United Kingdom & Ireland Local Pages - The Church of Jesus ...

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 1

MarketLine Industry Profile

Coal in the United Kingdom September 2013

Reference Code: 0183-2400

Publication Date: September 2013

WWW.MARKETLINE.COM

MARKETLINE. THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 2

EXECUTIVE SUMMARY

Market value The United Kingdom coal market grew by 13.6% in 2012 to reach a value of $6,419.3 million.

Market value forecast In 2017, the United Kingdom coal market is forecast to have a value of $7,522 million, an increase of 17.2% since 2012.

Market volume The United Kingdom coal market grew by 10.9% in 2012 to reach a volume of 60.9 million short ton.

Market volume forecast In 2017, the United Kingdom coal market is forecast to have a volume of 52.9 million short ton, a decrease of 13.1%

since 2012.

Geography segmentation The United Kingdom accounts for 6.6% of the European coal market value.

Market rivalry The UK coal market is tending towards increased consolidation. In 2013, Hargreaves Services took over five Scottish

Coal mines following the collapse of the company. Additionally, UK Coal, the biggest coal miner in Britain, is restructuring

its activities following the closure of Daw Mill, which represented a third of the UK Coal's revenue.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 3

TABLE OF CONTENTS

Executive Summary ....................................................................................................................................................... 2

Market value ............................................................................................................................................................... 2

Market value forecast ................................................................................................................................................. 2

Market volume ............................................................................................................................................................ 2

Market volume forecast .............................................................................................................................................. 2

Geography segmentation ........................................................................................................................................... 2

Market rivalry .............................................................................................................................................................. 2

Market Overview ............................................................................................................................................................ 7

Market definition ......................................................................................................................................................... 7

Market analysis .......................................................................................................................................................... 7

Market Data ................................................................................................................................................................... 8

Market value ............................................................................................................................................................... 8

Market volume ............................................................................................................................................................ 9

Market Segmentation ................................................................................................................................................... 10

Geography segmentation ......................................................................................................................................... 10

Market Outlook ............................................................................................................................................................. 11

Market value forecast ............................................................................................................................................... 11

Market volume forecast ............................................................................................................................................ 12

Five Forces Analysis .................................................................................................................................................... 13

Summary .................................................................................................................................................................. 13

Buyer power ............................................................................................................................................................. 14

Supplier power ......................................................................................................................................................... 15

New entrants ............................................................................................................................................................ 16

Threat of substitutes ................................................................................................................................................. 17

Degree of rivalry ....................................................................................................................................................... 18

Leading Companies ..................................................................................................................................................... 19

Hargreaves Services Plc .......................................................................................................................................... 19

Rio Tinto ................................................................................................................................................................... 23

Scottish Coal ............................................................................................................................................................ 26

UK Coal Production Limited ..................................................................................................................................... 27

Macroeconomic Indicators ........................................................................................................................................... 28

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 4

Country Data ............................................................................................................................................................ 28

Appendix ...................................................................................................................................................................... 30

Methodology ............................................................................................................................................................. 30

Industry associations ................................................................................................................................................ 31

Related MarketLine research ................................................................................................................................... 31

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 5

LIST OF TABLES

Table 1: United Kingdom coal market value: $ million, 2008–12 .................................................................................... 8

Table 2: United Kingdom coal market volume: million short ton, 2008–12 ..................................................................... 9

Table 3: United Kingdom coal market geography segmentation: $ million, 2012 ......................................................... 10

Table 4: United Kingdom coal market value forecast: $ million, 2012–17 .................................................................... 11

Table 5: United Kingdom coal market volume forecast: million short ton, 2012–17 ..................................................... 12

Table 6: Hargreaves Services Plc: key facts ................................................................................................................ 19

Table 7: Hargreaves Services Plc: key financials ($) ................................................................................................... 20

Table 8: Hargreaves Services Plc: key financials (£) ................................................................................................... 20

Table 9: Hargreaves Services Plc: key financial ratios ................................................................................................. 21

Table 10: Rio Tinto: key facts ....................................................................................................................................... 23

Table 11: Rio Tinto: key financials ($) .......................................................................................................................... 24

Table 12: Rio Tinto: key financial ratios ....................................................................................................................... 24

Table 13: Scottish Coal: key facts ................................................................................................................................ 26

Table 14: UK Coal Production Limited: key facts ......................................................................................................... 27

Table 15: United Kingdom size of population (million), 2008–12.................................................................................. 28

Table 16: United Kingdom gdp (constant 2000 prices, $ billion), 2008–12 .................................................................. 28

Table 17: United Kingdom gdp (current prices, $ billion), 2008–12 .............................................................................. 28

Table 18: United Kingdom inflation, 2008–12 .............................................................................................................. 29

Table 19: United Kingdom consumer price index (absolute), 2008–12 ........................................................................ 29

Table 20: United Kingdom exchange rate, 2008–12 .................................................................................................... 29

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 6

LIST OF FIGURES

Figure 1: United Kingdom coal market value: $ million, 2008–12................................................................................... 8

Figure 2: United Kingdom coal market volume: million short ton, 2008–12 .................................................................... 9

Figure 3: United Kingdom coal market geography segmentation: % share, by value, 2012 ........................................ 10

Figure 4: United Kingdom coal market value forecast: $ million, 2012–17 ................................................................... 11

Figure 5: United Kingdom coal market volume forecast: million short ton, 2012–17 .................................................... 12

Figure 6: Forces driving competition in the coal market in the United Kingdom, 2012 ................................................. 13

Figure 7: Drivers of buyer power in the coal market in the United Kingdom, 2012 ....................................................... 14

Figure 8: Drivers of supplier power in the coal market in the United Kingdom, 2012 ................................................... 15

Figure 9: Factors influencing the likelihood of new entrants in the coal market in the United Kingdom, 2012 ............. 16

Figure 10: Factors influencing the threat of substitutes in the coal market in the United Kingdom, 2012..................... 17

Figure 11: Drivers of degree of rivalry in the coal market in the United Kingdom, 2012 ............................................... 18

Figure 12: Hargreaves Services Plc: revenues & profitability ....................................................................................... 21

Figure 13: Hargreaves Services Plc: assets & liabilities ............................................................................................... 22

Figure 14: Rio Tinto: revenues & profitability ............................................................................................................... 25

Figure 15: Rio Tinto: assets & liabilities ....................................................................................................................... 25

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 7

MARKET OVERVIEW

Market definition The coal market is defined as revenues due to the sale of coal for industry and power generation.

