WPP Annual Report 2005 - AnnualReports.com

196

Annual Report & Accounts 2005

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of WPP Annual Report 2005 - AnnualReports.com

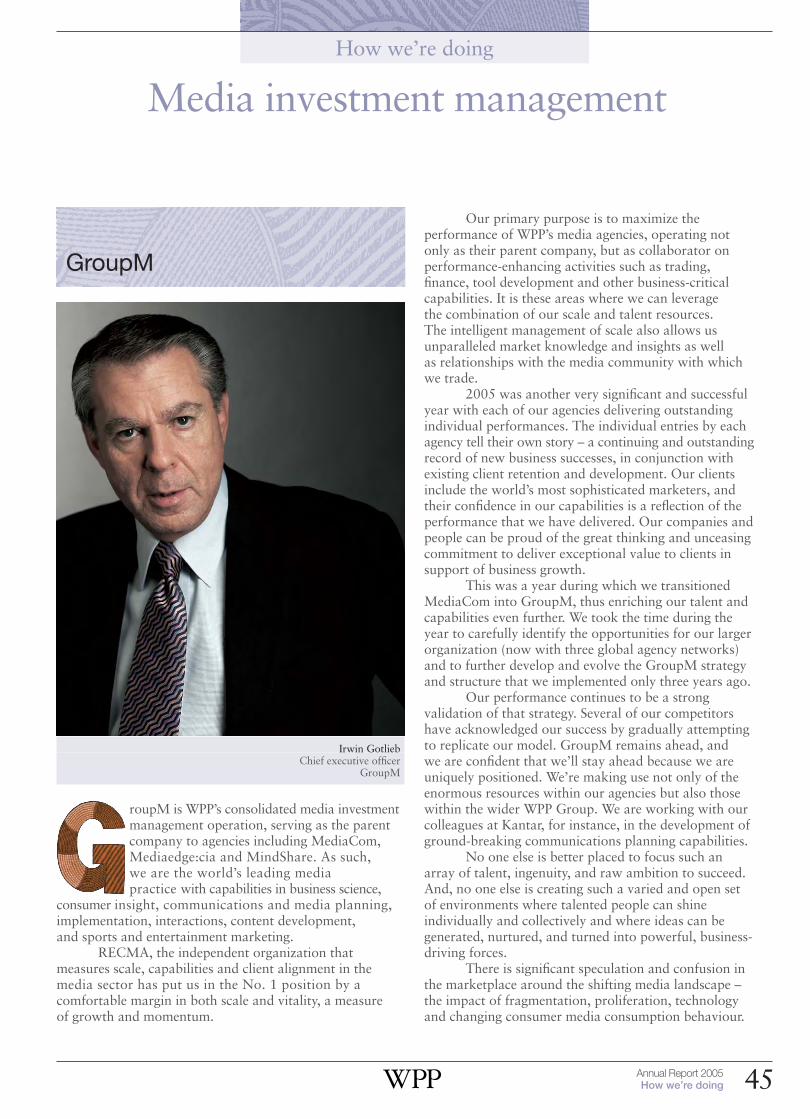

AdvertisingMedia investment management

Information, insight & consultancyPublic relations & public affairs

Branding & identityHealthcare communications

Direct, promotion & relationship marketingSpecialist communications

27 Farm StreetLondon W1J 5RJ

Telephone +44 (0)20 7408 2204Fax +44 (0)20 7493 6819

125 Park AvenueNew York NY 10017-5529

Telephone +1 (212) 632 2200Fax +1 (212) 632 2222

www.wpp.com

Annual Report &Accounts 2005

Annual R

eport&A

ccounts 2005

Contents

The fast readA six-minute read 2

Who we areAbout WPP 8Our companies and associates 10

Why we existWhy we exist 12Our mission 13

How we’re doingFinancial summary 15Letter to share owners 18Reports from our operating brands 26Ogilvy & Mather Worldwide 28JWT 33Young & Rubicam Brands 35Grey Global Group 41The Voluntarily United Group of Creative Agencies 43Bates Asia 44GroupM 45MediaCom 46Mediaedge:cia 48MindShare 49The Kantar Group 51Public relations & public affairs: overview 55Hill & Knowlton 56Ogilvy Public Relations Worldwide 58B to D Group: overview 60Enterprise IG 61Fitch 62CommonHealth 63Specialist communications 64

What we thinkThe Advertising & Marketing Services Industry:New markets and new technologies by Sir Martin Sorrell 70The Life & Works of Stephen Kingby Jeremy Bullmore and Judie Lannon 90

Who runs WPPBoard of Directors 94Senior officers and advisors to the Board 97

How we behaveDirectors’ reportReview of the Company’s governance

and the Nomination committee 100Review of the Audit committee 102Review of the Compensation committee 103The Board of Directors 105Committee meetings 106Share owner relations 106Internal control 106Adoption of IFRS 107Scheme of Arrangement 108Sarbanes-Oxley S404 108Going concern 108Responsibilities in respect of the preparation

of financial statements 108Substantial share ownership 108Election of directors 109Profits and dividends 109Parent company charitable donations 109Group activities 109Intangible assets 109Share capital 109Authority for purchase of own shares 109Supplier payment policy 109Auditors 109Corporate responsibilityBusiness impact 110How we manage corporate responsibility risk

and opportunity 110Corporate responsibility goals 111The impact of our work 111WPP as an employer 111Social investment 114Environment and supply chain 115

Annual Report 2005The Fast Read 1

How we’re rewardedCompensation committee report

on behalf of the BoardIntroduction 1162005 highlights 116Remit of the Compensation committee 116Composition of the Compensation committee 116Advisors to Compensation committee 118Principles of remuneration 118Review of compensation 119Impact of IFRS 120Policy on directors’ service contracts,

notice periods and termination payments 120Elements of remuneration 122Directors’ remuneration 125Directors’ interests 126US-style proxy disclosures 130

Operating & financial reviewCompetitive performance 133Geographic performance 134Sector performance 135Review of operations 137Adoption of IFRS 137Reconciliation to 2004 UK GAAP 137Group financial performance 138Operating margins 138Like-for-like performance 139Headcount 139Acquisitions and start-ups 139Parent company initiatives 139Treasury activities 139Cash flow and balance sheet 140New corporate structure 141Pensions funding 141Future prospects 141

Our 2005 financial statementsAccounting policies 145Consolidated income statement 150Consolidated cash flow statement 151Consolidated statement of recognised

income and expense 151Consolidated balance sheet 152Notes to the consolidated financial statements 153Company balance sheet 170Notes to the Company balance sheet 171Transition to IFRS 172Reconciliation to US Accounting Principles 177Notes to the Reconciliation to US Accounting

Principles 178Independent auditors’ report 181Five-year summary 183Financial glossary 184

About share ownershipInformation for share ownersShare owners’ register 187Analysis of shareholdings at 31 December 2005 187Dividends 187American Depositary Receipts (ADRs) 188Financial calendar 188Share price 188Access numbers/Ticker symbols 189Online information 189Registrar and transfer office 189American Depositary Receipts (ADRs) office 189WPP registered offices 189Tax information 189

Where to find usContact points 191

WPP offices 191Investor relations 191Media relations 191

Group information 191

Current and historical financial information, including trading statements, newsreleases and presentations are available online at www.wpp.com/investor

You can sign up to receive WPP news and announcements by e-mail atwww.wpp.com/emailservices

For a quick, pre-digested, highly-compressed version ofthis Annual Report: read the next six pages.The full story starts on page 8.Please read that, too.

The fast readWPP is one of the world’s largest communicationsservices groups, made up of leading companies in:

•Advertising

•Media investment management

• Information, insight & consultancy

•Public relations & public affairs

•Branding & identity

•Healthcare communications

•Direct, promotion & relationship marketing

•Specialist communications

WPP companies provide communications servicesto clients worldwide including more than 300 of theFortune Global 500; over one-half of the NASDAQ 100and over 30 of the Fortune e-50.

Our companies work with over 390 clients in threeor more disciplines. More than 270 clients are served infour disciplines; these clients account for around 60% ofGroup revenues. The Group also works with nearly 220clients in six or more countries.

Collectively, the Group has 92,000* people workingin over 2,000 offices in 106 countries.Our companies and their websites are listed on pages 10 and 11.

* Including associates.

Who we are

Annual Report 2005The Fast Read2

Within the WPP Group, our clients have access tocompanies with all the necessary marketing andcommunications skills; companies with strong anddistinctive cultures of their own; famous names, many of them.

WPP, the parent company, complements these companies in three distinct ways.

First, it relieves them of much administrative work.Financial matters (such as planning, budgeting,reporting, control, treasury, tax, mergers, acquisitions,

investor relations, legal affairs and internal audit) are co-ordinated centrally. For the operating companies, every administrative hour saved is an extra hour to bedevoted to the pursuit of professional excellence.

