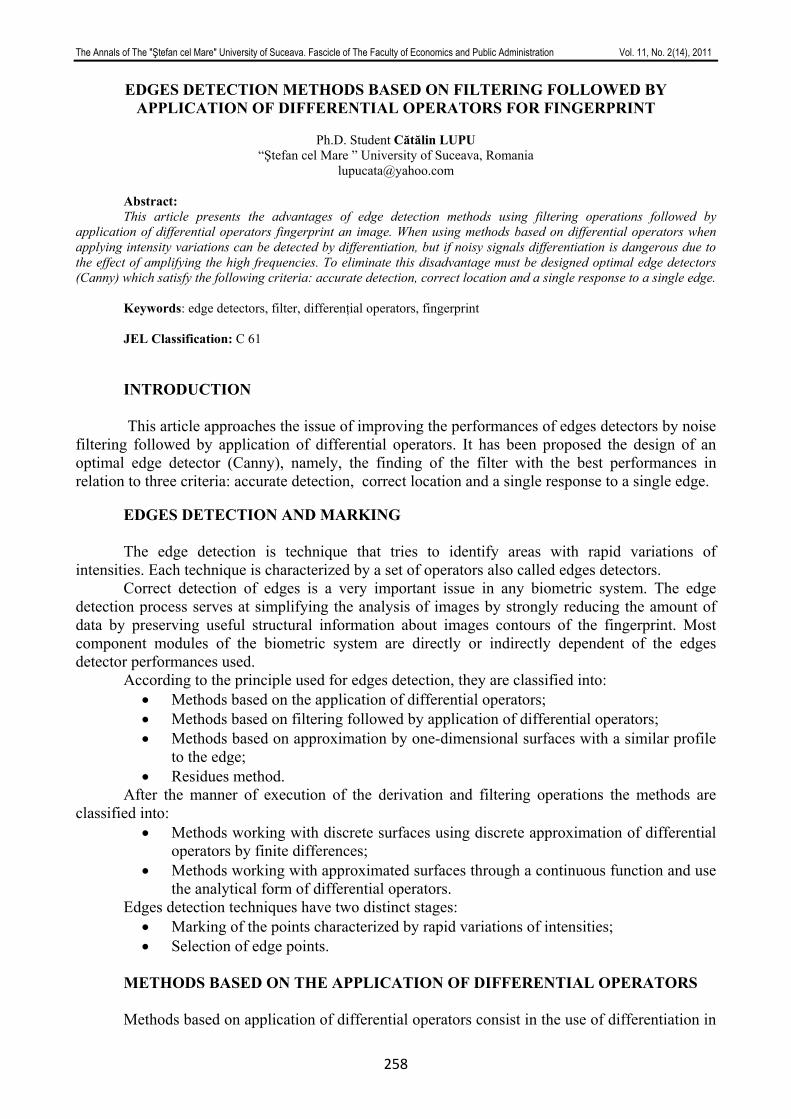

THE PRESTIGE DISASTER AND THE PROPOSAL FOR A EUROPEAN FUND FOR THE COMPENSATION OF OIL POLLUTION...

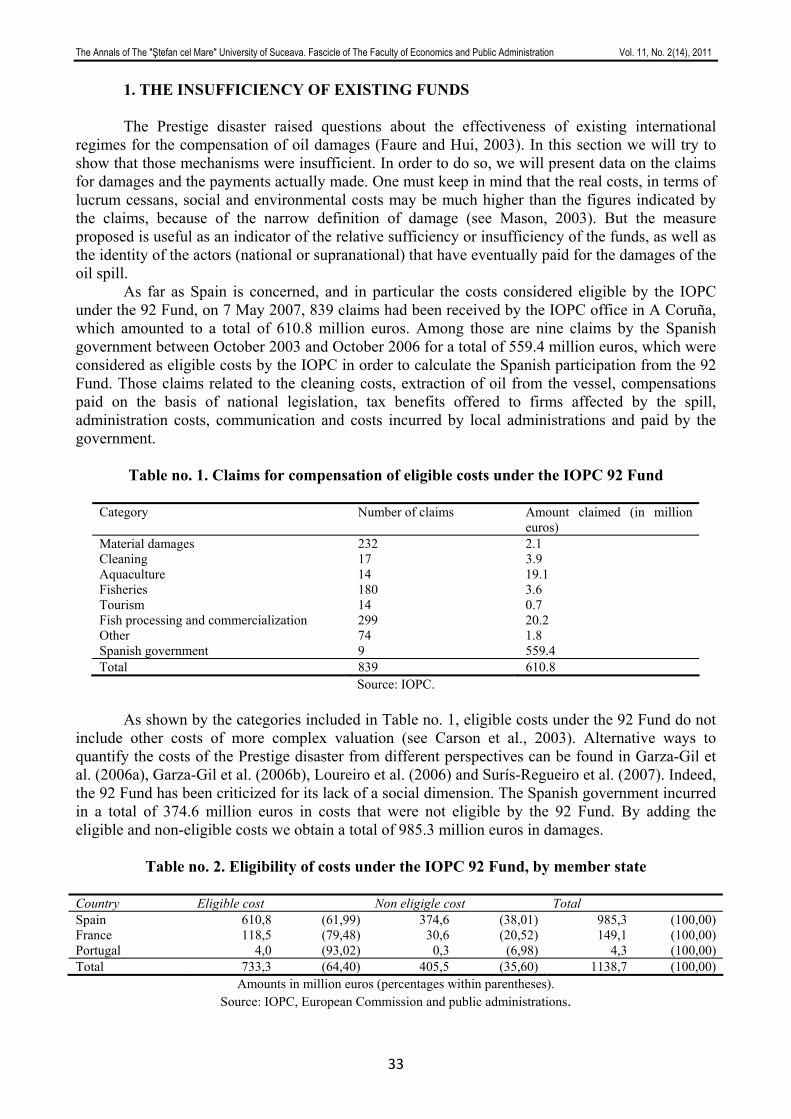

305

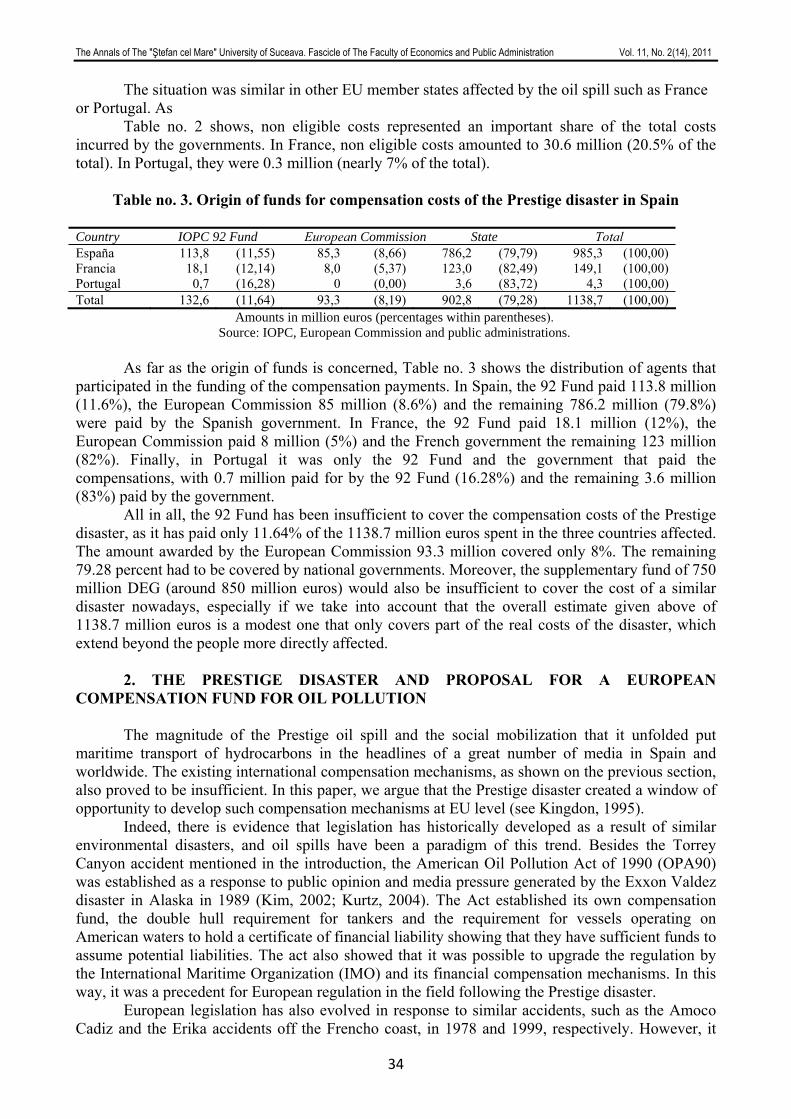

ISSN 2066-575X www.seap.usv.ro/annals Revistă cotată CNCSIS, categoria B+ / Indexată în baze de date internaţionale THE ANNALS OF THE "ŞTEFAN CEL MARE" UNIVERSITY OF SUCEAVA. FASCICLE OF THE FACULTY OF ECONOMICS AND PUBLIC ADMINISTRATION VOLUME 11, NO. 2(14), 2011 Editura Universităţii Ştefan cel Mare din Suceava

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of THE PRESTIGE DISASTER AND THE PROPOSAL FOR A EUROPEAN FUND FOR THE COMPENSATION OF OIL POLLUTION...

ISSN 2066-575X www.seap.usv.ro/annals

Revistă cotată

CNCSIS, categoria B+ /

Indexată în baze de date

internaţionale

THE ANNALS OF THE "ŞTEFAN CEL MARE"

UNIVERSITY OF SUCEAVA. FASCICLE OF THE FACULTY OF

ECONOMICS AND PUBLIC ADMINISTRATION

VOLUME 11, NO. 2(14), 2011

Editura Universităţii Ştefan cel Mare din Suceava

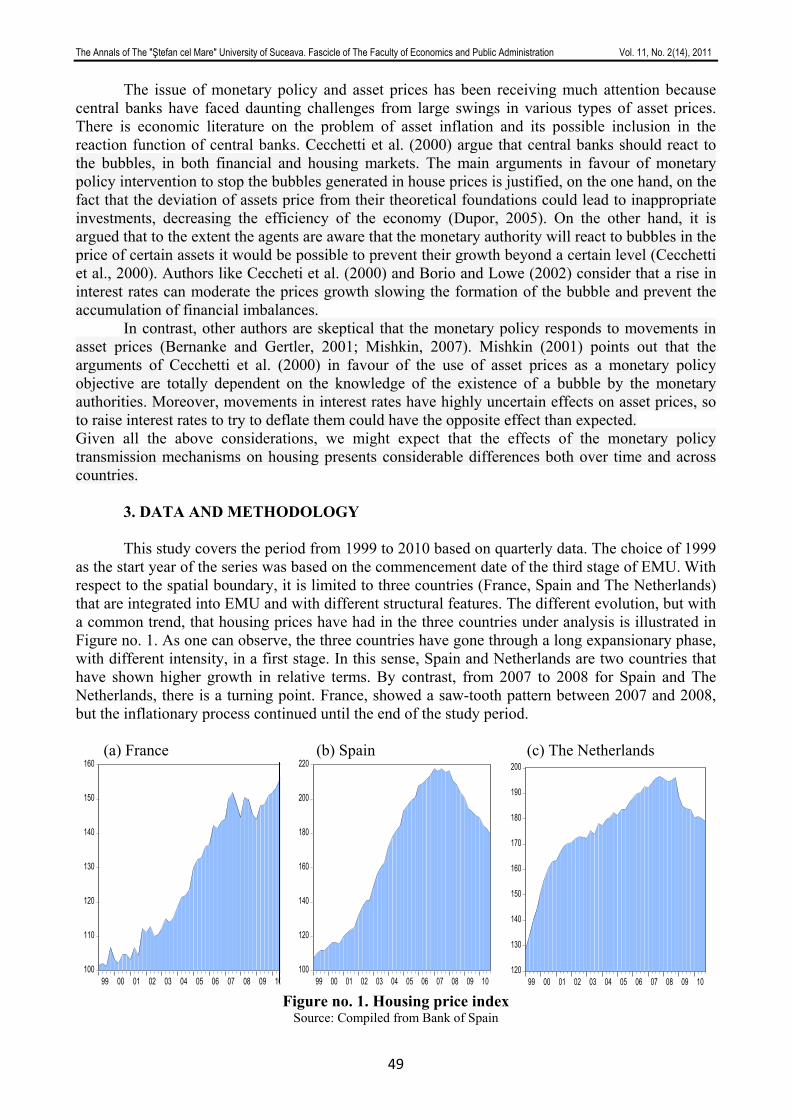

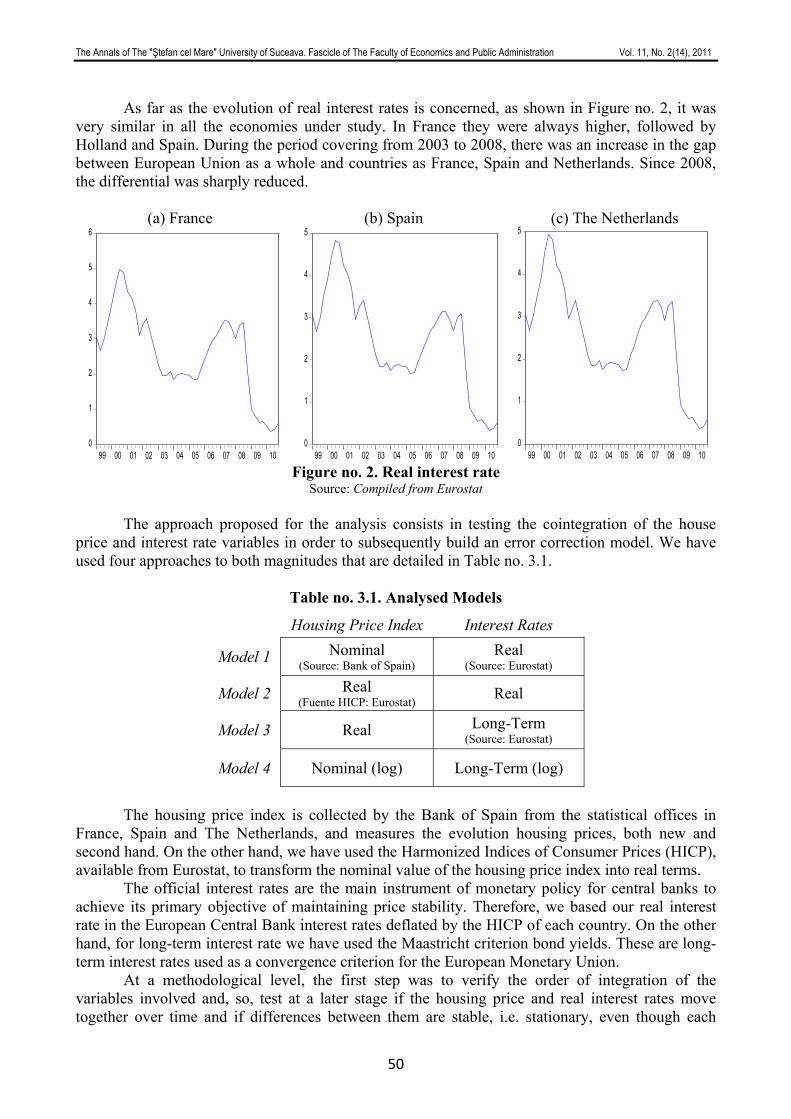

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

2

EDITORIAL BOARD:

Editor‐in‐chief: Carmen NĂSTASE General editorial secretary: Adrian Liviu SCUTARIU Editors: Elena HLACIUC, Carmen CHAŞOVSCHI, Mariana LUPAN, Ovidiu Florin HURJUI SCIENTIFIC COMMITTEE:

Angela ALBU, „Ştefan cel Mare” University of Suceava, Romania Paolo ANDREI, University of Studies in Parma, Italy Stefano AZZALI, University of Studies in Parma, Italiy George P. BABU, University of Southern Mississippi, USA Christian BAUMGARTNER, International Friends of Nature, Austria Grigore BELOSTECINIC, ASEM, Chi şinău, Republic of Moldova Ionel BOSTAN, „Alexandru Ioan Cuza” University of Iaşi, Romania Aurel BURCIU, „Ştefan cel Mare” University of Suceava, Romania Gheorghe CÂRSTEA, Academy of Economic Studies, Bucharest , Romania Slobodan CEROVIC, Singidunum University, Belgrade, Serbia Simion CERTAN, State University of Chişinău, Republic of Moldova Carmen CHAŞOVSCHI, „Ştefan cel Mare” University of Suceava, Romania Liliana ELMAZI, Tirana University, Albania Cristian Valentin HAPENCIUC, „Ştefan cel Mare” University of Suceava, Romania Elena HLACIUC, „Ştefan cel Mare” University of Suceava, Romania Elena IFTIME, „Ştefan cel Mare” University of Suceava, Romania Marian JALENCU, State University of Chişinău, Republic of Moldova Miika KAJANUS, Savonia University of Applied Sciences, Iisalmi, Finland Alunica MORARIU, „Ştefan cel Mare” University of Suceava, Romania Maria MUREŞAN, Academy of Economic Studies, Bucuresti, Romania Carmen NĂSTASE, „Ştefan cel Mare” University of Suceava, Roman ia Alexandru NEDELEA, „Ştefan cel Mare” University of Suceava, Romania Ion PÂRȚACHI, ASEM, Chişinău, Republic of Moldova Rusalim PETRIŞ, „Ştefan cel Mare” University of Suceava, Romania Abraham PIZAM, University of Central Florida, Orlando, Florida Ion POHOAȚĂ, „Alexandru Ioan Cuza” University of Iaşi, Romania Gabriela PRELIPCEAN, „Ştefan cel Mare” University of Suceava, Romania Gheorghe SANDU, „Ştefan cel Mare” University of Suceava, Romania Petru SANDU, Elizabethtown College, Pennsylvania, USA Doru TILIUȚE, „Ştefan cel Mare” University of Suceava, Romania Viorel ȚURCANU, ASEM, Chişinău, Republic of Moldova Diego VARELA PEDREIRA, University of A Coruna, Spain Răzvan VIORESCU, „Ştefan cel Mare” University of Suceava, Romania Text review: Adrian Liviu SCUTARIU. Cover design: Adrian Liviu SCUTARIU Contact: Faculty of Economics and Public Administration „Ştefan cel Mare” University of Suceava Str. Universităţii nr. 13, Corp H, Camera H108 720229 SUCEAVA, ROMANIA Phone: (+40) 230 216147 ext. 294 E-mail: [email protected] Journal web site: www.seap.usv.ro/annals Faculty web site: www.seap.usv.ro University web site: www.usv.ro

Întreaga răspundere asupra conţinutului articolelor publicate revine autorilor. The entire responsability for the content of the published articles rests with the authors.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

3

CONTENT

SECTION 1. ECONOMY, TRADE, SERVICES ................................................................... 6 DOES EU MEMBERSHIP AFFECT THE SOCIAL AND LABOUR INCLUSION OF FOREIGN PRISONERS IN SPAIN? AN ANALYSIS OF SELF-PERCEPTIONS AND ATTITUDES TOWARDS LEARNING ..........................................................................................7

Isabel NOVO-CORTI María RAMIL María BARREIRO-GEN

SUSTAINABLE DEVELOPMENT IN BUCOVINA REGION – ANALYSIS OF TOURISTIC POTENTIAL IN SUCEAVA BASIN.............................................................................................16

PhD. Student Constantin COCERHAN Professor PhD. Carmen NĂSTASE

ONLINE EDUCATION - AN IMPORTANT ISSUE FOR THE LABOR MARKET..............25 Assoc. Prof. PhD. Diana-Mihaela POCIOVĂLIŞTEANU PhD. Lecturer Liana BADEA

THE PRESTIGE DISASTER AND THE PROPOSAL FOR A EUROPEAN FUND FOR THE COMPENSATION OF OIL POLLUTION DAMAGE: A MISSED OPPORTUNITY FOR THE EUROPEAN UNION? ...........................................................................................................32

Javier PRADO-DOMÍNGUEZ Diego VARELA

QUALITATIVE OBSERVATION APPLIED IN PROMOTIONAL STRATEGY DESIGN .40 Associate Professor Adriana MANOLICĂ Teaching assistant, PhD. Claudia BOBÂLCĂ Teaching assistant, PhD. Oana CIOBANU

IS THERE A STABLE RELATIONSHIP BETWEEN REAL INTEREST RATES AND HOUSING PRICES? EVIDENCE FROM SEVERAL EURO AREA COUNTRIES ..............46

