UC RUSAL - AnnualReports.com

219

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of UC RUSAL - AnnualReports.com

UC

RU

SAL

www.rusal.com

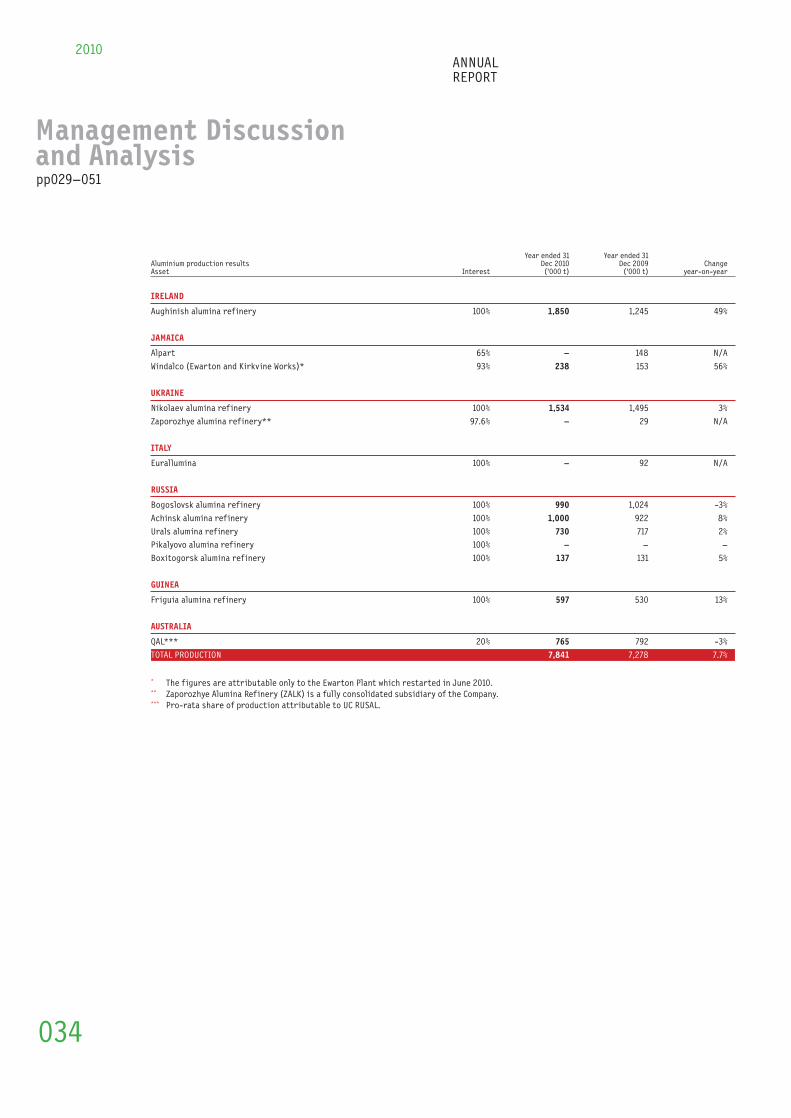

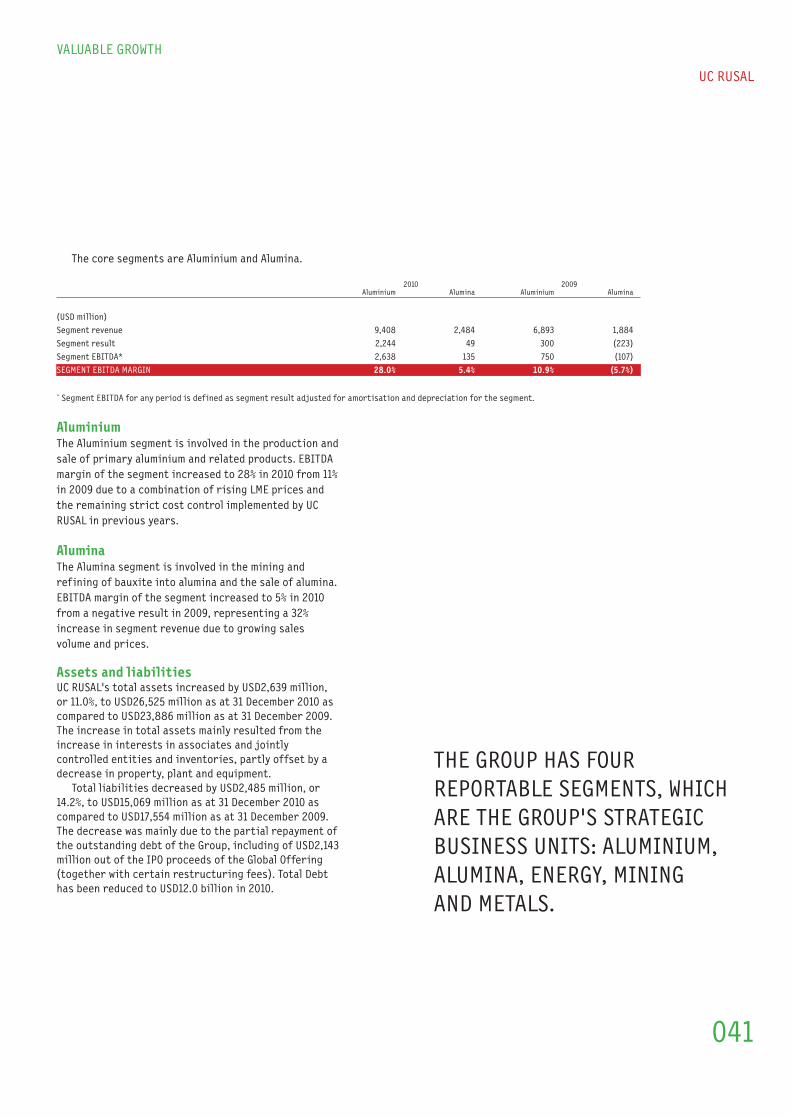

USD million 2010 2009 2008 2007 2006

Revenue 10,979 8,165 15,685 13,588 8,429Adjusted EBITDA 2,597 596 3,526 4,620 3,680Adjusted EBITDA Margin 23.7% 7.3% 22.5% 34.0% 43.7%EBIT 2,031 (63) (1,228) 3,647 3,312Income from Associates 2,435 1,417 (3,302) (14) (16)Pre Tax Profit/(Loss) 3,011 839 (6,053) 3,225 3,223Net Profit/(Loss) 2,867 821 (5,984) 2,806 2,897Net Profit/(Loss) Margin 26.1% 10.1% (38.2%) 20.7% 34.4%Earnings/(Loss)Per Share (in USD) 0.19 0.06 (0.49) 0.32 NA*Total Assets 26,525 23,886 24,005 22,063 9,252Equity Attributableto Shareholdersof the Company 11,456 6,332 4,488 10,095 3,078Net Debt 11,472 13,633 13,170 8,395 4,319* Earnings/Loss Per Share was not calculated for the year ended 31 December 2006, since transfer of the

interest in RUSAL was not completed until 27 March 2007

MANAGED PRODUCTION FINANCIAL PERFORMANCETHROUGH THE RECOVERY AND DEBT REDUCTION

FOCUS ONPROFITABILITY

MLN USD1,738Aluminaproduction

Aluminiumproduction

MLN USDMLN T

MLN T

4.1

7.8

24%

3

2,867

TIMES

EBITDAmargin

Increase inearnings per share

Net operatingcash flow

Netprofit

MLN USD367

MLN USD11,472Netdebt

Capitalexpenditure

unless otherwisespecified

Financial and OperationalHighlights

vAluablegrowth

ANNUAL REPORT2010

UC RUSAL

UC RUSAL

ANNUAL REPORT2010

content CorporateProfile 03

Chairman’sStatement 07

CEO’sReview 011

BusinessOverview 015

Management Discussionand Analysis 029

Profiles of Directorsand Senior Management 053

Directors’Report 069

Corporate GovernanceReport 101

Independent Auditors’Report 112

Glossary 194

Appendix A - Principal terms of theShareholders’ Agreement withthe Company 201

Appendix B - Principal terms of theShareholders’ Agreementbetween MajorShareholders Only 203

CorporateInformation 208

2010 0.8 MLN T

+52%Russia & The Other CISCountries AluminiumConsumption SOURCE: UC RUSAL

VALUABLE GROWTH

UC RUSAL

Our GlobalFootprint

2010ANNUALREPORT

UC RUSAL IS THE WORLD’S LARGEST PRODUCER of primaryaluminium, alloys and value-added products with aparticular focus on the production and sale of primaryaluminium, which is the higher margin upstreamsegment of the industry.

In 2010, UC RUSAL maintained its position as thelargest aluminium producer in the world.

PRIMARY ALUMINIUMPRODUCTION IN 2010

UC RUSAL is one of the industry leaders in aluminaproduction.

ALUMINA PRODUCTION IN2010

Within its upstream business, UC RUSAL is verticallyintegrated to a high degree, having secured substantialsupplies of bauxite and alumina production capacity.The Company’s core smelters, located in Siberia, Russia,benefit from access to stranded low cost hydrogenerated electricity enabling it to be one of the lowestcost producers of aluminium globally with principalSiberian facilities in close proximity to importantChinese and Asian markets.

IN 2010 UC RUSALMAINTAINED ITS POSITIONAMONG THE LEADINGCOMPANIES ON THEALUMINIUM COST CURVE

* The methodology used by Brook Hunt (an independent research andconsulting firm specialising in the mining and metals industries) tocalculate the C1 costs used in the preparation of the aluminium costproduction curve presented differs from the methodology used by UCRUSAL for the calculation of its Cash Operating Cost (FOB basis).Specifically, Brook Hunt does not include in C1 costs, corporateoverheads (including selling, general and administrative expenses) andcasthouse costs.

