VietnAM - Stockbiz

85

Q3 2011 www.businessmonitor.com FOOD & DRINK REPORT ISSN 1749-3072 Published by Business Monitor International Ltd. VIETNAM INCLUDES BMI'S FORECASTS

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of VietnAM - Stockbiz

Q3 2011www.businessmonitor.com

food & drink report

iSSn 1749-3072published by Business Monitor international Ltd.

VietnAMINCLUDES BMI'S FORECASTS

Vietnam Food & Drink Q3 2011INCLUDES BMI'S 5-YEAR FORECASTS

Part of BMI's Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: April 2011

Business Monitor InternationalMermaid House,2 Puddle Dock,London, EC4V 3DS,UKTel: +44 (0) 20 7248 0468Fax: +44 (0) 20 7248 0467Email: [email protected]: http://www.businessmonitor.com

© 2011 Business Monitor InternationalAll rights reserved.

All information contained in this publication iscopyrighted in the name of Business MonitorInternational, and as such no part of thispublication may be reproduced, repackaged,redistributed, resold in whole or in any part, or usedin any form or by any means graphic, electronic ormechanical, including photocopying, recording,taping, or by information storage or retrieval, or byany other means, without the express written consentof the publisher.

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time ofpublishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business MonitorInternational accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of thepublication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind asto the accuracy or completeness of any information hereto contained.

CONTENTS

BMI Industry View .................................................................................................................................. 7

SWOT ..................................................................................................................................................... 9

Drink Industry SWOT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Food Industry SWOT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Grocery Retail Industry SWOT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Industry Business Environment Overview ............................................................................................ 12

Global Food & Drink View . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Commodity Prices Pressuring Margins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Signs Of A Consumer Recovery In Developed Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Emerging Markets Look Ever More Attractive . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Big Deals Could Be Back On The Agend . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Table: BMI FOOD & DRINK CORE VIEWS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Asia Pacific Risk/Reward Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Table: ASIA PACIFIC FOOD & DRINK RISK/REWARD RATINGS -Q3 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Vietnam Food & Drink Business Environment Rating .......................................................................... 25

Consumer Outlook ................................................................................................................................ 27

Industry Forecast Scenario ................................................................................................................... 31

Food . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Table: Table: Vietnam Food Consumption Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Table: Table: Vietnam Canned Food Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Table: Table: Vietnam Confectionery Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Table: Table: Vietnam Food & Drink Trade Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

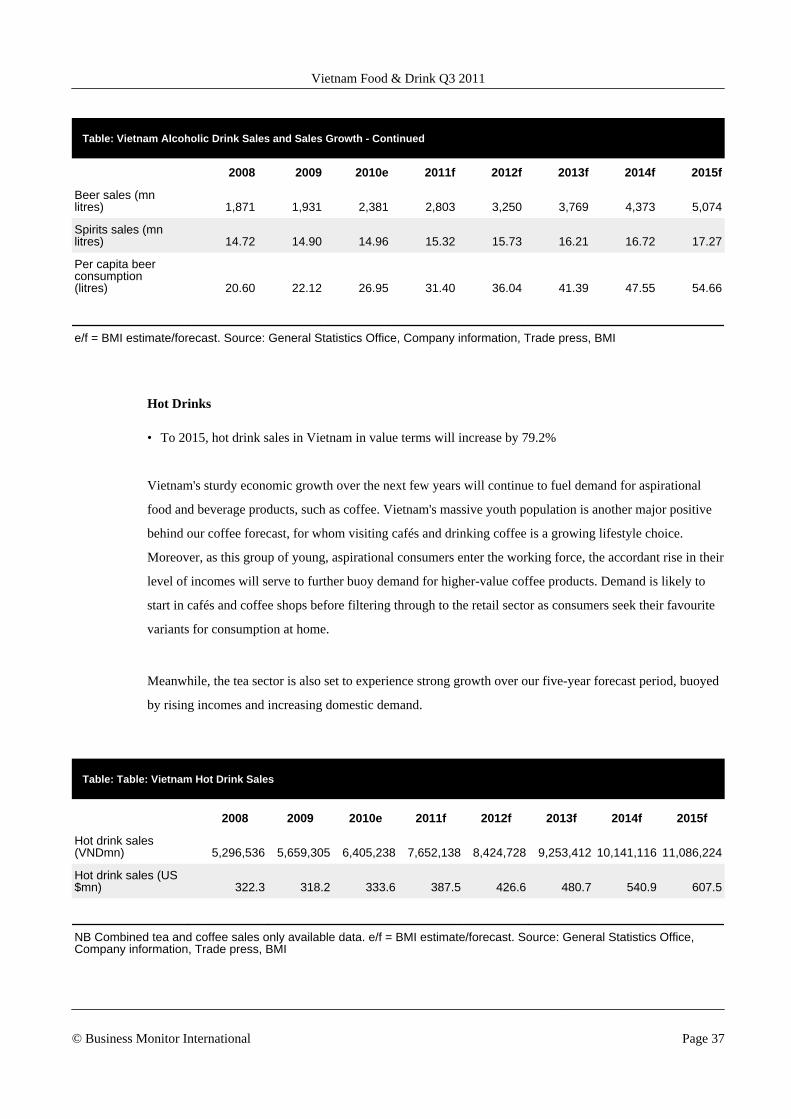

Drink . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Table: Table: Vietnam Alcoholic Drink Sales and Sales Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Table: Table: Vietnam Hot Drink Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

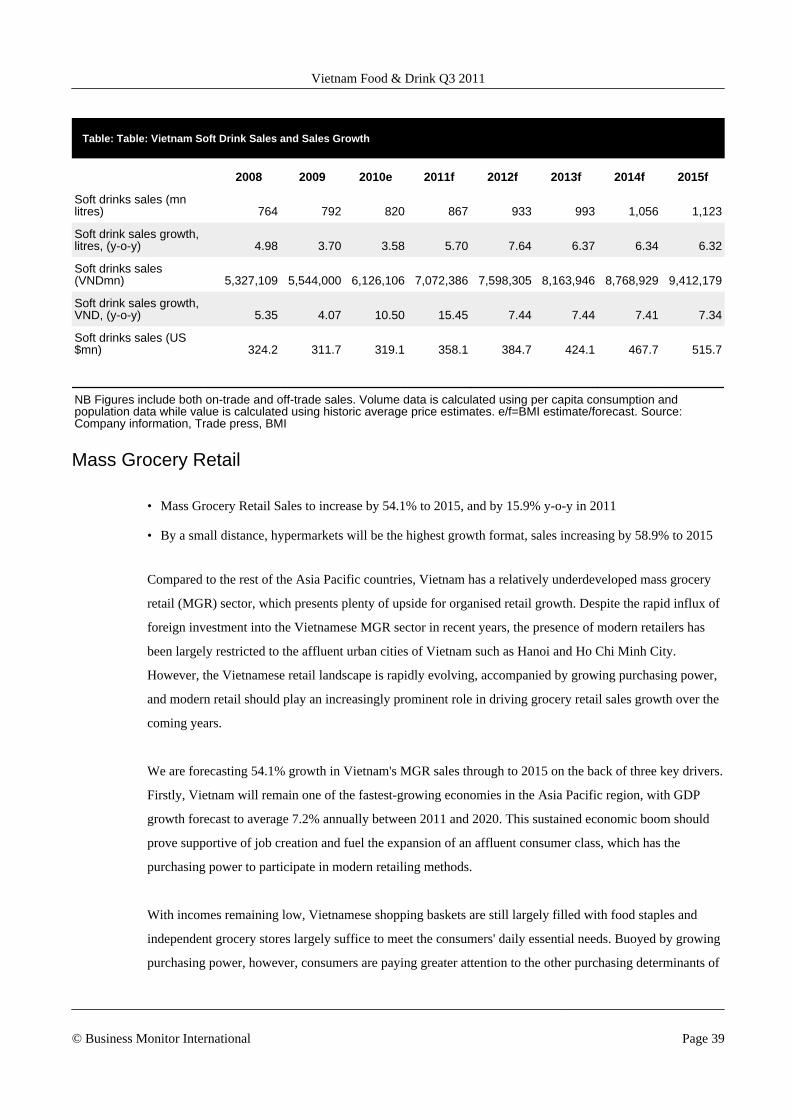

Table: Table: Vietnam Soft Drink Sales and Sales Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Mass Grocery Retail . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

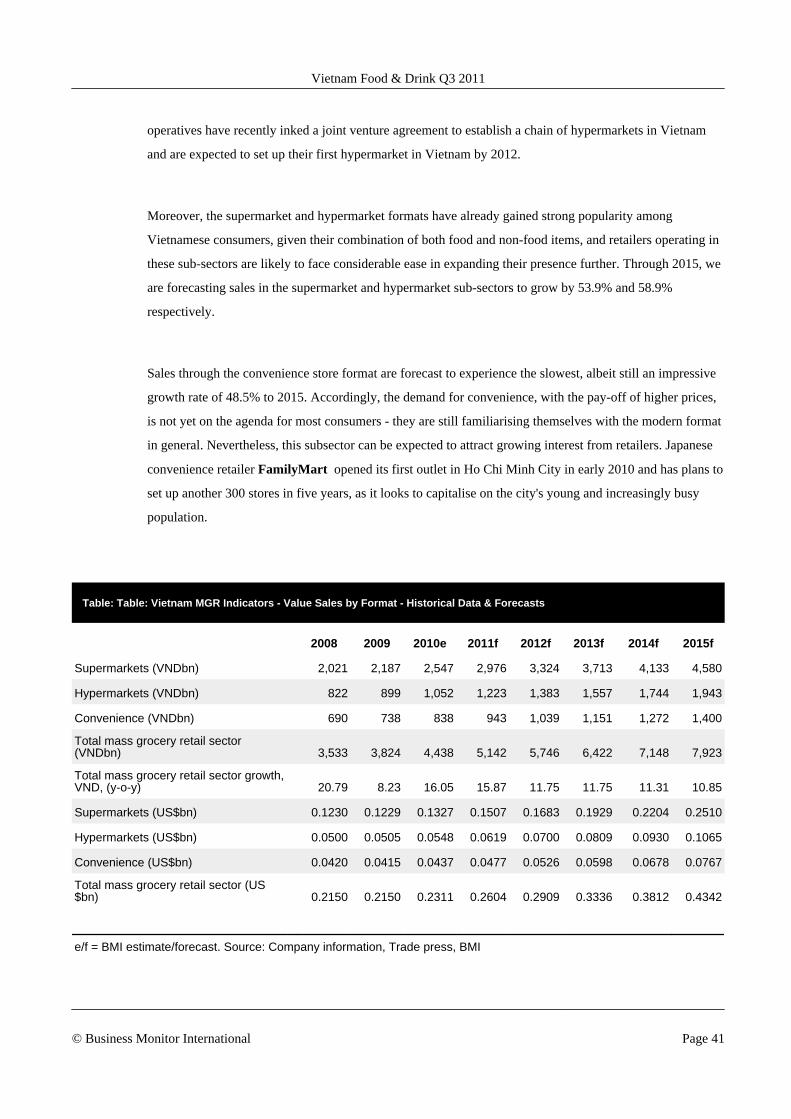

Table: Table: Vietnam MGR Indicators - Value Sales by Format - Historical Data & Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

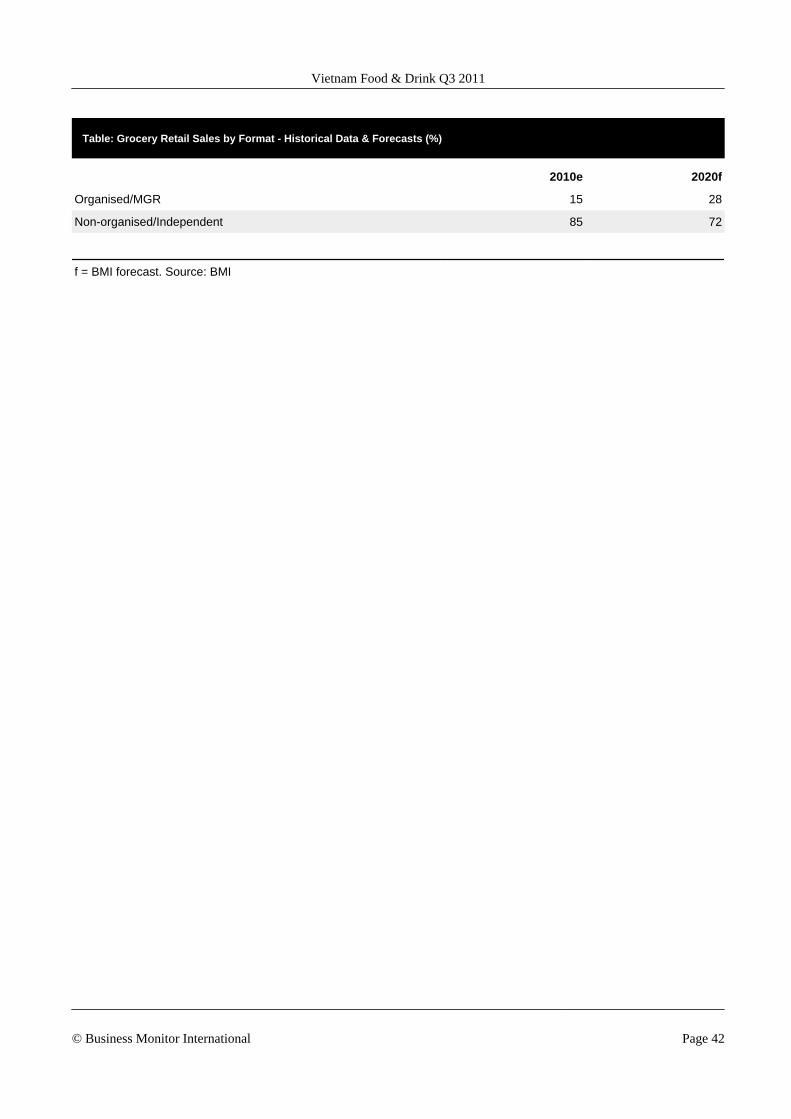

Table: Grocery Retail Sales by Format - Historical Data & Forecasts (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Food ..................................................................................................................................................... 43

Industry Trends And Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Market Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Drink ..................................................................................................................................................... 47

Industry Trends And Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Market Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