José Manuel SÁNCHEZ SANTOS José Pablo ABEAL VÁZQUEZ

CHARACTERISTICS OF THE ILLEGAL DRUG MARKETS IN EUROPEAN UNION ....56 Scientific Researcher PhD. Irina CAUNIC Professor PhD. Gabriela PRELIPCEAN

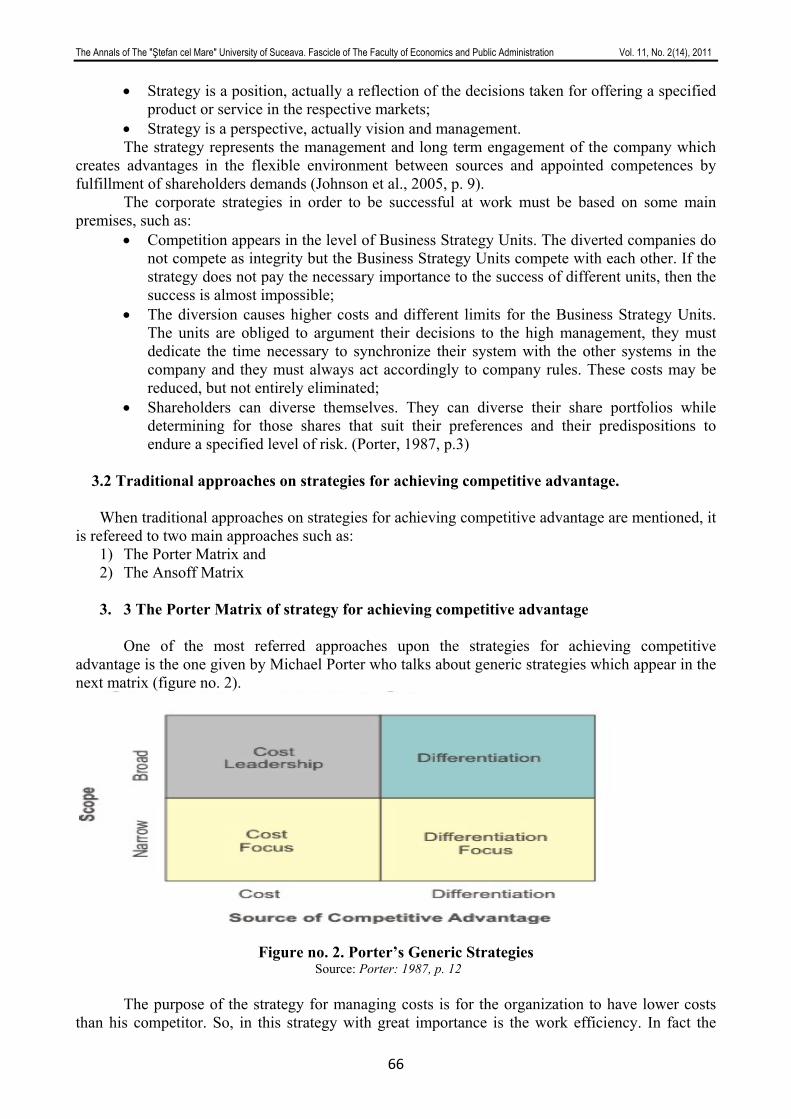

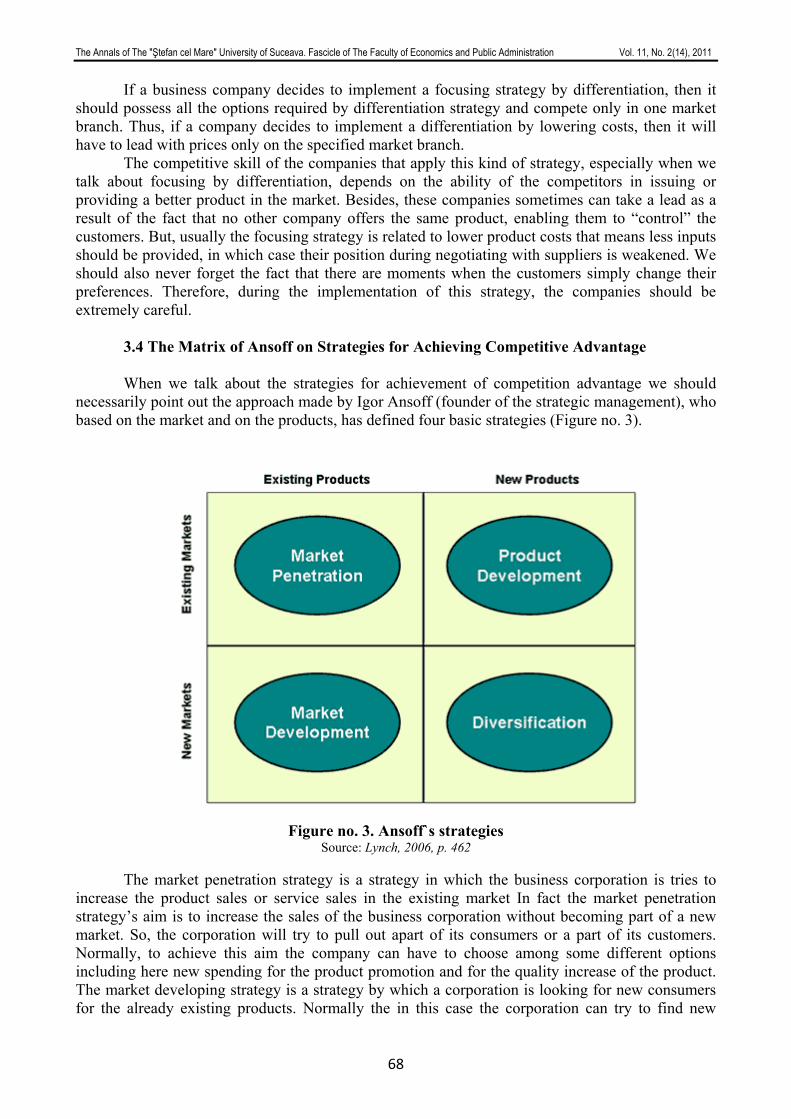

STRATEGIES FOR ACHIEVING COMPETITIVE ADVANTAGE .......................................63 Assistant Professor Jusuf ZEKIRI Associate Professor Ph.D. Alexandru NEDELEA

TEA PRODUCTION, CONSUMPTION AND EXPORTS IN GLOBAL AND BANGLADESHI PERSPECTIVE.................................................................................................74

Tasnuba NASIR Mohammad SHAMSUDDOHA

COMBINING COMPANIES – A SOLUTION FOR OVERCOMING THE ECONOMIC CRISIS EFFECTS ...........................................................................................................................81

Lecturer Ph.D. Nicoleta Cristina MATEI THE EVOLUTION OF THE CUSTOMS UNION.......................................................................86

Lecturer PhD. Marius BOIŢĂ Professor PhD. Dorina ARDELEAN Professor PhD. Cristian HAIDUC

THE ROLE OF COMMERCIAL BANKS FROM ROMANIA IN THE ATTRACTION OF STRUCTURAL FUNDS..................................................................................................................91

PhD. Corina BERICA

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

4

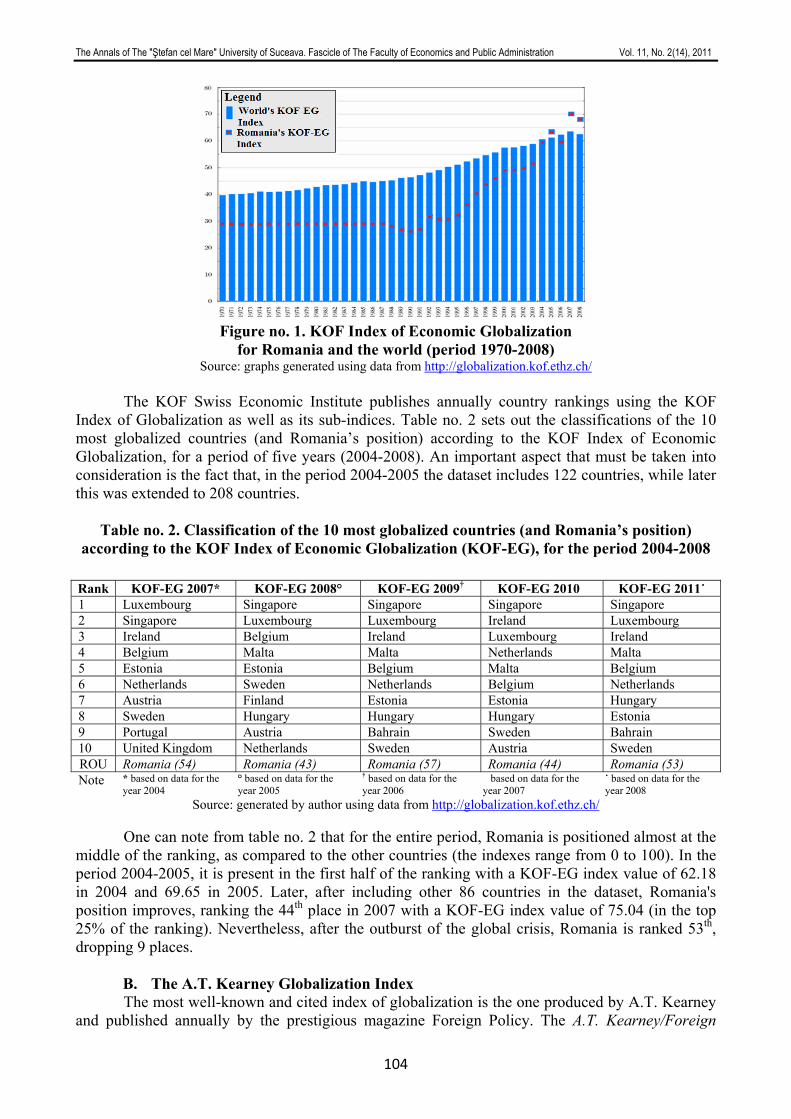

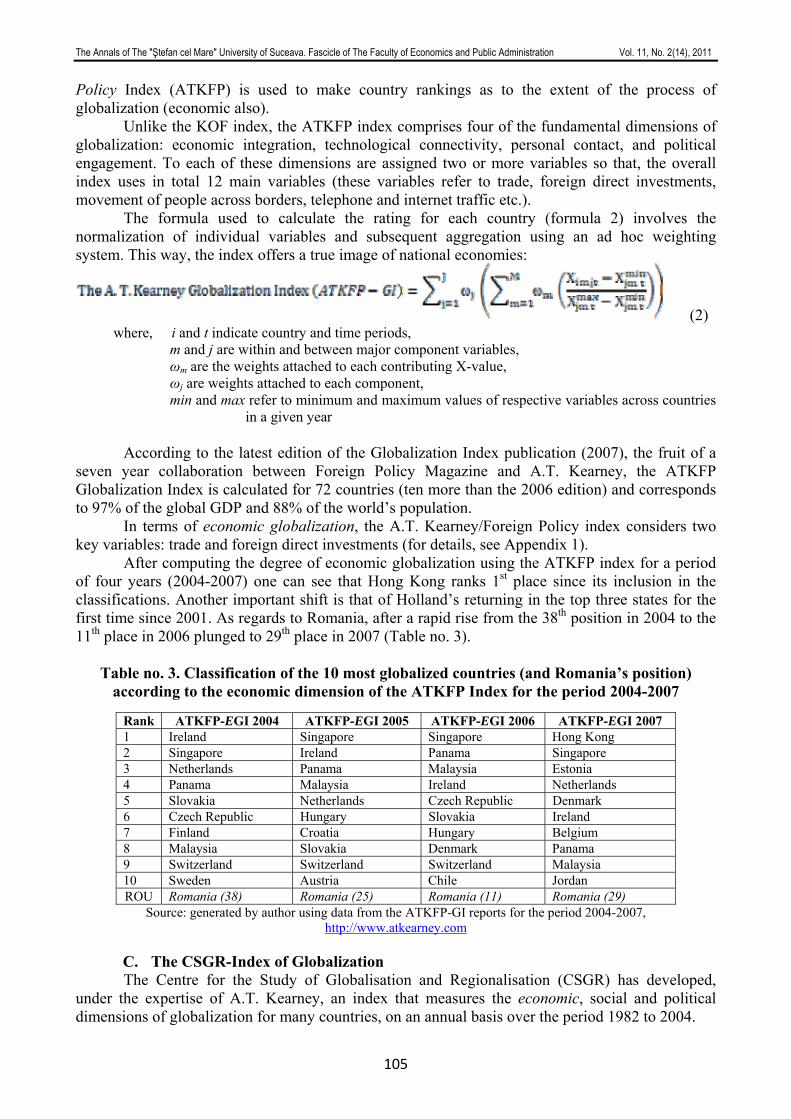

MEASURING ECONOMIC GLOBALIZATION – FACTS AND FIGURES..........................99 Ph. D. Student Marius C. APOSTOAIE

PHARE CROSSBORDER GRANTS AND CHANGES IN THE CROSSBORDER ECONOMY. STUDY CASE – ROMANIAN-UKRAINIAN BORDER ...................................110

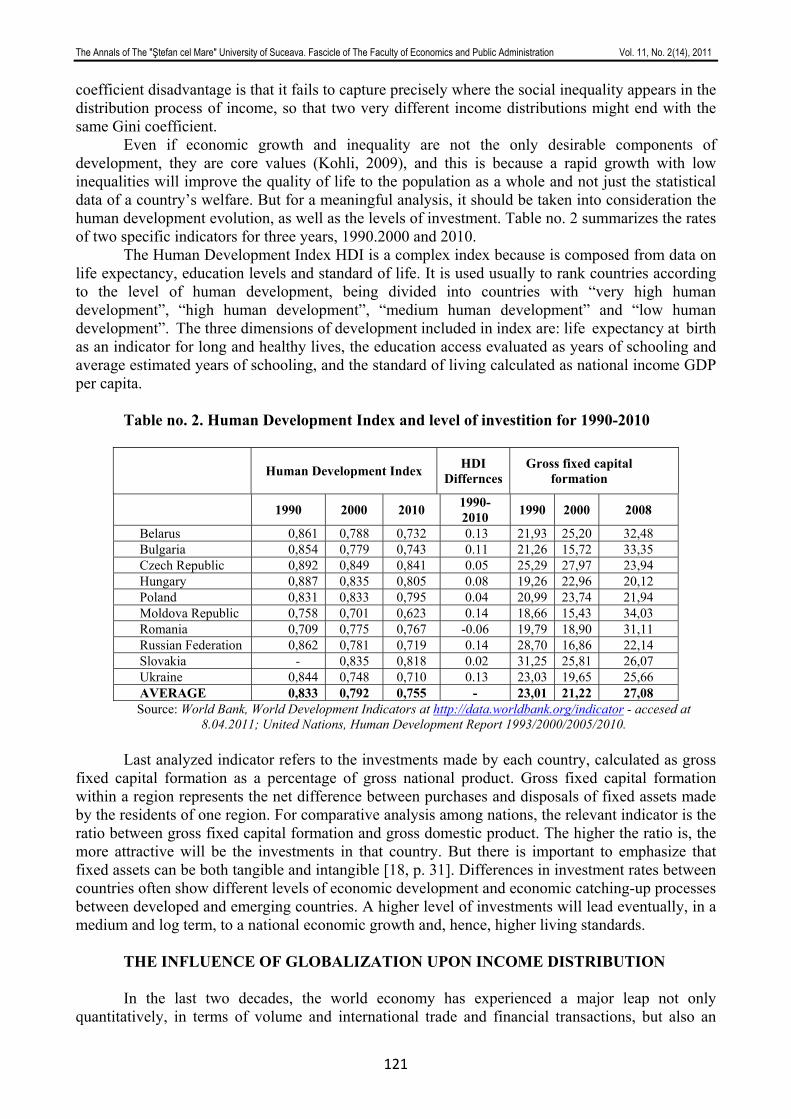

PhD. Student Marcela SLUSARCIUC THE INCOME INEQUALITY IN THE EASTERN EUROPEAN COUNTRIES: A COMPARATIVE STUDY FOR THE PERIOD 1990-2010.......................................................119

PhD. Student Cristina Gabriela SUSANU HOW CAN WE ANTICIPATE CRISES? ..................................................................................128

Ph.D. student Elena Bianca VIERU

SECTION 2. MANAGEMENT AND BUSINESS ADMINISTRATION ............................. 135 SUSTAINABLE DEVELOPMENT POLICIES IMPACT ON FOREIGN DIRECT INVESTMENT...............................................................................................................................136

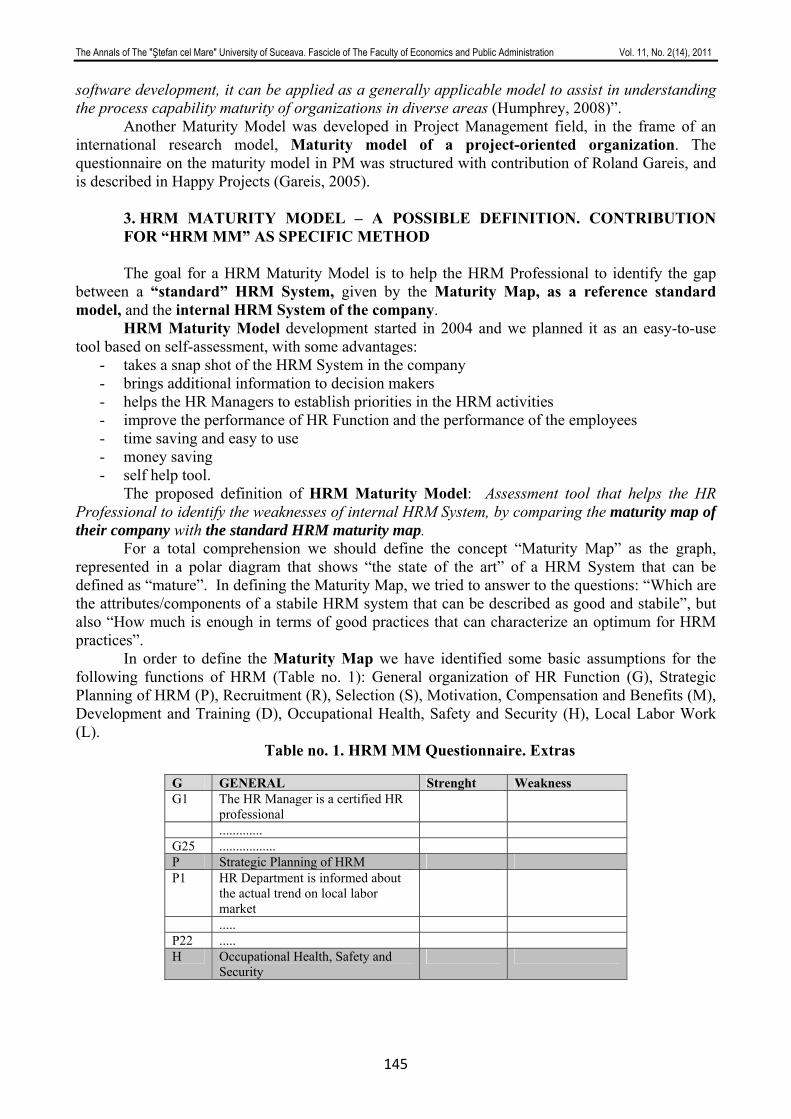

Associate Professor PhD. Costică MIHAI HUMAN RESOURCES MANAGEMENT MATURITY MODEL..........................................143

Associate Professor PhD. Carmen CHAŞOVSCHI EMPLOYABILITY MANAGEMENT: IS HIGHER EDUCATION IN CRISIS? .................149

Assistant Professor Nikhil Chandra SHIL Alok Kumar PRAMANIK

SOME FEATURES OF POSTWAR BUSINESS CYCLES ......................................................166 Assistant PhD. Student. Mihaela IFRIM

THE ROLE OF EMOTIONAL INTELLIGENCE IN TRANSFORMATIONAL LEADERSHIP AND REAL ESTATE MARKET IN POST-COMMUNIST MARKETS.....173

Teaching Assistant PhD. Student Sorin ANAGNOSTE Teaching Assistant PhD. Student Costin DAMAŞARU

SECTION 3. ACCOUNTING ‐ FINANCES ..................................................................... 180 DIFFERENTIAL FINANCIAL REPORTING FOR MICRO-ENTITIES: ADVANTAGES AND LIMITS .................................................................................................................................181

