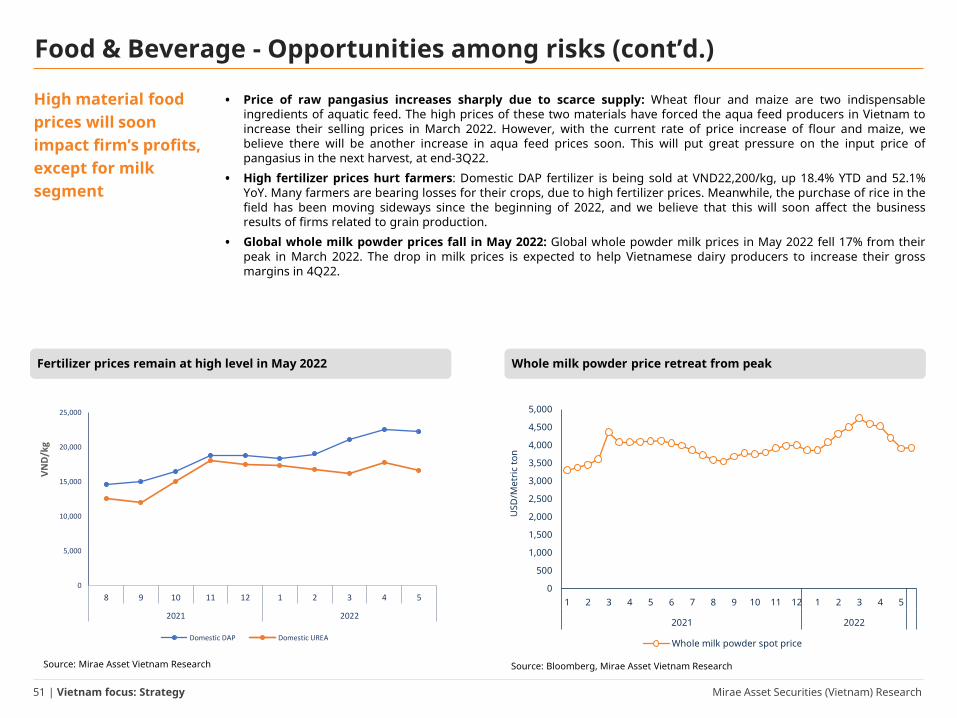

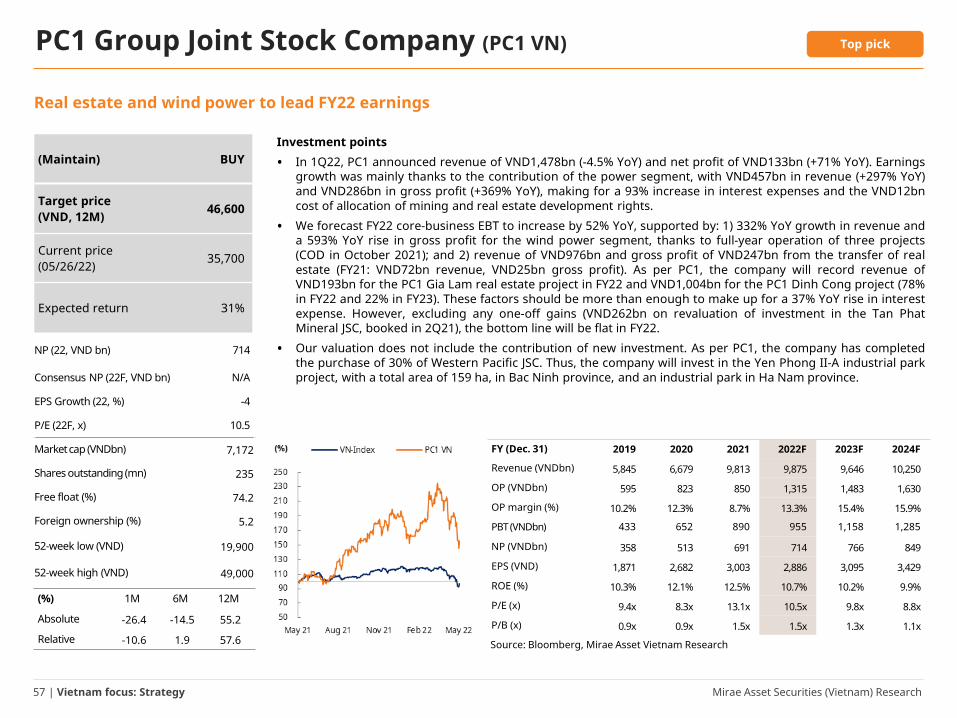

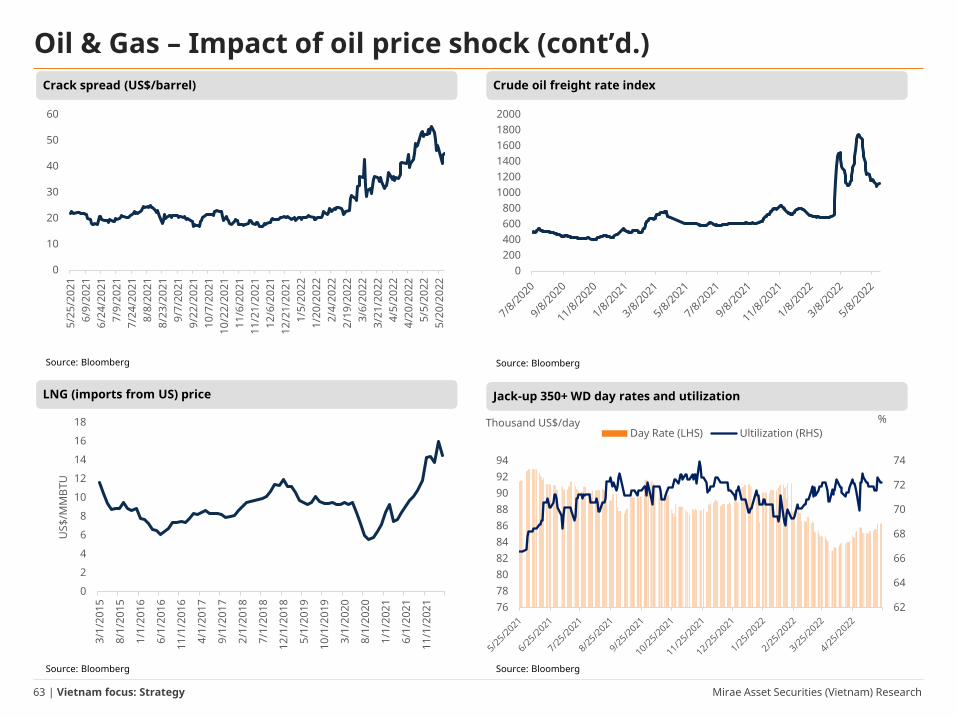

12-scheme-information-document---mirae-asset-savings-fund ...

Upload

khangminh22Category

view

0download

0

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

VIETNAM ECONOMY AND STOCK MARKETNavigating opportunities

Research teamMirae Asset Securities (Vietnam)

Strategy report | June 2022

Mirae Asset Securities (Vietnam) Research2 | Vietnam focus: Strategy

Contents

I. Vietnam economy in the first five months of 2022 3

II. Vietnam stock market May 2022 review 19

III.Vietnam stock market prospects 27

IV. Sector outlook and stock recommendations 33

Mirae Asset Securities (Vietnam) Research3 | Vietnam focus: Strategy

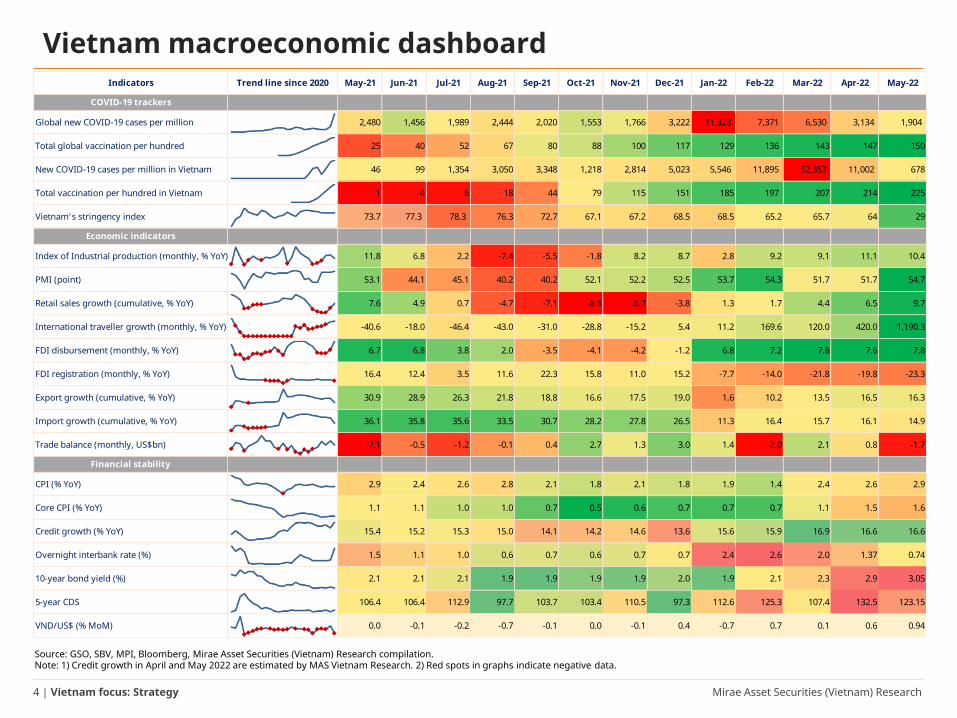

❑ Vietnam’s economy continued its recovery in May, as the number of new infectionstumbled and the economy fully returned to a new normalcy. Specifically, IndustrialProduction maintained its double-digit rally for a second consecutive month, with May’sproduction volume growing at the fastest pace since April 2021; Retail Sales of consumergoods and services achieved a strong YoY improvement; and disbursed FDI inflowsremained positive. Meanwhile, export growth slowed; registered FDI inflows continued todecline, and disbursed public investment capital grew at a slower pace compared withthe same period last year.

❑ CPI continued to accelerate in May (up 2.86% YoY), with increasing prices of food andfoodstuff, input materials, and gasoline rising in line with the world oil prices. Meanwhile,the CPI of Culture, Entertainment, and Tourism and Out-of-home Dining rose sharply onthe rebound in tourism demand and complete re-opening of the economy.

❑ We believe Vietnam's economy is supported by key growth drivers, including: 1) anexpected recovery in consumption; 2) exports regaining momentum, as domesticproduction returns and external demand recovers; 3) expectations for registered FDI torally, as travel between countries is gradually returning to normal, creating favorableconditions for foreign investors to survey and carry out investment procedures inVietnam; and 4) the government’s promotion of public investment.

❑ Key risks for Vietnam’s economic recovery include: 1) increased global supply disruptions;and 2) increasing inflation risks.

I. Vietnam economy in the first five months of 2022

Mirae Asset Securities (Vietnam) Research4 | Vietnam focus: Strategy

Vietnam macroeconomic dashboard

Source: GSO, SBV, MPI, Bloomberg, Mirae Asset Securities (Vietnam) Research compilation. Note: 1) Credit growth in April and May 2022 are estimated by MAS Vietnam Research. 2) Red spots in graphs indicate negative data.

Indicators Trend line since 2020 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22 Apr-22 May-22

COVID-19 trackers

Global new COVID-19 cases per million 2,480 1,456 1,989 2,444 2,020 1,553 1,766 3,222 11,328 7,371 6,530 3,134 1,904

Total global vaccination per hundred 25 40 52 67 80 88 100 117 129 136 143 147 150

New COVID-19 cases per million in Vietnam 46 99 1,354 3,050 3,348 1,218 2,814 5,023 5,546 11,895 62,353 11,002 678

Total vaccination per hundred in Vietnam 1 4 6 18 44 79 115 151 185 197 207 214 225

Vietnam's stringency index 73.7 77.3 78.3 76.3 72.7 67.1 67.2 68.5 68.5 65.2 65.7 64 29

Economic indicators

Index of Industrial production (monthly, % YoY) 11.8 6.8 2.2 -7.4 -5.5 -1.8 8.2 8.7 2.8 9.2 9.1 11.1 10.4

PMI (point) 53.1 44.1 45.1 40.2 40.2 52.1 52.2 52.5 53.7 54.3 51.7 51.7 54.7

Retail sales growth (cumulative, % YoY) 7.6 4.9 0.7 -4.7 -7.1 -8.6 -8.7 -3.8 1.3 1.7 4.4 6.5 9.7

International traveller growth (monthly, % YoY) -40.6 -18.0 -46.4 -43.0 -31.0 -28.8 -15.2 5.4 11.2 169.6 120.0 420.0 1,190.3

FDI disbursement (monthly, % YoY) 6.7 6.8 3.8 2.0 -3.5 -4.1 -4.2 -1.2 6.8 7.2 7.8 7.6 7.8

FDI registration (monthly, % YoY) 16.4 12.4 3.5 11.6 22.3 15.8 11.0 15.2 -7.7 -14.0 -21.8 -19.8 -23.3

Export growth (cumulative, % YoY) 30.9 28.9 26.3 21.8 18.8 16.6 17.5 19.0 1.6 10.2 13.5 16.5 16.3

Import growth (cumulative, % YoY) 36.1 35.8 35.6 33.5 30.7 28.2 27.8 26.5 11.3 16.4 15.7 16.1 14.9

Trade balance (monthly, US$bn) -2.1 -0.5 -1.2 -0.1 0.4 2.7 1.3 3.0 1.4 -2.0 2.1 0.8 -1.7

Financial stability

CPI (% YoY) 2.9 2.4 2.6 2.8 2.1 1.8 2.1 1.8 1.9 1.4 2.4 2.6 2.9

Core CPI (% YoY) 1.1 1.1 1.0 1.0 0.7 0.5 0.6 0.7 0.7 0.7 1.1 1.5 1.6

Credit growth (% YoY) 15.4 15.2 15.3 15.0 14.1 14.2 14.6 13.6 15.6 15.9 16.9 16.6 16.6

Overnight interbank rate (%) 1.5 1.1 1.0 0.6 0.7 0.6 0.7 0.7 2.4 2.6 2.0 1.37 0.74

10-year bond yield (%) 2.1 2.1 2.1 1.9 1.9 1.9 1.9 2.0 1.9 2.1 2.3 2.9 3.05

5-year CDS 106.4 106.4 112.9 97.7 103.7 103.4 110.5 97.3 112.6 125.3 107.4 132.5 123.15

VND/US$ (% MoM) 0.0 -0.1 -0.2 -0.7 -0.1 0.0 -0.1 0.4 -0.7 0.7 0.1 0.6 0.94

Mirae Asset Securities (Vietnam) Research5 | Vietnam focus: Strategy

I.1 – Covid-19 situation❑ The number of new infections plummeted in April and May, after peaking in March. In addition, the mortality

rate maintained a low level, thanks to high fully-vaccinated rates and the promotion of vaccine boosters. With

the trend of declining numbers of new infections and a sustained low mortality rate, Vietnam's economy has

fully returned to a new normalcy.

New Covid cases plunged;

mortality rate maintained

low level

Vietnam’s new covid cases tumbled after peaking in March

Source: Our World in Data, Mirae Asset Securities (Vietnam) Research compilationData updated as of 5/30/202

Vietnam’s Covid mortality rate

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jun

21

Jul 2

1

Aug

21

Sep

21

Oct

21

Nov

21

Dec

21

Jan

22

Feb

22

Mar

22

Apr

22

May

22

(%)

0

500

1000

1500

2000

2500

3000

Jun

21

Jul 2

1

Aug

21

Sep

21

Oct

21

Nov

21

Dec

21

Jan

22

Feb

22

Mar

22

Apr

22

May

22

New cases per million(# cases)

Mirae Asset Securities (Vietnam) Research6 | Vietnam focus: Strategy

I.2 – Industrial production❑ The May index of industrial production (IIP) continued to expand (+4% MoM and +10.4% YoY), with the IIP of

Manufacturing and Processing up 12.1% YoY. Businesses have adapted to the new normalcy, recovered, and

expanded their production, thanks to the successful containment of Covid-19 and re-opening of the economy.