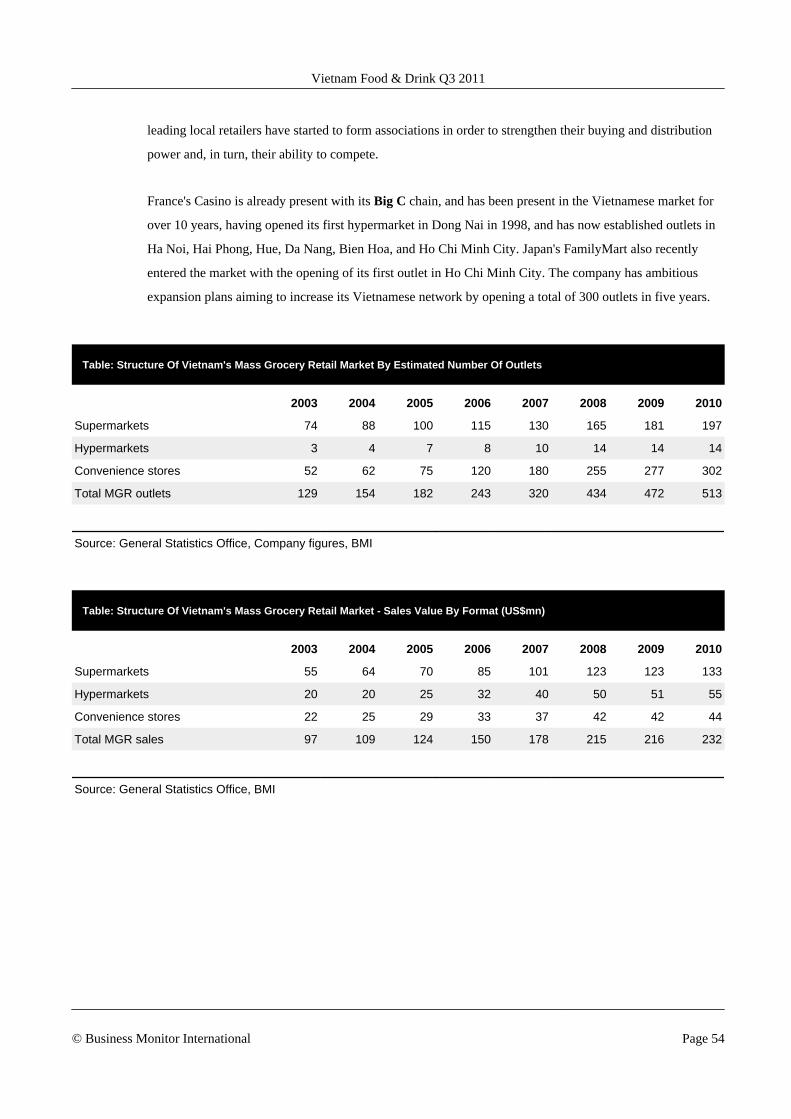

Mass Grocery Retail .............................................................................................................................. 51

Industry Trends And Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Market Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

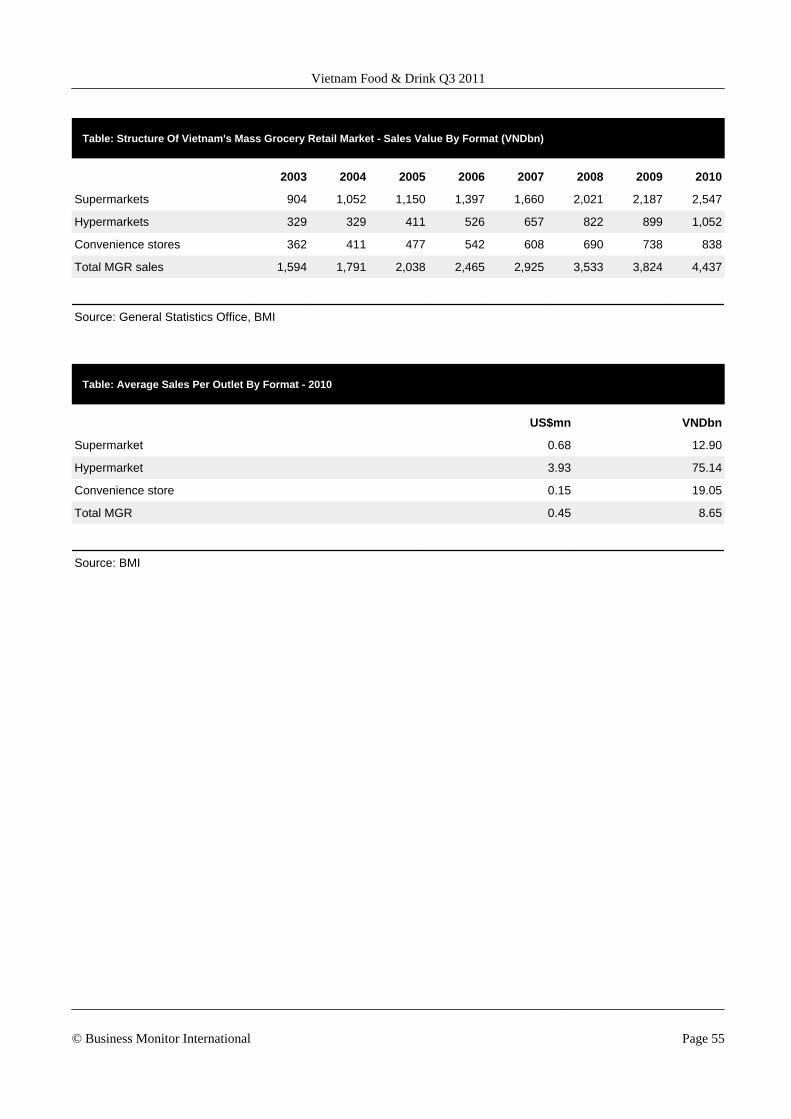

Table: Structure Of Vietnam's Mass Grocery Retail Market By Estimated Number Of Outlets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Table: Structure Of Vietnam's Mass Grocery Retail Market - Sales Value By Format (US$mn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 5

Table: Structure Of Vietnam's Mass Grocery Retail Market - Sales Value By Format (VNDbn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Table: Average Sales Per Outlet By Format - 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

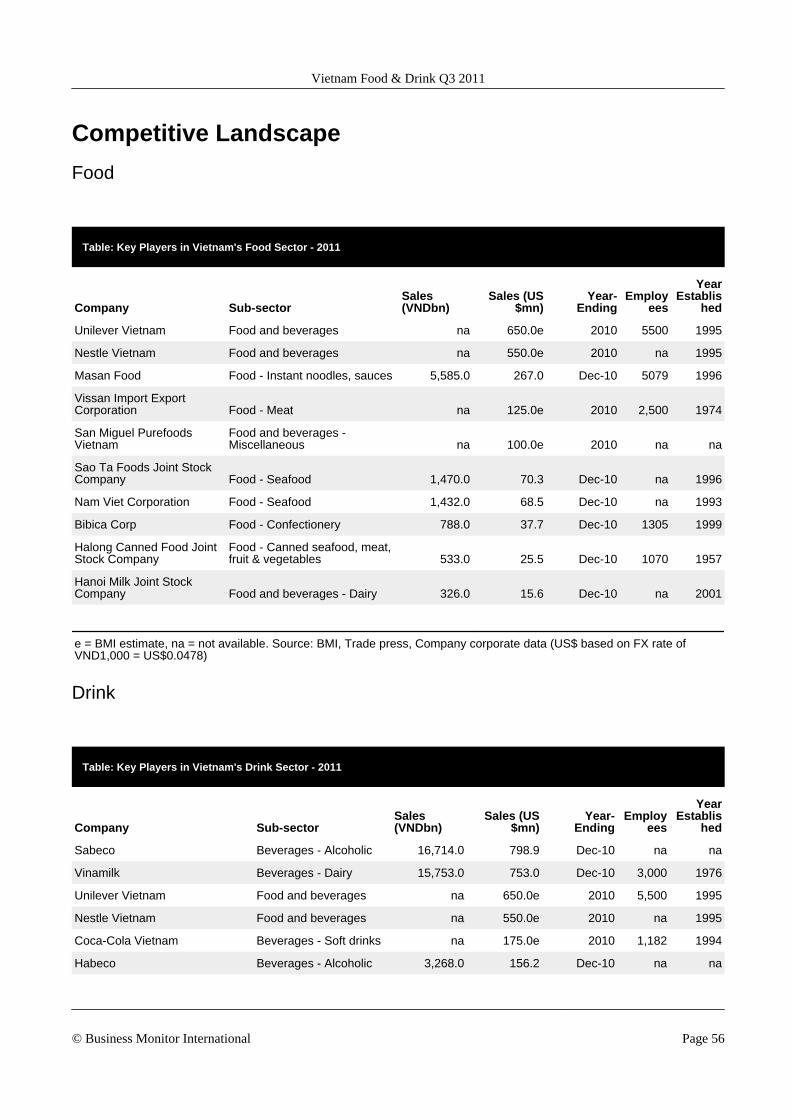

Competitive Landscape ........................................................................................................................ 56

Food . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

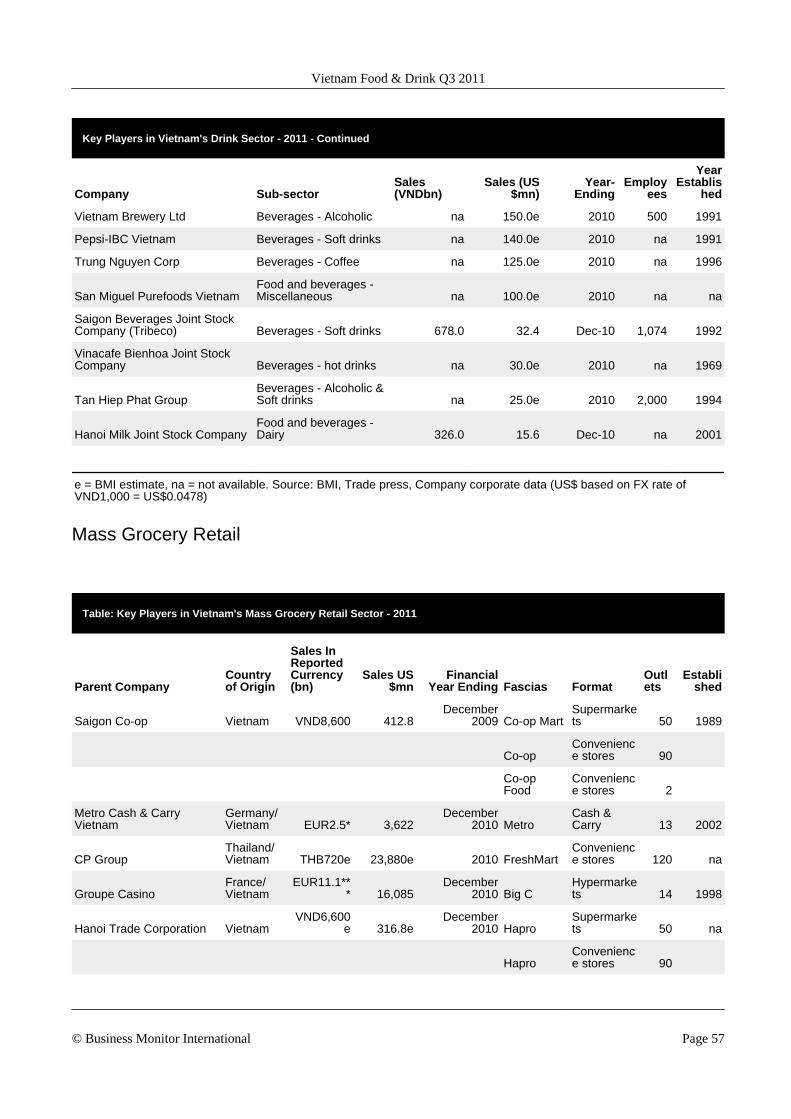

Table: Key Players in Vietnam's Food Sector - 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Drink . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Table: Key Players in Vietnam's Drink Sector - 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Mass Grocery Retail . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Table: Key Players in Vietnam's Mass Grocery Retail Sector - 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Company Analysis ................................................................................................................................ 59

Unilever Vietnam . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Nestlé Vietnam . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Masan Consumer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Vietnam Dairy Products Joint Stock Company (Vinamilk) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

San Miguel Pure Foods (VN) Co Ltd . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Hanoi Beer Alcohol Beverage Corp (Habeco) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Saigon Beer Alcohol and Beverage Corporation (Sabeco) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Carlsberg . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Metro Cash & Carry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Saigon Co-op . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Methodology ......................................................................................................................................... 79

Risk/Reward Ratings Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Ratings System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Table: Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Glossary ............................................................................................................................................... 81

Food & Drink . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Mass Grocery Retail . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

BMI Food & Drink Forecasting and Sources ......................................................................................... 83

How We Generate Our Industry Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

Sourcing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 6

BMI Industry View

A large, youthful population and a rapid influx of foreign direct investment as firms seek to take advantage

of this favourable demographic picture underline the enormous potential of Vietnam's food, drink and mass

grocery retail markets, as evidenced by our latest industry forecasts. Investment will continue to flow into

the industry, helping to drive double-digit annual sales growth across many market sub-sectors, especially

given the level of maturity being reached within sectors of the industry in other South East Asian markets.

That said, we note that an inflationary environment and government measures to stem inflation and put

economic growth on a more sustainable footing could serve to undermine demand in the short term.

Headline Industry Data

• Food Consumption will grow by 72.3% to 2015, albeit from a very low base thanks to rising consumeraffluence and the ongoing spread of mass grocery retail

• We have revised up our 2011 Vietnam beer consumption forecast from high single digits to 17.7% on theback of sustained industry investment and the strong performance of leading industry players

• To 2015 we expect mass grocery retail sales to increase by 54.1% (2011 growth is forecast at 15.9%),with hypermarkets set to be the outperformers in growth terms

Key Industry Trends

Weaker Retail Sales Data - Vietnamese retail sales of goods and services rose by 22.6% year-on-year in

Q111 to reach VND451.8trn. Adjusted for inflation, which remains elevated, sales increased by 8.7%. The

inflation-adjusted increase is far lower than the growth rate experienced for the same period of 2010 and

2009 (24.1% and 14.4% respectively). Weaker growth has been attributed to the severity of inflationary

pressures and the impact this has had on consumer spending power. A number of retailers have already

unveiled measures that attempt to address this problem by launching significant promotional campaigns,

offering discounts across a range of daily essential items (among them are Big C and Lotte Mart) in an

attempt to show that they are sharing the burden of elevated costs with consumers and thus retaining

consumer loyalty.

Inflation Remains A Concern - The inflationary burden on the Vietnamese consumer is getting heavier.

With Brent crude prices reaching highs not seen since mid-2008, Vietnamese manufacturers and suppliers

have increased their sale prices, as they contend with soaring electricity and fuel prices. In response to the

respective 20% and 15% increases in petrol and electricity prices announced by the government, the

majority of Vietnamese manufacturers and suppliers raised their sale prices from March 1 2011. Faced with

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 7

the threat of surging transportation costs and sale prices from manufacturers, Vietnamese retailers have

hiked prices of perishable products, which are directly exposed to petrol and electricity price increases, by

10-18%. On the other hand, prices of non-perishable goods, which bear indirect influences from inflationary

trends in fuel and electricity, have been increased by 5%.

