l'esprit de Toulouse - International Federation for Information ...

Upload

khangminh22Category

view

1download

0

Trading Complex RisksJob Market Paper

Felix Fattinger∗

November 13, 2019

AbstractThis paper studies how complexity impacts markets’ ability to aggregate informa-tion and distribute risks. I amend fundamental asset pricing theory to reflect agents’imperfect knowledge about complex dividend distributions and test its clear-cut pre-dictions in the laboratory. Market equilibria corroborate complexity-averse tradingbehavior. Despite being overpriced, markets efficiently share complex risks betweenbuyers and sellers. While complexity induces noise in individual trading decisions,market outcomes remain theory-consistent. This striking feature reconciles with arandom choice model, where bounds on rationality are reinforced by complexity.By adjusting for estimation biases, traders reduce the variation in market-clearingprices of complex risks.

Keywords: Complexity, risk sharing, information aggregation, boundedrationalityJEL Classification: G12, G14, G41

∗Department of Finance & Brain, Mind and Markets Laboratory, University of Melbourne, 198 Berke-ley Street, Victoria 3010, Australia. Phone: +61-3-8344-9336. E-mail: [email protected] thank Elena Asparouhova, Hedi Benamar, Peter Bossaerts, Markus Brunnermeier, Adrian Buss, ClaireCelerier, Sylvain Chassang, Marc Chesney, Soo Hong Chew, Sebastian Dorr, Thierry Foucault, An-dreas Fuster, Dan Friedman, Zhiguo He, Cars Hommes, Philipp Illeditsch, Chad Kendall, Carsten Mu-rawski, Corina Noventa, Michaela Pagel, Jean Paul Rabanal, David Redish, Jean-Charles Rochet, MartinSchonger, Nicolas Treich, Roberto Weber, Alexandre Ziegler, participants at the TSE Finance Workshop,the University of Zurich Brown Bag Seminar, the 2018 AFA, the University of Melbourne Brown BagSeminar, the 2018 Experimental Finance Conference, the 2018 RBFC, the 2018 FIRN Annual Conference,the 2018 Paris December Meeting, the 2nd MPI Experimental Finance Workshop, the 2019 WFA, and the2019 EFA for helpful comments. I am especially grateful to Sebastien Pouget, Sophie Moinas, and BrunoBiais for countless discussions while visiting Toulouse School of Economics, where part of this researchwas conducted. I also thank Kathrin De Greiff, Sara Fattinger, Sandra Gobat, Rene Hegglin, JonathanKrakow, Ferdinand Langnickel, Patrick Meyer, Lukas Munstermann, and Carlos Vargas for participatingin the pilot session. Last but not least, I am indebted to Cornelia Schnyder for her invaluable supportin conducting the main sessions of the experiment. Financial support by the Swiss National ScienceFoundation is gratefully acknowledged.

That economic decisions are made without certain knowledge of the consequences is prettyself-evident.Kenneth J. Arrow

The essence of the situation [the problems of life] is action according to opinion, of greater orless foundation and value, neither entire ignorance nor complete and perfect information, but

partial knowledge.Frank H. Knight

1. Introduction

Risk is ubiquitous to decision-making in financial markets, where investors’ trading deci-sions directly affect their financial well-being. In their seminal work, Debreu (1959) andArrow (1964) provide an elegant theory of value and choice under risk in the contextof perfect and complete markets. In sharp contrast to this theoretical benchmark, theinherent complexity of real-world markets only allows for an imperfect measurement offinancial risks (Knight, 1921) with varying levels of confidence (Keynes, 1921). Thus, itmay come as little surprise that the predictions by Debreu and Arrow’s theory are gener-ally rejected in the field. Acknowledging this particular discrepancy between theory andreality, I ask the following three questions: (i) How powerful is the neoclassical theory indescribing market outcomes, i.e., prices and allocations, if one accounts for the complexrisk structure of financial assets? (ii) Can such an amended theory improve our under-standing of the highly non-trivial process that transforms individual trading decisions intocollective market outcomes? (iii) How does complexity impact financial markets’ abilityto aggregate information and distribute risk? I try to answer these questions in two steps.

I begin with the theory. For the most simple two-state setting, I extend traditionalconsumption-based asset pricing theory to reflect agents’ partial knowledge about thedistribution of future dividends (Knight, 1921). The source of complexity that impairsinformation quality is exogenous to the model. To increase generality, I incorporate bothkinked as well as smooth complexity preferences by applying two canonical decision theo-ries under ambiguity (Ghirardato, Maccheroni, and Marinacci, 2004; Klibanoff, Marinacci,and Mukerji, 2005). In a Walrasian market, both preference classes provide similar qual-itative implications regarding the trading of complex risks: In the absence of aggregateuncertainty, competitive market prices are sensitive to mispricing, whereas risk alloca-tions are relatively more robust to incorrect beliefs. Intuitively, the latter is the resultof increased risk sharing incentives in the face of imperfect information. Contrary to the

1

above decision theories, subjective expected utility (Savage, 1954), i.e., the theoreticalfoundation of choice under uncertainty, implies relatively less efficient risk sharing underpartial knowledge.

Clearly, whether preferences known to explain behaviour under (pure) ambiguity pre-serve any explanatory power (over subjective expected utility) for partially measurablerisks remains an empirical question. In a second step, I therefore test the theory’s clear-cut predictions in the laboratory, constructing a one-to-one replication of the underlyingmodel economy. The lab is the sole environment that enables me to simultaneously con-trol for both individual beliefs and strategic uncertainty, a virtual impossibility in thecontext of field data. In my main treatment, I introduce complexity in traded risks byrelying on the seminal description of financial risks by Bachelier (1900) and Black andScholes (1973).

My findings shed light on the above questions. First, in the presence of complexrisks, asset market equilibria corroborate complexity-averse trading behavior. In linewith markets’ awareness of traders’ imperfect information, complexity reduces the priceelasticity of risk-minimizing supply and demand schedules. Complex risks are generallyoverpriced, suggesting that individuals overestimate the drift relative to the volatilitycomponent of financial risks. However, the reduction in price sensitivity overcomes thesizeable variation in subjective beliefs, allowing complex risks to be shared almost perfectlybetween buyers and sellers. This striking feature of market equilibrium under partialknowledge demonstrates the explanatory power of a conditional rational choice paradigmthat accounts for informational imperfections.

Second, at the individual level, complexity causes more mistakes in trading decisions,where mistakes are defined as adopting strategies that are strictly dominated in termsof their risk-return profile.1 Both frequencies and distributions of dominated actionsconfirm that individual trading strategies become increasingly noisy under more complexrisks. Crucially, as the number of participants becomes larger, this noise cancels outin equilibrium and theory-consistent prices and optimal risk allocations prevail. Thisaggregation result can be explained by a random choice model in which the relativelikelihood of a given action is increasing in its anticipated utility.2

Third, combining complexity aversion with random choice provides an effective settingto investigate how complex risks generically impact market outcomes. While complexity

1 Conditions for strict dominance are derived under perfect and imperfect information about dividends.In the latter case, the conditions hold for both kinked (Ghirardato, Maccheroni, and Marinacci, 2004)and smooth (Klibanoff, Marinacci, and Mukerji, 2005) preferences.

2 See Section 3 for a formal definition of anticipated utility under imperfect information.

2

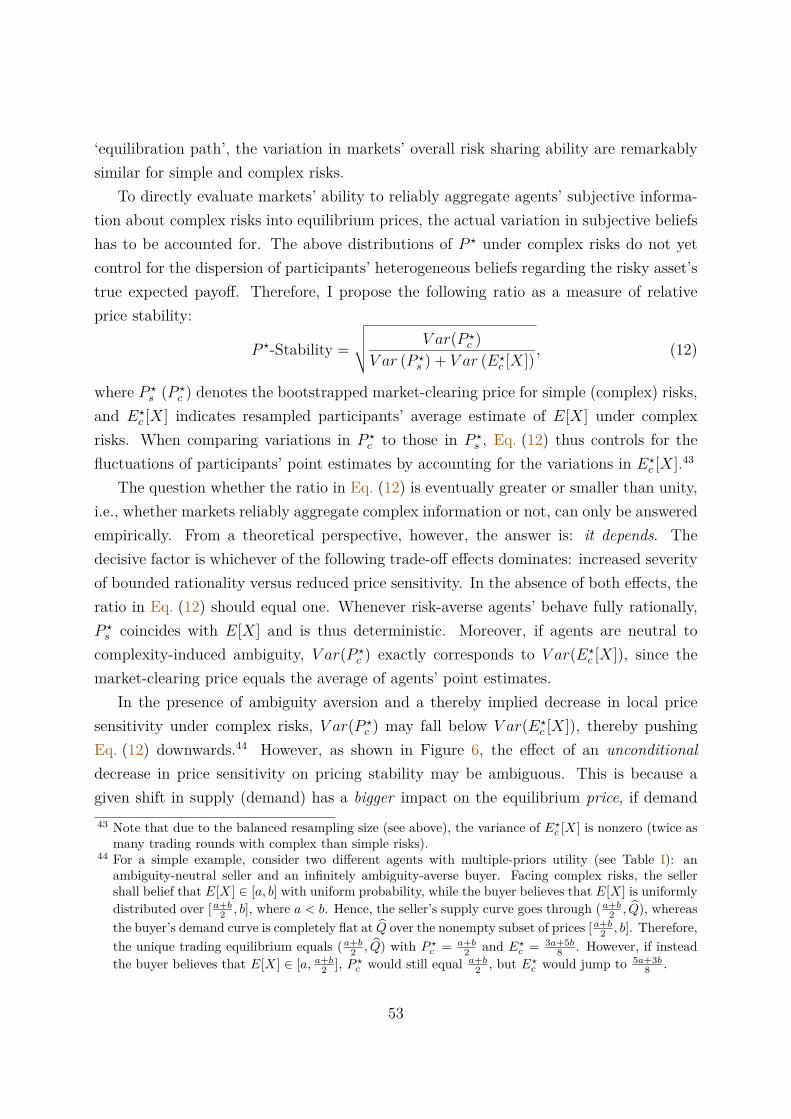

aversion facilitates robust risk sharing, its implication on the informativeness of pricesis per se ambiguous. However, I find evidence that individual trading behavior exhibitsself-awareness of prevailing estimation biases. More specifically, the bigger the distancebetween individual point estimates and the true dividend probability, the less price sensi-tive the submitted supply and demand curves. Eventually, self-awareness translates intocollective awareness which decreases the variation in market-clearing prices relative tothe variation in subjective beliefs. This showcases the stabilizing effect of discontinuoustrading periods during times of high price uncertainty. In general, markets’ ability toaggregate subjective beliefs into prices is therefore determined by the trade-off betweenreduced price sensitivity and amplified bounded rationality.

