CMC Corp (CMG VN)

13

ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ARE LOCATED IN APPENDIX A. Yuanta does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Share price performance relative to VNI Market cap US$262mn 6M avg. daily turnover US$210k Outstanding shares 100mn Free float 53% FINI ownership 38.9% Major shareholders 48.5% P/E TTM 31.2x P/B Current 3.0x Trading platform HOSE FOL Room 10.1% Financial outlook (VND bn) Year to Dec 2019A 2020A 1H20A 1H21A Sales 5,032 4,924 2,132 2,632 Op. profit 261 244 76 105 Net profit 137 171 52 73 EPS (VND) 1,368 1,701 n.m. n.m. EPS chg (%) (28.5) 24.4 n.m. n.m. P/E TTM (x) 43.6 35.0 n.m. n.m. CMC Corp (CMG VN) An under-covered cloud computing play The second largest technology solution provider. CMG is an ICT services provider focused on telecommunications (cloud computing & data centers) and technology solutions (system integration & digitalization). CMG is among Vietnam’s top four data service providers and is the second largest listed ICT firm by market cap, after FPT (Not rated). Digital transformation market has ample room for growth. The total number of companies in Vietnam has posted 8.2% CAGR in 2011-2020 to reach 800K firms. The government projects this figure to reach 1.3- 1.5 mn by 2025, representing a solid runway for the growth of digital transformation services. In the short-term, IDC forecasts Vietnam’s IT services market to grow by 10.3% YoY in 2021 to reach USD 636mn, with software services to rise 13.1% YoY to reach USD 564mn. Specific catalyst: CMG is expanding its cloud service capacity with a VND 1.5tn investment in two state-of-the-art data centers: a 1,200-rack data center in HCMC in Dec 2021, and another one in Hanoi to be launched in Feb 2022. The additional capacity amid growing demand appears to be a sensible strategy that should enable CMG to expand its cloud computing/telecommunication service revenues. Ambitious projections. CMG guides for 2021 revenue growth of 20% YoY to reach VND6.1tn and PBT by 11% YoY to reach VND324bn. CMG plans to expand in the global market, with revenue projected to grow to USD1bn by 2025, equivalent to 36% CAGR in 2020-2025. This would substantially outpace the World Bank’s 16% industry CAGR forecast. Valuations: CMG is trading at 31.2x trailing PE, which is significantly higher than the regional peer’s median of 18.6x. This may be justified given CMG’s ambitious growth strategy in cloud computing, as underpinned by its substantial investments in data center capacity. Unrated Company Report Vietnam: Industrials 21 October 2021 CMG VN Not Rated Close 20 October 2021 Price VND 59,600 12M Target N/A What’s new? ► CMG is the second largest domestic technology solutions provider in Vietnam. ► CMG projects 36% revenue CAGR in 2020- 2025 on the back of expanding market and business capacity. ► CMG is expanding its telecommunication capacity by adding two data centers in HCMC and Hanoi with total investment of VND1 trillion (US$44mn). Key inferences ► Demand for digital transformation services is soaring and will continue to rise in the years ahead. ► As Vietnam’s second largest technology service provider, CPG appears to be well-positioned to capture the growing domestic and international demand. ► In contrast to sector leader FPT, CMG is not well covered by the Street (yet), and the stock has ample FOL room (for now). Company profile: CMC Corp (HSX: CMG) is a provider of digital products and services, with a core strength in digital transformation solutions. As Vietnam’s second-largest listed IT sector firm by market capitalization, we think the stock should be of interest to clients seeking exposure to the country’s burgeoning IT industry, especially considering the stock’s c. US$27mn of FOL room (for now). Samsung SDS is CMG’s largest shareholder. Source: Bloomberg, Fiinpro Research Analysts: Binh Truong +84 28 3622 6868 ext 3845 Binh.truong@yuanta.com.vn http://yuanta.com.vn Bloomberg code: YUTA

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of CMC Corp (CMG VN)

ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ARE

LOCATED IN APPENDIX A. Yuanta does and seeks to do business with companies covered in its

research reports. As a result, investors should be aware that the firm

may have a conflict of interest that could affect the objectivity of this

report. Investors should consider this report as only a single factor in

making their investment decision.

Share price performance relative to VNI

Market cap US$262mn

6M avg. daily turnover US$210k

Outstanding shares 100mn

Free float 53%

FINI ownership 38.9%

Major shareholders 48.5%

P/E TTM 31.2x

P/B Current 3.0x

Trading platform HOSE

FOL Room 10.1%

Financial outlook (VND bn)

Year to Dec 2019A 2020A 1H20A 1H21A

Sales 5,032 4,924 2,132 2,632

Op. profit 261 244 76 105

Net profit 137 171 52 73

EPS (VND) 1,368 1,701 n.m. n.m.

