The safe haven - Bank zweiplus

19

bank zweiplus customer magazine, 1/2009 The safe haven Your “surplus” for more security surrounding your money. So you can sleep soundly. And still not miss any opportunity. In focus New e-banking system: Security with simplicity Money tips New Swiss depositor protection: You can be well-diversified at just one bank too Interview Dr. Jan Amrit Poser, Chief Economist at Bank Sarasin, talks about the security of investments Where is my safe haven? Financial services put to the test. Dossier on page 8

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of The safe haven - Bank zweiplus

bank zweiplus customer magazine, 1/2009

The safe havenYour “surplus” for more security surrounding your money. So you can sleep soundly. And still not miss any opportunity.

In focus New e-banking system: Security with simplicity

Money tips New Swiss depositor protection: You can be well-diversified at just one bank too

InterviewDr. Jan Amrit Poser, Chief Economist at Bank Sarasin, talks about the security of investments

Where is my safe haven? Financial services put to the test. Dossier on page 8

ALSO WITH BOXER DIESEL ALSO WITH BOXER DIESEL ALSO WITH BOXER DIESEL ALSO WITH BOXER DIESEL

www.subaru.ch SUBARU Switzerland AG, Industriestrasse, 5745 Safenwil, Tel. 062 788 89 00. Subaru dealers: around 200. www.multilease.ch Net non-binding price recommendation inclusive of 7.6% VAT.

Spacious: The new Forester AWD.Great value: From CHF 32.800.–.

Increased safety for all.ABS with electronic brake-force distribution and brake assist; driver, passenger andside airbags at the front; head airbags in the front and back; all-round impact pro-tection; active head rests in the front; electronic vehicle dynamics control and Isofixchild seat anchors.

More comfortable ride.Comfort chassis with rear automatic level control. Dual-range 2x5 speed manualwith hill start assist or automatic with SPORTSHIFT® in 2.0 liter models or 5-speedmanual or automatic with SPORTSHIFT® in 2.5 liter models. Large panoramic glasswindscreen (2.0XS Limited and 2.5XT Executive). Excellent panoramic view. Blue il-luminated interior.

Increased all-wheel safety.Only Subaru offers Symmetrical AWD (the Subaru 4x4 system). The longitudinally in-stalled SUBARU BOXER engine gives the car a low center of gravity. Coupled withthe symmetrical all-wheel powertrain, this makes for greater road grip and stability.

More car for the money.For example, in the Forester 2.5XT AWD Executive (starting at CHF 46.800.–): Aluminumalloy 4-cylinder 16V SUBARU BOXER engine, 2457 cm3, 230 hp, keyless entry-and-gosystem with a start-and-stop button, automatic air-conditioning including pollen filters, leather interior, radio/CD player with MP3, WMA and DVD readers and 7 speakers, cruisecontrol, navigation system and Bluetooth®-ready, ground clearance of 22.5 cm, bootcapacity of up to 1610 liters (VDA).

SPORTSHIFT® is a registered trademark of Prodrive Ltd. Energy efficiency category D, CO2 198/199 g/km, total consumption 8.4 l/100 km (2.0, man./auto.).Average for all the new models available: 204 g/km.

The perfect combination of dynamic SUV andcomfortable limousine. A high-performance, modern crossover. Be inspired by its accelerationand smooth running, with features that leave nothing to be desired. Boundless potential for use.

JUSTY TWO, 5-doorFront wheel drive, 51 hpCHF 16.000.–. From March 2009

IMPREZA AWD, 5-doorfrom 1.5 l /107 hp to 2.5 l Turbo/300 hpfrom CHF 25.800.– to CHF 59.200.–

FORESTER AWD, 5-doorfrom 2.0 l /147 hp to 2.5 l Turbo/230 hpfrom CHF 32.800.– to CHF 49.800.–

LEGACY AWD, 4/5-doorfrom 2.0 l /150 hp to 3.0 l /6 cyl. /245 hpfrom CHF 29.900.– to CHF 58.300.–

OUTBACK AWD, 5-doorfrom 2.0 l /150 hp to 3.0 l /6 cyl. /245 hpfrom CHF 40.100.– to CHF 57.300.–

TRIBECA AWD, 5-door3.6 l /6 cyl. /258 hp 5 or 5+2 seatsfrom CHF 59.000.– to CHF 67.500.–

118938_210x297_e_K_Fore 19.12.2008 11:50 Uhr Seite 1

3surplus 1/2009 Editorial The safe haven

Contents

Dear readersIt’s a great pleasure for me to present today the very first edition of “surplus” – the new bank zweiplus customer magazine.

“surplus” offers our customers interesting and useful information surrounding the key topic “safe haven.” This issue addresses the topic in a series of editorial articles, complemented in a report in the middle of the magazine and featuring an interview with Dr. Jan Poser, Chief Economist at Bank Sarasin.

As significant as 2008 is anchored in the history of bank zweiplus as the founding year of the company, noteworthy is that it will also go down in the annals of history of the global economy as “the year of the worst banking and financial crisis.” In my view, it therefore seems even more essential that “surplus” provides specific, useful tips enabling our customers to navigate their investments into a “safe haven,” even amid turbulent times. At the same time, of course, the employees of bank zweiplus are always eager to stand by your side as well, with their sound know-how and efficient performance. Indeed, it’s our declared goal that your assets are always in safe hands with bank zweiplus.

In the future, “surplus” should also convey our most important organizational objective to the same extent as our Bank: i.e., consistently offering extra tangible advantages to our valued customers in accordance with our guiding principle, “one plus one equals zweiplus.”

I hope you thoroughly enjoy reading this first issue of “surplus.”

Sincerely,

Marco WeberCEO

Current issues4 Range of cards is now complete Following Visa and Swiss Travel Cash, now comes the Maestro Card4 News5 Investing with buy and hold Holding stocks for ten years?

In focus6 New e-banking system Security with simplicity

Dossier8 Where is my safe haven? Financial services put to the test12 Secure investing in the crisis: The Swiss franc is a safe haven. Interview with Dr. Jan Amrit Poser, Chief Economist at Bank Sarasin 14 Our forecasts

Money tips16 The new Swiss depositor protection You can be well-diversified at just one bank too

Personal 17 Column The heart shows us the right way

Sponsoring 18 Sponsoring The zweiplus talent team Art on Ice19 Davidoff Swiss Indoors Efficient advertising

4 surplus 1/2009Current issues bank zweiplus

Whether shopping or paying hotel and restaurant bills: With bank zweiplus cred-it cards, you can pay simply by signing your name, or using your personal PIN code – and at more than 9.4 million shops, hotels and restaurants worldwide. bank zweiplus credit cards also offer direct debit as a unique additional function. In fact, you pay no commissions when mak-ing cash withdrawals with direct debit at any ATMs in Switzerland or Liechtenstein. The withdrawals are immediately and di-rectly debited to your bank account. More information on our range of credit cards can be found at www.bankzweiplus.ch › About us › Range of cards.

With a bank zweiplus Maestro Card, you can make cash-free payments in Switzer-land and abroad, or make cash withdraw-als around the clock at over one million ATMs worldwide in the currency of the respective country. But that’s not all: You can also pay for your purchases and expenditures with your bank zweiplus Maestro Card at more than 9.4 million shops, hotels and restaurants worldwide.

