Distribution and Sustainable Management of Roadside Trees in Bahawalpur, Pakistan

OCCASIONAL PAPER 105

Towards a sustainable coal power

Syed Akhtar Ali

v.1.20

1/5/2014

Research on Economy & Politics of Pakistan

2 | P a g e

Towards a sustainable coal power

NEPRA has announced a new coal tariff, revising the earlier tariff within less than a year .There is

confusion among people regarding the quantum nature and motivation of change .We will try in this

space to understand and elaborate upon a number of issues to the market, economics and technology

of coal power and venture to make some submissions and recommendations. Fortunately, only a press

release has been issued containing some key data and details and a formal gazette announcement has

still to be made.

The new tariff has been announced on the request of the GoP in the context of Gadani Coal Power Park

on which GoP is moving on a fast track basis and is trying to attract investors. GoP in a letter to NEPRA

requested NEPRA to study and make the appropriate changes in tariff and its structure. Following points

were raised;

Reconsideration of per MW cost of the project

Realistic adjustment of Thermal efficiency(downwards)

Reconsideration of Fixed and variable O&M costs

Change in the plant factor(capacity factor)

NEPRA incorporated those points and presented the new tariff, of which we provide a comparison in

table 1.Similarly, we have provided a comparison of basic assumptions of the two tariffs in Table2.

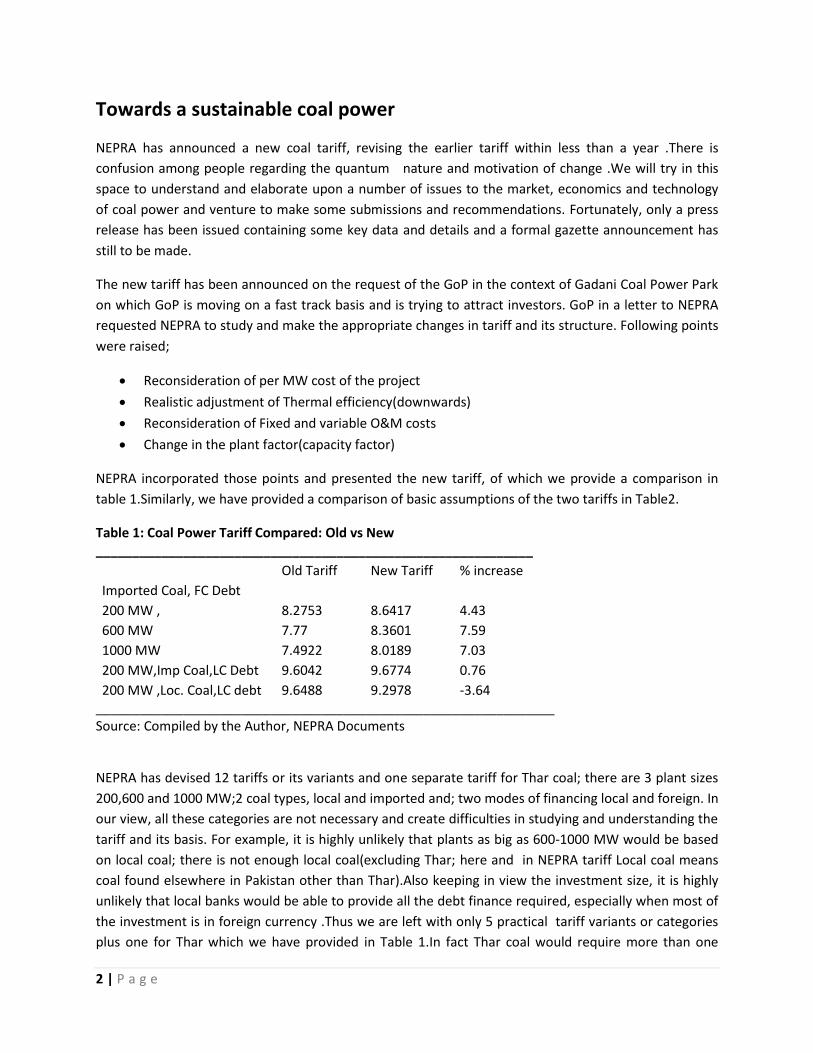

Table 1: Coal Power Tariff Compared: Old vs New ____________________________________________________________

