Isolating Advertisements from Mobile Applications in Android

The resource-based view revisited:

Comparative firm advantage,

willingness-based isolating mechanisms

and competitive heterogeneityAnoop Madhok1, Sali Li2, Richard L Priem2

1Schulich School of Business, York University, Toronto, Canada;2Lubar School of Business, The University of Wisconsin–Milwaukee, Milwaukee, Wisconsin, USA

Correspondence:Anoop Madhok, Schulich School of Business, York University, 4700 Keele Street, Toronto, ON L4S 1S8, Canada.Tel: þ 416 736 2100, Ext. 20578;Fax: þ 416 736 5687;E-mail: [email protected]

AbstractWe take a step beyond the resource-based view that resource characteristics (i.e., valuable,rare, inimitable and non-substitutable) are the sole basis for isolating mechanisms. Instead,we apply Ricardo’s principle of Comparative Advantage in a two-firm, two-product scenario toshow how additional isolating mechanisms can result from economic incentives that providemanagers with distinct strategic choices. Specifically, our analysis indicates that managers’strategic decisions based on comparative firm advantage (CFA) affect their willingness toimitate competitors, even when their firms are fully capable of such imitation. This willingness,in turn, helps to determine the direction of firm expansion. We discuss how Ricardo’s CFAlogic can provide specific guidance for managers regarding effective firm strategies in specificcomparative advantage situations by factoring in both internal efficiencies and competitivepressures when designing and implementing rent-seeking strategies.European Management Review (2010) 7, 91–100. doi:10.1057/emr.2010.6;published online 29 April 2010Keywords: comparative firm advantage; competitive heterogeneity; resource-based view; isolatingmechanisms

Introduction

Comparative advantage and competitive advantage aretwo important concepts in the economics and manage-ment literatures. Scholars typically have used com-

parative advantage to predict trade patterns betweennations and competitive advantage to predict a firm’ssuperior performance relative to competitors. Recently,however, these level-of-analysis boundaries have begun toblur. For instance, Porter (1990) has applied the competi-tive advantage rationale at the nation level in establishinghis dynamic, ‘diamond’ model: namely, that a nation’sdemand conditions, rivalry conditions, factor conditions,and supporting industries determine its competitiveadvantage in a particular industry relative to other nations.In going beyond the more static factor conditions (such asland) that provided the basis for David Ricardo’s landmarkwork, Porter has enriched, extended and reformulatedRicardo’s (1821) theory of comparative advantage, offering

a more comprehensive explanation for why some nationsadvance and prosper in certain industries while others donot. Moreover, Porter’s nation-level work has sincestimulated research examining the competitive advantageof ‘industry clusters’ at the sub-national level (e.g., Storper,1993; Maskell and Malmberg, 1999).

This successful application of competitive advantageconcepts upward to the nation level begs two exploratoryquestions: Can we likewise apply Ricardo’s concepts of com-parative advantage downward to the firm level? And if wedo, might new implications result for theory in strategicmanagement? For example, the issues of why firms differ andthe durability of such differences have been fundamental tostrategy research associated with the resource-based view(RBV). We show in this paper how comparative advantageconcepts can be applied at the firm level of analysis, and howthis application produces novel insights into such elemental

European Management Review (2010) 7, 91–100& 2010 EURAM Macmillan Publishers Ltd. All rights reserved 1740-4754/10

palgrave-journals.com/emr/

strategy issues as the determinants (sources) of heterogeneityamong competing firms and the sustainability of firm-levelcompetitive advantages.

Resource inimitability – due to the inability of rivals toreplicate a focal competitor’s rare and valuable resources –is central to the RBV’s explanations of sustainablecompetitive advantage. In contrast to this ability-basedargument, we use the logic of comparative advantageto demonstrate situations wherein a focal competitor’sresources are imitable, yet potential rivals are unwilling tomake the investments necessary to replicate or imitatethose resources because the rivals’ current resourceconfigurations can be applied more profitably elsewhere.That is, even if they are able to imitate, some rivals orpotential rivals choose to refrain from imitation (i.e., areunwilling to imitate) based on their internal logics ofcomparative advantage. We term this comparative firmadvantage (CFA). Moreover, we show how this previouslyunexamined source of competitive heterogeneity can leadto sustainable advantage in contexts where either: (1) therivals continue to have more profitable opportunitieselsewhere; or (2) when delay by rivals pursuing otheropportunities allows the focal competitor time to convert‘second class’, imitable resources into ‘first class’, inimi-table resources. Thus, we demonstrate how comparativeadvantage-based reasoning complements the RBV in itscurrent form and has important implications for thecapture of rents – a key aspect of strategy theory (Rumeltet al., 1994) – by factoring in both internal efficiencies andcompetitive pressures when designing and implementingrent-seeking strategies.

Our paper is organized as follows. We first investigatewhat constitutes comparative advantage in the context ofstrategic management. In the process of doing so, we linkfirms’ rent-earning capacities with their resource deploy-ment and accumulation decisions in a novel manner thatrevisits the role and functioning of (comparative) oppor-tunity costs in this decision. In contrast to past work in theRBV, we combine both use- and user-based opportunitycosts as the underlying basis for such decisions. Havingestablished the theoretical basis of our argument, we thenrelate managers’ resource allocation decisions to ability andwillingness-based isolating mechanisms (WIM) and to thesustainability of competitive advantage. We then discussthe implications of these ideas.

The comparative advantage of firmsMcGraw-Hill’s Dictionary of Modern Economics (1983: 88)defines comparative advantage1 as ‘the special ability of acountry to provide one product or service relatively morecheaply than other products or services. This concept isgenerally used in international trade theory, although it alsoapplies to cost comparisons among firms in an industryand among individual workers’.2 Unlike the notion ofcompetitive advantage – which before Porter (1990) hadbeen strictly applied at the firm level – comparativeadvantage can be broadly applied at multiple levels ofanalysis (Ricardo, 1821). To better examine firms’ com-parative advantage, however, we must take one step beyondthe dictionary definition and place the concept within thecontext of strategic management.

The RBV views firms as collections of resources andevolving capabilities ‘that are managed dynamically for thepurpose of earning rent’ (Williams 1994: 229). In linewith this logic, firms deploy strategies to serve the ends ofcreating, enhancing and capturing economic rents (Barney,1991; Peteraf, 1993; Makadok, 2001; Peteraf and Barney,2003), with rents defined as ‘returns to a factor in excess ofits opportunity costs’ (Peteraf and Barney, 2003: 315).

Opportunity costs underpin many important theoreticalissues in the strategic management literature. As Coase(1973: 108) claimed, ‘opportunity cost would seem to be theonly one which is of use in the solution of businessproblems because of its focus on the alternative courses ofaction which are open to the executive’ (emphasis added).The alternative courses of action, embedded in the conceptof opportunity costs, acknowledge managers’ optionsand liberties in making strategic choices (Child, 1972),with managers being economically motivated to pursuethat strategy and to choose that course of actionamong alternatives which further enhances their firms’search for rents.

