THE EFFECT OF TAX INCENTIVES ON INVESTMENT DECISIONS

39

THE IMPACT OF TAX INCENTIVES ON THE INVESTMENT DECISIONS OF LARGE SCALE PRIVATE INDUSTRIES IN NAKAWA INDUSTRIAL AREA. A CASE STUDY OF SHUMUK INDUSTRIES LIMITED . GODFREY BIMANYWARUGABA 2015 A RESEARCH REPORT SUBMITTED TO THE DEPARTMENT OF ECONOMICS AND STATISTICS IN PARTIAL FULFILMENT OF THE REQUIREMENT FOR THE AWARD OF THE DEGREE OF BACHELOR OF ECONOMICS AND STATISTICS OF KYAMBOGO UNVERSITY. SEPTEMBER, 2013

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of THE EFFECT OF TAX INCENTIVES ON INVESTMENT DECISIONS

THE IMPACT OF TAX INCENTIVES ON THE INVESTMENT DECISIONS OF

LARGE SCALE PRIVATE INDUSTRIES IN NAKAWA INDUSTRIAL AREA.

A CASE STUDY OF SHUMUK INDUSTRIES LIMITED

.

GODFREY BIMANYWARUGABA

2015

A RESEARCH REPORT SUBMITTED TO THE DEPARTMENT OF ECONOMICS AND

STATISTICS IN PARTIAL FULFILMENT OF THE REQUIREMENT FOR THE AWARD

OF THE DEGREE OF BACHELOR OF ECONOMICS AND STATISTICS OF

KYAMBOGO UNVERSITY.

SEPTEMBER, 2013

ii

Table of contents

List of tables ....................................................................................................................................v

List of figures .................................................................................................................................vi

Abstract ........................................................................................................................................viii

CHAPTER ONE..............................................................................................................................1

INTRODUCTION...........................................................................................................................1

1.0 Background to the study ...................................................................................................... 1

1.1 Problem statement ............................................................................................................... 2

1.2 Objectives of the study ........................................................................................................ 3

1.2.1 General objective .......................................................................................................... 3

1.2.2 Specific objectives ........................................................................................................ 3

1.3 Research questions............................................................................................................... 3

1.4 Scope of the study.............................................................................................................. 4

1.5 Significance of the study ..................................................................................................... 4

1.6 Justification for the study.................................................................................................... 4

1.7 Operation definitions ........................................................................................................... 5

1.7.1 Tax incentives ............................................................................................................... 5

1.7.2 Large scale private industries........................................................................................ 5

1.7.3 Investment ..................................................................................................................... 5

CHAPTER TWO.............................................................................................................................6

LITERATURE REVIEW................................................................................................................6

2.0 Introduction.......................................................................................................................... 6

2.1 Types of tax incentives in large scale private organizations ............................................... 6

2.1.1 Tax holidays .................................................................................................................. 6

iii

2.1.2 Tax discounts ................................................................................................................ 6

2.1.3 Tax exemptions. ............................................................................................................ 7

2.2 Tax incentive contribution on human capital investment decisions.................................... 8

2.3 Tax incentive contribution on inventory capital investment decisions ............................... 8

2.4 Tax incentive contribution on gross investment levels........................................................ 9

CHAPTER THREE.......................................................................................................................10

METHODOLOGY........................................................................................................................10

3.0 Introduction........................................................................................................................ 10

3.1 Research Design ................................................................................................................ 10

3.2 Area and population of study............................................................................................. 10

3.3 Sample selection ................................................................................................................ 10

3.4 Data types and sources....................................................................................................... 11

3.5 Data collection methods .................................................................................................... 11

3.5.1 Use of interviews ........................................................................................................ 11

3.5.2 Observation ................................................................................................................. 11

3.6 Data analysis...................................................................................................................... 11

3.7 Limitations to the study. .................................................................................................... 12

CHAPTER FOUR .........................................................................................................................13

PRESENTATION AND DISCUSSION OF FINDINGS .............................................................13

4.0 Introduction........................................................................................................................ 13

4.1 Background characteristics of the respondents.................................................................. 13

4.2 Various tax incentives enjoyed by Shumuk....................................................................... 17

4.3 Impact of tax incentives on Human capital investment decision ...................................... 18

4.4 Impact of tax incentives on inventory investment decision............................................... 20

4.5 Impact of tax incentives on Gross investment decision..................................................... 21

iv

CHAPTER FIVE...........................................................................................................................24

SUMMARY OF RESULTS, CONCLUSION AND RECOMMENDATIONS...........................24

5.0 Introduction........................................................................................................................ 24

5.1 Summary of results ............................................................................................................ 24

5.1.1 Various tax incentives ................................................................................................. 24

5.1.2 Tax incentives and human capital investment decision. ............................................. 24

5.1.4 Tax incentives and inventory investment decision ..................................................... 24

5.1.5 Tax incentives and gross investment decision. ........................................................... 24

5.2 Conclusion ......................................................................................................................... 25

5.3 Recommendations.............................................................................................................. 26

REFERENCES..............................................................................................................................27

Appendix A: Questionnaire...........................................................................................................28

v

List of tables

Table 4.3.1: Recruitment rate and tax incentives ........................................................................ 18

Table 4.3.2: Rate of training workers and tax incentives ............................................................ 18

Table 4.3.3: Rate of productivity of workers and tax incentives ................................................ 19

Table 4.3.4: Current state of Welfare of workers and tax incentives .......................................... 19

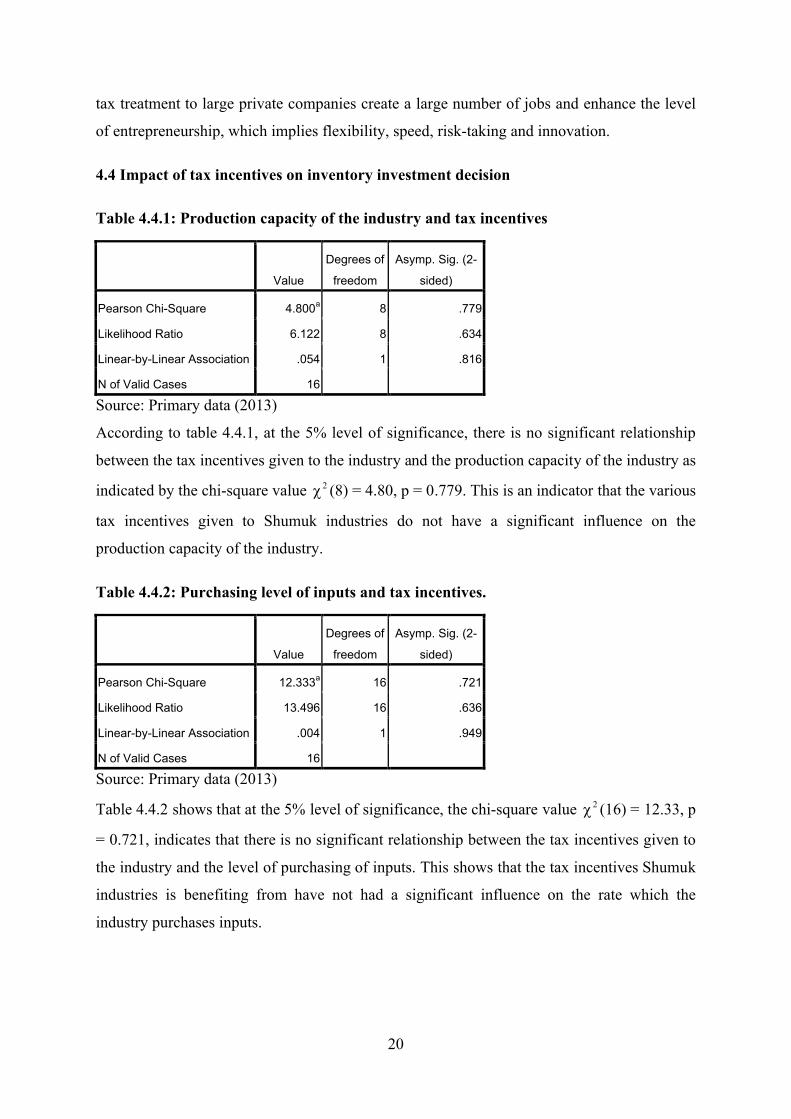

Table 4.4.1: Production capacity of the industry and tax incentives........................................... 20