VALUABLE GROWTH

UC RUSAL

2010ANNUALREPORT

CorporateProfile

03

2010ANNUALREPORT

04

Key Shareholders1

* Amokenga Holdings is ultimately controlled by Glencore InternationalAG.** Including 0.22% directly held by the CEO of the Company

Key customersThe favourable location of UC RUSAL’s Siberian assets

has enabled UC RUSAL to develop a strong client base onall 5 continents spanning the major construction,packaging and automotive consumption segments. In2010, the Company sold primary aluminium, alloys andvalue added products to almost 50 countries. Theregional breakdown of these sales are shown below.

2010 revenue splitThe table below indicates sales of primary aluminium,

alloys and value-added products to end-users, excludingglobal traders:

Looking to the future, UC RUSAL wishes to furtherdevelop sales to key customers in the major growthregions with an emphasis on establishing directexposure to end-use segments for UC RUSAL’s products,tied to a broader suite of service options. As aconsequence, the role of global trading companies in theoverall sales portfolio will reduce, while regionaldistributors will adopt a stronger role in the portfolio.

On a regional basis, the net deficit markets ofEurope and North America will remain key targets for UCRUSAL’s value added products. UC Rusal expects to see astrong shift in sales to Asia due to growth in thisregion, in particular, in China. It is anticipated that by2015, 30% of the Company’s exports will be sold tosupport growing urbanisation and infrastructuredemand in Asia.

Vertically integrated asset base

Our scale, upstream focus and position on the costcurve provide unique exposure to the aluminiumindustry. UC RUSAL operates bauxite and nepheline oremines, alumina refineries, aluminium smelters, foil millsand packaging production centres as well as power-generating facilities. The Company employs more than72,000 people who work in 19 countries over 5continents.

In 2010 UC RUSAL produced the following:

Mining Refineries

alumina

bauxite

nepheline aluminium

SOURCE: UC RUSAL internal company report

11.7 MLN T

7.8 MLN T 4.1 MLN T 4.9 MLN T

Smelters

Production, 2010

In addition, UC RUSAL produced approximately 81,400tonnes of aluminium foil and foil-containing packagingmaterials.

Key factsIn 2010, UC RUSAL accounted for about 10% of the world’saluminium output and about 10% of the world’s aluminaproduction generated from the following facilitieslocated throughout the world:> 16 aluminium smelters> 12 alumina refineries> 8 bauxite mines> 4 foil mills> 2 cathode plants

UC RUSAL is listed on The Stock Exchange of HongKong Limited and is also listed on Euronext Paris in theform of Global Depositary Shares and on MICEX and RTSin the form of Russian Depository Receipts.

1 Source: Thisinformation was takenfrom www.rusal.com on31 March 2011.2 Source: CRU, based onproduction in 2010

VALUABLE GROWTH

UC RUSAL

05

Strong technology baseUC RUSAL has developed its own in-house R&D, designand engineering centres and has RA-300 and RA-400smelting technologies. Further, new energy efficientand environmentally friendly RA-500 technology isunder design.

Commodity diversification throughsignificant investments> UC RUSAL has a 25% plus one share interest in Norilsk

Nickel, the largest nickel and palladium producer2

and one of the leading producers of platinum andcopper in the world.

> UC RUSAL’s 50/50 LLP Bogatyr Komir coal jointventure in the Ekibastuz coal basin, one of thelargest coal basins in the CIS, provides UC RUSAL witha natural energy hedge.

Near-term growth projects> BEMO Project that involves the construction of the

3,000 megawatt BEMO HPP and Boguchanskyaluminium smelter in the Krasnoyarsk region whichhas a design capacity of 588,000 tonnes of aluminiumper annum. In 2010, UC RUSAL and RusHydro receivedcredit funds from VEB and resumed works at theconstruction site in January 2011.

> Taishet aluminium smelter in Irkutsk region with750,000 tonnes of aluminium per annum of designcapacity. The company is in the process ofnegotiating project financing from various lenders.

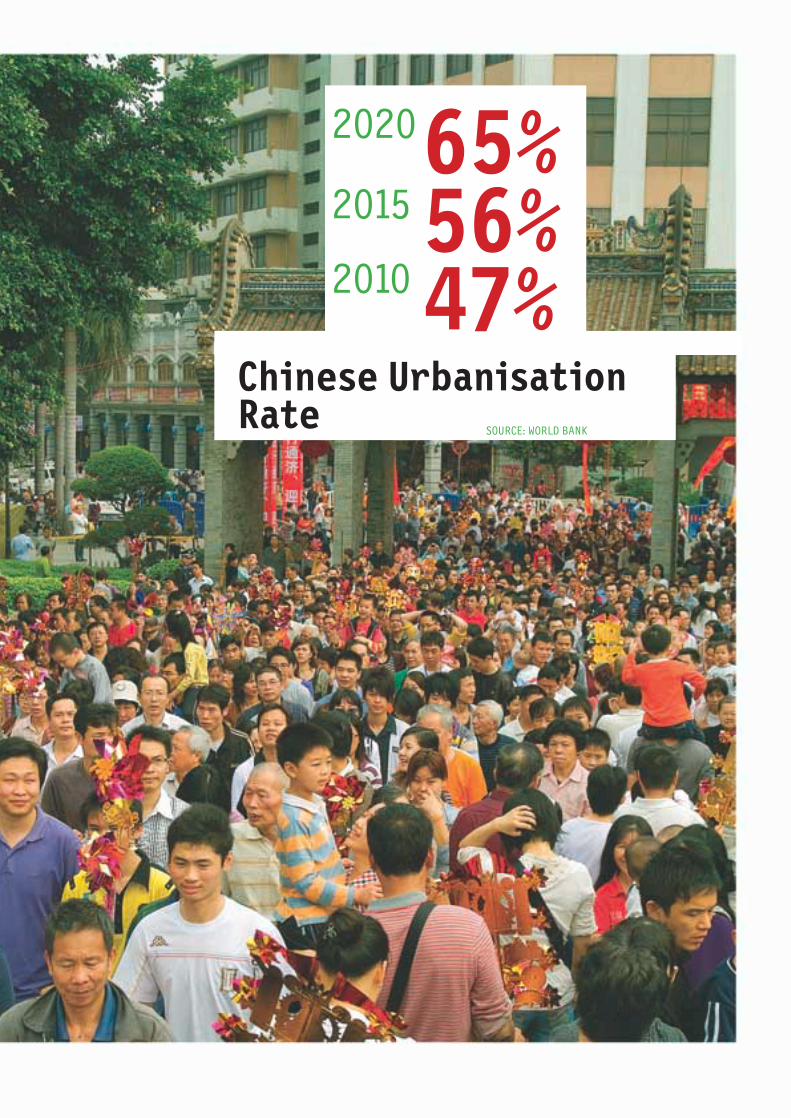

2020

2015

2010

65%56%47%

SOURCE: WORLD BANK

Chinese UrbanisationRate

VALUABLE GROWTH

UC RUSAL

2010ANNUALREPORT

07

pp07–09

Chairman’sStatement

Dear Shareholders,

I am pleased to present the Annual Report of UnitedCompany RUSAL Plc for the year ended 31 December 2010.

2010 was another year of significant developmentand progress for UC RUSAL, our first as a listed companyfollowing the successful listing of the Company’s Shareson the Hong Kong Stock Exchange and Global DepositaryShares on the Euronext in Paris. Despite the first partof 2010 being affected by the global economic crisis, wewere able to maintain our global leadership position inthe aluminium production industry. The Company’sstrategy and core values of efficiency, transparencyand courage enabled us to deliver significant value, notjust for our Shareholders but also for our partnersacross the globe. As a result of our operationalf lexibility, diversified assets and sustainable low costproduction, we were able to meet the rising demand foraluminium by increasing production volumes at many ofour economically and environmentally efficientfacilities.

UC RUSAL’s listing was a historic event and we areextremely proud to be the first company with Russianassets to be listed on the Hong Kong Stock Exchange andto conduct a simultaneous listing on exchanges in HongKong and Paris. Our belief and faith in the listing hasbeen validated by the continuing demand for, andinterest in, the Company’s Shares and we are delightedthat Russian investors are now also able to investindirectly in the Company following the landmark listingof Russian Depositary Receipts representing theCompany’s Shares on the MICEX and the RTS. I have great

pleasure in welcoming our new investors and lookforward to sharing the future success of the Companywith you.

2010 was the first year for us as a listed company andwe have made considerable efforts to meet marketstandards of disclosure and investor relations as wellas the requirements of regulatory authorities andstock exchanges.

During the past year, we reduced the initial minimumboard lot size on the Hong Kong Stock Exchange from24,000 Shares to 1,000 Shares. This resulted in asubstantial increase in Asian retail investor activityand improvements in Share liquidity. During the fourth

THE COMPANY’S STRATEGY ANDCORE VALUES OF EFFICIENCY,TRANSPARENCY AND COURAGEENABLED US TO DELIVERSIGNIFICANT VALUE, NOT JUSTFOR OUR SHAREHOLDERS BUTALSO FOR OUR PARTNERSACROSS THE GLOBE

2010ANNUALREPORT

08

Chairman’sStatementpp07–09

quarter of 2010, the average daily trading volume of theShares was 2.3 times greater than the average dailytrading volume of the Shares in the third quarter.

The broad Shareholder base of the Company,representing each of the continents and all types andsize of investors, has obliged us to focus significantattention on addressing the rights and interests ofminority Shareholders. The Company’s managementregularly visits key investment centres in the world toprovide stakeholders and potential investors withupdates on the Company’s performance.

UC RUSAL continues to be proud of its approach ofpractising the highest standards of internationalcorporate governance and the Board is committed toensuring that formal and transparent procedures are inplace to protect and maximise the interests of theShareholders. We demonstrated this in 2010 with thecreation of UC RUSAL’s Department of Control, InternalAudit and Business Co-ordination as well as thecontinuous efforts by the Board and its AuditCommittee and Corporate Governance and NominationsCommittee.