The Travel Cash Card is regarded as the most secure travel money and is a more sophisticated version of the trusted Swiss Bankers Travelers Cheques. The card bears the Maestro Card brand and is a so-called pre-paid card, with which you can withdraw cash in local currency at any of more than one million ATMs worldwide. And if lost or stolen, your Travel Cash Card is replaced worldwide at no cost, with the remaining balance credited. In addition, the card is protect-ed with a PIN code and not linked to your

bank account – which makes it even more secure. More information on the Maestro Card and Travel Cash Card can be found at www.bankzweiplus.ch › About us › Range of cards.

Our customer advisor team is looking for-ward to offering you advice and assist-ance in selecting the most appropriate card, via the toll-free telephone number 00800 0800 55 55 from Monday to Friday, between 08:30 and 19:00. You can also access a simplified overview of bank zweiplus prices and fees online at www.bankzweiplus.ch › Paying › Services › Prices and fees. (bz)

NewsChange in minority shareholderAabar Investments PJSC recently an-nounced the purchase of AIG Private Bank Ltd. from its parent company American International Group, Inc. (AIG).

The sale of AIG Private Bank to Aabar Investments PJSC still requires the approval of the relevant supervisory authority: namely, the Swiss Federal Banking Commission (SFBC). Aabar In-vestments PJSC is a global investment firm headquartered in Abu Dhabi.

Bank Sarasin & Co. Ltd. continues to hold a 57.5% equity stake in bank zwei-plus ltd., so the Bank is in fact still a subsidiary of Bank Sarasin & Co. Ltd. from a legal perspective.

For bank zweiplus customers, nothing will change. All AIG Private Bank Ltd. products will continue to be available to you in the same form. (bz)

Launch of the Managed Fund Portfoliobank zweiplus’s objective is to offer a selection of various asset managers with comparable general conditions. As a customer, you then choose your preferred asset manager based on a se-lected list.

Each asset manager will offer the same strategies, which can vary within a pre-defined spectrum ranging from cash, bonds, stocks and alternative in-vestments, depending on the relevant strategy (i.e. “conservative,” “balanced, “growth” or “dynamic”). These available strategies are denominated in the cur-rencies CHF, EUR and USD. (bz)

Range of cards is now completebank zweiplus now features a full assortment of bank cards. Since the outset of 2009, we offer you the new Maestro Card, in addition to credit cards and the Travel Cash Card.

5

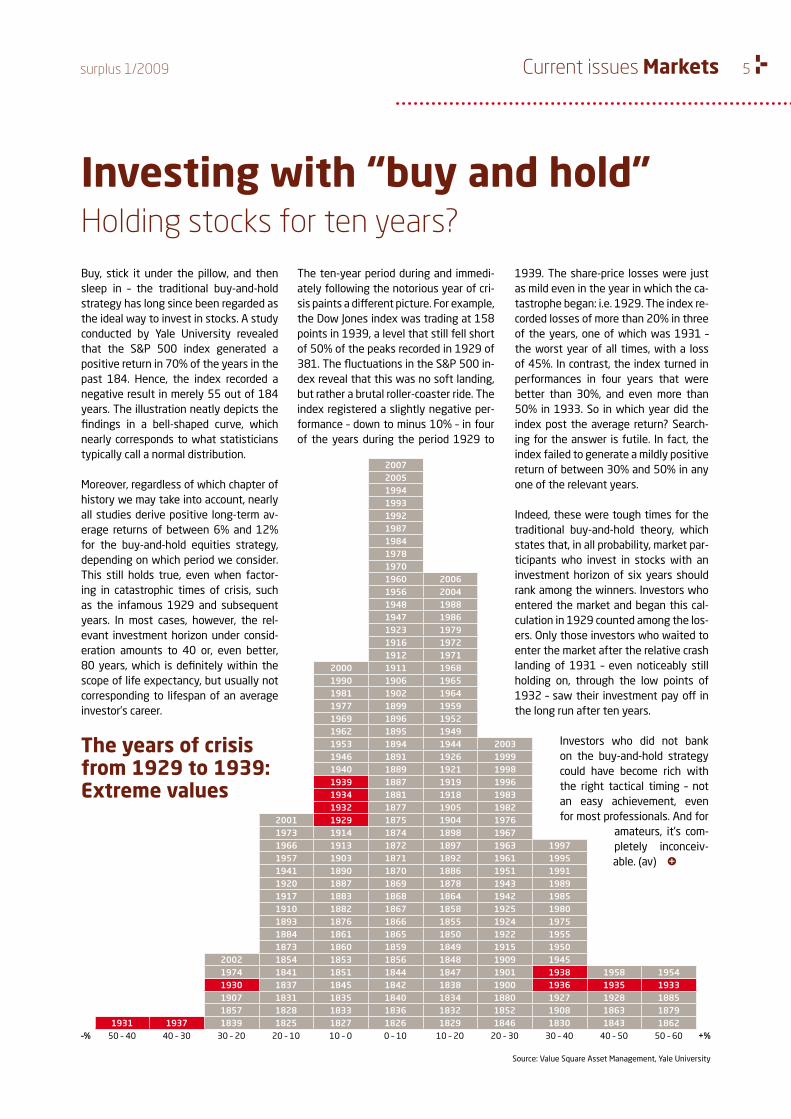

–% +%

2007200519941993199219871984197819701960 20061956 20041948 19881947 19861923 19791916 19721912 1971

2000 1911 19681990 1906 19651981 1902 19641977 1899 19591969 1896 19521962 1895 19491953 1894 1944 20031946 1891 1926 19991940 1889 1921 19981939 1887 1919 19961934 1881 1918 19831932 1877 1905 1982

2001 1929 1875 1904 19761973 1914 1874 1898 19671966 1913 1872 1897 1963 19971957 1903 1871 1892 1961 19951941 1890 1870 1886 1951 19911920 1887 1869 1878 1943 19891917 1883 1868 1864 1942 19851910 1882 1867 1858 1925 19801893 1876 1866 1855 1924 19751884 1861 1865 1850 1922 19551873 1860 1859 1849 1915 1950

2002 1854 1853 1856 1848 1909 19451974 1841 1851 1844 1847 1901 1938 1958 19541930 1837 1845 1842 1838 1900 1936 1935 19331907 1831 1835 1840 1834 1880 1927 1928 18851857 1828 1833 1836 1832 1852 1908 1863 1879

1931 1937 1839 1825 1827 1826 1829 1846 1830 1843 186250 – 40 40 – 30 30 – 20 20 – 10 10 – 0 0 – 10 10 – 20 20 – 30 30 – 40 40 – 50 50 – 60

surplus 1/2009 Current issues Markets

Investing with “buy and hold”Holding stocks for ten years?

Source: Value Square Asset Management, Yale University

Buy, stick it under the pillow, and then sleep in – the traditional buy-and-hold strategy has long since been regarded as the ideal way to invest in stocks. A study conducted by Yale University revealed that the S&P 500 index generated a positive return in 70% of the years in the past 184. Hence, the index recorded a negative result in merely 55 out of 184 years. The illustration neatly depicts the findings in a bell-shaped curve, which nearly corresponds to what statisticians typically call a normal distribution.

Moreover, regardless of which chapter of history we may take into account, nearly all studies derive positive long-term av-erage returns of between 6% and 12% for the buy-and-hold equities strategy, depending on which period we consider. This still holds true, even when factor-ing in catastrophic times of crisis, such as the infamous 1929 and subsequent years. In most cases, however, the rel-evant investment horizon under consid-eration amounts to 40 or, even better, 80 years, which is definitely within the scope of life expectancy, but usually not corresponding to lifespan of an average investor’s career.

