vilniaus gedimino technikos universitetas - vilnius tech

84

1 VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETAS VERSLO VADYBOS FAKULTETAS Ʋ021,Ǐ (.2120,.26 ,5 VADYBOS KATEDRA 6LOYLMD 'REURYROVN\Wơ EVALUATION OF VILNIUS CITY LARGEST SHOPPING CENTERS LEASING USING MULTIPLE CRITERIA METHOD VI/1,$86 0,(672 ','ä,Ǐ-Ǐ 35(.<%26 &(175Ǐ 1UOMOS DAUGIAKRITERINIS VERTINIMAS Baigiamasis magistro darbas Verslo vadybos VWXGLMǐ SURJUDPD YDOVW\ELQLV NRGDV 62403S121 Tarptautinio verslo specializacija Vadybos ir verslo administravimo VWXGLMǐ NU\SWLV Vilnius, 2011

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of vilniaus gedimino technikos universitetas - vilnius tech

1

VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETAS

VERSLO VADYBOS FAKULTETAS

VADYBOS KATEDRA

EVALUATION OF VILNIUS CITY LARGEST SHOPPING CENTERS LEASING USING MULTIPLE CRITERIA METHOD

VI UOMOS DAUGIAKRITERINIS VERTINIMAS

Baigiamasis magistro darbas

Verslo vadybos 62403S121

Tarptautinio verslo specializacija

Vadybos ir verslo administravimo

Vilnius, 2011

2

VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETASVERSLO VADYBOS FAKULTETAS

VADYBOS KATEDRA

TVIRTINU

______________________

(Varda

______________________ (Data)

EVALUATION OF VILNIUS CITY LARGEST SHOPPING CENTERS LEASING USING MULTIPLE CRITERIA METHOD

NUOMOS DAUGIAKRITERINIS VERTINIMAS

Baigiamasis magistro darbas

Tarptautinio verslo specializacijaVadybos ir verslo ad

Vadovas __________

(Data)

Konsultantas_________________________________ ____________ __________

(Data)

Konsultantas_________________________________ ____________ _________

(Data)

Vilnius, 2011

3

VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETAS

Verslo vadybos(Fakultetas)

Verslo vadyba, TVmitu09

BAIGIAMOJO DARBO (PROJEKTO)

2011 m. d.(Data)

Patvirtinu, kad mano baigiamasis darbas (projektas) tema

patvirtintas 20 m. d. dekano potvarkiu Nr. ,

mokslini kai ir specialistai:

Mano darbo (projekto) vadovas

-usi).

4

VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETASVERSLO VADYBOS FAKULTETAS

TVIRTINU

_______________________

)

_____________________(Data)

BAIGIAMOJO MAGISTRO DARBO

……......................Nr. ...............Vilnius

Studentui (ei) Silvijai Dobrovolskytei..........…............................................…........

Baigiamojo darbo tema:

............................................................................................................................................................patvirtinta 201…m. ……………….…… d. dekano potvarkiu Nr. ………….

kai

Baigiamojo darbo rengimo konsultantai: …….………………………………………………………………………………………………................................................................................................ ...............................................................

Vadovas

…………………………………..

……………………………..….... (Data)

Tarptautinio verslo specializacija

5

Vilnius Gediminas Technical University

Business Management faculty

Economics and management of enterprises department

ISBN ISSN

Copies No. ………

Date ….-….-….

Business Management study programme master thesis.

Title: Evaluation of Vilnius city largest shopping centers leasing using multiple criteria method

Author Silvija Dobrovolskyt Academic supervisor prof. habil. Dr. R.

Thesis language

Lithuanian

Foreign (English)X

Annotation

The purpose of this master thesis is to evaluate three major shopping centers of Vilnius

city, using a multiple criteria method and to provide the methodology for choosing the right

retail location.

The work consists of four parts. The review of shopping centers‘ classification and

importance in social and economic life is provided in first part of the thesis. The hierarchical

system of choosing retail location criteria is created in the second part of this paper. The third

section provides an overview of the Vilnius City shopping centers‘ market and identifies

three major shopping centers in Vilnius. The survey of commercial real estate professionals

and calculations according the hierarchical criteria system are carried out in part four of this

thesis. The leasing opportunities of three major shopping centers of Vilnius are evaluated and

the methodology of choosing a retail location in shopping center is provided in the end.

Structure: introduction, theoretical part, analytical part, survey and calculations,

conclusions and suggestions, references.

Thesis consists of: 77 pages text without appendixes, 34 tables, 10 graphic schemes, 32

references. The attached Appendix 1.

Keywords: criteria, leasing, multiple criteria method, shopping center, shopping mall, retail location

6

Vilniaus Gedimino technikos universitetas

Verslo vadybos fakultetas

katedra

ISBN ISSN

Egz. sk. ………..

Data ….-….-….

Verslo vadybos gistro darbas

Pavadinimas vertinimasAutorius Vadovas prof. habil. dr. R.

Kalba

X

AnotacijaBaigiamajame magistro darbe

Baigiamojo magistro darbo tikslas yra

keturios dalys. Pirmoje dalyje

ekonominiame gyvenime. Antroje dalyje yra sudaroma hi

. Ketvirtoje nimo metodas ir, remiantis, turima

vadas dalis dalis, ir .

Darbo apimtis: 77 p. teksto be , 3 2. Pridedamas 1 priedas.

patalpos

7

VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETASVERSLO VADYBOS FAKULTETAS

VADYBOS KATEDRA

……..................Nr. ...............Vilnius

vidurkis..................…...........….....………….........................…...balo.

Baigiamojo darbo tema:

Vadovo atsiliepimas

……………………......................................................................................... ...................................................................

............................................................................................................................................................

............................................................................................................................................................

..................................................................................................................................... .......................

............................................................................................................................................................

............................................................................................................................................................

............................................................................................................................................................

Vadovas .....................……..........

Tarptautinio verslo specializacija

8

VILNIAUS GEDIMINO TECHNIKOS UNIVERSITETASVERSLO VADYBOS FAKULTETAS

VADYBOS KATEDRA

RECENZIJA

…….......................Nr. ...............Vilnius

vertinimas ………………………………………………………………………………....................................

RECENZIJA…………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………

……………………...….………………………………………………………………………………………………

…………………………..….……………………………………………………………………………………………

………………………………...…………………………………………………………………………………………

………………………………..….………………………………………………………………………………………

…………………………………..….……………………………………………………………………………………

…………………………………...…….………………………………………………………………………………

…………………………………………...….…………………………………………………………………………

………………………………………………………………………………………………………………………....

Magistro laipsnio suteikimo komisijos narys

………………………… ……………………………………………………..

9

CONTENT

INTRODUCTION………………………………………………………………………………14

1. SHOPPING CENTRE ............................................................................................................ 16

1.1 RETAIL LOCATIONS ....................................................................................................... 16

1.2 SHOPPING CENTER DEFINITION ................................................................................. 17

1.3 SHOPPING CENTRE TYPES ........................................................................................... 19

1.3.1 Types by size ................................................................................................................ 19

1.3.2 Types by concept .......................................................................................................... 20

1.3.3 Types by location.......................................................................................................... 22

1.3.4 Types by layouts ........................................................................................................... 23

1.4 SHOPPING CENTRE IMPORTANCE.............................................................................. 25

1.5 EUROPEAN MARKET AND PERSPECTIVES............................................................... 27

1.5.1 Market review............................................................................................................... 27

1.5.2 Shopping centers perspectives...................................................................................... 28

2. CHOOSING RETAIL LOCATION ..................................................................................... 30

2.1 Importance of retail location ............................................................................................... 30

2.2 Multiple criteria decision making ....................................................................................... 31

2.3 Criteria................................................................................................................................. 31

2.3.1 Location ........................................................................................................................ 34

2.3.2 Price .............................................................................................................................. 36

2.3.3 Tenant Mix ................................................................................................................... 37

2.3.4 Customers ..................................................................................................................... 39

2.3.5 Shopping center characteristics .................................................................................... 40

2.3.6 Premises characteristics ................................................................................................ 42

2.3.7 Recognition................................................................................................................... 44

3 SHOPPING CENTERS IN VILNIUS.................................................................................... 46

3.1 Market review 2010 ............................................................................................................ 46

3.1.1 Economy....................................................................................................................... 46

10

3.1.2 Retail............................................................................................................................. 46

3.1.3 Major shopping centers ................................................................................................ 48

4. MULTIPLE CRITERIA ANALYSIS OF MAJOR SHOPPING CENTERS IN VILNIUS....................................................................................................................................................... 53