In 2010, UC RUSAL held its first annual generalmeeting as a listed company, with voter participation ofalmost 95%. All resolutions proposed at the meeting,which included the reappointment of Board members andthe Company’s auditor and the refreshing of mandatesfor the Board to issue and repurchase shares, werepassed by an overwhelming majority.

UC RUSAL is a truly global company and our corevalues underpin our approach of working incollaboration with all partners and local stakeholders toensure that environmental and sustainability interestsare given the highest priority. Over the last five years,UC RUSAL has invested in excess of USD1 billion intechnical and environmental upgrades aimed at reducingharmful emissions. As an example of our focus on theenvironment, our project to reduce perf luorocarbonemissions at the Krasnoyarsk aluminium smelter (one ofthe largest smelters in the world) has been included inthe list of approved projects carried out in accordancewith Article 6 of the Kyoto Protocol.

We have continued to invest in communities throughour sustainable development initiatives. The Companyre-launched a number of corporate and socialresponsibility programmes worldwide, including “TheTerritory of RUSAL”, a unique programme which assiststhe development of social infrastructure and civilsociety initiatives in regions where the Companyoperates. UC RUSAL also runs a special programme called“Computers for School Students” which is aimed atsupporting education in various Russian regions.Following the devastating forest fires that ravagedlarge areas of Russia during the unprecedented heat ofthe 2010 summer, the Company funded the constructionof homes in the Nizhny Novgorod region of Russia, whichsuffered the most from this disaster.

As an indication of our commitment to the Asianmarkets and in order to encourage communication andpromote greater understanding between Russia andAsia, UC RUSAL launched a five-year educationalpartnership with the Hong Kong University of Scienceand Technology (HKUST). This joint project is aimed atfostering joint scientific research, addressingpressing environmental issues and promoting co-operation between young scientists from the tworegions.

2010 has seen the Company make significant stridesin the repayment of its debt ahead of schedule andcontrol its production costs even further to achieveone of the lowest production costs across the wholealuminium industry. Throughout the year, the Companyremained true to its core values that helped steer itthrough the global economic downturn. This, combinedwith the tireless work of our employees, means that weare excellently positioned to meet the growing globaldemand for aluminium. Our renewed financial strengthand the ongoing support of our major lenders hasenabled UC RUSAL to refocus on delivering increasedproduction in 2011 and beyond.

The Company would not be the world’s leadingaluminium producer without the dedication andcommitment of our staff across the globe. Ourcorporate culture and values remain at the centre of

UC RUSAL IS A TRULY GLOBALCOMPANY AND OUR COREVALUES UNDERPIN OURAPPROACH OF WORKING INCOLLABORATION WITH ALLPARTNERS AND LOCALSTAKEHOLDERS TO ENSURETHAT ENVIRONMENTAL ANDSUSTAINABILITY INTERESTSARE GIVEN THE HIGHESTPRIORITY.

VALUABLE GROWTH

UC RUSAL

09

everything we do and on behalf of the Board, I would liketo thank all of the members of our global team for theircontribution to our success.

Aluminium continues to be at the forefront ofadvancements in a number of industries, most notablywithin the automotive sector, where the drive toincrease fuel efficiency by using lighter weightmaterials like aluminium is leading to radical changes inproduction processes. Looking towards the future, weare well positioned to take advantage of this and otherpositive long term industry fundamentals as wecontinue to forge ahead with our growth strategy.

We are grateful to all the investors who continue tobelieve in UC RUSAL and look forward to the brightfuture that lies ahead of us. On behalf of the Board, Iwould like to thank you for your continued trust andinvestment.

VICTOR VEKSELBERG

CHAIRMAN OF THE BOARD

28 April 2011

010

2010 73.4 MLN UN

+20%Global Productionof Cars

SOURCE: CRU

VALUABLE GROWTH

UC RUSAL

2010ANNUALREPORT

011

CEO’SReview

pp011–013

THE YEAR’S KEY HIGHLIGHTS

2010 was a momentous year for UC RUSAL characterisedby the recovery in demand and prices for our metal andthe transformation of the business into a listed publiccompany. UC RUSAL’s strategy, which focused on costefficiency and value creation, delivered significantreturns through the year. While dealing with the impactof the global economic crisis and having now returnedto growth, the Company’s outlook continues to improve.

FINANCIAL RESULTS HIGHLIGHTS

UC RUSAL’s financial performance in 2010 was strong.Our net profit for 2010 increased to USD2,867 millionfrom a net profit of USD821 million in 2009. OurAdjusted EBITDA for 2010 increased to USD2,597 millionas compared to USD596 million in 2009, with theAdjusted EBITDA margin significantly improving up to23.7%. These achievements are a positive signal to ourpartners, employees and investors that we aredelivering on our stated strategy of focusing oncreating investor value. Our resilient financialperformance was helped by our commitment tomaintaining long term sustainable growth and thecontinuous efforts to counter the adverse effects ofboth the downturn in the global economy and of thecommodity markets, by keeping costs at the lowestlevels possible and improving business processes toensure the Company is able to maximise the benefitarising from the economic recovery.

INDUSTRY REVIEW

In 2010, we operated in a vibrant, improving economicenvironment. Demand in markets where we operatestrengthened throughout the year and was driven bystrong economic activity in Germany, South Americaand, most of all, Asia. LME prices for aluminium rose by30% from a weighted average price of USD1,668 pertonne in 2009 to USD2,173 per tonne in 2010. This priceincrease was accompanied by a 9% growth in 2010 of theworldwide production of primary aluminium, which hasbeen estimated at 40.4 million tonnes, and growth inaluminium consumption to an estimated 40.6 million

THESE ACHIEVEMENTS ARE APOSITIVE SIGNAL TO OURPARTNERS, EMPLOYEES ANDINVESTORS THAT WE AREDELIVERING ON OUR STATEDSTRATEGY OF FOCUSING ONCREATING INVESTOR VALUE.

2010ANNUALREPORT

012

CEO’sReviewpp011–013

tonnes, 14% higher than 2009 aluminium consumptionlevels. The increases in both aluminium production andconsumption were driven by demand from China, thanksto the continued growth, urbanisation andindustrialisation occurring throughout that country.

OPERATIONS REVIEW

In 2010, UC RUSAL continued its implementation ofvarious cost saving initiatives and productivityenhancement programs which have assisted the Group tomaintain its global industry leadership position.However, its efforts were somewhat hampered by costinf lation (due, in particular, to rising raw materialprices and LME - linked costs components due to thegrowth in the underlying aluminium price). The entirealuminium sector experienced this cost inf lation andalthough UC RUSAL generally fared better than the restof the industry in managing costs, its aluminiumoperating costs increased by 17% from USD1,471 pertonne in 2009 to USD1,724 per tonne in 2010.

Throughout 2010, UC RUSAL responded to theimproving market conditions by launching new, andrestarting previously idle operations. April saw thecompletion of the commissioning of potline 5 at theIrkutsk aluminium smelter (IrkAZ). Production graduallyrestarted at the Novokuznetsk aluminium smelterbetween March and May 2010. Operations also restartedat the Ewarton Works Plant in May 2010 and the bauxitefeed in the same plant commenced on 1 June 2010.

As a result, each of the key production figuressignificantly improved. Total aluminium outputamounted to 4,083 thousand tonnes in 2010, an increase

of 3.5% as compared to the 2009 output. Alumina outputtotalled 7,841 thousand tonnes in 2010, an increase of7.7% over the 2009 figure. Bauxite production totalled11.7 million tonnes in 2010 and increased by 3.5% ascompared to 2009.

MARKETING STRATEGY

In 2010, UC RUSAL focused on increasing sales of alloysand value-added products and creating a sales platformin Asia to take advantage of growth consumption in theregion and the potential net-importer position ofChina.

The share of alloys in our total production volumegrew from 18% in 2009 to 32% in 2010. The Company hasplans to further expand sales of high value-addedproducts to end-users through improving anddeveloping foundry manufacturing within the aluminiumdivision. This will enable the Company to meet thedemand from consumers representing the globalautomotive and construction industries.

In 2010, UC RUSAL continued to pursue its Chinagrowth initiative. UC RUSAL expects that China willcontinue to increase its imports of primary aluminiumand potentially become a net importer in the mediumterm. In order to be well-prepared to benefit fromattractive China growth fundamentals, we have focusedon establishing a strong foothold in the largest andfastest-growing aluminium market in the world. InNovember 2010, we announced that the Company would beentering into a Framework Agreement with China NorthIndustries Corporation (NORINCO) which sets out thebasic principles for the acquisition by the Company of a33% stake in Shenzhen North Investments CorporationLimited, an affiliate of NORINCO and a Chinese tradingcompany with more than 15 years of experience inselling primary aluminium in China and Asia. The partiesalso intend to sign a memorandum of understandingrelating to the establishment of a joint venture toproduce aluminium alloys. UC RUSAL’s future growthplans in China therefore have strong support.

DEBT REPAYMENT

Our debt repayment and restructuring programmeprogressed positively during 2010. In October 2010, UCRUSAL completed the refinancing of its VEB

Loan,

defined at page 042, with a new USD4.58 billion creditfacility from Sberbank. Refinancing the VEB Loan wasthe final step in a comprehensive program torestructure the Company’s loan portfolio. UC RUSAL hastherefore now succeeded in executing long-termagreements with all of its creditors with conditionswhich will help to ensure the stable development of the

UC RUSAL CONTINUED ITSIMPLEMENTATION OF VARIOUSCOST SAVING INITIATIVES ANDPRODUCTIVITY ENHANCEMENTPROGRAMS WHICH HAVEASSISTED THE GROUP TOMAINTAIN ITS GLOBALINDUSTRY LEADERSHIPPOSITION.

