Western Sydney & Aerotropolis Investment Seminar - Austrade

19

NSW ECONOMIC UPDATE Western Sydney & Aerotropolis Investment Seminar September 2019 | Michael Bradley, Corporate & Institutional Banking

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Western Sydney & Aerotropolis Investment Seminar - Austrade

NSW ECONOMIC UPDATEWestern Sydney & Aerotropolis Investment Seminar

September 2019 | Michael Bradley, Corporate & Institutional Banking

PRESENTATION OVERVIEW

Introduction to National Australia Bank (“NAB”)

NSW economy

NSW infrastructure

Australia Outlook

INTRODUCTION TO NAB

NAB GROUP snapshot

4

customers globally~10 MILLION

employees1~33,000

Established more than

150yearsago

One of Australia and New Zealand’s biggest banking groups and largest institutions, managing relationships with retail, corporate and institutional clients in its core franchise in Australia and internationally.

One of the world’s safest banking groups2, with a strong balance sheet contributing to a AA- credit rating.

GLOBAL FOOTPRINT

150 YEARSIN THE UK

United StatesWholesale banking,

institutional markets, business and treasury

activity

AsiaNetwork of offices in China, HK, Japan,

Singapore, India and Indonesia providing banking services and market products to

corporate and institutional customers

40+ YEARSIN THE USAND ASIA

Seven branches and two representative offices outside Australia & NZ

New ZealandRetail, private, wealth, business, corporate and

institutional and markets via Bank of New Zealand (BNZ)

AustraliaFull service bank across retail,

business, private, corporate and institutional banking, and wealth

A$5.7BNFY18 Group

Cash Earnings3

CORE BUSINESS SEGMENTSSplit across:

Corporate & Institutional Banking

Consumer Banking & Wealth

New Zealand Banking

Business & Private Banking

1. Represents full time equivalent employees as at 30 September 2018 for NAB Group.2. Most recently, NAB ranked 29th in Global Finance magazine’s World’s Safest Banks 2017. Ratings apply to the world’s largest 500 banks by asset size and are

based on the long-term foreign currency ratings issued by Fitch Ratings, Standard & Poor’s and Moody’s Investors Service. (Global Finance magazine, 2017)3. Including restructuring-related costs and customer-related remediation as at 30 September 2018 for NAB Group

United KingdomWholesale banking,

institutional markets, business and treasury

activity

6%

51%23%

20%

Acquisition FinanceInfrastructureEnergyCommodities

A LEADING AUSTRALIAN BANK global capability in specialised finance

~AUD18BN EXPOSURE IN AUSTRALIA, NORTH AMERICA & EUROPE

DIVERSIFICATION ACROSS KEY INDUSTRY SEGMENTS GLOBALLY

NAB PROVIDES SPECIALIST INSIGHT AND TRANSACTION EXPERTISE IN THE STRUCTURING, NEGOTIATION AND EXECUTION OF M&A AND EVENT DRIVEN FINANCING ACROSS A VARIETY OF SECTORS

65%

2%

28%

5%

AustraliaAsiaUKNorth America

Infrastructure Energy Resources and commodities

**Excluding those with resource risk

United StatesNew York based team with

connectivity across North America

Australia & NZAustralia’s no.1 infrastructure

financier* with an active presence in NZ (via BNZ)

AsiaExperience supporting

infrastructure investment in Asian centres

UK & EuropeLondon based team with reach across major European markets

World-class franchise Top 15 in infrastructure finance globally*

Lead Arranger on 58 global infrastructure transactions with combined value of A$5.6b in 2018*

$100b Australian infrastructure commitment, leveraging our global networks and capability

Global reach Global platform, with coverage presence in Australia and NZ (via BNZ) as

well as major financial centres – New York, London, Hong Kong and Singapore

Coverage of global financial sponsors, strategic investors and industrial groups

Supporting key clients expand into new markets and facilitating inbound capital and trade flows