Secondly, the parent company encourages andenables operating companies of different disciplinesto work together for the benefit of clients. Such

collaborations have the additional benefit of enhancing thejob satisfaction of our people. The parent company alsoplays an across-the-Group role in the following functions:the management of talent, including recruitment andtraining; in property management; and in procurement,information technology and knowledge sharing.

And, finally, WPP itself can function as the 21stcentury equivalent of the full-service agency. Forsome clients, predominantly those with a vast

geographical spread and a need for marketing servicesranging from advertising through design and websiteconstruction to research and internal communications,WPP can act as a portal to provide a single point ofcontact and accountability.Read more about our role on page 12.

Why we exist What we think

Our mission

To develop and manage talent;to apply that talent,throughout the world,for the benefit of clients;to do so in partnership;to do so with profit.

The Advertising & Marketing Services Industry:New markets and new technologies

2005 was WPP’s best ever year by all metrics. 2006 has already shown more growth. It should – in theory – be better still.

It didn’t, however, look that way at the beginning of 2005. The calendar offered no big events to boostadvertising and marketing services spending, suggestingit would be the weakest of the four-year cycle to 2008.Moreover, 2004 was a hard act to follow. In that year, the world fully recovered from the internet bust of 2000,boosted in part by politics and sport. But, in the end, 2005confounded expectations – achieving for the first time 15%operating margins under ‘old’ 2004 UK GAAP measures.

2006 should benefit from a ‘mini-quadrennial’ –mid-term Congressional elections in the US, the TurinWinter Olympics and soccer’s World Cup in Germany.And 2007 will be the platform for 2008 – a ‘maxi-quadrennial’ dominated by the US presidential elections.The blockbuster Beijing Olympics and the EuropeanFootball Championships will also accelerate spending.

The short-term picture for the communicationsservices industry has improved. The immediate issues of government extravagance, consolidation amongclients, media owners, retail and agencies, increasingtrade and price promotion, fees, procurement andoutsourcing, media fragmentation and super-agencies are opportunities as much as threats.

In the long term, advertising and marketing servicesas a proportion of GNP will better the cyclical peakestablished in 2000. Globalisation and the growth of Asia Pacific, overcapacity and the shortage of humancapital, the web, the demand for internal communicationsand retail concentration should continue to assure ourindustry’s importance.Sir Martin Sorrell’s article begins on page 70.

The Life & Works of Stephen King

Jeremy Bullmore and Judie Lannon pay tribute to one ofthe founding fathers of modern advertising practice with a brief biography, an analysis of Stephen’s publishedwritings and edited highlights from them.The tribute appears on pages 90 to 93.

A collection of Jeremy Bullmore’s acclaimed Annual Report essays is nowavailable in book form. Please see page 90.

Annual Report 2005The Fast Read 3

How we’re doing

Financial summary*

2005 2004 Change %

Turnover (billings) £26,674m £19,598m +36.1

Revenue £5,374m £4,300m +25.0

Headline EBITDA1 £877m £664m +32.1

Headline operating profit1 £721m £531m +35.8

Reported operating profit £653m £476m +37.2

Headline PBIT1 £755m £560m +34.8

Headline PBIT margin 14.0% 13.0% +1.0

Headline PBT1 £669m £490m +36.5

Reported PBT £592m £434m +36.4

Headline diluted earnings per share1,3 36.0p 27.9p +29.0

Headline diluted earnings per ADR1,2,3 $3.27 $2.56 +27.7

Ordinary dividend per share 9.34p 7.78p +20.1

Ordinary dividend per ADR2 85.0¢ 71.3¢ +19.2

Net debt at year-end £804m £555m +44.9

Average net debt4 £1,212m £1,083m +11.9

Ordinary share price at year-end 629.0p 573.0p +9.8

ADR price at year-end $54.00 $54.67 -1.2

Market capitalisation at year-end £7,881m £6,792m +16.0

At 10 May 2006

Ordinary share price 681.5p

ADR price $63.35

Market capitalisation £8,524m

Notes*These figures have been prepared under IFRS (International Financial Reporting Standards,incorporating International Accounting Standards).

1 The calculation of ‘headline’ measurements of performance (including Headline EBITDA, Headlineoperating profit, Headline PBIT, Headline PBT and Headline earnings) is shown in note 32 of thefinancial statements.

2 One American Depositary Receipt represents five ordinary shares. These figures have beentranslated for convenience purposes only using the income statement exchange rates shown onpage 150. This conversion should not be construed as a representation that the pound sterlingamounts actually represent, or could be converted into, US dollars at the rates indicated.

3 Earnings per share is calculated in note 10 of the financial statements.4 Average net debt is defined on page 184.

2005 results

Our twentieth year was a record one. Our results for2005 reflect the continued, steady strength of the worldeconomy positively impacting almost all disciplines andgeographies, and, in addition, include the results of Grey Global Group (‘Grey’) with effect from 7 March 2005,which has performed well and made a strong contributionto the Group’s results.

Revenues were up 25% to £5.4 billion. Operatingmargin was up 1.0 margin points to 14.0%, ahead of our objective of 13.7%. Headline PBIT – that is beforegoodwill impairment, amortisation of acquired intangibles,interest, tax and investment gains and write-downs – was up almost 35% to £755 million.

Headline profit before tax was up over 36% to£669 million. Reported profit before tax was up over 36%to £592 million. Headline diluted earnings per share wereup 29% to 36.0p and reported diluted earnings per shareup almost 27% to 29.7p.

Total share owner return improved, with your shareprice rising by almost 10% to 629.0p over the year anddividends rising 20% to 9.34p. The share price hasadvanced a further 8% to 681.5p at the time of writing.

Based on constant currency comparisons, on alike-for-like basis, revenues were up 5.5% for the year, up 6% in the first half and 5% in the second half. Thisappears to have been at or above the growth in theworldwide market, with the Group maintaining orincreasing market share.

Sector and geographic performance

By sector, Media investment management led the way,along with direct, internet and interactive-related activitiesand Healthcare communications. Advertising, Information,insight & consultancy, Branding & identity and Specialistcommunications, showed consistent growth. Publicrelations & public affairs also continued to show significantimprovement following a strong year in 2004.

Marketing services contributed 52% of ourrevenues in 2005.

By geography, Asia Pacific, Africa and the MiddleEast, Latin America and Central and Eastern Europe ledthe way. Western Continental Europe, although relativelymore difficult, improved slightly in the second half. Marketsoutside North America represented 61% of our revenues,a similar level to 2004, due to the impact of Grey.

Our long-term objectives are to increase thecombined geographic share of revenues of Asia Pacific,Latin America, Africa and the Middle East, and Centraland Eastern Europe, from around 20% to one-third. Wealso aim to increase the share of revenues of marketingservices from 52% to two-thirds; and to increase the shareof more measurable marketing services – such as Insight,information & consultancy, and direct, interactive andinternet – from around one-third of our revenues to 50%.

Annual Report 2005The Fast Read 4

Cash flow

The objective introduced in 2003 of covering outgoings by free cash flow was achieved, excluding the net cashelement of the acquisition of Grey. We now generate over $1 billion per annum of cash flow – available forenhancing share owner value through capital expenditure,acquisitions, dividends and share buybacks.

Future objectives

We will continue to focus on our key objectives – improvingoperating profits and margins, increasing cost flexibility,using free cash flow to enhance share owner value andimprove return on capital employed, continuing to developthe role of the parent company in adding value to ourclients and people, developing our portfolio in high-revenuegrowth areas, both geographically and functionally, andimproving our creative quality and capabilities.

Outlook

Worldwide economic conditions seem set to continue to show steady growth in 2006, although concernsremain over the Middle East, oil and commodity pricesand the twin deficits of the US economy.

Although growth in the world economy continues to be led by Asia Pacific, Latin America, Africa and theMiddle East, Russia and the CIS countries, even WesternContinental Europe may continue the improvement seenin the second half of 2005, although the UK looks soft.

2006 should benefit from the ‘mini-quadrennial’impact of the mid-term US Congressional elections, the FIFA World Cup and the Winter Olympics in Turin.

2007 should also benefit from the build-up to theUS Presidential elections and the Beijing Olympics in 2008,which, as a maxi-quadrennial year, should be a very strongone, buoyed by those events plus heavy US politicaladvertising and the European Football Championships.Our letter to share owners starts on page 18.

Our 2005 operating & financial review and financial statements arepresented in full on pages 132 to 185 and at www.wpp.com/investor

Notes1 Percentages are calculated on a constant currency basis. See definition on page 184.2 Headline PBIT: The calculation of Headline PBIT is set out in note 32 of the financial statements.