Old Tariff New Tariff % increase

Imported Coal, FC Debt 200 MW , 8.2753 8.6417 4.43

600 MW 7.77 8.3601 7.59

1000 MW 7.4922 8.0189 7.03

200 MW,Imp Coal,LC Debt 9.6042 9.6774 0.76

200 MW ,Loc. Coal,LC debt 9.6488 9.2978 -3.64 _______________________________________________________________ Source: Compiled by the Author, NEPRA Documents

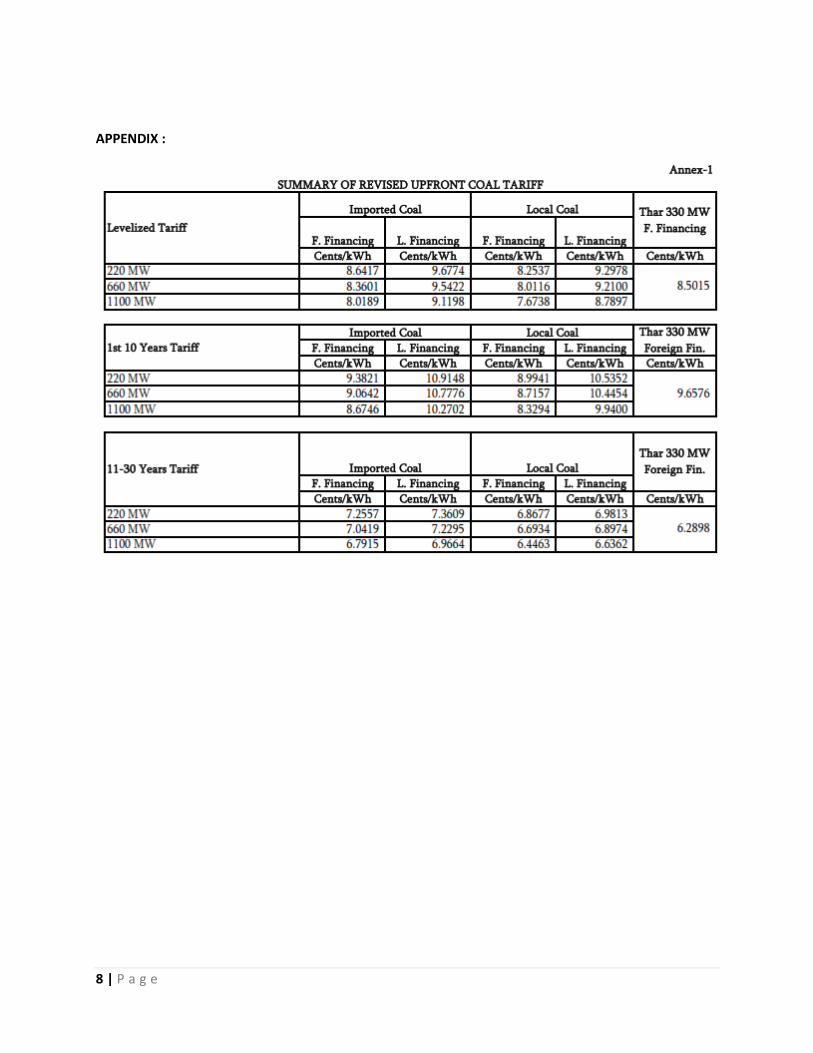

NEPRA has devised 12 tariffs or its variants and one separate tariff for Thar coal; there are 3 plant sizes

200,600 and 1000 MW;2 coal types, local and imported and; two modes of financing local and foreign. In

our view, all these categories are not necessary and create difficulties in studying and understanding the

tariff and its basis. For example, it is highly unlikely that plants as big as 600-1000 MW would be based

on local coal; there is not enough local coal(excluding Thar; here and in NEPRA tariff Local coal means

coal found elsewhere in Pakistan other than Thar).Also keeping in view the investment size, it is highly

unlikely that local banks would be able to provide all the debt finance required, especially when most of

the investment is in foreign currency .Thus we are left with only 5 practical tariff variants or categories

plus one for Thar which we have provided in Table 1.In fact Thar coal would require more than one

3 | P a g e

variant. The present one caters to the project proposal of Engro .One would note that there is an

apparent increase of only 7-7.5 % and not more. Although in reality, the change is larger(10-13%) due to

the changes in capacity (utilization) factor; older tariff assumed a CF of 60% while the new one takes a

CF of 85%, from one extreme to another .This factor alone is responsible for understatement of the old

tariff by about 1 cent. In that sense, the quantum of change is larger. I have been on record to have

proposed to PPIB and NEPRA to adopt a more realistic CF. However, free advice is never respected and

now the muscle of the GoP has managed to bring about the same change.

