TIVO PART II - CiteSeerX

42

1 High Technology, Entrepreneurship and Strategy TiVo – TV, Your Way Dewole Aradeon Ilia Dub Vadim Kosin Sharon Lee Per Levin Dimitrios Pazaitis

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of TIVO PART II - CiteSeerX

1

High Technology, Entrepreneurship and Strategy

TiVo – TV, Your Way Dewole Aradeon Ilia Dub Vadim Kosin Sharon Lee Per Levin Dimitrios Pazaitis

2

"Here is, in a nutshell, what a PVR can do for you: empower you to take control of what you watch on TV. The consumer electronics industry has finally delivered on what the VCR promised more than 25 years ago: the ability to time-shift TV."

- e-town.com, July 2000

1. Introduction

Context for Innovation

The history of TiVo goes back as far as the early 1990s, when Silicon Graphics

collaborated with Time Warner in one of the first attempts to create something they

called “Interactive TV”. The trial the two companies eventually started in Orlando failed,

but the idea was born: the TV viewer should be in the “driver’s seat” of creating a

programming schedule that suits him.

In 1997, two former Silicon Graphics executives got together and founded TiVo, the

company dedicated to providing “personal television” – a technology that would allow

the viewer to watch his favorite movies any time, no matter when they were shown on

TV or on which network channel. This has critical implications for the TV network

industry.

At the same time, in 1997, the TV industry and the industry for consumer electronics

were undergoing major changes related to the proliferation of cable and satellite TV. This

brought with it up to 500 TV channels at the disposal of television viewers.

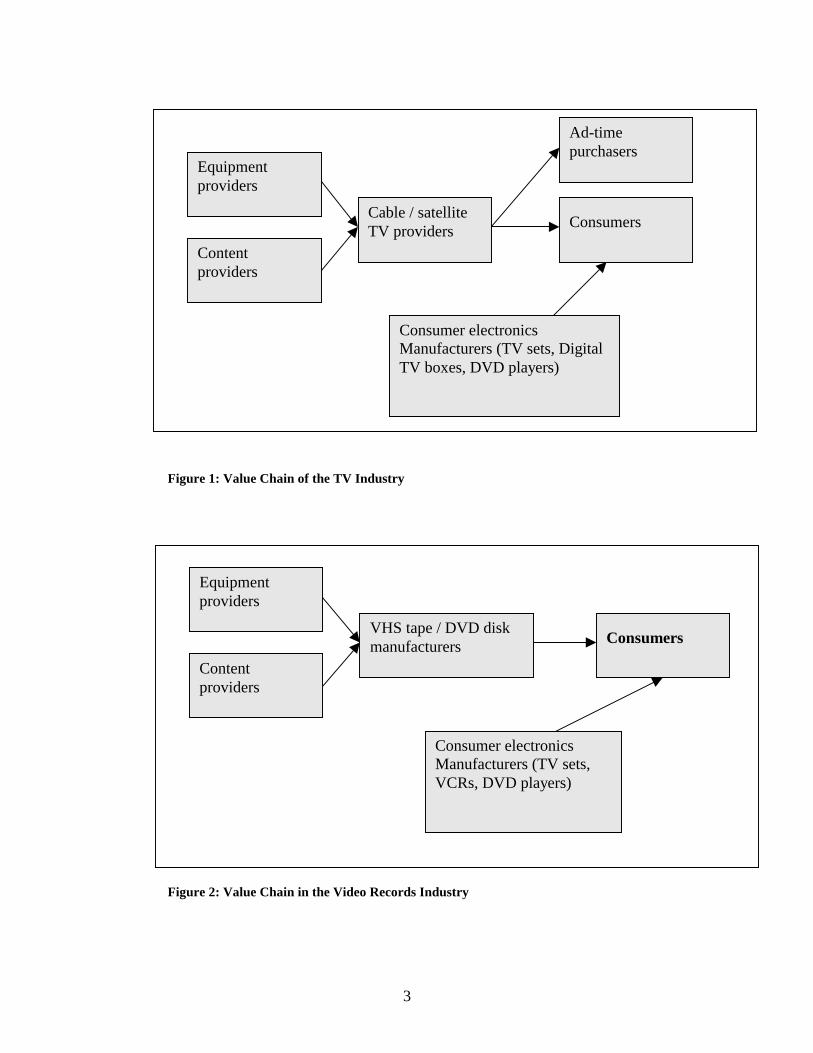

This was the setting, when TiVo Inc. was born. The relevant value chains of that time, are

depicted below in figure 1 and figure 2.

3

Figure 1: Value Chain of the TV Industry

Figure 2: Value Chain in the Video Records Industry

Equipment providers

Content providers

VHS tape / DVD disk manufacturers

Consumers

Consumer electronics Manufacturers (TV sets, VCRs, DVD players)

Equipment providers

Content providers

Cable / satellite TV providers

Consumers

Consumer electronics Manufacturers (TV sets, Digital TV boxes, DVD players)

Ad-time purchasers

4

Technology Description

As TiVo Inc. puts it: “TiVo DVRs are like VCRs, but with a hard disk and without the

hassles of videotapes”. Essentially TiVo is a smart video recorder that “knows” which

movies its owner prefers and automatically records them. Furthermore: TiVo enables a

TV viewer to watch a live show, pause it for a moment, get himself a coffee and continue

watching the same movie with a “time-shift”. And of course, when watching a recorded

(or time-shifted) movie, the user can fast-forward through the much-hated commercials.

This of course has implications for TV advertisers and indirectly on the TV network

studios that sell air time to these advertisers based on when their spots were aired (now

irrelevant).

From the technological point of view, TiVo is an amazingly simple device: it consists of

a basic PowerPC with an MPEG encoder / decoder and a universal Remote Control. The

PowerPC runs Linux OS and a piece of TiVo’s proprietary software. In addition the

company maintains a TiVo Broadcast Center. The Broadcast Center is a series of

computer servers that store the TV Guide and some additional content, such as the

TiVolution Magazine. Every TiVo device needs to be connected to a phone line, so that it

can regularly dial into the Broadcast Center in order to get up-to-date content and

information.

It is interesting to compare the technological development of TiVo with the development

of DVD, especially because both are considered to be direct successors of the VCR. DVD

arose from a common effort of a consortium of the most influential consumer electronics

and media companies. The technology was developed in the best labs backed by huge

R&D budgets with a single goal: to create a replacement for the VCR. TiVo on the other

5

hand can be considered a “by-product” of the development in several technological areas:

PCs, hard drives, media compression (MPEG) and the Internet. This has implications on

how TiVo has had to struggle with a fragmented and evolving base of strategic backers,

some of whom are also demonstrating the potential to be rivals.

Industry analysis

To analyze the competitive situation in TiVo’s industry we are using Porter’s five forces

model:

- Biggest part of the technology, such as PC, hard-drives, MPEG is available to anyone

- Information for the TV Guide is available

- There is almost no network effect, so that existing installed base doesn’t represent an entry barrier

Easy Entry

- A few electronic component manufacturers supply critical parts

- Satellite / cable TV providers: high bargaining power, thanks to direct access to large customer bases

- Powerful TV networks supply program content

Strong Suppliers

- VCR offers some of the functions of the PVR and has much higher acceptance and lower price

- It might be possible to add PVR functionality to VCRs so that they will become a perfect substitute

- DVD writers are a potential substitute

- Set-top boxes with DVR incorporated

Substitutes

- Individual buyers have low bargaining power, however since PVR is a new technology, mass acceptance is crucially important

- Buyers are price sensitive - Consumer electronics manufacturers: high bargaining power, due to established brands, manufacturing capabilites, distribution channels and financial strenght.

Buyers - Two direct competitors (Moxi Digital, ReplayTV) backed by large corporations competing in a very small market

- Cable TV providers in the process of creating their own set-top boxes with DVR technology incorporated (AT&T Broadband).

Intense Rivalry

6

The five forces analysis show, that it will be difficult for TiVo to remain market leader in

this market and even to survive. On one hand its very uncertain whether the consumers

will accept TiVo’s product (and PVRs in general) and whether the market will take off.

