1 - IPO delisting and underwriter prestige in China

29

- 1 - IPO delisting and underwriter prestige in China Chi-Yih YANG* Business School Xi’an Jiaotong-Liverpool University, China Xiaoming DING Business School Xi’an Jiaotong-Liverpool University, China Xinru NI School of Economics, Finance and Management University of Bristol, U.K. * Corresponding author: Dr. Chi-Yih YANG Associate Professor Business School, Xi’an Jiaotong-Liverpool University, No.111 Ren'ai Road, Suzhou Dushu Lake Higher Education Town, Suzhou Industrial Park, Jiangsu Province 215123, China Tel: +86 (0)512 88161708 E-mail: [email protected]

Transcript of 1 - IPO delisting and underwriter prestige in China

- 1 -

IPO delisting and underwriter prestige in China

Chi-Yih YANG*

Business School

Xi’an Jiaotong-Liverpool University, China

Xiaoming DING

Business School

Xi’an Jiaotong-Liverpool University, China

Xinru NI

School of Economics, Finance and Management

University of Bristol, U.K.

* Corresponding author:

Dr. Chi-Yih YANG Associate Professor Business School, Xi’an Jiaotong-Liverpool University, No.111 Ren'ai Road, Suzhou Dushu Lake Higher Education Town, Suzhou Industrial Park, Jiangsu Province 215123, China Tel: +86 (0)512 88161708 E-mail: [email protected]

- 2 -

IPO delisting and underwriter prestige in China

ABSTRACT

Previous western literature about the effect of underwriter prestige on IPO performance

reveals incongruous results but the majority is in support of the positive relationship between

the two. This paper focuses on a sample of 1376 IPO firms in China and aims to examine

whether underwriter prestige has an explanatory effect on IPO failure under the

certification/screening hypothesis and the sociopolitical shield hypothesis. Logit regression

model is employed and underwriter prestige is measured by three proxies: the number of

managing underwriters, the market share and corporate classification for lead underwriter. For

a sample with large offering size, only number of managing underwriters appears significant

and is positively related with delisting risk, which contradicts western literature.. Nevertheless,

for a sample with small offering size, only state ownership is significant and negatively

related with delisting risk. This result is consistent with western literature. The results suggest

that underwriter prestige is not formally established in China and there is a lack of mutual

certification between underwriters and issuing firms.

Keywords: Corporate Governance, Initial Public Offerings, Underwriter Reputation,

People’s Republic of China

- 3 -

1. Introduction

1.1. Institutional Background

Although the People’s Republic of China was established in 1949, China’s securities

market has been formally developed since the late 1980s, with a short history of more than 20

years. Over the past two decades, China has achieved great success in the economic

development with the annual GDP growth above an average of eight percent. Moreover,

following the U.S., China became the No. 2 country in attracting foreign direct investment

(FDI) in 2010 (Hu, 2011) and the No. 1 in holding foreign currency reserve in 2011 (Yin &

Lin, 2011). However, such great achievement was not reflected in the performance of its

securities market as Shanghai A Shares shrunk over 50 percent since 2001 till 2005

(Securities Daily, 2012) and a considerable amount of companies have been suffering from

financial distress. Nevertheless, under this circumstance, China's stock market has

experienced an annual average delisting rate of less than 1 percent in the past 10 years, which

is much lower than other major capital markets in the world. For example, approximately 6

percent of listed companies are removed annually from the New York Stock Exchange

(NYSE) (Cao, 2010).

From 1949 to 1978, the Chinese government adopted a centrally planned economic

structure, and it was only from the 1980s that the Chinese economy began transitioning from

a government-planned economy to a market-oriented one. Similar to economic structure, the

IPO system in China has also experienced two stages of development, the quota allocation

system and the examination and ratification system. In the quota allocation system period

(from 1990 to 1999), the regulatory authorities had absolute discretion over the issuance

volume and pricing of IPO shares. A quota for the number of IPOs to be launched each year

was set and the quota was allocated evenly among all central and local government ministries.

The situation at that time became so absurd that even the Commission of Family Planning and

- 4 -

the Military Commission received an IPO quota. As a result of this system, IPO quotas

became a rare and precious resource, leading to the problem of rent seeking by government

institutions with IPO quotas, serious information asymmetry and price distortion between the

primary and secondary stock markets. The environment for IPOs became better after the

introduction of an examination and ratification system. In the examination and ratification

system period (from 2000 to the present), a special Stock Issuance Examination and

Ratification Commission was established to independently investigate the listing

qualifications of companies. The most significant reform implemented via this system is that

the pricing of newly listed shares is determined by market demand rather than by the

regulatory authorities (Ma, Song and Yang, 2010).

Under the current examination and ratification system, a firm seeking IPO must go

through a multi-step and tightly controlled selection process. The first step is to get approval

from the China Securities Regulatory Commission (CSRC) followed by permission from the

relevant national and local authorities. The next step is to pass the examination of the listing

committees of the stock exchanges followed by a formal announcement of the IPO. Some

major listing requirements for IPOs in China include at least three fiscal years of operation

with cumulative earnings of more than 30 million RMB, registered capital of no less than 30

million and etc.

On the other hand, in order to protect the interests of investors and send messages of

default risk, CSRC decided in 1998 to distinguish firms in financial distress by launching a

new policy to enforce “special treatment” (ST) upon those firms. These “ST” firms share

certain features and they are:

(1) Companies that had negative cumulative earnings over two consecutive years or had net

asset value (NAV) per share below its par value (book value).

- 5 -

(2) Companies that had negative earnings for one year, but the current year shareholders’

equities are below its registered capital.

(3) Companies that received the auditors’ “going concern opinions”.

The “ST” firms are forced to improve their financial condition through efforts such as

reorganization, mergers etc. Those that exhibit no sign of financial improvement in the

subsequent year will receive “particular transfer” (PT) warning from CSRC. If the “PT” firms

are still unable to revitalize in the following year, they will have to face their destiny - to be

delisted from stock exchanges. (Zhang et al., n.d)

Delisting is treated as a vital step to improve the performance of China’s securities

market. Take the period from 1999 to 2003 as an example, only four companies were deleted

from the securities market. The first delisted company in Chinese stock market was Narcissus

Electric Appliance Company which was floated on the Shanghai Stock Exchange. On 23rd of

April, 2001, the CSRC decided to terminate the listing of this company’s stock because it had

been making a loss for four successive years and it failed to provide solid proposals to stop

losses and to make profits in the short-term. The other three companies (Anshan No. 1

Construction Machinery Company, Shanghai Citic-Jiading Industrial Company, and Hubei

Jianghu Ecology Company) were delisted as a result of reporting successive losses in the first

half-year after suspension, a decision to stop the listing by the shareholder meeting, and a

denial opinion issued for the first year annual report after restarting the listing (Green,

Czernkowski and Wang, 2009). However, given the short history of China’s securities market,

the delisting mechanism is not complete yet. The only quantified indicator for delisting is loss

for four consecutive years.

- 6 -

1.2. Research objective

This study will use delisting as an indicator to measure financial distress of IPO firms.

The underlying reason is that apart from some common financial distress indicators like ST

and PT, CRSC also use other indicators like *ST, S*ST and SST to refer to firms with

different financial situation before delisting and these indicators can be removed or altered if

the situation has been improved. Hence, delisting is clearer and more straightforward than ST,

PT or other indicators.

