2002 - AnnualReports.com

176

2002 Annual Report Inter-American Development Bank Annual Report 2002

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of 2002 - AnnualReports.com

INTER-AMERICAN DEVELOPMENT BANK1300 New York Avenue, N.W.

Washington, D.C. 20577

Tel. (202) 623-1000 Fax (202) 623-3096

www.iadb.org

ISSN 0074-087X

INT

ER

-AM

ER

ICA

N D

EV

EL

OP

ME

NT

BA

NK 2002

Annual ReportInter-American Development Bank

An

nu

al Re

po

rt 2002

The Inter-American Development Bank, the oldest and

largest regional multilateral development institution,

was established in 1959 to help accelerate economic

and social development in Latin America and the

Caribbean.

Efforts to create a development institution to

focus on pressing problems in the region date to the

First Inter-American Conference in 1890. A specific

proposal toward that end by President Juscelino

Kubitschek of Brazil in 1958 received support through-

out the hemisphere. Shortly thereafter, the Organi-

zation of American States drafted the Articles of

Agreement establishing the Inter-American

Development Bank.

Today, the Bank’s membership totals 46 nations,

including 26 Latin American and Caribbean countries,

the United States, Canada, and 18 nonregional

countries.

The Bank has become a major catalyst in mobi-

lizing resources for the region. Its principal functions

are to utilize its own capital, funds raised in financial

markets, and other available resources to finance the

development of its borrowing member countries; to

supplement private investment when private capital is

not available on reasonable terms and conditions; and

to provide technical assistance for the preparation,

financing and implementation of development

projects.

In carrying out its mission, the Bank has

approved $118 billion for projects that represent a

total investment of $282 billion.

The Bank’s operations cover the entire spec-

trum of economic and social development, with an

emphasis on programs that benefit low-income popu-

lations. In the past, Bank lending focused on the pro-

ductive sectors of agriculture and industry, the physi-

cal infrastructure sectors of energy and transportation,

and the social sectors of environmental and public

health, education and urban development. In 1995, the

IDB began lending up to 5 percent of its ordinary capi-

tal resources directly to the private sector, without

government guarantees. Current lending priorities

include poverty reduction and social equity, modern-

ization of the State, competitiveness, and integration.

The IDB group also includes the Inter-American

Investment Corporation (IIC), an autonomous affiliate

that promotes economic development by financing

small and medium-scale private enterprises, and the

Multilateral Investment Fund (MIF), which supports

investment reforms and private sector development.

The financial resources of the Bank consist of

the ordinary capital account—comprised of subscribed

capital, reserves and funds raised through borrow-

ings—and Funds in Administration, comprised of con-

tributions made by member countries. The Bank also

has a Fund for Special Operations for lending on con-

cessional terms in countries classified as economically

less developed.

Member country subscriptions to the Bank's

ordinary capital consist of both paid-in and callable

capital. Paid-in capital in the form of cash or notes

represents 4.3 percent of total subscriptions. The

major part of member subscriptions is for callable cap-

ital, which may be drawn only to service the Bank's

borrowings and guarantees.

The Bank has borrowed funds for its operations

from the capital markets of Europe, Japan, Latin

America, the Caribbean and the United States. The

Bank’s debt is AAA rated by the three major rating

services in the United States, and is accorded equiva-

lent status in the other major capital markets.

The Bank’s highest authority is the Board of

Governors, on which each member country is repre-

sented. Governors are usually Ministers of Finance,

Presidents of Central Banks or officers of comparable

rank. The Board of Governors has delegated many of

its operational powers to the Board of Executive

Directors, which is responsible for the conduct of the

Bank’s operations.

The Bank, whose headquarters are in

Washington, D.C., has Country Offices in each of its

borrowing member countries and in Paris and Tokyo.

THE INTER-AMERICAN DEVELOPMENT BANK COUNTRY OFFICES AND REPRESENTATIVES

ARGENTINA, Jorge ElenaCalle Esmeralda 130, pisos 19 y 20(Casilla de correo N 181, Sucursal 1)Buenos Aires Tel: 4320-1800

BAHAMAS, Frank J. MarescaIDB House, East Bay Street(P.O. Box N-3743)Nassau Tel: 393-7159

BARBADOS, Jeremy S. GouldMaple Manor, Hastings(P.O. Box 402)Christ Church Tel: 427-3612

BELIZE, Hugo Souza1024 Newtown Barracks101 1st FloorMarina Towers Building(P.O. Box 1853)Belize City Tel: 223-3900

BOLIVIA, Carlos MeloEdificio “BISA”, 5 pisoAvda. 16 de Julio, N 1628(Casilla N 5872)La Paz Tel: 235-1221

BRAZIL, Waldemar F. WirsigSetor de Embaixadas NorteQuadra 802 Conjunto FLote 39 - Asa Norte70.800-400 Brasília, D.F. Tel: 317-4200

CHILE, Julio AngelAvda. Pedro de Valdivia 0193, 11 piso(Casilla N 16611)Correo 9 (Providencia)Santiago Tel: 431-3700

COLOMBIA, Fernando CossioCarrera 7a N 71-21Torre B, 19 pisoEdificio BancafeBogotá Tel: 325-7000

COSTA RICA, Bertus J. MeinsEdificio Centro Colón, piso 12Paseo Colón, entre calles 38 y 40San José Tel: 233-3244

DOMINICAN REPUBLIC Moisés A. PinedaAvda. Winston Churchill esquinacalle Luis F. Thomen, Torre BHD(Apartado postal N 1386)Santo Domingo Tel: 562-6400

ECUADOR, Dora P. CurreaAvda. 12 de Octubre 1830 y CorderoEd. World Trade Center - Torre II, piso 9(Apartado postal N 17-07-9041)Quito Tel: 256-3453

EL SALVADOR, Luis VergaraEdificio World Trade Center, 4 piso89 Avda. Norte y Calle El MiradorColonia EscalónSan Salvador Tel: 233-8900

GUATEMALA, Carlos BarberyEdificio Géminis 1012 Calle 1-25, Zona 10, Nivel 19(Apartado postal N 935)Guatemala Tel: 335-2650

GUYANA, Sergio Varas-Olea47 High Street, Kingston(P.O. Box 10867)Georgetown Tel: 225-7950

HAITI, Gerard S. JohnsonBanque interaméricaine de

développementBourdon 389(Boîte postale 1321)Port-au-Prince Tel: 45-5711

HONDURAS, Helge SembBoulevard MorazánEdificio Los Castaños, 5 y 6 pisosColonia Los Castaños(Apartado postal N 3180)Tegucigalpa Tel: 232-4838

JAMAICA, Keith Evans40-46 Knutsford Blvd., 6th floor(P.O. Box 429)Kingston 10 Tel: 926-2342

JAPAN, Toshio KobayashiFukoku Seimei Bldg. 16F2-2-2 Uchisaiwaicho, Chiyoda-kuTokyo 100 Tel: 3591-0461

MEXICO, David B. AtkinsonAvda. Horacio N 18556 piso (Esquina Periférico)Los Morales-Polanco11510 México, D.F. Tel: 5580-2122

NICARAGUA, Eduardo BalcarcelEdificio BIDKm. 4-1/2 Carretera a Masaya(Apartado postal 2512)Managua Tel: 67-0831

PANAMA, John J. HastingsAvda. Samuel LewisEdificio Banco Unión, piso 14(Apartado postal 7297)Panamá 5 Tel: 263-6944

PARAGUAY, Alvaro CubillosEdificio Aurora I, pisos 2 y 3Calle Caballero esquinaEligio Ayala (Casilla N 1209)Asunción Tel: 49-2061

PERU, Vladimir RadovicPaseo de la República 3245, piso 14(Apartado postal N 270154)San Isidro, Lima 27 Tel: 215-7800

SURINAME, Pablo AdamPeter Bruneslaan 2-4Paramaribo Tel: 46-2903

TRINIDAD AND TOBAGOWilliam Robinson19 St. Clair Avenue(P.O. Box 68)Port of Spain Tel: 622-8367

URUGUAY, Martin StabileAndes 1365, piso 13(Casilla de correo 5029)Sucursal 1Montevideo Tel: 902-0444

VENEZUELA, Román MayorgaEdificio Centro Federal, piso 3Avda. Venezuela, El RosalCaracas 1060 Tel: 951-5533

INSTITUTE FOR THE INTEGRATIONOF LATIN AMERICA AND THE CARIBBEAN

Juan José TacconeCalle Esmeralda 130, pisos 16 y 17(Casilla de correo N 39)Sucursal 1Buenos Aires Tel: 4320-1850

SPECIAL REPRESENTATIVE IN EUROPE

Carlo BinettiBanque interaméricaine de

développement66, Avenue d’Iéna75116 Paris France Tel: 40 69 31 00

i

CONTENTS

INTER-AMERICAN DEVELOPMENT BANK

Latin America and the Caribbean in 2002 . . 1

Part I: THE BANK IN 2002

Key AreasOverview . . . . . . . . . . . . . . . . . . . . . . . 11Board of Governors . . . . . . . . . . . . . . . 16Board of Executive Directors . . . . . . . . 17Poverty Reduction and Social Equity . . 20Sustainable Economic Growth . . . . . . . . 22Modernization of the State . . . . . . . . . . 24Competitiveness . . . . . . . . . . . . . . . . . . . 25Social Sectors . . . . . . . . . . . . . . . . . . . . 27Integration . . . . . . . . . . . . . . . . . . . . . . 31The Environment . . . . . . . . . . . . . . . . . 36Private Sector . . . . . . . . . . . . . . . . . . . . . 37Portfolio Management . . . . . . . . . . . . . . 43Development Effectiveness . . . . . . . . . . . 47