NEPRA maintains that capacity factor is notional and that is what our understanding was as well.

However, in a recent TV discussion Economic Advisor to GoP Dr. Miftah Ismail opined that due to CF

effect , IPPs were already earning a RoE of 30% or so. It is incumbent on NEPRA to clarify this to the

public. This also raises an issue on the black box of Capacity Payments to IPPs. NEPRA should either

include such statements in its valuable SOI Report or ask NTDC/CPPA to issue a separate report in this

respect. Audits do not replace the role of public information and oversight, especially, when doubts

have been expressed by some quarters in this respect.

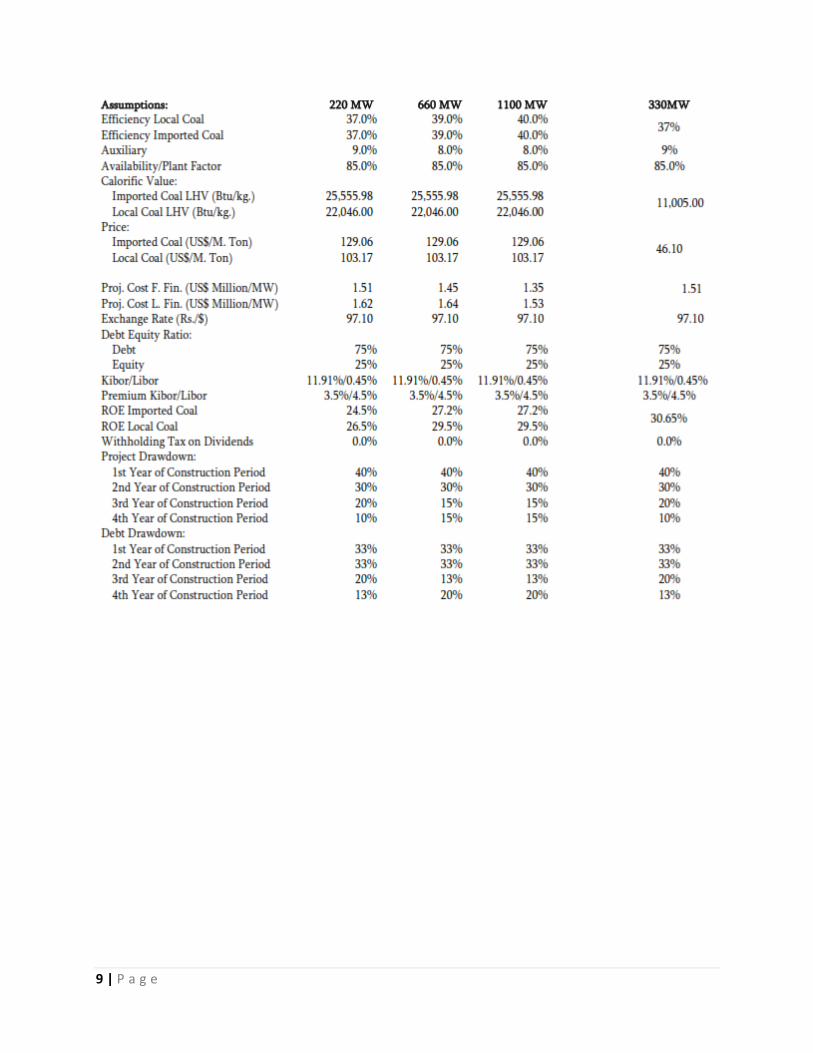

Also in the new tariff, higher coal prices have been taken (129 USD/ton, an increase of about 10 USD

per ton; amusingly coal prices have come down since the last tariff); CAPEX has also been enhanced to

around 1.5 Mn USD per MW. With escalation provided, this may further go up by another 20%.The

bomb shell is unbelievably high RoEs up to 30% after tax (no tax).The professionals at NEPRA had an

impossible job of coming up with the desired or dictated coal power tariff. And still more difficult stage

remains of writing down the tariff determination report for the gazette notification.

