Vietnam: Country on the move - VN – INVESTOR

70

Vietnam: Country on the move Primer II April 2007 Deutsche Bank AG/Hong Kong All prices are those current at the end of the previous trading session unless otherwise indicated Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Independent, third-party research (IR) on certain companies covered by DBSI's research is available to customers of DBSI in the United States at no cost. Customers can access this IR at http://gm.db.com, or call 1-877-208-6300 to request that a copy of the IR be sent to them. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Vietnam: Country on the move - VN – INVESTOR

Vietnam: Country on the move

Primer II April 2007

Deutsche Bank AG/Hong Kong All prices are those current at the end of the previous trading session unless otherwise indicated Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Independent, third-party research (IR) on certain companies covered by DBSI's research is available to customers of DBSI in the United States at no cost. Customers can access this IR at http://gm.db.com, or call 1-877-208-6300 to request that a copy of the IR be sent to them. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1

Table of Contents

Economic update.......................................................................................2

Fiscal policy................................................................................................9

Monetary policy.......................................................................................11

SOCB and SOE reform ............................................................................13

Capital market .........................................................................................17

Sectoral analysis......................................................................................21

Market dynamics .....................................................................................32

FPT Corporation (FPT VN, VND460,000)................................................36

Vietnam Dairy (VNM VN, VND175,000).................................................39

Sacom Bank (STB VN, VND 98,000).......................................................42

PV Drilling (PVD VN, VND292,000) ........................................................45

VSH Hydro (VSH VN, VND82,500)..........................................................47

REE Corporation (REE VN, VND215,000) ...............................................49

Kinh Do Corp (KDC VN, VND220,000)....................................................52

Tan Tao Industrial Park (ITA VN, VND140,000).....................................55

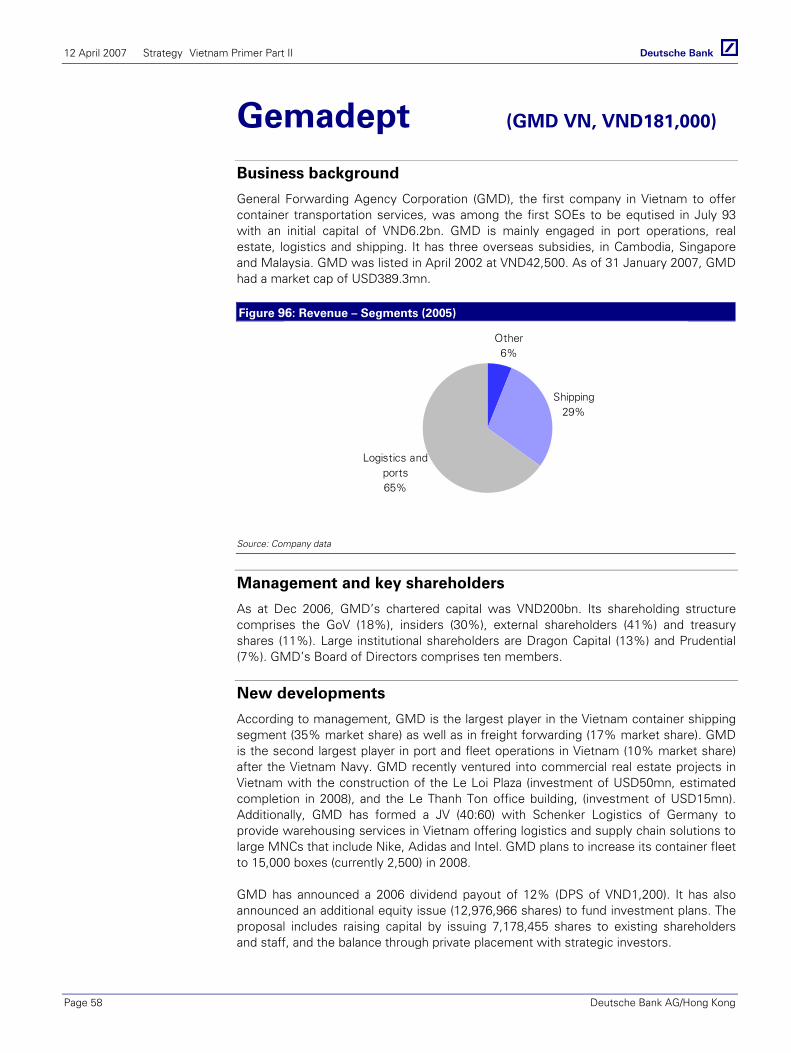

Gemadept (GMD VN, VND181,000) .......................................................58

HCMC Infrastructure (CII VN, VND76,000) ............................................61

Bibliography.............................................................................................64

DB Contact Benjamin Chandler at (852) 2203-6936 or [email protected] (HK) Charles-J Donley at (852) 2203-6918 or [email protected] (HK). Blair Richmond at (212) 250 8802 or [email protected] (NYC) "The author of this report wishes to acknowledge the contribution made by Tariq Aboosally Mohamed, employee of Amba Research Lanka (Private) Ltd a third-party provider to Deutsche Bank of offshore research support services."

GEMS: Asia Vietnam Strategy

12 April 2007

Vietnam Primer Part II Country on the move

Juliana Lee Economist 852 2203 8312 [email protected]

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies.

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their investment decision.

Independent, third-party research (IR) on certain companies covered by DBSI's research is available to customers of DBSI in the United States at no cost. Customers can access this IR at http://gm.db.com, or call 1-877-208-6300 to request that a copy of the IR be sent to them.

DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1

Digest

Sustaining strong growth Both domestic and external demand remained robust in 2006, leading to a GDP growth of 8.2%, well above 7.5% in the period of 2001-2005 and one of the highest GDP growth rates in the world. Highlighting its emergence in the international scene, Vietnam became a formal member of the WTO on 13 January 2007. Meanwhile, the US granted Vietnam a permanent normal trade relations (PNTR) status on 12 December 2006. Vietnam’s WTO membership demonstrates its commitment to market liberalization and globalization.

Reform continues Apart from Agribank, which is scheduled to be equitised in 2008, all state-owned commercial banks are to be privatised in 2007. The state will continue to hold the majority of stake of at least 51% in state run commercial banks while limiting foreign ownership to 30% and individual ownership to 10%. Moreover, PM Decision 112 stipulates that the CAR should be no less than 8% and that the banking standards should be fully consistent with Basel I by 2010. As for state-owned enterprises, 1,500 out of 2,100 are to be equitised over the next five years.

Fast-track market development, presenting risks and opportunities Supported by the GoV, the number of listed companies rose to 196 by the end of 2006, up sharply from 44 in 2005, with the market capitalization rising to USD13.9bn, 25% of Vietnam’s GDP. Meanwhile, the VNINDEX rose sharply to 751.8 by end-2006 from 307.5 at end-2005, trading at 74.9x compared to 15.4x in 2005. This sharp increase prompted regulatory measures to shield the banking system from the possible fall-out of market instability. There are, however, concerns that more restrictive measures may be forthcoming.

GDP growth (2006)8.2%yoy

Population84.4 million 0-14 years: 27%15-64 years: 67%65 over: 9%

GDP per capita (2006)USD725

Top exports

Oil, Textile/garments

Top Imports

Machinery/equip, Petro prod

Main trading partnerUSA, JapanChina/Hong KongTaiwan, Singapore

S&P BB Stable

Market capitalization (2006)HSTC USD9.7bnHaSTC USD7.2bn

Avg daily turnoverUSD5.2mn

Top 5 companies by mkt capFinancing and Promoting TechPha Lai Thermal PowerVietnam Dairy Sacom BankPetrovietnam

Form of governmentSocial Republic

Chief of statePresident Nguyen Minh TRIET

Head of governmentPrime Minister Nguyen Tan DUNG

Community Party of VietnamSecretary General Nong Duc MANH

12 April 2007 Strategy Vietnam Primer Part II

Page 2 Deutsche Bank AG/Hong Kong

Economic update I. Strong growth

Both domestic and external demand remained robust in 2006, leading to a GDP growth of 8.2%, well above the 7.5% growth achieved in the 2001-2005 period – one of the highest GDP growth rates in the world. Vietnam’s GDP per capita stood at USD725 in 2006, up from USD413 in 2001.

Figure 1: Growth comparison (2006)

0

2

4

6

8

10

12C

hina

Indi

a

Vie

tnam

Pak

ista

n

Mal

aysi

a

Indo

nesi

a

Phi

lippi

nes

Thai

land

%

Sources: CEIC, DB Global Markets Research

Highlighting its emergence in the international scene, the General Council of the World Trade Organization (WTO) approved Vietnam’s membership after 11 years of negotiations on 7 November 2006 and, following the approval of the National Assembly, Vietnam became a formal member on 13 January 2007. Meanwhile, the US granted Vietnam a permanent normal trade relations (PNTR) status on 12 December 2006.

Industrialization Vietnam’s economy continued to evolve from an agrarian economy to one driven by industry. Last year, the GDP growth was again led by the industry and construction sectors, which grew 10.4% yoy, while the services and agricultural sectors expanded 8.3% and 3.4%, respectively. The industrial and construction sectors’ share of GDP continued to rise, to 41.5% in 2006 from 25.2% in 1990, while the share of the agricultural sector fell to 20.4% from 31.8%. Meanwhile, the share of the services sector stood relatively stable at 38.1% in 2006, down from 43% in 1990.