On the other hand the established consumer electronics manufacturers have the biggest

power in this market, because they find themselves not only in a strong bargaining

position as suppliers (in the case of cable TV providers) as gateways to large customer

populations. In addition these players are also potential entrants in the market. In fact we

expect that they will enter the market by embedding PVR functionality into TV sets,

DVD players and set-top boxes as soon as the market takes off. In any case, even if no

new players enter the market, the bargaining power of the suppliers and the intense

rivalry in the market will make it very difficult for TiVo to capture value. We will expand

on these points in the next two sections.

7

2. TiVo: Business Model and Strategic Alliances

TiVo’s primary objective is to establish TiVo as the leader in convergence technology,

specifically with regards to household entertainment. TiVo would like to see its

technology, particularly its core digital video recording technology, licensed by

manufacturers of consumer electronics products, and its use and functionality extended

by content and other providers who will pay it co-development fees. This is of course, in

addition to a constant stream of subscription fees, although the sustainability of this over

the long term is in question, given the fierce competition on the horizon and the general

unpopularity of monthly fees.

Business Model

TiVo currently cites four sources of revenue: subscription revenue, non-subscription

revenue, licensing revenue and engineering professional services. Subscription revenue

comes from a monthly or lifetime fee charged to TiVo users. Non-subscription revenue

primarily includes charter advertising and sponsorship revenue from consumer

companies and media networks that have provided content on the TiVo Service.

Licensing revenue consists of revenues generated from licensing technology to consumer

electronics companies and service providers. Engineering professional services revenue

includes revenues earned for engineering services performed.

To date, $8.2 million of its latest quarter revenue (ended April 2002) of $9.9 million is

made up of recurring subscription revenue. Non-subscription and services revenue have

8

been insignificant to date. And until the battle around patents and an industry standard

has been conclusively won, it will be difficult to expect a steady stream of licensing

revenue.

Non-subscription revenue may hold some promise. This includes revenue streams from

the following: advertising, audience measurement research, revenues from programmers

and electronic commerce. In early May of 2002, TiVo debuted a new advertising

campaign with partner Best Buy, dubbed “advertainment” that had some innovative

elements to it, including “telescoping” 30-second commercials that allow viewers to opt-

in to view interesting, branded entertainment and then return to their ‘live’ viewing

without skipping a beat. Contrary to popular opinion, this is not as ridiculous as people

think (who would deliberately choose to watch commercials?), as it appears that

advertisers are beginning to sit up now and to craft more interesting forms of

“advertainment” – an example here would be the BMW film shorts that were wildly

successful in driving viewers to the BMW website. A second would be the research done

by TiVo indicating that TiVo viewers did more instant replays of the Super Bowl

commercials than of the game itself, with the Pepsi ads featuring Britney Spears being

the unacknowledged “MVP.” Such entertainment is automatically stored on the TiVo

hard drive on reserved space (so as not to infringe on the viewer’s allotted recording

hours) and hence can be accessed whenever desired – a boon to advertisers.

Other aspects of this commercial included the ability to enter a free CD giveaway as well

as to order a CD using only the TiVo remote. Obviously, one can see how this can

9

translate to lead generation and Request for Information capabilities although

unfortunately, it is still too early to determine what the uptake will be. TiVo also plans to

offer brand marketers near real-time audience measurement data on their campaigns,

including when it was viewed and how often.

This evolution represents a fundamental change in advertising. A ‘pull’ model is

replacing the traditional ‘push’ model, where consumers pick and choose which

advertising they wish to consume. However, while exciting, this is still a nascent

development which success will depend heavily on mass adoption.

Ultimately, it appears that TiVo would like to see licensing revenue make up the bulk of

the business’s revenues. The licensing model recently gained credibility - the Sony

licensing deal inked in October 2001 (see Exhibit 1), was worth an estimated $10-15

million, and hopefully hailed as a ‘proxy licensing deal.’ Last month, Sony shipped its

first DVR powered by TiVo-licensed technology to the Japanese market. TiVo also

recently received $1.6 million in revenues for helping DirectTV develop their next

generation combined set-top/DVR box.

TiVo was also recently awarded several key patents, one around the pausing and

recording of live television broadcasts (“Multimedia Timewarping”) in May 2001 which

led to a 72% spike in the stock and one in December 2001 around core DVR technology

and home networking capabilities. TiVo expects that by 2003, between 30-40% of its

revenue will come from licensing revenue. Already, it is attempting to shift as much as

10

possible of the sales, marketing and distribution responsibilities to its partners (see details

in Exhibit 1 below), with TiVo providing only co-development efforts and technical

support. Clearly, in the long term TiVo sees itself as a technology company.

Manufacturing was outsourced from the very beginning (although not without cost in

terms of revenue sharing and equity). In fact, in October 2001, TiVo formed a separate

business unit just to support TiVo’s licensing strategy.

There are several risks associated with this business model. In the near and midterm,

subscription revenue is expected to be the bulk of their revenue. This reliance on

subscription revenue is unhealthy, given that portions of this revenue have been promised

to more than a few strategic partners. This is exacerbated by the nature of some of their

revenue sharing arrangements that, according to their 10K, “require us to share a portion

of our subscription fees whether or not we increase or decrease the price of the TiVo

Service.” This also makes TiVo’s pricing strategy a little inflexible. One of the biggest

points of psychological resistance for users is the need to pay both a cable/satellite

subscription fee, and a TiVo fee on top of that. If a competitor somehow manages to

disguise or do away with this cost, they will be at an instant advantage. The 10K

revelation implies the limitations of TiVo’s ability to match any changes in the

subscription model.

Another shortcoming is that the TiVo hardware alone, without the $9.95 TiVo

subscription, can already record, pause, rewind and fast-forward through live and

recorded programming. All the fee buys you is the ability to do a daily callback to TiVo’s

11

servers to get the TV guide data. The possibility of free riding thus exists, if to an

unknown extent.

In addition, as acknowledged in their 10K, the emerging enhanced-television industry is

highly litigious, particularly in the area of on-screen program guides. “Many patents

covering interactive television technologies have been granted but have not been

commercialized. For example, we are aware of at least seven patents for pausing live

television.”1 TiVo currently faces at least four lawsuits around intellectual property

infringement, and is counter-suing at least one of them (Sonicblue). Needless to say, this

is a costly endeavor.

And ultimately, the success of all these revenue streams hinges on broad-based mass

adoption. It has been a disappointment to many that TiVo has only sold just over 400,000

boxes in 3+ years. However, now that the product is hitting what is called the ‘magic’

number of $299, the price point at which popular devices like the DVD and the VCR

took off, the DVR may yet emerge as the new ubiquitous device. Whether it will be TiVo

that succeeds will be discussed in Part III.

Strategic Partnerships: The Drive Toward Marketing, Distribution, ADOPTION

TiVo’s selection and timing of strategic partners/equity investors display an excellent use

of alliances to simultaneously manage both development and adoption. The earliest

alliances for example, essentially represented a co-opting of three of the most threatened

segments: home electronics manufacturer (Philips, March 1999), satellite TV provider 1 TiVo Form 10K for year ended Jan 3, 2002, 40

12

(DirecTV, April 1999) and television network (NBC, June 1999, followed by CBS,

Comcast, Cox, Walt Disney, Liberty Digital, Discover, TV Guide Interactive and

Advance/Newhouse, July 1999). These were also the segments that would be critical to

the development and deployment of the product. Philips (and later Sony in September

1999) would undertake the manufacturing of the hardware, subsidized by TiVo, while

DirecTV would open up its base of over 10 million subscribers and provide much needed

marketing and distribution resources.

The evolution of this network of strategic partners was followed by a sequential

accumulation of complementary resources in accordance to TiVo’s lifecycle needs. As

pointed out above, central to TiVo’s success is the need to promote the mass deployment

of digital video recording technology (TiVo has deliberately promoted an open standards,

Linux-based platform for this reason.) As such, TiVo began broadening its strategic

partners to make this technology more attractive, affordable and ubiquitous. Providers of

online entertainment and content such as AOL, Real Networks and AtomFilm were

added. Sony’s new satellite recorder will come bundled with TiVo technology at no extra

cost, ditto for DIRECTV’s 2nd generation box.