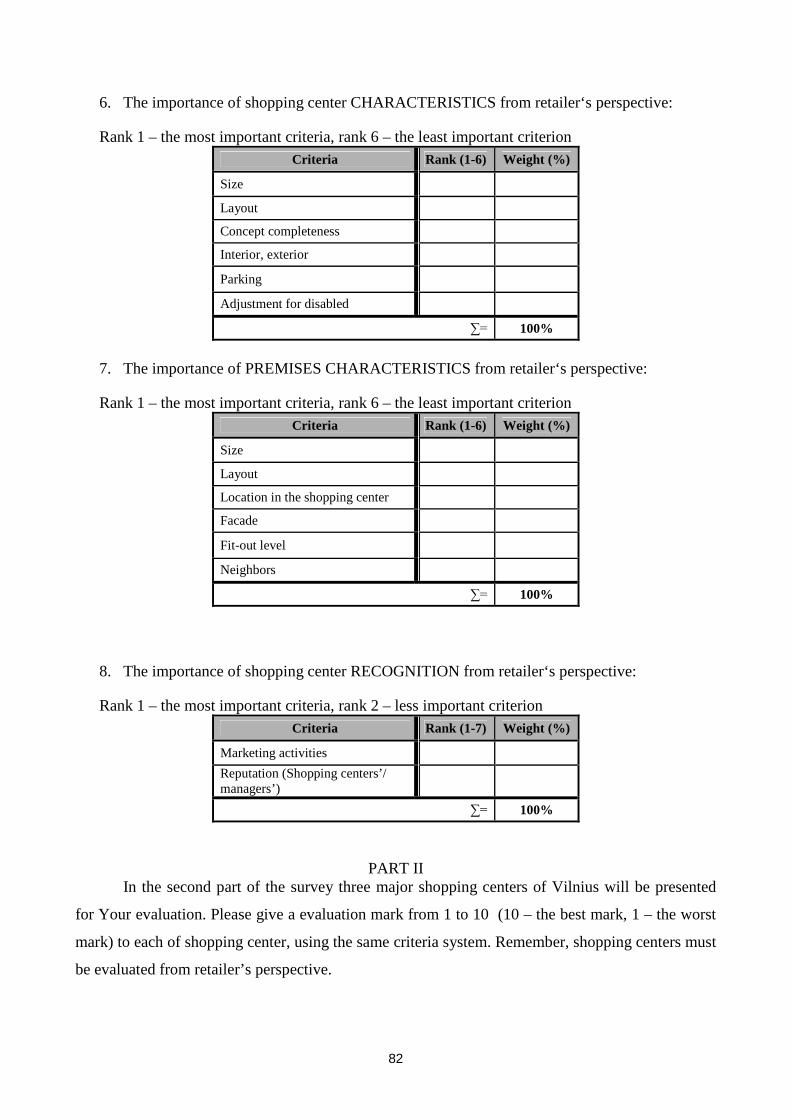

4.1 Survey.................................................................................................................................. 53

4.2 Evaluation of criteria ........................................................................................................... 54

4.3 Evaluation of shopping centers ........................................................................................... 61

4.4 Calculations and conclusions .............................................................................................. 67

CONCLUSIONS ......................................................................................................................... 73

REFERENCES............................................................................................................................ 75

APPENDIXES ............................................................................................................................. 78

11

List of Tables:

1. Table 1. International Standard for European Shopping Center Types (Lambert, 2006)

2. Table 2. Types of shopping centers (ICSC, 1999)

3. Table 3. Key figures of the main shopping centers in Vilnius (made by author)

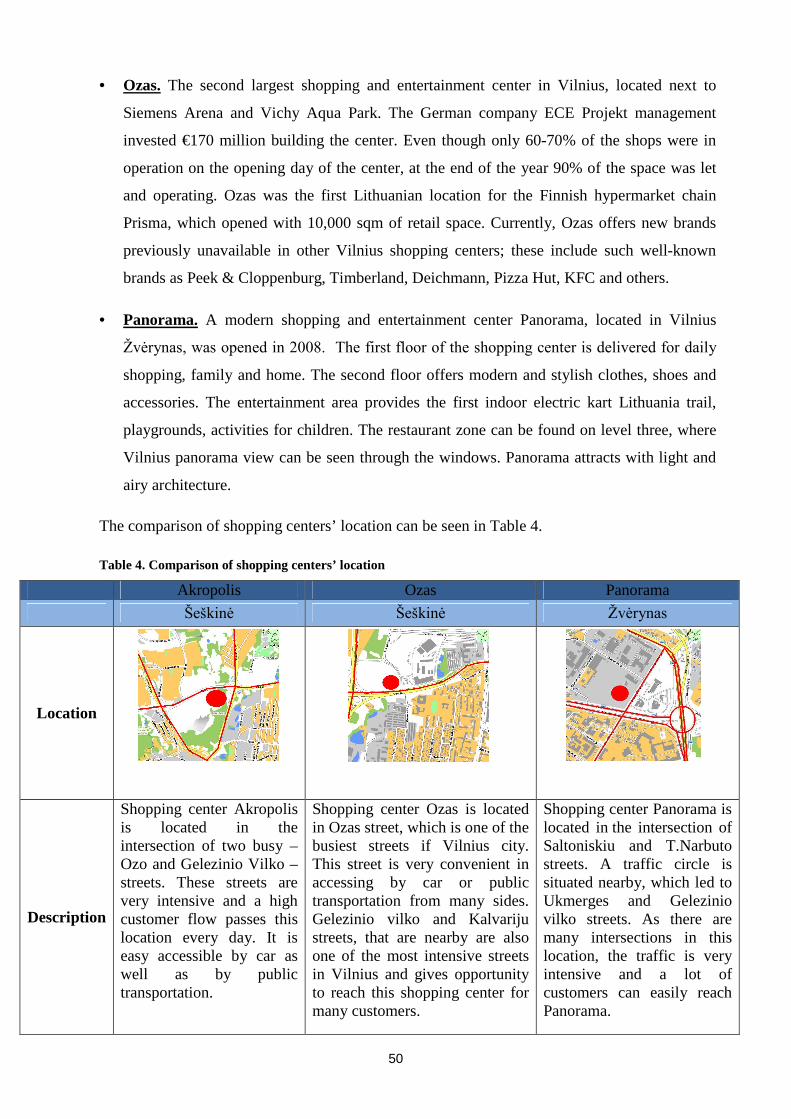

4. Table 4. Comparison of shopping centers’ location (made by author)

5. Table 5. Comparison of shopping centers’ parking (made by author)

6. Table 6. Comparison of shopping centers’ layouts and concepts (made by author)

7. Table 7. Comparison of shopping centers’ tenant mix (made by author)

8. Table 8. Ranks of the main criteria elicited from experts (made by author)

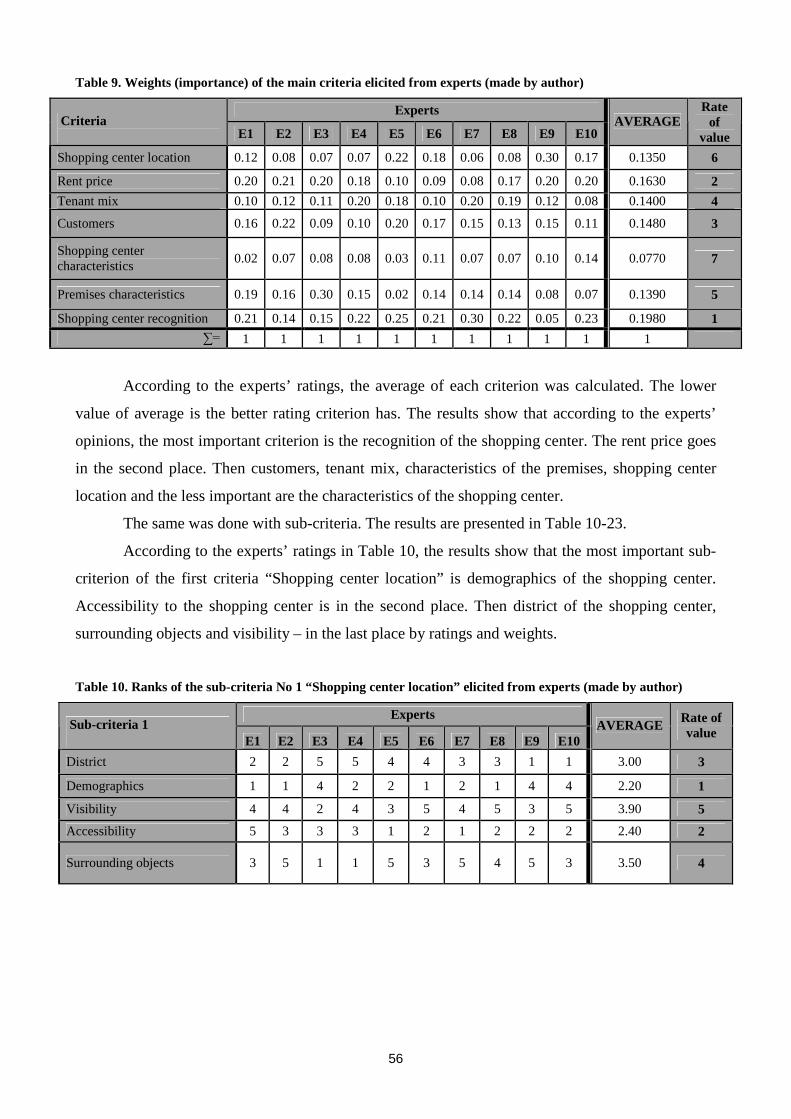

9. Table 9. Weights (importance) of the main criteria elicited from experts (made by author)

10. Table 10. Ranks of the sub-criteria No 1 “Shopping center location” elicited from experts

(made by author)