Table 4.4.2: Purchasing level of inputs and tax incentives. ........................................................ 20

Table 4.4.3: Inventory level and tax incentives........................................................................... 21

Table 4.5.1: Rate of finance distribution to departments and tax incentives. ............................. 21

Table 4.5.2: Salary payment rate and tax incentives. .................................................................. 22

Table 4.5.3: Rate of auditing financial books and tax incentives................................................ 22

Table 4.5.4: Ratio of output to GDP and tax incentives.............................................................. 23

vi

List of figures

Figure 4.1.1: Gender distribution of the respondents .................................................................. 13

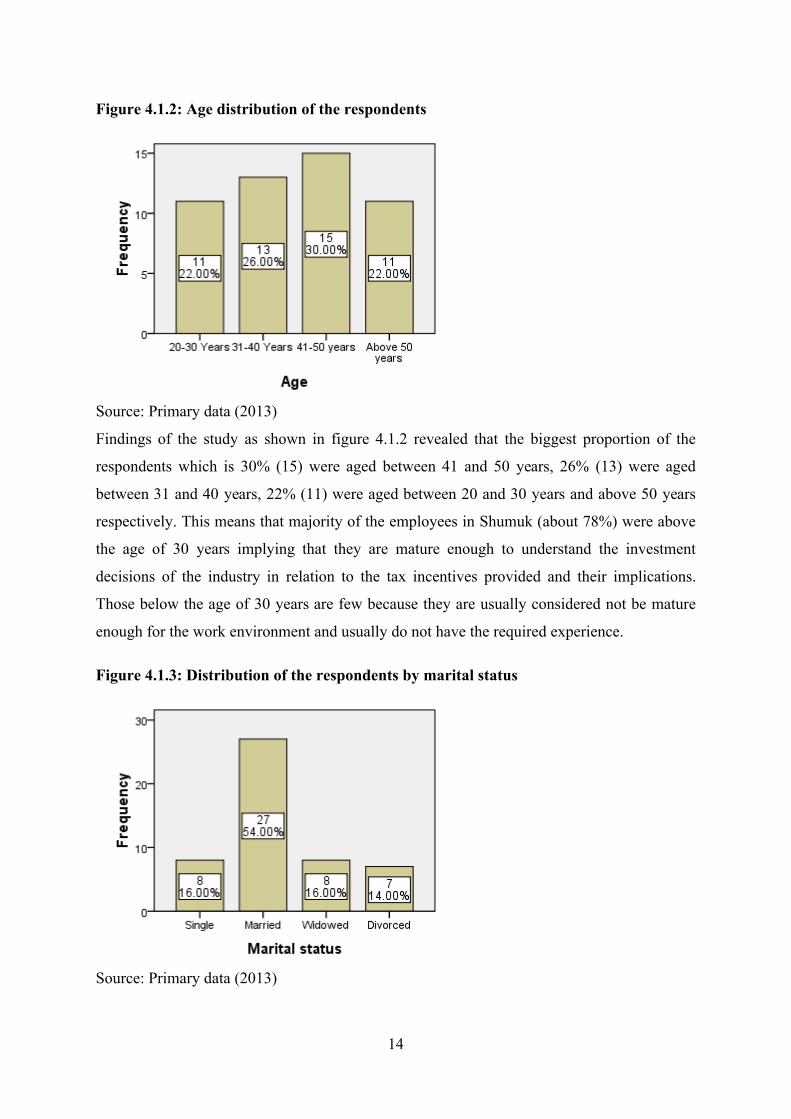

Figure 4.1.2: Age distribution of the respondents ....................................................................... 14

Figure 4.1.3: Distribution of the respondents by marital status .................................................. 14

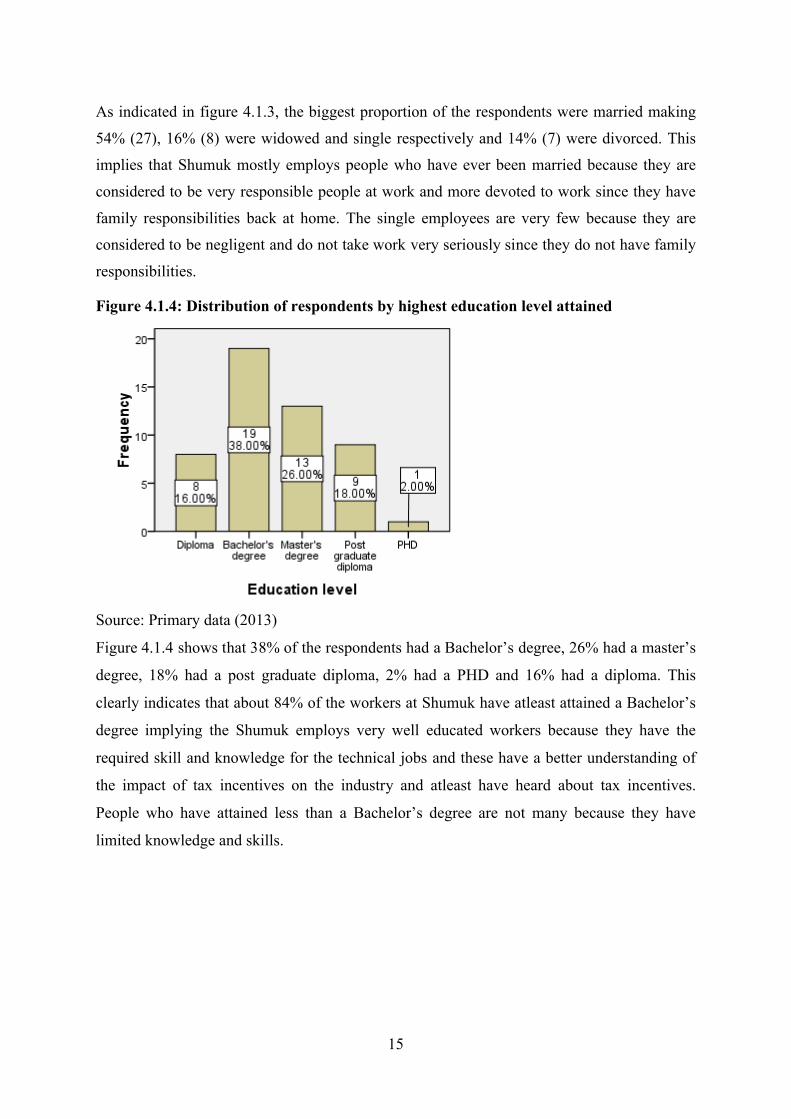

Figure 4.1.4: Distribution of respondents by highest education level attained ........................... 15

Figure 4.1.5: Distribution of respondents by period worked in company................................... 16

Figure 4.2.1: Tax incentives given to the industry ...................................................................... 17

vii

List of abbreviations

CIT Corporate Income Tax

EPRC Economic Policy Research Centre

FDI Foreign Direct Investment

GDP Gross Domestic Product

IMF International Monetary Fund

OECD Organisation for Economic Co-operation and Development

UNCTAD United Nations Conference on Trade and Development

URA Uganda Revenue Authority

VAT Value Added Tax

viii

Abstract

A tax incentive is a deduction, exclusion or exemption from a tax liability, offered as an

enticement to engage in a specified activity such as investment in capital goods for a certain

period. In Uganda, a number of tax incentives are given to investors both foreign and local so as

to encourage investment in an effort to create jobs and enhance economic growth. The study

was carried out to assess the impact of tax incentives on the investment decisions of large scale

private manufacturing industries in Nakawa industrial area.

