Systematic review of the clinical effectiveness and cost ...

Upload

khangminh22Category

view

0download

0

University of Chicago Law School University of Chicago Law School

Chicago Unbound Chicago Unbound

Coase-Sandor Working Paper Series in Law and Economics Coase-Sandor Institute for Law and Economics

2003

Transfer Regulations and Cost Effectiveness Analysis Transfer Regulations and Cost Effectiveness Analysis

Eric A. Posner [email protected]

Follow this and additional works at: https://chicagounbound.uchicago.edu/law_and_economics

Part of the Law Commons

Recommended Citation Recommended Citation Eric Posner, "Transfer Regulations and Cost Effectiveness Analysis" (John M. Olin Program in Law and Economics Working Paper No. 184, 2003).

This Working Paper is brought to you for free and open access by the Coase-Sandor Institute for Law and Economics at Chicago Unbound. It has been accepted for inclusion in Coase-Sandor Working Paper Series in Law and Economics by an authorized administrator of Chicago Unbound. For more information, please contact [email protected].

POSNER.DOC 07/07/04 1:39 PM

TRANSFER REGULATIONS ANDCOST-EFFECTIVENESS ANALYSIS

ERIC A. POSNER†

ABSTRACT

Recent scholarship on regulatory oversight has focused on cost-benefit analysis of prescriptive regulations—regulations that restrictbehavior such as pollution—and their use to cure market failures, andhas overlooked the vast number of transfer regulations. Transferregulations are regulations that channel funds to beneficiaries. Theseregulations are authorized by statutes that establish entitlementprograms like Medicare and Social Security, pay one-timedistributions to victims of misfortunes such as natural disasters andthe 9/11 terrorist attack, and fund pork barrel spending. Cost-benefitanalysis cannot be used to evaluate transfer regulations because alltransfer regulations fail cost-benefit analysis; cost-effectivenessanalysis, however, can be used to evaluate transfer regulations.Although executive orders appear to require agencies to use cost-effectiveness analysis to evaluate transfer regulations that have a largeeconomic impact, the agencies’ record is dismal. Most agencies fail toperform cost-effectiveness analysis, and other agencies perform cost-effectiveness analysis incorrectly. More vigorous Office ofManagement and Budget and, possibly, judicial review could improvethe quality of distributive regulations.

Copyright © 2003 by Eric A. Posner.† Kirkland & Ellis Professor of Law, University of Chicago. Thanks to Matthew Adler,

John Duffy, Beth Garrett, Tom Merrill, Arti Rai, Cass Sunstein, and Adrian Vermeule for theircomments, and to J.T. Bloch for research assistance. The Sarah Scaife Foundation Fund andThe Lynde and Harry Bradley Foundation Fund provided financial support.

POSNER.DOC 07/07/04 1:39 PM

1068 DUKE LAW JOURNAL [Vol. 53:1067

INTRODUCTION

Every year the Office of Management and Budget (OMB) sendsa report to Congress that discusses federal regulations reviewed byOMB during the prior year.1 These reports include a calculation ofthe aggregate costs and benefits of most major or significantregulations, so that Congress and the public may be given a sense ofthe welfare impact of regulatory policy. But excluded from thiscalculation is a class of regulations that OMB calls “agency transferrules.”2 The draft 2003 OMB report lists twenty-five such rules, issuedby a diverse group of agencies, including Agriculture, Defense,Health and Human Services, and Transportation.3 The 2002 OMBreport lists seventy-two rules issued over an eighteen-month period.4

Most of these rules implemented a congressional authorization ormandate to spend money. An appropriation statute would providethat a certain amount of money be given to farmers, or dairyproducers, or victims of the 9/11 attack, and would direct an agency,in very general language, to give the money to the intendedbeneficiaries. Other transfer rules were issued pursuant toentitlement programs such as Medicare or Social Security. Agenciescharged with the task of distributing money under these programsissued regulations that specified who would receive money, how muchthe person would receive, and how one should apply for it.

OMB has not explained why it excludes transfer regulations fromthe calculation of the aggregate net benefits of federal regulation, butthe reason is clear. Ordinary regulations aim to correct marketfailures, and a regulation that successfully corrects a market failuregenerates social value. Cost-benefit analysis distinguishes regulationsthat generate social value and those that do not, and an aggregatecost-benefit analysis of all federal regulations reveals whether the

1. The most recent published report is OFFICE OF MGMT. & BUDGET, STIMULATING

SMARTER REGULATION (2002) [hereinafter 2002 OMB REPORT], available athttp://www.whitehouse.gov/omb/inforeg/2002_report_to_congress.pdf. The draft report for 2003can be found at Office of Mgmt. & Budget, Draft 2003 Report to Congress on the Costs andBenefits of Federal Regulations, 68 Fed. Reg. 5,492 (Feb. 3, 2003) [hereinafter Draft 2003 OMBReport]. The reports also discuss regulations issued by independent agencies, make proposalsfor regulatory reform, and discuss related matters. The 2002 OMB REPORT covers eighteenmonths. All of the reports can be downloaded from http://www.whitehouse.gov/omb/inforeg/regpol-reports_congress.html (last visited Dec. 15, 2003).

2. See, e.g., 2002 OMB REPORT, supra note 1, at 36 n.30.3. Draft 2003 OMB Report, supra note 1, at 5,479.4. 2002 OMB REPORT, supra note 1, at 5,497.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1069

regulations as a group increase or decrease efficiency. Transferregulations, unlike ordinary market-correcting regulations, are notdesigned to generate value in the economic sense. A transferregulation that pays $100 to farmers also costs taxpayers $100; thecosts and benefits wash out, producing a social loss if administrativecosts are greater than zero, as they always are. Thus, a conventionalcost-benefit analysis of a transfer regulation will always yield anegative outcome. Treating every transfer regulation as a social cost,and subtracting the costs of transfer regulations from the net benefitsof ordinary regulations, would not reveal anything about the qualityof agency rulemaking. Rather it would indicate that Congress hasdecided to use agencies to implement transfers, something that isalready known. The purpose of the OMB reports is not to tellCongress that agencies implement transfers; it is to tell Congressabout the quality of agency rulemaking.

But this does not mean that transfer regulations cannot beevaluated. The difference between an ordinary regulation and atransfer regulation is, on a rough approximation (to be refinedbelow), that the transfer regulation achieves a distributional goal oroutcome mandated by Congress. Ordinary cost-benefit analysiscannot be used for evaluating a transfer regulation, but cost-benefitprinciples can be used. The term of art for a cost-benefit analysis thattakes distributional goals as fixed and evaluates the means forachieving them is cost-effectiveness analysis, a decision procedure thatis used widely by policy analysts outside the government.5 Cost-effectiveness analysis is a procedure for comparing the differentmeans for achieving a given regulatory end; it identifies the leastcostly means as the most cost-effective.

Cost-effectiveness analysis is the correct decision procedure forevaluating transfer regulations. The main reason for using cost-effectiveness analysis is that a cost-effective regulation will morecheaply achieve the regulatory goal than a cost-ineffective regulation.This point can be made in two ways: Given a regulatory goal likeproviding lunches to schoolchildren, a cost-effective regulation willcost less (say $20 million) than a cost-ineffective regulation (say $30million) while providing the same lunches to the same children.Alternatively, given a fixed cost (say $25 million), a cost-effectiveregulation will provide lunches to more schoolchildren than a cost-

5. It is used frequently for evaluating regulations of medical practices; see infra Part II.A.for an example.

POSNER.DOC 07/07/04 1:39 PM

1070 DUKE LAW JOURNAL [Vol. 53:1067

ineffective regulation. Although many alternative regulations will bedifficult to compare because they affect different people in differentways, monetization of benefits, akin to the practice of cost-benefitanalysis, can be used to make comparison possible.6

A subordinate but also important goal of cost-effectivenessanalysis is regulatory transparency. Agencies have many advantagesover their nominal overseers such as executive branch officials,members of Congress, and judges: agencies set the regulatory agendawithin their domain and also have more information about the effectsof different kinds of regulation. To the extent that agency officialshave goals or values that differ from those of their superiors, or areespecially vulnerable to interest group pressure, they may chooseregulations that their principals would not choose. By requiringagencies to perform cost-effectiveness analysis of their regulationsand report the results, the principals can force agencies to divulgeinformation in a digestible form, thus reducing the agencies’ ability toregulate in ways that the principals would not like.7

Executive Order 12,8668 requires agencies to use cost-benefitanalysis or cost-effectiveness analysis when evaluating regulations,whichever is appropriate.9 Its reference to cost-effectiveness analysisis explicit: “When an agency determines that a regulation is the bestavailable method of achieving the regulatory objective, it shall designits regulations in the most cost-effective manner to achieve theregulatory objective.”10 The same language can be found in theexecutive order’s predecessor, Executive Order 12,291,11 which wassigned by President Reagan in 1981.12 These executive orders, andsome other related executive orders and statutes, have caused asignificant shift in the practices of regulatory agencies, and over thelast two decades it has become standard practice for agencies toperform and report cost-benefit analyses for important regulations

6. For a discussion of cost-benefit analysis, see Matthew D. Adler & Eric A. Posner,Rethinking Cost-Benefit Analysis, 109 YALE L.J. 165 (1999).

