UWI (MONA) & COMMUNITY CO-OPERATIVE CREDIT ...

63

UWI (MONA) & COMMUNITY CO-OPERATIVE CREDIT UNION LIMITED FINANCIAL STATEMENTS 31 DECEMBER 2014

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of UWI (MONA) & COMMUNITY CO-OPERATIVE CREDIT ...

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

FINANCIAL STATEMENTS

31 DECEMBER 2014

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

FINANCIAL STATEMENTS

31 DECEMBER 2014

I N D E X Page Independent Auditors' Report to the Registrar 1 - 2 FINANCIAL STATEMENTS Statement of Comprehensive Income 3 Statement of Financial Position 4 - 5 Statement of Changes in Equity 6 - 8 Statement of Cash Flows 9 Notes to the Financial Statements 10 - 61

Page 1 INDEPENDENT AUDITORS’ REPORT To: The Registrar of Co-operative and Friendly Societies Re: UWI (Mona) & Community Co-operative Credit Union Limited Report on the Financial Statements

We have audited the financial statements of UWI (Mona) & Community Co-operative Credit Union Limited set out on pages 3 to 61 which comprise the statement of financial position as at 31 December 2014 and the statements of comprehensive income, changes in equity and cash flows for the year then ended and a summary of significant accounting policies and other explanatory notes. Management Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and the Co-operative Societies Act, and for such internal control as management determines is necessary to enable the preparation of the financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors‟ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal controls relevant to the Credit Union‟s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Credit Union‟s internal controls. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Page 2 INDEPENDENT AUDITORS’ REPORT (CONT’D) To: The Registrar of Co-operative and Friendly Societies Re: UWI (Mona) & Community Co-operative Credit Union Limited Opinion In our opinion, the financial statements give a true and fair view of the Credit Union‟s financial position at 31 December 2014 and of its financial performance, changes in equity and its cash flows for the year then ended in accordance with International Financial Reporting Standards and comply with the provisions of the Co-operative Societies Act. Report on additional requirements of the Co-operative Societies Act. We have obtained all information and explanations which, to the best of our knowledge and belief, were necessary for the purpose of our audit. In our opinion, proper accounting records have been kept, and the financial statements, which are in agreement therewith, give the information required by the Act, in the manner so required. Chartered Accountants

30 March 2015

________________________________

Page 3

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF COMPREHENSIVE INCOME

YEAR ENDED 31 DECEMBER 2014

Note 2014 2013 $’000 $’000 INTEREST INCOME: Loans to members 184,798 167,591 Liquid assets 1,747 4,988 Financial investments 3,579 4,232 Reverse repurchase agreements 7,095 8,235 197,219 185,046 INTEREST EXPENSE AND OTHER FINANCIAL COSTS: Members deposits 48,161 43,218 Members‟ voluntary shares 11,786 11,287 Other financial costs 8,622 1,579 68,569 56,084 NET INTEREST INCOME 128,650 128,962 Provision for loan impairment 11 ( 2,174) ( 822) NET INTEREST INCOME AFTER PROVISION FOR LOAN IMPAIRMENT 126,476 128,140 Cambio gain 1,864 4,207 Non-interest income 7 38,716 47,946 NET INTEREST AND OTHER INCOME 167,056 180,293 OPERATING EXPENSES 8 155,608 146,026 NET SURPLUS FOR THE YEAR 11,448 34,267 OTHER COMPREHENSIVE INCOME: Item that may be reclassified to surplus Unrealised losses arising on financial instruments ( 570) ( 668) Item that will not be reclassified to surplus Gain on revaluation of property 38,820 - - TOTAL COMPREHENSIVE INCOME FOR THE YEAR 49,698 33,599

Page 4

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF FINANCIAL POSITION

31 DECEMBER 2014 Note 2014 2013 $’000 $’000 ASSETS NON-CURRENT ASSETS: Earning: Financial investments 10 43,238 43,825 Loans, after provision for loan impairment 11 1,762,305 1,244,576 1,805,543 1,288,401 Non-Earning: Property, plant and equipment 12 93,516 59,374 TOTAL NON-CURRENT ASSETS 1,899,059 1,347,775 CURRENT ASSETS: Earnings Assets: Liquid assets 13 49,389 49,894 Reverse repurchase agreements 14 121,174 145,549 Financial investments 10 33,069 32,233 Loans, after provision for loan impairment 11 67,362 380,470 270,994 608,146 Non-Earnings Assets: Cash and bank balances 15 12,162 11,340 Inventories 939 516 Other assets 16 48,068 17,802 61,169 29,658 TOTAL CURRENT ASSETS 332,163 637,804 TOTAL ASSETS 2,231,222 1,985,579 EQUITY AND LIABILITIES CAPITAL AND RESERVES: Institutional capital 17 207,529 203,062 Non-institutional capital 18 68,718 47,607 276,247 250,669

Page 5

UWI (MONA) & COMM UNITY

CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF FINANCIAL POSITION

31 DECEMBER 2014 Note 2014 2013 $’000 $’000 NON-CURRENT LIABILITIES: Interest Bearing: Members‟ voluntary shares 19 276,433 279,209 Members‟ deposits 21 26,118 82,539 External credit 22 72,110 - 374,661 361,748 CURRENT LIABILITIES: Interest Bearing: Members‟ voluntary shares 19 341,602 324,990 Members‟ deposits 21 1,200,189 1,029,078 External credit 22 17,249 - External 3 1,559,040 1,354,068 Non-Interest Bearing: Accruals 23 3,504 2,697 Payables 24 17,770 16,397 21,274 19,094 TOTAL CURRENT LIABILITIES 1,580,314 1,373,162 TOTAL EQUITY AND LIABILITIES 2,231,222 1,985,579 Approved for issue by the Board of Directors on 30 March 2015 and signed on its behalf: _____________________ ____________________ R. Eytle - President N. Morgan - Treasurer

Page 6

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF CHANGES IN EQUITY

YEAR ENDED 31 DECEMBER 2014

Non - Institutional Institutional Capital Capital Total Note $’000 $’000 $’000

Balance at 1 January 2013 191,317 42,299 233,616 Total comprehensive income - Net surplus for the year - 34,267 34,267 - Other comprehensive income - ( 668) ( 668) Transactions with owners - Entrance fees 115 - 115 - Dividends on permanent shares - ( 1,580) ( 1,580) - Increase in permanent shares 1,350 ( 22) 1,328 Transfer to statutory reserve 10,280 ( 10,280) - Decrease in other reserves 20(a) - (16,409) ( 16,409) Balance at 31 December 2013 203,062 47,607 250,669 Total comprehensive income - Net surplus for the year - 11,448 11,448 - Other comprehensive income - ( 570) ( 570) Transactions with owners - Entrance fees 185 - 185 - Dividend on permanent shares - ( 1,790) ( 1,790) - Increase to permanent shares 1,992 ( 48) 1,944 Transfer to statutory reserve 2,290 ( 2,290) - Revaluation surplus - 38,820 38,820 Decrease in other reserves 20(a) - (24,459) ( 24,459) Balance at 31 December 2014 207,529 68,718 276,247

Page 7

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF CHANGES IN EQUITY

YEAR ENDED 31 DECEMBER 2014

INSTITUTIONAL CAPITAL

Statutory Capital Special Permanent Reserve Reserve Reserve Share Total $’000 $’000 $’000 $’000 $’000

Balance at 1 January 2013 151,012 22,390 2,000 15,915 191,317 Transactions with owners - Increase in permanent shares - - - 1,350 1,350 - Entrance fee 115 - - - 115 Transfer to statutory reserve 10,280 - - - 10,280 Balance at 31 December 2013 161,407 22,390 2,000 17,265 203,062

Transactions with owners - Increase in permanent shares - - - 1,992 1,992 - Entrance fee 185 - - - 185 Transfer to statutory reserve 2,290 - - - 2,290 Balance at 31 December 2014 163,882 22,390 2,000 19,257 207,529

Page 9

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF CASH FLOWS

YEAR ENDED 31 DECEMBER 2014

2014 2013 $’000 $’000 CASH FLOWS FROM OPERATING ACTIVITIES: Net Surplus 11,448 34,267 Adjustments for: Interest received 194,126 195,623 Interest income ( 197,219) ( 185,046) Interest expense 59,947 54,505 Interest paid ( 53,227) ( 47,232) Depreciation 8,861 479 Write back of property, plant and equipment - 189 Provision for loan impairment 2,174 822 Operating cash flows before movement in working capital 26,110 53,607 Changes in operating assets and liabilities - Members‟ deposit 107,970 133,282 Members‟ voluntary shares 13,836 21,115 Inventories ( 423) ( 57) Other assets ( 30,266) ( 630) Loans ( 205,053) ( 267,937) Decrease in other reserves ( 24,459) ( 16,409) Payables and accruals 2,180 8,364 Cash used in operating activities ( 110,105) ( 68,665) CASH FLOWS FROM INVESTING ACTIVITIES: Purchase of property, plant and equipment ( 4,183) ( 18,322) Reverse repurchase agreement 23,814 ( 23,906) Financial investment 1,093 16,517 Cash provided by/(used in) investing activities 20,724 ( 25,711) CASH FLOWS FROM FINANCING ACTIVITIES: External credit 89,359 - Increase in members‟ permanent shares 1,944 1,328 Dividends paid ( 1,790) ( 1,580) Entrance fees 185 115 Cash provided by/(used in) financing activities 89,698 ( 137) INCREASE/(DECREASE) IN CASH AND CASH EQUIVALENTS 317 ( 94,513) Cash and cash equivalents at beginning of year 61,234 155,747 CASH AND CASH EQUIVALENTS AT END OF YEAR (Note 15) 61,551 61,234

Page 10

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 1. STATUS AND PRINCIPAL ACTIVITIES: The UWI (Mona) & Community Co-operative Credit Union Limited is incorporated under the laws of Jamaica and is registered under the Co-operative Societies Act, and has its registered office at 2 Gibraltar Camp Way, Mona Campus, Kingston 7, Jamaica.