The years of crisis from 1929 to 1939: Extreme values

The ten-year period during and immedi-ately following the notorious year of cri-sis paints a different picture. For example, the Dow Jones index was trading at 158 points in 1939, a level that still fell short of 50% of the peaks recorded in 1929 of 381. The fluctuations in the S&P 500 in-dex reveal that this was no soft landing, but rather a brutal roller-coaster ride. The index registered a slightly negative per-formance – down to minus 10% – in four of the years during the period 1929 to

1939. The share-price losses were just as mild even in the year in which the ca-tastrophe began: i.e. 1929. The index re-corded losses of more than 20% in three of the years, one of which was 1931 – the worst year of all times, with a loss of 45%. In contrast, the index turned in performances in four years that were better than 30%, and even more than 50% in 1933. So in which year did the index post the average return? Search-ing for the answer is futile. In fact, the index failed to generate a mildly positive return of between 30% and 50% in any one of the relevant years.

Indeed, these were tough times for the traditional buy-and-hold theory, which states that, in all probability, market par-ticipants who invest in stocks with an investment horizon of six years should rank among the winners. Investors who entered the market and began this cal-culation in 1929 counted among the los-ers. Only those investors who waited to enter the market after the relative crash landing of 1931 – even noticeably still holding on, through the low points of 1932 – saw their investment pay off in the long run after ten years.

Investors who did not bank on the buy-and-hold strategy could have become rich with the right tactical timing – not an easy achievement, even for most professionals. And for

amateurs, it’s com-pletely inconceiv-able. (av)

6 surplus 1/2009

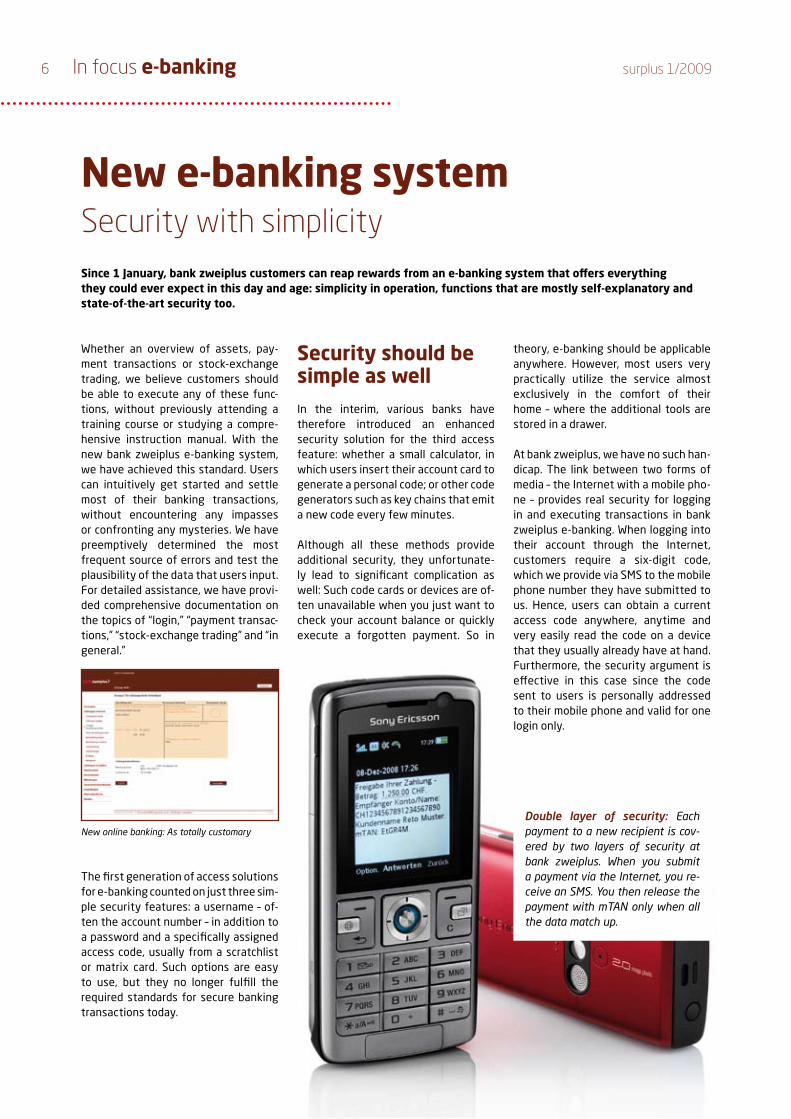

New e-banking systemSecurity with simplicity Since 1 January, bank zweiplus customers can reap rewards from an e-banking system that offers everything they could ever expect in this day and age: simplicity in operation, functions that are mostly self-explanatory and state-of-the-art security too.

In focus e-banking

Security should be simple as well In the interim, various banks have therefore introduced an enhanced security solution for the third access feature: whether a small calculator, in which users insert their account card to generate a personal code; or other code generators such as key chains that emit a new code every few minutes.

Although all these methods provide additional security, they unfortunate-ly lead to significant complication as well: Such code cards or devices are of-ten unavailable when you just want to check your account balance or quickly execute a forgotten payment. So in

theory, e-banking should be applicable anywhere. However, most users very practically utilize the service almost exclusively in the comfort of their home – where the additional tools are stored in a drawer.

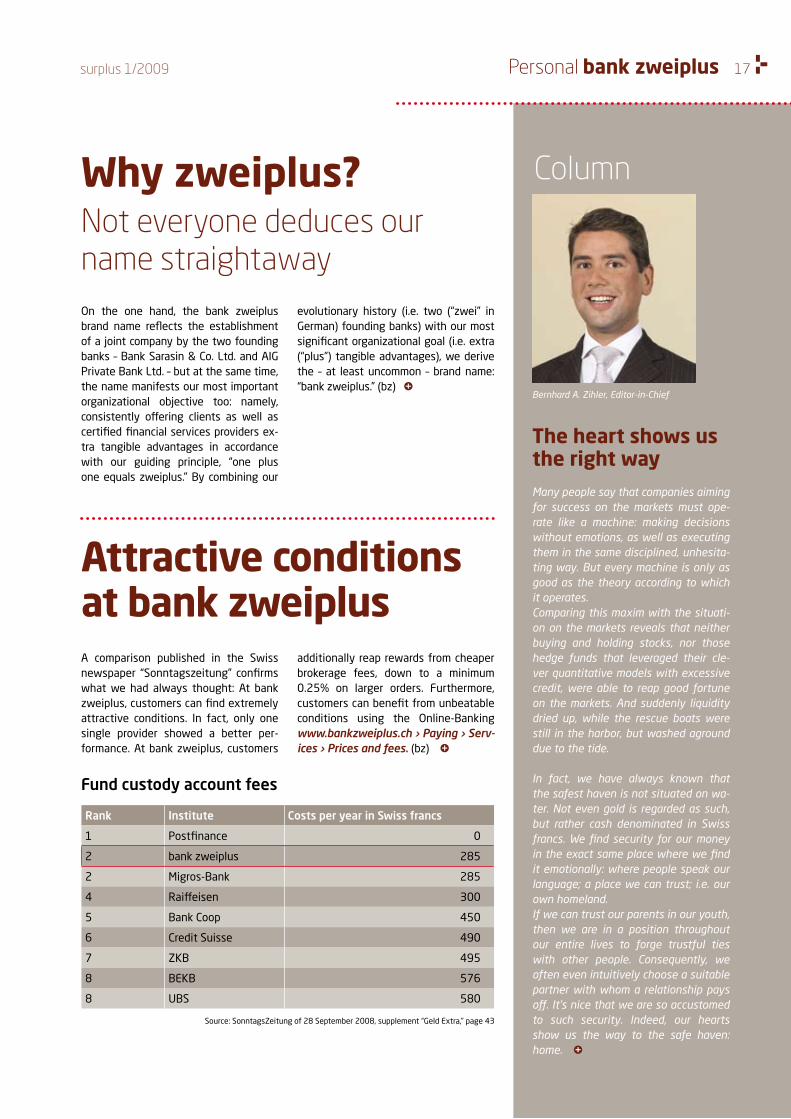

At bank zweiplus, we have no such han-dicap. The link between two forms of media – the Internet with a mobile pho-ne – provides real security for logging in and executing transactions in bank zweiplus e-banking. When logging into their account through the Internet, customers require a six-digit code, which we provide via SMS to the mobile phone number they have submitted to us. Hence, users can obtain a current access code anywhere, anytime and very easily read the code on a device that they usually already have at hand. Furthermore, the security argument is effective in this case since the code sent to users is personally addressed to their mobile phone and valid for one login only.