EPS chg (%) (28.5) 24.4 n.m. n.m.

P/E TTM (x) 43.6 35.0 n.m. n.m.

CMC Corp (CMG VN)

An under-covered cloud computing play

The second largest technology solution provider. CMG is an ICT services

provider focused on telecommunications (cloud computing & data

centers) and technology solutions (system integration & digitalization).

CMG is among Vietnam’s top four data service providers and is the

second largest listed ICT firm by market cap, after FPT (Not rated).

Digital transformation market has ample room for growth. The total

number of companies in Vietnam has posted 8.2% CAGR in 2011-2020

to reach 800K firms. The government projects this figure to reach 1.3-

1.5 mn by 2025, representing a solid runway for the growth of digital

transformation services. In the short-term, IDC forecasts Vietnam’s IT

services market to grow by 10.3% YoY in 2021 to reach USD 636mn,

with software services to rise 13.1% YoY to reach USD 564mn.

Specific catalyst: CMG is expanding its cloud service capacity with a VND

1.5tn investment in two state-of-the-art data centers: a 1,200-rack

data center in HCMC in Dec 2021, and another one in Hanoi to be

launched in Feb 2022. The additional capacity amid growing demand

appears to be a sensible strategy that should enable CMG to expand its

cloud computing/telecommunication service revenues.

Ambitious projections. CMG guides for 2021 revenue growth of 20% YoY

to reach VND6.1tn and PBT by 11% YoY to reach VND324bn. CMG plans

to expand in the global market, with revenue projected to grow to

USD1bn by 2025, equivalent to 36% CAGR in 2020-2025. This would

substantially outpace the World Bank’s 16% industry CAGR forecast.

Valuations: CMG is trading at 31.2x trailing PE, which is significantly

higher than the regional peer’s median of 18.6x. This may be justified

given CMG’s ambitious growth strategy in cloud computing, as

underpinned by its substantial investments in data center capacity.

Unrated Company Report

Vietnam: Industrials 21 October 2021

CMG VN

Not Rated

Close 20 October 2021

Price VND 59,600

12M Target N/A

What’s new?

► CMG is the second largest domestic

technology solutions provider in Vietnam.

► CMG projects 36% revenue CAGR in 2020-

2025 on the back of expanding market and

business capacity.

► CMG is expanding its telecommunication

capacity by adding two data centers in

HCMC and Hanoi with total investment of

VND1 trillion (US$44mn).

Key inferences

► Demand for digital transformation services is

soaring and will continue to rise in the years ahead.

► As Vietnam’s second largest technology service

provider, CPG appears to be well-positioned to

capture the growing domestic and international

demand.

► In contrast to sector leader FPT, CMG is not well

covered by the Street (yet), and the stock has ample

FOL room (for now).

Company profile: CMC Corp (HSX: CMG) is a provider of digital products and services, with a core strength in digital transformation solutions. As

Vietnam’s second-largest listed IT sector firm by market capitalization, we think the stock should be of interest to clients seeking exposure to the

country’s burgeoning IT industry, especially considering the stock’s c. US$27mn of FOL room (for now). Samsung SDS is CMG’s largest shareholder.

Source: Bloomberg, Fiinpro

Research Analysts:

Binh Truong

+84 28 3622 6868 ext 3845

http://yuanta.com.vn

Bloomberg code: YUTA

CMG: the second largest technology

solution provider

Provider of integrated services. CMC Corp provides a range of ICT services including

telecom (cloud computing, data centers, internet, and other data services),

technology solutions (system integration, digital transformation, security, IT

services, smart production). Major domestic clients markets include substantial

firms in the banking sector (e.g. PVcombank), government sector, and large private

sector corporations (e.g., HPG). The company targets substantial growth from the

global market; it currently exports software outsourcing/IT/cloud services. Japan

and Korea are its largest markets, and management aims to expand sales to

Southeast Asia, the US, and EU.

Fig. 1: FY2020 Revenue mix Fig. 2: FY2020 Profit before tax composition

Source: CMG, Yuanta Vietnam Source: CMG, Yuanta Vietnam

IDC estimates that Vietnam’s IT services market will reach USD 636mn in 2021, an

increase of 10.3% YoY. Seeking to capture this growth, CMG has expanded its

technology solutions capacity by launching its securities operation center (SOC)

which offers technologies from IBM and Samsung as well as CMB’s in-house

solutions. Based on IDC’s estimates, CMG’s technology solutions account for about

24.5 % of market share, just behind FPT’s dominant 37% market share. CMG is also

the second largest ICT company in terms of market capitalization in Vietnam.