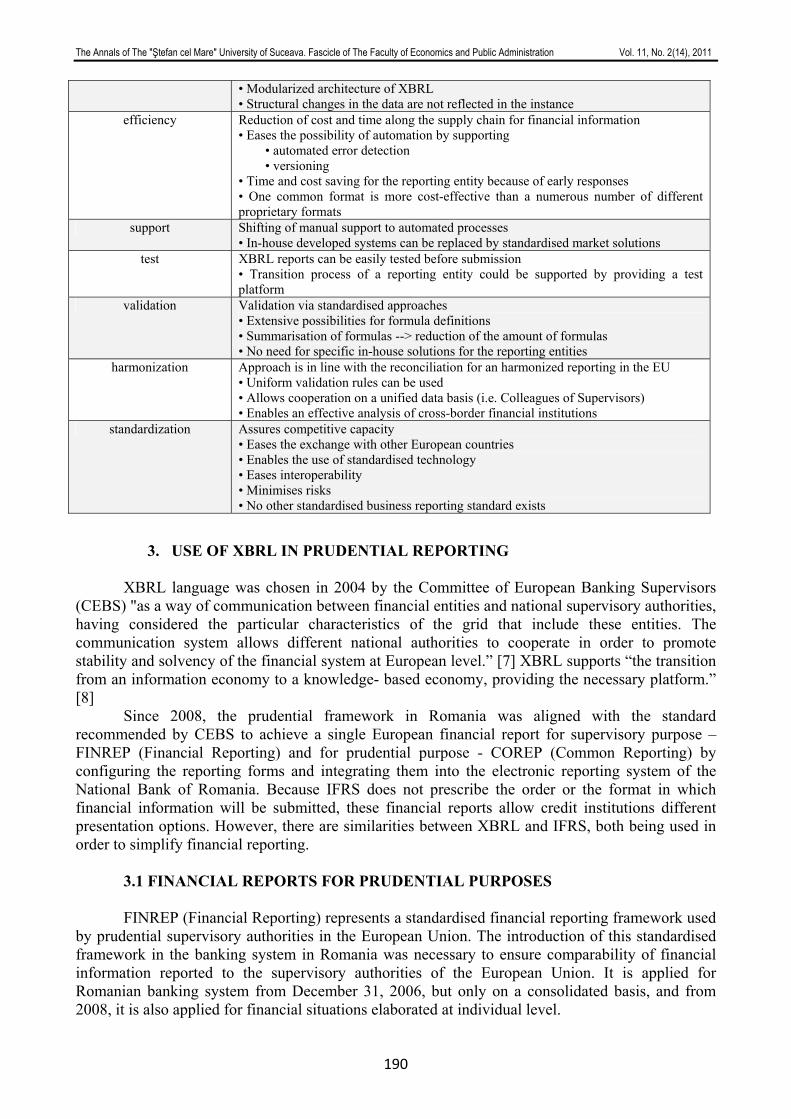

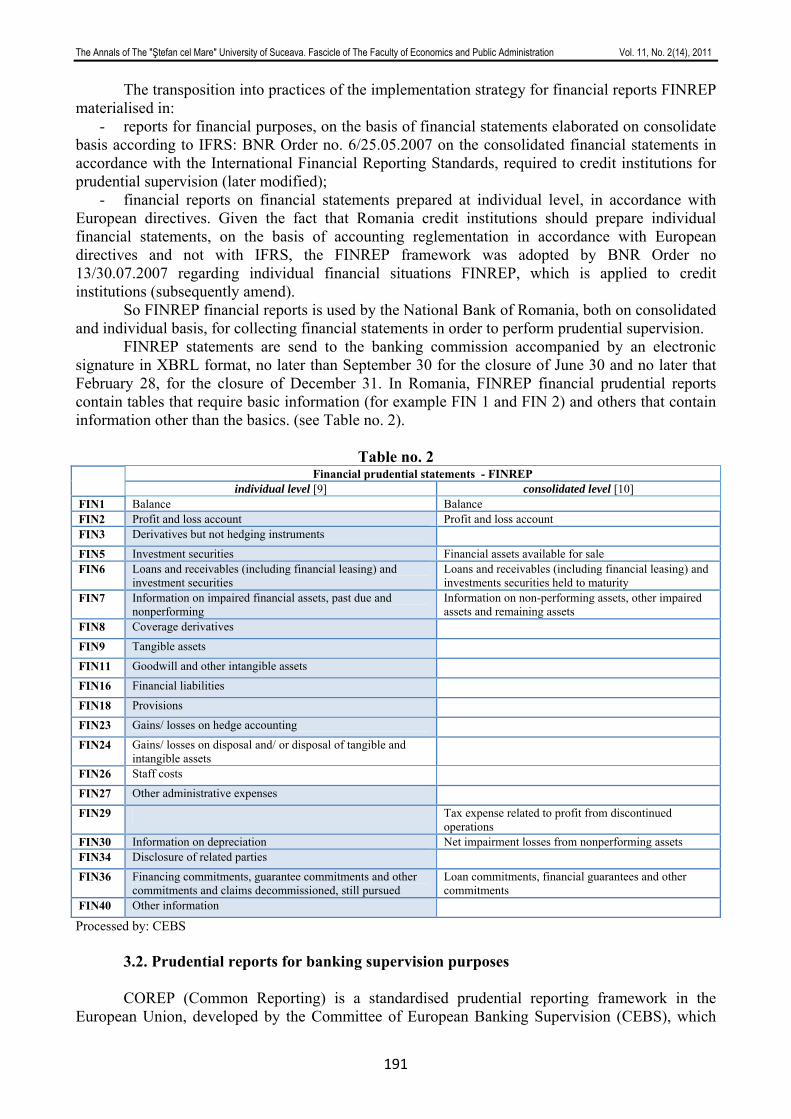

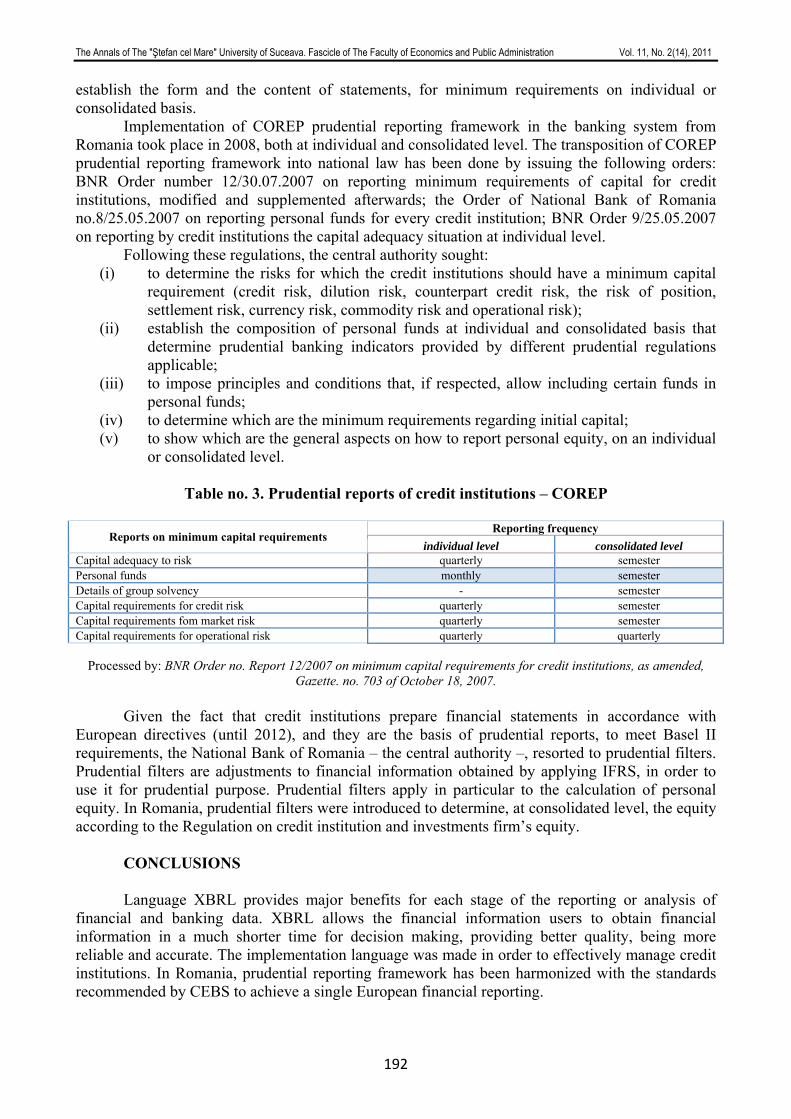

Professor PhD. Ramona NEAG ASSESSING THE IMPACT OF XBRL IN RAPORTATIONS ISSUED BY CREDIT INSTITUTIONS.............................................................................................................................188

Lecturer Ph.D. Mariana VLAD Ph.D. Student Ioana COLBU PhD. Student Alexandra Narcisa CIOBAN

QUALITY THROUGH EDUCATION IN AUDITING.............................................................194 Lecturer Ph.D. Ionela-Corina CHERSAN Lecturer Ph.D. Maria BERHECI (căs. GROSU)

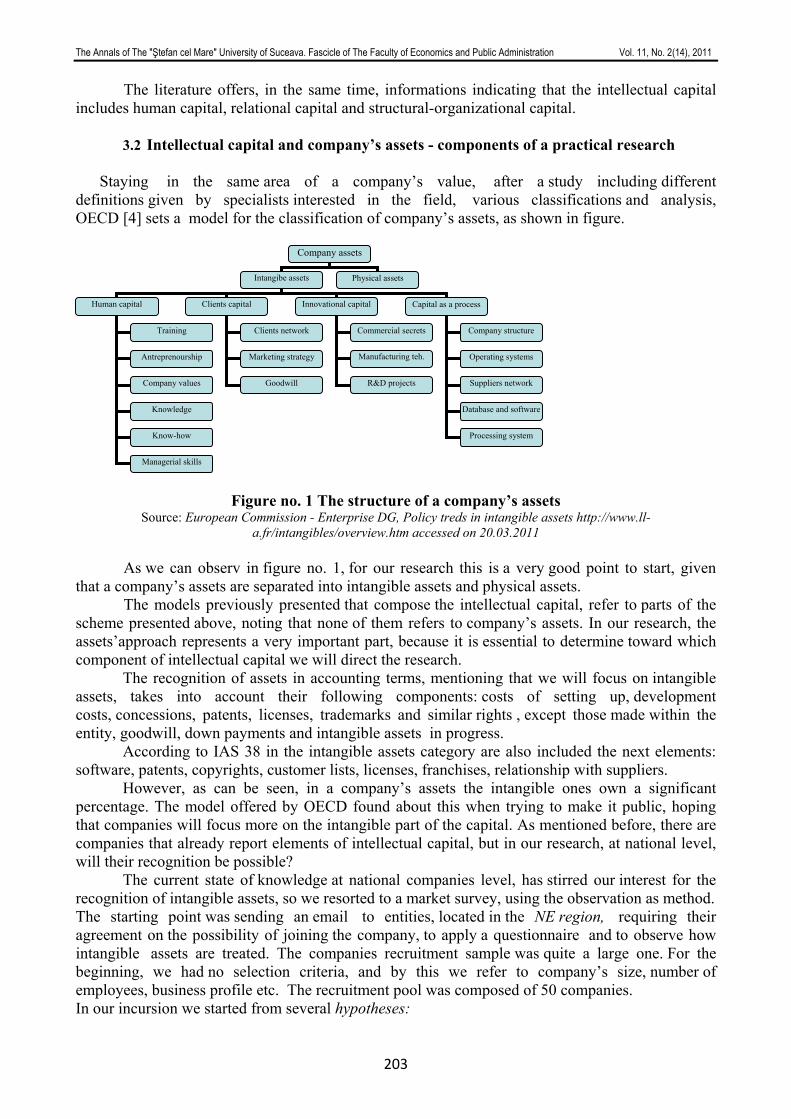

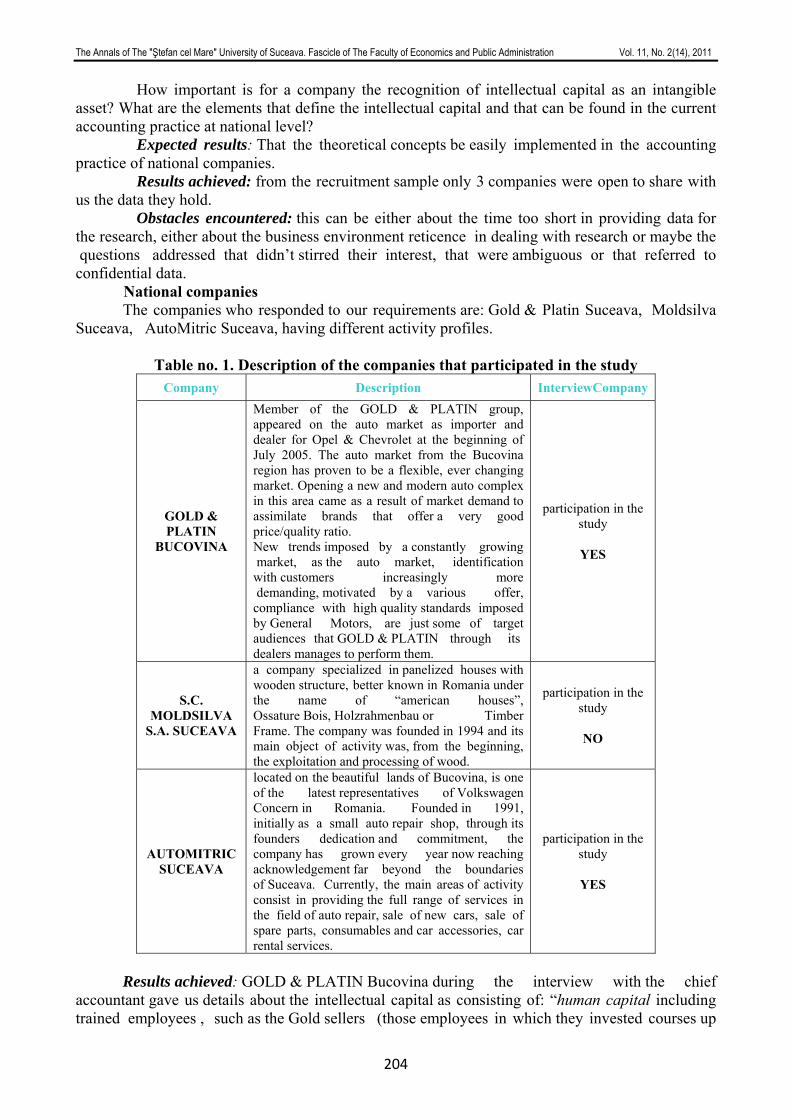

THE ASSETS OF THE COMPANY – A THEORETICAL AND PRACTICAL APROACH RELATING PARTICULARLY TO INTELLECTUAL CAPITAL ........................................201

Assistant PhD. Student Irina MIHAI PhD. Student Alexandra-Daniela SOCEA Assistant PhD. Student Marius CIUBOTARIU

THE TREASURY OPERATING MECHANISM IN ROMANIA............................................208 Nicoleta IONESCU (EFTENE) Gabriela MIHAI (ANDREESCU)

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

5

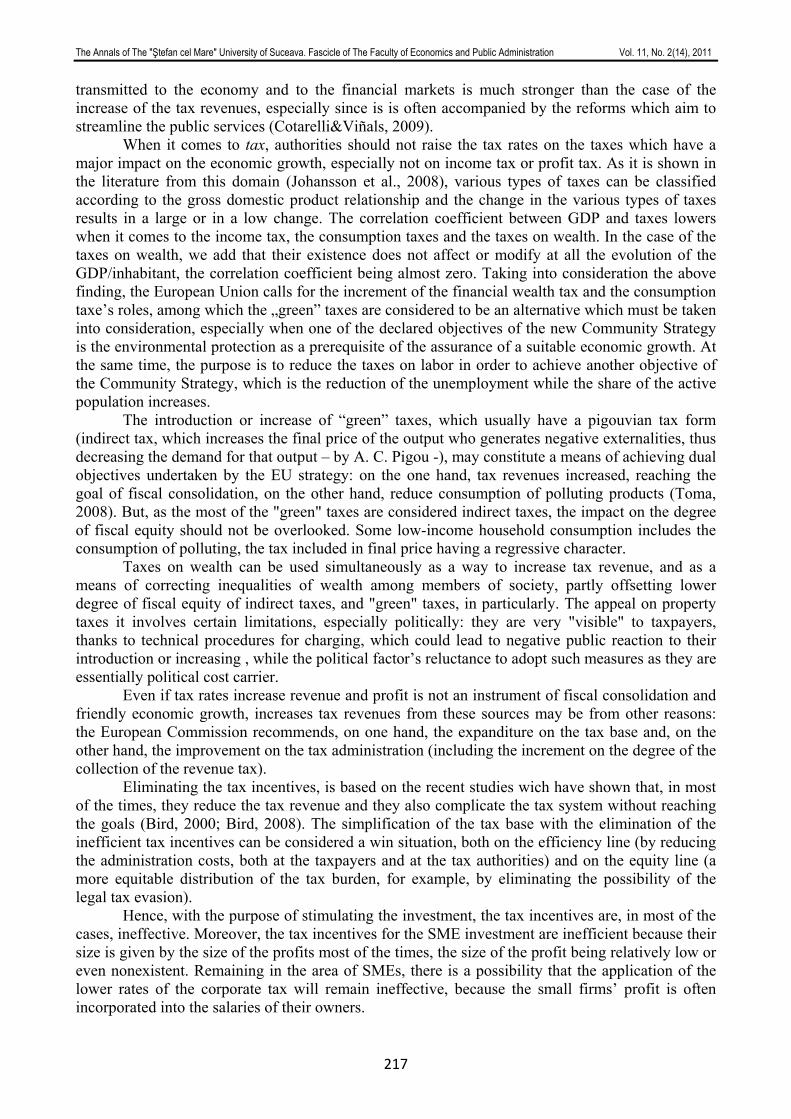

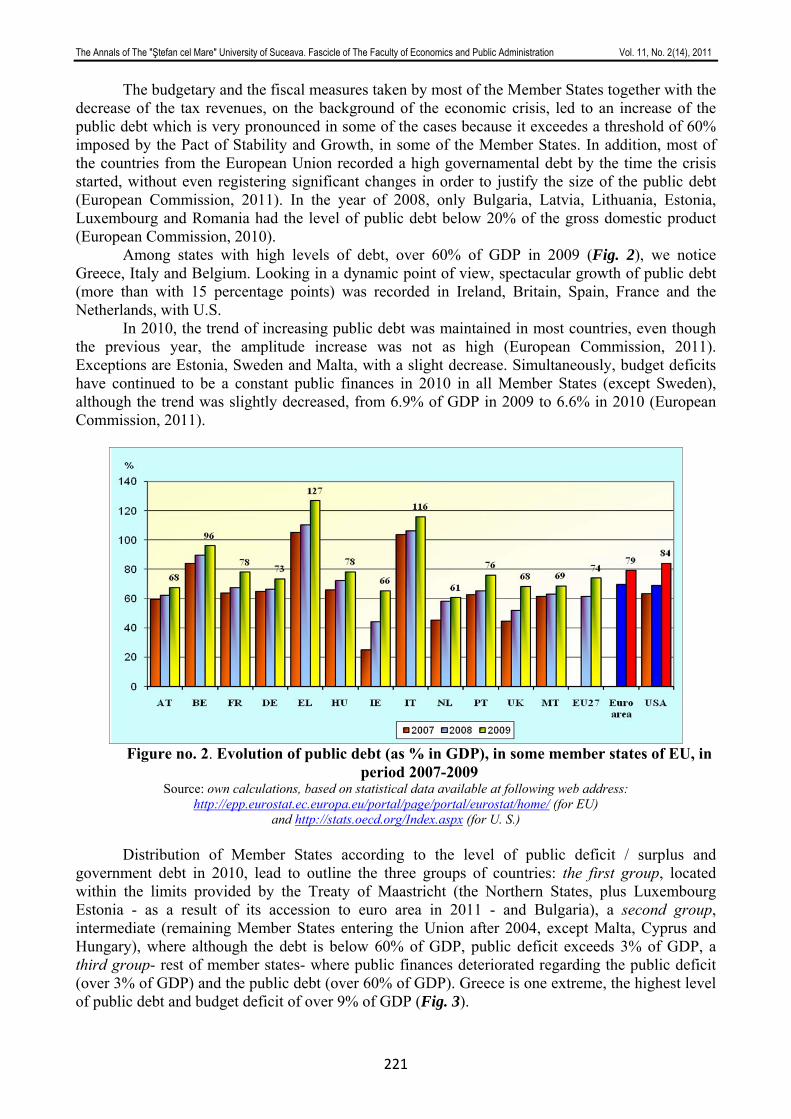

IMPLICATIONS OF FISCAL CONSOLIDATION IN EU ON THE BACKGROUND OF PROMOTING SUSTAINABLE ECONOMIC GROWTH.......................................................214