This seems to be a residual calculated RoE for reaching the required tariff level and does not seem to be

a result of a well thought out or articulated policy rate, unless the Gazette notification offers some

wisdom in this respect. The good and bad thing about NEPRA’s upfront tariff system is that it is only a

Reference Tariff and all kind of indexation is provided to eliminate the investor’s risk. In India for

example, a skeleton indexation mechanism has created a major issue in a 5000 MW coal power project

of Tata Power who quoted a prices as low as IRs 2.24 per kWh basing its price on a long term contract

with mine owners in Indonesia. Government of Indonesia subsequently changed the rules of the game

and made retrospective changes applicable to contracts finalized prior to the new law. Tata contracts

with power purchasers in India did not provide indexation to include such eventuality and based its

calculations on the historical trend and the currency factor. As a result, Tata Power had to go to the

Supreme Court of India to get a raise of 25% in the agreed tariff. So, for a change, our system appears to

be better than that in India. However, NEPRA system is too detailed and exposes the dirty linen of

excessive RoE.

4 | P a g e

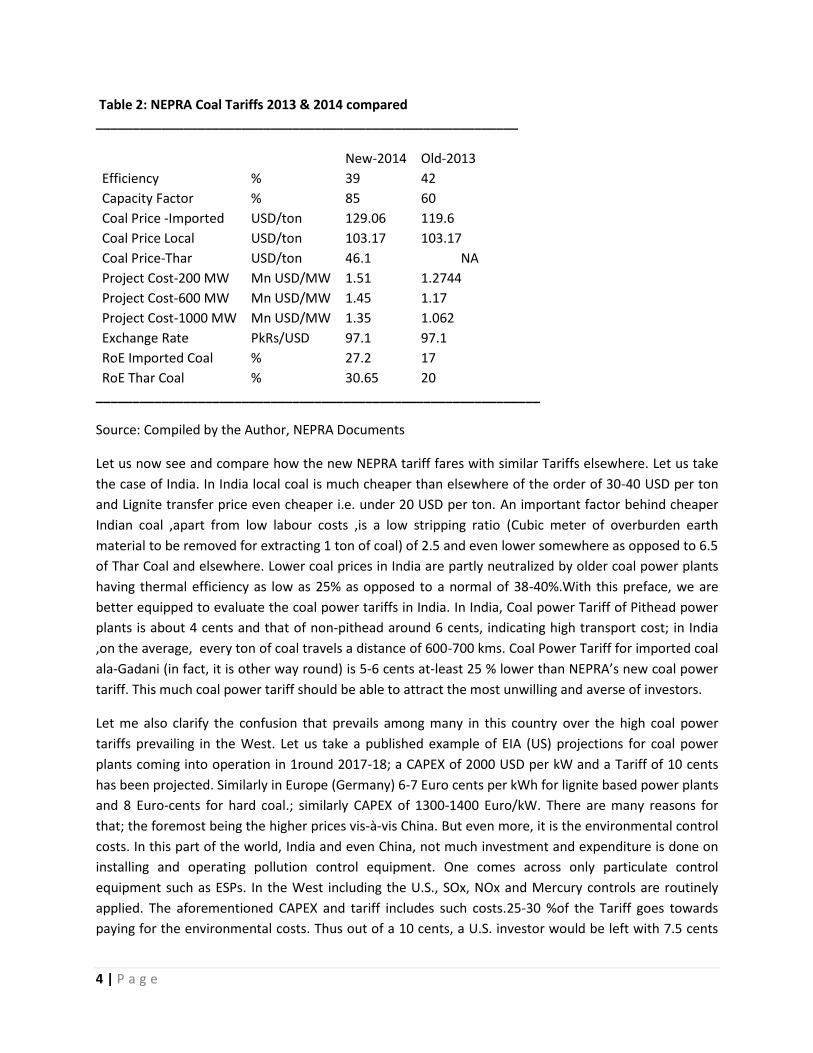

Table 2: NEPRA Coal Tariffs 2013 & 2014 compared __________________________________________________________

