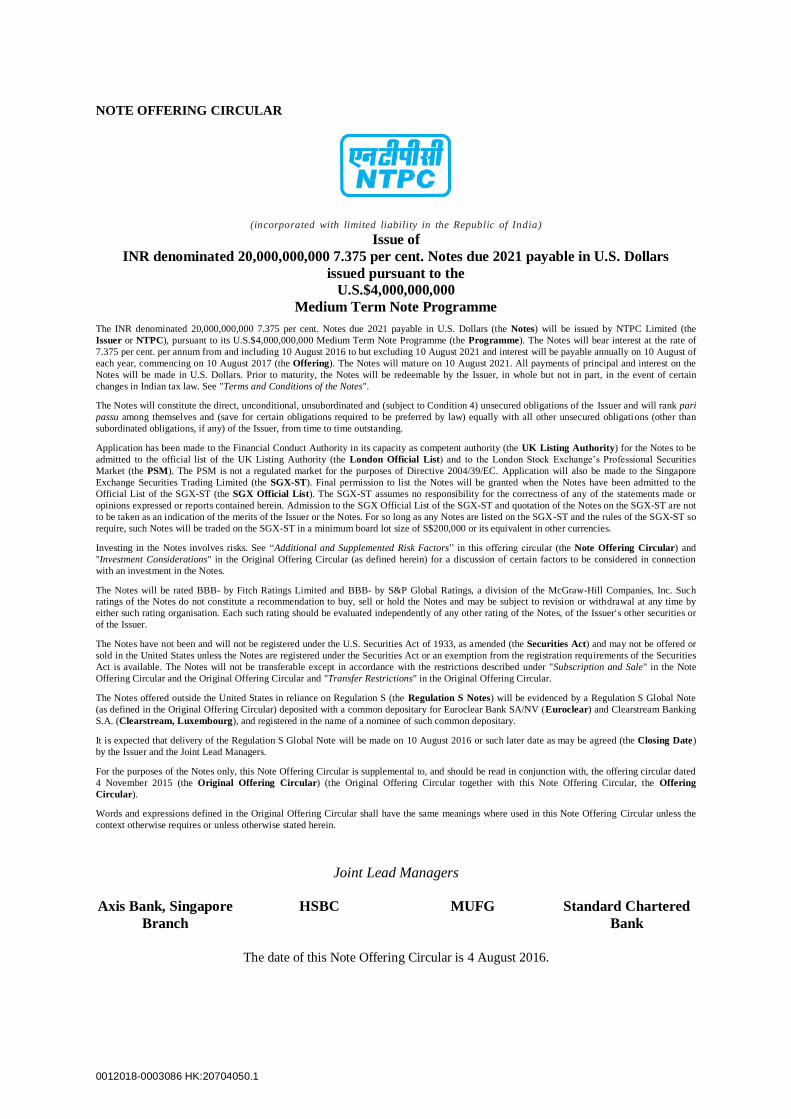

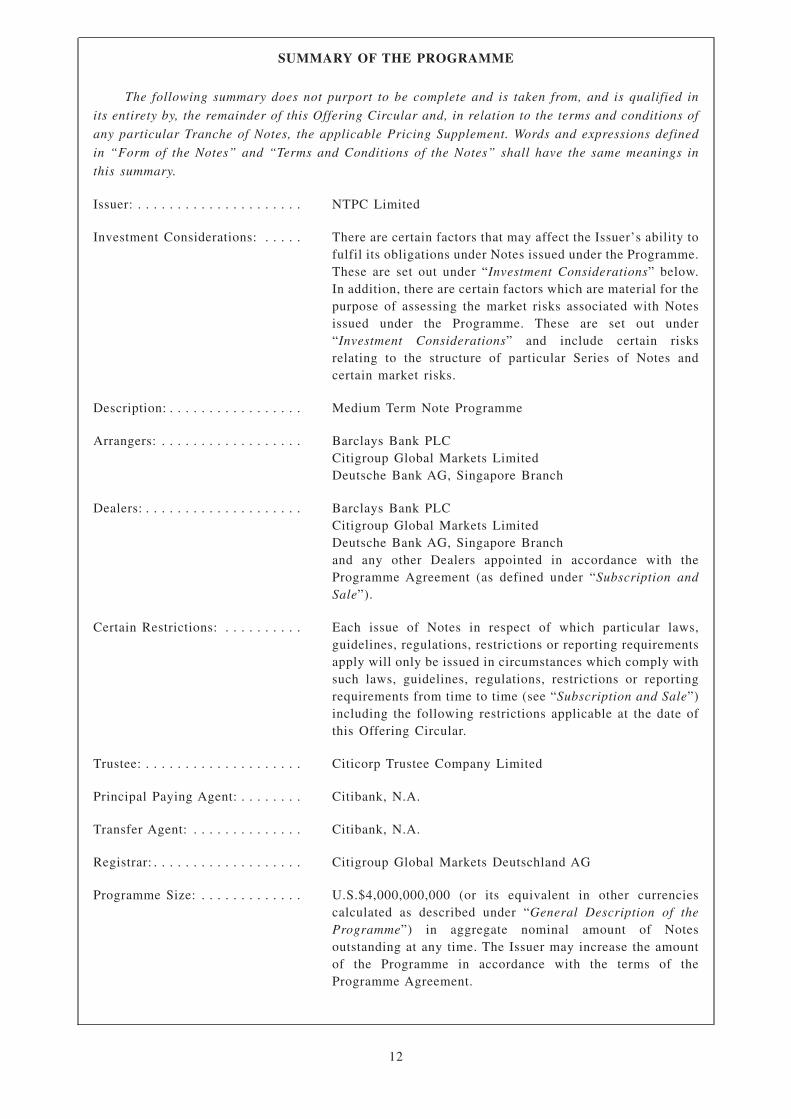

NOTE OFFERING CIRCULAR

(incorporated with limited liability in the Republic of India)

Issue of

INR denominated 20,000,000,000 7.375 per cent. Notes due 2021 payable in U.S. Dollars

issued pursuant to the

U.S.$4,000,000,000

Medium Term Note Programme

The INR denominated 20,000,000,000 7.375 per cent. Notes due 2021 payable in U.S. Dollars (the Notes) will be issued by NTPC Limited (the

Issuer or NTPC), pursuant to its U.S.$4,000,000,000 Medium Term Note Programme (the Programme). The Notes will bear interest at the rate of

7.375 per cent. per annum from and including 10 August 2016 to but excluding 10 August 2021 and interest will be payable annually on 10 August of

each year, commencing on 10 August 2017 (the Offering). The Notes will mature on 10 August 2021. All payments of principal and interest on the

Notes will be made in U.S. Dollars. Prior to maturity, the Notes will be redeemable by the Issuer, in whole but not in part, in the event of certain

changes in Indian tax law. See "Terms and Conditions of the Notes".

The Notes will constitute the direct, unconditional, unsubordinated and (subject to Condition 4) unsecured obligations of the Issuer and will rank pari

passu among themselves and (save for certain obligations required to be preferred by law) equally with all other unsecured obligations (other than

subordinated obligations, if any) of the Issuer, from time to time outstanding.