Advertising and Media investment management

53

Information, insight & consultancy 11

Branding & identity, Healthcare and Specialist communications

26 Public relations & public affairs 10

2005 Headline PBIT1, 2 by sector %

2005 revenue2 by sector %

Branding & identity, Healthcare and Specialist communications

Advertising and Media investment management

27 Public relations & public affairs 10

48

Information, insight & consultancy 15

2005 Headline PBIT1, 2 by geography %

Continental Europe 24

Asia Pacific, Latin America, Africa & Middle East

19

North America 46

UK 11

2005 revenue2 by geography %

Continental Europe 27

Asia Pacific, Latin America, Africa & Middle East

19

UK 15

North America 39

Annual Report 2005The Fast Read 5

Non-executive chairman

Philip LaderChairman of the Nomination committeeMember of the Compensation committee

Executive directors

Sir Martin SorrellChief executive

Paul RichardsonFinance director

Howard PasterDirector

Mark ReadStrategy director

Non-executive directors

Colin Day

Esther DysonMember of the Compensation committeeMember of the Audit committee

Orit Gadiesh

David KomanskyMember of the Nomination committee

Christopher MackenzieMember of the Compensation committeeMember of the Nomination committee

Stanley (Bud) MortenCurrent chairman of the Compensation committeeMember of the Audit committeeSenior independent director

Koichiro Naganuma

Lubna Olayan

John Quelch

Jeffrey Rosen Future chairman of the Compensation committeeMember of the Audit committee

Paul SpencerChairman of the Audit committee

Members of the Advisory BoardJeremy BullmoreJohn Jackson

Company SecretaryMarie CapesDirectors’ biographies appear on pages 94 to 96.

Who runs WPP How we behave

Corporate governance

The Board of Directors as a whole is collectivelyaccountable to the Company’s share owners for goodcorporate governance and is committed to achievingcompliance with the principles of corporate governanceset out in the Combined Code.

Our goal is to comply with relevant laws,regulations, and guidelines such as the Combined Code,the US Sarbanes-Oxley Act of 2002 the NASDAQ rules,and their related regulations and, as far as is practicable,policies such as the Hermes Principles and those issuedby the Association of British Insurers (ABI), the NationalAssociation of Pension Funds (NAPF), the PensionsInvestment Research Consultants (PIRC).

WPP operates a system of internal control, which ismaintained and reviewed in accordance with the CombinedCode and the guidance in the Turnbull Report as well as therelevant provisions of the Securities Exchange Act of 1934as they currently apply to the Company. In the opinion ofthe Board, the Company has complied throughout the yearwith the Turnbull Report and has also complied with therelevant provisions of the Securities Exchange Act of 1934.

Corporate responsibility

Paul Richardson is the Board director responsible forassessing corporate responsibility risks for 2006. He chairsWPP’s Corporate responsibility committee, established in2003, which advises on policy, monitors emerging issuesand co-ordinates communication among Group companies.The Committee is made up of senior representatives fromWPP’s major business categories. It identifies andassesses significant corporate responsibility risks andopportunities for the business.

WPP’s three most significant corporateresponsibility issues are:The impact of our work including marketing ethics,compliance with marketing standards, protection ofconsumer privacy, social and cause-related marketing.The work our operating companies produce is part of ourcorporate responsibility performance. They are expectedto comply with all laws, regulations and codes of marketingpractice as well as our own Code of Business Conduct.Employment including diversity and equal opportunities,business ethics, employee development, remuneration,communication and health and safety. Our goal is to havea talent base that reflects the communities in which weoperate. We believe diversity contributes to creativity, newideas and a richer workplace. In 2005, WPP invested£32.7 million in training and well-being across the Group. Social investment including pro bono work, donationsto charity and employee volunteering. In 2005, our totalsocial investment was worth £17.3 million, equivalent to0.32% of revenue (2.9% of reported pre tax profits). This includes £13.9 million in pro bono work (based onthe fees the benefiting organisations would have paid forour work) and £3.4 million in donations.Full details of our governance policies and practices, and our corporateresponsibility activities, can be found on pages 99 to 115.

Annual Report 2005The Fast Read6

Executive remuneration policy is set by WPP’sCompensation committee and is governed by threeguiding principles:

•Competitiveness

•Performance

•Alignment to share owner interests

During 2005, the Compensation committeeundertook a thorough review of the Group’s currentcompensation and incentive strategy.

The committee subsequently decided to make a number of significant changes to the way in whichcompensation is to be delivered whilst at the same timestaying true to the principles of compensation describedabove. In summary this entailed:

•Single-year performance awards, delivered as restrictedstock awards and vesting a further two years after the end of the one-year performance period, replaced awardspreviously made under the operating company Long TermIncentive Plans.

•Similarly at the parent company, the use of ExecutiveShares Awards replaced awards previously made underthe Performance Share Plan. Again, these awards will vesttwo years after the end of the one-year performance period.

•A significantly reduced use of stock options. Awards ofstock options have not been made to executive directorssince 1995. Below this level, options will now only be usedin special circumstances, such as a recruitment incentive.

•Future awards of stock made on an annual basis to theWPP Leaders, Partners and High Potential Groups will allbe in the form of restricted stock which vest three yearsafter grant.Our directors’ remuneration and interests are described on pages 122 to131. A full report from the Compensation committee starts on page 116.

How we’re rewarded About share ownership

WPP is quoted on the London Stock Exchange andNASDAQ in New York.

Analysis of shareholdings

Issued share capital as at 31 December 2005: 1,252,899,372ordinary shares, owned by 11,572 share owners.

Substantial share ownership

As at 4 May 2006, the Company is aware of the followinginterests of 3% or more in the issued ordinary sharecapital of the Company:

Legal & General 4.15%

WPP ESOPs 4.05%

Legg Mason 3.98%

Barclays 3.11%

AIM Management 3.05%

The disclosed interests of all of the above refer to therespective combined holdings of those entities and tointerests associated with them. The Company has not been notified of any other holdings of ordinary sharecapital of 3% or more.

Share owner relations

WPP has a well-developed continuous program to addressthe needs of share owners, investment institutions andanalysts, supplying a regular flow of information about thecompany, its strategy, performance and competitive position.

WPP’s website, www.wpp.com, provides currentand historical financial information including tradingstatements, news releases and presentations.More information relating to share ownership can be found on pages 186to 189.

Share owners by type • Institutional investors 95%

• Employees 4%

• Other individuals 1%

Share owners by geography • UK 41%

• US 43%

• Asia Pacific, Latin America, Africa & Middle East and Continental Europe 16%

Annual Report 2005The Fast Read 7

Who we are

WPP is one of the world’s largest communications services groups, made up of leading companies in:

AdvertisingMedia investment management

Information, insight & consultancyPublic relations & public affairs

Branding & identityHealthcare communications

Direct, promotion & relationship marketingSpecialist communications

Annual Report 2005Who we are8

Every WPP company is a distinctive brand in its own right; all withtheir own identities and own areas of expertise. That is their strength.What they have in common is in harnessing intelligence, talent andexperience to bring competitive advantage to their clients.

Through our companies and associates, WPP offers a comprehensiveand, when appropriate, integrated range of communications services tonational, multinational and global clients.

Our companies work with more than 300 of the Fortune Global500; over one-half of the NASDAQ 100 and over 30 of the Fortune e-50.Over 390 clients are served in three or more disciplines. More than 270clients are served in four disciplines; these clients account for around 60%of Group revenues. The Group also works with nearly 220 clients in six ormore countries.

Collectively, the Group has 92,000* people working in over 2,000offices in 106 countries.* Including associates.