❑ In 5M22, the IIP grew 8.3% YoY. Notably, production in some secondary industries increased sharply compared

with the same period last year, such as Clothing (+22% YoY); Electrical Equipment (+20.4% YoY); Pharmaceuticals

(+16.8%); and Leather and Related Products (+13.5% YoY).

Monthly IIP Manufacturing IIP in 5M22

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

Industrial production

has maintained double-

digit growth for two

consecutive months

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

-15

-10

-5

0

5

10

15

20

25

30

35

Jan

19

Mar

19

May

19

Jul 1

9

Sep

19

Nov

19

Jan

20

Mar

20

May

20

Jul 2

0

Sep

20

Nov

20

Jan

21

Mar

21

May

21

Jul 2

1

Sep

21

Nov

21

Jan

22

Mar

22

May

22

IIP Processing and manufacturing IIP(% YoY)

Seasonal effects

Covid-19 wave

-13.8-9.8

-2.63.53.54.24.44.64.7

7.07.38.18.68.99.2

11.111.211.511.6

13.516.8

20.422.0

Rubber and plastic productsMachinery and equipment installation/repair

Coke, refined petroleum productsBasic metals

Motor vehiclesProcessed wood products

TobaccoChemicals and chemical products

TextilesFood products

FurnitureOther non-metallic mineral products

BeveragesPaper and paper products

ManufacturingPrinting, recorded media reproduction

Machinery and equipmentPrefabricated metal products

Computer, electronic, optical productsLeather and related products

PharmaceuticalsElectrical equipment

Clothing

(% YoY)

Mirae Asset Securities (Vietnam) Research7 | Vietnam focus: Strategy

I.2 – Industrial production (cont’d.) ❑ Vietnam's manufacturing PMI has remained above the 50-point threshold for eight consecutive months, reaching

54.7 in May, up from 51.7 in April. Production output recovered at the fastest pace since April 2021 .

❑ We believe that the main drivers, such as the high vaccination rate, improved demand in both the domestic and

global markets, gradual return of operating capacity to pre-pandemic levels, and increase in working hours, will

continue to support the recovery of industrial production in 2022.

❑ Risks to watch: 1) Possibility of disruption to the material supply chain; and 2) adverse affects on global growth by

the Russia-Ukraine war shock and China's Zero Covid policy. However, China has reopened since June 1, after a

two-month lockdown, so the risks related to China’s “Zero Covid" policy will probably gradually decline in the

coming months.

Industrial production

to continue to

rebound

Vietnam’s PMI has remained above 50-point threshold

Source: Bloomberg, Mirae Asset Securities (Vietnam) Research compilation

Monthly IIP

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

Year 2021 2022

Month 5 6 7 8 9 10 11 12 1 2 3 4 5

IIP 11.8 6.8 2.2 -7.4 -5.5 -1.8 8.2 8.7 2.8 9.2 9.1 11.1 10.4

Mining -5.9 -4.9 -8.0 -2.4 -7.1 -8.2 6.2 -7.1 -1.7 2.2 7.5 7.9 4.2

Processing and manufacturing 14.4 8.1 2.9 -9.2 -4.9 -0.8 8.6 10.9 2.9 9.7 9.7 11.7 12.1

Production and distribution of electricity 12.7 8.2 6.7 1.5 -9.7 -4.8 6.8 9.1 5.2 11.9 6.5 8.6 2.4

Water supply; waste management and treatment, sewage

4.1 6.0 4.3 0.2 -2.0 -0.5 0.4 0.8 4.1 4.3 -4.6 2.7 5.5

30

35

40

45

50

55

60

Jan

12M

ay 1

2Se

p 12

Jan

13M

ay 1

3Se

p 13

Jan

14M

ay 1

4Se

p 14

Jan

15M

ay 1

5Se

p 15

Jan

16M

ay 1

6Se

p 16

Jan

17M

ay 1

7Se

p 17

Jan

18M

ay 1

8Se

p 18

Jan

19M

ay 1

9Se

p 19

Jan

20M

ay 2

0Se

p 20

Jan

21M

ay 2

1Se

p 21

Jan

22M

ay 2

2

PMI 3-month average PMI(Point)

Mirae Asset Securities (Vietnam) Research8 | Vietnam focus: Strategy

I.2 – Industrial production (cont’d.) Manufacturing PMI

Source: Bloomberg, Mirae Asset Securities (Vietnam) Research compilation

Year 2020 2021 2022

Month 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5

Global

Euro Area

US

UK

Emerging Markets

China

Japan

South Korea

Vietnam

ASEAN

Mirae Asset Securities (Vietnam) Research9 | Vietnam focus: Strategy

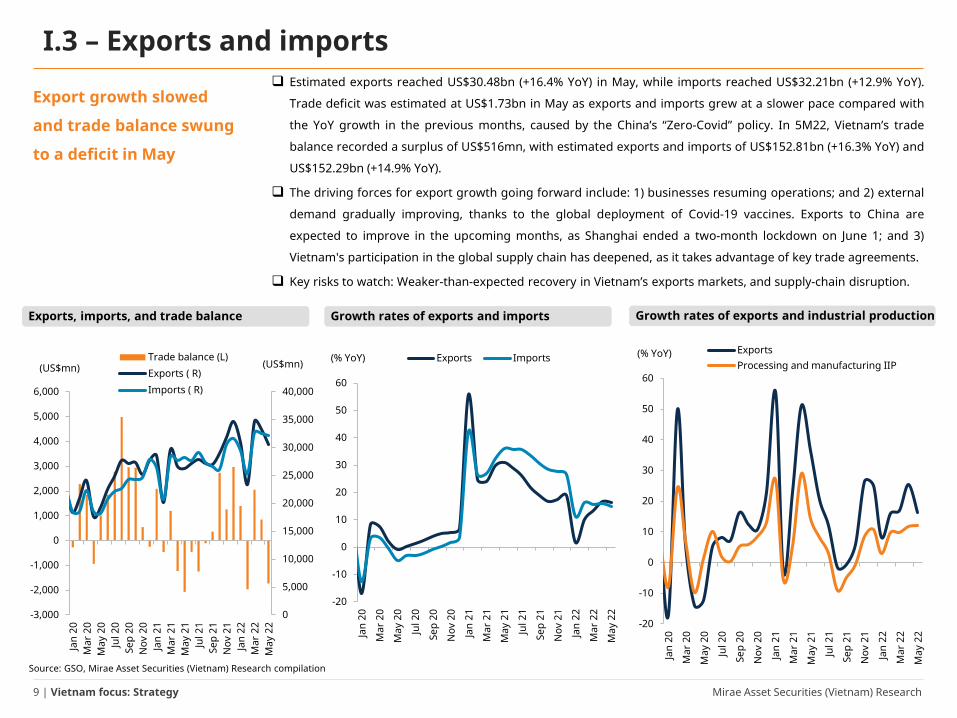

I.3 – Exports and imports❑ Estimated exports reached US$30.48bn (+16.4% YoY) in May, while imports reached US$32.21bn (+12.9% YoY).

Trade deficit was estimated at US$1.73bn in May as exports and imports grew at a slower pace compared with

the YoY growth in the previous months, caused by the China’s “Zero-Covid” policy. In 5M22, Vietnam’s trade

balance recorded a surplus of US$516mn, with estimated exports and imports of US$152.81bn (+16.3% YoY) and

US$152.29bn (+14.9% YoY).

❑ The driving forces for export growth going forward include: 1) businesses resuming operations; and 2) external

demand gradually improving, thanks to the global deployment of Covid-19 vaccines. Exports to China are

expected to improve in the upcoming months, as Shanghai ended a two-month lockdown on June 1; and 3)

Vietnam's participation in the global supply chain has deepened, as it takes advantage of key trade agreements.

❑ Key risks to watch: Weaker-than-expected recovery in Vietnam’s exports markets, and supply-chain disruption.

Export growth slowed

and trade balance swung

to a deficit in May

Exports, imports, and trade balance

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

Growth rates of exports and imports Growth rates of exports and industrial production

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

Jan

20M

ar 2

0M

ay 2

0Ju

l 20

Sep

20N

ov 2

0Ja

n 21

Mar

21

May

21

Jul 2

1Se

p 21

Nov

21

Jan

22M

ar 2

2M

ay 2

2

Trade balance (L)Exports ( R)Imports ( R)

(US$mn)(US$mn)

-20

-10

0

10

20

30

40

50

60

Jan

20

Mar

20

May

20

Jul 2

0

Sep

20

Nov

20

Jan

21

Mar

21

May

21

Jul 2

1

Sep

21

Nov

21

Jan

22

Mar

22

May

22

Exports Imports(% YoY)

-20

-10

0

10

20

30

40

50

60

Jan

20

Mar

20

May

20

Jul 2

0

Sep

20

Nov

20

Jan

21

Mar

21

May

21

Jul 2

1

Sep

21

Nov

21

Jan

22

Mar

22

May

22

ExportsProcessing and manufacturing IIP

(% YoY)

Mirae Asset Securities (Vietnam) Research10 | Vietnam focus: Strategy

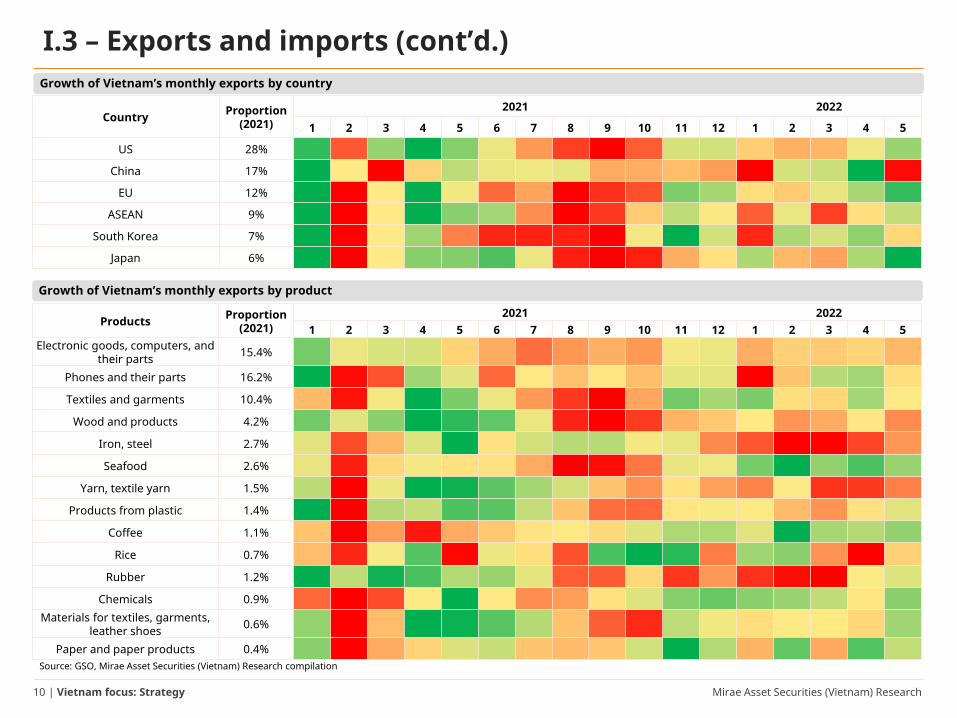

I.3 – Exports and imports (cont’d.)

Growth of Vietnam’s monthly exports by product

Growth of Vietnam’s monthly exports by country

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

Country Proportion (2021)

2021 2022

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5

US 28%

China 17%

EU 12%

ASEAN 9%

South Korea 7%

Japan 6%

Products Proportion (2021)

2021 20221 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5

Electronic goods, computers, and their parts 15.4%

Phones and their parts 16.2%

Textiles and garments 10.4%

Wood and products 4.2%

Iron, steel 2.7%

Seafood 2.6%

Yarn, textile yarn 1.5%

Products from plastic 1.4%

Coffee 1.1%

Rice 0.7%

Rubber 1.2%

Chemicals 0.9%Materials for textiles, garments,

leather shoes 0.6%

Paper and paper products 0.4%

Mirae Asset Securities (Vietnam) Research11 | Vietnam focus: Strategy

I.4 – Public investment❑ In 5M22, realized investment capital from the State budget was estimated at VND147.8tr, equivalent to

27.7% of the annual plan and up by 9.5% YoY (versus 26.9% of the annual plan and +15.6% YoY in 5M21).

The disbursement of public investment capital grew at a slower pace compared with the same period last

year, partly due to the increase in construction material prices, which has led to delays in construction.

Investment capital from state budget

Public investment

disbursement expected

to be key growth driver

in 2022

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

-15

-10

-5

0

5

10

15

20

25

30

0

10

20

30

40

50

60

Jan

21

Mar

21

May

21

Jul 2

1

Sep

21

Nov

21

Jan

22

Mar

22

May

22

Monthly investment capital from the State budget YoY growth (accumulative)(VNDtr) (% YoY)

Mirae Asset Securities (Vietnam) Research12 | Vietnam focus: Strategy

I.5 – FDI❑ In 5M22, newly-registered FDI capital reached US$4.1bn (-53.4% YoY), declining 5.7% YoY in terms of the number of

newly-registered FDI projects. Meanwhile, additionally-registered FDI capital (US$5.61bn; +45.4% YoY) and disbursed

FDI capital (US$7.71bn; +7.8% YoY) remained positive in 5M22.

❑ We believe the wave of FDI into Vietnam will improve going forward, thanks to the following: 1) Vietnam’s

vaccination rate has reached a high level and businesses have adapted to the “new normalcy”; 2) travel between

countries is gradually returning to normal, creating favorable conditions for foreign investors to survey and carry out

investment procedures in Vietnam; and 3) Vietnam continues to benefit from the restructuring of the global supply

chain, with the advantage of geographical location and labor costs.

❑ Risks to watch: Increasing competition among countries in attracting foreign investment.

FDI attraction and disbursement

Source: Mirae Asset Securities (Vietnam) Research compilation, GSO, updated as of 05/20/2022

Some major FDI projects in 5M22

Project Country Registered capital

Project of LEGO Group Denmark ~ US$1.32bn

Investment in infrastructure building of Bac Ninh VSIP urban areas and services

SingaporeAdditionally-

registered capital of US$941mn

Project of Samsung Electro-mechanics Vietnam Co., Ltd South Korea

Additionally-registered capital of US$920mn

Factory to manufacture electronic products, media, network equipment and multimedia audio products

Hong KongAdditionally-

registered capital of nearly US$306mn

Registered FDI

plunged, while

disbursed FDI

maintained its

growth momentum

Source: MPI, Mirae Asset Securities (Vietnam) Research compilation

-30

-20

-10

0

10

20

30

40

50

0

5,000

10,000

15,000

20,000

25,000

30,000

2014 2015 2016 2017 2018 2019 2020 2021 5M22

Registered FDI (L)FDI disbursement (L)Registered FDI growth (R)FDI disbursement growth (R)

(US$mn) (% YoY)

Mirae Asset Securities (Vietnam) Research13 | Vietnam focus: Strategy

I.6 – Domestic consumption❑ Retail Sales of consumer goods and services continued to recover in May (+22.6% YoY), reaching a higher scale and growth

rate compared with the same period in pre-pandemic years. Notably, Accommodation and Catering Services and Travel

Services recovered strongly, with revenue up by 69.3% YoY and 324.3% YoY, respectively, thanks to Vietnam’s return to

normalcy, accompanied by the tourism re-opening policy. In 5M22, Retail Sales of consumer goods and services rose 9.7% YoY.

