Emart - When will SSG.com turn a profit? - Mirae Asset ...

10

Emart ( 139480 KS) When will SSG.com turn a profit? Use of offline stores is key to shortening time to breakeven for SSG.com With the widespread adoption of fast delivery services, we believe SSG.com will continue to expand its core fulfillment center capabilities. In particular, we think the use of Emart stores to increase SSG.com’s core fulfillment capabilities could shorten the online platform’s time to breakeven. In our view, SSG.com, which has lower fixed costs than offline operations, needs to reduce variable costs. Aside from commissions that inevitably arise from sales, transportation costs account for the biggest percentage of SSG.com’s SG&A expenses. This is because, unlike Coupang or Market Kurly, SSG.com does not have an in-house delivery network. If SSG.com increases its delivery capacity by expanding picking & packing (PP) centers (e.g., the Cheonggyecheon Emart store) and setting up core fulfillment centers, this would allow the online platform to 1) save costs related to last-mile delivery (by reducing delivery distances) and 2) improve its transportation spending efficiency. The expansion of core fulfillment centers could also lower the need for spending on large distribution centers (core fulfillment centers cost W3-6bn vs. W80-180bn for large distribution centers). Transfer of fixed costs could improve offline profits If Emart uses some or all of its stores as core fulfillment centers for SSG.com (i.e., reducing sales floor space and using it instead for delivery), we think this could lead to fixed cost savings and thus improve profits. Emart’s same-store sales (SSS) growth was -0.6% in 2017, -2.8% in 2018, and -3.4% in 2019. Even if Emart’s floor space is partially used for fulfillment, the resulting revenue decline of the offline business should be fairly limited. For the offline business, the biggest source of costs (aside from commissions) are labor and depreciation. If Emart utilizes some of its stores to boost SSG.com’s delivery capabilities, this could help it transfer fixed costs to the online segment. SSG.com’s cost pressures could increase as a result, but the impact on SG&A expenses is likely to be partially offset by a decrease in transportation costs tied to sales. Maintain Buy and TP of W190,000 We maintain our Buy call and target price of W190,000 on Emart. We believe downside risks to 2020-21 EPS stemming from the spread of COVID-19 are limited, as a rise in average ticket caused by panic buying is likely to offset the impact of in-store traffic declines. SSG.com, meanwhile, is seeing 1) new customer inflows and 2) higher average ticket. We expect SSG.com to be able to retain these new customers, resulting in a quantum leap for its customer base and transaction value compared to pre- outbreak levels; this is a factor that justifies Emart’s valuation. Emart is currently trading at a 2020F P/E of 13.7x, higher than the level seen in 2018, when offline weakness and online expectations had not been priced in. Looking ahead, we believe the aggressive utilization of Emart’s stores will improve overall profits, supporting a valuation re-rating. We hence continue to recommend Buy on the stock and maintain it as our top pick in retail. FY (Dec.) 12/16 12/17 12/18 12/19 12/20F 12/21F Revenue (Wbn) 14,615 15,515 17,049 19,063 20,045 21,270 OP (Wbn) 569 585 463 151 232 312 OP Margin (%) 3.9 3.8 2.7 0.8 1.2 1.5 NP (Wbn) 376 616 450 234 219 288 EPS (W) 13,497 22,101 16,150 8,391 7,844 10,323 ROE (%) 5.1 7.7 5.5 2.8 2.5 3.2 P/E (x) 13.6 12.3 11.3 15.2 13.7 10.4 P/B (x) 0.7 0.9 0.6 0.4 0.3 0.3 Dividend Yield (%) 0.8 0.6 1.1 1.6 1.9 1.9 Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests Source: Company data, Mirae Asset Daewoo Research estimates Retail Company Report March 31, 2020 (Maintain) Buy Target Price (12M, W) 190,000 Share Price (03/30/20, W) 107,500 Expected Return 77% OP (20F, Wbn) 232 Consensus OP (20F, Wbn) 253 EPS Growth (20F, %) -6.5 Market EPS Growth (20F, %) 25.0 P/E (20F, x) 13.7 Market P/E (20F, x) 9.7 KOSPI 1,717.12 Market Cap (Wbn) 2,997 Shares Outstanding (mn) 28 Free Float (%) 68.2 Foreign Ownership (%) 32.7 Beta (12M) 0.51 52-Week Low 97,900 52-Week High 181,500 (%) 1M 6M 12M Absolute 2.4 -4.9 -37.5 Relative 18.5 14.3 -22.1 Mirae Asset Daewoo Co., Ltd. [ Retail ] Myoungjoo Kim +822-3774-1458 [email protected] Minjeong Kyeong +822-3774-1437 [email protected] 50 60 70 80 90 100 110 3.19 7.19 11.19 3.20 Emart KOSPI

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Emart - When will SSG.com turn a profit? - Mirae Asset ...

Emart (139480 KS)

When will SSG.com turn a profit?

Use of offline stores is key to shortening time to breakeven for SSG.com

With the widespread adoption of fast delivery services, we believe SSG.com will

continue to expand its core fulfillment center capabilities. In particular, we think the

use of Emart stores to increase SSG.com’s core fulfillment capabilities could shorten

the online platform’s time to breakeven. In our view, SSG.com, which has lower fixed

costs than offline operations, needs to reduce variable costs.

Aside from commissions that inevitably arise from sales, transportation costs account

for the biggest percentage of SSG.com’s SG&A expenses. This is because, unlike

Coupang or Market Kurly, SSG.com does not have an in-house delivery network. If

SSG.com increases its delivery capacity by expanding picking & packing (PP) centers

(e.g., the Cheonggyecheon Emart store) and setting up core fulfillment centers, this

would allow the online platform to 1) save costs related to last-mile delivery (by

reducing delivery distances) and 2) improve its transportation spending efficiency. The

expansion of core fulfillment centers could also lower the need for spending on large

distribution centers (core fulfillment centers cost W3-6bn vs. W80-180bn for large

distribution centers).