PhD. Candidate Elena TOMA PhD. candidate Marius FRUNZĂ

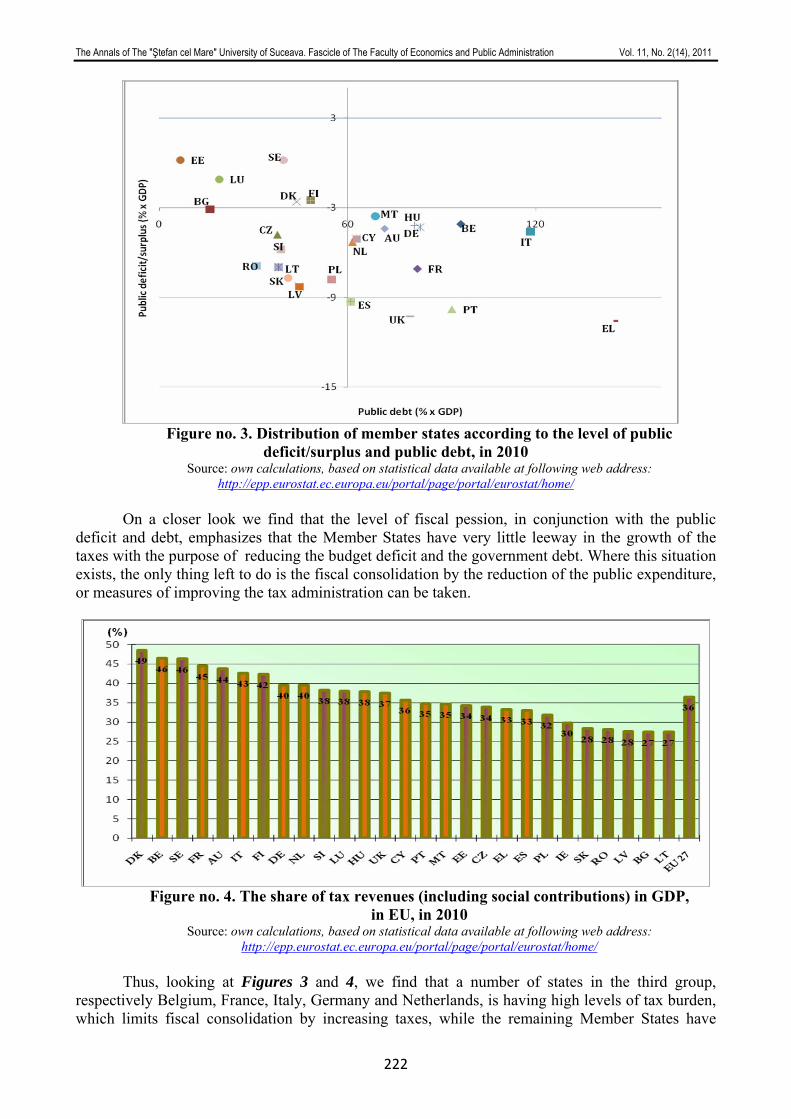

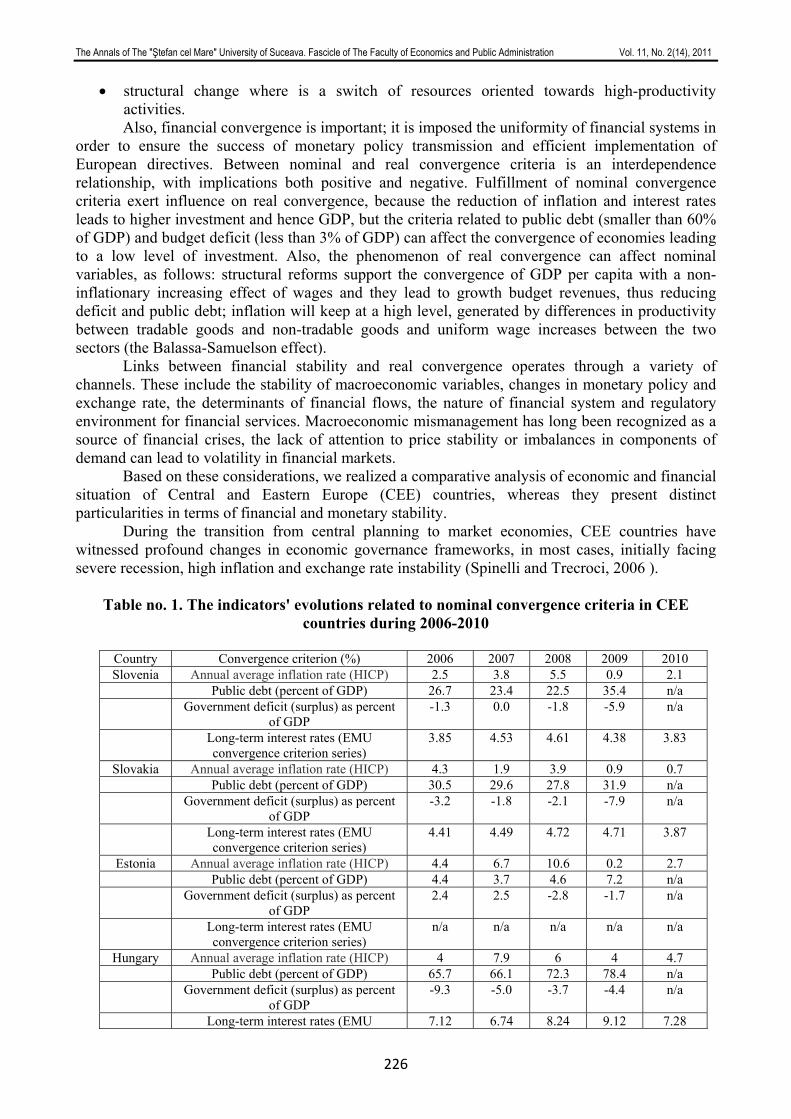

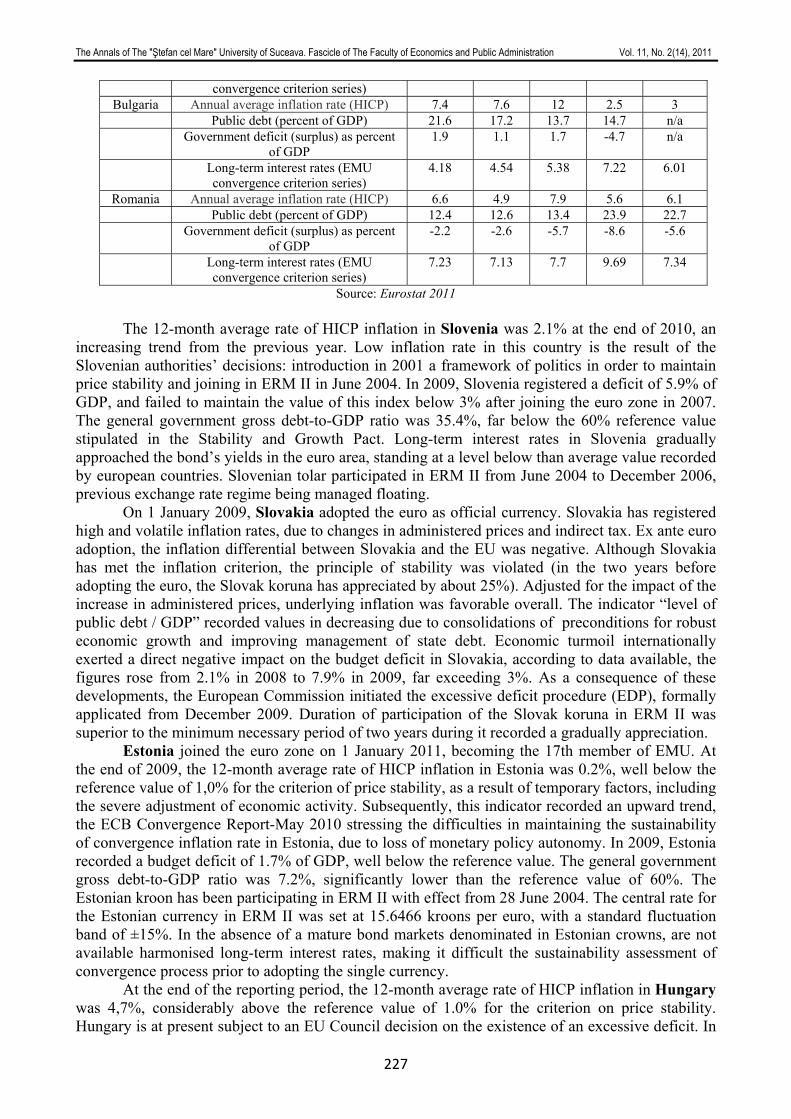

CONVERGENCE PROCESS- PRECONDITION FOR ENSURING FINANCIAL AND MONETARY STABILITY IN EURO AREA.............................................................................225

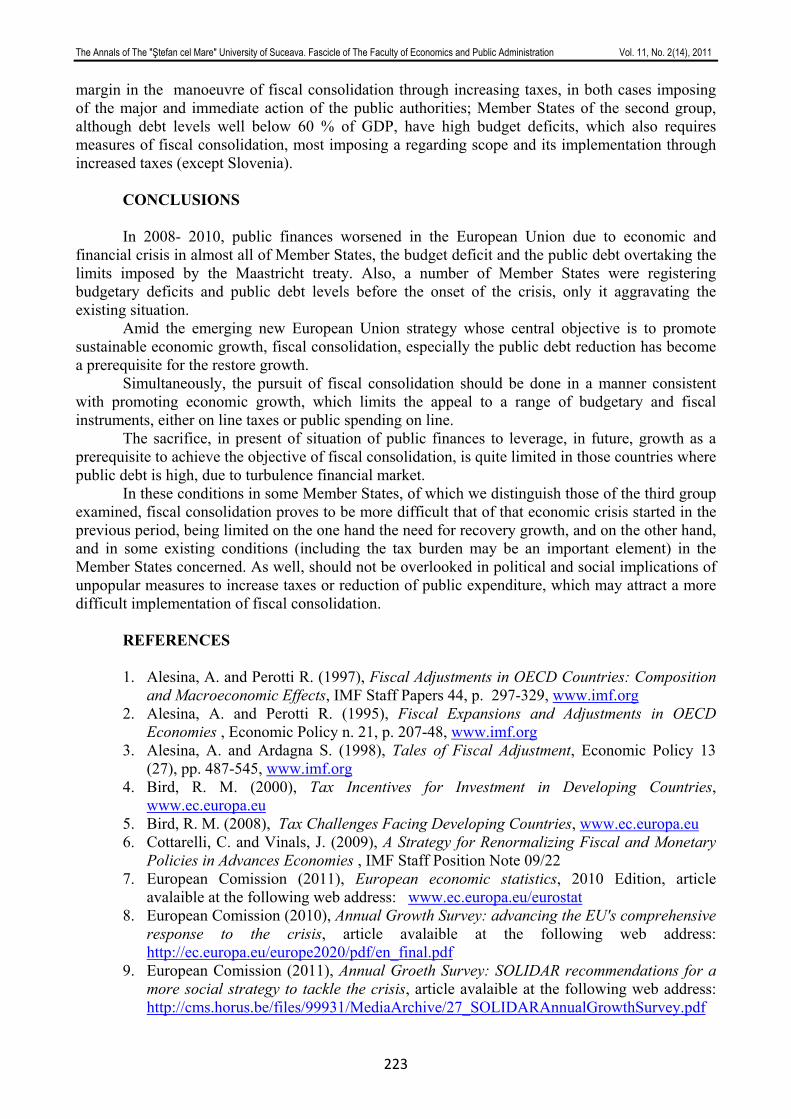

PhD. Student Anca Elena NUCU OCKHAM’S RAZOR IN THE ANALYSIS OF INTANGIBLE CAPITAL? .........................233

PhD. student Cristina Ionela FĂDUR PhD. student Daniela CIOTINĂ

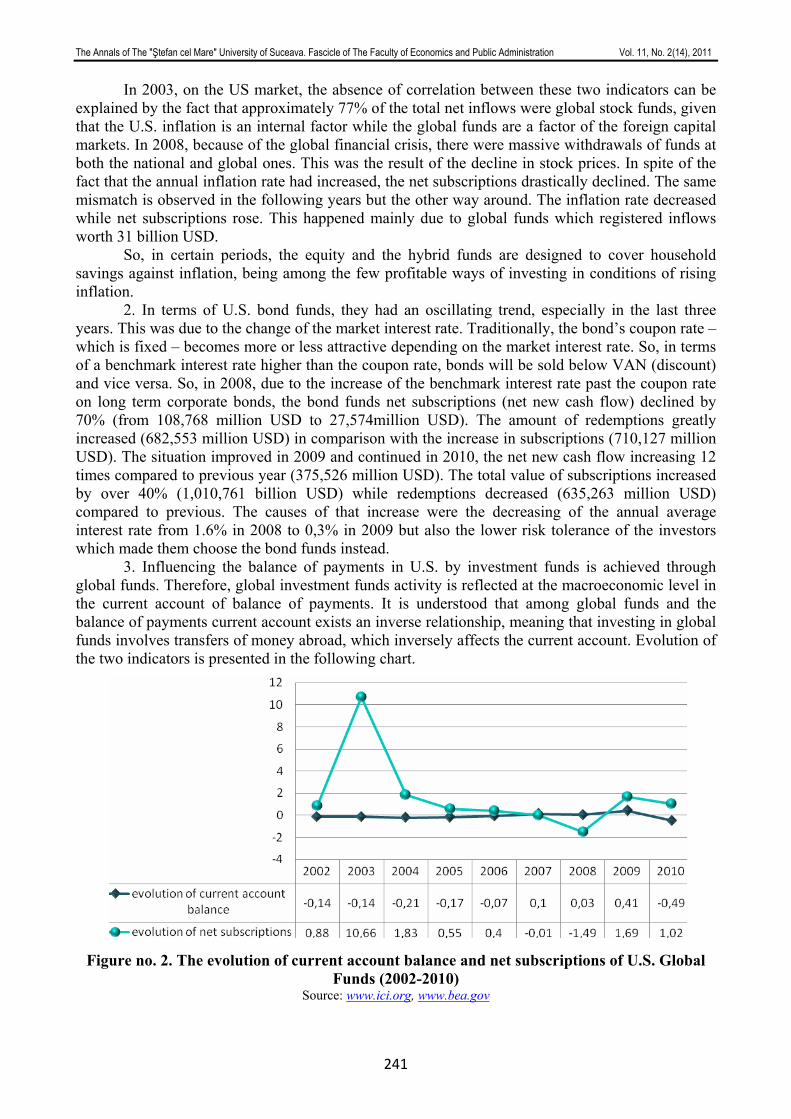

THE ROLE OF MUTUAL FUNDS IN U.S. ECONOMY .........................................................239 PhD. Student Delia-Elena DIACONAŞU

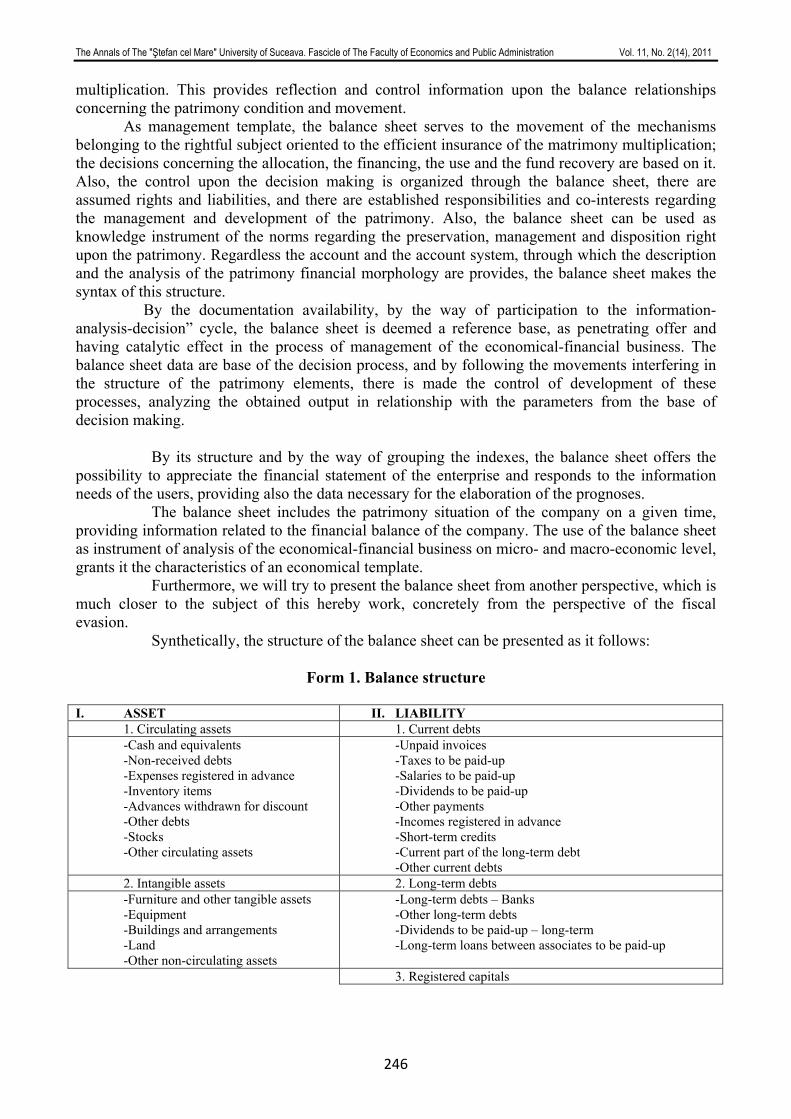

ANALYSIS OF THE ECONOMICAL-FINANCIAL BUSINESS OF THE CONTRIBUTORS – SUPPORT OF THE TAX EVASION FIGHT .........................................................................245

PhD. Student George Dorin DEDU

SECTION 4. STATISTICS, DATA PROCESSING (INFORMATICS) & MATHEMATICS... 251 STATISTICAL WAVES OF THE BUDGETARY FINANCING OF EDUCATION AND SCIENE IN UKRAINE .................................................................................................................252

Associate Professor Ph.D. Olesia TOTSKA EDGES DETECTION METHODS BASED ON FILTERING FOLLOWED BY APPLICATION OF DIFFERENTIAL OPERATORS FOR FINGERPRINT .......................258

Ph.D. Student Cătălin LUPU SECTION 5. LAW AND PUBLIC ADMINISTRATION ................................................... 265 MODELS OF THE IMPLEMENTATION IN ROMANIAN CIVIL SERVICE AT THE LOCAL LEVEL.............................................................................................................................266

Assoc. Prof. PhD. Dorina ŢICU THE LEGAL EUROPEAN CUSTOMS REGIME ....................................................................274

Lecturer PhD. Dumitrita FLOREA (IONESCU) Lecturer PhD. Parascheva NISIOI

LAW FROM AUGUST 14, 1938 BETWEEN TRADITION AND INNOVATION, NECESSITY AND OPPORTUNITY...........................................................................................281

Lecturer PhD. Student Marilena-Oana NEDELEA AUTONOMY AND DECENTRALIZATION - CURRENT PRIORITIES IN THE LOCAL PUBLIC ADMINISTRATION MANAGEMENT......................................................................288

University Assistant Ph.D. Candidate Petronela ZAHARIA LEGAL SYSTEM OF PUBLIC LIMITED LIABILITY COMPANIES .................................293

University Assistant Ph.D. Candidate Eugenia Gabriela LEUCIUC

INSTRUCȚIUNI UTILE PENTRU AUTORI / AUTHOR GUIDELINES ............................. 303

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

6

SECTION 1

ECONOMY, TRADE, SERVICES

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

DOES EU MEMBERSHIP AFFECT THE SOCIAL AND LABOUR INCLUSION OF FOREIGN PRISONERS IN SPAIN? AN ANALYSIS OF SELF-PERCEPTIONS AND

ATTITUDES TOWARDS LEARNING

Isabel NOVO-CORTI University of A Coruña, Faculty of Economics and Business, Campus de Elviña, 15071 A Coruña, Spain

[email protected] María RAMIL

University de A Coruña, Faculty of Economics and Business, Campus de Elviña, 15071 A Coruña, Spain [email protected]

María BARREIRO-GEN University de A Coruña, Faculty of Economics and Business, Campus de Elviña, 15071 A Coruña, Spain

Abstract: Movements of people linked to the processes of globalization lead to the formation of foreign cultural and

ethnical groups, which may generate risk of exclusion. When these people have committed crimes, and have been punished for them, this risk is increased. In this paper we analyze the case of foreign prisoners in the Northwest region of Spain. We rely on qualitative and quantitative research conducted in prisons. By means of statistical analysis of equality-of-means t-test, we found greater difficulties for the inclusion of foreign prisoners, as well as significant differences in self-perceptions of this group in relation to Spaniards, especially in the groups of non-EU foreigners. These differences are particularly apparent in matters relating to the education processes and employment training conducted within prisons. Taking into account these differences would allow designing specific education and training policies to promote the social integration and employment of the foreign-born inmate population, minimizing thus the risk of exclusion.