❑ International visitors recovered strongly compared with the same period last year, thanks to a re-opening of tourism and

many international flight routes. International visitors to Vietnam reached 365,300 arrivals, 4.5 times the figure in the same

period last year, but still down 95% compared with the same period in 2019.

❑ We remain optimistic about the recovery of retail and consumer services (although it will take some time to return to pre-

pandemic levels), thanks to: 1) an expected rebound in consumer demand; 2) improvement in workers’ incomes upon a return

to the labor market, thus boosting spending; 3) the reduction of value-added tax, which may help stimulate consumption; and

4) expectations for the tourism industry to gradually prosper in 2022.

❑ The biggest risk to retail and consumption is a resurgence of Covid-19.

Retail sales and consumption services (% YoY)

Consumption

remained the

growth

momentum

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

International visitors to Vietnam

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

-80

-60

-40

-20

0

20

40

May

19

Aug

19

Nov

19

Feb

20

May

20

Aug

20

Nov

20

Feb

21

May

21

Aug

21

Nov

21

Feb

22

May

22

Retail sales of consumer goods and servicesRetail sales of goodsAccommodation & Catering ServicesTravel ServicesOther Services

(% YoY)

-100

100

300

500

700

900

1,100

1,300

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan

19M

ar 1

9M

ay 1

9Ju

l 19

Sep

19N

ov 1

9Ja

n 20

Mar

20

May

20

Jul 2

0Se

p 20

Nov

20

Jan

21M

ar 2

1M

ay 2

1Ju

l 21

Sep

21N

ov 2

1Ja

n 22

Mar

22

May

22

International visitors (L)

Growth rate (R)

('000 arrivals)(% YoY)

-80

-60

-40

-20

0

20

40

60

Feb

20

May

20

Aug

20

Nov

20

Feb

21

May

21

Aug

21

Nov

21

Feb

22

May

22

Retail and recreationGrocery and pharmacyParksTransit stations

(% change frombaseline)

Vietnam’s community mobility trend

Source: Covid-19 Community Mobility Reports, Mirae Asset Securities (Vietnam) Research compilation

Mirae Asset Securities (Vietnam) Research14 | Vietnam focus: Strategy

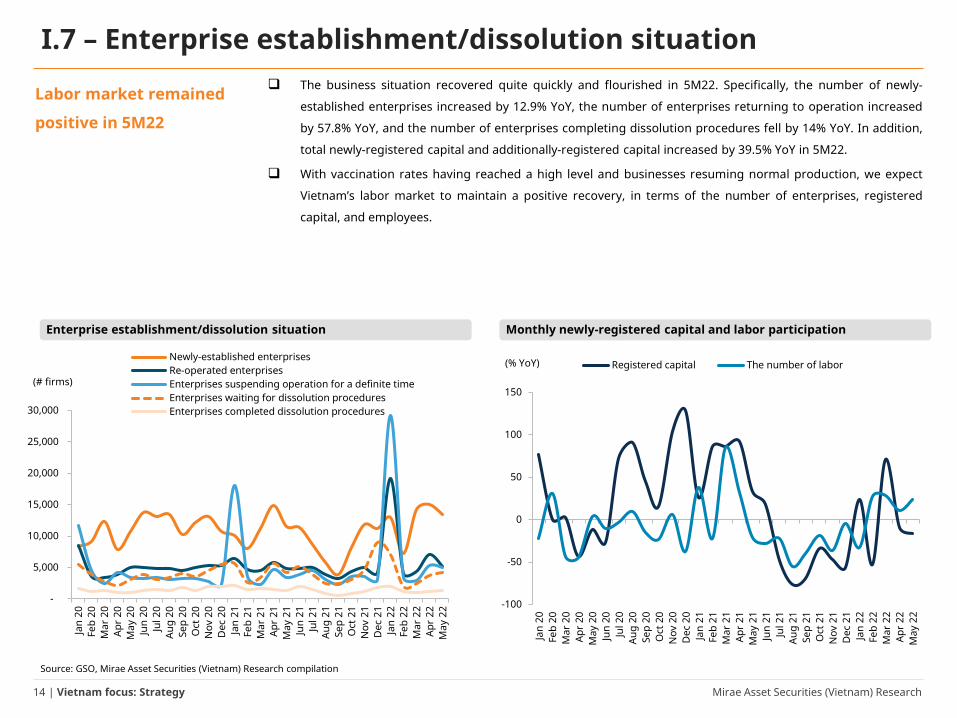

I.7 – Enterprise establishment/dissolution situation❑ The business situation recovered quite quickly and flourished in 5M22. Specifically, the number of newly-

established enterprises increased by 12.9% YoY, the number of enterprises returning to operation increased

by 57.8% YoY, and the number of enterprises completing dissolution procedures fell by 14% YoY. In addition,

total newly-registered capital and additionally-registered capital increased by 39.5% YoY in 5M22.

❑ With vaccination rates having reached a high level and businesses resuming normal production, we expect

Vietnam’s labor market to maintain a positive recovery, in terms of the number of enterprises, registered

capital, and employees.

Monthly newly-registered capital and labor participation

Labor market remained

positive in 5M22

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation

Enterprise establishment/dissolution situation

-

5,000

10,000

15,000

20,000

25,000

30,000

Jan

20Fe

b 20

Mar

20

Apr

20M

ay 2

0Ju

n 20

Jul 2

0Au

g 20

Sep

20O

ct 2

0N

ov 2

0D

ec 2

0Ja

n 21

Feb

21M

ar 2

1Ap

r 21

May

21

Jun

21Ju

l 21

Aug

21Se

p 21

Oct

21

Nov

21

Dec

21

Jan

22Fe

b 22

Mar

22

Apr

22M

ay 2

2

Newly-established enterprisesRe-operated enterprisesEnterprises suspending operation for a definite timeEnterprises waiting for dissolution proceduresEnterprises completed dissolution procedures

(# firms)

-100

-50

0

50

100

150

Jan

20Fe

b 20

Mar

20

Apr

20M

ay 2

0Ju

n 20

Jul 2

0Au

g 20

Sep

20O

ct 2

0N

ov 2

0D

ec 2

0Ja

n 21

Feb

21M

ar 2

1Ap

r 21

May

21

Jun

21Ju

l 21

Aug

21Se

p 21

Oct

21

Nov

21

Dec

21

Jan

22Fe

b 22

Mar

22

Apr

22M

ay 2

2

Registered capital The number of labor(% YoY)

Mirae Asset Securities (Vietnam) Research15 | Vietnam focus: Strategy

I.8 – Exchange rate❑ As of end-May, the VND/US$ exchange rate increased by 0.94% MTD and by 1.56% YTD. The VND depreciated relative to

the US dollar; however, the level of depreciation of the VND was medium compared with the depreciations of other Asian

currencies, partly thanks to a trade surplus, abundant foreign exchange reserves, and optimistic disbursal of FDI capital.

❑ In 2022, the VND is expected to be stable and depreciate within a range of around 1% against the US dollar, in light of: 1)

the SBV's flexible mechanism for regulating foreign currency supply and demand; 2) an expected surplus for the trade

balance in 2022, once exports accelerate; 3) growth of FDI inflows into Vietnam, thanks to production shifts; 4) Vietnam’s

foreign exchange reserves reaching a high level and tending toward increases; and 5) the US Treasury’s mid-April 2021

removal of Vietnam from its list of currency manipulators and end to the tariff threat on the end-July 2021 currency-

dispute truce, which should ease pressure on the VND/US$ exchange rate.

VND/US$ exchange rate and US Dollar Index (DXY) VND depreciated relative to US$ in 5M22

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg, as of 05/30/2022

VND depreciated

relative to US$ in

5M22

Source: Bloomberg, as of 05/30/2022, Mirae Asset Securities (Vietnam) ResearchNote: JPY = Japanese yen, PHP = Philippines peso, CNY = Chinese yuan, VND = Vietnamese dong, INR = Indian rupee, KRW = Korean won, MYR = Malaysian ringgit, THB = Thailand baht, IDR = Indonesian Rupiah

-4

-2

0

2

4

6

8

10

12

14

16

CNY VND PHP

INR MYR IDR

KRW THB JPY

(End 2021 = 0%)

85

90

95

100

105

110

22600

22800

23000

23200

23400

23600

23800

Mar

18

May

18

Jul 1

8Se

p 18

Nov

18

Jan

19M

ar 1

9M

ay 1

9Ju

l 19

Sep

19N

ov 1

9Ja

n 20

Mar

20

May

20

Jul 2

0Se

p 20

Nov

20

Jan

21M

ar 2

1M

ay 2

1Ju

l 21

Sep

21N

ov 2

1Ja

n 22

Mar

22

May

22

VND/US$ (L) DXY (R)(VND) (Point)

Mirae Asset Securities (Vietnam) Research16 | Vietnam focus: Strategy

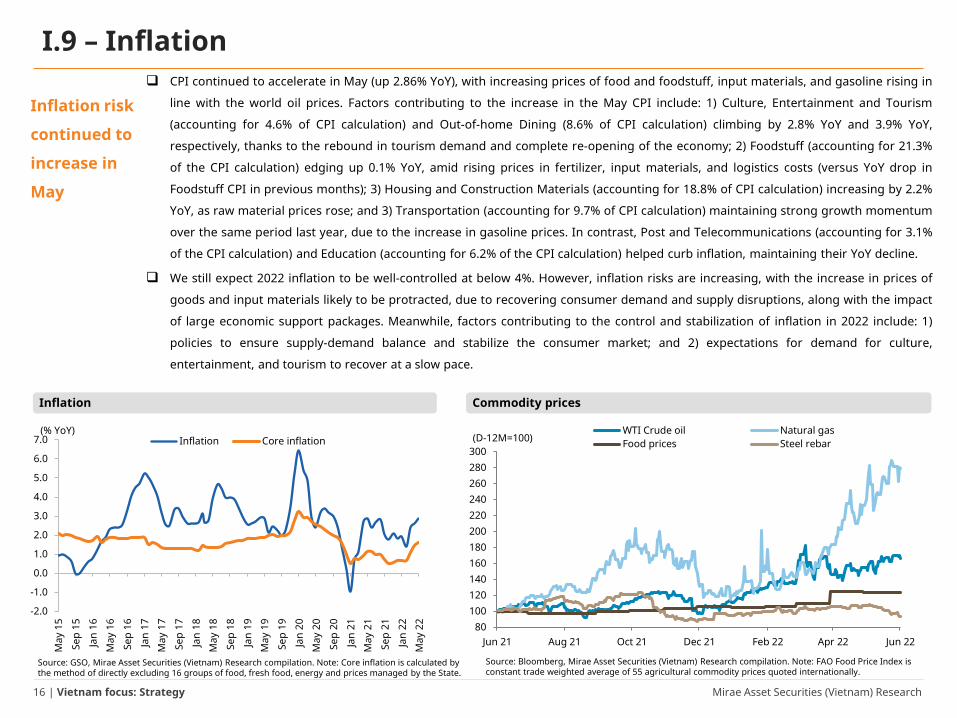

I.9 – Inflation❑ CPI continued to accelerate in May (up 2.86% YoY), with increasing prices of food and foodstuff, input materials, and gasoline rising in

line with the world oil prices. Factors contributing to the increase in the May CPI include: 1) Culture, Entertainment and Tourism

(accounting for 4.6% of CPI calculation) and Out-of-home Dining (8.6% of CPI calculation) climbing by 2.8% YoY and 3.9% YoY,

respectively, thanks to the rebound in tourism demand and complete re-opening of the economy; 2) Foodstuff (accounting for 21.3%

of the CPI calculation) edging up 0.1% YoY, amid rising prices in fertilizer, input materials, and logistics costs (versus YoY drop in

Foodstuff CPI in previous months); 3) Housing and Construction Materials (accounting for 18.8% of CPI calculation) increasing by 2.2%

YoY, as raw material prices rose; and 3) Transportation (accounting for 9.7% of CPI calculation) maintaining strong growth momentum

over the same period last year, due to the increase in gasoline prices. In contrast, Post and Telecommunications (accounting for 3.1%

of the CPI calculation) and Education (accounting for 6.2% of the CPI calculation) helped curb inflation, maintaining their YoY decline.

❑ We still expect 2022 inflation to be well-controlled at below 4%. However, inflation risks are increasing, with the increase in prices of

goods and input materials likely to be protracted, due to recovering consumer demand and supply disruptions, along with the impact

of large economic support packages. Meanwhile, factors contributing to the control and stabilization of inflation in 2022 include: 1)

policies to ensure supply-demand balance and stabilize the consumer market; and 2) expectations for demand for culture,

entertainment, and tourism to recover at a slow pace.

Inflation Commodity prices

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation. Note: Core inflation is calculated by the method of directly excluding 16 groups of food, fresh food, energy and prices managed by the State.

Inflation risk

continued to

increase in

May

Source: Bloomberg, Mirae Asset Securities (Vietnam) Research compilation. Note: FAO Food Price Index is constant trade weighted average of 55 agricultural commodity prices quoted internationally.

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

May

15

Sep

15

Jan

16M

ay 1

6

Sep

16

Jan

17M

ay 1

7

Sep

17

Jan

18M

ay 1

8

Sep

18

Jan

19M

ay 1

9

Sep

19

Jan

20M

ay 2

0

Sep

20

Jan

21M

ay 2

1

Sep

21

Jan

22M

ay 2

2

Inflation Core inflation(% YoY)

80100120140160180200220240260280300

Jun 21 Aug 21 Oct 21 Dec 21 Feb 22 Apr 22 Jun 22

WTI Crude oil Natural gasFood prices Steel rebar(D-12M=100)

Mirae Asset Securities (Vietnam) Research17 | Vietnam focus: Strategy

I.9 – Inflation (cont’d.)CPI by industry (% YoY)

Source: GSO, Mirae Asset Securities (Vietnam) Research compilation Note: Core inflation is calculated by the method of directly excluding 16 groups of food, fresh food, energy and prices managed by the State.

Item Proportion (%)2021 2022

5 6 7 8 9 10 11 12 1 2 3 4 5

CPI 2.9 2.4 2.6 2.8 2.1 1.8 2.1 1.8 1.9 1.4 2.4 2.6 2.9

Core CPI 1.1 1.1 1.0 1.0 0.7 0.5 0.6 0.7 0.7 0.7 1.1 1.5 1.6

Food and Foodstuff 33.6 0.2 -0.3 0.5 1.2 1.3 0.1 -0.1 0.5 -0.1 -0.2 1.0 1.1 1.3

Food 3.7 4.3 4.4 5.0 5.1 4.7 4.3 3.9 3.9 3.1 1.7 1.8 2.1 2.4

Foodstuff 21.3 -1.1 -2.0 -0.8 0.1 0.4 -1.4 -1.7 -0.8 -1.7 -1.8 -0.1 -0.2 0.1

Out-of-home dining 8.6 2.0 1.9 1.9 2.1 2.1 2.2 2.3 2.4 2.4 3.1 3.4 3.8 3.9

Beverage and Tobacco 2.7 1.6 1.6 1.8 1.9 2.0 2.2 2.4 2.5 2.8 2.2 2.6 2.7 3.0

Garment, Footwear and Hats 5.7 1.0 1.0 0.9 0.9 0.8 0.9 1.0 1.1 0.9 0.7 1.0 1.1 1.3

Housing and Construction Materials 18.8 2.9 4.0 4.4 4.3 1.6 1.1 1.5 1.0 3.5 0.4 1.7 2.7 2.2

Household Appliances and Equipment 6.7 0.6 0.6 0.6 0.6 0.7 0.8 0.9 1.1 1.2 1.2 1.4 1.6 1.8

Medicines and Healthcare 5.4 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.3 0.3 0.3 0.3 0.4

Transportation 9.7 21.2 15.5 13.8 13.6 13.6 16.5 20.7 15.8 14.5 15.5 18.3 16.6 18.4

Post and Telecommunications 3.1 -0.9 -0.8 -0.9 -0.9 -0.9 -0.9 -0.7 -0.7 -0.7 -0.7 -0.6 -0.5 -0.3

Education 6.2 4.1 4.1 4.1 4.0 -1.1 -2.2 -3.1 -3.5 -3.8 -3.3 -3.2 -2.3 -2.2

Culture, Entertainment and Tourism 4.6 -0.6 -0.7 -1.1 -0.9 -0.7 -0.5 -0.3 -0.2 -0.1 0.3 0.5 1.8 2.8

Mirae Asset Securities (Vietnam) Research18 | Vietnam focus: Strategy

I.10 – Key macroeconomic indicators

Source: GSO, Vietnam Customs, MPI, Bloomberg, IMF, Mirae Asset Securities (Vietnam) Research Note: Public debt (% GDP) in 2021 is estimated by MOF.