The objectives of the study were to identify the various tax incentives offered to Shumuk

industries in Nakawa industrial area, to assess the tax incentive contribution on human capital

investment decisions of Shumuk industries in Nakawa industrial area, to assess the tax incentive

contribution on inventory capital investment decisions of Shumuk industries in Nakawa

industrial area and to assess the tax incentive contribution on gross investment levels of Shumuk

industries in Nakawa industrial area.

Primary data was collected using an interview guide and observation methods from a sample of

50 employees in the different departments at Shumuk selected using cluster and simple random

sampling techniques. Data analysis was done in SPSS to generate descriptive statistics

describing the variables of interest.

The findings of the study reveal that Shumuk receives tax incentives in form of withholding, tax

discounts and tax exemptions. These tax incentives have no significant impact on the

investment decisions at Shumuk industries as regards human capital investment, inventory

investment and gross investment. The other factors that influence investment decision are the

Bank lending rates, tax levels in the economy and the availability of raw materials.

According to the findings of the study, recommendations were made as follows: Government

should also advocate for reduced commercial bank lending rates to investors so as to encourage

more investments and The government of Uganda should give more tax incentives to both the

new and already existing investors through giving tax holidays, tax exemptions and tax

discounts so as to encourage investment in the country.

1

CHAPTER ONE

INTRODUCTION

This section presents the background to the study, statement of the problem, objectives of the

study, the scope of the study, justification of the study and significance of the study.

1.0 Background to the study

A tax incentive is a deduction, exclusion or exemption from a tax liability, offered as an

enticement to engage in a specified activity such as investment in capital goods for a certain

period (Feibel, 2012).

A multiplicity of tax incentives exist including; tax holidays, reduction on CIT (corporate

income tax) rate for certain sectors, exemption of CIT(corporate income tax) for export

companies, accelerated capital (investment) allowances; Buildings facilitates investment in

new equipment and machinery Could result in excessive investment (e.g. unutilized buildings);

Plant and machinery, investment tax credits, location based incentives, reduced taxes on

dividends tax-shifting and interests paid abroad, preferential treatment of long term, deductions

for qualifying; expenses transfer of technology if considered with other measures major capital

gains including; training expenses, export marketing expenses, exemptions from indirect taxes

(VAT, import tariffs), Export processing zones (OECD, 2001), (United Nations, 2000),

(Fletcher, 2002).

Every country strives for private investors. They create jobs, increase production and exports

and pay taxes. However, (Walubiri, 2012) notes that the investment climate in Uganda

currently has become very competitive in that investors not waived from or some whose tax

components have not been reduced face high competition. In line with the above, (Manson,

2011) observes that from meat packers and cement makers to banks and hotels, Uganda

exempts more than 1,200 businesses from certain taxes. The various large scale private

industries in various parts of Kampala (Nakawa inclusive) including; Picfare Industries

Limited, Quality Chemicals, Roofing's Rolling Mills, Bidco Uganda Limited, Sameer

Agriculture and Livestock, Southern Range Nyanza Ltd and Shumuk Industries limited are

beneficiaries of tax incentives (Walubiri, 2012).

There is a continuous increment in the Foreign Direct Investments (Private Investments) in

Kampala which are mostly concentrated in Nakawa division despite the relatively few

incentives offered to the private large scale investors. As (UNCTAD, 2011) further notes, the

following figures showing FDI including their years were observed; 644 US$ million in

2

2006, 792 US$ million in 2007, 729 US$ million in 2008, 816 US$ million in 2009 and 848

US$ million in 2010. This shows that tax incentives have had more less no effect on the gross

investments more so decision making pertaining investment of large private industries. The

high investments were mainly attributed to the precious market, urbanization,

industrialization and political stability to mention but a few but not tax incentives. This is

further avowed by (Walubiri, 2012) which while quoting a World Bank report asserts that

over 92% of investors in Uganda currently enjoying tax incentives can invest their capital

even without these incentives. And as a result, the report notes that Uganda lost

approximately 2% of its GDP in potential tax revenue amounting to US$ 272m in financial

year 2009/10.

With vast tax incentive arrangements that have come under the spotlight, IMF calls for

Uganda to eliminate tax exemptions in its latest report at the end of June. In Uganda’s budget

2010/2011, it was shown that tax exemptions on hoes, kerosene sugar excise duty were

granted to some of the agricultural, petroleum and sugar large scale private industries in

Kampala (Nakawa) inclusive. Despite these incentives, pump prices were still high, however,

and headline inflation stood at 15.8 percent in that year to June. “The exemptions list is too

huge: to raise tax the single most important thing they can do is to reduce exemptions,” said

Governor Mutebile Tumusime. The high inflation was a discouraging factor to the investing

ability of any private large scale investor, in other words, IMF to some extent attributed the

deteriorated economic environment of Uganda to the many existing tax incentives, that tax

incentives had done more harm than good, including the reduction of investment (Manson,

2011). The study seeks to examine the impacts of tax incentives on the investment decisions

of large scale private industries in Nakawa.

1.1 Problem statement

Tax incentives are a very effective tool of attracting private investors. (Feibel, 2012)

observes that tax exemptions and incentives are given to about 300, mostly elite and well-

funded private investors in Nakawa division. As observed by (Byensi, 2011), most of the

large scale private industries in Uganda more so in Kampala (especially Nakawa) today

have in one way or the other benefited from tax incentives. They give them enough time to

get used to the economy and later start paying taxes. To be more specific, amidst the various

private industries in Nakawa division in Kampala, it has been observed by different scholars

including; (Manson, 2011)); (Mwesigwa, 2012); (Walubiri, 2012) and (Mayende, 2012) that

tax incentives like tax holidays, exemptions and discounts granted to some of these large

3

scale private industries have reduced their gross investment, human capital investment (used

more machines than labor and increased their inventory investment. (IMF, 2012) together

with (Feibel, 2012) conclusively note that tax incentives are one of the least important

impact ants in the investment decisions of large scale private industries in Nakawa. These

two argue that tax incentives have promoted harmful tax competition among the private

industries in the division. Most private industries in Nakawa industrial area Shumuk

industries inclusive can’t ascertain the impact of most tax incentives on their investments

since they are unfair, string attached in other words, they are not transparent to the extent that

some investors would prefer to invest without tax incentives. (Nandala, 2012) observes that

various tax incentives are given to the large scale private investors whose impact to not only

the country but also to investment decisions of private investors is anonymous. Thus the

study seeks to assess the impact of tax incentives on the investment decisions of large scale

private industries in Nakawa

1.2 Objectives of the study

1.2.1 General objective

The general objective of the study is to assess the impact of tax incentives on the investment

decisions of Shumuk industries in Nakawa industrial area.

