WDP-98 - World Bank Documents

284

WDP-98 SECOND GLOBAL PROSPECTS CONFERENCE Background Papers 98 U231 World Bank Discussion Papers Problems of Developing Countries in the 1990s Volume II Country Studies F. Desmond McCarthy Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of WDP-98 - World Bank Documents

WDP-98SECOND GLOBAL PROSPECTS CONFERENCE

Background Papers

98 U231 World Bank Discussion Papers

Problems ofDeveloping Countriesin the 1990s

Volume IICountry Studies

F. Desmond McCarthy

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Recent World Bank Discussion Papers

No. 39 Livestock Production in North Africa and the Middle East: Problems and Perspectives. John C. Glenn [Also available inFrench (39F)]

No. 40 Nongovemmental Organizations and Local Development. Michael M. Cernea [Also available in Spanish (40S)]

No. 41 Patters of Development: 1950 to 1983. Moises Syrquin and Hollis Chenery

No. 42 Voluntary Debt-Reduaion Operations: Bolivia, Mexico, and Beyond... Ruben Lamdany

No. 43 Fertility in Sub-Saharan Africa: Analysis and Explanation. Susan Cochrane and S.M. Farid

No. 44 Adjustment Programs and Social Welfare. Elaine Zuckerman

No. 45 Primary School Teachers' Salaries in Sub-Saharan Africa. Manuel Zymelman and Joseph DeStefano

No. 46 Education and Its Relation to Economic Growth, Poverty, and Income Distribution: Past Evidence and Further Analysis.Jandhyala B.G. Tilak

No. 47 International Maaoeconomic Adjustment, 1987-1992. Robert E. King and Helena Tang

No. 48 Contract Plans and Public Enterprise Pe!formance. John Nellis [Also available in French (48F)]

No. 49 Improving Nutrition in India: Policies and Programs and Their Impact. K. Subbarao

No. 50 Lessons of Financial Liberalization in Asia: A Comparative Study. Yoon-Je Cho and Deena Khatkhate

No. 51 Vocational Education and Training: A Review of World Bank Investment. John Middleton and Terry Demsky

No 52 The Market-Based Menu Approach in Action: The 1988 Brazil Financing Package. Ruben Lamdany

No. 53 Pathways to Change: Improving the Quality of Education in Developing Countries. Adriaan Verspoor

No. 54 Education Managersfor Business and Govemment. Samuel Paul, Jacob Levitsky, andJohn C. Ickis

No. 55 Subsidies and Countervailing Measures: Critical Issuesfor the Uruguay Round. Bela Balassa, editor

No. 56 Managing Public Expenditure: An Evolving World Bank Perspective. Robert M. Lacey

No. 57 The Management of Common Property Natural Resources. Daniel W. Bromnley and Michael M. Cernea

No. 58 Making the Poor Creditworthy: A Case Study of the Integrated Rural Development Program in India. Robert Pulley

No. 59 Improving Family Planning, Health, and Nutrition Outreach in India: Experiencefrom Some World Bank-AssistedPrograms. Richard Heaver

No. 60 Fighting Malnutrition: Evaluation of Brazilian Food and Nutrition Programs. Philip Musgrove

No. 61 Staying in the Loop: International Alliancesfor Sharing Technology. Ashoka Mody

No. 62 Do Caribbean Exporters Pay Higher Freight Costs? AlexanderJ. Yeats

No. 63 Developing Economies in Transition. Volume I: General Topics. F. Desmond McCarthy, editor

No. 64 Developing Economies in Transition. Volume II: Country Studies. F. Desmond McCarthy, editor

No. 65 Developing Economies in Transition. Volume III: Country Studies. F. Desmond McCarthy, editor

No. 66 Illustrative Effects of Voluntary Debt and Debt Service Reduction Operations. Ruben Lamdany and John M.Underwood

No. 67 Deregulation of Shipping: What Is to Be Learnedfrom Chile. Esra.Bennathan with Luis Escobar and GeorgePanagakos

No. 68 Public Sector Pay and Employment Reform: A Review of World Bank Experience. Barbara Nunberg

(Continued on the inside back cover.)

SECOND GLOBAL PROSPECTS CONFERENCE

Background Papers

98 = World Bank Discussion Papers

Problems ofDeveloping Countnresin the 1990s

Volume IICountry Studies

F. Desmond McCarthy, editor

The World BankWashington, D.C.

Copyright C 1990The International Bank for Reconstructionand Development/THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing November 1990

Discussion Papers present results of country analysis or research that is circulated to encourage discussionand comnment within the development community. To present these results with the least possible delay, thetypescript of this paper has not been prepared in accordance with the procedures appropriate to fomialprinted texts, alnd the World Bank accepts no responsibility for errors.

The findings, interpretations, and conclusions expressed in this paper are entirely those of the author(s) andshould not be attributed in any manner to the World Bank, to its affiliated organizations, or to members ofits Board of Executive Directors or the countries they represenit. The World Bank does not guarantee theaccuracy of the data included in this publication and accepts no responsibility whatsoever for anyconsequence of their use. Any maps that accompany the text have been prepared solely for the convenienceof readers; the designations and presenltatioml of material in them do not imply the expression of any opinionwhatsoever on the part of the World BanLk, its affiliates, or its Board or member countries concerning thelegal status of any country, territory, city, or area or of the authorities thereof or concerning the delimitationof its boundaries or its national affiliation.

The material in this publication is copyrighted. Requests for permission to reproduce portions of it shouldbe sent to Director, Publications Departnment, at the address shown in the copyright notice above. TheWorld Bank encourages dissemination of its work and will normally give permission promptly and, when thereproduction is for noncommercial purposes, without asking a fee. Pemlission to photocopy portions forclassroom use is not required, though notification of such use having been made will be appreciated.

The complete backlist of publications from the World Bank is shown in the annual Index of Publications,which contains an alphabetical title list (with full ordering information) and indexes of subjects, authors, andcountries and regions. The latest edition is available free of charge from the Publications Sales Unlit,Department F, The World Bank, 1818 H Street, N.W., Washington, D.C. 20433, U.S.A., or fromPublications, The World Bank, 66, avenue d'1ena, 75116 Paris, France.

ISSN: 0259-210X

F. Desmond McCarthy is principal econonmist in the Internationial Economic Analysis and ProspectsDivision of the World Bank's International Economics Department.

Library of Congress Cataloging-in-Publication Data

Global Prospects Conference (2nd : 1990 : World Bank)Problems of developing countries in the 1990s / F. Desmond

McCarthy, editor.p. cm. -- (World Bank discussion papers ; 97-98)

At head of title: Second Global Prospects Conference, backgroundpapers.Conference held at the World Bank, Washington, D.C., Apr. 30-May

1, 1990.Contents: v. 1. General topics -- v. 2. Country studies.ISBN (invalid) 0-8213-1623-X (v. 1). -- ISBN 0-8213-1633-8 (v. 2)1. Economic forecasting--Developing countries--Congresses.

2. Developing countries--Economic conditions--Congresses.3. Economic forecasting--Europe, Eastern--Congresses. 4. Europe,Eastern--Economic conditions--1989- --Congresses. I. McCarthy, F.Desmond, 1936- . II. Title. III. Series.HC59.7.C57 1990330.9'009172'4--dc20 90-12855

CIP

- iii -

ACKNOWLEDGMENTS

The second Global Prospects Conference was held at the World Bank,Washington, D.C. on April 30-May 1, 1990. It was sponsored by the InternationalEconomics Department (IEC) and Development Economics (DEC). The stated purposeof the conference was to help strengthen the analysis and forecasting capabilityfor global sample of countries: (a) in their view what will be the leadingeconomic issues of the nineties at the country and global level; (b) how eachviews his own economy evolving; and (c) how they view the linkage to the globaleconomy.

There were nine country studies presented at the conference byrepresentatives from selected developing countries while two papers by Bankstaff were on the economic issues for the nineties and the global accountingframework: DEC analytical database. The conference closed with a round tablediscussion on methodology and developing country policy issues. Three othergeneral topics were discussed by representatives from academia: (a) foreignresource flows and developing country growth; (b) problems and prospects forEastern Europe in the 1990s; and (c) role of government.

Volume 1 contains an overview paper, two Bank staff papers, andgeneral topics.

Volume 2 contains an overview paper, nine country studies and notesfrom the Round Table discussion.

I would like to thank Ms. Milagros Divino and Ms. Allison Strongfor their contribution in the preparation of these two volumes.

- iv -

CONFERENCE PARTICIPANTS

Johannes Linn, Director, IECPaul Armington, Division Chief, IECAPCharles Blitzer, Principal Industrial Economist, LACF. Desmond McCarthy, Principal Economist, IECAP*Shahrokh Fardoust, Senior Economist, IECAP*Richard Eckaus, Chairman, MIT Department of Economics**Korkut Boratav, Professor, University of Ankara, Turkey*James Hanson, Lead Economist, IECDI**Stanley Fischer, Vice President and Chief Economist, DECVPLance Taylor, Professor, MIT*Sweder van Wijnbergen, Lead Economist, LA2CO**Michael Gavin, Professor, Columbia University*Sue Collins, Professor, Harvard University/CEA**Felipe Morande, ILADES/Georgetown University, Chile*Luca Barbone, Senior Economist, LAC**Miroslaw Gronicki, Professor, University of Pennsylvania*Timothy King, Division Chief, EDIST**Azizur Rahman Khan, Professor, University of California, Riverside, California*Nora Lustig, Brookings Institute*V. Fitzgerald, Professor, Institute of Social Studies, The Hague**Claudio Frischtak, Principal Industrial Economist, IENINJ. Dirck Stryker, Professor, Tufts University*Patrick Honohan, Senior Economist, CECFP**Kenneth K. Meyers, Consultant, World Bank*Charles Humphreys, Principal Economist, AFTTF**Helen Shapiro, Professor, Harvard University*Enzo Grilli, Chief Economist, EAS**V.N. Gnanathurai, EPU, Government of Malysia*Frank Lysy, Principal Economist, LA3C1Andrew Steer, Economic Adviser, DECVPManuel Montes, East-West Center, Hawaii*Rob Vos, Professor, Institute of Social Studies, The Hague**E. Mick Riordan, Consultant, IECAP*D.C. Rao, Director, FRS

* Presentor of paper** Lead discussant of paper

CONTENTS OF THE SERIES

VOLUME 1. GENERAL TOPICS

ACKNOWLEDGMENTS

CONFERENCE PARTICIPANTS

OVERVIEW OF THE CONFERENCEF. Desmond McCarthy

ECONOMIC ISSUES FOR THE NINETIESby F. Desmond McCarthy and Shahrokh Fardoust(Discussant: Richard Eckaus)

FOREIGN RESOURCE FLOWS AND DEVELOPINGCOUNTRY GROWTH: A THREE-GAP MODEL

by Lance Taylor(Discussant: Sweder van Wijnbergen)

PROBLEMS AND PROSPECTS FOR ECONOMICDEVELOPMENT IN EASTERN EUROPE IN THE 1990s

by Miroslaw Gronicki and Joshua Charap(Discussant: Timothy King)

RENT SEEKING OR RENT REDISTRIBUTION?AUTOMOBILE FIRMS AND THE BRAZILIAN STATE1956-68

by Helen Shapiro(Discussant: Enzo Grilli)

GLOBAL ACCOUNTING FRAMEWORK: DECANALYTICAL DATABASE

by E. Mick Riordan(Discussant: Rob Vos)

VOLUME 2. COUNTRY STUDIES

CHILE: RECENT PAST, PROSPECTS, AND CHALLENGESby Felipe Morande(Discussant: Luca Barbone)

JAMAICA: CAN THE RECOVERY BE SUSTAINED?by Michael Gavin(Discussant: Sue Collins)

THE MEXICAN ECONOMY IN THE EIGHTIES: ANOVERVIEW

by Nora Lustig(Discussant: V. Fitzgerald)

- vi-

ECONOMIC PERFORMANCE IN BANGLADESH DURINGTHE 1970s AND THE 1980s AND PROSPECTS FOR THEFUTURE

by Azizur Rahman Khan(Discussant: Richard Eckaus)

MALAYSIA: PATHWAYS TO STABLE GROWTH WITHEQUITY

by V.N. Gnanathurai(Discussant: Frank Lysy)

THE PHILIPPINE ECONOMY IN 1990: RECOVERY ANDRESTORATION

by Manuel Montes(Discussant: Rob Vos)

ADJUSTMENT IN WEST AFRICA: THE GUINEAEXPERIENCE

by J. Dirck Stryker(Discussant: Patrick Honohan)

EMERGING MAIAWIby Kenneth K. Meyers(Discussant: Charles Humphreys)

THE MEDIUM-TERM PROSPECTS FOR THE TURKISHECONOMY

by Korkut Boratav(Discussant: James Hanson)

ROUND TABLE DISCUSSIONChaired by: Paul Armington

- vii -

TABLE OF CONTENTS

Page No.