Transparency on the market value of cloud computing (a component of CMG’s

telecommunication services segment) is unfortunately very limited. Our admittedly

rough understanding is that the Big 3 foreign players (i.e., AWS (Amazon), Azure

(Microsoft), and Google Cloud) account for approximately 80% of total cloud

revenues in Vietnam. This is actually higher than the three tech giants’ global

market share of roughly 60%.

However, CMG’s management considers themselves to be the market leader in this

field amongst domestic cloud providers. Specifically, the company offers a complete

software-as-a-service (SaaS) package for cloud computing. This package enables

the management of applications, data, operating systems, storage, and networking.

Using outsourced SaaS solutions means that client firms do not need to develop

their own internal IT capabilities, thus allowing them to simply focus on developing

their core business.

Fig. 3: CMG provides cloud computing and SaaS services

Source: bigcommerce.com

CMG plans to expand its cloud computing capacity by investing VND 1.5tn in two

tier-3 data centers in Ho Chi Minh City (expected launch: December 2021) and

Hanoi (to be launched in 2022). The tier-3 designation indicates the second-highest

level of data center complexity, with substantial power, cooling, and other

infrastructure redundancies leading to total expected annual downtime of just 1.6

hours.

The telecommunication segment is CMG’s most profitable business with PBT margin

of 12%-13% in the past 4 years. Based on our discussions with senior industry

managers, very few Vietnamese companies offer cloud computing facilities due to

the substantial investment required to develop them. This represents a high entry

barrier.

Currently, just four domestic companies provide tier 3 data centers: VNPT, FPT,

Viettel, and CMC. Technically, a Tier 3 data center has multiple paths for power and

cooling and systems in place to update and maintain it without taking it offline. By

expanding its tier-3 data centers, we believe that CMG is in a solid position to

capture the growing demand for cloud services in Vietnam.

Strategic shareholder potentially offers additional benefits. Samsung SDS (0018620

KS, Rated BUY by Yuanta Korea analyst Lee Chang-Young) is CMG’s largest

shareholder with a 30% stake. Samsung SDS is a global digital transformation

services provider. We consider it to be a strong strategic partner for CMG as the

latter firm expands its business capacity and seeks to broaden its global market

share in the years ahead, especially in Korea, Japan, and South East Asia.

ICT sector: Ample room for growth in

Vietnam

We expect Vietnam’s Internet economy to post strong growth over the next several

years. Vietnam boasts the largest proportion of online shoppers in Southeast Asia,

with 53% of the population (49.3 million individuals) shopping online in 2020,

according to the Vietnam E-Commerce and Digital Economy Agency (IDEA).

The World Bank estimates that Vietnam’s e-commerce market reached USD 11.8bn

or 2.5% GDP in 2020, and it forecasts market CAGR of 16% in 2020-25E. This is

dwarfed by the Vietnam government’s forecast of 23.9% for the same period, with

the market value expected to reach USD35bn in 2025. Regardless, both forecasts

are significantly higher than a screen of global e-commerce sales growth forecasts,

which range from 7% to 12% CAGR.

This fast-growing market should attract firms to join the digital transformation

trend as they seek to capture market share.

Fig. 4: Vietnam’s e-commerce sales value should outgrow that of the world

over the next several years

Source: World Bank estimates

Digital transformation market has ample room for growth. The number of registered

companies in Vietnam has posted CAGR of 8.2% in 2011-2020 to reach 800k firms

as of end-2020. But Vietnam also has 5.4 million sole proprietor businesses, which

have potential to grow and become limited companies over time. The government

targets 1.3mn to 1.5 mn companies by 2025.

The World Bank estimates that the use of digital platforms is associated with 4.3%

growth in sales after controlling for firm size, location, and sector. Thus, the

increasing number of companies represents solid potential for digital

transformation service providers, including listed ICT firms such as FPT Corp (FPT

VN, Not rated) and CMG.

Fig. 5: Growth potential

Source: World Bank estimates for 2011-2020, Vietnam government target for 2025E

Government support for digital transformation. The government has clearly

indicated that it wants Vietnam to be in the race by emphasizing digital

transformation as one of the core objectives of its 2021–2030 National Development

Strategy. The Prime Minister has set the rather ambitious goal for Vietnam to rank

among the world’s 50 leading countries in IT development by 2025. The number of

government digital services has increased by tenfold from Feb 2020 to April 2021,

albeit from a low base, and the authorities have adopted accommodative policies to

support the digital transformation of state-owned enterprises.

Digital transformation is further triggered by the pandemic. Needless to say, Covid-

19 has changed the way we work, study, and live. Online consumer spending has

blossomed during the pandemic (and the related lockdowns) allowing online

platforms to gain market share, including MWG’s Bach Hoa Xanh and MSN’s Vinmart.