Finally, my empirical findings have several implications for the experimental and the-oretical asset pricing literature: (i) Extending the finding in Biais, Mariotti, Moinas,and Pouget (2017), I show that, in absence of complex risks, second-order stochasticdominance is sufficient for generating competitive market outcomes in line with rationalchoice.3 (ii) In the presence of complex risks, individual behavior is highly heteroge-neous, i.e., trading strategies implied by subjective expected utility as well as kinked andsmooth ambiguity preferences are observed. (iii) Notwithstanding individual heterogene-ity and complexity-induced bounded rationality, incorporating partial knowledge into aneoclassical asset pricing model convincingly explains market equilibria under imperfectinformation. Hence, subjective expected utility a la Savage (1954) is insufficient to un-derstand market behavior if traders have access to partial knowledge only. Moreover, mybottom-up approach demonstrates how aggregate stability results from individual hetero-geneity. This stands in contrast to the rational of representative agent models motivatedby specific singular behavior.

The merits of taking the study of how (complex) individual trading translates into tomarket outcomes to the lab are manifold. By design, the lab allows for the constructionof complete markets and—by comparing market-clearing prices to random price draws—provides a direct test of their competitiveness. Also, the experimenter can exercise fullcontrol over each market participants’ information set and how their individual decisionsinteract towards equilibrium. Crucial for any study of complex information, the labora-tory environment offers the unique virtue of measuring subjective beliefs (expectations).This generally constitutes an impracticality when confronted with real-world data. Mostimportantly, the treatment effect under investigation can be analyzed in isolation, while

3 In the setting studied by Biais, Mariotti, Moinas, and Pouget (2017), rational choice is implied byfirst order stochastic dominance.

3

controlling for any kind of endogeneity concerns.The obvious benchmark for this study is the case in which traders face ‘simple’ risks

and hence everybody has perfect information about the objective dividend distribution. Inmy experiment, complexity is introduced by linking risky dividends directly to the payoffof a digital option, i.e., making dividends depending on the realizations of a particular‘reference path’. In this case, the reference path follows a geometric Brownian motion.More specifically, participants are provided with the parameters of the reference path inaddition to a dynamic visualization of its past trajectory. Thus, the presence of complexrisks requires them to deductively determine dividend distributions by solving a stochasticdifferential equation. Although solvable by hand for certain parameters, deriving theproblem’s closed-form solution proves infeasible for most participants.4 The advantageof this implementation is the simple structure of the complicated but yet well-definedtask at heart. The problem’s comprehensible form together with its visualization allowsparticipants to appraise—with more or less certainty—the apparently objective dividendrisk.5 Note, the objectivity of the complex dividend distribution is a necessary conditionfor contrasting the empirical data to any kind of theoretical benchmark.

In the absence of perfect information, participants acquire a more or less precise es-timate of the relevant dividend distribution, i.e., are faced with a smaller or wider set ofpossible priors. Being aware of the incompleteness of their knowledge, “it would be irra-tional for an individual who has poor information about her environment to ignore thisfact and behave as though she were much better informed” (Epstein and Schneider, 2010,p. 5). Thus, I theoretically study trading decisions under complex risks as a departurefrom subjective expected utility by applying two seminal ambiguity models: a general-ization of the multiple-priors model by Gilboa and Schmeidler (1989), and the smoothambiguity model by Klibanoff, Marinacci, and Mukerji (2005). While the former implieskinked ambiguity preferences, the later allows for smooth ambiguity effects.

In my setting, the main implication of both models is intuitive. If agents are averse4 This is not surprising given the means at hand and the limited time available during the experiment.

Presenting participants with an obviously solvable but complicated problem represents the design’sintegral treatment.

5 Although this notion of complexity is arguably specific, it naturally extends to real-world financialmarkets’ perceived risk structure. There is a vast scientific literature on various notions of complexity.In computer science and machine learning one distinguishes, e.g., between computational complexity(required resources), sample complexity (minimum number of draws), and Kolmogorov complexity(minimum descriptive length) of problem solving. Interestingly enough, recent contributions in deci-sion science provide evidence for commonalities between the human brain and computer algorithmssolving and reacting to problems with varying levels of complexity (see, e.g., Bossaerts and Murawski(2016)).

4

to perceived ambiguity, they, ceteris paribus, prefer to avoid being exposed to imper-fectly understood risks. When starting from a zero ambiguity exposure, this leads to ano-trade interval.6 For nonzero endowments in the risky asset, as pointed out by Dowand da Costa Werlang (1992), engaging in trade is generally optimal. In my model econ-omy, incentives to trade stem from nontradable but hedgeable consumption risk. In short,under both models, agents’ price sensitivity of their perfect hedging strategy decreasesin the presence of complex risks. Intuitively, being completely hedged insures not onlyagainst risk but also against potential complexity-induced ambiguity. The main differencebetween the two models lies in their implied conditions for mispricing. Within the smoothambiguity model, incorrect beliefs immediately impact equilibrium prices, whereas thisdoes not unconditionally hold for the multiple-priors model. As noted above, my experi-ment finds evidence for both preference classes.

To compare the above documented complexity effects to those induced by the canonicalambiguity instrument in experimental economics, I additionally study both individualbehavior and market allocations in an Ellsberg (1961) environment. My results indicatethat complex risks have similar but more pronounced implications on individual tradingand market outcomes than ambiguity induced by conventional Ellsberg urns.

The remainder of the paper is organized as follows. Section 2 reviews the literature.Section 3 introduces the model economy and develops the necessary theory for generatingpredictions about trading both simple and complex risks. Section 4 describes the exper-imental design. Section 5 confronts the theoretical predictions with the data. Section 6concludes.

2. Literature

This paper relates to four distinctive strands of the literature. First, my design directlybuilds on the experimental setup proposed by Biais, Mariotti, Moinas, and Pouget (2017).Relying on a two-state world with two nonredundant assets (a risk-free bond and a riskystock), it offers the simplest possible setting to test the rational paradigm of general equi-librium asset pricing theory. Controlling for participants competitive behavior, they findmarket outcomes to be consistent with the theory of complete and perfect markets: Onaverage, (simple) risk is perfectly shared and only aggregate risk is priced. Therefore,Biais, Mariotti, Moinas, and Pouget’s (2017) parameter-free test of the most fundamental

6 For example, this phenomenon serves Dimmock, Kouwenberg, Mitchell, and Peijnenburg (2016) inexplaining known household portfolio puzzles, e.g., the equity home bias.

5

theory constitutes the ideal benchmark upon which the trading of simple and complexrisks can be compared.7 Moreover, its simple market-clearing pricing scheme based onindividual supply and demand functions can be controlled for any kind of strategic uncer-tainty. This constitutes an impracticality in the context of the continuous double auctionthat is most commonly used in experimental asset market studies.

Second, the herein presented analysis naturally relates to experimental studies ontrading ambiguous or complex assets. Implementing a continuous double auction of state-contingent claims based on an Ellsberg urn, Bossaerts, Ghirardato, Guarnaschelli, andZame (2010) analyze how participants’ ambiguity aversion affects asset prices and finalportfolio holdings. Similar to the no-trade result, they find that, for certain subsets ofprices, ambiguity-averse agents prefer to hold nonambiguous portfolios. Furthermore,Bossaerts, Ghirardato, Guarnaschelli, and Zame (2010) show how, in the presence ofaggregate risk, sufficiently ambiguity-averse investors indirectly impact asset prices byaltering the per capita risk to be shared among marginal investors.

Asparouhova, Bossaerts, Eguia, and Zame (2015) show how ambiguity preferencescan explain asset prices under asymmetric reasoning. They consider a continuous doubleauction of arrow securities, where, midway through the auction, agents are confronted withan involved updating problem regarding the relative likelihood of the underlying states.8

In line with Fox and Tversky’s (1995) comparative ignorance proposition, Asparouhova,Bossaerts, Eguia, and Zame (2015) argue that agents perceive irreconcilable post-updatingmarket prices as ambiguous. Hence, if ambiguity-averse, agents who apply incorrectreasoning become price-insensitive. Consistent with ambiguity aversion, the more price-sensitive agents there exist, the less severe is the experimentally documented mispricing.

Carlin, Kogan, and Lowery (2013) study how computational complexity alters biddingbehavior in a deterministic environment.9 They find higher complexity to increase volatil-ity, lower liquidity, and decrease trade efficiency, i.e., to reduce gains from trade. Moreover,Carlin, Kogan, and Lowery (2013) provide evidence that, additionally to any noise arisingfrom estimation errors, traders’ bidding strategies are influenced by a complexity-inducedadverse selection problem. Intuitively, given traders’ private values of the tradable asset

7 For their most general predictions, Biais, Mariotti, Moinas, and Pouget (2017) only rely on first orderstochastic dominance. When allowing for deviations from their symmetric payoff distribution, myanalysis assumes expected utility maximization instead.

8 The updating task in Asparouhova, Bossaerts, Eguia, and Zame’s (2015) experimental design is anadaptation of the famous ‘Monty Hall problem’.

9 In the experimental design by Carlin, Kogan, and Lowery (2013) participants trade different assetswhose values have to be determined deductively by solving systems of linear equations, where theauthors differentiate between simple and complex computational problems.

6

are affiliated, the fear of winner’s curse, i.e., to systematically lose by trading against abetter informed counterparty, leads traders to submit more conservative price quotes.