VALUABLE GROWTH

UC RUSAL

013

Company and provide it with opportunities forstrengthening competitiveness. Amongst other factors,lower debt levels and reduced interest rates will be apositive contribution to the Group’s overall ability toobtain an advantage over its competitors.

UC RUSAL met and was in fact able to exceed its 2010scheduled debt repayment obligations. Looking forward,the Company also intends to explore other refinancingoptions. In March and April 2011, the Companysuccessfully completed two consecutive RUR15 billionbond issues, marking the Company’s return to the publicdebt capital markets. The issue was positively receivedby the market, as evidenced by a more than two-timesoversubscription. The issue size was large by Ruble bondmarkets’ standards and the significant demand furtherdemonstrates the high level of investor confidence inUC RUSAL.

INVESTMENT PROJECTS

In 2010, the Company pursued its strategic goal ofdeveloping new smelter capacity in low cost captiveenergy regions. A financing package amounting toRUR50 billion (approximately USD1.7 billion) wasapproved by VEB for the BEMO Project to complete theconstruction of the BEMO HPP and the first phase of the588,000 tonnes per annum capacity Boguchanskyaluminium smelter.

The BEMO Project is being implemented jointly by theCompany and RusHydro. The construction of the BEMOHPP will enable UC RUSAL to maintain an abundant supplyof hydro-power for its smelters in Siberia. A majorconsumer of electricity generated by the BEMO HPP willbe the Boguchansky aluminium smelter. With everincreasing energy costs and the urgent need to addressclimate change, the BEMO Project is at the forefront ofmodern and sustainable developments in aluminiumproduction.

In the medium term, UC RUSAL expects to pursueanother growth option, namely the completion of theTaishet aluminium smelter in Russia with maximumcapacity of 750,000 tonnes per annum.

With the launch of these two smelters, UC RUSAL willreceive new technologically advanced andenvironmentally friendly smelting facilities. They willadd 1.3 million tonnes per year of smelting capacity (1million tonnes on an attributable basis) and will helpenhance UC RUSAL’s world leadership position duringthe global economic recovery and the expected growthin demand for aluminium.

OUTLOOK

Our expectation is that aluminium will outperform other

base metals due to fundamental price support frommarginal production costs. Already there are signs ofcontinued improvement in the underlying globalmacroeconomic environment which should providefundamental support to performance in the aluminiummarket. China is once again expected to lead the worldin aluminium demand. UC RUSAL believes that aluminiumconsumption in China in 2011 will grow by 12% and reach18.5 million tonnes driven by continued urbanisation.The ongoing restrictions on power consumption acrossthe country as the Chinese Government looks to improveenergy efficiency by reducing smelter capacity meansan increasing amount of aluminium supply will comefrom metal imported from overseas countries – mostnotably Russia, which is just across the Chinese border.Medium term growth outlook remains robust and UCRUSAL believes that China will continue to increase itsimports of primary aluminium.

Given the encouraging outlook for aluminium pricesand increasing consumer demand, we anticipate that UCRUSAL should be in a position to continue to strengthenits world leadership position.

PRODUCTION INCREASES

Assuming the continuing restoration of the market in2011, UC RUSAL is well placed for further growth. TheCompany plans to increase production of aluminium by2% in 2011, compared to 2010 and reach almost fullproduction capacity. The major increase in productionis expected at the environmentally friendly andtechnologically advanced Siberian smelters. In addition,UC RUSAL expects to increase alumina output by 8% in2011 compared with 2010 output, mainly by increasingproduction at the Windalco-Ewarton Plant in Jamaica,which restarted in June 2010.

In conclusion, we have reaffirmed our commitment tothe values that have guided the Company for many yearsand which have helped us navigate through the economicdownturn. As a result, UC RUSAL is well placed tocontinue delivering value for all stakeholders in 2011and beyond. We approach the year ahead with theconfidence befitting our position as a truly globalcompany and the world’s leading aluminium producer.

OLEG DERIPASKA

CHIEF EXECUTIVE OFFICER

28 April 2011

014

2010 RECORD SINCE 2000

US$197.5/TPremium on AluminiumSupplies to WesternEurope SOURCE: METAL BULLETIN

VALUABLE GROWTH

UC RUSAL

2010ANNUALREPORT

015

BusinessOverview

pp015–027

UC RUSAL IS THE WORLD’S LARGEST PRODUCER ofaluminium, producing 4.1 million tonnes in 2010 whichaccounts for approximately 10% of the global output.

The Group’s business is focused on the upstreamsegment of the industry — the production and sale ofprimary aluminium (including alloys and value-addedproducts, such as aluminium sheet ingot and aluminiumbillet). Within its upstream business, the Group isvertically integrated to a high degree, having securedsubstantial supplies of bauxite and having the capacityto produce alumina in excess of its currentrequirements. The Group is the world’s fourth largestproducer of alumina, producing approximately 7.8million tonnes in 2010 which accounts for approximately10% of the global output3. Alumina production volumes in2010 fully satisfied the Company’s aluminium productionneeds, achieving 100% self sufficiency. The Group’srevenue was USD10,979 million for the year ended31 December 2010.

OUR STRENGTHS

UC RUSAL is uniquely positioned to benefit from theattractive fundamentals of the global aluminiumindustry:

BUSINESS UNITS

AluminiumUC RUSAL operates 16 aluminium smelters which arelocated in four countries: Russia (13 plants), Ukraine(one plant), Sweden (one plant) and Nigeria (one plant).The Company’s core asset base is located in Siberia,Russia, accounting for some 85% of the Company’saluminium output in 2010. Among those, Bratsk andKrasnoyarsk smelters together account for nearly halfof UC RUSAL’s aluminium production and are the largestaluminium smelters in the world.

The Company’s aluminium smelters benefit fromaccess to low-cost and renewable energy sources,particularly in Siberia where smelting facilities rely onstranded hydro power as their principal source ofelectricity.

As a result of the Company’s competitive advantagein accessing low cost captive power, UC RUSAL’saluminium production was placed in the second quartileof Brook Hunt’s 2010 C1 cash cost curve (refer to thechart at page 03).

Access to low-cost and relatively abundant hydropower generation will allow the Company to retain itscurrent competitive position on the global cost curvegoing forward, as environmental concerns andcompetition for energy sources continue to putpressure on the cost base of other aluminium producersthat rely more on thermal or gas power.

During 2010, UC RUSAL continued to implement acomprehensive program designed to control costs,optimise the production process and strengthen theCompany’s position as one of the world’s most cost-efficient aluminium producers.

2010ANNUALREPORT

016

BusinessOverviewpp015–027

The table below4 provides an overview of UC RUSAL’saluminium smelters as at 31 December 2010:

CapacityNameplate utilisation

Asset Location %Ownership capacity, kt rate

SIBERIA

Bratsk aluminium smelter Russia 100% 1,006 97%Krasnoyarsk aluminium smelter Russia 100% 1,008 97%Sayanogorsk aluminium smelter Russia 100% 542 99%Novokuznetsk aluminium smelter Russia 100% 322 84%Khakas aluminium smelter Russia 100% 297 100%Irkutsk aluminium smelter Russia 100% 529 74%Alukom Taishet aluminium smelter Russia 100% 11 —

OTHER RUSSIA

Bogoslovsk aluminium smelter Russia 100% 187 61%Urals aluminium smelter Russia 100% 75 96%Volgograd aluminium smelter Russia 100% 168 92%Volkhov aluminium smelter Russia 100% 24 77%Nadvoitsy aluminium smelter Russia 100% 81 88%Kandalaksha aluminium smelter Russia 100% 76 85%

OTHER COUNTRIES

KUBAL Sweden 100% 128 73%ALSCON Nigeria 85% 96 18%Zaporozhye aluminium smelter Ukraine 97.6% 114 22%TOTAL NAMEPLATE CAPACITY 4,664UC RUSAL ATTRIBUTABLE CAPACITY 4,664 88%

UC RUSAL intends to further expand its aluminiumsmelting base in Russian Siberia. The two f lagshiporganic growth projects are the Boguchansky andTaishet smelter projects, which together will increaseproduction capacity by an additional 1.3 million tonnesper annum post completion (1 million tonnes on anattributable basis).

BEMO ProjectThe BEMO Project involves the construction of the 3,000megawatt BEMO HPP and the Boguchansky aluminiumsmelter in the Krasnoyarsk region in Siberia which willproduce approximately 588,000 tonnes of aluminium perannum.

The construction of the Boguchansky aluminiumsmelter is divided into two stages, with the first start-up complex (with production capacity of 147,000 tonnesof aluminium per annum) scheduled for completion by2013 and the second complex scheduled for completionby the end of 2015.

In 2010, UC RUSAL together with RusHydro receivedcredit funds from VEB for the completion ofconstruction of the first start-up complex of theBoguchansky aluminium smelter and resumed works atthe construction site in January 2011.

The capital expenditure for the Boguchanskyaluminium smelter is currently estimated at

3 According to CRU.4 The table presentstotal nameplatecapacity of the plants,each of which is aconsolidated subsidiaryof the Group.5 Capital expenditureamounts are based onUC RUSAL’s managementaccounts, and differfrom amounts disclosedin annual consolidatedfinancial statements asthe managementaccounts ref lect thelatest best estimate ofthe capital costsrequired to completethe project, whereasamounts disclosed inthe consolidatedfinancial statementsref lect commitments asat 31 December 2010.6 See footnote 5.7 See footnote 5.8 OHSAS 18001 is astandard of occupa-tional health and safetymanagement system,which is part of thegeneral managementsystem. Theseinternational standardscomply with the world’sbest practices inoccupational health andsafety managementsystems.

approximately USD1,590 million5 (UC RUSAL’s share of thiscapital expenditure will be approximately USD795 million).

The capital expenditure for the first start-upcomplex of the Boguchansky aluminium smelter iscurrently estimated at approximately USD826 million6

(UC RUSAL’s share of this capital expenditure will beapproximately USD413 million), of which approximatelyUSD296 million has been incurred as of 31 December2010 (UC RUSAL’s share of this amounted toUSD148 million).