Application has been made to the Financial Conduct Authority in its capacity as competent authority (the UK Listing Authority) for the Notes to be

admitted to the official list of the UK Listing Authority (the London Official List) and to the London Stock Exchange’s Professional Securities

Market (the PSM). The PSM is not a regulated market for the purposes of Directive 2004/39/EC. Application will also be made to the Singapore

Exchange Securities Trading Limited (the SGX-ST). Final permission to list the Notes will be granted when the Notes have been admitted to the

Official List of the SGX-ST (the SGX Official List). The SGX-ST assumes no responsibility for the correctness of any of the statements made or

opinions expressed or reports contained herein. Admission to the SGX Official List of the SGX-ST and quotation of the Notes on the SGX-ST are not

to be taken as an indication of the merits of the Issuer or the Notes. For so long as any Notes are listed on the SGX-ST and the rules of the SGX-ST so

require, such Notes will be traded on the SGX-ST in a minimum board lot size of S$200,000 or its equivalent in other currencies.

Investing in the Notes involves risks. See “Additional and Supplemented Risk Factors” in this offering circular (the Note Offering Circular) and

"Investment Considerations" in the Original Offering Circular (as defined herein) for a discussion of certain factors to be considered in connection

with an investment in the Notes.

The Notes will be rated BBB- by Fitch Ratings Limited and BBB- by S&P Global Ratings, a division of the McGraw-Hill Companies, Inc. Such ratings of the Notes do not constitute a recommendation to buy, sell or hold the Notes and may be subject to revision or withdrawal at any time by

either such rating organisation. Each such rating should be evaluated independently of any other rating of the Notes, of the Issuer's other securities or

of the Issuer.

The Notes have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the Securities Act) and may not be offered or

sold in the United States unless the Notes are registered under the Securities Act or an exemption from the registration requirements of the Securities

Act is available. The Notes will not be transferable except in accordance with the restrictions described under "Subscription and Sale" in the Note

Offering Circular and the Original Offering Circular and "Transfer Restrictions" in the Original Offering Circular.

The Notes offered outside the United States in reliance on Regulation S (the Regulation S Notes) will be evidenced by a Regulation S Global Note

(as defined in the Original Offering Circular) deposited with a common depositary for Euroclear Bank SA/NV (Euroclear) and Clearstream Banking

S.A. (Clearstream, Luxembourg), and registered in the name of a nominee of such common depositary.

It is expected that delivery of the Regulation S Global Note will be made on 10 August 2016 or such later date as may be agreed (the Closing Date)

by the Issuer and the Joint Lead Managers.

For the purposes of the Notes only, this Note Offering Circular is supplemental to, and should be read in conjunction with, the offering circular dated

4 November 2015 (the Original Offering Circular) (the Original Offering Circular together with this Note Offering Circular, the Offering

Circular).

Words and expressions defined in the Original Offering Circular shall have the same meanings where used in this Note Offering Circular unless the

context otherwise requires or unless otherwise stated herein.

Joint Lead Managers

Axis Bank, Singapore

Branch

HSBC MUFG Standard Chartered

Bank

The date of this Note Offering Circular is 4 August 2016.

0012018-0003086 HK:20704050.1

TABLE OF CONTENTS

PAGE

ABOUT THIS DOCUMENT ............................................................................................................ S-1

GLOSSARY OF TERMS USED IN THIS OFFERING CIRCULAR ................................................. S-2

NOTES BEING ISSUED AS GREEN MASALA BONDS ................................................................ S-3

ADDITIONAL AND SUPPLEMENTED RISK FACTORS .............................................................. S-4

DESCRIPTION OF THE ISSUER .................................................................................................. S-18

SUPERVISION AND REGULATION ............................................................................................ S-19

USE OF PROCEEDS ...................................................................................................................... S-20

THE ISSUER'S GREEN BOND FRAMEWORK ............................................................................ S-21

SUBSCRIPTION AND SALE ......................................................................................................... S-23

PRICING SUPPLEMENT FOR GREEN MASALA BONDS .......................................................... S-25

TAXATION .................................................................................................................................... S-35

RECENT DEVELOPMENTS ......................................................................................................... S-37

AUDITED FINANCIAL RESULTS FOR THE YEAR ENDED 31 MARCH 2016 ......................... S-40

0012018-0003086 HK:20704050.1 S-1

ABOUT THIS DOCUMENT

This document is in two parts. The first part is the Note Offering Circular, which describes the

specific terms of the Notes being offered as Green Masala Bonds and also adds to and updates information contained in the Original Offering Circular. The second part, the Original Offering

Circular, provides more general information about the Issuer and the terms and conditions of the

Notes.

This Offering Circular comprises as a whole listing particulars in compliance with the listing rules

made under Section 73A of the Financial Services and Markets Act 2000 by the UK Listing Authority.

In the event of any conflict between the description of the Notes in this Note Offering Circular and the

description of the Notes in the Original Offering Circular, the description of the Notes in this Note

Offering Circular shall prevail.

No future financial statements are to be incporated by reference into this Offering Circular.

The Issuer accepts responsibility for the information contained in this Offering Circular. To the best

of the knowledge of the Issuer (having taken all reasonable care to ensure that such is the case) the

information contained in this Offering Circular is in accordance with the facts and does not omit

anything likely to affect the import of such information.

The reference to the specified office of the Paying Agent being “in London” appearing on page 212 of

the Original Offering Circular shall be deemed to be deleted and replaced “in Dublin”.

0012018-0003086 HK:20704050.1 S-2

GLOSSARY OF TERMS USED IN THIS OFFERING CIRCULAR

All references to the Rupee Bond Circular or the ECB Guidelines in the Original Offering Circular

should be read as the Foreign Exchange Management (Borrowing or Lending in Foreign Exchange)

Regulations, 2000 and the circulars issued thereunder by the RBI, including the Master Direction – External Commercial Borrowing, Trade Credit, Borrowing and Lending in Foreign Currency by

Authorised Dealers and Persons other than Authorised Dealers dated 1 January 2016, as amended.

0012018-0003086 HK:20704050.1 S-3

NOTES BEING ISSUED AS GREEN MASALA BONDS

The Notes being offered as “green masala bonds”, are in alignment with the pre-issuance

requirements of the Climate Bonds Standard Version 2.0 issued by the Climate Bonds Initiative

(Green Masala Bonds). In that regard, KPMG India (KPMG) has issued an independent limited

assurance statement (the Assurance Report) and the Climate Bonds Initiative has issued a certificate

that the issue of the Notes has met the relevant criteria set by the Climate Bonds Standard Board (the

CBI Certificate), in each case with respect to the Issuer's Green Bond Framework (as defined and

described in further detail in the following pages of this Note Offering Circular).

0012018-0003086 HK:20704050.1 S-4

ADDITIONAL AND SUPPLEMENTED RISK FACTORS

Investors should carefully consider the following Risk Factors as well as the other information

contained in this Offering Circular prior to making an investment in the Notes. In making an

investment decision, each investor must rely on its own examination of the Issuer and the terms of the

offering of the Notes. The risks described below are not the only ones that may affect the Notes.