Despite the importance of opportunity costs, researchershave yet to reach a consensus on what they really entail.The conventional approach treats opportunity costs as thevalue (for a focal resource user) of a resource in itsalternative best use (Coase, 1973; Chiles and McMackin,1996). Consider this to be use-based opportunity costs. Asa corollary, for use-based opportunity costs rent wouldbe the excess in value of a resource in a particular userelative to its next best use. Notably, this treatment isprimarily focused on resource use, but it implicitly neglectsthe role of competition in determining resource valueand rent-earning capacity. In contrast, Peteraf (1993) citedKlein et al. (1978) in her influential article to distinguishbetween use-based and user-based opportunity costs,with user-based opportunity costs determined by the valueof a resource to its second-highest valuing potential user.As a corollary, for user-based opportunity costs rent wouldbe the excess in value of a resource in a particular userelative to its value in such use by its next best user.3

The distinction between use-based and user-basedopportunity cost is subtle but significant. In the firstcase, the next best use refers to the application of theparticular resource by the same firm to another use. In thesecond case, it refers to the application of the particularresource by another firm for the same or similar use. Thekey difference between these two approaches is that theformer is about what can be done better within a firm as itseeks to earn rents, whereas the latter focuses on who cando it better between two firms. In this latter sense,the marginally productive resource refers to the resourceheld by the inferior user/producer. We illustrate these twologics, and the limitations of considering only one of thetwo in strategic analysis, through the following stylizedscenarios.

Types of opportunity costs and strategic choiceConsider a single-firm, two-product case following theconventional approach – that is, a focal firm can employ itsinternal resources in making two products – and assumefor simplicity that these two products have the same level of

Comparative firm advantage Anoop Madhok et al.

92

perceived consumer value. If the firm can produce oneproduct more efficiently than it can produce the other,then Ceteris paribus it should choose to produce theproduct that it can produce most efficiently. This is becausethe firm’s use-based opportunity costs are greater if itforgoes producing the more efficient product than ifit forgoes producing the less efficient one. Thus, forconventional, use-based logic the emphasis is on efficiencyin resource utilization between two products, and a firmcan capture greater rents by producing one than it can byproducing the other. This is hardly controversial.

More recently RBV scholars such as Peteraf and Barney(2003) have questioned the conventional argument of rentcreation above. They instead take inter-firm competitioninto consideration and view opportunity costs from a moreuser- and competitor-focused perspective. From thisperspective even if the firm can produce one productmore efficiently than another, choosing a strategy dependsalso on the productivity ratios of potential rivals. In otherwords, can the focal firm discussed above still earn rentsby producing its most efficient product given the existenceof competition?

In contrast to the conventional view, where the focuswas on the difference between two uses within a particularfirm, the focus of user-based opportunity cost logic is onthe difference between two competitors (or resourceusers) in their efficiency in making a particular product.In this two-firm, single-product case the differencebetween the efficient use of a productive resource by oneparticular user over another becomes the source ofrent (Peteraf, 1993; Peteraf and Barney, 2003); that is, rentrepresents a return to efficiency differences betweentwo firms with respect to resources in a particularuse. Given the definition of competitive advantage as afirm’s ability ‘to create relatively more economic value’(Peteraf and Barney, 2003: 314) that ‘is an indicatorof a firm’s potential to best its rivals in terms of rents y ’(p. 313), we can determine Ceteris paribus that the moreefficient firm holds a competitive advantage in thetwo-firm, single-product case. Again, this is hardlycontroversial.

Both of these approaches to opportunity costs clearlyhave contributed to the development of strategic manage-ment theory. Yet, the lack of integration between themhinders a more comprehensive understanding of appro-priate strategies for firms as they deploy and accumulateresources in the search for rents. On the one hand, theconventional argument overlooks the role of competition.On the other hand, although the second argument high-lights the competitive dimension in the rent-earningprocess it neglects the possibility for firms to takealternative courses of action with their productive re-sources. By assuming ‘two single-business firms competingin a production market, one of which has a competitiveadvantage over the other’ (Peteraf and Barney, 2003: 315;italics added)4 and that ‘(t)he use to which the potentialuser may wish to put it may be exactly the same (asthe focal firm)’ (Peteraf, 1993: 184; italics added), theRBV argument over-simplifies competitive processes. AsLippman and Rumelt (2003) point out, without consideringthe alternative courses of action the single-product marketmodel jeopardizes the operational meaning of opportunity

cost, because opportunity cost only has meaning whenfirms have multiple options for creating and capturingvalue through different resource allocation strategies.

To begin integrating these two perspectives, we next turnto a two-firm, two-product world5 wherein the notionof CFA can naturally be introduced. Extending the previousdiscussions, consider a situation in which both firms canproduce the same product more efficiently than the otherproduct, and one firm can produce each of the twoproducts more efficiently than can the other firm. In thatcase, the more efficient firm will make the strategic choicebased on its internal efficiency advantage, but the situationis a little more complicated for the second firm. Specifically,the second firm may choose the product at which it is lessefficient if its relative advantage for that product is greaterwhen compared to the other firm. Thus, both efficiencyadvantage and comparative advantage should be consid-ered by the second firm in making the product decision.Moreover, as we will discuss, if the first firm has anefficiency advantage both internally and relative tocompetitors, it will apply conventional thinking and, Ceterisparibus, choose to produce the product where it has theinternal efficiency advantage and will forgo productionof the second product in order to achieve the greatestpossible profitability. The second firm is then protectedin producing the second product, even though it is lessefficient with the second product than is the first firm, bythe first firm’s unwillingness (due to insufficient economicincentive) to produce the second product. This is theessence of WIM.

A recent example illustrates this argument. When Ebayentered the Korean market it acquired AuctionCo, one ofthe online auction leaders in Korea for both business-to-consumer (B-to-C) and consumer-to-consumer (C-to-C)auctions. Ebay soon learned, however, that with AuctionCoit had a sharper edge over other Korean competitors in theC-to-C auction market than it did in the B-to-C market.Given limited managerial resources, Ebay chose to abandonthe B-to-C market in Korea and largely focus on the C-to-Cmarket. Consistent with the two firm–two product argu-ments in this paper, we see that Ebay has competitiveadvantages over its Korean competitors for both B-to-Cand C-to-C models, but Ebay found its greatest CFA in itsC-to-C business. On the other hand, although a local onlinebusiness site like Lycos Korea may not have a competitiveadvantage in either the B-to-C or C-to-C markets overEbay’s AuctionCo, Lycos Korea has a relative CFA in theB-to-C market and can be successful there due towillingness-based mechanisms isolating it from Ebay.

Thus, there are many differences that can be foundamong our three stylized scenarios. Table 1 summarizessome key differences between the conventional view, theRBV and CFA reasoning.