As at 31 December 2010, the first start-up complex ofthe Boguchansky aluminium smelter was estimated to be25% to 30% complete, which included the following works:> earth works comprising 9,014 thousand cubic metres

of ground excavation and back-filling of6,031 thousand cubic metres;

> erection of 29.7 thousand cubic metres of cast-in-place reinforced concrete structures; and

> construction of 2.7 thousand tonnes of metalstructures.In January 2011, UC RUSAL issued a press release

stating that it had resumed works at the Boguchanskyaluminium smelter as follows:> construction of a number of production facilities of

the first start-up complex;> drilling of wells to secure a water supply for the site;> construction of a railroad leading to the smelter;

3 According to CRU.4 The table presentstotal nameplatecapacity of the plants,each of which is aconsolidated subsidiaryof the Group.5 Capital expenditureamounts are based onUC RUSAL’s managementaccounts, and differfrom amounts disclosedin annual consolidatedfinancial statements asthe managementaccounts ref lect thelatest best estimate ofthe capital costsrequired to completethe project, whereasamounts disclosed inthe consolidatedfinancial statementsref lect commitments asat 31 December 2010.6 See footnote 5.7 See footnote 5.8 OHSAS 18001 is astandard of occupa-tional health and safetymanagement system,which is part of thegeneral managementsystem. Theseinternational standardscomply with the world’sbest practices inoccupational health andsafety managementsystems.

VALUABLE GROWTH

UC RUSAL

017

UC RUSAL'S ALUMINIUMSMELTERS BENEFIT FROMACCESS TO LOW-COSTAND RENEWABLE ENERGYSOURCES, PARTICULARLY INSIBERIA WHERE SMELTINGFACILITIES RELY ONSTRANDED HYDRO POWER ASTHEIR PRINCIPAL SOURCE OFELECTRICITY

> preparation of design documentation for thepriority objects of the first start-up complex,namely the approach line, warehousing and objects ofelectricity and water supply.Construction of reduction potrooms and the foundry

commenced in March 2011; and the workers’ camp isnearly completed, with the first workers scheduled tomove in by April 2011. The construction of three blocksin a ten-block apartment house for the staff in thenearby town of Tayezhny is expected to be completed inApril 2011.

Taishet aluminium smelterThe Taishet aluminium smelter is located in Irkutsk,Russia, and will be constructed in the medium term. Thesmelter’s design capacity is 750,000 tonnes per annum.The total capital expenditure for the smelter (excludingconstruction of the anode plant) is currently estimatedat approximately USD2,437 million7, of which USD551.2million, had been spent as of 31 December 2010.

As a consequence of the global economic crisis,construction of the smelter was temporarily suspended.The Company is in the process of negotiating projectfinancing for the construction of the first phase of thesmelter from various banks.

AluminaThe Group operates 12 alumina refineries. In recentyears, the Company has substantially increased itsrefining capacities by means of new acquisitions andincreased holdings in existing assets. UC RUSAL’salumina refineries are located in six countries: Ireland(one plant), Jamaica (two plants), Ukraine (two plants),Italy (one plant), Russia (four plants) and Guinea (oneplant). In addition, the Company holds a 20% equity stakein QAL, the second largest alumina refinery in the worldin terms of production capacity. Most of the Group’srefineries have ISO 9001 certified quality controlsystems, ten refineries and QAL have been ISO 14001certified for their environmental management andthree have received OHSAS 180018 certification fortheir health and safety management system.

UC RUSAL’s six largest alumina refineries in terms ofproduction accounted for 88% of its aggregate aluminaproduction for the year ended 31 December 2010.

The Company’s long position in alumina capacityhelps to secure sufficient supply for the prospectiveexpansion of the Company’s aluminium productioncapacity and allows the Company to take advantage offavourable market conditions through third-partyalumina sales.

2010ANNUALREPORT

018

BusinessOverviewpp015–027

The table below9 provides an overview of UC RUSAL’salumina refineries as at 31 December 2010:

NameplateAsset Location % ownership capacity, kt Process

Achinsk alumina refinery Russia 100% 1,069 NephelineBoksitogorsk alumina refinery Russia 100% 149 SinterBogoslovsk alumina refinery Russia 100% 1,074 Bayer & SinterUrals alumina refinery Russia 100% 740 Bayer & Sinter

Friguia alumina refinery Guinea 100% 618 Bayer

QAL Australia 20% 4,020 Bayer

Eurallumina Italy 100% 1,085 Bayer

Aughinish alumina refinery Ireland 100% 1,890 Bayer

Alpart Jamaica 65% 1,673 BayerWindalco Jamaica 93% 1,240 Bayer

Zaporozhye alumina and aluminium complex Ukraine 97.6% 260 Bayer & SinterNikolaev alumina refinery Ukraine 100% 1,570 BayerTOTAL NAMEPLATE CAPACITY 15,388UC RUSAL attributable capacity 11,500

9 Calculated based onthe pro rata share ofthe Group’s ownershipin correspondingalumina refineries.Zaporozhye AluminaRefinery (ZALK) is afully consolidatedsubsidiary of theCompany.10 See Footnote 5.

BauxiteThe aggregate attributable bauxite production from theGroup’s mines for the year ended 31 December 2010 was11.7 million tonnes. As at 31 December 2010, the Grouphad aggregated JORC bauxite Mineral Resources of1,823 million tonnes, of which 603 million tonnes wereMeasured, 620 million tonnes were Indicated and600 million tonnes were Inferred.

Securing the supply of high quality bauxite atadequate volumes and cost competitive prices for itsalumina facilities is an important task for the Company.Additional exploratory work is being undertaken to findnew deposits of bauxite in the existing operationalbauxite mining areas of the Group and new projectareas. Each of the Group’s mining assets is operatedunder one or more licences. The following table providesan overview of the Company’s bauxite mines as at 31December 2010:

VALUABLE GROWTH

UC RUSAL

019

Mineral Resources(1)

Annual% Measured Indicated Inferred Total Capacity(2)

Asset Location ownership mt mt mt mt mt

Timan Bauxite(3) Russia 80% 111 67 — 178 2.5North Urals bauxite mine Russia 100% 10 178 114 302 3.4

Compagnie des Bauxites de Kindia Guinea 100% — 34 62 96 3.2Friguia Bauxite and Alumina Complex Guinea 100% 34 142 153 329 2.1

Bauxite Company of Guyana, Inc.(3) Guyana 90% 3 41 4 48 2.2

Alpart Jamaica 65% 15 41 38 94 3.2Windalco Jamaica 93% 28 46 12 86 3.7

Dian-Dian Project Guinea 100% 402 71 217 690 —TOTAL 603 620 600 1,823 20.3

ENERGY ASSETS

BEMO ProjectIn May 2006, UC RUSAL and RusHydro, a companycontrolled by the Russian Government, entered into acooperation agreement to jointly construct the BEMOProject. In 2010, UC RUSAL together with RusHydroreceived credit funds from VEB for the construction ofthe BEMO HPP and the first start-up complex of theBoguchansky aluminium smelter and as of January 2011,works at both construction sites had resumed.

As at 31 December 2010, key construction andassembly works of the BEMO HPP for the first start-upcomplex (3 turbines) have been completed to thefollowing extent:> 93% of the concrete placing and assembly of pre-cast

reinforced concrete has been completed;> 89% of the hydromechanical equipment and metal

structures have been assembled;> 61.5% of the cranes have been assembled;> 25% of the hydraulic power equipment has been

assembled;> 99.8% of the earth and rock excavation has been

carried out;> 100% of the asphalt concrete has been placed; and> 95% of the cement injection has been completed.

UC RUSAL’s proportion of capital expenditure for theBEMO Project is 50%, with total 100% capital expenditurefor the BEMO HPP currently estimated at approximatelyUSD1,769 million10 (UC RUSAL's share of this capitalexpenditure will be approximately USD884 million), ofwhich USD1,263 million had been spent as of 31 December2010 (UC RUSAL’s share of this amounted to

USD631 million). The Investment Fund of the RussianFederation finances the necessary infrastructure (thecosts of which are not included in the project budget).The total investment from the Investment Fund approvedby the Russian Government for the BEMO Projectamounted to RUR26 billion, including RUR18 billioninvested in the period between 2008 and 2009 and RUR1.9billion in 2010.

MINING ASSETS

UC RUSAL’s mining assets comprise of 16 mines and minecomplexes, including eight bauxite mines, two quartzitemines, one f luorite mine, two coal mines, one nephelinesyenite mine and two limestone mines. The Companyjointly operates the two coal mines with Samruk-Energo,the energy division of Samruk-Kazyna under a 50/50joint venture, LLP Bogatyr Komir. The long position inalumina capacity is supported by the Company’s bauxiteand nepheline syenite resource base.

LLP Bogatyr KomirLLP Bogatyr Komir, which is located in Kazakhstan, is a50/50 joint venture between the Company and Samruk-Energo. LLP Bogatyr Komir, which produced 39 milliontonnes of coal in 2010, has approximately 790 milliontonnes of JORC Proved and Probable Ore Reserves andhas Measured Mineral Resources and Indicated MineralResources together of approximately 2.0 billion tonnesas at 31 December 2010. LLP Bogatyr Komir generatedsales of USD422 million in 2009 and USD559 million in2010. Sales are divided almost evenly between Russianand Kazakh customers in terms of physical volumes.

(1) Mineral Resources:> are recorded on an unattributable basis, equivalent to 100% ownership; and> are reported as dry weight (excluding moisture).Mineral Resources tonnages include Ore Reserve tonnages.

(2) Annual capacity is calculated based on the pro rata share of the Group’s ownership in corresponding bauxite mines and mining complexes.(3) The total annual capacity of the Group’s fully consolidated subsidiaries Timan and Bauxite Co. De Guyana is included in annual capacity figures,

notwithstanding that minority interests in each of these subsidiaries are held by third parties.