7. In this way, cost-effectiveness analysis reduces agency costs (in the economic sense) inthe same way that cost-benefit analysis does. See Eric A. Posner, Controlling Agencies withCost-Benefit Analysis: A Positive Political Theory Perspective, 68 U. CHI. L. REV. 1137, 1140–42(2001) (arguing that cost-benefit analysis saves costs by “ensur[ing] that elected officialsmaintain power over agency regulation”).

8. Exec. Order No. 12,866, 58 Fed. Reg. 51,735 (Oct. 4, 1993).9. Id. at 51,735–36.

10. Id. at 51,736.11. Exec. Order No. 12,291, 46 Fed. Reg. 13,193 (Feb. 19, 1981).12. Id. at 13,193.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1071

other than transfer regulations.13 OMB reviews agencies’ cost-benefitanalyses and issues guidelines for good practice, as well as drafts thereports to Congress discussed above.14 With the prodding of OMB,the agencies’ cost-benefit analyses have gradually improved. Theseregulatory changes have in turn generated an enormous academicliterature on cost-benefit analysis and its influence on regulatoryoutcomes.15

There has been no comparable activity with respect to transferregulations. Agencies that implement transfer regulations recognizethat Executive Order 12,866 applies, but they rarely provide the cost-effectiveness analysis that the executive order requires. Althoughagencies do, usually, say something about the costs of a regulation,their comments are rarely illuminating and often incoherent. Someagencies simply state that the regulation complies with the executiveorder without further elaboration.16 Other agencies provide only theamount of the disbursement.17 Still other agencies do perform, orclaim to perform, a cost-effectiveness analysis, but in fact make claimsinconsistent with cost-effectiveness principles.18 OMB does not appearto engage in a strict review, as it does for cost-benefit analysis ofordinary, nontransfer regulations;19 and, as noted above, its annual

13. ROBERT W. HAHN & MARY BETH MUETHING, AM. ENTERPRISE INST.-BROOKINGS

JOINT CTR. FOR REGULATORY STUDIES, THE GRAND EXPERIMENT IN REGULATORY

REPORTING 3–5 (2003).14. For information on OMB’s activities, see its website at http://www.whitehouse.gov/

omb/inforeg/regpol.html (last visited Dec. 15, 2003).15. See, e.g., STEPHEN BREYER, REGULATION AND ITS REFORM 4–7, 111, 117 (1982)

(creating a general framework for analyzing agencies and noting instances of cost-benefitanalyses and how they are often prepared to support agency decisions already reached); CASS

SUNSTEIN, RISK AND REASON 19–22 (2002) (describing the rise of cost-benefit analysis and itseffect on agencies). Neither of these books mentions transfer regulations or says much aboutcost-effectiveness analysis. Nor can one find discussions in the major case books.

16. See, e.g., Disaster Assistance; Cerro Grande Fire Assistance, 66 Fed. Reg. 15,948,15,958 (Mar. 21, 2001).

17. See, e.g., New Markets Venture Capital Program, 66 Fed. Reg. 28,602, 28,608–09 (May23, 2001) (describing the Small Business Association’s and applicants’ administrative costs for aloan guarantee program); Wool and Mohair Market Loss Assistance Program and AppleMarket Loss Assistance Program, 66 Fed. Reg. 13,839, 13,840–41 (Mar. 8, 2001) (describing theamounts to be paid to various producers).

18. See infra Part III for examples.19. There is some evidence that OMB has recently decided to pressure agencies to perform

cost-effectiveness analysis on transfer regulations. See Letter from John D. Graham,Administrator, Office of Information and Regulatory Affairs, OMB, to Hon. Hector H.Barreto, Administrator, SBA, at http://www.whitehouse.gov/omb/inforeg/sba_eidl-rtnltr.html(Feb. 11, 2002) (on file with the Duke Law Journal) (sending a rule back to the SBA for cost-effectiveness analysis); Letter from John D. Graham, Administrator, Office of Information and

POSNER.DOC 07/07/04 1:39 PM

1072 DUKE LAW JOURNAL [Vol. 53:1067

reports to Congress do not discuss the quality of the cost-effectivenessanalyses performed by agencies during the prior year. The academicliterature on transfer regulations is nil.

What explains the contrast between the intensity of interest incost-benefit analysis of regulations designed to solve market failures,and cost-effectiveness analysis of transfer regulations? OMB saysnothing about this topic in its reports to Congress: it lists the transferregulations without explaining why their costs and benefits are notdiscussed. A separate document, the Best Practices Guidelines,implies without saying explicitly that transfer regulations are notsusceptible to cost-benefit analysis because cost-benefit analysis is notdesigned to evaluate transfers.20 But the obvious rejoinder, that cost-effectiveness analysis can be used to evaluate transfer regulations, isnot discussed. In short, there has been virtually no discussion—not byOMB or the agencies, not by academics—about the use of cost-effectiveness analysis to evaluate transfer regulations that disbursemoney or other benefits to specified groups.

This Essay is a first effort to fill this gap. Part I defines transferregulations and discusses their purposes and effects. Part II discussescost-effectiveness analysis and explains how it can be used to evaluateboth transfer regulations and the statutes that authorize transferregulations. Part III provides some examples of how agenciesevaluate transfer regulations. Agencies sometimes claim to performcost-effectiveness analysis on transfer regulations, but they rarelyperform it correctly. Throughout, it should be understood that there

Regulatory Affairs, OMB, to Hon. Bill Hawks, Undersecretary for Marketing and RegulatoryPrograms, United States Department of Agriculture, at http://www.whitehouse.gov/omb/inforeg/usda_ee_for_nonhuman_primates_rtnltr012902.html (Jan. 29, 2002) (on file with theDuke Law Journal) (sending proposed policy back to USDA for cost-effectiveness analysis).The Draft 2003 OMB Report contains greater attention to cost-effectiveness analysis than in thepast, see Draft 2003 OMB Report, supra note 1, at 5,499–503, but the context suggests thatOMB has cost-effectiveness analysis of market-correcting regulations in mind, not of transferregulations. In addition, the administrator of Medicare has recently decided to use cost-effectiveness analysis to evaluate Medicare coverage. See Robert Pear, U.S. Limiting Costs ofDrugs for Medicare, N.Y. TIMES, Apr. 21, 2003, at A1 (describing how the Bush administrationhas begun to weigh cost as a factor in deciding whether Medicare should pay for new drugs andmedical procedures).

20. See OFFICE OF MGMT. & BUDGET, ECONOMIC ANALYSIS OF FEDERAL REGULATIONS

UNDER EXECUTIVE ORDER 12866 § III(c)(2), at http://www.whitehouse.gov/omb/inforeg/print/riaguide.html (1996) (on file with the Duke Law Journal) (“While transfers should not beincluded in the [executive order’s] estimates of the benefits and costs of a regulation, they maybe important for describing the distributional effects of a regulation.”).

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1073

is no presumption that transfer regulations are undesirable; they canbe used to good and bad ends, just like any other kind of regulation.

I. WHAT ARE TRANSFER REGULATIONS?

A. A Typology of Regulations

Regulations, as Table 1 shows, can be divided into two types:prescriptive regulations and transfer regulations. Prescriptiveregulations are rules that place restrictions on behavior; examplesinclude rules that restrict factory emissions, mandate safe workplaces,and require testing before drugs are marketed. Transfer regulationsare rules that distribute money and other resources to firms orindividuals. A regulation that distributes cash to victims of a naturaldisaster is a transfer regulation. However, transfer regulations do notalways involve the disbursement of cash. Some transfer regulationsdistribute in-kind benefits such as food stamps, housing, or licenses touse the radio spectrum. The Appendix lists significant transferregulations reviewed by OMB between April 1 and September 30,2001.21

TABLE 1TYPES OF REGULATIONS

Type Definition Example

PrescriptiveA regulation thatrestricts behavior

Limitation on emissionof a pollutant

TransferA regulation that transfers

money or goods tobeneficiaries

Distribution of funds tovictims of a natural disaster

The regulations on OMB’s list are diverse. They governapplication procedures and eligibility criteria for cash relief forfarmers whose crops have been destroyed by bad weather or drivenfrom the market by foreign competition; the ingredients of thenational school lunch and breakfast program; Medicare

21. The list includes “[s]ignificant regulatory action[s]” under Exec. Order No. 12,866, 58Fed. Reg. 51,735, 51,738 (Oct. 4, 1993), which are regulations that have an impact of at least$100 million; “major” rules under the Congressional Review Act, 5 U.S.C. § 804(2) (2000); andrules above the threshold of the Unfunded Mandates Reform Act, 2 U.S.C. §§ 1531–1538(2000).