Market volumes given within this profile are for both primary (anthracite, bituminous, and lignite) and secondary

(anthracite, bituminous, and lignite briquets but excluding metallurgical coke) coal consumption.

The market has been valued at annual average minemouth prices and does not include any transportation costs.

Any currency conversions used in the creation of this report have been calculated using constant annual average 2012

exchange rates.

For the purposes of this report, Europe consists of Western Europe and Eastern Europe.

Western Europe comprises Belgium, Denmark, France, Germany, Greece, Italy, the Netherlands, Norway, Spain,

Sweden, Switzerland, Turkey, and the United Kingdom.

Eastern Europe comprises the Czech Republic, Hungary, Poland, Romania, Russia, and Ukraine.

Market analysis The UK coal market witnessed some strong growth recently, after recovering from a steep contraction in 2009.

Significant deceleration is however expected, with annual rate not exceeding 4.5%.

The UK coal market had total revenues of $6.4bn in 2012, representing a compound annual growth rate (CAGR) of 1.1%

between 2008 and 2012. In comparison, the French market declined with a compound annual rate of change (CARC) of

-1.7%, and the German market increased with a CAGR of 4.0%, over the same period, to reach respective values of

$2.3bn and $38.8bn in 2012.

Market consumption volumes declined with a CARC of -1.4% between 2008 and 2012, to reach a total of 60.9 million

short tons in 2012. The market's volume is expected to fall to 52.9 million short tons by the end of 2017, representing a

CARC of -2.8% for the 2012-2017 period.

The performance of the market is forecast to accelerate, with an anticipated CAGR of 3.2% for the five-year period 2012

- 2017, which is expected to drive the market to a value of $7.5bn by the end of 2017. Comparatively, the French and

German markets will grow with CAGRs of 5.0% and 6.1% respectively, over the same period, to reach respective values

of $3.0bn and $52.1bn in 2017.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 8

MARKET DATA

Market value The United Kingdom coal market grew by 13.6% in 2012 to reach a value of $6,419.3 million.

The compound annual growth rate of the market in the period 2008–12 was 1.1%.

Table 1: United Kingdom coal market value: $ million, 2008–12

Year $ million £ million € million % Growth

2008 6,13 .8 3,874.1 4,776.3

2009 4,514.0 2,848.7 3,512.1 (26.5%)

2010 5,136.2 3,241.4 3,996.3 13.8%

2011 5,652.8 3,567.3 4,398.2 10.1%

2012 6,419.3 4,051.1 4,994.6 13.6%

CAGR: 2008–12 1.1%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 1: United Kingdom coal market value: $ million, 2008–12

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 9

Market volume The United Kingdom coal market grew by 10.9% in 2012 to reach a volume of 60.9 million short ton.

The compound annual rate of change of the market in the period 2008–12 was -1.4%.

Table 2: United Kingdom coal market volume: million short ton, 2008–12

Year million short ton % Growth

2008 64.5

2009 53.3 (17.4%)

2010 55.4 3.9%

2011 54.9 (0.9%)

2012 60.9 10.9%

CAGR: 2008–12 (1.4%)

SOURCE: MARKETLINE M A R K E T L I N E

Figure 2: United Kingdom coal market volume: million short ton, 2008–12

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 10

MARKET SEGMENTATION

Geography segmentation The United Kingdom accounts for 6.6% of the European coal market value.

Germany accounts for a further 39.9% of the European market.

Table 3: United Kingdom coal market geography segmentation: $ million, 2012

Geography 2012 %

Germany 38,789.9 39.9

United Kingdom 6,419.3 6.6

Spain 2,438.6 2.5

France 2,347.8 2.4

Italy 1,608.4 1.7

Rest of Europe 45,576.0 46.9

Total 97,180 100%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 3: United Kingdom coal market geography segmentation: % share, by value, 2012

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 11

MARKET OUTLOOK

Market value forecast In 2017, the United Kingdom coal market is forecast to have a value of $7,522 million, an increase of 17.2% since 2012.

The compound annual growth rate of the market in the period 2012–17 is predicted to be 3.2%.

Table 4: United Kingdom coal market value forecast: $ million, 2012–17

Year $ million £ million € million % Growth

2012 6,419.3 4,051.1 4,994.6 13.6%

2013 6,473.1 4,085.0 5,036.4 0.8%

2014 6,632.4 4,185.6 5,160.4 2.5%

2015 6,924.9 4,370.1 5,387.9 4.4%

2016 7,220.8 4,556.9 5,618.2 4.3%

2017 7,522.0 4,747.0 5,852.5 4.2%

CAGR: 2012–17 3 2%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 4: United Kingdom coal market value forecast: $ million, 2012–17

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 12

Market volume forecast In 2017, the United Kingdom coal market is forecast to have a volume of 52.9 million short ton, a decrease of 13.1%

since 2012.

The compound annual rate of change of the market in the period 2012–17 is predicted to be -2.8%.