Annual Report 2005Who we are 9

EWABespoke Communications

Who we are

Advertising

ADK 1

www.adk.jpBates Asiawww.batesasia.comBrandBuzz ■

www.brandbuzz.comDentsu Y&R 1, 2, ■

www.yandr.comDiamond Ogilvywww.diamond.co.krGrey Worldwide ◆

www.greyglobalgroup.comLG Ad 1

www.lgad.co.krJWTwww.jwt.comMarsteller Advertising ■

www.marsteller.comOgilvy & Mather Worldwidewww.ogilvy.comRed CellSoho Squarewww.sohosq.comThe Voluntarily United Group of CreativeAgencieswww.group-united.comY&R ■

www.yandr.com

Media investmentmanagement

GroupM:MAXUSwww.maxusglobal.comMediaComwww.mediacom.comMediaedge:ciawww.mecglobal.comMindSharewww.mindshareworld.comOutrider ▲

www.outrider.comOther media agenciesKinetic Worldwide 2

www.kineticww.comKR Media 3

Information, insight &consultancy

The Kantar Group:www.kantargroup.comAdded Valuewww.added-value.comBPRIwww.bprigroup.comCannondale Associateswww.cannondaleassoc.comCenter Partnerswww.centerpartners.comEverystonewww.everystonegroup.comFocalyst 2

www.focalyst.comFusion 5www.fusion5.comGlendinningwww.glendinning.comHenley Centre HeadlightVisionwww.hchlv.comIMRB Internationalwww.imrbint.comKMR Groupwww.kmr-group.com– AGBNielsen Media Research 2

www.agbgroup.com– BMRB International

www.bmrb.co.uk– IBOPE Media Information 1

www.ibope.com.br– Marktest 1

– Mediafaxwww.mediafax-pr.com

Lightspeed Researchwww.lightspeedresearch.comMVIwww.mventures.comMattson Jack Groupwww.mattsonjack.comMillward Brownwww.millwardbrown.comResearch Internationalwww.research-int.comRMS Instorewww.rms-uk.comZiment Groupwww.zimentgroup.comOther marketing consultanciesohalwww.ohal-group.com

Public relations & public affairs

BKSH ■

www.bksh.comBlanc & Otuswww.blancandotus.comBuchanan Communicationswww.buchanan.uk.comBurson-Marsteller ■

www.bm.comChime Communications PLC 1

www.chime.plc.ukClarion Communicationswww.clarioncomms.co.ukCohn & Wolfe ■

www.cohnwolfe.comFinsburywww.finsbury.comGCI Group ◆

www.gcigroup.comHill & Knowltonwww.hillandknowlton.comOgilvy Public Relations Worldwidewww.ogilvypr.comPenn, Schoen & Berland ■

www.psbsurveys.comQuinn Gillespiewww.quinngillespie.comRobinson Lerer & Montgomery ■

www.rlmnet.comTimmons and Companywww.timmonsandcompany.comWexler & Walker Public Policy Associateswww.wexlergroup.com

Branding & identity

Addison Corporate Marketing•www.addison.co.ukBDGMcCollwww.bdg-mccoll.comBDGworkfutureswww.bdgworkfutures.comColey Porter Bellwww.cpb.co.ukDovetailwww.dovetailfurniture.comEnterprise IG•www.enterpriseig.comFitchwww.fitchww.comLambie-Nairn•www.lambie-nairn.comLandor Associates ■•www.landor.comThe Partners ■•www.thepartners.co.ukVBAT•www.vbat.nlWalker Group •www.wgcni.comWarwickswww.warwicks-uk.com

Annual Report 2005Who we are10

Our companies & associates

Who we are

Healthcare communications

CommonHealthwww.commonhealth.comFeinstein Kean Healthcarewww.fkhealth.comGrey Healthcare Group ◆

www.ghgroup.comOgilvy Healthworldwww.ogilvyhealthworld.comSudler & Hennessey ■

www.sudler.com

Direct, digital, promotion & relationship marketing

A. Eicoff & Cowww.eicoff.comBridge Worldwidewww.bridgeworldwide.comBrierley & Partners 1

www.brierley.comDialogue Marketingwww.dialmkg.comDigitwww.digitlondon.comEinson Freemanwww.einsonfreeman.comEWAwww.ewa.ltd.ukFullSIX 3

www.fullsix.comGood Technology ▲ ■

www.goodtechnology.comGrass Roots 1

www.grg.comG2 ◆

www.g2.com– G2 Branding & Design– G2 Interactive– G2 Direct & Digital– G2 Promotional MarketingHeadcount Worldwide Field Marketingwww.headcount.co.ukHigh Co 1

www.highco.fr KnowledgeBase Marketing ■

www.knowledgebasemarketing.comMando Brand Assurancewww.mando.co.ukMaxx Marketingwww.maxx-marketing.comOgilvyOne Worldwidewww.ogilvy.comRMG Connectwww.rmgconnect.comRTC Relationship Marketing ■

www.rtcrm.comsyzygy 1

www.syzygy.netVML ■

www.vml.comWunderman ■

www.wunderman.com141 Worldwidewww.141worldwide.com

Specialist communications

Corporate/B2BBrouillardwww.brouillard.comOgilvy Primary Contactwww.primary.co.ukCustom mediaForwardwww.theforwardgroup.comSpafaxwww.spafax.comDemographic marketingThe Bravo Group ■

www.thebravogroupyr.comKang & Lee ■

www.kanglee.comMosaicaMDUniWorld 1

www.uniworldgroup.comWINGLATINO ◆

www.winglatino.comEmployer branding/recruitmentJWT Specialized Communicationswww.jwtworks.comEvent/face-to-face marketingMJMwww.mjmcreative.comPCI Fitchwww.fitch.comThe Event Union– MJM– Pro Deo

www.prodeo.com– facts + fiction

www.factsfiction.deFoodservice marketingThe Food Groupwww.thefoodgroup.comSports marketingGlobal Sportnetwww.globalsportnet.comPerformance SportEntwww.performance-worldwide.comPSMwww.premiere.co.uk PRISM Groupwww.prismteam.com

Entertainment marketingAlliance ◆

www.alliance-agency.comYouth marketingThe Geppetto Groupwww.geppettogroup.comG Whiz ◆

www.thinkgwhiz.comReal estate marketingPacewww.paceadv.comTechnology marketingBanner Corporation ■

www.b1.comMedia & production servicesClockwork Capital 1

www.clockworkcapital.comThe Farm Groupwww.farmpost.co.uk MEDIAPRO Group 1

www.mediapro.esMetro Groupwww.metrobroadcast.co.uk

WPP knowledge communities

The [email protected] [email protected]

Key1 Associate2 Joint venture3 Minority investment■ A Young & Rubicam Brands company▲ A Mediaedge:cia company• A member of B to D Group ◆ A Grey Global Group company

As at May 2006

Annual Report 2005Who we are 11

Annual Report 2005How we’re doing Contents12

WPP, the parent company, complements thesecompanies in three distinct ways.

First, it relieves them of much administrative work.Financial matters (such as planning, budgeting,reporting, control, treasury, tax, mergers, acquisitions,

investor relations, legal affairs and internal audit) are co-ordinated centrally. For the operating companies, every administrative hour saved is an extra hour to bedevoted to the pursuit of professional excellence.

Secondly, the parent company encourages and enablesoperating companies of different disciplines to worktogether for the benefit of clients. Such collaborations

have the additional benefit of enhancing the job satisfactionof our people. The parent company also plays an across-the-Group role in the following functions: the managementof talent, including recruitment and training; in propertymanagement; and in procurement, information technology and knowledge sharing.

And finally – a relatively recent development,this – WPP itself can function as the 21st centuryequivalent of the full-service agency. For some clients,

predominantly those with a vast geographical spread anda need for marketing services ranging from advertisingthrough design and website construction to research andinternal communications, WPP can act as a portal toprovide a single point of contact and accountability.

No two clients are structured in preciselythe same way. Within WPP’s operating companies, teams can be tailor-made to match any and all.

etween them, WPP companies have tens ofthousands of individual clients. They rangefrom Fortune 500 global giants through single-nation start-ups to the smallest of specialistcharities. Diverse as they are, they have onething in common: in pursuing their objectives,

they face formidable competition.Growing affluence in many parts of the world –

combined with over-capacity and over-supply in almostevery significant consumer market – have put more andmore power into the hands of consumers, accelerated by technology.

As always, if they are to succeed – or even to survivewith profit – every competitive company needs anintrinsically appealing product or service. But that, thoughit remains the most fundamental of requirements, is nolonger enough. Just as competitive costermongers arrangetheir apples in appealing displays, and polish them lovinglyto catch their customers’ eyes, so all companies need todisplay their wares compellingly.

They need access to high-quality information,strategic advice and specialist communications skills. And it’s in the nature of specialist and creative talent that it is unlikely to flourish within the confines of amanufacturing or service company. People with specialisttalents work best – and contribute more – when recruited,trained and inspired by specialist companies.

Within the WPP Group, our clients have access tocompanies of all the necessary marketing and communicationsskills; companies with strong and distinctive cultures of their own; famous names, many of them.

Why we exist

Our missionTo develop and manage talent;

to apply that talent, throughout the world,

for the benefit of clients;to do so in partnership;

to do so with profit.