A few scholars (e.g. Liu, Yin & Yi, 2005) have already studied underwriter prestige

effect on China’s stock market but to the best of our knowledge none has ever tested whether

the factors that have frequently appeared in Western literature have a similar explanatory

effect on China’s IPOs. Thus, it is of great significance and practical value to compare and

contrast the effect of underwriter prestige on China’s primary securities market with that on

western markets. In order to establish a comprehensive sample for study, this research will

focus on a long sample period from 1990 to 2010 and aims to examine whether underwriter

prestige has an explanatory effect on the failure of an IPO, particularly A-Shares, in China

under two hypotheses that will be provided in Section 2.2, certification/screening hypothesis

and sociopolitical shield hypothesis. This research is expected to shed light on the relationship

between underwriter prestige and IPO failure risk in China and provide insight for investment

companies and individual investors as well.

The organization of the rest of this article is as follows. Section 2 provides literature

review and hypotheses development. Section 3 describes the methodology of the research

with regression model, explanatory variables and control variables in detail. Section 4

discusses the results obtained and explains the robustness of the model. Finally, Section 5

summarizes the whole paper with limitations and implications for future research.

- 7 -

2. Literature review and hypothesis development

2.1. Literature review

In the seminal paper “The Market for "Lemons: Quality Uncertainty and the Market

Mechanism”, Akerlof (1970) argues that the difficulty of distinguishing good quality from

bad is inherent in the business world and further proposes that "business in underdeveloped

countries is difficult". In such markets social and private returns differ, and therefore, in some

cases, numerous institutions can arise to reduce the effects of quality uncertainty. One obvious

institution is guarantees.

China is a developing country and its securities market is far from efficient due to its

special political and economic situation, thus guarantees play an important part in ensuring

information symmetry between issuers and investors. There are usually two types of

guarantees in the process of issuing stocks, namely underwriter and sponsor. An underwriter

takes the risk of distributing securities and is responsible for raising investment capital from

investors on behalf of corporations and governments. A sponsor is responsible for the

information disclosure of listed firms. However, sometimes the lead underwriter also acts as

the sponsor. Since the mechanism of sponsors was not introduced in China until 2004, this

paper will only focus on the other type of guarantees - underwriters.

Although Akerlof suggests that the presence of guarantees may ensure the quality of

products, research results related to the effect of underwriter prestige on stock performance

diverge. Using an investment bank's capital as a proxy for its prestige, Michaely and Shaw

(1994) demonstrate that IPOs managed by high prestige underwriters tend to have smaller

initial returns and less severe long-run underperformance. They find out that the difference of

long-run performance between the IPOs issued by more reputable and the less reputable

underwriters is prominent. The latter group displays a two-year negative excess return of 26.8

percent, while the former group only shows a 1.5 percent negative excess return. Consistent

- 8 -

with Michaely and Shaw (1994), Carter, Dark & Singh (1998) examine the initial returns and

the three-year returns after IPO as well as the relationship between those returns and

underwriter prestige measured by several existing proxies. They discover that, on average,

market-adjusted returns in the long-run are less negative for those IPOs marketed by more

reputable underwriters. They further claim that investing in IPOs is risky to investors’ wealth.

However, one can mitigate the risk by investing in IPOs underwritten by more reputable

underwriters. Additionally, Chemmanur and Fulghieri (1994) argue that investors use

underwriters’ past performance, which is measured by the quality of firms that they have

previously underwritten, to assess their prestige. In order to protect investment banks’ own

reputation, they will underwrite IPOs with relatively better long-term performance and

invariably attempt to reduce the probability of marketing ‘lemons’, since such business will

ultimately damage the reputation of the underwriters. Consequently, these prestigious

underwriters will tend to set much stricter standards in their evaluation of firms which in turn

results in the firms they choose having high quality and high survival potential in the

aftermarket.

On the contrary, others hold an opposite stance towards this issue. Carter and Manaster

(1990) document an adverse relationship between underwriter reputation and IPO

performance. After examining the aftermarket returns of IPOs, they find out that an

underwriter’s reputation reflects the expected level of ‘informed’ activity. According to

Rock’s (1986) work, IPO returns are required by uninformed investors as compensation for

the risk of trading against inside information. The value of an issuing firm is private

information to the firm but the skills of underwriters to evaluate the values of the firms and to

disclose this information through the issue prospectus varies with their abilities. That is to say,

reputable underwriters are proficient at discovering the volatility of issuing firms’ value in

secondary market and these reputable underwriters are associated with lower risk offerings.

With less risk, there is less incentive to acquire information and there will be fewer informed

- 9 -

investors. Since Carter and Manaster (1990) find out that more informed investors require a

higher return, consequently, prestigious underwriters are associated with IPOs that have poor

performance.

A third school holds the opinion that there is no direct relationship between

underwriter prestige and IPO performance. Logue et al. (2002) suggest that consideration of

underwriter reputation and marketing activities at the same time is important if proper

implications about the IPO issuing process and IPO performance are to be drawn. Their

finding reveals that long-term investor returns are more associated with aftermarket

underwriter activities than underwriter reputation, issue-date pricing, or premarket

underwriter activities. An issuing firm chooses reputable underwriter because the reputation

of an underwriter is an indicator of its ability in price stabilization activities. Thus,

underwriter reputation per se has no significant impact on the post-IPO stock returns after

accounting for the services provided by the underwriters.

As the literature review has presented so far, the effect of underwriter prestige on IPO

performance is quite controversial in Western literature and scholars cannot reach a consensus

on this issue. Therefore it is interesting to investigate this topic to see if China’s situation fit

into any of these categories or if it exhibits totally different behavior.

2.2. Hypotheses

Generally speaking, the positive side outweighs the other two sides based on the

literature review, so two hypotheses in support of the positive relationship between IPO

performance and underwriter prestige are developed in this research.

2.2.1. The Certification/Screening Hypothesis

Initially, the certification hypothesis derives from the literature on reputational

signaling. In Klein and Leffler’s (1981) work, a non-refundable investment is perceived by

- 10 -

customers as a commitment to product quality and they demonstrate the conditions under

which the non-refundable expenditure can function to guarantee the quality of a firm’s equity.

The certification hypothesis is based on the assumption of information asymmetry between

insiders who are shareholders, and outsiders who are prospective subscribers to IPOs.

Services provided by investment banks act as a way to reduce information asymmetry in the

IPO market. According to Booth and Smith (1986), certification is a significant function

carried out by underwriters. By agreeing to underwrite an offering, high-quality investment

banks ‘lease’ the brand name, “certify” the quality of the issue and guarantee that the issue

price is consistent with inside information about the firm’s investors’ returns in the future.

Thus certification by a high-quality underwriter can guarantee the quality of an issuing

company and boost the demand for the issue.

Another related function performed by underwriter is screening IPO candidates and

discovering firm values. For instance, Michaely and Shaw (1994) claims that underwriter

quality lowers the need to underprice because the information asymmetry between

uninformed and informed investors is reduced. As discussed in Carter, Dark & Singh (1998),

underwriters’ ability of screening may be accountable for the superior performance of IPOs

marketed by high reputation underwriters. Therefore, with this line of reasoning, high quality

underwriters screen and certify IPOs with good business prospects, contributing to a positive

relationship between underwriter reputation and IPO returns over long-run period.