Third, a growing literature investigates the drivers and implications of financial com-plexity both from a theoretical as well as an empirical perspective. Ellison (2005) andGabaix and Laibson (2006) demonstrate theoretically that inefficient levels of financialcomplexity can prevail in a competitive equilibrium. Carlin (2009) finds that financialcomplexity increases with the degree of competition among financial institutions. Carlinand Manso (2011) show how educational initiatives aiming to foster financial literacy mayeventually cause welfare diminishing obfuscation, i.e., the strategic acceleration of com-plexity by financial service providers to preserve industry rents (see Ellison and Ellison(2009)). From an investor’s view, Brunnermeier and Oehmke (2009) discuss three differ-ent ways to deal with complexity: (i) applying separation results, (ii) relying on models,or (iii) via standardization. Arora, Barak, Brunnermeier, and Ge (2011) illustrate howcomputationally complex derivatives may worsen asymmetric information costs.

Celerier and Vallee (2017) empirically test the implications of the Carlin (2009) modeland indeed find complexity to be increasing in issuer competition. Furthermore, severalstudies analyze the steadily growing market for complex securities, in particular theirpricing, historical performance, as well as the characteristics of the involved issuers andinvestors (Henderson and Pearson (2011), Ghent, Torous, and Valkanov (2017), Grif-fin, Lowery, and Saretto (2014), Sato (2014), and Amromin, Huang, Sialm, and Zhong(2011)). Relying on expected utility theory, Hens and Rieger (2008) moreover rejectthe often-claimed market completing effect of structured products. Hence, there existsboth theoretical and accumulating empirical evidence that financial institutions rely on acontinuing increase in complexity to shield industry rents from competitors and learningby investors rather than to create higher quality products. My paper complements thisliterature by investigating the effects of rising complexity on agents’ trading behavior,deliberately abstracting from financial innovation’s potential market completion role andthe strategic use of complexity to mitigate competition.10

10 In reality, most markets, including those for financial assets, can hardly be characterized as being com-plete in a static sense, i.e., in the absence of retrading opportunities. Hence, the financial innovationindustry’s touted services towards market completion have to be evaluated against dynamic complete-ness as developed in Kreps (1982) and Duffie and Huang (1985). Assuming dynamic completeness, theexistence of a Radner equilibrium (Radner, 1972) crucially depends on agents’ ability of perfect fore-sight, i.e., to perfectly forecast today all future prices depending on information revealed tomorrow.Asparouhova, Bossaerts, Nilanjan, and Zame (2016) experimentally show how the inability of perfectforesight can cause considerable deviations from equilibrium prices. Thus, one reasonable concernimplied by the increasing complexity of traded risks is that agents lacking the required resources tofully understand their complicated nature may fail to correctly forecast future price movements.

7

Finally, this paper also relates to an emerging literature comparing individuals’ pref-erences towards pure Ellsberg-like ambiguity and complex risk(s), where, as in this paper,the latter is uniquely defined by an objective probabilistic structure. The findings inHalevy (2007) give support to a close relation between individuals’ ability to correctlyreduce compound lotteries and their attitudes to pure ambiguity. The vast majorityof participants (95%) who failed to disentangle compound objective lotteries, displayednonambiguity-neutral behavior.

In their recent paper, Armantier and Treich (2016) provide strong empirical evidencefor “a tight link between attitudes toward ambiguity and attitudes toward complex risk”(Armantier and Treich, 2016, p. 5). In their ambiguity treatment, participants are con-fronted with lotteries whose outcomes depend on draws from an opaque Ellsberg urn,while complex risks are represented by lotteries that get settled by simultaneous drawsfrom multiple transparent urns. Based on estimated certainty equivalents for both lotterytypes, Armantier and Treich (2016) elicit ambiguity as well as complex risk premiums.They find a strong positive correlation between the two premiums across participants.

3. Theory

This section introduces the simple model economy for which I study individual tradingbehavior conditional on agents’ information quality. If risks are simple, implications ofvarying risk-preferences are analyzed within the classical framework of expected utility. Incontrast, if risks are complex, individual preferences are adjusted to account for agents’imperfect information. The former case provides a clear-cut benchmark for investigat-ing the latter. At the end of Section 3.3, I provide a summary of the theory’s generalpredictions in contrast to subjective expected utility.

3.1. Model

I start from the simple setting of Biais, Mariotti, Moinas, and Pouget (2017). In thetwo-period interpretation of this trading economy, t ∈ 1, 2, uncertainty gets resolved int = 2, where there exist two possible states of the world, Ω = u, d. The probability ofreaching state u is denoted by π, i.e. P(ω=u) = π and P(ω=d) = 1 − π, respectively.Contrary to Biais, Mariotti, Moinas, and Pouget (2017), I allow for any nontrivial binary

8

payoff distribution π ∈ (0, 1).11 This generalization is crucial, given agents’ subjectivebeliefs in the context of complex risks.

The economy offers access to a complete asset market, where shares of a risky asset(stock) can be traded in exchange for units in the risk-free asset (numeraire). The stockpays a state-dependent dividend X per share in t = 2, but nothing beforehand. Thedividend fully transfers the stock’s final value to shareholders, i.e., after dividends havebeen paid, all shares expire worthless (no continuation value). Without loss of generality,I assume that X(u) > X(d). The time difference between t = 1 and t = 2 is consideredto be very short, allowing to abstract from any time discounting. Therefore, in-betweenperiods, the risk-free asset simply serves as pure storage device (cash) that does not payany interests.

There is an infinite number of agents populating the economy. I denote the unboundedset of agents by I. Agent i ∈ I is endowed with nonnegative holdings in the risk-freeasset Bi, Si shares of the risky stock, and some state-contingent nontradable income Ii(ω)in t = 2. Moreover, every agent belongs to one of two types, i.e., either she is allowedto buy (potential buyer) or to sell (potential seller) shares. There are as many buyers assellers and their respective endowments are identical within each type. Every agent onlycares about her utility of consumption Ci(ω) in t = 2, where consumption equals the sumof final holdings in the risk-free asset, dividend payments, and nontradable income. Inthe first period, potential buyers and sellers are able to trade shares via a call-mechanismto maximize their increasing utility from consumption Ui(Ci) in the second period.12

Importantly, agents’ nontradable income is set to exactly offset the aggregate con-sumption risk generated by the stock’s dividend payments. For constant aggregate wealth(across states), I show in the following that, under risk aversion, the unique rational ex-pectation equilibrium is independent from heterogeneous attitudes towards simple con-sumption risks. In particular, under simple risks, the stock market-clearing price andquantity remain unaffected by the shape of agents’ utility functions (Ui)i∈I . If, despitethe income Ii(ω), aggregate risk prevailed, market equilibrium would necessarily reflect11 Biais, Mariotti, Moinas, and Pouget (2017) only consider the symmetrical case, i.e., π = 1/2. Imposing

symmetry has the advantage of delivering robust predictions even under the inapplicability of expectedutility theory, i.e., by only assuming the absence of first order stochastically dominated actions.

12 To trade, agents submit either demand or supply schedules for a closed discrete set of prices. In thespirit of a Walrasian clearinghouse (Friedman (2018)), the call-mechanism then maximizes trade byminimizing the gap between demand and supply.

9

agents’ (average) risk preferences.13

3.2. Trading Simple Risks: The Expected Utility Benchmark

In the presence of simple risks, the probability π is common knowledge, and thus, agentspossess perfect information about the stock’s payoff distribution. According to classicalconsumption-based asset pricing theory, the stochastic discount factor then corresponds tothe representative agent’s marginal rate of intertemporal substitution. In Biais, Mariotti,Moinas, and Pouget’s (2017) simple economy, with consumption restricted to t = 2, ex-pected utility theory implies an equilibrium stock price P equal to the stock’s normalizedexpected payoff weighted by her marginal utilities across states.14 If (Ii(ω))(i∈I) eliminatesaggregate consumption risk, the interconnectedness between P and marginal utilities dis-appears, allowing for predictions robust to any set of increasing utility functions (Ui)i∈I .Next, I generalize the analysis in Biais, Mariotti, Moinas, and Pouget (2017), who focuson π 6= 1/2 only, to any possible dividend distribution.

Recalling the two-state nature of the economy in t = 2, one can write agent i’s expectedutility from consumption as

E[Ui(Ci(ω))

]= π Ui(Ci(u)) + (1− π)Ui(Ci(d))

= π Ui

µi +√

1− ππ

σi

+ (1− π)Ui(µi −

√π

1− πσi), (1)

where µi ≡ πCi(u) + (1− π)Ci(d) and σ2i ≡ π(1− π) (Ci(u)− Ci(d))2. Thus, any agent’s

expected utility can be rewritten as a function of the probability π, her expected con-sumption, and the standard deviation of consumption across states.13 Constantinides (1982) shows that if agents with different risk attitudes all maximize expected utility

subject to a common prior, equilibrium prices can always be rationalized in a representative agentframework. Hence, in the absence of complex risks, market equilibrium can be explained by the riskpreferences of this representative agent.

14 When deciding on her optimal trading strategy Q in t = 1, the representative agent solves the followingproblem (where Q > 0 implies buying)

maxQ

E[Ui(Ci(ω))] s.t. Ci(ω) = (Si +Q)X(ω) + (Bi −QP ) + Ii(ω),

maximizing her expected utility from consumption in t = 2 subject to her budget constraint (neglectingany borrowing constraints). Hence, the first order condition yields

P = E

[U ′

i(Ci(ω))E[U ′

i(Ci(ω))]X(ω)].

10

In the absence of aggregate risk, i.e., if aggregate wealth Σi (SiX(ω) + Ii(ω)) is con-stant across states, there must exist a tradable quantity Q at which every seller and buyeris perfectly hedged against any consumption risk in t = 2.15 If agents are risk-averse, i.e.,whenever Ui is strictly concave for every agent i, there exists a unique equilibrium for thecall-mechanism in t = 1.

Proposition 1. If Ui is differentiable and strictly concave ∀i ∈ I, and there exists atradable quantity Q such that every seller and buyer is perfectly hedged, i.e., σi = 0 ∀i ∈ I,then seller i’s supply and buyer j’s demand curve for the risky asset have the uniqueintersection point (E[X], Q) ∀i, j ∈ I × I.

Proof. For proof see Appendix A.

The driving force behind Proposition 1 is the strict concavity of the utility functions, i.e.,agents’ aversion to consumption risk. To see this, it is helpful to separately consider theshape of both seller i’s supply and buyer j’s demand curve for the risky stock.