Transfer of fixed costs could improve offline profits

If Emart uses some or all of its stores as core fulfillment centers for SSG.com (i.e.,

reducing sales floor space and using it instead for delivery), we think this could lead to

fixed cost savings and thus improve profits. Emart’s same-store sales (SSS) growth was

-0.6% in 2017, -2.8% in 2018, and -3.4% in 2019. Even if Emart’s floor space is partially

used for fulfillment, the resulting revenue decline of the offline business should be

fairly limited.

For the offline business, the biggest source of costs (aside from commissions) are labor

and depreciation. If Emart utilizes some of its stores to boost SSG.com’s delivery

capabilities, this could help it transfer fixed costs to the online segment. SSG.com’s cost

pressures could increase as a result, but the impact on SG&A expenses is likely to be

partially offset by a decrease in transportation costs tied to sales.

Maintain Buy and TP of W190,000

We maintain our Buy call and target price of W190,000 on Emart. We believe downside

risks to 2020-21 EPS stemming from the spread of COVID-19 are limited, as a rise in

average ticket caused by panic buying is likely to offset the impact of in-store traffic

declines. SSG.com, meanwhile, is seeing 1) new customer inflows and 2) higher

average ticket. We expect SSG.com to be able to retain these new customers, resulting

in a quantum leap for its customer base and transaction value compared to pre-

outbreak levels; this is a factor that justifies Emart’s valuation.

Emart is currently trading at a 2020F P/E of 13.7x, higher than the level seen in 2018,

when offline weakness and online expectations had not been priced in. Looking ahead,

we believe the aggressive utilization of Emart’s stores will improve overall profits,

supporting a valuation re-rating. We hence continue to recommend Buy on the stock

and maintain it as our top pick in retail.

FY (Dec.) 12/16 12/17 12/18 12/19 12/20F 12/21F

Revenue (Wbn) 14,615 15,515 17,049 19,063 20,045 21,270

OP (Wbn) 569 585 463 151 232 312

OP Margin (%) 3.9 3.8 2.7 0.8 1.2 1.5

NP (Wbn) 376 616 450 234 219 288

EPS (W) 13,497 22,101 16,150 8,391 7,844 10,323

ROE (%) 5.1 7.7 5.5 2.8 2.5 3.2

P/E (x) 13.6 12.3 11.3 15.2 13.7 10.4

P/B (x) 0.7 0.9 0.6 0.4 0.3 0.3

Dividend Yield (%) 0.8 0.6 1.1 1.6 1.9 1.9

Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests

Source: Company data, Mirae Asset Daewoo Research estimates

Retail

Company Report

March 31, 2020

(Maintain) Buy

Target Price (12M, W) 190,000

Share Price (03/30/20, W) 107,500

Expected Return 77%

OP (20F, Wbn) 232

Consensus OP (20F, Wbn) 253

EPS Growth (20F, %) -6.5

Market EPS Growth (20F, %) 25.0

P/E (20F, x) 13.7

Market P/E (20F, x) 9.7

KOSPI 1,717.12

Market Cap (Wbn) 2,997

Shares Outstanding (mn) 28

Free Float (%) 68.2

Foreign Ownership (%) 32.7

Beta (12M) 0.51

52-Week Low 97,900

52-Week High 181,500

(%) 1M 6M 12M

Absolute 2.4 -4.9 -37.5

Relative 18.5 14.3 -22.1

Mirae Asset Daewoo Co., Ltd.

[Retail]

Myoungjoo Kim +822-3774-1458 [email protected]

Minjeong Kyeong +822-3774-1437 [email protected]