The conventional view, as in the first scenario, is basedon a one firm-two product model; accordingly, the greatestinterest is in the issue of what can be done better in a firm,and the focus is on how to enhance a firm’s internalefficiency with respect to resource utilization. In contrast,the second scenario as put forward by Peteraf and Barney(2003) in their elaboration of the RBV is based on thesituation of two firms and one product; accordingly, itsinterest is on the issue of which one of the two firms can

Comparative firm advantage Anoop Madhok et al.

93

produce the product in a more efficient manner andthereby capture more value.

In the third scenario, CFA reasoning is based on a twofirm–two product model that better reflects the complexityand dynamics of business competition; accordingly, theinterest is in the issue of what can be done better by whichfirm. CFA reasoning goes one step beyond extantapproaches – it looks both within and across firms andthus incorporates both use- and user-driven criteria in itscalculus regarding product production choices. CFA is amore comprehensive approach because it recognizes thatfirms have alternative opportunities for utilizing theirspecific resources in their search for rents, and that firmscan and should make optimal choices among thesealternatives by factoring in both internal efficiencies andcompetitive pressures when designing and implementingrent-seeking strategies. The resulting strategic choices,based on both use- and user-driven compulsions, canaffect a firm’s resource accumulation and allocationprocesses and thus with time can cause durable differencesacross firms. CFA reasoning can therefore complementthe RBV by helping to better explain managers’ strategicchoices and actions and how these choices contribute tointer-firm heterogeneity.

In the next section, we introduce some variations to ourbasic argument to further elaborate on how firms’economic incentives in rent-seeking affect managers’resource accumulation and allocation decisions. We alsoshow how CFA reasoning identifies an important but as yetunaddressed aspect of competitor heterogeneity. Specifi-cally, by extending the concept of isolating mechanismbeyond ability to also include willingness, we use CFAreasoning to address the issue of inter-firm heterogeneityacross rivals more comprehensively than does the currentRBV. In this process, we also extend current understandingof sustainable competitive advantage and identify thetype(s) of advantage (comparative, competitive, or both)that are truly sustainable.

Re-examining competitive heterogeneityThe question of why firms differ can be subdivided into twocomponent parts. First, when and why are firms unable toimitate one another effectively? Second, and equallyimportant, when and why would rivals or potential rivals

that are able to imitate instead choose to refrain fromimitation (i.e., be unwilling to imitate)?

The RBV has focused largely on the first part of thequestion. Traditionally, three general isolating mechanismshave been identified that prevent the imitation of resourceallocations: property rights, learning and developmentalcosts, and causal ambiguity (Rumelt, 1984; Hoopes et al.,2003). All three mechanisms focus on the fact thatcompetitors lack the ability to imitate; thus, they can beconsidered as ability-based isolating mechanisms (AIM).However, as Hoopes et al. (2003: 891) pointed out in theirdiscussion of competitive heterogeneity, ‘if resources orcapabilities associated with sustained performance hetero-geneity are not protectable, then its persistence must bedue to something other than costly imitation’. Supportingthis line of thought, Knott (2003) found in her study thatclose but able rivals did not copy superior but imitablefranchise routines that they recognized as important. Shetherefore questioned whether the RBV has been overly (andtoo narrowly) concerned with resource imitability, sincethere may be other factors reducing the incentive of rivalsto imitate. Similarly, Christensen (1997) highlighted anumber of different cases where incumbents chose not to(i.e., were not willing to) imitate a potential future rivalbecause the incentives to do so were weak. This line ofargument underlines the existence of what we term as WIM,characterized by firms’ different economic incentives asthey pursue rent-seeking strategies.

In other words, WIM exists as a consequence of firms’economic incentives to profit logic. The CFA rationalewe have described functions as a WIM. Consider againEbay’s strategy in the Korea market. Although Ebay has thecapabilities to employ its resources in a similar way as itsKorean competitors in the B-to-C business model, Ebay’sdecision makers foresee greater profit potential fromfocusing their resources on the C-to-C business frameworkand thus differentiating the firm from its competitors. Thisrepresents a WIM from the perspective of the firmsoperating in the B-to-C market.

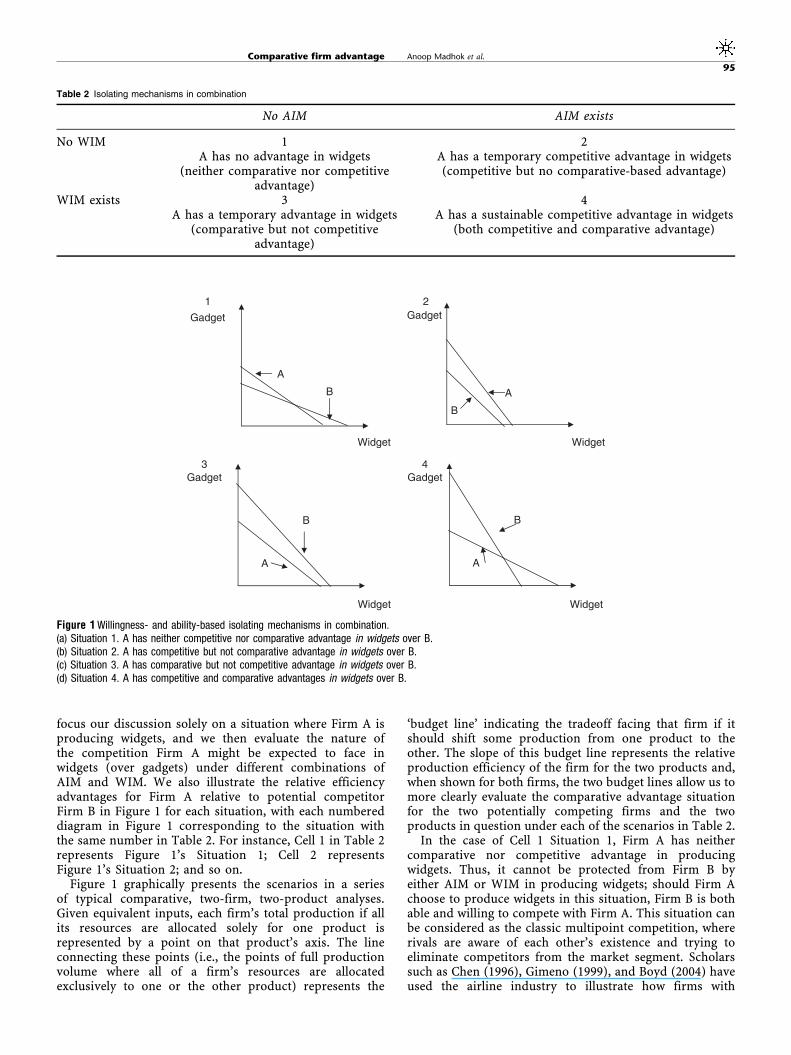

Both types of isolating mechanisms are clearly importantin competition between firms. To better illustrate how thetraditional RBV reasoning and CFA reasoning – andtherefore correspondingly AIM and WIM – can worktogether in the two-firm, two-product case, we use thesimple two-by-two matrix shown in Table 2. For clarity, we

Table 1 Summary of the three perspectives

The conventional view The RBV The comparative firmadvantage (CFA) view

Basic model One firm two products Two firms one product Two firms two productsKey approach towardsopportunity costs

Use based User based Both

Key area of focus Internal efficiency; Withina firm

Efficiency relative tocompetition; between twofirms

Both; within and betweenfirms

Key question What can be done betterinside a firm?