On the other hand, the agriculture sector remained the top source of employment, accounting for a 57% share of the total, with about three-quarters of the population residing in rural areas. The country’s workforce is estimated at 42mn and is growing at 3.5-4% on average, well above the population growth rate of 1.4%.

Sustaining strong growth

Growth driven by industry

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 3

Figure 2: GDP and employment share by sector 1995 Figure 3: GDP and employment share by sector 2006

Share of GDP

32%

17%7%

44%

Employment

70%

10%

3%

17%

Agric'e Industry Const'n Services

Employment

56%

14%

5%

25%

Agric'e Industry Const'n Services

Share of GDP

19%

32%

9%

40%

Sources: GSO, CEIC, DB Global Markets Research Sources: GSO, CEIC, DB Global Markets Research

Sustaining high growth The socioeconomic development plan (SEDP) 2006-2010 aims to bring Vietnam out of its “less” developed condition by 2010, raising per capita income to above USD1,000 by 2010, with emphasis on globalisation and industrialisation of the economy. The Government of Vietnam (GoV) aims to raise the industry/construction share of GDP to 43-44% by 2010, up from 41% in 2001-2005.

The GoV’s GDP growth target for the period 2006-2010 stands at 7.5-8.0%, led by export growth of 16%, slightly higher than the 14.7% growth in imports. The GoV expects the investment share of GDP to rise to 40% in 2010 from 37.5% in 2001-2005, which implies 10-11% annual growth, compared to the consumption growth target of 6-7% for the same period.

Figure 4: SEDP 2006-2010, growth by sector Figure 5: SEDP 2006-2010, share of GDP

4.5 5.53.1

13.1

15.9

10

6.27.6 8

-

5

10

15

20

2001-05planned

2001-05 actual

2006-10 planned

Agriculture Industry Services%yoy

20 21

16

38.541 43.541.5

38 40.5

-

10

20

30

40

50

2001-05planned

2001-05 actual

2006-10 planned

Agriculture Industry Services% of GDP

Sources: MPI, DB Global Markets Research Sources: MPI, DB Global Markets Research

II. Diversifying trade

Vietnam’s economic growth in 2006 was underpinned by strong export growth. Exports rose 22.1% yoy in 2006, down slightly from the 24% in 2005. Although rising relatively modestly in 2006, by 12.9% yoy, oil remained Vietnam’s top export item with its share of total exports at 21%. This was followed closely by textile and garments, whose exports rose 19.9% yoy, accounting for 15% of the total exports in 2006. Meanwhile, exports of coffee and rubber (which together make up about 6% of total exports) rose 51.9% yoy and 61.8% yoy, respectively. Growth in computer exports also remained strong, at 22.8% yoy, although down from the 33.9% in 2005, reflecting the global trend. We expect the importance of computer and electrical components to increase

GoV supporting higher

social investment

Strong export growth

12 April 2007 Strategy Vietnam Primer Part II

Page 4 Deutsche Bank AG/Hong Kong

meaningfully, supported by investments from Intel, Microsoft, Samsung and Canon. Meanwhile, import growth accelerated to 20.4%yoy in 2006 from 17% in 2005, led by imports of machinery and spare parts and textile-related products, leaving the trade deficit at USD4.8bn in 2006, compared to a deficit of USD4.5bn in 2005.

Figure 6: Composition of exports by value (2006) Figure 7: Composition of imports by goods (2006)

Agriproducts

12%

Other31%

Aquaproducts

8% Computer&

Electronics4%

Footwear9%

Textile &garments

15%

Crude oil21%

Other45%

Tools &spare parts

15%

Electronics5%

Petroleum13%

Steel7% Leather

4%

Fabrics7%

Plastics4%

Sources: CEIC, DB Global Markets Research Sources: CEIC, DB Global Markets Research

While we expect the WTO membership will further integrate Vietnam into the global economy, we expect only a limited impact on the net trade as Vietnam liberalises and reduces import barriers. On the other hand, we expect a far greater impact on the economy as a whole as the WTO membership keeps Vietnam on the path of liberalisation and reform.

Figure 8: Export by destination Figure 9: Import by destination

0%

20%

40%

60%

80%

100%

2001 2005

Others

U S

Japan

China + HK

Australia

Singapore

Germany

0%

20%

40%

60%

80%

100%

2001 2005

Others

Thailand

Korea

Japan

Taiwan

Singapore

China + HK

Sources: CEIC, DB Global Markets Research Sources: CEIC, DB Global Markets Research

III. Balance of payment

Remittances, an alternative resource for investment In 2005, despite the trade account deficit of USD2.3bn (BoP), Vietnam recorded a current account surplus of USD0.2bn, supported by large remittance inflows. In contrast to the goods, service and income accounts, which continued to record deficits, the transfer account remained strongly positive, helping to limit the current account deficit.

WTO membership reflects

Vietnam’s commitment to

liberalization and reform

Currenct account deficit

limited by large remittance

inflows

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 5

Net transfers stood at USD3.4bn in 2005, up from USD2.5bn in 2004 and higher than the official development assistance (ODA)1 and foreign direct investment combined, which stood at USD2.5bn in 2005. These inflows left the overall balance of payment at USD2.1bn, yielding FX reserves which were higher at USD9.2bn in 2005, up from the USD8.8bn in 2004.

Figure 10: Transfers Figure 11: ODA and FDI

-5-4-3-2-1012345

1995 1997 1999 2001 2003 2005

Trade+Service+Income

Transfers

CA

USD bn

-3

-2

-1

0

1

2

3

4

5

1995 1997 1999 2001 2003 2005

ODA

FDI

CA

USD bn

Sources: CEIC, DB Global Markets Research Sources: CEIC, DB Global Markets Research

Disbursed ODA stood largely unchanged at USD1.4bn in 2005. About 80% of the ODA is collected and allocated by the Development Assistance Fund (DAF), which was restructured in July 2006 as Vietnam Development Bank (VDB), with the rest channeled through state-owned commercial banks. Japan remains the top source of ODA for Vietnam, followed by the World Bank and the Asian Development Bank. ODA remains a significant funding source for infrastructure investment, for transport projects in particular.

Figure 12: ODA by sector (2006) Figure 13: FDI (newly licensed) by sector (2005)

Transport,20.9%

Other,31.0%Water

supply &sanitation,

5.0%

Education,5.7%

Commodity& general

assistance,6.3%

Banking &financial,

6.3%

Agriculture,7.5%

Health,7.1%

Energy,10.2%

Manufactg,64.3%

Other, 8.4%Const, 3.4%

Realestate/rentg& businessactivities ,

8.5%

Health &social work,

4.3%

Transport,storage &communi,

14.5%

Sources: UNDP DAD Vietnam, DB Global Markets Research Sources: UNDP DAD Vietnam, DB Global Markets Research

Vietnam is likely to lose access to the cheapest donor funds by 2010, as it crosses the threshold GNI per capita of USD898 to be eligible for International Development Association (IDA) loans. Vietnam would then have to borrow from Bank for Reconstruction and Development (IBRD), which could raise borrowing costs more than

1 ODA comprises all grants and loans to developing countries, which are undertaken by the official sector and given at concessional financial terms (if loans, have a grant element of at least 25%)

ODA remains a significant

funding source for

infrastructure investment

12 April 2007 Strategy Vietnam Primer Part II

Page 6 Deutsche Bank AG/Hong Kong

twofold.2 Hence, it is vital that Vietnam not only take full advantage while concessional finance is available but also use the opportunity to find and secure alternative financing sources.

The Ministry of Planning and Investment (MPI) is targeting an ODA commitment of USD20-24bn in 2006-2010, USD11-12bn of which is likely to be disbursed. In 2001-2005, the donors pledged USD14.9bn but disbursed less than 50%. According to the MPI estimate, ODA disbursed in 2006 stood at USD1.7bn.

Meanwhile, MPI expects FDI of USD23-25bn in 2006-2010. FDI stood at USD2.0bn in 2005 and MPI estimates it to be USD3.1bn in 2006. South Korea, Singapore, Taiwan Japan and Hong Kong remain Vietnam’s five top investors which account for about 61% of registered capital.