50

60

70

80

90

100

110

3.19 7.19 11.19 3.20

Emart KOSPI

Emart

Mirae Asset Daewoo Research 2

March 31, 2020

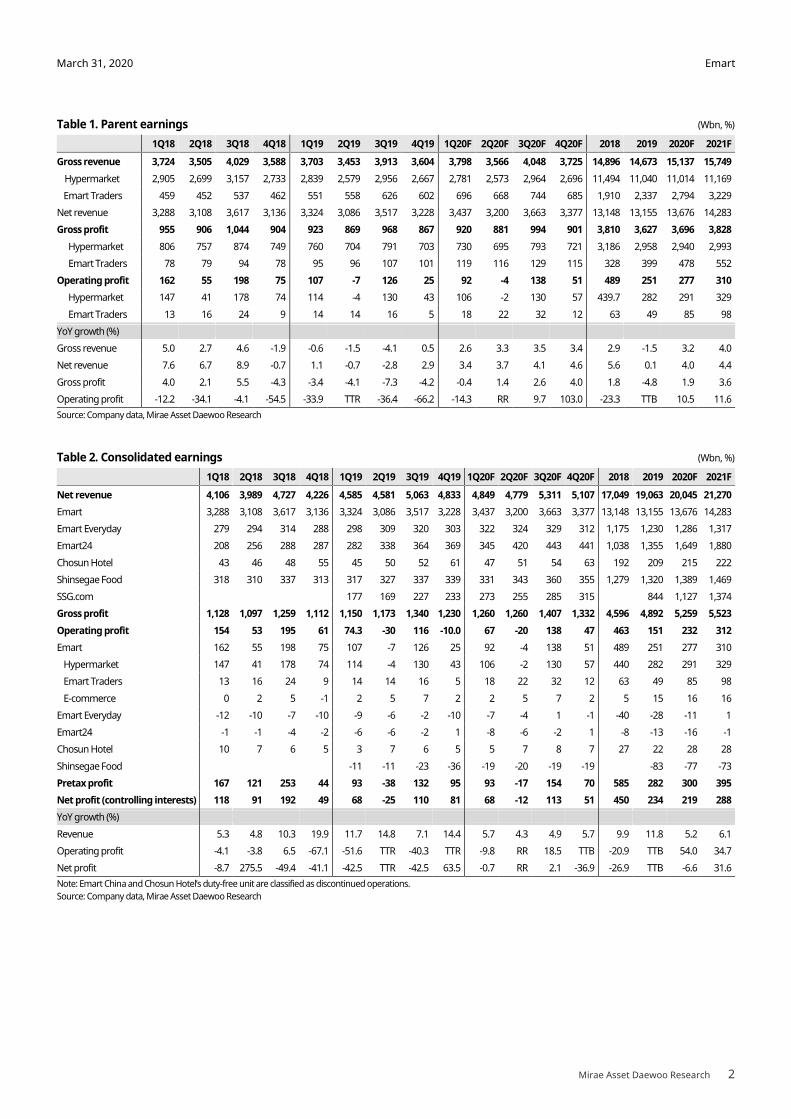

Table 1. Parent earnings (Wbn, %)

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20F 2Q20F 3Q20F 4Q20F 2018 2019 2020F 2021F

Gross revenue 3,724 3,505 4,029 3,588 3,703 3,453 3,913 3,604 3,798 3,566 4,048 3,725 14,896 14,673 15,137 15,749

Hypermarket 2,905 2,699 3,157 2,733 2,839 2,579 2,956 2,667 2,781 2,573 2,964 2,696 11,494 11,040 11,014 11,169

Emart Traders 459 452 537 462 551 558 626 602 696 668 744 685 1,910 2,337 2,794 3,229

Net revenue 3,288 3,108 3,617 3,136 3,324 3,086 3,517 3,228 3,437 3,200 3,663 3,377 13,148 13,155 13,676 14,283

Gross profit 955 906 1,044 904 923 869 968 867 920 881 994 901 3,810 3,627 3,696 3,828

Hypermarket 806 757 874 749 760 704 791 703 730 695 793 721 3,186 2,958 2,940 2,993

Emart Traders 78 79 94 78 95 96 107 101 119 116 129 115 328 399 478 552

Operating profit 162 55 198 75 107 -7 126 25 92 -4 138 51 489 251 277 310

Hypermarket 147 41 178 74 114 -4 130 43 106 -2 130 57 439.7 282 291 329

Emart Traders 13 16 24 9 14 14 16 5 18 22 32 12 63 49 85 98

YoY growth (%)

Gross revenue 5.0 2.7 4.6 -1.9 -0.6 -1.5 -4.1 0.5 2.6 3.3 3.5 3.4 2.9 -1.5 3.2 4.0

Net revenue 7.6 6.7 8.9 -0.7 1.1 -0.7 -2.8 2.9 3.4 3.7 4.1 4.6 5.6 0.1 4.0 4.4

Gross profit 4.0 2.1 5.5 -4.3 -3.4 -4.1 -7.3 -4.2 -0.4 1.4 2.6 4.0 1.8 -4.8 1.9 3.6

Operating profit -12.2 -34.1 -4.1 -54.5 -33.9 TTR -36.4 -66.2 -14.3 RR 9.7 103.0 -23.3 TTB 10.5 11.6

Source: Company data, Mirae Asset Daewoo Research

Table 2. Consolidated earnings (Wbn, %)

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20F 2Q20F 3Q20F 4Q20F 2018 2019 2020F 2021F

Net revenue 4,106 3,989 4,727 4,226 4,585 4,581 5,063 4,833 4,849 4,779 5,311 5,107 17,049 19,063 20,045 21,270

Emart 3,288 3,108 3,617 3,136 3,324 3,086 3,517 3,228 3,437 3,200 3,663 3,377 13,148 13,155 13,676 14,283

Emart Everyday 279 294 314 288 298 309 320 303 322 324 329 312 1,175 1,230 1,286 1,317

Emart24 208 256 288 287 282 338 364 369 345 420 443 441 1,038 1,355 1,649 1,880

Chosun Hotel 43 46 48 55 45 50 52 61 47 51 54 63 192 209 215 222

Shinsegae Food 318 310 337 313 317 327 337 339 331 343 360 355 1,279 1,320 1,389 1,469

SSG.com 177 169 227 233 273 255 285 315 844 1,127 1,374

Gross profit 1,128 1,097 1,259 1,112 1,150 1,173 1,340 1,230 1,260 1,260 1,407 1,332 4,596 4,892 5,259 5,523

Operating profit 154 53 195 61 74.3 -30 116 -10.0 67 -20 138 47 463 151 232 312

Emart 162 55 198 75 107 -7 126 25 92 -4 138 51 489 251 277 310

Hypermarket 147 41 178 74 114 -4 130 43 106 -2 130 57 440 282 291 329

Emart Traders 13 16 24 9 14 14 16 5 18 22 32 12 63 49 85 98

E-commerce 0 2 5 -1 2 5 7 2 2 5 7 2 5 15 16 16

Emart Everyday -12 -10 -7 -10 -9 -6 -2 -10 -7 -4 1 -1 -40 -28 -11 1

Emart24 -1 -1 -4 -2 -6 -6 -2 1 -8 -6 -2 1 -8 -13 -16 -1

Chosun Hotel 10 7 6 5 3 7 6 5 5 7 8 7 27 22 28 28

Shinsegae Food -11 -11 -23 -36 -19 -20 -19 -19 -83 -77 -73

Pretax profit 167 121 253 44 93 -38 132 95 93 -17 154 70 585 282 300 395

Net profit (controlling interests) 118 91 192 49 68 -25 110 81 68 -12 113 51 450 234 219 288

YoY growth (%)

Revenue 5.3 4.8 10.3 19.9 11.7 14.8 7.1 14.4 5.7 4.3 4.9 5.7 9.9 11.8 5.2 6.1

Operating profit -4.1 -3.8 6.5 -67.1 -51.6 TTR -40.3 TTR -9.8 RR 18.5 TTB -20.9 TTB 54.0 34.7

Net profit -8.7 275.5 -49.4 -41.1 -42.5 TTR -42.5 63.5 -0.7 RR 2.1 -36.9 -26.9 TTB -6.6 31.6

Note: Emart China and Chosun Hotel’s duty-free unit are classified as discontinued operations.