Which firm can do it better? What can be done betterby which firm?

Key argument oninter-firm heterogeneity

Not applicable Ability to imitate Willingness to imitate

Comparative firm advantage Anoop Madhok et al.

94

focus our discussion solely on a situation where Firm A isproducing widgets, and we then evaluate the nature ofthe competition Firm A might be expected to face inwidgets (over gadgets) under different combinations ofAIM and WIM. We also illustrate the relative efficiencyadvantages for Firm A relative to potential competitorFirm B in Figure 1 for each situation, with each numbereddiagram in Figure 1 corresponding to the situation withthe same number in Table 2. For instance, Cell 1 in Table 2represents Figure 1’s Situation 1; Cell 2 representsFigure 1’s Situation 2; and so on.

Figure 1 graphically presents the scenarios in a seriesof typical comparative, two-firm, two-product analyses.Given equivalent inputs, each firm’s total production if allits resources are allocated solely for one product isrepresented by a point on that product’s axis. The lineconnecting these points (i.e., the points of full productionvolume where all of a firm’s resources are allocatedexclusively to one or the other product) represents the

‘budget line’ indicating the tradeoff facing that firm if itshould shift some production from one product to theother. The slope of this budget line represents the relativeproduction efficiency of the firm for the two products and,when shown for both firms, the two budget lines allow us tomore clearly evaluate the comparative advantage situationfor the two potentially competing firms and the twoproducts in question under each of the scenarios in Table 2.

In the case of Cell 1 Situation 1, Firm A has neithercomparative nor competitive advantage in producingwidgets. Thus, it cannot be protected from Firm B byeither AIM or WIM in producing widgets; should Firm Achoose to produce widgets in this situation, Firm B is bothable and willing to compete with Firm A. This situation canbe considered as the classic multipoint competition, whererivals are aware of each other’s existence and trying toeliminate competitors from the market segment. Scholarssuch as Chen (1996), Gimeno (1999), and Boyd (2004) haveused the airline industry to illustrate how firms with

Table 2 Isolating mechanisms in combination

No AIM AIM exists

No WIM 1A has no advantage in widgets

(neither comparative nor competitiveadvantage)

2A has a temporary competitive advantage in widgets(competitive but no comparative-based advantage)

WIM exists 3A has a temporary advantage in widgets

(comparative but not competitiveadvantage)

4A has a sustainable competitive advantage in widgets

(both competitive and comparative advantage)

A

Widget

B

Gadget

1

A

Widget

B

Gadget4

A

Widget

B

Gadget 2

A

Widget

B

Gadget3

Figure 1 Willingness- and ability-based isolating mechanisms in combination.(a) Situation 1. A has neither competitive nor comparative advantage in widgets over B.(b) Situation 2. A has competitive but not comparative advantage in widgets over B.(c) Situation 3. A has comparative but not competitive advantage in widgets over B.(d) Situation 4. A has competitive and comparative advantages in widgets over B.

Comparative firm advantage Anoop Madhok et al.

95

superior resources in multiple markets tend to either pushcompetitors out from the markets or relegate the compe-titors to very small secondary or niche positions.

Now take the case (Cell 2 Situation 2) where only AIMexists and WIM does not exist for Firm A to producewidgets. Firm A has competitive but no comparativeadvantage in producing widgets. Traditionally, AIM hasbeen considered a necessary and sufficient condition forthe existence of sustainable competitive advantage. How-ever, when only AIM exists but WIM does not, competitorslack the capability to imitate in the short-to-medium runbut they do not lack the motivation. This is a situationwherein Firm A has would-be and motivated imitators whoat some point may attempt imitation. Once the situationallows it, these imitators will make the investmentsnecessary to catch up with the Firm A, and Firm A maylose its competitive advantage. Scholars such as Mitchell(1991) and Giarratana (2008) argue that in high-techindustries, despite the fact that start-up firms tend todominate in newly emerged market segments, the start-ups’success and first mover advantage cannot prevent largefirms that were incumbents in the previously dominantsegments from entering the new market segments. In thissituation, the start-ups’ advantageous positions are onlytemporary, and depend upon the speed with whichprevious incumbents can imitate and catch up.

From a dynamic perspective, we may find that with timeand environmental change the competitive relationshipbetween Firm A and Firm B in producing widgets easilycould evolve from Cell 2 to Cell 1. For instance, the holderof a unique patent is protected by an AIM, and hassustainable competitive advantage due to the legal protec-tion that prevents potential competitors from imitating.Such competitive advantage is limited by calendar time,geographic scope and institutional or technologicalchanges, however. More important to our argument, asevident from the short period within which most patentsare circumvented (Levin et al., 1987), is that concertedeffort by a motivated imitator can result in cultivation ofthe desired capabilities over time. This implies that withthe protection of AIM many firms can only achievetemporary competitive advantages which could be over-come by would-be and well-motivated competitors.

In Cell 3 Situation 3, only WIM exists and AIM does not.Firm A has comparative but no competitive advantage inproducing widgets. Here, suppose that Firm A specializesin widgets. Even though as a result of competitiveadvantage Firm B has the ability and knowledge to producewidgets, given its limited managerial resources (Penrose,1959) Firm B’s managers will not be economicallymotivated (i.e., will be unwilling) to attempt imitationand compete in widgets, because their greatest potentialprofit is in gadgets. That is, even though AIM does not existand hence cannot prevent Firm B from imitating Firm A,WIM can still protect Firm A because Firm B can achievehigher rents by pursuing CFA-based rents, which in thisscenario is represented by gadgets.

Arora et al.’s (2009) recent research on the US drugindustry provides an excellent example for this situation.They analyzed more than 3000 drug R&D projects in the USduring 1980–1994, and found that pharmaceutical firms aresuperior to biotech firms in both the discovery of new

compounds and in the clinical development of thosecompounds. Yet because pharmaceutical firms have agreater comparative advantage in clinical developmentthan in the discovery of new compounds, they tend tospecialize downstream in clinical developments and leavebiotech firms to conduct upstream discoveries. Thus,pharmaceutical firms are analogous to Firm B, and clinicaldevelopment is what we have called ‘gadget’ in our example;and biotech firms are analogous to Firm A and compounddiscovery is ‘widget’.

Unless strategic decision making is distorted by otherfactors (e.g., to spread investment risk, better strategicpositioning, etc), or unless there is an increase in availablemanagerial services (Penrose, 1959), Firm B’s managerswill be unwilling to launch an attack in the widget market.To put it differently, if only WIM exists, Firm A’scompetitors may have the ability to attack its marketsegment but may choose not to do so because that wouldbe a suboptimal resource allocation. Under this marketsituation the WIM is not a strategic failure of Firm B;rather it is a ‘natural’ side effect of Firm B pursuing amaximization-based rent-seeking strategy in its productionchoices.