Key Company Trends

Largest Ever PE Deal - Global private equity (PE) firm Kohlberg Kravis Roberts & Co (KKR) has agreed

to acquire a 10% stake in Vietnamese consumer goods producer Masan Consumer. Vietnam is emerging

on the radars of PE investors looking to entrench themselves in the favourable consumer plays of emerging

markets (EMs). KKR has agreed to acquire the stake in Masan Consumer, the largest producer of

condiments like fish, soy and chilli sauce and the second biggest producer of instant noodles in Vietnam, for

US$159mn, marking the largest PE investment in the country. Masan Consumer is a subsidiary of Masan

Group, one of the largest private sector conglomerates in Vietnam. Upon completion of the acquisition,

Masan Group's equity stake in Masan Consumer will decrease from 86.6% to 78%.

Key Risks to Outlook

We remain concerned that excessive monetary tightening in an attempt to battle rising inflationary pressures

could result in a hard landing for the Vietnamese economy. Nonetheless, inflation remains a problem that

must be tackled. Manufacturers have already had to implement a number of price hikes and while larger

retailers have tried to counter the impact of these via loyalty problems, they will not be able to profitably

sustain these indefinitely, meaning higher costs will have to be passed on to consumers.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 8

SWOT

Drink Industry SWOT

Vietnam Drink Industry SWOT

Strengths • Vietnamese consumers, particularly the young and affluent, are interested in brands, and,accordingly, renowned Western products backed by investment in marketing and promotionstend to have highly successful launches.

• The wealthy urban centres of Hanoi and Ho Chi Minh City now provide highly receptiveconsumer audiences.

• Alcoholic drinks are widely consumed and have gained popularity in recent years.

• Vietnam has been one of the fastest-growing economies in Asia in recent years, with GDPgrowth averaging 7.6% annually between 2000 and 2009

Weaknesses • There are wide income disparities between urban and rural areas, and local consumptionpatterns vary significantly according to income.

• The drinks industry remains largely fragmented except for a few key sectors, such as alcoholicand soft drinks.

• Vietnam's infrastructure is still weak. Roads, railways and ports are inadequate to cope with thecountry's economic growth and links with the outside world.

Opportunities • Accession to the WTO, in January 2007, will continue to benefit Vietnamese exporters, with thegradual removal of market barriers and trade restrictions set to increase competition.

• Vietnam's large domestic market, growing export opportunities and low labour costs, as well asthe prospect of acquiring newly privatised drink companies, offer further investmentopportunities.

• A growing tourism sector is fuelling interest in convenience categories, in addition to sub-sectorssuch as soft and alcoholic drinks.

• In line with consumers' rising disposable incomes, there are opportunities for premium-brandedproducts in the soft and alcoholic drinks sub-sectors.

• The global trend towards health-consciousness provides an opportunity for drinks manufacturersto diversify into perceived healthier options.

Threats • Vietnam's WTO membership may result in smaller companies unable to cope with the increasedcompetition being forced out of business.

• Rising raw-material costs threaten profitability in this competitive market in which higher pricescannot easily be passed on to consumers.

�

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 9

Food Industry SWOT

Vietnam Food Industry SWOT

Strengths • The food-processing sector accounts for a sizeable proportion of industrial output and GDP, withthe sector attracting significant foreign investment in recent years from the likes of Unilever,Nestlé and San Miguel.

• Vietnamese consumers, particularly the young and affluent, are interested in brands and,accordingly, renowned Western products backed by investment in marketing and promotionstend to have highly successful launches.

• The wealthy urban centres of Hanoi and Ho Chi Minh City now provide highly receptiveconsumer audiences.

• Large and diverse domestic agricultural output aids the stability of ingredient supplies and pricesfor local producers -- a vital strength during this period of global volatility.

Weaknesses • There are wide income disparities between urban and rural areas, and local consumptionpatterns vary significantly according to income.

• The food-processing industry remains largely fragmented except for a few key sectors, such asdairy and confectionery.

• The country's agricultural sector has been criticised for being too slow to adapt to newtechnologies to be globally competitive in the long term, although the government is workinghard to address this.

• Vietnam's infrastructure is still weak. Roads, railways and ports are inadequate to cope with thecountry's economic growth and links with the outside world.

• The lack of white goods among large sections of the consumer base slows down thedevelopment of the high-potential dairy sector

Opportunities • Accession to the WTO continues to benefit Vietnamese exporters, with the gradual removal ofmarket barriers and trade restrictions set to increase competition.

• Rising income levels and changing lifestyles, particularly in urban areas, are increasingconsumer demand for snacks, convenience and luxury food items.

• Vietnam's large domestic market, growing export opportunities and low labour costs, as well asthe prospect of acquiring newly privatised food companies, offer further investment opportunities.

• The country's agricultural sector is in need of significant investment and willing investors canexpect assisted entry.

• A growing tourism sector fuels interest in convenience categories

Threats • Vietnam's WTO membership may result in smaller companies unable to cope with the increasedcompetition being forced out of business.

• Rising commodity costs will remain a risk for the profitability of processed-food manufacturers;farmers themselves also claim this as a threat, with the primary level reportedly seeing little inthe way of these higher prices.

�

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 10

Grocery Retail Industry SWOT

Vietnam Mass Grocery Retail Industry SWOT

Strengths • The potential size of the MGR market makes it an attractive target for foreign retailers onceimproved market terms are granted. Further growth is expected, especially in the supermarketformat.

• Hypermarkets, supermarkets and convenience stores have all proved popular in Vietnam,catering to different types of consumers and different shopping occasions.

• A growing multinational presence in the retail sector has aided the acceptance of modern retailbest-practices in Vietnam, particularly things like added-value in-store services.

• The formation of buying groups has proved an effective means of facilitating quicker expansionamong smaller industry players.

Weaknesses • Vietnam's retail distribution networks remain underdeveloped and expansion-oriented firms mustinvest in infrastructural development as well as new store openings.

• Regulations governing international participation in modern retail in Vietnam have resulted inslow rates of expansion, and aspects of government policy continue to make life challenging forforeign firms in spite of WTO accession.

• Poverty levels among the country's vast rural population hugely inhibit the potential audiencesize for modern retail in Vietnam.

■ .

Opportunities • The hypermarket concept is still in its infancy and, as familiarity with modern retailing grows, thisformat will represent an immense growth opportunity.

• Modern retail is currently focused on the major urban centres of the north and south, which stillboast space for new entrants, and central Vietnam and the provinces provide furtheropportunities still.

• Modern retail concepts, such as discounting and private labelling, should prove popular withprice-conscious Vietnamese consumers as familiarity with modern retailing builds.

• Rapid urbanisation and the development of new housing complexes provide ideal locations forthe rolling out of modern retail outlets with a large and receptive audience.

Threats • Were industry majors Tesco, Carrefour and Wal-Mart all to enter Vietnam, the window ofopportunity for other entrants would rapidly close.

• Rising operating costs will threaten retailer profit margins; with it difficult to pass price increaseson to consumers in such a price sensitive environment.

�

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 11

Industry Business Environment Overview

Global Food & Drink View

Developments within the global food and drink industry in the past three months have continued to reflect

and support BMI's core industry views. Of particular importance in the last quarter has been the impact of

rising commodity prices - a factor that BMI was particularly quick to recognise was likely to impact

margins and also the valuation of food and drink firms. Rising global prices are also becoming an

increasingly important factor in emerging markets, where surging inflation threatens to undermine

confidence and put downwards pressure on growth in spending power.

Over the quarter we have seen encouraging signs of a consumer recovery in several important developed

markets, including the US, Germany and France. However, we expect high unemployment, fiscal austerity

measures and looming rate hikes to put pressure on growth rates over the longer term. Growth in emerging

markets has continued to impress and for many firms has acted to offset the lacklustre rates of growth in

developed markets.

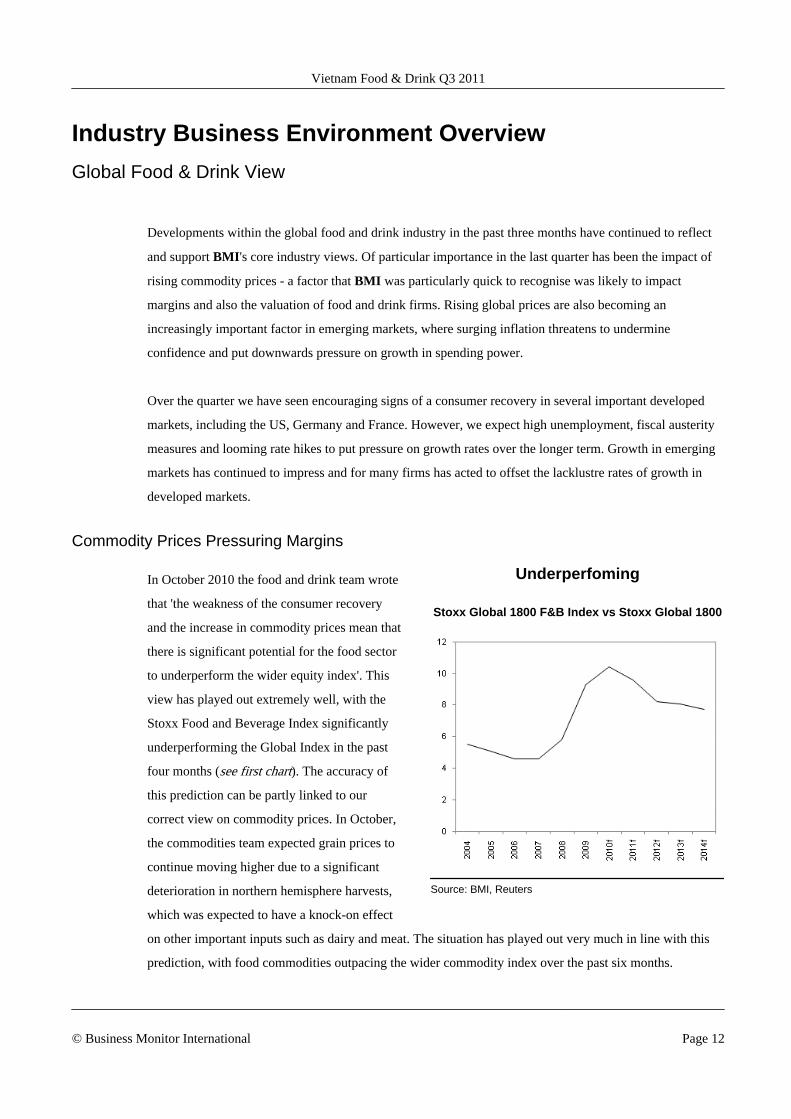

Commodity Prices Pressuring Margins

In October 2010 the food and drink team wrote

that 'the weakness of the consumer recovery

and the increase in commodity prices mean that

there is significant potential for the food sector

to underperform the wider equity index'. This

view has played out extremely well, with the

Stoxx Food and Beverage Index significantly

underperforming the Global Index in the past

four months (see first chart). The accuracy of

this prediction can be partly linked to our

correct view on commodity prices. In October,

the commodities team expected grain prices to

continue moving higher due to a significant

deterioration in northern hemisphere harvests,

which was expected to have a knock-on effect

on other important inputs such as dairy and meat. The situation has played out very much in line with this

prediction, with food commodities outpacing the wider commodity index over the past six months.

Underperfoming

Stoxx Global 1800 F&B Index vs Stoxx Global 1800

Source: BMI, Reuters

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 12

Most major food groups have now reported their results for the fourth quarter of 2010 and they tell a clear

story, with margins falling due to rising costs. In response food groups have announced that they will begin

to raise prices more aggressively in 2011 and firms such as Unilever have suggested that they have learnt

from the experience of 2008, when they priced up and down effectively. However, BMI is concerned that

the consumer environment could make price increases harder to implement than in the past, with the slow

pace of economic recovery continuing to weigh on consumer confidence and with retailers very reluctant to

accept price increases. In addition, since 2008 consumer savviness has increased in many important markets

- for example private labels and discount stores have made huge strides in the US and parts of Europe where

they had previously had little presence, such as in Spain and Italy, meaning that any attempt to pass on price

increases could simply strengthen the trend towards lower priced products and retail formats.

A general ramp up in commodity prices, including in a sharp increase in the price of energy, has acted to

drive up inflation in both developed and emerging markets. This has led to a general move towards

hawkishness among central banks. In emerging markets, food inflation has been particularly rampant, with

double-digit levels of growth seen in many parts of the market. Given the disproportionate impact of rising

prices on poorer sections of societies in countries such as China and Brazil, such governments are under

pressure to cool down their economies and they have already begun raising interest rates. We are pencilling

in further rate hikes in these and several other important emerging markets including India and Indonesia

over the coming year, which will put downwards pressure on growth momentum.

Signs Of A Consumer Recovery In DevelopedMarkets

In line with our expectations the consumer

sector in developed markets struggled to deliver

significant growth through much of 2010, with

price sensitivity the preeminent theme and

private labels and the discount sector gaining

ground. However, there were some positive

signs starting to emerge towards the end of the

year and we now believe that 2011 could be the

real year of recovery. For example, in the US

there were signs that the US discount sector -

characterised by the firms Family Dollar and

Dollar General - which delivered dynamic

Slow Improvement

Unemployment (% of labour force, year average)

f = BMI forecast. Source: BLS, BMI

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 13

growth during the downturn, started to slow

towards the end of 2010.

BMI believes this lower rate of growth (combined with improving results at mainstream retailers) can be

attributed to an upturn in consumer confidence in the second half of 2010, combined with an improved

outlook for GDP growth in 2011. The big downside risks for the US economy in 2011 - that taxes rise and

unemployment benefits are not extended - actually turned into a major upside surprise in December 2010,

after Congress not only approved an extension of the income tax regime and unemployment benefits, but

also cut payroll taxes by two percentage points. This improvement in the consumer outlook will be greeted

warmly by most retailers, but for discount operators, which have thrived thanks to the weak economic

environment, a stronger retail sector could actually have a detrimental impact on results. This is borne out

by Family Dollar's sales growth slowing as 2010 progressed, with comparable sales in December climbing

by just 4%.

A similar story was seen in Europe, where the movement towards discount stores seems to have peaked in

many important markets, including Germany, the UK and France. Germany proved to be one of the

country's best positioned to bounce back from the economic downturn and this has been reflected in the

relative growth of the retail sector. For example, German retailer Rewe registered growth of 4% in its

German sales during the year. This growth was driven by the company's supermarket outlets, with growth

up by 6.4%, but was weighed down by the underperformance of the company's Penny discount stores,

which registered a 1.2% contraction in revenues. The outperformance of the supermarket sector is in line

with a strengthening of the domestic consumer market and is reminiscent of the two years leading up to the

economic crisis, when questions were asked about the long-term prospects for the discount sector in the

German market.