Source: Company data, Mirae Asset Daewoo Research

Emart

Mirae Asset Daewoo Research 3

March 31, 2020

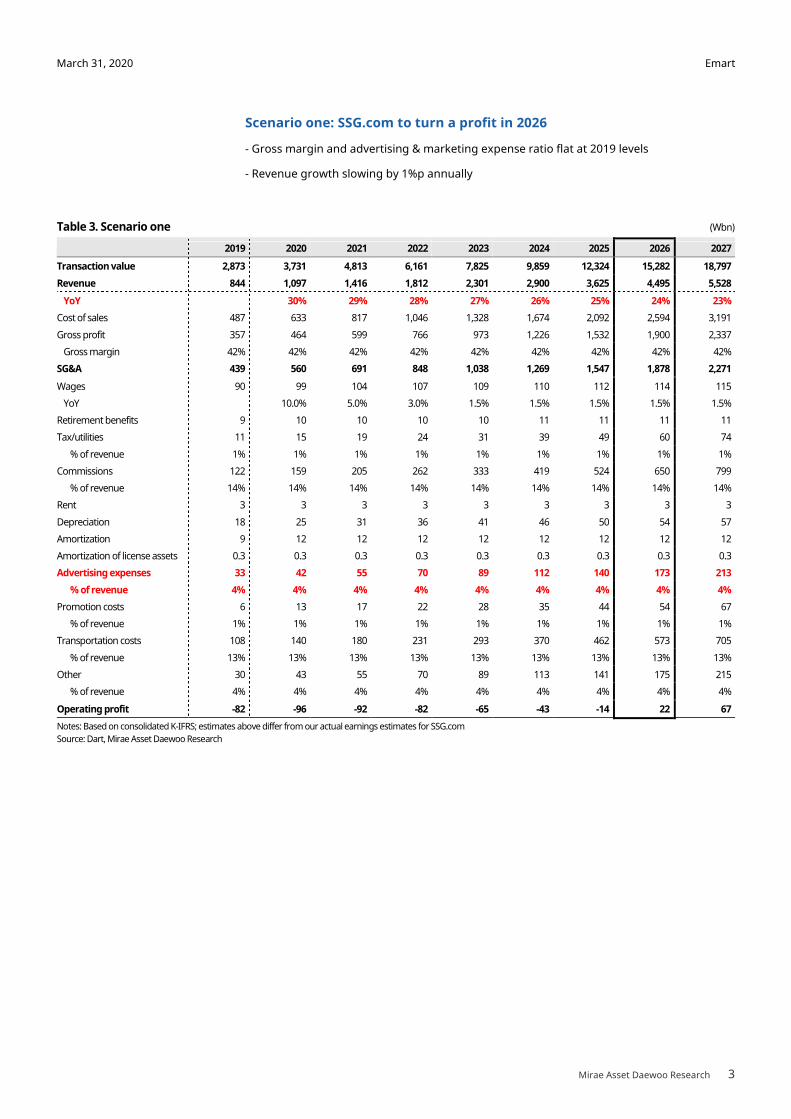

Scenario one: SSG.com to turn a profit in 2026

- Gross margin and advertising & marketing expense ratio flat at 2019 levels

- Revenue growth slowing by 1%p annually

Table 3. Scenario one (Wbn)

2019 2020 2021 2022 2023 2024 2025 2026 2027

Transaction value 2,873 3,731 4,813 6,161 7,825 9,859 12,324 15,282 18,797

Revenue 844 1,097 1,416 1,812 2,301 2,900 3,625 4,495 5,528

YoY

30% 29% 28% 27% 26% 25% 24% 23%

Cost of sales 487 633 817 1,046 1,328 1,674 2,092 2,594 3,191

Gross profit 357 464 599 766 973 1,226 1,532 1,900 2,337

Gross margin 42% 42% 42% 42% 42% 42% 42% 42% 42%

SG&A 439 560 691 848 1,038 1,269 1,547 1,878 2,271

Wages 90 99 104 107 109 110 112 114 115

YoY

10.0% 5.0% 3.0% 1.5% 1.5% 1.5% 1.5% 1.5%

Retirement benefits 9 10 10 10 10 11 11 11 11

Tax/utilities 11 15 19 24 31 39 49 60 74

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Commissions 122 159 205 262 333 419 524 650 799

% of revenue 14% 14% 14% 14% 14% 14% 14% 14% 14%

Rent 3 3 3 3 3 3 3 3 3

Depreciation 18 25 31 36 41 46 50 54 57

Amortization 9 12 12 12 12 12 12 12 12

Amortization of license assets 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

Advertising expenses 33 42 55 70 89 112 140 173 213

% of revenue 4% 4% 4% 4% 4% 4% 4% 4% 4%

Promotion costs 6 13 17 22 28 35 44 54 67

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Transportation costs 108 140 180 231 293 370 462 573 705

% of revenue 13% 13% 13% 13% 13% 13% 13% 13% 13%

Other 30 43 55 70 89 113 141 175 215

% of revenue 4% 4% 4% 4% 4% 4% 4% 4% 4%

Operating profit -82 -96 -92 -82 -65 -43 -14 22 67

Notes: Based on consolidated K-IFRS; estimates above differ from our actual earnings estimates for SSG.com