The short time-line of alliances below illustrates the focused campaign launched by TiVo

to drive 1) adoption and 2) the ubiquity of TiVo technology, particularly through pushing

the convergence of various types of entertainment.

13

Exhibit 1

Date Partner Details Financial Terms

May 2002 AOL (AOLTV service)

Joint development to converge PC and TV. TiVo users

can schedule recordings online, Live chat can be used

while watching TV.

$4M paid as

development fee to

TiVo

March 2002 Best Buy TiVo will be the only stand-alone personal video recorders

with electronic program guide-based service sold by Best

Buy. Under the agreement, Best Buy will be the exclusive

retail distributor of the TiVo-only branded Series2 digital

video recorders. Valid until Feb 2003.

TiVo will share with

Best Buy a portion of

the TiVo Service

revenue.

Feb 2002 DIRECTV (over 10.7 million subscribers)

TiVo to jointly develop 2nd generation Digital Satellite

Receiver with inbuilt DVR, removing adoption barrier of

“teeter factor” (too many entertainment devices).

DIRECTV also to take over manufacturing of the set-top

boxes, which should greatly reduce cost of boxes. Also

responsible for marketing and distribution of boxes.

DIRECTV pays per-

account monthly fees to

provide server support

and limited customer.

Jan 2002 RealNetworks, and Jellyvision

RealNetworks to bundle its music player into TiVo

allowing customers to download, manage and play their

favorite music, streaming video and other digital content

on TV. Jellyvision will co-develop video party games for

the mass audience. In addition, new TiVo will allow

digital photos to be stored and viewed as well as prints

ordered.

Unknown

Nov 2001 AT&T Broadband (14 million subscribers)

AT&T to introduce DVRs to cable customers. Note

AT&T regards this as an interim strategy to provide

customers with PVR service while developing integrated

box with same functions. Unsure if licensing structure will

then follow. NOTE: AT&T is not exclusively committed

to TiVo for future PVR rollouts. Recently concluded a

service trial with TiVo competitor ReplayTV

AT&T Broadband gets

portion of subscription

fee. Also portion of

revenues received from

advertising and

promotional activities

October 2001 Sony Signed 7-year licensing deal to allow it to incorporate Sony pays upfront fee

14

TiVo technology into its line of consumer products

worldwide. “This deal is the cornerstone of TiVo’s

licensing strategy.” Deal expected to bring in $10-15M

over next 12 months. NOTE: This is a non-exclusive deal.

Sony plans to bundle TiVo technology with its satellite tv

set top controller at no extra cost (reducing ‘teeter factor’)

Predicts 100k more boxes to be sold as a result

for access to client

source code + royalties

on per product basis.

Option to license server

code as well.

May 2001 AtomFilms and IFILM

These web only short-film companies will distribute their

shorts to TiVo, allowing viewers to watch these films in

greater comfort than on a PC screen

Unknown

October 2000 BskyB Jointly developing and delivering the TiVo service on

stand-alone PVRs in the UK market

Equity investor. No

licensing revenue

recognized yet

July 2000 Comcast Deploying TiVo market by market to its captive cable

customers. Also jointly developing Comcast’s Personal

TV Service

Equity investor

This portfolio of alliances is perhaps TiVo’s biggest competitive advantage, apart from

its list of patents, which may be considered more contentious in its nature. In the

entertainment industry where “every technical innovation is viewed as an act of war,”2

TiVo has done a surprising job of keeping this network together despite evolving agendas

and occasional conflicts of interest. To date, this has been achieved through a careful

balancing act. For example, while allowing viewers to speed through advertisements at

warp speed, nonetheless, it didn’t go as far as ReplayTV in allowing viewers to

completely skip through commercials in 30 second passages. In addition, TiVo offers an

added carrot for advertisers – the ability to tap into an anonymous database (zipcode-

2 “End Of An Affair”, Damian Cave, Salon.com Technology, 20 June 2001

15

specific only) that reveals what ads have been fast-forwarded, saved and retrieved, and

how often.

Privacy-minded geeks/early adopters were placated by the use of an open Linux

architecture and by the officially lax attitudes toward the “hacking” of the TiVo core.

‘Backdoors’ were deliberately left open. Richard Bulwinkle, TiVo’s director of customer

relations even publicly announced that TiVo would not go after hackers who tried to

increased the capacity of the boxes.3 This created what was seen as a “mutually beneficial

relationship;” allegedly, some staunch Replay TV supporters even switched sides solely

because of this capability to increase the capacity of the TiVo receivers.

TiVo may also have capitalized on stiff competition in the cable TV market – the AT&T

Broadband deal for example materialized after AT&T rival EchoStar Communciations

announced a similar deal with Moxi Digital first.

Ironically, the very strengths of the alliance (which has resulted in TiVo’s heavy

dependence) may turn out to be TiVo’s undoing in the long term particularly as conflicts

of interest continue to evolve. For example, ABC, CBS, Viacom, Walt Disney, NBC,

AOL Time Warner and 20th Century Fox are asking the Federal Court to stop Sonicblue

from selling a new PVR that allows customers to skip commercials without hitting the FF

button, and which would allow owners to send shows to each other over the Internet.

3 "I essentially made a public statement saying we would not go after people for adding memory to their boxes," Bulwinkle says. "We did not say you can hack us ad infinitum, but we did say we would not prosecute people for putting in more memory," Ibid

16

Given that a group of four hackers have just released ExtractStream, a software code that

allows TiVo users to move compressed copies TV shows from their TiVo boxes to their

computers and share them, it is not difficult to see TiVo being the next target. Needless to

say, more than half of the above litigators are TiVo equity investors.

The rapid evolution of the industry, and of the underlying technology, has led to key

TiVo partners also holding equity stakes in rival companies, and to sign non-exclusive

contracts that do not preclude in-house development or multiple contractors. For

example, AOL Time Warner also holds a stake in Moxi Digital. AT&T Broadband,

although currently using TiVo technology, is still looking to develop its own integrated

DVR/satellite set top box. This could clearly influence the depth of AT&T’s commitment

to distributing TiVo, and leaves open the possibility that it may, one day, abruptly shut

TiVo out of the country’s largest cable subscriber base. More current is DIRECTV’s

pending merger with Echostar Communications. TiVo is heavily dependent on

DIRECTV for distribution - almost 50% of its new subscribers come through them.

A realization of this vulnerability may be a part of what’s driving TiVo to focus on

diminishing the importance of subscription fees to their revenues, and towards licensing

and other non-subscription revenues such as advertising.

III. TiVo: Challenges and Competition

Strategic Challenges

TiVo faces a number of serious challenges specific to the “early adopter phase.” The

issues in trying to establish its PVR technology as a standard for home entertainment are:

17

��Adoption/Education: educating customers on TiVo’s fairly large number of

technical features;

��Willingness to Pay: requiring customers to pay both a monthly cable service fee

and a TiVo service fee poses a psychological price barrier

��Competition: The entry of competition, both from powerful industry

‘incumbents’ and from start-ups

��Sustainable Competitive Advantage: Does TiVo have a competitive advantage

over its rivals and how sustainable is it?

��Product Longevity: Is TiVo a fad? Can TiVo make the leap from ‘geek toy’ to a

mass-market product?

The challenges inherent in its chosen business model, e.g. around patents and its strategic

partners have already been touched on. As such, in this section, we will only discuss the

above issues in the context of two broad categories: Competition and Adoption. Part IV

will then talk about the long-term prospects for TiVo and the sustainability of its

technology.

1. The Competitive Challenge

TiVo believes that principal competitive factors in the intensely competitive market for

home entertainment goods and services will be:

��Name recognition (brand)

��Level of performance

��Pricing

��Ease of use

��Functionality

18

Currently, although TiVo ranks comparably with its rivals on all of the above, none of

them really provides TiVo with any sustainable competitive advantages. Ease of use,

performance, pricing, and functionality can be easily imitated or out-matched, and as we

have noted, many brand name companies are considering entry into this market. TiVo

can defend its technology by suing based on its patents, but as we have mentioned, this

will be a difficult, lengthy and costly road.

