Bangkok Commercial Asset Management

25

0 Confidential Year-end 2019 Presentation Bangkok Commercial Asset Management March 2020

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Bangkok Commercial Asset Management

0

Confidential

Year-end 2019 Presentation

Bangkok Commercial Asset Management

March 2020

1

DisclaimerYou must read the f ollowing bef ore continuing. The conf idential inf ormation f ollowing this page, the oral presentation of such inf ormation and other materials distributed at, or in connection with, the presentation (the "Presentation") is

f or inf ormation purposes only , and does not constitute or f orm part of any offer or inv itation to sell or the solicitation of an off er or inv itation to purchase or subscribe f or, or any offer to underwrite or otherwise acquire any securities of

Bangkok Commercial Asset Management Public Company Limited (the “Company”) or any other securities, nor shall any part of the Presentation or the f act of its distribution or communication f orm the basis of, or be relied on in

connection with, any contract, commitment or inv estment decision in relation thereto in Thailand, Singapore, the United States, China, Japan or any other jurisdiction. This Presentation has been prepared solely f or inf ormational use

and made av ailable to y ou on a strictly conf idential basis, and may not be taken away , reproduced, ref erred to publicly or redistributed in whole or in part to any other person. By attending this presentation and/or reading this

Presentation, y ou are agreeing to be bound by the f oregoing and below restrictions . Any f ailure to comply with these restrictions may constitute a v iolation of applicable securities laws . If y ou are not the intended recipient of this

Presentation, please delete and destroy all copies immediately .

This Presentation is conf idential, and all contents of this Presentation are to be kept strictly conf idential. This Presentation is intended only f or the recipients thereof , and may not be copied, reproduced, retransmitted or distributed by a

recipient to any other persons in any manner, or used or relied upon by any party f or any other purpose.

Neither this Presentation nor any of its contents may be disclosed, distributed or used f or any other purpose without the prior written consent of the Company . By accepting deliv ery of this Presentation, y ou agree that y ou will promptly

return, delete or destroy this Presentation to the Company upon the Company ’s request .

This Presentation may contain f orward-looking statements that may be identif ied by their use of words like “plans,” “expects,” “will,” “anticipates,” “believ es,” “intends,” “depends, ” “projects,” “estimates” or other words of similar meaningand

that inv olv e risks and uncertainties. All statements that address expectations or projections about the f uture, including, but not limited to, statements about the strategy f or growth, product dev elopment, market position, expenditures,

and f inancial results, are f orward -looking statements. Forward -looking statements are based on certain assumptions and expectations of f uture ev ents. The Company does not guarantee that these assumptions and expectations are

accurate or will be realized . Actual f uture perf ormance, outcomes and results may diff er materially f rom those expressed in forward -looking statements as a result of a number of risks, uncertainties and assumptions. Although the

Company believ es that such f orward-looking statements are based on reasonable assumptions, it can giv e no assurance that such expectations will be met . Past perf ormance does not guarantee or predict f uture perf ormance.

A number o f i mportant factors could cause actual results or outcomes to differ materially fro m those expressed in any forward -looking statement . Representative examples of these factors include (without limitation) general industry and economic

conditions, interest rate trends, cost ofcapital and capital availability, currency exchange rates, co mpetition fro mother co mpanies, shifts in customer demands, customers and partners, changes in operating expenses including employee wages, benefits and

training, governmental and public policy changes and the continued availability of financing in the amounts and the terms necessary to support future business. You are cautioned not to place undue reliance on these forward -looking statements, which are

based on the current view of the Company's management on future events . The Co mpany does not assume any responsibility to amend, modi fy or revise any forwardlooking statements, on the basis ofany subsequent developments, information or events, or

otherwise.