The main activities of the Credit Union are to promote thrift among its members by affording them an opportunity to accumulate their savings and to create for them a source of credit for provident or productive purposes at reasonable rates of interest.

Membership to the Credit Union is obtained by the holding of members‟ shares which should be

at least one voluntary shares and one permanent share. Voluntary shares are deposits available for withdrawals on demand, while permanent shares are paid in cash and invested in risk capital and are redeemable only upon transfer to another member. Individual membership may not exceed 20% of the total of the members‟ shares of the credit union.

The Co-operative Societies Act requires, among other provisions, that at least 20% of the net surplus of the Credit Union be transferred annually to a reserve fund. Section 59 (1) & (11) of the Act provides for the exemption from income tax and stamp duty for the Credit Union.

2. FUNCTIONAL CURRENCY:

These financial statements are presented in Jamaican dollars which is the Credit Union‟s functional currency. Except where indicated to be otherwise, financial information presented are shown in thousands of Jamaican dollars.

3. SIGNIFICANT ACCOUNTING POLICIES:

The principal accounting policies applied in the preparation of these financial statements are set out below. The policies have been consistently applied to all the years presented.

(a) Basis of preparation -

These financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and have been prepared under the historical cost convention as modified by the revaluation of certain properties and financial assets that are measured at fair value or revalued amounts.

Page 11

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D):

(a) Basis of preparation (cont’d) -

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the credit union‟s accounting policies. Although these estimates are based management‟s best knowledge of current events and actions, actual results could differ from those estimates. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in note 4. Amendments to published standard effective in the current year that is relevant to the credit union’s operations There were no new standards or amendments and interpretations effective during the current period which was considered relevant to the Credit Union. Standards and amendments to published standards that are not yet effective and have not been early adopted by the credit union

IFRS 9, ‘Financial Instruments’, (effective for annual periods beginning on or after 1 January 2018). IFRS 9 addresses classification and measurement of financial assets and liabilities and replaces the multiple classification and measurement models in IAS 39 with a single model that has only two classification categories: amortised cost and fair value.

Classification of financial assets under IFRS 9 is driven by the entity‟s business model for managing the financial assets and the contractual characteristics of the financial assets. IFRS 9 also removes the requirement to separate embedded derivatives from financial asset hosts. It requires a hybrid contract to be classified in its entirety at either amortised cost or fair value,

For financial liabilities IFRS 9 retains most of the IAS 39 requirements including amortised cost accounting for most financial liabilities and the requirement to separate embedded derivatives. The main changer is where the fair value option is taken for financial liabilities, the part of a fair value change due to an entity‟s own credit risk is recorded in Other Comprehensive income rather that in profit or loss, unless this creates an accounting mismatch.

Page 12

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D): (a) Basis of preparation (cont’d) -

IFRS 15, Revenue from contracts with Customers’, (effective for annual periods beginning on or after 1 January 2017). IFRS 15 establishes principles for reporting useful information to users of financial statements about the nature, amount, timing and uncertainty of revenue and cash flows arising from an entity‟s contracts with customers. Revenue is recognized when a customer obtains control of a good or service and thus has the ability to direct the use and obtain the benefits from the goods or service. The standard replaces IAS 18. “Revenue” and IAS 11 “Construction contracts” and related interpretations. The directors anticipate that the adoption of the above standards, which are relevant in future periods, is unlikely to have any material impact on the financial statements.

(b) Foreign currency translation -

Foreign currency transactions are accounted for at the exchange rates prevailing at the dates of the transactions. Monetary items denominated in foreign currency are translated to Jamaican dollars using the closing rate as at the reporting date. Non-monetary items measured at historical cost denominated in a foreign currency are translated using the exchange rate as at the date of initial recognition; non-monetary items in a foreign currency that are measured at fair value are translated using the exchange rates at the date when the fair value was determined. Exchange differences arising from the settlement of transactions at rates different from those at the dates of the transactions and unrealized foreign exchange differences on unsettled foreign currency monetary assets and liabilities are recognized in surplus or deficit. Translation differences on non-monetary financial instruments, such as equities classified as available-for-sale financial assets, are included in equity.

(c) Financial instruments -

A financial instrument is any contract that gives rise to both a financial asset in one entity and a financial liability or equity in another entity.

Page 13

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D):

(c) Financial instruments (cont’d) Financial assets -

(i) Classification

The Credit Union classifies its financial assets into the following categories: loans and receivables and available-for-sale. The classification depends on the purpose for which the financial assets were acquired. Management determines the classification of its financial assets at initial recognition and re-evaluates this designation at every reporting date.

Loan and receivables

These assets are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They arise principally through the provision of services to customers (e.g loans), but also incorporate other types of contractual monetary asset. The Credit Union‟s loans and receivables comprise loans, cash and cash equivalents and reserve repurchase agreements in the statement of financial position.

A provision for impairment is established if there is objective evidence that a loan is impaired. The amount of the provision is the difference between the carrying amount and the recoverable amount, being the present value of expected future cash flows, including amounts recoverable from collateral, discounted at the original effective interest rate of the loans.

A loan is classified as impaired when, in management‟s opinion, there has been deterioration in credit quality to the extent that there is no longer reasonable assurance of timely collection of the full amount of principal and interest. If the payment on a loan is contractually 3 months in arrears, the loan will be classified as impaired.

Page 14

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D):

(c) Financial instruments (cont’d) - Financial assets (cont’d)

(i) Classification (cont’d) Loans and receivables (cont’d)

Write-offs are made when all or part of a loan is deemed uncollectible or in the case of debt forgiveness. Write-offs are charged against previously established provisions for credit losses and reduce the principal amount of a loan. Recoveries in part or in full of amounts previously written off are credited to impairment loss expenses in the statement of comprehensive income.

The Credit Union‟s impairment loss provision requirements, as stipulated by the Jamaica Co-operative Credit Union League if it exceeds the IFRS impairment provision are dealt with in a non-distributable loan loss reserve as an appropriate of accumulated surplus.

Available-for-sale financial assets

Available-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other categories. Financial investments are classified as available-for-sale on the statement of financial position.

(ii) Recognition and Measurement

Regular purchases and sales of financial assets are recognized on the trade-dates the date on which the Credit Union commits to purchase or sell the asset. Financial investments are initially recognized at fair value plus transaction costs for all financial assets not carried at fair value through surplus or deficit. Financial assets are derecognized when the rights to receive cash flows from the financial assets have expired or have been transferred and the Credit Union has transferred substantially all risks and rewards of ownership. Available-for-sale financial assets are subsequently carried at fair value, with fair value gains or losses being recorded in other comprehensive income. Loans and receivables are subsequently carried at amortised cost using the effective interest method.

Page 15

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D):

(c) Financial instruments (cont’d) -

Financial assets (cont’d) (ii) Recognition and Measurement (cont’d)

Changes in fair value of monetary securities denominated in a foreign currency and classified as available-for-sale are analysed between translation differences resulting from changes in amortised cost of the security and other changes in the carrying amount of the security. The translation differences on monetary securities are recognized in surplus or deficit; translation differences on non-monetary securities are recognized in other comprehensive income. Changes in the fair value of monetary and non-monetary securities classified as available for sale are recognized in other comprehensive income. When securities classified as available for sale are sold or impaired, the accumulated fair value adjustments previously recognized in other comprehensive income are included in the income statement as gains and losses from investment securities.