The pandemic has reinforced and hasten the need for businesses to adapt to the

changed environment. Digital transformation thus offers superior sales growth with

enhanced consumer satisfaction and cost savings by allowing retailers to ship goods

directly from factories, thus lowering overhead and labor costs while increasing

convenience. Experts suggest that the growth of cloud services rather than

expensive in-house development is inevitable because it is cheaper and requires

less resources to scale up core business capacities.

Short-term growth sector growth. According to IDC, the total size of Vietnam’s ICT

market should reach USD8.3bn in 2021, an increase of 6.7% YoY. Within the broad

ICT market, software services should grow by 13.1% YoY to reach USD 563mn in

2021; and IT services should expand by 10.3% YoY to reach USD 636.3mn,

according to IDC.

Fig. 6: Software revenue to outgrow others items in 2021

Source: IDC

.

Techonology group

(USD mn) 2018 2019 2020 2021

2021 YoY

growth

Hardware 6,187 6,482 6,868 7,118 3.6%

IT services 465 520 577 636 10.3%

Software 391 442 499 564 13.1%

IT total 7,042 7,443 7,944 8,318 4.7%

Financial snapshot

Profit margin is improving. Although CMG’s 2020 revenue slowed due to the impact

of Covid-19, the company posted a record high profit margin. This was mainly

attributable to a shift in the product mix in favor of high-margin telecommunication

revenues. CMG’s telecommunication segment typically has the highest PBT margin

of 12.1%, compared to the company’s overall blended PBT margin of 5.8%.

Fig. 7: Profit margin is expanding Fig. 8: Revenue mix

Source: CMG, Yuanta Vietnam Source: CMG, Yuanta Vietnam

Aggressive capex to facilitate future growth. ROE has decelerated over the last three

years, mainly becuase of declining asset turnover as CMG invested heavily in its new

IT facilities (i.e., the VND1.5 trillion state-of-the-art office building and data centers

in HCMC).

Fig. 9: Dupont Analysis Fig. 10: Liquidity ratios are safe and stable

Source: CMG, Yuanta Vietnam Source: CMG, Yuanta Vietnam

CMG’s cash conversion cycle is stable despite lengthened recievables period, as it

has been offset by the increase in payable days outstanding. The company’s free

cash flow has been volatile and was negative in 2019, primarily due to its investment

in the new facilities.

Fig. 11: Cash conversion cycle remains stable Fig. 12: Free cash flow

Source: CMG, Yuanta Vietnam Source: CMG, Yuanta Vietnam

YTD Operational review: Growth is sailing on the Cloud

2Q21 revenue increased by 23% YoY to VND1,301bn. Gross profit margin slightly

slid to 18.1%, down from 18.3% in 2Q20. Operating expenses rose by 12% YoY to

VND172.2bn, but SG&A/Revenue ratio stood at 13.2%, 1.3 ppt below that of 2Q20.

2Q21 PATMI rose by 13.2% YoY to VND 44.1bn.

6M21 revenue increased by 23.5% YoY to VND 2,632bn. Although gross profit

margin contracted to 15.9% from 18.6% in 6M20, net profit reached VND 107.3bn,

up by 29.2% YoY, so net profit growth outpaced that of revenues. This is mainly

attributable to the efficient control of operating costs, as 6M21 SG&A expenses

declined by 2.3% YoY.

In 1H21, CMG fulfilled 39% of its 2021 PAT guidance of VND275bn.

Fig. 13: CMG saw improvement in financial performance in 6M21

Source: CMG

Key metric (VND bn) 2Q20 2Q21 6M20 6M21

Revenue 1,058 1,301 2,132 2,632

Revenue growth (%) -4.4% 23.0% -12.3% 23.5%

Gross profit margin (%) 18.3% 18.1% 18.6% 15.9%

Operating profit 40.1 62.7 75.9 105.0

PATMI 28.4 44.1 52.0 72.6

Valuation and Risks

Valuation

CMG is trading at 31.2x trailing PE, which is significantly higher than the regional

peer’s median of 18.6x. This is potentially justifiable given that CMG has

aggressively invested in the new facilities to enable future growth. Management

guides for 36% revenue CAGR in 2020- 2025. From a different perspective, CMG is

trading at just 1.1x trailing sales, which is significantly lower than the regional peers’

median of 2.9x.

Available room for foreign investor. Foreign investors currently hold 38.9% of CMG,

which leaves 10.1% foreign room. In contrast to the sector leader FPT, foreign clients

do not have to pay an FOL premium to buy shares in CMG. As illustrated in Fig 13,

FPT is cheaper on a trailing PE (23x vs. CMG’s 31x) and EV/EBITDA bases (9.7x vs

CMG’s 15.7x). This is wonderful if you’re a domestic investor (or married to one).