POSNER.DOC 07/07/04 1:39 PM

1074 DUKE LAW JOURNAL [Vol. 53:1067

reimbursement for the cost of self-management training for diabetics;prescription drug benefits for military personnel; disability criteria forchildren in the Social Security system; affirmative action reportingrequirements for government contractors; disaster relief; andrequirements for receiving certain small business loans.22 The threadrunning through the regulations on OMB’s list is that they areauthorized by a congressional appropriation or budgetary statute, or astatute that establishes an entitlement program.

The purposes of regulation can be divided into two categories:correcting market failures and redistributing wealth. For example, apollution regulation corrects a market failure, and a regulation thatreimburses farmers who lost crops redistributes wealth. One might betempted to generalize from these examples and conclude that allprescriptive regulations are designed to correct market failures andall transfer regulations are designed to redistribute resources tofavored groups. But although this assumption is roughly true as anempirical matter, it is not an analytic truth. A transfer regulation canbe designed to improve efficiency, and a prescriptive regulation canbe designed to transfer resources to a group.

Consider, for example, a regulation that implements acongressional appropriation for monetary relief to victims of a naturaldisaster. This regulation looks like a straightforward transfer ofmoney from the government to individuals, but it might be justifiedby a failure in the insurance market. If the insurance market fails toprovide disaster insurance, the government might be justified inproviding that insurance. One way to provide such insurance is towait for a disaster to occur and then make payments to victims. If, asseems likely, people anticipate these transfers ex ante, then theregulation (in theory) enhances efficiency by enabling people to poolrisk.

As for prescriptive regulations that serve distributional purposes,consider regulations that implement a congressional plan to supportfarm prices through a quota system. The regulations do not transfermoney to farmers, but rather limit the amount of production. Yetthrough the limitation on production, prices are increased andfarmers are benefited. Although the regulation prescribes behavior, itserves a distributional aim, not efficiency.

22. See the Appendix, infra.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1075

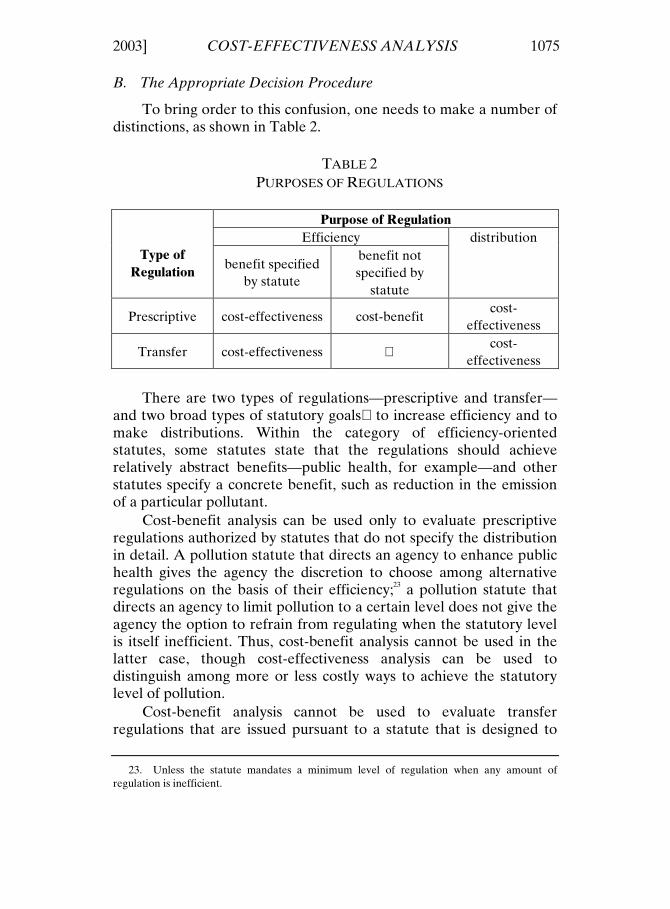

B. The Appropriate Decision Procedure

To bring order to this confusion, one needs to make a number ofdistinctions, as shown in Table 2.

TABLE 2PURPOSES OF REGULATIONS

Purpose of RegulationEfficiency

Type ofRegulation

benefit specifiedby statute

benefit notspecified by

statute

distribution

Prescriptive cost-effectiveness cost-benefitcost-

effectiveness

Transfer cost-effectiveness ∅ cost-effectiveness

There are two types of regulations—prescriptive and transfer—and two broad types of statutory goals to increase efficiency and tomake distributions. Within the category of efficiency-orientedstatutes, some statutes state that the regulations should achieverelatively abstract benefits—public health, for example—and otherstatutes specify a concrete benefit, such as reduction in the emissionof a particular pollutant.

Cost-benefit analysis can be used only to evaluate prescriptiveregulations authorized by statutes that do not specify the distributionin detail. A pollution statute that directs an agency to enhance publichealth gives the agency the discretion to choose among alternativeregulations on the basis of their efficiency;23 a pollution statute thatdirects an agency to limit pollution to a certain level does not give theagency the option to refrain from regulating when the statutory levelis itself inefficient. Thus, cost-benefit analysis cannot be used in thelatter case, though cost-effectiveness analysis can be used todistinguish among more or less costly ways to achieve the statutorylevel of pollution.

Cost-benefit analysis cannot be used to evaluate transferregulations that are issued pursuant to a statute that is designed to

23. Unless the statute mandates a minimum level of regulation when any amount ofregulation is inefficient.

POSNER.DOC 07/07/04 1:39 PM

1076 DUKE LAW JOURNAL [Vol. 53:1067

enhance efficiency. Consider a statute that funds general scientificresearch on the theory that the market undersupplies such research.An agency is directed to issue transfer regulations that provide therules for applying for grants. The statute might or might not have theeffect of enhancing efficiency through regulation, but the agencycannot veto the statute, so there is no point in doing a cost-benefitanalysis of the entire statutory scheme. The agency can only do cost-effectiveness analysis, which will reveal whether a given regulation isless costly than alternative regulations for accomplishing the statutorygoal of converting money into knowledge.

When one turns to statutes that have distributional aims, onesees that neither prescriptive regulations nor transfer regulations canbe evaluated using cost-benefit analysis. Again, when a statutespecifies a distribution, cost-benefit analysis cannot be used. But cost-effectiveness analysis is appropriate, as will be seen.

Statutory distributional schemes generally have two distinctpurposes. The first purpose is to benefit a politically influential group,such as dairy producers or tobacco farmers. No serious scholardefends these transfers, and their unattractiveness might explain whythe academic literature has ignored them. The implicit assumptionseems to be that if these transfers are bad, then the regulations thatimplement them are bad, and there is no reason to discuss how tomake them cost-effective. This response, however, is wrong. Even ifpolitically motivated transfers are regrettable, they are a fact of life,and it is an important task to analyze how to implement them in away that minimizes their disruptive impact on the economy.

The second purpose of transfer regulations is to benefit poorpeople, people who suffer from discrimination, and people who havesuffered a misfortune. Social Security, Medicare, and Medicaidauthorize transfer regulations that provide benefits to the poor andnot-so-poor. Regulations implementing affirmative action programsfor government contractors benefit victims of discrimination.24 Theregulations governing both the disbursements of 9/11 moneys andmoneys for natural disasters benefit victims of a misfortune.25

24. See, e.g., Participation by Disadvantaged Business Enterprises in Procurement UnderEnvironmental Protection Agency (EPA) Financial Assistance Agreements, 68 Fed. Reg.43,823, 43,824 (proposed July 24, 2003) (to be codified at 40 C.F.R. pts. 30, 31, 33, 35, 40)(describing the EPA’s efforts to ensure its affirmative action program is in line with decisions ofthe United States Supreme Court).

25. See, e.g., September 11th Victim Compensation Fund of 2001, 28 C.F.R. § 104 (2003)(outlining the final rules regarding the disbursement of funds to victims of the attacks).

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1077

Although market-correcting rationales are sometimes given for theseprograms, their thrust seems to be redistributive. Regulations areneeded because Congress does not want to determine every detailabout how funds are allocated and disbursed; that is why Congresstransfers these functions to an agency. Limited transfers to poor andunfortunate people are relatively uncontroversial, and it is thus apuzzle that the question of how to evaluate agency regulations thatimplement these transfers has been neglected by legal scholars.