Emerging Markets Look Ever More Attractive

Despite these signs of recovery in developed markets, we continue to believe that the pace of growth in the

consumer sector over the next five years is unlikely to match the boom levels seen in the years leading up to

the financial crisis. Fiscal austerity measures are only now starting to be felt by the average consumer, while

rising inflation means that consumers may also soon have to contend with rising interest rates and mortgage

repayments. Unemployment across the US and eurozone is also remaining stubbornly high and looks

unlikely to fall significantly until we are some way into the economic recovery. BMI has a relatively

pessimistic outlook for employment in the US, believing that the credit boom actually masked massive

structural problems in the US economy, for which there is no quick fix. Because of this, we are forecasting

that unemployment will not go back to its pre-crisis lows over the next ten years (see second chart).

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 14

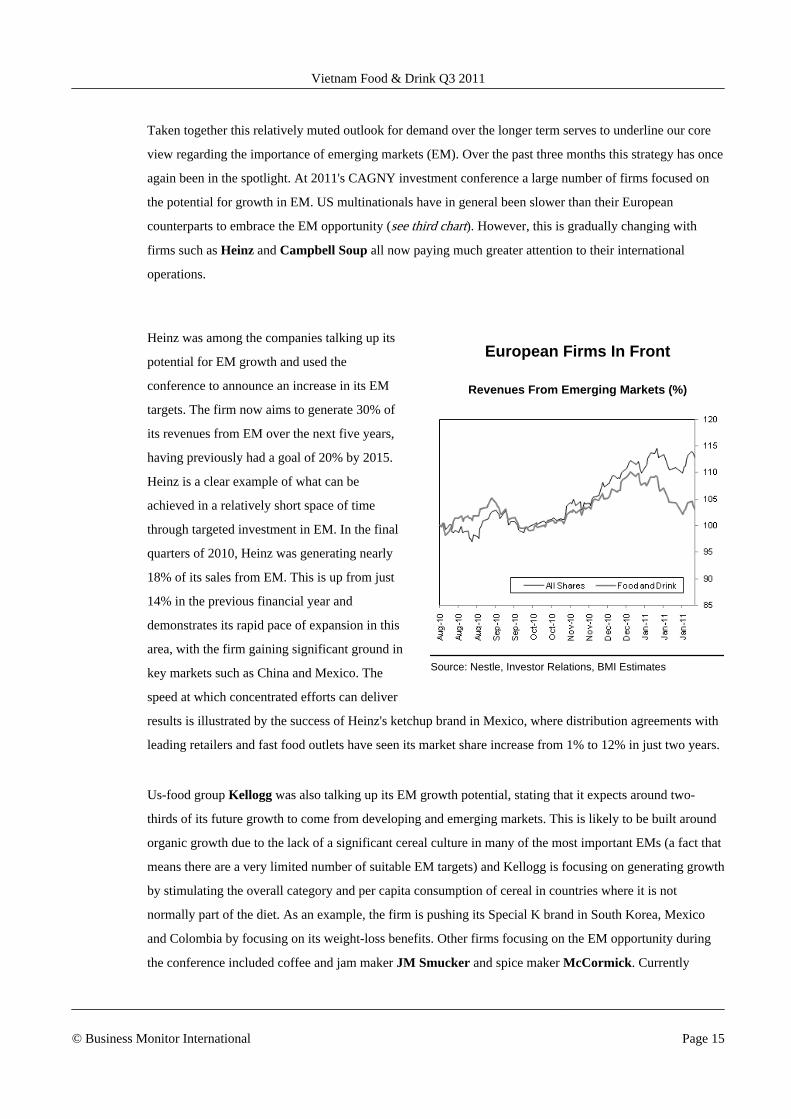

Taken together this relatively muted outlook for demand over the longer term serves to underline our core

view regarding the importance of emerging markets (EM). Over the past three months this strategy has once

again been in the spotlight. At 2011's CAGNY investment conference a large number of firms focused on

the potential for growth in EM. US multinationals have in general been slower than their European

counterparts to embrace the EM opportunity (see third chart). However, this is gradually changing with

firms such as Heinz and Campbell Soup all now paying much greater attention to their international

operations.

Heinz was among the companies talking up its

potential for EM growth and used the

conference to announce an increase in its EM

targets. The firm now aims to generate 30% of

its revenues from EM over the next five years,

having previously had a goal of 20% by 2015.

Heinz is a clear example of what can be

achieved in a relatively short space of time

through targeted investment in EM. In the final

quarters of 2010, Heinz was generating nearly

18% of its sales from EM. This is up from just

14% in the previous financial year and

demonstrates its rapid pace of expansion in this

area, with the firm gaining significant ground in

key markets such as China and Mexico. The

speed at which concentrated efforts can deliver

results is illustrated by the success of Heinz's ketchup brand in Mexico, where distribution agreements with

leading retailers and fast food outlets have seen its market share increase from 1% to 12% in just two years.

Us-food group Kellogg was also talking up its EM growth potential, stating that it expects around two-

thirds of its future growth to come from developing and emerging markets. This is likely to be built around

organic growth due to the lack of a significant cereal culture in many of the most important EMs (a fact that

means there are a very limited number of suitable EM targets) and Kellogg is focusing on generating growth

by stimulating the overall category and per capita consumption of cereal in countries where it is not

normally part of the diet. As an example, the firm is pushing its Special K brand in South Korea, Mexico

and Colombia by focusing on its weight-loss benefits. Other firms focusing on the EM opportunity during

the conference included coffee and jam maker JM Smucker and spice maker McCormick. Currently

European Firms In Front

Revenues From Emerging Markets (%)

Source: Nestle, Investor Relations, BMI Estimates

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 15

Smucker generates nearly all of its revenues in North America, but used the conference to reveal it was

exploring plans to enter the attractive Chinese market. The firm revealed it was exploring a number of

avenues for market entry, including an acquisition of or partnership with a local firm. With a debt-to-

EBITDA ratio of only 0.89, Smucker looks well positioned to make acquisitions and it has previously

demonstrated an appetite for large-scale transformational takeovers.

Meanwhile, McCormick announced a target of generating 12% of its revenues from EM by 2015, which

compares to 9% at present. The firm highlighted the tremendous opportunity in India, where consumers

traditionally buy spices in bulk, but where middle-class consumers are increasingly 'seeking the higher

quality and convenience of branded products'. With even medium-sized producers now seeking out

acquisitions in EM, the battle to acquire attractive assets can only intensify, with a positive result for EM

valuations. While acquisitions can be a straightforward way to gain EM exposure, particularly for firms that

have little or none, the success of Heinz has also demonstrated the enormous amount that can be done by

simply investing in distribution and marketing, with many developed market firms already in possession of

brands and products that have enormous potential for growth in EM countries.

Big Deals Could Be Back On The Agend

Strong growth in EMs combined with a return to growth in developed markets means that many firms look

to be feeling more confident about their long-term prospects and we believe that this could spur a significant

ramp up in M&A activity in 2011. During much of 2010 there was a general attitude of caution, with firms

waiting to see which way the global economy was moving before committing to any big deals. In Q111 we

saw the first tentative steps in this direction, with PepsiCo purchasing a 66% stake in Russia's Wimm-Bill-

Dann for US$3.8bn, General Mills looking set to buy a 50% stake in Yoplait for EUR800mn and Diageo

agreeing to acquire Turkey's Mey Icki for US$2.1bn.

All of the major deals concluded by consumer groups in Q111 were bolt-on acquisitions and we are yet to

see a return to the more transformative deals seen in the years leading up to the financial crisis, such as

InBev's acquisition of Anheuser-Busch or Pernod Ricard's purchase of Absolut Maker Vin & Spirit.

However, with economies of scale such an important force in the food and drink sector, these kinds of deals

are sure to eventually re-emerge and we think that they could once again be on the cards in 2011. Firms that

we think are in a strong financial position to fund major acquisitions during 2011 include Diageo, Nestlé

and SABMiller, with acquisitions seen as a viable way to prop up relatively lacklustre sales growth in

developed markets.

One of our long-term core views is that multinationals with balanced developed and EM portfolios are best

positioned for growth. For EM-based firms this means that we see acquisitions in developed markets are a

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 16

priority as they look to develop better rounded companies with less volatile earnings. This trend has been

evident over the last six months with Colombia's largest food company Grupo Nacional de Chocolates

announcing it is to purchase US cookie producer Fehr Foods for US$84mn, while Chilean wine producer

Concha y Toro is to buy California-based Fetzer Vineyards from US drinks firm Brown Forman. This

follows on from Mexican bakery firm Grupo Bimbo announcing in November it is to acquire Sara Lee's

North American bakery business for US$925mn and is a trend that we expect to gather pace as major firms

in the EMs of Asia and Latin America start to look to develop businesses that can truly compete on a global

scale.

Table: BMI FOOD & DRINK CORE VIEWS

Short-term Outlook

Higher input costs will affect margins and raise tensions between producers and retailers

Rising inflation will put pressure on demand in emerging markets

Developed market growth returning but unlikely to match levels seen years leading up to the financial crisis due to:

Government fiscal policy - austerity

Government monetary policy - increasing likelihood of rate hikes due to rising inflation

Long-term Outlook

MNCs with balanced developed and EM portfolios are best positioned for growth

Companies with strong Emerging Market exposure will continue to outperform

Multinationals will increasingly pursue frontier market investments

Investment in innovation will increase as producers seek differentiation; emphasis will be placed on protecting innovations

Brand builders will continue to leave sectors under threat from private labels

Government legislation will play an increasing role in marginalising unhealthy food and beverage products

Premiumisation will re-emerge as a key driving force behind revenue growth

Demand for convenience in retail and food will continue to grow

Functional foods will be the highest growth sector in developed markets

Consolidation will continue as producers seek greater efficiencies

Beverage companies will continue to invest in diversification away from carbonated beverages and into healthier sub-sectors

Source: BMI

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 17

Asia Pacific Risk/Reward Ratings

The 9.0 magnitude earthquake and tsunami that struck Japan on March 11 2011 has inevitably placed a

damper on the country's investment appeal. Although Japan was top in our Q211 Asia Pacific food and

drink (F&D) risk/reward ratings, thanks to an enviable balance of a low-risk operating environment and

high consuming levels, the recent spate of natural catastrophes in Japan saw the country slip to the second

position this quarter. Indeed, the extensive damages caused to Japan's transport infrastructure and tough

domestic picture are likely to keep potential investors at bay in the near term, thus dimming the

attractiveness of Japan.

Meanwhile, high-growth economies such as China, India and Indonesia continue to feature strongly in our

risk/reward ratings, underlining the massive abundance of opportunities in Asian Pacific emerging markets

(EMs). More noteworthy of mention is, however, the upward shifts in rankings for India and Indonesia. We

have repeatedly stressed that the developed economies of the Asia Pacific region will gradually lose their

investment appeal over the coming decades as opportunities for long-term growth dwindle, and our updated

risk/reward ratings for this quarter bear out this view.

Quake Deals Japan A Blow, China Now Tops

The recent dynamics in Japan has tipped the country off its top spot in our Q311 Asia Pacific F&D risk/

reward ratings. Japan's risk/reward rating score has declined from 63.7 in the last quarter to 61.8 presently,

implying a shaky operating environment for consumer goods investors.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 18

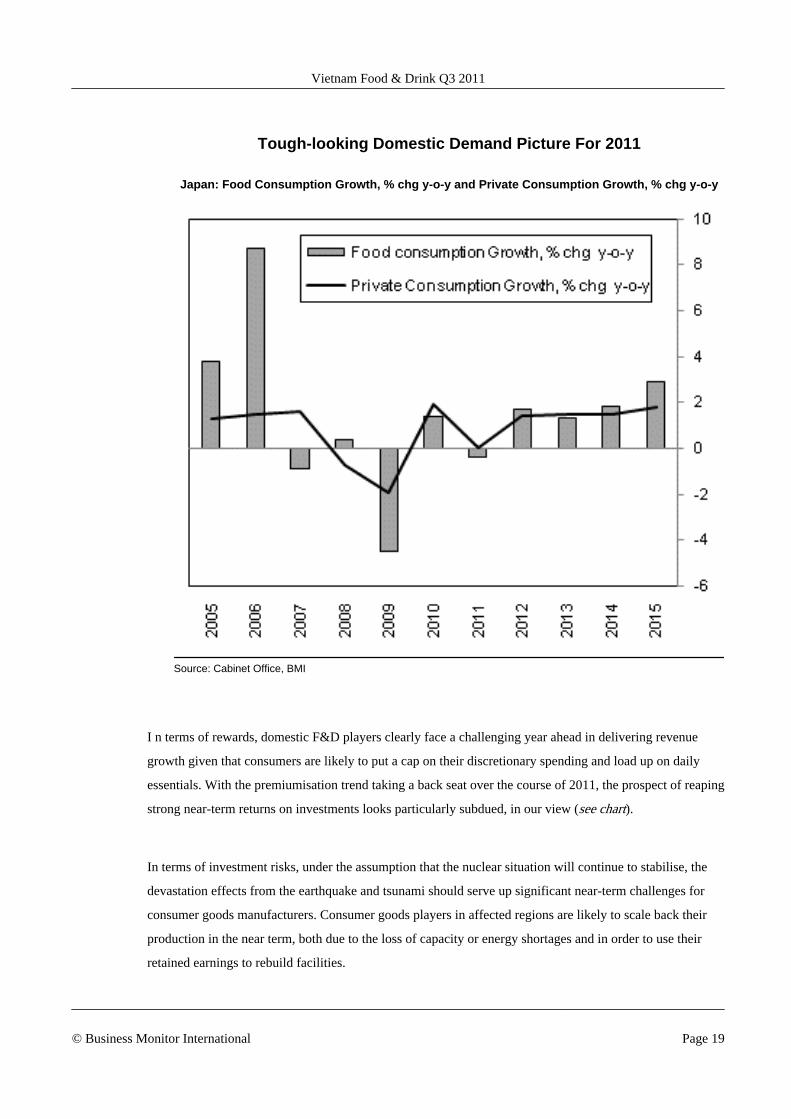

Tough-looking Domestic Demand Picture For 2011

Japan: Food Consumption Growth, % chg y-o-y and Private Consumption Growth, % chg y-o-y

Source: Cabinet Office, BMI

I n terms of rewards, domestic F&D players clearly face a challenging year ahead in delivering revenue

growth given that consumers are likely to put a cap on their discretionary spending and load up on daily

essentials. With the premiumisation trend taking a back seat over the course of 2011, the prospect of reaping

strong near-term returns on investments looks particularly subdued, in our view (see chart).