The Year’s LendingSummary . . . . . . . . . . . . . . . . . . . . . . . 51Argentina . . . . . . . . . . . . . . . . . . . . . . . 55Bahamas . . . . . . . . . . . . . . . . . . . . . . . . 55Barbados . . . . . . . . . . . . . . . . . . . . . . . . 56Belize . . . . . . . . . . . . . . . . . . . . . . . . . . 56Bolivia . . . . . . . . . . . . . . . . . . . . . . . . . 57Brazil . . . . . . . . . . . . . . . . . . . . . . . . . . 59Chile . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Colombia . . . . . . . . . . . . . . . . . . . . . . . 63Costa Rica . . . . . . . . . . . . . . . . . . . . . . 65Dominican Republic . . . . . . . . . . . . . . . 65Ecuador . . . . . . . . . . . . . . . . . . . . . . . . 67El Salvador . . . . . . . . . . . . . . . . . . . . . . 68Guatemala . . . . . . . . . . . . . . . . . . . . . . 68Guyana . . . . . . . . . . . . . . . . . . . . . . . . . 70Haiti . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Honduras . . . . . . . . . . . . . . . . . . . . . . . 71Jamaica . . . . . . . . . . . . . . . . . . . . . . . . . 73Mexico . . . . . . . . . . . . . . . . . . . . . . . . 73Nicaragua . . . . . . . . . . . . . . . . . . . . . . . 75Panama . . . . . . . . . . . . . . . . . . . . . . . . 77Paraguay . . . . . . . . . . . . . . . . . . . . . . . . 78Peru . . . . . . . . . . . . . . . . . . . . . . . . . . . 78Suriname . . . . . . . . . . . . . . . . . . . . . . . 80Trinidad and Tobago . . . . . . . . . . . . . . . 80Uruguay . . . . . . . . . . . . . . . . . . . . . . . . 81Venezuela . . . . . . . . . . . . . . . . . . . . . . . 82Regional . . . . . . . . . . . . . . . . . . . . . . . . 83Technical Cooperation . . . . . . . . . . . . . . 86Cofinancing . . . . . . . . . . . . . . . . . . . . . 87Funds in Administration . . . . . . . . . . . . 89Procurement . . . . . . . . . . . . . . . . . . . . . 92Statement of Approved Loans

and Guarantees . . . . . . . . . . . . . . . . 97

Institutional AspectsEvaluation and Internal Audit . . . . . . . . 100Country Offices . . . . . . . . . . . . . . . . . . 102Special Office in Europe . . . . . . . . . . . . . 103Office in Japan . . . . . . . . . . . . . . . . . . . . 105Administration . . . . . . . . . . . . . . . . . . . 106

Financial MattersHighlights . . . . . . . . . . . . . . . . . . . . . . . 109Borrowings . . . . . . . . . . . . . . . . . . . . . . 111

Part II: FINANCIAL STATEMENTS

Ordinary Capital . . . . . . . . . . . . . . . . . . . 115Fund for Special Operations . . . . . . . . . . 143Intermediate Financing Facility Account . 157

Annual Report 2002

ii

APPENDICES

Governors and Alternate Governors . . . . . 163Executive Directors and Alternates . . . . . . 164Channels of Communication

and Depositories . . . . . . . . . . . . . . . . . 165Principal Officers . . . . . . . . . . . . . . . . . . . 166

BOXES

1. Colpatria: First Private Sector Mortgage Bond Guarantee . . . . . . . . . 14

2 Poverty Reduction Initiatives in Belize . . . 213. MECOVI Program . . . . . . . . . . . . . . . . . 234. Regional Security . . . . . . . . . . . . . . . . . . 255. Advancing Social Inclusion . . . . . . . . . . . 296. The New Regionalism in the Americas . . 327. The Follow-up to the Summit

of the Americas . . . . . . . . . . . . . . . . . . 358. Reconstruction of the Coffee-Growing

Region in Colombia . . . . . . . . . . . . . . . 389. Corporate Social Responsibility . . . . . . . 4010. Microenterprise Forum . . . . . . . . . . . . . . 4111. Participatory Project Design:

Brazil’s Favela/Bairro . . . . . . . . . . . . . . . . 46

TABLES

I. Ten Years of Operations, 1993-2002 . . vII. The External Environment . . . . . . . . 1

III. Distribution of Loans by Sector . . . . . 51IV. Yearly (2002) and Cumulative Loans

and Guarantees (1961-2002) . . . . . . . . 52V. Yearly (2002) and Cumulative

Disbursements (1961-2002) . . . . . . . . 53VI. Yearly (2002) and Cumulative (1961-2002)

Total Cost of Projects . . . . . . . . . . . . . 54VII. Nonreimbursable and Contingent-

Recovery Technical Cooperation . . . . . 86VIII. Cofinancing . . . . . . . . . . . . . . . . . . . . . 88

IX. Funds in Administration . . . . . . . . . . . 90X-XII. Disbursements for Purchase

of Goods and Services by Country of Origin . . . . . . . . . . . . . . . 94-96

XIII. Consolidated Administrative Expenses . . . . . . . . . . . . . . . . . . . . . . . 107

XIV. Capital of the Bank . . . . . . . . . . . . . . . 109XV. Contribution Quotas to the Fund

for Special Operations . . . . . . . . . . . . . 110XVI. Outstanding Borrowings by Currency 110

XVII. Borrowings, Fiscal Year 2002 . . . . . . . 111

CONTENTS

ArgentinaAustriaBahamasBarbadosBelgiumBelizeBoliviaBrazilCanadaChileColombiaCosta Rica

CroatiaDenmarkDominican RepublicEcuadorEl SalvadorFinlandFranceGermanyGuatemalaGuyanaHaitiHonduras

IsraelItalyJamaicaJapanMexicoNetherlandsNicaraguaNorway PanamaParaguayPeruPortugal

SloveniaSpainSurinameSwedenSwitzerlandTrinidad and TobagoUnited KingdomUnited StatesUruguayVenezuela

MEMBER COUNTRIES

iii

Inter-American Development BankWashington, D.C.

January 31, 2003

Mr. Chairman:

Pursuant to Section 2 of the By-Laws of the Inter-American Development Bank, I trans-mit to you the Annual Report of the Bank for 2002, which the Board of ExecutiveDirectors submits to the Board of Governors.

The Report contains a brief summary of the economic situation of Latin Americaand the Caribbean and a review of the Bank’s operations in 2002.

In addition, the Report contains a description on a country-by-country basis and aregional basis of the Bank’s various operations—loans, guarantees, financings for smallprojects and technical cooperation—on behalf of Latin America’s development; a summarystatement of the loans approved in 2002; the financial statements of the Bank, and its gen-eral appendices.

Complying with Article III, Section 3(a), of the Agreement Establishing the Bank,the Report contains separate audited financial statements for its various sources of funds.For the ordinary capital resources, these are presented pursuant to the provisions of ArticleVIII, Section 6(a) of the Agreement; for the Fund for Special Operations, in accordancewith the provisions of Article IV, Section 8(d), of the Agreement; and for the IntermediateFinancing Facility Account, complying with Section 5(d) of Resolution AG-12/83 of theBoard of Governors.

Sincerely yours,

Enrique V. Iglesias

Chairman, Board of GovernorsInter-American Development Bank

iv

Editor John Ferriter, Office of External Relations

Design by Valkiria Amaro Peizer, Office of External Relations

Photographers Text photos: Willie Heinz, Office of External Relations

Cover photo: Willie Heinz and Diana Lesbines

This report can be obtained online in PDF format at www.iadb.org

This report is printed on recycled paper.