Source: Dart, Mirae Asset Daewoo Research

Emart

Mirae Asset Daewoo Research 4

March 31, 2020

Scenario two: SSG.com to turn a profit in 2025

- Gross margin expanding 0.1%p annually; advertising & marketing expense ratio falling

0.1%p annually

- Revenue growth slowing by 1%p annually

Table 4. Scenario two (Wbn)

2019 2020 2021 2022 2023 2024 2025 2026 2027

Transaction value 2,873 3,731 4,813 6,161 7,825 9,859 12,324 15,282 18,797

Revenue 844 1,097 1,416 1,812 2,301 2,900 3,625 4,495 5,528

YoY 30% 29% 28% 27% 26% 25% 24% 23%

Cost of sales 487 632 814 1,041 1,319 1,659 2,070 2,563 3,147

Gross profit 357 465 601 772 982 1,240 1,554 1,932 2,382

Gross margin 42% 42% 42% 43% 43% 43% 43% 43% 43%

SG&A 439 559 688 843 1,029 1,254 1,525 1,847 2,227

Wages 90 99 104 107 109 110 112 114 115

YoY 10.0% 5.0% 3.0% 1.5% 1.5% 1.5% 1.5% 1.5%

Retirement benefits 9 10 10 10 10 11 11 11 11

Tax/utilities 11 15 19 24 31 39 49 60 74

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Commissions 122 159 205 262 333 419 524 650 799

% of revenue 14% 14% 14% 14% 14% 14% 14% 14% 14%

Rent 3 3 3 3 3 3 3 3 3

Depreciation 18 25 31 36 41 46 50 54 57

Amortization 9 12 12 12 12 12 12 12 12

Amortization of license assets 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

Advertising expenses 33 41 52 64 79 97 118 142 169

% of revenue 4% 4% 4% 4% 3% 3% 3% 3% 3%

Promotion costs 6 13 17 22 28 35 44 54 67

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Transportation costs 108 140 180 231 293 370 462 573 705

% of revenue 13% 13% 13% 13% 13% 13% 13% 13% 13%

Other 30 43 55 70 89 113 141 175 215

% of revenue 4% 4% 4% 4% 4% 4% 4% 4% 4%

Operating profit -82 -93 -86 -71 -47 -14 29 85 155

Notes: Based on consolidated K-IFRS; estimates above differ from our actual earnings estimates for SSG.com

Source: Dart, Mirae Asset Daewoo Research

Emart

Mirae Asset Daewoo Research 5

March 31, 2020

Scenario three: SSG.com to turn a profit in 2026

- Gross margin remaining at 2019 level; advertising & marketing expense ratio expanding

by 0.1%p annually

- Revenue growth picking up 0.1%p annually

Table 5. Scenario three (Wbn)

2019 2020 2021 2022 2023 2024 2025 2026 2027

Transaction value 2,873 3,731 4,854 6,321 8,236 10,739 14,015 18,303 23,922

Revenue 844 1,097 1,428 1,859 2,422 3,159 4,122 5,383 7,036

YoY 30% 30% 30% 30% 30% 31% 31% 31%

Cost of sales 487 633 824 1,073 1,398 1,823 2,379 3,107 4,061

Gross profit 357 464 604 786 1,024 1,335 1,743 2,276 2,975

Gross margin 42% 42% 42% 42% 42% 42% 42% 42% 42%

SG&A 439 561 698 871 1,093 1,382 1,758 2,249 2,892

Wages 90 99 104 107 109 110 112 114 115

YoY 10.0% 5.0% 3.0% 1.5% 1.5% 1.5% 1.5% 1.5%

Retirement benefits 9 10 10 10 10 11 11 11 11

Tax/utilities 11 15 19 25 32 42 55 72 94

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Commission 122 159 206 269 350 457 596 778 1,017

% of revenue 14% 14% 14% 14% 14% 14% 14% 14% 14%

Rent 3 3 3 3 3 3 3 3 3

Depreciation 18 25 31 36 41 46 50 54 57

Amortization 9 12 12 12 12 12 12 12 12

Amortization of license assets 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

Advertising expenses 33 43 58 77 103 137 183 245 327

% of revenue 4% 4% 4% 4% 4% 4% 4% 5% 5%

Promotion costs 6 13 17 22 29 38 50 65 85

% of sales 1% 1% 1% 1% 1% 1% 1% 1% 1%

Transportation costs 108 140 182 237 309 403 525 686 897

% of revenue 13% 13% 13% 13% 13% 13% 13% 13% 13%

Other 30 43 55 72 94 123 160 209 273

% of revenue 4% 4% 4% 4% 4% 4% 4% 4% 4%

Operating profit -82 -97 -94 -85 -69 -46 -15 27 82

Notes: Based on consolidated K-IFRS; estimates above differ from our actual earnings estimates for SSG.com

Source: Dart, Mirae Asset Daewoo Research

Emart

Mirae Asset Daewoo Research 6

March 31, 2020

Scenario four: SSG.com to turn a profit in 2024

- Aggressive utilization of offline stores as online fulfillment centers

- Last-mile delivery cost reductions � Ratio of transportation costs to total revenue falling

0.5%p annually

- Use of offline stores � Higher labor and depreciation expenses vs. previous assumptions

- Revenue growth picking up 0.1%p annually

Table 6. Scenario four (Wbn)