The information in this Presentation has been prepared by the Company and has not been independently verified, approved or endorsed by any advisor retained by the Company . No representation or warranty, express or implied, is made as to, and no

reliance, in whole or in part, should be placed on, the fairness, accuracy, co mpleteness or correctness of the information and opinions in this Presentation. It is not intended that these materials provide, and you may not rely on these materials as providing, a

complete or co mprehensive analysis of the Company . The information and opinions in these materials are provided as at the date of this Presentation, and are subject to change without notice. None of the Company or any of their respective affiliates,

directors, officers, employees, agents, advisers or representatives, makes any representation as to, or assumes any responsibility or liability with regard to, the accuracy or co mpleteness of any information contained here (whether prepared by it or by any

other person) or undertakes any responsibility or liability for any reliance which is placed by any person on any statements or opinions appearing herein or which are made by the Co mpany or any third party, or undertakes to update or revise any information

subsequent to the date hereof, whether as a result ofnew information, future events or otherwise and none of them shall have any liability (in negligence or otherwise) for nor shall they accept responsibility for any loss or damage howsoever arising fro many

information or opinions presented in these materials or use of this Presentation or its contents or otherwise arising in connection with this Presentation .

This Presentation also contains certain statistical data and analyses (the “Statistical Information”) which have been prepared in reliance upon information furnished by the Company and /or third party sources for which the Company has either obtained or is in

the process of obtaining the necessary consents for use. Numerous assumptions were used in preparing the Statistical Information, which assumptions may or may not appear herein . As such, no assurance can be given as to the Statistical Information ’s

accuracy, appropriateness or completeness in any particular context, nor as to whether the Statistical Information and /or the assumptions upon which they are based reflect present market conditions or future market performance. Moreover, any information

from third party sources contained in this Presentation may not be used or relied upon by any other party, or for any other p urpose, and may not, directly or indirectly, be reproduced, disseminated or quoted without the prior written consent of such third

party. This Presentation does not purport to be complete description of the terms of or the inherent risks in any actual or p roposed transaction described herein.

This Presentation may not be taken or transmitted into the United States, Canada or Japan or distributed directly or indirect ly, in the United States, Canada or Japan or any other jurisdiction where it is unlawful to do so. No portion of these materials is an

offer of securities for sale in the United States, Canada or Japan, or any other jurisdiction. This presentation is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country

or other jurisdiction where such distribution, transmission, publication, availability, or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction. Under the terms of any proposed offering , no

securities will be offered or sold in the United States absent registration or an exemption from registration. No public offe ring of securities will be made in the United States, and the Company does not intend to register any part of a proposed offerin g in the

United States.

2

Contents

Section 2 : Industry Overview and Outlook

Appendix A : NPLs and NPAs Management

Section 1 : Business and Financial Performance

Business and

Financial Performance

Section 1

4

• NPAs management method: straight sale of assets or asset

enhancement, taking into account the expected return and cost of renovation

• Source of NPAs: conversion from NPLs or direct purchase of NPAs

• NPAs primarily consists of real estate assets such as commercial and residential properties, vacant land, and hotels

• NPAs value as of 2019:

(Unit: THB mn)

32,5881

54,4671

Gross NPAs(record at cost)

Appraisal valueof NPAs

40.8% discount to

the appraised value

NPLs and NPAs management are the columns of BAM's business

• NPLs management method: debt restructuring or court process

• Source of NPLs: purchased from financial institutions in Thailand through bilateral negotiations or a bidding process

• NPLs are mostly collateralized by real estate-related assets

which are secured by a first priority mortgage• NPLs value as of 2019:

Distressed debt assets (NPLs) management Properties foreclosed (NPAs) management

(Unit: THB mn)

83,621

192,189

Gross NPLs(record at cost)

Appraisal valueof NPLs collateral

56.5% discount

to the appraised value

NPAs outstanding (gross) by asset type

26.4%

1.6%

24.9%

46.1%

1.1%

Vacant land Hotels Commercial properties

Residential properties Movable assets

(As of Y2019)

Note:

1 Excludes instalment sales

2 Unsecured NPLs are mainly NPLs that debtor has transferred all underlying collateral to repay the debt or w e purchased it at a public auction at a price below the balance of the NPLs.