Keywords: social exclusion, prisoners, foreign, comparison of means JEL Classification: J00 INTRODUCTION The sustainability of any social structure necessarily involves the inclusion of each and

every one of its members. A society with ghettos or groups without their own space will hardly achieve those levels of development needed for its survival over time (Wiliamson & Pickett, 2008).

Globalization is characterized by the high speed and increasing size of international relations and exchanges. People's mobility is thus growing, and societies become much more pluralistic, with the growing presence of cultural and ethnic minority groups. If societies are not flexible and tolerant enough, situations where the is a risk of exclusion will soon arise (Sen, 2000).

When these minority groups, for whatever reason, are, in addition, part of another minority group (disabled, elderly, homosexuals, drug addicts, criminals, etc.), the risk of exclusion increases and therefore, society can see its own structure and sustainability threatened.

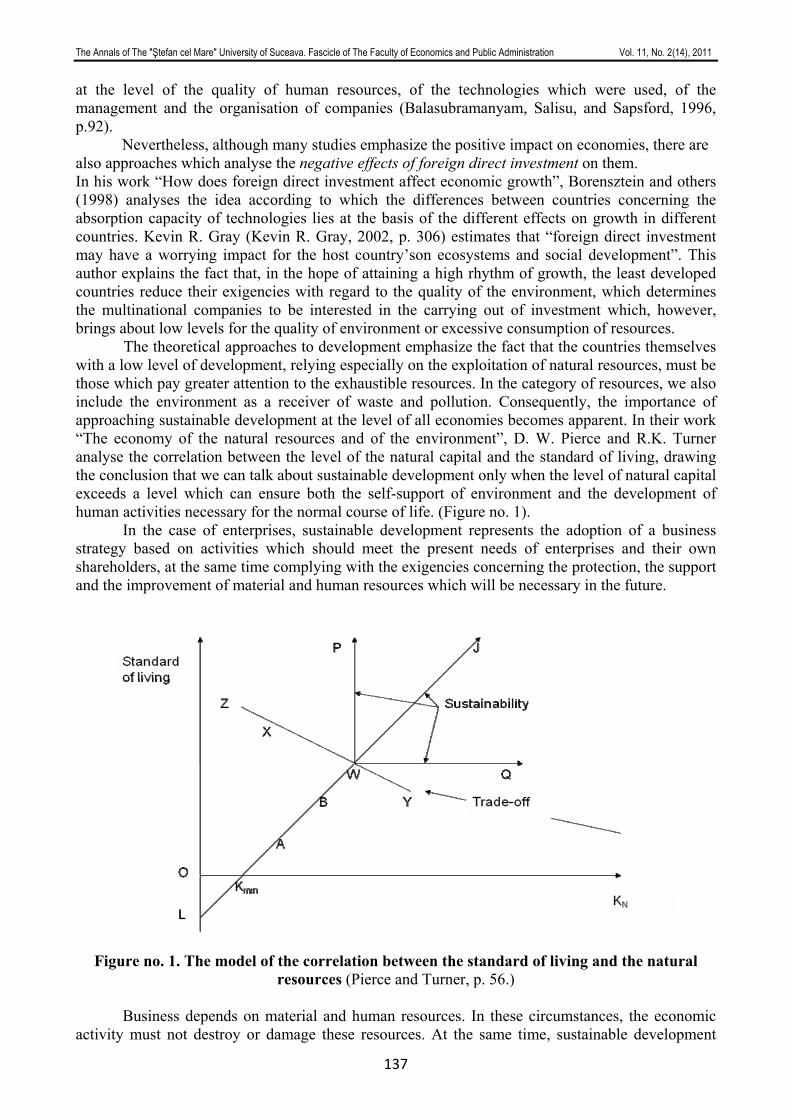

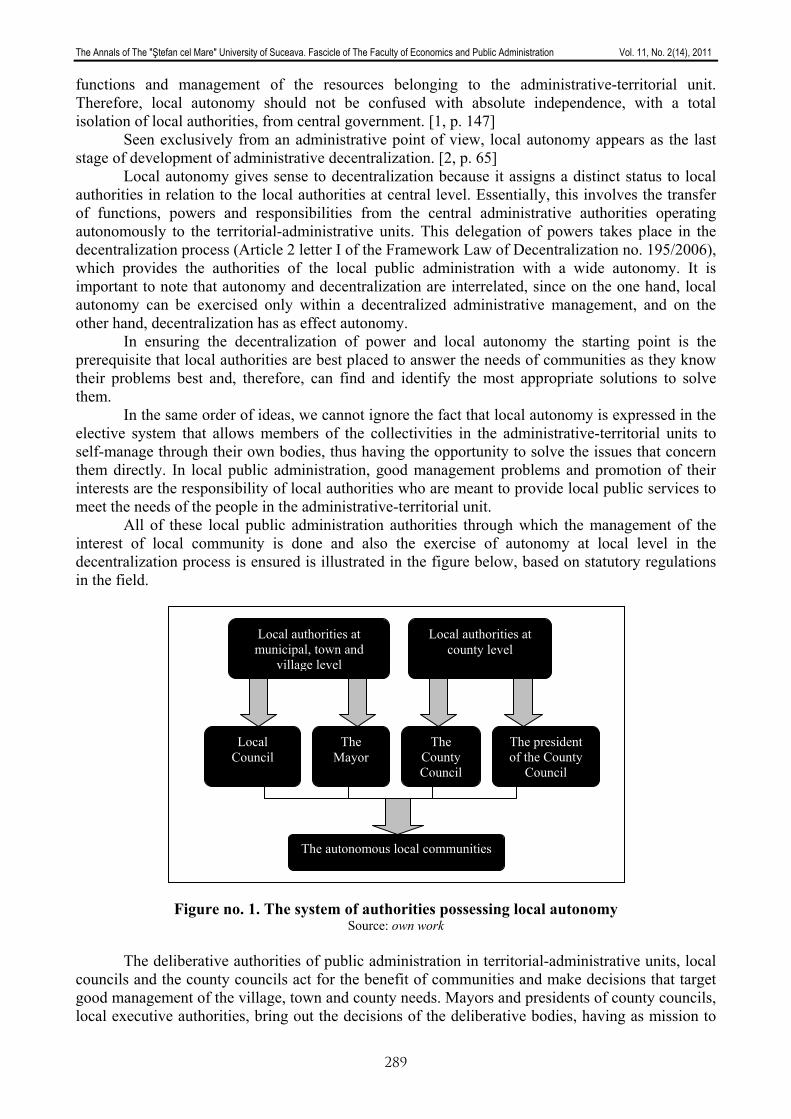

The process of multiple risk of exclusion faced by foreign prisoners is shown in Figure no. 1, which states that migration is linked to globalization, which creates social groups, which for the only fact of being composed by foreigners, gives them different cultural characteristics (sometimes also ethnic), linked to the emergence of the risk of exclusion, which increases the risk of marginalization and/or crime, thus reinforcing the group qualitative differences and increasing the differential characteristics, entering a into a vicious circle. This allows the accumulation of reasons that lead to the risk of multiple exclusion, entering into a feedback mechanism in which the exclusion processes are reinforced and augmented. That is, exclusion causes crime, which in turn leads to exclusion, and so on.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

8

THEORETICAL BACKGROUND Inclusion is therefore a goal for all societies pursuing the survival of their own

organizational and operational schemes, i.e. whose goal is sustainable social development. But inclusion cannot be achieved without a strong knowledge of each and every groups that should be included. Thus, the consideration of all the social groups is essential in a developed society. The fight against social exclusion in general, and multiple exclusion in particular, becomes a prime target (Silver, 1995). In fact, this concern is reflected in world declarations, such as the Millennium Development Goals (UN, 2000), or the European Agenda 2020, that sets the achievement of sustainable and inclusive growth as one of its objectives (COM, 2010).

Sometimes, situations of exclusion lead to crime, which in turn leads to exclusion (Herrero, 2003), so that the wheel of multiple exclusion begin to roll.

In this paper we present a study based on the convicted population in the northwest region of Spain (region NUTS at level 2), in order to know their home country peculiarities, and then be able to know if nationality really affects the opportunities for inclusion. If so, it would be possible to carry out some actions to reverse the situation of multiple exclusion of this group. For that reason, we made a survey among prisoners in the prisons of Galicia to evaluate possible differences in attitudes linked to nationality that could affect future opportunities for convicts.

In order to to perform the analysis, we developed a questionnaire that we distributed among the convict population of Galician prisons. This survey reflects the opinions and perceptions of inmates. We are aware that prisoners may belong to organized criminal gangs internationally, as part of a superstructure, and escape, to some extent, to the exclusion processes discussed here. However, their individual assessments on the prison system would remain valid. Similarly, we see that the group of foreign inmates as a heterogeneous group, which should be subject to further analysis.

The importance of taking into account the views and perceptions of the group of foreign prisoners relies on the high risk of social exclusion they face. But we must also bear in mind that they are a significant part of the prison population. According to the Ministry of Home Affairs (Government of Spain), 35 percent of inmates in Spanish prisons are foreigners (Ministry of Home Affairs, 2009). Therefore, the proportion of non-nationals is high, and represents over a third of the prison population. In recent years, in absolute terms, there was an increasing trend in the number of foreign prisoners, although it decreased in 2011. However, since the total convicted population has also declined, foreigners account for a similar share of the population as in the previous year.

With respect to the country of origin, the largest foreign inmate population come from South America, followed by North Africa. Foreign prisoners from the European Union amounted, in 2009, to 18.9% of the foreign prison population in Spain, according to the Ministry of Home Affairs. The number of Romanian prisoners in Spanish jails was 2169, accounting for 8% of all the foreigners in prison. Thus, Romania is at the top of EU, followed by Portugal, with 557 inmates (2.1% of total foreigners).

In this paper, we investigate how foreign prisoners, particularly, the ones that comes from the European Union, perceive their future outlook, and if their perceptions and attitudes differ (or not) from those of Spanish prisoners.

METODOLOGY The work is divided into two parts: in the first one, we analyzed the different areas pointed

out for Subirats i Humet, Carmona and Brugué Gomà Torruella (2005) as the essential pillars of social inclusion, namely labour and economy, education and training, and famili and society..Our aim is to study the nature and magnitude of the differences between the possibilities of inclusion for Spanish and foreign prisoners.

Subsequently, we carried out a fieldwork focused on the study of the prisoners perceptions on these pillars (Family and Society, Education and Labor), depending on their nationality, and also

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

9

related to their language and their belonging or not to the European Union. In order to do this, we used a statistical analysis for comparison of means, analyzing the values of the "Student t" in order to find statistically significant differences in the responses. The questionnaire was based on a set of questions that we asked to inmate population so that they expressed how much they agree or disagree with specific statements, according to a Likert scale, where the value 1 corresponds to strongly disagree and 5 is complete agreement. We performed a pretest to 50 inmates, after that, we proceeded to the purification of the questionnaire, eliminating redundant questions and wrong understanding. The final test was translated into Arabic, with support from the Official School of Languages in A Coruña, due to the presence of prisoners of Arabic origin, with whom the research team had some communication problems.

Family and Social Area: In this regard, we found that public visibility is a major factor, essential for inclusion. In

Spain there is a high level of the condemned "without papers", we mean that they are not in legal status. Illegal residence of foreigners in the country of destination makes the problems of exclusion grow and multiply, worsening the situation considerably. That is the main reason to analyze the foreign prison population separately from that of European Union countries, which enjoy the status of EU citizens, and do not have this problem. However, they still have their own language and cultural differences, such as those from Central and Eastern Europe. This is a differential issue that may generate groups at risk of exclusion.

On the other hand, having support from family or friends is essential to achieve a normal life after leaving prison. In the case of foreigners, they often have their family abroad and, in many cases, the family does not know that they are in prison, so they must face alone this difficult situation. Foreigners face limitations on family reunification and they are expelled from the country as a preferential sanction (foreigners are given the option not to pay the whole of their term in prison if they accept to leave the country and commit not to return for a number of years), making it more difficult to leave the prison and quickly begin a normal life (Ribas et al, 2005). Furthermore, the social networks of the inmate are often the only way they have, for example, to get a job, being one of the most important mechanisms for achieving social inclusion. If they lack these networks, the adaptation process is complicated, so they need the help of an intermediary, such as an association (Ribas et al, 2005).

Economic and Labor sphere: Leaving prison with a lawful source of income, such as a job or a pension, is decisive for

non-recidivism. Those prisoners who have good prospects in the labor market reoffend less, while those who do not, among which are almost always foreigners, relapse more easily, especially if they have drug problems (Entford, 2009 ).

Education and Training sphere: Having previous training and undertaking training courses in prison are a definite plus for

inmates to find a job after they leave prison. Education is therefore a precondition to make reintegration easier (Smerotkina, 2010). An attempt, for example, to make the prison environment more relaxed and facilitate education is the implementation of the "modules of respect", which promote the activity of prisoners and good manners (Cantero, 2010). Despite these efforts, we must take into account the high percentage of illiteracy in prison. Often, even if inmates can read and write, they have considerable difficulties, because they lack reading and writing habits (Bhatti, 2009). Among foreigners, an important part do not speak Spanish well. For this reason, we have dedicated a special section to the differentiation of the foreign prison population between Spanish-speakers and the rest.

Consequently, the potential inclusion of foreign prisoners is lower overall than that of national prisoners, even those that enjoy European citizenship. After considering these spheres, we decided to conduct a questionnaire for the inmates to further examine these aspects of prisoners’ life

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

10

and see the aspects that can be targeted in order to get out of the situation of social exclusion they face.

EMPIRICAL ANALYSIS The study has been carried out in the region of Galicia, located in the Northwest of Spain.

There are five prisons in Galicia: Teixeira, Bonxe, Monterroso, Pereiro de Aguiar and A Lama. There are also two Social Integration Centres (CIS), with third grade prison population (semi-freedom).

One of the main difficulties in the implementation of this work has been the access to the prison population. Entry into prisons has required nominal permits for each of the members of the research team from the Ministry of Interior of the Government of Spain (Penitentiary Institutions).

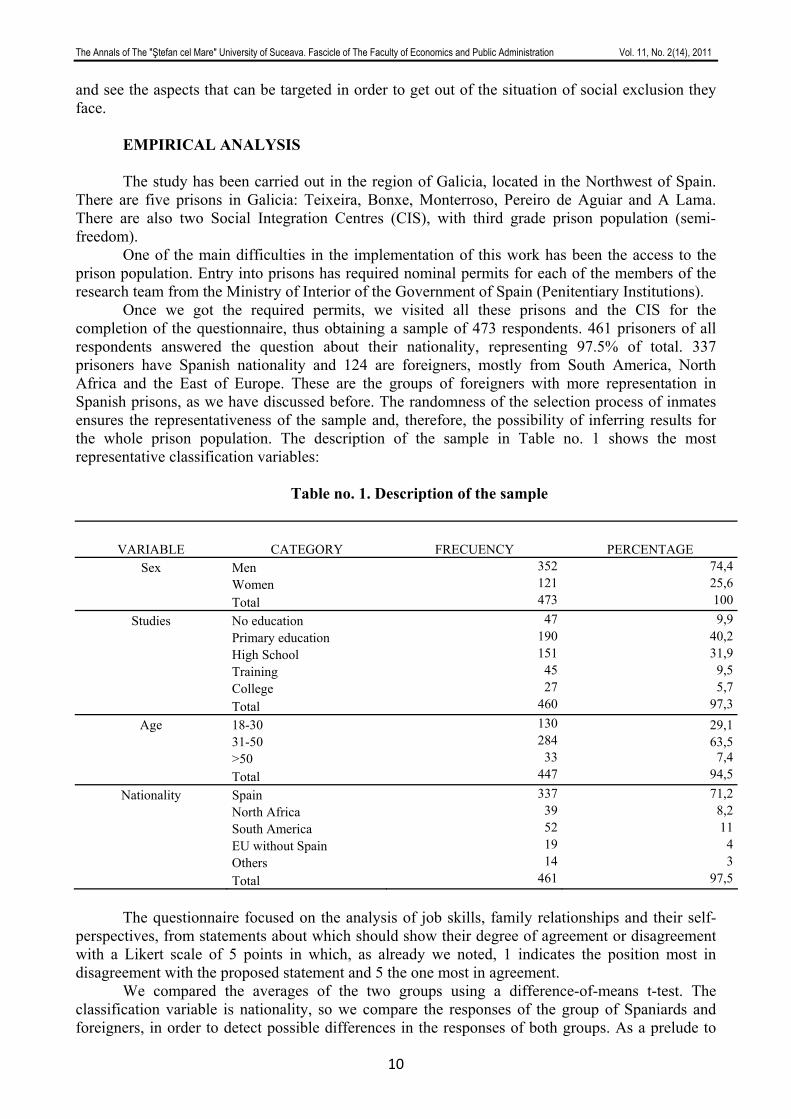

Once we got the required permits, we visited all these prisons and the CIS for the completion of the questionnaire, thus obtaining a sample of 473 respondents. 461 prisoners of all respondents answered the question about their nationality, representing 97.5% of total. 337 prisoners have Spanish nationality and 124 are foreigners, mostly from South America, North Africa and the East of Europe. These are the groups of foreigners with more representation in Spanish prisons, as we have discussed before. The randomness of the selection process of inmates ensures the representativeness of the sample and, therefore, the possibility of inferring results for the whole prison population. The description of the sample in Table no. 1 shows the most representative classification variables:

Table no. 1. Description of the sample

VARIABLE CATEGORY FRECUENCY PERCENTAGE Sex Men 352 74,4

Women 121 25,6 Total 473 100

Studies No education 47 9,9 Primary education 190 40,2 High School 151 31,9 Training 45 9,5 College 27 5,7 Total 460 97,3

Age 18-30 130 29,1 31-50 284 63,5 >50 33 7,4 Total 447 94,5

Nationality Spain 337 71,2 North Africa 39 8,2 South America 52 11 EU without Spain 19 4 Others 14 3 Total 461 97,5

The questionnaire focused on the analysis of job skills, family relationships and their self-

perspectives, from statements about which should show their degree of agreement or disagreement with a Likert scale of 5 points in which, as already we noted, 1 indicates the position most in disagreement with the proposed statement and 5 the one most in agreement.

We compared the averages of the two groups using a difference-of-means t-test. The classification variable is nationality, so we compare the responses of the group of Spaniards and foreigners, in order to detect possible differences in the responses of both groups. As a prelude to

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

11

the t-test, we conducted Levene's test, which indicates whether it is possible to assume equal variances or if they are different.

We have analyzed the responses grouped into the fields we have commented previously: Family and Social sphere: We found significant differences in certain questions. The foreign prison population has a

more positive perception than the Spanish because they think that will be received better in their environment when they leave prison. However, foreign prisoners often have their families abroad. Their family supports them, but they must rebuild their lives by themselves.