2010ANNUALREPORT

020

BusinessOverviewpp015–027

GROUP WIDE INITIATIVES

Changes to the organisational structure ofthe CompanyIn 2010, the Company’s organisational structure wasmodified to increase management efficiency and createa more distinct specialisation of production facilitiesthrough maximising the concentration of specifictasks, while ensuring a clear coordination of, andconstant interaction between, elements of theCompany’s structure.

The aluminium business was divided into two separatedivisions, based on the operations’ geographicallocations and objectives. Aluminium facilities in Siberiawere grouped together to create Aluminium DivisionEast, which focuses on exports of primary aluminium.Given their proximity to key Russian and Europeancustomers, aluminium facilities located in the Uralsregion and the North-Western regions of Russia wereintegrated to form Aluminium Division West, tospecialise in the manufacture of value-added products.More information on these aluminium divisions isprovided on page 032 of this Annual Report.

A similar process was applied to the Company’salumina division. Foreign alumina facilities weregrouped together to form the International AluminaDivision, which was to focus on delivering products tocustomers outside of Russia, while Russian facilitieswere integrated to form Alumina Division East,responsible for the supply of the Company’s aluminiumoperations with alumina.

Furthermore, the First Deputy Chief ExecutiveOfficer of the Company, Vladislav Soloviev, was maderesponsible for the overall operating control of all ofthe Company’s assets.

The sales directorate was also divided to coverexternal markets, on the one hand, and Russian and CISmarkets, on the other hand. The decision to do so wasprompted by the significant differences in customerrequests in the domestic and external markets.

Structural changes also resulted in theestablishment of the Commercial Directorate. Thisbusiness unit was created to centralise and optimisethe procurement function and centralise the sales ofby-products.

Engineering and Construction Division (ECD)The ECD was established by UC RUSAL in July 2005.Historically, aluminium companies would implementrepairs and maintenance, engineering and constructionprojects using their own resources. The outsourcing ofthese services has resulted in the emergence of repair,engineering and construction service companiesembodied by the ECD, which incorporates over 70 years

of Russian know-how in aluminium.The key advantage of the ECD is its ability to provide

comprehensive repairs, maintenance, engineering andconstruction services, resulting in the reduction ofcapital expenditure and operational costs. It is theGroup’s major investment for ensuring dynamic andsustainable growth through continuation of newprojects and refurbishing of existing productionfacilities.The major functional areas of the ECD are as follows:> implementation of complex engineering and

construction projects with an EPCM approach; and> maintenance, repair and replacement of process

equipment at all Group facilities.

The ECD, including design institutes RUSAL VAMI11, GIDEP(Krasnoyarsk) and the SibVAMI (Irkutsk), provides a fullrange of engineering and designing services, startingfrom site selection, process development and feasibilitystudy to basic and detailed engineering in thealuminium, alumina, chemical and energy industries.

During the execution of projects, the ECD acts as thein-house EPCM contractor to the Group. The ECDperforms a full range of activities related to execution,including the preparation of detail design,documentation, the purchase of equipment andconstruction, commissioning and start-up activities.

The advantages of the ECD’s EPCM and engineeringcapabilities can be illustrated by the construction ofthe Group’s Khakas smelter which was designed andconstructed by the ECD. Work commenced on the facilityin March 2005, the first metal production was broughton line in December 2006, and the smelter became fullyoperational in November 2007. Capital expenditure inthe Khakas project amounted to USD2,415 per tonne ofinstalled RA-300 aluminium smelting capacity.

Maintenance and RepairsThe ECD performs maintenance, repairs, overhauls andreplacement of process equipment of all equipment unitsat each of the Group’s facilities in Russia and Ukraine.

It has more than 10 branches and subsidiaries inRussia and Ukraine and about 18,000 employees areinvolved in maintenance and repair activities.

InnovationsAluminium production technologies developed by theCompany are among the leading three forms ofaluminium production technologies which have beendeveloped worldwide. In 2006, the Khakas smelter – thefirst aluminium production site commissioned in Russiain the last 20 years – was built to utilise RA-300

11 Situated in Saint-Petersburg, the largestdesign institute wasfounded in 1931. Morethan 40 industrialenterprises in theworld have beenconstructed on thebasis of its designprojects. It has over460 patents andlicenses its proprietarytechnologies foralumina, aluminium andmagnesium production.

VALUABLE GROWTH

UC RUSAL

021

technology which had been developed by the Company. Inthe near future the Company plans to completeconstruction of two aluminium smelters – Boguchanskyand Taishet – which will run using the RA-300 and RA-400 technologies created by UC RUSAL.

UC RUSAL has developed innovative and revolutionaryaluminium production technology which will facilitatethe emission of almost no greenhouse gases. In 2010, arecently created anode material allowed UC RUSALexperts to produce aluminium with lower levels ofproduction contaminants, which would assist the Groupin reducing its overall greenhouse gas emissions.Furthermore, UC RUSAL plans to have developed, by 2015,the first electrolytic cell with inert anodes.

The Company has converted smelters which wereconstructed many years ago, replacing their agedtechnology with “Environmental Soederberg” technologywhich allows high process and environment indicators tobe reached. Approximately 100 pots in the Krasnoyarskaluminium smelter have converted to “EnvironmentalSoederberg” technology. This technology allows anodepaste consumption to be reduced by 7%, f luoridealuminium consumption to be decreased by 30% andf luoride emissions to be reduced by 75%.

In 2011, the Company intends to launch a project todevelop non-waste alumina production which will make itpossible to use red mud in ferrous metallurgy,significantly reducing the volumes of disposed waste.

In addition UC RUSAL, in cooperation with variousinstitutes, has worked on the development of newaluminium-based alloys for use in the automotive, powergeneration and aircraft construction industries with aview to reduce the negative environmental impact ofthese industries and facilitating power savings.

Technological achievementsPreparation has been completed for the large-scaleconversion of UC RUSAL’s smelters to resource-saving“greener” technology - this includes the installation of88 “New Soederberg” design cells which have beentested for the upgrade of the Krasnoyarsk,Novokuznetsk and Irkutsk aluminium smelters.Engineering documentation has been developed for theconstruction of cells and an automatic alumina pointfeeding system at the Bratsk aluminium smelter.Redesigned tools and process equipment have beentested to reduce manual labour. In addition, feasibilitystudies are being carried out in connection with theupgrade of the Krasnoyarsk, Bratsk, Novokuznetsk,Volgograd and Irkutsk aluminium smelters.

Work is underway for the design of an industrialprocess for inert anodes production, anode testing at

higher amperage and for the design of a new electrodetype for converting Soederberg pots to inert anodes.Inert anodes from new alloys have been tested in 100Apots for a period of 20 days and aluminium with a 99.0%purity level was produced and the cost of anodes wasreduced by 30%.

RA-300 and RA-400 pot designs have been enhancedto improve their energy consumption and increasepotlife. Start-up devices have been designed and testedwhich allow line loads not to be disconnected during thealuminium production process. Updated engineeringdocumentation has been circulated to the Khakasaluminium smelter. This documentation will also be usedfor the construction of the Boguchansky and Taishetaluminium smelters. Work is underway to improve theenergy consumption of cells with a view to reduceconsumption by 1,500 to 2,000 kWh per tonne ofaluminium produced.

The value-added product range has been expandedthrough process improvements and the production of abetter quality of lithographic slab for Krasnoyarskaluminium smelter, a higher foil production grade forSayanogorsk aluminium smelter and better packagingquality at the Bratsk aluminium smelter. In addition, anenergy-efficient process for the production of EC-grade wire-rod with better parameters which addressthe needs of the industry is being developed.

Other technological achievements by the Company in2010 include:> potline 5 at the Irkutsk aluminium smelter (reaching

of design capacity);> the upgrade of 4 calcining furnaces at Krasnoyarsk

and Bratsk aluminium smelters, increasing calcined

ALUMINIUM PRODUCTIONTECHNOLOGIES DEVELOPED BYTHE COMPANY ARE AMONG THELEADING THREE FORMS OFALUMINIUM PRODUCTIONTECHNOLOGIES WHICH HAVEBEEN DEVELOPED WORLDWIDE.

2010ANNUALREPORT

022

BusinessOverviewpp015–027

coke output by 64 tpa;> the improvement of the pre-bake anode production

at Sayanogorsk aluminium smelter, allowing cheapcoke to be calcined at OOO Slantsy;

> the design and implementation of new engineeringsolutions at the Bogoslovsk and Urals aluminiumsmelters to increase the capacity of mud disposalareas, allowing for the operation of these plantswithout having to construct new mud lakes for 10 and17 years respectively;

> the stabilisation of the existing production processat Krasnoyarsk and Bratsk aluminium smelters,increasing current efficiency by over 0.75%, reducingpower consumption by 220 kWh per tonne ofaluminium produced and increasing higher gradesoutput by 12%12;

> the improvement of liquor processing at aluminarefineries with the aim of maintaining and boostingthe throughput capacity of existing facilities whenintroducing low-quality bauxites into production.Heat exchange efficiency has also been increased atthese refineries; and

> the upgrade of rotating calciners to stabilisecalcination, improve alumina quality and reducespecific fuel oil consumption.

Quality PolicyThe Company has adopted and implemented a qualitymanagement system, which aims to ensure that all of itsproducts are in full compliance with the highestinternational standards and customer requirements. Inaddition, in early 2011 UC RUSAL adopted a corporatequality policy which specifies unified qualityrequirements and principles for all of its subdivisionsand operations.

One of the key principles of the corporate qualitypolicy is the requirement for all aspects of the Companyto be customer-oriented. UC RUSAL consistentlyanalyses the demands and expectations of its customersand aims to improve the levels of customer satisfactionwith the quality of its products and services as well asmaintaining its reputation as a reliable businesspartner. To do so, UC RUSAL pays special attention totraining its employees on how to use the tools of theProduction System, improving the levels ofprofessionalism of its personnel and involving them inthe process of developing a “quality-orientated”culture for the Company.