11. Table 11. Weights (importance) of the sub-criteria No 1 “Shopping center location”

elicited from experts (made by author)

12. Table 12. Ranks of the sub-criteria No 2 “Rent price” elicited from experts (made by

author)

13. Table 13. Weights (importance) of the sub-criteria No 2 “Rent price” elicited from

experts (made by author)

14. Table 14. Ranks of the sub-criteria No 3 “Tenant mix” elicited from experts (made by

author)

15. Table 15. Weights (importance) of the sub-criteria No 3 “Tenant mix” elicited from

experts (made by author)

16. Table 16. Ranks of the sub-criteria No 4 “Customers” elicited from experts (made by

author)

17. Table 17. Weights (importance) of the sub-criteria No 4 “Customers” elicited from

experts (made by author)

18. Table 18. Ranks of the sub-criteria No 5 “Shopping center characteristics” elicited from

experts (made by author)

19. Table 19. Weights (importance) of the sub-criteria No 5 “Shopping center characteristics”

elicited from experts (made by author)

20. Table 20. Ranks of the sub-criteria No 6 “Premises characteristics” elicited from experts

21. Table 21. Weights (importance) of the sub-criteria No 6 “Premises characteristics”

elicited from experts (made by author)

12

22. Table 22. Ranks of the sub-criteria No 7 “Shopping center’s recognition” elicited from

experts (made by author)

23. Table 23. Weights (importance) of the sub-criteria No 7 “Shopping center’s recognition”

elicited from experts (made by author)

24. Table 24. Evaluation of Akropolis shopping center by the main criteria (made by author)

25. Table 25. Evaluation of Akropolis shopping center by the sub – criteria (made by author)

26. Table 26. Evaluation of Ozas shopping center by the main criteria (made by author)

27. Table 27. Evaluation of Ozas shopping center by the sub – criteria (made by author)

28. Table 28. Evaluation of Panorama shopping center by the main criteria (made by author)

29. Table 29. Evaluation of Panorama shopping center by the sub – criteria (made by author)

30. Table 30. Shopping centers’ evaluation (the main criteria) (made by author)

31. Table 31. Shopping centers’ evaluation (sub – criteria) (made by author)

32. Table 32. Shopping centers’ comparison (the main criteria) (made by author)

33. Table 33. Shopping centers’ comparison (sub- criteria) (made by author)

34. Table 34. Comparison of one-level and hierarchical systems calculations (made by

author)

13

List of Figures:

1. Figure 1. Shopping centers in city center

2. Figure 2. Shopping centers equidistant from city center

3. Figure 3. Shopping centers on the boundaries of the city

4. Figure 4. Shopping centers out of town

5. Figure 5. Shopping center layouts

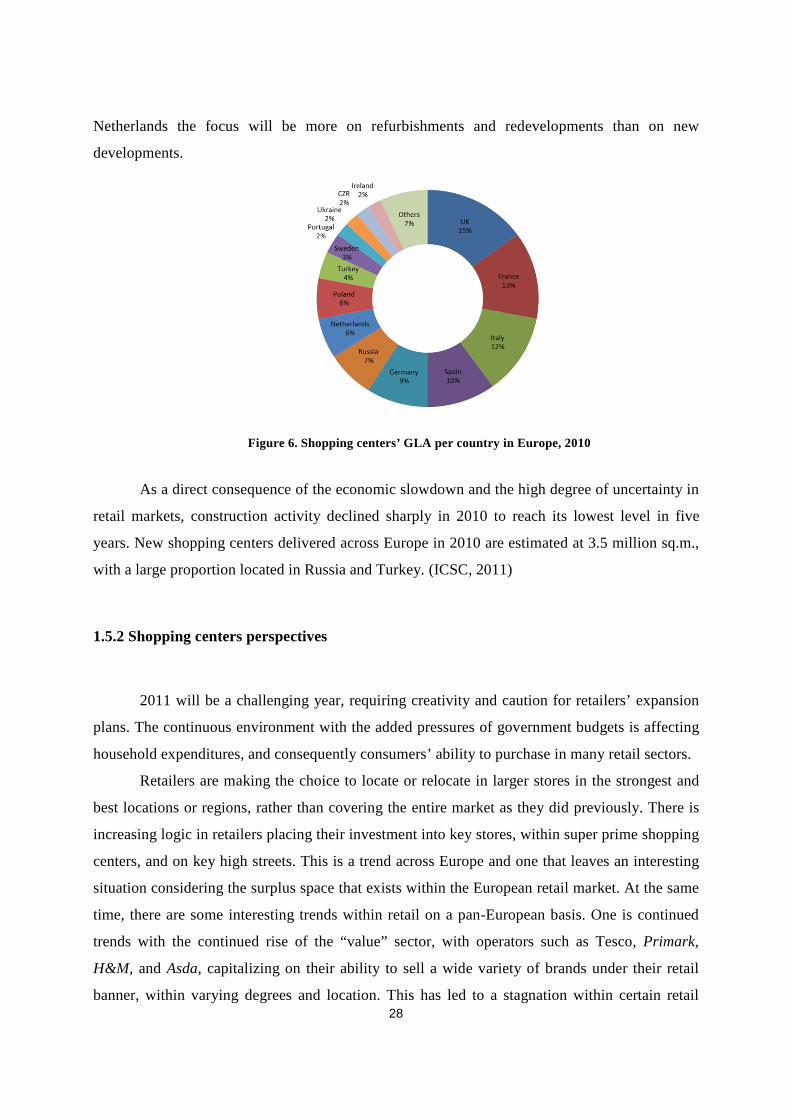

6. Figure 6. Shopping centers’ GLA per country in Europe, 2010

7. Figure 7. Retail Location criteria

8. Figure 8. Shopping center’s distribution by cities (%), 2010, IInd quarter

9. Figure 9. Shopping center’s area for 1000 people, 2010 (Ober-Haus, 2010)

10. Figure 10. Growth of shopping centers’ area in Vilnius

14

INTRODUCTION

Over the years shopping center concept and value has strongly changed. Today the

shopping center is not just a place for shopping or spending free time, but it actively participate

in country’s economic and social life. Even a third part of country’s retail sales is generated in

shopping centers. Moreover, shopping centers are a great catalyst for retail growth and many job

positions are created through shopping centers as well. Today shopping centers contribute to

forming citizenries’ style and shopping culture.

Over the past decade the rapid boom of shopping centers created not only a wide

variety for customers, increased competition among traders, but also tasked the process for

retailers of choosing the right retail location for their business. The success of retailer’s business

is strongly determined by right choice of retail location. However, for the reason to choose the

best option, many factors are needed to be evaluated: location, rent price, tenant mix, customer

flow, shopping center recognition, marketing activities, etc. To evaluate correctly each of the

criteria and to estimate the weight (importance) of it is one of the toughest and most difficult

tasks for retailer when choosing a retail location.

Over the past years Vilnius city shopping centers’ market has also increased significantly.

In consequence of intensive development of shopping centers a great variety of choice for

costumers was created. On the other hand, the competition between shopping centers has also

increased significantly, which complicates the selection of store locations for retailers.

The aim of this paper is to analyze the most important criteria for shopping centers, and

according to them, to evaluate the major Vilnius city shopping centers from retailer’s position.

For processing criteria and evaluating shopping centers, the multiple criteria method was chosen,

which is used as a decision support system.

Objective of the work raises the following tasks:

1. To explore the shopping centers’ development and classification;

2. To review the importance of shopping centers’ market to European economy;

3. To analyze the choice of retail location importance and the main criteria;

4. To explore the major Vilnius city shopping centers;

5. To perform multiple analysis, which help to identify the best shopping center for

leasing in Vilnius;

15

6. Based on the results to draw conclusions and suggestions.

A variety of literature sources of foreign authors scientific articles, various reviews and

analysis of specialists are used in this paper.

This paper consists of four parts. The shopping center concept, development trends,

classification and importance for social and economic life is analyzed in first part of this paper.

After a brief review about shopping center’s market in Europe, an importance for the economy is

analyzed. In the second part of the paper the importance of choice for retail location and the main

criteria groups are analyzed. The third part of this paper provides an overview of the Vilnius city

shopping centers’ market and a more detailed review of three major shopping centers –

Akropolis, Ozas and Panorama. For the reason to process all the criteria a multiple criteria

method is used in part four of this paper. Through the survey, which was intended to commercial

real estate professionals, the ranks and weights (importance) of criteria was identified and three

major Vilnius city shopping centers were evaluated.

Based on the results of multiple criteria analysis, the best Vilnius city shopping center for

leasing is chosen and the suggestions of choosing the right retail location for retailers are

provided.

This paper provides wider understanding about shopping center importance to social and

economic life as well as an importance of right choice of retail location. The analysis of Vilnius

city major shopping centers leasing using multiple criteria method shows what criteria are the

most important for retailers in a process of choosing the best retail location and which shopping

center of Vilnius city is the most attractive for retailers.

.