Indicator 2014 2015 2016 2017 2018 2019 2020 2021 2022F

Real GDP growth (%, YoY) 6.0 6.7 6.2 6.8 7.1 7.0 2.9 2.6 5.9

Export growth (%, YoY) 13.8 8.1 9.0 21.1 13.2 8.4 6.5 19 22

Import growth (%, YoY) 12 12.1 5.6 20.8 11.1 6.8 3.6 26.5 21

Trade balance (US$ bn) 2.0 -3.2 2.6 2.7 6.8 11.1 19.1 4.1 8.2

FDI disbursement (US$ bn) 12.4 14.5 15.8 17.5 19.1 20.4 20.0 19.7 21

Retail growth, excluding inflation (%, YoY) 6.2 8.5 8.3 9.3 9.4 9.2 -3.0 -6.2 6.5

Average CPI (%) 4.1 0.6 2.7 3.5 3.5 2.8 3.2 1.8 3.9

Foreign exchange reserve (US$bn) 34.5 30.5 36.7 49.2 55.3 78.5 94.8 107.4 130

Credit growth (%, YoY) 14.2 17.3 18.2 18.3 10.7 13.6 12.2 13.6 13

Exchange rate VND/US$ 21,388 22,485 22,761 22,698 23,175 23,314 23,267 22,826 23,054

Change in VND/US$ (%) 1.4 5.1 1.2 -0.3 2.1 0.5 -0.2 -1.6 1.0

Public debt (%/GDP) 43.6 46.1 47.6 46.3 43.6 43.4 46.6 43.7 46.9

Mirae Asset Securities (Vietnam) Research19 | Vietnam focus: Strategy

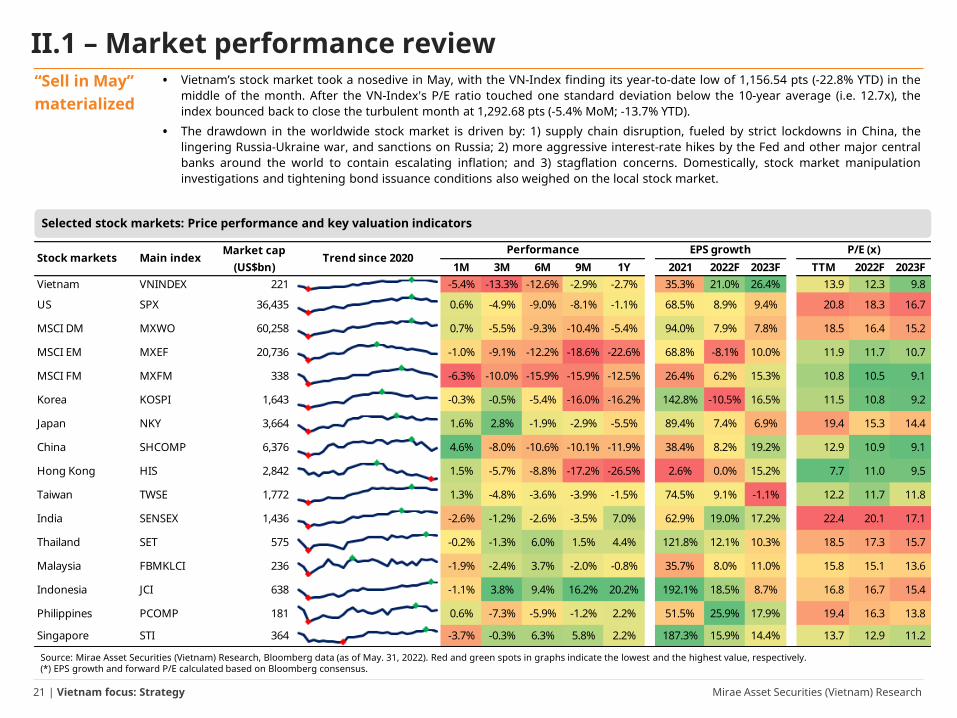

❑ Vietnam’s stock market took a nosedive in May, with the VN-Index finding its year-to-datelow of 1,156.54 pts. After the VN-Index's P/E ratio touched one standard deviation belowthe 10-year average (i.e., 12.7x), the index bounced back to close the turbulent month at1,292.68 pts (-5.4% MoM; -13.7% YTD).

❑ The drawdown in the worldwide stock market is driven by: 1) supply chain disruption,fueled by strict lockdowns in China, the lingering Russia-Ukraine war, and sanctions onRussia; 2) more aggressive interest-rate hikes by the Fed and other major central banksaround the world to contain escalating inflation; and 3) stagflation concerns.Domestically, stock market manipulation investigations and tightening bond issuanceconditions also weighed on the local stock market.

❑ According to our liquidity metric, Consumer Durables & Apparel, Insurance, Retailing,and Software & Services attracted the most market cash flow during the resumption ofmarket momentum, while the liquidity scores of Utilities, Energy, and Transportationimproved to Neutral. By contrast, many mainstays — such as Banks, Real Estate,Materials, and Diversified Financials — continued to trade at low levels.

❑ Domestic individuals (accounting for 82% of total trading value) and local institutions(~8% of total trading value) sold in May, with net amounts of VND489bn and VND2.7tr,respectively, all offset by the VND3.2tr in net buying by foreign investors (~10% of totaltrading value). ETFs poured in a net inflow of US$213.5mn in May, for a total ofUS$265.3mn YTD, mainly from DCVFMVN Diamond ETF and Fubon FTSE Vietnam ETF.

II. Vietnam stock market May 2022 review

Mirae Asset Securities (Vietnam) Research20 | Vietnam focus: Strategy

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg

II.2 – VN-Index and key driving events

1,000

1,100

1,200

1,300

1,400

1,500

Jan 21 Feb 21 Mar 21 Apr 21 May 21 Jun 21 Jul 21 Aug 21 Sep 21 Oct 21 Nov 21 Dec 21 Jan 22 Feb 22 Mar 22 Apr 22 May 22 Jun 22

(Point)

Third Covid-19 wave

The State Bank of Vietnam (SBV) issued Circular 03/2021/TTNHNN on April 2, 2021, amending Cir. 01/2020/TT-NHNN to extend the debt moratorium for loans hit by Covid-19 and allow banks to apply a 3-year provisioning roadmap for these loans.

The Government promulgates Decree 52/2021/ND-CP on extension of time limit for payment of value-added tax, corporate income tax, personal income tax, and land rental in 2021.

Fourth Covid-19 resurgence

Resolution No. 68/NQ-CP is issued, with a support package of VND26,000bn

Social distancing period

Vietnam officially launches its largest-ever vaccination campaign

Social distancing eased

Resolution No. 128/NQ-CP of the Government promulgating the regulation "Safely and flexibly adapting, effectively controlling the Covid-19 pandemic"

The Government issuesOfficial Letter 7776/CD-VPCP on accelerating the disbursement of public investment capital in 2021

Government submits the Economic Restructuring Plan for the 2021−2025 period to the National Assembly

A new Covid variant —Omicron —detected in South Africa

The first case of Omicron variant appears in Vietnam

Resolution No. 105/NQ-CP on supporting businesses, cooperatives, and business households negatively affected by Covid-19

Package of tax exemptions,reductions for businesses and individual business households worth VND21tr

RCEP officially takes effect

Promulgating Resolution 43/2022/QH15 on fiscal and monetary policies to support the socio-economic recovery and development program

Main events in the past five months of 2022:1) VAT officially reduced by 2 percentage points to 8% from Feb. 1, 2022 to the end of 2022.2) Resolution No. 18/NQ-CP issued, implementing Resolution No. 44/2022/QH15, dated January 11, 2022, of the National Assembly on investment policy of the East South–North expressway construction project in the period of 2021–2025.3) The government announces full reopening of tourism from Mar. 15.4) Russia’s President orders military operation in Ukraine.5) Vietnam reopens international and domestic tourism activities.6) The Government promulgates the program to prevent and control the Covid-19 pandemic for the period of 2022–2023.7) The Government approved the Resolution of the National Assembly extending the application period of Resolution 42 on bad debtsettlement to August 15, 2025.8) Deputy Prime Minister signed and promulgated Official Dispatch No. 304/CD-TTg of the Prime Minister, dated April 7, 2022, on rectification of corporate bond market activities and land use rights auctions.9) The National Assembly agrees to extend pilot resolution 42/2017/QH14 on bad debt settlement until the end-2023.10) The Federal Reserve raises the Fed Funds Rate by half a point to 0.75%–1%.

1

2

3

4

56

7 8

9

10

Mirae Asset Securities (Vietnam) Research21 | Vietnam focus: Strategy

• Vietnam’s stock market took a nosedive in May, with the VN-Index finding its year-to-date low of 1,156.54 pts (-22.8% YTD) in themiddle of the month. After the VN-Index's P/E ratio touched one standard deviation below the 10-year average (i.e. 12.7x), theindex bounced back to close the turbulent month at 1,292.68 pts (-5.4% MoM; -13.7% YTD).

• The drawdown in the worldwide stock market is driven by: 1) supply chain disruption, fueled by strict lockdowns in China, thelingering Russia-Ukraine war, and sanctions on Russia; 2) more aggressive interest-rate hikes by the Fed and other major centralbanks around the world to contain escalating inflation; and 3) stagflation concerns. Domestically, stock market manipulationinvestigations and tightening bond issuance conditions also weighed on the local stock market.

“Sell in May” materialized

Selected stock markets: Price performance and key valuation indicators

II.1 – Market performance review

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data (as of May. 31, 2022). Red and green spots in graphs indicate the lowest and the highest value, respectively.(*) EPS growth and forward P/E calculated based on Bloomberg consensus.

1M 3M 6M 9M 1Y 2021 2022F 2023F TTM 2022F 2023FVietnam VNINDEX 221 -5.4% -13.3% -12.6% -2.9% -2.7% 35.3% 21.0% 26.4% 13.9 12.3 9.8

US SPX 36,435 0.6% -4.9% -9.0% -8.1% -1.1% 68.5% 8.9% 9.4% 20.8 18.3 16.7

MSCI DM MXWO 60,258 0.7% -5.5% -9.3% -10.4% -5.4% 94.0% 7.9% 7.8% 18.5 16.4 15.2

MSCI EM MXEF 20,736 -1.0% -9.1% -12.2% -18.6% -22.6% 68.8% -8.1% 10.0% 11.9 11.7 10.7

MSCI FM MXFM 338 -6.3% -10.0% -15.9% -15.9% -12.5% 26.4% 6.2% 15.3% 10.8 10.5 9.1

Korea KOSPI 1,643 -0.3% -0.5% -5.4% -16.0% -16.2% 142.8% -10.5% 16.5% 11.5 10.8 9.2

Japan NKY 3,664 1.6% 2.8% -1.9% -2.9% -5.5% 89.4% 7.4% 6.9% 19.4 15.3 14.4

China SHCOMP 6,376 4.6% -8.0% -10.6% -10.1% -11.9% 38.4% 8.2% 19.2% 12.9 10.9 9.1

Hong Kong HIS 2,842 1.5% -5.7% -8.8% -17.2% -26.5% 2.6% 0.0% 15.2% 7.7 11.0 9.5

Taiwan TWSE 1,772 1.3% -4.8% -3.6% -3.9% -1.5% 74.5% 9.1% -1.1% 12.2 11.7 11.8

India SENSEX 1,436 -2.6% -1.2% -2.6% -3.5% 7.0% 62.9% 19.0% 17.2% 22.4 20.1 17.1

Thailand SET 575 -0.2% -1.3% 6.0% 1.5% 4.4% 121.8% 12.1% 10.3% 18.5 17.3 15.7

Malaysia FBMKLCI 236 -1.9% -2.4% 3.7% -2.0% -0.8% 35.7% 8.0% 11.0% 15.8 15.1 13.6

Indonesia JCI 638 -1.1% 3.8% 9.4% 16.2% 20.2% 192.1% 18.5% 8.7% 16.8 16.7 15.4

Philippines PCOMP 181 0.6% -7.3% -5.9% -1.2% 2.2% 51.5% 25.9% 17.9% 19.4 16.3 13.8

Singapore STI 364 -3.7% -0.3% 6.3% 5.8% 2.2% 187.3% 15.9% 14.4% 13.7 12.9 11.2

Trend since 2020Stock markets Main indexMarket cap

(US$bn)Performance EPS growth P/E (x)

Mirae Asset Securities (Vietnam) Research22 | Vietnam focus: Strategy

• In general, most industries plummeted in the first haft of the month, and subsequently saw uneven recoveries, withincreasingly divergent performances. For the whole month, many mainstays — namely, Banks, Materials, RealEstate, Diversified Financials, F&B, and Capital Goods — weighed heavily on the benchmark. By contrast, Utilities,Software and Services, and Telecommunications posted positive returns in May and made positive contributions tothe VN-Index.

Increasingly divergent performances

Banks, Materials, and Real Estate weighed on the market, partly offset by Utilities, and Software and Services

II.3 – Performance review by industry

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data (as of May. 31, 2022). Red and green spots in graphs indicate the lowest and the highest value, respectively.

Market cap VN-ndex impacts in May(VNDbn) 1M 3M 6M 9M 1Y (monthly change, points)

Automobiles & Components 9,501 0.2% 0.5% 2.0% -5.6% 3.0% 15.5% 0.01

Banks 1,563,909 30.5% -6.9% -16.4% -10.6% -3.0% -12.5% -29.46

Capital Goods 260,470 5.1% -5.9% -21.0% -14.8% 28.8% 47.5% -4.65

Commercial & Professional Services 5,435 0.1% -1.9% 2.0% -8.7% 4.4% 21.4% -0.03

Consumer Durables & Apparel 54,544 1.1% -4.9% 2.2% 6.3% 24.9% 23.6% -0.67

Consumer Services 7,684 0.1% -19.3% -26.0% -18.9% -9.7% -1.5% -0.20

Diversified Financials 129,453 2.5% -13.6% -27.8% -36.0% 3.1% 45.9% -5.20

Energy 78,314 1.5% -4.5% -26.8% -15.2% -3.2% -8.7% -0.94

F&B 533,612 10.4% -4.0% -9.9% -9.7% -2.6% 1.9% -4.97

Health Care 3,198 0.1% -14.4% -24.4% -29.4% -9.0% 50.6% -0.14

Household & Personal Products 1,442 0.0% -10.4% -12.4% -14.1% -21.5% -22.9% -0.04

Insurance 52,870 1.0% -13.5% -8.3% -11.9% -4.3% 6.0% -2.10

Materials 432,161 8.4% -15.0% -20.9% -24.3% -20.2% -11.6% -18.57

Media & Entertainment 1,517 0.0% -1.2% -18.9% 1.9% 15.2% -1.3% 0.00

Pharmaceuticals 30,480 0.6% -5.5% -10.0% -7.0% -11.2% 3.4% -0.45

Real Estate 1,143,569 22.3% -2.8% -7.7% -14.5% -3.4% -3.5% -8.83

Retailing 135,525 2.6% -4.7% 7.5% 10.5% 40.8% 70.0% -1.69

Software & Services 108,005 2.1% 4.4% 17.6% 13.0% 19.8% 32.3% 0.97

Telecommunication 2,131 0.0% 2.9% -7.7% -4.0% 35.8% 70.4% 0.02

Transportation 195,221 3.8% -5.0% -10.2% -2.1% 4.5% 24.4% -2.60

Utilities 361,450 7.0% 6.1% -4.9% 25.5% 38.5% 50.4% 5.31

VN-Index 5,131,527 100% -5.4% -13.3% -12.6% -2.9% -2.7% -74.12

GICS industry groupPerformance

Weight Trend since 2020

Mirae Asset Securities (Vietnam) Research23 | Vietnam focus: Strategy

Top leading and lagging contributors to VN-Index’s performance in May

II.3 – Performance review by industry (cont’d.)