Interest on available-for-sale securities calculated using the effective interest method is recognized in the income statement as part of revenue, other income and finance income. Dividends on available-for-sale equity instruments are recognised in the income statement as part of other income when the Credit Union‟s right to receive payments is established. The Credit Union assesses at each reporting date whether there is objective evidence that a financial asset or a group of financial asset is impaired. In the case of equity securities classified as available for sale, a significant or prolonged decline in the fair value of the security below its cost is considered as an indicator that the securities are impaired. If any such evidence exists, the cumulative loss, measured as the difference between the acquisition cost and the current fair value, less any impairment loss on the financial assets previously recognized other comprehensive income is removed and recognized in surplus or deficit.

Page 16

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D): (c) Financial instruments (cont’d) - Financial liabilities

The Credit Union‟s financial liabilities net of transaction costs, are initially measured at fair value, and are subsequently measured at amortised cost using the effective interest method. At the reporting date, the items classified as financial liabilities are members‟ voluntary shares, members‟ deposits and external credits.

(d) Reverse repurchase agreement - Securities purchased under agreements to resell are recorded as collaterised financing

transactions and are classified as loans and receivables. The related interest income is recorded on the accruals basis.

(e) Property, plant and equipment -

Items of property, plant and equipment are recorded at historical less accumulated depreciation. Historical cost includes expenditure that is directly attributable to the acquisition of the items. Freehold buildings are subsequently carried at fair value, based on periodic valuations by a professionally qualified valuer. These revaluations are made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period. Changes in fair value are recognised in other comprehensive income and accumulated in the revaluation reserve except to the extent that any decrease in value in excess of the credit balance on the revaluation reserve, or reversal of such a transaction, is recognised in profit or loss.

Depreciation is calculated on the straight-line method at annual rates estimated to

write off the costs of the assets over the period of their estimated useful lives. Annual rates are as follows:

Buildings 2½% Leasehold Improvement 14 1/3% Computer and Equipment 20% Computer software 33 1/3% Furniture and Fixtures 10% Motor vehicle 20%

Page 17

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT’D): (f) Employee benefit -

The Credit Union operates a contribution based pension scheme, which is administrated by a separate trustee. The scheme is funded by employees‟ contribution of 5% of salary or optional of 10% and employer‟s contribution of 10%.

(g) Other assets - Receivables are carried at anticipated realisable value. An estimate is made for doubtful receivables based on all outstanding amounts at year end. Bad debts are written off in the year in which they are identified.

(h) Cash and cash equivalents -

Cash and cash equivalents are carried in the statement of financial position at cost. For the purposes of the cash flow statement, cash and cash equivalents comprise cash in hand and in bank and deposits not held to satisfy statutory requirements and short term highly liquid investments with original maturities of three months or less, net of bank overdraft.

(i) Inventories -

Inventories are stated at the lower of cost and fair value less cost to sell cost being determined on the first-in-first-out basis.

(j) Impairment of non-current assets - Non-current assets are reviewed for impairment losses whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognized for the amount by which the carrying amount of the assets exceeds its recoverable amount, which is the greater of an asset‟s net selling price and value in use. For the purpose of assessing impairment, assets are grouped at the lowest level for which there are separately identified cash flows. Non financial assets that suffered an impairment are reviewed for possible reversal of the impairment at each reporting date.

Page 18

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D): (k) Borrowings -

Borrowings are recognized initially as the proceeds received, net of transaction costs incurred. Borrowings are subsequently stated at amortised cost using the effective yield method. Any difference between proceeds, net of transaction costs, and the redemption value is recognized in surplus or deficit over the period of the borrowings.

(l) Deposits -

Deposits are recognized initially at the nominal amount when funds are received. deposits are subsequently stated at amortised cost using the effective yield method.

(m) Revenue recognition -

The Credit Union recognises revenue when the amount of revenue can be reliably measured, it is probable that future economic benefit will flow to the entity and when specific criteria have been met for each of the Credit Union‟s activities. Interest income is recognized in the income statement for all interest bearing instruments on an accrual basis unless collectability is doubtful.

Interest income and expense

Interest income includes the amortization of any discount or premium, transaction costs or other differences between the initial carrying amount of an interest-bearing instrument and its amount at maturity calculated on an effective interest rate basis. When financial assets become doubtful of collection, they are written down to their recoverable amounts and interest income is thereafter recognized based on the rate of interest that was used to discount the future cash flows for the purpose of measuring the recoverable amount, which is the original effective interest rate of the instrument calculated at the acquisition or origination date.

Fees and other income Fees and other income are recognized on an accrual basis. Loan origination fees are recognized over the life of the loan, as an adjustment to the effective yield on the loans.

Dividend income from equity financial investments is recognised when the shareholder‟s right to receive payment has been established.

Page 19

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

3. SIGNIFICANT ACCOUNTING POLICIES (CONT’D): (n) Leases - Leases of property where the entity has substantially all the risks and rewards of ownership are classified as finance leases. Finance charges are expensed in the statement of comprehensive income over the lease period. Leases where a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments under operating leases are charged as an expense in the statement of comprehensive income on the straight- line basis over the period of the lease.

(o) Members’ shares - Permanent shares Permanent shares may be redeemable subject to the sale, transfer, or repurchase of

such shares. Dividends may be paid on permanent shares subject to the profitability of the Credit Union. Permanent shares are equity shares and form part of the capital of the Credit Union.

Voluntary shares Members‟ voluntary shares represent deposit holdings of the Credit Union‟s members,

to satisfy membership requirements and to facilitate eligibility for loans and other benefits. These shares are classified as financial liabilities. Dividends payable on these shares are determined at the discretion of the Credit Union and reported as interest in the statement of income in the period in which they are approved.

Institutional capital -

Institutional capital includes the statutory reserve fund, as well as various other reserves established from time to time which, in the opinion of the directors, are necessary to support the operations of the Credit Union and, thereby, protect the interest of the members. These reserves are not available for distribution.

Page 20

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY:

Judgements and estimates are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. (a) Critical judgements in applying the credit union’s accounting policies -

In the process of applying the credit union‟s accounting policies, management has not made any judgements that it believes would cause a significant impact on the amounts recognized in the financial statements.

(b) Key sources of estimation uncertainty -

The credit union makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts and assets and liabilities within the next financial year are discussed below:

(i) Fair value estimation

A number of assets included in the Credit Union‟s financial statements require measurement at, and/or disclosure of, at fair value. Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm‟s length transaction. Market price is used to determine fair value where an active market (such as a recognized stock exchange) exists as it is the best evidence of the fair value of a financial instrument.

The fair value measurement of the Credit Union‟s financial and non financial assets and liabilities utilises market observable inputs and data as far as possible. Inputs used in determining fair value measurements are categorized into different levels based on how observable the inputs used in the valuation technique utilized.

Page 21

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY (CONT’D):

(b) Key sources of estimation uncertainty (cont’d) -

(i) Fair value estimation (cont’d)

The standard requires disclosure of fair value measurements by level using the following fair value measurement hierarchy:

(i) Level 1 – Quoted prices (unadjusted) in active markets for indentical assets or liabilities.

(ii) Level 2 – Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices). (iii) Level 3 - Inputs for the asset or liability that are note based on observable market data (that is, derived from prices).

The classification of an items into the above levels are based on the lowest level of the inputs used that has a significant effect on the fair value measurement of these items.

The credit union measures a number of items at fair value - Revalued building – property, plant and equipment (note 12) Financial instrument – (note 10)

Page 22

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY (CONT’D):

(c) Key sources of estimation uncertainty (cont’d) -

(ii) Impairment losses on loans to members

In determining amounts recorded for impairment losses on loans to members in the financial statements, management makes judgements regarding indicators of impairment, that is, whether there are indicators that suggest there may be measurable decrease in estimated future cash flows from loans, for example, through unfavourable economic conditions and default. Management uses estimate based on historical loss experience for assets with credit risk characteristics and objective evidence of impairment similar to those in the portfolio when scheduling future cash flows. The methodology and assumptions used for flows. The methodology and assumptions used for estimating both the amount and timing of future cash flows are reviewed regularly to reduce any differences between loss estimates and actual loss experience.

5. FINANCIAL RISK MANAGEMENT:

The Credit Union‟s activities are principally related to the use of financial instruments, which involves analysis, evaluation and management of some degree of risk or combination of risks. The Credit Union manages risk through a framework of risk principles, organizational structures and risk management and monitoring processes that are closely aligned with the activities of the Credit Union. The Credit Union‟s risk management policies are designed to identify and analyze the risks faced by the Credit Union, to set appropriate risk limits and controls, and to monitor risks and adherence to limits by means of regularly generated reports. The Credit Union‟s aim is therefore to achieve an appropriate balance between risks and return and minimize potential adverse effects on the Credit Union‟s financial performance.