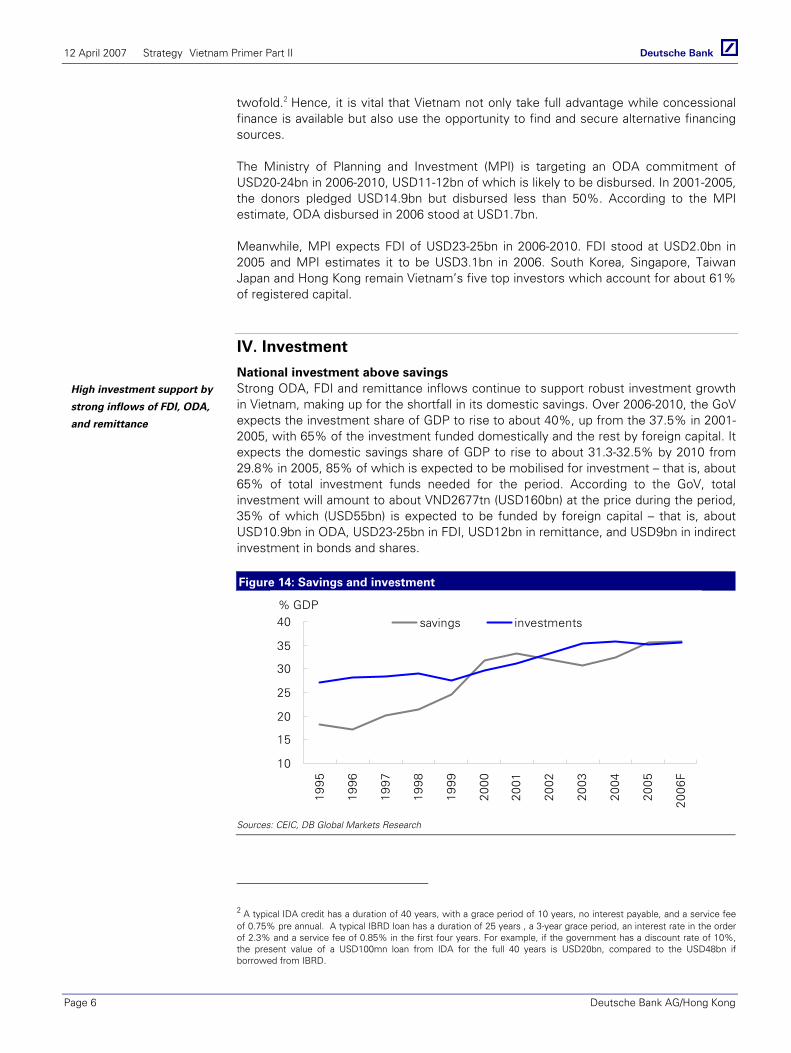

IV. Investment

National investment above savings Strong ODA, FDI and remittance inflows continue to support robust investment growth in Vietnam, making up for the shortfall in its domestic savings. Over 2006-2010, the GoV expects the investment share of GDP to rise to about 40%, up from the 37.5% in 2001-2005, with 65% of the investment funded domestically and the rest by foreign capital. It expects the domestic savings share of GDP to rise to about 31.3-32.5% by 2010 from 29.8% in 2005, 85% of which is expected to be mobilised for investment – that is, about 65% of total investment funds needed for the period. According to the GoV, total investment will amount to about VND2677tn (USD160bn) at the price during the period, 35% of which (USD55bn) is expected to be funded by foreign capital – that is, about USD10.9bn in ODA, USD23-25bn in FDI, USD12bn in remittance, and USD9bn in indirect investment in bonds and shares.

Figure 14: Savings and investment

10

15

20

25

30

35

40

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

F

savings investments% GDP

Sources: CEIC, DB Global Markets Research

2 A typical IDA credit has a duration of 40 years, with a grace period of 10 years, no interest payable, and a service fee of 0.75% pre annual. A typical IBRD loan has a duration of 25 years , a 3-year grace period, an interest rate in the order of 2.3% and a service fee of 0.85% in the first four years. For example, if the government has a discount rate of 10%, the present value of a USD100mn loan from IDA for the full 40 years is USD20bn, compared to the USD48bn if borrowed from IBRD.

High investment support by

strong inflows of FDI, ODA,

and remittance

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 7

Infrastructure needs 3 According to the GoV plan, about 25% of the total investment will be dedicated to addressing the infrastructure bottleneck. Infrastructure investment accounted for about 9.4% of GDP in recent years (2002/2003) and the GoV plans to increase it to 11.4% of GDP in 2006-2010.

Figure 15: Infrastructure expenditure by area and source

% GDP Transport Elect Tel Water Total %TotalUsers 0.0 0.9 0.3 0.1 1.3 14ODA 1.7 1.2 0.3 0.3 3.5 37Budget 0.8 0.1 0.0 0.1 1.0 11Govt bonds 1.2 0.0 0.0 0.0 1.2 13SOCBs 0.1 0.0 0.2 0.0 0.3 3Private 0.2 1.2 0.6 0.0 2.0 21Community 0.0 0.0 0.0 0.1 0.1 1Total (2002-2003) 4.0 3.4 1.4 0.6 9.4 100Developt goal 4.1 4.7 1.4 1.2 11.4

Sources: World Bank

In the electricity sector, investments required to meet the Fifth Power Master Plan amount to VND215.1tn (USD13.7bn, 3.9% of GDP) in 2005-2010. This figure is now regarded as an underestimate because of a higher-than-expected demand growth in recent years. The financial model used by EVN to plan future investments suggests that capital expenditure will amount to VND237.3tn (USD16bn), 4.7% of GDP annually in the same period.

Figure 16: Energy overview

Proven Oil Reserves (Jan 1, 2006E) 600 mn barrelsOil Production (2005E) 366,400 barrels per dayOil Consumption (2005E) 259,400 barrels per dayNet Oil Exports 67,000 barrels per dayCrude Oil Distillation Capacity (2006E) None Proven Natural Gas Reserves (Jan 2006E) 6.8 trillion cubic feetNatural Gas Production (2003E) 0.1 trillion cubic feetNatural Gas Consumption (2003E) 95.4 billion cubic feet Recoverable Coal Reserves (2003E) 165.3 million short tonsCoal Production (2003E) 17.6 million short tonsCoal Consumption (2003E) 10.4 million short tons Electricity Installed Capacity (2003E) 8.7 gigawattsElectricity Production (2003E) 39.7 billion kilowatt hoursElectricity Consumption (2003E) 36.9 billion kilowatt hours

Total Energy Consumption (2003E)

1 quadrillion Btus*, of which Oil (46%), Coal(22%), Hydroelectricity (22%), Natural Gas(10%), Nuclear (0%), Other Renewables (0%)

Per Capita Energy Consump'n (2003E) 12.1 million BtusEnergy Intensity (2003E) 5,148.3 Btu per $2000 PPP*

Sources: Energy Information Agency Note: VoV has taken various measures to increase the life of the fields, including cutting production (to about 350,000 in 2005 from 402,000bbl per day in 2004) and promoting exploration efforts. In 2004, new stocks of oil were discovered in Vietsovpetro’s Dragon field and a 100mn barrel was discovered off Vietnam’s northeast coast.

3 Borrowed heavily from World Bank: Vietnam’s Infrastructure Challenge (2006)

Addressing the

infrastructure bottleneck

12 April 2007 Strategy Vietnam Primer Part II

Page 8 Deutsche Bank AG/Hong Kong

According to the Energy Information Agency, much of Vietnam’s rural population relies mainly on non-commercial biomass energy sources such as wood, dung, and rice husks, leaving per capita commercial energy consumption among the lowest in Asia. However, this is expected to change, with rapid growth in the commercial sector, urbanization, and improvement in living standards.

In particular, electricity demand is forecast to grow 15% per year until 2010. Until very recently, Vietnam relied heavily on hydropower for its electricity generation. This dependence on hydropower poses risks to the stable supply of electricity as it is vulnerable to changing weather conditions. In response, the GoV has promoted the construction of thermal power generation plans. In 2004, the share of hydro power generation stood at about 38%, down from 47% in 2002, while that of oil/gas and coal stood at 49% and 13%, respectively, compared to 39% and 14% in 2002.

Capital spending on transportation infrastructure remains the highest. The Ministry of Transport has proposed capital spending of about VND69.2tn (USD4.3bn, 4.2% of GDP per year) in 2006-2008.

In the water and sanitation sector the government has set coverage targets to achieve its 2010 development goals. The targets are 85% coverage for urban water and sanitation, and 75% for rural water and sanitation, which would require investment of VND57.5tn (USD3.62 billion, 1.2% of GDP annually) in 2005-2010.

In the telecommunications sector, in October 2005 the Ministry of Post and Telematics adopted a target of 32-42 total telephone lines per 100 people by 2010. Achieving 35 lines per 100 people would require about VND57tn (USD3.6bn, 1.4% of GDP per year) in 2006-2010.

GoV promoting thermal

power

Capital spending on

transportation infrastructure

remains the highest

GoV targets 85% and 75%

water and sanitation

coverage for the urban and

rural areas, respectively

32-42 telephone lines per

100 people by 2010

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 9

Fiscal policy Public debt remains manageable, but risks remain Although public debt remained at a manageable level of 45.5% of GDP in 2006, much better than the average rate of 61% for low-income countries in Asia and about the same rate as ASEAN-4, there are lingering concerns over fiscal sustainability due to continued extensive reliance on government budget and off-budget expenditure to fund investment projects and also due to a high degree of uncertainty regarding the contingent costs of bank reform. While the state’s share of investment has trended downward to 52% in 2005, the budget remained the top source, constituting about 47% of total state investment. Meanwhile, the loan share of state investment rose to 31% in 2005, from 20% in 1995, while the SOE equities’ share stood at 17% in 2005. In response, the GoV has increased its efforts to finance infrastructure investments via equitisation/privatisation of state-owned enterprises (SOEs).

Figure 17: Investment by sector Figure 18: State source of investment

10

15

20

25

30

35

1995 1997 1999 2001 2003 2005

40

45

50

55

60

65

Non-state Foreign invested sectorState (rhs)

% %

0

10

20

30

40

50

1995 1997 1999 2001 2003 2005

LoanEquities of State EnterpriseOtherState Budget

%

Source: GSO Source: GSO

Off-budget items remain a risk to fiscal soundness While the fiscal deficit appears to have remained low in recent years, there are ongoing concerns over the government’s extensive reliance on off-budget expenditures. In particular, according to an IMF estimate, the 2006 official budget balance stood at 1.3% of GDP, but, including off-budget expenditure, the deficit stood at 6.3% of GDP.