The Company applies the most advanced technologiesto constantly optimise and standardise all of itsprocesses to improve cost-efficiency ratios. Eachproduction facility of the Company is certified inaccordance with the ISO 9001 quality managementsystem. The Company plans to adopt the requirements ofthe ISO TS 16949 international standard in the future to

further improve current production processes.UC RUSAL also intends to establish a customer supportcentre, responsible for the detailed analysis ofcustomer requirements and a supplier developmentcentre to formalise requirements for incoming rawmaterials for the purpose of minimising stock-relatedrisks, improving product quality and increasingsatisfaction of both (internal and external customers).

CORPORATE STRATEGY

UC RUSAL’s mission is to create value for Shareholdersthrough sustainable growth. The strategy to achievethis focuses on:> maintaining its position among the most efficient

and lowest cost producers in the industry:> maintaining low cost electricity supply through

long term contracts;> investing, where appropriate, to develop its own

power generation capacity and energy productionfacilities to create a natural hedge for electricitycosts;

> developing enhanced technologies that reduceenergy consumption and maintaining the Company’scapability to allow further innovation;

> increasing aluminium production capacity inSiberia where there is low cost captive energysupply;

> shifting production towards higher value addedproducts and expanding direct contact with end-users;

> redoubling its commitment to company wide costmanagement programs;

> optimising other raw material sourcing, transportand logistics to minimise costs; and

> continuing actively to manage production torespond to changes in the market.

> increasing its presence in the rapidly growingconsumption segments of automotive, packaging/printing and electronics:> exploiting the manufacturing capabilities of the

Siberian operations to increase sales of highvalue products; and

> expand sales to Asia, in particular China, takingfull advantage of UC RUSAL’s operating proximityto Asian end-users.

> maintaining an efficient capital structure thatprovides a sound platform for growth by:> continuing to use cash f low generation to reduce

financial debt; and> proactively exploring opportunities to refinance

debt obligations under more favourable terms.> pursuing value accretive growth opportunities

organically or through acquisitions or asset swaps by:

12 In 2010, UC RUSALcompleted amperageincrease programmes,reduced materialsconsumption throughimproved processparameters and controlalgorithms, improvedcapacity of castingmachines and theadaptation of newproduct types.

VALUABLE GROWTH

UC RUSAL

023

> enhancing upstream vertical integration whilemaintaining a focus on higher margin upstreamprimary aluminium production;

> exploring growth opportunities in regions withstranded low cost captive electricity supply;

> enhancing its bauxite and alumina self-sufficiencyby exploring growth opportunities ingeographically diverse regions and exploitingregional supply/demand imbalances; and

> securing access to and self-sufficiency in keyproduction inputs.

> managing environmental protection matters andutilising natural resources responsibly by making allof UC RUSAL’s production facilities meet emissionstandards set by the local laws in the jurisdictionswhere UC RUSAL conducts business.

Near term initiatives that ref lect theimplementation of UC RUSAL’s strategy, whichposition the Company to benefit fully from theincrease in aluminium consumption driven by theurbanisation of China and other emerging economiesand the attractive long term fundamentals of theindustry, include:> steady progress towards completing the

construction of the Boguchansky and Taishetsmelters in Siberia, which are expected toproduce an additional 1.3 million tonnes perannum of aluminium using low cost, captiveelectricity generated by hydroelectric powergenerators in the region; and

> securing long term power supply contracts fromthe Ministry of Energy of the Russian Federationwhich allows the Company to purchase electricityfrom the Russian wholesale market until 2027.These new contracts guarantee long-term accessto electricity at stable rates through thewholesale market and ensure the continuation oflong-term capacity location contracts with majorsuppliers of electricity.

ENVIRONMENTAL AND SAFETYPOLICIES

As with other natural resources and mineral processingcompanies, the Group’s operations create hazardousand non-hazardous waste, eff luent emissions into theatmosphere, water and soil and safety concerns for itsworkforce. Consequently, the Group is required tocomply with a range of health, safety and environmentallaws and regulations. The Group believes its operationsare in compliance in all material respects with theapplicable health, safety and environmental legislationof the Russian Federation, its regions and the countriesand regions where the Group’s plants are situated. The

Group intends to upgrade where feasible to comply withthe best international standards.

Operating on five continents and being involved inthe metal production and processing, mining and powergeneration industries, UC RUSAL shares responsibilityfor addressing regional and global environmental issuesand finding cutting edge approaches to solving suchproblems. The Company considers its environmentalprotection activities to be an inherent part of itsbusiness as well as its contribution to publicsustainable development projects.

UC RUSAL’s goal is to facilitate the gradualimprovement of environmental indicators, while at thesame time taking into account practical possibilitiesand social and economic factors.

The following guidelines are adhered to when makingmanagement decisions at all levels and in all areas ofthe Company’s business:> Risk Management: define and assess environmental

risks, set targets and plan work taking into accountenvironmental risk management issues;

> Compliance: comply with environmental legislativerequirements of the countries where UC RUSAL hasoperations as well as comply with environmentalcovenants assumed by the Company;

> Prevention: apply the best available techniques andmethods to prevent pollution, minimise risks ofenvironmental accidents and other negative impacton the environment;

> Training: train employees of the Company to meet theenvironmental requirements applicable to their

OPERATING ON FIVECONTINENTS AND BEINGINVOLVED IN THE METALPRODUCTION AND PROCESSING,MINING AND POWERGENERATION INDUSTRIES, UCRUSAL SHARES RESPONSIBILITYFOR ADDRESSING REGIONAL ANDGLOBAL ENVIRONMENTAL ISSUESAND FINDING CUTTING EDGEAPPROACHES TOSOLVING SUCH PROBLEMS.

2010ANNUALREPORT

024

BusinessOverviewpp015–027

business areas to give employees a betterunderstanding of the environmental consequencesshould such requirements not be met;

> Cooperation: note the opinions and interests ofrelated parties, establish environmentalrequirements when selecting suppliers andcontractors and assist them in complying with therequirements;

> Measurability and evaluation: establish, measureand evaluate environmental indicators and assesscompliance with environmental legislation of thecountries where UC RUSAL operates and withenvironmental covenants assumed by the Company;and

> Openness: openly demonstrate the Company’s plansand results of its environmental activities includingthrough public reports issued by the Company.Key goals of UC RUSAL’s environmental strategyinclude:

> reducing emissions, including greenhouse gases;> creating a closed-circuit water supply system for the

main production processes of the Company’sfacilities;

> increasing the volume of treated and used wasteproducts and their safe disposal;

> replacing and disposing of electrical equipmentcontaining polychlorbiphenyls (PCBs);

> rehabilitating land which has been negativelyimpacted and assisting in the maintenance ofbiodiversity; and

> creating corporate systems to manage environmentalaspects and risks.By following this environmental policy and

undertaking to regularly update its provisions, theCompany has tasked itself with constantly developingand improving its environmental management systemand following up on its principles at all productionfacilities of UC RUSAL, including all those which are inoperation and those which are still under construction.

The Group has also taken steps to lessen theenvironmental impact of its operations and comply withall applicable environmental laws and regulations. TheGroup’s mines, refineries, smelters and other plantslocated in Russia are subject to statutory limits on airemissions and the discharge of liquids and othersubstances. Russian authorities may permit, inaccordance with the relevant Russian laws andregulations, a particular Group facility to exceedstatutory emission limits, provided that the Groupdevelops a plan for the reduction of the emissions ordischarge and pays a levy based on the amount ofcontaminants released in excess of the limits. Fees areassessed on a sliding scale in accordance with therelevant laws and regulations: the lowest fees areimposed for pollution within the statutory limits,

intermediate fees are imposed for pollution within theindividually approved limits and the highest fees areimposed for pollution exceeding such limits.

In 2007, the Company signed a memorandum ofunderstanding with the United Nations DevelopmentProgram. The aim of the memorandum is to implementmeasures to minimise the impact of the Group onclimate change by reducing greenhouse gas emissions.The Group is actively participating in the InternationalAluminium Institute’s activities related to targetingthe reduction of greenhouse gas emissions and energyefficiency. The Group has achieved significantimprovements in greenhouse gas emission reductions.For instance, the Group’s aluminium smelters reducedgreenhouse gas emissions in 2010 by more than 43%compared to 1990.

The Group is a member of the National Carbon Unionin Russia, a partnership of leading businesses createdin July 2003. The National Carbon Union aims to create aregulatory structure for the control of greenhouse gasemissions and to develop a strategy for the applicationof the Kyoto Protocol in Russia. The Group alsoparticipates in activities conducted by the RussianMinistry for Economic Development concerning thedevelopment of Russia’s carbon market. The “Reductionof Perf luorocarbons emission at Krasnoyarsk Smelter”project was approved by the Ministry of EconomicDevelopment on 31 December 2010 as a JointImplementation Project13. The total emission reductionfor the years 2008-2012 is estimated to be 1.2 millionCO

2 eql14. A similar Joint Implementation Project at Bratsk

aluminium smelter (for an estimated emission reductionof 1.2 million CO

2 eql

14) is being prepared forparticipation in the third carbon tender15. A decision isexpected to be made in the first half of 2011.

The Group’s social performance is guided by the tenuniversal social and environmental principles of the UNGlobal Compact to which the Company is a signatory. TheCompany measures its social performance in accordancewith the requirements of the Global ReportingInitiative’s Business Guide to the SustainabilityReporting Guidelines. The principles of the GlobalReporting Initiative’s reporting system are fullycompatible with the principles of the UN Global Compact.The Company released its communication on progressreporting in accordance with the UN Global Compactin April 2010.