Table 5: United Kingdom coal market volume forecast: million short ton, 2012–17

Year million short ton % Growth

2012 60.9 10.9%

2013 57.1 (6.2%)

2014 56.1 (1.8%)

2015 55.0 (1.9%)

2016 54.0 (1.9%)

2017 52.9 (1.9%)

CAGR: 2012–17 (2.8%)

SOURCE: MARKETLINE M A R K E T L I N E

Figure 5: United Kingdom coal market volume forecast: million short ton, 2012–17

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 13

FIVE FORCES ANALYSIS

The coal market will be analyzed taking coal mining companies as players. The key buyers will be taken as power

generation companies, and mining equipment suppliers and landowners/regulators as the key suppliers.

Summary

Figure 6: Forces driving competition in the coal market in the United Kingdom, 2012

SOURCE: MARKETLINE M A R K E T L I N E

The UK coal market is tending towards increased consolidation. In 2013, Hargreaves Services took over five Scottish

Coal mines following the collapse of the company. Additionally, UK Coal, the biggest coal miner in Britain, is restructuring

its activities following the closure of Daw Mill, which represented a third of the UK Coal's revenue.

The size and strength of buyers in this market, grants them significant leverage; however, the high level of dependency

on coal as a vital energy source restrains buyer power somewhat.

Supplier power is weakened, as mining equipment is specialized and manufacturers are restrained by this dependency

on what constitutes a niche demand.

Large, multinational, diversified mining companies are the dominant players. They benefit from economies of scale, with

bulk coal production translating into a minimal per unit selling price for coal.

Coal, as an energy source, faces several possible substitutes, including: oil, gas, nuclear fuels, wind power and solar

power. Some are more beneficial for the environment; however, switching would involve high investment for traditional

power generation companies.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 14

Buyer power

Figure 7: Drivers of buyer power in the coal market in the United Kingdom, 2012

SOURCE: MARKETLINE M A R K E T L I N E

Buyers in this market are generally power generation companies. In the UK market, buyers include both power

companies that are exclusively involved in upstream activities, such as power generation and more vertically integrated

entities, such as RWE Group, which both generates and supplies electricity to end users through its service provider

Npower. Buyers can also be industrial and retail users. Coal companies are therefore not just selling to one or two

dominant buyers, which decreases the power of buyers here.

Amongst buyers, there are also steel makers, who use coking coal in the manufacture of steel.

Due to the high coal consumption of coal-fired power generators, vertical integration between electricity generation and

coal mining is possible and one example is BHP Billiton. Also steel companies are often additionally involved in the

mining of coal. However, the capital outlay needed to integrate vertically is very high.

With markets, such as electricity, controlled at the level of regional provinces, liberalization originally led to an increase in

competition and a weakening of established players. Coal is a commodity and once certain uniform standards have been

achieved there is only limited potential for product differentiation. Competition within the market is therefore largely driven

by price, increasing the buyer power.

Overall buyer power in this market is moderate.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 15

Supplier power

Figure 8: Drivers of supplier power in the coal market in the United Kingdom, 2012

SOURCE: MARKETLINE M A R K E T L I N E

Suppliers in this market, include producers of mining and production equipment and land owners, amongst others.

In general, supplier power is weakened by the fact that the mining market is important to supplier s’ revenues. Mining

equipment is often highly specialized and manufacturers are restrained by this dependency on what constitutes a niche

demand.

Innovation in the mining technology and equipment allows suppliers to differentiate their services and establish some

loyalty with market players.

Major landowners and governmental bodies can also be considered as suppliers within this market in some respect. The

well recognized nature of coal as a non-renewable source of energy, transforms the region, in which reserves are

located, into a critical supply input. The legal stranglehold over access to such reserves forms the strongest supply force.

Backward integration is unlikely as market players and buyers operate in distinctly different industries.

Overall, supplier power is only moderate.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 16

New entrants

Figure 9: Factors influencing the likelihood of new entrants in the coal market in the United Kingdom, 2012

SOURCE: MARKETLINE M A R K E T L I N E

Large multinational mining companies act as the dominant players within the coal market. These companies derive great

advantage from economies of scale, with bulk coal production translating into a minimal per unit selling price for coal.

Smaller companies within the market may therefore struggle to compete on an equal footing. This structural inequality

pushes the market towards consolidation.

The assets required for coal mining are considerable, including a large amount of specialized machinery. This serves as

a significant entry barrier. In addition, the complex logistics of coal mining and the prohibitive start-up costs, necessary

for securing a mine, constitute a further obstruction. The lack of serious product differentiation and the absence of brand

loyalty in this area undermine the security of current actors.

Stringent environmental regulations are increasingly putting pressure on the production of coal and it is becoming

increasingly expensive for companies to comply with such regulations. Coal is said to be the most environmentally

damaging fossil fuel. Organizations, such as the European Commission, are restricting the amount of emissions that are

allowed to be produced. However coal conversion technologies, such as coal-to-liquids and coal-to-gas, are expected to

create new markets for coal supplies which could encourage new entrants.

While mining companies involved in other activities, such as metals and iron ore, can alter their portfolio to include coal,

this transition would require investment in new mines, which constitutes a high switching cost if the company does not

operate on a large scale and therefore have the funds necessary for the investment.

Despite healthy market value growth within the last few years, the production volume is expected to contract going

forward, which tends to discourage newcomers in the coal market.

The threat from new entrants is assessed as weak in the current economic climate.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 17

Threat of substitutes

Figure 10: Factors influencing the threat of substitutes in the coal market in the United Kingdom, 2012

SOURCE: MARKETLINE M A R K E T L I N E

Coal, in principle, faces several possible substitutes in the power generation market, including: oil, gas, and nuclear

fuels.

Other substitutes include renewable sources, i.e. wind power and solar power, geothermal energy, etc. These can be

seen as quite a strong threat with the current emphasis on utilizing more environmentally friendly fuels, but involve high

investment for traditional power generation companies in order to make the transition to renewable energy sources.

In practice, power companies can only exploit low switching costs to a limited degree. The balance of their primary

energy mix can easily be altered, shifting the emphasis in accordance with the demands or dangers of the market.