In terms of investment risks, under the assumption that the nuclear situation will continue to stabilise, the

devastation effects from the earthquake and tsunami should serve up significant near-term challenges for

consumer goods manufacturers. Consumer goods players in affected regions are likely to scale back their

production in the near term, both due to the loss of capacity or energy shortages and in order to use their

retained earnings to rebuild facilities.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 19

While the near-term dynamics bode poorly for Japan, investors are also likely to lose interest in the country

over the longer horizon due to its limited prospects for growth and high level of market maturity. Yes,

Japan's high F&D consumption levels, well-developed labour force and low levels of bureaucracy will

remain strong attractions for investors but realistically the market is mature and clearly would not be the

best place to search for solid long-term revenue growth.

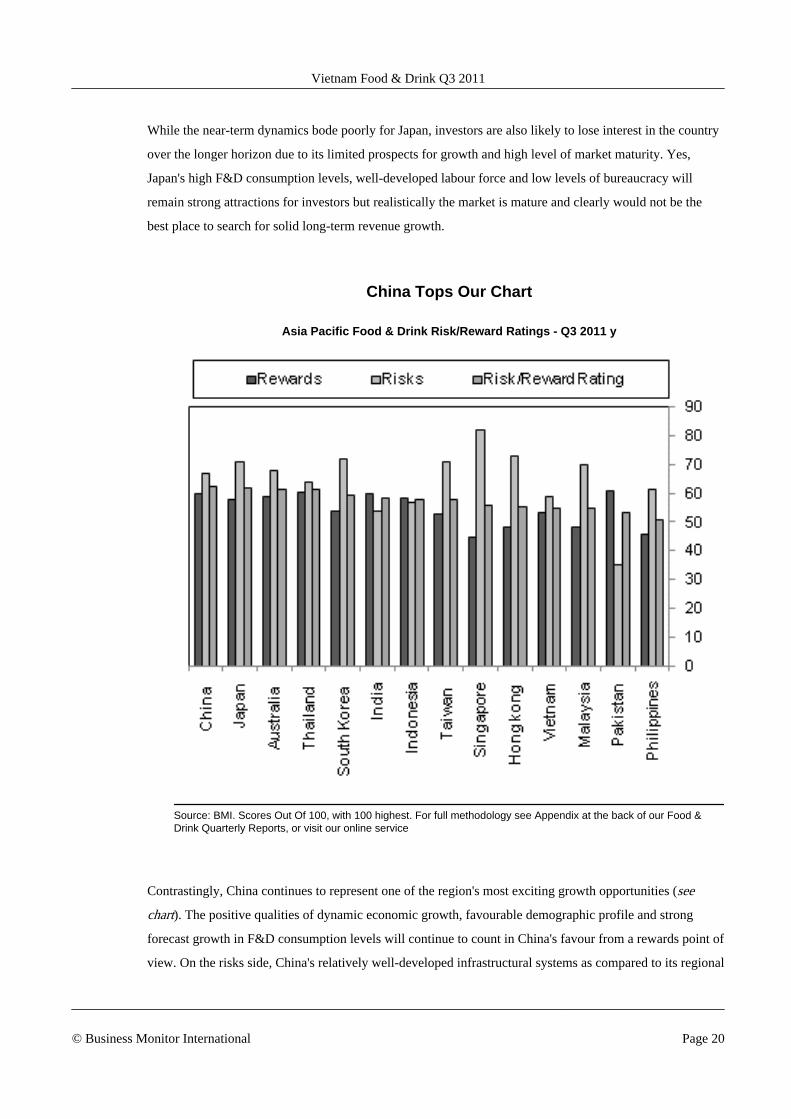

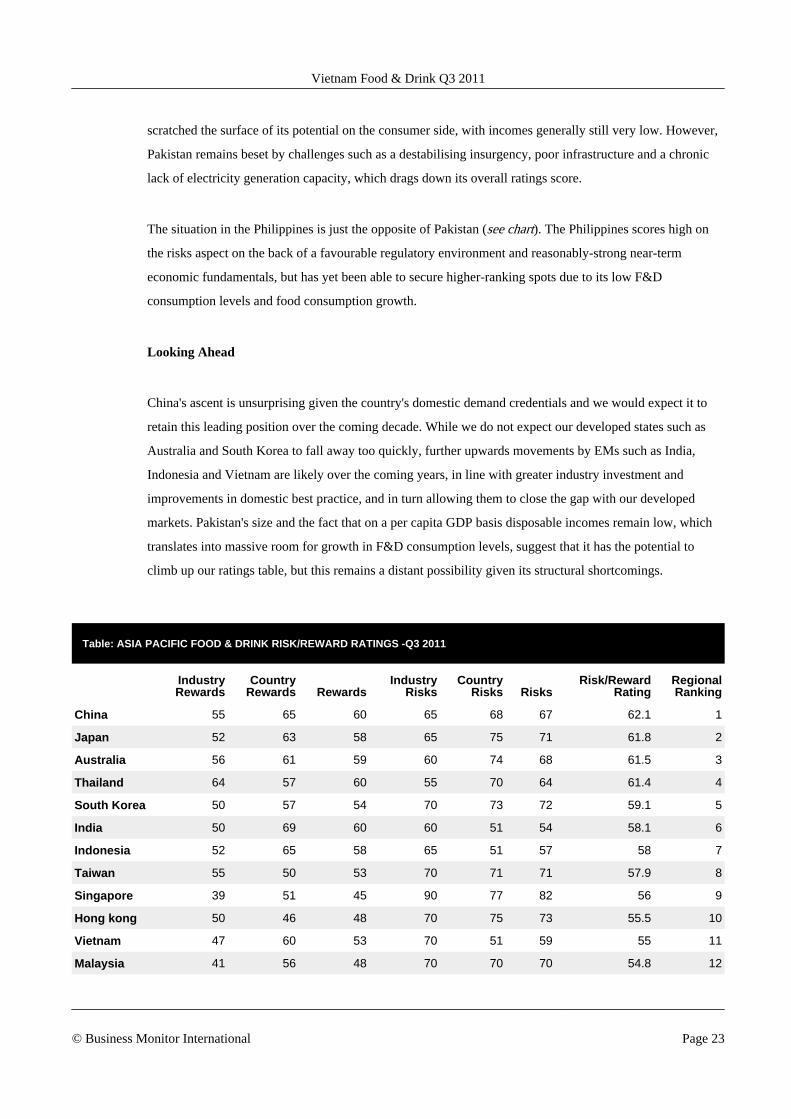

China Tops Our Chart

Asia Pacific Food & Drink Risk/Reward Ratings - Q3 2011 y

Source: BMI. Scores Out Of 100, with 100 highest. For full methodology see Appendix at the back of our Food &Drink Quarterly Reports, or visit our online service

Contrastingly, China continues to represent one of the region's most exciting growth opportunities (see

chart). The positive qualities of dynamic economic growth, favourable demographic profile and strong

forecast growth in F&D consumption levels will continue to count in China's favour from a rewards point of

view. On the risks side, China's relatively well-developed infrastructural systems as compared to its regional

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 20

developing market peers and sturdy near-term economic fundamentals further accentuates the country's

reputation as an enticing foreign direct investment (FDI) destination. This healthy balance of risk to reward

ensures that China remains one of the largest recipients of foreign investment and also explains its top

position in our rankings.

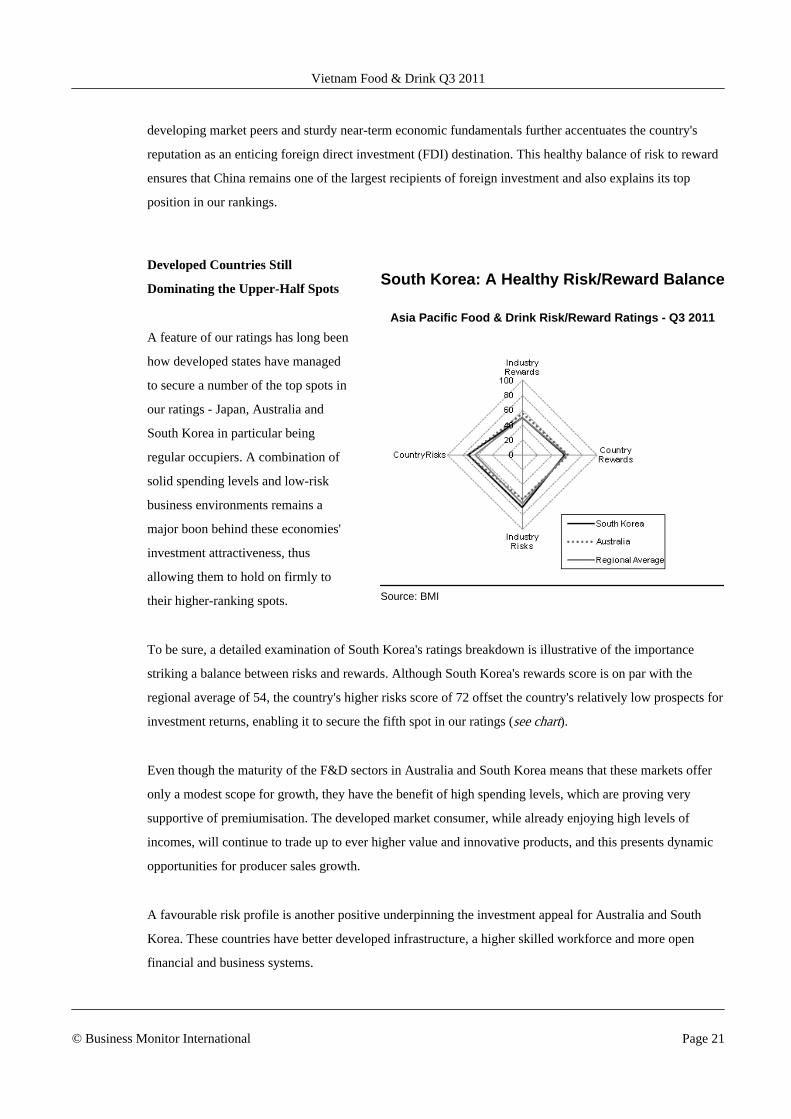

Developed Countries Still

Dominating the Upper-Half Spots

A feature of our ratings has long been

how developed states have managed

to secure a number of the top spots in

our ratings - Japan, Australia and

South Korea in particular being

regular occupiers. A combination of

solid spending levels and low-risk

business environments remains a

major boon behind these economies'

investment attractiveness, thus

allowing them to hold on firmly to

their higher-ranking spots.

To be sure, a detailed examination of South Korea's ratings breakdown is illustrative of the importance

striking a balance between risks and rewards. Although South Korea's rewards score is on par with the

regional average of 54, the country's higher risks score of 72 offset the country's relatively low prospects for

investment returns, enabling it to secure the fifth spot in our ratings (see chart).

Even though the maturity of the F&D sectors in Australia and South Korea means that these markets offer

only a modest scope for growth, they have the benefit of high spending levels, which are proving very

supportive of premiumisation. The developed market consumer, while already enjoying high levels of

incomes, will continue to trade up to ever higher value and innovative products, and this presents dynamic

opportunities for producer sales growth.

A favourable risk profile is another positive underpinning the investment appeal for Australia and South

Korea. These countries have better developed infrastructure, a higher skilled workforce and more open

financial and business systems.

South Korea: A Healthy Risk/Reward Balance

Asia Pacific Food & Drink Risk/Reward Ratings - Q3 2011

Source: BMI

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 21

Fast-Growing EMs Closing The Gap

While the likes of Australia, Japan and South Korea are likely to stay put in their top-ranking positions in

the near-to-medium term, we acknowledge that the Asian Pacific EMs are quickly catching up with their

developed market counterparts.

We like the long-term promise of domestic-demand oriented countries such as India, Indonesia and

Vietnam, which backed by massive consumer bases, provides dynamic long-term growth potential for

consumer-facing players. Although the negative attributes of weak distribution and labour infrastructure,

perceived excessive bureaucracy and corruption will remain key stumbling blocks to attracting foreign

investment in these EMs, which explains their weak risks scores, these markets will continue to climb up

our ratings ladder and potentially take over the leading positions from developed markets over the long

horizon.

Specifically, India and Indonesia have overtaken Taiwan and moved up the rankings by one spot to the sixth

and seventh position respectively in this quarter, underlining the countries' increasingly attractive

investment appeal. At the bottom half of our risk/reward table, Vietnam and Malaysia are also closing the

gap with their developed market peers.

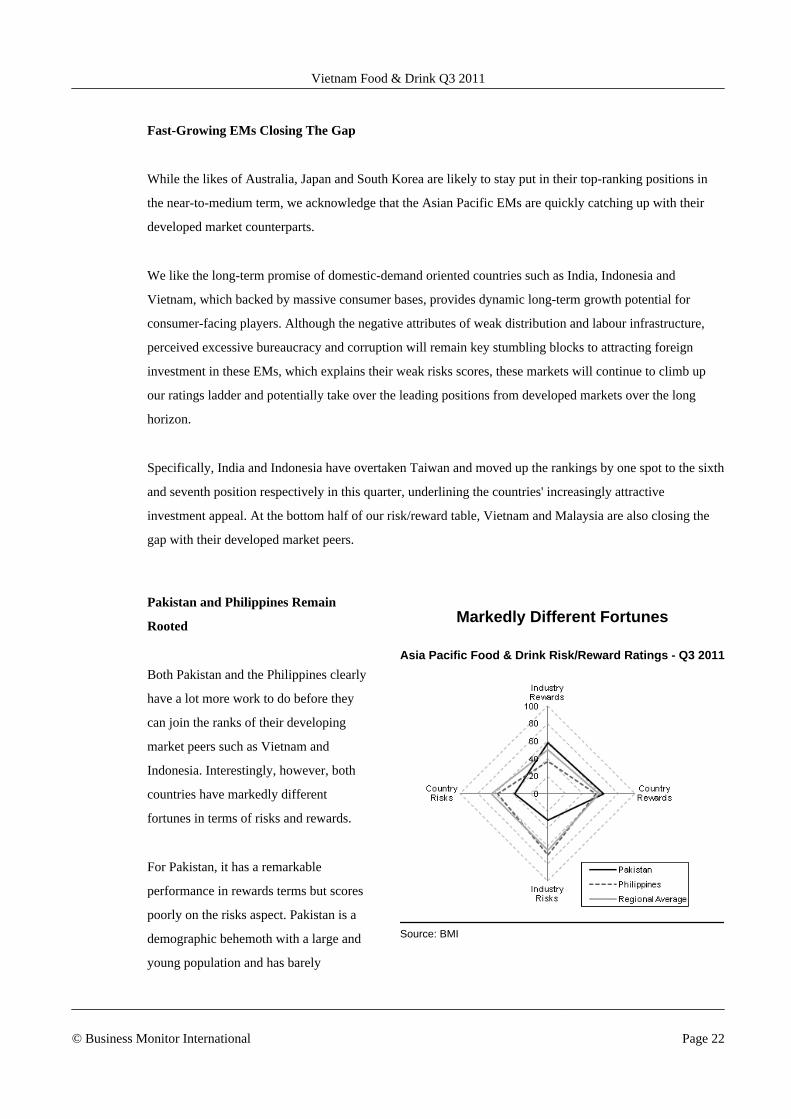

Pakistan and Philippines Remain

Rooted

Both Pakistan and the Philippines clearly

have a lot more work to do before they

can join the ranks of their developing

market peers such as Vietnam and

Indonesia. Interestingly, however, both

countries have markedly different

fortunes in terms of risks and rewards.