The Group considers the health and safety of itsemployees a fundamental responsibility that is centralto its business. To this end, the Group has formulated aseries of health and safety principles, policies andguidelines and established a health and safetymanagement system. Ten of the Group’s sites andfacilities are already OHSAS 1800116 certified and it is

13 As defined in article6 of the Kyoto Protocol.14 Carbon dioxideequivalent.15 The “third carbontender” is a projectselection processinitiated by Sberbank (acarbon units operator,designated by theRussian government)which selects projectsbased on certaincriteria. On selection,the projects arereferred to an expertcommittee for a finaldecision and approvalby the Minister forEconomic Development.16 See footnote 8.

VALUABLE GROWTH

UC RUSAL

025

the objective of the Group to acquire OHSAS 18001certification for all of its operating facilities.

Care for the health of the Group’s employees is a keyelement of the Group’s social policy. The Group providesa full range of medical services for its employees andpromotes a healthy lifestyle. The Group emphasisespreventive medicine and the reduction of lost workingtime resulting from occupational illnesses throughcorporate medical centres it has established in mostregions where the Group operates.

CHARITY AND SPONSORSHIPINITIATIVES

Leadership means ResponsibilityWith activities spanning 19 countries on 5 continents,as a global company UC RUSAL believes that it has aresponsibility to ensure that sustainable businessdevelopment helps ensure the social and economicdevelopment in the regions and countries where theCompany operates. The Company views social investmentas an important element of sustainable development.

Through social activities in the regions of itspresence, UC RUSAL tries to promote the development ofpartnership between businesses, governments andnations, helping local communities find solutions tosocial problems, supporting charity and volunteerinitiatives, and as a result helping local development.The establishment and development of a network ofSocial Programme Centres (“SPC”) is an indication of theCompany’s commitment to its social developmentpolicies. The SPCs were established in 2004 and sincethen the Company has been able to transform them intoa modern, professional non-profit organisation capableof quickly responding to any sort of externalchallenges.

The charity projects implemented by UC RUSAL SPCsare based on a constant dialogue with localcommunities, contest-based selection of the bestprojects, long-term orientation and on-goingefficiency assessment. The local communities are giventhe chance to put forward their needs, call attention tothe most pressing problems they face and offersolutions to them, develop their own proposals andparticipate in contests which are designed to select thebest and most efficient projects.

Partnership ProjectsSince 2006, UC RUSAL has been implementing a socialprogramme “Partnership Programmes” aimed atdeveloping multilateral social partnerships toencourage sustainable regional development. Theprogramme is being implemented in Russia (Khakasiaand Krasnoyarsk, Irkutsk and Sverdlovsk regions) and

Ukraine (Nikolaev region). One of the key events in theprogramme was the Charity Season.

In 2010, the Charity Season included events such asthe Social Star contest, the Russian national volunteerweek “Spring Week of Charity”, “Auto-quest for GoodDeeds”, a cross country bike race combined with takingpictures dubbed “City of the Young”, the “SocialPartnership: New Challenges” chat show and the “Ball ofVolunteers”.

1,112 organisations partnered up with Charity Seasonin 2010. In total, 800 events were held and socialinvestments made by the partners exceeded USD140,000.

“The Territory of RUSAL” ProgrammeIn September 2010 the Company launched a new socialprogramme in addition to other charity activities thatit has been engaging in over the past six years. TheTerritory of RUSAL programme has three focuses:> financing of projects aimed at developing the social

infrastructure in cooperation with the governmentsof the Krasnoyarsk region and the Sverdlovsk regionas well as the municipal administrations;

> offering grants to support and develop initiativesproposed by children and young adults; and

> improving computer literacy of primary schoolstudents as part of a joint project with the “Actionwith No Limits” fund.The largest grant offered by UC RUSAL for the

construction, renovation, repairs and equipment forsocial infrastructure facilities was USD160,000, while thelargest grant given to the development of initiativesproposed by children and young adults was USD3,000.

The New Village ProjectIn the summer of 2010, wildfires broke out throughoutcentral Russia, causing significant property damage andloss of life. In particular, the Nizhny Novgorod regionsuffered the most. To reduce the consequences of thewildfires, UC RUSAL decided to implement an aidprogramme called “New Village” in the Nizhny Novgorodregion.

The New Village Project involved the construction of49 new houses for people whose homes had burned downin the Borsky district of the Nizhny Novgorod region. InNovember 2010, the construction of the new houses wascompleted and the victims of the natural disaster movedinto their new homes.

In total, over USD3 million was spent on the NewVillage project.

Computers for School StudentsIn cooperation with the charity fund “Action with NoLimits”, UC RUSAL is implementing a project called“Computers for School Students” under which theschools of the Sovetsky district in Krasnoyarsk as well

2010ANNUALREPORT

026

BusinessOverviewpp015–027

as the schools in Achinsk, Kodinsk, Divnogorsk andNikolaev (Ukraine) will be given laptops for theirstudents. More than 15,000 laptops have already beenbought as part of the project which is beingimplemented as a partnership between the state and theprivate sector. The fund has invested USD3.5 million inthe project.

Once these schools have laptops available to theirstudents, and other programmes to introduce computertechnologies into schools being taken into account,these schools should reach new levels in terms of theutilisation of such technology and innovative teachingmethods.

Programme of Private DonationsIn 2010, the Company continued with its traditionalprogramme of private donations by employees. The fundscollected under the programme provided support to 8not-for-profit organisations working with seriously illand disabled children and troubled adolescents. Theywere also used to finance a number of emergencysurgeries, to buy supplies for orphans studying in artsand creative classes, clothes for orphanages as well asto buy first aid supplies for the victims of the summerwildfires in Central Russia.

In total, the Company’s employees collected overUSD42,000.

Joint Project with the Hong Kong Universityof Science and Technology (HKUST)In June 2010, UC RUSAL launched a 5 year joint projectwith the Hong Kong University of Science and Technology(“HKUST”). The main goal of this project is to developjoint scientific research activities, offer solutions toimprove environmental performance and promotecooperation between young scientists from the twocountries. UC RUSAL expects to invest a total of USD1.5million in this project.

The joint project between UC RUSAL and HKUST willcomprise three main parts. As part of the project a UCRUSAL President’s forum has been established which willcooperate with the Institute of Special Research toarrange lectures by world-famous politicians, businesspeople, educators and scientists at HKUST. The secondpart of the project is a student exchange programmethat will allow senior students and postgraduates fromRussia and Hong Kong to learn about the highereducation system of their host country with all theirexpenses being paid for by UC RUSAL grants. The thirdpart of the project is a 3-year joint researchprogramme to develop pre-insulated fibre-reinforcedaluminium envelope and roof systems using aluminium asit is the most easily manufactured and environmentallyfriendly choice for this use. The goal of this programme

17 The Leaders ofCorporate Charitycontest is a jointproject of the businessdaily newspaper TheVedomosti,PricewaterhouseCoopersand “Donors’ Forum”, anon-commercialpartnership of grantproviders. The aim ofthe project is to bringout the best practicesin creation andrealisation ofcorporate charityprogrammes and toraise the attention ofbusiness and society tothese practices. Thecontest was organisedwith the support of theMinistry of EconomicDevelopment of theRussian Federation, theRussian Union ofIndustrialists andEntrepreneurs and theCommission for CivilSociety Development ofthe Civic Chamber ofthe Russian Federation.

is to find innovative solutions and new uses foraluminium in the construction industry. It is expectedthat the products developed as part of this project willmake use of new energy efficient and environmentallyfriendly composite materials and will begin to beintroduced into mass production in just a few years,making construction a more innovative industry.

In 2010, UC RUSAL’s partnership projects became thelaureate of the Leaders of Corporate Charity contest17

in the nomination for “Best Project helping theDevelopment of Charity Culture in Society”.

VALUABLE GROWTH

UC RUSAL

027

The table below sets out the Group’s expenditure oncharity and sponsorship projects in 2010:

ExpenditureCharity and sponsorship projects (USD’000)

New Village Project 3,400“The Territory of RUSAL” Programme 145Computers for School Students

(in cooperation with the Actionwith No Limits fund) 700

Partnership projects 6.5Private Donations Programme 42Russian National Union of Martial Arts 334

DEVELOPED MARKETS

2010 6 MLN T

+8.6%Packaging IndustriesAluminium Consumption

SOURCE: BROOK HUNT

VALUABLE GROWTH

UC RUSAL

2010ANNUALREPORT

029

pp029–051

Management Discussionand Analysis

OVERVIEW OF TRENDS IN INDUSTRYAND BUSINESS

Aluminium industry in 2010 and UC RUSAL’sindustry view and outlookThe aluminium market demonstrated significant pricevolatility during 2010, with prices below USD2,000 pertonne at times and reaching maximum levels aroundUSD2,500 per tonne.

Demand for aluminium continued to improvethroughout 2010 driven by strong economic activity inGermany, South America and Asia. Demand in the USA andJapan stabilised in the second half of 2010 following anincrease in consumption driven by the automotive andengineered products sectors. Global auto productionaccounted for 35% of aluminium consumption, which hadreached the level it was prior to the global financialcrisis of 73.4 million tonnes and was supported byaggressive Chinese and US car sales growth of 33% and35% respectively.

Underlying demand for consumer products, includingpackaging and beverage cans, continued to support therolled products segment.

Investors’ appetite for commodities remained strongwith oil soaring above USD90 per barrel and copperreaching above USD9,000 per tonne in December 2010and aluminium prices rose as a consequence. The USdollar, weakened over December 2010, also supportingthe increase in aluminium prices.

Based on robust growth in demand for aluminiumfrom China and the recovery of physical demand in theUSA, Europe and Japan, demand for aluminium in 2010surged by around 14% from 2009 levels to 40.6 milliontonnes. Worldwide production of primary aluminium in2010 was 40.4 million tonnes, 9% higher than the 37.0

million tonnes of production in 2009.UC RUSAL expects strong global demand for aluminium