While one of TiVo’s major advantages is its alliances with strong partners who are

equally interested in seeing widespread deployment of the TiVo technology and are

hence incented to help drive the price down e.g. AOL Time Warner and Sony. However,

even this advantage does not seem to be sustainable as few of these contracts are

exclusive, and we see major rival Replay TV adopting the same strategy, partnering with

powerful industry players, and in some cases, even partnering with the same people.

TiVo faces competition from 2 different sources. The first comes from established

companies in consumer electronic market, especially VCRs (DVD) and cable TV. The

second comes from ‘pure-plays’ such as ReplayTV and Moxi Digital.

VCR

When PVR technology was first made available on a large scale to consumers—with

products such as the Replay TV and the TiVo PTV 100—it was seen as interesting but

not quite as functional as the good old-fashioned VHS standard. Some observers find

PVRs cool but question whether they're really worth the higher price. Others like all the

new functions and options that PVRs provide but don't consider these devices permanent

19

recording solutions. Over time, with the help of technological improvements and a loyal,

almost cult-like following (TiVo claims that over 97% of TiVo users have recommended

it to a friend), TiVo has emerged as a strong competitor to VCR. (See Appendix II for a

full comparison of TiVo and VCR).

VCR’s Advantages:

• The technology is well established and has been around for a long time – no fear

factor to overcome

• Millions of users own VCRs – network effect. Users can easily swap tapes with

each other

• Both the device and the medium are inexpensive.

TiVo’s Advantages:

• Longer recording times (14-60 plus hours of hard drive space available);

• No need to buy or label or store tapes

• Automatic recording process so that you always automatically record the latest

episode even if the scheduling changes;

• “Intelligent” recording; automatically records shows you might like based on your

preferences. Also allows you to record by actor or genre of show

• Pause control over live programs, so you can leave the TV without missing

anything, and

• A single button that lets you speed through commercials

Cable TV

Current trends in cable and satellite TV providers are a major concern to TiVo and other

set-top boxes companies that are the first movers in this space. They face the risk of

having created value (through developing the technology), only to ultimately be locked

20

out of the value capture process. They are bearing the cost of consumer education

currently, and face the risk that once people have been converted to the idea, cable TV

companies may offer TiVo-like services directly to their customers. These players

currently have the advantage of owning the channels into people’s homes and most are

already thinking of incorporating TiVo-like technology directly into the set top boxes.

Whether they license the technology from TiVo as Sony did, or choose to create their

own (as AT&T Broadband has said it will do), or use a competing technology (like

EchoStar using Moxi Digital) will greatly morph the competitive landscape.

There is no question that TiVo has the potential to be a disruptive technology as it

continues to improve. Eventually, consumer demand will require cable TV operators to

provide such services with each set top box. The only question that remains then is how

they will go about meeting this demand.

Replay TV

TiVo’s biggest competitor has traditionally been Replay TV. Unlike TiVo’s business

model, i.e. one based on subsidizing retail products and making it up on service revenues,

Replay did not charge a monthly or lifetime fee – the money was built into the higher

price tags on these units. The major difference was that Replay TV has allowed the

viewer to completely skip all commercials, while TiVo only fast-forwarded the

commercials. In February 2001, Replay TV was acquired by SONICblue. After merging

with SONICblue, their business model has been changed to model of licensing the

technology – like TiVo.

21

Replay TV’s latest debut features a broadband Internet connection and home networking

capabilities which allows programming to be shared with up to 15 users. The current

focus of Replay TV is to develop and market next generation digital platform, and while

the company does not have enough resources on its own, the SONICblue acquisition

should provide all the required assets.

Ultimate TV

In February 2001, Microsoft dove into the personal video-recorder market with Ultimate

TV, buoyed by a $50 million marketing campaign. The pitch for Microsoft's Ultimate TV

was designed to crack one problem TiVo couldn't: effectively communicating how the

technology works and how it can benefit viewers. Ultimate TV only works with DirecTV

satellite - not with Dish Network, not with digital cable, not with traditional cable, and

not with broadcast TV. If customer is already a DirecTV subscriber, he can't use his

current receiver; he needs to replace it. Storage is limited to a single hard drive. The

much-hyped ability to record two channels at the same time only works with the more

expensive "dual LNB" dish antennas and Microsoft's isn't the only system capable of

doing it. Microsoft was first to offer dual DirecTV satellite tuner design--allowing viewer

to watch one program while recording another, or even record two programs while

watching something recorded previously. But TiVo quickly added the feature, requiring

only a software change since its units already had the dual-tuner hardware (See Appendix

2 for full comparison)

22

Early this year, Microsoft announced its exit from the Ultimate TV hardware business.

One report had Microsoft selling only 1,200 units a month since Ultimate TV’s

introduction in March 2001! Lack of market acceptance is the obvious reason for this

decision mainly stemming from resistance to the high price and monthly fees. Microsoft

charges $9.95 a mont0h for the program guide necessary for Ultimate TV to function.

Ironically, this is not the best news for TiVo, which had been secretly hoping to leverage

off Microsoft’s deep pockets and marketing expertise to aid in the uphill task of

educating the mass market.

Dish Network

In 2001, Open TV and Echo Star Communication Corporation released Dish 501, which

is a product that combines basic VCR-like disk recording with a program guide and the

ability to pause life television. Later, Dish Network and Web TV offered a “complete

enhanced TV”, package with four products built into one. It includes a single set-top box

with digital video recording, games, Internet access and interactive TV shows. They

adopted the strategy, which allowed customers not to pay for the box; service was

bundled with the box and attractiveness of the product substantially increased as a result.

Moxi Digital

The latest entrant in the product category is Moxi Digital. They announced that their

product will not be sold directly to consumers, but to cable TV operators, who will then

lease the boxes out to their customers.

23

2. The Adoption Challenge

The early expectations for the volume of TiVo sales have been very high, many predicted

the adoption rate to be much higher that that of VCR in the late 1970s. Unfortunately for

TiVo, these predictions have turned to be unrealistic. When the first recorders hit the

market couple years ago, the reason for the low adoption rate was attributed to consumers

not completely understanding what the machine could do. One of the reasons was

deemed to be TiVo’s over clever and hence somewhat cryptic 30-second TV spots.

Another reason contributing to relatively low adoption rate was the price of the unit,

which at $699, eventually turned to be higher that consumer’s willingness to pay.

Yet, several price drops two years later, there have been no major explosion in sales -

only 300,000 to 400,000 units have been sold over the past 3 years – an adoption rate

comparable with VCR’s in the late 1970’s, but nowhere near the amount projected or the

amount needed to crack the 21 million-unit cable box-market.

A challenge related to this issue of adoption is often called “crossing the chasm.” As is

common with the rollout of new technologies, a high level of technological performance

is often deemed a major competitive advantage. What this often leads to is a cycle of

R&D for the sake of R&D, a technology push as opposed to a pull by mass market

demand. In the case of TiVo, considerable engineering resources are still being devoted

to improving its essential technologies. While this has endeared TiVo to the “early

adaptors” and the “techno-geeks” who adore the eminently hackable Linux platform used

by TiVo, there has been a price to pay. This price is usually, literally, higher prices and

24

more complex features which end up pigeonholing the product to a narrow niche

segment. Hence, the product never quite “crosses the chasm” to the much larger mass

market segment which is generally the key to profitability and break even. While TiVo

recognizes the need to keep finding ways to drop the price and increase mass market

accessibility, the rush toward incorporating more interactive features, internet capabilities

(a la Replay TV), digital photo storage smacks dangerously of the “more technology for

technology’s sake” syndrome.

To sum up the adoption challenge: It is estimated that TiVo will need approximately

675,000 subscribers to break even. As of April 2002, TiVo hit the 425,000 mark. The

recent slew of deals inked by TiVo, as described in Part II, ranging from exclusive

distribution deals inked with Best Buy and AT&T to the rollout of TiVo boxes priced

below $200 may well boost the numbers further and faster, but whether this will be in

time to avert a cash crunch or to firmly establish TiVo in the ranks of ubiquity before the

next hot product/technology hits the market remains to be seen.