Whether an overview of assets, pay-ment transactions or stock-exchange trading, we believe customers should be able to execute any of these func-tions, without previously attending a training course or studying a compre-hensive instruction manual. With the new bank zweiplus e-banking system, we have achieved this standard. Users can intuitively get started and settle most of their banking transactions, without encountering any impasses or confronting any mysteries. We have preemptively determined the most frequent source of errors and test the plausibility of the data that users input. For detailed assistance, we have provi-ded comprehensive documentation on the topics of “login,” “payment transac-tions,” “stock-exchange trading” and “in general.”

The first generation of access solutions for e-banking counted on just three sim-ple security features: a username – of-ten the account number – in addition to a password and a specifically assigned access code, usually from a scratchlist or matrix card. Such options are easy to use, but they no longer fulfill the required standards for secure banking transactions today.

Double layer of security: Each payment to a new recipient is cov-ered by two layers of security at bank zweiplus. When you submit a payment via the Internet, you re-ceive an SMS. You then release the payment with mTAN only when all the data match up.

New online banking: As totally customary

7surplus 1/2009 In focus e-banking

For the security of our customers, we have integrated SMS and the Internet to create one of the most state-of-the-art e-banking solutions in Switzerland. Users reap benefits from this integra-ted approach not just in terms of se-curity, but also quite simply in terms of the latest up-to-date, customized information.

This underlying simplicity is not only featured in the payment transactions service, but also applied consistently to all e-banking functions, including stock-exchange trading, which begins with the securities search. Supporting menus are available here, with which users can very swiftly call up the desi-red security number. With the stock-exchange trading function, e-banking precisely follows the logic of an order. Furthermore, bank zweiplus customers can now enjoy this user-friendliness for trading on other stock exchanges such as the XETRA in Frankfurt, NYSE and NASDAQ in New York as well as Euronext in Paris and Amsterdam, in addition to the Swiss exchanges SWX and Virt-X.

With new reports, customer portfolios are presented in e-banking with even more transparency. The asset analysis breaks down investments according to asset classes and currencies. Moreover, the maturity analysis provides a quick overview of the expiration dates of fixed-term deposits, fiduciary invest-ments and bonds, so customers are al-ways up-to-date with regard to the ti-ming of re-investment considerations. Hence, users have quick access to an overview of their assets, enabling them to better plan their financial affairs

The simplicity of our e-banking system, which enables customers to navigate their way through their financial infor-mation, is something we do not want to sacrifice for the sake of security. This poses a real challenge since most me-thods based on security are not really that user-friendly.So-called notifications constitute ano-ther function for providing heightened security as well as for boosting the pro-vision of information. For instance, an account can notify or warn customers if their account balance falls below a

specified amount, or if unusually large outgoing transfers are debited to their account – by whatever means they desire, whether via e-mail or SMS, or even both. (vp)

Customers generally have the possibi-lity of carrying out their banking tran-sactions via our banking line or their customer advisor. In this case, users can request e-banking in “read-only mode,” whereby utilizing the service can never trigger a transaction from e-banking. Customers are able to view the value and positions of their portfolio and have access to all overviews of assets.

Transparent and user-friendlyIn addition to read-only mode, e-ban-king users can also request payment transactions and/or stock-exchange trading services. In developing these functionalities, the focal point was di-rected on security and simplicity in the sense of a user-friendly context. For example, with payment transactions we have designed the screen layout precisely in line with the familiar ori-ginal paper-based documents. Hence, an orange-colored payment slip looks just like its paper counterpart. Moreo-ver, the information that users enter appears exactly in the same place. We have therefore adapted the system to customer conventions, and the users can settle their payment transactions faster and easier – without confusing the input fields or misunderstanding the data to be entered. Regarding other domestic and foreign payment transac-tions, we have also consolidated as many steps as possible to enable users to very quickly and accurately input a payment. The system identifies obvi-ously implausible data already during input: For example, if a bank clearing number is entered that does not even exist, the user is immediately notified.

When users effect payments, the money is debited from their respective account. This is where the greatest potential for danger looms in e-banking. So we have applied a double layer of protection for such transactions: i.e. e-banking requi-res an additional code for each payment to a new recipient. As a result, we send another message to the user via mobile phone, containing a mobile Transaction Authorization Number, or in short, the acronym mTAN (for more details, see the report titled „No chance for hackers“).

No chance for hackersManipulating payment transactions entered into e-banking systems is one of the latest trends pursued by criminal hackers. While users believe that they are sending a pay-ment to their chosen recipient, the hacker is manipulating the transaction during the online cession and instead transferring the payment (sometimes even with the amount revised upward) to another recipient.

At bank zweiplus, this kind of manipulation has no chance of succeeding. We very tho-roughly check each and every time a custo-mer effects a payment to a new recipient to which a transfer has not previously been made. We safeguard against such cases of manipulation through a special means: with mTAN, which stands for mobile Transaction Authorization Number.

bank zweiplus e-banking users receive an mTAN via SMS – together with the amount to be transferred as well as the name of the recipient of their payment – which they should closely scrutinize in terms of whe-ther the information in the SMS actually corresponds to the data they input through the Internet. If the data match, users enter a confirmation of the mTAN via the Internet.

The longer customers use our e-banking system, the less often they are subject to such checks: i.e. bank zweiplus e-banking is engaged in a continuous learning process. Recipients that receive regularly recurring payments from users are placed on their per-sonal positive list. In addition, government authorities, doctors and other institutions, to which many of our customers regularly execute transfers, have possibly long since been placed on the system-wide positive list before users have even made their very first payment. Hence, not every single outgoing payment must be subject to an mTAN. Ne-vertheless, noteworthy is that if customers receive an SMS with an mTAN they should also thoroughly control the contents since this is the only way of preventing manipula-tion of the payment transaction.

8 surplus 1/2009Dossier The safe haven

But the world is no longer so simple. Since banks have filed for bankruptcy in the USA, Iceland and Great Britain, en-tirely different risks have stepped into the spotlight, which can no longer be overlooked as of autumn of last year. Suddenly people are asking themselves the questions: Just how safe is my bank, really? Will I still be able to withdraw my money tomorrow? Is it possible that my bank will go bankrupt too? And how well is my money protected by the govern-ment, or other security system, in case of such an event? The experts call this systemic risk.