First, note that for a price equal to the stock’s expected dividend, seller i’s expectedconsumption in Eq. (1) is independent of the number of shares sold. Since seller i isrisk-averse, for P = E[X], she will therefore always decide to sell exactly Q shares andthereby be perfectly hedged against future fluctuations in consumption. However, forP < E[X] (P > E[X]), her expected consumption only increases, if she sells less (more)than Q shares. Because she is only willing to bear risk, i.e., deviate from selling Q

shares, if appropriately compensated in return, her supply curve must lie somewhere inthe lower left and upper right quadrant of the price-quantity space shown in Subfigure(a) of Figure 1.

Second, note that for P = E[X], similarly buyer j’s expected consumption in Eq. (1) isindependent of the number of shares bought. Given her risk-aversion, she chooses to buyexactly Q shares for P = E[X], and more (less) than Q shares if P < E[X] (P > E[X]),as illustrated in Subfigure (b) of Figure 1. Thus, when there is no aggregate risk, selleri’s supply and buyer j’s demand curve exhibit the unique intersection point (E[X], Q) asdepicted in Subfigure (c).

Interestingly enough, depending on the shape of Ui, a large opposite income effect candominate the corresponding substitution effect of a given price change. Hence, seller i’ssupply or buyer j’s demand curve can effectively be nonmonotonic within the respectivedominating quadrants of the PQ-plane. The following remark provides an example of anonmonotonic supply curve.15 Recall that endowments only differ between types.

11

P

Q

dominated(µi ↓ , σi ↑)

dominated(µi ↓ , σi ↑)

E[X]

(∆µi

=0)

(∆µi

=0)

Q

(a) Supply

P

Q

dominated(µi ↓ , σi ↑)

dominated(µi ↓ , σi ↑)

E[X]

(∆µi

=0)

(∆µi

=0)

Q

(b) Demand

P

Q

P ? = E[X]

Q? = Q

(c) Equilibrium

Figure 1. Trading equilibrium for simple risks

Notes: This figure shows the unique equilibrium for risk-averse agents in the absence of aggregateconsumption risk.

Remark 1. Suppose, seller i’s utility function is defined piecewise as follows

Ui(C) =

c1C1−ε

1−ε , for 0 ≤ C < C,

c2 − e−αC , for C ≤ C,

where α > ε > 0 and ε small, and c1 and c2 are positive constants such that Ui isdifferentiable ∀C ≥ 0. For certain parameter pairs (α, π), seller i’s supply curve can benonmonotonic over a nonempty subset of P .

Proof. For proof see Appendix A.

12

Figure D.1 in the Appendix D shows an example of a nonmonotonic supply curve forsimilar parameter values as in the actual experiment. 16

Absence of Risk Aversion

In case agents are not averse to consumption risk, for all P 6= E[X], an even stricterseparation between dominating and dominated strategies than shown in Figure 1 applies.From the proof of Proposition 1 it directly follows that whenever Ui is either linear orconvex, seller i always strictly prefers to sell zero shares for P < E[X]. In contrast,for P > E[X], her expected utility is maximized if and only if she sells her full initialendowment in shares. The symmetric behavior applies to risk-neutral and risk-lovingbuyers, respectively.

For P = E[X], risk-neutral agents are indifferent between trading Q shares or anyother quantity, whereas risk-loving agents are indifferent between trading zero shares orthe maximum number possible. In summary, as long as they do not consistently chooseamong their set of indifferent strategies in an asymmetric manner, the equilibrium inFigure 1 remains unaffected by a nonzero mass of nonrisk-averse agents.

3.3. Trading Complex Risks: Heterogeneous Complexity Preferences

When agents’ information about the distribution of X(ω) is imperfect, I consider theassociated consumption risk to be (more) complex. In the presence of such complex risks,‘rationality’ in decision making requires some form of acknowledgment of the information’sinherent degree of (im)precision. The literature provides a vast number of models intendedto account for individuals’ degree of confidence in their relative likelihood estimates. Inthe following, I analyze individual trading of complex risks within two classes of seminalambiguity models: multiple-priors utility and the ‘smooth ambiguity’ model proposedby Klibanoff, Marinacci, and Mukerji (2005). In the former, agents’ information qualityhas a first-order effect on their trading decision (change in mean), whereas for the latter,lower information precision increases the total amount of perceived ‘risk’ (see Epsteinand Schneider (2010)). For multiple-priors utility, there exists a direct mapping to rank-dependent expected utility, which I briefly discuss.16 The intuition behind this exemplary nonmonotonicity effect is simple. For every seller and any givenQ, both C(d) and C(u) are strictly increasing in P > 0. If prices are high enough, seller i’s higherCARA coefficient α, relevant for C(ω) > C, can dominate her lower CRRA coefficient ε. Thus, foreven higher prices, she is willing to bear less and less risk, causing her supply curve to decrease untilit eventually reaches Q, thereby completely eliminating her consumption risk.

13

Multiple-priors Utility

Agents facing complex risks are unable to determine π with certainty, but rather haveto consider several payoff distributions possible. Hence, intuitively, when making theirtrading decisions, they are guided by a set of potential probability laws. I denote agenti’s subjective set of possible priors on the state space Ω by Ci.

Based on this idea of multiple priors, Gilboa and Schmeidler (1989) axiomatize amultiple-priors maxmin decision rule that assumes infinite ambiguity-aversion. In orderto allow for a full spectrum of ambiguity preferences, I employ the generalization proposedby Ghirardato, Maccheroni, and Marinacci (2004), the so-called α-maxmin model, instead.Assuming the set Ci of subjective priors to be convex, agent i’s utility from consumptionin t = 2 is then given by

Ui(Ci(ω)) = αi minπ∈Ci

(E[Ui(π)

])+ (1− αi) max

π∈Ci

(E[Ui(π)

]), (2)

where E[Ui(π)

]≡ π Ui(Ci(u)) + (1 − π)Ui(Ci(d)), Ui, as before, is a differentiable and

strictly concave utility function, and αi ∈ [0, 1]. First, note the straightforward interpreta-tion of Eq. (2). On the one hand, the cardinality or wideness of Ci measures agent i’s ambi-guity perception: The bigger her set of subjective priors, the more ambiguity she perceives.On the other hand, her preferences towards ambiguity are expressed by αi: If αi > 1/2,she puts more weight on the minimal expected utility, implying ambiguity-aversion. Incontrast, if αi < 1/2 (αi = 1/2), then she is ambiguity-loving (ambiguity-neutral). Fortheir axiomatization, Gilboa and Schmeidler (1989) assume maximal ambiguity-aversion,i.e., αi = 1. Second, whenever Ci is a singleton, Eq. (2) reduces to Eq. (1) with subjectiveprobability πi, i.e., Eq. (2) converges to subjective expected utility as Ci → πi. For easeof notation, I furthermore rely on the following definition:

Ei[X]

:= αiEi[X]

+ (1− αi)Ei[X], (3)

where Ei[X]≡ Eπi [X] with πi := arg min

π∈Ciµi(π), and Ei

[X]≡ Eπi [X] with πi :=

arg maxπ∈Ci

µi(π).

When risks are complex, agents perceive ambiguity regarding the probability π. Inorder to analyze individual trading behavior within the α-maxmin model, a case-by-caseanalysis is required, whereby agent i can behave differently from agent j in two dimensions:First, agent i is either averse to (αi > 1/2) or even favors (αi ≤ 1/2) perceived ambiguity.Second, she can either have correct or incorrect beliefs about the true payoff probability

14

Table I. Agent types with multiple-priors utilityBeliefs about π

Correct (π ∈ Bi) Incorrect (π 6∈ Bi)

Ambiguity-averse Yes (αi > 1/2) Type AC Type AINo (αi ≤ 1/2) Type NC Type NI

Notes: In the presence of complexity-induced ambiguity, I distinguish between four differenttypes of agents with multiple-priors utility. Agent i can either be ambiguity-averse or doesnot dislike ambiguity. Additionally, she can either apply correct or incorrect reasoning whenprocessing her imperfect information about π.

π. More precisely, I classify agent i as having incorrect beliefs, if π is not sufficiently closeto the midpoint of her set of priors, i.e., if π 6∈ Bi ⊂ Ci, where Bi itself depends on herambiguity-aversion:

Bi =

[πM −∆(2αi − 1), πM + ∆(2αi − 1)], for αi > 12 ,

πM for αi ≤ 12 ,

(4)

where πM denotes the midpoint of Ci with length (or maximum difference) 2∆. We notethat Bi → Ci as αi → 1 and Bi → πM as αi → 1/2. Table I summarizes the four possiblecombinations of different types.