ACKNOWLEDGMENTS . . . . . . . . . . . . . . . . . . . . . . . . iii

CONFERENCE PARTICIPANTS ... . . . . . . . . . . . . . . . . . iv

OVERVIEW OF THE CONFERENCE ................F. Desmond McCarthy

CHILE: RECENT PAST, PROSPECTS, AND CHALLENGES . . . . . .7by Felipe MorandeDiscussant: Luca Barbone

JAMAICA: CAN THE RECOVERY BE SUSTAINED? . . . . . . . . . . . 37by Michael GavinDiscussant: Sue Collins

THE MEXICAN ECONOMY IN THE EIGHTIES: AN OVERVIEW . . . . . . . 71by Nora LustigDiscussant: V. Fitzgerald

ECONOMIC PERFORMANCE IN BANGLADESH DURING THE 1970s ANDTHE 1980s AND PROSPECTS FOR THE FUTURE . . . . . . . . . . . . 99

by Azizur Rahman KhanDiscussant: Richard Eckaus

MALAYSIA: PATHWAYS TO STABLE GROWTH WITH EQUITY . . . . . . . 121by V.N. GnanathuraiDiscussant: Frank Lysy

THE PHILIPPINE ECONOMY IN 1990: RECOVERY AND RESTORATION . . . 151

by Manuel MontesDiscussant: Rob Vos

ADJUSTMENT IN WEST AFRICA: THE GUINEA EXPERIENCE . . . . . . . 183by J. Dirck StrykerDiscussant: Patrick Honohan

EMERGING MALAWI .... . . . . . . . . . . . . . . . . . . . . 203by Kenneth K. MeyersDiscussant: Charles Humphreys

THE MEDIUM-TERM PROSPECTS FOR THE TURKISH ECONOMY . . . . . . . 229by Korkut BoratavDiscussant: James Hanson

ROUND TABLE DISCUSSION . . . . . . . . . . . . . . . . . . . . 257Chaired by: Paul Armington

OVERVIEW

OF THE SECOND GLOBAL PROSPECTS CONFERENCE

APRIL 30-MAY 1, 1990

PROBLEMS OF DEVELOPING COUNTRIES IN THE 1990s

F. Desmond McCarthy

- 3 -

SECOND GLOBAL PROSPECTS CONFERENCE

Problems for the Nineties

The decade of the nineties is expected to result in significantimprovement over what has now come to be known as the 'lost decade of theeighties. " The Second Global Prospects Conference sought to address the problemsfacing developing countries for the coming decade by inviting a number of expertsto present views on selected topics of general interest together with arepresentative sample of country studies. The broad objective was to identifyand discuss the problems of development to be faced by policy makers in thenineties with a bias towards the practical perspective.

There were five papers on general topics: economic issues for thenineties, role of government, foreign resource flows and developing countrygrowth, Eastern Europe and finally a paper updating work on the global accountingframework. There were nine country studies. The countries were chosen toreflect a number of criteria--offer a reasonable geographic distribution,successful and not so successful experiences, small and large countries, togetherwith some of the less fashionable countries. From Latin America, Mexico andChile were chosen; from the Caribbean, Jamaica; from South Asia, Bangladesh; fromSouth East Asia, Malaysia and the Philippines; from the Mediterranean region,Turkey, while East and West Africa were represented by Malawi and Guinearespectively. Each paper had an official discussant and the conference concludedwith a Round Table discussion on issues for the nineties.

General Topics

The opening paper provided a review of global economic developmentsin the eighties together with a broad tour d'horizon of economic issues for thenineties. The industrial countries enjoyed a strong performance largelyresulting from policy changes introduced at the beginning of the decade.Typically these involved restrictive monetary policy to contain inflationarypressures and a wide range of structural reforms to enhance supply conditionsand improve the functioning of markets. The performance among developingcountries varied greatly. Those that did well, largely in Asia, had investmentto GDP ratios above 22 percent and were able to achieve a policy mix that enabledthem to take advantage of opportunities in the global market. In the ninetiesthis broad pattern is expected to continue. The industrial countries areprojected to maintain robust growth but at a slightly lower level than in thelate eighties. Increased globalization of the world economy is expected astrade, financial and production linkages are intensified. Among developingcountries the more dynamic economies especially in Asia are expected to achievegrowth rates of around 6 percent while the prospects for many of the countriesin Latin America and especially in Africa are about half that level. When onefactors in population growth rates the new decade does not hold too much promisefor many of the poorer countries in Africa. The financing of development hasundergone major changes during the past decade. The most notable change hasbeen the precipitous decline of flows from commercial banks compared with the

- 4 -

levels earlier in the decade. This in turn has led to an increasing role forthe official lending agencies. In short this means that for the great majorityof developing countries resources for development will have to be increasinglygenerated domestically. This in turn implies the need for a credible governmentpolicy that can ensure the flow of adequate fiscal resources and at the same timeprovide the right milieu for private investors. Among events on theinternational scale are Europe '92 and structural changes in Eastern Europe.The former is expected to lead to a larger and freer market in Europe in a morecompetitive environment. There is also increasing discussion of reciprocitywhich may be a vehicle for some protectionist forces. This may lead to somedifficulties especially for the dynamic export-oriented economies of Asia.Developments in Eastern Europe are likely to lead to some resources beingchanneled in that direction. Over time it is expected that this region willattract significant direct investment flows and maybe some redirection of flowsto other LMICs. As these economies restructure it is expected that they willgenerate increased competition in the global economy but over time it is alsoexpected that increased effective demand will result. Perhaps an even moreinteresting fallout will be the lessons or new paradigms that may result fordevelopment from the rapid changes occurring in Eastern Europe.

A major theme that pervaded a number of the papers was what shouldbe the appropriate role of the state. The paper by Shapiro offered anilluminating case study of the automobile industry in Brazil in the period 1956-1968. The analysis indicated that in this instance the state was able to extractrents from the private sector and use them to shape investment behavior. Thusshe argues that, with stable policy and concomitant credibility, the state wasable to reduce the role of uncertainty and essentially eliminate the role ofdirectly unproductive rent seeking activities. This offers one possible approachto ensure that state intervention does not necessarily lead to an inefficientoutcome in either a static or dynamic sense.

The paper by Taylor focussed on the role of foreign resource flowsin the growth of developing countries. Based on a set of studies of 17developing countries he estimated that an additional inflow of about US$40billion would be needed to support an extra one percentage point in fastercapacity growth in the medium term. In order to restore historical growth ratesto Sub-Saharan Africa and Latin America much larger transfers would be needed.

Gronicki discussed the recent changes in Eastern Europe and thelikely economic evolution in the next few years. The demise of the centralplanning paradigm in those countries marks a watershed in economic policy making.The debate will continue on the appropriate role for the state and how to easethe transition towards more market-based economies. Many problems remain to beaddressed, from determining the ownership of property to putting some form ofsecurity net in place, to moderate the social costs and concomitant pressuresfrom the consequences of restructuring the economy. The problems faced by policymakers vary across these countries from the relatively well managedCzechoslovakia to the impoverished Romania.

In a somewhat more technical vein Riordan reviewed progress on theGlobal Accounting Framework. This is part of an ongoing effort at the World

-5

Bank to develop a unified data system for all major global economic accounts.The author indicated that country-specific data bases are now being added andhe provided examples of both cross-section and time-series views of selectedcountry databases. It is expected that this data base will be made availableto the public at large in a format that can be readily adopted to suit individualcountry groupings.

Country Studies

There were three Latin American studies which covered a wide rangeof experiences: Chile, Jamaica and Mexico. Chile has managed to generate astable economic milieu while Mexico, after rescheduling its external debt, isbeginning to resume growth. Jamaica had a number of stabilization plans in theearly eighties which failed to induce the needed reforms. Presently it seemsthat it will need some restructuring of its official debt.

The two African case studies were symptomatic of many of the problemsof that continent. Guinea has seemingly a whole plethora of problems ofunderdevelopment ranging from poor institutions through illiteracy tomalnutrition. In addition Malawi is faced by a major challenge from the AIDSepidemic.

The one country from the Mediterranean region, Turkey, presented aninteresting analysis of winners and losers under a structural reform program.It was argued that the traditional rentiers, the industrialists, were graduallyreplaced by financiers.

The three countries from Asia were Bangladesh, Malaysia and thePhilippines. Bangladesh continues to face major problems of poverty exacerbatedby a high population growth rate. The Philippines is torn by domestic politicalstrife. Perhaps one of the few good stories is Malaysia, where a pragmaticpolicy mix seems to be achieving remarkable results.

In short, many of the problems of the eighties are still with us aswe enter the nineties. In many countries these have become exacerbated.However, the debate has become less polemical and more practical. Perhaps thenineties will see a much more pragmatic approach to policy so that the majorproblems of development will begin to be redressed.

Economists studying the development process have always been readyto admit that economics is only part of the problem. Social, legal andinstitutional factors, together with the historical perspectives, were recognizedby many to be of major importance. However, it now seems that economists maynot be able to solve even the economic problems; in many instances a new paradigmis needed. Countries such as Malawi seem to have followed the "right"prescription but with little success while Malaysia seems to have achieved agreat deal of success with policies that traditionalists might eschew.

CHILE

RECENT PAST, PROSPECTS, AND CHALLENGES

Felipe Morande

With commentary by Luca Barbone

- 9 -

ACKNOWLEDGMENTS

The author wishes to thank Klaus Schmidt-Hebbel and Raimundo Soto forhelpful comments, and Eduardo Saavedra for comments and research assistance.

- 11 -

TABLE OF CONTENTS

Page No.