16

I SHOPPING CENTRE

1.1 RETAIL LOCATIONS

Before starting business or just opening one more store, the most important stage is to

choose location. The difference between selecting the wrong location and the right site could be

the difference between business failure and success.

Commercial retail locations are available in many different forms, depending upon the

demand of products or services and target group. Retailers must consider many store location

factors in order to choose the perfect location, generating the maximum amount of profit. The

main types of retail locations are:

1) Shopping Mall. From small kiosks to large floor areas for big stores, a shopping mall is a

wise choice for any type of retailing businesses. There are generally 1 to 3 anchor stores,

or large chain stores, and then dozens of smaller retail shops. Typically the rent in a mall

location is much higher than other retail locations. This is due to the high amount of

customer traffic a mall generates.

2) Community Shopping Center. Most of the neighborhoods have their community

shopping centers in various sizes. These are small areas where not more than 40 to 50

shops can be found. Also the types of retailers, and the goods or services available in a

community shopping center differs a lot depending upon the location and the type of

customers. One area to investigate before choosing this type of store location is parking.

Smaller shopping centers and strip malls may have a limited parking area for your

customers.

3) Downtown Area. Any traditional market area offers more freedom and fewer rules for

retail business owners. Along with many older, well-established specialty stores and well

known retail franchise outlets in such market areas, there are many new brands thriving

to start their business there. The lack of parking is generally a big issue for downtown

retailers.

4) Airports. The airport retail hub may differ from malls because it is only open to travelers

but retail stores offer welcome relief to travelers to utilize their free time. Today in most

of the airports products are being showcased as never before as retailers have realized the

revenue potential of retailing business in airports. (Waters, 2008)

17

5) Office Building. The business park or office building may be another option for a

retailer, especially when they cater to the needs and requirements of other businesses.

Here the target customers are very specific, but if the marketing is done well, one can

enjoy high profit on investments.

6) Free standing locations. This type of retail location is basically any stand-alone

building. It can be tucked away in a neighborhood location or right off a busy highway.

Depending on the landlord, there are generally no restrictions on how a retailer should

operate his business. The price for all that freedom may be traffic.

7) Home-based. More and more retail businesses are getting a start at home. For this type

of location, a retailer does not need to invest much and the growth might also be limited

to some extent. This type of location is an inexpensive option, but growth may be limited.

It is harder to separate business and personal life in this setup and the retailer may run

into problems if there isn't a different address and/or phone number for the business.

(StartFranchiseNow, 2010).

All the options, mentioned above, had their pluses and minuses, but the tendency shows

that retailers mostly seek out and locate next to other retailers in one place or in a nearby

geographical area (Berman and Evans, 2007). Retailers increasingly react by working together in

order to enhance the attractiveness of their common location (Warnaby, Bennison, Davies and

Hughes, 2004). Shopping malls are planned, constructed, managed and marketed as integrated

unit and this has a strong impact on the retail mix – tenant mix, atmosphere, merchandise value,

accessibility, etc. The opportunity to find everything in one place, saving time and energy, not

depending on weather, staying away from traffic, attractive marketing events and many other

advantages attract customers and put the shopping mall to the very top of retail location choices.

(Teller, 2008)

1.2 SHOPPING CENTER DEFINITION

Commercial buildings are one of the oldest building types in the world history. The

exchange of goods was one of the key driving forces behind the development of civilizations that

have affected all areas of life and led to the emergence of cities and their expansion.

With the development of the economy and changing needs of society, the shopping center

definition and importance has also changed. To understand shopping center, that is also usually

called as a shopping mall, only as a shopping place is not entirely accurate. As shopping centers

18

become more and more multifunctional, their role is growing not only in social life, but in the

country‘s economic life too.

Different references provide different definitions for the shopping center’s concept.

According to the International Council of Shopping Centers1, a shopping center is a

group of retail and other commercial establishments that is planned, developed, owned, and

managed as a single property, typically with on-site parking provided. The center’s size and

orientation are generally determined by the market characteristics of the trade area served by the

center. (ICSC, 2007)

According to the insights of Lithuanian real estate professionals, shopping center is a

centrally managed commercial establishment, which operates more than 10 independent stores

(tenants), leasable area is not less than 5 000 square meters and anchor tenant takes not more

than 70% of leasable area. (Macijauskas, 2009)

Various dictionaries define shopping center in such ways:

1) One or more buildings forming a complex of shops representing merchandisers, with

interconnecting walkways enabling visitors to easily walk from unit, along with a parking

area – a modern, indoor version of the traditional marketplace; (Wikipedia, 2004)

2) A specialty built covered area containing shops and restaurants, which people can walk

between, and where cars are not allowed; (Reverso, 2005)

3) A collection of retail stores with a common parking area, usually containing a

combination of department stores, grocery stores, retail and food stores. (InvestorWords,

2005)

So, the study of shopping center‘s definition in different sources showed that the

main shopping center‘s features are:

• A complex of retail and other commercial establishments;

• Planned, developed, owned, and managed as a single property;

• With a common parking area.

1 The International Council of Shopping Centers (ICSC) is the global trade association of the shopping centerindustry. Its 60,000 members in the U.S., Canada and more than 80 other countries include shopping center owners, developers, managers, marketing specialists, investors, lenders, retailers and other professionals as well as academics and public officials. (ICSC, 2004)

19

1.3 SHOPPING CENTRE TYPES

The main historical events mentioned above indicate that the changing society,

developing technology and economic growth made changes in shopping center functions, layouts

and concept too. For example, in the middle of 20th century the rise of the suburb and

automobile culture influenced the creation of new formats.

1.3.1 Types by size

According to European standards, the International Council of Shopping Centers

identifies that there are traditional and specialized shopping centers (Table 1). It is also identifies

that there are two types of small traditional centers:

• Comparison – based: include retailers typically selling fashion apparel and

shoes, home furnishings, electronics, general merchandise, toys, luxury goods,

gifts and other discretionary goods. They are often a part of larger retail areas,

most likely found in city centers and not anchored.

• Convenience – based: include retailers that sell essential goods and are typically

anchored by a grocery store (supermarket or hypermarket). Additional stores

include drugstores, convenience stores, retailers’ selling household goods, basic

apparel, flowers and pet supplies. Those centers are typically located at the edge

or out of town.

Table 1. International Standard for European Shopping Center Types (Lambert, 2006)

h

t

t

p

:

/

/

Format Type of Scheme Gross Leasable Area (GLA)

Very Large 80 000 sq.m. and aboveLarge 40 000 – 79 999 sq.m.Medium 20 000 – 39 999 sq.m.

Traditional

Small 5 000 – 19 999 sq.m.Retail Park Large

MediumSmall

20 000 sq.m. and above10 000 – 19 999 sq.m.5 000 – 9 999 sq.m.

Factory Outlet Center 5 000 sq.m. and above

Specialized

Theme–Oriented Center

Leisure – BasedNon–Leisure–Based

5 000 sq.m. and above5 000 sq.m. and above

20

1.3.2 Types by concept

Given the maturity of the industry, numerous types of centers currently exist that go

beyond the standard definitions. According to the International Council of Shopping Centers, the

first classification for shopping centers was: Neighborhood, Community, Regional and

Superregional centers.

Due to the growing industry, more types of shopping centers were developed. Now the

International Council of Shopping Centers classifies shopping centers in eight types (Table 2):

• Neighborhood Center: This center is designed to provide convenience shopping

for the day-to-day needs of consumers in the immediate neighborhood. According to the

International Council of Shopping Centers, roughly half of these centers are anchored by a

supermarket, while about a third has a drugstore anchor. These anchors are supported by stores

offering pharmaceuticals and health-related products, sundries, snacks and personal services. A

neighborhood center is usually configured as a straight-line strip with no enclosed walkway or

mall area, although a canopy may connect the storefronts.

• Community Center: A community center typically offers a wider range of

apparel and other soft goods than the neighborhood center does. Among the more common

anchors are supermarkets, super drugstores, and discount department stores. Community center

tenants sometimes contain off-price retailers selling such items as apparel, home

improvement/furnishings, toys, electronics or sporting goods. The center is usually configured

as a strip, in a straight line, or “L” or “U” shape. Of the eight center types, community centers

encompass the widest range of formats.

• Regional Center: This center type provides general merchandise (a large

percentage of which is apparel) and services in full depth and variety. Its main attractions are its

anchors: traditional, mass merchant, or discount department stores or fashion specialty stores. A

typical regional center is usually enclosed with an inward orientation of the stores connected by a

common walkway and parking surrounds the outside perimeter.

• Superregional Center: Similar to a regional center, but because of its larger

size, a superregional center has more anchors, a deeper selection of merchandise, and draws from

a larger population base. As with regional centers, the typical configuration is as an enclosed

mall, frequently with multilevels.

21

• Fashion/Specialty Center: A center composed mainly of upscale apparel shops,

boutiques and craft shops carrying selected fashion or unique merchandise of high quality and

price. These centers need not be anchored, although sometimes restaurants or entertainment can

provide the draw of anchors. The physical design of the center is very sophisticated, emphasizing

a rich decor and high quality landscaping. These centers usually are found in trade areas having

high income levels.