Additional risks not currently known to the Issuer or that the Issuer, based on the information

currently available to it, currently deems immaterial may also impair the Issuer’s business operations.

All of these risks are contingencies which may or may not occur and the Issuer is not in a position to

express a view on the likelihood of any such contingency occurring. If any of the following or any

other risks actually occur, the Issuer’s business, prospects, results and financial condition could be

adversely affected and the price of and the value of investment in the Notes could decline and all or

part of the investments may be lost. These Risk Factors should be read in conjunction with those in

the Original Offering Circular under “Investment Considerations”.

In the event of any conflict between the descriptions under this “Additional and Supplemented

Risk Factors” in this Note Offering Circular and the descriptions under “Investment

Considerations” in the Original Offering Circular, the following descriptions in this Note

Offering Circular shall prevail.

The following Risk Factors are in addition to, and should be read in conjunction with, those in

the Original Offering Circular under “Investment Considerations”.

The Notes may not be a suitable investment for all investors seeking exposure to green assets.

At the Issuer’s request, KPMG has issued the Assurance Report and the Climate Bonds

Initiative has issued the CBI Certificate, in each case with respect to the Issuer's Green Bond

Framework. Neither of the Assurance Report or the CBI Certificate is incorporated into, nor does

either form part of, the Offering Circular. Neither the Issuer nor the Dealers make any representation

as to the suitability of the Assurance Report or the CBI Certificate. Neither of the Assurance Report or

the CBI Certificate is a recommendation to buy, sell or hold securities and each is only current as of

the respective date that it was initially issued. The Issuer has agreed to certain reporting and use of

proceeds obligations as described herein; however, it will not be an Event of Default under the Terms

and Conditions of the Notes if the Issuer fails to comply with such obligations. A withdrawal of the

Assurance Report or the CBI Certificate may affect the value of the Notes and may have

consequences for certain investors with portfolio mandates to invest in green assets.

The following risk factor appearing on page 90 of the Original Offering Circular shall be

deemed to be deleted in its entirety and replaced by the following:

The proposed adoption of Indian Accounting standards converged with IFRS (IND-AS) could have

a material adverse effect on the presentation of the Issuer’s financial statements.

The Issuer has historically prepared its annual and interim financial statements under Indian

GAAP. Public companies in India, including the Issuer, are now required to prepare annual and

interim financial statements under IND-AS in accordance with the roadmap announced on 2 January

2015 by the Ministry of Corporate Affairs, Government of India (the MCA), in consultation with the

National Advisory Committee on Accounting Standards (the MCA Press Release) for convergence

with IFRS. On 16 February 2015, the MCA notified the public of the Companies (Indian Accounting

Standards) Rules, 2015, which have come into effect from 1 April 2016. The Issuer intends to

announce its quarterly financial results pursuant to IND-AS for the first time for the quarter ended 30

0012018-0003086 HK:20704050.1 S-5

June 2016. There can be no assurance that the Issuer’s financial condition, results of operations, cash

flows or changes in shareholders’ equity will not appear materially worse under IND-AS than under

Indian GAAP. In the Issuer’s transition to IND-AS reporting, we may encounter difficulties in the

ongoing process of implementing and enhancing the Issuer’s management information systems.

Moreover, there is increasing competition for the small number of IND-AS-experienced accounting

personnel available as more Indian companies begin to prepare IND-AS financial statements.

Furthermore, there is no significant body of established practice on which to draw in forming

judgments regarding the new system’s implementation and application. There can be no assurance

that the Issuer’s adoption of IND-AS will not adversely affect the Issuer’s reported results of

operations or financial condition and any failure to successfully adopt IND-AS could adversely affect

the Issuer’s business, financial condition and results of operations. In addition, in its transition to

IND-AS reporting, the Issuer may encounter difficulties in the on-going process of implementing and

enhancing its management information systems.

The following risk factor appearing on page 97 of the Original Offering Circular shall be

deemed to be deleted in its entirety and replaced by the following:

Rupee Denominated Notes are subject to selling restrictions and may be transferred only to a

limited pool of investors.

Rupee Denominated Notes can only be issued to and held by investors resident in

jurisdictions who are a member of the Financial Action Task Force (FATF) or a member of a FATF-

Style Regional Body and whose securities market regulator is a signatory to the International

Organisation of Securities Commission's (IOSCO’s) Multilateral Memorandum of Understanding

(Appendix A Signatories) or a signatory to bilateral Memorandum of Understanding with the

Securities and Exchange Board of India (SEBI) for information sharing arrangements. Additionally,

investors should not be resident of a country identified in the public statement of the FATF as: (i) a

jurisdiction having a strategic Anti-Money Laundering or Combating the Financing of Terrorism

deficiencies to which counter measures apply; or (ii) a jurisdiction that has not made sufficient

progress in addressing the deficiencies or has not committed to an action plan developed with the

FATF to address the deficiencies.

The following Risk Factors supplement and update the corresponding risk factor in the Original

Offering Circular under “Investment Considerations”

The Issuer’s operations and the Issuer’s expansion plans have significant fuel requirements and

the Issuer may not be able to ensure the availability of fuel at competitive prices.

The success of the Issuer’s operations and the proposed expansion of its generation capacity

will be dependent on, among other things, the Issuer’s ability to ensure unconstrained availability of

fuels at competitive prices during the life cycle of its existing and planned thermal power stations. The

Issuer’s primary fuels are coal, gas and naphtha, with approximately 87.25 per cent. of its directly

owned installed generating capacity as of 30 June 2016 being coal-fired and approximately 9.99 per

cent. being gas or naphtha-fired. Fuel costs represent the Issuer’s largest operating expense,

constituting approximately 75.0 per cent. of total operating expenses on a stand-alone basis.

The Issuer purchases substantially all of its coal from subsidiaries of Coal India Limited

(CIL) and Singareni Collieries Company Limited (SCCL). The Issuer had signed long-term coal

supply agreements (CSAs) covering units commissioned as of 31 March 2009 for 23,895 MW at its

15 directly owned coal-fired power stations and covering units with a total capacity of 9,620 MW

0012018-0003086 HK:20704050.1 S-6

commissioned after 31 March 2009 or currently under construction. The Issuer has entered into long-

term gas supply agreements with GAIL (India) Limited (GAIL) for the supply of gas to its directly

owned gas-fired power stations. The Issuer has also entered into a long-term regasified liquefied

natural gas (RLNG) supply agreement with GAIL. However, no assurance can be given that the

Issuer’s suppliers will be able to satisfy its contractual commitments and that alternative sources of

supply would be available on reasonable terms.

If the Issuer is unable to obtain supplies from these suppliers on acceptable terms and

conditions, no assurance can be given that it will be able to obtain supplies from alternative suppliers.

Further, coal and gas allocations and gas prices are currently determined by the Government, whilst

coal prices are set by CIL or SCCL, as the case may be. In the event that coal and gas supplies or gas

prices were to be deregulated, no assurance can be given that the Issuer will be able to obtain supplies

of coal and gas at competitive prices and in the required quantities.