1.2.2 Specific objectives

i. To identify the various tax incentives offered to Shumuk industries in Nakawa industrial

area.

ii. To assess the tax incentive contribution on human capital investment decisions of

Shumuk industries in Nakawa industrial area.

iii. To assess the tax incentive contribution on inventory capital investment decisions of

Shumuk industries in Nakawa industrial area.

iv. To assess the tax incentive contribution on gross investment levels of Shumuk industries

in Nakawa industrial area.

1.3 Research questions.

i. What are the various tax incentives offered to Shumuk industries in Nakawa industrial

area?

ii. What is the tax incentive contribution on human capital investment decisions of Shumuk

industries in Nakawa industrial area?

4

iii. What is the tax incentive contribution on inventory capital investment decisions of

Shumuk industries in Nakawa industrial area?

iv. What is the tax incentive contribution on gross investment levels of Shumuk industries in

Nakawa industrial area?

1.4 Scope of the study

The research design was conducted with the main interest of the private large scale investors

of Shumuk Aluminium Industries. Shumuk Aluminium Industries Limited (SAIL) originated

from “SHUMUK ENTERPRISES” in 1984. It commenced its business with moderate trading

of commodities with a retail/wholesale outlet on South Street in Uganda in 1984. Shumuk

Aluminium industries limited is located on Plot 24 Mukabya Road, Nakawa industrial area in

Nakawa division.

The main focus of the research was limited to the impact of tax incentives on the investments

decisions of private large scale industries in Nakawa division, Kampala district.

1.5 Significance of the study

i. The study will provide information to the government of Uganda on some of the crucial

effects of tax incentives on investment decision making by private large scale investors

in Nakawa division and thus the study providing a base for them to easily formulate

policies that will be geared towards this either supplementing or removing these tax

incentives.

ii. To the private large scale industries, the study will flaunt the relevance of the tax

incentives in their investment decisions.

iii. The study will also contribute to a pool of knowledge and thus will provide literature

that will cover the existing gaps thus new reference material for use by academicians

and other researchers.

1.6 Justification for the study

The Ugandan government has done a lot of attempts to spur the private investments in

Kampala, more so Nakawa division including provision of tax incentives. Most of the large

scale private investors were lagging to craft investment decisions in Nakawa due to the high

taxes, so the government established tax incentives. A lot of funds of the government have

been lost through the provision of these incentives which funds would have been used

elsewhere to impact the lives of the poor. This sets a baseline for the researcher to ascertain

5

whether the tax incentives have influenced the investment decisions of large scale private

investors in Nakawa.

1.7 Operation definitions

1.7.1 Tax incentives

A tax incentive is a deduction, exclusion or exemption from a tax liability, offered as an

enticement to engage in a specified activity such as investment in capital goods for a certain

period

1.7.2 Large scale private industries

These are large organisations established by private individuals to venture in various

productive activities with the aim of mainly gaining profits.

1.7.3 Investment

Investment is the amount purchased per unit time of goods which are not consumed but are to

be used for future production (i.e. capital).

6

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

In this, a review of the related literature and details of the research about the topic of study

has been done; more literature will be analyzed on the various impacts of tax incentives on

the investment decisions in Shumuk industries specifically analyzing tax incentive

contribution to their human, inventory capital investment decisions and gross investment

levels.

2.1 Types of tax incentives in large scale private organizations

2.1.1 Tax holidays

According to the 1998 firm survey, one third of Ugandan firms in urban sites of Nakawa

were in a tax-loss position in 1997, that is, they never a tax holiday. The 1994 firm survey

among the private large scale industries in Kampala (Nakawa) inclusive suggested that one

strong source of a sense of unfairness in taxes were tax holidays. Although the structure of

tax incentives is changing, the unevenness of tax holidays continues. For example, the 1998

survey, which collected information for three years, found that roughly 35 percent of

respondents reported receiving corporate tax holidays in 1997, while 32 percent reported

receiving them in 1995. Import tax holidays were enjoyed by 16 percent of all firms in 1997

but only by 12 percent three years earlier. This situation is expected to change in the next few

years, given that tax holidays were repealed in 1997. Consistent with the new policy, firms

reported that their tax holidays will expire on average in the year 2000. Despite their

important role as policy instrument, tax holidays do not seem to explain either the probability

that a firm invests, or the level of investment of Ugandan firms in 1996-97. However, if the

practice is that tax-holiday firms do not file their income tax returns at all and hence manage

to claim for the full tax depreciation allowance after the tax holiday ends, then their real

effective tax burden can be much lower than predicted by the standard model (Duanjie Chen,

1999); (Ritva Reinikka, 1999).

2.1.2 Tax discounts

Uganda's tax base remains low and experts warn that this won't sustain the economic growth

that the country craves. Uganda Revenue Authority (URA) had always consistently failed to

7

beat monthly tax collection targets. The tax body collected Shs 474.44bn against a target of

shs 473.08bn in February, 2012, registering a surplus of Shs 1.36bn (Mwesigwa, 2012).

However, as Mwesigwa (2012) further averred, experts warned that these collections were

still low. During a budget consultative meeting held in Kampala recently, donors, who funded

about 25% of the national budget, delivered a joint statement expressing dissatisfaction with

the persistent weaknesses shown by the low domestic revenue mobilization from private

investors in Kampala more so Nakawa. Particularly, the donors cited the practice of granting

ad hoc tax discounts, which not only eroded the revenue base, but also undermined the

efficiency of these private industries.

It was thus from a study by Mwesigwa (2012) that various private industries in Nakawa that

dealt in hand hoes, solar equipment, home utensils, aluminum steels, parts and inputs for the

assembly of refrigerators and freezers, motor vehicles imported in respect to the

transportation of tourists, building materials as well as scholastic materials ,that is, Picfare,

Spear motors, Shumuk industries, Master Industries received huge tax discounts which

fostered their decision making and thus spurred their human capital investment including not

only job training but also provision of free on-job training though this was not reflected in the

level of GDP. It was established by (Mwesigwa, 2012) that tax incentives had a moderate

impact on the level of human capital investment in Kampala (particularly Nakawa).

2.1.3 Tax exemptions.

A study that Uganda’s provision of tax incentives more so exemptions to large scale private

individuals in Kampala (Nakawa inclusive) was behind the colossal competition among the

various large scale private industries in the city. Analysis insinuated that the primary

beneficiaries of Uganda’s tax exemptions were large domestic firms and foreign

multinational companies found in the heart of Kampala city as well as Nakawa such as Spear

Motors and Shumuk industries (Mwesigwa, 2012).

From the regional study by Tax Justice Network, (2012) the tax exemptions on the side of the

large scale private investors created a larger regional market, and meant that firms located in

the neighbourhood of Nakawa division serviced this market. At the same time, however,

Government of Uganda was being tempted to increase tax incentives more so exemptions in

order to attract FDI and, they believed that this would cultivate decision making culture of

private individuals as pertains to investment and would thus increase output, spur inventories

of these private industries as well as their exports. Analysis however unveiled that the

8

provision of tax exemptions across the large scale private industries though fostered the

investment decision making culture through increased output and inventory investment , it

presented harmful tax competition, reduced exports and lead to a “race to the bottom” in the

city.