• Power Center (Retail Park): A consistently designed, planned and managed

scheme that comprises mainly medium- and large-scale specialist retailers (“big boxes” or

“power stores”). (Lambert, 2006)

• Theme/Festival Center: A consistently designed, planned and managed scheme

that can either be leisure based or non-leisure based. This scheme includes some retail units and

typically concentrates on a narrow but deep selection of merchandise within a specific retail

category. A leisure-based center is usually anchored by a multiplex cinema and includes

restaurants and bars with any combination of bowling, health and fitness and other leisure-

concept uses. A non-leisure-based center concentrates on a niche market for fashion/apparel or

home furnishings or can target specific customers such as passengers at airports. The biggest

appeal of these centers is to tourists; they can be anchored by restaurants and entertainment

facilities. These centers, generally located in urban areas, tend to be adapted from older,

sometimes historic, buildings, and can be part of mixed use projects.

• Factory Outlet Center: Consistently designed, planned and managed scheme

with separate store units, where manufacturers and retailers sell merchandise at discounted prices

that may be surplus stock, prior – season or slow selling. These centers are typically not

anchored. A strip configuration is most common, although some are enclosed malls, and others

can be arranged in a "village" cluster. (ICSC, 1999)

It is not always easy to identify precisely the type of shopping center. There are shopping

centers that combine elements from different types such mixing is one more way how new

concepts of shopping centers begin.

22

Table 2. Types of shopping centers (ICSC, 1999)

TYPE CONCEPT SQ.M. NUMBER TYPEANCHOR

RATIONEIGHBORHOOD CENTER

Convenience 2 800 –14 000

1 or more Supermarket 30-50%

COMMUNITY CENTER

Convenience 9 300 –32 500

2 or more Supermarket, drugstore, home improvement, specialty apparel

40-60%

REGIONAL CENTER Fashion 37 200 –74 300

2 or more Department stores, fashion apparel

50-70%

SUPERREGIONAL CENTER

Similar to regional, but wider assortment

74 300 and above

3 or more Department stores, fashion apparel

50-70%

FASHION / SPECIALTY CENTER

Fashion 7 400 –23 200

N/AFashion

N/A

POWER CENTER Dominant anchors, few small tenants

23 200 –55 700

3 or more Home improvement, warehouse

75-90%

THEME / FESTIVAL CENTER

Leisure: tourists-oriented, retail and services

7 400 –23 200

N/A Restaurants, entertainment

N/A

OUTLET CENTER Manufacturers‘ outlet stores

4 600 –37 200

N/A Manufacturers‘ outlet stores

N/A

1.3.3 Types by location

Shopping center‘s location is one of the most important factors affecting the shopping

1) Standing in historical city center (Figure 1);

Figure 1. Shopping centers in city center

2) Situated in central districts of the city, equidistant from city center and suburbs

(Figure 2);

Figure 2. Shopping centers equidistant from city center

23

3) Built in suburbs, outskirts and city boundaries (Figure 3);

Figure 3. Shopping centers on the boundaries of the city

4) Situated out of town, at the farthest distance from city center. Location allows build

larger shopping centers, with convenient access and spacious parking lot. (Figure

4).

Figure 4. Shopping centers out of town

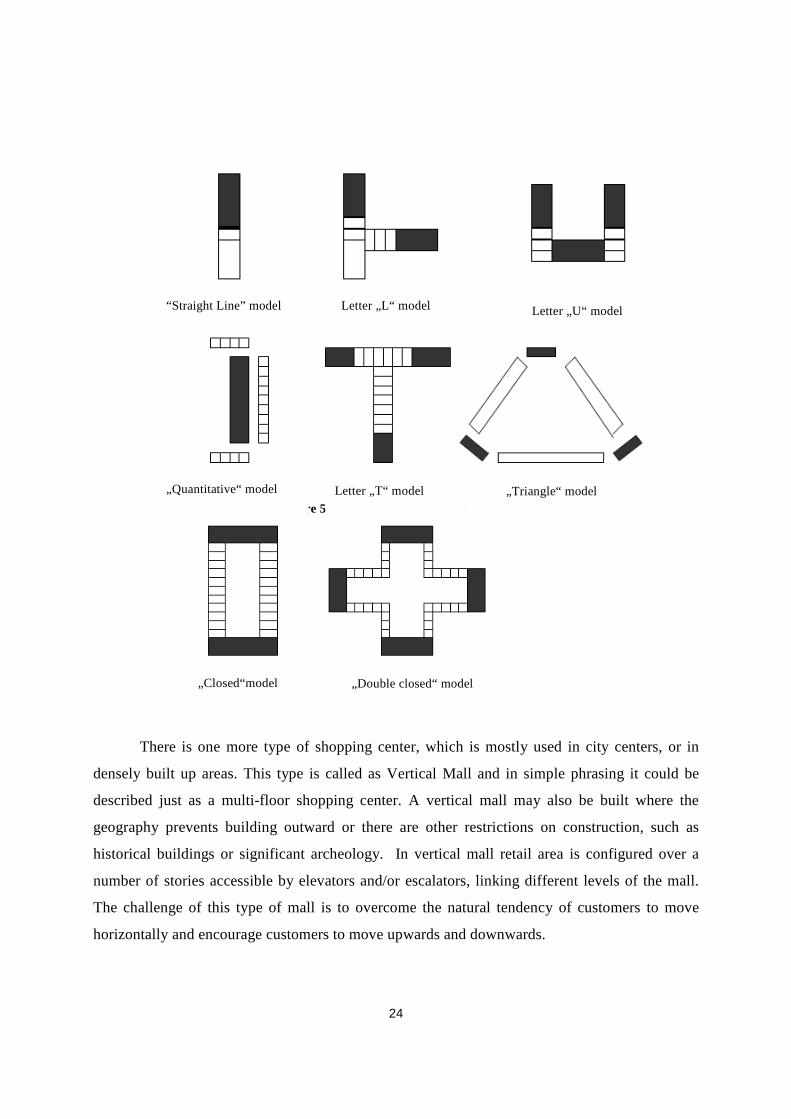

1.3.4 Types by layouts

Shopping center‘s location has a significant influence not only to its concept, but also to

the layout of the shopping center. Shopping centers in the city center and densely built up

districts usually are smaller than shopping centers in suburbs. Broad area, which is intended to

shopping center, gives developers more freedom in developing the concept and layout. Shopping

center’s layout must be planned and designed considering not only constructional and

architectural requirements, but human psychology as well. The following types of shopping

centers are shown in Figure 5 (Levitt, Berens, Beyard, 1997):

24

Figure 5. Shopping center layouts

There is one more type of shopping center, which is mostly used in city centers, or in

densely built up areas. This type is called as Vertical Mall and in simple phrasing it could be

described just as a multi-floor shopping center. A vertical mall may also be built where the

geography prevents building outward or there are other restrictions on construction, such as

historical buildings or significant archeology. In vertical mall retail area is configured over a

number of stories accessible by elevators and/or escalators, linking different levels of the mall.

The challenge of this type of mall is to overcome the natural tendency of customers to move

horizontally and encourage customers to move upwards and downwards.

„Quantitative“ model Letter „T“ model „Triangle“ model

“Straight Line” model Letter „L“ model Letter „U“ model

„Closed“model „Double closed“ model

25

1.4 SHOPPING CENTRE IMPORTANCE

Shopping centers in many parts of Europe have existed for many centuries, but it

is only in the past 50 years that modern purpose-built shopping centers have been developed in

Europe. The consumer is the linchpin of the retail real estate industry and, for that matter, the

European economy. With consumption accounting for approximately 60 percent of the Gross

Domestic Product (GDP) in Europe, it is a backbone and catalyst for European growth.

For the retailer and the consumer, shopping centers provide a clustering of goods

and services that benefit both. Retailers benefit from the concentration of shoppers (footfall) and

consumers benefit from the choice of shops, wide-selection of goods and services offerings and

retailer competition. For the community, shopping centers provide economic benefit, including

jobs and tax revenues through new or expanded hubs of commerce or regeneration of areas. For

the investor, shopping centers are a unique real-estate asset on par, as an asset class, with office,

industrial and residential properties.

Here are 8 key reasons why shopping centers are important to the European

economy and its commerce:

1. Commerce depends on shopping centers. Nearly a quarter of all retail sales in Europe are

estimated to occur in shopping centers. The value of retail sales is approximately equivalent

to a fifth of GDP.

2. Retailers depend on shopping centers. Shopping centers are a good platform for retailer

growth, especially in new markets. Over the next ten years, the retail sector is expected to

grow more rapidly than GDP, and therefore become an increasingly more important driver of

economic activity. The growth in retail activity has been driven, in part, by the growth and

proliferation of large multinational retailers. The development of new centers offers retailers

the opportunity to occupy larger and more efficient stores from scratch, tailored to their

requirements, within a professionally built and run environment.

3. Shopping centers create and support millions of jobs. Shopping centers make a significant

contribution to retail employment. Shopping centers directly employ 4.0 million workers

across Europe—equivalent to a fifth of retail employment. Shopping centers generate

26

employment opportunities for women. About three-fifths of overall retail employment is

female.