MACROECONOMIC VARIABLES IN THE LAST TWO DECADES . . . . . . . . . . . 13

ECONOMIC POLICIES IN RECENT YEARS . . . . . . . . . . . . . . . . . . 15

MAIN PROBLEMS AND RISKS FOR THE FUTURE . . . . . . . . . . . . . . . 18

POLITICS AND THE SOCIAL COSTS OF ADJUSTMENT . . . . . . . . . . . . . 21

CLOSING REMARKS . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

TABLES

1 National Accounts . . . . . . . . . . . . . . . . . . . . . . . . 242 Current Account Data . . . . . . . . . . . . . . . . . . . . . . . 253 Public Sector . . . . . . . . . . . . . . . . . . . . . . . . . . 264 Incentive Indicators Prices . . . . . . . . . . . . . . . . . . . . 27

CHARTS

1 Gross Domestic Product . . . . . . . . . . . . . . . . . . . . . . 282 Investment .... . . . . . . . . . . . . . . . . . . . . . . . . 283 Inflation .... . . . . . . . . . . . . . . . . . . . . . . . . 294 Real Copper Prices . . . . . . . . . . . . . . . . . . . . . . . . 305 Real Exchange Rate Index ... . . . . . . . . . . . . . . . . . . 306 Exports of Goods . . . . . . . . . . . . . . . . . . . . . . . . . 317 Imports of Goods . . . . . . . . . . . . . . . . . . . . . . . . . 318 Foreign Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

APPENDIX . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

COMMENTARY BY LUCA BARBONE ..................... 35

- 13 -

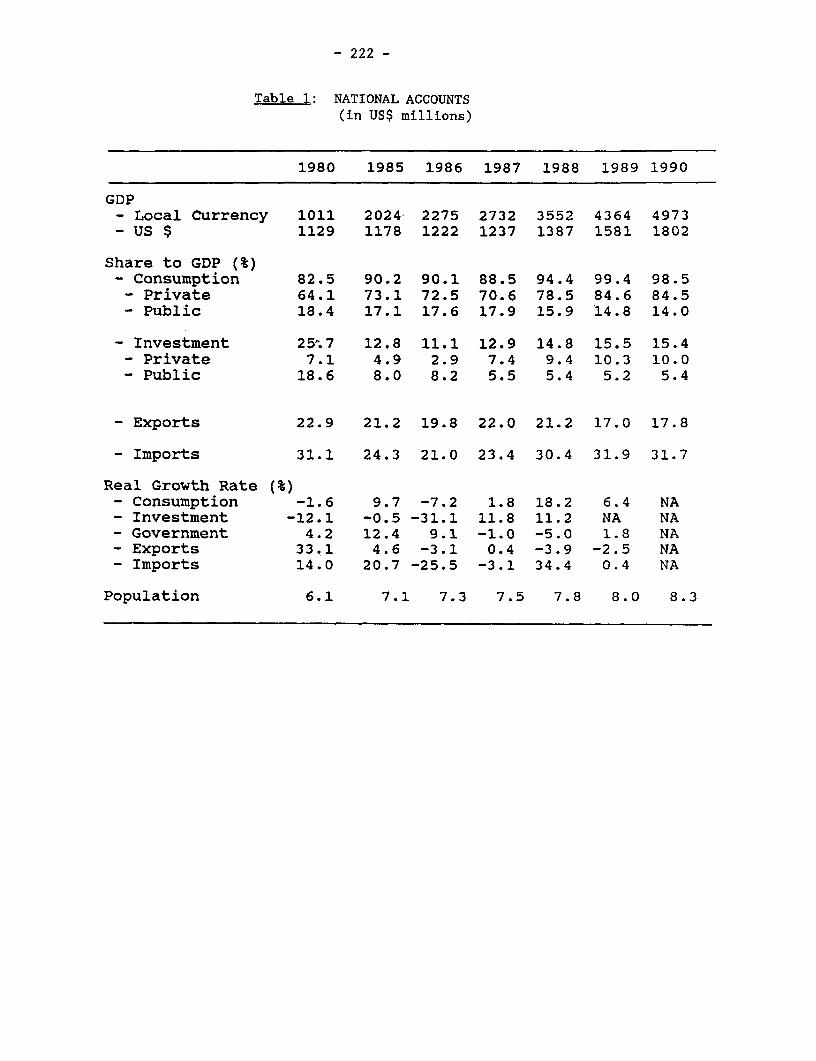

In recent years, the performance of the Chilean economy has beenpositive--a sharp contrast to the rest of Latin America. While the rest of theregion has been beset by severe recession and widespread inflation, Chile hasenjoyed significant growth for six years, while inflation has been kept undercontrol at rates close to or below 20 percent per year. In the meantime,progress in servicing foreign debt has helped widen access to foreign creditmarkets.

This economic improvement was achieved through structural reformscarried out in the last two decades. This paper discusses the strengths andshortcomings of these reforms.

The strong recent macroeconomic performance of the Chilean economy isno guarantee of sustained growth and stable prices in the 1990s. Severalproblems may hamper future progress, ranging from insufficient national savingsand investment to the recurrence of external shocks. The social cost of theadjustment undertaken since 1982-83 deserves a special mention. Chile's worstdepression since the 1930s left many people feeling that the gains from recoverywere unevenly distributed among the population. This discontent played a keyrole in the political reforms that began in 1988, culminating with free electionsat the end of 1989. Now, the greatest challenge facing the new government ishow to balance a popularly mandated income redistribution effort with the needfor sustained economic growth.

MACROECONOMIC VARIABLES IN THE LAST TWO DECADES

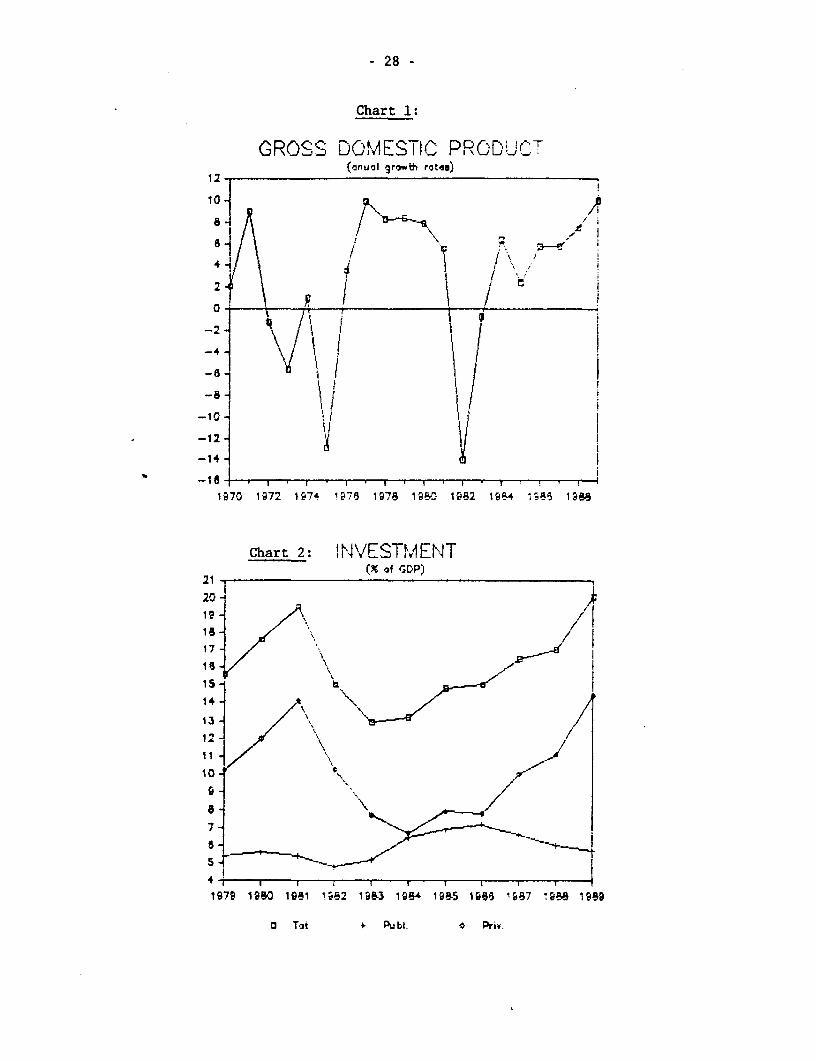

Sharp macroeconomic fluctuations have been the hallmark of the Chileaneconomy in the last two decades. After mediocre but sustained growth at ratesaround 4 percent per year from the late 1940s to the late 1960s, the 1970s inChile saw an early fiscal spending-led miniboom in 1971 followed by severeinflation and an economic crisis, with the public sector deficit growing to 25percent of gross domestic product (GDP) in 1973. Pursuant cuts in public sectorexpenditures, tax reforms, and a sharp decline in terms of trade in 1975 led toa severe recession: GDP plunged more than 12 percent in a single year. A strongrecovery followed in 1977, then evolved into a significant boom, with privatespending rising dramatically and incomes increasing moderately. The boom lastedfrom 1978 to 1981 and ended abruptly in 1982 when the Chilean economy experiencedits worst depression since the 1930s: GDP dropped by 14.1 percent in 1982 anda further 0.7 percent in 1983. The business cycle entered another expansionaryphase in 1984; this time it is lasting longer than ever before. It prevailedlast year, and growth of at least 4 percent is expected this year. From 1984to 1987, expansion was led by growth in exports, while from 1988 to the presentit has been spurred by improved terms of trade primarily in the price of copper.

Unemployment trends over the last two decades have followed closely thefortunes of economic activity, although some qualifications should be made.Indeed, it is clear that structural reforms carried out in the second half ofthe 1970s--ranging from trade reforms to a complete overhaul of the publicsector--had a significant effect on unemployment rates; they went up from

- 14 -

historical rates of between 4 and 5 percent to close to 23 percent during the1975-76 recession. Even when the economy experienced a boom in 1978-81, ratesnever fell below 11 percent (and were greater if emergency employment programswere included). Since the 1984 expansionary phase began, unemployment rates havedeclined steadily from a high of 25.2 percent in September 1982 (more than 30percent if emergency programs are included) to about 6 percent by the end of lastyear.

Inflation remains a persistent problem. It was exacerbated in theearly 1970s, and was close to 1,000 percent in 1973. Then it dropped graduallyfrom 375 percent in 1974 to 39 percent in 1979 as a result of a contractionaryfiscal policy that turned the prospects of a huge deficit in 1975 to surplusesafter 1976. In early 1978, when trade reform was close to completion and tariffson most imports were approaching a flat rate of 10 percent, economic authoritiesjudged that Chile's economy was "open." Following this diagnosis, an activeexchange rate policy was initiated with the aim of stabilizing prices. First,it involved predetermined, monthly minidevaluations, and, after June 1979, theexchange rate was pegged to the U.S. dollar. However, domestic inflation easedslowly and did not fall below two digits until 1981. When the fixed rate wasabandoned in June 1982 and a passive crawling peg system was adopted, inflationincreased rapidly to levels close to 20 percent per year. These levels havepersisted, except in 1988, when they fell to 12.7 percent.