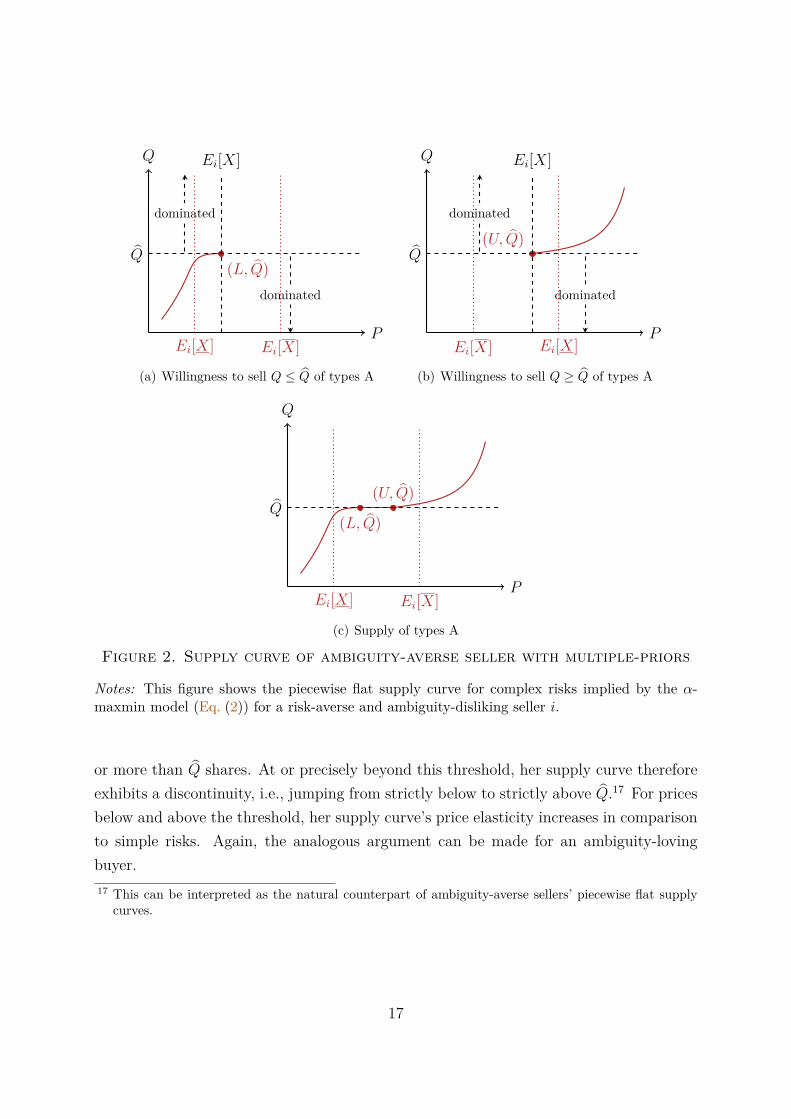

Price Sensitivity

To deduce the effect(s) of complexity-driven ambiguity on agents’ trading behavior, thedifferent types presented in Table I have to be considered separately. I start with the firstrow of Table I. If aggregate endowments are constant, any risk-averse agent, as shownabove, prefers to trade exactly Q shares for P = E[X]. Now, given their distaste forthe perceived ambiguity regarding π, agents of type AC and AI eventually both prefer totrade Q for prices significantly different from E[X]. More precisely, for any given degreeof risk-aversion, the subset of prices for which they wish to be perfectly hedged againstconsumption risk is increasing in both their ambiguity aversion and ambiguity perception.

Proposition 2. In the presence of perceived ambiguity and if there exists a tradablequantity Q such that σi = 0 ∀i ∈ I, then agents of types AC and AI exhibit constantsupply or demand curves over closed subsets of P . Their absolute price elasticity is adecreasing function in both αi and the cardinality/length of Ci.

Proof. For proof see Appendix A.

15

In case of no aggregate risk, it holds for any seller i that πi < πi for Q < Q and πi > πi

for Q > Q, respectively. Intuitively, if seller i is hedged against varying consumption byselling exactly Q shares, her expected consumption µi decreases in 1 − πi (πi) whenevershe sells less (more) than Q shares. Analogously, for any buyer j it holds that πj > πj

for Q < Q and πj < πj for Q > Q, respectively. These shifts in relative size of πiand πi around Q in combination with ambiguity-aversion are the driving force behindProposition 2.

To foster the reader’s intuition, the result in Proposition 2 is illustrated in Figure 2from the perspective of an ambiguity-averse seller—the analogous reasoning also appliesto any ambiguity-averse buyer. First, due to seller i’s risk-aversion, it can be shown thatfor P = Ei[X], selling exactly Q shares strictly dominates trading any other quantity ofthe risky asset. Moreover, given Eq. (2), she is only willing to sell less than Q shares forprices strictly below Ei[X] (see proof of Proposition 2). This is illustrated in Subfigure(a) of Figure 2. Analogously, seller i only agrees to sell more than Q shares in return forP > Ei[X] (see Subfigure (b)). Second, due to the above discussed order effect of πi andπi, it follows that the lower price bound L in Subfigure (a) and the upper price bound Uin Subfigure (b) do not coincide. Therefore, putting everything together, the piecewiseconstant supply curve depicted in Subfigure (c) prevails, where seller i’s supply of therisky asset is constant over the closed subset [L,U ].

In comparison to the analysis under simple risks in Section 3.2, a nice and intuitiveinterpretation of Proposition 2 emerges. Since agents of types AC and AI are averse toambiguity, selling or buying Q shares becomes even more attractive compared to situationswith objective payoff distributions. By trading exactly Q units of the risky asset, agentsnot only are able to avoid risk, but additionally to dispose any exposure to perceivedambiguity. Trading Q shares hence simultaneously corresponds to the perfect hedgingstrategy against both risk and ambiguity. In return for this dual insurance, agents arewilling to forego potential gains from trade.

I now turn to the second row in Table I. For nonambiguity-averse agents, there aretwo cases to be distinguished between. First, if αi equals 1/2, agent i is ambiguity-neutral.For a seller with αi = 1/2, L and U in Figure 2 coincide, i.e., under complex risks, shebehaves as a subjective expected utility-maximizer. The analogous argument applies foran ambiguity-neutral buyer. Second, if αi < 1/2, agent i is ambiguity-loving. The samereasoning as in the proof of Proposition 2 implies that for an ambiguity-loving seller, itholds that L > U . Hence, when risks are complex, there exists a certain price between Uand L for which she is indifferent between gaining exposure to ambiguity from selling less

16

(L, Q)

P

Q

dominated

dominated

Ei[X]

Ei[X] Ei[X]

Q

(a) Willingness to sell Q ≤ Q of types A

(U, Q)

P

Q

dominated

dominated

Ei[X]

Ei[X] Ei[X]

Q

(b) Willingness to sell Q ≥ Q of types A

(L, Q)

(U, Q)

P

Q

Ei[X] Ei[X]

Q

(c) Supply of types A

Figure 2. Supply curve of ambiguity-averse seller with multiple-priors

Notes: This figure shows the piecewise flat supply curve for complex risks implied by the α-maxmin model (Eq. (2)) for a risk-averse and ambiguity-disliking seller i.

or more than Q shares. At or precisely beyond this threshold, her supply curve thereforeexhibits a discontinuity, i.e., jumping from strictly below to strictly above Q.17 For pricesbelow and above the threshold, her supply curve’s price elasticity increases in comparisonto simple risks. Again, the analogous argument can be made for an ambiguity-lovingbuyer.17 This can be interpreted as the natural counterpart of ambiguity-averse sellers’ piecewise flat supply

curves.

17

Mispricing and Suboptimal Risk Sharing

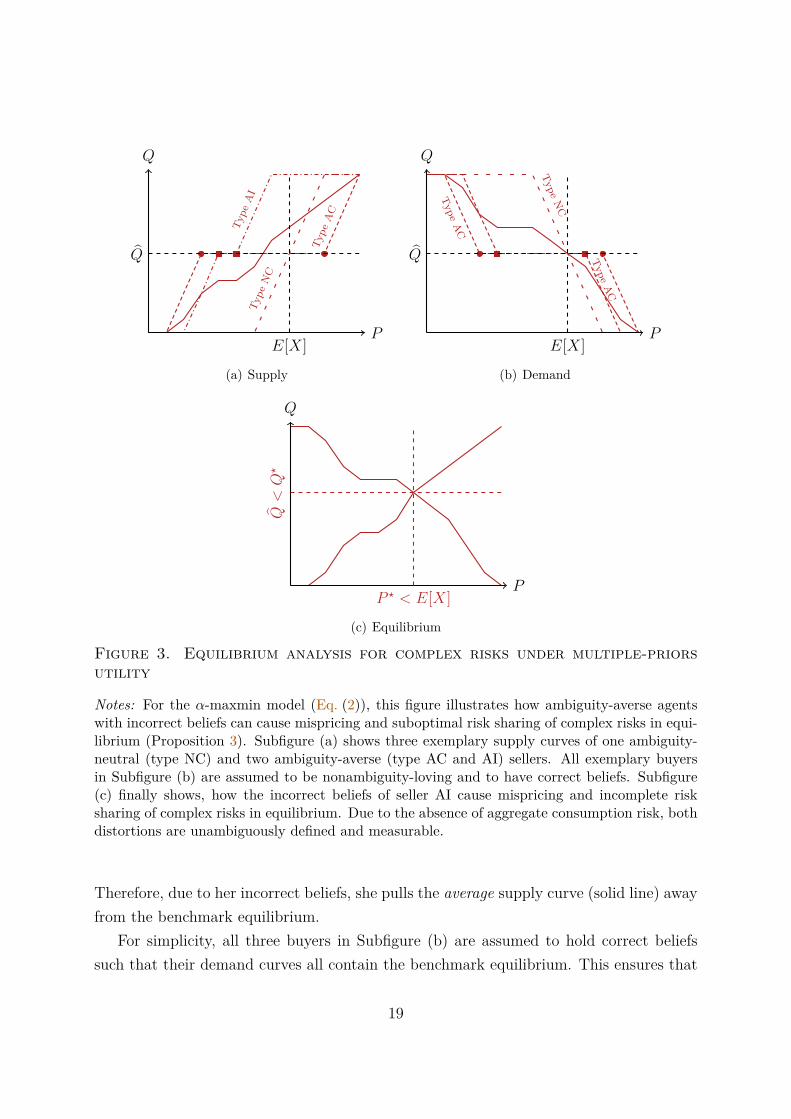

How complex risks are priced and shared in equilibrium, crucially depends on agents’beliefs regarding π. If aggregate wealth is constant, the risky asset is mispriced when-ever the market-clearing price deviates from its expected dividend.18 Hence, wheneverthe market-clearing quantity (per capita) is different from Q, consumption risk is onlysuboptimally shared between risk-averse buyers and sellers. I therefore subsequently referto the market-clearing price and quantity for simple risks, i.e., (E[X], Q), as benchmarkequilibrium.

Nonambiguity-loving agents (αi ≥ 1/2) with correct beliefs (π ∈ Bi) never cause anymispricing or incomplete risk sharing, simply because their supply or demand curvesalways contain the benchmark equilibrium (see above). Due to the jump of their supply(demand) curve between U and L, an ambiguity-loving seller (buyer) almost surely neverchooses to sell (buy) Q shares at P = E[X], independently of her beliefs regarding π.While it is clear why ambiguity-neutral agents with incorrect beliefs provoke mispricingand suboptimal risk sharing (due to their piecewise constant supply and demand curves)this is, however, less clear for ambiguity-averse agents whose subsets of beliefs Bi doesnot contain π.

Proposition 3. In the presence of perceived ambiguity and if there exists a tradablequantity Q such that σi = 0 ∀i ∈ I, then any nonzero mass of type AI sellers (buyers)moves aggregate supply (demand) away from the benchmark equilibrium under simplerisks.