For foreign investors, the discussion on the “market’s” valuation is relevant when

considering CMG, but the decision on FPT is complicated by the need to factor in

an FOL premium (and what may be a very prolonged settlement period – and

relatively recent experience indicates that this settlement period can be longer than

one might normally expect).

Fig. 13: CMG is trading at 1.1 x Sales, which is significantly lower than the regional peers’ median

Source: Bloomberg

Samsung SDS Asia Pacific Pte. Ltd, a global player in digital transformation, is

currently CMG’s largest shareholder with a 30% stake. CMG expects the partnership

will help companies to expand the business capacity and broaden the market

overseas such as Korea, Japan, South East Asia, EU, North America. Another 8.9% of

the company is in the hands of other foreign investors, but this still leaves plenty

of FOL room.

Risks

Covid-19 has clearly impacted the operations of CMG’s clients and the company

itself. The restrictions in HCMC have been loosened, but they may still impact the

launch of the new data center in the city. COVID may also impact the financial

stability and liquidity of clients and thus the drive to adopt new technology. It may

also impact CMG’s ability to acquire new contracts.

Ticker Name Mkt Cap

(VND)

ROE

(%)

ROA

(%)

Net D/E

(x)

P/E (x) P/B (x) EV /

EBITDA

(X)

P/S (X)

FPT VM Equity FPT CORPORATION 88,569 5.3 2.4 39.7 23.1 5.3 9.7 2.7

300645 CH EquityZHEJIANG ZHENGYUAN ZHIHUI -A 9,689 5.3 2.4 39.7 75.4 4.0 52.6 3.1

RSYS IN Equity R SYSTEMS INTERNATIONAL LTD 7,843 -69.3 N/A 5.5 11.9 N/A

600289 CH EquityBRIGHT OCEANS INTER-TELECO-A7,702 -27.9 -12.9 -40.2 N/A 1.4 N/A 4.0

300588 CH EquityXINJIANG SAILING INFORMATI-A 7,403 -27.7 -10.9 12.1 N/A 7.0 N/A 7.6

003007 CH EquityBEIJING ZZNODE TECHNOLOGIE-A6,162 9.8 8.0 -65.0 21.2 1.9 29.2 3.2

DATA IN Equity DATAMATICS GLOBAL SERVICES5,838 11.4 8.3 -33.3 24.1 2.7 4.7 1.7

AIT TB Equity ADVANCED INFORMATION TECHNOL5,562 19.3 8.0 27.9 15.1 2.8 6.5 1.0

NCS IN Equity NUCLEUS SOFTWARE EXPORTS LTD5,174 19.1 14.3 -73.9 14.4 2.5 7.8 3.3

CIGN IN Equity CIGNITI TECHNOLOGIES LTD 5,128 32.9 20.8 -43.7 15.9 4.5 5.4 1.9

1075 HK Equity CAPINFO CO LTD-H 4,834 11.9 5.4 -63.3 10.2 1.2 N/A 1.0

PIA VH Equity PETROLIMEX INFORMATION 109 5.3 2.4 39.7 8.0 2.0 5.0 0.8

DAD VH Equity DANANG EDUCATION 108 5.3 2.4 39.7 9.1 1.3 2.7 N/A

VLA VH Equity VAN LANG TECHNOLOGY 20 5.3 2.4 39.7 N/A 1.6 N/A 3.1

Median 5,700 5.3 2.4 -10.6 18.6 2.6 7.1 2.9

CMG VN Equity CMC CORP 5,960 9.7 3.7 -2.9 31.2 3.0 15.7 1.1

2021 profit guidance now looks aggressive and may be missed. CMG only fulfilled

39% of its annual profit guidance in 1H21, and this was before the tightened

mobility and other restrictions were adopted in 3Q21. CMG’s profit has been highly

seasonal, with peak levels typically in 3Q and 4Q in most years. However, CMG is at

risk of missing its annual guidance for 2021 given the widespread lockdowns in

3Q21.

Low trading liquidity and smallish market cap may keep the stock off the radar

screen of sell-side analysts (current coverage is nonexistent as far as we know) and

institutional investors. On the other hand, this low visibility may also represent an

opportunity.

Fig. 14: Financial performance typically peaks in the Fourth Quarter (VND bn)

Source: CMG

Competition in cloud computing is intense. Giant multinational companies such as

Amazon (AWS), Azure, and Google dominate the Vietnam market, and the IT market

leader, FPT, is clearly a strong competitor in this area as well. CMG has invested

heavily in the new data centers to enhance its own competitiveness and to capture

domestic market share. We believe that growth in the overseas business provides

additional upside potential, and evidence of meaningful traction in this business

could catalyze the share price.