However, a wholesale switch to alternative substitutes would involve significant investment – and divestment – of highly

specialized generation facilities.

Therefore, despite an ongoing challenge from cleaner energy sources, the coal market continues to hold significant

ground. Gas prices, global instability and concern over national energy independence, and resistance to the expansion

of nuclear power, conjoin to drive coal back into a strong position. Heavy investment in cleaner coal aims to

accommodate this movement, whilst undercutting environmental opposition. The implementation of clean coal

technology (CCT) strategies, such as carbon capture and storage (CCS), within coal fired power stations, may decrease

the environmental impact of using coal and reduce the threat of more environmentally friendly substitutes moving

forward.

In the short term, EIA forecasts that electricity generation from coal should increase by about 7.0% and generation from

natural gas should fall by 3.0% in 2013, as projected coal prices to the power sector fall slightly, while natural gas prices

increase, allowing coal to regain some of its power sector generation share. The combined impact from the usage of

natural gas and renewable sources to generate power is however expected to gradually reduce the share of coal to

produce electricity to 39.0% in 2035 from the high of 49.0% in 2007.

The threat from substitutes remains moderate.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 18

Degree of rivalry

Figure 11: Drivers of degree of rivalry in the coal market in the United Kingdom, 2012

SOURCE: MARKETLINE M A R K E T L I N E

The coal market is tending towards increased consolidation, with a local player, UK Coal, dominating the scene. The

presence of strong players boosts the competition within the market.

Exit barriers are high, as many of the major tangible assets are highly specialized and therefore divestment is difficult.

Although some of the players have other businesses, such as mining of metals, a relative lack of diversification sustains

rivalry. Geographical diversification is, however, often achieved, insulates companies from fluctuations within particular

countries’ markets.

Despite healthy market value growth within the last few years, the production volume is expected to contract going

forward which may boost the threat of competiton.

Overall, rivalry is strong.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 19

LEADING COMPANIES

Hargreaves Services Plc

Table 6: Hargreaves Services Plc: key facts

Head office: West Terrace, Esh Winning, Durham DH7 9PT, GBR

Telephone: 44 191 373 4485

Fax: 44 191 373 3777

Website: www.hargreavesservices.co.uk

Financial year-end: May

Ticker: HSP

Stock exchange: London

SOURCE: COMPANY WEBSITE M A R K E T L I N E

Hargreaves Services (Hargreaves) is a UK-based company engaged in sourcing, producing, processing, handling and

transporting bulk materials to the customers in the energy, waste and transport sectors. The group also imports coal into

the UK; coke and refractory minerals into Europe; and operates a haulage transport fleet in the UK.

The group operates through four segments: production, energy and commodities, transport, and industrial services.

Hargreaves's production segment produces coal, coke, and smokeless fuel briquettes. It also recycles tires for

customers throughout the UK and Europe. The group produces coal, coke, and smokeless fuel briquettes through its

subsidiaries: Maltby Colliery, Monckton Coke & Chemical Company, Maxibrite Ltd, Monckton Rubber Technologies, and

Rocpower.

Maltby Colliery is a mine located near Rotherham, South Yorkshire, which produces around 1.2 million tons of coal.

Monckton Coke & Chemical Company is an independent coke works company that produces metallurgical coke through

its site located near Barnsley, South Yorkshire. Maxibrite Ltd is a South Wales-based company engaged in

manufacturing of solid fuel, and smokeless fuel briquettes for domestic heating markets in the UK and Europe. Monckton

Rubber Technologies is a company engaged in recycling of waste vehicle tires into rubber crumb and wire at its

processing center in Sheffield. Rocpower is a company engaged in developing small biomass power plants.

The group's energy and commodities segment provides coal, coke, minerals and biomass products to industrial,

wholesale and public sector energy consumers. Hargreaves offers raw materials such as coal and biomass products and

services including port operations, storage, processing, handling and redistribution through road, rail and waterways to

the electricity supply industries. The group through its joint ventures is engaged in marketing of combustion by-products.

The group through its subsidiary, Coal4Energy, is engaged in the supply and distribution of coal products to industrial

and domestic consumers. Hargreaves offers raw materials including pulverized fuel ash, furnace bottom ash, lightweight

aggregates, fireclay, brick shale, foundry coke, metallurgical coke, coke breeze, calcined pet-coke, ferro-alloys, fluorspar

and bauxite to the foundry, steel, smelting and refractory industries.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 20

Hargreaves's transport segment is engaged in the provision of logistics services to the individuals in the UK. The group

offers transportation services through its subsidiaries: Hargreaves Transport Services, Imperial Tankers, and Hargreaves

Waste Services. Hargreaves Transport Services is a bulk haulage operator. It operates through a fleet of around 200

vehicles that provides its services to the customers in markets including power generation, coal mining, quarrying, port

services, industrial chemicals, construction, recycling, and agriculture. The group's subsidiary Imperial Tankers is a road

tanker haulier. It transports liquid products including hazardous and non-hazardous chemicals, petroleum products,

bitumen, pitches and tars, pressurized gasses, and controlled liquid wastes. Hargreaves's subsidiary, Hargreaves Waste

Services is a bulk and roll on-off hauliers in the UK. It provides haulage and management solutions to the waste industry

and local authorities through its depots located around the UK.

The group's industrial services segment provides contract management services to the power generation, utilities,

chemicals, minerals and steel industries through its subsidiaries Norec, AJS Contracts, Killingholme Storage and

Distribution, and DWL Engineering Services. Its service offerings include: engineering design, fabrication and project

management, plant operation and maintenance, facilities management, and ash and residual product recovery services.

Hargreaves's clients in industrial services segment include: E.ON UK, Scottish Power, Scottish & Southern Energy,

International Power, EFD Energy, ConocoPhillips and Eggborough Power Ltd. In 2013, Hargreaves acquired assets of

the Scottish coal miner ATH Resources.