Proof. For proof see Appendix A.

Figure 3 illustrates the mechanics behind Proposition 3 for the simplified case of onlythree sellers and buyers, respectively. Subfigure (a) depicts the exemplary supply curves(for a given discrete price grid) for three different types of sellers. Assuming type NC tobe ambiguity-neutral, she rationally chooses—in line with her correct beliefs—to sell Qshares for P = E[X]. Because of AC’s pronounced ambiguity-aversion, her supply curveis constant over a considerable subset of prices (delimited by circles in Subfigure (a)).Importantly, since π ∈ BAC, the constant part still contains the benchmark equilibrium.In contrast, the constant piece of type AI’s supply curve (delimited by squares) doesnot include the point (E[X], Q). Hence, neither the length of CAI nor the degree of herambiguity-aversion αAI > 1/2 are sufficiently large to prevent that π 6∈ BAI (see Eq. (4)).18 The absence of aggregate risk in combination with a complete market allows for perfect risk sharing.

18

Type

NC

Type

AC

Type

AI

P

Q

Q

E[X]

(a) Supply

TypeN

C

TypeA

C

TypeA

C

P

Q

Q

E[X]

(b) Demand

P

Q

Q<Q?

P ? < E[X]

(c) Equilibrium

Figure 3. Equilibrium analysis for complex risks under multiple-priorsutility

Notes: For the α-maxmin model (Eq. (2)), this figure illustrates how ambiguity-averse agentswith incorrect beliefs can cause mispricing and suboptimal risk sharing of complex risks in equi-librium (Proposition 3). Subfigure (a) shows three exemplary supply curves of one ambiguity-neutral (type NC) and two ambiguity-averse (type AC and AI) sellers. All exemplary buyersin Subfigure (b) are assumed to be nonambiguity-loving and to have correct beliefs. Subfigure(c) finally shows, how the incorrect beliefs of seller AI cause mispricing and incomplete risksharing of complex risks in equilibrium. Due to the absence of aggregate consumption risk, bothdistortions are unambiguously defined and measurable.

Therefore, due to her incorrect beliefs, she pulls the average supply curve (solid line) awayfrom the benchmark equilibrium.

For simplicity, all three buyers in Subfigure (b) are assumed to hold correct beliefssuch that their demand curves all contain the benchmark equilibrium. This ensures that

19

any mispricing and incomplete risk sharing in equilibrium is solely driven by the AI-typeseller’s supply curve in Subfigure (a). The solid line constitutes the resulting averagedemand curve. Finally, Subfigure (c) depicts the market-clearing price P ? and quantityQ? (per capita) that corresponds to the intersection of the average supply and demandcurves. Due to seller AI’s underestimation of π, the market-clearing price is smaller thanthe stock’s expected dividend, implying mispricing equal to |P ?−E[X]|. Furthermore, theaverage market-clearing quantity of shares is greater than Q, i.e., in equilibrium, agentsdo not share complex risks perfectly.

Intuitively, Proposition 3 establishes a condition under which ambiguity-induced priceinsensitivity is sufficiently large to offset any equilibrium effects of incorrect beliefs aboutcomplex risks. Given the midpoint of agent i’s set of priors Ci, the more ambiguity-averseshe is, i.e., the larger her αi, the wider becomes the subset of payoff distributions Bi forwhich incorrect beliefs do not cause any deviations from the benchmark equilibrium. Notethat for any αi < 1, the subset Bi in Eq. (4) is strictly smaller than Ci. Thus, as longas agent i is not maximally ambiguity-averse, requiring the true payoff distribution π tobe contained in Ci is not sufficient for precluding differences between simple and complexequilibria.

Another implication of the multiple-priors model’s constant supply (demand) curve isthe arising possibility of multiple equilibria. In an economy with heterogeneous agents(with respect to their beliefs as well as their preferences towards risk and ambiguity),multiple equilibria are nevertheless unlikely to prevail. For instance, if the supply curveof a given mass of sellers equals Q for a nonsingleton subset of prices, a nonzero massof sellers whose supply is not constant over the same subset is sufficient for the averagesupply curve to be nonconstant.

From Multiple-priors to Rank-dependent Expected Utility

Since the seminal work by Tversky and Kahneman (1992), cumulative prospect theoryhas become the most prominent alternative to expected utility for modeling decision mak-ing under uncertainty. Therefore, a reasonable question to ask is how trading decisionsunder complex risks of agents with rank-dependent utility differ from the above analysis?For binary acts, e.g., the herein considered risky asset, Chateauneuf, Eichberger, andGrant (2007) show that ‘neo-additive’ decision weights allow for a one-to-one correspon-dence from αi and Ci in Eq. (2) to (i) a likelihood sensitivity index and (ii) a pessimism

20

(optimism) index as generally used in rank-dependent expected utility models.19

Smooth Ambiguity Preferences

Proposition 2’s somehow extreme result of (local) perfect price inelasticity is clearly linkedto the kinked preferences induced by the maxmin property of Eq. (2). To emphasize thegeneralizability of its main implications, I now analyze individual trading behavior underthe ‘smooth ambiguity’ model by Klibanoff, Marinacci, and Mukerji (2005). Adoptingthe above notation, agent i’s utility from consumption in t = 2 can then be written as

Ui(Ci(ω)) =∫

∆(Ω)φi(E[Ui(π)

])dµi(π), (5)

where ∆(Ω) is the simplex of all possible payoff distributions on Ω, µi is agent i’s subjec-tive probability measure on ∆(Ω), and φi is a continuous, strictly increasing, real-valuedfunction.

Eq. (5) has an intuitive interpretation: On the one hand, the more payoff distributionsexhibit a nonzero probability mass under µi, the bigger agent i’s set of possible priors.On the other hand, the curvature of φi(·) expresses her ambiguity preferences: As forutility functions for simple risks, concavity of φi(·) implies ambiguity-averse, linearityambiguity-neutral, and convexity ambiguity-loving preferences. Hence, similar to the α-maxmin model in Eq. (2), the smooth ambiguity model allows for a separation betweenthe level of perceived ambiguity as well as agent i’s general preferences towards it. Forease of notation and analog to Eq. (3), I rely on the following definition:

Ei[X] :=∫

∆(Ω)Eπ[X]dµi(π), (6)

where Eπ[X] denotes the expected payoff of the risky asset based on P(ω=u) = π andP(ω=d) = 1− π, respectively.

Proposition 4. Let µi(π) be the normalized Lebesgue measure on agent i’s set of possiblepriors [πi, πi] ⊂ [0, 1], i.e., µi(π) := 1/(πi − πi)dπ ∀π ∈ [πi, πi]. In the presence of perceivedambiguity, if there exists a tradable quantity Q such that σi = 0 ∀i ∈ I, then

(i) agent i’s price elasticity is an increasing function in the second order derivative ofφi(·).

19 In rank-dependent expected utility models, the likelihood sensitivity index measures the steepness ofthe probability weighting function and the optimism (pessimism) index its intersection point with the45-degree line.

21

P

Q

Ei[X]

Q

Figure 4. Supply curve of ambiguity-averse seller with smooth prefer-ences

Notes: This figure shows the decreased price elasticity of the supply curve for complex risksimplied by the smooth ambiguity model (Eq. (5)) for a risk-averse and ambiguity-disliking selleri.

(ii) any nonzero mass of sellers (buyers) for whom πi+πi2 6= π moves aggregate supply

(demand) away from the benchmark equilibrium under simple risks.

Proof. For proof see Appendix A.

As implied by the proof of Proposition 4, with utility as in Eq. (5), any agent’s supply(demand) curve goes through (Q, Ei[X]). Thus, independently of her ambiguity pref-erences, she always finds it optimal to sell (buy) Q shares for a price P equal to hersubjective expected payoff per share given her subset of priors.

For prices below and above Ei[X], Figure 4 exemplary illustrates how imperfect infor-mation about π affects an ambiguity-averse seller’s supply curve. The demand curve forany ambiguity-averse buyer behaves analogously. If, under complex risks, seller i dislikesany perceived ambiguity regarding π, selling Q shares generally becomes more attractivethan under simple risks. Due to her smooth distaste for ambiguity, i.e., the concavity ofφi(·), she smoothly decreases her supply’s price elasticity for prices different from Ei[X],as displayed in Figure 4. However, in contrast to Figure 2, her supply curve never becomesperfectly inelastic for any interior nonempty subset of prices.

In case seller i is ambiguity-loving, i.e., φi(·) is convex, the slope of her supply curveamplifies when moving from simple to complex risks. Comparing Figure 4 to Subfigure(a) in Figure 1 moreover shows how increasing complexity under Eq. (5) manifests itselfsimilarly as a shift in sellers’ risk aversion under Eq. (1): If seller i is ambiguity-averse,

22

she is always willing to accept a lower µi in return for a gradual reduction in σi.For equally probable priors, the second part of Proposition 4 states that whenever

there is a critical mass of agents for whom π is different from their respective midpointof priors, they shift aggregate supply (demand) away from the benchmark equilibrium.Under the smooth ambiguity model, the pricing and allocation of complex risks is thereforemore sensitive to agents’ ex-ante beliefs than under kinked ambiguity-preferences. Forsmooth preferences, ambiguity-induced price insensitivity can never offset a critical mass’distorting equilibrium effects of incorrect beliefs, no matter how small the respectivedeviations from π.

In contrast to the multiple-priors model, the pricing of complex risks by ambiguity-averse agents with smooth preferences is more sensitive to incorrect beliefs. Under themultiple-priors model, the necessary mispricing condition requires the exclusion of thetrue probability π from a set of priors, i.e., π 6∈ Bi, instead of ‘only’ a pointwise deviation.

Summary

In general, for both kinked and smooth ambiguity preferences, complexity has (quali-tatively) similar implications for individual trading behavior and aggregate market out-comes. This is illustrated in Figure 5. If averse to complexity-induced ambiguity, the pricesensitivity of agents with nonsingleton priors decreases under complex risks. In the pres-ence of incorrect beliefs, these agents can cause mispricing and potentially trade towardssuboptimal risk allocations. However, their reduced price sensitivity is likely to mitigateaverse effects on risk sharing. This is intuitive, since, under complexity, ambiguity-averseagents always prefer to trade towards lower consumption risk for a wider range of prices.Importantly, the latter is not true under subjective expected utility (Savage, 1954).20

To summarize, decision theory under ambiguity implies the following two predictionsregarding the trading of complex risks:

P1: Mispricing–Equilibrium prices are a function of subjective beliefs.