Skilled human resources are in high demand. Competition is fierce among

companies seeking ICT talent. This is a global issue that is being driven by global

operators who may be less likely to quibble over a few million VND per month than

the traditional Vietnam manager would be. We expect this chase for IT talent to

continue, and the costs of acquiring and retaining qualified staff are very likely to

expand rapidly going forward.

PROFIT AND LOSS (VND bn) BALANCE SHEET (VND bn)

FY Dec 31 (VND’bn) 2017A 2018A 2019A 2020A FY Dec 31 (VND’bn) 2017A 2018A 2019A 2020A

Revenue 4,892 4,956 5,032 4,924 Total assets 3,121 3,594 4,724 5,101

Technology solution 3,006 3,459 3,112 3,106 Cash & cash equivalents 356 193 270 361

Telecommunication 1,445 1,690 1,903 2,032 ST Investment 168 224 1,089 1,069

Overseas business 87 170 252 413 Accounts receivable 1,009 1,344 1,253 1,264

Others 796 363 114 114 Inventories 238 267 294 202

Cost of goods sold (4,137) (4,167) (4,116) (3,999) Other current assets 135 151 137 159

Gross profits 755 789 916 925 Net fixed assets 767 1,067 1,112 1,183

Operating expenses (525) (575) (655) (682) Others 448 348 570 863

Operating profits 230 214 261 244 Total liabilities 1,852 2,223 2,461 2,756

Net interest expenses (11) (22) (20) 13 Current liabilities 1,648 1,878 1,687 2,008

Net investments income/(loss) 17 19 25 21 Accounts payable 564 615 478 699

Net other incomes 16 21 1 6 ST debts 450 430 437 554

Pretax profits 252 232 267 283 Long-term liabilities 204 345 774 748

Income taxes (36) (44) (48) (47) Long-term debts 11 293 720 689

Minority interests 43 50 82 66 Others 193 52 54 59

Net profits 173 138 137 171 Shareholder's equity 1,269 1,370 2,263 2,345

Core earnings 173 138 137 171 Share capital 673 721 1,000 1,000

EBITDA 356 371 441 458 Treasury stocks - - - -

EPS (VND) 2,567 1,912 1,368 1,701 Others 112 135 135 133

KEY RATIOS Retained earnings 169 165 178 227

KEY RATIOS Minority interest 281 316 351 385

2017A 2018A 2019A 2020A

Growth (% YoY) CASH FLOW (VND bn)

Sales 1.3 1.5 (2.1) FY (VND’bn) 2017A 2018A 2019A 2020A

Technology solution 15.1 (10.0) (0.2)

Telecommunication 17.0 12.6 6.8 Operating cash flow 422 330 1,212 3,382

Overseas business 94.7 47.9 64.1 Net income 173 138 137 171

Others (54.4) (68.5) (0.2) Dep, & amortisation 126 156 173 209

Operating profit (7.0) 21.9 (6.5) Change in working capital (2) (130) (121) 263

EBITDA 4.3 18.7 4.0 Others 125 166 1,023 2,739

Net profit (20.3) (0.7) 24.8 Investment cash flow (229) (719) (2,415) (3,276)

EPS (VND) (25.5) (28.5) 24.4 Net capex (261) (363) (405) (3,021)

Profitability ratio (%) Change in LT investment (42) (199) (267) (365)

Gross margin 15.4 15.9 18.2 18.8 Change in other assets 74 (157) (1,743) 110

Operating margin 4.7 4.3 5.2 5.0 Cash flow after invt. 192 (390) (1,203) 106

EBITDA margin 7.3 7.5 8.8 9.3 Financing cash flow 4 226 1,280 (14)

Net margin 3.5 2.8 2.7 3.5 Change in share capital 20 47 845 -

ROA 6.2 4.1 3.3 3.5 Net change in debt 66 262 435 86

ROE 14.3 10.4 7.5 7.4 Change in other LT liab. (81) (83) - (100)