New-2014 Old-2013

Efficiency % 39 42

Capacity Factor % 85 60

Coal Price -Imported USD/ton 129.06 119.6

Coal Price Local USD/ton 103.17 103.17

Coal Price-Thar USD/ton 46.1 NA

Project Cost-200 MW Mn USD/MW 1.51 1.2744

Project Cost-600 MW Mn USD/MW 1.45 1.17

Project Cost-1000 MW Mn USD/MW 1.35 1.062

Exchange Rate PkRs/USD 97.1 97.1

RoE Imported Coal % 27.2 17

RoE Thar Coal % 30.65 20 _____________________________________________________________

Source: Compiled by the Author, NEPRA Documents

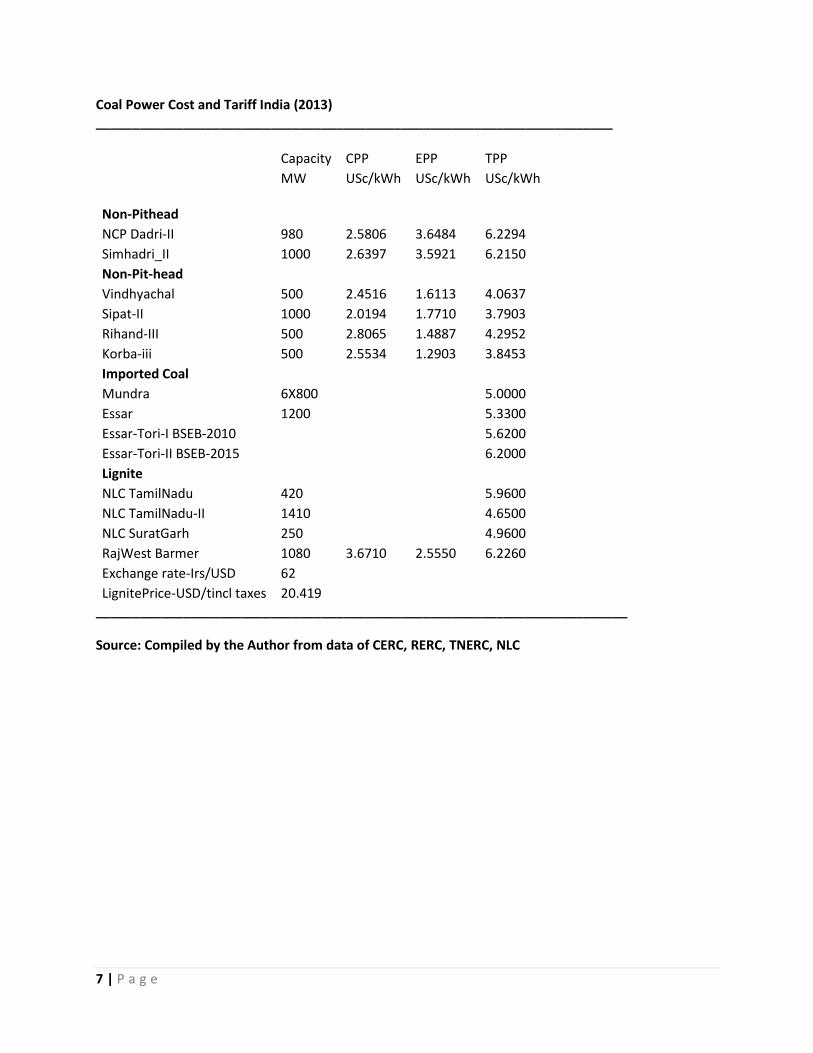

Let us now see and compare how the new NEPRA tariff fares with similar Tariffs elsewhere. Let us take

the case of India. In India local coal is much cheaper than elsewhere of the order of 30-40 USD per ton

and Lignite transfer price even cheaper i.e. under 20 USD per ton. An important factor behind cheaper

Indian coal ,apart from low labour costs ,is a low stripping ratio (Cubic meter of overburden earth

material to be removed for extracting 1 ton of coal) of 2.5 and even lower somewhere as opposed to 6.5

of Thar Coal and elsewhere. Lower coal prices in India are partly neutralized by older coal power plants

having thermal efficiency as low as 25% as opposed to a normal of 38-40%.With this preface, we are

better equipped to evaluate the coal power tariffs in India. In India, Coal power Tariff of Pithead power

plants is about 4 cents and that of non-pithead around 6 cents, indicating high transport cost; in India

,on the average, every ton of coal travels a distance of 600-700 kms. Coal Power Tariff for imported coal

ala-Gadani (in fact, it is other way round) is 5-6 cents at-least 25 % lower than NEPRA’s new coal power

tariff. This much coal power tariff should be able to attract the most unwilling and averse of investors.