* Source: Inframation5

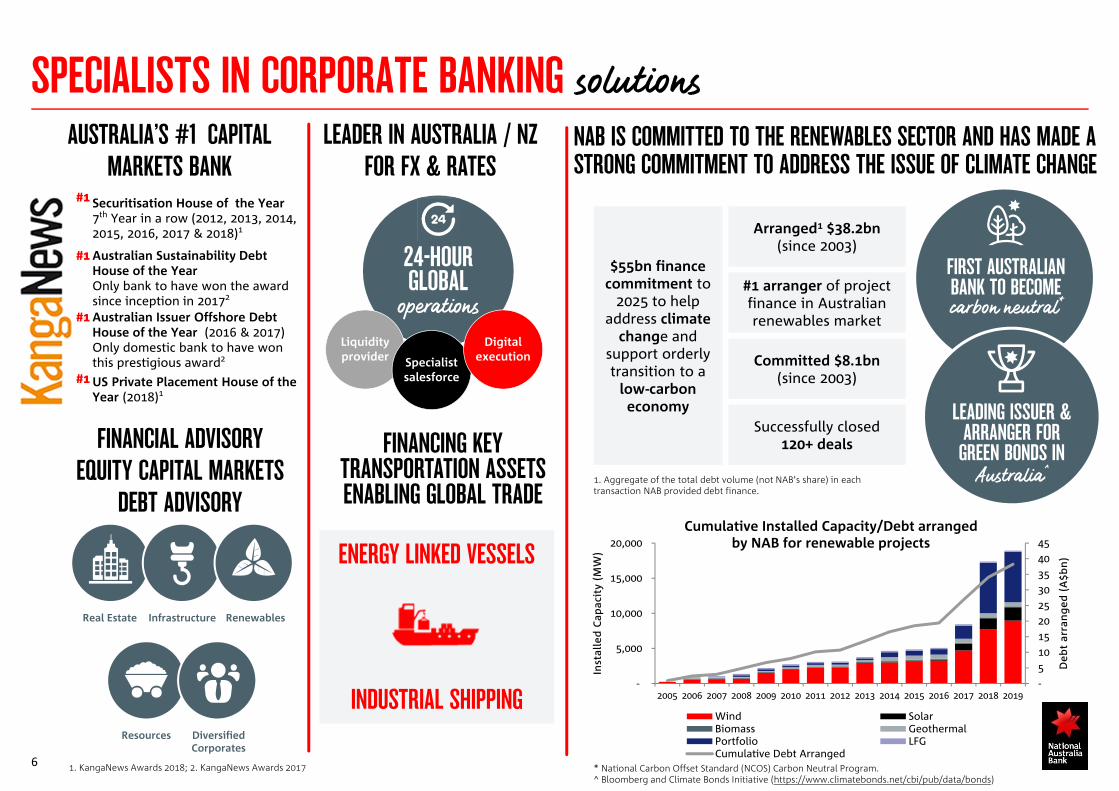

SPECIALISTS IN CORPORATE BANKING solutions

6

1. Aggregate of the total debt volume (not NAB’s share) in each transaction NAB provided debt finance.

Arranged1 $38.2bn(since 2003)

Committed $8.1bn(since 2003)

$55bn finance commitment to

2025 to help address climate

change and support orderly transition to a

low-carbon economy

#1 arranger of project finance in Australian renewables market

Successfully closed 120+ deals

carbon neutral*

FIRST AUSTRALIAN BANK TO BECOME

LEADING ISSUER & ARRANGER FOR GREEN BONDS IN

Australia^

- 5 10 15 20 25 30 35 40 45

-

5,000

10,000

15,000

20,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Deb

t ar

ran

ged

(A

$bn

)

Inst

alle

d C

apac

ity

(MW

)

Cumulative Installed Capacity/Debt arranged by NAB for renewable projects

Wind SolarBiomass GeothermalPortfolio LFGCumulative Debt Arranged

* National Carbon Offset Standard (NCOS) Carbon Neutral Program.^ Bloomberg and Climate Bonds Initiative (https://www.climatebonds.net/cbi/pub/data/bonds)

NAB IS COMMITTED TO THE RENEWABLES SECTOR AND HAS MADE A STRONG COMMITMENT TO ADDRESS THE ISSUE OF CLIMATE CHANGE

24-HOUR GLOBAL

operationsLiquidity provider Specialist

salesforce

Digital execution

LEADER IN AUSTRALIA / NZ FOR FX & RATES

FINANCING KEY TRANSPORTATION ASSETSENABLING GLOBAL TRADE

ENERGY LINKED VESSELS

INDUSTRIAL SHIPPING

AUSTRALIA’S #1 CAPITAL MARKETS BANK

#1 Securitisation House of the Year 7th Year in a row (2012, 2013, 2014, 2015, 2016, 2017 & 2018)1