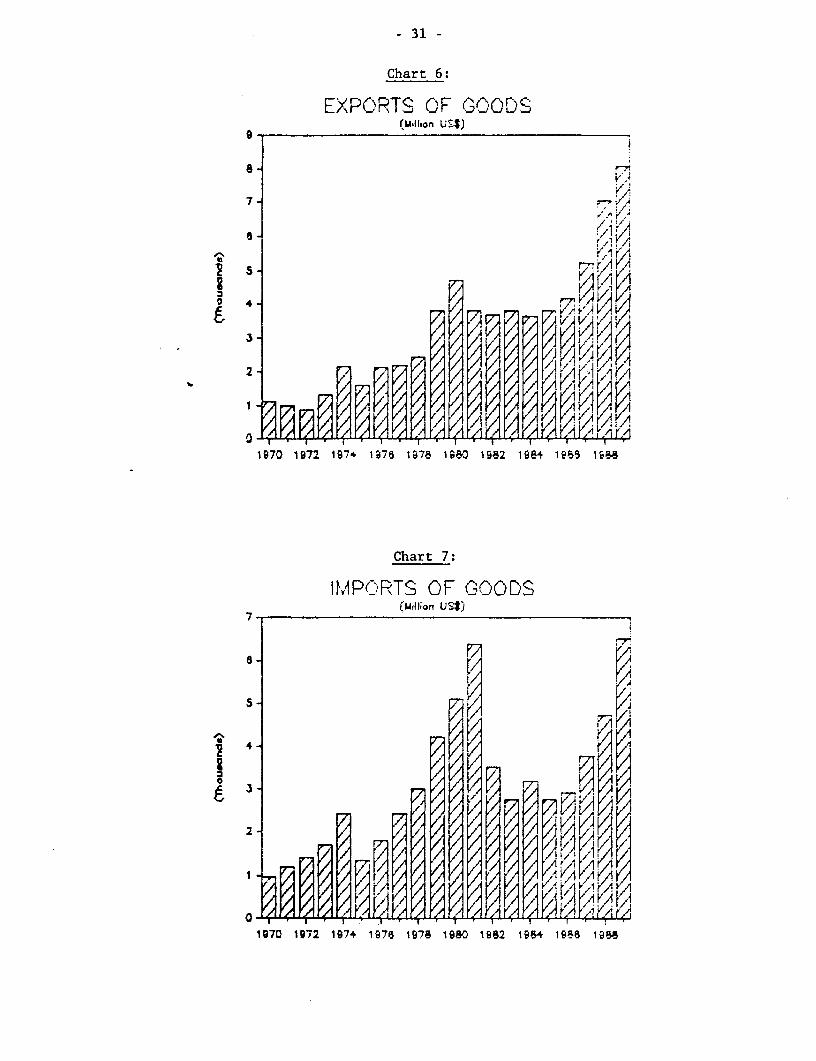

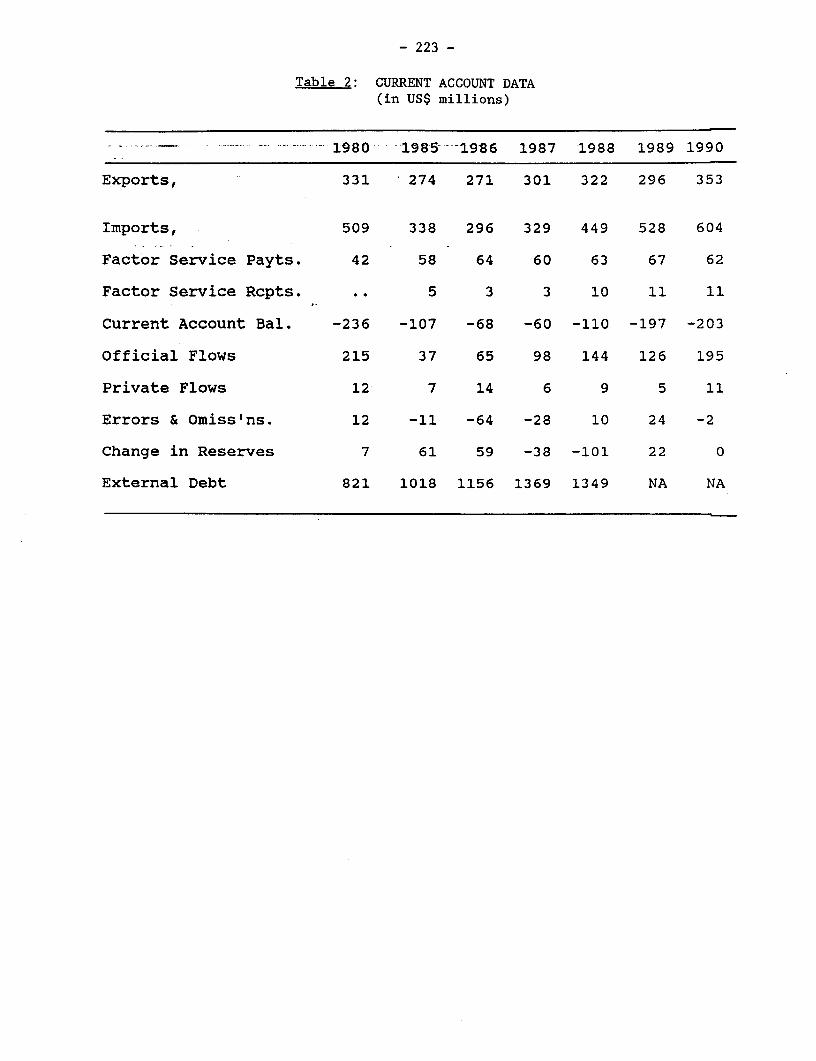

Chile's debt position during this period followed a similar pattern tothat of other Latin American countries: as petrodollars were recycled in thelate 1970s and world liquidity increased, Chile borrowed enough to triple itsforeign debt in just six years. The composition of Chile's foreign debt was,however, very different from that of other highly-indebted countries. Indeed,of the US$9.6 billion!/ increase in foreign debt between 1976 and 1982, US$6.8billion (71 percent) was private sector debt. For most other Latin Americancountries, most foreign debt was incurred by the public sector.

When the Chilean government refinanced and rescheduled its foreign debtfollowing the 1982 crisis, the public sector incurred new debt--mostly withmultilateral agencies--to ease the burden of the private sector. Thus, by 1989,more than 85 percent of total foreign debt was held by the public sector.

As a result of a very aggressive debt conversion program started in1985, total foreign debt has declined in the last few years, from a peak ofUS$17.8 billion in December 1986, to US$13.5 billion in November 1989. Theamount converted in the same period was much higher, though, reaching almost US$9billion through various mechanisms implemented by the economic authorities.

While external factors have played an important role in the economicfluctuations and recurrent crises during the last two decades, the most criticalelement contributing to economic instability was government waste andmismanagement. External factors prompted needed adjustments in domesticpolicies. Indeed, the 1975 recession was the result of a deep contraction in

1/ All foreign debt figures correspond to medium- and long-term obligations.

- 15 -

public sector spending, as the authorities tried to compensate for a sharpdecline in the price of copper. The ensuing "miniboom" of 1978-81 was spurredpartly by the wide availability of foreign savings, but there were also someinternal factors that activated domestic private spending. Similarly, while the1982-83 depression occurred as a result of foreign financing being abruptly cut,domestic authorities created the conditions for disaster: first, they alloweduncontrolled spending during the 1970s, and subsequently they contracted moneysupply and fiscal spending, and increased taxes in hopes of preventing recessionin 1982.

The sharp drop in the price of copper between 1984 and 1987, combinedwith problems in servicing foreign debt, pushed up the real exchange rate (tothe U.S. dollar) by more than 40 percent. In 1988 and 1989 economic activitypicked up and export prices (particularly copper) increased sharply. Domesticmoney supply also expanded significantly.

ECONOMIC POLICIES IN RECENT YEARS

Economic policies in recent years have been shaped mainly by twofactors: first, that the most important structural reforms were carried out inthe late 1970s, and second, the deep depression suffered in 1982-83.

The three stages that should have characterized adjustment followingthe 1982-83 depression were stabilization, recovery, and growth. The typicalWorld Bank prescription is that stabilization requires spending cuts (typicallyon the fiscal side) and expenditure switching policies (primarily realdevaluations). The recovery and growth stages require structural reforms toreduce public sector waste and reforms to allow relative prices to truly reflectcomparative advantages and scarcity. Most Latin American countries have foundit difficult to sustain initial stabilization and have realized that maintaininga "high" real exchange rate is not sufficient to significantly increaseproduction of tradeable goods. What are lacking in many Latin American countriesare reforms to liberalize the economy. Such reforms could include measures toloosen trade restrictions and reduce the size of the government. Strong interestgroups are likely to resist such reforms, and may be powerful enough to preventthem.

By contrast, Chile achieved recovery and growth more easily because itsliberalizing reforms occurred in the late 1970s. Consequently, the bulk of theadjustment in Chile in 1982-85 focused on allowing the real exchange rate toreflect the new external payments situation--an absence of voluntary foreignlending and depressed terms of trade. Soon after, the volume of exportsincreased, in index terms, from 88.2 in 1983 to approximately 130 in 1989, whileindustrial production increased 50 percent, agricultural production 44 percent,and general tradeable production 41 percent.

The 1982-83 crisis changed the design of economic policies in manyways. Perhaps the most drastic was in the exchange rate policy. After threeyears of a policy that pegged the exchange rate to the U.S. dollar, in June 1982there was a 15 percent devaluation (judged clearly as insufficient by the privatesector), then a move toward a floating rate, and then a crawling peg mechanism

- 16 -

that started at almost twice the initial value, all in a span of five months.The passive crawling peg involves adjusting the nominal exchange rate accordingto the previous month's domestic inflation rate less an arbitrary estimation ofthe world inflation rate. The estimated world inflation rate has beenartificially manipulated from time to time to effect gradual real devaluationsor revaluations (in terms of deviations of a PPP rate).

The peso depreciated by about 50 percent between 1982 and 1987--aperiod when the foreign exchange constraint was most acute. Subsequently, termsof trade improved and pressure for a real appreciation grew, despite theexistence of a copper price stabilization fundZ/ (most of the fund's resourceshave been spent). By the end of 1989, the real exchange rate was about 40percent higher than in 1982. The economic authorities have been reluctant,however, to allow a drastic and more significant real appreciation, althoughimproved external conditions and strong export performance may have led to thatunder a floating system. As a result of not appreciating further, inflation hassurged. This, in turn, will lead to a real appreciation, despite thegovernment's exchange rate policies.

The crisis also affected monetary policy. Between 1978 and 1982,domestic credit was consistently decreased in real terms in order to balanceincreases in base money caused by the massive inflows of foreign capital.Despite this effort, total Ml went up in real terms by 41 percent between 1978and 1982. A significant demonetization of the economy occurred in 1982, withMl falling 16 percent in three years. Between 1983 and 1985, monetary policywas strongly determined by the authorities' decision to allow the Central Bankto bail out certain domestic debtors who suffered as a result of the domesticfinancial crisis.

In 1985, a new team at the Central Bank and the Ministry of Financeinitiated a monetary policy to manage domestic credit based on manipulatinginterest rates, inflation, and imports. Lower foreign exchange reserves duringthat period made the policy easier to implement. This policy is, to some extent,credited with achieving a relatively stable inflation rate of around 20 percentbetween 1985 and 1989.

In the case of fiscal policy, the 1982-83 crisis put strong pressureon the government to increase spending. This was especially acute after thegovernment's bail-out of the banking system in January 1983, which revealed themagnitude of Chile's domestic debt. Prior to the banking crisis, declining taxrevenues had already put the fiscal sector in deficit--something the governmentdid not want to reveal during its negotiations with the IMF and the World Bank.Ultimately, over four years, the domestic debt crisis and bail-outs by theCentral Bank resulted in accumulated quasi-fiscal losses of close to US$5

./ The fund was created in 1985 to provide a buffer stock of foreign exchangereserves that accumulate when the price of copper is above a "normal" level,and which can be spent when the price of copper temporarily falls below thatnormal level. In 1988 and 1989, this money was used by fiscal authoritiesto prepay Central Bank debt.

- 17 -

billion. In 1988 the government agreed to treat the US$5 billion as debt owedto the Central Bank.

A related policy matter was the regulation of capital markets. Indeed,many analysts attribute the rising debt between 1978 and 1982 to the lack ofappropriate regulations over domestic financial activities. Domestic banks didnot adhere to conservative lending criteria and distortions of relative pricesled to unrealistic valuations of assets. Further, regulations on banks' loansto related corporations were minimal. In some cases, more than one third of thebanks' portfolios were loans to corporations whose owners were the same as thebanks'. In addition, it was widely believed that deposits in private financialinstitutions were insured by the state. Such a ubiquitous insurance mechanismfacilitated risk-taking by banks' managers as depositors did not discriminatebetween institutions by the quality of their portfolios.

The link between inadequate regulations and high indebtedness promptedradical legislative reforms. In 1986, new laws were enacted that set stricterregulations for all types of financial activities. One law forbids a bank tolend more than 2 percent of its capital to related corporations. Another lawdecrees that the state can only insure demand deposits of private financialinstitutions. It is early to say yet whether the new legislation has beeneffective, but it seems to have helped.

However, perhaps the most relevant feature of the depression-inducedpolicy changes was that they left untouched the basic resource allocationmechanisms implemented by the structural reforms of the late 1970s. In effect,in spite of strong pressures to swiftly increase the involvement of the statein economic activities and reverse the liberalization of prices, trade, andinterest rates--in Chilean words, to abandon the "modelo neo-liberal"--thegovernment only introduced some marginal and transitory counterreforms. Forinstance, in the case of trade policy, tariffs were increased from flat ratesof 10 percent to 20 percent in 1982; then to a cascade structure with a maximumof 35 percent for a brief period in 1984; and then back to the 20 percent flatrate in 1985. They were reduced a further 5 percent in 1987. No quantitativerestrictions were enacted during this period.

Following the crisis, the price of most consumer goods continued to bedetermined by supply and demand. The only exceptions are prices of certainagricultural products, such as wheat and corn, which were benefitted by "bandas."