2.2.2. The Sociopolitical Shield Hypothesis

One vital and non-repeatable event during an organization’s life cycle is the

conversion from private to public ownership. Although an initial public offering provides

several benefits to firms that successfully go through the transition, the conversion also brings

about several costs and risks (Pollock, Porac, & Wade, 2004). However, valuable external

social capital that companies have access to can be used to mitigate the risk of failure. Social

- 11 -

capital has been defined in different ways by various scholars in the social and organizational

sciences. Nevertheless, all of these definitions have two elements in common: (1) social

capital stems from the structure of relationships among participants in a network and (2) a

participant has the ability to access these networks or social-structural benefits (Coleman,

1988).

When an entity’s or product’s quality and characteristics are hard to determine, their

relationships with prestigious others can provide important signals to help reduce

uncertainties perceived by stakeholders (Podolny, 1994). There are two types of ties in such

context, internal and external ties. Internal ties are ties within organizations and they are

defined as "bonding" or "communal" forms of social capital, while external ties are defined as

"bridging" or "linking" forms of social capital.

To illustrate, one of the key external links an IPO firm has when going public is its tie

with the underwriter leading the IPO (Carter & Manaster, 1990; Pollock, Porac, & Wade,

2004). The lead underwriter works closely with the top management team, including lawyers

and auditors of an IPO firm, as well as with the Securities and Exchange Commission (SEC)

to guide the firm through the offering process (Husick & Arrington, 1998). One of the most

important functions of the lead underwriter of an IPO is to create a network of investors who

will become the IPO firm's initial shareholders. The relationships established by the

underwriter with these investors can influence the stability of these networks and the

aftermarket performance and survival probability of an IPO. More stable investor networks

can reduce the volatility of stock price and trading volume in the secondary market (Carter &

Dark, 1993; Ellis, Michaely, & O'Hara, 2000).

Under both hypotheses mentioned above, IPOs underwritten by prestigious underwriters

are associated with lower probability of failure.

- 12 -

3. Methodology

3.1. Data and variables

The data used for this research comes from China Stock Market Accounting Research

(CSMAR) database of GTA Finance and Education Group. The sample contains 1376 IPOs

listed on the Shanghai Stock Exchange and the Shenzhen Stock Market during the period

1990-2005. Each firm is tracked until December 31, 2010 to determine if it continues to trade

or fails. 69 IPOs in the sample had been delisted by the end of the year 2010.

Detailed definitions of the variables are provided in Table 1. In this research, the long-run

performance of an IPO is measured by its survival. The dependent variable is a binary factor

that indicates whether an IPO is delisted (equals to 1) or is still listed (equals to 0) during the

period of observation. The independent variable of primary interest is underwriter prestige

which is measured by 3 proxies: the number of managing underwriters, market share of lead

underwriter and credit rating of lead underwriter. The estimated signs of the three proxies

should all be positive in accordance with the two hypotheses.

The first proxy for underwriter prestige is the number of managing underwriters (NU)

during the process of initial public offering. Corwin and Schultz (2005) find strong evidence

of information production by syndicate members. That is, more co-managers that are attracted

by the reputation of lead underwriter can result in more analyst coverage and additional

market makers following the offering, promoting market price and demand discovery.

Therefore, large NU is associated with good reputation of lead underwriter. This measure is

used by Dong, Michel and Pandes (2011) as a proxy for underwriter quality in their study for

long-run IPO performance.

- 13 -

The second measure of this research is the market share (MS) of the lead underwriter.

In the process of initial public offering, the lead underwriter maintains the prospectus and its

name appears first in the tombstone. Megginson and Weiss (1991) are among the first to focus

on the relative market share of the underwriter. In the Megginson-Weiss (MW) measure, the

lead manager for each IPO is given full credit for the total amount underwritten. In Beneda’s

(2006) study on the performance and distress indicators of new public companies, underwriter

market share is used as a measure of underwriter quality as well. Due to data limitation in

China, this study applies Herfindahl index instead of the MW measure. Securities Association

in China (SAC) published the market share of China’s top 20 underwriters in 2006 which

totals 96.61%. While altogether the remaining 80 underwriters only account for 3.39% of the

market share, which is ignored in this study.

The last proxy for underwriter reputation is security-firm classification or rating (CR)

of the lead underwriter published by CSRC in July 2010. Underwriters are classified into five

big categories (A, B, C, D and E) and eleven sub-categories as shown in Table 1 based on the

following 6 aspects: adequacy of capital, corporate governance and compliance, dynamic risk

control, security of information system, customer protection, and transparency. Nevertheless,

CSRC emphasizes that this classification should not be used for commercial purposes like

advertising or marketing. It is assumed in this study that investors can refer to this publicly

available rating as underwriters’ reputation and quality. It is worth mentioning that the

classification only includes existing securities companies, thus the classification for

underwriters that went bankrupt before the year 2010 and underwriters that are not securities

companies (e.g. commercial banks) are denoted as not rated (CRO) in this research.

Apart from the three variables of underwriter reputation, a major characteristic of

China’s corporate governance structure is its highly concentrated equity structure. Most of the

listed firms in China are transformed from SOEs and the central government very often is still

the major shareholder. For example, average shareholding held by the PRC government in

- 14 -

2001 was estimated at 60% (CFA Institute, 2007). Economists generally view government

ownership as being detrimental to corporate performance. For example, Shleifer and Vishny

(1998) show that private ownership is preferable to state ownership because the government

has a “grabbing hand” that extorts firms for the benefit of politicians and bureaucrats at the

expense of corporate wealth. However, Parker, Peters and Turetsky (2002) find that higher

levels of blockholder and insider ownership are positively associated with the likelihood of

firm survival. Thus, this study also investigates whether state ownership (STATE) affect the

survival profile of IPOs in China.

In terms of control variables, a large body of literature has provided evidence of the

significance of variables like firm age, offering size, IPO activity, and industry effect in

explaining long-run performance of IPOs. The first control variable included is LNAGE. The

age of a firm is suggested as a proxy for the risks of the IPO firm (Ritter, 1984). It is

reasonable that older firms are less risky and may have established reputations. The next

control variable is LNSIZE defined by the natural logarithm of gross proceeds, which is the

total number of shares offered during the IPO multiplied by the offering price. Size of the

offering has been considered as a proxy for the extent of information asymmetry regarding the

prospects of the IPO issuer. IPO firms raising higher proceeds at the offering are presumed to

have less uncertainty regarding their future prospects and, hence, are expected to perform

better (Jain and Kini, 2000). Larger offerings also provide IPO firms with more cash, which

can serve as a resource-based transformational shield following the IPOs (Fischer and Pollock,

2004). The third control variable in this research is initial return (IR). Grinblatt and Hwang

(1989) and Welch (1989) find out that IPO issuers use underpricing to signal their quality to

the investors. Hence, signaling models predict that initial return of an IPO or the degree of

underpricing should be positively associated with the firm’s aftermarket performance. On the

contrary, Ritter (1991) documents higher initial returns accompanying more evident long-run

underperformance for younger IPOs and interprets this finding as being over-optimism. Initial

- 15 -

return is included in this research and is defined by the difference between closing price at the

day and offering price divided by offering price. Last but not least is the industry effect. EI

Hennawy and Morris (1983) used a dummy variable to describe industry and shown an

industry effect when predicting firm failure. Audretsch (1991) found that survival rates do

vary considerably across industries, and they are shaped by the conditions of technology and

demand underlying the industry. As Table 1 indicates, according to the CSRC industry

classification code (SIC), the sample contains IPOs from six industries namely

banking/financing, public/utilities, real estate, general, industrial and commercial respectively.