(As of Y2019)

Real estate Real estate & other security/collateral

Other security/collateral Unsecured 2

80.0%

14.3%

0.6% 5.0%

NPLs (gross) by collateral type

5

Distressed asset management—flow chart summaryBAM's principal business is to acquire and manage NPLs and NPAs

Purchase of NPLs

and NPAs

NPLs

NPAs (including

investment in

securities)

NPAs management NPAs disposal Cash

Court enforcement

process

Enforcement of

collateral via public

auction

NPAs

Cash

Pay by cash

Pay by debt to

equity conversion

Debt restructuring

Settlement

reached

Settlement

not reached

Dispute

settled

Dispute not

settled

BAM successfully

purchases

3rd party purchases

Sourcing1

73.3% of total income in 2019

26.5% of total income in 2019

Pay by collateral

transfer (NPAs and

investment in securities)

NPLs management2

NPAs management3

Note

1. Income from NPLs management constituted a larger portion of total income in Q1.2019, primarily due to cash payments

received from a significant debtor in the amount exceeding our cost of credit for purchase of receivables

65.2%

34.4%

0.4%

NPL management NPA management Other

(FY2019)

73.3%1

26.5%

0.2%

BAM total income

70.8%

28.6%

0.6%

(FY2017) (FY2018)

6

2019 Performance and 2020 Target

Growth (YoY)

+19.10%+ 3,164 MB

Growth (YoY)

+26.56%+ 2,117 MB

Growth (YoY)

+25.90%+ 1,347 MB

19,733 MB 10,088 MB

Cash Collection Gross Profit

6,549 MB

Net Profit

2020 Target

• Grow asset base by purchasing NPLs and NPAs from financial institutions 10,000 – 12,000 MB

• Target Cash collection 15,000 – 17,000 MB

7

Note:

1 Signif icant increase in cash collection for NPL in Y2019 due to the increase of cash collected from the Legal Execution Department, w hich was

attributable to (i) our policy to proactively continue to collect cash from auction sales from the Legal Execution Department; and (ii) the receipt of the

payment of the auction sale from the Legal Execution Department in respect of the sale of collateral assets of one signif icant debtor during year

ended 31 December 2019

Total cash collected for NPLs Total cash collected for NPAs

0

3,000

6,000

9,000

12,000

15,000

2017 2018 2019

(TH

B m

n)

9,159

10,791

14,0591

0

3,000

6,000

9,000

12,000

15,000

2017 2018 2019

(TH

B m

n)

4,356

5,778 5,674

Source: Company’s MD&A

Cash Collection : Breakdown

8

Financial performance – operating profitabilityProven track record evidenced by solid financial performance

Source: Company’s Financial Statements and MD&A

Notes:

1 Gross profit margin is calculated from the sum of (i) total interest income (excluding interest income on deposits); (ii) gain (loss) on investment in securities – net; (iii) gain on credit for purchase of receivables; (iv) gain on sale of properties foreclosed; (v) gain on installment sales; and (vi) other

operating income less total interest income and further divided by the sum of ( i) – (vi)

2 Net profit margin is calculated from net profit divided by the sum of (i) total interest income; (ii) gain (loss) on investment in securities – net; (iii) gain

on credit for purchase of receivables; (iv) gain on sale of properties foreclosed; (v) gain on installment sales; and (vi) other operating income; 3Q

2018 margin not disclosed

Revenue breakdown Cash collections

Net profit and net profit marginGross profit and gross profit margin

5,401 6,353

8,974

2,181

3,372

3,237

44

26

25

7,626

9,751

12,236

0

2,000

4,000

6,000

8,000

10,000

12,000

2017 2018 2019

(TH

B m

n)

NPL management NPA management Other income

4,5015,202

6,549

59%53% 54%

0%

20%

40%

60%

80%

0

3,000

6,000

9,000

12,000

2017 2018 2019

(TH

B m

n)

Net profit Net profit margin

5,981

7,971

10,088

79%82% 83%

-20%

10%

40%

70%

100%

0

3,000

6,000

9,000

12,000

15,000

2017 2018 2019

(TH

B m

n)

Gross profit Gross profit margin

9,159 10,791

14,059

4,356

5,778

5,674

13,516

16,569

19,733

2017 2018 2019

0

4,000

8,000

12,000

16,000

20,000

(TH

B m

n)

Cash collection from NPL Cash collection from NPA Total cash collection

1 2

9

99.9107.7

115.8

0.0

35.0

70.0

105.0

140.0

2017 2018 2019

(TH

B b

n)

Financial performance – balance sheet

Credit for purchase of receivables (net NPL) Properties foreclosed (net NPA)

Total assets Total shareholder's equity

72.9 75.4 77.4

0.0

25.0

50.0

75.0

100.0

2017 2018 2019

(TH

B b

n)

17.7

20.6

23.9

0.0

6.0

12.0

18.0

24.0

2017 2018 2019

(TH

B b

n)

Source: Company’s Financial Statement and MD&A

.