Page 23

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D): The Credit Union has exposure to the following risks from its use of financial instruments:

Credit risk

Liquidity risk

Market risk

Operational risk

In common with all other businesses, the Credit Union‟s activities expose it to a variety of risks that arise from its use of financial instruments. This note describes the Credit Union‟s objectives, policies and processes for managing those risks to minimize potential adverse effects on the financial performance of the Credit Union and the methods used to measure them. There have been no substantive changes in the Credit Union‟s exposure to financial instrument risks, its objectives, policies and processes for managing those risks or the methods used to measure them from previous periods unless otherwise stated in this note. (i) Principal financial instruments

The principal financial instruments used by the Credit Union from which financial instrument risk arises, are as follows:

- Financial investments - Loans, after provision for impairment - Liquid assets - Reverse repurchase agreements - Cash and bank balances - Members‟ voluntary shares - Members‟ deposits - External credit

Page 24

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D):

(ii) Financial instruments by category

Financial assets

Loans and receivables Available-for-sale 2014 2013 2014 2013 $’000 $’000 $’000 $’000 Cash and bank balances 12,162 11,340 - - Liquid assets 49,389 49,894 - - Reverse repurchase agreements 121,174 145,549 - - Loans, after provision for loan impairment 1,829,667 1,625,046 - - Financial investments - - 76,307 76,058 2,012,392 1,831,829 76,307 76,058

Financial liabilities

Financial liabilities at amortised cost .

2014 2013 $’000 $’000 Members‟ voluntary shares 618,035 604,199 Members‟ deposits 1,226,307 1,111,617 External credit 89,359 - - 1,933,701 1,715,816 (iii) Financial instruments not measured at fair value

Financial instruments not measured at fair value includes cash and bank balances, liquid assets, reverse repurchase agreements, loans, after provision for impairment, unquoted equity, members‟ voluntary shares, members‟ deposits and external credits. Due to their short term nature, the carrying amounts of liquid assets, reverse repurchase agreements and cash and bank balances maturing within one year is assumed to approximate their carrying amount.

Page 25

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D):

(iii) Financial instruments not measured at fair value (cont’d)

Unquoted equities classified as available-for-sale are measured at historical cost less impairement as their values cannot be reliably determined.

(iv) Financial risk factors -

The Board of Directors is ultimately responsible for the establishment and oversight of the Credit Union‟s risk management framework. The Board has established committees for managing and monitoring risks.

Three key committees for managing and monitoring risks are as follows:

(i) Supervisory Committee

The Supervisory Committee oversees the Internal Audit function of the Credit Union and ensures that internal procedures and controls are adhered to. The Supervisory Committee is assisted in its oversight role by Internal Audit. Internal Audit undertakes both regular and ad hoc reviews of management controls and procedures, the results of which are reported to the Supervisory Committee.

(ii) Credit Committee

The Credit Committee oversees the approval of the credit facilities to members. It is also primarily responsible for monitoring the quality of the loan portfolio

(iii) Finance Committee

The Finance Committee is responsible for overseeing the management of the Credit Union‟s assets and liabilities and the overall financial structure. It is also primarily responsible for managing the funding and liquidity risks of the Credit Union.

Page 26

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

These committees comprise persons independent of management and reports to the Board on a monthly basis. There have been no significant changes to the Credit Union‟s exposure to financial risks or the manner in which it manages and measures these risks. (i) Credit risk -

The Credit Union takes on exposure to credit risk, which is the risk that a counterparty will cause a financial loss by being unable to pay amounts in full when due. Credit exposures arise principally in lending activities.

For loans, strategic decisions are primarily made by the Board of Directors, with some delegation of credit approval authority to the Credit Committee and certain members of executive management. The Credit Union‟s credit policy forms the basis for all its lending operations. The policy aims at maintaining a high quality loan portfolio, as well as enhancing the Credit Union‟s mission and strategy. The policy sets the basic criteria for acceptable risk and identifies risk areas that require special attention.

Additionally, the Credit Union is exposed to credit risk in its treasury activities, arising from financial assets that the Credit Union uses for investing, its liquidity and managing currency and interest rate risks, as well as other market risks. There is also credit risk in off-statement of financial position financial items, such as loan commitments.

Credit review process

The Credit Union has established a credit quality review process involving regular analysis of the ability of borrowers and other counterparties to meet interest and loan repayment obligations.

Loans

The Credit Union assesses the probability of default of individual borrowers using internal ratings. The Credit Union assesses each borrower on four critical factors. These factors are the member‟s credit history, ability to pay linked to the industry benchmarked debt service ratio of 75%, character profile and the member‟s economic stability, based on employment and place of abode.

Page 27

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(i) Credit risk (cont’d)

Loans (cont‟d)

Borrowers of the Credit Union are segmented into two rating classes, performing and non-performing.

The credit quality review process allows the Credit Union to assess the potential loss as a result of the risk to which it is exposed and take corrective action. Exposure to credit risk is managed, in part, by obtaining collateral and personal guarantees.

Investments and resale agreements

The Credit Union limits its exposure to credit risk by investing mainly in liquid securities, with counterparties that have high credit quality. As a consequence, management‟s expectation of default is low.

The Credit Union has documented policies which facilitate the management of credit risk on investment securities and resale agreements. The Credit Unions exposure and credit ratings of its counterparties are continually monitored.

Credit limits

The Credit Union manages concentrations of credit risk by placing limits on the amount of risk accepted in relation to a single borrower or groups of related borrowers, and to product segments. Borrowing limits are established by the use of the system described above. Limits on the level of credit risk by product categories, and for investment categories, are reviewed and approved bi-annually by the Board of Directors.

Collateral

The amount and type of collateral required depends on an assessment of the credit risk of the borrower. Guidelines are implemented regarding the acceptability of different types of collateral. The principal collateral types provided for loans and advances are charges over member balances, real property and motor vehicles.

Page 28

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D):

(iv) Financial risk factors (cont’d) -

(i) Credit risk (cont’d) Collateral (cont‟d)

Management monitors the market value of collateral, requests additional collateral in accordance with the underlying agreement, and monitors the market value of collateral obtained during its review of the adequacy of the provision for credit losses.

Liquid assets and bank balances

Liquid assets and bank balances are held in financial institutions which management regards as strong and there is no significant concentration. The strength of these financial institutions is constantly reviewed by the finance committee.

Impairment

The Credit Union assesses on a monthly basis whether there is evidence of impairment in accordance with the general principles and methodology set out in IAS 39 and the relevant implementation guidance. These procedures include the following steps:

Identification of events that provide objective evidence that a loan is impaired.

Establishment of criteria for assessment on an individual or collective basis.

Establishment of groups of assets with similar characteristics.

Establishing methodology to be used in determining cash flows from impaired loans.

Determining interest income recognition.

Recoveries. The main considerations for the loan impairment assessment include whether

any payment of principal or interest are overdue by more than 30 days based on the established PEARLS grid recommended by the League or based on any known difficulties in the cash flows of counterparties, credit rating downgrades or infringement of the original terms of the contract.

Page 29

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5 FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(i) Credit risk (cont’d) Impairment (cont‟d)

The Credit Union addresses impairment assessment in two areas: individually assessed allowances and collectively assessed allowances. The assessment applied to individually significant accounts normally encompassed collateral held and the anticipated receipts for that individual account. Collectively assessed allowances are determined through the application of PEARLS prescribed percentages to the aging profiles of the loan portfolio.

The internal rating tool assists management to determine whether objective

evidence of impairment exists, based on the following criteria set out by the Credit Union:

Delinquency in contractual payments of principal and interest;

Cash flow difficulties experienced by the borrower (e.g. equity ratio, net income percentage of revenue);

Breach of loan covenants or conditions;

Initiation of bankruptcy proceedings;

Deterioration of the borrower‟s competitive position; and

Deterioration in the value of collateral.

The impairment provision shown in the statement of financial position at year end is derived from the two internal rating grades. However, the impairment comes from the non-performing rating class.

Repossessed collateral The Credit Union was in the process of negotiating the sale of assets which was used as collateral for loans as follows: Carrying amount 2014 2013

$’000 $’000 Motor vehicle - 1,400

Page 30

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(i) Credit risk (cont’d) Repossessed collateral

Title for the above asset was not transferred to the Credit Union at the end of the reporting period. Consequently the Credit Union did not recognized the asset on the statement of financial position.

Credit risk exposure

Maximum exposure to credit risk before collateral held or other credit enhancements are as follows:

For items on the statement of financial position, the exposures are based on the net carrying amounts as reported as follows: 2014 2013 $’000 $’000

On the statement of financial position- Loans to members, net of provision for impairment 1,829,667 1,625,046 Liquid assets - earning 49,389 49,894 Financial investments 76,307 76,058 Securities purchased under agreements to resell 121,174 145,549 2,076,537 1,896,547

Items not on the statements of financial position the table represents a worst case scenario of credit risk exposure to the Credit Union at 31 December 2013 and 2014, without taking account of any collateral held or other credit enhancements.

2014 2013 $’000 $’000

Loan commitments 28,305 22,599

.