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

5

10

15

20

25

30

GAS VN POW VN VSH VN GEG VN FPT VN PVD VN PVT VN PNJ VN REE VN BCG VN VJC VN GMD VN KDC VN BAF VN ANV VN VHM VN KBC VN EIB VN HDB VN CTG VN

Utilities Software& Services

Energy ConsumerDurables& Apparel

Capital Goods Transportation F&B Real Estate Banks

1M change (L) Impact (R)(% MoM) (index points)

-12

-10

-8

-6

-4

-2

0

-30

-25

-20

-15

-10

-5

0VPB VN TCB VN VIB VN STB VN BID VN VCB VN MBB VN OCB VN HPG VN GVR VN BCM VN NVL VN DXG VN VND VN SAB VN VNM VN MSN VN HVN VN BVH VN PLX VN

Banks Materials Real EstateDiversifiedFinancials F&B Transportation

InsuranceEnergy

Mirae Asset Securities (Vietnam) Research24 | Vietnam focus: Strategy

• The daily average trading value in May plunged by more than 33% MoM to around VND13.8tr/day. That said, marketcash flow has improved slightly in recent weeks, since the VN-Index’s bottoming.

• According to our liquidity metric, Consumer Durables & Apparel, Insurance, Retailing, and Software & Services attractedthe most market cash flow during the market momentum resumption, while the liquidity scores of Utilities, Energy, andTransportation improved to Neutral. By contrast, many mainstays — such as Banks, Real Estate, Materials, andDiversified Financials — continued to trade at low levels.

Market cash flow has diverged during the bounceback

Market liquidity heatmap

II.4 – Market liquidity heatmap

Source: Mirae Asset Securities (Vietnam) Research. Red and green spots in graphs indicate the lowest and the highest value, respectively.Note: To rank liquidity levels, we use percentile scores that allow for comparing the current trading level to its historic trading levels over the trailing twelve-month period. The score ranges from 0% (the lowest) to 100% (the highest). For visualization, we use a heat map, with red signifying the lowest, green the highest, and yellow the middle.

Liquidity Trend4/29/2022 5/6/2022 5/13/2022 5/20/2022 5/27/2022 6/3/2022 score last 10 weeks

Consumer Durables & Apparel 75%Insurance 73%Retailing 69%Software & Services 65%Utilities 59%Transportation 45%Energy 43%F&B 27%Capital Goods 25%Health Care 20%Diversified Financials 12%Materials 4%Consumer Services 2%Real Estate 2%Automobiles & Components 0%Banks 0%Pharmaceuticals 0%VN-Index 2%

GICS Industry groupHeat map

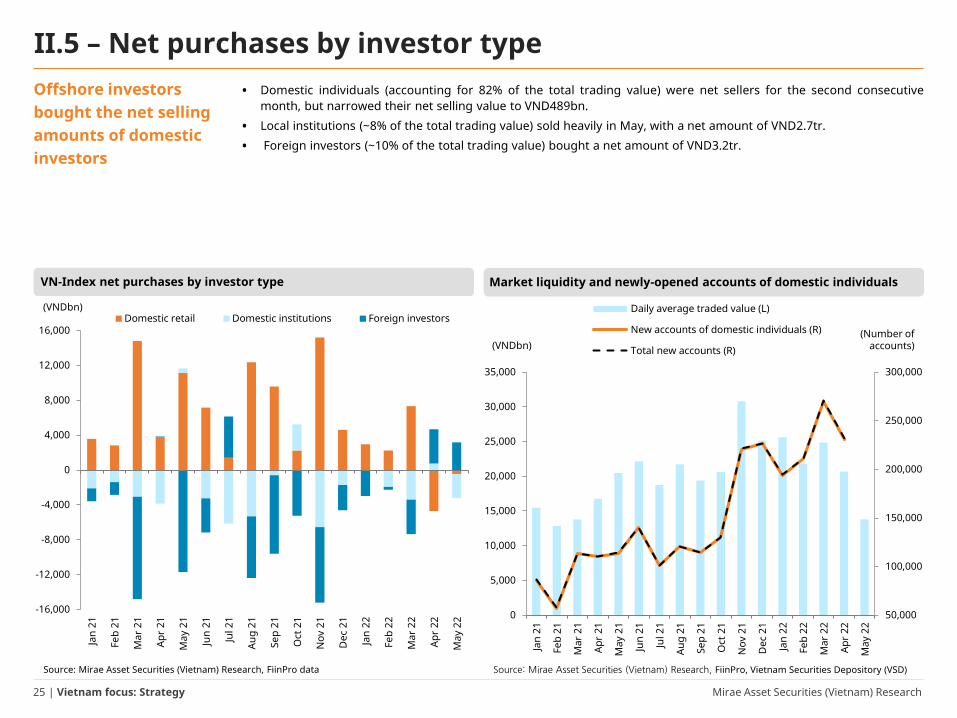

Mirae Asset Securities (Vietnam) Research25 | Vietnam focus: Strategy

Offshore investors bought the net selling amounts of domestic investors

II.5 – Net purchases by investor type• Domestic individuals (accounting for 82% of the total trading value) were net sellers for the second consecutive

month, but narrowed their net selling value to VND489bn.

• Local institutions (~8% of the total trading value) sold heavily in May, with a net amount of VND2.7tr.

• Foreign investors (~10% of the total trading value) bought a net amount of VND3.2tr.

Source: Mirae Asset Securities (Vietnam) Research, FiinPro data

VN-Index net purchases by investor type Market liquidity and newly-opened accounts of domestic individuals

Source: Mirae Asset Securities (Vietnam) Research, FiinPro, Vietnam Securities Depository (VSD)

-16,000

-12,000

-8,000

-4,000

0

4,000

8,000

12,000

16,000

Jan

21

Feb

21

Mar

21

Apr

21

May

21

Jun

21

Jul 2

1

Aug

21

Sep

21

Oct

21

Nov

21

Dec

21

Jan

22

Feb

22

Mar

22

Apr

22

May

22

Domestic retail Domestic institutions Foreign investors(VNDbn)

50,000

100,000

150,000

200,000

250,000

300,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan

21

Feb

21

Mar

21

Apr

21

May

21

Jun

21

Jul 2

1

Aug

21

Sep

21

Oct

21

Nov

21

Dec

21

Jan

22

Feb

22

Mar

22

Apr

22

May

22

Daily average traded value (L)

New accounts of domestic individuals (R)

Total new accounts (R)(Number of

accounts)(VNDbn)

Mirae Asset Securities (Vietnam) Research26 | Vietnam focus: Strategy

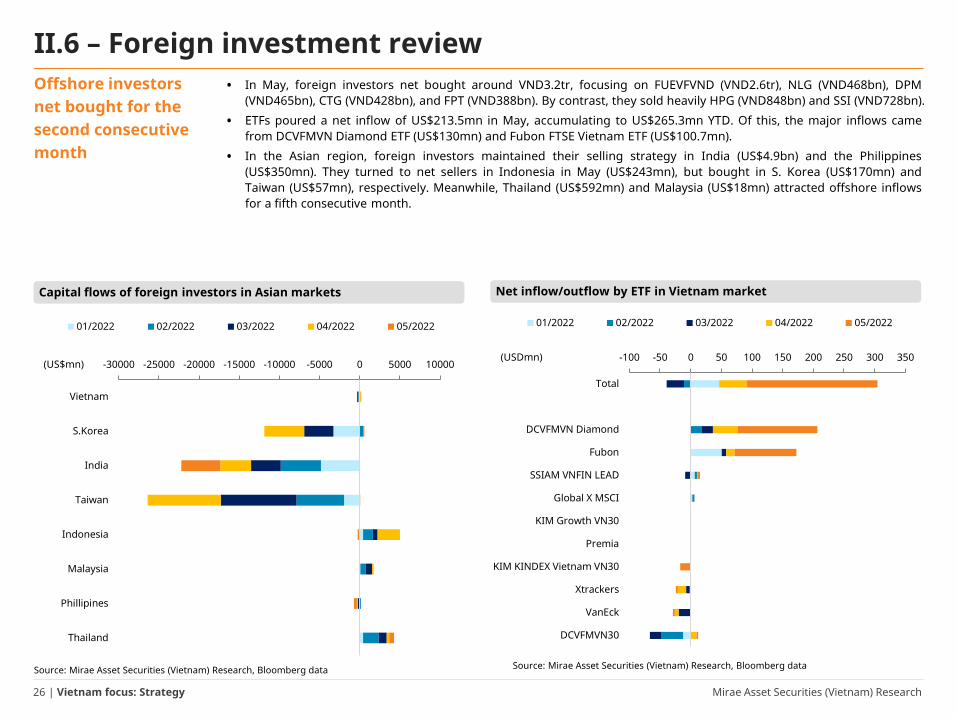

II.6 – Foreign investment reviewOffshore investors net bought for the second consecutive month

• In May, foreign investors net bought around VND3.2tr, focusing on FUEVFVND (VND2.6tr), NLG (VND468bn), DPM(VND465bn), CTG (VND428bn), and FPT (VND388bn). By contrast, they sold heavily HPG (VND848bn) and SSI (VND728bn).

• ETFs poured a net inflow of US$213.5mn in May, accumulating to US$265.3mn YTD. Of this, the major inflows camefrom DCVFMVN Diamond ETF (US$130mn) and Fubon FTSE Vietnam ETF (US$100.7mn).

• In the Asian region, foreign investors maintained their selling strategy in India (US$4.9bn) and the Philippines(US$350mn). They turned to net sellers in Indonesia in May (US$243mn), but bought in S. Korea (US$170mn) andTaiwan (US$57mn), respectively. Meanwhile, Thailand (US$592mn) and Malaysia (US$18mn) attracted offshore inflowsfor a fifth consecutive month.

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data

Capital flows of foreign investors in Asian markets Net inflow/outflow by ETF in Vietnam market

-30000 -25000 -20000 -15000 -10000 -5000 0 5000 10000

Vietnam

S.Korea

India

Taiwan

Indonesia

Malaysia

Phillipines

Thailand

01/2022 02/2022 03/2022 04/2022 05/2022

(US$mn)-100 -50 0 50 100 150 200 250 300 350

Total

DCVFMVN Diamond

Fubon

SSIAM VNFIN LEAD

Global X MSCI

KIM Growth VN30

Premia

KIM KINDEX Vietnam VN30

Xtrackers

VanEck

DCVFMVN30

01/2022 02/2022 03/2022 04/2022 05/2022

(USDmn)

Mirae Asset Securities (Vietnam) Research27 | Vietnam focus: Strategy

• VN-Index experienced a nasty sell-off, with its P/E plunging from a standard deviation (SD)above the 10-year average to one below the average. After bouncing back recently, the VN-Index is trading at 13.9x on a trailing P/E basis, below the 10-year average of 15x.Historically, the current valuation level of the VN-Index is attractive, offering buyingopportunities for strong fundamental stocks boasting long-term growth prospects atbargain prices.

• Despite having a relatively high ROE, the VN-Index is still trading at discount level, lowerthan peers, such as Indonesia (16.8x), Malaysia (15.8x), Thailand (18.5x), and thePhilippines (19.4x). Of note, the VN-Index has been trading at a discount compared withregional peers over the past 10 years. Furthermore, with its economic growth andcorporate earnings prospects (both of which are forecast to outperform those of othermarkets), Vietnam is likely to maintain a relatively attractive valuation. Meanwhile,emerging-market classification visibility in the foreseeable future, along with initiatives forimproving stock market transparency, is a plus in terms of the market attractiveness to FII.

• We priced in the increasing inflationary pressure on earnings in the coming quarters; thus,we cut our whole-year EPS growth projection for the VN-Index to 17.5% YoY (from 22% theprior forecast), lower than the Bloomberg consensus of 21% YoY. As a result, we expect theVN-Index to regain lost ground and return to the 1,300–1,530 range this year,corresponding to a fair P/E range from 12.8–15.1x.

III. Vietnam stock market prospects

Mirae Asset Securities (Vietnam) Research28 | Vietnam focus: Strategy

Attractive valuation at current discount level

III.1 – Relative valuations• VN-Index experienced a nasty sell-off, with its P/E plunging from a standard deviation (SD) above the 10-year average

to a SD under the average. After bouncing back recently, the VN-Index is trading at 13.9x on a trailing P/E basis, belowthe 10-year average of 15x.

• Correspondingly, the earning yield of the VN-Index also corrected from its 10-year average plus a SD before the maketentered the correction rout. On the other hand, domestic bond yields have soared since end of March, reflectingexternal risks (i.e., supply chain disruptions, China’s zero-Covid policy, the Russia-Ukraine war and sanctions on Russia,the Fed’s rate hikes and its balance sheet runoff, and global stagflation concerns), as well as domestic inflationarypressure. Currently, VN-Index is trading at 7.2x on a trailing earning yield, slightly above its 10-year average.

• Historically, the current valuation level of the VN-Index is attractive, offering buying opportunities for strongfundamental stocks boasting long-term growth prospects at bargain prices.

The VN-Index is currently trading below its 10-year P/E average

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data

Rising domestic bond yields reflected inflation risk

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data

10.5

12.8

15.1

17.3

19.6

10

12

14

16

18

20

22

May 12 May 13 May 14 May 15 May 16 May 17 May 18 May 19 May 20 May 21 May 22

P/E -2SD -1SD

10-year average +1SD +2SD

(x)

0

2

4

6

8

10

12

May 12 May 13 May 14 May 15 May 16 May 17 May 18 May 19 May 20 May 21 May 22

Earnings yield -1SD 10-year average+1SD 2-year yield 5-year yield10-year yield

(%pa)

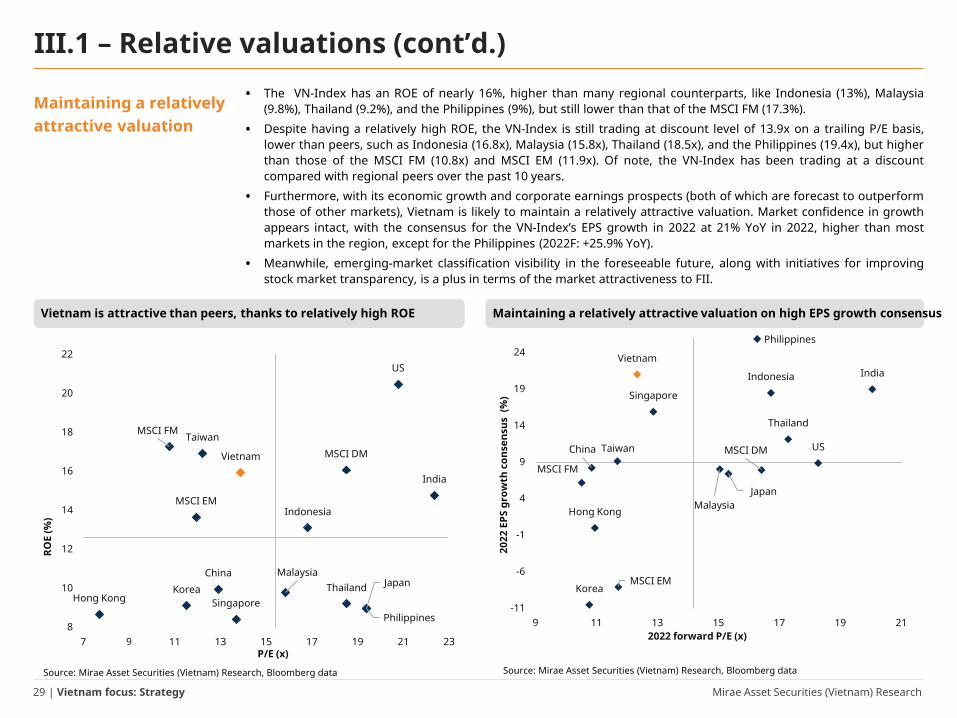

Mirae Asset Securities (Vietnam) Research29 | Vietnam focus: Strategy

• The VN-Index has an ROE of nearly 16%, higher than many regional counterparts, like Indonesia (13%), Malaysia(9.8%), Thailand (9.2%), and the Philippines (9%), but still lower than that of the MSCI FM (17.3%).