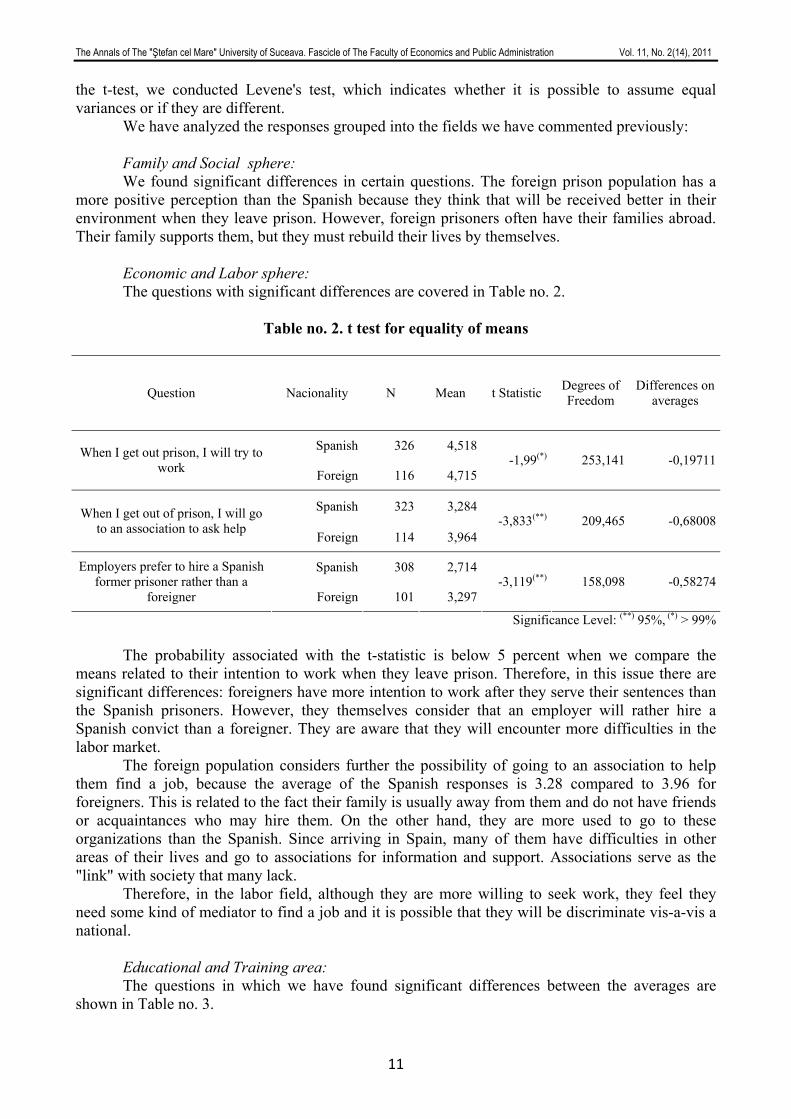

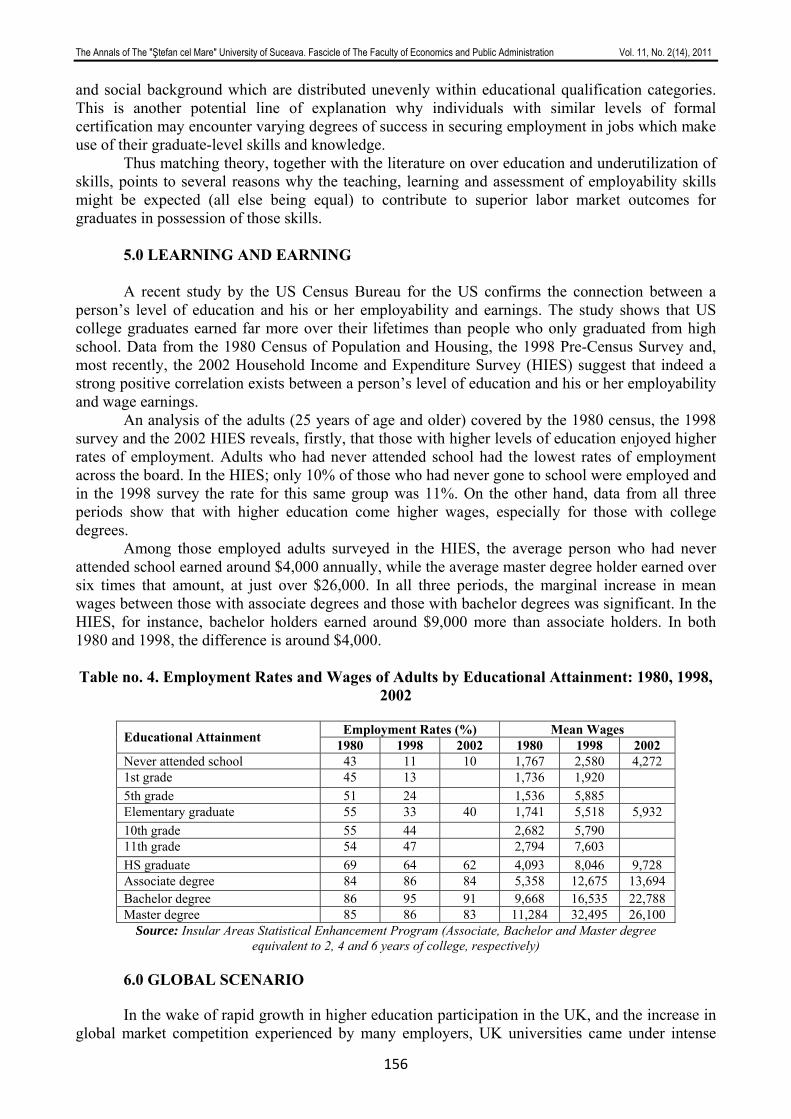

Economic and Labor sphere: The questions with significant differences are covered in Table no. 2.

Table no. 2. t test for equality of means

Question Nacionality N Mean t Statistic Degrees of Freedom

Differences on averages

Spanish 326 4,518When I get out prison, I will try to work Foreign 116 4,715

-1,99(*) 253,141 -0,19711

Spanish 323 3,284When I get out of prison, I will go to an association to ask help Foreign 114 3,964

-3,833(**) 209,465 -0,68008

Spanish 308 2,714Employers prefer to hire a Spanish former prisoner rather than a

foreigner Foreign 101 3,297-3,119(**) 158,098 -0,58274

Significance Level: (**) 95%, (*) > 99% The probability associated with the t-statistic is below 5 percent when we compare the

means related to their intention to work when they leave prison. Therefore, in this issue there are significant differences: foreigners have more intention to work after they serve their sentences than the Spanish prisoners. However, they themselves consider that an employer will rather hire a Spanish convict than a foreigner. They are aware that they will encounter more difficulties in the labor market.

The foreign population considers further the possibility of going to an association to help them find a job, because the average of the Spanish responses is 3.28 compared to 3.96 for foreigners. This is related to the fact their family is usually away from them and do not have friends or acquaintances who may hire them. On the other hand, they are more used to go to these organizations than the Spanish. Since arriving in Spain, many of them have difficulties in other areas of their lives and go to associations for information and support. Associations serve as the "link" with society that many lack.

Therefore, in the labor field, although they are more willing to seek work, they feel they need some kind of mediator to find a job and it is possible that they will be discriminate vis-a-vis a national.

Educational and Training area: The questions in which we have found significant differences between the averages are

shown in Table no. 3.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

12

Table no. 3. t test for equality of means

Question Nationality N Mean t Statistic Degrees of Freedom

Differences on averages

Spanish 319 2,589Courses and professions that I have learned in prison will

help me find a job Foreign 108 3,25-3,643(**) 425 -0,66066

Spanish 322 1,729Courses in prison are sufficient Foreign 110 2,345

-3,786(**) 156,352 -0,61564

Spanish 316 1,744Institutions promote enough programs for inmates Foreign 107 2,327

-3,475(**) 153,577 -0,58343

Significance Level: (**) > 99%

The foreign prison population has a higher educational level than the national average, although it should be noted that the courses of studies are not always equivalent. Also, foreigners know, in general, more languages than Spaniards. Their interest in languages is explained, often, by the need to communicate in the host country and in prison, where in many cases they can not communicate with others in the language of their home country.

When inmates are asked about the usefulness of what they have learned in prison at the time they go free, we get an average of 2.59 points in the case of the Spanish and 3.25 in the foreign; about their opinion on the existence of sufficient training in prison, the means are of 1.73 points compared to 2.35 and as to whether they consider that institutions promote sufficient support programs, the average values obtained are of 1.74 points in the national group of prisoners against 2.33 for foreigners.

In all three cases, the average response of the Spanish prisoners and foreigners differs significantly, as indicated by the low probability associated with the t-statistic, far below the reference value 0.05. Foreigners have a more positive opinion of these three aspects. They value more positively the programs and courses held in prison. It is possible that foreigners are more eager to learn than national prisoners, but it is possible to accept the help offered by the institutions further than domestic ones, because they have fewer resources to rely on.

The greater effectiveness of actions taken in the educational field was verified. However, in order to clarify this result, we divided the foreign prison population into three groups: from South America, North Africa and the European Union without Spain. Then, we did the same comparison of means, three times, first comparing the group of South American with the other foreigners, second to the North Africans with other foreigners. Thirdly, we compared the EU's collective without Spain with other foreign prison population. Despite the differences, according to this analysis, are not significant, the average of Africans responses is the highest. This group may not only be influenced by the factor of foreignness. The level of studies which this group has is lower than the level of other foreigners. The mean difference in this respect is shown significantly at a 98% level. Moreover, inmates who come from the European Union show in these questions a lower average compared to other foreigners. This group has also a higher education level.

In order to determine the influence of factors such as language or belonging to any EU Member State, we proceeded to a new analysis for the comparison of means.

First, we split the sample into Spanish speakers and other inmates. We have obtained very similar results to those discussed above (Table no. 4). The non-Spanish speakers valued more positively the courses and programs offered in prison. With respect to the knowledge acquired in

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

13

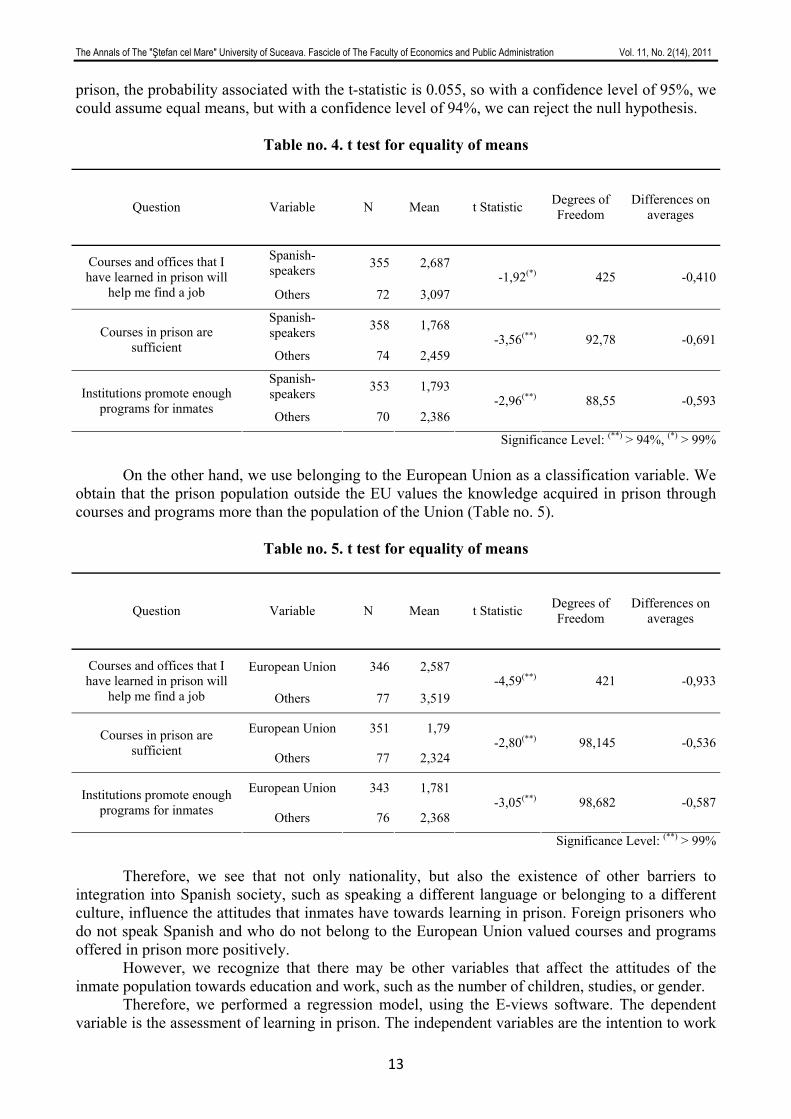

prison, the probability associated with the t-statistic is 0.055, so with a confidence level of 95%, we could assume equal means, but with a confidence level of 94%, we can reject the null hypothesis.

Table no. 4. t test for equality of means

Question Variable N Mean t Statistic Degrees of Freedom

Differences on averages

Spanish-speakers 355 2,687Courses and offices that I

have learned in prison will help me find a job Others 72 3,097

-1,92(*) 425 -0,410

Spanish-speakers 358 1,768Courses in prison are

sufficient Others 74 2,459-3,56(**) 92,78 -0,691

Spanish-speakers 353 1,793Institutions promote enough

programs for inmates Others 70 2,386-2,96(**) 88,55 -0,593

Significance Level: (**) > 94%, (*) > 99% On the other hand, we use belonging to the European Union as a classification variable. We

obtain that the prison population outside the EU values the knowledge acquired in prison through courses and programs more than the population of the Union (Table no. 5).

Table no. 5. t test for equality of means

Question Variable N Mean t Statistic Degrees of Freedom

Differences on averages

European Union 346 2,587Courses and offices that I have learned in prison will

help me find a job Others 77 3,519-4,59(**) 421 -0,933

European Union 351 1,79Courses in prison are sufficient Others 77 2,324

-2,80(**) 98,145 -0,536

European Union 343 1,781Institutions promote enough programs for inmates Others 76 2,368

-3,05(**) 98,682 -0,587

Significance Level: (**) > 99%

Therefore, we see that not only nationality, but also the existence of other barriers to integration into Spanish society, such as speaking a different language or belonging to a different culture, influence the attitudes that inmates have towards learning in prison. Foreign prisoners who do not speak Spanish and who do not belong to the European Union valued courses and programs offered in prison more positively.

However, we recognize that there may be other variables that affect the attitudes of the inmate population towards education and work, such as the number of children, studies, or gender.

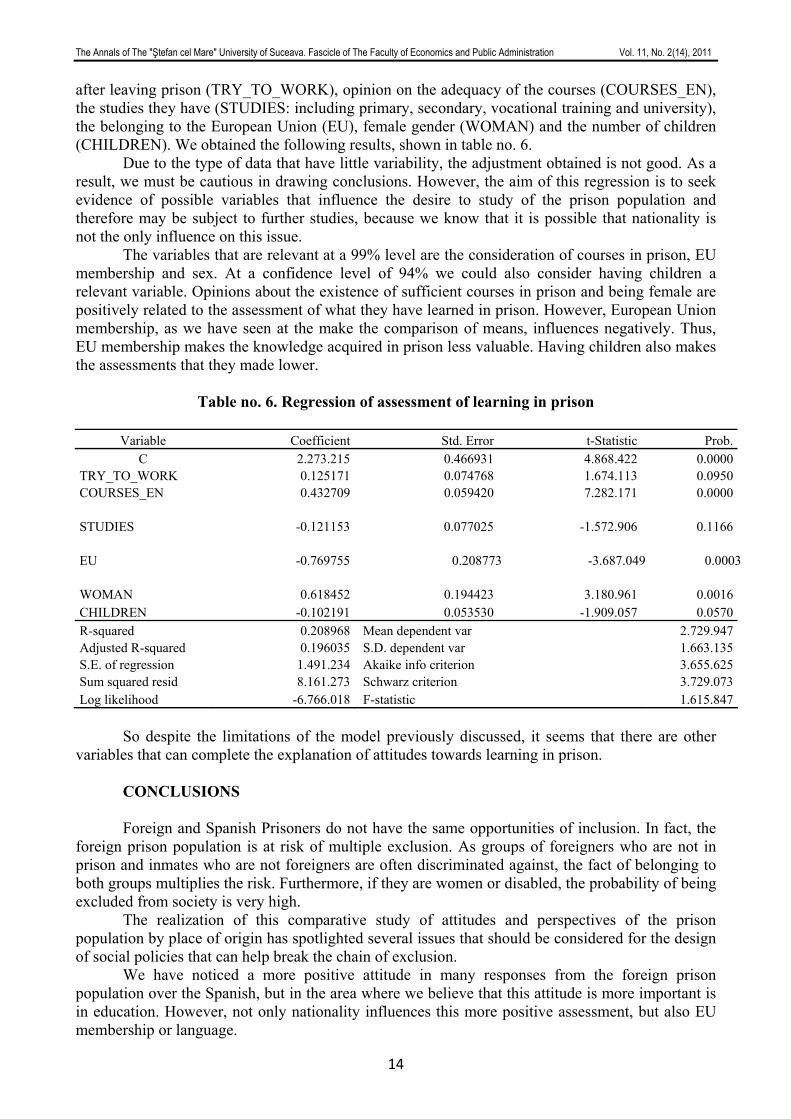

Therefore, we performed a regression model, using the E-views software. The dependent variable is the assessment of learning in prison. The independent variables are the intention to work

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

14

after leaving prison (TRY_TO_WORK), opinion on the adequacy of the courses (COURSES_EN), the studies they have (STUDIES: including primary, secondary, vocational training and university), the belonging to the European Union (EU), female gender (WOMAN) and the number of children (CHILDREN). We obtained the following results, shown in table no. 6.

Due to the type of data that have little variability, the adjustment obtained is not good. As a result, we must be cautious in drawing conclusions. However, the aim of this regression is to seek evidence of possible variables that influence the desire to study of the prison population and therefore may be subject to further studies, because we know that it is possible that nationality is not the only influence on this issue.

The variables that are relevant at a 99% level are the consideration of courses in prison, EU membership and sex. At a confidence level of 94% we could also consider having children a relevant variable. Opinions about the existence of sufficient courses in prison and being female are positively related to the assessment of what they have learned in prison. However, European Union membership, as we have seen at the make the comparison of means, influences negatively. Thus, EU membership makes the knowledge acquired in prison less valuable. Having children also makes the assessments that they made lower.

Table no. 6. Regression of assessment of learning in prison Variable Coefficient Std. Error t-Statistic Prob.

C 2.273.215 0.466931 4.868.422 0.0000TRY_TO_WORK 0.125171 0.074768 1.674.113 0.0950COURSES_EN 0.432709 0.059420 7.282.171 0.0000

STUDIES -0.121153 0.077025 -1.572.906 0.1166

EU -0.769755 0.208773 -3.687.049 0.0003

WOMAN 0.618452 0.194423 3.180.961 0.0016CHILDREN -0.102191 0.053530 -1.909.057 0.0570R-squared 0.208968 Mean dependent var 2.729.947Adjusted R-squared 0.196035 S.D. dependent var 1.663.135S.E. of regression 1.491.234 Akaike info criterion 3.655.625Sum squared resid 8.161.273 Schwarz criterion 3.729.073Log likelihood -6.766.018 F-statistic 1.615.847

So despite the limitations of the model previously discussed, it seems that there are other

variables that can complete the explanation of attitudes towards learning in prison.

CONCLUSIONS Foreign and Spanish Prisoners do not have the same opportunities of inclusion. In fact, the

foreign prison population is at risk of multiple exclusion. As groups of foreigners who are not in prison and inmates who are not foreigners are often discriminated against, the fact of belonging to both groups multiplies the risk. Furthermore, if they are women or disabled, the probability of being excluded from society is very high.

The realization of this comparative study of attitudes and perspectives of the prison population by place of origin has spotlighted several issues that should be considered for the design of social policies that can help break the chain of exclusion.

We have noticed a more positive attitude in many responses from the foreign prison population over the Spanish, but in the area where we believe that this attitude is more important is in education. However, not only nationality influences this more positive assessment, but also EU membership or language.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

15

So foreign inmates value the learning they do in prison, as well as programs and courses that are offered in a prison environment, more positively,. Therefore, we believe that certain training courses adapted to the needs of this group would provide additional mechanisms to rebuild their lives, and could be one of the key elements to achieve reintegration. However, in the case of foreigners outside the EU the development of these programs may not be an effective mechanism for labor integration, since within the group of foreigners in prison are those who give a lower valuation of these activities, probably motivated by the higher education level or the possibility of obtaining inclusion in other ways.

Also, we leave the analysis of the influence of other variables such as sex or the number of children on the assessment of education in prison open to possible further detailed investigation.

ACKNOWLEDGMENTS

This work has been done with the financial support from the Ministry of Education, Government of Spain, the General Secretary of Penitentiary Institutions under the Ministry of Home Affairs (Government of Spain), the General Secretary for Equality (Government of the Xunta de Galicia) and the assistance of the Official School of Languages of A Coruña (Galicia).

REFERENCES

1. Bhatti, G. (2010), Learning behind bars: Education in Prisons, Teaching and Teacher Education 26, 31-36

2. Cantero, F. (2010), The pedalogical action in jails. Possibilities and limits, Revista española de psicología 68 (245), 49-64.

3. COM. (2010), Comunicación de la Comisión: Europa 2020: Una estrategia para un crecimiento inteligente, sostenible e integrador 2020, Bruselas 3.3.2010

4. Entorf, H. (2009), Crime and the labour market: Evidence from a survey of inmates, Jahrbucher Fur Nationalokonomie Und Statistik 229(2-3), 254-269.

5. Ministry of Home Affairs. (2009) Anuario estadístico del Ministerio del Interior 2009, Chapter 4. Consulted in: http://www.institucionpenitenciaria.es/web/portal/documentos/publicaciones.html

6. United Nations. (2000), Declaración del Milenio, Asamblea General 13.09.2000 7. Ribas, N; Almeda, E y Bodelón, E. (2005), Rastreando lo invisible: Mujeres extranjeras

en las cárceles Anthropos. 8. Sen, A. (2000), Social exclusion: concept, application and scrutiny, Asian Development

Bank. 9. Silver, H. (1995), Reconceptualizing Social Disadvantage: Three Paradigms of Social

Exclusion. En Rodgers,G. Gore, G Y Figueiredo, J. (Ed.) Social Exclusion: Rhetoric, Reality, Responses. Geneva: International Institute for Labour Studies

10. Smerotkina, K. (2010), Education as a Prerequisite for Inclusion of Prisioners in the Society, Society, Integration, Education 453-460.