Off-budget expenditure includes on-lending for investment projects through DAF (now VDB), which has amounted to about 2-3% of GDP since 2000. DAF has outstanding loans equivalent to about 12% of GDP. Off-budget investment also includes education and infrastructure bonds, SOCB bonds, municipal bonds and extra-budgetary recurrent expenditure.4

4 DAF provided soft loans for the financing of eligible investment projects on a priority list approved by the Prime Minister. DAF operations are funded in part through ODA loans, the issuance of DAF’s own bonds, loans from the Postal Savings Service Company, loans from the Social Security Fund, funds mobilised by DAF branch offices (deposits) and project bonds. Education bonds are typically used to finance improvements in school buildings and related facilities, while infrastructure bonds are used primarily to finance investments in, and maintenance of, transportation and irrigation projects. SOCB recapitalization bonds. In 2001, as a part of the government’s restructuring programme for SOCBs, (State-owned commercial banks) non-performing loans worth VND23tn (5.2% of GDP as of 2000) were identified for resolution. Under this programme, the four largest SOCBs received capital injections totaling

Extensive reliance on

off-budget expenditure to

fund investment projects

12 April 2007 Strategy Vietnam Primer Part II

Page 10 Deutsche Bank AG/Hong Kong

Figure 19: Fiscal balance Figure 20: Revenue by source 2006

-8

-6

-4

-2

0

2

2002 2003 2004 2005E 2006E

Official budget balance

Overall fiscal bal. including off-budget expenditure

% Foreigninvested

enterprises9%

Others18%

Oil31%

SOE's18%

Customs16%

Non stateenterprises

8%

Sources: IMF, MoF, DB Global Markets Research Note: Excludes debt amortization payments and adjusted for carried over revenues and expenditure, which the government definition includes

Sources: MoF, DB Global Markets Research

Oil remains the top source of government revenue Government revenue is highly dependent on oil, tax revenue from state-owned enterprises, and customs duties, with their share of total revenue estimated to be 26.6%, 17.8%, and 16.9%, respectively, in 2006. In 2005, the oil share of total revenue stood at 26.4%, compared to the personal income tax share of around 2.1%. There are concerns over this high dependency on oil and customs taxes due to the volatility in international oil prices and further trade liberalisation with the WTO membership, among other things.

External position also still manageable Vietnam’s external debt remains low by global standards, at 32.2% of GDP – about USD19.3bn in 2006 (IMF estimate). The public share of total external debt (including guarantees) stood at 80% and there are concerns that the country’s large investment needs will translate into a greater debt burden. At the same time, although the private share of total external debt remains relatively small (at 20%), concerns remain over the private sector’s ability to hedge against foreign exchange (FX) risks. Moreover, Vietnam’s official FX reserves stood well below the external debt at USD11.2bn in 2006.

Figure 21: Public debt Figure 22: External debt (% of GDP) 2002 2003 2004 2005 2006 (% of GDP) 2002 2003 2004 2005 2006 Public debt 38.2 40.8 42.7 43.7 45.5 External 35.0 33.8 33.9 32.5 32.6

Domestic 10.1 13.4 15.3 17.1 18.2 Long term 31.3 30.0 30.6 29.5 29.6

Foreign 28.1 27.4 27.4 26.6 27.3 Short term 3.7 3.8 3.3 3.0 3.0

Source: IMF, Ministry of Finance Note: Includes public and publicly guaranteed debt

Source: IMF, Ministry of Finance Note: Includes public and publicly guaranteed debt

VND10.9tn (2.5% of 2000 GDP), of which VND9.7tn was provided in the form of recapitalisation bonds and the remainder in cash. Municipal bonds. Ho Chi Minh City and Hanoi are permitted to issue bonds equivalent to 100% of their annual investment budget (for other cities, the applicable limit is 30%), subject to MOF approval. Extra-budgetary recurrent expenditure by local governments resulting in arrears to the transport and irrigation sectors. The World Bank estimated the arrears to the transportation sector at end-2003 to be about VND14.4tn (2.3% of GDP) and arrears to irrigation as of end-June 2004 of VND1.3tn (0.2% of GDP and equivalent to one-quarter of annual public investment in agriculture). The clearance of these arrears is reportedly being financed through the issuance of government bonds and special budgetary allocations. (IMF)

Heavy reliance on oil

revenue, SOE tax revenue

and customs duties

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 11

Monetary policy High inflation and credit growth Inflation rose sharply in 2004 and remained high due to strong growth and supply shocks. Increases in oil prices have translated into higher inflation as the government cut fuel subsidies to reduce its fiscal burden and improve energy efficiency. While the domestic oil prices were increased nine times between end-2003 and August 2006, labour costs continued to increase, resulting in second-round effects on prices. The GoV raised the common minimum wage by 38% in January 2003, 20.7% in October 2005, and 28.6% in October 2006. Average civil service wages were raised by an additional 20% in October 2004 and minimum wages in foreign-invested firms were raised by 42% (on average) in February 2006. Meanwhile, the country also suffered other supply-driven inflation, due to avian influenza and floods. Still, the impact on inflation was limited with administered prices accounting for about 10% of Vietnam’s CPI basket. Meanwhile, credit growth rose sharply to 41.7% yoy in 2004 from 28.4% in 2003, as a result of financial deepening. The ratio of broad money (M2) to GDP continued to rise from 58% in 2001 to 75% in 2004.

In response to a sharp increase in inflation and credit growth, the SBV raised its policy rates5 and reserve requirements. In particular, in July 2004, the SBV raised reserve requirement for corporate deposits with tenor less than one year to 5% (for VND) and 8% (for USD) from 2% and 4%, respectively. Discount and refinancing rates were also raised 50bps to 4.5% and 6.5%, respectively, in December 2005.

In 2006, credit growth fell to 18%, lower than the set target of 20%, while inflation also eased further to 6.6% in 2006 from 8.4% in 2005, although remaining relatively high compared to that of its trading partners, raising concerns over its impact on the nation’s export competitiveness. We expect inflation to remain relatively high, due to the second-round effect of wage hikes and strong demand.

Figure 23: Inflation and monetary policy rates

0

2

4

6

8

10

12

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07

%

Refinancing rate

Discount rate

Base rate

CPI inflation

Sources: State Bank of Vietnam, CEIC, DB Global Markets Research

5 The discount and refinancing facility rates form the lower and upper bands of an interest rate corridor, for Open Market Operation rate. Through the discount facility, credit institutions can access SBV funds subject to quotas, and the maximum term of drawing is 91 days. The refinancing facility is a collateralised lending facility. The SBV also announced a base rate to provide a reference rate for commercial banks’ lending rates, although the relationship between the base rate and other interest rates has been very weak. However, the SBV continues to rely on other monetary instruments such as reserve requirements as it remains the most effective policy instrument. The SBV pays interest on required reserves in dong and on excess reserves in foreign currency. (IMF)

Credit growth and inflation

have fallen but still higher

than trading partners’

12 April 2007 Strategy Vietnam Primer Part II

Page 12 Deutsche Bank AG/Hong Kong

Challenges to the monetary policy transmission The conduct of monetary policy faces various institutional and structural constraints as the SBV faces conflicting policy objectives of fighting inflation and meeting the GoV’s growth target. In particular, state-owned commercial banks (SOCBs) frequently operate on a non-commercial basis to support growth, while increasing internationalisation of the banking system (dollarisation) has complicated monetary policy transmission.

Although there is no comprehensive data on foreign currency circulation in Vietnam, the amount involved is believed to be much larger than what is in the banking system, due to the increasing use of foreign currency as the medium of exchange, with nonresidents in particular, and investment. Although falling from the high of 32% in 2001, the share of foreign currency deposits in broad money remained high at 23% in 2Q2006.

A de facto pegged currency 6 Vietnam officially maintains a managed floating exchange rate regime. Between 1999 and 2000, the SBV had maintained a +/-0.25% trading band on the dong against the US dollar. In 2000 and 2001, however, the dong was allowed to depreciate sharply in response to the depreciation of the currencies of the neighbouring countries as the GoV tried to protect Vietnam’s export competitiveness following the 25% devaluation of the dong in 1997-1998.

Figure 24: Dong vs USD

13000

14000

15000

16000

17000

1999 2000 2001 2002 2003 2004 2005 2006 2007

Source: Bloomberg

The SBV expects the dong to depreciate against the US dollar by 1-2% per year in 2006-2007. However, after the SBV widened the trading band to +/-0.5% on 2 January 2007, the dong fell below 16,000 against the US dollar by mid-February, from 16,066 at the beginning of the year, suggesting that a steady depreciation of the dong is no longer guaranteed, although we expect the annual change to be limited to 1-2%. While we expect Vietnam to remain on the path of liberalisation, broadly abiding by its WTO commitments, we think that the GoV will continue to prioritise the stability of the dong and its export competitiveness.