Key Metrics

The company recorded revenues of $1,091m in the fiscal year ending May 2012, an increase of 24.6% compared to

fiscal 2011. Its net income was $47m in fiscal 2012, compared to a net income of $39m in the preceding year.

Table 7: Hargreaves Services Plc: key financials ($)

$ million 2008 2009 2010 2011 2012

Revenues 641.6 797.2 728.6 875.2 1,090.7

Net income (loss) 20.1 29.6 32.6 39.0 46.7

Total assets 315.0 358.8 446.9 488.5 644.9

Total liabilities 239.0 245.1 304.7 306.8 428.9

Employees 1,900 1,979 2,209 2,399 2,426

SOURCE: COMPANY FILINGS M A R K E T L I N E

Table 8: Hargreaves Services Plc: key financials (£)

£ million 2008 2009 2010 2011 2012

Revenues 404.9 503.1 459.8 552.3 688.3

Net income (loss) 12.7 18.7 20.6 24.6 29.5

Total assets 198.8 226.4 282.0 308.3 407.0

Total liabilities 150.8 154.7 192.3 193.6 270.7

SOURCE: COMPANY FILINGS M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 21

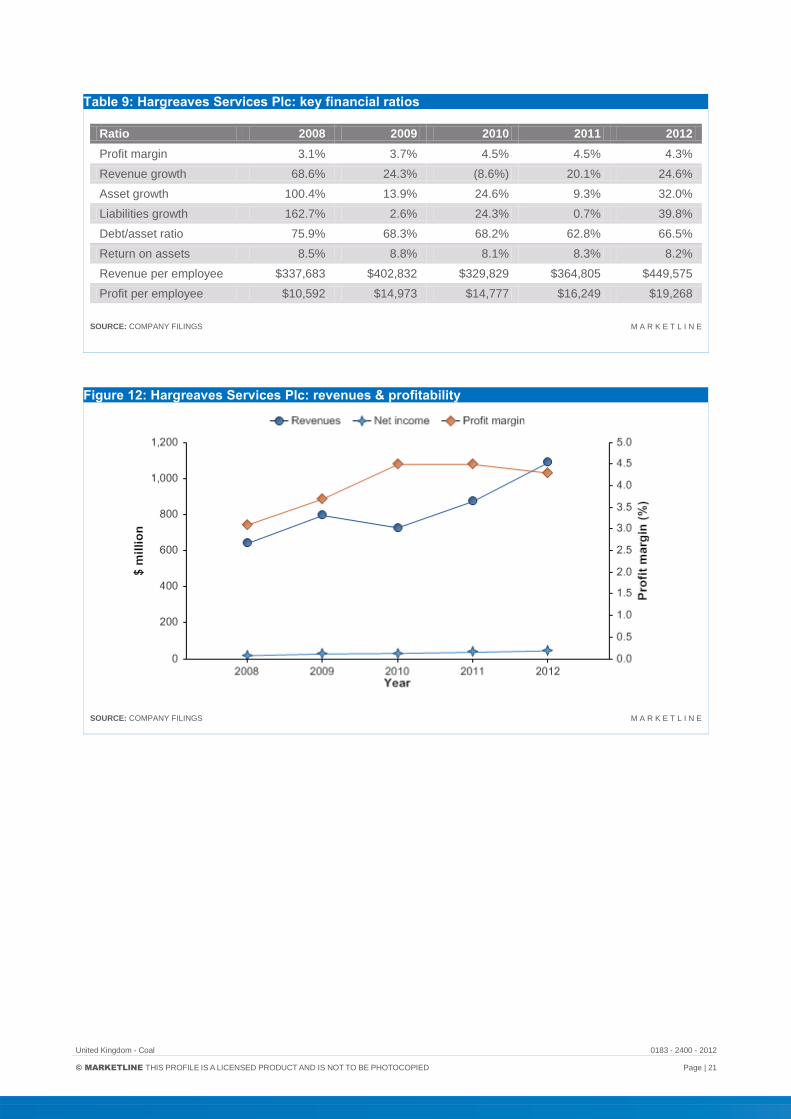

Table 9: Hargreaves Services Plc: key financial ratios

Ratio 2008 2009 2010 2011 2012

Profit margin 3.1% 3.7% 4.5% 4.5% 4.3%

Revenue growth 68.6% 24.3% (8.6%) 20.1% 24.6%

Asset growth 100.4% 13.9% 24.6% 9.3% 32.0%

Liabilities growth 162.7% 2.6% 24.3% 0.7% 39.8%

Debt/asset ratio 75.9% 68.3% 68.2% 62.8% 66.5%

Return on assets 8.5% 8.8% 8.1% 8.3% 8.2%

Revenue per employee $337,683 $402,832 $329,829 $364,805 $449,575

Profit per employee $10,592 $14,973 $14,777 $16,249 $19,268

SOURCE: COMPANY FILINGS M A R K E T L I N E

Figure 12: Hargreaves Services Plc: revenues & profitability

SOURCE: COMPANY FILINGS M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 22

Figure 13: Hargreaves Services Plc: assets & liabilities

SOURCE: COMPANY FILINGS M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 23

Rio Tinto

Table 10: Rio Tinto: key facts

Head office: 2 Eastbourne Terrace, London, W2 6LG, GBR

Telephone: 44 20 7781 2000

Fax: 44 20 7781 1800

Website: www.riotinto.com

Financial year-end: December

Ticker: RIO

Stock exchange: New York, Australia, London

SOURCE: COMPANY WEBSITE M A R K E T L I N E

Rio Tinto is engaged in international mining which encompasses exploring for, mining, and processing the earth's

mineral resources. The group offers products which include aluminum, coal, copper, diamonds, industrial minerals

(borax, titanium dioxide, and salt), gold, and iron ore. The group has global operations with significant businesses in

Australia, North America, South America, Asia, Europe, and South Africa.