41.1 41.837.1

0.0

20.0

40.0

60.0

2017 2018 2019

(TH

B b

n)

Growth in asset based and yield played company

10

Financial performance –profitability and leverage

ROAA ROAE

Total liability-to-equity ratio1

Source: Company’s Financial Statement and MD&A

Notes:

1 Total liability divided by shareholders' equity

Interest-bearing debt to equity ratio

56.9 57.775.7

41.1 41.837.1

1.4 1.4

2.0

0.0

0.5

1.0

1.5

2.0

2.5

0.0

50.0

100.0

150.0

200.0

2017 2018 2019

(x)

(TH

B b

n)

IBD Equity IBD to equity

1.41.6

2.1

0.0

0.5

1.0

1.5

2.0

2.5

2017 2018 2019

(x)

4.75.0

5.9

0.0

2.0

4.0

6.0

8.0

2017 2018 2019

(%)

11.012.6

17.7

0.0

5.0

10.0

15.0

20.0

25.0

2017 2018 2019

(%)

11

Financial performance – cash collection and allowances

Cash collection from NPL1 Allowance for NPL2

Cash collection from NPA3 Allowance for NPA4

Source: Company ’s Financial Statement and MD&A

Notes:

1 Cash collection f rom our NPL is calculated f rom the sum of cash collection receiv ed f rom our NPL management business div ided by credit f or purchase of receiv ables –

net (av erage).

2 Allowance f or NPL is calculated f rom allowance f or doubtf ul accounts of credit f or purchase of receiv ables div ided by credit f or purchase of receiv ables (bef ore deducting

allowances)

3 Cash collection f rom NPA is calculated f rom the sum of cash collection receiv ed div ided by the sum of (i) properties f oreclosed – net; (ii) installment sale receiv ables-net

(av erage)

4 Allowance f or impairment of NPAs to NPAs is calculated f rom allowance f or impairment of NPAs div ided by properties f oreclosed (af ter rev aluation).

8.70 7.69 7.47

0.0

3.5

7.0

10.5

14.0

2017 2018 2019

(%)

24.88

29.12

24.75

0.0

11.0

22.0

33.0

44.0

2017 2018 2019

(%)

2.97

2.47

2.04

0.0

1.3

2.5

3.8

5.0

2017 2018 2019

(%)

12.83 14.55

18.40

0.0

10.0

20.0

30.0

2017 2018 2019

(%)

3 year average of 15.26%

3 year average of 26.25%

12

54.1% 55.7% 59.3%

45.9% 44.3% 40.7%

2017 2018 2019

Debentures Borrowings and Notes Payable

32%

21%5%

42%

31%

22%5%

42%

Well diversified and sustainable sources of funding to support business expansion

Funding breakdown

Funding strengths and relationships

THB97.9bn THB99.6bn THB112.8bn

2017

Debentures Borrowing Notes payable Equity

2018Total debt: 56.9bn58% of sources

of funding2

Total debt: 57.7bn58% of sources

of funding2

Sources of funding mix

Strong financial position allows us to adopt flexible capital structures and financing strategies

Source: Company filing and Financial Statement

Note:

1 In July 2019, w e issued THB 20,000.0mn of Debentures. These Debentures have a maturity date ranging from January 2021 to July 2034 and bear interest at a rate ranging from 2.3% to 3.9% per annum

Relationships with over 10 financial

institutions allows us to have access to various sources of funding

As of 31Dec. 19

❑ Avg. funding cost of ͂ 3.06%1

❑ Avg. Duration of ͂ 6 Years

40%

25%

2%

33%

2019Total debt: 75.7bn67% of

sources of funding2

13

84 327 46 133 20 0.83,733 4,930

1,3011,469

32,619

789 609 525 87942 0.2 1,831 2,618 868 764

17,317

Less than 1 year 1 to less than 2

years

2 to less than 3

years

3 to less than 4

years

4 to less than 5

years

5 to less than 6

years

6 to less than 7

years

7 to less than 8

years

8 to less than 9

years

9 to less than 10

years

10 years and

above

Cash collection Acquisition cost

Large cash collections have been generated, and BAM possesses considerable outstanding balances for future cash

collection

Distressed debt assets (NPLs) and properties foreclosed from NPLs as of December 31, 2019 (in THB million unless specified)