Annual Report 2005Why we exist 13

Annual Report 2005How we’re doing14

2005 2004 Change %

Turnover (billings) £26,674m £19,598m +36.1Revenue £5,374m £4,300m +25.0Headline EBITDA1 £877m £664m +32.1Headline operating profit1 £721m £531m +35.8Reported operating profit £653m £476m +37.2Headline PBIT1 £755m £560m +34.8Headline PBIT margin 14.0% 13.0% +1.0Headline PBT1 £669m £490m +36.5Reported PBT £592m £434m +36.4Headline diluted earnings per share1,3 36.0p 27.9p +29.0Headline diluted earnings per ADR1,2,3 $3.27 $2.56 +27.7Ordinary dividend per share 9.34p 7.78p +20.1Ordinary dividend per ADR2 85.0¢ 71.3¢ +19.2Net debt at year-end £804m £555m +44.9Average net debt4 £1,212m £1,083m +11.9Ordinary share price at year-end 629.0p 573.0p +9.8ADR price at year-end $54.00 $54.67 -1.2Market capitalisation at year-end £7,881m £6,792m +16.0

At 10 May 2006

Ordinary share price 681.5pADR price $63.35Market capitalisation £8,524m

Notes*These figures have been prepared under IFRS (International Financial Reporting Standards, incorporating International Accounting Standards).1 The calculation of ‘headline’ measurements of performance (including Headline EBITDA, Headline operating profit, Headline PBIT, Headline PBT and Headline earnings) is shown in note 32 of the financial statements.2 One American Depositary Receipt represents five ordinary shares. These figures have been translated for convenience purposes only using the income statement exchange rates shown on page 150. This conversion should not be construed as a representation that the pound sterling amounts actually represent, or could be converted into, US dollars at the rates indicated.

3 Earnings per share is calculated in note 10 of the financial statements.4 Average net debt is defined on page 184.

How we’re doing*Financial summary*

Our twentieth year was a record one. All the key measures were better, reflecting growth

across almost all disciplines and geographies.

Annual Report 2005How we’re doing 15

How we’re doing

The Group has made the transition to IFRS and the figures for 2004 and 2005 are presented onthis basis. Information for 2003 and prior years is on a UK GAAP basis, as previously reported.1

Notes1 Figures for 2005 and 2004 have been prepared in accordance with IFRS (International FinancialReporting Standards, incorporating International Accounting Standards), which the Group adoptedin 2005. Figures for prior years have been prepared under UK GAAP, as previously disclosed in theGroup’s Annual Report and Accounts for those years.

2 The calculation of ‘headline’ measurements of performance (including Headline EBITDA, HeadlinePBIT and Headline earnings) is shown in note 32 of the financial statements.

3 Calculated gross of goodwill and using profit after taxation before goodwill impairment and othergoodwill write-downs, and gains/losses arising from the revaluation of financial instruments,amortisation of acquired intangible assets, and investment gains and write-downs.

Annual Report 2005How we’re doing16

Revenue1

£m05

04

03

02

01

5,374

4,300

4,106

3,908

4,022

Headline EBITDA1, 2

£m05

04

03

02

01

877

664

661

574

607

0504030201

Headline PBIT1, 2

£m

0

20

2468

1012141618

755560534468561

Headline PBIT2

margin

Headline diluted earnings per share1, 2

p

36

30

24

16

8

0

36.027.929.023.830.9

0504030201Dividends per share p

After tax return on average capital employed1, 3

%

0

10

123456789

9.18.57.56.89.4

0504030201

Weighted average cost of capital (WACC)

WPP total return to share owners relative to relevant comparators rebased to 31 December 2000

WPP

150

100

50

031 Dec 00 31 Dec 01 31 Dec 02 31 Dec 03 31 Dec 04

10 May0631 Dec 05

FTSE 100 Omnicom Interpublic

Financial summary

Annual Report 2005How we’re doing 17

How we’re doing

Notes1 Figures for 2005 and 2004 have been prepared in accordance with IFRS (International FinancialReporting Standards, incorporating International Accounting Standards), which the Group adoptedin 2005. Figures for prior years have been prepared under UK GAAP, as previously disclosed in theGroup’s Annual Report and Accounts for those years.

2 Percentages are calculated on a constant currency basis. See definition on page 184.3 The calculation of Headline PBIT is set out in note 32 of the financial statements.4 Interest in 2005 excludes finance costs arising from the revaluation of financial instruments.5 Average net debt includes amounts drawn down in each year on the Group’s working capital facility(the advance of cash financing against which certain trade debts have been assigned). This facilitywas repaid and cancelled on 31 August 2005.

6 Includes corporate bonds, convertible bonds and bank loans payable at par value, excluding anyredemption premium due.

Average net debt1, 5 £mand interest cover multiples

0

10

123456789

1,2121,0831,4801,5371,069

0504030201Net interest4 cover on Headline PBIT1,3

Debt maturity6

£m– 450

20072006

506

2008

–

2009

–

2010

–

2011

–

2012

–

2013

378

2014

87

2015+

2005 revenue2 by geography%North America 39

UK 15

Continental Europe 27

Asia Pacific, Latin America,Africa & Middle East

19

2005 Headline PBIT2, 3 by geography%North America 46

UK 11

Continental Europe 24

Asia Pacific, Latin America,Africa & Middle East

19

2005 revenue2 by sector%Advertising and Mediainvestment management

48

Information, insight & consultancy 15

Public relations & public affairs 10Branding & identity, Healthcareand Specialist communications

27

2005 Headline PBIT2, 3 by sector%Advertising and Mediainvestment management

53

Information, insight & consultancy 11

Public relations & public affairs 10Branding & identity, Healthcareand Specialist communications

26

How we’re doing

Annual Report 2005How we’re doing18

PP’s twentieth year was our best ever withkey measures exceeding the previous peakyears of 2001 and 2004.

Most importantly, total share ownerreturn improved, with your share pricerising by almost 10% to 629p over the

year and dividends rising 20% to 9.34p. Pleasingly, yourshare price has advanced a further 8% to 681.5p at thetime of writing.

Revenues were up 25% to £5.4 billion. Operatingmargin was up one margin point to 14% (15% under 2004 UK GAAP). Headline PBIT – that is before goodwillimpairment, amortisation of acquired intangibles, interest,tax and investment gains and write-downs (what a mouthful!)– was up almost 35% to £755 million. Headline profitbefore tax was up over 36% to £669 million.

Profit before tax was up over 36% to £592 million.Headline diluted earnings per share were up 29% to 36.0pand reported diluted earnings per share up almost 27% to 29.7p.

These results reflect faster growth in almost all regions– North America, Eastern Europe, Asia Pacific, LatinAmerica, Africa and the Middle East – the slower growtharea being Western Europe. Similarly, growth wasencouraging across all communications services sectors –Advertising, Media investment management, Information,insight & consultancy, Public relations & public affairs,Branding & identity, Healthcare and Specialistcommunications. As in 2004, we were firing on all cylinders.

These results also reflected continued improvementin productivity, with like-for-like revenues up 5.5% andaverage headcount on the same basis up 5.2%. Liquidityimproved with average net debt up only £132 million (at 2005 exchange rates) despite a net cash outflow of£195 million. Operating margins improved significantly,too – up one margin point after incentives and 0.9 marginpoints before incentives.

The rest of this letter to you is based on constantcurrency comparisons, which are more meaningful given

Dear share owner

Letter to share owners

currency movements. On a like-for-like basis revenues wereup 5.5% for the year, up 6% in the first half and 5% in thesecond half. This appears to have been above the growth inthe worldwide market, with the Group increasing marketshare.

Revenue growth was also consistently strong insuccessive quarters, on a like-for-like basis up 5.7%, 6.2%,4.8% and 5.2%. The momentum was maintained in thefirst quarter of 2006, with like-for-like revenues up almost5%. Our like-for-like revenue objective for 2006 remainsover 4%, well in line with or above forecasts for theadvertising and marketing services industry and worldwideGNP growth.

Media investment management continuesto lead growth

By sector, Media investment management led the way,together with Healthcare and Specialist communications,the latter particularly in direct, interactive and internet. But Advertising, Information, insight & consultancy, andBranding & identity also registered good performances.Public relations & public affairs registered its strongestyear since 2000. Marketing services fell to 52% of ourrevenues in 2005 from 54% in the previous year, due tostrong growth in Media investment management and theacquisition of Grey Global Group (‘Grey’), which wasmore concentrated in Advertising and Media investmentmanagement. We are still, however, more than just anadvertising company.

By geography, Asia Pacific, Africa and the MiddleEast, Latin America and Central and Eastern Europe ledthe way. The only laggard was Western Europe,particularly France, Germany and the UK, although therewas some improvement towards the end of the year andinto 2006. As a result, and because of the acquisition ofGrey, which was more concentrated in North America,markets outside North America remain at around 61% ofour revenues, as compared to 58% in 2003 and 56% in

How we’re doing

2002. The influence of the faster-growing markets outsideNorth America is increasing rapidly.

Profits up; liquidity improved

Headline PBIT margins rose to 14.0% from 13.0%, aheadof our original objective of 13.2%. This was particularlyencouraging as our income statement reflected our largest-ever incentive pools for record performance. Pre-incentiveheadline PBIT margins rose by 0.9 margin points to 18.3%from 17.4%. Incentive payments rose to £228 million, ormore than four margin points, from £190 million in 2004.Total incentive payments (including share-based payments)were more than 24% of operating profits before bonuses,taxes and income from associates. Our objective remainsto pay out approximately 20% at maximum and 15% attarget, excluding share option costs. Variable staff costs(freelance, consultants and incentive payments, includingshare option charges) now account for 7.6% of revenues,almost at last year’s peak of 7.8%. This provides a usefulshock absorber for operating margins, should revenuesagain come under pressure.