Rio Tinto operates through eight business groups: iron ore; aluminum; coal, copper; industrial minerals; diamonds; gold;

and other operations.

Rio Tinto's iron ore group wholly owns Hamersley Iron mines in Brazil. Hamersley Iron operates ten mines including

three mines in joint venture. It also includes the Dampier Salt operations at three sites in Western Australia. Rio Tinto

has 53.0% interest in Robe River mines in Australia and 58.7% interest in Iron Ore Company of Canada. The company

has 50.35% interest in the Simandou iron ore project in Guinea.

Rio Tinto's aluminum group operates through the wholly-owned, integrated aluminum subsidiary, Rio Tinto Alcan. Rio

Tinto Alcan is one of the world's largest producers of bauxite, alumina, and aluminum. Rio Tinto Alcan provides bauxite,

alumina, specialty aluminas, and aluminum products.

The coal business group is one of the biggest suppliers of thermal and coking coal to the Asian seaborne market. Rio

Tinto Coal Australia manages eight coal mines in Queensland and New South Wales. In the US, the group operates the

Colowyo coal mine. It also offers higher-value coking, or metallurgical, coal which, when mixed in furnaces with iron ore,

produces steel.

Rio Tinto's copper group is the sixth largest supplier of copper. It has a diverse mix of operations and projects located in

North and South America, Africa, Asia, and Australia. The group offers copper, molybdenum, silver, and nickel.

The industrial minerals group comprises Rio Tinto Minerals (RTM) and Rio Tinto Iron & Titanium (RTIT). RTM is a global

leader in borates supply and RTIT is a market leader in high grade titanium dioxide. The segment provides borates,

titanium dioxide feedstocks, high purity iron, metal powders, zircon, and rutile products. It has five mines: Dampier Salt

holding 68.4% interest located at Dampier, Lake MacLeod, and Port Hedland in Western Australia; Rio Tinto Minerals -

Boron at California in the US; Rio Tinto Fer et Titane in Havre-Saint-Pierre, Quebec in Canada; QIT Madagascar

Minerals with 80% interest located at Fort-Dauphin in Madagascar; and Richards Bay Minerals with 74% interest located

at Richards Bay, KwaZulu-Natal in South Africa.

The diamonds group operates through Rio Tinto Diamonds (RTD), one of the world's leading rough diamond producers,

active in mining and sales and marketing. Rio Tinto's diamond assets comprises the Argyle diamond mine in Australia,

the Diavik diamond mine in Canada, Murowa diamonds in Zimbabwe, and the Bunder diamond project in India.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 24

The gold business group is one of the top 15 gold producers in the world, and the largest among the diversified miners.

Rio Tinto has interests in two of the largest gold resources, at Oyu Tolgoi and Grasberg. The Grasberg contains the

largest gold reserves in the world.

The other operations business group of Rio Tinto comprises its exploration, and technology and innovation business

groups.

The exploration group is organized into five geographically based teams in North America, South America, Australasia,

Asia, and Africa/Europe. The exploration group focuses on discovering new mineral resources to replace and/or

supplement those already mined by Rio Tinto. Its exploration teams, along with a small project generation team, are

constantly seeking new finds of these important products plus deposits of bauxite, iron ore, coal, uranium, borate, and

other industrially viable minerals.

The technology and innovation group has bases in Australia, Canada, the UK, and the US. Its role is to identify and

promote best operational technology practice across the group and to pursue step change innovation of strategic

importance to ore bodies of the future.

Key Metrics

The company recorded revenues of $50,967m in the fiscal year ending December 2012, a decrease of 15.8% compared

to fiscal 2011. Its net loss was $2,990m in fiscal 2012, compared to a net income of $5,826m in the preceding year.

Table 11: Rio Tinto: key financials ($)

$ million 2008 2009 2010 2011 2012

Revenues 54,264.0 41,825.0 56,576.0 60,537.0 50,967.0

Net income (loss) 4,609.0 5,335.0 14,324.0 5,826.0 (2,990.0)

Total assets 89,616.0 97,236.0 112,402.0 119,545.0 117,573.0

Total liabilities 67,155.0 51,311.0 47,128.0 60,337.0 59,552.0

Employees 54,264 56,894 76,894 67,930 71,219

SOURCE: COMPANY FILINGS M A R K E T L I N E

Table 12: Rio Tinto: key financial ratios

Ratio 2008 2009 2010 2011 2012

Profit margin 8.5% 12.8% 25.3% 9.6% (5.9%)

Revenue growth 82.7% (22.9%) 35.3% 7.0% (15.8%)

Asset growth (11.4%) 8.5% 15.6% 6.4% (1.6%)

Liabilities growth (10.5%) (23.6%) (8.2%) 28.0% (1.3%)

Debt/asset ratio 74.9% 52.8% 41.9% 50.5% 50.7%

Return on assets 4.8% 5.7% 13.7% 5.0% (2.5%)

Revenue per employee $1,000,000 $735,139 $735,766 $891,167 $715,638

Profit per employee $84,937 $93,771 $186,282 $85,765 ($41,983)

SOURCE: COMPANY FILINGS M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 25

Figure 14: Rio Tinto: revenues & profitability

SOURCE: COMPANY FILINGS M A R K E T L I N E

Figure 15: Rio Tinto: assets & liabilities

SOURCE: COMPANY FILINGS M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 26