Page 31

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(i) Credit risk (cont’d)

The table below shows the Credit Union‟s loans and the associated impairment provision for each internal rating class:

2014 2013 $’000 $’000 Performing - Neither past due nor impaired 1,798,816 1,592,107 Non-performing - Past due but not impaired 16,718 21,852 Impaired 15,493 12,015 32,211 33,867 1,831,027 1,625,974 Less provision for loan losses ( 5,159) ( 2,985) 1,825,868 1,622,989 Aged analysis of past due but not impaired loans: 2014 2013 $’000 $’000 2 to 3 months 11,758 19,053 3 to 6 months 3,866 2,113 6 to 12 months 1,094 1 Over 12 months - 685 16,718 21,852 There are no financial assets other than loans that are past due.

Of the aggregate amount of gross past due but not impaired loans, the fair value of collateral that the company held was $63,156,814 (2013 - $37,603,307).

Page 32

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(i) Credit risk (cont’d) Concentration of risk Loans

The following table summarises the Credit Union‟s credit exposure for consumer loans at their carrying amounts.

2014 2013 $’000 $’000 Home Improvement 138,928 83,638 Motor vehicle 323,599 318,568 Other 1,368,500 1,223,768 1,831,027 1,625,974 Less: Allowance for loan impairment ( 5,159) ( 2,985) 1,825,868 1,622,989 Interest receivables 3,799 2,057

1,829,667 1,625,046 Debt securities

The following table summaries the Credit Union‟s credit exposure for debt securities at their carrying amounts, as categorized by issuer: 2014 2013 $’000 $’000

Government of Jamaica Bonds and debentures 36,388 36,968

Page 33

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(ii) Liquidity risk -

Liquidity risk is the risk that the Credit Union is unable to meet its payment obligations associated with its financial liabilities when they fall due and to replace funds when they are withdrawn. The consequence may be the failure to meet obligations to repay depositors and fulfil commitments to lend.

The Credit Union‟s approach to managing liquidity is to ensure as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damages to the Credit Union‟s reputation.

Liquidity risk management process

The Credit Union‟s liquidity management process, as carried out within the Credit Union, includes:

(i) Monitoring future cash flows and liquidity on a daily basis. This

incorporates an assessment of expected cash flows and the availability of high grade collateral which could be used to secure funding if required;

(ii) Maintaining a portfolio of highly marketable and diverse assets that

can easily be liquidated as protection against any unforeseen interruption to cash flow;

(iii) Optimising cash returns on investments;

(iv) Managing the concentration and profile of debt maturities.

Monitoring and reporting take the form of an analysis of the cash balances and expected investment maturity profiles for the next day, week and month, respectively, as these are key periods for liquidity management. The starting point for those projections is an analysis of the contractual maturity of the financial liabilities and the expected collection date of the financial assets.

Page 34

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(ii) Liquidity risk (cont’d)

The maturities of assets and liabilities and the ability to replace, at an acceptable cost, interest-bearing liabilities as they mature, are important factors in assessing the liquidity of the Credit Union and its exposure to changes in interest rates and exchange rates.

The tables below present the undiscounted cash flows payable (both interest and principal cash flows) of the Credit Union‟s financial liabilities based on contractual repayment obligations. The Credit Union expects that many customers will not request repayment on the earliest date the Credit Union could be required to pay.

Within 3 3 to 12 1 - 5 Over 5 Months Months Years Years Total $‟000 $‟000 $‟000 $‟000 $‟000

As at 31 December 2014: Members‟ deposits 1,069,802 130,387 26,118 - 1,226,307

Members‟ voluntary shares 323,837 17,765 129,479 146,954 618,035 External credit 4,174 13,075 72,110 - 89,359 Total financial liabilities (contractual dates) 1,397,813 161,227 227,707 146,954 1,933,701

As at 31 December 2013: Members‟ deposits 839,732 189,346 67,620 14,919 1,111,617 Members‟ voluntary Shares 297,155 27,835 162,821 116,388 604,199 Total financial liabilities (contractual dates) 1,136,887 217,181 230,441 131,307 1,715,816

Page 35

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(iii) Market risk

The Credit Union takes on exposure to market risk, which is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices. Market risk mainly arise from changes in foreign currency exchange rates and interest rates. Market risk is monitored by the Finance Committee which carries out extensive research and monitors the price movement of financial assets on the local and international markets. Market risk exposures are measured using sensitivity analysis.

Currency risk

Currency or foreign exchange risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate because of changes in foreign exchange rates.

The Credit Union‟s exposure to foreign currency risk at statement of financial position date was as follows: 2014 2013 ’000 ’000 Liquid assets earning - USD 7 111 CAD 2 - - GBP 2 5 .

Reverse Repurchase Agreement- USD 3 116 GBP 30 29 Cash in hand - GBP 4 _-_ CAD 6 - - GBP 2 2

Page 36

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

6. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(iii) Market risk (cont’d)

Foreign currency sensitivity

The following tables indicate the currencies to which the Credit Union had significant exposure on its monetary assets and its forecast cash flows. The change in currency rates below represents management assessment of the possible change in foreign exchange rates.

Change in Effect on % Change in Effect on Currency Rate Net Surplus Currency Rate Net Surplus 2014 2014 2013 2013 % $‟000 % $‟000 Currency:

USD +1 16 +15 2,013 CAD +1 8 +15 - GBP +1 61 -15 937 USD -10 (160) -15 (135) CAD -10 ( 77) -1 - GBP -10 (599) -1 12

Page 37

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 6. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(iii) Market risk (cont’d)

Interest rate risk -

Interest rate risk is the risk that the value or future cash flows of a financial instrument will fluctuate because of changes in market interest rates, and arises mainly from investments, loans, deposits reverse repurchase agreements and external credit.

Floating rate instruments expose the Credit Union to cash flow interest risk, whereas fixed interest rate instruments expose the Credit Union to fair value interest risk. The Credit Union‟s interest rate risk policy requires it to manage interest rate risk by maintaining an appropriate mix of fixed and variable rate instruments as determined by the Finance committee. The policy also requires it to manage the maturities of interest bearing financial assets and interest bearing financial liabilities. The Board sets limits on the level of mismatch of interest rate re-pricing that may be undertaken, which is monitored daily by the Finance department. The following tables summarize the Credit Union‟s exposure to interest rate risk. They include the Credit Union‟s financial instruments at carrying amounts, categorized by the earlier of contractual re-pricing or maturity dates.

Page 38

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 6. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(iii) Market risk (cont’d)

Interest rate risk (cont‟d) -

A summary of the Credit Union‟s interest rate gap position is as follows: 2014 Within 3 3 to 12 1-5 Over 5 Non-interest Months Months Years Years Bearing Total $‟000 $‟000 $‟000 $‟000 $‟000 $‟000

Assets: Liquid assets 49,389 - - - - 49,389 Reverse repurchase agreements 121,174 - - - - 121,174 Financial investments 33,069 - 26,238 9,235 7,765 76,307 Loans, after provision after impairment 13,055 54,307 579,133 1,183,172 - 1,829,667 Total 216,687 54,307 605,371 1,192,407 7,765 2,076,537 Liabilities: Members‟ deposits1,069,802 130,387 26,118 - - 1,226,307 Members‟ voluntary shares 323,837 17,765 129,479 146,954 - 618,035 External credit 4,174 13,075 72,110 - - 89,359 Total 1,397,813 161,227 227,707 146,954 - 1,933,701 Total Interest Rate Sensitivity Gap (1,181,126) ( 106,920) 377,664 1,045,453 7,765 142,836 Cumulative Gap (1,181,126)(1,288,046) ( 910,382) 135,071 142,836 -

Page 39

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(iii) Market risk (cont’d)

Interest rate risk (cont’d)

2013 Within 3 3 to 12 1-5 Over 5 Non-interest Months Months Years Years Bearing Total $‟000 $‟000 $‟000 $‟000 $‟000 $‟000

Assets: Liquid assets 49,894 - - - - 49,894 Reverse repurchase agreements 145,549 - - - - 145,549 Financial investments 32,233 - 26,825 9,235 7,765 76,058 Loans, after provision for impairment 12,422 71,706 618,488 922,430 - 1,625,046 Total assets 240,098 71,706 645,313 931,665 7,765 1,896,547 Liabilities: Members‟ deposits 839,732 189,346 67,620 14,919 - 1,111,617 Members‟ voluntary Shares 297,155 27,835 162,821 116,388 - 604,199 Total 1,136,887 217,181 230,441 131,307 - 1,715,816 Total Interest Rate Sensitivity Gap ( 896,789) (145,475) 414,872 800,358 7,765 180,731 Cumulative Gap ( 896,789)(1,042,264) (627,392) 172,966 180,731 -

Page 40

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d) -

(iii) Market risk (cont’d)