Distributional statutes, then, are sometimes normativelydefensible and sometimes not. But it is important to see thatprescriptive regulations and transfer regulations authorized bydistributional statutes all fail a standard cost-benefit analysis, that is,one that does not use a multiplier to adjust for the lower purchasingpower of the poor.26 When a regulation disburses cash, the benefitscan be no greater than the costs, and will be lower as long as there issome administrative cost. Consider a payment of $100 to a dairyproducer. The benefit of the regulation is $100, and the cost of theregulation is $100 plus administrative expenses (and tax distortions ifsuch is the case). This remains true for transfers to the poor. Thebenefit of a $100 transfer to a poor person is $100, and the cost is $100plus administrative expenses. It is true that a poor person is likely tovalue $100 more than a rich person (or dairy producer) is, but suchdifferences are excluded from cost-benefit analysis as it is usuallyperformed.27 Cost-benefit analysis does not take account of the factthat the poor person values $100 more than the rich person does.Thus, cost-benefit analysis will also conclude that transfers to interestgroups and poor people produce negative net benefits; it does notallow one to distinguish between these types of transfers, and it doesnot allow one to distinguish between better and worse regulationsgiven a particular distributional goal.

In sum, cost-benefit analysis cannot be used to evaluate transferor prescriptive regulations that have distributional aims, or to

26. At one time economists believed that multipliers could be used to reflect variation inthe valuation of marginal dollars by people of different wealth, but this project foundered ontechnical, empirical, and philosophical difficulties. For a brief discussion, see HARVEY S.ROSEN, PUBLIC FINANCE 259–60 (3d ed. 1992).

27. There are some limited exceptions. See, e.g., Matthew D. Adler & Eric A. Posner,Implementing Cost-Benefit Analysis When Preferences Are Distorted, 29 J. LEGAL STUD. 1105,1136–37 (2000) (analyzing cost-benefit analyses where the marginal utility of money based onwealth is factored in); Adler & Posner, supra note 6, at 194–97 (describing the need to factor indistorted preferences, such as those that arise from wealth differences, when performing cost-benefit analyses).

POSNER.DOC 07/07/04 1:39 PM

1078 DUKE LAW JOURNAL [Vol. 53:1067

evaluate transfer regulations that implement statutes with efficiencygoals that do not leave the benefit or distribution decision to agencies.For all these purposes, cost-effectiveness analysis is necessary. Thenext Part focuses on the simplest case—the use of cost-effectivenessanalysis to evaluate transfer regulations authorized by statutes withdistributional goals—though most of what is said will apply to theother cases as well.

II. ANALYSIS OF TRANSFER REGULATIONS AND STATUTES

A. Analysis of Regulations

A cost-effective transfer regulation distributes resources lesswastefully than alternative transfer regulations do. To take a simpleexample, consider a statute that authorizes an agency to distribute$10 million to victims of a natural disaster. The agency considers twotransfer regulations. The first provides a lump sum payment of $1,000to each of the 10,000 people living in the affected area. The secondrequires individuals to apply for reimbursement of their losses and toprovide evidence of the losses. The first regulation willovercompensate some people and undercompensate others, but it willsave administrative costs. The second regulation will provide moreaccurate compensation, but will also generate sizable administrativecosts. A cost-effectiveness analysis permits comparison of the tworegulations. The more cost-effective regulation is the one thatprovides the fullest compensation to the most people—the firstregulation if the natural disaster caused everyone about the sameamount of harm greater than or equal to $1,000; the secondregulation if the disaster affected people unequally and proof is nottoo costly because records are complete and losses can be easilycomputed.

Cost-effectiveness analysis comes in many flavors. Somedecisionmakers evaluate medical interventions by taking as fixed thegoal of increasing “quality adjusted life years” (QALY), andcomparing medical interventions on the basis of the ratio of QALYssaved to cost. A quality adjusted life year is a measure that representsthe value to a person of living a year with a medical condition thatdegrades the quality of life. A government medical agency with afixed budget and the mandate to increase QALYs will purchasemedical devices with higher QALY/cost ratios until the budget is

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1079

exhausted.28 The budgetary outlay and the mandate to maximizeQALYs are fixed; cost-effectiveness analysis tells the agency whichmedical devices maximize QALYs given the budgetary constraint.

Another example of cost-effectiveness analysis comes from itsuse to evaluate environmental projects. Suppose that a certainenvironmental goal—a reduction of air pollution, for example—isprovided by statute, but the agency is given the discretion to chooseamong means. The agency can mandate the washing of coal prior toits use in power plants, or the use of scrubbers attached tosmokestacks, or some combination; or it can choose to put limits onthe amount of pollution generated by factories while allowing factoryowners to choose among different technologies; or it can create asystem of tradable emission permits; or it can choose some other ruleor framework for achieving the ends set by statute.29 For a givenreduction of air pollution, each regulatory instrument will have adifferent cost. Cost-effectiveness analysis compares the costs of thedifferent means and identifies the least-cost means as the most cost-effective.30

A third example of cost-effectiveness analysis is its use toevaluate income redistribution programs. The goal is redistribution ofwealth from rich to poor; the constraint is the willingness of taxpayersto pay for the redistribution. The policy analyst must evaluatedifferent mechanisms, none of which is perfect. Tax and transfersystems, for example, require administratively costly determinationsof need or else result in the inclusion of wealthy people with lowincome or the exclusion of poor people with higher incomes (forexample, because they have many children or high medical costs).Minimum wage laws are less complex, but they exclude nonworkersand may hurt low-income workers. Tax and transfer systems distort

28. See, e.g., Robert Fabian, The Qualy Approach, in VALUING HEALTH FOR POLICY: AN

ECONOMIC APPROACH 118, 118–19 (George Tolley et al. eds., 1994); Arti K. Rai, RationingThrough Choice: A New Approach to Cost-Effectiveness Analysis in Health Care, 72 IND. L.J.1015, 1048–52 (1997). For an example from the medical literature, see Daniel Polsky et al.,Economic Evaluation of Breast Cancer Treatment: Considering the Value of Patient Choice, 21 J.CLINICAL ONCOLOGY 1139, 1139 (2003).

29. See LAWRENCE H. GOULDER ET AL., THE COST-EFFECTIVENESS OF ALTERNATIVE

INSTRUMENTS FOR ENVIRONMENTAL PROTECTION IN A SECOND-BEST SETTING 1–3 (Nat’lBureau of Econ. Research, Working Paper No. 6464, 1998) (analyzing the costs of variousmethods to reduce pollution).

30. For a well-known example, see BRUCE A. ACKERMAN & WILLIAM T. HASSLER,CLEAN COAL/DIRTY AIR 66–72 (1981) (arguing that the most cost-effective, short-term methodfor reducing air pollution from coal involves coal washing, not factory scrubbing).

POSNER.DOC 07/07/04 1:39 PM

1080 DUKE LAW JOURNAL [Vol. 53:1067

labor-leisure choices; minimum wage laws impose deadweight costson consumers or shareholders. A cost-effectiveness analysis cutsthrough these apparent incommensurables and shows that tax andtransfer systems are likely to be superior: holding constant thepayments to beneficiaries, they result in lower social cost.31

The basic idea behind cost-effectiveness analysis is that ofcomparing alternative regulations or projects when either the costs orthe benefits are fixed.32 The right form of cost-effectiveness analysisdepends heavily on the statutory goal. Suppose, for example, thatCongress appropriates $100 million and authorizes the United StatesDepartment of Agriculture (USDA) to spend it on lunches for needyschoolchildren. Consider three alternative regulations: (1) give themoney to schools in poor census districts; (2) give the money toschools in proportion to the number of needy students in each school;or (3) give school lunch vouchers to parents whose family income fallsbelow the poverty line.33

Each alternative has different costs. Under (1), USDA mustprocess applications from schools and monitor their behavior toensure that the money is used to buy lunches, but this approachavoids the need to determine the poverty level of individual students.Under (2), USDA deals with a larger number of schools and engagesin more intensive monitoring, but it will also deliver lunches to morepoor students. Under regulation (3), USDA must print and distributevouchers and ensure that they are used properly, but it will also reachchildren who are not at school, and children at schools that fail toapply for school lunch benefits. The regulations provide, respectively,increasing accuracy at increasing cost.

Cost-effectiveness analysis of these alternatives can be illustratedwith a few numbers. If USDA itself paid all of the administrativecosts (including those of the schools and parents) from theappropriation, the calculation would be simple. Just choose theregulation that gets the most lunches to needy children. If, as is morelikely, USDA’s administrative costs come from anotherappropriation, and schools and parents must absorb their own

31. EDWARD M. GRAMLICH, BENEFIT-COST ANALYSIS OF GOVERNMENT PROGRAMS

123–33 (1981).32. I follow the simple discussion in EDITH STOKEY & RICHARD ZECKHAUSER, A

PRIMER FOR POLICY ANALYSIS 153–55 (1978).33. This example is based loosely on the regulation discussed infra in Part III.B.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1081

administrative costs, then a slightly more complex calculation isneeded, as illustrated by Table 3.