• Despite having a relatively high ROE, the VN-Index is still trading at discount level of 13.9x on a trailing P/E basis,lower than peers, such as Indonesia (16.8x), Malaysia (15.8x), Thailand (18.5x), and the Philippines (19.4x), but higherthan those of the MSCI FM (10.8x) and MSCI EM (11.9x). Of note, the VN-Index has been trading at a discountcompared with regional peers over the past 10 years.

• Furthermore, with its economic growth and corporate earnings prospects (both of which are forecast to outperformthose of other markets), Vietnam is likely to maintain a relatively attractive valuation. Market confidence in growthappears intact, with the consensus for the VN-Index’s EPS growth in 2022 at 21% YoY in 2022, higher than mostmarkets in the region, except for the Philippines (2022F: +25.9% YoY).

• Meanwhile, emerging-market classification visibility in the foreseeable future, along with initiatives for improvingstock market transparency, is a plus in terms of the market attractiveness to FII.

Maintaining a relatively attractive valuation

III.1 – Relative valuations (cont’d.)

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data

Vietnam is attractive than peers, thanks to relatively high ROE Maintaining a relatively attractive valuation on high EPS growth consensus

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data

Vietnam

USMSCI DM

MSCI EM

MSCI FM

Korea

Japan

China

Hong Kong

Taiwan

India

Thailand

Malaysia

Indonesia

Philippines

Singapore

-11

-6

-1

4

9

14

19

24

9 11 13 15 17 19 21

2022

EPS

gro

wth

con

sens

us (

%)

2022 forward P/E (x)

Vietnam

US

MSCI DM

MSCI EM

MSCI FM

Korea JapanChina

Hong Kong

Taiwan

India

ThailandMalaysia

Indonesia

PhilippinesSingapore

8

10

12

14

16

18

20

22

7 9 11 13 15 17 19 21 23

ROE

(%)

P/E (x)

Mirae Asset Securities (Vietnam) Research30 | Vietnam focus: Strategy

• As Vietnam economy is still on road to a post-pandemic recovery, 1Q22 earnings growth is still robust, with the totalNPATMI of HOSE-listed firms increasing 34% YoY (2021: +37.6% YoY). However, companies have set conservativetargets for 2022, with the total PBT of 320 out of the 404 HOSE-listed firms (~92% of total market cap) set to grow by15.8% YoY.

• We priced in the rising inflationary pressure on earnings in the coming quarters; thus, we cut our full-year EPSgrowth projection for the VN-Index to 17.5% YoY (from 22% the prior forecast), lower than the Bloomberg consensusof 21% YoY.

o After a strong recovery in 2021, earnings growth is expected to be normalized in 2022.o As global inflation rises, profit margins are under pressure from surging transportation and material costs.o Due to increased inflationary pressure, along with the hawkish path of the Federal Reserve, local interest

rates are on the rise.o With a 2022 EPS growth expectation of 17.5%, we expect the VN-Index to regain lost ground to return to the 1,300–

1,530 range this year, corresponding to a fair P/E range from 12.8–15.1x.

We cut our 2022 EPS growth projection for the VN-Index to 17.5% YoY to reflect inflationary pressure

III.2 – Earnings review and 2022 outlook

Source: Mirae Asset Securities (Vietnam) Research, Bloomberg data Source: Mirae Asset Securities (Vietnam) Research

VN-Index’s EPS growth consensus for 2022 VN-Index forecast for 2022: Sensitivity analysis

2022

EPS

gro

wth

con

sens

us

10-year P/E band

-2SD -1SD Average +1SD +2SD

10.5 12.8 15.1 17.3 19.6

16.0% 1,050 1,281 1,512 1,742 1,973

16.5% 1,055 1,286 1,518 1,750 1,981

17.0% 1,059 1,292 1,525 1,757 1,990

17.5% 1,064 1,297 1,531 1,765 1,998

18.0% 1,068 1,303 1,538 1,772 2,007

18.5% 1,073 1,308 1,544 1,780 2,015

19.0% 1,077 1,314 1,551 1,787 2,024 19%

20%

21%

22%

23%

24%

25%

26%

Jan 22 Feb 22 Mar 22 Apr 22 May 22

Bloomberg consensus(% YoY)

Mirae Asset Securities (Vietnam) Research31 | Vietnam focus: Strategy

III.2 – Earnings review and 2022 outlook (cont’d.)

Source: Mirae Asset Securities (Vietnam) Research, FiinPro data (update as of May. 31, 2022)

Total earnings growth by industry for HOSE-listed firms: 1Q21 review and 2022 AGM stats

2020 2021 YoY growth% of totalmarket cap

PBT growth target

Automobiles & Components 9,501 13.2% 0.3% 11.9% 90% 13%Banks 1,563,909 16.4% 32.1% 31.9% 100% 33%Capital Goods 260,470 1.2% 19.9% 28.8% 93% 31%Commercial & Professional Services 5,435 -21.3% -4.2% 28.0% 95% 1%Consumer Durables & Apparel 54,544 37.0% 8.7% 37.6% 89% 32%Consumer Services 7,684 -89.2% 46.6% 168.2% 43% 13%Diversified Financials 129,453 38.4% 152.6% 29.0% 80% 14%Energy 78,314 -58.7% 92.1% -46.4% 15% -23%F&B 533,612 -12.1% 28.9% 44.4% 98% -3%Health Care 3,198 -37.0% 65.6% 873.9% 63% 5%Household & Personal Products 1,442 28.7% -27.3% -0.2% 100% 7%Insurance 52,870 28.5% 27.1% 5.8% 26% -8%Materials 432,161 56.9% 117.7% 45.8% 72% -16%Media & Entertainment 1,517 59.1% 140.5% 108.7%Pharmaceuticals 30,480 8.4% 8.0% 31.6% 93% 5.5%Real Estate 1,143,569 -1.6% 8.4% -11.9% 98% 12.4%Retailing 135,525 0.3% 41.3% 19.7% 100% 22.0%Software & Services 108,005 13.3% 23.8% 37.4% 93% 20.5%Telecommunication 2,131 -3.5% 38.9% 516.3% 82% 192.7%Transportation 195,221 -176.2% -10.9% 94.4% 75% 47.5%Utilities 361,450 -20.5% 12.0% 54.0% 85% -23.3%Total HOSE-listed firms 5,131,527 -0.5% 37.6% 34.0% 92% 15.8%

GICS Industry groupTotal market cap

(VNDbn)

2022 AGM statsEarnings growth (% YoY)

Mirae Asset Securities (Vietnam) Research32 | Vietnam focus: Strategy

III.3 – Upcoming eventsKey events in the last seven months of 2022

Source: Mirae Asset Securities (Vietnam) Research compilationNote: BoJ: Bank of Japan, FOMC: Federal Open Market Committee (US), BoE: Bank of England, ECB: European Central Bank

World events Vietnam’s events

Date Country Event Date Event

June

6/7/2022 AU RBA Interest Rate Decision 6/3/2022 Announcement of FTSE Vietnam ETF portfolio restructuring 6/8/2022 IN RBI Interest Rate Decision 6/10/2022 Announcement of VanEck Vectors Vietnam (VNM) ETF portfolio restructuring 6/9/2022 EA ECB Interest Rate Decision 6/16/2022 Expiry date of the VN30 futures contract

6/16/2022 US Fed Interest Rate Decision 6/17/2022 Restructuring of FTSE Vietnam Index ETF6/16/2022 GB BoE Interest Rate Decision 6/17/2022 Restructuring of VanEck Vectors Vietnam ETF6/17/2022 JP BoJ Interest Rate Decision 6/29/2022 Announcement of Vietnam economic data

July

7/5/2022 AU RBA Interest Rate Decision 7/18/2022Announcement of member change of VN30 and VNFINLEAD

Announcement of members’ information update of VN30, VNFIN LEAD, VNFIN SELECT, VNDIAMOND

7/7/2022 US FOMC Minutes 7/21/2022 Expiry date of the VN30 futures contract7/21/2022 JP BoJ Interest Rate Decision 7/29/2022 Announcement of Vietnam economic data7/28/2022 US Fed Interest Rate Decision

August8/2/2022 AU RBA Interest Rate Decision 08/01/2022 Changes in VN30, VNFINLEAD, VNFIN SELECT, and VNDIAMOND take effect8/4/2022 GB BoE Interest Rate Decision 8/18/2022 Expiry date of the VN30 futures contract

8/18/2022 US FOMC Minutes 8/29/2022 Announcement of Vietnam economic data

September

9/6/2022 AU RBA Interest Rate Decision 09/02/2022 Announcement of FTSE Vietnam ETF portfolio restructuring 9/8/2022 EA ECB Interest Rate Decision 09/09/2022 Announcement of VanEck Vectors Vietnam (VNM) ETF portfolio restructuring

9/15/2022 GB BoE Interest Rate Decision 9/15/2022 Expiry date of the VN30 futures contract9/22/2022 US Fed Interest Rate Decision 9/16/2022 Restructuring of FTSE Vietnam Index ETF and VanEck Vectors Vietnam ETF9/22/2022 JP BoJ Interest Rate Decision 9/29/2022 Announcement of Vietnam economic data

October10/13/2022 US FOMC Minutes 10/17/2022

Announcement of member change of VNFIN SELECT and VNDIAMONDAnnouncement of members’ information update of VN30, VNFIN LEAD, VNFIN SELECT,

VNDIAMOND10/27/2022 EA ECB Interest Rate Decision 10/29/2022 Expiry date of the VN30 futures contract10/28/2022 JP BoJ Interest Rate Decision 10/29/2022 Announcement of Vietnam economic data

November

11/1/2022 AU RBA Interest Rate Decision 11/07/2022 Changes in VN30, VNFINLEAD, VNFIN SELECT, and VNDIAMOND take effect11/3/2022 US Fed Interest Rate Decision 11/17/2022 Expiry date of the VN30 futures contract11/3/2022 GB BoE Interest Rate Decision 11/29/2022 Announcement of Vietnam economic data

11/24/2022 US FOMC Minutes

December

12/6/2022 AU RBA Interest Rate Decision 12/2/2022 Announcement of portfolio restructuring of FTSE Vietnam ETF and VanEck Vectors Vietnam ETF12/15/2022 US Fed Interest Rate Decision 12/15/2022 Expiry date of the VN30 futures contract12/15/2022 GB BoE Interest Rate Decision 12/16/2022 Restructuring of FTSE Vietnam Index ETF and VanEck Vectors Vietnam ETF12/15/2022 EA ECB Interest Rate Decision 12/29/2022 Announcement of Vietnam economic data12/20/2022 JP BoJ Interest Rate Decision

Mirae Asset Securities (Vietnam) Research33 | Vietnam focus: Strategy

• Industrial Real Estate: In general, the IP industry performance was strong in 1Q22. Total revenue of the eight leading enterprises increased by 13% YoY, whiletheir after-tax profit surged by 35% YoY. Some IP developers posted triple-digit growth rates in after-tax profit, such as IDC (+381% YoY) and VGC (+153%).

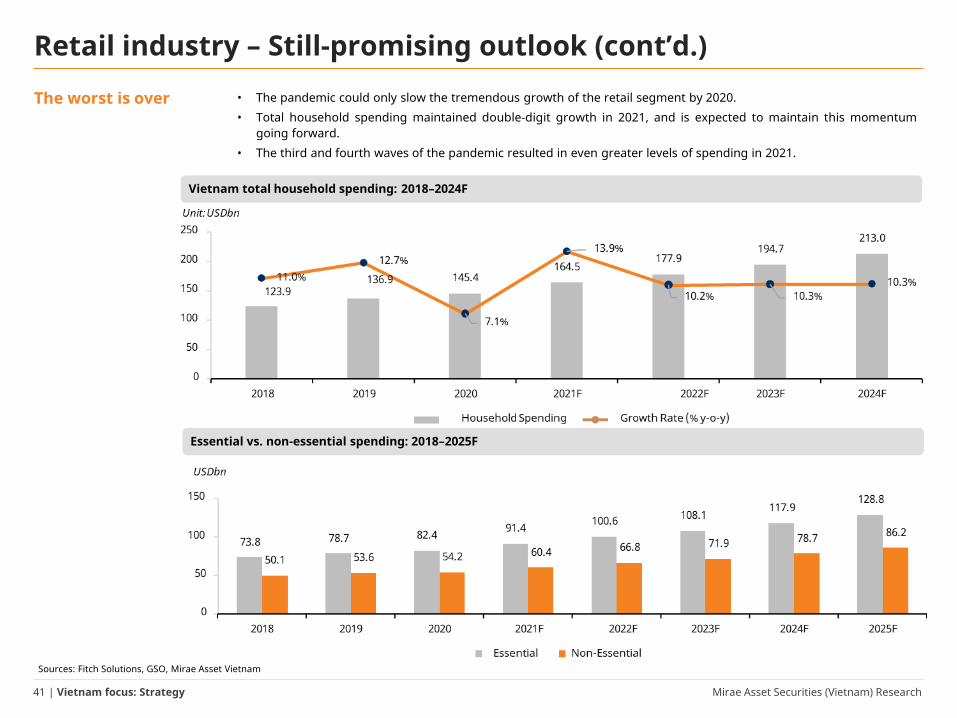

• Retail: We expect the retail industry to sustain double-digit growth in the long term. The recovery of non-essential sectors should be the key driver of the industry,thanks to depressed demand over the past two years. Total household spending maintained double-digit growth in 2021, and is expected to maintain thismomentum going forward.