Interest rate sensitivity The following table indicates the sensitivity to a reasonable possible change in interest rates, with all other variables held constant, on the Credit Union‟s net surplus and other components of equity. The sensitivity of the net surplus is the effect of the assumed changes in interest rates on net surplus based on the floating rate financial assets and financial liabilities. The sensitivity of equity is calculated by revaluing fixed rate available-for-sale financial assets for the effect of the assumed changes in interest rates. The correlation of variables will have a significant effect in determining the ultimate impact on market risk, but to demonstrate the impact due to changes in variable, variables had to be on an individual basis. It should be noted that movements in these variables are non-linear. Effect on Effect on Net Surplus Equity 2014 2014 $‟000 $‟000 Change in basis points: +250 6,496 6,496 -100 ( 2,599) ( 2,599) Effect on Effect on Net Surplus Equity 2013 2013 $‟000 $‟000 Change in basis points: +250 5,088 5,088 -100 (2,035) (2,035)

Page 41

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D): (iv) Financial risk factors (cont’d)

(iii) Market risk (cont’d)

Equity price risks

Equity price risk arises out of equity securities held by the Credit Union as part of its investment portfolio. Management monitors the mix of debt and equity securities in its investment portfolio based on market expectations. The primary goal of the Credit Union‟s investment strategy is to maximize investment returns while managing risk so as to minimize potential adverse effects on the Credit Union‟s financial performance.

(v) Operational risk -

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associated with the Credit Union‟s processes, personnel, technology and infrastructure, and from external factors other than credit, market and liquidity risks such as those arising from legal and regulatory requirements and generally accepted standards of corporate behaviour. Operational risks arise from all of the Credit Union‟s operations.

The Credit Union‟s objective is to manage operational risks so as to balance the avoidance of financial losses and damage to the Credit Union‟s reputation with overall cost effectiveness and to avoid control procedures that restrict initiative and creativity. The primary responsibility for the development and implementation of controls to address operational risk is assigned to senior management within each department. This responsibility is supported by the development of overall standards for the management of operational risk in the following areas: • requirement for appropriate segregation of duties, including the independent

authorisation of transactions; • requirements for the reconciliation and monitoring of transactions; • compliance with regulatory and other legal requirements; • documentation of control and procedures;

Page 42

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D):

(v) Operational risk (cont’d) - • requirement for the periodic assessment of operational risks faced, and the

adequacy of controls and procedures to address the risks indentified; • requirements for the reporting of operational losses and proposed remedial action; • development of a contingency plan; • risk mitigation, including insurance where this is effective. Compliance with the Credit Union‟s standards is supported by a programme of periodic reviews undertaken by Internal Audit. The results of internal audit reviews are discussed with the department heads, with summaries submitted to senior management.

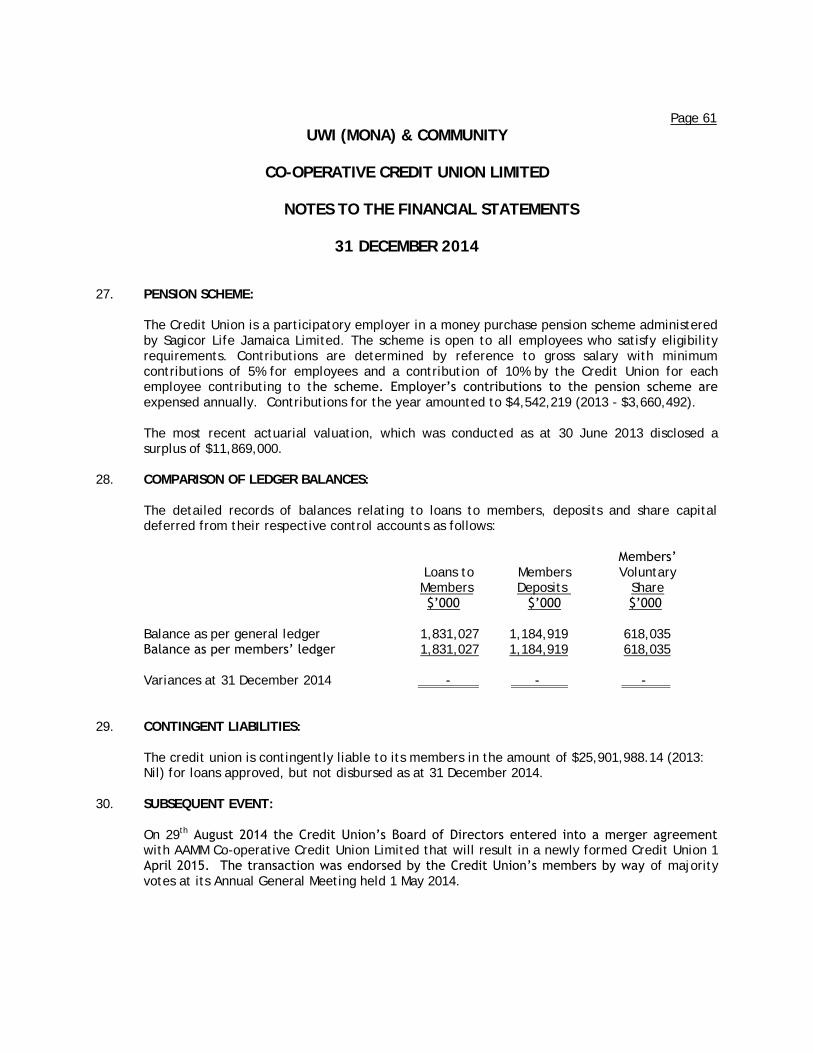

(vi) Capital management - The Credit Union‟s objectives when managing institutional capital, which is a broader concept than the „equity‟ on the face of the statement of financial position. (i) To comply with the capital requirements set by the Jamaica Co-operative

Credit Union League and the Bank of Jamaica for the financial sector in which the Credit Union operates;

(ii) To safeguard the Credit Union‟s ability to continue as a going concern so that it

can continue to provide returns and benefits for members;

(iii) To maintain an 8% ratio of institutional capital to total assets; and (iv) To maintain a strong capital base to support the development of its business

through the allocation of 20% (minimum) of net surplus to institutional capital. Capital adequacy and the use of regulatory capital are monitored by the Credit Union‟s management, based on the guidelines in its Capital Asset Management Policy.

Page 43

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

5. FINANCIAL RISK MANAGEMENT (CONT’D):

(vi) Capital management (cont’d) -

The Jamaica Co-operative Credit Union League currently requires member Credit Unions to maintain a minimum level of the institutional capital at 8% of total assets. At the statement of financial position date, this ratio was 10% which is in compliance with the requirements. The proposed Bank of Jamaica regulations require the Jamaica Co-operative Credit Union League to ensure that member Credit Unions: (i) Hold a minimum level of regulatory capital of 6% of total assets; and (ii) Maintain a ratio of total regulatory capital to risk-weighted assets at or above

10%. The table below summaries the composition of regulatory capital and the ratios of the Credit Union as at 31 December 2013 and 2014. During the year, the Credit Union complied with all externally imposed capital requirements to which they are subject. Actual Required Actual Required 2014 2014 2013 2013 $’000 $’000 $’000 $’000 Total regulatory capital 207,529 223,122 203,062 198,624 Risk – weighted assets: Total risk-weighted assets 1,574,576 1,417,135 BOJ primary ratio 9.30% 6% 10.23% 6% Risk weighted capital adequacy ratio 17.43% 10% 13,27% 10% Institutional capital ratio 10.23% 8% 10.23% 8%

Page 44

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 6. FAIR VALUE ESTIMATION:

Fair value is the amount for which an asset could be exchanged, or liability settle, between knowledgeable willing parties in an arm‟s length transaction. The following tables provide an analysis of Credit Union‟s financial instruments held as at at 31 December, that, subsequent to initial recognition, are measured at fair value. The financial instruments are grouped into level 1 to 3 based on the degree to which the fair values are observable as follows:

Level 1 includes those instruments which are measured based on quoted prices in active markets for identical assets or liabilities.

Level 2 includes those instruments which are measured using inputs other than quoted prices within level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices).

Level 3 includes those instruments which are measured using valuation techniques that include inputs for the instrument that are not based on observable market date (unobservable inputs).

Level 2 .

2014 2013 $’000 $’000 Financial assets measured at fair value

Available-for-sale financial investments Government of Jamaica Securities 36,388 36,968 Other 32,154 31,325 68,542 68,293

Page 45

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 6. FAIR VALUE ESTIMATION (CONT’D): Financial investments which has being categorized as level 2 valuation model is based on yields derived from pricing services which may include data not observed in actual market transaction but indicative information Measurement of fair real estate

The fair value of building was determined by independent property valuers, having aappropriate recognized professional qualification and recent experience in the location and categorizing of property, plant and being valued.

The fair vale measurement of building has been categorized as a level 3 for fair value based on inputs to the valuation techniques relating to expected market yields, see note 12 for further details.