#1 Australian Sustainability Debt House of the Year Only bank to have won the award since inception in 20172

#1 Australian Issuer Offshore Debt House of the Year (2016 & 2017)Only domestic bank to have won this prestigious award2

#1 US Private Placement House of the Year (2018)1

1. KangaNews Awards 2018; 2. KangaNews Awards 2017

FINANCIAL ADVISORYEQUITY CAPITAL MARKETS

DEBT ADVISORY

Real Estate Infrastructure Renewables

Diversified Corporates

Resources

NSW ECONOMIC REVIEW

AUTHORS:Gareth Spence, Senior Economist Tony Kelly, Senior Economist John Sharma, Economist Phin Ziebell, Economist

Photo Mai Thai

Falls in house prices accelerating up until March Qtr(more on this later)

Dwelling construction contracting sharply –apartments weakest

NAB and property industry professionals predict further declines

Business conditions have also fallen, possible stabilisation

Business conditions have eased from highs in 2017/2018

Retail and wholesale weakest

Consumption is being held back by low wage growth

SYDNEY HOUSE PRICES CONTRACTING STEEP DROP IN HOUSEBUILDING APPROVALSDec 2009 = 100

100

110

120

130

140

150

160

170

180

190

Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19

Dwellings

Houses

Units

0

5000

10000

15000

20000

25000

1987

1991

1995

1999

2003

2007

2011

2015

2019

ApprovalsCommencements

Number

FIRST, A LITTLE BIT OF NOT SO GOOD NEWS (MARCH QTR)

BUSINESS CONDITIONS DOWN FROM LAST YEAR BUT STABILISED IN MARCH NSW INDUSTRY – CONFIDENCE & CONDITIONS

Index –Mar Qtr’19

-20

-15

-10

-5

0

5

10

15

20

25

30

Ma

r-03

Ma

r-05

Ma

r-07

Ma

r-09

Ma

r-11

Ma

r-13

Ma

r-15

Ma

r-17

Ma

r-19

NSW

AUS

Index, trend

-30-25-20-15-10

-505

10152025 Conditions

Confidence

Sources: ABS; NSW Treasury, NAB Economics

UNEMPLOYMENT FAVOURABLE VS OTHER STATES VERY STRONG INFRASTRUCTURE PIPELINE

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Other

Water/sewerage

Energy

Transport infrastructure

$Bn

HOWEVER, SUPPORT FOR GROWTH (MARCH QTR)

LOW UNEMPLOYMENT PROVIDES SUPPORT OFFICE MARKET FUNDAMENTALS REMAIN SOUND$000’s, LHS %ge - RHS

4

5

6

7

8

9

10

11

120

50

100

150

200

250

300

350

400

2006 2008 2010 2012 2014 2016 2018

Office approvals Office vacancies (rhs)

2

3

4

5

6

7

8

9

10

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

NSW

Greater Sydney

Rest of NSW

%ge

Sources: ABS; NSW Treasury, NAB Economics, OECD

Downside cushioned somewhat by a strong labour market

Commercial property looking much better than Residential

Labour market remains robust

Commercial property market in a healthy state

NSW compares favourably

Unemployment lowest of major states

0

2

4

6

8

NSW Vic. Qld SA WA Tas. NT ACT

Feb-18

Feb-19

80

90

100

110

120

130

140

150

160

170

180

2012 2014 2016 2018

NSW

Qld

Vic.Tas.