P2: Robust risk sharing–Equilibrium allocations are less sensitive to incorrect beliefsrelative to subjective expected utility.

20 Under subjective expected utility, the trading of complex risks can be modeled according to Propo-sition 1, while simply accounting for subjective beliefs πi. Hence, there does not exist any a priorimechanism that decreases the sensitivity of either equilibrium prices nor risk allocation with respectto subjective beliefs.

23

P

Q

P ? = E[X]

Q? = Q

(a) Simple Risks

P

Q

Ei[X]

Ej[X]

Q

(b) Complex Risks

P

Q

P ?

Q? ≈ Q

E[X]

(c) Equilibria Comparison

Figure 5. General comparison between equilibria for simple versus com-plex risks

Notes: This figure summarizes the main implications of trading simple versus complex risks.Subfigure (a) shows the uniquely defined equilibrium for simple risks. Subfigure (b) showsexemplary supply and demand curves for complex risks of two traders with different subjectivebeliefs. Subfigure (c) illustrates (i) that, in the presence of complexity, incorrect beliefs cancause mispricing, whereas (ii) the local reduction in price sensitivity mitigates their averse effecton risk sharing.

Finding conclusive evidence in favour or against the above predictions remains an empir-ical matter. Crucially, doing so requires compliance with the underlying model assump-tions.

Finally, note that, in contrast to risk allocations, the impact of incorrect subjectivebeliefs on equilibrium prices can be reinforced by a complexity-induced decrease in pricesensitivity. Figure 6 illustrates how a (relatively) large and small supply shift can lead to

24

P

Q

∆P ?

(a) Price impact under low price sensitivity

P

Q

∆P ?

(b) Price impact under very low price sensi-tivity

Figure 6. Price impact of incorrect beliefs about complex risks

Notes: This figure illustrates the ambiguous price impact of incorrect subjective beliefs undervarying levels of price (in)sensitivity. Subfigure (a) shows the price impact from a large shiftof a relatively more price-sensitive supply curve. Subfigure (b) shows the price impact from asmall shift of a less price-sensitive supply curve. Due to the lower price sensitivity of the demandcurve in Subfigure (b), the two price impacts exactly coincide.

identical price impacts in case of an offsetting difference in demand price (in)sensitivities.However, a negative21 (positive) correlation between the magnitude of estimation errorsand individual price sensitivities clearly decreases (increases), ceteris paribus, the mis-pricing effect of the former. An empirical correlation analysis should therefore providevaluable insights into the price stability of complex risks in equilibrium.

3.4. Price-taking Behavior, Asymmetric Information, and Strategic Uncer-tainty

Before turning to the experimental test of the above theory, three potentially interferingeffects need to be addressed more carefully. First, my model economy assumes infinitelymany agents. When implementing it in the laboratory, complying with this particularassumption constitutes an apparent impossibility. I meet this practical constraint byrunning all sessions with a relatively high number of at least 16 participants.22 Moreover, I21 As opposed to the supply shifts in Figure 6.22 This minimum number is in line with the average number of 17.6 participants per session in Biais,

Mariotti, Moinas, and Pouget (2017).

25

alternate between two different pricing schemes: market-clearing—as persistently assumedabove—and random price draws (see below). Comparing participants’ supply and demandfunctions between these two pricing schemes allows me to control for their price-takingbehavior.

Second, and more importantly, depending on how agents self-assess their informationprocessing capabilities relative to others, they might perceive considerable informationasymmetries in the presence of complex risks. In a Grossman and Stiglitz (1980) rational-expectation equilibrium, market-clearing prices imperfectly reflect informed traders’ costlyinformation about the risky stock’s expected payoff. Applied to my setting, there existsa dominant strategy for (completely) uninformed agents whose implications are in linewith the ambiguity preference-based theory above: Agents who perceive themselves asuninformed (i.e., face too high information processing costs) and simultaneously believemarkets to generate, at least partially, informative prices should always submit perfectlyinelastic supply (demand) functions, i.e., Qi(P ) = Q ∀P .

Somewhat similar to Grossman and Stiglitz (1980), I require some unobservable het-erogeneity in agents’ information processing abilities (costs) to prevent market-clearingprices to be fully informative.23 Otherwise, given the implied conditionality of agents’supply (demand) functions on market-clearing prices, no one would have an incentive toengage in processing complex information in the first place. Thus, Grossman and Stiglitz’s(1980) informational efficiency paradox would prevail.

Third, any further potential implications caused by strategic uncertainty must be ac-counted for. In a trading game such as the one considered herein, agent i generally facesstrategic uncertainty about the behavior of the remaining −i traders. Whenever agent iforms subjective beliefs about her opponents’ actions, these beliefs—whether rationaliz-able or not—may affect her trading decisions ex-ante.

Alternating between market-clearing and random price draws not only allows for test-ing the price-taking hypothesis, but additionally enables me to control for any potentialeffects from either perceived asymmetric information or strategic uncertainty.23 Whenever agent i believes that there is a nonzero mass of agents submitting supply (demand) functions

based on relatively less informative beliefs, she finds herself better off trading according to her ownmore informative beliefs.

26

4. Experiment

In this section, I first present the parameterization of the model economy that balancestradable and nontradable income such to eliminate aggregate risk. This is followed by amotivation of the main design feature of my experiment, i.e., the creation of simple andcomplex risks in the laboratory. Second, I provide a detailed overview of the conductedsessions, including summary statistics and randomizations checks.

4.1. Design and Parameterization

The selection process of the model parameters is twofold. On the one hand, the distri-bution of the stock’s binary dividend needs to be fixed. In order to control for a naturalfocal point effect, I alternate between two values of π, i.e., π ∈ 1/3, 1/2. Furthermore, tosimplify calculations of expected payoffs, I set the stock’s dividend X(ω) equal to ECU150 (experimental currency units) in state u and ECU 0 in state d, respectively.

On the other hand, agents’ endowments need to be as such that aggregate consumptionis constant across states. Table II presents the endowments for both sellers and buyersthat independently apply at the beginning of every trading round. Note, in the presenceof equally many sellers and buyers, consumption risk is zero on the aggregate level. Inparticular, if any seller i and any buyer j agree to trade Q = 2 shares at a price per shareof P , both are perfectly hedged with constant consumption equal to ECU 300 + 2P andECU 600− 2P , respectively. The symmetry between sellers’ and buyers’ potential overallconsumption is intentional. When comparing local sensitivities between their supply anddemand, symmetry arguments allow me to isolate and solely analyze preference-drivendifferences.24

Complex versus Simple Risks in the Laboratory

When implemented in the laboratory, complex risks need to satisfy two necessary condi-tions to generate data that can be analyzed in the light of the above theory:

(i) complex risks have to follow an objective underlying probability distribution, and

(ii) participants have to be aware of the problem’s well-defined nature and the existenceof its unique solution.

24 Despite the symmetry in total consumption, endowment effects and reference-dependent preferences(see, e.g., Kahneman, Knetsch, and Thaler (1991)) could still be at play. However, I find no evidenceof this in my experimental data.

27

Table II. Endowments for sellers and buyers

Seller BuyerStock 4 0Bond 0 300Cont. income I(ω)

State u: I(u) 0 0State d: I(d) 300 300

Agg. wealth constant

Notes: This table shows the respective endowments for sellers and buyers that apply at thebeginning of every independent trading round. All figures except the number of shares arein experimental currency units (ECU). The state-contingent nontradable income I(ω) exactlyoffsets the aggregate risk from stock endowments.

Moreover, when aiming for informative empirical data, the (imperfect) information aboutcomplex risks should:

(iii) not be too complex, i.e., imposing nontrivial restrictions on participants’ sets ofpriors, but still be complex enough such that subjective priors neither are singletons.

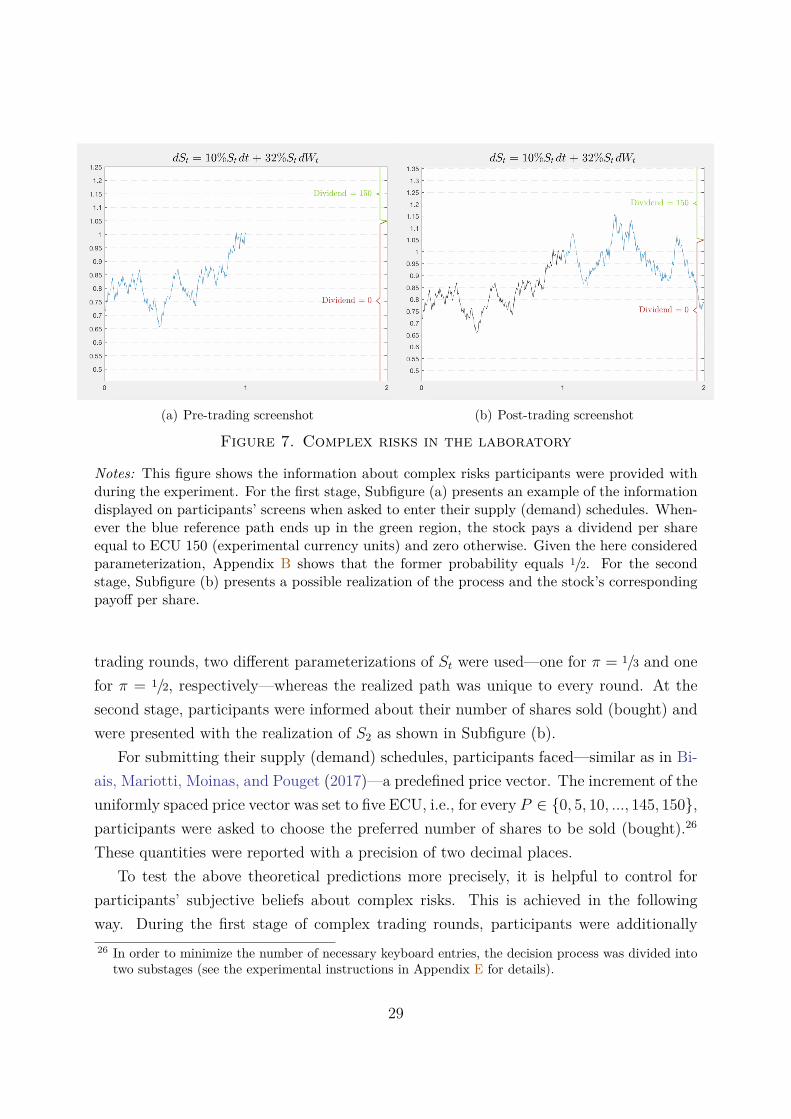

I argue that the following implementation satisfies (i), (ii), and (iii). Consider thegeometric Brownian motion shown in Subfigure (a) of Figure 7. In the ‘complex risktreatment’, participants were provided with both the dynamic visualization of a referencepath between t = 0 and t = 1, as well as the formal specification of the stochasticdifferential equation governing its evolution. To map this continuous process St into therequired binary payoff distribution,25 a simple threshold approach was applied. Morespecifically, whenever the reference path in t = 2 was greater or equal than a predefinedthreshold L, i.e., if S2 ≥ L, the risky stock paid a dividend X(u) equal to 150 andzero otherwise. As demonstrated in Appendix B, the problem of determining P(S2≥L)in Figure 7 can be solved with a back-of-the-envelope calculation applying Ito calculus.Essentially, this implementation of complex risks links the stock’s dividend to the payoffof a digital option in a Black and Scholes (1973) model.