The size and role of the state has not changed significantly althoughthe bail-outs of several financial institutions in early 1983 put the governmentin the position of virtually controlling more than 50 percent of the financialsystem. This was transitory, however, and after three to four years, all of theinstitutions involved had been sold or dissolved.

In the end, the crisis was overcome by correcting the policyinstruments that helped to bring the crisis in the first place, but not byreversing the liberalizing reforms of the 1970s. This strategy is to some extentresponsible for the depression's depth. For example, calls for massive domesticdebt bail-outs, which would have required a revision in fiscal reforms but would

- 18 -

have alleviated the need for reducing private spending, were resisted; also,pressures for stricter regulations or more state intervention in labor marketsto "protect" employment were also resisted. Ultimately, the response to thecrisis played a key role in the quick restoration of economic activity and thestrong supply response of tradeable goods.

MAIN PROBLEMS AND RISKS FOR THE FUTURE

Four main problems can affect Chile's prospects for medium- to long-term growth. First are the chronic low rates of national saving and domesticinvestment; second is the fragile fiscal situation. The third one concerns therecurrence of external shocks. And the fourth problem relates to politics andthe social cost of adjustment, which will be key issues for Chile in the 1990s.I will refer to the first three now and take up the latter in the next section.

Saving and Investment. The prospects of growth for the Chilean economyare to a large extent constrained by low domestic saving and investment rates.In the 1970s, the domestic saving rate fell to 12 percent of GDP, then droppedto 8.5 percent in the 1980s. During the 1980s, gross investment as a percentageof GDP reached a 16.3 percent average, which compares favorably to the 14.8percent during the 1970s. However, based on the experience of other countries,these rates are not high enough to sustain long-term growth in Chile. Besides,20 years ago, when Chile had a 14 percent national saving rate and a 15 percentgross investment rate, it was able to sustain only modest average growth ratesof 4 percent a year.

In the last three years, both investment and saving seem to haveimproved significantly, although it is uncertain whether the higher rates willpersist once the current expansion and the copper price bonanza end. Nationalsaving was 16.3 percent in 1988 and was estimated at 17 percent in 1988, whilegross investment grew by 17 percent in 1988 and an estimated 20.1 percent lastyear.2/ Several studies on prospects for economic growth in Chile concur thatthese rates are barely sufficient to sustain a 5 percent growth rate (or a 3.3percent growth rate in per capita terms). However, there is less agreement onthe effects that decontrolled prices will have on resource allocation andefficiency.

A key question is whether the structural reforms and the businessclimate, combined with a 20 percent investment to GDP ratio, will yield a growthrate of more than 5 percent. While data are available on the effects ofstructural reforms, information tracing the climate for business is scarce. Thebusiness climate has been volatile, first during the depression (1982-83), andthen during the recent political upheaval. Structural reforms and an appropriatebusiness climate during the 1990s are essential to Chile's economic growth.

Low saving and investment ratios must also be corrected. It seems thatin Chile (as in several other Latin American countries) saving--particularly

.i/ These figures include inventory changes.

- 19 -

household saving- -is low because the cultural incentive to save is not as strongas in, say, industrializing Asian countries. This can also be attributed tothe strong dependence on the state. In this sense, a more frugal governmentwould help reverse this low-saving tradition.

The balance between public and private investment is important forfuture growth. Since 1985, private investment increased, while the share ofpublic investment in GDP tended to remain constant. Should this trend continue,severe problems could arise if, as some analysts believe, an urgent need arisesto improve and expand Chile's infrastructure. However, public infrastructuremust be financed either by increased public saving or through loans from foreigncreditors. The first option is not feasible in the current political context:thus, over the next few years, Chile may turn to foreign sources to help financepublic infrastructure.

An "appropriate business climate" constitutes a clear legal frameworkwith stable rules favoring private business and controlling key economic factors.In particular, these rules should maintain the resource allocation mechanismsbrought by the reforms in the 1970s. In particular, laws protecting propertyrights should be immutable. Further, the rules should not contain loopholesallowing for an arbitrary change in the regulations in the future.

Chile has gone a long way in developing an institutional and legalframework that preserves reforms in the long run. Actually, the process wasinitiated with the reforms themselves, in the late 1970s, and strongly testedby the 1982-83 depression.

The Chilean government's decision not to retract the liberalizationreforms instituted in the 1970s was decisive in convincing private agents thatreforms were credible and, thus, the supply response to the adjustment was high.This, in turn, made the outcome different in Chile than in other Latin Americancountries, where the lack of confidence in public institutions contributed toa low tradeable supply response.

During the political reforms of the late 1980s, the economic and fiscalpolicies of the 1970s and early 1980s were subject to close scrutiny. Now,however, an implicit consensus has been reached not to alter these policies.If the new administration's income redistribution plan succeeds, within thislegal and institutional framework, the "appropriate business climate" will befortified.

Fiscal Risks. The second threat to Chile's growth is the fragilefiscal situation stemming from pressures on expenditures. On one side, thereis the debt owed by the government to the Central Bank, amounting to US$6.3billion. The government is paying half a percent over the London InterbankOffered Rate in interest, or about US$600 million a year. The government isrequired to pay a minimum of 2 percent of the total debt, or about US$120million. This debt was even higher at the end of 1988, but during 1989, theformer government paid more than US$1 billion in amortization and tied anadditional US$400 million payment into the 1990 budget. The resources came from

- 20 -

the copper stabilization fund, which accumulated significant reserves in the lasttwo years as the price of copper rose above the predetermined "normal" price.V/

For the coming years, with the price of copper closer to normal, itwill be difficult for the government to pay any extra amortization. Besides,the interest bill on this debt could become a heavy burden if it approaches thestipulated US$600 million--approximately 12 percent of total expenditures andabout 2.3 percent of GDP--and it cannot be too much less than that because theCentral Bank's financial position remains critical. In other words, any interestpayment less than LIBOR plus 1/2 percent will risk a cash deficit at the CentralBank that will have to be financed by an inflation tax.

Social demands could also threaten fiscal stability. The newgovernment is well aware of the fiscal pressures and may adopt a strategy linkingincreased fiscal spending to increased taxes. Indeed, tax legislation that willgenerate about US$600 million a year in additional revenues between 1991 and 1993is currently being discussed in Congress. The law will allow for US$400 toUS$500 million more in social spending. The remainder will be used for fiscalsaving. (These extra funds could be used to increase interest payments to theCentral Bank.)

While the proposed legislation contains some tax increases that couldreduce profits from private investment, the government has agreed to partiallyreverse the reform in 1994 and give some compensation to small and medium-sizecorporations. These tax reforms, coupled with other more political argumentsclaiming that investment is more sensitive to a politically stable environmentthan to a (small) reduction in after-tax profitability, would lead to a minor,negative aggregate effect on private investment. What is important is tomaintain fiscal austerity and control private spending and saving.

Recurrent External Shocks. The third problem that can affect Chile'sgrowth prospects concerns recurrent external shocks. Positive and negativeexternal shocks have spurred booms and recessions, respectively, in the last twodecades. Each time the authorities reacted after the fact by changing policiesand regulations to diminish the influence of future external shocks. In the nearfuture, the most likely shock is a fall in the price of copper. The metal'scurrent price is widely viewed as unsustainable given the medium- to long-termprospects for supply and demand.

While the copper price stabilization fund was designed to absorb sucha shock, economic authorities chose instead to use foreign reserves from the fundto prepay debt owed to the Central Bank. In the future the government shouldshow restraint and use the fund only as a buffer. Unfortunately, it may be toolate to accumulate more resources before the copper price drops.

V./ This "normal" price has been set jointly by the government of Chile and theWorld Bank, within the framework of the 1985 First Structural AdjustmentLoan (SAL 1).

- 21 -

Other negative shocks are possible but cannot be predicted. Forinstance, a world recession in the next five years is possible, especially ifthere is a financial collapse in the United States.

In any event, any eventual negative shocks would impinge on Chile'sability to comply with its external obligations and/or its capacity to import.The extent of any damage will depend on access to foreign resources and on theduration of the shock. Chile's access to voluntary lending is likely to increasein the next few years (although not to the extent reached in 1979-81) as a resultof its "good behavior" as a debtor, which is expected to continue under the newadministration. However, negotiations will have to take place before 1991 toreschedule about US$600 million in annual interest payments due between 1991 and1994. Even if no other negative shock but the reduction in the copper priceoccurs, the financing for imports needed to achieve a 5 percent growth ratebetween 1991 and 1994 will be inadequate unless additional foreign lending isobtained.

POLITICS AND THE SOCIAL COSTS OF ADJUSTMENT

The adjustment, recovery, and growth experienced since late 1983 hasnot been without a social cost. First, the depression brought extremely highunemployment (close to 30 percent of the labor force, including state emergencyemployment programs) and a large contraction of real wages. Real wages fell 16percent between 1981 and 1983. Cuts in real wages were an important prerequisitefor the increase in the real exchange rate: the contraction in employment wasbusinesses' response to macro policies that reduced aggregate spending. Risingunemployment and declining real wages had a severe effect on people's welfare.Although there are no data on factor income distribution after 1982, a roughcalculation based on unemployment and real wage figures indicates that workers'income could have decreased by almost 20 percent between 1981 and 1983.V/

The bulk of the adjustment affected private spending. Fiscal spending,meanwhile, was not reduced by much between 1981 and 1984: without debtservicing, it went from US$3.37 billion in 1981 to US$3.29 billion in 1982,US$3.16 billion in 1983, and US$3.36 billion in 1984. GDP jumped from 23.3percent in 1981 to 25.7 percent in 1984, while the fiscal deficit moved from asurplus of 1.7 percent of GDP in 1981 to a deficit of 4 percent of GDP in 1984.Part of this is due to the government's support of the employment emergencyprograms, but also to the decision not to default completely on growing socialsecurity obligations. Other more permanent social spending items, such as healthcare for the poor and food and housing programs, were reduced in some cases andmaintained in others. But the needs stemming from the depression clearlyoverwhelmed the government's capacity to help.

2/ During the same period, GDP decreased 15 percent. The 20 percent figurementioned in the text should be taken with care, since unemployed people'sincome did not fall to zero.

- 22 -

The problems of unemployment and low real wages have eased, althoughat different rates. Employment generation has been very strong since 1985(close to 900,000 new jobs through 1989), and unemployment declined to 6 percentlast year. Meanwhile, real wages have been increasing more slowly. By the endof 1989, after two years of growth that put GDP beyond the 1981 level of 23.1percent, real wages were still 3 percent lower than in 1981. The per capitaincome for Chileans has dropped 10 percent since 1981, and real incomes haverisen only 3.1 percent since 1981.

On the fiscal side, spending on health, welfare, and educationalprograms has decreased by more than 20 percent between 1984 and 1989 (28 percentper capita) ..6/ Much of this decrease was forced by the big deficit of the socialsecurity system (21 percent increase), but also by a 108 percent increase inhousing programs.

Despite these reductions in social spending, hard evidence that thequality of life has declined is lacking, although improvements in livingstandards have slowed since the depression.

Nonetheless, despite strong macroeconomic performance in the last fewyears, low- and middle-income people have not regained the living standards(measured by income) that they had in 1981. Some people assert that a "socialdebt" is owed to those groups, who constitute the majority of Chile's population.These social inequities provided the backdrop to the 1988 and 1989 electionresults, which granted the new government a mandate to carry out an incomeredistribution program that will involve fiscal and tax reforms. At the sametime, people have grown accustomed to moderate inflation rates and recognize thebenefits of economic growth. With this in mind, the new administration will alsomaintain the macroeconomic policies that have so profoundly changed Chile'seconomy.

The big challenge for the new administration will be how to balancesocial and economic policy goals in a democratic context. The previousadministration left behind strong macroeconomic indicators, and any worseningof them could be politically dangerous. Besides, it is clear that newpolicymakers are eager to demonstrate that they could be at least as efficientin administering the state as their predecessors and that Chile will not fallinto the economic morass of some of its neighbors.