11. Subirats i Humet, J, Gomà Carmona, R. y Brugué Torruella, J. (2005) Riesgos de exclusión social en las Comunidades Autónomas, Documentos de Trabajo. Bilbao: Fundación BBVA e Institut d’Estudis Autonòmics, Generalitat de Catalunya.

12. Wiliamson, R., Pickett, K. (2008) Desigualdad: un análisis de la infelicidad colectiva, Turner.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

16

SUSTAINABLE DEVELOPMENT IN BUCOVINA REGION – ANALYSIS OF TOURISTIC POTENTIAL IN SUCEAVA BASIN

PhD. Student Constantin COCERHAN

„Simion Mehedinţi” Doctoral School Bucharest University Bucureşti, Faculty of Geography

[email protected] Professor PhD. Carmen NĂSTASE

"Ştefan cel Mare" University of Suceava, Romania Faculty of Economics and Public Administration

[email protected] Abstract: Tourism has always been an economic pillar of European countries, in addition to building understanding and

enlightening travellers. New considerations, sustainability, environment and socio-economics are calling for a new pardigm of how tourism operates. This article present the touristic potential of Suceava Basin, the infrastucture and how tourism can be considered as a fundamental opportunity for social and economic development in North East Region – Bucovina. The research investigated innovative strategies, solutions and recommandations to improve infractucture and supporting services for tourism, overcoming many barriers.

Keywords: Bucovina Region, innovative strategies, touristic infractucture, touristic potential, sustainability

JEL Classification: A12, O18

1. INTRODUCTION 1.1. Motivation of the theme selection, scope and purpose of research

World tourism has acquired in the second half of the XXth century, a bigger importance,

which was illustrated mainly by the continued growth in the number of tourists and revenue collected. National tourism, constitutes in the perspective of the present approach, a real chance to relaunch the economic growth and sustainable development of market economy in Romania.

The goal of the research was to create a synthesis work to present, in a realistic picture, the overall characteristics of the infrastructure and tourist facilities in the area studied and to evaluate possibilities to improve the infrastructure in terms of sustainable tourism development of the area.

The aims pursued were: - Identification, analysis and description of existing infrastructure elements in the area

studied; - The achievement of some synthesis cartographic representation; - Assessing the adequacy of infrastructure of communications routes to the current

requirements of tourism; - Advancing proposals for infrastructure development / tourism base from the perspective of

the growing importance of this sector in all economic activities of the area and from the European integration and sustainable development.

1.2. The scientific fundamentation, methods and research procedures used

The methods and procedures mainly used in our research have been the observation, the analysis (functional - to highlight the role of some elements in the overall, statistical which has focused particularly reporting series of data and formulating hypotheses, cartographic conducting spatial mapping of elements, diagnostic reflecting the features of the current situation, prognostic on the possible developments, synthesis, comparative method (comparing the elements, phenomena of the same kind to capture the similarities and differences between them in order to reflect the logical links), computerized data.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

17

Personal contribution to this paper is to process and summarize data obtained from sources or from direct observation in the field and drawing a picture of the topic studied, realization of some thematic synthetic maps: Suceava Basin –The infrastructure of the ways of communications, Suceava Basin - Accommodation capacity, computerized data processing, advancing proposals to improve tourism resources.

2. THE ANALYSIS OF THE TURISTIC POTENTIAL IN THE SUCEAVA BASIN

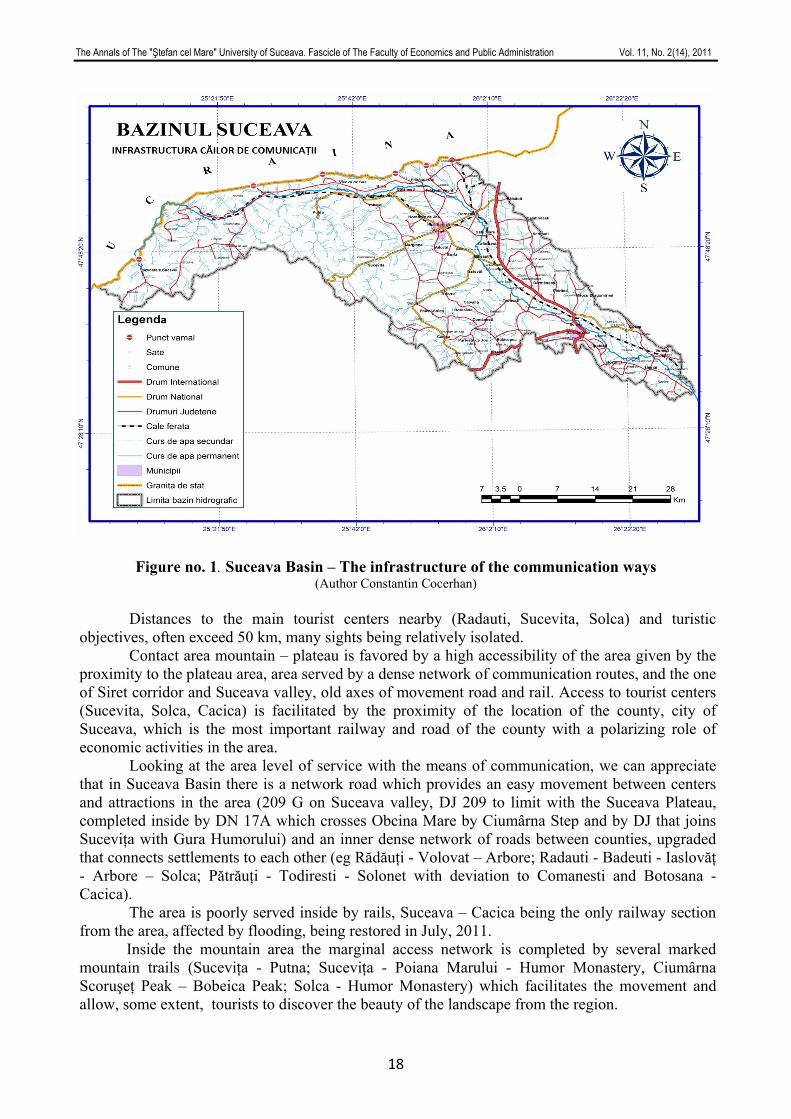

2.1. The infrastructure of the communication ways

Suceava Basin is located in the north of the country, is included in the touristic province of Carpatho- Pericarpatica, being included in touristic region Bukovina and overlaps Suceava complex tourism area, touristic region known worldwide, which has a base and a tourism potential varied and complex. Regarding the accessibility of the area, it is in a plateau region, with favorable conditions to develop communication networks.

For this area, the most important road artery is European road E 85 which crosses the county from north to south, in Suceava and liaises with Ukraine in Chernovtsy and the capital, Bucharest. To this is added E576 highway from Suceava to Gura Humorului - Câmpulung Moldovenesc – Vatra Dornei.

Suceava is the main railway junction of the area, and most important railway bus is bus 5: Bucharest - Suceava - Vicsani and on to Moscow, thus having an international character. From this emerges bus line that provides contact Transcarpathian northwest, namely Suceava - Câmpulung Moldovenesc – Vatra Dornei, to Timisoara, Oradea, Baia Mare - Satu Mare.

The entire area from north of Moldova benefits from the presence of the International Airport "Stefan cel Mare" Salcea located in the city, 12 km from the city of Suceava.

The map analysis (Fig. 1) reveals a series of regional differences in the level of service with ways of communication to the area studied.

Analyzing the network of communications from the space of the upper basin of Suceava, we note that the main access roads are particularly roads (DJ 209 G on Suceava valley, DJ 209 to the limit with Suceava plateau), the railway from Suceava valley provides access only to Putna beyond this village, to Nisipitu is not operational because of damage caused by floods in the summer of 2008. Movement within the mountain area is served and a dense network of roads upgraded interior and forest roads. From the perspective of tourists traveling within the area said that there are few marked trails (eg Putna-Suceviţa) which constitutes an impediment to tourism development perspective in the area.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

18

Figure no. 1. Suceava Basin – The infrastructure of the communication ways

(Author Constantin Cocerhan) Distances to the main tourist centers nearby (Radauti, Sucevita, Solca) and turistic

objectives, often exceed 50 km, many sights being relatively isolated. Contact area mountain – plateau is favored by a high accessibility of the area given by the

proximity to the plateau area, area served by a dense network of communication routes, and the one of Siret corridor and Suceava valley, old axes of movement road and rail. Access to tourist centers (Sucevita, Solca, Cacica) is facilitated by the proximity of the location of the county, city of Suceava, which is the most important railway and road of the county with a polarizing role of economic activities in the area.

Looking at the area level of service with the means of communication, we can appreciate that in Suceava Basin there is a network road which provides an easy movement between centers and attractions in the area (209 G on Suceava valley, DJ 209 to limit with the Suceava Plateau, completed inside by DN 17A which crosses Obcina Mare by Ciumârna Step and by DJ that joins Suceviţa with Gura Humorului) and an inner dense network of roads between counties, upgraded that connects settlements to each other (eg Rădăuţi - Volovat – Arbore; Radauti - Badeuti - Iaslovăţ - Arbore – Solca; Pătrăuţi - Todiresti - Solonet with deviation to Comanesti and Botosana - Cacica).

The area is poorly served inside by rails, Suceava – Cacica being the only railway section from the area, affected by flooding, being restored in July, 2011.

Inside the mountain area the marginal access network is completed by several marked mountain trails (Suceviţa - Putna; Suceviţa - Poiana Marului - Humor Monastery, Ciumârna Scoruşeţ Peak – Bobeica Peak; Solca - Humor Monastery) which facilitates the movement and allow, some extent, tourists to discover the beauty of the landscape from the region.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

19

Distances between major tourist centers (Radauti, Suceviţa, Gura Humorului, Solca) and attractions are included frequently between 10-50 km.

For Suceava area and its surroundings, the most important road artery is European road E 85 which crosses the county from north to south, in Suceava and liaises with Ukraine in Chernovtsy and the capital, Bucharest. This is compounded by the national road E 576 from Suceava to Gura Humor - Câmpulung Moldovenesc – Vatra Dornei. An important role have and other county or municipal roads that are linking tourist objectives: Suceava - Pascani by Bosanci-Udeşti-Dolhasca, Suceava - Dorohoi by Adancata, Suceava - Radauti and Suceava - Dragomirna.

Railway circulation is done in the area on the route Suceava - Milisauti - Dornesti - Radauti, but lately decreased a lot the frequency of using of this type of transport, road transport being preferred, more quickly and conveniently, which is well served by private entrepreneurs.

Among the analyzed sub areas we can appreciate that the latter is characterized by the dense network of communication routes, the movement of people realizing easy and efficient. In conclusion, we appreciate that road densities decrease from the middle and lower basin area to the one of contact with the mountain, the most poorly served in this regard remains the upper basin of Suceava, although there are operational railways in this area, their importance in movement of people and tourists has decreased greatly over the past decade, their functions being taken over by road transport.

2.2. Tourist accommodation structures

Bucovina region, in which limits falls Suceava basin, is a touristic area with national and

international recognition. Tourism potential which is available, accessibility in the area were used locally in recent years by increasing the number of tourist reception and overall development of tourism infrastructure.

In the area we have identified the presence of the following types of tourist accommodation structures: structures with accommodation (hotels, motels, villas, camps, campgrounds, boarding houses, farmhouses, rented rooms in family homes), structures with functions of catering (inside structures belonging to companies and accommodation), recreational structures with functions (clubs, swimming pools, small football fields, tennis, winter sports equipment) and structures with functions of transport (buses, rental cars).

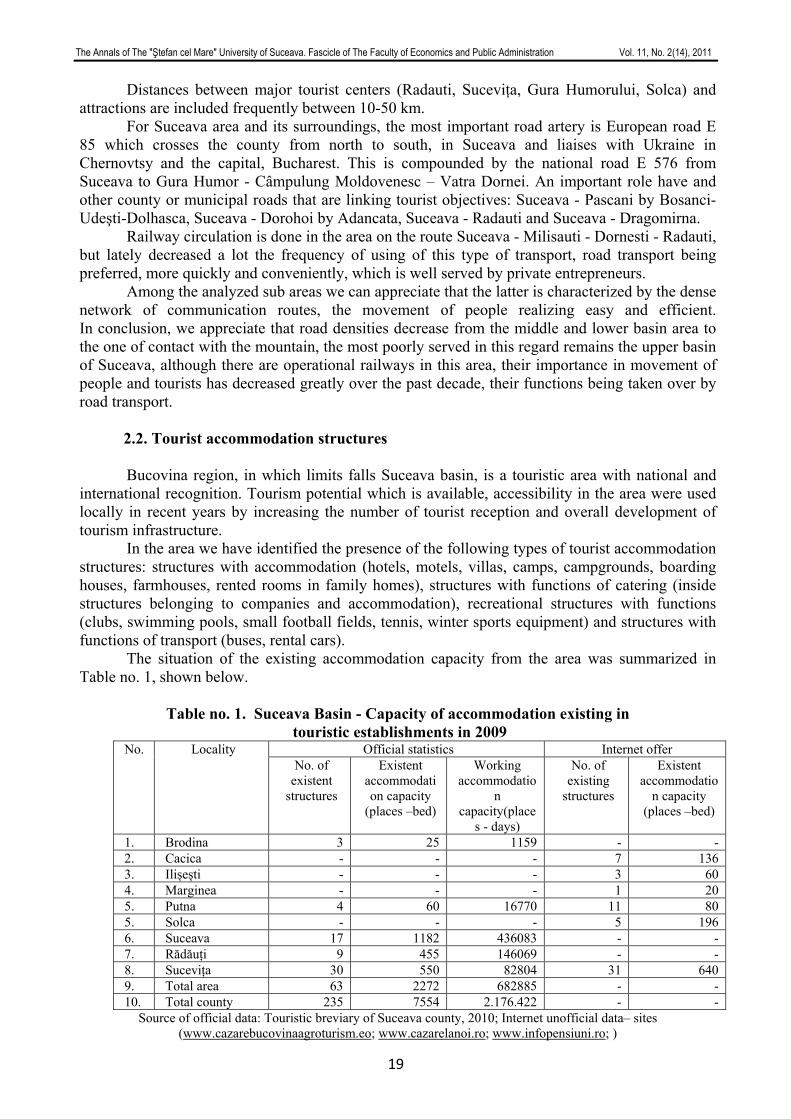

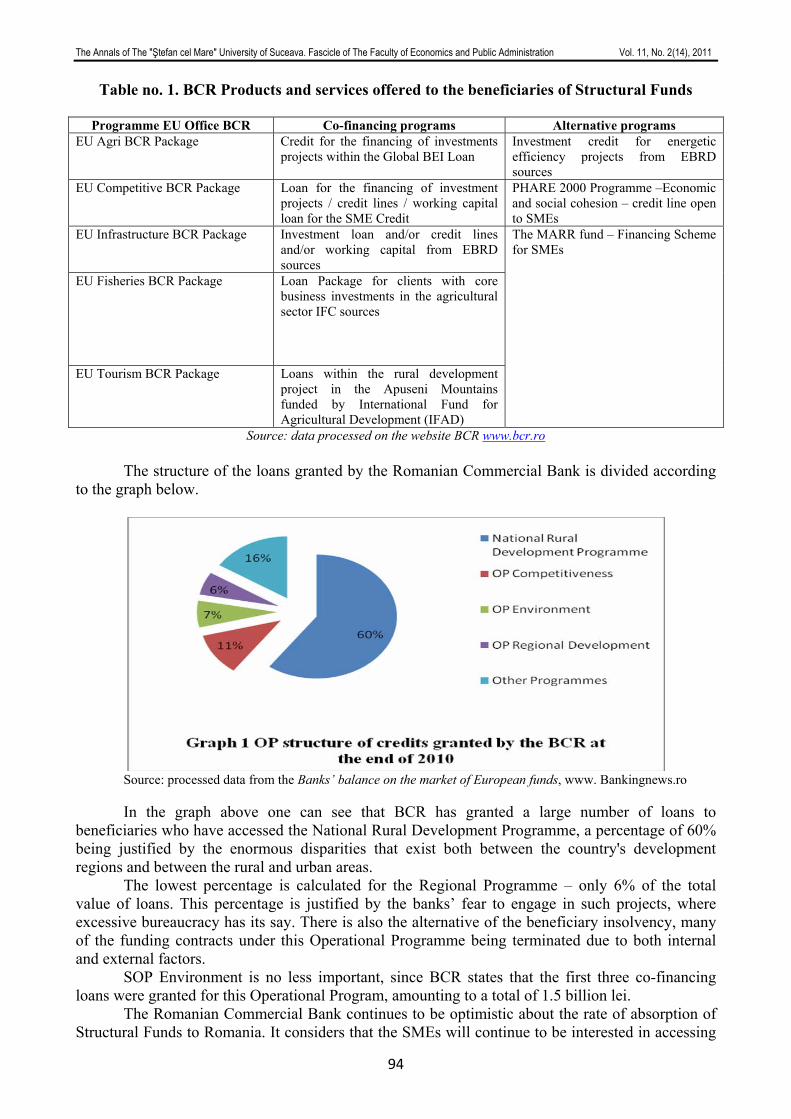

The situation of the existing accommodation capacity from the area was summarized in Table no. 1, shown below.

Table no. 1. Suceava Basin - Capacity of accommodation existing in touristic establishments in 2009

Official statistics Internet offer No. Locality No. of

existent structures

Existent accommodation capacity

(places –bed)

Working accommodatio

n capacity(place

s - days)

No. of existing

structures

Existent accommodatio

n capacity (places –bed)

1. Brodina 3 25 1159 - - 2. Cacica - - - 7 136 3. Ilișești - - - 3 60 4. Marginea - - - 1 20 5. Putna 4 60 16770 11 80 5. Solca - - - 5 196 6. Suceava 17 1182 436083 - - 7. Rădăuți 9 455 146069 - - 8. Sucevița 30 550 82804 31 640 9. Total area 63 2272 682885 - - 10. Total county 235 7554 2.176.422 - -

Source of official data: Touristic breviary of Suceava county, 2010; Internet unofficial data– sites (www.cazarebucovinaagroturism.eo; www.cazarelanoi.ro; www.infopensiuni.ro; )

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

20

Reporting the existing accommodation capacity in the analyzed area to the total of the

county shows that 26.8% of accommodation structures in the county is concentrated in the area studied, 30.07% of the capacity of accommodation (bed spaces) and 31.37 % of operational accommodation capacity (seats-days).

Analyzing the distribution of accommodation capacity on the two parts of the Suceava basin - mountain and plateau - we stated that the middle and lower basin has a capacity of significant relative to the mountain, all indicators analyzed, holds 44.06% respectively the number of structures, 74% of the capacity of existing accommodation (bed spaces) and 87.39% of operational accommodation capacity (seats-days).

Data obtained from consulting official sources were filled in the table with a series of data corresponding to touristic offer published for April of 2010 on the internet.

As can be seen, these data reflect the fact that in reality, the accommodation capacity is higher than reflected by the data in official statistics.

The differences between the two possible sources of information have the first question non-coverage in official statistics the localities with less than three structures of accommodation. Other probable causes are: non-inclusion of some farmhouses in the permanent tourist circuit, registration of more rooms in Easter touristic offers to attract more tourists, commissioning of new pensions etc.