For Pakistan, it has a remarkable

performance in rewards terms but scores

poorly on the risks aspect. Pakistan is a

demographic behemoth with a large and

young population and has barely

Markedly Different Fortunes

Asia Pacific Food & Drink Risk/Reward Ratings - Q3 2011

Source: BMI

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 22

scratched the surface of its potential on the consumer side, with incomes generally still very low. However,

Pakistan remains beset by challenges such as a destabilising insurgency, poor infrastructure and a chronic

lack of electricity generation capacity, which drags down its overall ratings score.

The situation in the Philippines is just the opposite of Pakistan (see chart). The Philippines scores high on

the risks aspect on the back of a favourable regulatory environment and reasonably-strong near-term

economic fundamentals, but has yet been able to secure higher-ranking spots due to its low F&D

consumption levels and food consumption growth.

Looking Ahead

China's ascent is unsurprising given the country's domestic demand credentials and we would expect it to

retain this leading position over the coming decade. While we do not expect our developed states such as

Australia and South Korea to fall away too quickly, further upwards movements by EMs such as India,

Indonesia and Vietnam are likely over the coming years, in line with greater industry investment and

improvements in domestic best practice, and in turn allowing them to close the gap with our developed

markets. Pakistan's size and the fact that on a per capita GDP basis disposable incomes remain low, which

translates into massive room for growth in F&D consumption levels, suggest that it has the potential to

climb up our ratings table, but this remains a distant possibility given its structural shortcomings.

Table: ASIA PACIFIC FOOD & DRINK RISK/REWARD RATINGS -Q3 2011

IndustryRewards

CountryRewards Rewards

IndustryRisks

CountryRisks Risks

Risk/RewardRating

RegionalRanking

China 55 65 60 65 68 67 62.1 1

Japan 52 63 58 65 75 71 61.8 2

Australia 56 61 59 60 74 68 61.5 3

Thailand 64 57 60 55 70 64 61.4 4

South Korea 50 57 54 70 73 72 59.1 5

India 50 69 60 60 51 54 58.1 6

Indonesia 52 65 58 65 51 57 58 7

Taiwan 55 50 53 70 71 71 57.9 8

Singapore 39 51 45 90 77 82 56 9

Hong kong 50 46 48 70 75 73 55.5 10

Vietnam 47 60 53 70 51 59 55 11

Malaysia 41 56 48 70 70 70 54.8 12

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 23

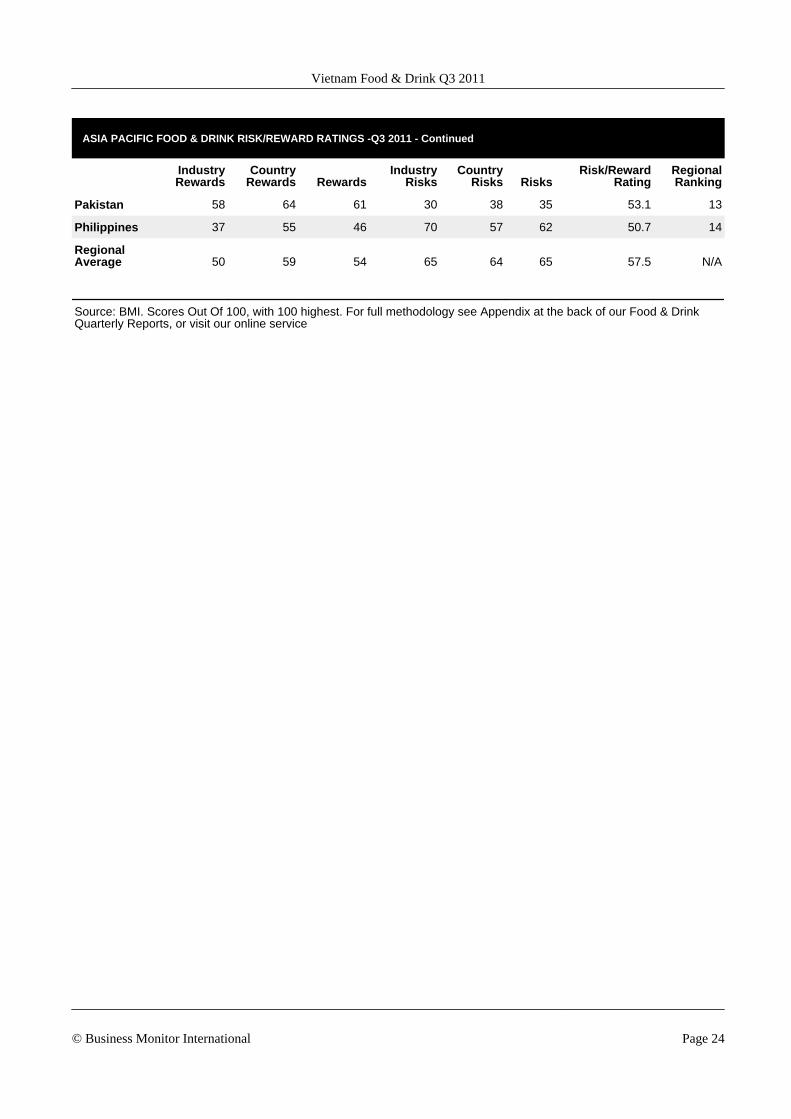

ASIA PACIFIC FOOD & DRINK RISK/REWARD RATINGS -Q3 2011 - Continued

IndustryRewards

CountryRewards Rewards

IndustryRisks

CountryRisks Risks

Risk/RewardRating

RegionalRanking

Pakistan 58 64 61 30 38 35 53.1 13

Philippines 37 55 46 70 57 62 50.7 14

RegionalAverage 50 59 54 65 64 65 57.5 N/A

Source: BMI. Scores Out Of 100, with 100 highest. For full methodology see Appendix at the back of our Food & DrinkQuarterly Reports, or visit our online service

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 24

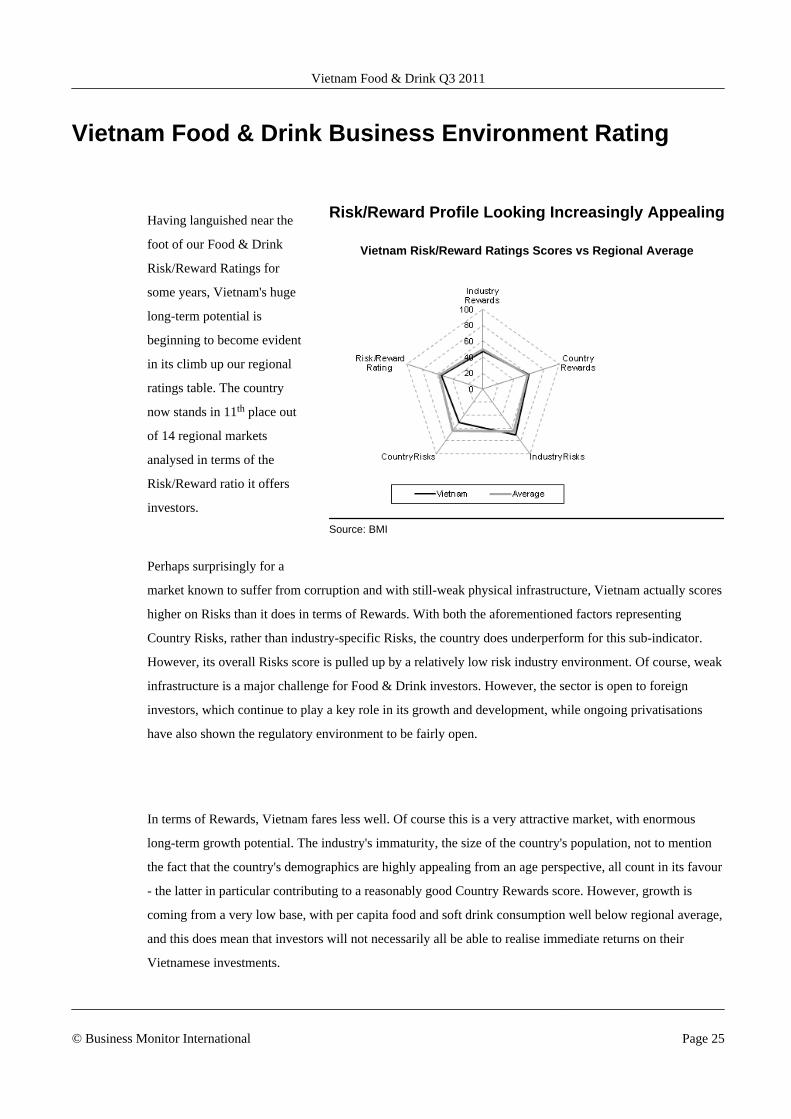

Vietnam Food & Drink Business Environment Rating

Having languished near the

foot of our Food & Drink

Risk/Reward Ratings for

some years, Vietnam's huge

long-term potential is

beginning to become evident

in its climb up our regional

ratings table. The country

now stands in 11th place out

of 14 regional markets

analysed in terms of the

Risk/Reward ratio it offers

investors.

Perhaps surprisingly for a

market known to suffer from corruption and with still-weak physical infrastructure, Vietnam actually scores

higher on Risks than it does in terms of Rewards. With both the aforementioned factors representing

Country Risks, rather than industry-specific Risks, the country does underperform for this sub-indicator.

However, its overall Risks score is pulled up by a relatively low risk industry environment. Of course, weak

infrastructure is a major challenge for Food & Drink investors. However, the sector is open to foreign

investors, which continue to play a key role in its growth and development, while ongoing privatisations

have also shown the regulatory environment to be fairly open.

In terms of Rewards, Vietnam fares less well. Of course this is a very attractive market, with enormous

long-term growth potential. The industry's immaturity, the size of the country's population, not to mention

the fact that the country's demographics are highly appealing from an age perspective, all count in its favour

- the latter in particular contributing to a reasonably good Country Rewards score. However, growth is

coming from a very low base, with per capita food and soft drink consumption well below regional average,

and this does mean that investors will not necessarily all be able to realise immediate returns on their

Vietnamese investments.

Risk/Reward Profile Looking Increasingly Appealing

Vietnam Risk/Reward Ratings Scores vs Regional Average

Source: BMI

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 25

That said, notwithstanding the low base from which growth is coming, we would expect Vietnam to

continue its climb up the Ratings over the medium-term, as spending picks up and growth remains at hugely

attractive levels.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 26

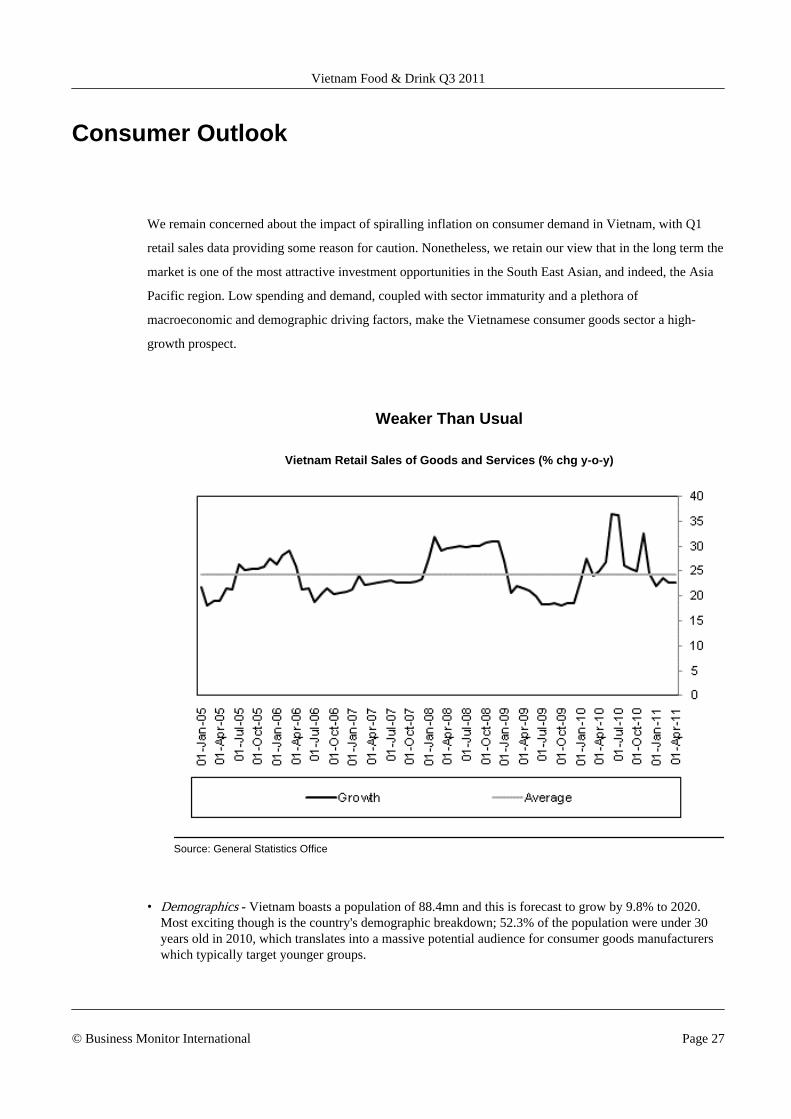

Consumer Outlook

We remain concerned about the impact of spiralling inflation on consumer demand in Vietnam, with Q1

retail sales data providing some reason for caution. Nonetheless, we retain our view that in the long term the

market is one of the most attractive investment opportunities in the South East Asian, and indeed, the Asia

Pacific region. Low spending and demand, coupled with sector immaturity and a plethora of

macroeconomic and demographic driving factors, make the Vietnamese consumer goods sector a high-

growth prospect.