25

4.Predictions for Future of TiVo

Financial

Until now, TiVo has not been able to generate revenues at a significant rate and has

suffered big net losses every year since the start-up of the company in 1997. TiVo will

need considerably more funds to continue its research and development program and to

market and launch new products. In January 31, 2002, TiVo had $52.3 million of cash

and cash equivalents. The management of TiVo believes that these funds should keep the

company liquid for one more year. TiVo launched a savings program earlier this year,

slashing jobs to reduce cash outflow. It may be difficult for TiVo to raise more funding

from venture capitalists since many of these are focusing on projects with a track record

of profitability theses days. AOL holds a 30% equity stake in TiVo but has until now

refused to increase its ownership in the company. Unless the market takes off seriously

during 2002 and generates revenue through subscription revenues, TiVo will be in a

situation where more capital is needed. See appendix IV and V for full income statement

and balance sheet.

Patents/Intellectual Property

Until January 31, 2002, TiVo had filed 131 patent applications and been awarded 33.

According to the management of TiVo, the patent applications have been kept broad in

nature to try to cover the basic technology, rather than special technical details or

features. The patent applications are supposed to cover the entire TiVo technology,

including hardware, software and the TiVo service. TiVo has also filed numerous

trademark applications on brands and slogans related to TiVo’s field of activities. Patents

26

are very important since TiVo (and its competitor Replay TV) wants to make the cable

TV operator and consumer electronics manufacturers dependent on their technology. It is

however at this point unclear how strong the patents that TiVo and its competitors hold

are. TiVo’s patents are currently being contested in lawsuits filed by several companies

(Sonicblue, Command Audio, Pause Technology) holding other patents on PVR. TiVo

has also filed a lawsuit against SonicBlue for patent infringement. If TiVo would lose

these trials, it is likely that their business would be harmed considerably. Many of the

companies that TiVo is meeting in court have considerably better financial strength TiVo

can just not afford to fight off their competitors through lengthy legal procedures.

International Expansion

United Kingdom is the only country outside the United States where TiVo has chosen to

establish itself. Until now, the only market TiVo has entered is UK, where subscriptions

are being acquired at a very slow pace. In most European countries the offering of TV

channels is much more limited than in the United States, making TiVo’s key value

proposition (the ability to organize a wealth of channels and programming) considerably

weaker. Cable TV is less built out in Europe, which makes it more difficult for TiVo to

reach out to a captive audience of TV viewers. Considering TiVo’s limited resources it is

probably wise to focus on the US market. If TiVo is not able to establish a market in

America where the TV has a very strong position it is unlikely that they will have success

on other continents.

27

Concluding Remarks

TiVo’s ambition to create an open standard for personal TV and earn revenues on

licensing their technology to producers of consumer electronic goods is tenuous. The key

to success in this field would be strong patents. The value of TiVo’s patents have

however not yet been tested in court. We doubt that TiVo will have enough resources to

win long, drawn-out battles against their more financially solid rivals.

All new consumer electronic products are subject to some inertia in the market at the

beginning of their lifetime. We feel that it will very difficult for TiVo to educate the

customers and reach the critical mass of consumers they so desperately need in order to

earn revenues on boxes and subscriptions while disciplining their cash outflow. The only

viable option for TiVo to survive is to gain access to a secure source of cash to enable

them to continue the education process of its viewers and to adequately defend its

patents. A possible option would be a merger or and acquisition of TiVo by a larger firm.

TiVo has been able to create partnerships with important players in the whole value

chain. While this has probably been TiVo’s strongest competitive advantage so far, TiVo

will face a major challenge in balancing the different interests of their partners and

continue keeping the alliance together.

If more people begin using a PVR, there is a risk that cable companies and broadcasting

companies will lose a big part of their advertising revenues. As mentioned earlier in this

report, co-opting advertisers through the sale of interactive commercials and sponsored

28

TV may be one way around the problem. If TiVo does not succeed here, it is likely that

the powerful networks will try to drive TiVo out of business by lawsuits and other means.

To conclude, we believe that the road ahead for TiVo will be a difficult one due to the

slow market growth, the TV networks’ interest in maintaining advertising in the form it is

today, the unclear patent situation, and the financial burden involved in fending off

determined rivals while growing a brand and a customer base.

29

5. List of References

[1] www.tivo.com - Tivo Inc. Homepage

[2] SEC filing 10-K for the fiscal year ended January 31, 2002, Tivo Inc.

[3] “TiVo - Don't Buy One Just Yet”, Phil Karn, January 2000

[4] “TiVo Revisited”, Phil Karn, October 2001

[5] “End of an affair?”, Damien Cave, Salon.com June 2001

[6] “ReplayTV vs. TiVo, the comparison chart”, Eric W. Lund, January 2001

[7] “10 ways Tivo will change your life”, BBC News, Septembet 2000

[8] “TiVo Or Not TiVo?”, Chris Taylor, Time.com, May 2001

[9] “Entertainment; Clicking Outside the Box”, Saul Hansell, The New York Times,

September 2000

[10] “Outlook 2000: Technology & Media; Technology Could Soon Hand TV

Control to the Viewer”, Bernard Weinraub, The New York Times,

December 1999

[11] “In the U.S., Interactive TV Still Awaits An Audience”, Jennifer 8. Lee, The

New York Times, December 2001

[12] “Technology; Networks See Threat in New Video Recorder”, LAurie J. Flynn,

The New York Times, November 2001

[13] “Skip-the-Ads TV Has Madison Ave. Upset”, Amy Harmon, The New York

Times, May 2002

[14] “TiVo Shares Soar on Patent Win”, Reuters, May 2001

[15] “Don't People Want to Control Their TV's?”, Roy Furchgott, The New York

Times, August 2000

30

[16] “TiVo revamps business plan, sheds workers”, Richard Shim, CNET News.com,

April 2001

[17] “TiVo vs. UltimateTV, Part I”, David Coursey, AnchorDesk, April 2001

[18] “TiVo vs. UltimateTV”, Fresh Gear, January 2002

[19] “TiVo Shifts Marketing Focus, Unveils AOL Deal”, Bob Tourtellotte, Reuters,

January 2001

[20] “Great Gadget, But...”, Daniel Kadlec, ON Magazine, July 2001

[21] “The Next Digital TV Recorders”, Arik Hesseldahl, Forbes.com, January 2002

[22] “TiVo Buys Itself Time by Raising $51 Million”, George Mannes,

TheStreet.com, August 2001

[23] “TiVo files for IPO, teams with Sony”, Stephanie Miles, CNET News.com,

September 1999

[24] “Sony to make TiVo personal TV”, Robert Lemos, ZDNet News, September

1999

[25] “ReplayTV revisits recorder strategy”, Anna Mathews, Wall Street Journal,

November 2000

[26] “Digital TV in the UK: the story so far”, Luke Goode, University of Auckland

[27] “TiVo and the Internet: A Portent of Things to Come”, Justin Belinski, January

2001

[28] “The digital TV Revolution – Setting the Pace, Analysis of the Digital Set-Top

Box Industry”, High Technology Strategy and Entrepreneurship, INSEAD,

June 2001

[29] “DVD”, High Technology Strategy and Entrepreneurship, INSEAD

31

[30] “TiVo and Replay Drive Media Companies Nuts”, Josh Bernoff and Joseph L.

Butt, Jr., Forrester Research, August 1999

[31] “Is TiVo’s Signal Fading?”, Business Week Online, September 2001

[32] “One to watch”, Deborah Claymon, RedHerring, August 1998

[33] “Vulcan hedges bet on personalized TV”, Georgie Raik-Allen, RedHerring,

January 1999

[34] “The VCR, version 2.0”, Rafe Needleman, RedHerring, April 1999

[35] “Tivo IPO winners include…”, Tom Davey, RedHerring, October 1999

[36] “Revenge of Tivo (and ReplayTV)”, Rafe Needleman, RedHerring, August 2000

[37] “A media merger in your living room”, Rafe Needleman, RedHerring,

February 2002

[38] “TiVo Inc. Financials”, Hoover’s Online

32

APPENDIX I4: TiVo INVESTORS AND PARTNERS

Equity Investors

America Online (AOL), Advance/Newhouse, CBS, Comcast Corporation, Cox Communications,

DIRECTV, Discovery Communications, Encore Media Group, Liberty Media subsidiaries, Liberty

Digital, NBC, Philips Electronics, Showtime Networks, SONY, TV Guide Interactive and The Walt

Disney Company — leading companies from every facet of both the television and

communications industries have embraced TiVo's concept of personal television and made equity

investments in the company.