Stability Net change in cash flow 196 (163) 77 91

Net debt/equity (x) -5.0 22.3 -8.9 -8.0 Beginning cash flow 160 356 193 270

Int. coverage (x) 8.2 5.2 4.2 3.0 Ending Cash Balance 356 193 270 361

Int. &ST debt coverage (x) 0.7 0.5 0.7 0.6

Cash conversion days 41.2 50.8 62.9 54.1 KEY METRICS

Current ratio (X) 1.2 1.2 1.8 1.5 2017A 2018A 2019A 2020A

Quick ratio (X) 1.0 1.0 1.6 1.4 PE (x) 23 31 44 35

Net cash/(debt) (VND mn) 64 (306) 201 187 Diluted PE (x) 23.2 31.2 43.6 35.0

Efficiency PB (x) 3.2 3.1 2.6 2.5

Days receivable outstanding 61 80 86 85 EBITDA/share 5,288 5,152 4,407 4,585

Days inventory outstanding 19 22 25 23 DPS 800 700 1,000 -

Days payable outstanding 39 52 48 54 Dividend yield (%) 1.3 1.2 1.7 -

EV/EBITDA (x) 11.1 12.4 13.1 12.6

Source: Company data, YSVN EV/EBIT (x) 17.2 21.5 22.1 23.7

Appendix A: Important Disclosures

Analyst Certification

Each research analyst primarily responsible for the content of this research report, in whole or in part, certifies that with respect

to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal

views about those securities or issuers; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related

to the specific recommendations or views expressed by that research analyst in the research report.

Ratings Definitions

BUY: We have a positive outlook on the stock based on our expected absolute or relative return over the investment period. Our

thesis is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile. We

recommend investors add to their position.

HOLD-Outperform: In our view, the stock’s fundamentals are relatively more attractive than peers at the current price. Our thesis

is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile.

HOLD-Underperform: In our view, the stock’s fundamentals are relatively less attractive than peers at the current price. Our thesis

is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile.

SELL: We have a negative outlook on the stock based on our expected absolute or relative return over the investment period. Our

thesis is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile. We

recommend investors reduce their position.

Under Review: We actively follow the company, although our estimates, rating and target price are under review.

Restricted: The rating and target price have been suspended temporarily to comply with applicable regulations and/or Yuanta

policies.

Note: Yuanta research coverage with a Target Price is based on an investment period of 12 months. Greater China Discovery Series

coverage does not have a formal 12 month Target Price and the recommendation is based on an investment period specified by

the analyst in the report.

Global Disclaimer © 2019 Yuanta. All rights reserved. The information in this report has been compiled from sources we believe to be reliable, but

we do not hold ourselves responsible for its completeness or accuracy. It is not an offer to sell or solicitation of an offer to buy

any securities. All opinions and estimates included in this report constitute our judgment as of this date and are subject to change

without notice.

This report provides general information only. Neither the information nor any opinion expressed herein constitutes an offer or

invitation to make an offer to buy or sell securities or other investments. This material is prepared for general circulation to clients

and is not intended to provide tailored investment advice and does not take into account the individual financial situation and

objectives of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness

of investing in any securities, investments or investment strategies discussed or recommended in this report. The information

contained in this report has been compiled from sources believed to be reliable but no representation or warranty, express or

implied, is made as to its accuracy, completeness or correctness. This report is not (and should not be construed as) a solicitation

to act as securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on such

business in that jurisdiction.

Yuanta research is distributed in the United States only to Major U.S. Institutional Investors (as defined in Rule 15a-6 under the

Securities Exchange Act of 1934, as amended and SEC staff interpretations thereof). All transactions by a US person in the

securities mentioned in this report must be effected through a registered broker-dealer under Section 15 of the Securities Exchange

Act of 1934, as amended. Yuanta research is distributed in Taiwan by Yuanta Securities Investment Consulting. Yuanta research is

distributed in Hong Kong by Yuanta Securities (Hong Kong) Co. Limited, which is licensed in Hong Kong by the Securities and

Futures Commission for regulated activities, including Type 4 regulated activity (advising on securities). In Hong Kong, this

research report may not be redistributed, retransmitted or disclosed, in whole or in part or and any form or manner, without the

express written consent of Yuanta Securities (Hong Kong) Co. Limited.

Taiwan persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Attn: Research

Yuanta Securities Investment Consulting

4F, 225,

Section 3 Nanking East Road, Taipei 104

Taiwan

Hong Kong persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Attn: Research

Yuanta Securities (Hong Kong) Co. Ltd

23/F, Tower 1, Admiralty Centre

18 Harcourt Road,

Hong Kong

Korean persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Head Office

Yuanta Securities Building

Euljiro 76 Jung-gu

Seoul, Korea 100-845

Tel: +822 3770 3454

Indonesia persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Attn: Research

PT YUANTA SECURITIES INDONESIA

(A member of the Yuanta Group)

Equity Tower, 10th Floor Unit EFGH

SCBD Lot 9

Jl. Jend. Sudirman Kav. 52-53

Tel: (6221) – 5153608 (General)

Thailand persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Research department

Yuanta Securities (Thailand)