2019 2020 2021 2022 2023 2024 2025 2026 2027

Transaction value 2,873 3,731 4,854 6,321 8,236 10,739 14,015 18,303 23,922

Revenue 844 1,097 1,428 1,859 2,422 3,159 4,122 5,383 7,036

YoY 30% 30% 30% 30% 30% 31% 31% 31%

Cost of sales 487 633 824 1,073 1,398 1,823 2,379 3,107 4,061

Gross profit 357 464 604 786 1,024 1,335 1,743 2,276 2,975

Gross margin 42% 42% 42% 42% 42% 42% 42% 42% 42%

SG&A 439 560 693 858 1,064 1,325 1,678 2,136 2,730

Wages 90 102 110 117 122 127 133 139 145

YoY 13.0% 8.0% 6.0% 4.5% 4.5% 4.5% 4.5% 4.5%

Retirement benefits 9 10 11 11 12 12 13 13 14

Tax/utilities 11 15 19 25 32 42 55 72 94

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Commissions 122 159 206 269 350 457 596 778 1,017

% of revenue 14% 14% 14% 14% 14% 14% 14% 14% 14%

Rent 3 3 3 3 3 3 3 3 3

Depreciation 18 27 37 46 56 66 75 85 94

Amortization 9 12 12 12 12 12 12 12 12

Amortization of license assets 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

Advertising expenses 33 42 55 72 93 122 159 207 271

% of revenue 4% 4% 4% 4% 4% 4% 4% 4% 4%

Promotion cost 6 13 17 22 29 38 50 65 85

% of revenue 1% 1% 1% 1% 1% 1% 1% 1% 1%

Transportation costs 108 134 168 209 260 324 422 552 721

% of revenue 13% 12% 12% 11% 11% 10% 10% 10% 10%

Other 30 43 55 72 94 123 160 209 273

% of revenue 4% 4% 4% 4% 4% 4% 4% 4% 4%

Operating profit -82 -96 -90 -72 -40 10 64 140 244

Notes: Based on consolidated K-IFRS; estimates above differ from our actual earnings estimates for SSG.com

Source: Dart, Mirae Asset Daewoo Research

Emart

Mirae Asset Daewoo Research 7

March 31, 2020

Emart (139480 KS/Buy/TP: W190,000)

Comprehensive Income Statement (Summarized) Statement of Financial Condition (Summarized)

(Wbn) 12/18 12/19 12/20F 12/21F (Wbn) 12/18 12/19 12/20F 12/21F

Revenue 17,049 19,063 20,045 21,270 Current Assets 2,286 3,650 3,742 3,914

Cost of Sales 12,453 14,170 14,786 15,747 Cash and Cash Equivalents 284 681 638 647

Gross Profit 4,596 4,893 5,259 5,523 AR & Other Receivables 584 668 706 752

SG&A Expenses 4,133 4,742 5,027 5,211 Inventories 1,123 1,279 1,352 1,439

Operating Profit (Adj) 463 151 232 312 Other Current Assets 295 1,022 1,046 1,076

Operating Profit 463 151 232 312 Non-Current Assets 14,468 17,445 16,693 16,089

Non-Operating Profit 122 131 68 83 Investments in Associates 718 836 884 941

Net Financial Income -54 -105 -144 -139 Property, Plant and Equipment 10,404 10,004 9,210 8,537

Net Gain from Inv in Associates 37 74 82 95 Intangible Assets 288 1,319 1,269 1,225

Pretax Profit 585 282 300 395 Total Assets 16,754 21,095 20,435 20,003

Income Tax 126 58 74 97 Current Liabilities 4,998 5,406 5,535 4,811

Profit from Continuing Operations 459 224 226 298 AP & Other Payables 1,560 1,779 1,880 2,001

Profit from Discontinued Operations 17 0 0 0 Short-Term Financial Liabilities 1,674 1,657 1,574 594

Net Profit 476 224 226 298 Other Current Liabilities 1,764 1,970 2,081 2,216

Controlling Interests 450 234 219 288 Non-Current Liabilities 2,898 5,482 4,521 4,568

Non-Controlling Interests 26 -10 8 10 Long-Term Financial Liabilities 2,165 4,789 3,789 3,789

Total Comprehensive Profit 19 108 226 298 Other Non-Current Liabilities 733 693 732 779

Controlling Interests -4 122 372 490 Total Liabilities 7,896 10,888 10,056 9,380

Non-Controlling Interests 23 -13 -146 -192 Controlling Interests 8,172 8,809 8,973 9,207

EBITDA 993 1,033 1,077 1,029 Capital Stock 139 139 139 139

FCF (Free Cash Flow) -125 -139 1,206 1,178 Capital Surplus 4,237 4,237 4,237 4,237

EBITDA Margin (%) 5.8 5.4 5.4 4.8 Retained Earnings 2,773 2,794 2,959 3,193

Operating Profit Margin (%) 2.7 0.8 1.2 1.5 Non-Controlling Interests 685 1,398 1,406 1,416

Net Profit Margin (%) 2.6 1.2 1.1 1.4 Stockholders' Equity 8,857 10,207 10,379 10,623

Cash Flows (Summarized) Forecasts/Valuations (Summarized)

(Wbn) 12/18 12/19 12/20F 12/21F 12/18 12/19 12/20F 12/21F

Cash Flows from Op Activities 770 816 1,206 1,178 P/E (x) 11.3 15.2 13.7 10.4

Net Profit 476 224 226 298 P/CF (x) 4.8 3.1 2.6 2.6

Non-Cash Income and Expense 579 931 940 836 P/B (x) 0.6 0.4 0.3 0.3

Depreciation 503 849 794 673 EV/EBITDA (x) 9.2 10.0 7.6 7.0

Amortization 27 33 50 44 EPS (W) 16,150 8,391 7,844 10,323

Others 49 49 96 119 CFPS (W) 37,841 41,426 41,839 40,694

Chg in Working Capital -296 -217 135 163 BPS (W) 293,262 319,802 325,712 334,100

Chg in AR & Other Receivables 60 -9 -30 -36 DPS (W) 2,000 2,000 2,000 2,000

Chg in Inventories -163 -157 -72 -87 Payout ratio (%) 11.7 24.1 23.8 18.1

Chg in AP & Other Payables 43 58 67 81 Dividend Yield (%) 1.1 1.6 1.9 1.9

Income Tax Paid -63 -126 -74 -97 Revenue Growth (%) 9.9 11.8 5.2 6.1

Cash Flows from Inv Activities -817 -1,005 -65 -78 EBITDA Growth (%) -6.9 4.0 4.3 -4.5