WASA

NT

ACT

HOUSING STILL UP OVER LONG TERM

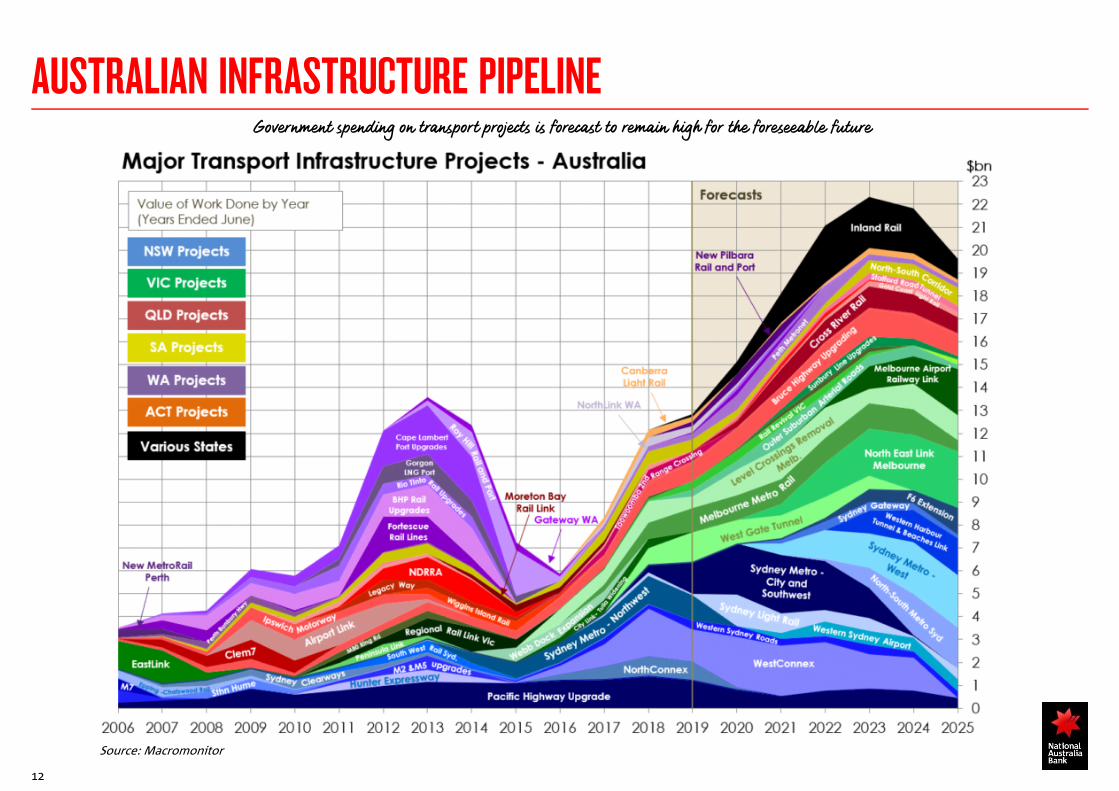

NSW INFRASTRUCTURE PIPELINE

11

KEY INFRASTRUCTURE THEMES

PRIVATISATION & ASSET

RECYCLING

TRANSPORT FOCUSED PIPELINE

URBANISATION &

POPULATION GROWTH

EXPANDING INVESTMENT APPETITES

Popu

lati

on

(m)

$’b

20 22 24 26 28 30 32 34 36 38

Low Medium High

Up to 36 m people by

2040

0

5

10

15

20

25

30

35

NSW VIC OtherStates

Sydney Desalination Plant, Macquarie Generation, Port of Newcastle, Land &

Property Information, Endeavour Energy, NSW Ports, Ausgrid, TransGrid,

Westconnex Port of

Melbourne, VIC Land Titles

SA & WA Land Titles

12

AUSTRALIAN INFRASTRUCTURE PIPELINEGovernment spending on transport projects is forecast to remain high for the foreseeable future

Source: Macromonitor

AUSTRALIA OUTLOOKSynopsis of market commentary from Kieran Davies, NAB Group Economics and Ray Attrill NAB Market Research

INTEREST RATES RBA

Uncertainty around consumer spending

Income in real terms stagnating

Real household wealth falling

Wage growth remains low and forward indicatorspoint to rising unemployment

However:

– Boost to incomes from lower interest rates and taxcuts... and

– House prices stabilising = lower drag on realwealth… but

– These take time to drive a recovery… and

– Global risks persist

Therefore, additional policy stimulus is expected

And, additional 25bp cut to the cash rate from the RBAby November, to 0.75%

Commonwealth focus on generating surplus remains arisk to the fiscal stimulus being forthcoming

Could lead to further rate cuts

Government has plenty of fire power

14

Source: NAB Group Economics, Australian Markets Weekly, 26 August 2019

Australia has significant capacity to use fiscal policy to support the economy

House prices have stabilised since June 2019

Note: Monthly prices were seasonally adjusted by NAB. The estimate for August 2019 is based on daily data for the month to date.