From this CFA perspective we can further explain thedilemma proposed by Pisano (2006) – why is it thatbiotech firms usually only achieve near zero profitability,yet have survived for more than 30 years? CFA suggeststhat biotech survival may be due to the fact thatpharmaceutical firms have an absolute advantage, but nota comparative advantage, in new compound discovery.On the one hand, if biotech firms try to increase revenuesby selling compounds at higher prices to the pharmaceu-tical firms, the pharmaceutical companies will move intothe discovery arena given that they have an absoluteadvantage if they do so. On the other hand, biotech firmsare allowed enough profits to survive by the pharmaceuticalfirms precisely because the pharmaceutical firms can moreprofitably focus their resources on clinical development.Thus, Pisano’s (2006) biotech–pharmaceutical question isconsistent with Cell 3 Situation 3; we can say using ourterminology that Firm A enjoys a temporary competitiveadvantage in producing widgets due to WIM until Firm Bchooses to attack for some other strategic reason.

In Cell 4 Situation 4, both AIM and WIM exist. Firm Ahas both comparative and competitive advantage in makingwidgets. Only when both WIM and AIM work togethercan a competitive advantage be sustained for a long term.In this scenario, potential rivals are limited in their abilitiesto imitate and have little incentive to do so. It is only this‘double protection’ that results in a truly sustainablecompetitive advantage.

We once again can use a dynamic perspective to showcompetitive evolution, this time from Cell 3 to Cell 4.Suppose in Cell 3 Firm B chooses to specialize in gadgets.Through lack of use, its routines and capabilities inproducing widgets likely would erode with time (i.e., theintercept of Firm B on the widget axis will shift inwardsfrom the original position in Situation 3 towards theposition in Situation 4). On the other hand, by specializingin widgets Firm A will benefit from a learning-by-doingprocess that is unavailable to Firm B (i.e., the intercept ofFirm A on the widget axis will shift outwards from its

Comparative firm advantage Anoop Madhok et al.

96

original position in Situation 3 towards the position inSituation 4). As a result of experiential learning and path-dependence, even though the initial condition for Firm Awas inferior to Firm B for producing widgets, Firm A maybecome more efficient in producing widgets than Firm B ina later stage (Penrose, 1959). Moreover, once Firm Abecomes more efficient in producing widgets, even if FirmB were to attempt to duplicate the greater efficiency of FirmA in producing widgets, this would be difficult for Firm Bdue to the firms’ different historical paths (Teece et al.,1997). This indicates that the early stage WIM due tocomparative advantage later will be augmented by AIM thatalso will begin to protect Firm A (i.e., an evolution to Cell4), thus making the competitive position between Firm Aand B more sustainable.

This dynamic overall process is illustrated well by Adnerand Snow’s (forthcoming) recent argument concerningthe efficacy of ‘graceful technological retreats’ by dominantincumbents when they face a new entrant possessing adramatically-improved new technology. This work also canhelp illustrate the potential for transition from Cell 3 to Cell4 that we just discussed. Adner and Snow (forthcoming)argue that incumbents under threat from new technologyneed not try to imitate the new technological breakthrough,even when they have the capabilities and resources to do so.Instead, another strategic option is to cede the customersfor the new technology to the entrant while focusinginstead on those existing customers whose preference is tostay with the familiar-but-less-effective older technology.According to Adner and Snow (forthcoming), this focuson continuing to dominate the older technology can bethe most effective response for an incumbent when thecustomer segment favoring the older technology – due toinertia, lack of investment, or occupying a niche requiringspecial use characteristics – is sufficiently large. This wouldbe another Cell 3 case wherein the incumbent firm mayhave the ability but not the willingness to choose tocompete with the new technology. Following CFA logic,as time passes the new entrant and the incumbent willgain further experience with their respective technologies.As this experience increases the ability-related barriersfor each firm, should they later wish to expand into theother’s technology, their AIM-based competitive advantagewill increase and the competitive situation will shift intoCell 4.

The example from Adner and Snow (forthcoming) alsohelps to illuminate an important but as yet ignored factorthat works in concert with CFA reasoning when managersare making strategic decisions. For Ricardo’s (1821) nation-level analysis of production decisions, the motivation for aparticular product focus is the potential for ‘gains fromtrade’ that may accrue to both nations, and the mechanismthrough which this occurs is trade among nations. Theanalogous motivation for comparative advantage analysisat the firm level is profit for each firm individually, butthere is no corresponding direct product transfer or benefitsharing among competing firms. Instead, the additionalfactor necessary for CFA reasoning to be useful is thepresence of consumer segments with heterogeneouspreferences for the products available in our two-firm,two-product scenarios. That is, as Adner and Snow(forthcoming) note, for a ‘graceful technological retreat’

to make economic sense there must be a sufficiently largesegment of consumers whose preferences can be satisfied –or perhaps even be best satisfied – by the incumbent’spreviously dominant technology. Absent this – that is,with homogenous consumers or buyers who all preferone product over the other – then it becomes a two-firm,single-product model, where CFA logic would not apply forthe firms’ strategic decisions.

DiscussionRicardo’s seminal work ‘On the Principles of PoliticalEconomy and Taxation’ (1821) has left two major legaciesfor economic and managerial thought: the theory of rentand the theory of comparative advantage (Sraffa, 1981).Although deeply embedded and well integrated in Ricardo’soriginal work, the two theories have evolved ratherdivergently. On the one hand, comparative advantagetheory has with some exceptions been applied rathernarrowly to the domain of international economics, despiteRicardo’s intention that it be applied to other levels ofanalysis as well (Ricardo, 1821). On the other hand, thetheory of rent has reached well beyond Ricardo’s originalintention – which was to explain how countries canenhance their wealth – and has permeated microeconomicsand strategic management. In strategic management, forexample, Ricardian rents provide the foundation of theRBV, which has become over the past 20 years one ofthe most influential theories in the field (Lockett et al.,2009). In the words of one of its foremost proponents,the RBV is ‘simply an extension of Ricardian economicsbut with the assertion that many more factors – besidesland – are inelastic in supply’ (Barney, 2001b: 645), andshares Ricardo’s basic assumption that (some) resourcesare heterogeneous, valuable, rare and imperfectly mobile(Barney, 1991, 2001a; Peteraf and Barney, 2003).

Despite having experienced divergent developmentpaths, the two legacies of Ricardian economics neverthelessshare the same roots; they can and should be reintegrated.Given the commonalities, integrating Ricardo’s compara-tive advantage theory with the RBV likely can improve ourunderstanding of both rents and sustainability of advantageat the firm level. We have revisited Ricardo’s work oncomparative advantage, for example, and used it inaddressing one of the most fundamental issues in strategy:inter-firm differences and competitive heterogeneity(Rumelt et al., 1994; Hoopes et al., 2003).