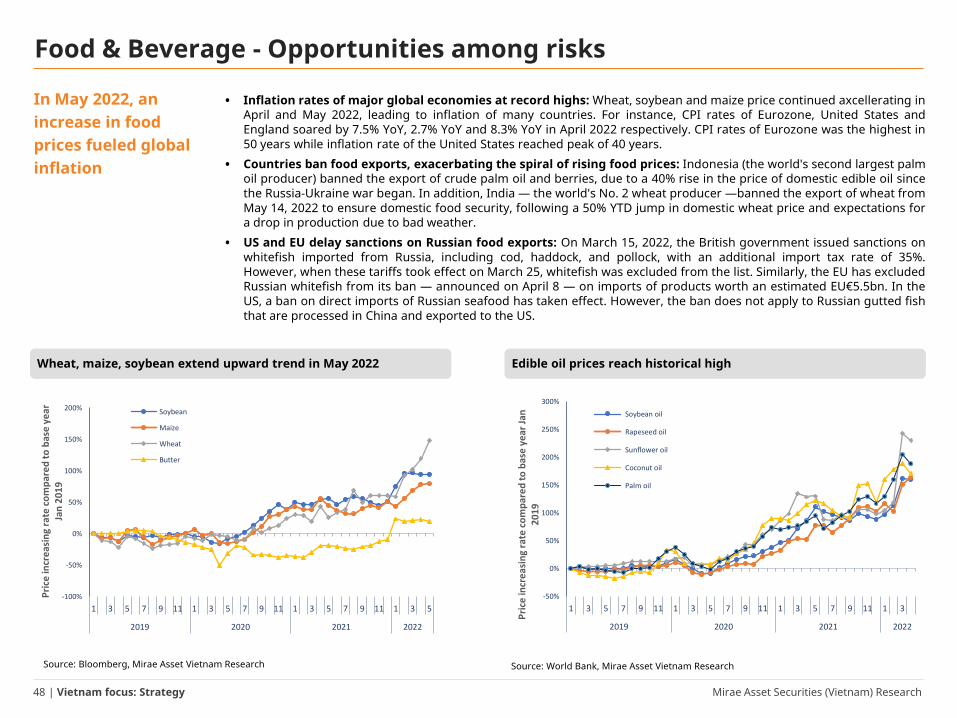

• F&B: Seafood exporters are expected to have outstanding results in last-9M22. We believe that 2Q22 will see a boom in both the revenue and profit of seafoodexporters. However, it should be noted that this positive trend is likely to gradually fade in the last two quarters of 2022, as the 2021 low-priced inventory has beenexhausted and the new harvest, with higher prices, will arrive at end-3Q22. Beverages, food exports, and sugar production will see slight growth in 2022, with animproved performance for beverages expected, as domestic demand recovers from 2021’s low base.

• Utilities: According to Vietnam Electricity Corporation, electricity consumption increased by 6.3% YoY in 4M22. Wind power was the biggest beneficiary, with a500% YoY increase in April 2022 and a 369% YoY increase in 4M22, in terms of volume. Solar power output grew by 53% YoY in April 2022 and 6.6% YoY in 4M22. Themobilization of hydropower generators also improved by 27% YoY in April 2022 and 21% YoY in 4M22. According to the meteorological agencies, hot weather isforecast to arrive later than usual for the Northern and Central provinces, with lower-than-usual intensity and shorter duration. The water levels of some of themain rivers in the Northern region saw a slight recovery in 5M22.

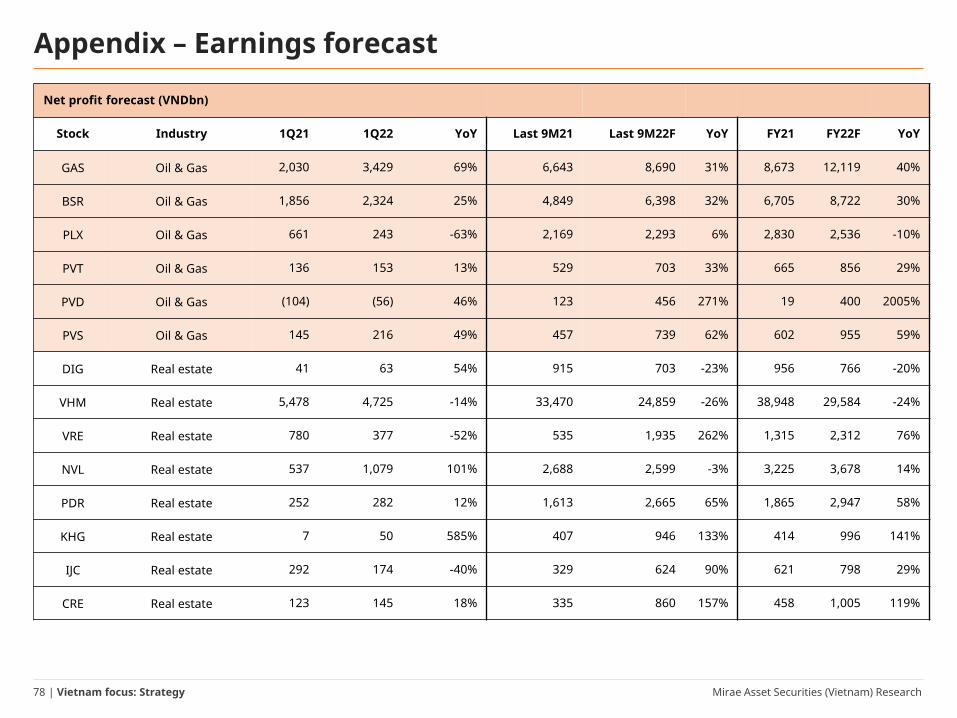

• Oil & Gas: In total, O&G listed companies recorded growth rates of 46% in revenue and 74% in NPAT. Major oil and gas companies, namely GAS and PVS, deliveredstrong performances in the first quarter. GAS reported a surge of 52% YoY in revenue and and 69% YoY in NPAT. PVS also posted excellent results, with revenuegrowth of 44% YoY and after-tax profit growth of 50% YoY. It is estimated that O&G enterprises hold the largest cash balances among companies listed onVietnam’s stock market.

• Construction: In 4M22, government disbursement totaled VND85,712bn, achieving 14.86% of the Prime Minister’s FY22 target. Of this, domestic disbursementreached VND83,234bn, while foreign disbursement made up VND2,177bn. The Ministry of Finance estimated total capital disbursement at VND117,937VND by theend of May, achieving 20.45% of the FY22 plan. For 2022, the public investment capital allocated to the Ministry of Transport (MT) is expected to be VND50,000bn.By April 30, 2022, the total amount disbursed was VND10,096bn, while by the end of May, disbursement is expected to reach VND11,728bn.

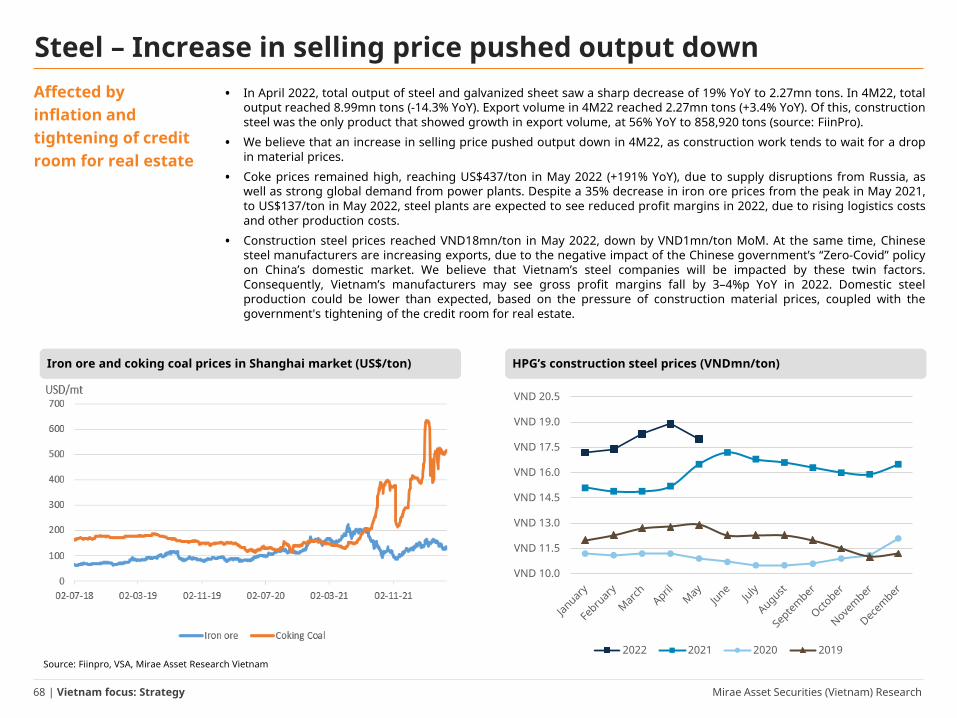

• Steel: Coke prices remained high, reaching US$437/ton in May 2022 (+191% YoY), due to supply disruptions from Russia, as well as strong global demand frompower plants. Despite a 35% decrease in iron ore prices from the peak in May 2021, to US$137/ton in May 2022, steel plants are expected to see reduced profitmargins in 2022, due to rising logistics costs and other production costs. Construction steel prices reached VND18mn/ton in May 2022, down by VND1mn/ton MoM.

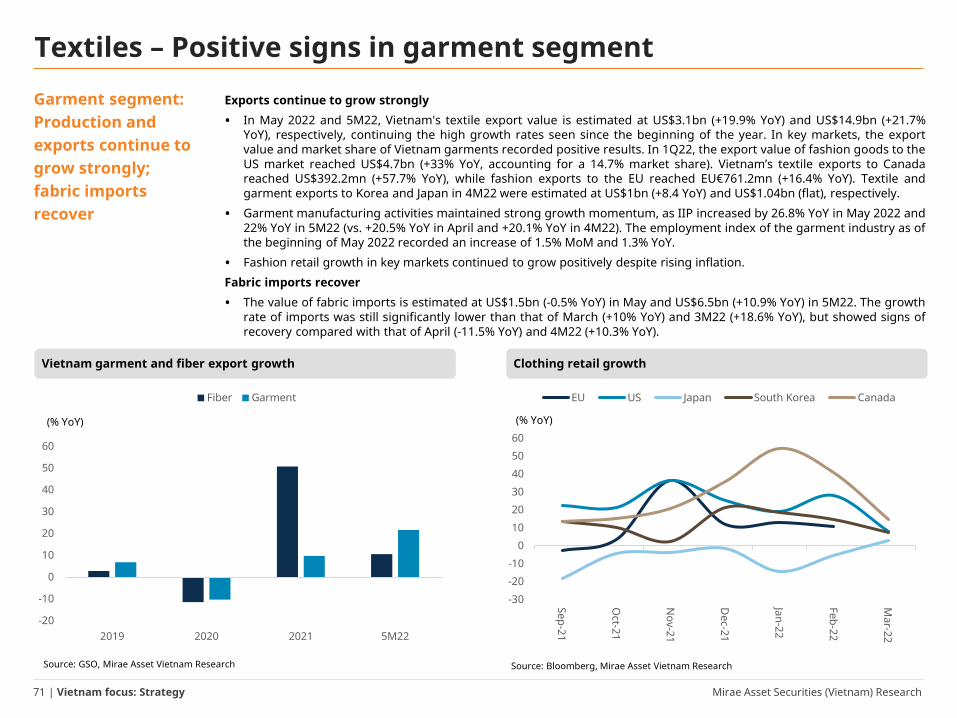

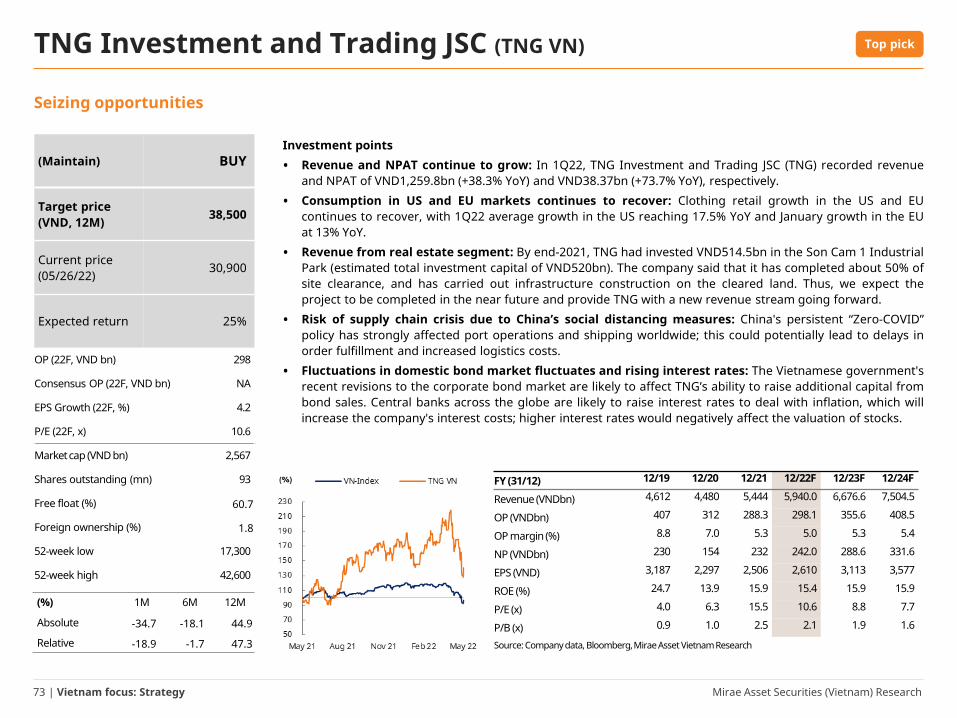

• Textiles: In May 2022 and 5M22, Vietnam's textile export value is estimated at US$3.1bn (+19.9% YoY) and US$14.9bn (+21.7% YoY), continuing the high growthrates seen since the beginning of the year. In key markets, the export value and market share of Vietnam garments recorded positive results. In 1Q22, the exportvalue of fashion goods to the US market reached US$4.7bn (+33% YoY, accounting for 14.7% of the market share). Vietnam’s textile exports to Canada reachedUS$392.2mn (+57.7% YoY), while fashion exports to the EU reached EU€761.2mn (+16.4% YoY). Textile and garment exports to Korea and Japan in 4M22 wereestimated at US$1bn (+8.4 YoY) and US$1.04bn (flat), respectively.

• Seaports: In 5M22, the volume of seaport clearance was estimated at 304.2mn tons (+2.9% YoY). Clearance container volume was estimated at 10.4mn TEU (+4.3%YoY). Container clearance activities maintained their growth for three consecutive months, after a slight decline of 1% in 2M22. Export-import value maintainedgood growth rates, with total export-import value estimated at US$306bn (+16.5% YoY, vs. +16.3% YoY in 4M22) in 5M22. The shipping price index of main routeswas on a downward trend, due to shipping activities declining amid the COVID-19 pandemic in China and the Ukraine crisis pushing up transport costs globally.