The simplest means for severe crisesSo it’s about time to shed some light on all the financial services in terms of where they stand a few months in the wake of these dark days. It’s time to take a look at all the risks, to realize against which risks we should take action as well as identify the other risks over which we should not lose any sleep. ATMs functioned, so people were able to withdraw their money, take it home and stick it under their mattress. Or after fur-

When it comes to money, historically there has been only one area where in-vestors have taken security into consid-eration: investment risk. This involved weighing the risks against the expected returns as well as contemplating which investment is better suited to an in-vestor’s personal profile. Conservative, fixed-income investments in bonds, medium-term notes or savings books all generate lower returns, but with lower risk too. On the other hand, investments in growth-accentuated stocks are sub-ject to the fluctuations on the financial markets and therefore harbor greater risks in the near term, but have generat-ed much better returns in the long run.

Where is my safe haven? Financial services put to the test.There’s a light emerging at the end of the tunnel. The central banks of countries with major currencies have concurred that no more large banks should be allowed to go bankrupt. In addition, these governments are taking action to underpin the banking system and economy with a sense common purpose that has not been seen in decades. This dossier features interesting background information for investors on the topic of security revolving around money and serves as a useful guide for secure investing. By Bernhard A. Zihler and Arne Voelker

Now, fulfill your dreams. There’s no time like the present for solid value. Mortgage interest rates are low, and real estate prices in Swit-zerland are stable. So now is the time to secure long-term financing of your dream house.

9surplus 1/2009 Dossier The safe haven

Spending money leads to security The simplest method to lend a boost to the economy is to spend your money now. But a few expenditures won’t al-leviate the situation either: We all must pay taxes. So don’t put off the payments any longer than necessary. In fact, you earn interest on advance payments at tax offices in most cantons at higher rates than on savings books.

When you pay bills, you should execute the transactions mainly via bank trans-fer. The payment transactions system – the core of the banking system – is situ-ated on solid ground and was never

endangered in any phase of the crisis. The risks relating to payments lie out-side the banking system and particu-larly result from individual behavior. For example, always keep your ATM PIN code confidential; don’t let anyone see it. And when using an e-banking system, you should expect a bank to employ the most state-of-the-art security measures possible. In this area, bank zweiplus is a significant step ahead of most other banks, with the integration of Internet and mobile phone (for more details, see the “In focus” section on page 6).

ther consideration, they put their money in a safe. In fact, sales of personal safes hit record highs last autumn, just as new rental agreements for safe-deposit box-es at banks surged as well.

The decisive disadvantage for every-thing that is held in a safe is that these assets become immovable. Gold gener-ates no dividends (but harbors price risks, see the “Interview” on page 12). And cash that’s not held in an account loses value in most years due to infla-tion. Actually, cash must be utilized in order to offset the effect of inflation – or even more than outweigh the impact.

Who is your counterparty?There was a time not so long ago when people laughed at investors who invested in funds instead of putting their money into the numerous innovative structured products, which came to market so ostensi-bly amid each newly emerging investment theme, often featuring more favorable con-ditions too. But since the emergence of the financial market crisis, this perspective has shifted once again. We would recommend contacting your bank zweiplus customer advisor team, which would be happy to further help you.

Where should I invest my pensi-on capital? When I draw pension funds at retirement, how should I actually invest the money? Per-plexed, many retirees decide on an annuity. In this regard, you can definitely get more for your money than with your pension plan – even amid times of crisis. We‘re looking forward to helping you.

10

The solid ground on which our bank stands is also underpinned by our par-ent company, Bank Sarasin, as well as its parent company, Rabobank – a Netherlands-based cooperative bank and the only bank in Europe that‘s not under state control, with the best credit rating a bank can earn: AAA.(For more details on counterparty risk, see the box “Who is your counterparty?”).

Or invest favorably now?Governments of industrialized coun-tries most certainly rank among the first-class counterparties. Their credit ratings enjoy a top-notch reputation; their government bonds are sought by investors as a safe haven in times of crisis. In fact, the bonds issued by the Swiss Confederation are among the most coveted in the world. Hence, prices for such bonds have also surged strongly since the outset of the crisis, and the yields have therefore declined at the same time. If the crisis were to escalate once again, further price gains could be expected, however. Investors

Although some expenditures are not necessarily essential, they especially pay off at the present time. Because confidence diminishes amid a crisis, people tend to save their money. This particularly affects providers of luxury goods as well as high-value consumer goods. Consequently, watch and jewelry stores are now luring customers with the biggest discounts in the wake of the Christmas sales season, when con-sumption has noticeably dwindled. This is also the case for a new automobile or furniture.

Amid a crisis, it’s important to maintain liquidity Cash can be well preserved with a sav-ings book, where it’s secure until such time as the markets offer opportunities once more. Then, your money should be quickly available again. Hence, don’t disperse your money among too many banks in order to better maintain an overview. Thanks to the new deposi-tor protection in Switzerland, up to CHF 100,000 per depositor and bank is now secure (see the article “Money tips” on page 16). And even better, savings book deposits at bank zweiplus currently earn favorable interest at above-average rates of 1.1% on investment savings accounts and even 1.25% on youth sav-ings accounts and senior-citizen’s sav-ings accounts.

Take a close look at the terms of the savings book offered at the bank you trust with your money and, incidentally, all bank deposits, including private ac-counts for payment transactions. In-deed, only the bank itself is liable for your deposits, so it should be on solid ground. bank zweiplus is just such a solid bank; it neither develops its own financial products nor executes its own trading operations: meaning, we only engage in stock-exchange activities on your behalf, but never in our own specu-lative interests.

looking for that extra return in the realm of bonds can browse through corporates (for more details, see the box “Cheaper than stocks”).

Even though stocks have already lost substantial ground, perhaps they’re not yet really that cheap (for more details on stock valuations, see the box “Stocks with a margin of safety”) because the risks are still rather aligned to the down-

surplus 1/2009Dossier The safe haven

11

side. But a little courage cannot hurt: For instance, investors could enter the stock market with a small share of their assets, maybe 5%, thereafter emotion-ally experiencing the ups and downs, but not so bad as to prevent them from sleeping soundly. Still, it’s a sufficient investment to participate when the

market stages a recovery again. At that moment, such investors would be a step ahead of all those participants who have now exited the market once and for all. Investors who are still fully invested in the stock market are possibly swearing about the pain of their losses: “never again stocks.” But it’s precisely at that moment in time, when the last remain-ing private investor has exited the mar-ket, at which the next bull market begins for those hardened investors with per-severance.

Investors don’t have to make a small investment in the stock market with just one stroke. For example, how about planning the investment in in-stallments? It’s no problem with a fund savings plan: After first selecting the relevant fund, investors make regular-recurring monthly payments, acquiring additional fund units, month for month – sometimes more, sometimes less – de-pending on market fluctuations. In this way, the fund unitholders can obtain an attractive average acquisition price. From a long-term perspective, this has been one of the most successful meth-ods of investing and, for most investors, much more rewarding than looking for the right timing.

Furthermore, an investment in funds also holds another advantage: Investors have to give little thought to counter-party risk because funds are classified as extraordinary assets – unlike struc-tured products – for which only the issu-ing bank is liable (for more details, see the box “Who is your counterparty?“).

The systemic risks have been recognized It appears that we could re-focus our attention perhaps already this year just on the risk classes that have always been, and will always be, associated with the financial markets: i.e. the in-vestment risk relating to totally normal market fluctuations.