6 See Vietnam Primer published in August 2006 for FX history

Conflicting goal of SBV

Depreciation of the dong is

no longer guaranteed

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 13

SOCB and SOE reform7 SOCBs dominate the banking sector The banking sector is dominated by five SOCBs, which account for more than 78% of the total bank assets, and are segmented by sectoral lines. In order of asset size, the five SOCBs are VBARD (Vietnam Bank for Agriculture and Rural Development), Vietcombank (Bank for Foreign Trade of Vietnam, trade financing bank), BIDV (Bank for Investment & Development of Vietnam, infrastructure bank), ICB (Industrial and Commercial Bank of Vietnam, industrial development bank), and MHB (Mekong Housing Bank, housing development bank). The rest of the banking system is relatively more market oriented. Semi-private joint stock banks (JSBs) operate on a limited local scale, servicing the domestic private sector. They are capitalised by SOCBs, SOEs (state-owned enterprises), private businesses and individuals, including foreign investors. Joint venture banks are 50% owned by a foreign bank and 50% by an SOCB. SOCBs maintained its dominant position in the sector, while the total assets of the banking system rose to 68% of GDP in 2005, from 10% in 1990.

Figure 25: Banking sector Figure 26: Market share of banks in lending

5 State-owned commercial banks

BIDV, Vietcombank, VBARD, ICB, MHBVietnam Bank for Social Policies

34 Joint stock commercial banks

4 Joint venture banks

28 Foreign bank branches

901 People’s credit fund

5 Finance companiesz

8 Leasing companies

Foreign,

8%JVBs, 2%

JSBs,12%

SOCBs,78%

Source: SBV, 2005 Source: Fitch

Reforming SOCBs Banking reform efforts initiated in 2001 centered on restructuring SOCBs, which included recapitalisation, NPL resolution and operational measures (such as improving credit risk management or undertaking of audit based on International Accounting Standards). Note that banks were traditionally not required to maintain a minimum capital adequacy ratio but rather just a minimum amount in Vietnam. For example, minimum capital requirement for SOCBs was VND1100-2200bn. Moreover, SOCBs suffered from the culture of policy directing. Based on the IAS (which includes not only the non-performing amount due but not paid, but also the whole loan balance), the NPL ratio stood as high as 10% (World Bank estimate), not 4% in 2004 as suggested by the Vietnamese Accounting Standards.

According to the Decision 457 issued in April 2005, all credit institutions, except foreign banks, are required to meet a minimum CAR (risk weighted) of 8% by 2008. This decision was followed by the PM Decision 112 (in 2006), which stipulates, among others, that the CAR should be no less than 8% and that the banking standards should be fully consistent with Basel I by 2010. The CAR of SOCBs hovered around 4-5% in 2005 and has yet to meet the minimum requirement. However, other banks are close to

7 Borrowed heavily from World Bank: Taking Stock (June 2006)

Banking sector is dominated

by SOCBs

Equitisation of SOCBs

12 April 2007 Strategy Vietnam Primer Part II

Page 14 Deutsche Bank AG/Hong Kong

meeting (if they have not already met it) the requirement, by raising capital through profit and convertible bond issuance and/or NPLs reduction (by rescheduling).

The financial reform plan also includes the equitization of all SOCBs. The process of equitisation has already begun for two SOCBs. Apart from Agribank (VBARD), which is scheduled to be equitised in 2008, all SOCBs are to be privatised in 2007. The state will continue to hold the 51% majority stake in state-run commercial banks while limiting foreign ownership to 30% and individual ownership to 10%.

Meanwhile, the SBV has submitted a proposal to amend the State Bank Law and the accompanying decree to increase its autonomy in areas of monetary policy and regulation of the banking sector and to free itself from the ownership role of SOCBs. Banking supervision will be enhanced by establishing an independent financial supervision board. The SBV has initiated an assessment of its supervision practices against international standards, the Basel Core Principles.

Figure 27: GDP by ownership

30

35

40

45

50

55

1995 1997 1999 2001 2003 20054

6

8

10

12

14

16

18

StateNon-StateForeign investment sector (rhs)

% %

Sources: CEIC, DB Global Markets Research

SOE reform gaining better traction With Doi Moi, the government embarked on a gradual transformation of ownership structures. This, however, did not lead to a sharp reduction in the state’s share of the economy. Instead, the state focused on the decentralisation of power to state-owned enterprises (SOEs). Meanwhile, the government allowed the entry of foreign invested enterprises (FIEs) into Vietnam, but typically in joint ventures with SOEs.

Figure 28: Completed SOE transformation 2001 2002 2003 2004 2005 2001-05Equitization 198 213 358 643 709 2121Sales/Assignments 59 39 48 44 70 260Liquidation/Bankruptcy 21 24 29 41 40 155Single Member LLCs 0 2 8 34 0 44Subtotal 278 278 443 762 820 2581Mergers 2 60 118 43 6 229Total 280 338 561 805 826 2810

Sources: National Steering Committee for Enterprise Reform and Development (NSCERD) and World Bank

The State pursued a gradual equitisation of non-strategic SOEs, focusing on small- and medium-sized enterprises. The SOE reform plan provided for equitization, liquidation, and merger of a significant number of smaller and medium-sized enterprises. By 2006, the number of SOEs fell to well below what it was in 2001 (5,771) and the amount of bank debt of restructured SOEs has risen, reducing risks to the state’s finances and the banking system.

SBV seeks to increase its

autonomy

Decentralisation of power to

SOEs

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 15

Figure 29: Transformed SOEs 2001 2002 2003 2004 2005Avg charter capital (VND bn) 7.7 7.1 8.8 9.9 17.3Avg bank debt (VND bn) 5.4 5.4 8 9.9 21.7Avg number of employees 199 198 195 238 329Share of transformed SOEs withstate holding above 35% 26 27 45 55 57Share of transformed SOEs with noshares sold to outsiders 50 50 52 46 26

Sources: National Steering Committee for Enterprise Reform and Development (NSCERD) and World Bank

There are about 2,100 SOEs at present and about 1,500 to be equitised over the next five years. This suggests that close to 80 corporations and large firms will have to go public, while enterprises in 28 business activities will remain 100% state-owned.

In compliance with the latest decision of the prime minister, on 29 December 2006, 1 state-run group and 52 corporations will have to undergo equitisation in 2007-2010. The list of those groups and state-owned corporations consists of 1 economic conglomerate Vinatex Group, 6 state-run Corporations 91 (the largest SOEs), 6 state-run corporations of the Ministry of Industry, 14 state-run corporations of the Ministry of Construction, 10 state-owned corporations of the Ministry of Public Transport, 3 of the Ministry of Fisheries, 12 state-owned corporations of the Ministry of Agriculture and Rural Development and 1 state-owned corporation under the management of the Ministry of Health.

In 2007, GoV is targeting equitization of 550 SOEs. Those to be listed in HSTC include Vietnam Petroleum Transport Company (Vipco), Tan Tien Plastic Packaging Company (Tapack) and Dry Cell and Storage Battery Co (Pinaco). Under The Ministry of Transport and Telecommunications plans, Civil Engineering Construction Corporation’s eight subsidiaries (Cienco1 to Cienco 8), Thang Long construction Corporation, Vietnam Waterway Construction Corporation (Vinawaco) and Southern Waterborne Transport Corporation (Sowatco) will be equitized. While Saigon Beer-Alcohol-Beverage Corp (Sabeco) and Hanoi Beer-Alcohol-Beverage Corp (Habeco) are to be equitised as early as 2007, Vinatex Group and Vietnam Airlines are scheduled to be equitised in 2008. The other large state-owned corporations, including Vietnam National Chemical Corp (Vinachem), Vietnam National Cement Corp, Song Da Corp, Vietnam Machinery Installation Corp (Lilama) and others, are to be equitised in 2010.

The GoV established the State Capital Investment Corporation (SCIC) in July 2005 to take over and manage state capital. By taking over the ownership rights from ministries and provinces, it is expected to remove the conflict of interest between ownership and regulation. The SCIC reportedly plans to take ownership of VND23tn (USD1.43bn) in state holdings at 1,000 equitised companies by the end of 2007. SCIC has so far taken over state capital at 294 businesses in various sectors, ranging from energy, IT and telecom to health care and consumer goods, with a book value of VND2.96tn, calculated at the time of equitisation. The market value of its portfolio is estimated to be VND29.25tn (SD183mn). In particular, as of 25 January 2007, SCIC held a 7.37% stake in FPT (Corporation for Financing and Promoting Technologies), 91% in Pacific Airlines, 48% in Vinamilk (Vietnam Dairy Products Joint Stock Company), and 63% in Bao Minh, a non-life insurer.

Improvements in legal framework Vietnam has shown a marked improvement in its legal framework in promoting private sector activities. The 2005 Law on Investment was passed to create a level playing field for all investors, domestic and foreign, based on WTO principles. Meanwhile, the 2005 Enterprise Law sought to eliminate discrimination against non-state and foreign-invested

1500 of 2100 SOEs to be

equitized over the next five

years.

550 SOEs to be equitized in

2007

SCIC to remove the conflict

of interest between

ownership and regulation

Upgrading legal framework

based on WTO principles

12 April 2007 Strategy Vietnam Primer Part II

Page 16 Deutsche Bank AG/Hong Kong

enterprises, to reduce non-market interference measures inconsistent with WTO regulations and to encourage private participation in industries that are not specified in a “negative list”. The law is also expected to provide a basis for improvement in corporate governance and performance of enterprises, SOEs in particular.