Before submitting their respective supply (demand) functions during the first stage oftrading complex risks, participants were presented the type of information displayed inSubfigure (a) of Figure 7. Simultaneously, they were given the possibility to repeatedlyobserve the reference path’s dynamic evolution between t = 0 and t = 1. Across complex25 Not to be confused with seller i’s share endowment Si in Section 3.

28

(a) Pre-trading screenshot (b) Post-trading screenshot

Figure 7. Complex risks in the laboratory

Notes: This figure shows the information about complex risks participants were provided withduring the experiment. For the first stage, Subfigure (a) presents an example of the informationdisplayed on participants’ screens when asked to enter their supply (demand) schedules. When-ever the blue reference path ends up in the green region, the stock pays a dividend per shareequal to ECU 150 (experimental currency units) and zero otherwise. Given the here consideredparameterization, Appendix B shows that the former probability equals 1/2. For the secondstage, Subfigure (b) presents a possible realization of the process and the stock’s correspondingpayoff per share.

trading rounds, two different parameterizations of St were used—one for π = 1/3 and onefor π = 1/2, respectively—whereas the realized path was unique to every round. At thesecond stage, participants were informed about their number of shares sold (bought) andwere presented with the realization of S2 as shown in Subfigure (b).

For submitting their supply (demand) schedules, participants faced—similar as in Bi-ais, Mariotti, Moinas, and Pouget (2017)—a predefined price vector. The increment of theuniformly spaced price vector was set to five ECU, i.e., for every P ∈ 0, 5, 10, ..., 145, 150,participants were asked to choose the preferred number of shares to be sold (bought).26

These quantities were reported with a precision of two decimal places.To test the above theoretical predictions more precisely, it is helpful to control for

participants’ subjective beliefs about complex risks. This is achieved in the followingway. During the first stage of complex trading rounds, participants were additionally26 In order to minimize the number of necessary keyboard entries, the decision process was divided into

two substages (see the experimental instructions in Appendix E for details).

29

asked to provide their point estimate regarding the stock’s expected payoff per share.27

Independently of subjective preferences, the so elicited point estimates allow to anchorparticipants’ individual sets of priors.

In contrast, during the first stage of the ‘simple risks treatment’, participants knew theexact probability of the stock paying a dividend equal to 150. For the case where π = 1/2,participants were confronted with an urn containing 15 green and 15 red balls, as depictedin Subfigure (a) of Figure 8. At the second stage, the color of one randomly drawn ball wasrevealed. Whenever this ball happened to be green, the stock paid a dividend per shareequal to ECU 150 and zero otherwise.28 Finally, as a control treatment, the tradablerisks of the last trading round were purely ambiguous. Instead of a ‘transparent urn’,participants were confronted with the Ellsberg (1961)-like urn shown in Subfigure (b),whose composition of green and red balls was unknown.

For both treatments, two different pricing schemes were applied: market clearingversus random price draws. Whereas the former maximizes trade by minimizing thedifference between supply and demand,29 the latter randomly picks one price from thegiven price vector, each with equal probability.30

4.2. Sessions Structure, Incentivization, and Participant Summary Statis-tics

Table III provides an overview of the six sessions conducted in the ‘Laboratory for Ex-perimental and Behavioral Economics’ at the University of Zurich during fall 2016.31 Thenumber in parenthesis indicates the number of participants in a given session.32 Eachsession consisted of ten independent trading rounds. All participants only participated inone session. For every single trading round, Table III lists the actual payoff distribution,the nature of the underlying consumption risk, simple (S) versus complex (C), and theapplied pricing scheme, market clearing (MC) versus random price draw (random). A27 Depending on participants’ respective preferences, the risky asset’s expected payoff under complex

risks is either defined by the mean of Eq. (3) for trading more or less than Q shares, or by Eq. (6),respectively.

28 Similarly, for π = 1/3, the presented urn contained ten green and 20 red balls.29 To prevent any effects due to anticipated rationing, following Biais, Mariotti, Moinas, and Pouget

(2017), all orders at the market-clearing price were fully executed.30 The inherent logic of the random price draw is equivalent to the standard mechanism proposed by

Becker, DeGroot, and Marschak (1964).31 The experiment was fully computerized using z-Tree (Fischbacher, 2007).32 To be eligible, participants were required to have some basic finance knowledge (i.e., major or minor

in finance, internship or other work experience in the field of finance, or free-time trading experience).

30

GR

?

1Ballisrandomlydrawn.

R G R

G G GR R

GR R G R

G G GR R

GR R G R

G G GR R

15x/15xG R

G

R

Dividend=150if

Dividend=0if

(a) Pre-trading screenshot for simple risks

GR

?

1Ballisrandomlydrawn.

R G R

G G GR R

GR R G R

G G GR R

GR R G R

G G GR R

30x=orG RG

G

R

Dividend=150if

Dividend=0if

(b) Pre-trading screenshot for ambiguous risks

Figure 8. Simple and ambiguous risks in the laboratory

Notes: This figure shows the information about simple and ambiguous risks participants wereprovided with at the first stage during the respective trading rounds of the experiment. When-ever the randomly drawn ball is green, the stock pays a dividend per share equal to ECU 150(experimental currency units) and zero otherwise. In contrast to simple risks in Subfigure (a),the distribution of green and red balls in Subfigure (b) is arbitrary.

‘high’ (‘low’) π refers to an integer parameterization of the stochastic reference path St

that results in a probability P(S2≥L) of 84.21% (15.89%). ‘P’ denotes a practice round.To control for potential ‘comparative ignorance effects’ (see Fox and Tversky (1995)), thesequential ordering of simple and complex risks was reversed between the first three andthe last three sessions.

In each session, after the ten trading rounds shown in Table III, participants were ad-ditionally presented with two lotteries, each based on one of the two urns in Figure 8. Forboth lotteries, their certainty equivalents were elicited via Abdellaoui, Baillon, Placido,and Wakker’s (2011) computerized iterative choice list method.33 Importantly, the lotter-ies’ payoffs were chosen such that they exactly matched the range of possible consumptionlevels in each of the previous trading rounds (see Figure D.2 in Appendix D). Overall,one session lasted approximately 90 minutes.

At the end of every session, one out of the seven nonpractice trading rounds or one ofthe two lottery outcomes was randomly chosen, each with equal probability. Participantsthen were paid either their final wealth of the selected trading round or the outcome ofthe selected lottery (divided by twelve in either case). Additionally, if their point estimateregarding π was correct (within ±3%), they earned an extra three Swiss francs, whenever33 No risk or ambiguity aversion is assigned to participants with multiple switching points for either the

simple (one) or the ambiguous lottery (two).

31

Table III. Sessions overview

Session 1 (#16) Session 2 (#18) Session 3 (#16)

Round π Type Pricing π Type Pricing π Type Pricing1 1 C (P) MC 1 C (P) MC 1 C (P) MC2 high C (P) random high C (P) random high C (P) random3 low C (P) MC low C (P) MC low C (P) MC4 1/2 C MC 1/3 C random 1/3 C MC5 1/3 C MC 1/2 C random 1/3 C random6 1/2 C random 1/3 C MC 1/2 C MC7 1/3 C random 1/2 C MC 1/2 C random8 1/2 S MC 1/2 S random 1/2 S MC9 1/3 S random 1/3 S MC 1/3 S random10 ambig A MC ambig A random ambig A MC

Session 4 (#16) Session 5 (#16) Session 6 (#16)

Round π Type Pricing π Type Pricing π Type Pricing1 1/2 S (P) MC 1/2 S (P) MC 1/2 S (P) MC2 9/10 S (P) random 9/10 S (P) random 9/10 S (P) random3 1/2 S MC 1/2 S random 1/2 S MC4 1/3 S random 1/3 S MC 1/3 S random5 high C (P) MC high C (P) MC high C (P) MC6 1/2 C MC 1/3 C random 1/3 C MC7 1/3 C MC 1/2 C random 1/3 C random8 1/2 C random 1/3 C MC 1/2 C MC9 1/3 C random 1/2 C MC 1/2 C random10 ambig A MC ambig A random ambig A MC

Notes: This table provides an overview of the six conducted sessions. Each session consisted often independent trading rounds. The number in parenthesis indicates the number of participantsin a given session. For every session, the first column lists the actual payoff distribution, thesecond column the nature of the underlying consumption risk (simple (S) versus complex (C)),and the third column the applied pricing scheme (market clearing (MC) versus random pricedraw (random)). The ‘high’ (‘low’) π refers to an integer parameterization of the geometricBrownian motion that implies a 84.21% (15.89%) probability of a dividend per share equal to150. Trading rounds with a ‘P’ in parenthesis are practice rounds.

the corresponding trading round was selected for payment. On average, participantsreceived 38.40 Swiss francs, with a maximum of CHF 50 and a minimum of CHF 25.