3.2. Regression model

Logit analysis is used in a multivariate setting to investigate the characteristics of Chinese

IPOs that went delisted afterwards. The logit model used in this study is:

LNSIZELNAGE

ICICICICICIR

STATECRBCRAMSNUDELIST

i

iiiiii

iiiiii

1312

11109876

543210

65432

αααααααα

αααααα

++++++++

+++++= (2)

DELIST, the dependent variable, is a dichotomous variable with the value equal to 1 if

the firm is delisted from the stock exchange. In addition to the proxies of underwriter

reputation (NU, MS, CRA and CRA), STATE represent the unique governance mechanisms

in China and IR, IC, LNAGE and LNSIZE represent the control variables of firm i as defined

in the section above. If the jth variable is effective in improving survivability of an IPO firm,

the coefficient αj is expected to be negative.

Two measures of goodness-of-fit will be used in this study to compare the logit models.

One is the fitted log-likelihood. Another metrics is Pseudo-R2, which is R2 generalized to

nonlinear models to measure goodness of fit using the likelihood function. We can see which

model fits better if that model has a larger Pseudo-R2.

- 16 -

4. Empirical results and analysis

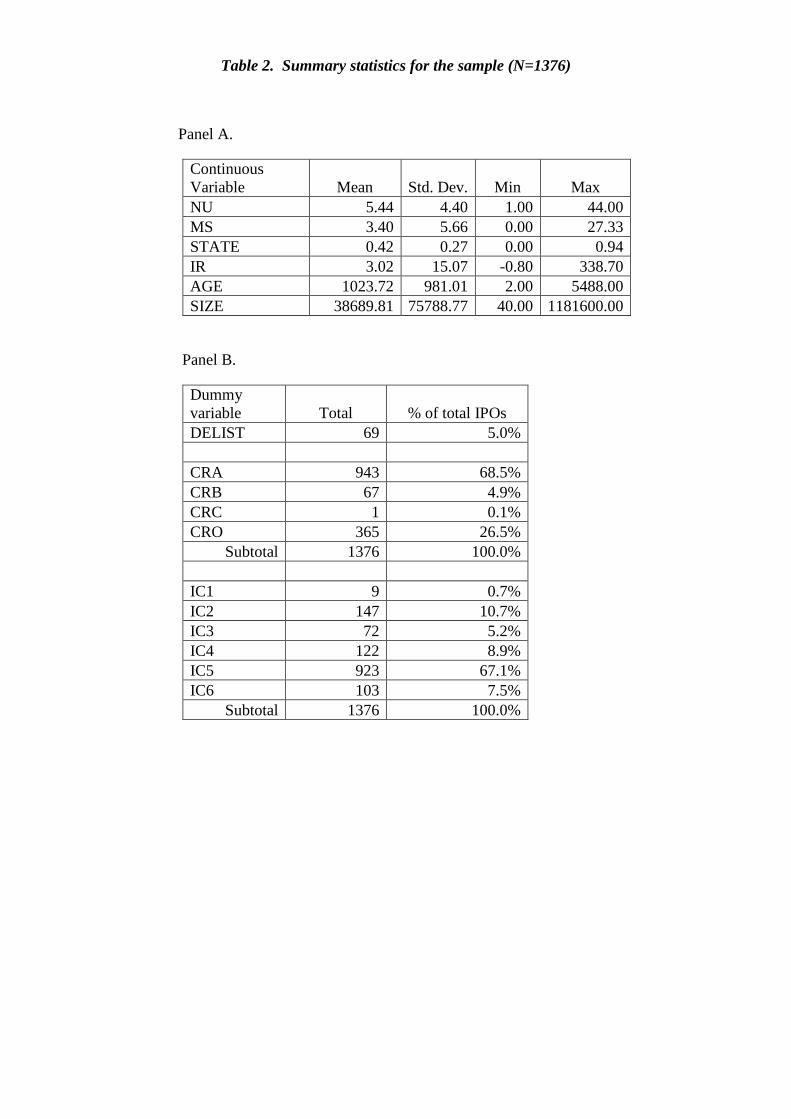

4.1. Descriptive statistics

Table 2 displays summary statistics for the sample. An IPO is brought to market by 5.4

underwriters on average and the maximum number of syndicate members is 44. Although the

market share of lead underwriter varies between 0 and 27.33%, the mean is only 3.4%. This

situation is the same for initial return, which has a big range (-0.8% to 338.7%) but a small

mean (3.02%). The mean of state ownership for IPO firms in China is 42.0%, suggesting that

ownership structure for Chinese SOEs is still concentrated even after IPO. As for dummy

variables, percentage of total sample for each category is provided. 5% of observed IPOs were

delisted from the market during the period of study. It is also observed that 68.5% IPOs are

underwritten by securities companies with credit rating A and only 0.1% IPOs are

underwritten by credit rating C companies. Moreover, in China, the majority of listed

companies come from the industrial sector which occupies a percentage of nearly 67%.

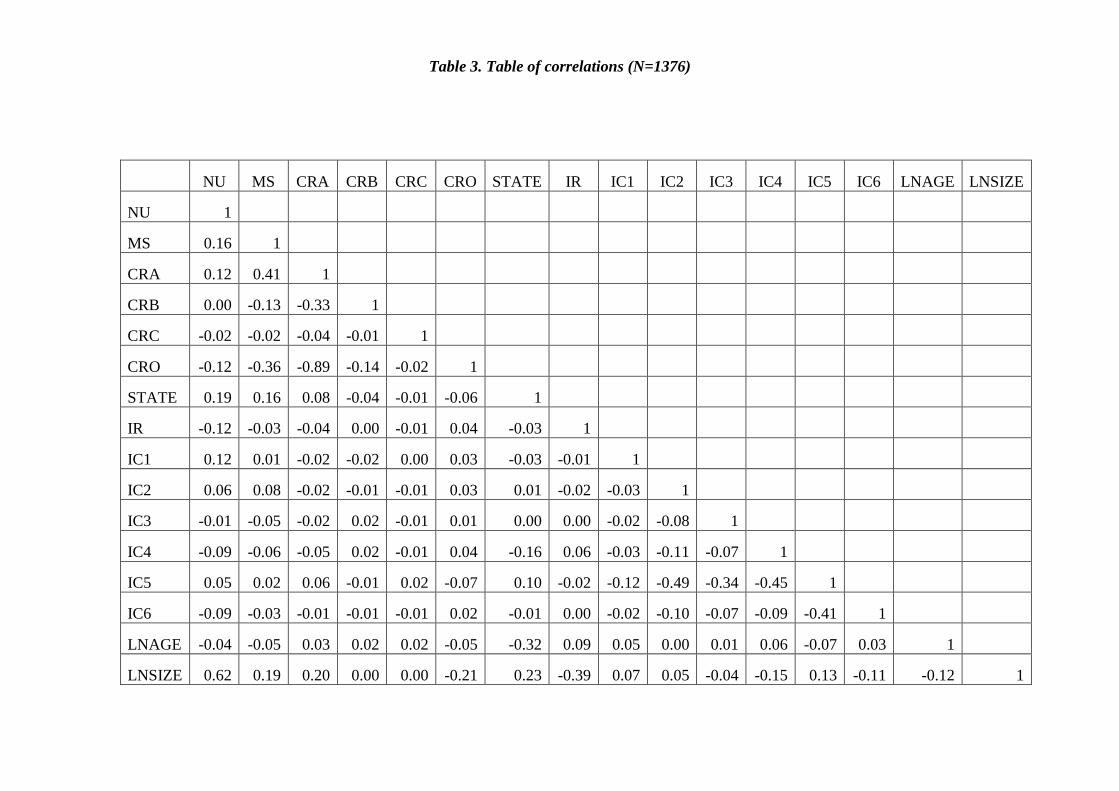

Table 3 presents the correlation matrix for the variables used in the model. As it can be

observed, within the three variables of main interest (NU, MS and CRA), the correlation is

positive between each pair since they all measure underwriter prestige in the same direction.