Tips on the InternetComparing pension fundsWhich pension funds are healthy? Which offer the best performance?www.pensionskassenvergleich.ch

Selecting bondsHundreds of financial pages show share prices, but where should investors look for bonds?www.finanzen.net/anleihen

On the lookout for cheap stocksSearch for price/book ratios smaller than one, or numerous other criteria.www.finviz.com/screener

Stocks with a margin of safety.Investors should only buy stocks of com-panies when the price falls below the book value. That was Benjamin Graham‘s motto, author of the book titled “The Intelligent Investor,” and guru to Warren Buffett – one of the biggest investors of all times. The idea behind the strategy: If the price doesn’t increase, then the individual parts of the company are still worth more than the price paid for the stock. This is referred to as the “margin of safety.” If investors followed this radical principle, in most years there would be few firms remaining in whose stocks they could even invest at all.

surplus 1/2009 Dossier The safe haven

Additional readingBenjamin Graham

Published in 1949, this book became the bible of conservative investors and is more up-to-date today than ever be-fore.

The Intelligent Inves-tor, the bestseller about the right invest-ment strategy. Re-vised by Jason Zweig, Finanzbuch Verlag GmbH, hardcover, 630 pages

12 surplus 1/2009Interview The safe haven

Secure investing in the crisis The Swiss franc is a safe haven

Dr. Jan Amrit Poser, 38, is Chief Economist at Bank Sarasin. Born in Germany, Dr. Poser now lives in Zurich, is married and has one son (age two).

where that’s gaining ground?Higher commodity prices will certainly return at some point in time. But that won’t be an issue until such time as awareness of the long-term shortage is rekindled – after the recession.

Does that mean that nearly all markets are retreating at the same time – and the money has not merely changed hands or flowed to other markets? The financial markets are not a zero-sum game. One investor’s loss is not always another investor‘s gain. In most cases, market movements affect everyone. The majority of investors enjoy growth in as-set values when the market advances. And most suffer when it falls, leading to destruction of asset value.

as a safe haven too. Why?One motive is to hedge against inflation. But the inflation problem has been rath-er relegated to the background. The sec-ond motive is the flight to real value that would even withstand a collapse of the banking sector. In the interim, however, the central banks have made it clear that no more major banks are going to declare bankruptcy. So this motive is ac-tually inapplicable. And the third motive is of course speculation itself. But I fear that the so-called credit boom, which we had experienced prior to the current cri-sis, also excessively drove up the price of gold. Consequently, I really wouldn’t view the precious metal as a safe haven as long as there are still speculative po-sitions in the gold market.

Could gold prices tumble as severely as we have seen with other commodi-ties? The price of gold is unlikely to undergo such a pronounced drop as oil prices. In the Middle East, India and China, people use traditional jewelry to preserve value and as wedding gifts, which stabilizes prices on the downside. But the specu-lative phase must first come to an end.

Is there a commodity market any-

Dr. Poser, welcome to bank zweiplus. The overriding topic of discussion in this issue of “surplus” is “safe haven.” Is a savings book really the only safe haven at the present time?A savings book is a safe haven that in-vestors should take into consideration. Government bonds are also interesting because they still harbor price gains. These are essentially the safe havens.

Government bonds have already un-dergone strong price advances. Nev-ertheless, do they still hold upside potential?I think so. On the one hand, they still have potential because benchmark in-terest rates are shrinking; on the other, because the economic picture is rather still deteriorating and disinflationary fears are emerging. But one point should be clarified: Bonds don‘t offer the same gains that investors would anticipate from stocks in the long run. Moreover, investors must be flexible too, divesting bonds when signs of an economic turna-round emerge. And we expect such a recovery to happen in mid-2009.

The Swiss franc has gained terrain, from which many Swiss investors have very unwittingly reaped rewards amid the crisis. How?The Swiss currency is a safe haven be-cause it appreciates in value in times of crises. We expect the franc to strengthen further in the coming quarters. Thereaf-ter, investors can also contemplate re-investing in bonds denominated in other currencies. But that point has yet to come. And very generally, it’s advisable to have a certain home bias: meaning, investing the lion’s share of assets in the home country to avoid being subject to currency fluctuations, which can be quite significant.Gold has been traditionally regarded

Dr. Jan Amrit Poser, Chief Economist at Bank Sarasin, forecasts that the Swiss economy will begin to stage a recovery in mid-2009 at the earliest. Until then, Switzerland will pass through a recessionary phase, in which conservative forms of investing will offer the greatest security. Bernhard A. Zihler and Arne Voelker spoke to Dr. Jan Amrit Poser.

13surplus 1/2009 Interview The safe haven

Have we come to the end of down-swing?Destruction of asset value will prob-ably continue to prevail at the outset of 2009 as well. Even more negative eco-nomic news is forthcoming: The corpo-rate earnings outlook will turn weaker. Deleveraging – i.e. the reduction in the proportion of borrowed capital – will also continue to play out in the financial sys-tem. It will still take some time before the banking system has shrunk to a healthy state.

Why must the banking system shrink?Many people obtained mortgage loans during the US real estate boom, even if these borrowers were entirely unable to afford the loans in terms of their in-comes and assets. But since house prices continued to climb further and further, these loans never became non-perform-ing. Mortgage banks securitized these loans as securities and re-sold them as investment vehicles, which were listed as off-balance sheet assets that no one was able to see. But as the trend in real estate prices headed south, the problems became more apparent: Banks were faced with numerous mortgages suddenly surfacing on their balance sheets for which there was no collateral and whose values continued dwindling more and more. These loans must now be written down and eliminated.

Should I join in the trend toward delev-eraging too? Is the best investment today the repayment of my credit?No, certainly not. If you obtain a loan now, you should benefit from the low interest rates that we already have at present and even lower in the foresee-able future as well. If investors want to purchase real estate, or can refinance their mortgage on their house, then the time is now.

But isn’t the Swiss real estate market vulnerable?Prices are still far from the previous record highs. Switzerland learned its lessons from the last real estate crisis of the 1990s. There are no signs of over-exuberance here in this country – in sharp contrast to the USA, Spain or Great Britain.

Is that also the case with bank stocks? Indeed, some bank shares occasionally rebound quite rapidly, don’t they?There’s still much too much uncertainty looming in the banking sector, surround-ing the valuation of mortgage securities and, in addition, what credit losses may still be pending, with regard to credit cards or automobile loans, for exam-ple. Add to that the uncertainty about whether the government must once again step in to provide financial assist-ance. All these factors lead to sharp fluc-tuations in share prices. We recommend staying away from investments in larger commercial banks at the present time – even if the stocks have lost considerable ground and the prices seem low.

So which sectors would currently be interesting?Day-to-day, bread-and-butter stocks such as Nestlé are interesting, as well as the telecommunications sector, be-cause it holds substantial amounts of cash. We also favor the pharma sector since drug sales are not dependent on economic cycles. Incidentally, it’s not always stocks that are interesting in-vestments; corporate bonds have fallen even more sharply than stocks in terms of valuation models. The bond sector should soon stage a strong recovery. But I would only invest in first-class is-suers, or entrust the task of selection and diversification of individual bonds to a good investment fund.

Aren’t these really conservative rec-ommendations and not that far away from a savings book?Our current investment policy remains the same: overweight cash. I would rec-ommend that investors keep their cash handy and wait for the right situation. And – if at all – only very slowly begin building up positions. There are no mar-kets that investors should be chasing at the present time.

Pension funds also suffered losses in the crisis. How safe are these invest-ments?The year 2008 will be recorded in the annals of history as one of the worst years for the stock markets, together with the crisis of 1929. This relative fact should be clarified: meaning, it’s an extraordinary time. Of course, the situation strongly weighed on pension funds too. But we should not expect this climate to prevail as such through the coming years. In the wake of weak years, stronger times return, so the sys-tem stabilizes over the medium term.