2.2 Tax incentive contribution on human capital investment decisions

Uganda's tax base remains low and experts warn that this won't sustain the economic growth

that the country craves. Uganda Revenue Authority (URA) had always consistently failed to

beat monthly tax collection targets. The tax body collected Shs 474.44bn against a target of

Shs 473.08bn in February, 2012, registering a surplus of Shs 1.36bn. However, experts warn

that these collections are still low. During a budget consultative meeting held in Kampala

recently, donors, who fund about 25% of the national budget, delivered a joint statement

expressing dissatisfaction with the persistent weaknesses shown by the low domestic revenue

mobilization from private investors in Kampala more so Nakawa. Particularly, the donors

cited the practice of granting ad hoc tax exemptions, which not only eroded the revenue base,

but also undermined the efficiency of these private organizations. From the study, on that

note, showed that various private organizations in Nakawa dealing in hand hoes, solar

equipment, parts and inputs for the assembly of refrigerators and freezers, and motor vehicles

imported in respect to the transportation of tourists, building materials as well as scholastic

materials like Picfare, spear motors, Shumuk industries, Master Industries that received tax

incentives, spurred their human capital investment including not only job training but also

provision of free on-job training though this was not reflected in the level of GDP. Further to

the above, (Alon Mweisgwa, 2012) conclusively inferred that tax incentives had a moderate

impact on the level of human capital investment in Kampala (particularly Nakawa).

2.3 Tax incentive contribution on inventory capital investment decisions

Uganda’s provision of tax incentives more so in Kampala (Nakawa inclusive) was part of the

tax competition among the various private organizations in the city. Analysis insinuated that

the primary beneficiaries of Uganda’s tax exemptions and incentives are large domestic firms

and foreign multinational companies found in the heart of Kampala city as well as Nakawa

such as Spear Motors and Shumuk industries (Mwesigwa, 2012).

From the regional study by Tax Justice Network, the tax incentives on the side of the private

investors created a larger regional market, and meant that firms located in the neighbourhood

of Nakawa division serviced this market. At the same time, however, Government of Uganda

9

was being tempted to increase tax incentives in order to attract FDI and, they believed that

this would, increase output, spur inventories of these private organizations as well as their

exports. Analysis suggested that the provision of tax incentives across the private

organizations though increased the output and inventory investment, presented harmful tax

competition, reduced exports and lead to a “race to the bottom” in the city.

2.4 Tax incentive contribution on gross investment levels

A major tax reform took place in Uganda in 1997. This reform included complete elimination

of new tax holidays in favor of a rate of 30 per cent on company income, with generous

capital allowances for all investors and unlimited loss-carry forward. A zero import duty was

also set on a wide range of capital goods. The elimination of selective incentives also greatly

simplified investment licensing. The main effects of this tax reform were (comparing

averages of three years before and after 1997): an increase of one percentage point in the ratio

of investment to GDP, 70 per cent increase in foreign investment inflows, and a one percent

of GDP increase in tax revenue (Ritva Reinikka, 1999). Every year Uganda sacrificed an

amount equal to nearly twice its entire health budget due to its use of tax incentives such as

tax holidays for foreign businesses. Worse still, research showed that these incentives were

not necessary to attract investments to Uganda since they didn’t not increase the gross

investment of the private organizations which was reflected by the GDP. Government needs

to remove excessive tax incentives, promote transparency on the tax incentives they give, and

coordinate with the East African Community to avoid harmful tax competition (Reinikka,

1999).

10

CHAPTER THREE

METHODOLOGY

3.0 Introduction

This section shows the design methods and techniques of collecting and analyzing data that

were used to achieve the stated objectives. These are; research design, design concepts,

sources of data collection, procedure of data collection, data quality control, data processing

and analysis.

3.1 Research Design

The researcher adopted a descriptive survey study design, where both qualitative and

quantitative descriptive data were used. The researcher’s study consisted of two variables of

interest, the dependent variable which is the investment decision and the independent variable

tax incentives.

3.2 Area and population of study

The study was carried out in Shumuk industries in Nakawa industrial area, Kampala district

in Central Uganda. The study targeted the executives and a few employees from different

departments of Shumuk industries. The executives were precisely those who mainly

participated in the day to day operation decisions Shumuk industries. At some instances,

views from the employees of these private industries were an added advantage as regards to

the accuracy of the data to be collected.

3.3 Sample selection

The researcher used cluster sampling technique. The researcher divided the study area that is,

Shumuk industries into clusters. Since in each cluster (department), there were study units all

having a different characteristic that is, people with different positions in the industry. So

from the sampling frame made of clusters, simple random sampling was done in each cluster

independently. The researcher therefore used cluster sampling as the probability sampling

technique together with a non-probability sampling technique (purposive technique) at some

point in the study, so as to get a sample of 50 respondents.

11

3.4 Data types and sources

The researcher collected data using primary sources.

Primary data was collected from consultations and discussions with executive personnel of

Shumuk industries in the Nakawa industrial area who mainly participated in the day to day

operation decisions of the industry. At some instances, views from the employees of Shumuk

industries were an added advantage as regards to the accuracy of the data that was collected.

This data was efficient in that it offered adequate information as it was centered on the live

events from the field through interviews and also because of the availability of respondents.

3.5 Data collection methods

The researcher employed the use of interviews and the observation method, as instruments

for data collection.

3.5.1 Use of interviews

The interviews were structured and the reliability of information gathered was of high

essence since similar questions were asked to the employers/shareholders/employees and it

gave in-depth information about particular cases of interest to the researcher. However, the

research was limited by the responses given because the respondents assumed that they are

under investigation hence being cautious.

3.5.2 Observation

Through the on field observation of the different categories of respondents, the data in

relation to the impacts of tax incentives to the investment decisions of Shumuk industries in

Nakawa was collected. Attributes such as gender, type of industries were also measured.

3.6 Data analysis

The design that was used to present data was a descriptive survey design and it is justified

because it describes an issue as it exists. The results are in digital form and they were

analyzed using a statistical package called SPSS.

In data analysis, the researcher organized and extracted meaning from the data collected. The

data from respondents were collected, recorded and discussed for the better choice of the

design specifications.

The process of data processing mainly constituted of two major processes and they included;

editing and tabulation;

12

Editing involved crosschecking for errors and omissions in the instruments in order to ensure

accuracy, uniformity and completeness. Here, the researcher ensured that each of the research

instruments is clear, logical and hence achievement of comprehensive responses.

Tabulation was the last stage of data processing where counting and adding of all answers to

particular questions was done for the whole study. It involved allocating individual answers

of individual respondents to particular questions under the guidance of appropriate codes.

Under tabulation, computer packages like EXCEL were used to handle the quantitative data

processing.

The process of data analysis entailed qualitative data analysis and quantitative data analysis.

Qualitative data analysis was applied on qualitative data which of course was not numerical.

This entailed analysis of contents of an interview so as to identify the main themes that

emerged from the responses that were given by the respondents. Codes were assigned to the

main themes and thereafter responses classified under the main themes and finally the themes

and responses were integrated in the report.

Otherwise, for quantitative data, the researcher did not use manual means since the

respondents are many, it would be straining. So the researcher analyzed using computer and

to be more specific, the researcher used SPSS.

3.7 Limitations to the study.

While carrying out the study, the researcher met the following problems.

i. Time limitation. The time allocated for conducting the research and analyzing findings

was not enough to win the deadlines. However the researcher critically did whatever was

possible so that she gave the most reliable and efficient data.

ii. Financial limitation. High research costs were incurred during the course of the research

investigations. However proper budgeting enabled proper executions and spending.

iii. Sudden power costs. Unpredicted load shedding hindered the study arrangements as per

the allocated time. However schedules of the power available were followed.

iv. Non-response errors. The researcher got some non-responses from some of the

respondents but solved this by replacing those who were not available.