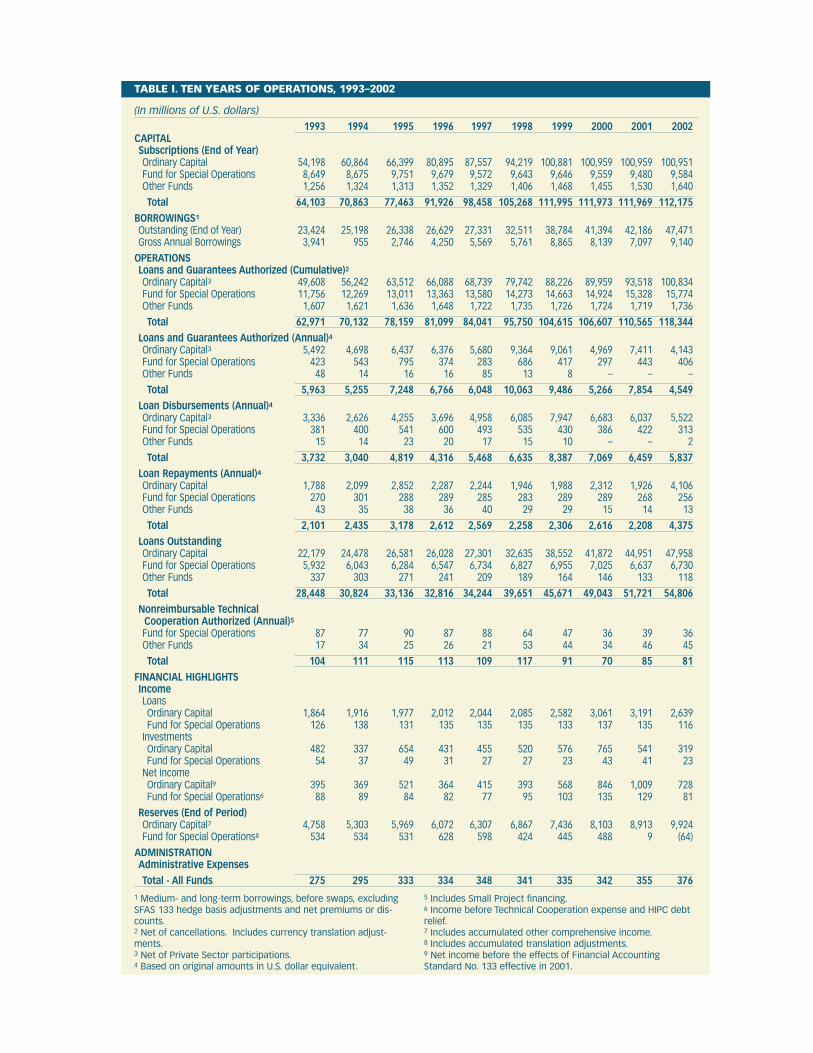

TABLE I. TEN YEARS OF OPERATIONS, 1993–2002

(In millions of U.S. dollars)

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002CAPITALSubscriptions (End of Year)Ordinary Capital 54,198 60,864 66,399 80,895 87,557 94,219 100,881 100,959 100,959 100,951Fund for Special Operations 8,649 8,675 9,751 9,679 9,572 9,643 9,646 9,559 9,480 9,584Other Funds 1,256 1,324 1,313 1,352 1,329 1,406 1,468 1,455 1,530 1,640

Total 64,103 70,863 77,463 91,926 98,458 105,268 111,995 111,973 111,969 112,175BORROWINGS1

Outstanding (End of Year) 23,424 25,198 26,338 26,629 27,331 32,511 38,784 41,394 42,186 47,471Gross Annual Borrowings 3,941 955 2,746 4,250 5,569 5,761 8,865 8,139 7,097 9,140

OPERATIONSLoans and Guarantees Authorized (Cumulative)2Ordinary Capital3 49,608 56,242 63,512 66,088 68,739 79,742 88,226 89,959 93,518 100,834Fund for Special Operations 11,756 12,269 13,011 13,363 13,580 14,273 14,663 14,924 15,328 15,774Other Funds 1,607 1,621 1,636 1,648 1,722 1,735 1,726 1,724 1,719 1,736

Total 62,971 70,132 78,159 81,099 84,041 95,750 104,615 106,607 110,565 118,344Loans and Guarantees Authorized (Annual)4Ordinary Capital3 5,492 4,698 6,437 6,376 5,680 9,364 9,061 4,969 7,411 4,143Fund for Special Operations 423 543 795 374 283 686 417 297 443 406Other Funds 48 14 16 16 85 13 8 – – –

Total 5,963 5,255 7,248 6,766 6,048 10,063 9,486 5,266 7,854 4,549 Loan Disbursements (Annual)4Ordinary Capital3 3,336 2,626 4,255 3,696 4,958 6,085 7,947 6,683 6,037 5,522Fund for Special Operations 381 400 541 600 493 535 430 386 422 313Other Funds 15 14 23 20 17 15 10 – – 2

Total 3,732 3,040 4,819 4,316 5,468 6,635 8,387 7,069 6,459 5,837Loan Repayments (Annual)4Ordinary Capital 1,788 2,099 2,852 2,287 2,244 1,946 1,988 2,312 1,926 4,106Fund for Special Operations 270 301 288 289 285 283 289 289 268 256Other Funds 43 35 38 36 40 29 29 15 14 13

Total 2,101 2,435 3,178 2,612 2,569 2,258 2,306 2,616 2,208 4,375Loans OutstandingOrdinary Capital 22,179 24,478 26,581 26,028 27,301 32,635 38,552 41,872 44,951 47,958Fund for Special Operations 5,932 6,043 6,284 6,547 6,734 6,827 6,955 7,025 6,637 6,730Other Funds 337 303 271 241 209 189 164 146 133 118

Total 28,448 30,824 33,136 32,816 34,244 39,651 45,671 49,043 51,721 54,806 Nonreimbursable Technical

Cooperation Authorized (Annual)5Fund for Special Operations 87 77 90 87 88 64 47 36 39 36Other Funds 17 34 25 26 21 53 44 34 46 45

Total 104 111 115 113 109 117 91 70 85 81FINANCIAL HIGHLIGHTSIncomeLoansOrdinary Capital 1,864 1,916 1,977 2,012 2,044 2,085 2,582 3,061 3,191 2,639Fund for Special Operations 126 138 131 135 135 135 133 137 135 116

InvestmentsOrdinary Capital 482 337 654 431 455 520 576 765 541 319Fund for Special Operations 54 37 49 31 27 27 23 43 41 23

Net IncomeOrdinary Capital9 395 369 521 364 415 393 568 846 1,009 728Fund for Special Operations6 88 89 84 82 77 95 103 135 129 81

Reserves (End of Period)Ordinary Capital7 4,758 5,303 5,969 6,072 6,307 6,867 7,436 8,103 8,913 9,924Fund for Special Operations8 534 534 531 628 598 424 445 488 9 (64)

ADMINISTRATIONAdministrative ExpensesTotal - All Funds 275 295 333 334 348 341 335 342 355 376

1 Medium- and long-term borrowings, before swaps, excludingSFAS 133 hedge basis adjustments and net premiums or dis-counts.2 Net of cancellations. Includes currency translation adjust-ments.3 Net of Private Sector participations.4 Based on original amounts in U.S. dollar equivalent.

5 Includes Small Project financing.6 Income before Technical Cooperation expense and HIPC debtrelief.7 Includes accumulated other comprehensive income.8 Includes accumulated translation adjustments.9 Net income before the effects of Financial AccountingStandard No. 133 effective in 2001.

Latin America and the Caribbean in 2002

LATIN AMERICA AND THE CARIBBEAN IN 2002 1

TABLE II. THE EXTERNAL ENVIRONMENT

(In percent)

2001 2002eOutput growthDeveloped countries 0.7 1.5Developing countries 2.9 2.8

Growth — World trade volume –0.5 2.9

Short-term interest ratesU.S. Dollar 3.6 1.8Euro 4.2 3.4

Commodity prices(% change)Petroleum –13.8 2.7Agricultural Products –9.1 8.5Minerals and Metals –9.5 –3.6

Developed country (G-7) manufactured goods –1.4 0.5

e = EstimatesSource: World Bank, Global Economic Prospects, 2003.

Economic performance in Latin America andthe Caribbean remained sluggish in 2002.Although the United States emerged from itsrecession, fear of risk dominated the interna-tional environment. The region continued tobe affected by the severe crisis in Argentina,which had repercussions on trade and finan-cial stability in neighboring countries and con-tributed to weakening capital inflows to theregion.

Latin America is now experiencing one ofits most critical periods in several decades.While some economies experienced modestgrowth, not a single country has escaped thedownturn, and at least five economies are inthe midst of an outright recession. Per capitaincome in Latin America is now less than itwas five years ago, consumption is stagnant,and investment has slid back to its lowestpoint in the past decade. After almost half a

decade of external financial constraints andlow domestic growth, any maneuvering roomto offset the effects of the cycle has all but dis-appeared in most countries.

Many factors are contributing to theuncertainty about the future of the region. Theinternational economic scenario continues tobe clouded by the fragile recovery of growth inthe United States. Argentina has not yetfound a way out of its protracted economiccrisis. In Brazil, fears of macroeconomic insta-bility have not fully dissipated, due to the fis-cal pressure exerted by the heavy debt burden.In several countries, economic uncertainty iscompounded by social unrest.

Nevertheless, in the midst of the currentproblems the region has shown its commit-ment to macroeconomic stability, internationaleconomic integration and democracy. Thesefoundations, absent from the scene two

decades ago, must now be strengthened inorder to foster sustained recovery throughoutthe region.

International Scenario

The international environment for LatinAmerican economies was highly adverse in2002, due to slow growth in developed coun-tries, deterioration in the terms of trade for theregion as a whole, greater aversion to risk onthe part of international investors, and thereverberations from the severe crisis inArgentina.

Thanks to interest rate reductions by theFederal Reserve and an expansionary fiscalpolicy, the recession in the United Statesproved less pronounced and more short-livedthan was initially feared after the events ofSeptember 11, 2001.The U.S. economy grew2.3 percent in 2002. However, growth in theEuropean Union was a mere 0.8 percent and inJapan was completely stagnant.The recovery inthe United States had a healthy effect on worldtrade, as the country’s imports rose 4.4 percent.As a result, world trade, which had fallenslightly in 2001, rose 2.9 percent in 2002.