Consumer Electronics

Philips Electronics, Sony Corporation of America and Thomson Multimedia — top consumer

electronic manufacturers — have incorporated TiVo Personal TV Service into their own branded

personal video recorders.

4 TiVo website

33

Programming

Animal Planet, Cinemax, CNBC, Discovery, E! Entertainment, Encore, FLIX, HBO, Home &

Garden Television, The Learning Channel, The Movie Channel, NBC, Showtime, Starz!,

Sundance Channel, Travel Channel, and Westerns Encore — TiVo has created "Network

Showcases," branded areas in which TiVo users can search for and record from daily updates of

the best shows these networks have to offer.

Technology Suppliers

Liberate — interactive capabilities for the TiVo-enabled personal video recorder will be enabled

by Liberate's TV set-top box software. OpenTV — integration with OpenTV will further allow

multiple service offerings to run on the TiVo platform, including the ability for TiVo and its partners

to author content for the TiVo Service using standard protocols such as HTML and JavaScript.

Quantum — the Consumer Electronics Business Unit (CEBU) of Quantum Corporation's Hard

Disk Drive Group is a premier partner and supplier of digital storage technology for TiVo's

Personal TV Service. Powered from the beginning by Quantum QuickView audio/video

technology, the TiVo Personal TV Service digitally records television shows without videotape.

Satellite Service Providers

DIRECTV - Developing personal video recorders that incorporate both the TiVo Personal TV

Service and its own service offerings into one receiver. British Sky Broadcasting Group and TiVo

Inc. are jointly developing and delivering the TiVo service on stand-alone personal video

recorders in the U.K. market.

34

Interactive TV

America Online - AOL will develop a co-branded AOLTV and TiVo-enabled personal video

recorder.

Video on Demand

Blockbuster - Working together to develop a video on demand-like service that will eventually

allow TiVo subscribers to obtain movies directly through their TiVo recorders.

Content AtomFilms and IFILM — These innovative web-based short-film companies have partnered with

TiVo to deliver their programming on "TiVo Takes," TiVo's weekly guide to the best programming

on television.

Promotions

Creative Artists Agency - A talent agency that is promoting TiVo to bring it into the mainstream of

American entertainment.

35

APPENDIX II: COMPARISON OF TiVo, REPLAY TV AND VCR5

Feature Replay TV TiVo VCR

Manual deletion of recordings

Yes, with "Are you sure?" confirmation. Deleting a Replay Channel removes all recordings belonging to that Channel.

Yes, with "Are you sure?" confirmation.

May overwrite whole tape or any portion.

Automatic deletion of recordings

Repeating, non-guaranteed recordings deleted oldest-first. New episodes overwrite old ones, keeping up to seven shows at once (for a show-based Replay Channels) or within a maximum space allotment (for zone and theme-based Replay Channels). Guaranteed recordings will never be auto-deleted.

TiVo Suggestions deleted as needed to make room for other recordings. Scheduled recordings are saved for at least as long as their expiration (default is two days), and are deleted in order of their expiration dates when room is needed for more scheduled recordings. Only individual shows (not Season Passes) may have their expiration extended when scheduling them, but all recordings may be extended after they are recorded. Shows may also have their expiration shortened, at your option, when there is a scheduling conflict After software release this year, Season Passes may be extended at scheduling time, and may be limited to keeping only a certain number at once.

If you leave a rewound tape in, new recordings will overwrite old ones.

Save a recording

permanently

Yes, any show may be saved permanently after it has been recorded. Since Guaranteed recordings are never auto-deleted, marking a show as guaranteed let's you save a show

Yes, any show may be saved permanently after it has been recorded, but not at scheduling time. However, see "Automatic deletion of recordings" regarding extending a show's expiration date at

Yes, take out the tape and hide it in your sock drawer.

5 Source: Internet website

36

permanently when scheduling it. Still, you might want to explicitly mark a guaranteed recording as saved to move it out of its Replay Channel.

scheduling time.

Video editing No, get over it. No, don't even think it. May overwrite portions of recordings; some allow audio dubbing; programs may be duped (and in some cases edited) in two-machine setups.

Delete portions of recordings

No. No. No, short of cutting the tape with scissors.

Dump to videotape

(convenience features)

Displays an episode slate" with show name and details while displaying a countdown timer from 10.

Philips boxes display a countdown timer from 10 (but no episode slate). Sony units display an episode slate with show name and details while pausing ten seconds (but no countdown shown). SVR-2000 has VCR control for Sony VCRs only. VCR control for other models in future software release.

It's already on tape, silly.

37

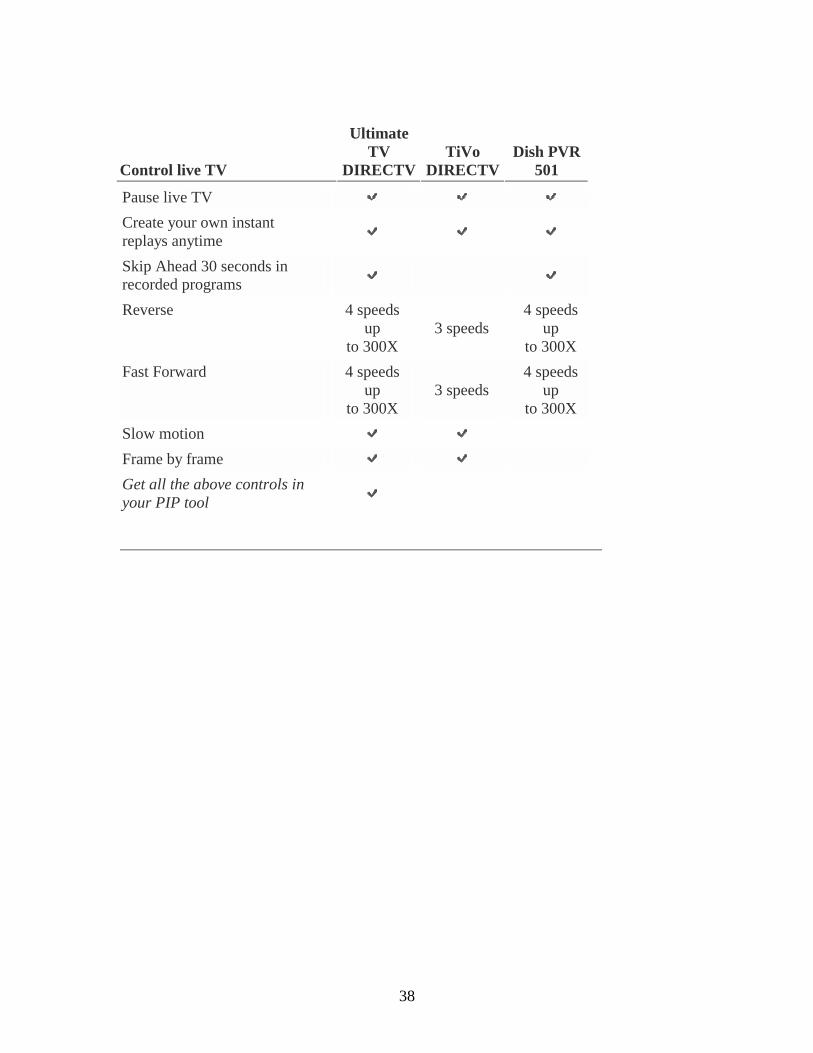

APPENDIX III: COMPARISON OF TiVo, ULTIMATE TV AND DISH PVR 5016

Record

Ultimate TV

DIRECTVTiVo

DIRECTVDish PVR

501 Up to 35 hours of digital video recording (actual recording capacity depends on the type of programming being recorded)

Guide to future programs Up to 14 days

Up to 14 days 2 days

Watch two live shows at once using Picture-In-Picture (PIP)