Source: Australian Bureau of Statistics, CoreLogic, National Australia Bank

Source: Australian Bureau of Statistics, Reinhart and Rogoff, Reserve Bank of Australia, various national statistical agencies, National Australia Bank

Significant fall in house prices

Stabilising period preceding growth

FOREIGN EXCHANGE AUD AUD volatility of late all about USD/CNY, though

commodity prices also weakening

RBA will need to do more than cut the Cash Rate to0.5% to further weaken AUD by its own hand

AUD/USD correlation to base metals index

AUD/KRW has sustained position well below 10 yearaverage level

NAB forecast is for this to continue on trend in band of800-825

15

AUD/USD vs. USD/CNY

AUD/USD vs. base metals

10yr average AUDKRW, LHS

Source: NAB Markets Research, Macrobond

Source: National Australia Bank, Macrobond

10yr AUD/KRW vs. USD/KRW

Source: NAB Markets Research, Bloomberg

AUDKRW, LHS

AUDUSD, RHS

FORECASTS FX and IR

16

Source: NAB Group Economics, Australian Markets Weekly, 26 August 2019

KEY CONTACTS

18

KOREA CONTACTS

• Based in Hong Kong, leads Corporate Coverage for NAB’s corporate relationships in Hong Kong and Korea• 14+ years’ banking and finance experience in Australia, Hong Kong, China and Korea• Broad range of experience across a wide range of corporate banking solutions including cross-border M&A, DCM, Markets, Trade

Finance, Cash Management

Michael Bradley, Head of Corporate Coverage, Hong Kong (includes Korea)E: [email protected] M: +852 6468 5540

IMPORTANT notice

19

Disclaimer: National Australia Bank Limited (ABN 12 004 044 937), its related bodies and any officer, employee, agent, adviser or contractor thereof (“NAB”) do not warrant or represent that the information, recommendations, opinions or conclusions contained in this document ("Information") is accurate, reliable, complete or current. The Information has been prepared for dissemination to professional investors for information purposes only and any statements as to past performance do not represent future performance. The Information does not purport to contain all matters relevant to any particular investment or financial instrument and all statements as to future matters are not guaranteed to be accurate. In all cases, anyone proposing to rely on or use the Information should independently verify and check the accuracy, completeness, reliability and suitability of the Information and should obtain independent and specific advice from appropriate professionals or experts. The Information is not intended as an offer or solicitation for the purchase or sale of any financial instrument.

This presentation is for discussion purposes only and may provide indicative terms and conditions which National Australia Bank may submit for credit approval to provide finance. The issue of these materials is not intended in any manner, and should not be interpreted as, representing or creating any offer of financing or the provision of any financial accommodation, or that financing will be available on these or any other terms. Any offer of finance is subject to satisfactory completion of National Australia Bank’s usual due diligence requirements and internal credit and pricing assessment processes. These materials are also provided subject to legal advice, financial modelling and all necessary financing documentation.

To the extent permissible by law, NAB shall not be liable for any errors, omissions, defects or misrepresentations in the Information or for any loss or damage suffered by persons who use or rely on such Information (including by reasons of negligence, negligent misstatement or otherwise). If any law prohibits the exclusion of such liability, NAB limits its liability to the re-supply of the Information, provided that such limitation is permitted by law and is fair and reasonable. NAB, its affiliates and employees may hold a position or act as a price maker in the financial instruments of any issuer discussed within this document or act as an underwriter, placement agent, adviser or lender to such issuer.

The Information is governed by, and is to be construed in accordance with, the laws in force in the State of Victoria, Australia, and any dispute or claim arising from, or in connection with, the Information is subject to the non-exclusive jurisdiction of the courts of that State.

Please be aware that any telephone calls to NAB may be recorded. If you would like more details regarding the privacy of your information at NAB, please visit the NAB website.

The Information contained within this presentation that has been prepared is confidential and must not be disclosed to third parties without NAB’s consent.

© 2019 National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.