7. NON-INTEREST INCOME: 2014 2013

$’000 $’000 Dividends from equity securities 546 467 Miscellaneous income 38,170 47,479

38,716 47,946

Page 46

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

8. OPERATING EXPENSES: 2014 2013 $’000 $’000 Utilities 3,927 4,035 Depreciation and amortization 8,861 479 Audit and supervision 3,249 2,603 Repairs and maintenance 2,769 2,328 Telecommunication 4,950 5,122 Printing, stationery and supplies 4,730 3,353 Insurance premium 2,259 2,308 Professional and consulting 6,550 4,596 Subscription 351 573 Administrative expense 6,873 6,521 Security 3,433 2,817 Bad debts 598 6,617 Members‟ security 7,498 6,876 Marketing and promotion 2,042 4,115 Representation and affiliation 8,226 11,506 Staff costs (note 9) 89,292 82,177 155,608 146,026 9. SALARIES AND OTHER STAFF COST: 2014 2013

$’000 $’000 Employee salaries and allowances 80,242 74,856 Other staff benefits 4,508 3,661 Pension 4,542 3,660 89,292 82,177 The number of persons employed at December 31:

Full-time 26 24 Contract 14 19 40 43

Page 47

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 10. FINANCIAL INVESTMENTS: 2014 2013 $’000 $’000 Non-current: Available-for-sale at fair value - Government of Jamaica Securities 35,473 36,060 Available-for-sale, at historical value - Unquoted equities 5,583 5,583 QNET 2,182 2,182 43,238 43,825 Current: Available-for-sale at fair value - Government of Jamaica Securities 915 908 Victoria Mutual Building Society 32,154 31,325 33,069 32,233

(a) Government of Jamaica securities includes interest receivable amounting to $915,047

(2013 - $908,233). (b) Unquoted equities represent shares held in Credit Union Fund Management Company

and the League. A minimum of 1,000,000 shares, each with a par value of $1.00, must be held with the League for the Credit Union to retain membership status. The equivalent of amounts held in the statutory reserve (Note 17) must either be used to purchase League shares or placed in League term deposits (Note 13).

(c) The QNET deposit represents investment by the Credit Union in the company which will

provide information services to participating credit unions. In total, the participating credit unions will account for 80% of the cost of the project and the remaining 20% will be funded by the League.

(d) The Victoria Mutual Building Society deposits includes interest receivables amounting

to $827,878 (2013 - $138,121).

Page 48

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

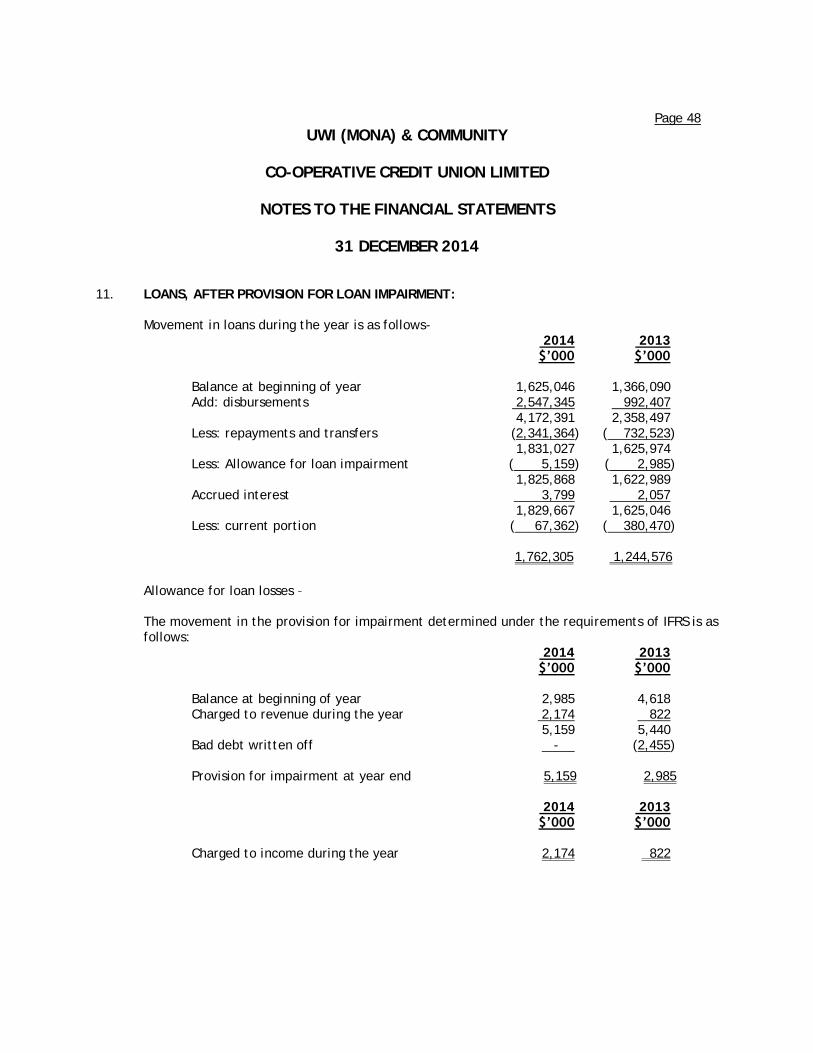

31 DECEMBER 2014 11. LOANS, AFTER PROVISION FOR LOAN IMPAIRMENT: Movement in loans during the year is as follows- 2014 2013 $’000 $’000 Balance at beginning of year 1,625,046 1,366,090 Add: disbursements 2,547,345 992,407 4,172,391 2,358,497 Less: repayments and transfers (2,341,364) ( 732,523) 1,831,027 1,625,974 Less: Allowance for loan impairment ( 5,159) ( 2,985) 1,825,868 1,622,989 Accrued interest 3,799 2,057 1,829,667 1,625,046 Less: current portion ( 67,362) ( 380,470) 1,762,305 1,244,576

Allowance for loan losses – The movement in the provision for impairment determined under the requirements of IFRS is as follows:

2014 2013 $’000 $’000 Balance at beginning of year 2,985 4,618 Charged to revenue during the year 2,174 822 5,159 5,440 Bad debt written off - (2,455). Provision for impairment at year end 5,159 2,985

2014 2013 $’000 $’000 Charged to income during the year 2,174 822

Page 49

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

11. LOANS, AFTER PROVISION FOR LOAN IMPAIRMENT (CONT’D): The provision for impairment determined under JCCUL regulatory requirement is as follows -

2014 2013 $’000 $’000

IFRS provision as per above 5,159 2,985 Loan loss reserve (note 18 (b)) 1,675 1,809 6,834 4,794 The provision for impairment under the JCCUL regulatory requirement for 2014 is in excess of

the provision required under IFRS provisioning rules. The excess of the League‟s provision over the IFRS provision is dealt with through a transfer from undistributed surplus to a loan loss reserve.

Delinquent loans - The following is a summary of delinquent loans as at 31 December 2014: Portion of Number of Loans not Statutory Months in accounts Delinquent Savings held covered Loan Loss Provision Arrears in arrears Loans against loans by savings Provision Rate $‟000 $‟000 $‟000 $‟000 % 2 – 3 months 22 160 10 150 16 10 3 – 6 months 6 4,392 493 3,899 1,318 30 7 – 12 months 4 7,353 399 6,954 4,412 60 12 months and over 12 1,089 61 1,028 1,089 100 Totals 24 12,994 963 12,031 6,835

The interest in respect to non-performing loans which have been excluded from the revenue and expenditure statement was $1,184,535 (2013 - $945,064).