IV. Sector outlook and stock recommendations

Mirae Asset Securities (Vietnam) Research34 | Vietnam focus: Strategy

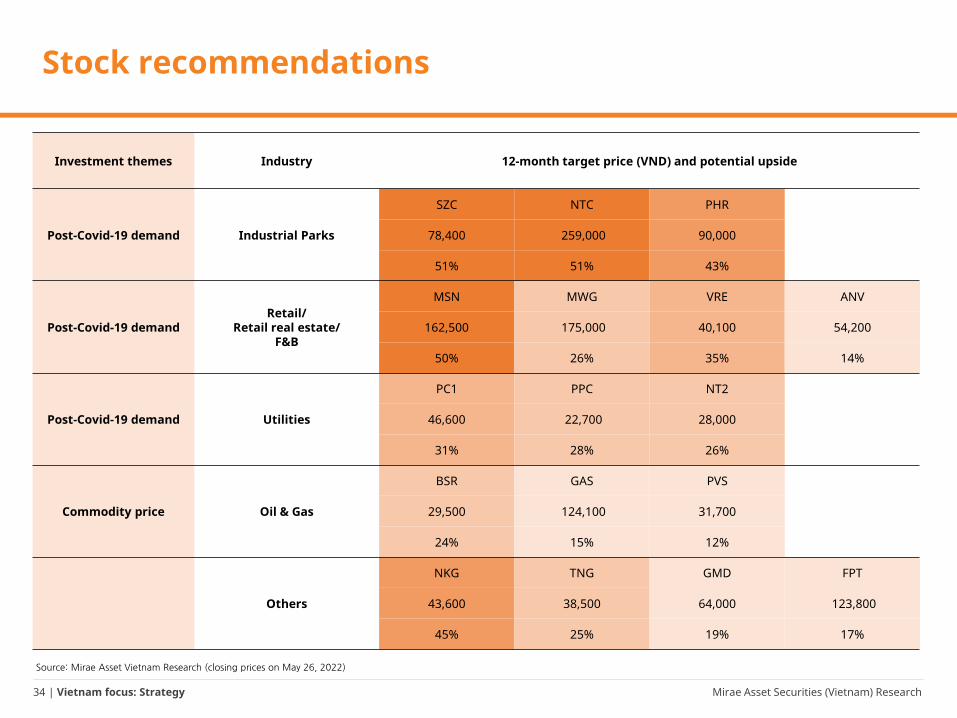

Stock recommendations

Source: Mirae Asset Vietnam Research (closing prices on May 26, 2022)

Investment themes Industry 12-month target price (VND) and potential upside

Post-Covid-19 demand Industrial Parks

SZC NTC PHR

78,400 259,000 90,000

51% 51% 43%

Post-Covid-19 demandRetail/

Retail real estate/F&B

MSN MWG VRE ANV

162,500 175,000 40,100 54,200

50% 26% 35% 14%

Post-Covid-19 demand Utilities

PC1 PPC NT2

46,600 22,700 28,000

31% 28% 26%

Commodity price Oil & Gas

BSR GAS PVS

29,500 124,100 31,700

24% 15% 12%

Others

NKG TNG GMD FPT

43,600 38,500 64,000 123,800

45% 25% 19% 17%

Mirae Asset Securities (Vietnam) Research35 | Vietnam focus: Strategy

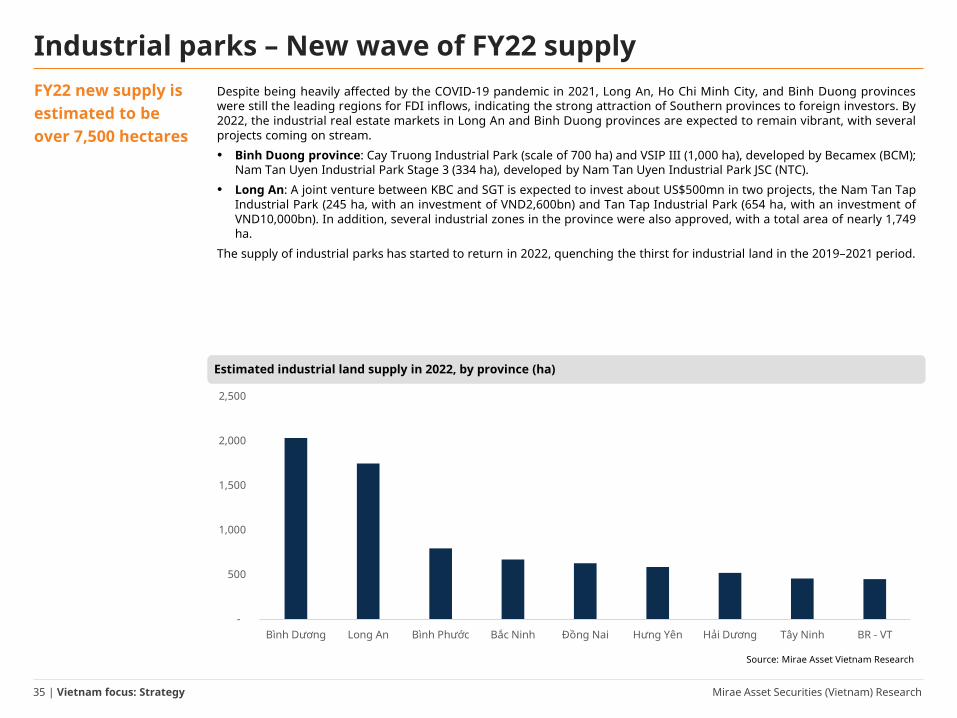

Industrial parks – New wave of FY22 supplyFY22 new supply is estimated to be over 7,500 hectares

Despite being heavily affected by the COVID-19 pandemic in 2021, Long An, Ho Chi Minh City, and Binh Duong provinceswere still the leading regions for FDI inflows, indicating the strong attraction of Southern provinces to foreign investors. By2022, the industrial real estate markets in Long An and Binh Duong provinces are expected to remain vibrant, with severalprojects coming on stream.

• Binh Duong province: Cay Truong Industrial Park (scale of 700 ha) and VSIP III (1,000 ha), developed by Becamex (BCM);Nam Tan Uyen Industrial Park Stage 3 (334 ha), developed by Nam Tan Uyen Industrial Park JSC (NTC).

• Long An: A joint venture between KBC and SGT is expected to invest about US$500mn in two projects, the Nam Tan TapIndustrial Park (245 ha, with an investment of VND2,600bn) and Tan Tap Industrial Park (654 ha, with an investment ofVND10,000bn). In addition, several industrial zones in the province were also approved, with a total area of nearly 1,749ha.

The supply of industrial parks has started to return in 2022, quenching the thirst for industrial land in the 2019–2021 period.

Estimated industrial land supply in 2022, by province (ha)

Source: Mirae Asset Vietnam Research

-

500

1,000

1,500

2,000

2,500

Bình Dương Long An Bình Phước Bắc Ninh Đồng Nai Hưng Yên Hải Dương Tây Ninh BR - VT

Mirae Asset Securities (Vietnam) Research36 | Vietnam focus: Strategy

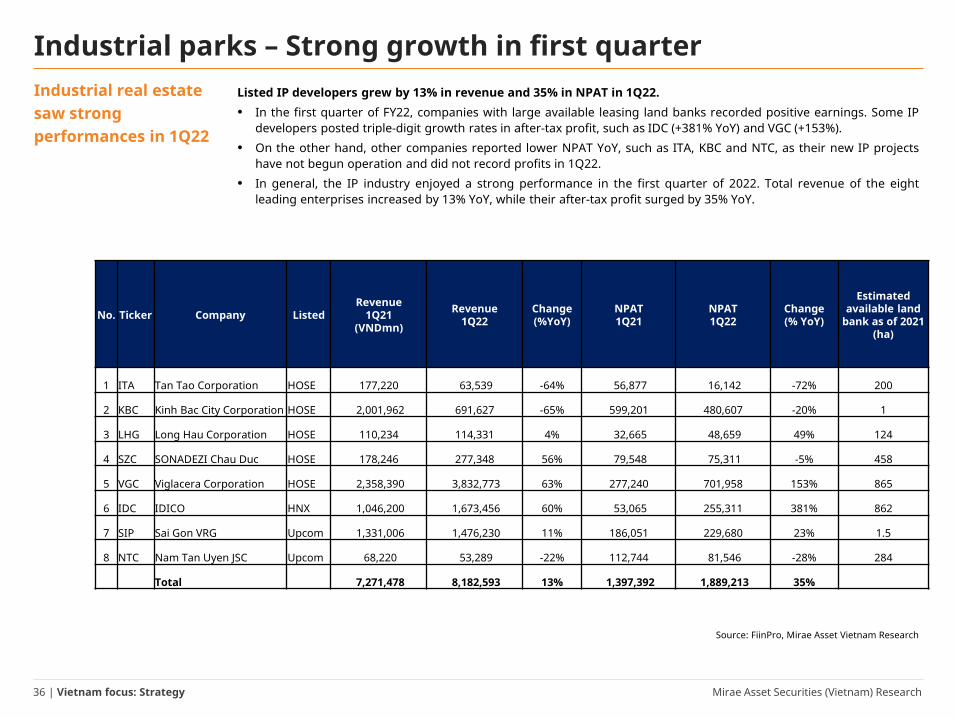

Industrial parks – Strong growth in first quarterIndustrial real estate saw strong performances in 1Q22

Listed IP developers grew by 13% in revenue and 35% in NPAT in 1Q22.

• In the first quarter of FY22, companies with large available leasing land banks recorded positive earnings. Some IPdevelopers posted triple-digit growth rates in after-tax profit, such as IDC (+381% YoY) and VGC (+153%).

• On the other hand, other companies reported lower NPAT YoY, such as ITA, KBC and NTC, as their new IP projectshave not begun operation and did not record profits in 1Q22.

• In general, the IP industry enjoyed a strong performance in the first quarter of 2022. Total revenue of the eightleading enterprises increased by 13% YoY, while their after-tax profit surged by 35% YoY.

Source: FiinPro, Mirae Asset Vietnam Research

No. Ticker Company Listed Revenue

1Q21(VNDmn)

Revenue1Q22

Change(%YoY)

NPAT1Q21

NPAT1Q22

Change(% YoY)

Estimated available land

bank as of 2021(ha)

1 ITA Tan Tao Corporation HOSE 177,220 63,539 -64% 56,877 16,142 -72% 200

2 KBC Kinh Bac City Corporation HOSE 2,001,962 691,627 -65% 599,201 480,607 -20% 1

3 LHG Long Hau Corporation HOSE 110,234 114,331 4% 32,665 48,659 49% 124

4 SZC SONADEZI Chau Duc HOSE 178,246 277,348 56% 79,548 75,311 -5% 458

5 VGC Viglacera Corporation HOSE 2,358,390 3,832,773 63% 277,240 701,958 153% 865

6 IDC IDICO HNX 1,046,200 1,673,456 60% 53,065 255,311 381% 862

7 SIP Sai Gon VRG Upcom 1,331,006 1,476,230 11% 186,051 229,680 23% 1.5

8 NTC Nam Tan Uyen JSC Upcom 68,220 53,289 -22% 112,744 81,546 -28% 284

Total 7,271,478 8,182,593 13% 1,397,392 1,889,213 35%

Mirae Asset Securities (Vietnam) Research37 | Vietnam focus: Strategy

Residential segment to enjoy strong earnings

SONADEZI Chau Duc Shareholding Company (SZC VN)

Investment points1Q22: Revenue up, but profit down

• In 1Q22, SZC announced revenue of VND277.3bn (+56% YoY), thanks to land leasing and managementrevenue. However, COGS/sales ratio increased sharply to 63.1%, compared with 39.3% in 1Q21, leading toNPAT of VND75.3bn (-5% YoY).

• The sharp increase in COGS/revenue ratio in 1Q22 came from the higher proportion of wholesale revenuefrom related parties. Wholesale revenue in 1Q22 reached VND192bn, accounting for 69.3% of total revenue,compared with 25.8% in 1Q21.

Strong earnings momentum starts from 2022In 2022, we expect earnings momentum to be maintained, with NPAT of VND601bn (+85% YoY), thanks to thefollowing:

• The launch 25.2 ha in the first phase of the Huu Phuoc project, which we expect to contribute about VND280–330bn to FY22 after-tax profit.

• SZC’s expected leasing of about 40 ha of industrial land, with revenue of VND670bn and NPAT of VND300bn.

(%) 1M 6M 12M

Absolute -33.3 -17.5 33.1

Relative -17.5 -1.0 35.5

NPAT (22F, VNDbn) 601

Market consensus (22F, VNDbn) n/a

EPS Growth (22F, %) 85

P/E (22F, x) 7.8

Marketcap (VND bn) 4,705

Outstanding (mn) 100

Freefloat (%) 89.2

Foreignownership(%) 2.6

52 week-high (VND) 31,550

52 week-low (VND) 83,400

(Maintain) BUY

Target price (VND, 12M) 78,400

Current price (05/26/22) 51,800

Expected return 51%

FY (31/12) 12/18 12/19 12/20 12/21 12/22F 12/23FRevenue (VNDbn) 290 329 433 713 1,269 1,396 Operating profit (VNDbn) 111 139 213 392 747 803 OP margin 38.2 42.2 49.2 55.0 58.9 57.5 NP (VNDbn) 97 134 186 324 601 646 EPS (VND) 779 1,140 1,860 3,236 6,012 6,462ROE (%) 6.8 9.7 15.3 23.7 35.9 30.7P/E (x) 15.5 21.2 22.8 7.8 7.2P/B (x) 1.5 3.1 5.0 3.9 3.2Source: Bloomberg, Mirae Asset Vietnam Research

Mirae Asset Securities (Vietnam) Research38 | Vietnam focus: Strategy

A step forward with NTC3 project

Nam Tan Uyen Joint Stock Company (NTC VN)

Investment pointsIn 1Q22, revenue for Nam Tan Uyen Joint Stock Company (NTC) reached VND53bn (-22% YoY), with financialrevenue of VND61bn (-29% YoY). Profit after tax was VND81.5bn (-27.7% YoY), with EPS of VND3,398. The NTC3project has completed total estimated investment of VND871bn, and is undergoing the final legal process tobegin official operations.NTC3 project to provide growth momentum: After receiving the land in the 2019–2020 period, NTC3'sinvestment and development process has been completed. The project is expected to be put into operation in2022.With a commercial land area of 288.52 ha and an estimated rental price in this area of around US$100–110/m2/lease cycle, we believe that NTC is capable of leasing its entire NTC3 land bank within five years andgenerating total revenue of nearly VND7,400bn. NTC has paid off most of the loan for the NTC3 project, which iscurrently the company’s only loan. Based on a change in the accounting— from annual allocation to one-timerecognition — for revenue from IP leasing activities, NTC's profit should show a dramatic increase in FY22.High dividend payout ratio: Cash dividend remains above 80% of charter capital (equivalent to 65–73% of NPAT),indicating NTC’s healthy business performance and strong cash flow.

(%) 1M 6M 12M

Absolute -13.0 -10.4 2.7

Relative 2.7 6.0 5.1

NPAT (22F, VNDbn) 846

Market consensus (22F, VNDbn) n/a

EPS Growth (22F, %) 187

P/E (22F, x) 5.1

Marketcap (VND bn) 4,320

Outstanding (mn) 24

Freefloat (%) 20.1

Foreignownership(%) 4.5

52 week-high (VND) 158,200

52 week-low (VND) 226,900

(Maintain) BUY

Target price (VND, 12M) 259,000

Current price (05/26/22) 172,000

Expected return 51%

FY (31/12) 12/18 12/19 12/20 12/21 12/22F 12/23F

Revenue (VNDbn) 532 194 264 271 1,220 1,247

Operating profit (VNDbn) 438 86 344 343 1,057 1,148

OP margin 82.3 44.5 130.5 126.6 86.7 92.0

NP (VNDbn) 470 237 291 294 846 918

EPS (VND) 19,357 9,855 12,123 12,274 35,248 38,253

ROE (%) 95.9 40.4 46.04 46.3 113.0 70.8

P/E (x) 2.7 11.2 16.3 15.8 5.1 4.7

P/B (x) 2.1 4.6 10.1 7.4 5.9 3.0

Source: Bloomberg, Mirae Asset Vietnam Research

Mirae Asset Securities (Vietnam) Research39 | Vietnam focus: Strategy

PHR looks to boost FY22 earnings from VSIP

Phuoc Hoa Rubber Joint Stock Company (PHR VN)

Investment points

• In 1Q22, PHR's revenue and net profit reached VND365bn (+30% YoY) and VND299bn (+239% YoY),respectively, mainly thanks to VND289bn in compensation from the transfer of 209 ha from VSIP.

• PHR received Decision No. 40/QD-TTg (dated January 10, 2022) on adjustment of the investment policy of theVietnam-Singapore Industrial Park III project as a basis for the People's Committee of Binh Duong province toapprove compensation for PHR. We expect PHR to be able to realize the compensatory profit from VSIP IIIfrom 2Q22. We forecast that PHR will book VND630bn in 2022 and VND368bn in 2023 in compensation fromVSIP III. We expect associated profit from VSIP to start from FY24 onward, with a profit of VND75bn in FY24.

• We believe that rubber prices will continue to increase in 2022 to an average of JPY240/ton, with a forecast ofworld supply of 13.8mn tons and demand of 14mn tons. PHR can increase its gross profit by VND150bn fromthis segment.

• Tan Lap and Hoi Nghia Industrial Parks (IP), with the advantage of low costs, as well as the lack of IP landbankin Binh Duong province, will be the key growth catalyst for PHR in the 2023–2025 period. The total area of IPsthat PHR plans to develop in the 2023–2027 period is 2,972ha, making PHR one of the largest industrial parkdevelopers in Vietnam.