However, the correlation between MS and CRA is relatively large (0.41). The correlations

between LNSIZE and variables of main interest such as NU, MS, CRA and STATE are too

big to be ignored. The problem of potential multicollinearity would be considered in choosing

the regressors.

4.2. Logit Regression Results

4.2.1. Results for the whole sample

- 17 -

Table 4 and Table 5 provide the estimation results for the Logit regression model. In

total, six models are run under two different settings: one includes all IPOs and the other

separates IPO into two groups by offering size. With all control variables introduced, Model 1

contains only one underwriter reputation variable NU, Model 2 only MS, and Model 3 only

CRA and CRB (CRC is not included since its group size is negligible while CRO is not

included due to multicollinearity). Model 4 considers all underwriter reputation variables: NU,

MS, CRA and CRB. It can be observed in Table 4 that NU is significant in both Model 1 and

Model 4 while MS or CRA or CRB never present evidence of significance.

As for the control variables, only LNSIZE shows great significance across Model 1

through Model 4. This may result from the relatively high correlations among lnSIZE and

other independent variables which have been observed in Table 3.

With increasing goodness-of-fit measured by Pseudo R2, the results for Model 1 to

Model 4 can be summarized as follows. Controlling for state ownership (STATE), initial

return (IR), industry effect (IC), firm age (LNAGE) and offering size (LNSIZE), we can

conclude only that number of managing underwriters (NU) exerts positively significant

impact on delisting risk (DELIST).

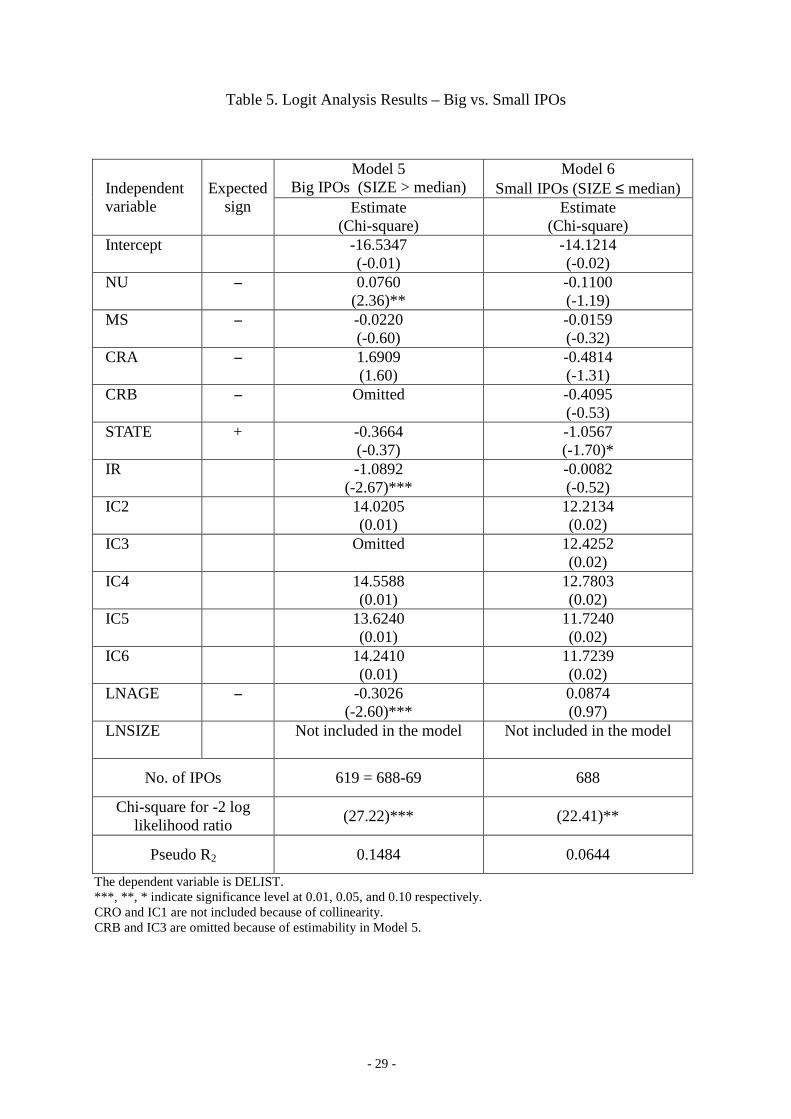

4.2.2. Results for sample sorted into small and large size groups

Because of the potential multicollinearity among lnSIZE and the proxies for

underwriter reputation, the full sample is sorted into two groups according to the sample

medium of LNSIZE. Model 5 only contains big IPOs while Model 6 small IPOs. The control

variable LNSIZE is this eliminated in Table 5 since the effect related to offering size is

already considered by sorting the sample into the big versus the small groups.

- 18 -

The estimation results shown in Table 5 indicate that for different offering sizes,

different variables of main interest are significant in China’s securities market. For big IPOs,

only NU appears significant and the positive sign it carries indicates that IPOs issued by large

underwriter syndicates are associated with higher risk of delisting, while IR and LNAGE have

negatively significant effect on delisting probability for large IPOS. For small IPOs, only

STATE appears significant and the negative sign it carries indicates that IPOs with higher

government shareholdings are associated with lower risk of delisting.

4.3. Discussion

Our results of the significantly positive values of NU for big IPOs contradict the

findings of Dong, Michel & Pandes (2011) and Corwin & Schultz (2005). Traditionally, more

managing underwriters can provide an issuer more channels for the distribution of shares as

the sociopolitical shield hypothesis predicts in section 2.2. Sometimes, it is better to form a

syndicate to spread the risk simply because the offering size is so big. However, this line of

reasoning may not apply well to China’s stock market. One possible explanation may be that

there is a lack of mutual certification among underwriters and issuers in China. Instead, they

collude for mutual benefits (Xiao, 2012). Moreover, Jin, Wu and Chen (2003) suggest that the

relationship between underwriters and issuers are distorted in China because CSRC acts not

only as a regulator but also as a guarantor. The majority of Chinese underwriters have been

devoted to the ‘packaging’ of issuers for a long period of time. Nevertheless, they just provide

channels for floating while services like financial and management consultations are ignored.

Jin, Wu and Chen (2003) also state that different from mature market, China’s stock market

has just been developed for a short period of over 20 years. In the initial stage of development,

underwriters have homogenous market influence. Reputations will be formed only when the

market becomes relatively mature. Put it another way, underwriters in emerging markets like

- 19 -

China are busy competing with each other for market share and they are not like underwriters

in mature markets that market IPOs with good quality to maintain their established reputation.