CFA and the sustainability of competitive advantageBarney defines a sustainable competitive advantage asoccurring when a strategy that creates value for the firm is‘not simultaneously being implemented by any current orpotential competitors and when these other firms areunable to duplicate the benefits of this strategy’ (1991: 102).This suggests that not all competitive advantages can or willbecome sustainable. The key, then, is to identify thosesituations that have the attributes and thus potential forfirms to achieve sustainable advantage. Through ourdiscussion of Table 2 and Figure 1 we have distinguishedscenario types and paths of evolution among types that canlead to truly sustainable competitive advantage. When aneconomic activity has both comparative and competitive

Comparative firm advantage Anoop Madhok et al.

97

advantage, both WIM and AIM function together to resultin a more robust sustainability. Our scenarios have shownhow CFA reasoning can complement the RBV to provide amore comprehensive understanding of isolating mechan-isms. By emphasizing managers’ decisions to structuretheir activities in line with comparative opportunity costs,CFA logic shows that firm managers may have rationalincentives not to imitate other firms and that systematicdifferences in preferences across managers may be causedby the incentives to pursue CFA rent-seeking strategies.Extant study on the RBV has not yet recognized and builtupon this distinction.

CFA and the RBVLippman and Rumelt (1982: 419) contend that ‘a theoryexplaining the dispersion of firm efficiencies within anindustry must address both the origins of inter-firmdifferences and the mechanisms that impede their elimina-tion through competition and entry’. With respect to theRBV framework our most direct focus and contributionis on the dimension of inimitability, which we havepartitioned into two aspects: ability and willingness. Wequestion the RBV’s nearly exclusive emphasis on AIM;given resource value, AIM is considered a necessary andsufficient condition for sustainability in the RBV. Yet, ifmechanisms exist that make able competitors unwillingto imitate, then inimitability via ability is no longer thesole necessary condition or sufficient condition forsustainable advantage. In contrast to Oliver (1997), whodemonstrated firms’ unwillingness to imitate because ofinstitutional constraints, our argument rests on an eco-nomic logic. The challenge to RBV scholars is theintegration of WIM into the theoretical framework ofthe RBV.

Our introduction of CFA reasoning and WIM into thestrategy conversation is a step toward a more holistic andrealistic view of competitive heterogeneity. This step isnotable for RBV scholars in part because Peteraf andBarney have stated that ‘so fundamental is the conditionof heterogeneity, that it is the sine qua non of this [RBV]theory’ (2003: 311; italics in original). In a sense, AIM andWIM as we have proposed it are complementary to oneanother in determining firms’ resource allocations anddeployments. That is, they in part co-determine thecompetitive heterogeneity phenomena in an industry.

CFA and other approaches to strategyBesides extending the RBV’s view of competitive hetero-geneity, our CFA argument also can be applied to dynamiccapabilities that center around firms’ routines, inertia andpath-dependence (Nelson and Winter, 1982; Teece et al.,1997; Eisenhardt and Martin, 2000). In short, routines aredeveloped through experience and tend to differ in theirefficiency and effectiveness. Nelson and Winter (1982)demonstrated through simulation the conditions whereinsome routines are more conducive to sustainable advantagethan are others. By placing the firm along differentexperiential paths based on relative opportunity costs,the CFA argument provides an additional and novel set ofconditions that can further strengthen sustainable compe-titive advantage. This in turn contributes to a more

comprehensive and robust framework for inter-firmheterogeneity than do conventional RBV arguments.

CFA also has potential to add to the literature on theboundaries of the firm. When a firm is no longer able toorganize a new economic activity in-house because theassociated costs do not justify doing so, the firm willlimit its scope/boundaries (e.g., Coase, 1937; Williamson,1975). The following question arises from CFA reasoning,however: Before firms reach their ability limitations (i.e.,where the incremental cost of adding a new economicactivity exceeds the potential benefits), are their managersalways willing to expand? CFA logic emphasizes thewillingness aspects of firms’ activities, and potentiallycan lend new insight into the question: ‘[Given limitedresources], why does a firm organize a particular economicactivity internally and not any other?’

Finally, CFA also may be useful in bringing customersback more directly into the strategy equation. As shownearlier during our discussion of the Adner and Snow(forthcoming) paper, CFA-based decisions by managersoften must take into account market segments andconsumer preferences. Such demand side considerationsof course are not new to either strategy or entrepreneurshipscholars; Edith Penrose (1959) asserted 50 years ago thatcompanies realize successful business growth when theyattend to consumers. More recently, arguments areresurfacing that ‘resources gain economic value from theiruse by customers’ (Kor et al., 2007: 1198). Some strategyscholars have begun using customer-focused approaches inexamining strategic issues such as: the influences ofconsumer demand on technological innovation and com-petitive advantage (Adner and Levinthal, 2001; Adner, 2002;Adner and Zemsky, 2006; Tripsas, 2008); consumer-focusedstrategies for value creation and appropriation (Zanderand Zander, 2005; Priem, 2007; Gans et al., 2008; Adner andSnow, forthcoming); and users’ roles in entrepreneurialinnovation (Sawhney et al., 2005; Shah and Tripsas, 2007;Faulkner and Runde, 2009). As shown by our earlierdiscussion of Adner and Snow (forthcoming), CFA reason-ing may represents one step toward a needed integration ofdemand side and producer side approaches to strategicmanagement.

The managerial usefulness of CFABecause CFA and WIM shift the frame from the ability toimitate to the managerial incentives to do so, we have movedbeyond the idea that the characteristics of resources inand of themselves (i.e., valuable, rare, inimitable and non-substitutable) are the sole isolating mechanisms that con-tribute to competitive heterogeneity. Instead, additionalisolating mechanisms like WIM also may be found withinthe domain of managerial choice (Child, 1972). The currentlyaccepted RBV and the dynamic capabilities approach tostrategic management have been criticized repeatedly asbeing singularly lacking in actionable prescriptions formanagers (e.g., Priem and Butler, 2001a, b; Ambrosini andBowman, 2009; Lockett et al., 2009). Consistent with thesecriticisms, Birger Wernerfelt noted in a recent interviewthat the capital asset pricing model in finance hasconsiderable utility for managerial problem-solving, butwent on to say: ‘I think the RBV is not that. Instead I think

Comparative firm advantage Anoop Madhok et al.

98

it just says okay, here are some of the resources that areimportant, but it doesn’t tell you what to do with themreally. So I think unfortunately it is not that’ (Lockett et al.,2008: 1133). Recent RBV-based studies still fall prey to the‘lack of prescription’ problem (e.g., Holcomb et al., 2009);these studies reconfirm that great managers are importantand that managers’ heterogeneous ability (in this case, atbundling resources) explains more variance in outcomeswhen there is resource parity (see Thomas (1988) for anearlier empirical demonstration), but they have little to sayabout specific actions that should be taken by ‘great’managers in different contexts. CFA studies may illuminateone path for moving beyond this problem, because CFAlogic can indicate what strategies are likely to be effectivealternatives in specific comparative advantage situations, aswe have shown in our explanations of Table 2 and Figure 1.