2

Raw material and commodity pricesaround the world recovered somewhat, afterdeclining for several years. Agricultural prod-uct prices rose by over 8 percent on average,although metals and minerals fell by 3.6 per-cent while the price of petroleum rose 2.7 per-cent. Nevertheless, several major LatinAmerican commodities declined significantly:sugar dropped 26.5 percent, coffee 8.8 per-cent, bananas 7.4 percent, aluminum 6.5 per-cent and copper 0.2 percent. Hence, the termsof trade for the region as a whole were onceagain weakened. Various factors also weakenedtrade for some groups of countries. The crisisin Argentina had adverse effects on tradewithin the MERCOSUR countries, and alsoaffected the tourism industry in Uruguay andParaguay, as well as family remittances toBolivia and Paraguay. The tourism industry inCaribbean countries remained depressed as aresult of the events of September 11.However, contrary to what had been feared,family remittances from the United States toMexico, Central America and other countriesdid not decline.

Despite the return of positive growthrates in the United States, the risk-averse cli-mate in 2002 deterred capital inflows to LatinAmerica and the Caribbean, especially afterthe second quarter of the year, due in largepart to domestic factors in the United States.The accounting fraud scandals sharpened theperception of risk in the capital market to pro-portions even greater than those noted in theweeks following September 11. The spread onU.S. high-yield corporate bonds jumped from650 basis points (above the yield on U.S.Treasury bonds) at the end of April to over1,000 basis points in October, when it peaked(a year earlier, just after the terrorist attacks, ithad reached 950 basis points). This increase inperceived risk was reflected in investments inemerging markets, compounded in certaincases by domestic or regional situations. Thiswas the case in Brazil, affected by the uncer-tainty surrounding the presidential election,and by the crisis in neighboring Argentina: thecost of international debt issues rose from 700

75

85

95

105

115

125

135

COMPONENTS OF DEMAND(Index: 1998.II = 100)

Note: Includes Argentina, Brazil, Chile, Colombia, Peru andVenezuela.

Consumption Exports Investment

1998

.II

1998

.III

1998

.IV

1999

.I

1999

.II

1999

.III

1999

.IV

2000

.I

2000

.II

2000

.III

2000

.IV

2001

.I

2001

.II

2001

.III

2001

.IV

2002

.I

2002

.II

basis points in the first quarter of 2002 to over2,000 basis points in October before beginningto decline. There were also sharp increases inthe cost of securities in Uruguay, because of itsclose ties to Argentina. The cost of internation-al financial resources rose for other countriesas well, although to a lesser degree. InArgentina, the spreads remained above 4,000basis points after the country defaulted on itsdebt at the end of 2001.

The adverse international financial envi-ronment for Latin America has translated intoa substantial decrease in capital inflows. In theseven largest economies in Latin America (rep-resenting 90 percent of regional GDP), capitalinflows in mid-2002 plummeted to one-thirdof the amount recorded four years earlier. Forthe full year, total capital inflows to the regiontotaled an estimated $50 billion, well below theannual average of $74 billion posted from 1996to 1998. Discounting the emergency fundingdisbursed to alleviate crisis situations, inde-pendent capital inflows added up to less then$40 billion. Since 1999, foreign direct invest-ment has been the only source of net inflowsto the region. The figure for 2002 represents a

sharp decline, from over $60 billion in 2001and a peak of $72 billion in 1999. Foreigndirect investment concentrated in only twocountries, Mexico and Brazil, which are receiv-ing over 80 percent of such funds.

Capital other than foreign investment hasbeen fleeing the region since the Russian crisisin mid-1998, and the situation worsened dur-ing some months in 2002. The outflow offunds from the region has now exceeded thecapital flight that occurred from 1983 to 1989during the debt crisis (in amounts adjusted forinflation). In the past two years alone, theregion has foregone funds amounting toroughly 5 percent of its GDP.

The reduction in capital inflows hasspread to virtually all the countries in theregion that had gained access to the interna-tional financial markets in the second half ofthe 1990s. Mexico and some of the CentralAmerican countries have been the least affect-ed. In the final months of the year, Colombiaand Peru were able to return to the marketwith successful bond offerings at rates thatwere relatively moderate, given the generalconditions of the market. While various inter-

LATIN AMERICA AND THE CARIBBEAN IN 2002 3

0

20

40

60

80

100

120

CAPITAL FLOWS(In billions of U.S. dollars)

Note: Includes Argentina, Brazil, Chile, Colombia, Mexico, Peruand Venezuela. Data refer to the cumulative value for the last 12months.

1997

-I

1997

-III

1998

-I

1998

-III

1999

-I

1999

-III

2000

-I

2000

-III

2001

-I

2001

-III

2002

-I20

02-II

10

8

6

4

2

0

-2

-4

-6

GDP GROWTH IN LATIN AMERICA (In percent)

Note: Includes Argentina, Brazil, Chile, Colombia, Mexico, Peruand Venezuela.

Decline Recession Recovery Stagnation Recession

1997

.II

1997

.IV

1998

.II

1998

.IV

1999

.II

1999

.IV

2000

.II

2000

.IV

2001

.II

2001

.IV

2002

.II

national events have influenced the behavior ofinvestors, the bond market has shown greatability to distinguish between countries. Infact, there have never been such differences inthe debt margins of the various countries inthe region, from the extremely high level ofArgentina to the very low levels of Chile andMexico, with Brazil and Uruguay occupyingpositions in between.

In short, despite a measured recovery inthe United States and lower U.S. interest rates,external conditions for Latin America becamemore difficult in 2002, thereby aggravating atrend that began in 1998. The terms of tradehave been unfavorable since then, and on thewhole changed little in 2002. Aversion to riskon the part of international investors increaseddue to domestic factors in the United States,and when combined with the crisis inArgentina and political uncertainty in Brazil,caused a new reduction in net capital inflowsin the region.

Macroeconomic Results andAdjustment Policies

Economic growth in the region over the pastfew years has been closely associated with the

behavior of external capital inflows other thanforeign investment, which, as noted above, hasbeen very unstable. As a result of the Asian cri-sis in mid-1997 and the Russian debt moratori-um a year later, capital inflows to the regionbecame negative. A partial recovery of inflowsin mid-1999 coincided with a period of robustbut very short-lived growth, which ended ayear later. Since then growth rates in the regionhave been modest and in 2002 were negative.Overall GDP for the region is estimated tohave fallen by 0.5 percent, thereby cancelingout the modest 0.4 percent increase that hadbeen achieved in 2001. As ECLAC has report-ed, the region has now accrued half a decade oflost growth, inasmuch as per capita income hasfallen 0.3 percent per year since 1998.

The decrease in GDP in 2002 was due inparticular to the collapse of production inArgentina. Although in mid-2002 there weresome signs of a modest recovery in demandand certain sectors of production, the year wasexpected to close with a 12 percent drop in thecountry’s GDP. Haiti, Paraguay, Uruguay andVenezuela also saw declines in their GDP.Although Peru and Ecuador achieved thehighest growth rates in South America, thoserates were only around 4 percent. Growth

4

75

80

85

90

95

100

105

CREDIT TO THE PRIVATE SECTOR(Index: June 1998 = 100)

Note: Loans in constant value, three-month moving average.Includes Argentina, Brazil, Chile, Colombia, Mexico, Peru andVenezuela.

Jan

1998

July

199

8

Jan

1999

July

199

9

Jan

2000

July

200

0

Jan

2001

July

200

1

Jan

2002

July

200

2

PUBLIC SECTOR BALANCE(Percent of GDP)

Source: International Monetary Fund, World Economic Outlook.Note: Includes 33 Latin American and Caribbean countries.

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

0.0

-0.5

-1.0

-1.5

-2.0

-2.5

-3.0

-3.5

-4.0

-4.5

rates in Bolivia, Chile and Colombia, althoughpositive, were even more modest. Spurred bythe United States, Mexico emerged fromrecession, but grew less than 2 percent. Thegrowth rate of the Central American countriesas a whole was slightly higher than 2 percent,while Caribbean economies, despite problemsin tourism, grew by an estimated 3.6 percent.Given that virtually no country experiencedhigh growth, it can be said for the first time inover a decade that the region was in a situationof widespread stagnation.

Investment has been the component ofaggregate demand that has been most sensitiveto the fluctuations in capital inflows and thedownturn in productive activity. In 2002 itdropped again, to at least 20 percent below itspeak in 1997, representing the lowest point inthe past ten years. Mexico is the only one ofthe larger countries in the region to escapethese tendencies. Over the past four years,investment is estimated to have fallen 60 per-cent in Argentina, 15 percent in Chile, and 10percent in Brazil. Consumption has beenmuch more stable, but without any upwardtrend, entailing gradual erosion of per capitaconsumption over the past few years for theregion as a whole. There was a sudden drop in

consumption in Argentina. Decreases were alsonoted in the other countries in recession.

Exports have been the only component ofaggregate demand consistently contributing togrowth in the region in recent years. Thistrend was reversed in 2002, as the region’sexports as a whole fell 3 percent. Exportsfrom the MERCOSUR countries fell 4 per-cent, particularly due to the crisis in Argentina,whose imports from neighboring countries fellto a third of their 2001 level. Uruguay is esti-mated to have suffered a two percentage pointdrop in its growth rate for this reason.Exports from the Andean countries as a groupare estimated to have fallen by 4 percent.Mexico and the Central American countrieswere helped by the recovery in the UnitedStates, but likewise did not make great gains inexport growth. The lack of growth in exportsis one of the most worrisome features of theregion’s current situation, especially in view ofthe fact that several countries received thestimulus of significant exchange rate devalua-tions, described below.