Note:

1 Outstanding balance for converted properties excluding revaluation of properties foreclosed and allow ance, to reflect the actual cost of

acquiring the assets

Cash collection equals c.129.61% of the

acquisition cost for NPL portfolios acquired >10

years ago

Cash collection equals c.188.37% of the

acquisition cost for NPAs directly acquired >10

years ago

375 842 1,920 3,070 5,226 4,943 5,61426,281

5,7897,523

141,240

12,819 10,97810,678 12,635 15,191 13,852 8,333

18,0465,789

6,049

108,970

Less than 1 year 1 to less than 2

years

2 to less than 3

years

3 to less than 4

years

4 to less than 5

years

5 to less than 6

years

6 to less than 7

years

7 to less than 8

years

8 to less than 9

years

9 to less than 10

years

10 years and

above

Credit for purchase of receivables and converted properties foreclosed:

Cash collection/ acquisition cost (%)

2.95 7.67 35.68 100.00 124.36

Outstanding balance1

12,517 10,393 10,836 6,225 2,689

Properties foreclosed (directly purchased):

Break even

Recovery periodPreparation, negotiation and restructuring period

24.30 34.4017.98 67.36 145.64129.61

9,341 10,648 12,551 5,495 2,854 20,005

Cash collection/ acquisition cost (%)

10.71 53.70 451.24 149.92 192.21

Outstanding balance1

663 349 0.2 890 50

15.09 47.688.68 203.88 188.34 188.37

437 739 32 390 194 2,261

14

12.4 9.9 8.2 9.1 9.8 8.3 3.5 4.5 1.9 1.4 14.6

83.6

26.0 19.5 18.8 17.5 21.7 16.3 8.1 21.2 5.6 4.333.1

192.2

<1 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 >10 Total

High appraisal value relative to book value

NPLs and NPAs portfolio – outstanding balance / appraisal value split by year, as of December 31, 2019

Distressed debt assets

Properties foreclosed (converted from distressed debt assets)

(THB bn)

Appraisal / outstanding balance coverage

% of Outstanding balance of the portfolio

2.3x

100%

2.3x

17%

3.0x

2%

3.0x

2%

4.7x

5%

2.0x

10%

2.2x

12%

1.9x

11%

2.3x

4%

2.3x

10%

2.0x

12%

2.1x

15%

0.1 0.9 0.9 1.6 2.7 1.7 2.3 1.3 1.0 1.0 5.5

19.0

0.3 1.7 1.6 2.9 4.9 3.2 4.8 3.8 2.0 2.512.0

39.7

<1 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 >10 Total

(THB bn)

2.1x

100%

2.2x

27%

2.4x

6%

2.2x

5%

3.0x

9%

1.8x

13%

1.9x

14%

1.7x

8%

2.0x

10%

2.0x

5%

1.8x

3%

2.0x

1%

Properties foreclosed (direct purchased)

0.7 0.3 0.4 0.7 0.03 0.0 0.4 0.9 0.2 0.0 2.36.0

1.3 0.7 0.9 1.3 0.05 0.0 1.0 3.00.5 0.2

7.3

16.2

<1 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 >10 Total

Outstanding Balance Appraisal value

(THB bn)

Appraisal / outstanding balance coverage

% of Outstanding balance of the portfolio

100%38%1%3%15%0%0.5%12% 6%7%6%11%

Appraisal / outstanding balance coverage

% of Outstanding balance of the portfolio

2.7x3.2x3.8x2.4x3.4x1.4x1.7x1.7x 2.4x2.2x1.9x1.9x

Industry overview and Outlook

Section 2

16

THB107,653mn1.6x D/E ratio

SAM THB43,056mn

-1.2x D/E ratio

(10)

0

10

20

30

(2,000) (1,000) 0 1,000 2,000 3,000 4,000 5,000

Debt-

to-e

quity

ratio

Shareholders’ equity (THB mn)