As of the date of this Offering Circular, the Issuer has planned to source coal for some of the

power projects under construction from the coal mines allotted to it and is working towards starting

coal production from these mines commensurate with the start of power generation from the linked

end-use power projects. In order to meet the coal requirement in case of any delay in the start of coal

production from the captive mines, the Issuer has already approached the Government for allocation

of tapering coal linkages from the coal mines of CIL. If the Issuer is unable to timely produce coal

from these mines or as per the requirement of the related projects and does not obtain tapering coal

linkages, no assurance can be given that the Issuer will be able to obtain supplies from alternative

sources. Though transportation of coal from two captive mines to its linked end-use power projects

shall be through the Issuer’s own system, the transportation of coal from other mines to the linked

power projects will be made through the Indian railways network (some of which network, as of the

date of this Offering Circular, requires further strengthening). Any delays in development of the

related infrastructure by the railways could constrain the fuel supplies to the Issuer’s projects and no

assurance can be given that the Issuer will be able to transport the coal through alternative means.

Any such constraints on sourcing of coal could have a negative impact on the Issuer’s business,

prospects and financial condition as well as on current and future capacity addition plans.

With respect to coal, while India has substantial proven reserves, significant investments

would be required to exploit and mine these reserves. No assurance can be given that such

investments will be made. The domestic demand for coal is expected to increase significantly in the

future, driven by significant capacity addition in the Indian power sector. High dependence on

domestic coal could therefore expose the Issuer to potential price and availability risks. In the event of

a shortage of coal, not only will the productivity of the Issuer’s coal-fired power stations be reduced

but it will also hinder the Issuer’s expansion plans. The Issuer also sources coal through bilateral short

term memoranda of understanding (MoUs) with SCCL or subsidiaries of CIL, through imports and

through e-auctions conducted by the subsidiaries of CIL. However, there is no assurance that such

sources of coal will continue to be available to the Issuer in the future at reasonable prices or terms or

at all.

With respect to gas, the Issuer’s use has been limited in the past due to inadequate supply of

domestic gas. The Issuer has arranged for the supply of RLNG through long- and short-term contracts

to meet part of its requirements. The short-term RLNG contracts are agreed on a “reasonable

endeavours” basis with no obligation on the part of the Issuer such as “ship-or-pay” or, “take-or-pay”

and no supply or pay obligation on the part of the suppliers. However, due to high RLNG prices, the

offtake of power by distribution companies and beneficiaries and, consequently, RLNG consumption

0012018-0003086 HK:20704050.1 S-7

have been low. The Issuer estimates that it will require 16.39 million metric standard cubic metres of

gas per day in fiscal 2016 to operate its directly owned gas-fired power stations at a plant load factor

(which is a measure equal to the percentage of capacity actually utilised) (PLF) of 85.0 per cent. If

the Issuer experiences a shortage in the supply of gas to its gas-fired power stations, the productivity

of those power stations would be reduced. Although the Issuer is in the process of securing a supply

of gas for the Issuer’s projects at Kawas and Gandhar, there is no assurance that it will be able to

secure an adequate supply of gas for its current gas-fired power stations or future gas-fired projects.

The Issuer’s ability to secure adequate fuel supply for its Kawas and Gandhar projects may also be

affected by its dispute with Reliance Industries Limited (RIL) on the sale and purchase agreement for

gas supply for those projects. See “The Issuer has executed a letter of intent with RIL for the purchase

of gas, which, if not declared as a valid and binding contract between the Issuer and RIL, may

negatively impact the Issuer’s financial condition and results of operation.” below. Any such

constraints on sourcing gas would have a negative impact on the Issuer’s business, prospects and

financial condition as well as current and future capacity addition plans.

The State Electricity Boards (SEBs) and state owned distribution companies account for more than

88 per cent. of the Issuer’s sales of electricity generated from its directly owned power stations and

any change that adversely affects the Issuer’s ability to recover dues from them would adversely

affect its financial position.

The SEBs and the state owned distribution companies are the largest purchasers of power

from the Issuer and accounted for more than 88 per cent. of the Issuer’s sales of electricity generated

from its directly owned power stations in fiscal 2015. The Issuer is obligated to supply power to them

in accordance with the terms of the allocation letters issued by the Government for each of the

Issuer’s power stations. Historically, the Issuer has had significant problems recovering payments

from the SEBs. The Scheme for One Time Settlement of Outstanding Dues (the OTSS) introduced

several measures to address these problems. Tripartite agreements (the Tripartite Agreements) were

signed under which the receivables for past due amounts from the SEBs were securitised, resulting in

the issue to the Issuer of 8.5 per cent. tax free state government special bonds issued under the OTSS

(the Tax Free Bonds). The Tax Free Bonds matured in various stages from 1 October 2006 until 1

April 2016. These agreements, inter-alia, provide that in case of any default in payment of current

dues by any state utility, the outstanding dues can be deducted from the state’s RBI account and paid

to the Issuer. In addition, the Tripartite Agreements require the SEBs to establish letters of credit

(LCs) to cover 105 per cent. of current payments for the sale of electricity generated from the Issuer’s

directly owned power stations. In addition to the Tripartite Agreements, the Issuer’s sales to the SEBs

from its directly owned power stations after 31 October 2016 are secured through supplementary

agreements with the SEBs under which the SEBs have agreed to create a charge over their own

receivables in favour of the Issuer, and in the event of a payment default, to assign their receivables

into an escrow account. If receivables of these SEBs are not received into such escrow accounts for

any reason whatsoever or if the security over such receivables is flawed, payments to the Issuer would

not be secured. Any change that adversely affects the Issuer’s ability to recover its dues from the

SEBs will adversely affect its financial position.

In fiscal 2014, the SEBs incurred losses of approximately Rs.985,950 million without

accounting for subsidy and Rs.624,620 million after accounting for subsidy received. (Source: Power

Finance Corporation Limited report on the performance of state power utilities: July 2015.) In

addition, there have also been instances of state governments promising free power to certain sections

of society, such as farmers. The adoption of such policies by state governments would adversely

affect the financial health of the SEBs, which would in turn adversely affect their ability to make

0012018-0003086 HK:20704050.1 S-8

payments to the Issuer. See “The unbundling of the SEBs pursuant to the Electricity Act could have

an adverse impact on the Issuer’s revenues.” below and the section entitled “The Power Industry in

India.”

There may be other changes to the regulatory framework that could adversely affect the Issuer.

The statutory and regulatory framework for the Indian power sector has changed significantly

in recent years and the full impact of these changes is unclear. There are likely to be more changes in

the next few years, some of which could potentially impose greater legal, compliance and

administrative burdens on the Issuer. The Electricity Act has put in place a framework for reforms in

the sector, but in many areas the details and timing of reforms are yet to be determined. It is expected

that many of these reforms will take time to be implemented. Furthermore, there could be additional

changes in tariff policy, requirements for unbundling of the SEBs, restructuring of companies in the

power sector, open access and parallel distribution and licensing requirements for, and tax incentives

applicable to, companies in the power sector. Such additional changes could adversely affect the

Issuer’s business prospects, financial condition and results of operations. For a discussion on the

regulatory framework of the electricity industry in India, see “Regulations and Policies in India”.

The Issuer’s expansion plans and diversification plans require significant capital expenditure and

if the Issuer is unable to obtain the necessary funds for expansion, its business plans and prospects

may be adversely affected.