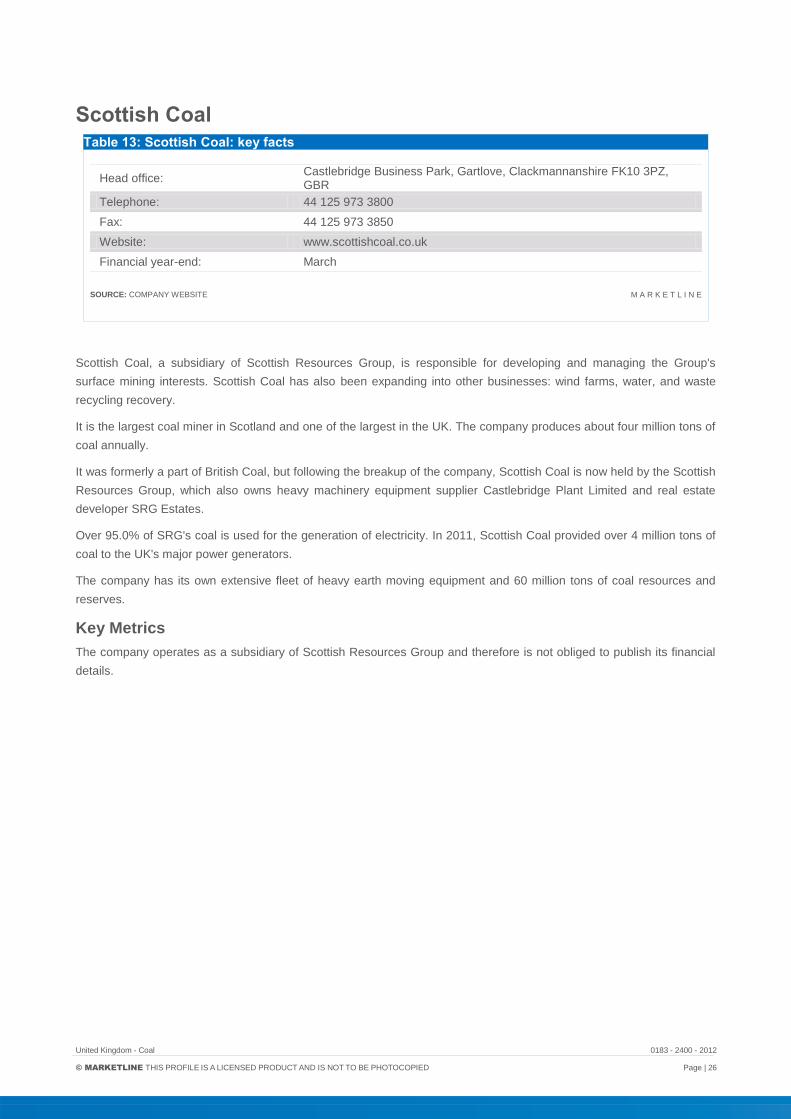

Scottish Coal

Table 13: Scottish Coal: key facts

Head office: Castlebridge Business Park, Gartlove, Clackmannanshire FK10 3PZ, GBR

Telephone: 44 125 973 3800

Fax: 44 125 973 3850

Website: www.scottishcoal.co.uk

Financial year-end: March

SOURCE: COMPANY WEBSITE M A R K E T L I N E

Scottish Coal, a subsidiary of Scottish Resources Group, is responsible for developing and managing the Group's

surface mining interests. Scottish Coal has also been expanding into other businesses: wind farms, water, and waste

recycling recovery.

It is the largest coal miner in Scotland and one of the largest in the UK. The company produces about four million tons of

coal annually.

It was formerly a part of British Coal, but following the breakup of the company, Scottish Coal is now held by the Scottish

Resources Group, which also owns heavy machinery equipment supplier Castlebridge Plant Limited and real estate

developer SRG Estates.

Over 95.0% of SRG's coal is used for the generation of electricity. In 2011, Scottish Coal provided over 4 million tons of

coal to the UK's major power generators.

The company has its own extensive fleet of heavy earth moving equipment and 60 million tons of coal resources and

reserves.

Key Metrics

The company operates as a subsidiary of Scottish Resources Group and therefore is not obliged to publish its financial

details.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 27

UK Coal Production Limited

Table 14: UK Coal Production Limited: key facts

Head office: Harworth Park, Blyth Road, Harworth, Doncaster, South Yorkshire, DN11 8DB

Telephone: 44 1302 751 751

Website: www.ukcoal.com

SOURCE: COMPANY WEBSITE M A R K E T L I N E

UK COAL Production Limited is involved in coal mining. The group primarily operates in the UK.

The group operates through two business segments: deep mining, surface mining.

The group operates three deep mines located in central and northern England. The group estimated total reserves of

approximately 100 million tons and produces 3.2 million tons per year. The closed/sold deep mines consist of the closed

Rossington colliery. UK COAL generates electricity from mines methane at both operating and closed sites.

The group's surface mining segment includes all mining activities at surface level together with the plant hire operations

of the group. It consists of six active coaling surface mines and consent to mine one further site. This segment produces

1.8 million tons of coal per year.

Key Metrics

UK Coal Production Limited is a private company and does not publish its financial details.