127 Gaysorn Tower, 16th floor

Ratchadamri Road, Pathumwan

Bangkok 10330

Vietnam persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Research department

Yuanta Securities (Vietnam)

4th Floor, Saigon Centre

Tower 1, 65 Le Loi Boulevard,

Ben Nghe Ward, District 1, HCMC, Vietnam

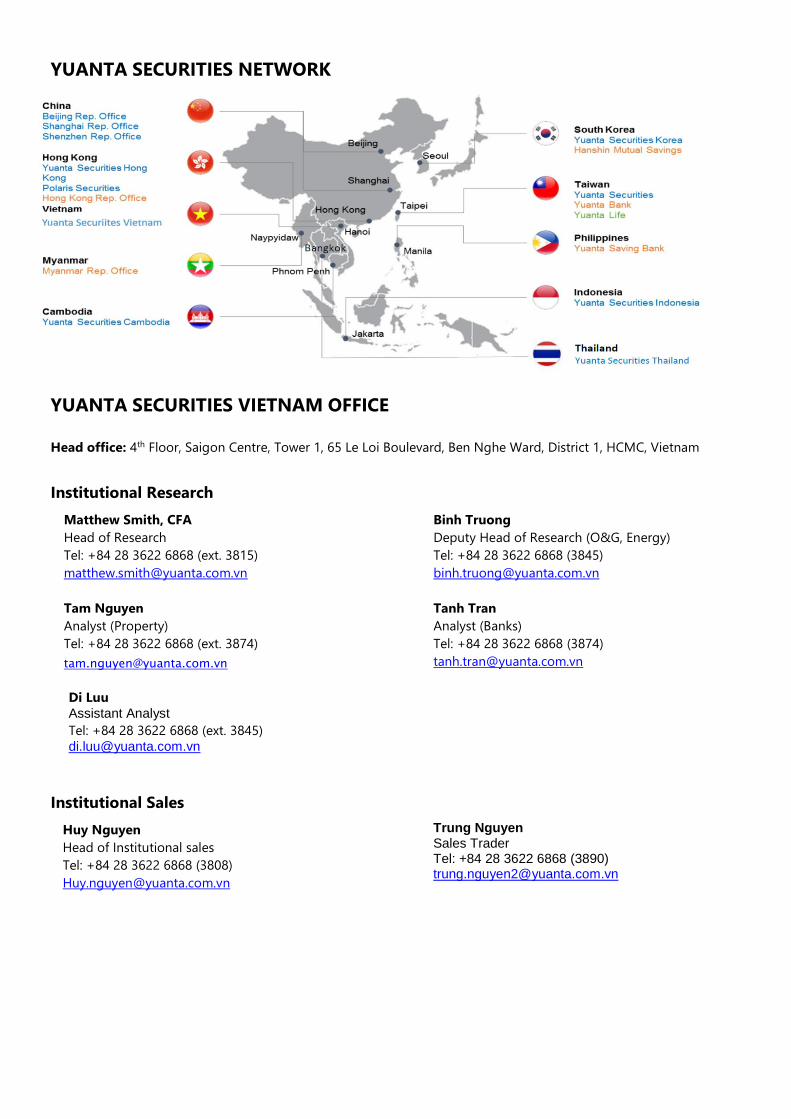

YUANTA SECURITIES NETWORK

YUANTA SECURITIES VIETNAM OFFICE

Head office: 4th Floor, Saigon Centre, Tower 1, 65 Le Loi Boulevard, Ben Nghe Ward, District 1, HCMC, Vietnam

Institutional Research

Matthew Smith, CFA

Head of Research

Tel: +84 28 3622 6868 (ext. 3815)

Binh Truong

Deputy Head of Research (O&G, Energy)

Tel: +84 28 3622 6868 (3845)

Tam Nguyen

Analyst (Property)

Tel: +84 28 3622 6868 (ext. 3874)

Tanh Tran

Analyst (Banks)

Tel: +84 28 3622 6868 (3874)

Di Luu

Assistant Analyst

Tel: +84 28 3622 6868 (ext. 3845)

Institutional Sales

Huy Nguyen

Head of Institutional sales

Tel: +84 28 3622 6868 (3808)

Trung Nguyen Sales Trader Tel: +84 28 3622 6868 (3890) [email protected]

![[kenhxaydung vn] - COFFA MAIKHOANAM](https://static.fdokumen.com/doc/165x107/631a6c43bb40f9952b01fff5/kenhxaydung-vn-coffa-maikhoanam.jpg)

![[123doc vn] - phan tich swot vinamilk nhom 1](https://static.fdokumen.com/doc/165x107/631a8092fd704e1d390a28a2/123doc-vn-phan-tich-swot-vinamilk-nhom-1.jpg)