13

CHAPTER FOUR

PRESENTATION AND DISCUSSION OF FINDINGS

4.0 Introduction

In this chapter, the results on background characteristics, various tax incentives, the impact of

tax incentives on human capital investment decision, the impact of tax incentives on

inventory investment decision, the impact of tax incentives on gross investment decision and

the general respondent personal views about the impact of tax incentives on investment

decision are presented.

4.1 Background characteristics of the respondents

Figure 4.1.1: Gender distribution of the respondents

Source: Primary data (2013)

According to figure 1, most of the respondents which is 62% (31) were males and 39% (19)

were females. This means that Shumuk employs male workers to a large extent because they

considered to be more energetic and hence guarantee greater productivity in terms of output.

The females are less preferred because they are thought to be less efficient and productive

because they are less energetic and have other responsibilities like looking after their

families.

14

Figure 4.1.2: Age distribution of the respondents

Source: Primary data (2013)

Findings of the study as shown in figure 4.1.2 revealed that the biggest proportion of the

respondents which is 30% (15) were aged between 41 and 50 years, 26% (13) were aged

between 31 and 40 years, 22% (11) were aged between 20 and 30 years and above 50 years

respectively. This means that majority of the employees in Shumuk (about 78%) were above

the age of 30 years implying that they are mature enough to understand the investment

decisions of the industry in relation to the tax incentives provided and their implications.

Those below the age of 30 years are few because they are usually considered not be mature

enough for the work environment and usually do not have the required experience.

Figure 4.1.3: Distribution of the respondents by marital status

Source: Primary data (2013)

15

As indicated in figure 4.1.3, the biggest proportion of the respondents were married making

54% (27), 16% (8) were widowed and single respectively and 14% (7) were divorced. This

implies that Shumuk mostly employs people who have ever been married because they are

considered to be very responsible people at work and more devoted to work since they have

family responsibilities back at home. The single employees are very few because they are

considered to be negligent and do not take work very seriously since they do not have family

responsibilities.

Figure 4.1.4: Distribution of respondents by highest education level attained

Source: Primary data (2013)

Figure 4.1.4 shows that 38% of the respondents had a Bachelor’s degree, 26% had a master’s

degree, 18% had a post graduate diploma, 2% had a PHD and 16% had a diploma. This

clearly indicates that about 84% of the workers at Shumuk have atleast attained a Bachelor’s

degree implying the Shumuk employs very well educated workers because they have the

required skill and knowledge for the technical jobs and these have a better understanding of

the impact of tax incentives on the industry and atleast have heard about tax incentives.

People who have attained less than a Bachelor’s degree are not many because they have

limited knowledge and skills.

16

Figure 4.1.5: Distribution of respondents by period worked in company

Source: Primary data (2013)

The findings of the study in figure 5 show that majority of the respondents which is 60% (30)

had been in the company for over five years, 26% had been in the company for 3-4 years,

10% had been in the company for 2-3 years and 2 % had been in the company for 6 months-

1year and less than 6 months respectively. This implies that majority of the respondents

(about 86%) have been in the company for over 3 years meaning that they were well

experienced and atleast had good information about the company and the effects of tax

incentives on investment decisions in the company. The remaining 14% had been in the

company for less than three years had therefore knew little about the company and the effect

of tax incentives.

17

4.2 Various tax incentives enjoyed by Shumuk

Figure 4.2.1: Tax incentives given to the industry

Source: Primary data (2013)

The findings in figure 4.2.1 show that 34% (17) of the respondents said the company is given

withholding, 30% (15) said the company received tax discounts, 18% (9) said the company

received tax exemptions, 16% (8) said the company received tax holidays and 2% (1) said the

company received tax deferments. This means that Shumuk is receiving mostly withholding

and tax discount incentives therefore pays less taxes which helps it to save and invest the

other part that would be paid in taxes. The findings are in agreement with the findings by

Mwesigwa (2012) where various industries in Nakawa including Shumuk were receiving tax

discounts. The other tax incentives given to Shumuk are tax holidays and tax exemptions

which agrees to the findings by Mwesigwa (2012). Chen (1999) also noted that tax holidays

were being given to large scale private companies in Kampala, Nakawa division inclusive.

18

4.3 Impact of tax incentives on Human capital investment decision

Table 4.3.1: Recruitment rate and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 8.008a 12 .784

Likelihood Ratio 9.645 12 .647

Linear-by-Linear Association .400 1 .527

N of Valid Cases 17

Source: Primary data (2013)

According to table 4.3.1, at the 5% level of significance, there is no significant relationship

between the tax incentives given to the industry and the rate of recruitment of workers at

Shumuk industries at 2 (12) = 8.01, p = 0.784. This implies that the tax incentives given to

Shumuk industries are not playing a significant role in influencing the recruitment of workers

Table 4.3.2: Rate of training workers and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 11.931a 12 .451

Likelihood Ratio 12.592 12 .399

Linear-by-Linear Association .176 1 .675

N of Valid Cases 17

Source: Primary data (2013)

The chi-square value 2 (12) = 11.93, p = 0.451 in table 4.3.2 shows that there is no

significant relationship between the tax incentives given to the industry and the rate of

training of workers at the 5% level of significance. This means that the various tax incentives

given to Shumuk industries have got no influence on the rate at which the workers are being

trained in the industry.

19

Table 4.3.3: Rate of productivity of workers and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 16.843a 12 .156

Likelihood Ratio 19.828 12 .070

Linear-by-Linear Association 1.709 1 .191

N of Valid Cases 17

Source: Primary data (2013)

The findings in table 4.3.3 show that with a chi-square value 2 (12) = 16.84, p = 0.156, there

is no significant relationship between tax incentives given to the industry and the rate of

productivity of workers in the industry at the 5% level of significance. This shows that the tax

incentives given to Shumuk industries do not have any significant impact on the productivity

of workers.

Table 4.3.4: Current state of Welfare of workers and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 10.327a 12 .587

Likelihood Ratio 10.267 12 .593

Linear-by-Linear Association .189 1 .664

N of Valid Cases 17

Source: Primary data (2013)

According to table 4.3.4, the value of the chi-square 2 (12) = 10.33, p = 0.587, indicates that

at the 5% level of significance, there is no significant relationship between the tax incentives

given to the industry and the state of welfare of workers in the industry. This means that the

tax incentives given to Shumuk industries do not play any role in influencing the state of

welfare of workers at the industry.

The findings are in agreement with a study by Joyce (2002) found out that tax incentives have

a statistically significant positive effects on human capital investment especially rate and

growth employment growth through affecting labour market participation decisions. However a

study by Leuven and Oosterbeek, (2004) found that a former Dutch tax incentive aimed at stimulated

training of workers over the age of 40 resulted in the postponement of training but did not increase

total training investments. Chen et al., (2002) also found out that fiscal incentives and preferential

20

tax treatment to large private companies create a large number of jobs and enhance the level

of entrepreneurship, which implies flexibility, speed, risk-taking and innovation.

4.4 Impact of tax incentives on inventory investment decision

Table 4.4.1: Production capacity of the industry and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 4.800a 8 .779

Likelihood Ratio 6.122 8 .634

Linear-by-Linear Association .054 1 .816

N of Valid Cases 16

Source: Primary data (2013)

According to table 4.4.1, at the 5% level of significance, there is no significant relationship

between the tax incentives given to the industry and the production capacity of the industry as

indicated by the chi-square value 2 (8) = 4.80, p = 0.779. This is an indicator that the various

tax incentives given to Shumuk industries do not have a significant influence on the

production capacity of the industry.