Page 50

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

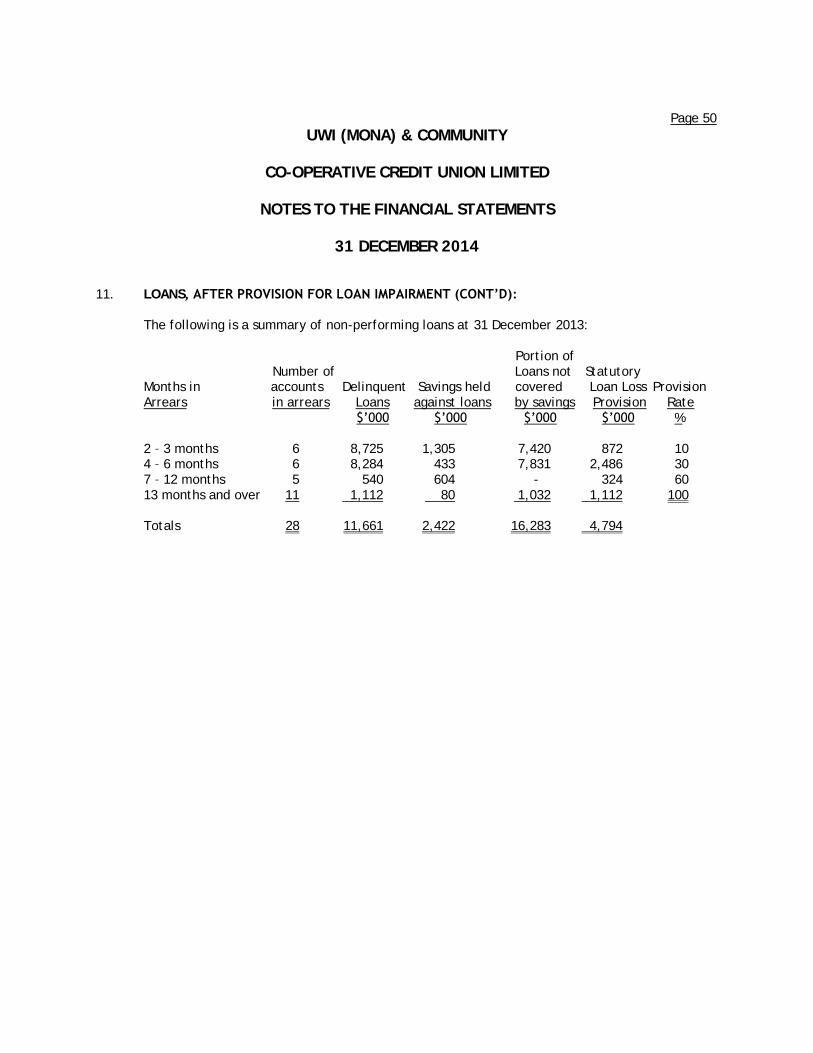

11. LOANS, AFTER PROVISION FOR LOAN IMPAIRMENT (CONT’D): The following is a summary of non-performing loans at 31 December 2013: Portion of Number of Loans not Statutory Months in accounts Delinquent Savings held covered Loan Loss Provision Arrears in arrears Loans against loans by savings Provision Rate $‟000 $‟000 $‟000 $‟000 % 2 – 3 months 6 8,725 1,305 7,420 872 10 4 – 6 months 6 8,284 433 7,831 2,486 30 7 – 12 months 5 540 604 - 324 60 13 months and over 11 1,112 80 1,032 1,112 100 Totals 28 11,661 2,422 16,283 4,794

Page 51

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014 12. PROPERTY, PLANT AND EQUIPMENT: Office Fixed Asset Computer Computer Leasehold Motor Building Furniture Work in Progress Hardware Software Equipment Signs Improvement Vehicle Total $‟000 $‟000 $‟000 $‟000 $‟000 $‟000 $‟000 $‟000 $‟000 $‟000 At cost - 1 January 2013 39,682 7,212 197 8,612 14,664 17,305 461 11,618 3,994 103,745 Additions - 2,028 12 1,509 1,727 12,498 - 548 - 18,322 Disposals - ( 132) - (1,344) - ( 798) - - - ( 2,274) Transfers 5,905 727 - - - - - ( 6,632) - - Adjustments - - ( 92) - - - - ( 97) - ( 189) At 30 December 2013 45,587 9,835 117 8,777 16,391 29,005 461 5,437 3,994 119,604 Additions 549 374 - 1,431 107 1,722 - - - 4,183 Transfer - 220 (117) - - - - (103) - - Revaluation adjustments 25,464 - - - - - - - - 25,464 71,600 10,429 - 10,208 16,498 30,727 461 5,334 3,994 149,251 Depreciation - 1 January 2013 11,087 5,294 - 7,949 13,904 16,576 393 6,689 133 62,025 Charge for the year 1,145 1,157 - 1,117 1,059 1,543 46 319 799 7,185 Transfers 2,408 182 - - - - - ( 2,590) - - Eliminated on disposal - ( 132) - (1,344) - ( 798) - - - ( 2,274) Adjustments ( 2,436) ( 540) - (1,769) (1,287) ( 556) 22 ( 140) - ( 6,706) At 31 December 2013 12,204 5,961 - 5,953 13,676 16,765 461 4,278 932 60,230 Charge for the year 1,152 702 - 1,442 1,459 3,019 - 288 799 8,861 Transfers - 10 - - - - - (10) - - Revaluation adjustment (13,356) - - - - - - - - (13,356) - 6,673 - 7,395 15,135 19,784 461 4,556 1,731 55,735 Net Book Value - 31 December 2014 71,600 3,756 - 2,813 1,363 10,943 - 778 2,263 93,516 31 December 2013 33,383 3,874 117 2,824 2,715 12,240 - 1,159 3,062 59,374

Page 52

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

31 DECEMBER 2014

12. PROPERTY, PLANT AND EQUIPMENT (CONT’D):

The credit Union‟s building was revalued on 4 December 2014 using the replacement cost method carried out by independent qualified valuers. The valuation surplus was credited to other comprehensive income and is shown in non-institutional capital. The fair value of land and building are grouped into levels 1 to 3 based on the degree to which the fair value are observable as follows:

Quoted price (unadjusted) in active markets for identical assets or liabilities (level

1).

Inputs other than quoted prices included within level 1 that are observable for the

assets or liability, either directly (that is, as prices) or indirectly (that is, derived

from prices) (Level 2).

Inputs for the asset or liability that are not based on observable market date (that is,

unobservable inputs) (Level 3).

The fair value of the building is a level 3 fair value measurement. A reconciliation to the

closing fair value balance is as follows –

2014

$’000

Opening balance historical cost 32,231

Purchases 549

Gains included in „other comprehensive income‟

- Gain on property revaluation 38,820

Closing balance (level 3 fair values) 71,600

Page 53

UWI (MONA) & COMMUNITY

CO-OPERATIVE CREDIT UNION LIMITED

NOTES TO THE FINANCIAL STATEMENTS

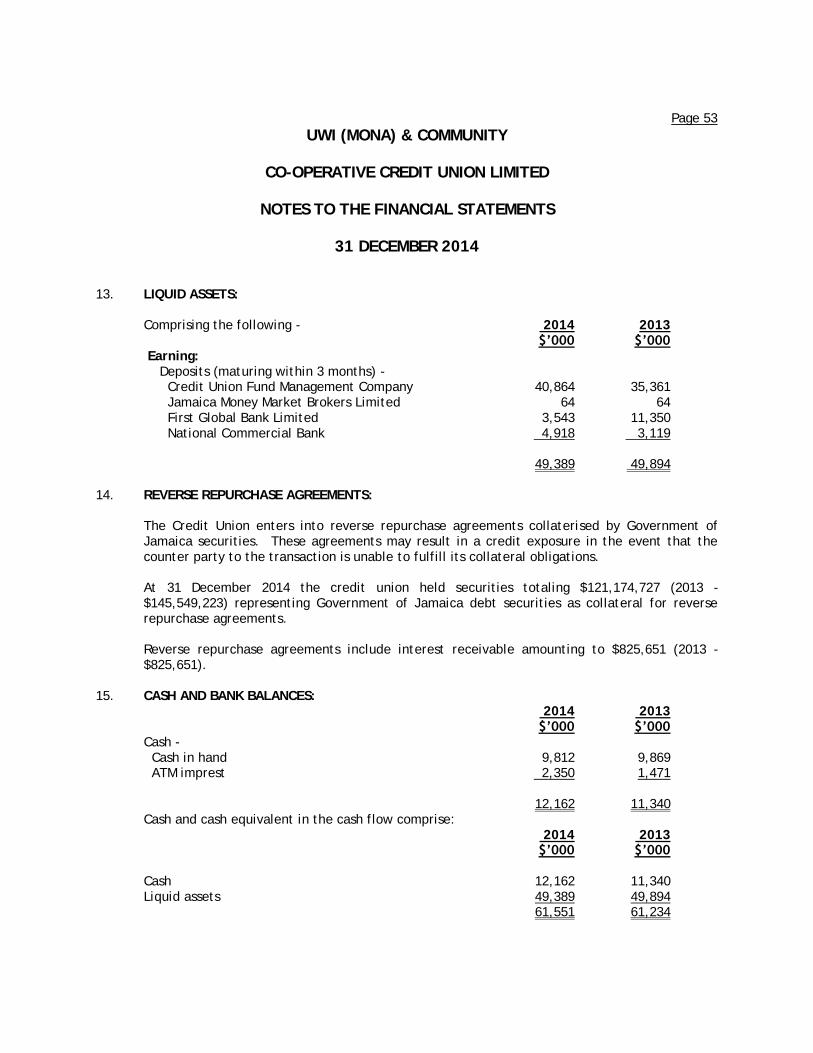

31 DECEMBER 2014 13. LIQUID ASSETS: Comprising the following - 2014 2013 $’000 $’000 Earning:

Deposits (maturing within 3 months) - Credit Union Fund Management Company 40,864 35,361