In contrast, the previous administration's performance on the socialside was inadequate, at least according to Chile's tradition of state welfaresupport and income distribution favoring the poor. Much can be done to correctmany of these social "debts." However, the extent to which the cost of improvingsocial services will be detrimental to private sector growth and investment isunknown.

i./ The figures are more dramatic if one compares 1989 with 1981, before thecrisis.

- 23 -

CLOSING REMARKS

Chile's prospects for the 1990s are fairly good, if policymakersconfront the main problems affecting the economy and find an appropriate mix ofpolicies that spur national savings and private investment, keep the fiscalbudget under tight control, permit a flexible absorption of eventual negativeexternal shocks, and contribute to a more equitable society. A basic frameworkshould be the liberalized economy inherited from the 1980s, amended in a way thatshows more solidarity with the poor. In the end, this would be the only roadto a modern and economically sound democracy.

- 24 -

Table I : NATITNAL ACCOUNTS

1980 1985 1986 1987 1988 1933 1990

GDPLocal Currency (NMMS) 363.4 356.4 376.6 398.2 427.5 470.2MM uss 27571 16018 16825 18959 22084 25536

Share to GDP (2)Consumption 83.17 83.53 81.57 79 75.83 76.3

Private 70.72 69.2E 68.92 67.58 65.32 66.41Public 12.45 14.25 12.65 11.42 10.51 9.89

Investment a/ 17.6 14.8 15 16.5 17 20.1Private 12 7.9 7.8 10 11.1 14.4Public 5.6 6.9 7.2 6.5 5.9 5.7

Exports 22.82 29.08 30.63 33.52 37.37 37.67Imports 27 26.32 26.81 29.42 30.18 34.4

Real 6rowth Rate 7.8 2.4 5.7 5.7 7.4 10.1Consumption 6.8 -1.1 4.9 4.8 9.6 8.3Investsent 21.9 14.8 7.1 16.2 10.7 20.8Goverment -8.1 -0.3 -2.1 -2.1 4.7 0.9Exports 14.3 6.9 9.8 8.8 6.1 16.2Imports 18.7 -11 9.7 17 12.1 25.3

Population (thousands) 11144.8 12127.7 12327 12536.4 12748.2 12963.6

a/ Gross fixed capital formation.

- 25 -

Table 2: CURRENT ACCOUNT DATA (fMUSS)

1980 1965 1986 1987 1988 1989 1990 1995-2000

Exports USS Current 4705 3084 4199 5224 7051 80980leports USS Current 5469 2955 3099 3994 4833 6502Factor Service Payments 1320 2097 2108 1878 2101 1987factor Service Receips 197 221 178 181 339Current Account Balance -1971 -1329 -1137 -888 -167 -622

Direct Investaent 170 26 57 98 117 20uOfficial flow 85 1144 450 603 298 n.aPrivate Flow 1003 10 88 -85 111 n.aErrors and Omissions 50 -3 -49 -91 -110 52.9Change in Reserves a/ 1244 -99 -228 45 732 437.4

External Debts 11084 17431 18887 19444 17649 16250

a/ Balance of payments.

- 26 -

Table 3: PUBLIC SECTOR(All Data as % of GDP)

Consolicated Non-Financiai Puolic Sector

(including Public Enterprises)Financ:ng of Deficit

Central 6overeent ------------------------------------------------------------------------------- ------------------------------------ Doaestic External Inflation

Revenue Expenditure Baiance ;eyenue cxpenditure Deficit Loss Loss Loss CtnerCurrent Capital (deficit" a/ Current Capital &2)

1981 32.1 26.6 2.6 -2.9 34.2 29.1 4.7 -0.4 -3.6 2.71982 29.9 31.9 0.3 2.3 33.9 35 .2 2.6 3.9 1.1 2.219B3 27.7 30.5 0.2 3.0 3.3.5 34.0 3.v 3.5 ¢ -1384 28.7 30.7 1.5 3.5 34.3 33.8 4.9 4.5 1.7 2.71985 28.6 29.6 2.7 3.7 36.7 33.1 6.4 2.9 -1.4 4.11986 28.2 26.6 2.7 1.1 i.5 -1.0 3.11987 28.7 25.9 2.6 -0.2 -0.3 -2.5 2.21988 28.7 23.3 2.1 - -3.6 -7.3 3.71989

a/ Revenue between 1986-88 corresponds to the saving (net current income)..QTES: Capital Expenditure is investsent i2,- net capital expenditures

- 27 -

Table 4 : INCENTIVE iNDICATORS PRICES

1380 1985 19E6 1987 1988 198 13C 1995-2010

Iiflation Rate 31.2 26.4 17.4 21.5 12.7 21.4 25

Real Eff. Exchange Rate 100 :58.92 i7h.36 170.64 178.28 172.06(1980=100)

ILdex Real Wages 100 93.21 95.06 94.9 101.12 103.06(1980:100)

Real Eff. Interest RateBorrowing rates 5.03 4.13 1.47 3.15 2.03 5.08LOaning rates 12.23 11.05 7.64 3.39 7.44 11.83

Ritio: Donestic-ForeingEnergy PriceGasolineOther

Uneaployuent Rate 10.4 12 6.8 7.9 6.3 6

- 28 -

Chart 1:

GROSS -DOMESTIC PRODUCT(Onual growth roteeu)

-12l

, g *~j I fll

-14l

1970 1972 1974 1978 1978 1280 1982 19A_4 1X68

Chart 2: INVESTM-AENT(X of GOP)

11,

15'

14

17-

12 -

7-~~~~~~~~~~~~~~~~~~~~~~~~~~~~..

179 1980 i9:i 1;,8 l2 3i 191 5 19686 1987 ISe.8 1ie19

O To t 4 Pu bII Priv.

- 29 -

Chart 3a: INFLAT,'ON(Dea to C'a X tanation)

5000

400-

200-

10017 'I r-r

i970 1972 1974 1978 1978 1Wj 1962 19+4 1966 1696.

Chart 3b: INFLATIONa(o. to Dea. X variation)

GO I

sro

40

30 1

20-

10

0'1077 19781979 1960&D1961 1962 19&3 1964 195196881987 1968 1296

- 30 -

Chart 4:

cUES oanta jr Pound, 1-;ja)

750

1-OI |r [E

1.30

120

1000

190 17- i7 1?75 /97 /~018-!

Io / I.

1970 1972 1;-74 ?975 197Ri 1980 1982 19 ,A 1 9A6

Chart 5:

sREAL -IHA.NGr -ZATCE

1 S^L

1 40-

130

VAV

.,~~~~~~~~~~~~~~~~~i

170 -

100

190 17 174-7498 SO18 1/*./ !I5 i/-i8

- 31 -

Chart 6:

EXPORTS CF GOODSrmsilion USS)

4- 4

7 A~~~~~~~~~~73 x~~~~~~~~~~~~A

2

1970 1972 1974 1976 1978 1980 1982 1984 1985 l1938

Chart 7:

It-,PcRTS OF GOODS(Million USt)

7-i

2

100197 2 1974 1976 1978 1980 1982 198-4 19856 1938

- 32 -

Chart 8:

FOREIGN DEBT(Million UZI)

17 -~

14 -

13 t

12 --

-~11

4 - ~ ~ ~ ~ ~ ~ ~ 4

2-

1970 1972 1974 1976 1978 1 980 1E82 19634 186 1988

0 Tota! * Priv. Pubi.

- 33 - APPENIXPage 1 of 2

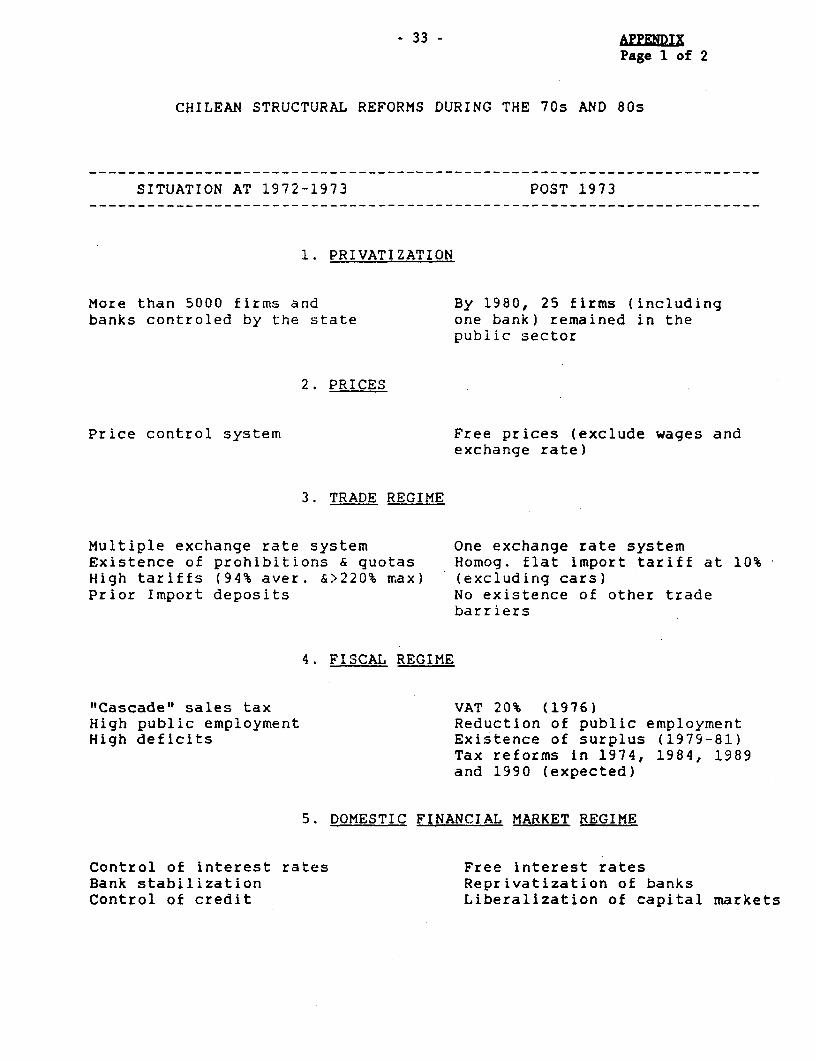

CHILEAN STRUCTURAL REFORMS DURING THE 70s AND 80s

SITUATION AT 1972-1973 POST 1973

1. PRIVATIZATION

More than 5000 firms and By 1980, 25 firms (includingbanks controled by the state one bank) remained in the

public sector

2. PRICES

Price control system Free prices (exclude wages andexchange rate)

3. TRADE REGIME

Multiple exchange rate system One exchange rate systemExistence of prohibitions & quotas Homog. flat import tariff at 10%High tariffs (94% aver. &>220% max) (excluding cars)Prior Import deposits No existence of other trade

barriers

4. FISCAL REGIME

"Cascade" sales tax VAT 20% (1976)High public employment Reduction of public employmentHigh deficits Existence of surplus (1979-81)

Tax reforms in 1974, 1984, 1989and 1990 (expected)

5. DOMESTIC FINANCIAL MARKET REGIME

Control of interest rates Free interest ratesBank stabilization Reprivatization of banksControl of credit Liberalization of capital markets