Chg in PP&E -692 128 0 0 Operating Profit Growth (%) -20.9 -67.4 53.6 34.5

Chg in Intangible Assets -20 -20 0 0 EPS Growth (%) -26.9 -48.0 -6.5 31.6

Chg in Financial Assets 1,334 -227 -65 -78 Accounts Receivable Turnover (x) 40.0 38.2 37.1 37.1

Others -1,439 -886 0 0 Inventory Turnover (x) 16.0 15.9 15.2 15.2

Cash Flows from Fin Activities 103 581 -1,137 -1,034 Accounts Payable Turnover (x) 12.1 12.3 12.1 12.1

Chg in Financial Liabilities 139 2,608 -1,083 -980 ROA (%) 2.9 1.2 1.1 1.5

Chg in Equity 0 0 0 0 ROE (%) 5.5 2.8 2.5 3.2

Dividends Paid -82 -104 -54 -54 ROIC (%) 3.9 1.1 1.7 2.5

Others 46 -1,923 0 0 Liability to Equity Ratio (%) 89.1 106.7 96.9 88.3

Increase (Decrease) in Cash 60 397 -43 9 Current Ratio (%) 45.7 67.5 67.6 81.3

Beginning Balance 224 284 681 638 Net Debt to Equity Ratio (%) 38.0 53.2 36.5 26.1

Ending Balance 284 681 638 647 Interest Coverage Ratio (x) 5.7 1.0 1.6 2.2

Source: Company data, Mirae Asset Daewoo Research estimates

Emart

Mirae Asset Daewoo Research 8

March 31, 2020

APPENDIX 1

Important Disclosures & Disclaimers

2-Year Rating and Target Price History

Company (Code) Date Rating Target Price

Emart (139480) 05/28/2019 Buy 190,000

05/15/2019 Buy 240,000

05/15/2019 Buy 190,000

02/06/2019 Buy 240,000

07/24/2018 Buy 320,000

02/25/2018 Buy 375,000

Equity Ratings Distribution & Investment Banking Services

Buy Trading Buy Hold Sell

Equity Ratings Distribution 84.05% 9.82% 6.13% 0.00%

Investment Banking Services 76.67% 13.33% 10.00% 0.00%

* Based on recommendations in the last 12-months (as of December 31, 2019)

Disclosures

As of the publication date, Mirae Asset Daewoo Co., Ltd. has acted as a liquidity provider for equity-linked warrants backed by shares of Emart as an underlying

asset; other than this, Mirae Asset Daewoo has no other special interests in the covered companies.

Analyst Certification

The research analysts who prepared this report (the “Analysts”) are registered with the Korea Financial Investment Association and are subject to Korean

securities regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws or regulations thereof. Each Analyst

responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the personal views of the Analyst about

any and all of the issuers and securities named in this report and (ii) no part of the compensation of the Analyst was, is, or will be directly or indirectly

related to the specific recommendations or views contained in this report. Mirae Asset Daewoo Co., Ltd. (“Mirae Asset Daewoo”) policy prohibits its Analysts

and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer,

director or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or

any other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this report. Like all

employees of Mirae Asset Daewoo, the Analysts receive compensation that is determined by overall firm profitability, which includes revenues from,

among other business units, the institutional equities, investment banking, proprietary trading and private client division. At the time of publication of this

report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or Mirae Asset Daewoo except as

otherwise stated herein.

Disclaimers

This report was prepared by Mirae Asset Daewoo, a broker-dealer registered in the Republic of Korea and a member of the Korea Exchange. Information

and opinions contained herein have been compiled in good faith and from sources believed to be reliable, but such information has not been

independently verified and Mirae Asset Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy,

completeness or correctness of the information and opinions contained herein or of any translation into English from the Korean language. In case of an

English translation of a report prepared in the Korean language, the original Korean language report may have been made available to investors in

advance of this report.

The intended recipients of this report are sophisticated institutional investors who have substantial knowledge of the local business environment, its

common practices, laws and accounting principles and no person whose receipt or use of this report would violate any laws or regulations or subject Mirae

Asset Daewoo or any of its affiliates to registration or licensing requirements in any jurisdiction shall receive or make any use hereof.

This report is for general information purposes only and it is not and shall not be construed as an offer or a solicitation of an offer to effect transactions in

any securities or other financial instruments. The report does not constitute investment advice to any person and such person shall not be treated as a

client of Mirae Asset Daewoo by virtue of receiving this report. This report does not take into account the particular investment objectives, financial

Stock Ratings Industry Ratings

Buy : Relative performance of 20% or greater Overweight : Fundamentals are favorable or improving

Trading Buy : Relative performance of 10% or greater, but with volatility Neutral : Fundamentals are steady without any material changes

Hold : Relative performance of -10% and 10% Underweight : Fundamentals are unfavorable or worsening

Sell : Relative performance of -10%

Ratings and Target Price History (Share price (─), Target price (▬), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆))

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at Mirae Asset Daewoo Co., Ltd., we may call a trading opportunity in case there is a technical or short-term material

development.

* The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of future

earnings.

* The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic

conditions.