Weaker Than Usual

Vietnam Retail Sales of Goods and Services (% chg y-o-y)

Source: General Statistics Office

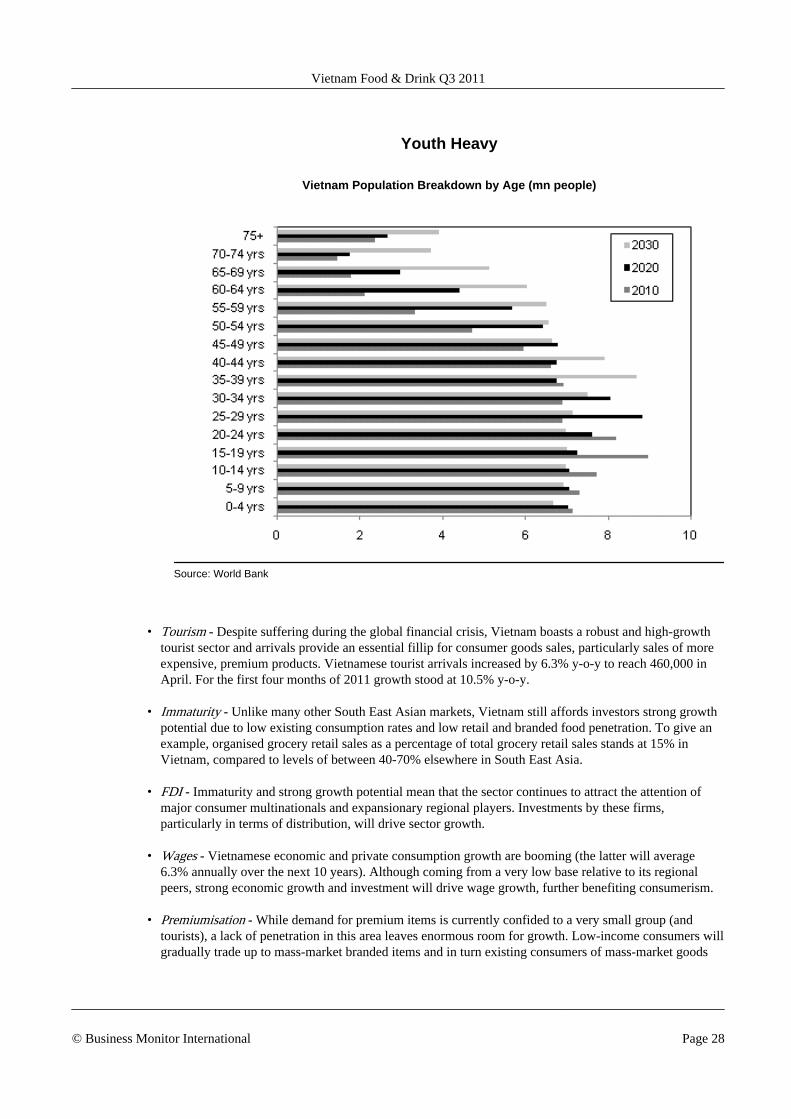

• Demographics - Vietnam boasts a population of 88.4mn and this is forecast to grow by 9.8% to 2020.Most exciting though is the country's demographic breakdown; 52.3% of the population were under 30years old in 2010, which translates into a massive potential audience for consumer goods manufacturerswhich typically target younger groups.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 27

Youth Heavy

Vietnam Population Breakdown by Age (mn people)

Source: World Bank

• Tourism - Despite suffering during the global financial crisis, Vietnam boasts a robust and high-growthtourist sector and arrivals provide an essential fillip for consumer goods sales, particularly sales of moreexpensive, premium products. Vietnamese tourist arrivals increased by 6.3% y-o-y to reach 460,000 inApril. For the first four months of 2011 growth stood at 10.5% y-o-y.

• Immaturity - Unlike many other South East Asian markets, Vietnam still affords investors strong growthpotential due to low existing consumption rates and low retail and branded food penetration. To give anexample, organised grocery retail sales as a percentage of total grocery retail sales stands at 15% inVietnam, compared to levels of between 40-70% elsewhere in South East Asia.

• FDI - Immaturity and strong growth potential mean that the sector continues to attract the attention ofmajor consumer multinationals and expansionary regional players. Investments by these firms,particularly in terms of distribution, will drive sector growth.

• Wages - Vietnamese economic and private consumption growth are booming (the latter will average6.3% annually over the next 10 years). Although coming from a very low base relative to its regionalpeers, strong economic growth and investment will drive wage growth, further benefiting consumerism.

• Premiumisation - While demand for premium items is currently confided to a very small group (andtourists), a lack of penetration in this area leaves enormous room for growth. Low-income consumers willgradually trade up to mass-market branded items and in turn existing consumers of mass-market goods

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 28

will gradually increase their discretionary spending on these products, creating opportunities for premiumproduct sales.

The aforementioned factors and a relatively relaxed regulatory environment will stand Vietnam in good

stead to attract investments from the world's major F&D players, which could further stimulate consumer

interest in modern retailing methods and higher-value F&D products.

Singapore MGR operator NTUC Fairprice is the latest company to jump aboard the inbound investment

bandwagon in Vietnam, joining the likes of South Korean retailer Lotte, Japan's FamilyMart and German

retailer Metro as it looks to capitalise on the country's emerging market potential. While UK retailer Tesco

has stayed silent on speculation that it is weighing up an entry into the Vietnamese market, we would not be

surprised if Vietnam were to pop up on the retailer's long-term radar, given the country's high-growth retail

prospects. Clearly, investments in the retail sector will only intensify and consumption habits should move

up several notches over the coming years, as the variety of consumer products and demand increase.

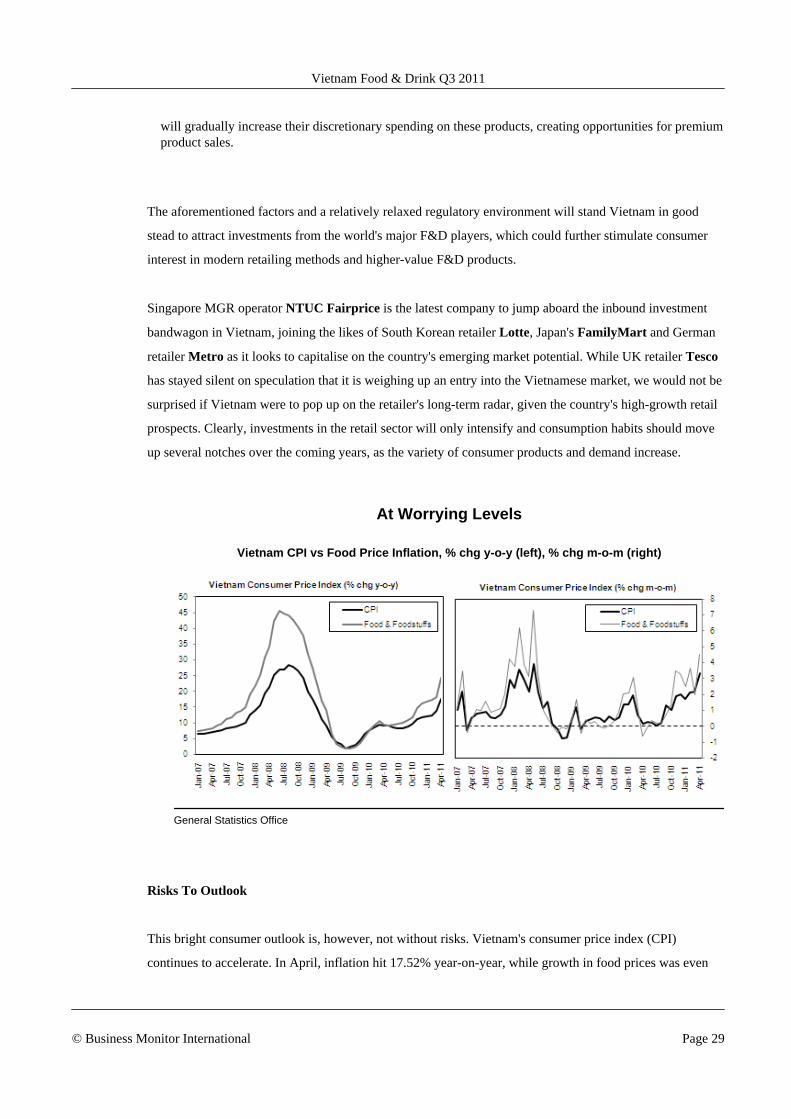

At Worrying Levels

Vietnam CPI vs Food Price Inflation, % chg y-o-y (left), % chg m-o-m (right)

General Statistics Office

Risks To Outlook

This bright consumer outlook is, however, not without risks. Vietnam's consumer price index (CPI)

continues to accelerate. In April, inflation hit 17.52% year-on-year, while growth in food prices was even

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 29

more dramatic at 24.43%. Monthly growth figures underline the severity of this trend. Month-on-month GPI

growth in April stood at 3.32%, a third consecutive monthly gain.

The need to get inflation under control raises the risk of further rate hikes in 2011 (following a 100 basis

point hike in April). Of course the downward pressure that inflation places on demand makes inflation the

greater risk and yet aggressive tightening does increase the risk of a hard landing for the Vietnamese

economy and this would of course also pose a threat to consumer goods players even if it could ultimately

translate into greater long-term economic stability.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 30

Industry Forecast Scenario

Food

Food Consumption

• To 2015, food consumption in Vietnam is forecast to experience strong growth of 72.3%, at which pointconsumption is expected to reach VND496.7trn.

• Per capita food consumption is forecast to grow by 64.0% over the same time period, reaching a fairlymodest VND5.4mn by 2015, reflecting the low starting base.

This impressive level of growth in food consumption could be attributed to two key factors: the rising

affluence among Vietnamese consumers and an ongoing expansion of the country's mass grocery retail

(MGR) industry.

At present, income levels in Vietnam are a long way behind developed economies and consumer purchases

remain largely centred on food staples and daily necessities. However, as incomes start to accelerate off a

low base on the back of sturdy economic growth, consumer tastes and preferences are expected to calibrate

towards the higher-value food and beverage segments, which should guarantee a receptive and growing

audience for branded food and beverage products in the medium term.

The ongoing expansion of the MGR industry will also drive up per capita food consumption levels,

provided goods sold through such outlets remain competitively priced. Ultimately, food consumption

growth will be driven by the government's ability to harness rural spending power and by modern retailers'

ability to find a model that stirs consumer interest, without forgetting that price will remain the major

purchasing determinant.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 31

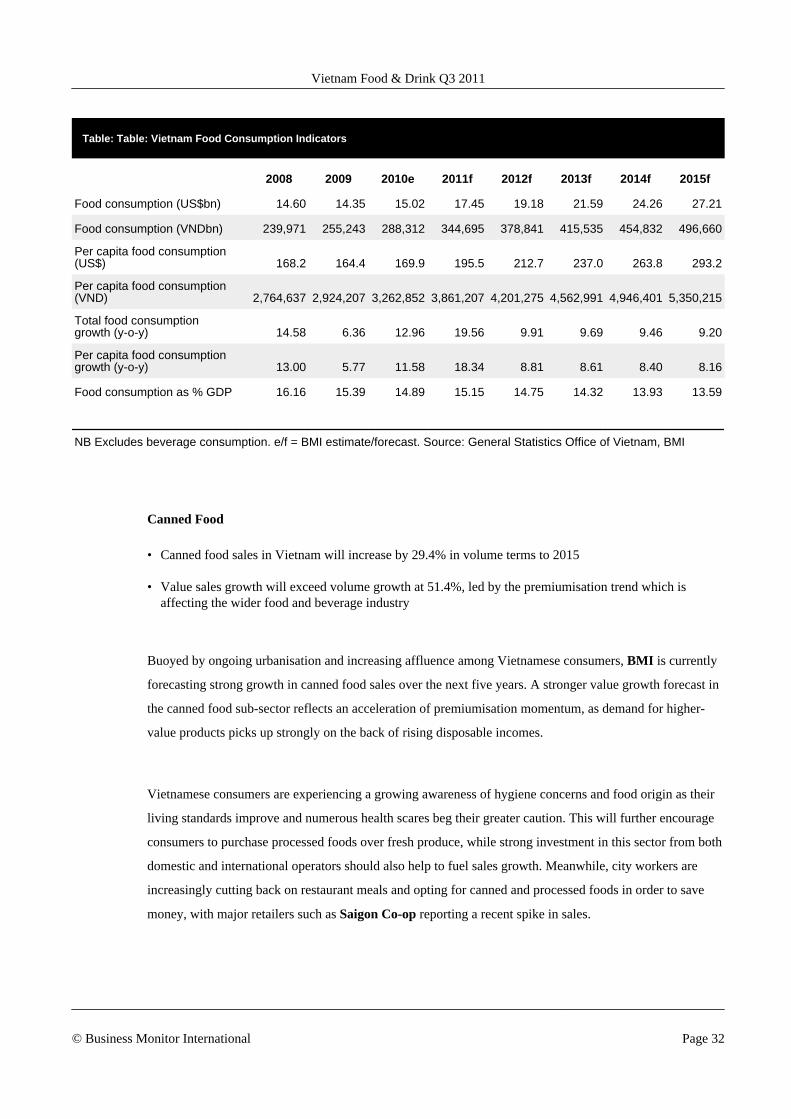

Table: Table: Vietnam Food Consumption Indicators

2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Food consumption (US$bn) 14.60 14.35 15.02 17.45 19.18 21.59 24.26 27.21

Food consumption (VNDbn) 239,971 255,243 288,312 344,695 378,841 415,535 454,832 496,660

Per capita food consumption(US$) 168.2 164.4 169.9 195.5 212.7 237.0 263.8 293.2

Per capita food consumption(VND) 2,764,637 2,924,207 3,262,852 3,861,207 4,201,275 4,562,991 4,946,401 5,350,215

Total food consumptiongrowth (y-o-y) 14.58 6.36 12.96 19.56 9.91 9.69 9.46 9.20

Per capita food consumptiongrowth (y-o-y) 13.00 5.77 11.58 18.34 8.81 8.61 8.40 8.16

Food consumption as % GDP 16.16 15.39 14.89 15.15 14.75 14.32 13.93 13.59

NB Excludes beverage consumption. e/f = BMI estimate/forecast. Source: General Statistics Office of Vietnam, BMI