Given the protracted deterioration of theinternational economic environment for LatinAmerica, governments have had less and lesslatitude for domestic policy measures. Fiscal

LATIN AMERICA AND THE CARIBBEAN IN 2002 5

60

50

40

1990

30

20

10

0

1997 1999 2000/e 2001/e

POVERTY(Percent of the population)

Source: ECLAC.

1995

1996

1997

1998

1999

2000

2001

2002

UNEMPLOYMENT(In percent)

Source: ECLAC.

9.5

9.0

8.5

8.0

7.5

7.0

Indigent Non-indigent poor

25.8

24.5 25.324.3 24.4

22.519 18.5 17.8 18.6

deficits increased, especially between 1997 and1999, leading to major increases in public sec-tor debt ratios. For example, in six of thelargest economies of Latin America, the aver-age fiscal deficit rose from 0.9 percent of GDPin the second quarter of 1997 to 3.7 percent inthe last quarter of 1999, and public debtincreased from 27 percent to 35 percent ofGDP. Since then, despite slow economicgrowth, governments have tightened fiscalpolicies in an effort to limit the fiscal deficit.However, two factors have worked againstthem. First, fiscal income suffered from thestagnation or recession, and was in someinstances weakened by the very same austeritymeasures. Argentina and Uruguay have bothexperienced this problem. Second, the cost ofpublic debt increased, due to both the increasein domestic interest rates and the devaluationof the local currencies. Brazil was particularlyhard hit by this problem, which was exacerbat-ed by the fact that the cost of a large part of itsdomestic debt is also directly or indirectlylinked to the exchange rate. Despite the imple-mentation of fiscal austerity measures, theaverage fiscal deficit in the region as a wholefell from 3.9 percent of GDP in 2001 to 3.1percent in 2002, still well above the levels ofaround 2 percent that were the norm until1997.

Because fiscal policy has not been suffi-cient to reduce the excess of spending overrevenue (or to compensate for the lessenedavailability of external savings since the 1998Russian crisis), the burden of adjustment hasfallen on the private sector. In the sevenlargest economies in the region, the averagecurrent account deficit (external savings) fellfrom 5 percent of GDP in 1998 to less than 1percent four years later. However, the averagefiscal deficit in these economies fell onlyaround 1 percent on average. Thus, the adjust-ment was made through a reduction in net pri-vate sector spending of around 3 percent ofGDP, which occurred essentially through asharp drop in investment. Within this average,however, the modalities of adjustment havediffered sharply from country to country.

Brazil and Venezuela have sharply reducedtheir fiscal deficits, making room for the pri-vate sector (which in Venezuela has translatedinto capital outflow and a massive surplus inthe current account, given the depression ofprivate investment for reasons other than theavailability of external savings). In Argentinaand Colombia, attempts at fiscal adjustmenthave ultimately not succeeded in reducing thefiscal deficit, and so sharp reductions in theavailability of external savings have been com-pletely absorbed by cutbacks in private sectorspending. In Chile and Peru, initially morefavorable fiscal positions have allowed forrelaxation of the fiscal deficit, thereby moder-ating the social cost of the adjustment.However, the private sectors in these countrieshave experienced significant changes in theirinvestment and financing patterns in order toadjust to the change in external conditions.

Exchange rates have been a central vari-able in recent adjustment processes in a num-ber of economies in the region. Faced withreduced external financing, a number of coun-tries have loosened the exchange rate as a toolfor strengthening the current account positionabroad. Argentina and Venezuela in particularhave allowed a (managed) float of their curren-cies. In Argentina, the convertibility that hadbeen in place for almost ten years wasdropped, and in Venezuela, the system of con-trolled devaluation was abandoned. Brazil,Colombia and Uruguay also devalued theircurrency by over 20 percent over the past 12months. Increasingly since mid-1998, whenrestrictions on foreign financing began, realexchange rates have risen on average byaround 70 percent in the seven largest coun-tries in the region. In Argentina and Brazil,rates had risen by the end of 2002 by over 150percent; in Chile and Colombia by close to 50percent, and in Venezuela and Peru by around25 percent. Mexico is the only one of the largeeconomies whose currency has appreciated inreal terms since 1998.

The devaluations have been a necessarystep, although in many cases not a trouble-freeone. While devaluing the currency is a com-

6

mon response to externally-generated disrup-tions, such as those experienced by most coun-tries in the region in recent years, it can alsohave a painful impact when the government,the financial sector or private firms have majormismatches between their assets and liabilitiesin foreign exchange. Several countries initiallysought to avoid adjustments in the exchangerate, only to be forced to yield to persistent,deepening external turbulence. In some cases,the devaluations have had devastating effectson the financial sector and the sustainability ofthe fiscal situation. The countries that havebeen best able to address these problems, suchas Chile, are the ones that are more open tointernational trade, with lower ratios of publicsector debt and smaller foreign exchange mis-matches in the balances of the public sector,the financial sector and private firms.

The desire to retain international reserveshas been among the reasons for looseningexchange rates. Contrary to what happened inperiods of external constraints in previousdecades, virtually all countries have avoidedsignificant reductions of their internationalreserves. With the exception of Paraguay,international reserves in South Americancountries at the end of 2002 in all instances aregreater than six months’ worth of imports, andnot substantially less than in 1998, when theconstraints on external financing began.

Given the limited latitude for fiscal policymeasures, several countries have turned moreactively to monetary policy to stimulatedomestic demand. This was the case in thefirst few months of 2002, when internationalfinancial conditions were less unfavorable andthe risks of losing international reserves wereconsequently lower. Several central banks inthe region substantially increased the basicmoney supply, at least until May, and somereduced their intervention rates. However,these trends were later reversed. For example,in Brazil, after a period of decline, the refer-ence rate rose to 24 percent by the end of2002, over eight points higher than the rate ofa year earlier. Although the rate also increasedin Mexico, the level remained far below where

it had stood until 2000. On the other hand,Colombia, Chile and Peru achieved more last-ing reductions in interest rates in comparisonwith the previous two years. These recent dif-ferences in behavior notwithstanding, wheninterest rates for 2002 are compared with thoseimmediately after the Russian crisis, it is clearthat recent levels are substantially lower inmost countries, with the notable exceptions ofArgentina and Uruguay.

Attempts to stimulate aggregate demandthrough monetary policy were limited by thecautious attitude on the part of the financialsector and investors in general. Domestic cred-it grew at very modest rates in most countries,in many cases at rates below the basic moneysupply. In the seven largest countries in theregion, bank credit for the private sector hasfallen by 20 percent in real terms since mid-1998. Rather than a situation of tight credit,which would be reflected in pressures for rais-ing bank lending rates, most countries are in astate of financial paralysis, in which demandfor credit has fallen and banks are hesitant tolend due to slow economic growth and theincreased risk associated with possible devalu-ations and other macroeconomic adjustmentpolicies.

For the first time since 1991, averageinflation in the region increased in 2002, from6 percent in 2001 to 8 percent. Although anumber of countries implemented expansion-ary monetary policies at some point in 2002,higher inflation was actually due to the sharpdevaluations in the exchange rates of a fewcountries, particularly Argentina andVenezuela, and to a lesser extent, Brazil andUruguay. By contrast, inflation declined con-siderably in Ecuador, and also in Colombia,Costa Rica and Nicaragua. Higher inflationrates are not yet a threat to macroeconomicstability in any country in the region.Nevertheless, rising inflation does reflect thelimitations of monetary policies, because fiscalproblems are so great that they limit themaneuvering room of monetary authorities.In a number of countries the level and struc-ture of government debt limits the room for

LATIN AMERICA AND THE CARIBBEAN IN 2002 7

raising interest rates and creates a preconditionfor inflation.

Social Situation

Due to the stagnation and recession in LatinAmerica, the labor market has weakened. Theaverage unemployment rate is estimated tohave risen to 9.1 percent in 2002, almost onepercentage point higher than in the past twoyears and the highest on record. Argentina,Colombia, the Dominican Republic, Panama,Uruguay and Venezuela had unemploymentrates of over 15 percent. In addition, there isevidence that real wages have deteriorated inArgentina, Brazil, Paraguay, Uruguay andVenezuela. In Chile and Colombia, real wagestended to increase despite unemployment, sus-tained by the effectiveness of the minimumwage. Real wages also rose in Bolivia, Mexico,Nicaragua and Peru.

The weakening of the labor market in thelast few years has had a worrisome effect ontrends in poverty. During the 1990s, thepoverty rate (defined as the number of personsliving on less than $2 daily income) had fallenfrom 48.3 percent to around 42 percent, andextreme poverty (less than $1 a day) haddeclined from 22.6 percent to 17.8 percent.Because of slow growth in the past two years,these trends have reversed. According toECLAC calculations, the poverty rate rose to43 percent in 2001, and extreme poverty roseto 18.6 percent. Thus, by 2001 the total num-ber of poor people had risen from 207 millionto 214 million (and those in extreme povertyfrom 88 million in 2000 to 93 million).Although estimates for 2002 are provisional,the poverty index is believed to have risen to44 percent and the figure for extreme povertymay have reached 20 percent. Argentina,Paraguay, Uruguay and Venezuela suffered anincrease in poverty, whereas rates may havefallen slightly in Peru and the DominicanRepublic. ECLAC projections for 2002 indi-cate a rise in poverty by around seven millionpeople, six million of whom are in dire need.