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 28

MACROECONOMIC INDICATORS

Country Data

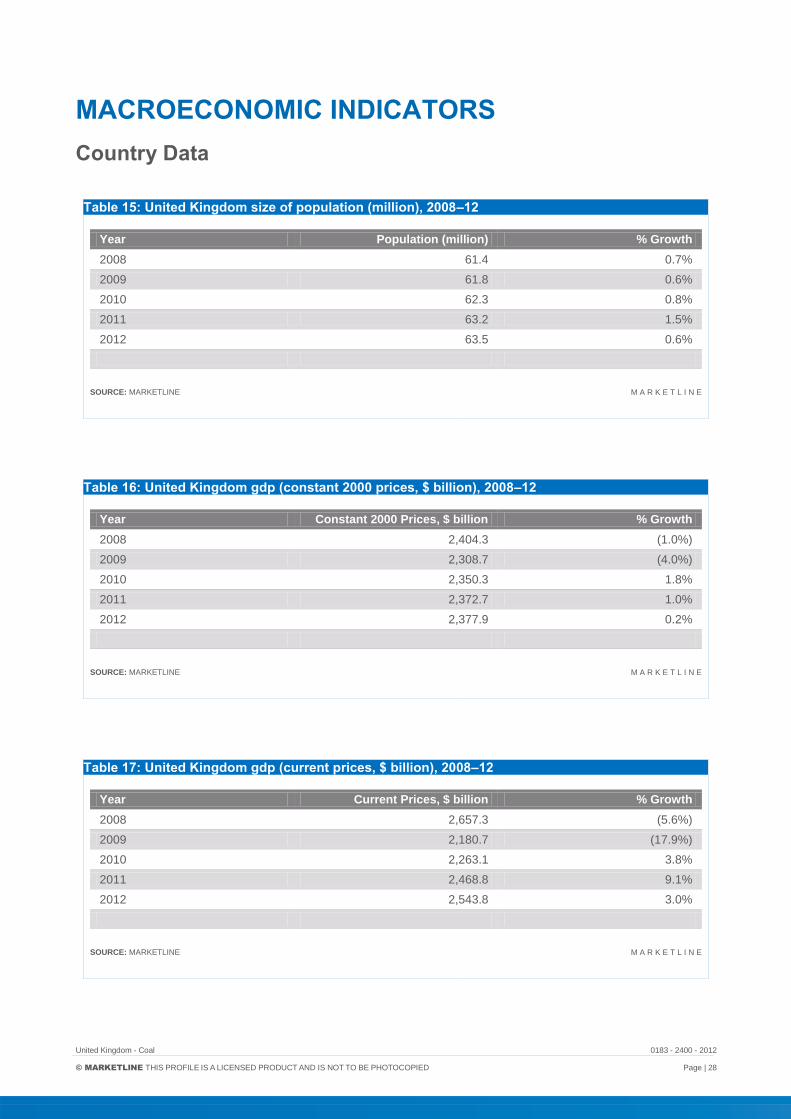

Table 15: United Kingdom size of population (million), 2008–12

Year Population (million) % Growth

2008 61.4 0.7%

2009 61.8 0.6%

2010 62.3 0.8%

2011 63.2 1.5%

2012 63.5 0.6%

SOURCE: MARKETLINE M A R K E T L I N E

Table 16: United Kingdom gdp (constant 2000 prices, $ billion), 2008–12

Year Constant 2000 Prices, $ billion % Growth

2008 2,404.3 (1.0%)

2009 2,308.7 (4.0%)

2010 2,350.3 1.8%

2011 2,372.7 1.0%

2012 2,377.9 0.2%

SOURCE: MARKETLINE M A R K E T L I N E

Table 17: United Kingdom gdp (current prices, $ billion), 2008–12

Year Current Prices, $ billion % Growth

2008 2,657.3 (5.6%)

2009 2,180.7 (17.9%)

2010 2,263.1 3.8%

2011 2,468.8 9.1%

2012 2,543.8 3.0%

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 29

Table 18: United Kingdom inflation, 2008–12

Year Inflation Rate (%)

2008 3.6%

2009 2.2%

2010 3.3%

2011 4.5%

2012 2.8%

SOURCE: MARKETLINE M A R K E T L I N E

Table 19: United Kingdom consumer price index (absolute), 2008–12

Year Consumer Price Index (2000 = 100)

2008 108.5

2009 110.8

2010 114.5

2011 119.6

2012 123.0

SOURCE: MARKETLINE M A R K E T L I N E

Table 20: United Kingdom exchange rate, 2008–12

Year Exchange rate ($/£) Exchange rate (€/£)

2008 0.5449 0.7973

2009 0.6416 0.8921

2010 0.6475 0.8589

2011 0.6235 0.8 74

2012 0.6311 0.8111

SOURCE: MARKETLINE M A R K E T L I N E

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 30

APPENDIX

Methodology MarketLine Industry Profiles draw on extensive primary and secondary research, all aggregated, analyzed, cross-

checked and presented in a consistent and accessible style.

Review of in-house databases – Created using 250,000+ industry interviews and consumer surveys and supported by

analysis from industry experts using highly complex modeling & forecasting tools, MarketLine’s in-house databases

provide the foundation for all related industry profiles

Preparatory research – We also maintain extensive in-house databases of news, analyst commentary, company

profiles and macroeconomic & demographic information, which enable our researchers to build an accurate market

overview

Definitions – Market definitions are standardized to allow comparison from country to country. The parameters of each

definition are carefully reviewed at the start of the research process to ensure they match the requirements of both the

market and our clients

Extensive secondary research activities ensure we are always fully up-to-date with the latest industry events and

trends

MarketLine aggregates and analyzes a number of secondary information sources, including:

- National/Governmental statistics

- International data (official international sources)

- National and International trade associations

- Broker and analyst reports

- Company Annual Reports

- Business information libraries and databases

Modeling & forecasting tools – MarketLine has developed powerful tools that allow quantitative and qualitative data to

be combined with related macroeconomic and demographic drivers to create market models and forecasts, which can

then be refined according to specific competitive, regulatory and demand-related factors

Continuous quality control ensures that our processes and profiles remain focused, accurate and up-to-date

United Kingdom - Coal 0183 - 2400 - 2012

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 31

Industry associations

Energy Information Administration

1000 Independence Avenue, SW, Washington, DC 20585, US

Tel.: 1 202 586 8800

Fax: 1 202 586 9753

www.eia.doe.gov

World Coal Institute Cambridge House, 180 Upper Richmond Road, Putney, London SW15 2SH, UK

Tel.: 44 20 8246 6611

Fax: 44 20 8246 6622

www.wci-coal.com

Related MarketLine research

Industry Profile

Coal in Belgium

Coal in the Netherlands

Coal in Canada

Coal in Western Europe

Coal in Eastern Europe

MARKETLINE | 119 FARRINGDON ROAD | LONDON,

UNITED KINGDOM, EC1R 3DA

T: +44 161 238 4040 | F: +44 870 134 4371

df

Copyright © 2022 FDOKUMEN