As a result of all this, headline PBIT rose to £755million, well over $1 billion for the second year in a row,up more than 31% in constant currencies. Although 2005was a strong year, some of our first-generation businessescontinued to suffer and a non-cash impairment chargereflecting accelerated amortisation of goodwill of £46million was taken, compared to £41 million in 2004. Pre-tax profits, therefore, rose by almost 32% to £592million, more than $1 billion for the first time, and dilutedheadline earnings per share by more than 25% to 36p.

Free cash flow was up strongly at £565 million,compared to £466 million in 2004. Excluding the cashpayment for Grey, for the third year in a row we morethan achieved our recently introduced cash flow objectiveof covering all acquisition payments and share re-purchases,and managed to cover dividend payments, too.

Liquidity improved as well, and even after the part-cash acquisition of Grey, your company remainscomfortably geared. Net debt averaged £1.212 billion –up £132 million (at 2005 exchange rates) – despite a grosscash payment of £376 million in respect of the acquisitionof Grey. In the first quarter of 2006, liquidity has continuedto strengthen, with average net debt only up £215 millionto £1.043 billion (at 2006 exchange rates) compared withthe same period in 2005, again despite the gross cashpayment for Grey. Headline interest cover in 2005 waswell over eight times. Analysts appear comfortable withaverage net debt levels of more than twice EBITDA, orover £2 billion, versus our current levels of approximately£1.2 billion.

Industry prospects

Theoretically, 2005 should have been the weakest year ofthe 2005-2008 quadrennial cycle, with no special events to stimulate growth. In fact, it was the contrary – perhapsreflecting a growing realisation among clients that the only way to succeed is by generating like-for-like revenuegrowth through innovation and branding. 2006 should,again in theory, be a stronger year, with the Turin WinterOlympics, the FIFA World Cup in Germany and the USCongressional elections stimulating growth. The industrywill probably grow at 4-5% in 2006, compared to 3-4% in 2005, with marketing services outpacing advertising,driven primarily by growth in direct, interactive andinternet marketing. 2007 should again be a good year,reflecting the build-up to the Beijing Olympics and the2008 US Presidential election, in which both parties areexpected to have well-financed, multi-candidate fields.2008 should be a blockbuster year not only because of the Summer Olympics and the US elections, but also withthe European Championship in Austria and Switzerland.Spending beyond one’s means may finally catch up withthe US economy in 2009 and result in a global slow-down.2007 should see growth similar to 2006’s or slightlystronger growth, with 2008 escalating to 5-6%.

2005 was an excellent year; 2006, we believe, willsee WPP strengthen more. The Company continues to bein its most robust position since 2000. Revenue growth,cost management, productivity, liquidity and balance sheetstrength all continued to improve over last year andcontinue to do so in 2006. Most importantly, our talentbase continues to strengthen, particularly as we invest inincreasing headcount in 2005 and in 2006.

As far as 2006 and beyond is concerned, there are two principal concerns: America’s twin deficits, andWestern Europe’s stagnation. How long growth cancontinue when the US government continues to run current account and fiscal deficits remains to be seen. The American consumer remains sluggish, and chairmenand CEOs do not seem willing as yet to raise corporatecapital spending consistently to bolster the economy, which – in our view – remains patchy. The 2000 recessionwas stimulated by a sharp decline in corporate capitalspending, which was then ameliorated by strongerconsumer spending. The reverse has not happened yet,notwithstanding the strength in corporate profitability,liquidity and margins. Profits as a proportion of GNP areat a 50-year high. At the same time inflation, stimulated by commodity price inflation, in oil and steel in particular,has increased, and the dollar has weakened. Perhaps this is an old-fashioned approach, but operating beyond your

Annual Report 2005How we’re doing 19

How we’re doing

means seems perilous to us. And a country’s currency, we think, comes close to representing its ‘stock price’.

Our second worry is that Western Europecontinues to stagnate, although there are signs of a slightimprovement. France, Germany, Italy and, to a lesserextent the UK, resemble a mature company in a matureindustry. There is little top-line growth. With healthcareand pension costs becoming an increasing burden, unlessrelative interest rates decline and growth is stimulated byfurther broadening of the European Union, for example by the early entry of Turkey or by more liberal corporateand social tax policies, Western Europe may be trapped in a sluggish, lack-of-growth scenario, falling furtherbehind the US and Asia Pacific. Social and structural costs are significant elements of this concern. The recentintroduction of transfer of undertakings legislation in theEU (‘TUPE’), for example, represents another burden tobear. In certain circumstances, it is possible that havingwon an account, the winning agency would have to takeon the losing team or pay severance.

Despite these issues, there is evidence – particularlyin 2004, 2005 and the early part of 2006 – of a growingfocus on top-line growth. Given a low-inflationaryenvironment, limited pricing power and more concentratedretail distribution, clients are increasingly coming to theview there is only one way to compete – throughinnovation and branding. Promote on price and you createcommodities. Innovate and differentiate, you create brandsand the right to demand a premium from the consumer.There is a growing realisation that cutting costs alone willnot deliver growth targets promised to Wall Street and theCity of London. There is a limit to cost reduction, but noceiling on top-line growth – at least until you reach 100%market share. Further reinforcing this trend, strategicadvisors, such as management consultants like McKinsey,counsel a switch in focus from costs to revenues.Corporate strategic plans are increasingly concentrating onmanaging for growth, instead of managing for value.

Finally, managements are just plain tired ofgrappling with debilitating cost-management programmes.For the past three or four years, there has been aninexorable focus on cost. It is much more fun to focus on growth – perhaps this partially explains the recent surgein merger and acquisition activity, too.

Annual Report 2005How we’re doing20

‘‘

‘‘

’’

’’Clients are increasinglycoming to the view there is only one way to compete – throughinnovation and branding.

For the past three or fouryears, there has been aninexorable focus on cost. It is much more fun to focuson growth – perhaps thispartially explains the recentsurge in merger andacquisition activity, too.

How we’re doing

Grey delivers benefits

Grey, which accounts for about 15% of the enlargedCompany, has now been fully integrated and has brought tothe Group important strategic assets and strong people. Ithas a powerful planning and account handling advertisingagency led by Jim Heekin, with relationships with majormultinational clients of WPP. And it is now raising its levelsof creativity. Its strong Media investment managementcapability, led by Alexander Schmidt-Vogel, is now fullyintegrated into GroupM, winning large accounts usingGroupM networks and planning and research tools. Its public relations capability, led by Jeff Hunt, is now co-ordinating and co-operating with Cohn & Wolfe, ably led by Donna Imperato. Its very strong healthcarecapability, probably our fastest growing, is run by Lynn O’Connor Vos. Its strong direct, sales promotion,interactive and internet capability, now uniformly brandedG2, is led by Joe Celia. Geographic strengths include theUS and Europe (including Eastern Europe) in particular,with interesting bases in Asia Pacific, Latin America, Africaand the Middle East, which are being built up further,organically and by acquisition. Grey also presents bigopportunities to build on existing common clientopportunities, and explore new relationships.

Our margins

Our 2006 budgets indicate organic growth of 4%, equallybalanced between first and second halves, and skewed togreater growth in marketing services. Operating marginsare projected to reach 14.5%. So far, we are ahead ofbudget. The margin objective for 2007 is 15.0% and in2008 we will aim even higher.

2006 should be a better year for the industry,stimulated by an additional 1% growth through the mini-quadrennial factors, such as the mid-term US Congressionalelections, the Turin Winter Olympics and the FIFA WorldCup in Germany. The following year should be its equal or even better, as we gear up for the maxi-quadrennial in2008. As previously noted, that year should be a blowout.In February, when we announced our results for 2005, we already had given guidance on life beyond 15%, andhow we might improve further our margin to 19% or 20%under 2004 UK GAAP. This is not so outrageous as somebelieve, given that our best performing companies in eachservices sector already perform at a combined Groupmargin of 17%.

Our top priorities

Our reason for being, the justification for WPP’s existence,continues to be to add value to our clients’ businesses andour people’s careers. Our goal remains to be the world’smost successful provider of communications services tomultinational and local companies.

To that end, we have three top strategic priorities.First, in the short term, having weathered the internetbust successfully, we need to build on the solid base wehave established. Our people are stronger: they are

better resourced, motivated and incentivised than when we exited the last recession in the early 1990s.