4. Shopping centers are a catalyst for non-retail development and area regeneration.

Shopping centers directly provide positive economic benefits to the community, including

employment, income and tax revenue, as well as physical improvements to the environment

in terms of better buildings and infrastructure. Indirectly, through the “multiplier” and

“accelerator” economic effects on the economy, shopping-center development (including

redevelopment and renovation) lifts the broader economy.

5. Social role. Shopping centers respond to changes in consumer tastes and needs. Retailers and

shopping-center owners are recognizing that consumers work, live and play differently today

as demographics and societies evolve and intersect ever more. Shopping centers are

providing a greater range of entertainment to connect with the consumer desire for

experiential environments. (DTZ Research, 2011)

6. Spending leisure time. Now shopping centers have a dual functionality, not only to sell and

make money, but also to cater for consumers’ immediate pleasure and enjoyment. Cinema,

bowling, pool club, theatre, karting tracks, laser spaces and many other entertainments are

being incorporated in shopping malls now and attract customers not only to spend time for

shopping, but to spend their free time as well. Moreover, parents are satisfied with shopping

malls, as it has become a good place for their children with guarantees of a gun-, drug-, and

crime free environment. (Socyberty, 2007)

7. Shopping centers are an investment-grade asset. Shopping centers are popular with cross-

border investors as they provide large good quality assets, benefiting from secure incomes

and relatively low risk compared to alternative real estate assets. Shopping centers also have

attracted investors—directly or indirectly through real estate investment trusts—because of

their relatively strong investment returns in many European countries. Total real estate

investment activity in Europe reached €95.9vbn in 2010.

8. Activity for tourists. Tourism is one of the worlds’ largest industries, and shopping is one of

the most popular activities for tourists. Given the size of this market with the growth in both

the tourism industry and tourist destinations, identifying the desires of this consumer segment

is increasingly important in the contemporary marketplace. Shopping center, being one of the

tourists’ sightseeing objects, contributes to creating the image of cities and countries.

(Kinley, Kim, Forney, 2001)

27

Shopping centers serve a number of important roles for consumers, retailers,

investors and policymakers. The ubiquitous shopping center is more than just a fixture in

thousands of towns and cities. It is a dynamic source of development, commerce and growth and,

at the same time, fills an important delivery role—efficiently and cost-effectively—for European

retailers’ products and services. Thus, shopping centers play an important role not only in public

life, but in country’s economy too.

1.5 EUROPEAN MARKET AND PERSPECTIVES

1.5.1 Market review

New shopping center development in Europe fell sharply in 2010, representing the largest

decline since 1983, according to a report from Cushman & Wakefield. Around 55.9 million

square feet of shopping center space was completed last year, a fall of 30 percent from 2009. It

was the second consecutive year of falling completion levels and represented the lowest annual

completion total since 2004. (ICSC, 2011)

In the end of 2010 Gross Leasable Area (GLA) of shopping centers across approximately

6 500 schemes of the Europe was over 120 million sq.m. The UK, France, Italy, Germany and

Spain have the largest shopping centers stocks, accounting for 60% of total European stock.

Western Europe accounts for more than 90% of shopping center stock in Europe, with the new

entrant countries accounting for the remaining 10%, they have had high growth rates in recent

years. There were delivered approximately 18 million sq.m. of Gross Leasable Area in Europe

between 2006 and 2009, including 76% in the Europe 15 countries and 24% in Europe accession

countries.

The shopping center stock per capita shows some wide differences between the European

countries. Comparing to the European average of 238 sq.m. per thousand capita, Sweden, Ireland

and the Netherlands seem largely over-supplied with a stock per capita over 400 sq.m. The

shopping center stock in the three major European markets – the UK, France and Italy – are

within the European average while the Central and Eastern European countries and Germany are

below the European average (Figure 6). Russia, which posted the strongest increase in the recent

years and has also the most significant pipeline for the short term, is far below with a stock of 60

sq.m. of shopping center per thousand of capita. Based on this analysis, it is expected to see an

increasing development pipeline in Romania, Russia and Turkey, whilst in the Nordics and the

28

Netherlands the focus will be more on refurbishments and redevelopments than on new

developments.

Figure 6. Shopping centers’ GLA per country in Europe, 2010

As a direct consequence of the economic slowdown and the high degree of uncertainty in

retail markets, construction activity declined sharply in 2010 to reach its lowest level in five

years. New shopping centers delivered across Europe in 2010 are estimated at 3.5 million sq.m.,

with a large proportion located in Russia and Turkey. (ICSC, 2011)

1.5.2 Shopping centers perspectives

2011 will be a challenging year, requiring creativity and caution for retailers’ expansion

plans. The continuous environment with the added pressures of government budgets is affecting

household expenditures, and consequently consumers’ ability to purchase in many retail sectors.

Retailers are making the choice to locate or relocate in larger stores in the strongest and

best locations or regions, rather than covering the entire market as they did previously. There is

increasing logic in retailers placing their investment into key stores, within super prime shopping

centers, and on key high streets. This is a trend across Europe and one that leaves an interesting

situation considering the surplus space that exists within the European retail market. At the same

time, there are some interesting trends within retail on a pan-European basis. One is continued

trends with the continued rise of the “value” sector, with operators such as Tesco, Primark,

H&M, and Asda, capitalizing on their ability to sell a wide variety of brands under their retail

banner, within varying degrees and location. This has led to a stagnation within certain retail

29

sectors, which have been unable to maintain momentum and created potential risk areas, include

retailers who sell music, books and games- all of which can operate across mobile, and key to

this, cheaper retail platforms. It is expected that some alignment of retail estate to follow this

trend in 2011. (DTZ Research, 2011)

In 2011 new supply should come back to the market, especially in the eastern part of the

region, with Russia and Turkey again leading the way with 2.1 and 2.8 million sq.m.,

respectively, planned for delivery. International Council of Shopping Centers estimates 13

million sq.m. of new shopping centers’ space will be delivered in 2011 and 2012.

Russia, Romania and Turkey are leading the first positions regarding the volume of new

supply of shopping centers to be delivered in 2011 – 2012 compared to the existing stock as at

the end of 2010. The expected pipeline for the next two years represents more than 30% of the

stock. These figures illustrate the huge differences between the far Eastern Europe, with its really

“booming” development trend and Western Europe where developers and investors are much

more focused on redevelopments and refurbishments than on new supply. (ICSC, 2011)

Development is expected to pick up in 2011. Cushman & Wakefield expects to see an

upturn in activity in more than half of the European markets surveyed. About 7 million sq.m. of

new space is scheduled for completion by year’s end. If all of the schemes are finished on time,

this year’s development total will exceed that of last year by 33%, Cushman & Wakefield notes.

In total, 165 new shopping centers opened in 2010, bringing Europe's total amount of retail space

to 130 million sq.m. As with previous years, Central and Eastern Europe accounted for the

majority (63%) of new space opened. Russia and Turkey continue to dominate the European

development pipeline with their combined 2011 – 2012 pipeline accounting for more than 40%

of the European total. Both markets are expected to see large increases in development activity in

2011. In Russia approximately 3 million sq.m. of new GLA is due to open between 2011 and

2012. In Turkey nearly 1.8 million sq.m. of new space is scheduled for completion before the

end of 2012.

There was a rebound in investment activity across all commercial property sectors in

2010. European retail investment volumes amounted to $54.5 billion, a 72% increase from the

previous year. Investment activity is expected to increase slightly across Europe in 2011, and cap

rates are predicted to remain stable. Retail’s share of total European commercial property

investment continued to rise in 2010, to 33% - up from 30% in 2009 - confirming its popularity

as an asset class. (ICSC, 2011)

30

2. CHOOSING RETAIL LOCATION

2.1 Importance of retail location

Retail locations provide retailers with physical access to their target customers and can

generate operating advantages that can prove difficult for competitors to overcome. The growth

intensity of retail competition due to the emergence of new formats and technology as well as

shifts in customer needs is forcing retailers to devote more attention to strategic thinking. Retail

mix depends on strategic thinking, includes customer service, store display and design,

communication mix, pricing, merchandise assortment, and location strategy. With the increasing

need to plan for the opening and parallel operation of multiple stores, the strategic nature of these

decisions has significantly intensified (Ghosh and Craig, 1983). Store location decisions have

long been among the most crucial ingredients for any retail business that relies on customers. It

is also one of the most difficult issues to plan and make correct decision when locating the store

in the retail environment. The retail environment is in a state of flux, and what bides well today

may not be accepted in the future. The location of the retailer also indicates what sort of retailer

he / she is. Whether the retailer is searching for a new retail site or relocating an existing

business, retail management has the power to increase profits by choosing the right location.

Location decisions are complex but can be used to develop a sustainable competitive

advantage. These decisions are harder to change because retailers frequently have to either make

substantial investments to buy and develop a real estate or commit to long-term leases with

developers. Location decisions have become even more important in recent years, as there are

more retailers opening up in new locations and making the better locations harder to obtain. The

importance of a suitable location strategy for retailers is clear, particularly in relation to

marketing and financial strategy considerations. The location decisions of retailers are also

significant for other stakeholders, like consumers, planners, and property investment firms.