ECLAC has reconsidered the feasibility of

Latin America and the Caribbean meeting theobjective proposed in the United Nations’Millennium Development Goals of reducingextreme poverty by half between 1990 and2015. The progress achieved thus far by thevarious countries in the region is uneven, inas-much as some have already reached the goal,while others have receded from it. The situa-tion is best in Chile and Panama, which in2000 achieved the goal of lowering extremepoverty by half. Brazil, the DominicanRepublic and Uruguay have advanced partiallybut significantly toward the goal: 95 percent inthe first two countries and 82 percent in thethird. Costa Rica, El Salvador, Guatemala,Mexico and Nicaragua have advanced byabout 40 percent. Bolivia, Honduras and Perualso showed advances toward meeting the goal,although at their current pace, they would notbe able to reach it. A more critical picture canbe seen in Colombia, Ecuador, Paraguay andVenezuela, where levels of extreme poverty in2000 were higher than they were in 1990.

According to ECLAC calculations, ifextreme poverty is to be cut in half by 2015,total GDP would have to grow by 2.7 percenta year for 15 years: 5.7 percent for countrieswith the greatest poverty, 2.7 percent for coun-tries in the middle and 2.5 percent for coun-tries with the least poverty. With regard tocutting total poverty by half, a goal that is inprinciple more in tune with the region’s levelof development, some of poorest countries havepractically no chance of doing so, because theywould have to reach levels of growth consider-ably higher than their historic performance.

Prospects for 2003 and PolicyChallenges

The prospects for the region in 2003 areuncertain. In the international environment,perceived risk remains very high, particularlybecause of various fears about the U.S. econo-my. Although growth recovered in the thirdquarter of 2002, there are still doubts aboutvarious parts of the corporate sector, and thehigh current account deficit of the United

8

States with the rest of the world may be asource of instability for the world economy.The implications of a possible armed conflictadd to uncertainty, and in certain circles, thereis speculation about possible deflation, whichcould mire the U.S. economy in more perma-nent problems, similar to what Japan experi-enced in the 1990s.

There are also serious causes for concernin Latin America. The Argentine crisis remainsunresolved, despite signs of recovering produc-tion and a gradual renewal of financial confi-dence. The goal of reaching a full agreementwith the International Monetary Fund, whichis crucial for reestablishing relations with theinternational financial markets, has proven tobe particularly troublesome. Brazil alsoemerged as a focus of concern in 2002, due tothe increase in the spread on its public debt,increased domestic interest rates, and devalua-tion of the currency. However, these concernshave subsided, improving prospects for debtsustainability.

Against this difficult political and eco-nomic backdrop, the region has nonethelessreaffirmed its commitments to democracy andinternational integration. Democracy is theregion’s best asset in terms of responding to

the current crisis, together with participatoryand inclusive policies aimed at resolving notonly macroeconomic problems, but also thelarge-scale social challenges.

The new processes of international inte-gration are the region’s best opportunity forimproving its medium-range prospects forgrowth.The challenge facing Latin Americaand the Caribbean is to combine the varioussubregional integration initiatives with themore ambitious objective of achieving integra-tion with other groups of countries, especiallyfrom the developed world. The countries ofCentral America and the Caribbean haverecently revitalized their subregional integra-tion programs, and are now aiming at the U.S.market. Chile has opted for a strategy of bilat-eral agreements and signed a free trade agree-ment with the United States in late 2002. TheAndean countries and the members of MER-COSUR are exploring what their best optionsmay be. The experiences of the region and ofother regions of the world show that there is nosingle path for advancing toward internationalintegration. In any case, the region now has arange of possibilities that must be seized inorder to open up new possibilities for invest-ment, trade and international cooperation.

LATIN AMERICA AND THE CARIBBEAN IN 2002 9

Part I:The Bank in 2002

THE BANK IN 2002 11

Key Areas

Overview

For the ninth year in a row, the Inter-American Development Bank was the largestsource of multilateral financing for LatinAmerica and the Caribbean in 2002. Includedin the lending program were loans and guaran-tees to finance public and private sector invest-ment programs, an emergency operation, andsector loans supporting policy reformprograms.

The Bank’s operational program for theyear responded to the needs of the borrowingmember countries and reflected the use of agreater variety of instruments and productsthan ever before. These included innovationloans, multi-phase loans and sector facility

loans—three product lines that, taken together,make up the flexible lending instrumentsestablished by the Bank’s Board of Governorsin 2001.

Over the course of 2002, the IDB com-mitted $4.55 billion in 86 loan operations tofund projects totaling an estimated $7.6 bil-lion. Of these, seven loans and guarantees tothe private sector without government guaran-tees totaled $316.4 million. The Bank alsofinanced 336 technical cooperation projectstotaling $65.4 million. In addition, theMultilateral Investment Fund approved 67projects, most of them technical assistanceoperations, for a total of $98.6 million.

Distributed among the principal areas ofconcentration of activity as defined in theBank’s Institutional Strategy, social sectorprojects accounted for $2.13 billion, or 46.8percent of the year’s non-emergency loanapprovals; projects for modernization of thestate and reform totaled $667.2 million, or 14.7percent of new commitments; and projects toimprove the competitiveness of the region’seconomies reached $1.26 billion, or 27.6 per-cent of the portfolio. A single emergency loanof $500 million, not included in the distribu-tion above, was approved for Uruguay to shoreup social expenditures at a time of severe fiscalconstraint. When this operation is included asa social sector program, the total of the year’slending in that sphere rises to 57.6 percent of2002 approvals.

The Bank’s Board of Governors stipulatedin the Eighth General Replenishment ofResources in 1994 that lending for povertyreduction and social equity should reach 40percent in terms of volume of resources and 50percent in terms of the number of operationsin succeeding years. Investments in povertyreduction and social equity are cross-sectoraland include financings in the social sectors as

well as other sectors. In 2002, 69 percent ofthe total lending volume ($2.8 billion) and 58percent of the number of operations (42) wereclassified under these headings.

Sorted by country group, the Bankapproved $2.52 billion for Group I countries,whose 1997 per capita income was above$3,200 (Argentina, Bahamas, Barbados, Brazil,Chile, Mexico, Trinidad and Tobago, Uruguayand Venezuela) and $2.01 billion for Group IIcountries, with incomes below $3,200 per capi-ta (Belize, Bolivia, Colombia, Costa Rica, theDominican Republic, Ecuador, El Salvador,Guatemala, Guyana, Haiti, Honduras, Jamaica,Nicaragua, Panama, Paraguay, Peru andSuriname).

As part of the Heavily Indebted PoorCountries (HIPC) Initiative, the Bank in 2002delivered debt relief to each of the four eligiblemember countries: Bolivia, $47 million;Guyana, $10 million; Honduras, $20 million;and Nicaragua, $46 million, for a total ofapproximately $123 million.

The Bank provided financing for policy-based reform programs in 2002 in Guatemala,Peru and Nicaragua, with funding of $500 mil-lion from the ordinary capital and $30 millionfrom the Fund for Special Operations. Thetotal of $530 million was well below the Bank’slending authority for policy-based lending. Itis expected that total approvals for this instru-ment will be higher in the coming year.

In the social sectors taken as a whole, theleading areas of concentration were socialinvestment (10 projects representing over 13percent of the total number of approvals and42 percent of all loan commitments) and theenvironment and natural disaster preventionand mitigation (11 projects totaling over $146million). Oportunidades in Mexico was a par-ticularly noteworthy social investment project.By targeting resources to indigent families andimplementing measures to continuously moni-tor key project components—incentives toencourage children to remain in school and forparents to make better use of health care andnutrition services—the operation will build onsuccess already achieved by the government of

Mexico in the social sectors, while looking forways to strengthen the replicability and evalu-ability of expenditures in these vital sectors.

In the area of the environment and natu-ral disasters, projects in Bolivia and Peru willminimize, control and compensate for thedirect and indirect social and environmentalimpacts of construction and operation ofmajor infrastructure investments. InBarbados, Ecuador, Guatemala, Honduras andPanama, the Bank helped underwrite programsfor the management and conservation of eco-logically fragile areas.

Seven urban development projects werefinanced during the year. One key effort wasto modernize local governments to make thembetter able to mobilize investment, more agileand transparent in the administration of publicfunds, and more attractive as future investmentdestinations. In terms of meeting more imme-diate needs, the Bank financed housing andsettlement projects in Ecuador, Nicaragua andTrinidad and Tobago.

Five projects were approved in the watersupply and sanitation sector, including one forthe city of Goiânia in Brazil that will con-tribute directly to achieving the MillenniumDevelopment Goal of halving by 2015 thenumber of people lacking access to safe drink-ing water or an adequate wastewater disposalsystem.

In education, the Bank supported threeprojects, including an $80 million loan toimprove the achievement of primary schoolstudents in rural and marginal urban areas inthe Dominican Republic. A $30 million loanto the Ministry of Education in Guyana willimprove literacy and numeracy at the primaryschool level while improving attendance ratesfor pupils and training for teachers. In health,the Bank approved another project for Guyanathat will improve nutrition for infants by usingthe flexible sector facility instrument.