TABLE 3SCHOOL LUNCH EXAMPLE APPROPRIATION FIXED

Reg.Lunchesto NeedyChildren

Lunchesto OtherChildren

TotalAdmin.Costs

Approp. +Admin.Costs

Cost perLunch to

NeedyChild

(1) 15 million 5 m. $10 m. $110 m. $7.33(2) 18 m. 2 m. $20 m. $120 m. $6.67(3) 19 m. 1 m. $30 m. $130 m. $6.84

The cost of a regulation includes all its costs, not just the costsdirectly incurred by the agency. If beneficiaries, such as families, orintermediaries, such as schools, must incur costs in order to receivethe benefits, then their costs must be included in the cost-effectiveness analysis. As such, the fifth column of Table 3 lists thecombined cost of each regulation. Dividing the combined cost of eachregulation by the number of beneficiaries under each regulation thenumber of needy children listed in the second column yields theaverage cost of delivering a lunch to a needy child (column six).According to this column, regulation (2) is the most cost-effective: itsends lunches to needy children at the least cost per child.

Congress might alternatively pass a statute that directs USDA toprovide lunches for, say, 20 million needy children, to be paid out of ageneral appropriation. Again, USDA would come up with variousalternative regulations, and then it would compare them, as inTable 4.

POSNER.DOC 07/07/04 1:39 PM

1082 DUKE LAW JOURNAL [Vol. 53:1067

TABLE 4SCHOOL LUNCH EXAMPLE BENEFIT FIXED

Reg.Lunchesto NeedyChildren

Lunchesto OtherChildren

TotalAdmin.Costs

Cost ofLunches($5 perlunch)

Cost perLunch to

NeedyChild

(1) 20 million 8 m. $13 m. $140 m. $7.65(2) 20 m. 4 m. $23 m. $120 m. $7.15(3) 20 m. 1.5 m. $33 m. $107.5 m. $7.03

All three of the regulations provide the same benefits (secondcolumn). The most cost-effective regulation is regulation (3) becauseit costs least per lunch to deliver these benefits (last column).

I have simplified in order to convey the basic principles of cost-effectiveness analysis. A few observations are now necessary. First,note the difference between cost-benefit analysis and cost-effectiveness analysis. All of these regulations would fail a standardcost-benefit analysis, because a transfer to needy children is not a“benefit” in the conventional economic sense—it’s just a transfer. Thecost to the taxpayer offsets the benefit to the needy child, and theadministrative costs are a deadweight loss. To fulfill the congressionalmandate to transfer resources to needy children, USDA could not usecost-benefit analysis.

Second, the cost-effectiveness analysis, as I have performed it,assumes that the value of getting a lunch to a non-needy child is zero.This might be a reasonable assumption, but it also might not be true.Congress could worry that non-needy children do not always havenutritional lunches and want to remedy this situation. Thus, a moreaccurate cost-effectiveness analysis might attach some weight to alunch received by a non-needy child—say, 10 percent of the value of alunch to a needy child—and the agency could use this weighting in thecost-effectiveness analysis; it should also make the weighting explicit,so that elected officials would know the basis of the decision. In somesituations, this might produce different results—regulation (1) mightbe better than regulation (2) or regulation (3)—but it also seemsreasonable for the agency to take its lead from Congress, and notattach value to the receipt of lunches by non-needy children unlessCongress says otherwise.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1083

Third, one might argue in the first example that the choice ofregulation (2) defeats Congress’s purpose: Congress wants to get asmany lunches to needy children as possible, and for that purposeregulation (3) is better, even if more costly per lunch. But it would bebetter for USDA to return to Congress and ask for a largerappropriation, so that 19 million needy children would be benefitedusing regulation (2), explaining that the extra budgetary expense isless than the administrative costs under regulation (3).

Fourth, one should note that Congress could choose differentends—at a higher or lower level of abstraction. Congress could askUSDA to ensure that all children have adequate nutrition,understanding that poorer children need more aid. Congress couldgive USDA the option to provide school breakfasts as well as lunches,or more food stamps, or cash assistance, or educational programsabout good eating habits, and so forth. Congress might also stipulatethe nutritional content of the lunches, or leave that decision up toUSDA. The more discretion that USDA has, the more complex thecost-effectiveness analysis will be. As the level of abstractionincreases, cost-effectiveness analysis becomes the same as cost-benefitanalysis.

One problem with using cost-effectiveness analysis to evaluatetransfer regulations is that if the underlying transfer statute itself isbad, then one is firmly in the world of the second best, and cost-effectiveness analysis might have perverse effects. Consider a statutethat appropriates $100 million for dairy producers because of theirpolitical influence and not because of any legitimate need. A highlycost-effective statute will result in more money in the pockets of thedairy producers and less squandered on administrative expenses, butthat just means more slops in the political trough, and more lobbyistssidling up to it.34 (This problem is not as severe for regulations thatsurvive cost-benefit analysis.35) Cost-effectiveness is not an ultimatemoral value; the social value of even a highly cost-effective regulationdepends on the social value of the statutory program that itimplements. For that reason, it might be desirable for agencies to

34. Cf. Gary Becker & Casey Mulligan, Deadweight Costs and the Size of Government, 46J. LAW & ECON 293 (1998).

35. Though there are some potential similar problems. See Posner, supra note 7, at 1163–65(describing problems with cost-benefit analysis where, for example, the president transfersmoney to special interest groups simply to get elected).

POSNER.DOC 07/07/04 1:39 PM

1084 DUKE LAW JOURNAL [Vol. 53:1067

evaluate the authorizing statute as well as the regulations. This is thetopic of the next Section.

B. Analysis of the Authorizing Statute

When Congress authorizes a distribution to a particular group,agencies cannot usually prevent the distribution from occurring asintended.36 But there are actions short of interference that mightimprove distributional outcomes and the political process that leadsto them. Of special interest are reporting requirements, such as thosecreated by the National Environmental Policy Act (NEPA),37 whichrequires agencies to issue environmental impact statements.38 Ratherthan banning activity that harms the environment, NEPA requiresagencies to estimate and report the environmental impact of projectssuch as the construction of highways.39 Opponents of the regulationcannot seek relief from a court unless an agency fails to issue anadequate environmental impact statement. If the environmentalimpact statement is adequate, opponents must take their case toelected officials and seek a political remedy.

Agencies that issue transfer regulations could similarly berequired to report the welfare costs and distributional effects of theseregulations—that is, to issue “welfare impact statements.” If thewelfare impact is objectionable, then critics can bring this information

36. I put aside the controversy over whether the president or agencies have the authority torefuse to spend appropriated moneys. Regarding presidential impoundment, see Train v. City ofNew York, 420 U.S. 35, 49 (1975). See also Ralph S. Abascal & John R. Kramer, PresidentialImpoundment Part I: Historical Genesis and Constitutional Framework, 62 GEO. L.J. 1549, 1549(1974) (describing the history of the federal budgetary system and concluding that the executivecannot derive impoundment authority from statutes); Ralph S. Abascal & John R. Kramer,Presidential Impoundment Part II: Judicial and Legislative Responses, 63 GEO. L.J. 149, 149(1974) (describing the courts’ undue deference to the executive and the probable impact of theCongressional Budget and Impoundment Control Act of 1974, Pub. L. No. 93-344, 88 Stat. 297(codified as amended at 2 U.S.C. §§ 681–688 (2000))). Regarding the line item veto, seeElizabeth Garrett, Accountability and Restraint: The Federal Budget Process and the Line ItemVeto Act, 20 CARDOZO L. REV. 871, 872–74 (1999) (arguing that the Act was inappropriatelyanalyzed by the Supreme Court, and that the Act should be constitutionally viewed as acongressional delegation to the president of the power to withhold all spending, regardless ofthe form of the spending). See also J. Gregory Sidak, The President’s Power of the Purse, 1989DUKE L.J. 1162, 1162 (1989) (arguing that the president has implied powers to get money fromthe treasury, even without congressional appropriation).

37. National Environmental Policy Act of 1969, Pub. L. No. 91-190, 83 Stat. 852 (1970)(codified as amended in scattered sections of 42 U.S.C.).

38. 42 U.S.C. § 4332(c) (2000).39. There is no substantive review under NEPA.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1085

to politicians and lobby for reform. The welfare impact statementwould include the following information.