Although location decisions are a primary consideration in customer’s store choice, most

retailers traditionally rely on intuition guided by experience and “common sense”. A more

scientific and refined approach to evaluate possible retail locations is needed. The decision

makers, who should evaluate a series of trade-offs, can be aided in their decisions with a

multiple-criteria decision-making process. (Burnaz, Topcu, 2007)

31

2.2 Multiple criteria decision making

Each shopping center has its own strengths and weaknesses, several incommensurate and

conflicting criteria exist for evaluating shopping centers. Identifying these evaluation criteria,

defining the effects of them on each other, assessing their importance, and choosing a particular

retailer necessitate a well-designed multiple-criteria decision making (MCDM) – based

evaluation.

Multi-Criteria Decision Making (MCDM) is a discipline aimed at supporting decision

makers, faced with making numerous and sometimes conflicting evaluations. MCDA aims at

highlighting these conflicts and deriving a way to come to a compromise in a transparent

process. (Wikipedia, 2005)

Multi-Criteria Decision Making methods are noted to be helpful in reaching important

decisions that cannot be determined straightforwardly. The underlying principle of MCDM is

that decisions should be made by use of multiple criteria. By applying the concept of MCDM,

Professor Thomas Saaty created the analytic hierarchy process (AHP) and the analytic network

process (ANP). Both methods are claimed to possess qualitative and quantitative components.

On one hand they are used to identify decision criteria (qualitative component). This involves the

creation of a structural model for the decision problem. On the other hand, they employ the

procedure for assigning weights to the criteria (quantitative component). (Cheng, 2005)

The Analytic Hierarchy Process (AHP) is a theory of relative measurement with absolute

scales of both tangible and intangible criteria based on the judgment of knowledgeable and

expert people. The AHP reduces a multidimensional problem into a one dimensional one.

Decisions are determined by a single number for the best outcome or by a vector of priorities that

gives an ordering of the different possible outcomes. (Saaty, 2007)

2.3 Criteria

Shopping center is a commercial land use that is more than a real estate venture. It is

also a retail merchandising complex that not only provides many of the basic goods and services

that a community requires but also functions to a greater or lesser extent as a social and

community center. Shopping center is distinguished by several basic precepts: a coordinated

development strategy, a unified spatial arrangement, a carefully planned tenant mix of mutually

supportive tenants, and centralized management control. There are many criteria that must be

considered before choosing the best retail location for business. There are seven main groups:

32

Location, Rent price, Tenant mix, Customers, Shopping center characteristics, Premises

Characteristics, Recognition. Each of them has sub – criteria:

1) Location: District, Demographics, Visibility, Accessibility, Surrounding objects;

2) Rent Price: Rent Price, Financial model flexibility, Additional fees;

3) Tenant mix: Anchor tenants, Number of tenants, Balance of tenants, Occupation rate,

Number of competitors;

4) Customers: Target Group, Customer flow, Weekly repartition, Customer flow in

proposed location;

5) Shopping centers’ characteristics: Size, Layout, Concept, Design, Parking, Adjustment

for disabled people;

6) Premises characteristics: Size, Layout, Location in the shopping center, Façade, Fit-out

level, Neighbors;

7) Recognition: Marketing activities, Reputation.

The hierarchical structure of retail location criteria lay out in Figure 7.

33

Figure 7. Retail Location criteria

CRITERIA

1. LOCATION 2. RENT PRICE

3. TENANT MIX

4. COSTUMERS

5. SC CHARAC-TERISTICS

6. PREMISES CHARAC-

TERISTICS

CONVENIENCE

7. RECOGNITION

MARKETING2.1 Rent Price

2.2 Financial flexibility

1.1 District

1.2 Demographics

1.3 Visibility

1.4 Accessibility

1.5 Surrounding objects

3.1 Anchor tenants

3.2 Number of tenants

3.3 Balance of tenants

3.4 Occupation rate

3.5 Number of competitors

4.1 Target group

4.2 Customer flow

4.3 Weekly repartition

4.4 Customer flow in proposed

location

5.1 Size

5.2 Layout

5.3 Concept

5.4 Design

5.5 Parking

5.6 Adjustment for disabled people

6.1 Size

6.2 Layout

6.3 Location in the shopping center

6.4 Facade

6.5 Fit-out level

6.6 Neighbours

7.1 Marketing activities

7.2 Reputation

2.3 Additional fees

34

2.3.1 Location

Location is of paramount importance in the success of all types of shopping center. The site

must qualify by virtue of its trade area, the income level of the households in the area, competition,

highway access, and visual exposure. The site should represent an impregnable economic position.

Its superior access, greater convenience, better merchant array, and improved services make it

impractical for another similar project to be developed nearby. Recommended distances between

shopping centers cannot be established precisely, either for the same or different type centers. It is

not mere distance between centers, but population density, convenience, accessibility, and diverse

merchandise that count. (Levitt, Berens, Beyard, 1997)

2.3.1.1District

Analysis of shopping center district is one of those first and important steps before

developing a shopping center. It is highly related with transportation and accessibility to the

shopping center and it determines shopping center type, size, layout, anchor tenants, tenant mix and

many other components. The character of a district and the nature of the competition in it shape the

character of a shopping center, including type, quality and tone. The district traditionally is the

geographic area that provides the majority of the steady customers necessary to support a shopping

center. The boundaries of the trade area are determined by a number of factors, including the type

of shopping center, accessibility, physical barriers, the location of competing facilities, and driving

time and distance. For retailers, who are seeking for a location, district is also important criterion,

which lets to assess what customer target and purchasing power can be expected.

2.3.1.2 Demographics

For both, shopping center owners and retailers it is important to have a full understanding

about the shopping center‘s catchment area and demographics. Shopping center‘s financial success

depends on retailers‘ operation, whereas success of their business is mainly determined by customer

flow. So, it is essential to know potential customers and constantly analyze their changing needs.

Catcment area is the area and population, from which a shopping center attracts customers. What is

really needed to know about those customers, is number of population, living around; the average

age of population and distribution in the area; the average family income and distribution by income

level; employment and professions analysis; private ownership and rental housing assesment; ethnic

and racial consist, cultural defferences; psichological analysis, etc. All these aspects let understand

the needs of pupolation and their buying habits, and according to this, to form shopping center‘s

concept and tenant mix.

35

2.3.1.3 Visibility

Good visibility improves shopping center’s accessibility. A customer, driving at local traffic

speed, can easily overshoot the entrance to the parking lot if he or she has not seen the shopping

center and its entrance from the access road. Clear signage helps direct customers, increases

visibility, and heightens awareness that a shopping center is near. Overpasses, hills, curves in the

road, and heavy vegetation all impede visibility. Even though traffic flow attracts retail business, a

site that fronts on a highway heavily built up with strings of competing distractions (including

signs) is actually less accessible. (Levitt, Berens, Beyard, 1997)

2.3.1.4 Accessibility

Location of the shopping center must be easy to reach, and the roads must have extra

capacity to avoid congestion during periods of high-volume traffic. The shopping center must be

easy to enter and safe to leave for customers and employees. Shopping centers need to be easily

accessible from the street regardless of what your mode of transportation is.

Automobile traffic may be classified according to the reason for the trip. There are the work

trip, the shopping trip, and the pleasure trip. A good location for a retailer seeking the customer on a

planned shopping trip is along the right – hand side of the main street leading into a shopping

district and adjacent to other streets carrying traffic into, out of, or across town. The beginning or

end of a row of stores rather than across the street from the stores is preferable.

In smaller communities, where the major streets lead to and from the downtown area, the traffic

pattern can be readily identified. In larger cities, where there are suburban shopping center

locations, the traffic moves in many different directions. Because shopping centers tend to generate

traffic, an analysis of the traffic flow to centers and between centers may show that a particular

store location is outstanding.

2.3.1.5 Surrounding objects

Surrounding objects of the shopping center are usually associated with the district where the

shopping center is. In the residential district shopping center will be surrounded by houses, in the

industrial districts – surrounded by factories, warehouses, offices, etc. Shopping center in the center

of the city probably will be surrounded by more luxurious architecture buildings and historical

heritage and so on. Surrounding objects can strongly influence the customer flow into the shopping

center. For example, business center, located near the shopping center will attract more customers

in the lunch time and in the evening, when employees from the business center come to shopping

36

before going home. Other shopping center in the near neighborhood is also a very important

indicator, that should be assessed, but in this case, it may be more negative affected as a competitor.

2.3.2 Price

2.3.2.1 Rent Price

Rent price is the main criterion that usually determine retailer‘s decision in choosing a retail

location. There might be various combinations of financial model, but International Council of

Shopping Centers separate two main types of rent: Minimum rent and Percentage rent. May

shopping center owners require the tenant to pay both – a fixed minimum rent and a percentage

rent. Percentage rent is calculated as a percentage of tenant‘s annual sales made in the premises.

Under the cost sharing between the tenant and lanlord, rental income may take such forms:

• Gross Lease – paid only the base rent and the landlord accepts payment on the cost

of other risks;

• Net Rent – the tenant with a base rent fee also pays all operating costs.