The Issuer will need significant additional capital to finance its business plan and in

particular, its plan for capacity expansion. As of the date of the Original Offering Circular, the Issuer

was engaged in construction activities for projects representing 23,004 MW, including 4,495 MW

undertaken by its joint venture companies and subsidiaries, which are in different stages of progress

As of 30 June 2016, 24,059 MW is under construction, including 4,300MW through joint ventures

companies and subsidiaries. The Issuer is also pursuing a number of additional projects, representing

a further increase of more than 27,000 MW of capacity, which are in various stages, including

projects for which tenders have been invited or a feasibility report has been or is being prepared. The

scheduled completion dates of the Issuer’s expansion plans and budgets with respect to its expansion

plans are management estimates only and there is no assurance that such proposed expansion will be

completed or, if completed, that there will not be cost or time overruns.

The Issuer expects approximately 30 per cent. of its proposed capital expenditure to be funded

by internal accruals and/or through the issue of equity shares and the remaining approximately 70 per

cent. to be funded by debt financing. The Issuer’s ability to finance its planned capital expenditure is

subject to a number of risks, contingencies and other factors, some of which are beyond its control,

including the Issuer’s results of operations generally, tariff regulations, interest rates, borrowing or

lending restrictions, if any, changes to applicable laws and regulation, the amount of dividend

required to be paid to the Issuer’s shareholders and other costs and the Issuer’s ability to obtain

financing on acceptable terms. In addition, as of the date of this Offering Circular, there were a

number of large-scale infrastructure projects under development in India which may impair the

Issuer’s ability to obtain additional funding and it may not be able to receive adequate debt funding on

commercially reasonable terms in India. In such event, the Issuer may be required to seek funding

internationally, which would result in exposure to foreign exchange risks and which may require

approvals under, or be restricted by, laws and regulations in India. For further details, see also the

section entitled “Regulations and Policies in India — Foreign Exchange Laws”. If the Issuer is unable

0012018-0003086 HK:20704050.1 S-9

to raise required funds for expansion, its business plans and prospects may be adversely affected. See

also the section entitled “Description of the Issuer — Business — Capacity Expansion”.

The Issuer is also in the process of progressively diversifying the fuel mix of its power

stations. In addition, the Issuer plans to invest in power trading, electricity distribution, coal mining

and oil exploration. These diversification efforts will also require significant additional capital. There

can be no assurance that the Issuer will be able to raise the required capital to implement its

diversification plans on acceptable terms or at all. In the event that the Issuer cannot raise the funds to

diversify its business, its business, financial condition, prospects and results of operation may be

materially and adversely affected.

The Issuer’s expansion plans are subject to a number of risks and uncertainties.

The Issuer’s expansion plans are subject to a number of factors, including the state of the

local and global economy, difficulties in assimilating personal and integrating operations and cultures,

laws and regulations, governmental action, delays in obtaining permits or approvals, global prices of

crude oil and other fuels for transportation, prices of fuel supplies required for power station

operations, accidents, natural calamities, and other factors beyond its control. Power projects

generally have long gestation periods due to the process involved in their commissioning. Contracts

for construction and other activities relating to the projects are awarded at different times during the

course of the projects. In addition, the Issuer’s projects are dependent on external contractors for

construction, installation, delivery and commissioning, as well as the supply and testing of key plant

and equipment. The Issuer may only have limited control over the timing, quality of services,

equipment or supplies provided by these contractors. The Issuer is highly dependent on some of the

external contractors who supply specialised services and sophisticated and complex machinery. There

can be no assurance that the performance of the external contractors will meet the Issuer’s

specifications or performance parameters or that they will remain financially sound. The failure or

delay of the external contractors to perform could result in incremental cost or time overruns, or the

termination of a power project development. For example, the work at the Issuer’s Barh project has

been delayed by the non-performance of the contractor’s work in relation to constructing a steam

generator, pursuant to which the contractor’s contract with the Issuer has been terminated. There can

be no assurance that the Issuer would be able to complete its expansion plans in the time expected, or

at all, or that their gestation period would not be affected by any or all of these factors.

Furthermore, the Issuer’s ability to acquire sites for its expansion plans depends on many

factors, including whether the land is private or state-owned, whether the land is classified in a

manner that allows it to be used as contemplated by the Issuer’s projects, and the willingness of the

owners to sell or lease their land. In many cases, the area identified as a suitable site is owned by

numerous small landowners. Acquisition of private land in India can involve many difficulties,

including litigation relating to ownership, liens on the land, inaccurate title records, negotiations with

numerous land owners and obtaining Government approvals. Acquisition of Government land may

also involve a number of difficulties relating to rehabilitation and resettlement where people’s

livelihood is dependent on the land. Further, in instances where forest land is required to set up a

project, as of the date of this Offering Circular, Government clearance for diversion of forest land for

non-forest purposes is mandatory for a power project as well as its connected mines, and project

development could be severely affected in case of any delay in obtaining such clearances.

The Issuer may also face competing interests with respect to usage of land, as in the case of

the Issuer’s North Karanpura Thermal Power Project where work was put on hold for several years

0012018-0003086 HK:20704050.1 S-10

due to objections that the proposed location of the project is on coal-bearing land. Work on the project

has since been re-started.

The power industry in which the Issuer operates is highly regulated. For example, with

respect to the power business, several licences are required under the Electricity Act, including a

transmission licence, a distribution licence and an electricity trading licence. There is no assurance

that the Issuer or the concerned agency will be able to obtain all the necessary approvals or clearances

with respect to its expansion plans. Any of these factors could have a material adverse effect on the

Issuer’s business, financial condition and results of operation.

The Issuer may be adversely affected by changes in the Government’s policy relating to the Issuer.

The Government owns 69.74 per cent. of the Issuer’s paid-up capital. To date, the

Government’s ownership has been an important factor in some aspects of the Issuer’s business,

including the settlement of electricity dues payable by the SEBs to the Issuer. Any significant changes

in the Government’s shareholding in the Issuer, and/or pursuit by the Government of policies that are

not in the interests of the Issuer, could adversely affect the Issuer’s business.

The Issuer generally manages its business on a day to day basis independently from the

Government. The Government has named the Issuer as a “Maharatna” company as a consequence of

which the Issuer enjoys enhanced autonomy in making financial and other decisions. Adverse changes

in the terms of, or the loss of, “Maharatna” status may decrease the Issuer’s autonomy and the Issuer’s

ability to compete with other participants in the Indian power sector.

The Issuer’s operations create difficult environmental challenges, and changes in environmental

laws and regulations may expose the Issuer to liability and result in increased costs.