Record two shows at the same time*

Watch one show while recording another

Record two live shows while watching a recorded one

Record with one touch of a button

Protect recordings so they don't get erased

Custom record segments of shows

6 Source: Internet website

38

Control live TV

Ultimate TV

DIRECTVTiVo

DIRECTVDish PVR

501 Pause live TV Create your own instant replays anytime

Skip Ahead 30 seconds in recorded programs

Reverse 4 speeds up

to 300X 3 speeds

4 speeds up

to 300X Fast Forward 4 speeds

up to 300X

3 speeds 4 speeds

up to 300X

Slow motion Frame by frame Get all the above controls in your PIP tool

39

It's Easy

Ultimate TV

DIRECTVTiVo

DIRECTVDish PVR

501 Search TV for your favorite shows

Personalized TV Favorite Channel lists 6 2 4

Reminders when your favorite TV shows are on

Order Pay Per View programs with your remote control

Parental Locks - lock channels or shows based on content and rating

Limit spending on Pay Per View programs

Software upgrades via the satellite

Dolby Digital enabled

40

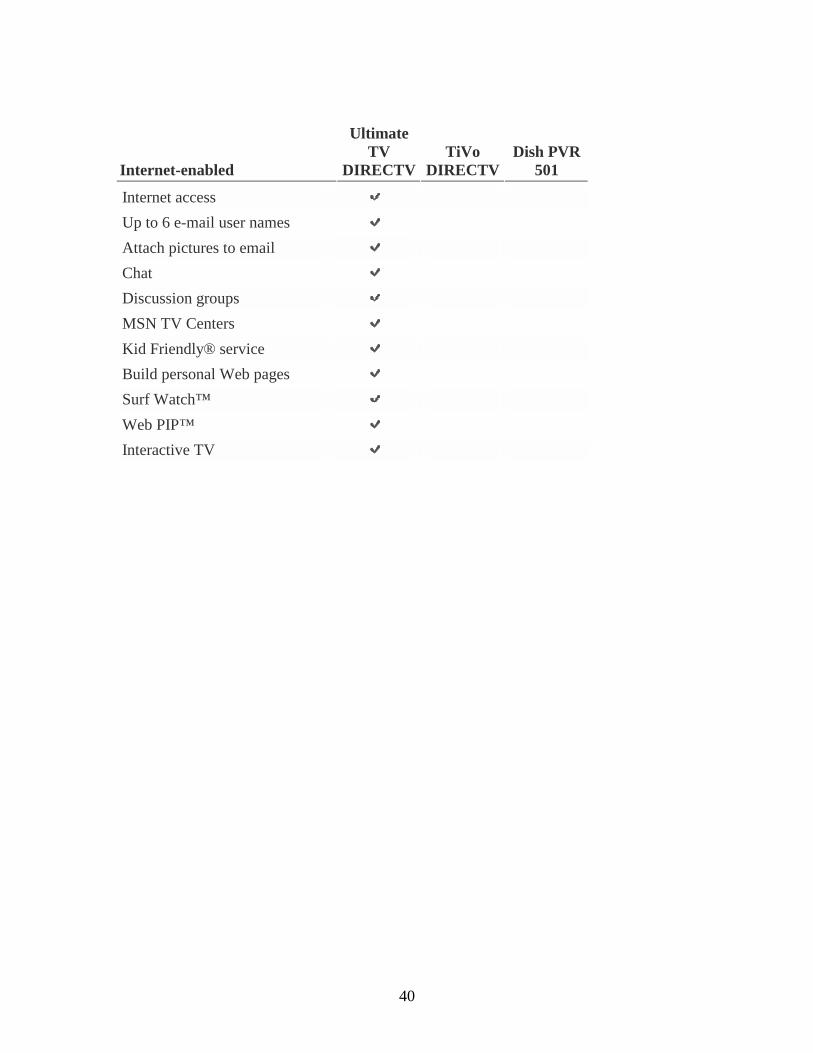

Internet-enabled

Ultimate TV

DIRECTVTiVo

DIRECTVDish PVR

501 Internet access Up to 6 e-mail user names Attach pictures to email Chat Discussion groups MSN TV Centers Kid Friendly® service Build personal Web pages Surf Watch™ Web PIP™ Interactive TV