And if I want to do something to supple-ment my pension provision right now? There will be a need for restructuring in-dividual pension funds, and the results are not always immediately visible. If you want to supplement your pension provision, you can always invest in the third-pillar scheme.

Or how about in stocks? Aren’t they cheap at present?Ultimately, it always comes down to the stock valuation in terms of the price in-vestors are willing to pay for a particular stock. This price can be higher at certain times and lower again at other times. It’s possible that valuations can remain lower for an extended period, if inves-tors have no confidence and ascribe a reduced value to such investments. But the stock markets have now suffered so severely that they have reached a point where they are trading substantially be-low their long-term average valuations.

So is it worth entering the market now?Entering the stock market now is only for investors with nerves of steel and sufficient perseverance to withstand a continuing bear market. The risks are currently rather still geared to the down-side and caution is advisable. We do not expect stabilization until mid-2009. But since we can never gauge the exact mo-ment of the low point on the stock mar-kets, there‘s certainly nothing wrong with soon resuming the build-up of eq-uity positions, piece-by-piece.

Overview of all forecasts

Outlook on page 14

14

Sector weighting

Asset classes: Overweight the money market

Forecasts Macroeconomic outlook

The US economy is suffering from a financial-sector cardiac arrest

Escalating recession is imminent, with no recovery in sight until the third quarter of 2009.

Consumption must adjust over the next ten years.

Europe is following in the footsteps of the US recession

A recovery in Europe will lag behind the USA, into 2010.

Switzerland is falling into recession too.

The money market

Benchmark interest rates continue to decline

USA: Interest rates continue to fall, while the slope of the yield curve flattens. The US dollar is unable to stage a sustainable recovery.

EU: The European Central Bank (ECB) must cut its interest rates. The euro is subject to downside risks due to rate cuts.

Switzerland: The Swiss National Bank (SNB) is cutting interest rates too. Demand for the Swiss franc as a safe haven is growing.

In all the regions around the world, eco-nomic indicators are pointing to the dee-pest recession in decades. And we do not expect to see a recovery until the second half of 2009. Government bonds have been the only asset class to show a positive trend in recent weeks. Although government bond yields are hovering at historical lows, further upside potential is still in the cards. Tumbling inflation rates – as well as further interest rate cuts and the prospect of unconventional monetary policy measures on the part of the central banks – should continue to un-derpin government bonds. In light of the credit crunch, credit risk premiums have surged to record highs, implying a marked increase in default rates in the corporate bond sector. But since bonds of healthy

The world is on the verge of recessi-on: “cash is king.”

Bonds are underpinned by declining inflation expectations.

Earnings estimates must be revised further downward, but valuations are becoming increasingly attractive.

companies have also fallen victim to the crisis and been excessively punished too, spectacular investment opportunities have emerged as a result.

Meanwhile, the picture on the currency markets reveals a trend toward safer ha-vens. Consequently, the Swiss franc has gained terrain versus the euro. This, in turn, prompted the Swiss National Bank (SNB) to initiate a surprising interest rate cut in order to somewhat weaken the Swiss franc against the euro, aiming to additionally counteract the diminishing economy. The US dollar should continue to reap rewards in the near term from the deleveraging process, but the greenback will be unable to stage a longer-term re-covery. (jp)

Risks remain high, so we recommend slightly underweighting equities following the crash.

The uncertainty surrounding the fair value of an investment remains elevated.

Deleveraging: Underweight alterna-tive investments

Economic outlookIt is probably hard to find a period in history in which economic growth came to a standstill on a global basis in such a short time. The recession already underway will continue to deepen even further for the time being. Corporate earnings estimates are still too high, so stock valuations are not attractive at the moment, but fair.

Investment strategy

Overweight

Neutral

Underweight

Source: Bank Sarasin

Money market Bonds

Equities Other assets

surplus 1/2009Outlook Our forecasts

Healthcare Telecommunications Consumer goods

Energy Financials Utilities

Commodities / materials Industrials Technology Cyclical consumer goods

Autographed photo with Miss Switzerland Whitney Toyloy

Come take your picture together with Miss Switzerland Whitney Toyloy on Thursday, 5 February 2009 at stand P.06 and, at the same time, learn more about bank zweiplus services.

Guest appearance at FONDS’09.

bank zweiplus ltd., P.O. Box, CH-8048 Zurich www.bankzweiplus.ch

16 Money tips Depositor protection

extraordinary assets. Whether invest-ment funds are invested in stocks, bonds or gold, they all have one thing in com-mon: They are regarded as extraordinary assets from a legal perspective. Such in-vestments are never the property of the bank or company that manages the fund and selects the assets. To the same ex-tent, these investments are not the property of the bank that manages your custody account either – the custodian bank where your assets are merely held in safekeeping. Investments in funds always belong solely to the unitholders of the respective investor community. If the fund company goes bankrupt, the extraordinary assets remain intact. If the custodian bank is affected, the cus-tody account holdings remain the sole property of the customer and in the full amount.

Investors who scattered their cash hold-ings among various banks amid the cri-sis took a logical step toward greater diversification. Buy now it’s important for these investors to ideally re-position themselves for the available buying op-portunities that emerge in the coming months. bank zweiplus opens the door to an independent and broadly diversified selection of first-class fund providers (i.e. offering a choice of investment funds from more than 50 fund companies). The maximum brokerage fee amounts to just 1% and even decreases with larger in-dividual orders to a minimum of 0.25%. Custody account fees are also uniformly and attractively structured, amounting to a maximum of 0.19% or minimum CHF 75 per year. Your bank zweiplus cus-tomer advisor team is looking forward to offering you advice and assistance, via the toll-free telephone number 00800 0800 55 55, or +41 (0)58 059 22 17 from Monday to Friday, between 08:30 and 19:00.

each of their banks, for the sake of the security of a savings book or even a non-interest-bearing private account. And in particular, these customers will have to dispense with the advantage of having all the services provided under one roof. The good news: Switzerland’s National Council and Council of States shortly before Christmas approved raising the depositor protection ceiling to CHF 100,000. Consequently, most people can now begin to confidently rebundle their assets at a single bank. Swiss de-positor protection is based on two prin-ciples. One is the so-called bankruptcy privilege. Customer deposits are paid out first if a bank files for bankruptcy. Only thereafter are the claims of the bank’s other creditors satisfied, for example suppliers. Hence, customer deposits en-joy precedence according to law.

The second principle is joint and several liability. All banks should be mutually accountable for customer deposits held by other banks if one of them files for bankruptcy. This of course necessitates that the majority of banks are still in good shape and profitable. Should all the banks fail, depositor protection is of no help here. However, the government would hardly let the situation escalate to such a point. Even without legal obli-gation, the government is ready to come to the rescue of troubled banks. Indeed, the banking sector is too important for the Swiss economy. Incidentally, deposi-tor protection directly covers only those deposits held by banks. The system only protects money held in accounts: i.e. more explicitly, sight deposits (such as private accounts for payment trans-actions, savings accounts, fixed-term deposits) and medium-term notes (i.e. bank notes). But depositor protection does not cover the investments held in your custody account. Funds count as

Long lines of customers standing at the door of their banks is something Switzer-land had never seen before. But in October 2008, it actually came to that: investors gathering at the big banks to withdraw their money. While at other banks – partic-ularly the cantonal banks and Raiffeisen banks – people looking to open up a new account were backed up in lines.