'34 'APPENDIXPage 2 of 2

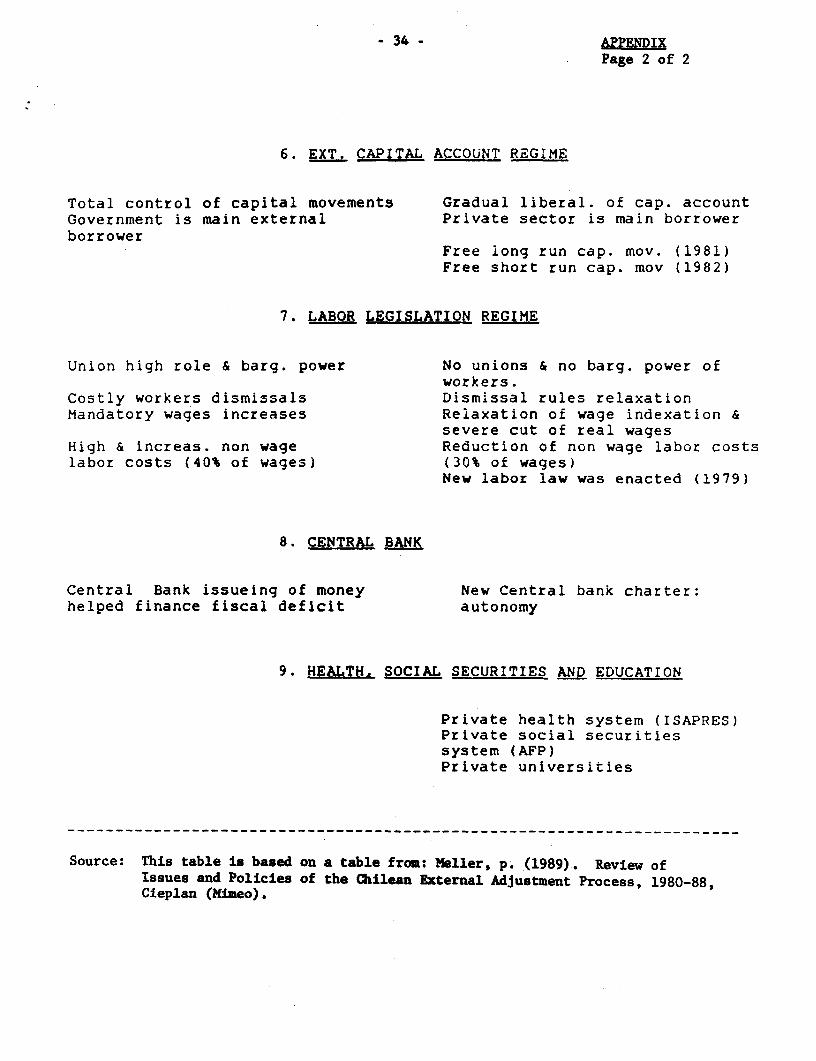

6. EXT. CAPITAL ACCOUNT REGIME

Total control of capital movements Gradual liberal. of cap. accountGovernment is main external Private sector is main borrowerborrower

Free long run cap. mov. (1981)Free short run cap. mov (1982)

7. LABOR LEGISLATION REGIME

Union high role & barg. power No unions & no barg. power ofworkers.

Costly workers dismissals Dismissal rules relaxationMandatory wages increases Relaxation of wage indexation &

severe cut of real wagesHigh & increas. non wage Reduction of non wage labor costslabor costs (40% of wages) (30% of wages)

New labor law was enacted (1979)

8. CENTRAL BANK

Central Bank issueing of money New Central bank charter:helped finance fiscal deficit autonomy

9. HEALTH. SOCIAL SECURITIES AND EDUCATION

Private health system (ISAPRES)Private social securitiessystem (AFP)Private universities

Source: This table is based on a table from: Meller, p. (1989). Review ofIssues and Policies of the Chilean External Adjustment Process, 1980-88,Cieplan (Mimeo).

- 35 -

COMMENTARY BY LUCA BARBONE

I found this paper quite interesting. Most people who has beenworking on Latin America in the past few years view Chile as an outlier, astumbling block in the comparison of growth and economic performance. Althoughit is true that other countries in Latin America have enjoyed relatively goodperformance--Colombia or Paraguay--it is also easy to come up with very specificreasons for their performance that make them less of a challenge in terms ofdefining a paradigm of what good economic management in a Latin American country,in particular, may mean.

I have two sets of comments.

The first is on some of the interpretation in the paper as to thereasons for the economic success in Chile.

And second, to draw some lessons. The lessons may be more grim thanthe interpretation.

Let me start by the two elements that I think the paper rightlydispels as not being relevant, not being a sufficient condition for explainingChile's performance. As it is made clear, an authoritarian government is nota sufficient condition for good performance, nor is the ability to compress realwages as low as they can go.

Although these features were present in Chile, they have also beenpresent in most Latin American countries, including those with the leastenjoyable economic records such as Argentina or Brazil, or even Peru.

Where a military government does help is being able to guaranteecontinuity in economic management. The paper rightly stresses that the abilityto insist on certain basic parameters, despite setbacks along the way, is oneof the key aspects that contributed to the successful restoration of what hasbeen defined as the appropriate business climate.

Thus, while I agree with the basic message of the paper, namely thatgood and consistent economic management is eventually rewarded by good economicperformance, I would have liked to see a more focused analysis on two relevantissues: (a) the relative role played by the reversal of macroeconomic policies,particularly the exchange rate policy, in obtaining a turnaround in performanceafter the banking crisis; and (b) the extent to which "excessive" structuraladjustment policies may have contributed to the crisis, or reinforced the effectsof inappropriate macro policies. In fact, if we had been here in 1983, probablythe consensus would have been that the experiment was a disaster and the adviceof this group to the government would have been to try to change policies asquickly as possible to avoid a serious depression. In fact, the government didchange policies after 1982. Although the emphasis on free markets, the emphasison reducing the role of the state, the emphasis on deregulation remained to alarge extent, some excesses that led to the banking crisis were pruned, andmacroeconomic policies (particularly the exchange rate policy) reoriented. Thus,

- 36 -

the question remains as to which of these two elements was crucial in allowingChile to recover from the 1982-83 crisis.

But still, one must agree that consistency of policies is somethingthat has also given an important contribution (with a bit of luck coming fromexternal conditions) to the average 4 or 5 percent per capita growth in the lastfive years. One aspect that remains striking, however, and that might be ofcrucial importance in deciding whether the current economic success is likelyto be sustainable in the future, relates to the external vulnerability of Chile,which is underlined in this paper. Unlike Mexico, for instance, which has beenable to diversify its exports to an extent that was certainly unimaginable a mere10 years ago, Chile still has basically half of its export revenues dependenton one commodity, copper, and that, despite the enormous growth in non-traditional exports. Can we consider the process of structural reform completedunder these conditions? If the answer is yes, i.e., that heavy dependence onone or few commodities is not something of concern for an economy where marketsignals have been allowed to operate freely, then I think this carriesimplications for a number of other countries where structural adjustment policiesare routinely identified with policies for diversification of exports.

New for the political economy lessons, particularly for LatinAmerica, I think that the paper gives a sobering message although severalcountries are now, for own conviction or for lack of alternative, being pushedtowards adopting the same type of policies that Chile adopted in the seventiesand in the early eighties. It is very difficult to envisage--at least for anumber of them--that the same conditions of stability and economic managementmay prevail for a sufficiently long period of time, if it is true that it takesa long time for the shift from a constellation of policies where the priceincentives and the market incentives are wrong to a constellation of policieswhere the right price and market incentives take effect on output and employmentand stability.

In this sense, I read the message of the paper as one of extremedifficulty for the task ahead, as the lags between the implementation ofstructural adjustment policies and any rewards are sufficiently long andunpredictable that the political cycle may make a reversal much more likely thanone would like to expect.

JAMAICA: CAN THE RECOVERY BE SUSTAINED?

Michael Gavin

With commentary by Sue Collins

- 39 -

TABLE OF CONTENTS

Page No.

CRISIS AND RECOVERY . . . . . . . . . . . . . . . . . . . . . . . 42

Economic Crisis and Collapse, 1972-80 . . . . . . . . . . . . 42Recovery, 1980-88 .... . . . . . . . . . . . . . . . . . . 44