Thus, underwriters may be attracted by the large issue size and want to have a slice of the

cake. These underwriters are not concerned about their reputation since fighting for market

share seems more important under current circumstances. For the above reasons, an

underwriter syndicate may not exert its positive impact on IPO performance.

For the sample with small offering size, the negative relationship between the PRC

government stockholding and IPO hazard rate indicates the importance of government’s

commitment to the survivability of a privatized SOE in China. A potential interpretation is

that relationships or Guanxi between the business and the government may represent a way to

bypass laws and regulations through personal connections with government officials. Through

this relationship, special treatment is guaranteed (Braendle, Gasser and Noll, 2005). Our

finding is also consistent with Wang and Deng (2006) and Chen, Jiang, Liang and Wang

(2011). Wang and Deng (2006) empirically found state ownership reduces the likelihood of

financial distress for a listed firm in SHSE or SZSE since PRC government would try to

rescue the problematic SOEs even though they have gone public. Chen, Jiang, Liang and

Wang (2011) analyzed 201 instances of violation by Chinese listed firms during 1994-2008

and found that companies with a state-owned background are more likely to escape serious

punishment by the CSRC. One possible reason may be that the CSRC does not apply the law

strictly to avoid colliding with the government goal which SOEs may help to achieve, such as

employment.

5. Conclusions and future research

In conclusion, this research focuses on the sample period of 1990 to 2005 and aims to

examine whether underwriter prestige has an explanatory effect on the failure of an IPO,

- 20 -

particularly A-Shares in China under two hypotheses, certification/screening hypothesis and

sociopolitical shield hypothesis. Literature review reveals that the effect of underwriter

prestige on IPO performance is quite controversial in Western literature. But generally

speaking, the positive side outweighs the other two sides.

By using delisting as an indicator to measure financial distress of IPO firms, this research

demonstrates that western literature can only partially explain the situation in China. The

independent variable of primary interest is underwriter prestige which is measured by number

of managing underwriters, market share of lead underwriter and credit rating of lead

underwriter. Besides, there are one governance variable and four control variables in the

research namely STATE, lnAGE, lnSIZE, IR (initial return) and IC (industry code). Logit

model is applied to analyze the data. Two metrics, the fitted Log likelihood and Pseudo-R2 are

used to compare the two models.

The main finding of this paper is that for different IPO sizes, different factors appear

important in China’s securities market. The significantly negative values of STATE in the

small size group are consistent with the Chinese literature that IPO firms controlled by PRC

government are less likely to delist. On the contrary, the significantly positive values of NU in

the large size group contradict the hypotheses derived from western literature, indicating that

IPOs brought to market by large underwriter syndicate are more likely to fail. The main

account for this result may be that in the initial stage of development, underwriters in China

are not concerned about their reputation.

However, the research has certain limitation with regard to one of the proxies for

underwriter reputation, the market share of China’s top 20 underwriters in 2006 is employed

and it is assumed that the market share has not fluctuated over the period of observation.

Carter, Dark & Singh (1998) points out that the Carter and Manaster (CM) system is more

appropriate for measuring underwriter rankings. The CM system reflects the company an

- 21 -

underwriter keeps and is analogous to the starring order appearing in Hollywood's billboards

because the measure uses underwriters' relative placements in stock offering "tombstone"

announcements. However, the problem for implementation is that the compilation of the CM

measure is quite tedious because each tombstone has the potential to impact the order of each

underwriter's relative position. Moreover, it is not feasible to collect the "tombstone"

announcements for all listed firms at the moment of the completion of this paper either.

Further research on this topic may try CM measure to see if different results can be obtained.

The implication of this research is threefold. For investors, different factors should be

paid close attention to according to IPO’s size when investing. Big size IPOs underwritten by

fewer managing underwriters and small size IPOs backed-up by high state ownership have a

lower delisting risk. For issuers, an underwriter syndicate does not necessarily guarantee the

prospect of an IPO in the context of China’s stock market. Market share is not a reliable

indicator for underwriter reputation either. Lastly, the implication for regulators is that a more

complete and strict delisting mechanism needs to be set in order to promote market efficiency.

ST stocks warned several times by CSRC would long be delisted if they were subject to

regulations in developed markets. Sponsors, who should bear legal liability of an offering,

should play his/her positive role in issuing process as well. CSRC can also set up rules to

forbid the dual roles of investment companies as underwriter and sponsor at the same time.

- 22 -

References

Akerlof, G. (1970) ‘The market for ‘lemons’: quality uncertainty and the market mechanism’, The Quarterly Journal of Economics, 84 (3), pp.488-500.

Audretsch, D.B. (1991), “New firm survival and the technological regime”, Review of Economics and Statistics, 60(3), pp.441-450.

Beneda, N. (2007) ‘Performance and distress indicators of new public companies’, Journal of Asset Management 8, pp.24–33.

Booth, J. & Smith, R. (1986) ‘Capital raising, underwriting and the certification hypothesis’,

Journal of Financial Economics, 15, pp.261—281.

Cao, Z (2010) ChiNext delisting may not be as direct as planned, Shenzhen Daily [Online] Available from: http://www.szdaily.com/content/2010-11/04/content_5054644.htm (Accessed: April 25th, 2012)

Carter, R. & Dark, F. (1993) ‘Underwriter reputation and initial public offers: The detrimental effects of flippers’, Financial Review, 28 pp.279-301.

Carter, R., Dark, F. & Singh, A. (1998) ‘Underwriter reputation, initial returns, and the long-run performance of IPO shares’, Journal of Finance, 53, pp.285-311.

Carter, R. & Manaster, S. (1990) ‘Initial public offerings and underwriter reputation’, Journal of Finance, 45, pp.1045-1067.

Chemmanur, T. & Fulghieri, P. (1994) ‘Investment bank reputation, information production, and financial intermediation’, Journal of Finance, 49 (1), pp.57-79.

Coleman, J. (1988) ‘Social capital in the creation of human capital’, American Journal of Sociology, 94, pp.95-121.

Corwin, S. & Schultz, P. (2005) ‘The role of IPO underwriting syndicates: pricing, information production, and underwriter competition’, Journal of Finance 60, pp.443-486.

Dong, M., Michel, J. & Pandes, J. (2011) ‘Underwriter Quality and Long-Run IPO Performance’, Financial Management, Spring 2011, pp.219 – 251.

EI Hennawy, R.H.A and Morris, R.C. (1983), “The significance of base year in developing failure prediction models”, Journal of Business Finance & Accounting, 10(2), pp.209-223.

Ellis, K., Michaely, R. & O'Hara, M. (2000) ‘When the underwriter is the market maker: An examination of trading in the IPO aftermarket’, Journal of Finance, 55, pp.1039-1074.

Fischer, H.M. and Pollock, T.G. (2004), “Effects of social capital and power on surviving transformational change: The case of initial public offerings”, Academy of Management Journal, 47(4), pp. 463-481.

Green, W., Czernkowski, R. & Wang, Y. (2009) ‘Special treatment regulation in China: potential unintended consequences’, Asian Review of Accounting, 17(3), pp.198-211.

- 23 -

Grinblatt, M. & Hwang, C. (1989) ‘Signalling and the pricing of new issues’, Journal of Finance 44, pp.393-420.

Herfindahl, O. (1950) ‘Concentration in the U.S. steel industry’, unpublished doctoral dissertation, Columbia University.

Husick, G. & Arrington, J. (1998) The initial public offering: A practical guide for executives. New York: Bowne & Co.