Let me also clarify the confusion that prevails among many in this country over the high coal power

tariffs prevailing in the West. Let us take a published example of EIA (US) projections for coal power

plants coming into operation in 1round 2017-18; a CAPEX of 2000 USD per kW and a Tariff of 10 cents

has been projected. Similarly in Europe (Germany) 6-7 Euro cents per kWh for lignite based power plants

and 8 Euro-cents for hard coal.; similarly CAPEX of 1300-1400 Euro/kW. There are many reasons for

that; the foremost being the higher prices vis-à-vis China. But even more, it is the environmental control

costs. In this part of the world, India and even China, not much investment and expenditure is done on

installing and operating pollution control equipment. One comes across only particulate control

equipment such as ESPs. In the West including the U.S., SOx, NOx and Mercury controls are routinely

applied. The aforementioned CAPEX and tariff includes such costs.25-30 %of the Tariff goes towards

paying for the environmental costs. Thus out of a 10 cents, a U.S. investor would be left with 7.5 cents

5 | P a g e

for installing and operating the plants comparable to ours in environmental terms. Sooner or later, we

may have to also pay attention to these aspects, especially when a large number of power plants are

installed around one location. Separate tariff components may have to be provided for environmental

controls. Alternatively controls may have to be applied on upper limit of Sulphur (say 1%)in the

imported coals.

A little backgrounder seems to be in order to understand the RoE issue. India offers a RoE of 15-16%

taxable and in local currency. If one examines, the annual reports of the companies in energy sector, the

usual profitability rates are 10-12 % after tax. This is despite there are all kinds of risks. In our case, there

are all kinds of price and purchasing commitments and indexations, single buyer PPA and sovereign

guarantees. There is literally no project risk except country risk. Standard rates of 17% are quite

reasonable and for Thar 20.5 % given as a special rate. There is hardly a case for further enhancing it. In

an interview published recently in this very newspaper, a very suave and major player in the energy and

banking sector, indicated his nervousness over a RoE of 17% in foreign currency and without tax and

that people may criticize him of excessive profits. How would he react to profit rates of up to 30%.Some

trimming of the proposed tariff rates seem to be in order. A reduction in RoE, coupled with a more

realistic and usual CF of 80% and retaining the coal price (which in any case is a variable and a pass-

through) at the previous level, should enable the calculators to bring down the proposed tariff

significantly. The bosses should feel contented and relieved when all the four requirements as

mentioned in the beginning of this essay have been complied with; the most important being increase in

per MW capital costs. An attempt to increase the tariff with impossible RoEs would be

counterproductive and would invite criticism and controversy. Calculated tariffs, however, do suffer

from problems and may be out of sync with the market sentiments. A much better approach is of

competitive bidding which discovers the real market numbers.

In the early days of Gadani idea, PM Nawaz Sharif spoke of competitive bidding. One does not hear

much of it now. However, competitive bidding occurs when there is competition. Presently there does

not appear to be much of a diversity or competition. Only Chinese and some Arab parties are visible.

This may be mostly due to the poor law and order situation. Western companies normally abstain from

a market where Chinese are active, as they have no chance to match Chinese prices. Also multilateral

institutions generally oppose coal power. However, there may be other countries like Russia, Czeck-Slav,

South Korea and Poland who may take interest, if approached. Russians have money, technology and

manpower resources to be able to compete with Chinese technology and capital.

A high tariff alone may not be enough. Projects may have to be structured catering to a variety of

investors; some may not be interested to get involved with the operations; some may be loathe to

private sector; some may not be interested in coal procurement risks. Some may require government to

government deals .In the upfront tariff as it is there, all coal price risks are loaded against the power

purchaser. There is no incentive for bringing in savings and efficiency in coal procurement. Some

creative thinking should be put in this direction and also the possibilities of pooling coal imports under

TCP mechanism. However, time is short to be wasted in ideas, how good these may appear to be. There

is no harm in checking with the stake-holders or considering such conditional provisions into the PPA

frameworks. Providing for Coal storages and warehouses for third party coal traders may also be looked

6 | P a g e

into. A lot can be done to create diversity, openness and flexibility for promoting competition and

efficiency.