0

100,000

200,000

300,000

400,000

Apr 18 Apr 19 Mar 20

(W) Emart

Emart

Mirae Asset Daewoo Research 9

March 31, 2020

situations, or needs of individual clients. The report is not to be relied upon in substitution for the exercise of independent judgment. Information and

opinions contained herein are as of the date hereof and are subject to change without notice. The price and value of the investments referred to in this

report and the income from them may depreciate or appreciate, and investors may incur losses on investments. Past performance is not a guide to future

performance. Future returns are not guaranteed, and a loss of original capital may occur. Mirae Asset Daewoo, its affiliates and their directors, officers,

employees and agents do not accept any liability for any loss arising out of the use hereof.

Mirae Asset Daewoo may have issued other reports that are inconsistent with, and reach different conclusions from, the opinions presented in this report.

The reports may reflect different assumptions, views and analytical methods of the analysts who prepared them. Mirae Asset Daewoo may make

investment decisions that are inconsistent with the opinions and views expressed in this research report. Mirae Asset Daewoo, its affiliates and their

directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale, or

offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each case

either as principals or agents. Mirae Asset Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the

subject companies to provide investment banking, market-making or other financial services as are permitted under applicable laws and regulations.

No part of this document may be copied or reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written

consent of Mirae Asset Daewoo.

Distribution

United Kingdom: This report is being distributed by Mirae Asset Securities (UK) Ltd. in the United Kingdom only to (i) investment professionals falling within

Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other

persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as

“Relevant Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of

its contents.

United States: Mirae Asset Daewoo is not a registered broker-dealer in the United States and, therefore, is not subject to U.S. rules regarding the

preparation of research reports and the independence of research analysts. This report is distributed in the U.S. by Mirae Asset Securities (USA) Inc., a

member of FINRA/SIPC, to “major U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6(b)(4) under the U.S.

Securities Exchange Act of 1934, as amended. All U.S. persons that receive this document by their acceptance hereof represent and warrant that they are a

major U.S. institutional investor and have not received this report under any express or implied understanding that they will direct commission income to

Mirae Asset Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed herein should contact

and place orders with Mirae Asset Securities (USA) Inc. Mirae Asset Securities (USA) Inc. accepts responsibility for the contents of this report in the U.S.,

subject to the terms hereof, to the extent that it is delivered to a U.S. person other than a major U.S. institutional investor. Under no circumstances should

any recipient of this research report effect any transaction to buy or sell securities or related financial instruments through Mirae Asset Daewoo. The

securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered

or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements.

Hong Kong: This report is distributed in Hong Kong by Mirae Asset Securities (HK) Limited, which is regulated by the Hong Kong Securities and Futures

Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for distribution only to

professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws of Hong Kong) and

any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Mirae

Asset Daewoo or its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject

Mirae Asset Daewoo and its affiliates to any registration or licensing requirement within such jurisdiction.

Emart

Mirae Asset Daewoo Research 10

March 31, 2020

Mirae Asset Daewoo International Network

Mirae Asset Daewoo Co., Ltd. (Seoul) Mirae Asset Securities (HK) Ltd. Mirae Asset Securities (UK) Ltd.

Global Equity Sales Team

Mirae Asset Center 1 Building

26 Eulji-ro 5-gil, Jung-gu, Seoul 04539

Korea

Units 8501, 8507-8508, 85/F

International Commerce Centre

1 Austin Road West

Kowloon

Hong Kong

41st Floor, Tower 42

25 Old Broad Street,

London EC2N 1HQ

United Kingdom

Tel: 82-2-3774-2124 Tel: 852-2845-6332 Tel: 44-20-7982-8000

Mirae Asset Securities (USA) Inc. Mirae Asset Wealth Management (USA) Inc. Mirae Asset Wealth Management (Brazil) CCTVM

810 Seventh Avenue, 37th Floor

New York, NY 10019

USA

555 S. Flower Street, Suite 4410,

Los Angeles, California 90071

USA

Rua Funchal, 418, 18th Floor, E-Tower Building Vila

Olimpia

Sao Paulo - SP

04551-060

Brasil

Tel: 1-212-407-1000 Tel: 1-213-262-3807 Tel: 55-11-2789-2100

PT. Mirae Asset Sekuritas Indonesia Mirae Asset Securities (Singapore) Pte. Ltd. Mirae Asset Securities (Vietnam) LLC

Equity Tower Building Lt. 50

Sudirman Central Business District

Jl. Jend. Sudirman, Kav. 52-53 Jakarta Selatan

12190

Indonesia

6 Battery Road, #11-01

Singapore 049909

Republic of Singapore

7F, Saigon Royal Building

91 Pasteur St.

District 1, Ben Nghe Ward, Ho Chi Minh City

Vietnam

Tel: 62-21-515-3281 Tel: 65-6671-9845 Tel: 84-8-3911-0633 (ext.110)

Mirae Asset Securities Mongolia UTsK LLC Mirae Asset Investment Advisory (Beijing) Co., Ltd Beijing Representative Office

#406, Blue Sky Tower, Peace Avenue 17

1 Khoroo, Sukhbaatar District

Ulaanbaatar 14240

Mongolia

2401B, 24th Floor, East Tower, Twin Towers

B12 Jianguomenwai Avenue, Chaoyang District

Beijing 100022

China

2401A, 24th Floor, East Tower, Twin Towers

B12 Jianguomenwai Avenue, Chaoyang District

Beijing 100022

China

Tel: 976-7011-0806 Tel: 86-10-6567-9699 Tel: 86-10-6567-9699 (ext. 3300)

Shanghai Representative Office Ho Chi Minh Representative Office

38T31, 38F, Shanghai World Financial Center

100 Century Avenue, Pudong New Area Shanghai

200120

China

7F, Saigon Royal Building

91 Pasteur St.

District 1, Ben Nghe Ward, Ho Chi Minh City

Vietnam

Tel: 86-21-5013-6392 Tel: 84-8-3910-7715