OUTLOOK: CAN THE RECOVERY BE SUSTAINED? . . . . . . . . . . . . . 54

REFERENCES .56

TABLES

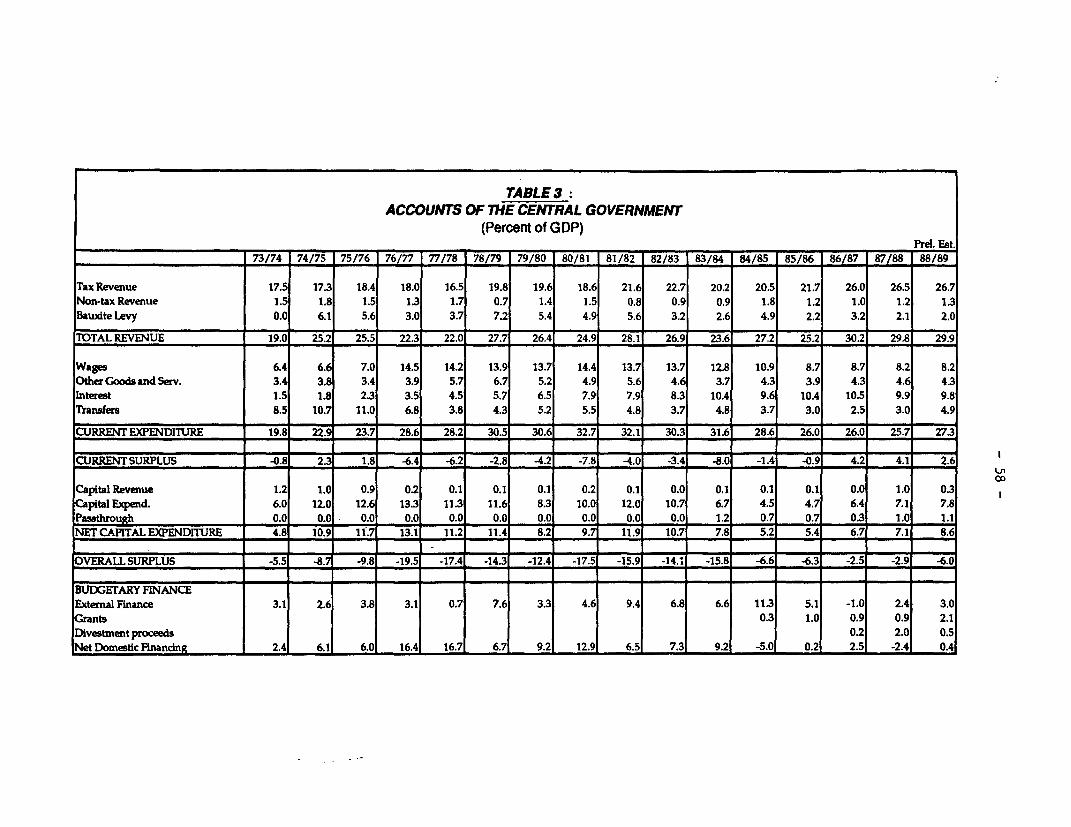

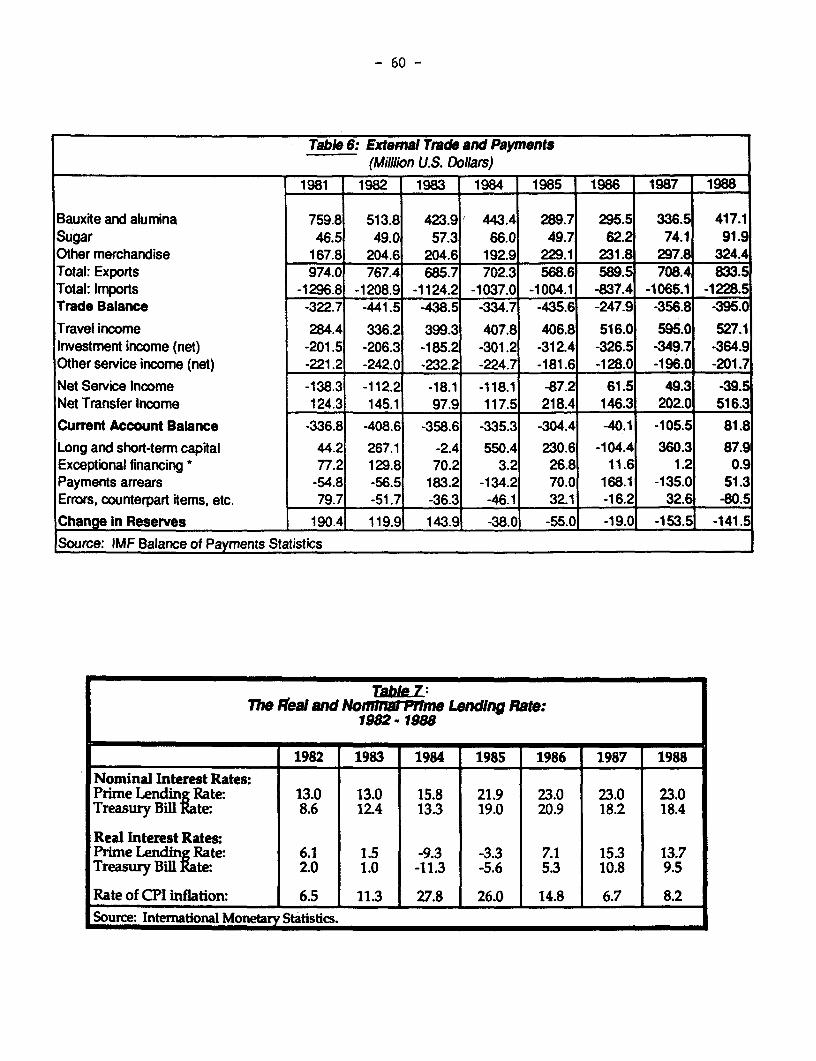

1 Macroeconomic Performance in Jamaica . . . . . . . . . . . . . 572 The Bauxite Sector in Jamaica. . . . . . . . . . . . . . . . . 573 Accounts of the Central Government . . . . . . . . . . . . . . 584 Economic Growth in Jamaica .... . . . . . . . . . . . . . . 595 National Accounts .... . . . . . . . . . . . . . . . . . . 596 External Trade and Payments ... . . . . . . . . . . . . . . 607 The Real and Nominal Prime Lending Rate, 1982-1988 . . . . . . 608 Employment and Unemployment, 1983-1988 . . . . . . . . . . . . 619 External Public Debt, 1977-1987 . . . . . . . . . . . . . . . 61

CHARTS

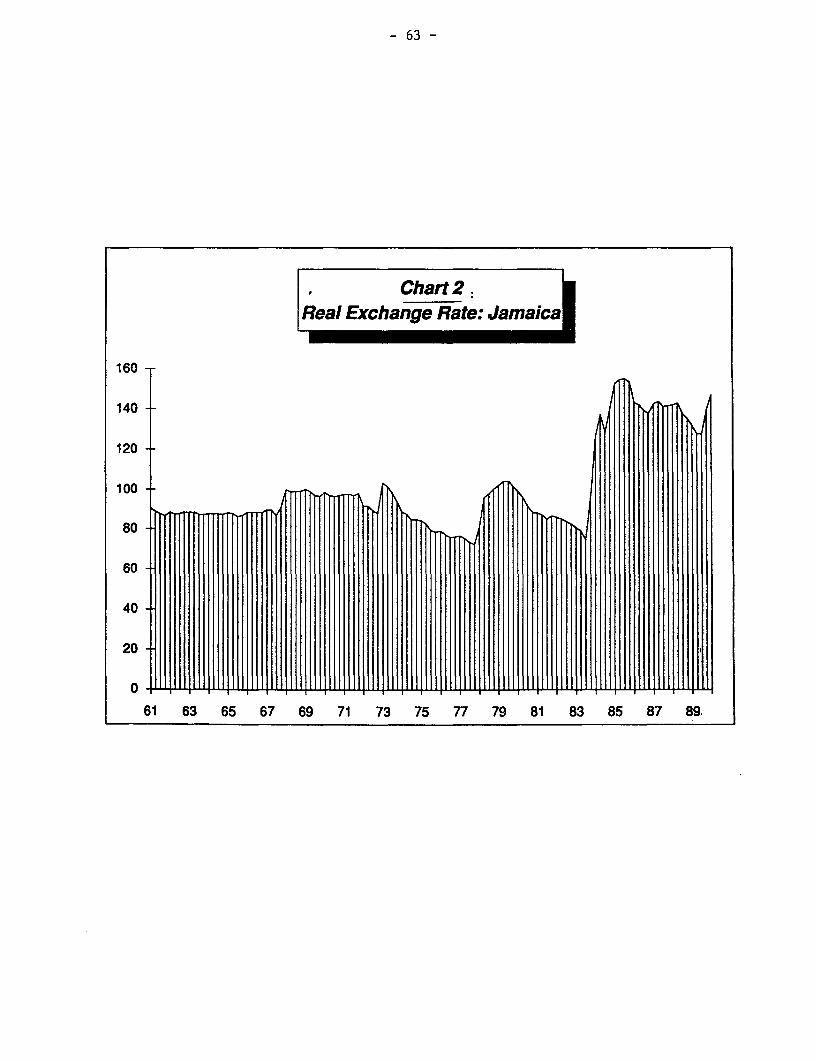

1 Terms of Trade: Jamaica . . . . . . . . . . . . . . . . . . . 622 Real Exchange Rate: Jamaica . . . . . . . . . . . . . . . . . 633 Net Investment in Jamaica ..... . . . . . .. . . . . . . 644 Private and Public Saving . . . . . . . . . . . . . . . . . . 655 Real GDP in Jamaica, 1964-1987 ..... . . . . . . . . . . . 66

COMMENTARY BY SUE COLLINS . . . . . . . . . . . . . . . . . . . . 67

I

- 41 -

Jamaica relies heavily on international trade: its imports andexports equal roughly half the GDP. The country's bauxite reserves and beacheswould have little value without foreign markets, and there are no domesticsubstitutes for such imported goods as petroleum. But with gains from tradecomes a vulnerability to external macroeconomic events, vulnerability worsenedby Jamaica's immense foreign debt.

Jamaica is poor but not desperately poor. Its GDP of roughly US$1,000per capita places the country in the ranks of the lower-middle-income countries.But the highly skewed income distribution means that much of the population livesin genuine poverty, and past and contemplated austerity measures threaten theprecarious living conditions of that group. Even so, the long-standingcommitment of the two major Jamaican political parties to a welfare state,combined with the gentle Caribbean environment, makes Jamaica compare favorablyto wealthier countries in such development indicators as education, infantmortality, and the availability of doctors and nurses. The life expectancy of74 years compares well with many industrial countries.

Jamaica enjoyed, in the quarter century to 1973, robust economicgrowth, driven by high rates of savings and investment, in an environment ofstable prices and generally manageable external deficits (Table 1). Jamaica'seconomic decline began abruptly in 1973. Indeed, production fell dramaticallyduring most of the 1970s, making only a feeble recovery in the 1980s. Savingsand investment collapsed, inflation accelerated, and external imbalancesintensified and became chronic. By the end of 1988 the country's external debtwas nearly 150 percent of GDP. If that decline now seems inevitable to someobservers, it certainly was not foreseen in 1973. For example, 1974 World Bankanalysis of economic prospects for Jamaica presented optimistic and pessimisticscenarios for 1972-80. The pessimistic scenario foresaw growth of "only" 5.7percent a year, the optimistic scenario 7 percent a year.;/ In fact, real GDPdeclined an average of 2.5 percent a year over this period, winding up in 1980almost 20 percent below the 1972 level. This outcome would have been viewed asincredible in the early 1970s.

Which is the real Jamaica? Did the halting but real recovery thatJamaica experienced in the 1980s lay the foundation for renewed growth in the1990s - growth that Jamaica has shown itself capable of achieving? Or was itmerely a brief interruption of a secular decline? The answer depends on domesticpolicy and the external environment. This paper lays out recent historicalexperience and prospects for both determinants of Jamaican economic growth anddevelopment. It presents a brief overview of Jamaica's recent economic history,which illustrates the role of various determinants and explains how Jamaicareached its current macroeconomic position. The paper then discusses prospectsfor the future and emphasizes problems and risks that the Jamaican policymakersmust cope with in the 1990s.

.1/ World Bank 1974.

- 42 -

CRISIS AND RECOVERY

The watershed years, 1972-80, created the conditions with which recenteconomic policy has had to cope. After a brief discussion of 1972-80, the paperdetails economic policy and its outcomes in the 1980s, setting the stage for adiscussion of economic prospects for the 1990s.

Economic Crisis and Collapse. 1972-80

When Michael Manley led the Peoples National Party (PNP) to victory inthe 1972 elections, he inherited an economy that seemed sound. The Jamaicaneconomy had for a quarter century experienced rapid growth, substantial monetaryand financial stability, and a fairly strong international payments position.To be sure, worrisome trends can with hindsight be identified. The governmenthad since the early 1960s been increasingly active in economic affairs, reflectedin gradually growing government expenditures. Extending to a wide variety ofmicroeconomic, trade, and industrial policies,2/ this more active role of thegovernment was not always conducive to economic efficiency and growth. On thecontrary, it was widely believed that the government was rewarding politicalsupporters and punishing political opponents.i./ But increased governmentspending was not matched by increased revenues, and the trend throughout the1960s was increased budgetary deficits and rapid monetary growth and inflation.

In addition, the gradual decline in the terms of trade during the 1960sthreatened the generally strong international payments positioniJ (see Chart 1).In particular, the petroleum price increases that rocked the world economy in1973 were painful for Jamaica because it depends on imported petroleum for nearlyall its domestic energy needs. These increases occurred while Jamaica was inthe midst of a payments crisis that, while then minor, was an ominous harbingerof subsequent developments.

With the benefit of hindsight, the basis for economic growth wasdangerously narrow, as Jamaica's growth depended heavily on bauxite and tourism.But it is also possible to make too much of this dependence. The bauxite andtourism boom were major factors in the buoyant postwar years, but economic growthextended to all major sectors of the economy, including manufacturing,construction, and agriculture. In the late 1960s the bauxite sector contributedonly about 13 percent of Jamaica's GDP, 1 percent of employment, 14 percent ofgovernment revenue, and less than 20 percent of retained foreign exchange

2./ See Wellisz and Stone 1989 for a comprehensive, and critical, summary ofgovernment economic policies during this period.

iJ/ Wellisz and Stone 1989.

i/ See, for example, Jefferson 1972.

- 43 -

earnings.5/ And the petroleum price increases, though painful, were offset byfavorable trends in Jamaica's export prices. Indeed, although Jamaica's termsof trade were substantially less favorable than in the 1950s and early 1960s,they show no further decline until after 1978, long after the start of Jamaica'seconomic decline.V/

There were, in fact, many positive aspects of the economic situationthat the PNP government inherited in 1972. The government's external andinternal debt amounted to only about one fourth of GDP at the beginning of the1970s.7/ Until about 1969, almost all of Jamaica's current accounts had beenfinanced by direct foreign investment, and at the end of 1972 the public-sectorexternal debt amounted to only about US$200 million, less than 15 percent of GDP.Jamaica's international payments problems in 1972 and 1973 were clearlyassociated with a temporary investment boom and the completion of some bauxiteprojects.f./ In brief, while the international economic environment of the 1970swas in many respects more hostile toward Jamaica than that of the 1960s, theeconomy that the PNP inherited was basically sound. Nothing in Jamaica'seconomic development during the previous decades made subsequent disastrousevents inevitable.2/

Manley and the PNP came to office committed to the establishment ofdemocratic socialism. This translated into, among other things, a desire toreduce economic inequalities within Jamaica and throughout the world, and toreduce the role of markets and capital--particularly foreign capital--in thenational economy. From the time the PNP took power to just after the December1976 elections, the government made economic policy in a relatively unconstrainedenvironment. It made no effort to adjust to the 1973 petroleum price increases,sponsored massive wage increases, and engaged in a dramatic expansion of thepublic sector. Government consumption rose from 18 percent of GDP in 1972, to27 percent in 1976, and 32 percent in 1978. Revenue did not keep pace with therise in government spending, and the result was the familiar pattern of public-sector deficits, monetary and price inflation, exchange-rate overvaluation, andexternal deficits. This situation was exacerbated in Jamaica by emigration ofthe professional and business class to the United States and Canada as economicprospects deteriorated.

5. Jefferson 1972.