41

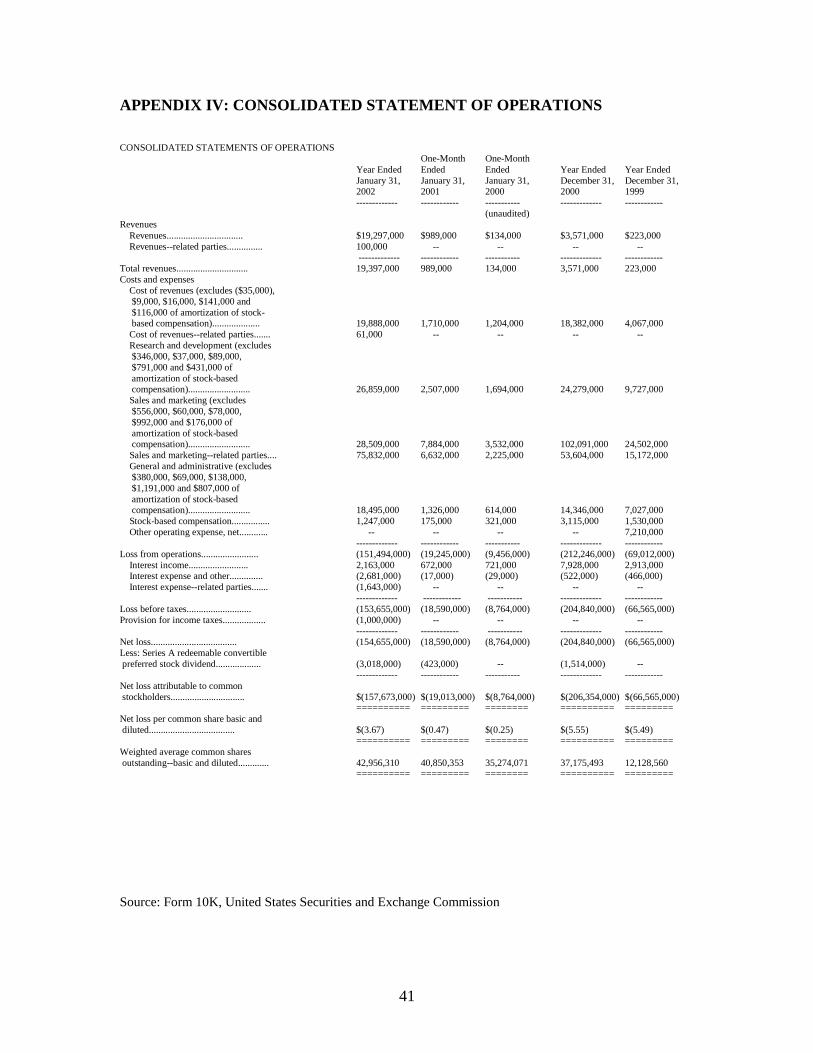

APPENDIX IV: CONSOLIDATED STATEMENT OF OPERATIONS

Source: Form 10K, United States Securities and Exchange Commission

CONSOLIDATED STATEMENTS OF OPERATIONS One-Month One-Month Year Ended Ended Ended Year Ended Year Ended January 31, January 31, January 31, December 31, December 31, 2002 2001 2000 2000 1999 ------------- ------------ ----------- ------------- ------------ (unaudited) Revenues Revenues................................ $19,297,000 $989,000 $134,000 $3,571,000 $223,000 Revenues--related parties............... 100,000 -- -- -- -- ------------- ------------ ----------- ------------- ------------ Total revenues.............................. 19,397,000 989,000 134,000 3,571,000 223,000 Costs and expenses Cost of revenues (excludes ($35,000), $9,000, $16,000, $141,000 and $116,000 of amortization of stock- based compensation).................... 19,888,000 1,710,000 1,204,000 18,382,000 4,067,000 Cost of revenues--related parties....... 61,000 -- -- -- -- Research and development (excludes $346,000, $37,000, $89,000, $791,000 and $431,000 of amortization of stock-based compensation).......................... 26,859,000 2,507,000 1,694,000 24,279,000 9,727,000 Sales and marketing (excludes $556,000, $60,000, $78,000, $992,000 and $176,000 of amortization of stock-based compensation).......................... 28,509,000 7,884,000 3,532,000 102,091,000 24,502,000 Sales and marketing--related parties.... 75,832,000 6,632,000 2,225,000 53,604,000 15,172,000 General and administrative (excludes $380,000, $69,000, $138,000, $1,191,000 and $807,000 of amortization of stock-based compensation).......................... 18,495,000 1,326,000 614,000 14,346,000 7,027,000 Stock-based compensation................ 1,247,000 175,000 321,000 3,115,000 1,530,000 Other operating expense, net............ -- -- -- -- 7,210,000 ------------- ------------ ----------- ------------- ------------ Loss from operations........................ (151,494,000) (19,245,000) (9,456,000) (212,246,000) (69,012,000) Interest income......................... 2,163,000 672,000 721,000 7,928,000 2,913,000 Interest expense and other.............. (2,681,000) (17,000) (29,000) (522,000) (466,000) Interest expense--related parties....... (1,643,000) -- -- -- -- ------------- ------------ ----------- ------------- ------------ Loss before taxes........................... (153,655,000) (18,590,000) (8,764,000) (204,840,000) (66,565,000) Provision for income taxes.................. (1,000,000) -- -- -- -- ------------- ------------ ----------- ------------- ------------ Net loss.................................... (154,655,000) (18,590,000) (8,764,000) (204,840,000) (66,565,000) Less: Series A redeemable convertible preferred stock dividend................... (3,018,000) (423,000) -- (1,514,000) -- ------------- ------------ ----------- ------------- ------------ Net loss attributable to common stockholders............................... $(157,673,000) $(19,013,000) $(8,764,000) $(206,354,000) $(66,565,000) ========== ========= ======== ========== ========= Net loss per common share basic and diluted.................................... $(3.67) $(0.47) $(0.25) $(5.55) $(5.49) ========== ========= ======== ========== ========= Weighted average common shares outstanding--basic and diluted............. 42,956,310 40,850,353 35,274,071 37,175,493 12,128,560 ========== ========= ======== ========== =========

42

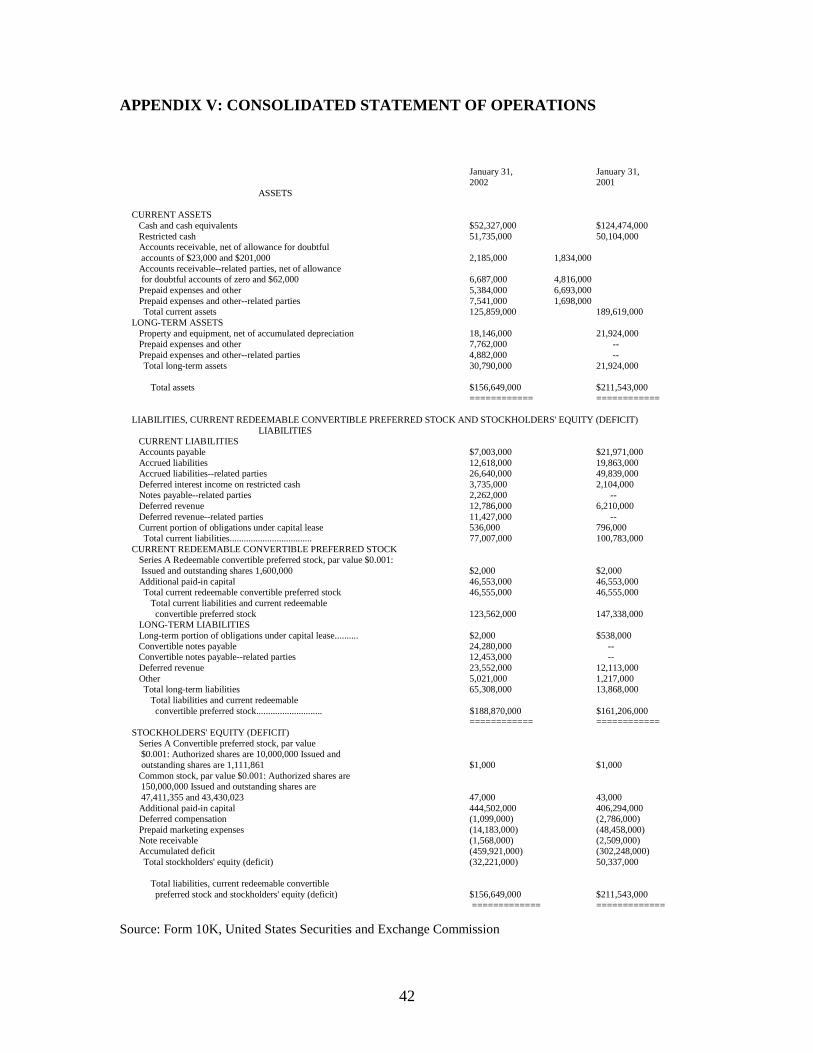

APPENDIX V: CONSOLIDATED STATEMENT OF OPERATIONS

Source: Form 10K, United States Securities and Exchange Commission

January 31, January 31, 2002 2001

ASSETS CURRENT ASSETS Cash and cash equivalents $52,327,000 $124,474,000 Restricted cash 51,735,000 50,104,000 Accounts receivable, net of allowance for doubtful accounts of $23,000 and $201,000 2,185,000 1,834,000 Accounts receivable--related parties, net of allowance for doubtful accounts of zero and $62,000 6,687,000 4,816,000 Prepaid expenses and other 5,384,000 6,693,000 Prepaid expenses and other--related parties 7,541,000 1,698,000 Total current assets 125,859,000 189,619,000 LONG-TERM ASSETS Property and equipment, net of accumulated depreciation 18,146,000 21,924,000 Prepaid expenses and other 7,762,000 -- Prepaid expenses and other--related parties 4,882,000 -- Total long-term assets 30,790,000 21,924,000 Total assets $156,649,000 $211,543,000 ============ ============ LIABILITIES, CURRENT REDEEMABLE CONVERTIBLE PREFERRED STOCK AND STOCKHOLDERS' EQUITY (DEFICIT)

LIABILITIES CURRENT LIABILITIES Accounts payable $7,003,000 $21,971,000 Accrued liabilities 12,618,000 19,863,000 Accrued liabilities--related parties 26,640,000 49,839,000 Deferred interest income on restricted cash 3,735,000 2,104,000 Notes payable--related parties 2,262,000 -- Deferred revenue 12,786,000 6,210,000 Deferred revenue--related parties 11,427,000 -- Current portion of obligations under capital lease 536,000 796,000 Total current liabilities................................... 77,007,000 100,783,000 CURRENT REDEEMABLE CONVERTIBLE PREFERRED STOCK Series A Redeemable convertible preferred stock, par value $0.001: Issued and outstanding shares 1,600,000 $2,000 $2,000 Additional paid-in capital 46,553,000 46,553,000 Total current redeemable convertible preferred stock 46,555,000 46,555,000 Total current liabilities and current redeemable convertible preferred stock 123,562,000 147,338,000 LONG-TERM LIABILITIES Long-term portion of obligations under capital lease.......... $2,000 $538,000 Convertible notes payable 24,280,000 -- Convertible notes payable--related parties 12,453,000 -- Deferred revenue 23,552,000 12,113,000 Other 5,021,000 1,217,000 Total long-term liabilities 65,308,000 13,868,000 Total liabilities and current redeemable convertible preferred stock............................ $188,870,000 $161,206,000 ============ ============ STOCKHOLDERS' EQUITY (DEFICIT) Series A Convertible preferred stock, par value $0.001: Authorized shares are 10,000,000 Issued and outstanding shares are 1,111,861 $1,000 $1,000 Common stock, par value $0.001: Authorized shares are 150,000,000 Issued and outstanding shares are 47,411,355 and 43,430,023 47,000 43,000 Additional paid-in capital 444,502,000 406,294,000 Deferred compensation (1,099,000) (2,786,000) Prepaid marketing expenses (14,183,000) (48,458,000) Note receivable (1,568,000) (2,509,000) Accumulated deficit (459,921,000) (302,248,000) Total stockholders' equity (deficit) (32,221,000) 50,337,000 Total liabilities, current redeemable convertible preferred stock and stockholders' equity (deficit) $156,649,000 $211,543,000

============= =============