ConclusionRumelt et al. (1994) have argued that a comprehensiveunderstanding of inter-firm heterogeneity requires differentstreams of theories. The CFA reasoning we have introducedextends strategy scholars’ current understanding of com-petitive advantage and isolating mechanisms in a distinc-tive manner and sheds new light on the phenomenon ofinter-firm heterogeneity. This matter is important becausecompetitive advantages, when sustainable, potentiallyculminate in performance differences across rival firms.The implication for managers is that they should analyzecomparative opportunity costs when deciding which rentenhancing strategies to pursue.

One potential avenue for future research is to uncoverother sources of WIM based on managerial choices, whichin turn would further enhance our understanding of inter-firm heterogeneity. With respect to CFA reasoning,additional questions that might be addressed could include:How does the relationship among alternative products(e.g., are they complementary or supplementary) affectfirms’ strategic choices and resource allocations? Or withrespect to firms’ search for rents: What is the substitut-ability attribute of the RBV (Priem and Butler, 2001a)? Wehope that CFA-related issues such as these will be picked upby other scholars in future research.

Notes

1 A detailed illustration of comparative advantage using Ricardo’soriginal example is shown in the Appendix.

2 There is an implicit ceteris paribus assumption in thisdefinition: that all these products or services render a similarlevel of perceived consumer benefit. That is, the profit margin ofa product or service is determined solely by costs. Otherwisefirms/nations need not provide the relatively lower cost productor service but instead can pursue the ones that promise thelargest difference between perceived benefits and cost (i.e., valuecreation, Peteraf and Barney, 2003).

3 Later, Peteraf and Barney (2003) define rent as a return abovethe opportunity cost of the marginally productive resources, thelatter referring to the value generated by the resources held bythe inferior producer/user.

4 Note that Peteraf and Barney (2003: 313) consider competitiveadvantage as a ‘fundamental type of competitive edge y anindicator of the firm’s potential to best its rivals in terms of

rents, profitability, market share, and other outcomes ofinterest’. To keep our argument consistent with the RBV, wesubscribe to this interpretation of competitive advantage herein.Moreover, this interpretation is also applied to the laterdiscussion of comparative firm advantage.

5 Of course resources can be applied to multiple products andface multiple competitors. Our model, however, is concernedonly with the next best use and the next best competitor.

References

Adner, R., 2002, ‘‘When are technologies disruptive? A demand-based view of

the emergence of competition’’. Strategic Management Journal, 23: 667–688.

Adner, R. and D. Levinthal, 2001, ‘‘Demand heterogeneity and technology

evolution: Implications for product and process innovation’’. Management

Science, 47: 611–628.

Adner, R. and D. Snow, 2010, ‘‘ ‘Old’ technology responses to ‘New’ technology

threats: Demand heterogeneity and graceful technology retreats’’. Industrial

and Corporate Change (forthcoming).

Adner, R. and P. Zemsky, 2006, ‘‘A demand-based perspective on sustainable

competitive advantage’’. Strategic Management Journal, 27: 215–239.

Ambrosini, V. and C. Bowman, 2009, ‘‘What are dynamic capabilities and are

they a useful construct in strategic management? International Journal of

Management Reviews, 11: 29–49.

Arora, A., A. Gambardella, L. Magazzini and F. Pammolli, 2009, ‘‘A breath of

fresh air? Firm type, scale, scope, and selection effects in drug development’’.

Management Science, 55: 1638–1653.

Barney, J., 1991, ‘‘Firm resources and sustained competitive advantage’’.

Journal of Management, 17: 99–120.

Barney, J., 2001a, ‘‘Is the resource-based ‘view’ a useful perspective for strategic

management research? Yes’’. Academy of Management Review, 26: 41–56.

Barney, J., 2001b, ‘‘Resource-based theories of competitive advantage: A ten-

year retrospective on the resource-based view’’. Journal of Management, 6:

643–650.

Boyd, J., 2004, ‘‘Intra-industry structure and performance: Strategic groups and

strategic blocks in the worldwide airline industry’’. European Management

Review, 1: 132–144.

Chen, M. -J., 1996, ‘‘Competitor analysis and interfirm rivalry: Toward a

theoretical integration’’. Academy of Management Review, 21: 100–134.

Child, J., 1972, ‘‘Organizational structure, environment and performance:

The role of strategic choice’’. Sociology, 6: 1–22.

Chiles, T. and J. McMackin, 1996, ‘‘Integrating variable risk preferences, trust,

and transaction cost economics’’. Academy of Management Review, 21:

73–100.

Christensen, C., 1997, The innovator’s dilemma – When technologies cause great

firms to fail. Boston, MA: Harvard Business School Press.

Coase, R., 1937, ‘‘The nature of the firm’’. Economica, 4: 386–405.

Coase, R., 1973, ‘‘Business organization and the accountant’’. In J. Buchanan

and G. Thirlby (eds.) L.S.E. essays on cost. London: London School of

Economics and Political Science, pp: 95–132.

Eisenhardt, K. and J. Martin, 2000, ‘‘Dynamic capabilities: What are they?

Strategic Management Journal, 21: 1105–1121.

Faulkner, P. and J. Runde, 2009, ‘‘On the identity of technological objects

and user innovations in function’’. Academy of Management Journal, 34:

442–462.

Gans, J., G. MacDonald and M. Ryall, 2008, The two sides of competition and

their implications for strategy Working paper, Melbourne Business School,

Melbourne, Australia.

Giarratana, M., 2008, ‘‘Missing the starting gun: De Alio entry order in new

markets, inertia and real option capabilities’’. European Management Review,

5: 115–124.

Gimeno, J., 1999, ‘‘Reciprocal threats in multimarket rivalry: Staking out

‘spheres of influence’ in the U.S. airline industry’’. Strategic Management

Journal, 20: 101–128.

McGraw-Hill Dictionary of Modern Economics, 1983 Edited by D. Greemwald

A handbook of terms and organizations. New York: McGraw-Hill.

Holcomb, T., M. Holmes and B. Connelly, 2009, ‘‘Making the most of what you

have: Managerial ability as a source of resource value creation’’. Strategic

Management Journal, 30: 457–485.

Comparative firm advantage Anoop Madhok et al.

99

Hoopes, D., T. Madsen and G. Walker, 2003, ‘‘Guest Editors’ introduction to the

special issue: Why is there a resource-based view? Toward a theory of

competitive heterogeneity’’. Strategic Management Journal, 24: 889–902.

Klein, B., R. Crawford and A. Alchian, 1978, ‘‘Vertical integration, appropriable

rents, and the competitive contracting process’’. Journal of Law and

Economics, 21: 297–326.

Knott, A., 2003, ‘‘The organizational routines factor market paradox’’. Strategic

Management Journal, 24: 929–943.