The Company is also more profitable, more liquid,less leveraged and better structured than then. In the mostrecent economic cycle, margins peaked at 14.5% andbottomed at 12.3%, as opposed to 10.5% and 5.6% theprevious time.

Second, in the medium term, to build upon thesuccessful base we have established with theacquisition of Young & Rubicam Brands and Grey.

At Grey,the new management structure is now in place andwhatever integration targeted, now completed. At Young& Rubicam Brands, our plans are also largely completed,the one remaining task being to complete the managementstructure at the Y&R advertising agency, where momentumhas picked up recently.

Our third priority, in the long term or over the next five to 10 years, is to increase the combinedgeographic share of revenues of Asia Pacific, Latin

America, Africa and the Middle East, and Central andEastern Europe, from around 20% to one-third. We shallalso aim to increase the share of revenues of marketingservices from around 52% to two-thirds; and to increasethe share of more measurable marketing services – suchas Information, insight & consultancy, and direct,interactive and internet – from around one-third of ourrevenues to 50%.

Our six objectives

Our six objectives remain as follows:First, to continue to raise operating margins to the levels of the best-performing competition. 15% (under 2004 UK GAAP) has finally been

achieved. 20%, or 19% under IFRS, is much tougher, but not out of the question. BBDO, Dentsu and McCannhave done so historically, although the pressure becametoo great in some instances.

Annual Report 2005How we’re doing 21

How we’re doing

Second, to continue to increase flexibility in the coststructure. Great strides were made in 2004 and 2005on this. Peak flexibility historically was in 2000,

at 6.6% of revenues in variable staff costs. Now at 7.6% in 2005, and 7.8% in 2004, we have seen new peaks; and once again we have a sufficient ‘shock absorber’ in our cost structure, if revenue growth weakens.

Third, to improve total share owner return bymaximising the return on investment on theCompany’s £600 million free cash flow. There

are broadly three alternative uses of funds:

•Capital expenditure, which usually approximates thedepreciation cost. Pressure here has eased as technologypricing has fallen, although we are investing more in realestate, particularly in the US, to secure greater efficiencies.

•Mergers and acquisitions, which have historically takenthe lion’s share of free cash flow. Here we have raised thehurdle rate on capital utilised so that our return on capitalemployed may be increased. Even so, there are stillinteresting opportunities, particularly outside the US,where pricing remains lower and where there is a closer fit with the Company’s strategic objectives. Privatetransactions remain more attractively priced at single-digitprice-earnings multiples. Happily, return on capital fromGrey exceeded our cost of capital in the first year, and thereturn from Young & Rubicam Brands, although stillbelow the cost of capital, is rising satisfactorily.

•Dividends or share buy-backs. We have been the onlyFTSE 100 company to increase its dividend by 20% perannum over the past 10 years. Given dividend cover ofmore than four times headline earnings and a dividendyield of just over 1%, we can continue to increase thedividend. However, a rolling share buy-back programmeappears to offer a more significant benefit to total shareowner returns, and we are looking at boosting the level of the share buy-back programme from 1.5-2% of theoutstanding share capital to over 2%. In the first quarter of 2006, we were buying back shares at an annualised rate of 2.5%.

Fourth, we will continue to enhance the contributionof the parent company. WPP is not just a holdingcompany focused on planning, budgeting, reporting

and financial issues, but a parent company that can addvalue to our clients and our people. We will continue to do this through a limited group of 250 or so people at thecentre in London, New York, Hong Kong and São Paulo.This does not mean that we seek to diminish the strengthof our operating brands. Our objective is to maximise theadded value for our clients with their businesses and ourpeople with their careers.

Annual Report 2005How we’re doing22

‘‘

‘‘’’

’’

It is a relatively recentdevelopment for certainmultinational marketingcompanies, when looking to satisfy their globalcommunications needs, tomake their initial approach notto operating companies butdirectly to parent companies.

All our clients, whether global,multinational or local, continueto focus on the quality of ourthinking, co-ordination ofcommunications, and price. In response, we focus on talent, structure and incentives.

How we’re doing

Many of our initiatives are possible because of thescale on which we now operate. In the optimum use ofproperty, in information technology and in procurementgenerally, we are able to achieve efficiencies that would be beyond the reach of any individual operating company.But it is also clear that there is an increasing requirementfor the centre to complement the operating companies inprofessional development and client co-ordination.

It is a relatively recent development for certainmultinational marketing companies, when looking tosatisfy their global communications needs, to make theirinitial approach not to operating companies but directly to parent companies. Such assignments present major, andincreasingly frequent, opportunities for the few groups of our size. It is absolutely essential that we have theprofessional resources and the practice developmentcapability to serve such clients comprehensively, activelyand creatively.

All our clients, whether global, multinational orlocal, continue to focus on the quality of our thinking, co-ordination of communications, and price. In response,we focus on talent, structure and incentives.

People, people, people

Talent and its management therefore remain the lynchpinof our reason for existence: that is what our clients pay usfor. Development of our people and the way we managethat talent is a critical driver of performance; and on that critical dimension, we continue to make significantprogress. In the creation of extremely attractive workingenvironments, with highly competitive incentives, weincreasingly differentiate ourselves from our competitorsand improve the attraction of WPP companies asdestinations for talent.

Our quarterly reviews with the operatingcompanies have been restructured, consequently, to give more time and attention to talent and to clients. Our recruiting efforts throughout 2005 were dedicated and especially fruitful as we successfully targeted andattracted top talent within and beyond our industry,often competing with investment banking, managementconsulting, and private equity offers. The war for talent is fierce, and there is more to be done.

The blueprint for our executive developmentcurriculum has been completed, and our new clientleadership training programme has been successfullyintroduced. Each of our operating companies installed its own approach to performance assessment andsuccession planning, aimed at developing the careers of their people, improving the quality of feedback,coaching and mentoring they receive and providing for

orderly succession. We continued to scrutinise and modifyour compensation practices: both to offer competitive andjustly based rewards to our existing people and to attractoutstanding talent from elsewhere. For the first time Grey was included in our performance and assessmentapproach in 2005. Our incentives assessment and rewardsmethodology have been enthusiastically received.

A communications services company must be amodel of excellent external and internal communications.To that end, we are broadening the understanding of the Group’s vast resources through a raft of regularcommunications: our regular FactFiles profiling Groupresources/companies/products; our monthly public onlinenews bulletin, e.wire; our quarterly global newspaper, TheWIRE; our annual Atticus Journal of original marketingthinking; and our annual Corporate Responsibility Report.Our online communications continue to be expanded witha comprehensive redevelopment of the WPP intranet andGroup website (www.wpp.com).

In property management, we continue to improvethe return on our investment in real estate through theWPP Space Program, with planned investment in propertydatabase and systems, innovative design and continuousreview of key locations. Surplus space, primarily inheritedthrough recent acquisitions, is steadily released from theportfolio, resulting in a reduction of 1,000,000 square feetduring the past two years; on our average cost per squarefoot equivalent to a saving of £24 million. Following thisreduction, at the end of 2005 our portfolio was 18.2million square feet and a further release of 300,000 squarefeet is expected during 2006.

In procurement, we have set ourselves the goal ofbecoming the undisputed leader of procurement practice in the global advertising and marketing services industry.With intensified internal training in this area, we havefocused on our major markets and categories morefavourable for global, regional or country contracts suchas IT, telecoms, facilities, travel, professional services and production. This program’s success has beendemonstrated by improvement of the non-staff costs to revenue ratio in recent years.

In information technology, we continue to integratecore infrastructure support across our offices. As withCordiant, Grey operations have been quickly integratedinto our IT platform, which has allowed the operatingcompanies to concentrate on client-related IT systemsdevelopment. Convergence of transmission of electronicdata, internet, wireless, IP and traditional voice telephonypresents us with a further opportunity to standardise ourapproach to technology at the regional if not global level,and to take advantage of current overcapacity in many ofthese sectors.

Annual Report 2005How we’re doing 23

How we’re doing

Finally, in practice development we continue todevelop horizontal initiatives in a focused set of high-potential areas across our vertical operating brands: inmedia investment management, healthcare, privatisation,new technologies, new faster-growing markets, internalcommunications, retail, entertainment and media, financialservices, and hi-tech and telecommunications. Specifically,we continue to invest in sharing insights and developinginitiatives through The Channel (in media and research)and The Store (in distribution and retail).

In key geographic markets we are increasingly co-ordinating our activities through WPP CountryManagers. Despite events at WPP Italy, we continue tobelieve that increasing co-ordination is required betweenour brands at the country and global levels, as thearguments for investment in regional management becomeweaker. However, the activities of Country Managers mustbe closely aligned and monitored. In addition, we areappointing a small number of WPP Global Client Leadersto co-ordinate our efforts on behalf of clients and to ensurethey get maximum benefit from their relationships withWPP operating brands.