IAM

THB24,551mn

17.7x D/E ratio

Mahanakorn:

THB9,742mn

3.9x D/E ratio

Sinnsuptaw ee

THB6,649mn

0.9x D/E ratio

LSF

SWP

J AMC

Ayudhya

RCAM

Alpha Capital

NFS

Chayo

Knight Club

Rutchayothin

Phethai

Thanapatr

BAM47.3%

SAM18.9%

IAM10.8%

Mahanakorn4.3%

Sinnsuptawee2.9%

LSF1.9%

SWP1.7%

J AMC1.5%

Others10.7%

Peer Ranking and Financial Figure Highlights of Top Market Players

(as at 31 December 2018) Total assets of AMCs as of 31 Dec 2018

Competition Outlook:

We are the largest AMC company by far to our competitors

2018

AMC industry assets THB227.7bn

50,000

3,000

Illustration on the size of the assets

Source: IPSOS report

(200,000)

BAM is by far largest not only

in terms of asset size but our

shareholder equity based and

ability to leverage in the future

#1

#2

#3

#4

#5

17

• Renovate to create more value to NPAs

• Launch more campaigns to promote sales

• NPAs sale via Online channel

NPAs Management

• Shorten Negotiation Process

• Increase Number of new TDR debtors

• Expedite the receipt of payment from auction

sales from the Legal Execution Department

• Debt Restructuring via Online Channel

NPLs Management

Key strategies to shorten turnaround time

18

NPAs Renovation ------Budget > 600 MB per annum

Before After

19

NPAs Campaign

Condo House & Commercial Land Investment

• คอน โด โดน ใ จสบ ายกระ เ ป๋ า

• คอน โดกล างเ มื อ ง

• บ้ านสบ าย

• บ้ านแ บ รนด์ ดั ง

• บ้ านสวนสุ ข ใ จ

• ท่ี ดิ น เ พื่ อ การอ อม

• ท่ี ดิ น แ ห่ งอ นาคต

• B A M fo r S ME

• I n ves t m en t Proper t y / Fa c t o r y

20

Thank you

NPLs & NPAs Management

Appendix A

22

79.8 81.7 83.6

0.0

20.0

40.0

60.0

80.0

100.0

2017 2018 2019

(TH

B b

n)

NPLs Management

Distressed debt assets (gross NPLs)

Source: Company f iling

Note:

1 Before allow ance for doubtful accounts under BOT guidelines

2 Unsecured NPLs are mainly NPLs that debtor has transferred all underlying collateral to repay the debt or w e purchased it at a public auction at a price below the balance of the NPLs.

Growing assets based Collateral values exceed acquisition cost NPLs backed by majority real estate

collateral

NPLs acquisition amounts

10,252.610,971.3

12,810.4

0

3,000

6,000

9,000

12,000

15,000

2017 2018 2019

(TH

B m

n)

(As of Y2019)

Breakdown of NPL portfolio

4%

13%

6%

14%

8%23%

31%

< THB 1 mn THB 1 - 5 mn THB 5 - 10 mn THB 10 - 50 mn

THB 50 - 100 mn THB 100 - 500 mn > THB 500 mn

(As of Y2019)