The Issuer’s power stations and power generation projects are subject to environmental laws

and regulations promulgated by the Ministry of Environment and Forests (MoEF) and the pollution

control boards of the relevant states. These include laws and regulations that limit the discharge of

pollutants into the air, land and water and establish standards for the treatment, storage and disposal of

hazardous waste materials. The Issuer expects that environmental laws and compliance requirements

will continue to become stricter. Compliance with current and future environmental regulations,

particularly by the Issuer’s older power stations, may require substantial capital expenditure and, in

certain cases, may require the closing down of non-complying power stations. In particular, the Issuer

generates high levels of ash in its operations. There are limited uses for ash and therefore demand for

ash is low. While the Issuer continues to explore methods to utilise or dispose of ash, its ash

utilisation activities are insufficient to dispose of the ash it generates. Furthermore, the Issuer is

required to achieve 100 per cent. ash utilisation on a progressive basis under the MoEF notification

dated 3 November 2009. Compliance with this requirement, as well as any future norms with respect

to ash utilisation, may add to the Issuer’s capital expenditures and operating expenses. In certain cases

where it may not be possible to increase the Issuer’s utilisation of ash to comply with this

requirement, the Issuer may need to reduce the generation of ash through a partial or full shutdown of

its operating power stations, thereby reducing its average PLF which could have a material adverse

effect on the Issuer’s business, financial condition and results of operation.

The Issuer could be subject to substantial civil and criminal liability and other regulatory

consequences in the event that an environmental hazard was to be found at the site of any of its power

stations or if the operation of any of the Issuer’s power stations results in material contamination of

the environment. For instance, in 2006, the Chattisgarh Environment Conservation Board through its

0012018-0003086 HK:20704050.1 S-11

regional officer filed a criminal complaint against the Issuer’s Korba unit alleging air and water

pollution. Financial losses and liabilities as a result of increased compliance costs or due to

environmental damage or criminal liability due to such environmental breaches may affect the

Issuer’s reputation and financial condition.

Furthermore, there is a possibility that environmental compliance norms may be drastically

altered, resulting in substantial capital and operating expenditure to the Issuer, which may have an

adverse impact on the Issuer’s financial condition.

To note a recent example, in December 2015, the Government put forth the Environment

(Protection) Amendment Rules, 2015, stipulating strict requirements regarding water consumption

and emissions of particulate matter, sulphur dioxide, oxides of nitrogen and mercury for thermal power plants. The standards have been revised under three categories in terms of thermal power plants

brought online before 31 December 2003, between 1 January 2003 and 31 December 2016 and after 1

January 2017. The notice provides that thermal power stations brought online before 31 December 2016 shall meet the revised limits prior to 7 December 2017. The Issuer has written to the

Government for certain amendments to the notification citing difficulties in its implementation and for

extending the timeline.

There is no assurance that we can complete the required modifications in the plants to ensure

compliance to the revised regulations before the stipulated date or at all and this can have adverse

implications for the Group.

The Issuer’s business involves numerous risks that may not be covered by insurance.

While the Issuer maintains insurance of its operating plants with ranges of coverage that the

Issuer believes to be consistent with industry practice, the Issuer is not fully insured against all

potential hazards and events incidental to its business and there is no assurance that the Issuer’s

insurance coverage will be adequate and available to cover any loss incurred in relation to such types

of incidents. The Issuer is not covered for certain risks such as war, damage or destruction of data or

records or damage or loss due to pollution or contamination. Further, notwithstanding the Group’s

insurance coverage, any damage to the Group’s buildings, facilities, equipment, or other properties as

a result of occurrences such as fires, floods, water damage, explosions, power losses, typhoons and

other natural disasters may have an adverse effect on the Group’s business, financial condition, results

of operations and growth prospects. The occurrence of any such events not covered by insurance may

have a material adverse effect on the Issuer’s business, financial condition and results of operations

and the trading price of the Notes.

The Issuer may encounter problems relating to the operations of its joint ventures.

As of the date of this Offering Circular, the Issuer has formed 22 joint venture companies

with various third parties for undertaking specific business activities. The Issuer’s joint venture

partners may:

be unable or unwilling to fulfil their obligations, whether of a financial nature or otherwise;

have economic or business interests or goals that are inconsistent with the Issuer’s;

take actions contrary to its instructions or requests or contrary to the Issuer’s policies and

objectives;

take actions that are not acceptable to regulatory authorities;

become involved in litigation;

have financial difficulties; or

0012018-0003086 HK:20704050.1 S-12

have disputes with the Issuer.

Any of the foregoing may have an adverse effect on the business, prospects, financial

condition and results of operations of the Issuer.

The Issuer’s ability to raise foreign capital is constrained by global economic conditions and

conditions in foreign financial markets.

The Issuer has raised and expects to continue to raise capital in foreign markets. The Issuer’s

ability to raise foreign capital is constrained by the conditions of these markets. The global capital and

credit markets have recently been experiencing periods of extreme volatility and disruption. The

global financial crisis, including the continuing sovereign debt crisis in Europe, concerns over

recession, inflation or deflation, energy costs, geopolitical issues, commodity prices and the

availability and cost of credit, have contributed to unprecedented levels of market volatility and

diminished expectations for the global economy and the capital and credit markets. On 23 June 2016,

the United Kingdom held a referendum on its membership of the European Union and voted to leave

(Brexit). There is significant uncertainty at this stage as to the impact of Brexit on general economic

conditions in the United Kingdom and the European Union and any consequential impact on global

financial markets. For example, Brexit could give rise to increased volatility in foreign exchange rate

movements and the value of equity and debt investments. A lack of clarity over the process for

managing the exit and uncertainties surrounding the economic impact could lead to a further

slowdown and instability in financial markets. These factors, combined with others, may impact the

Issuer’s ability to raise capital in foreign markets. An inability to raise foreign capital or access

foreign credit markets would have a material adverse effect on its business and financial condition.

The Issuer’s business, financial condition and results of operations may be materially and

adversely affected if the Issuer is unable to take advantage of certain tax benefits or if there are any

adverse changes to the tax regime in the future.

Section 80-IA of the Income Tax Act, 1961 (the Income Tax Act) provides that, subject to

certain conditions being fulfilled, 100 per cent. of the profits derived from the projects for the

generation, distribution or transmission of power would be entitled for deduction from total income

for 10 consecutive assessment years out of 15 years, beginning from the year in which the project

commences power generation, transmission or distribution of power, if the activity is commenced

before 31 March 2017. If such or other tax benefits become unavailable, the Issuer’s financial

condition, results of operations and business could be materially and adversely affected.

The draft bill on goods and services tax was introduced in December 2014 and the bill has

been pending before the upper house of the parliament for its approval. As the bill has not been

approved, the Issuer is unable to ascertain the full impact of the proposed tax changes on its revenues.

See the investment consideration “The proposed new taxation system could adversely affect the

Issuer’s business and the trading price of the Notes.”

The Issuer has not appointed the requisite number of independent directors on its Board

As the Issuer is a Government company, the power of appointment of its Board is vested with

the President of India, acting through the administrative ministry. As of the date of this Offering

Circular, the Issuer has not been able to maintain the minimum Board composition as required under

the Companies Act, 2013, the rules thereunder and the listing agreements with the Indian stock

exchanges. If the Indian stock exchanges decide to undertake any action against the Issuer including

0012018-0003086 HK:20704050.1 S-13

levying of penalties or if there is any communication with the regulatory agencies in that regard, it

may have a material adverse effect on the Issuer’s reputation, materially and adversely affect the

Issuer’s business, prospects and results of operations.