Furthermore, we continue to encourage internalstrategic alliances and promote co-operation. Practicedevelopment initiatives have thereby been reinforced insuch areas as healthcare, internal communications, andmedia and entertainment. This has been especiallyimportant to manage our portfolio of direct investments in new media.

All these initiatives are designed to ensure that we, the parent company, really do (and are perceived to)inspire, motivate, coach, encourage, support andincentivise our operating companies to achieve theirstrategic and operational goals.

Fifth, as we move up the margin curve, we intend to place greater emphasis on revenue growth. Onelegitimate criticism of our performance against the

best-performing competition is our comparative level oforganic revenue growth. 2000 was a bumper year butunsustainable. In 2001, we disappointingly moved backinto the middle of the pack. But there was a significantrevival in 2002 and 2003, when we were one of only twoof the major companies that showed revenue growth. 2004 was punctuated with a number of high-profile wins,resulting in the second strongest organic growthperformance in the industry, and 2005 saw strong growthagain among the leaders in the industry.

Our practice development activities are also aimedat helping us position our portfolio in the faster-growingfunctional and geographic areas. So far in 2006, the Grouphas made acquisitions or increased equity interests inAdvertising and Media investment management in the US,

the UK, Germany, South Africa, Israel, China, Singaporeand Brazil; in Public relations & public affairs in India;and in Direct, internet & interactive in the US and China.

These acquisitions continue to move us forward to our aforementioned strategic priorities; expanding themarket shares of our businesses in Asia Pacific, LatinAmerica, Africa and the Middle East to one-third; inmarketing services to two-thirds; and in Information,insight & consultancy, direct and interactive, to one-half.

We will expand our strong networks – Ogilvy &Mather, JWT, Y&R, Grey, United, BatesAsia, MindShare,Mediaedge:cia, MediaCom, Research International,Millward Brown, KMR, Hill & Knowlton, Ogilvy Public Relations Worldwide, Burson-Marsteller, Cohn &Wolfe, GCI, OgilvyOne, Wunderman, 141 Worldwide, G2, CommonHealth, Sudler & Hennessey, OgilvyHealthworld, Grey Healthcare, Enterprise IG, Landor and Fitch – in high-growth markets or where their market share is insufficient.

In 2005, in addition to the completion of theacquisition of Grey, we strengthened our position inAdvertising and Media investment management in the US,the UK, Denmark, the Netherlands, Spain, Russia, Israel,Argentina, Hong Kong and Australia; in Information,insight & consultancy in the US, the UK, Poland, China,Hong Kong, Korea and New Zealand; in Public relations& public affairs in the US, Denmark, Bahrain, Argentina,India, China and Australia; in Healthcare communicationsin the US, the Netherlands and Switzerland; and in direct,internet and interactive in the US.

We will also enhance our leadership position in Information, insight & consultancy by furtherdevelopment of our key brands with particular emphasison North America, Asia Pacific and Latin America. We will accelerate our growth of panels and haveestablished a Kantar-wide operational capability.We will reinforce our growing position in media research through KMR, which includes our investments in television audience research through IBOPE,AGBNielsen Media Research and Marktest, which,combined, are the market leader outside North America. In addition, we will reinforce our worldwide strength indirect and interactive marketing and research through ourtraditional channels such as The Digital Edge, OgilvyOne,Wunderman, Blanc & Otus and Lightspeed. Although the early 2000-2001 compressions in financial valuationsinitially offered significant opportunities, we will now also invest directly in the new channels through start-ups,particularly as US valuations in search, for example, havebecome prohibitive. Lastly, we will continue to develop our specialist expertise in areas such as healthcare, retail and interactive and to identify new high-growth areas.

Annual Report 2005How we’re doing24

How we’re doing

Creativity remains paramount

Our sixth objective is to improve still further thequality of our creative output. Despite the growingimportance of co-ordinated communications and

price effectiveness, the quality of the work remains andwill remain paramount. If you drew a graph plottingcreative awards (as a proxy for creativity) against marginsfor any group of agencies, there would be a very strongcorrelation. The more awards, the stronger the margins.The client’s procurement department fades into thebackground when the work is strong. Of the three thingswe do – strategic thinking, creative execution and co-ordination – creative execution is undoubtedly the mostimportant, and that means creativity in its broadest sense.

Clients look for creative thinking and output notjust from advertising agencies, public relations and design companies, but also from our media investmentmanagement companies, MindShare, Mediaedge:cia,MAXUS and MediaCom, and our research companies.Millward Brown remains arguably one of our mostcreative brands. Witness its new global brands survey with the Financial Times.

We will achieve this objective by stepping up ourtraining and development programs; by recruiting thefinest external talent; by celebrating and rewardingoutstanding creative success tangibly and intangibly; byacquiring strong creative companies; and by encouraging,monitoring and promoting our companies’ achievements in winning creative awards. For additional leadership inthis regard, Robyn Putter, still worldwide creative directorat Ogilvy, has agreed to take on the additional role ofWPP’s worldwide creative head.

We are committed to achieving these objectives as a substantively responsible corporate citizen of theworld at large and the communities in which we operate.

Looking forward

A colossal amount remains to be done – challengingour clients, and therefore us. It seems certain that once theseobjectives are achieved, they will be replaced by new ones.

As companies grow in size, most chairmen andCEOs become concerned that their organisations maybecome flabby, slow to respond, bureaucratic and sclerotic.

Any sensible business leader aggressively resists thisphenomenon; we all seek the benefits of size and scalewithout sacrificing the suppleness and energy of a smallerfirm. And, for the first time, new technologies now makethis possible on a global platform.

WPP wants the scale and resources of the largestfirm together with the heart and mind of a small one.

As a parent company, we continue to developpractical principles and policies for our companies’charitable giving and services to the environment,education, the arts and healthcare based on best-practiceguidelines. We conservatively calculate that the WPPorganisation contributed an estimated £17.3 million worth of time, skills, materials and money to social andcommunity causes in 2005. A summary of the Group’sapproach to corporate responsibility can be found onpages 110 to 115.

And finally… a reminder

Those who own shares in WPP – and those who analyseand comment on its performance – quite rightly see it as a single entity; they rate it according to its overallachievements. And it’s those achievements that this Reportfeatures. It’s been a very good year.

But of course, what those aggregate numbers fail toreveal are the extraordinary number, range and diversity of quite separate achievements that go to make up thoseimpressive company totals.

By applying their brains and their talent and theirexperience to the service of their clients, every company in every discipline on every continent has contributed tothat parent company total. The contribution of some92,000 individual people, representing a vast variety ofskills, has gone to make up that parent company total.

And, as always, it is those individual skills that ourclients value, and pay for. Project by project, some tens ofthousands of them in all, as WPP companies helped maketheir clients more successful, so, project by project, theyadded inexorably to the final figures presented here.

So it is entirely right that we should end this letterby acknowledging the true source of our success – andoffering our wholehearted gratitude to all those manypeople who made it happen.

Philip LaderChairman

Sir Martin SorrellGroup chief executive

Annual Report 2005How we’re doing 25

How we’re doing

Annual Report 2005How we’re doing26

How we’re doing

Reports from our operating brands

Annual Report 2005How we’re doing 27

s the marketplace, the media, andconsumers’ expectations have evolved, wehave structured our offering to seize theinitiative. It could not be more clear whatclients want. They want great ideas thatcan move effortlessly through multiple

channels. They want thinking unfettered to specific media.They want diverse capabilities and they want experiencedpartners. They want leaders who can work together. We aredelivering. We have the partners in place who are working

How we’re doing

Agency networks

across regions and disciplines, creating new and compellingcommunication solutions. Yes, we are a long way from justthe “ad business.” And that is a good thing.

Last year we reaped the benefit of more than adozen years of honing 360 Degree Brand Stewardship®.This business platform enables us to integrate successfullyour growing range of disciplines which now include 141,Ogilvy’s brand activation company, Ogilvy PR and OgilvyHealthworld. We also have brought digital and directmedia back into our operations this year as Neo@Ogilvy.

We have made changes in leadership that haveallowed us to further our 360 agenda. In North America,where Ogilvy Advertising and OgilvyOne are alreadyclosely collaborating, the appointment of Carla Hendra andBill Gray as co-CEOs of North America promises morecohesion. (They succeed Tro Piliguian who is now WPP’schief operating officer.) Gary Leih, formerly at Ogilvy SouthAfrica, has dramatically reorganized Ogilvy in London;uniting our companies as the single largest marketingcommunications group in the UK.

While changes like these promise better 360execution, as practitioners we know that capability alone is not enough. If there is not a great idea at the heart of acampaign, it is a missed opportunity. Great ideas are whatclients come to us for. And we’ve had a number of those big ideas over this past year.