We expect Vietnam’s WTO membership to keep Vietnam on the path of liberalisation and further institutional and legal reform. In particular, Vietnam is expected to implement TRIPS (intellectual property), TRIMS (investment measures), CVA (Customs Valuation Agreements), TBT (technical barriers to trade), SPS (sanitary and phytosanitary measures), ILP (import licensing provisions), A/D & C/V (antidumping) and ROO (rules of origin).

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 17

Capital market Rapid increases in stock market capitalisation8 There are two stock market trading platforms in Vietnam, in Ho Chi Minh City (HSTC, which was set up in July 2000 with two stocks) and Hanoi (HaSTC, set up in March 2005). Although relatively small by regional standards, stock market capitalisation has risen rapidly over the past year due largely to new listings prompted by government initiatives to increase market capitalisation. The GoV not only directed joint-stock companies with dominant stakes held by the state and SOEs to list or auction their shares on the securities trading centers but also provided tax incentives to support development of the capital market.

Figure 30: Market capitalisation (% GDP)

GDP per capita USD

Malaysia

India

Thailand Phillipines

Indonesia Pakistan Sri Lanka

V ietnam

China

-

40

80

120

160

200

0 1,000 2,000 3,000 4,000 5,000 6,000

Mkt cap (% of GDP)

Source: Reuters Note: Vietnam only takes into account HSTC

As a result, the number of companies listed in the HSTC rose to 106 in end-2006 from 38 in end-2005, leading to a market capitalisation of VND161.4tn (USD9.7bn) up from VND8.9tn (USD565m). During the same period, the number of listed stocks in the HaSTC rose to 87 from 6, with the market capitalisation rising to VN70tn (USD4.2bn) from VN2.1tn (USD125m). By end-2006, the market capitalisation of the two stock markets reached USD13.9bn, 25% of Vietnam’s GDP in 2006.

On the demand front, the government (via Decision 238 in September 2005) increased the ceiling on foreign shareholdings in listed companies, from 30% to 49%, with the ceiling on bank ownership maintained at 30%. There are plans to further relax constraints on foreign ownership in some sectors. By some estimates, foreign investors currently own around 20-30% of the shares listed in the stock market. On the domestic side, public interest in the stock market increased as real estate activity slowed down.

Meanwhile, Vietnam has a much more active, bigger informal (unregulated) market, which is not burdened by strict disclosure requirements. By some estimates, the information market is about four to five times the size of the trading centres. Reportedly, there are 6,532 companies trading in the informal market, mostly solid performers and

8 See Vietnam Primer published in August 2006 for regulations

Rapid development of

capital market

12 April 2007 Strategy Vietnam Primer Part II

Page 18 Deutsche Bank AG/Hong Kong

considered more attractive than the listed companies, as the premium is usually low at the early stage of the company’s privatisation.

The Securities Law which took effect on 1 January 2007 seeks to bring many of the companies whose shares are being informally traded under the regulation of the State Securities Commission. Under the law, a company with shares issued to the public, with shares listed on HSTC, or with shares owned by 100 or more investors and the charter capital over VND10bn would be considered “publicly held”. This gives the SSC the authority to regulate. Note that the SSC can regulate the issuer, intermediaries and investors as long as the issuance is a public offering, the securities are publicly traded, and the issuer is a publicly held company. All public companies would be subject to formal standards of disclosure and governance.

The new securities law also stipulated a higher minimum registered capital of VND80bn and VND10bn for the HSTC and HaSTC, respectively, up from VND5bn for both. Meanwhile, the capital requirement for securities companies was raised: to VND25bn from VND2bn for brokerage; to VND100bn from VND12bn for self-trading; and to VND165bn from VND22bn for issue guarantee.

If a securities company wants to do business in all of the five fields (depository, brokerage, investment consultancy, issue guarantee and self-trading), the minimum capital requirement now stands at VND200bn, up from VND43bn previously. In addition, the securities companies will not be allowed to operate in stock investment list management that will be under the charge of fund management companies. Listed firms and securities companies are given a period of time (slated for one or two years) to chalk out a capital-raising roadmap. After this period, if the firms cannot meet the new requirements, they will be removed from HSTC or forced to move to HaSTC.

The law also stipulates that brokers and intermediaries dealing in securities are to be licensed by the SSC. Investors are now allowed only one account in a securities company. The limitation aims to prevent fake transactions to influence share prices in the stock market and cause losses for other investors. The law also laid the ground for the transformation of the Ho Chi Minh City Stock Trading Center into a “privately” owned entity.

Figure 31: VNINDEX

0

200

400

600

800

1000

1200

2001 2002 2003 2004 2005 2006 2007

Source: Reuters

Reigning in the informal

market

Upgrading the securities law

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 19

Regulatory risks In response to a sharp rise in stock markets, the Ministry of Finance and State Securities Committee have decided on the following: 1) Temporarily retain the foreign holding cap in listed companies on the stock market. The cap is now still 49% of the shares of a listed company and 30% of the shares of a listed bank. 2) Curb securities investment lending, repo transactions and share mortgage loans and supervise foreign portfolio investment and apply administrative measures on cash withdrawal out of Vietnam by foreign investors. 3) Inspect securities companies facing investor complaints and impose administrative penalties if violations are found. 4) Accelerate the disclosure of information by listed firms on their finances; 5) Re-registration with the SSC by foreign funds, even those licensed by the Ministry of Trade. 6) The SSC to provide investors with analysis and assessment of the stock market, including information on financial indicators.

The prime minister also instructed the Ministry of Finance and SSC to closely work with the SBV and authorized agencies to further strengthen the supervision of operations of the stock market, ensuring compliance with the Securities Law by public companies, foreign investment funds, and institutions and individuals dealing in the stock market. They also called to supervise brokering, investment consulting, and business appraisal activities to boost the high quality of these services for investors and apply suitable management tools to ensure the management of foreign investment capital flows in the stock market in the relationship between the stock market and monetary market, which may calls for revision of the guiding decrees on implementing the Ordinance on FX Administration. The SBV must also enhance the supervision of banks in trading shares, investing and contributing capital as well as transferring shares of joint stock banks aimed at ensuring transparency and security for the banking system. Meanwhile, the Ministry of Finance is mandated to submit to the GoV a plan for establishing one working team to supervise stock market operations.

Bond market Vietnam’s bond market remains relatively underdeveloped and illiquid. Most of bonds are government bonds (85%) and limited corporate bond market due to the absence of rating agencies. As at end-2006, there were over 450 bonds outstanding in the domestic market, with a market value of about VND130tn, 13.3% of GDP. Other papers include municipal bonds (HCMC and Hanoi). DAF bonds, education and infrastructure bonds, SOCB recapitalisation bonds, BIDV bonds, and the Vietcombank convertible bonds.9 In October 2005, the government issued its first international bond since the Brady issues in the 1990s, amounting to USD750mn, with a yield of 7.125%, which was lower than Indonesian and Philippines bonds. Meanwhile, Standard & Poor’s raised Vietnam’s credit rating outlook from BB- positive to BB stable in September 2006.

9 Municipal bonds. Ho Chi Minh City and Hanoi are permitted to issue bonds equivalent to 100% of their annual investment budget (for other cities, the applicable limit is 30%), subject to MOF approval. HCMC has so far issued bonds in the amount of VND2tn (0.2% of GDP), and is to issue another VND2tn in 2005; while Hanoi has not yet issue any municipal bonds, it is expected to issue bonds on the order of VND1.5tn in 2005. DAF bonds The DAF (now VDB) has become one of the largest financial institutions in Vietnam, and has outstanding loans equivalent to about 12 percent of GDP, half of which are financed through ODA. Education and infrastructure bonds The National Assembly has authorized issuance of a total of VND110tn (about USD7 billion, or 15.6% of 2004 GDP) of education and infrastructure bonds for the period 2005–2010. SOCB recapitalization bonds In 2001, as a part of the government’s restructuring program for SOCBs, non-performing loans worth VND23tn (5.2% of GDP as of 2000) were identified for resolution. Under this program, the four largest SOCBs received capital injections totaling VND10.9tn (2.5% of 2000 GDP), of which 9.7tn was provided in the form of recapitalization bonds and the remainder in cash. (IMF)

Strengthening prudential

regulations

Bond market dominated by

government due to the

absence of rating agencies

12 April 2007 Strategy Vietnam Primer Part II

Page 20 Deutsche Bank AG/Hong Kong

Figure 32: Size of debt market

0

20

40

60

80

100

Mal

aysi

a

Thai

land

Chi

na

Phi

lippi

nes

Indo

nesi

a

Vie

tnam

Pak

ista

n

% of GDP

Source: ADB

Although improving, the market remains relatively illiquid as investors hold them until maturity. Long-term (10-15-year) bonds (9.06%), which make up about 40% of the total, are typically purchased by insurance companies and held to maturity, while 60% of 2-3-5-year bonds (mostly 5yr; 7.7%) are held by SOCBs. Reportedly, GoV is expected to adopt various administrative and structural measures (including issuing government bonds with the same maturity date although auctioned at separately) to increase liquidity and depth of its bond market.