Kor, Y., J. Mahoney and S. Michael, 2007, ‘‘Resources, capabilities and

entrepreneurial perceptions’’. Journal of Management Studies, 44:

1187–1212.

Levin, R., A. Klevorick, R. Nelson and S. Winter, 1987, ‘‘Appropriating the

returns from industrial research and development’’. Brookings Papers on

Economic Activity, 3: 783–820.

Lippman, S. and R. Rumelt, 1982, ‘‘Uncertainty imitability: An analysis of

interfirm differences in efficiency under competition’’. Bell Journal of

Economics, 13: 418–439.

Lippman, S. and R. Rumelt, 2003, ‘‘The payments perspective: Micro-

foundations of resource analysis’’. Strategic management Journal, 24:

1069–1087.

Lockett, A., R. O’Shea and M. Wright, 2008, ‘‘The development of the RBV:

Reflections from Birger Wernerfelt’’. Organization Studies, 29: 1125–1141.

Lockett, A., U. Morgenstern and S. Thompson, 2009, ‘‘The development of the

resource-based view of the firm: A critical appraisal’’. International Journal

of Management Reviews, 11: 9–28.

Makadok, R., 2001, ‘‘Toward a synthesis of the resource-based and dynamic-

capability views of rent creation’’. Strategic Management Journal, 22:

387–401.

Maskell, P. and A. Malmberg, 1999, ‘‘Localised learning and industrial

competitiveness’’. Cambridge Journal of Economics, 23: 167–185.

Mitchell, W., 1991, ‘‘Dual clocks: Entry order influences on incumbents and

newcomer market share and survival when specialized assets retain their

value’’. Strategic Management Journal, 12: 85–100.

Nelson, R. and S. Winter, 1982, An evolutionary theory of economic change.

Cambridge, MA: Harvard University Press.

Oliver, C., 1997, ‘‘Sustainable competitive advantage: Combining institutional

and resource-based views’’. Strategic Management Journal, 18: 697–713.

Penrose, E., 1959, The theory of the growth of the firm. Oxford, UK: Basil

Blackwell.

Peteraf, M., 1993, ‘‘The cornerstones of competitive advantage: A resourced-

based view’’. Strategic Management Journal, 14: 179–191.

Peteraf, M. and J. Barney, 2003, ‘‘Unraveling the resource-based tangle’’.

Managerial and Decision Economics, 24: 309–323.

Pisano, G., 2006, ‘‘Can science be a business? Lessons from biotech’’. Harvard

Business Review, 84: 114–124.

Porter, M., 1990, Competitive advantage of nations. New York: Free Press.

Priem, R., 2007, ‘‘A consumer perspective on value creation’’. Academy of

Management Review, 32: 219–235.

Priem, R. and J. Butler, 2001a, ‘‘Is the resource-based ‘view’ a useful perspective

for strategic management research? Academy of Management Review’’, 26:

22–40.

Priem, R. and J. Butler, 2001b, ‘‘Tautology in the resource-based view and the

implications of externally determined resource value: Further comments’’.

Academy of Management Review, 26: 57–66.

Ricardo, D., 1821, On the principles of political economy and taxation.

Albemarle-Street, London, UK: John Murray.

Rumelt, R., 1984, ‘‘Toward a strategic theory of the firm’’. In R. Lamb (eds.)

Competitive strategic management. Englewood Cliffs, NJ: Prentice-Hall,

pp: 556–570.

Rumelt, R., D. Schendel and D. Teece, 1994, ‘‘Fundamental issues in strategy’’.

In R. Rumelt, D. Schendel and D. Teece (eds.) Fundamental issues in strategy:

A research agenda. Boston, MA: Harvard Business School Press, pp: 9–47.

Sawhney, M., G. Verona and E. Prandelli, 2005, ‘‘Collaborating to create: the

Internet as a platform for customer engagement in product innovation’’.

Journal of Interactive Marketing, 19: 4–17.

Shah, S. and M. Tripsas, 2007, ‘‘The accidental entrepreneur: the emergent and

collective process of user entrepreneurship’’. Strategic Entrepreneurship

Journal, 1: 123–140.

Sraffa, P., 1981, The works and correspondence of David Ricardo. Cambridge,

UK: Cambridge University Press.

Storper, M., 1993, ‘‘Regional ‘worlds’ of production: Learning and innovation in

technology districts of France, Italy and the USA’’. Regional Studies, 27:

433–456.

Thomas, A., 1988, ‘‘Does leadership make a difference to organizational

performance?’’ Administrative Science Quarterly, 33: 388–400.

Tripsas, M., 2008, ‘‘Customer preference discontinuities: A trigger for radical

technological change’’. Managerial and Decision Economics, 29: 79–97.

Teece, D., G. Pisano and A. Shuen, 1997, ‘‘Dynamic capability and strategic

management’’. Strategic Management Journal, 18: 507–534.

Williams, J., 1994, ‘‘Strategy and the search for rents: The evolution of diversity

among firms’’. In R. Rumelt, D. Schendel and D. Teece (eds.) Fundamental

issues in strategy: A research agenda. Boston, MA: Harvard Business School

Press, pp: 229–246.

Williamson, O., 1975, Markets and hierarchies: Analysis and antitrust

implications. New York: Free Press.

Zander, I. and U. Zander, 2005, ‘‘The inside track: On the important (but

neglected) role of customers in the resource-based view of strategy and firm

growth’’. Journal of Management Studies, 42: 1519–1548.

AppendixFirst, Let us look at Portugal. If with 80 men, Portugal canproduce 1 unit of wine in a year. However, with the samenumber of men, Portugal can produce only 80/90 (0.88)unit of cloth in a year. If Portugal chooses to produce 1 unitof wine, she is giving up the opportunity to produce 0.88unit of cloth. On the other hand, if Portugal chooses toproduce 1 unit of cloth, she is giving up 1/.88 (1.125) unitsof wine.

Now, let us look at England. If with 120 men, England canproduce 1.2 units of cloth in a year. However, with the samenumber of men, England can produce only 1 unit of wine ina year. If England chooses to produce 1 unit of wine, she isgiving up the opportunity to produce 1.2 units of cloth. Onthe other hand, if England chooses to produce 1 unit ofcloth, she is giving up 1/1.2 (0.833) unit of wine.

As shown in Table A1, we can see that the opportunitycost of producing one unit of cloth is lower for England(0.8333) than for Portugal (1.125). On the other hand, theopportunity cost of producing one unit of wine for Portugal(0.88) is lower than for England (1.2). Therefore, Portugalhas comparative advantage in producing wine; while eventhough England does not have any absolute advantage inproducing either cloth or wine, but she has comparativeadvantage in producing cloth.

Table A1 Comparative advantage

England Portugal

1 unit of cloth 0.833 unit of wine 1.125 unit of wine1 unit of wine 1.2 unit of cloth 0. 88 unit of cloth

Comparative firm advantage Anoop Madhok et al.

100

Copyright © 2022 FDOKUMEN