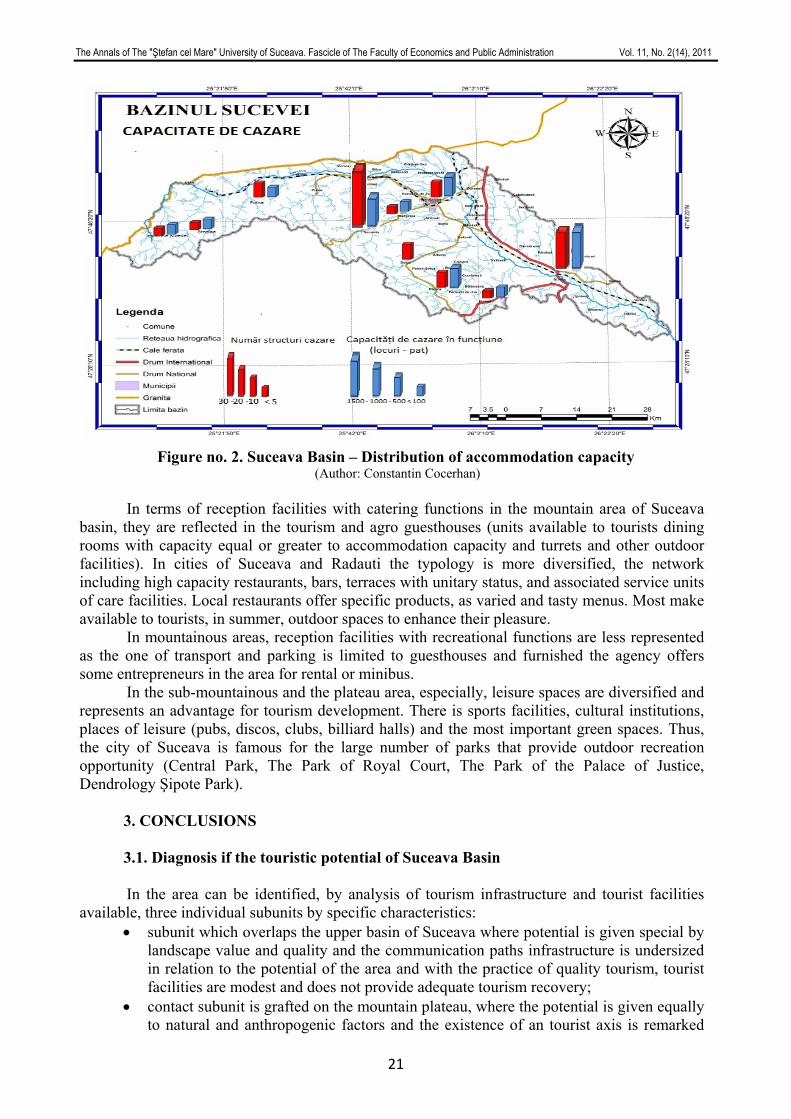

On the map in Fig. 2 is shown the territorial distribution of tourist accommodation structures of Suceava Basin.

Analyzing the accommodation capacity estimated as number of structures we see large disparities between analyzed subunits of the Suceava basin. In the upper basin of Suceava, the accommodation capacity is reduced, being concentrated in Putna town in mountain-plateau contact area with the highest accommodation capacity falls Suceviţa city, which owns the largest number of structures in the basin of Suceava, followed by Cacica and Solca, and in the middle and lower basin is dominated by the city of Suceava, followed by city Radauti.

In terms of accommodation capacity in operation, with the greatest capacity is part of the middle and lower basin which is dominated by the city of Suceava, followed by mountain-plateau contact area where Suceviţa city includes the largest capacity. In the upper basin of Suceava official statistics include only data for Putna area, accommodation capacity in operation is very small compared to that of the other two areas analyzed.

In the typology of tourist accommodation structures with functions stands the predominance in the plateau area of the basin of the hotel type structures and the sub-mountainous and mountainous of agro-touristic guesthouses, service quality is appreciated in most cases with 2-3 flowers for hostels and 2-3 stars for hotels and restaurants, with only 4 units classified with 4 stars across the area (1 in Suceava, 1 in Radauti and 2 in Suceviţa).

Campings satisfy partially the requests of the automobilist tourism; is remarkable in this respect Ilişeşti camping, Dragomirna camping and Burac camping, near Dragomirna Monastery, offering tourists the possibility of camping in a very picturesque area.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

21

Figure no. 2. Suceava Basin – Distribution of accommodation capacity (Author: Constantin Cocerhan)

In terms of reception facilities with catering functions in the mountain area of Suceava

basin, they are reflected in the tourism and agro guesthouses (units available to tourists dining rooms with capacity equal or greater to accommodation capacity and turrets and other outdoor facilities). In cities of Suceava and Radauti the typology is more diversified, the network including high capacity restaurants, bars, terraces with unitary status, and associated service units of care facilities. Local restaurants offer specific products, as varied and tasty menus. Most make available to tourists, in summer, outdoor spaces to enhance their pleasure.

In mountainous areas, reception facilities with recreational functions are less represented as the one of transport and parking is limited to guesthouses and furnished the agency offers some entrepreneurs in the area for rental or minibus.

In the sub-mountainous and the plateau area, especially, leisure spaces are diversified and represents an advantage for tourism development. There is sports facilities, cultural institutions, places of leisure (pubs, discos, clubs, billiard halls) and the most important green spaces. Thus, the city of Suceava is famous for the large number of parks that provide outdoor recreation opportunity (Central Park, The Park of Royal Court, The Park of the Palace of Justice, Dendrology Şipote Park).

3. CONCLUSIONS

3.1. Diagnosis if the touristic potential of Suceava Basin

In the area can be identified, by analysis of tourism infrastructure and tourist facilities available, three individual subunits by specific characteristics:

• subunit which overlaps the upper basin of Suceava where potential is given special by landscape value and quality and the communication paths infrastructure is undersized in relation to the potential of the area and with the practice of quality tourism, tourist facilities are modest and does not provide adequate tourism recovery;

• contact subunit is grafted on the mountain plateau, where the potential is given equally to natural and anthropogenic factors and the existence of an tourist axis is remarked

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

22

with touristic resorts located in contact depressions with the mountain valleys (Suceviţa - Solca - Cacica ), where the infrastructure of communications channels has a higher density, where there are adequate tourist facilities that can meet various requirements, the image potential and resources of the area but not sufficiently exploited and promoted;

• the subunit which is grafted on the mountain-plateau contact in which touristic potential is given equally to natural and anthropogenic factors and is remarked the existence of an axis with tourist resorts located in contact with the mountain valleys (Suceviţa - Solca - Cacica) where communications infrastructure routes have a higher density, where there are adequate tourist facilities that can meet various requirements, the image potential and resources of the area but not sufficiently exploited and promoted;

• subunit which overlaps the plateau area of the Suceava basin, which has human touristic resources of international value, where the infrastructure requirements are approaching to practice a civilized tourism, with tourist facilities which can meet various requirements under the complex when they would be effectively promoted and that are valued in a relatively high measure, especially in tourist centers as polarizing activity zone (Suceava and Radauti).

3.2 Sustainable tourism in Suceava Basin

In sustainable development perspective, tourism potential of the Suceava Basin can be a valuable resource and a planning and recovery to a similar level to other tourist regions in the world can ensure sustainable development of the region for the benefit of current and future generations.

Valence elements for the practice of sustainable tourism in the area are to maintain a large natural background, there is a distinct ethno-folkloric background, objectives of exceptional cultural-historical, hospitality people, with specific cuisine Bucovina, the existence of higher schools profile of tourism in the area, availability of people for practicing tourism. Currently, in the Suceava area and in Bucovina is practiced a conventional tourism, tourist offer being focused on visiting religious monuments and fund capitalization traditions and customs of Bucovina region, addressing in particular the adult population.

From the perspective of sustainable development this area should be seen as an area where you can develop many forms of tourism: ecological, rural, cultural, spa, entertainment, religious. Although some forms are already present, the recovery of the tourism potential is not satisfactory or brings important environmental damage.

In the situation of Suceava Basin for inclusion in sustainable development and reducing human pressure on the environment is required:

• protection and conservation of world heritage from the area (churches with mural paintings from Suceviţa, Arbore, Pătrăuţi);

• protection and conservation of cultural heritage in urban areas; • establishment of a tourist information center in the city Radauti; • Increase tourism in the region's tourism offer; • modernization of tourist infrastructure in mountain areas (Brodina Valley); • developing and promoting improved specificity tourist area; • increasing the professionalism of those involved in tourism activities; • ensuring quality of tourism services for visitors to provide valuable experience; • ensuring continuity of natural resources and culture of host communities; • ensuring a balance between the needs of the tourism industry and the need to preserve

the environment; • promotion of ecological tourism.

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

23

• accessing European funds for modernization funding of tourism activities and technical and material base for tourism.

AKNOLEDGEMENT This work was supported by the project "Post-Doctoral Studies in Economics: training

program for elite researchers - SPODE" co-funded from the European Social Fund through the Development of Human Resources Operaţional Programme 2007-2013, contract no. POSDRU/89/1.5/S/61755.)”

BIBLIOGRAPHY

1. Băltăreţu, Andreea (2007), Ecoturism și dezvoltare durabilă, Edit. PRO Universitaria, București

2. Barbu, N.; Ionesi, L. (1987), Obcinile Bucovinei, Ghid turistic, colecția Munții noștri, Edit. Sport-Turism, București

3. Bibirigea, I.,R., Managementul integrării turismului românesc în Uniunea Europeană,autoreferat teza de doctorat, www.cnaa.md

4. Ielenicz, M., Comănescu, Laura (2006), România potențial turistic, Edit. Universitară, București.

5. Bahre Heike, Chasovschi Carmen, Năstase Carmen (2009), The Profile of the Tourism Information Center Officer in Romania, Amfiteatru Economic Journal, ISSN 1582-9146, Vol 11, no. 25/2009, pages 51-61, February

6. Hrenciuc, D. (2010), Patrimoniu 2010-Buletin de informare, lucrare editată de Direcția pentru Cultură, Culte și Patrimoniu Cultural Național Suceava, Edit. Terra Design, Suceava.

7. Năstase, Carmen, (2007), Dezvoltare durabilă și turism durabil, Revista de turism, nr. 3, Universitatea ”Ștefan cel Mare”, Suceava.

8. Pompei Cocean, Gh. Vlăsceanu, Bebe Negoescu, (2005), Geografia generală a turismului, Editura Meteor Press, București

9. Răduianu, I.D., (2009), Resursele de apă din bazinul hidrografic al râului Suceava și valorificarea lor, rezumatul tezei de doctorat,

10. Scutariu Adrian Liviu, Năstase Carmen (2010), Comparative evolution of tourism in the Nord Eastern Region of Romania, Subcarpathia of Poland and Central Slovakia, Bulletin of University of Agricultural Sciences and Veterinary Medicine Cluj Napoca. Horticulture, Volume 67, No. 2, pp. 229 – 237

11. Velcea, Valeria, Savu, A., (1982), Geografia Carpaților și Subcarpaților Românești, Edit.. Didactică și pedagogică București.

12. Direcția Județeană de Statistică Suceava – Breviarul turistic al județului Suceava, ediția 2007.

13. Direcția Județeană de Statistică Suceava – Breviarul turistic al județului Suceava, ediția 2010.

14. www.alpinnetorg.ro –Puncte de acces în Obcinile Bucovinei, accessed 12.04.2010. 15. www.carpatiorg.ro – Trasee în Obcinile Bucovinei, accessed 12.04.2010, 16.06.2010. 16. www.cazarebucovinaagroturism.eo – pensions data, accessed 12.04.2011 . 17. www.cazarelanoi.ro- pensions data, accessed 12.04.2010. 18. www.comune.ro – localities data Suceava county, accessed 17.05.2010 19. www.hartainfoturism.ro – pensions data, accessed 17.05.2010 20. www.harta-suceava.ro – Touristic map of the Suceava county, accessed 17.05.2010 21. www.infopensiuni.ro – pensions data, accessed 12.04.2011. 22. www.lasuceava.ro – pensions data, accessed 7.05.2010

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

24

23. www.pensiuni-vile.ro - pensions data, accessed 12.04.2010 24. www.romaniaturistica.ro – Info ski, accessed 20.06.2010 25. www.travelworld.ro – Human settlements map from Obcinile Bucovinei, accessed

7.05.2010 26. www.turism365.ro – date pensiuni, accessed 7.05.2010 27. www.vileonline.ro – date pensiuni, accessed 15.04.2010

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

25

ONLINE EDUCATION - AN IMPORTANT ISSUE FOR THE LABOR MARKET

Assoc. Prof. PhD. Diana-Mihaela POCIOVĂLIŞTEANU “Constantin Brâncuşi” University of Targu Jiu, West University of Timişoara, Romania

[email protected] PhD. Lecturer Liana BADEA

Academy of Economic Studies, Bucharest, Romania [email protected]

Abstract: Crises come and a crisis go and during any period of insecurity there is invariably an outcry for “change”,

change to the law, the rules, the system, our behaviour etc. It is then, during the crisis when people start asking questions about the causes, the effects and the remedies for the crisis. They usually blame others for what happens to them and start observing what it is obvious – the factors that change the world. Nowadays, population face a number of significant new trends in the global environment. These shifts are affecting not only the shape and mode of operation but also the purpose of higher education systems. Some of these trends represent sources of opportunities; others constitute potential threats. Among the most critical dimensions of change are the growing role of knowledge, the information and communication revolution, the emergence of a worldwide labour market, and global socio-political changes. Increasing the level of education is became a priority for individuals and society. Starting from such aspects, this paper aims to emphasize the fact that a high level of education obtained in the classical way or online, increases the chance of adapting to labour market demands and it contributes to increasing the quality of life.

Keywords: online education, higher education, labour market, employment

JEL Classification: I20, I25

INTRODUCTION

In the context of a globalised society, one may observe that knowledge accumulation has become one of the major factors in economic development and is increasingly at the core of a country’s competitive advantage, which is itself determined by the ability to innovate in a continuous manner. Starting from this, it is easy to understand that countries are struggling to adapt their higher education systems to meet the challenges brought about by rapid societal change over recent years. Thus, new types of higher institutions and new forms of competition are appearing, inducing traditional institutions to change their modes of operation and delivery and take advantage of opportunities offered by the new information and communication technologies.

As the majority of individuals know, in the present, as in the past, one of the factors that made a huge difference between the stages of developments of countries was the educational system. It was also one of those factors that assured the functionality of the labour market. This is why, in our era confronted with many changes, the rapid adaption of the educational system to the markets evolution become very important.

Employment is, in any society, including in developed countries, a balance which is essential for macroeconomic and socio-political stability. It is a complex dynamic process of major interest to all economic and social partners for the present and future of society, with varying implications: economic, psychosocial, educational, cultural, political. Increasing the employment of the workforce and reducing the phenomenon of unemployment are now key economic policy objectives of all countries, made possible by establishing equilibrium between supply and demand for skilled labor market.

In accordance with the objectives of Europe 2020, the European Strategy on Employment aims to create more and better jobs throughout the European Union. The European Strategy encourages measures to ensure the achievement by 2020 of three major objectives:

75% of people aged between 20 and 64 to be active on the labor market reducing school dropout to less than 10% and increasing to at least 40% the proportion of

higher education graduates among the population aged 30-34;

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

26

reduction by at least 20 million the number of people who suffer or may suffer from poverty and social exclusion. The Europe 2020 strategy for smart, sustainable and inclusive growth rightly recognises the

key role education and higher education must play if the ambitions for Europe in a fast-changing global reality are to be realised. It is obviuos that the labour markets increasingly require more graduates with the knowledge and competences provided by higher education; countries will have to invest substantially in their higher education systems to ensure that this demand is met. However, as we all know, while demands are increasing, public funding is diminishing and the new tehnologies require important funds.

As James D. Wolfensohn said in 2000: „It is impossible to have a complete education system without an appropriate and strong higher education system... I am not for a moment suggesting that primary education and secondary education are not at the very essence of development... [but that is] not enough. You have to have centers of excellence and learning and training if you are going to advance the issue of poverty and development in developing countries... the key... is higher education, not just on the technological side, but to create people with enough wisdom to be able to use it.”

In order to realise that objective, one must first understand what the trends in this area are and how they affect the general mentality. The paper is going to emphasize the importance of the online education in our days and the fact that it became one of the trusted forms of education.

ONLINE EDUCATION Nowadays we can see that quality higher education and training is crucial for economies that

want to move up the value chain beyond simple production processes and products. In particular, today’s globalizing economy requires countries to nurture pools of well-educated workers who are able to adapt rapidly to their changing environment and the evolving needs of the production system. Today’s world asks to well train people which are able to give practical solutions for economic problems. And we ask ourselves: is the educational system ready to provide such a thing? Is it enough to teach students how to memorize a bunch of theories? Is it enough to tell them which are the economic variables and how they evolve? Is it enough to stay to the classical forms of education? Do we have to adapt the educational system to the global trends?

Thus is why it is particularly important to examine how research can energize and re-engage the brain and the voice of online classes in achieving a more effective strategic positioning in the context of the modern university.

The Internet has changed the way people get informed, interact, communicate and learn in the 21st century. Distribution of information and knowledge is nowadays carried out more and more via the Internet. The growing demands for highly skilled and educated labour force claim for changing traditional teaching and learning processes. One way of changes is related with an integration of various kinds of computer-based learning systems as supplements to conventional teaching methods, as it is said that nowadays there are three major new challenges which bear heavily on the role and functions of higher education: economic globalization; the increasing importance of knowledge as a driver of growth, and the information and communication revolution (Salmi, 2001).

Historically, the rush of online education may be located in the decade 1990-2000, a period characterised by a boom in the ICT and the invention and evolution of the Web. This not only led to the foundation of many Open Universities around the world (Doukas and Andreatos, 2007), but also pushed many traditional universities to offer distance learning courses. It is estimated that, as far as continuing education in higher education institutions is concerned, distance learning will grow at least ten times faster than on-campus learning over the years to come (Burns, 2006). Thus is why many universities around the world started to use means of online education in order to adopt their management strategies to the evolution of the humankind.

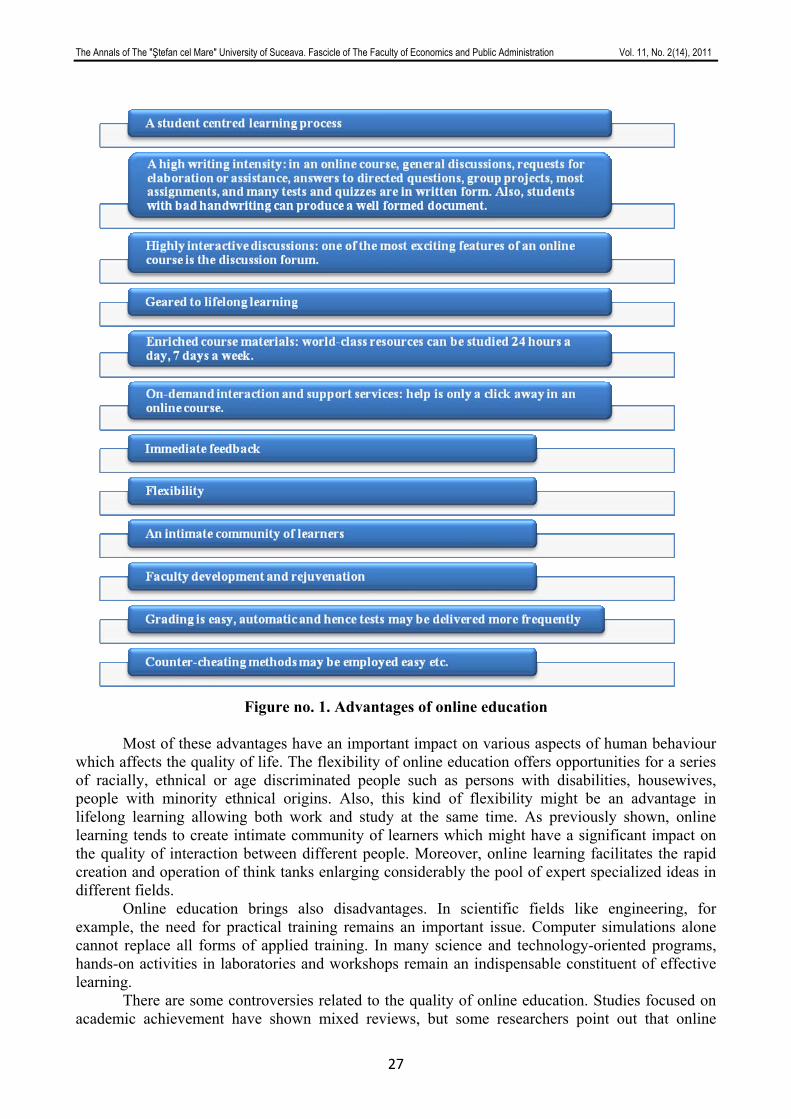

It is well recognized that online education brings a lot of advantages (Figure no. 1)

The Annals of The "Ştefan cel Mare" University of Suceava. Fascicle of The Faculty of Economics and Public Administration Vol. 11, No. 2(14), 2011

27

Figure no. 1. Advantages of online education

Most of these advantages have an important impact on various aspects of human behaviour

which affects the quality of life. The flexibility of online education offers opportunities for a series of racially, ethnical or age discriminated people such as persons with disabilities, housewives, people with minority ethnical origins. Also, this kind of flexibility might be an advantage in lifelong learning allowing both work and study at the same time. As previously shown, online learning tends to create intimate community of learners which might have a significant impact on the quality of interaction between different people. Moreover, online learning facilitates the rapid creation and operation of think tanks enlarging considerably the pool of expert specialized ideas in different fields.