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 21

Sectoral analysis Vietnam’s 2006 economic growth of 8.2%yoy was led by the manufacturing sector. Meanwhile, the service sector expanded 8.3%, led by growth in the hotel and restaurant sector, while the agricultural sector remained a laggard, growing by only 3.4% yoy in 2006.

Figure 33: Real GDP growth by sector Real GDP VNDbn %yoy % of GDP

2005 2006* 2005 2006*

Agriculture, forestry, fishery 76,874 79,488 3.4 19.6 18.7

Agriculture 64,098 65,918 2.8 16.3 15.5

Fishery 10,141 10,905 7.5 2.6 2.6

Forestry 2,635 2,665 1.1 0.7 0.6 Industry & construction 157,846 174,210 10.4 40.2 41.0

Manufacturing 89,514 100,593 12.4 22.8 23.7

Construction 34,428 38,232 11.0 8.8 9.0

Mining & quarrying 22,663 22,845 0.8 5.8 5.4

Electricity, water supply 11,241 12,540 11.6 2.9 2.9 Services 158,276 171,390 8.3 40.3 40.3

Trade 63,957 69,423 8.5 16.3 16.3

Transport, communication, tourism

15,318 16,871 10.1 3.9 4.0

Real estate business 14,809 15,244 2.9 3.8 3.6

Hotel, restaurant 13,466 15,139 12.4 3.4 3.6

Education & training 13,126 14,231 8.4 3.3 3.3

State management 10,477 11,270 7.6 2.7 2.7

Finance, banking, insurance 8,197 8,867 8.2 2.1 2.1

Other 18,926 20,345 7.5 4.8 4.8 Total 392,996 425,088 8.2

Source: GSO Note: * Provisional

Agriculture

Growth in the agriculture sector slowed to 3.4%yoy in 2006 from 4.0% in 2005, adversely affected by prolonged cold weather in the north, floods in the central area and the Mekong delta, and avian flu.

Rice Vietnam is the world’s fifth largest producer of rice. The Mekong Delta is Vietnam’s largest rice granary, responsible for over 50% of the national output and over 90% of rice exports (in volume). In 2006, rice production remained largely unchanged from the previous year, at 35.8mn tons, while rice exports fell to 4.7mn tons from 5.2mn tons in 2005. In value terms, however, rice exports stood stable at USD1.3bn as prices rose due to subdued supply and strong demand.

Coffee Vietnam is the second largest producer and exporter of coffee in the world, after Brazil, with a market share of 12% in terms of production. Vietnam has more than 500,000ha for coffee production, 450,000ha of which are for Robusta and the remainder for Arabica, with the Mekong Delta and the Central Coast area as the main place of production in the last ten years. Coffee is one of the Vietnam’s top ten export items, with the US and EU as the top two destinations. In 2006, Vietnam exported 897,000 tons of coffee valued at USD1.1bn.

Fifth largest producer of rice

Coffee is one of the

Vietnam’s top ten export

items

12 April 2007 Strategy Vietnam Primer Part II

Page 22 Deutsche Bank AG/Hong Kong

Upon accession to the WTO, Vietnam has pledged to eliminate export subsidies for agricultural products while maintaining 10% subsidies for domestic use. In particular, there will be no more state awards for coffee exports (several dollars for each ton). Moreover, average tariff for agricultural products will be cut to 20.9% from 23.5%, although maintaining the import quota for certain agricultural products such as sugar, eggs, cigarettes and salt.

The Ministry of Agriculture and Rural Development (MARD) drafted the “Vietnamese Rice Development Strategy for the 21st Century” aimed at increasing rice-cultivating areas in the Mekong and Red River Deltas. The strategy includes researching the structure of agricultural products, evaluating the competitive edge of each agricultural product, and mapping out strategies and measures for each period of development. According to the MARD, the agricultural sector has been allocated VND2.1tn (0.7% of the total budget) from the State Budget in 2007. VND1.2tn is for the construction of irrigation plants with VND298bn and VND210bn allocated for agriculture and forestry development, respectively. While the GoV encourages investments in agriculture and food processing, investments in dairy products, production of vegetable oil and cane sugar is subject to the condition that it includes investment in raw material sources. At end-2006, the agriculture sector had attracted 53 FDI projects with a combined registered capital of USD7.5bn.

Market capitalisation The agriculture and food-processing sector commanded 19% (USD2.5bn) of market capitalisation by end-January 2007, compared to 55% (USD947mn) in 1H06. The largest listed players in the industry by market cap were Vietnam Dairy Products (USD1.73bn) and Kinh Do Corp (USD411mn) at end-January 2007.

Fisheries

Vietnam has a relatively favourable environment to support the sector, with its long coastline, a favourable climate and water environment and a large number of experienced workers (more than 4mn). Seafood was ranked fourth among the nine staple items exported from Vietnam in 2006. While the fisheries sector expanded 7.5% yoy in 2006, seafood exports rose 23% yoy to USD3.4bn in 2006, surpassing the Ministry of Fisheries’ forecast of USD2.8bn. The strong growth was due largely to higher global prices for shrimp/fish and increased demand for white fish in European countries, as the latter faced fishing restrictions. The GoV plans to achieve an export target of USD3.5bn in 2007 and USD4.5bn by 2010.

The Ministry of Fisheries is targeting 2.0mn tons from fishing and 1.8mn tons from aquaculture, in 2007. Aquaculture accounted for 50% of the fisheries sector’s total output with 3.7mn tons in 2006. The ministry plans to invest USD222.5mn in 2007-10 in aquatic product processing and trading and invest USD62.5mn to build an information system by 2015 to help fishermen from coastal areas receive pertinent information, including weather forecasts and rescue effort details.

Market capitalisation The fisheries sector contributed to 1% (USD148mn) market capitalisation at end-Jan 07 compared to 2% (USD34mn) as of 1H06. The largest listed companies in the sector were An Giang Fisheries Import Export Co (market capitalisation of USD67mn) and Sao Ta Foods Joint Stock Co (mkt cap USD24mn) at 31 Jan 07.

Aquaculture accounted for

50% of the fisheries sector’s

total output

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 23

Mining

The mining sector, which accounts for 5.4% of GDP, rose 0.8%yoy in 2006, down from 1.1% in 2005, due to regulatory constraints on FDI in the sector, protection for natural resources, shortage of equipment, and higher costs (energy and labour). According to the Department of Geology and Minerals of Vietnam, the main identified mineral resources are coal, natural gas, and crude oil. Under the master plan, the GoV has allocated about VND64bn (compared to the total of VND2.7tn) for exploring lead and zinc mines. The GoV expects demand for lead and zinc to rise to 45,000 tons and 165,000 tons in 2005-2010.

Coal Coal dominates Vietnam’s mining industry. Most of the coal produced in Vietnam is anthracite, mined mainly in the province of Quang Ninh in north eastern Vietnam. According to the Vietnam Coal and Mineral Group, Vietnam had 220bn tons of anthracite coal, 78m tons of semi-anthracite coal, 38m tons of coking coal, 96m tons of thermal coal and 306m tons of lignite as of 2006. Coal production increased 18.3%yoy to 37mn tons in 2006 due to an improved mining technology and higher coal prices amid increased energy demand. Meanwhile, coal exports grew 65.6%yoy in 2006 to 29.7m tons. According to the Ministry of Industry, coal mining is expected to increase 9.3% yoy with annual production of 42mn tons by 2010. The key coal producer is the Vietnam National Coal and Mineral Industries Group (Vinacomin) and is targeting production of over 37mn metric tons of coal in 2007. Vinacomin has approximately 30 subsidiaries operating in both strip mines and underground mines, 15 of which are expected to be equitised by 2010, with the process beginning in 2007.

The GoV estimates a requirement of 10.2mn metric tons of coal per annum to meet the projected power demand of 20,000MW by 2010. Vinacomin is constructing several large thermo-electronic power plants, with a combined capacity of 1,100-1,400MW. In addition, Vinacoal, the country largest coal producer is seeking a foreign investment of USD750mn to construct seven coal-fired plants with a total capacity of 1,232MW by 2010.

Vietnam is the largest anthracite coal exporter globally, with 13% of world market share as of 2005. Under the coal export plan for the year 2006-2010, Vietnam is estimated to reduce the coal export volume to 11mn tons in 2007, compared to 18mn tons in 2005. Moreover, during 2006, a new export tax of 10% on coal for 2007 was introduced.

Gas Vietnam extracted about 6.4bn cubic meters (up 1.2% yoy) of natural gas and 3,43,000 tons of liquidised gas in 2006. As per the Socioeconomic Development Plan (2006-2010), natural gas extraction is expected to reach 13.2bn cubic meters by 2010. The much-expected opening of the gasoline retail industry is not covered by the WTO agreements. State-owned enterprises will keep their monopoly in importing and distributing.

Crude Oil Vietnam extracted about 16.6mn tons of oil in 2006, down 10.3% from 18.5mn tons in 2005 and lower than the GoV’s target of 17.3mn tons. Foreign investment is expected to increase annual crude oil extraction to 22mn tons and gas extracted to 13.2bn cubic meters by 2010.