With this run on banks, many investors did not merely deposit their money in another individual bank, but rather diver-sified their funds among various banks. Such a move was attributable primarily to the fact that depositor protection in Switzerland had covered only up to CHF 30,000 per depositor and bank. So it was not just the big banks that suffered losses; these investors came out on the short end as well.

Indeed, these investors must now pay several banking fees for their various ac-counts. They have also lost the overview of their scattered portion of assets and relinquished control over the structure of the overall portfolio. Furthermore, these investors may let investment opportu-nities just slip away if they have not opened a securities custody account at

New Swiss depositor protectionYou can be well-diversified at just one bank too The Swiss federal government presented one of the greatest Christmas gifts last year: Now, up to CHF 100,000 is covered by depositor protection. Those who diversified their money among various banks due to security reasons can now begin to gather together their funds under one roof again. By Roland Gassmann

Roland Gassmann,

Head of Switzerland and Austria

surplus 1/2009

17surplus 1/2009 Personal bank zweiplus

A comparison published in the Swiss newspaper “Sonntagszeitung” confirms what we had always thought: At bank zweiplus, customers can find extremely attractive conditions. In fact, only one single provider showed a better per-formance. At bank zweiplus, customers

additionally reap rewards from cheaper brokerage fees, down to a minimum 0.25% on larger orders. Furthermore, customers can benefit from unbeatable conditions using the Online-Banking www.bankzweiplus.ch › Paying › Serv-ices › Prices and fees. (bz)

The heart shows us the right wayMany people say that companies aiming for success on the markets must ope-rate like a machine: making decisions without emotions, as well as executing them in the same disciplined, unhesita-ting way. But every machine is only as good as the theory according to which it operates.Comparing this maxim with the situati-on on the markets reveals that neither buying and holding stocks, nor those hedge funds that leveraged their cle-ver quantitative models with excessive credit, were able to reap good fortune on the markets. And suddenly liquidity dried up, while the rescue boats were still in the harbor, but washed aground due to the tide.

In fact, we have always known that the safest haven is not situated on wa-ter. Not even gold is regarded as such, but rather cash denominated in Swiss francs. We find security for our money in the exact same place where we find it emotionally: where people speak our language; a place we can trust; i.e. our own homeland. If we can trust our parents in our youth, then we are in a position throughout our entire lives to forge trustful ties with other people. Consequently, we often even intuitively choose a suitable partner with whom a relationship pays off. It’s nice that we are so accustomed to such security. Indeed, our hearts show us the way to the safe haven: home.

Bernhard A. Zihler, Editor-in-Chief

On the one hand, the bank zweiplus brand name reflects the establishment of a joint company by the two founding banks – Bank Sarasin & Co. Ltd. and AIG Private Bank Ltd. – but at the same time, the name manifests our most important organizational objective too: namely, consistently offering clients as well as certified financial services providers ex-tra tangible advantages in accordance with our guiding principle, “one plus one equals zweiplus.” By combining our

evolutionary history (i.e. two (“zwei” in German) founding banks) with our most significant organizational goal (i.e. extra (“plus”) tangible advantages), we derive the – at least uncommon – brand name: “bank zweiplus.” (bz)

Why zweiplus?Not everyone deduces our name straightaway

Attractive conditions at bank zweiplus

Column

Rank Institute Costs per year in Swiss francs

1 Postfinance 0

2 bank zweiplus 285

2 Migros-Bank 285

4 Raiffeisen 300

5 Bank Coop 450

6 Credit Suisse 490

7 ZKB 495

8 BEKB 576

8 UBS 580

Source: SonntagsZeitung of 28 September 2008, supplement “Geld Extra,” page 43

Fund custody account fees

18 surplus 1/2009Sponsoring Events

bank zweiplus warmly congratulates the young athletes and wishes them the ut-most success in their future careers in sports. (bz)

bank zweiplus impressively boosted its level of recognition thanks to the advertising scheme – in the form of a 15-second TV ad – used during the ten-nis matches broadcast by Swiss TV sta-

tions SF2, TSR and TSI. In fact, nearly two million spectators in Switzerland tuned in to see the ad during a total of 139 broadcasts. (bz)

The talent team of Art on Ice Produc-tion AG has acquired a new primary sponsor with bank zweiplus.

Due to an advance nomination proc-ess, the talent team screening day took place in Olten (Solothurn) on 20 Sep-tember 2008. The event was regarded as the testing ground for being accepted on the zweiplus talent team Art on Ice. The following nine athletes succeeded in making the zweiplus talent team and henceforth will receive financial and technical support: Romy Bühler, Joos Kündig, Anaïs Morand & Antoine Dorsaz (pair-skating), Alisson Perticheto, Tomi Pulkkinen, Noah Scherer, Tina Stürzinger and Diana Zanta.

bank zweiplus acted as TV sponsor of the Davidoff Swiss Indoors at the live broadcast of the tennis match, from 20 to 26 October 2008.

Davidoff Swiss IndoorsAdvertisement draws nationwide attention

We promote Swiss talent on the way to a breakthrough

19surplus 1/2009 Contact bank zweiplus

Important information

This publication released by bank zweiplus ltd. (hereinafter referred to as “bzp”) has been compiled with publicly ac-

cessible information and data (hereinafter referred to as “information”) that are deemed to be reliable. Nevertheless,

bzp assumes no representation or warranty, express or implied, as to the accuracy or completeness of the information.

Possible errors in this information constitute no basis for direct or indirect liability on the part of bzp. In particular, bzp

assumes no responsibility for any changes in the opinions expressed herein, plans or details about products, the rele-

vant strategies and the economic environment, as well as market, competitive or regulatory conditions, etc. Although

bzp has done everything within its power to create a reliable publication, we cannot rule out that it may contain errors or

is incomplete. Neither the Bank, nor its shareholders or employees, assumes any responsibility regarding the relevance

of the opinions, assessments and conclusions conveyed herein. Despite the release of this publication in connection

with an existing contractual relationship, any liability on the part of bzp is limited to gross negligence or willful intent

only. Furthermore, bzp accepts no liability for any immaterial inaccuracies. In such case, any liability on the part of bzp

is limited to an amount that would normally be expected. bzp explicitly accepts no liability for indirect damages. This

publication does not constitute a solicitation or an invitation to make an offer to buy or sell any securities or other

specific products. We recommend that you obtain detailed information regarding the respective product prior to making

an investment.

ImprintIssue 1/2009“surplus” is published in the languages German and English

Publisherbank zweiplus ag, Zurich

Publishing and editorialbank zweiplus ag Bändliweg 20 CH-8048 Zurich [email protected]

Editor-in-chiefBernhard A. Zihler (bz)[email protected]

Editorial staff Marco Weber (mw), Roland Gassmann (rg), Dr. Jan Armit Poser (jp), Volker Platz (vp),Nathalie Taiana (Photos), Arne Völker (av)

Layout, graphic design, art directionAebi, Völker, Und, AGBinzallee 31CH-8055 Zurich

Head of Advertising Silvan Franchetto [email protected]

SubscriptionsNew subscriptions can be submitted via e-mail to [email protected].

bank zweiplus Customer Centers

*Opening hours: Monday to Friday from 09:00 to 17:00

**Cash withdrawals are only possible at the Customer Centers in Zurich and Basel, not at the headquarters in Zurich

Customer Center Basel*

Wallstrasse 1CH-4002 Basel

Customer Center Zurich*

Talstrasse 62CH-8001 Zurich

Headquarters**

bank zweiplus agP.O. BoxBändliweg 20CH-8048 Zurich