Hu, X. (2011) China’s FDI reaches its record new, Jinghua Daily [in Chinese] [Online] Available from: http://epaper.jinghua.cn/html/2011-01/19/content_624416.html (Accessed: April 25th, 2012)

Jain, B.A. and Kini, O. (2000), “Does the presence of venture capitalists improve the survival profile of IPO firms? ”, Journal of Business Finance and Accounting, 27(9/10), pp. 1139-1176

Jin, X., Wu, S. & Chen, D. (2003) ‘Underwriter reputation, IPO quality and issue innovation in China’, research from Haitong Securities Co.,Ltd. [in Chinese]

Klein, B. & Leffler, K. (1981) ‘The role of market forces in assuring contractual performance’, Journal of Political Economy 89, pp.615-641.

Logue, D., Rogalski, R., Seward, J. & Foster-Johnson, L. (2002) ‘What is special about the roles of underwriter reputation and market activities in initial public offerings?’, Journal of Business, 75 (2), pp. 213-243.

Liu, J., Yin, B. & Yi, X. (2005) ‘An empirical study on underwriter reputation and IPO quality in China’, Finance and Trade Economics, 3. [in Chinese]

Ma, J., Song, F. & Yang, Z. (2010) ‘The dual role of the government: securities market regulation in China 1980-2007’, Journal of Financial Regulation and Compliance, 18, pp.158-177.

Megginson, W. & Weiss, K. (1991) ‘Venture capitalist certification in initial public offerings’, Journal of Finance, 46, pp.879-904.

Michaely, R. & Shaw, W. (1994) ‘The pricing of initial public offerings: tests of adverse-selection and signaling theories’, The Review of Financial Studies, 7 (2), pp.279-319.

Podolny, J. 1994, ‘Market uncertainty and the social character of economic exchange’, Administrative Science Quarterly, 39, pp.458-483.

Pollock, T., Porac, J. & Wade, J. (2004) ‘Constructing deal networks: Brokers as network ‘architects’ in the U.S. IPO market and other examples’ Academy of Management Review, 29, pp.50-72.

Ritter, J. (1984) ‘The ‘hot’ issue market of 1980’, Journal of Business, 57, pp.215–240.

Ritter, J. (1991) ‘The long run performance of initial public offerings’, Journal of Finance, 46, pp.3-27.

- 24 -

Rock, K. (1986) ‘Why new issues are underpriced’, Journal of Financial Economics 15, pp.187-212.

Securities Daily (2012) The implication of Shanghai index returning to 10- year-ago’s performance [Online] Available from: http://www.foundersc.com/financialComm/12/01/31/5K14944668FS.shtml (Accessed: April 25th, 2012) [in Chinese]

Welch, I. (1989) ‘Seasoned offerings, imitation costs and the underpricing of initial public offerings’, Journal of Finance 44, pp.421-449.

Xiao, H. (2012) ‘IPOs rejected by underwriters’, Securities Daily [Online]. Available from: http://www.ccstock.cn/ipo/xingupinglun/2012-02-01/A689416.html (Accessed: March 19th, 2012) [in Chinese]

Yin, H. (2010) ‘Underwriter reputation and IPO quality under sponsor mechanism’,

Reformation and Strategy, 8(Cumulatively,NO.204) [in Chinese]

Yin, X. & Lin, C. (2011) China ranked 6th in global gold reserve [Online] Available from: http://finance.ifeng.com/news/hqcj/20110815/4395030.shtml (Accessed: April 25th, 2012) [in Chinese]

Zhang, L., Chen, S., Yen, J., Altman, E. & Heine, M. (n.d.) ‘Corporate financial distress diagnosis in China’, supported by Natural Science Foundation of China (NSFC)-Project (70172018).

* Market share of China’s top 20 underwriters in 2006 published by Securities Association in China (SAC) is available from: http://www.sac.net.cn/hysj/zqgsjysj/200704/t20070409_11408.html (Accessed: 10 August 2012) [in Chinese]

* Corporate classification published by China Securities Regulatory Commission (CSRC) in 2010 is available from: http://www.csrc.gov.cn/pub/zjhpublic/G00306205/201007/t20100714_182487.htm (Accessed: 10 August 2012) [in Chinese]

- 25 -

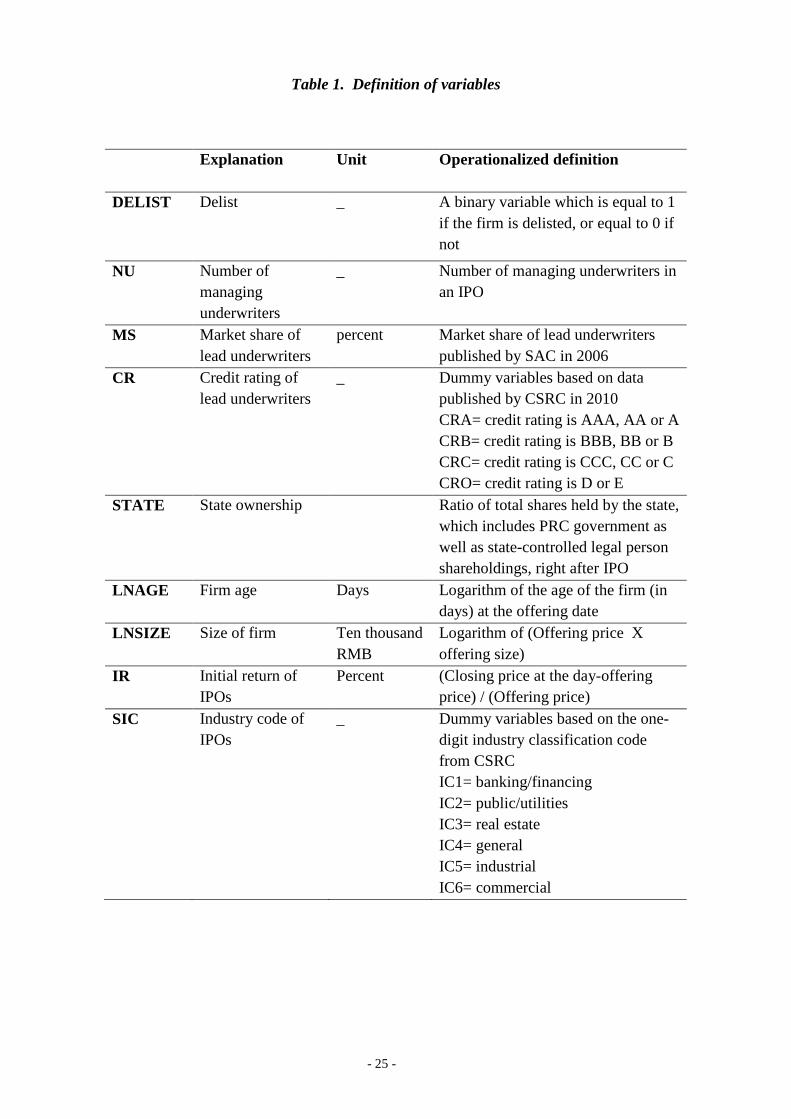

Table 1. Definition of variables

Explanation Unit Operationalized definition

DELIST Delist _ A binary variable which is equal to 1 if the firm is delisted, or equal to 0 if not

NU Number of managing underwriters

_ Number of managing underwriters in an IPO

MS Market share of lead underwriters

percent Market share of lead underwriters published by SAC in 2006

CR Credit rating of lead underwriters

_ Dummy variables based on data published by CSRC in 2010 CRA= credit rating is AAA, AA or A CRB= credit rating is BBB, BB or B CRC= credit rating is CCC, CC or C CRO= credit rating is D or E

STATE State ownership Ratio of total shares held by the state, which includes PRC government as well as state-controlled legal person shareholdings, right after IPO

LNAGE Firm age Days Logarithm of the age of the firm (in days) at the offering date

LNSIZE Size of firm Ten thousand RMB

Logarithm of (Offering price X offering size)

IR Initial return of IPOs

Percent (Closing price at the day-offering price) / (Offering price)

SIC Industry code of IPOs

_ Dummy variables based on the one-digit industry classification code from CSRC IC1= banking/financing IC2= public/utilities IC3= real estate IC4= general IC5= industrial IC6= commercial

Table 2. Summary statistics for the sample (N=1376)

Panel A.