1. Distribution of Benefits. In 1999 Congress passed anappropriations bill that provided relief to dairy producers who hadincurred large losses after the collapse of dairy prices. The billdirected USDA to give money to dairy producers, but did not say (a)which dairy producers would receive money, or (b) how much moneyeach would receive.40 USDA promulgated a transfer regulation that,among other things, distributed moneys to dairy producers on thebasis of their production in 1997 and 1998. As I discuss in Part III.C,USDA used both years in order to avoid the cost of collecting newinformation from producers who had provided 1997 productionfigures when enrolled in the program the year before, but as a result,some firms, including firms that had stopped production, wouldreceive payments even though they did not lose money in 1998 as aresult of the market collapse.

The statement that accompanied the USDA’s transfer regulationdid not explicitly describe the distributive consequences, though theycould have been inferred from the formula in the regulation bysomeone who had data about the structure of the industry. Theagency had information about the industry and could have providedmore detailed information about the distributional effects of theregulation. It could, for example, have broken down producers bysize, and described the average level of compensation for each groupof producers—both in absolute terms and as a percentage of eachproducer’s loss. The agency could also have provided correlationsbetween compensation level and other attributes, such as location,number of employees, and so forth.

The reason for requiring the agency to provide this informationis that it facilitates monitoring of the agency by Congress, affectedparties, and the public.41 To the extent that agencies can provide aconcise, numerical account of the distribution of benefits, Congress,relevant staffers, or committees can relatively easily check that theagency is acting consistently with statutory goals. If the agency is not,

40. See infra Part III.C.41. Regarding the effects of informational regulations, see SUNSTEIN, supra note 15, at

191–228.

POSNER.DOC 07/07/04 1:39 PM

1086 DUKE LAW JOURNAL [Vol. 53:1067

Congress can in the future exercise greater oversight or enact moreprecise statutes.42

2. Deadweight Costs. It is possible that these distributionaleffects of the dairy market regulation, though not intended byCongress, could have been justified by a cost-effectiveness analysis,which would show that a more accurate distribution of benefits wouldhave entailed excessive administrative costs. But even if this is thecase, there is the further question whether the basic statutory goal ofcompensating dairy producers is desirable, given the inevitablewelfare losses that accompany any distributional scheme. One mightthink that Congress took these costs into account when it enacted thestatute, or that the agency has no basis for questioning Congress’sdecision in any event. But NEPA suggests a different view: Congressboth authorizes agencies to approve projects that have harmfulenvironmental impacts and requires agencies to issue a reportdescribing these impacts. The reason is presumably to provide acheck on agencies that focus too much on their mission and discountenvironmental concerns. Similarly, Congress could ask agencies bothto redistribute wealth and to report the welfare distortions caused byredistribution.

In welfare economics, it is often said that a transfer does nothave any efficiency effects, but this statement is a simplification thatdoes not take account of so-called indirect costs. Every transferrequires taxation, and all taxation causes distortions. The $200 millionappropriated for dairy producers comes from the pockets oftaxpayers, and will distort their choices between labor and leisure aswell as other activities. There are standard, albeit rough, ways tomeasure this welfare loss, and the welfare loss could be reported bythe agency.43 Prescriptive regulations that redistribute wealth throughmarket restrictions cause even greater distortions, which can also becalculated and reported.44 In addition, the behavior of recipients oftransfers can also be distorted as long as the transfer is not a surprise.The dairy industry knows that it will receive transfers from Congresswhen dairy prices collapse; as a result, producers do not allocate

42. Exec. Order No. 12,866, 58 Fed. Reg. 51,735 (Oct. 4, 1993), already requires adiscussion of distribution, see id. at 51,735–36, but agencies usually respond with boilerplate.

43. See ROSEN, supra note 26, at 305–22 (describing the concept of welfare loss andmethods for measurement).

44. See GRAMLICH, supra note 31, at 123–33 (providing an analytical model for thedistorting effects of wealth redistribution programs).

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1087

resources efficiently. Some should not be in business in the first place;others should diversify or take other steps to protect themselvesagainst downturns. Every transfer reinforces the expectation thatCongress will intervene in the future, and thus results in distortions.These distortions can be calculated and reported.

The reason for reporting this information is that Congress andthe public might not know the economic cost of the transfers thathave been authorized. The report of deadweight costs makes itexplicit that the transfer of money to dairy producers and otherinterest groups has effects beyond the obvious distributional changes.People who are willing to tolerate the distributional changes mightchange their minds when they learn the accompanying deadweightcost. In many circumstances, there will not be the political will torepeal statutory transfers or resist enacting them in the first place, butgreater public awareness of their costs might have a desirable effecton the margin.

3. Pareto Superior Regulations. As a supplement to theinformation on deadweight costs, an agency could propose a statutoryscheme that is Pareto superior to the authorizing statute.45 Frequently,this will be impractical or pointless, but in many cases the proposalwould make clear the problems with the statute. For example, it isoften the case that giving cash to beneficiaries is Pareto superior tousing price controls or quantity limits. Consider a statutory programthat benefits farmers by increasing prices and revenues throughrestrictions on production. If, instead, the quotas were eliminated andfarmers were given cash equal to the implicit subsidy created by thequotas, there would be money left over for taxpayers or otherbeneficiaries.

One might imagine that when an agency proposes a quotaregulation pursuant to a statute that provides for quotas, it will alsoreport the Pareto superior statutory scheme. The report could be sentto Congress, which might then decide to stop the regulation and

45. Cf. IVAN LITTLE, A CRITIQUE OF WELFARE ECONOMICS 86–88 (1950) (describing therise of the Pareto approach and its relevance to social welfare analysis in the first half of thetwentieth century); Stephen Coate, An Efficiency Approach to the Evaluation of PolicyChanges, 110 ECON. J. 437, 437 (2000) (proposing an approach whereby different policy changesare compared for Pareto superiority).

POSNER.DOC 07/07/04 1:39 PM

1088 DUKE LAW JOURNAL [Vol. 53:1067

appropriate money for the proposed transfer.46 Although Congressmight often refuse to enact the Pareto superior appropriation becauseof inertia, time constraints, or a desire to retain the disguise on thetransfer, in some cases it might well prefer the Pareto superiorappropriation, and act accordingly.

I have argued that regulatory oversight of transfer regulationswould be improved if agencies reported three kinds of information:(1) the distributive effects of the regulation, (2) its welfare costs, and(3) any Pareto superior alternatives. As Part IV discusses, ExecutiveOrder 12,866 already authorizes the first type of reporting, andprobably the other two as well, but a statute modeled on NEPAmight also be desirable. Just as NEPA requires agencies to report theenvironmental impact of regulations without directly banningenvironmentally unsound regulations, the proposed statute wouldrequire agencies to report the welfare impact of regulations withoutdirectly banning distributively unjust regulations. The agency would,in effect, route opponents of the regulation to the political process.47

The benefits to the political process could be expected to be similar tothose that NEPA has produced.

There is, however, an important objection to reportingrequirements. NEPA has, in practice, imposed considerableadministrative and litigation costs on agencies. Environmentalistshave used NEPA to delay and block regulations: Agencies frequentlyhave decided that the administrative and litigation costs, and perhapsthe political costs as well, are so high that an otherwise legalregulation is not worth defending.48 The NEPA experience suggeststhat reporting requirements for transfer regulations might involvehigh administrative costs, and be used as a weapon against transferregulations. Whether this is good or bad depends on how high thecosts will be, and on what kinds of regulations are likely to beblocked. It is possible that reporting requirements can, in the

46. A legislative veto is illegal, INS v. Chadha, 462 U.S. 919, 959 (1983), but informalpressure on the agency might be sufficient, or else a statutory injunction against the regulationwould be necessary.

47. There are other programs designed to regulate through information disclosure; oneprominent example is the toxics release inventory. See Madhu Khanna et al., Toxics ReleaseInformation: A Policy Tool for Environmental Protection, 36 J. ENVTL. ECON. & MGMT. 243,243–45 (1998) (detailing the regulatory effect the disclosure of environmental information canhave on firms and how firm behavior changes after such disclosures).

48. For a discussion of the high cost and low quality of lengthy NEPA reports, see BradleyC. Karkkainen, Toward a Smarter NEPA: Monitoring and Managing Government’sEnvironmental Performance, 102 COLUM. L. REV. 903, 917–23 (2002).

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1089

American legal and political system, only generate either boilerplate(if the legal standard is low) or excessive litigation (if the legalstandard is high), in which case reporting requirements for transferregulations would be inadvisable. Much depends on whether thereare groups that will monitor welfare impact statements and takeagencies to court when they fail to issue adequate welfare impactstatements, as environmental groups have done for environmentalimpact statements. Too much enthusiasm for litigation might lead tointerference with normal agency functions; however, too littleenthusiasm might again lead to statements containing nothing butboilerplate.