The Issuer has contingent liabilities under Indian Accounting Standards, which may adversely

affect its financial condition.

As of 31 March 2015, the contingent liabilities appearing in the Issuer’s consolidated

financial statements were as follows:

Category Amount

(Rs. in million) Claims against the Company not acknowledged as debts in respect of:

Capital works ..................................................................................................

81,272 Land compensation cases ................................................................................. 3,143

Fuel claims ...................................................................................................... 5,672

Statutory claims ............................................................................................... 8,964

Disputed income tax/sales tax/excise demand .................................................. 52,595

Other contingent liabilities ............................................................................... 9,142

Total ............................................................................................................... 160,788

Some of the beneficiaries have filed appeals against the tariff orders of the CERC. The

amount of contingent liability relating to these appeals is not ascertainable.

Natural calamities could have a negative effect on the Indian economy and cause the Issuer

business to suffer.

India has experienced natural calamities such as earthquakes, floods, droughts including

the flash flood that affected the state of Uttarakhand in June 2013 and the cyclone which affected

various parts of Odisha in October 2013. In fiscal 2015, the agricultural sector was adversely

affected by unseasonal rains and hailstorms in northern India in March 2015. As a result, the gross

value added, which is the value of output less the value of intermediate consumption, in the

agricultural sector decreased by 0.2% in fiscal 2015 as compared to 4.2% growth in fiscal 2014. In

addition, in July 2012, three of India’s inter-connected northern power grids collapsed for several

hours, resulting in widespread power outages across the country. Prolonged power outages, spells

of below normal rainfall in the country or other natural calamities could have a negative impact on

the Indian economy, affecting the Issuer’s business and potentially causing the trading price of the

Notes to decrease.

Political, economic and social developments in India could adversely affect the Issuer’s business.

The Issuer derives virtually all of its revenues and resources such as fuel, equipment and

materials from India. All of the Issuer’s electricity generating facilities and other assets are located

in India and all of the Issuer’s officers and directors are resident in India. The Issuer’s operations

and financial results and the market price and liquidity of the Notes may be affected by changes in

Government policy or taxation or social, ethnic, political, economic or other developments in or

affecting India. Since achieving independence in 1947, India has had a mixed economy with a

large public sector and an extensively regulated private sector. The Government and the state

governments have in the past, among other things, imposed controls on the prices of a broad range

of goods and services, restricted the ability of businesses to expand existing capacity and reduce

the number of employees, and determined the allocation to businesses of raw materials and foreign

0012018-0003086 HK:20704050.1 S-14

exchange. Since 1991, the Government has significantly relaxed most of these restrictions.

Nonetheless, the role of the Government and state governments in the Indian economy as

producers, consumers and regulators, remains significant in ways that directly affect the Issuer and

the electricity industry in India. Moreover, most recent parliamentary elections were completed in

May 2014, which was won by the Bhartiya Janta Party led National Democratic Alliance.

Although the current government has continued India’s economic liberalisation and deregulation

programmes, there can be no assurance that these will continue in the future. The rate of economic

liberalisation is subject to change and specific laws and policies affecting banking and finance

companies, foreign investment, currency exchange and other matters affecting investment in the

Issuer’s securities are continuously evolving as well. Other major reforms that have been proposed

are the goods and services tax, the direct tax code and the general anti-avoidance rules. Any

significant change in India’s economic liberalisation, deregulation policies or other major

economic reforms could adversely affect business and economic conditions in India generally and

the Issuer’s business in particular. India has also witnessed civil disturbances in the past. While

these civil disturbances did not directly affect the Issuer’s operations, it is possible that future civil

unrest as well as other adverse social, economic and political events in India could have an adverse

impact on the Issuer.

Trade deficits could have a negative effect on the Issuer’s business and the trading price of the

Notes.

India’s trade relationships with other countries can influence Indian economic conditions. In

fiscal 2016, the merchandise trade deficit was estimated at U.S.$118.5 billion compared with

U.S.$137.7 billion in fiscal 2015 and U.S.$135.8 billion in fiscal 2014. This large merchandise trade

deficit neutralises the surpluses in India’s invisibles, which are comprised of international trade in

services, income from financial assets, labour and property and cross-border transfers of mainly

workers’ remittances in the current account, resulting in a current account deficit. If India’s trade

deficits increase or become unmanageable, the Indian economy, and therefore the Issuer’s business,

future financial performance and the trading price of the Notes could be adversely affected.

Any downgrading of India’s debt rating by an international rating agency could have a negative

impact on the Issuer’s business.

On 25 April 2012, Standard and Poor’s Ratings Services, a Division of the McGraw Hill

Companies Inc. (S&P) revised the outlook on the long-term ratings on India from “stable” to

“negative” citing the slowdown in India’s investment and economic growth and the widened current

account deficit, resulting in a weaker medium term credit.

On 18 June 2012, Fitch Ratings Ltd. (Fitch) scaled down India’s sovereign credit rating

outlook from “stable” to “negative,” citing structural challenges such as corruption, inadequate

economic reforms, and slow economic growth combined with elevated inflation. On 25 April 2012

and 18 June 2012, respectively, as a result of their downgrading of India’s outlook, both S&P and

Fitch downgraded the outlook on the Issuer’s rating from “stable” to “negative”. In June 2012 and

January 2013, S&P and Fitch, respectively, announced that they may lower India’s sovereign credit

rating below investment grade, citing slowing GDP growth, setbacks or reversals in India’s economic

policy, a widening fiscal deficit and/or increasing spreads of credit default swaps for Indian banks.

S&P reiterated in May 2013 that, although there had been some easing of pressure towards a

downgrade of the rating, there is still a likelihood of such a downgrade unless significant

improvements are seen in factors such as a high fiscal deficit and levels of government borrowing.

0012018-0003086 HK:20704050.1 S-15

However, on 12 June 2013 Fitch revised the outlook on India’s sovereign credit rating from

“negative” to “stable” and consequently the outlook of the Issuer’s rating has been revised from

“negative” to “stable”. Subsequently, in August 2013 Fitch warned that India’s sovereign rating may

be lowered if the India is unable to meet its fiscal deficit target. In September 2013, Moody’s

Investors Service Inc. (Moody’s) put India’s sovereign credit rating on notice, warning that any

changes Moody’s makes to India’s sovereign rating outlook will depend on the depth and extent of

the current economic downturn and the trends in the balance of payments situation. In April 2015,

Moody’s revised India’s sovereign rating outlook from “stable” to “positive” and retained the long-

term rating at “Baa3” as it expected actions of policymakers to enhance India’s economic strength in

the medium term. Similarly, Standard & Poor’s upgraded its outlook on India’s sovereign debt rating

to “stable” in September 2014 and retained such rating in October 2015, while reaffirming the “BBB”

long-term rating. Standard & Poor’s stated that the revision reflects the view that India’s improved

political setting offers an environment which is conducive to reforms that could boost growth

prospects and improve fiscal management.

There can be no assurance that these ratings will not be further revised, suspended or

withdrawn by S&P, Moody’s or Fitch or that any other global rating agency will not also downgrade

the Issuer’s or India’s sovereign credit ratings.