Continuous Variable Mean Std. Dev. Min Max NU 5.44 4.40 1.00 44.00 MS 3.40 5.66 0.00 27.33 STATE 0.42 0.27 0.00 0.94 IR 3.02 15.07 -0.80 338.70 AGE 1023.72 981.01 2.00 5488.00 SIZE 38689.81 75788.77 40.00 1181600.00

Panel B.

Dummy variable Total % of total IPOs DELIST 69 5.0% CRA 943 68.5% CRB 67 4.9% CRC 1 0.1% CRO 365 26.5%

Subtotal 1376 100.0% IC1 9 0.7% IC2 147 10.7% IC3 72 5.2% IC4 122 8.9% IC5 923 67.1% IC6 103 7.5%

Subtotal 1376 100.0%

Table 3. Table of correlations (N=1376)

NU MS CRA CRB CRC CRO STATE IR IC1 IC2 IC3 IC4 IC5 IC6 LNAGE LNSIZE

NU 1

MS 0.16 1

CRA 0.12 0.41 1

CRB 0.00 -0.13 -0.33 1

CRC -0.02 -0.02 -0.04 -0.01 1

CRO -0.12 -0.36 -0.89 -0.14 -0.02 1

STATE 0.19 0.16 0.08 -0.04 -0.01 -0.06 1

IR -0.12 -0.03 -0.04 0.00 -0.01 0.04 -0.03 1

IC1 0.12 0.01 -0.02 -0.02 0.00 0.03 -0.03 -0.01 1

IC2 0.06 0.08 -0.02 -0.01 -0.01 0.03 0.01 -0.02 -0.03 1

IC3 -0.01 -0.05 -0.02 0.02 -0.01 0.01 0.00 0.00 -0.02 -0.08 1

IC4 -0.09 -0.06 -0.05 0.02 -0.01 0.04 -0.16 0.06 -0.03 -0.11 -0.07 1

IC5 0.05 0.02 0.06 -0.01 0.02 -0.07 0.10 -0.02 -0.12 -0.49 -0.34 -0.45 1

IC6 -0.09 -0.03 -0.01 -0.01 -0.01 0.02 -0.01 0.00 -0.02 -0.10 -0.07 -0.09 -0.41 1

LNAGE -0.04 -0.05 0.03 0.02 0.02 -0.05 -0.32 0.09 0.05 0.00 0.01 0.06 -0.07 0.03 1

LNSIZE 0.62 0.19 0.20 0.00 0.00 -0.21 0.23 -0.39 0.07 0.05 -0.04 -0.15 0.13 -0.11 -0.12 1

Table 4. Logit Analysis Results – All IPOs

Independent variable

Expected sign

Model 1 NU only

Model 2 MS only

Model 3 CR only

Model 4 All

Estimate (Chi-square)

Estimate (Chi-square)

Estimate (Chi-square)

Estimate (Chi-square)

Intercept -10.6509 (-0.02)

-12.3541 (-0.01)

-12.4815 (-0.01)

-10.7806 (-0.02)

NU − 0.0800 (2.35)**

0.0800 (2.33)**

MS − 0.0005 (0.02)

0.0105 (0.00)

CRA − -0.1824 (-0.67)

-0.1923 (-0.64)

CRB − -0.7258 (-0.96)

-0.7213 (-0.95)

STATE + -0.7225 (-1.46)

-0.6229 (-1.26)

-0.6230 (-1.27)

-0.7242 (-1.45)

IR -0.0113 (-0.85)

-0.0085 (-0.69)

-0.0081 (-0.66)

-0.0109 (-0.82)

IC2 12.6737 (0.02)

13.0066 (0.01)

13.0662 (0.01)

12.7418 (0.02)

IC3 12.4719 (0.02)

13.8157 (0.01)

12.8818 (0.01)

12.5484 (0.02)

IC4 13.2196 (0.02)

13.5428 (0.01)

13.6143 (0.02)

13.3006 (0.02)

IC5 12.2301 (0.02)

12.5377 (0.01)

12.6095 (0.01)

12.3120 (0.02)

IC6 12.3624 (0.02)

12.6380 (0.01)

12.7021 (0.01)

12.4338 (0.02)

LNAGE − -0.0728 (-1.14)

-0.0683 (-1.07)

-0.0636 (-0.99)

-0.0682 (-1.06)

LNSIZE − -0.4507 (-3.08)***

-0.2729 (-2.26)**

-0.2545 (-2.08)**

-0.4326 (-2.93)***

No. of IPOs 1376 1376 1376 1376

Chi-square for -2 log likelihood ratio

(26.86)*** (22.19)** (23.44)** (28.12)***

Pseudo R2 0.0491 0.0405 0.0428 0.0514

The dependent variable is DELIST. ***, **, * indicate significance level at 0.01, 0.05, and 0.10 respectively. CRO and IC1 are not included because of collinearity.

- 29 -

Table 5. Logit Analysis Results – Big vs. Small IPOs

Independent variable

Expected sign

Model 5 Big IPOs (SIZE > median)

Model 6 Small IPOs (SIZE ≤ median)

Estimate (Chi-square)

Estimate (Chi-square)

Intercept -16.5347 (-0.01)

-14.1214 (-0.02)

NU − 0.0760 (2.36)**

-0.1100 (-1.19)

MS − -0.0220 (-0.60)

-0.0159 (-0.32)

CRA − 1.6909 (1.60)

-0.4814 (-1.31)

CRB − Omitted -0.4095 (-0.53)

STATE + -0.3664 (-0.37)

-1.0567 (-1.70)*

IR -1.0892 (-2.67)***

-0.0082 (-0.52)

IC2 14.0205 (0.01)

12.2134 (0.02)

IC3 Omitted 12.4252 (0.02)

IC4 14.5588 (0.01)

12.7803 (0.02)

IC5 13.6240 (0.01)

11.7240 (0.02)

IC6 14.2410 (0.01)

11.7239 (0.02)

LNAGE − -0.3026 (-2.60)***

0.0874 (0.97)

LNSIZE Not included in the model

Not included in the model

No. of IPOs 619 = 688-69 688

Chi-square for -2 log likelihood ratio

(27.22)*** (22.41)**

Pseudo R2 0.1484 0.0644

The dependent variable is DELIST. ***, **, * indicate significance level at 0.01, 0.05, and 0.10 respectively. CRO and IC1 are not included because of collinearity. CRB and IC3 are omitted because of estimability in Model 5.