Canned Food

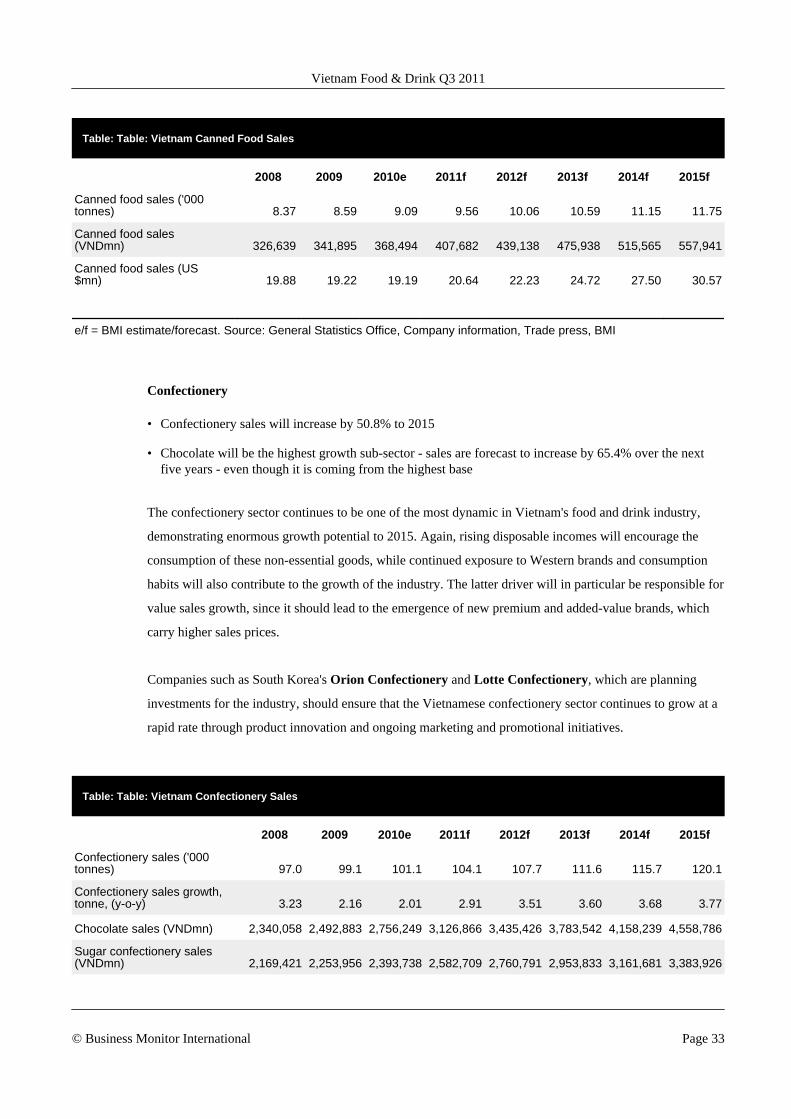

• Canned food sales in Vietnam will increase by 29.4% in volume terms to 2015

• Value sales growth will exceed volume growth at 51.4%, led by the premiumisation trend which isaffecting the wider food and beverage industry

Buoyed by ongoing urbanisation and increasing affluence among Vietnamese consumers, BMI is currently

forecasting strong growth in canned food sales over the next five years. A stronger value growth forecast in

the canned food sub-sector reflects an acceleration of premiumisation momentum, as demand for higher-

value products picks up strongly on the back of rising disposable incomes.

Vietnamese consumers are experiencing a growing awareness of hygiene concerns and food origin as their

living standards improve and numerous health scares beg their greater caution. This will further encourage

consumers to purchase processed foods over fresh produce, while strong investment in this sector from both

domestic and international operators should also help to fuel sales growth. Meanwhile, city workers are

increasingly cutting back on restaurant meals and opting for canned and processed foods in order to save

money, with major retailers such as Saigon Co-op reporting a recent spike in sales.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 32

Table: Table: Vietnam Canned Food Sales

2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Canned food sales ('000tonnes) 8.37 8.59 9.09 9.56 10.06 10.59 11.15 11.75

Canned food sales(VNDmn) 326,639 341,895 368,494 407,682 439,138 475,938 515,565 557,941

Canned food sales (US$mn) 19.88 19.22 19.19 20.64 22.23 24.72 27.50 30.57

e/f = BMI estimate/forecast. Source: General Statistics Office, Company information, Trade press, BMI

Confectionery

• Confectionery sales will increase by 50.8% to 2015

• Chocolate will be the highest growth sub-sector - sales are forecast to increase by 65.4% over the nextfive years - even though it is coming from the highest base

The confectionery sector continues to be one of the most dynamic in Vietnam's food and drink industry,

demonstrating enormous growth potential to 2015. Again, rising disposable incomes will encourage the

consumption of these non-essential goods, while continued exposure to Western brands and consumption

habits will also contribute to the growth of the industry. The latter driver will in particular be responsible for

value sales growth, since it should lead to the emergence of new premium and added-value brands, which

carry higher sales prices.

Companies such as South Korea's Orion Confectionery and Lotte Confectionery, which are planning

investments for the industry, should ensure that the Vietnamese confectionery sector continues to grow at a

rapid rate through product innovation and ongoing marketing and promotional initiatives.

Table: Table: Vietnam Confectionery Sales

2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Confectionery sales ('000tonnes) 97.0 99.1 101.1 104.1 107.7 111.6 115.7 120.1

Confectionery sales growth,tonne, (y-o-y) 3.23 2.16 2.01 2.91 3.51 3.60 3.68 3.77

Chocolate sales (VNDmn) 2,340,058 2,492,883 2,756,249 3,126,866 3,435,426 3,783,542 4,158,239 4,558,786

Sugar confectionery sales(VNDmn) 2,169,421 2,253,956 2,393,738 2,582,709 2,760,791 2,953,833 3,161,681 3,383,926

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 33

Table: Vietnam Confectionery Sales - Continued

2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

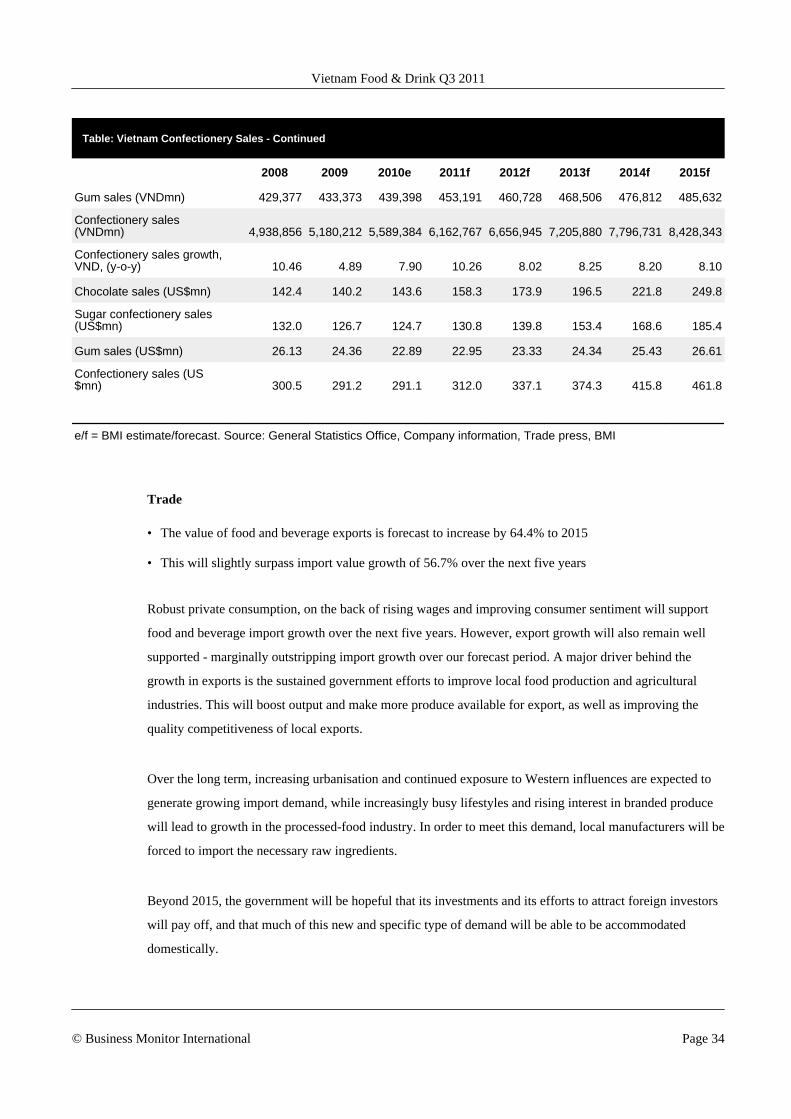

Gum sales (VNDmn) 429,377 433,373 439,398 453,191 460,728 468,506 476,812 485,632

Confectionery sales(VNDmn) 4,938,856 5,180,212 5,589,384 6,162,767 6,656,945 7,205,880 7,796,731 8,428,343

Confectionery sales growth,VND, (y-o-y) 10.46 4.89 7.90 10.26 8.02 8.25 8.20 8.10

Chocolate sales (US$mn) 142.4 140.2 143.6 158.3 173.9 196.5 221.8 249.8

Sugar confectionery sales(US$mn) 132.0 126.7 124.7 130.8 139.8 153.4 168.6 185.4

Gum sales (US$mn) 26.13 24.36 22.89 22.95 23.33 24.34 25.43 26.61

Confectionery sales (US$mn) 300.5 291.2 291.1 312.0 337.1 374.3 415.8 461.8

e/f = BMI estimate/forecast. Source: General Statistics Office, Company information, Trade press, BMI

Trade

• The value of food and beverage exports is forecast to increase by 64.4% to 2015

• This will slightly surpass import value growth of 56.7% over the next five years

Robust private consumption, on the back of rising wages and improving consumer sentiment will support

food and beverage import growth over the next five years. However, export growth will also remain well

supported - marginally outstripping import growth over our forecast period. A major driver behind the

growth in exports is the sustained government efforts to improve local food production and agricultural

industries. This will boost output and make more produce available for export, as well as improving the

quality competitiveness of local exports.

Over the long term, increasing urbanisation and continued exposure to Western influences are expected to

generate growing import demand, while increasingly busy lifestyles and rising interest in branded produce

will lead to growth in the processed-food industry. In order to meet this demand, local manufacturers will be

forced to import the necessary raw ingredients.

Beyond 2015, the government will be hopeful that its investments and its efforts to attract foreign investors

will pay off, and that much of this new and specific type of demand will be able to be accommodated

domestically.

Vietnam Food & Drink Q3 2011

© Business Monitor International Page 34

Table: Table: Vietnam Food & Drink Trade Indicators

2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Exports (US$mn) 10,585 9,706 10,713 11,517 12,587 13,883 15,335 16,961

Imports (US$mn) 3,479 3,206 3,354 3,638 3,982 4,363 4,786 5,256

Balance (US$mn) 7,106 6,500 7,359 7,879 8,605 9,520 10,549 11,705

e/f = BMI estimate/forecast. Source: UNCTAD, BMI

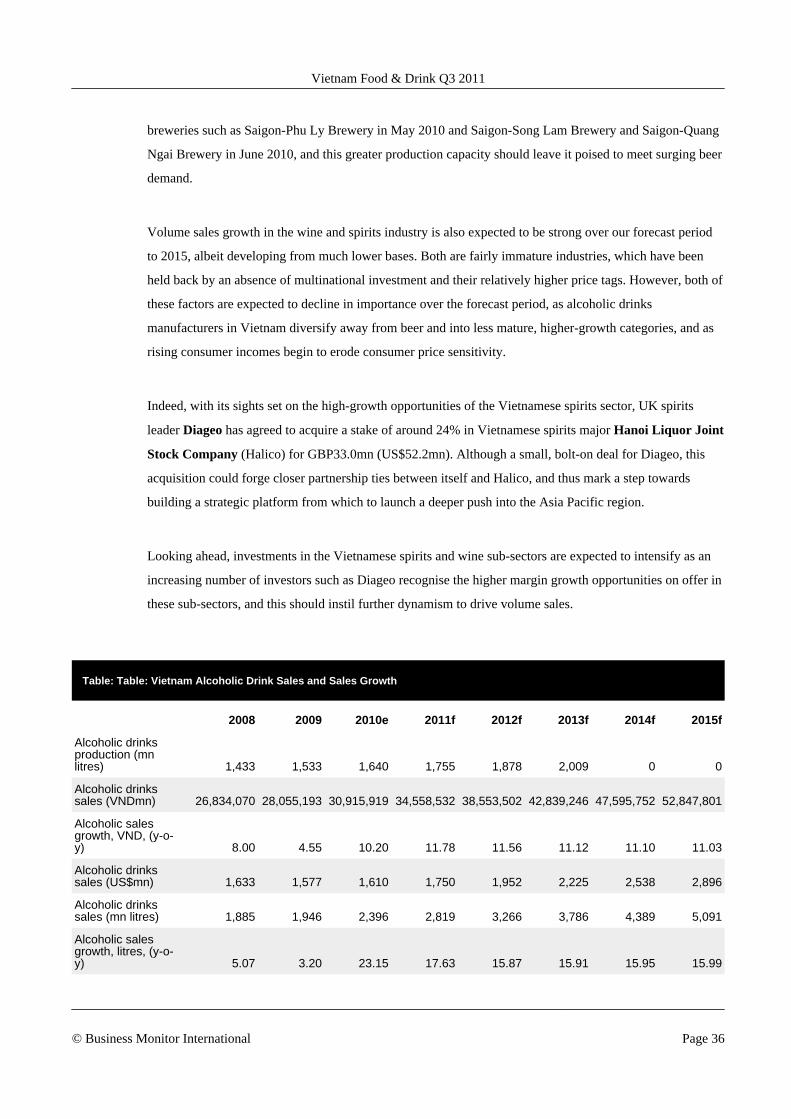

Drink

Alcoholic Drinks

• To 2015, alcoholic drinks sales in value terms are forecast to increase by 70.9%

• Beer will be the main driver of sector growth - in fact we recently revised up our forecast for Vietnamesebeer consumption growth in 2011 from high-single digits to 17.7%

The outlook for Vietnam's alcoholic drinks industry remains very strong, as it continues to attract

considerable interest from foreign investors. A number of industry majors such as Diageo, Asia Pacific

Breweries and Carlsberg have been attracted by the alcoholic drinks sector's bright outlook. Beer will

continue to dominate the alcoholic drinks sector, accounting for the vast majority of volume sales, and will

remain the main contributor to value sales. This is in part due to the strong interest the beer sector has been

attracting from both local and international brewers.

In fact, this level of interest, coupled with impressive sales figures from leading brewers

Habeco and Sabeco have prompted us to revise our 2011 forecast for beer volumes upwards. Over the long

term, beyond the current forecast period, the outlook for the Vietnamese beer sector is very positive as well,

as the brewing industry gradually moves towards premiumisation on the back of rising consumer affluence.

Ongoing strengthening in the Vietnamese tourism sector further spells optimism for higher beer sales over

the coming quarters. Vietnam remains a developing, low-income country and the domestic beer sector is

arguably more reliant on tourist arrivals to drive value sales. Tourists generally have a greater penchant for

higher-value items and have the purchasing power to afford the higher-priced consumer goods.

In light of this outlook market leaders Sabeco and Habeco, which control an estimated 35% and 20% of the

domestic beer market respectively, have continued to ramp up their production capacities and these

expansionary activities should stimulate stronger value sales. Sabeco, for instance, started operating new

Vietnam Food & Drink Q3 2011