Before concluding, a word is in order on technological choices. Engro has chosen CFC boilers which are

best suited for low quality coals like Lignite of Thar. It also solves Sox pollution problem within the boiler

itself obviating the need of treatment of flue gases. NOx are produced comparatively in lesser quantities

in CFC boilers where lower temperatures are involved .There is a few percentage points sacrifice for

thermal efficiency. Although in Germany RWe is using PC Boilers for firing Lignite and achieves thermal

efficiency of 43 % by drying-preheating Lignite by exhaust gases before firing into the furnace, it may be

advisable to standardize on CFC boilers for a variety of reasons. Imported coal projects would most likely

prefer the Pulverized Coal technology which is more in vogue for hard coals. Some provision has to be

there to mix a percentage (say 10-20%) of Thar coal into the hard coal of imported coal projects.

Concluding coal and hydro power are the only two cheap and large energy options; all others are too

expensive or lack capacity and other constraints. If by hasty decisions, we make these expensive, there

would be no way to bring down the retail tariff which to-date is unaffordable and has given rise to many

problems. A balance must be struck between the desire to attract maximum investment and the ability

to pay. RoE decisions are very fundamental decisions which set a precedence and benchmark against

which all other sector projects base their expectations. A lot more thinking ought to have gone into it

than what appears to be the [email protected]

7 | P a g e

Coal Power Cost and Tariff India (2013) _______________________________________________________________________

Capacity CPP EPP TPP

MW USc/kWh USc/kWh USc/kWh

Non-Pithead

NCP Dadri-II 980 2.5806 3.6484 6.2294

Simhadri_II 1000 2.6397 3.5921 6.2150

Non-Pit-head Vindhyachal 500 2.4516 1.6113 4.0637

Sipat-II 1000 2.0194 1.7710 3.7903

Rihand-III 500 2.8065 1.4887 4.2952

Korba-iii 500 2.5534 1.2903 3.8453

Imported Coal Mundra 6X800

5.0000

Essar 1200

5.3300

Essar-Tori-I BSEB-2010

5.6200

Essar-Tori-II BSEB-2015

6.2000

Lignite NLC TamilNadu 420

5.9600

NLC TamilNadu-II 1410

4.6500

NLC SuratGarh 250

4.9600

RajWest Barmer 1080 3.6710 2.5550 6.2260

Exchange rate-Irs/USD 62 LignitePrice-USD/tincl taxes 20.419 _________________________________________________________________________

Source: Compiled by the Author from data of CERC, RERC, TNERC, NLC

8 | P a g e

APPENDIX :

9 | P a g e

10 | P a g e

Brief Profile: Syed Akhtar Ali

Akhtar Ali is an eminent energy expert and consultant, advising public and private sector clients on

energy policy, investments and tariff issues and has authored a number of books on the subject. He is a

visiting Professor of Energy at IoBM and teaches energy management to MBA students. He has held

top management appointments in Pakistan’s public and private sector. He was Research Fellow

Energy at Harvard University’s Kennedy School of Government. He is an author of eight books on

various subjects such as energy, governance, political economy and resources. He heads Proplan

Associates, a consulting company having a current focus on Energy. He is also Chairman (REAP)

Research on Economy and Politics of Pakistan, a think tank that brings out research publications on

national issues. [email protected]/[email protected]

Books by Syed Akhtar Ali

1. The Political Economy of Pakistan: an Agenda for Reforms. (1994).

1. Pakistan’s Development Challenges :Federalism, Security and Governance 2010

2. Pakistan’s development; economy, resources and technology, 2012.

3. Pakistan Nuclear Dilemma: Energy & Security Dimensions. (1984).

4. Pakistan Energy Development: the Road Ahead.(2010).

5. Pakistan Issues in Energy Policy, 2012-2014

6. Nuclear Politics and Challenges of Governance. (1998)

7. South Asia: Nuclear Stalemate or Conflagration. (1987).

Copyright © 2022 FDOKUMEN