C. Mixed Regulations and Distributional Questions

Many statutes authorize agencies to issue prescriptive regulationsthat both cure market failures and effect transfers to particulargroups. A statute designed to restrict pollution might provide thatfactories in one region cut emissions more than factories in anotherregion, or that all factories use a technology that is cheaper for somefactories than for others. If Congress could have achieved its goalsequally well or better without making these distinctions, then thestatute self-consciously redistributes wealth compared to a statutewhose distributional effects follow naturally from the primary goal ofcorrecting a market failure. The agency must accept statutoryconstraints, and when it performs cost-benefit analysis, it mustexclude alternative regulations that have a higher benefit-cost ratiobut do not have the prescribed distributional effects.49

More interesting, when agencies have a broad mandate to solvemarket failures, they will face two possible situations: (1) a singleoptimal regulation that might or might not have desirabledistributional effects, and (2) multiple regulations with equal benefit-cost ratios and different distributional effects.

In the first case, cost-benefit analysis supports one outcome. Ifthe agency promulgates a different regulation with a more attractivedistributive effect, that regulation is a mixed regulation. There isreason to think that agencies do this. When agencies justifyregulations, they often explain how they designed the regulation sothat the burden is not concentrated on the poor, or on a particular

49. One might prefer to say that the decision procedure is cost-effectiveness analysis, butthis is just a matter of labeling.

POSNER.DOC 07/07/04 1:39 PM

1090 DUKE LAW JOURNAL [Vol. 53:1067

segment of the population, or on residents of a particulargeographical area; or they note that the regulation favors smallbusinesses at the expense of big businesses. For example, in 1982, theEPA promulgated regulations governing the lead content limits forgasoline that imposed stricter standards on larger refineries than onsmall refineries.50 And agencies are directed to do this, in part byexecutive orders, and perhaps also in part by a political sense of thegroups that Congress or oversight committee members care about.51

In all these cases, the agency’s decision procedure is most accuratelydescribed not as cost-benefit analysis, but as cost-effectivenessanalysis of various routes to some distributional goal.

In the second case, cost-benefit analysis does not distinguishamong multiple regulations with different distributional effects, andfor that reasons the agency must issue a mixed regulation that reflectsan implicit or explicit decision about distribution. In the absence oflegislative guidance, the agency might rely on any of the factorsdescribed in the previous paragraph, or on its own beliefs aboutdistributional equities. In this case, the agency’s decision procedure iscost-benefit analysis, but supplemented with (not constrained by) adistributive judgment.

A related question—but one that can only be mentioned and notanswered here—is why there is no distributional analogy to ExecutiveOrder 12,866’s mandate to use cost-benefit analysis. In theory, anexecutive order could require agencies that are given vague statutorydirection to promulgate prescriptive or transfer regulations that meetcertain distributional criteria. Indeed, it appears that agencies alreadydo this, albeit in an ad hoc way.52 The question is why OMB does notdemand more consistent and specific distributional results—forexample, regulations that improve the Gini coefficient, or some othermeasure of equality.53 No doubt the answer has to do with thedifficulty of specifying distributional criteria that are as clear as the

50. Regulation of Fuels and Fuel Additives, 40 C.F.R. pt. 80 (1982) (amended 1996).51. See Draft 2003 OMB Report, supra note 1, at 5,514 (general requirements); Exec.

Order No. 13,132, 64 Fed. Reg. 43,255, 43,255 (Aug. 4, 1999) (federalism); Exec. Order No.12,898, 59 Fed. Reg. 7,629, 7,629–30 (Feb. 11, 1994) (environmental justice); Exec. Order No.12,866, 58 Fed. Reg. 51,735, 51,736 (Oct. 4, 1993) (distributive impact).

52. See the farm relief regulation discussed infra in Part III.A; the agency imposed a cap onthe size of the transfer without any statutory authority, thus favoring smaller producers relativeto larger producers (though not necessarily wealthier producers relative to poorer producers).

53. For a discussion of the Gini coefficient, the Poverty Index, and other measures ofdistributional inequality, see JOSEPH E. STIGLITZ, ECONOMICS OF THE PUBLIC SECTOR 230–35(1986).

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1091

cost-benefit standard, but this difficulty itself is something ofa mystery.54

D. The Opportunities and Limits of OMB Review

The OMB has been the chief force behind the spread of cost-benefit principles among agencies, and it could serve a similar role forcost-effectiveness analysis. How cost-effectiveness analysis of transferregulations might improve the political process depends on the goalsand incentives of the relevant political actors. One can distinguish twobroad possibilities—both are caricatures intended only to make clearthe forces at work.

1. Congress Is Honest but Agencies Are Not. Suppose thatCongress honestly legislates in the public interest, but that agencieshave specific goals or missions that deviate from congressional goals.Congress has diverse methods for disciplining agencies, but withagenda setting power and superior information about their regulatorydomain, agencies can issue regulations that differ from Congress’sideal. However, if agencies were required to perform cost-effectiveness analyses on transfer regulations, and faced sanctions ifthey did not, they would be forced to divulge some of their privateinformation, which would facilitate monitoring by Congress or therelevant committees. Here, cost-effectiveness analysis, like cost-benefit analysis of prescriptive market-correcting regulations, is adevice for solving a principal-agent problem.55

2. Congress Is Dishonest but the President Is Not. Suppose thatCongress seeks to pay off interest groups, while the president, withhis broad national mandate, prefers to regulate in the public interest.Transfer statutes, then, do not distribute wealth to deservingbeneficiaries, but to interest groups. However, because Congressenacts vague statutes that delegate a great deal of discretion toagencies, the president can use his authority over the agencies tocounter Congress’s efforts. Consider a tax credit law that has theovert aim of creating jobs but is in fact intended to, or partly intendedto, benefit firms that fill out the forms for companies that claim the

54. See LARRY TEMKIN, INEQUALITY 91, 118 (1996) (discussing various possibilities forthe correct criteria of equality).

55. Cf. Posner, supra note 7, at 1140 (discussing “cost-benefit analysis as a method bywhich the President, Congress, or the judiciary controls agency behavior”).

POSNER.DOC 07/07/04 1:39 PM

1092 DUKE LAW JOURNAL [Vol. 53:1067

tax credit.56 If the statute is vague enough, and does not explicitlyrequire contracting with members of the interest group, then aregulation that does involve that group is likely to fail a cost-effectiveness analysis. Thus, the president, through OMB, can use thecost-effectiveness obligation to resist congressional efforts to disguisetransfers, forcing Congress either to make the transfers explicit—which entails political costs—or to abandon them.

E. Judicial Review

Judicial deference to agency action is justified by division oflabor: agencies are specialists, judges are generalists. The problemwith judicial deference is that agencies can use their discretion inways that are inconsistent with social welfare and congressionalpolicy, as the case may be. Agencies might transfer resources topolitically powerful interest groups or indulge ideological passions notshared by the public. The virtue of cost-benefit analysis (as a statutorymandate) is that it harnesses the power of quantification, permittingcourts to scrutinize an agency’s decision without reproducing it. Whenmonetization of costs and benefits does not otherwise distort theagency’s mission too much, judicial enforcement of cost-benefitanalysis will produce better regulations, regulations that do not reflectthe internal biases of the agency or its chief.57

As has been seen, cost-benefit analysis is not suitable forevaluating transfer regulations. If judges enforced cost-benefitanalysis, all transfer regulations would be struck down. However, withlegislative authorization—or through aggressive interpretation of thearbitrary and capricious standard58—courts could use cost-effectiveness analysis to review transfer regulations. This reviewcould take many forms. At the lowest level, courts would remandregulations when the accompanying statement in the Federal Registerdoes not include cost-effectiveness ratios for the regulation itself and

56. Compare to the Targeted Jobs Tax Credit, 26 U.S.C. § 51 (2000) (now the WorkOpportunity Tax Credit), discussed in Elizabeth Garrett, Harnessing Politics: The Dynamics ofOffset Requirements in the Tax Legislative Process, 65 U. CHI. L. REV. 501, 521–22 (1998)(arguing that “the most vociferous supporters of the targeted jobs tax credit were not thedisadvantaged groups covered by the provision nor the businesses that claimed the credit,” butrather the “firms that helped employers determine which employees qualified for the tax creditand complete the necessary tax forms”).

57. This is Sunstein’s view, see SUNSTEIN, supra note 15, at 191–228, although he thinksjudges should be highly deferential because of their lack of expertise, id. at 225.