Crude oil is Vietnam's largest foreign exchange earner and the country is Southeast Asia's third largest crude producer. In 2006, crude oil contributed 21% of Vietnam’s total export turnover at USD8.3bn, the same as in 2005. To ensure sufficient supply of crude

The largest anthracite coal

exporter globally

Oil is Vietnam's largest

foreign exchange earner

12 April 2007 Strategy Vietnam Primer Part II

Page 24 Deutsche Bank AG/Hong Kong

for domestic industries, the Ministry of Planning and Investment proposed to lower crude oil exports, to 15.6mn tons by 2010. Meanwhile, to reduce reliance on petroleum imports, the GoV is investing USD2.5bn in constructing its first oil refinery, Dung Quat, in the central Quang Ngai Province with annual processing capacity of 6.5 million tons. The project is scheduled to come onstream in early 2009, meeting about 40% of the domestic demand for petroleum products. A further two oil refineries are scheduled to become productive in 2009. The GoV expects Vietnam to become a net importer of crude oil by 2015, when all three refineries become operational and demand for crude oil rises.

Vietnam’s oil sector is dominated by the state-owned Vietnam oil and gas corporation (Petrovietnam). Established in 1975, Petrovietnam, along with its subsidiaries, covers operations of oil and gas exploration, production, storage, transportation and distribution services in Vietnam. Petrovietnam transported, processed, and delivered 5.6bn cubic meter of dry gas, 107,000 tons of condensate and 338,000 tons of liquid petroleum gas, reporting a revenue of USD906mn in 2006, 20% yoy. Petrovietnam plans to extract 25-30mn tons per year until 2010, of which inland crude oil extraction would account for 60%, natural gas 33% and the rest is to be extracted abroad. Chevron (USA) and Petronas (Malaysia) are active partners of Petrovietnam, operating petroleum contracts in Vietnam. According to management, Petrovietnam is likely to sign two oil exploration contracts in 2007, one in Nigeria and other in Cuba. However, the GoV has plans to privatise this state-owned enterprise by 2008.

Market capitalisation There are three mining companies listed on the HSTC with a combined market capitalisation of USD49m as of 31 Jan 2007, constituting less than 0.5% of the total market cap. In particular, in December 2005, Petrovietnam’s newly equitised subsidiary Petrovietnam Drilling and Well Services (PVD) was listed on the HCSTC with Petrovietnam retaining a 51% stake.

Manufacturing

The manufacturing sector led the industry sector growth, rising 12.4% yoy in 2006, constituting about 23.7% of GDP, up from 22.8% in 2005. According to GSO estimate, IP was 10.2% in 2006, compared to 10.6% in 2005.

Figure 34: Key manufacturing industry subsector growth 2005

-

40,000

80,000

120,000

Food &B

everages

Minerals

Electrical

andelectronic

Chem

icals

Textiles

Rubber andplastic

Leather

Machinery

0

5

10

1520

25

30

351994 price

Growth

VND bn % yoy

Sources: GSO, DB Global Markets Research

On becoming a member of the WTO, industrial subsidies will be scrapped within five years of the accession. Moreover, the import duties would be reduced to 13.6% within

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 25

five to seven years (2007-2014) from the date of accession to the WTO from the current average of 17.6%.

Market capitalisation The manufacturing and engineering sector commanded 12% (USD1,9bn) of HSTC market capitalisation at end-January 2007, down from the 24% (USD414mn) at end-1H06. The largest players were Cable And Telecommunications Materials Co (with market capitalisation of USD522mn) and Refrigeration Electrical Engineering (market cap of USD451mn) at end-January 2007.

Steel Steel production increased 4.7% yoy to 3.8mn tons in 2006, the only ASEAN country to record growth in the year. According to the Steel Association, domestic steel manufacturers met 100% of the domestic demand for construction steel, pipe steel and galvanised steel but only 30% of the domestic demand for steel plate. According to the SEDP 2006-2010, the GoV expects the steel industry to grow 7.5-8.0% yoy to reach an annual capacity of 10.2mn tons by 2010. POSCO, a Korean steel maker, plans to set up a cold-rolled steel plant in Vietnam (in October 2007, to be commissioned by end- 2009.

Due to its dependence on imports for steel ingots (over 70% imported), the steel industry faced a loss of VND70bn (USD4.4mn) in 2006. The Steel Association submitted a proposal to the Ministry of Trade to reduce imports of steel ingot to 50% of demand in 2007, down from 70% in 2005 and 2006.

Market capitalisation The VND100bn Vietnam-Italy Steel Joint Stock Company is the only steel company listed on the HCSTC, with a market capitalisation of USD27.3mn at end-January 2007. It was listed on 25 December 2006 at VND45,000 per share. Vietnam Steel Corporation (VSC) is the largest steel maker in Vietnam with a 40% market share but is not listed and remains a 100% state-owned company.

Cement According to Vietnam Economic Times, the Vietnam National Cement Association (VNCA) expects annual demand for cement to reach 50mn tons by 2010, a 10.5-11.5% yoy growth over the next five years. According to the Ministry of Construction, Vietnam requires USD3.4bn worth of cement between now and 2010. The industry expects to produce 60mn tons of cement by 2010, up from the 31mn tons produced in 2006. Cement production in 2006 grew 11.2%yoy in 2006, up from 10% in 2005, supported by infrastructure projects and strong economic growth.

Japanese manufacturer Bim Son Cement Company and Ishikawajima-Harima Heavy Industries Co. has entered into a Joint-Venture to set up a manufacturing facility (annual production capacity 2mn tons), scheduled to be commissioned by end-2008 in the central Thanh Hoa province.

Market capitalisation To date, there is no cement company listed on the HCSTC. Vietnam National Cement Corporation (VNCC), a 100% state-owned company, is the largest cement manufacturer in Vietnam, with a market share of 46%.

Chemicals Chemical production grew 7.9% in 2006, compared to 6.9% in 2005. The chemical industry in Vietnam is highly fragmented with 2,070 individual players. The state sector owns 4% of the companies, foreign investors own 10% and the remaining 86% is owned by Vietnamese domiciles. The state sector contributed to 65% of the total industry output, in value.

Building its steel industry

Strong growth in cement

production

A highly fragmented sector

12 April 2007 Strategy Vietnam Primer Part II

Page 26 Deutsche Bank AG/Hong Kong

According to the Ministry of Industry, the chemicals industry targets a growth of 14% per annum by 2010 in order to satisfy 100% domestic demand for phosphorous and fertilizers and 70% of domestic demand for urea.

Market capitalisation To date, there are no chemical manufacturing companies listed on the HSTC.

Plastics Vietnam’s plastic industry is considered to be in its infancy compared to Malaysia, Singapore, Thailand and China’s and is characterised by under-capitalisation and lack of technology. The output per capita was 25kg per person in 2005. Countries like Singapore and Malaysia had far exceeded this number in 1999 with 94kg per person and 49kg per person, respectively. However, the industry has been growing at 30% p.a. in recent years and the Vietnam Plastics Association (VPA) expects Vietnam’s Plastics output to reach 4.5m tons by 2010 from 1.7m tons in 2006.

According to the Vietnam Plastics Association, the sector expects to earn USD580m (21.3% yoy) from exports in 2007. The Association also expects Vietnam’s Plastics output to reach 3.8mn tons by 2010 from 1.7mn tons in 2006.

The Vietnam South Plastics Association (VSPA) and the Vietnam Plastics Association (VPA), both 100% state-owned, are the two key players in the plastics sub-sector. VPA commanded a 20% share of the total plastics market in Vietnam as of 2006. Vietnam is home to 1,400 plastic manufacturers with c. 80% of them operating in Ho Chi Minh City.

Market capitalisation There are four plastic companies listed on the HCSTC with a combined market cap of US$289.2mn as of 31 Jan 07 constituting c. 2% of the total market cap. Binh Minh Plastics Joint Stock Company is the largest with a market cap of US$60.4m as at that date.

Textile and Garments In 2006, textile and garment production rose 9.9% yoy in 2006, down from 18.2% yoy in 2005. Textile and garment exports rose 22% yoy to USD5.8bn, representing 14.7% of the total exports – second most important export item, after oil.

According to the SEDP 2006-2010, the GoV is targeting production of 1.1bn square meters of fabric and 1.5bn pieces of garments, with an annual export growth of 15%, or USD10bn. The sector continued to attract foreign investment. Teachang corporation of Korea signed a contract with Thein Nam to contribute 60% of the capital in building a denim cloth factory in Vietnam. According to Vinatex, the factory is expected to operate by 2008, with an output capacity of 30mn meters per year. Meanwhile, Taiwan’s Formosa Group injected USD500mn in the garment factory in the Nhon Trach IP and is planning to invest an additional USD400mn into expanding its production capacity. Malaysia’s Parmatex Berhad plans to invest USD100mn in a garment factory in the Chu Lai Economic Zone. In Feb 2007, three projects were launched in the Pho Noi B Textile and Garment industrial Zone. The Pho Noi Knitting centre, The Ha Noi Thread Factory and the Waste Water Treatment centre were newly launched by Vietnam textile and garment group (Vinatex) with a combined capital of VND282bn, aimed at addressing the problem of inadequate infrastructure and water treatment systems. Vinatex management expects these projects to meet the growing demand in the export market. Vinatex is targeting a revenue of USD900mn in 2007 (17% yoy) and an export revenue of USD1.5bn, an 18% yoy increase.

Infant industry

Textile and garments are

Vietnam’s second most

important export item

12 April 2007 Strategy Vietnam Primer Part II

Deutsche Bank AG/Hong Kong Page 27