Table 4.4.2: Purchasing level of inputs and tax incentives.

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 12.333a 16 .721

Likelihood Ratio 13.496 16 .636

Linear-by-Linear Association .004 1 .949

N of Valid Cases 16

Source: Primary data (2013)

Table 4.4.2 shows that at the 5% level of significance, the chi-square value 2 (16) = 12.33, p

= 0.721, indicates that there is no significant relationship between the tax incentives given to

the industry and the level of purchasing of inputs. This shows that the tax incentives Shumuk

industries is benefiting from have not had a significant influence on the rate which the

industry purchases inputs.

21

Table 4.4.3: Inventory level and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 12.644 12 .395

Likelihood Ratio 14.717 12 .257

Linear-by-Linear Association .993 1 .319

N of Valid Cases 16

Source: Primary data (2013)

According to table 4.4.3, the chi-square value 2 (12) = 12.64, p = 0.395, indicates that at the

5% level of significance there is no significant relationship between the tax incentives

enjoyed by the industry and the inventory level of the industry an indicator that the tax

incentives do not have a significant impact on the level of inventory at Shumuk industries.

The findings agree with the findings by and Pirnia (2001) who noted that in Europe when

firms are given tax incentives, they save large sums of money which they use to purchase

more inputs and expand their scale of production. A similar study in India by OECD (2001)

noted that when tax incentives are given to manufacturing companies, they stock large

amounts of raw material to use over a long period of time.

4.5 Impact of tax incentives on Gross investment decision

Table 4.5.1: Rate of finance distribution to departments and tax incentives.

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 7.782 12 .802

Likelihood Ratio 9.172 12 .688

Linear-by-Linear Association .231 1 .630

N of Valid Cases 17

Source: Primary data (2013)

According to table 4.5.1, the findings of the study show that there is no significant

relationship between the tax incentives given to Shumuk industries and the rate of financial

distribution to the departments at Shumuk at the 5% level of significance basing on the chi-

square value 2 (12) = 7.78, p = 0.802. This implies that the tax incentives from which

22

Shumuk industries benefits do not play any significant role in decisions involving the

distribution of finances to the different departments.

Table 4.5.2: Salary payment rate and tax incentives.

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 22.029a 12 .037

Likelihood Ratio 12.991 12 .370

Linear-by-Linear Association 2.196 1 .138

N of Valid Cases 17

Source: Primary data (2013)

The chi-square value 2 (12) = 22.03, p = 0.037 in table 4.5.2 shows that there is a significant

relationship between the tax incentives given to Shumuk industries and the salary payment

rate in Shumuk industries at the 5% level of significance. This means that the benefits from

the tax incentives given to Shumuk industries are having an influence on the rate at which

workers at Shumuk are paid.

Table 4.5.3: Rate of auditing financial books and tax incentives

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 11.657a 12 .474

Likelihood Ratio 10.160 12 .602

Linear-by-Linear Association .393 1 .531

N of Valid Cases 17

Source: Primary data (2013)

Table 4.5.3 shows that basing on the chi-square value 2 (12) = 11.66, p = 0.474, at the 5%

level of significance, there is no significant relationship between the tax incentives given to

Shumuk industries and the rate at which financial books are audited. This implies that the tax

incentives given to Shumuk industries have no significant impact on the rate at which

financial books are audited.

23

Table 4.5.4: Ratio of output to GDP and tax incentives.

Value

Degrees of

freedom

Asymp. Sig. (2-

sided)

Pearson Chi-Square 13.331 12 .345

Likelihood Ratio 13.049 12 .365

Linear-by-Linear Association .537 1 .464

N of Valid Cases 17

Source: Primary data (2013)

According to table 4.5.4, the chi-square value 2 (12) = 13.33, p = 0.345, shows that there is

no significant relationship between the tax incentives given to the industry and the ratio of

out of the industry to GDP at the 5% level of significance. This means that the tax incentives

enjoyed by Shumuk industries does not have any significant impact on the ratio of the output

of the industry to the GDP of the country.

In line with these findings are the findings by Nathan, (2004) who found out that tax

incentives clearly enhance returns on investment; they may be justified by positive

externalities stemming from investments; they are relatively easy to target and fine tune; they

signal openness to private investment; they are useful in a world of capital mobility; they are

necessary for responding to tax competition from other jurisdictions; and they compensate for

other deficiencies in the investment climate. Wells, (1986) also found that tax incentives

given to large companies enable these companies to expand their investments thus increasing

output. He also found that multination corporations decide to invest in foreign countries by

comparing the tax incentives across nations.

24

CHAPTER FIVE

SUMMARY OF RESULTS, CONCLUSION AND RECOMMENDATIONS

5.0 Introduction

In this chapter the summary of results as regards the various tax incentives, the effect of tax

incentives on the investment decisions of the industry and the conclusions and

recommendations made are presented.

5.1 Summary of results

5.1.1 Various tax incentives

All the respondents in the study had heard about tax incentives which included tax holidays,

tax exemptions, tax discounts and withholding tax. All respondents said the industry was a

beneficiary of tax incentives benefiting majorly from withholding tax and tax discounts.

5.1.2 Tax incentives and human capital investment decision.

The study established that tax there is no significant relationship between the tax incentives

and the recruitment rate of employees ( 2 (12) = 8.01, p = 0.784), rate of training workers

( 2 (12) = 11.93, p = 0.451), productivity of workers ( 2 (12) = 16.84, p = 0.156) and the

state of welfare of the workers ( 2 (12) = 10.33, p = 0.587).

5.1.4 Tax incentives and inventory investment decision

The findings of the study show that there is no significant relationship between tax incentives

given to the industry and the production capacity of the industry ( 2 (8) = 4.80, p = 0.779),

purchasing level of inputs ( 2 (16) = 12.33, p = 0.721) and inventory level of the industry

( 2 (12) = 12.64, p = 0.395).

5.1.5 Tax incentives and gross investment decision.

There is a significant relationship between tax incentives and the salary payment rate to

workers ( 2 (12) = 22.03, p = 0.037), and there was no significant relationship between the

tax incentives and the rate of finance distribution to departments ( 2 (12) = 7.78, p = 0.802),

25

the rate at which financial books are audited ( 2 (12) = 11.66, p = 0.474) and the ratio of

output of the industry to national output ( 2 (12) = 13.33, p = 0.345).

5.2 Conclusion

According to the study, the following conclusions were made;

Tax incentives do not significantly affect the human capital investments of large scale private

industries since there is no significant relationship between the tax incentives given to

Shumuk industries and the components of human investment decisions.

Tax incentives do not significantly affect the inventory investment decisions of large scale

private industries since there is no relationship between the tax incentives given to the

industry and the different components of the inventory investment decisions.

Tax incentives affect the gross investment decision to a small extent since there was only a

significant relationship between the salary payment rate to workers and there was no

significant relationship between the tax incentives and the rate of finance distribution to

departments, the rate at which financial books are audited and the ratio of output of the

industry to national output.

Generally, tax incentives do not significantly affect the investment decisions of large scale

private scale industries in Nakawa.

26

5.3 Recommendations.

Basing on the findings of the study, the following recommendations were made;

i. The private large scale industries should also use the benefits of tax holidays to

benefit the economy through re-investing the savings and expanding businesses and

expanding their scales of production to enhance economic growth and development.

ii. Large scale private industries should try to inform their employees of the benefits of

tax incentives through meetings and involving them in decision making so that they

are aware of the benefits because in this study most of them were undecided about

some issues implying they were not sure.

iii. Government should also advocate for reduced commercial bank lending rates to

investors so as to encourage more investments. This could be achieved throught he

central bank reducing the interbank lending rates that result in reduced lending rates

to the public.