58. See the discussion infra in Part III.C.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1093

for a range of plausible alternative regulations. In addition, a transferregulation that is less cost-effective than an alternative within theagency’s authority would be vacated on judicial review, and onremand the agency would be required to issue the cost-effectivetransfer regulation. There would still be a place for judicial deference,as in the case for cost-benefit analysis; determining the distributionalgoals of a statute would need to be discretionary within a broadrange. But this would not mean that the agency is unconstrained. At aminimum, agencies would be required to act consistently acrossregulations. In a similar way, if agencies have some discretion tochoose discount factors and valuations of life for cost-benefit analysis,a consistency requirement across regulations and agencies wouldconstrain their behavior in useful ways.59

My suggestion is not radical. Courts already review agencies’cost-effectiveness analyses when transfer regulations are the subjectof litigation. Part III discusses some examples.60 But, as will be seen,the judicial efforts are dispiriting. Although courts focus on the rightissues—whether inaccurate distributions should be tolerated in orderto reduce administrative costs—courts rarely demand that agenciesprovide data that support their cost-effectiveness analyses, so it isalways hard to see why courts approve some transfer regulationswhile rejecting others. One senses that courts rely on a rough sense ofthe ideal distributional outcome intended by the statute and areimpatient with arguments that administrative cost savings justifyreliance on crude proxies or bright-line rules that result indistributions that deviate from the ideal. If courts think it proper todefer to agency judgments, then they should not reject thesearguments; if they think it proper to scrutinize the agency’s claims,they should demand data and base their own judgment on anassessment of the facts. Currently, they do neither.

59. See Posner, supra note 7, at 1191–92 (arguing that agencies, when performing cost-benefit analyses, should be forced to be consistent with all kinds of valuations, includingvaluations of life and discount factors).

60. Here are two others: McDaniels v. United States, 300 F.3d 407, 411 (4th Cir. 2002),where the court defended the agency’s decision to use gross revenues as a proxy for net incomeon grounds of administrative cost, and Michigan Head Start Directors Ass’n v. Butz, 397 F. Supp.1124, 1140 (W.D. Mich. 1975), where the court rejected a similar proxy on the ground that theadministrative cost savings (nowhere specified) were insufficient.

POSNER.DOC 07/07/04 1:39 PM

1094 DUKE LAW JOURNAL [Vol. 53:1067

III. SOME EXAMPLES

According to OMB reports to Congress, agencies havepromulgated several hundred transfer regulations, counting onlythose regulations that have had an impact of at least $100 million orare otherwise considered “major” under OMB’s conventions. Eachone of these regulations was published in the Federal Register alongwith a statement that the regulation complied with Executive Order12,866. Many of the statements contain boilerplate, but a significantnumber contain a cost-effectiveness analysis, or at least a gesture inthat direction.

No scholar has tried to determine whether these regulations are,as a group, cost-effective. At first sight, this gap in the literatureseems odd, for there is a large literature on the related question ofwhether prescriptive regulations issued under market-correctingstatutes are cost-justified.61 But the reason for the different levels ofattention devoted to these questions is probably that agencies’ cost-benefit analyses supply much more data than agencies’ cost-effectiveness analyses, making scholarly review of the cost-benefitanalyses easier.

In the absence of agency supplied data about cost-effectiveness,the best way to determine whether agencies issue cost-effectivetransfer regulations would be through an empirical study thatcollected all the regulations and determined whether their cost-effectiveness ratios were superior to plausible alternatives. Such astudy, however, would be nearly impossible. One cannot knowwhether a regulation that provides school lunches at $5 per lunch iscost-effective unless one knows what alternatives are available, and ifthe agency does not provide a thorough and credible discussion of thealternatives (and they never do, as far as I have found), one could notknow what these alternatives would be without becoming an expert inevery field of regulation.62 As a result, one cannot evaluate transfer

61. See, e.g.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1095

regulations on the basis of their cost-effectiveness in the samesystematic way that John Morrall evaluated health and safetyregulations on the basis of their implicit valuations of life.63

For these reasons, I will take the less ambitious route andevaluate the quality of the cost-effectiveness analysis in a smallsample of regulations. The point here is not to defend or criticize theregulations themselves, but to evaluate the reasoning of the agency.

A. Farm Relief

After the collapse of farm prices in 1998, Congress appropriated$3 billion for farm relief, of which $200 million was directed to dairyproducers “in a manner determined by the Secretary” of USDA.64

The Secretary thus had to develop a formula for distributing the $200million among the many dairy producers who lost money. This is notas easy as it sounds: the problem is determining how much aparticular producer lost as a result of the price decline. One ideawould be to look at how much milk the producer manufactured in theyear prior to the market collapse, and give the producer an amount ofmoney equal to the industry-wide average level of profits per unit ofmilk that the affected producer manufactured in the prior year. Thisformula, however, would overcompensate unprofitable producers: ifthese producers would have made no profits in 1998 even if prices hadnot declined, any payment would overcompensate them. On the otherhand, it would have been very difficult to determine the lost incomeof each producer on the basis of a projection to 1998. Apparently forthis reason, the Secretary chose a bright-line rule that awarded a fixedamount per unit of milk produced in the earlier year. She also cappedcompensation at 2.6 million pounds of milk.65 This cap favored smallerproducers.

In 2000, Congress appropriated another $325 million for dairyproducers (and livestock producers as well), directing the Secretary touse the money “to compensate producers for economic losses

David M. Cutler, Health Care and the Public Sector, in 4 HANDBOOK OF PUBLIC ECONOMICS

2145 (Alan J. Auerbach & Martin Feldstein eds., 2002).63. Morrall, supra note 61, at 29–34.64. Omnibus Consolidated and Emergency Supplemental Appropriations Act of 1999,

Pub. L. No. 105-277, sec. 101(a), tit. XI, § 1111(d), 112 Stat. 2681, 2681−744 (1998).65. 7 C.F.R. §§ 1430.502–.506 (2003).

POSNER.DOC 07/07/04 1:39 PM

1096 DUKE LAW JOURNAL [Vol. 53:1067

incurred during 1999.”66 The Secretary maintained the cap issuedunder the prior regulation, and also provided that producers signedup in the first year of the program would be automatically enrolled inthe second year of the program. Payments would be based onproduction in 1997 and 1998.67 As a result, producers who had goneout of business in 1999, or even 1998, would nonetheless obtaincompensation as though they had been in business but had lostmoney. Milk Train, a consortium of large milk producers, broughtsuit against the Secretary, arguing that the cap and the automaticenrollment provisions favored smaller dairy producers.68 The capclearly prevented larger producers from obtaining compensation fortheir losses beyond the cap, and the automatic enrollment provisionsextended this preferential treatment to producers (presumably,smaller producers) who were no longer in the dairy business.

The Secretary argued that the rule complied with ExecutiveOrder 12,866 (the most recent cost-benefit executive order) andpassed a cost-benefit test,69 a claim that was apparently accepted bythe D.C. Circuit Court.70 Although the agency’s description of thecost-benefit analysis is hard to follow, the Secretary seemed to believethat a payment of $173 million to dairy producers could createbenefits of $400 to $600 million. “The differences between outlays,which are virtually all direct transfers to program participants, andincome, are made up of increased dairy prices . . . .”71 This explanationis incoherent. Cash transfers to dairy producers would not normallyincrease dairy prices, but even if they did, the loss to consumers—notmentioned anywhere—would offset the gain in income.

The Crop and Market Loss Assistance rule fails a cost-benefitanalysis, as indeed does any rule that determines how moneyappropriated by Congress would be distributed to beneficiaries. But itdoes not follow that any rule that the Secretary might promulgate

66. Agriculture, Rural Development, Food and Drug Administration, and RelatedAgencies Appropriations Act of 2000, Pub. L. No. 106-78, §§ 805, 822, 825, 113 Stat. 1135, 1179,1186–87 (1999) (codified as amended in scattered sections of 7 U.S.C.).

67. 7 C.F.R. §§ 1430.502.–.506.68. Milk Train, Inc. v. Veneman, 310 F.3d 747, 750 (D.C. Cir. 2002).69. 1999 Crop and Market Loss Assistance, 65 Fed. Reg. 7,942, 7,948 (Feb. 16, 2000).70. See Milk Train, 310 F.3d at 754, 756 (relying on the existence of the cost-benefit

analysis in holding that the cap and automatic enrollment provisions were proper). ExecutiveOrder 12,866 cannot be enforced by a court; the argument probably was made because a cost-justified regulation would not seem arbitrary and capricious under the APA.

71. 1999 Crop and Market Loss Assistance, 65 Fed. Reg. at 7,948.

POSNER.DOC 07/07/04 1:39 PM

2003] COST-EFFECTIVENESS ANALYSIS 1097

would be equally bad or good. The Milk Train case centered on justthis question. Milk Train complained that the rule violated the statuteby favoring smaller producers, and the Secretary argued thatdeviations from the statutory goal were justified by administrativecost savings.