Any adverse revisions to India’s credit ratings for domestic and international debt by

international rating agencies may adversely impact the Issuer’s ability to raise additional financing,

and the interest rates and other commercial terms at which such additional financing is available. This

could have a material adverse effect on the Issuer’s business and future financial performance, the

Issuer’s ability to obtain financing for capital expenditures, and the trading price of the Notes.

Depreciation of the Rupee against foreign currencies may have an adverse effect on the Issuer’s

results of operations and financial conditions.

As of 31 March 2015, the Issuer’s consolidated foreign currency borrowings of approximately

Rs.256.68 billion were denominated in U.S. dollars, Japanese yen and euros, while substantially all of

the Issuer’s revenues are denominated in Rupees. The Rupee has been quite volatile during fiscal

2014 and 2015 when compared against the U.S. dollar. First, it depreciated by 26.7 per cent. from

54.28 per U.S.$1.00 as at 31 March 2013 to an all-time low of 68.82 per U.S.$1.00 as at 28 August

2013 and then appreciated by 12.9 per cent. to close the fiscal 2014 at 59.89 per U.S.$1.00. In fiscal

2015, the Rupee depreciated by 4.4 per cent. to close the year at 62.50 per U.S.$1.00 and in fiscal

2016, the Rupee depreciated by 6.0 per cent., to close the year at 66.25 per U.S.$1.00. Overall, the

Rupee depreciated by 10.6 per cent. over the course of fiscal 2014 through to 2016. Volatility in

India’s currency and the possibility of slower growth pose significant risks for the financial prospects

of companies in India, as well as a greater default risk for Indian companies with foreign-denominated

debt. Depreciation of the Rupee against foreign currencies will increase the Rupee cost to the Issuer of

servicing and repaying the Issuer’s foreign currency borrowings. In addition, in fiscal 2015, imported

coal accounted for 9.8 per cent. of the total coal purchased by the Issuer for its directly owned power

stations. A depreciation of the Rupee would also increase the costs of coal imports by the Issuer. If as

a result of future changes in tariff regulations the Issuer is unable to recover the costs of foreign

exchange variations through its tariffs, the Issuer may be required to use hedging arrangements, which

may not fully protect the Issuer from foreign exchange fluctuations.

0012018-0003086 HK:20704050.1 S-16

Indian accounting principles and audit standards differ from those which prospective investors

may be familiar with in other countries.

As stated in the report of the Issuer’s independent auditors included in this Offering Circular,

the Issuer’s financial statements are in conformity with Indian GAAP, consistently applied during the

periods stated, except as provided in such report, and no attempt has been made to reconcile any of

the information given in this Offering Circular to any other principles or to base it on any other

standards. Indian GAAP differs from accounting principles and auditing standards with which

prospective investors may be familiar in other countries. See “Summary of Significant Differences

between Indian GAAP and IFRS”. Public companies in India, including the Issuer, have been required

to prepare financial statements under the Indian Accounting Standards (IND-AS) according to the

implementation roadmap drawn up by the Indian Ministry of Corporate Affairs. The Issuer may be

adversely affected by this transition.

The insolvency laws of India may differ from other jurisdictions with which holders of the Notes

are familiar.

As the Issuer is incorporated under the laws of India, an insolvency proceeding relating to the

Issuer, even if brought in another jurisdiction, would likely involve Indian insolvency laws, the

procedural and substantive provisions of which may differ from comparable provisions of another

jurisdiction.

An outbreak of avian, swine influenza, MERS or other contagious diseases may adversely affect

the Indian economy and the Issuer’s business.

A number of countries in Asia, including India, as well as countries in other parts of the

world, have had confirmed cases of the highly pathogenic H5N1 strain of avian influenza in birds.

Certain countries in Southeast Asia have reported cases of bird to human transmission of avian

influenza resulting in numerous human deaths. In 2009, there was a global outbreak of a new strain of

influenza virus commonly known as swine flu. Since 2012, an outbreak of the Middle East

Respiratory Syndrome corona virus (MERS) has affected several countries, primarily in the Middle

East. Future outbreaks of avian influenza, swine flu, MERS or a similar contagious disease could

adversely affect the Indian economy and economic activity in the region. As a result, any present or

future outbreak of avian influenza, swine flu or other contagious diseases could have a material

adverse effect on the Issuer’s business.

The Notes are not guaranteed by the Republic of India.

The Notes are not the obligations of, or guaranteed by, the Republic of India. Although the

Government owned 69.74 per cent. of the Issuer’s issued and paid up share capital as of the date of

the Offering Circular, the Government is not providing a guarantee in respect of the Notes. In

addition, the Government is under no obligation to maintain the solvency of the Issuer. Therefore,

investors should not rely on the Government ensuring that the Issuer fulfils its obligations under the

Notes.

The following Risk Factor is deleted in its entirety from the Original Offering Circular

under “Investment Considerations” as it is no long applicable.

0012018-0003086 HK:20704050.1 S-17

Interest on the Notes may be subject to EU withholding under the Savings Directive.

Under Council Directive 2003/48/EC on the taxation of savings income in the form of interest

payments (the Savings Directive), EU Member States are required to provide to the tax authorities of

other EU Member States with details of certain payments of interest or similar income paid or secured

by a person established in an EU Member State to, or for the benefit of, an individual resident in

another EU Member State or certain limited types of entities established in another EU Member State.

For a transitional period, Austria is required (unless during that period it elects otherwise) to operate a

withholding system in relation to such payments (subject to a procedure whereby, on meeting certain

conditions, the beneficial owner of the interest or other income may request that no tax be withheld).

The end of the transitional period is dependent upon the conclusion of certain other agreements

relating to information exchange with certain other countries. A number of non-EU countries and

territories including Switzerland have adopted similar measures (a withholding system in the case of

Switzerland).

On 24 March 2014, the Council of the European Union adopted a Council Directive (the

Amending Directive) amending and broadening the scope of the requirements described above. The

Amending Directive requires EU Member States to apply these new requirements from 1 January

2017, and if they were to take effect the changes would expand the range of payments covered by the

Savings Directive, in particular to include additional types of income payable on securities. They

would also expand the circumstances in which payments that indirectly benefit an individual resident

in a Member State must be reported or subject to withholding. This approach would apply to

payments made to, or secured for, persons, entities or legal arrangements (including trusts) where

certain conditions are satisfied, and may in some cases apply where the person, entity or arrangement

is established or effectively managed outside of the European Union.

However, the European Commission has proposed the repeal of the Savings Directive from 1

January 2017 in the case of Austria and from 1 January 2016 in the case of all other EU Member

States (subject to on-going requirements to fulfil administrative obligations such as the reporting and

exchange of information relating to, and accounting for withholding taxes on, payments made before

those dates). This is to prevent overlap between the Savings Directive and a new automatic exchange

of information regime to be implemented under Council Directive 2011/16/EU on Administrative

Cooperation in the field of Taxation (as amended by Council Directive 2014/107/EU). The new

regime under Council Directive 2011/16/EU (as amended) is in accordance with the Global Standard

released by the Organisation for Economic Co-operation and Development in July 2014. Council

Directive 2011/16/EU (as amended) is generally broader in scope than the Savings Directive,