• NN (Double Net) Lease – along with the basic tenants of rental fee also pays all

operating costs;

• NNN (Triple Net) Lease – the tenant pays all operating expenses, insurance and

property taxes. This is a lease, commonly used in shopping centers.

2.3.2.2 Flexibility of financial model

Probably the key point of negotiations and retailer’s decisions is flexibility of the financial

model. In the beginning of negotiations for retailers it is important to feel that landlord is flexible

and cares about coming tenant and its needs. There are many forms, how this flexibility can show –

step rent (when increased rent is dispensed gradually); free month for fitting – out, lower

indexation, and many other.

2.3.2.3 Additional fees

One of the most contentious elements of the landlord – tenant relationship is common area

costs, including common area maintenance (CAM), insurance, taxes, repairs and replacements, and

the marketing fund. These are referred to as the operating costs of the shopping center and are paid

according to the size of premises.

37

2.3.3 Tenant Mix

International Council of Shopping Centers describes tenant mix as the combination of store

types and price levels of retail and service businesses in a shopping center. An effective tenant mix

strengthens the center by creating a synergy calculated to appeal to a range of center customers,

increase customer flow and – through placement and price – encourage customers to make multiple

purchases. Tenant mix typically includes different percentages of the following retailers: clothing,

shoe, accessories, gifts, jewelry, food, specialty shops, restaurants, entertainment, services, etc.

(ICSC, 2000)

The exact tenant for a specific center is naturally affected by the specific circumstances of

leasing, financing and availability of tenants for a particular trade area. Shopping centers’

developers base their choices of selection on varying income ranges and other characteristics of the

market area, local buying habits, store sizes, and merchandising practices in different site conditions

and various geographic areas. (Levitt, Berens, Beyard, 1997)

In addition to the shops and catering provided in shopping destinations, a complementary

range of leisure activities is also being added to the larger centers for the reason to attract a wider

catchment and to extend the activity of the center throughout the day and evening. Leisure uses,

which are increasingly integral to regional centers, include cinemas, bowling alleys, family

entertainment centers, amusements, health clubs, night clubs and entertainments venues. The

synergy and compatibility of leisure uses alongside shops and catering produce a matrix of different

types of center. (Coleman, 2006)

The most important parts of tenant mix for retailer are: anchor tenant, number and balance

of tenants, vacancy rate and number of competitors.

2.3.3.1 Anchor tenants

Anchor tenants are an important factor in determining the effectiveness of a shopping center.

An anchor store is a unit integrated within a shopping center with a mixed variety of stores, whose

purpose is to significantly increase the mall’s appeal. It contains all or most of the following

features: it is large (usually more than 600 sq.m. GLA), multiple (national or international chain – a

minimum of three stores), has a strong brand (high awareness and positive response levels),

contributes significant traffic (specifically generates footfall), has widespread appeal (meaning it

would trade successfully as a stand-alone unit) and usually enjoys a privileged position with regard

to rent and services charges (Damian, 2011).

38

The placement of anchor tenants usually follows two guidelines: located so that customers

must walk past the storefronts of supplementary tenants to reach them, and separated so that all

supplementary tenants are passed on the way to and from the anchors. They usually are placed at

opposite ends of a mall. The anchor tenants normally are tied in closely with the development team

at the planning stage. The anchor tenants heavily influence site design, building design, layout, and

overall composition of tenants. Anchor tenants determine the center’s basic character and image.

(Levitt, Berens, Beyard, 1997)

2.3.3.2 Number of tenants

A number of shopping centers’ tenants is closely connected with the shopping center size

and layout. The higher number of stores in shopping center is, the greater variety of choices can be

provided and the higher customer flow to the center can be expected. Number of tenants is also

closely linked to the tenancy balance. Regardless of the shopping center size, when forming a tenant

mix, it is important thoroughly allocate number of tenants by type of merchandise. However,

shopping centers’ managers should focus not only on the quantity of stores, but on quality as well.

2.3.3.3 Balance of tenants

It is very important that tenant mix would be balanced in the shopping center. Balanced

tenancy occurs when stores in a planned shopping center complement each other as to the quality

and variety of their product offerings. A tenant mix cannot be decided by a formula – each shopping

center is different. A tenant appropriate for one center can be a mistake in another. Any list of

tenant classifications most frequently found in a given type of center can serve only as a guide in

selecting tenants for shopping centers’ developers and managers. It is not easy to reach the balance

of tenant mix in the shopping center, but it is one of the keys to success in attracting stronger brands

and more customers.

2.3.3.4 Occupation rate

One more indicator, which shows the success of the shopping center, is occupation rate.

Every shopping center is thought to be good with a 100% occupation rate. It is difficult not only to

achieve such level, but to preserve it as well. The result of this indicator is the responsibility of the

shopping center’s management.

39

2.3.3.5 Number of competitors

Before renting premises in the shopping center, it is recommended to make a small market

research and to analyze what is the depth of retailer’s category and how many competitors there are.

It is important to evaluate this in order to forecast results and possible threats.

2.3.4 Customers

Retailers’ revenue depends on the number of customer flow and purchasing power, so it is

important to assess the potential customers of the shopping center – to evaluate target group,

number of customer flow, repartition of customer flow in week – days and customer flow in

specific proposed location in the shopping center. Retailers divide visitors in such groups: those

who enter a store; those who after looking at the windows may become customers; and those who

pass without entering or looking.

2.3.4.1 Target group

The target group, which shopping center focuses on, is closely related to shopping center

location (district, demographics), concept and tenant mix (brand and price level). It is important that

retailer’s target group more or less coincide with the whole shopping center target group. For

example, if the shopping center is positioning itself as lower price center, so it might be difficult for

store of high price level.

2.3.4.2 Customer flow

Customer flow is one of the main criteria for retailers, when choosing a retail location. The

size of customer flow shows, how successfully shopping center is operating. Shopping center’s

customer flow reflects the results of general shopping center’s concept, strength of tenant mix,

shopping center management and marketing activities. Customer flow allows for retailer to evaluate

expected traffic to specific store and to forecast tentative income.

2.3.4.3 Weekly repartition

Customer flow in week days’ context distributes according to the shopping center district,

demographics, accessibility and surrounding objects. For example, the highest customer flow of the

shopping center in suburbs will be on weekends, whereas a shopping center somewhere in industrial

district will attract the highest customer flow on working days. It is important for retailer to evaluate

repartition of customer flow in week days’ context for the reason to plan business, number of

employees and expected income.

40

2.3.4.4 Customer flow in proposed location

Customer flow in proposed location is tightly related with characteristics of the premises –

location in the shopping center, neighbors, façade (visibility) and the main customer flow of the

center. The higher it is, the higher number of customers in specific premises can be expected. What

is also important for customers’ attraction – marketing activities (common shopping center

marketing activity, as well as individual retailer’s activity). Every shopping center has less

attractive locations, so retailers always draw strong attention to this criterion, which lets evaluate

tentative income.

2.3.5 Shopping center characteristics

Shopping center characteristics define shopping center size, layout, concept, design,

parking, accessibility and many other smaller factors. This is not the most significant criteria for

choosing a retail location, but the interface between all those factors forces to draw attention to all

of these criteria too.

2.3.5.1 Size

Mainly shopping center’s size depends on land area. The second important thing is planning

the shopping center, and designing its layout. Each square meter must be carefully considered,

trying to make the shopping center area as much effective as it is possible. Shopping center’s size

includes both: Gross Building Area (GBA) and Gross Leasable Area (GLA).

2.3.5.2 Layout

Shopping center’s configuration is very important for both – owner and tenants. In the

planning stage, the developer’s main consideration should be placement of the anchor tenants,

which must be positioned so that they draw customers between them and past other tenants.

Shopping center’s configurations have been adapted in countless variations and there is no one

formula, which one of them works the best. And no matter how spectacular the design of a

shopping center is, the layout is much more important. Moreover, retail spaces should be built of

materials that can be easily altered to allow for tenant’s changing needs. The design should provide

for future reallocation of store space and for readjustments in fixtures needed as tenants expand or

shift their locations in the center. (Levitt, Berens, Beyard, 1997)

2.3.5.3 Concept

Shopping center’s concept, as it was mentioned earlier in this paper, is an important factor,

especially related to shopping center district, demographics, surrounding objects, target group, etc.

41

Shopping center’s concept might be: Neighborhood center, Community center, Regional center,

Superregional center, Fashion / Specialty center, Power center (Retail Park), Theme / Festival

center, Factory Outlet center. When seeking for a retail location, retailers pay attention to clearness

and completeness of shopping center’s concept.

2.3.5.4 Design

Good shopping center’s design plays an important role in attracting customers. The

shopping center must be a complex of merchandising as well as a pleasant place for spending free

time. All the components are important and must be considered: interior, exterior, lighting, etc.

When benches, plants, sculptures, fountains and other mall furnishings are provided, the shopping

center creates a setting for even greater vitality in merchandising and promotion of the center.

Before choosing the right design, it is important to analyze, what market segment will be served.

For example, in a low income catchment area, it may be counterproductive to make the shopping

center too elegant, as this might result in scaring potential customers away who seek high value for