A global microenterprise credit programfor the northeast of Brazil will add 120,000new clients to CrediAmigo, tripling the num-ber of participants in this program initiated bythe Banco do Nordeste do Brasil in 1997.

12

In the second major category of lending,modernization of the state, there was anemphasis on projects for reform and decentral-ization of public sector administration. In all,eight such projects were approved in 2002 fora total of $105 million. Examples included anoperation in Chile to modernize theComptroller’s Office and a program inColombia to decentralize government serviceadministration. In terms of lending volume,an even greater amount of resources wasdirected toward projects in the realm of fiscalpolicy and the management of fiscal institutions.The single largest operation in the moderniza-tion of the state category was for fiscal reformin Peru, to be disbursed in two tranches total-ing $300 million. The project focuses on rev-enue enhancement and improved budget man-agement; social expenditure policy (gearingprograms to serve the country’s poorest popu-lations); and curbing public pension costs.Stand-alone projects included programs tostrengthen national foreign trade departmentsin Bolivia, Nicaragua and Peru; a fiscal reformprogram in Guatemala that will institute keybenchmarks for measuring the efficacy andpace of legal reforms and new regulations; andan innovative project to modernize the admin-istration of justice in Honduras.

In the third and final area of major activi-ty for the year—competitiveness—projectsinclude the subsectors of energy and trans-portation (including loans to both public andprivate sector borrowers), telecommunications(one loan to a private sector borrower inBolivia), agriculture and rural development,science and technology, tourism, industry andcredit and capital markets. In addition, a proj-ect approved for Panama addresses “competi-tiveness development” in general by financingdiagnostic studies that include inputs fromcivil society organizations, the public sectorand businesses, as well as preinvestment activi-ties for projects in the productive sectors.There were six transportation projectsapproved for highways, ports and airports inBolivia, Brazil, Colombia, the DominicanRepublic, Honduras and Uruguay. Energy sec-

tor projects included electricity transmissionand distribution in Guatemala and Guyana,and partial financing by the Bank’s PrivateSector Department for the Transredes, S.A. gaspipeline project in Bolivia, a major initiative toexpand the country’s capacity to export gas toBrazil.

In 2002, the Bank provided $242 millionin support for multisector credit programs. Aloan of $42 million to El Salvador’s BancoMultisectorial de Inversiones (BMI) will channelresources to start-up businesses as well asexisting firms in manufacturing, trade andservices. A $180 million loan for the thirdphase of a program administered by theCentral Bank of Uruguay will make up part ofthe shortfall in the domestic market of bothshort- and long-term savings needed byUruguayan businesses to invest in the produc-tive sectors. A particularly innovative projectin local capital market development was theColpatria partial credit guarantee on a mort-gage-based bond issue by a Colombian finan-cial institution (see Box 1). The Colpatriaproject will address a serious impediment togrowth for the entire region: the lack of a deepand efficient financial intermediation systemthat can stimulate private savings to enablesmaller and medium-sized businesses, in par-ticular, to make the investments they need tocompete with their counterparts in other partsof the world.

Projects in the productive sectors of agri-culture and agribusiness totaled $156 million,roughly 4 percent of the total lending volumefor the year. Resources were provided forprograms in Costa Rica, the DominicanRepublic, Nicaragua and Panama. In additionto concentrating on efforts to integrate nation-al and international markets, increase produc-tivity and combat rural poverty, each projectcontained a component to make more effectiveuse of technology in the area of plant and ani-mal health and food safety. The Bank financedtourism projects in Bolivia and Brazil. A rela-tively small but significant flexible-instrumentcredit of $500,000 was provided for Jamaica touse information and communications technol-

THE BANK IN 2002 13

BOX 1

ogy to foster greater competitiveness by localbusinesses.

A credit to the Caribbean DevelopmentBank (CDB) will continue the IDB’s ongoingefforts, as outlined in the Bank’s Charter, toassist non-IDB member countries from theCaribbean. The IDB and the CDB haveenjoyed a close and constructive relationship.The current loan, building upon the achieve-ments of past credits, will make concessionalresources available to qualifying countries(Dominica, Grenada, St. Lucia and St.Vincent) at a time when these countries havebeen forced to undertake broad and deep eco-nomic reconstruction programs in the after-math of September 11.

The Bank’s private sector operations in2002 amounted to $316.4 million. Six of theseven operations approved were for projects inthe region’s relatively poorer and smaller coun-tries, including the first private sector loan toGuatemala. Despite an unfavorable interna-tional context, the Bank was able through useof direct loan resources and an additional$63 million in syndicated cofinancing throughB loans, to marshal a total of more than

$1.15 billion for infrastructure investment.This is the equivalent of roughly three dollarsfor each dollar of funding approved by theBoard of Executive Directors.

The IDB’s 336 national and regionaltechnical cooperation programs totaled$65.4 million. National technical cooperationaccounted for the lion’s share (278 operationsfor $49.1 million), but regional projects(58 operations for $16.3 million) were also sig-nificant. The portfolio includes projects tocollect census data on the ethnic compositionof national populations so as to combat socialexclusion; promote corporate social responsi-bility; prevent the transmission of HIV/AIDS;improve educational opportunities for girls inprimary and secondary school; and reducechild labor.

The Bank’s Social EntrepreneurshipProgram continued to provide financing forsmall productive and commercial enterprisesand to support community-based projectsaimed at the poor and the excluded through-out Latin America and the Caribbean. In2002, 18 projects were approved totaling$8.1 million. They ranged from efforts to

14

In November 2002, the Bank backed the introduction

of a new securitization instrument into the Colombian

capital market by approving its first private sector

mortgage bond guarantee in support of the equiva-

lent of $50 million in mortgage bonds to be issued by

Banco Colpatria to local institutional investors.

The IDB partial credit guarantee will backstop

up to $5 million, or 10 percent of the total face value,

of the mortgage bond obligation, thereby leveraging

the Bank's participation tenfold.

The guarantee is designed to support

Colombia’s pioneering effort to establish the mort-

gage bond as a new instrument in the country’s cap-

ital markets, with Colpatria as the first issuer of such

a security, as permitted by new financial regulations

in 1999. This transaction may provide a demonstra-

tion effect for other private issuers as well as for

investors in Colombia, increasing the volume of secu-

ritization instruments locally and benefiting the

depth and diversity of the Colombian capital market.

The guarantee operation advances the IDB strategy

for Colombia of promoting private sector growth,

modernizing capital markets and developing housing

for less advantaged segments of the population.

Colombia’s once flourishing mortgage sector

suffered a setback in 1998 due to the unfavorable

macroeconomic climate and increasing interest

rates. The IDB support for a mortgage-backed bond

issue in national currency will improve Colpatria’s

capacity to provide residential mortgages, especially

for the low-income sector, and thus help resume

housing finance activity and raise the level of home

ownership in Colombia.

COLPATRIA: FIRST PRIVATE SECTOR MORTGAGE BOND GUARANTEE

develop sheep farms in Nicaragua to supportfor growers of sugar cane in the province ofTucumán in Argentina, honey producers inSan Bernardino, Guatemala and cashew farm-ers in El Salvador.

In October 2002, the Bank and theGovernment of Italy established the ItalianTrust Fund for Microenterprise Developmentwith an initial endowment of 5 million eurosto promote microcredit and social entrepre-neurship in the region.

The Multilateral Investment Fund(MIF), administered by the Bank, continuedas the major source of technical assistancegrants for microenterprise and small businessdevelopment, testing new approaches to devel-opment and reaching out to involve a broaderspectrum of populations. MIF approvals in2002 amounted to $98.6 million. Since itsinception in 1993, the MIF has providedalmost $800 million to finance more than 500projects to strengthen workforce capabilities,skills and standards, broaden the economicparticipation of smaller enterprises, and bolsterthe overall environment for entrepreneurialactivities in the region.

The Inter-American InvestmentCorporation (IIC) approved 20 projectstotaling $123.3 million in 2002. Anautonomous affiliate of the Bank, the IIC pro-motes the establishment, expansion and mod-ernization of the region’s small and medium-sized enterprises.

In terms of financial performance, theBank showed continued profitability duringthe year, with strong financial ratios. Amid aturbulent and uncertain climate, the Bankdelivered its borrowing program for 2002 andagain received a AAA credit rating from themajor credit-rating agencies, as it has everyyear since the founding of the institution.The Bank’s bond issues for the year totaled aface amount of $9.1 billion equivalent, with anaverage maturity of six years (two years longerthan the comparable figure for 2001) and aver-age adjustable-rate cost of 22 basis pointsbelow U.S. dollar LIBOR (five basis pointsbelow the previous year).

As described in greater detail in ensuingsections, the Bank’s Board of Governorsadopted on the occasion of the Bank’s AnnualMeeting in March a resolution implementingan Agreement of Measures for Enhancing theResponse Capacity of the Bank, thereby creat-ing a new lending framework for 2002-2004.The framework consists of three permanentlending categories: investment loans, policy-based loans (PBL) and emergency loans. Inaddition, the Governors established severalparameters for the lending program including:a) a numerical cap of $4.5 billion (an averageof $1.5 billion per annum) on policy-basedloans for 2002-2004 and subsequent three-yearperiods; b) minimum disbursement periods of36 months for investment loans and 18 monthsfor policy-based loans; c) an increase in themaximum percentage of IDB financing forinvestment loans of 10 percent for all countrygroups; and d) creation of a permanent win-dow for emergency loans with amounts anddisbursement profiles of operations to be con-sidered in any given year subject to maintain-ing the financial soundness of the Bank andwith floors to ensure availability of theseemergency resources for the smaller and lesserdeveloped countries.