27

REFERENCES

"http://www.taxjusticeafrica.net/sites/all/themes/simple_custom/favicon.ico"

Chen, D., F. C. Lee and J. Mintz (2002), Taxation, SMEs and Entrepreneuship, STI Working

Paper 2002/9, OECD, Paris.

Duanjie Chen & Ritva Reinikka (1999) “Business Taxation in a Low-Revenue Economy: A

Study on Uganda in Comparison With Neighbouring Countries” Africa Region Working

Paper June Series No. 3

Gujarati, (2004). Basic Econometrics, 4th edition, The McGraw−Hill Companies.

IMF (2012) “Uganda’s Macroeconomic Outlook in Global Perspective June” Budget 2012/13

Vol 1. No. 1 pp27.

Manson, 2011 “IMF criticises Uganda’s extensive tax breaks” The Financial Times Limited

press.

Mayende Stephen, (2012) “Effects of tax incentives on firms and tax efforts in Uganda” pdf

statistical abstract.

Mweisgwa Alon, (2012) “Experts warn against tax incentives”: Business- The Observer

Tuesday, 03 April 2012

Nandala Mafabi, (2012) “A race to the bottom? Tax Incentives” Kampala blog- Action aid

OECD (2001), “Corporate Tax Incentives for Foreign Direct Investment ”; OECD Tax Policy

Studies No. 4.

OECD (2007) “Tax Incentives for Investment – A Global Perspective: experiences in MENA

and non-MENA countries” Draft Version June 2007

Rajul Awasthi, (2012) “How effective is the tax incentive regime in Uganda”: Business- The

Observer- Tuesday, 03 July 2012

Tax Justice Network - Africa, (2012). “Country Tax Reports”

Tax Justice Network-Africa & Action Aid International, (2012) “Tax competition in East

Africa: A race to the bottom?” Tax incentives and Revenue losses in Uganda- Action aid

Walubiri Moses, (2012) “MPs, Kasami Clash over Tax Incentives to Investors” The New

vision, 29th August 2012.

Wells L., (1986.) “Investment Incentives: An unnecessary Debate”, CTC Reporter, autumn,

28

Appendix A: Questionnaire

Dear respondent, Iam Ainembabazi Racheal a final year student of Bachelor of Economics

and Statistics. As part of the mentioned course, Iam carrying out an academic study assessing

the impact tax incentives on investment decisions on large scale private industries in Nakawa

industrial area with a case study of SHUMUK industries limited. For the same reason, all the

information provided will be strictly academic and will not be disclosed to any third party for

whatsoever reason. Please tick or fill in where necessary.

SECTION A: BIO DATA

1. Gender of the respondent. A. Male B. Female

2. Age of the respondent (in years).

A. Below 20 B. 20-30 C. 31-40 D. 41-50 E. Above 50

3. Marital status of the respondent.

A. Single B. Married C. Widowed D. Divorced

4. Highest level of education attained.

A. Diploma B. Bachelor’s degree C. Master’s degree

D. Post graduate diploma E. PHD F. Others specify………………………

5. How long have you worked in this company?

A. Less than 6 months B. 6months-1year C. 2-3 years B. D. 3-4years E. Above 5 years

SECTION B: VARIOUS TAX INCENTIVES

6. Have you ever heard about tax incentives? A. Yes B. No

7. Which tax incentives have you heard about?

A. Tax holidays B. Tax discounts C. Tax exemptions B. D. Other (specify)………………………………………..

8. Is this industry a beneficiary of tax incentives? A. Yes B. No

9. If yes which of the incentives above are given to the industry?

A. Tax holidays B. Tax discounts C. Tax exemptions D. Other (specify)………………………………………..

29

SECTION C: TAX INCENTIVE CONTRIBUTION ON HUMAN CAPITAL, INVENTORY AND GROSS INVESTIMENT DECISION

Instructions.

From questions 10-13, write the number that best indicates your opinion on the statements using the following scale.

scale 1 2 3 4 5Strongly agree(SA)

Agree(A) Undecided(UD) Disagree(D) Strongly disagree(SD)

Human capital investment decision. (To be directed to the human resource department)

Item no.

statement Opinion no.

10. Tax incentives are responsible for the current recruitment rate of the industry.

11. Tax incentives are responsible for the current rate of training workers in the industry.

12. Tax incentives are responsible for the current rate of productivity of workers in the industry.

13. Tax incentives are responsible for the current state of welfare of the employees in the industry.

14. In your own view, do you think tax incentives play a significant role in the investment decisions of private large scale manufacturing? A. Yes B. No

15. If yes, explain the role tax incentives play.

……………………………………………………………………………………………………………………………………………………………………………………………………

16. If not, why?

……………………………………………………………………………………………………………………………………………………………………………………………………

17. Whether yes or no, conclusively in your own view, what other than tax incentives affects investment decisions of private large scale manufacturing industries?

……………………………………………………………………………………………………………………………………………………………………………………………………

THANK YOU FOR YOUR COOPERATION

30

SECTION C: TAX INCENTIVE CONTRIBUTION ON INVENTORY INVESTMENT DECISION

Instructions.

From questions 10-12, write the number that best indicates your opinion on the statements using the following scale.

scale 1 2 3 4 5Strongly agree(SA)

Agree(A) Undecided(UD) Disagree(D) Strongly disagree(SD)

Inventory investment decision (to be directed to the operations department)

Item no.

statement opinion

10 The production capacity of this industry and tax incentives.11 The purchasing level of the inputs of this industry and tax incentives

provided to it.12 The current inventory level of this industry and the tax incentives

provided to it.

13. In your own view, do you think tax incentives play a significant role in the investment decisions of private large scale manufacturing? A. Yes B. No

14. If yes, explain the role tax incentives play.

……………………………………………………………………………………………………………………………………………………………………………………………………

15. If not, why?

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

16. Whether yes or no, conclusively in your own view, what other than tax incentives affects investment decisions of private large scale manufacturing industries?

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

THANK YOU FOR YOUR COOPERATION

31

SECTION C: TAX INCENTIVE CONTRIBUTION ON GROSS INVESTIMENT DECISION

Instructions.

From questions 10-13, write the number that best indicates your opinion on the statements using the following scale.

scale 1 2 3 4 5Strongly agree(SA)

Agree(A) Undecided(UD) Disagree(D) Strongly disagree(SD)

Gross investment decision (to be directed to the finance department)

Item no.

Statement Opinion

10 The current rate of distribution to the various departments for their activities in the industry and the tax incentives provided to it.

11 The current salary payment rate to the workers in this industry and the tax incentives provided to it.

12 The current rate at which financial books are edited and the tax incentives provided to it

13 The current ratio rate of the output of the industry to the national (GDP) and the tax incentives provided to it

14. In your own view, do you think tax incentives play a significant role in the investment decisions of private large scale manufacturing? A. Yes B. No

15. If yes, explain the role tax incentives play.

……………………………………………………………………………………………………………………………………………………………………………………………………

16. If not, why?

……………………………………………………………………………………………………………………………………………………………………………………………………

17. Whether yes or no, conclusively in your own view, what other than tax incentives affects investment decisions of private large scale manufacturing industries?

……………………………………………………………………………………………………………………………………………………………………………………………………

THANK YOU FOR YOUR COOPERATION