Real estate Real estate & other security/collateral

Other security/collateral Unsecured 2

80.0%

14.3%

0.6% 5.0%

NPLs (gross) by collateral type

23

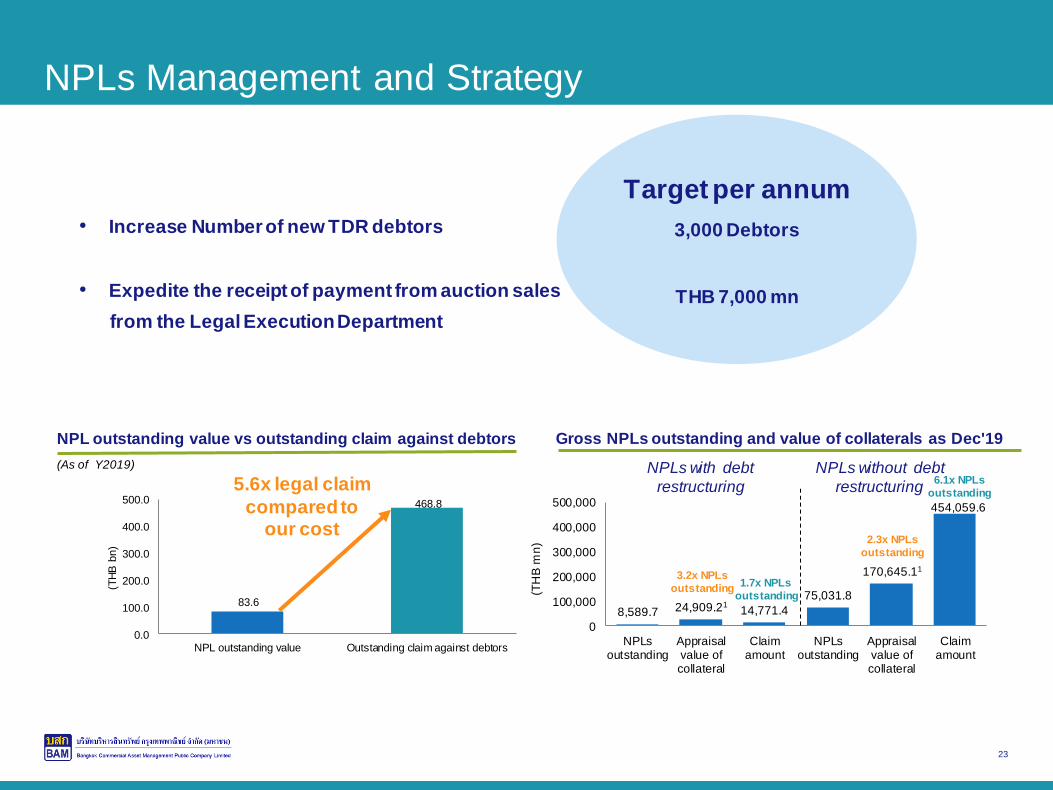

• Increase Number of new TDR debtors

• Expedite the receipt of payment from auction sales

from the Legal Execution Department

NPLs Management and Strategy

8,589.7 24,909.2114,771.4

75,031.8

170,645.11

454,059.6

0

100,000

200,000

300,000

400,000

500,000

NPLsoutstanding

Appraisalvalue ofcollateral

Claimamount

NPLsoutstanding

Appraisalvalue ofcollateral

Claimamount

(TH

B m

n)

Gross NPLs outstanding and value of collaterals as Dec'19

NPLs with debt

restructuring

NPLs without debt

restructuring

3.2x NPLs

outstanding1.7x NPLs

outstanding

2.3x NPLs

outstanding

6.1x NPLs

outstanding

83.6

468.8

0.0

100.0

200.0

300.0

400.0

500.0

NPL outstanding value Outstanding claim against debtors

(TH

B b

n)

NPL outstanding value vs outstanding claim against debtors

(As of Y2019)

5.6x legal claim

compared to our cost

Target per annum

3,000 Debtors

THB 7,000 mn

24

5,258.15,967.20

8,064.80

269.6

1,117.1

544.27

5,527.8

7,109.90

8,609.10

0

2,000

4,000

6,000

8,000

2017 2018 2019

(TH

B m

n)

From NPLs¹ From financial institutions

23.2

23.2

32.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2017 2018 2019

(TH

B b

n)

NPAs breakdown

Source: Company filing

Note:

1 Including assets acquired from bidding of collateral through public auction and transfer of collateral in satisfaction of debt

NPAs acquisition amounts (excluding investment in securities)

NPAs outstanding (net) by region

Properties foreclosed (gross NPAs)

Active NPA managementMajority of assets in Bangkok and

Central and Eastern Thailand Well-diversified type of NPAs

41.8%

25.7%

14.4%

9.0%

8.2% 0.9%

Bangkok and its vicinity Central and Eastern Thailand

Northern Thailand Northeastern Thailand

Southern Thailand Moveable properties

(As of Y2019)

NPAs outstanding (net) by asset type

21.9%

1.9%

27.0%

48.3%

0.9%

Vacant land Hotels Commercial properties

Residential properties Movable assets

(As of Y2019)