Efforts to implement the Bank’sInstitutional Strategy continued on severalfronts, including:

Adoption of the MillenniumDevelopment Goals, within the context of theparticular circumstances and priorities of IDBmember countries;

Presentation by the Board ofExecutive Directors to the Board of Governorsof a Progress Report on the New LendingInstruments;

Completion of a risk-assessment studyfor private sector operations; and

Preparation of a work plan for a reviewof the entire set of the Bank’s operational poli-cies.

The backdrop for the definition of thenew lending framework and the follow-up onrecommendations contained in the InstitutionalStrategy—in fact for virtually all areas of Bank

THE BANK IN 2002 15

activity during 2002—was the focus ondevelopment effectiveness. Together with theGovernors’ instructions to Management toadopt a series of measures to improve both thequality at entry and quality of the portfolio,the focus on this broad topic engendered avariety of concrete alternatives for improvingthe design, monitoring and evaluation of Bankinterventions.

In its second full year of operations fol-lowing a substantial overhaul, the Bank’sOffice of Evaluation and Oversight (OVE)produced a major report on the broad topic ofeffectiveness and issued a number of CountryProgram Evaluations (CPEs). The CPEs wereintended to serve as important inputs for theBank’s Country Strategy documents, them-selves a product reformulated according tonew guidelines adopted during the year. Forthe first time, performance-based criteria wereestablished for the allocation of the conces-sional resources of the Fund for SpecialOperations and Intermediate FinancingFacility.

As reported in the Annual Report onProjects in Execution prepared in 2002 basedon the portfolio as of the end of 2001, 91 per-cent of projects were classified as likely toachieve their development objectives asdefined in the Bank’s Portfolio PerformanceMonitoring and Reporting (PPMR) system.This compared with the figure of 88 percentestimated for the portfolio as of December 31,2000. The full deployment of a new ProjectAlert Identification System (PAIS) and thelaunching of a Lessons Learned RetrievalNetwork (LERN), both part of the ongoingredesign of the Project and OperationsInformation System (POIS), were evidence ofthe Bank’s efforts to improve accountabilitythroughout the project cycle and in all of theBank’s line departments.

The need to increase transparency in allaspects of Bank operations was felt keenly in2002. The Oversight Committee on Fraud andCorruption (OCFC) began its first full year ofoperations and instituted a toll-free hotline forthe anonymous reporting of allegations to a

permanent secretariat of the high-level bodychaired by the Executive Vice President. Inaddition, Management initiated a series ofactions aimed at making available to the publica greatly expanded amount of informationabout the Bank and its activities, includingprocurement, projects in implementation, and,in particular, areas of finance and institutionalprocedures and structure. A draft of a broadrevision of the Bank’s seven year-old informa-tion disclosure policy was prepared and dis-tributed to the Board of Executive Directorsfor consideration early in the new year.

Mechanisms to enhance consultation withcivil society groups and other stakeholdersinvolved in Bank operations continued to bedeveloped and used throughout the year. AStrategy for Promoting Citizen Participationin Bank Activities was prepared and sent to theBoard for consideration. Numerous consulta-tions were held by Civil Society AdvisoryCouncils (CASC) in the IDB Country Offices,many of them focused on discussions of theBank’s draft strategies on poverty, sustainablegrowth, social sector reform, competitiveness,integration and modernization of the state. TheBank’s Office of Learning concluded a two-year program of 20 workshops on IncorporatingCivil Society Participation in IDB Activities.Throughout the year, the Bank continued itsdialogue with the Inter-American RegionalOrganization of Workers (ORIT).

Board of Governors

The highest authority of the Bank is vested inthe Board of Governors, composed of oneGovernor and an Alternate Governor appoint-ed by each member country. Governors areusually Ministers of Finance, Presidents ofCentral Banks or officials in positions of com-parable rank in their respective governments.

The Forty-third Annual Meeting of theBoard of Governors took place in Fortaleza,Brazil from March 11-13, 2002. On that occa-sion, the Board approved the financial state-ments of the ordinary capital, the Fund forSpecial Operations (FSO), and the

16

Intermediate Financing Facility (IFF) accountfor 2001. The Board also approved the trans-fer of $70,200,000 equivalent in convertiblecurrencies to the IFF account, drawn from theFSO.

During its deliberations, the Board ofGovernors considered a range of topics includ-ing matters related to the international finan-cial scenario, the impact of external agents onthe stability of the region’s economies, thefight against poverty, and the role of the pri-vate sector in the development of the region.

The Board approved a resolution to rein-force the Bank’s ability to offer new productsand improve some of its current instruments;to respond more efficiently and effectively tocrisis; and to pay special attention to specificaspects such as mitigating social impacts andreducing poverty. By passing this resolution,the Board approved a new financing frame-work consisting of three types of loans: invest-ment, support of policy reform, and emer-gency. The Board of Executive Directors wasinstructed to analyze the outcome of imple-menting this financing framework, and tosubmit a report to the Governors during the2005 Annual Meeting.

In addition, the Governors stressed theneed to combat corruption and money laun-dering in the region, reinforce judicial systems,and foster private sector development. TheBoard emphasized the need to increase privatesector operations for the smaller countries inthe region, and to draft and implement a planof action to tend to the needs of the smallerand less developed countries. The Governorsrequested that the Bank assist in draftingnational strategies and planning for increasingcompetitiveness, take an active role in formu-lating strategies to reduce poverty, and providesupport to improve efficiency and transparen-cy in public expenditures. Lastly, the Boardrecommended improving supervision andevaluation systems in order to assess the effec-tiveness of Bank operations.

In addition to the Fortaleza meeting, theCommittee of the Board of Governors alsomet in Washington, on January 17-18. During

this meeting, the Committee worked on theproposals submitted by Management toincrease the Bank’s ability to respond to thenew requirements of the borrowing countriesand to engage in financing in foreignexchange. At its second meeting, theCommittee examined the report submitted tothe President entitled “The Challenge of BeingRelevant: The Future Role of the IDB,” pre-pared by the External Advisory Group, andanalyzed the topic of effectiveness in develop-ment.

As for effectiveness in development, theCommittee acknowledged the inherent diffi-culty in questions of measurement, particularlyin social sector projects, and suggested thatefforts be made to develop an assessment sys-tem that would take into account the specificsituation in each country. The Committeeunderscored the importance of reinforcing thesense of project ownership in each country inorder to strengthen sustainability. In addition,it stressed that Millennium DevelopmentGoals should be considered during the processof approving operations. Lastly, the Committeeagreed to the creation of a unit that will reportto the Executive Vice President and be incharge of assessing the impact of developmentand the “evaluability” of all Bank operations.

On November 8, 2002, the Board held anextraordinary meeting to elect the President ofthe Bank. On that occasion, it approved a res-olution electing Mr. Enrique V. Iglesias for afive-year term, starting April 1, 2003.

Board of Executive Directors

The IDB has 14 Executive Directors whorepresent the Bank’s 46 member countries.Directors serve full-time for a period of threeyears. In the absence of a Director, the Bank’sAlternate Executive Directors, appointed bytheir respective Directors, have full authorityto represent their constituencies.

During 2002, the Board of ExecutiveDirectors approved loan and technical cooper-ation operations as detailed below in the sec-tion on the year’s lending. The principal corpo-

THE BANK IN 2002 17

rate issues resolved by the Board are describedin the following section detailing the activitiesof Board Committees.

During early 2002, the Board, in an AdHoc Committee created for this purpose, heldintensive discussions on means for increasingthe Bank’s capacity to respond to evolvingregional needs.

Permanent Committees of the Board of Executive Directors

Steering Committee

The Steering Committee of the Board coordi-nates the work of the Board StandingCommittees and deals with administrativeissues related to Board management. TheCommittee is made up of the Chairs of thefour Standing Committees, Dean and ViceDean. In 2002, the Board approved expandingits membership to include the Director repre-senting the Bank’s largest shareholder, theUnited States.

Throughout 2002, the SteeringCommittee worked closely with the Office ofthe Executive Vice President to coordinate themanagement of the Board’s work program. Toshape the development of the 2003 work pro-gram, the Committee coordinated a series ofmeetings to review Management’s proposalsand allow Directors to set priorities for thecoming year. To that same end, the Committeehelped set the agenda for a Board retreat inNovember that focused on equipping theBank with the instruments needed to respondefficiently to the challenges facing its borrow-ing members. In addition, the Committee con-sidered issues concerning management of theBoard budget and the travel program of Boardvisits to borrowing countries.

Organization, Human Resources and Board Matters Committee

This Committee deals with Bank organization-al issues such as adjustments to the structureof the institution, human resources topics

including those related to the new humanresources strategy, and matters related toBoard functioning and efficiency.

During the course of the year, theCommittee reviewed Management’s progressin implementing the human resources strategyas well as Management’s progress in using thecontingency reserve for mutually agreed sepa-rations.

In the area of personnel policy, theCommittee recommended approval of a newsecondment policy for the Bank.